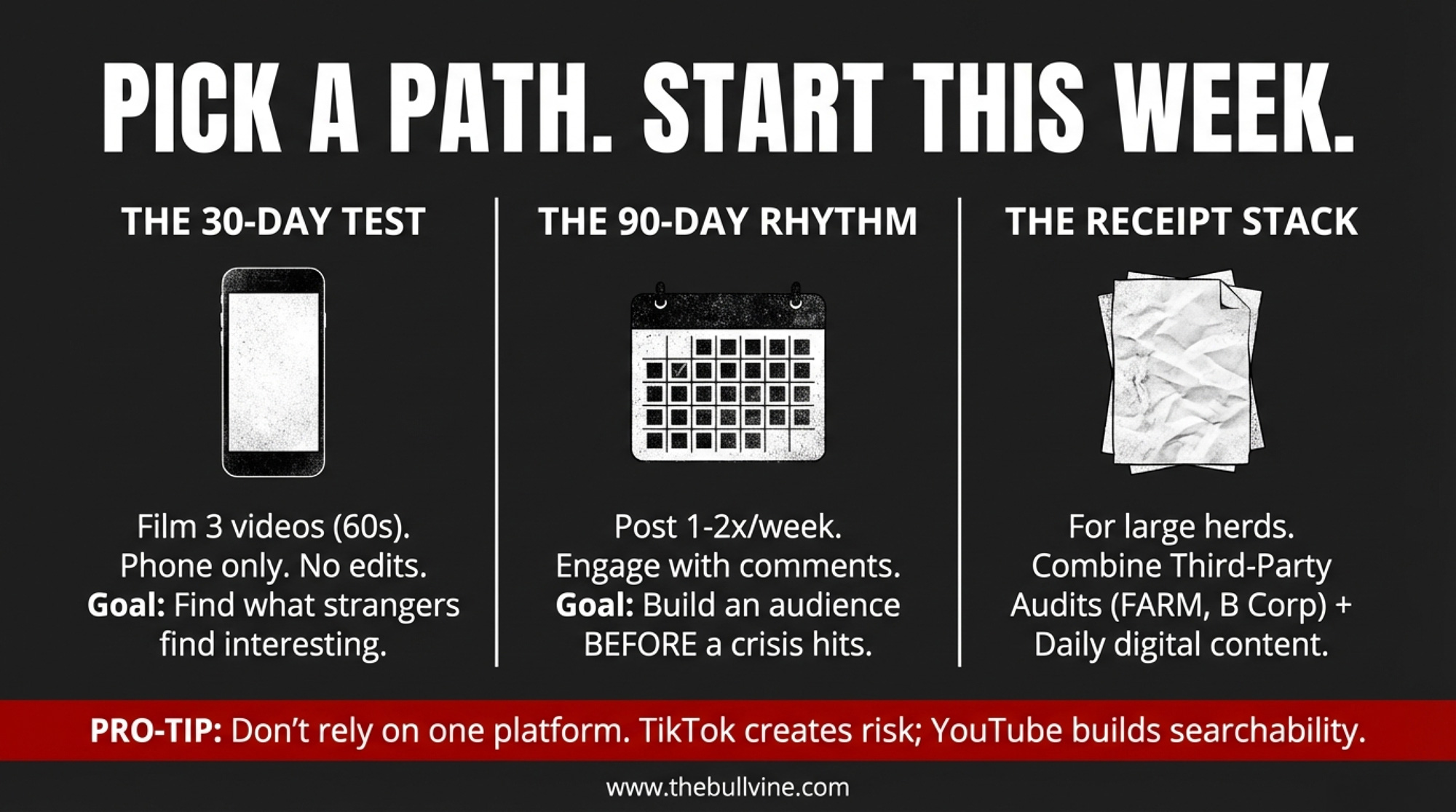

The National Dairy Shrine 2026 Awards slate just dropped — and it’s a landmark one. Pine-Tree Dairy takes the Distinguished Dairy Cattle Breeder Award, four Pioneers join a roll that now exceeds 360 names, Vita Plus’s Bob Hagenow is named Guest of Honor, and a brand-new Emerging Leader category debuts with four under-40 honorees.

Executive Director Mike Opperman announced the winners live on the Uplevel Dairy Podcast with host Peggy Coffeen, broadcasting from the Shrine’s Fort Atkinson office beside the original 1949 Dairy Shrine Club sign.

Pine-Tree Dairy: A Legacy That Rewrote the Pedigree Chart

If you’ve opened a Holstein sire summary in the last decade, you’ve probably read Pine-Tree’s fingerprints without realizing it. The Steiner family operation in Marshallville, Ohio — now in its fourth generation — takes the 2026 Distinguished Dairy Cattle Breeder Award, a category dating to 1973.

The operation today: 1,400 milking cows, 1,500 heifers, and 140 bulls across Holstein, Jersey, and Brown Swiss, with a 28,658-lb rolling herd average, 1,000+ embryos produced annually, and 19 consecutive years of Progressive Genetic Herd designation.

Why they reshaped the breed: Matt Steiner was selecting for NM$, cheese merit, daughter fertility, productive life, and calving ability before those traits carried real weight in official indexes. That commercial-first philosophy traced back to one $8,100 phone bid in 2003 — Wesswood-HC Rudy Missy at the Wisconsin Holstein Convention Sweetheart Sale. She grew into an EX-92 GMD DOM brood cow, exceeded 40,000 lbs of milk, and earned Holstein International Global Cow of the Year honors in 2014. (Read more: The $8,100 Gamble on Missy, 198 Dragged Genes, and the 20-Year Breeding Blind Spot Hiding in Your Herd)

Seagull-Bay Supersire — generational commercial sire, from the Missy branch via Ammon-Peachey Shauna

Mountfield SSI Dcy Mogul — one of the most-used Holstein sires in history, from the Missy Miranda branch

De-Su Balisto — highest-ranked Holstein sire ever in Australia, majority Rudy Missy maternal line

AltaOak, Pursuit, Sid, Burley (2021 HI Outcross Sire of the Year), Heroic — all trace back to Pine-Tree

The kicker stat from Opperman’s announcement: 48 of 50 heifers at the 2025 World Dairy Expo World Classic Sale traced back to a Pine-Tree prefix. Matt, Gail, and the next generation also supply A2A2 milk to two small processors, farm entirely on non-GMO inputs, and earned Wayne County Soil & Water Conservation District’s Conservation Farm of the Year — a stewardship legacy started when grandfather Ezra co-founded Wayne SWCD in 1947.

The 2026 Pioneers: Four Careers That Built the Modern Industry

Over 360 Pioneer Awards have been handed out since 1949. Four more join in 2026 — three academics and the duo behind “send her to Sunshine.”

Dr. Larry Chase — Professor Emeritus, Cornell University. Built a dairy nutrition research and extension program where applied research answered real producer questions and moved rapidly into on-farm practice. His research and extension arms reinforced each other, creating immediate industry impact.

Dr. Dennis “Denny” Funk. BS, MS, PhD from Iowa State. Managed Holstein sire development at Holstein Association USA starting in 1988, moved to an assistant professor role at UW–Madison, then joined ABS Global in 1995 as director of genetic programs. His career spans research, education, genetic evaluation systems, global germplasm commerce, and the commercial rollout of reproductive and genomic tech.

Dr. Rick Grant — Past President and Trustee, William H. Miner Agricultural Research Institute. 13 years at the University of Nebraska as professor of ruminant nutrition and extension dairy specialist, then 28 years at Miner with adjunct appointments at Vermont, Cornell, and SUNY Plattsburgh. Thirty-five years of field-shaping work in dairy nutrition, cow comfort, and producer-focused outreach.

Drs. Chris Simon and Dr. Dan Hornickel — the “Sunshine Boys.” University of Illinois vet school classmates in the 1970s who left their practices in 1983 to found Sunshine Genetics in Whitewater, Wisconsin. They built one of the world’s most respected embryo transfer operations — so respected that “send her to Sunshine” became industry shorthand for flushing your best cow at the gold-standard facility.

Emerging Leader Award: Dairy Finally Honors the Under-40s

Dairy has always honored grey hair. It hasn’t always honored the 30-somethings quietly reshaping the industry right now. The Shrine closed that gap in 2026 with a new category for leaders 40 and under — Opperman admits he missed eligibility himself by about six months.

The inaugural class (alphabetical, not ranked):

Bo Harstine — VP Technical Initiatives and Innovation, Select Sires. Driving innovation management and strategic alignment at Select, plus curriculum work with Ohio’s Department of Education ag and environmental systems advocacy committee.

Allison Ryan — Director of Marketing and Communications, MVP Dairy. The force behind two state-of-the-art dairy education visitor centers in Ohio and Kansas, plus active roles with Mercer County Farm Bureau and Fairgrounds.

Lucas Sjostrom — Account Manager, Specialty Herd Solutions; head distiller at Redhead Creamery. By 39, he’d logged trade missions with Russian investors, federal milk marketing order hearings, and leadership roles with Midwest Dairy and Midwest Milk — while co-building Redhead Creamery with his wife Elise as a value-added model for family farm sustainability.

Emily Yeiser Stepp — Senior Director of Industry Affairs, Fairlife. Helped establish the Center for Dairy Excellence Foundation, trained 400+ evaluators through the National Dairy FARM Program, and managed an on-farm social responsibility program covering 99% of U.S. fluid milk supply, 150+ co-ops and processors, and 26,000+ farms.

Guest of Honor: Bob Hagenow

The 84th Guest of Honor in Shrine history is Bob Hagenow, sales manager at Vita Plus Corporation, where he’s clocked 39 years. Dairy knows Bob from somewhere else entirely — the colored shavings at World Dairy Expo, where he’s served as ringmaster for the Holstein and Brown Swiss shows and as secretary-treasurer on the WDE board of directors, keeping Expo on solid financial footing.

Bob Hagenow’s firm handshake reaches your soul, reflecting his 40-year commitment to transforming the dairy industry. From the show ring to the boardroom, Bob’s servant leadership and genuine passion for helping others succeed have made him a trusted voice and mentor, shaping the future of dairy one connection at a time. (Read more: Bob Hagenow: A Legacy Built on a Handshake)

Beyond Expo, he’s board president of the Wisconsin 4-H Dairy Fund, coaches county 4-H judging teams, announces state youth shows including Wisconsin State Fair, serves as off-campus advisor to UW–Madison’s Badger Dairy Club, and mentors University of Minnesota students. As Opperman put it, nobody’s ever seen Bob on a bad day — and if he had one, he’d smile through it.

Save the Date: 2026 Awards Banquet

All 2026 honorees will be recognized at the National Dairy Shrine Annual Awards Banquet on Monday, September 28, 2026, at the Alliant Energy Center Exhibition Hall in Madison, Wisconsin — kicking off World Dairy Expo week.

Capacity is roughly 320 seats, and the 2025 banquet sold out a couple of weeks early. Tickets open July 1 via dairyshrine.org/banquet/. World Dairy Expo itself runs September 29 through October 2, 2026, at the Alliant Energy Center. Winners are permanently installed in the Hall of Fame at the Shrine’s Fort Atkinson museum, with accompanying video interviews.

Also on deck from the Shrine: scholarship winners from a record 207 applications will be announced over the coming weeks, and the May 13 webinar at noon Central tackles “Maximizing Internships in Dairy and Agriculture Careers” with panelists from Midwest Dairy, Oklahoma State, Holstein Association USA, and Cargill.

Your Genetics Rep Has Bad News – But Won’t Tell You Until January — Secure your genetics contracts before an impending $12,000 annual price hike hits your operation. The latest financial data follows the money on the Select Sires combination, exposing why replacement costs are surging and how to strategically defend your margins.

David vs. Goliath: Strategies for Small Dairy Farmers to Challenge Large Processors — Margin protection requires outsmarting the massive processors currently strangling farms with 1-3% profits. Our team dismantles the rigged dairy pricing system and delivers a proven value-added blueprint—inspired by today’s emerging leaders—to help you drastically increase per-cwt revenue.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

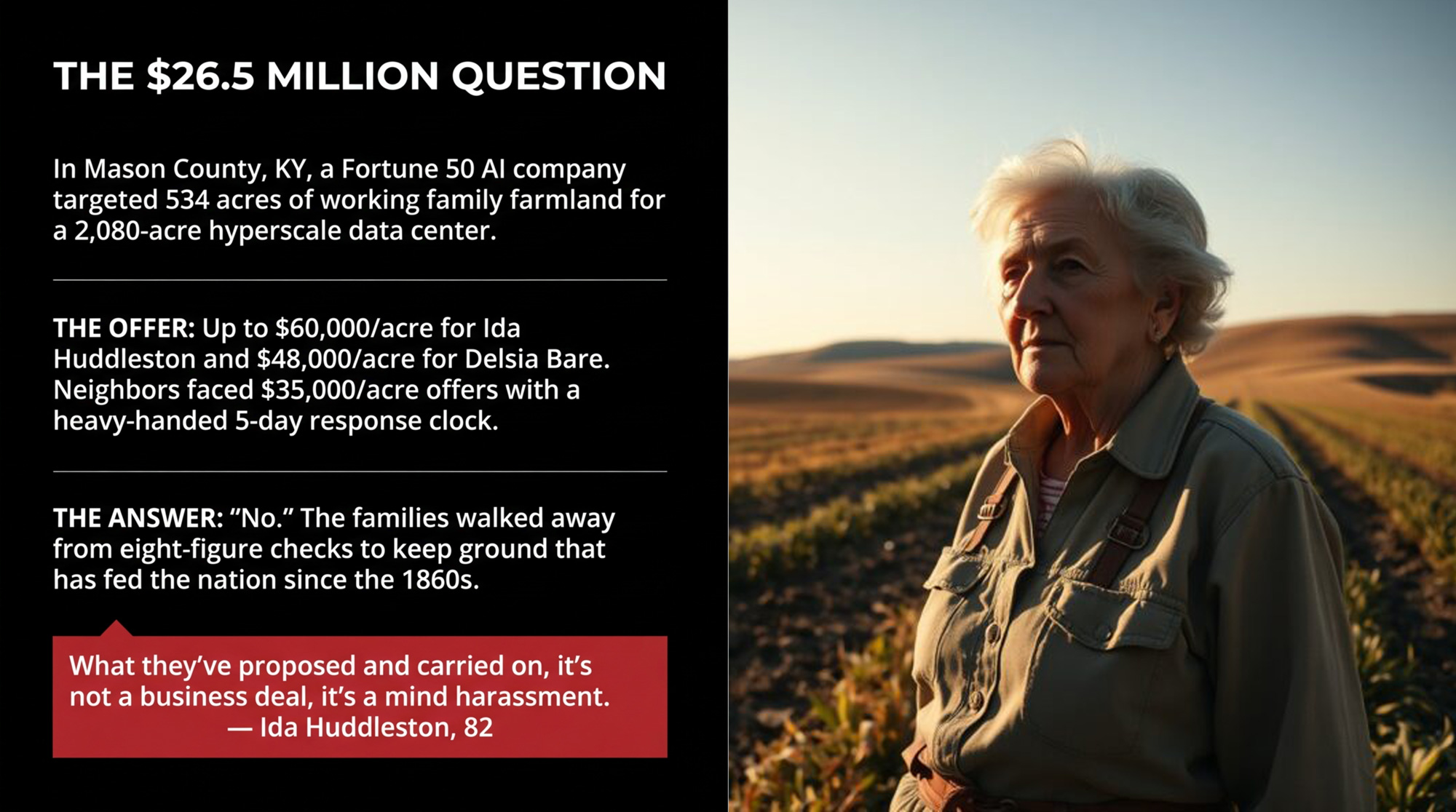

In Mason County, up to $60,000 an acre was on the table for working farmland — and at least four families still walked away, forcing every serious producer in a growth corridor to ask what their own ground is really worth.

