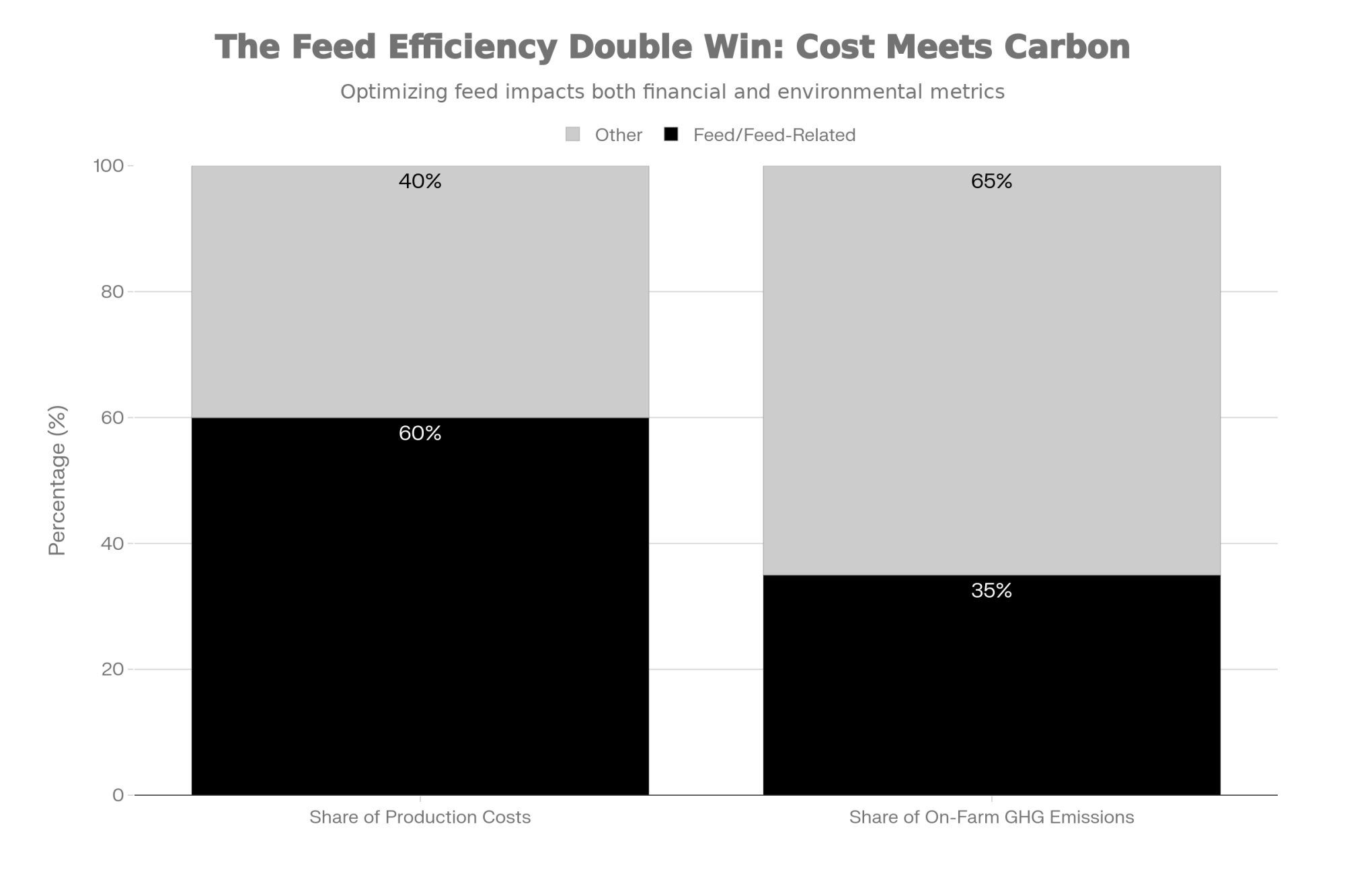

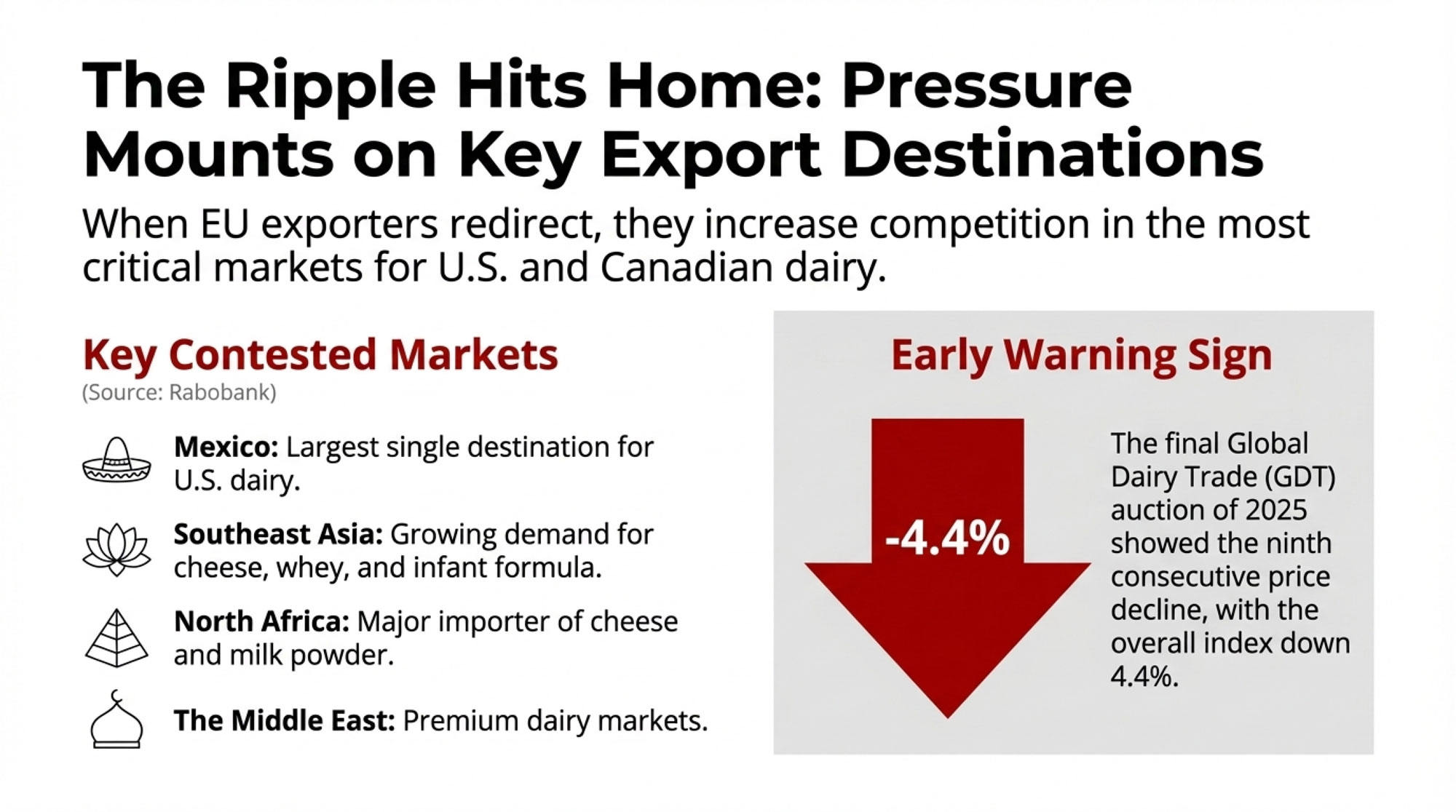

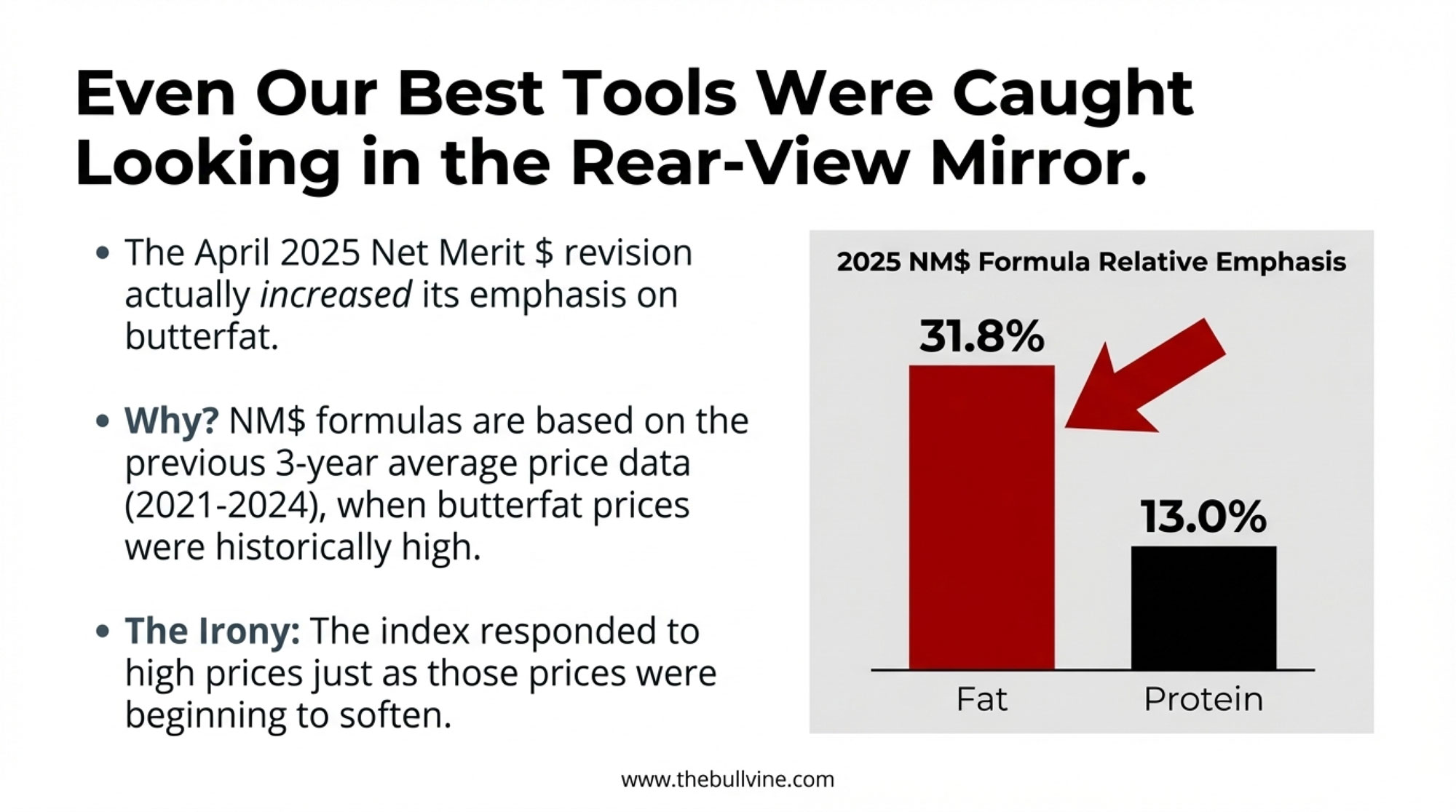

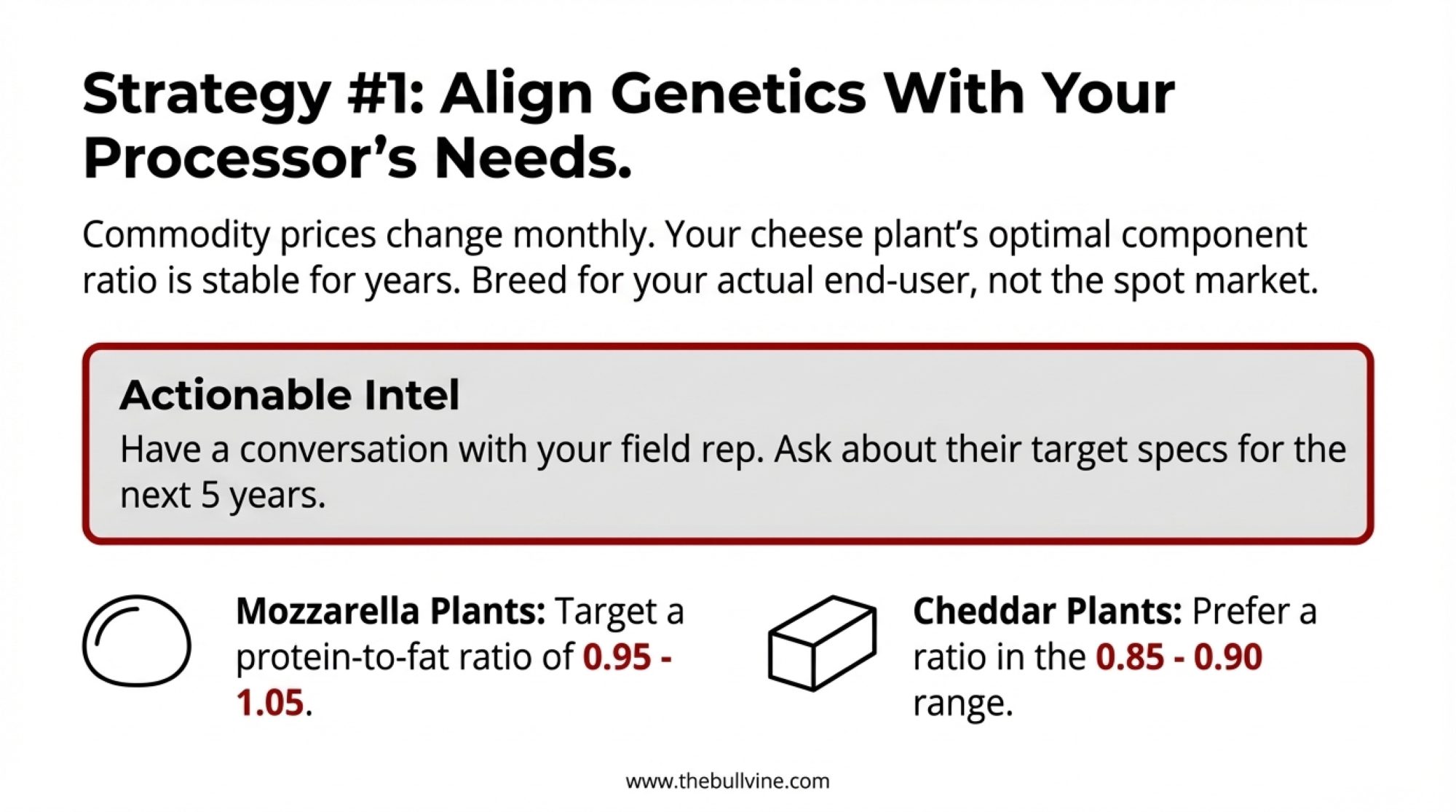

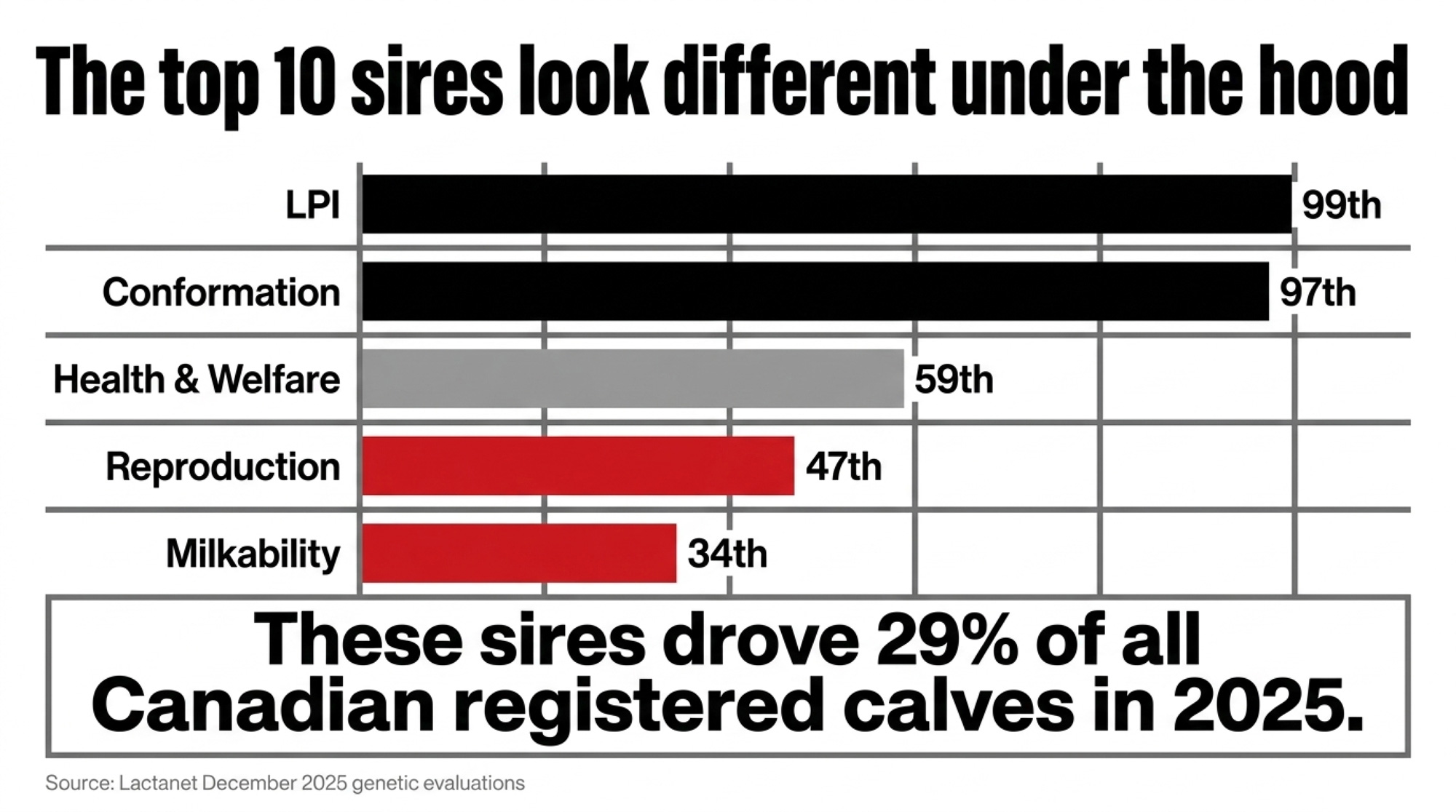

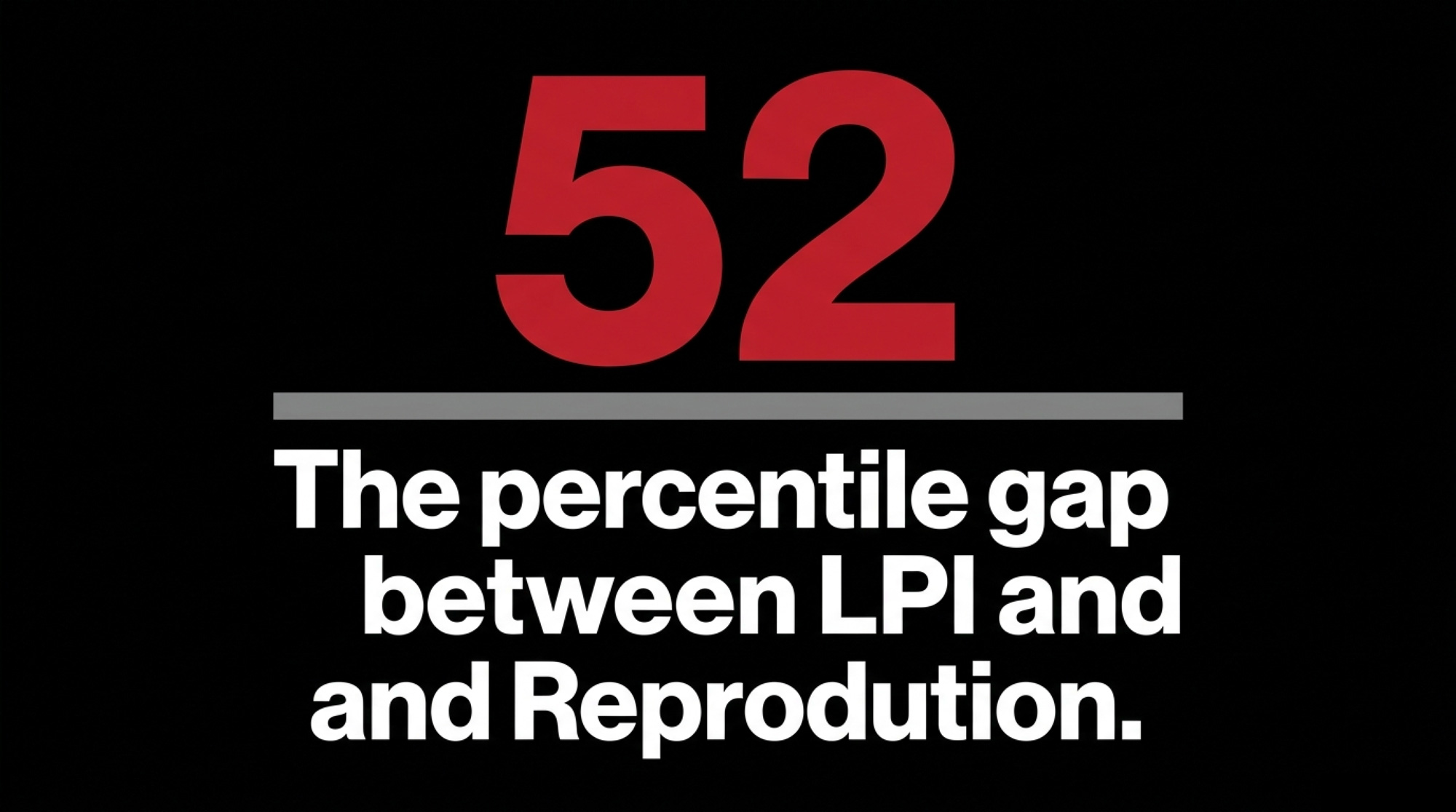

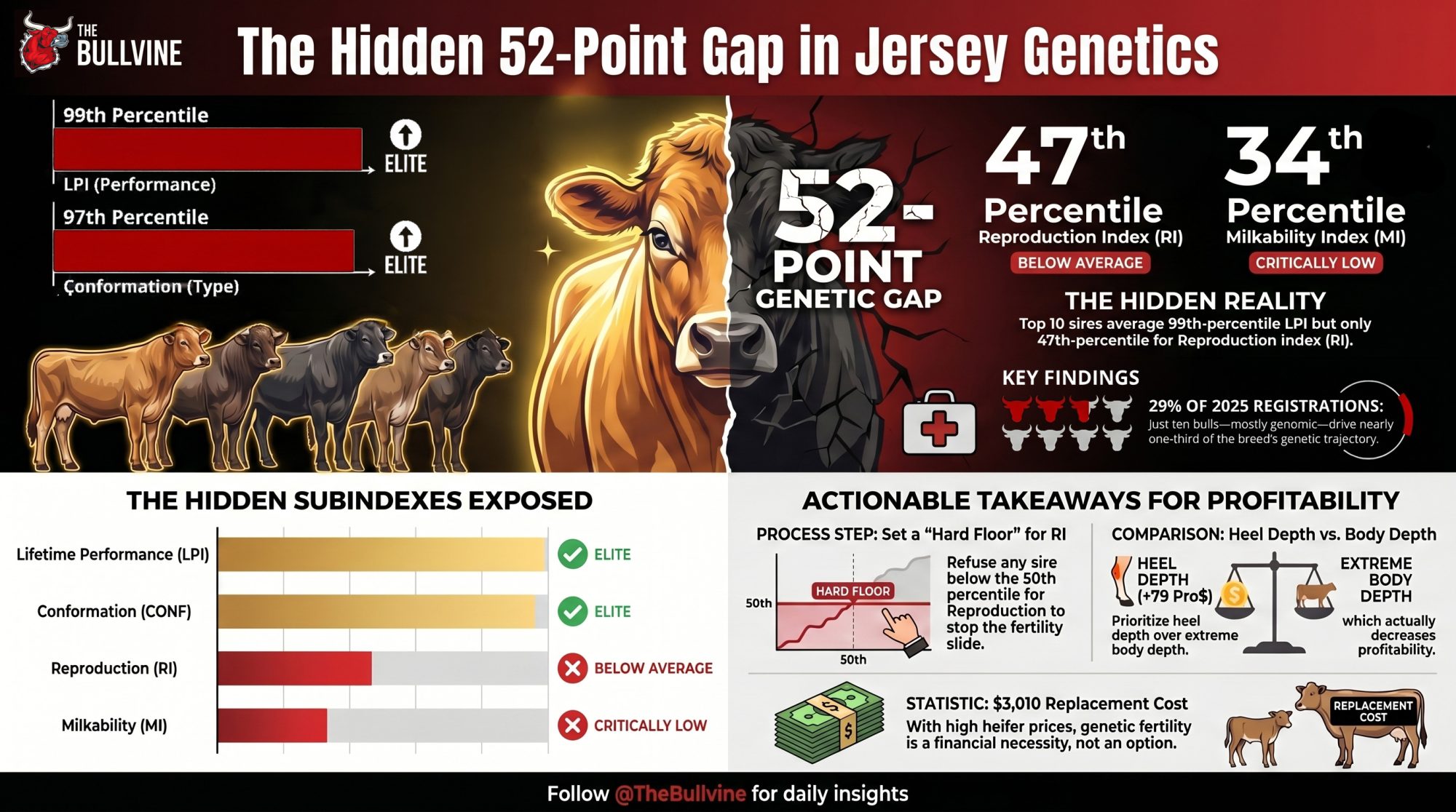

Canada’s top ten Jersey sires average 99th-percentile LPI and 47th-percentile Reproduction. That 52-point gap sired 29% of 2025 registrations — and never shows up on a single catalog page.

Jersey Canada’s record registration year produced a top ten sire group with elite LPI and conformation. Yet a look under the hood, and the Reproduction and Milkability subindexes tell a very different story for the future cows filling Canadian barns.

When I sat down in March 2026 with Jersey Canada’s 2025 registration data and Lactanet’s December 2025 genetic evaluations, I expected to see what the catalog pages were already shouting. Record registrations, up 9.74% over the previous high. Ten sires averaging Lifetime Performance Index (LPI) at the 99th percentile. Conformation at the 97th. Every bull A2A2. On paper, the Canadian Jerseys looked like they were winning on every front.

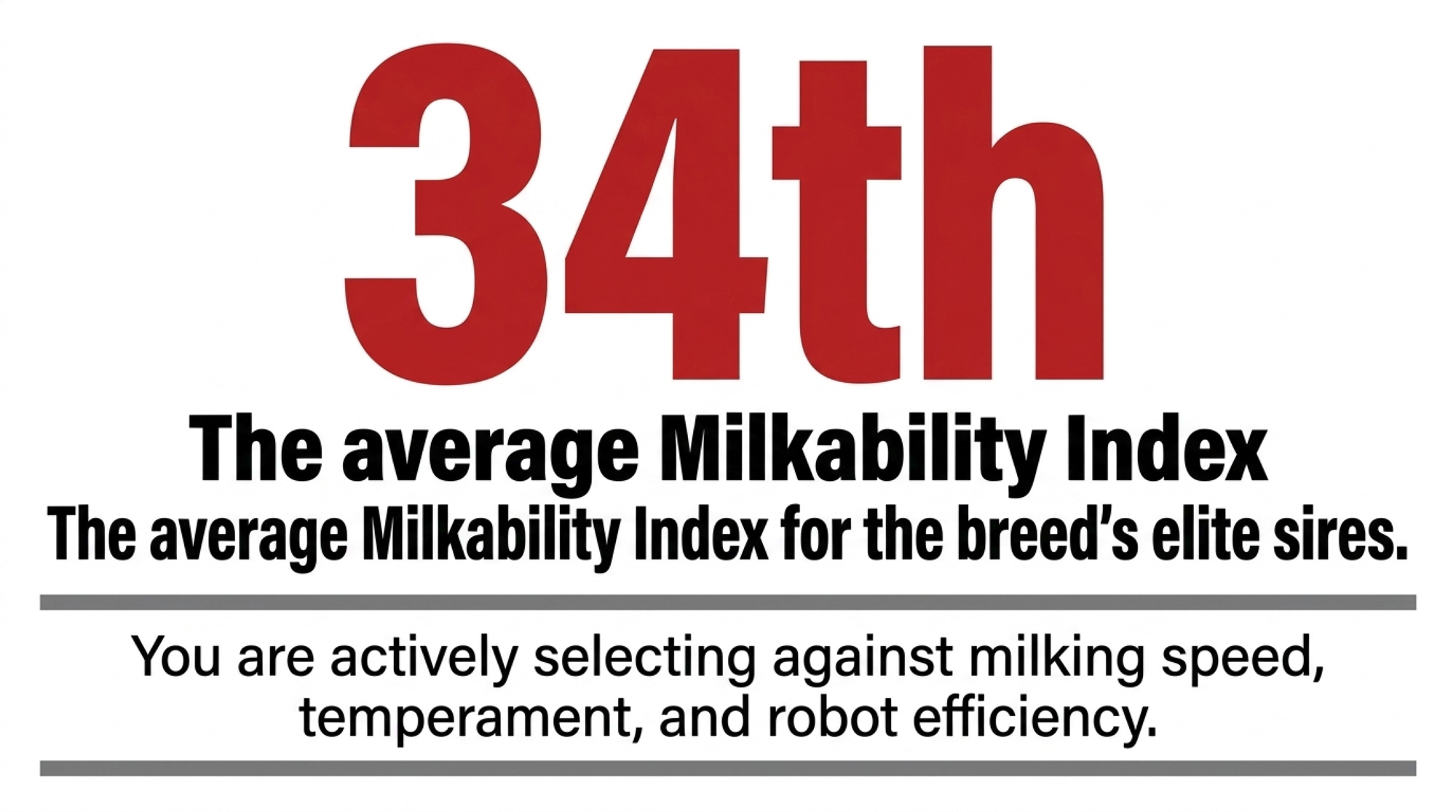

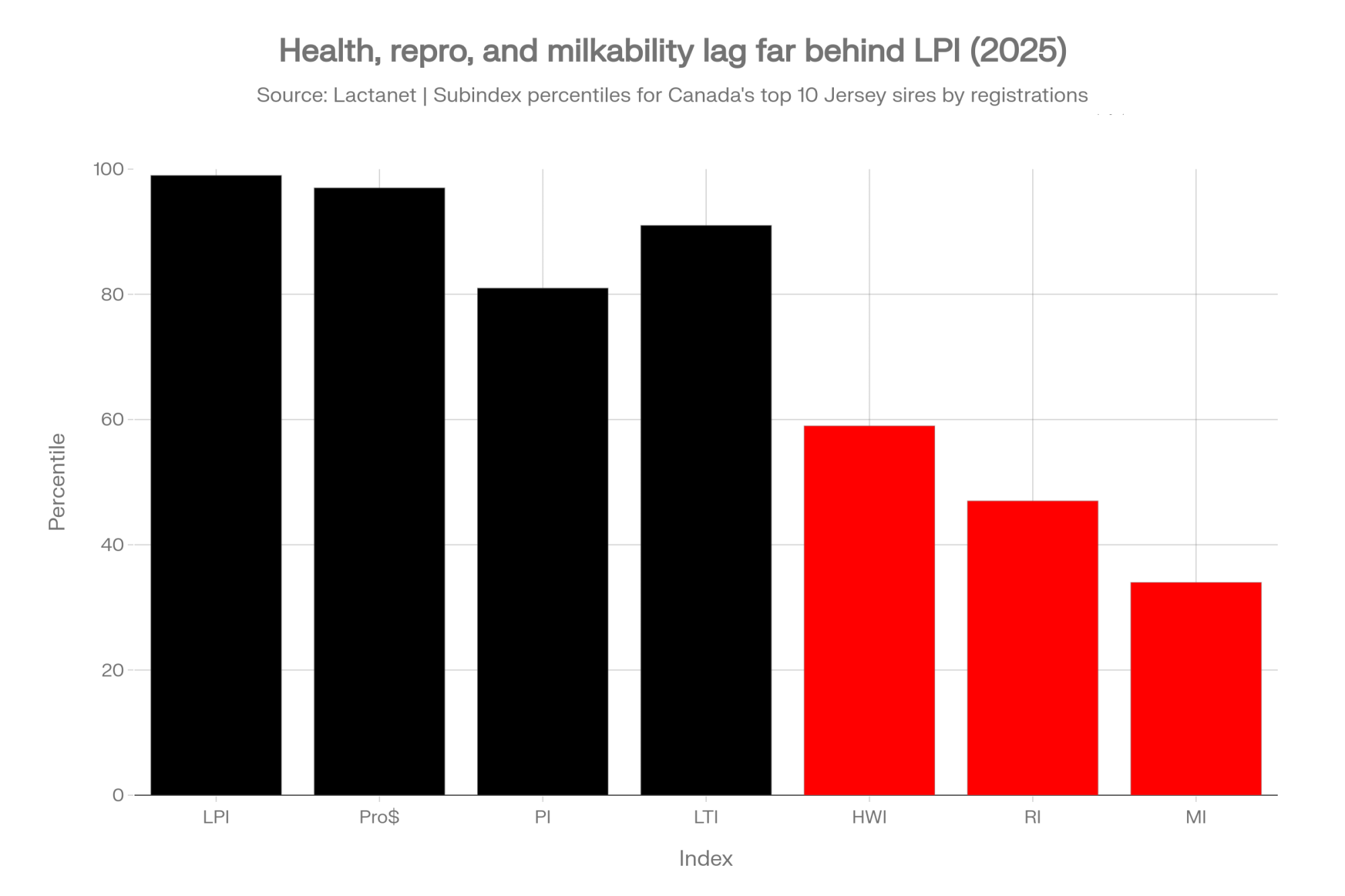

Then I pulled the LPI subindex profile on that same top ten group. The Reproduction Index (RI) across those bulls averaged the 47th percentile — below breed average. Five of ten fell below the median for fertility. The Milkability Index (MI), Lactanet’s subindex covering milking speed, temperament, and mammary milking traits, sat at the 34th percentile. And the Health & Welfare Index (HWI) — the one that captures Metabolic Disease Resistance, Mastitis Resistance, and Cystic Ovaries — averaged just the 59th percentile, with four bulls below the 50th.

Let me say this plainly: neither the breed associations nor the A.I. companies are publishing or promoting subindexes, and very little has been published on understanding or using them. After six decades of breeding cattle and working on dairy cattle improvement — including the original Dollar Difference Formula and Holstein Canada’s Type Classification overhaul in the 1980s — I’m still pushing the industry to look past the numbers it celebrates and toward the economically important ones it quietly ignores.

That’s not breeders failing to read the fine print. That’s a system that never printed it.

What Do Canada’s Top 10 Jersey Sires Actually Look Like Genetically?

Let’s start with which sires are actually driving the breed.

The ten bulls leading Jersey Canada’s 2025 registrations — ToBeFamous and Ghost tied at No. 1, followed by Victorious, Skyfall, Xenial, Artemis, Goldorak, Honeymoon, Cinnamon, and Tekashi — averaging 402 registered daughters each. Together, they sired 29% of all Jersey registrations in Canada that year. Eight of the ten were genomic sires when used, and those eight alone account for 81% of the group’s registered daughters.

When eight genomic bulls shape roughly one in four registered calves in a country, their genetic profile isn’t just interesting. It’s the trajectory of the breed.

Here’s how the Lactanet December 2025 evaluations stack up for that top ten:

Index

Average

Percentile Rank

Range

Bulls Below 50th

LPI

1,918

99th

39th–99th

1 of 10

Pro$

$1,542

~97th

—

—

Production Index (PI)

—

81st

56th–99th

0 of 10

Longevity & Type (LTI)

—

91st

21st–99th

1 of 10

Health & Welfare (HWI)

—

59th

17th–88th

4 of 10

Reproduction (RI)

—

47th

19th–84th

5 of 10

Milkability (MI)

—

34th

2nd–90th

5 of 10

Milk

358 kgs

50th

−121 to 1,071

6 of 10

Fat

49 kgs

79th

12–84

2 of 10

Fat %

+0.37%

—

0.07–0.83

0 of 10

Protein

25 kgs

60th

12–52

4 of 10

Protein %

+0.16%

—

0.07–0.31

0 of 10

Conformation (CONF)

+11.4

97th

−2 to +18

1 of 10

The gap between the 99th-percentile LPI and the 47th-percentile RI — 52 percentile points — might be the most revealing number in this dataset. It also never shows up on a sire card.

Why Don’t Breeders See the Fertility and Milkability Gap?

The short version: nothing in the current sire selection pipeline forces RI, HWI, or MI onto the table when you’re actually ordering semen.

Fat percentage is loud. When a bull adds +0.83%F — the high end of this top ten’s range — the economic reward shows up on every milk settlement. The A2A2 and BB casein story works the same way: processors put a premium on paper, breeders respond, and by 2025, the breed hit 100% A2A2 and 90% BB kappa-casein among its most-used sires. That’s the market signal doing exactly what it’s supposed to do.

Fertility costs are quiet. When a cow takes an extra cycle or two to settle, the penalty spreads across the vet bill, the semen line, the replacement purchase, and a longer calving interval that drags down lifetime milk and drives up lifetime days dry. None of those line items show up with a bold “this is what 47th-percentile RI genetics cost you this month” stamped on them.

Timed AI programs like Double-Ovsynch and Presynch-Ovsynch deepen the blind spot. They override a cow’s own biology, delivering conception rates that hide genetic fertility deficits. The protocol works — but it costs more to maintain with every percentile point of genetic fertility you give away. More shots. Tighter labour timing. More resynchronization cycles.

The Milkability Index gap tells its own story. MI combines milking speed, temperament, and milking-related mammary traits — exactly the traits that determine how quickly and smoothly cows move through a parlour or a robot box. A 34th-percentile MI average means the daughters of the breed’s most popular sires are, on balance, below average for the traits that drive milking efficiency and robot throughput. That’s real money in labour and robot capacity, especially as more Canadian herds adopt automated milking.

