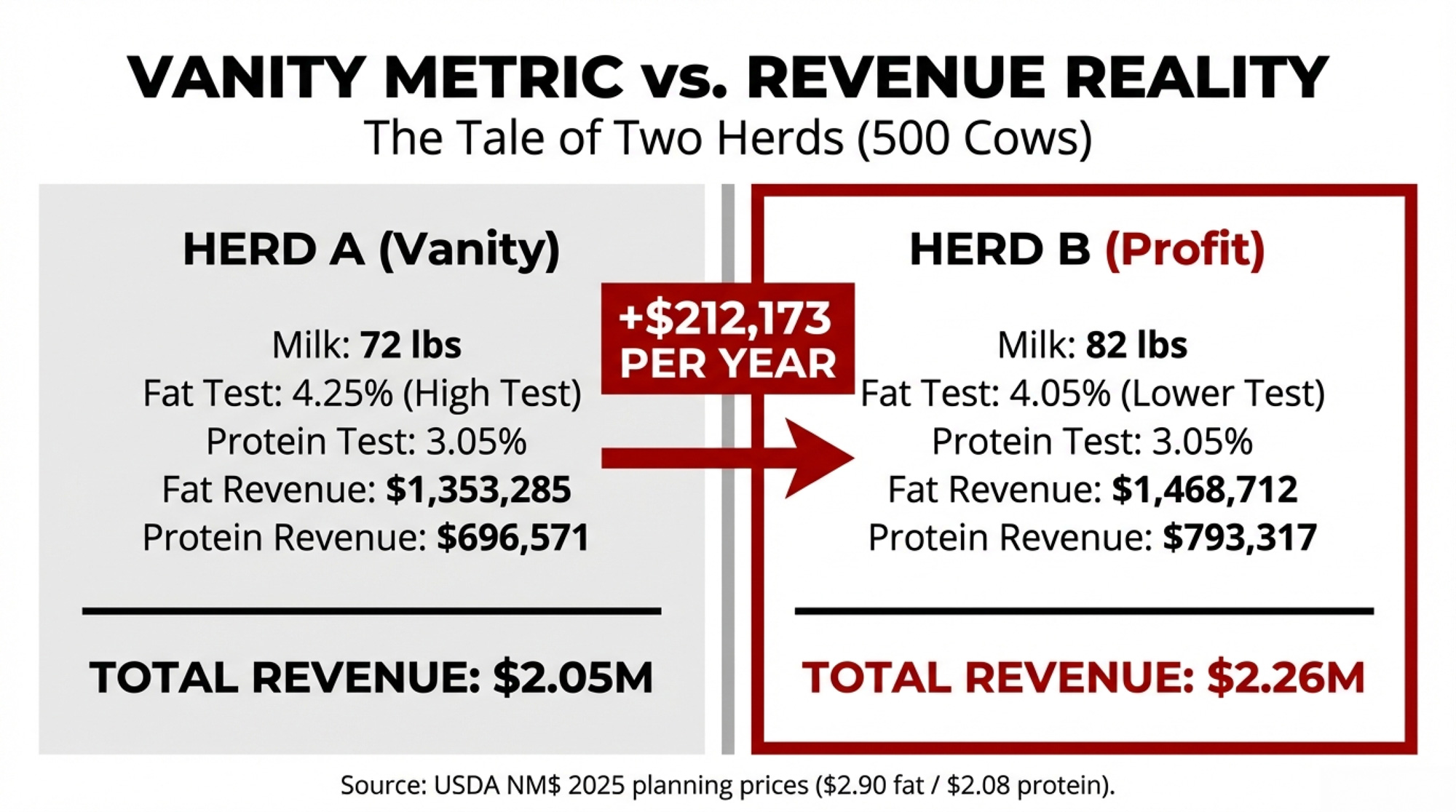

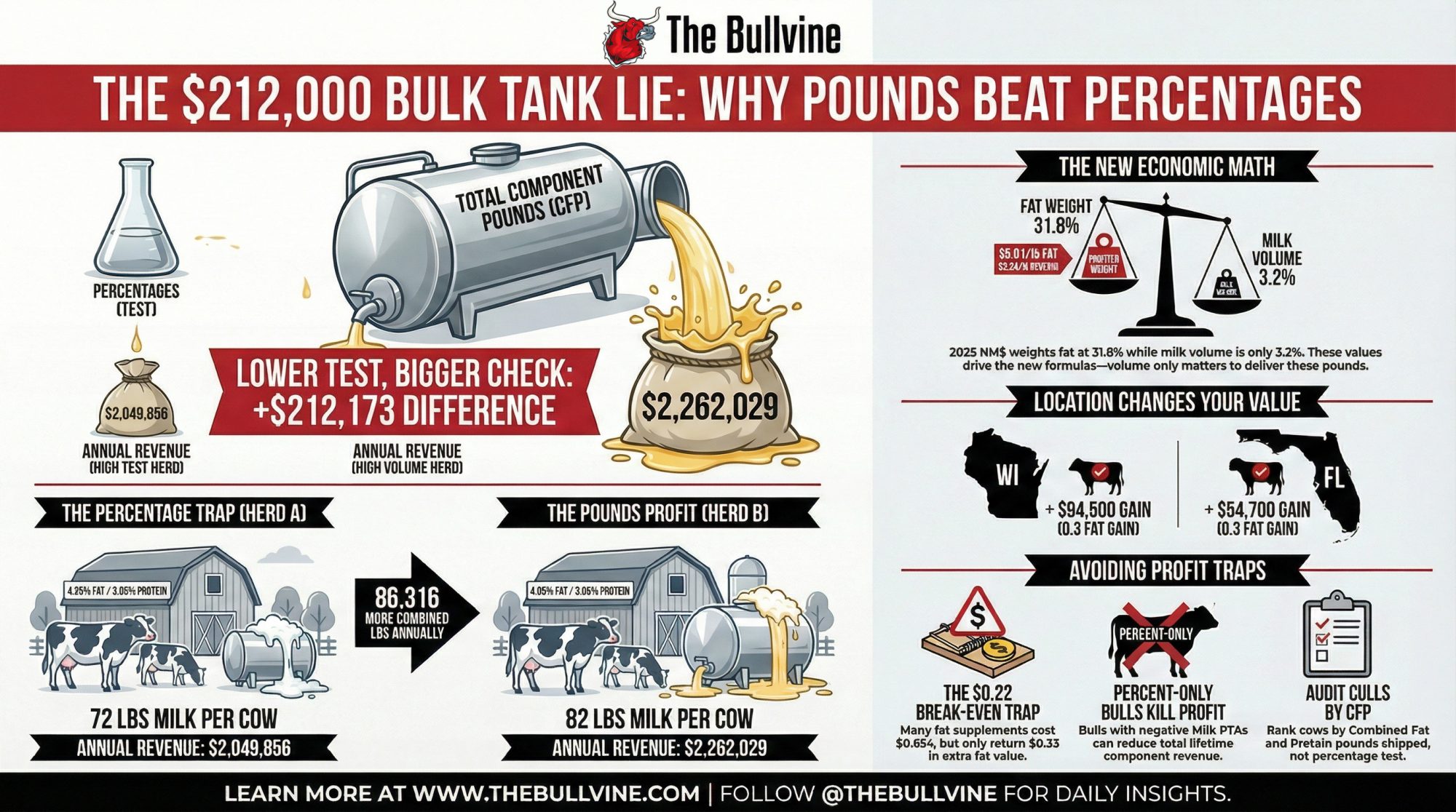

A lower-test herd shipped $212,000 more than its 4.25% neighbor. If you’re chasing percentages, this barn math is your wake-up call.

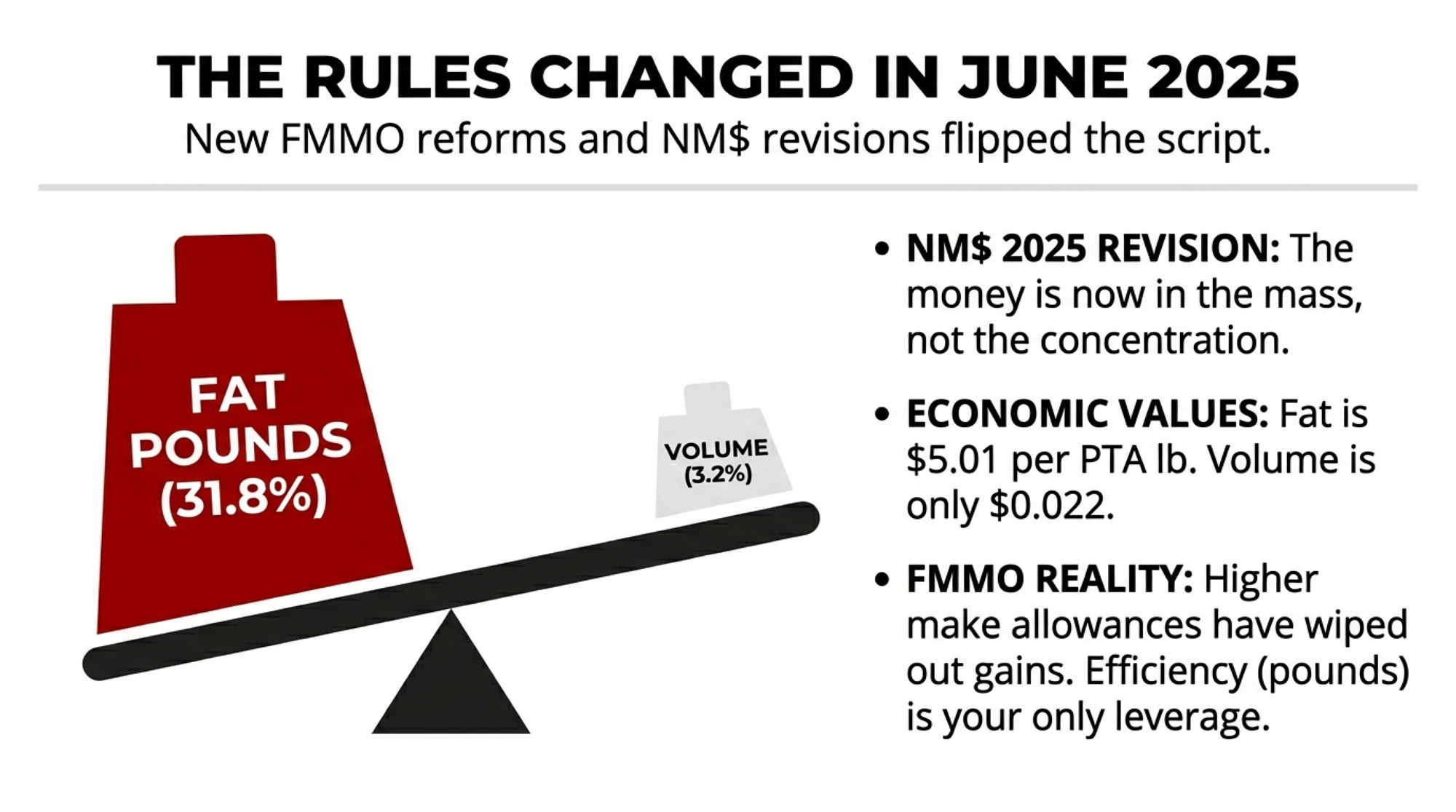

Executive Summary: June 2025 FMMO reforms and the 2025 NM$ revision have flipped the script so that fat and protein pounds shipped, not test percentages, drive your milk check. A side‑by‑side model of two 500‑cow Upper Midwest herds shows the lower‑test herd (4.05% fat at 82 lbs) shipping $212,000 more fat and protein value per year than a 4.25% herd at 72 lbs, using the USDA’s NM$ planning prices. NM$ now gives 31.8% weight to fat and only 3.2% to volume, which means “percent‑only” bulls with negative Milk PTAs can quietly cut lifetime component revenue even when their proofs look good on fat percentage. On the ration side, C16:0 supplement programs that add +0.10 fat test often cost three to four times more than the extra fat is worth once you do the barn math at $0.65–$1.00/cow/day. Your federal order then decides how much of that value you actually see: the same 0.3‑point fat gain is worth roughly $94,500 in a Wisconsin MCP plant but closer to $54,700 in a fluid‑heavy Florida order. The article walks through these calculations step by step and finishes with a four‑point playbook — track CFP, cull on pounds, match spending to your order, and pick sires on component pounds — so you can stress‑test your own numbers instead of trusting what the bulk tank report says.

