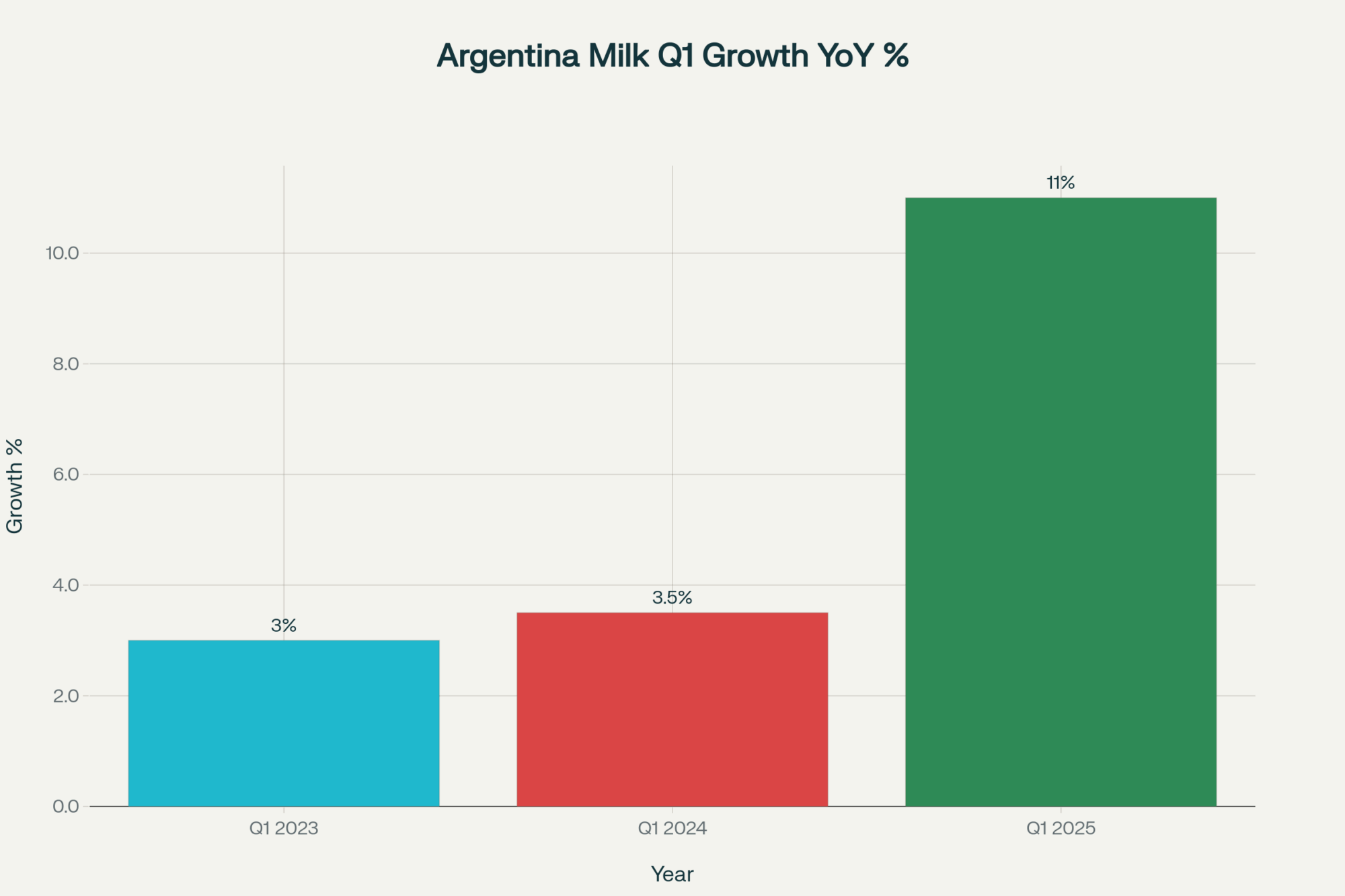

Argentina’s milk output jumped 11% in Q1—that’s reshaping global dairy prices faster than you think.

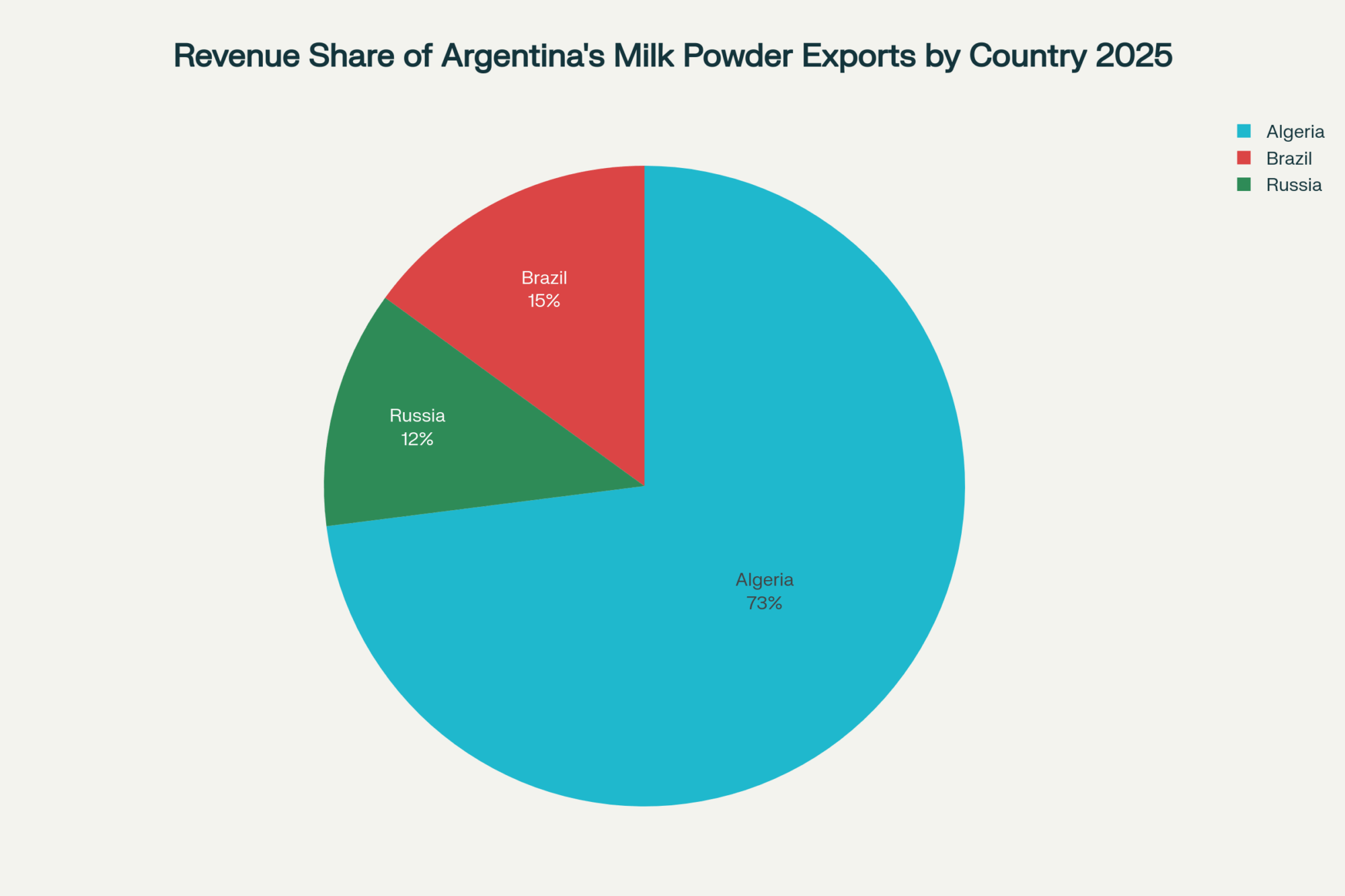

EXECUTIVE SUMMARY: Here’s what’s really goig on: Argentina just became the world’s fastest-growing major dairy producer with 11% growth in Q1 2025—and that’s going to hit your bottom line whether you like it or not. They scrapped those 9% export duties last August, making their milk powder suddenly way more competitive on global markets. We’re talking about 11.2 billion liters projected for this year, with 73% of their powder heading to Algeria alone. The thing is, while EU and U.S. production stays flat due to environmental regs and costs, Argentina’s ramping up fast with smart tech adoption. If you’re not watching milk powder futures and thinking about your operational efficiency right now, you’re missing the boat. This isn’t just another recovery story—it’s a complete reshuffling of who’s calling the shots in global dairy.

KEY TAKEAWAYS

Monitor your commodity exposure now—Argentina’s supply surge could drop global milk powder prices by 5-10%, directly impacting your marketing strategy and contract timing.

Audit your feed efficiency immediately—With new global competition, farms achieving 5-8% efficiency gains through precision monitoring (like Argentina’s Grupo Chiavassa) will separate winners from losers.

Review your supply chain positioning—Argentina’s export growth into Algeria, Brazil, and Russia could create opportunities or headaches depending on where your milk goes and what you buy.

Consider technology investments that boost margins—Argentine producers are using rumination collars and automated health systems to stay competitive; falling behind on farm tech isn’t an option anymore.

Prepare for price volatility through 2025—With traditional powerhouses struggling and Argentina surging, expect more market swings and plan your risk management accordingly.

Look, the bottom line? Argentina went from crisis to global growth leader in 18 months. That kind of speed should wake us all up about how fast things can change in this business. Whether this creates opportunity or problems for your operation depends entirely on how quickly you adapt to the new reality.

Argentina’s dairy industry is sprinting ahead, reshaping the global market in a way that demands serious attention. Production gains reached nearly 11% in the first quarter of 2025, with forecasts suggesting total output close to 11.2 billion liters this year. This rapid expansion signals a significant market shift that could affect operations worldwide.

Argentina’s production surge isn’t just numbers on a chart. It’s a structural recovery driven by policy reforms and operational improvements that will influence global milk flows and pricing. This is critical for producers worldwide.

Farm-level optimism is notable, even if expressed cautiously in public. Many producers are reinvesting in their herds. Grupo Chiavassa, a leading dairy in Santa Fe, uses rumination collars and health monitoring tech from Allflex to enhance productivity and animal health. Though exact 2025 numbers aren’t published yet, previous data confirms technology adoption is delivering real benefits.

