Most 2,800-cow dairies chase volume. Curtis Vanden Berge chased components — and hit 4.17% fat while one cow, Halogen 516-ET, seeded 200-plus descendants in his Bakersfield barn.

When Holstein Association USA CEO Lindsey Worden called with the news, Curtis Vanden Berge didn’t see it coming. “When CEO Lindsey Worden called me to tell me the news, I was truly surprised,” he says. “It’s nice to be recognized for the work we do every day.”

That recognition is the 2026 Distinguished Young Holstein Breeder award, which he’ll receive at the National Holstein Convention in Orlando in June. But the real story has been building for decades on a family dairy that uprooted once, expanded, and grew into one of California’s most genetics-driven Holstein herds.

Leaving Mira Loma, Building in Bakersfield

Curtis didn’t “find” dairying — he grew up in the middle of it. He was raised on his family’s dairy near Mira Loma, California, where his father and grandfather sparked his passion for dairy farming and genetic progress.

In 2004, the family relocated to Bakersfield, expanding the farm and creating opportunities for the next generation. By 2010, Curtis had stepped into day-to-day management at Vanden Berge Dairy. Five years later he became a partner. Today the operation is run by Curtis and his wife Stacey, alongside his brother Trevin and his wife Heidi, while Curtis and Stacey raise their three children — Case, Tessa, and Payton — on the farm.

2,800 Holsteins, Three Times a Day, Components First

Vanden Berge Dairy now milks about 2,800 Holstein cows in California’s Central Valley, running three-times-a-day milking.

The numbers behind the award aren’t fluff:

Rolling herd average: 27,895 lb milk

Fat: 1,163 lb (4.17%)

Protein: 928 lb (3.33%)

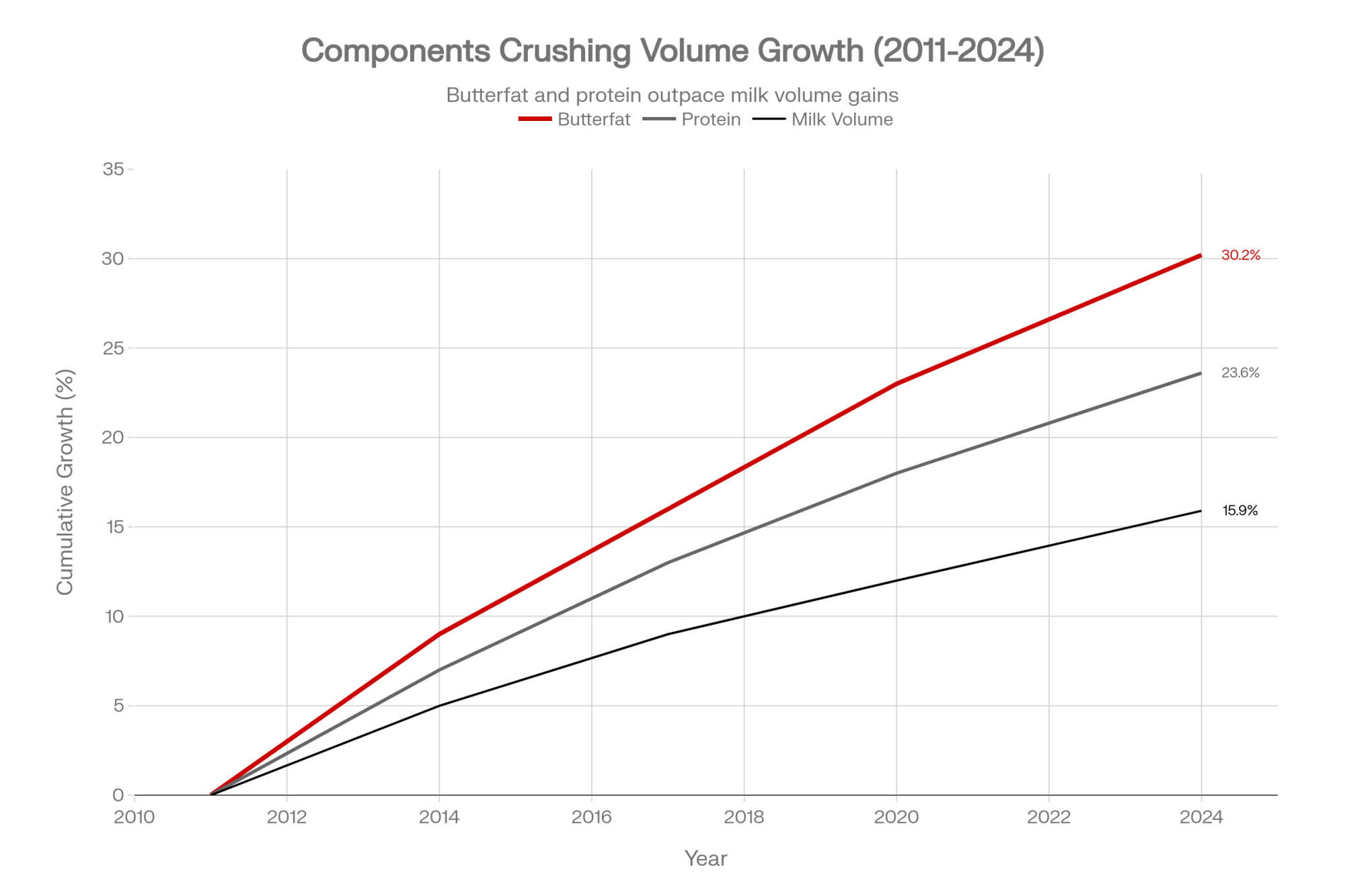

That profile isn’t accidental. Curtis is driven to continuously improve herd genetics, focusing on increasing components and making sure each generation is better than the last. Higher fat and protein pounds are the priority — and in a market where components carry more of the milk cheque every year, that focus lines up with where progressive Holstein breeders have pushed for the past decade.

The Cows Behind the Strategy

The genetic shift took off when the first group of Registered Holsteins arrived at Vanden Berge Dairy nearly 15 years ago. One cow in particular, Longfellow Boxer Bianca, showed Curtis what Registered Holsteins could do — her performance in the herd demonstrated their value firsthand.

Another foundation piece is Seagull-Bay Halogen 516-ET, whose influence keeps spreading through the milking string and heifer pens. Curtis can trace more than 200 descendants of that cow in the herd today, including Vanden-Berge Trpc Daphne-ET EX-90 — proof you don’t have to choose between commercial performance and high-end pedigrees.

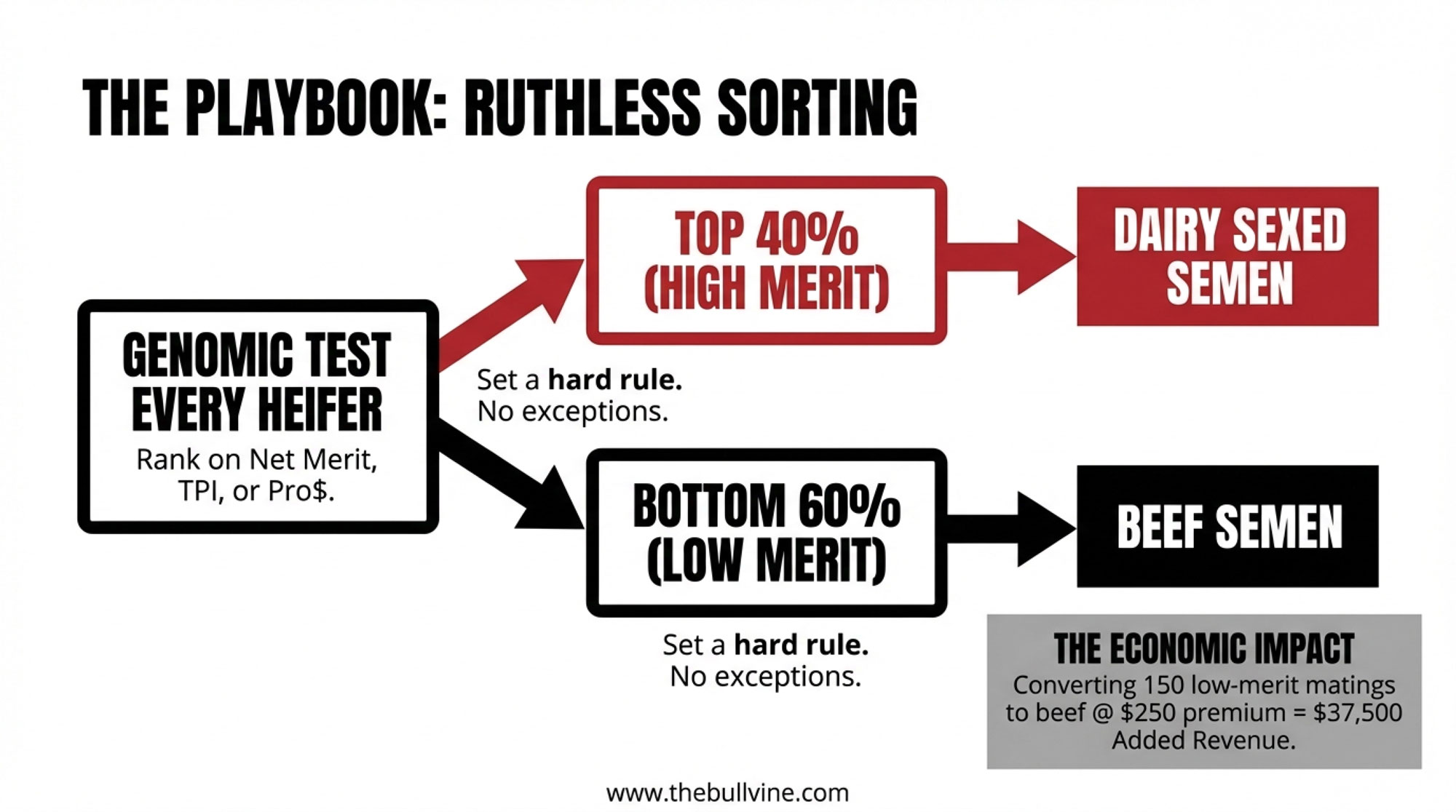

Genomics, Embryos and Beef-on-Dairy — With Discipline

On the tools side, Curtis isn’t dabbling. Vanden Berge Dairy leans on:

Genomic testing to sort heifers early and line up matings that move indexes, not just pedigrees

Embryo transfer and IVF to multiply the most profitable cow families faster

Beef-on-dairy to turn lower-genetic-value pregnancies into higher-value calves instead of replacements they don’t need

That package, combined with Holstein Association USA’s programs and services, gives Curtis a feedback loop: what the cows look like, what they produce, and how it ties back to mating decisions made years earlier. It’s the same shift across top Holstein herds — genomics isn’t a “technology project” anymore, it’s just how breeding decisions get made.

More Than Genetics: Association Leadership

This award doesn’t just recognize a numbers game. Curtis has been active with the California Holstein Association for years, serving on the board and two years as president — no small commitment while managing a large Western herd.

That role has put him in the middle of the big questions: how to keep Registered Holsteins relevant to large-pen commercial setups, how to protect breed identity and data integrity in a world of crossbreeding and beef-on-dairy, and how state associations stay valuable when breeders are stretched thin.

Why This Young Breeder Award Matters

The Distinguished Young Holstein Breeder Award targets breeders ages 21 to 40 who run a profitable Registered Holstein herd and contribute back to the industry. Winners receive travel and lodging for up to two people to the National Holstein Convention, complimentary tickets to the Awards Luncheon, a $2,000 cash award, and a plaque — plus their name engraved on a permanent plaque at Holstein Association USA headquarters in Brattleboro.

Recent recipients include Tim Rauen of Iowa, Trent Hendrickson of Wisconsin, and Ty Etgen of Ohio. Curtis joins that list at a moment when Western dairies face hard scrutiny on water, emissions, and economics — and a 2,800-cow, components-driven Holstein herd run by a breeder comfortable with both genomic data and a board agenda is exactly the kind of operation that will help decide what the Holstein cow looks like fifteen years from now.

Curtis Vanden Berge will be recognized as Holstein Association USA’s 2026 Distinguished Young Holstein Breeder during the National Holstein Convention in Orlando, Florida, on Wednesday, June 24.

Key Takeaways

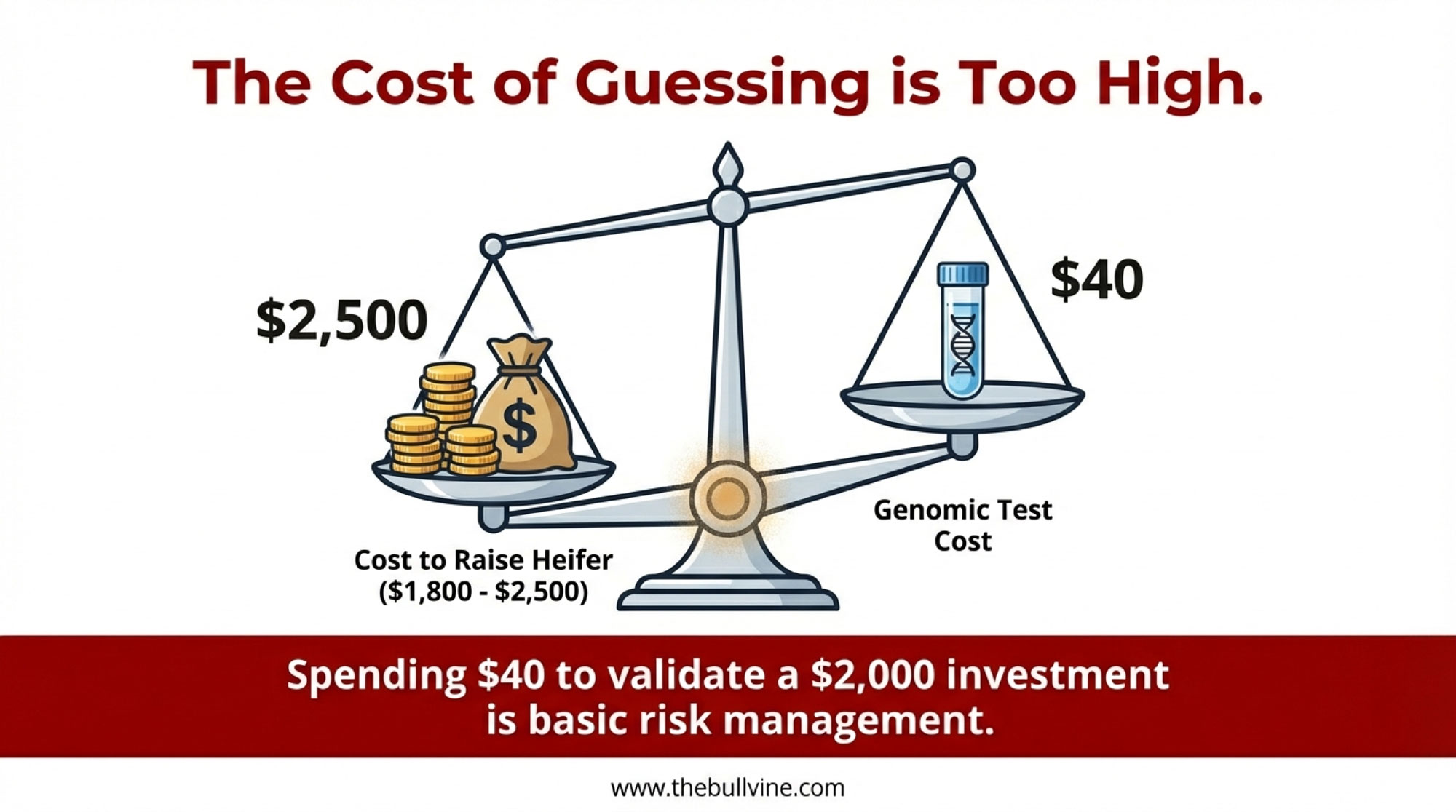

Components are the play. Vanden Berge runs nearly 28,000 lb of milk at 4.17% fat and 3.33% protein because fat and protein pounds are what cash the milk cheque — not raw volume.

Genomics, IVF, and beef-on-dairy only pay when they’re part of one system. Test heifers early, multiply your best cow families, and breed the bottom end to beef instead of making replacements you don’t need.

One cow can carry a herd. Halogen 516-ET left 200-plus descendants in this string — proof that finding and propagating your best family beats chasing the hot bull every proof run.

The award rewards more than numbers. Curtis built it with herd results plus state-association leadership, and that combination is what gets a young breeder recognized at the national level.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

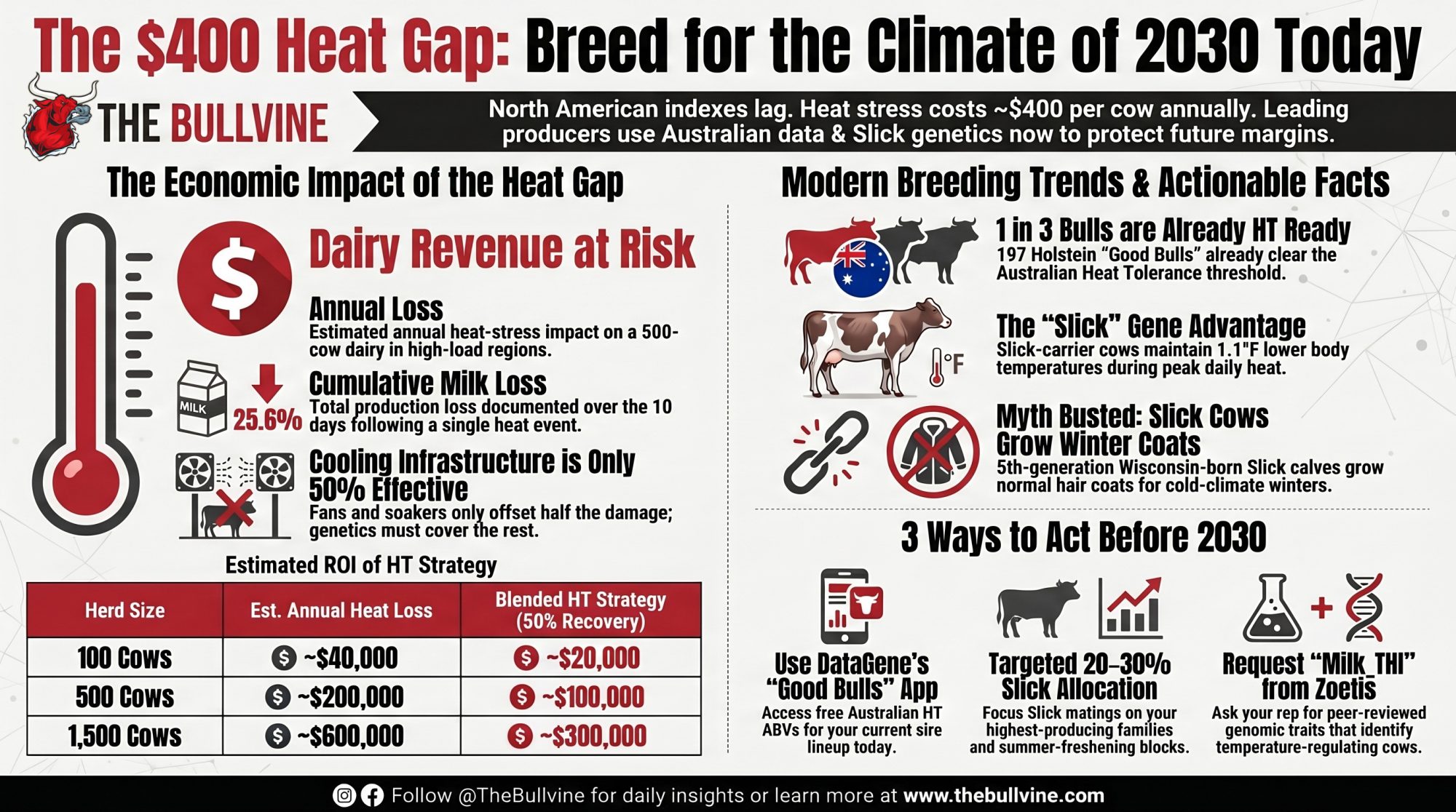

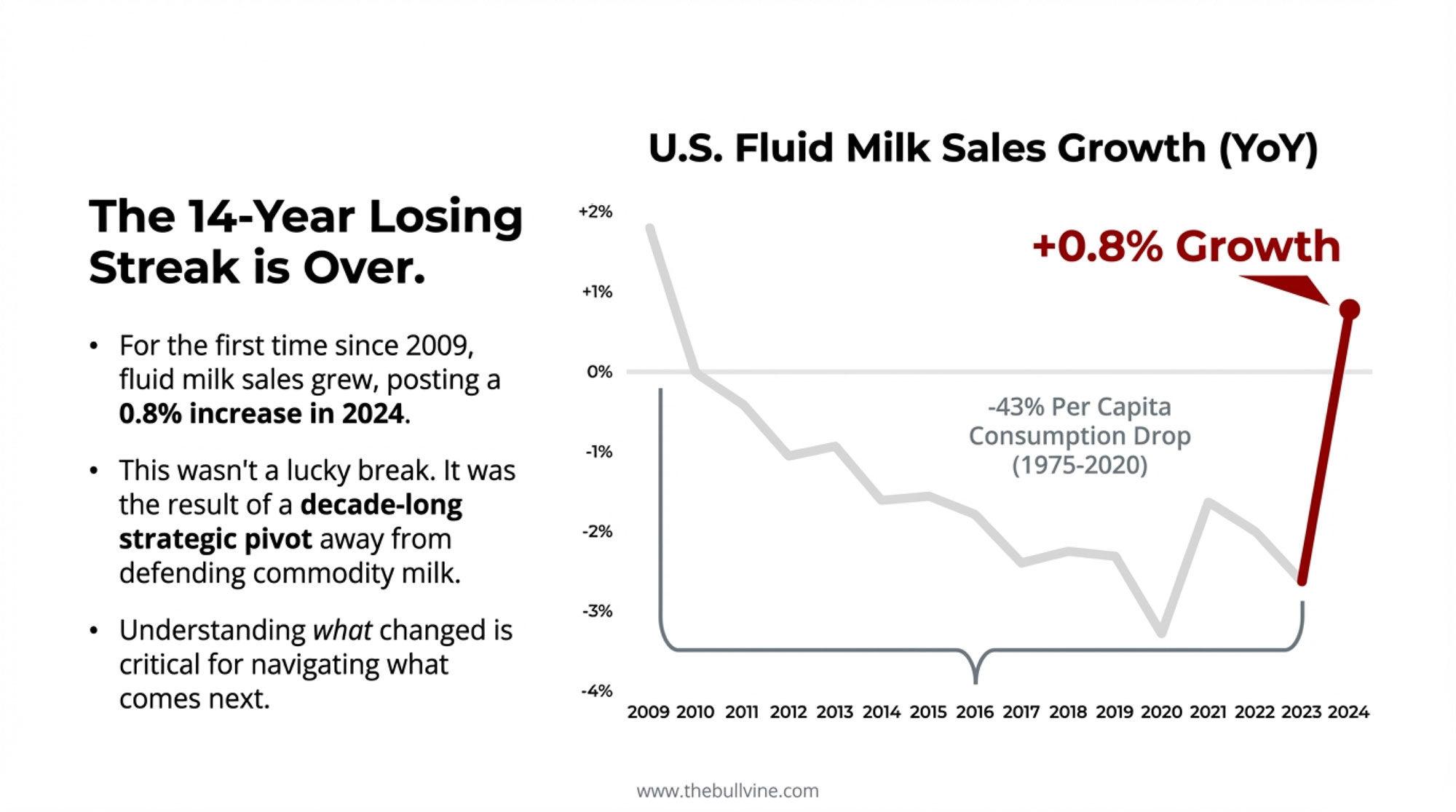

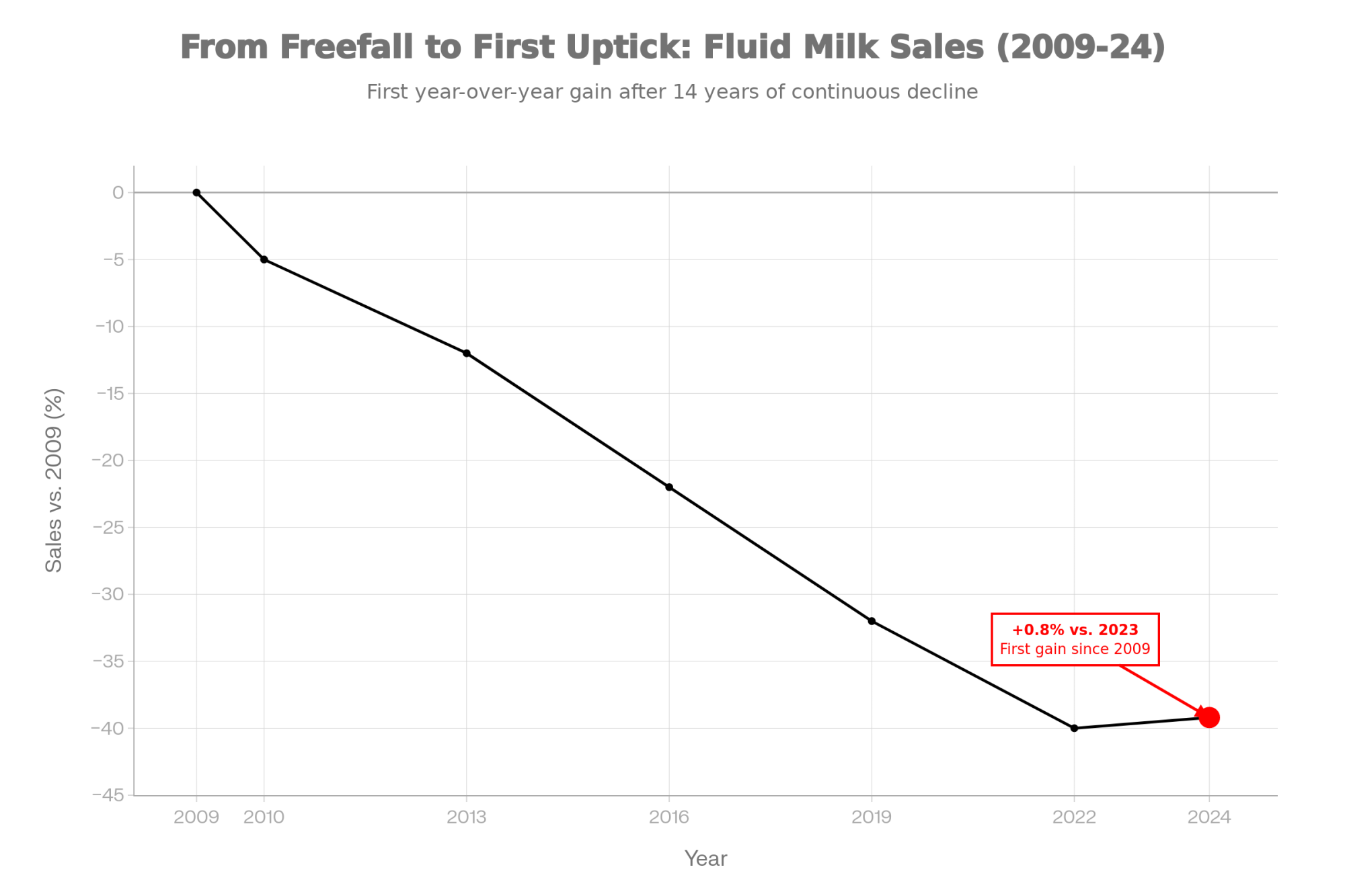

Trevor Parrish in NSW started filtering sires on HT ABV in 2017. By August 2024, 197 Holstein Good Bulls cleared the threshold. CDCB’s April 2025 NM$ revision added none of it.

