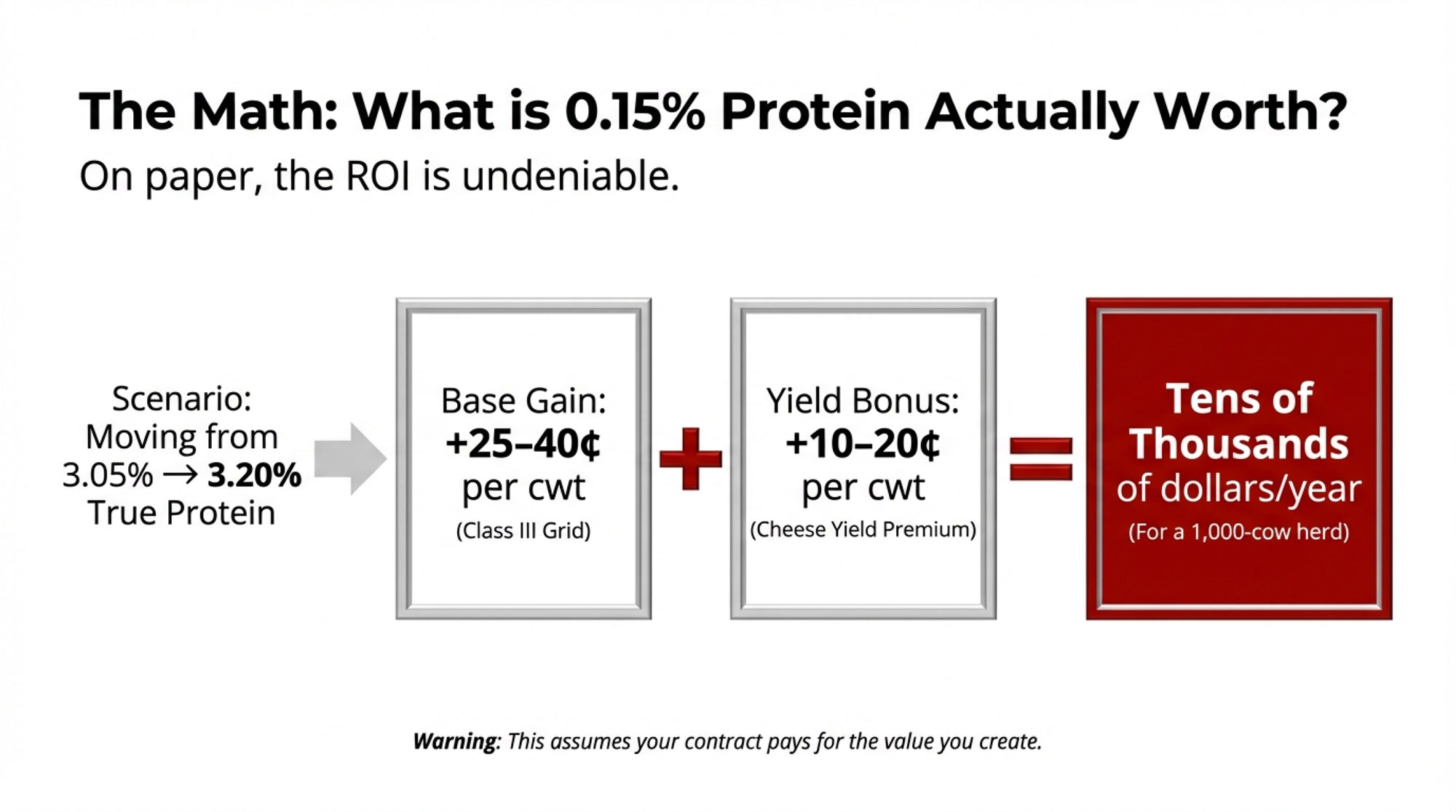

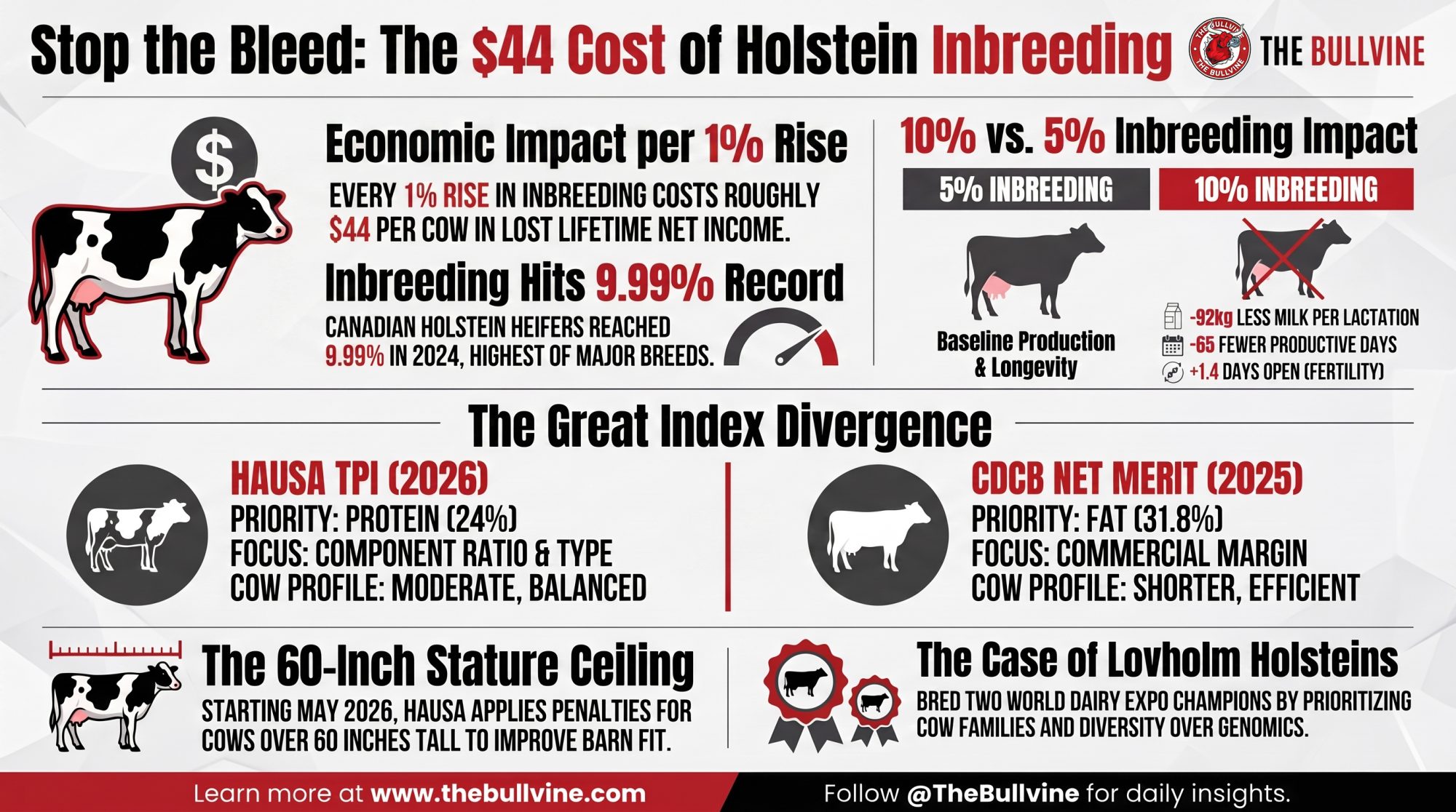

At 9.99% inbreeding, every extra point can quietly strip up to $44 per cow — before you even argue TPI vs Net Merit.

Lovhill Sidekick Kandy Cane takes the fist-bump and the banner — Grand Champion of the International Holstein Show at World Dairy Expo. Bred by Michael and Jessica Lovich on 72 tie-stall cows in Balgonie, Saskatchewan, and later classified EX-97, she’s living proof that a deep, functional udder and real longevity still win the ring — the same traits a narrowing gene pool is quietly pricing every breeder out of.