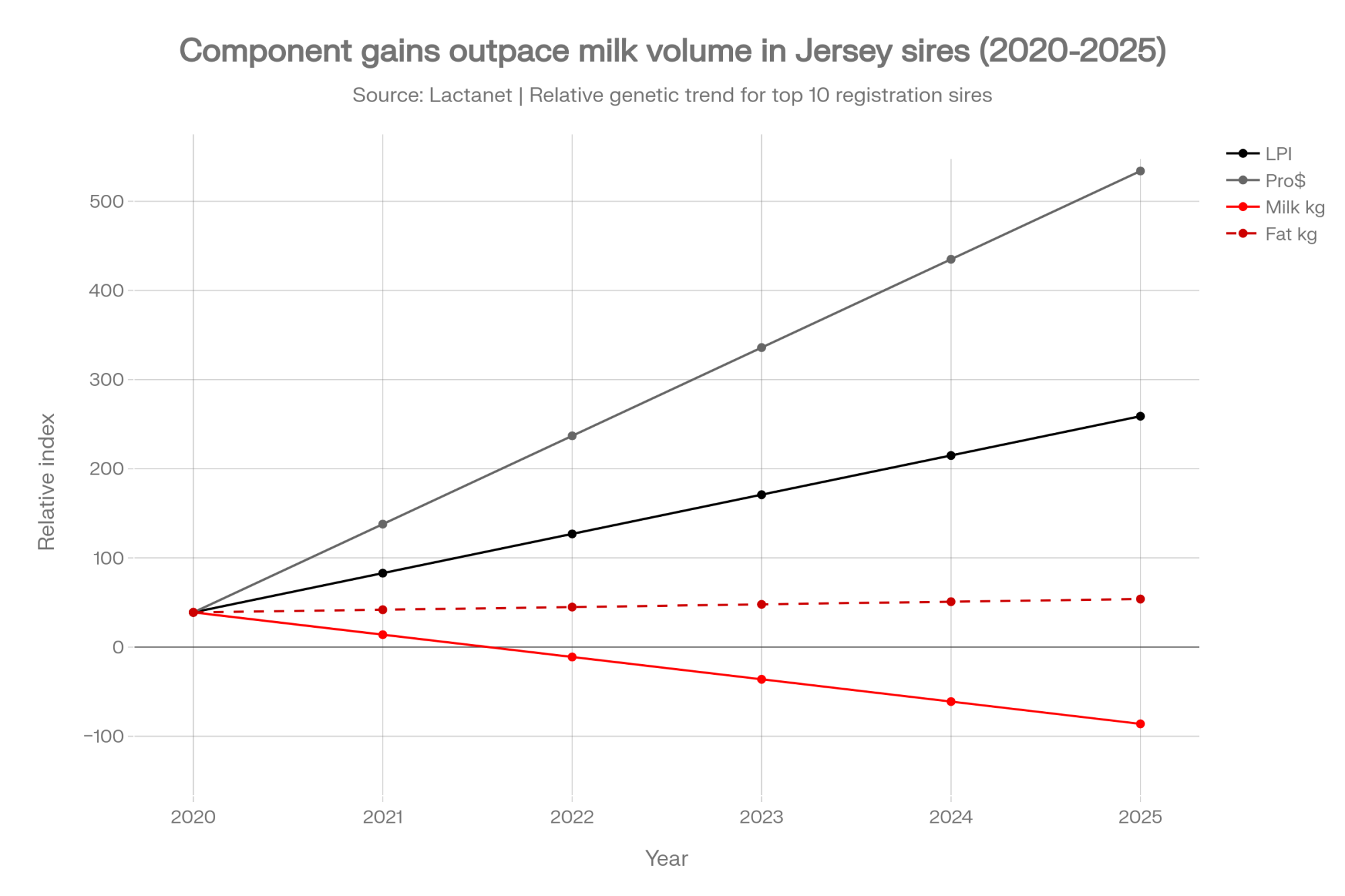

Fat Gains Up, Fertility Drifting: Five Years of Jersey Genetic Trends

Zoom out to the five-year trend for the top ten registration sires from 2020 to 2025, and the selection pattern comes into focus:

Trait

Annual Gain (Top 10 Registration Sires, 2020–2025)

LPI

+44 points/year

Pro$

+$99/year

Milk Volume

−25 kgs/year

Fat Yield

+3 kgs/year

Fat %

+0.05%/year

Protein Yield

+1 kg/year

Protein %

+0.03%/year

Conformation

+0.8/year

Mammary System

+0.8/year

Dairy Strength

+0.90/year

Feet & Legs

+0.75/year

Rump

+0.66/year

Inbreeding

−0.28%/year

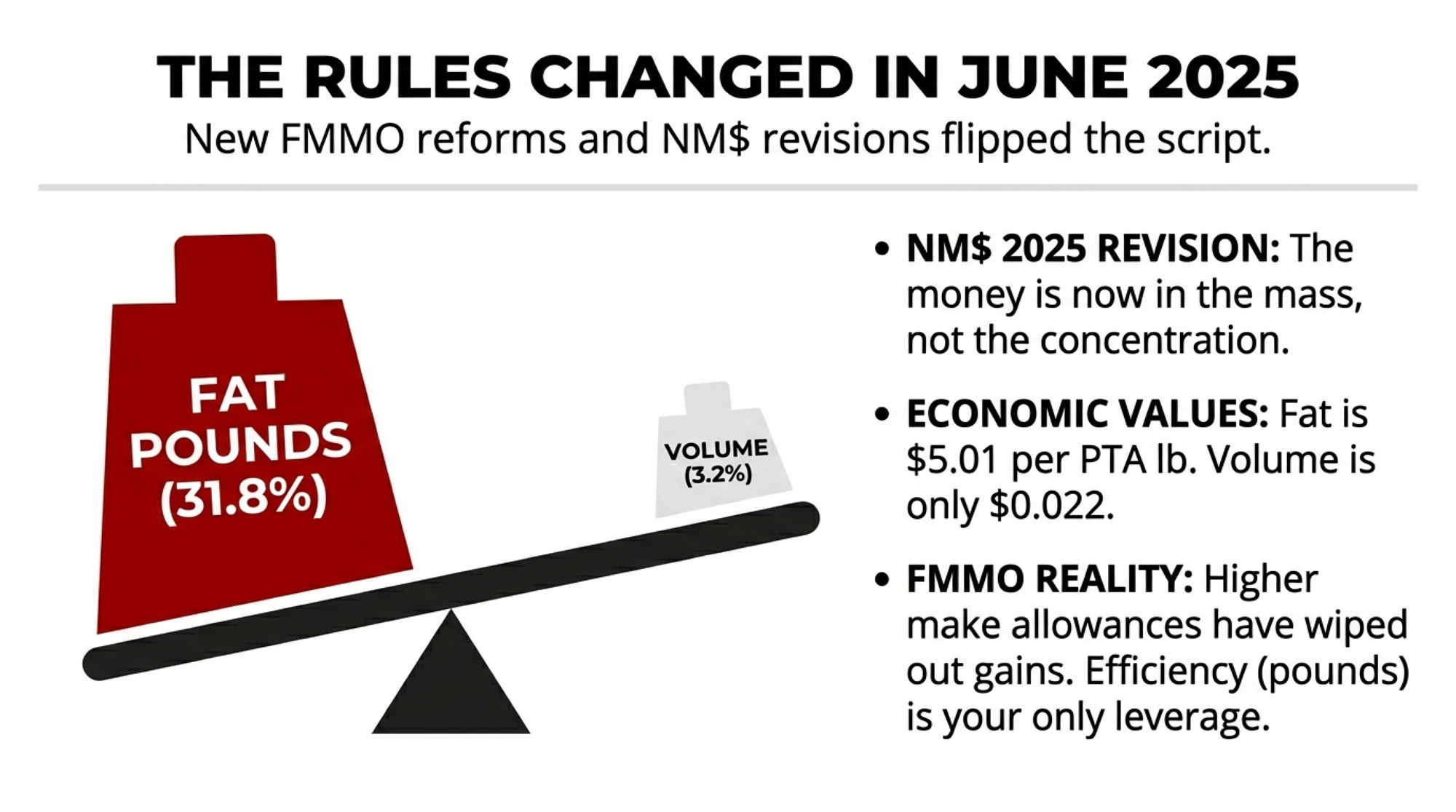

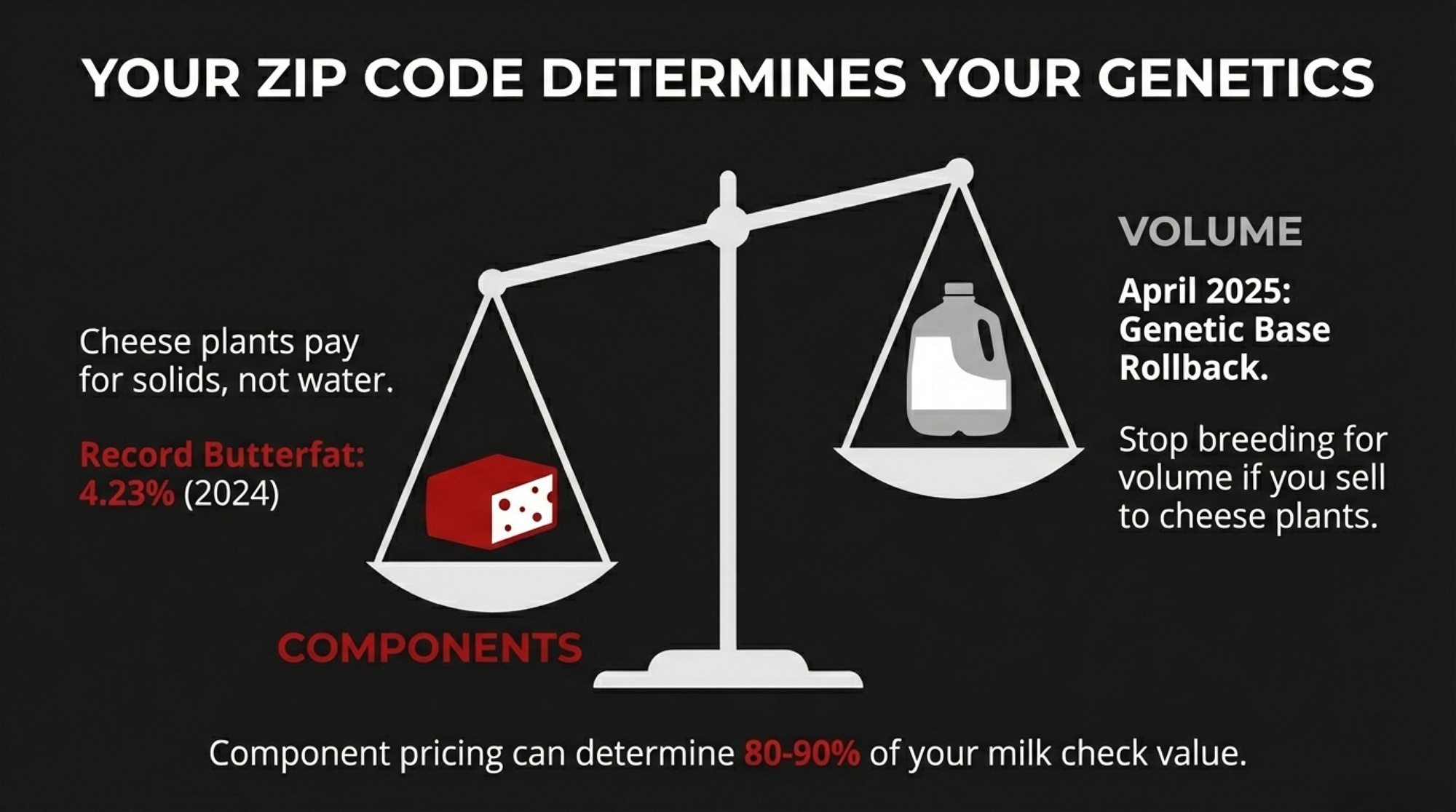

Milk volume is deliberately sliding while fat and protein percentages climb. That’s component pricing at work, and breeders are delivering exactly what processors reward.

What’s missing in that trend table are equivalent progress numbers for RI, HWI, or MI. The traits everyone tracks, publishes, and celebrates are the ones getting selected. The ones buried in PDF footnotes are drifting. The 47th-percentile RI average is a pretty good hint of which direction.

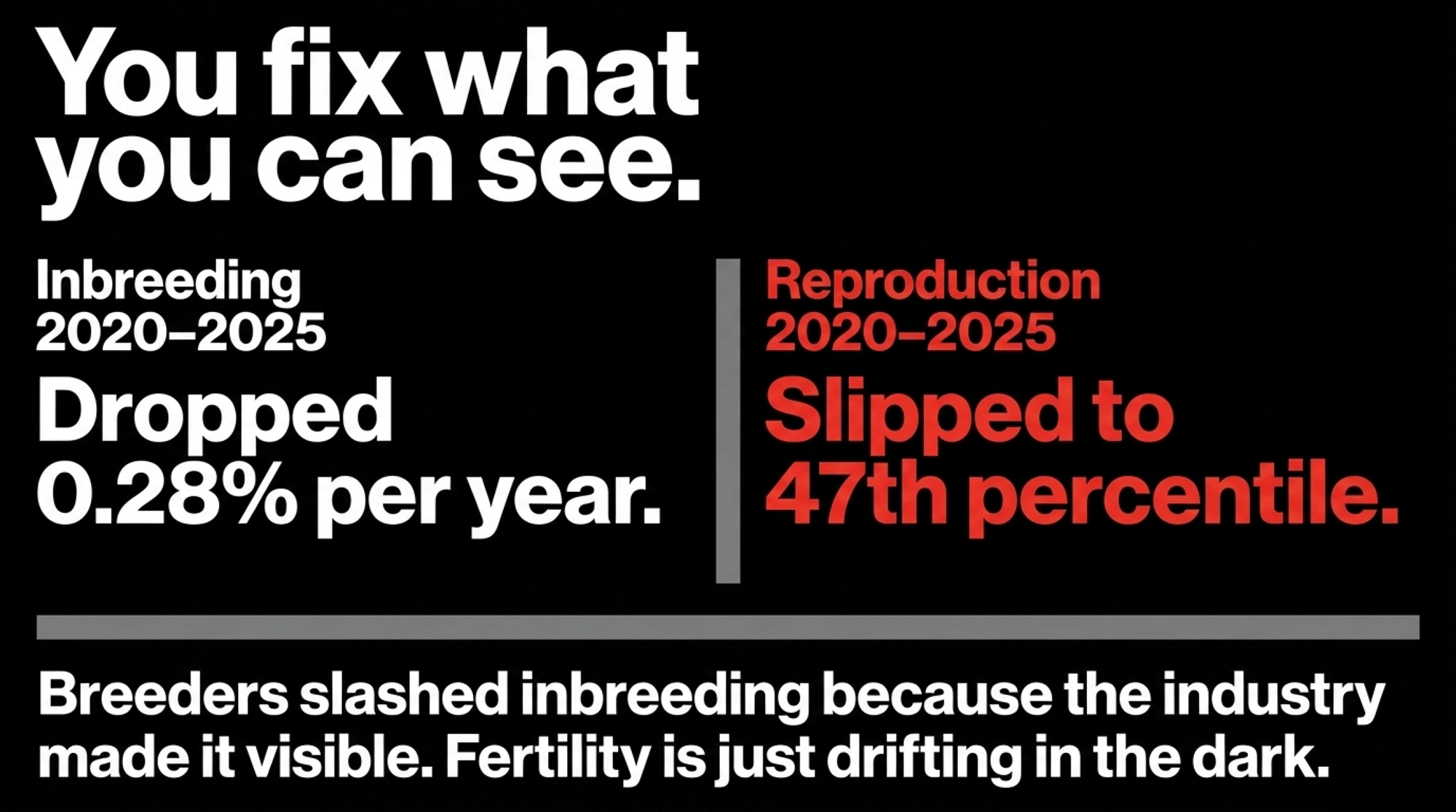

On the positive side, the inbreeding story is exactly what you’d hope to see. The average for the top ten drops from 9.77% in 2020 to 8.10% in 2025 — a reduction of 0.28% per year, with seven of ten bulls sitting under 9.0%. That proves something important: Canadian Jersey breeders can manage a trait that isn’t on the milk cheque when the industry makes it visible and gives them tools. It’s fair to ask why the same thing hasn’t happened for reproduction, health, and milkability yet.

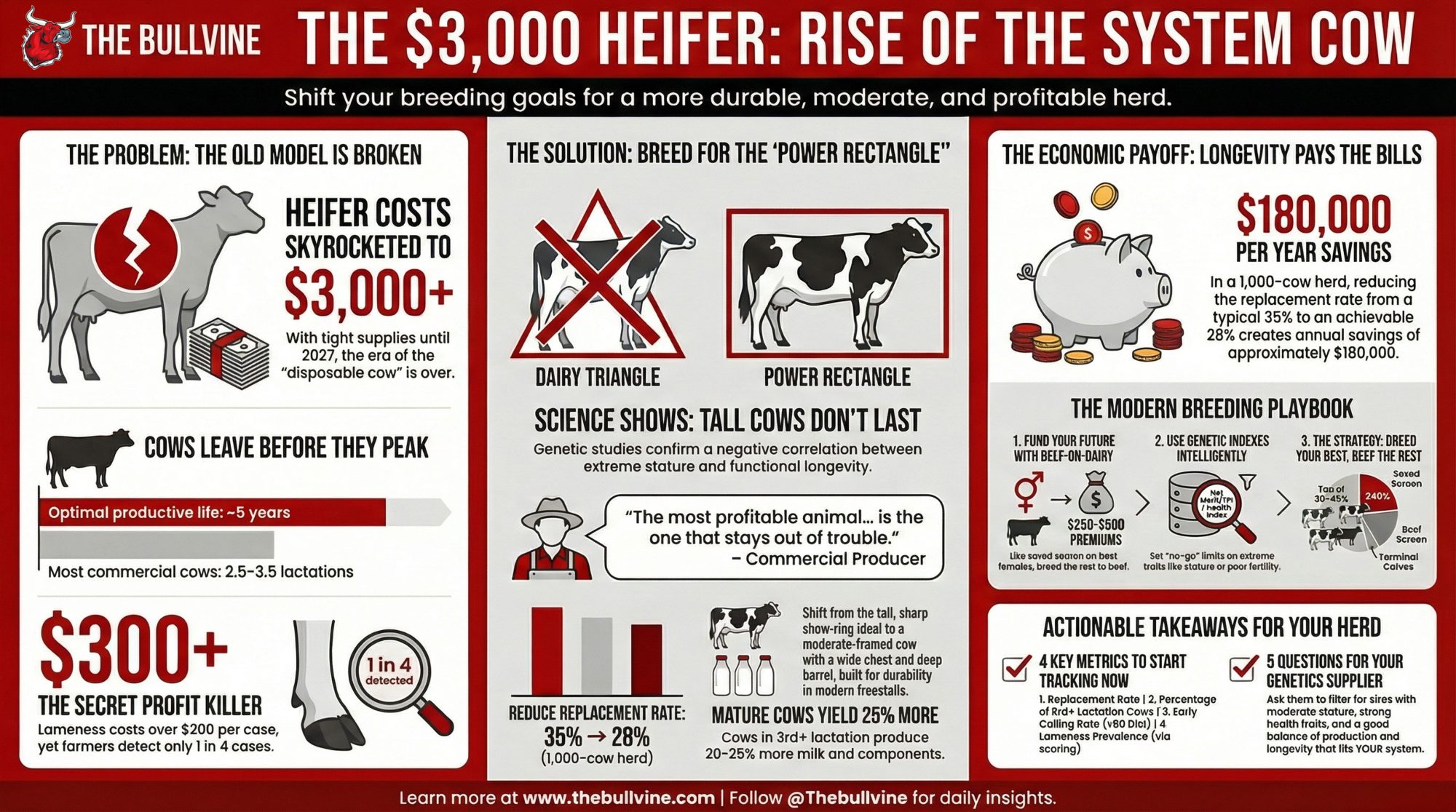

The Barn Math Behind 47th-Percentile Fertility

Here’s where you can feel it in your own numbers.

A 200-cow Jersey herd turning over 35% annually needs about 70 replacement heifers a year. That’s just barn math: 200 × 0.35 = 70.

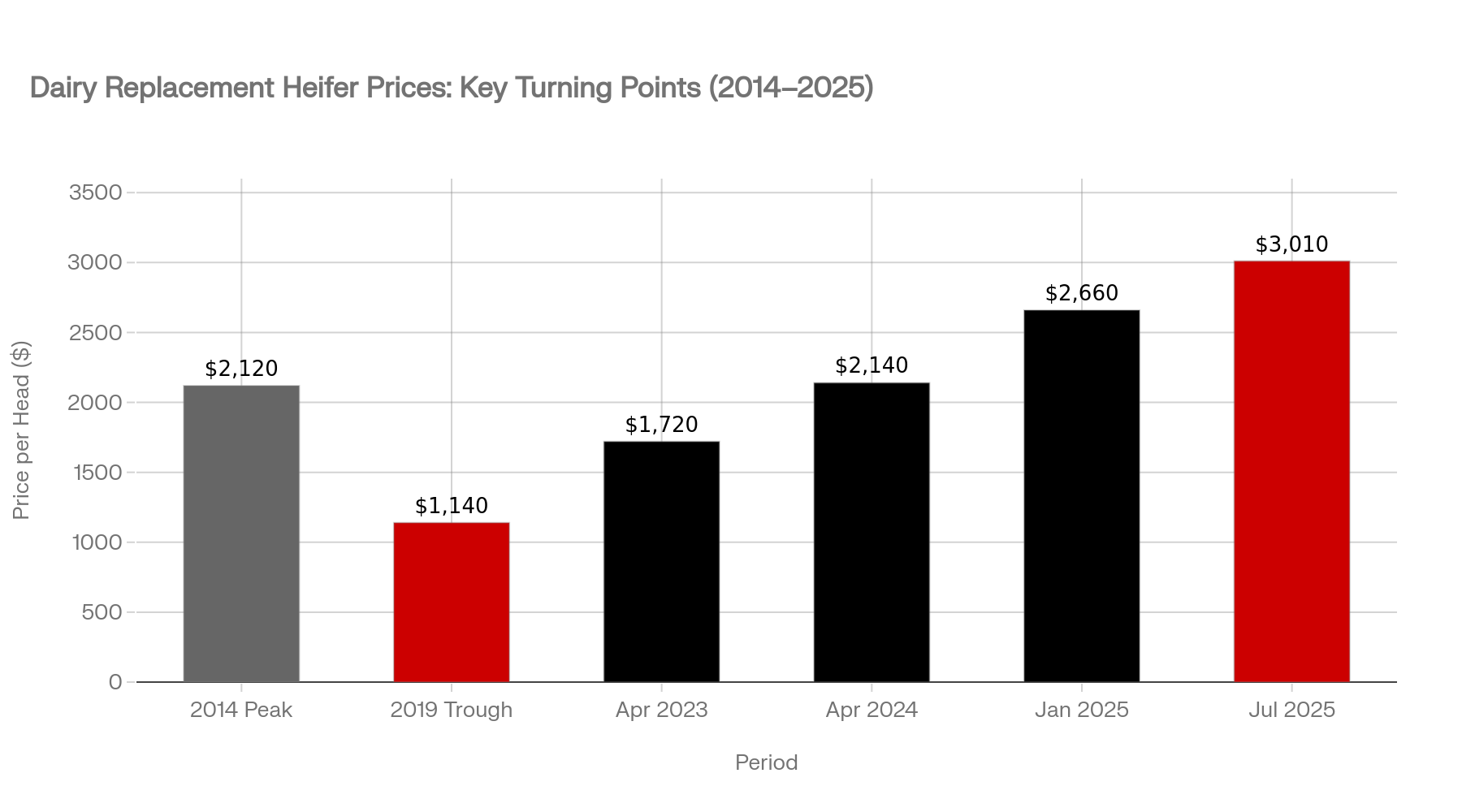

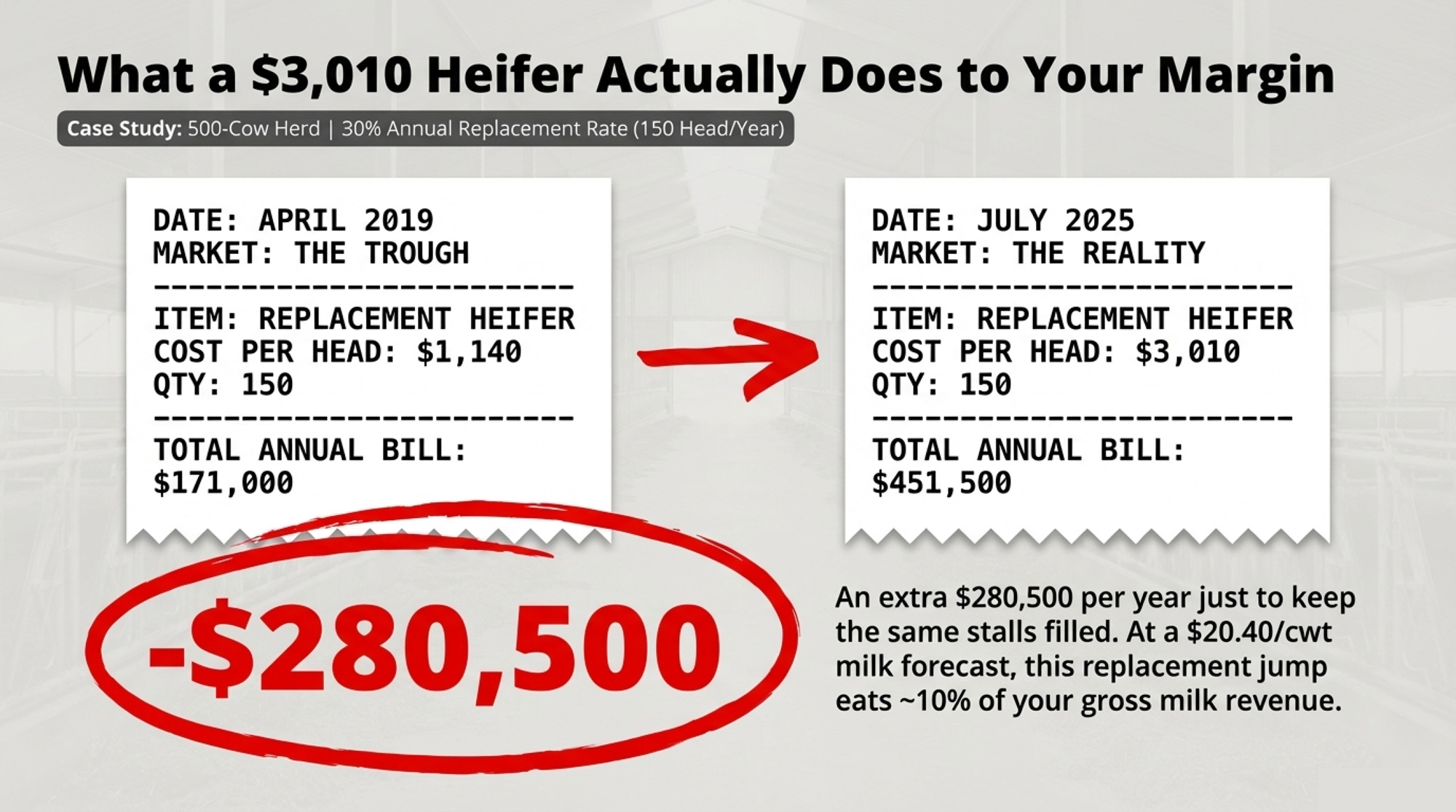

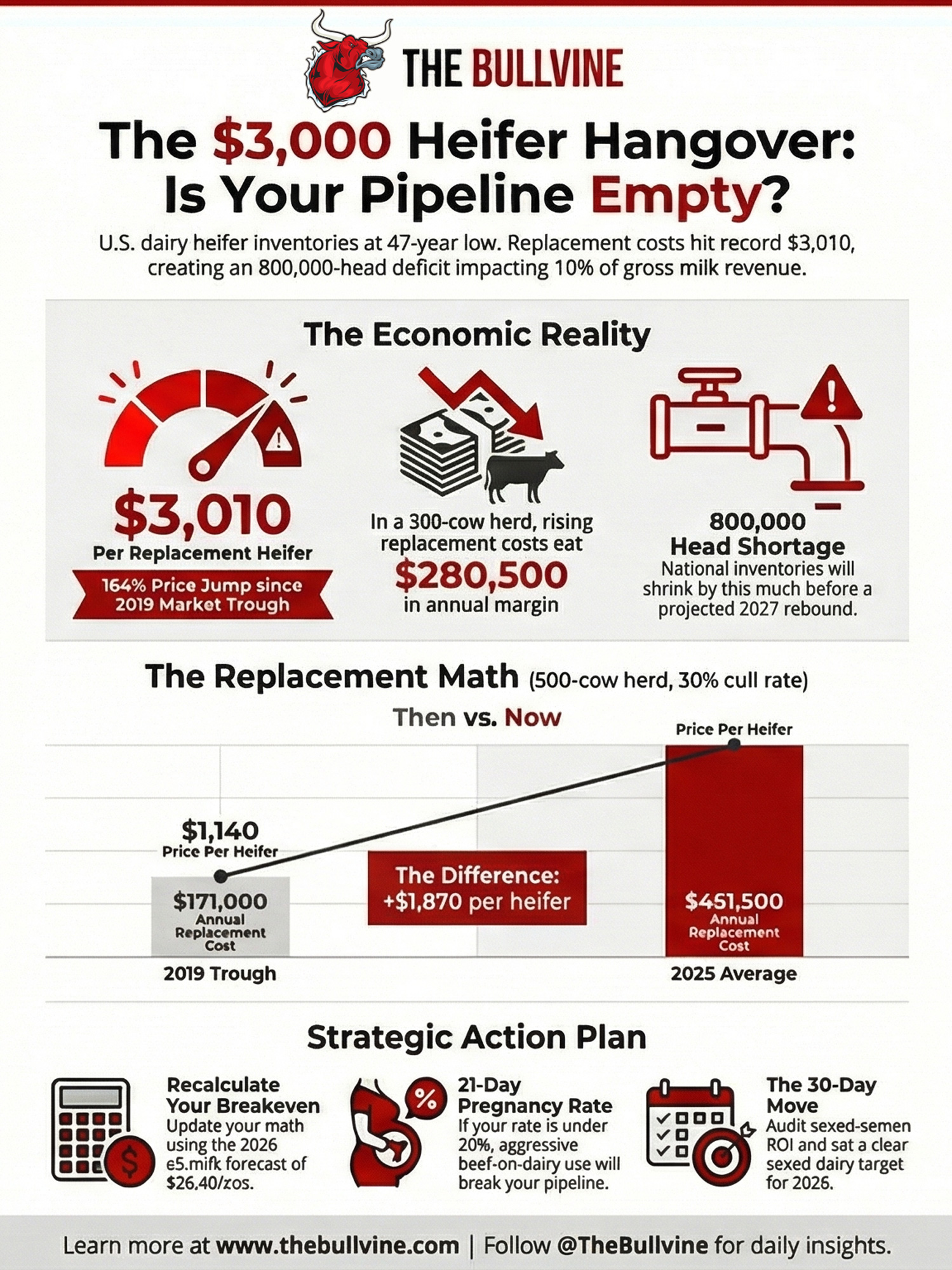

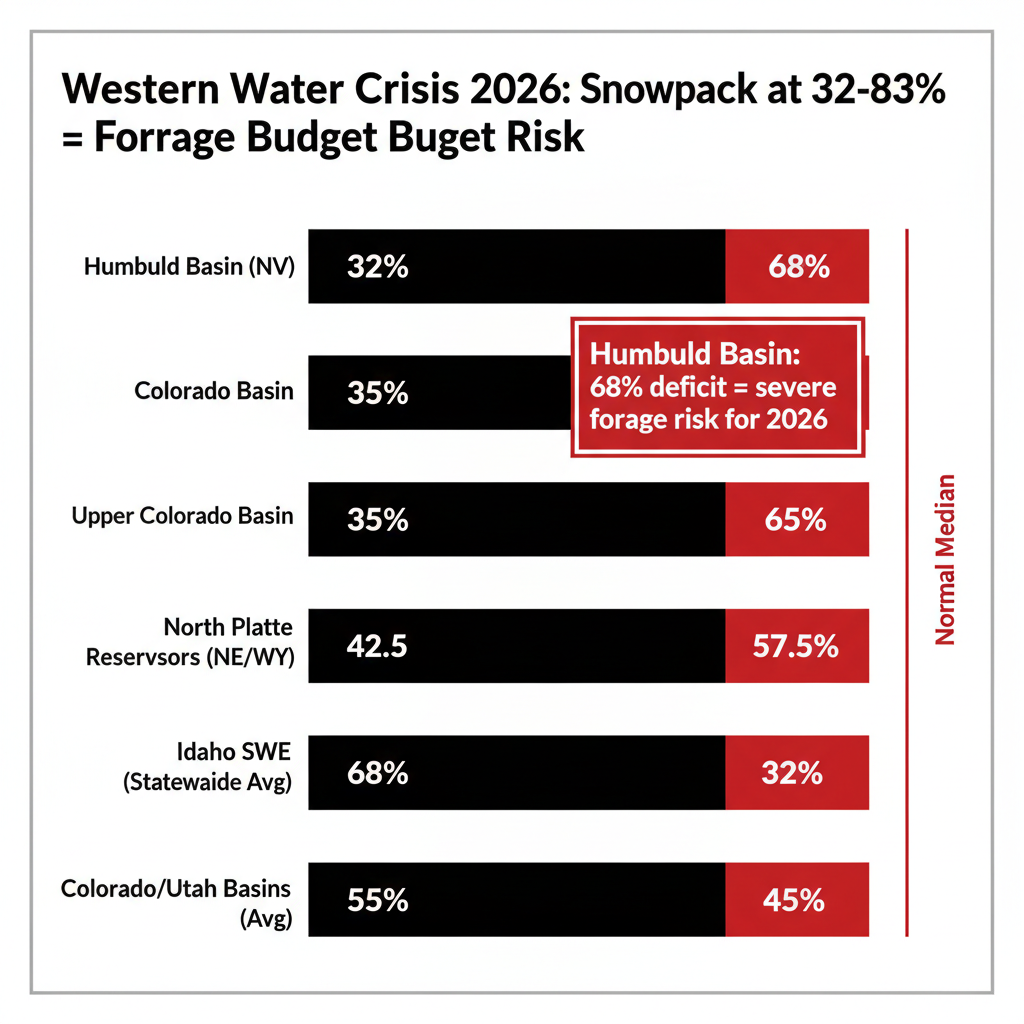

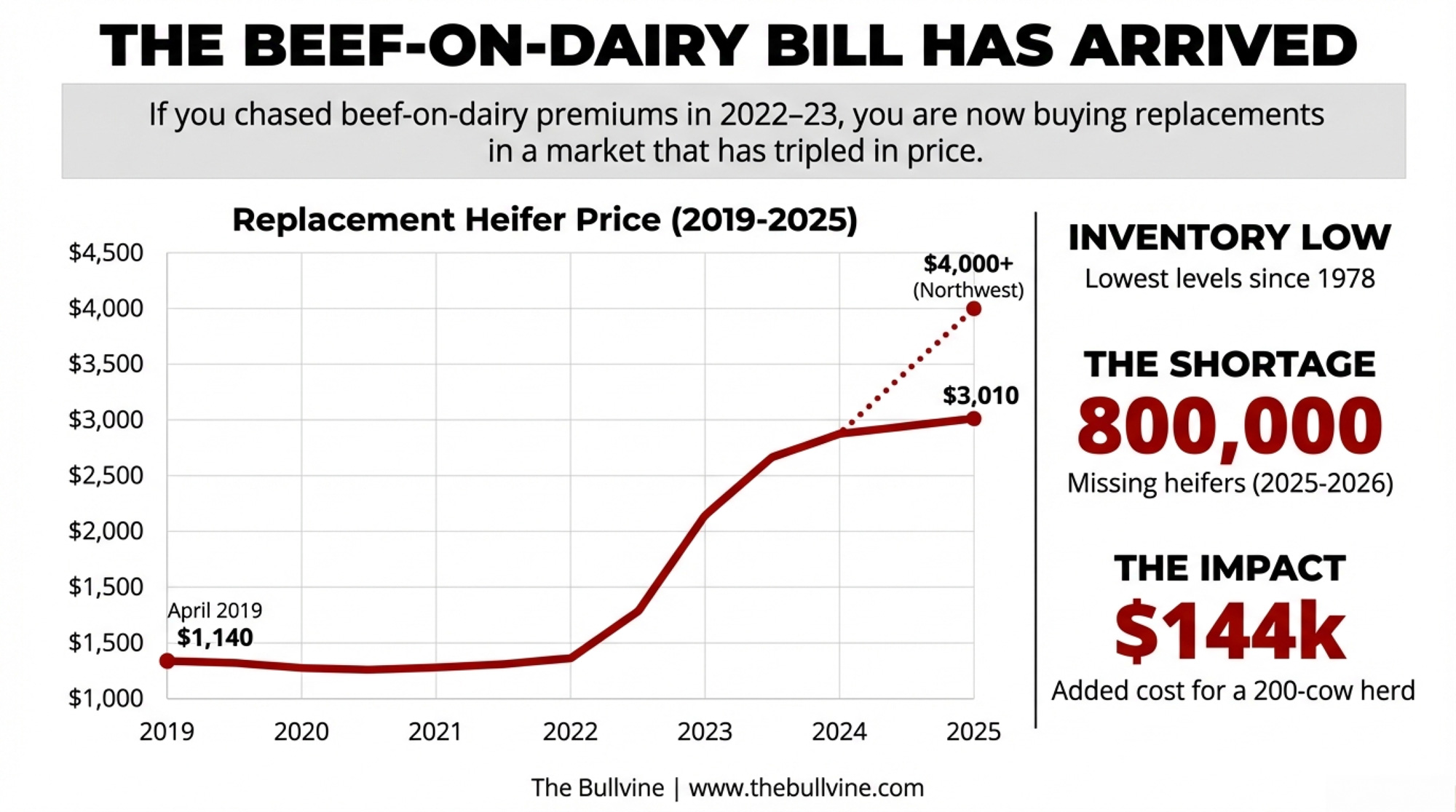

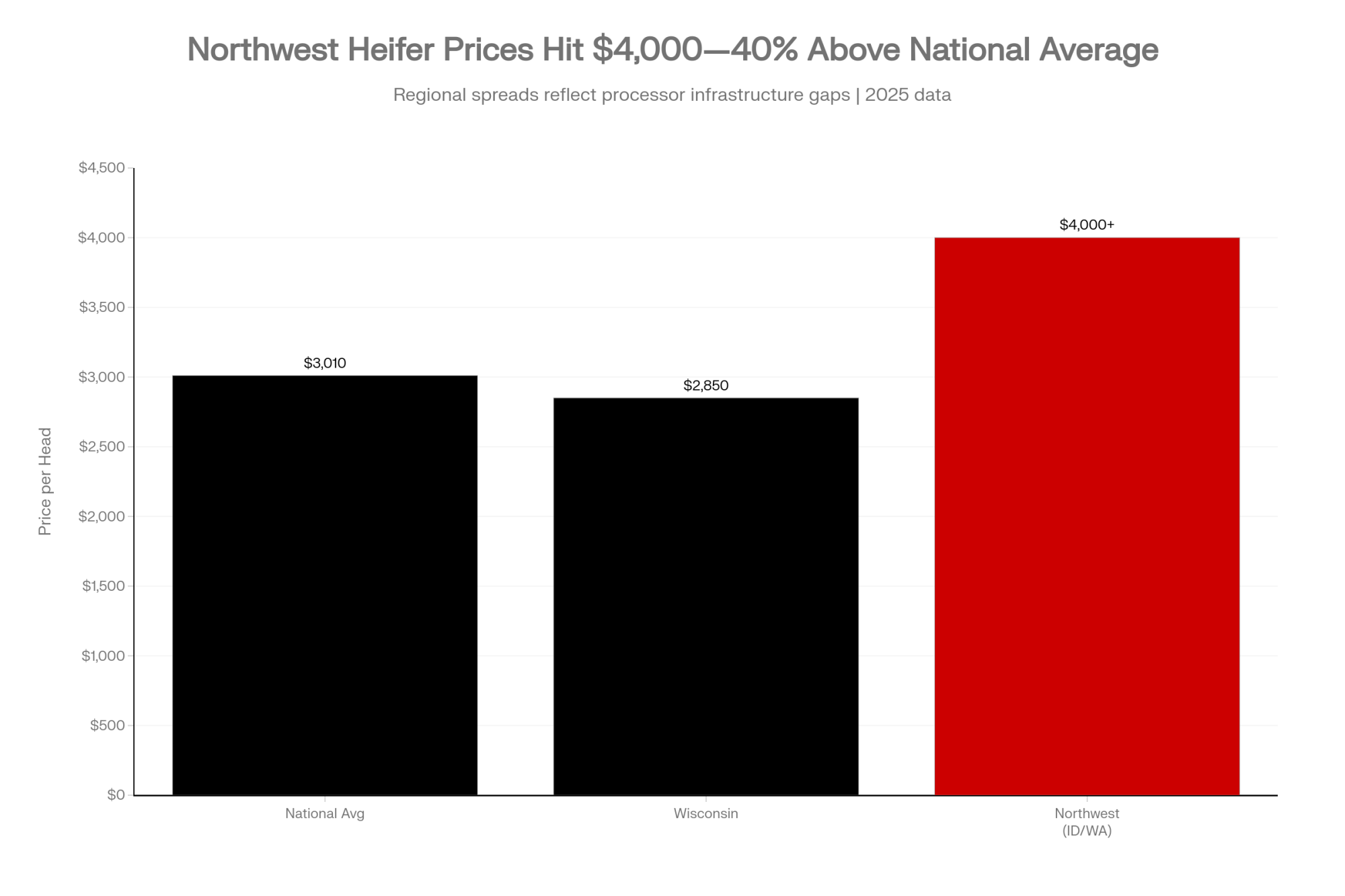

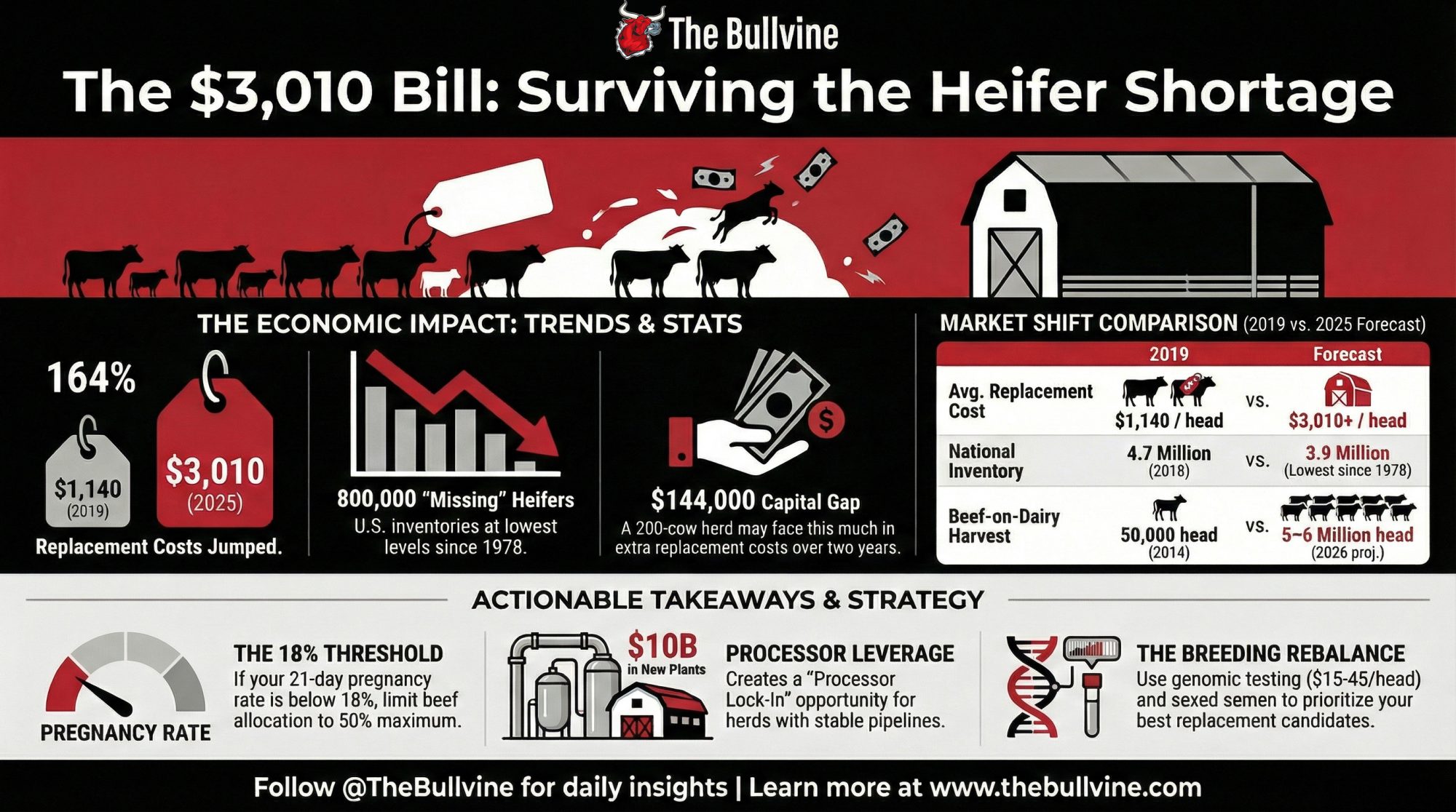

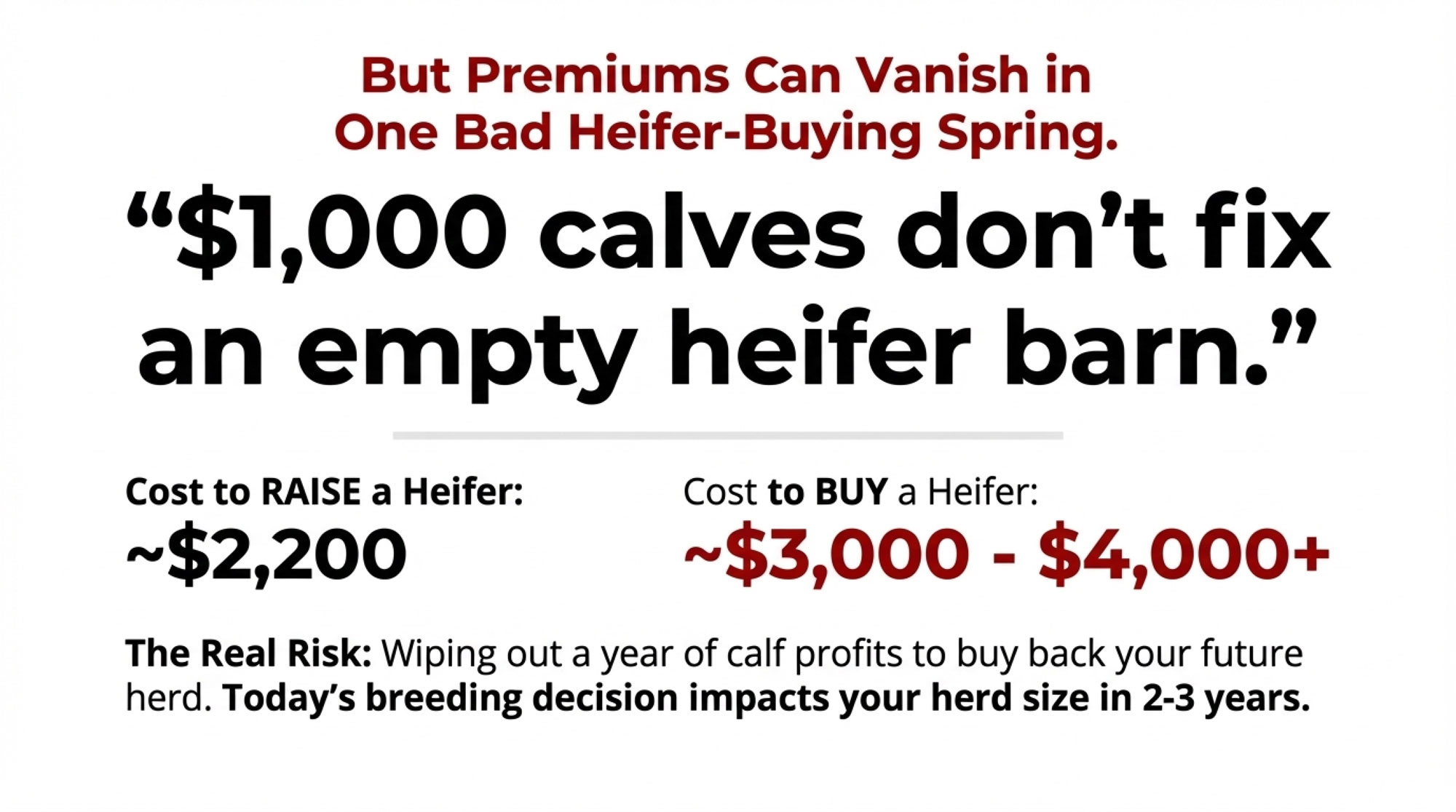

On the cost side, U.S. dairy replacement prices hit about $3,010 per head in July 2025, up 164% from the 2019 bottom of around $1,140, with top heifers bringing $4,000 or more in some auction barns. In Ontario, replacement heifers over 900 lbs were selling around $326–$328 per hundredweight at recent auctions — not the same absolute price, but the direction of travel is similar.