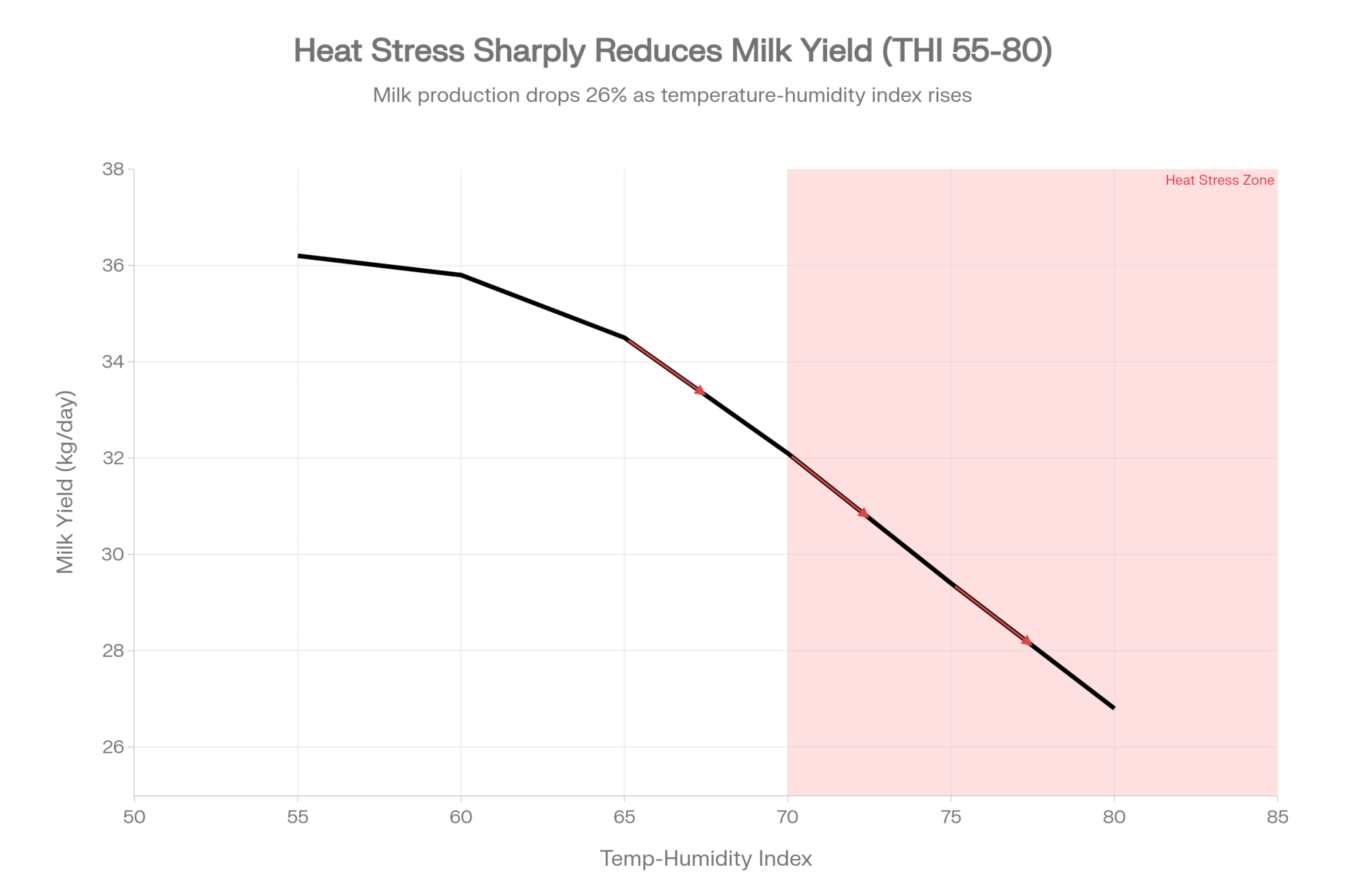

Executive Summary: Australia’s DataGene released a Heat Tolerance ABV in December 2017, and by the August 2024 run, 197 Holstein Good Bulls — roughly one in three — cleared the 100 threshold. CDCB’s April 2025 NM$ revision moved butterfat from 28.6 to 31.8 and dropped protein from 19.6 to 13, but added no heat tolerance trait; Lactanet hasn’t weighted it in LPI or Pro$ either, despite University of Guelph models hitting 0.97 rank correlation. The economic exposure for North American herds sits around $400/cow/year in heat-load regions — roughly $200,000 annually on a 500-cow dairy in southwestern Ontario or the Central Valley — based on the St-Pierre 2003 baseline adjusted for inflation and the 10% single-day, 25.6% 10-day cumulative milk losses documented in Science Advances (July 2025). Zoetis has peer-reviewed Milk_THI and CFS_THI traits in JDS (September and November 2025) that identify cows with measurably better rectal-temperature regulation. Select Sires’ ART program is now five Slick generations deep in Wisconsin, with parent averages tracking close to non-Slick matings and calves that still grow winter coat. The heifer you breed in May peaks in the early 2030s — waiting on CDCB locks in three more replacement cycles of thermal vulnerability, while DataGene’s Good Bulls App, Zoetis Clarifide, Australian proofs through Semex/Genex/ABS, and a 20–30% Slick allocation on your top cow families are all workable today. The question isn’t whether the margin math favours acting; it’s whether your AI rep can answer the HT question when you call tomorrow.

In late 2017, Holstein breeder Trevor Parrish of Kangaroo Valley, New South Wales, began weighting Heat Tolerance ABV into his sire selections — a decision still uncommon among his Australian peers at the time, according to DataGene’s adoption reporting and Parrish’s own May 2025 comments to Dairy News Australia. DataGene had just released the trait publicly: a quarterly-updated breeding value measuring how well a cow holds production when the Temperature-Humidity Index climbs past comfort. From that release forward, per his Dairy News Australia interview, Parrish treated Heat Tolerance as part of his standard sire-evaluation toolkit.

Eight years on, DataGene’s adoption data and Parrish’s published commentary tell the story of a breeder who treated the trait like calving ease — a filter you apply, not a debate you have. Meanwhile in Woodstock, Tulare, or Fond du Lac, no official North American genetic evaluation — not NM$, not TPI, not LPI — currently publishes a heat tolerance number at all. That gap has a dollar value. And it compounds every summer your replacement heifers come into the milking string.

What Australia Actually Did, Starting in 2017

DataGene released the Heat Tolerance ABV publicly in December 2017. The trait measures a cow’s ability to hold milk, fat, and protein output as THI rises past comfort thresholds. An ABV of 100 is breed average, and the trait sits inside the Balanced Performance Index (BPI) rather than floating as a standalone curiosity. A 2024 update lifted Holstein reliability by 10 percentage points and re-ranked the HT list more substantially for Holsteins than for Jerseys.

The adoption curve tells the more interesting story. In late 2016, during DataGene’s pilot work, only a handful of Good Bulls ranked meaningfully above 100 for HT. By the August 2024 ABV release, DataGene reported that one in three Holstein Good Bulls — 197 bulls — carried a Heat Tolerance ABV of 100 or above. That shift tracked a broader story of how climate pressure is reshaping dairy breeding priorities worldwide — but unlike most of the global picture, Australia already had the trait on the catalog page.

Speaking to Dairy News Australia in May 2025, Parrish framed the trait as part of a complete-cow picture: “Heat tolerance is part of that efficiency. As a breeder, you are trying to cover all the bases, and heat tolerance, now it has an ABV, is part of a solid, good quality cow.”

That isn’t a regulator’s decision. It’s a market filter, and it happened inside a decade.

Is the Science Strong Enough to Act On Without the Official Index?

Short answer: yes. And the research isn’t Australian-only. Three independent research pipelines — Australian, Canadian, and U.S. — now converge on the same conclusion: heat tolerance is a heritable, measurable, and economically significant trait in Holsteins.

Evidence stream

Metric

What it proves

Australia DataGene

197 Holstein Good Bulls at HT ABV ≥100 by Aug. 2024

Catalog-level selection signal exists

Canada Guelph / Lactanet-ready models

Rank correlations above 0.97 for Canadian Holstein bulls

Canadian evaluation framework is technically stable

U.S. Zoetis genomic traits

Milk_THI: -1.3 to 1.0 kg/day/THI; CFS_THI: -6.2 to 5.3 pts/THI

Heat tolerance can be genomically ranked in U.S. Holsteins

Slick allele field physiology

1.1°F lower vaginal temperature at noon–3 p.m.

Slick carriers regulate body temperature better under heat

The Three Scientific Proofs

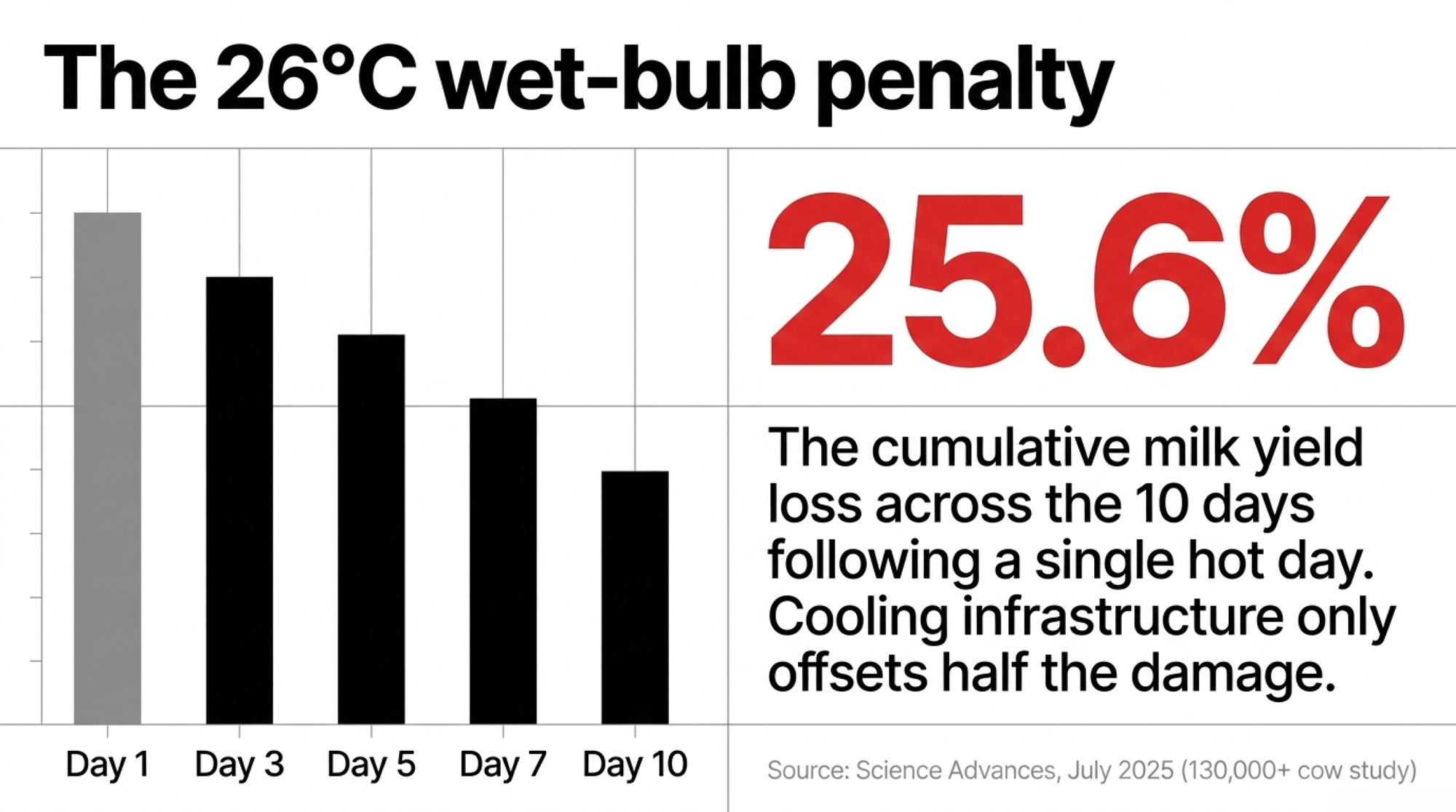

Australia — University of Chicago Climate Impact Lab (Science Advances, July 2025). Gong, Hsiang, Moscona and collaborators drew on production records from more than 130,000 cows over 12 years. Cooling infrastructure only offsets about half of the damage on the hottest days — fans and soakers cut losses by roughly 50% at a 20°C wet bulb, less than half overall at the top of the range.

Bottom line: Milk yield falls up to 10% on days when wet-bulb temperature exceeds 26°C. Cumulative loss across the 10 days following a single hot day reaches 25.6% of a single day’s baseline output.

Canada — University of Guelph (Schenkel, Miglior et al., Journal of Dairy Science). The Guelph group developed a Canadian heat tolerance evaluation framework using test-day production records and reaction-norm models. A follow-up 2025 JDS paper validated alternate models. Methodology is Canadian-ready; what’s missing is integration into LPI and Pro$.

Bottom line: Alternate models produce rank correlations above 0.97 for Canadian Holstein bulls — Lactanet has a validated, publication-ready HT evaluation sitting on the shelf.

United States — Zoetis research team (Vukasinovic et al., Journal of Dairy Science, September 2025). The team published validated genomic breeding values for heat tolerance in U.S. Holsteins. The specific traits are Milk_THI (change in daily milk yield per unit of THI, ranging from -1.3 to 1.0 kg per day per THI unit) and CFS_THI (change in conception at first service per unit of THI, ranging from -6.2 to 5.3 percentage points). A November 2025 JDS validation confirmed that higher standardized transmitting abilities on both traits corresponded to reduced rectal temperatures during heat stress.

Bottom line: The cows the Zoetis model ranks as heat-tolerant actually regulate body temperature better in the barn — the trait does what it says on the label.

The traits exist and are peer-reviewed. Whether Zoetis has integrated Milk_THI and CFS_THI into its customer-facing Clarifide reports is a question for your Zoetis rep. The September 2025 JDS paper establishes the methodology, not the commercial rollout timeline.

What Does the Barn Math Actually Look Like?

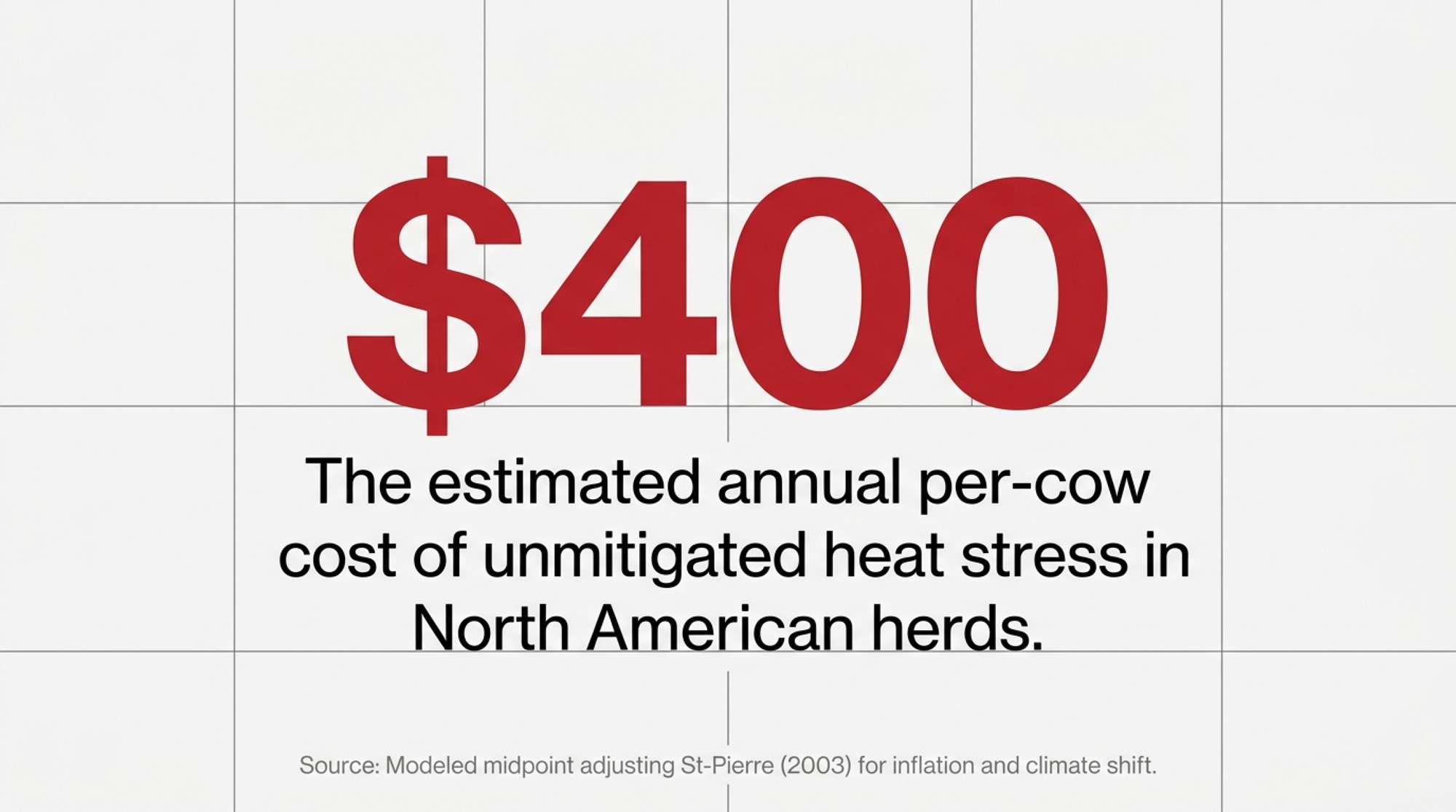

Published heat stress loss estimates for U.S. dairy herds anchor around 4 per cow per year as the unmitigated baseline, from St-Pierre, Cobanov and Schnitkey’s work in Journal of Dairy Science (2003) — early-2000s dollars. Aggregate U.S. dairy losses are modeled near $897 million annually at minimum heat abatement intensity, pulling back toward $500–$600 million with optimum abatement.

For herds in southwestern Ontario or California’s Central Valley — regions carrying a heavier seasonal heat load than the historical “temperate” framing suggests — a working midpoint of roughly $400 per cow annually is a reasonable illustrative figure once the St-Pierre baseline is adjusted for two decades of inflation and the climate shift documented in the Science Advances work. It’s a modeled estimate, not a published regional number. Operations still trying to cool their way out of the problem should also read our companion piece on where cooling infrastructure stops paying back.

The table below is an illustrative model built from that midpoint and a modeled 50% reduction assumption — the upper end of what combined cooling investment, Australian-style HT selection, and targeted Slick matings can plausibly deliver together. Actual results will vary with climate zone, milk price, Slick adoption percentage, and the sire mix already in the tank.

Herd Size

Est. Annual Heat Loss (Conventional)

Blended HT Strategy (50% Reduction)

Year-1 Implementation Cost (Est.)

100 cows

~$40,000

~$20,000

~$10,000

500 cows

~$200,000

~$100,000

~$40,000

1,500 cows

~$600,000

~$300,000

~$115,000

Underlying inputs: $400/cow annual heat loss (modeled midpoint); 50% recovery assumption from combined cooling + HT selection + Slick matings; Year-1 costs scaled for genomic testing on replacement heifers and semen premium on targeted Slick matings.

On a 500-cow operation, the Year-1 cost sketch roughly covers genomic testing on replacement heifers plus a modest semen premium on about 150 targeted Slick matings (roughly a 30% allocation of annual breedings). Under those modeled assumptions, payback clears inside the second summer. The arithmetic isn’t the weak point. The inputs are. But the direction and order of magnitude hold up in almost any scenario a North American breeder plugs in.