Weather remains unpredictable. The La Niña pattern caused pasture challenges in southern provinces, but the Pampas largely received adequate rainfall to support production growth.

Argentina’s dairy surge is changing global markets. Learn how 11% Q1 growth impacts your farm’s profitability and how to adapt your strategy for a competitive edge

Key facts worth noting:

Production growth near 11% in Q1 2025

Total milk volume projected near 11.2 billion liters for 2025

Algeria absorbs about 73% of Argentina’s whole milk powder exports, with Brazil and Russia also major markets

Export duties permanently eliminated in August 2024

Some recent chatter has centered on Nestlé’s Villa Nueva plant, but the major capacity expansion there took place in 2019. The real bottleneck today, as the Argentine Dairy Observatory highlights, is the need for broad upgrades to processing and cold-storage infrastructure across the country.

Farm gate prices have nudged higher, but increasing feed, fertilizer, and land rent costs mean margins remain tight despite growing volumes.

Globally, with growth stalling in the EU and U.S. due to environmental regulations and rising costs, Argentina’s rapid rise creates new competitive dynamics that affect everyone in dairy.

What This Means for Your Operation

Watch milk powder futures closely—Argentina’s rising supply could push prices downward, affecting your margin planning. Audit your operational efficiencies and consider tech investments that might help you stay competitive. If you’re part of a supply chain, whether trading or processing, identify how Argentina’s expanding exports might overlap with your operations.

According to recent Extension work from the University of Minnesota, farms implementing precision monitoring systems are seeing 5-8% improvements in feed efficiency. That’s the kind of edge that matters when global competition intensifies.

What strikes me about Argentina’s transformation is the speed and scale of change. Two years ago, they were struggling with crisis-level inflation and production declines. Now they’re leading global growth and grabbing market share. It’s a powerful reminder that in dairy, staying nimble and informed isn’t just smart—it’s essential for survival.

Argentina’s back, they’re competitive, and they’re rewriting the rules for global dairy markets. Whether that creates opportunity or challenges for your operation depends entirely on how quickly you adapt to this new reality.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The Robotics Revolution: Embracing Technology to Save the Family Dairy Farm – This deep dive into robotic milking systems provides actionable insights on the ROI, labor savings, and production gains of implementing cutting-edge technology. Learn how to evaluate if this investment can boost your farm’s efficiency and competitiveness.

How to Attract and Retain Exceptional Labor for Your Dairy Farm – A strong team is your ultimate competitive advantage. This guide offers practical strategies for improving employee retention, using technology to simplify scheduling and communication, and building a farm culture that supports long-term profitability.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

The dairy industry in 2025 is splitting into distinct paths, a divergence that breeders, producers, and consultants feel directly.

EXECUTIVE SUMMARY: Here’s what’s happening — the real money isn’t in pumping more milk, it’s in making better milk. US producers figured this out already… they’ve bumped production about 2% while cranking up butterfat and protein levels, adding over $110 per cow straight to the bottom line. Meanwhile, Europe’s struggling with disease outbreaks and shrinking herds, which actually creates opportunities for the rest of us. Feed prices? They’re all over the map, but smart operators are locking in contracts now. Don’t just milk more cows — make every drop work harder through genomics and precision tech. The farms winning in 2025 are the ones making data-driven moves, not just gut decisions.

KEY TAKEAWAYS FOR ACTION

Bump your milk protein 0.2% and butterfat 0.3% using genomic selection — we’re talking potentially $120+ more per cow annually. Start by pulling up your herd’s genomic profiles this week.

Cut feed waste with precision feeding tech — early adopters report 12% savings on feed costs. Begin with a pilot zone to test and optimize feed intake before rolling it out.

Lock in feed prices NOW before the predicted 10% spike hits — call your supplier today about volume contracts. Don’t wait and regret it later.

Use real-time monitoring to catch mastitis and lumpy skin early — quick intervention can prevent 5%+ production losses. Disease prevention beats treatment every time.

Diversify your milk sales channels to protect against trade chaos — use market intelligence from USDA and Rabobank reports to find new opportunities while others scramble.

Let me break it down for you. The US is absolutely charging ahead right now. According to the latest USDA Livestock, Dairy, and Poultry Outlook from July 2025, milk production is expected to reach approximately 228 billion pounds in 2025, with a slight increase to around 229 billion in 2026. But here’s the kicker: it’s not just about adding more cows. Producers are dialing in higher butterfat and protein yields—that’s the new competitive edge that’s propelling American cheese and butter to the top tier globally.

Now look to Europe, where a different reality is unfolding. The EU’s milk output is forecast to decline slightly, from 149.6 million tonnes last year to approximately 149.4 million tonnes this year. The herd is shrinking by an estimated 3 percent, squeezed by tighter environmental controls and soaring costs. Toss in some serious disease outbreaks—such as bluetongue and lumpy skin, particularly affecting Italy and France—and you’ve got producers pivoting hard toward cheese production, where margins still hold solid.

Regional Winners and Losers Keep Emerging

What strikes me about Argentina is how producers there are riding a solid wave. DairyNews reports roughly 11% growth in milk production for the first half of 2025, though much of that surge is feeding growing domestic consumption rather than export markets.

Australia’s story is more nuanced. Despite some conflicting forecasts, multiple sources indicate that production is expected to settle around 8.6 million tonnes for 2025—reflecting the ongoing impacts of drought and rising input costs that continue to squeeze smaller farms out of the market.

In New Zealand, the picture is both steady and unstable. Fonterra’s forecast ranges between NZ$8 and NZ$11 per kg of milk solids for 2025-26, with a midpoint around NZ$10. That volatility means cash flow management has become absolutely essential for Kiwi farmers.

Here’s an interesting twist: the broader economic outlook from the World Bank predicts that commodity prices will soften overall, yet dairy bucks the trend, propped up by tight supplies and robust demand.

Feed Markets and Growing Trade Tensions

Feed markets are painting a mixed picture. The latest forecast from the International Grains Council signals a strong corn crop for 2025-26, although it is flagging volatility driven by weather and biofuel policy shifts. Smart operators are locking in feed prices early—I’ve seen operations save $150-$ 200 per cow annually simply by timing their grain purchases correctly.

But watch out—risks are mounting. Disease challenges like bluetongue and lumpy skin disease continue pressing hard in Europe. Meanwhile, the escalating US-China tariff conflict—which involves tariffs of up to 125% imposed by the US on certain dairy categories and retaliatory tariffs exceeding 120% by China—continues to disrupt traditional trade flows.

What Smart Operators Are Doing Right Now

So, what’s a savvy dairy operator to do in this fractured landscape?

Genomic testing isn’t optional anymore. Focus on breeding for higher fat and protein yields—this is where the real premiums are. A Wisconsin producer I know increased his component premiums by $0.45 per hundredweight just by selecting bulls with superior genetic merit for milk components.

Lock in feed contracts early—don’t get caught off guard by market swings. One Iowa operation saved nearly $180 per cow last year by forward contracting corn when prices dipped in spring.

Embrace precision technology—whether it’s robotic milking systems or precision feeding platforms, the ROI is becoming clearer every quarter. A 1,200-cow California dairy reported a 12% improvement in feed efficiency after installing automated systems.

Monitor disease developments constantly. With what’s happening in Europe, proactive health protocols aren’t just good practice—they’re survival tactics.

Diversify your market strategies—don’t put all your eggs in one basket, especially with trade policies shifting so rapidly.

The margins for error are shrinking; however, the opportunities for those who adapt quickly are substantial. US producers who understand their competitive position in components—the European processors pivoting to maximize value from limited milk, the New Zealand farmers managing cash flow through price volatility—they’re all writing the playbook for what works in this new reality.

For smaller operations, this might mean forming partnerships to access elite genetics and technology. For larger farms, it’s about leveraging scale to implement comprehensive strategies faster than competitors can react.

This isn’t the dairy landscape our grandparents knew. It’s faster, more complex, and honestly, more unforgiving to those who don’t stay ahead of the curve. However, for producers ready to embrace change and think strategically about their positioning, there are real opportunities not only to survive but also to thrive.

The key takeaway? Success in 2025 hinges not only on volume but also on strategic, data-driven decisions that capitalize on regional strengths and navigate global market challenges.

Keep your eyes sharp—this year is shaping up to reshape everything we thought we knew about dairy.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Your 2025 Dairy Gameplan: Three Critical Areas Separating Profit from Loss – Get tactical with this how-to guide on immediate operational improvements. It offers practical strategies for optimizing silage, utilizing key feed additives, and perfecting transition cow management to save thousands of dollars and boost your bottom line this year.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