Now layer in genetics. If below-average RI bulls add even one extra service per conception across your dairy-bred matings, that’s more semen, more time open, and more risk that cows fall out of the dairy pipeline and into beef because they didn’t settle. It’s not just a $30–$50 sexed semen straw that didn’t stick. It’s a heifer that never existed, and a cow that probably gets bred to beef because everyone’s tired of missing her.

My read of the Production Index adds another twist. The PI averages the 81st percentile across the top ten — good, but notably lower than the LPI at the 99th and the LTI at the 91st.. In other words, the composite LPI for these bulls is being carried more by longevity and type than by yield. That raises a fair question: how much of that 1,918-point LPI reflects real lifetime profitability, and how much is the formula letting strong CONF and LTI paper override weak RI and MI?

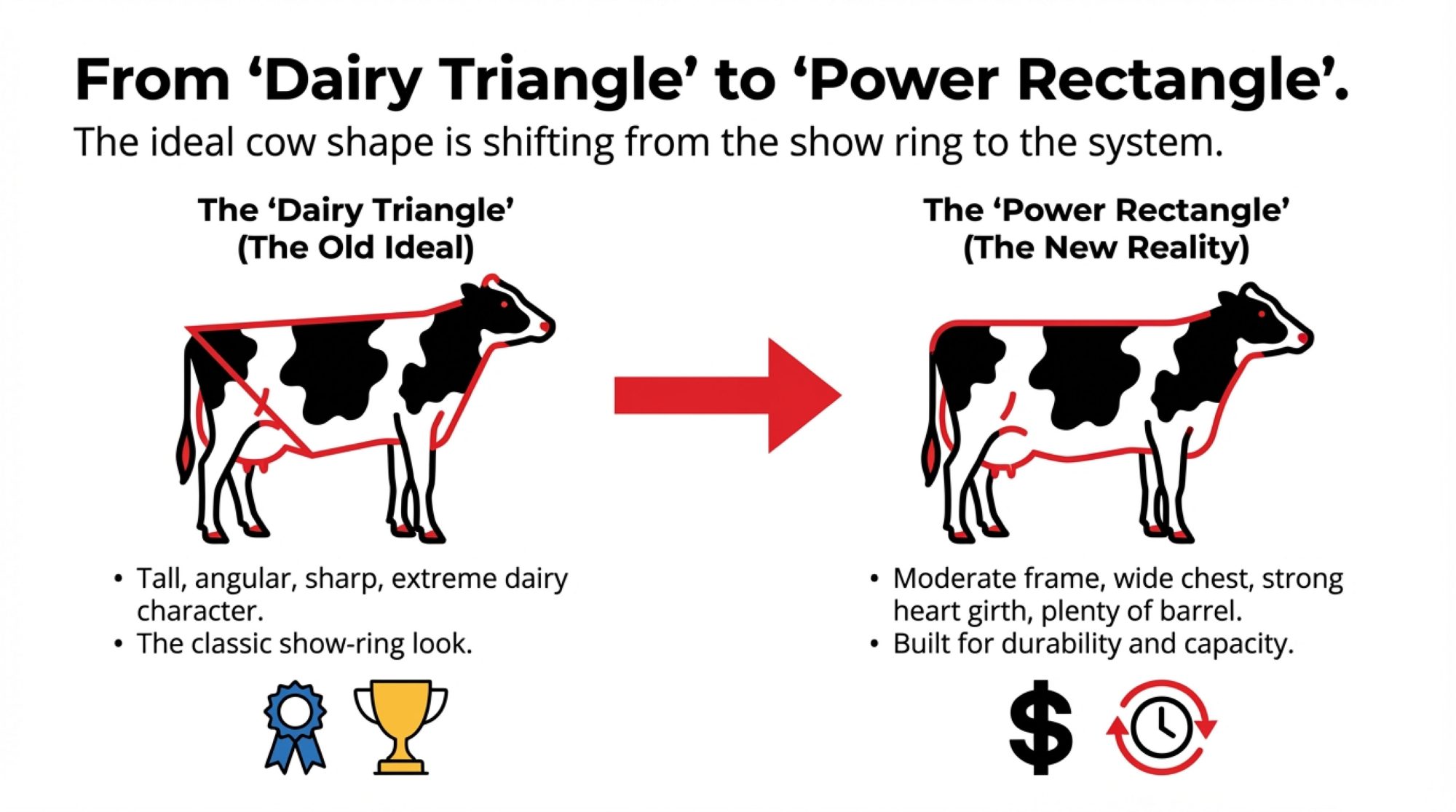

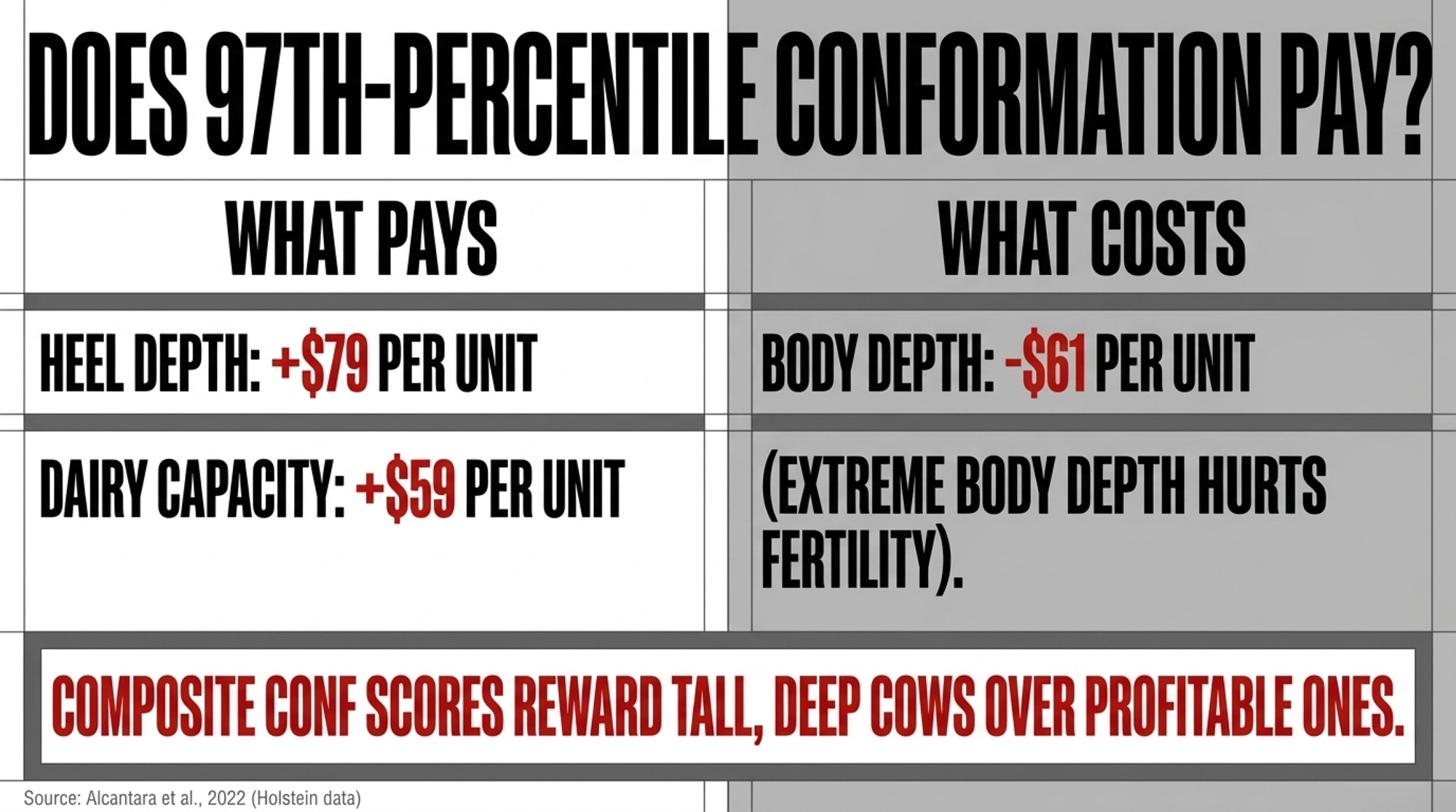

Does 97th-Percentile Conformation Actually Drive Jersey Profitability?

On paper, this top ten group is a type breeder’s dream. The average conformation score sits at +11.4 — the 97th percentile — with a range from −2 to +18. Mammary system averages +8.9. Feet and legs average +8.5. Those are big numbers.

The real question is what those numbers actually buy you.

Canadian work from Agriculture and Agri-Food Canada on longevity found that udder depth and milking ease accounted for 84% of the total contribution of type traits to functional longevity, and that rear teat placement, udder depth, and udder texture had a significant influence on functional survival. Cows with tight, well-attached udders stayed in the herd longer.

Alcantara, Baes, de Oliveira Junior, and Schenkel (2022), in the Canadian Journal of Animal Science, put hard-dollar values on the type traits involved. Analyzing 9,351 proven Holstein bulls, they found heel depth had the strongest positive effect on Pro$ of any conformation trait, at +$79.13 per unit RBV increase.

In plain terms: heel depth pays you; extreme body depth costs you.

That same paper showed dairy capacity (especially body length) was also positive, at +$59.00 per unit RBV. More capacious, angular cows tended to stay productive longer. But body depth told the other side of the story: it had the largest negative effect on Pro$ at –$61.95 per unit RBV because deeper-bodied cows ate more, tended to lose condition more quickly after calving, and showed poorer fertility in later lactations.

The problem is that composite CONF rewards all of it. Stature, angularity, body capacity, and dairy character are assigned the same number as functional mammary and feet-and-legs traits. So, a bull could rank in the 97th percentile for CONF largely on height and style, while another sits in the 72nd percentile with rock-solid udders and feet. The composite score doesn’t tell you which one actually puts more money in your pocket over five lactations. And neither does the catalog page.

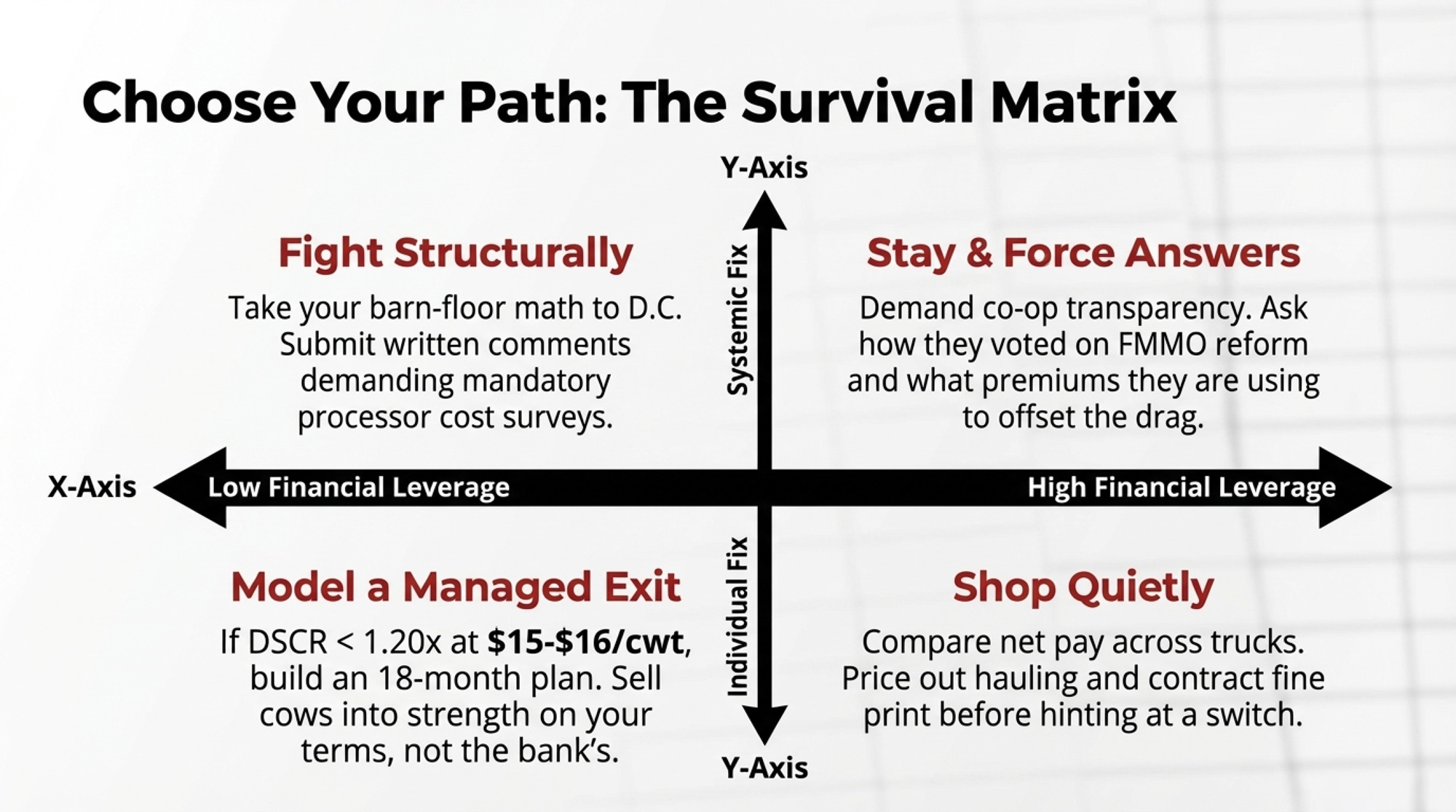

What Would a Balanced Jersey Sire Stack Look Like in 2026?

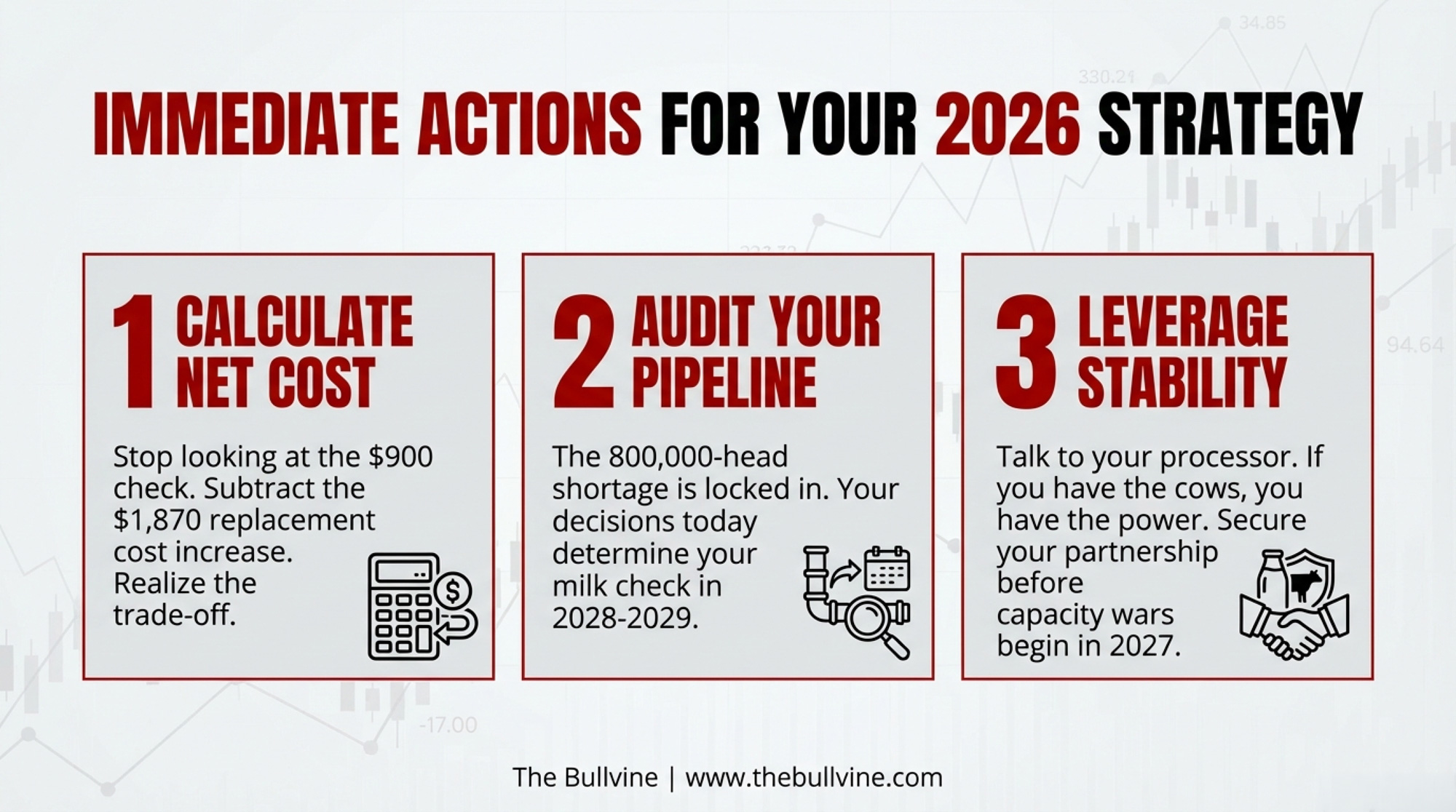

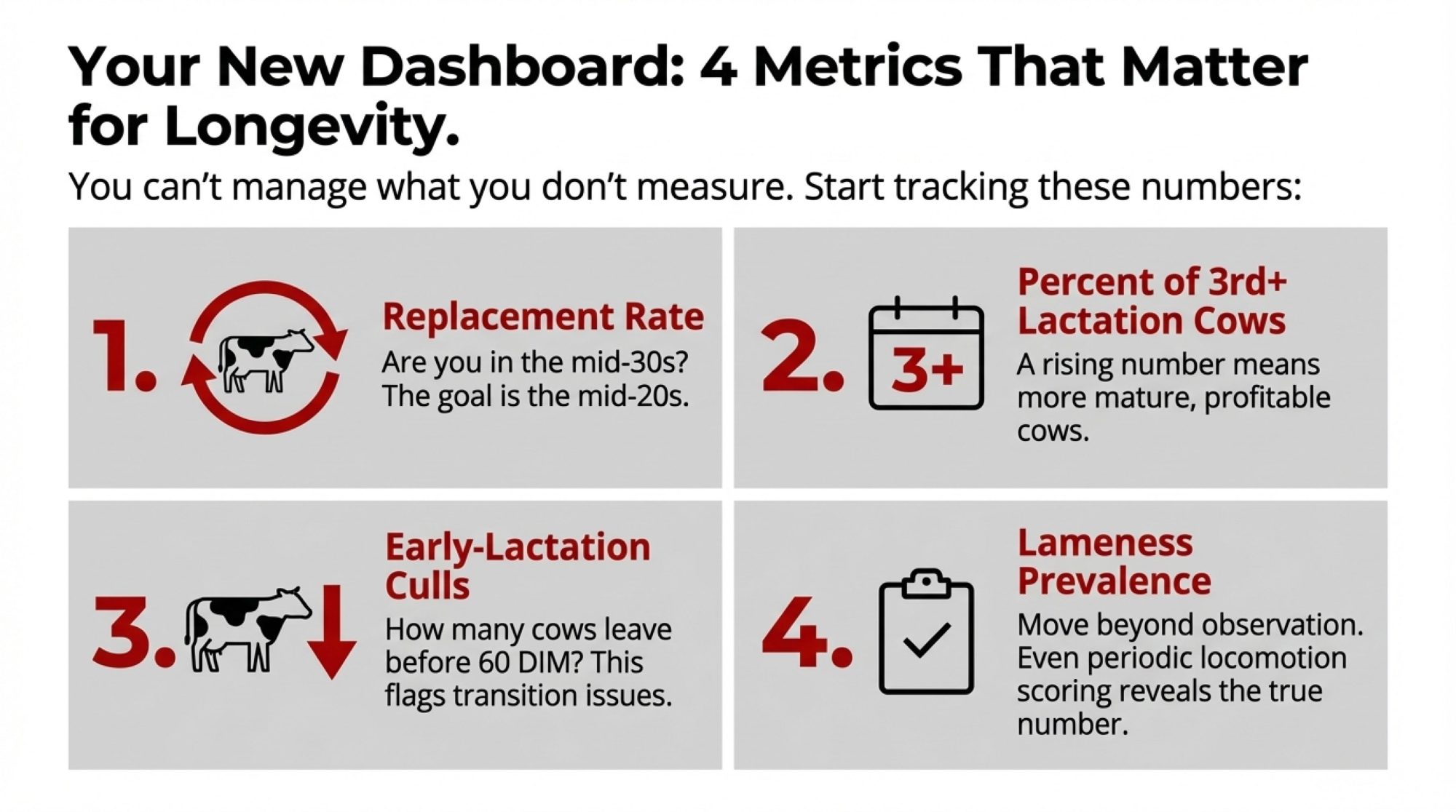

The 2025 data doesn’t say you need to blow up your sire list and start over. It says you need an index floor when selecting sires. And you need it on traits and subindexes where no one has put one to date.

Set a hard RI minimum at the 50th percentile for every bull in your stack. That’s not aggressive — it just means refusing to use sires whose daughters carry below-average fertility genetics. Apply this filter to the current top ten, and five of the ten drop out immediately. If you actually want to improve fertility, not just stop the slide, aim for RI in the 65th percentile or better. This month, pull the Lactanet subindex breakdown for every sire in your current mating plan. If any bull sits below the 50th-percentile for RI, flag him for replacement or for use only on your most fertile cows.

Give HWI a seat at the table. The top ten average just the 59th percentile for the Health & Welfare Index, with four bulls below the median. HWI is where Metabolic Disease Resistance, Mastitis Resistance, and Cystic Ovaries live in the modernized LPI. A 55th percentile floor keeps you from actively weakening your health genetics; 65th and up start building a real health advantage into your replacements.

Use MI as a robot and labour filter. With a 34th-percentile average, MI is the weakest subindex for this top ten group. Suppose you’re milking with robots — or thinking about it — milking speed, temperament, and teat placement matter just as much as litres. Even in a parlour, slow or difficult milkers chew up labour. Set your own MI floor at the 45th percentile, so you’re not selecting against milkability. In a robot environment, you might want a higher percentile.

Cap CONF expectations and target the right pieces. Instead of chasing 97th-percentile CONF across your whole stack, think in a 65th–80th percentile window and focus on mammary and feet-and-legs sub-scores. The Alcantara et al. work backs this up: heel depth and dairy capacity drive Pro$, while body depth drags it down. Select accordingly.

Use high-LPI/low-RI sires as specialty tools, not blanket-herd bulls. A bull sitting at 99th-percentile LPI with poor subindex scores might still earn a place, on the 15–20% of cows with outstanding fertility and health backgrounds where you can safely chase an outcross, special pedigree, or type shot. He shouldn’t be breeding 80% of the herd.

Before your fall semen order (90-day action), write a simple sire selection protocol. One page. Minimum RI and HWI percentiles. Plus a desired MI floor. Target range for CONF with mammary and feet/legs priorities. Share it with your AI rep and your genetic advisor. If they can’t work within it, that’s a data point too.

By spring 2027 (365-day action), pull services-per-conception data by sire group from your own herd records. That’s where you’ll see RI genetics and timed AI protocols separate. A bull who looks fine on paper but needs 3.2 services per conception in your barn is telling you something your sire catalog won’t.

What This Means for Your Operation

You don’t have to be running a big registered show string for this to matter. If you’re milking Jerseys and buying semen in Canada, you’re already living with the top ten bulls’ subindex profile. The only question is whether you’re steering it or just going along for the ride.

Run the subindex numbers on your current sire stack. Pull RI, HWI, and MI for every active bull you’re using. Calculate the weighted averages across your stack. If RI or HWI sits below the 50th percentile, you’ve quantified your genetic risk for fertility and health.

Decide what you’re actually willing to tolerate. A 47th-percentile RI average is what you get if you follow the registration leaderboard without asking questions. The minute you set a hard floor — even just at the 50th — you’re back in control.

Look at your conformation priorities through an economic lens. How much of your type selection pressure is going into the mammary system and feet/legs, and how much is chasing body depth and stature that the research says doesn’t pay? Adjust your eye accordingly.

If you’re running robots, treat MI as a non-negotiable. A 34th-percentile MI stack is basically selecting against robot efficiency. Put a line in the sand. Then ask yourself how many of your current sires clear it.

Double-check your replacement economics. On your own numbers, what does it cost to buy a bred Jersey heifer, with profit potential, right now? What’s your actual replacement rate? How much room do you have to play with fertility genetics before you start buying more herd replacements than you’d like?

Ask your AI rep better questions. Before you talk pedigrees or price, start with: “What are the RI, HWI, and MI percentiles on your top five Jersey sires for my herd?” If the answers come quickly — with printed subindex charts — you’re dealing with someone who’s reading the full proof sheet. If not, you’ve learned something about whose problems are being solved by that catalog page.

Key Takeaways

If half of the ten most-used Jersey sires in Canada sit below breed average for reproduction, the problem isn’t that breeders don’t care about fertility — it’s that the system never put RI, HWI, and MI on equal footing with LPI and CONF. I’ve been making that argument in one form or another for years: the numbers the industry promotes are the numbers that get selected. The numbers it buries get ignored.

The A2A2 success story proves breeders respond fast when the signal is clear. Processors put a premium on paper; within a few proof runs, the top ten registration bulls went 100% A2A2 and 90% BB. There’s no reason the same can’t happen for RI and MI once those numbers get the same font size in sire marketing and herd discussions.

The inbreeding trajectory shows it can be done. Dropping from 9.77% to 8.10% in five years didn’t happen by accident. It happened because inbreeding became visible and manageable. RI, HWI, and MI are sitting where inbreeding was a decade ago — important, but underused.

The Milkability Index might be the quietest and most expensive number on the page for robot herds. A 34th-percentile MI stack means you’re effectively selecting against milking speed and temperament in a system where every extra minute per cow at the robot is lost throughput. That’s not a small leak.

If you can write your sire selection protocol on one page — with hard subindex floors and a clear role for each bull — you’re ahead of most of the industry. The herds that do that over the next five years will be the ones with the replacements, the robot-friendly udders, and the health genetics that give them room to experiment elsewhere.

Five years from now, the real test of whether this analysis mattered won’t be on a Bullvine page. It’ll be in your own Lactanet login when you pull up your 2030 sire stack and see where your RI, HWI, and MI averages landed. Pull that same screen up tonight. What’s your average RI percentile — and are you honestly okay living with that number for the next five years?

Learn More

The Profit Index Paradox: Choosing Dollars Over Rankings — Arms you with the $869-per-cow lifetime profit gap data needed to override generic sire rankings. Rebuild your selection filter to prioritize Net Merit over LPI and stop leaving thousands on the table.

The Triple Cushion Trap: Why 2025’s Strong Margins Won’t Save You in 2026 — Dismantles the false security of 2025’s high margins by exposing the looming replacement heifer shortage. Prepares your operation for 2026 by mapping out critical moves for beef-on-dairy revenue and herd right-sizing.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