A 500-cow Upper Midwest dairy can leave $212,000 in combined fat and protein revenue on the table by chasing a higher bulk tank test instead of shipping more component pounds. That’s not a hypothetical — it’s what the math shows when you model two herds side by side using USDA’s own NM$ planning prices.

A nutritionist working with herds in the region described the pattern: a 500-cow operation watches butterfat climb from 3.9% to 4.1% over six months. Everyone celebrates. Then somebody runs the real numbers — 78 lbs/day at 3.9% versus 74 lbs/day at 4.1% — and realizes they’re shipping nearly identical fat pounds. The test improved. The milk check didn’t.

What June 2025 Changed — And What It Cost

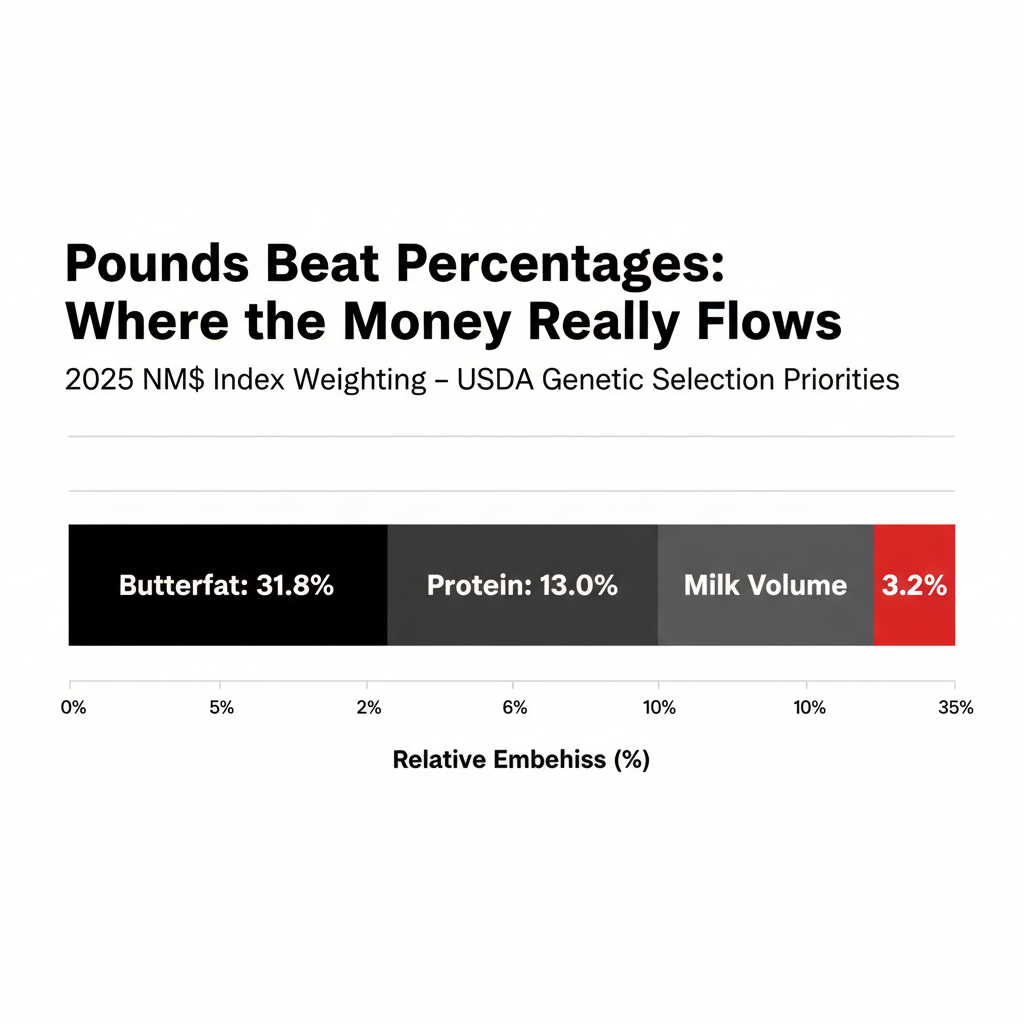

USDA’s April 2025 Net Merit revision pushed butterfat to 31.8% relative emphasis in NM$ — up from 28.6% in 2021 (VanRaden et al., NM$8 and NM$9). Protein carries 13.0%. Milk volume? Just 3.2%. The economic values are blunter still: fat at $5.01 per PTA pound, protein at $3.33, volume at $0.022.

Then the FMMO reforms hit on June 1, 2025. AFBF economist Daniel Munch calculated that in the first three months, producers lost more than $337 million in combined pool value — class price reductions of 85 to 93 cents per hundredweight depending on the order (AFBF Market Intel, September 2025). As Munch told Brownfield Ag News, the higher make allowances “more than wipe out” the gains from other reforms.

Upper Midwest Order 30 absorbed the worst of it. Roughly 69% of pooled milk went to Class III cheese in October 2025, with just 11.3% to Class I fluid (FMMA30 Dairy News, November 2025). That heavy cheese utilization means component value flows directly to producers — but the make allowance increase hit just as directly.

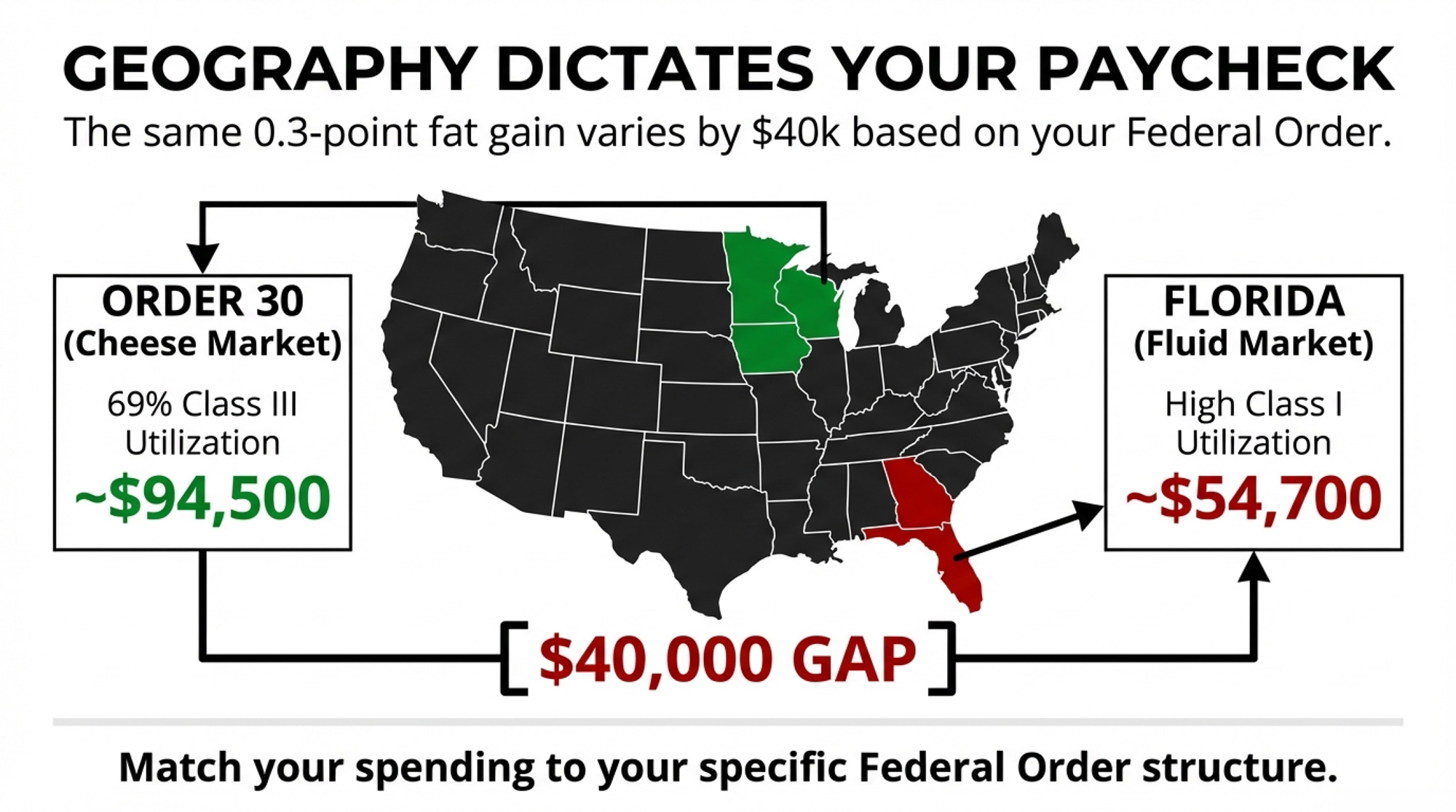

And regional structure amplifies everything. A 0.3-point butterfat improvement on a 500-cow herd captures an estimated $94,500 annually in Wisconsin’s MCP system versus approximately $54,700 in Florida’s skim-fat system. Same genetics. Same nutrition. A $40,000 gap from the order structure alone.

How $212,000 Disappears Into a Better Bulk Tank Test

Two 500-cow herds, both running 305-day lactations, were modeled using NM$ 2025 planning prices of $2.90/lb fat and $2.08/lb protein (VanRaden et al., January 2025). These are multi-year forecast prices; USDA built the index on non-spot prices. Actual FMMO butterfat ran about $2.95/lb in January 2025 and fell to approximately $1.45/lb by January 2026. The pounds principle holds at any price level; the dollar gap moves with the market.

Metric

Herd A (High Test)

Herd B (High Volume)

Difference

Milk/Cow/Day

72 lbs

82 lbs

+10 lbs

Fat Test

4.25%

4.05%

−0.20 points

Protein Test

3.05%

3.05%

Same

Annual Fat Shipped

466,650 lbs

506,453 lbs

+39,803 lbs

Annual Protein Shipped

334,890 lbs

381,403 lbs

+46,513 lbs

Fat Revenue @ $2.90/lb

$1,353,285

$1,468,712

+$115,427

Protein Revenue @ $2.08/lb

$696,571

$793,317

+$96,746

Combined F+P Revenue

$2,049,856

$2,262,029

+$212,173

Herd B — the lower-test herd — ships nearly 40,000 more pounds of fat and over 46,500 more pounds of protein. At actual January 2025 FMMO prices ($2.95 fat, $2.33 protein), the gap widens to roughly $226,000 because protein is priced higher than the NM$ assumption.