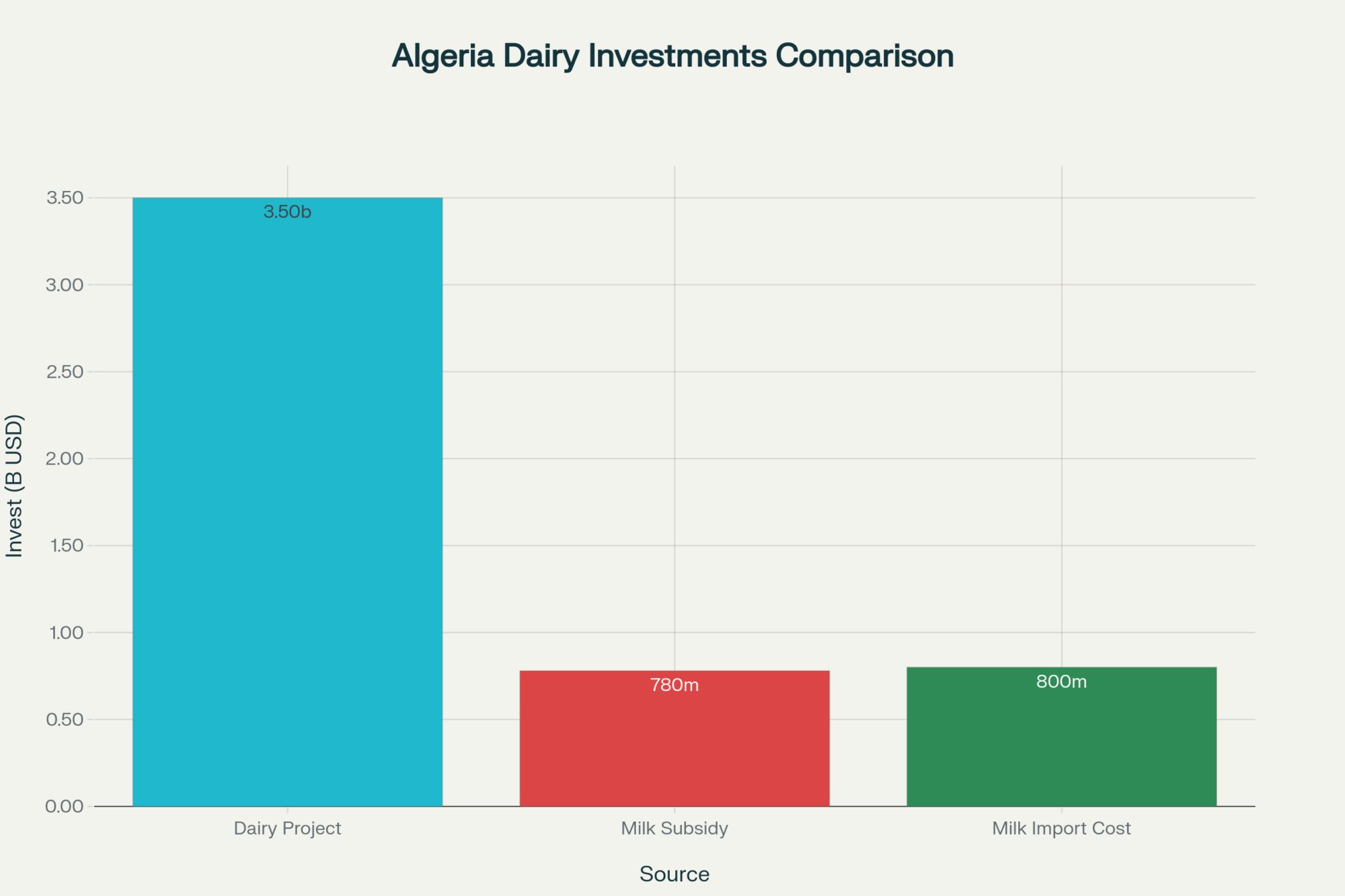

This $3.5 billion desert dairy will displace $400 million in global exports. The producers who survive will master the same feed efficiency and heat tolerance traits.

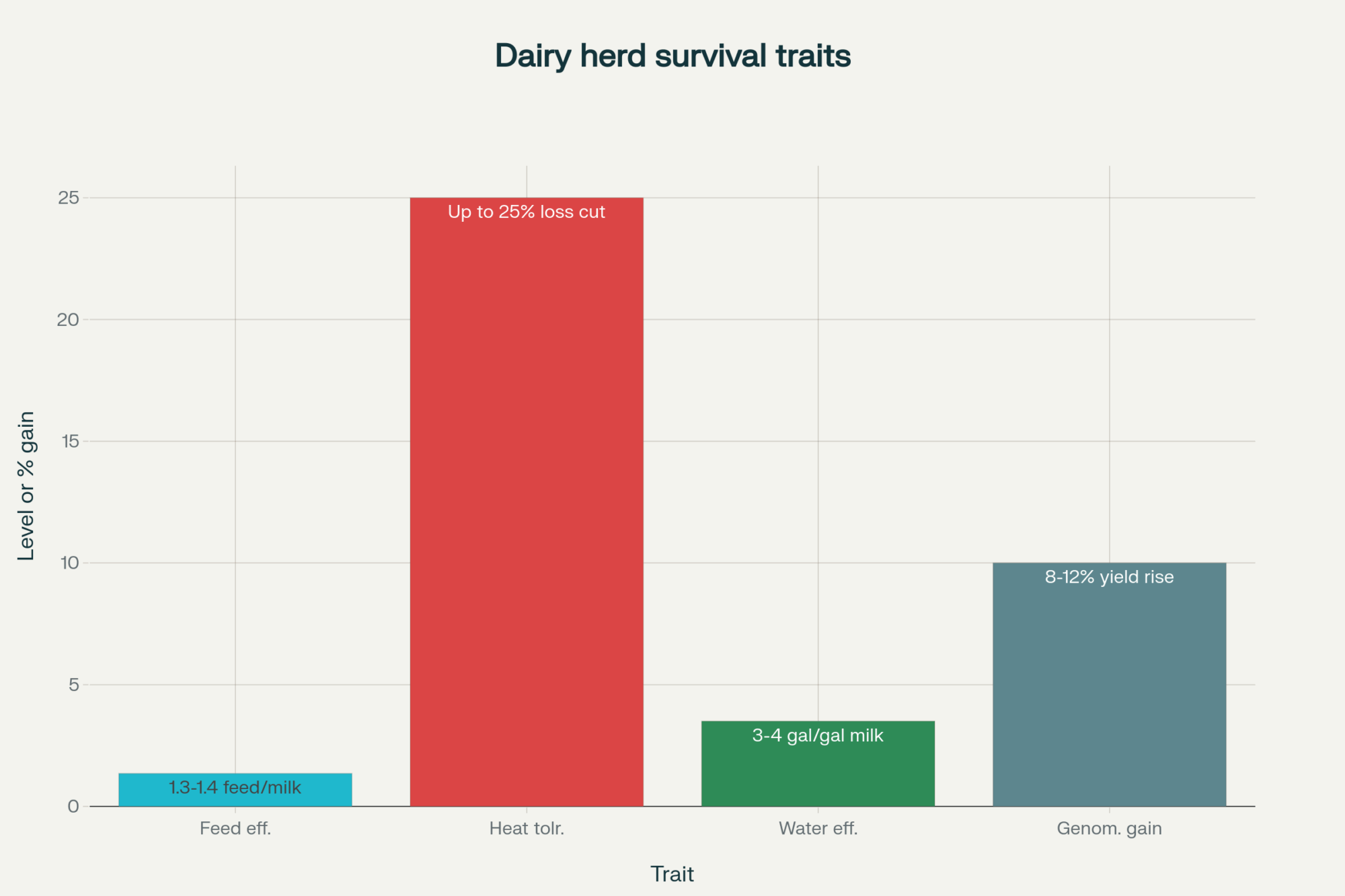

EXECUTIVE SUMMARY: Algeria’s national dairy initiative isn’t just about one big project—it’s about challenging everything we thought we knew about efficient milk production. They’re spending $800 million a year importing powder because they’re producing 2.5 billion liters but consuming 4.5 billion liters. Algeria’s targeting feed conversion ratios of 1.3-1.4 kg of milk per kg of dry matter in desert conditions—that’s competitive with temperate operations. Water use is high at 3-4 gallons per gallon of milk, but they’re managing it with smart tech. The real kicker? When this 270,000-cow operation hits full stride, it’ll cut global powder exports by $400 million annually. For us, this means that feed efficiency and genomic selection are no longer nice-to-haves—they’re survival tools. Start optimizing now or get left behind.

KEY TAKEAWAYS:

Boost milk production 15-20% through precision feed management → Start tracking your feed conversion ratios weekly and adjust TMR formulations based on real data. With feed costs volatile in 2025, every 0.1% improvement in efficiency adds $0.08-$ 0.12 per cow per day.

Cut heat stress losses by up to 25% with proactive cooling systems → Install shade structures and misting fans before summer peaks hit. Research shows dairy operations lose 15-20% of milk yield during heat stress events—preventable losses that directly impact your bottom line.

Leverage genomic testing for 8-12% yield improvements within 18 months → Begin incorporating genomic evaluations into breeding decisions this season. Focus on feed efficiency and heat tolerance traits—the same characteristics making Algeria’s desert dairy viable.

Optimize water efficiency to reduce operational costs 10-15% → Implement water recycling systems and monitor usage per liter of milk produced. Desert operations demonstrate that you can maintain production with effective water management—essential as water costs continue to rise globally.

Prepare for shifting global markets by strengthening local efficiency. Algeria’s project is expected to displace major powder exporters by 2027. Farms with superior feed conversion and genomic programs will capture market share as traditional suppliers scramble to compete.

Algeria’s national dairy initiative is more than just a massive construction project—it’s a comprehensive strategic move that’s already making waves in dairy circles everywhere.

Algeria has partnered with Qatar’s Baladna, agreeing to invest $3.5 billion into what might just be the most ambitious dairy setup on the planet. And honestly, if you’re in this business, this is big news.

Comparison of key financial figures related to Algeria’s dairy sector investment and operations

