Two robots, 100 cows, a calm barn — and a milk cheque that only balances because mom, the kid who “helps out,” and the farmer at hour fourteen all work for free.

Scroll through the parenting and ethics corners of Reddit, and you’ll keep hitting the same question: is more humane, ethical dairy even possible? Every so often an actual dairy farmer wanders in to answer it, describing a cow‑health‑first operation milking around 100 cows on a pair of robots — cows coming and going as they please, nobody setting a 4 a.m. alarm. It’s the dream a lot of tired producers and ethics‑minded consumers want to believe in. And honestly, parts of it are real.

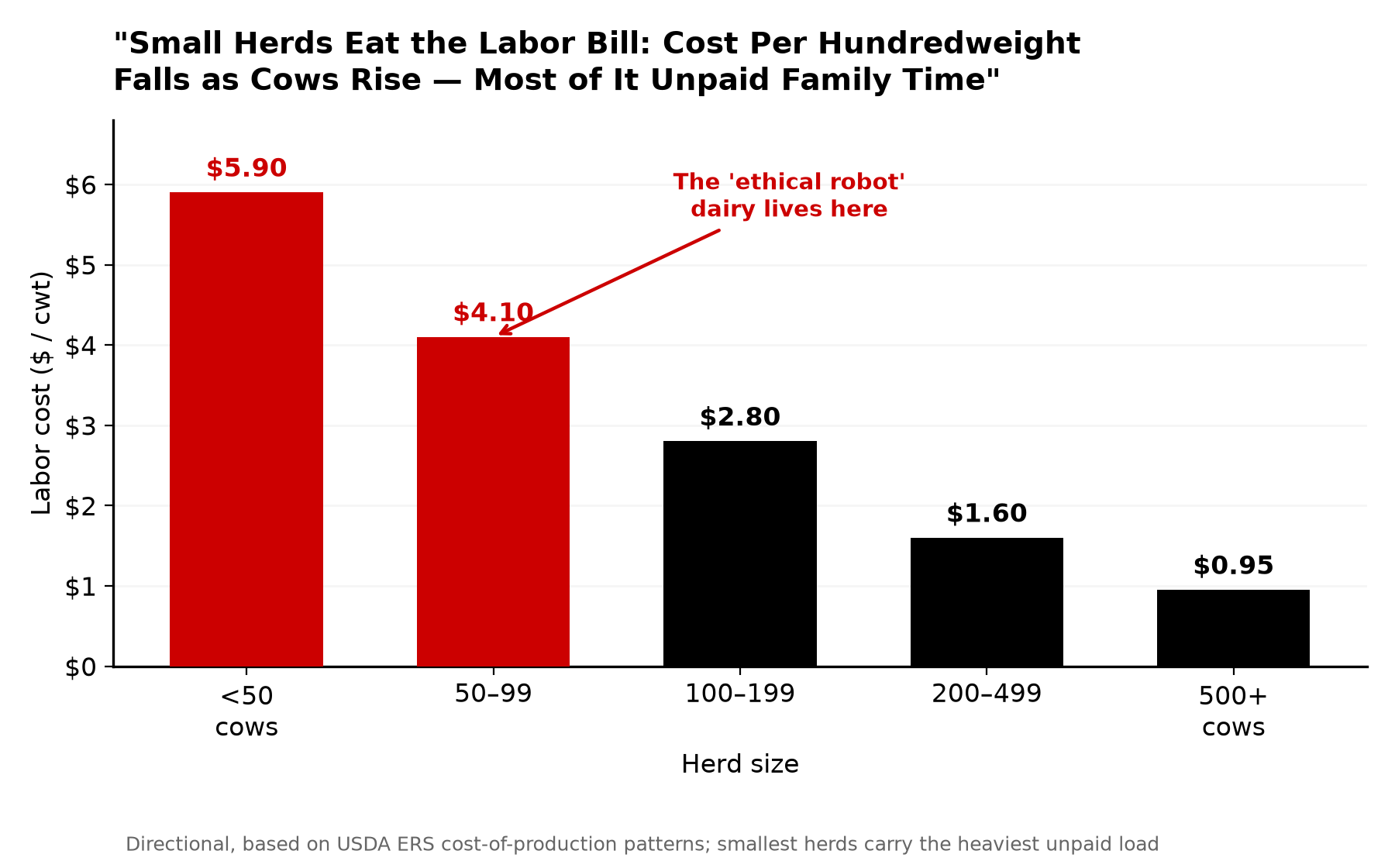

Here’s the part those threads never price. At 100 cows on commodity milk, that “ethical robot dairy” usually only balances because somebody’s labor is valued at zero. USDA’s Economic Research Service shows small herds carry far more labor cost per hundredweight than big ones — and on the smallest operations, most of it is the imputed value of unpaid family hours that never hit a payroll line. Robots don’t erase that line. They make it easier to pretend the time is free. Who’s actually paying for the “ethical” part is the question this whole story turns on.

What’s Changing and Why

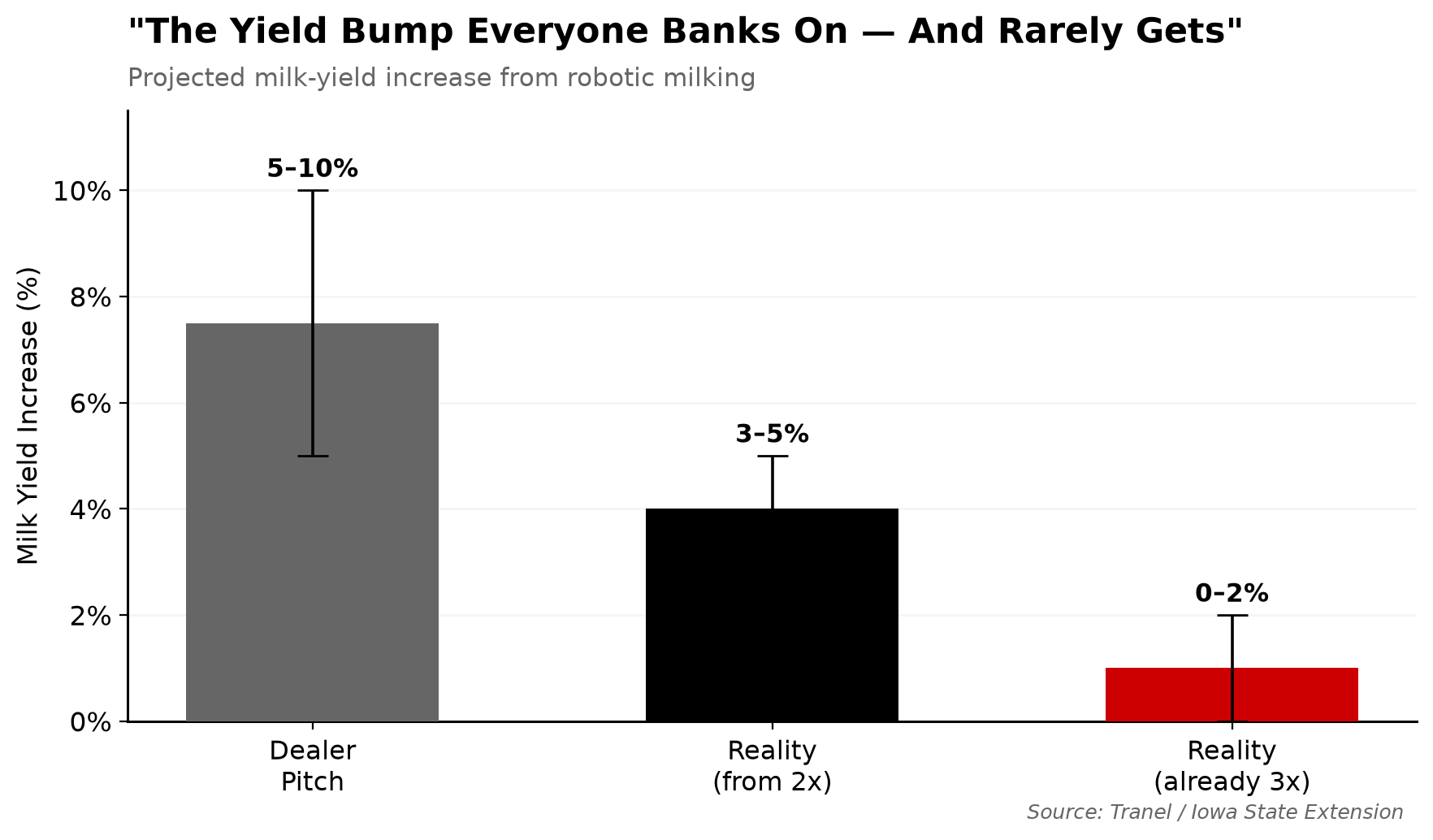

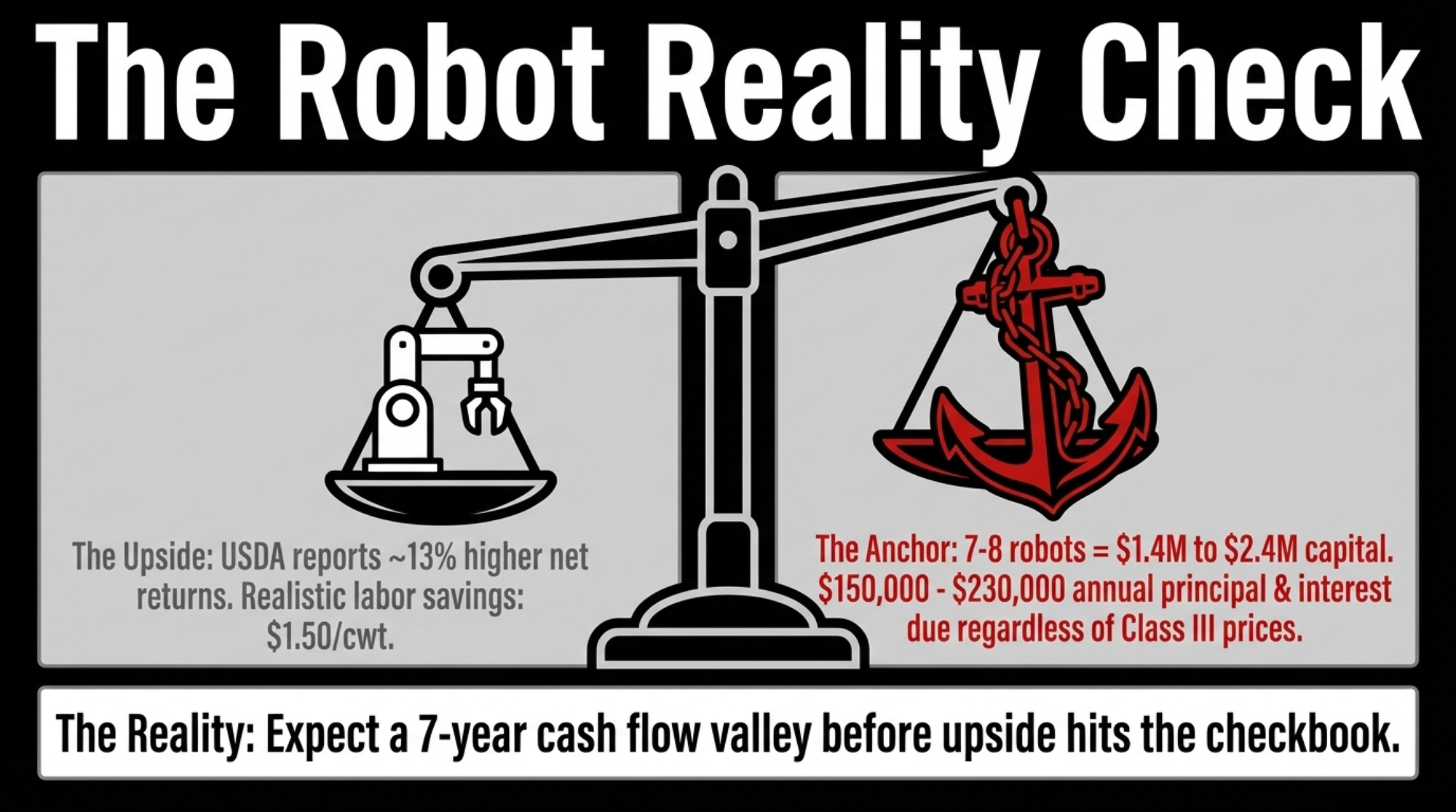

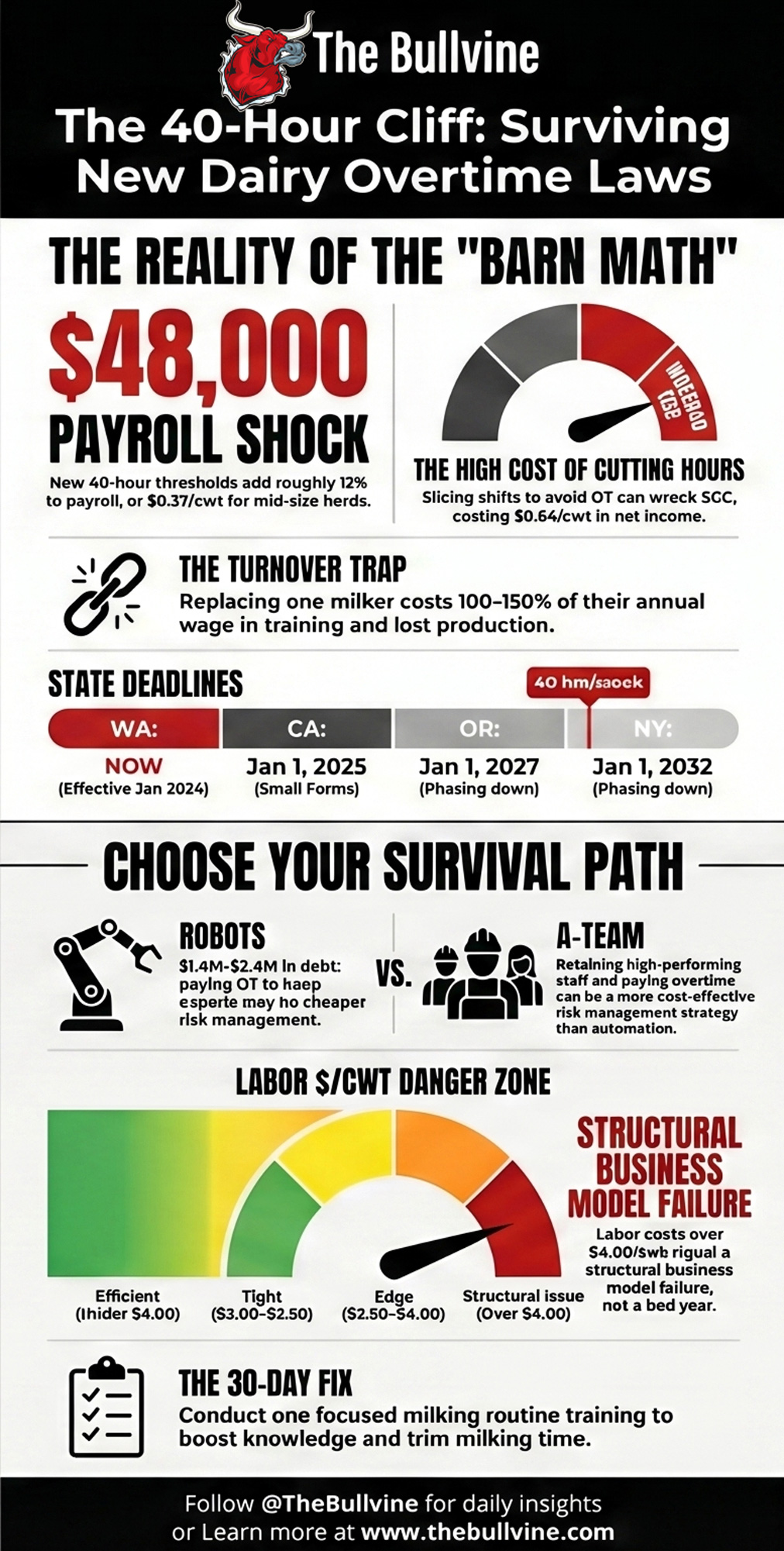

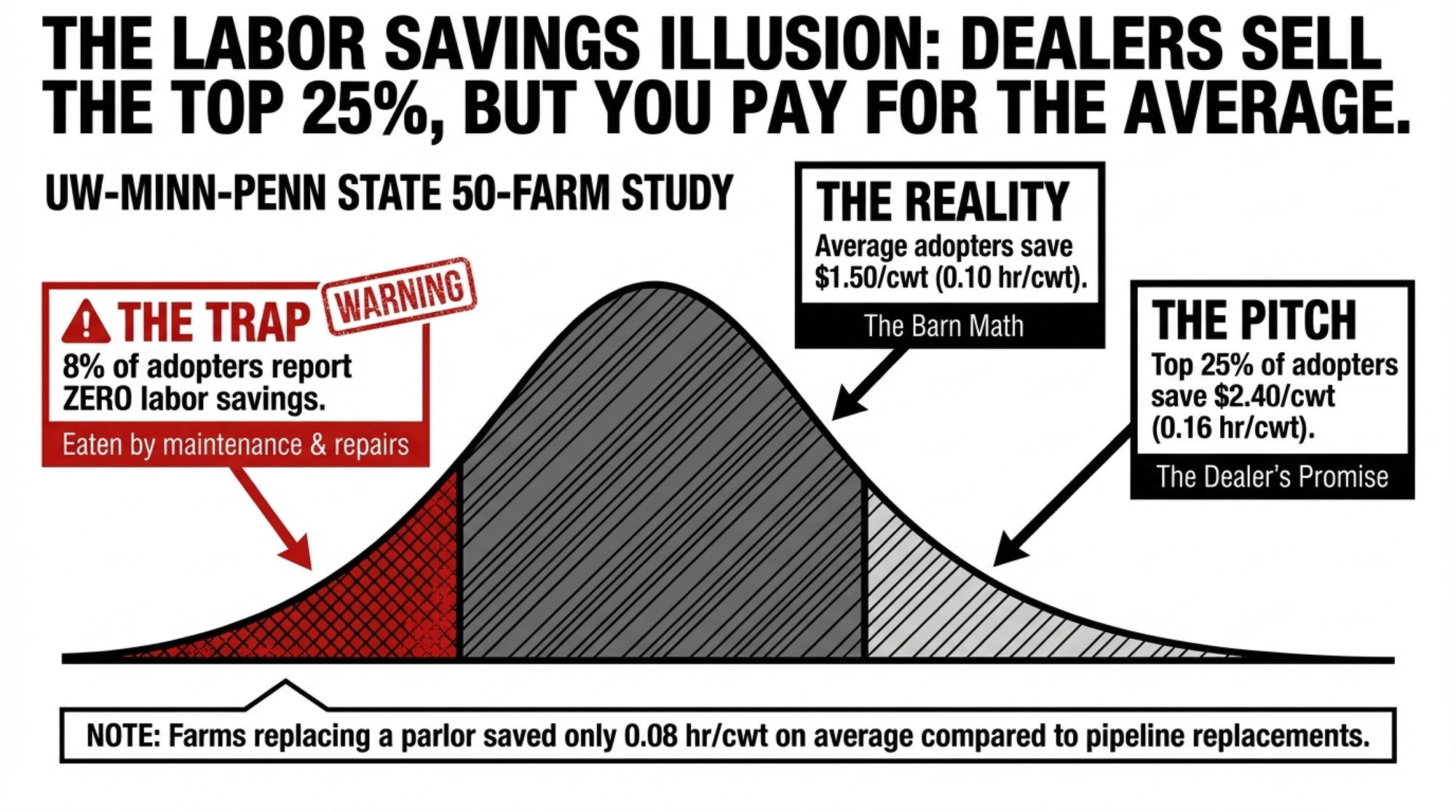

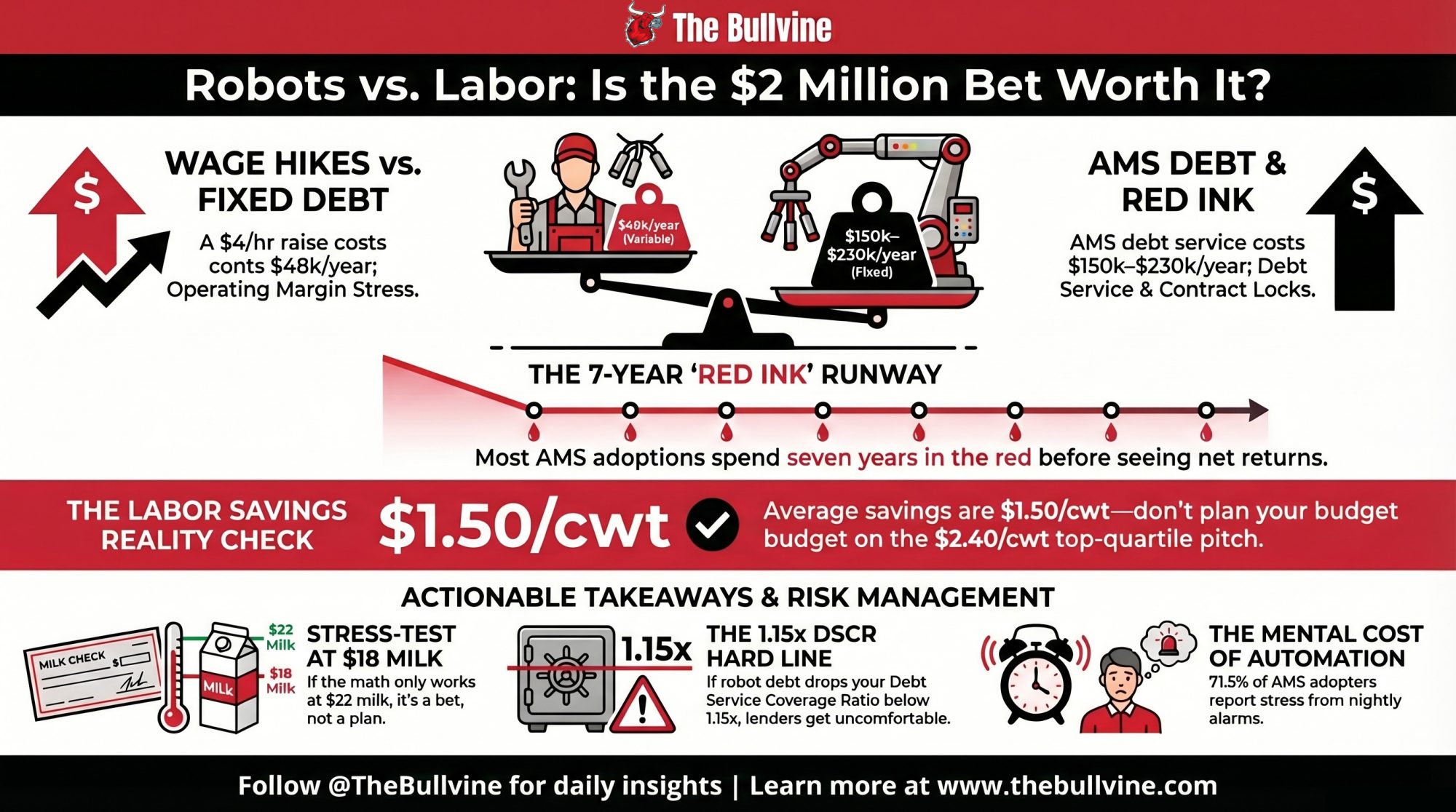

Robotic milking has stopped being exotic. USDA’s ERS reports box robots milked about 6% of U.S. milk by 2021, with the fastest uptake on 150‑to‑499‑cow farms. And the headline finding everyone repeats holds up: in ERS’s June 2026 analysis, robotic milking raised dairy net returns by $3.15/cwt on average, relative to non‑adopters.