Three Places the Trap Compounds Silently

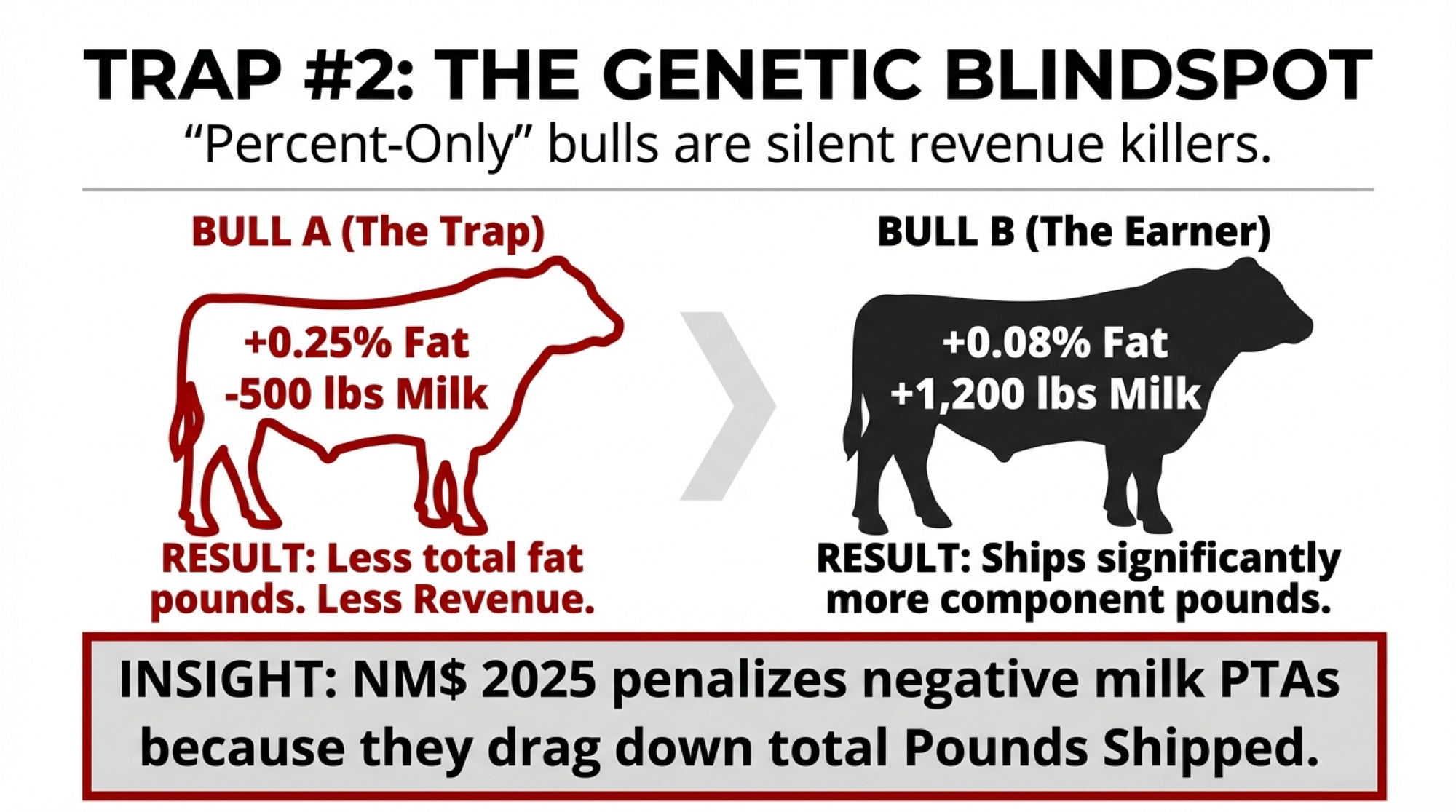

Genetics. The 2025 NM$ penalizes “percent-only” bulls with deeply negative Milk PTAs. A bull posting +0.25% fat but −500 lbs Milk loses on all three lines — less volume means fewer total fat pounds, fewer protein pounds, and less volume revenue. A bull at +0.08% fat with +1,200 lbs Milk often ships more total component pounds per lactation. That’s exactly what the $5.01/lb and $3.33/lb economic values reward.

Nutrition. Research from Prof. Kevin Harvatine’s lab at Penn State found C16:0 palmitic acid boosts fat test by +0.30 to +0.50 percentage points at ~2% of diet DM (Dairy Global, November 2023). Michigan State’s de Souza lab (J. Dairy Sci., 2024) showed mid-lactation cows at 40–50 kg/day responded best. But supplements run $0.65–$1.00/cow/day, and the protein test can slip 0.02–0.03 points. If milk yield doesn’t climb with the fat test, the P&L can go negative while the bulk tank report looks great.

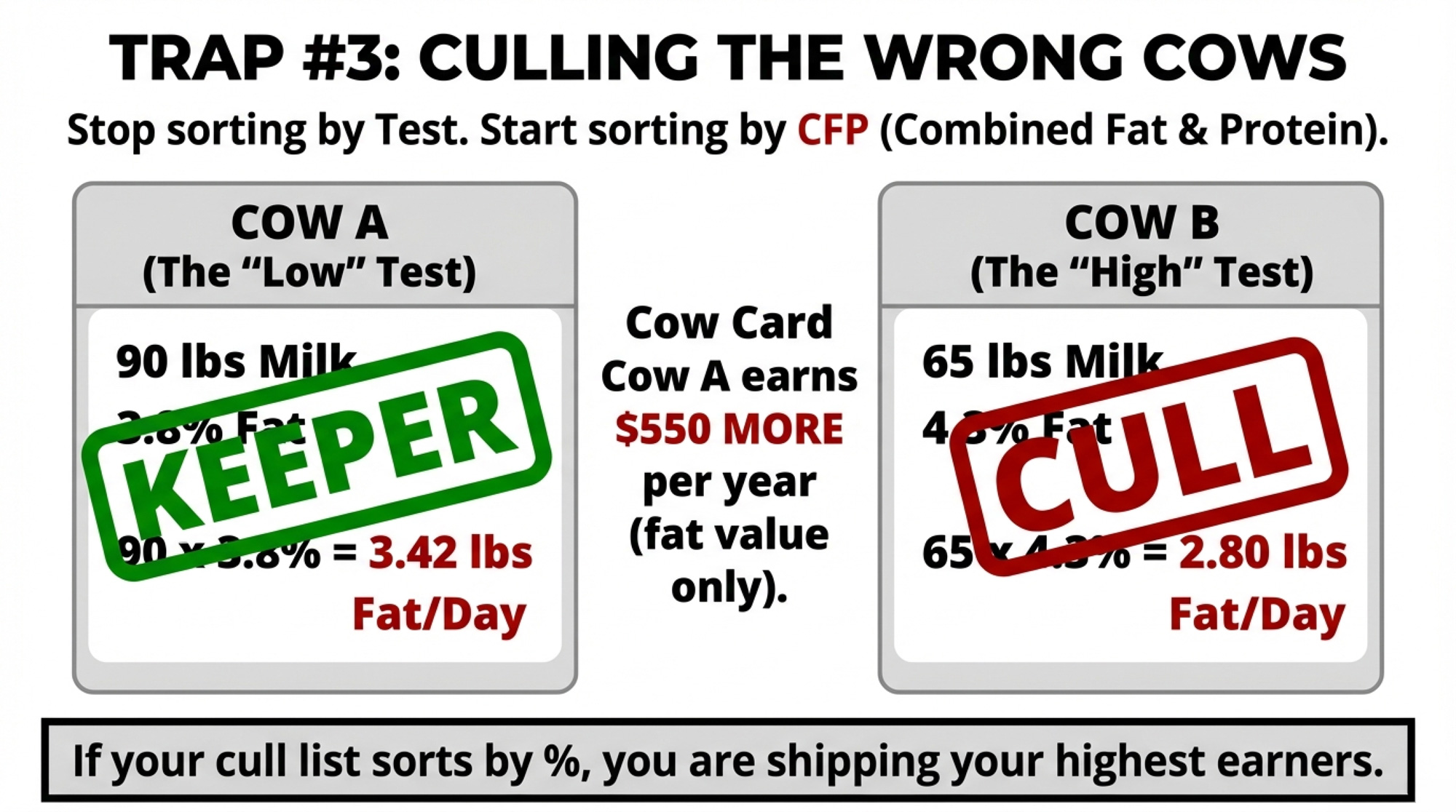

Culling. Cow 1 at 90 lbs/day and 3.8% fat ships 3.42 lbs fat/day. Cow 2 at 65 lbs/day and 4.3% ships 2.80 lbs. The “low test” cow delivers 0.62 more lbs of fat daily — about $550/year at $2.90/lb. If your cull list sorts by test instead of CFP (combined fat and protein pounds shipped), you may be shipping the wrong animals.

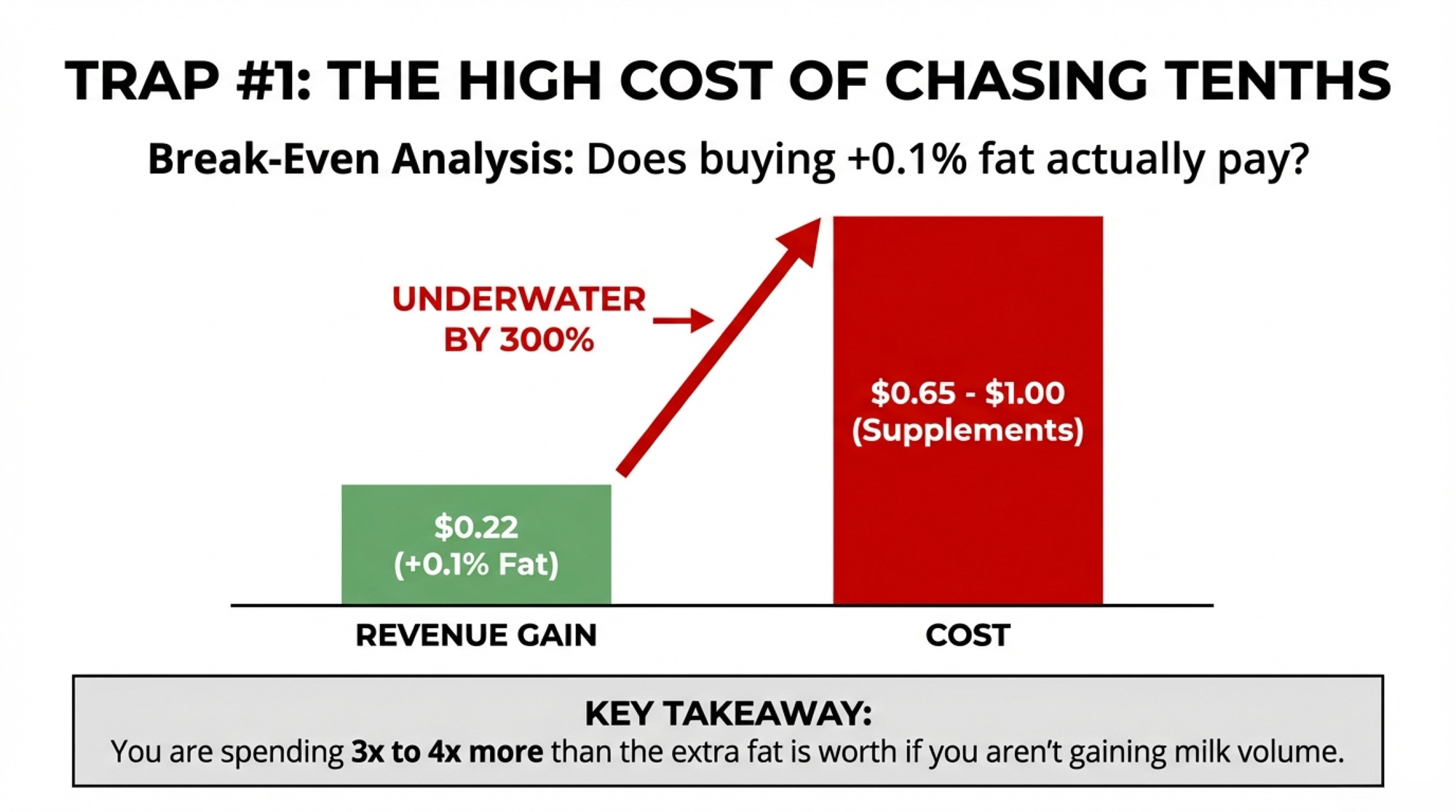

Does Chasing +0.1% Fat Actually Pay Under Component Pricing?

Full walkthrough: a program promising +0.10 points fat test on 500 cows averaging 75 lbs/day.

Break-even: about $0.22/cow/day. That’s three to four times below what any published C16:0 program costs. If a tenth of a point on fat test is the only gain — and you’re losing milk or protein in the process — the math is underwater.

The Shift: From Test Reports to Pounds Shipped

For herds getting ahead of this, the pivot starts with one change: they stop celebrating test and start tracking CFP per cow per day. Instead of “Our herd’s at 4.1% fat,” they’re asking: “How many pounds of fat and protein did we ship per cow today?”