Ida Huddleston is 82 and owns 71 acres of farmland outside Maysville, Kentucky. Her daughter, Delsia Bare, holds another 463 acres nearby. Together, according to local coverage, the family operates roughly 1,200 acres of ground that has supported them since the 1860s— through wheat in the Depression and working farmland still today.

Last year, a group representing an unnamed Fortune 100 company — described as Fortune 50 in more recent reporting — came looking to buy a big piece of that ridge for an AI data center. WLEX reporting cited by People magazine says the group offered Huddleston $60,000 per acre for her 71 acres and Bare $48,000 per acre for her 463 acres — more than $26 million combined for 534 acres.

“My grandfather and great-grandfather and a whole bunch of family have all lived here for years, paid taxes on it, fed a nation off of it,” Bare told CBS affiliate WKRC. “Even raised wheat through the Depression and kept bread lines up in the United States of America when people didn’t have anything else.”

They said no.

The offers that came with a five-day clock

The Huddleston family’s story hit regional news in mid-March 2026 and went national within days. But the land chase started much earlier — and their neighbors felt the same pressure.

Down the road, cattleman Dr. Timothy Grosser and his son Andy raise cattle on their place along KY 3056. In March 2025, a group representing the same data-center development offered them $35,000 per acre, according to LEX18 — nearly $8 million for their farm.

“They stressed that time was of the essence and they wanted responses really fast, like within the next five days,” Andy told LEX18. Despite the money and the rush, he was blunt: “We do not want to sell. The farm is my dad’s, and it means everything to him.”

Local 12’s segment on the Grossers emphasized the same theme: that kind of money “can buy a lot,” one line went, but Dr. Grosser made it clear it couldn’t buy what the place means to him.

Local 12 also reported in late March 2026 that the company’s representatives now have contracts “ready to go” on 28 properties as part of the proposed data-center complex. The company itself hasn’t been publicly identified “because of nondisclosure agreements,” the station said.

So you’ve got a Fortune 50–caliber tech client that no one is allowed to name yet, dozens of farms under contract, and a handful of families — like the Huddlestons and the Grossers — who’ve decided they won’t cash out, even at numbers that would make most advisors choke on their coffee.

“It’s not a business deal, it’s mind harassment.”

Huddleston didn’t sugarcoat how the process felt. In an interview with NBC affiliate WLEX, she described months of pressure in plain language: “What they’ve proposed and carried on, it’s not a business deal, it’s a mind harassment.”

She also told WKRC she doubted the data center would deliver the kind of jobs and growth its boosters promised. “It’s a scam,” she said in that interview, according to TechCrunch and WKRC’s original report. These are Huddleston’s characterizations of the proposals she received, reflecting her experience as a landowner who’s been repeatedly approached. The Bullvine hasn’t independently investigated the company’s economic claims, and the company itself hasn’t been publicly identified.

Bare talked less about the meetings and more about what the land means. “There’s nothing that can destroy me if I’ve got this land,” she told WKRC.

Huddleston has been just as blunt about how she thinks farmers are being treated in the process. “They call us old stupid farmers, you know, but we’re not,” she told WKRC in a separate segment. “We know whenever our food is disappearing, our lands are disappearing, and we don’t have any water — and that poison. Well, we know we’ve had it.”

Whatever you make of their language, there’s no question they’re speaking from long experience, not from a tweet. When a family that fed people through the Depression and kept bread on other tables says the money doesn’t move them, that hits differently than a talking point in a planning meeting.

The 2,080-acre plan: what’s actually coming to Mason County?

On the power side, the outlines are more concrete than the company name. East Kentucky Power Cooperative owns the Spurlock Station power plant in Mason County, a four-unit coal facility capable of generating about 1,608 megawatts— a little over 40 percent of EKPC’s total capacity. Planning documents from regional grid operator PJM show EKPC studying new transmission and substation options near Maysville, including a new Mason County substation tied into a 345-kV line to serve a potential large industrial load.

In a March 19, 2026 opinion piece in Kentucky Living and Building Kentucky, EKPC president and CEO Don Mosierwrote that the co-op has been in talks “for more than a year” with a Fortune 100 company evaluating a data-center site near Maysville and Spurlock Station. Mosier said any such customer would be responsible for paying the costs of required transmission upgrades under EKPC’s tariff.

At a special meeting at Maysville Community and Technical College, attorney Tanner Nichols of FBT Gibbons outlined a plan for a six-building “hyperscale” data-center complex on more than 2,080 acres, with about 2,000 construction jobs and 400 permanent positions, at a cost of more than 5 million — costs he told the commission the company would cover 100 percent. Coverage from WEKU described the company as a “Fortune 50 tech firm,” while WCPO summarized it as “Fortune 500” in a separate report from the same hearing. For consistency, this article follows WEKU’s “Fortune 50” phrasing and flags the discrepancy for readers.

Opponents, including We Are Mason County treasurer Janet Garrison, argue the permanent job number could be far lower. “We are not anti–data center or anti–progress at all,” she told Realtor.com. “But we want this thing to go in an industrial park. They want farmland, and that’s just not a very efficient use of 2,000 acres when they might only hire 50 people.”

Attorney Hank Graddy, representing residents, pressed Nichols on why the public had to address questions to an attorney for the industrial development authority and not directly to the company itself. A grassroots citizens’ group called We Are Mason County filed suit on March 27 against the Mason County Fiscal Court and Planning Commission, arguing the rezoning that enables the data center violates the county’s comprehensive plan and that “zoning without planning is illegal.”

For any dairy or mixed-livestock producer, this isn’t just a tech story in Kentucky. It’s about whether land that grows your forages — or your neighbor’s corn silage and hay — ends up under barns and pivots, or server halls and parking lots. When 534 acres of mostly working ground disappear into an industrial site, you’re not just losing asset value. You’re punching a hole in the local forage base that might be impossible to patch later.

What Does $26 Million Buy That 534 Acres of Kentucky Farmland Can’t?

Here’s where the barn-math gets real, and it starts with the fact that the offers were not one flat number.

Based on WLEX reporting cited by People magazine:

Huddleston’s 71 acres at $60,000/acre ≈ , $4,260,000.

Bare’s 463 acres at $48,000/acre ≈ , $22,224,000.

Together, those two offers total roughly $26.5 million for 534 acres.

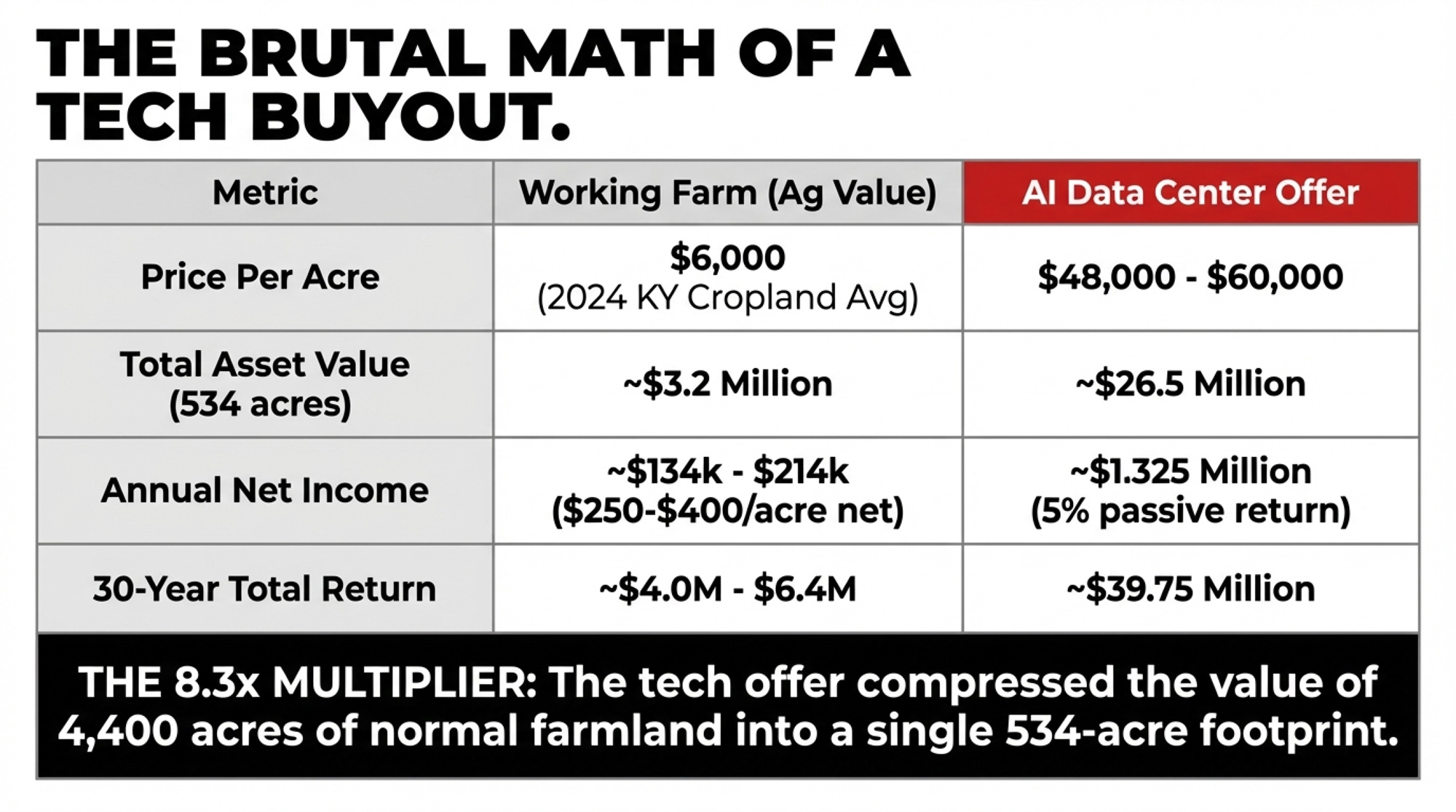

Now, stack that against what farmland is usually worth. USDA’s 2024 Land Values Summary puts average U.S. farm real estate at $4,170 per acre, with cropland at about $5,570 and pasture at $1,830. Kentucky-specific data puts average farm real estate around $5,300/acre and cropland near $6,220/acre. Bare herself told WKRC that land in Mason County is valued at “about $6,000 an acre,” and that the offer she received was roughly ten times that amount.

If you use a ballpark $6,000 per acre as a benchmark for good Kentucky cropland — consistent with both USDA data and Bare’s own description of local values — the math looks like this:

At that ag value, 534 acres ≈ $3.2 million.

The AI offer of ≈ $26.5 million is roughly 8.3× that number.

Or, said differently: the company compressed the land value of more than 4,400 acres of average U.S. farmland into one family’s 534-acre footprint.

Now switch from asset values to income, because that’s the part you live on.

If the family took the .5M and invested it at a conservative 5% annual return, that portfolio could throw off about .325 million a year before tax. No drought risk. No $4 diesel. No 4 a.m. milking unless somebody wants to get up anyway.

There’s no single “standard” net-income-per-acre figure for Kentucky, but extension budgets and Census-level data suggest a lot of mixed grain/forage acres end up in the low hundreds after expenses in an average year. To keep this useful, not hypothetical, treat $150–$400 per acre as a rough net range you can swap your own numbers into.

At $250 net/acre, 534 acres × $250 = $133,500/year net farm income.

At $400 net/acre, 534 acres × $400 = $213,600/year.

Compare that to the $1.325M passive return. You’re talking about turning down something like six to ten times your likely annual net, every single year, for as long as you’d hold the investments.

Over 30 years, without even compounding that 5%, the simple math is:

Passive: $1.325M × 30 = $39.75M.

Farm net: $133,500–$213,600 × 30 = $4.0–$6.4M.

Here it is side-by-side:

Ag Value vs. AI Tech Offer (Huddleston–Bare, 534 Acres)

Metric

Working Farm (Ag Value)

AI Data Center Offer

Price Per Acre

$6,000 (ballpark benchmark, in 2024 KY cropland range)

$48,000–$60,000 (Bare at $48k, Huddleston at $60k)

Total Asset Value (534 acres)

~$3.2 million

~$26.5 million

Annual Income

~$134k–$214k (net farm income at $250–$400/acre, illustrative)

~$1.325 million (5% return on $26.5M)

30-Year Total (no compounding)

~$4.0–$6.4 million

~$39.75 million

The Multiplier

1×

~8.3× (offer vs. farm-use value)

On a yellow pad, that looks like a once-in-a-lifetime chance to cash out, erase debt, fund retirement, and maybe even restart somewhere cheaper if you wanted to. For a lot of operations, it would be.

But you’d also be permanently trading control over this dirt — this ridge, these fence lines, that water — for a brokerage balance somewhere else.

If you’ve just poured serious money into new barns, parlors, robots, or a creamery, that math gets even more brutal. High per-acre offers can blow up the amortization schedule you built for that infrastructure. Suddenly, you’re wondering whether to walk away from a system that hasn’t had time to earn its keep, just because the ground underneath it is now worth more to servers than to cows.

From what Bare and Huddleston have told reporters, keeping their family’s ground in production still matters more to them than what any spreadsheet says those acres could generate in passive income. You don’t have to land on the same answer. But you do need to know what your own numbers say before a truck pulls into your lane.

Is Your Estate Plan Ready for a $60,000-Per-Acre Offer You Didn’t Ask For?