Where CDCB and Lactanet Have — and Haven’t — Moved

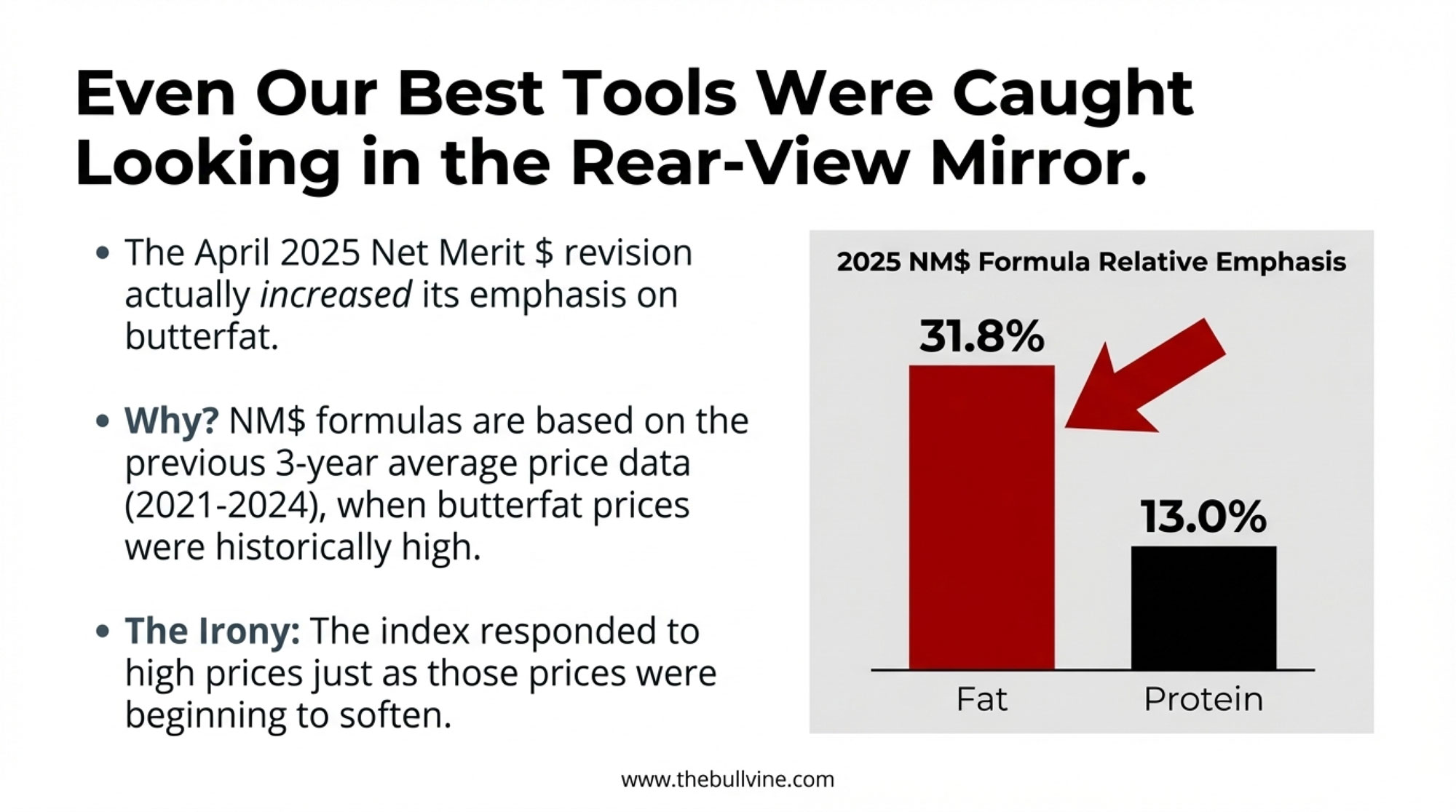

The CDCB’s April 2025 evaluation revision implemented the every-five-year base change (moving from cows born in 2015 to cows born in 2020) and updated income and cost variables inside NM$, Cheese Merit $, Fluid Merit $, and Grazing Merit $. Butterfat weight moved from 28.6 to 31.8 and protein dropped from 19.6 to 13, per the official CDCB April 2025 evaluation change documentation and the USDA-AGIL technical report by VanRaden, Toghiani, Basiel, and Cole. No new traits were added. No heat tolerance number. Those weight shifts carry their own strategic implications — which we unpack in our analysis of the April 2025 Net Merit revision’s butterfat-protein trade-off.

CDCB’s caution isn’t inertia for its own sake — the national evaluation’s credibility rests on trait reliability, and adding a trait prematurely carries real costs. But the cost of waiting now has a measurable dollar value. Realistic integration of Heat Tolerance into NM$ sits several evaluation cycles out. Lactanet is in a comparable position. The Guelph group has produced usable Canadian methodology and the 2025 JDS work validates it — but no heat tolerance index is currently published as part of LPI or Pro$.

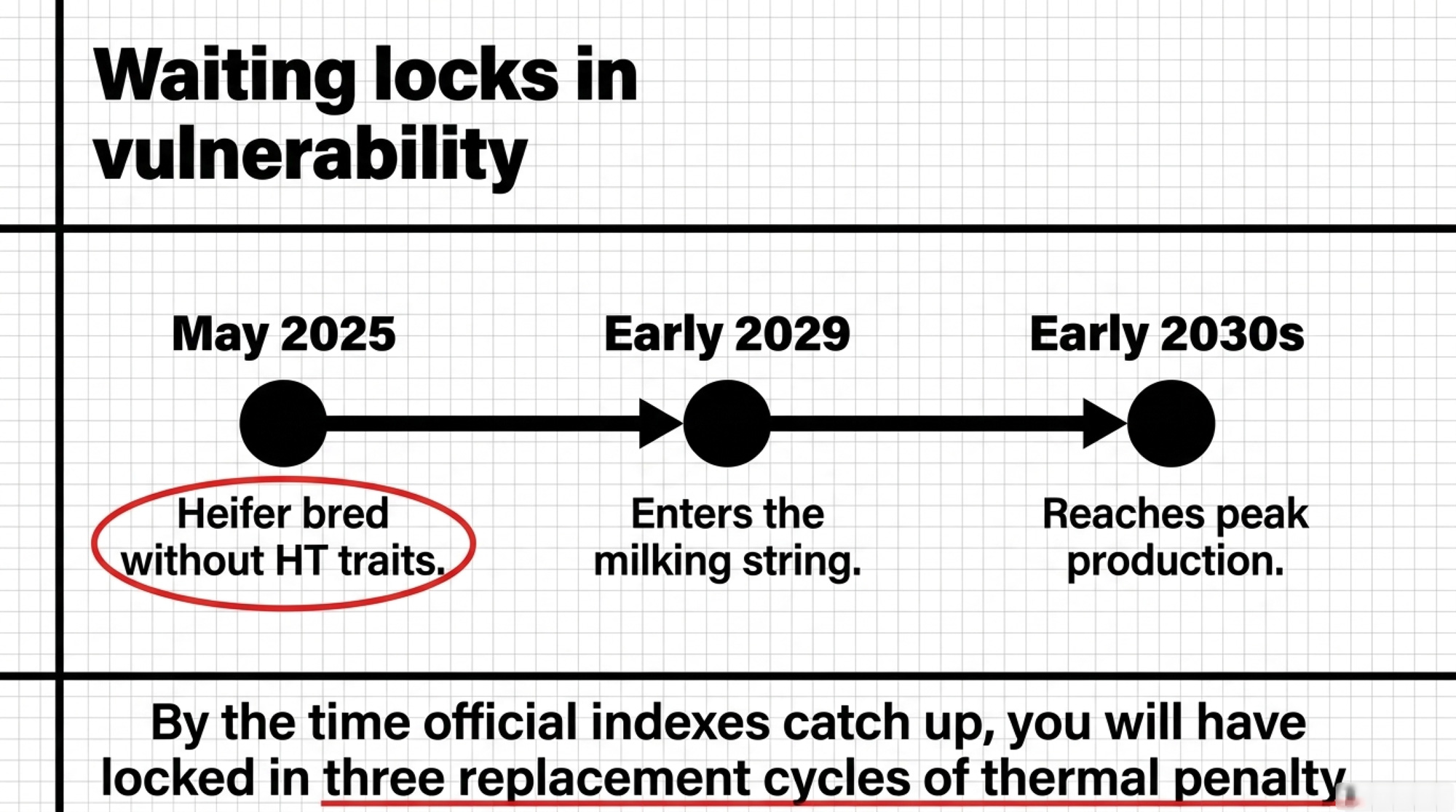

The replacement pipeline doesn’t care about governance timelines. A heifer bred this May enters the milking string in early 2029 and reaches peak production in the early 2030s — in a climate the Science Advances team projects will deliver materially more wet-bulb-26°C days across major dairy regions by midcentury, with 4% annual daily-yield losses baked in without adaptation. The genetic decision made this breeding cycle sets the thermal ceiling for that cow’s productive life.

The North American Program That’s Already Five Generations In

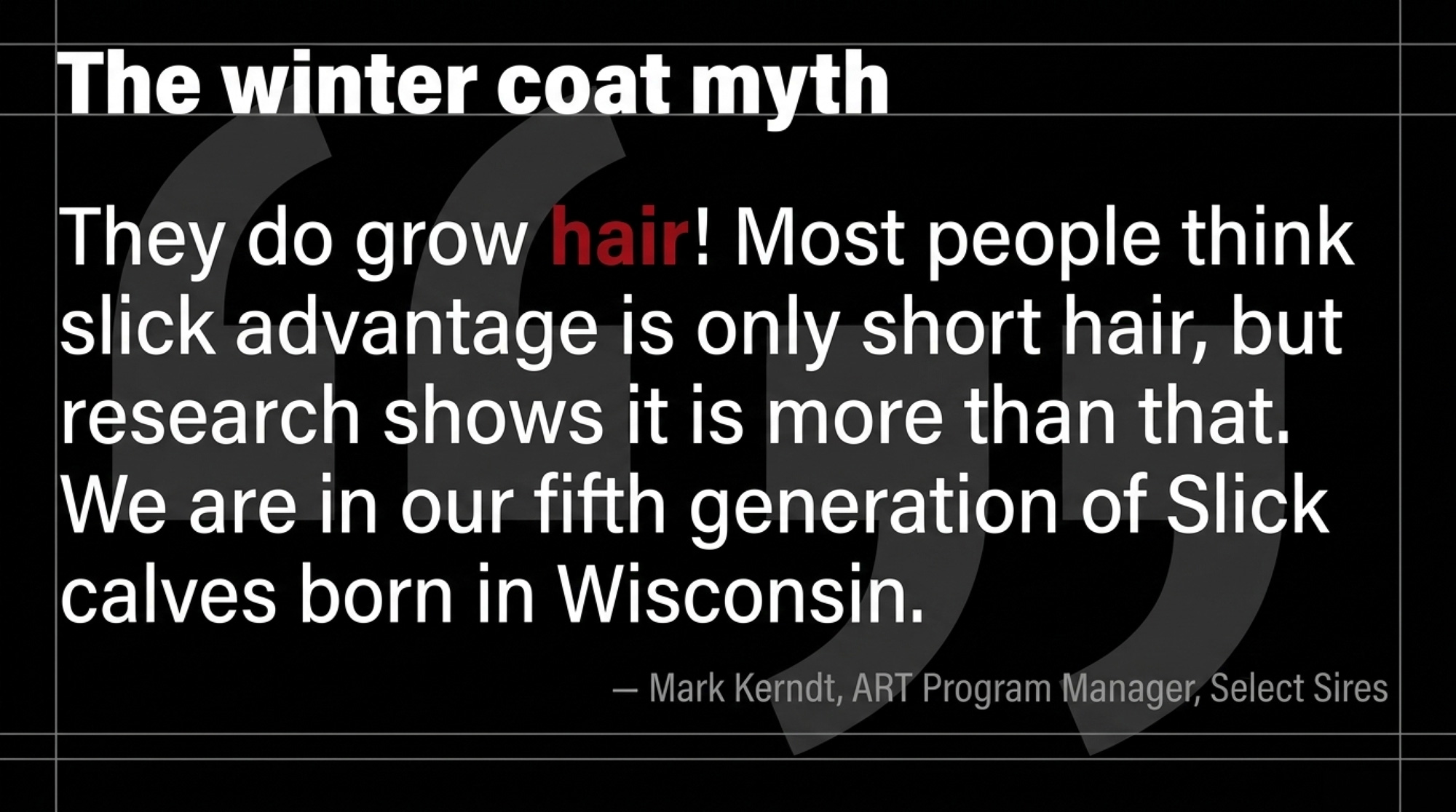

While CDCB hasn’t moved, Select Sires’ Aggressive Reproductive Technologies (ART) program has quietly been running the Slick playbook for years. Per an April 2026 blog authored by ART Program Manager Mark Kerndt, the program is now in its fifth generation of Slick calves, with all of them born in Wisconsin.

“We are breeding the horns out of the breed and are now also focusing on making the Holstein breed more heat tolerant, through the gradual introduction of the dominant slick allele into our cattle,” Kerndt wrote. “We expect several hundred potential slick calves to be born in our program in 2026 and the parent averages on these matings are very close to our non-slick matings.”

Two things worth holding onto from that. First: Wisconsin-born Slick calves grow hair in winter, which answers the most common North American objection before a breeder raises it. Kerndt again: “They do grow hair! Most people think slick advantage is only short hair, but research shows it is more than that.”

Second: parent averages on Slick matings sit close to non-Slick matings in the ART program. The production penalty breeders have long assumed isn’t showing up in the current generation. The piece of the picture North American breeders haven’t had — a named commercial program running the strategy long enough to produce fifth-generation data — is now on the record.

The piece still missing from the public record is the one that would close the circle: a named North American dairy producer, not an AI stud, who has been weighting HT or running Slick matings long enough to report two or three summers of their own production and fertility numbers. Those producers exist. Their data isn’t yet in the trade press. That’s the next story worth telling, and The Bullvine is actively reporting it — if you’re running one of these programs and willing to talk on the record, the editor’s line is open.

“But I Have -20°C Winters” — The Cold-Climate Objection That Isn’t Aging Well

The pushback from Ontario, Quebec, Wisconsin, and Minnesota breeders is almost always the same: “I don’t want a tropical cow in a -20°C barn.” Fair question. Until the data answers it.

Kerndt has answered it directly from Wisconsin, where January air temperatures regularly sit below -10°C. His fifth-generation Slick calves are born there, stay there, and — in his own words — “do grow hair!” The Slick allele isn’t producing tropical cattle incapable of holding coat in cold country. It’s producing cattle that thermoregulate more efficiently when THI climbs, while still growing a winter coat when the thermometer drops.

The framing error is calling it a “tropical gene” in the first place. Slick was characterized in Senepol cattle in tropical regions, yes — but the trait it delivers is heat dissipation efficiency, not tropical-only viability. And the climate the “temperate” label was built on doesn’t exist anymore. The Science Advances data shows that Ontario, the Upper Midwest, New York, and the Atlantic provinces are already accumulating enough wet-bulb-26°C days to put real dollars per cow per year on the table — the illustrative 0-per-cow midpoint in the Barn Math section lands squarely in those regions, not in Puerto Rico.

The decision has shifted. It used to be: “Is Slick worth the winter coat penalty?” The current data says: “Is holding onto an outdated temperate-climate mental model worth giving up 50% of the recoverable summer margin?”

Four Ways to Start Now — Without Waiting for CDCB

Active breeders split from waiters right here. Four approaches are already in use, each with a different cost, effort, and exposure profile. None require CDCB or Lactanet to move first.

MoveCost profileSignal usedBest fitDataGene Good Bulls AppFree lookupHT ABV; Holstein reliability around 48%Any breeder building a sire listZoetis Milk_THI / CFS_THI inquiryAccount / rep access dependentMilk-yield and first-service conception response to THILarge herds already using genomic servicesAustralian proof sheet requestRep request; sire coverage variesAustralian HT proof on eligible international siresHerds buying Semex, Genex, ABS or similar international geneticsCustom index layerGeneticist setup; usually 1–2 quartersNM$ or LPI floor plus HT as secondary filterOperations already using custom selection indexes

1. The Free Move — DataGene’s Good Bulls App. DataGene publishes HT ABVs quarterly in its freely available Good Bulls App. Pull it up, search a sire name, read the ABV. It costs nothing. DataGene’s own fact sheet recommends using a team of bulls because HT ABV reliability sits around 48% in Holsteins, lower than conventional production traits — but 48% on a trait that doesn’t exist in NM$ is still 48% more signal than you have today.

2. The Phone Call — Zoetis Milk_THI and CFS_THI. The Zoetis traits are peer-reviewed (Vukasinovic et al., JDS, September 2025; follow-up JDS validation, November 2025). Whether they’re accessible through Clarifide — and under what conditions — is a question for your Zoetis rep directly. Validation confirmed the traits identify cows that keep body temperature regulated during heat stress. Larger operations with existing account relationships are the ones most likely to get a useful answer first.

3. The Genetic Filter — Australian Proofs via International AI Partners. Sires distributed through international-facing AI partners — Semex, Genex, and ABS among them — may carry Australian proof data where their genetics are evaluated in the Australian system. Coverage varies by sire and stud. Ask your AI partner for the Australian proof sheet on specific bulls you’re considering. This is a phone call your rep can make today; no new account, no testing investment.

4. The Custom Index — Layering HT onto NM$ or LPI. For operations already running custom selection indexes, set NM$ or LPI as a floor and layer HT as a secondary filter — structurally how Australian farmers already use BPI alongside HT ABV. It takes a conversation with your AI partner’s geneticist and typically a quarter or two to implement cleanly. If you’re already building custom indexes, this is the obvious next add.

Slick Sires: What the Allele Actually Does — and Doesn’t

For operations ready to go further than a filter, weighting Slick sires into 20–30% of matings is the most direct structural play. Slick carriers are in commercial North American catalogs today, with Select Sires’ ART program the most openly documented pipeline — confirmed in the April 2026 Holstein Sire Directory. Swissgenetics also markets THERMO-ET P SL, the first European homozygous-polled Red carrier of the Slick gene. Coverage across other major studs varies; ask your AI partner what they currently carry or can source.

Here’s what the biology actually delivers. The Slick allele is a dominant mutation in the prolactin receptor gene that produces a short, sleek coat. University of Florida research by Dikmen and colleagues (Journal of Dairy Science, 2014) documented that Slick cows averaged 1.1°F lower vaginal temperatures at the hottest times of day (noon to 3 p.m.) compared with non-Slick herdmates housed in the same Florida freestall environment. And where summer-calving cows typically see a sharp first-90-day yield depression compared with winter-calving animals, that seasonal gap was substantially reduced in Slick carriers — Slick cows held closer to their winter-calving performance than wild-type animals in the same heat conditions. The regulatory and commercial path Slick has walked is worth comparing with how the PRLR-SLICK gene-edited variant stacks up on the 2029 milk cheque.

The strategy isn’t 100% Slick. It’s targeting Slick matings at your highest-producing cow families and summer-calving blocks, where heat stress hits the margin hardest. A 20–30% allocation blended with elite conventional sires selected on NM$ or LPI is where most breeders start. Per Select Sires’ own ART data, the production penalty Slick once carried isn’t showing up in the current generation.

Is Your Herd’s Genetic Strategy Already Behind Where Australia Was in 2019?

Not a rhetorical question. By the August 2024 ABV release, one in three Holstein Good Bulls cleared 100 for Heat Tolerance. Parrish told Dairy News Australia that Australian AI centres are moving toward filtering on HT the same way they already filter for calving ease: “AI centres won’t take bulls that aren’t good for Heat Tolerance. It will be like calving ease — now they won’t buy a bull that causes difficult calvings.”

That shift didn’t come from a regulator. It came from farmers like Parrish, year after year, building HT into what they asked their AI reps for.

North American studs respond to the same pressure. Kerndt has said plainly: “Heat tolerance is a valuable economic trait. By adding the slick trait to the elite genetic package offered by Select Sires, we can accomplish our goal of helping dairies everywhere become more profitable.”

When the conversation at the rep level shifts from “what’s your highest NM$ bull?” to “what’s your highest NM$ bull with Australian HT data above 100 or a validated Milk_THI value above zero?” — the catalogs move. Not in 2030. Sooner. The breeders best positioned will be the ones whose replacement heifers already carry heat-adapted genetics when that shift lands.

What This Means for Your Operation

If your herd regularly sees days with wet-bulb temperatures approaching or crossing 26°C, the Science Advances data says you’re already losing meaningfully on those days — even with fans and soakers running. Pull your summer milk-weight records against THI days from the last three years before your next breeding order.

If your replacement rate runs above 30%, you have enough genetic turnover to see measurable HT impact inside four years. Below 25%, stretch that timeline and adjust expectations accordingly.

If you already genomic-test 70% or more of your replacements, the incremental cost of adding HT screening at the sire level is effectively zero. The only reason not to add it is habit.

If your AI rep hasn’t raised heat tolerance in a sire presentation, that’s a conversation worth starting. The data exists. Whether your current stud has prioritized surfacing it is worth finding out before the next breeding order goes in.

If you breed for a specific milk market — components, cheese yield, A2A2 — weight HT as a filter on top of those targets, not a replacement for them. It stacks. It doesn’t substitute.

If you operate in what was traditionally called a “temperate” region — Ontario, Quebec, Upper Midwest, New York, Atlantic provinces — treat that label as historical, not current. The Science Advances midcentury projection work puts meaningful additional heat exposure in those regions.

If the winter-coat concern has kept you out of Slick matings: Select Sires’ fifth-generation Wisconsin-born Slick calves grow hair fine. The penalty isn’t what breeders have long assumed it was.

Key Takeaways

In the next 30 days: Pull your top 20 planned sires. Cross-reference each against DataGene’s Good Bulls App for HT ABV. Ask your Zoetis rep whether Milk_THI or CFS_THI values are accessible on those bulls. Request Select Sires’ April 2026 Holstein Sire Directory to identify current active Slick carriers. This is an afternoon’s work.

In the next 90 days: Identify your top-producing 20–30% of cow families and your May–July freshening block. Allocate Slick sire matings to those specific groups rather than broadcasting across the herd.

In the next 12 months: Begin documenting summer production and conception baselines now. When CDCB or Lactanet eventually integrates HT into NM$ or LPI, you’ll have your own performance delta in hand before your neighbor has results from their first Slick daughter.

If X, then Y: If your farm sits in a region that clears wet-bulb 26°C on more than a handful of days each summer and your replacement rate is above 30%, the cost of waiting another three years for CDCB exceeds the cost of starting a blended HT strategy now.

The wrong answers book-end the right one: 100% Slick is the wrong strategy for most North American herds in 2026. Zero Slick, in regions already carrying meaningful heat-day loads, is also the wrong strategy. The defensible position sits at 20–30%, targeted on your best, most heat-stressed genetics.

Parrish’s herd in Kangaroo Valley isn’t really the story. Select Sires’ fifth-generation Slick calves in Wisconsin aren’t quite it either. The story is that a producer in Woodstock, Tulare, or Fond du Lac could have started in 2019 or 2020 and closed most of the same distance by 2026. The tools have been sitting on the shelf. The question worth asking before the next breeding order goes in isn’t whether the climate will keep pressuring your margins. It’s whether the heifer you bred last Tuesday is built for the barn she’ll actually be milking in by the early 2030s — and if your AI rep can’t answer that question, what does that say about where the conversation needs to go next?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Transform Heat Stress into Your Carbon Strategy’s Secret Weapon — Follows the money on climate-linked regulatory risks, detailing how heat-stressed herds face a 23% methane penalty. Breaks down how selecting for heat-tolerant genomics secures your herd’s environmental compliance and long-term production floor.