That reframes every proposal — a new sire lineup, a nutrition tweak, or a cull list — around one question: does it raise CFP?

The Playbook: Four Ways to Manage for Pounds

1. Make CFP your primary metric. Calculate combined fat + protein pounds per cow per day, minimum monthly. 30-day action: pull last month’s data and establish your baseline. Trade-off: watching fat test flatten while CFP climbs feels wrong. It’s not.

2. Rebuild the cull list around CFP. Rank by shipped CFP first, then overlay fertility, health, and age. 90-day action: audit last quarter’s culls against CFP. Trade-off: you still need to watch for milk fat depression — tests aren’t irrelevant, just not the sorting metric.

3. Match spending to what your order actually pays. Order 30’s 69% Class III utilization means component value flows through relatively directly. In skim-fat orders with heavy Class I, the math is different. 30-day action: call your field rep and ask how much component value hits your check. Trade-off: even within the same order, different handlers deliver different capture.

4. Run genetics and nutrition on parallel tracks. Long-term: component-pound genetics (NM$, CFP). Short-term: nutrition for quick wins. 365-day action: rebalance your sire lineup at the next proof run using pound PTAs, not percentage PTAs. Trade-off: if component prices sag — January 2026 butterfat at ~$1.45/lb is a reminder — nutrition plays may need to scale back. The genetics keep compounding regardless.

What This Means for Your Operation

Run your own Herd A vs. Herd B table. Plug in your daily lbs, fat test, protein test, cow count, and your most recent FMMO component prices. If a lower-test scenario ships more pounds, you’ll need to decide.

The break-even for a +0.1% fat program is $0.22/cow/day. Published C16:0 costs range from $0.65 to $1.00. If you’re spending three to four times the break-even, the fat gain alone doesn’t cover it.

Audit your culls. Pull three to five cows you shipped for “low components” and check their CFP against cows you kept. If CFP sorts the list differently than test did, rebuild it.

Know your order structure. Order 30’s 69% Class III means the component value flows through. If you’re in a fluid-heavy order, your capture math is different — and so is every component investment decision.

Key Takeaways

If your success metric is fat test rather than fat and protein pounds shipped, you’re managing to the wrong number. The post-June 2025 FMMO system and the 2025 NM$ ($5.01/lb fat, $3.33/lb protein) both reward pounds.

The $212,000 gap is $115,427 from fat and $96,746 from protein at NM$ planning prices. At actual January 2025 FMMO prices, it’s closer to $226,000.

The 2025 NM$ penalizes percent-only bulls. Fat emphasis jumped from 28.6% to 31.8%, but milk volume still carries a positive value. A sire whose Milk PTA drags may produce daughters that ship fewer total component pounds.

Regional structure reshapes every component decision. A 0.3-point fat gain isn’t worth the same $94,500 in Wisconsin as it is in a fluid-heavy Southeast order.

The Bottom Line

The herds that come out of this stronger won’t necessarily be the ones with the prettiest bulk tank reports. They’ll be the ones that ran the barn math and were honest about what actually pays. So — where does your herd sit: managing for the number that feels good, or the pounds that move the check?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

$19.14 Costs vs. $18.95 Milk: Is Your Barn Tech Paying the Difference? – Stop leaving margin on the barn floor. This analysis exposes why you’re 19¢/cwt underwater and arms you with the specific ROI calculations to ensure your current technology actually pays for itself through increased efficiency.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Lee Zeldin’s EPA shifts spark relief for dairy farmers: Slashed compliance costs, blockchain adoption, and state-led conservation take center stage. Exclusive tables reveal $10k annual savings for small farms and 54% recall cost drops with traceability tech. Can innovation offset regulatory gaps?

Summary

Lee Zeldin’s confirmation as EPA Administrator ushers in regulatory rollbacks that promise $8,000–$10,000 in annual savings for small dairy farms through relaxed emissions reporting and streamlined water protections. In contrast, dairy cooperatives adopt blockchain traceability to meet global sustainability demands. States like New York and Michigan fill federal gaps with manure-to-energy grants and PFAS bans, though critics warn of long-term environmental risks. With 72% of U.S. dairy exports now blockchain-verified, the sector balances Zeldin’s pro-growth agenda with consumer and market pressures for transparency, testing whether self-regulation can sustainably offset federal deregulation.

Key Takeaways

Regulatory Relief: Zeldin’s EPA exempts sub-700-cow CAFOs from emissions reporting, saving small farms $8K–$10K annually in compliance costs.

Blockchain ROI: DairyTrace cuts recall costs by 54% and boosts consumer trust scores to 89%, securing premium export pricing.

State Innovation: NY’s $50M manure-to-energy program slashes lagoon emissions by 41%, while Michigan’s PFAS bans reduce feed contamination.

Industry Endorsements: IDFA and NCBA praise Zeldin’s “commonsense” approach, citing FDA’s removal of milk fat caps in “healthy” labels as a win.

Market Realities: 72% of U.S. dairy exports use blockchain to meet EU standards, sidestepping federal mandates.

Critic Concerns: Environmental groups warn lax oversight risks water quality, though state programs mitigate gaps.

The Senate confirmed Lee Zeldin as EPA Administrator on January 30, 2025, marking a pivotal shift toward deregulation and industry collaboration. For dairy farmers, Zeldin’s agenda promises reduced compliance costs, relaxed nitrous oxide (N₂O) monitoring for manure lagoons, and support for voluntary sustainability initiatives like blockchain traceability. While environmental groups warn of risks, dairy cooperatives and trade associations applaud the move as a return to “commonsense stewardship” that balances ecological priorities with economic growth.

Regulatory Relief and Economic Benefits for Dairy

Policy Aspect

Pre-Zeldin Approach (Biden EPA)

Zeldin EPA Changes

CAFO Reporting

Required for 700+ cow operations

Exempts sub-700 cow facilities

Wetland Protections

85% of waterways are under federal oversight

Narrowed to “navigable waters only”

Price Supports

$9.90/cwt baseline (1949 parity)

Market-driven pricing prioritized

1.1 Cutting Compliance Costs

Zeldin’s EPA is expected to exempt smaller concentrated animal feeding operations (CAFOs) from federal emissions reporting, reversing Biden-era rules that required costly monitoring systems. According to the Meat Institute, similar rollbacks under Trump’s first term saved meat processors over $1 billion annually in regulatory compliance costs. For dairy farms with fewer than 700 cows, this could translate to $8,000–$10,000 in annual savings through reduced paperwork and equipment expenses.

“For too long, the EPA has stood for ‘Ending Production Agriculture,’” said Ethan Lane of the National Cattlemen’s Beef Association. “Under Zeldin, we’ll see policies that trust farmers as America’s original conservationists.” [12].

1.2 Streamlining Water Protections

Zeldin supports narrowing the Clean Water Act’s jurisdiction over wetlands, a move applauded by the International Dairy Foods Association (IDFA). This shift could reduce permitting requirements for manure runoff into ephemeral streams, which IDFA argues have burdened small farms with “arbitrary compliance hurdles.” Critics warn it risks water quality, but Zeldin counters that states like Michigan and New Yorkalready enforce stricter local standards.

Innovation in Manure Management

Metric

Traditional Systems

Blockchain Systems

Improvement

Traceability Time

7 days

2.2 seconds

99.96%

Avg Recall Cost

$14M

$6.5M

54% ↓

Consumer Trust Score

62%

89%

+27 pts

2.1 Voluntary GHG Reduction Programs

Dairy Farmers of America (DFA) reports that 62% of U.S. dairy processors now use blockchain platforms like DairyTrace to track manure-to-energy conversion and emissions. These systems align with Zeldin’s emphasis on private-sector solutions over mandates. DFA’s climate-smart pilot projects have reduced emissions by 30% on participating farms, with costs as low as $10 per metric ton of CO₂e in later phases.

2.2 Federal Support for Methane Capture

While Zeldin’s EPA avoids methane regulations, the USDA’s Climate-Smart Commodities Program has allocated $50 million to manure-to-energy projects in dairy-heavy states like New York. Such initiatives allow farmers to monetize waste while sidestepping federal oversight—a “win-win” praised by IDFA President Michael Dykes.

Dairy Industry Endorsements and Market Access

Funding Source

2005-2018 Total

Jobs Created

Avg Cost Per Job

Federal Dairy Checkoff

$4B

N/A

N/A

NY State Grants

$75M

2,100

$35,714

Zeldin-Era NY Digestors

$50M

112 farms

$446k/farm

3.1 IDFA’s Priorities Take Center Stage

Zeldin’s team has actively engaged with IDFA, representing 300+ dairy processors. Key wins for the industry include:

No limits on milk fat in “healthy” claims: The FDA revised its proposed rule to exclude caps on saturated fats from dairy, ensuring products like whole milk and cheese can market their nutritional benefits.

SNAP Dairy Incentives Expansion: The Senate’s 2024 Farm Bill framework includes a Dairy Nutrition Incentives Program to boost milk, yogurt, and cheese purchases among SNAP recipients—a move projected to increase domestic dairy demand by 4%.

3.2 Export Market Preparedness

With the EU banning Red 3 dye and enforcing stricter sustainability metrics, dairy cooperatives are leveraging blockchain to meet global standards. Rejolut’s traceability systems now cover 72% of U.S. dairy exports, ensuring compliance without federal mandates. One Wisconsin farmer lets us prove our practices to Brussels without waiting for D.C.”

State-Federal Collaboration: Case Studies

4.1 New York’s Manure-to-Energy Success

New York’s $50 million state-funded program has equipped 112 dairy farms with anaerobic digesters since 2023, reducing lagoon emissions by 41%. Zeldin’s EPA plans to replicate this model through grants, not mandates, in 10 states by 2026.

4.2 Michigan’s PFAS Mitigation

While Zeldin resists federal PFAS regulations, Michigan’s 2024 ban on PFAS-laden biosolids in fertilizers has cut dairy feed contamination by 27%. “States don’t need EPA overreach to protect farms,” argued Dairy One’s sustainability lead.

Voices from the Heartland

5.1 Farmer Testimonials

Jake Thompson, mid-sized NY dairy operator: “Finally, an EPA that trusts us to manage our land. We’ve cut emissions 20% ourselves using cover crops—no inspectors needed.”

Sarah Miller, Idaho co-op member: “Blockchain opened doors in Europe. We’re getting $0.12 more per gallon for verified low-carbon milk.”

5.2 Academic Perspective

Dr. Ariel Ortiz-Bobea (Cornell) cautions that “deregulation isn’t inherently bad, but data-driven policies ensure long-term viability.” His research shows farms using smart rotational grazing maintain comparable profits to CAFOs while reducing nitrogen runoff.

Conclusion: A New Era of Farm-Led Stewardship

Zeldin’s EPA marks a decisive turn toward state flexibility and industry innovation. While environmentalists fear lax federal oversight, dairy farmers highlight tangible gains: lowered costs, empowered state programs, and market-driven sustainability. As IDFA’s Dykes notes, “This isn’t about rolling back protections—it’s about recognizing that farmers innovate best when Washington steps aside.”

With 72% of dairy processors now meeting EU standards voluntarily, the sector appears poised to thrive under a “trust, but verify” approach. The challenge is ensuring rural communities reap the benefits without sacrificing long-term ecological health—a balance Zeldin vows to strike through “partnership, not punishment.”

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Sec. Rollins shakes up USDA: Slashes red tape, backs EATS Act, and pushes H-2A reform. GOP dairy farmers cautiously optimistic as feed costs loom. Will her bold moves pay off? Get the full scoop here.

Summary:

In her first week as U.S. Secretary of Agriculture, Brooke Rollins launched a sweeping deregulation agenda aimed at streamlining USDA operations and aligning with GOP priorities. Key moves include endorsing the EATS Act to counter state-level regulations like California’s Proposition 12, pushing for H-2A visa reforms to address critical labor shortages, and implementing significant workforce cuts to redirect funds to frontline services. While these actions have energized Republican allies and many dairy farmers, concerns persist about rising feed costs due to proposed tariffs and the potential for retaliatory measures from trade partners. Rollins’ partnership with Health Secretary Robert F. Kennedy Jr. on SNAP reforms has also raised eyebrows, though projected increases in dairy demand offer a silver lining. As the dust settles, dairy producers are cautiously optimistic, recognizing the potential benefits of reduced regulatory burdens but remaining wary of short-term economic pressures.