That number’s real. It’s just shown at the wrong resolution. ERS measures it as an average across adopters — and the strongest returns lean toward larger, well‑utilized herds, not the 80‑to‑120‑cow place. The “ethical robot” dairy that keeps getting shared online sits on commodity milk, often with no premium channel at all. That average wasn’t built on farms like that one.

So the farms most exposed to the gap are exactly the ones the humane‑dairy story celebrates — small, family‑run, welfare‑forward, betting on robots to make the lifestyle last. They’re not wrong that robots improve daily life. They’re wrong if they assume the average return shows up on their balance sheet just because they bought the box.

How This Plays Out on Real Farms

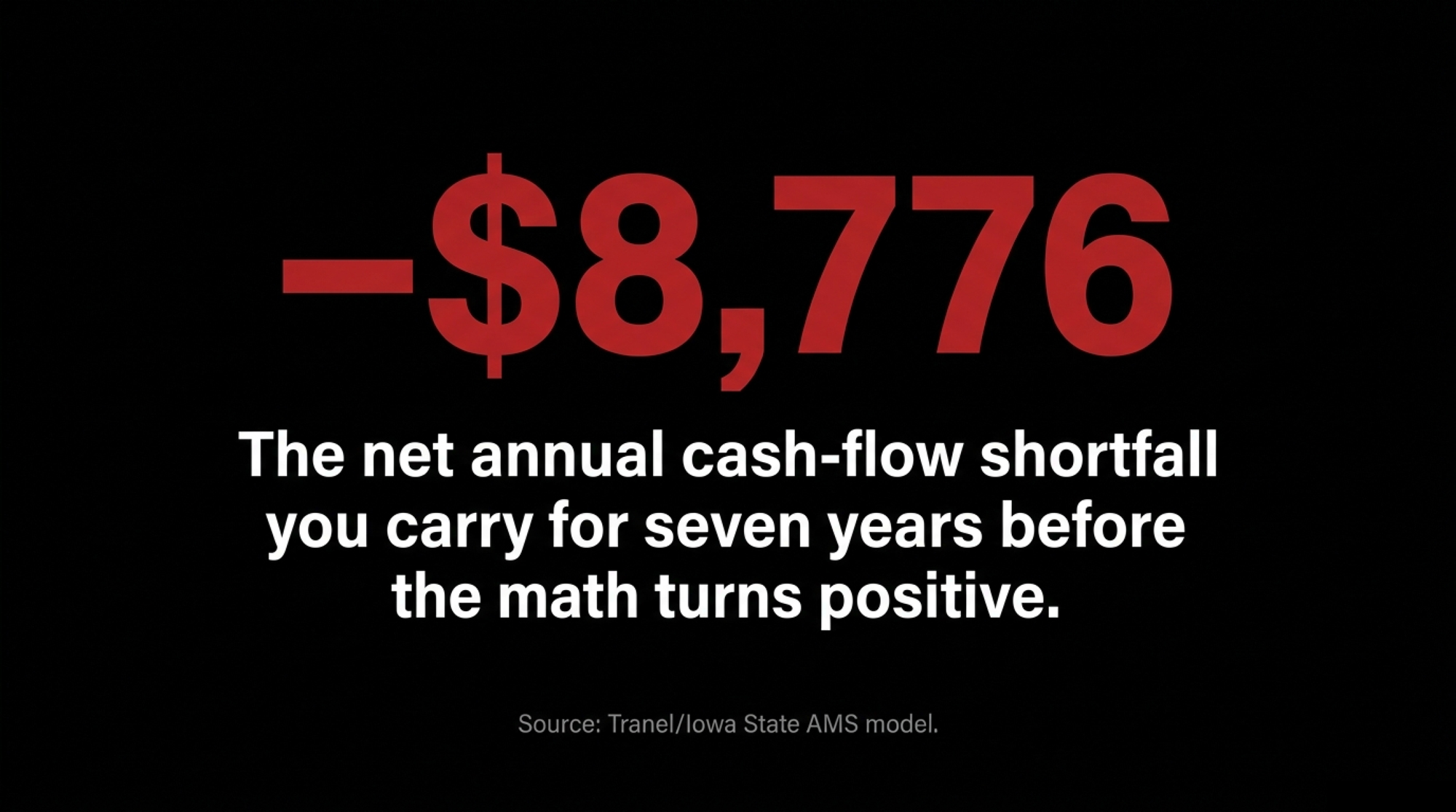

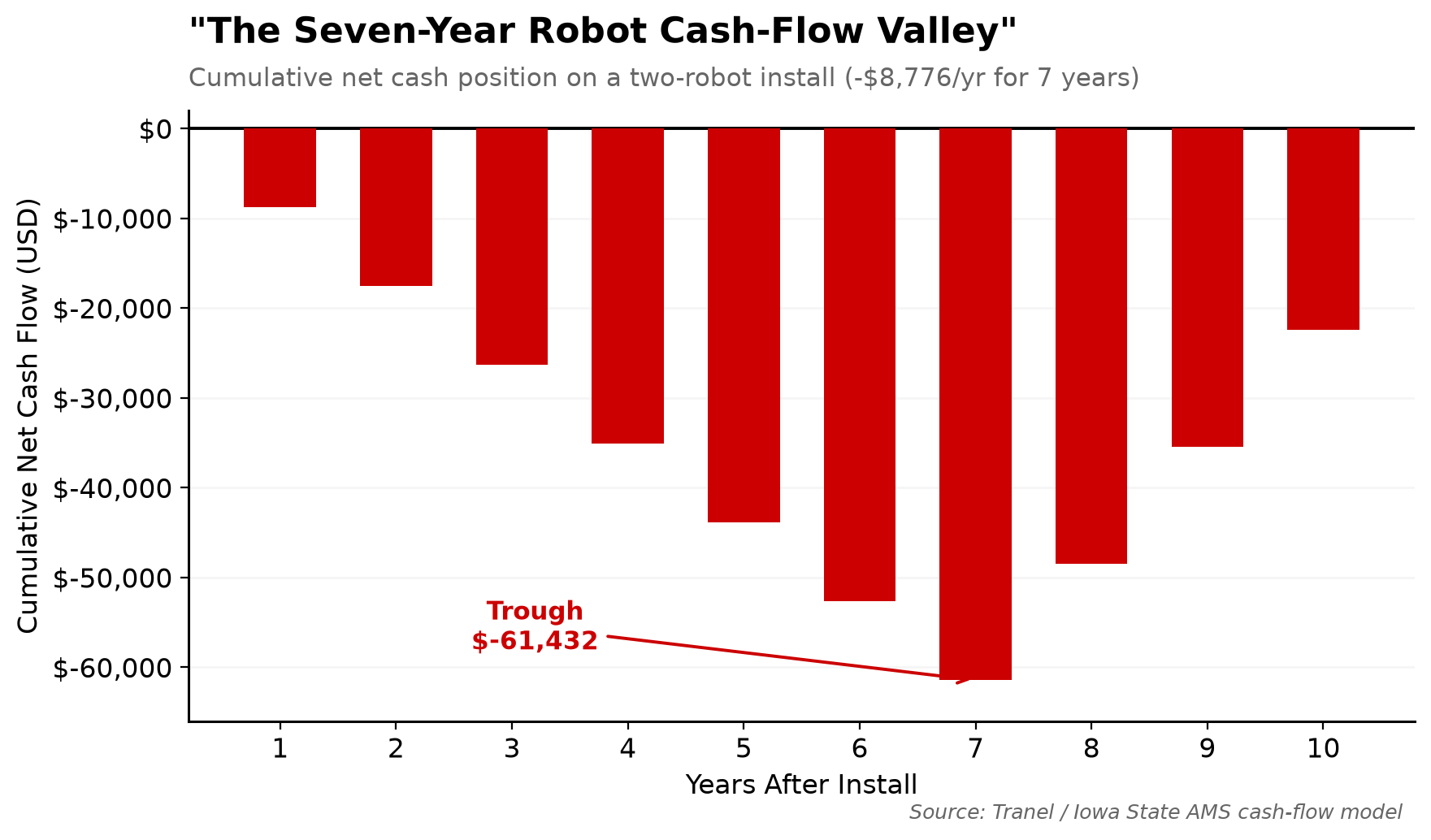

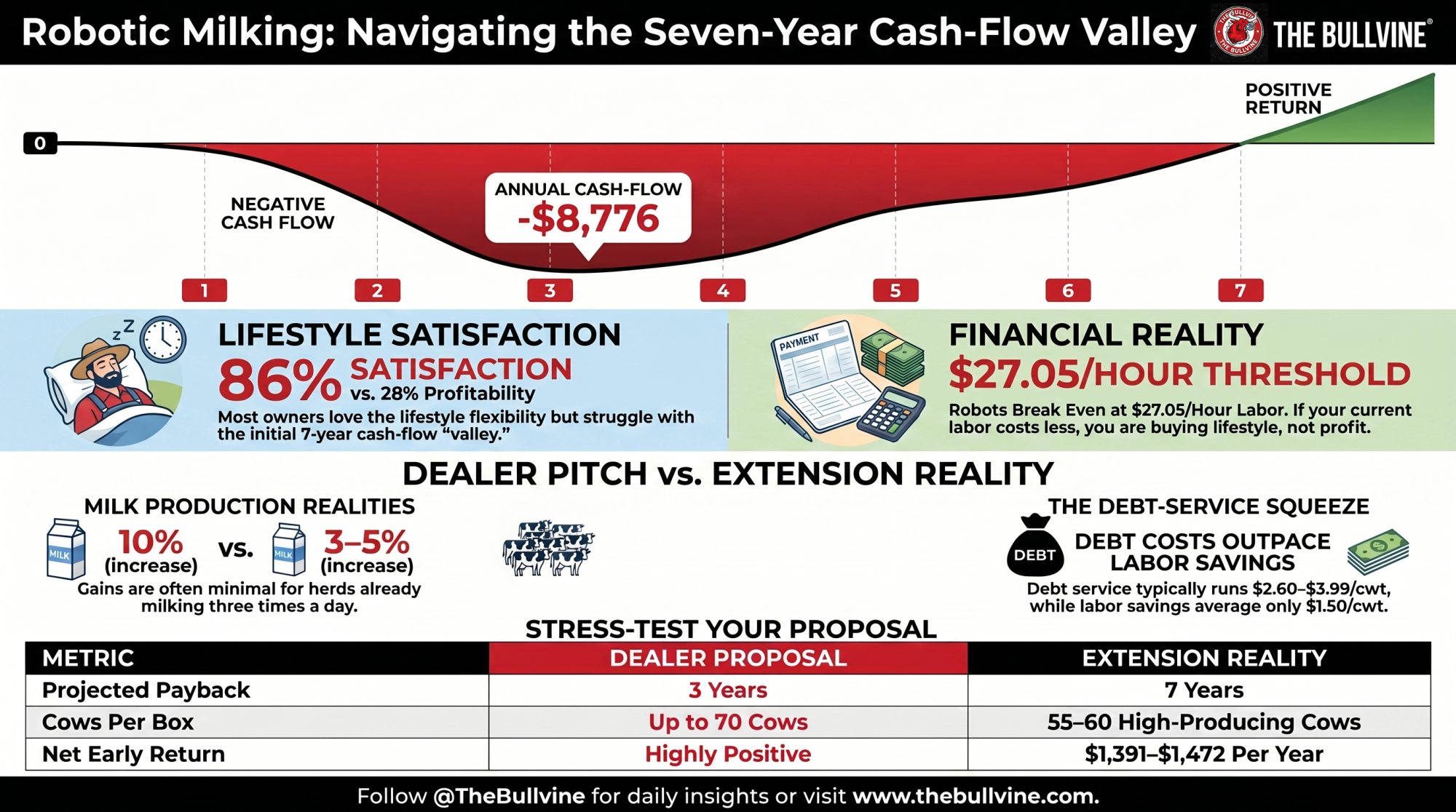

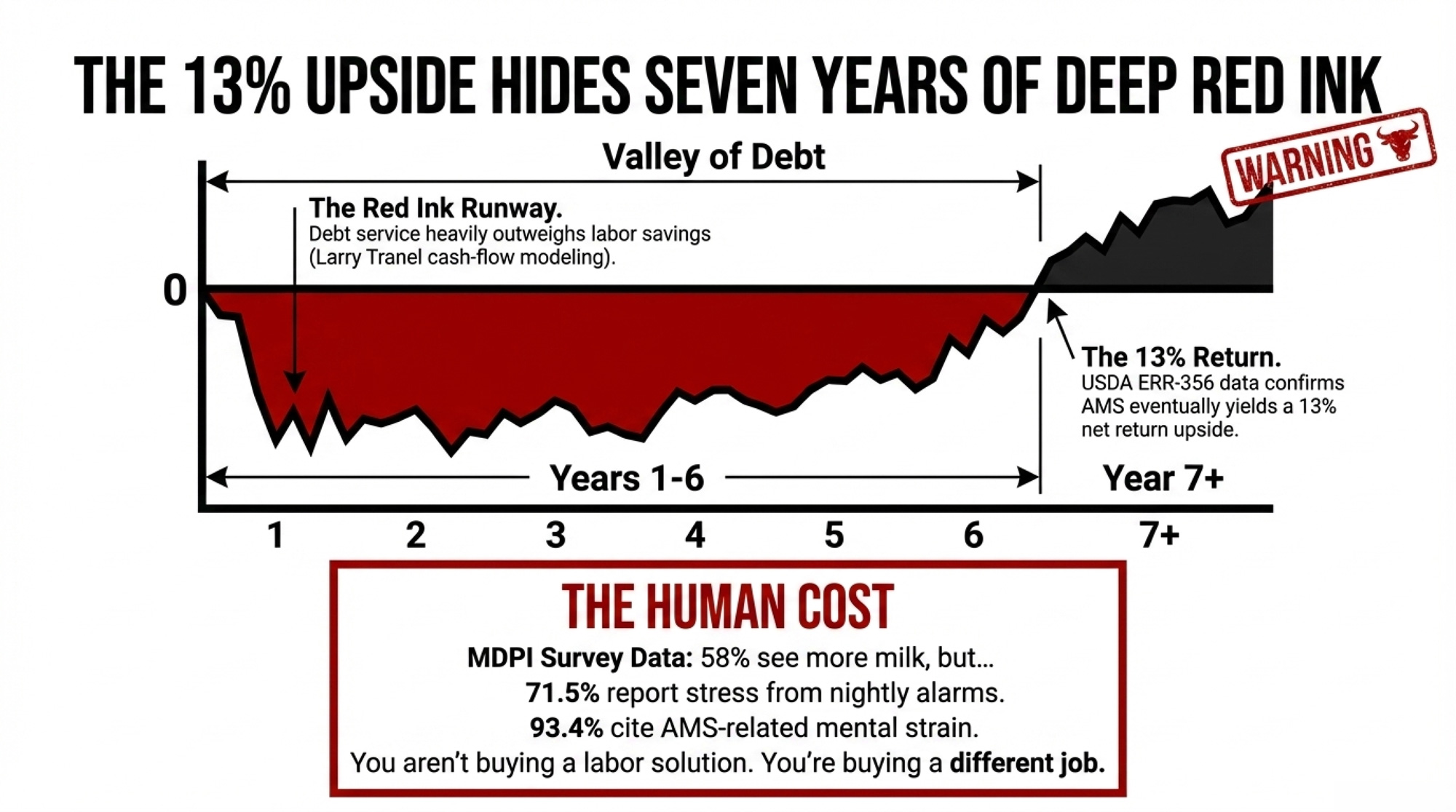

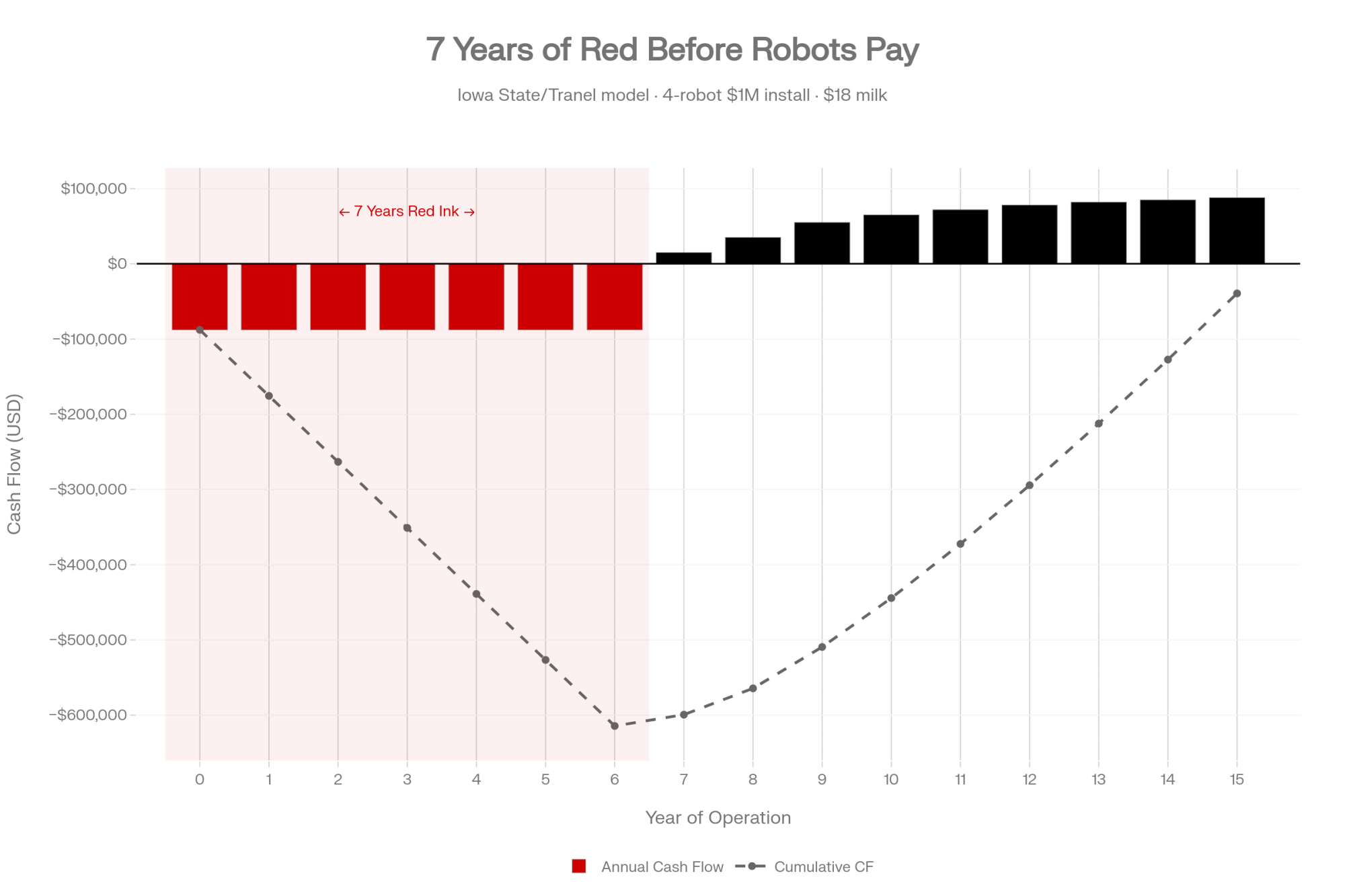

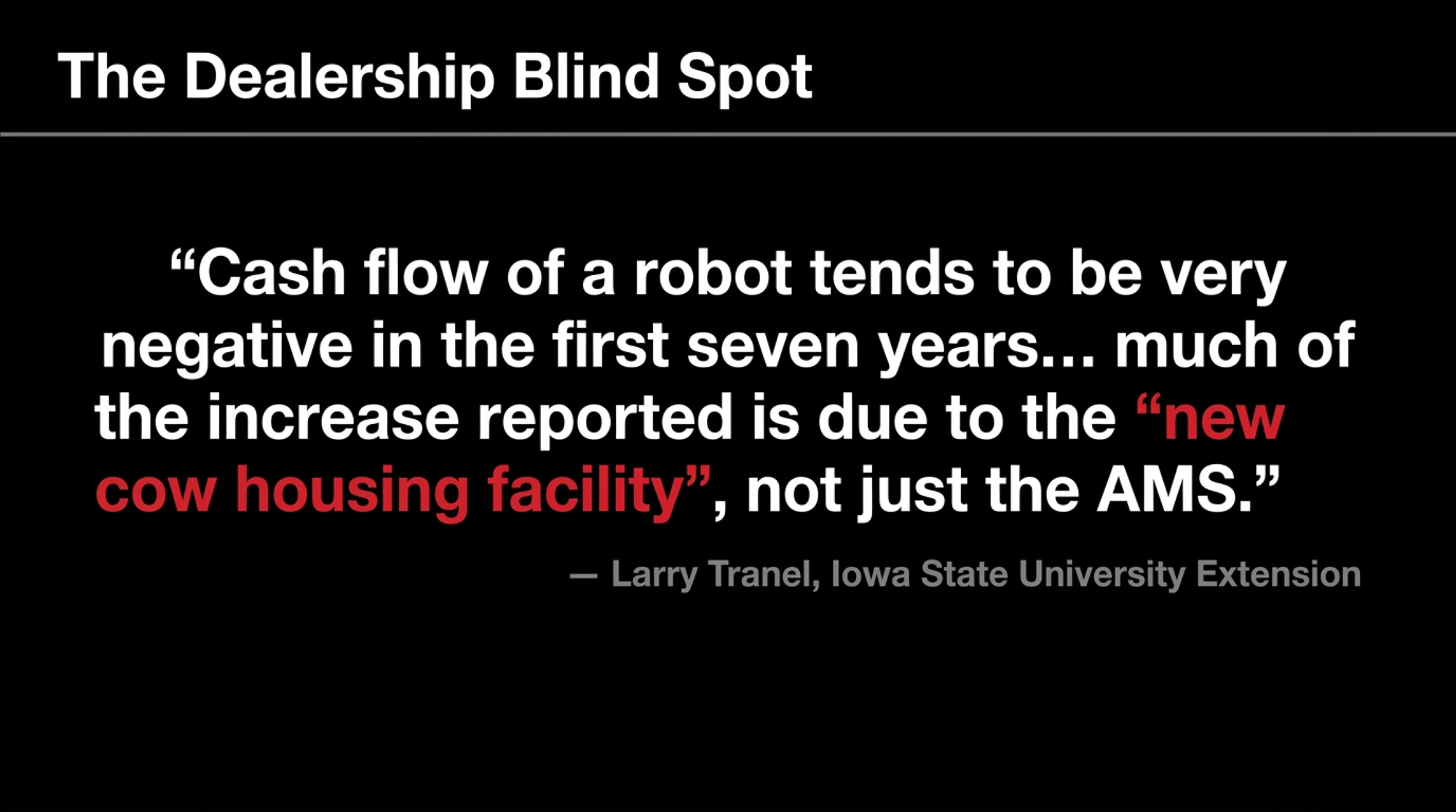

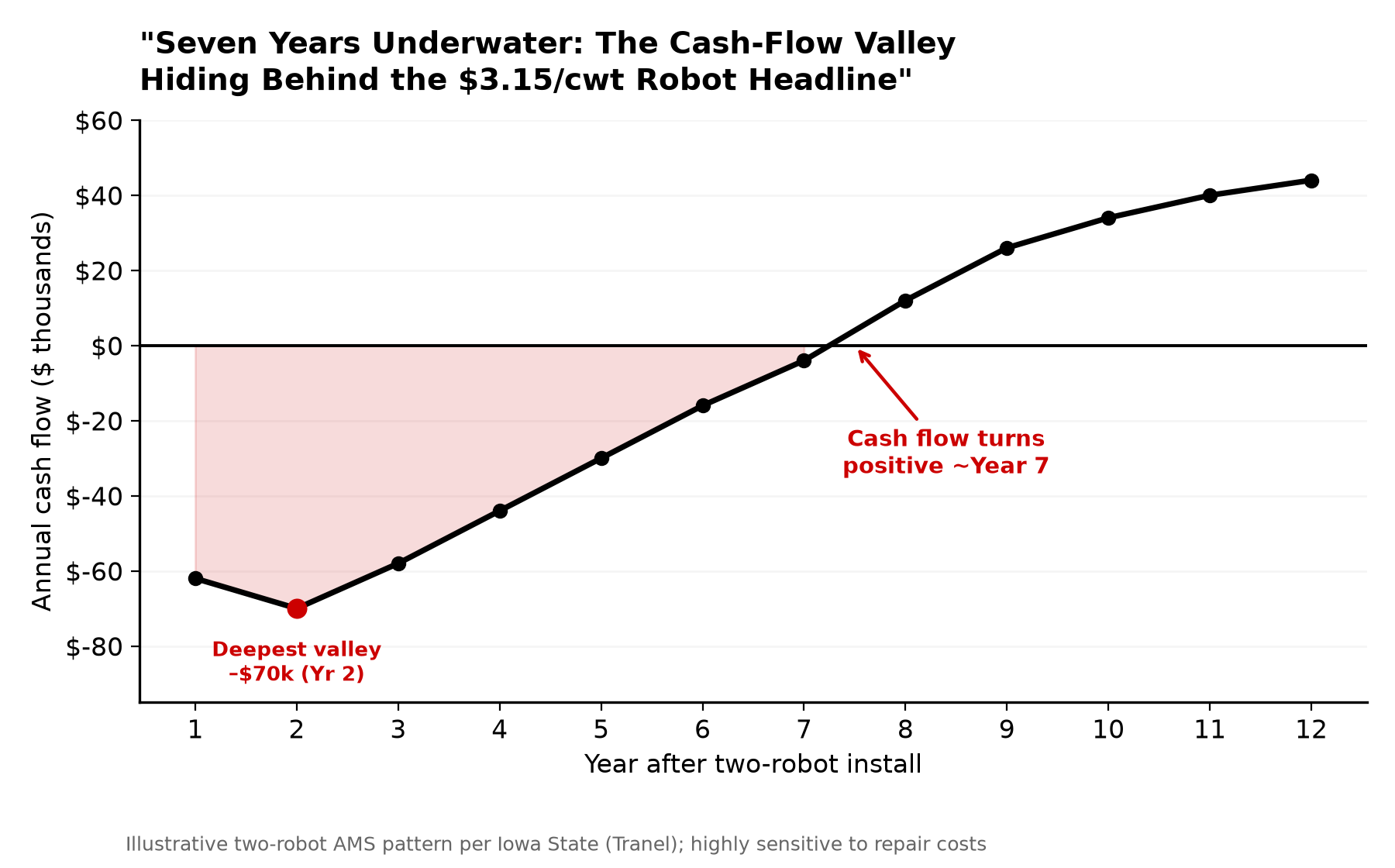

Iowa State extension economist Larry Tranel has run AMS cash flow for years, and his models tell the part the dealer’s payback chart skips.

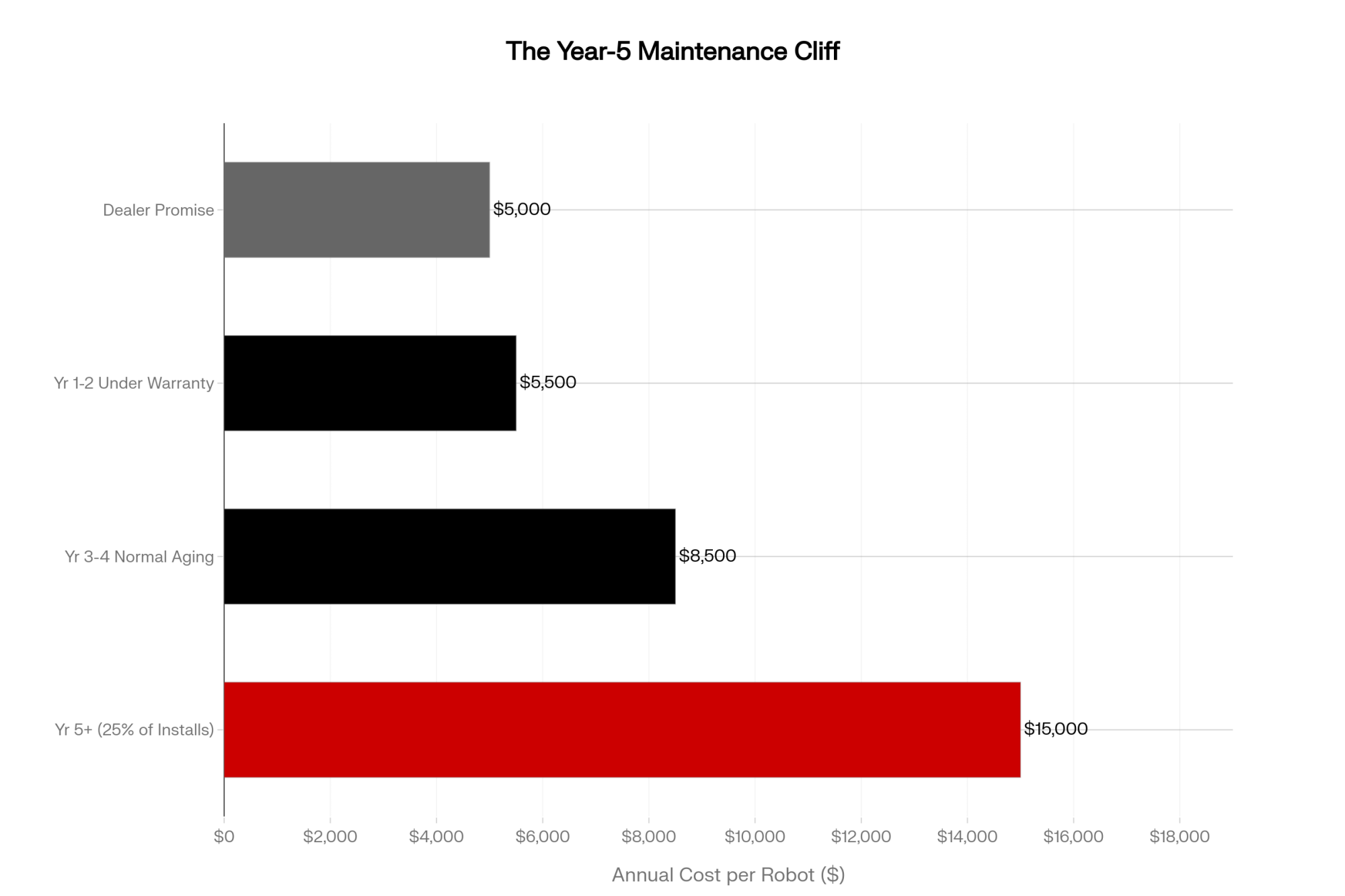

“Cash flow of a robot tends to be very negative in the first seven years, then pretty positive for the rest of the life of the AMS — but that is dependent on many variables, especially repair costs across the whole life of the robot.” — Larry Tranel, Iowa State University Extension.

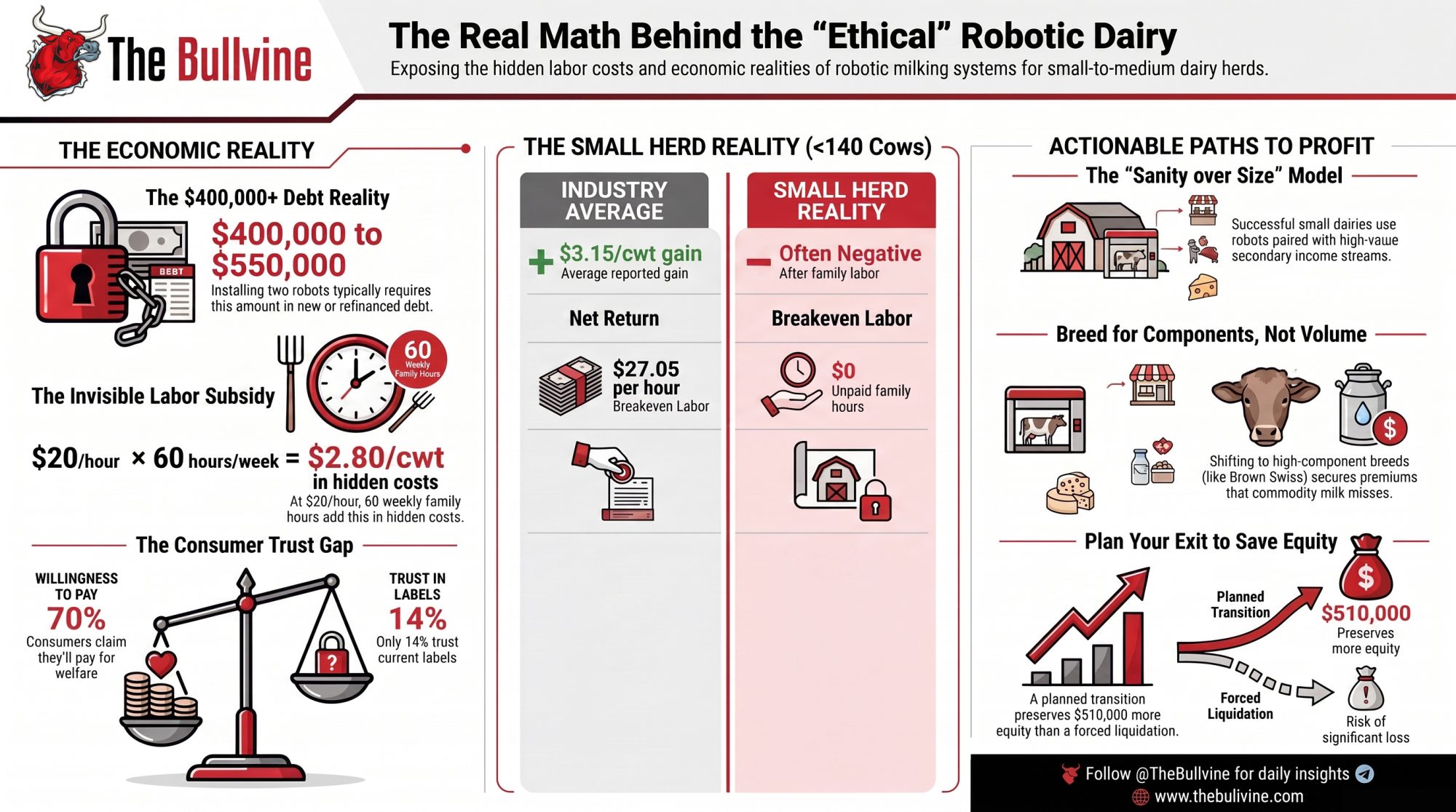

Two robots plus barn work routinely lands a family $400,000 to $550,000 in new or refinanced debt. And there’s a trap hiding inside the production bump. Tranel warns that “much of the increase reported on AMS is due to the new cow housing facility, not just the AMS, as new facilities often increase production 6 to 8 percent over old, worn‑out facilities.” In plain terms: families credit the robot for gains the new barn delivered, then build their projections on repeating them.