Gene-Edited Cows Are Legal. Your 2029 Milk Cheque Isn’t Safe. — Exposes the massive regulatory shift making gene-edited Slick cattle a commercial reality. Highlights how PRLR-SLICK edits bypass decades of traditional breeding to deliver immediate thermal resilience and vital margin protection for the next decade.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

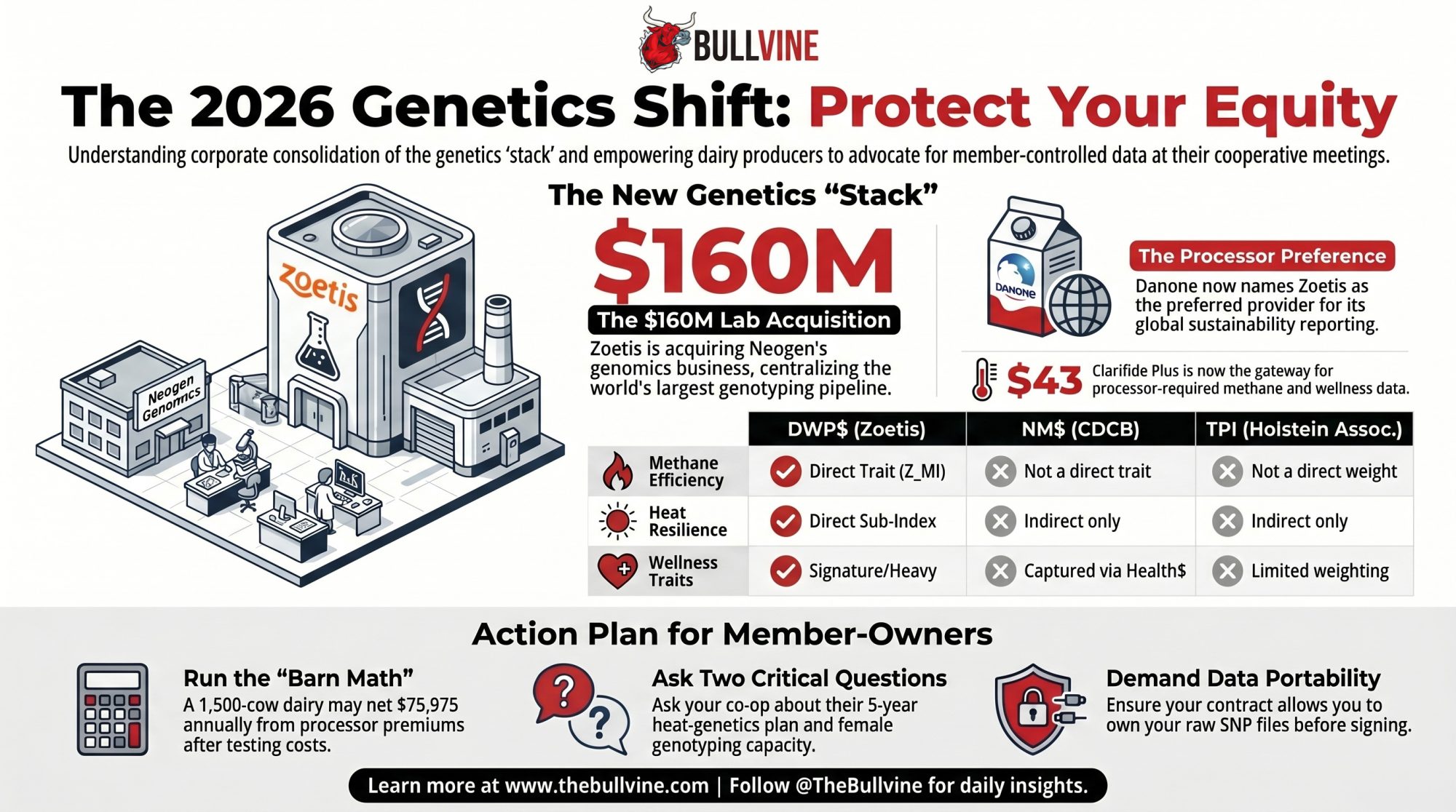

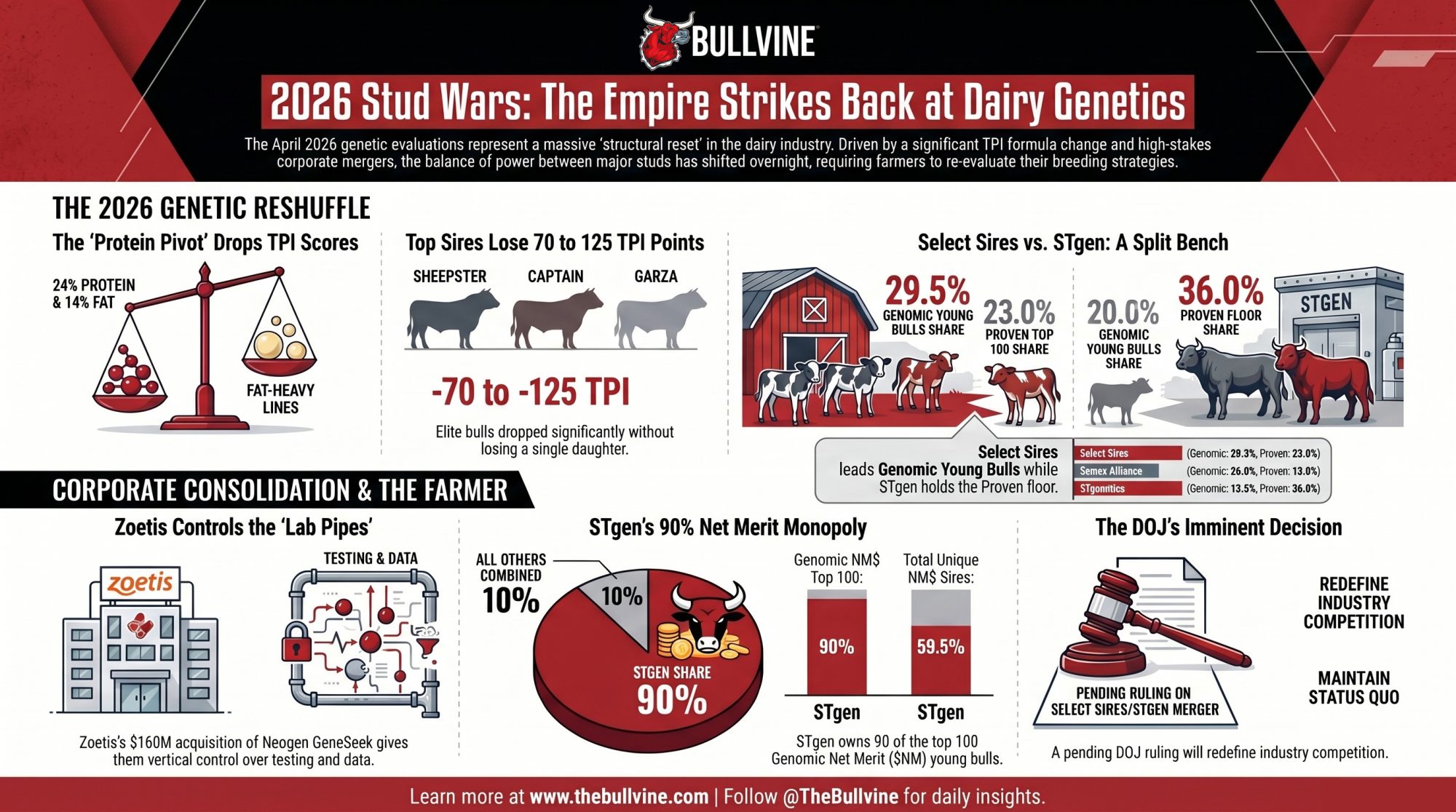

One $43 test, one $160 million lab acquisition, and one Danone preferred-provider letter — and the cooperative system 75 years of dairy farmers built has months, not years, to answer for itself.

The next time URUS, ABS Global, Genex/CRI, ST Genetics, or your Select Sires / Semex -affiliated co-op holds a district meeting on your calendar, look at the slide deck the regional manager hands out. Then ask, out loud, in front of your neighbors: “What’s our plan for the GeneSeek close?”

If the room goes quiet, you already have your answer. The publicly announced 2026 dairy genetics stack — Clarifide Plus at $43 a head, the $160 million Zoetis–Neogen lab deal, Danone’s Partner for Growth letter naming Zoetis as preferred testing provider — is reshaping every AI cooperative’s negotiating position through 2030. As of May 1, 2026, none of the major cooperatives most exposed to that shift has published a strategy response.

Your seat at that table. Your kids’ equity in the co-op. The genotyping pipeline three generations of member-owners built. All of it is being decided right now, in rooms where the question hasn’t been asked out loud yet.

This article is built on published program terms, public corporate filings, CDCB evaluation data, NAAB’s 2025 year-end report, USDA NASS Milk Production data, and a peer-reviewed 2025 Journal of Dairy Science study.

What Zoetis Built While the Cooperatives Were Quiet

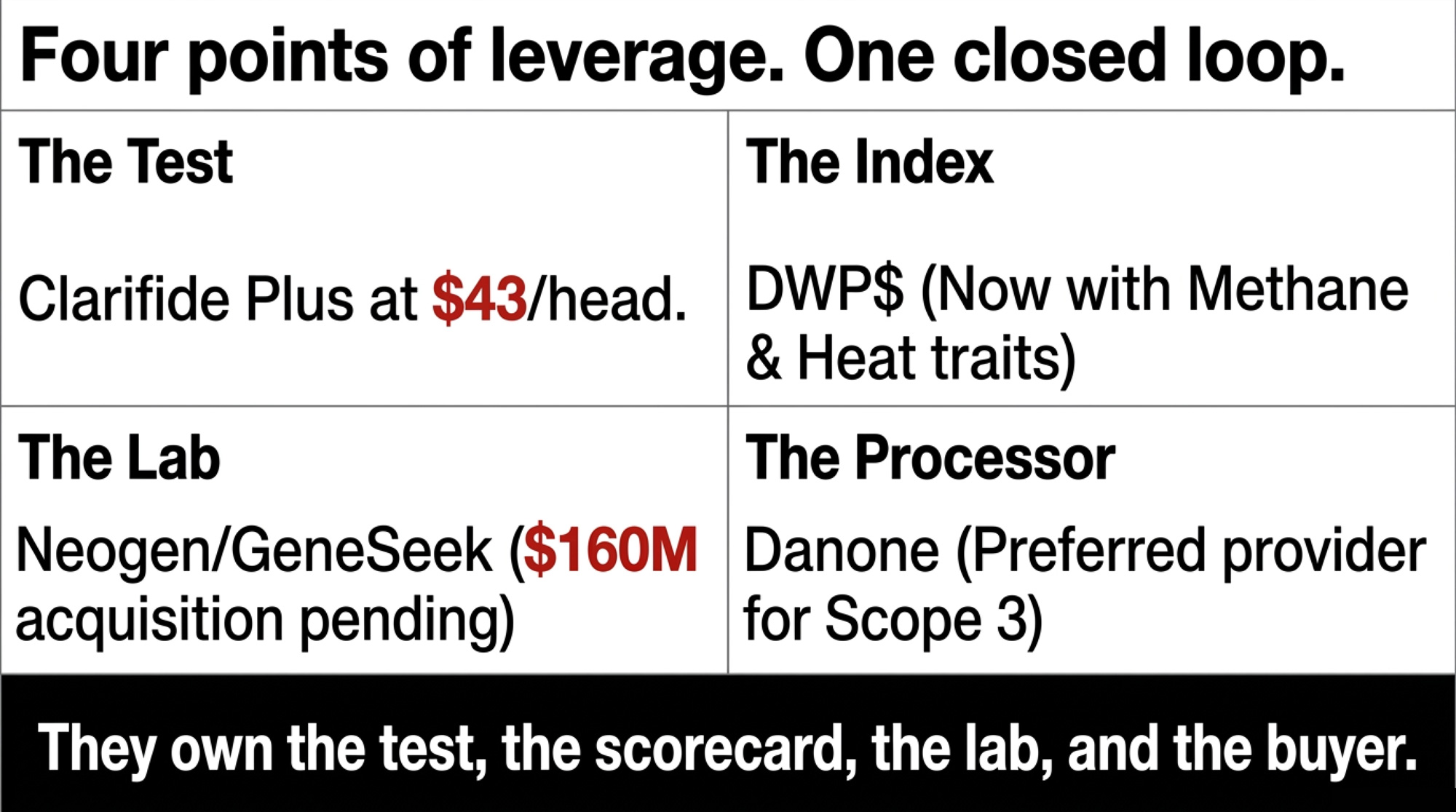

Zoetis doesn’t sell a single straw of semen. But it now sits at four points of leverage in the U.S. dairy genetics chain, and each one was announced publicly, in plain sight.

The test. Clarifide Plus runs $43 per Holstein head at Holstein Association USA’s published member rate, accessed May 1, 2026.¹ It’s already among the most widely used genomic tests in U.S. dairy.

The index. Zoetis owns DWP$, the Dairy Wellness Profit index. In April 2026, the company added Milk Methane Intensity (Z_MI) and a new sub-index called DWP$ Heat — built for herds experiencing heat stress 20% or more of the year, roughly 73 days. That’s Florida, Texas, Arizona, the southern San Joaquin, and increasingly the lower Midwest in late summer. For the back-story on how the index was assembled and what’s actually inside it, see our deeper piece on how Zoetis built the DWP$ index.

The lab. In March 2026, Zoetis announced it would acquire Neogen’s animal genomics business — including GeneSeek’s Igenity and GGP portfolios — for 0 million, subject to customary closing adjustments. That business runs roughly $90 million in annual genomics revenue, operates labs across the U.S., Brazil, Australia, China, and the U.K., and serves customers in more than 120 countries. Close is expected in the second half of 2026, pending regulatory approval.

The processor. Zoetis is the preferred genetic testing provider for Danone’s global Partner for Growth program, with DWP$ as the selection index. The two later expanded that partnership to scale testing across Danone’s supplier base for sustainability reporting — methane intensity, nitrogen efficiency, the metrics that feed scope 3 disclosures.

A company with no semen catalog is now the preferred testing provider for one of the world’s largest dairy processors, owns the index that ranks bulls inside that program, and is acquiring the lab that genotypes much of the rest of the industry. That’s the stack. On one page.

Leverage point

What it is

Key figure

Status / trigger date

The test

Clarifide Plus genomic panel

$43 / Holstein head

Holstein Assn. USA member rate, May 1, 2026

The index

DWP$ (Dairy Wellness Profit$)

Z_MI + DWP$ Heat sub-index added

April 2026

The lab

Neogen animal genomics (GeneSeek, Igenity, GGP)

$160M acquisition, ~$90M annual revenue

Close expected H2 2026, pending regulatory approval

The processor

Danone Partner for Growth preferred provider

DWP$ as selection index

Active; expanded for scope 3 reporting

What 75 Years of Member-Owners Actually Built

Three generations of dairy farmers pooled capital, semen, risk, and bull power so no single member would have to face the genetics market alone. Genex/CRI. Semex. Select Sires-affiliated co-ops — different banners, same logic. Member-owned, member-governed, member-equity. The genotyping pipeline that feeds every NM$ proof you’ve ever read off a sire summary was built on that infrastructure. What’s at stake in the post-GeneSeek environment isn’t whether your cooperative survives. It’s whether the genotyping data, the female reference population your co-op contributes to, and the negotiating leverage your manager carries into a Danone or Saputo or Schreiber meeting — whether all of that stays member-controlled, or gets routed around inside 18 months. That’s not a Zoetis policy question. It’s a member-governance question. And it’s the one your district director almost certainly hasn’t been asked yet.

To be fair to the boards at the major cooperatives, they’re navigating something the cooperative system wasn’t built for. Corporate entities move at the speed of capital. Cooperatives move at the speed of consensus — that’s a feature, not a bug, and it’s the same governance model that built the negotiating leverage worth protecting in the first place. But in 2026, consensus is a luxury members can no longer afford to wait through quietly. The fairness is real. The clock is also real. Both can be true.

Two Questions to Bring to Your Next District Meeting

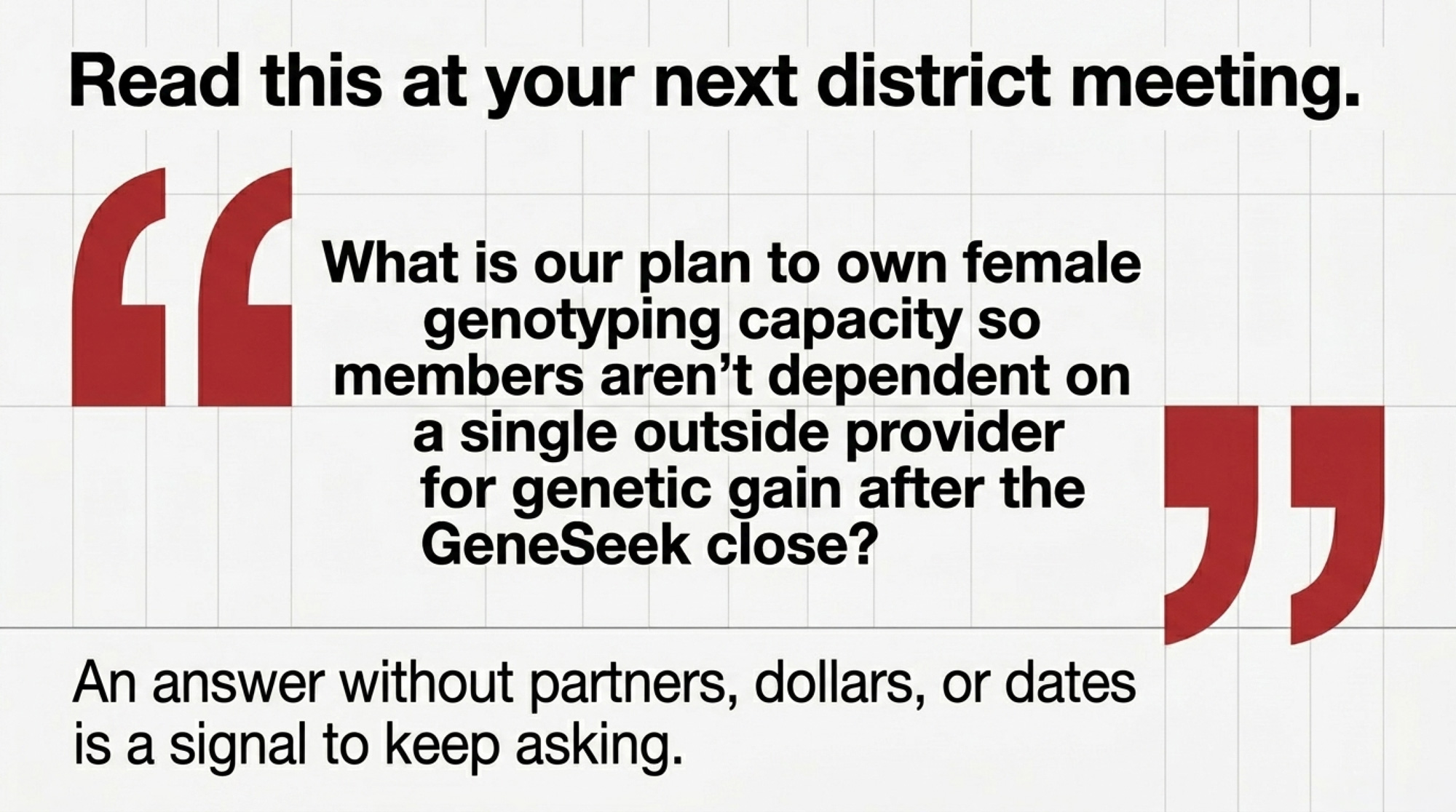

This is the action that matters most this month. Open the notes app on your phone. Type these two questions out. Read them aloud in front of the room when the floor opens for member questions:

“What’s our plan to own or control female genotyping capacity so members aren’t dependent on a single outside provider for health and fertility genetic gain after the GeneSeek close?”

Write the answer down. Date it. A serious answer names specific partners — Embrapa, Trans Ova, a domestic IVF lab — with dollar commitments and timelines beating 2028. An answer without partners, dollars, or dates is a signal to keep asking. Re-raise in 90 days. Document each round.

Boards move when members raise issues. The question is whether you’re the member raising this one.

What Data Are Processors Actually Building Their Scope 3 Programs Around?

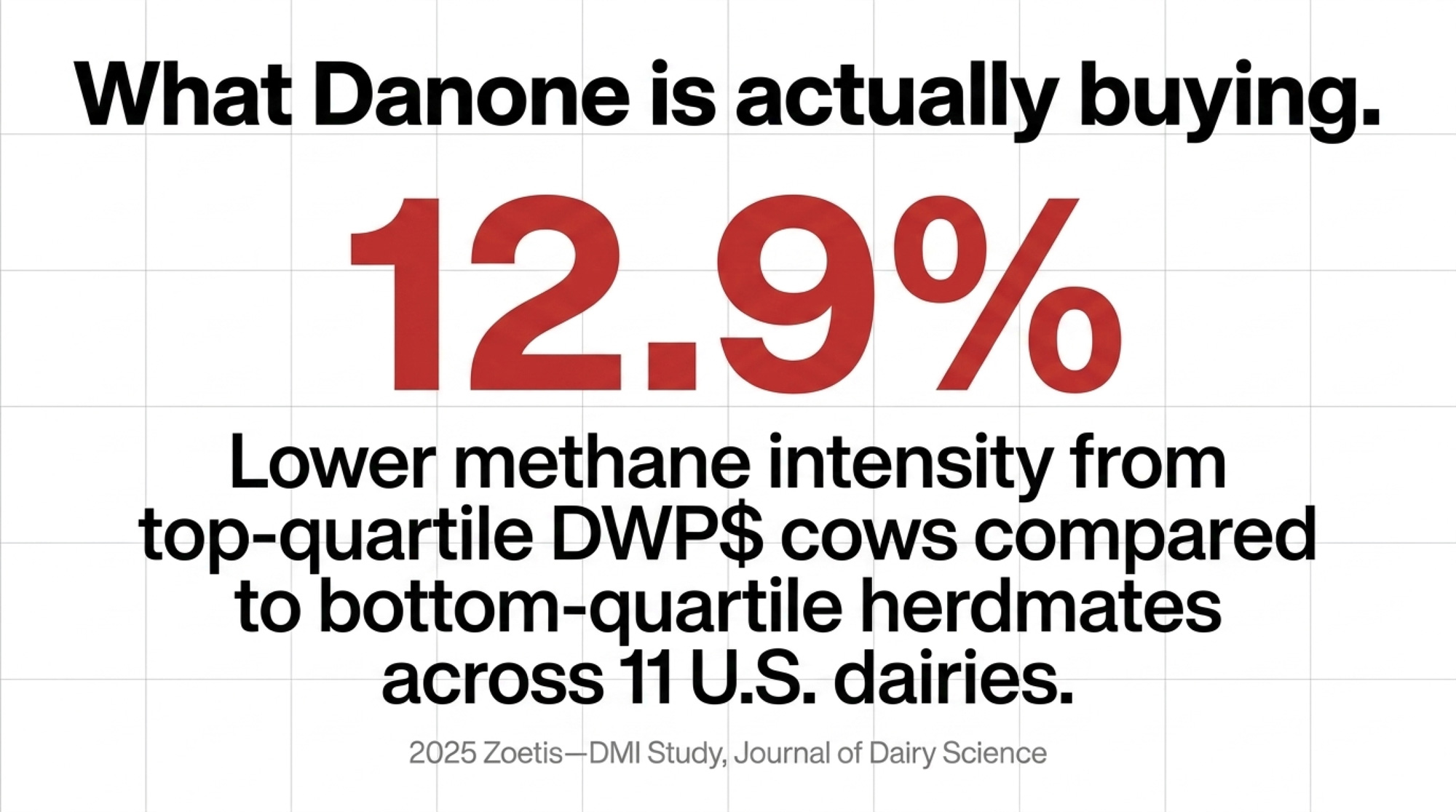

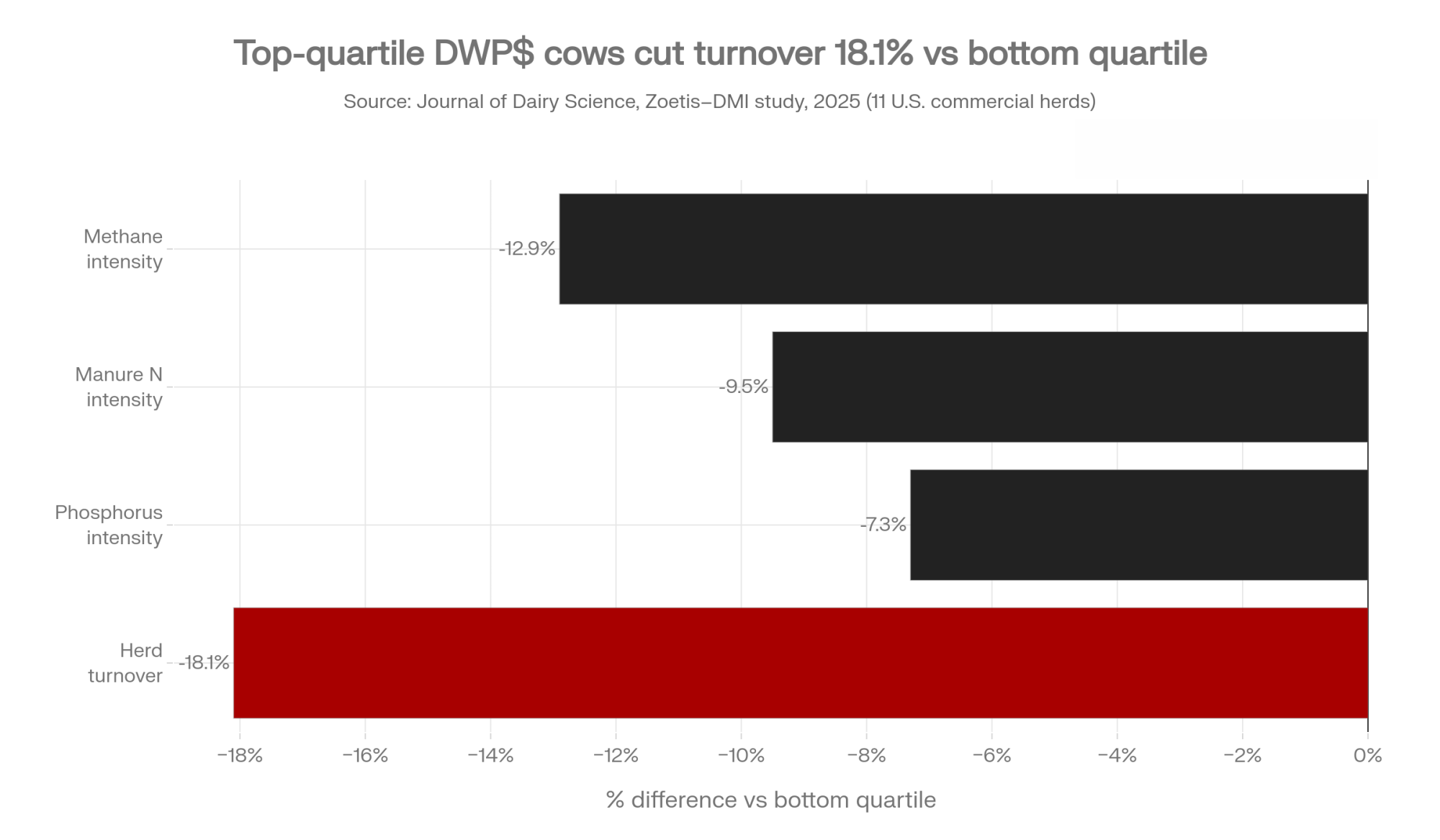

A 2025 Zoetis–Dairy Management Inc. study published in the Journal of Dairy Science— “Reduction of environmental effects through genetic selection” — analyzed cows from the top and bottom DWP$ quartiles across 11 U.S. commercial dairies. Top-quartile cows produced 12.9% lower methane intensity, 9.5% lower manure nitrogen intensity, 7.3% lower phosphorus intensity, and 18.1% lower herd turnover than bottom-quartile herdmates. That’s the dataset processors are now building scope 3 programs around.