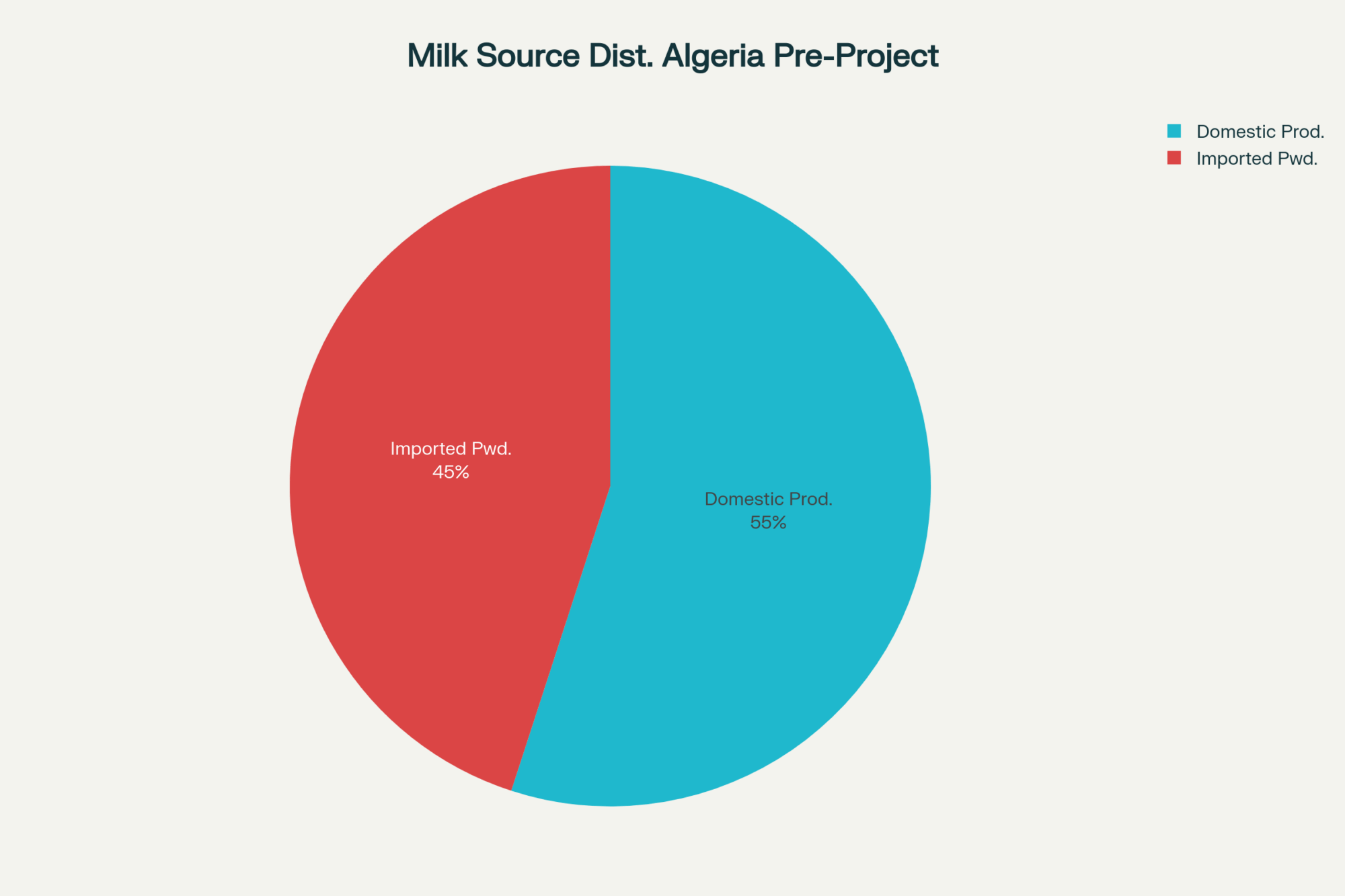

Algeria is shelling out a whopping $800 million a year on milk powder imports. Their domestic production clocks at around 2.5 billion liters, but people are guzzling about 4.5 billion liters annually. That’s a serious hole they’re trying to plug.

Current milk production sources in Algeria before the giant dairy project

That subsidy angle is crucial, and frankly, it’s what makes this whole thing possible. The government’s annual dumping of approximately DZD 105 billion—roughly $780 million—across the dairy chain. But here’s the million-dollar question: can they sustain that level of support when global commodity prices get volatile?

Desert Dairy on a Scale That’ll Blow Your Mind

Picture this: a dairy setup sprawling over land twice the size of New York City in Algeria’s arid Adrar province, housing 270,000 cows to churn out 1.7 billion liters yearly.

That’s huge, even by global standards. German engineering giant GEA—which knows its stuff when it comes to mega dairy projects—landed the contract valued between €140 and €170 million. Construction is expected to kick off in early 2026, with production reaching full stride by late 2027.

Notably, the project is expected to create 5,000 local jobs—that’s serious economic development for a region that desperately needs it.

The Desert Reality Check: Can They Really Make Milk in the Sahara?

Let’s talk feed first, because that’s where the rubber meets the road. Based on recent regional data, they’re looking at approximately $280 per metric ton for their ration mix, which includes maize, alfalfa, and TMR components. Not cheap, but pretty standard for what you’d expect in North Africa.

Regarding feed efficiency, the feed conversion ratio they’re targeting is around 1.3-1.4 kg of milk per kg of dry matter intake. Those are actually respectable numbers, especially when you consider the environmental challenges faced in the desert heat.

Water’s a whole different story. Current estimates put water usage at around 3-4 gallons per gallon of milk produced—and that’s a big deal in an arid place. However, that number fluctuates significantly depending on your cooling technology and recycling systems. Experts like Dr. Michael Hutjens have been vocal about the critical importance of water efficiency in these harsh environments—mismanage it, and you’re burning cash faster than you can say “dry lot.”

Only about 20-25% of Algeria’s current milk moves through official channels. The rest flows through informal markets, which honestly makes modernizing the whole supply chain a real headache.

Heat stress? It’s no joke out there. I’ve seen operations in Arizona and Saudi Arabia where butterfat numbers drop 15-20% during peak summer without proper cooling infrastructure. That’s why the projected 7-9 year payback period hinges so heavily on getting the technology implementation right.

What This Means for Your Bottom Line

Zooming out, the big picture is massive: Algeria aims to slash milk powder imports by half once this plant’s fully operational. That spells serious disruption for traditional exporters in the EU, US, New Zealand, and Argentina—we’re talking about displacing roughly $400 million worth of powder imports annually.

And about the commodity powder market? That’s going to get a lot more competitive—no doubt about it. If you’re an exporter who’s been counting on that Algerian business, it’s time to start thinking about plan B.

The timeline matters too. Construction is scheduled to start next year, but full production is expected to begin in late 2027. That gives traditional suppliers approximately 18 months to pivot before the real impact is felt.

The Bigger Picture

The project’s most significant implication is that it shatters conventional thinking about where large-scale dairy operations can be effective. Traditionally, you’d never look at the Sahara and think “perfect spot for a dairy farm.” But with the right technology, water management, and government backing?

This isn’t just about Algeria. Other resource-rich nations are watching this closely. If it works, expect to see similar projects emerging in the Middle East, Central Asia, and possibly even parts of sub-Saharan Africa, where governments are committed to achieving food security.

For those of us managing operations or advising producers, the lesson is clear: the game is changing faster than most people realize. Desert dairy used to be an oxymoron. Now it might be the future.

The real question for your operation isn’t whether these new production models will impact you—it’s when, and how you’ll adapt to a world where traditional geographic constraints no longer limit milk production.

Key survival traits for dairy herds in challenging environments

Algeria’s desert dairy gamble represents more than agricultural development—it’s a calculated bet on food sovereignty that will reshape global dairy trade. The producers who master extreme efficiency and heat tolerance now will be the ones still standing when the dust settles.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Dairy Cow Heat Stress: The Four Key Areas You Need To Address Now – This tactical guide provides actionable strategies for mitigating heat stress, focusing on the four critical areas of cow comfort and facility management. It reveals practical methods to prevent the 15-20% production losses mentioned in the main article.

The Global Dairy Market: A Tale of Two Halves – This strategic analysis breaks down the complex forces shaping today’s volatile global markets. It provides essential context for the trade disruptions discussed in the main article, helping you anticipate shifts and position your operation for long-term profitability.

Genomic Testing: Are You Leaving Money on the Table? – This article makes the definitive business case for genomic testing, a key takeaway from the Algeria analysis. It demonstrates how to leverage genetic data to accelerate progress on traits like feed efficiency and heat tolerance, directly boosting farm profitability.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Stop believing the “more milk = lower prices” myth. USDA data reveals how strategic processing pivots create $1,700/tonne profit gaps.

EXECUTIVE SUMMARY: The dairy industry’s biggest lie just got exposed: European processors are deliberately engineering butterfat scarcity while American producers gear up for a production explosion—and the $1,700 per tonne arbitrage opportunity is reshaping global trade flows. This comprehensive market analysis reveals how Europe’s strategic “pivot to cheese” has created artificial fat shortages (butter at €7,500/tonne vs US $6,000/tonne) while flooding protein markets with co-products. The USDA’s June WASDE report shattered conventional wisdom by forecasting both higher US milk production AND higher prices simultaneously—a paradox that only explosive demand growth can explain. German milk production dropped 2.9% year-over-year while UK production surged 6.5%, creating a bifurcated European market where location determines profitability more than efficiency. European cheese indices exploded with Cheddar Curd up 30.9%, Mild Cheddar +29.6%, and Mozzarella +38.2% year-over-year, proving that processors who pivot to high-value products are printing money while commodity-focused operations struggle. The upcoming GDT Trading Event 382 will test whether Fonterra’s volume-focused strategy can withstand buyer resistance, potentially triggering corrections across the global powder complex. Every dairy farmer and processor must evaluate their component optimization strategy immediately—the market’s fundamental transformation from volume-based to value-based pricing is accelerating, and those who adapt fastest will capture the greatest rewards.

KEY TAKEAWAYS

Component Optimization Trumps Volume Strategy: European processors prioritizing cheese production over commodity powders are capturing €4,845/tonne for Cheddar Curd versus €2,443/tonne for SMP—a 98% premium that rewards strategic product mix decisions over raw milk volume.

Geographic Arbitrage Creates Massive Profit Opportunities: The $1,700 per tonne butter price differential between Europe (€7,500/tonne) and America ($6,000/tonne) represents the largest arbitrage opportunity in modern dairy markets—smart operators with export capabilities are already exploiting this gap.

Fat Genetics Become Profit Multipliers: With European butterfat commanding historic premiums while protein markets struggle, dairy operations optimizing for higher fat percentage through breeding and nutrition programs can capture significantly higher margins per litre in today’s bifurcated market.

Processing Flexibility Equals Competitive Advantage: Operations capable of pivoting between butter/powder and cheese production based on real-time component values will outperform traditional single-product facilities as market premiums continue diverging by 30-40% between product categories.

Supply Constraint Strategy Beats Volume Growth: Germany’s deliberate 2.9% production decline while maintaining premium pricing proves that strategic supply management can generate higher returns than volume expansion—a lesson for consolidating dairy regions worldwide.

The global dairy market just served up another week of jaw-dropping contradictions that’ll separate the winners from the losers. Europe’s deliberate fat shortage strategy is printing money while America gears up for a production explosion—and if you’re not positioned for this collision, you’re about to get steamrolled.

Europe’s Billion-Dollar Chess Move

Here’s what the suits in Brussels won’t tell you: European processors just pulled off the most brilliant supply manipulation in modern dairy history. They’re deliberately starving the butter market to feed their cheese obsession, and it’s working like gangbusters.