Smaller robot stories can work — but rarely on the dairy alone. The ones that hold together almost always have a second income stream quietly carrying the cash‑flow valley. Marcus and Paige Dueck of Four Oak Farms near Kleefeld, Manitoba are the cleanest example you’ll find. When Western Canada’s first rail‑mounted Robomax milker rolled into their old tie‑stall barn in July 2020, it wasn’t a freedom play — it was a math problem. “My parents were looking to slow down their involvement in the barn, we had a new baby, and we had to make a decision,” Marcus told Farm Forum. “Expanding just wasn’t a financially feasible option.”

Notice what they didn’t do. They didn’t scale up to chase the robot’s economics — they kept a herd of about 50 cows and changed almost everything else. They swapped Holsteins for Brown Swiss, betting on temperament and component premiums over volume. “You don’t need more cows,” Marcus says. “You just need the right cows — ones that make milk that pays better.” Production per cow climbed roughly 40% over five years, driven by a shift to three‑times‑a‑day milking and cow‑level data — not more animals.

The dairy alone still wouldn’t carry it, and the Duecks are blunt about that. Half their roughly 900 acres goes to a high‑value hay business aimed at performance‑horse owners across Canada and the U.S., built around a German composite baler nobody else in their market runs. The other half is cash crop. On top of that sits Four Oak Ag Solutions, a manure‑and‑nutrient consulting firm Marcus grew from helping one neighbor with a manure plan. “In dairy, you can’t have all your eggs, or your milk, in one basket anymore,” he says. That diversification — not the robot — is what makes a 50‑cow operation work. It earned them Manitoba’s 2024 Outstanding Young Farmers title and a philosophy worth stealing: “We see a lot of farms chasing size, not sanity,” Paige says. “You can scale without losing peace.” Their model is the exception that proves the rule — robots fit inside a diversified business; they don’t rescue a bare commodity dairy.