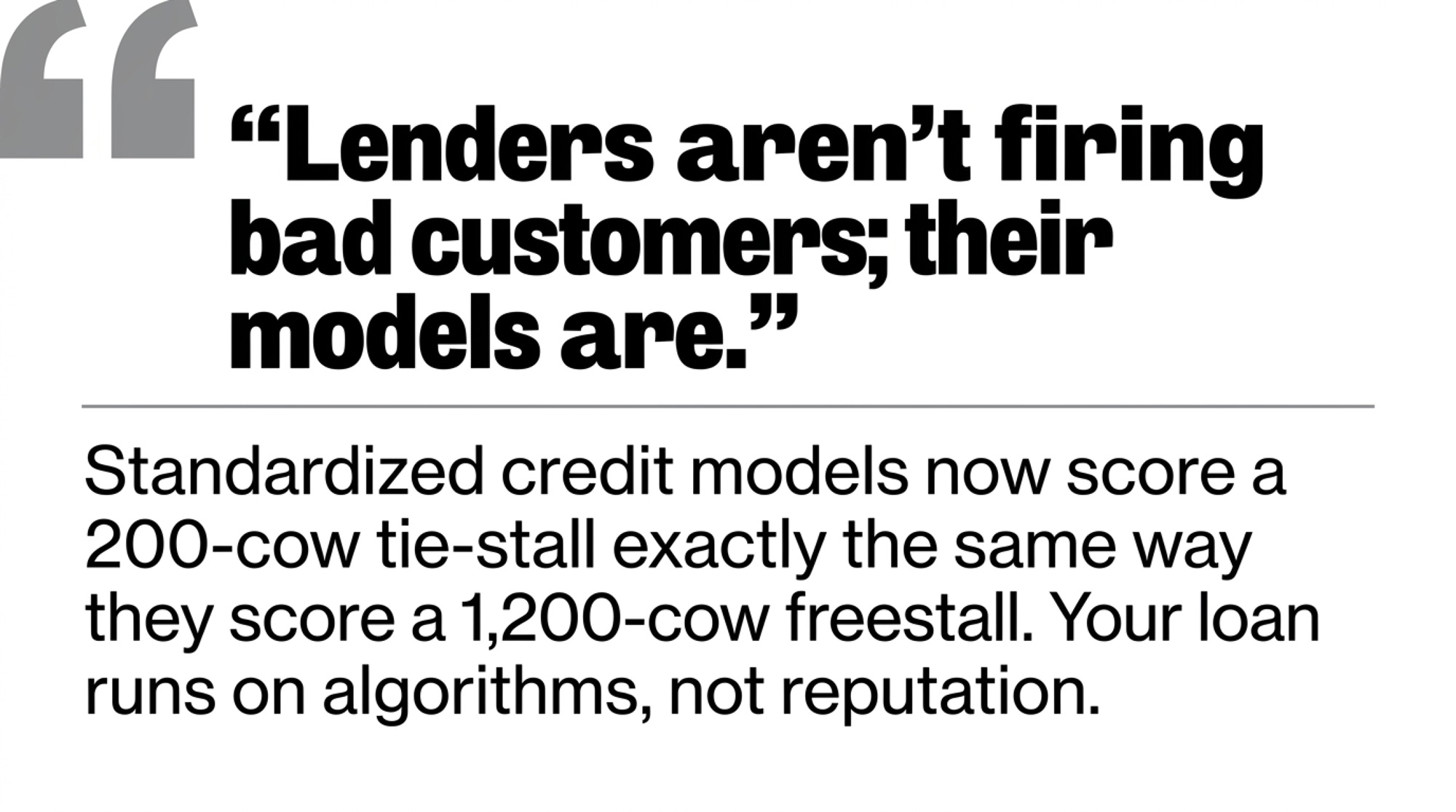

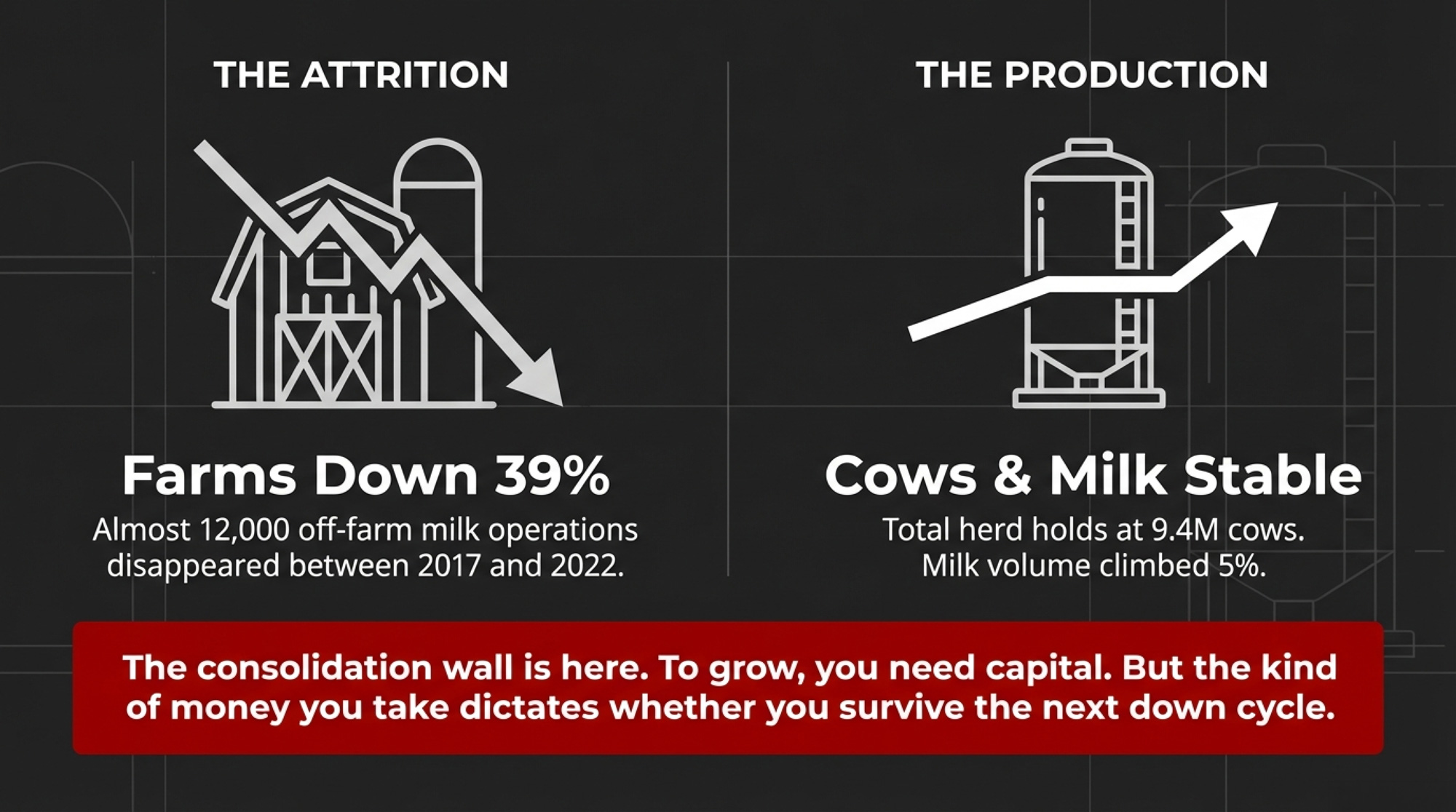

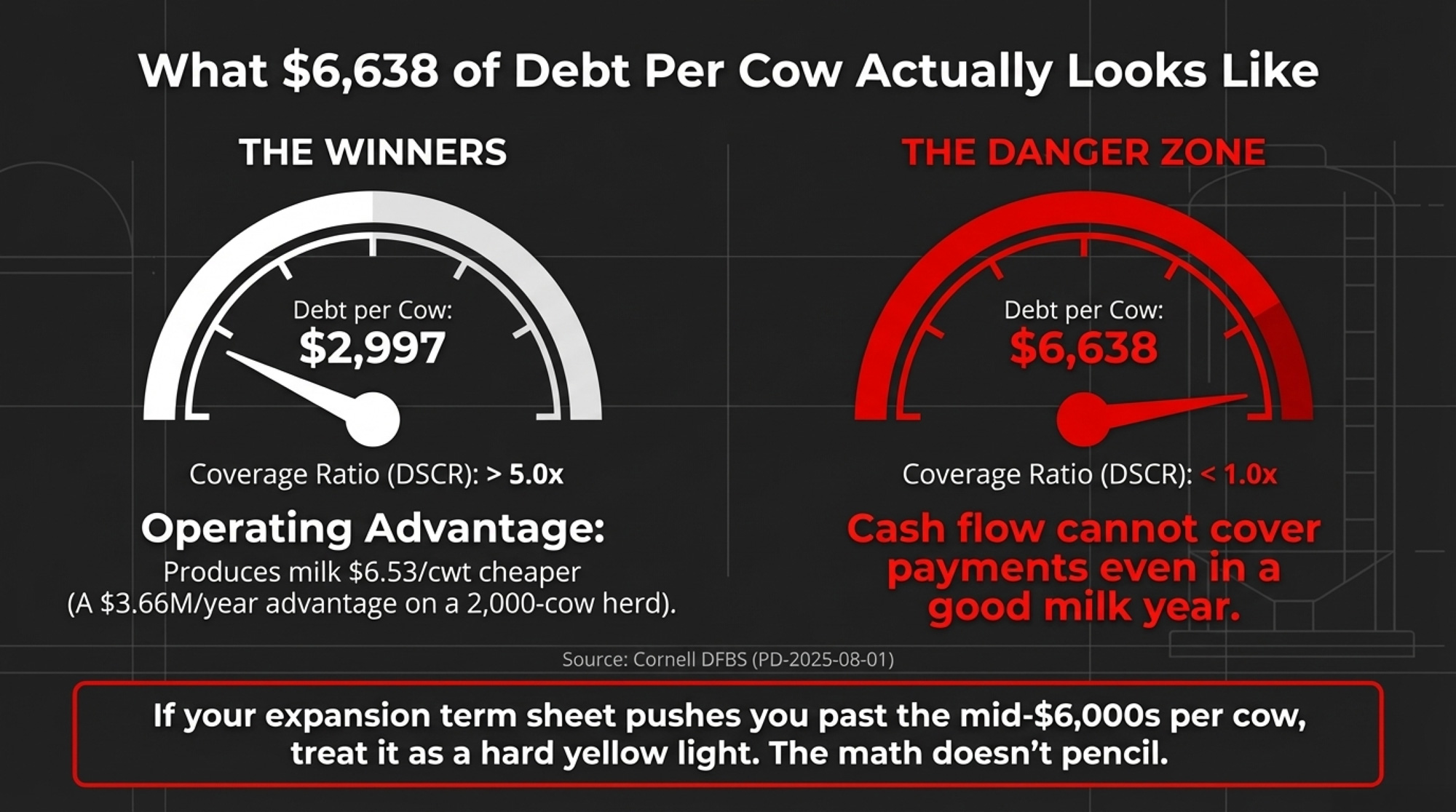

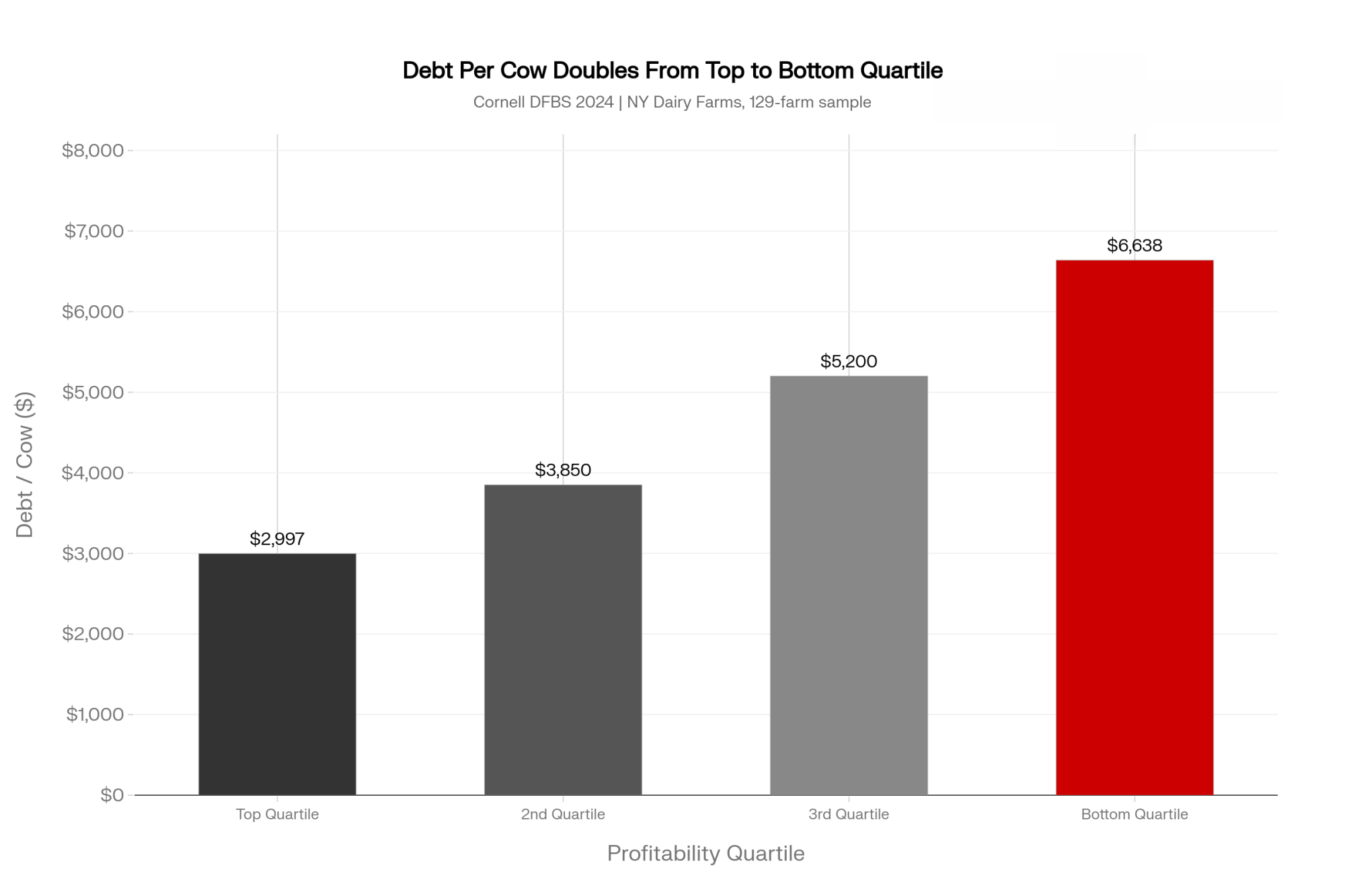

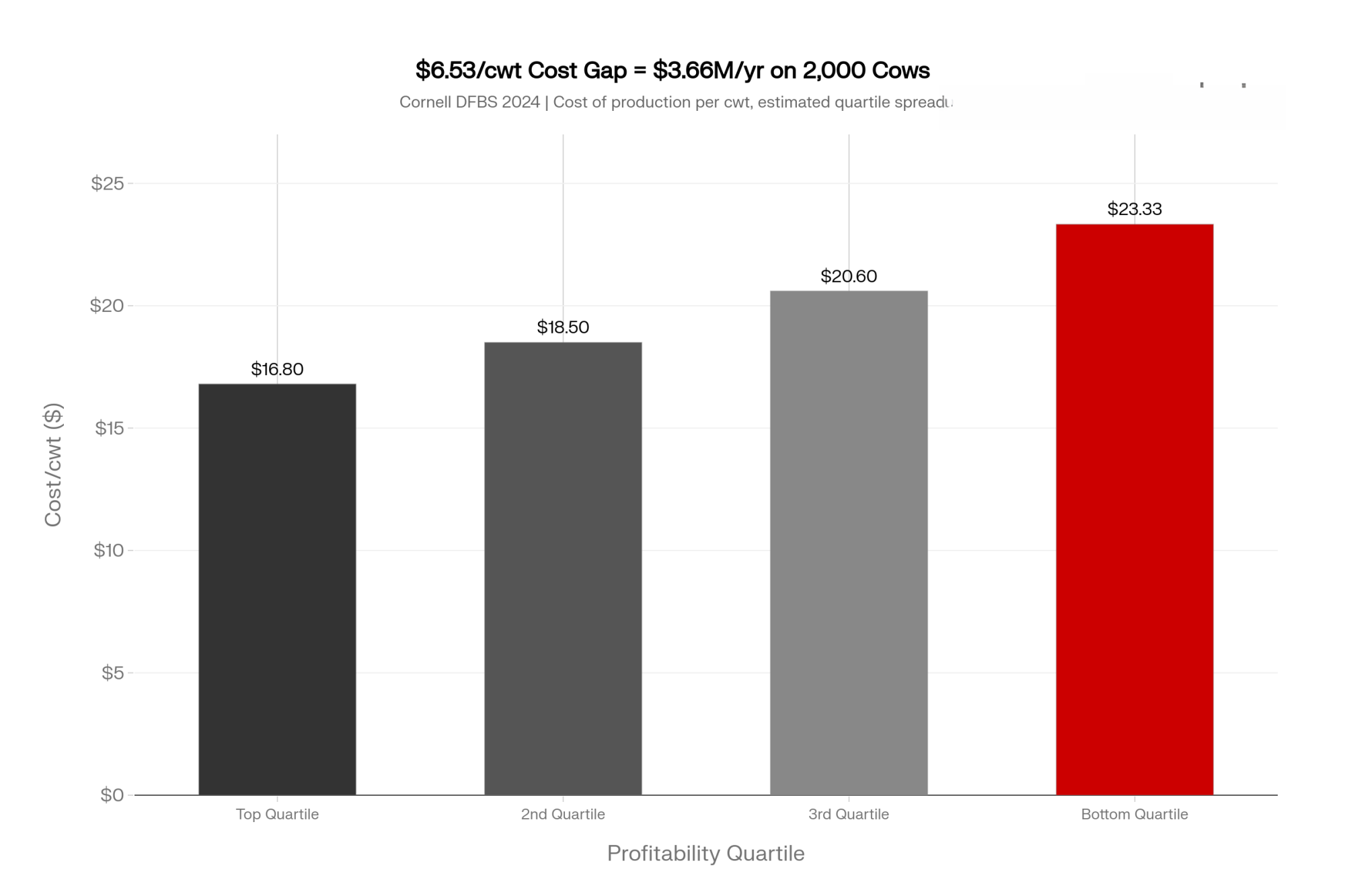

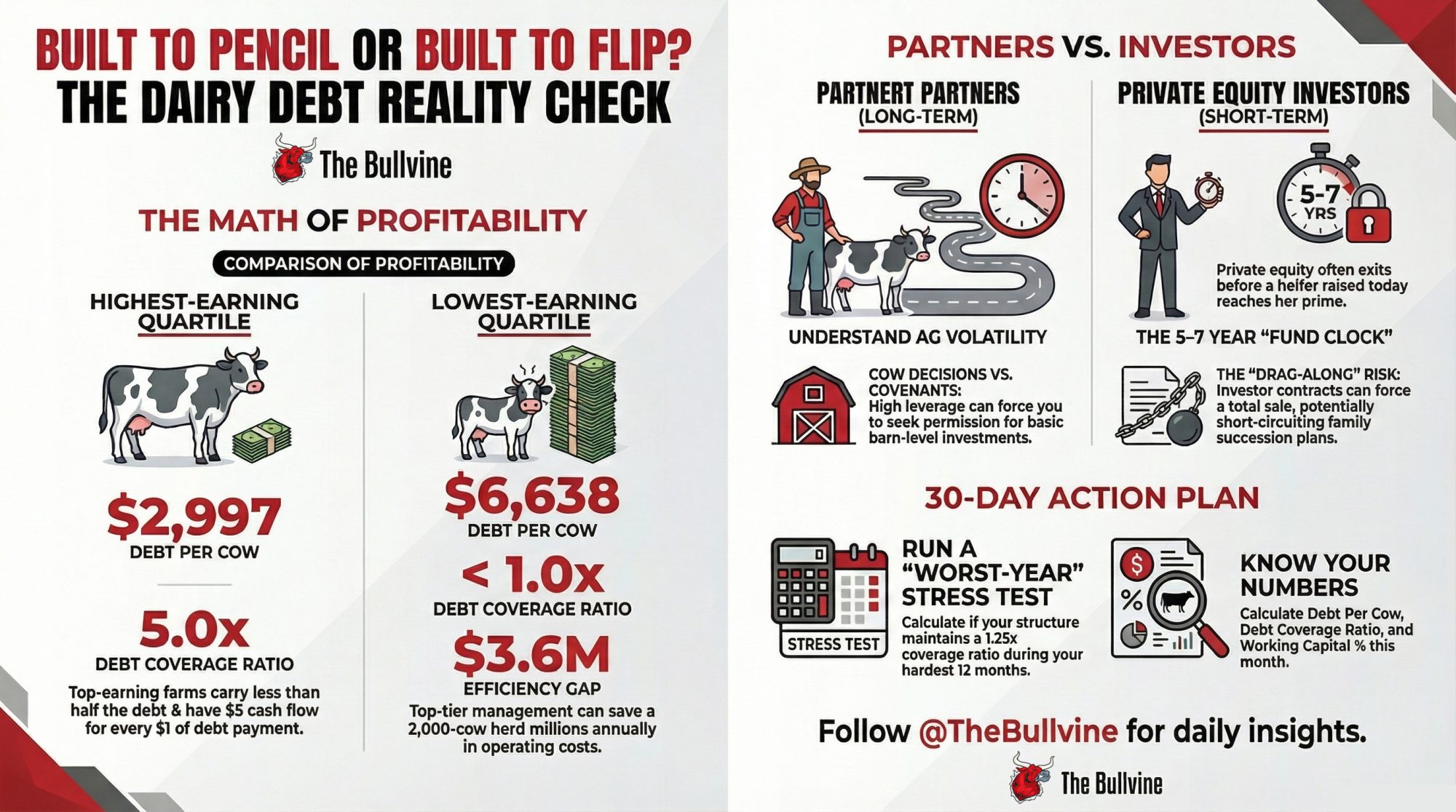

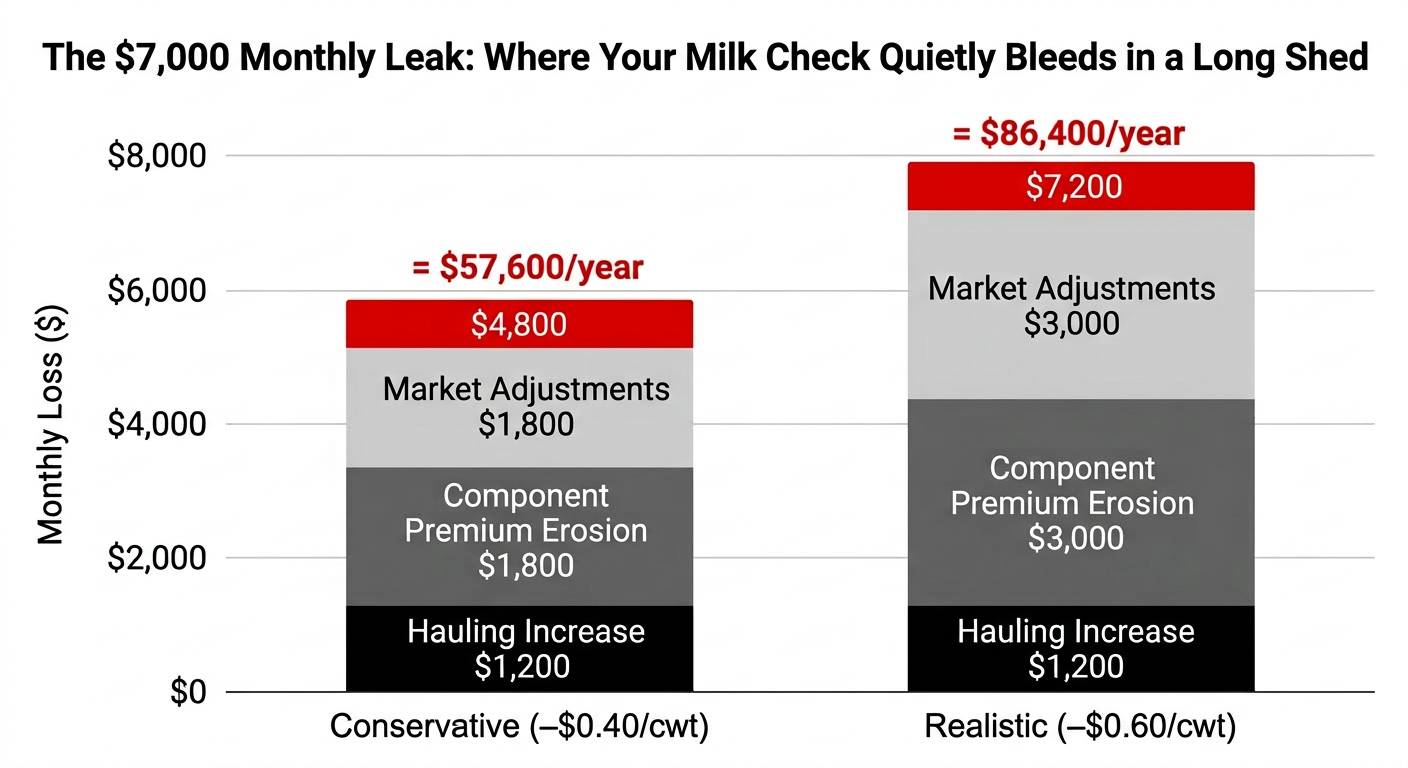

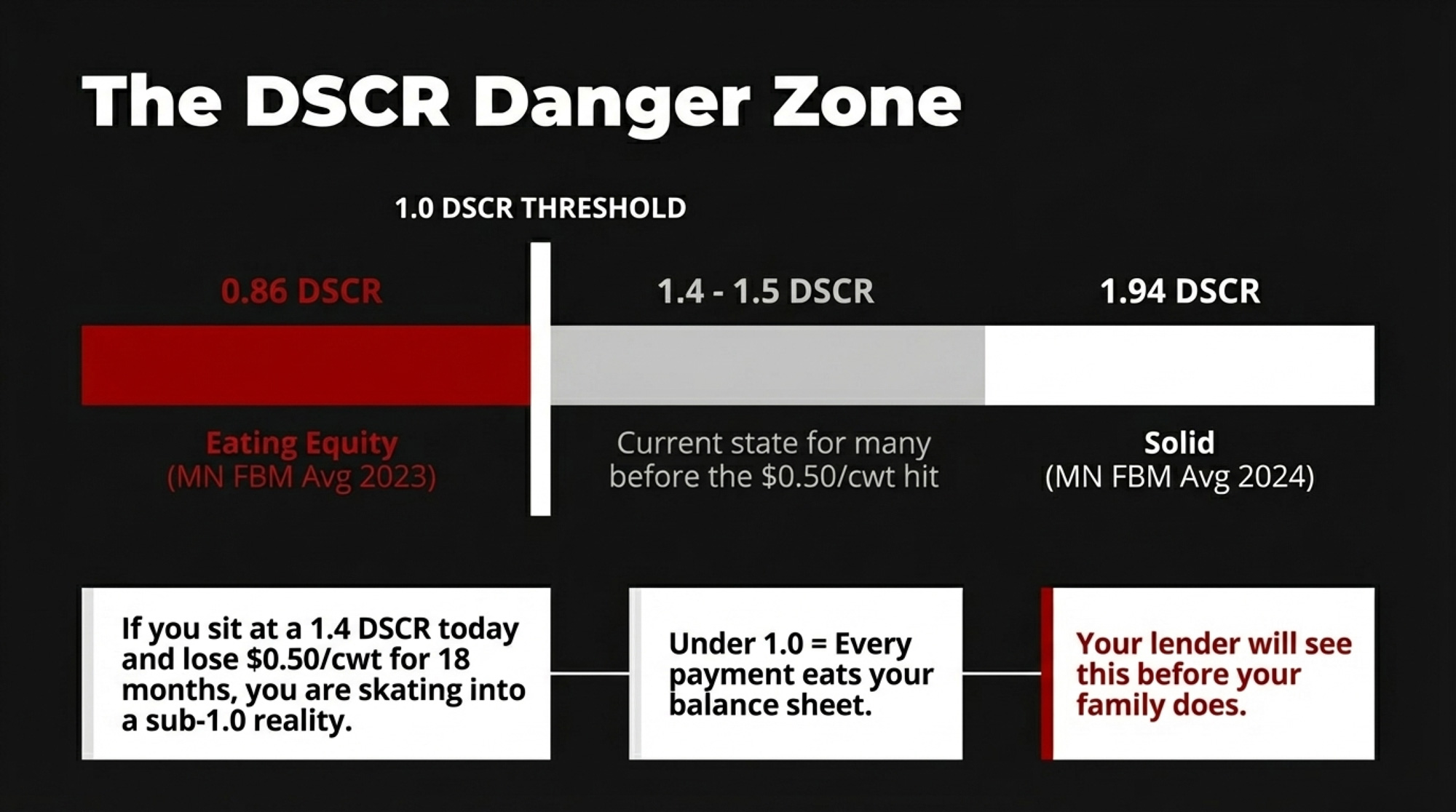

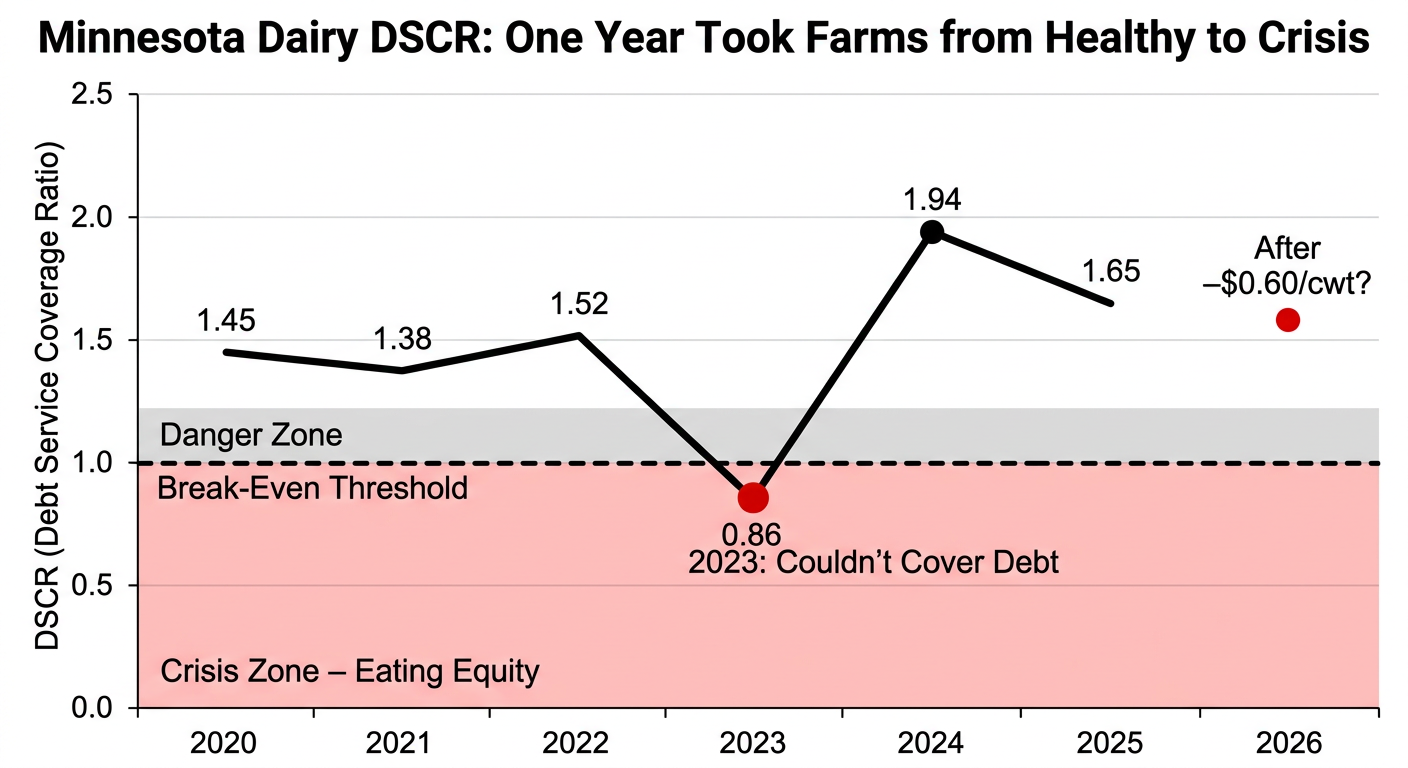

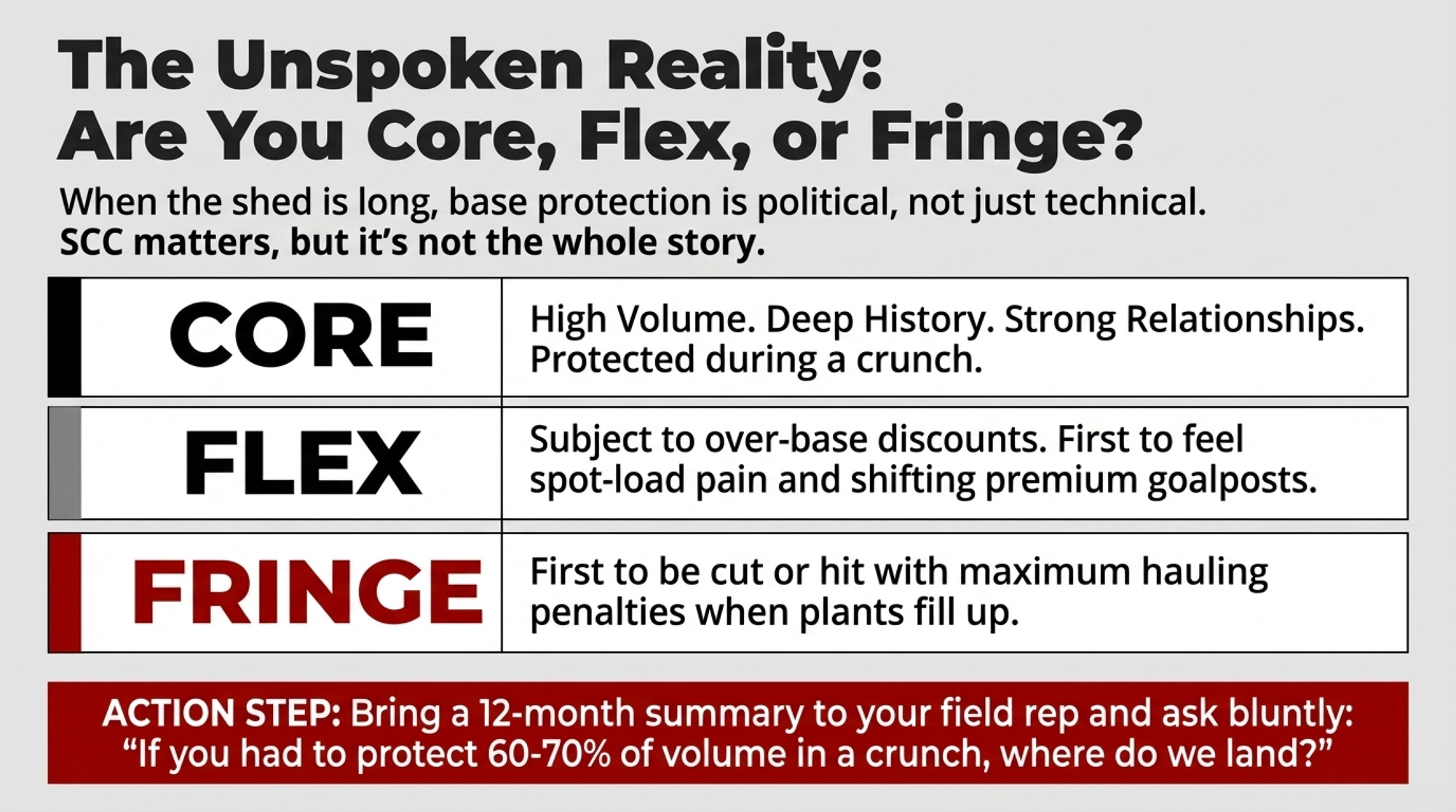

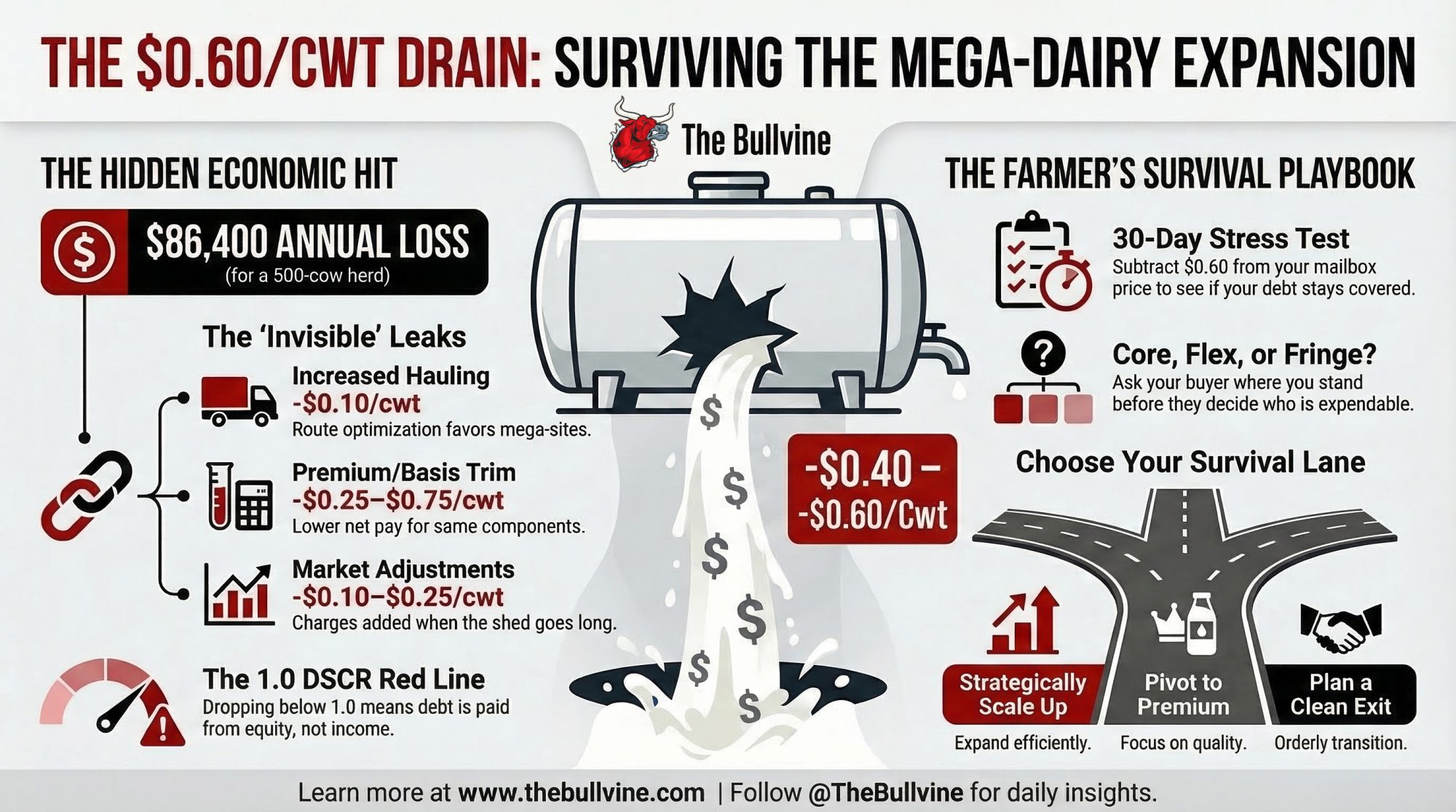

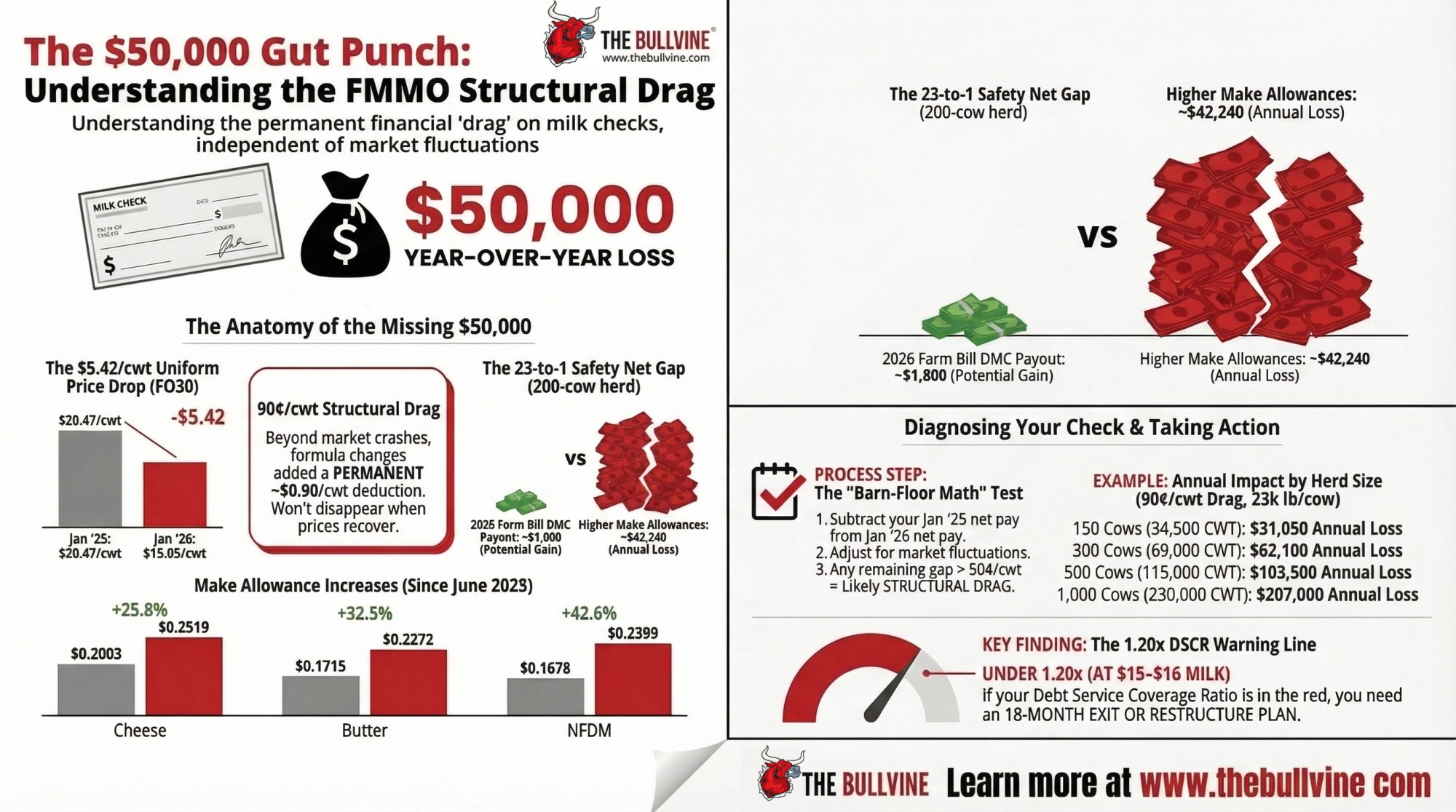

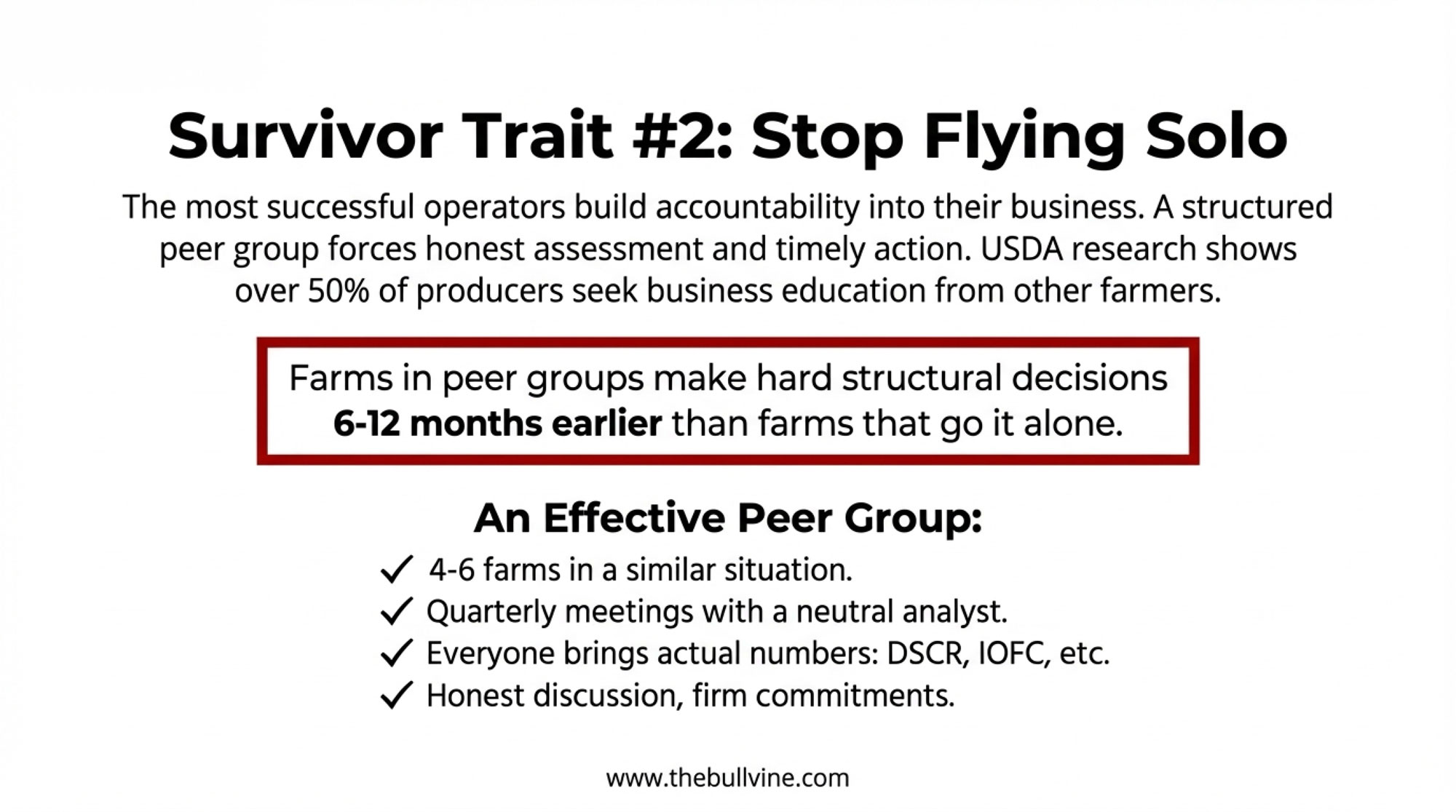

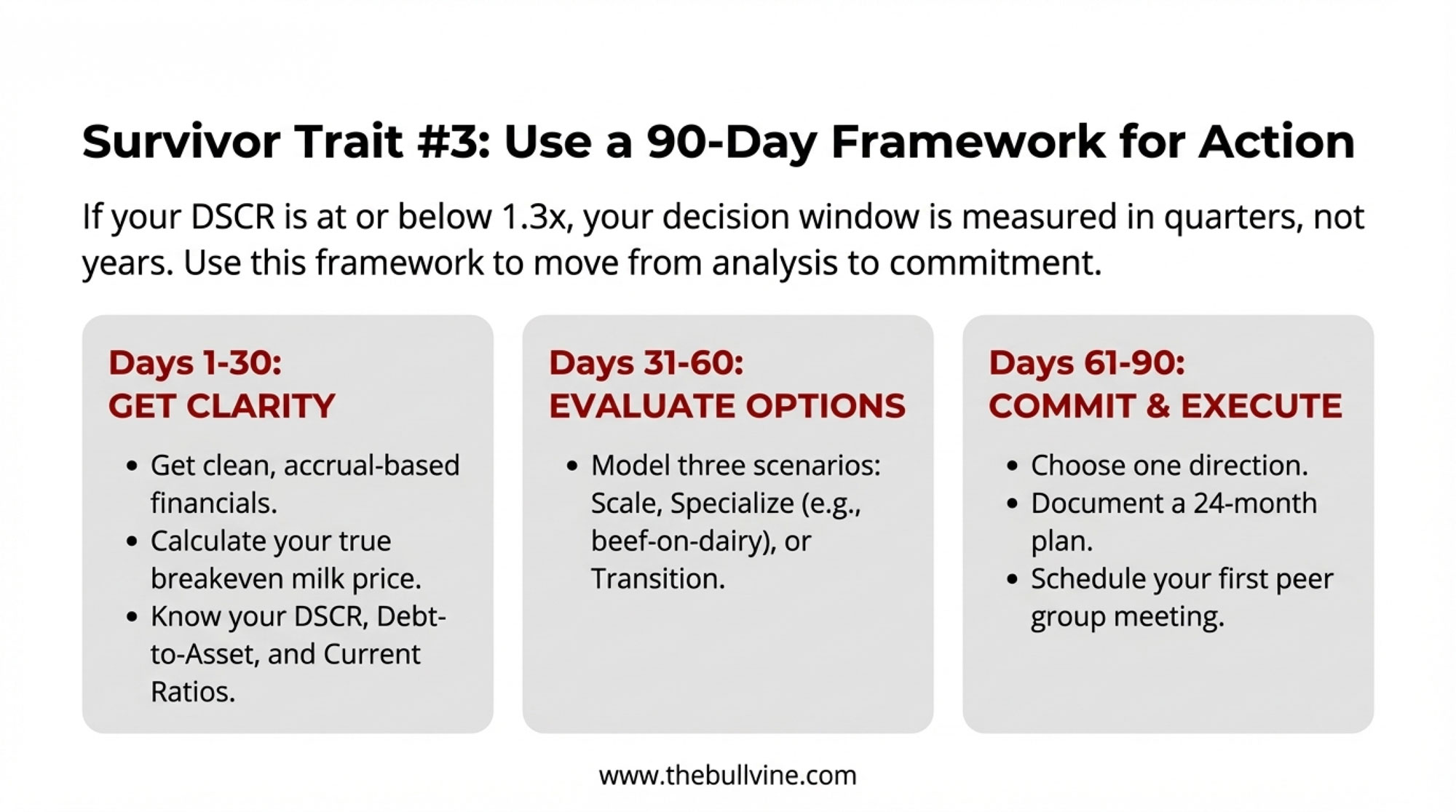

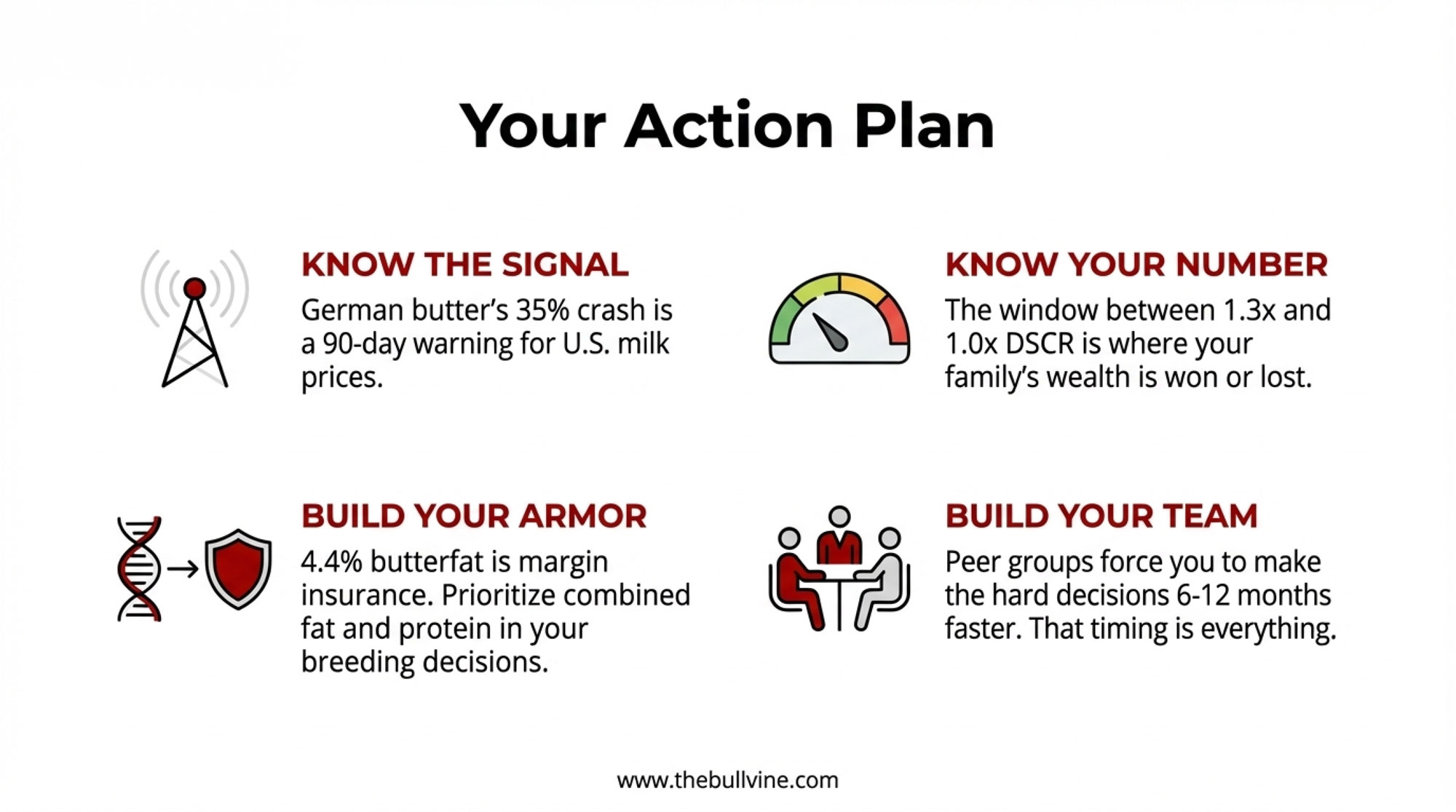

Cornell’s bottom‑quartile dairies sit at 0.36× DSCR. At 7% money on $4.5M of repriced debt, that’s about $118,000 more a year — and the reason your loan officer opened the laptop instead of the yellow pad.