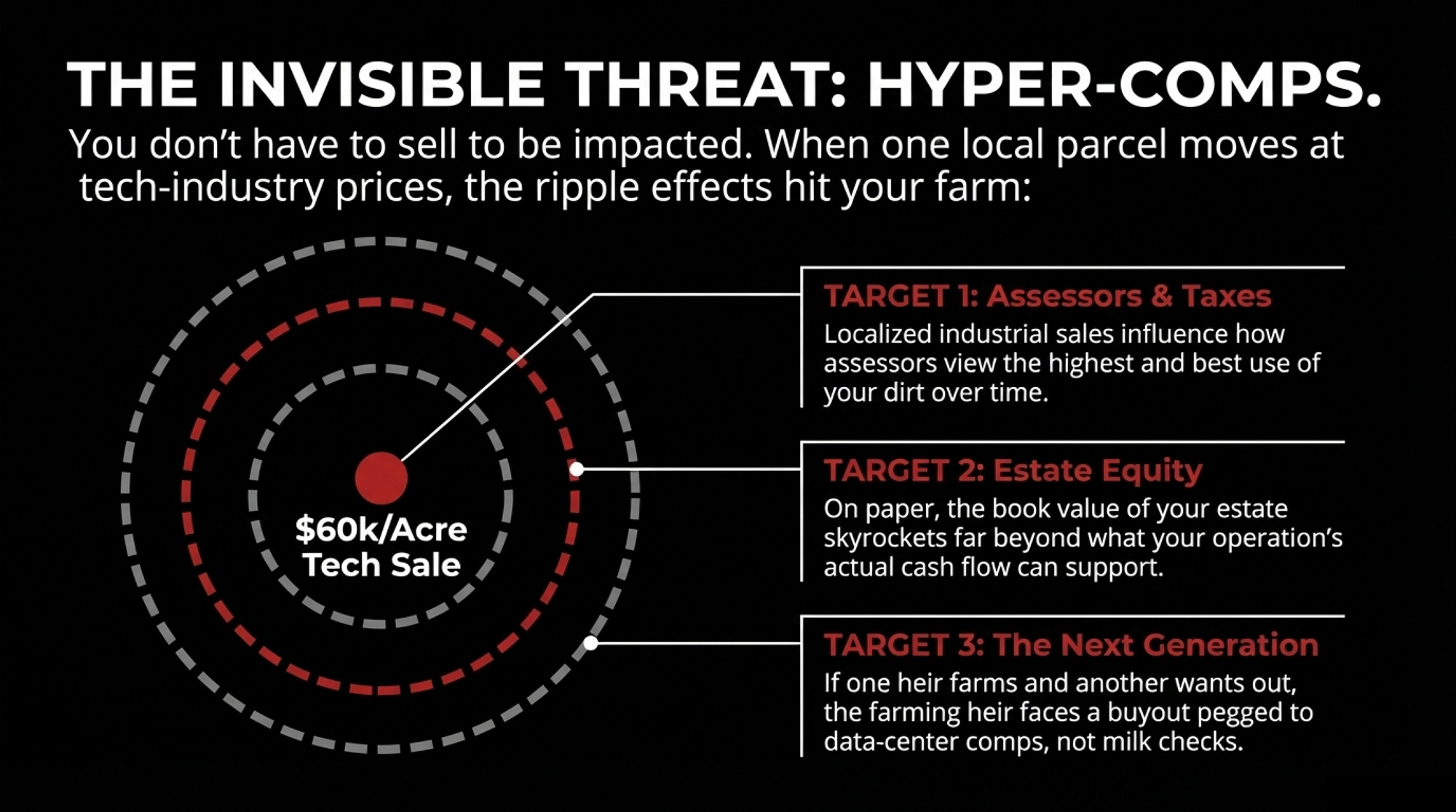

Most farm estate plans quietly assume your land will be valued somewhere near its agricultural use value. They weren’t built for a world where one project takes land from $6,000/acre to $48,000–$60,000/acre a couple of miles away.

Kentucky has an agricultural use-value system for property tax, where cropland assessments are based on capitalized rental income and typically work out to a few hundred dollars per acre, not full market value. That helps keep annual tax bills in line with what the ground earns. It doesn’t stop eye-popping industrial sales from influencing how your lender, your non-farming heirs, or a future buyer thinks about what the place is “worth.”

Even with use-value on the tax rolls, assessors and boards still see those comps, and over time that can change how they think about “updating” values.

On paper, the book value of your estate can jump far beyond what your operation’s cash flow supports.

If only one heir wants to farm and the others want a buyout, that farming heir could be staring at buyout numbers pegged to data-center comps, even though the ground still only earns like farmland.

When families like the Huddlestons and the Grossers refuse these offers, the ripple goes beyond their own payouts — it also shapes whether their kids or grandkids inherit land that’s still valued as farmland, or land priced at data-center comps that could force a sale on someone else’s terms.

The result, whether they’d frame it this way or not, is that they’re preserving a future where farming stays on the table for the next generation — even though it means walking away from a number that would solve a lot of short-term problems.

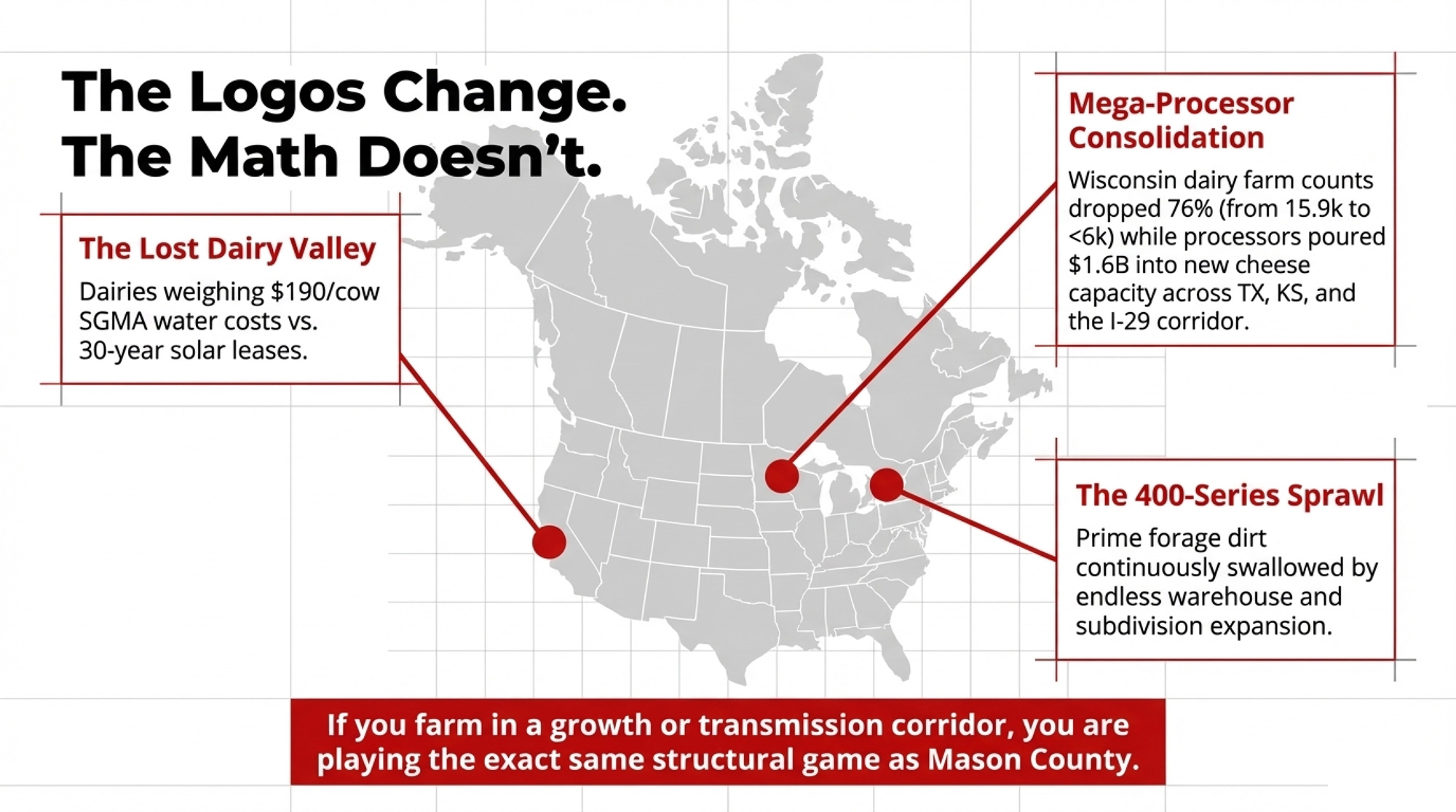

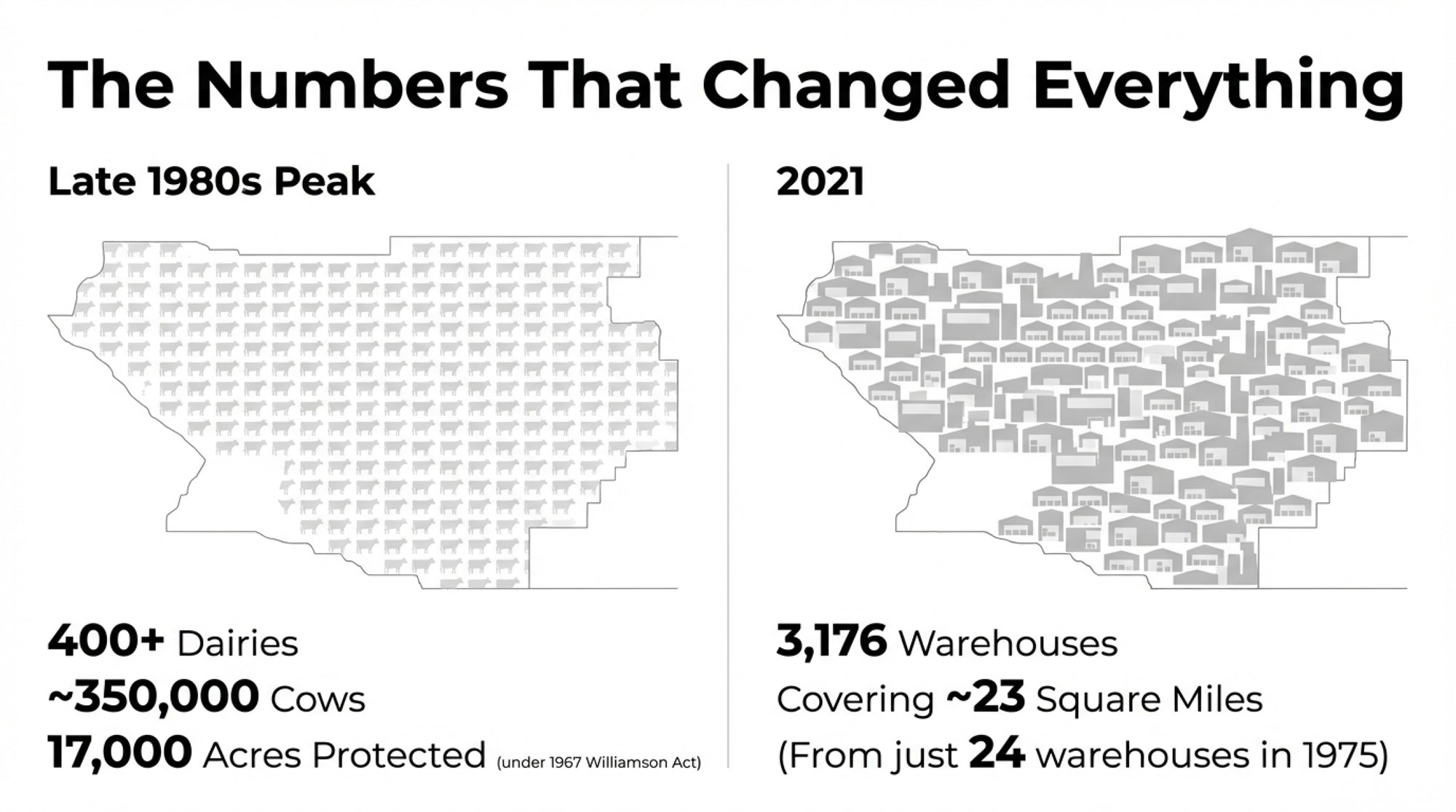

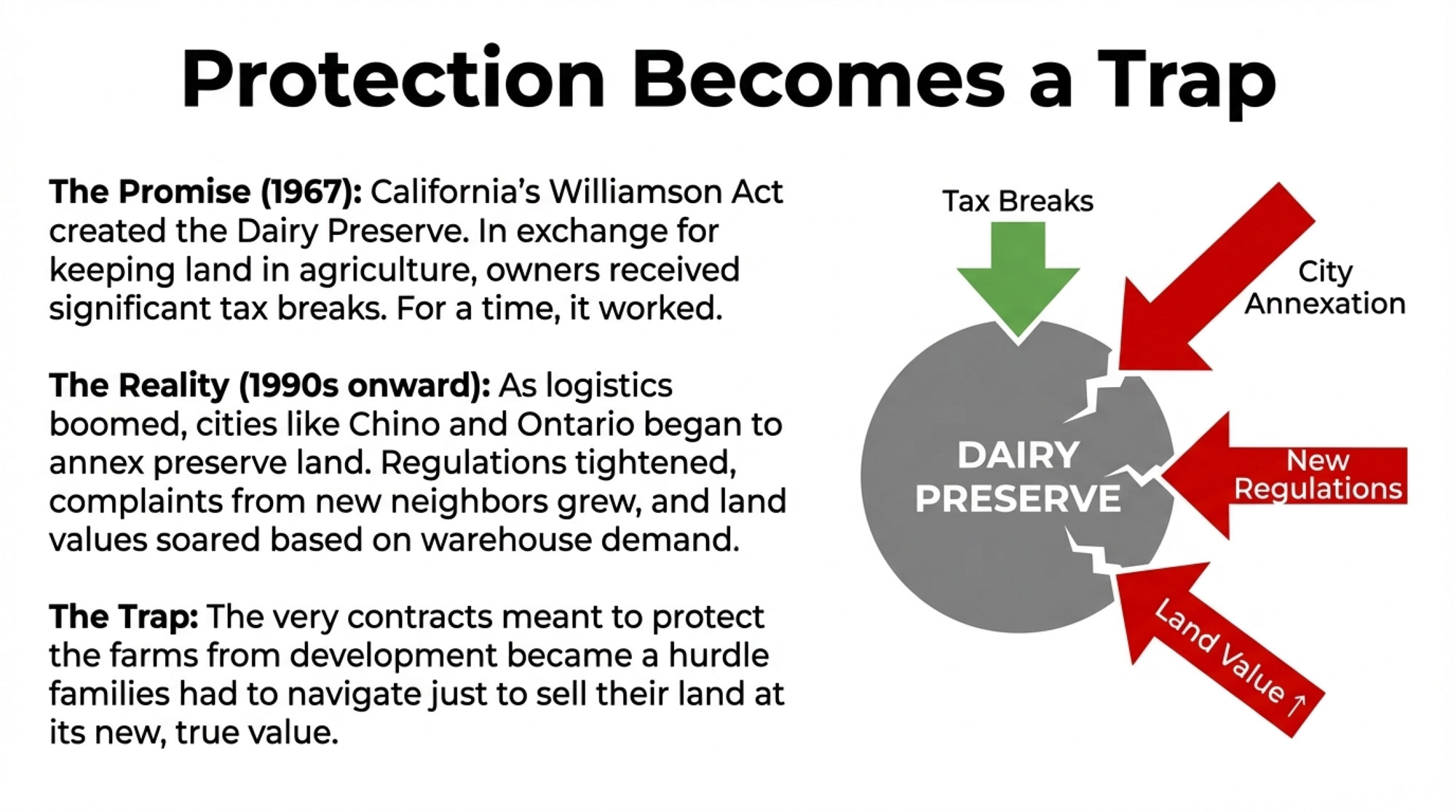

If you’ve got land in any kind of growth or transmission corridor — the I‑29 and I‑35 corridors, California’s Tulare and Kings counties, the Snake River plain, the I‑5/99 belt, or the outer rings of major Canadian cities — you’re in the same structural game. The names and logos change. The math doesn’t.