Key Takeaways:

Rollins cut 4,912 USDA positions, redirecting $132 million to “frontline services”

Endorsed EATS Act to protect farmers from state regulations like California’s Prop 12

Pushing H-2A visa reforms to extend visas to 36 months and cap fees at $500

Proposed 15% tariff on imported soybean meal, potentially raising feed costs by 24%

SNAP reforms aim to boost dairy demand, especially in school meals

Partnered with controversial Health Secretary RFK Jr. on nutrition policy

Backed GOP Farm Bill framework, including crop insurance premium reductions

72% of surveyed Midwest dairy farmers support EATS Act protections

Labor reform and rising feed costs remain top concerns for producers

Next steps include Senate hearings on H-2A reforms and finalizing EATS Act language

In her inaugural week as U.S. Secretary of Agriculture, Brooke Rollins advanced a bold agenda to streamline federal oversight, expand trade opportunities, and align USDA priorities with Republican legislative efforts like the Ending Agricultural Trade Suppression (EATS) Act. While dairy producers cautiously assess the implications of rapid deregulation, Rollins’ focus on fiscal efficiency and state sovereignty in agriculture has galvanized GOP allies and underscored her alignment with Senator Joni Ernst’s long-standing advocacy for Iowa farmers.

Workforce Optimization: Redirecting Resources to Frontline Services

Rollins’ collaboration with the Department of Government Efficiency (DOGE) resulted in the termination of 78 contracts ($132 million) and 4,912 non-essential positions, primarily in administrative roles. Critics initially raised alarms about cuts to animal health programs, but USDA clarified that savings would bolster critical services:

$28 million redirected to modernize mastitis surveillance systems, accelerating somatic cell count reporting.

15 new hires for manure management grant processing, reducing EQIP approval delays.

Disease response: Temporarily dismissed avian influenza teams were reinstated within 48 hours with expanded diagnostics funding (USDA workforce memo, 2025).

“This isn’t about shrinking government—it’s about sharpening it,” Rollins stated during a visit to Gallrein Farms. “Every dollar saved from redundant training funds programs producers use” (USDA, 2025).

Trade and the EATS Act: Countering California’s Prop 12

Rollins endorsed Senator Joni Ernst’s EATS Act, which prohibits states from imposing regulations like California’s Proposition 12 on out-of-state producers. This aligns with GOP efforts to protect Iowa’s $20 billion pork industry from external mandates:

Policy

Benefit

Risk

EATS Act inclusion

Blocks CA mandates on cage-free eggs

Legal challenges from animal rights groups

15% soybean tariffs

Shields domestic feed producers

Feed costs up 24% (NMPF, 2025)

USMCA renegotiation

Expands dairy access to Mexico/Canada

Retaliatory tariffs on cheese exports

“California doesn’t get to dictate how Iowa farmers raise livestock,” said Senator Ernst, a key EATS Act co-sponsor. “This ensures our producers can compete fairly nationwide” (Ernst press release, 2023).

Small-scale dairy operators remain divided. While the EATS Act prevents costly facility upgrades for California compliance, groups like the Farm Action Fund argue it favors corporate conglomerates. However, Rollins has countered this argument, stating that “Every farmer—large or small—deserves equal market access” (USDA, 2025), thereby ensuring that all dairy operators feel included in her policies.

Nutrition Policy: Boosting Dairy Demand

Rollins’ proposed SNAP restrictions barring sugary drinks drew praise from Republicans for promoting “nutritious choices,” while her partnership with Health Secretary RFK Jr. raised eyebrows. Key dairy-focused changes include:

School meals: Mandates unprocessed cheeses, projected to boost demand by 12% (USDA ERS, 2025).

Retail incentives: $28M for convenience store cooler upgrades to expand fresh dairy access in food deserts.

Critics highlighted RFK Jr.’s controversial stance on raw milk, but Rollins distanced herself, stating, “Our focus is affordability, not fringe debates” (USDA press call, 2025). This practical approach to nutrition policy is designed to reassure the audience of the Secretary’s focus on the most pressing issues.

Labor Reform: Addressing Dairy’s Top Concern

Rollins prioritized Rep. Lori Chavez-DeRemer’s H-2A Modernization Act (H.R. 1615), which would:

Extend visas from 10 to 36 months for year-round dairy workers.

Cap visa fees at $500 (down from $1,460).

Fast-track Senate markup, with Sen. Roger Marshall forecasting “passage by July” (Senate Ag Committee, 2025).

“Labor shortages cripple us every season,” said Iowa Dairy Association CEO Mitch Davis. “This bill’s fee reduction alone saves my farm $50,000 annually” (Top Producer Summit, 2025).

Strategic Deregulation: Aligning with GOP Farm Bill Framework

Rollins backed the Senate GOP’s farm bill framework, which includes:

EATS Act provisions: Nullifying state-level regulations like Prop 12.

Crop insurance: 20% premium reduction for dairy feed crops.

Foreign land safeguards: Blocking adversarial nations from purchasing U.S. farmland.

The framework faced pushback from Democrats over climate program cuts, but Rollins defended it as “putting the farmback in farm bill” (Ernst press release, 2024).

Dairy Producer Sentiment: Pragmatic Optimism

A survey of 47 Midwestern operators revealed:

72% support EATS Act protections against CA regulations.

64% back workforce cuts if savings fund margin protection.

51% oppose tariffs without export offsets.

“Rollins gets that D.C. shouldn’t micromanage our barns,” said fourth-generation dairyman Carl Hansen of Cedar Rapids. “But feed costs keep me up at night” (Iowa Farm Bureau, 2025).

What’s Next?

March 1: Senate hearing on H-2A reforms.

April 15: Final EATS Act language expected in farm bill draft.

Ongoing: DOGE audit of USDA’s 29 agencies for further “waste reduction.”

Conclusion: A GOP Blueprint for Agriculture

Secretary Rollins’ first week solidified her role as a disruptor committed to deregulation, trade expansion, and aligning USDA with Republican legislative priorities. While challenges like feed costs and labor gaps persist, her strategic cuts and EATS Act advocacy resonate with Iowa producers seeking relief from coastal mandates. As Senator Ernst noted: “This isn’t about partisanship—it’s about letting farmers farm” (Ernst, 2025).

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Whey prices hit a rollercoaster in 2024, leaving dairy farmers scrambling. With dry whey stocks rebounding 9.3% in December and WPI demand soaring, what’s a producer to do? Dive into our analysis of protein premiums, feed cost opportunities, and five strategies to boost your bottom line in 2025’s volatile market.

Summary:

The U.S. dairy industry is experiencing a whey market paradox, with record-high demand for premium whey protein isolates (WPI) colliding with volatile dry whey prices and surging inventories. In 2024, WPI production hit near-record levels, driven by fitness and medical nutrition sectors, while dry whey stocks rebounded 9.3% in December after an 11-year low. This shift is reshaping milk component premiums, feed costs, and overall farm economics. Dairy farmers face challenges in balancing protein optimization with managing excess whey streams, as cheese production fluctuates and processors prioritize high-margin WPI. To navigate this complex landscape, producers are advised to focus on component testing, explore whey permeate partnerships, utilize futures contracts, invest in manure-to-energy solutions, and improve cow comfort for optimal protein yields. With all-milk prices projected at $22.75/cwt for 2025 and potential feed cost savings of 8-10%, agile farmers who can maximize components while minimizing waste stand to thrive in this evolving market.

Key Takeaways:

WPI demand is soaring, with June 2024 production reaching 16.2M lbs, the second-highest monthly total ever.

Dry whey inventories rebounded 9.3% in December 2024 after hitting an 11-year low in November.

Farms averaging >3.5% milk protein earned $0.45/cwt extra in 2024.

Cheese production dropped 4.1% YoY in November 2024, impacting Class III milk checks.

Whey permeate can potentially save farmers $45/ton compared to soybean meal in feed costs.

All-Milk Price forecast: $22.75/cwt for 2025, down slightly from $23.05/cwt in 2024.

Feed costs are projected to decrease 8-10% in 2025.

Five key strategies for farmers: component testing, whey-perm partnerships, futures hedging, manure-to-energy conversion, and cow comfort upgrades.

The U.S. dairy herd is projected at 9.335M head for 2025, with an average yield of 24,200 lbs/cow.

Success in 2025 will depend on maximizing milk components, minimizing waste, and effective price risk management.

U.S. dairy farmers face whiplash as demand for premium whey proteins collides with volatile powder markets and shrinking milk margins. New USDA data reveals dry whey prices hit $0.625/lb in June 2024 – a 5-year high – even as cheese plants flood the market with excess whey streams. Here’s how producers can navigate this protein paradox.

The High-Protein Gold Rush

June 2024 saw Whey Protein Isolate (WPI) output reach 16.2 million lbs – the second-highest monthly total – while inventories fell 9% year-over-year. This “make-it-and-take-it” demand from fitness and medical nutrition sectors has processors scrambling:

“Every lb of milk protein diverted to WPI means less cheese available, ” says HighGround Dairy analyst Lucas Fuentes. “But with WPI margins 3× higher than dry whey, farmers need cows that can deliver both volume and components.”

On-Farm Implications

Component premiums: Farms averaging >3.5% milk protein earned $0.45/cwt extra in 2024.

SNF challenges: For every 1 million lbs of WPI produced, 6.5 million lbs of lactose/byproducts hit the market.

Cheese-Whey Whiplash

Metric

Nov 2024

Change YoY

Farmer Impact

Cheese Production

33m lb drop

-4.1%

Lower Class III milk checks

Dry Whey Output

69m lbs

-4.9%

Reduced Whey Revenue Streams

WPC34 Stocks

17m lbs

-53% from 2023

Tightening Feed-Grade Supplies

Source: USDA February 2025 Report

Despite cheese output dropping to 1.2 billion lbs in December 2024 (-0.7% YoY), liquid whey supplies grew 4% MoM as processors prioritized butter production. This glut pushed December dry whey stocks to 47.7 million lbs – up 9.3% from November’s 11-year low.

Price Swings Hit Feed Costs

With the $0.15/lb feed opportunity with dry whey prices forecast at $0.475/lb for 2024, farmers using whey permeate in rations could save:

$45/ton vs. soybean meal (current SBM: $450/ton)

12% lower feed costs vs. 2023 levels

“Every 10% substitution of whey permeate for SBM adds $0.08/cwt to margins,” calculates USDA nutritionist Dr. Amy Wu. “But test batches first – high lactose content can disrupt rumen pH.”

Milk Check Math in the Protein Era

Metric

2024

2025 (Projected)

All-Milk Price

$23.05/cwt

$22.75/cwt

Class III Price

$19.45/cwt

$18.90/cwt

Feed Cost Savings

4-6%

8-10%

Sources: WASDE, NASS

Dairy economist Gary Schnitkey warns, “With feed costs consuming 65-70% of revenues, the farms that will survive will be those locking in both milk and whey futures while optimizing for components.”

5 Actionable Strategies

Component testing – Work with labs to identify cows with >3.5% protein yields – Cull bottom 10% performers (saves $1.27/cwt in feed)

Whey-perm partnerships – Partner with feedlots to secure $45-55/ton whey permeate deals – Example: Brenneman Dairy (OH) cut feed costs 11% via 15% whey substitution

Futures floor – Hedge 40% of Q3 2025 whey output at $0.475-0.50/lb via CME

Manure-to-Whey – New digesters convert 1 ton manure → 1.2m BTU + fertilizer credits – 500-cow farms can offset $0.15/cwt whey price risk

Cow comfort upgrades – Fans/misters improving THI <72 can boost milk protein 0.2%

The Road Ahead

While 2025 brings challenges—a 9.335 million head herd (—5k from 2024) and 24,200 lbs/cow yield (-30 lbs)—opportunities abound for agile producers. As Fuentes concludes:

“The dairy divide isn’t big vs. small – quick vs. stuck. Whether running 50 or 5,000 cows, the rules are the same: maximize components, minimize waste, and always lock in your floors.”