Whether your milk check rewards those exact traits is a different question. Whether your cooperative has a counter-proof on the table is a third.

How DWP$, NM$ and TPI Differ on the Traits Processors Now Care About

Trait category

DWP$ (Zoetis)

NM$ (CDCB)

TPI (Holstein Assn.)

Methane efficiency

Direct trait (Z_MI), added 2026

Not a direct trait in 2025 NM$ revision

Not a direct trait weight

Heat resilience

Direct sub-index (DWP$ Heat), added 2026

Indirect (fertility, livability)

Indirect (fertility, longevity)

Wellness traits

Signature, heavy weighting

Captured via Health$ subindex

Limited direct weighting

Components (fat, protein)

Balanced vs wellness/longevity

Substantial weight

Heaviest weight historically

Productive Life

Strong weight

Strong weight

Strong weight

Type / Conformation

Modest direct weight

Modest direct weight

Heaviest of the three

Direction, not exact percentages. Each index answers a different question. Your milk check decides which one matters most. Your co-op’s catalog depth decides whether you have alternatives.

How Much Is the Processor Premium Really Worth on Your Operation?

Here’s the barn math. Plug your own herd into one of these and see where the net-out lands.

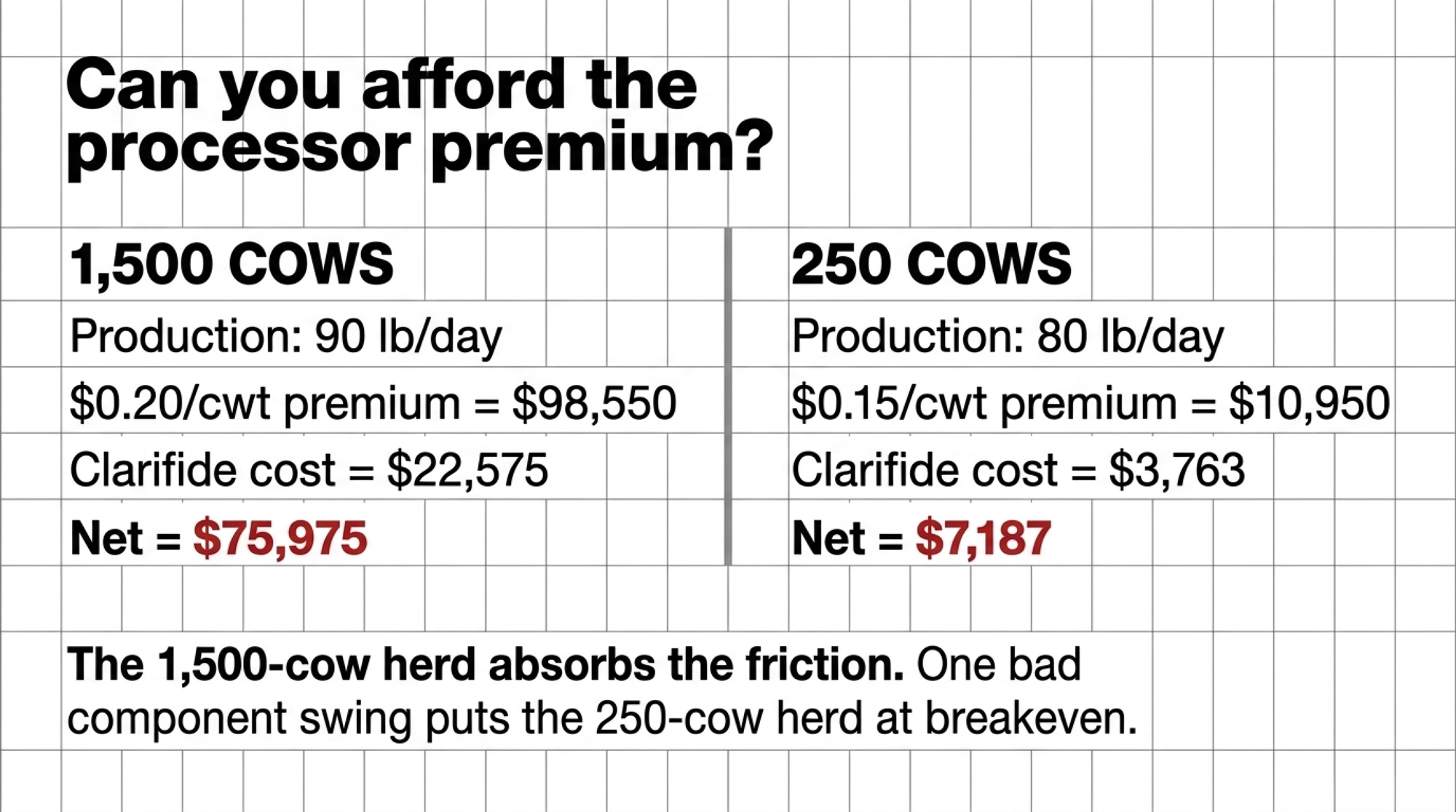

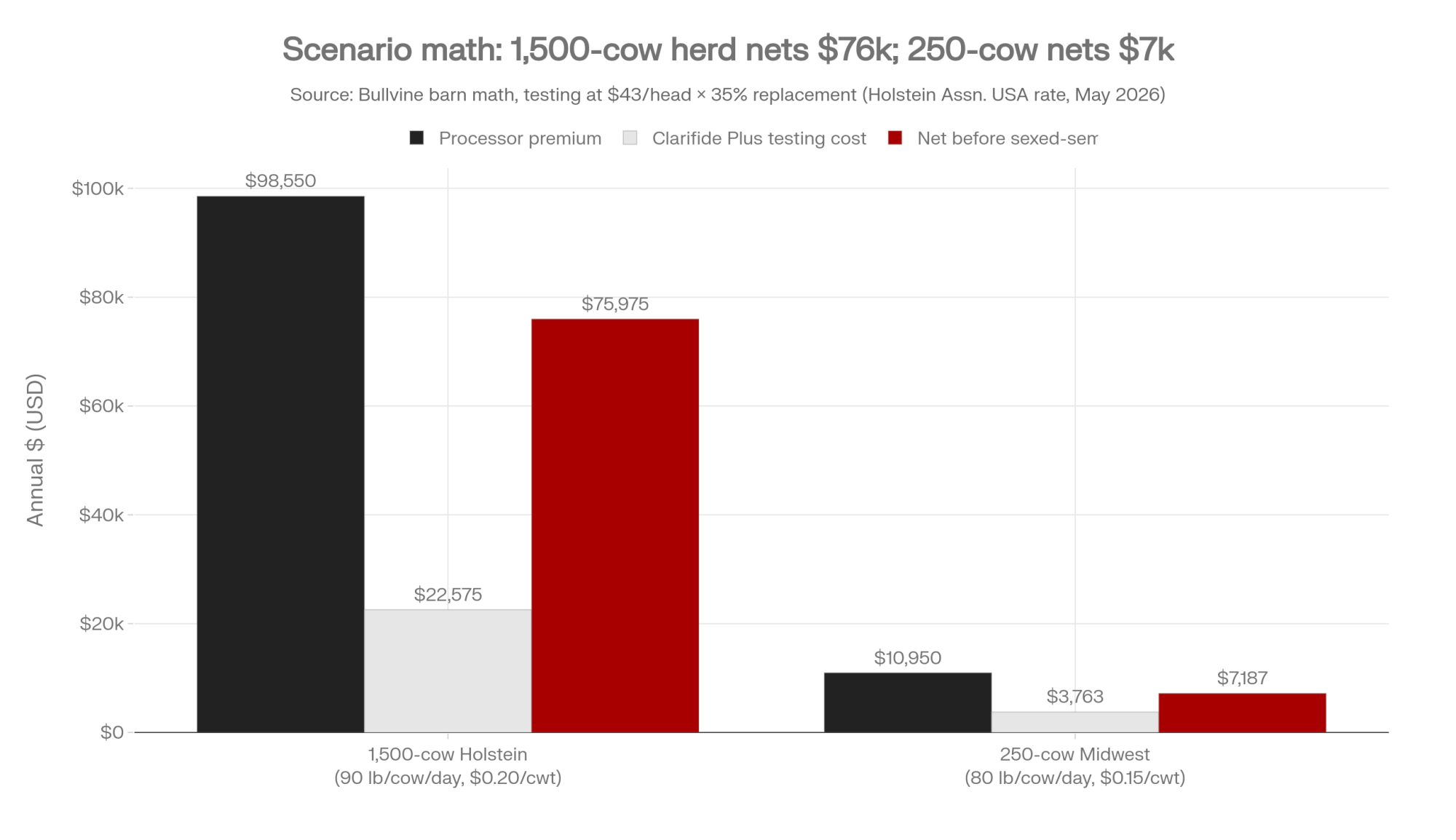

Scenario A — 1,500-cow Holstein operation, 90 lb/cow/day

Input

Value

Cows in milk

1,500

Daily production per cow

90 lb (above the U.S. herd average of ~66–67 lb/day implied by USDA NASS Milk Production, late 2025)²

Total annual production

49,275,000 lb = 492,750 cwt

Premium at $0.20/cwt

$98,550

Annual Clarifide Plus testing (1,500 × 35% × $43)³

~$22,575

Net at $0.20/cwt before sexed-semen differential

~$75,975

Scenario B — 250-cow Midwest herd, 80 lb/cow/day

Input

Value

Cows in milk

250

Daily production per cow

80 lb

Total annual production

7,300,000 lb = 73,000 cwt

Premium at $0.15/cwt

$10,950

Annual Clarifide Plus testing (250 × 35% × $43)³

~$3,763

Net at $0.15/cwt before sexed-semen differential

~$7,187

These are gross figures. Before the sexed-semen price differential. Before any component-yield drift if your contract pays butterfat and protein harder than DWP$ weights them. Before any year-one Danone signing subsidy.

The 1,500-cow operation has the volume to absorb the friction. The 250-cow operation is one bad component-pay swing from breakeven. If you’re a Wisconsin cheese-milk herd paid hard on components, or a Southern operation whose biggest profit leak is summer fertility — exactly the herds Zoetis is targeting with DWP$ Heat — DWP$ alignment may or may not match how your milk check actually gets built. Run your own math against your own contract before you renew.

Where Will Catalog Pressure Show Up First in Your AI Rep’s Order Sheet?

Indexes improve by consuming data. The one with preferred-provider testing across thousands of farms refines itself faster than one relying on voluntary contributions. Over five to seven years, in our analysis, DWP$ is on track to lead among major U.S. indexes on the traits processors care about — methane, feed efficiency, wellness — because of Zoetis’s vertically integrated testing-plus-index position. The 2025 JDS study is the first peer-reviewed proof point for that thesis.

The compounding runs downstream fast. More processors layer in Clarifide. Studs feel pressure to shift young-sire sampling toward DWP$-ranking bulls. Sampling slots are finite. A slot that doesn’t fit processor demand is a slot unlikely to recover cost.

That’s not Zoetis policy in any direct sense. It’s market dynamics responding to a structural shift. By April 2026, in our analysis of the public NAAB genomic young-sire list, the top tier of genomic Net Merit young bulls in the U.S. showed sharp concentration in a single stud’s NAAB code (methodology available on request). That’s the precedent for what catalog compression looks like when it works through to a published bull list.

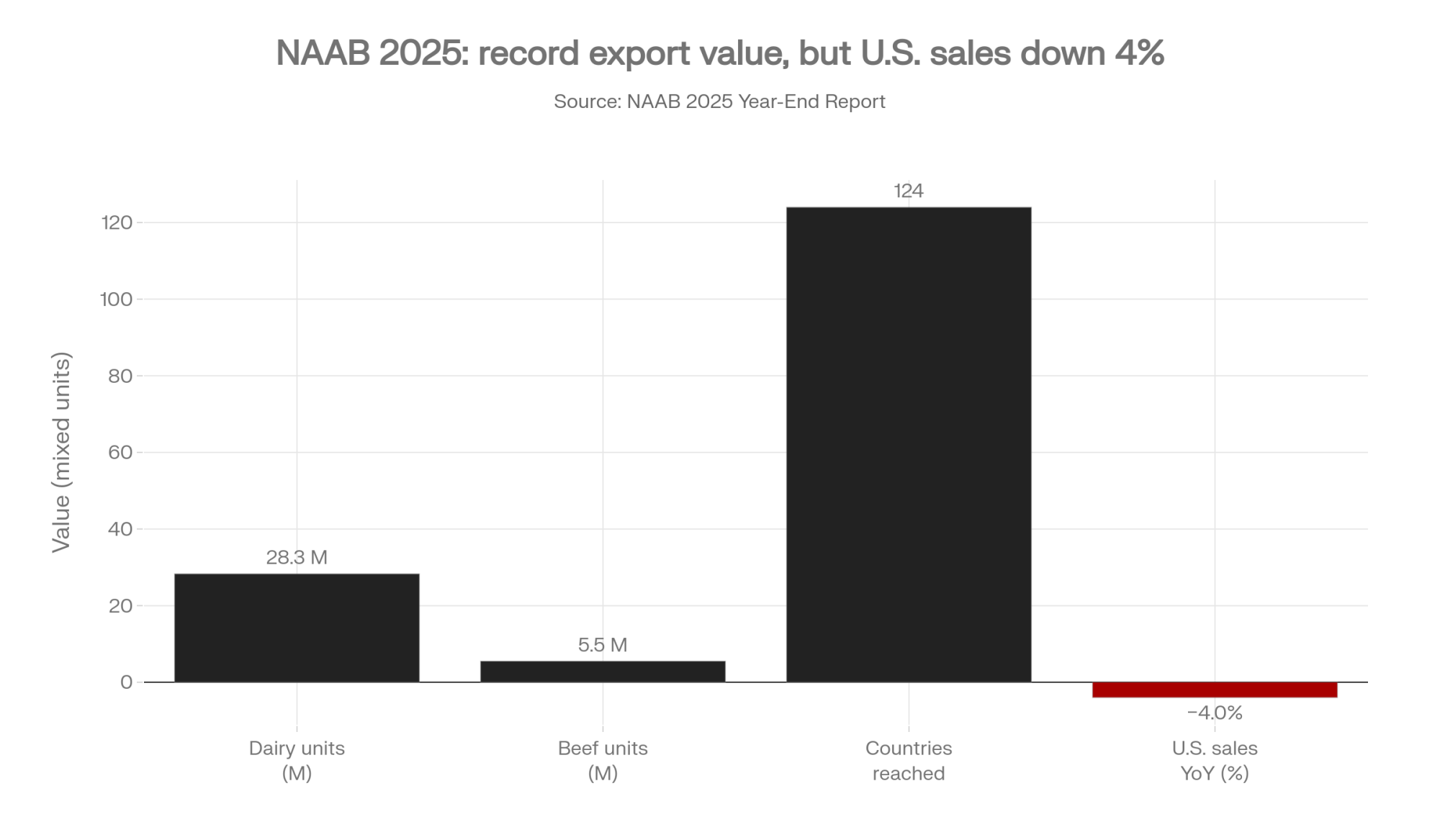

NAAB’s 2025 year-end report shows U.S. bovine semen sales down roughly 4% year-over-year. Export value reached a record $327.6 million even as total export units fell. China exited the U.S. market in early 2025. Dairy units exported settled at 28.3 million; beef exports rose to 5.5 million. U.S. genetics now reach 124 countries, up from 108 the prior year — and a clear majority of all dairy semen produced by NAAB members in 2025 left the country.

The structural pressure to watch is catalog compression outside the flagship top tier. The bulls most exposed in your cooperative’s next two catalogs are the slot 40–80 specialists: outcross health-trait sires, daughter-pregnancy-rate-leading bulls without methane-efficiency rank, show-type longevity sires whose proofs were built around classification rather than wellness data, A2A2-plus-component specialty sires for cheese-milk niches DWP$ doesn’t reward. That’s our read, not NAAB-confirmed sampling-mix data. Your cooperative’s next two catalogs will tell you if it’s right.

Pull slots 40–80 in the next catalog. Count what’s missing.

Options and Trade-Offs

Pick the path that fits how your milk check is built and how much room you’ve still got.

Path 1 — Participate with a parallel scorecard. Stay in Clarifide/DWP$ for processor compliance. Run your own mating logic underneath it, weighted to what your milk check actually pays for. Works when the processor premium is meaningful and your contract pays traits DWP$ underweights. Requires a breeding consultant or software workflow that shows DWP$ and NM$ rankings side by side. The risk: your AI rep’s default view is DWP$-framed. You have to actively ask for the second view every time.

Path 2 — Diversify your testing providers now, while you still can. Before you renew any testing contract, negotiate data-portability terms or split testing between Clarifide and an alternative — Neogen-GeneSeek pre-close, CDCB-based panels, a cooperative-run program. The H2 2026 close narrows the window on pre-close options. The risk: your nutrition software, vet platform, and mating program increasingly default to one data feed. Break one integration and three break with it.

The Switching-Cost Trap — read this before you sign anything.

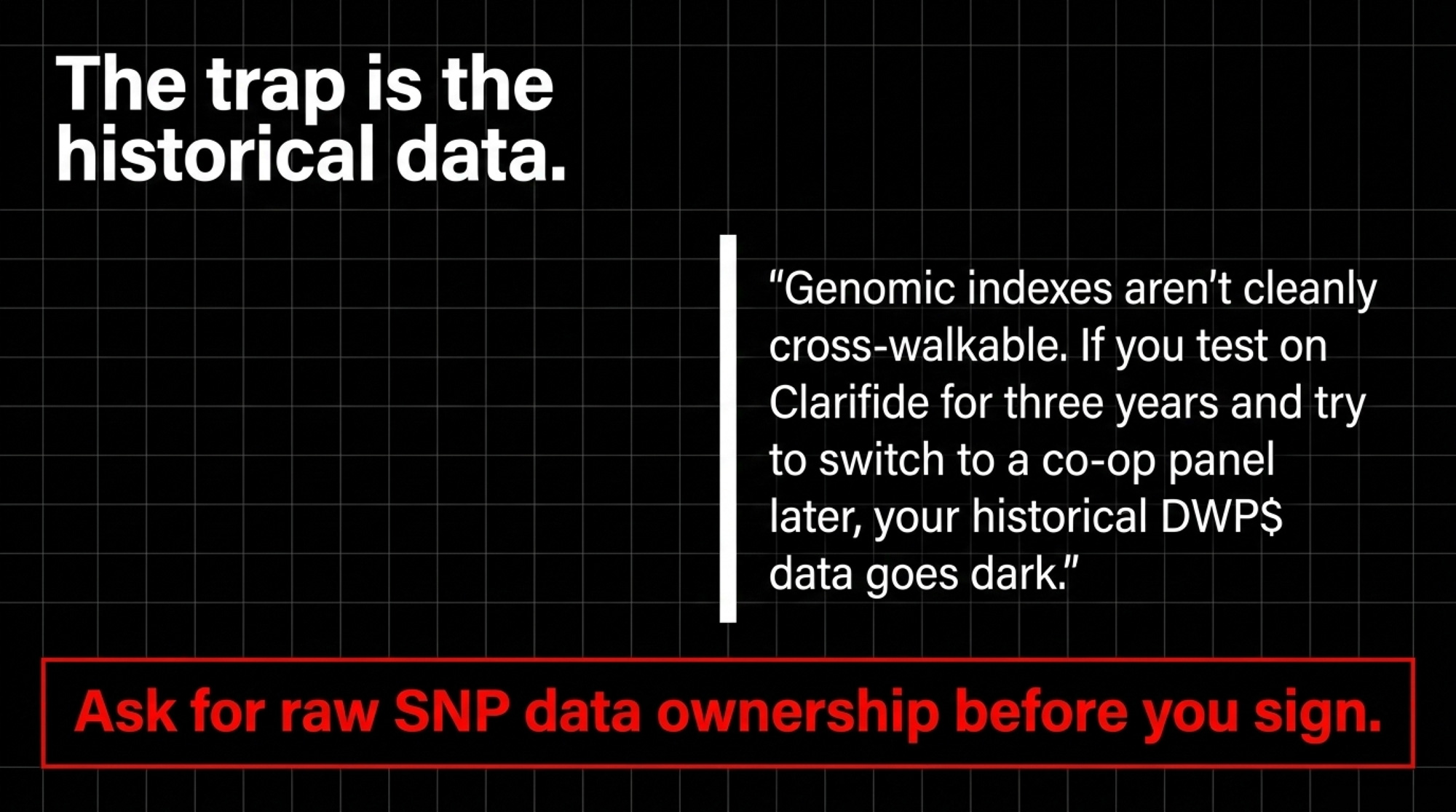

The harder cost in Path 2 isn’t the per-head test fee. It’s what happens to three years of historical rankings if you switch later.

Genomic indexes don’t translate cleanly across providers. The underlying SNP genotype usually does — once a genotype is on file with CDCB, it gets imputed to the same 80K-marker reference base regardless of which chip generated it. What doesn’t translate is the index ranking. DWP$ is Zoetis. NM$ is CDCB. TPI is Holstein Association. Each one weights traits differently, and a cow’s rank on one is not her rank on another.

So if you stay on Clarifide for three breeding crops and then want to move to a CDCB-based panel or a co-op program, the question isn’t whether to re-test the cattle. It’s whether your testing contract gives you export rights to the raw SNP file — and whether your genotypes were deposited with CDCB at the time of original testing. With those two boxes checked, a parallel evaluation costs a fraction of a re-test. Without them, you’re stuck either re-pulling samples or accepting that your historical DWP$ rankings and your forward-going scorecard live on different rulers.

Before you sign any testing contract this year, ask three questions in writing: Who owns the genotype file? Can you receive the raw SNP data, not just the index output? And can you re-run that data through a competing index without paying for a second test? Get the answers in the contract, not over the phone.

Path 3 — Source heat-tolerant genetics directly. If you’re in the South, parts of the West, or the lower Midwest, build a relationship with a Brazilian genetics supplier or a domestic IVF program working with Gyr-Holstein or SLICK-edited genetics. Trigger: summer THI in the upper-70s-to-low-80s range across an extended window — roughly where Zoetis itself recommends DWP$ Heat — and conception rates dropping by more than 5 percentage points across three consecutive summers. The risk: your traditional cooperative supplier probably can’t serve this need, creating a sourcing split you’ll need to manage.

Worth saying plainly as we head into the May–September heat window: DWP$ Heat is a software answer to a hardware problem. Genomic selection inside an existing Holstein population can shift what your daughters inherit at the margin. It cannot change what a Holstein is — a black-and-white animal selected over 75 years for cool-climate fluid-milk production, with body mass and coat type that limit how she dissipates heat at peak summer THI. Gyr-Holstein crosses and SLICK-edited cattle are a different physical platform: shorter coats, smaller body mass, sweat-gland density bred for the tropics. The honest question isn’t “is my DWP$ Heat score high enough?” It’s “do I need a different cow?” For most herds the answer is no — Holsteins still pay best where heat stress is occasional. For Florida, South Texas, Arizona, and the southern San Joaquin, where the answer is increasingly maybe, the Path 3 conversation isn’t optional anymore.