Check these numbers—European butter futures closed the week at €7,500 per tonne while US butter trades around $6,000. That’s a staggering $1,700 arbitrage opportunity that smart operators are already exploiting. But here’s the kicker: this isn’t some temporary market hiccup. This is strategic genius.

Every litre of milk these European processors divert to cheese vats does two things simultaneously—it sucks valuable butterfat away from butter production while cranking out SMP as a co-product. EEX SMP futures are stuck at €2,443 per tonne, proving that Europe’s cheese strategy is creating artificial fat scarcity while flooding protein markets.

Why does this matter for your operation? Because component values are diverging like never before. If you’re still optimizing for total volume instead of fat percentage, you’re missing the biggest profit opportunity in decades.

The UK’s Record Flush: Blessing or Curse?

While continental Europe tightens the screws, the UK’s drowning in milk. April production exploded 6.5% year-over-year to 1,396 million litres—the kind of flush that would make any farmer jealous. But here’s the plot twist: this abundance is creating its own nightmare.

UK farm-gate prices dropped 1.2 pence per litre to 43.69 ppl while the rest of Europe enjoys historically high returns. Sometimes too much of a good thing really isn’t good. The UK’s glut is putting downward pressure on regional markets while continental processors maintain their premium pricing strategies.

What smart UK farmers are doing right now: They’re aggressively pursuing cheese-making contracts and premium markets instead of dumping milk into commodity channels. Location matters more than ever in this bifurcated market.

Germany’s Structural Decline Accelerates

Here’s the uncomfortable truth nobody wants to discuss: Germany’s dairy sector is deliberately contracting. Raw milk deliveries for January-April fell 2.9% year-over-year to 10.65 million tonnes, and this isn’t weather-related. This is policy-driven destruction of production capacity.

Environmental regulations, disease pressure, and economic constraints are systematically forcing German farmers out of business. Belgium’s situation is even worse, with collections down 4.5% year-over-year. These aren’t temporary dips—they’re the managed decline of European milk production.

The opportunity here? Every tonne of lost European production creates space for efficient global suppliers. The question is whether you’re positioned to fill that gap.

America’s Production Juggernaut Nobody’s Talking About

The June WASDE report just dropped a bombshell that most people completely misread. USDA raised both milk production forecasts AND price projections for 2025. Wait, what? More milk AND higher prices?

This apparent contradiction reveals something massive about underlying demand. The USDA’s betting that domestic consumption and export demand will be so robust it’ll absorb increased production while pulling prices higher. That’s an incredibly bullish signal for US dairy.

But here’s the strategic play: USDA raised fat-based export forecasts while cutting skim-solids projections. Translation? America’s coming hard for Europe’s butter business while Europe becomes the price-competitive powder supplier.

Tomorrow’s $50 Million Poker Game

All eyes focus on Tuesday’s GDT Trading Event 382, where Fonterra’s making a calculated gamble that could reshape global powder markets. Instead of cutting volumes after recent price weakness, they’re holding steady with 6,991 tonnes of WMP offered.

Recent auctions showed SMP dropping 4.4% and WMP falling 3.7%. Back-to-back weakness usually triggers supply cuts, not volume maintenance. Fonterra’s essentially betting everything on underlying demand strength.

If buyers step up tomorrow, it validates their volume strategy. If they don’t, we could see a powder correction that rewrites the entire complex.

The H5N1 Wild Card That Changes Everything

Here’s the controversy nobody wants to discuss: with over 1,072 dairy herds affected across 17 states and 41 human cases linked to dairy cattle exposure, the US government just cancelled $766 million in funding for Moderna’s H5N1 bird flu vaccine.

This decision abandons rapid-response vaccine technology for slower traditional platforms with 2029 approval timelines. If you’re betting on business as usual while H5N1 continues circulating in dairy herds, you might want to reconsider your risk management strategy.

What Winners Are Doing Right Now

The processors dominating this game share three characteristics:

Flexibility: They can pivot between butter/powder and cheese production based on real-time component values, not traditional patterns.

Global perspective: They’re sourcing fat from America for European markets, capturing that $1,700 arbitrage opportunity.

Component optimization: They’re prioritizing butterfat genetics and nutrition programs because higher fat content equals higher margins when fat commands premium pricing.

The Cheese Market’s Money-Printing Machine

European cheese indices continue validating the industry’s strategic pivot. Recent data showed Cheddar Curd climbing €116 (+2.5%) to €4,845, with year-over-year gains of 30.9%. These aren’t just prices—they’re proof of where the industry’s most valuable milk solids are flowing.

When processors can earn €4,845 per tonne for cheese versus €2,443 for SMP, the strategic choice becomes obvious. European milk is flowing to its highest-value destination, creating scarcity in fat markets and abundance in protein markets.

The Bottom Line

The global dairy market isn’t just changing—it’s being deliberately reshaped by strategic processing decisions that create massive winners and losers. Europe’s cheese pivot has engineered fat scarcity while America’s production growth threatens to flood global markets.

Your action plan starts now:

Evaluate your fat genetics immediately. Higher butterfat content equals higher margins in today’s market.

Assess your processing flexibility. Can you pivot between product categories based on component values?

Watch Tuesday’s GDT results like a hawk. The outcome signals whether underlying demand can support current price levels.

Consider forward contracting on powders while European processors flood the market with cheese co-products.

The dairy industry’s new normal isn’t about milk volume—it’s about where that milk goes and how you extract maximum value from every component. Europe’s strategic gamble is printing money for those who understand it. America’s production explosion creates both opportunity and risk.

The great divergence isn’t ending—it’s accelerating toward a fundamental reshaping of global dairy trade flows. Make sure you’re positioned on the winning side when the dust settles.

Learn More:

Your 2025 Dairy Gameplan: Three Critical Areas Separating Profit from Loss – Practical strategies for implementing component optimization through targeted feeding programs, genetic selection, and transition cow management that can boost profitability by $500+ per cow within months of implementation.

5 Technologies That Will Make or Break Your Dairy Farm in 2025 – Demonstrates how smart calf sensors, robotic milkers, and AI-driven analytics deliver measurable ROI within 7 months while addressing labor shortages and efficiency challenges facing modern dairy operations.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Stop believing high trading volumes equal market strength. Record 20,641-tonne SGX week signals price chaos—smart money’s repositioning now.

EXECUTIVE SUMMARY: The biggest trading week in months just revealed what conventional market wisdom won’t tell you: massive volumes don’t mean bullish sentiment. While Singapore Exchange crushed records with 20,641 tonnes traded—nearly 14 times European volumes—whole milk powder prices still dropped 4.3% and skim milk powder fell 2.1%. China’s strategic 5% import reduction is permanently reshaping global demand patterns, forcing a fundamental supply-demand recalibration that conventional analysis misses entirely. Irish farmers capitalizing on 12.6% production growth while European butter prices climb €50 weekly demonstrates the bifurcated reality: consumer-facing products outperform industrial ingredients by massive margins. U.S. cheese exports hit all-time daily averages, yet spot Cheddar failed to break $2.00—proving that production records don’t automatically translate to price premiums. The data screams one truth: we’re witnessing early-stage rebalancing where efficiency and market positioning matter more than historical volume assumptions. Stop trading on yesterday’s patterns and start positioning for tomorrow’s supply-demand reality.

KEY TAKEAWAYS

Volume Deception Alert: Record SGX trading (20,641 vs 1,500 tonnes EEX) with simultaneous price drops signals smart money repositioning—not bullish sentiment. Farmers relying on volume indicators for pricing decisions are missing critical market shifts.

China’s Structural Pivot: 5% import reduction isn’t cyclical—it’s permanent domestic production strategy. Operations targeting Chinese export markets must diversify immediately or face chronic oversupply conditions through 2026.

Bifurcated Profit Zones: European butter gains €50 weekly while powder markets crater, revealing the €462 (+11.8% y/y) consumer-facing premium. Producers should prioritize cheese and butter over commodity powders for immediate margin protection.

Irish Production Surge: 12.6% collection growth (1,104kt April) creates supply pressure that traditional seasonal analysis underestimates. Competing regions must focus on cost efficiency and quality premiums to maintain market share.

The past week delivered a masterclass in market contradictions, with record-breaking trading volumes masking underlying price weakness across multiple dairy commodity platforms. While European butter prices continue their relentless climb and cheese markets show surprising resilience, powder markets send mixed signals that should have every dairy farmer paying attention.

Trading Floors Heat Up While Prices Cool Down

EEX’s Modest Performance Tells a Bigger Story

The European Energy Exchange saw 1,500 tonnes change hands last week, with Thursday emerging as the standout session at 525 tonnes. But here’s what the headline numbers don’t tell you: butter futures actually dropped 0.3% to €7,383, while skim milk powder fell to €2,541.

This isn’t just market noise. When you see heavy trading volumes alongside price declines, you’re witnessing real-time disagreement between buyers and sellers about where the fair value lies. The fact that 1,275 tonnes of butter traded while prices slipped suggests either profit-taking from earlier gains or genuine supply pressure building in European markets.

SGX Dominates with Massive Volume Surge

Now, let’s talk about where the real action happened. Singapore Exchange crushed it with 20,641 tonnes traded – nearly 14 times EEX’s volume. Whole milk powder led the charge with 11,115 lots, followed by SMP at 8,816 lots.

But here’s the kicker: even with this massive trading interest, WMP prices still dropped 0.1% to $3,841, and SMP fell harder at 1.0% to $2,866. The only bright spots were anhydrous milk fat jumping to $6,910 and butter edging up 0.5% to $6,862.

What does this tell us? Asian buyers are actively repositioning their portfolios, but they’re not paying premiums to do it. That’s either smart money sensing opportunity in the weakness or institutional selling creating the very pressure we’re seeing.

European Quotations Paint a Contradictory Picture

Butter Marches Higher Despite Futures Weakness

The EU weekly quotations delivered some head-scratching results. While EEX butter futures were declining, physical European butter prices gained €50 to €7,457 – a solid 0.7% weekly jump. Dutch butter led the charge with a €100 increase to €7,400, while French butter added €51 to €7,521.

This disconnect between physical and futures pricing isn’t accidental. It suggests immediate European demand remains robust while longer-term sentiment cools. For dairy farmers, this means current milk checks might stay strong even if forward contract prices are softening.