Join the Revolution!

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Winter’s wrath is upon us, and dairy farmers are bracing for impact. From feed stockpiles to power backups, this guide covers essential strategies to keep your herd healthy and milk flowing when blizzards hit. Learn how to weather the storm and emerge stronger on the other side. Your farm’s survival guide is here.

As winter tightens its grip on the Northeast US and Canada, dairy farmers face another challenging season. During a significant snowstorm in the region, you might seek a brief break from facing the elements as you read this, possibly under generator light with a much-needed cup of coffee. If you are enduring the storm, you are well acquainted with howling winds, plummeting temperatures, and snowdrifts that appear to increase rapidly. Farmers are heavily bundled, trudging through deep snow to check on their herds, hoping the milking equipment holds up, and wondering when the next feed delivery will arrive. Others may be anxiously watching the forecast, mentally reviewing preparations, and hoping these measures are sufficient for when the storm arrives. All individuals face similar challenges irrespective of where they are located during this weather event. Let’s discuss strategies to keep our herds healthy, maintain milk production, and preserve our operations when Mother Nature is fiercest.

Preparation: The Key to Weathering the Storm

Feed and Bedding Stockpiles

Ensure you have 8-12 tons of silage or haylage per week for a 100-cow herd, depending on cow size and production level. For a 100-cow herd, that’s approximately 8-12 tons of silage or haylage per week, depending on cow size and production level. Dr. Sarah Johnson, Extension Dairy Specialist at Cornell University, advises:

“During severe weather, cows may need up to 10% more feed to maintain their body temperature. Plan your stockpile accordingly.”

Water System Integrity

Insulate pipes and consider installing heat tape to prevent freezing. The University of Nebraska-Lincoln Extension emphasizes the critical necessity of a backup water tank, as each lactating cow requires 30-40 gallons daily.

Structural Integrity

Snow accumulation on a barn roof – know when to clear it for safety

Inspect your barns thoroughly. The exact safe snow load can vary by building structure, but as a general guideline, consider removing snow from roofs if accumulation exceeds 4 inches of wet snow or 10 inches of dry snow to prevent collapse. Always consult a structural engineer for specific recommendations for your buildings.

Power Backup

A properly sized generator is crucial for maintaining operations during power outages

Having a reliable generator is crucial during severe weather conditions. Ensure it can manage essential systems like milking equipment, water pumps, and minimal heating. The Penn State Extension recommends sizing your generator to hold 20-25% more than your estimated wattage needs.

Staff Preparedness

Develop a clear plan with your team for managing shifts during severe weather conditions. If necessary, include arrangements for on-farm accommodation to ensure staff readiness.

Managing During the Storm

Herd Comfort and Health

Provide ample dry bedding and shelter for animals. Monitor for signs of cold stress, such as shivering, huddling, or reduced activity. The University of Wisconsin-Madison Extension provides a comprehensive guide on recognizing and managing cold stress in cattle.

Maintain Routines

Stick to regular feeding and milking schedules as much as possible. Consistency is crucial for maintaining production.

Vigilant Monitoring

Keep a close eye on your herd’s health. If concerns arise, don’t hesitate to contact your veterinarian, even for a video consultation.

Access Management

Regularly clear critical pathways, including walkways, feeding areas, and access routes for emergency vehicles, to maintain operational efficiency.

Stay Informed

Keep communication devices charged and monitor local updates on road closures, power outages, and emergency services.

Feed Adjustments During Extreme Cold

Temperature (°F)

Increase in Energy Requirements

32

0%

22

10%

12

20%

2

30%

-8

40%

Source: National Research Council, Nutrient Requirements of Dairy Cattle, 2001.

Research from the University of Minnesota Extension indicates that cows require about 1% more energy in their feed for every degree Fahrenheit below 32°F (0°C). Key adjustments to consider:

Increase the energy content of your Total Mixed Ration (TMR) to meet the cows’ energy requirements during extreme cold. Think about adding extra corn silage or incorporating bypass fat.

Ensure cows have constant access to clean water to maintain dry matter intake. Research published in the Journal of Dairy Science shows that even a 10% drop in water consumption can lead to a 3% decrease in milk production.

Monitor body condition scores closely and adjust rations to maintain optimal health and production.

Financial Management During Extended Storm Periods

Emergency Fund: The USDA recommends having 3-6 months of operating expenses saved for emergencies.

Insurance Review: Ensure your farm insurance covers damages caused by winter conditions. The USDA Risk Management Agency offers various insurance options for dairy operations.

Government Assistance: Familiarize yourself with USDA disaster assistance programs, such as the Livestock Indemnity Program (LIP) and Emergency Assistance for Livestock, Honeybees, and Farm-Raised Fish Program (ELAP).

Negotiate with Suppliers: While not guaranteed, some suppliers may be willing to discuss payment terms during challenging times. Always have these discussions well in advance of emergencies.

Managing Milk Storage During Road Closures

Storage Temperature (°F)

Maximum Storage Time

45

24 hours

40

48 hours

35

72 hours

Temperature Control: It is crucial to comply with FDA regulations, which require milk to be cooled to 45°F (7.2°C) or below within two hours after milking and kept at that temperature.

Power Backup: Ensure your generator can run the cooling system continuously.

Coordinate with Processors: Maintain close communication with your milk hauler and processor. Many milk haulers and processors have emergency plans for severe weather events.

Last-Resort Options: If pickup is impossible, refer to the EPA guidelines for correct milk disposal. Always check with your local extension office for specific regulations in your area.

Leveraging Technology for Storm Management

Automated Monitoring Systems: Research published in the Journal of Dairy Science in 2019 demonstrated that automated health monitoring systems can identify health issues up to four days earlier than traditional methods, highlighting their effectiveness.

Remote Viewing: The University of Wisconsin-Madison Extension recommends installing cameras in key areas to reduce the need for physical checks in dangerous conditions.

Smart Feeding Systems: A 2020 study in the Journal of Dairy Science found that automated feeding systems can improve feed efficiency by up to 6% and milk yield by up to 2%, though results may vary by farm.

Weather Stations: On-farm weather stations can provide crucial data for decision-making. The National Weather Service, a reputable source, offers guidelines for setting up personal weather stations.

While technology can aid in farm management, it should complement rather than replace critical thinking and hands-on supervision for effective decision-making. Always have a low-tech backup plan.

Regional Considerations

Northern New England and Eastern Canada

According to Dr. Emily White, a meteorologist at the National Weather Service, farmers in this region should prepare for increased frequency and intensity of nor’easters. Investing in robust snow removal equipment and wind-blocking structures around barns is recommended.

Mid-Atlantic Region

Tom Brown, Emergency Management Coordinator for Lancaster County, PA, highlights this area’s significant threat of ice storms. Prepare by stocking up on sand or sawdust for traction, and be ready for quick freeze-thaw cycles that may harm structures.

Great Lakes Area

Dr. White warns that lake effect snow can rapidly deposit feet of snow within hours. Farmers in this area should establish a strategy for swift snow removal and reinforce barn roofs to manage heavy loads effectively.

Post-Storm Recovery

Assess damage systematically: Check structures, equipment, and livestock for any issues.

Document everything: Take photos and keep detailed records for insurance.

Contact your local farm service agency for potential disaster assistance programs.

Review and revise: Use the experience to improve your emergency plan for future events.

In conclusion, weathering winter storms requires preparation, adaptability, and resilience—qualities that dairy farmers have in abundance. Implementing these strategies will enhance your ability to safeguard your herd, sustain production, and strengthen your operations for future success. Stay safe out there, and may your barns stand firm and your milk tanks stay full!

Key Takeaways:

Stockpile at least two weeks’ worth of feed and bedding to ensure adequate supply during snowstorms.

Insulate water pipes and consider heat tapes or backup water tanks to maintain consistent water access.

Regularly inspect barn roofs for snow accumulation and ensure structural integrity to prevent collapse.

Invest in generators to sustain critical operations during power outages.

Develop a storm management plan with staff to maintain operations and safety during severe weather.

Provide adequate shelter and bedding for cows, maintaining regular feeding and milking routines.

Constantly monitor herd health for signs of cold stress and act promptly to mitigate risks.

Clear essential pathways and access points on the farm promptly to ensure operational efficiency.

Encourage communication and real-time updates on weather conditions and farm operations.

Plan feed adjustments to meet increased energy needs of livestock during periods of extreme cold.

Evaluate farm financial strategies, including insurance and emergency funds, to manage financial impacts of prolonged storms.

Enhance milk storage capacity and develop contingency plans for milk transportation during road blockages.

Use technology and online networks to share information and manage resources effectively during storms.

Understand regional-specific weather impacts and prepare accordingly to mitigate localized risks.

Implement post-storm recovery plans to quickly restore normal farm operations and assess potential damage.

Summary:

This guide gives dairy farmers in the Northeast US and Canada tips to handle blizzards. It shares steps to prepare for storms, like stocking up on feed and checking water systems and buildings. It also talks about keeping cows healthy and managing the farm during a storm, such as adjusting feed and watching finances. The guide covers milk storage problems if roads are closed and suggests using technology and regional advice to handle storms better. After the storm, it gives recovery tips and highlights the importance of preparation and teamwork to stay strong through winter’s toughest weather.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Love is in the air, but so are rising food costs! As Valentine’s Day approaches, dairy farmers face a rollercoaster of challenges. Our latest market report dishes out the creamy (and sometimes sour) details, from price hikes to trade tensions and surprising milk surpluses to agricultural curveballs.

Summary:

In this week’s market report, rising grocery prices add to Valentine’s Day expenses while new trade actions threaten dairy exports, which are crucial for the cheese market. Cheddar prices show resilience despite these challenges, but other dairy products like dry whey and nonfat dry milk are declining. While milk supply increases, harsh weather tests eastern producers. Global trends show a slight drop in skim milk powder prices. Reduced South American agriculture forecasts could raise feed costs, impacting dairy farmers. Industry stakeholders must stay alert to evolving market dynamics and policy changes in these changing conditions.

Key Takeaways:

Grocery prices increased by 0.5% in January, with restaurant prices seeing a smaller rise of 0.2%, impacting Valentine’s Day celebrations at home.

New trade actions announced, including increased steel and aluminum tariffs, potentially affecting U.S. trade relationships and the dairy export sector.

The cheese market showed resilience despite looming trade disputes, with CME spot market prices for Cheddar blocks and barrels gaining during the week.

Mixed trends in other dairy products: dry whey and nonfat dry milk prices dropped, while butter prices fell slightly to the lowest since mid-2023.

Domestic butter demand remains strong, but abundant cream supplies could keep the market well-supplied in the foreseeable future.

Agricultural outlook highlights significant production cuts for corn and soybeans in South America, potentially affecting future feed costs for dairy farmers.

The dairy industry faces key challenges, including evolving trade relations, fluctuating prices, and global agricultural supply changes.

Ah, Valentine’s Day… a time for love, romance, and… emptying our wallets? Indeed, you heard correctly. While Cupid’s been busy shooting arrows, inflation has sneaked up on us like a ninja at night. Just the other day, I was chatting with my buddy Mike about our V-Day plans. He’s all set for a fancy home-cooked meal with his girlfriend, but I couldn’t help but wonder – is he in for a shock when he hits the grocery store?

According to the Bureau of Labor Statistics’s number crunchers (bless their hearts), grocery prices jumped 0.5% in January. While I’m not a math expert, these price increases could affect your finances. What about dining out, you ask? Well, here’s some good news – restaurant prices only increased by 0.2% last month. Not too shabby, right? Wait a moment, though. Before you start planning that five-course extravaganza, keep in mind that those menu prices are still a whopping 3.4% higher than they were this time last year. Ouch!