Path 4 — Stay loud at the cooperative. This is the 30-day action. The two questions earlier in this article aren’t a one-time ask. Walk them into the next district meeting on your calendar. Bring them on your phone. Read them aloud. Write the answer down, date it. Talk to two neighbors before the meeting and ask them to do the same. Re-raise in 90 days. Boards respond to repeated, specific, member-coordinated pressure. They do not respond to a single member raising an issue once. The cost is your time and a little social friction. The alternative is having the answer handed to you in 2028 by someone who wasn’t elected by your district.

The 30/90/365 Horizon

Horizon

Action

Trigger

30 days

Read data-ownership clauses (raw SNP file, portability, re-run rights); bring district-meeting questions; talk to two neighbors

Renewal letter on file or expected within 12 months

90 days

Negotiate portability terms; open tropical-genetics conversation; re-raise at next district meeting

THI / fertility decline ORrenewal date inside H2 2026

365 days

Track slots 40–80; commit to scorecard or diversification path; document board responses

Next two catalog cycles published

Key Takeaways

If your processor has mentioned Clarifide, sustainability testing, or scope 3 reporting in any conversation this year, assume a similar letter could land within 6 to 18 months. Negotiate data-portability terms — including raw SNP file access — before you sign, not after.

If DWP$ rankings on your last 30 sire selections diverge from your NM$ or TPI rankings by more than your milk-check structure can absorb, you’re breeding against a scorecard that doesn’t match how you get paid.

If your summer conception rate has dropped more than 5 points across three consecutive summers, the question isn’t whether to chase a higher DWP$ Heat score. It’s whether the Holstein is the right physical platform for your zip code at all. Put tropical, SLICK-edited, or DWP$ Heat-aligned genetics on your supplier conversations this quarter.

If your cooperative can’t name partners, dollar commitments, and timelines when asked the Path 4 questions, treat that as an unanswered question. Re-raise in 90 days. Keep asking.

If thinning shows up at slots 40–80 in your cooperative’s next two catalogs, that’s the leading indicator of R&D compression — visible 18 to 24 months before it shows up in flagship marketing.

What Kind of Cooperative Do You Want to Belong to in 2030?

Three generations of dairy farmers decided no member should face the genetics market alone. That decision built shared genotyping pipelines, member-owned data, and the negotiating leverage that has kept U.S. genetics competitive in 124 export markets and in your own barn. None of that is guaranteed to survive a structural shift it doesn’t see coming.

The cow-level economics — full DWP$-versus-NM$ math broken down by contract type and herd size — live in next week’s Bullvine Weekly. That’s where the spreadsheet sits: plug in your own components, your own premium, your own replacement rate, and see where the net-out lands.

But the question that actually matters this month isn’t the spreadsheet. It’s the one you bring to your next district meeting, in front of the neighbors whose kids might still be milking cows in 2050. What kind of cooperative do you want them to belong to?

Editorial note: This article reflects publicly available information as of May 1, 2026. Updates and any post-publication responses will be reflected in subsequent coverage.

¹ Holstein Association USA, Genomic Testing Services price schedule, accessed May 1, 2026: Clarifide Plus Medium-Density SNP Test + Dairy Wellness Traits & Polled at $43 per Holstein animal (member rate). Industry-wide practical costs typically run $40–$50 per head depending on volume and program tier.

² USDA NASS Milk Production monthly report, late-2025 release: U.S. average production per cow for the most recent reported month was 1,963 lb, putting annualized U.S. herd-average in the 24,000–24,400 lb/cow/year band, equivalent to roughly 66–67 lb/day on a steady-state basis.

³ 35% reflects a typical Holstein heifer-replacement rate; operations generally run 30–40% depending on cull rate. Figures rounded to the nearest dollar; testing-cost rows reflect 35% of milking herd as a straight multiplier. Adjust to your own heifer inventory before applying.

Disclaimer: The Zoetis–Neogen $160 million transaction is structural in scope, but individual outcomes vary by state, processor contract, regional milk pricing, herd size, and cooperative affiliation. The barn-math figures above are illustrative benchmarks, not universal forecasts. Run your own numbers against your own contract before any breeding, testing, or supplier decision.

The Dairy Mirage: How the Industry’s ‘Fixes’ Are Finishing Off the Farmer — Dismantles the illusion that industry ‘solutions’—from co-ops to proprietary indices—are designed for your benefit. Exposes the extraction system that profits from farm losses, urging a pivot toward scale or specialization before the system cashes you out.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

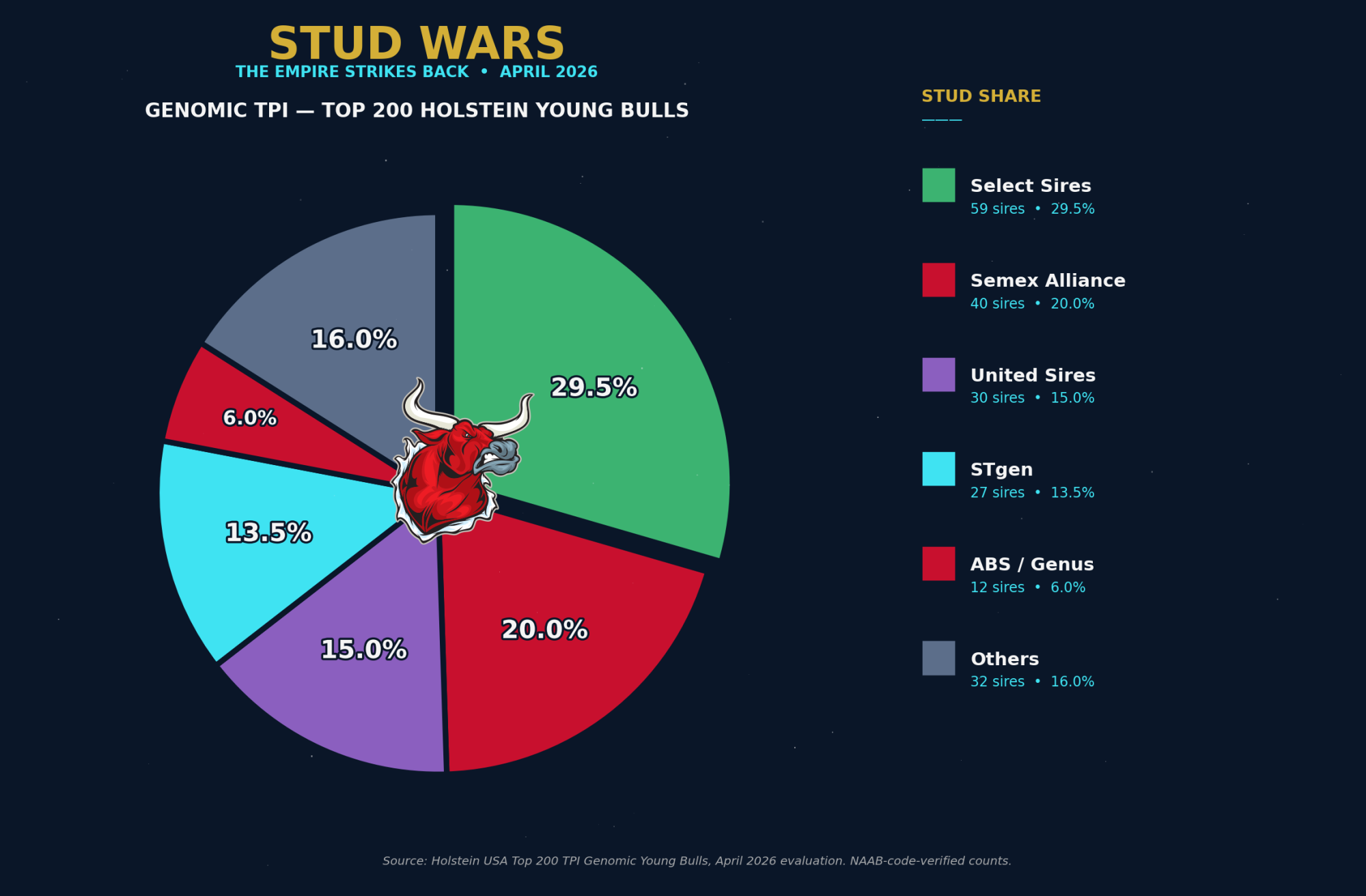

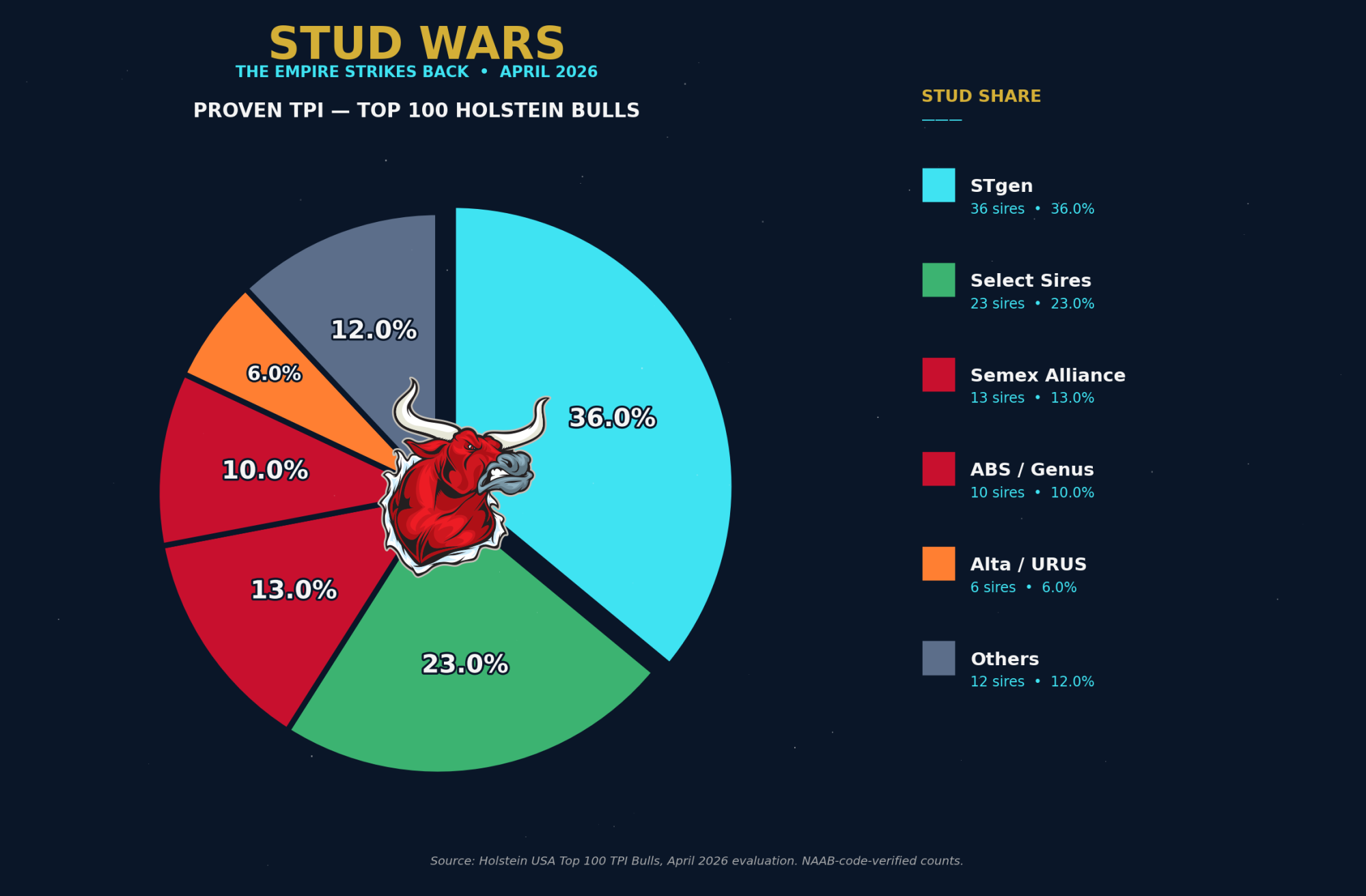

STgen owns 36% of the proven TPI top 100. Select Sires took 29.5% of the genomic top 200. United Sires — an independent breeder partnership founded in 2024 — grabbed 15% of the genomic top 200. And Zoetis just bought the lab pipes everyone else’s DNA flows through.

Three things hit at once on April 7, 2026.

Holstein Association USA detonated a TPI formula change that dropped Garza 125 points, Captain 72, and Sheepster 92 — without a single new daughter. STgen’s elite proven army still owns 36 of the top 100 proven TPI sires even after the formula loss — but the genomic young bull lists tell a different story. Select Sires now owns 59 of the top 200 genomic young bulls (29.5%) — the broadest genomic depth of any single stud. Semex took 40 sires (20%) of the top 200, with 9 of the top 20 spots. United Sires — the breeder-owned independent that launched in 2024 — has grabbed 30 sires (15%) of the top 200 out of nowhere. The genetic galaxy reshuffled overnight.

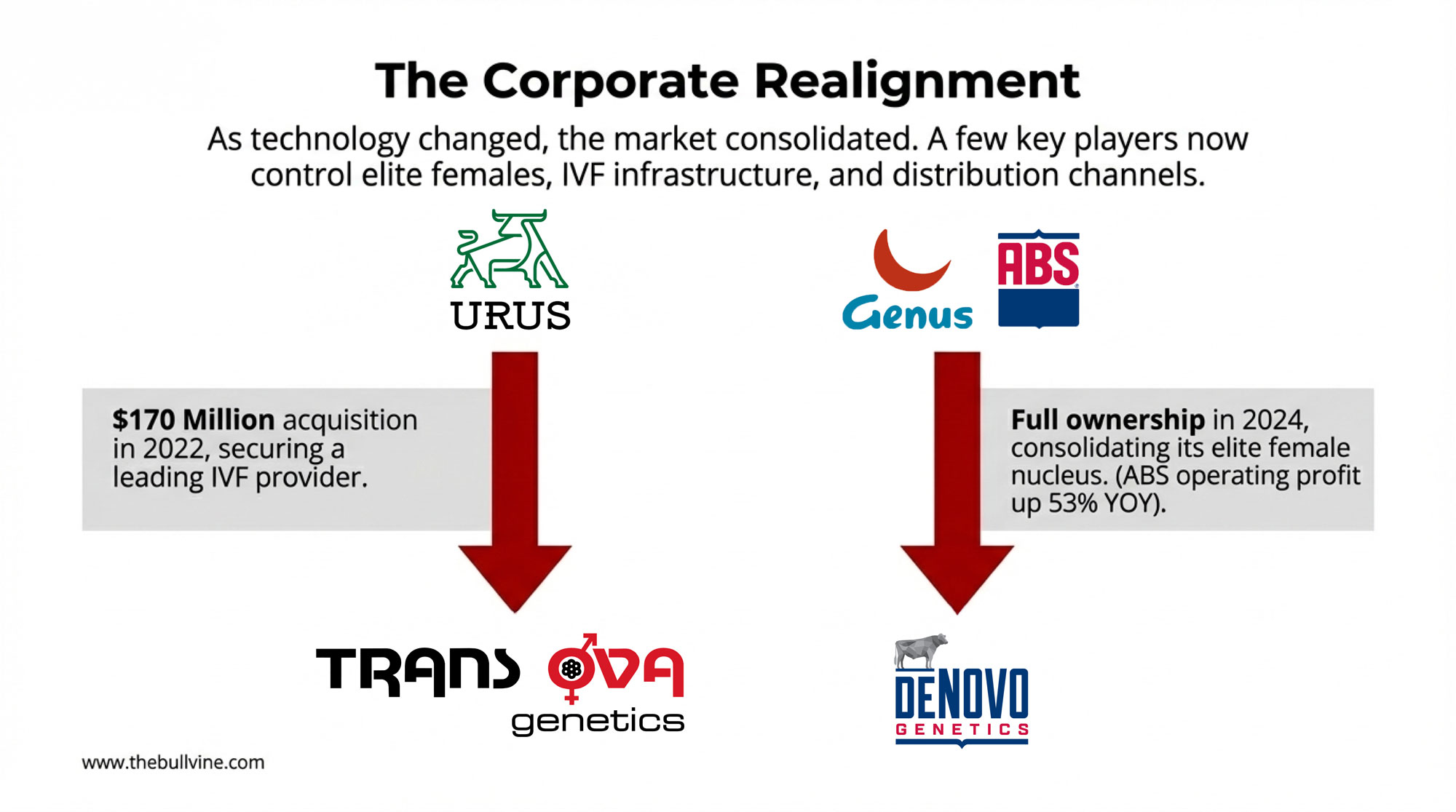

Meanwhile, the DOJ pulled the Select Sires + STgenetics merger off the shelf and is now “nearing a decision” on whether the largest cooperative distributor in North America gets to merge with the company that owns global sexed-semen patents. And Zoetis — a company that doesn’t sell a single straw of semen — wrote a 0 million check for the lab infrastructure that processes everyone else’s DNA. ABS, meanwhile, completed its full takeover of De Novo Genetics. Three consolidation moves. All upstream of the farmer.

The Bullvine’s position on consolidation hasn’t changed: it’s structural, it’s accelerating, and pretending it isn’t doesn’t help anyone. Whether the DOJ, the FTC, or anyone in Washington is paying attention is another question. The April 2026 sire share analysis isn’t a cleanup of 2025. It’s a structural reset.

Last April we called the run The Force Awakens — an emerging order taking shape, polled and gNM$ rebellions challenging the dominant studs. Twelve months later, the Empire is striking back: STgen holding its proven army through a hostile formula change, Select Sires lining up the largest cooperative consolidation in dairy genetics history, and Zoetis executing a vertical lock on the lab pipes that read everyone’s DNA. The rebels who took the genomic top 20 — Semex’s Progenesis line, a brand-new breeder partnership called United Sires — won a battle. The Empire is positioning to win the war.

Methodology: Same Battlefield, New Rules of Engagement

Following the precedent set in our April 2025 analysis, we again use top 200 sires for genomic TPI, top 100 for proven TPI, and the official Holstein Association USA April 2026 evaluation lists drawn from the official CDCB run published April 7, 2026 (Holstein USA; CDCB).

Holstein Association USA implemented the TPI 2026 formula change in this run — production weights shifted from 19% PTA Protein / 19% PTA Fat to 24% PTA Protein / 14% PTA Fat. That’s a 5-point bump for protein and a 5-point cut for fat. Daughter data didn’t change. The math behind the rankings did. This is the largest single TPI formula adjustment in recent memory, and it explains why bulls who were untouchable in December 2025 dropped 70 to 125 TPI points in April without milking a single new daughter (The Bullvine).

Methodology: All April 2026 stud-share figures in this analysis are independent counts of the official Holstein Association USA April 2026 lists, performed using the official NAAB marketing codes as the source of truth for stud assignment. Genomic TPI counts use the Holstein USA Top 200 TPI® Genomic Young Bulls (April 2026, 85% genomic reliability minimum). Proven TPI counts use the Holstein USA Top 100 TPI Bulls (April 2026, ACTIVE or LIMITED semen status, 80% traditional reliability minimum).

Key NAAB code → marketing organization assignments per the official NAAB table: 1 = GENEX Cooperative; 7/9/14/250/507/509 = Select Sires; 11 = Alta Genetics USA; 29/94 = ABS Global; 97 = CRV Holding; 200/777 = Semex Alliance; 288 = ASCOL; 523/551/646 = STgenetics (Inguran); 596/796 = United Sires, LLC (independent breeder partnership founded 2024); 599/799 = Blondin Sires; 719 = RuAnn Genetics. URUS-owned brands (GENEX, Alta, Jetstream, Trans Ova) are reported as separate codes per NAAB and consolidated where editorially useful. April 2025 baselines were independent counts performed at original publication using a different methodology that lumped some breeder codes together; year-over-year comparisons in this article are made cautiously.

Read that table. Five of the top 10 genomic young bulls in the world are 200HO — Semex Alliance. Two are Select Sires (S-S-I lines). Two are Alta/URUS (Peak AltaGoldenGate, Pen-Col AltaGlimpse). One is United Sires (OCD Whoops Sabotage, 796HO). Zero are STgen. The Progenesis line — Timetraveler, Superfreak, Tapas — locked down the top of the list. The 49-point spread between #1 (3563) and #10 (3514) is statistical noise at 65–80% genomic reliability. But the stud ownership pattern? That’s where the story lives.

Genomic TPI Stud Share — Top 200 Holstein Genomic Young Bulls (Verified Counts)

Stud (NAAB code)

Apr 2026 count

% of top 200

Select Sires (7, 14, 250)

59

29.5%

Semex Alliance (200, 777)

40

20.0%

United Sires (596, 796)

30

15.0%

STgen (523, 551)

27

13.5%

ABS / Genus (29, 94)

12

6.0%

Alta / URUS (11)

11

5.5%

GENEX / URUS (1)

9

4.5%

CRV (97)

8

4.0%

Independents (El Toro 508/708, A.I. Total 515, Genesis MX 706)

URUS umbrella — GENEX (1HO) + Alta (11HO) combined = 20 sires (10.0%), the third-largest cooperative group when consolidated.

Two notes on this table.

First, the April 2025 baseline used a different and less rigorous methodology — it lumped “Sexing Tech / Genosource” with breeder-affiliated codes that have since been revealed by official NAAB lookup to be a different organization entirely. With the corrected NAAB-code accounting, the year-over-year comparison should be read as: STgen alone has 13.5% of the genomic top 200 in April 2026 (down from the 39.5% “STgen / Genosource” lumped figure published in 2025). United Sires LLC — a separately-owned independent breeder partnership founded in 2024 with no ownership relationship to STgen — holds a separate 15.0%. The two are independent organizations with independent ownership and independent NAAB codes.

Second, Semex’s 20% matches their own self-reported claim closely. Their Facebook post on April 10 (Semex) reported “45% of the Top 20, 34% of the Top 50, 26% of the Top 100, 20% of the Top 200.” Our verified counts: 45% of top 20, 34% of top 50, 27% of top 100, 20% of top 200. They were on the money.

If you’re keeping score: the 24P/14F formula change penalized bulls heavy on fat — exactly the profile that built Captain, Garza, and Dominance into STgen’s elite proven army. STgen’s deep gNM$ pipeline still benefits from protein-heavy production traits. But on the genomic young bull TPI list — the leading indicator of where the next proven army comes from — Semex’s Progenesis and Beyond pipelines and Select Sires’ S-S-I and Stagger lines, protein-tilted by design, ate the formula change.

This is the imperial-consolidation reversal nobody scripted. STgen didn’t lose because their bulls got worse. They lost because Holstein Association USA changed what “best” means, and Select Sires, Semex, and a brand-new breeder cooperative were already breeding for the new definition.

Proven TPI: STgen’s Empire Holds Despite the Formula

First, STgen still owns three of the top 8 proven bulls — Dominance, Captain, Garza. Sheepster lost 92 TPI points without losing a daughter. He still sits at rank #1 with 2,359 daughters and 99% reliability. Garza lost 125 points. Captain lost 72. STgen’s elite proven army took the worst formula hit of any stud’s lineup, and they’re still here.

Second, the protein-formula winners are clear. Peak Powerhouse jumped +119 TPI in a single run to become the #2 proven bull in the world (Bullvine). Powerhouse carries the 1HO primary code = GENEX Cooperative (a URUS subsidiary), with secondary URUS codes 511HO and 122HO; the bull is the same Peak-branded URUS production line as the Alta-coded bulls. Peak AltaSamson at #10 carries 11HO = Alta Genetics, also URUS. Combined, URUS owns positions 2 and 10 of the proven top 10. Cookiecutter Horseshoe at #8 is registered under the 208HO Korean code as primary, but the bull is commercially distributed in North America via Semex (secondary codes 200HO and 777HO). Peak Powerstar’s debut at #9 gives Semex a new proven top-10 entry.

Third, the depth still belongs to STgen. 36 of the top 100 proven TPI bulls carry 551HO codes — STgenetics-Inguran, the largest single-stud share in any category we measured.

URUS umbrella — Alta (11HO) + GENEX (1HO) combined = 10 sires (10.0%) of the top 100, tied with ABS/Genus.

STgen’s depth on proven TPI is the most surprising finding in this entire run. Despite Garza, Captain, and Dominance each losing ground to the formula change, the broader STgen pipeline behind those flagship names — Brockington, Capn Miguel, Cap Mad Max, Captn Penza, Cap Volos, Cap Rivera, Capn Rodman, Cap Diggory, and dozens more — held position across the top 100. Select Sires gained ground on the genomic side; STgen held depth on the proven side. Both can be true simultaneously.