Powder Markets Show Resilience

SMP quotations gained €25 to €2,425, with Dutch SMP posting the strongest performance at €2,440 after a €50 increase. German SMP added €15 to €2,435, while French SMP gained €10 to €2,400. This strength in physical markets while futures decline creates an interesting arbitrage opportunity that smart traders are already exploiting.

Regional Production Patterns Reveal Critical Trends

Ireland’s Explosive Growth Continues

Irish milk collections jumped 12.6% in April to 1,104 thousand tonnes, pushing year-to-date volumes to 2.46 million tonnes – an impressive 8.5% ahead of 2024. Irish farmers deliver both volume and quality, with milkfat at 4.08% and protein at 3.47%.

This isn’t sustainable at current growth rates. Irish dairy expansion is happening faster than global demand growth, which means either prices have to adjust or production growth has to slow. The laws of supply and demand haven’t been suspended.

Southern Europe Struggles While Northern Europe Thrives

Spain’s milk production fell 1.0% to 641 thousand tonnes, while Italy dropped 0.6% to 1.17 million tonnes. Meanwhile, Ireland’s explosive growth creates a tale of two Europes. The weather patterns explain much of this – Ireland’s optimal grassland conditions contrast sharply with drought concerns across much of southern Europe.

China’s Farmgate Reality Check

Chinese farmgate prices at 3.07 Yuan/kg represent a brutal 9.4% year-over-year decline. At €37.00/100kg equivalent, Chinese farmers are getting paid roughly half what their European counterparts receive. This price differential explains why Chinese domestic production continues expanding while import demand weakens.

Weather Wildcards Reshape Production Landscapes

Europe’s Tale of Extremes

This spring ranks among the driest on record since 1991 across Benelux, northern France, Germany, western Poland, and Sweden. Most regions received only 50% of normal precipitation, raising serious concerns about crop yields.

But here’s the twist: Ireland’s grasslands remain in optimal condition with perfect growing weather. Meanwhile, Italy and Greece benefit from abundant rainfall and positive yield expectations. This creates a productivity gap that will influence milk production patterns for months ahead.

New Zealand’s Cautious Contraction

Dairy cow slaughters in New Zealand plummeted 25.2% in April, with 12-month rolling slaughters down 7.3% to 751 thousand head. This represents a deliberate herd size reduction that will constrain Oceania’s export capacity moving forward.

Smart Kiwi farmers are reading the global demand signals and adjusting accordingly. When your primary export markets show weakness, you don’t expand – you optimize.

US Market Dynamics Offer Global Lessons

Export Surge Masks Domestic Challenges

US cheese exports hit all-time daily averages in April, jumping 6.7% from already strong 2024 levels. American cheese and butter remain the world’s cheapest, creating a competitive export advantage that’s supporting domestic prices.

But there’s trouble brewing. Due to tariffs and trade tensions, Canadian butter buyers are looking elsewhere, causing US butter export momentum to slow from its February-March peak. When politics interfere with the dairy trade, everybody loses.

Powder Markets Face Structural Headwinds

The US-China trade war continues reshaping whey powder flows. China historically takes 40% of US whey exports, but tariff threats prompted massive March purchases followed by an April retreat to Belarus and New Zealand suppliers. CME spot dry whey rallied 0.75¢ to 58¢ per pound – its highest level in nearly four months.

US nonfat dry milk exports fell 20.9% in April to 113.5 million pounds as European suppliers gained market share in Southeast Asia. Mexico remains strong, but losing Asian market share to European competitors signals a fundamental competitiveness challenge.

Production Surge Creates Market Tensions

Cheese Plants Ramp Up Output

US cheese production reached 1.23 billion pounds in April – the highest daily average on record. Cheddar production jumped 8.1% year-over-year as new plants work through startup issues. This production surge explains why spot Cheddar failed to reach $2.00 and pulled back to close at $1.8575.

Butter Production Peaks Despite Price Strength

Manufacturers filled churns with cheap cream in April, pushing butter output to 215.8 million pounds – the highest April volume since 2020. Yet healthy domestic demand and improving exports offset this production increase, keeping prices climbing to $2.555 per pound.

This demonstrates that strong demand can absorb significant production increases when export markets remain competitive.

Class Prices Reflect Market Realities

Class III Futures Signal Caution

Cheese market weakness deflated nearby Class III prices, with June falling 41¢ to $18.80 per cwt and July dropping nearly 70¢ to $18.90. However, deferred contracts edged higher, promising milk revenues in the high-$18s and low $19s into early 2026.

Class IV Shows Strength

Class IV futures climbed across the board, with June settling at $18.42 and July reaching $19.16. September through December contracts returned above $20. Combined with record-high beef revenues, these milk checks easily cover operating costs.

Feed Markets Provide Stability

Corn Prices Hold Steady

July corn finished at $4.42 per bushel, down just 1.5¢ for the week. The December contract rallied over 10¢ to $4.49 as wet conditions in Ohio, Pennsylvania, and the Southeast forced some farmers to abandon unplanted acres.

Soybean Complex Gains on Policy Speculation

Soybean oil prices climbed on rumors that the Trump administration might announce renewable fuel credit decisions benefiting biodiesel. July soybeans closed at $10.58, up 16¢ weekly, while meal held steady at $296 per ton.

The Bottom Line

This week’s trading data reveals a global dairy market in transition. Record trading volumes reflect real disagreement about fair value, while regional production patterns create both opportunities and risks for forward-thinking farmers.

The key insight? We’re seeing the early stages of a supply-demand rebalancing that will favor producers who can maintain efficiency while competitors struggle with weather, feed costs, or market access.

European farmers should capitalize on current strength while monitoring powder market signals. US producers need to watch cheese production capacity and export market developments. And everyone should pay attention to China’s farmgate price trends – they’re previewing what happens when domestic production growth outpaces local demand.

Smart money is positioning for volatility. The question is whether you’re ready to navigate the choppy waters ahead or if you’re still fighting the last market cycle.

What’s your operation doing to prepare for these shifting global dynamics? The data suggests now’s the time to decide.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Stop expecting milk price crashes after record highs. Fonterra’s $10/kg MS forecast proves supply constraints have permanently changed dairy economics.

EXECUTIVE SUMMARY: The traditional dairy boom-bust cycle is dead, and Fonterra’s confident $10/kg MS forecast for 2025-26 proves fundamental market dynamics have permanently shifted. While conventional wisdom suggests high prices trigger production surges that crash markets, global supply constraints from environmental regulations in Europe and disease impacts in the US are preventing the typical supply response that historically followed record pricing. Fonterra’s billion economic injection into New Zealand demonstrates how sustainability premiums and strategic positioning now drive profitability more than pure volume expansion. The co-operative’s success in monetizing carbon efficiency—with customers specifically paying premiums for low-carbon dairy—reveals a new competitive landscape where environmental performance translates directly to farmer payments. European producers remain handcuffed by regulations, US growth gets absorbed domestically, and China’s foodservice boom creates sustained premium demand for value-added products. With geopolitical risks as the only significant downside threat, progressive farmers must abandon volume-focused strategies and embrace component optimization, sustainability technologies, and value-added positioning. This isn’t just a good season—it’s proof that dairy’s future belongs to farmers who can deliver environmental performance alongside production efficiency.

KEY TAKEAWAYS

Sustainability Pays Real Cash: Fonterra farmers meeting emissions criteria earn additional 1-5 cents per kg MS, with top performers capturing 10-25 cents per kg MS premiums—translating to $25,000 extra annual income for a 300-cow operation producing 100,000 kg MS, proving environmental stewardship drives profitability.

Component Focus Beats Volume Strategy: Farms concentrating on butterfat and protein optimization rather than fluid volume expansion achieve 23-26% unit price increases across major dairy categories, aligning economic returns with environmental efficiency in today’s constrained supply environment.

Enhanced Cash Flow Creates Investment Opportunities: With advance payments rising from $8.50 to $9.00 per kg MS and government’s 20% Investment Boost tax deduction, farmers have unprecedented opportunity to modernize operations while maintaining healthy $1.43/kg MS margins above breakeven forecasts.

Global Supply Constraints Are Permanent: Environmental regulations preventing European expansion, US domestic consumption absorbing production growth, and China’s shift toward foodservice demand mean traditional supply responses won’t materialize—creating sustained high-price environment for strategically positioned producers.

Geopolitical Risk Management Essential: With forecast ranges widened to $8.00-$11.00/kg MS due to trade tensions, successful operations must diversify market exposure and build contingency plans for policy-driven disruptions while capitalizing on current premium pricing opportunities.

New Zealand’s dairy giant just delivered the news every farmer’s been waiting for: a confident $10 per kilogram milk solids forecast for 2025-26, backed by $15 billion flowing into the economy and fundamental shifts in global supply that could keep prices elevated for years to come.

Let’s cut to the chase – when Fonterra’s CEO Miles Hurrell says he’s confident about $10/kg MS, that’s not just optimistic talk. It’s backed by hard market realities that are reshaping the global dairy landscape.

“We are not seeing that supply turn on. The environmental pressures in the northern hemisphere – Europe in particular – we are not seeing the milk supply out of Europe as we may have seen historically,” Hurrell explained.

Think about what that really means. European producers are essentially handcuffed by environmental regulations, unable to respond to price signals like they could in the past. The EU has lost over 1.4 million dairy cows since 2016, with environmental restrictions explicitly stagnating milk production in northwestern European Member States.

Meanwhile, the US is dealing with its own supply headaches. Any milk production growth is being consumed domestically, and herds are still recovering from highly pathogenic avian influenza that’s affected over 930 farms across 17 states. California alone saw a 9.2% drop in milk production since late 2024.

Are you starting to see the pattern? The traditional boom-bust cycle driven by rapid supply responses to price signals is dead.

China’s Foodservice Revolution Creates New Opportunities

The Chinese market story isn’t just about volume recovery – it’s about a fundamental shift in how dairy gets consumed. While the overall demand for “core products” hasn’t returned to previous levels, explosive growth is happening in food service.

“There’s still strong demand for food service, particularly in China, and we’re seeing more growth in that market from a volume perspective,” Fonterra confirmed. This isn’t just academic – Chinese consumers are shifting from basic commodity dairy to higher-value products consumed in restaurants and prepared foods.