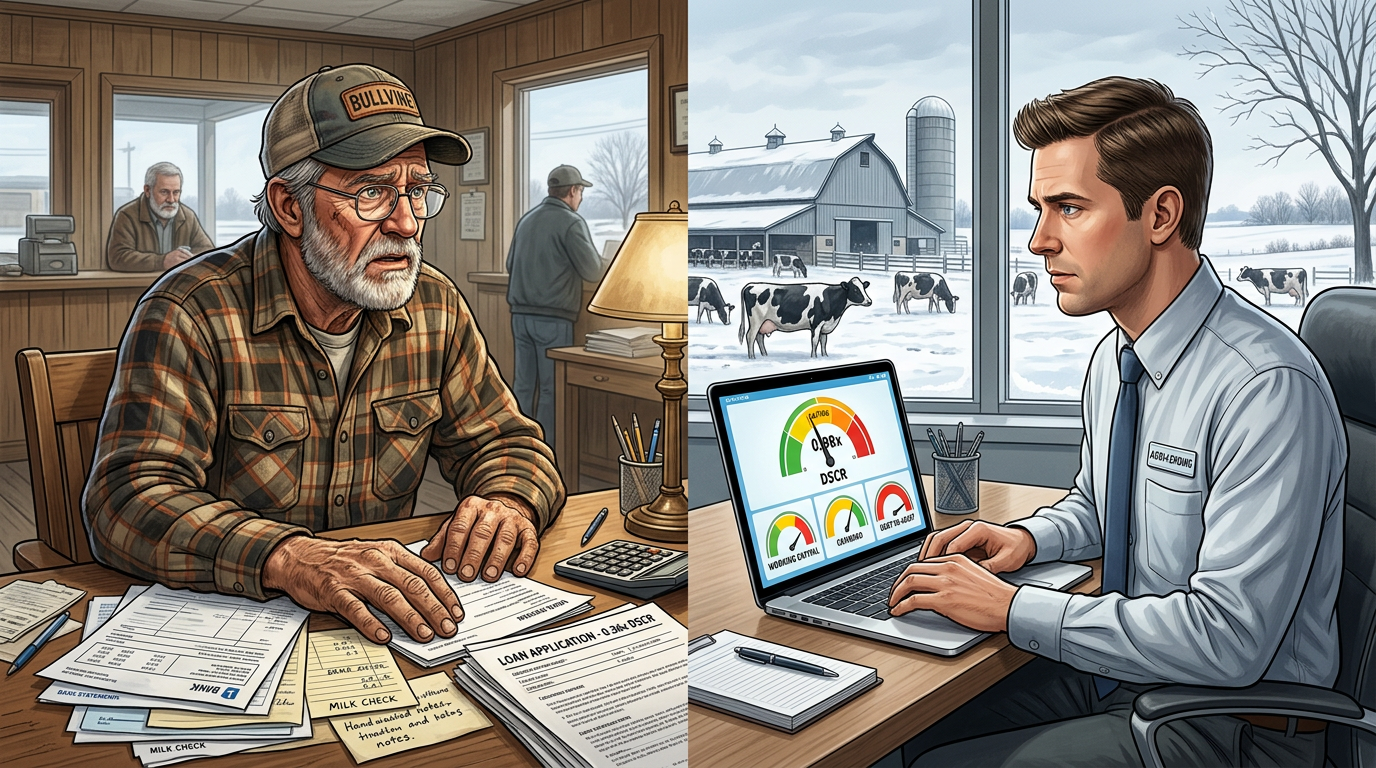

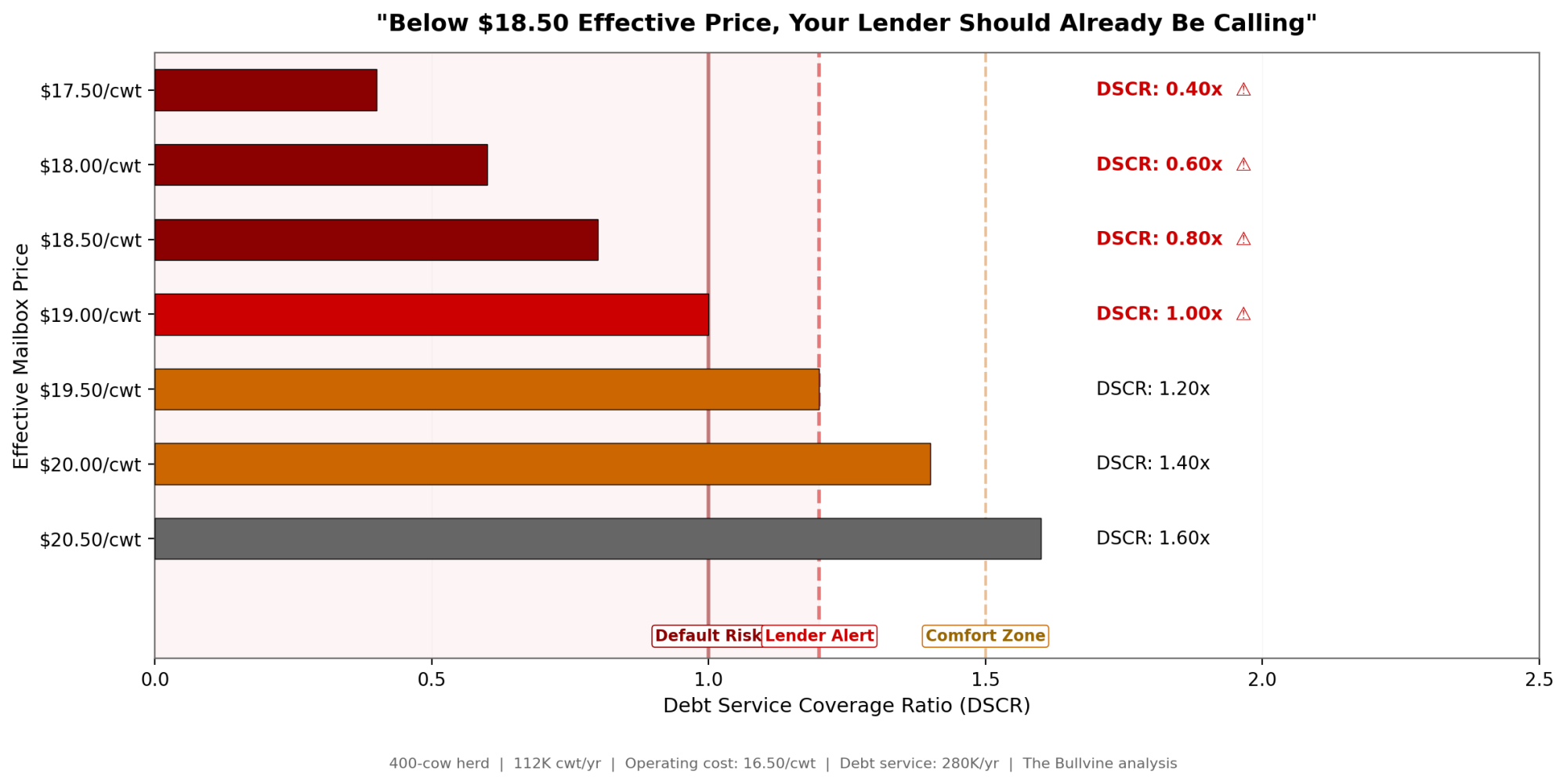

Executive Summary: Commercial ag operating rates sat in the mid‑7% range through late 2025 and early 2026, and Cornell’s 2023 DFBS shows the lowest‑profit quartile of New York dairies running a 0.36× DSCR — the exact number sending “good customer” files to the watch list. On $4.5M of repriced debt spread across real estate, equipment, and an operating line, the jump from 3.5–4% money to 7–8% adds roughly $118,000 a year in required payments, or about $1.07/cwt on a 400‑cow herd shipping 110,000 cwt. At USDA’s early‑2026 all‑milk forecast of $18.95/cwt, that same herd barely clears 1.0× DSCR; you need $20+ milk to breathe. Re‑amortizing a $1.8M parlor note from 14 to 25 years at 7.25% frees about $47,000 a year in cash flow — enough to pull a file out of the red, at the cost of more lifetime interest. Lenders aren’t firing bad customers; their models are. The farms getting flexibility walk in with a rolling 12‑month cost per cwt, their own DSCR math, a stress test at $17 milk, and at least one non‑correlated revenue line — beef‑on‑dairy, custom heifers, crop sales — that the dashboard can see. If your DSCR sits below 1.15× today and you can’t list every note and index on one page, your loan officer has more clarity on your risk than you do — and the next 30 days are when that changes.

Picture a gray February morning in central Wisconsin. A third‑generation dairyman walks into his Farm Credit office carrying 30 years of loan statements and the quiet confidence of a guy who’s never missed a payment.

He’s expecting a handshake. A quick renewal. Maybe a short gripe about milk prices over bad coffee.

Instead, the loan officer — younger, laptop already open — pulls up a screen. The numbers don’t work the way they used to. Red on debt service coverage. Yellow on working capital. A projected breakeven that has jumped nearly two bucks a hundredweight after a batch of loans repriced. For a 380‑cow herd, that’s not an abstract “dairy lending 2026” headline. That’s the morning the computer says no — and a family decides whether to catch up to the bank’s math or let the bank decide their future.

A note on these stories: The three dairies described below are illustrative composites, not real operations. They’re built from 2023–2026 industry patterns in Cornell’s Dairy Farm Business Summary, Chicago and Kansas City Fed ag credit surveys, and Bullvine case work. The math and thresholds are real. The names, scenes, and dialogue are not attributed to any specific producer. Real named sources — Nathan Kauffman at the Kansas City Fed and David Oppedahl at the Chicago Fed — are quoted or paraphrased only from their own published commentary and reporting by outlets like Brownfield Ag News. If you’re a producer willing to share your DSCR restructure story on the record, reach out — future “Dairy Lender Files” installments will feature real named operations.

The Day the Screen Replaced the Yellow Pad

For a long time, your dairy loan ran on three things: reputation, collateral, and whether your lender thought you kept a tight ship. You’d sit across from someone who knew your family and your fields. They’d scribble on a yellow pad, ask how the year went, and if you’d always paid your bills, the renewal slid through.

That world hasn’t vanished. It now sits underneath something colder — standardized credit models that score a 200‑cow tie‑stall in Minnesota the same way they score a 1,200‑cow freestall in New York.

Between 2015 and 2021, a lot of dairy debt went on the books at roughly 3.5–4.5% for conventional ag loans. Some FSA‑backed notes sat even lower. Then cheap money disappeared. The Chicago Fed’s 7th District AgLetter has pegged operating‑loan rates in the mid‑7% range and farm real‑estate loans in the high‑6% range through late 2025 and into early 2026 — still about double what many dairies locked in during their last expansion.

Those are effective rates on recently booked loans reported by participating banks — a blend of fixed and variable product. New paper is increasingly written as variable, typically priced as a spread over Prime or a term SOFR benchmark. Ask your lender which index your next renewal tracks. On a $3M loan, a 100‑basis‑point drift is roughly $30,000 a year in added interest; closer to $50,000 on $5M.

As of early 2026, USDA direct FSA operating loans sat in the mid‑4% range and ownership loans in the mid‑5% range — well below the commercial market, but only for borrowers who qualify. Check the current month’s FSA rate notice before you assume you’re priced in.

Kansas City Fed economist Nathan Kauffman told Brownfield Ag News in late 2025 that most producers can still service existing debt, helped by strong land values, but working capital is tight and some have already restructured heading into 2026. Chicago Fed policy advisor David Oppedahl has been more pointed in recent AgLetter commentary: repayment rates on non‑real‑estate loans are slipping, problem loans are creeping up, and roughly half of surveyed ag bankers expect more forced liquidations ahead.

At the system level, it’s “stress, not crisis.” At your kitchen table, sitting at 1.0× DSCR with repriced loans, that distinction feels academic.

What Your Lender’s Dashboard Actually Sees

When your lender opens your file, the model behind the screen scores you on ratios that sound cold but boil down to barn math once you cut the jargon. Every farm should be able to pull this snapshot in under five minutes.

The Dashboard Cheat Sheet

Metric

Target (Strong)

Danger Zone

Where the Numbers Come From

DSCR

> 1.25×

< 1.0×

Cornell DFBS 2023: top group 2.95×, bottom 0.36×

Debt per Cow

< $3,500

> $7,000

Progressive Dairy “Dairy Dozen” benchmarks

Working Capital

> 25% of gross revenue

< 10%

OSU “15 Measures of Dairy Farm Competitiveness”

Debt‑to‑Asset

< 0.25

> 0.40

DFBS 2023 average 0.29; top group 0.21

Now the barn‑math version of each.

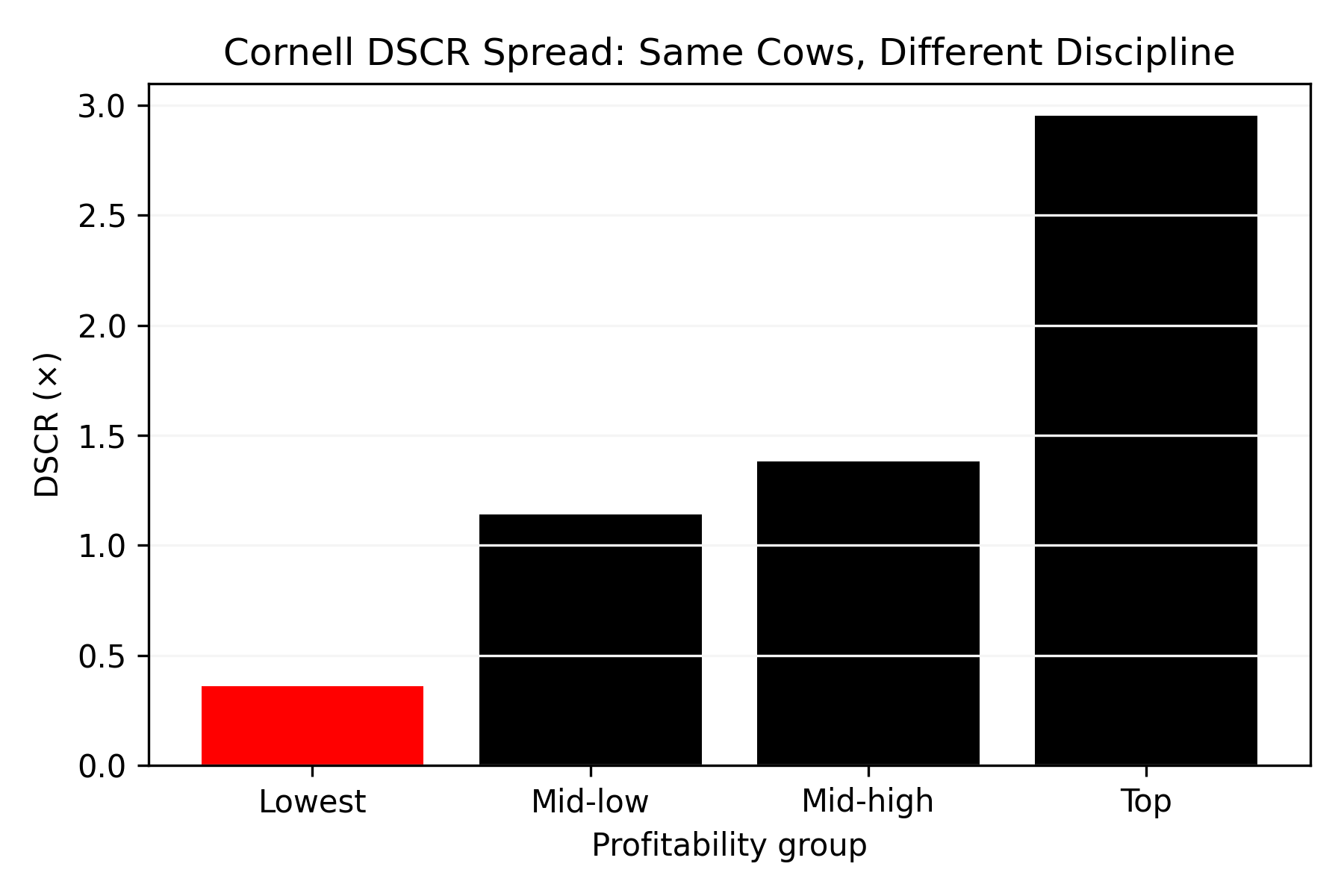

Debt service coverage ratio (DSCR). Net cash available for debt service divided by total annual principal and interest. A lot of lenders quietly target at least 1.25× as a comfort line. Cornell’s 2023 DFBS profitability comparison across 129 New York herds makes the spread vivid: the lowest‑profit group averaged just 0.36×, mid‑low hit 1.14×, mid‑high reached 1.38×, and the most profitable group sat at 2.95×. Below 1.0×, you’re not generating enough cash to cover your own debt.

Profitability Group

DSCR (×)

Lowest

0.36

Mid‑low

1.14

Mid‑high

1.38

Top

2.95

Working capital. Current assets minus current liabilities. Ohio State’s “15 Measures of Dairy Farm Competitiveness” calls anything above 25% of gross revenue competitive. In Brownfield’s 2025 coverage, Kauffman flagged working capital as the metric lenders are watching closest heading into 2026.

Debt per cow. Cornell’s lowest‑profit quartile carried about $5,007 of debt per cow versus roughly $3,097 for the top group — a gap of almost $1,900 per cow. Progressive Dairy’s “Dairy Dozen” benchmarks peg $3,000–$5,000 as manageable and flag $7,000 per cow as the point where servicing gets difficult.

Debt‑to‑asset ratio. The Cornell all‑farm DFBS average was 0.29 in 2023. Top‑profit farms ran about 0.21; the lowest‑profit group sat at 0.34. OSU flags anything above 0.30 as moving into higher‑risk territory.

Your grandfather knew these ratios. The difference? He had a year to fix them. You have a quarter.

The model pulls your numbers quarterly — sometimes monthly — and benchmarks them against thousands of farms in the bank’s footprint. Chicago Fed surveys through 2025 showed a rising share of 7th District banks reporting tighter collateral demands. If you’re not running these ratios yourself, your lender still is. You’re just not seeing the same screen.

Three Composite Farms, Three Outcomes

What follows are three composite dairy families — patterns, not people — built from 2023–2026 data in Wisconsin, New York, and Minnesota. Same industry, same rate environment. Very different results, depending on how they showed up at the bank.

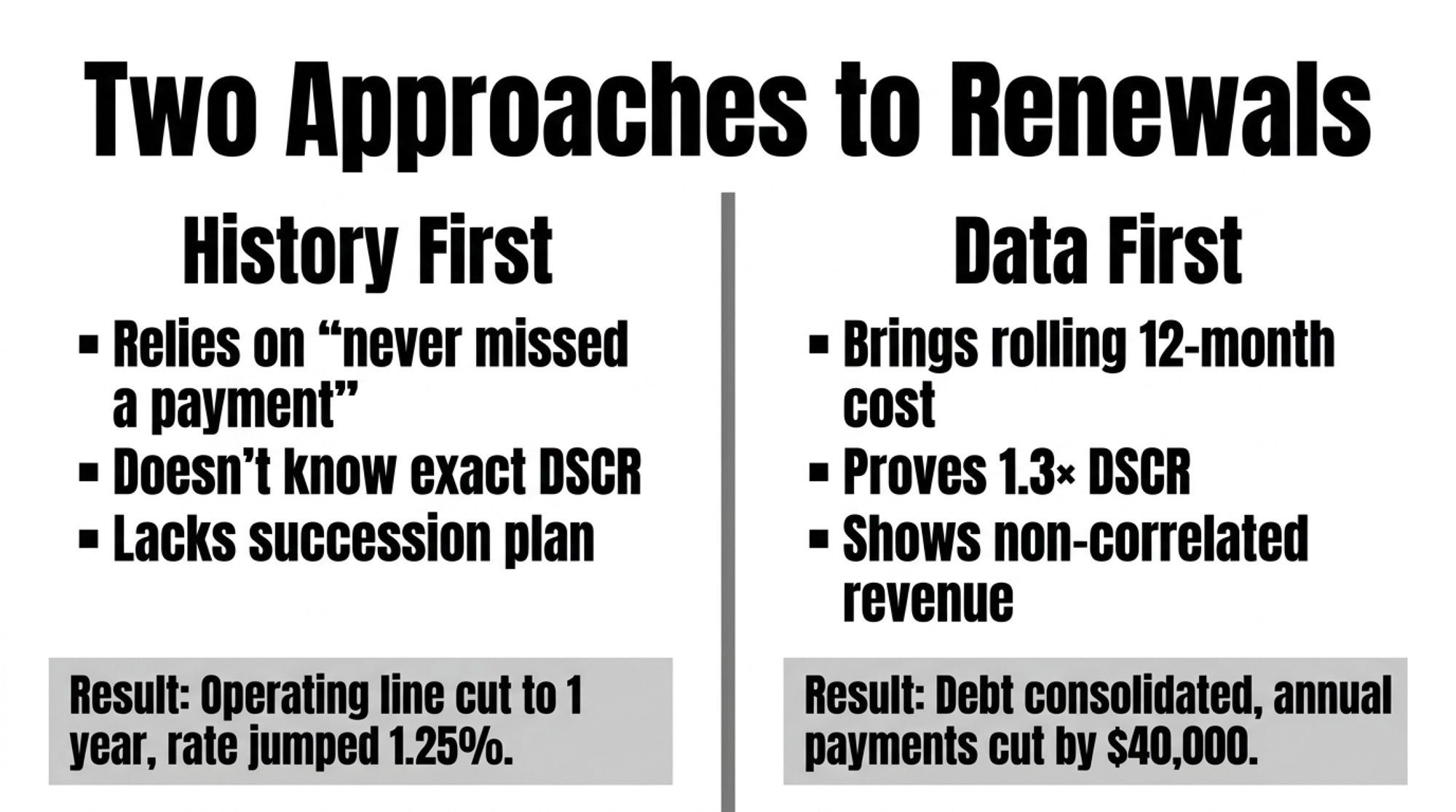

A 380‑Cow Wisconsin Dairy: “Good Customer” Meets New Math

Call this composite a 380‑cow Holstein herd in a sand‑bedded freestall in central Wisconsin. Rolling herd average in the high 70s. In 2019, a farm with this profile might have expanded the parlor and housing, taking on roughly $1.8 million in new term debt at around 3.75%. Payments fit fine at the time.

Those loans repriced in late 2025 to just over 7%, right in line with Chicago Fed survey rates. Bullvine’s own rate analysis suggests repricing typical mid‑size dairy debt from the mid‑3s to the mid‑7s can add more than $100,000 a year in debt service on $3–4M of repriced debt. For a 380‑cow herd on this trajectory, breakeven jumps from the high‑$17s into the low‑$19s per cwt.

A herd like this often has never missed a payment. Land still pencils as strong collateral — Oppedahl has noted in the Chicago Fed AgLetter that rising 7th District land values give some stressed farmers the option to sell off a portion of land to support operations. Even so, this kind of file typically shows DSCR sliding from above 1.4× to around 1.1×. That moves it off autopilot and onto the watch list.

At annual review, instead of a quick signature, the conditions now look like this: monthly financials instead of quarterly, a cap on new capital spending, and a clear ask to show a path back to at least 1.25× DSCR inside 18 months.

The common turning point on farms like this: somebody — often a younger family member — pulls 12 months of milk checks and expense reports, sits down with an Extension farm business educator, and builds a cash‑flow projection with three paths. Hold steady and hope for $20+ milk. Trim tail‑enders and push extra cash into principal — exactly the kind of move Kauffman has pointed to as risk reduction. Or lean harder into components and beef‑on‑dairy genetics.

That last path matters more to the bank than many producers realize. Lenders reward revenue that isn’t tied to the Class III/IV roller coaster. Beef‑on‑dairy calves sell into the fed‑cattle market, not the milk market, so they’re effectively non‑correlated revenue — cash that keeps flowing when milk prices tank. On a working balance sheet, a pen of high‑value crossbred calves and short‑bred heifers carries more weight than straight Holstein bull calves, strengthening the working‑capital line the model pulls every quarter. That kind of balance‑sheet signal often translates into more flexibility at renewal.

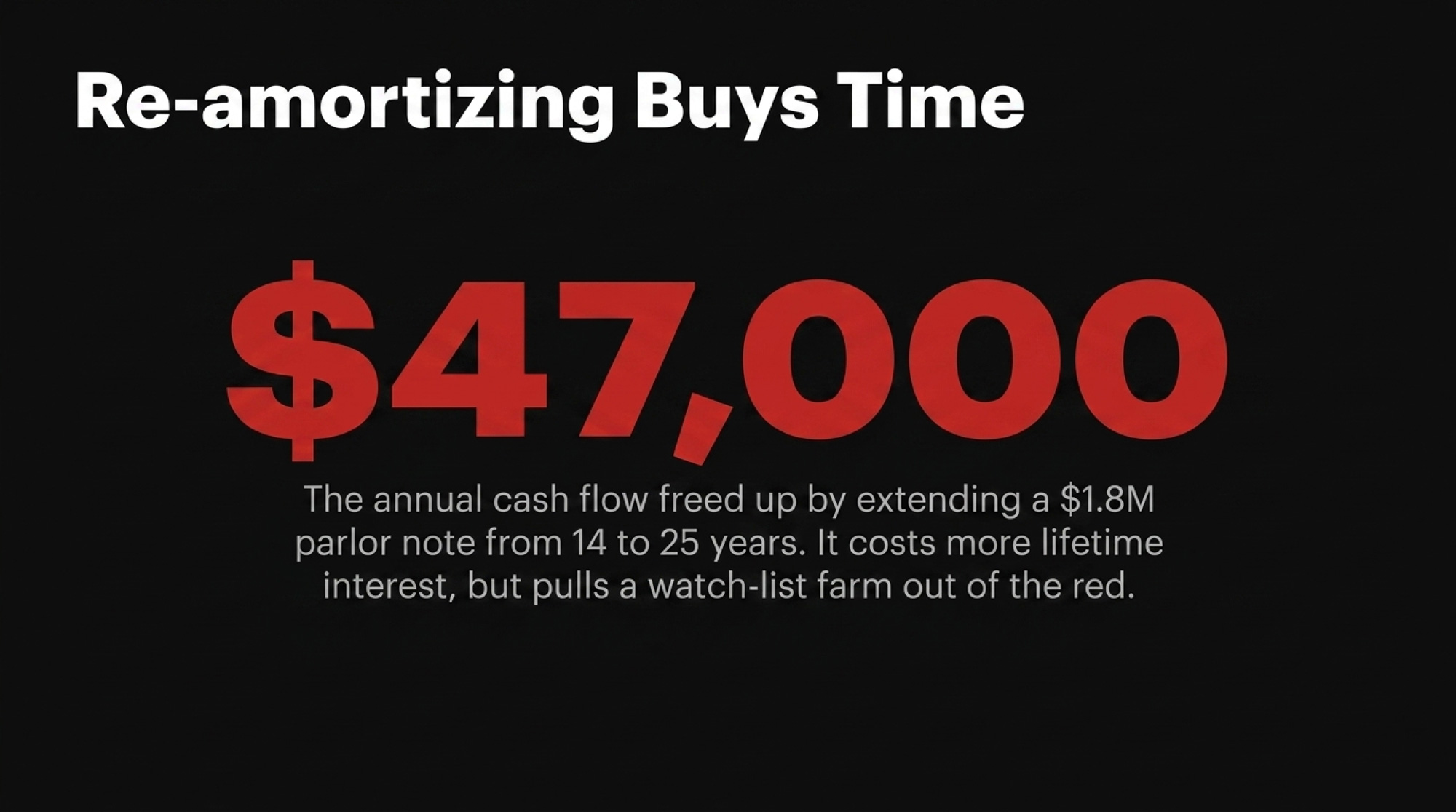

💡 The $47,000 Payment Gap On a $1.8M parlor note at ~7.25%, re‑amortizing from a 14‑year remaining term to a new 25‑year term drops annual P&I from roughly $203,000 to $156,000 — a gap of ~$47,000 per year. That’s the number in the headline. It’s also what often moves a watch‑list farm back into the “renewed” column. The trade‑off: more total interest over the life of the loan.

When a composite farm like this comes back to its lender with the same cows, same ground, same total debt, but a sharper story, the outcome typically shifts. A $47,000/yr payment drop nudges projected DSCR from about 1.14× into the low‑1.2× range. Not cushy. Out of the danger zone.

The relationship doesn’t carry farms like this. The data does.

Go deeper: “Profitable but Drowning: The Interest Rate Crisis Reshaping Mid‑Size Dairy” walks through the full repricing breakdown on herds in this exact position.

A 620‑Cow New York Dairy: Data Buys Better Terms

The second composite: a 620‑cow western New York dairy built from 200 over a decade by reinvesting profits and timing land buys around local retirements. Total debt near $6.8 million across a Farm Credit real‑estate package, a local bank equipment note, and an FSA‑guaranteed operating line. On paper, that leverage could make any lender twitch in a 7% rate world.

Files like this one earn the opposite reaction.

Operators on this trajectory track cost of production by month. Not just “feed, labor, other” — purchased feed per cow per day, hired labor per cwt, interest expense per cwt, repairs as a percent of gross. A rolling 12‑month cost around $16.80/cwt is plausible for a tightly run herd of this size. A 2023 Northeast Dairy Farm Summary reported a net cost of production of $22.64/cwt across member farms, so this composite would run well below the regional average. Cornell’s DFBS profitability comparison confirms the pattern from another angle: the highest‑profit group carried a debt coverage ratio of 2.95× versus 0.36× at the bottom.

A herd like this seeking $400,000 to upgrade manure storage under state rules would typically show DSCR holding in the high‑1.3× range even under a modeled $17 all‑milk year. Working capital comfortably positive. A simple written succession outline bringing a family member in over the next decade.

Rather than tightening terms, a lender looking for a reason to keep this file often goes the other direction — consolidating higher‑rate equipment debt into a longer real‑estate package. On the $1.2M chunk modeled here, stretching the term and picking up a better rate can cut annual debt service by roughly $40,000 (illustrative; exact savings depend on term and rate selected). That cash goes straight to working capital and strategic repairs.

The farm that walks in with a clear cost‑of‑production story gets the best tools when things get tight.

A 280‑Cow Minnesota Dairy: When “Good Customer” Isn’t Enough

The third composite: a 280‑cow tie‑stall in east‑central Minnesota. The cows do fine. The concrete, not so much.

No parlor, no robots, no big value‑added sideline. Total debt around $1.9 million, mostly land and building mortgages. A family farm like this often works with the same locally owned community bank for decades. The lender knows them by name and quietly rolls the operating line year after year.

Then, in 2024, that bank gets absorbed into a larger regional system — part of the wave of Midwest community‑bank consolidations over the last decade. When the file hits the new centralized risk model, three things flag: DSCR under 1.0× on recent tax returns (well below the Cornell all‑farm average of 1.84×), debt‑to‑asset ratio pushing 0.40 (versus the DFBS average of 0.29), and no documented succession plan. Kids with careers off‑farm.

That’s almost exactly the profile Kauffman has flagged in KC Fed commentary as most at risk — a producer who hasn’t built much land equity and carries heavier leverage on machinery or buildings.

Doors don’t slam on farms like this. The rules change. Operating line renewed for one year instead of three. Rate jumps about 1.25 percentage points, adding roughly $7,500 a year in added interest on a $600,000 line — on top of tighter covenants and a shorter renewal window. The bank asks for a formal transition or exit plan inside 12 months.

The typical next step on these files is a Minnesota Farm Business Management instructor — not to plan expansion, but to map an orderly wind‑down. A realistic three‑year exit: timing cow and equipment sales to avoid fire‑sale discounts, using Dairy Margin Coverage payouts and safety‑net checks to bridge cash flow, and listing land at current comparable values instead of waiting for a sheriff’s notice.

Bullvine’s own case work across several Midwest exits suggests families who planned 7–18 months ahead preserved roughly $400,000–$680,000 more equity than those pushed into forced liquidation. It isn’t the ending anyone dreams of. It beats letting the dashboard pick the date and the price.

▶ Next Step for Farms in This Position:Read “The 45‑Day Survival Guide for Mid‑Sized Dairy Operations” — the most logical playbook for operators whose DSCR is already under 1.0×.

What Happens to Your Milk Check When Your Interest Rate Jumps 1%?

Strip away the banker language and a big part of this shift is brutally simple: the same debt costs you a lot more than when you signed for it.

Take $2.5 million of term debt on a 20‑year amortization. At 6.5%, annual principal and interest runs about $223,700. Ship 100,000 cwt a year, and that’s roughly $2.24/cwt just to service that debt. At 7.5%, the payment climbs to about $241,700 — roughly $2.42/cwt. That’s about $18,000 more per year, or $1,500 less cash per month. (Standard amortization estimates; your exact number depends on payment structure and compounding.)

Interest Rate

Annual P&I (US$)

6.5%

223,700

7.5%

241,700

Now look at how that moves DSCR:

Net cash for debt service at $300,000 and a 6.5% payment: DSCR ≈ 1.34×.

Same cash, 7.5% payment: DSCR drops to about 1.24×.

If milk slides and net cash falls to $200,000 at the higher rate: DSCR ≈ 0.83×.

One percentage point of interest. One dollar of milk price. That’s the gap between “renewed with conditions” and “we need to talk about restructuring.”

How Much Does a Full Repricing Really Move Your Breakeven?

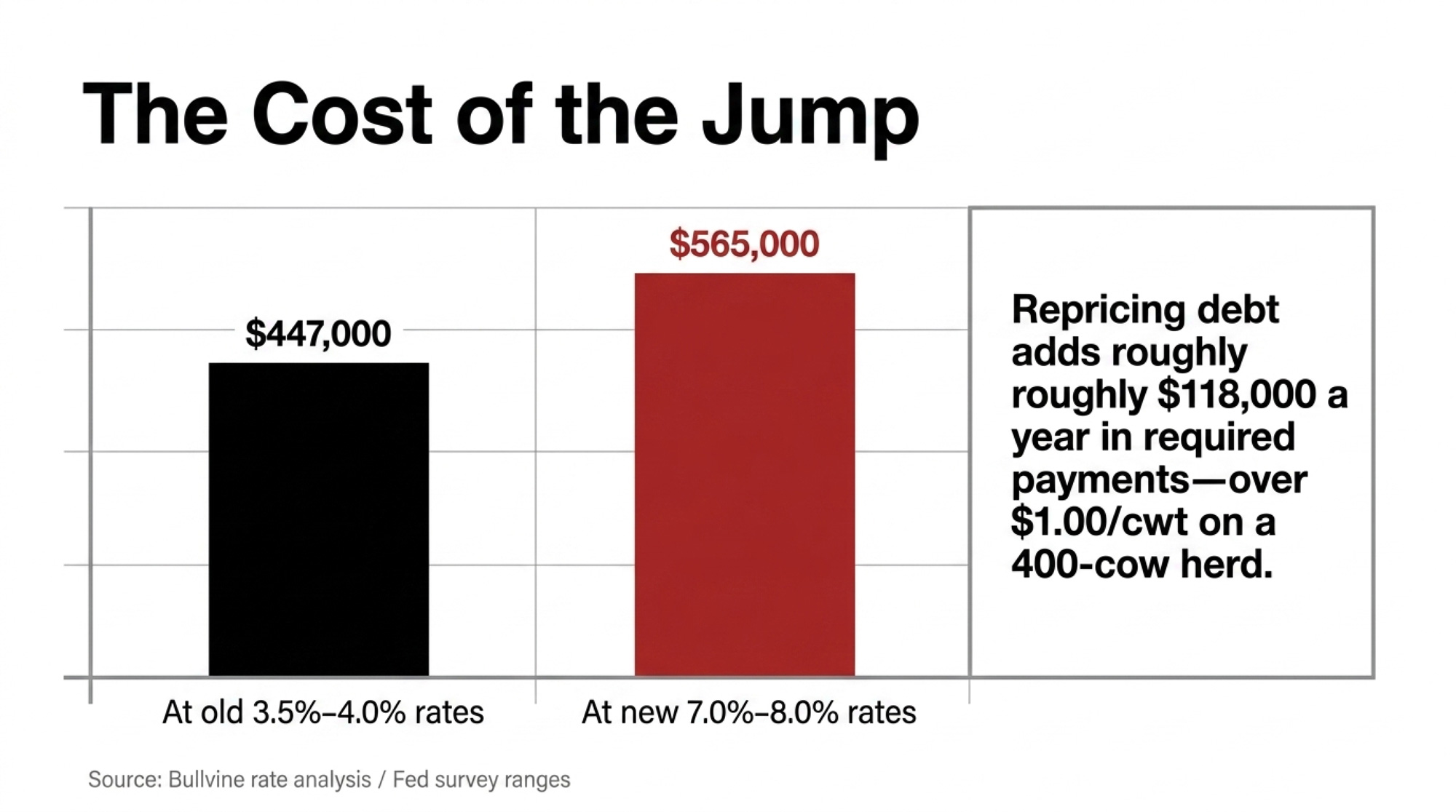

If you’re sitting on around $4.5 million in total debt, here’s what the repricing wave looks like using realistic chunks drawn from Fed survey ranges (standard amortization math, rounded for presentation):

Debt Type

Amount

Old Rate

New Rate

Old Annual P&I

New Annual P&I

Real estate (15‑yr)

$2.7M

3.5%

7.5%

~$232,000

~$300,000

Equipment (7‑yr)

$1.2M

4.0%

7.0%

~$197,000

~$217,000

Operating line (interest‑only)

$600K

3.0%

8.0%

$18,000

$48,000

Total

$4.5M

~$447,000

~$565,000

That’s about $118,000 more per year in required payments.

Spread across different herd sizes shipping milk:

Approximate Herd Size

Cwt Shipped

Added Cost (US$/cwt)

200 cows

55,000

2.15

280 cows

80,000

1.48

400 cows

110,000

1.07

The smaller you are, the bigger the per‑unit hit. And if your margin was only $0.50–$1.00/cwt to start with, that’s the whole ballgame.

Now stress‑test DSCR for that 400‑cow, $4.5M‑debt scenario. Assume 110,000 cwt shipped and non‑debt cash operating costs around .50/cwt — efficient by Cornell’s standards, given that DFBS profitability data shows far higher averages across most farms. USDA’s early‑2026 WASDE pegged the all‑milk forecast at $18.95/cwt, down from a revised $21.17 for 2025.

WASDE updates monthly. If a newer report has landed between filing and publication, refresh both the all‑milk row and the DSCR column below.

All‑Milk Price

Gross Revenue (110k cwt)

Cash Costs (@ $13.50)

Net Cash for Debt

DSCR vs ~$565K P&I

How Your Lender Reads It

$17.00

$1,870,000

$1,485,000

$385,000

~0.68×

“We have a problem.”

$18.00

$1,980,000

$1,485,000

$495,000

~0.88×

Below 1.0× threshold

$18.95

$2,084,500

$1,485,000

$599,500

~1.06×

Barely above water

$20.00

$2,200,000

$1,485,000

$715,000

~1.27×

Comfort zone

$22.00

$2,420,000

$1,485,000

$935,000

~1.66×

Strong

At $18.95 milk, you barely clear 1.0×. You need $20+ to breathe.

And that $13.50/cwt cost assumption is efficient. A 2023 Northeast summary reported a net cost of production of $22.64/cwt across member farms. If your cost base runs closer to $16–$17, the DSCR in this table deteriorates fast.

Go deeper: “$18.95 Milk, $19.14 Costs: USDA’s 2026 Milk Price ‘Upgrade’ Still Leaves Your Dairy in the Red” runs the full margin math band by band.

What DSCR Do Banks Really Want from Dairy Farms?

You can’t control your lender’s internal model. You can understand the target it’s aiming at.

At its simplest: DSCR = net cash available for debt service ÷ total annual principal and interest. If your net cash is $400,000 and total payments are $320,000, your DSCR is 1.25× — the farm generates 25% more cash than it needs to make debt payments.

DSCR Band

Typical Bank View

What It Feels Like on Farm

Lender Response

Below 1.0×

Not covering debt from cash flow

Scrambling to make payments, no buffer

Conditions, collateral pressure, restructure or exit talks

1.0–1.15×

Thin, one bad month from trouble

Every breakdown or milk dip hurts

Short‑term tolerance only with a written plan

1.15–1.30×

“Okay, not great”

Can sleep, but watch weather and milk price

Floor for flexible terms, new money around 1.25×

> 1.30×

Strong performer

Can invest and handle volatility

More freedom on terms, structure, and covenants

Pulling from Cornell’s 2023 DFBS profitability comparison (129 New York herds):

Below 1.0×. Not generating enough cash to cover debt. The lowest‑profit group averaged 0.36×. Expect conditions, collateral calls, or hard conversations.

1.0–1.15×. One bad month of milk, a feed mistake, or a breakdown can push you under. Some lenders will sit here short‑term, but only with a written plan to climb out.

1.15–1.30×. Where a lot of mid‑size herds land when things are “okay, not great.” Many lenders treat 1.25× as the floor for new money or flexible terms. Cornell’s mid‑high profit group averaged 1.38×.

Above 1.3×. Strong. The top‑profit group ran at 2.95×. These farms tend to get more freedom on amortization schedules and covenant structures because the numbers back the story.

Here’s the catch. Your lender isn’t just running DSCR at today’s mailbox price. Chicago Fed data confirm that extensions and renewals on non‑real‑estate lending are increasing — a sign more borrowers are asking for extra time and banks are testing harder before granting it. If you walk in having only looked at your best‑case price, and the dashboard is staring at your worst‑case, you’re not even arguing over the same math.

Are You Giving Your Lender Enough Data to Fight for You?

A lot of good operators will quietly admit they’ve never walked into the bank with a real data packet. The lender knew them. The cows looked fine. Bills got paid.

In a dashboard world, being a good operator still matters — but mostly after the numbers clear the first screen. If you want your lender to push for you with a credit committee that’s never set foot in your parlor, you’ve got to hand them ammunition.

The Minimum Data Packet (200–1,500‑Cow Dairy)

For your next scheduled meeting — not an emergency — walk in with:

Last three years of financials. Tax returns (Schedule F), year‑end balance sheets, depreciation schedules.

Rolling 12‑month cost per cwt. At least broken into feed, labor, and “all other” operating costs.

Your current DSCR. Today’s loan balances, current interest rates, total annual payments.

Working capital snapshot. Current assets minus current liabilities — the metric Kauffman has specifically flagged as the one lenders are watching closest.

Leverage snapshot. Total debt divided by total assets. The DFBS average was 0.29 in 2023; know where you sit.

That alone puts you ahead of more farms than you’d guess.

What Actually Earns Better Terms

Three forward scenarios. Base case, a “$2/cwt lower milk” stress case, and a slightly better‑than‑today case.

A simple succession plan. Even a one‑page outline of who’s likely running the place in 5–10 years. Farm Credit and Extension communications increasingly treat succession as a formal credit factor, not just a family story.

Real‑time production data. Rolling herd average, butterfat/protein trends, voluntary cull rate — anything that shows you manage cows, not just cash.

A non‑correlated revenue story. Beef‑on‑dairy receipts, custom heifer raising, crop sales, on‑farm processing. Anything not priced off the milk check strengthens your current‑asset picture in the bank’s model.

Rate‑index awareness. Know whether your current notes are fixed, variable over Prime, or tied to term SOFR. If you can’t tell the loan officer which index prices your operating line, you’re arguing blind.

FSA awareness. Know whether you qualify for USDA direct loans — well below commercial markets — and whether FSA‑guaranteed lending could improve terms with your current bank.

Red Flags That Trip Wires Fast

Patterns that, from lender and Extension farm‑management conversations, tend to push files straight into the risk bucket:

No updated personal financial statement after the lender asked for one.

No honest cost‑of‑production number.

No forward cash‑flow projection, even a simple one‑pager.

Farm and household expenses so tangled the lender can’t separate them.

A flat refusal to discuss succession.

No idea whether your rate is fixed or floating — or over what index.

When your dashboard numbers are already thin, any one of these pushes a lender toward higher rates, tighter covenants, or a quiet “no.”

Options and Trade‑Offs for Farmers

You don’t control interest rates. You control how you show up in front of the dashboard over the next 12 months.