Running the Numbers: What the 24P/14F Formula Costs (or Saves) Your Mating Program

Take Garza as the worked example. SDG Cap Garza-ET sat at +3464 TPI in December 2025 and dropped to +3339 TPI in April 2026 — a −125 TPI swing with zero new daughter data. His PTA Fat (+140 lbs) and PTA Protein (+50 lbs) didn’t move. The index weighting did.

Practical impact on a 500-cow Holstein herd: if your mating program selects service sires above a +3400 TPI threshold, Garza was in in December and is out in April — same bull, same daughters, same fertility. Multiply that across STgen’s elite proven army (Captain −72, Dominance −21) plus Sheepster (−92) on the Select Sires side, and roughly 30–40% of a typical commercial farm’s previous top-tier proven sire list now sits below older threshold cutoffs.

The fix is mechanical: drop your TPI cutoff by ~75–125 points, or rebuild your selection from PTA Protein and PTA Fat directly instead of relying on the headline index. The math hasn’t changed for milk in the tank. It’s changed for which bulls your computer flags as elite.

Specialty Forces: Type and Red & White

Headline gTPI and proven TPI tables tell you who’s winning the index war. Specialty rankings tell you who’s winning the niches — the breeders who keep buying for udder, feet, and frame; for component-heavy red herds; for a typier cow regardless of what TPI is doing this April. We’ve cross-referenced the EuroGenes April 2026 ranked top-50 lists for Type (PTAT) and Red & White TPI. Both pull from the same Holstein USA April 2026 evaluation as the headline gTPI lists but isolate subsets that don’t surface in the broader rankings.

Type (PTAT): The Spanish Empire You Forgot About

Rank

Bull

NAAB

TPI

PTAT

Stud

1

Ruann Karat-45955-ET

719HO45955

+2647

+3.92

RuAnn Genetics

2

Shg Lego

515HO00486

+2307

+3.84

A.I. Total (NL)

3

Redcarpet Story Arc-ET

730HO00005

+2215

+3.78

Redcarpet Sires

4

Stone-Front Eyecandy Apollo

288HO00352

+2448

+3.72

ASCOL (Spain)

5

Genosource Seenofear-ET

551HO05904

+2791

+3.71

STgen

6

Jimtown Nelson-ET

288HO00321

+2426

+3.69

ASCOL

7

Curlys Admire

734HO00157

+2600

+3.63

URUS (Jetstream)

8

Eclipse Milio-ET

551HO03708

+1982

+3.58

STgen

9

Eskdale Hulu Shoutout-ET

288HO00364

+2889

+3.56

ASCOL

10

Mr Legacy-Ranch E Atlas-ET

100HO12395

+2423

+3.55

JLG Custom

Source: Drawn from the official Holstein USA April 2026 evaluation.

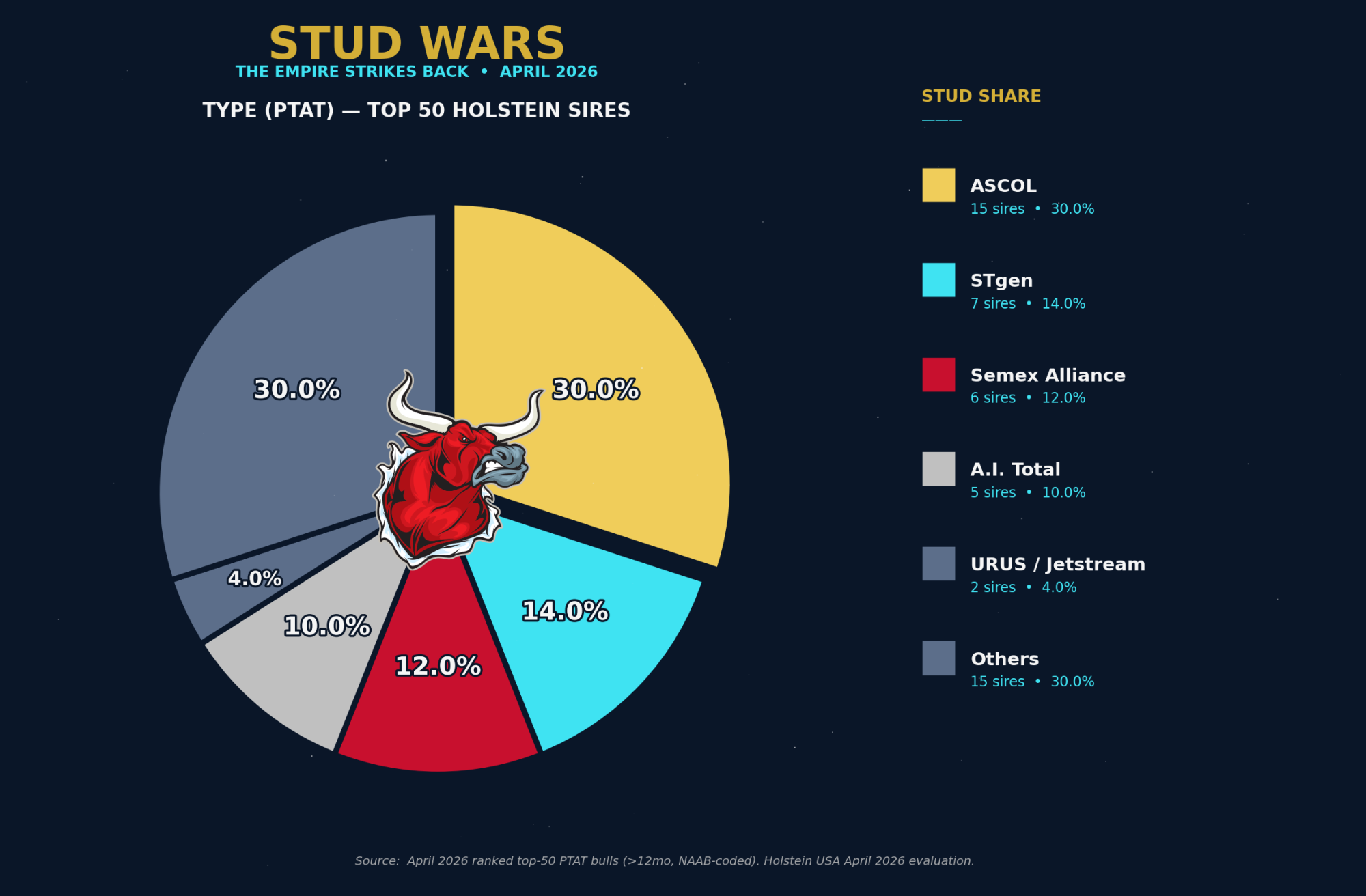

Type (PTAT) Stud Share — Top 50 Bulls

Stud (NAAB code)

Apr 2026 count

% of top 50

ASCOL (288)

15

30.0%

STgen (523, 551)

7

14.0%

Semex Alliance (200, 777)

6

12.0%

A.I. Total (515)

5

10.0%

Other independents (Showbox 744, Holstein Svc 712, AG3NexGen 733)

6

12.0%

Blondin (799)

2

4.0%

RuAnn (719)

2

4.0%

URUS / Jetstream (734)

2

4.0%

Redcarpet (730)

1

2.0%

ABS / Genus (94)

1

2.0%

Select Sires (250)

1

2.0%

Swissgenetics (196)

1

2.0%

The headline finding is the one nobody outside Europe will see coming: ASCOL — the Spanish breeder cooperative — owns 30% of the top 50 PTAT bulls in the U.S. evaluation, and 3 of the top 10. Stone-Front Eyecandy Apollo, Jimtown Nelson, and Eskdale Hulu Shoutout are all 288HO bulls, all PTAT ≥3.55. STgen has 7 (14%) and a top-10 presence with Genosource Seenofear at #5 and Eclipse Milio at #8. The big U.S. cooperatives — Select Sires (1), ABS (1), GENEX (0) — barely register at the top of the type rankings.

This is not new. PTAT has historically been the most fragmented stud-share category because elite type bulls come from individual breeder programs that license through niche distribution channels rather than the big-five cooperative pipelines. April 2026 just confirms the pattern with verified NAAB-code accounting.

Red & White TPI: ABS’s Quiet Empire

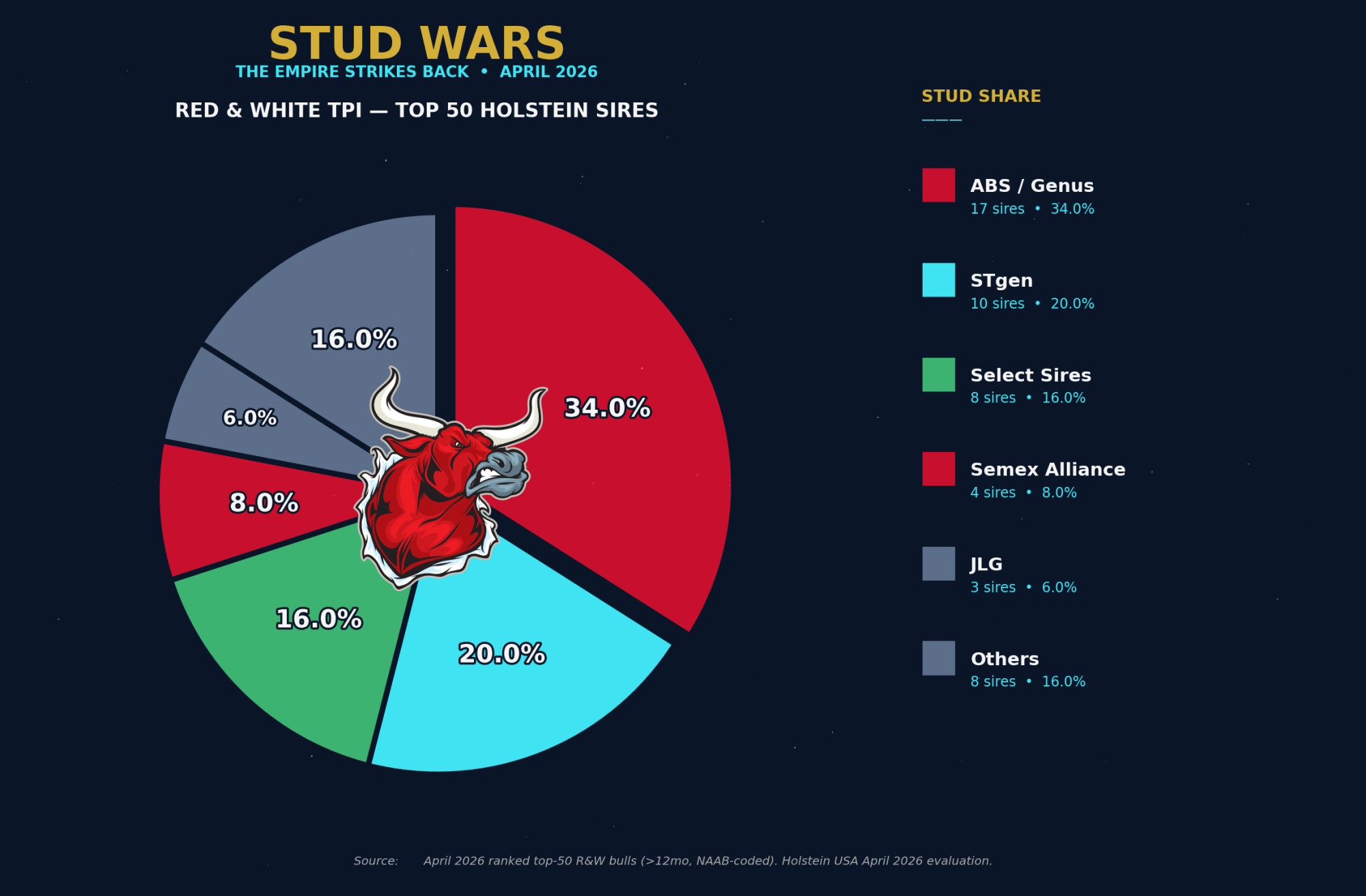

While the gTPI top 200 reshuffled around STgen and Select Sires, the R&W lineup tells a different story — ABS / Genus owns 17 of the top 50 R&W TPI bulls (34%) including 5 of the top 10. The De Novo acquisition is showing up in the rankings.

Rank

Bull

NAAB

TPI

Stud

1

Denovo 21873 Okafor-Red-ET

029HO00951

+3194

ABS / Genus

2

Aprilday Hrok Athens-Red-ET

250HO18217

+3180

Select Sires

3

Stgen Ocean-Red-ET

551HO06846

+3179

STgen

4

Ocd Morris Spirit-Red-ET

551HO06757

+3177

STgen

5

Aprilday Orphs Aesop-Red-ET

029HO00954

+3177

ABS / Genus

6

Sfh Scudetto Red ET

029HO22554

+3177

ABS / Genus

7

3star Patser-Red-ET

200HO08526

+3175

Semex

8

Siemers Rle Papaya-Red-ET

007HO17695

+3174

Select Sires

9

Sfh Saviero Red ET

029HO22562

+3170

ABS / Genus

10

Aprilday Orph Lyon-Red-ET

029HO00956

+3168

ABS / Genus

Source: Drawn from the official Holstein USA April 2026 evaluation.

Red & White TPI Stud Share — Top 50 Bulls

Stud (NAAB code)

Apr 2026 count

% of top 50

ABS / Genus (29, 94)

17

34.0%

STgen (523, 551)

10

20.0%

Select Sires (7, 14, 250)

8

16.0%

Semex Alliance (200, 777)

4

8.0%

JLG / Holstein Svc (100, 712)

3

6.0%

Alta / URUS (11)

2

4.0%

GENEX / URUS (1)

1

2.0%

United Sires (796)

1

2.0%

Other independents (Cogent 522, Inseme 643, A.I. Total 515, Intermizoo 198)

4

8.0%

The story in this table is the consolidation of red-and-white genetics under ABS/Genus’s roof. The top R&W bull, Denovo 21873 Okafor-Red-ET (029HO00951) at +3194 TPI, is a De Novo bull — the same De Novo program ABS completed its full takeover of in early 2026. Five of the top ten R&W bulls carry 029HO codes. Of the next 40, ABS owns another 12. Total: 17 of 50 (34%) — the largest single-stud share in any specialty category we counted.

STgen’s 20% share comes from a different angle. The 551HO R&W lineup — Ocean, Spirit, Red Lion, Redwood-P, Remington, Sizzler, Genosource Morris, Silver-Elite Ferrari, Silver-Elite Malibu — reflects STgen’s bid to keep R&W relevance through the Genosource production pipeline. Select Sires shows up with 8 bulls (16%), led by Aprilday Hrok Athens-Red at #2.

If you breed red Holsteins commercially, the practical implication is straightforward: the R&W elite is concentrating, not fragmenting. ABS, STgen, and Select Sires together own 70% of the top 50 R&W TPI bulls in April 2026. Independent breeder lines that historically carried R&W (Aprilday, Denovo, Genosource, Stgen) are increasingly inside one of those three corporate umbrellas.

The Economic Theater: NM$ and the Sire-Count Totals

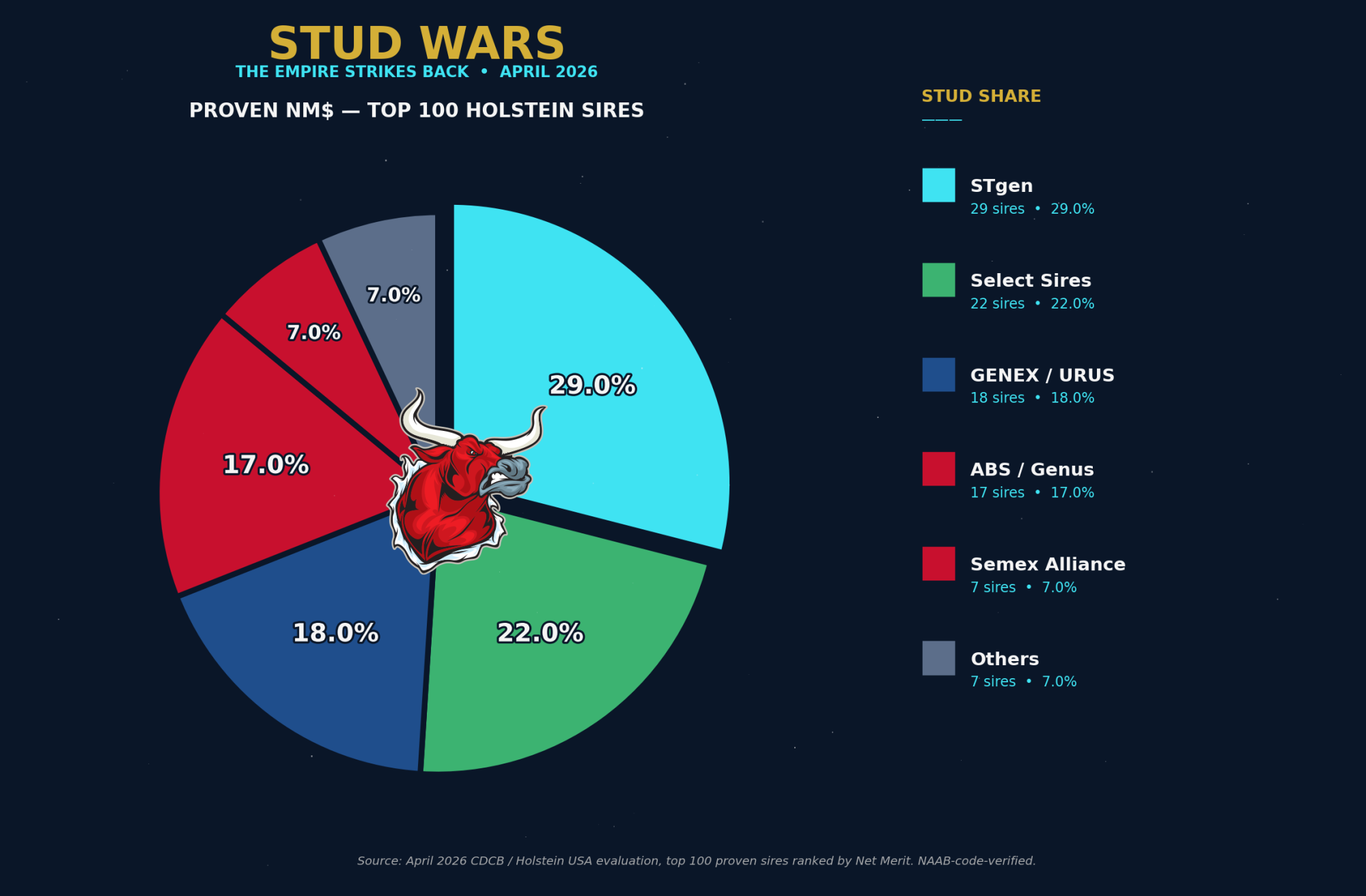

TPI is the breeding-decision proxy. Net Merit (NM$) is the dollars-per-cow-per-lactation proxy — USDA’s lifetime profit estimate for a daughter sired by that bull. If TPI tells you who’s winning the index war, NM$ tells you who’s winning the economics. And nobody who reads sire summaries will be surprised by what the NM$ tables show: STgen owns the NM$ rankings the way Saudi Arabia owns crude oil.

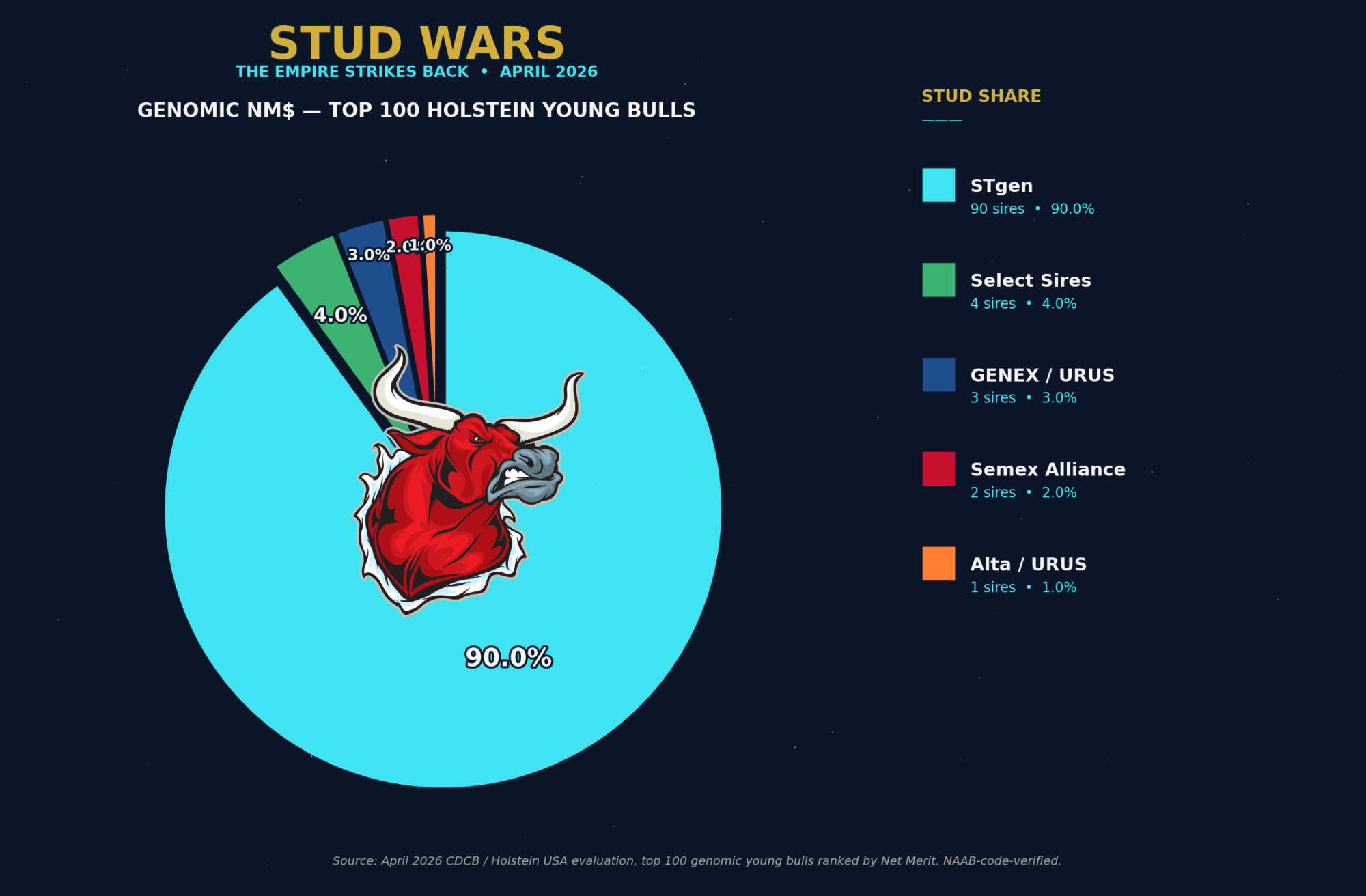

Genomic NM$: STgen’s 90% Empire

Rank

Bull

NAAB

NM$

TPI

Stud

1

Genosource Valkyrie-ET

551HO07040

+1308

+3464

STgen

2

Farnear Collateral-ET

551HO07100

+1304

+3410

STgen

Source: April 2026 CDCB / Holstein USA evaluation, top 100 genomic young bulls ranked by Net Merit. NAAB-code-verified.

Genomic NM$ Stud Share — Top 100 Bulls

Stud (NAAB code)

Apr 2026 count

% of top 100

STgen (523, 551, 558)

90

90.0%

Select Sires (7, 14, 250)

4

4.0%

GENEX / URUS (1)

3

3.0%

Semex Alliance (200, 777)

2

2.0%

Alta / URUS (11)

1

1.0%

This is not a typo. 90 of the top 100 genomic NM$ young bulls in the April 2026 evaluation carry STgen NAAB codes (551HO or 558HO). Select Sires has 4. GENEX/URUS has 3. Semex has 2. Alta has 1. Everyone else combined has zero. The Genosource production pipeline — anchored by Captain, Charl, Ripcord, Dominance, and Thorson as foundation sires — is producing genomic young bulls so deep on Net Merit that the rest of the industry barely registers.

This is also the strongest single argument for why the DOJ + Select Sires merger matters. If the deal clears, Select Sires gets distribution rights to 90% of the world’s top genomic NM$ pipeline. If it blocks, every cooperative in North America that wants to sell elite NM$ young bulls has to negotiate with STgen on STgen’s terms.

Proven NM$: A Different Five-Way Fight

The proven NM$ list is a different story — wider, more competitive, and shaped by which studs have managed to get high-NM$ Genosource-pipeline bulls daughter-proven before they age out of relevance.