What does this mean for your operation? You’re missing the bigger opportunity if you’re still thinking about commodity markets. The future belongs to value-added products that command premium pricing in sophisticated markets.

Environmental Premiums: From Cost to Profit Center

Here’s something that would have sounded like fantasy a decade ago: Fonterra is now receiving premium payments specifically for carbon efficiency, and they’re passing those premiums back to farmers.

“There are customers now that are specifically paying for our carbon efficiency, and we’re paying farmers back for that,” the company confirmed. Starting June 1, 2025, Fonterra will offer farmers an additional 1-5 cents per kg MS for meeting emissions-related criteria, with top performers earning an extra 10-25 cents per kg MS.

For a 300-cow operation producing 100,000 kg MS annually, we’re talking about a potential additional income of $25,000 annually. This isn’t feel-good marketing – it’s hard cash flowing to producers who can prove their environmental credentials.

Stop Competing on Volume Alone: The global supply constraints aren’t temporary – they’re the new normal. Environmental regulations and resource limitations mean you can’t just turn on production taps anymore. Focus on component optimization instead. Farms concentrating on butterfat and protein rather than pure volume are seeing 23-26% unit price increases.

Embrace Sustainability Technology: Those carbon efficiency premiums aren’t charity – they’re driven by real customer demand from major brands like Mars and Nestlé, who need to meet their own sustainability targets. Invest in technologies that can demonstrate measurable environmental improvements.

Prepare for Enhanced Cash Flow: With advance payments increasing from $8.50 to $9.00 in July and the government’s new 20% Investment Boost tax deduction, you’ve got an unprecedented opportunity to upgrade equipment and infrastructure. DairyNZ’s breakeven forecast sits at $8.57/kg MS for 2025-26, giving you a healthy $1.43/kg MS margin to work with.

Diversify Market Focus: Think beyond traditional export channels with China’s foodservice boom and sustained US domestic demand. Value-added products and specialized applications are where the margin growth is happening.

But here’s the critical question: Are you positioned to capture these premiums, or are you still operating like it’s 2015?

Geopolitical Wildcards Could Derail the Party

Let’s be honest about the risks. Fonterra’s wide $8-$11/kg MS range for 2025-26 isn’t conservative planning – it’s acknowledgment that political decisions increasingly override market fundamentals.

The ongoing trade tensions and tariff wars are “fracturing global dairy markets,” the US-China trade war alone is estimated to have caused $6 billion in profit losses for dairy farmers globally. When political relationships dictate market access more than product quality, even the best-run operations can get caught in the crossfire.

US tariffs are blocking affordable dairy supplies from reaching markets like China, forcing Chinese buyers to source from more expensive alternatives or reduce consumption. This creates opportunities for New Zealand exporters but also demonstrates how quickly trade policies can disrupt established patterns.

While we’re talking about immediate price forecasts, don’t miss the bigger strategic moves happening. New Zealand just launched a $25.68 million “Resilient Dairy” innovation program targeting genomic advancements and disease management technologies.

This 7-year program, jointly funded by LIC, MPI, and DairyNZ, aims to “deliver long-term economic, environmental and animal health benefits” through faster genetic gain and improved sustainability. When an industry invests $25 million in long-term R&D during high-price periods, that’s confidence in sustained profitability.

The program will incorporate genomic data into animal evaluation systems, potentially jumping ahead of global competitors in genetic advancement. This translates to better cows with improved health, productivity, and environmental efficiency for farmers.

The Bottom Line

Fonterra’s record $10/kg MS forecast isn’t just good news – it’s a roadmap for the industry’s future. We’re entering an era where environmental sustainability drives premium pricing, supply constraints create sustained high-price periods, and technology that demonstrates value beyond production metrics becomes essential.

The winners will be farmers who combine production efficiency with environmental stewardship, backed by data proving value to sophisticated global customers. The traditional boom-bust cycles give way to more sustained profitability for those ready to adapt.

Here’s your action plan:

Invest in component optimization over volume expansion

Implement sustainability technologies that qualify for premium payments

Take advantage of enhanced advance payments and tax incentives to upgrade operations

Develop value-added product strategies targeting foodservice and specialty markets

Prepare contingency plans for geopolitical trade disruptions

The question isn’t whether these trends will continue – it’s whether you’re positioned to capitalize on them. Fonterra’s confidence reflects more than current market conditions. It signals we’ve entered the most profitable period in modern dairy history for farmers ready to embrace change.

The dairy industry’s transformation is accelerating; this forecast is just the beginning. Are you ready?

The Robot Revolution: Transforming Organic Dairy Farms with Smart Tech in 2025 – Explores cutting-edge technologies that position forward-thinking dairy operations to capture sustainability premiums and operational efficiencies, showing how innovation investments align with the premium-driven future Fonterra’s success signals.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

EU’s €1.58B climate compliance burden hands competitive edge to NZ dairy—learn which sustainability moves pay vs. which drain profits.

EXECUTIVE SUMMARY: While Brussels celebrates hitting 54% emissions cuts, EU dairy farmers are unknowingly funding their own competitive disadvantage through €1.58 billion in annual compliance costs that add zero value to milk quality. Meanwhile, New Zealand producers achieve 46% lower carbon footprints than the global average—0.74 kg CO2e per kg milk versus 1.37 kg globally—without bureaucratic handcuffs, positioning them to capture growing market share in sustainability-driven premium markets. The brutal reality: EU climate policies are creating de facto trade barriers that benefit efficient producers in other regions while EU farmers drown in paperwork instead of investing in actual productivity improvements. Smart operations are already using carbon footprint metrics as operational optimization tools, achieving both emissions reductions and cost savings through improved feed efficiency and energy systems. Progressive dairy farmers need to stop treating sustainability as compliance theater and start leveraging it as a competitive weapon—because these EU-driven standards are becoming global requirements whether you’re ready or not.

KEY TAKEAWAYS

Follow the efficiency playbook, not the compliance manual: New Zealand dairy operations prove you can achieve 46% lower emissions intensity through pasture-based systems and operational efficiency—delivering both environmental performance and cost advantages without regulatory complexity.

Calculate your true sustainability ROI before jumping on bandwagons: EU farmers spending €1.58 billion annually on administrative compliance shows why you need to focus on technologies that improve feed conversion ratios and energy efficiency rather than chasing certification schemes that don’t hit your bottom line.

Position for premium market access now: EU sustainability standards are becoming global trade requirements through mechanisms like CBAM, creating opportunities for efficient producers to capture green premiums while less-prepared operations face market access restrictions.

Treat carbon metrics as operational KPIs: The most successful dairy operations use emissions intensity measurements the same way they track somatic cell counts—as indicators of system optimization that directly correlate with profitability improvements.

Build adaptable systems for regulatory uncertainty: Smart farmers are implementing technologies that deliver measurable productivity gains while meeting multiple sustainability frameworks, avoiding the trap of optimizing for specific regulations that could change with political winds.

While Brussels celebrates hitting a 54% emissions cut by 2030, here’s the brutal truth: EU dairy farmers are paying the price for climate virtue signaling that’s actually handing competitive advantages to their global rivals. The numbers tell a story most farmers haven’t heard yet—one that could reshape who wins and loses in the global dairy game.

The European Union just announced they’re projected to achieve a 54% net reduction in greenhouse gas emissions by 2030, tantalizingly close to their legally mandated 55% target. Sounds impressive, right? The kind of achievement that makes environmental ministers write glowing press releases about “decoupling economic growth from emissions.”

But here’s what they’re not telling you: while EU policymakers pat themselves on the back for nearly hitting their climate targets, the dairy sector tells a completely different story—one that could reshape global competitiveness in ways most farmers haven’t even considered yet.

The Numbers Don’t Lie: EU’s Climate “Success” Story

Let’s start with the headline-grabbing achievement. EU emissions dropped 37% since 1990, while the economy grew nearly 70%. That’s genuine decoupling of economic growth from emissions—proof that you can make money while cutting carbon.

More telling? The response to farmer protests across Europe resulted in a systematic weakening of environmental regulations that had taken years to negotiate.

Show Me the Money: Do Sustainability Premiums Actually Reach Your Bank Account?

Here’s where it gets interesting for progressive dairy farmers. While EU processors throw around impressive-sounding sustainability targets, let’s talk about what actually hits your bottom line.

The Reality Check:

The EU’s CAP Simplification Package projects to save farmers approximately €1.58 billion annually in administrative costs

Translation? EU dairy farmers were spending €1.58 billion yearly just on compliance paperwork

That’s money not going into actual production improvements

Meanwhile, the mandatory requirement for farmers to set aside 4% of arable land as non-productive areas—a cornerstone environmental measure—was effectively neutered, transformed from a binding obligation into a voluntary eco-scheme where farmers get paid to do what they previously required.

The €1.58 Billion Bureaucracy Tax: Why EU Farmers Pay While Competitors Profit

The protests weren’t just about fallow land. Here’s what actually got rolled back when farmers pushed back:

What Got Weakened:

Crop rotation requirements got more flexible

Permanent grassland protection was relaxed

The proposed Sustainable Use of Pesticides Regulation was withdrawn entirely

Farms under 10 hectares are proposed to be exempted from certain controls and penalties

This isn’t a policy adjustment; it’s a wholesale retreat under pressure. The European Economic and Social Committee noted that the “growing complexity of regulatory requirements linked to the Green Deal is imposing a significant burden on businesses, particularly Small and Medium-sized Enterprises (SMEs), potentially diverting resources from green innovation towards navigating administrative procedures.”

Global Competitive Reality: The Numbers Game

While EU dairy farmers navigate this regulatory maze, their competitors follow completely different rules. Here’s the uncomfortable truth about global dairy competitiveness:

Key Metric

EU Performance

Global Reality

Competitive Impact

Carbon Footprint

Improving but complex compliance

Varies by region

High compliance costs

Administrative Burden

€1.58B annually

Minimal in most regions

Direct cost disadvantage

Market Access

Protected but restrictive

Growing opportunities

Mixed benefits

Innovation Investment

High but bureaucracy-heavy

Focused on efficiency

Unclear ROI

The EU created the sustainability playbook, but everyone else uses it to compete more effectively against EU producers.