In California, dairies in what some now call the “Lost Dairy Valley” have already had to weigh roughly 0‑per‑cowSGMA water costs against 30‑year solar leases — and some concluded the land was worth more as someone else’s energy platform than as their own forage base.

In Wisconsin and the Upper Midwest, processors like Hilmar, Leprino, and Valley Queen have committed about $1.6 billion in new cheese capacity across Texas, Kansas, and the I‑29 corridor since 2020, according to prior Bullvine analysis and company announcements. Over the same stretch, Wisconsin’s dairy farm count fell from more than 15,900operations to fewer than 6,000, a drop of roughly 76% driven by consolidation, labor, and processing pull.

If you’re milking in the northern edge of the GTA — places like Vaughan, Caledon, or Bradford — you’ve watched good dirt along the 400‑series corridors disappear under warehouses and subdivisions. You don’t need an AI logo to know how fast the math can flip under your boots.

The Kentucky story adds AI data centers to that list. The real question isn’t “Would I sell?” It’s “Have we done enough math and paperwork that, if an offer comes, our answer doesn’t blow up the family?”

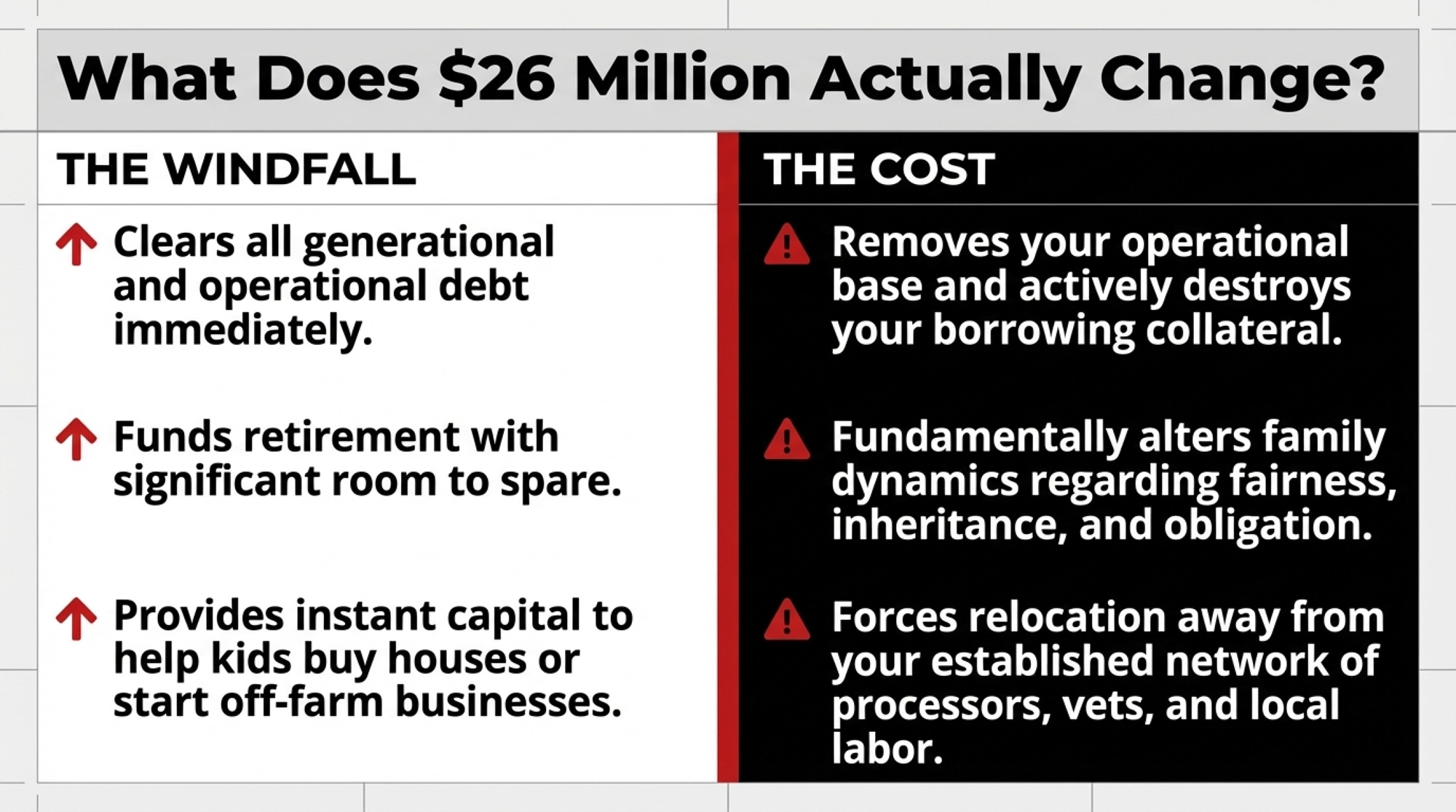

What Does $26 Million Really Change for Your Operation?

At one level, it’s obvious. A check in the eight figures:

Clears debt.

Funds retirement with room to spare.

Lets you help kids buy houses, go to school, or start their own businesses.

But it also:

Removes your operating base and, in many cases, your collateral.

Changes how your family thinks about fairness, inheritance, and obligation.

Might take you away from a region where your network, processors, and help are.

That’s why the barn-math in the last section matters. If your place looks anything like the Huddleston/Bare situation, an AI-style offer doesn’t just tilt the scales. It flips them.

The harder part is deciding whether you want to live in the world on the other side of that decision — and whether your current estate plan gives the next generation any chance to answer that question on their own terms.

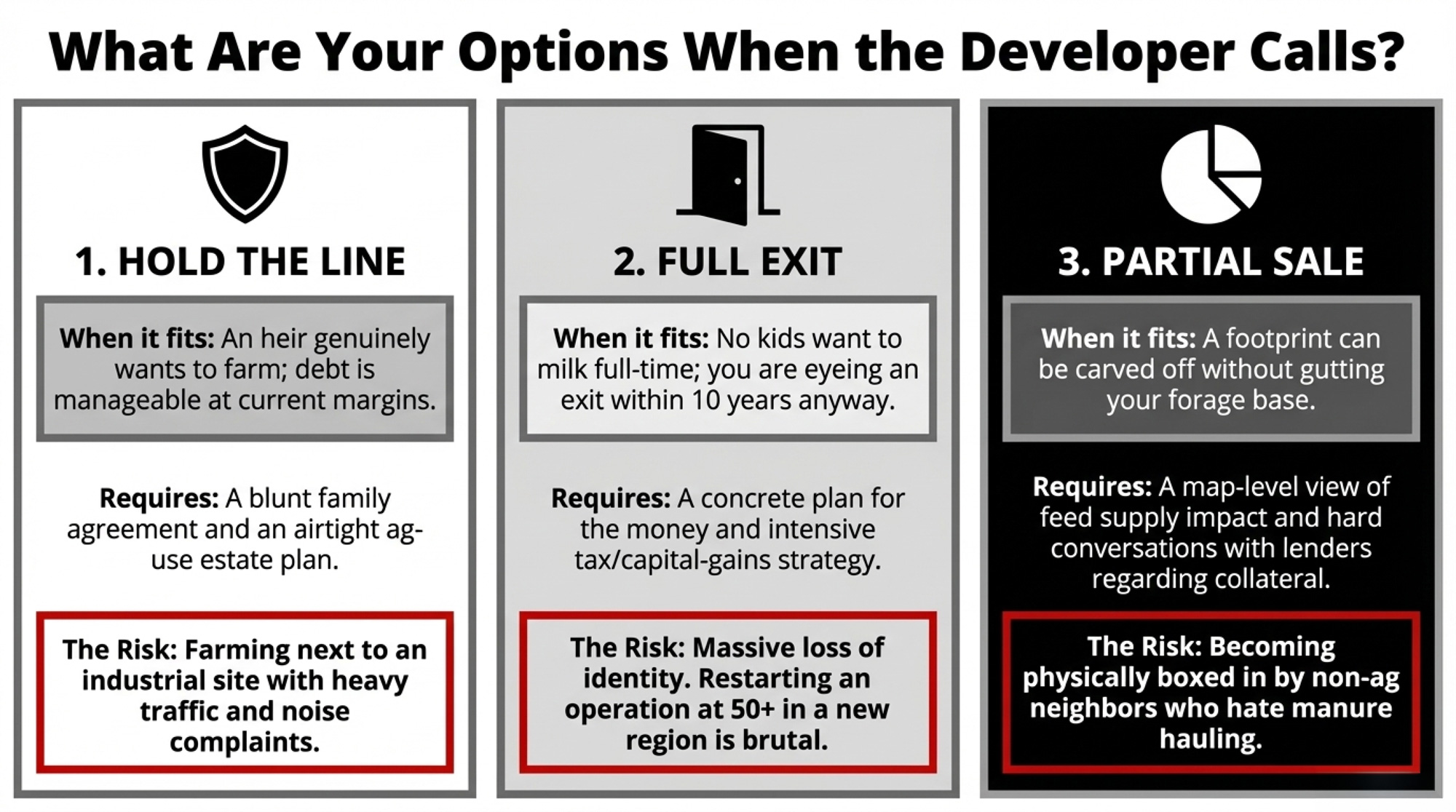

What Are Your Real Options If a Developer Shows Up?

You don’t get to pick whether a data center, warehouse, or solar farm wants your neighborhood. You do get to decide how prepared you are when their rep calls. Practically, you’ve got three real paths.

Decision Path

Best Fit For

Key Requirement

Financial Signal

Biggest Risk

Hold — Keep Producing

At least one heir wants to farm; manageable debt load

Written family agreement + updated estate plan using ag-use valuation

Farm net: ~4k–4k/yr on 534 ac

Creeping tax pressure as industrial comps arrive nearby

Full Exit — Cash Out

No farming heirs; already near a planned exit window

Concrete reinvestment plan + tax/legal advice before signing

Passive: ~.325M/yr at 5% on .5M

Loss of operating identity; starting over in a new region at 50+

Map-level analysis of feed, manure, expansion impact + lender review

Hybrid: debt cleared + partial passive income stream

Boxed in between non-ag neighbours; manure/silage haul complaints

Do Nothing / Ignore

—

—

—

Hands all decisions to someone else, usually on a bad day

1. Hold the line and keep producing

When it makes sense:

At least one heir genuinely wants to farm.

Your debt is manageable at current margins.

No per‑acre number anyone can write feels worth trading away the place.

What it requires:

A blunt family meeting where everyone agrees that below a certain number, you’re staying, and understands what that means for future buyouts, lifestyle, and retirement timing.

An estate plan that uses current‑use or ag‑use valuation tools where they exist and doesn’t leave heirs scrambling if nearby land sells high.

Risks and limits:

Property taxes and political pressure can still creep up as industrial projects arrive in the county.

You may end up farming next to an industrial site with heavier traffic and neighbors who don’t share farm‑country expectations about noise, manure, or late‑night lights.

2. Take a full exit and restart on your own terms

When it makes sense:

None of your kids or key family members want to milk or farm full‑time.

Your own numbers already have you eyeing an exit in the next decade.

The offer clearly exceeds what you’d reasonably earn from operating another 20–30 years on the same acres.

What it requires:

A concrete plan for where the money goes — debt settlement, retirement, a smaller place, off‑farm business, investments — not just “we’ll figure it out.”

Tax and legal advice before signing; long‑held land comes with capital‑gains and estate questions you don’t want to discover after closing.

Risks and limits:

Once you sell, you’re not a producer anymore. For people who built their identity around the farm, that’s a bigger shock than any interest‑rate change.

Moving to cheaper land in a new region means new markets, weather, rules, and community. Starting over at 50+ isn’t simple.

3. Partial sale or conversion — keep farming on fewer acres

When it makes sense:

The proposed site can be carved off one side without gutting your forage base or your core facilities.

The proceeds can fund debt retirement, facility modernization, or the purchase of replacement ground that has better cash flows.

What it requires:

A map‑level view of how losing those acres affects feed supply, manure management, and any long‑term expansion you were planning.

Hard conversations with your lender about how they view a farm that’s now part dirt, part liquid assets, and what that does to covenants and collateral.

Risks and limits:

You could end up boxed in between non‑ag neighbors and an industrial load, where hauling manure or silage turns into complaint calls to the county.

Replacement land that’s further out adds trucking time, fuel, and weather risk into a system that might already be running tight.

Not picking a path — not looking at fair‑market and ag‑use values, not updating your estate plan, not talking to your heirs — is still a choice. It just hands the toughest decisions to somebody else, usually on a bad day.

As you watch your own area, pay attention to forward‑looking signals:

New transmission lines or substation plans are hitting county maps.

Utility filings talking about a “large industrial load” or “data center.”

Land signs on neighboring farms with unfamiliar LLC names instead of local families or operations.

Each one is someone else already doing the math on your neighborhood.

Options and Trade-Offs for Farmers

Do this within 30 days.

Pull your county’s planning and zoning agendas, plus your power co‑op or utility filings. Search specifically for “data center,” “technology park,” or “solar” within about 10 miles of your home.