Proven NM$ Stud Share — Top 100 Bulls

Stud (NAAB code)

Apr 2026 count

% of top 100

STgen (523, 551)

29

29.0%

Select Sires (7, 14)

22

22.0%

GENEX / URUS (1)

18

18.0%

ABS / Genus (29, 94)

17

17.0%

Semex Alliance (200, 777)

7

7.0%

Alta / URUS (11)

7

7.0%

Proven NM$ is the most balanced category in the entire April 2026 analysis. Six studs all sit between 7% and 29%. STgen leads at 29% — their proven Genosource pipeline (Dominance #1, Thorson #2, Garza #3, Captain, Jack, John, Vito, Brockington) sweeps the top of the list. But Select Sires (22%), GENEX/URUS via Peak (18%), and ABS/Genus via De Novo (17%) are all within striking distance. The competitive structure here is healthier than anywhere else in the article — four studs have real depth, and any one of them can compete on commercial pricing.

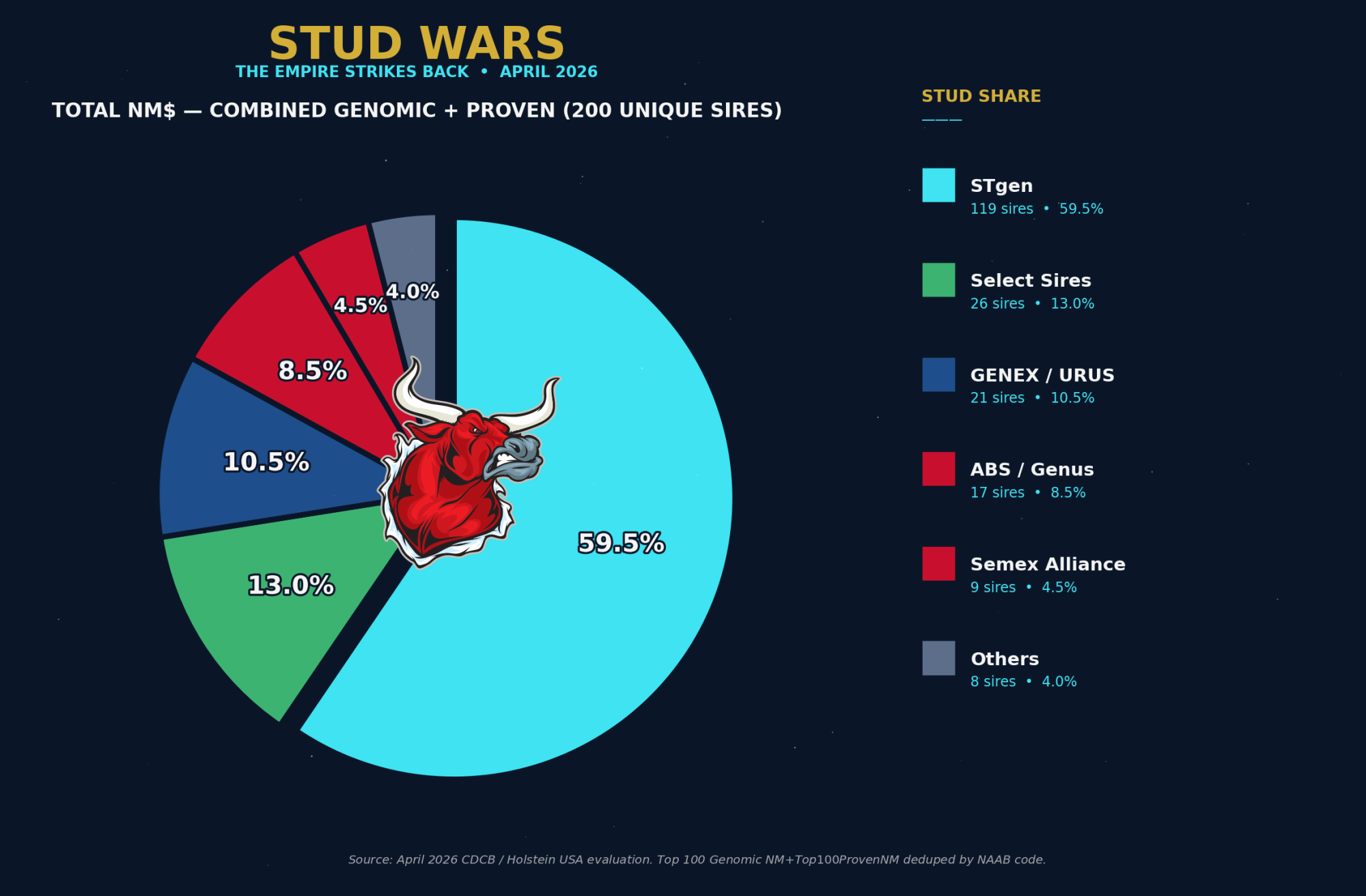

Total NM$: STgen Owns 60% of Both Lists Combined

When you dedupe the Genomic NM$ Top 100 and the Proven NM$ Top 100 by NAAB code, you get 200 unique sires(no bull appears on both lists at the same time). Of those 200, STgen owns 119.

Total NM$ Stud Share — 200 Unique Sires

Stud

Combined count

% of 200 unique sires

STgen

119

59.5%

Select Sires

26

13.0%

GENEX / URUS

21

10.5%

ABS / Genus

17

8.5%

Semex Alliance

9

4.5%

Alta / URUS

8

4.0%

STgen owns 59.5% of the combined NM$ map. Select Sires — the largest cooperative distributor in North America — owns 13%. URUS umbrella combined (Alta + GENEX) sits at 14.5%. The DOJ decision is, fundamentally, about who gets to sell the 60% slice that STgen currently produces.

The Combined Sire Count: Who Has the Deepest Bench

The per-category tables tell you who’s winning specific battles. The combined-count tables tell you whose bench is deepest — across every list a commercial breeder might shop from. We’ve deduped each combination by NAAB code so a bull that appears on both the TPI and the NM$ list only counts once.

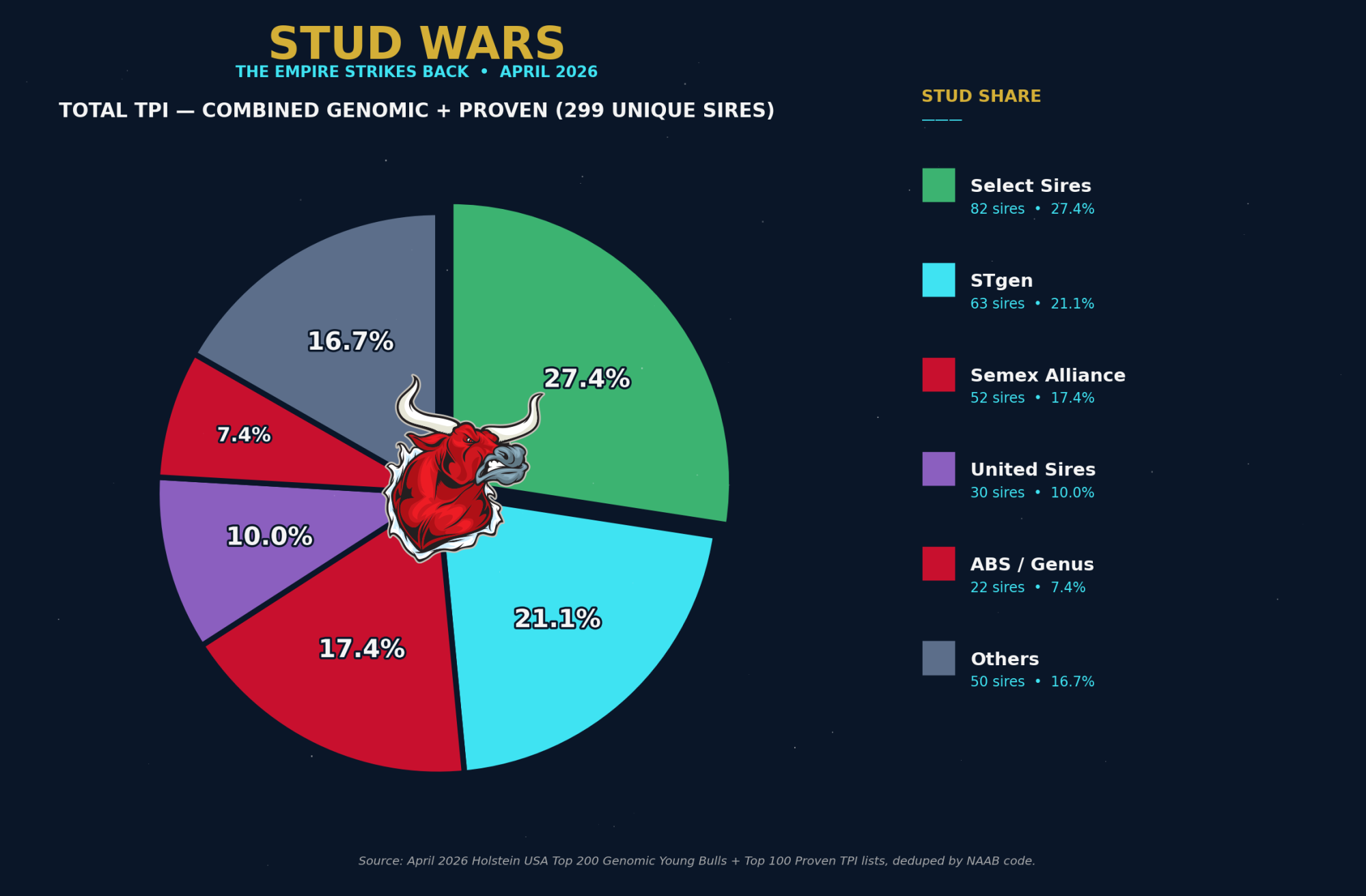

Total TPI — Genomic + Proven Combined (299 Unique Sires)

Stud

Combined count

% of 299 unique sires

Select Sires

82

27.4%

STgen

63

21.1%

Semex Alliance

52

17.4%

United Sires

30

10.0%

ABS / Genus

22

7.4%

Alta / URUS

17

5.7%

GENEX / URUS

13

4.3%

CRV

13

4.3%

Independents

7

2.4%

[CHART: Total TPI — Combined Genomic + Proven (299 Unique Sires), April 2026]

Select Sires owns the broadest TPI footprint at 27.4% of all unique TPI-ranked sires (genomic + proven combined). STgen sits at 21.1% — less depth than NM$ but still substantial. Semex’s 17.4% reflects their genomic top-200 strength (40 bulls). United Sires’ 10% from a single year of operation remains the most surprising data point in the entire analysis.

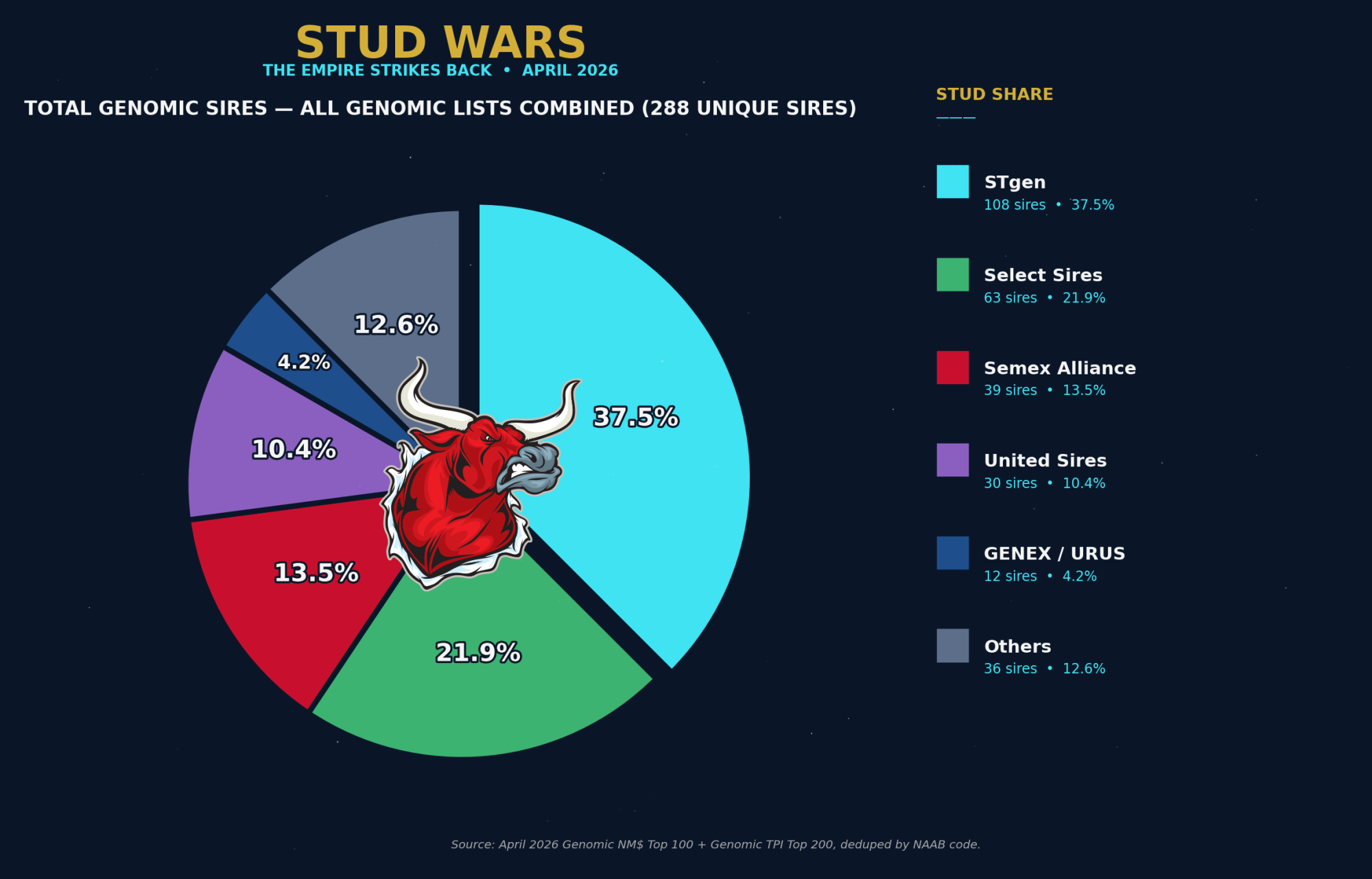

Total Genomic Sires — All Genomic Lists Combined (288 Unique Sires)

Stud

Combined count

% of 288 unique sires

STgen

108

37.5%

Select Sires

63

21.9%

Semex Alliance

39

13.5%

United Sires

30

10.4%

GENEX / URUS

12

4.2%

Alta / URUS

12

4.2%

ABS / Genus

12

4.2%

CRV

8

2.8%

Independents

4

1.4%

[CHART: Total Genomic Sires — All Genomic Lists Combined (288 Unique Sires), April 2026]

When you combine the Genomic TPI Top 200 and Genomic NM$ Top 100 — deduped — STgen pulls ahead of Select Sires at 37.5% to 21.9%. The NM$ dominance is what does it: 90 STgen genomic NM$ bulls plus 27 STgen genomic TPI bulls, deduped to 108 unique entries. The genomic future, on these two metrics combined, is overwhelmingly Genosource-pipeline genetics.

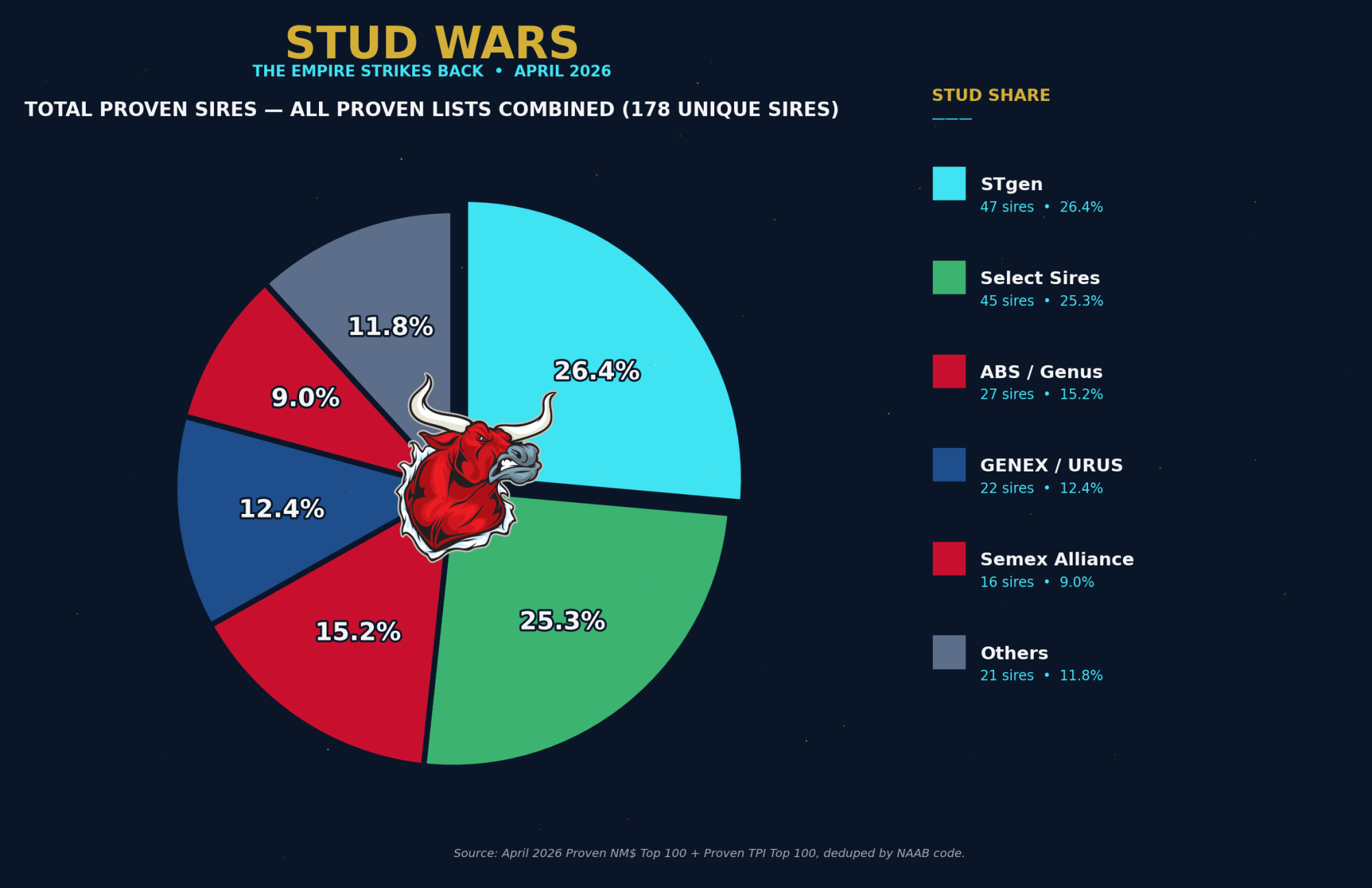

Total Proven Sires — All Proven Lists Combined (178 Unique Sires)

Stud

Combined count

% of 178 unique sires

STgen

47

26.4%

Select Sires

45

25.3%

ABS / Genus

27

15.2%

GENEX / URUS

22

12.4%

Semex Alliance

16

9.0%

Alta / URUS

13

7.3%

CRV

5

2.8%

Independents

3

1.7%

[CHART: Total Proven Sires — All Proven Lists Combined (178 Unique Sires), April 2026]

Proven sire counts — across both TPI and NM$ — are the most balanced in the entire article. STgen and Select Sires are within one bull of each other (47 vs 45). ABS, GENEX, and Semex all have meaningful proven depth. This is the category most resistant to consolidation pressure: proven sires take 5-7 years to develop, the pipeline can’t be acquired overnight, and four to five studs all have genuine elite proven inventory.

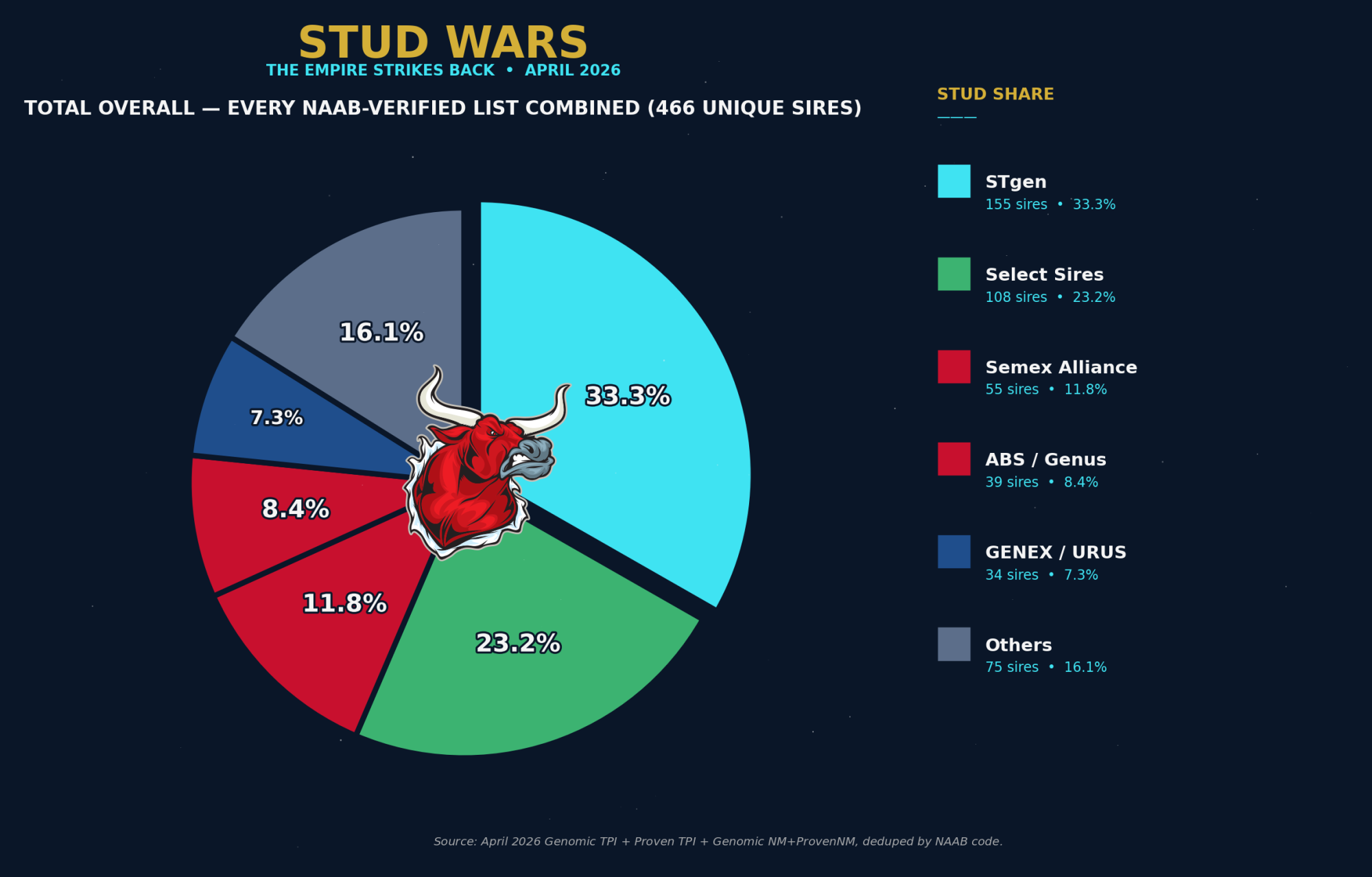

Total Overall — Every NAAB-Verified List Combined (466 Unique Sires)

Stud

Combined count

% of 466 unique sires

STgen

155

33.3%

Select Sires

108

23.2%

Semex Alliance

55

11.8%

ABS / Genus

39

8.4%

GENEX / URUS

34

7.3%

United Sires

30

6.4%

Alta / URUS

25

5.4%

CRV

13

2.8%

Independents

7

1.5%

This is the master scoreboard. Combine the Genomic TPI Top 200, Proven TPI Top 100, Genomic NM$ Top 100, and Proven NM$ Top 100 — dedupe everything by NAAB code — and you get 466 unique elite sires in the April 2026 evaluation. Of those, STgen owns 155 (one in three). Select Sires owns 108 (just under one in four). Together those two studs control 56.5% of the entire elite sire universe.