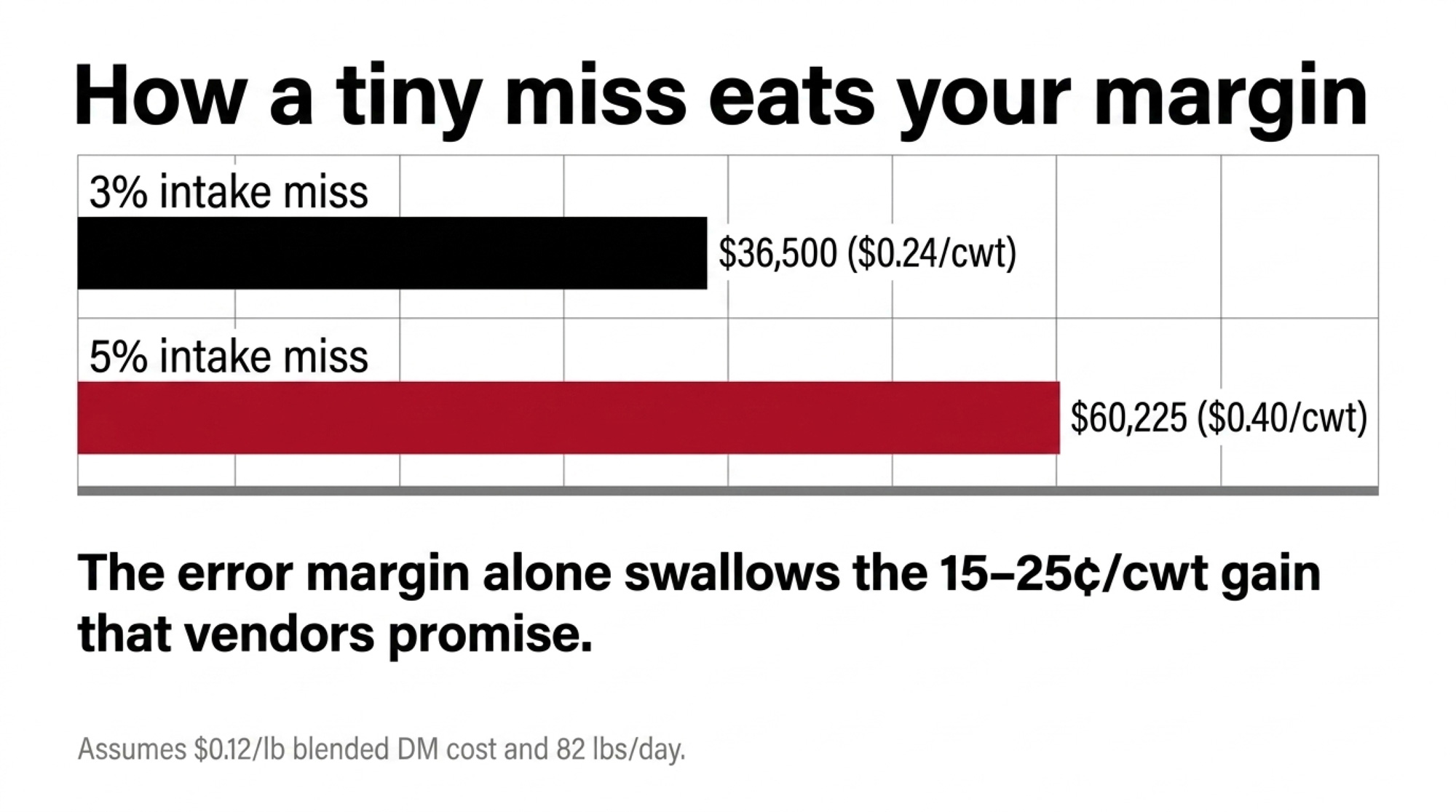

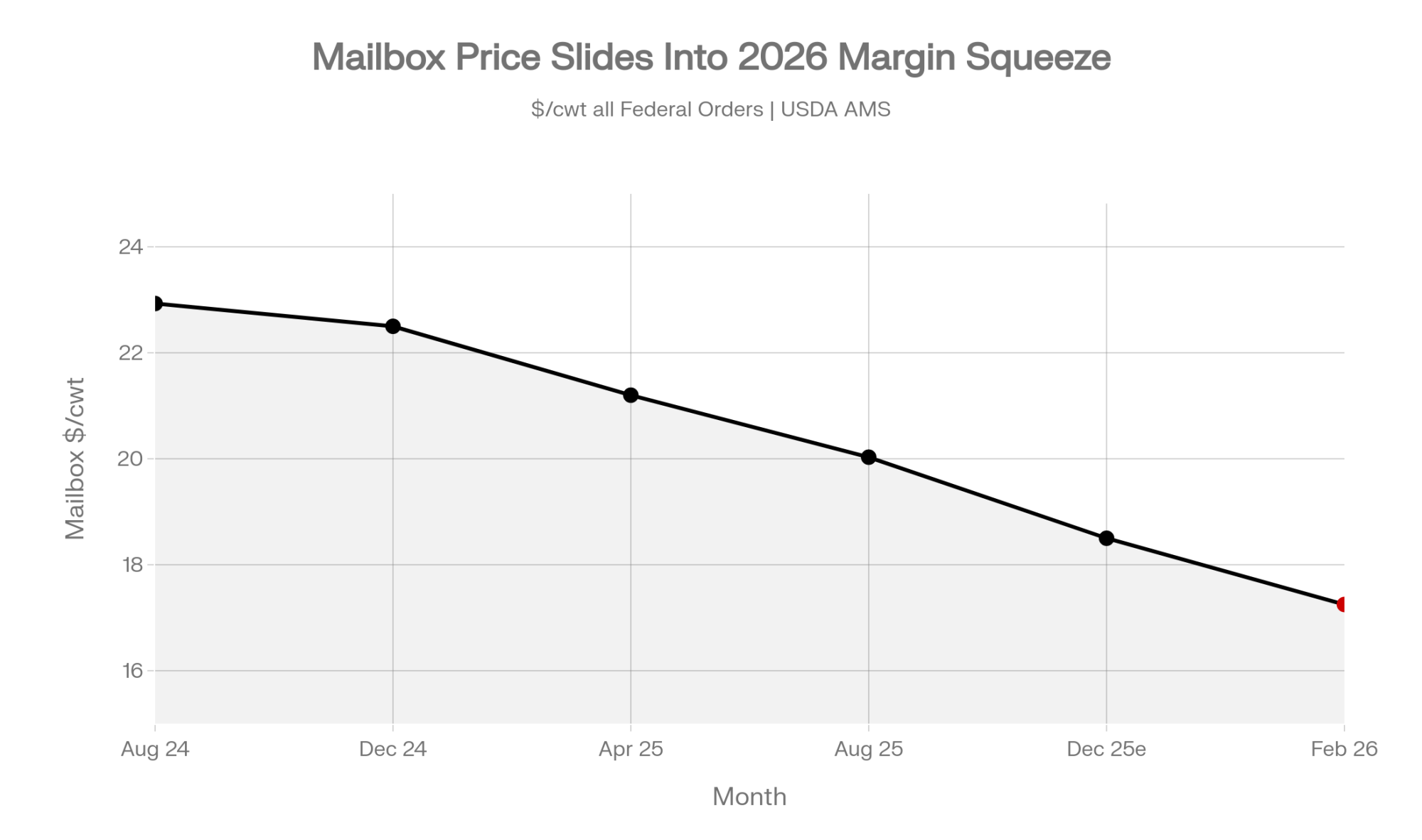

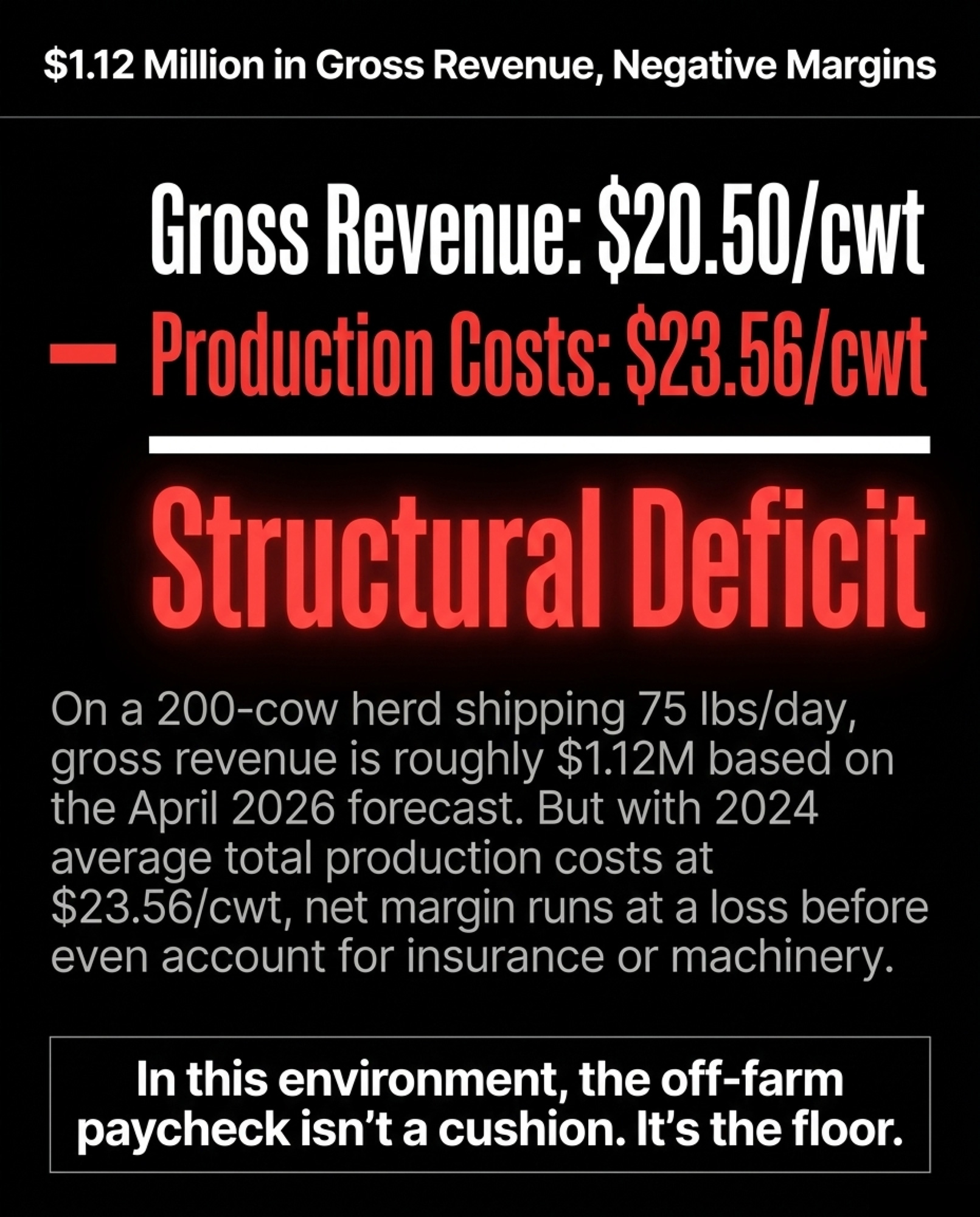

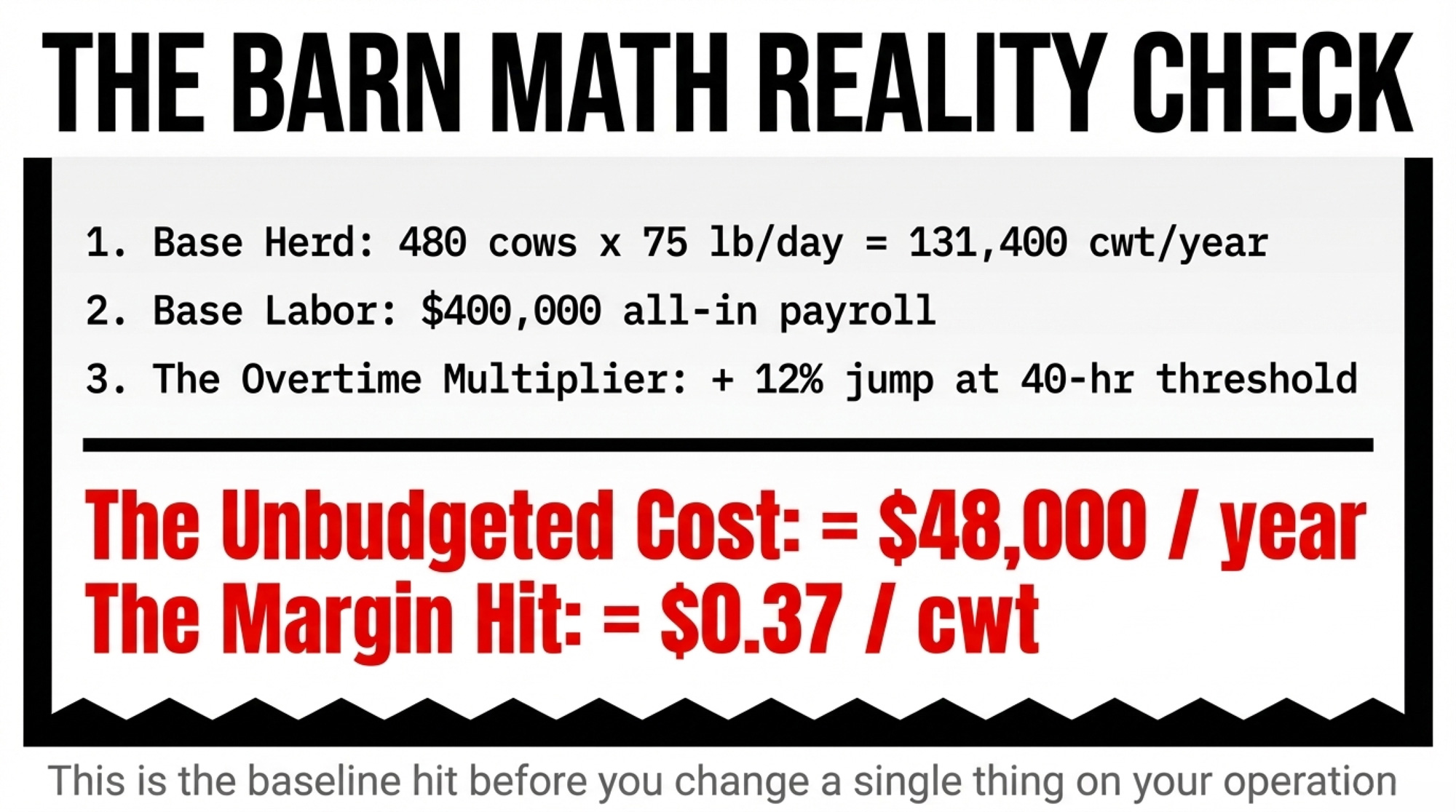

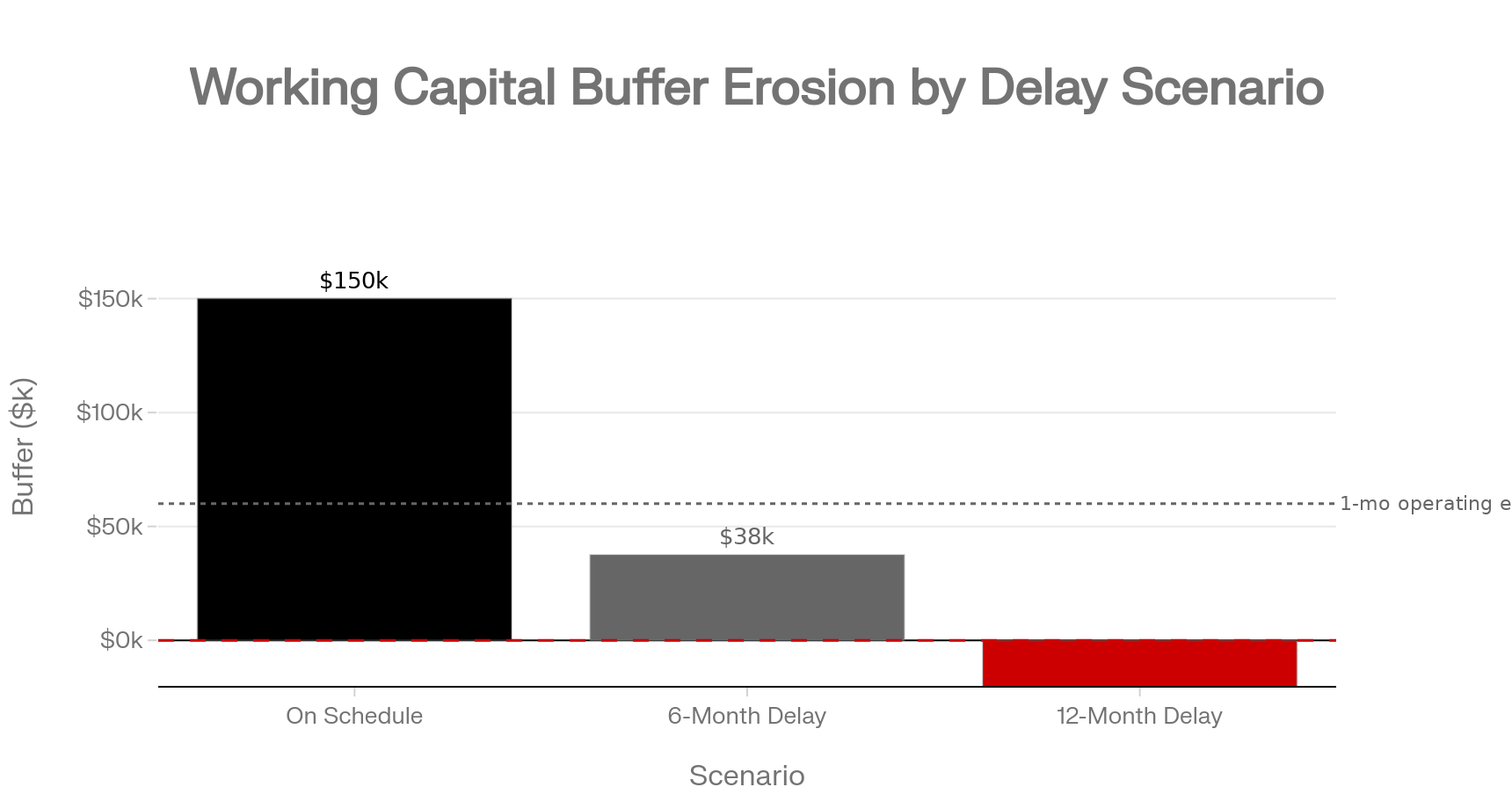

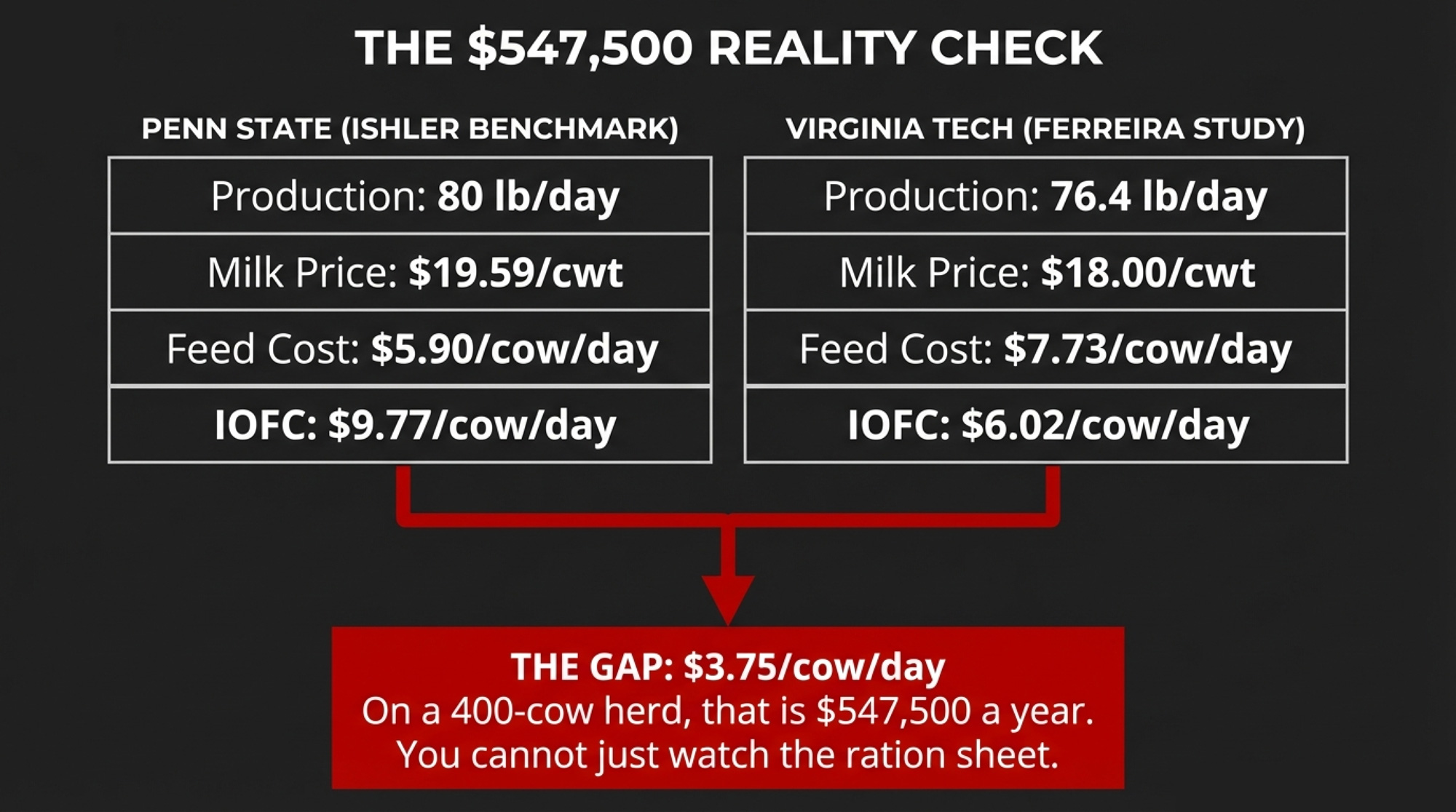

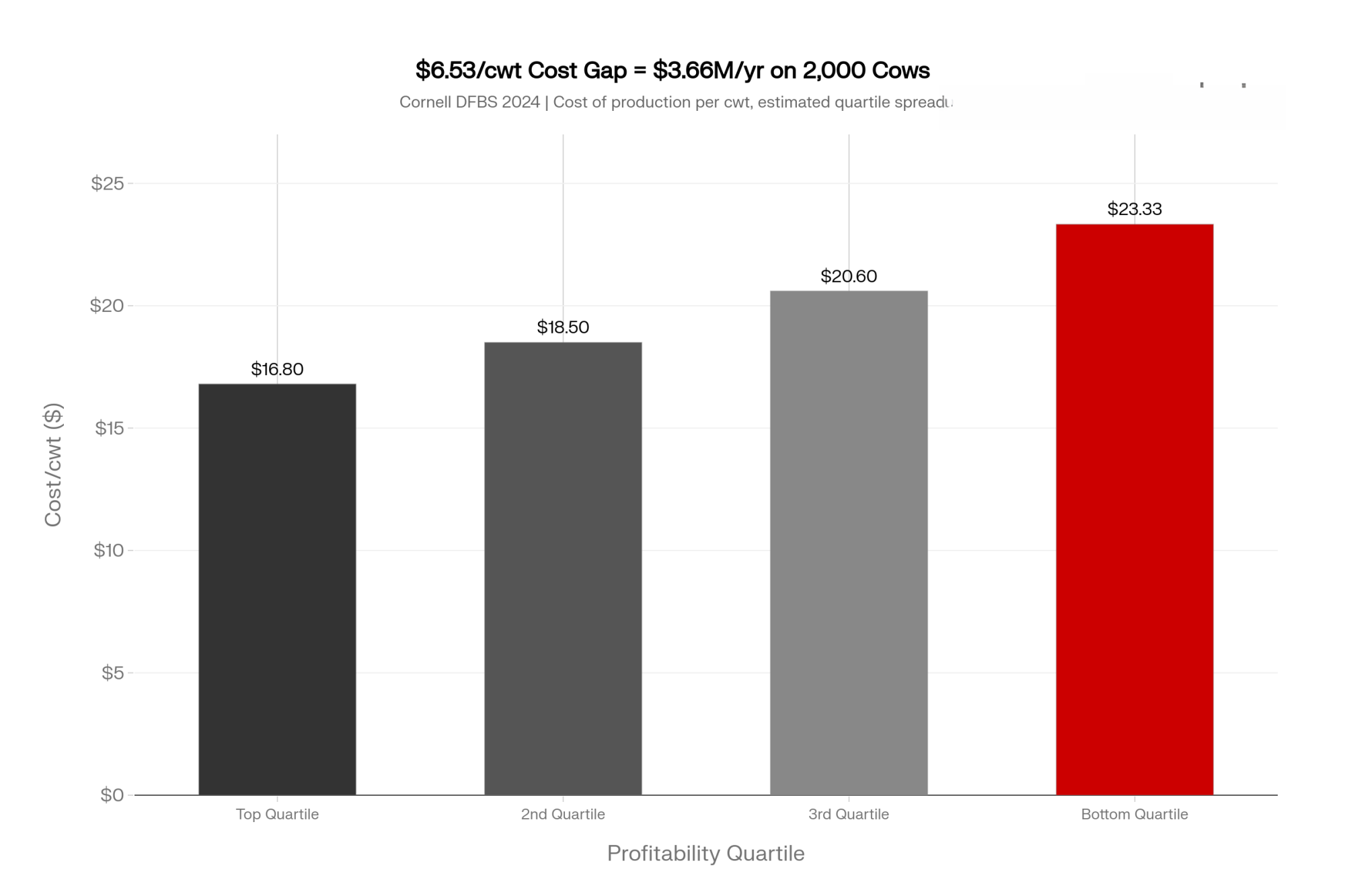

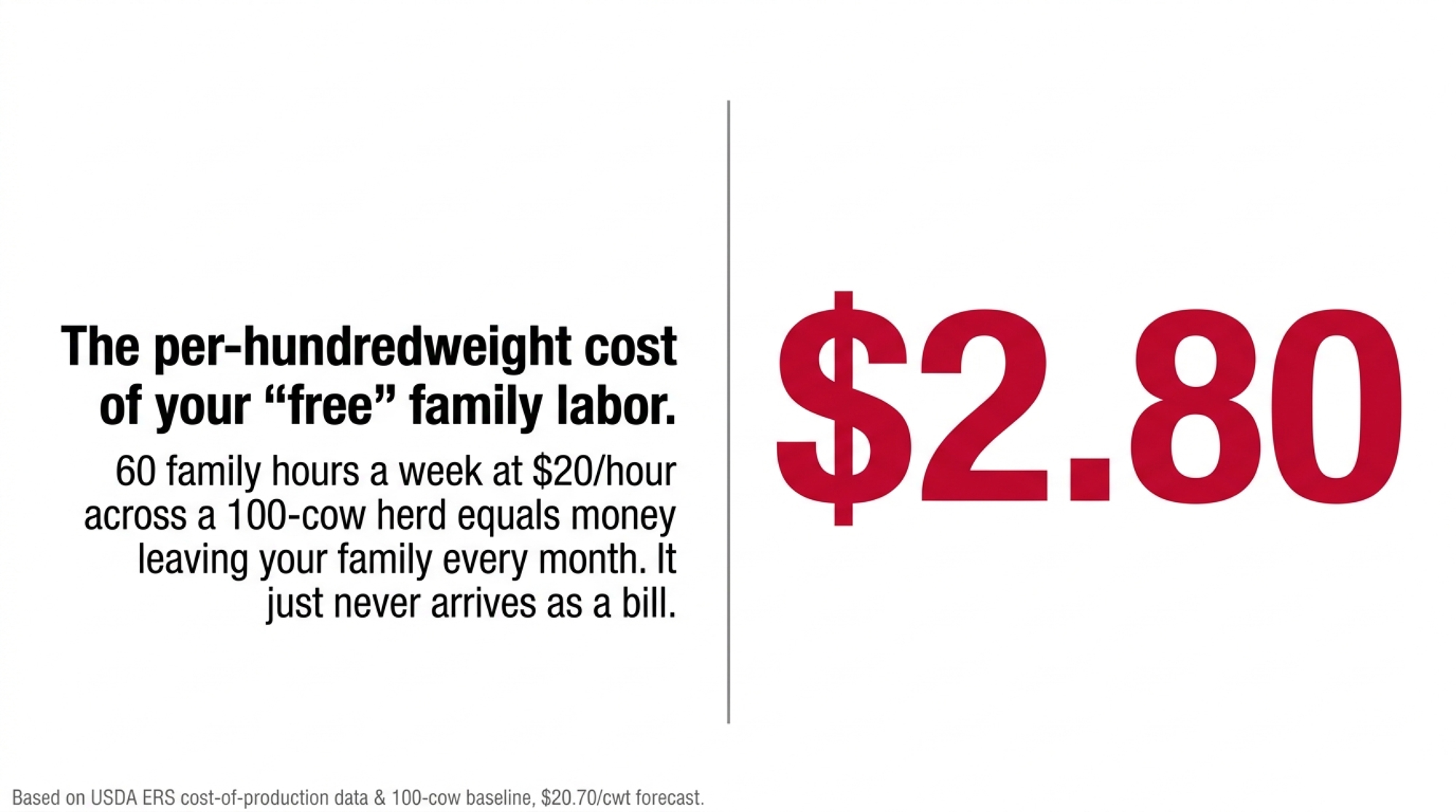

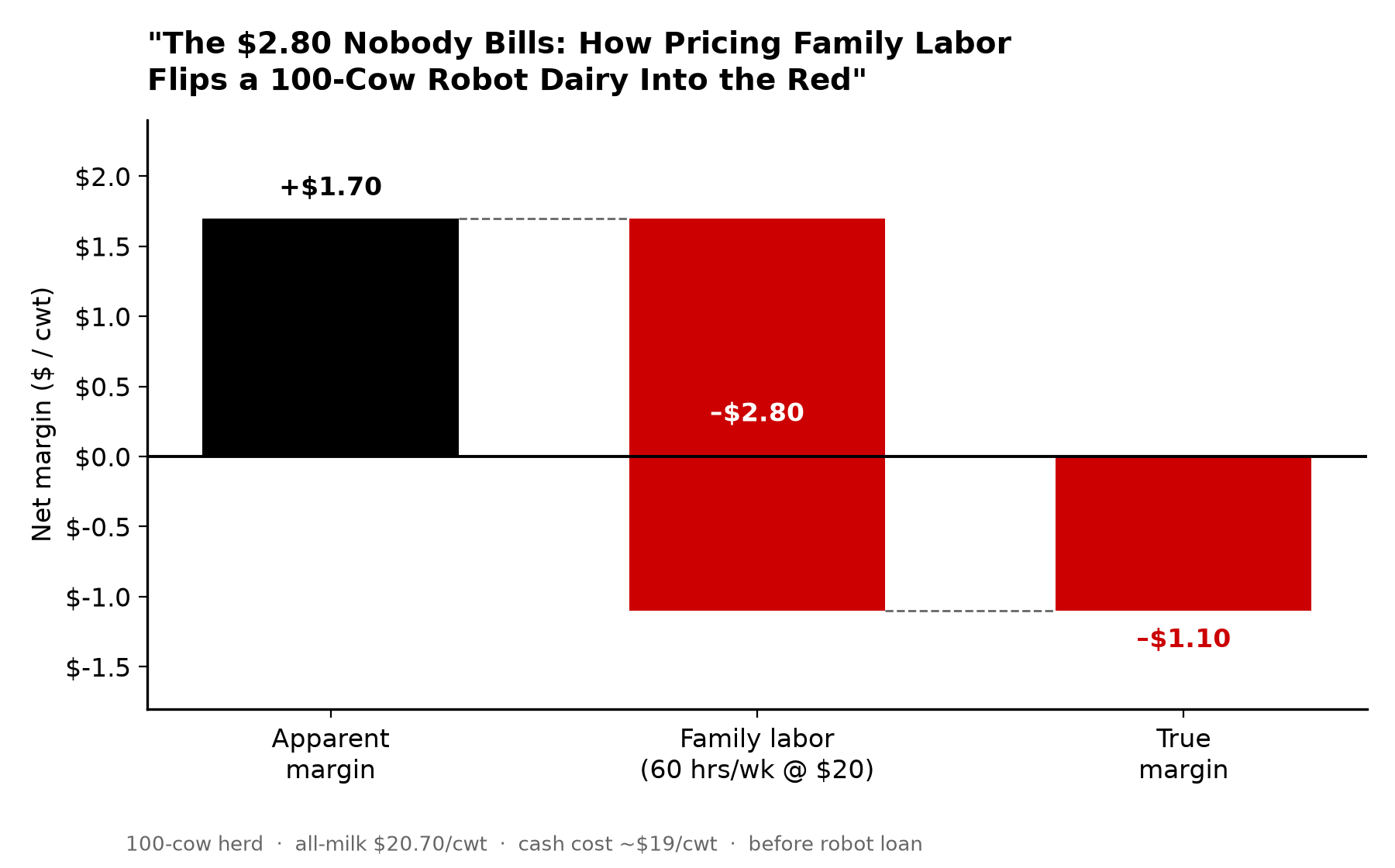

Now the micro barn‑math that should stop the room cold. USDA lowered its 2026 all‑milk forecast by 55 cents in June to $20.70/cwt, and the market’s still drifting. Say your 100‑cow place runs cash costs near $19/cwt and looks like it’s clearing a couple of dollars. Then you price the family hours honestly.

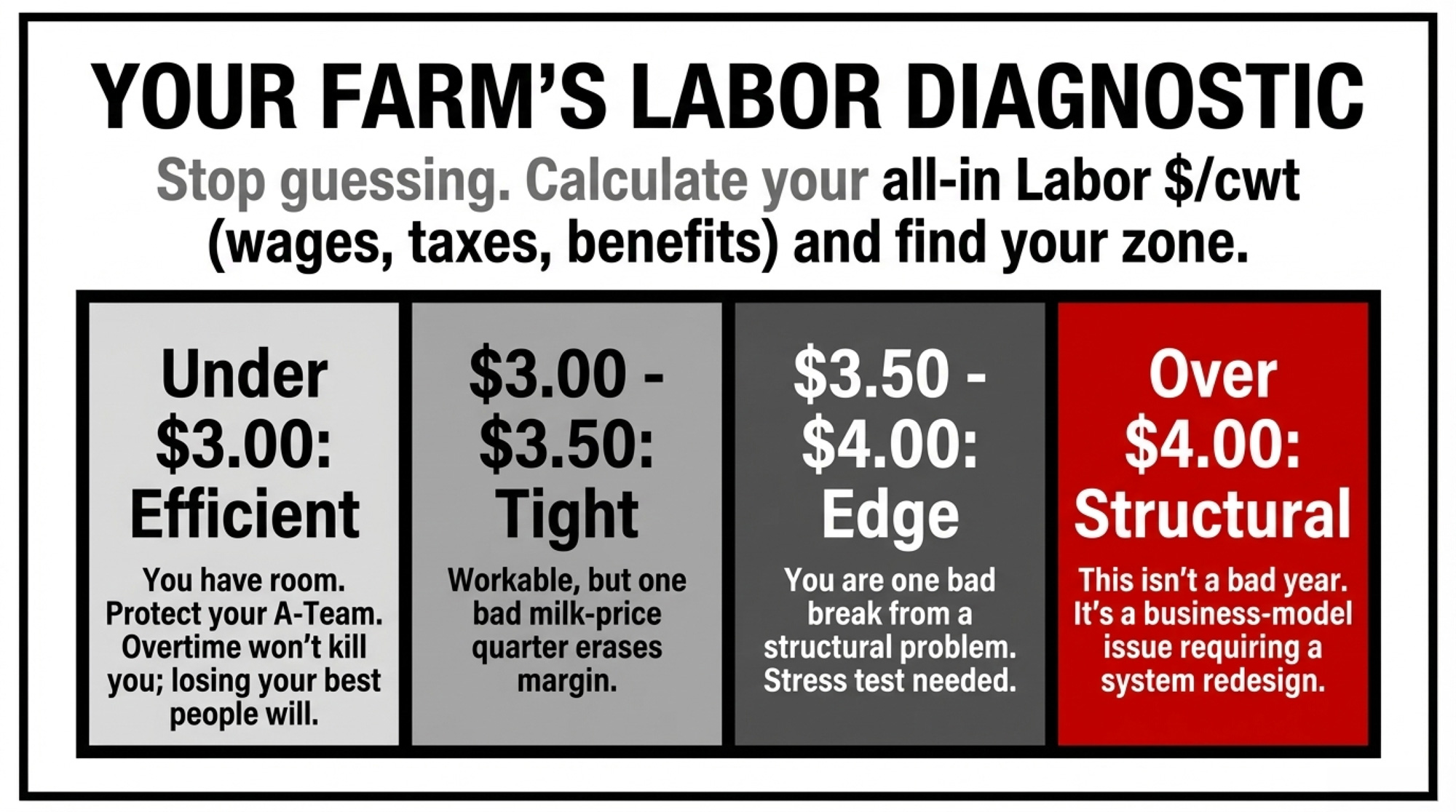

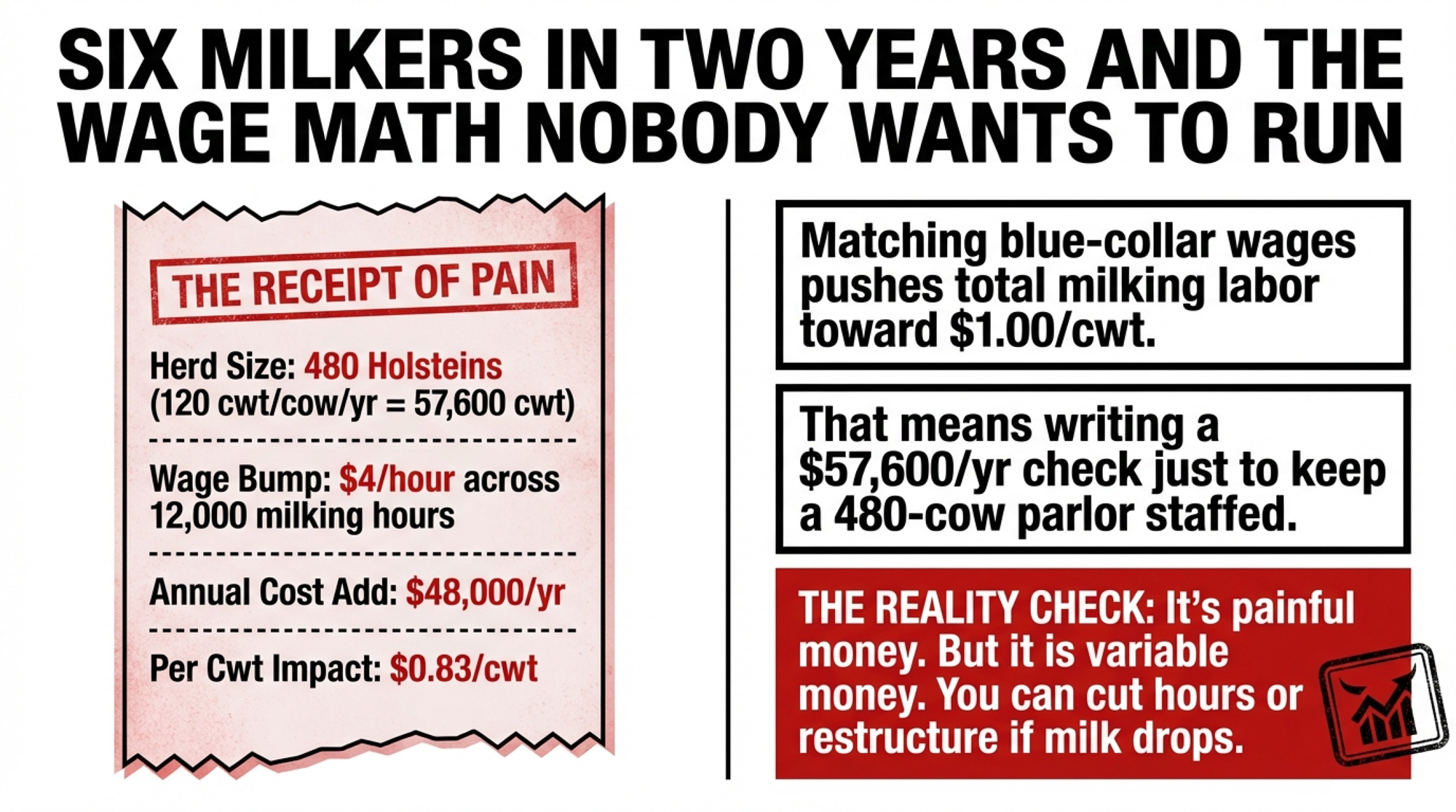

Run your own version: 60 family hours a week at $20/hour is about $62,400 a year — spread across roughly 2.2 million lbs of milk, that’s near $2.80/cwt you’re absorbing before you’ve paid a robot loan. ERS’s own cost‑of‑production work shows the smallest herds carry the heaviest labor load per hundredweight, much of it unpaid family time. Add that real labor bill back, and a comfortable‑looking margin can flip negative in a hurry. On 100 cows, that’s money leaving the family every month. It just never arrives as a bill.

The Mechanics Behind the Outcomes

Three hidden subsidies make the ethical robot story pencil on paper. None of them show up in the brochure, and all of them are load‑bearing.

| Hidden Subsidy | Who Pays It | What The Data Says |

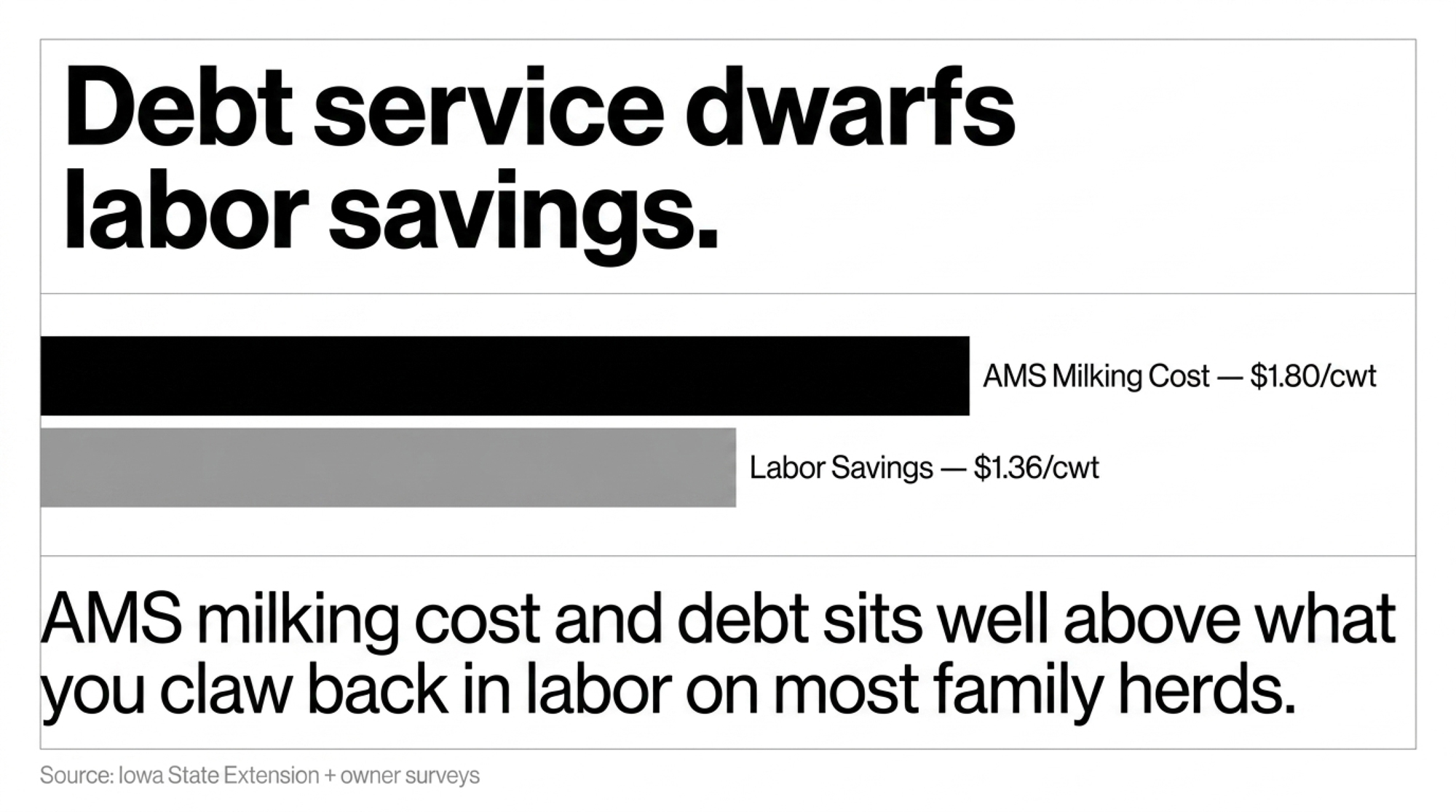

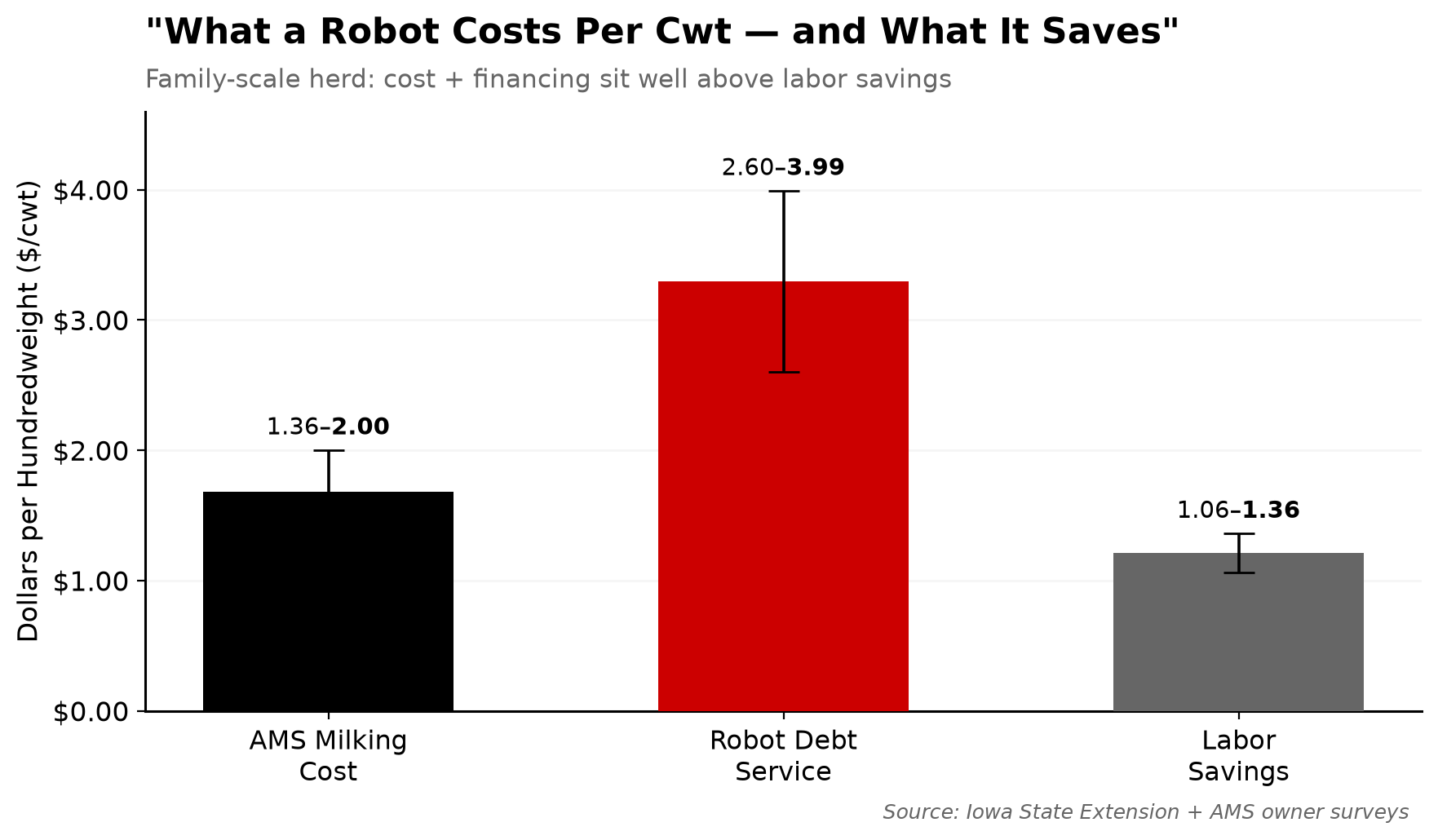

| Unpaid family labor | Mom, the kid, the farmer at hour 14 | Robots cut milking labor 21%+, but U. of Minnesota found robot herds less profitable per cow — the edge only appears per full-time worker |

| Paid-off land / off-farm income | The second business or the mortgage-free balance sheet | Four Oak Farms carries the cash-flow valley on hay + consulting income — not the robot |

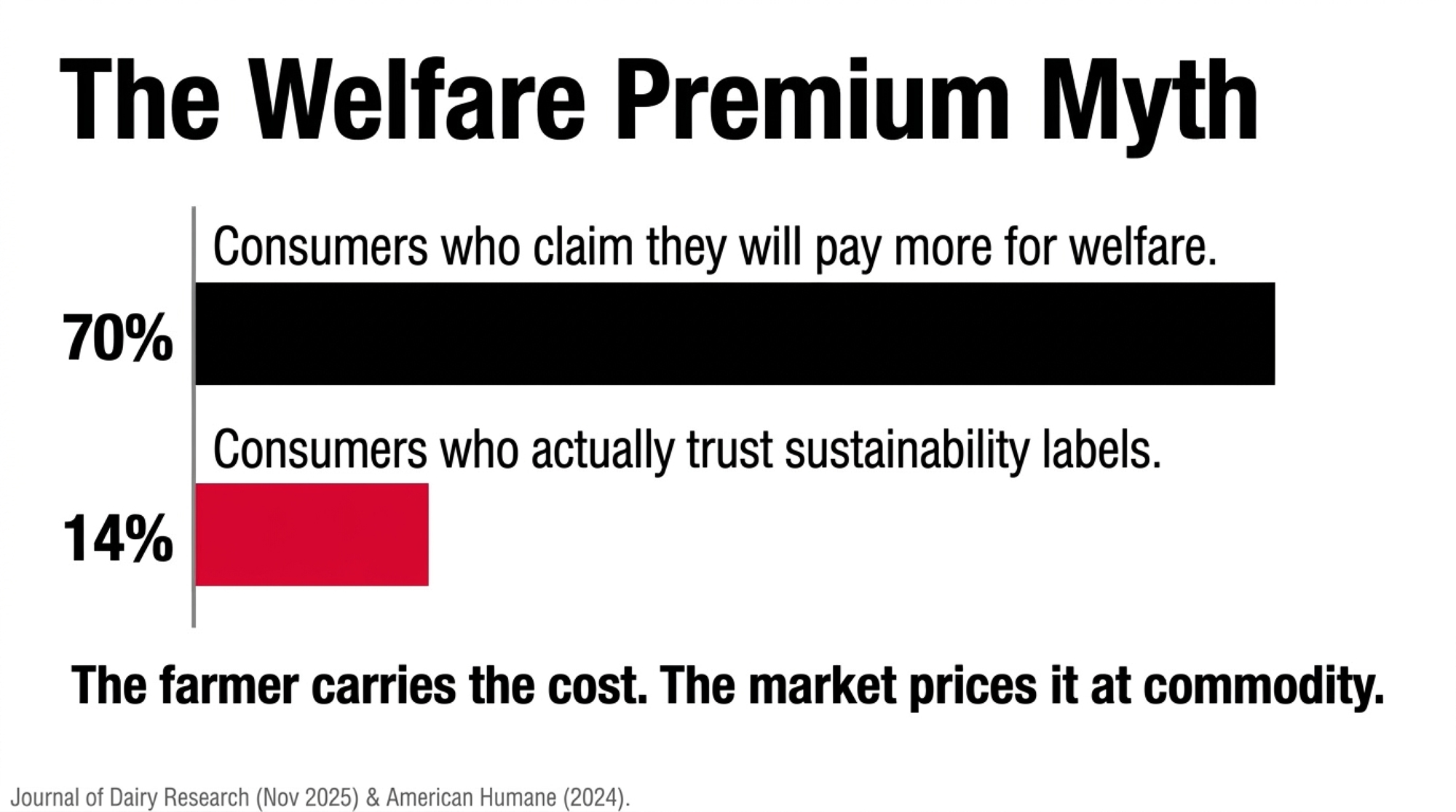

| Welfare premium that never arrives | The farmer’s conviction, priced at commodity | 70% say they’ll pay more; only 14% trust the label; 60% think brands are “just pretending” |

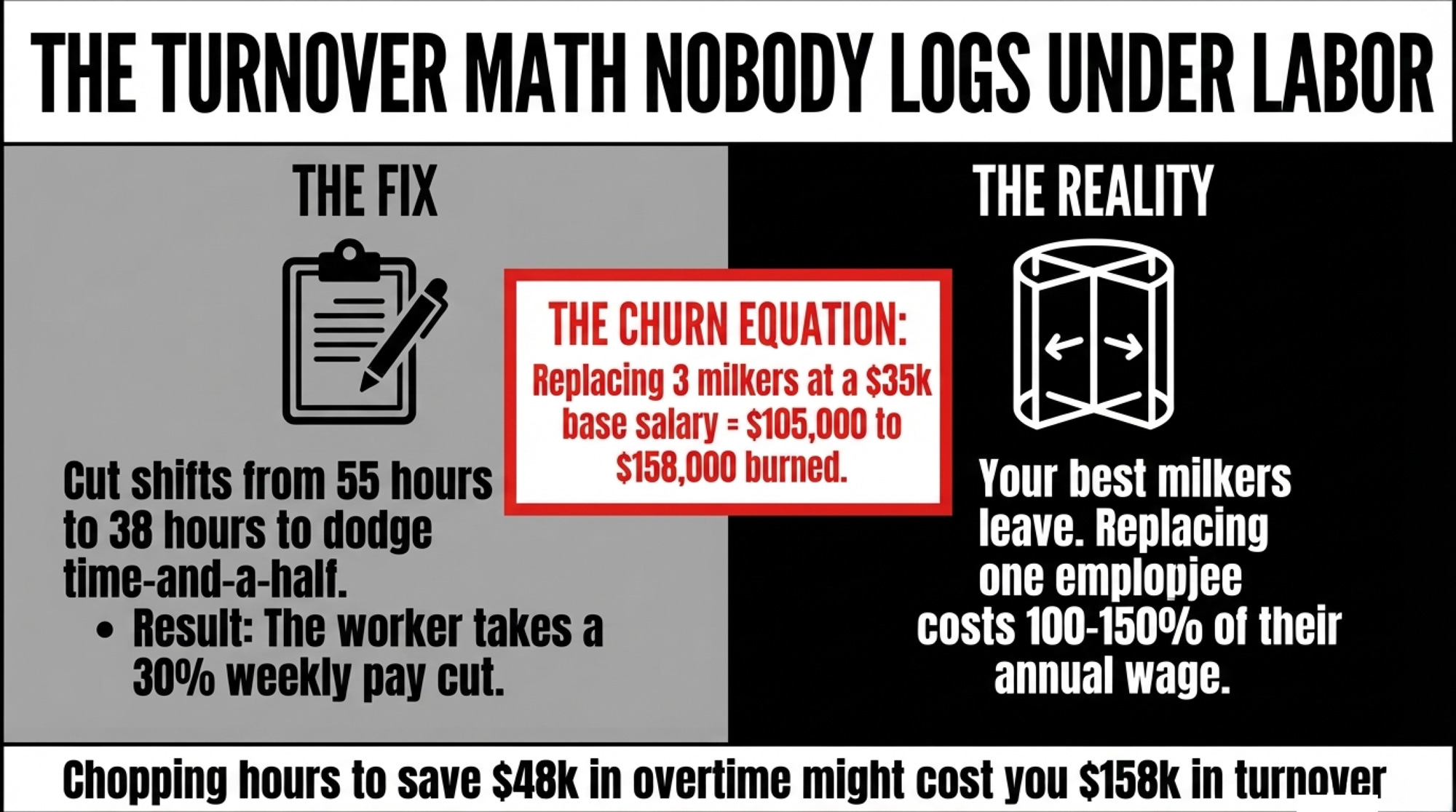

- Unpaid family labor. Robots cut hands‑on milking sharply — adopters in one multi‑box study reported labor‑cost cuts of over 21% — but they shift the rest of the work from physical to managerial and on‑call: the 2 a.m. alarm, the software, the fetch cows. University of Minnesota work found robot herds were actually less profitable per cow than conventional herds; the advantage only showed up once profit got measured per full‑time worker. Robots make your people more productive. They don’t make the labor free. They make it invisible.

- Paid‑off land or off‑farm income. The small robot farms that genuinely work tend to own their ground outright or run a second paycheck that quietly absorbs the cash‑flow valley. The Duecks’ hay and consulting income is exactly this — and they’ll tell you so. That’s an exception worth naming honestly, not a model to bolt onto a leveraged start‑up.

- The welfare premium that never reaches the milk cheque. A November 2025 study in the Journal of Dairy Research found 70% of consumers say they’ll pay more for animal‑welfare‑certified dairy. But only 14% of U.S. consumers fully trust sustainability claims on labels, and 60% figure companies are “just pretending.” The farmer carries the cost and the conviction of high‑welfare care while the market prices it at commodity. The handful who capture real premiums — Jasper Hill, Maple Hill, Alexandre Family Farm — do it through certification and brand, not by owning a robot.

| Metric | Figure | What It Means For The Cheque |

| Consumers who say they’ll pay more for welfare-certified dairy | 70% | Stated intent — the brochure number |

| Consumers who fully trust sustainability label claims | 14% | Intent evaporates without a trusted third party |

| Consumers who think brands are “just pretending” | 60% | Baseline skepticism working against you |

| Consumers emphasizing third-party certification (American Humane, 2024) | 67% | No independent label = no reliable premium |

How Much Does Your “Ethical” Story Cost Once You Price the Labor?

Run the reality check this month. Three questions, three numbers, and you’ll know more than most operators who’ve already signed.

What’s your true cost per cwt at your actual cows‑per‑robot utilization — not the dealer’s glossy target? How many unpaid family hours are propping up the story, and what are they worth at your local wage? And what premium per cwt would a processor or direct customer need to pay before the welfare narrative covers its own freight? If you can’t answer all three, you don’t yet know whether you own a business or a very expensive family project. Where does your breakeven actually sit right now?

Want to go deeper on that first number? See why small herds carry the heaviest labor cost per hundredweight.

Is the Robot the Reason Your Kids Stay — Or the Reason They Can’t Leave?

The succession pitch is powerful, and it’s not cynical: your kids won’t have to milk at 4 a.m. There’s real signal behind it. Bullvine’s own reporting has tied a tech‑savvy, balanced approach to a sharp rise in next‑generation interest — one figure put it as high as a 340% jump, though that stat traces to a single source and is best treated as directional, not gospel. Robots can genuinely make dairy a life a young person chooses instead of endures.

But technology doesn’t fix succession — economics and planning do. Only a small fraction of family operations survive to the third generation, and a robot doesn’t change those odds. When a heavily leveraged robot barn becomes the reason the next generation signs on, the “freedom” can quietly turn into a golden handcuff. They didn’t inherit cows and choice. They inherited $400,000‑plus in tech debt and an obligation to make it pay. The robot keeps them on the farm. It doesn’t necessarily keep the farm viable past their watch.

Options and Trade-Offs for Farmers

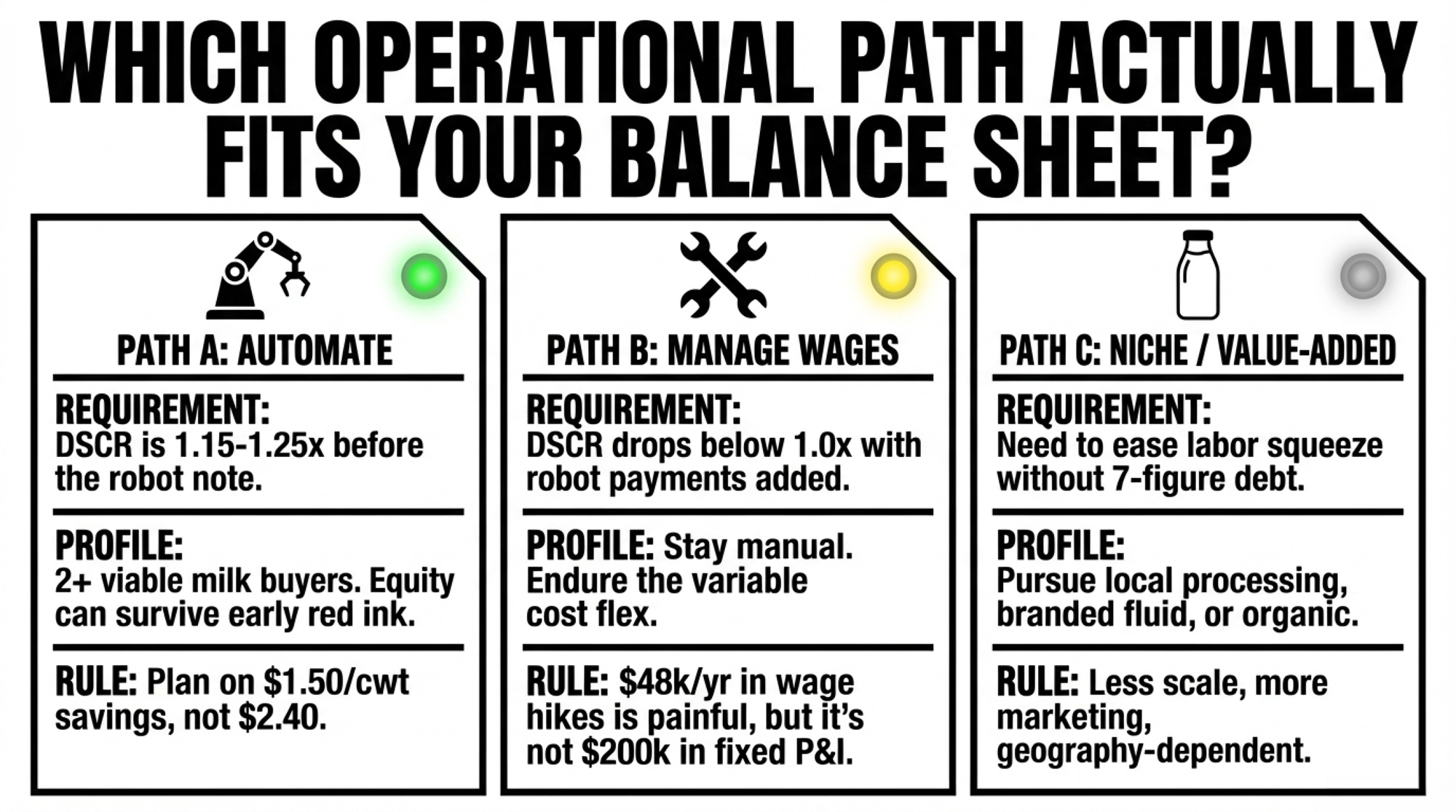

There’s no single right answer here. There are three honest paths, and your own math points to the one that fits.

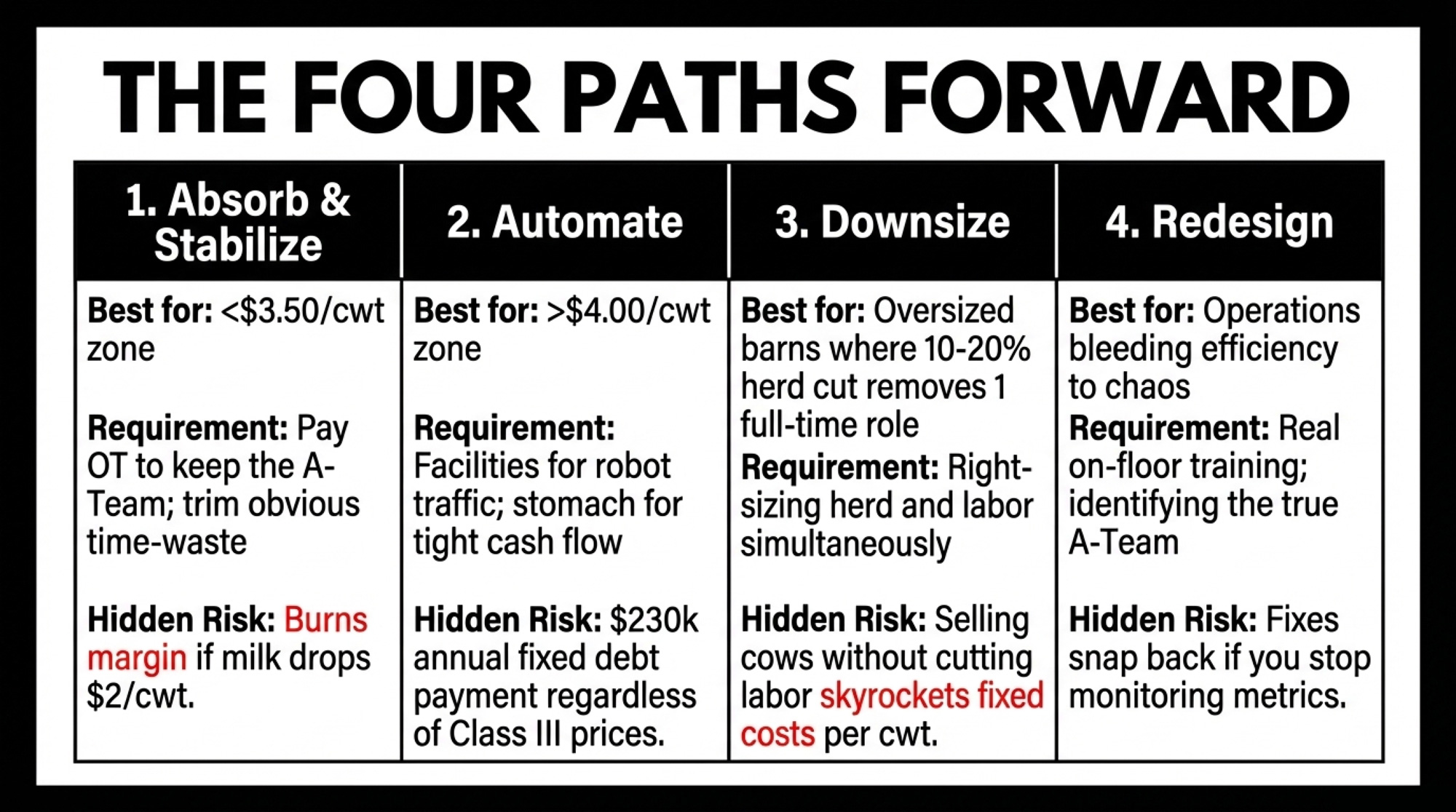

| Path | Works When | Required Condition | The Risk |

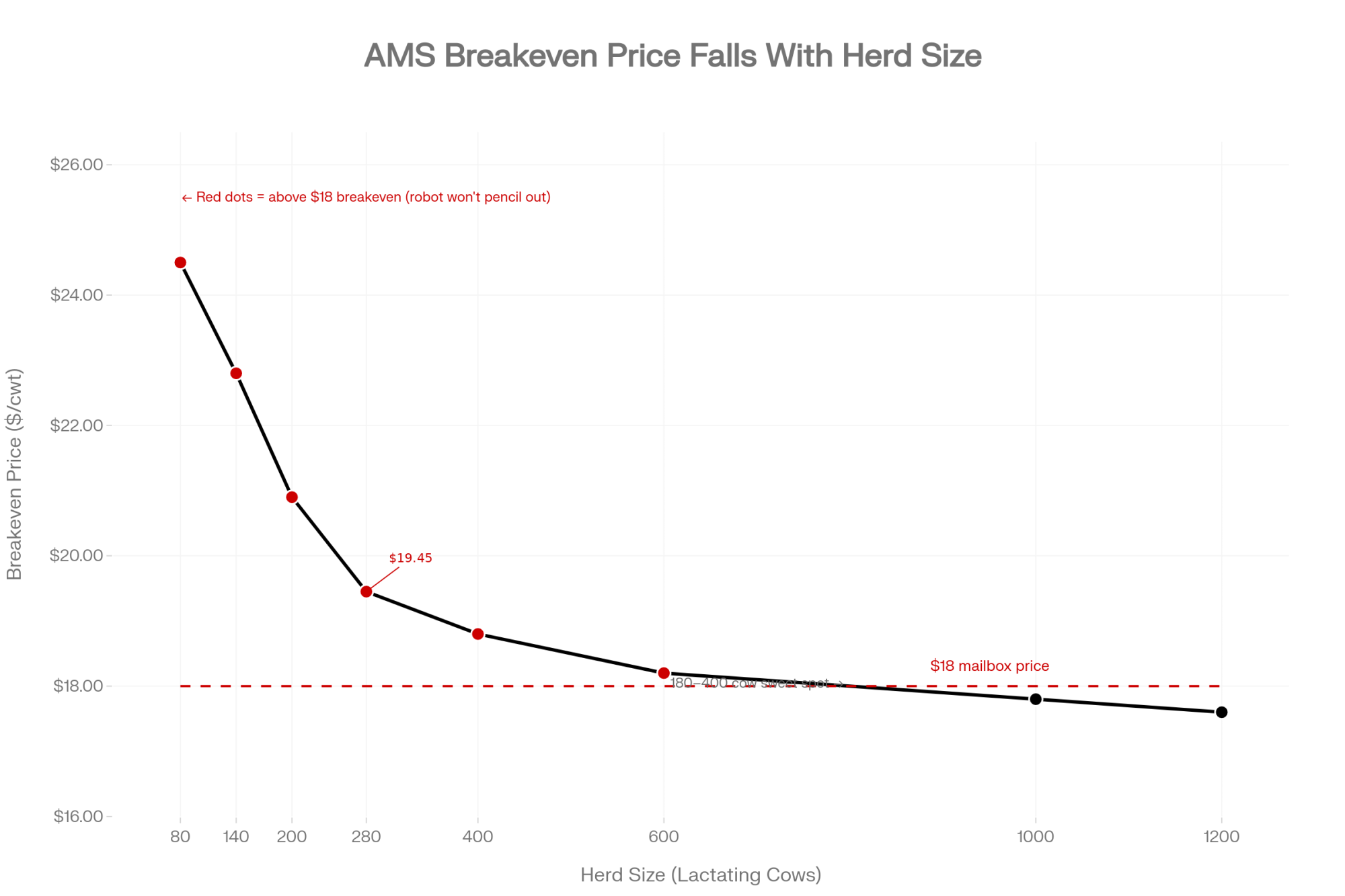

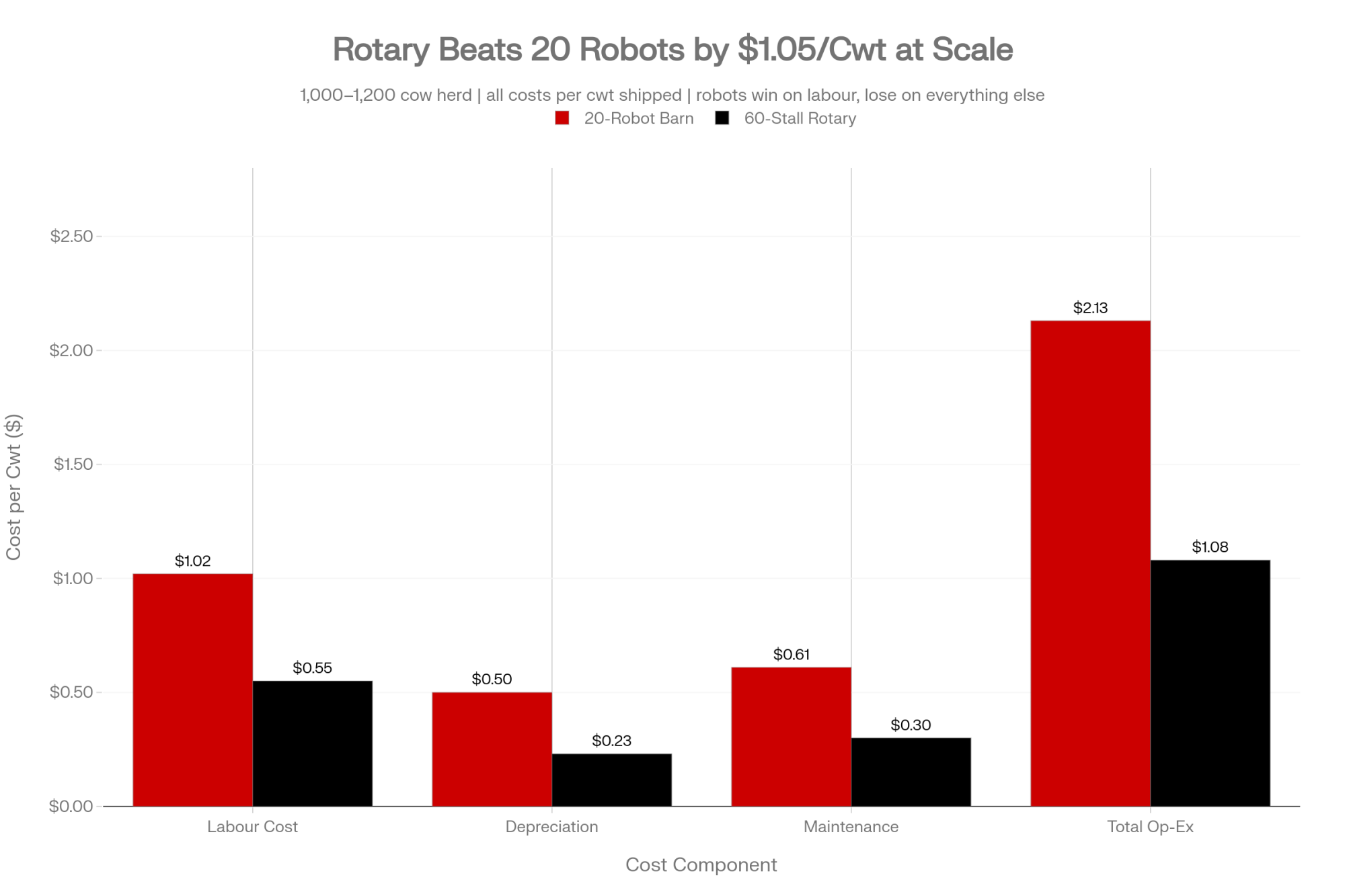

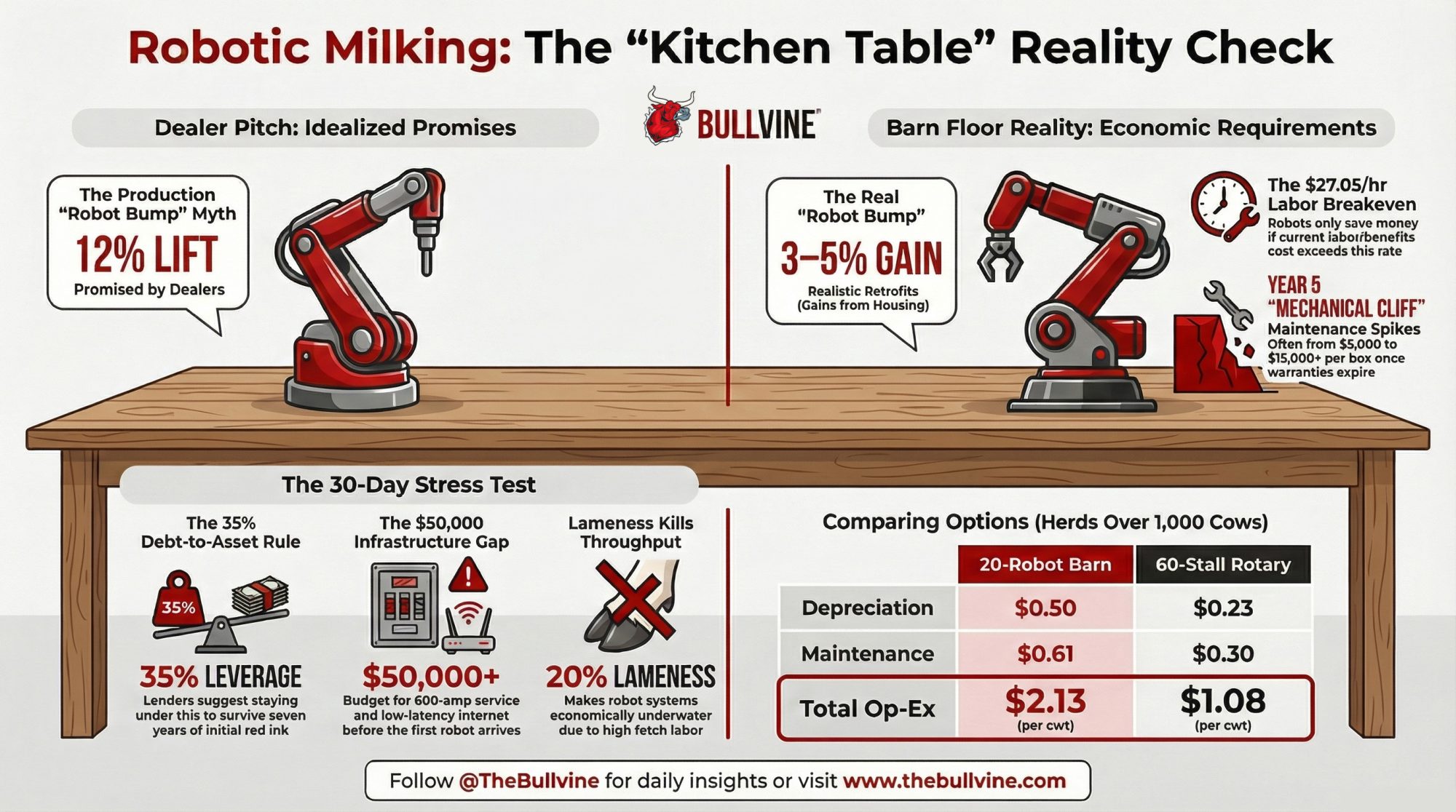

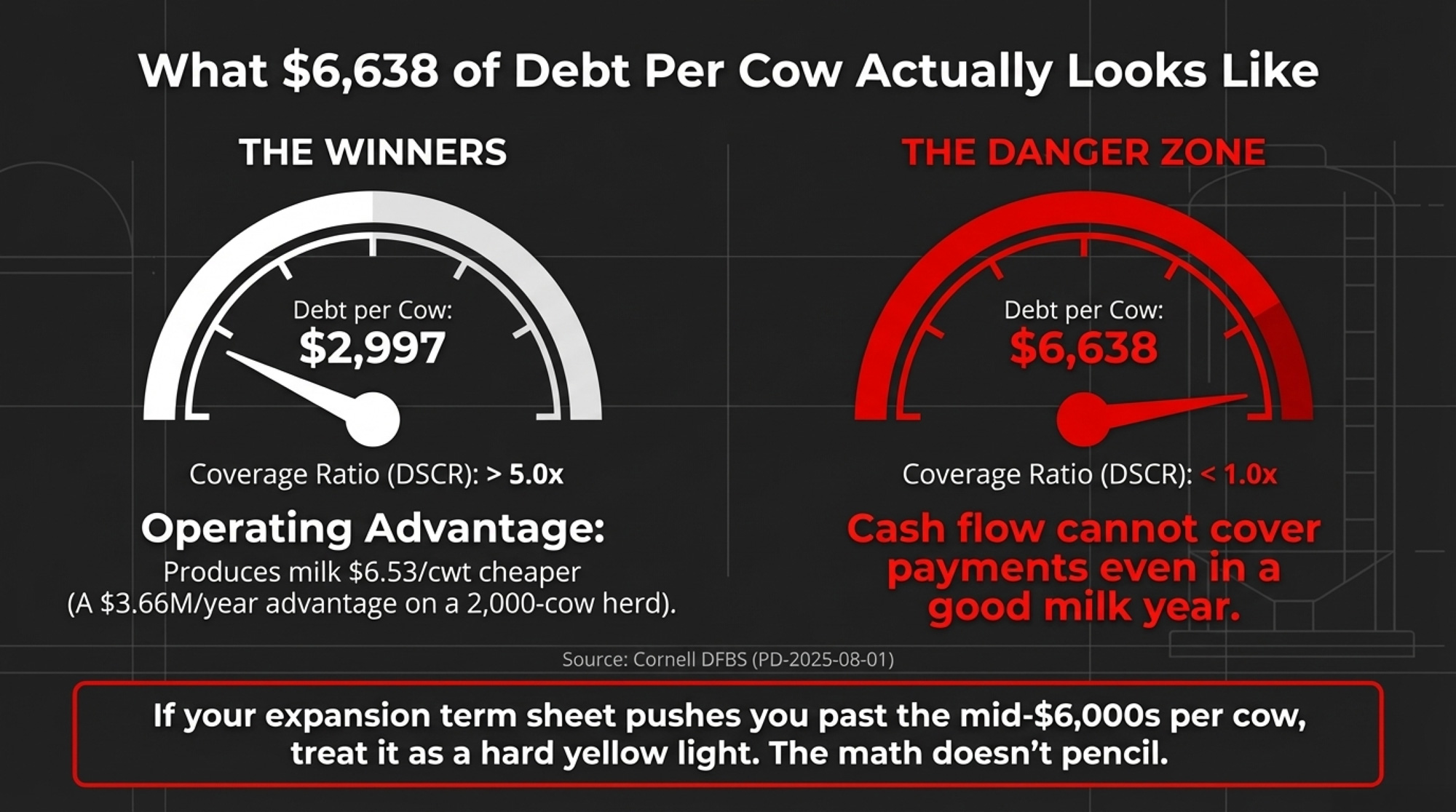

| 1 — Scaled, cost-competitive | Climbing toward larger, well-utilized herds | ~55 cows/robot utilization; labor valued at $27.05/hr breakeven | Below ~140 cows on commodity milk, the math rarely closes |

| 2 — Robot + 2nd income / real premium | You have a genuine second business or a paying market channel | The Four Oak model: diversified revenue + component-premium breed | WTP collapses at checkout — 67% demand third-party certification |

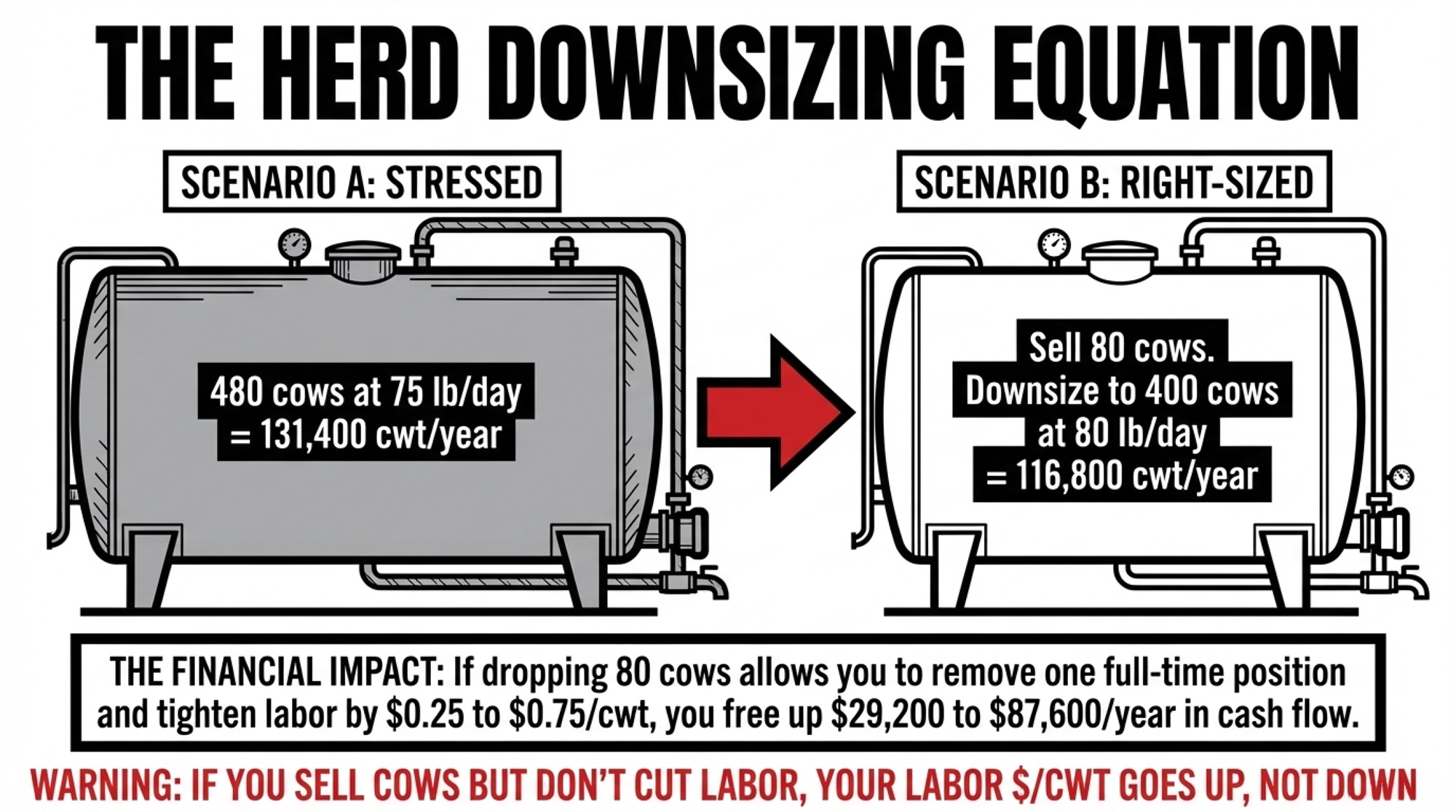

| 3 — Stop pretending robots fix it | Structurally negative 100-cow operation | Run true cost/cwt with family hours priced in | Waiting 18 months too long burns ~$575,000 in equity |

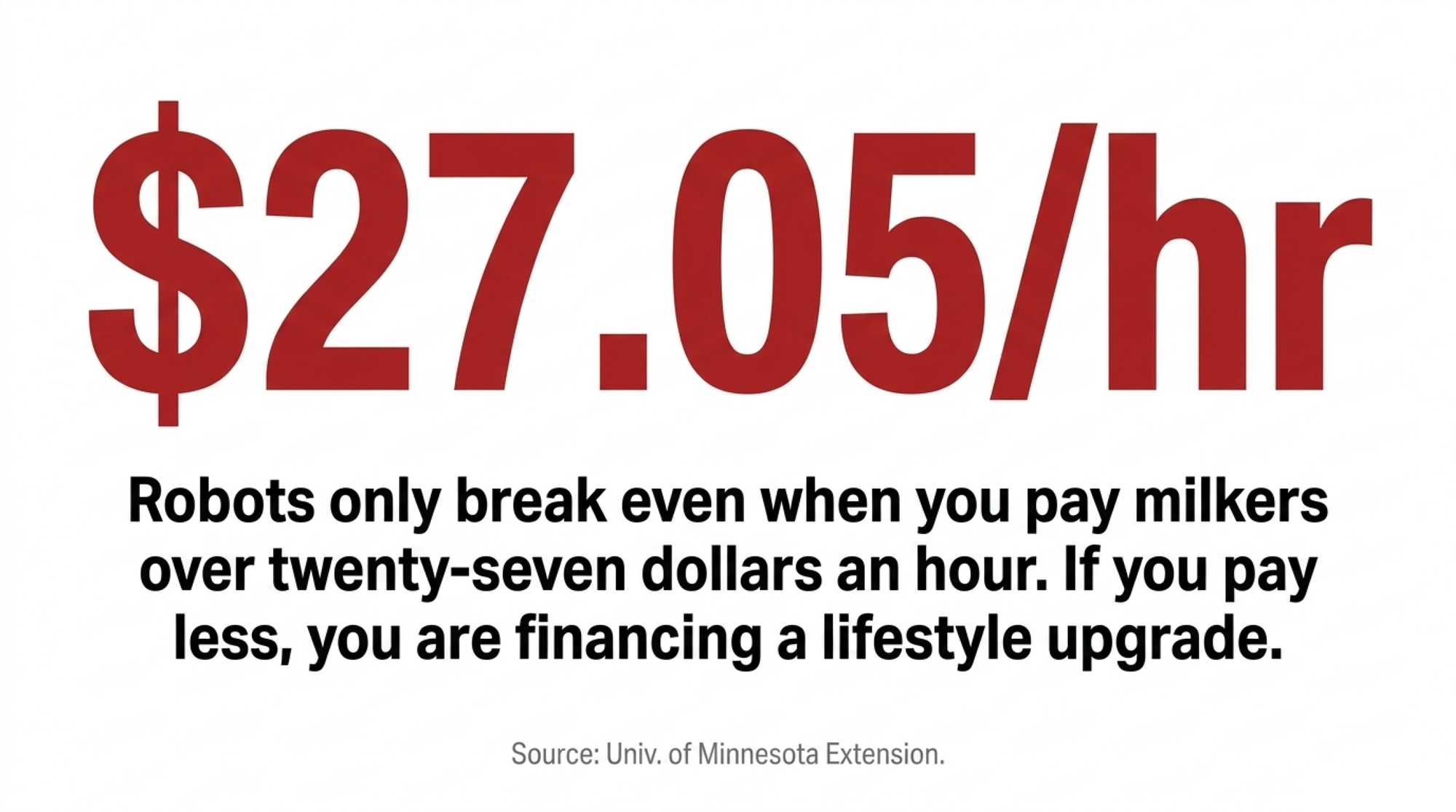

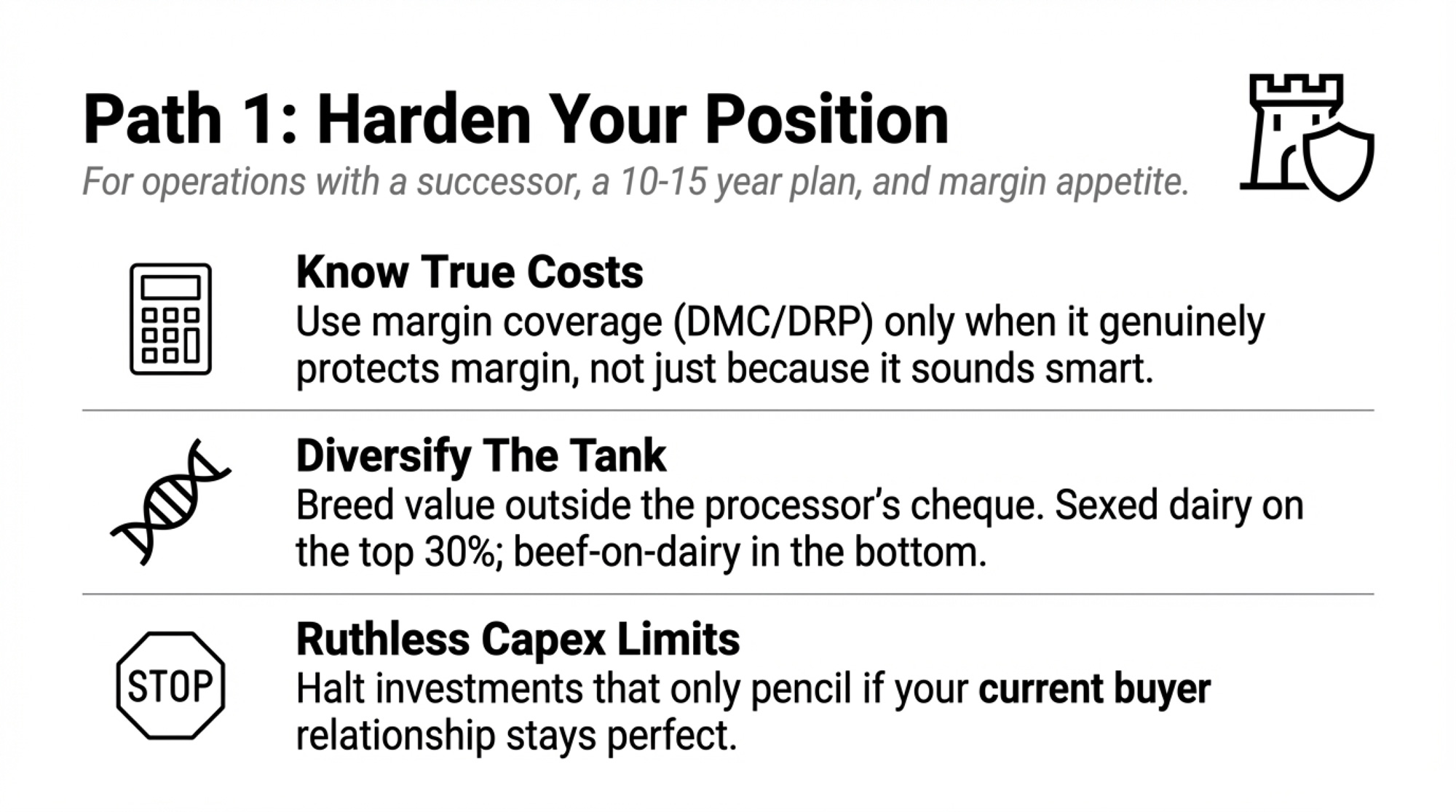

- Path 1 — Robots as a scaled, cost‑competitive system. Makes sense if you’re climbing toward the larger, well‑utilized herd size where ERS sees the strongest returns, with utilization near the 55 cows per robot extension benchmarks favor. Requires ruthless cost tracking and labor valued at market — University of Minnesota pegs the breakeven labor cost around $27.05/hour. The risk: below roughly 140 cows on commodity milk, the math rarely closes.

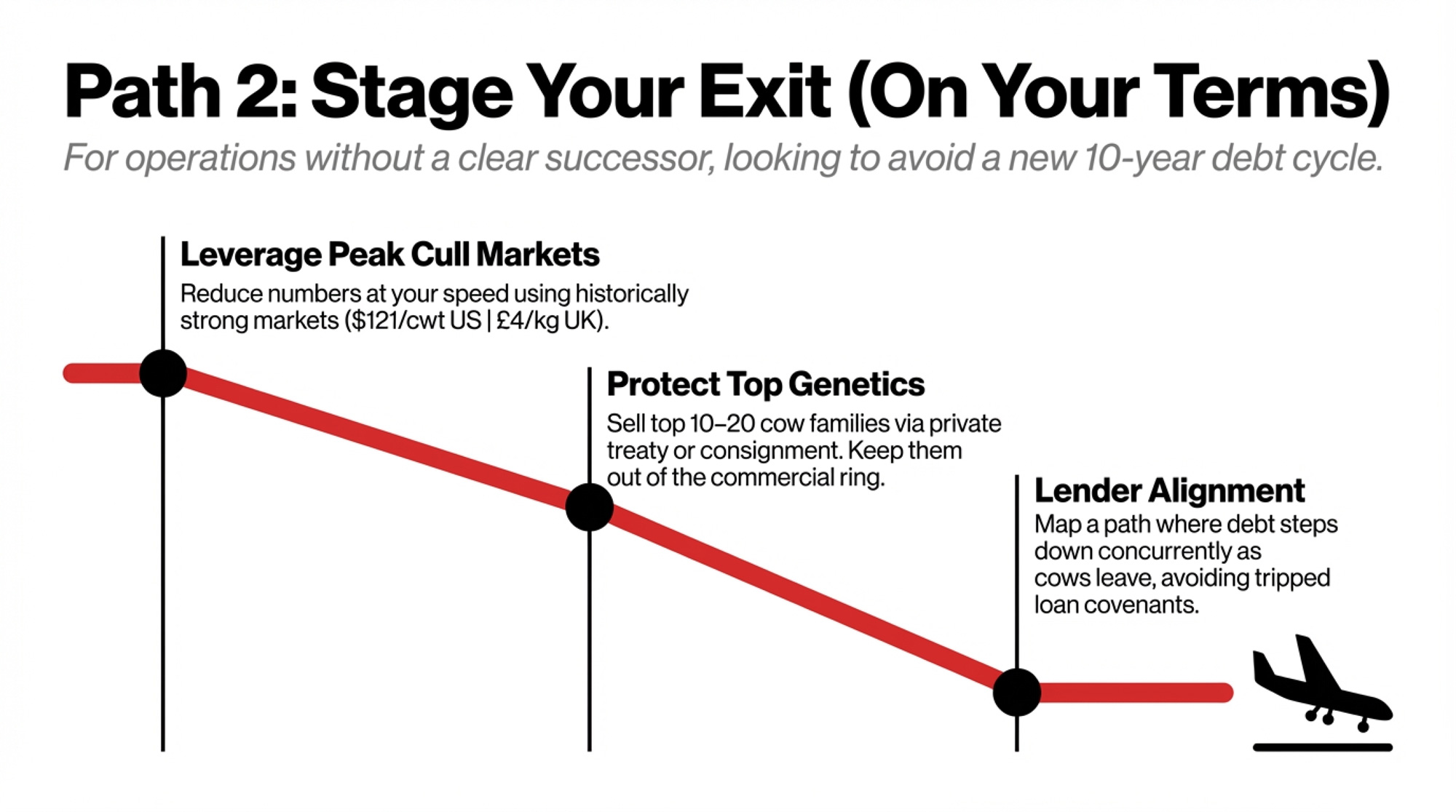

- Path 2 — Robots plus a second income or a real premium. This is the Four Oak Farms model — a robot paired with diversified off‑farm revenue (the Duecks’ hay business and Four Oak Ag Solutions consulting) and a breed strategy built on butterfat and protein premiums rather than volume. Requires either a genuine second business or a market channel paying a measurable $/cwt over commodity. The risk: stated willingness‑to‑pay collapses at the checkout without a trusted third‑party label — 67% of consumers in American Humane’s 2024 survey specifically emphasized third‑party certification.