Call your accountant or estate attorney and ask one simple question: “If land around me sold for $50,000 an acre next year, what would that do to my taxes and my estate plan?”

Within 90 days

Get both a fair‑market appraisal and an agricultural‑use appraisal on your ground. The gap between those two numbers is the same pressure the Huddlestons and the Grossers are staring at — and you need that gap on paper.

Sit down with your advisor and update your estate documents so they match today’s land reality, not the values you were carrying 15 years ago.

Within 365 days

If you’re in any growth or transmission corridor, put a written family agreement in place about if, when, and at what per‑acre number you’d even consider a non‑ag sale. It doesn’t lock anyone in. It just keeps your kids from having their first real conversation about it at the lawyer’s office.

Key Takeaways

If any serious offer on your land comes in at several times recent farm‑land sales in your county, treat it as a strategic decision that affects your heirs — not a side conversation — and run the barn‑math both ways before you say a word.

If you’ve got more than one heir and only one wants to farm, assume high‑value industrial comps will make future buyouts far more expensive, and bake that into your estate plan now with written agreements — not just good intentions.

If you decide you’ll “never sell,” back that conviction with paperwork: a current appraisal, a use‑value tax strategy where available, and an updated will or trust so your kids aren’t trying to manage big‑number assessments on a farm‑income business model.

If you’re already seeing power‑line upgrades, rezoning, or new tech projects within 10 miles, treat that as your 30‑day clock to check local filings, talk to your advisor, and start a family conversation — before someone else writes a number on your kitchen table for you.

The Bottom Line

Based on what Bare and Huddleston have told reporters, their answer, for now, is simple: land’s real value sits in what it grows and what it means, not just what someone’s willing to pay to pave it. They’ve chosen to keep producing food on Kentucky soil instead of trading their ridge for eight‑figure passive income backed by server halls and cooling ponds.

You don’t have to make the same call. But you should know your own numbers well enough that if a Fortune 50 company offered you eight times your current land value tomorrow, you wouldn’t be trying to do 30‑year math in a 30‑minute meeting. If you want the deeper economics — the full SGMA water‑vs‑solar math in California or the structural Dairy Curve that’s shrinking U.S. operations toward 10,000 by 2035 — dive into our Tier 2 and Tier 3 follow‑ups and make sure you’re getting the Bullvine Weekly so those playbooks land in your inbox, not just your feed.

Then ask one more question at your own kitchen table: what’s the real “make‑me‑move” number for your home farm — and have you actually told your heirs, or are you leaving them to guess when the offer shows up?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

When Land Is Worth More Than Milk in California’s Lost Dairy Valley – Navigate land-value wake-up calls with a kitchen-table framework used by families who watched 17,000 acres vanish into logistics. This case study delivers the courage to protect your legacy, whether in the barn or elsewhere.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Your plant may be modeling a $100K recall risk. The real odds point to $800K — and roughly $2,000 per cow quietly baked into your milk check.

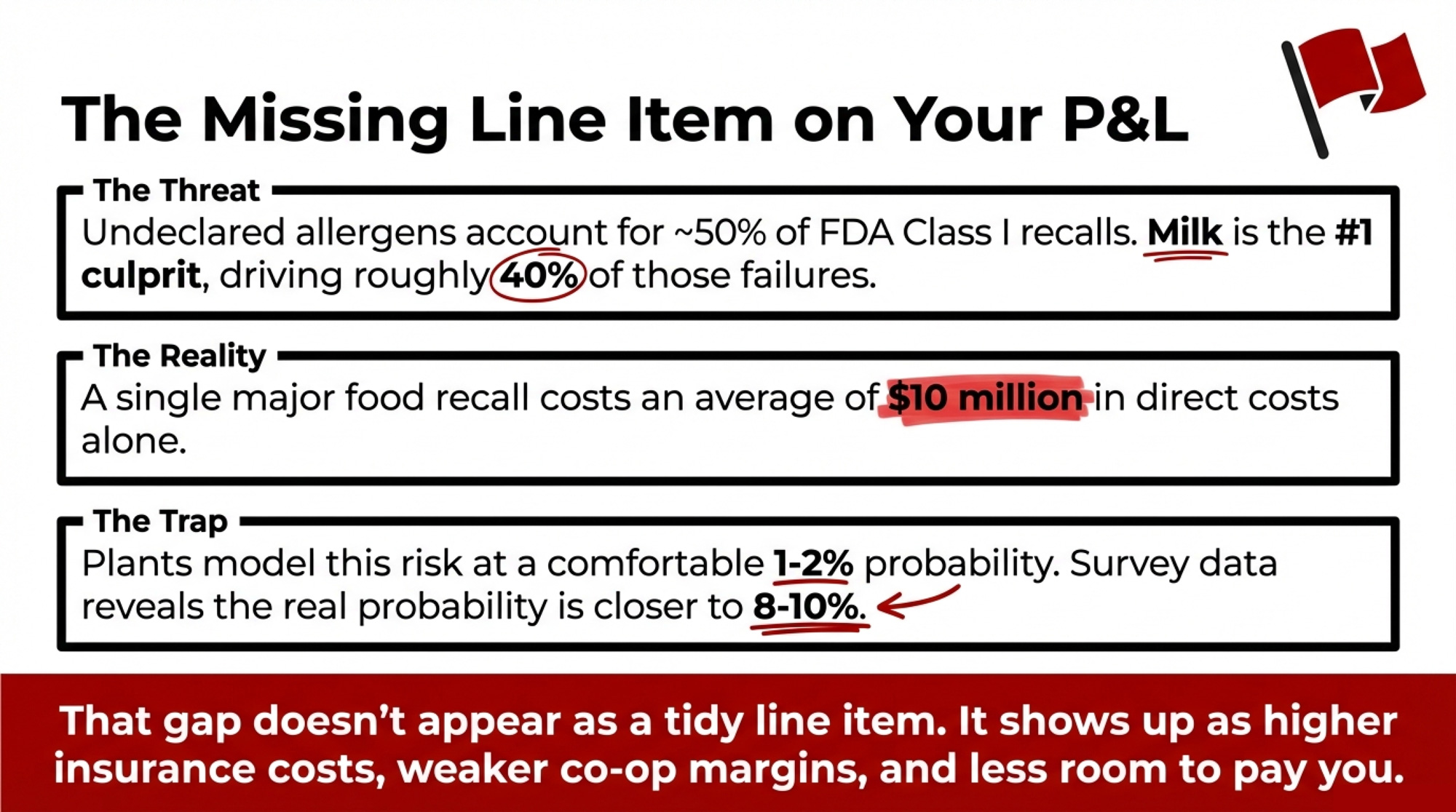

Executive Summary: Dairy’s allergen recall problem isn’t just a QA issue — it’s an invisible $2,000‑per‑cow risk that can end up baked into your milk check. Industry data puts the average direct cost of a food recall near $10 million, and undeclared allergens now account for almost half or more of FDA Class I recalls, with milk the single most commonly undeclared allergen. Many plants still model recall probability at 1–2%, but survey‑based numbers point closer to 8–10%, turning what looks like a $100,000 exposure into an $800,000 hit on a single high‑mix line supplied by about 400 cows. That gap doesn’t appear as a tidy line item; it shows up as higher insurance costs, weaker co‑op margins, and less room to pay you on components or volume. The story follows Ontario processor Mark Leduc and co‑op director Janet as they confront this math, run a targeted cleaning‑validation pilot on one yogurt line, and use real near‑miss data to renegotiate with insurers, customers, and their own board. You finish with a 30/90/365‑day playbook and specific questions to ask your plant and co‑op — from “What recall probability are we actually modeling?” to “Who pays if an in‑plant allergen failure triggers a $10 million recall?”

On paper, Mark’s 500‑cow supply base looks solid heading into 2026. Volumes are steady, co‑op contracts are locked, and the private‑label yogurt and ice cream runs are full. The allergen recall risk sits off to the side — until it doesn’t.

The $250 vs. $2,000 Per Cow Recall Gap

Before you get lost in SOPs and swab types, it helps to see the recall gap at a glance. This is the difference between the old “1–2% recall” rule of thumb and what more recent recall and survey data actually suggest for complex, multi‑allergen plants.

Industry and trade‑group analyses built on work from the Grocery Manufacturers Association and Food Marketing Institute often peg the average direct cost of a food recall around $10 million per event. At the same time, one published survey of food businesses with allergen plans reported that, while almost all respondents said they had a plan, roughly two in five still had at least one allergen‑related recall in five years. That works out closer to a high single‑digit annual probability than a comfortable 1–2%.

Here’s what that means for a 400‑cow supply block feeding a single high‑risk line:

Scenario

Annual Recall Probability

Average Recall Cost

Expected Annual Loss

Cost Per Cow (400-cow block)

Who’s Paying the Gap

“Rule of Thumb” (Plant Model)

1–2%

$10,000,000

$100,000–$200,000

$250–$500

Insurance premiums (manageable)

Survey Reality (Multi-Allergen Plants)

8–10%

$10,000,000

$800,000–$1,000,000

$2,000–$2,500

Your milk check

The Gap

6–8 percentage points

—

$600,000–$800,000

$1,500–$2,000

Underwritten by co-op members

Those numbers are simple math:

At 1% recall probability, expected annual cost = 0.01 × $10M = $100,000 → $250 per cow across 400 cows.

At 8% recall probability, expected annual cost = 0.08 × $10M = $800,000 → $2,000 per cow across the same 400 cows.

The plant’s profit‑and‑loss statement doesn’t show “,000 per cow allergen risk.” It shows higher insurance premiums, occasional big hits when things go wrong, and thinner margins for the co‑op and its members. If your co‑op owns or supplies that plant, you’re underwriting the difference, whether anyone has written it down or not.

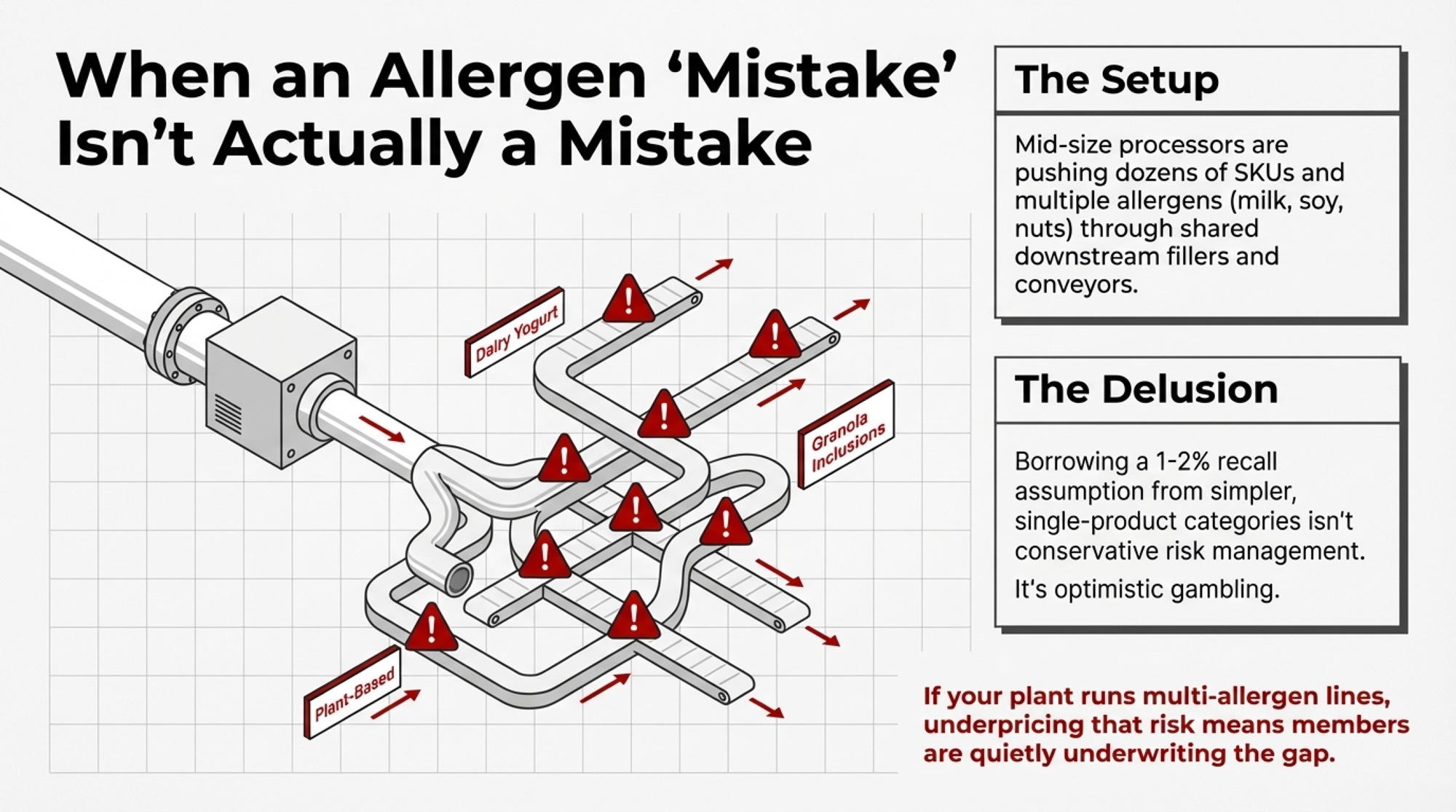

When the Dairy Allergen “Mistake” Isn’t Really a Mistake

Mark did what a lot of mid‑size processors have done over the past decade: he tried to push more SKUs through the same stainless. His highest‑risk yogurt line has all the classic features:

Dozens of SKUs — plain, fruit‑on‑the‑bottom, granola‑topped, high‑protein, kids’ flavors.

Multiple allergens — milk, soy from inclusions, sometimes nuts.

Shared downstream equipment — fillers, conveyors, packaging, and labels touching everything from whole‑milk Greek to “plant‑based” cups.

On the QA whiteboard, the plan looks fine: visual checks, routine cleaning, periodic swabs. On the risk model, the assumption is simple: if the chance of a major allergen recall is 1–2% per year and the average direct cost is about million, the expected annual hit is 0,000–0,000 — uncomfortable but “manageable” with insurance and standard controls.