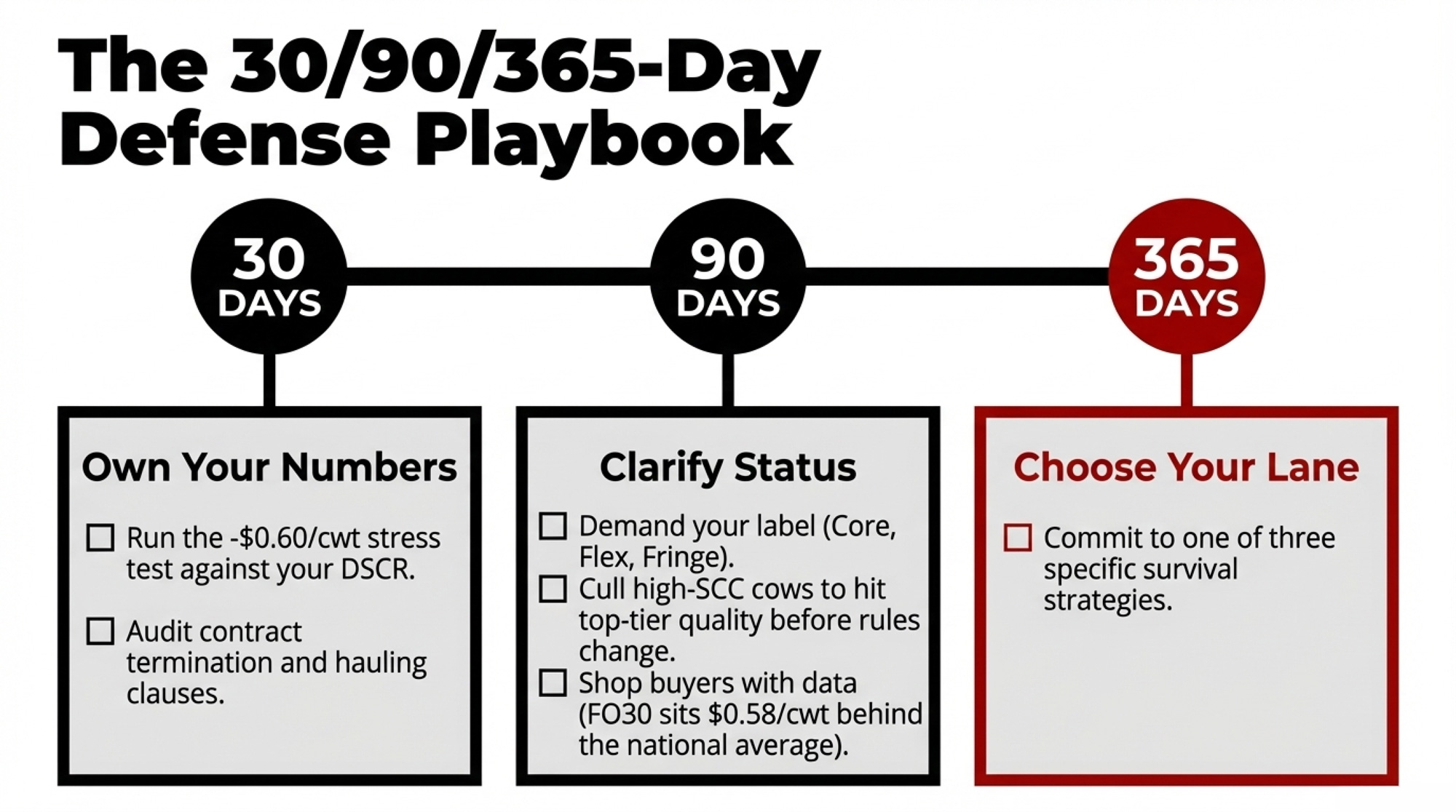

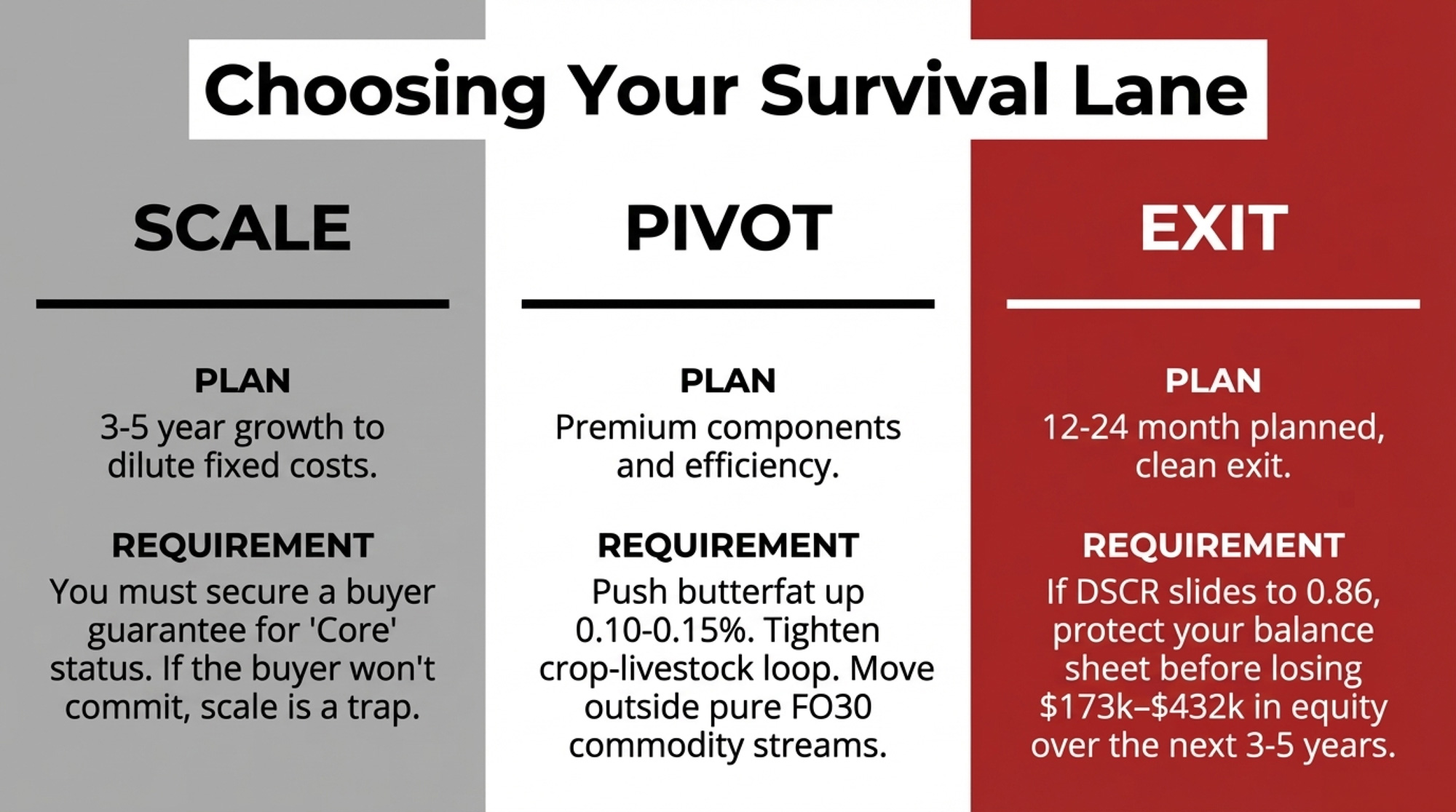

1. Upgrade Your Data Game (30‑Day Action)

Start here if you plan to keep milking at least 3–5 years, you’re not insolvent, but you honestly don’t know your DSCR or cost per cwt.

This month: Pull 12 months of milk checks and main expense categories. Build a rolling 12‑month cost per cwt using a simple spreadsheet or FINPACK template from Extension. Calculate your DSCR. Then book a meeting with your lender specifically to review your data — not to ask for money.

You walk in knowing where you stand instead of hoping. Your lender sees someone running toward the problem, not hiding.

The risk: You may not like that first DSCR number. But you can’t fix a ratio you won’t look at.

2. Restructure Before You’re Forced To

Move here if your DSCR is hovering near or just below 1.0×, you still have land equity, and your next big renewal is 6–24 months out.

What it takes: Map every loan on one page — balance, rate, index (fixed, Prime‑based, SOFR‑based), remaining term, payment. Model what happens if milk averages $2/cwt less than last year. Be open to extending terms on some debt or selling a non‑core asset. Oppedahl has pointed out in recent AgLetter commentary that some farms will need to sell land to help fund operations — it goes better if you initiate that conversation.

What you gain: Breathing room. A lender looking for a reason to keep you often will stretch a major note from 14 to 25 years, saving about $47,000 a year in payments on $1.8M at roughly 7.25% — enough to move DSCR out of the red.

What you give up: More total interest over the life of the loan. You’re buying flexibility today with future dollars. Move early and you help design the restructure. Wait, and somebody else does it for you.

3. Double Down on Margin, Not Size

This is the right path when you’re not set up to add cows cheaply, but there’s room to improve component premiums, beef‑on‑dairy revenue, or trim operating costs.

What it takes: Honest benchmarking of feed, labor, and machinery cost per cwt against peers. A focused 12‑month plan to raise butterfat/protein, add beef‑cross value, or shave specific costs. Cornell’s DFBS tells the story bluntly: the spread in debt coverage between the lowest‑profit group (0.36×) and highest (2.95×) wasn’t mainly about herd size or premiums — it was about cost discipline that drops straight to the DSCR line.

On a 600‑cow herd shipping 170,000 cwt, a $1.00/cwt cost reduction is worth $170,000 a year. Premiums help. Cost discipline changes your DSCR. A solid beef‑on‑dairy program gives the bank a revenue line that isn’t riding the Class III roller coaster.

The risk: Chasing premiums with extra labor or purchased feed can backfire if costs rise faster than the bonus. Measure tightly.

4. Plan an Exit While You Still Have Leverage

Consider this one when you’re past 60, heirs aren’t coming back, DSCR is under 1.0×, and you’re tired of wondering which letter from the bank is “the one.”

What it takes: A farm transition specialist or attorney. Early, blunt conversations with your lender about what a cooperative exit looks like. The willingness to say, “We might be better off leaving on our own terms.”

Across several Midwest cases, Bullvine’s analysis suggests strategic exits with 7–18 months of planning preserve roughly $400,000–$680,000 more family equity than forced sales — a margin close to the $480,000 equity gap between strategic exit and forced sale we’ve documented in prior case work. The difference between “retire with options” and “start over in town.”

The risk: Emotionally brutal. Some relationships fray. But the math usually gets worse, not better, if you delay.

Go deeper: “Only 12% of Dairy Farms Make It to Generation Three — Here’s What’s Different About the Ones That Do” is the companion read for families wrestling with this path.

Key Takeaways

If your DSCR sits below 1.15× today, treat it as a yellow light. Cornell’s lowest‑profit group averaged 0.36× — they didn’t get there in one quarter. Run your own stress test at $17 milk and talk with your lender before you drift under 1.0×.

If you can’t list your total annual debt payments on one sheet of paper, your lender has more clarity on your risk than you do. Within 30 days: list every note and operating line, add up annual P&I, calculate your DSCR.

If your plan assumes rates “go back to normal,” it’s not a plan. Commercial operating rates sat in the mid‑7% range through late 2025 and early 2026, and new paper is increasingly variable over Prime or term SOFR. Model your next two years at today’s rates and one notch higher.

If more than 90% of your revenue comes off the milk check, your balance sheet is more fragile than your lender’s model likes. Beef‑on‑dairy, custom work, or crop sales aren’t just extra cash — they’re non‑correlated revenue that strengthens how the dashboard reads your farm.

If you want your lender to fight for you in the credit committee room, hand them a story their dashboard can tell. A real cost‑of‑production number, a forward cash‑flow, and at least a rough succession outline.

The next time you sit across from your loan officer, the screen between you will quietly shape how hard they can push on your behalf.

You don’t control that dashboard. You do control whether it shows a fuzzy picture or a sharp one. For the deeper math — DSCR across five milk‑price bands, how Dairy Margin Coverage and FMMO changes interact with lender risk scoring, and the full cost‑of‑production playbook — watch for the next “Dairy Lender Files” installments in The Bullvine Weekly.

If the numbers are weighing on you, don’t carry it alone. Call or text 988 for the Suicide & Crisis Lifeline. For dairy‑specific support, reach out to Farm Aid at 1‑800‑FARM‑AID, your state farm‑mediation service, or your Extension farm management program.

Do you know your DSCR today? If not, the computer does. It’s time to see the same screen.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

The $19 Milk Trap: How 2026 Prices Quietly Drain a 400‑Cow Dairy’s Equity — Exposes the $144,000 annual equity drain facing mid-sized herds and delivers a high-stakes playbook to protect your balance sheet. Breaks down full-cost breakeven targets while providing the “action signals” needed to survive a $19.00 milk market.

Dairy farm economics 2026: pricing and margins — Reveals the structural reset hitting North American producers through FMMO modernization and the Canadian protein pivot. Arms you with the market intelligence to navigate the “higher-of” formula and identify the quiet margin leaks threatening long-term profitability.

Beef-on-Dairy’s $3,000 Trap: 800,000 Missing Heifers and Who Pays the Bill — Dismantles the “cash-flow hero” myth of beef-on-dairy by exposing the looming 800,000-head heifer shortage. Follows the money on $3,000 replacement costs, revealing why high-reproduction herds are the only ones winning the genetic revenue gamble.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

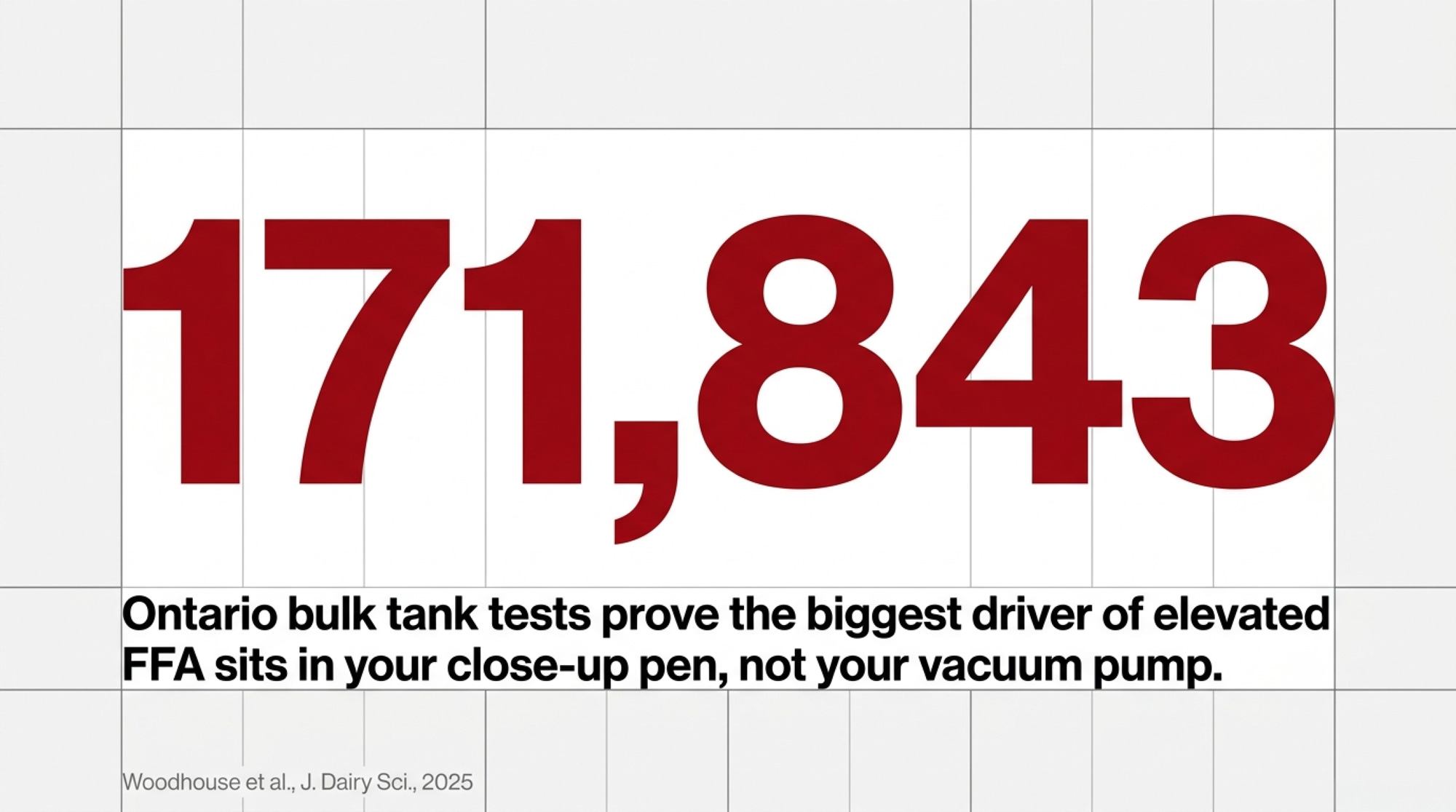

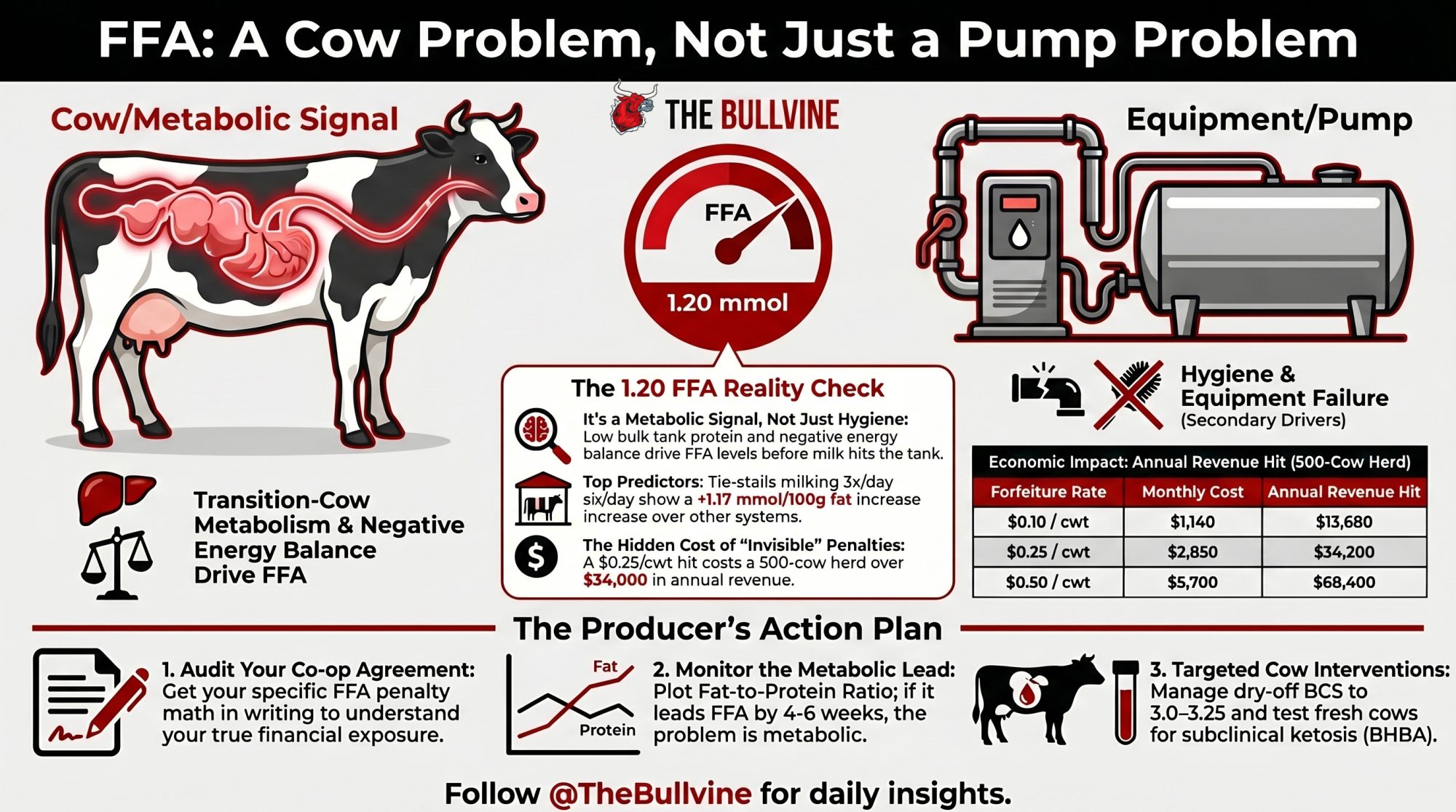

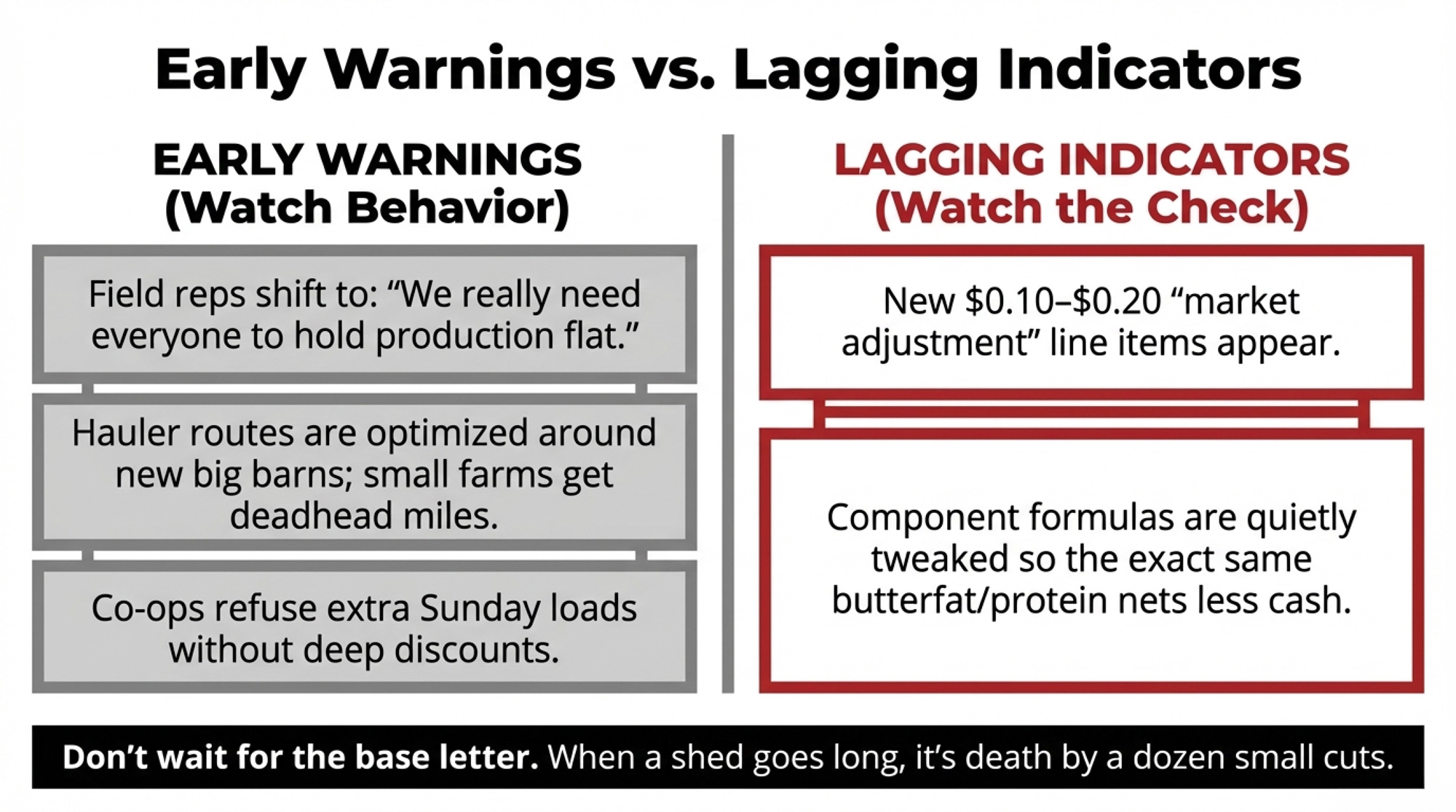

Guelph pulled 171,843 Ontario bulk tank tests and found the biggest FFA drivers weren’t your pump. They were your close-up pen, your ration, and three-incentive-day months.

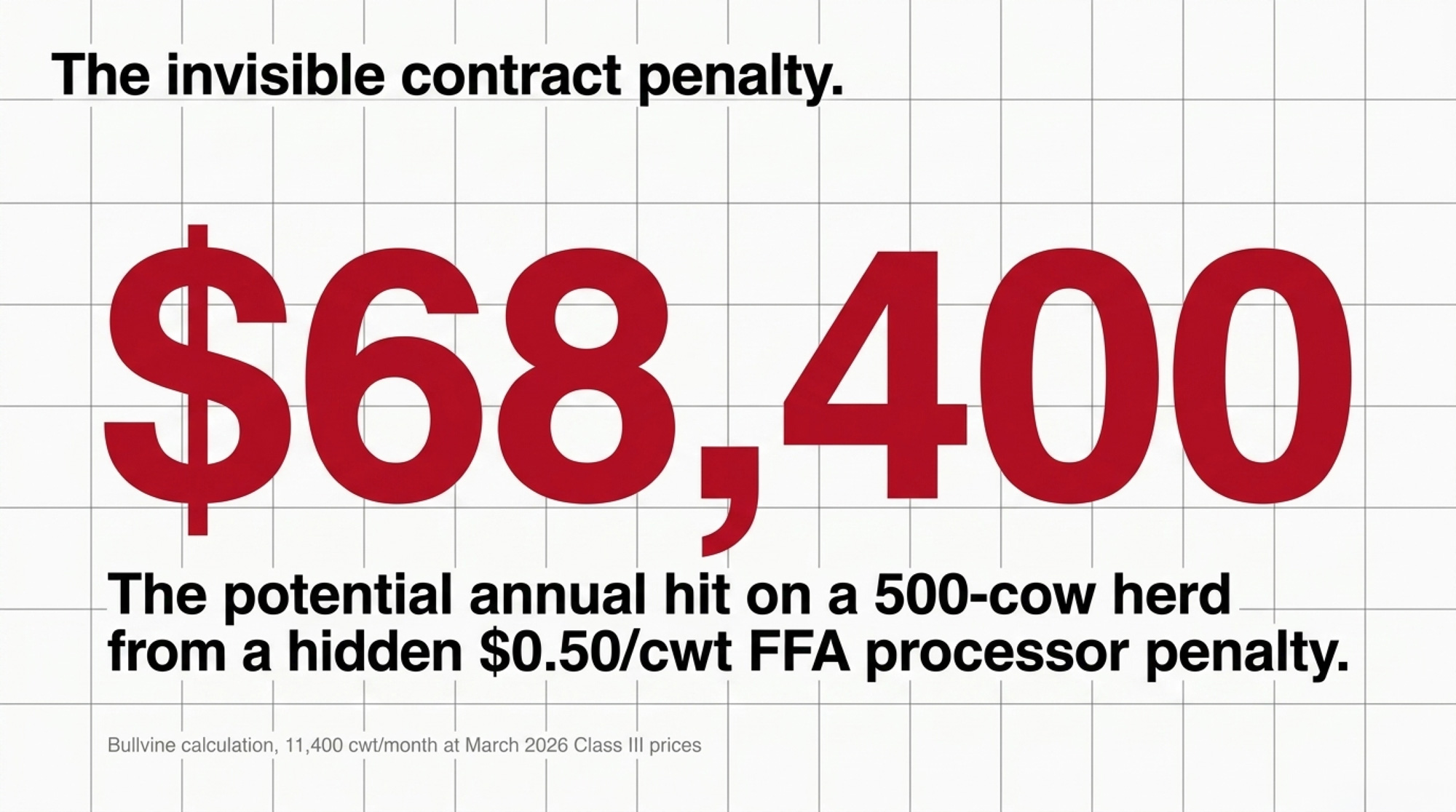

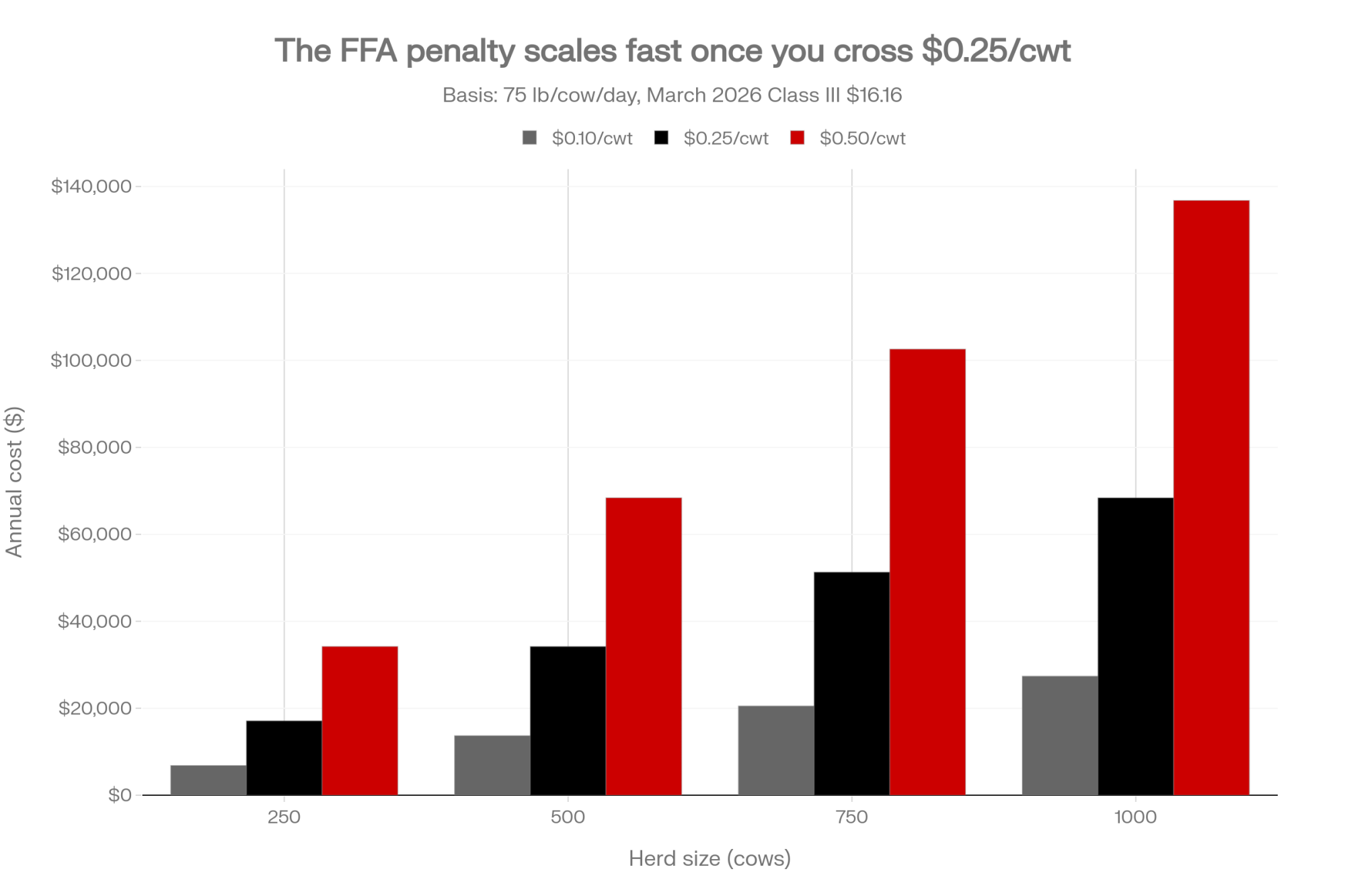

Executive Summary: Guelph researchers Hannah Woodhouse and Dr. David Kelton, working across 171,843 monthly bulk tank observations from every Ontario dairy farm over four years, have reframed the 1.20 mmol FFA sensory threshold as a transition-cow test, not a hygiene test — the significant predictors of an elevated month are lower bulk tank protein, non-parlor milking systems, three-incentive-day months, and higher bacteria counts, not your pump.¹ A companion 293-farm paper (J. Dairy Sci., Feb 2025) attached a 1.17 mmol/100g fat association to the tie-stall + ≥3×/day combination alone, and flagged that no operation in the 109-farm parlor freestall subsample posted a monthly average at or above 1.20.² The FFA penalty side lives almost entirely in the processor-specifications clause of your co-op supply agreement — BC Milk confirms FFA doesn’t affect provincial-pool pay, and no major North American processor posts its $/cwt FFA schedule publicly.³ On a 500-cow US herd producing 11,400 cwt/month at March 2026’s $16.16/cwt Class III, a $0.10–$0.50/cwt hit pencils at $13,680–$68,400/year, and FMMO reform’s 85–93¢/cwt Class-price reductions just tightened the margin in front of that number.⁴ The fastest intervention isn’t a facilities spend: plot FPR alongside FFA for six months, start fresh-cow BHBA testing at ≥1.2 mmol/L cutoff, move dry-off BCS into the 3.0–3.25 window, and layer in rumen-protected choline at the Arshad et al. (2020) dose.⁵ The demographic layer matters too — with US heifer inventories at a 20-year low and CoBank projecting 438,844 fewer dairy heifers in 2026, any parity-shift cull decision runs into $3,000+ replacement costs.⁶ The operator action: pull your last six bulk tank reports and your supply agreement this week, and get your co-op’s FFA penalty math in writing.

In January 2023, Dairy Farmers of Ontario field staff triggered an investigation on a 40-cow Holstein tie-stall that had averaged 1.32 ± 0.50 mmol FFA/100g fat across 752 samples between August 2018 and October 2022 — with more than 54% of samples at or above the 1.20 sensory threshold. The milking equipment tech had already been out. Vacuum fine. Liners fine. Filters changed at every milking, three times a day.

University of Guelph researcher Hannah Woodhouse and Dr. David Kelton walked into that barn and found what the data had been whispering all along: cracked milking unit claws with curdled milk inside, unequal milking intervals as short as three hours, and palm fat fed at 300 g/head/day with the dose pushed higher during fall DFO incentive months.¹ The equipment problems were real. But the ration, the intervals, and the calendar were doing most of the damage — and the equipment tech was never going to solve any of that alone.

That anonymized case farm sits at the clinical end of a bigger story. A body of peer-reviewed Guelph work covering every Ontario dairy farm over four years has reframed the 1.20 mmol bulk tank free fatty acids line as a transition-cow and management test, not a hygiene test.¹,² And the penalty exposure that follows it isn’t on your pay statement — it’s in the “processor specifications” pass-through buried in your co-op supply agreement.

What the 1.20 Bulk Tank Free Fatty Acid Threshold Is Really Measuring

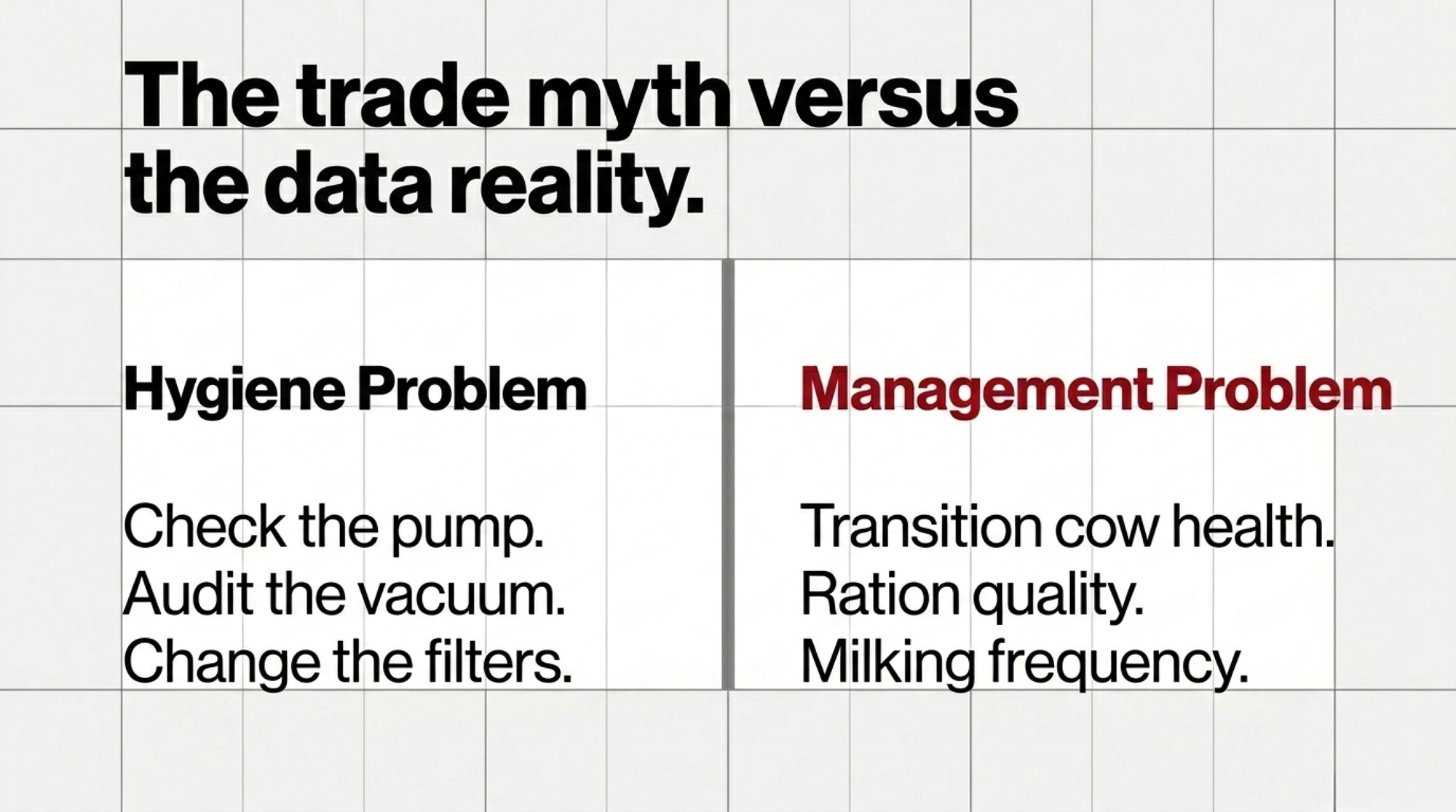

Start with what the 1.20 line does to milk. Above it, trained taste panels pick up rancid notes in butter and cheese, foam stability drops, and cheese-milk coagulation suffers.¹ That’s why processors penalize above threshold. And it’s why the trade spent a decade calling this a hygiene problem — check the pump, audit the vacuum, change the filters.

The Woodhouse et al. JDS Communications work tells a different story. Monthly bulk tank averages across all 3,771 Ontario dairy farms, August 2018 through December 2022, totaled 171,843 observations. Roughly 7% of those monthly averages sat at or above 1.20, and the significant predictors of an elevated month weren’t hardware — they were lower bulk tank milk protein, non-parlor milking systems, three-incentive-day months, and higher bulk tank bacteria counts.⁷

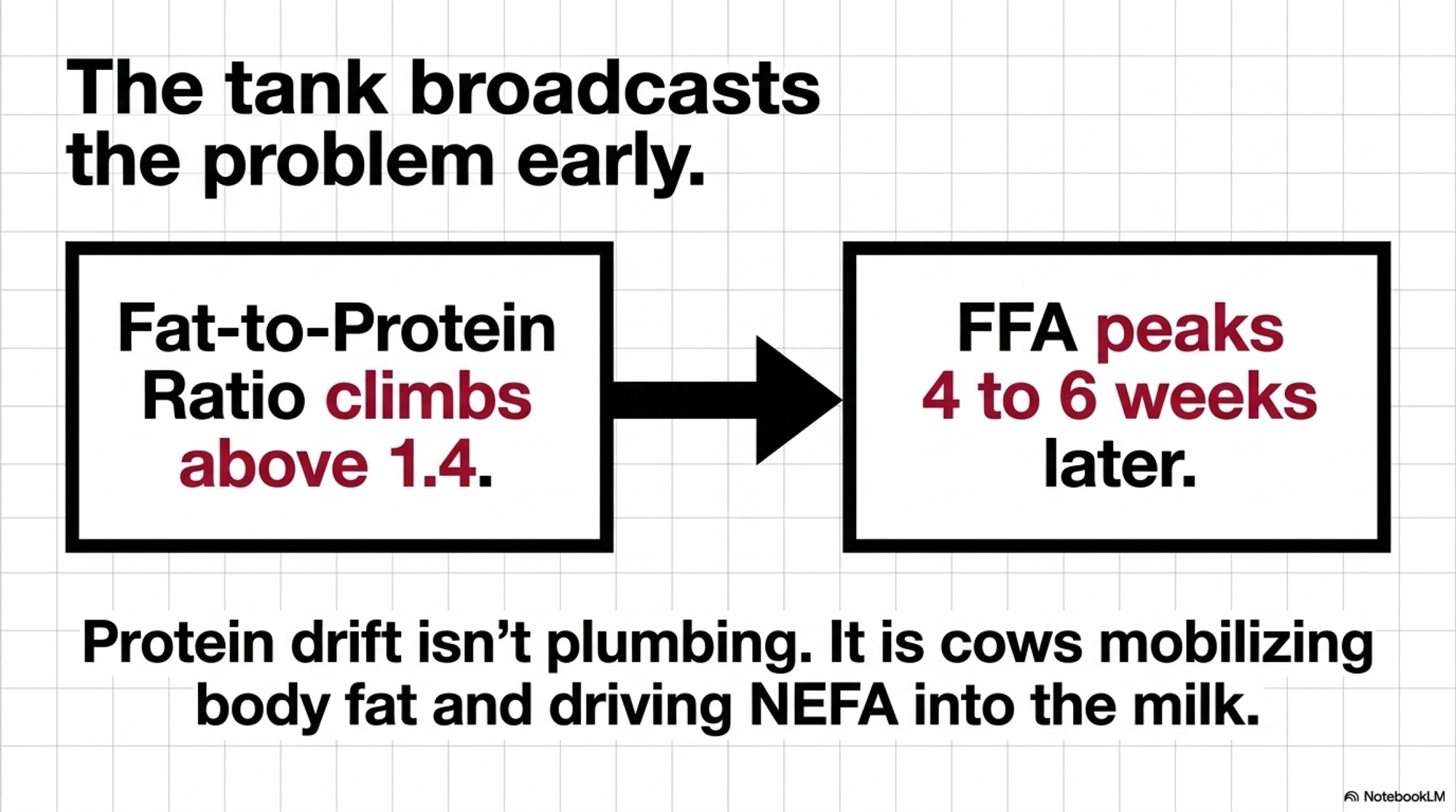

Protein drift in a bulk tank isn’t a plumbing signal. It’s a metabolic signal — cows in negative energy balance, mobilizing body fat, driving NEFA and lipase activity into milk that’s already biochemically compromised before it touches a single piece of stainless. The 1.20 line isn’t testing your milking system. It’s testing your transition cow program.