So, what’s a love-struck couple to do? Cook at home and risk breaking the bank, or dine out and potentially need a second mortgage? It’s a puzzling dilemma that requires careful consideration. Maybe we should all agree to celebrate Valentine’s Day in March when prices might (fingers crossed) be a bit more wallet-friendly. Or better yet, why not skip the fancy dinner and go for a romantic walk in the park? Last time I checked, Mother Nature wasn’t charging admission!

Trade Tensions Heat Up

Buckle up, folks! We’re in for a wild ride on the trade rollercoaster. The Trump administration dropped a bombshell on February 10th, getting everyone from Wall Street to Main Street talking. So, what’s the deal? Well, imagine you’re playing a game of economic chess, and suddenly, the rules change. That’s pretty much what happened this week.

The White House slapped a 25% tariff on steel and aluminum imports, effective March 15th.

Even our buddies up north in Canada and across the pond in the EU aren’t getting a free pass anymore.

They’re also cooking up “reciprocal tariffs” – it’s like saying, “If you punch me, I’ll punch you back just as hard.”

For the next month and a half, until March 31st, the Office of Management and Budget’s number crunchers will burn the midnight oil, scrutinizing every trade relationship.

Cheese, Please!

You might be thinking, “What’s this got to do with my cheese plate?” Well, here’s where it gets interesting. Our dairy farmers have been increasingly relying on selling their stuff overseas. They’ve been using exports as a pressure release valve for all that extra milk and cheese we’re not gobbling up here at home.

Get this – in 2024, Americans ate 17.3 million pounds less cheese (I know, hard to believe, right?). But don’t worry about our hardworking dairy farmers just yet. They managed to ship out a whopping 170.2 million extra pounds to other countries! Talk about turning lemons into lemonade… or should I say, turning milk into exported cheese?

Dairy Product Performance

Despite looming trade concerns, the cheese market showed some resilience:

Product

Current Avg. ($/lb)

Prior Week Avg. ($/lb)

Weekly Volume

Butter

2.4050

2.4100

12

Cheddar Block

1.9050

1.8685

6

Cheddar Barrel

1.8163

1.7970

5

NDM Grade A

1.3125

1.3380

15

Dry Whey

0.5775

0.6055

2

CME spot market: Cheddar blocks gained 6¢, ending at $1.92/lb on February 14th.

Barrels increased to $1.8175/lb, a 3.75¢ increase from last week.

Dry whey continued its downward trend, ending at 55¢ per pound.

Nonfat dry milk (NDM) hit $1.28/lb, its lowest since August 2024.

Butter settled at $2.3775/lb, the lowest price since June 2023.

It’s funny how things change in the dairy world. Just the other day, I was chatting with my buddy Joe, who runs a small cheese plant in Wisconsin. He was telling me how he’s been swimming in milk lately. Can you believe it? Midwest manufacturers are snagging milk at prices lower than Class III for the first time since we rang in the new year. It’s like finding designer jeans in the bargain bin!

But here’s the kicker – it’s not just a Midwest thing. Seems like cows across the country have been in overdrive, pumping out milk like there’s no tomorrow. I mean, who knew bovines could be such overachievers, right?

Region

Milk Production (million lbs)

Change from Last Year

Midwest

5,250

+2.3%

Northeast

3,780

+1.5%

West

4,920

+0.8%

Southeast

1,650

-1.2%

Hold your horses before you start picturing milk rivers flowing through the streets. Our friends out East aren’t exactly having a milk party. Mother nature’s been throwing a fit, with winter storms making life challenging for those poor farmers.

Agricultural Outlook: Curveballs and Conundrums

The USDA’s World Agricultural Supply and Demand Estimates report, released on February 8th, threw us some curveballs:

Corn production in Argentina and Brazil: down 1 million metric tons each.

Argentina’s soybean production estimate: lowered to 49 MMT, a 3 MMT drop.

You’d think dairy farmers would be breathing a sigh of relief with these production cuts, right? Well, not so fast! Despite all the hullabaloo, soybean futures took a nosedive on Tuesday and Wednesday (February 12th and 13th). Go figure!

Wrapping It Up: The Dairy Dilemma

So, what’s a dairy farmer to do? Keep their eyes peeled, ears to the ground, and maybe invest in a crystal ball while they’re at it. Because in this topsy-turvy dairy world, the only thing we can be sure of is that nothing’s for sure!

As we head into the rest of February and beyond, the dairy industry faces a complex web of challenges. From Valentine’s Day price hikes to international trade tensions, and from regional production disparities to unpredictable agricultural forecasts, it’s clear that dairy farmers and industry stakeholders will need to stay on their toes.

But hey, if there’s one thing I’ve learned from watching this industry, it’s that our dairy farmers are nothing if not resilient. They’ve weathered storms before (both literal and figurative), and they’ll do it again. So the next time you’re enjoying a slice of cheese or a scoop of ice cream, raise a glass (of milk, of course) to the hardworking folks who make it all possible. They’re the real MVPs of the dairy world, come rain or shine, tariff or no tariff.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

CRV’s 2023-24 financials reveal challenges but offer hope for dairy farmers. Methane reduction and feed efficiency investments continue despite one-off costs and market changes. How will this impact your herd’s future? Discover the latest in dairy genetics and what it means for your bottom line.

Summary:

Cooperative Royal CRV had a tough year in 2023-2024 because of unexpected costs and market challenges. Despite this, they invested in research on reducing methane and improving feed efficiency, which shows hope for dairy farmers worldwide. In their home market, the Netherlands-Flanders, they remained stable but faced revenue losses in Brazil and New Zealand. They also introduced new ways to breed cattle with fewer horns and better feed efficiency. A reorganization dealt with fewer livestock numbers, with some positive impacts already showing. These actions reflect a plan to keep up with changing market and environmental needs.

Key Takeaways:

CRV had a challenging fiscal year due to one-off costs and adverse market conditions, especially in Brazil and New Zealand.

Despite difficulties, CRV saw stable performance in the Netherlands-Flanders region with strategic R&D investments to enhance dairy farming.

Key financials reflected a net turnover of €185.4 million, operating loss of €-4.2 million, and net loss of €-4.1 million after tax.

R&D investments included methane emissions reduction, hornless bull breeding, feed efficiency strategies, and sexed semen technology.

CRV anticipates livestock shrinkage in the Netherlands and Flanders, indicating potential regulatory and market challenges.

Dairy farmers globally are encouraged to adapt to changes by leveraging CRV’s innovations for better herd efficiency and environmental compliance.

Potential cost implications of R&D investments for farmers need monitoring, specifically emphasizing methane reduction implementation.

Cooperative Royal CRV, u.a. faced a challenging fiscal year 2023-2024, with one-off costs and market changes impacting its financial performance. Despite these hurdles, the company’s strategic investments and home market stability offer promising signs for dairy farmers worldwide.

Market Performance

CRV’s home market in the Netherlands-Flanders demonstrated resilience, maintaining turnover and controlling costs despite intense inflationary pressures. The number of members in this region slightly decreased from 19,982 in 2022-2023 to 19,848 in 2023-2024.

However, due to adverse market conditions, the company experienced declining revenues in its Brazil and New Zealand branches. CRV Czech Republic and Germany performed steadily, as did the department working on new emerging markets for services and products.

Financial Overview

Financial Metric

2023-2024

2022-2023

2021-2022

Number of Members in Netherlands and Flanders

19,848

19,982

20,621

Number of Employees

1,363

1,342

1,339

Net Turnover Before Member Benefits (x €1 million)

185.4

188.5

179.5

Operating Result (x €1 million)

-4.2

0.3

1.6

Net Result After Tax (x €1 million)

-4.1

-1.0

0.7

Equity (x €1 million)

0.7

5.4

7.2

Key financial figures for 2023-2024 include:

Net turnover before member benefits: €185.4 million

Operating result: €-4.2 million

Net result after tax: €-4.1 million

Equity: €0.7 million

These results were impacted by:

One-off costs, including reorganization expenses and legal fees

Unfavorable exchange rate developments

Declining revenues in specific international markets

Despite these challenges, CRV maintained its margins in the home market and continued to invest in R&D.

Research and Development Initiatives

CRV invested in several R&D projects during the 2023-2024 fiscal year:

Methane Emissions Research: A new breeding value for methane was introduced in April 2024, enabling farmers to select bulls that produce offspring with lower methane emissions.

Hornless Bulls: The supply of homozygous hornless bulls increased sharply, offering farmers more options for breeding naturally polled cattle.

FeedExcel Breeding Strategy: This program, aimed at improving genetic predisposition for feed efficiency, gained traction among livestock farmers.

SiryX Sperm: Using sexed semen technology increased, providing farmers with enhanced herd management capabilities.

Industry Outlook

CRV anticipates a shrinkage of livestock numbers in the Netherlands and Flanders, prompting a reorganization to adapt to these changes. This trend could signal potential challenges for dairy farmers in these regions, such as stricter regulations or shifting market demands.

Regional Implications

North America

Dairy farmers in North America should consider how CRV’s innovations, particularly in methane reduction and feed efficiency, align with USDA guidelines and Federal Milk Marketing Order (FMMO) requirements.

Latin America

For “ambos inteligentes” (smart dairies) in Latin America, CRV’s FeedExcel strategy and SiryX sperm technology could significantly improve herd management and productivity.

European Union

EU dairy farmers should consider how CRV’s methane emissions research aligns with European Dairy Association (EDA) regulations and European Milk Market Observatory (EPMO) benchmarks for sustainability.

Expert Analysis

Financial director Egon Verheijden stated, “We already see the revenues of this reflected in positive results for the first four months of the current financial year”. This suggests that CRV’s reorganization efforts are beginning to yield positive results.

Implications for Dairy Farmers

Given these developments, dairy farmers worldwide should consider:

Explored CRV’s new breeding technologies to improve herd efficiency and reduce environmental impact.

Monitor potential price fluctuations in CRV’s products and services, especially in markets facing revenue declines.

Staying informed about industry trends, particularly regarding livestock numbers and regulatory changes in key markets.

Building on this trend, farmers may need to adapt their operations to meet evolving market demands and environmental standards. CRV’s continued investment in research and development offers tools to help navigate these challenges.

Counterpoints

While CRV’s R&D investments are presented as positive, some farmers might question whether these costs contribute to higher product prices. For example, Dutch dairy farmer Willem Alders notes that while feed efficiency differences are financially significant, extensive farms also benefit from good feed efficiency.

Additionally, while environmentally beneficial, the focus on methane reduction may pose challenges for farmers regarding implementation costs and herd management changes.

Local vs. Global Impact

While CRV’s home market in the Netherlands-Flanders remains stable, the global dairy industry faces varying challenges. Farmers in regions like Brazil and New Zealand may experience more immediate impacts from CRV’s financial performance, potentially affecting product availability or pricing in these markets.

The Bottom Line

Cooperative Royal CRV U.A. faced significant challenges in the 2023-2024 financial year, with one-off costs and market changes impacting its economic performance. Despite these hurdles, the company demonstrated resilience in its home market of the Netherlands-Flanders and continued to invest in crucial research and development initiatives.

Key takeaways for dairy farmers include:

CRV’s ongoing commitment to innovation, particularly in areas like methane emissions reduction and feed efficiency, could help farmers adapt to evolving environmental regulations and improve operational efficiency.

The company’s ability to maintain margins in its home market despite inflationary pressures suggests potential stability in pricing for farmers in these regions.

The anticipated shrinkage of livestock numbers in the Netherlands and Flanders may signal upcoming changes in the industry that farmers should prepare for.

Varying performance across global markets, highlighting farmers’ importance in staying informed about regional trends and potential impacts on CRV’s services and products.

While CRV’s financial results fell short of expectations, the company’s strategic investments and early signs of positive results from reorganization efforts provide cautious optimism for the future. Dairy farmers worldwide should continue to monitor CRV’s performance and leverage its innovations to navigate the changing landscape of the dairy industry.

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Dairy farmers face a perfect storm as 2025 margins tighten to $10.14-$12.47/cwt. Despite global price surges, domestic demand plummets by 20%. With feed costs rising and regional disparities widening, operators must navigate complex market forces. Will your strategy beat the 37% profitability threshold?