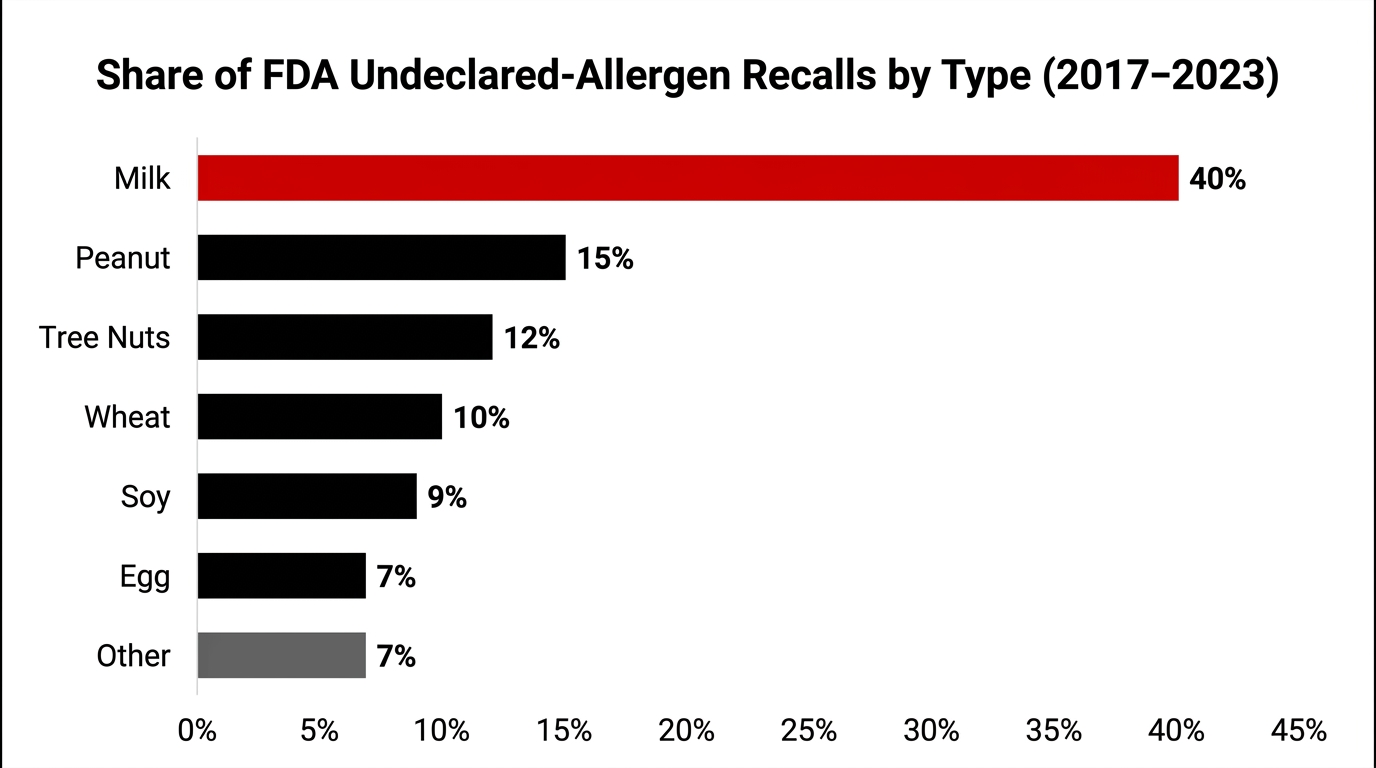

The reality is harsher. Undeclared allergens have become the leading cause of U.S. food recalls. One Trustwell analysis found that undeclared allergens accounted for 47% of all FDA Class I recalls in 2022 and 63% from January to August 2023. A 2024 review of U.S. recall patterns reported that undeclared allergens helped push total recall counts to a post‑pandemic high, with losses in the billions once direct and indirect costs are included.

Milk is at the center of that. An analysis of more than 620 FDA undeclared‑allergen recalls since 2017 found that around 40% were due to undeclared milk, making milk the single most commonly undeclared allergen.

So if your plant is built on milk and runs multi‑allergen, high‑mix lines, borrowing a 1–2% recall assumption from simpler categories isn’t conservative. It’s optimistic. And in a co‑op or supply‑based system, underpricing that risk is another way of saying your members are quietly underwriting the gap.

What Does a $10M Allergen Recall Really Mean for 400 Cows?

Mark’s highest‑risk yogurt line pulls milk from a group of farms totaling roughly 400 cows’ worth of production. Think of that as one 400‑cow block whose fortunes are tied to that line’s allergen performance.

From the available data:

The average direct recall costs $10 million per major event.

“Rule‑of‑thumb” recall probability: 1–2% per year.

Survey‑based probability for companies with allergen plans: roughly 8–10% per year over a five‑year window.

Step through the math so you can plug in your own numbers later.

How the $10M Recall Risk Lands on a 400‑Cow Block

Scenario A – Underpriced Risk (1% modeled annual probability)

Over the same 400 cows, that’s $2,000 per cow per year.

Now you’re not talking about a rounding error. You’re talking about a material drain on what that plant can afford to pay for milk, especially when margins are already tight from 2024–26 feed, labor, and energy costs.

The plant’s P&L doesn’t show “$2,000 per cow in allergen recall exposure.” It shows:

Higher recall and contamination insurance premiums.

Occasional large costs when the product is pulled and destroyed.

Less margin left for co‑op dividends, capital projects, and milk premiums.

If you sit on a board, the question isn’t, “Do we have an allergen control plan?” It’s, “Are we modeling recall probability at 1–2% when our own near‑miss data — and broader survey and recall stats — point much higher?”

The Boardroom Questions You Aren’t Asking Yet

Janet sits on the co‑op board and ships from a 350‑cow herd into Mark’s plant. She’s not just looking at somatic cell counts and butterfat anymore. She’s looking at who’s underwriting the plant’s allergen gamble.

The Question

Why It Matters

If You Can’t Answer This…

“Where exactly is the line between farm-origin hazards and plant-origin failures in our contracts?”

Residues at intake ≠ allergen cross-contact after the plant owns the milk. If contracts blur this line, your herd backs plant QA failures.

Your members may be underwriting recall costs they can’t control — and won’t know until the invoice arrives.

“How many allergen near-misses and label errors occurred on our highest-risk lines in the last 12–24 months?”

“We’re fine” isn’t data. Near-miss counts show whether your plant catches problems before they ship — or relies on luck and insurance.

You’re guessing at recall probability, not managing it.

“If there’s a $10M plant-origin allergen recall tomorrow, what indemnity rights do we have against members?”

Plant-side allergen failures can trigger member clawbacks if contracts aren’t clear. Know the split before the lawyer does.

You’ll find out during the recall — when it’s too late to negotiate.

If you’re in her chair — board member, delegate, advisory council — these are three questions that belong on your next agenda:

“Where exactly is the line between farm‑origin hazards and plant‑origin failures in our contracts?” Ask counsel and management to point to the clauses that separate residues or pathogens at intake from allergen cross‑contact and mislabeling that happen after the plant owns the milk. If they can’t show you that line in writing, your members may be underwriting risks they can’t control.

“In the last 12–24 months, how many allergen‑related near‑misses and label errors occurred on our highest‑risk lines — and who would pay if one of those shipped?” “We’re fine” isn’t an answer. You want a count of near‑misses, how they were caught, and how a miss would flow through your recall insurance, the co‑op’s balance sheet, and member returns.

“If there’s a $10 million plant‑origin allergen recall tomorrow, what specific indemnity or clawback rights do we have against members — and does that match our intent?” This isn’t about letting sloppy farms off the hook. It’s about making sure plant‑side allergen failures aren’t being patched with member‑funded indemnity language by default.

Once those questions hit the minutes, allergen control stops being just a QA metric. It becomes a risk‑underwriting decision, which is where it belongs for a co‑op.

Sesame’s Shortcut: When Labels Beat Cleaning

If you want to see how regulators behave when cleaning and labels collide, look at sesame.

The Food Allergy Safety, Treatment, Education, and Research (FASTER) Act made sesame the ninth major U.S. food allergen, with mandatory labeling and allergen‑control requirements taking effect January 1, 2023. After that date:

Allergy advocates and consumer groups documented cases where bakers and restaurants intentionally added sesame to products and updated labels rather than paying for full cleaning between runs.

The FDA said it was concerned about impacts on sesame‑allergic consumers but acknowledged that adding sesame and labeling it doesn’t automatically violate the law, as long as the label is accurate.

The message is uncomfortable: regulators were willing to accept cost‑saving allergen strategies as long as the label stayed accurate, even when those choices hurt allergic consumers. In practice, regulators have focused more on what’s on the label than what’s left on the stainless — at least so far.

If your plant runs “dairy‑free” or alt‑dairy products on shared equipment, that should get your attention. You can solve a milk‑protein problem on paper with wording, but if buyers and consumers lose confidence in “dairy‑free” claims coming out of your plant, that premium evaporates — and so does the extra value flowing back to your herd.

“May Contain Milk”: Precaution or Crutch?

Dairy doesn’t just live with milk as a top allergen. It also lives with a labelling tool that makes it easy to hedge liability in a grey zone: precautionary allergen labelling (PAL) — all the “may contain” and “processed in a facility” statements.

The research keeps pointing to the same problem:

PAL is often used inconsistently and, in many markets, without a specific regulatory framework, which reduces its value for people with food allergies.

Analytical surveys have found products with PAL that contained no detectable allergen, and products without PAL that did contain measurable allergens.

The 2024 paper “Time to ACT‑UP: Update on precautionary allergen labelling (PAL)” describes current PAL use as problematic and pushes for a risk‑based, regulated system tied to agreed reference doses and contamination data.

Regulators are tightening expectations:

FDA’s draft Compliance Policy Guide on major food allergen labeling and cross‑contact makes it clear that advisory statements can’t substitute for adequate cross‑contact controls and must be truthful and not misleading under the Federal Food, Drug, and Cosmetic Act.

Health Canada and CFIA guidance say PAL must be truthful and clear and “not be a substitute for Good Manufacturing Practices,” and should only be used where inadvertent presence of an allergen is unavoidable.

EU and UK guidance on “free‑from” claims increasingly expects “dairy‑free” to mean essentially no detectable milk protein, backed by documented risk assessments and agreed reference doses.

That leaves your plant or co‑op with two real PAL strategies:

PAL as a blanket shield. You put “may contain milk” on entire product lines to protect the lawyer, even when your own validation data shows very low actual risk.

PAL as a last resort. You reserve it for scenarios where documented risk assessments show you can’t get risk below a defined threshold despite fully applied controls.

If your own cleaning and testing suggest low milk‑protein risk but your labels still blanket “may contain milk,” you’re writing the plaintiff’s opening argument for them: you had enough information to do better and chose not to. And if a “dairy‑free” product tests positive for milk under that setup, PAL will look more like evidence of a business choice than a shield.

PAL isn’t going to carry this forever. As more regulators and retailers move toward risk‑based allergen labelling, plants that use “may contain” instead of validation will have a much weaker story to tell.

What Mark and His Co‑op Actually Did With One Yogurt Line

Once the recall math and near‑miss history were on the same page, Janet pushed for something simple: evidence instead of assumptions.

When QA first pitched a full allergen validation, Mark wanted more than theory before tying up his busiest line. The external numbers were ugly:

Validation for that filler and conveyor system sat in the five‑figure range per phase, with phases between $5,000 and $80,000 depending on scope and sample size.

The bigger fear was lost throughput — repeated clean–swab–reclean cycles on a line already overbooked with private‑label and alt‑dairy contracts.

Janet cut through the noise with one question:

“What’s actually cheaper for our members — validating one line properly, or living with the real recall odds on that filler and hoping our insurance and contracts keep us whole?”

Mark didn’t have an immediate answer. But he agreed to a focused first step: a pilot allergen cleaning validation on a single high‑risk yogurt line.

Over roughly a month, his team:

Picked the line with the widest allergen mix and the most sensitive customer contracts.

Left the core cleaning SOP in place but added high‑sensitivity ATP swabs on specific “worst‑case” surfaces after each changeover.

Used protein swabs where ATP passed, then ran milk allergen tests once ATP and protein were consistently passing.

The early results were uncomfortable:

Several “visually clean” changeovers failed ATP or protein — exactly the kind of runs that would have gone into production before.

After changing tools, chemistry, and a few SOP steps, first‑pass cleaning success climbed; once ATP and protein were reliably passing, milk allergen tests came back clean.

The pilot cost real money — test kits, labor, and some lost line time. But it bought three assets Mark and Janet had never had:

A measured first‑pass cleaning rate on their riskiest line.

A count of near‑misses that would have shipped under the old system.

A one‑pager that they could show their insurer, their biggest retail customer, and their members when they talked about risk and premiums.

Janet’s line at the next board meeting was blunt:

“I’d rather see us spend five figures hunting our own near‑misses than watch eight figures disappear from the milk check because we never bothered to look.”

That was the turn. Not a new law. Not a hardware upgrade. Just one pilot on one line and a decision to move allergen recall risk out of the shadows and into the budget.

The 90‑Day Allergen Recall Risk Playbook for Mid‑Size Dairy Plants

You don’t have to rebuild your whole plant to change your allergen recall risk profile. You need 90 days of disciplined work that puts real numbers next to your milk check.

In the Next 30 Days: Name Your Riskiest Line and Your Blind Spots

1. Pick your highest‑risk line on purpose.

Ask:

Which line runs the most SKUs and allergen combinations (milk plus soy, nuts, eggs)?

Which line has the tightest changeover windows?

Which line touches your “dairy‑free,” “non‑dairy,” or premium private‑label contracts?

That’s your pilot line. Don’t overthink it.

2. Pull a 12–24‑month allergen and label‑error history for that line.

With your QA team, pull:

All failed ATP, protein, and allergen swabs on that line.

All label or packaging deviations involving milk or other allergens.

Any incidents where the wrong product or label was caught before shipping.

If you can’t generate that report in a clean, credible way, you’re not managing recall risk. You’re gambling.

30‑Day Check:

By your next board or advisory meeting, you should be able to say:

“In the last 12 months, our riskiest line had [X] allergen‑related near‑misses, and here’s how we caught them.”

If you don’t know X, the recall model you’re using on your P&L isn’t reality.

Over the Next 90 Days: Run the Pilot and Put a Price Tag on Prevention

3. Run a 2–4 week cleaning validation pilot on that line.

You’re not trying to build a PhD thesis. You’re trying to establish a baseline:

Start from your existing cleaning SOP.

Add ATP swabs on 5–10 “worst‑case” surfaces after cleaning.

Add protein swabs where ATP passes.

Once ATP and protein are consistently passing, run milk allergen tests at agreed intervals (end of selected changeovers, high‑risk product switches).

Track:

How many first‑round cleans fail ATP or protein?

How many re‑cleans are needed to pass?

How many allergen tests do you run, and what are their results?

The goal isn’t zero failures in week one. The goal is a baseline you can act on.