Writing for AgProud in September 2024, Woodhouse put it in producer-ready terms: dairy producers can manage individual cows, ration quality, milking frequency, and milk filter changes to reduce FFA levels.⁸ Cows and ration come first on her own list. Filters last. The paper’s predictor ranking points squarely in the same direction.⁷

Dimension

Old industry assumption

Guelph 2024-2025 evidence

Operator action

Primary cause

Pump/vacuum/liner wear

Transition-cow energy deficit (low BT protein)

Call vet first

Key predictor

Equipment age

Tie-stall + ≥3×/day (β=1.17)

Audit housing × milking freq

Filter protocol

Replace more often

Filter <2×/day adds only β=0.27

Keep, don’t over-weight

Seasonality driver

Summer heat on equipment

3-incentive-day months

Map incentives to FFA peaks

Parlor freestall herds ≥1.20

Common

0 of 109 farms

Benchmark target

Is This a Metabolic Problem or an Equipment Problem?

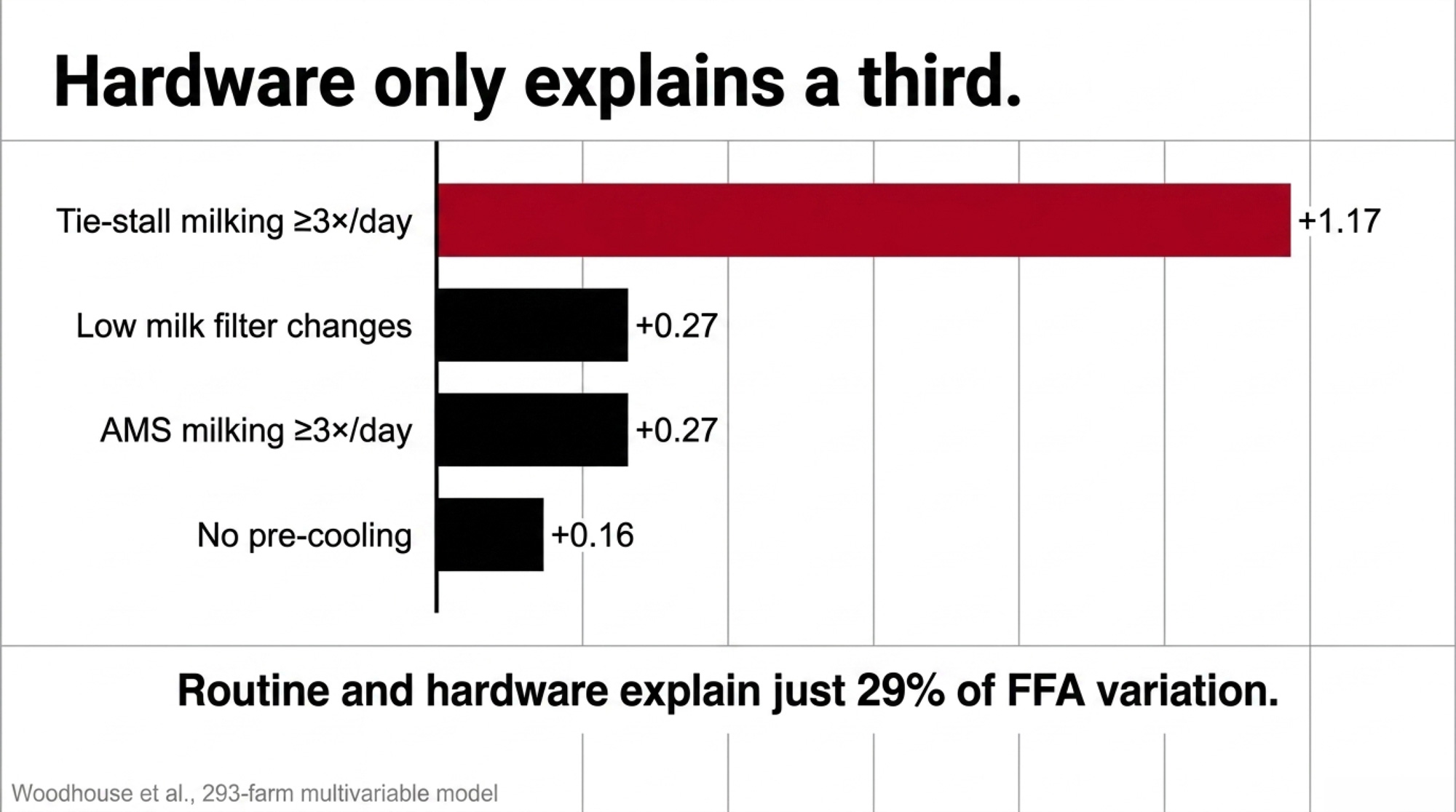

The Woodhouse et al. farm-factors paper (J. Dairy Sci., February 2025) put direct measurements on that question. It’s a cross-sectional study of 293 Canadian dairy farms — 238 in Ontario, 55 in British Columbia, split across 71 tie-stall, 109 parlor freestall, and 113 AMS freestall operations. Mean bulk tank FFA: 0.84 mmol/100g fat, SD 0.40, range 0.26–3.67. Ten percent of herds sat at or above 1.20.²

The final multivariable model is where the argument lands. Not in round numbers —in published beta coefficients:

AMS herds milking ≥3×/day: β = 0.27 (95% CI 0.12–0.41)

Not changing the milk filter at least 2×/day on ≥3×/d farms: β = 0.27 (95% CI 0.10–0.44)

No pre-cooling: β = 0.16 (95% CI 0.02–0.30)

And this one matters: **in the 109-farm parlor freestall subsample, no operation posted a monthly FFA average at or above 1.20 during the study window.**² That’s a snapshot, not a universal law. But it’s a loud snapshot.

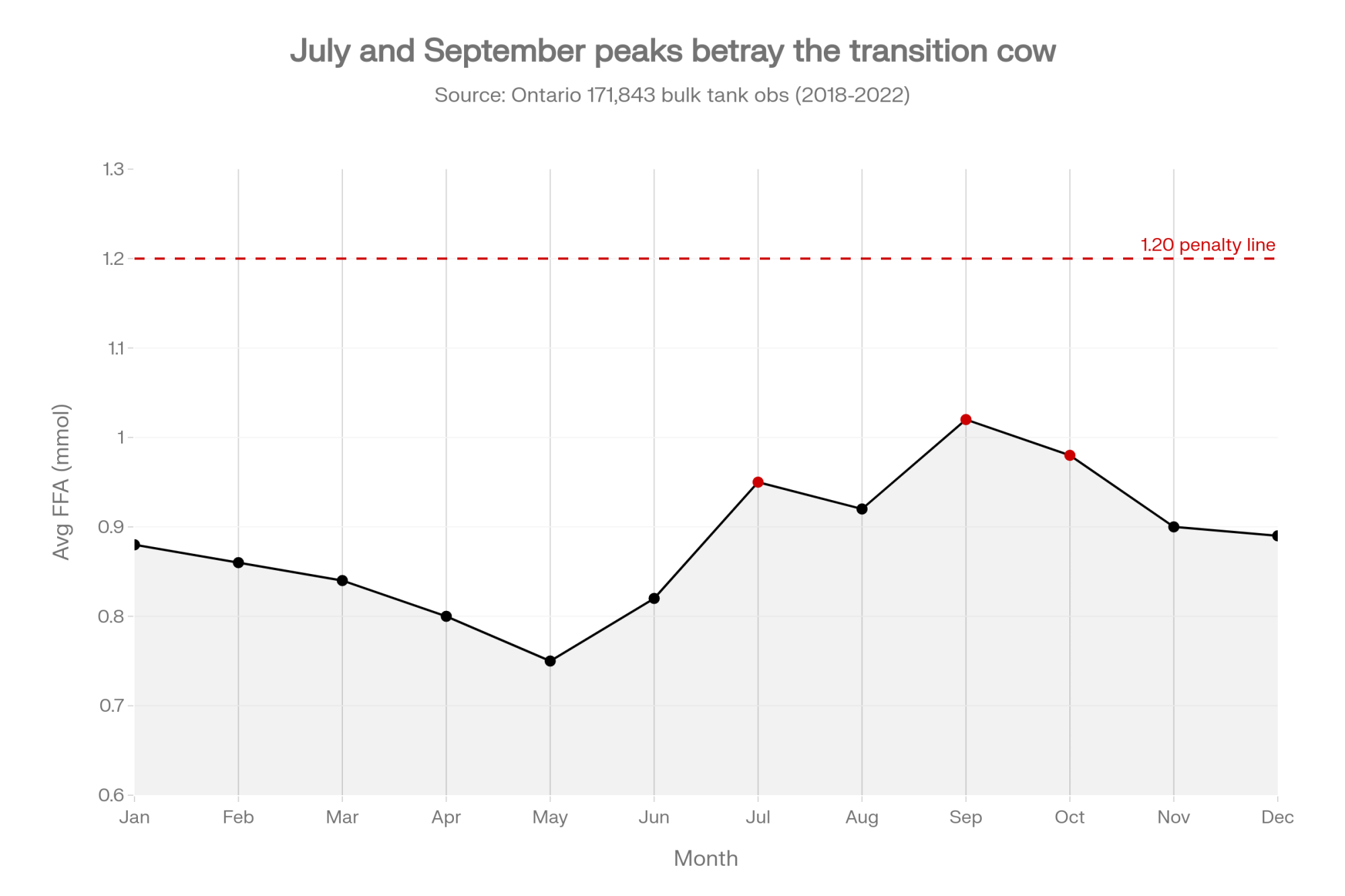

The adjusted R² on the model was 29%, which is an honest way of saying hardware and routine only explain about a third of the variation — the rest sits in cows, rations, and calendars.² Ontario’s broader surveillance closes the loop: FFA lowest in May, highest in July and September, every year.⁷ Equipment doesn’t know what month it is. Transition cows do.

What’s the FFA Penalty Actually Worth on Your Herd?

Here’s where most coverage of this paper waves a dollar figure around and hopes you don’t check the schedule behind it. We’re not going to do that.

The Canadian disclosure landscape is thinner than it looks. DFO reports FFA back to every Ontario producer on every bulk tank load.¹ BC Milk has reported FFA back to producers since August 1, 2019 — but the BC Milk Marketing Board’s own Component & Quality Testing page explicitly states that FFA “does not factor into producer’s component or quality results and has no impact to a producer pay” at the provincial-pool level.³,⁹ That doesn’t mean there’s no penalty. It means the penalty, if any, flows through the processor-specifications clause of the individual producer agreement — which is not public.

On the US side, FMMO pooling doesn’t set FFA penalties at all. Those live entirely in co-op supply agreements and processor contracts, and we could not locate a single publicly posted $/cwt FFA penalty schedule from a major North American processor or co-op at publication. What is public is the penalty mechanism: above threshold, the plant either discounts the load, downgrades it out of cheese milk, or diverts it to a lower-value class. The dollar hit depends on your co-op, your plant, and your class mix.

So the barn-math in this piece is a worked example with reader-supplied inputs, not a documented exposure. Here’s the frame for a 500-cow US herd:

At the USDA AMS-announced March 2026 Class III price of $16.16/cwt, gross milk value ≈ $184,224/month.¹⁰

Multiply 11,400 cwt by your own co-op’s FFA forfeiture ($/cwt) to size your exposure.

Illustrative $/cwt Forfeiture

v

Annual Cost

% of Annual Gross

$0.10/cwt

$1,140

$13,680

0.6%

$0.25/cwt

$2,850

$34,200

1.5%

$0.50/cwt

$5,700

$68,400

3.1%

Halve the herd to 250 cows at the same production and price and the middle line pencils at about $17,100/year. Whatever your co-op’s number is, it’s not a rounding error — and the only way you’ll know it is to pull the agreement. That’s the point of the contract-audit step in the next section.

Did FMMO Reform Make the US FFA Penalty Sharper?

Federal milk marketing order reform took effect June 1, 2025. The USDA AMS final rule, issued January 15, 2025, after a 49-day national hearing and producer referenda across all 11 orders, reshaped component pricing formulas and raised processor make allowances:¹¹

Product

New Make Allowance (per lb)

Cheese

$0.2519

Butter

$0.2272

Nonfat Dry Milk

$0.2393

Dry Whey

$0.2668

The butterfat recovery factor was adjusted to 91% (from 90%), and the composition factor upgrade — updating skim milk to 3.3% true protein, 6.0% other solids, 9.3% nonfat solids to reflect modern milk — was held back six months and took effect December 1, 2025.¹¹

AFBF economist Daniel Munch put hard numbers on the gap in his September 22, 2025, Market Intel piece. Higher make allowances pulled $337 million from pool revenues in the first three months alone, with Class price reductions of 85–93¢/cwt, and the six-month composition-factor delay cost farmers roughly $100 million in compensationagainst what full reform would have delivered on the original timeline.¹²

Margin pressure pushes operators harder toward co-op production incentive signals. The Ontario analysis flagged three-incentive-day months as a significant predictor of elevated FFA.⁷ Fat supplements rise. Marginal cows get pushed. The quality penalty — whatever your agreement says it is — then bites exactly the milk you overproduced. Neither side of that loop appears as a line item on the pay statement.

The Fastest Intervention That Doesn’t Cost $50,000

Before spending a dollar on facilities, run the JDS finding backward. Pull three bulk tank reports. Calculate fat-to-protein ratio. Penn State Extension flags a herd-level FPR above 1.4 as an energy-deficit and subclinical-ketosis signal when more than about 40% of the measured group exceeds it.¹³ A validation study refined the individual-cow cut-off to >1.42 (sensitivity 92%, specificity 65%) for subclinical ketosis.¹⁴ Twenty-minute diagnostic. Zero dollars.

Then the protocol. Do these now, not next quarter:

This week: Pull your last six bulk tank FFA reports from your co-op quality lab and plot FPR on the same months. If FPR leads FFA by 4–6 weeks, that’s your metabolic signal.

This week: Pull your co-op supply agreement. Find the “processor specifications” or “quality” clause and the line that references FFA. Then email your quality manager and ask, in writing, for (a) the exact $/cwt or class-downgrade math the plant applies above 1.20, and (b) what share of your last six quality adjustments was attributable to FFA. Save both answers. This is the barn-math input only you can get.

This month: Score every cow going dry. Anything above BCS 3.5 goes into a limit-fed pre-dry pen; dry-off BCS in the 3.0–3.25 range minimizes post-calving NEFA mobilization.¹⁵ Costs labor, not capital. Tank effect lags 6–8 weeks.

This month: Start fresh-cow BHBA testing. Blood BHBA ≥1.2 mmol/L is the widely used subclinical-ketosis cutoff with balanced sensitivity and specificity in hand-meter field work; Oetzel’s ≥1.4 mmol/L threshold marks the jump in DA and clinical ketosis risk.¹⁶ Test days 3–5 and 10–14. At ~40 calvings a month and roughly $1.00/test, that’s about $80/month.

Within 60 days: Work rumen-protected choline into the close-up ration at the Arshad et al. (2020) meta-analysis dose of 60 g/cow/day at 25% active, from 21 days pre-calving through at least 28 days postpartum.⁵ That meta-analysis of 21 trials reported an average milk response of ~2.3 kg/day and ~0.08 kg/day fat, with substantial between-trial and between-herd variation.⁵ Balchem’s published summary of pooled ReaShure trials puts the sustained response at roughly 700 kg more milk over a standard 305-day lactation — real, but not uniform across herds.¹⁷ Ask your nutritionist for a per-cow-per-day cost based on current feed contracts; it will move with commodity markets and isn’t a single published number.

And the longer horizon:

90 days: Six months of FFA + FPR plotted; at least two fresh-cow BHBA cohorts logged; your co-op’s FFA penalty math on file in writing; a decision on which of the three paths below you’re actually taking.

365 days: Re-plot your fall FFA peak year-over-year against parity distribution and incentive-day calendar. Decide whether you can document a structural shift worth bringing to a co-op board meeting.

Filter changes still matter. The Woodhouse TTR follow-up paper (J. Dairy Sci., February 2026) found “milk too cold” alarms associated with an average FFA of 1.31 mmol/100g fat — the only alarm type with a significant increase over baseline — and more than 15% of alarm-associated samples already sat at or above 1.20.¹⁸ Real. Measurable. Worth doing. But changing the filter without fixing the transition cow problem is putting a new battery in the smoke alarm while the fire burns.

When Does an FFA Problem Become a Culling Decision?

Some FFA problems aren’t managerial. They’re demographic.

When the fall peak climbs year over year and herd average parity sits above 3.2, protocol upgrades blunt the problem but don’t solve it. Older multiparous cows carry more metabolically active visceral fat, mobilize NEFA faster, and compound ketosis risk at every subsequent calving. The Woodhouse/Kelton case farm added another wrinkle: late-lactation cows carry higher LPL activity, so extending lactation to fill quota can amplify lipolysis risk.¹

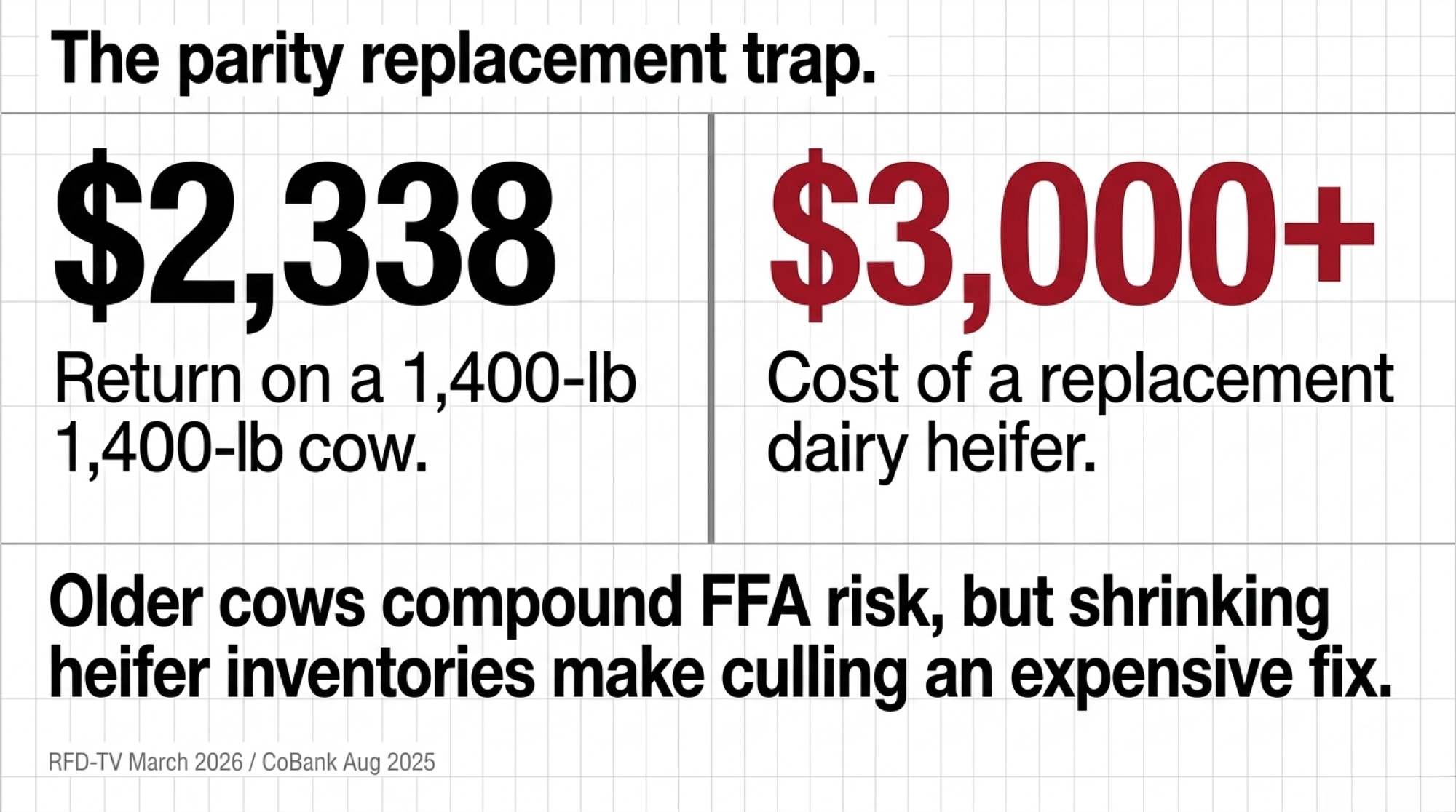

A working operator rule — Bullvine editorial rule-of-thumb, not a published threshold — if more than 30% of your parity 4+ cows test BHBA >1.4 mmol/L across two consecutive calvings, that cohort belongs on the voluntary cull list before the next dry-off. The cull market makes the call easier than it was two years ago: RFD-TV reported Southern Plains lean-cow (85–90%) auction prices at roughly $167/cwt in early March 2026, with bulls north of $200/cwt in parts of the South on tight supplies and strong grinding demand.¹⁹ A 1,400-lb parity 4+ Holstein at $167/cwt returns about $2,338 — real cash that partially funds her replacement.

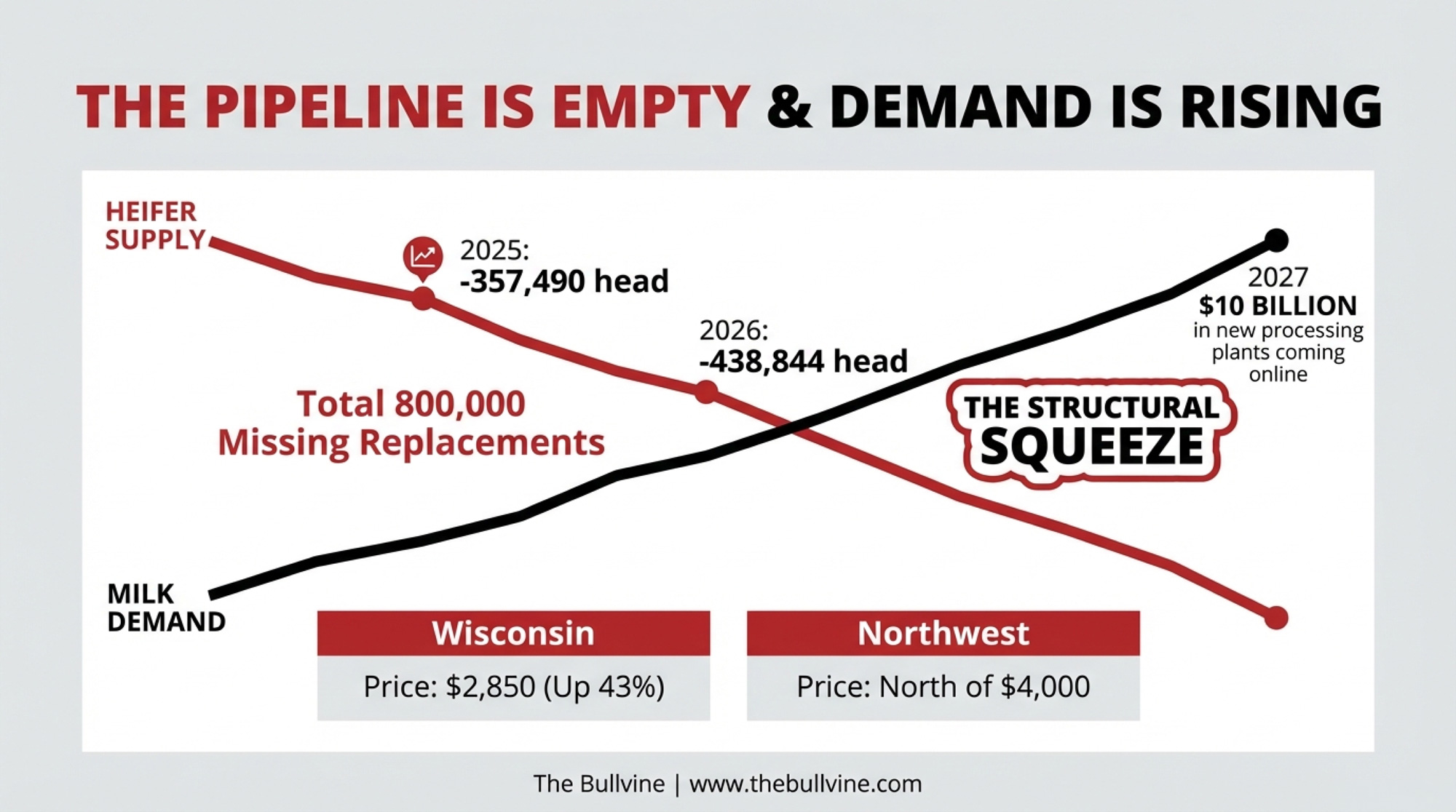

But the replacement side is brutal. CoBank’s August 2025 Knowledge Exchange outlook put US dairy heifer inventories at a 20-year low, with a predictive model showing 438,844 fewer dairy heifers in 2026 versus 2025 — driven largely by ~398,925 more beef-on-dairy calves — and total replacement inventories expected to shrink by roughly 800,000 head before rebounding in 2027, with heifer prices potentially above $3,000/head.²⁰

Walking herd average parity from 3.2 to 2.8 in that market isn’t cheap or fast. Typical structural FFA correction through parity shift runs 18–24 months under normal replacement supply, closer to 24–30 months under today’s conditions — a Bullvine analytical projection based on typical parity-turnover mechanics, not a sourced forecast. But running RPC forever on a metabolic age that keeps escalating is more expensive, slower, and quieter.

Options and Trade-Offs for Your Operation

Path

Best-fit trigger

Core spend / year (500-cow)

Payback window

Backfire risk

30/60/90 protocol only

Seasonal pattern, parity ≤3.2, no YoY escalation

RPC ~60 g/cow/day + BHBA testing (~$960/yr)

6–9 months

Misdiagnosed demographic problem

Protocol + parity 4+ culling

Parity >3.2, YoY peak climb >0.15 mmol

Above + ~$3,000/head replacement cost

18–24 months

Heifer market ($3,000+/head, 438,844 shortfall)

Add contract audit

Any herd, any pattern

Operator time only

Immediate

Co-op refusal = your new baseline

Status quo

“Filters and hope”

$13,680–$68,400/yr penalty exposure

Never

Compounding margin loss under FMMO reform (85–93¢/cwt)

Three paths, depending on what your six months of data say:

Run the 30/60/90-day protocol only. Works when the pattern is managerial — seasonal, spring-recovering, no year-over-year escalation. RPC plus BHBA testing is the core spend. Backfires if you’ve misdiagnosed a demographic problem and your fall peak climbs again next October.

Run the protocol plus targeted culling of parity 4+ repeat-ketosis cows. Works when herd average parity tops 3.2 and year-over-year peaks escalate more than 0.15 mmol/100g fat. Pays out over 18–24 months. Backfires if you can’t source replacements at workable economics at CoBank’s projected heifer prices.²⁰

Run the contract audit alongside either path. Even a clean-FFA herd benefits from knowing exactly what the FFA threshold in its supply agreement says and what share of quality adjustments the co-op will attribute to FFA in writing. The answer — or the refusal — is your baseline for every future conversation.

DFO publishes the mechanics of its FFA reporting to every Ontario producer.¹ BC Milk publishes the framework while clarifying that FFA does not affect provincial-pool pay — any producer-level penalty flows through the processor-specifications clause of the individual agreement.³ Most US co-op supply agreements reference a processor-level FFA threshold but don’t publish the penalty math. That absence isn’t universal bad faith — some co-ops share full component and quality schedules with members on request. It’s the absence of a public, standardized FFA penalty framework across North America that makes this a contract-audit problem, not a headline problem.

What This Means for Your Operation

When FFA climbs, your first call is your transition-cow vet. The equipment tech is the second call. That’s the core reframe the Guelph data demands.⁷,²

If April readings stay above 1.10 after a winter-stress recovery window, you’re not looking at a seasonal problem. You’re looking at a structural one — a parity question, not a filter question.

If FPR leads FFA by 4–6 weeks in your own six-month data, your tank is broadcasting the metabolic signal before the sensory threshold catches it. Act on the FPR.

If more than 30% of your parity 4+ cows throw BHBA >1.4 mmol/L across two consecutive calvings, that cohort is carrying your fall FFA peak — and at $167/cwt lean-cow prices, the market is paying to move them.¹⁹

If your co-op’s incentive-day calendar sits 3–5 weeks ahead of every FFA elevation on your statement, you’ve documented exactly the mechanism the Ontario data flagged.⁷ That’s a specific conversation to have with your quality manager, in writing.

If your co-op can’t — or won’t — put the FFA portion of your last six quality adjustments in writing, that silence is your baseline. Everything you do next sits against it.

If the 30-day protocol pencils at low four figures a month and your contract-audit reveals a meaningful $/cwt FFA hit, the expensive fix is cheaper than the invisible one.

Key Takeaways

If bulk tank milk protein is drifting down, the odds of elevated FFA climb sharply in the Ontario data — call your vet before the equipment tech.⁷

If your herd is tie-stall and milking ≥3×/day, the Woodhouse farm-factors paper attaches a 1.17 mmol/100g fat association to that single combination — the single biggest lever in the model.²

If herd average parity is above 3.2 and fall FFA peaks are escalating year over year, you’re looking at a demographic problem the 30-day protocol alone won’t solve, in a heifer market projected to shrink by 800,000 head before rebounding in 2027.²⁰

If you don’t know your co-op’s FFA penalty math in writing, you don’t know your exposure. Period.

If you execute the 24-month plan and document the before/after, you’ve earned a governance argument, not just a management win.

The Question You’ll Face Next October

The Woodhouse/Kelton case farm ran 1.32 mmol FFA on average over four years, with 54% of samples elevated.¹ That’s not an outlier. It’s a data point with a mailing address. The research doesn’t cull the parity 4+ cow for you. It doesn’t pull your supply agreement. It doesn’t translate the processor-specifications clause the pay statement leaves out.

What it does — through exact betas, seasonal patterns, and 171,843 monthly bulk tank observations across every Ontario dairy farm — is prove that the margin test hiding inside every bulk tank FFA reading is measurable, attributable, and fixable on a timeline shorter than the opacity of the system suggests.

Here’s the harder question. An operator who fixes their FFA and says nothing lets the current arrangement continue as designed — program worked, producer responded, questions about disclosure never get asked. An operator who fixes their FFA and walks a documented before/after into a co-op board meeting — with their own supply agreement in one hand and AFBF’s $337 million pool-revenue analysis in the other — is doing something different. So what are you going to bring to your co-op board next October — your FFA numbers, or your silence?

Editor’s note: This article contains editorial analysis and opinion by The Bullvine. It describes general industry patterns and does not refer to any specific named co-operative, processor, or producer other than those expressly attributed. Specific contract terms, quality schedules, and regulatory frameworks vary by co-op and jurisdiction; producers should consult their own agreements and advisors.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

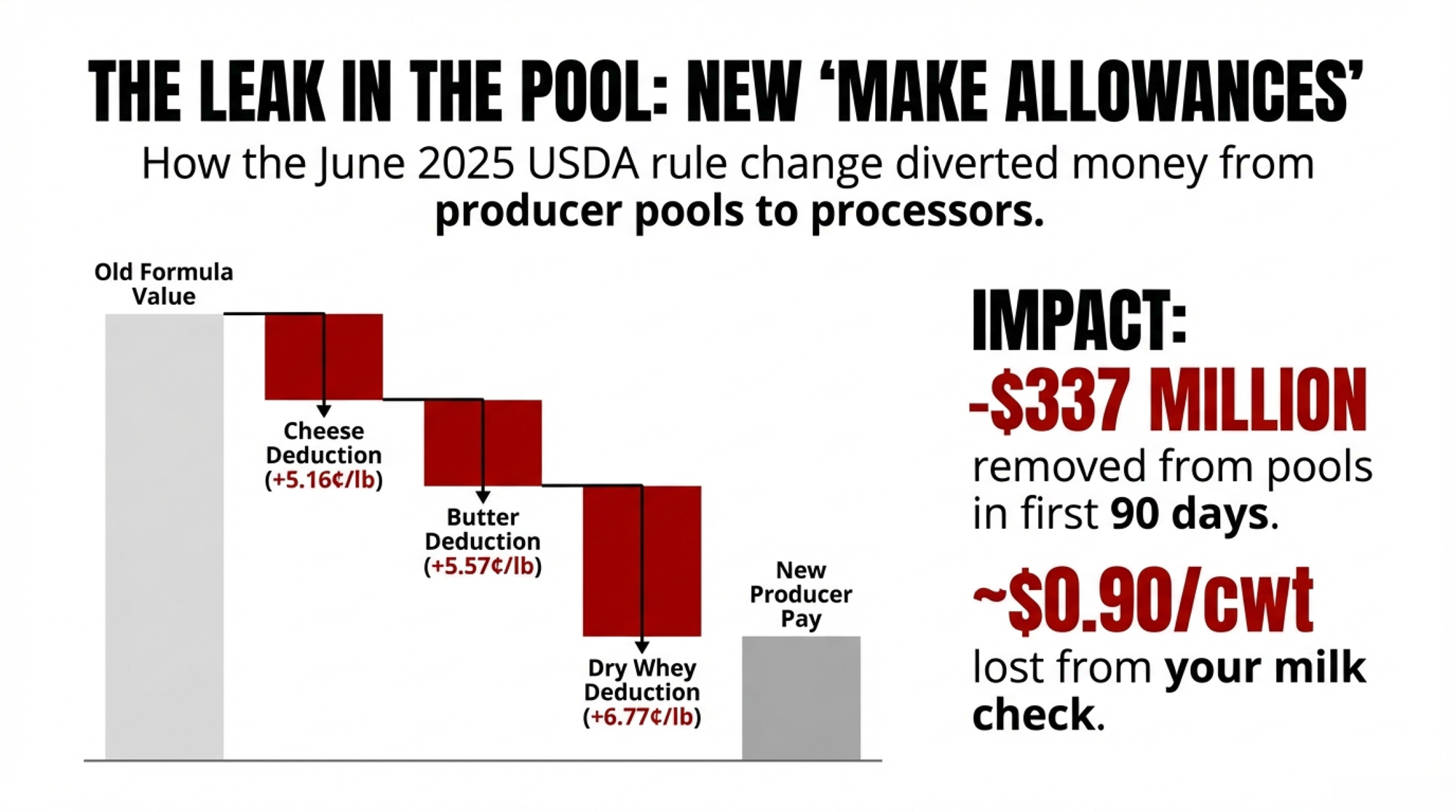

$15 Pizza. 73-Cent Milk Check. The Real Super Bowl Score for Dairy Farmers. — Follows the money on the June 2025 FMMO reform that diverted $337 million from producer pools to processors. This economic analysis arms you with specific calculations to recalibrate breakevens against widening farm-to-retail price spreads.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