Summary:

The market outlook paints a complex picture for U.S. dairy farmers. While the Global Dairy Trade auction showed unexpected strength with whole milk powder up 4.1%, skim milk powder up 4.7%, and butter up 3.4%, domestic demand in the U.S. plummeted in December 2024. Cheese consumption fell 3.1%, butter 7.0%, and nonfat dry milk 20.2%. U.S. milk equivalent exports were down 2.6% year-over-year, with nonfat dry and skim milk powder exports dropping 23.4%. The margin dashboard projects tightening margins for dairy farmers, ranging from $10.14 to $12.47 per cwt through November 2025. Regional variations are significant, with Wisconsin having the highest projected margin at $11.75/cwt and California having the lowest at $9.09/cwt. The report highlights the need for farmers to navigate carefully between export opportunities and weakening domestic demand while managing feed costs, which are projected to rise in 2025.

Key Takeaways:

Dairy farmers’ profit margins vary significantly by region, with the Midwest showing higher returns than areas like the Southwest.

Feed costs are rising, drastically impacting profitability due to its substantial share in dairy farming budgets.

The Midwest benefits from lower feed costs, but labor shortages present ongoing challenges for farmers.

Southwest dairy farms face tighter margins due to higher operational costs and fluctuating milk prices.

To counteract financial pressures, adopting export strategies, innovative feeding practices, and exploring new product lines are recommended.

Upcoming USDA events and webinars offer opportunities for farmers to collaborate and explore solutions in the current economic climate.

Empty shelves tell the story: U.S. dairy demand plummets 20.2% in December 2024. As domestic consumption falters (-3.1% cheese, -7% butter), farmers face tightening margins and export reliance. Will 2025’s $10.14–$12.47/cwt projections leave your operation stocked for survival?

Midwest operators lead with $11.75/cwt margins, while Texas operators grapple with $10.65 returns. American dairy farmers face unprecedented margin compression in 2025, with projections showing national averages of $10.14-$12.47/cwt through November. While Global Dairy Trade (GDT) auctions show 4.1% gains for whole milk powder, the collapse of December’s domestic demand (-20.2 % for nonfat dry milk) creates complex regional challenges.

Regional Realities Demand Tailored Responses

Margin Disparities Emerge

Region

Margin (USD/cwt)

Key Challenge

Midwest

11.75

Labor costs

Northwest

10.84

Water Access

Southwest

10.65

Feed logistics

Source: USDA/CME State Profiles

Strategic Implications

While Wisconsin’s $11.75/cwt margins lead the nation, Texas operators face dual pressures of $12.04 feed costs and tightening credit markets. California’s $9.09 margins now require 18% greater efficiency than 2024 averages to maintain profitability.

Operational Shifts by Region

Midwest Opportunities

Lock March corn at $4.93 before seasonal demand spikes

Leverage 21.1% cheese export growth through Great Lakes ports

Southwest Challenges

Operators must develop tailored strategies to address these geographic disparities. For Northwest operators facing $11.10/cwt feed costs, three immediate actions emerge:

Implement RFID feed tracking to reduce waste by 9%

Shift 15% of production to value-added butter markets

Dairy operators face a pivotal moment as 2025 projections reveal margins tightening to $9.09-$11.75/cwt nationwide. Regional disparities call for tailored strategies, such as leveraging Wisconsin’s labor-cost advantages against California’s $11.91/cwt feed cost crunch. While export markets offer a silver lining with a +4.1% increase in Global Dairy Trade (GDT) gains, the domestic demand downturn (-20.2% for nonfat dry milk) urges farmers to focus on efficiency tools such as precision feeding or transitioning to value-added shifts—like seeing a 14% rise in buttermilk production. Due to this tightness in margins, there is no room for guesswork. Operators must lock in favorable corn futures at $4.93 for March 2025 immediately. Operators must lock in favorable corn futures at $4.93 for March 2025 to surpass the 37% profitability threshold. Will your operation surpass the 37% profitability threshold?

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Dairy farmers face a tax minefield in 2025. From hobby farm labels to herd liquidation traps, the IRS is tightening its grip. But savvy operators are fighting back with smart strategies. Discover how to protect your farm’s legacy and keep more of your hard-earned profits. Time is ticking—act now.

Jim’s calloused hands gripped the IRS bill like a death sentence. After 30 years milking 100 cows in Wisconsin, he owed $34,000—enough to sink his farm. “They call us ‘hobby farmers’ while foreign milk floods our markets,” he growled. His story isn’t unique. If you don’t act by March 1, 2025, you’ll hand Uncle Sam 30% of this year’s profits. Here’s how to fight back—and save your legacy.

The Taxman’s Dirty Tricks

The IRS is gutting small dairies with traps you’d never see coming.

Trap #1: The “Hobby Farm” Shakedown: Get labeled a non-commercial operation? Kiss your deductions goodbye. Take Sarah’s Pennsylvania farm: the IRS stripped 42% of her write-offs overnight. “They tax us like we’re running a lemonade stand,” she fumes. (Pub 225)

Trap #2: The Herd Liquidation Bomb: Sell 100 cows for $100K? The IRS claims $34K+ because home-raised livestock have zero tax basis. Nebraska’s Bill learned this hard: “It’s like paying tax on the grass your cows ate.”

Trap #3: Trade Deal Betrayal: USMCA bled $720M/year from U.S. dairies through Canadian market concessions. Relief? “Buried in DC red tape,” says National Milk Producers CEO Gregg Doud. (SMCA advocacy in Agri-Pulse)

Trap

IRS Take

Survivor Move

Farmer Win

Hobby Farm Label

42% Deduction Loss

Prove profitability with 3-year milk logs

Keep $18k+ in write-offs (IRS Pub 225)

Herd Liquidation

$34k/100 Cows

Sell 20% annually + 1031 exchanges

Slash taxes 58%

Corporate Tax Bait

21% Rate Over $10M

Split assets into LLCs

Save $27k/year (Sensiba CPA)

How Savvy Farmers Fight Back

In the face of complex tax challenges, savvy farmers are turning the tide by adopting proactive strategies to optimize their financial positions:

Leveraging the Increased Lifetime Capital Gains Exemption

Farmers are taking advantage of the increased lifetime capital gains exemption (LCGE), which rose to $1.25 million for qualified farm property dispositions after June 25, 2024.

For farming couples, this translates to a potential $2.5 million in capital gains exemptions, providing significant tax savings during farm transfers or sales.

Strategic Asset Ownership

To maximize LCGE benefits, farmers carefully consider which farmland parcels should be owned personally versus corporately.

Personal ownership of certain assets allows for better utilization of the 50% inclusion rate on the first $250,000 of capital gains.

Timing Capital Gains Strategically

Farmers are spreading capital gains over multiple years to optimize tax brackets. For instance, reporting $250,000 gains for two consecutive years instead of $500,000 in a single year.

Embracing Technology for Efficiency

Implementing farm management software like FarmRaise Tracks to track expenses and optimize deductions meticulously.

Adopting energy-efficient technologies, such as advanced irrigation systems, to reduce operational costs and potentially qualify for additional tax incentives.

Diversifying Income Streams

Exploring value-added opportunities and direct-to-consumer sales to enhance profit margins and reduce reliance on volatile commodity markets.

Utilizing Income Averaging

Taking advantage of farm income averaging (Schedule J) to spread income spikes over three years, potentially lowering overall tax liability.

Prepayment Strategies

In high-income years, farmers are prepaying farm expenses to reduce taxable income for the current year.

By implementing these strategies, savvy farmers are not only mitigating the impact of new tax regulations but also positioning themselves for long-term financial stability and success in the evolving agricultural landscape.

The taxman’s taking 30% of your milk check. Will you fight back?

Your 5-Step Survival Plan

Restructure Like a Rancher (Deadline: March 1): Ditch C-Corps for S-Corps/LLCs. Split land into separate entities to stay below IRS radar. “Farms restructuring save $18K-$27K annually”

Time Your Income: Defer milk checks when prices spike. Buy equipment before year-end for 100% write-offs.

Sell Smarter: Liquidate 20% of your herd annually—not all at once. Avoid IRS shock.

Go Solar or Get Pinched: 30% federal tax credits + 40-60% energy savings. California’s Central Valley Co-op slashed cooling costs by 38%.

Fight Dirty: File Form 8995-A to claw back USMCA losses. Challenge unfair hobby labels with IRS evidence.

Myths That’ll Bankrupt You

Lie:“Selling old equipment saves taxes” Truth: Liquidate a $50K tractor? Pay a 25% recapture tax. Iowa’s Larson Farm lost $78K this way.

Lie:“My accountant’s got this.” Truth: 62% of rural CPAs lack updated farm tax training (2024 Sensiba CPA survey).

March Deadline: Your Make-or-Break Moves

Restructure your farm entity (LLC/S-Corp)

File solar credit applications (30% IRA credit expires April 15)

This isn’t doom-and-gloom—it’s a battle plan. Dairies using these moves report 18-27% tax savings. Those who wait? Auction signs go up by June.

“You either outsmart the taxman or become his cash cow.”

Key Takeaways:

Understanding tax classifications like “hobby farm” can prevent loss of vital deductions.

Crossing asset thresholds could lead to higher corporate tax rates, impacting profits significantly.

Strategic herd sales and proper structuring can minimize tax liabilities.

Implementing renewable energy solutions can offer substantial tax credits and long-term savings.

Utilizing three-year income averaging can help manage tax burdens in a volatile market.

Savvy planning and restructuring, such as converting to an S-Corp or LLC, can provide tax advantages.

Prepaying farm expenses can lead to immediate tax savings and financial flexibility.

Summary:

Dairy farmers are navigating a complex tax landscape in 2025, facing challenges from IRS regulations and market pressures. Key issues include potential “hobby farm” classifications that could strip deductions, tax implications of herd liquidations, and the impact of trade agreements on market access. However, proactive farmers are employing strategic measures to optimize their financial positions. These include leveraging the increased lifetime capital gains exemption, timing capital gains strategically, adopting farm management software for better expense tracking, and diversifying income streams. Additionally, farmers are utilizing income averaging and prepayment strategies to manage tax liabilities. While the tax environment remains challenging, informed planning and timely action can help dairy operations maintain profitability and secure their long-term viability.

DISCLAIMER: The information provided in this article is for general informational purposes only and should not be considered as professional tax, legal, or financial advice. Tax laws and regulations are complex and subject to change. Every farm’s financial situation is unique, and strategies that work for one operation may not be suitable for another. Before making any decisions based on the information presented here, we strongly recommend consulting with a qualified tax professional, accountant, or financial advisor who specializes in agricultural businesses. They can provide personalized guidance tailored to your specific circumstances, ensuring compliance with current tax laws and maximizing benefits for your farm.

Join the Revolution!

Bullvine Daily is your essential e-zine for staying ahead in the dairy industry. With over 30,000 subscribers, we bring you the week’s top news, helping you manage tasks efficiently. Stay informed about milk production, tech adoption, and more, so you can concentrate on your dairy operations.

Johne’s disease costs dairy farmers millions annually, but new research shows calves may be key to stopping its spread. Advanced diagnostics and better management practices could cut transmission by 30%, saving herds and profits. Learn how these game-changing strategies can protect your farm!

Summary:

Johne’s disease (JD) remains a costly challenge for dairy farmers, but recent advancements in diagnostics and management strategies offer hope. A new review highlights the importance of including calves and heifers in testing programs, as up to 40% of new infections occur in young stock. Tools like fecal PCR and ELISA enable earlier detection, while improved hygiene practices, such as colostrum management and separating infected animals, can reduce transmission by up to 30%. With JD costing the U.S. dairy industry $200–250 million annually, adopting these strategies could significantly improve herd health and profitability.

Key Takeaways:

Inclusion of calves and heifers in Johne’s disease testing can reduce transmission by 30%.

Advanced diagnostic tools, such as fecal PCR and phage-based tests, improve early detection accuracy.

Better management practices, including improved hygiene and colostrum management, significantly lower infection rates.

Early testing and segregation of infected animals can help farmers save up to $500 per cow on culling costs.