4. Track pilot costs and compare them to your modeled recall risk.

During that pilot:

Log extra minutes or hours per changeover.

Log overtime or schedule shifts caused by re‑cleans.

Log the cost of ATP, protein, and allergen kits plus any lab fees.

At the end, stack those numbers against your recall risk math:

A low‑thousands‑of‑dollars pilot is realistic on a line like this over a month.

At an 8% annual recall probability and a $10M recall cost, your expected annual exposure is $800,000 on that line — or $2,000 per cow on a 400‑cow block.

That’s a conversation your insurer, your retailer, and your members all understand: pay a known amount now to reduce the odds of an eight‑figure hit later.

Over the Next 365 Days: Move Recall Risk into Governance and Contracts

5. Put allergen recall risk in front of your board and members once, in writing.

At your next major meeting:

Share a one‑page pilot summary: cost, failures caught, changes made.

Walk through the recall math at 1–2% and 8–10% probabilities, using your own line as the example.

Ask in plain language:

“Are we comfortable modeling recall risk at 1–2% per year when our own near‑miss data — and broader survey and recall data — point much higher?”

Once that question is in the minutes, allergen recall risk becomes a governance item, not just a QA report.

6. Take your data to your insurer and your biggest retail or brand customer.

Use the pilot numbers:

With your insurer: “Here’s our high‑risk line and the validation data. How does this impact recall coverage and premiums at renewal?”

With your largest customer: “We’ve validated cleaning and reduced allergen risk on your line. Can we talk about longer terms, preferred status, or modest premiums tied to this control?”

You’re not asking for charity. You’re negotiating with evidence.

7. Rewrite one clause at renewal so producers aren’t underwriting plant‑side failures.

At the next contract renewal:

Make sure raw milk supply agreements clearly separate farm‑origin hazards (residues, pathogens at intake) from plant‑origin allergen and labeling failures (cross‑contact, mislabeling, wrong packaging) that occur after milk crosses the hose.

If you’re a producer, ask your co‑op or plant rep:

“If there’s an allergen recall caused by cross‑contact or mislabeling in the plant, how much of that cost can be pushed back onto members under our current wording?”

If plant‑origin failures can be pushed back on your herd, you’re underwriting risks you can’t directly control.

What This Means for Your Operation

You don’t need to own a plant to be tied to this. If your milk goes into a high‑mix facility, allergen recall risk is already baked into your milk check.

If your milk feeds a plant running yogurt, ice cream, cheese blends, or alt‑dairy on shared lines, assume your recall exposure looks more like an 8–10% scenario than a safe 1–2% — unless someone shows you data that says otherwise.

In the next 30 days, ask your plant or co‑op for a simple allergen near‑miss and label‑error report for their riskiest line. If they can’t pull it, you know they’re leaning harder on recall insurance and “may contain” labels than on validated allergen control.

If you sit on a board, push to have allergen recall risk discussed once a year alongside milk price, capital spending, and debt coverage. That discussion should include near‑miss counts, cleaning validation pass rates, and recall history on products made with your milk.

Before you sign your next supply agreement, read the indemnity and contamination clauses with allergens in mind. If in‑plant failures can be pushed back onto members, your herd is backing liabilities you never meant to underwrite.

If you ship into “dairy‑free” or alt‑dairy contracts, treat PAL as a last resort, not a business model. Premiums in that space exist because consumers trust the label; once that trust cracks, the premium disappears.

Use the $250 vs. $2,000 per cow math as a sanity check. If you can spend a low‑thousands‑of‑dollars pilot to materially reduce an $800,000 expected recall exposure on a single line, that’s not just QA spend. That’s risk management.

Key Takeaways

If your plant models allergen recall risk at 1–2% per year while survey data show roughly two in five companies with allergen plans still had a recall over five years, you’re probably underpricing that risk by a factor of four.

A focused cleaning‑validation pilot on your riskiest line is a realistic 90‑day project that can turn “we think we’re fine” into numbers your board, insurer, retailer, and members can actually use.

“May contain milk” is not a long‑term strategy. As regulators and retailers move toward risk‑based allergen labelling and tighter “dairy‑free” claims, plants that leaned on PAL instead of validation will have the weakest story to tell.

If your co‑op or plant contracts don’t clearly separate farm‑origin hazards from plant‑origin allergen and labeling failures, your herd may be backing liabilities you never agreed to carry.

The Bottom Line

Mark and Janet now expect one simple answer every year:

“On our highest‑risk line, what’s our real cleaning pass rate, what did it cost us to prove it, and how much of that recall risk is already baked into our milk check?”

Don’t wait for a $10 million mistake to discover who’s actually liable. Send this article to your co‑op field rep or plant contact and ask: “Where is our allergen validation data — and what recall probability are we really modeling?”

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

The Hidden Contract Clause That Could Cost Your Dairy $55,000 in 2026 – This tactical guide arms you with a 30-day action plan to dodge the massive liability shifts appearing in new milk contracts. It exposes how processor-level failures are being legally offloaded onto farms and delivers the leverage needed to protect your profit.

The $11 Billion Reality Check: Why Dairy Processors Are Banking on Fewer, Bigger Farms – This strategic deep dive reveals the $11 billion processing wave reshaping the industry through 2028. It breaks down why processors are locking in supply with mega-dairies, allowing you to position your operation before regional consolidation closes your window to negotiate.

More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – This disruptive analysis exposes the brutal “more milk, fewer farms” era and the $250,000 margin gap facing mid-size dairies in 2026. It delivers the precise math required to choose between scaling, specializing, or exiting while you still own your equity.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

When the same logo sits on your genomic test, your wellness index, and now the lab behind a big slice of the industry’s DNA cards, the number that matters isn’t just $160 million — it’s the $86,000 you quietly push through that pipeline over five years.

Executive Summary: Zoetis’ just-announced $160 million purchase of Neogen’s animal genomics business is a bet on owning the global DNA pipeline, not just another test brand. Neogen’s unit brings in $90 million in genomics revenue, operates five labs across the U.S., Brazil, Australia, China, and the U.K., and serves customers in 120+ countries, dropping a ready‑made lab network into Zoetis’ Precision Animal Health machine. For a 750‑cow Holstein herd using CLARIFIDE Plus at roughly $43/head, that means around $17,200 a year — about $86,000 over five years — flowing through one company’s genomic loop that now influences breeding, wellness traits, and health protocols. The article shows how that integration can genuinely help (sharper predictions, smoother software, simpler decisions) while also raising switching costs and shifting leverage away from herds, breed associations, and AI programs toward a handful of platforms. It then gives a concrete 30/90/365‑day playbook: audit genomics contracts for data ownership and use, secure export rights, pilot a non‑Zoetis lab as Plan B, and stop letting any single index be the only lens on your genetics and health risk. The core message: you can stay in the Zoetis ecosystem, but before this deal closes in the second half of 2026, you need to decide — and document — who owns your genotypes, how portable they are, and how hard it would really be to change course later.

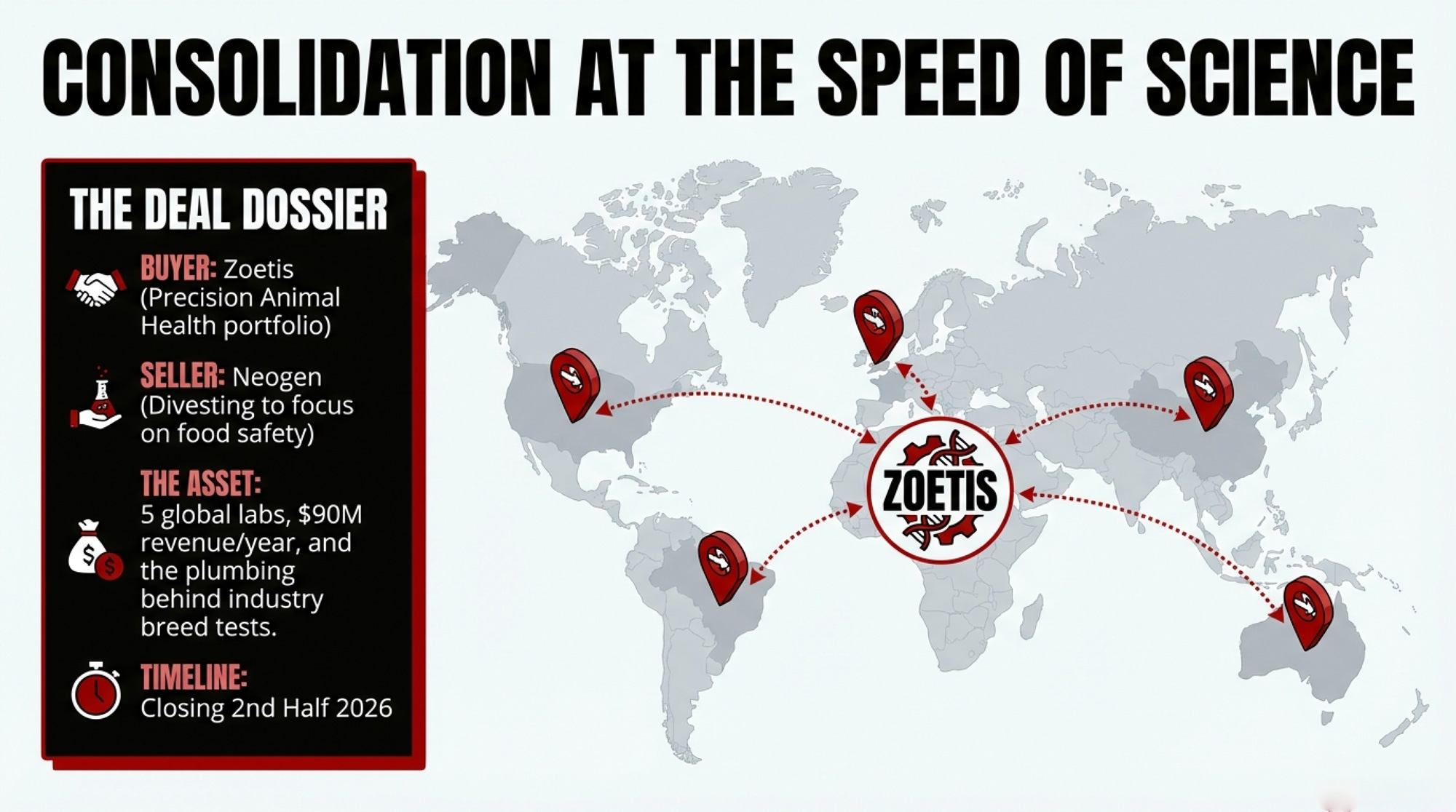

On March 2, 2026, Zoetis announced it would pay 0 million to acquire Neogen’s animal genomics business, including its GeneSeek laboratories and livestock/companion animal genomics portfolio. Neogen says the net proceeds will primarily go toward debt reduction and a tighter focus on its food safety and animal safety markets, and both companies expect the deal to close in the second half of calendar year 2026, subject to regulatory approvals.

The real question for 2026 is blunt: How much control over your genomics and data are you handing to one company — and on what terms — when this closes?

What $160 Million Actually Buys — and What It Doesn’t

Here’s what’s actually changing.

Buyer: Zoetis Inc. (NYSE: ZTS), “the world’s leading animal health company,” positioning the deal as strengthening its Precision Animal Health portfolio. Jamie Brannan, Zoetis’ Chief Commercial Officer, says the acquisition “brings complementary capabilities that expand predictive insights and individualized care, enabling us to deliver added value to customers.”

Seller: Neogen Corporation (NASDAQ: NEOG), calling this a “planned divestiture” of its animal genomics business, so it can simplify operations, focus on core food and animal safety markets, and reduce debt. CEO and President Mike Nassif says the sale “allows the company to accelerate de‑leveraging and improve profitability.”

Asset: Neogen’s animal genomics business, which:

Generates about $90 million in annual sales as of Neogen’s fiscal 2025.

Operates five laboratories in the United States, Brazil, Australia, China, and the United Kingdom, plus an office in Canada.

Serves customers in more than 120 countries, using fixed‑array and sequencing technologies with associated software to support genetic testing.

Zoetis describes it as a leader in U.S. beef and dairy genomics.

Price:$160 million, a clean ~1.8× revenue multiple on that $90 million sales base.

Timeline: Zoetis expects to complete the acquisition in the second half of 2026, and Neogen expects to close by the first half of its 2027 fiscal year, pending regulatory approvals.

That 1.8× revenue multiple tells you how each side sees this. For Neogen, it signals that genomics is a scale‑dependent service line — valuable, but not its primary growth engine, compared with food and animal safety. For Zoetis, rolling a ~$90‑million genomics business into a much larger animal health portfolio is easy to justify if it deepens their Precision Animal Health strategy and tightens the link between genetics, medicines, vaccines, diagnostics, and digital tools.

Zoetis isn’t starting from zero on genomics. They already had:

CLARIFIDE and CLARIFIDE Plus for dairy, built around genomic predictions and the Dairy Wellness Profit Index (DWP$), with wellness traits aimed at mastitis, metritis, displaced abomasum, ketosis, lameness, twinning, abortion, and more.

INHERIT Select for beef, positioned as a genomic tool for commercial herds.

A genetics lab in Kalamazoo, Michigan, is part of their existing Precision Animal Health infrastructure.

What they’re buying now is plumbing and reach: a global lab footprint, thousands of customers who’ve used GeneSeek as their processor, and a large base of Igenity and GGP genotypes feeding evaluations and management tools across species.

Asset

Zoetis Holdings (Before Deal)

After $160M Neogen Acquisition

Genomic Products

CLARIFIDE Plus (dairy), INHERIT Select (beef), DWP$ wellness index

All existing products + Neogen’s Igenity, GGP platforms, sequencing technologies

Lab Footprint

1 genetics lab (Kalamazoo, Michigan)

6 total labs: U.S., Brazil, Australia, China, U.K., Canada

Customer Reach

North America focus via existing distribution

120+ countries served through acquired lab network

Annual Genomics Revenue

Est. $400M+ (within Precision Animal Health segment)

Adds $90M from Neogen genomics business

Strategic Control

Owned genomic testing pipeline for proprietary indexes

Also processes DNA for competitors, associations, AI companies

Competitive Position

Leading dairy genomics brand

Owns both the test brand AND much of the third-party lab infrastructure

The 750‑Cow Herd Caught in the New Loop.

Now pull this into a barn you recognize.

Picture a family‑run 750‑cow Holstein herd that’s all‑in on CLARIFIDE Plus:

Every heifer gets genotyped through CLARIFIDE Plus.

The breeding program leans heavily on DWP$ and wellness traits that Zoetis positions as predictors of health and profitability.