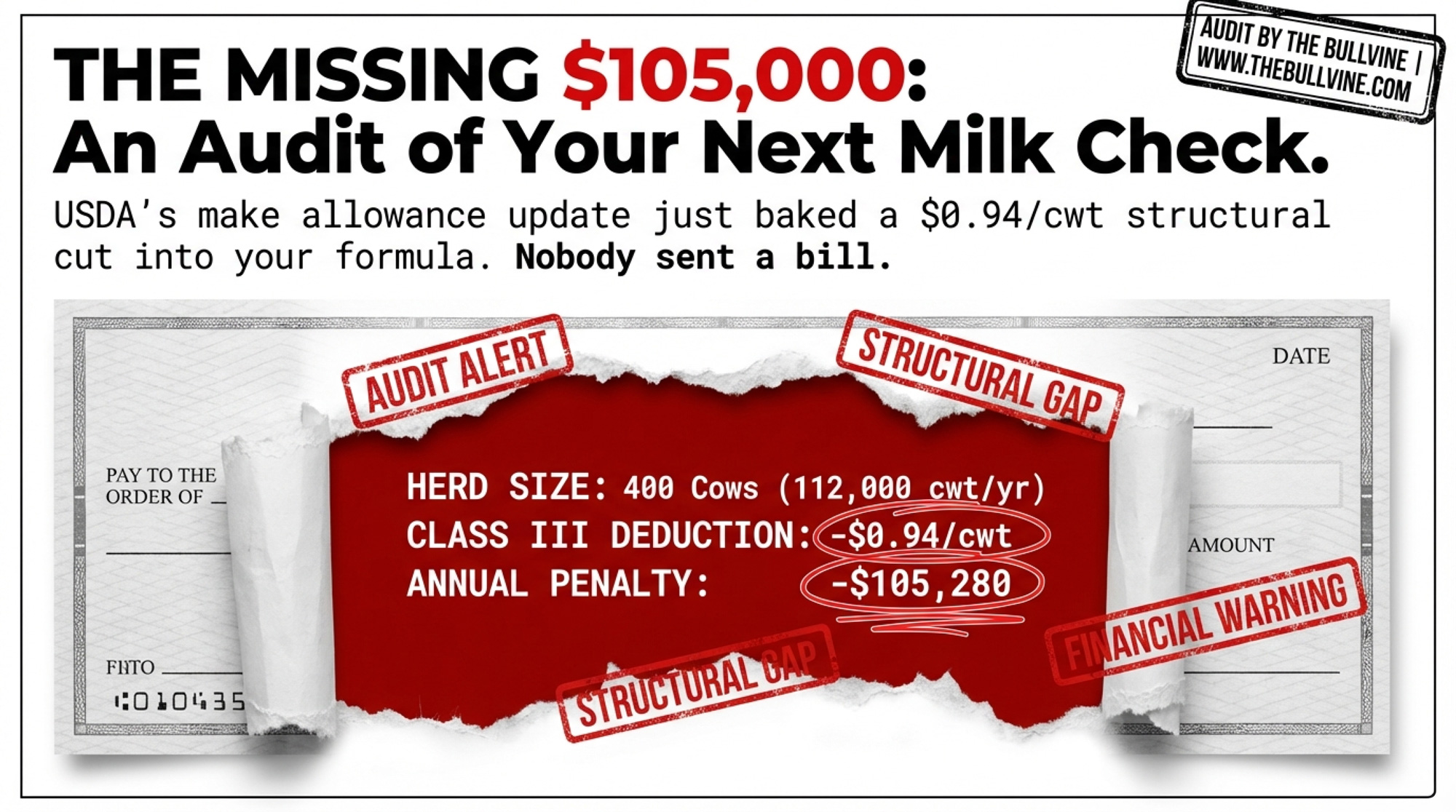

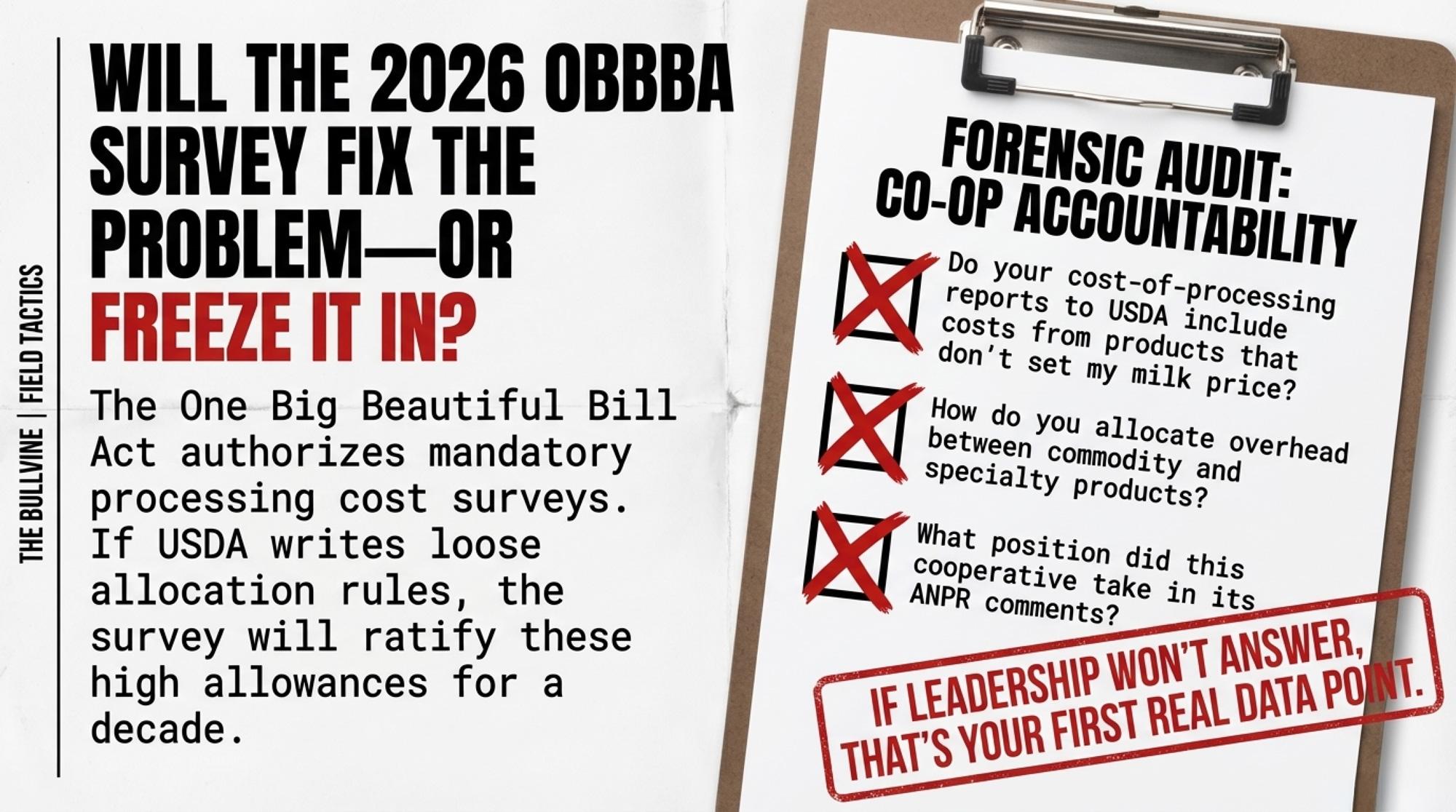

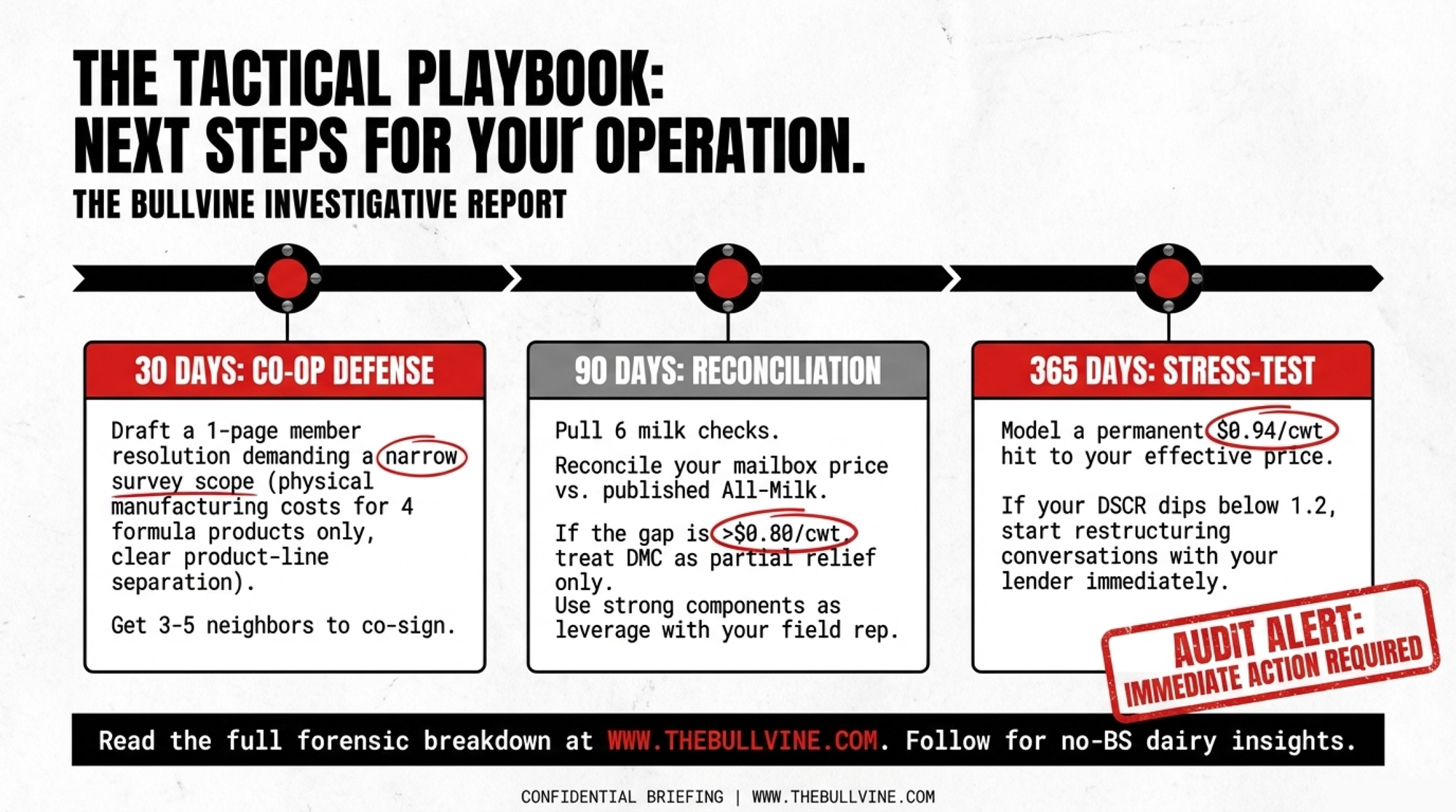

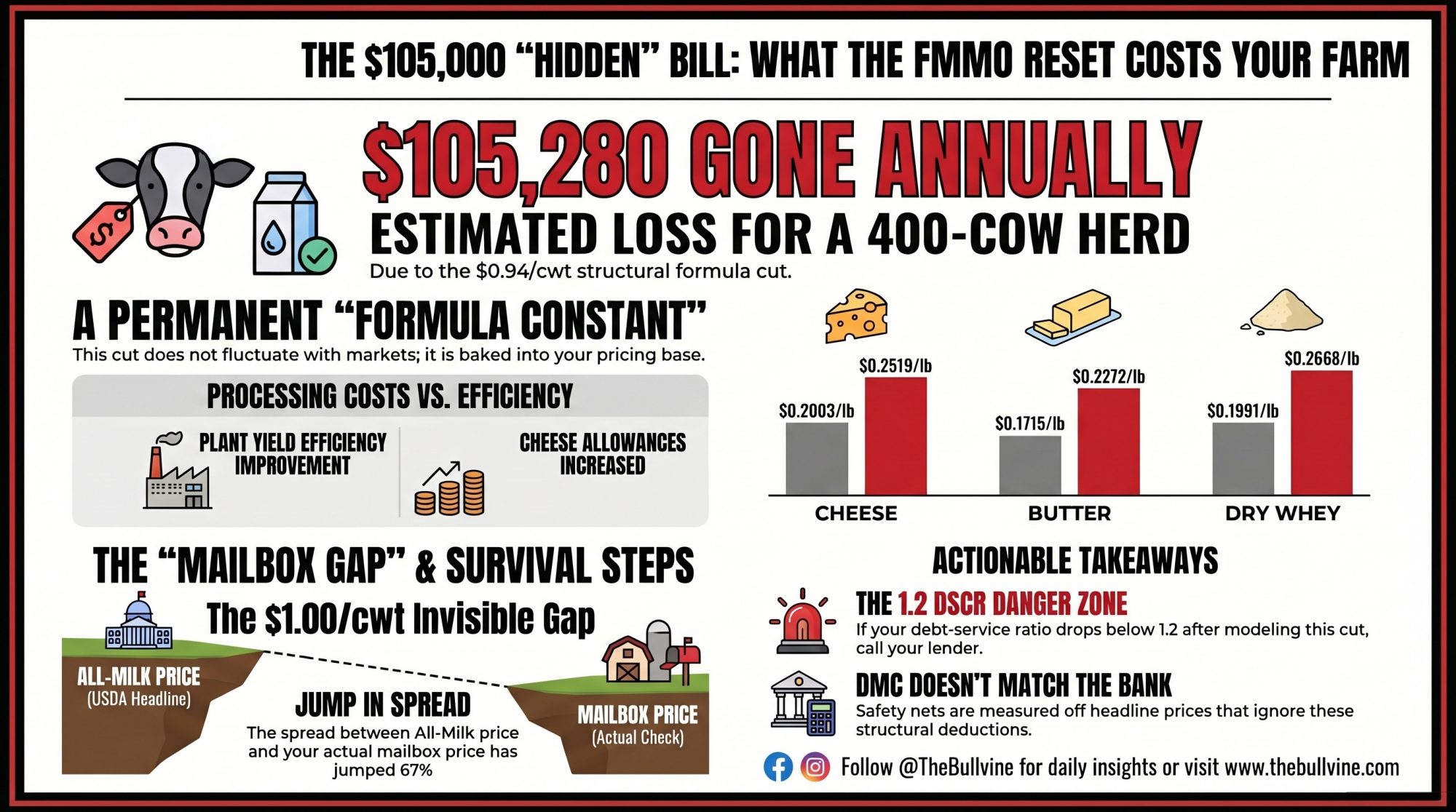

USDA’s make allowance update structurally cut Class III minimum prices by $0.94/cwt — and the mandatory survey that’s supposed to bring transparency could lock those numbers in for a decade.

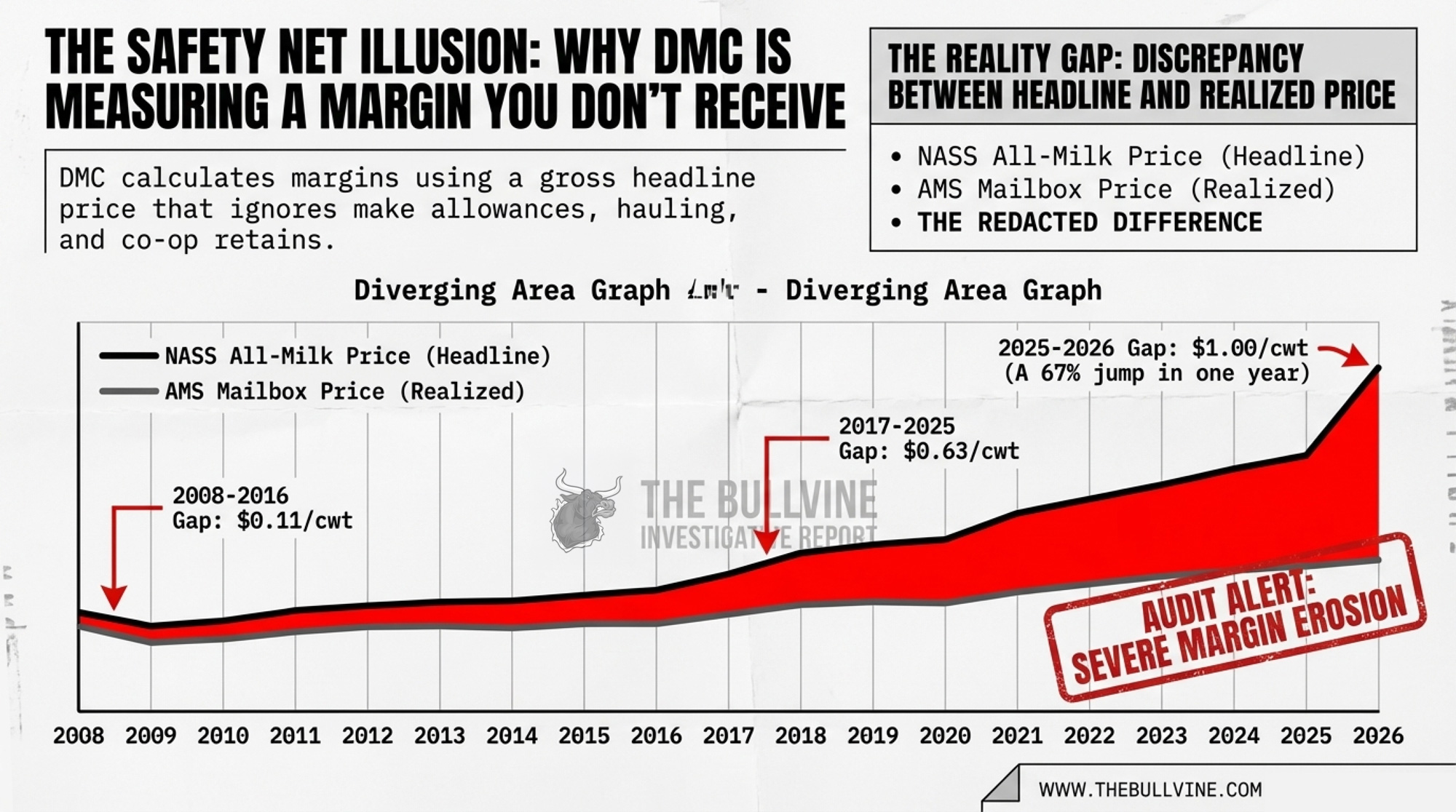

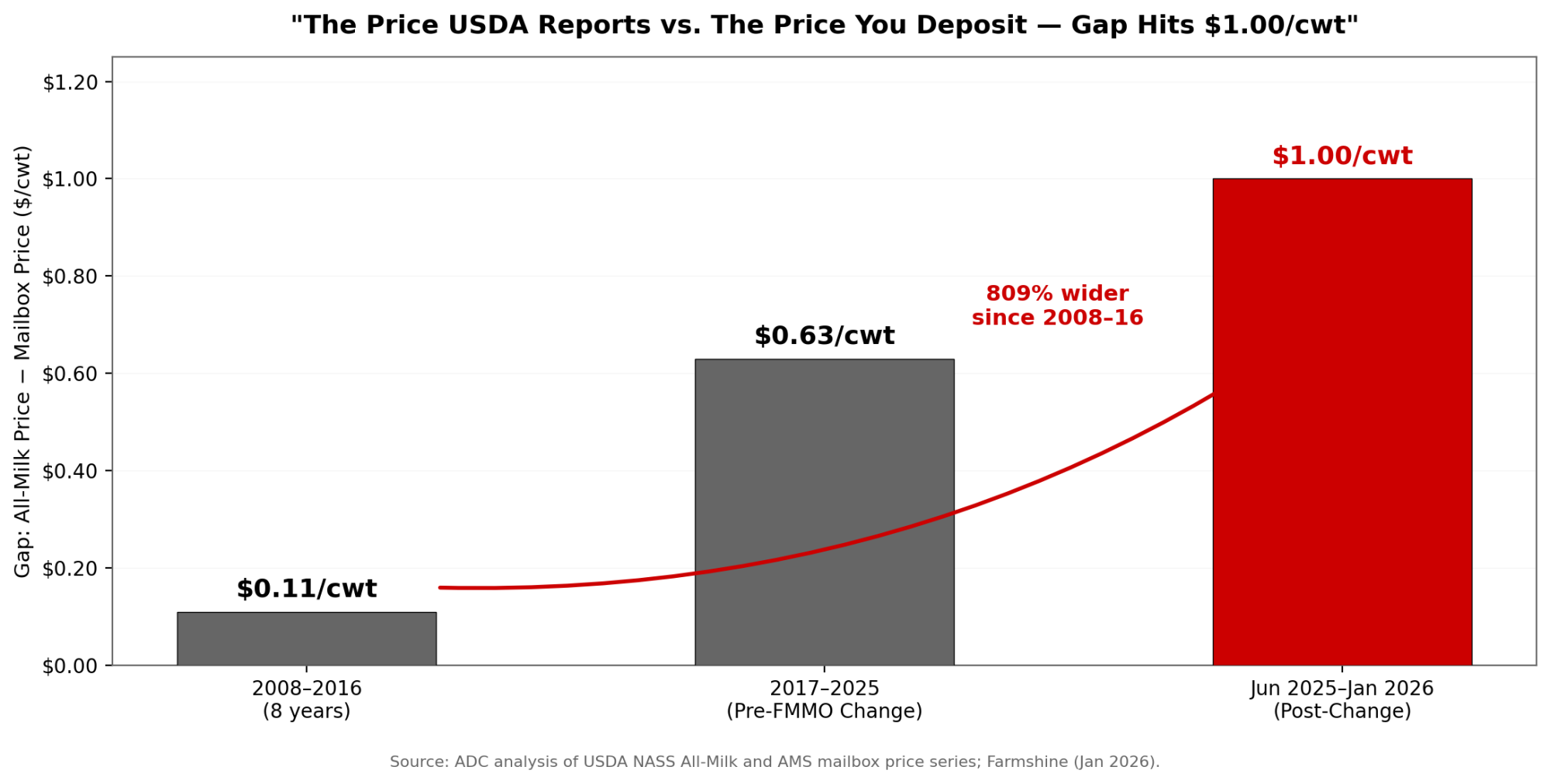

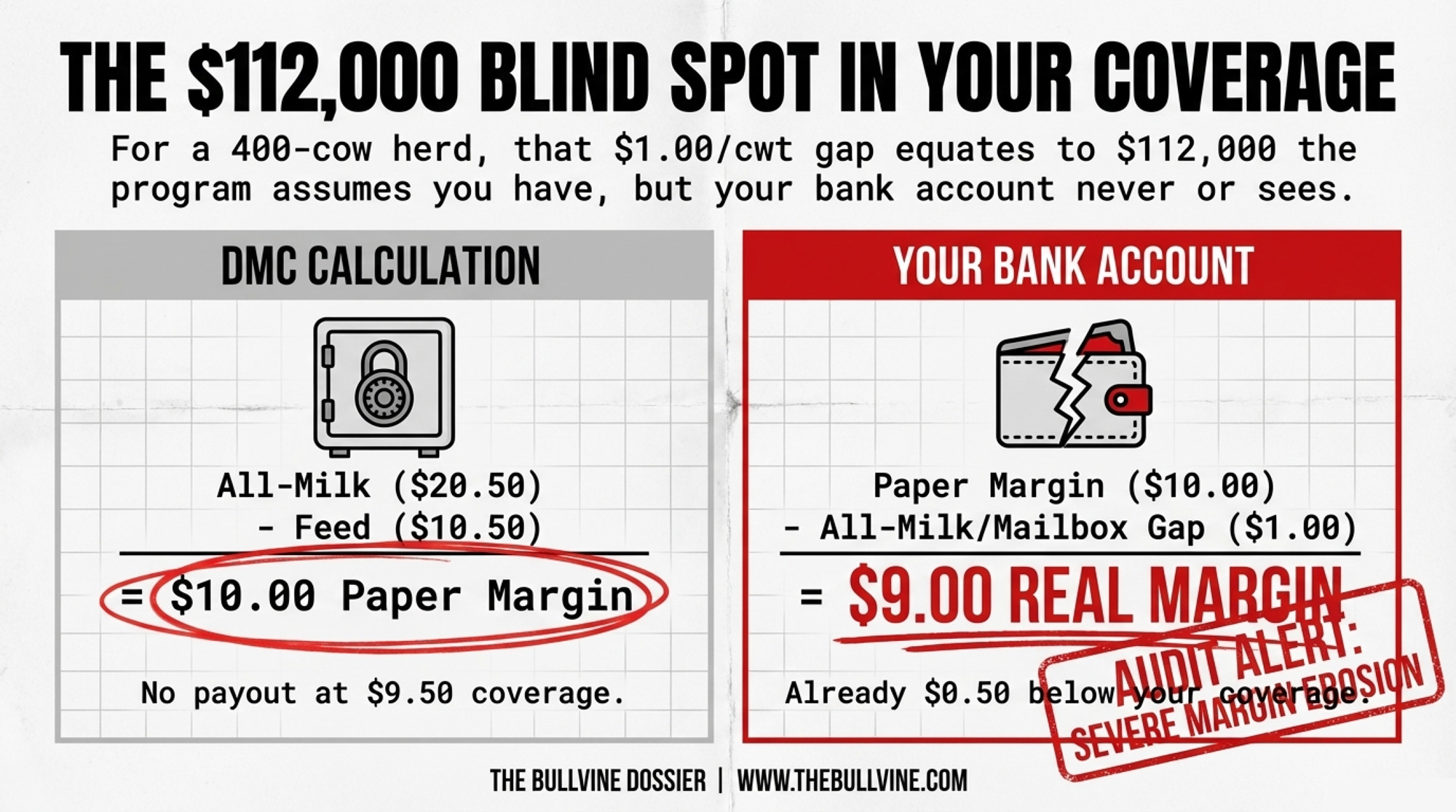

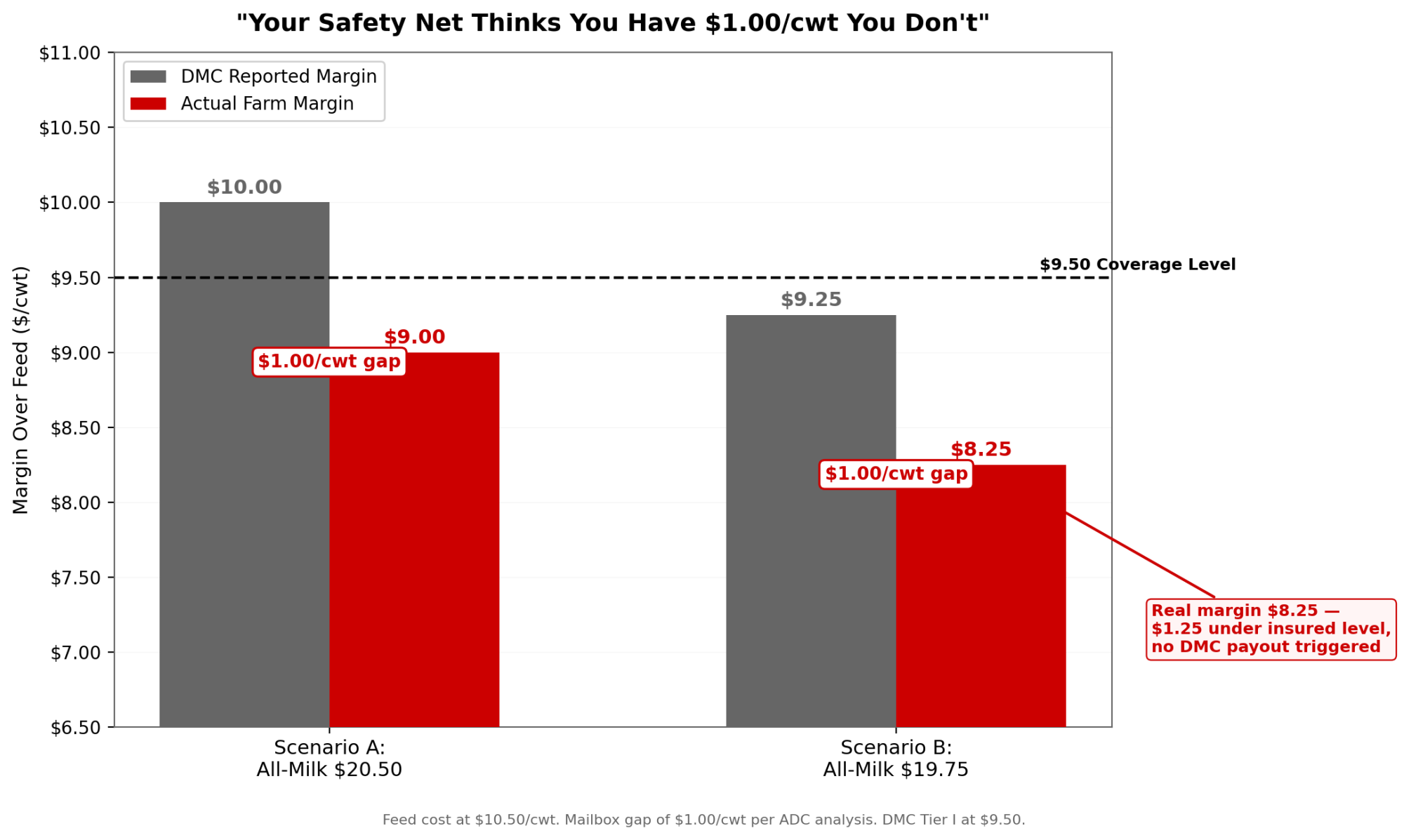

Executive Summary: USDA’s June 2025 make allowance increases baked a $0.94/cwt structural cut into every Class III milk check — not a market swing, a formula constant that hits at any commodity price. On a 400-cow herd, that’s $105,280 a year gone before your component values are even calculated. The cheese allowance alone jumped 25.8% — the first reset since 2008 — despite a 12% improvement in plant yield efficiency over that same stretch. Now add the All-Milk/mailbox gap, which has widened to roughly .00/cwt: DMC is measuring a margin your bank account doesn’t actually see. The real fight is the OBBBA’s mandatory processing cost survey, now in rulemaking, where USDA’s approach to cost categories will either audit these allowances down or lock them in for years. If your DSCR drops below 1.2 after you model this $0.94 deduction, the lender conversation needs to happen before the survey results — not after.

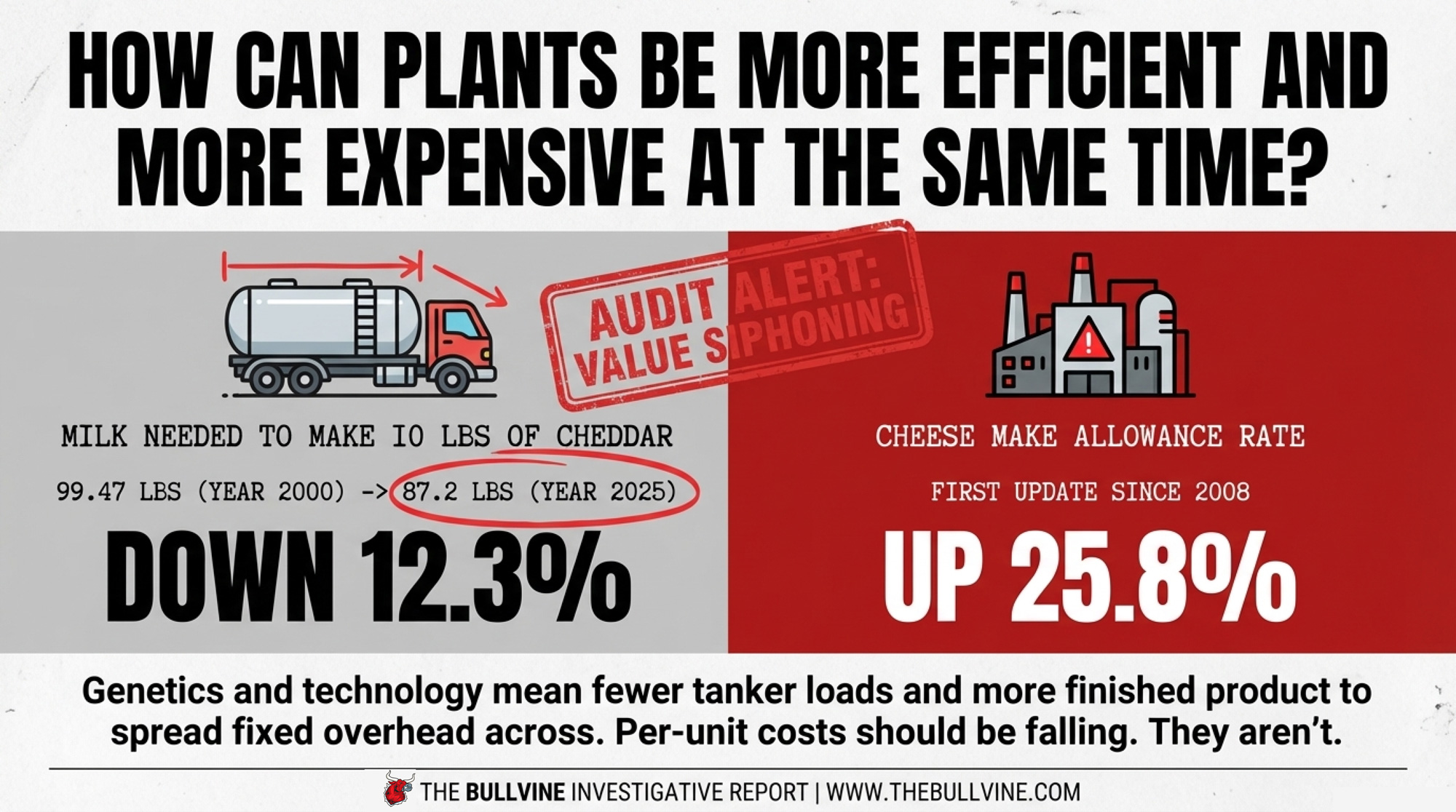

We ran the math ourselves — on the June 2025 FMMO change, month by month, through March 2026. Using USDA’s published pricing formulas and commodity prices from AMS Dairy Product Mandatory Reporting, The Bullvine calculated the make allowance impact independently.

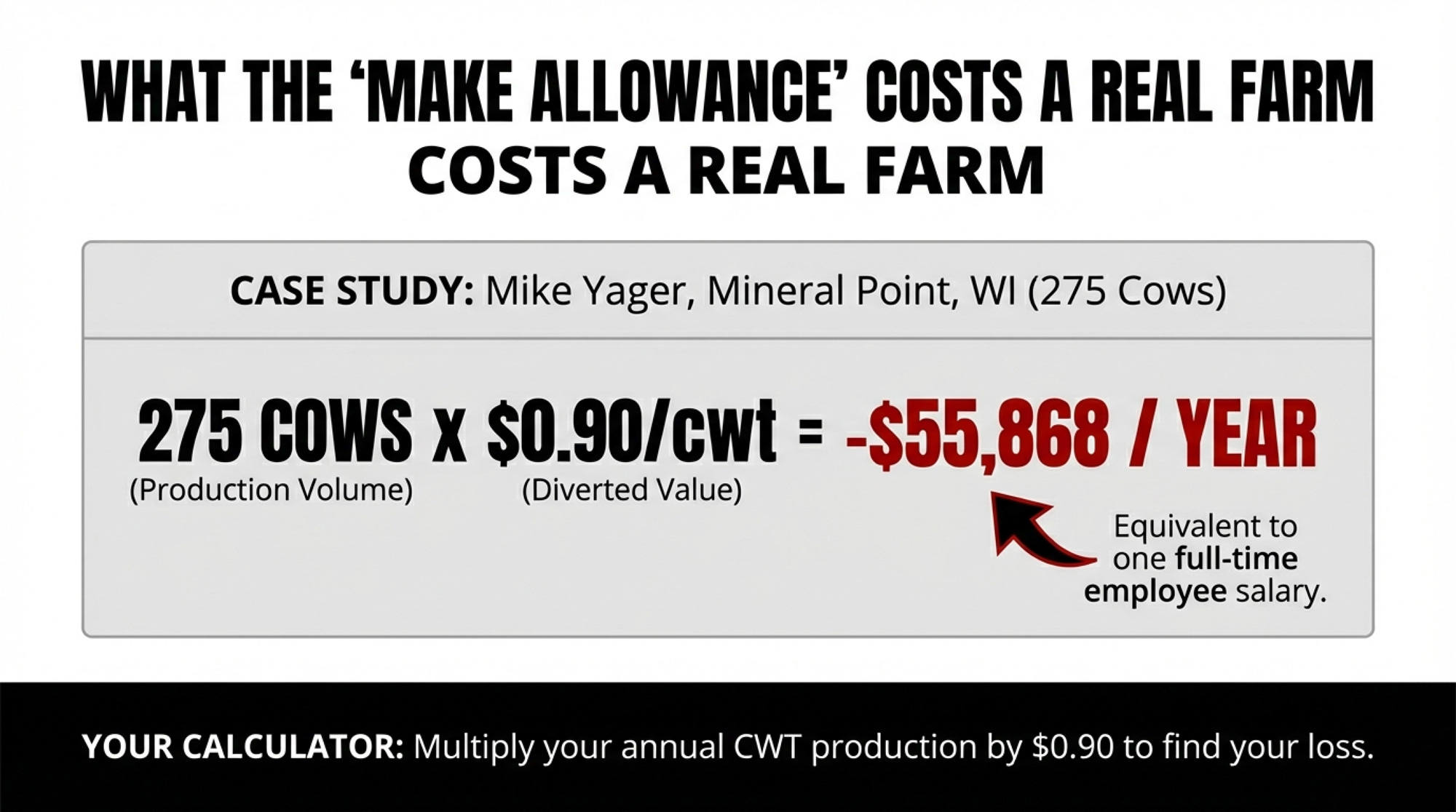

The result: $0.94 per cwt stripped from every Class III milk check, and $0.87 per cwt from every Class IV check. Every single month. It doesn’t fluctuate with cheese or butter markets — it’s baked into the formula constants. For a 400‑cow Holstein herd shipping about 112,000 cwt a year, the Class III hit alone works out to $105,280 per year at standard component tests, and closer to $112,000 at actual pool test levels.

“Dairy farmers remain the only participants in the supply chain without the ability to set prices or recover costs through a built‑in mechanism,” says Laurie Fischer, CEO of the American Dairy Coalition. “In practical terms, that’s a multi-dollar deduction built into the pricing system on the front end.”

The comfortable story in 2025 was that FMMO modernization gave everyone something. The formula math says processors got a margin reset. Family herds got deeper into a hole.

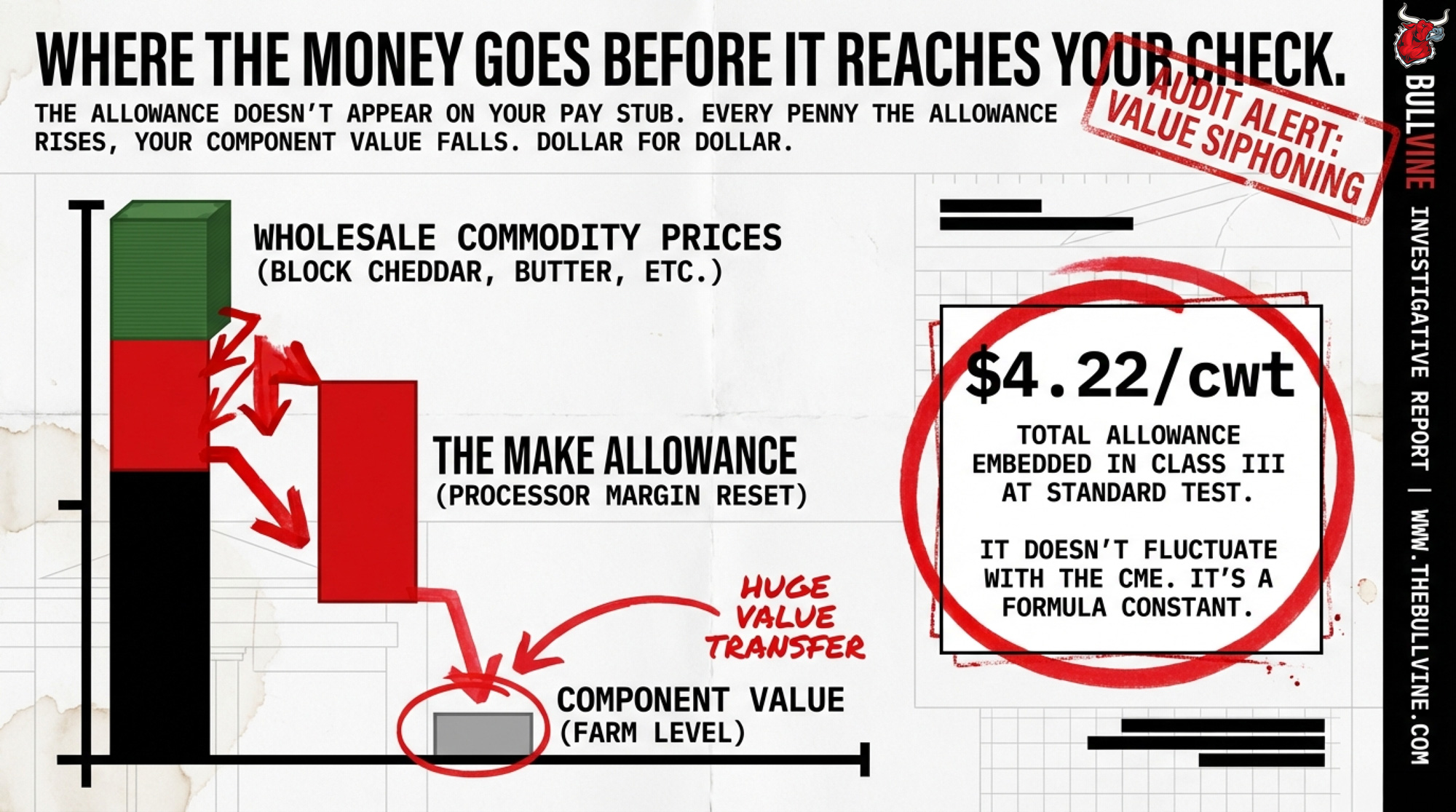

Where the Money Goes Before It Reaches Your Check

The allowance doesn’t appear on your pay stub. USDA starts with wholesale commodity prices — block cheddar, butter, nonfat dry milk, dry whey — then subtracts the make allowance before calculating component prices. Every penny the allowance rises, your component value falls. Dollar for dollar.

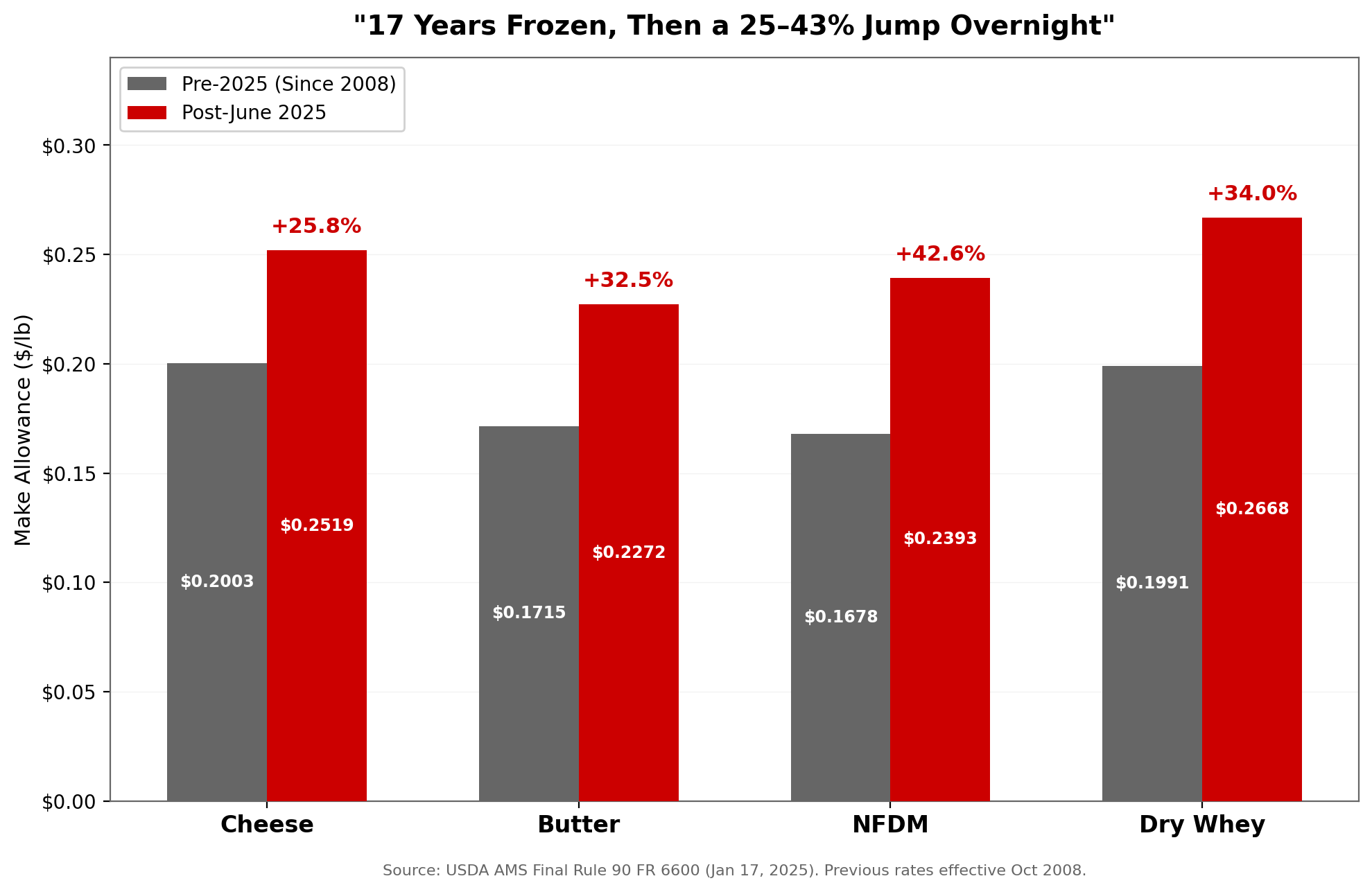

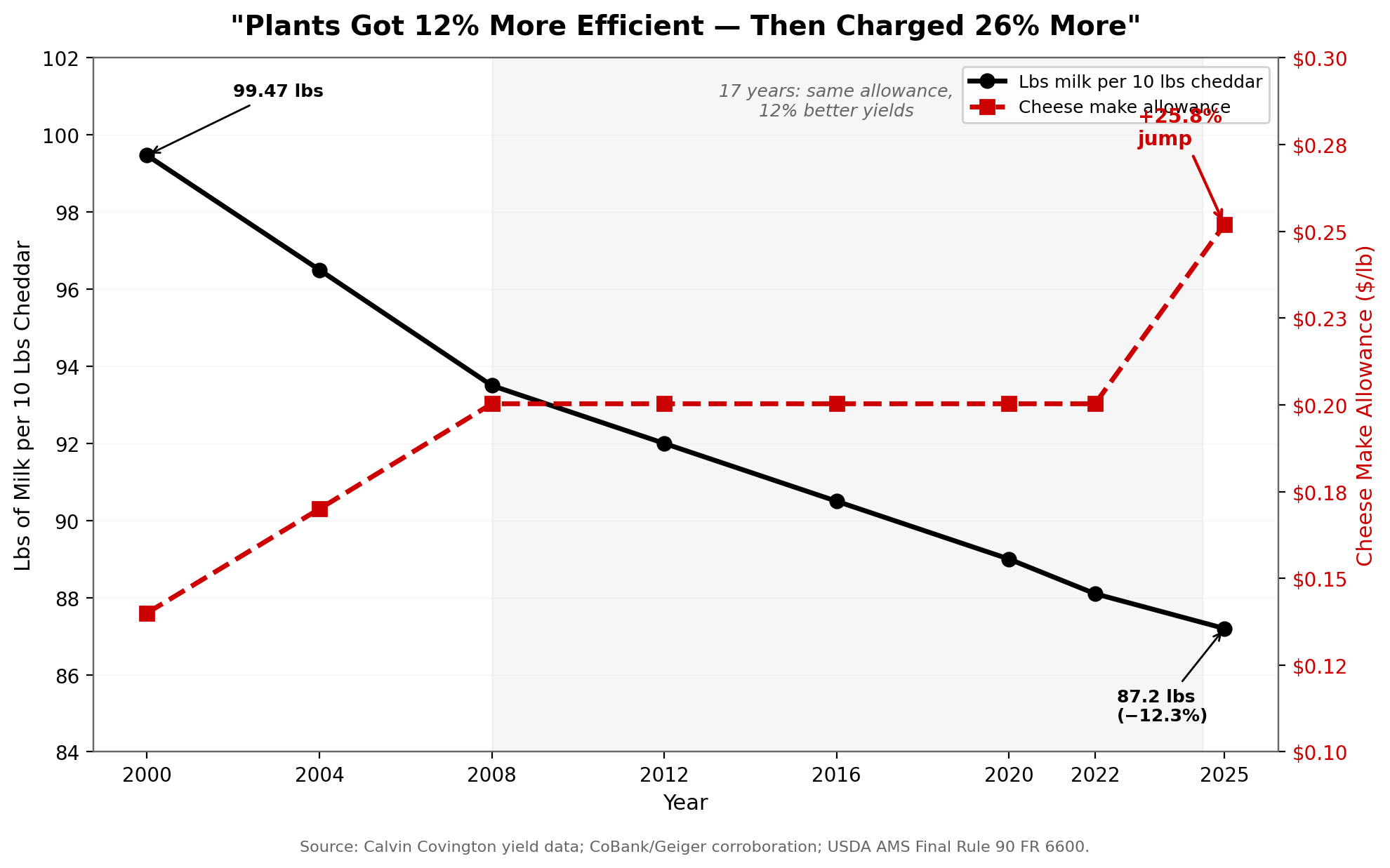

The June 2025 increases, finalized in rule 90 FR 6600 and effective across all 11 federal orders, were not pennies:

Product

Pre‑2025

Post‑2025

Increase

Cheese

$0.2003/lb

$0.2519/lb

+25.8%

Butter

$0.1715/lb

$0.2272/lb

+32.5%

Nonfat Dry Milk

$0.1678/lb

$0.2393/lb

+42.6%

Dry Whey

$0.1991/lb

$0.2668/lb

+34.0%

Source: USDA AMS Final Rule 90 FR 6600, January 17, 2025. Previous rates had been in effect since October 2008.