The Innovation Edge: What Actually Pays

Here’s where the story gets interesting. The pressure cooker of EU climate policy is driving innovation that could create lasting competitive advantages—if farmers can navigate the regulatory complexity long enough to benefit.

The Clean Industrial Deal, launched in February 2025, aims to mobilize over €100 billion for clean manufacturing and industrial decarbonization. But here’s the critical question: Will EU dairy farmers be the first to market these technologies, or will they be too busy complying with regulations to implement them effectively?

The Innovation Fund recently attracted 373 applications for clean technology projects, with funding requests far exceeding the €3.4 billion available budget. EU Climate Commissioner Wopke Hoekstra called this “a clear signal of European industry’s dedication to achieving climate neutrality objectives while enhancing competitiveness.”

But smart farmers are asking: Which sustainability investments actually deliver returns?

ROI Reality Check: What Actually Works

Based on the data and farmer experience, here’s what delivers:

Winners:

Improved feed efficiency delivers both emissions reductions and cost savings

Energy systems that reduce operational costs while meeting compliance requirements

Technologies that optimize production efficiency metrics

Losers:

Administrative compliance systems that don’t improve actual performance

Complex certification schemes with high overhead costs

Regulatory mandates with unclear or delayed payback periods

The most successful operations treat emissions reduction as a proxy for operational efficiency rather than a separate environmental goal.

What This Means for Your Operation

If you’re running a progressive dairy operation, here are the critical questions you should be asking:

1. Are you calculating true compliance costs vs. benefits received? The €1.58 billion EU farmers spend on compliance suggests many operations haven’t done this math properly.

2. Which EU-driven innovations should you adopt, regardless of local regulations? Focus on technology or practices that improve operational efficiency while reducing emissions intensity. These deliver competitive advantages independent of regulatory mandates.

3. How can you position for sustainability-driven market premiums without getting trapped in compliance complexity? Build systems that can adapt to different market requirements rather than optimizing for specific regulatory frameworks.

The Trade War Nobody’s Talking About

EU sustainability standards are becoming non-tariff trade barriers by stealth. The Carbon Border Adjustment Mechanism (CBAM) and sustainability certification requirements force global dairy producers to adopt EU-compatible systems or face market access restrictions.

This creates a fascinating competitive dynamic. Countries with naturally lower-emission production systems could benefit enormously from EU sustainability requirements. Meanwhile, intensive production systems in other regions face significant adaptation costs.

Implementation Reality: What Progressive Farmers Are Actually Doing

Talk to progressive dairy farmers across different regions, and you’ll hear consistent themes that cut through the policy rhetoric. The most successful operations aren’t just complying with regulations; they use sustainability metrics as operational optimization tools.

Smart farmers recognize that genetics, improved feeding strategies, and better manure management deliver emissions reductions and productivity improvements. This isn’t about environmental virtue signaling; it’s about operational efficiency that happens to reduce emissions as a valuable side effect.

The challenge? Smaller operations get crushed by compliance complexity, while larger farms gain competitive advantages through economies of scale in managing regulatory requirements.

The Bottom Line

The EU’s 54% emissions achievement isn’t the victory Brussels wants you to believe. Yes, emissions are down 37% while the economy grew 70%—impressive numbers proving sustainability and profitability coexist. But dig deeper, and you’ll find EU dairy farmers are becoming unwitting test subjects in a regulatory experiment that might be handing long-term competitive advantages to producers who achieve better environmental outcomes with less bureaucratic overhead.

Your move: Stop treating sustainability as a compliance exercise and use it as an operational optimization tool. Focus on metrics that improve both your environmental footprint AND your profit margins. The farmers who master this balance will thrive regardless of which way the regulatory winds blow.

Action items for progressive dairy farmers:

Calculate your true compliance costs vs. sustainability premiums received – Use the EU’s €1.58 billion administrative burden as a benchmark for what not to accept

Focus on efficiency-driven sustainability investments – Target technologies that deliver measurable productivity improvements alongside emissions reductions

Build adaptable systems – Create operational frameworks that can adapt to different market requirements rather than optimizing for specific regulatory frameworks

Monitor global trends – EU standards are becoming global benchmarks, so prepare for these requirements to reach your market

The EU created the sustainability playbook, but they’re still figuring out how to use it effectively. Smart farmers in other regions have the opportunity to learn from both their successes and their mistakes. The question isn’t whether sustainability requirements are coming to your market—it’s whether you’ll be ready to profit from them when they arrive.

The bottom line? EU climate policy is driving global dairy transformation whether you participate or not. The choice is whether you’ll lead or be disrupted by that change.

Learn More:

BST Reapproval: The Key to Unlocking Dairy Sustainability – Reveals practical strategies for implementing scientifically-proven technologies that reduce methane emissions by up to 12.7% while improving profitability—exactly what dairy farmers need to compete with EU sustainability standards without bureaucratic overhead.

EU Dairy Prices Plateau: What You Need to Know About the 2025 Market Split – Demonstrates how current EU market dynamics create both risks and opportunities for dairy operations, providing essential insights for positioning your operation in a landscape where sustainability regulations are reshaping product pricing and processor strategies.

European Dairy Future: Navigating Long-Term Milk Volume Decline and Market Shifts – Exposes the long-term implications of EU regulatory pressure with an 11% projected herd reduction by 2035, helping progressive farmers understand which adaptation strategies will determine winners and losers in the post-2025 dairy landscape.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

China’s dairy imports inch up as trade wars reshuffle global suppliers. New Zealand wins big while US struggles with tariff whiplash.

EXECUTIVE SUMMARY: China’s dairy powder imports showed modest growth in early 2025 (+2% YoY), driven by declining domestic milk production and strategic stockpiling ahead of volatile US-China tariffs. New Zealand captured 46% of imports through duty-free access, while US suppliers faced near-exclusion during peak 125% tariffs. Chinese domestic consumption remains tepid, whey imports surged 42% as buyers raced tariff deadlines. The 90-day tariff reprieve in May offers temporary relief, but long-term trade uncertainty favors diversified sourcing and geopolitical stability over traditional market fundamentals.

KEY TAKEAWAYS:

Trade wars redefine suppliers: New Zealand dominates with duty-free access; US whey exports collapsed under 125% tariffs.

Domestic pressures: China’s milk production declines (-1.5-2.6% forecast) and 24-month price slump drive import needs.

Strategic stockpiling: March whey imports hit 4-year highs as buyers rushed to beat tariff deadlines.

China’s dairy import landscape turned upside down in early 2025, with imports surging 23.5% in March amid unprecedented market chaos. Forget the modest 2% projected growth figure – the real story lies in the violent reshuffling of suppliers as Chinese buyers scramble to adapt. The market fell when Beijing hammered US dairy with punishing 125% duties before May’s reprieve. New Zealand emerged as the clear winner, snatching nearly 46% of China’s total dairy imports after securing duty-free access in January 2024. Meanwhile, US suppliers watched helplessly as their previously dominant position in China’s critical whey market evaporated overnight. For dairy producers worldwide, the rules have changed: trade policy now trumps quality, efficiency, and even price in a market increasingly driven by geopolitics rather than traditional fundamentals.

Tariff Whiplash Reshapes Global Dairy Supply Chains Overnight

The first half of 2025 delivered a gut punch to the US-China dairy trade. Starting with a seemingly manageable 10% tariff on US dairy products in March, tensions exploded when Beijing slapped 125% duties on American dairy by early April. Though mid-May negotiations yielded a 90-day reduction to approximately 20%, the damage to long-established trade relationships appears irreversible.

US dairy exporters took a direct hit. SMP exports to China vanished, plummeting to zero in February 2025. Considering the US previously directed 42% of its whey exports to China and controlled nearly half the Chinese whey market, this collapse represents nothing short of a disaster for American producers.

“We’re not just seeing a temporary trade hiccup,” warns Dr. Michael Harvey, Senior Dairy Analyst at Rabobank. “What’s happening is a fundamental realignment of global dairy flows that could outlast the current tensions. Chinese buyers have made it clear – they’ll pay premiums for supply stability and predictability, regardless of product quality or price advantages.”

Meanwhile, New Zealand dairy farmers are laughing to the bank. With complete duty-free access to China since January 2024 through their Free Trade Agreement, Kiwi producers now control an astonishing 46% of China’s dairy import market. This dramatic shift proves how rapidly trade policy can render traditional competitive advantages irrelevant, leaving producers at the mercy of political negotiations rather than rewarding efficiency or quality.

China’s whey imports skyrocketed a staggering 41.7% in March to 67,812 metric tons – the highest monthly volume in nearly four years – as panicked buyers raced against crushing tariff deadlines. This frenzied stockpiling pushed cumulative whey imports up 35.8% above last year’s levels. WMP imports jumped 30.7% to 43,232 metric tons, helping drive a remarkable 23.5% surge in total March dairy imports.

What makes this buying spree particularly remarkable? It happened despite sluggish domestic consumption, creating a market paradox where overall dairy demand remains weak yet import volumes temporarily explode. The pattern reveals how powerfully trade policy fears now override traditional market signals.

“Look at the whey market to understand what’s happening,” notes Wei Zhang, Asian Dairy Market Analyst at Global Dairy Intelligence. Despite weak overall consumption in China, whey imports shot up 41.7% in March. Trade policy concerns are now trumping traditional market signals, creating pitfalls and opportunities for producers who can read these new dynamics.”

This import surge doesn’t signal a return to China’s glory days. WMP imports are projected at 460,000 metric tons for 2025, but they still lag well below the historical average of the past decade. Instead, it highlights a market where success demands precise timing and category-specific strategies rather than broad expansion across dairy products.

Chinese Milk Production Crisis Creates Targeted Import Openings

China’s domestic milk production is taking a nosedive, projected to fall 1.5-2.6% in 2025 after dropping 0.5% in 2024. Farmgate milk prices have crashed for 24 straight months, hitting brutal lows around .40/cwt by early 2025 – a crushing 15% below last year and well under production costs for many farmers.

This price collapse has forced countless smaller operations to shut down while driving significant herd reductions. Curiously, China’s National Bureau of Statistics reported milk output increased 1.7% in Q1 2025 compared to Q1 2024 – a puzzling contradiction highlighting the challenges in getting reliable data on China’s dairy sector.