The herd‑management software — through Zoetis or partner integrations — pulls genomics directly into the cow card, so DWP$ and wellness scores sit alongside repro, health, and production records.

Meanwhile, another herd in the same region runs Igenity or GGP tests through a breed or AI program that sends DNA cards to Neogen’s GeneSeek labs.

As of March 2, 2026, those routes are set to converge:

Neogen’s animal genomics business — including its five labs and software — is under a definitive agreement to be sold to Zoetis.

Zoetis says integrating Neogen’s genomic technologies and data solutions will expand “predictive insights, individualized care, and greater value” across major livestock and companion species.

From the 750‑cow herd’s side of the fence, that means:

The lab processing a significant share of breed/AI genomics — Neogen’s business — is on track to have the same corporate parent as CLARIFIDE Plus and other Zoetis genomics offerings.

The company that runs your genomic test, defines your wellness index, integrates with your herd software, and sells you disease‑prevention products will also own a big chunk of the lab capacity behind your neighbors’ tests and some association pipelines you rely on.

That might pencil out just fine. But it’s no longer the same arm’s‑length relationship you started with.

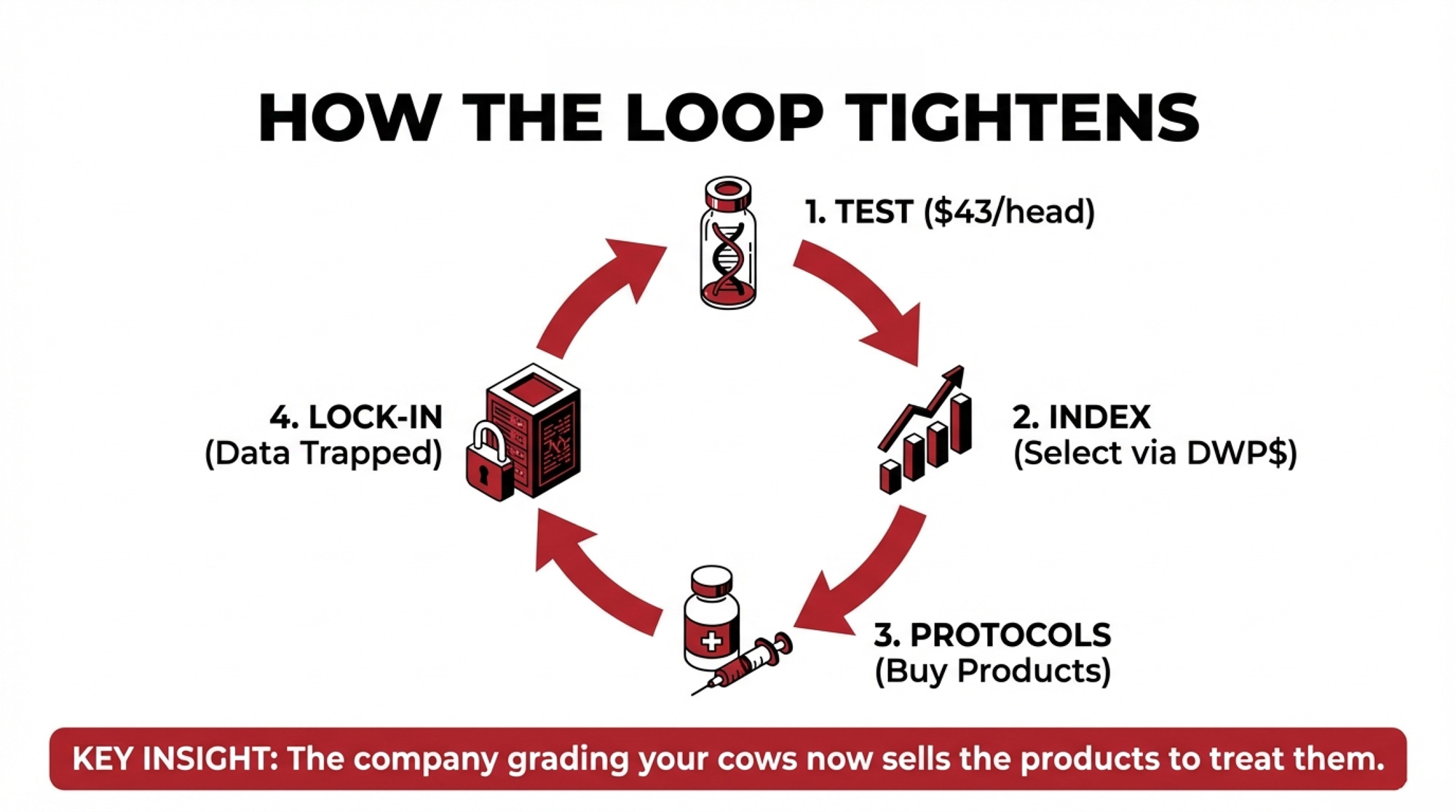

The Genomics Loop: $43 Per Head, 2,000 Animals, One Company

CLARIFIDE Plus isn’t a mystery line item. Holstein Association USA lists CLARIFIDE Plus at around $43 per Holstein animal, with practical costs for many herds in the $40–$50 per head band depending on volume and program.

Step

Annual Activity

5-Year Total

Who Benefits

Direct Testing

400 tests × $43 = $17,200/year

$86,000

Zoetis (lab revenue)

Genetic Direction

Selection/culling decisions based on DWP$ index

2,000 animals shaped by one platform’s trait priorities

Zoetis (proves index “works”)

Protocol Adjustments

Est. $10/cow/year targeted health spend (750 cows)

$37,500

Zoetis (wellness-linked product sales)

Switching Friction

Staff retraining, advisor realignment, dual-index period

Opportunity cost: $15,000–$25,000

Zoetis (customer retention)

Total Economic Exposure

$24,700/year

$123,500+

Platform lock-in achieved

Now run realistic barn math for that 750‑cow herd:

You test 400 head per year — heifers plus some key cows.

You keep that up for 5 years.

You use one platform’s genomic test and index to steer breeding and culling.

Step 1: Direct testing spend

Using $43 per head as a concrete, sourced test price:

400 tests/year × $43 = $17,200 in genomics fees per year.

5 years × 400 tests/year = 2,000 animals genotyped.

2,000 tests × $43 = $86,000 in direct testing spend over five years.

Your invoices might come in a little lower or higher with discounts and bundling, but you’re still in that neighborhood.

Step 2: Genetic direction

Each year, you and your advisors use those scores to:

Push sexed semen on the top DWP$ heifers.

Push beef semen or early culling on low‑index animals.

Make earlier do‑not‑breed calls when low‑index animals also underperform in the parlor or maternity pen.

After five years, a large share of your milking herd has been shaped by one company’s definition of “profitable genetics” — the way DWP$ weights milk, fat, protein, fertility, and wellness traits.

That’s powerful if DWP$ lines up with your economics. It’s limiting if you ever decide you want different trade‑offs.

Step 3: Downstream product spend

Those wellness traits don’t just sit in a report. They steer protocols.

Zoetis describes its Precision Animal Health vision as predicting, preventing, detecting, and treating disease using integrated tools across medicines, vaccines, diagnostics, and digital solutions. On a CLARIFIDE Plus herd, that often turns into:

High mastitis‑risk genetics? More aggressive mastitis prevention and treatment programs.

High lameness risk? Tighter hoof‑health schedules, trims, and monitoring.

Transition disease risk? Higher‑touch dry‑cow and fresh‑cow protocols backed by specific products.

Nobody’s forcing these choices, but when the same company provides the risk scores and sells the tools, it’s easy for more of your per‑cow health spend to gravitate there over time.

Even modest shifts add up. If wellness‑driven protocols increase targeted health spend by:

$10 per cow per year across 750 cows, that’s $7,500/year.

Over 5 years, it’s $37,500 in additional health spending guided by the same platform.

You may get every dollar of that back in avoided disease. The point is that your genomics, protocols, and product choices are now tightly coupled to one ecosystem.

Step 4: Switching cost

Fast‑forward to 2031.

You decide you’d like to:

Move some or all genotyping to a non‑Zoetis, CDCB‑approved service lab, or

Shift your primary emphasis from DWP$ to a national index like NM$, TPI, or PRO$, alongside your own KPIs.

You’re not just changing who prints your reports.

You’re:

Re‑training staff who’ve lived in DWP$ bands and wellness trait lists.

Re‑aligning conversations with genetics advisors, vets, and lenders.

Managing a period where different indexes don’t always agree on which cows are “top” and which are “bottom.”

Each turn of the loop made the system easier. It also raised the friction if you ever want to step partly outside it.

What Does This Deal Change for a 750‑Cow Herd?

Step

What You Do/Spend

What Zoetis Gains

1. Testing

400 tests/year → $17,200/year → $86,000over 5 years

Lab revenue and a larger genomic dataset

2. Selection

Herd bred and culled to a single platform index

Evidence their index “works” + genetic direction aligned to their trait priorities

3. Protocols

Wellness traits steer more targeted health programs

Product sales linked to genomic risk and integrated Precision Animal Health offerings

4. Switching

Higher friction if you try to move labs or indexes after 5+ years

Stickier customers and more leverage in commercial negotiations

That’s the decision pipeline Zoetis is paying $160 million to tighten.

Why Many Producers Will Choose the Loop Anyway

There are plenty of good reasons herds will lean into this ecosystem on purpose.

Zoetis and Neogen both emphasize that combining their genomics businesses will expand “predictive insights,” “individualized care,” and “highly accurate, scalable genetic testing,” giving customers deeper views on animal health, productivity, and sustainability across species.

For a 700‑cow operation juggling labor, data overload, and disease pressure, that upside looks like:

Sharper predictions. A larger combined genomics business — more samples, traits, and species — can support more robust trait predictions, especially for wellness and health.

Less friction. Results that feed directly into herd software and decision tools cut the time you spend moving files and reconciling systems.

Cleaner conversations. When your genomics, wellness traits, and protocols use the same language, it’s easier for your team to pull in the same direction.

So it’s perfectly rational for a herd to say: “We’ll accept more dependence if the tools keep improving and the economics hold up.”

The risk isn’t using the loop. It’s using the loop without knowing how to exit it or what happens to your data if you ever need to.

When “Neutral” Labs Aren’t Neutral Anymore

For breed associations, AI companies, and public genomics projects, the immediate tension isn’t about convenience. It’s about governance.

From Zoetis and Neogen’s own descriptions, Neogen’s genomics business has been:

Serving customers in more than 120 countries,

Operating five laboratories in the U.S., Brazil, Australia, China, and the U.K., plus an office in Canada, and

Acting as a leader in U.S. beef and dairy genomics.

For years, much of that work sat under Neogen as a third‑party service:

Associations sent member DNA for genotyping under genomic‑enhanced evaluations.

AI companies used Neogen’s platforms (Igenity, GGP) to genotype bulls and commercial heifers.

Government and research projects used its lab network for large‑scale testing.

Once those labs move under Zoetis’ roof, the questions change:

What do the firewalls really look like? Zoetis says it’ll integrate Neogen’s genomic technologies and data solutions into its Precision Animal Health offering while “supporting continuity for colleagues and customers” and building on Neogen’s genomics legacy. Partners will want clarity on how individual customer data is segregated and protected.

What visibility does a lab owner get, even without individual IDs? Aggregate volume, array choice, and project timing can reveal a lot about what breeds, studs, and associations are doing.

Who benefits most from data aggregation? Associations may own members’ genotypes, but Zoetis’ ownership of the lab business gives it more visibility into patterns than a standalone, service‑only lab would.

Zoetis is open about using this acquisition to “advance animal health through innovation, data, and technology,” and to empower customers with tools for healthier animals and sustainable production. That’s legitimate. The flip side is that it also concentrates influence — as both lab vendor and product competitor — in fewer hands.

If Consolidation Keeps Rolling, Where Does It End?

The Zoetis–Neogen deal fits a familiar pattern from seeds, crop protection, and precision ag:

Products evolve into platforms.

Platforms build data moats.

Data moats raise switching costs — and leverage shifts toward the platform owners.

In animal genetics, current signals already point to:

A global market where animal genetics and genomics continue to grow as producers chase productivity, health, and sustainability gains.

A small top tier of players — Zoetis, major genetics companies, and large animal health providers — controlling most of the genomics and evaluation stack.

If current consolidation trends continue, it’s easy to picture a world where:

Four to six dominant platforms effectively steer most genetics and health decisions on commercial herds.

Genomics becomes a feature inside integrated solutions (software + products + advisory) rather than a standalone service you can easily shop for.

Independent labs focus on niche work or act as backup routes for organizations that deliberately keep a second lane open.

For mid‑size dairies, the risk creeps in quietly:

Platform indexes and wellness scores become the default language for your team and advisors.

The easiest tools — usually the ones tied to your main platform — get used by default.

By the time you question the relationship, your replacement strategy, cull logic, and protocols may all be tuned to a single system.

The myth is: “If this stops working, we’ll just switch.”

The reality, if you don’t plan, is: “We’d like to switch, but the friction is too high, and the whole farm thinks in one platform’s numbers.”

The Turn: It’s Not “Stay or Go” — It’s “On What Terms?”

You’re not going to stop Zoetis and Neogen from closing this deal. Regulatory reviews may tweak conditions, but the labs will likely sit under Zoetis by late 2026.

What you do control is how boxed in you are when that happens.

The real decision over the next 12–18 months is:

Do you keep using Zoetis‑linked genomics on default terms, or

Do you keep using them while locking in better data and exit terms to maintain leverage?

Most producers and associations will stay in the ecosystem because:

The tools are strong and already integrated.

The workflows are familiar.

Evaluating alternatives takes time and focus.

That’s fine — as long as you treat lab and data contracts like infrastructure decisions, closer to choosing a milk buyer or lender than picking a glove supplier.

That means pushing for:

Clear language that your farm or organization owns your raw genotypes.

Guaranteed data portability — the right to export complete genotype files with IDs in standard formats if you move some or all volumes.

Tight data‑use provisions — especially around using your genotypes, even de‑identified, to train proprietary tools.

A transition clause that obligates cooperation if you shift business elsewhere.

You don’t have to leave. You don’t want to discover your options are gone the day you actually need them.

The Playbook Before This Deal Closes

Here’s a practical, time‑bound framework.

In the Next 30 Days: Read the Fine Print Like It’s a Milk Contract

Before the announcement fades:

Pull your genomics agreement or program terms. That might be with Zoetis directly, a stud, a breed association, or a vet/genetics service that bundles testing.

Circle language on:

Data ownership

Data use (especially “de‑identified,” “aggregated,” “research,” “product development”)

Term, automatic renewal, and termination

Ask your contact three blunt questions: