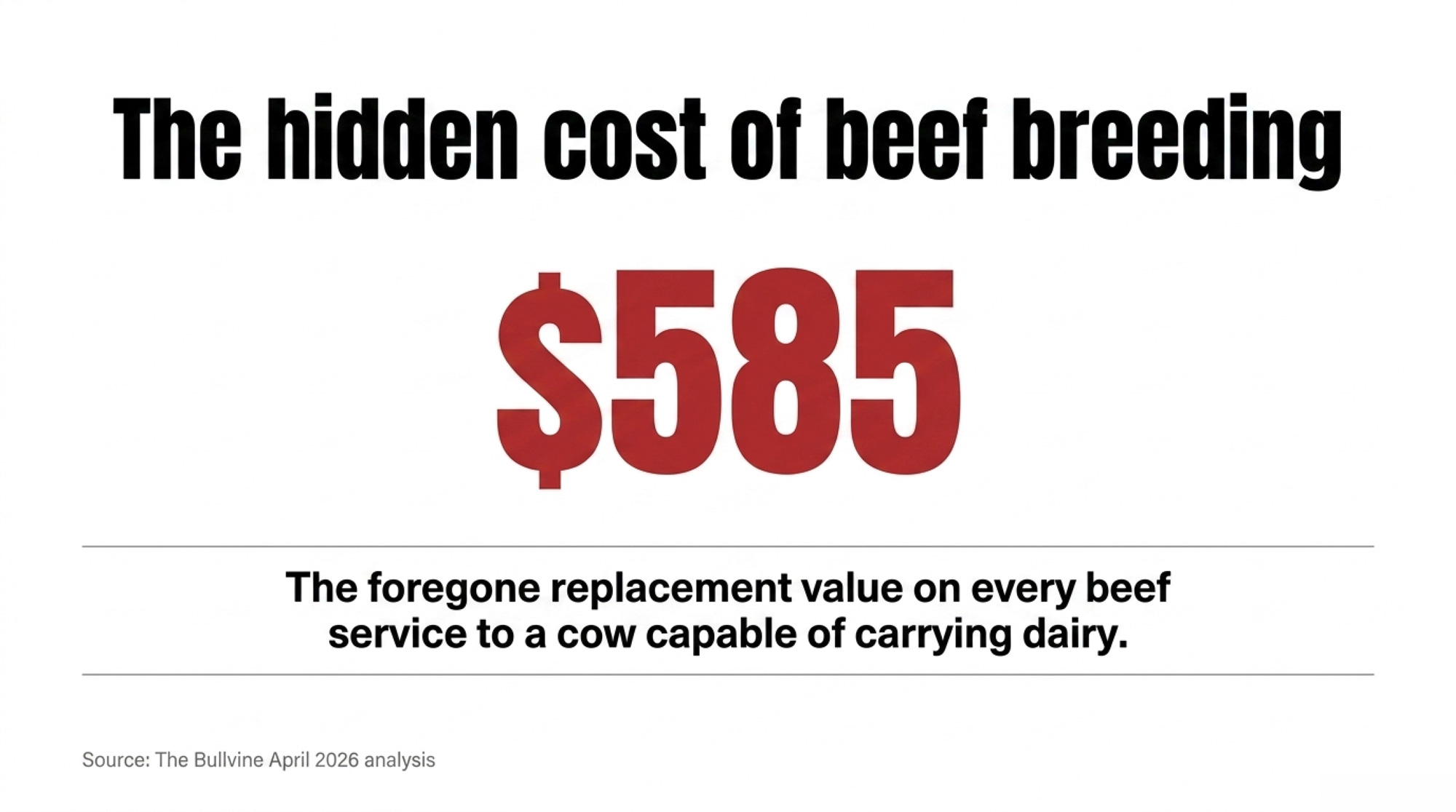

This Independence Day, the beef-on-dairy calf check is the quiet reason a lot of American dairy families still own their barns. But every beef straw you put in a viable dairy cow trades away roughly $585 in future heifer value — so the real question on the Fourth isn’t whether it works. It’s whether that calf check is funding your independence or slowly mortgaging it.

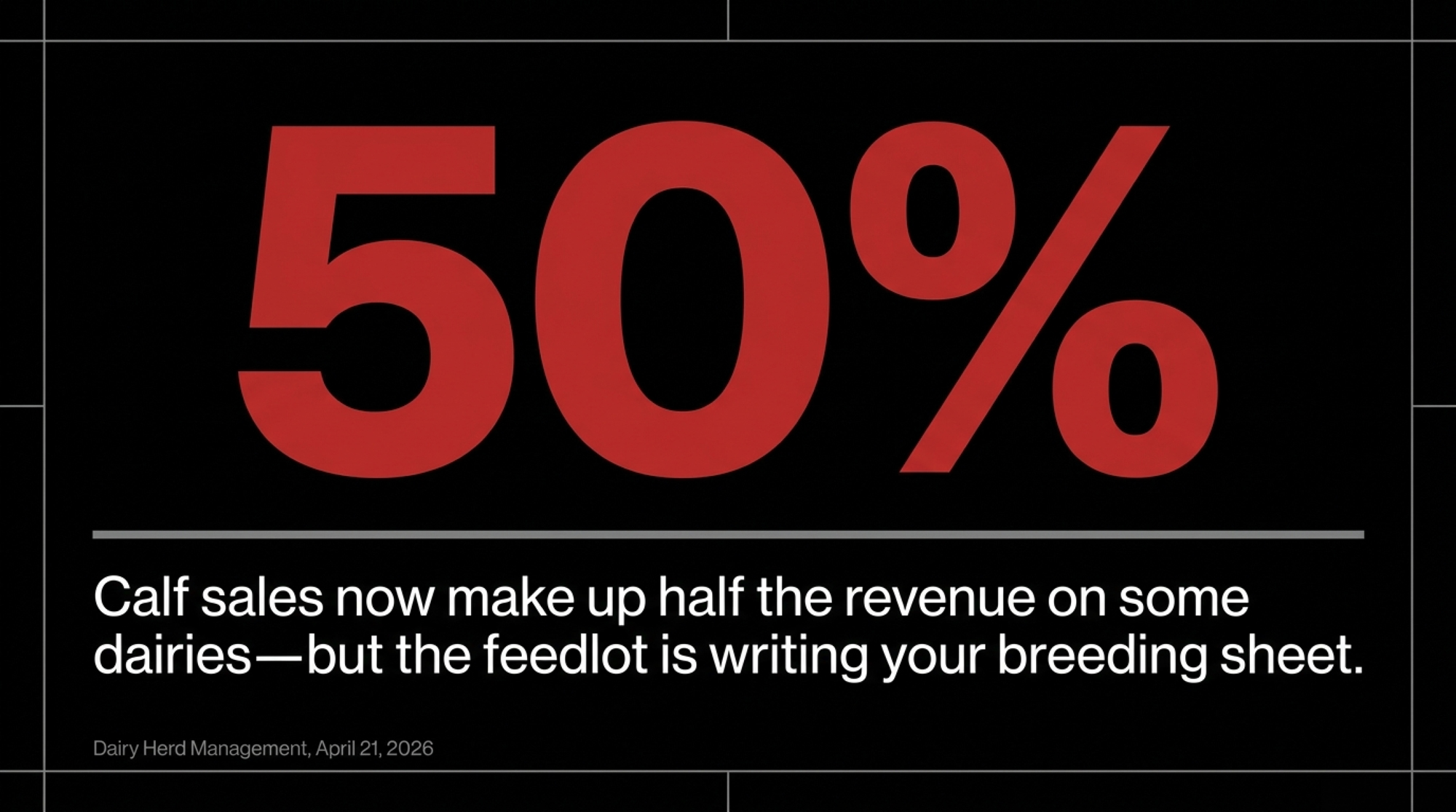

Ken McCarty used to barely glance at what his bull calves brought. On the McCarty family’s roughly 20,000-cow operation near Colby, Kansas, those calves were something you loaded out and forgot about. Then the math flipped. Today, McCarty shared that calf sales “went from something that you basically ignored in your budget to something that really today accounts for, depending on the month in the market, somewhere around 50% of our overall revenue”.

Half the revenue. From the calf nobody used to write up.

There’s something fitting about telling this story on the Fourth. Independence, for a dairy family, has never been an abstraction — it’s whether you still hold the deed, still call the shots, still decide what gets bred to what. And right now, for thousands of U.S. operations, the thing keeping that independence intact isn’t the milk check. It’s the calf that used to ride out on the cull trailer.

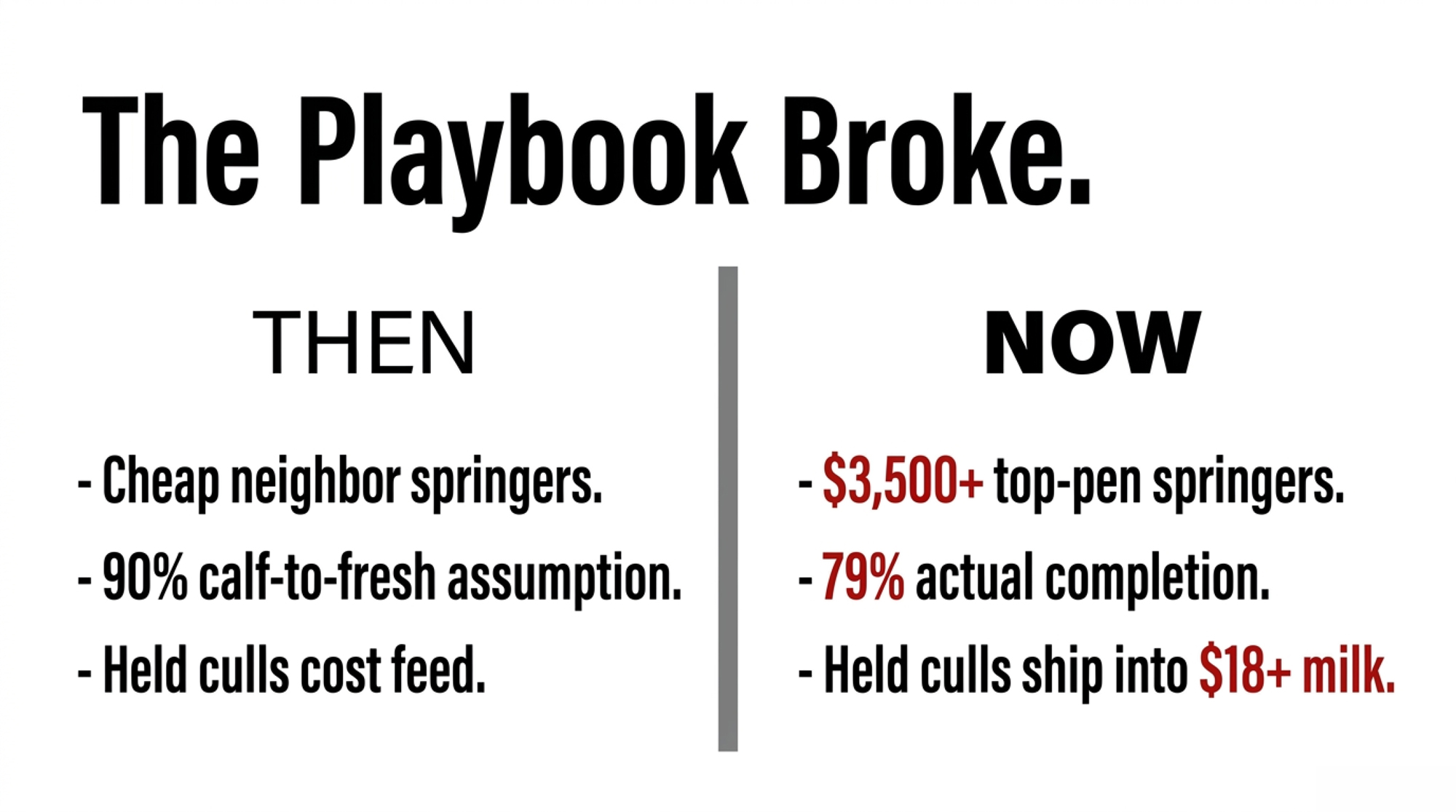

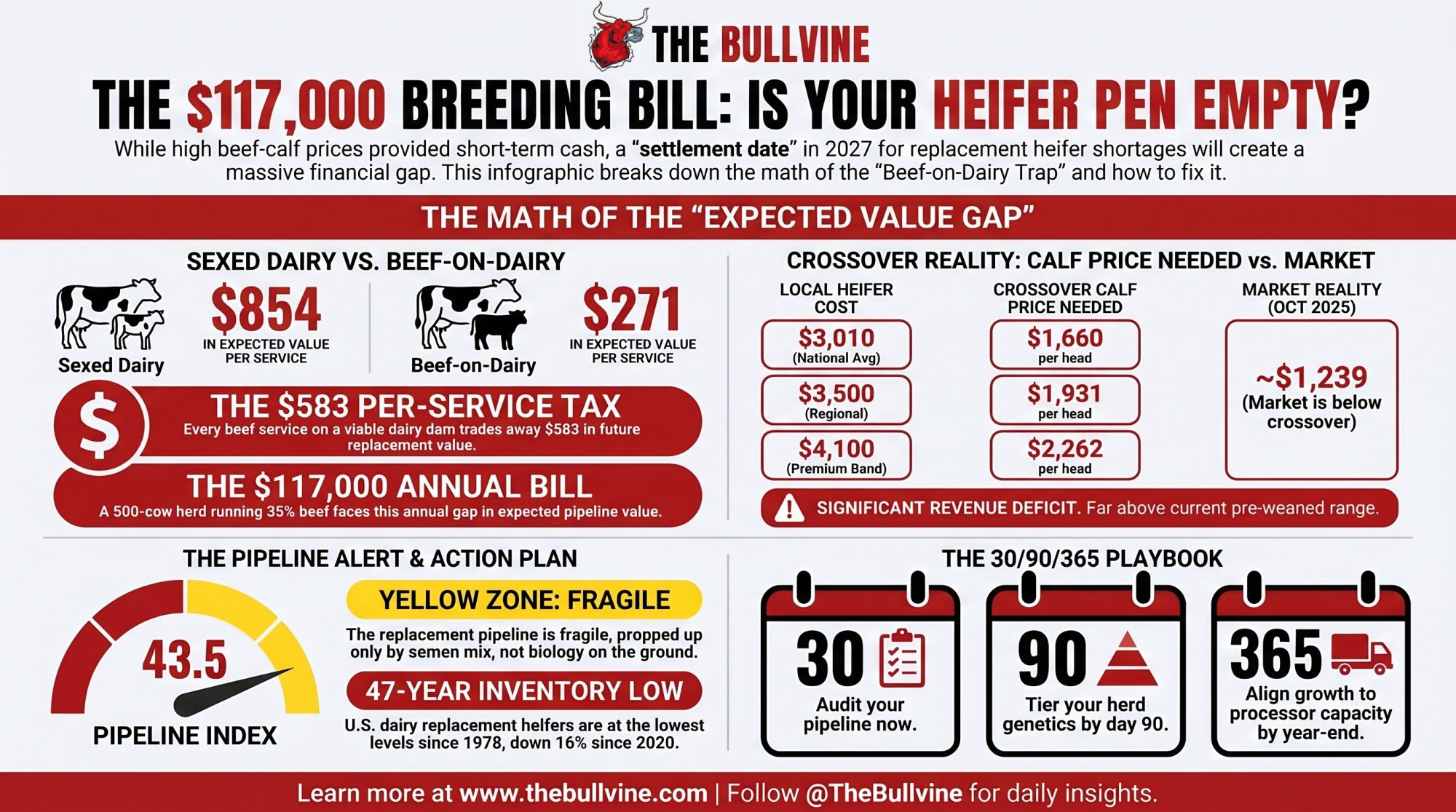

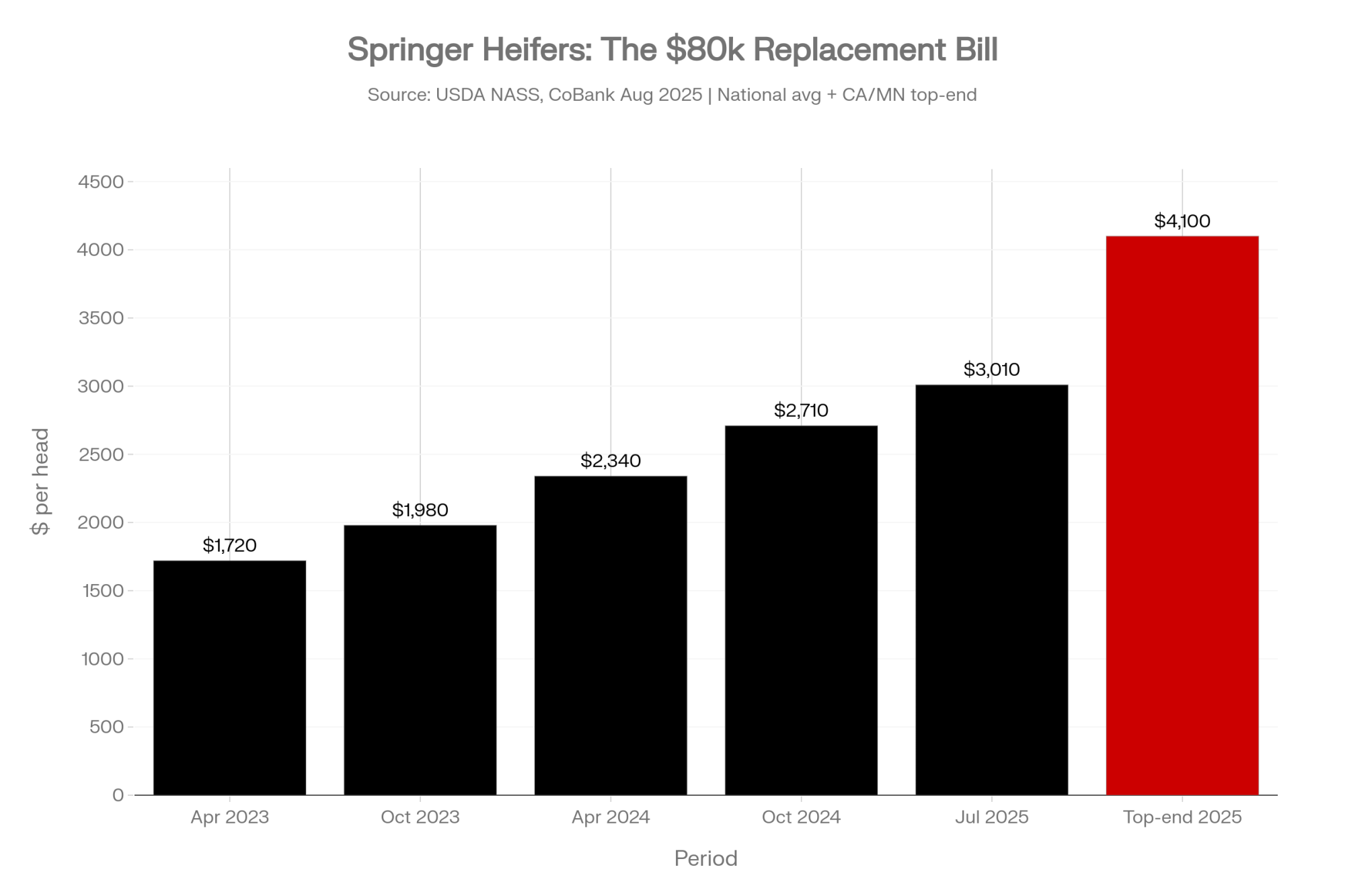

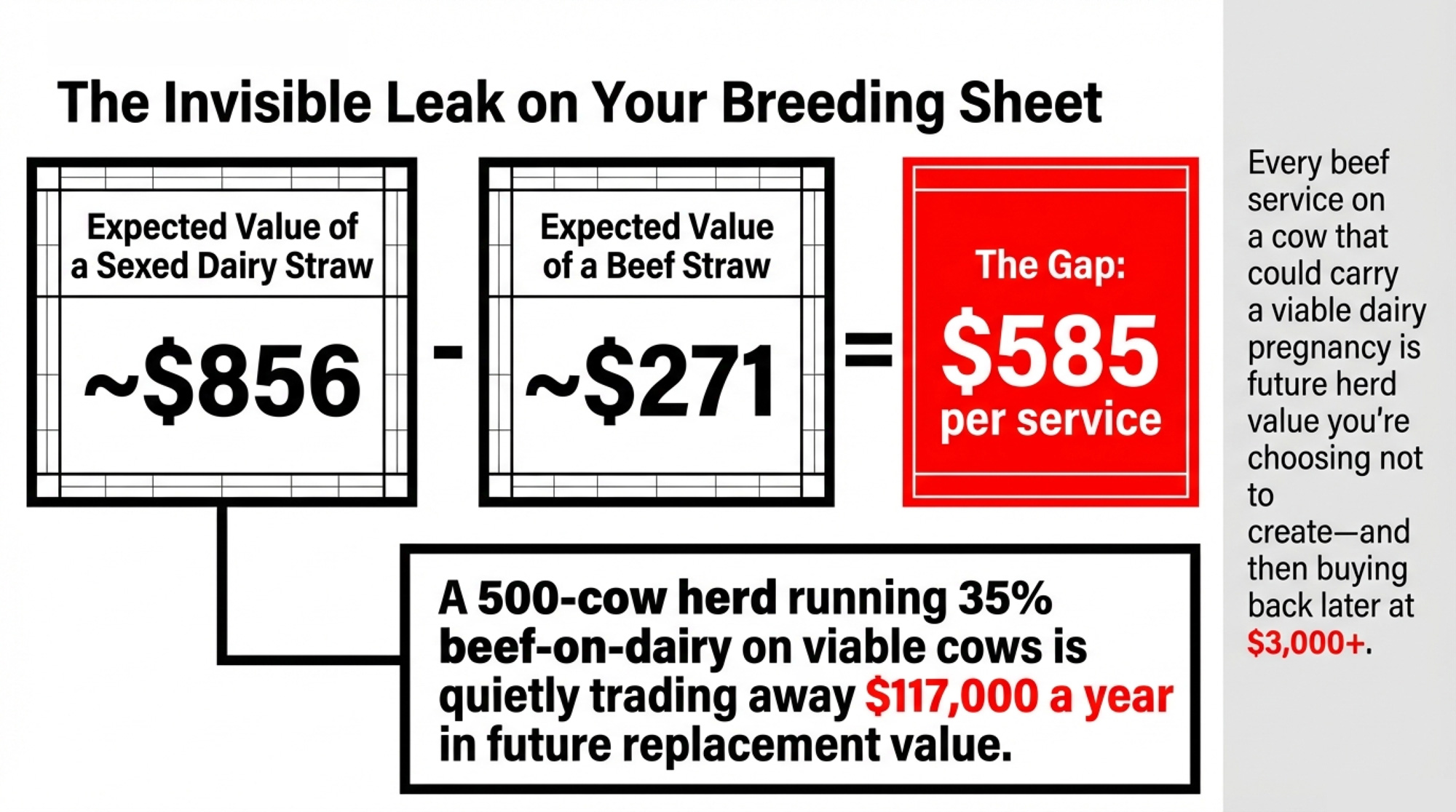

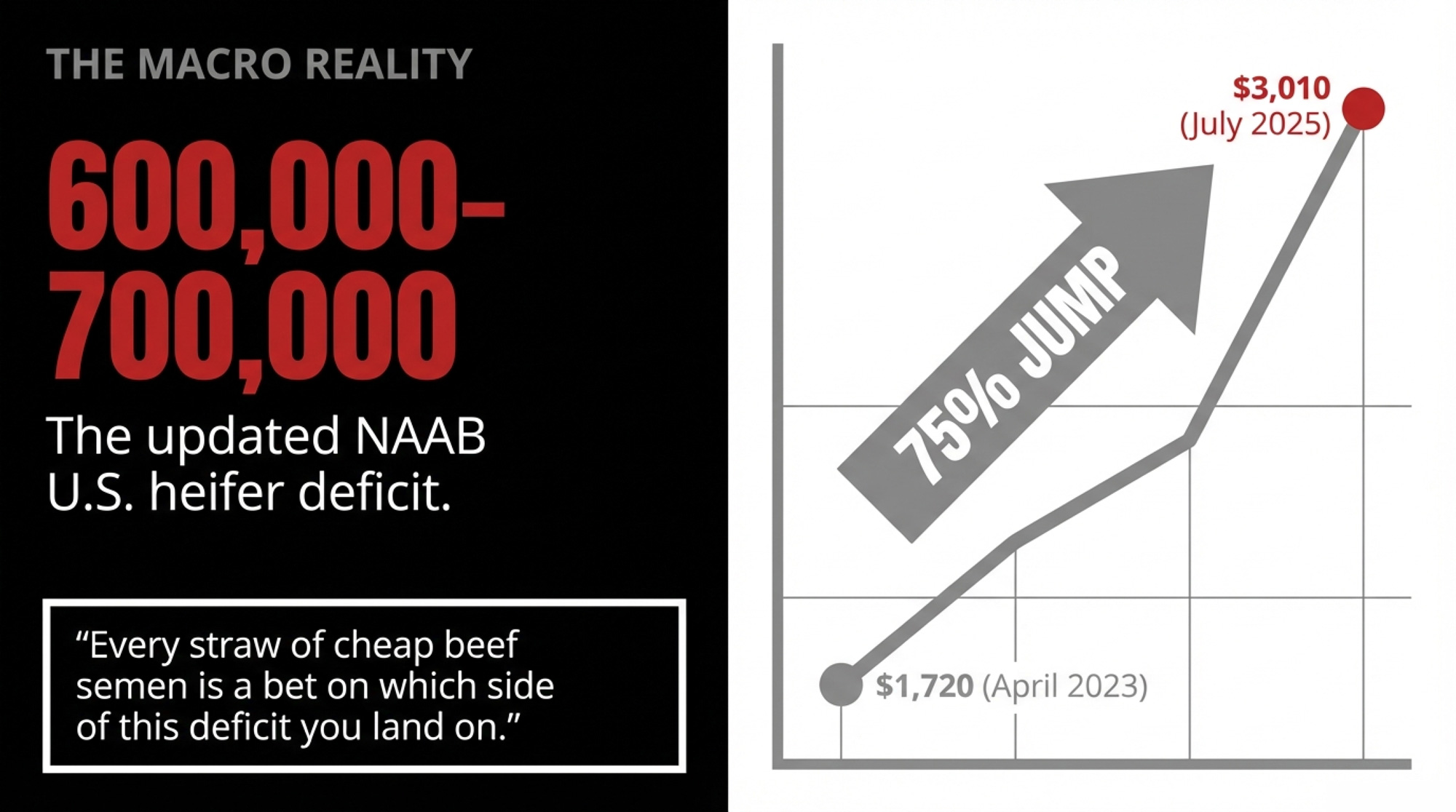

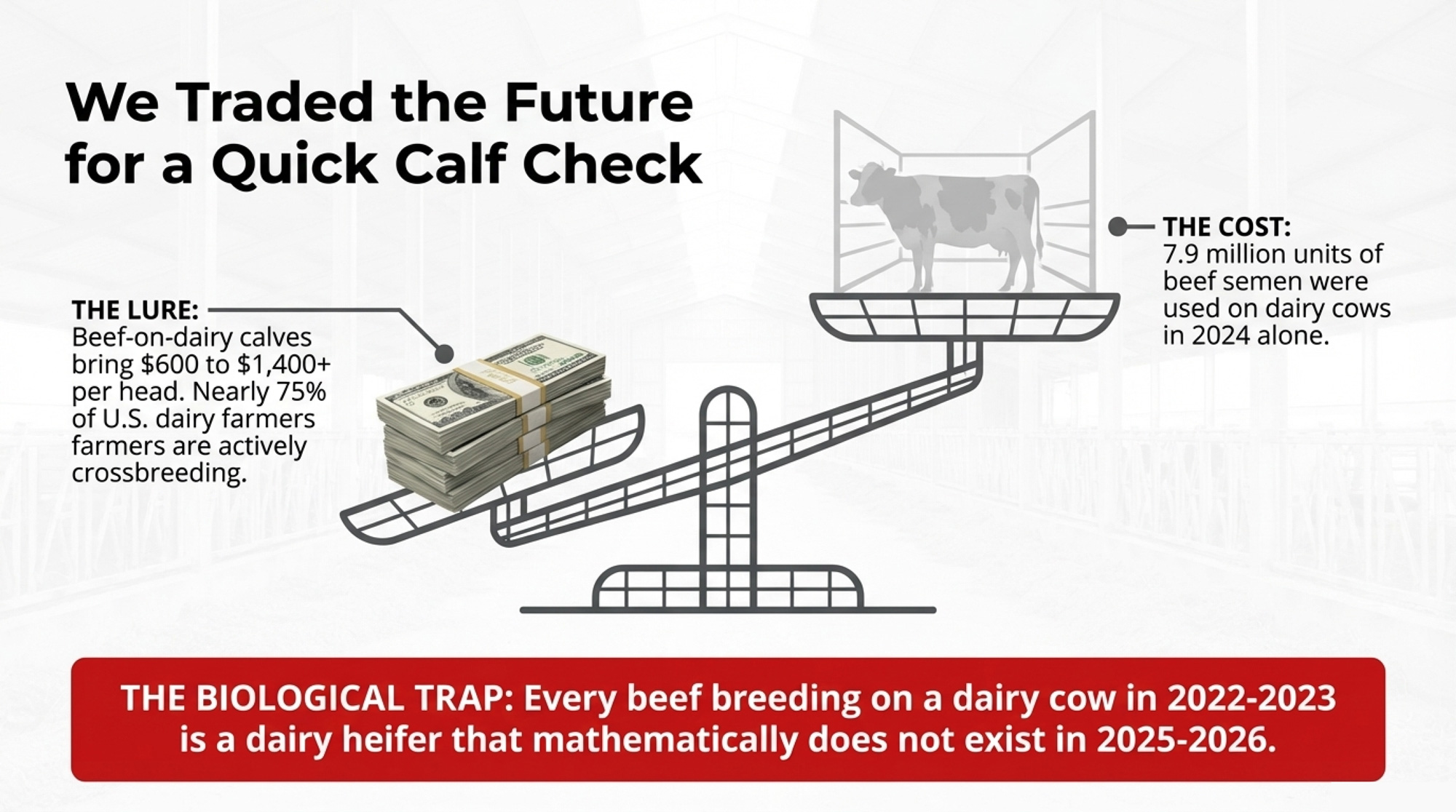

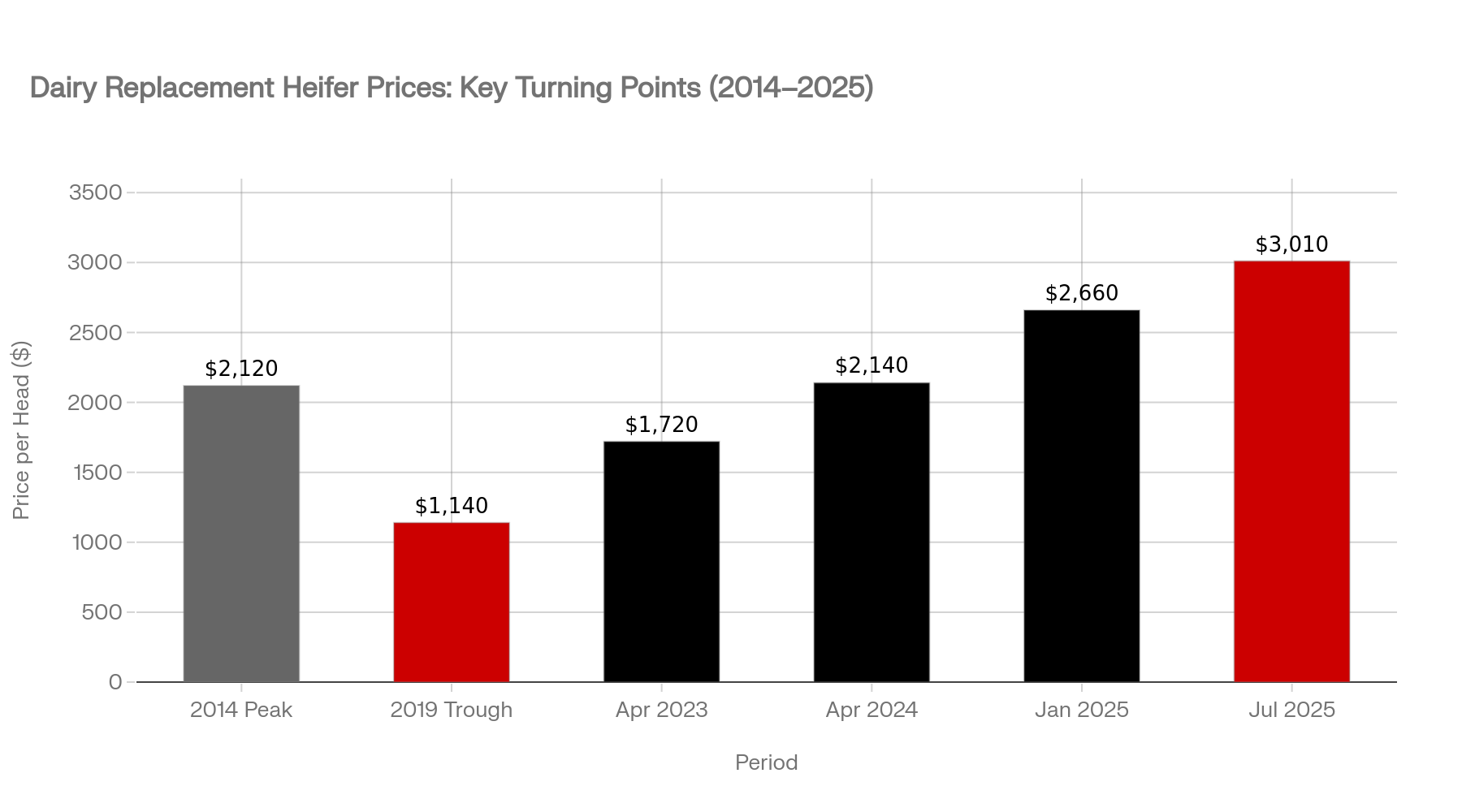

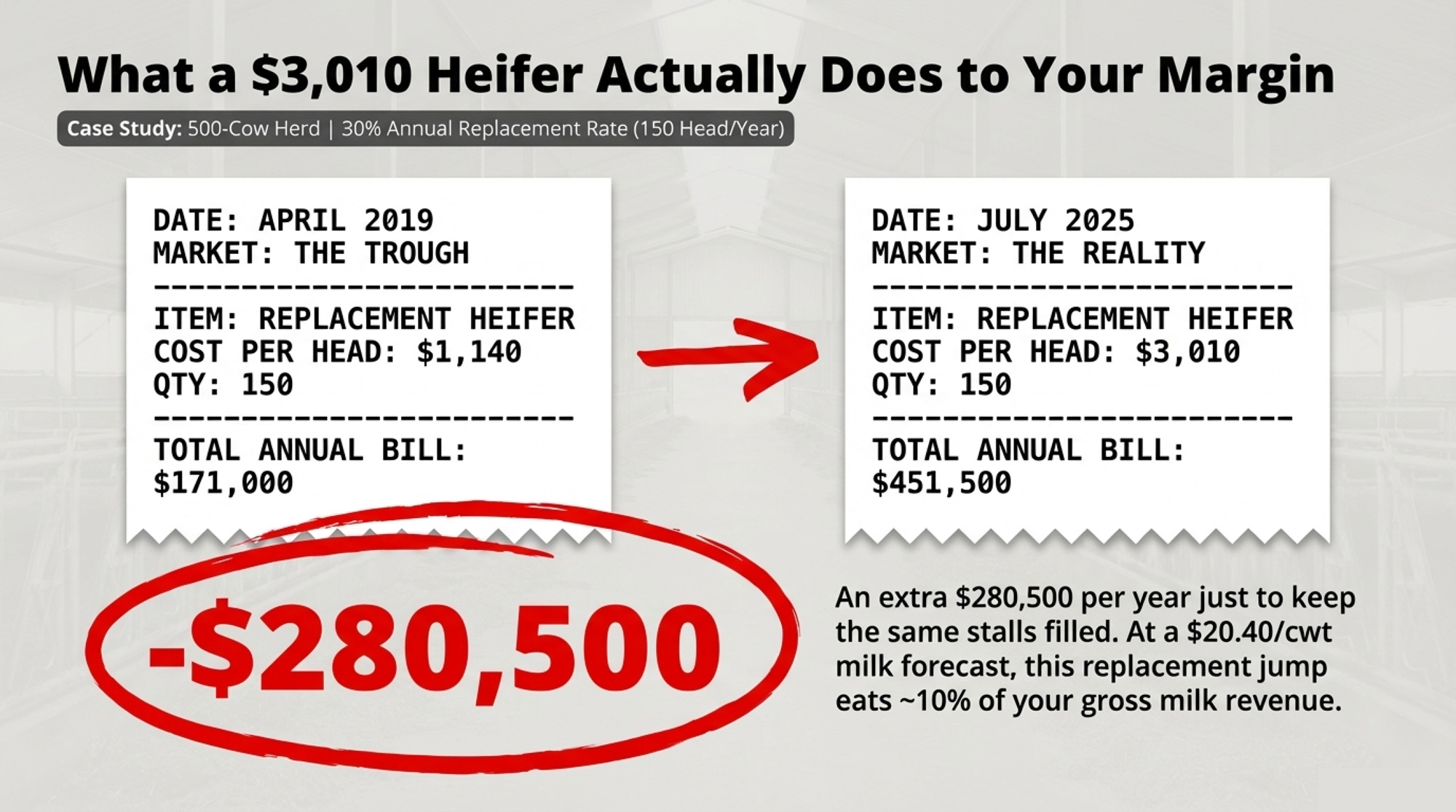

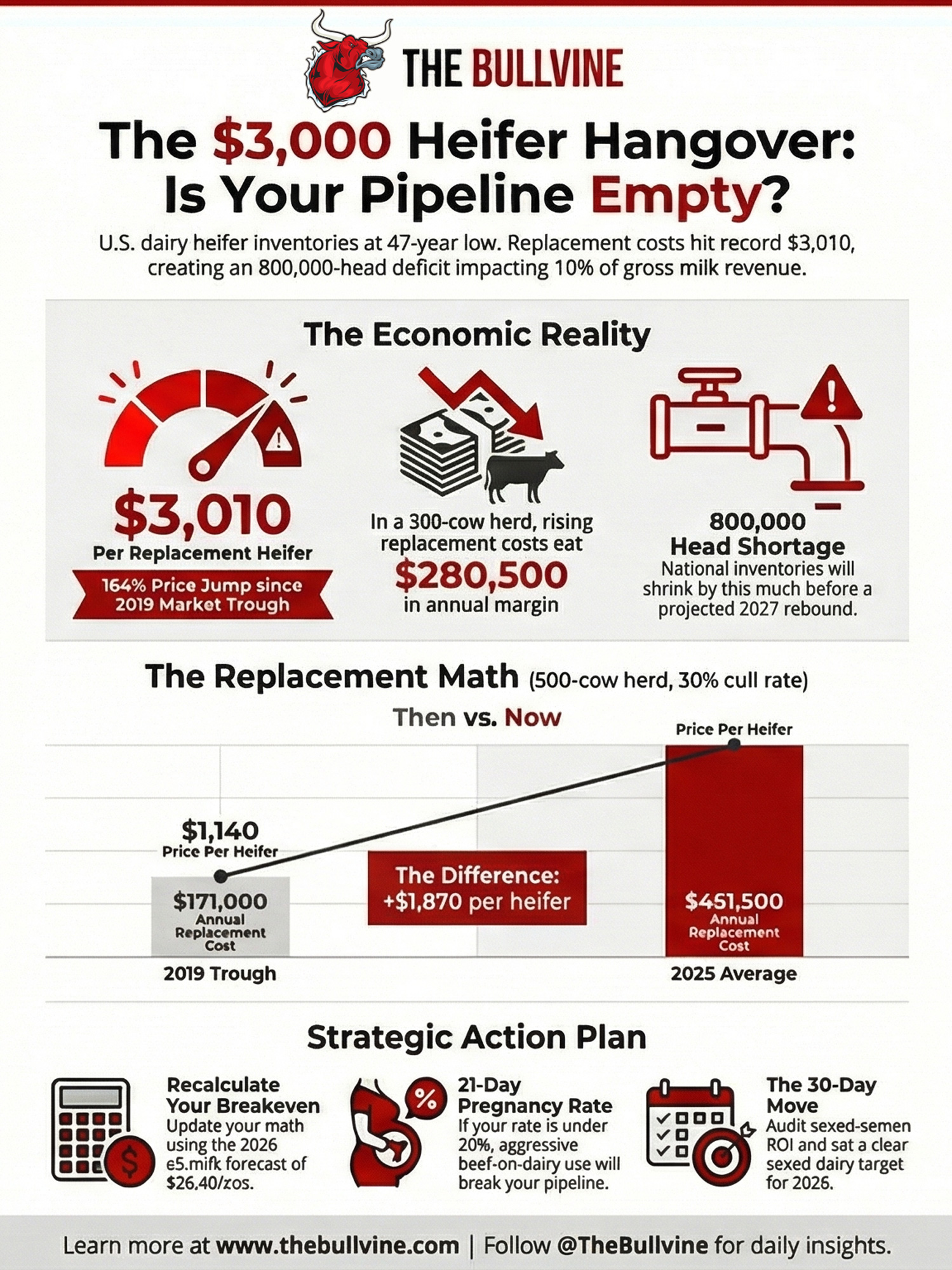

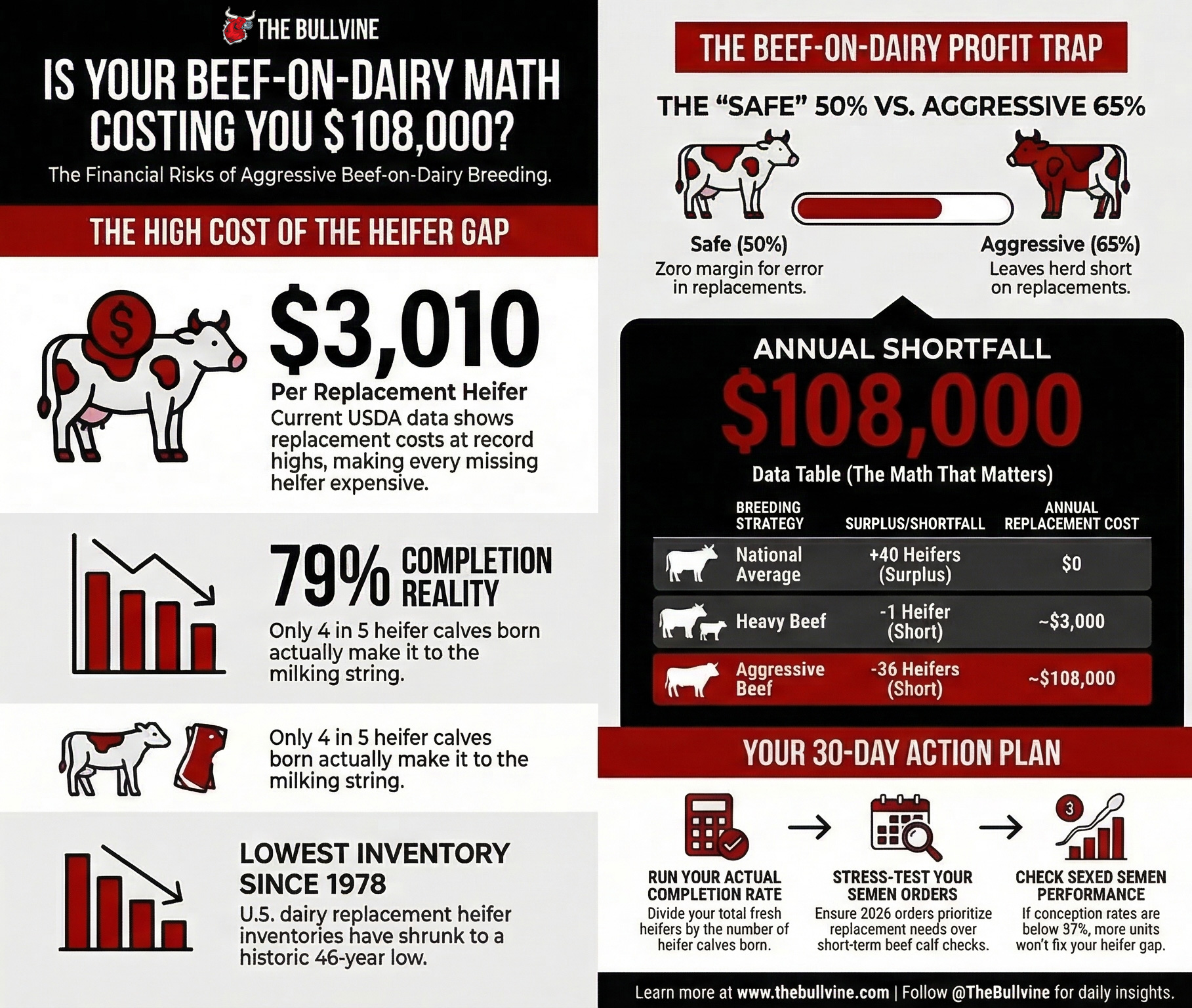

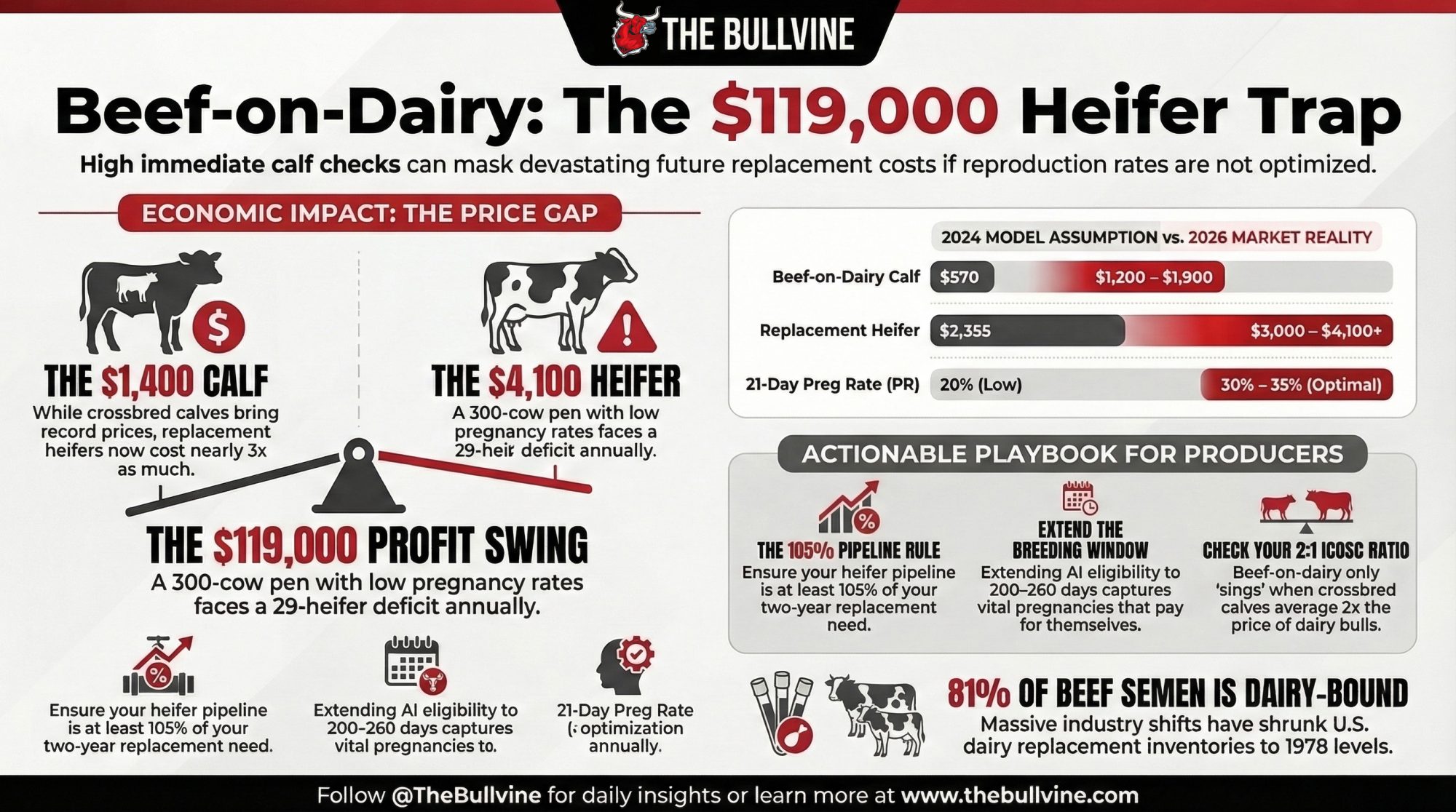

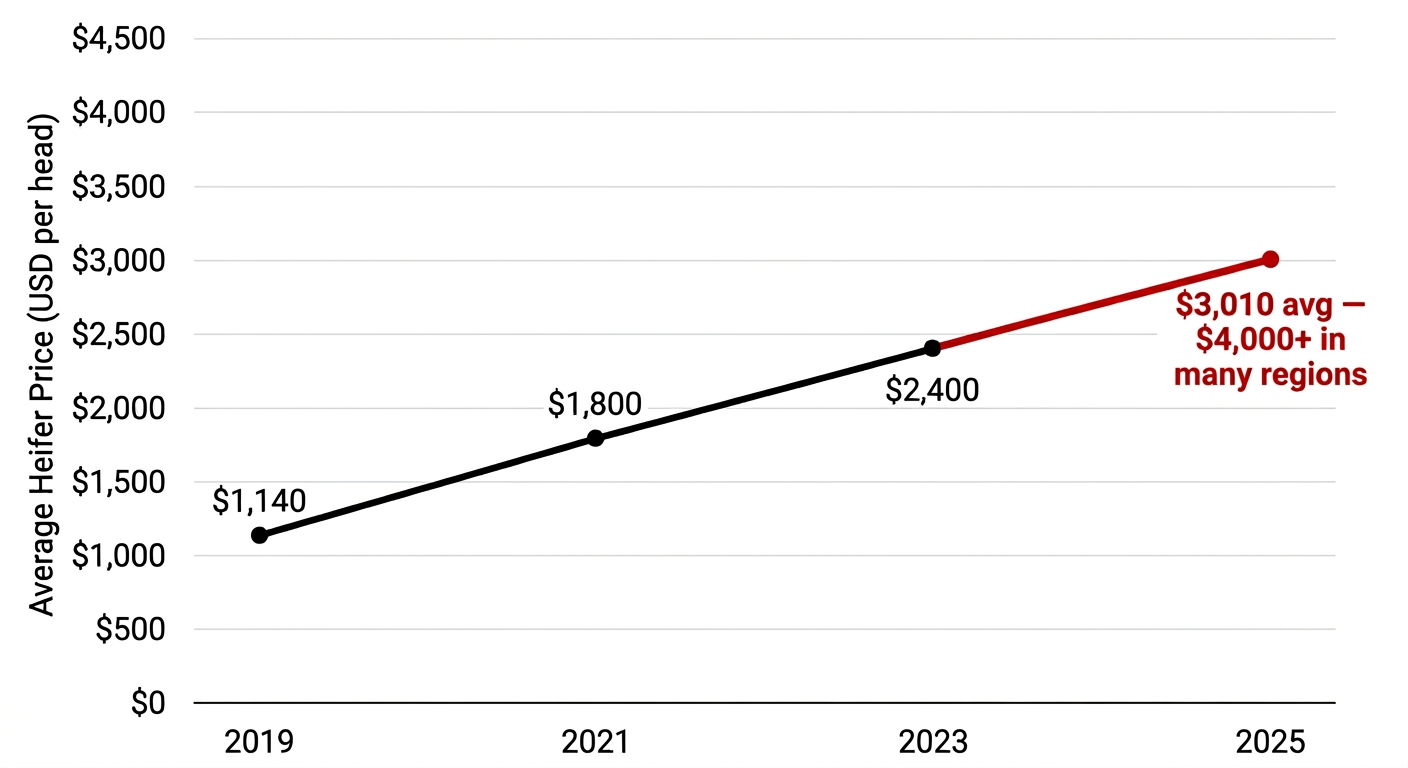

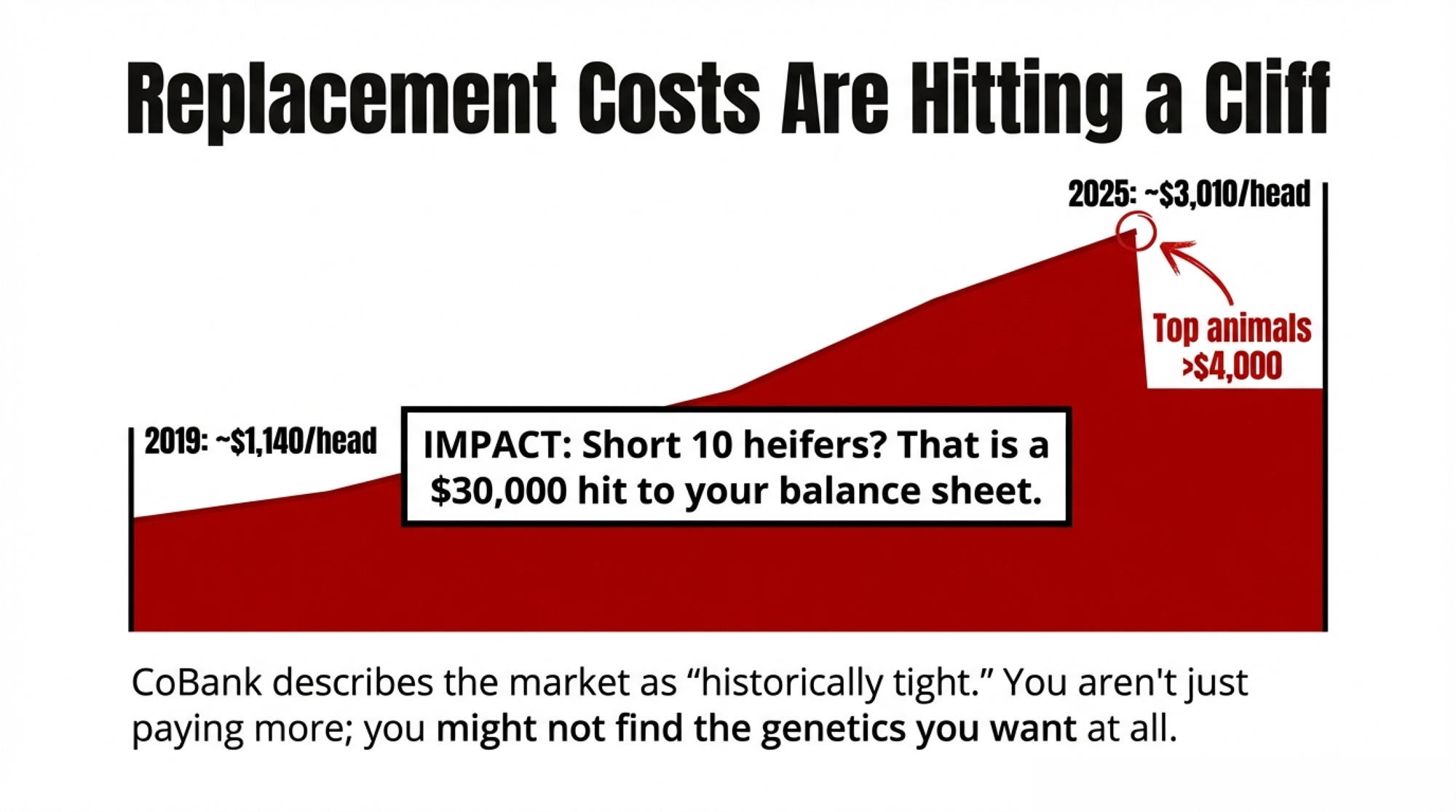

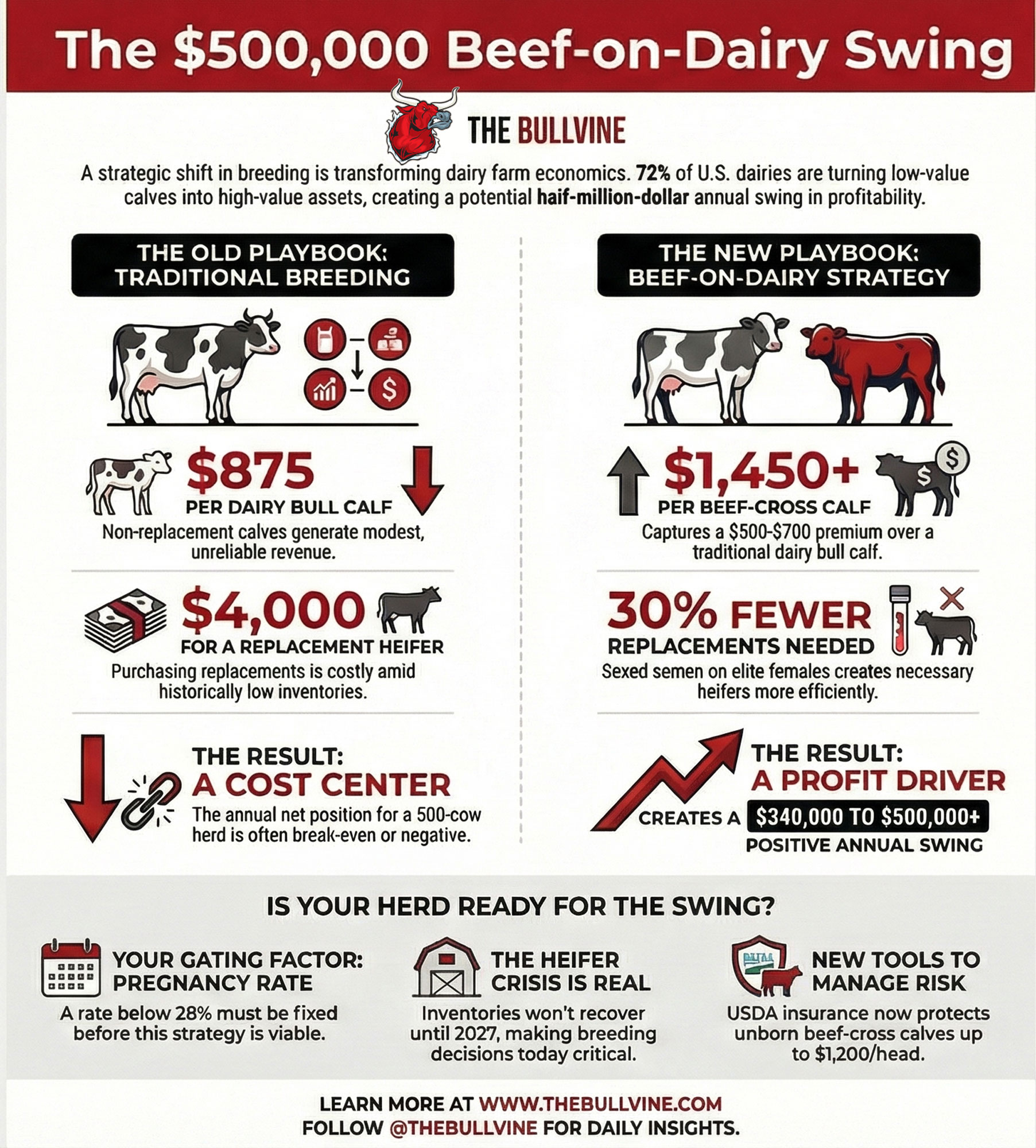

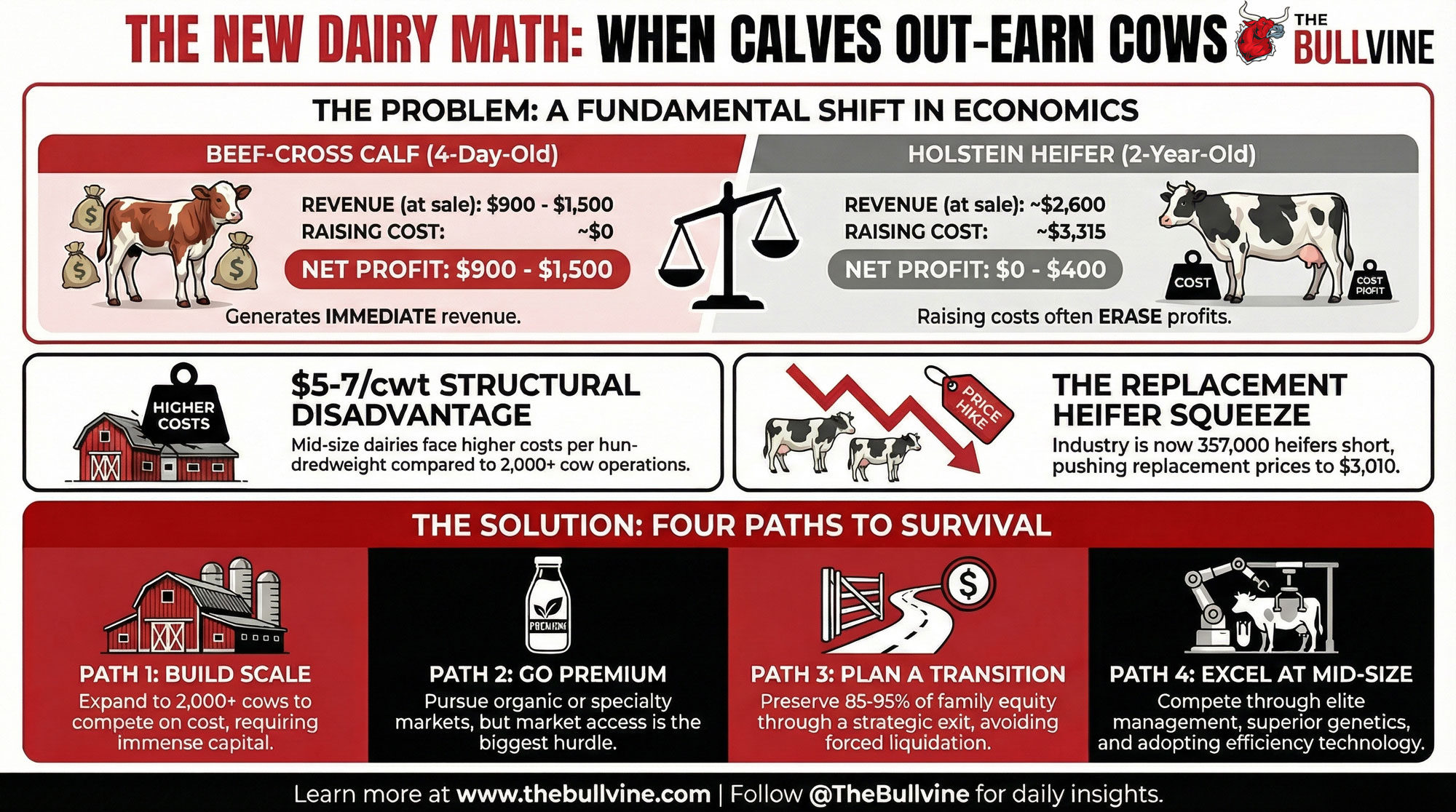

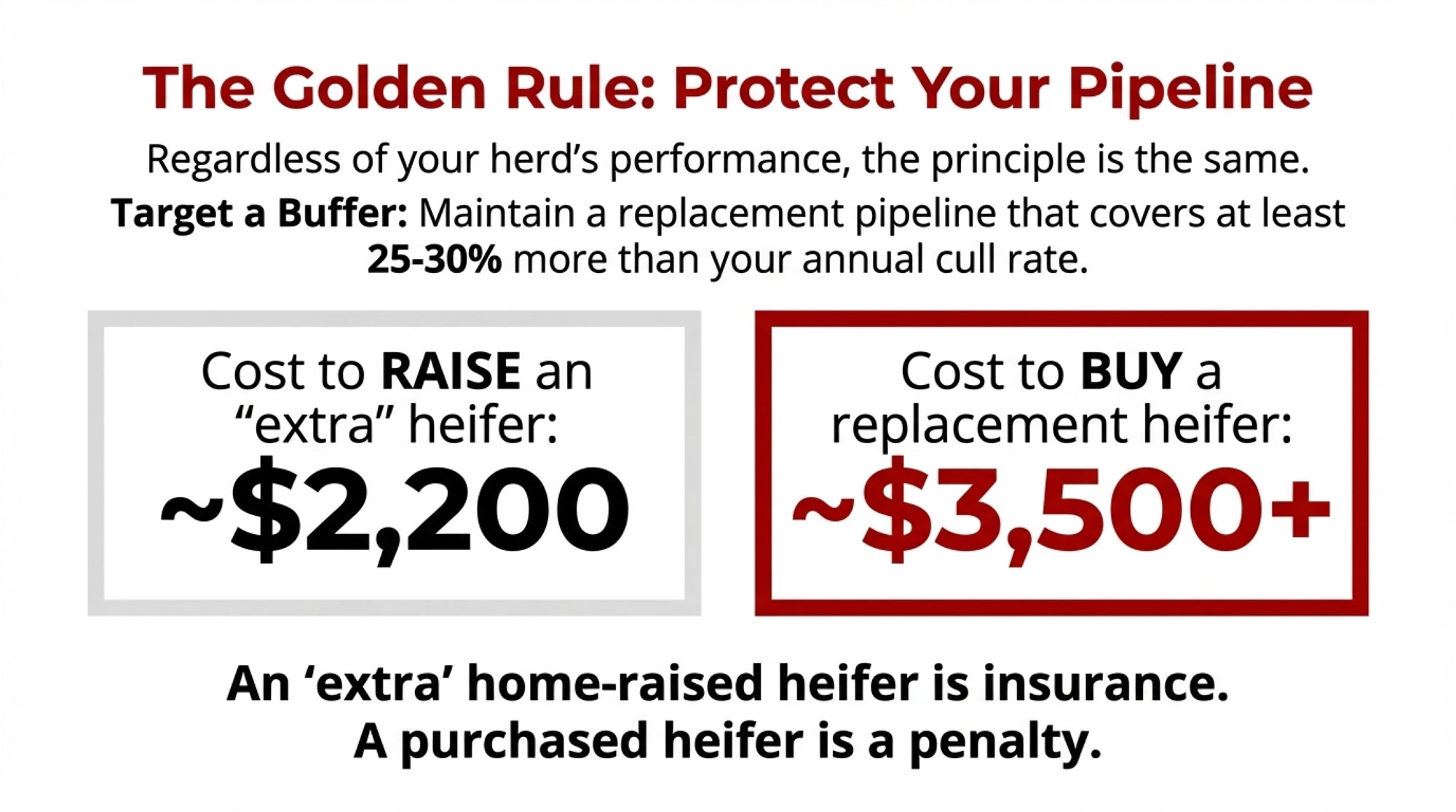

On a lot of American dairies this Fourth of July, that calf check isn’t a bonus — it’s the reason the family still owns the barn. And that’s exactly what’s worth pausing on. Independence you didn’t quite decide to buy can turn into dependence you never saw coming. Replacement heifers now run around $3,010 a head (USDA Agricultural Prices, mid-2025), up from $1,140 back in April 2019. So every time you breed a cow that could’ve thrown a viable dairy heifer to beef instead, you’re handing over roughly $585 in expected future value (Bullvine analysis; see Methodology Note). It’s a great trade until it isn’t. And most farms never sat down and decided to lean this hard on the calf check — they slid into it, one semen straw and one good sale barn check at a time.

From Throwaway to Half the Check

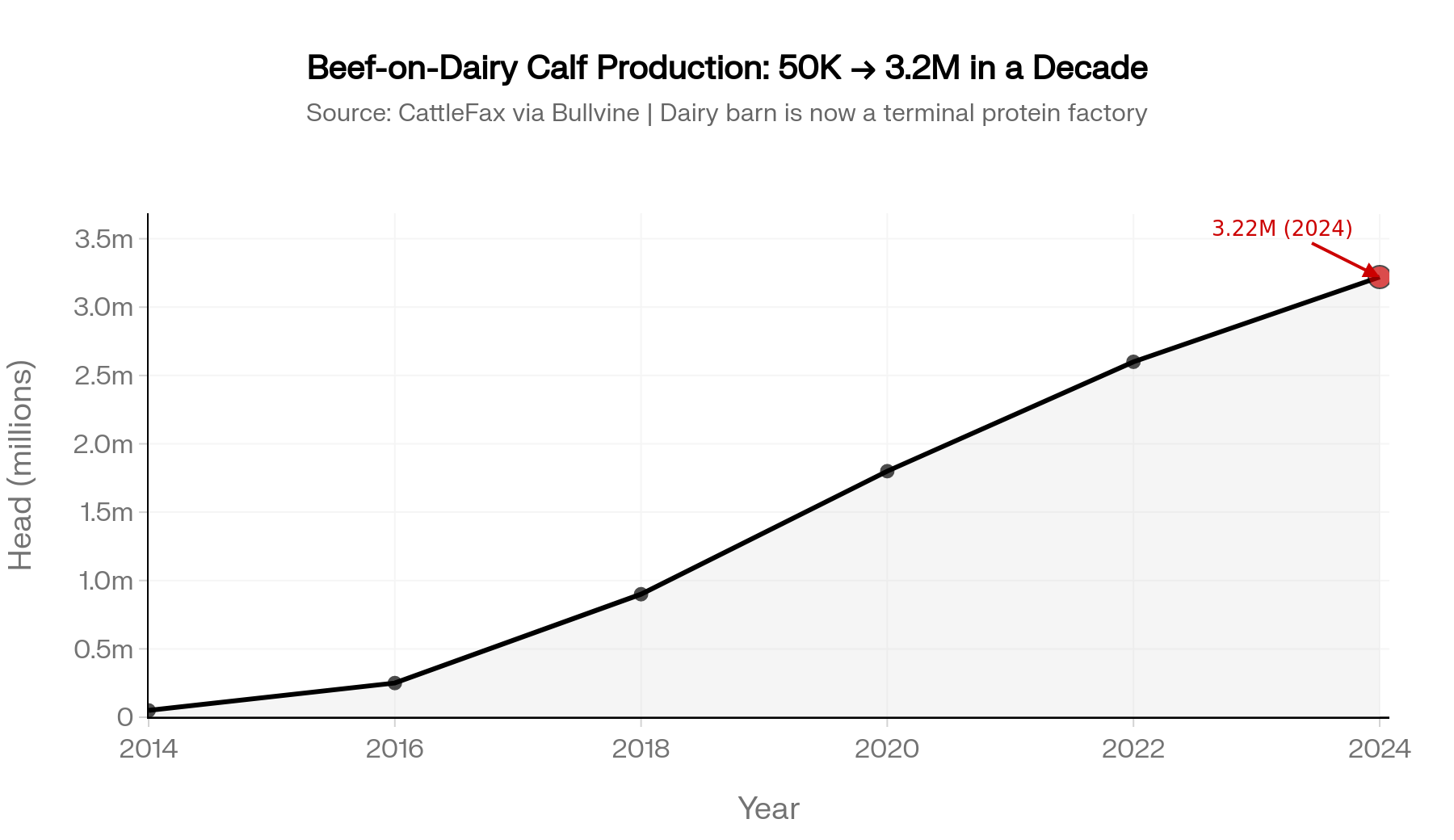

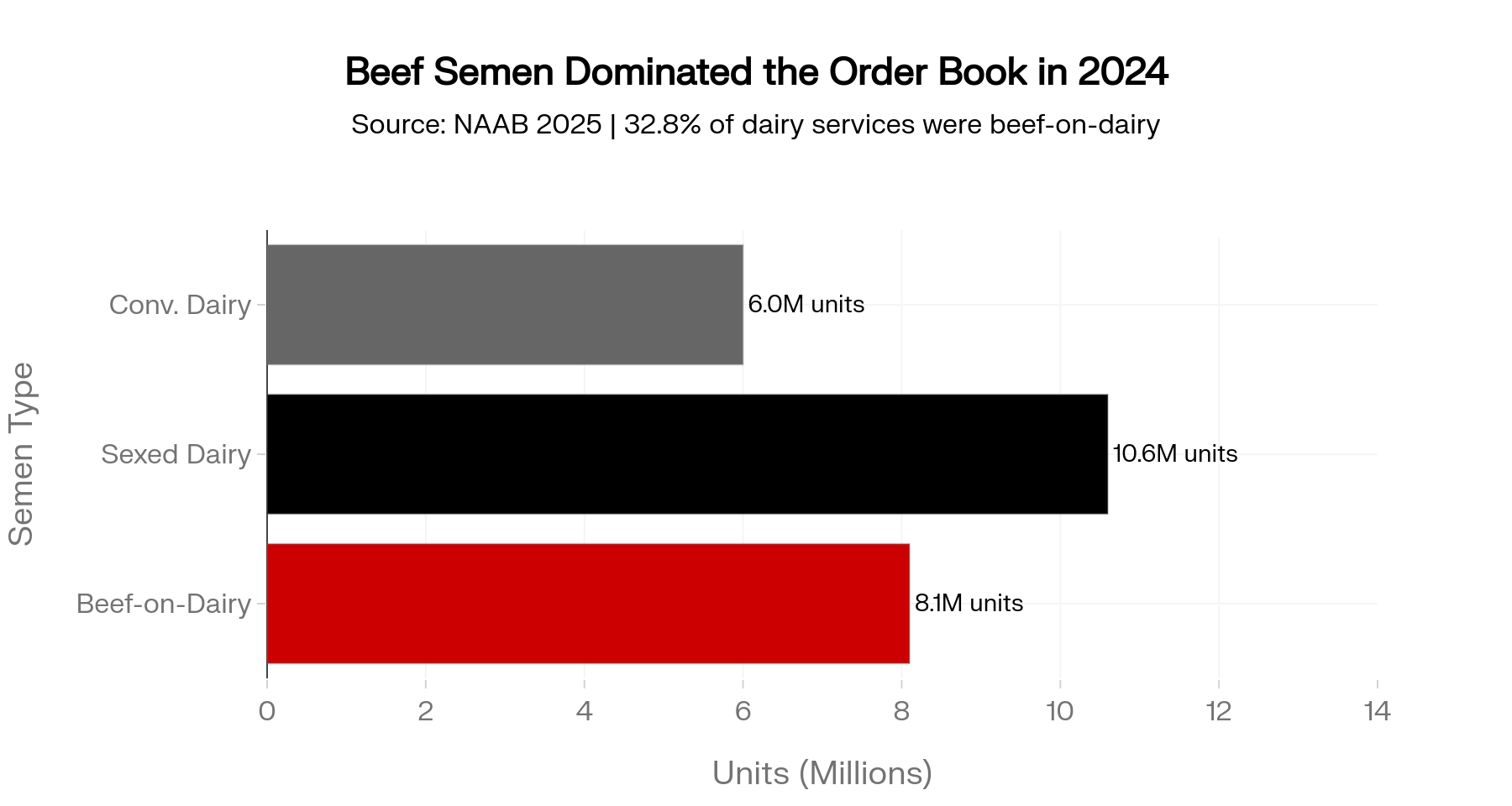

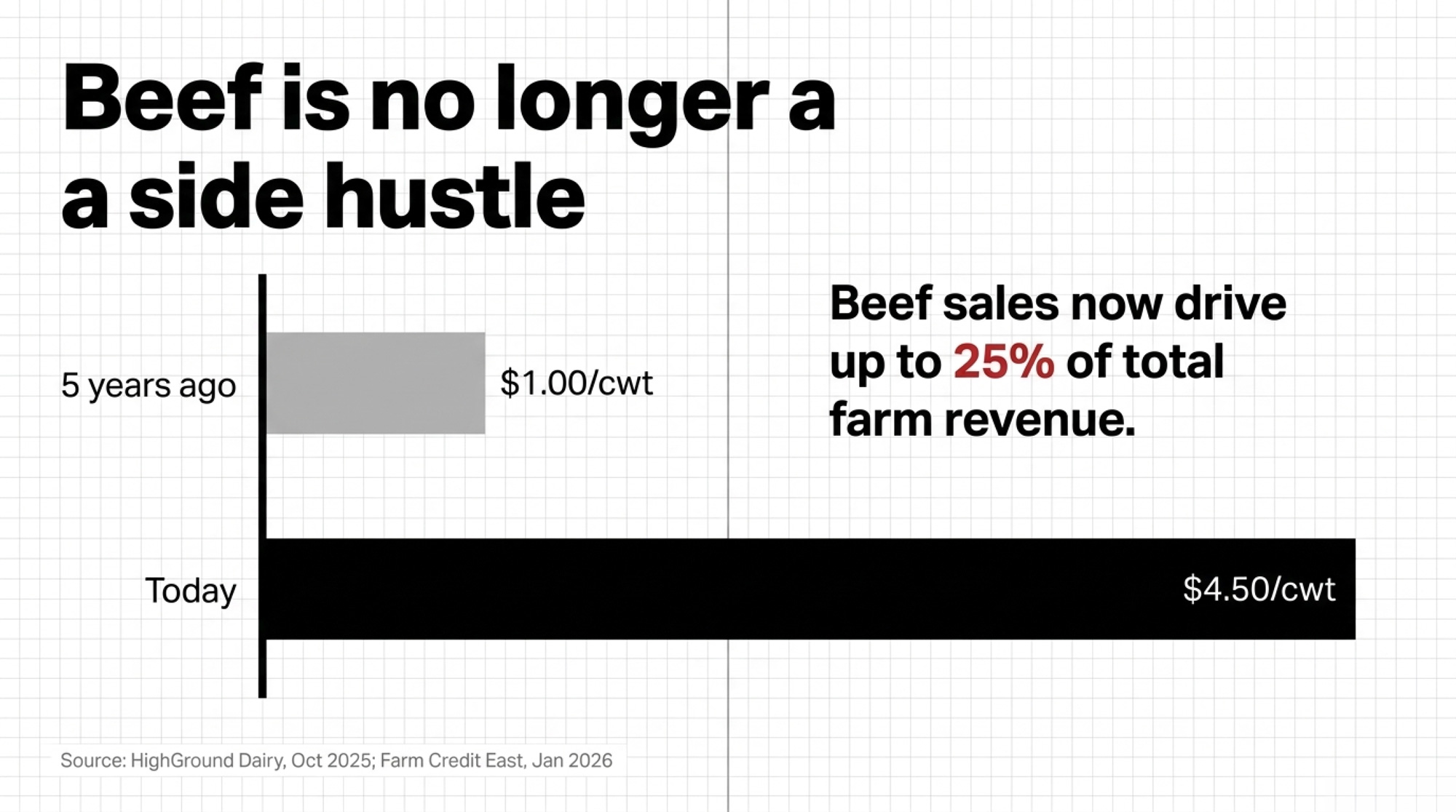

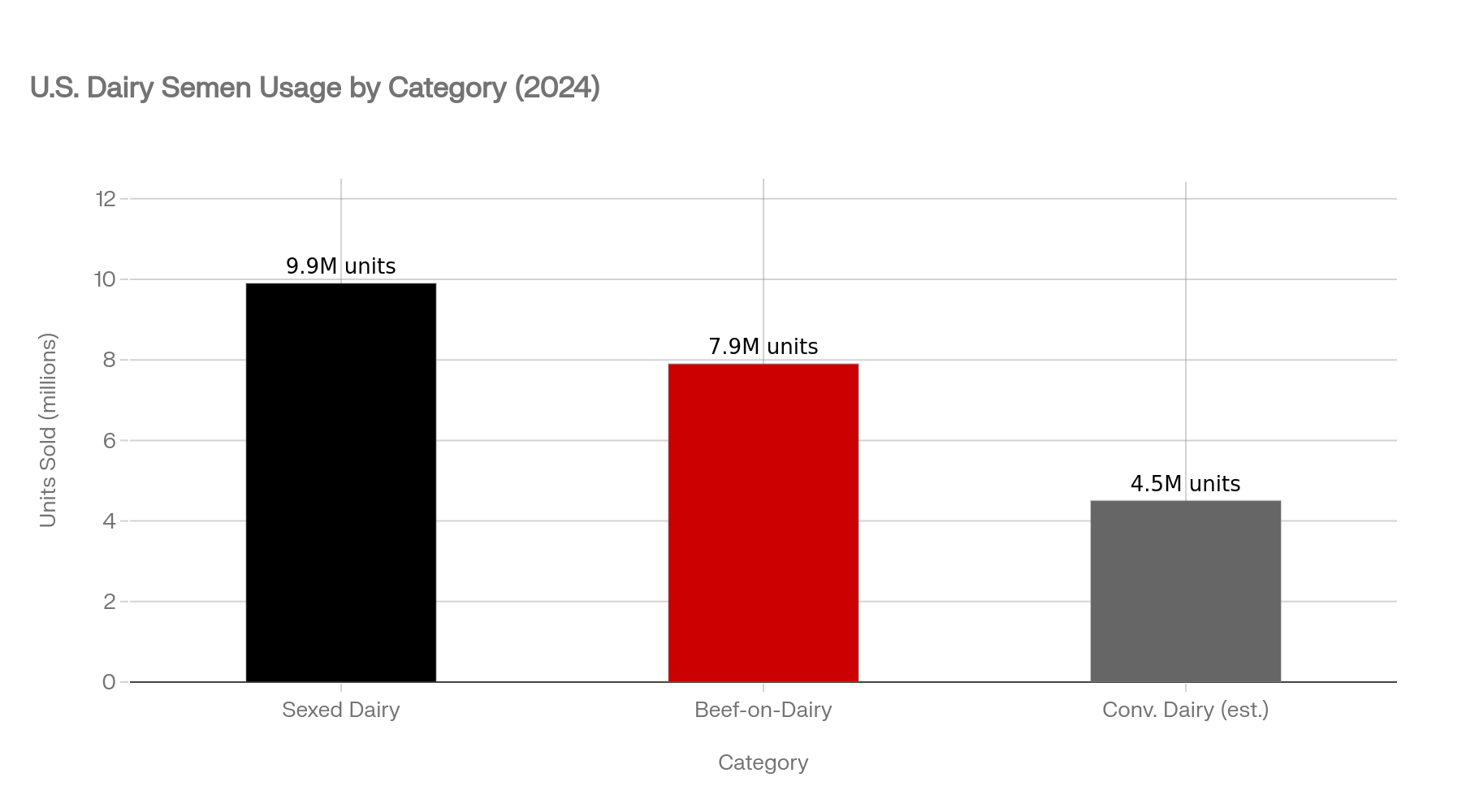

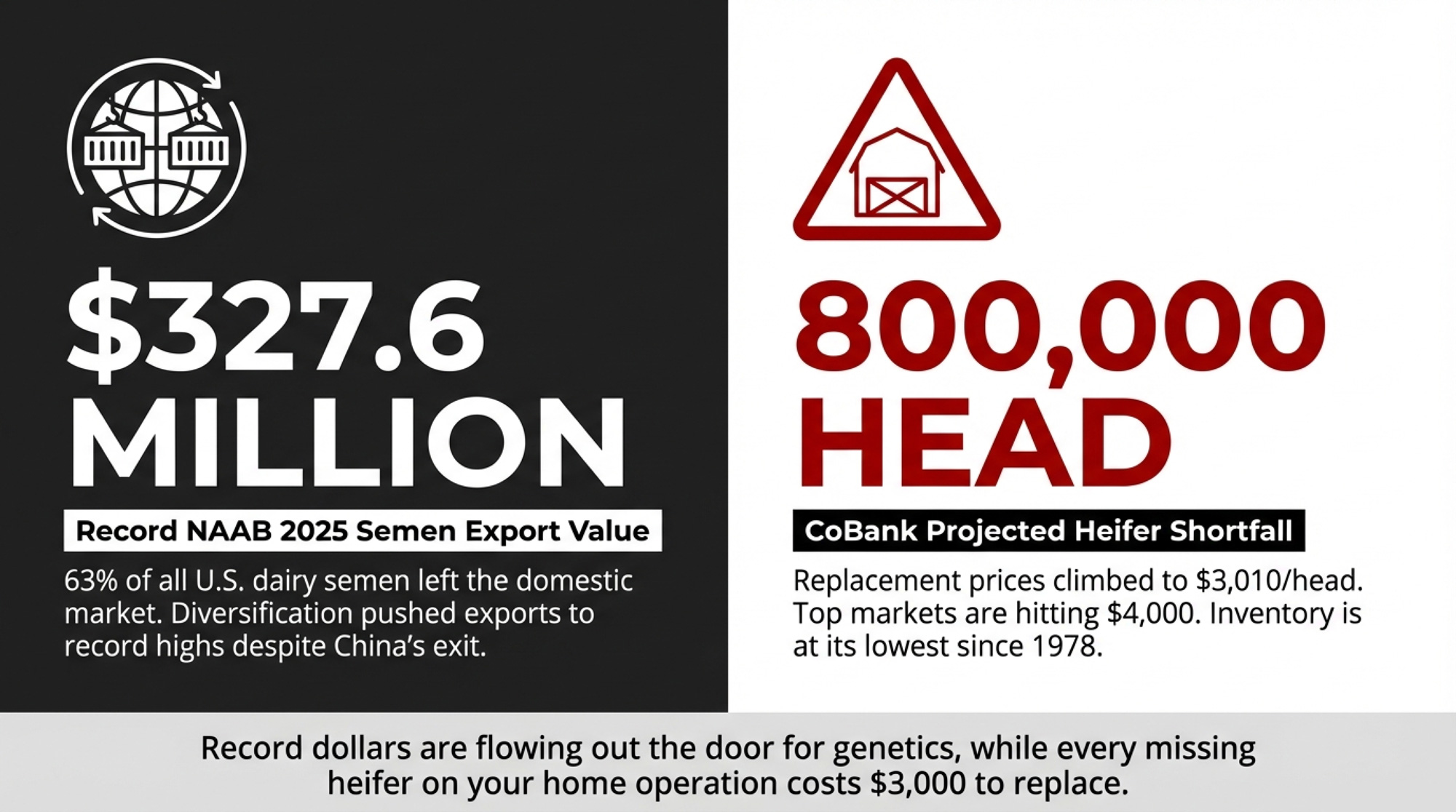

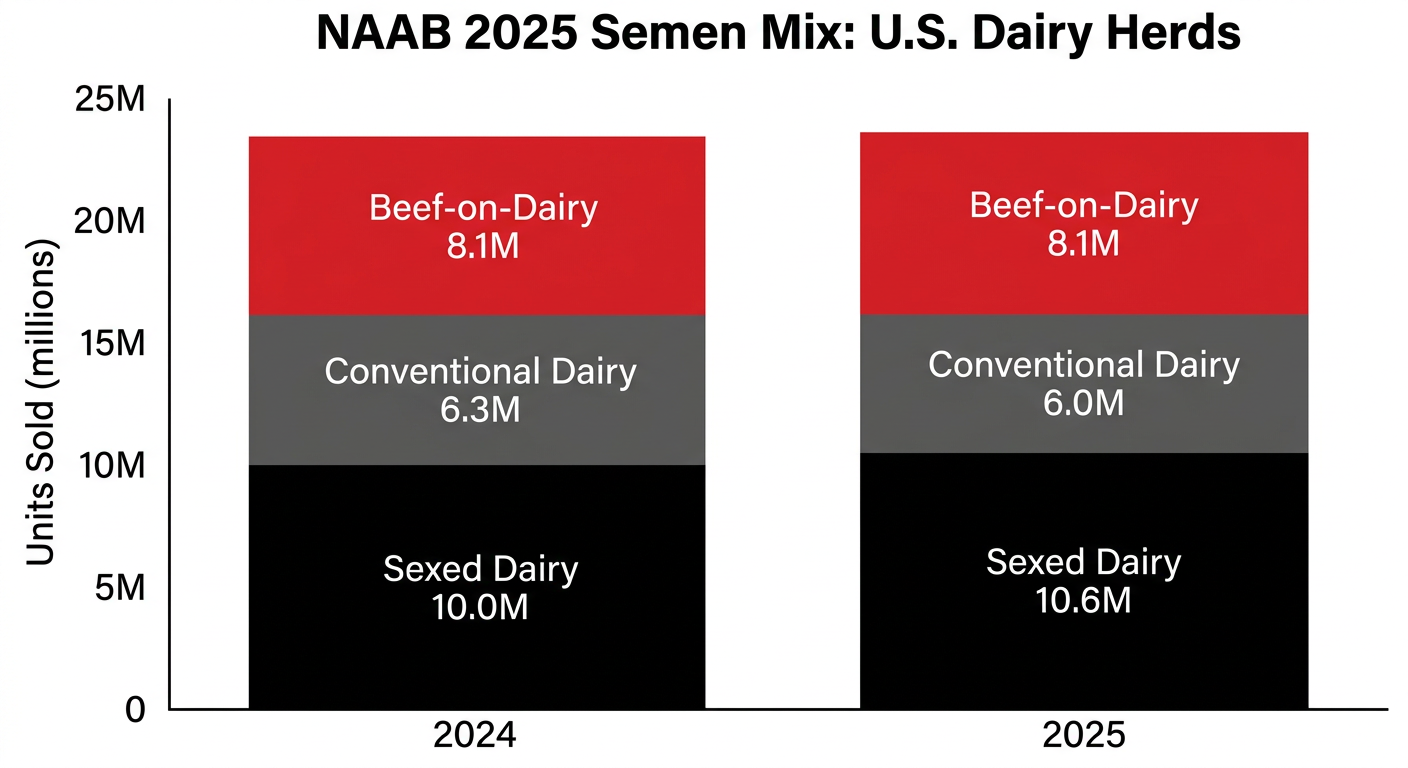

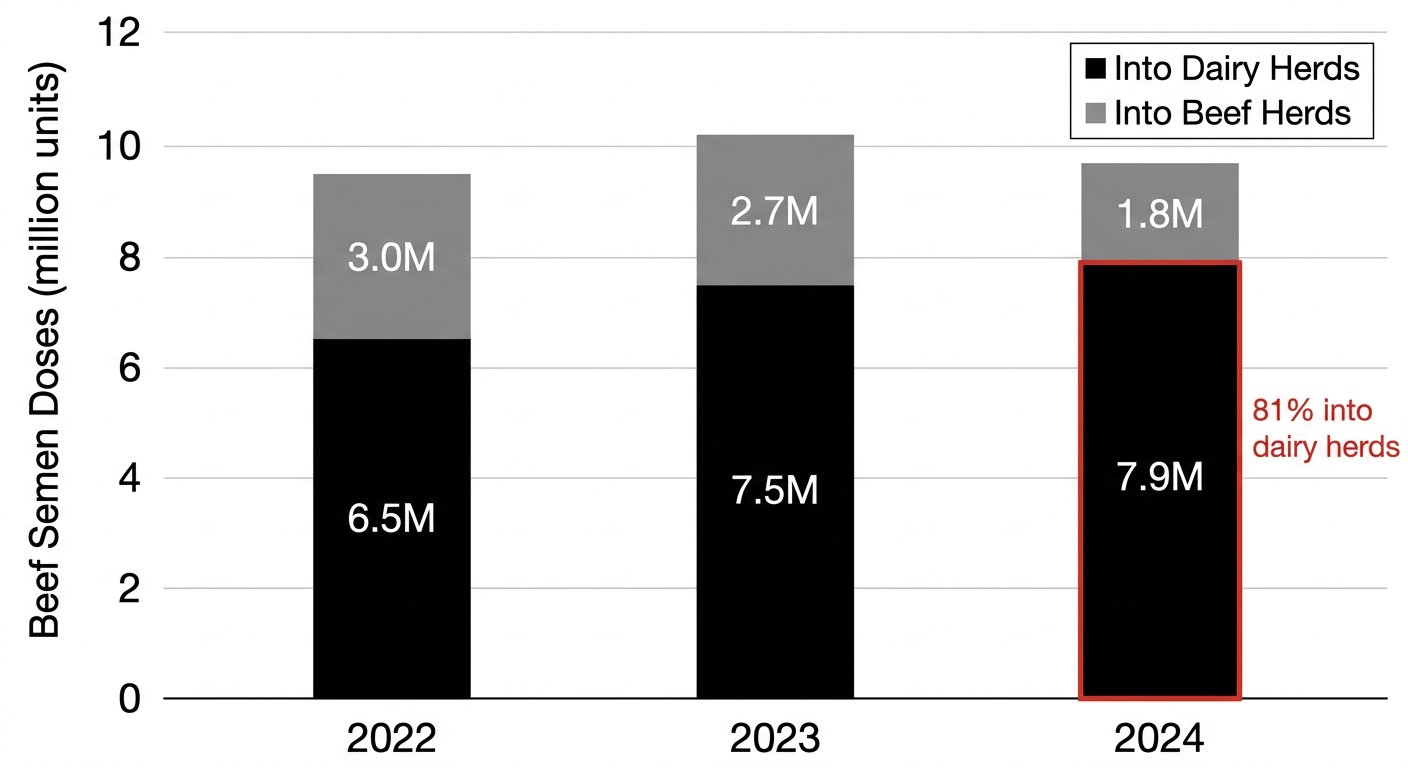

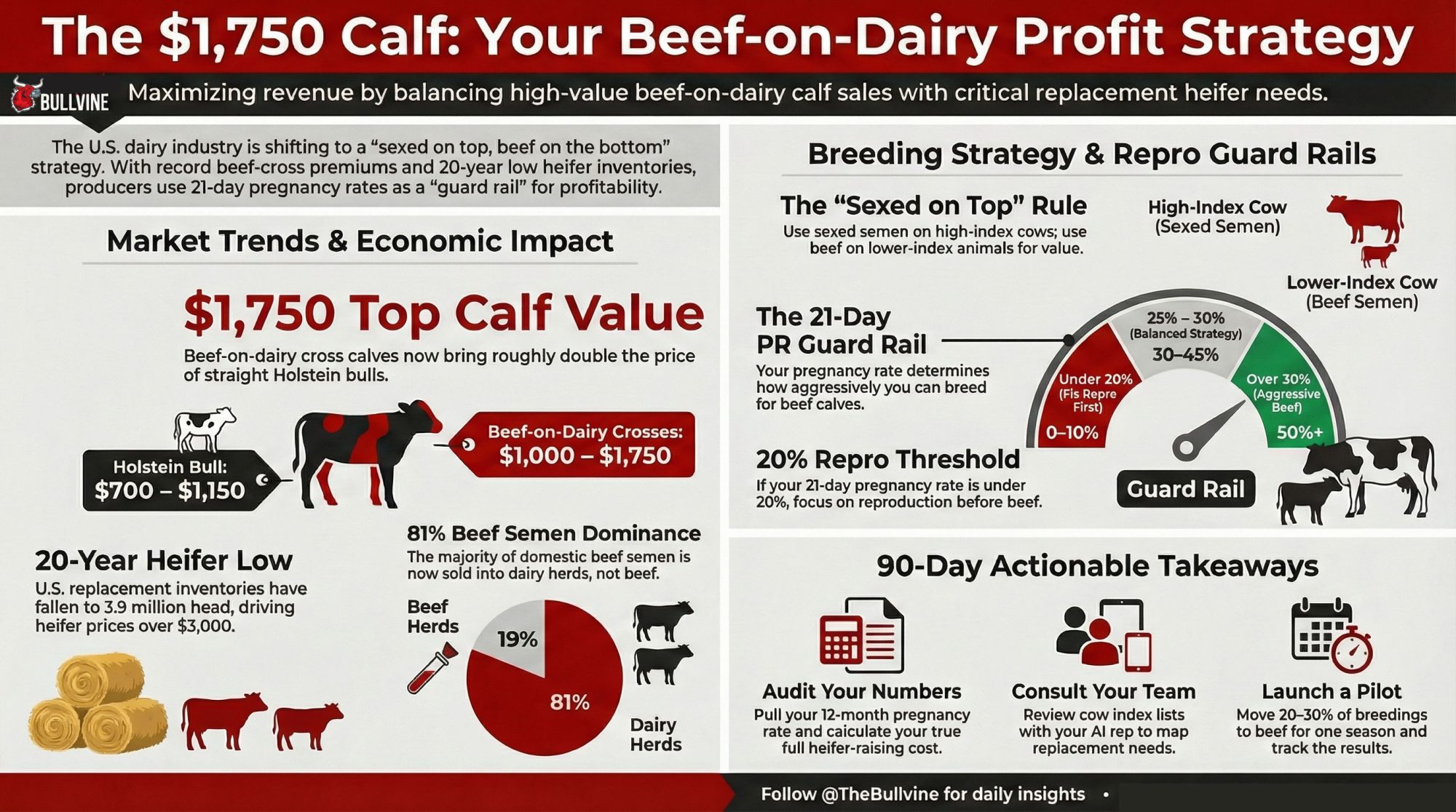

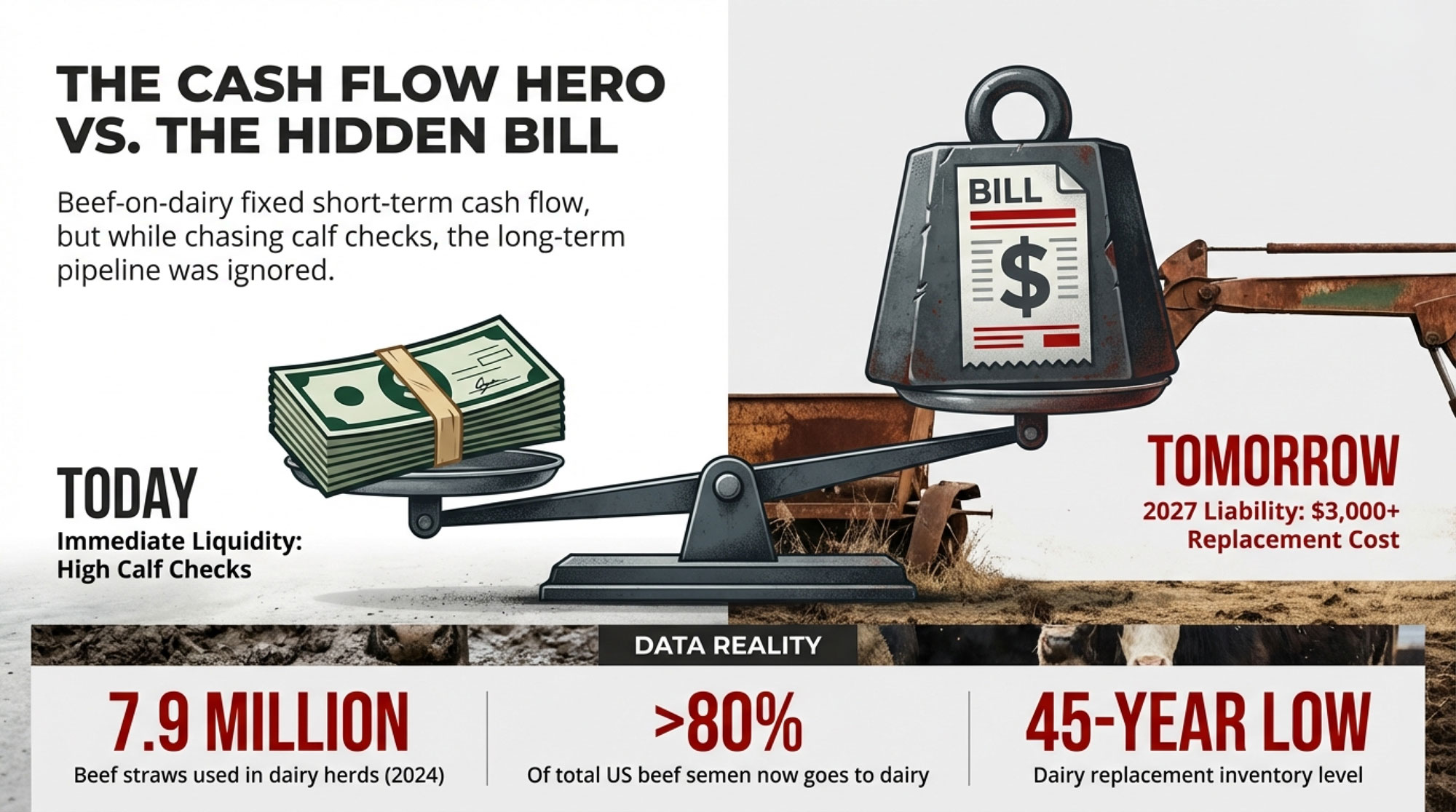

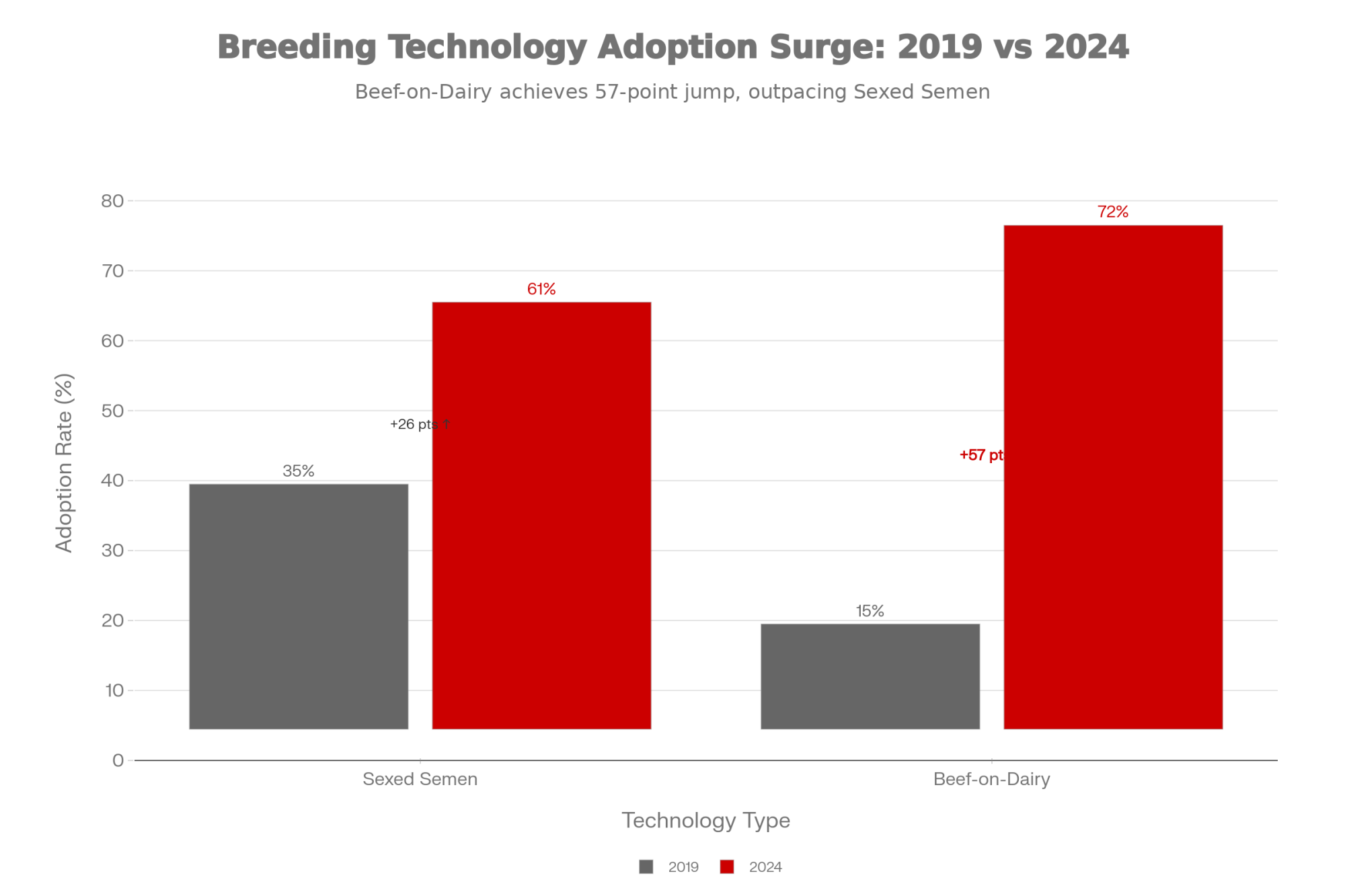

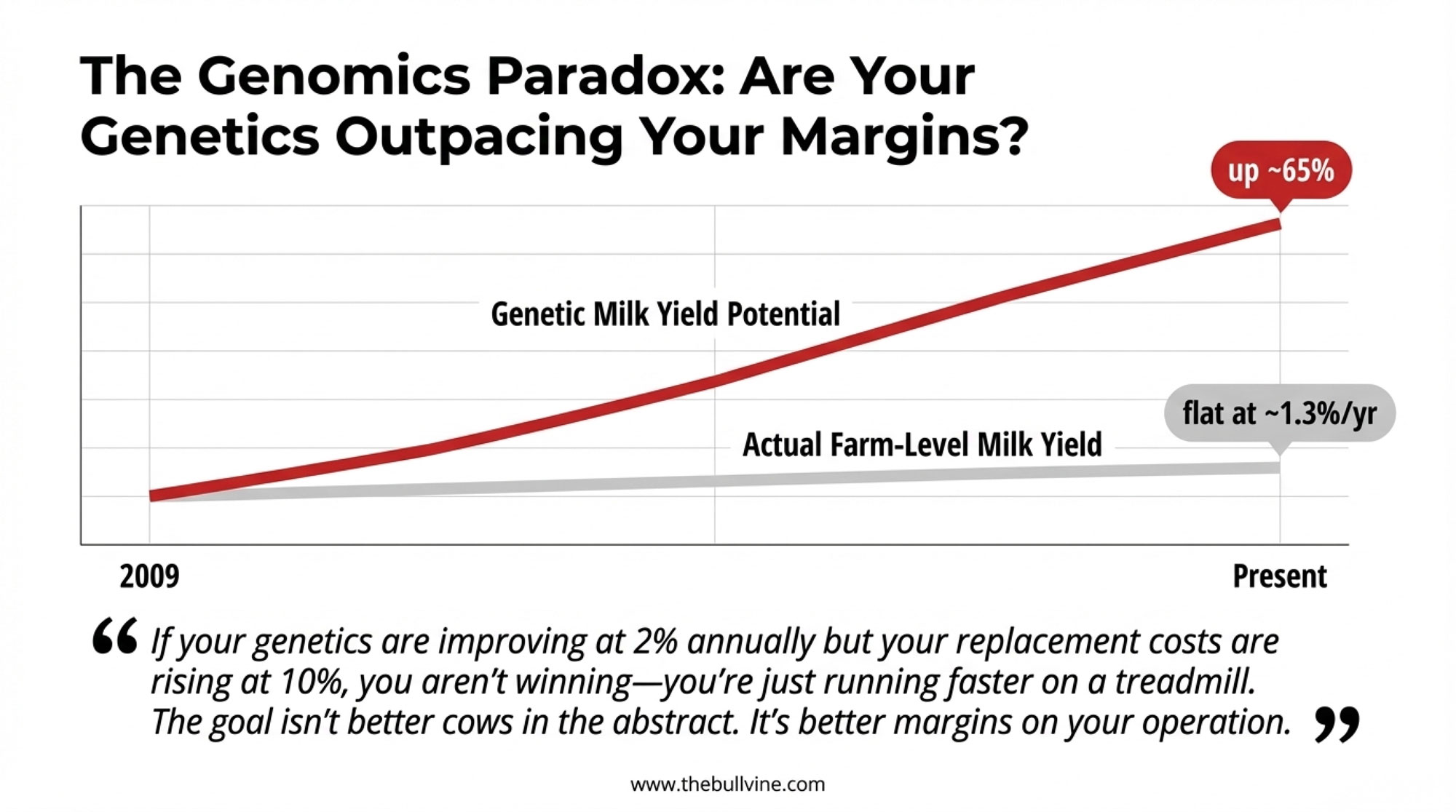

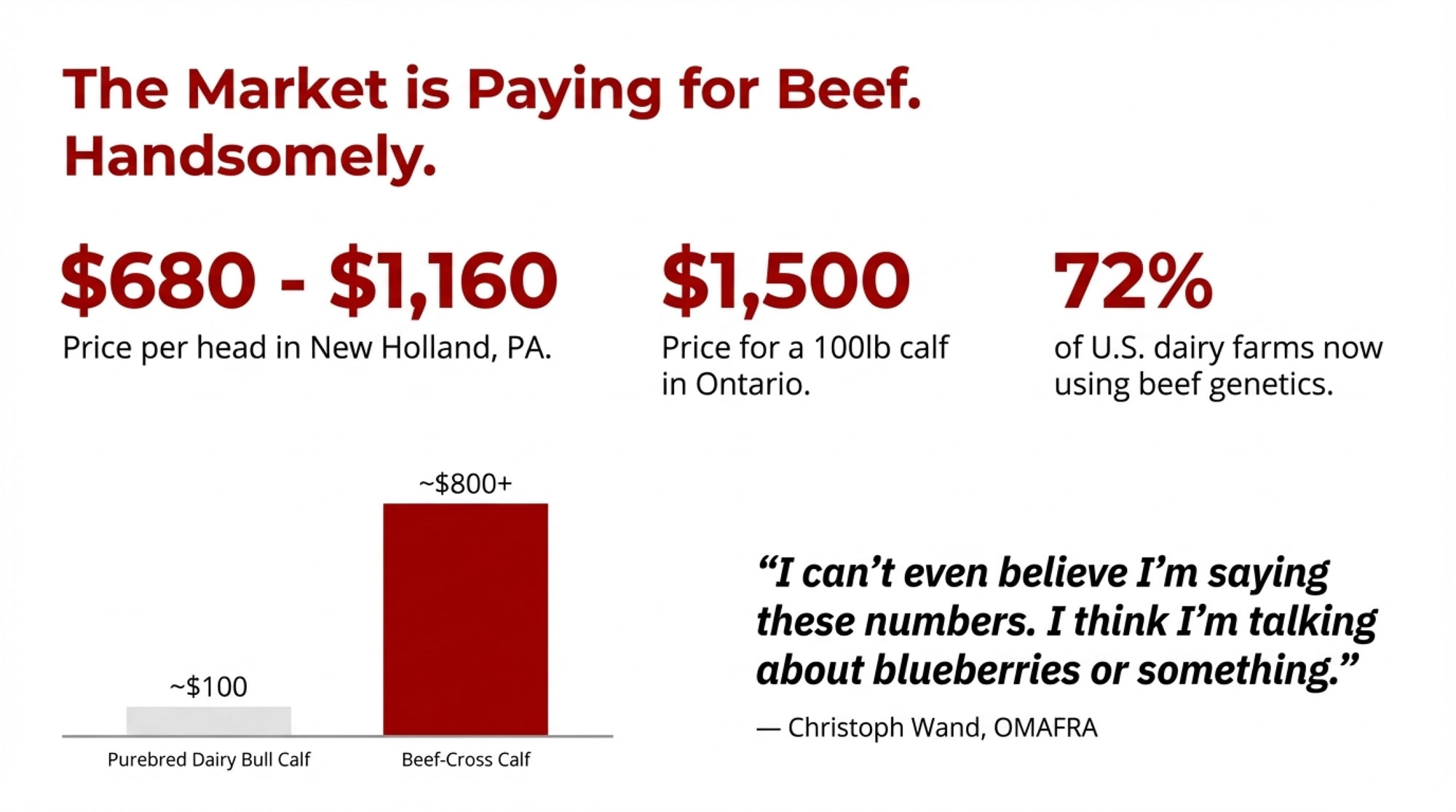

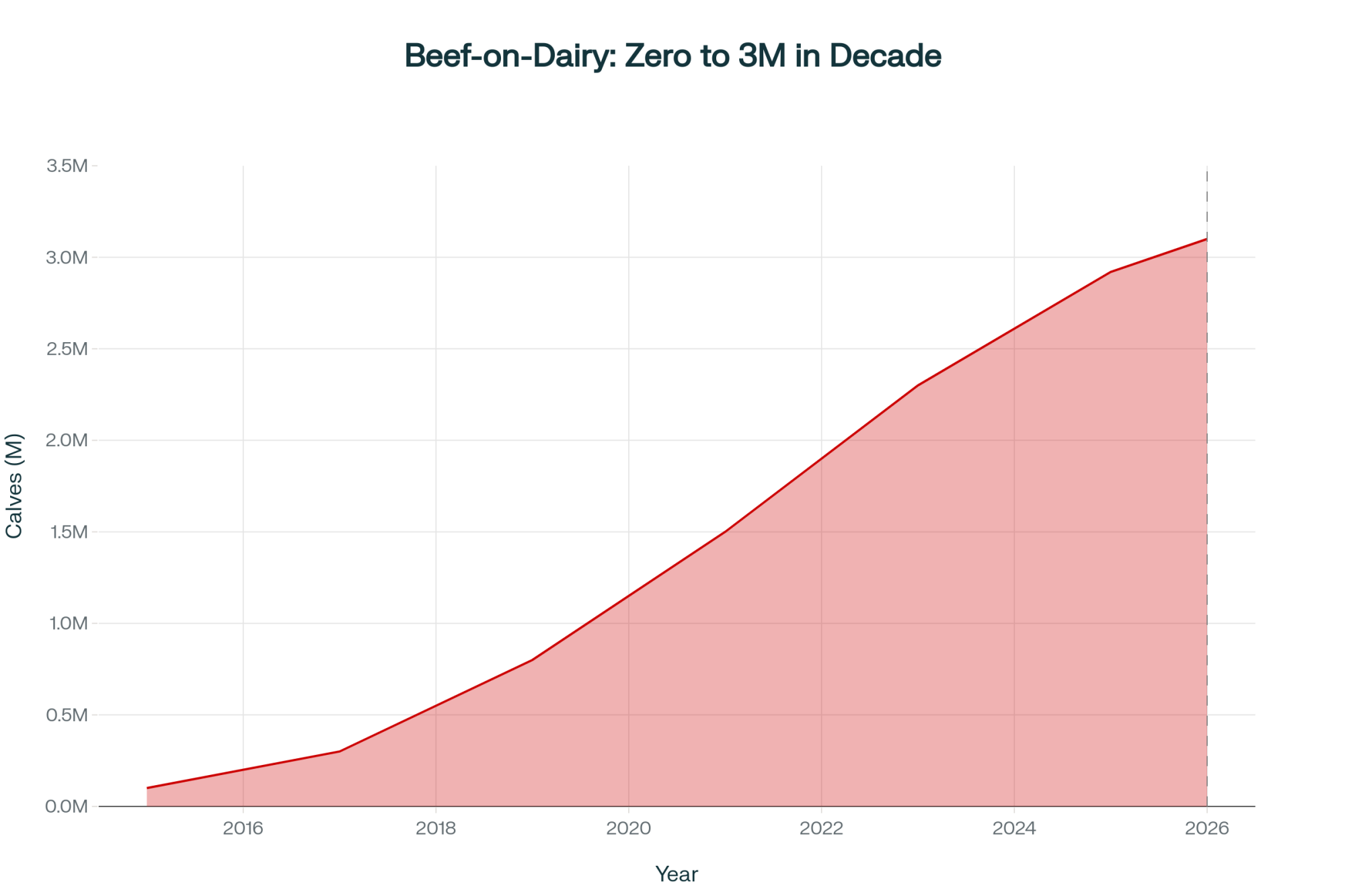

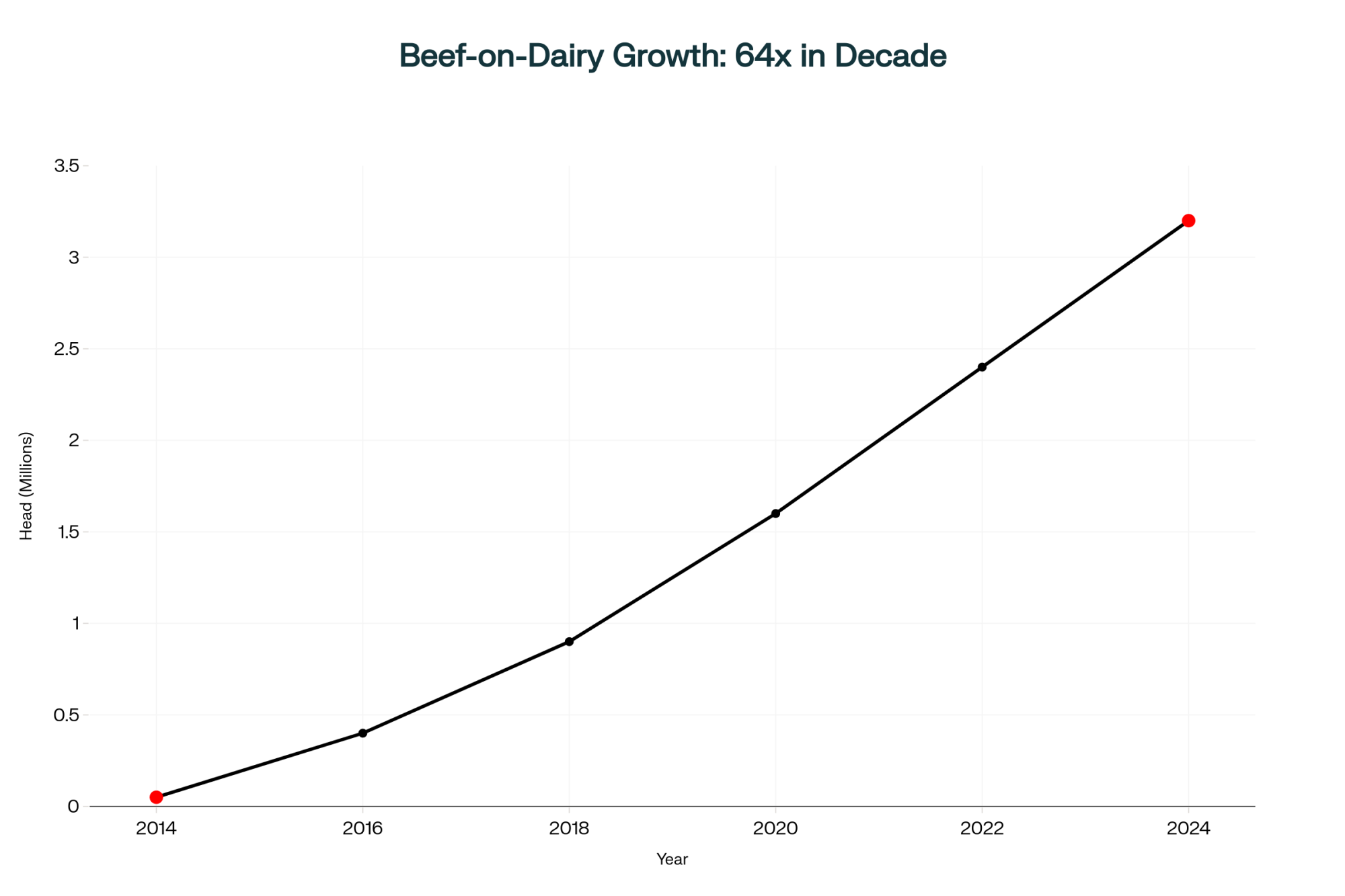

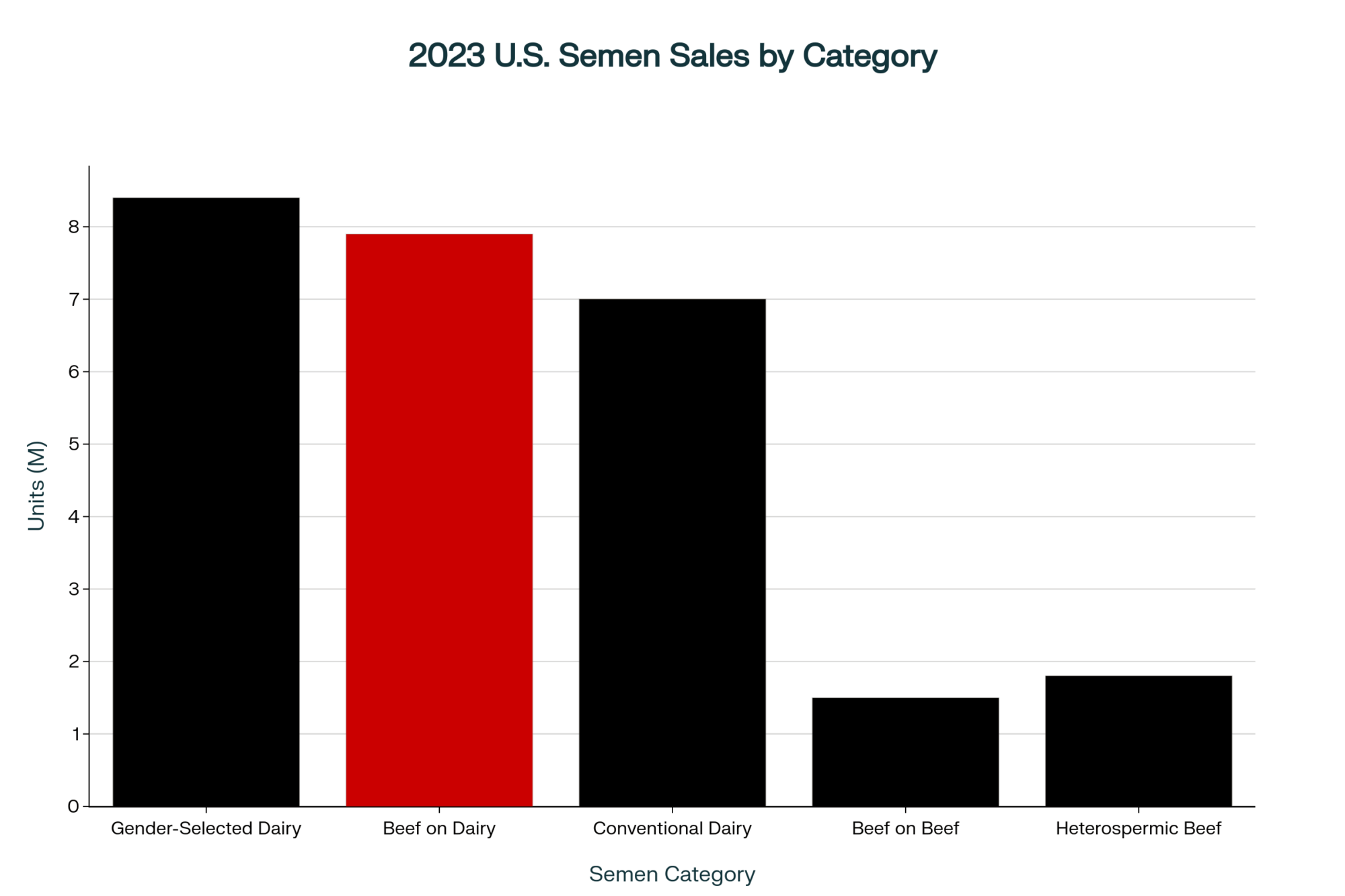

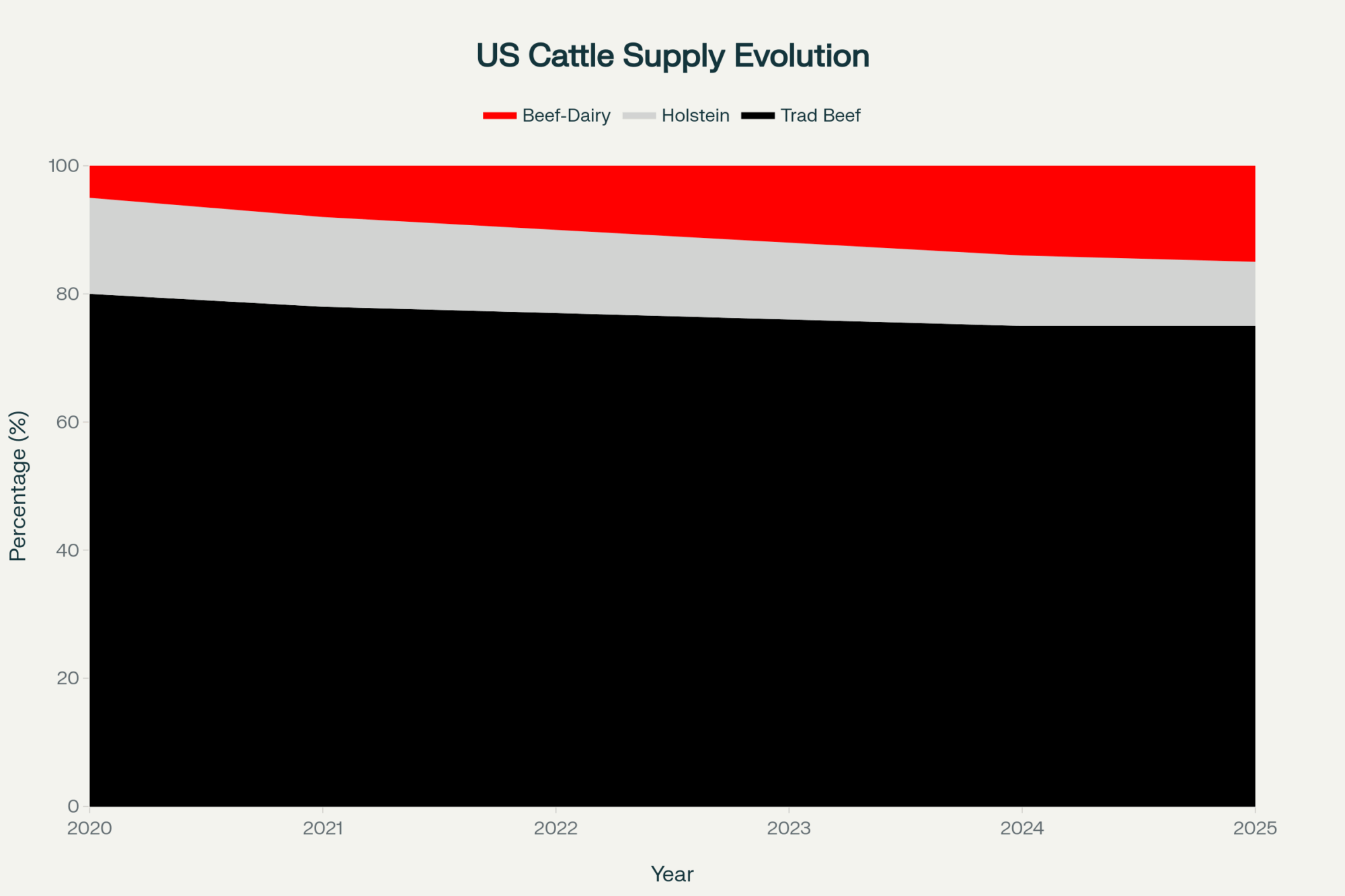

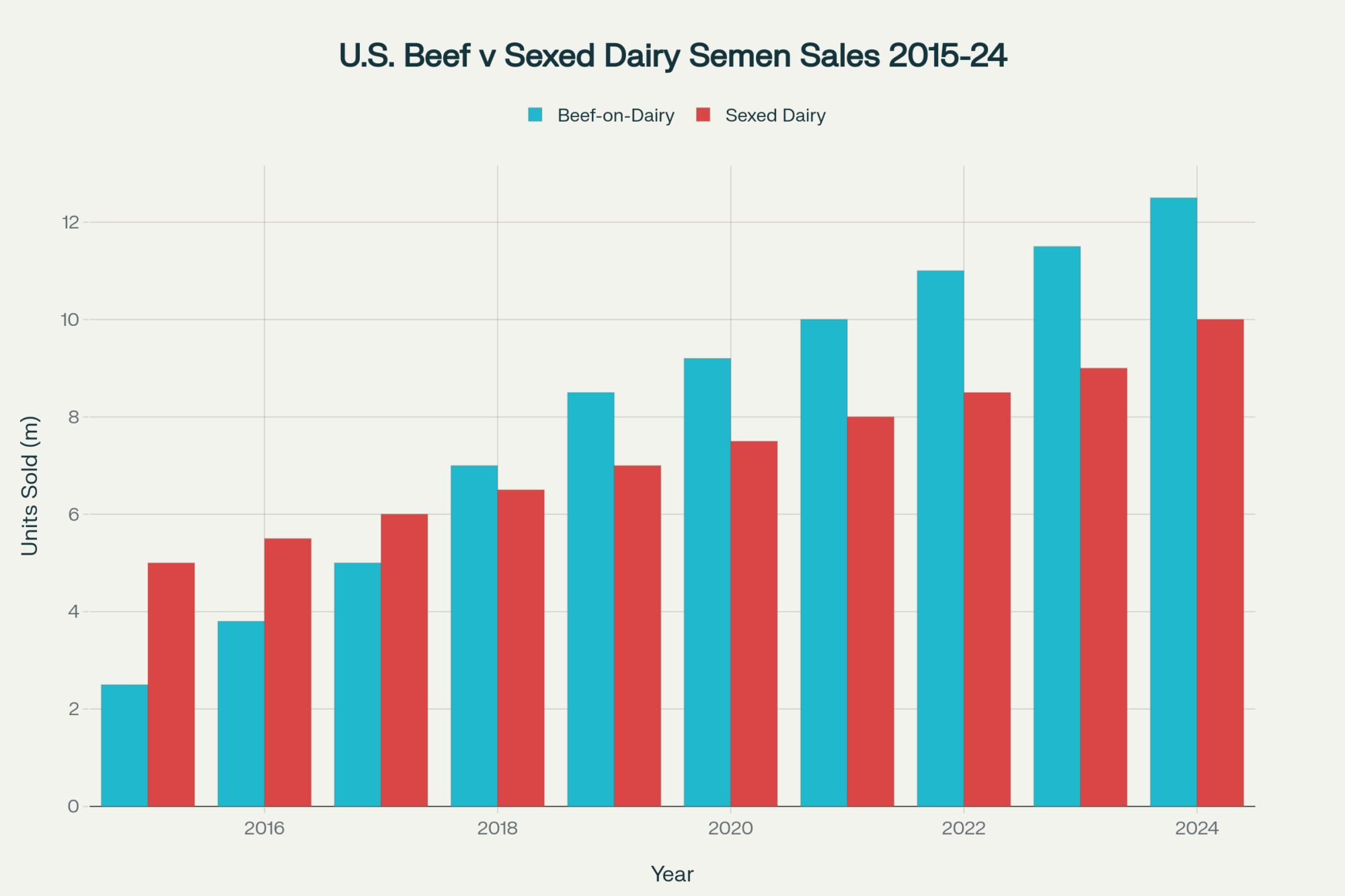

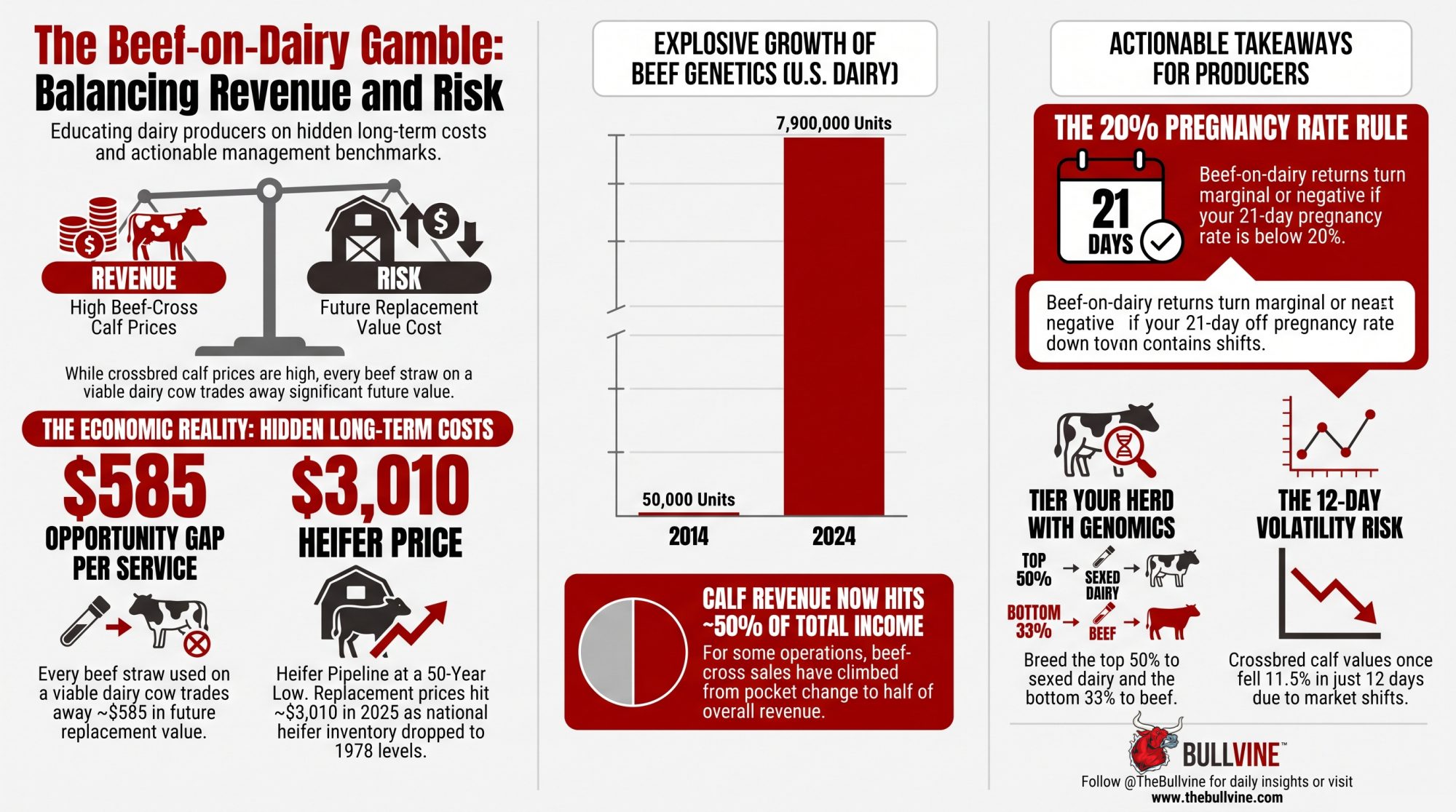

Beef-on-dairy stopped being a side hustle years ago. In 2014, U.S. dairies used around 50,000 units of beef semen. By 2024, the NAAB report put total U.S. beef units at 9.7 million — with 7.9 million going straight onto dairy cows and 1.8 million into beef herds (NAAB 2024 Regular Members Semen Sales Report). Beef-on-dairy now accounts for roughly a third of all U.S. dairy services (NAAB 2025), and about 72% of U.S. dairy herds run some beef genetics (American Farm Bureau). Nobody drifted into that by accident. They followed the check.

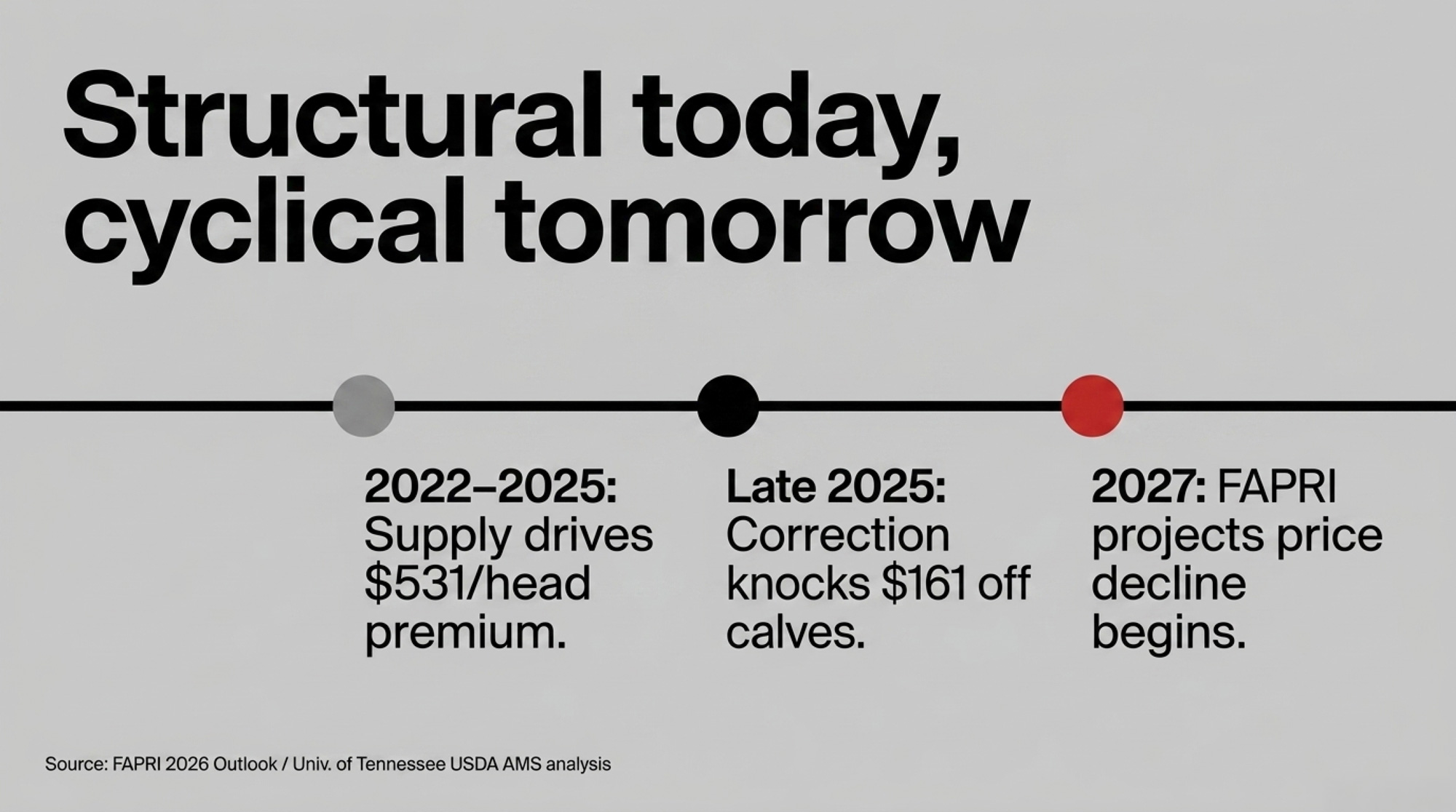

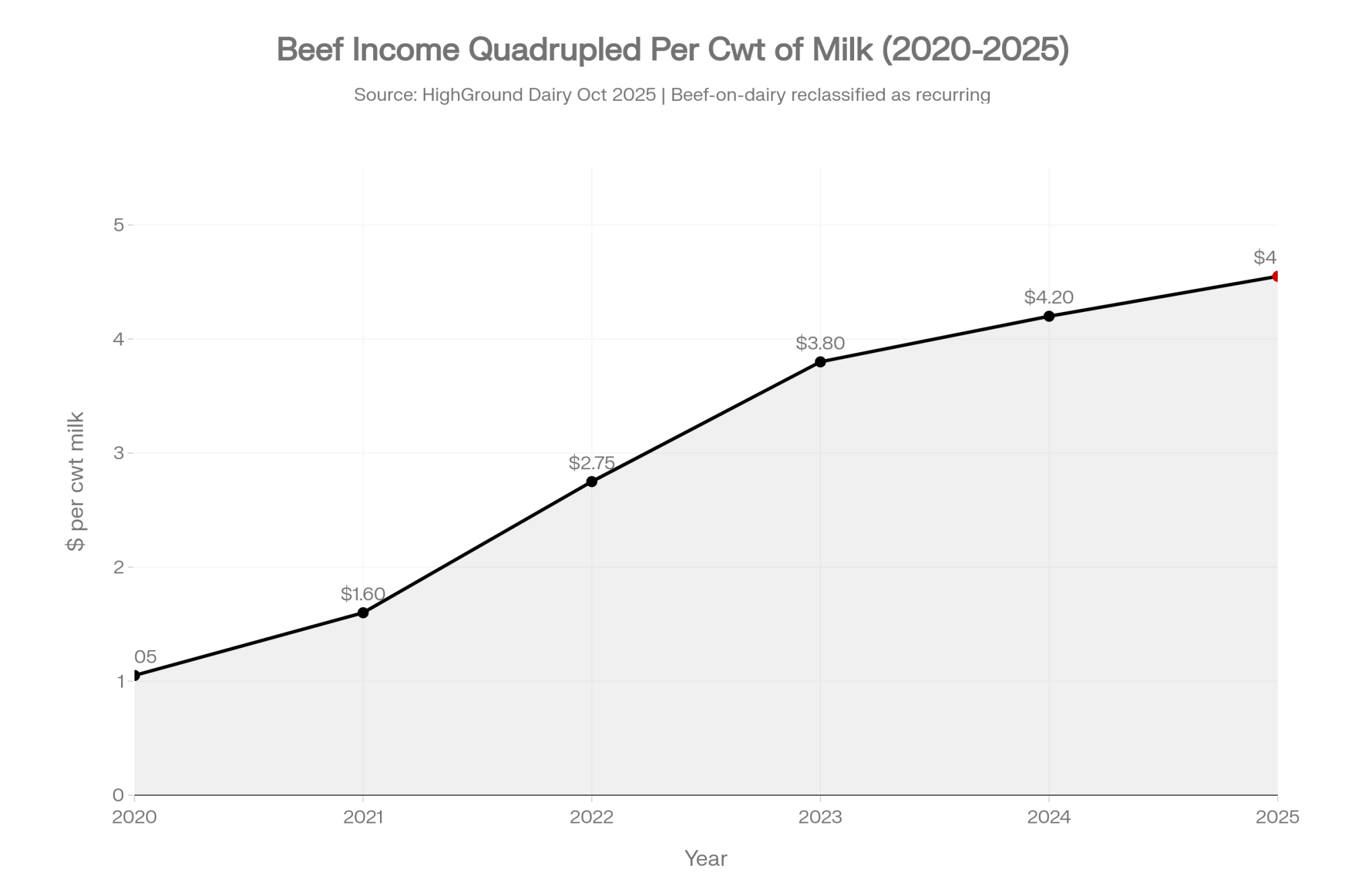

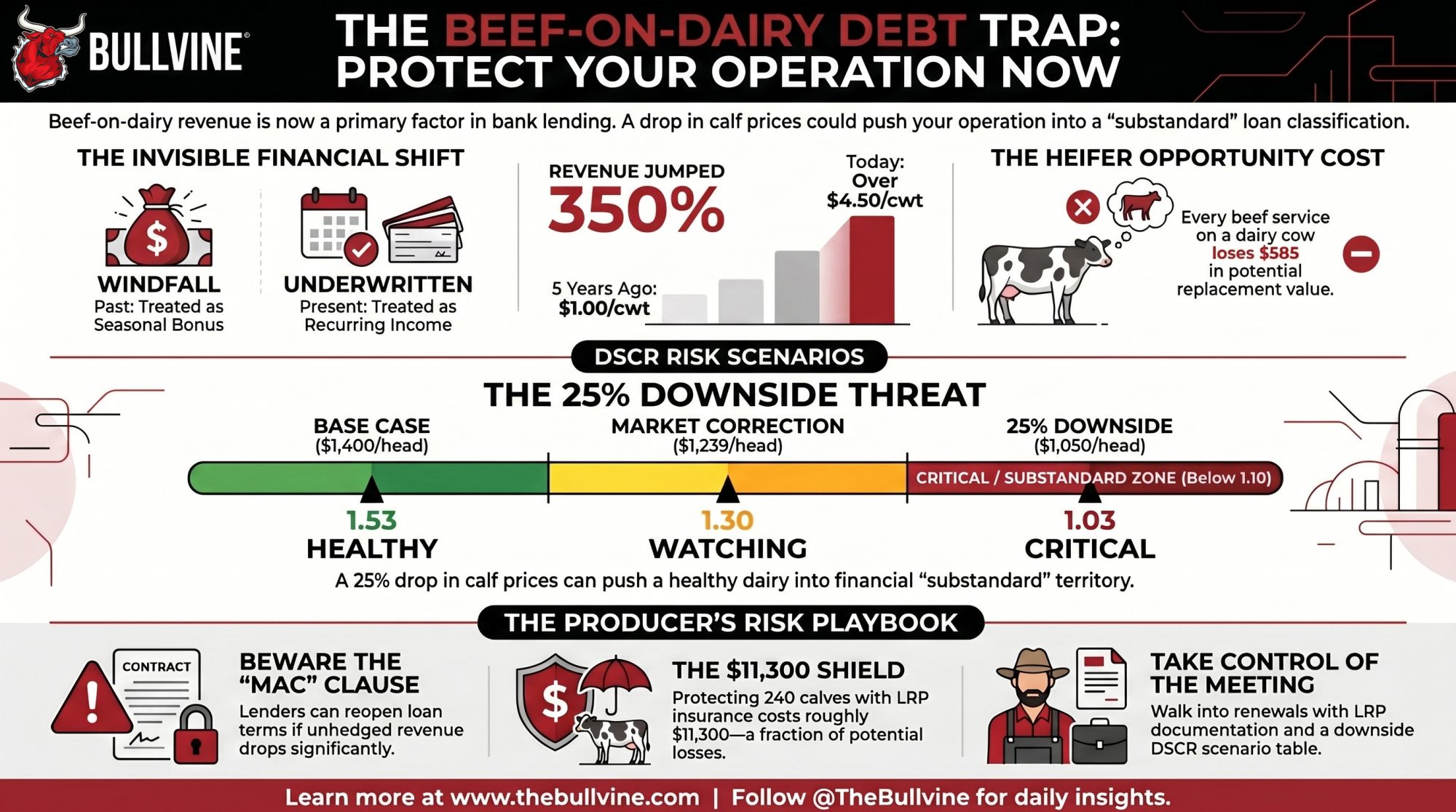

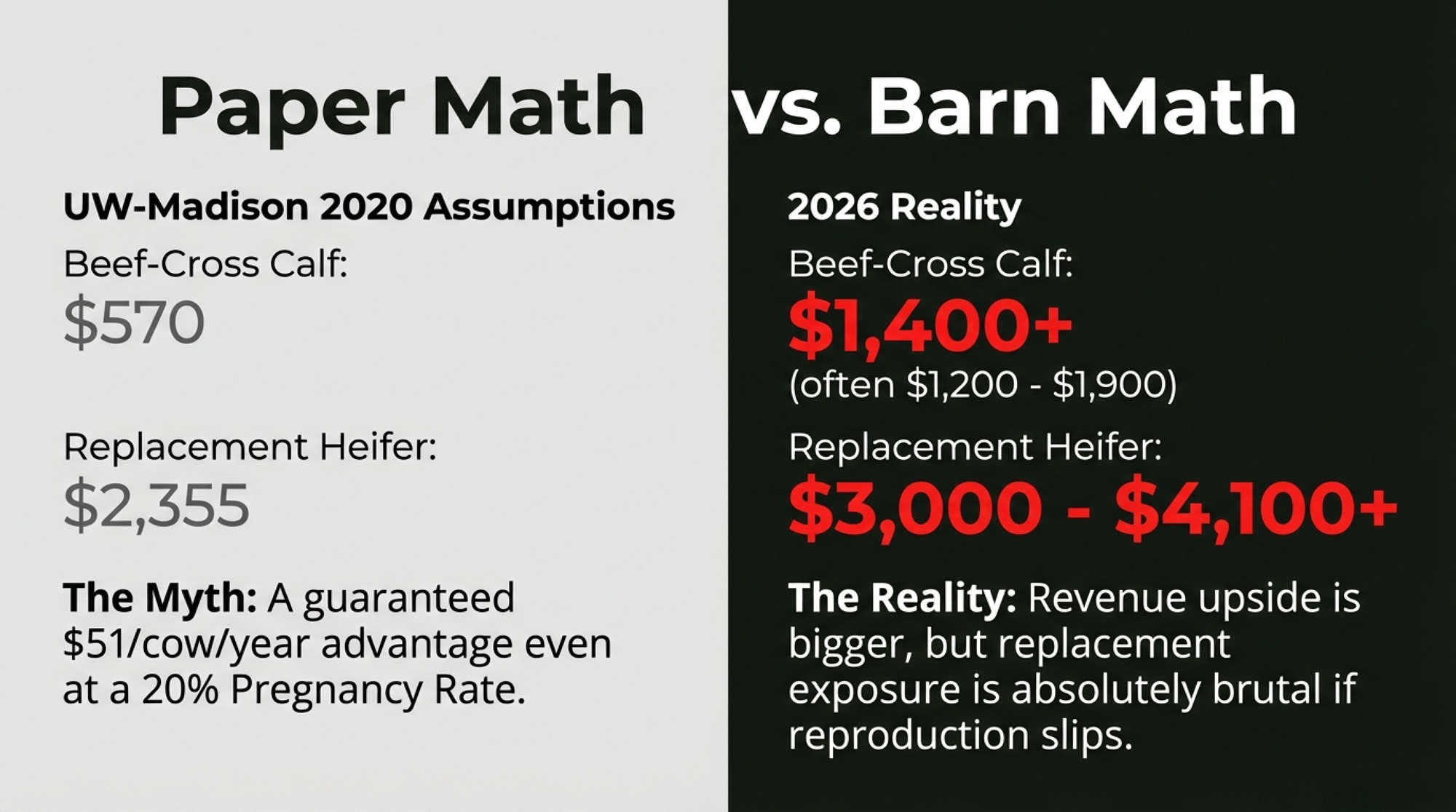

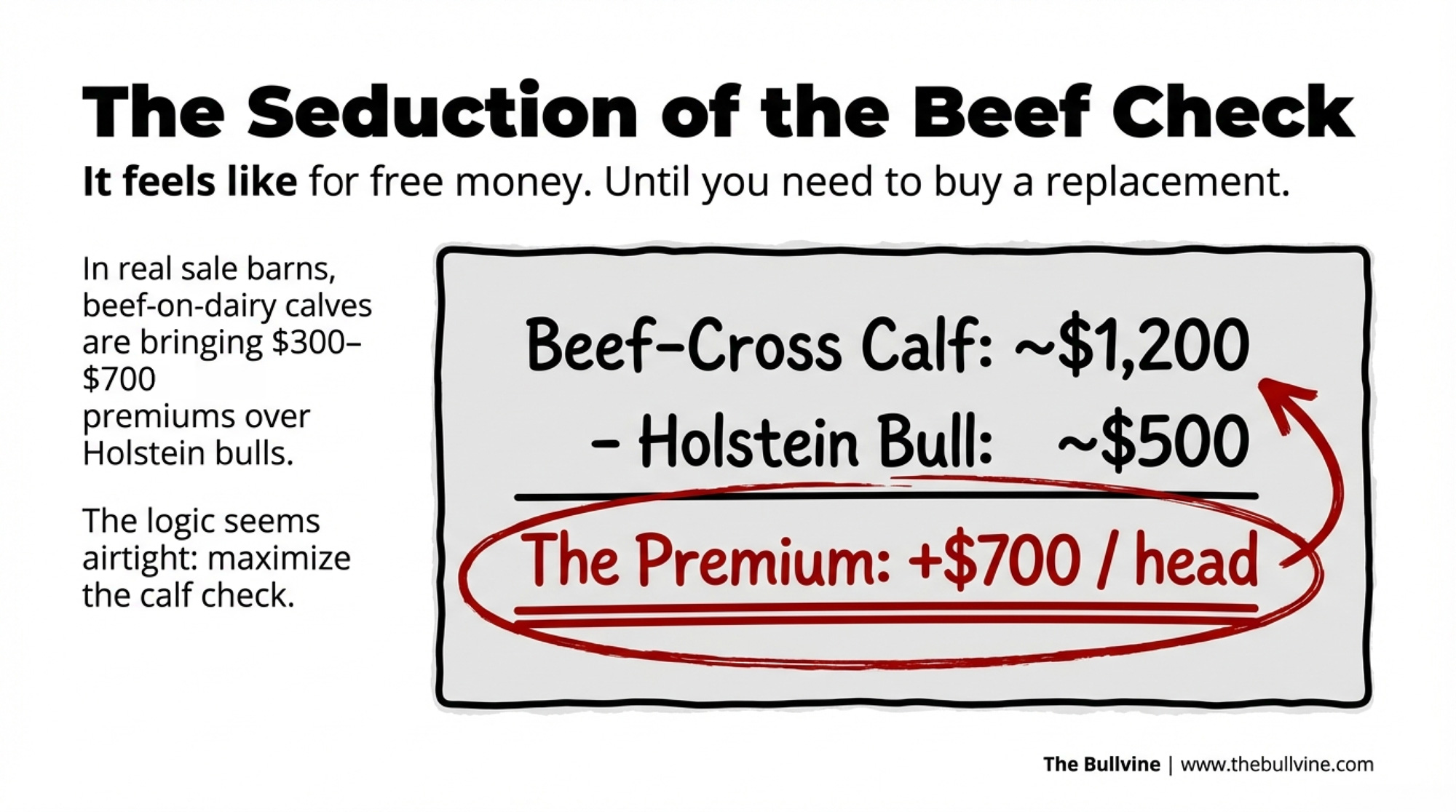

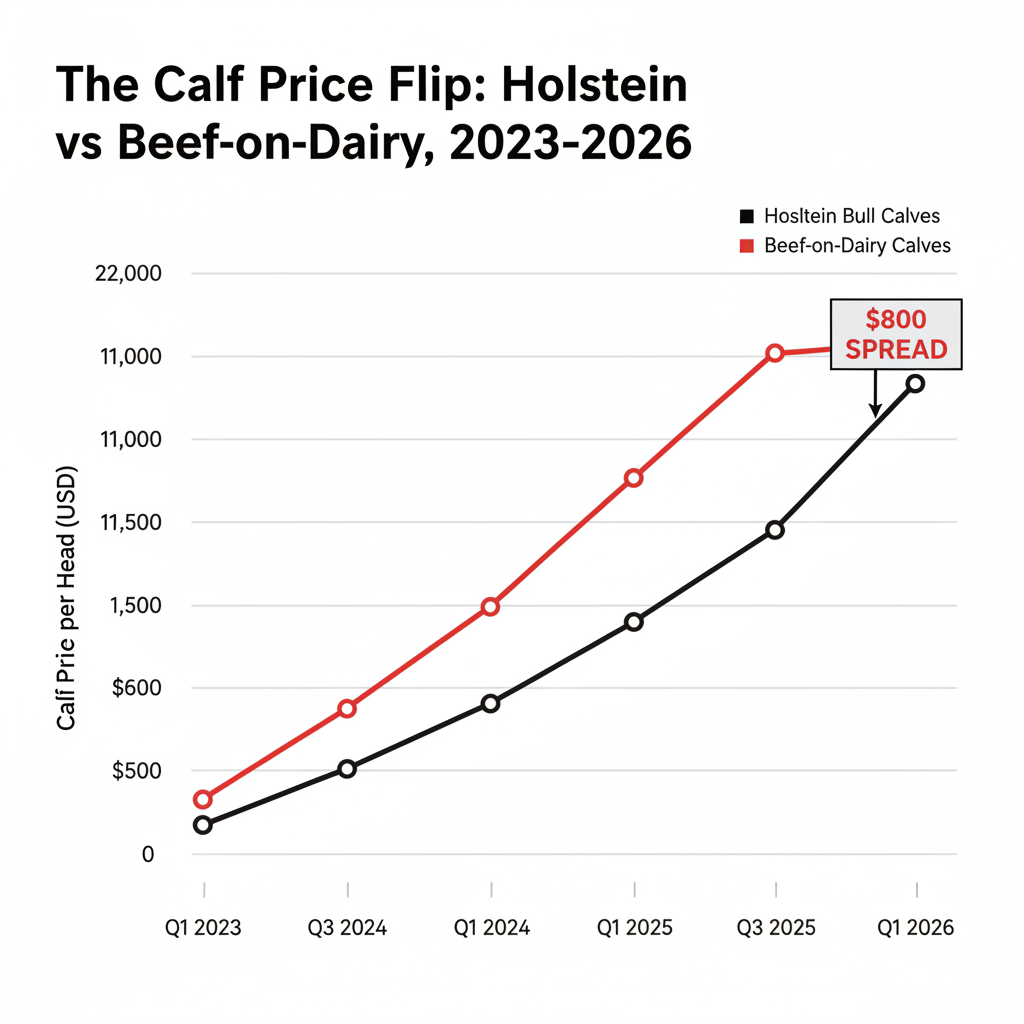

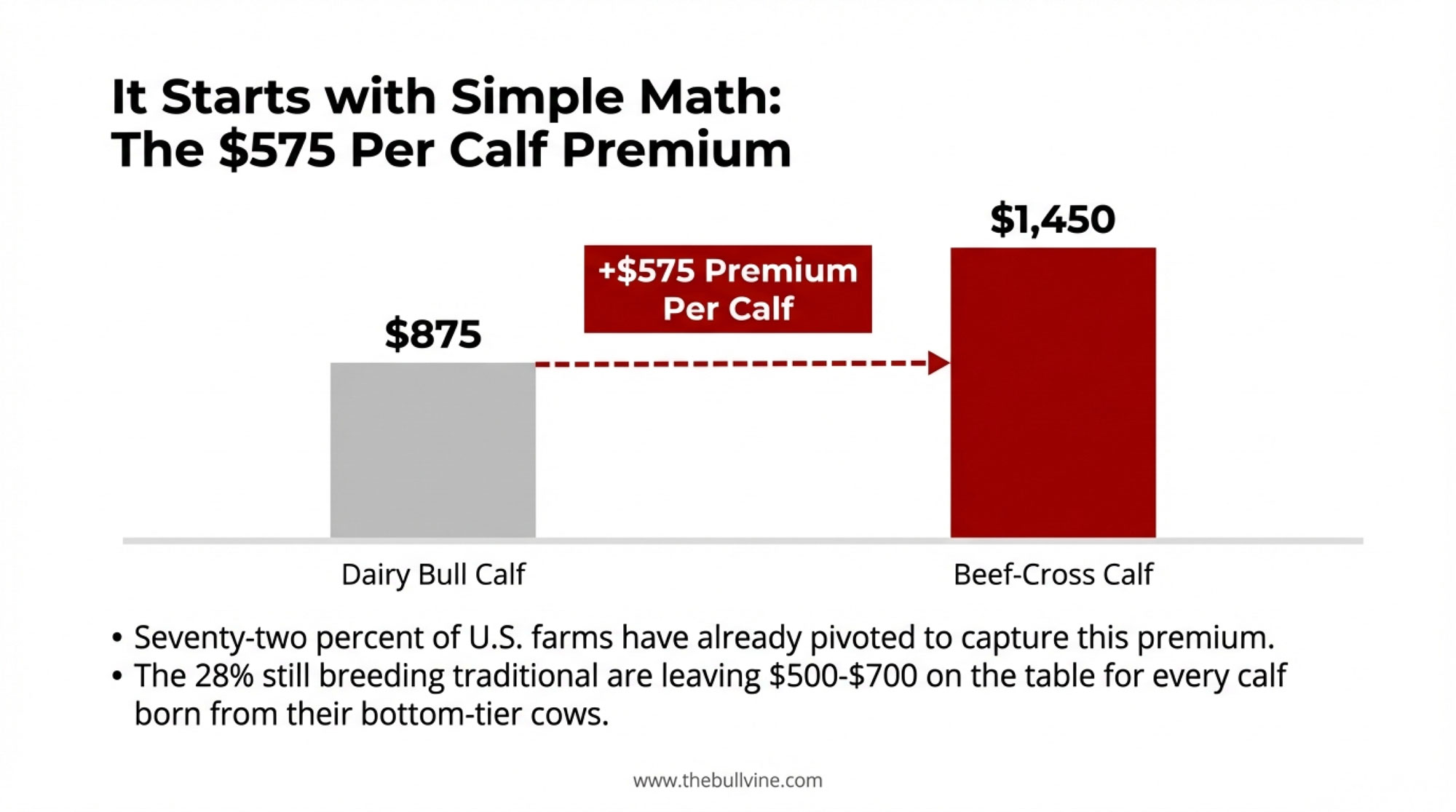

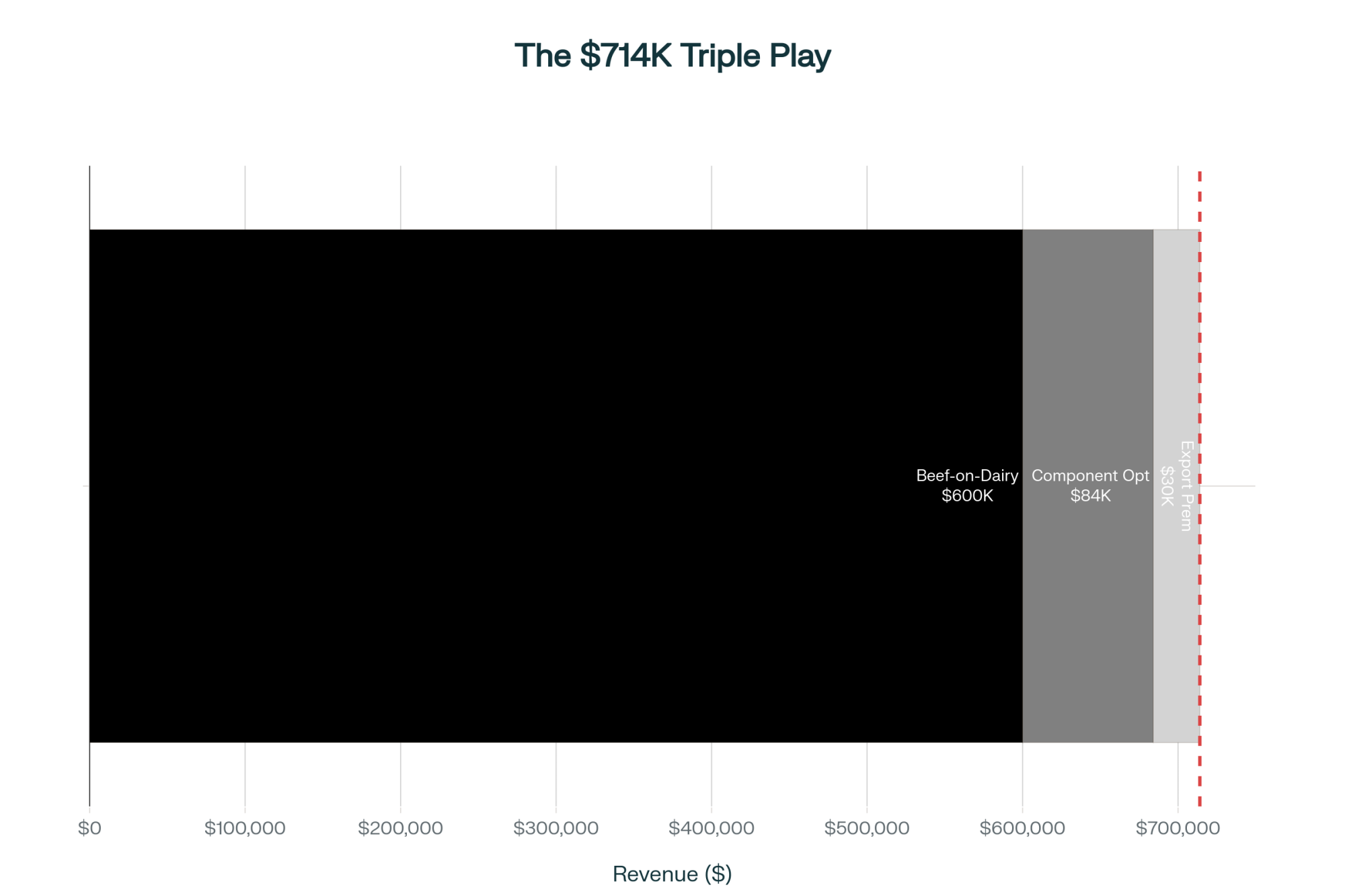

And the check got serious. Dairy market analyst Mike North lays out the scale plainly: beef revenue has climbed from around $1.00 to $1.50 per hundredweight of milk-equivalent in late 2022 to roughly $5.00 to $5.50/cwt today — tripled, in some cases quadrupled, in four years (Mike North interview, June 2, 2026). University of Wisconsin Dairy Research pegs the strategic beef-cross premium at $350 to $400 per calf (University of Wisconsin Dairy Research, 2025). When a calf line moves your milk-equivalent needle by five bucks a hundredweight, your lender stops treating it like pocket change.

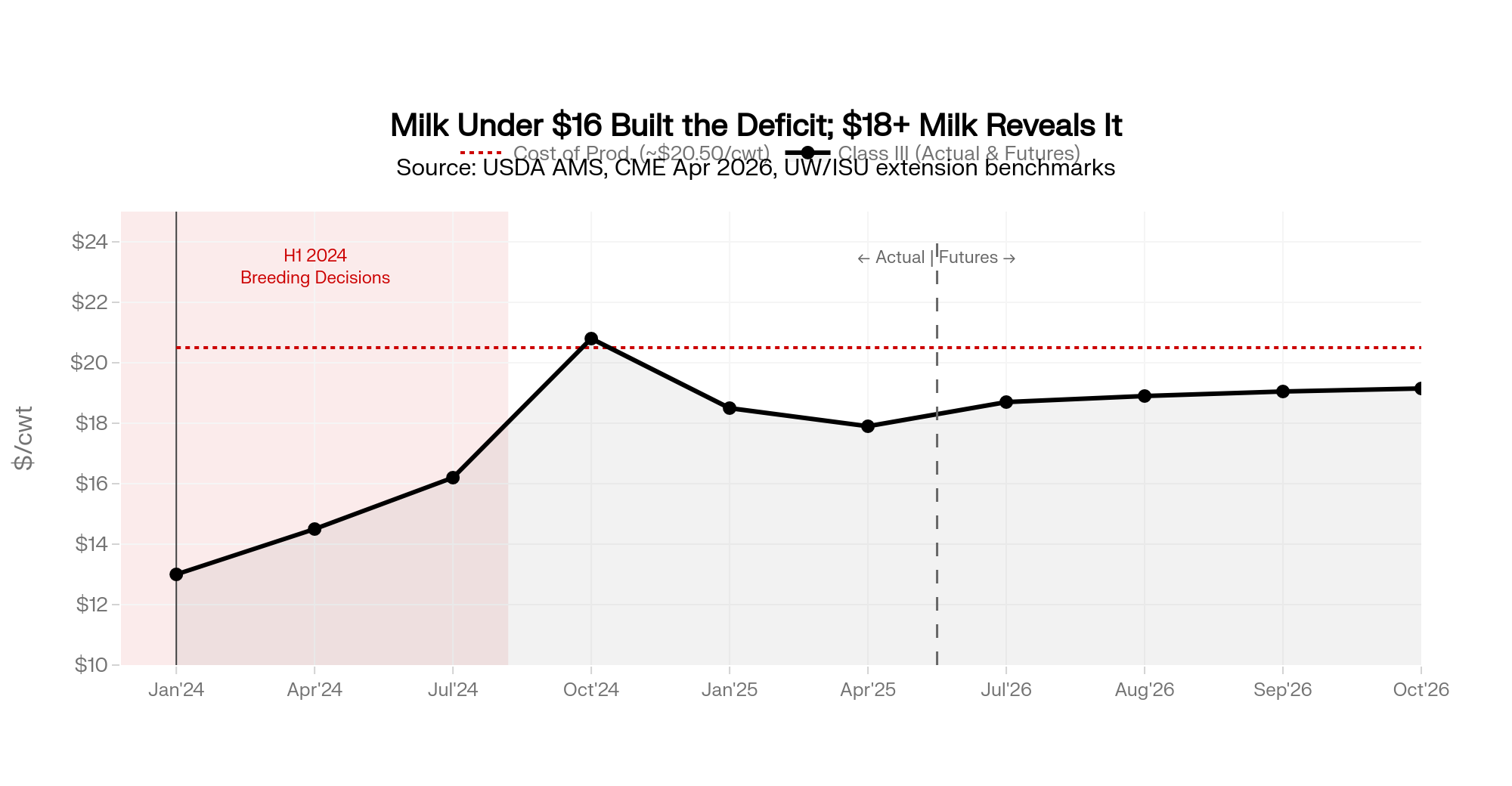

The timing is what makes this urgent right now. USDA cut its 2026 all-milk forecast to $20.70/cwt in June — down $0.55 in a single report — while CME spot milk sat near $16/cwt (USDA Economic Research Service, June 17, 2026;Southeast AgNET, June 22, 2026). For a lot of operations, the calf check is the thin line between red ink and black. That’s the reason it deserves a hard look, not a victory lap.

It’s Not Just the 20,000-Cow Crowd

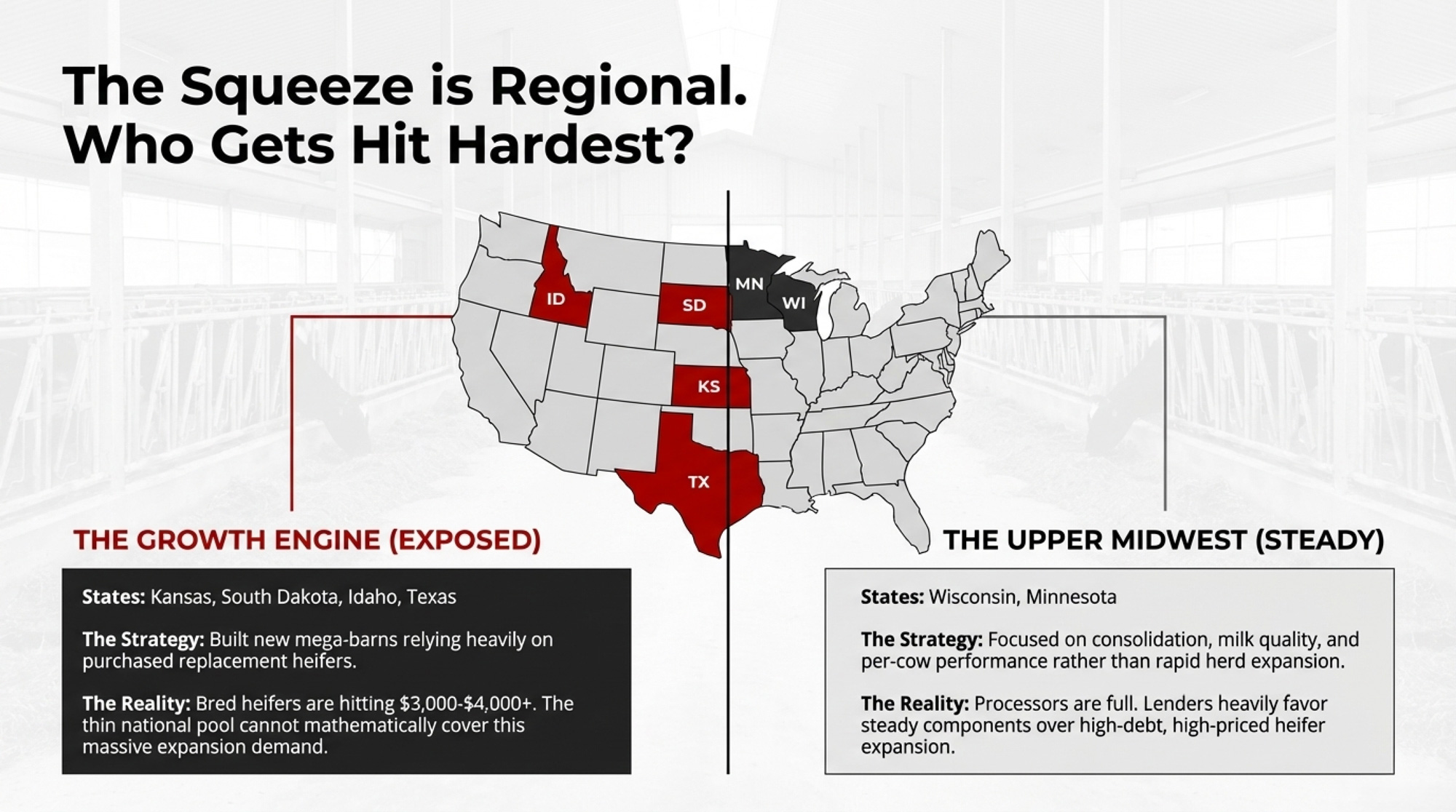

Randy Ebert saw this coming before most. He milks about 6,800 Holsteins at Ebert Enterprises near Algoma, in Kewaunee County, Wisconsin, and he’s been breeding Angus crosses for 14 years — back when the neighbors still treated a crossbred calf as a curiosity. He calls beef-on-dairy “one of the few things that is helping us combat inflation costs of what we do” (Brownfield Ag News, July 9, 2025). He didn’t chase a fad. He made a bet more than a decade ago and watched the market walk over to meet him. That runway matters — the farms doing this well didn’t start last Tuesday.

Smaller operations are in it too. Glacier Edge Dairy near Milton, Wisconsin was a 300-cow farm when the Wisconsin Beef Council profiled it, and it built beef cattle into the income “shortly after we started” — a plan, not a panic move. The Metcalf family has since grown the herd to about 750 registered Jerseys (The Bullvine, February 24, 2026). Different scale, different breed, same lesson: this works when you build it in on purpose instead of bolting it on in a bad month.

The Micro Barn-Math Breakdown

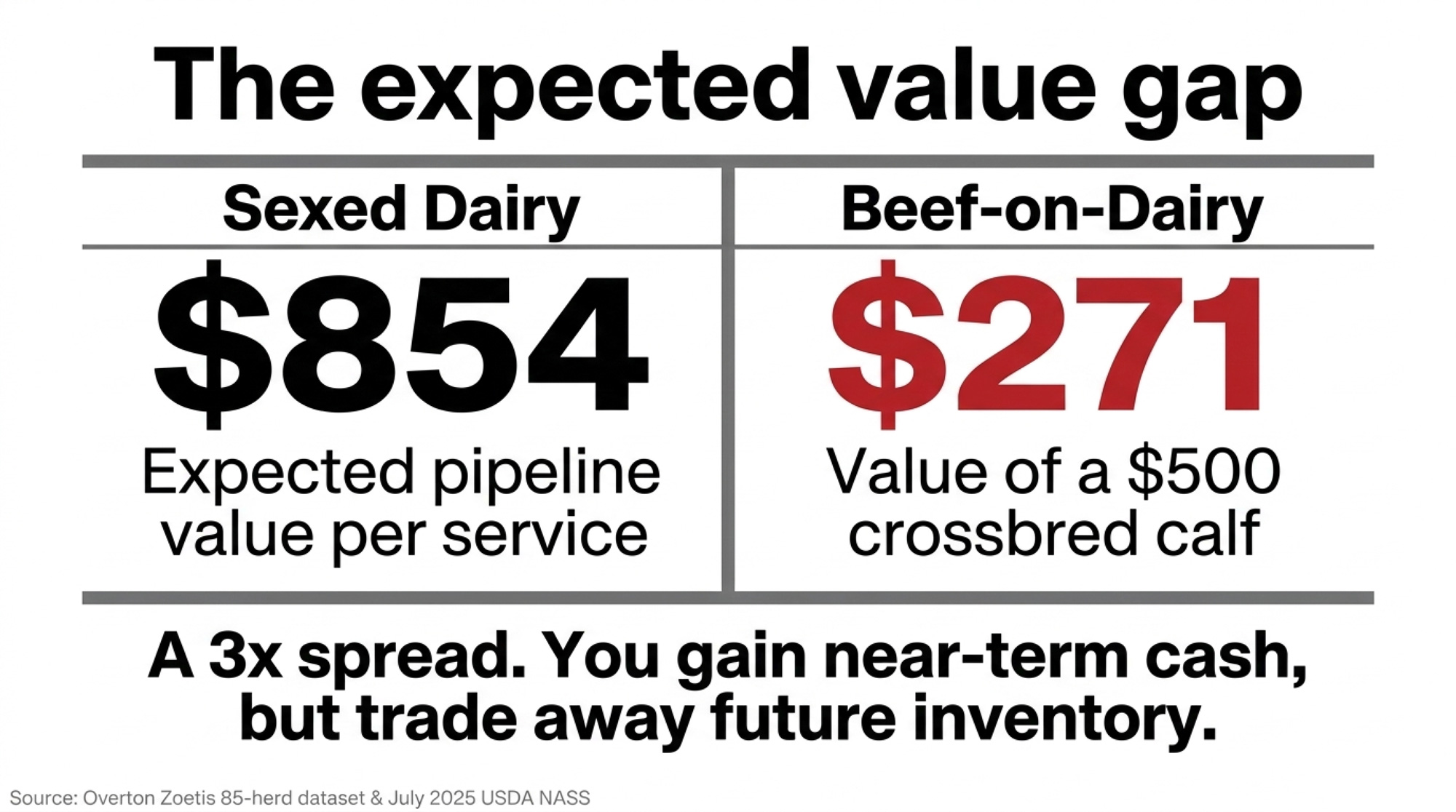

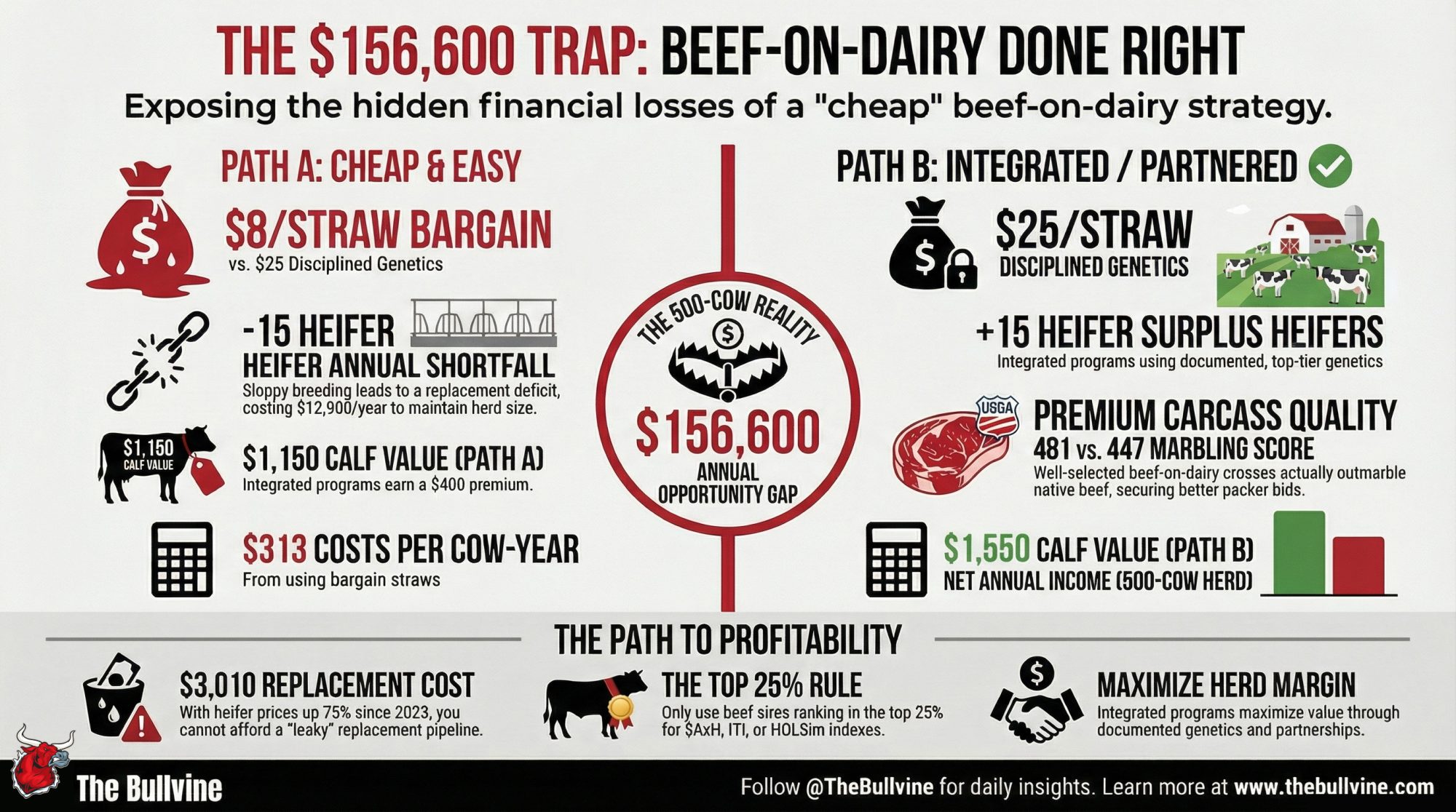

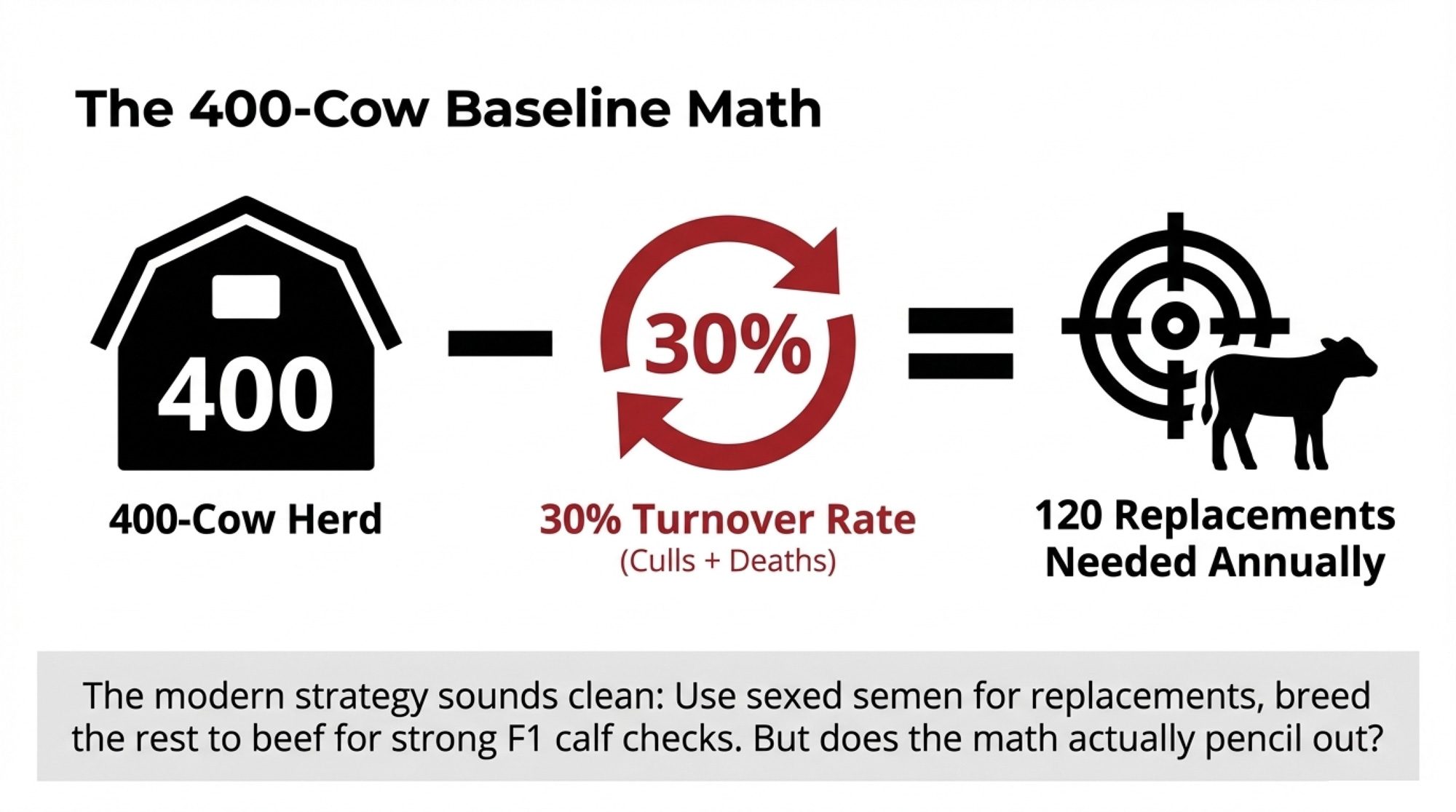

Independence looks great on a banner. It looks different on a spreadsheet. Here’s the piece you can map straight onto your own place. Take one viable dairy dam. At today’s prices, here’s what each breeding decision is really worth:

| Service Type | What It Can Become | Expected Value |

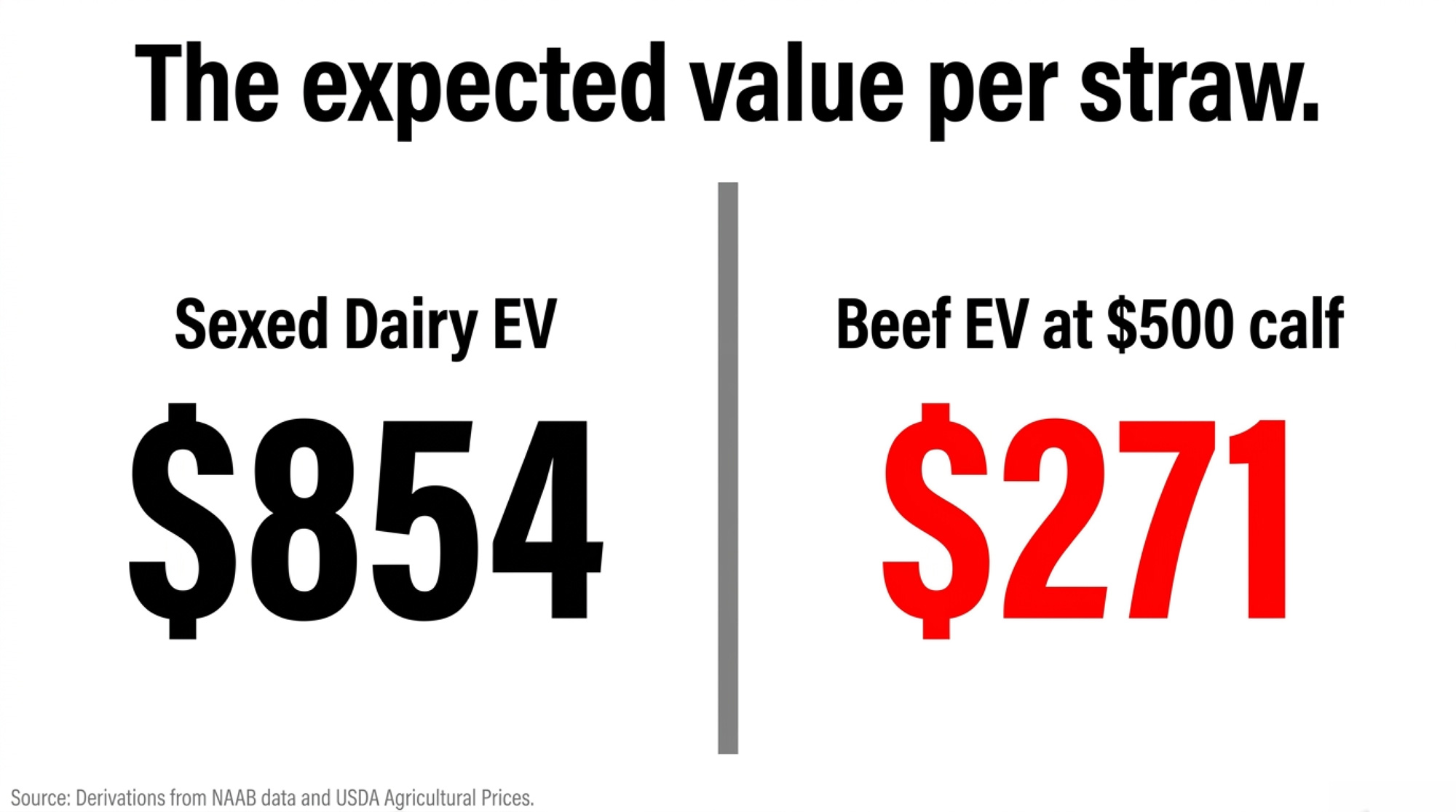

| Sexed dairy service | A $3,010 replacement heifer | $854 |

| Beef straw | A beef-cross calf | $271 |

| The opportunity gap | Value handed over per service | ~$585 |

Bullvine analysis; components round independently. See Methodology Note.

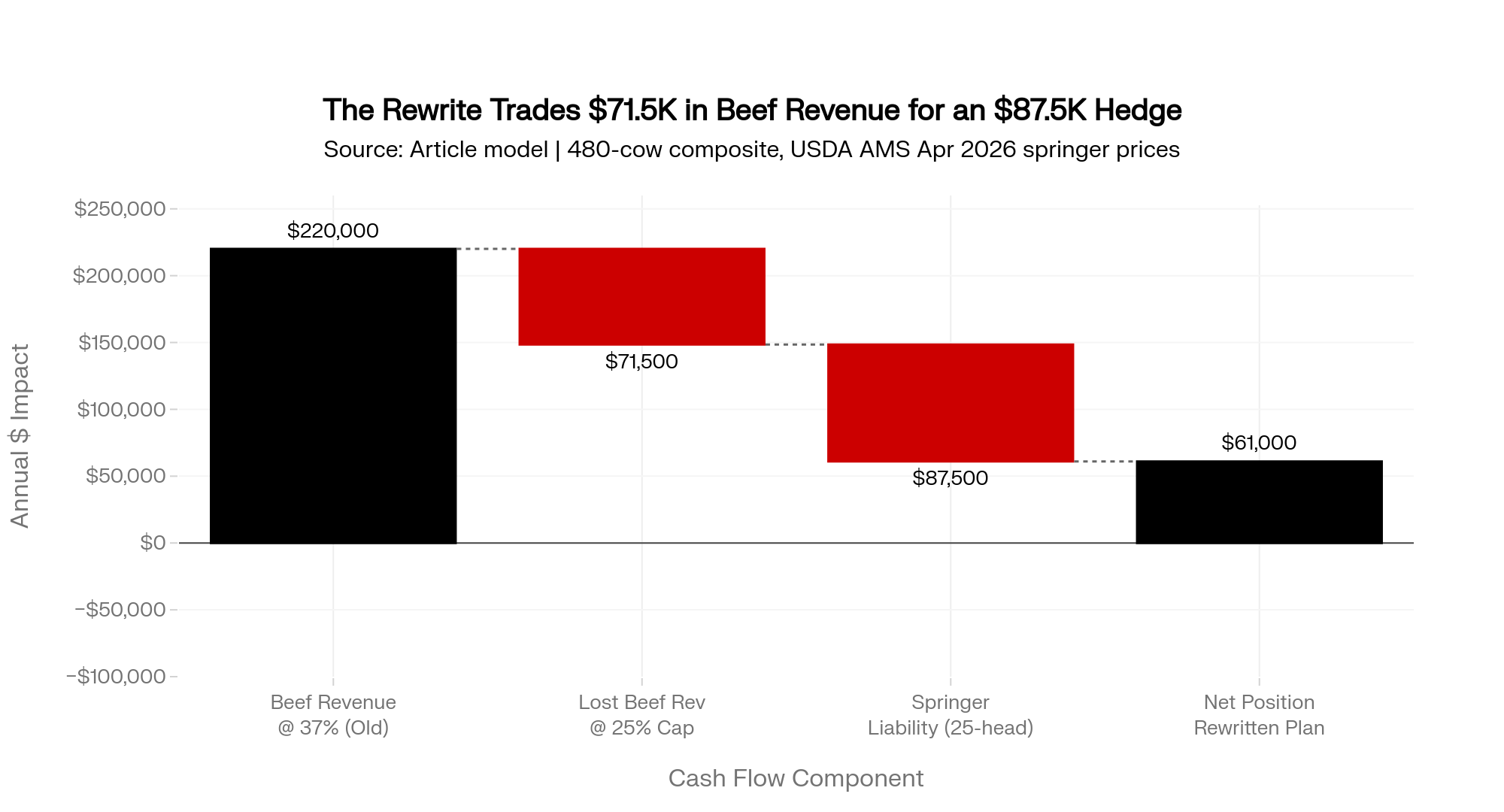

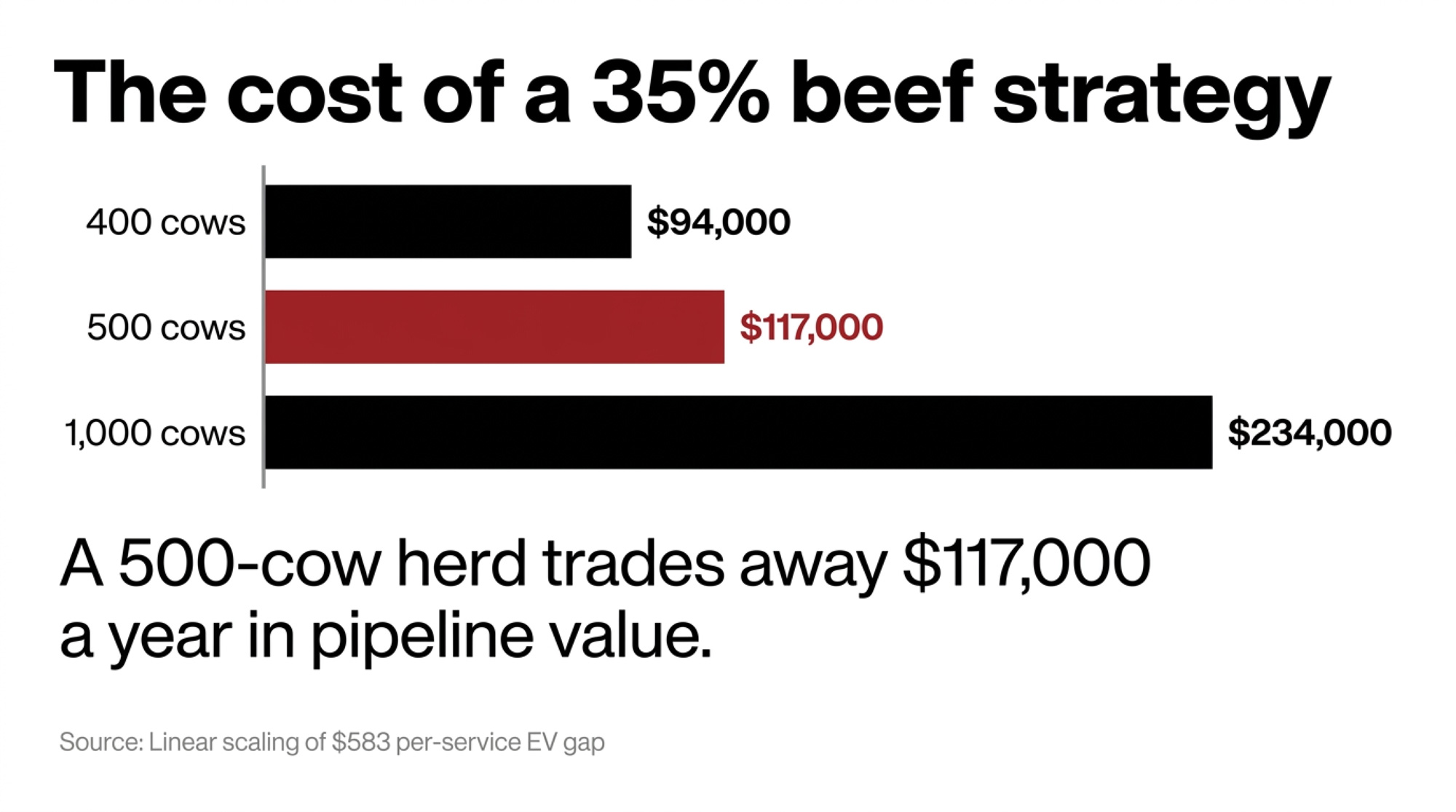

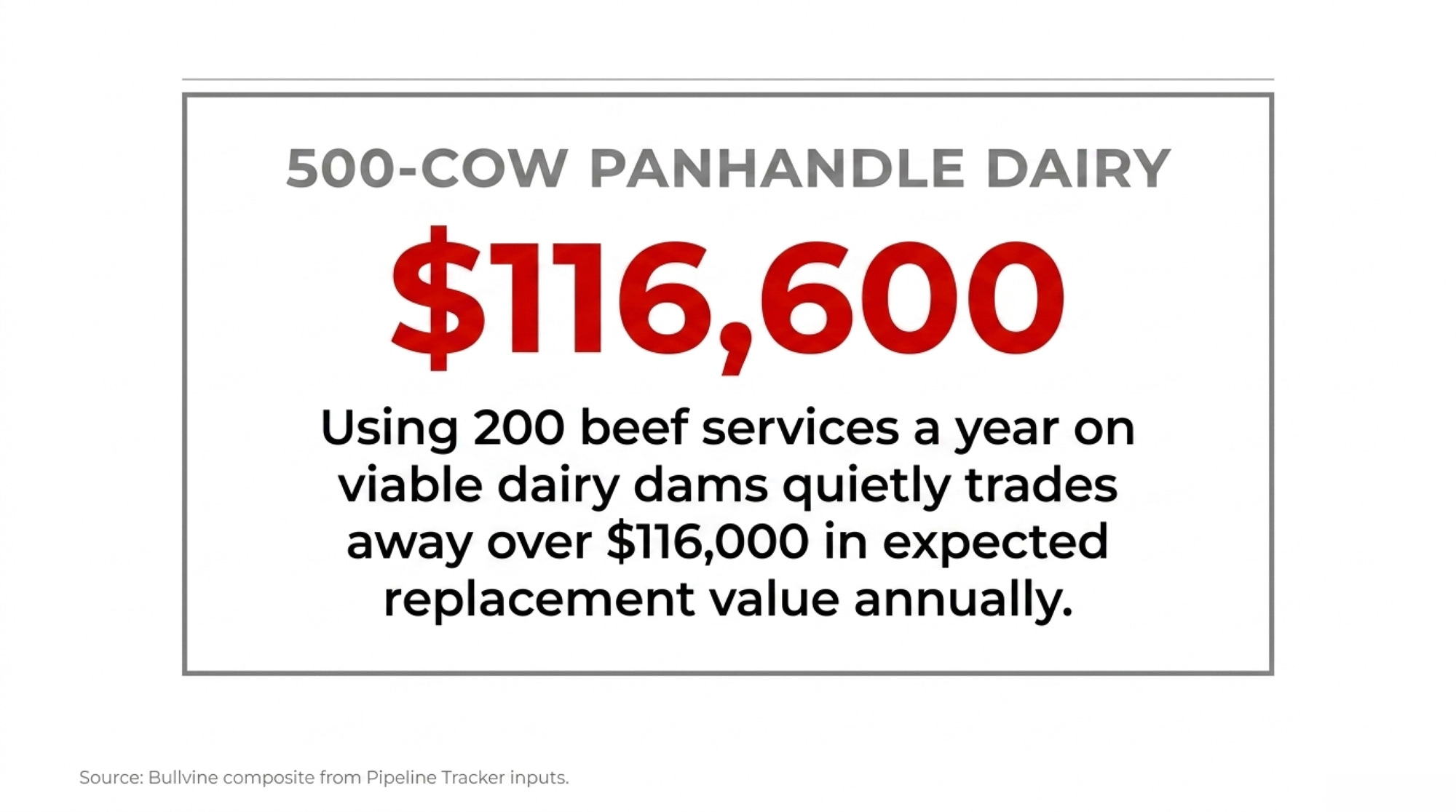

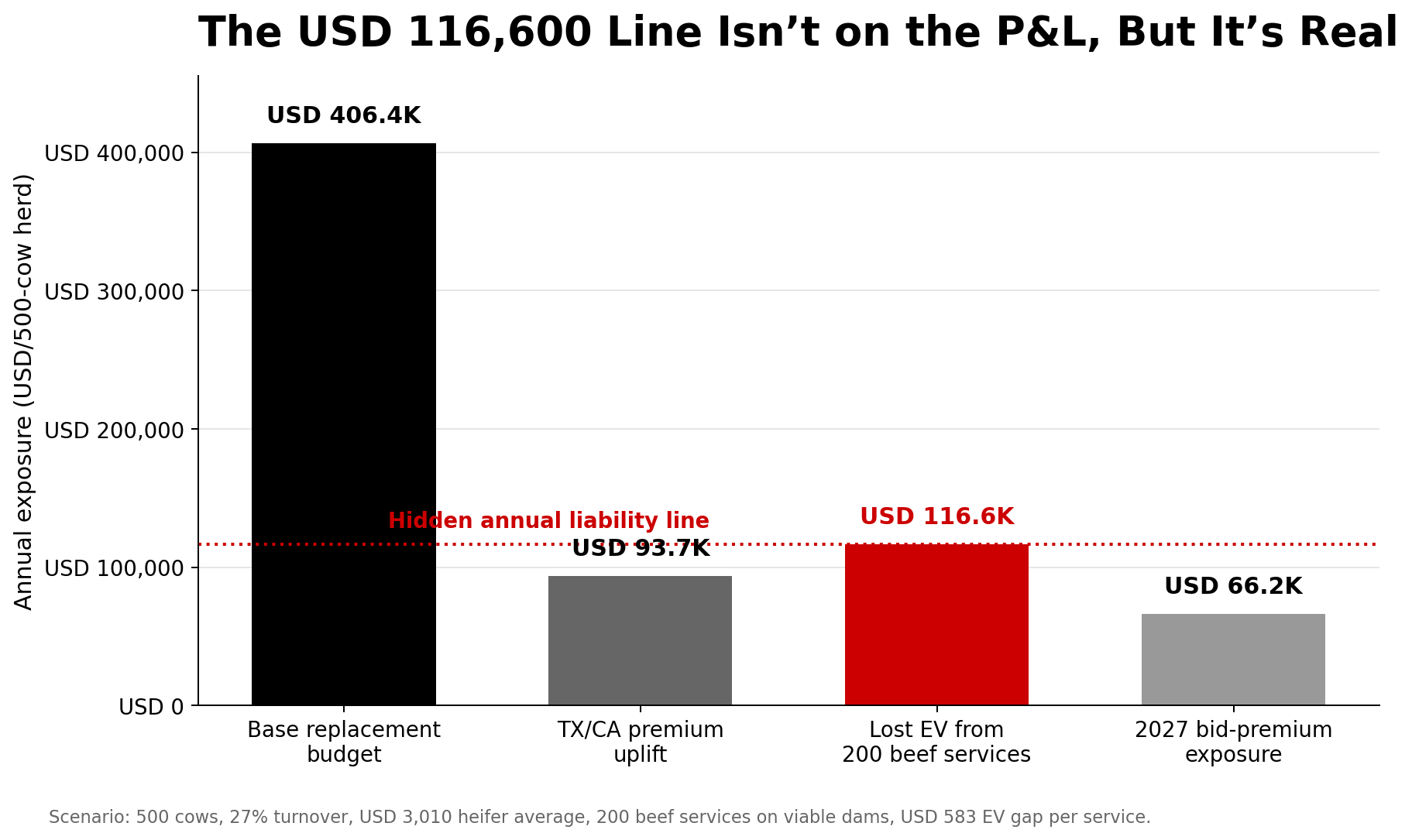

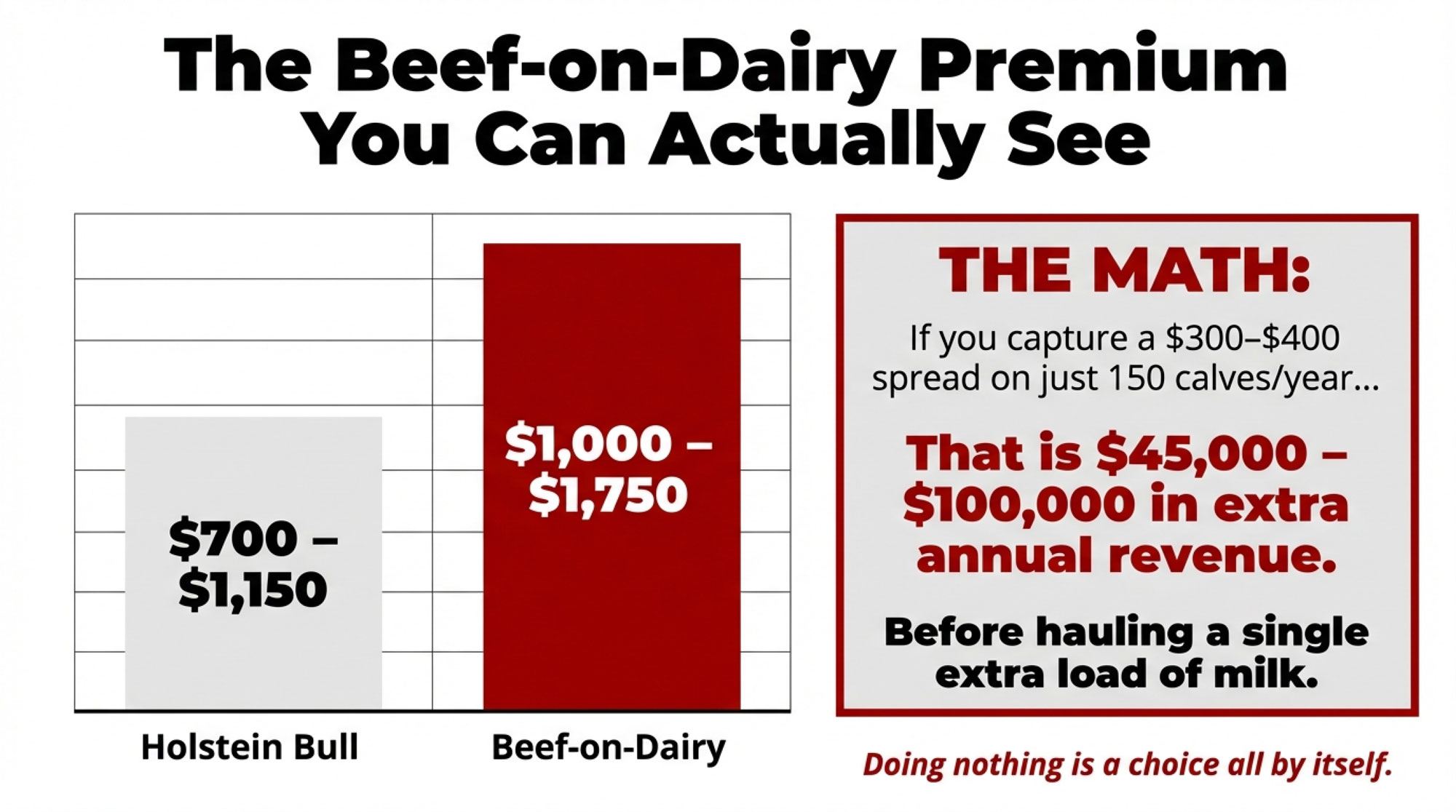

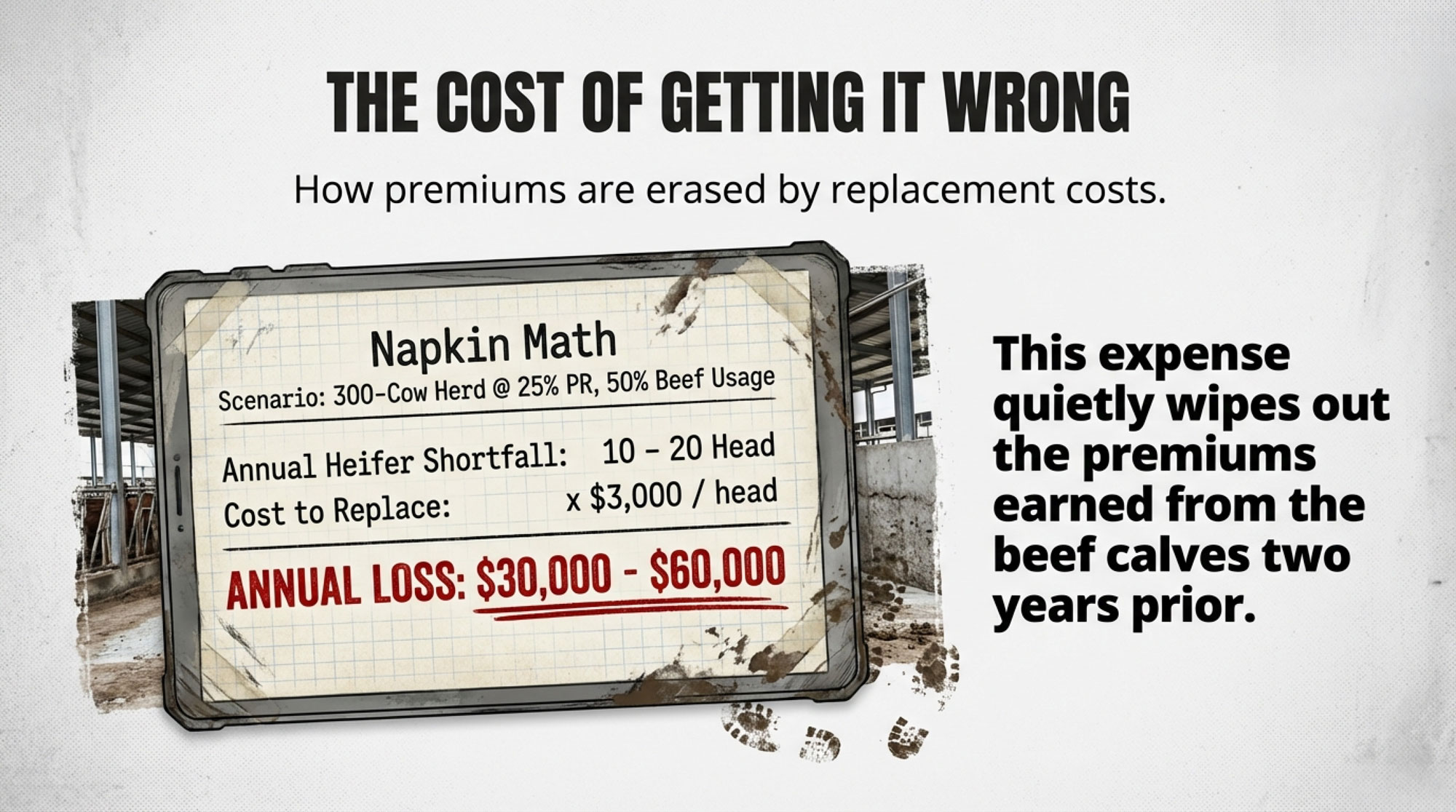

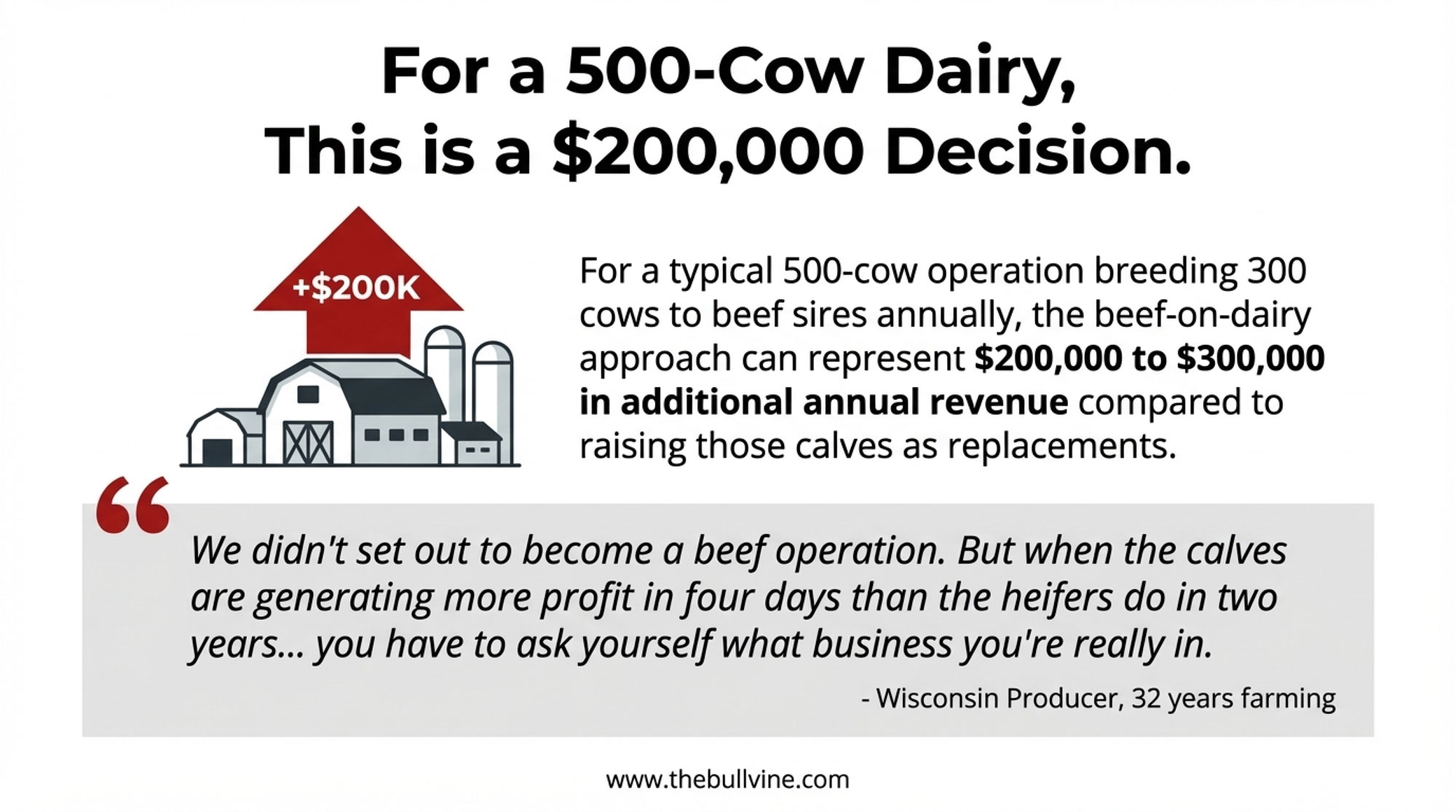

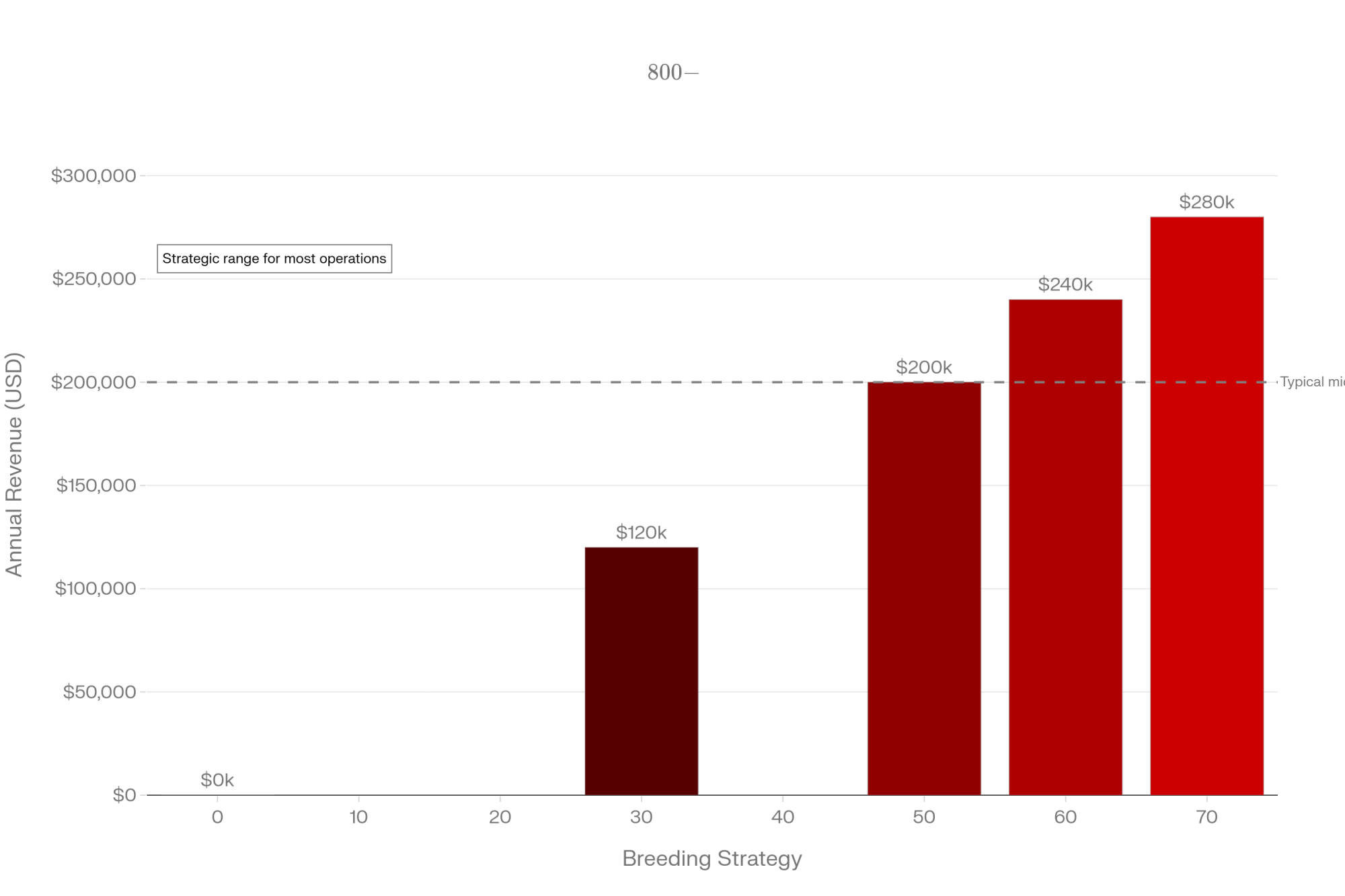

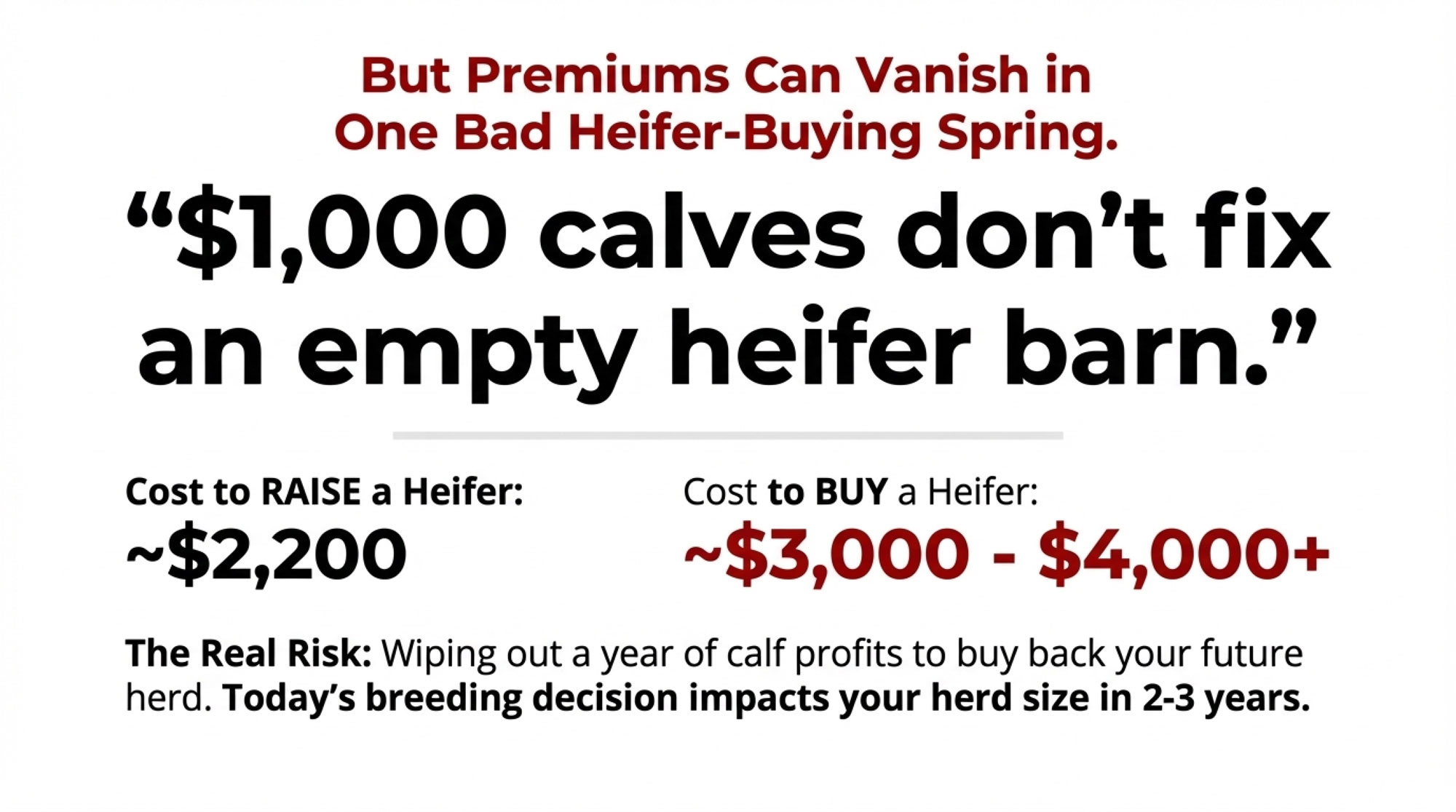

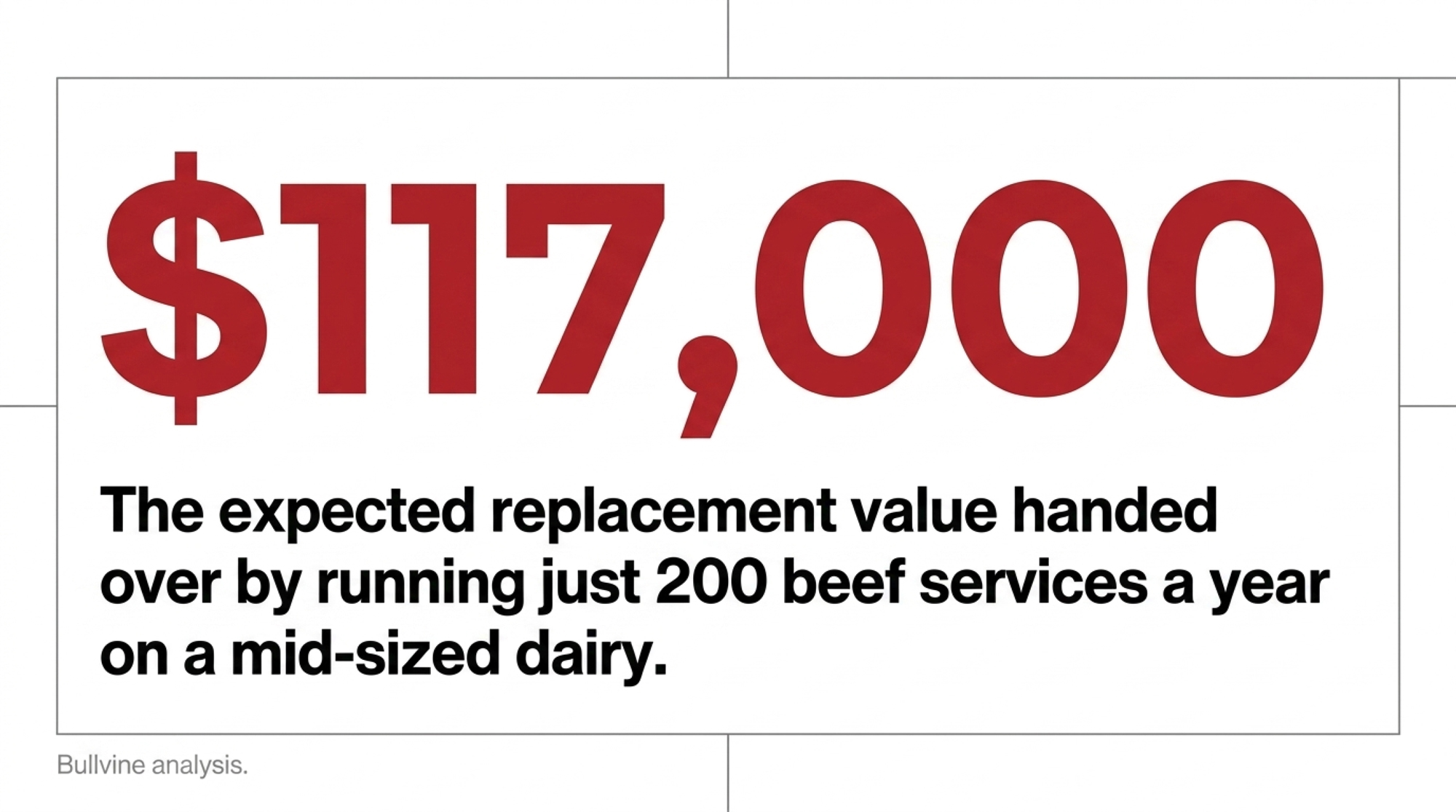

The whole-herd cost: Run 200 of those beef services a year on a mid-sized dairy and you’ve handed over about $117,000 in expected replacement value. On a 300-cow family herd making just 60 of those calls against its best cows, it’s still roughly $35,000 a year. That’s not cash out of the checkbook today. It’s heifers you won’t have tomorrow.

| Herd profile | Beef services/yr on viable dams | Annual value handed over | Warning flag |

| 300-cow family herd | 60 | ~$35,000 | Manageable if repro is strong |

| Mid-sized dairy | 200 | ~$117,000 | Calf check funding heifer drain |

| ~170+ service threshold | 170+ | North of $100,000 | Premium funded by your pipeline |

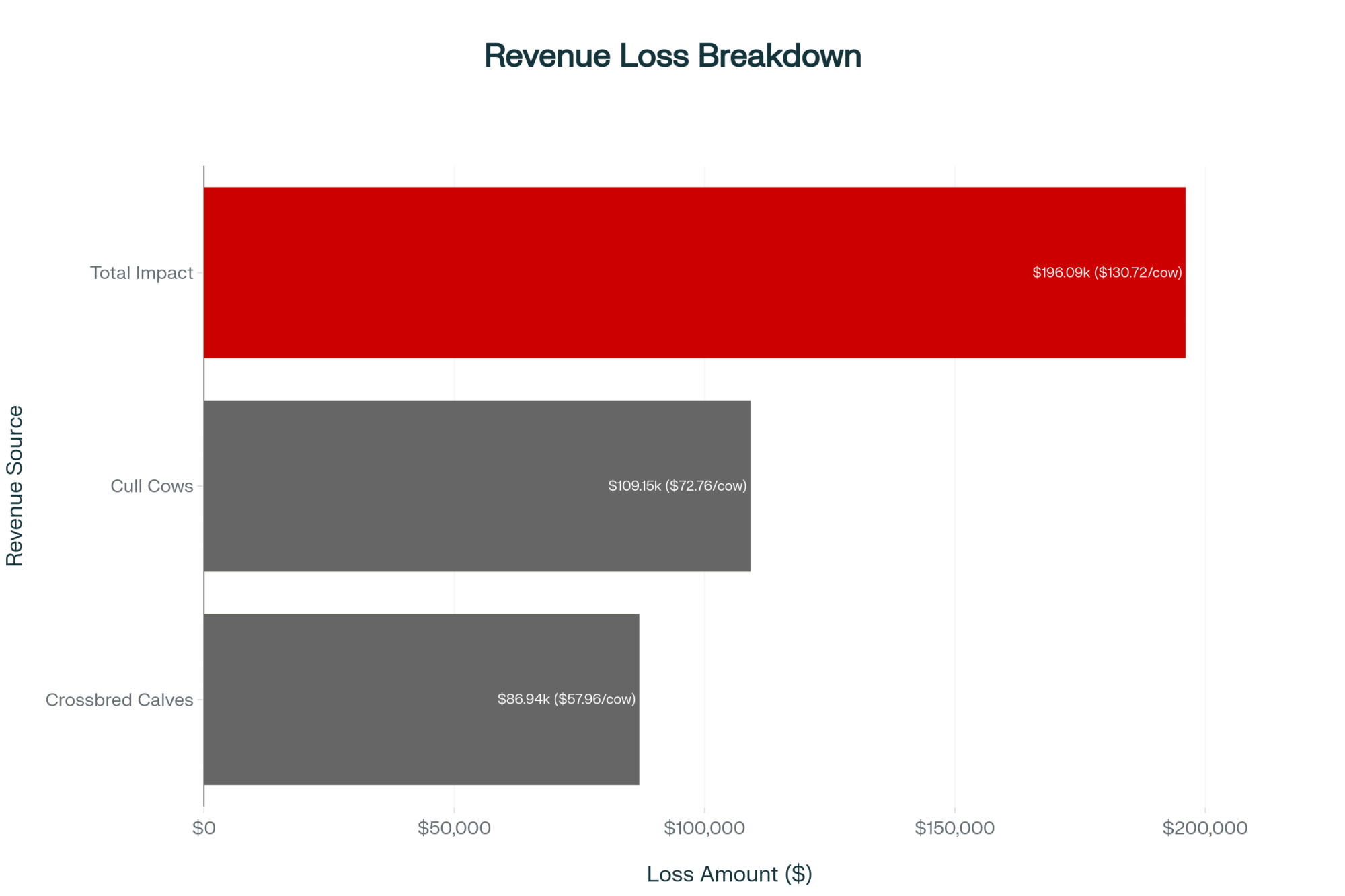

| 1,500-cow @ 40% beef | Oct 2025 price break | ~$196,000 revenue wiped | ~$130.72/cow in 12 days |

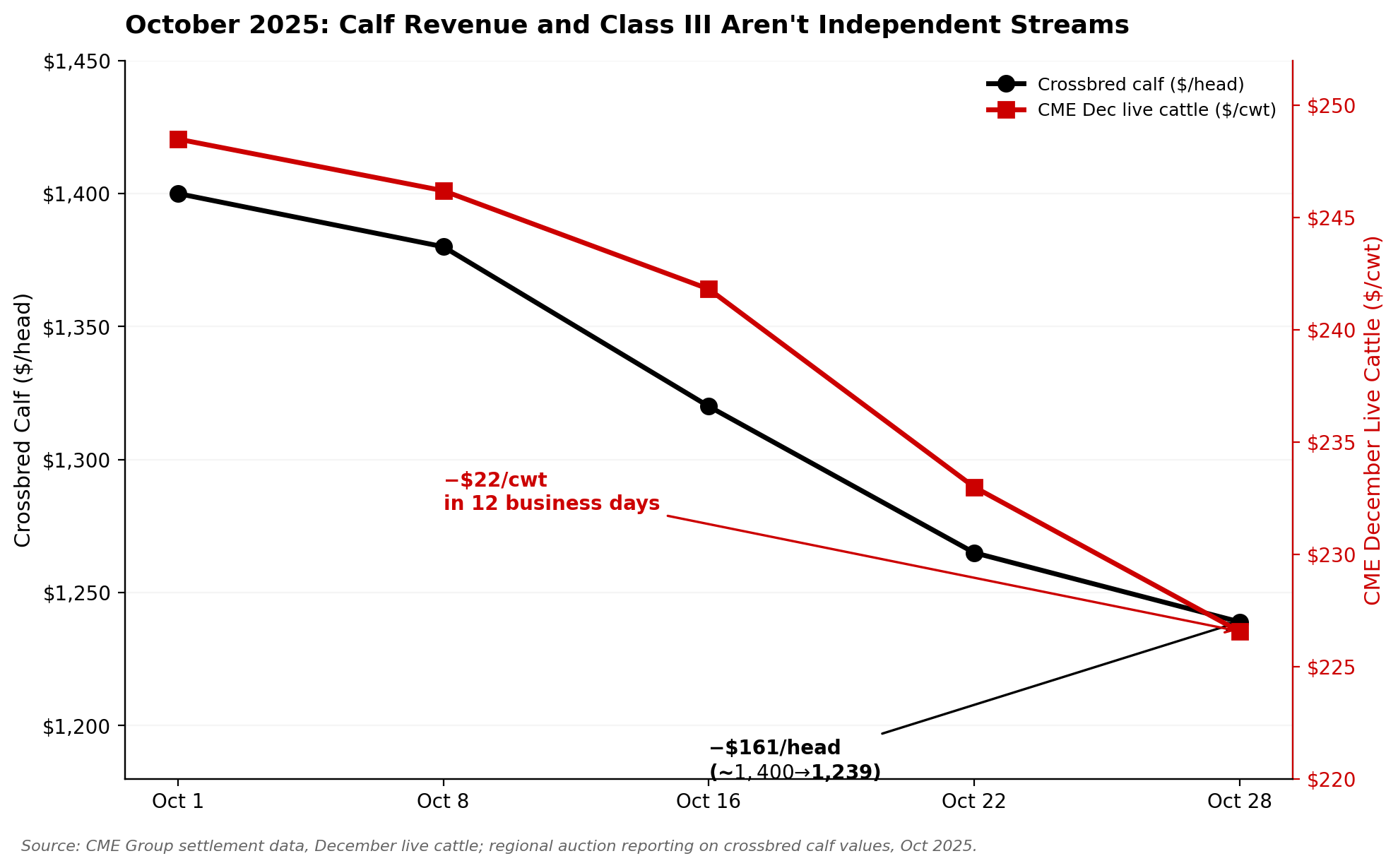

Now here’s the part that gets forgotten when the calf check is fat: the beef market can turn on you inside two weeks.

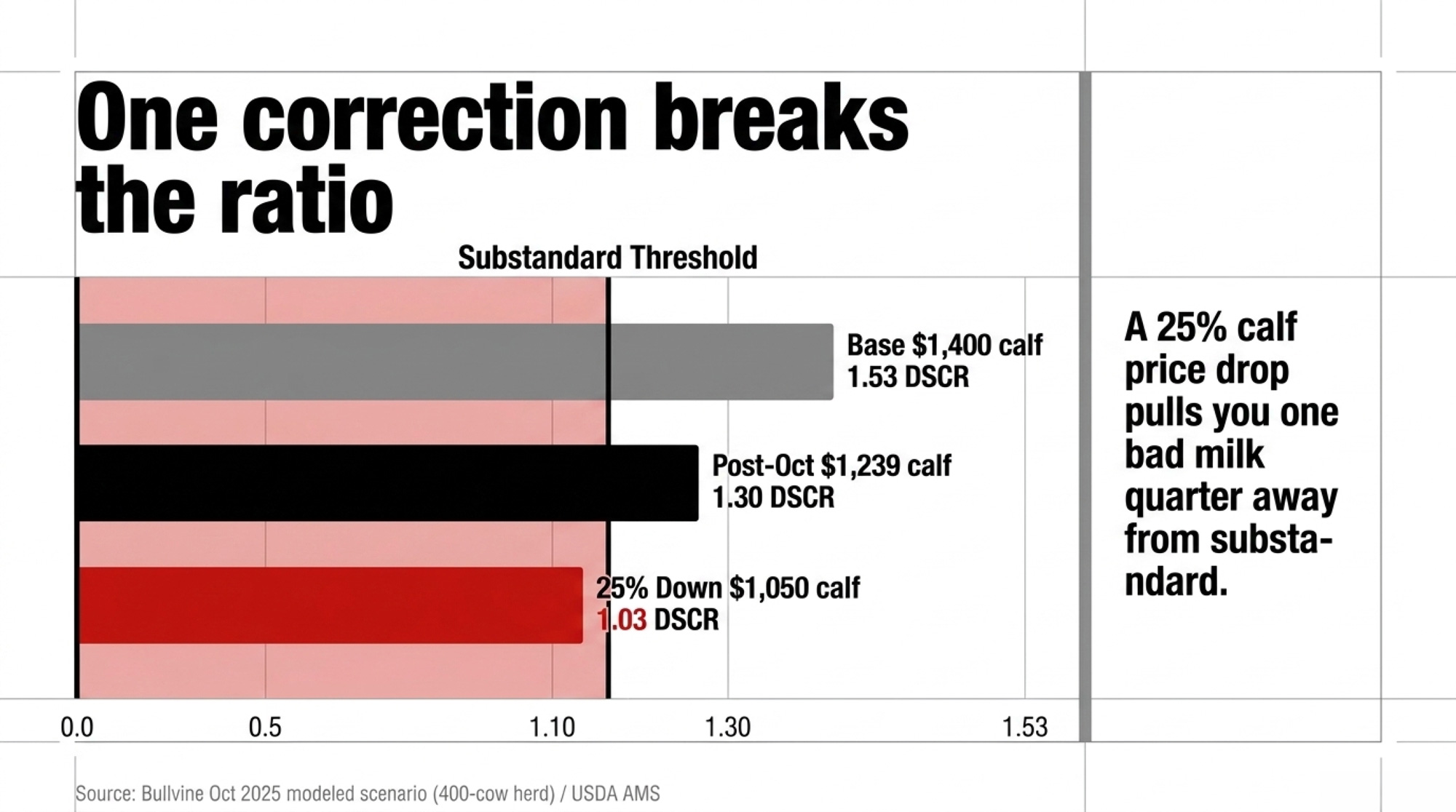

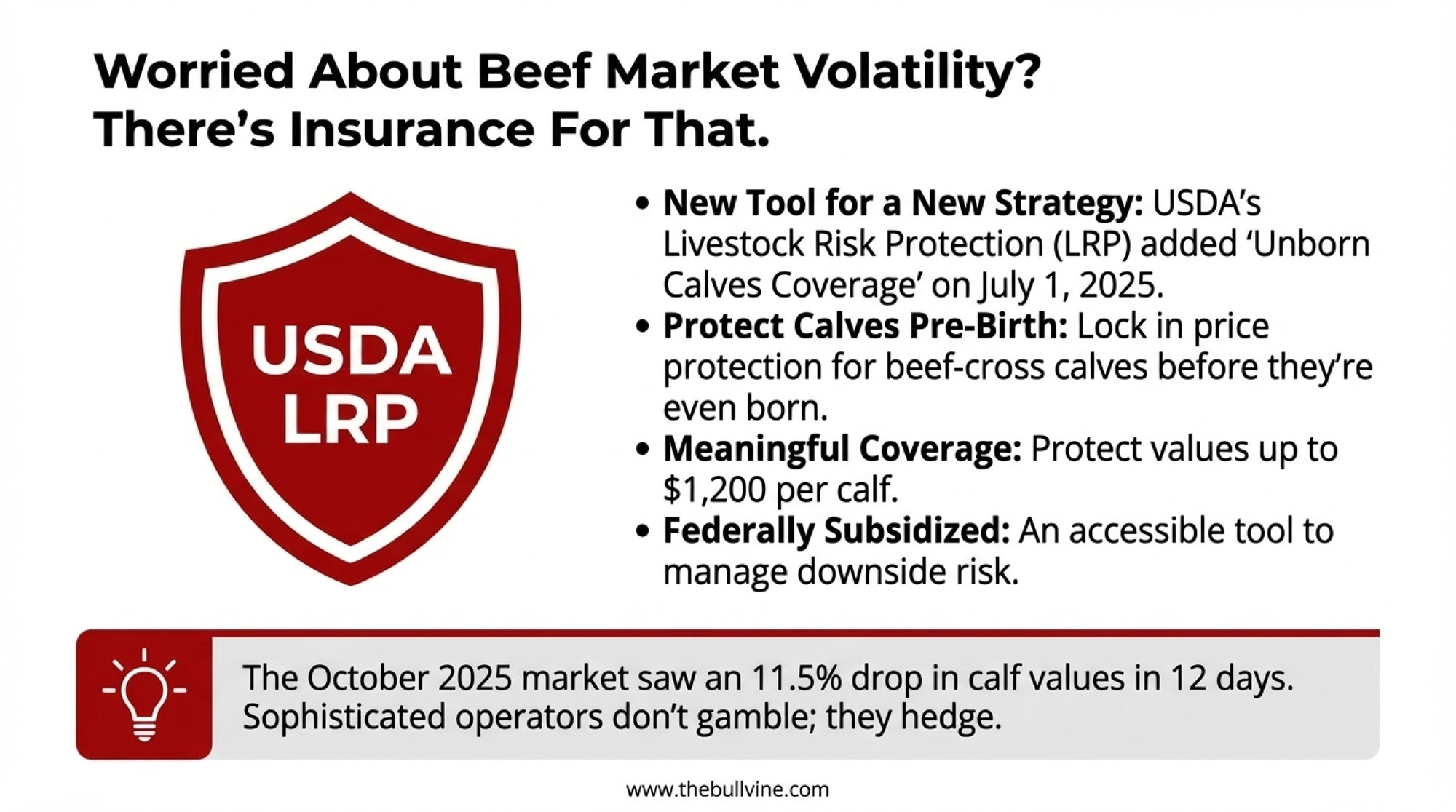

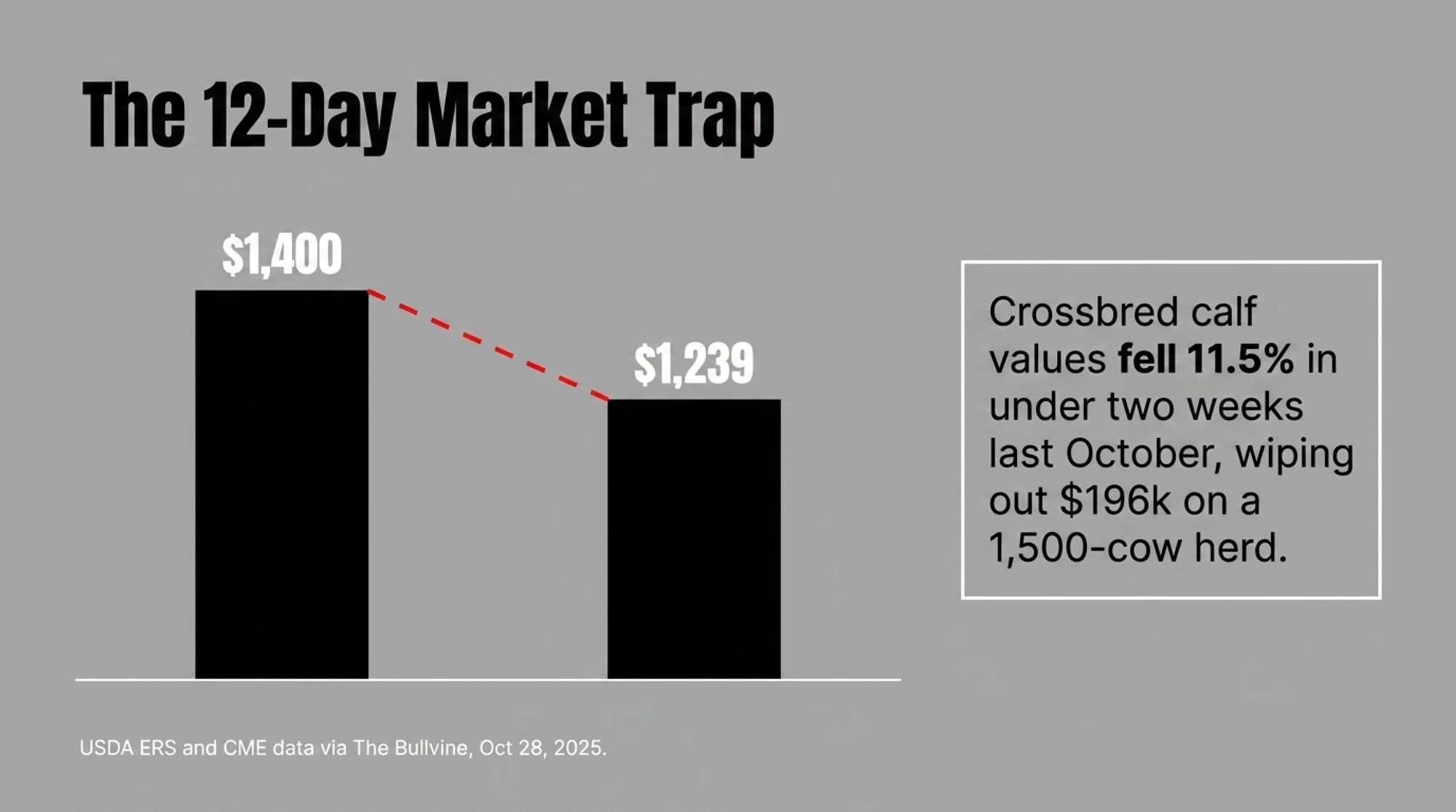

⚠ Twelve days. One import headline. Last October, crossbred calf values fell 11.5% — from about $1,400 to $1,239 a head — in roughly 12 days, after a market break tied to signals about reopening cattle and beef imports. For a modeled 1,500-cow herd breeding 40% to beef, that swing wiped out around $196,000 in annual calf revenue — about $130.72 per cow across the whole herd (The Bullvine, October 28, 2025, citing USDA ERS and CME data).

The futures moved just as hard. CME December Live Cattle dropped from $247.88/cwt on October 16 into the mid-$220s inside two weeks. None of that volatility shows up in the premium when the calf buyer quotes you a friendly price on a Tuesday.

How Much Does That Beef Straw Actually Cost You?

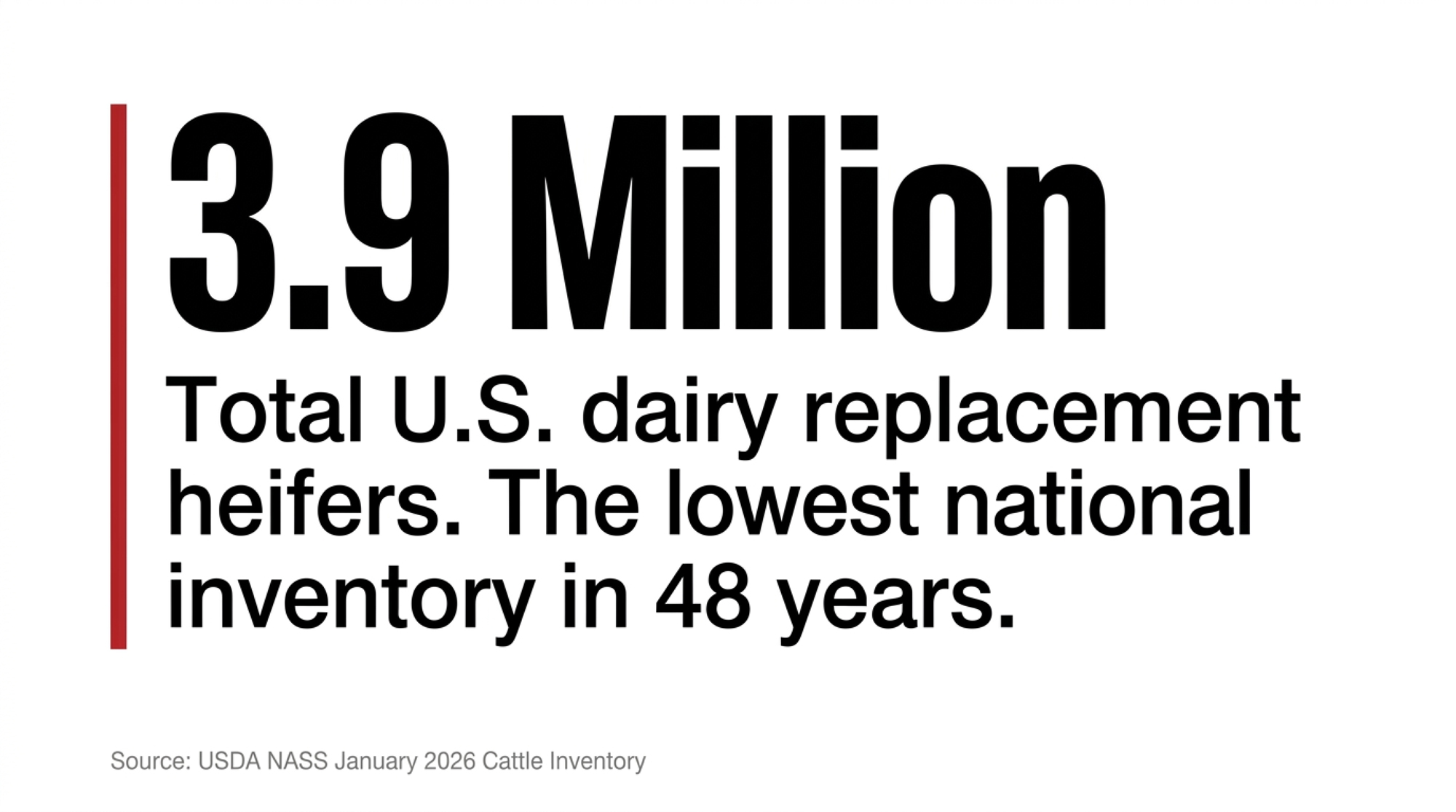

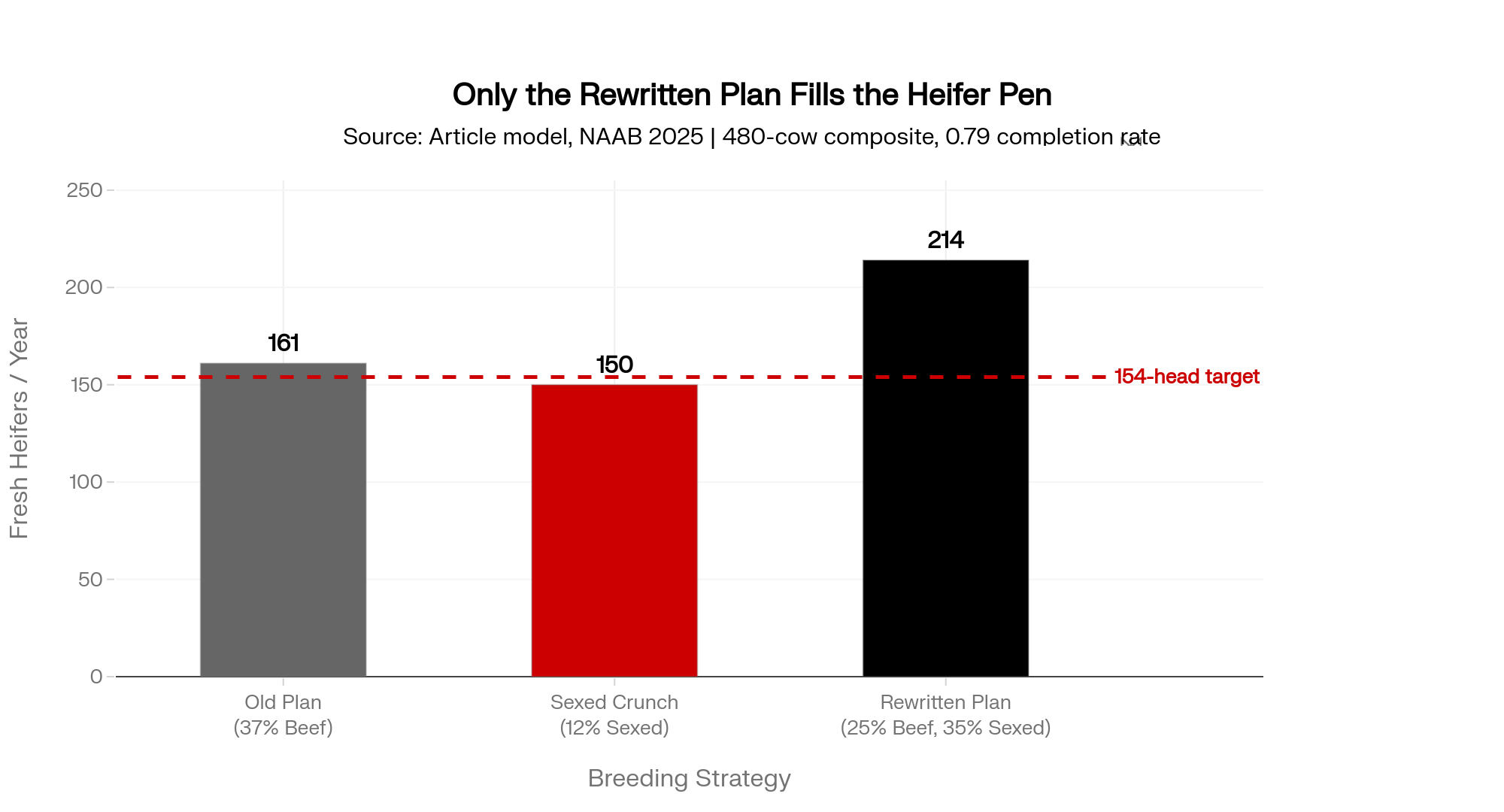

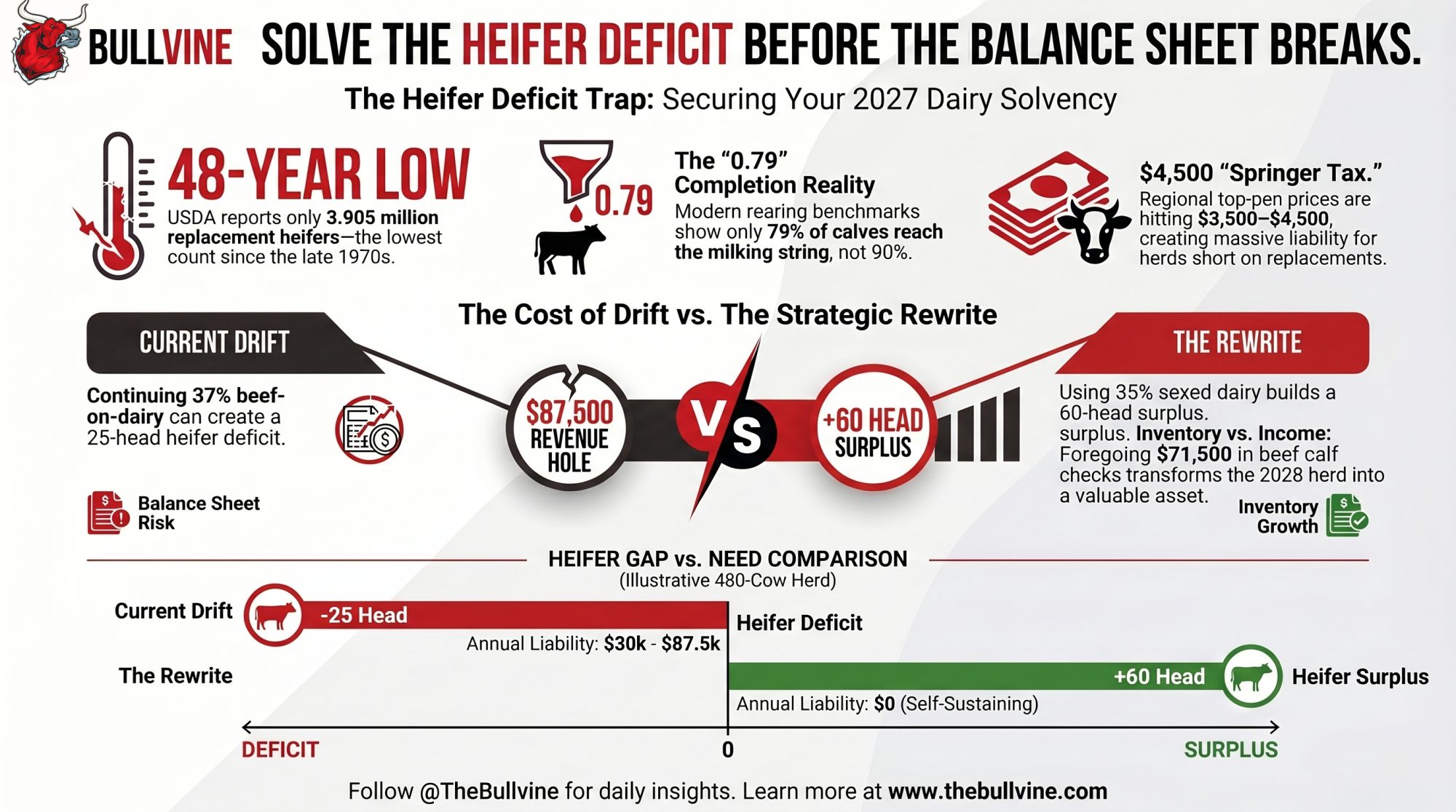

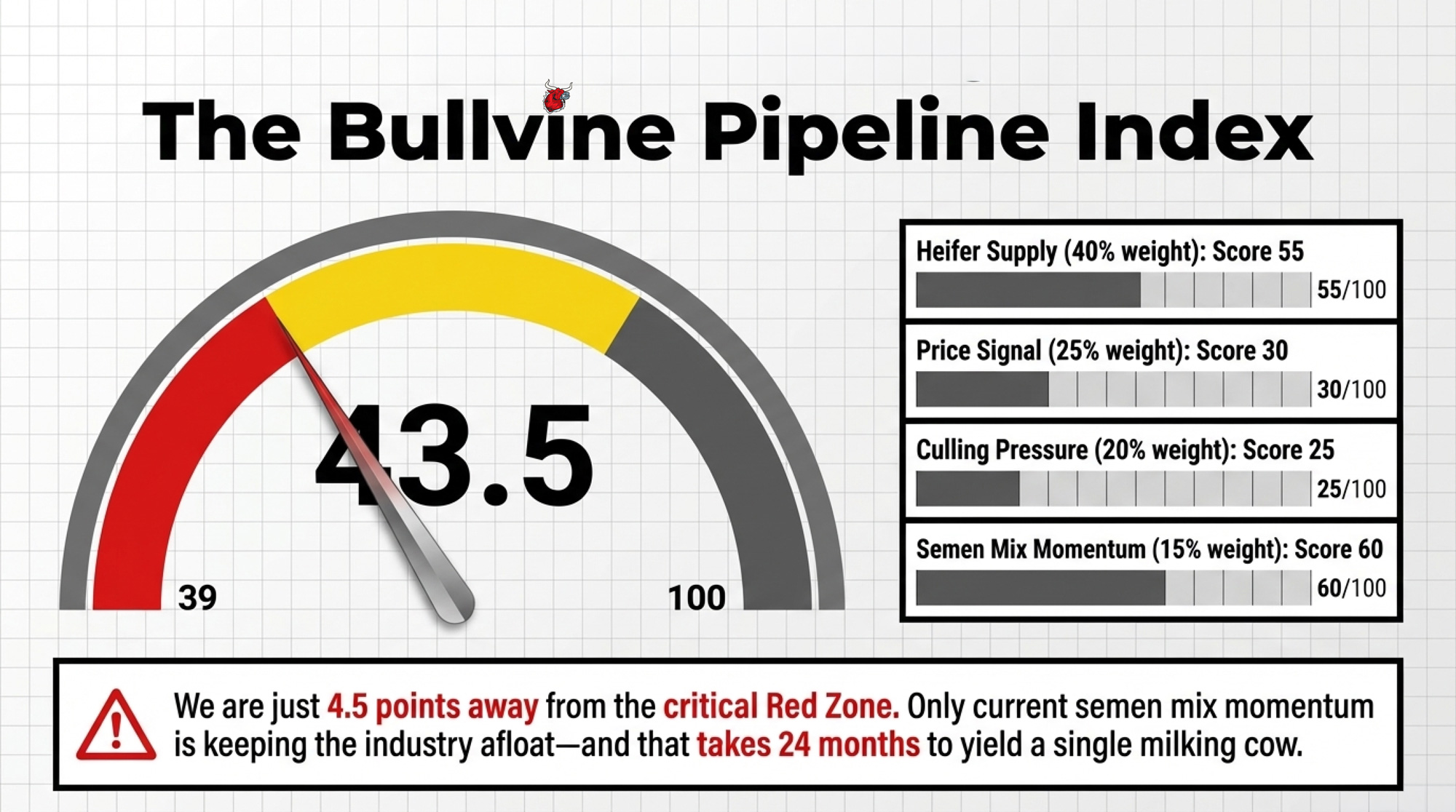

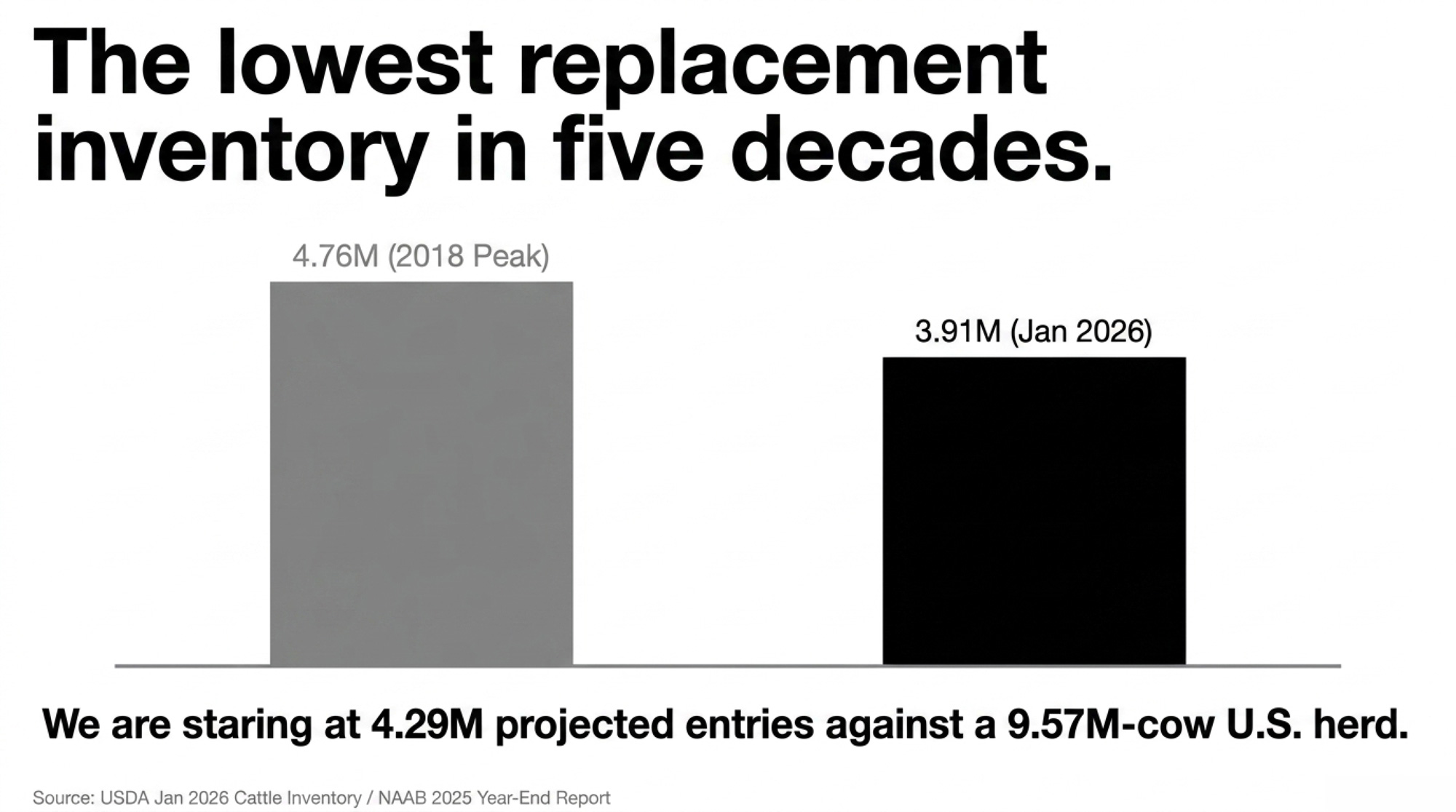

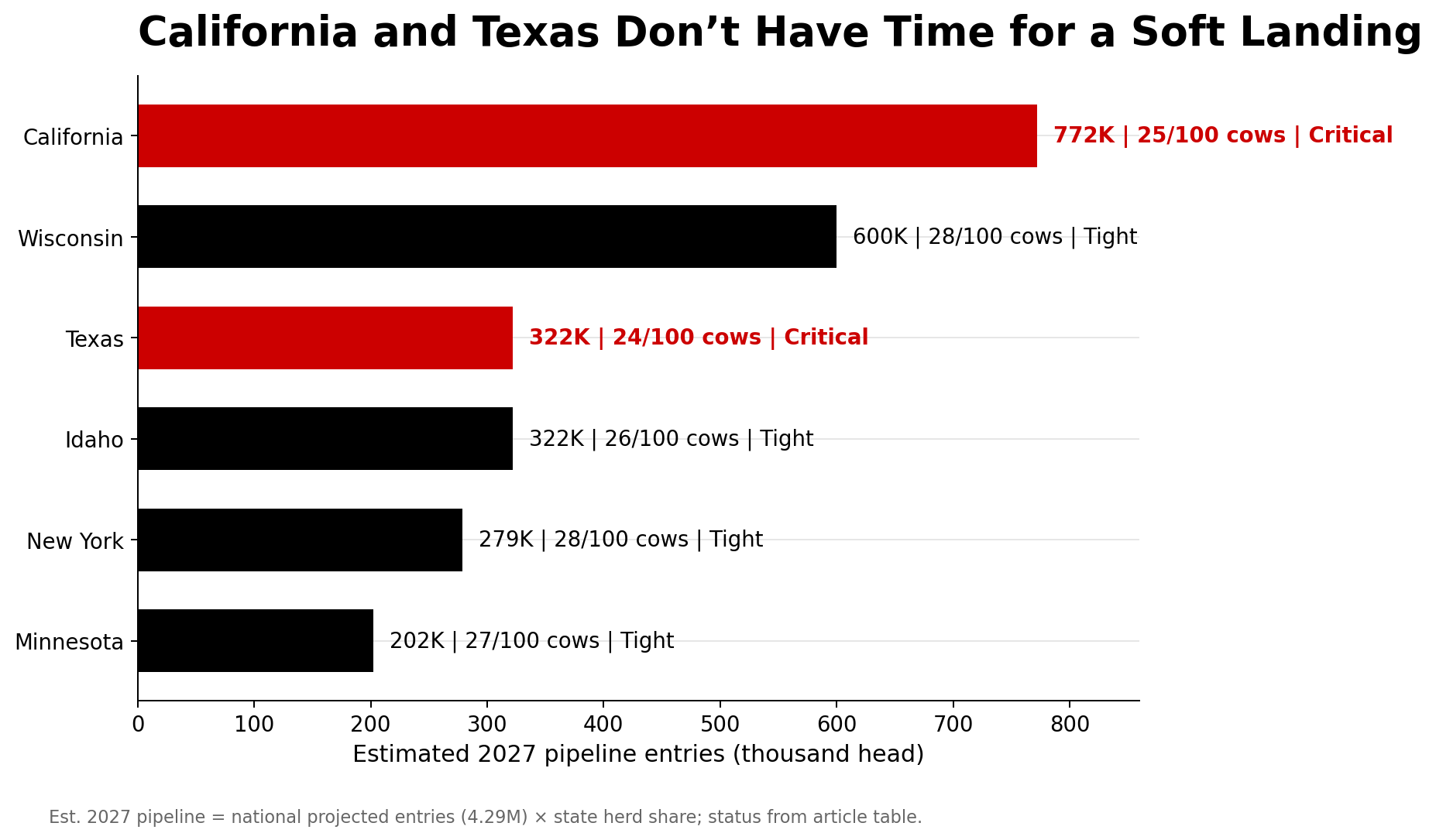

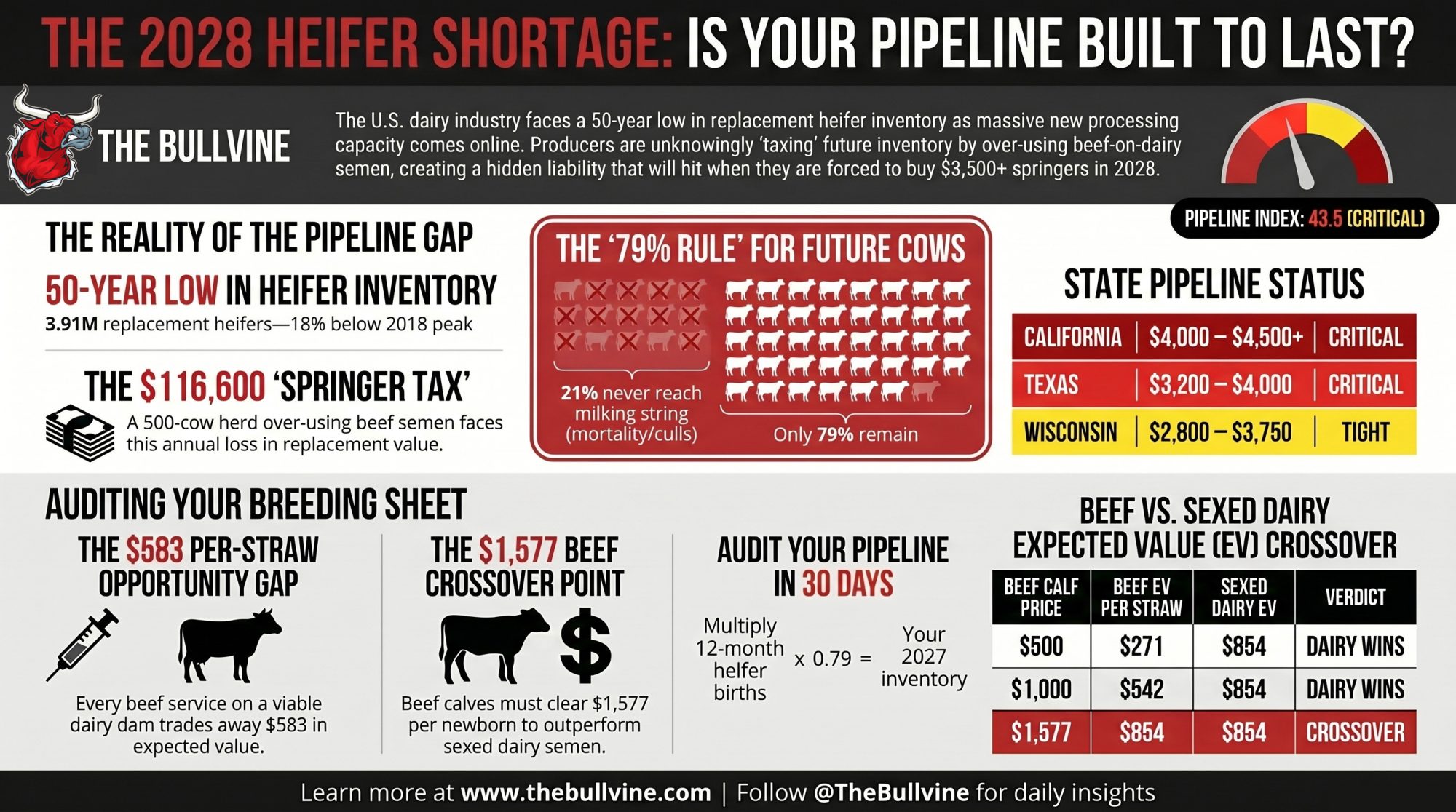

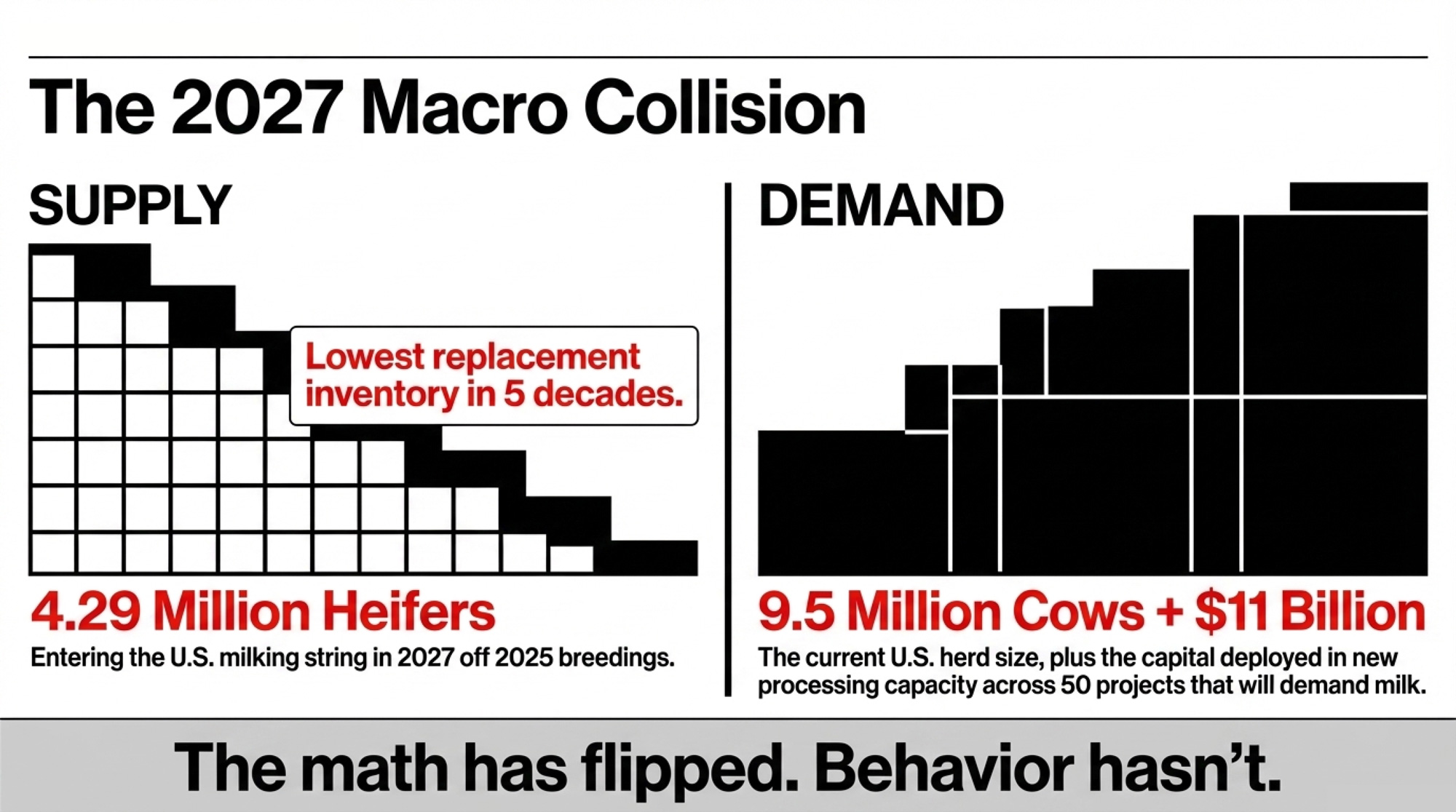

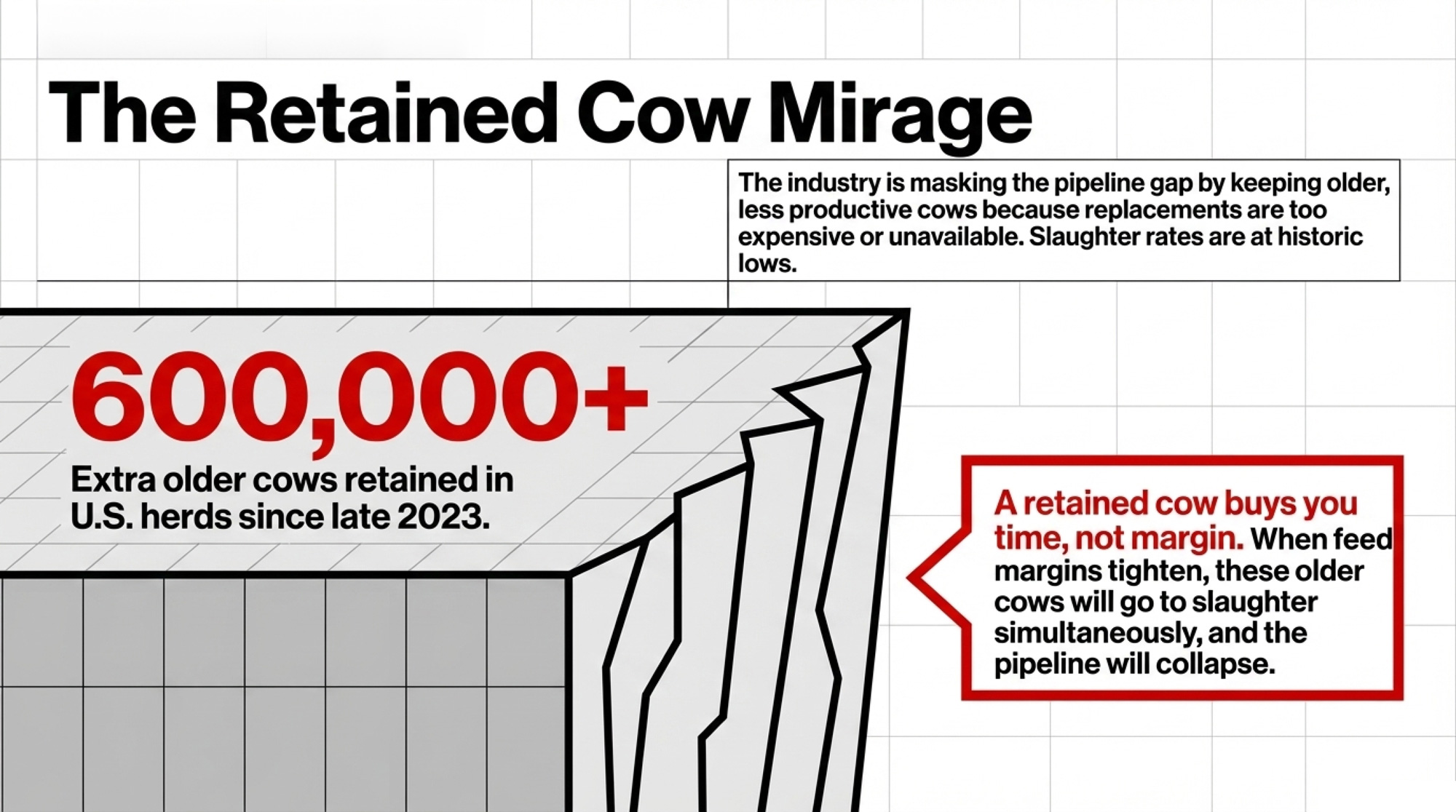

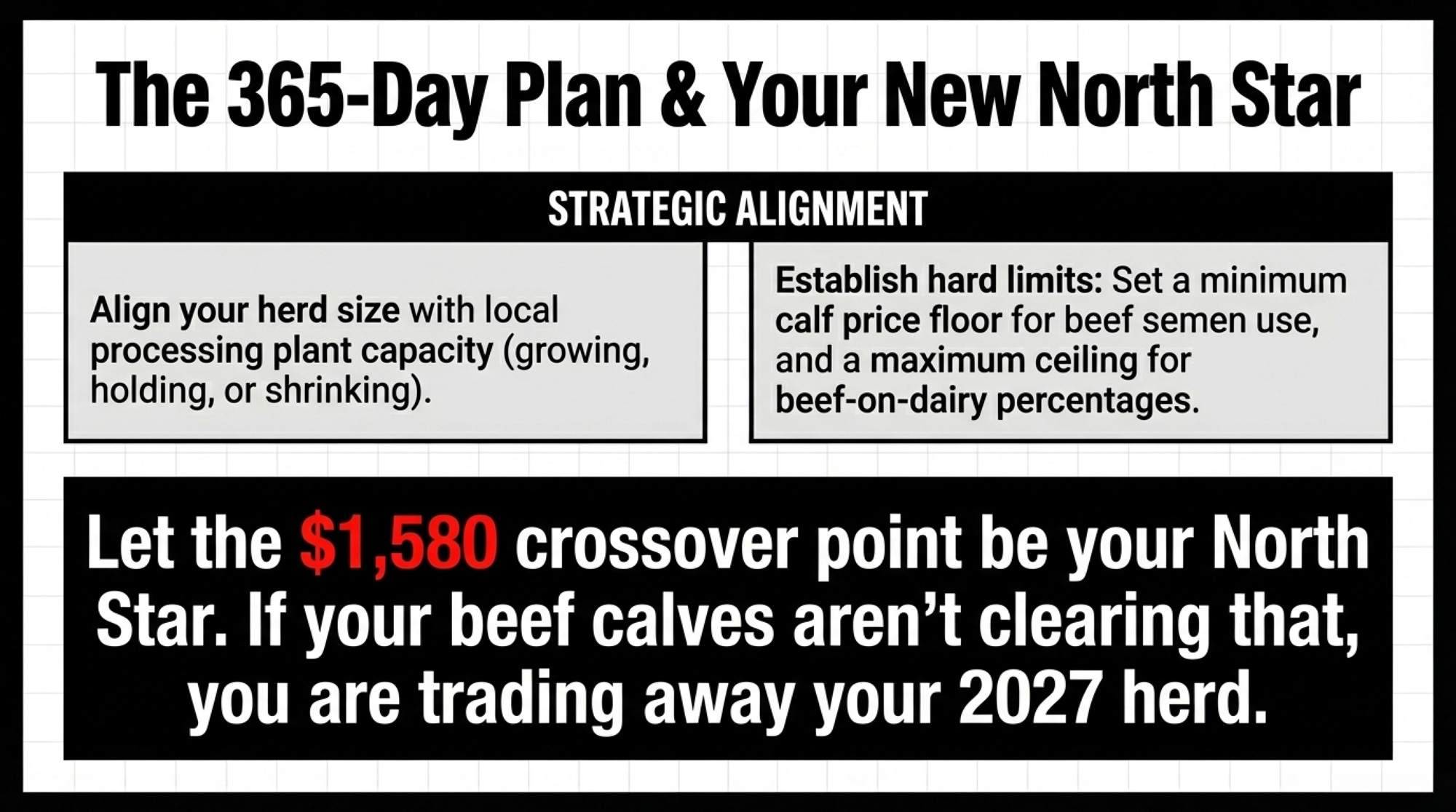

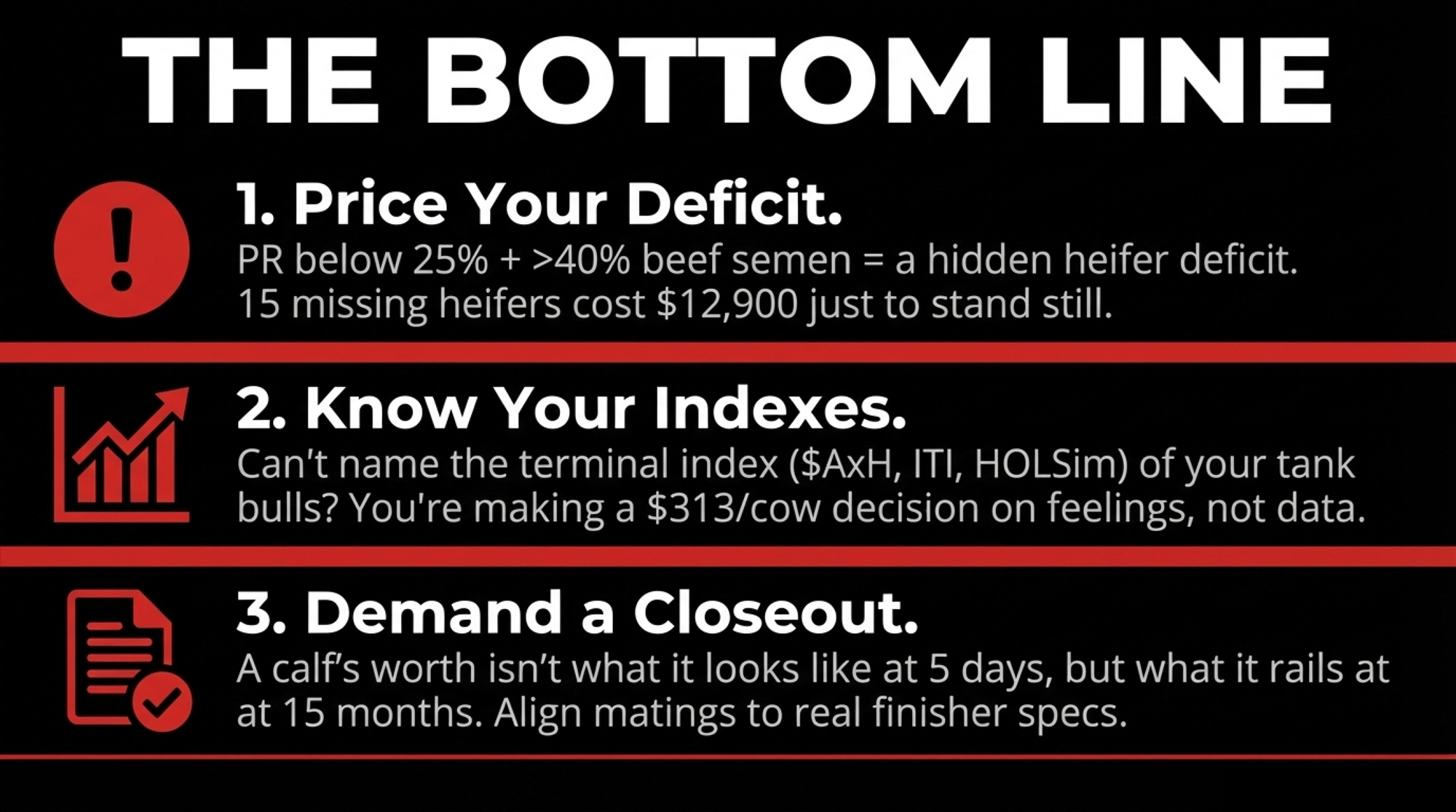

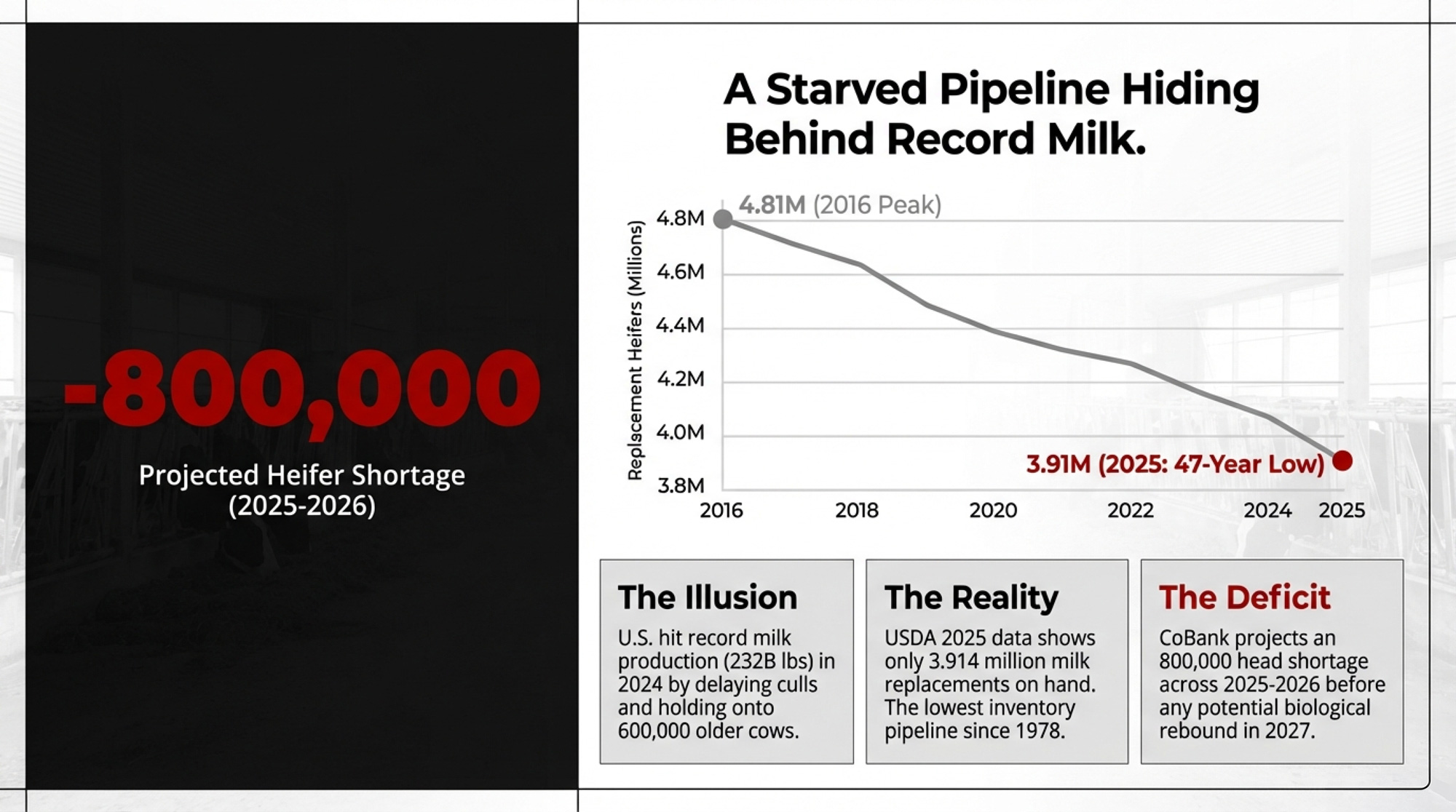

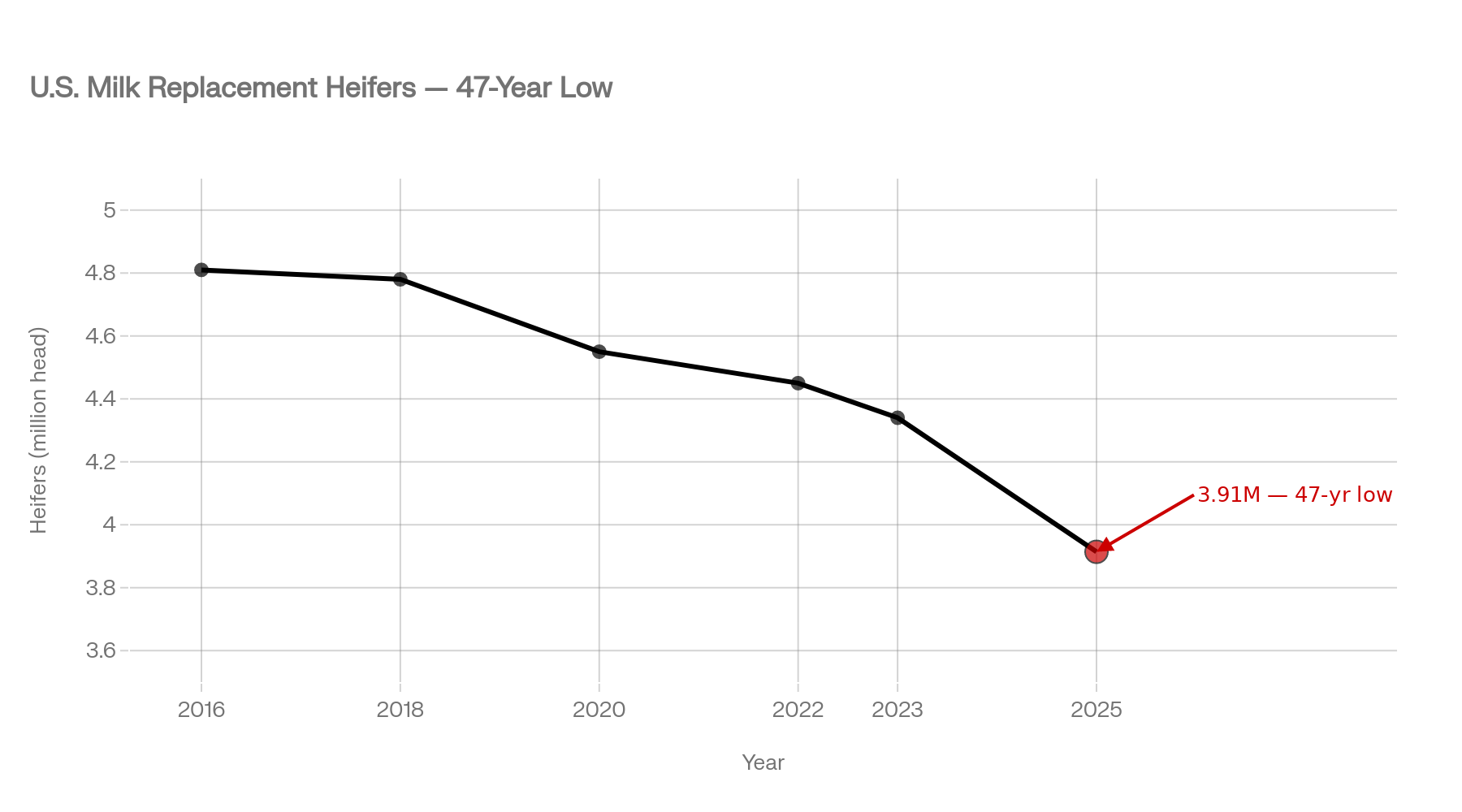

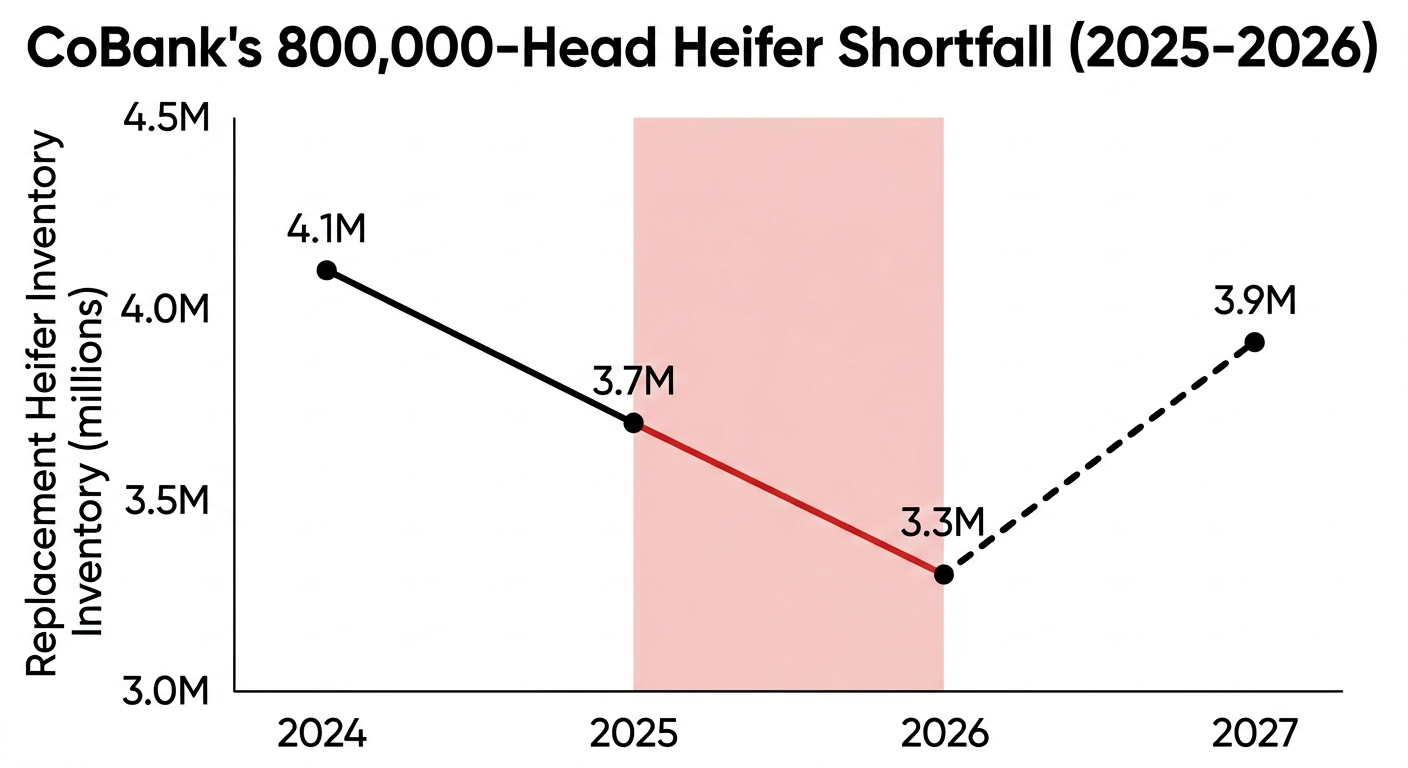

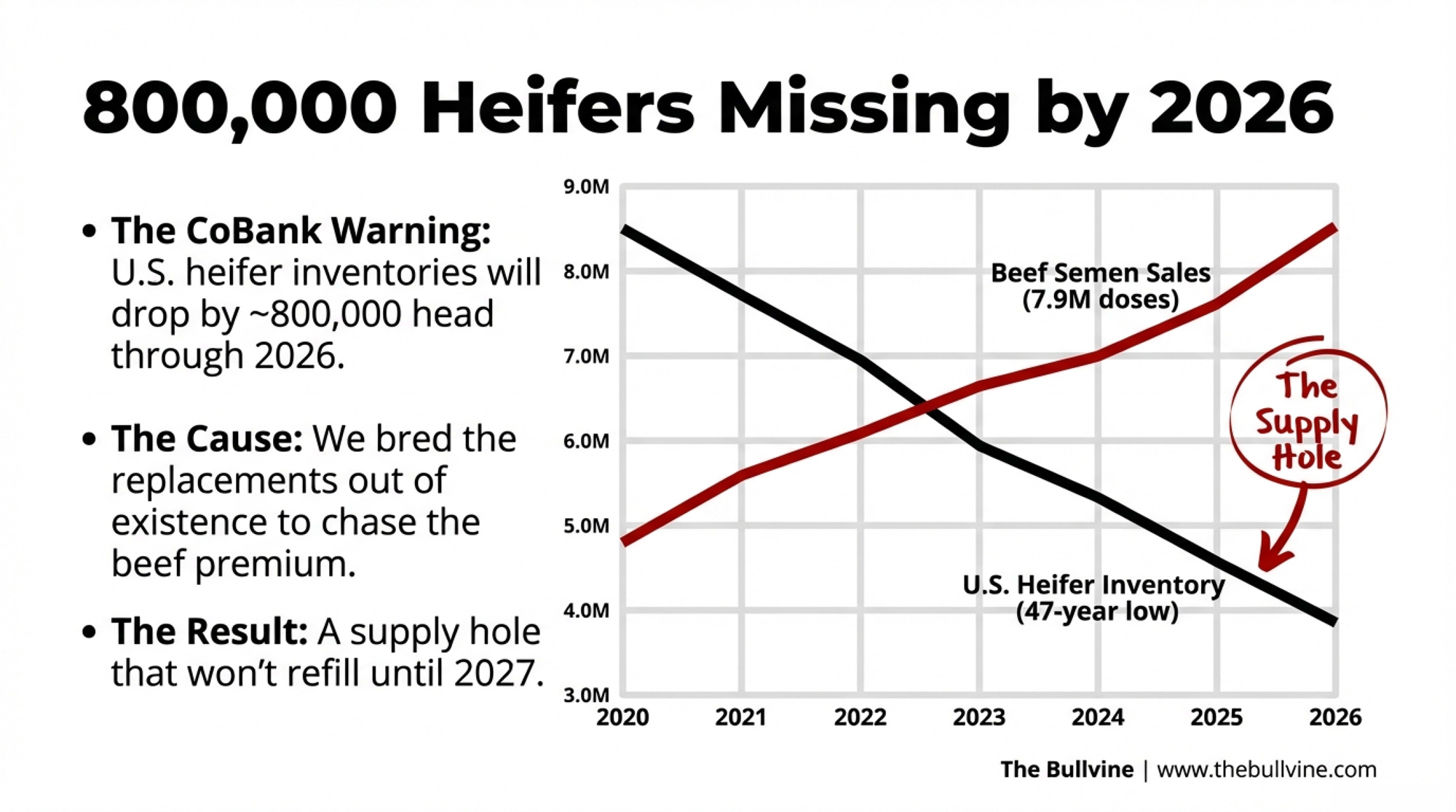

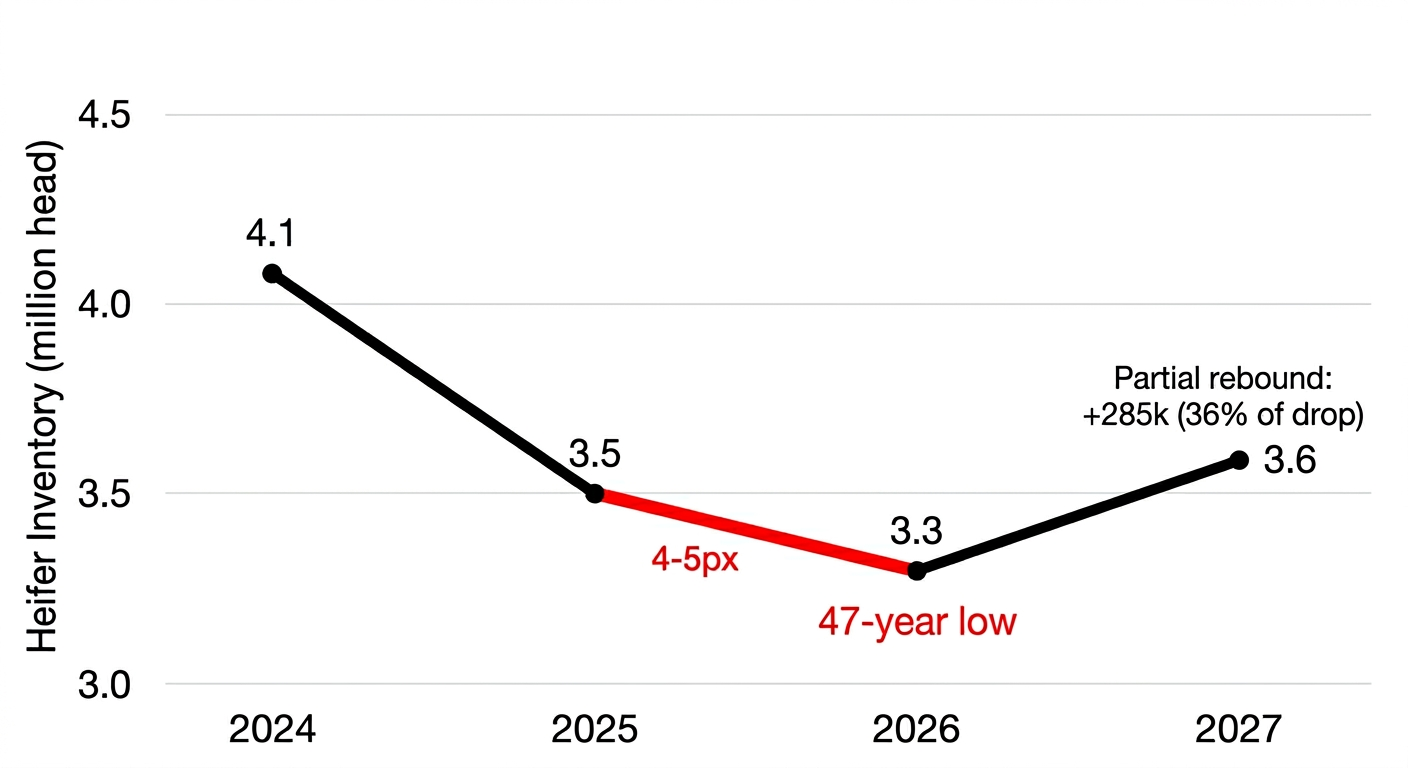

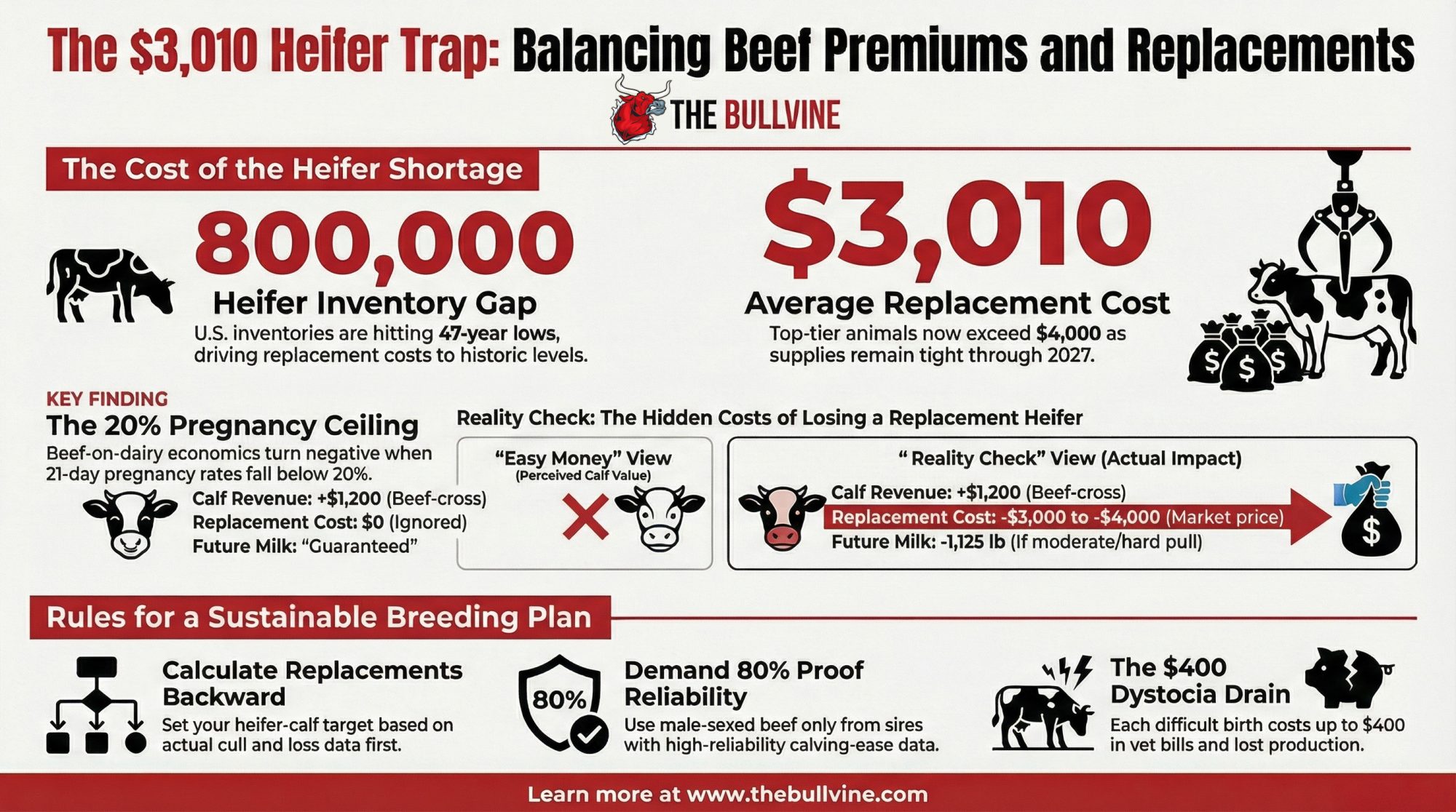

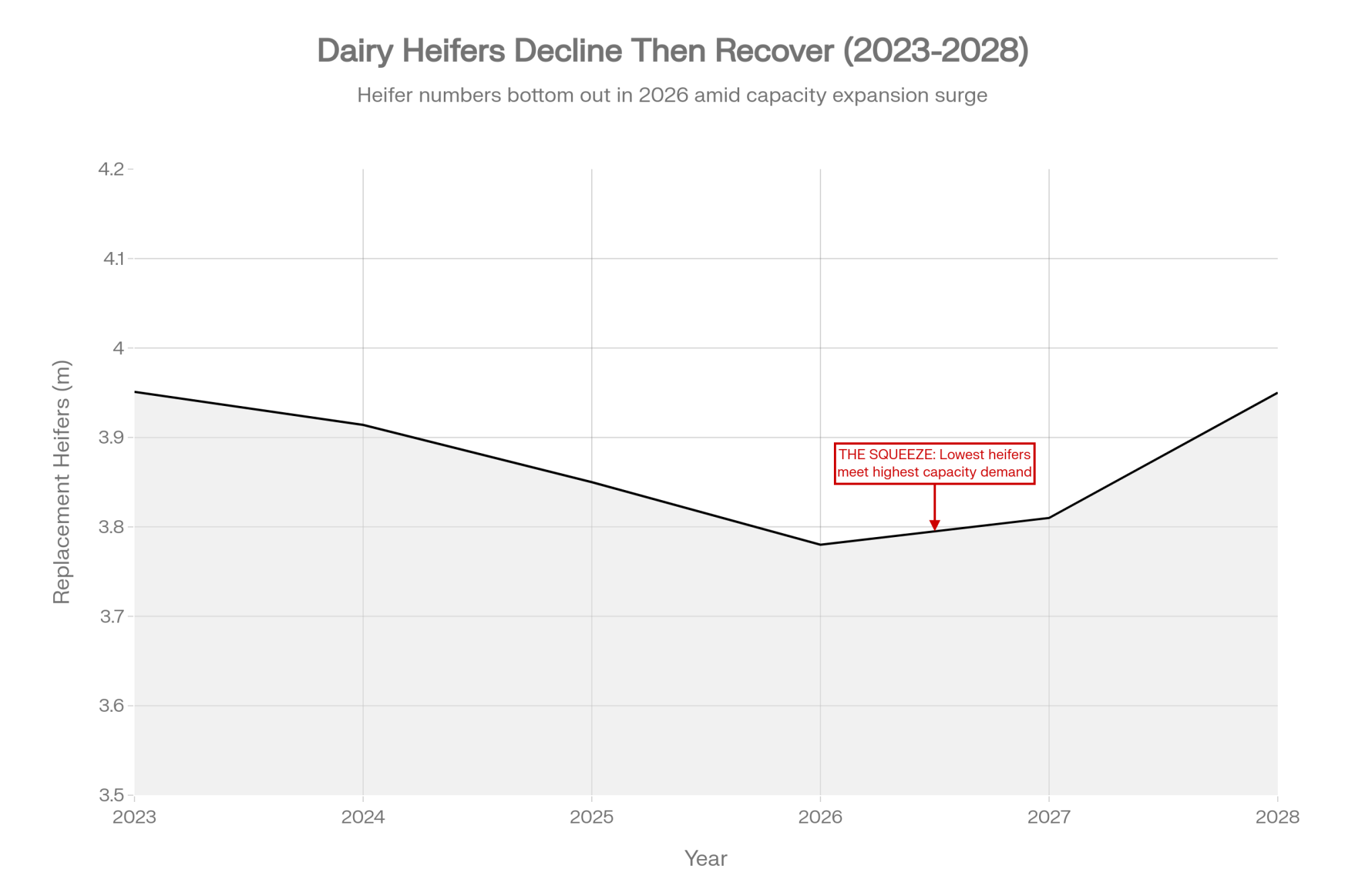

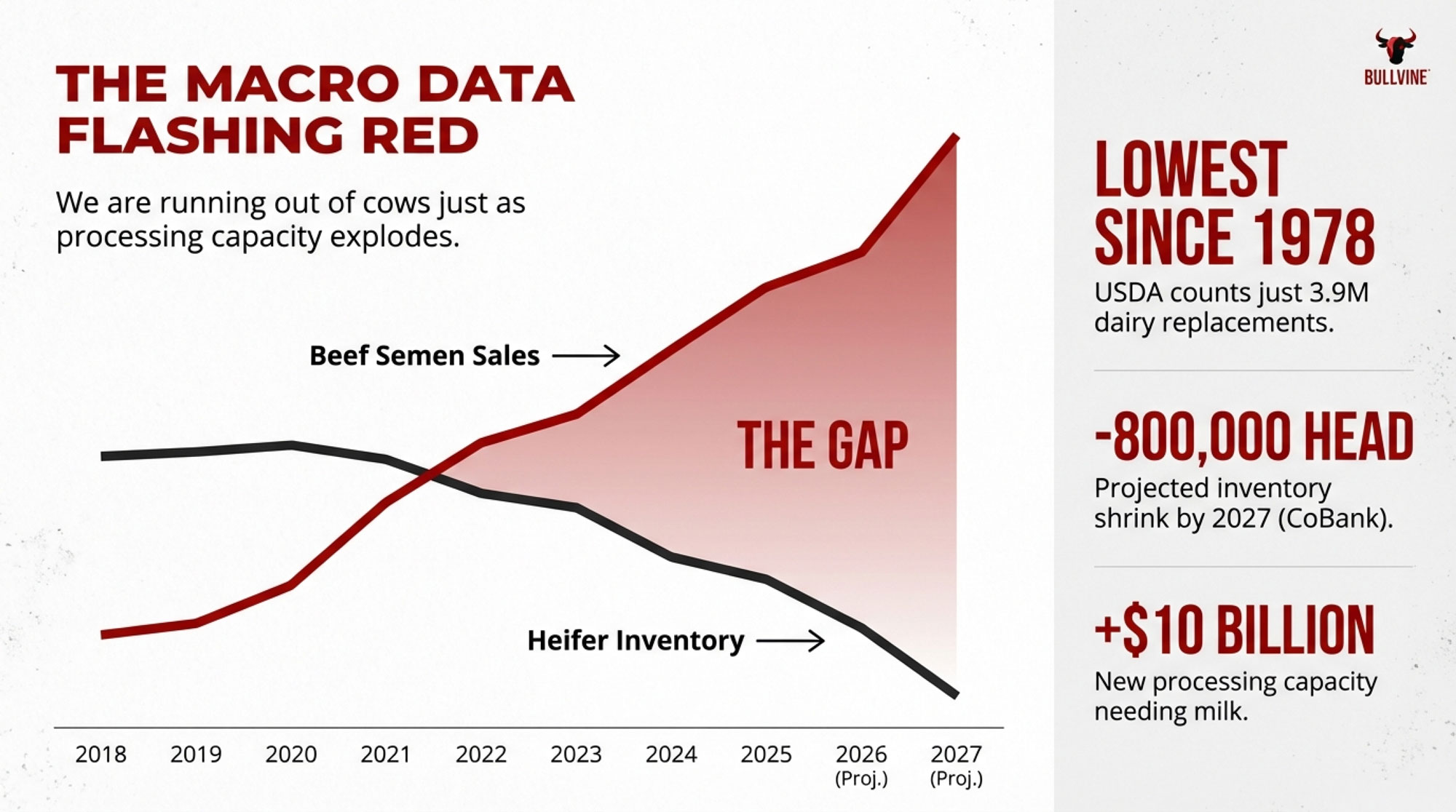

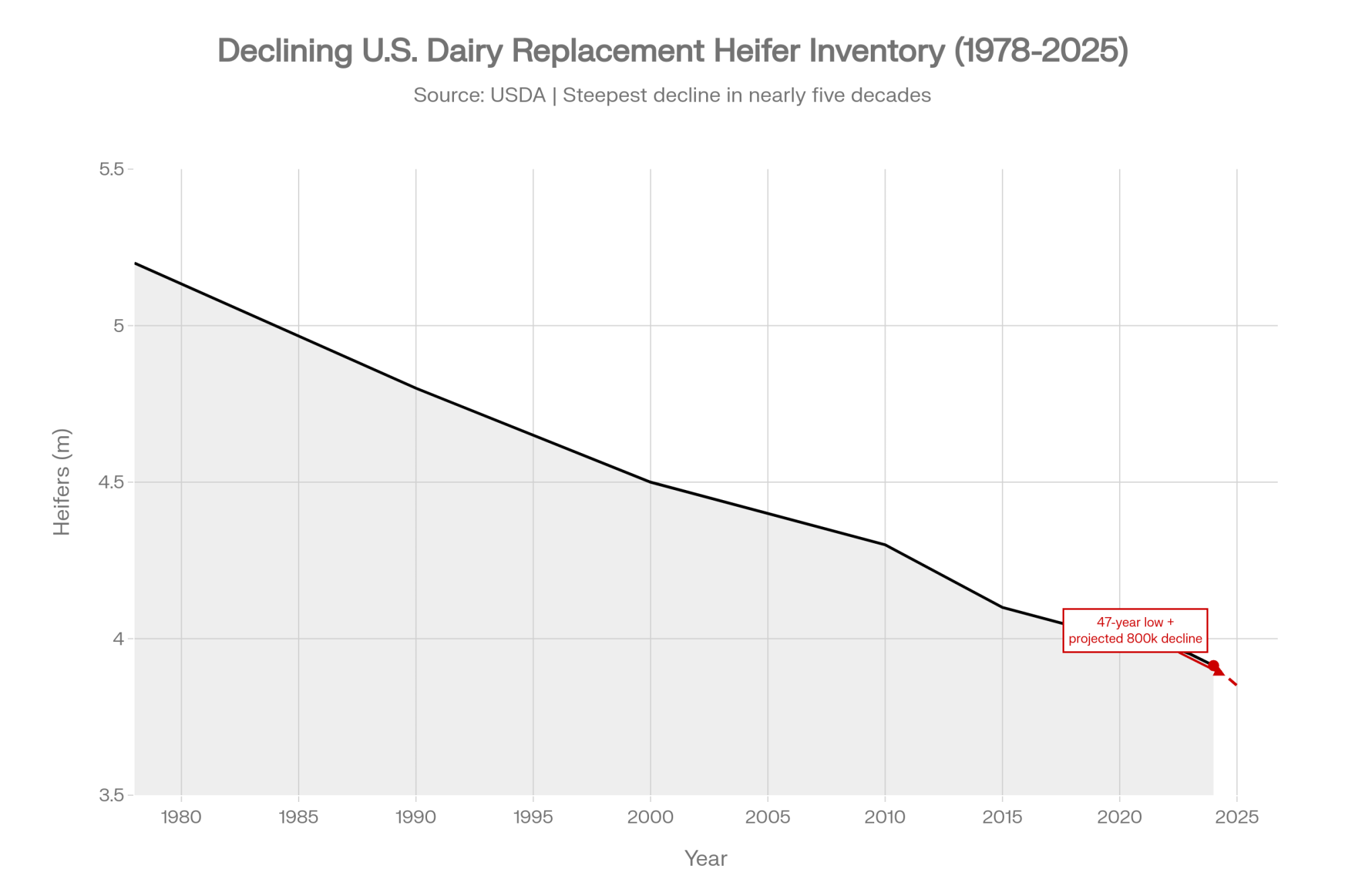

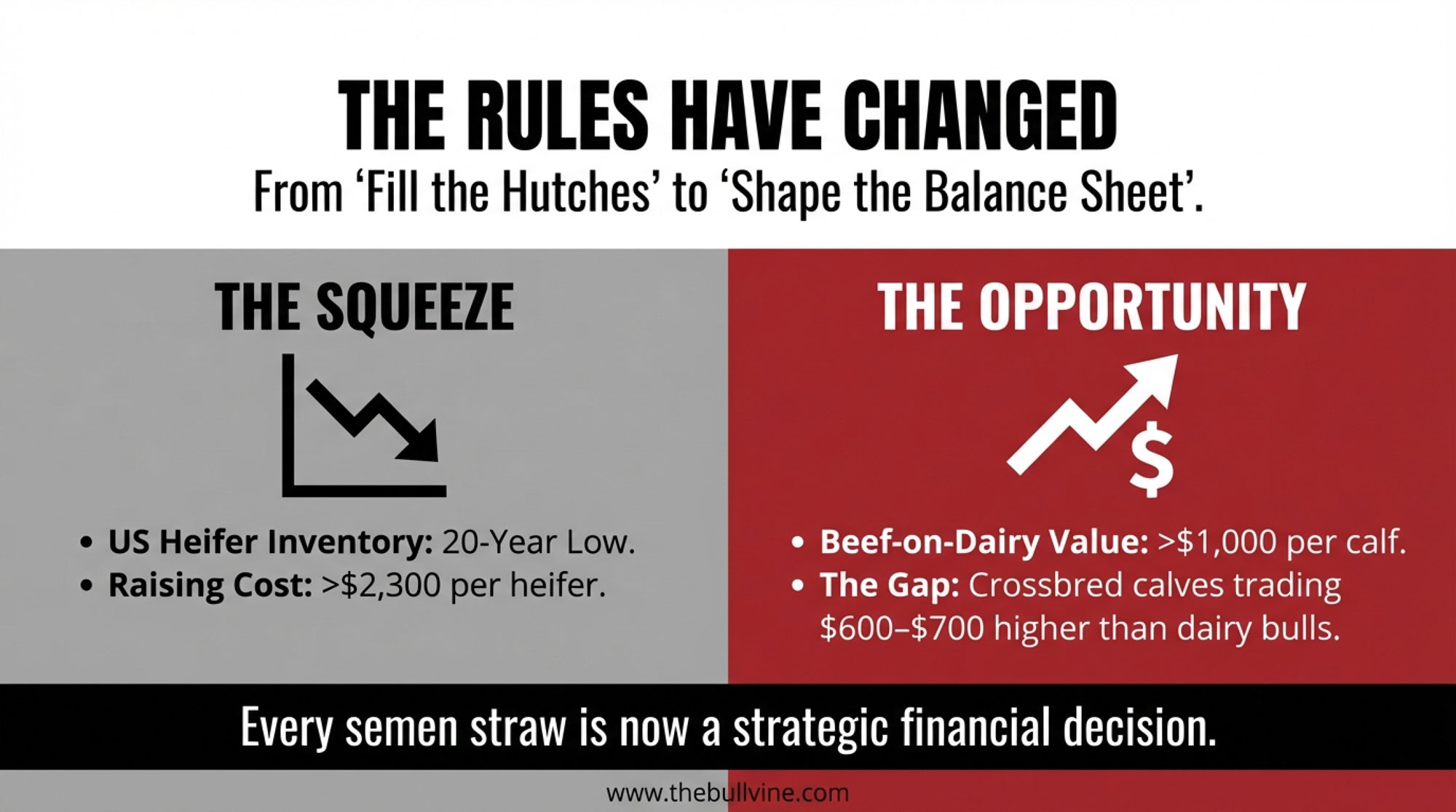

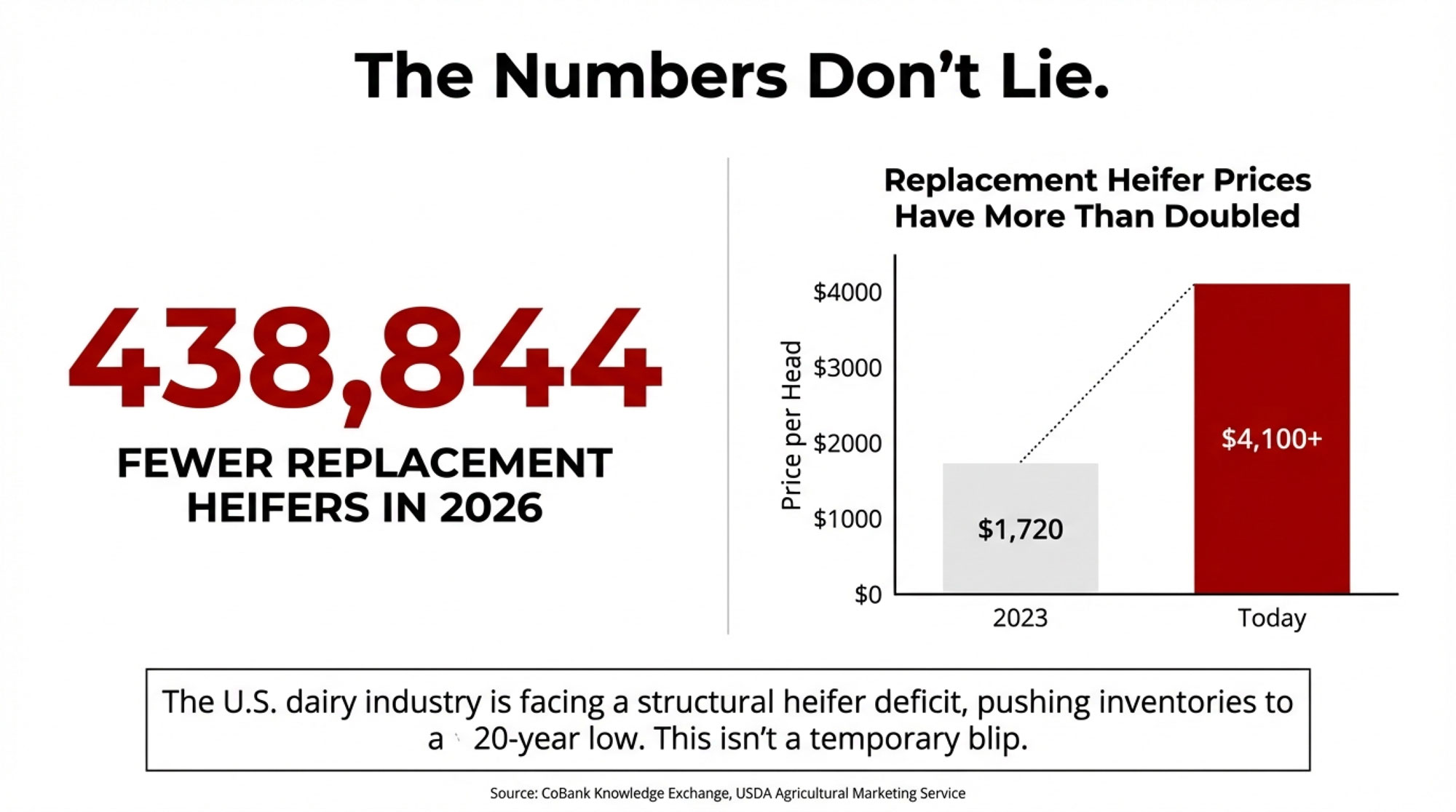

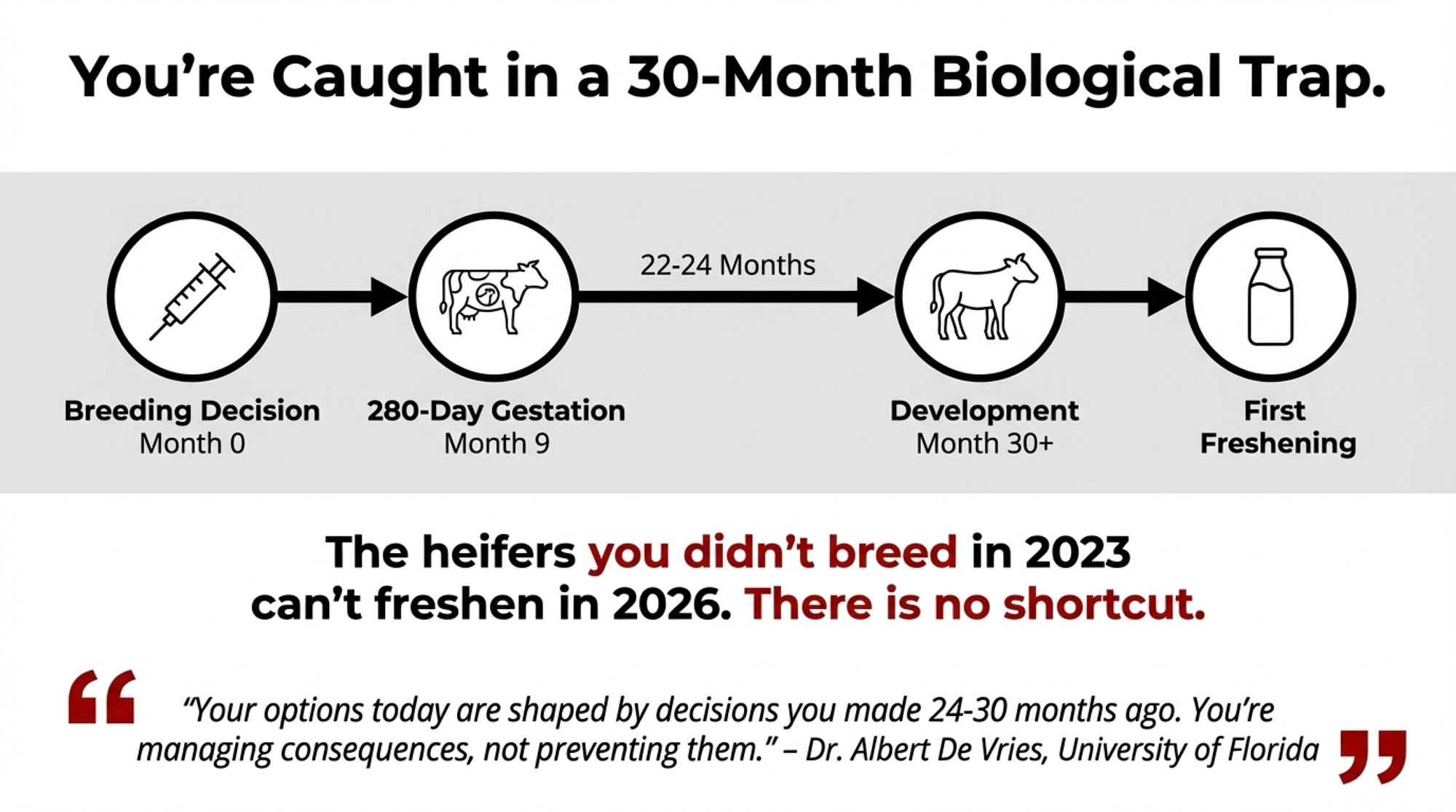

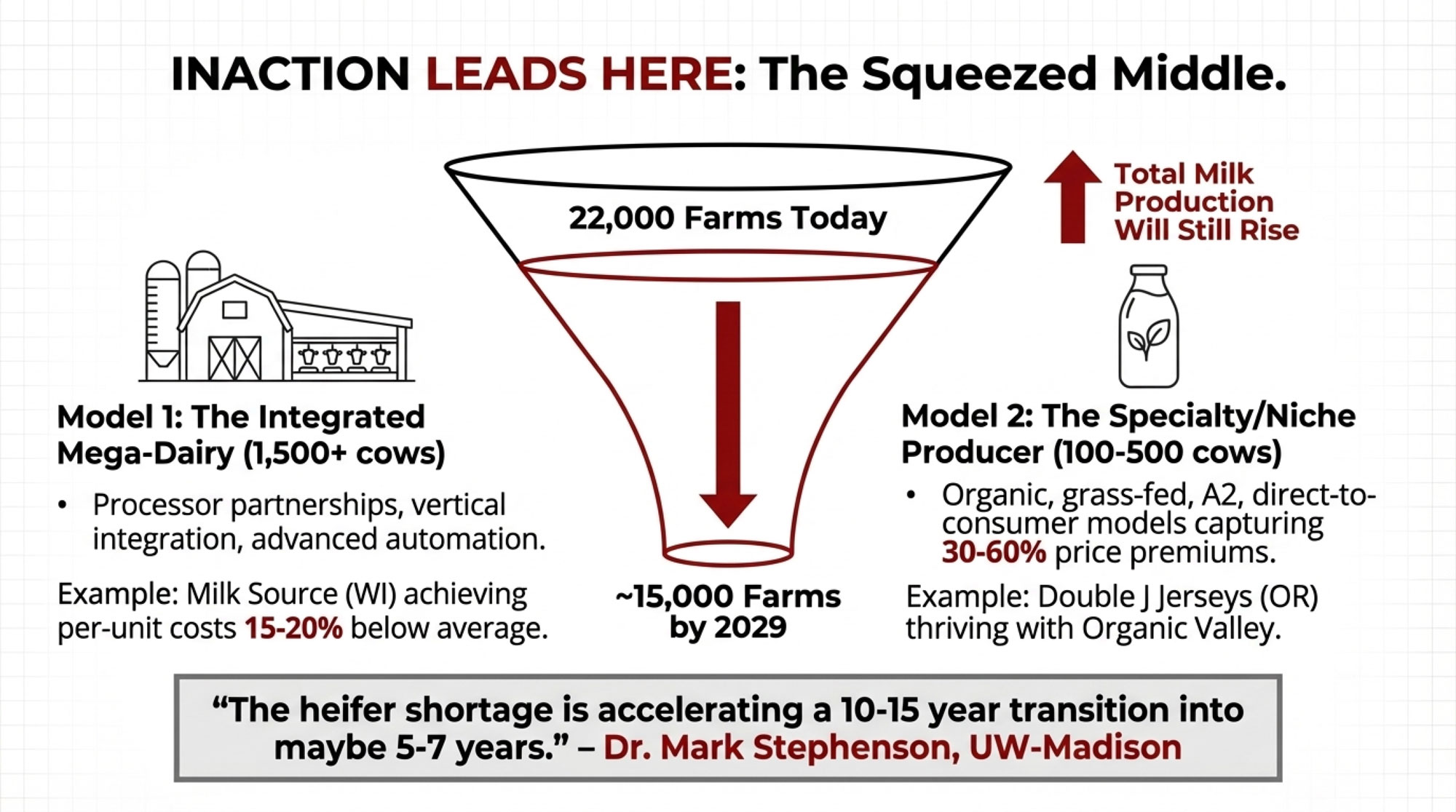

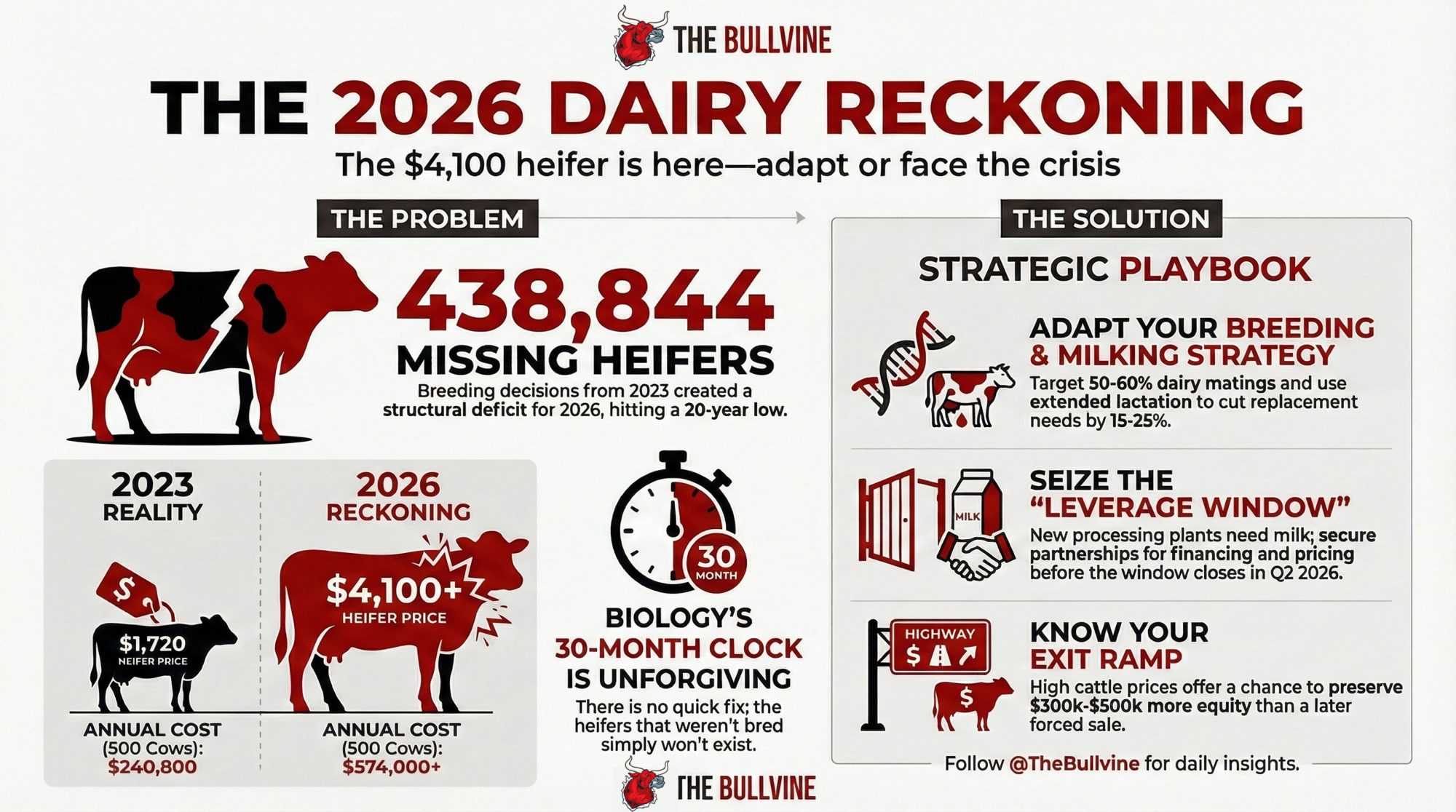

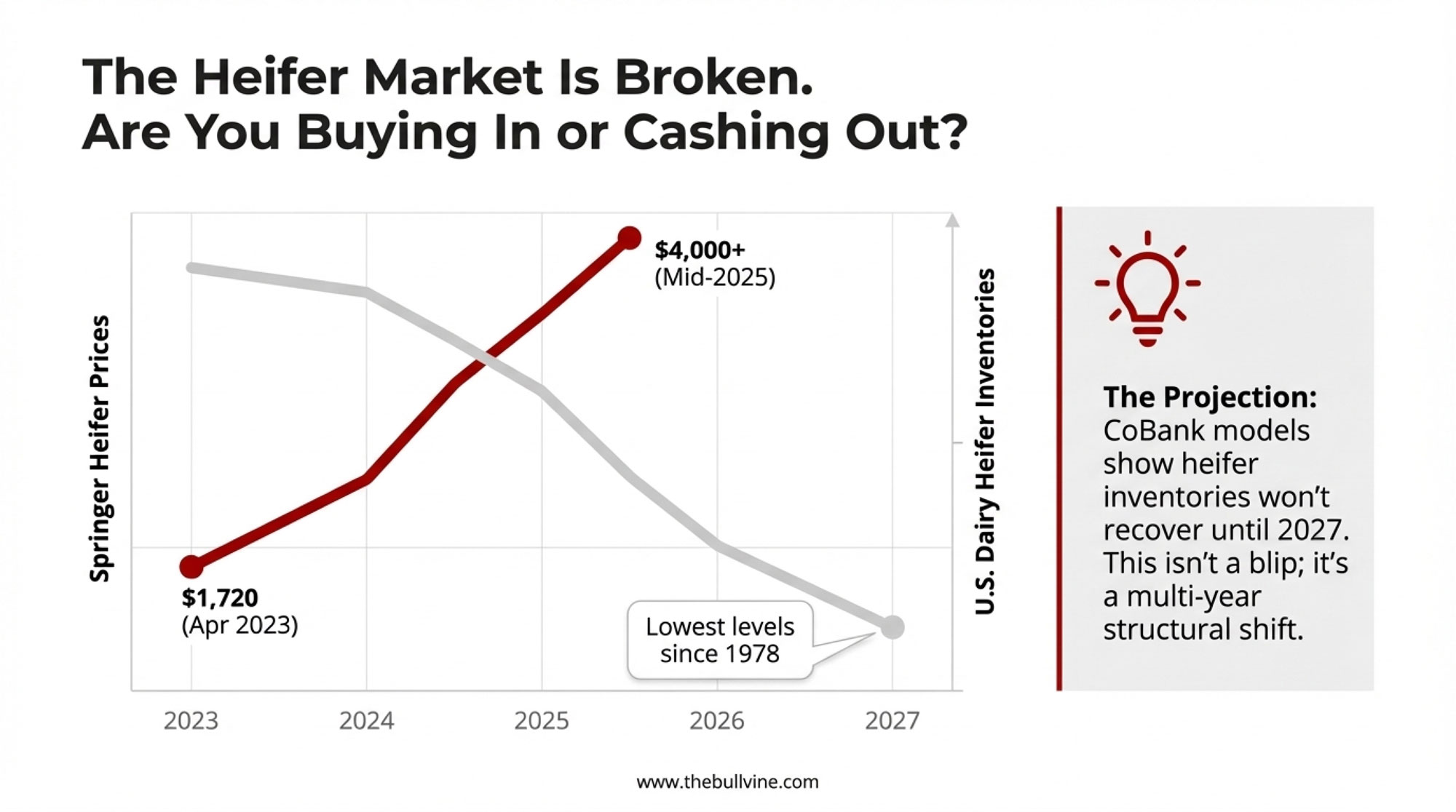

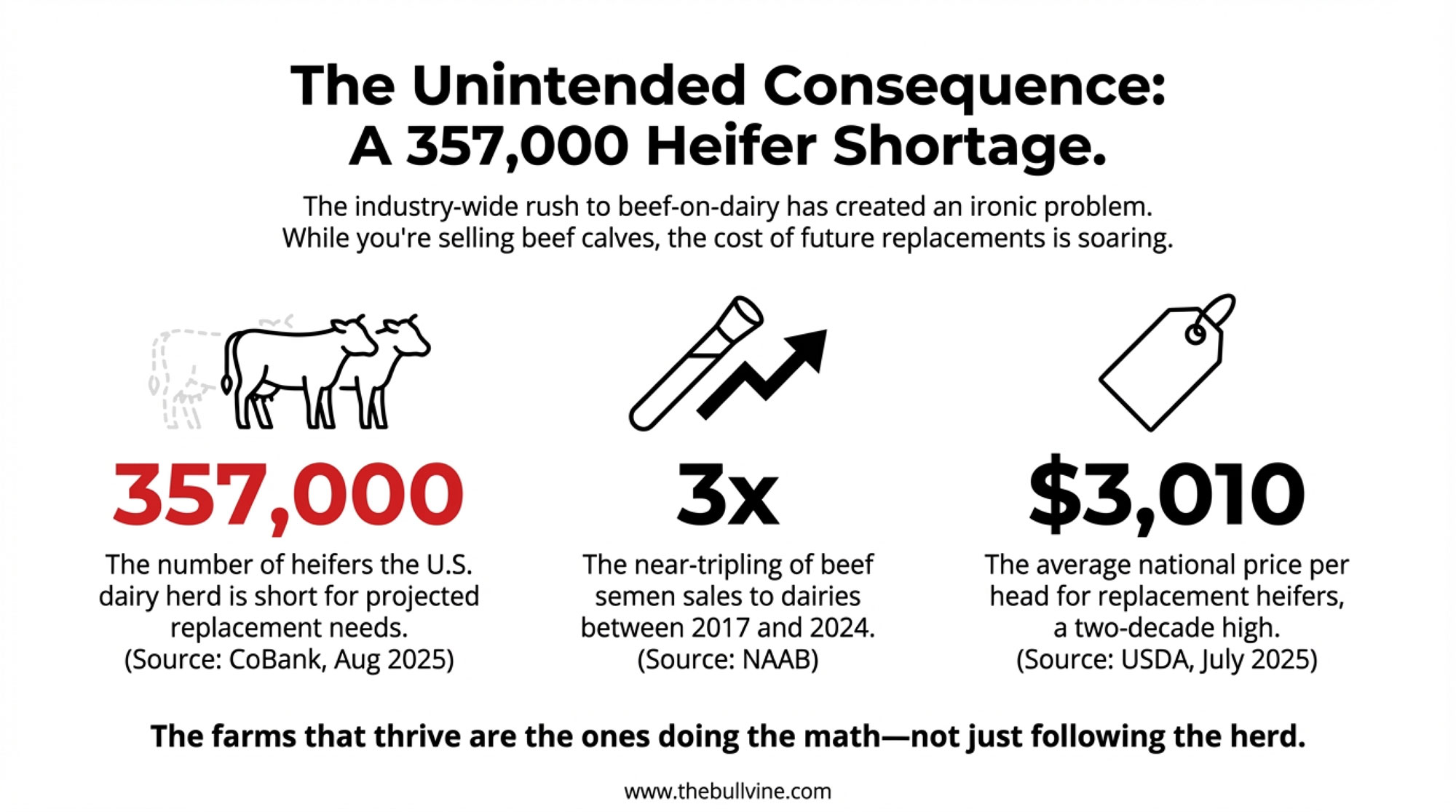

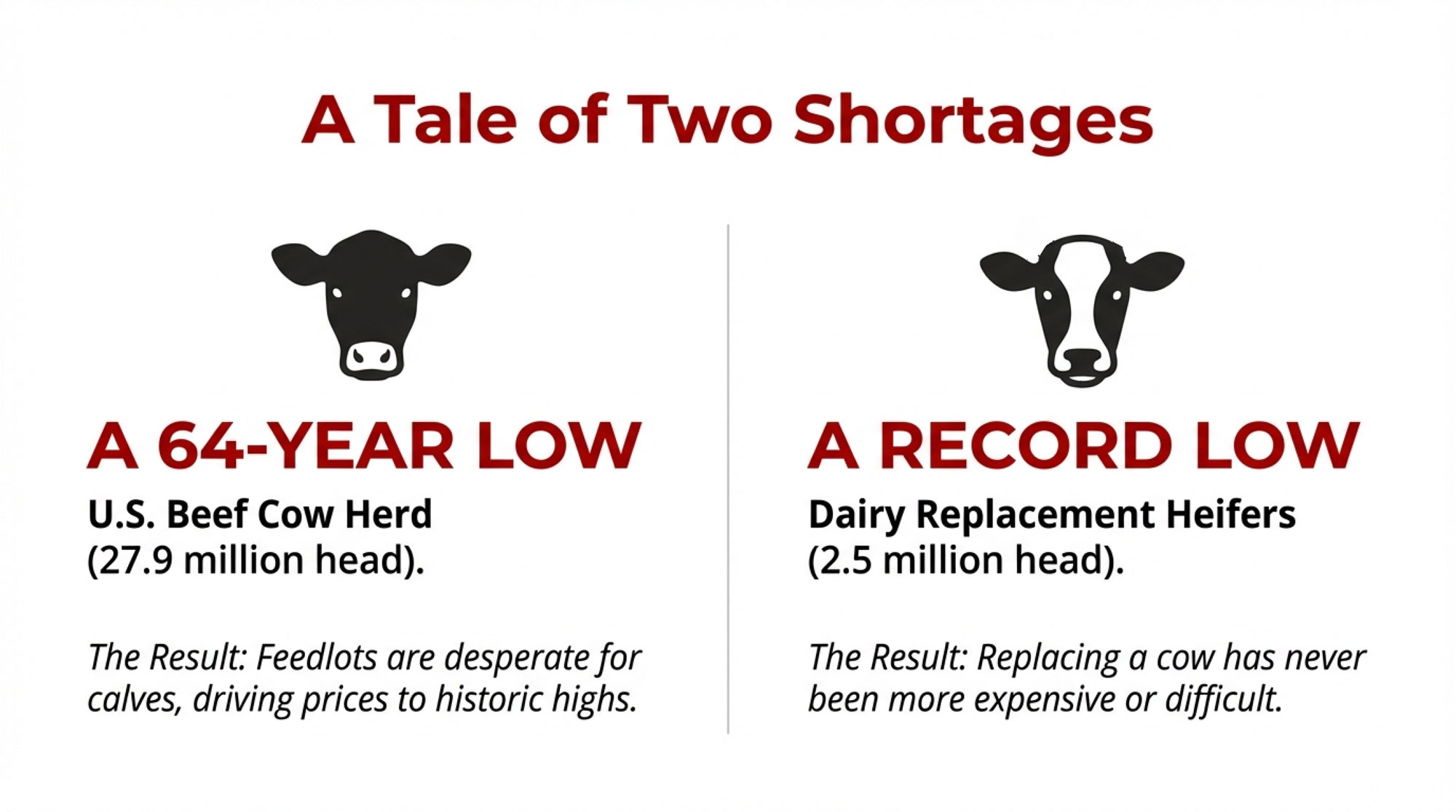

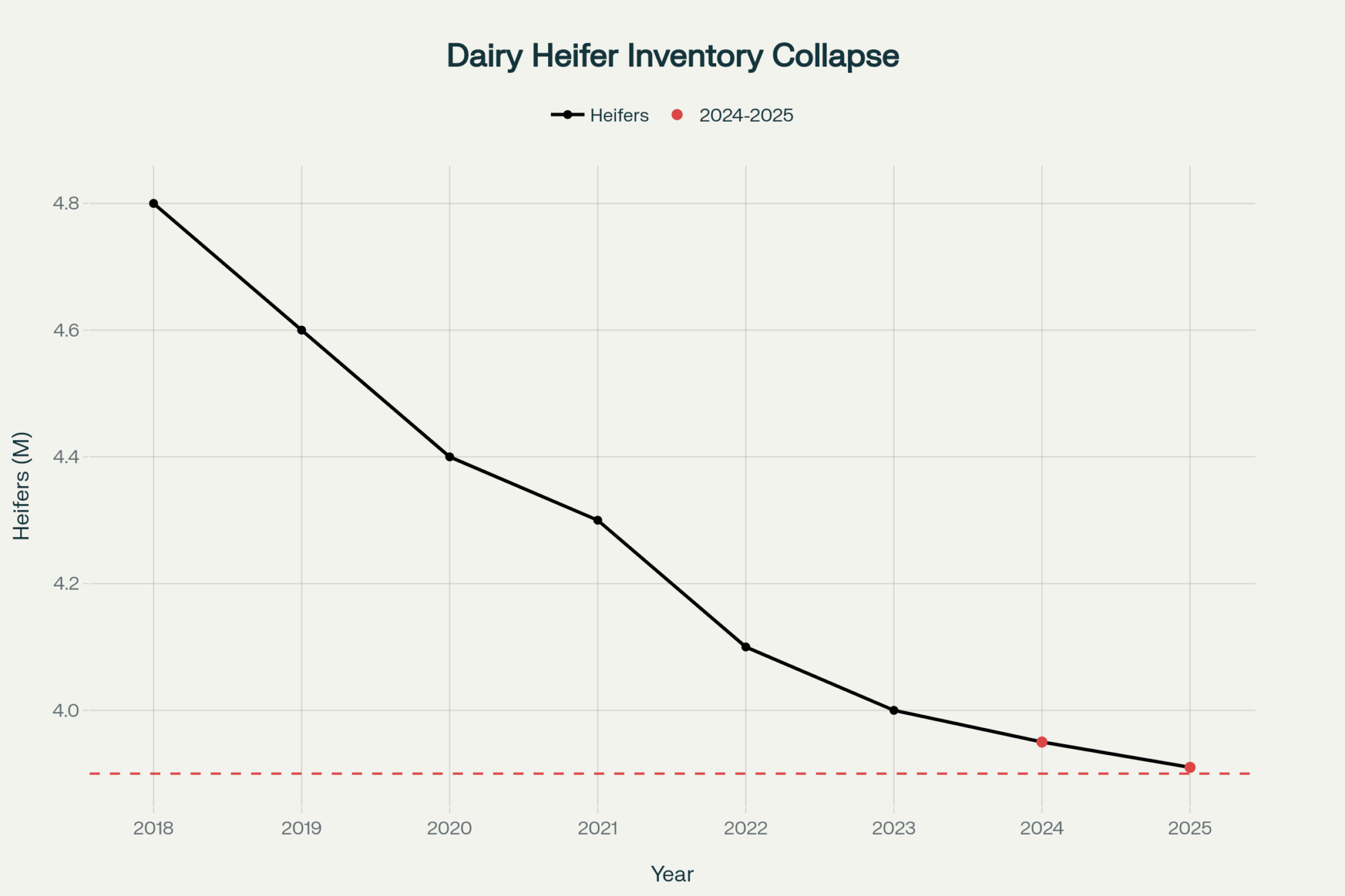

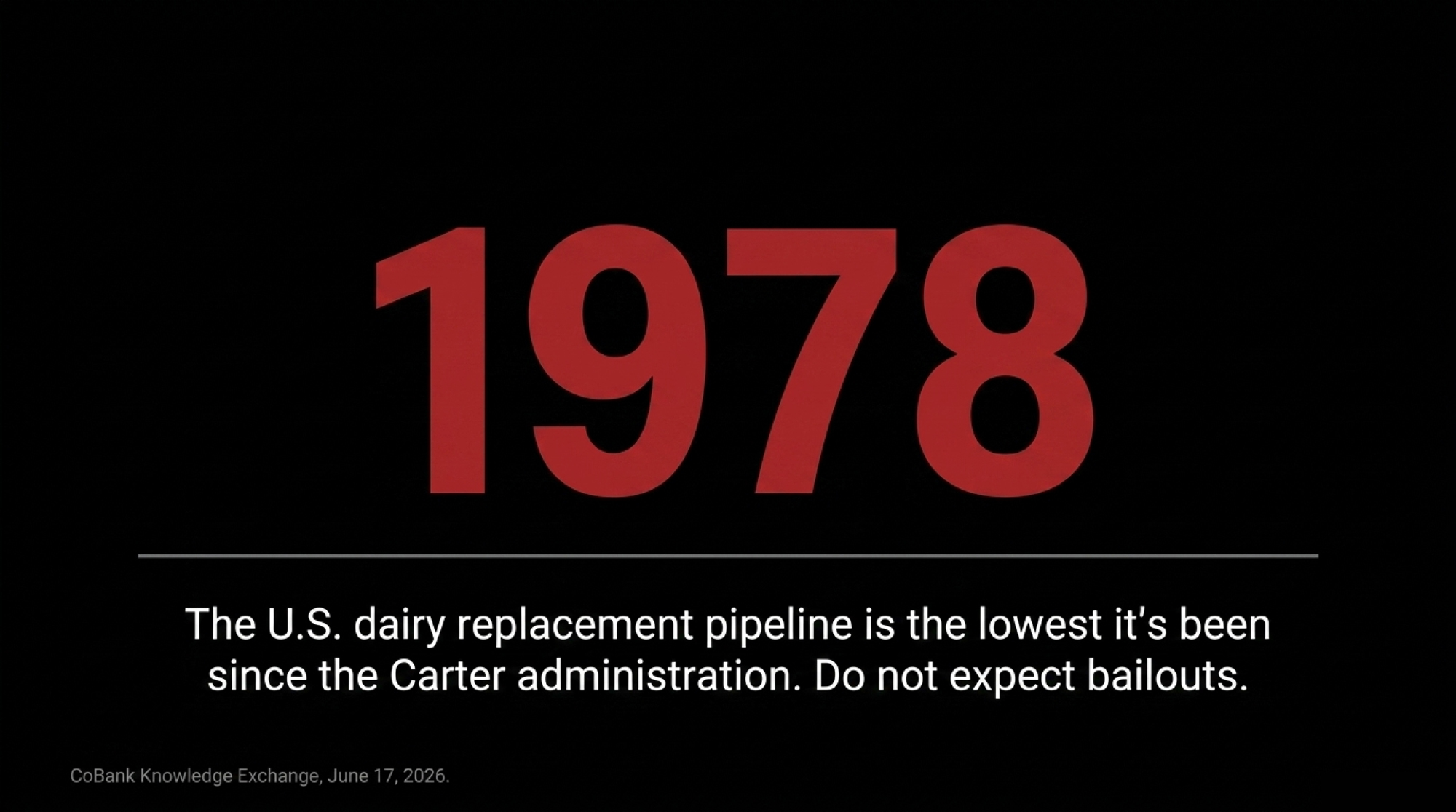

Start with why one straw is worth $585 in the first place. Two markets are fighting over the same cow. The replacement heifer pipeline is the tightest it’s been in nearly half a century — about 3.905 million dairy replacements as of January 1, 2026, the lowest count since 1978. CoBank projects the pipeline entering the milking herd shrank by a combined 796,000 head across 2025 and 2026 — 357,490 fewer in 2025, 438,844 fewer in 2026 (CoBank Knowledge Exchange, June 17, 2026). Fewer heifers, pricier heifers. Which makes the dairy pregnancy you didn’t create worth more every year the shortage runs.

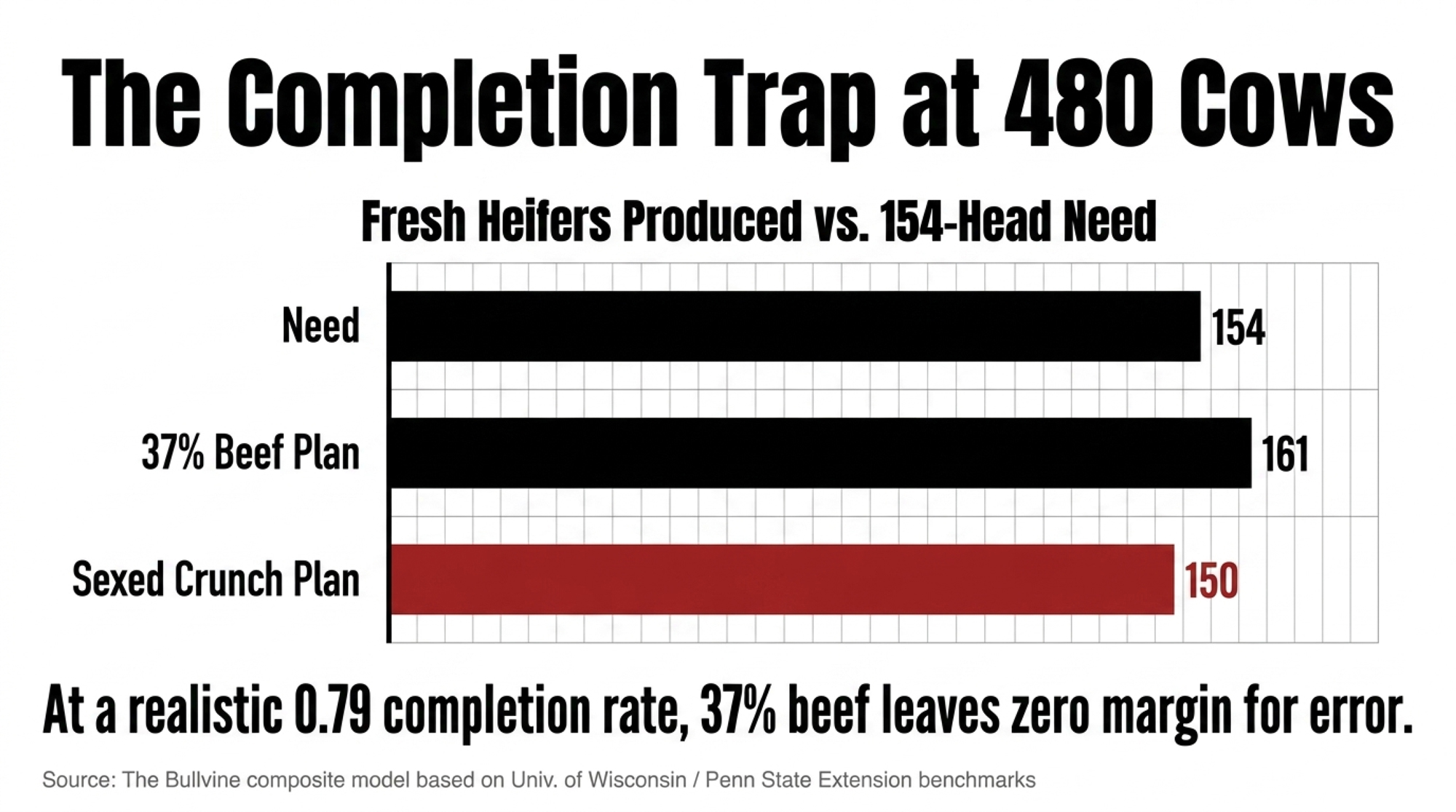

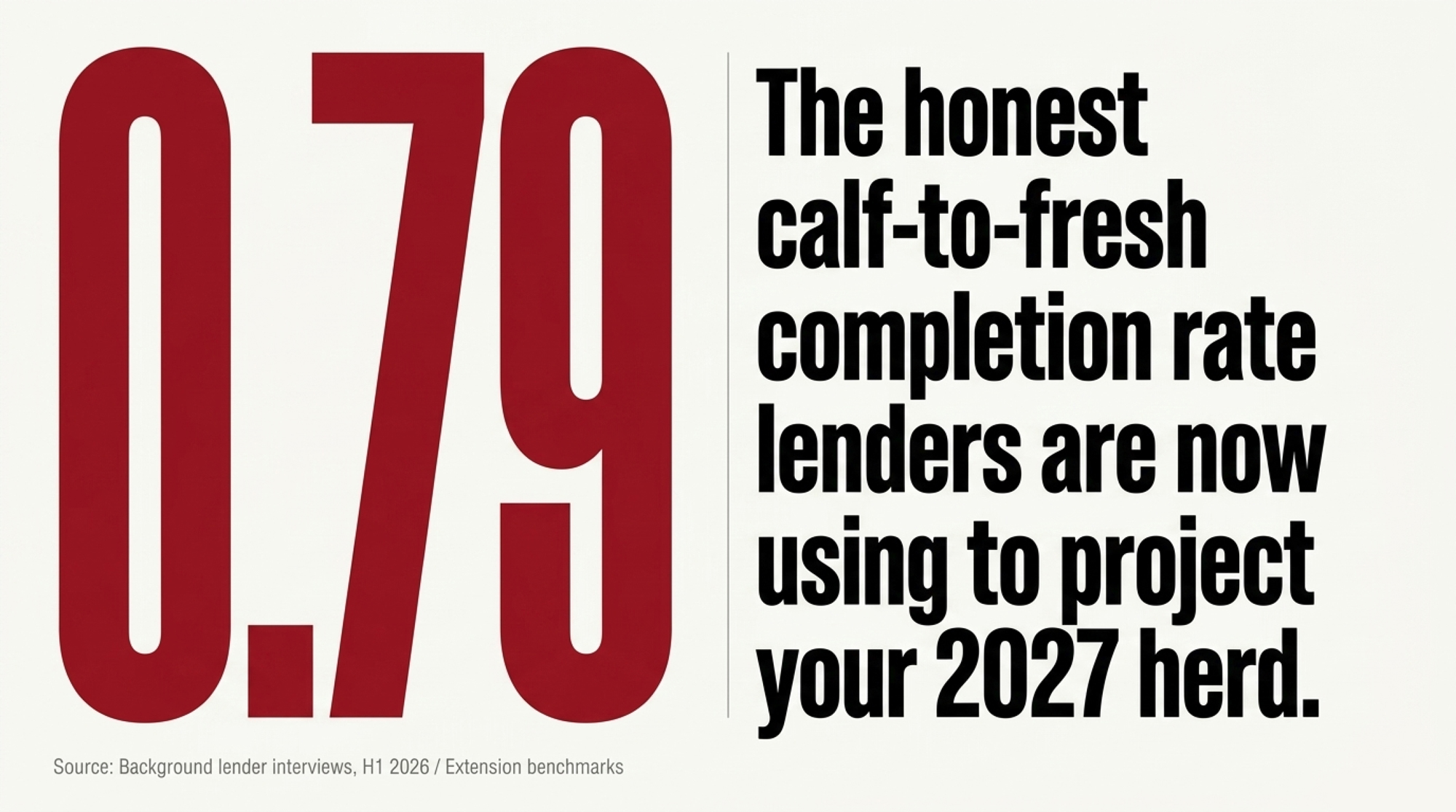

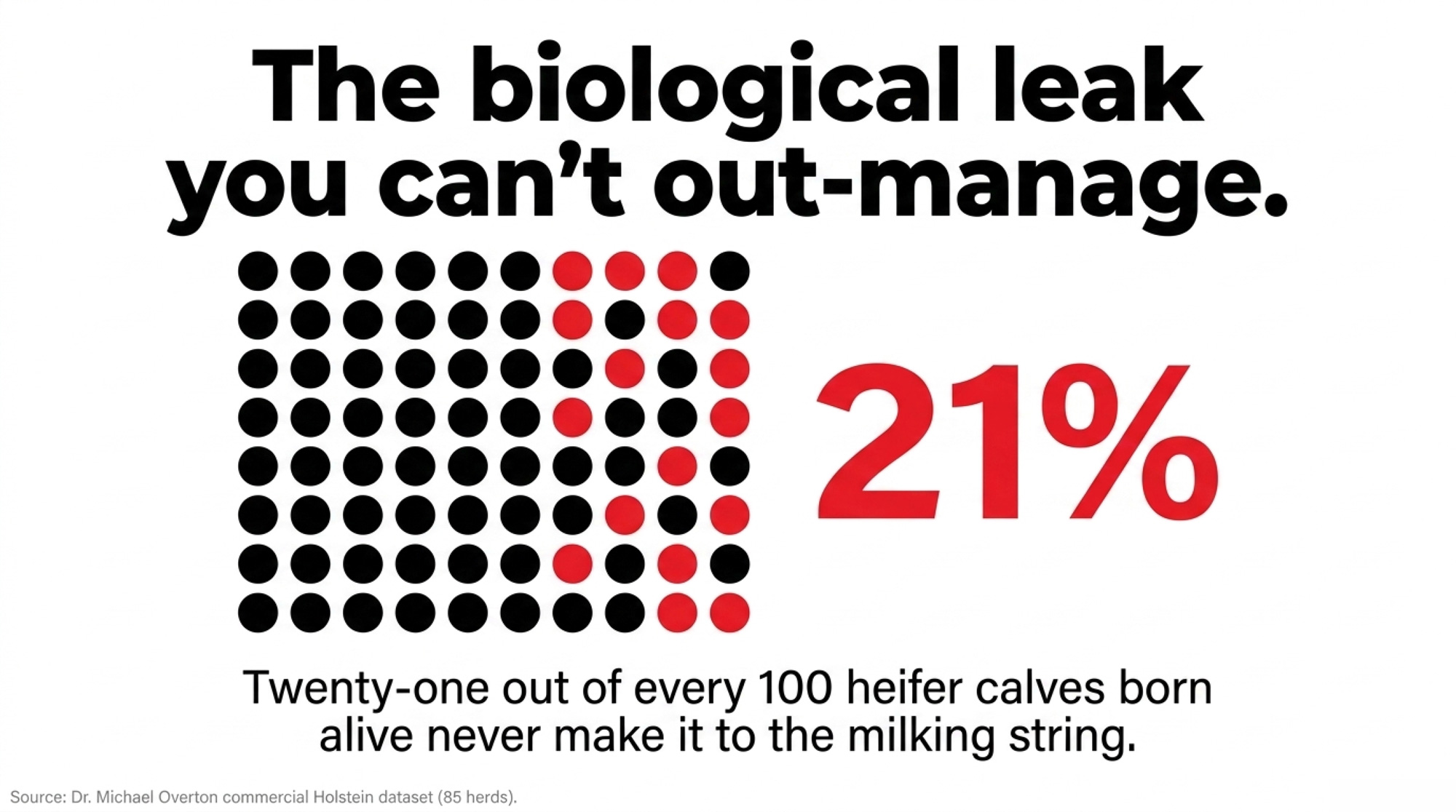

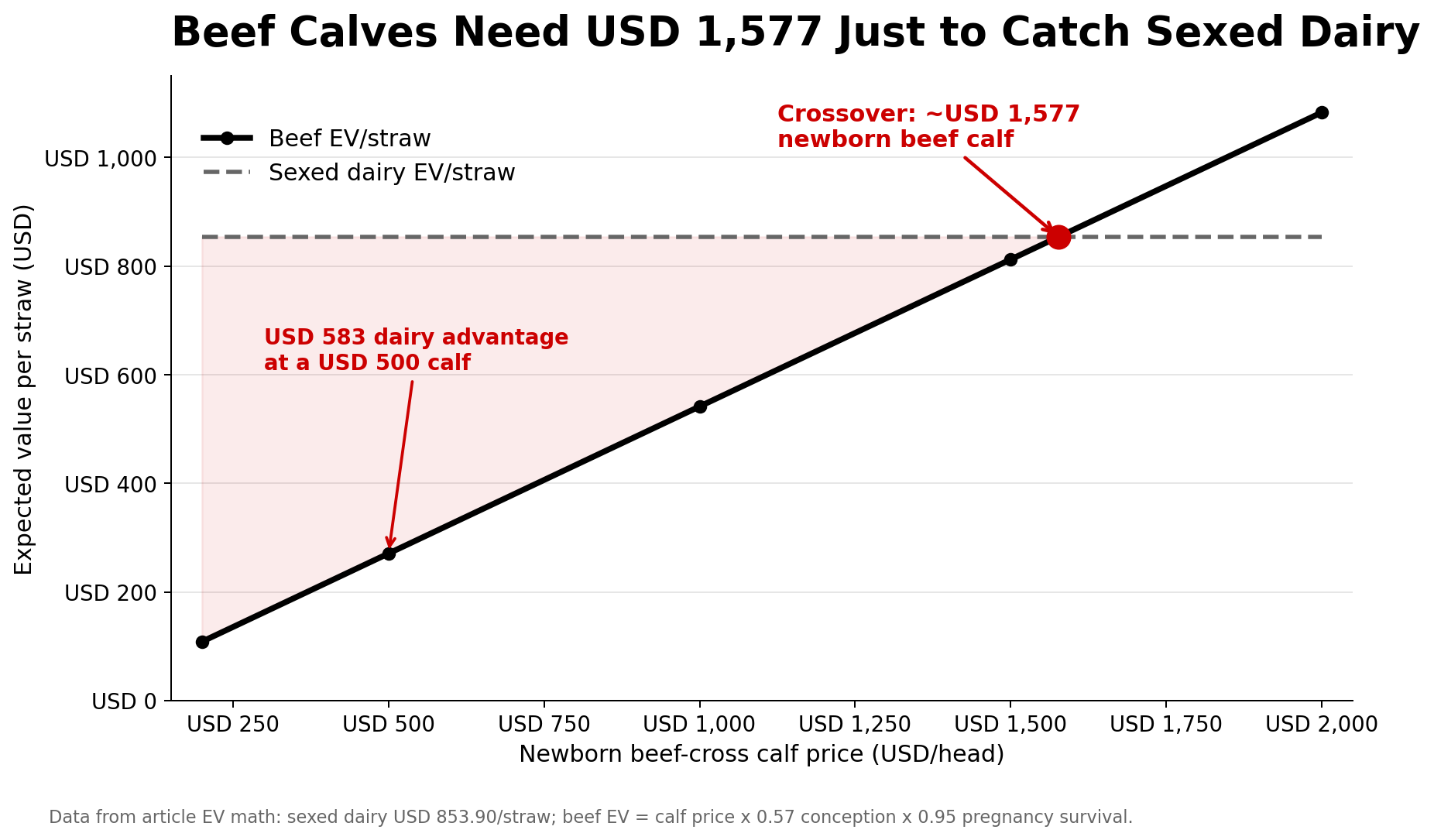

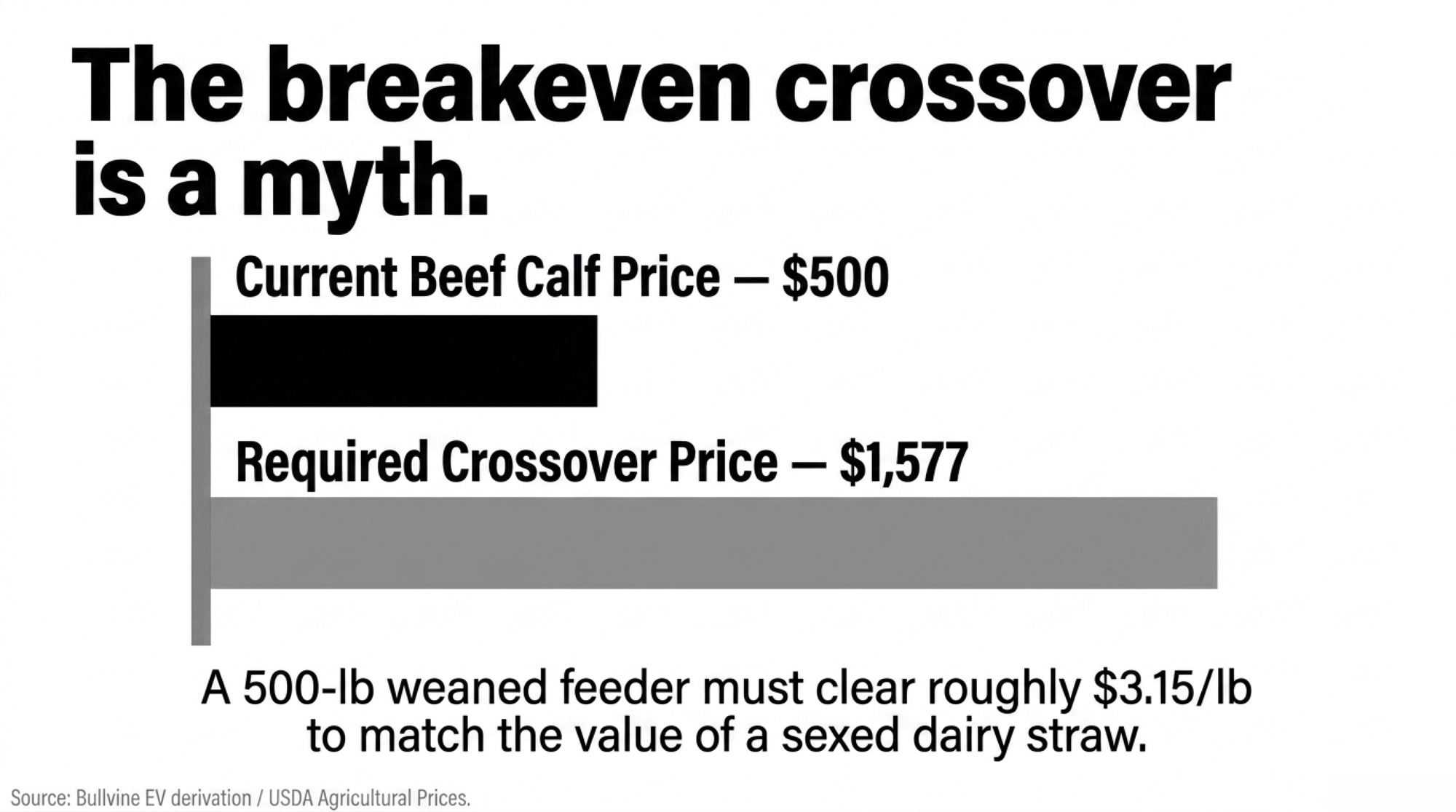

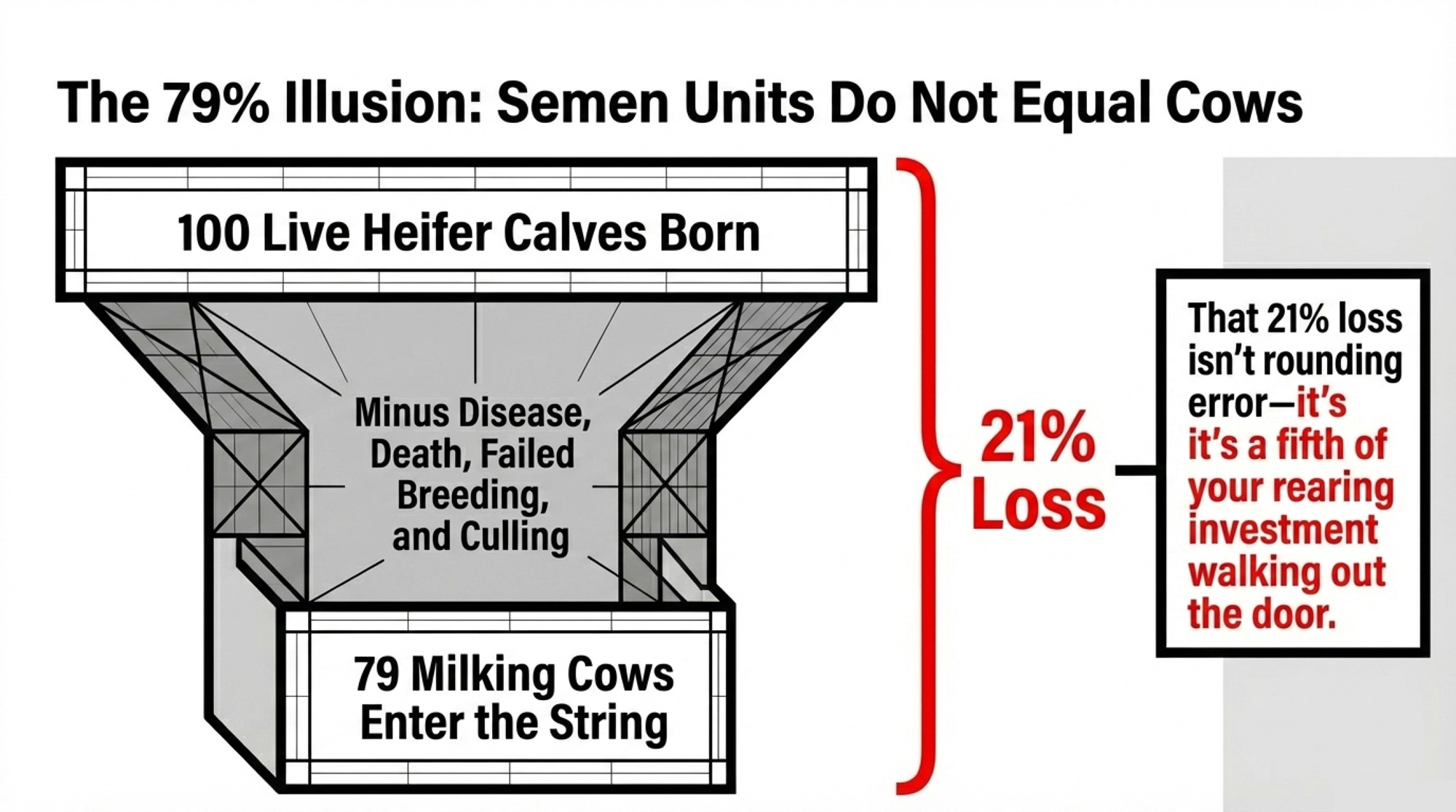

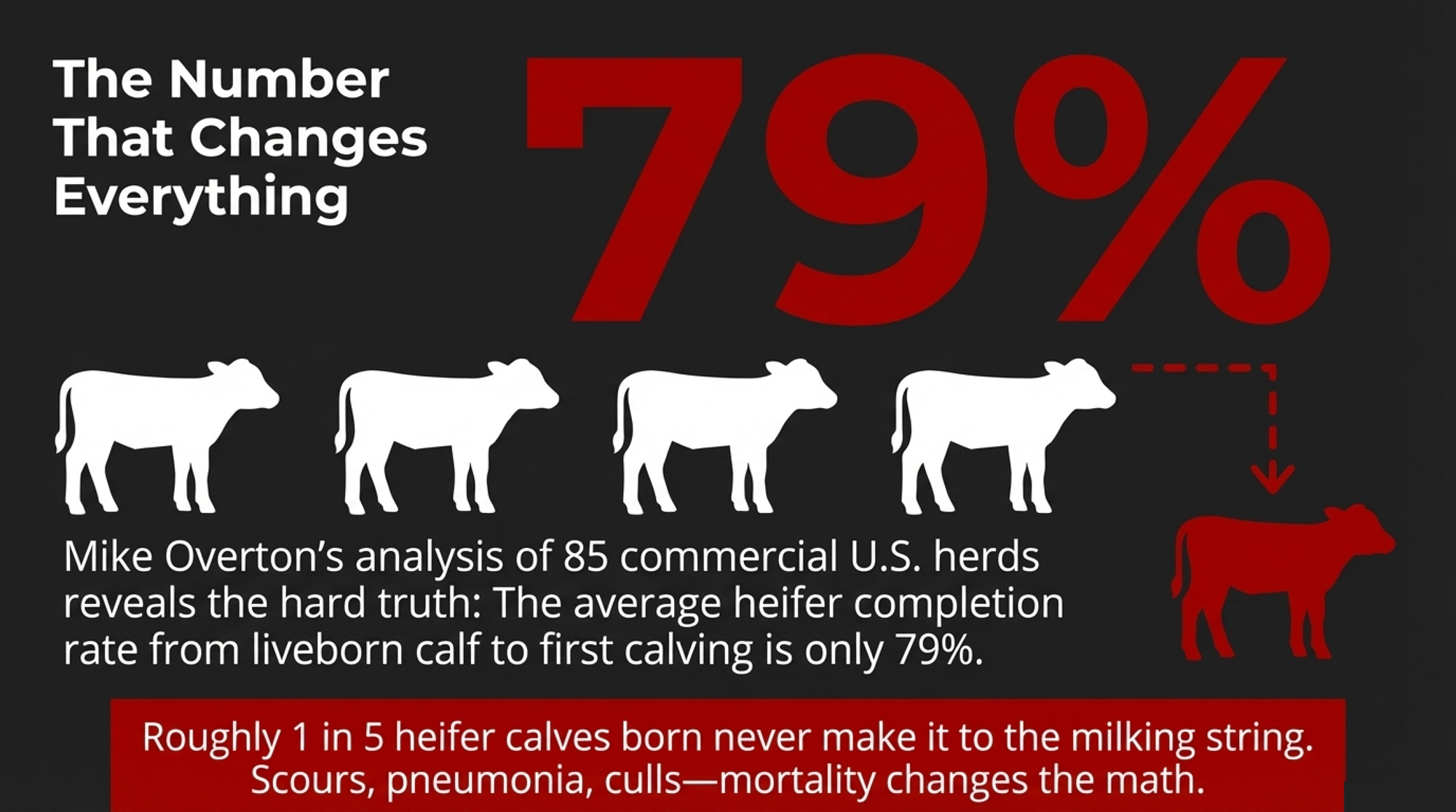

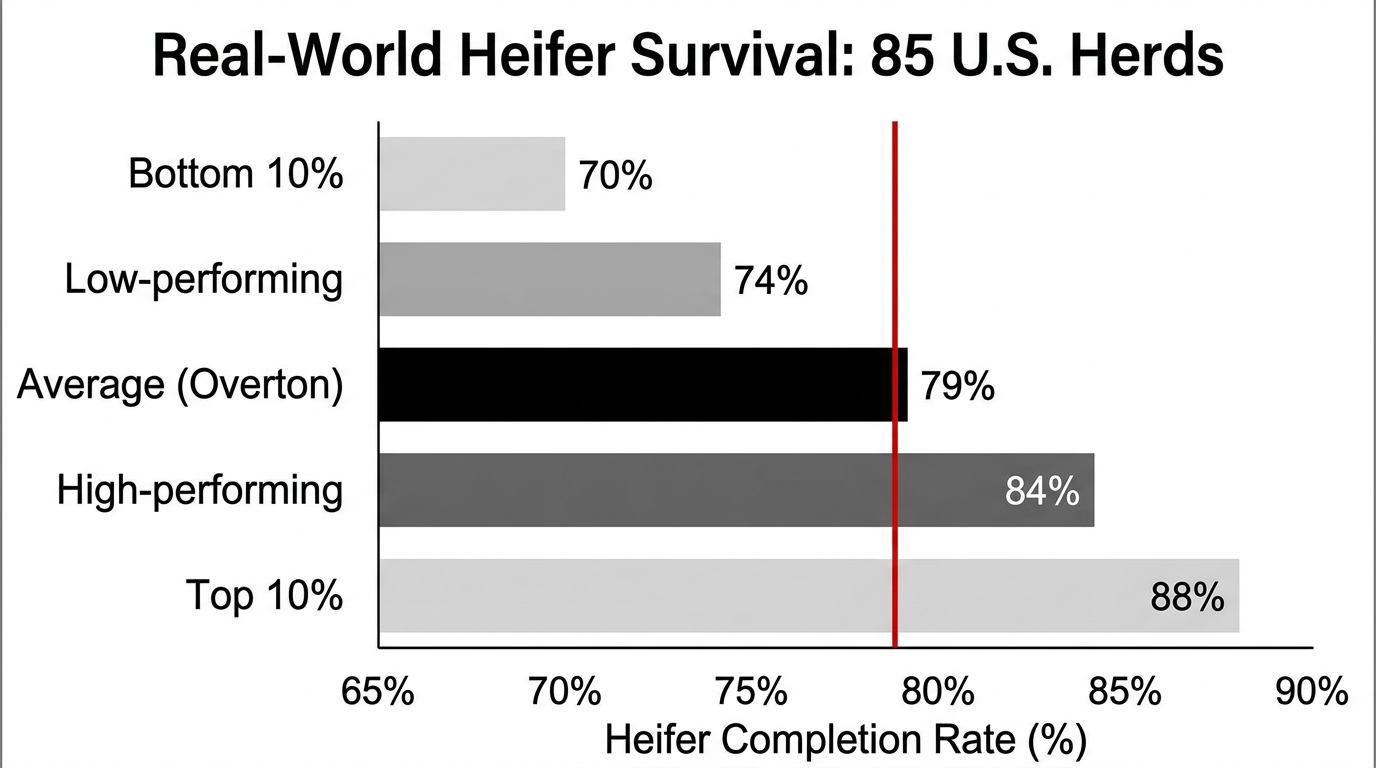

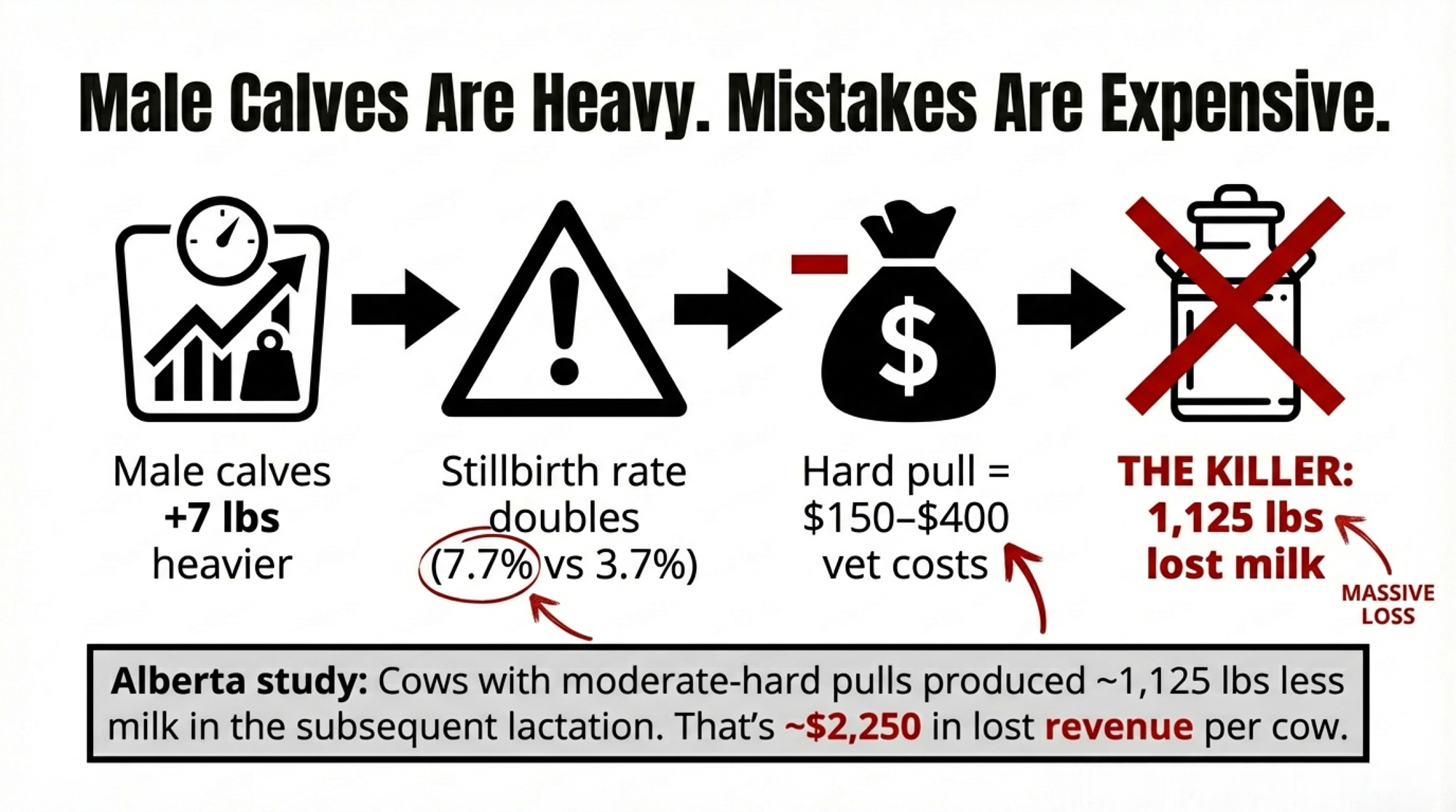

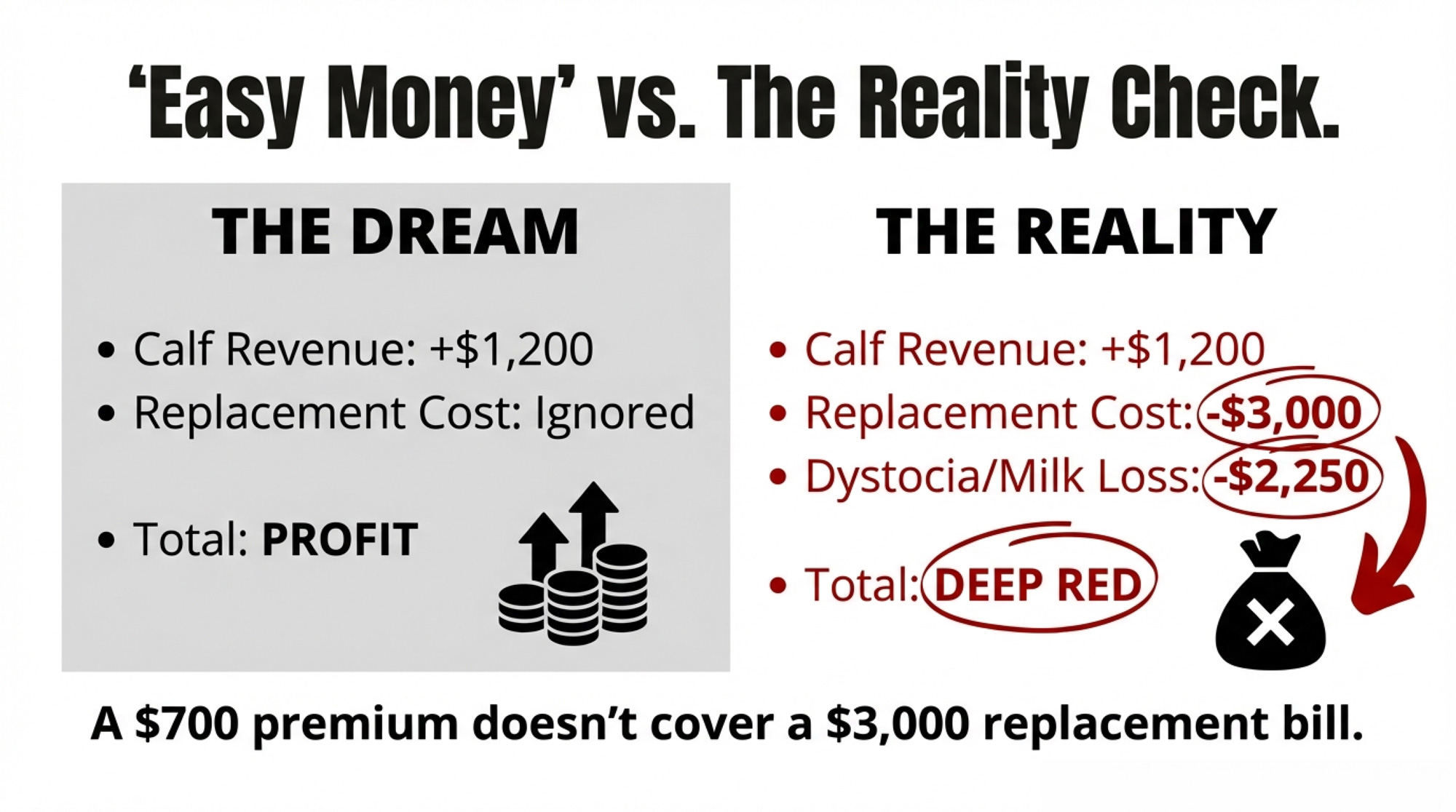

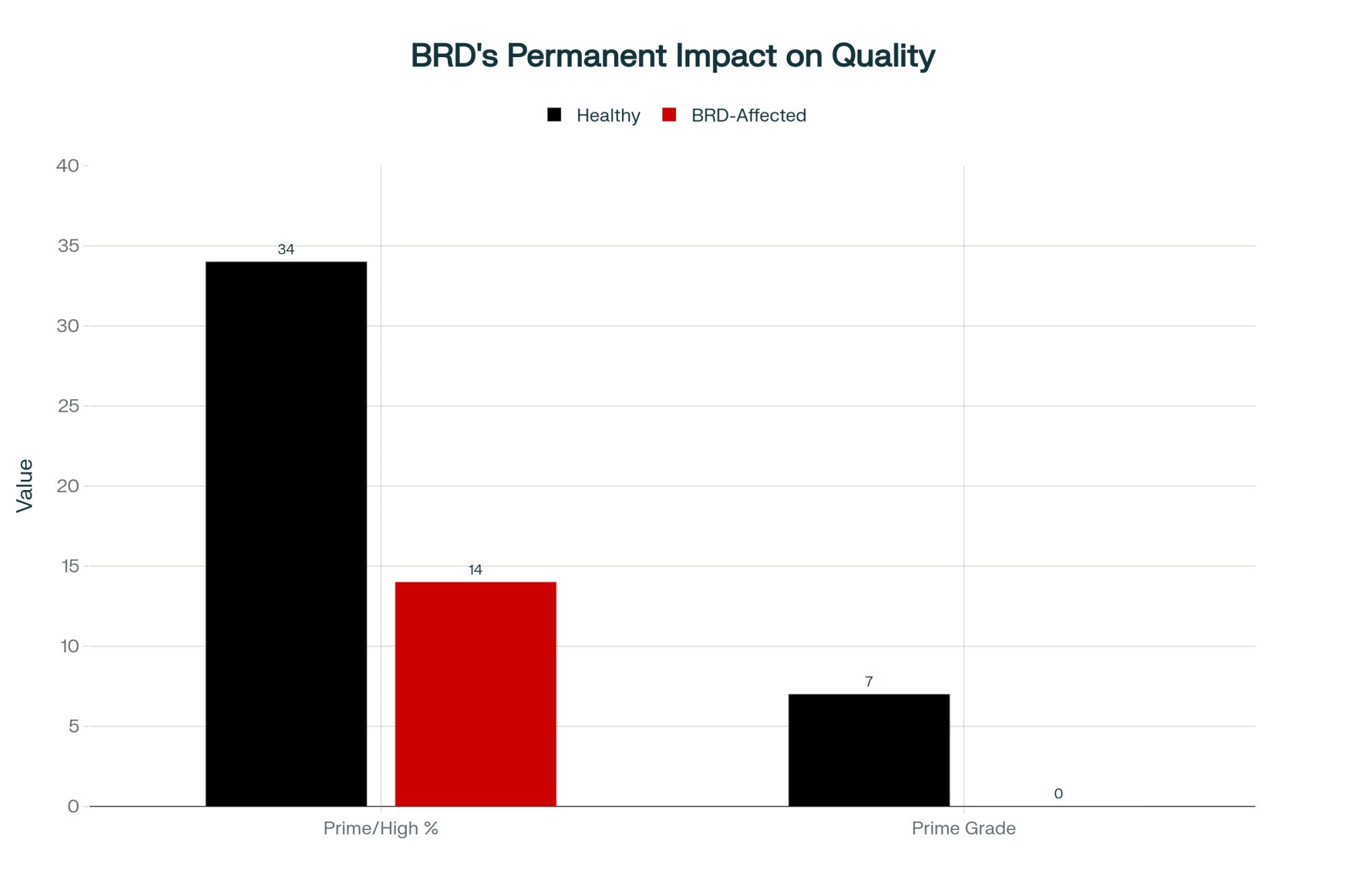

The math itself is just arithmetic once someone lays out the pieces. A beef service is worth your calf price times the odds it becomes a sellable calf. A sexed-dairy service is worth your local heifer cost times a stack of probabilities — conception, calf survival, heifer survival, and the share that actually make it all the way to first calving. That last one is where most people fool themselves. It’s roughly 79% (interquartile range 74–84%), out of Dr. Michael Overton’s 85-herd study presented at the 2026 High Plains Dairy Conference. Plug in a $3,010 heifer and a $500 calf, and a beef calf would have to clear about $1,580 a head to break even against sexed dairy. Most markets aren’t paying that right now.

So run your own version. The $585 isn’t a universal constant — it moves with your heifer price, your calf price, and your conception rates. But at today’s roughly $3,010 heifer and $500 calf, that’s where it lands. Multiply it by how many viable dairy dams you bred to beef last year. North of $100,000 in traded-away value — roughly 170-plus beef services at the $585 gap — and your calf premium is quietly being funded by your own heifer pipeline. Most producers have never run that exact multiplication. This week’s a good week to.

Here’s a faster gut check, the kind of stress test a lender runs. Take your last 12 months of calf and cull revenue per cwt and knock 35% off it. If that single change flips you from positive to negative cash flow, you’re not just a dairy anymore — you’re a leveraged beef play (The Bullvine, February 21, 2026). If you can’t answer that off the top of your head, that’s the first number to find.

Is Your Breeding Barn Quietly Working Against You?

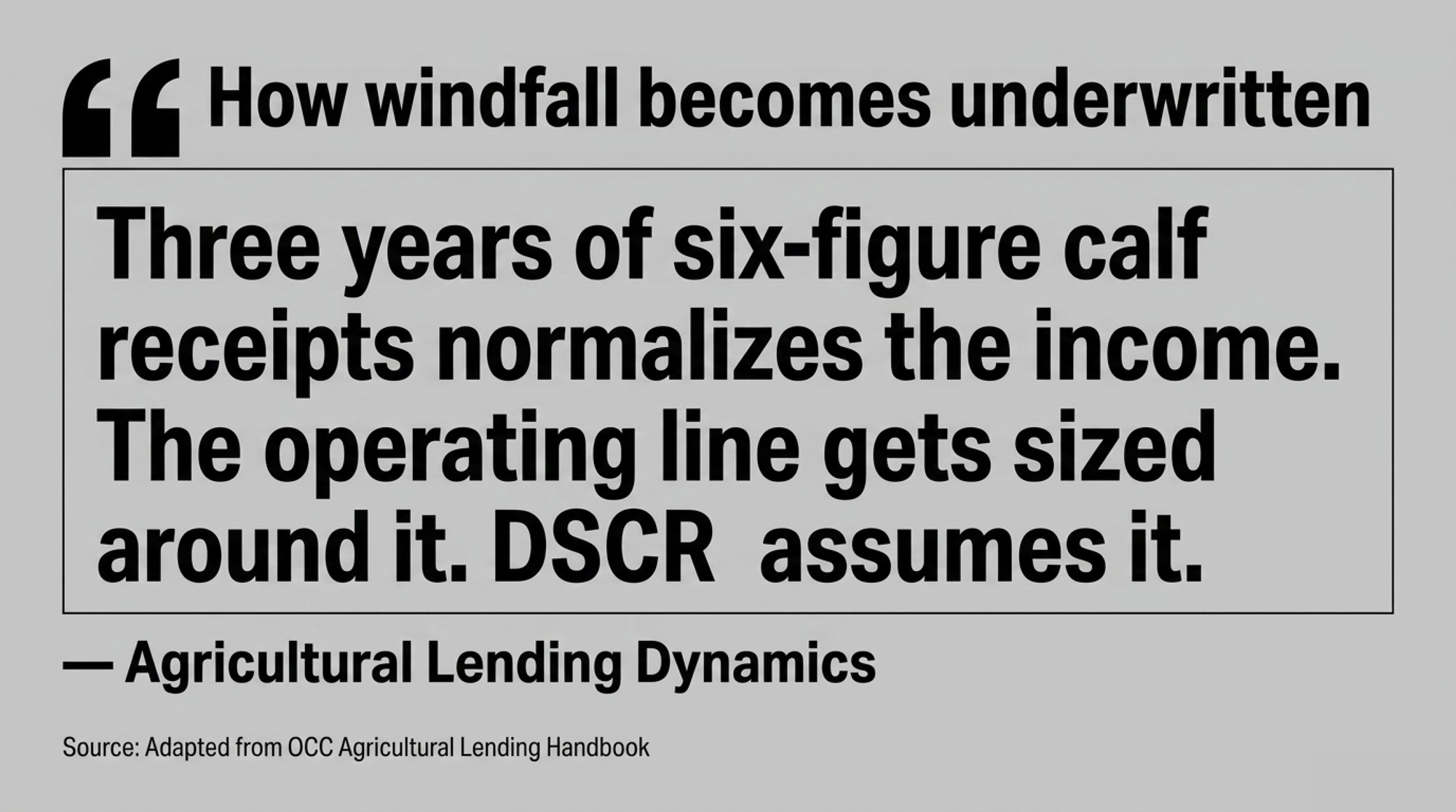

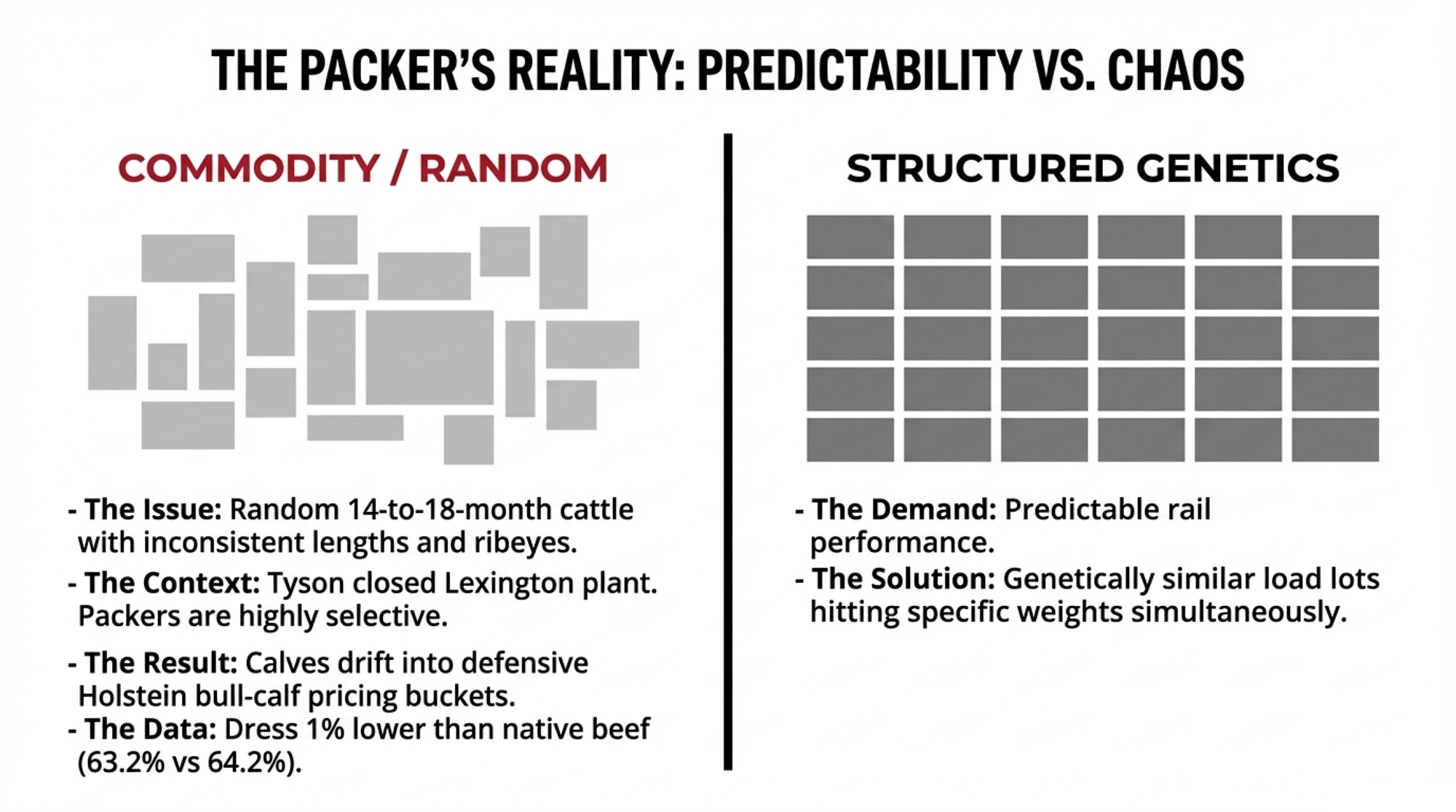

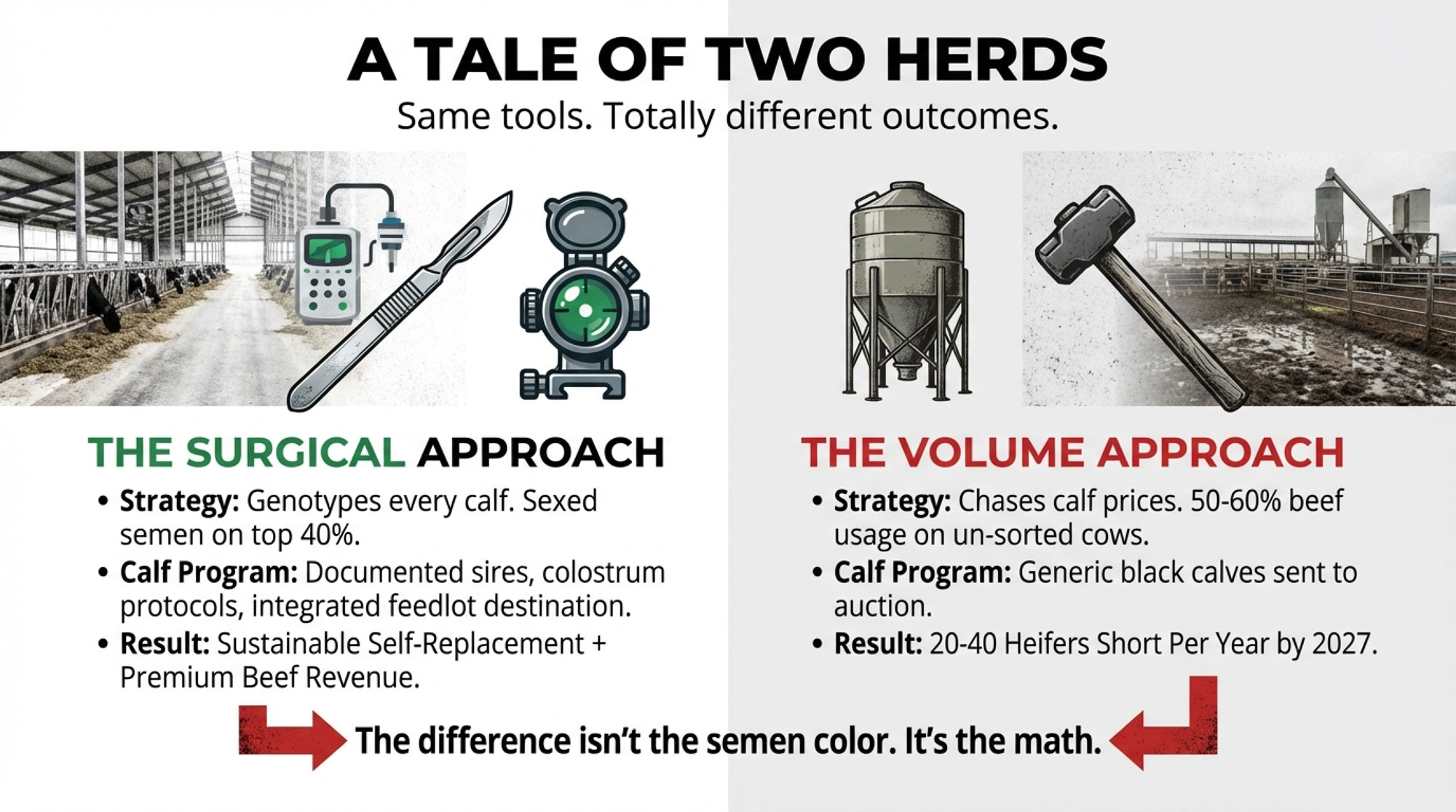

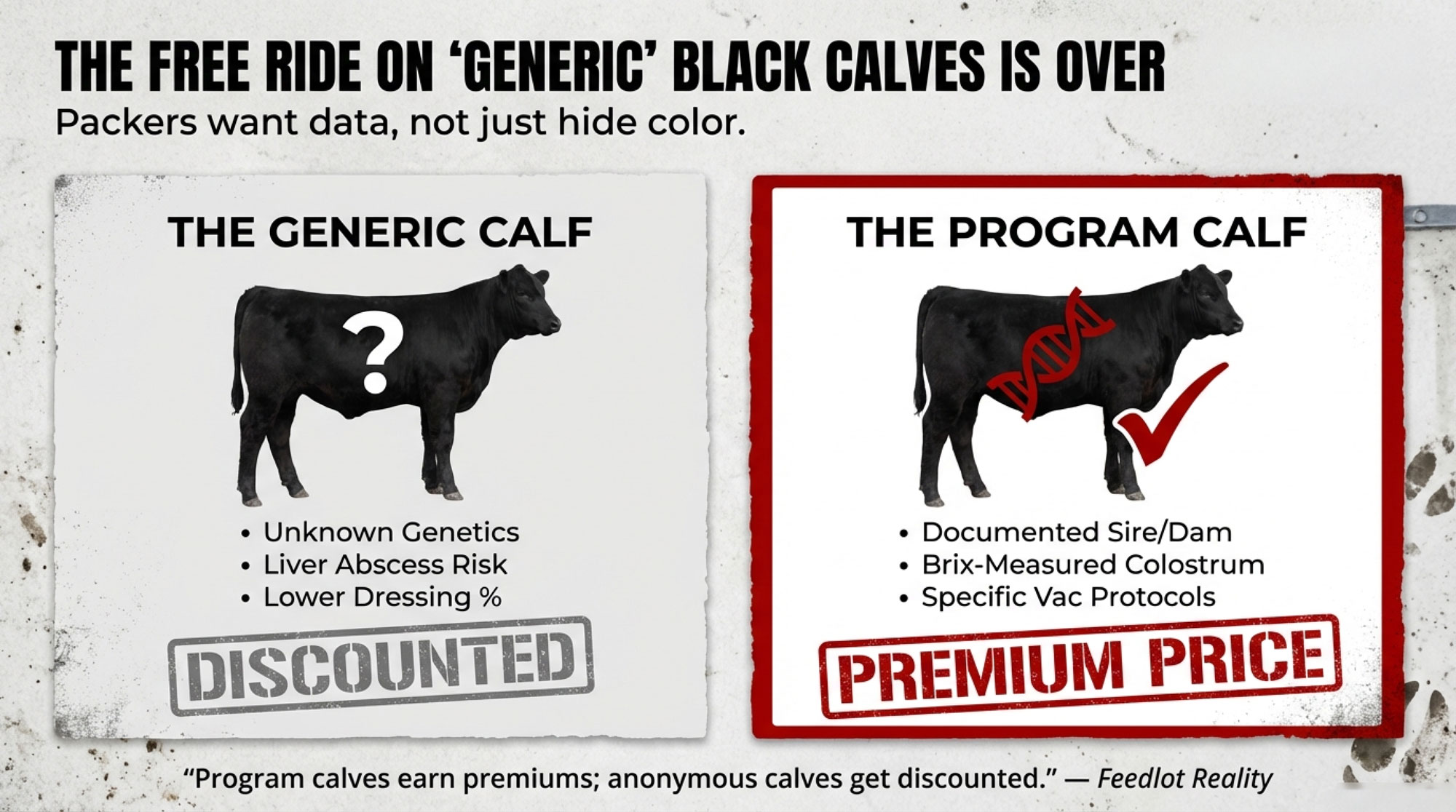

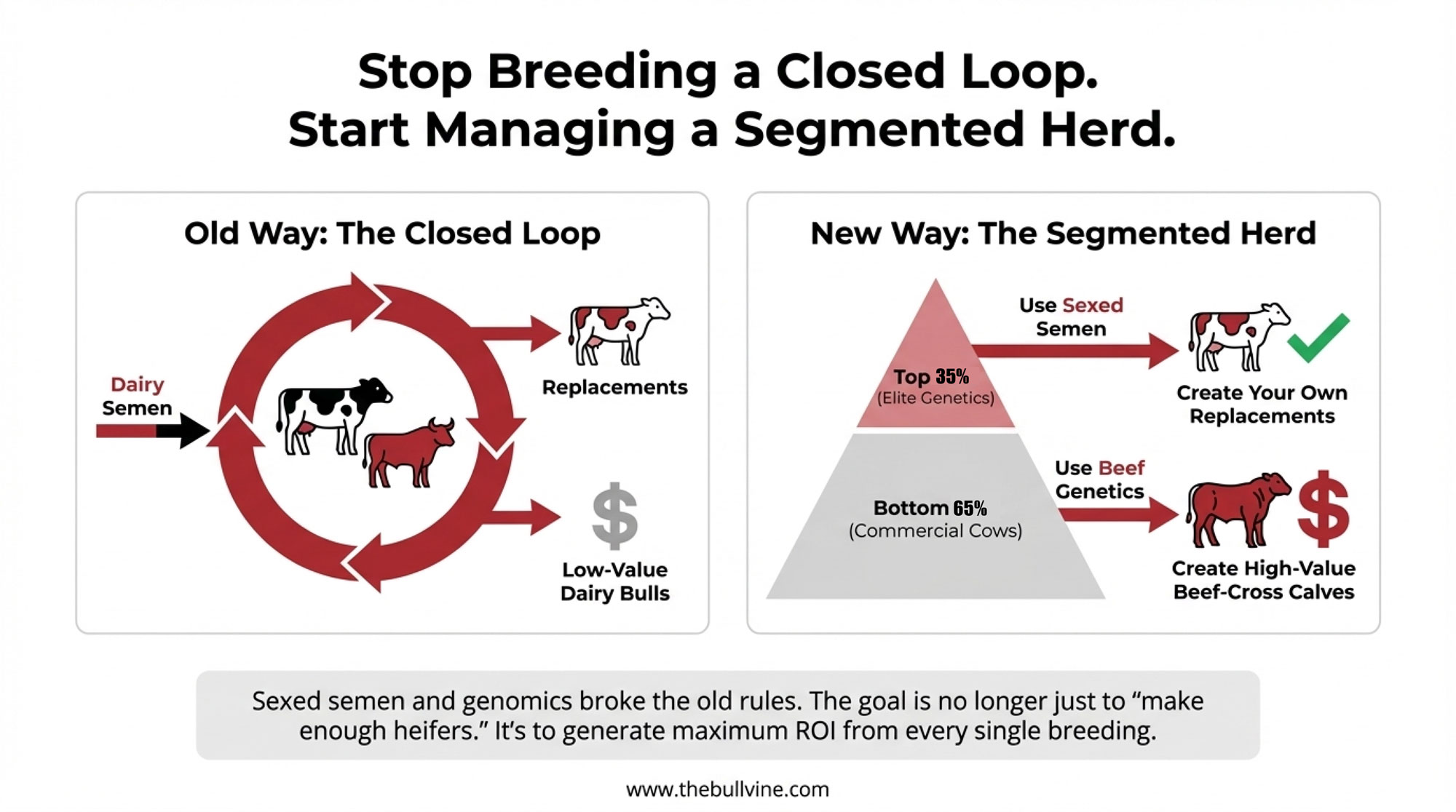

There’s a deeper mechanic hiding under the dollars, and it’s easy to miss until calf revenue climbs toward half your top line. When that happens, the buyer at the far end of the chain starts writing your breeding decisions for you. Packers pay for calves that hit carcass specs, so feedlots chase the calves most likely to hit them — and that pressure runs all the way back to the straw your breeder picks up at your farm gate. You still own the cows. But somewhere in there, the spec started co-authoring your breeding sheet.

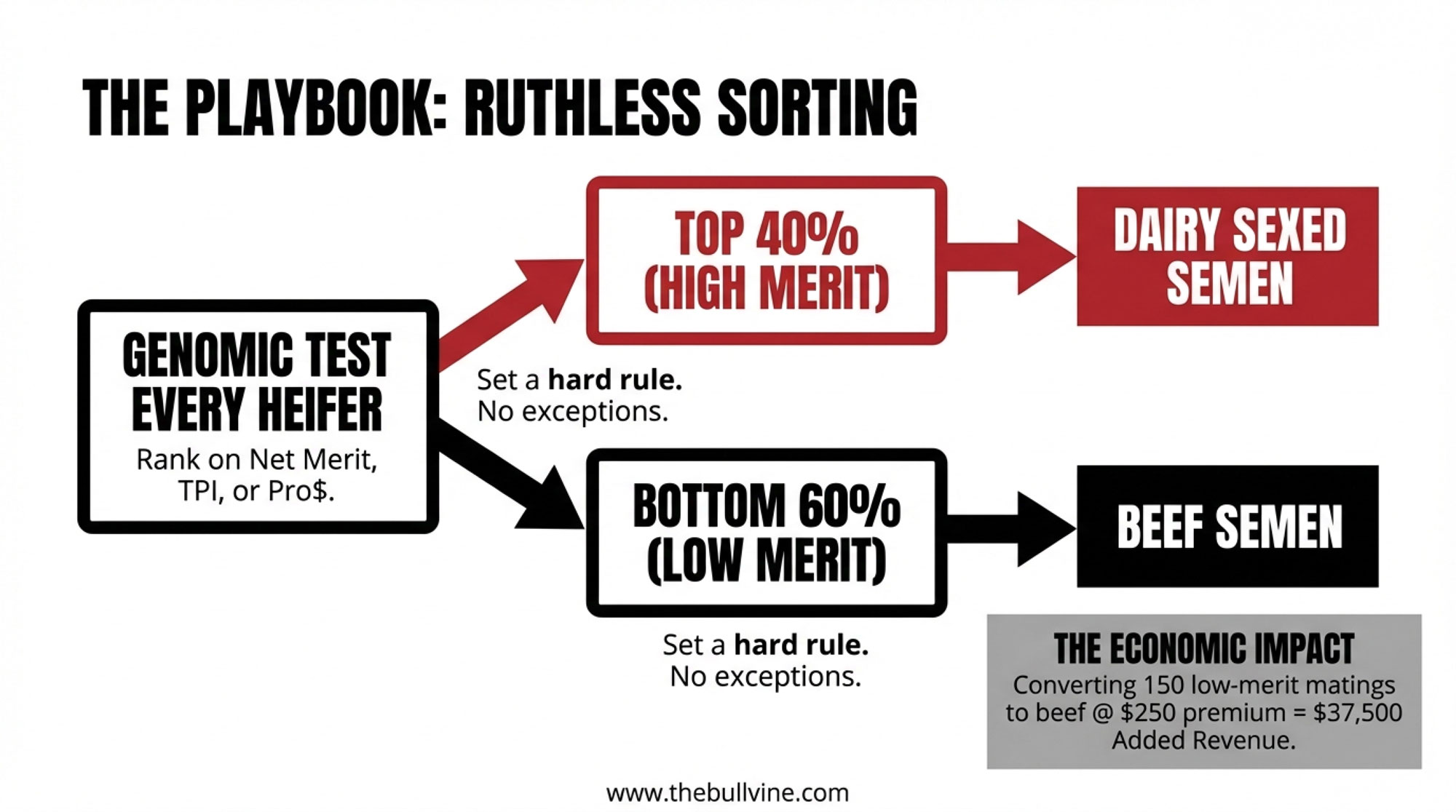

That’s exactly why operations like McCarty’s genomic-test every female, breed the top half to sexed dairy and the bottom to beef, and match sire selection to what the feedlot and packer actually want. The discipline isn’t optional at that scale. It’s the whole reason the 50%-of-revenue calf check is an asset instead of a liability. Even the researcher who built the industry’s beef-on-dairy model thinks the pendulum swung too far: “We used too much beef semen,” Dr. Victor Cabrera of UW-Madison told The Bullvine. “We entered into the problem — which I think now we are coming out of.” The farms that get burned are the ones running beef by feel, breeding good cows to Angus because last month’s check felt good — and not noticing they’ve over-beefed their best genetics until the heifer bill lands.

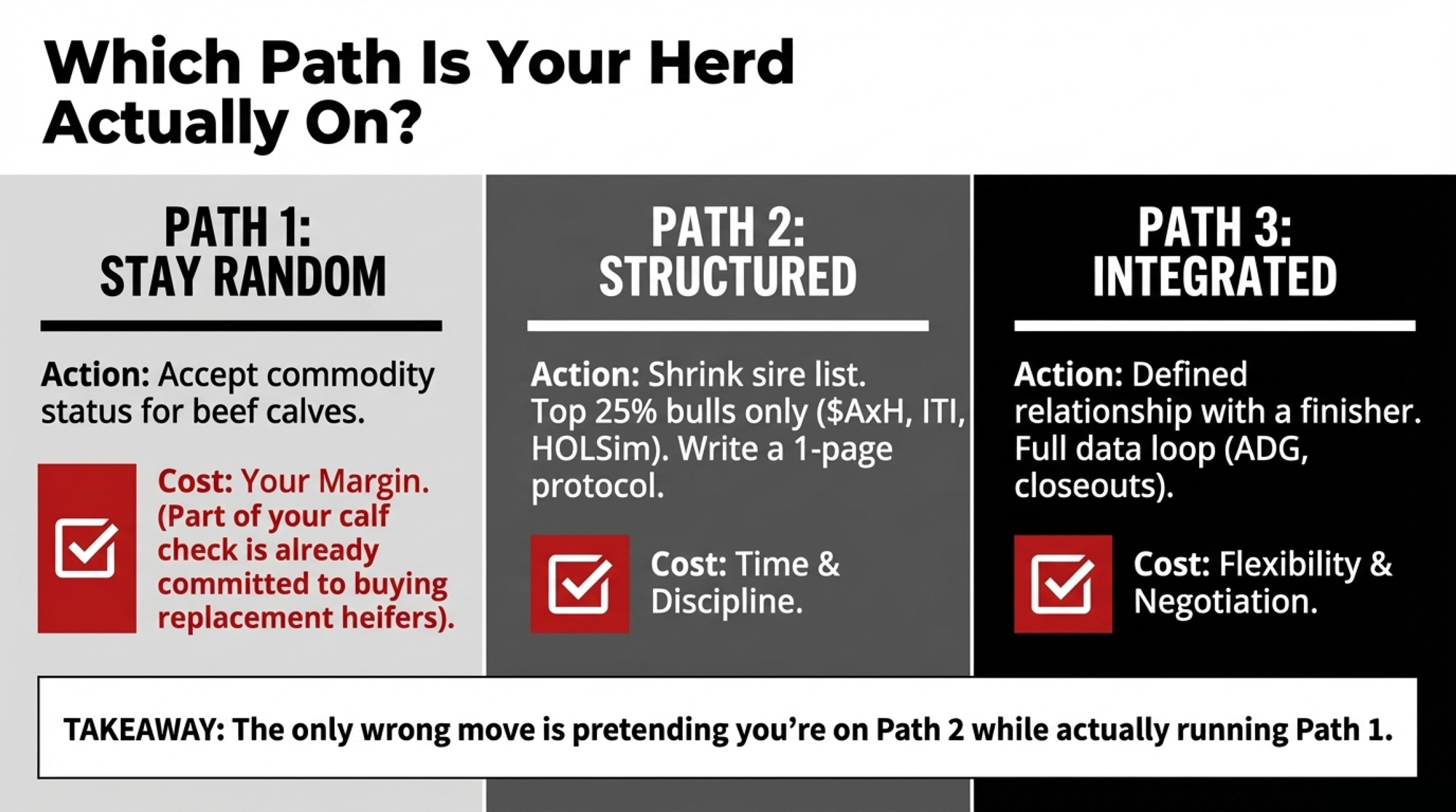

Options and Trade-Offs for Your Herd

There’s no single right answer here. There’s a right answer for your fertility, your debt, and your heifer needs — and it probably isn’t your neighbor’s. Here’s how farms are actually playing it.

| Strategy | Best-fit herd | When it works | Where it bites |

| Genomic-tier it (top½ dairy, bottom⅓ beef) | Any herd with repro discipline | Best genetics build your line; calf check rides the rest | Skip the annual recheck and you over-beef your best cows by drift |

| Cap beef ~⅓ of pregnancies | Herds in a $3,000+ heifer market | Bank calf income without draining the tank | Leaves short-term premium on the table |

| Insure the calf stream (LRP) | Beef ≥ ~20% of revenue | Insulates cash flow from a sudden break | Costs premium in the calm years |

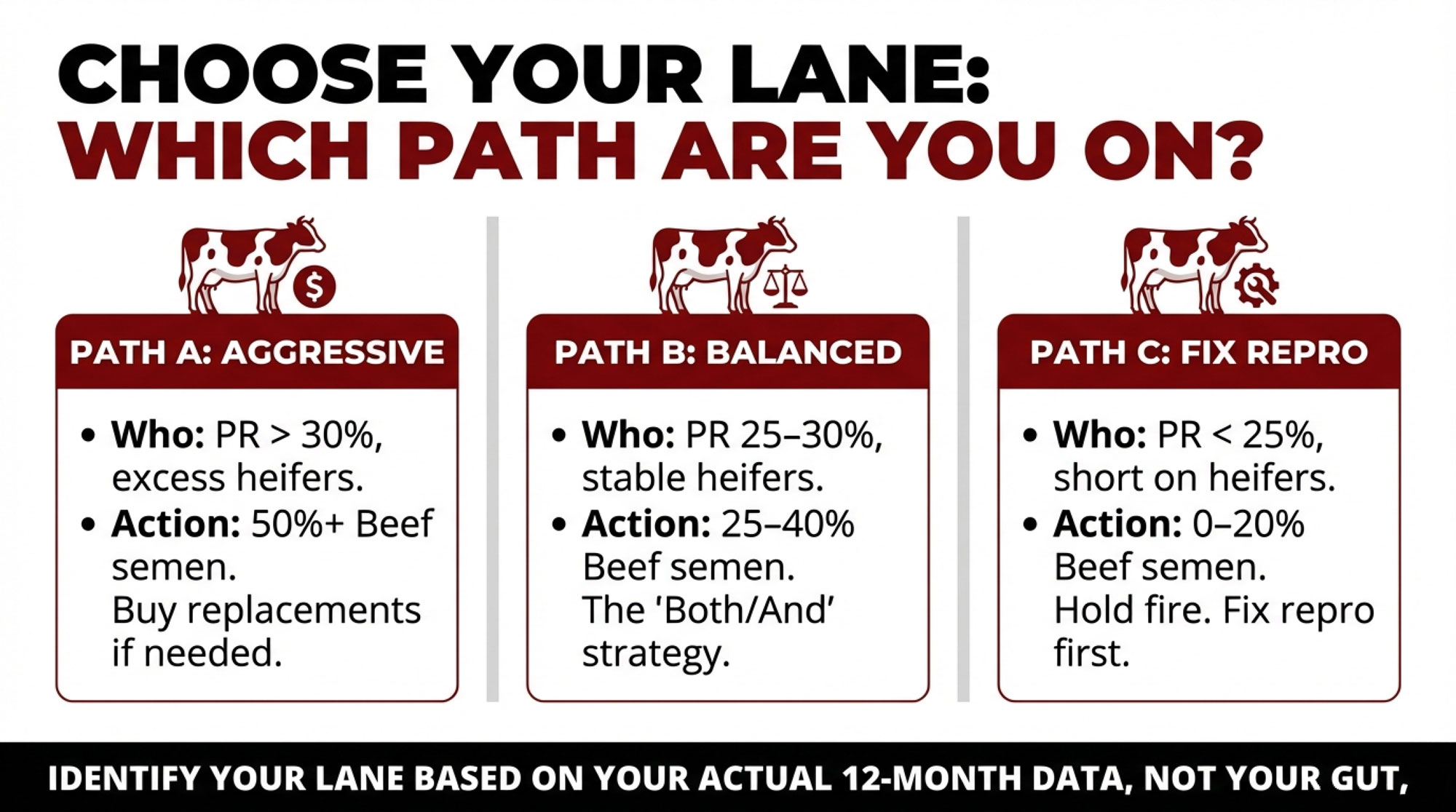

| Push beef harder | 21-day preg rate ≥ ~20–30% | Strongest calf income for high-fertility herds | Return goes negative/marginal below ~15–20% preg rate |

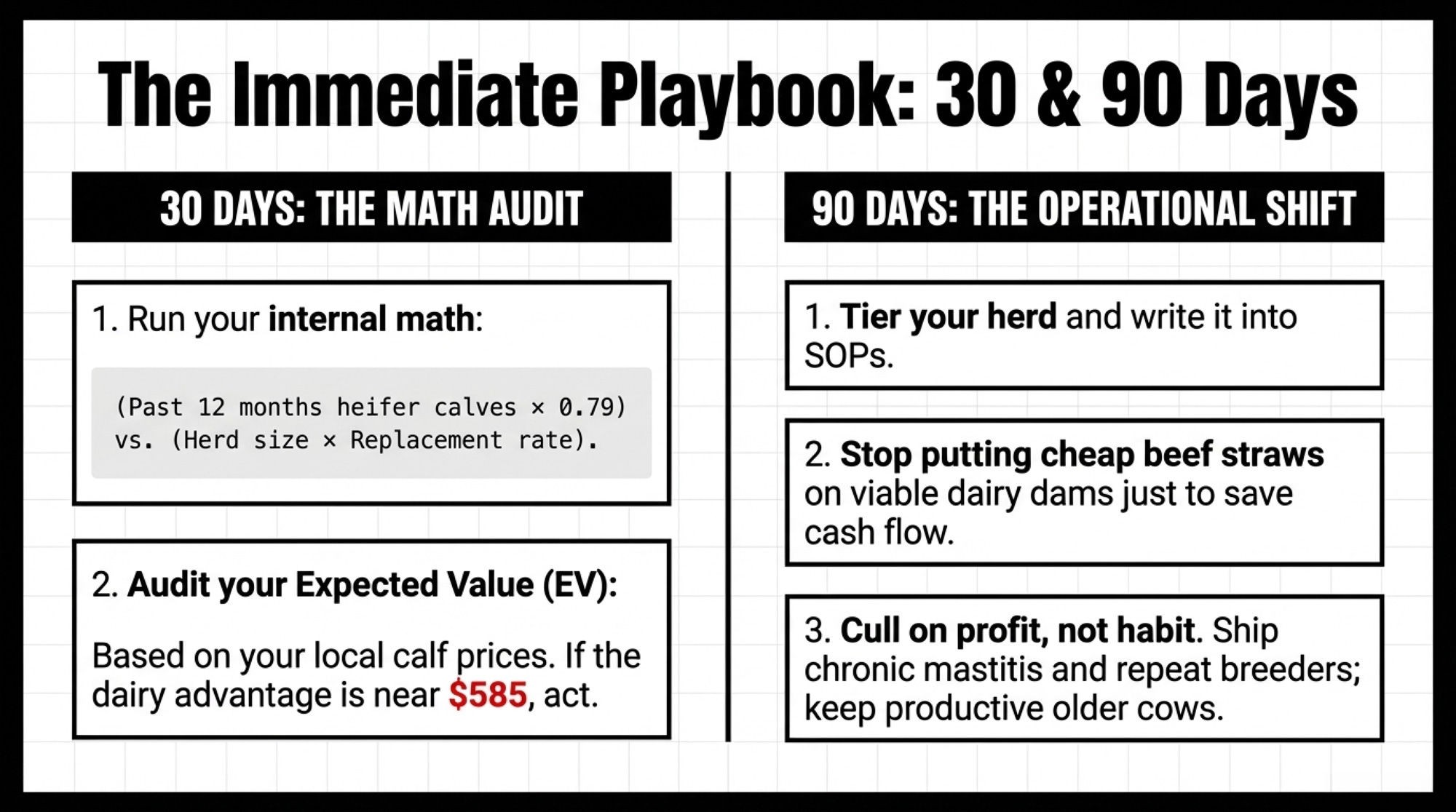

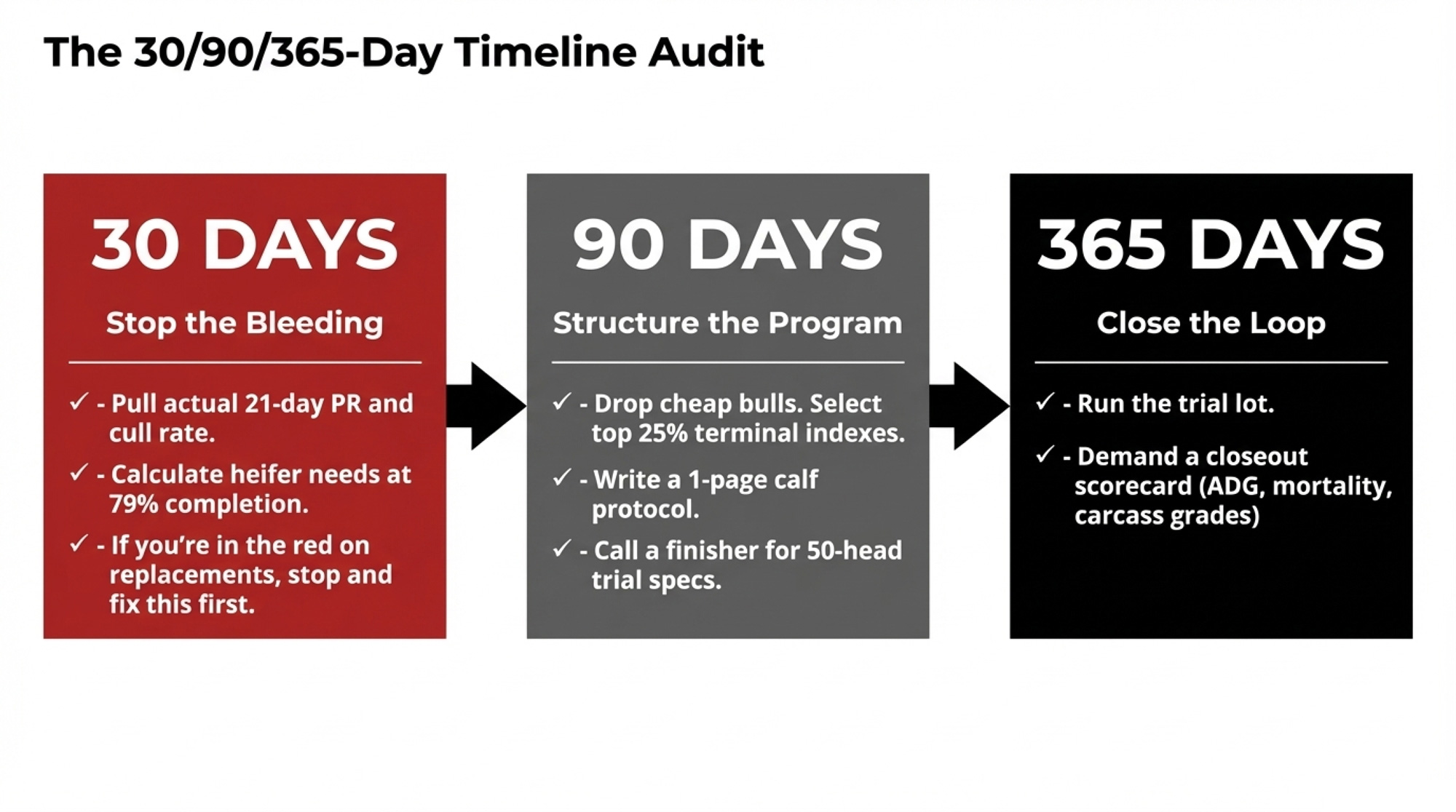

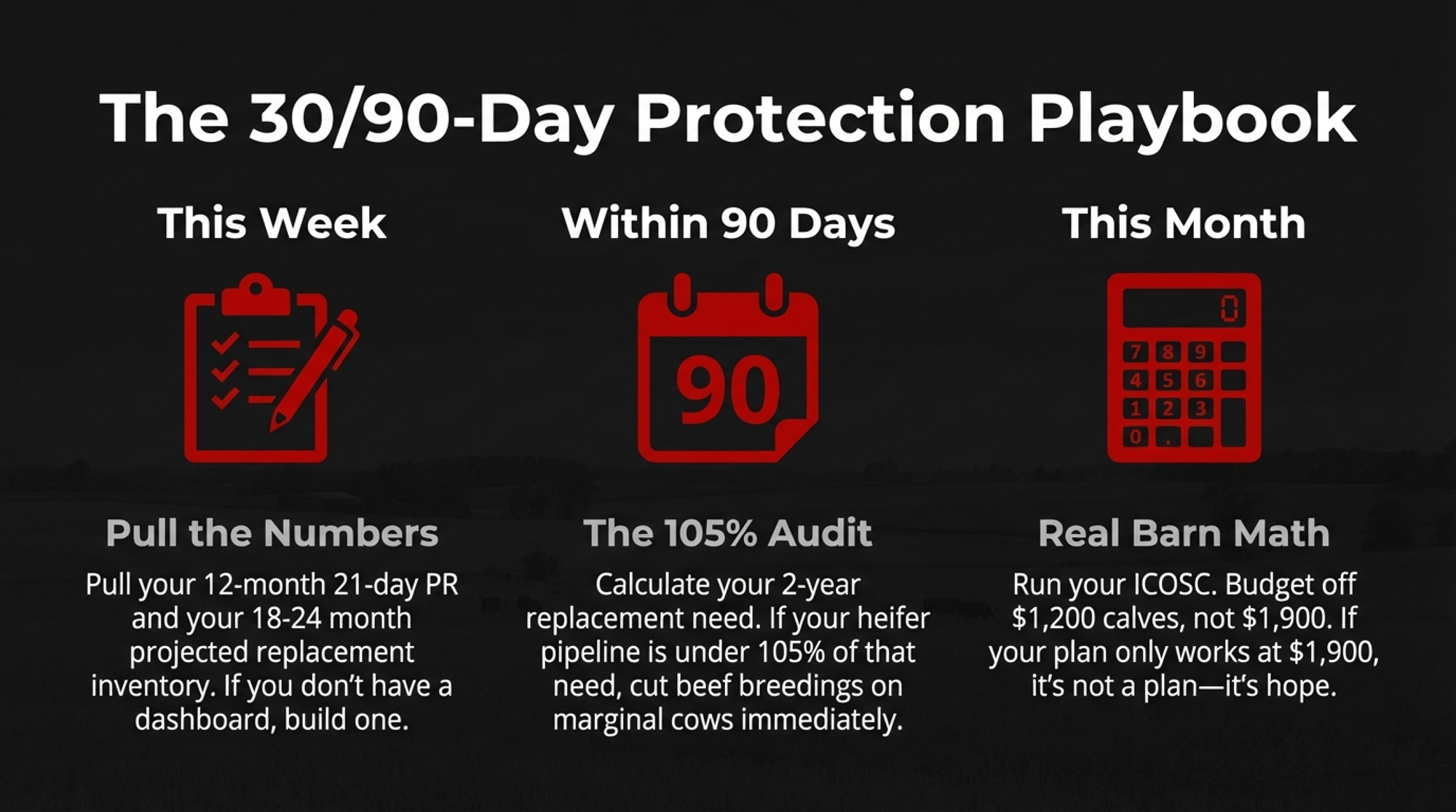

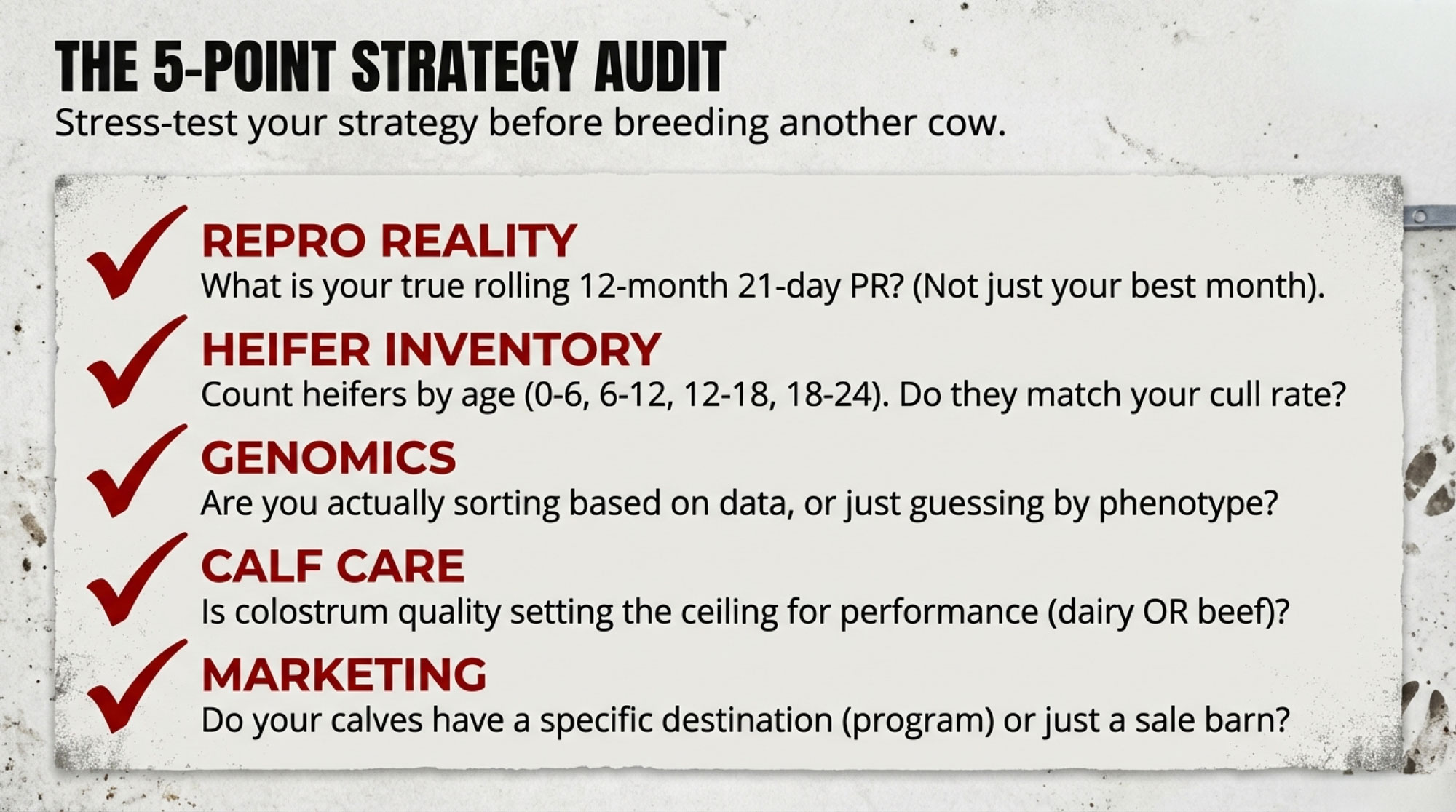

1. Genomic-tier it — and do this within 30 days

Rank every female. Breed the top half to sexed dairy, the bottom third to beef, and post the policy where the breeding calls actually get made. This fits almost any herd with reproductive discipline. It needs genomic testing and a written plan.

- When it works: You keep your best genetics building your line while the calf check rides on the animals you weren’t keeping anyway.

- Where it bites: Skip the annual recheck and you’ll over-beef your best cows by drift — and catch it too late.

2. Cap the beef share around one-third of pregnancies

Hold beef to roughly a third of pregnancies, in line with the broader industry mix — sexed dairy runs about 37% of the market and beef-on-dairy about 32% (Ag Proud, 2024; NAAB 2025).

- When it works: You bank calf income without draining the replacement tank in a $3,000-plus heifer market.

- The trade-off: You leave some short-term premium on the table today to keep from being a forced springer buyer tomorrow.

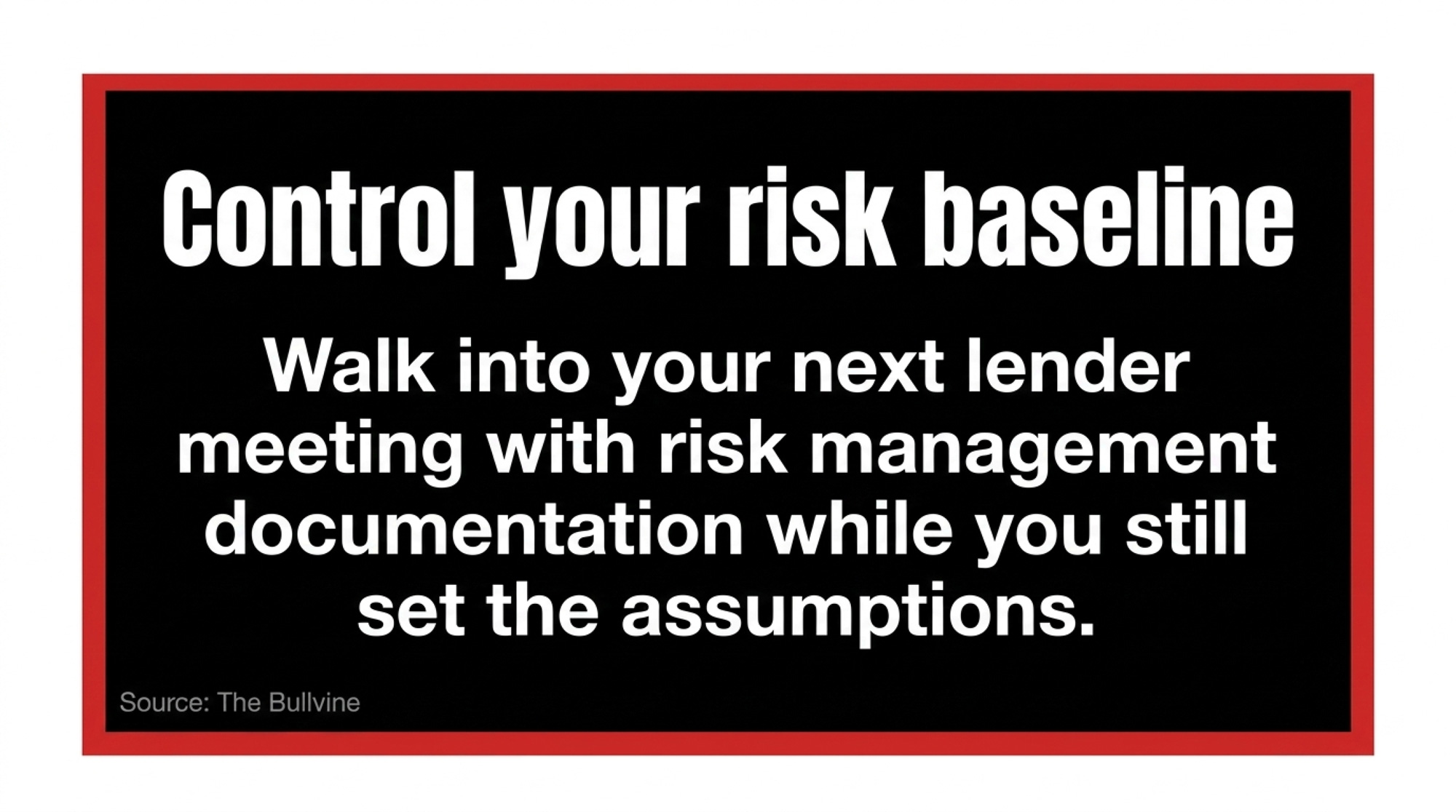

3. Insure the calf stream

Once beef is a real revenue line, price Livestock Risk Protection on it the way you’d run Dairy Revenue Protection on milk. Ag lenders are increasingly pushing producers to do exactly that.

- When it works: It insulates cash flow from a sudden break like last October’s.

- The trade-off: It costs premium dollars in the calm years — and last October is the entire reason it exists.

4. Push beef harder — but only if your reproduction has earned it

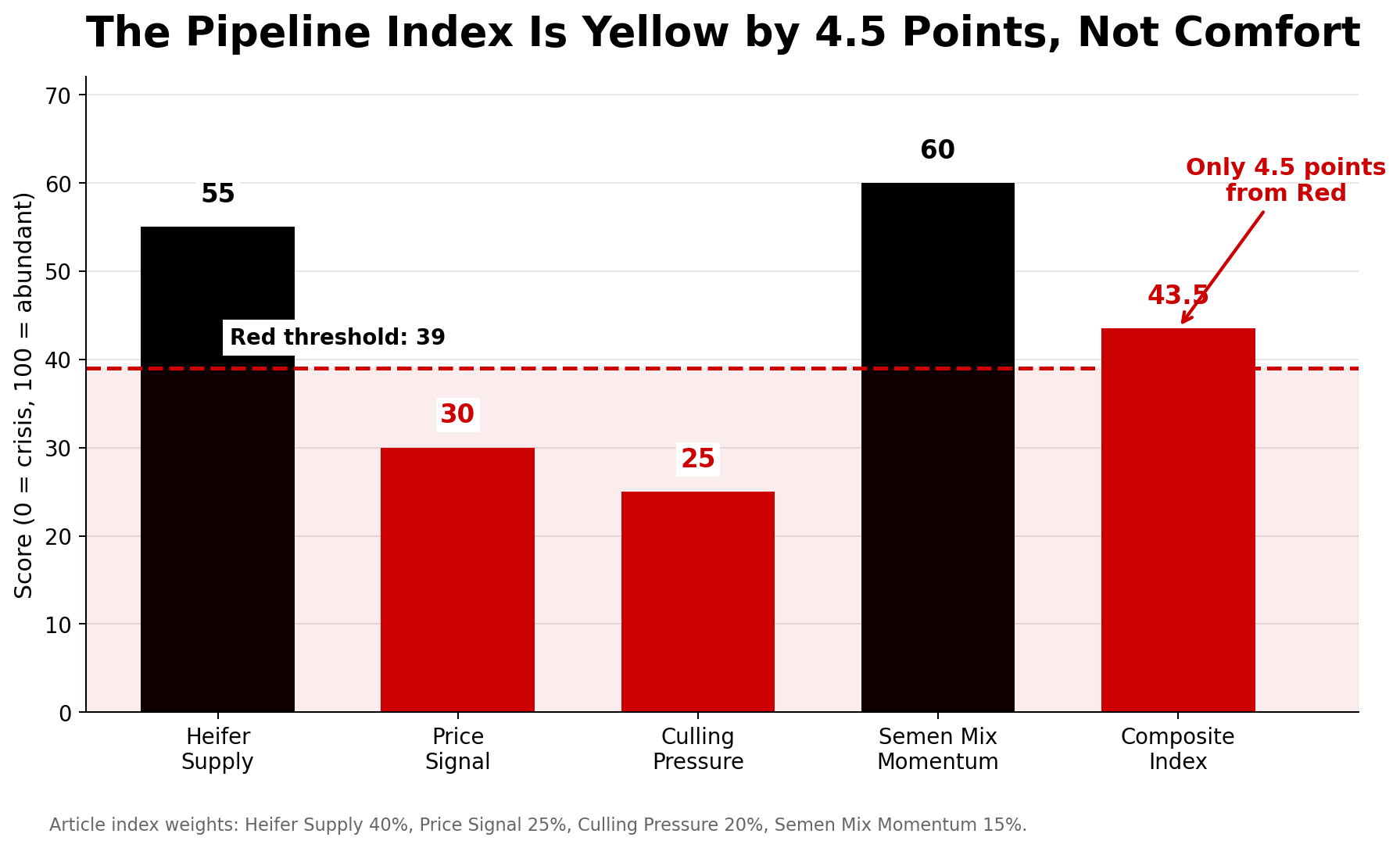

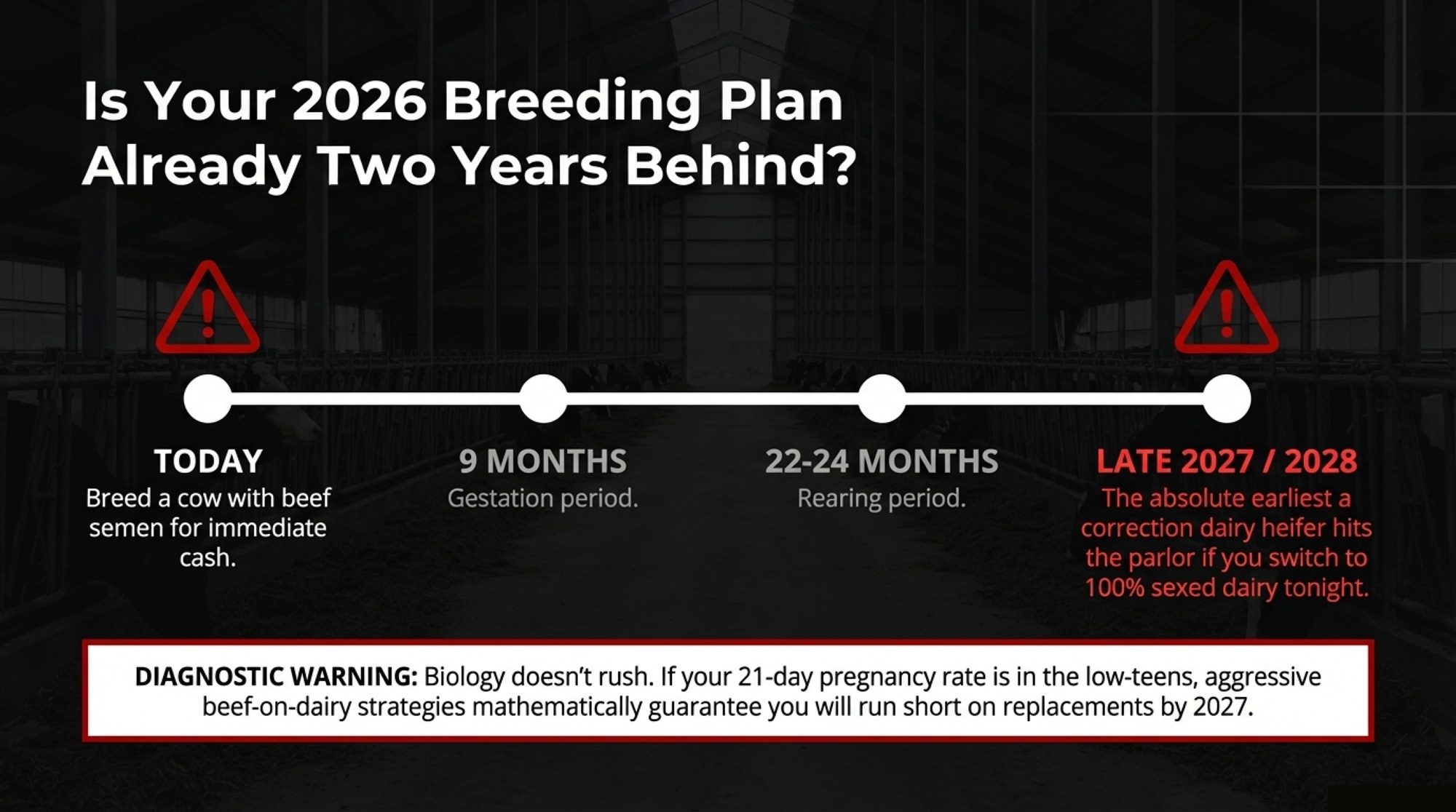

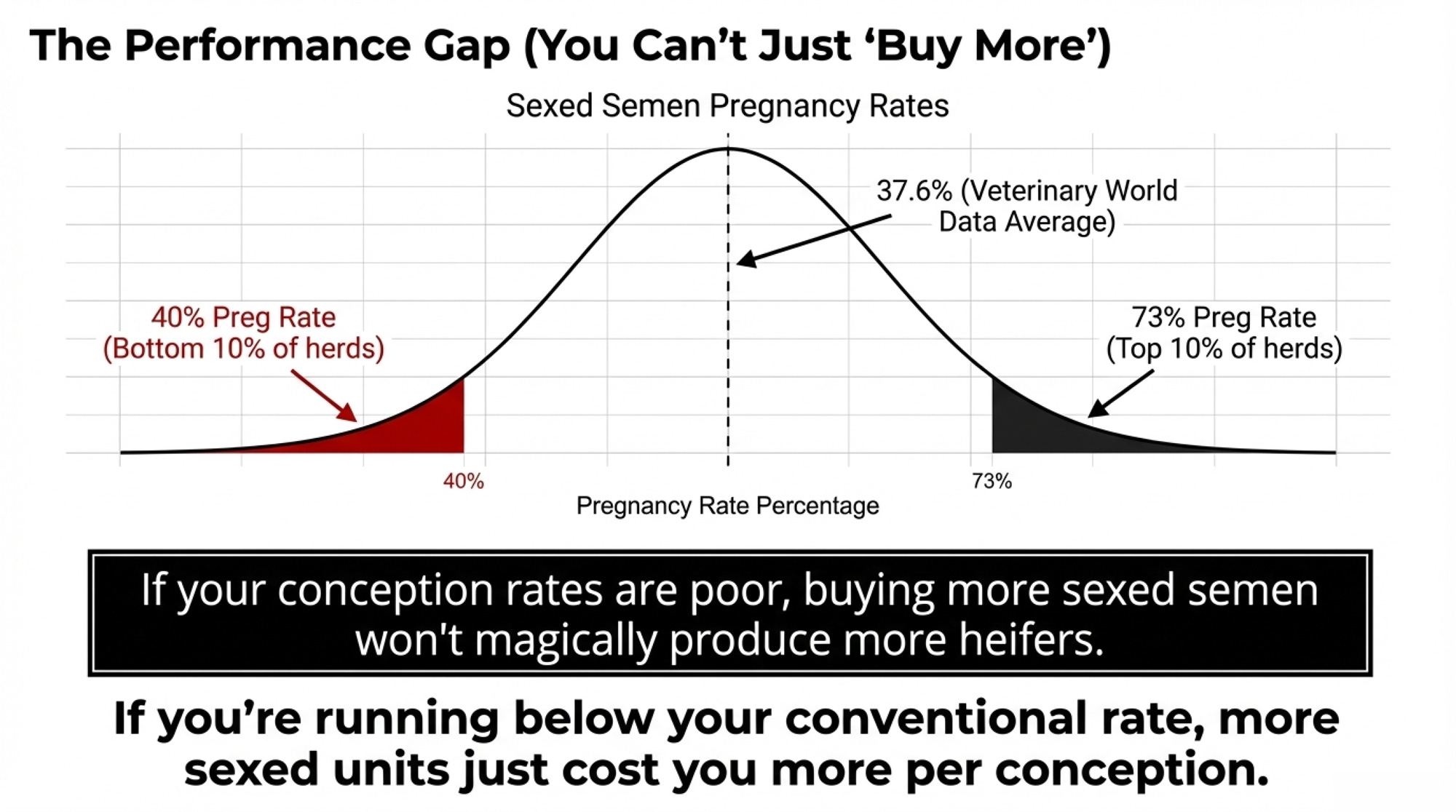

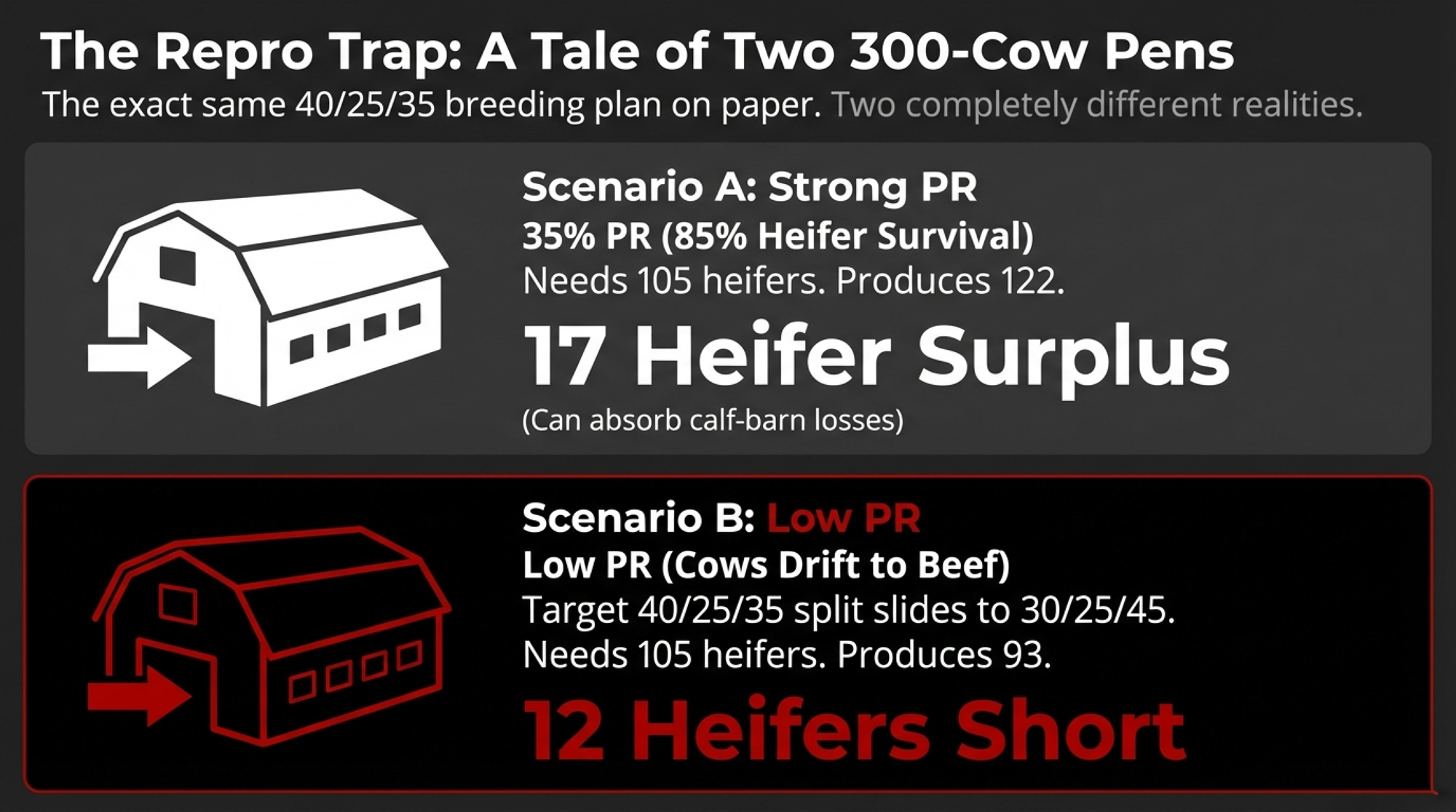

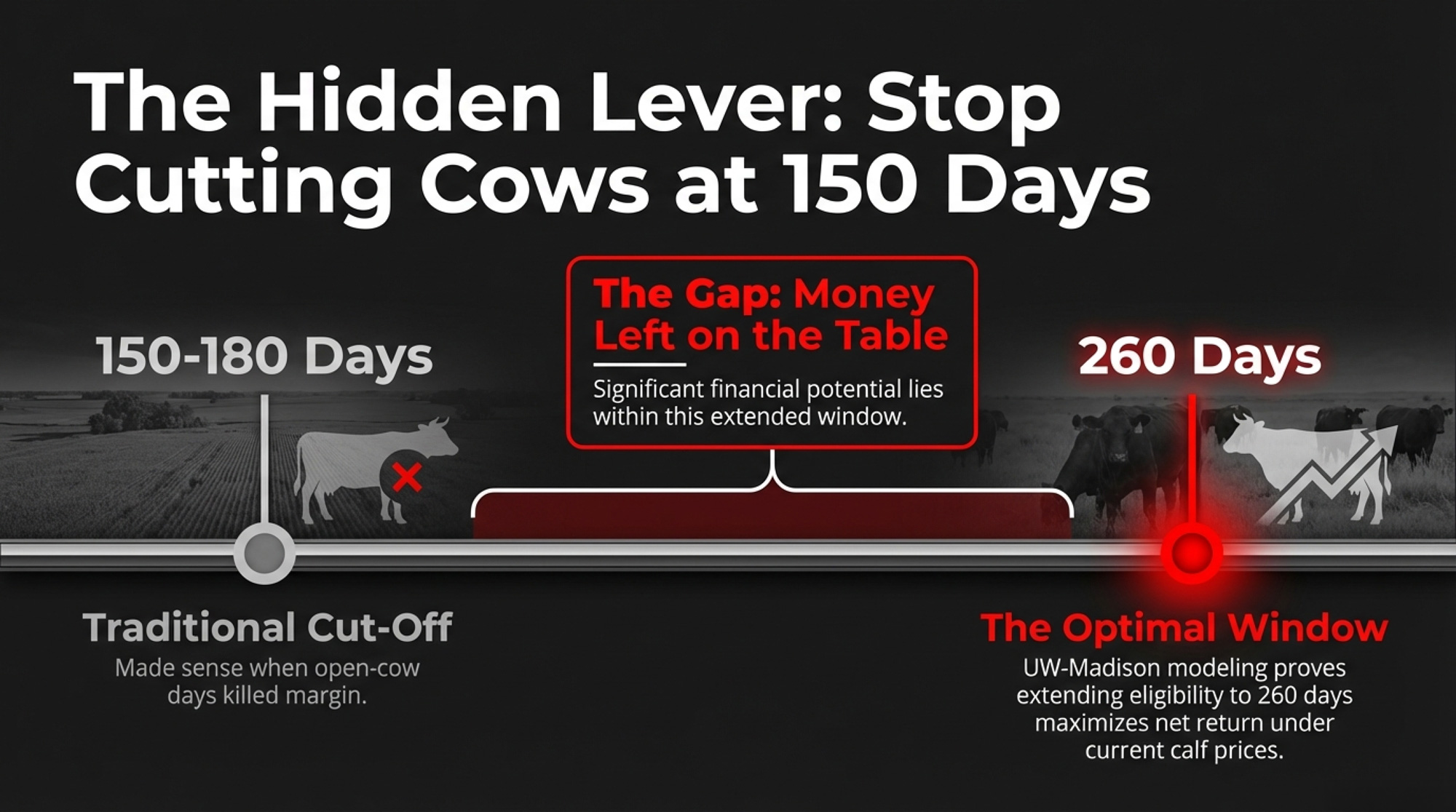

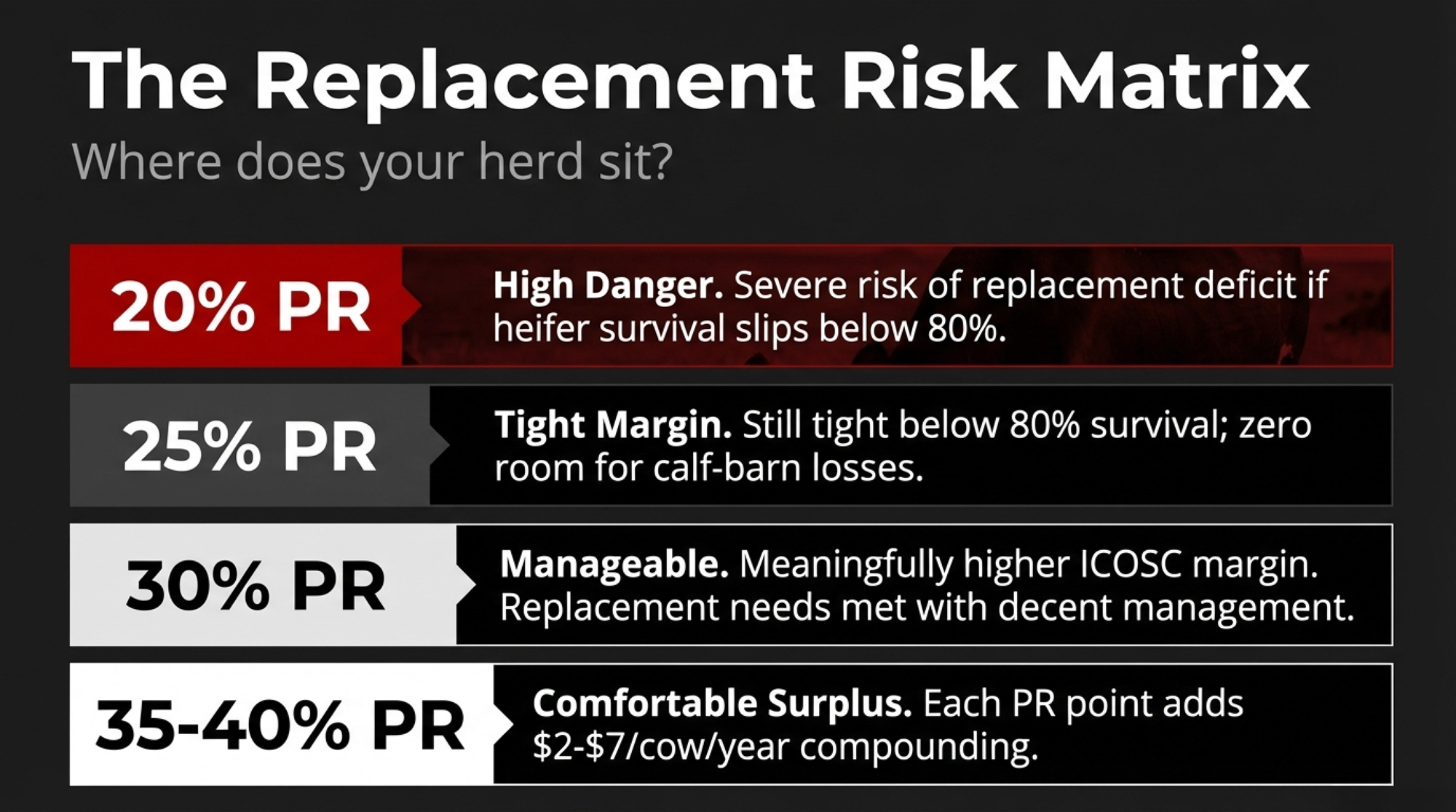

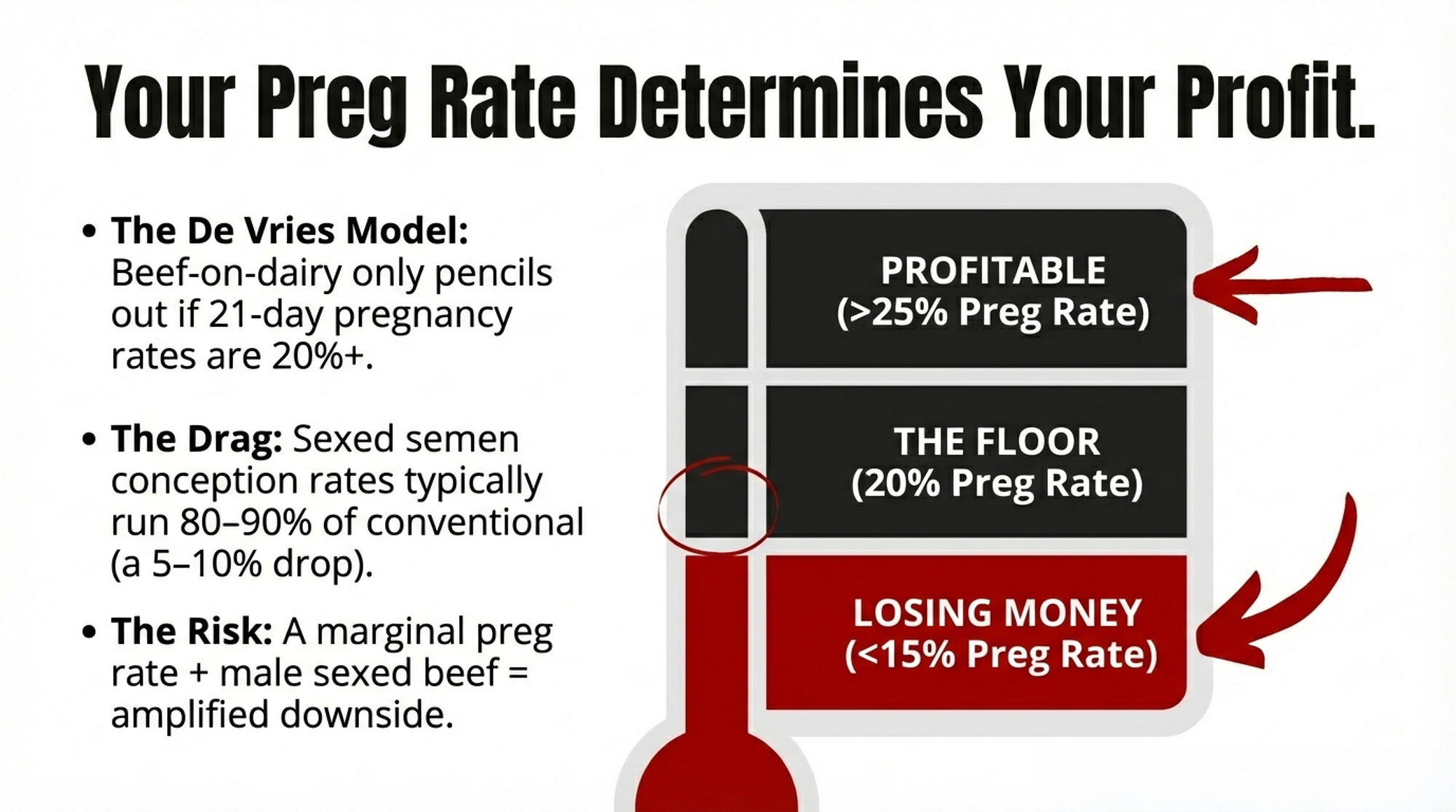

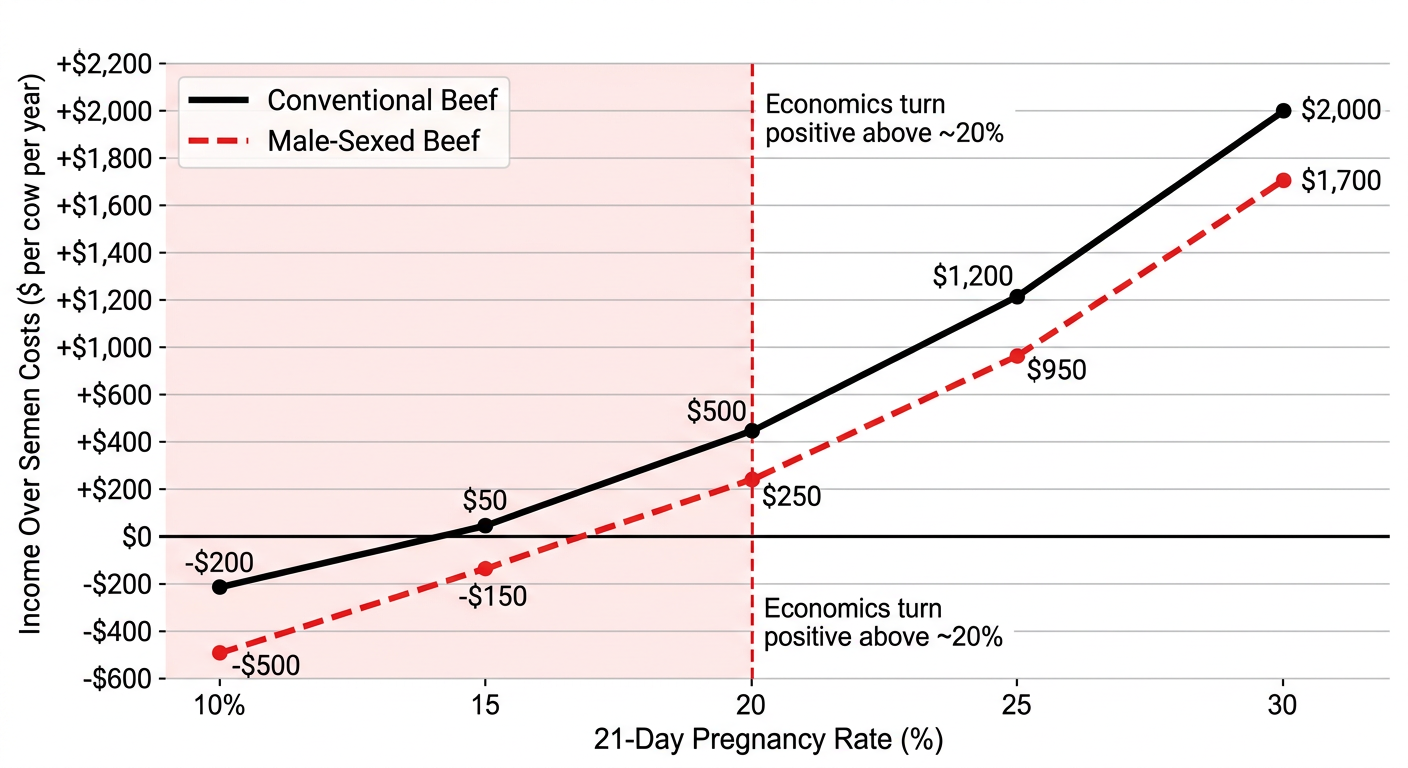

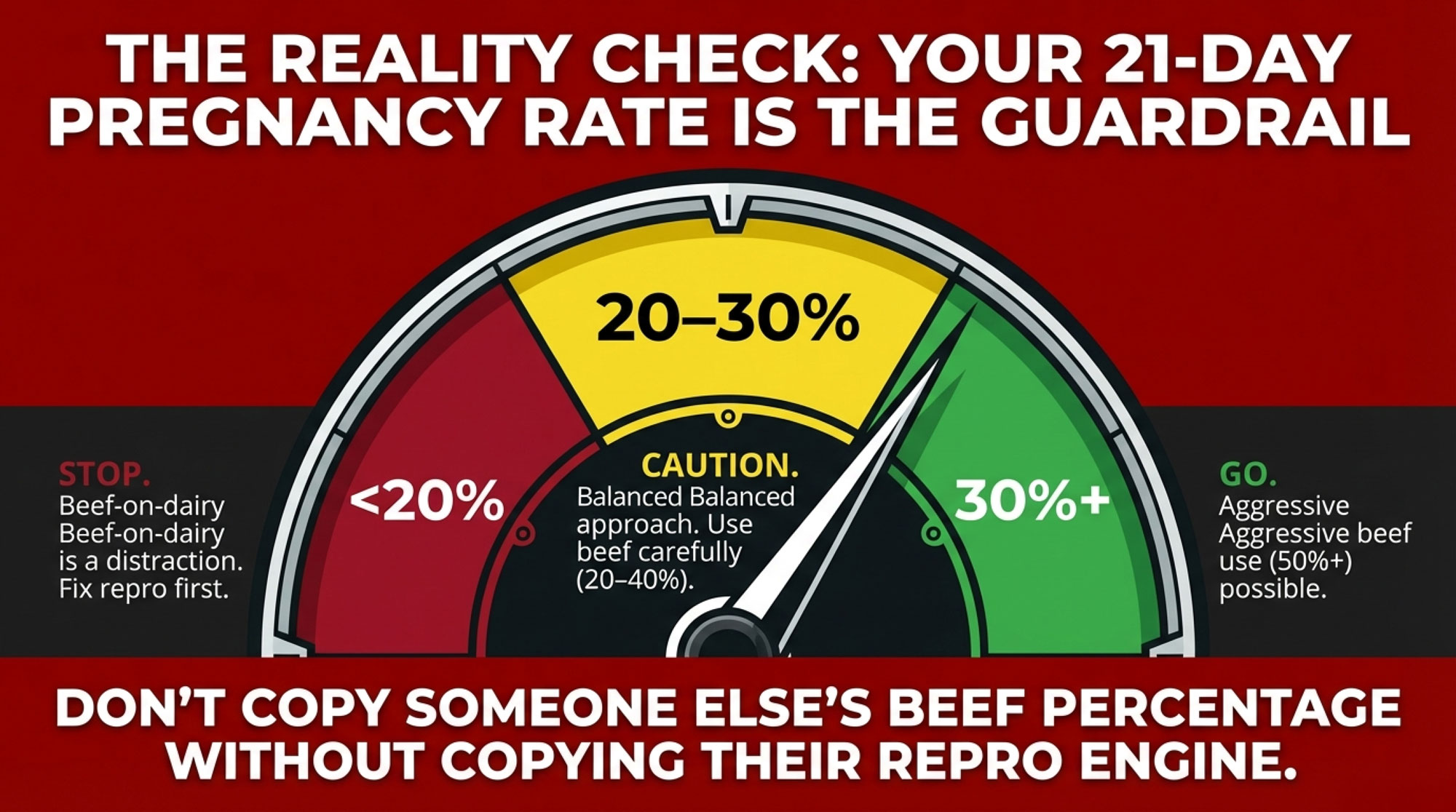

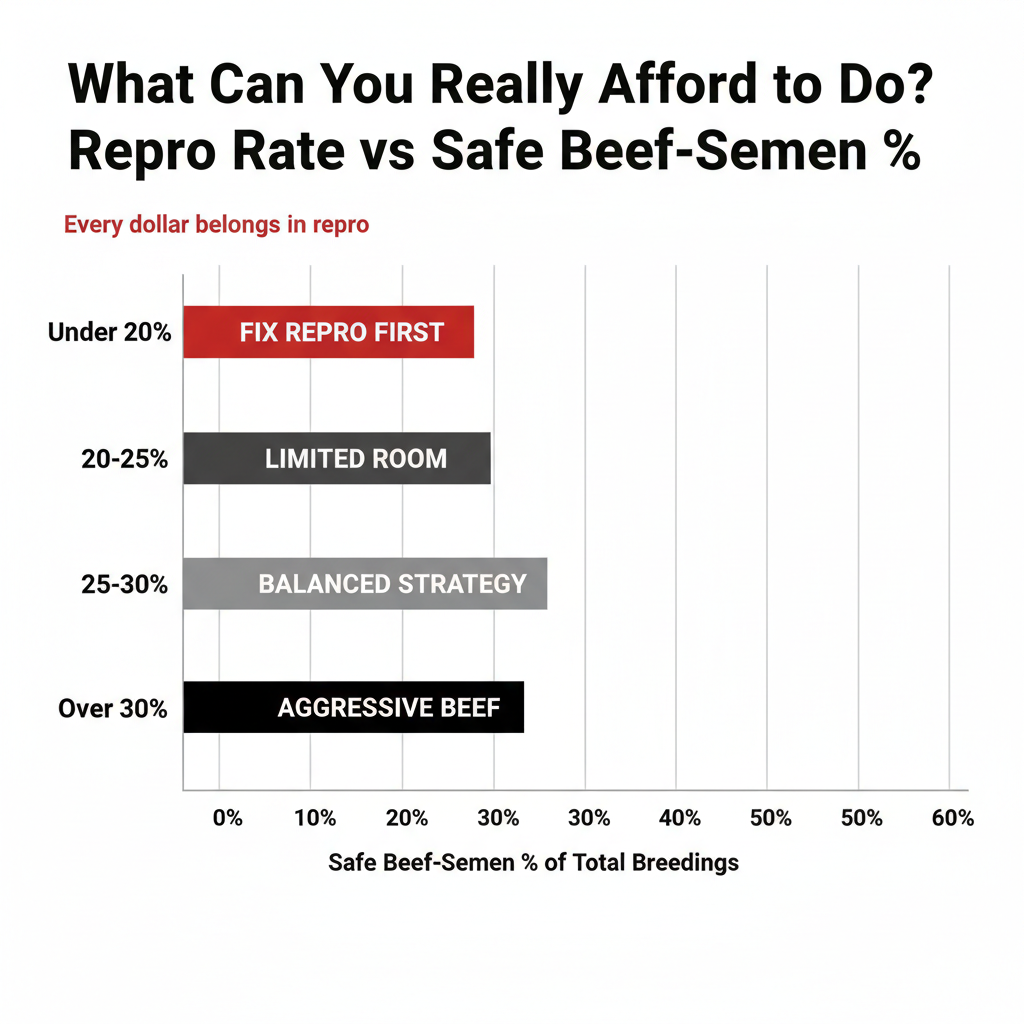

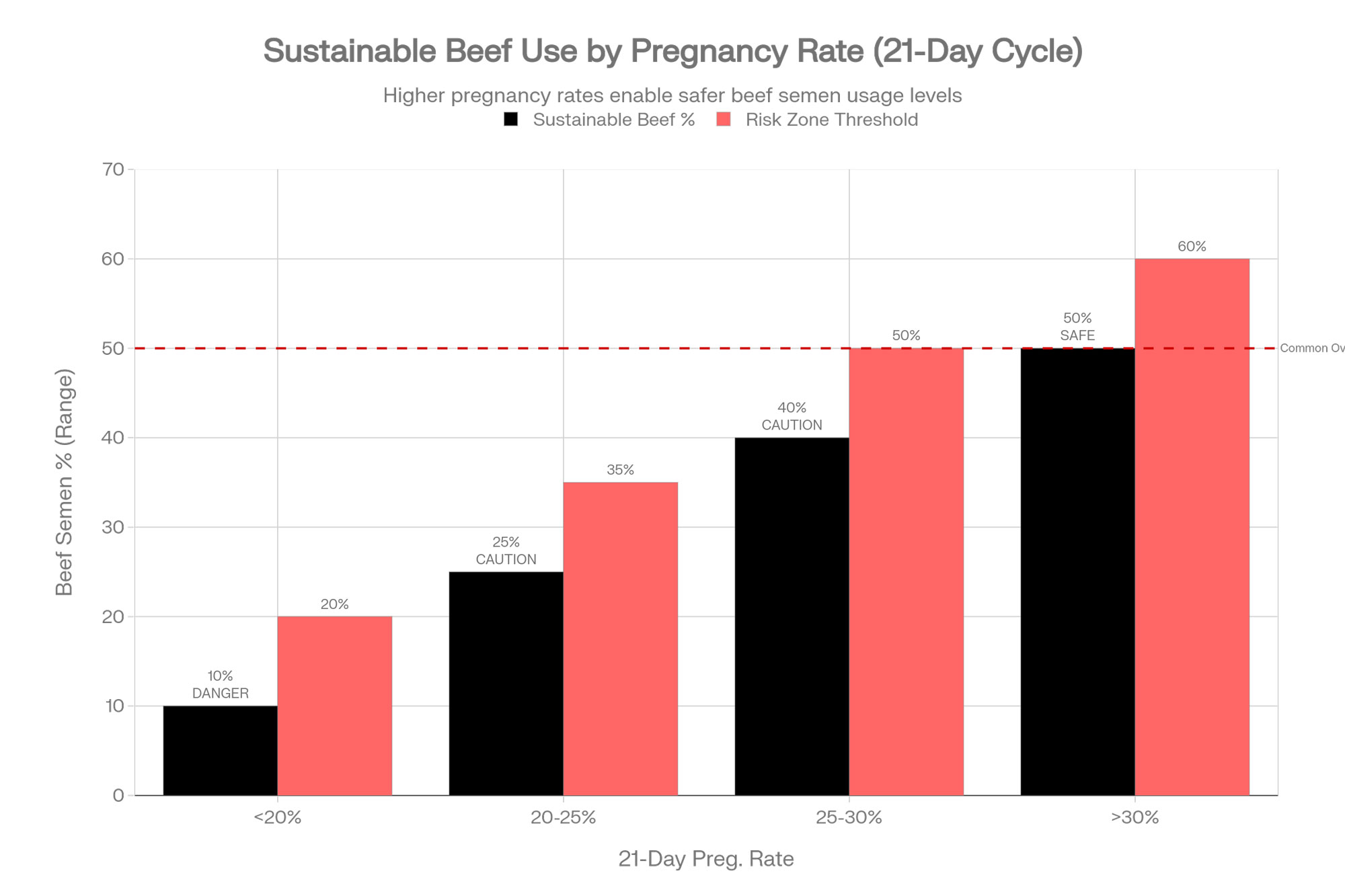

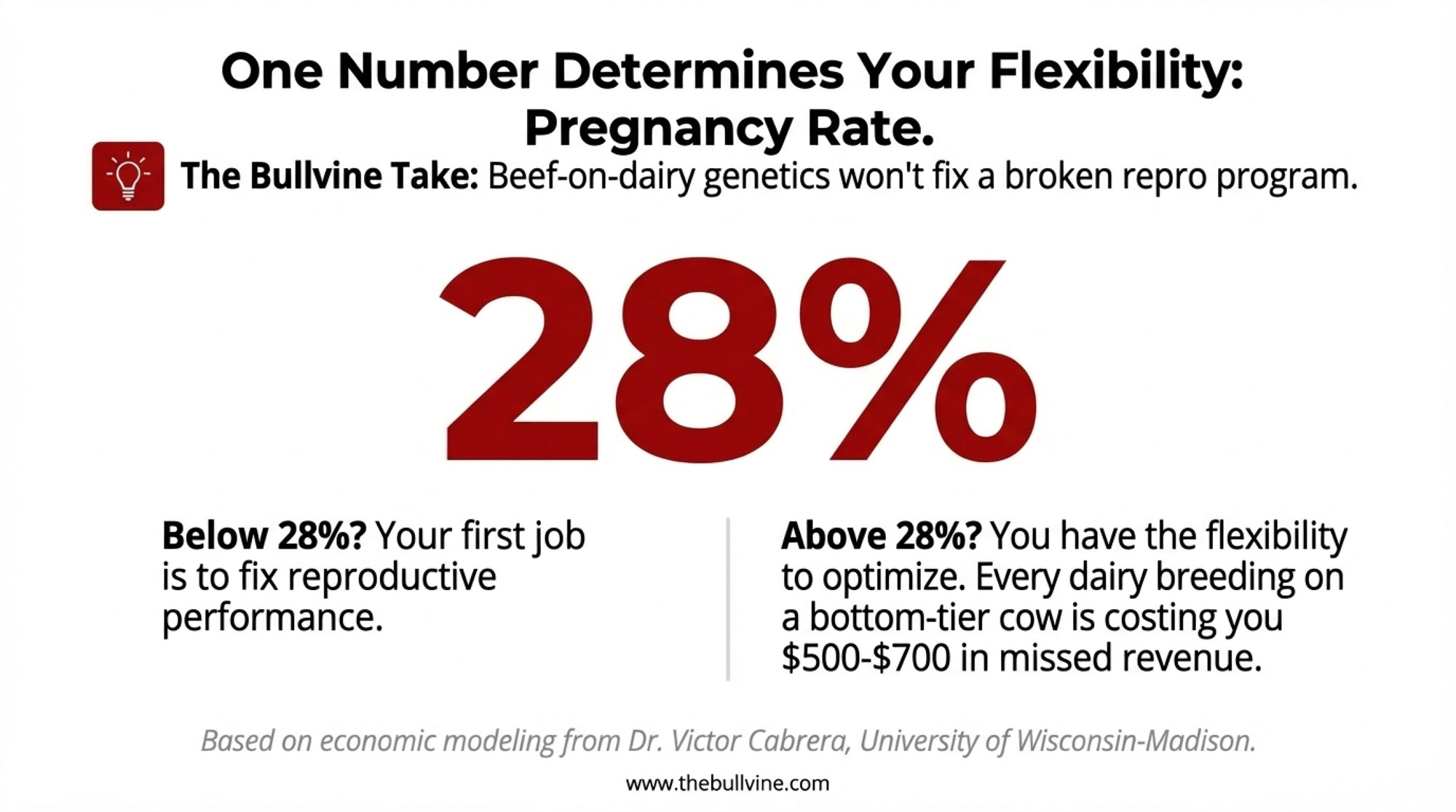

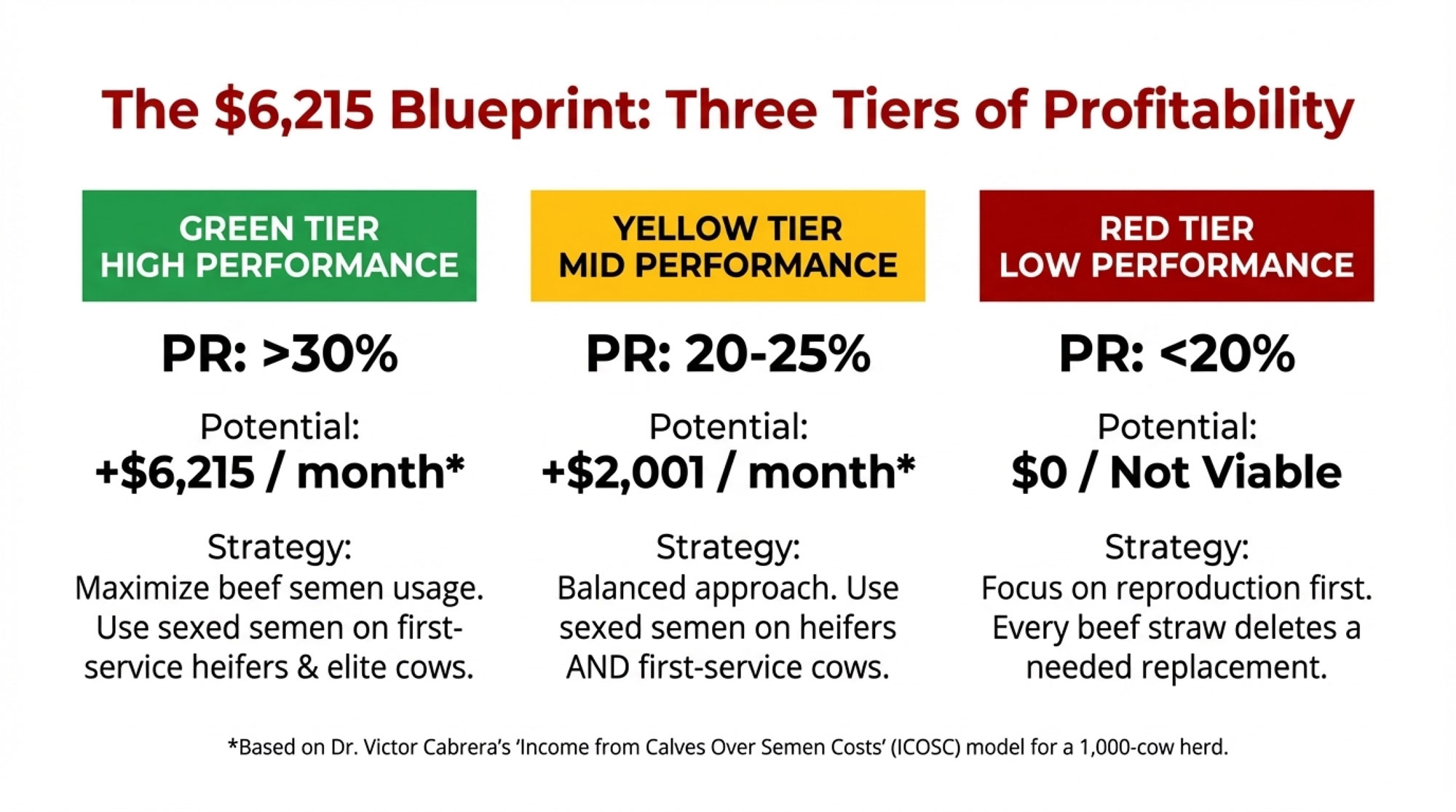

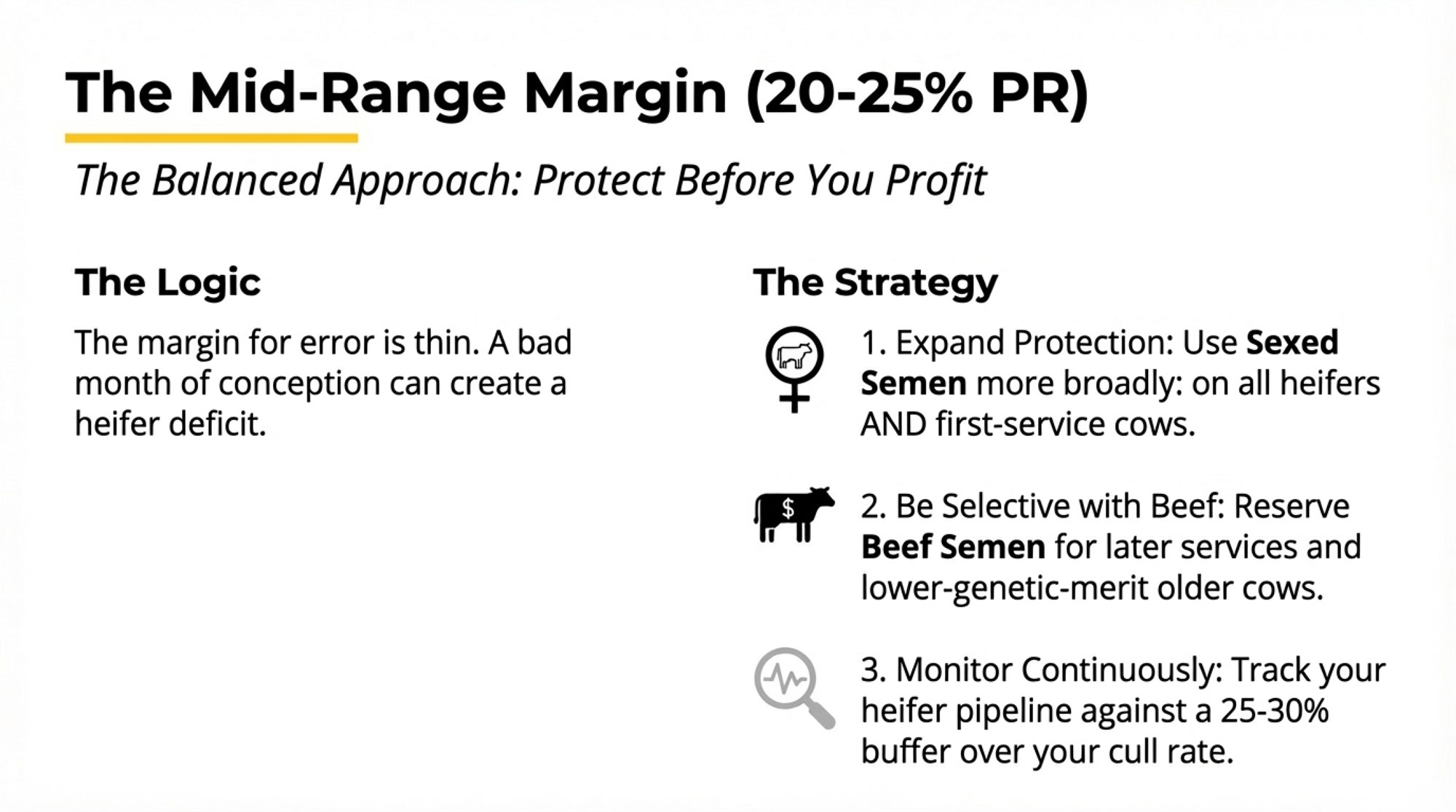

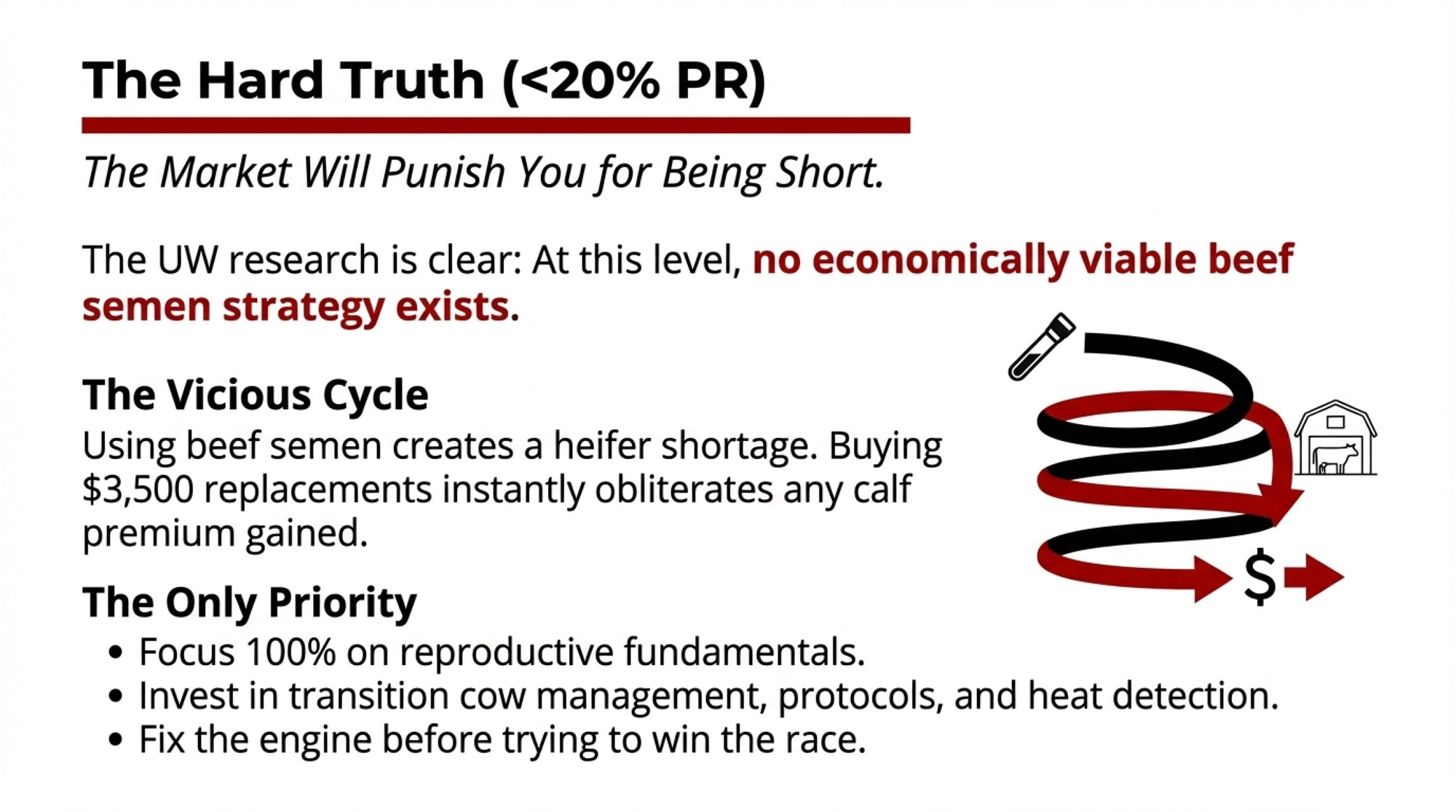

A genuinely high-fertility herd that consistently makes more dairy heifers than it needs can run more beef with a clear conscience, because it isn’t borrowing from a pipeline it can’t refill. Fix repro first. Cabrera’s peer-reviewed modeling found beef semen is an attractive proposition only for herds with at least a roughly 20% 21-day pregnancy rate — and that the return turns negative or marginal for low-performance herds around 15%, while herds at 30% can generate the strongest calf income (Cabrera et al., JDS Communications, 2021). The right beef share for a 30% pregnancy-rate herd is simply not the right share for one sitting at 17%.

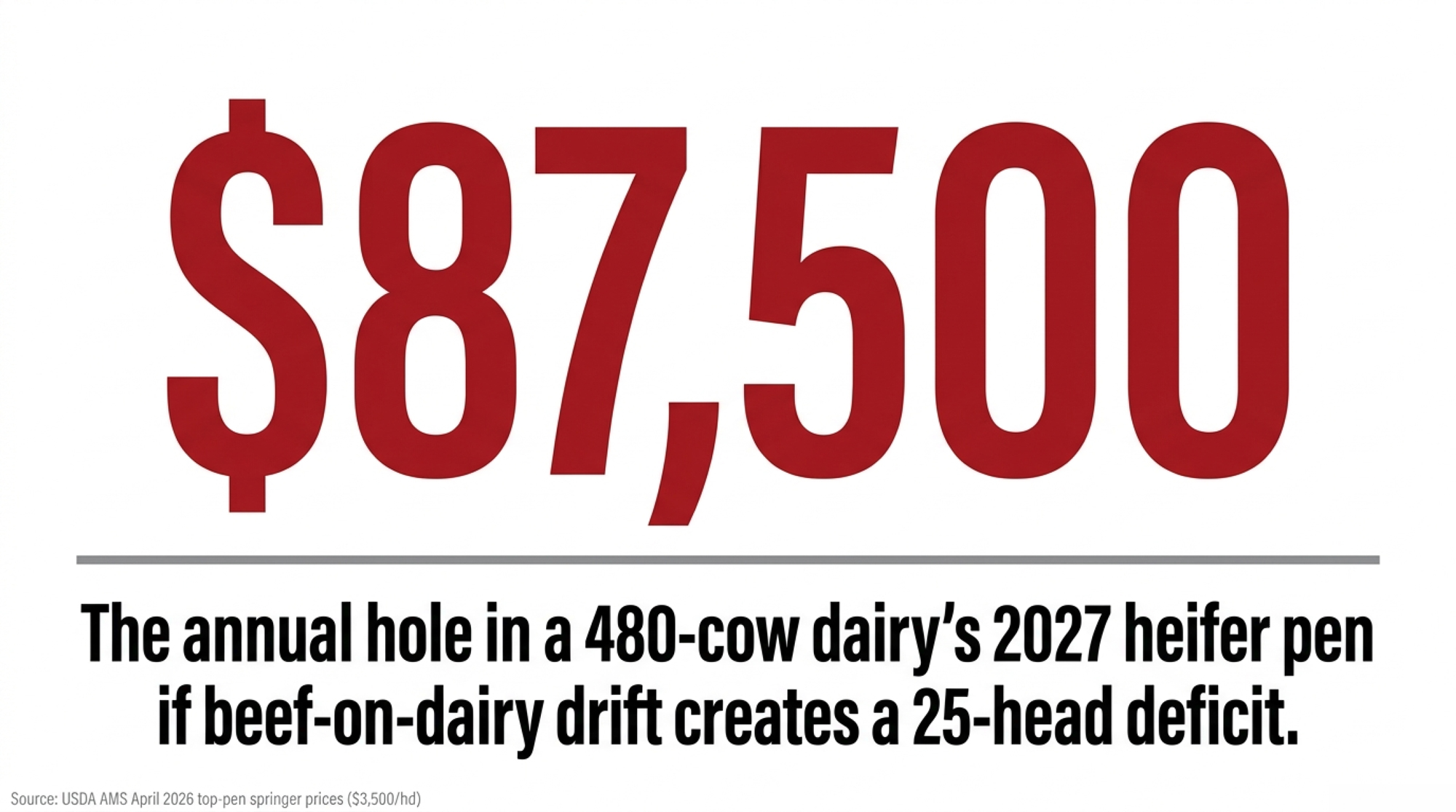

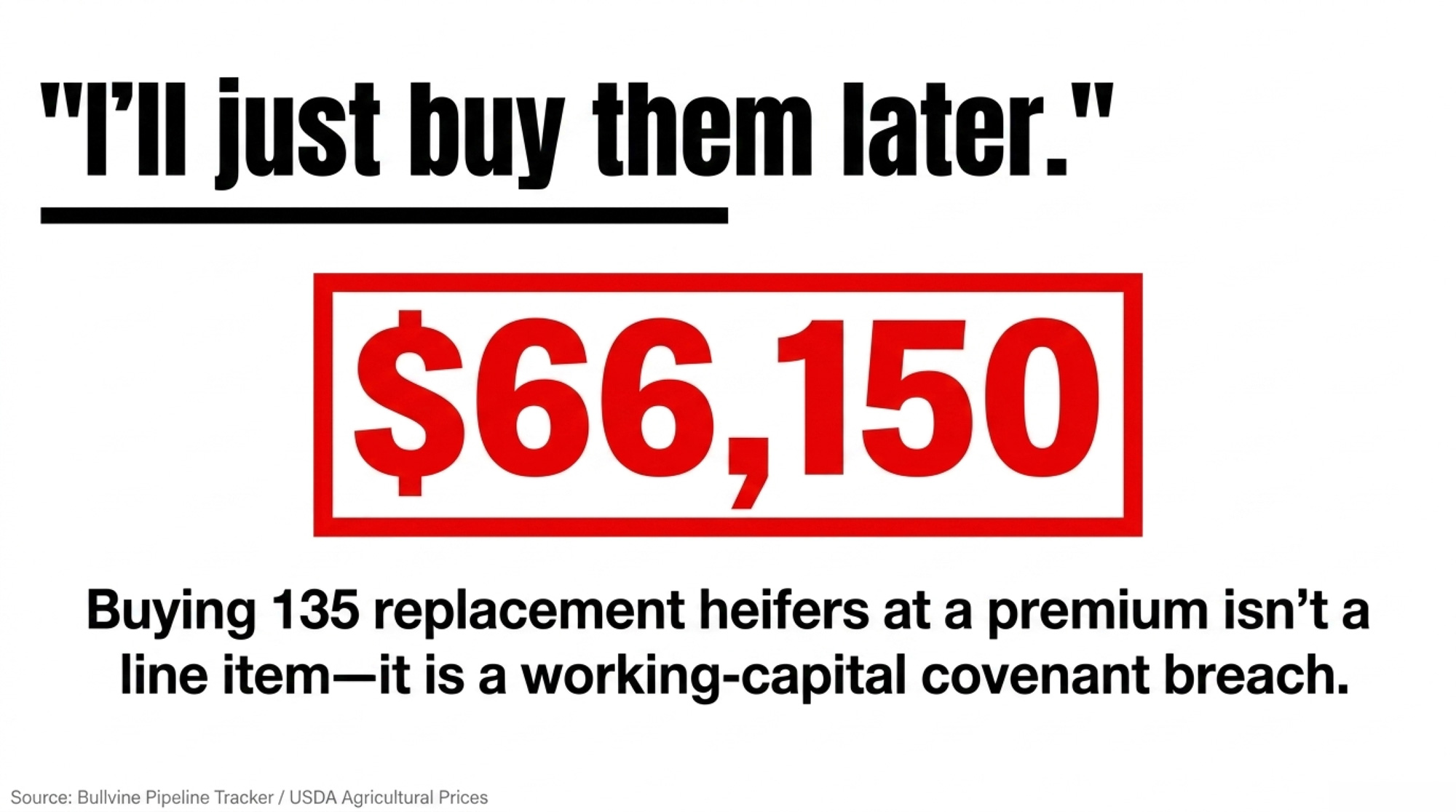

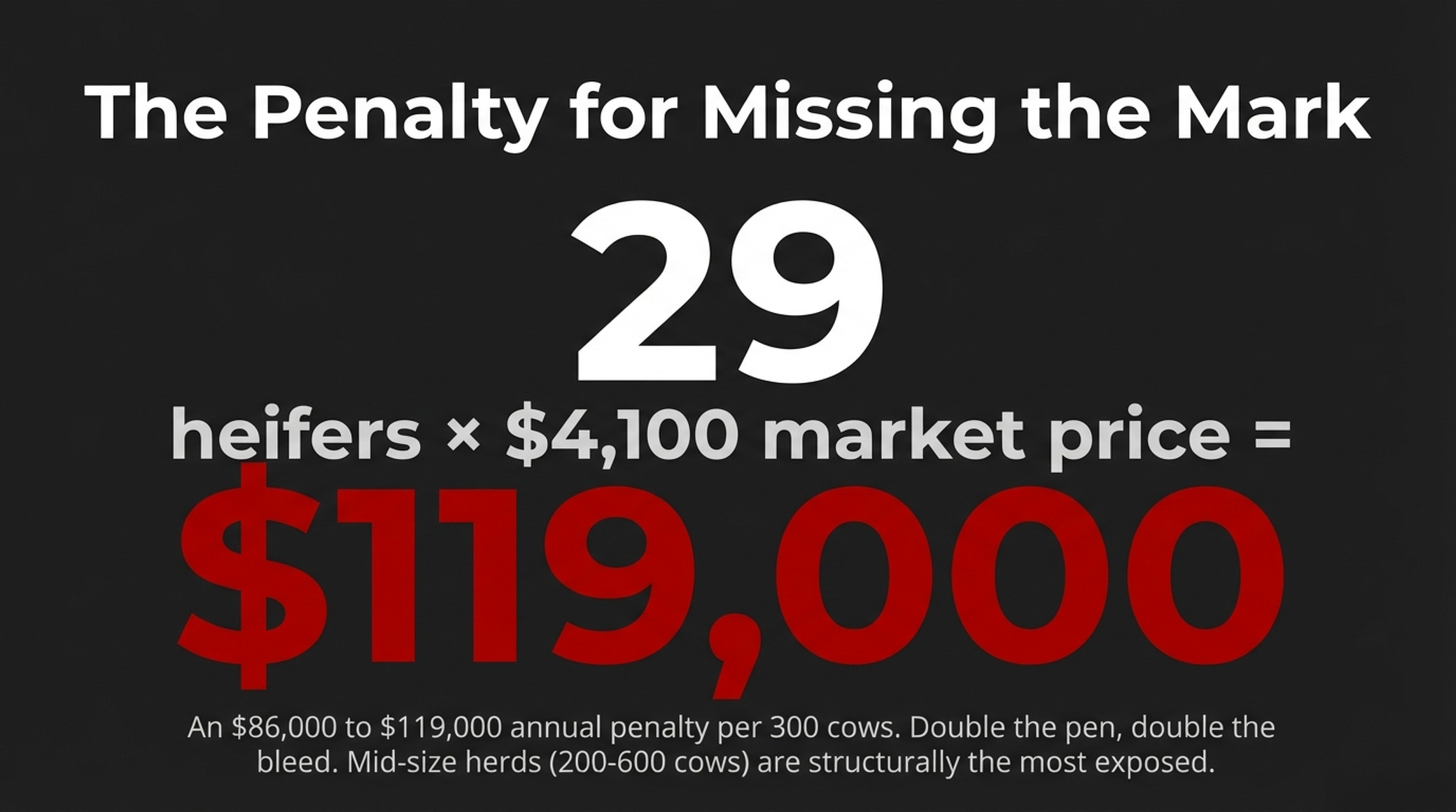

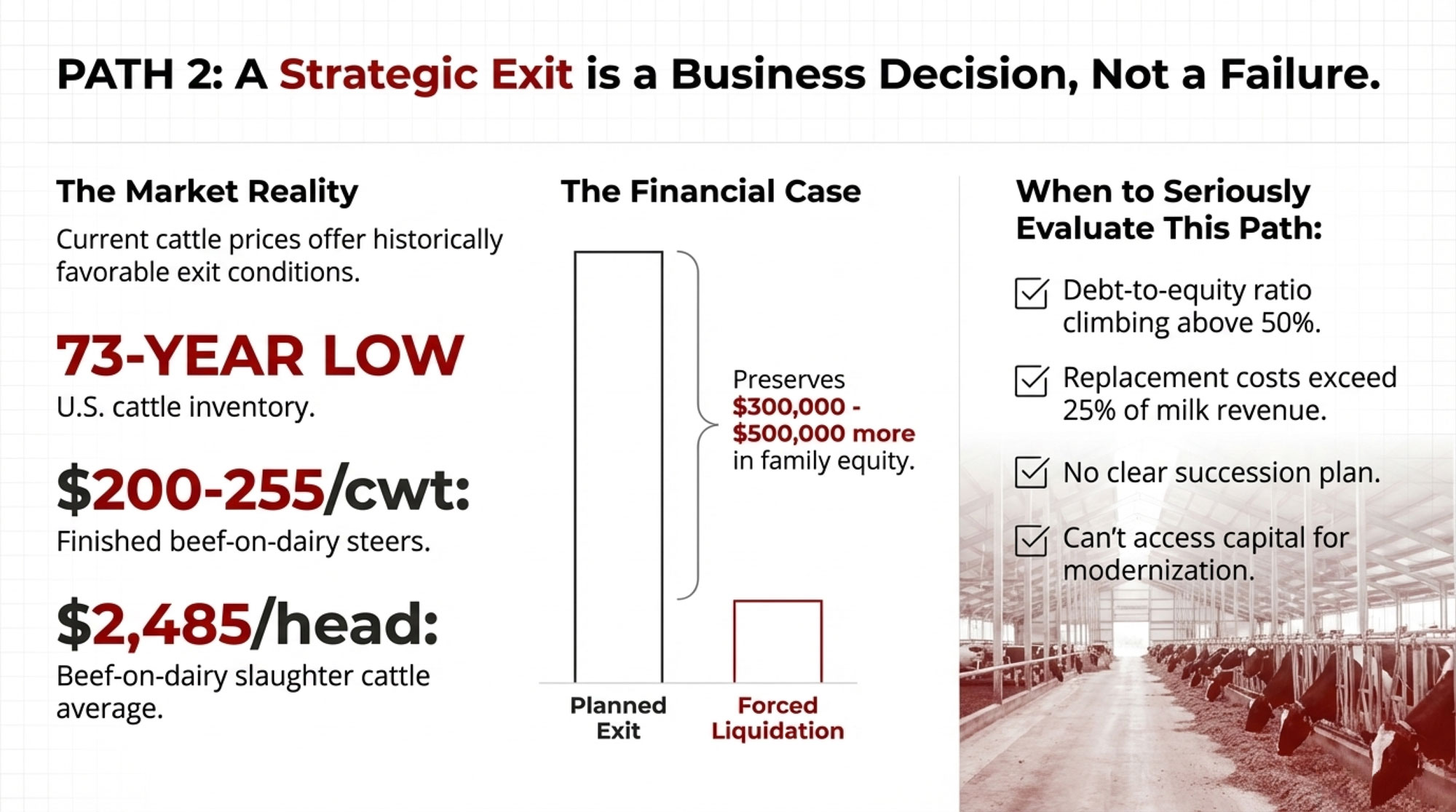

One forward-looking piece to fold into all of this: don’t count on the heifer market bailing you out. CoBank projects the rebuild finally starts in 2027 and 2028 — but adds back only about 360,200 head over the two years, with 285,400 entering the milking herd in 2027. Enough to slow the bleeding against a 796,000-head hole. Nowhere near enough to refill the tank. Budget replacements at $3,800 to $4,800 a head through the 2027 peak, and pencil it in before anyone at the kitchen table wants to say that number out loud.

Key Takeaways

- If you bred more than a handful of your good cows to beef last year, run the $585 multiplication before your next repro meeting. North of $100,000 in traded-away value means your calf premium is funded by your own heifer pipeline.

- If knocking 35% off last year’s calf and cull revenue would flip your cash flow negative, you’re a leveraged beef play — cap the exposure now.

- If your 21-day pregnancy rate is under 20%, park the beef-share debate and fix reproduction first.Cabrera’s modeling says beef semen’s return goes marginal or negative below that line.

- If you haven’t repriced replacements lately, budget $3,800–$4,800 a head through the 2027 peak. The rebuild is a crawl of about 360,200 head over two years, not a comeback.

- If beef sales clear ~20% of your revenue, price the LRP this quarter. Lenders already treat that income like milk. So should you.

- If you can’t state your beef-share ceiling out loud, you don’t have one. Write it down before drift decides it for you.

The Real Independence Question

There’s a fitting irony for the Fourth. The trade keeping so many farm families independent — on their own land, on their own terms — is the same trade that can hand your fate to one volatile market overnight. Independence was never the calf check. It’s knowing your own numbers well enough that no single price swing gets to decide whether you’re still farming next year.

McCarty sits at 50% of revenue from calves because he built a system precise enough to carry that weight. Plenty of farms never built the system — they just leaned harder on the beef straw because the check cleared and the milk price didn’t. So the honest question this Independence Day isn’t whether beef-on-dairy works. It clearly does. The sharper one: if calf prices dropped 11.5% again next month, would your operation feel a dip — or a hole?

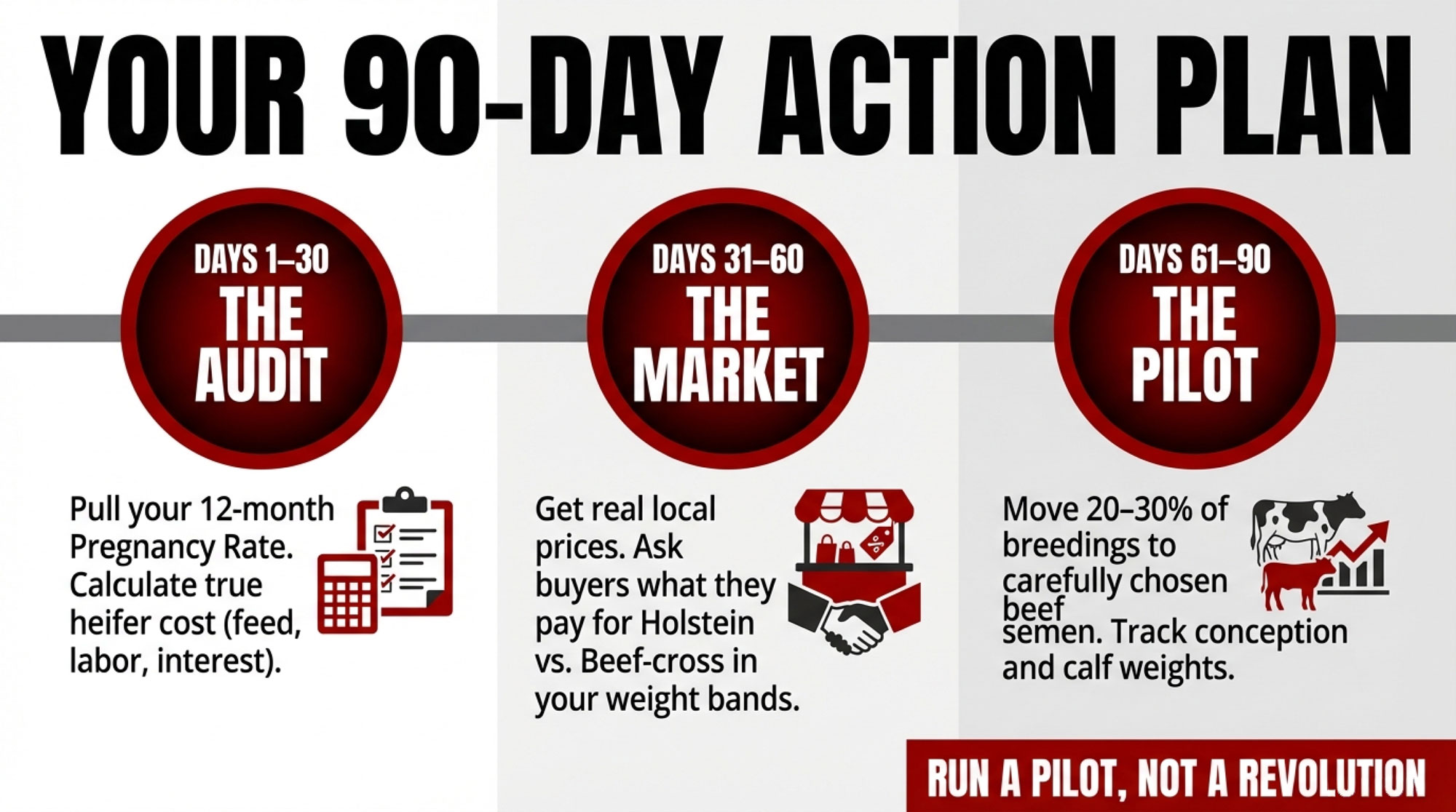

Pull your last breeding records and 12 months of calf revenue before your next repro meeting, run both the $585 math and the 35% test against your own numbers, then take them to your genetics rep and your lender in the same week. While the big systems argue over where dairy’s headed — the War of the Worlds fight over the industry’s future playing out over your head — this is how one farm actually survives the crossfire, one breeding decision at a time. We’re breaking down the full per-service and whole-herd model by herd size in the next Bullvine Weekly. That’s where the real numbers live.

Methodology Note. The $585-per-service figure and its components come from a single Bullvine model and are illustrative at today’s prices, not fixed constants. The model assumes a roughly $3,010 national-average replacement heifer (CoBank Knowledge Exchange, mid-2025) and a roughly $500 beef-cross calf. Expected value of a sexed-dairy service (about $854) is heifer cost times conception probability, calf survival, heifer survival to breeding, and heifer completion to first calving — the last using the ~79% completion rate (IQR 74–84%) from Dr. Michael Overton’s 85-herd dataset presented at the 2026 High Plains Dairy Conference. Expected value of a beef service (about $271) is calf price times beef conception and calf-survival probabilities. The components round independently, so the gap prints as roughly $583–$585. The ~$117,000 (200 services), ~$35,000 (60 services on a 300-cow herd), and $1,580 breakeven calf price all shift with your own inputs. Recalculate with your numbers. The arithmetic, not the specific dollar figure, is the part that transfers.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Transform Your Dairy Economics: How Beef-on-Dairy Crossbreeding Delivers 200% ROI — Arms your breeding program with actionable crossbreeding metrics like average daily gain and feed conversion. This protocol shifts focus onto genetic selection science, showing how matching specific beef sires can cut down feed costs by over $100 per head.

- $3010 Per Heifer. 800000 Short. Your Beef-on-Dairy Bill Is Due. — Exposes the long-term structural reality of the nation’s 800,000 missing replacements against a massive $10 billion processing plant expansion. Learn how to navigate four concrete paths to protect your herd turnover without sacrificing cash flow.

- The Angus Advantage: Revolutionizing Dairy Profitability Through Strategic Beef Crossbreeding — Dismantles traditional breeding models by leveraging data-driven Angus crossbreeding to capture an 840% increase in calf value over purebred lines. This approach reduces gestation length, speeding up your cows’ return to profitable milk production cycles.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.