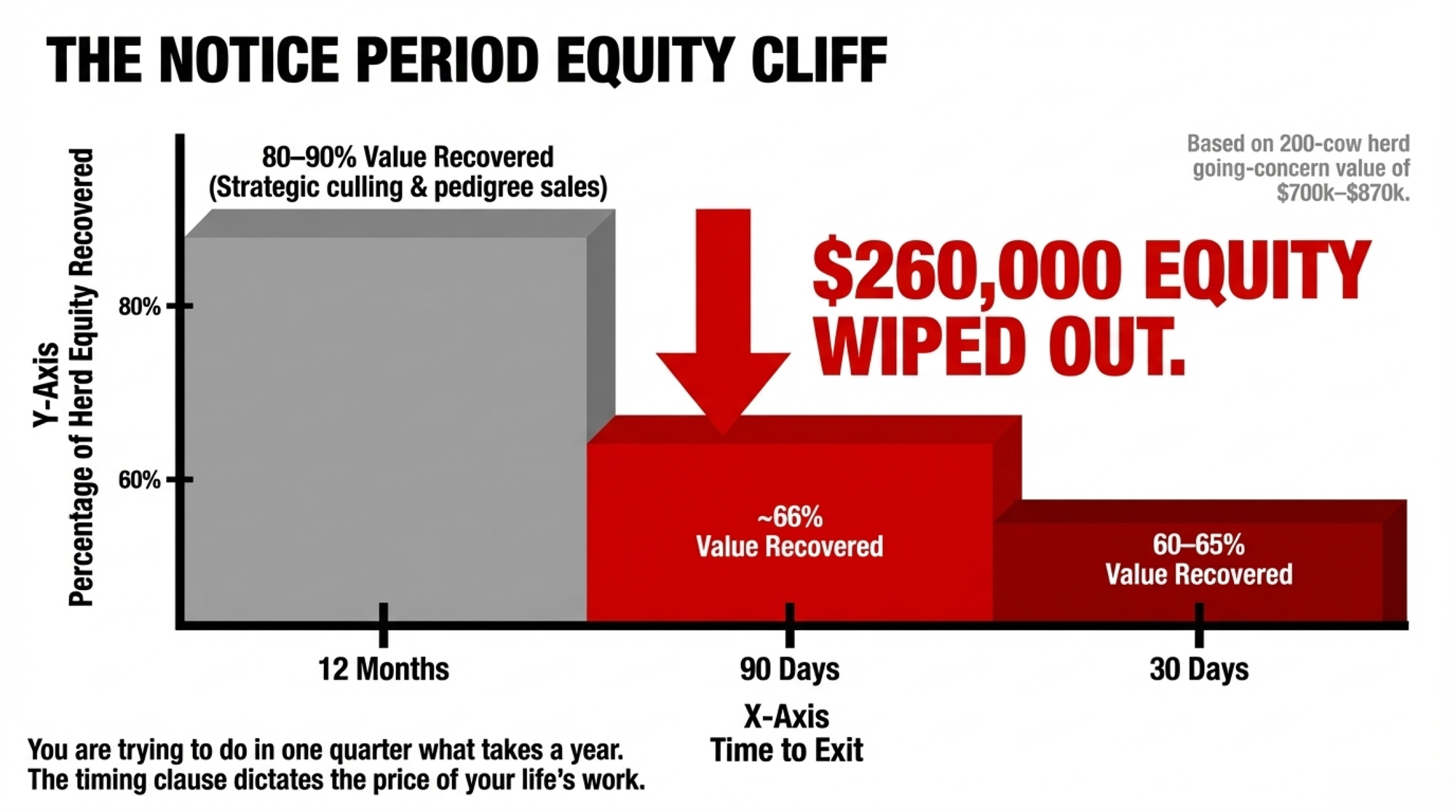

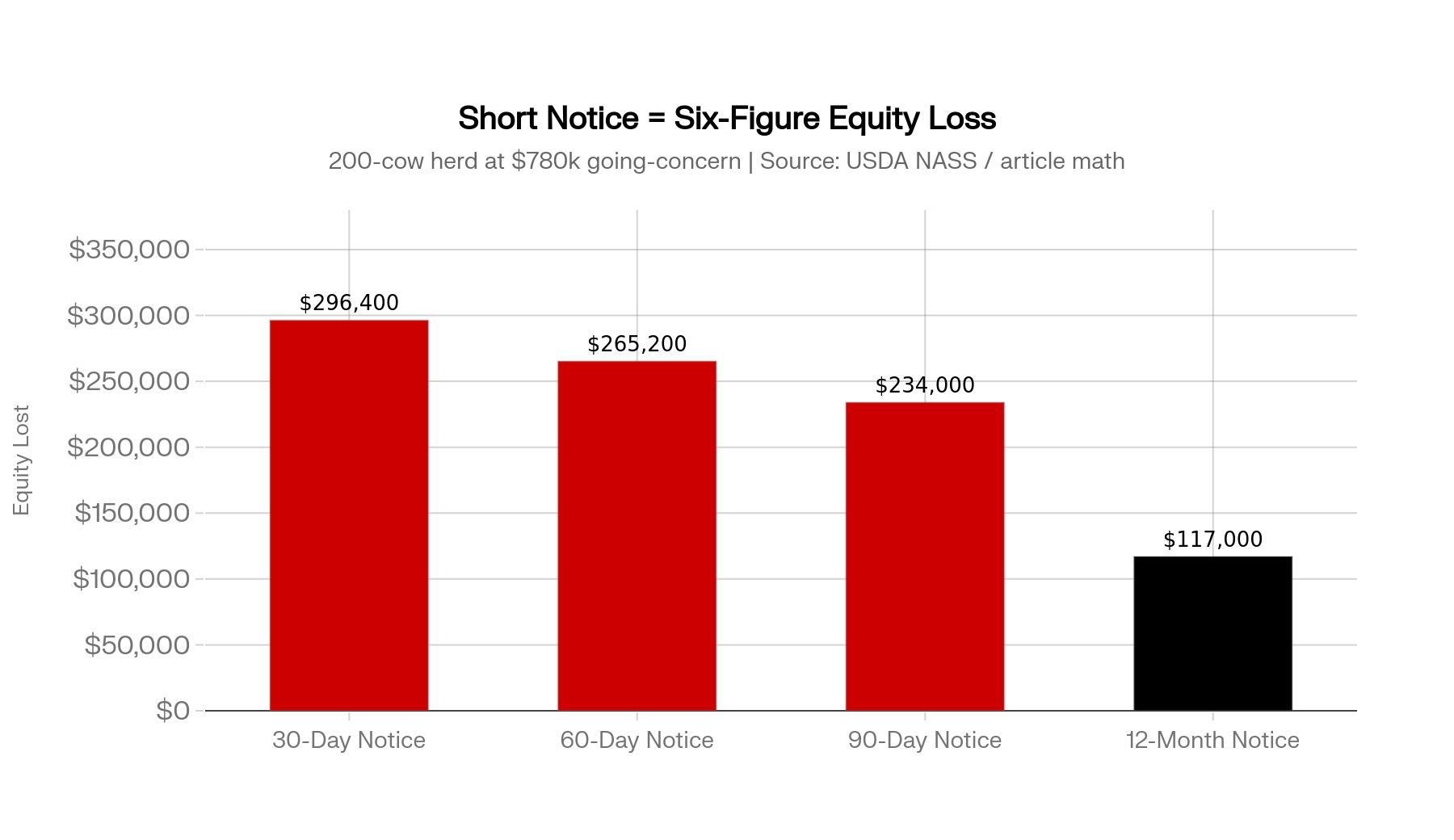

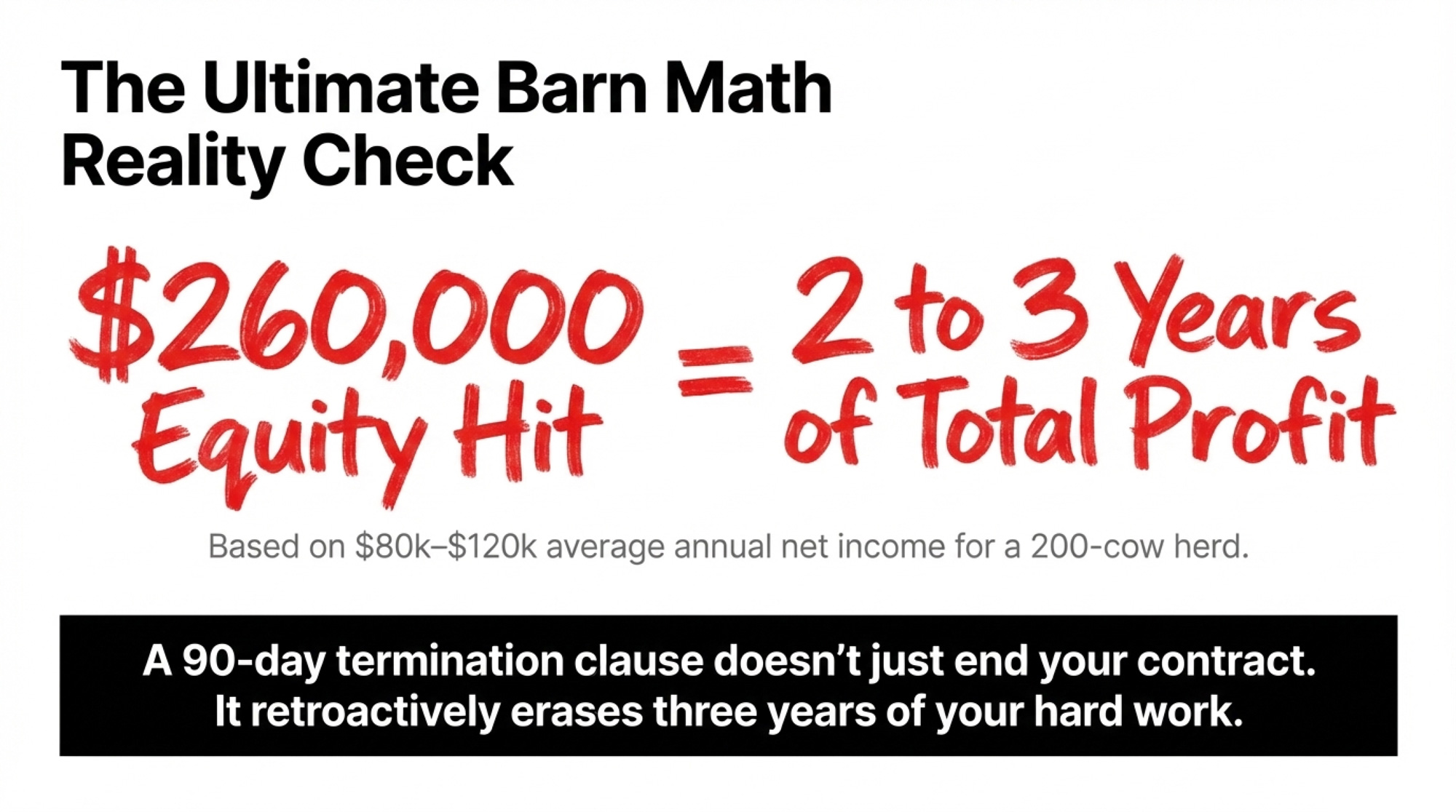

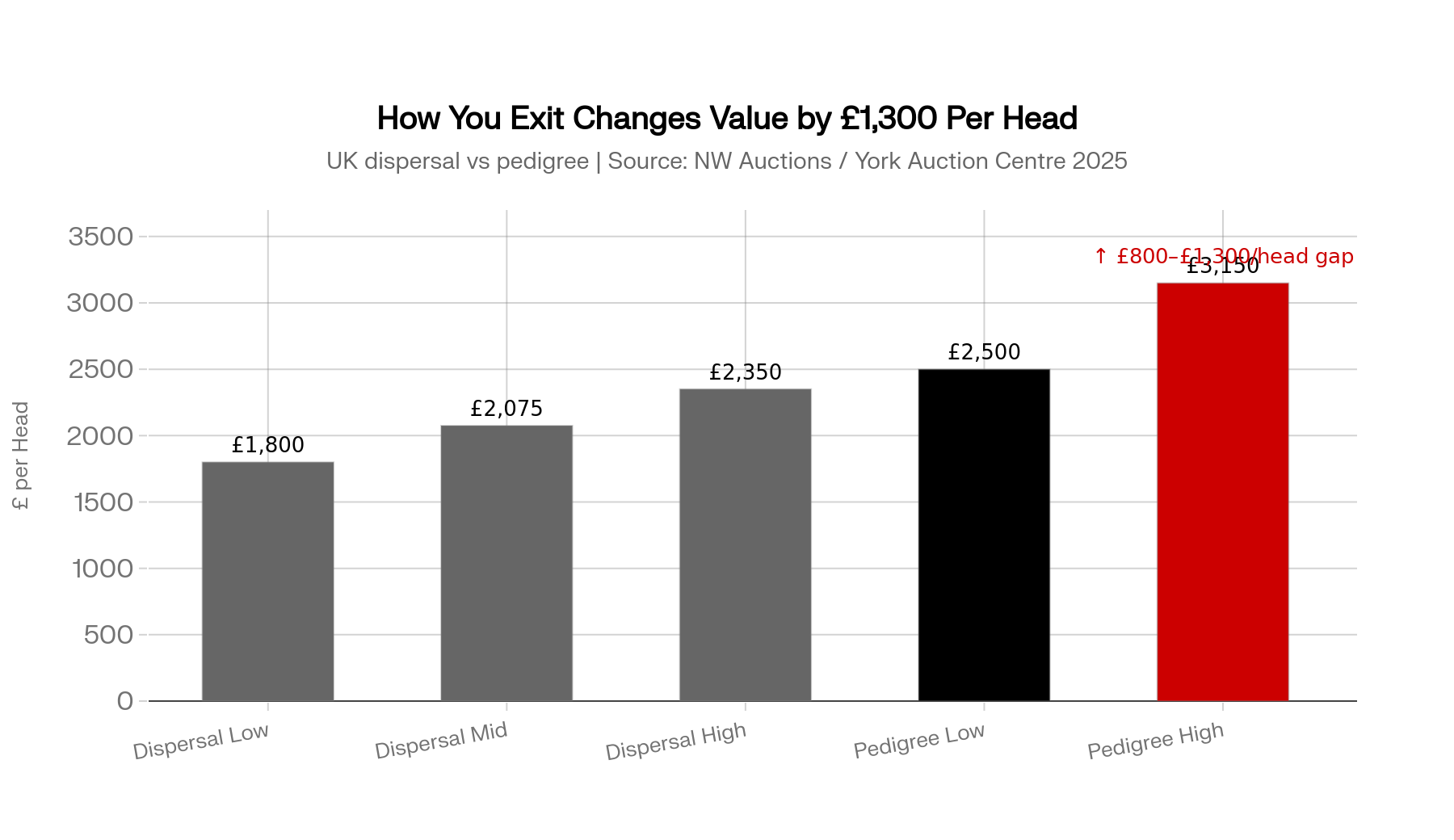

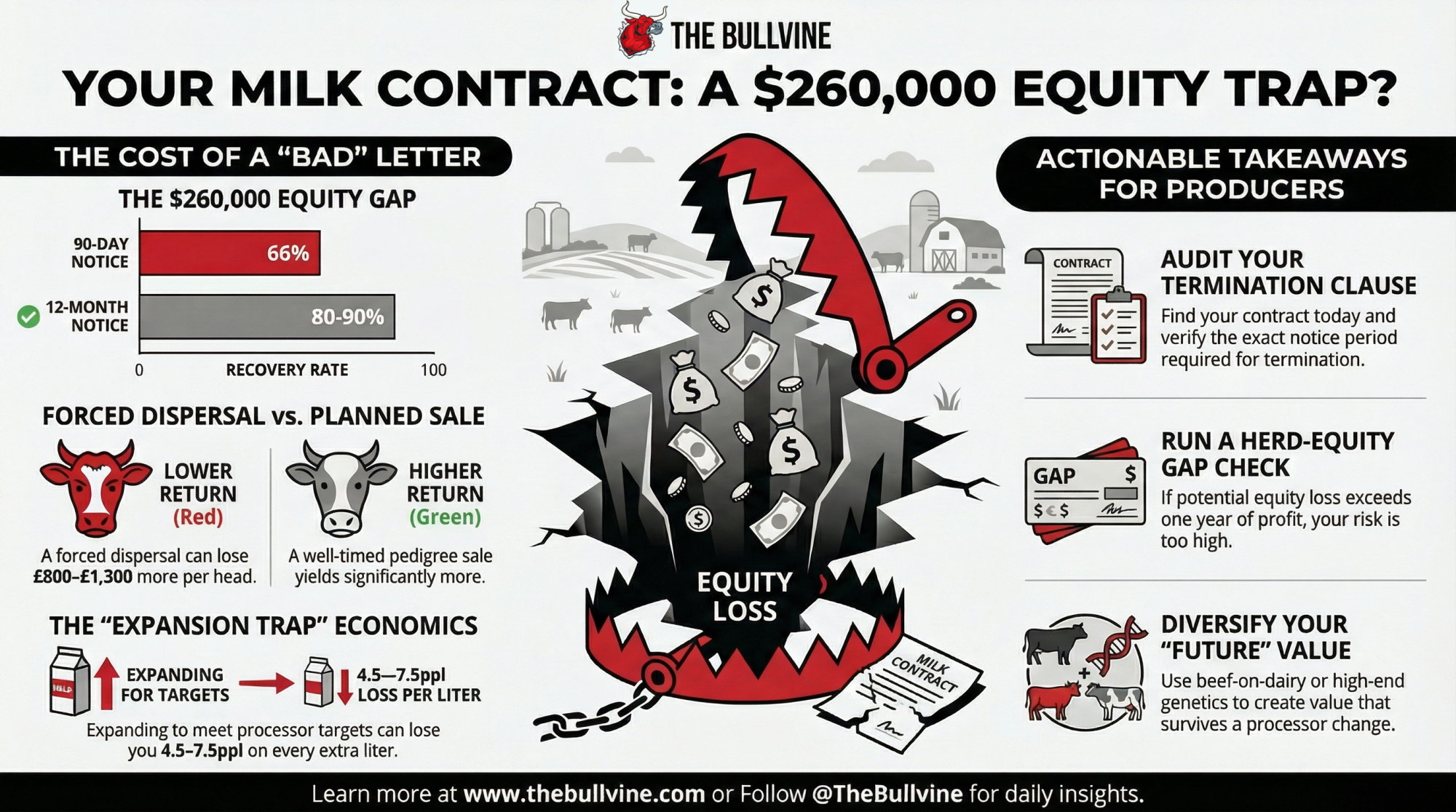

- Path 3 — Stop pretending robots fix an unprofitable commodity dairy. Sometimes the honest move within the next 30 days is to run your true cost per cwt — family hours priced in — and accept that a structurally negative 100‑cow operation needs a different decision than more debt. Bullvine’s exit‑math work shows waiting 18 months too long on a negative position can quietly burn around $575,000 in equity; a planned transition preserved $765,000 versus $255,000 in a forced liquidation. No robot out‑runs that gap.

We’re building the full seven‑year cash‑flow valley behind that $3.15/cwt return — laid out year by year by herd size — as a follow‑up; watch for it in the coming weeks.

Key Takeaways

- If your robot herd “breaks even” on paper, rerun it with every family hour priced at your local wage. If that move pushes you into the red, you’re subsidizing the operation, not running it.

- If you’re below ~140 cows on commodity milk with no premium channel, treat the $3.15/cwt average net return as somebody else’s number until your own utilization and labor math say different.

- If you’re banking on a welfare premium, get the contract or certification in writing first — 70% say they’ll pay, only 14% trust the label, and your co‑op rarely converts welfare compliance into $/cwt.

- If you’re going to make a small robot herd work, copy the Duecks before you copy the brochure: a second income stream and a component‑premium breed strategy did the heavy lifting, not the robot.

- If your operation’s been structurally negative for 18 months or more, run the exit‑versus‑reinvest math before you sign robot debt. The equity gap between a planned and a forced transition runs into six figures.

- If robots are the reason your kids are staying, separate the lifestyle promise from the balance sheet. Make sure they’re choosing a viable business, not inheriting an obligation.

The Question to Take to the Kitchen Table

That farmer answering the “is ethical dairy even possible” question isn’t wrong to want a calmer barn and cows that get to be cows. The question that decides whether the dream survives contact with the milk cheque is the one nobody in the showroom asks: at your herd size, your milk price, and your real labor bill, who’s quietly paying for the “ethical” part — the market, or your own family?

Run those three numbers this week. Then take them to your lender and your kids before you take them to the equipment rep. And if you want to see how a robot, Brown Swiss, hay, and consulting actually came together on one real Manitoba farm, read how the robots hum and the cows stay calm at Four Oak Farms.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Robotic Milking Pays 13% More – After 7 Years of Red Ink — Arms you with Larry Tranel’s full economic model to calculate the exact annual cash-flow gap your checking account will absorb during the multi-year startup phase.

- How 5 Dairy Farmers Got Out While They Were Still Winning — Exposes the massive $575,000 equity gap between a strategic, planned dispersal and a forced liquidation when a financially strapped operation waits too long to transition.

- The Myth of ‘Cheap’ Labor: H‑2A, Robots, and the Hard Math Dairies Need to Survive the Next 10 Years — Delivers critical comparative data pitting the upfront capital demands of box robots against the high administrative and compliance costs of structured immigrant labor programs.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.