Michael and Jessica Lovich milk 72 cows in a tie-stall barn in Balgonie, Saskatchewan. They mostly ignore genomics. They breed off cow families and their own eye. And they’ve now bred two separate World Dairy Expo Holstein Grand Champions — Lovhill Goldwyn Katrysha in 2015 and Lovhill Sidekick Kandy Cane in 2025. They’re the first and only breeders in history to pull that off. (Read more: Lovholm Holsteins: The Only Farm to Breed 2 World Dairy Expo Holstein Champions Milks 72 Cows in Tie-Stalls)

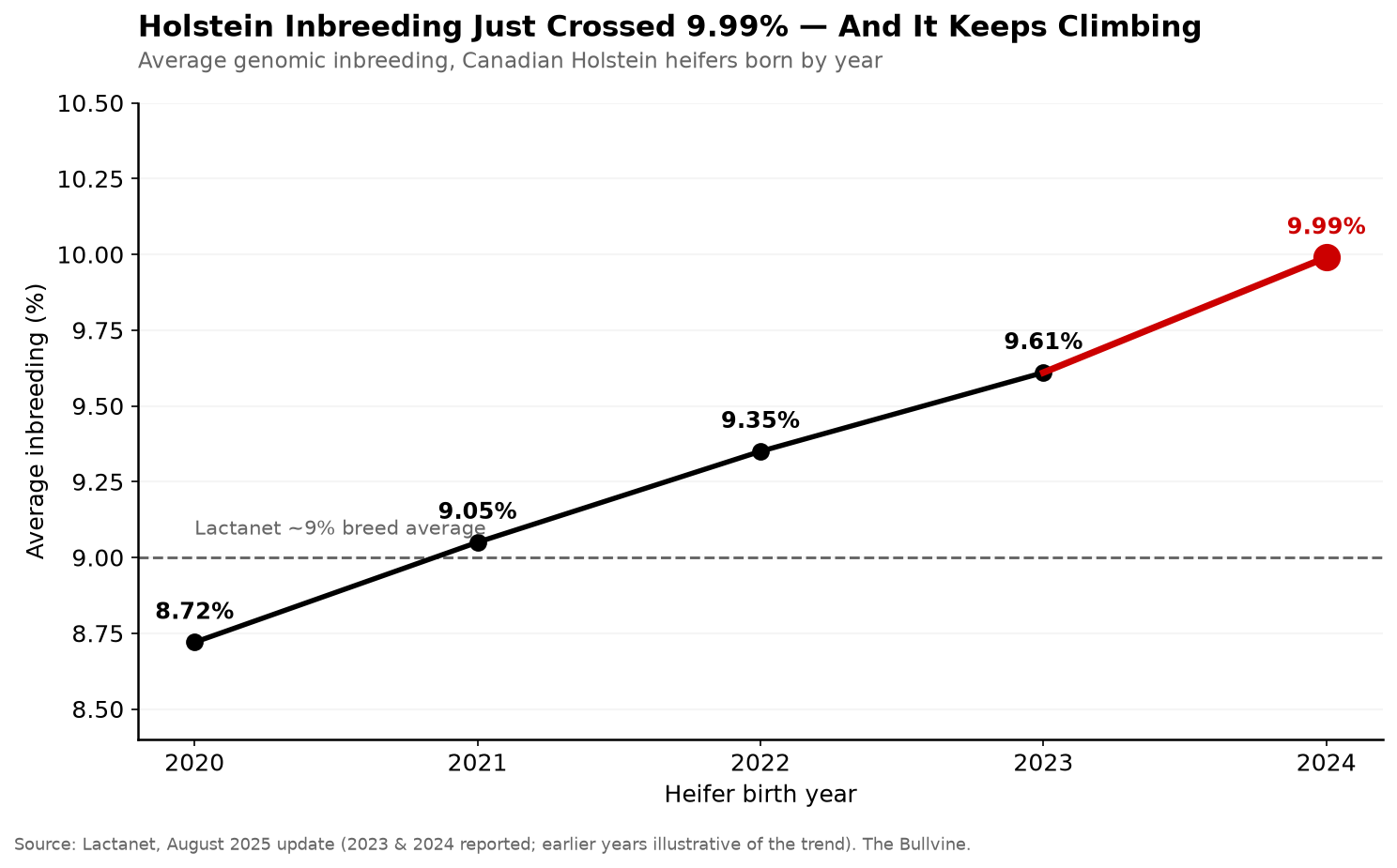

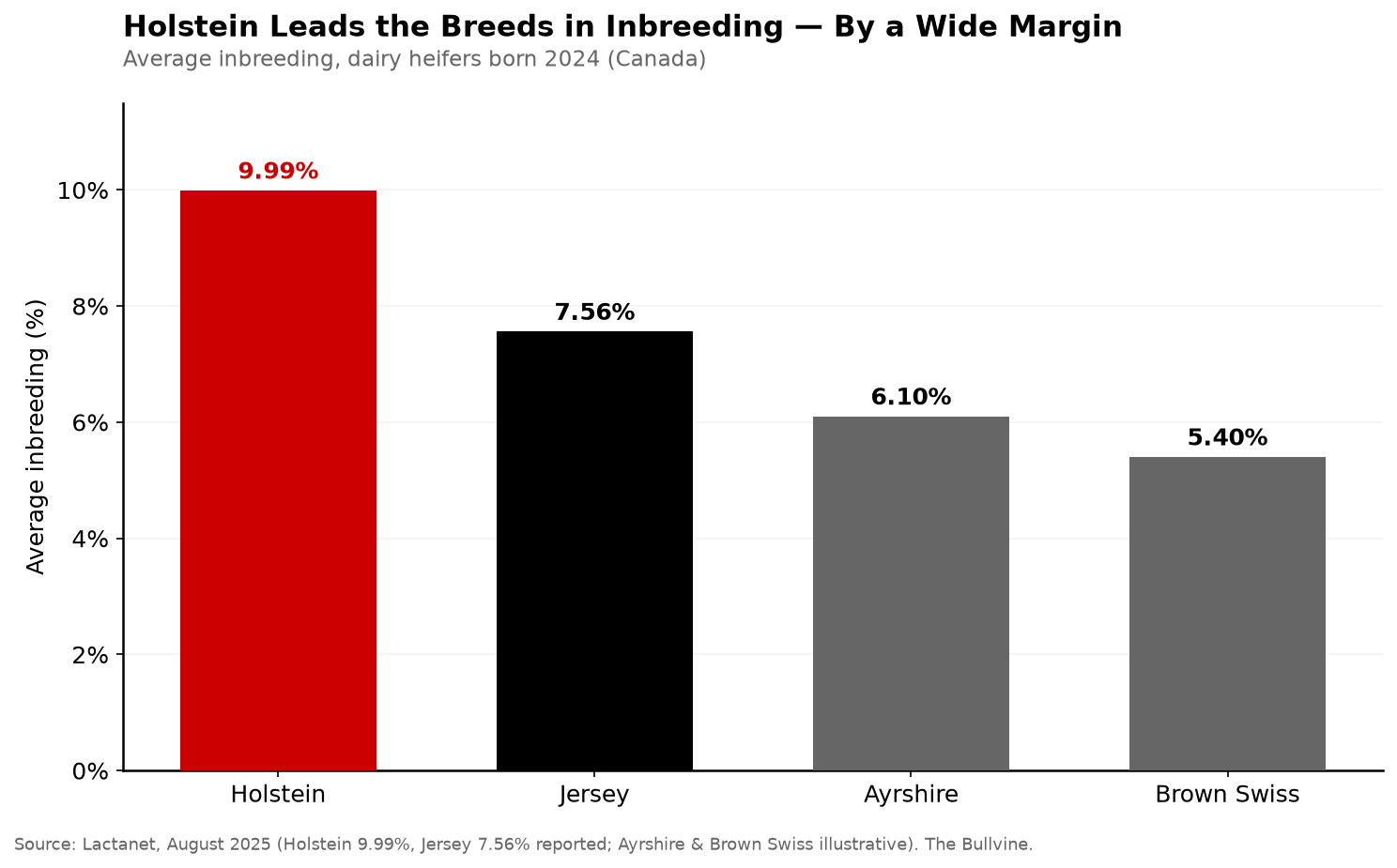

Here’s the part that should make you pause. The herd that walked away from the index list ended up breeding the kind of functional, long-lasting cows the commercial indices are quietly moving toward anyway. They succeeded by breeding out of a broader, more diverse gene pool — the exact opposite of where the rest of the industry is rushing. And while everyone keeps arguing about show cattle versus commercial cattle versus “just use the index,” a number nobody chose keeps climbing in the background: Holstein inbreeding hit 9.99% for Canadian heifers born in 2024 — the highest of the four major breeds, ahead of Jersey at 7.56%, and up from 9.61% the year before — according to Lactanet’s August 2025 update. That number lands on all three camps at once, no matter which side of the argument you stand on.

What’s Changing and Why

For thirty years, the dairy genetics argument has had two sides. One camp says the show ring proves what a valuable cow looks like. The other says the milk cheque does. This summer a third voice got loud enough to matter: “Both of you are wasting time — just breed off the top GTPI or Net Merit list.”

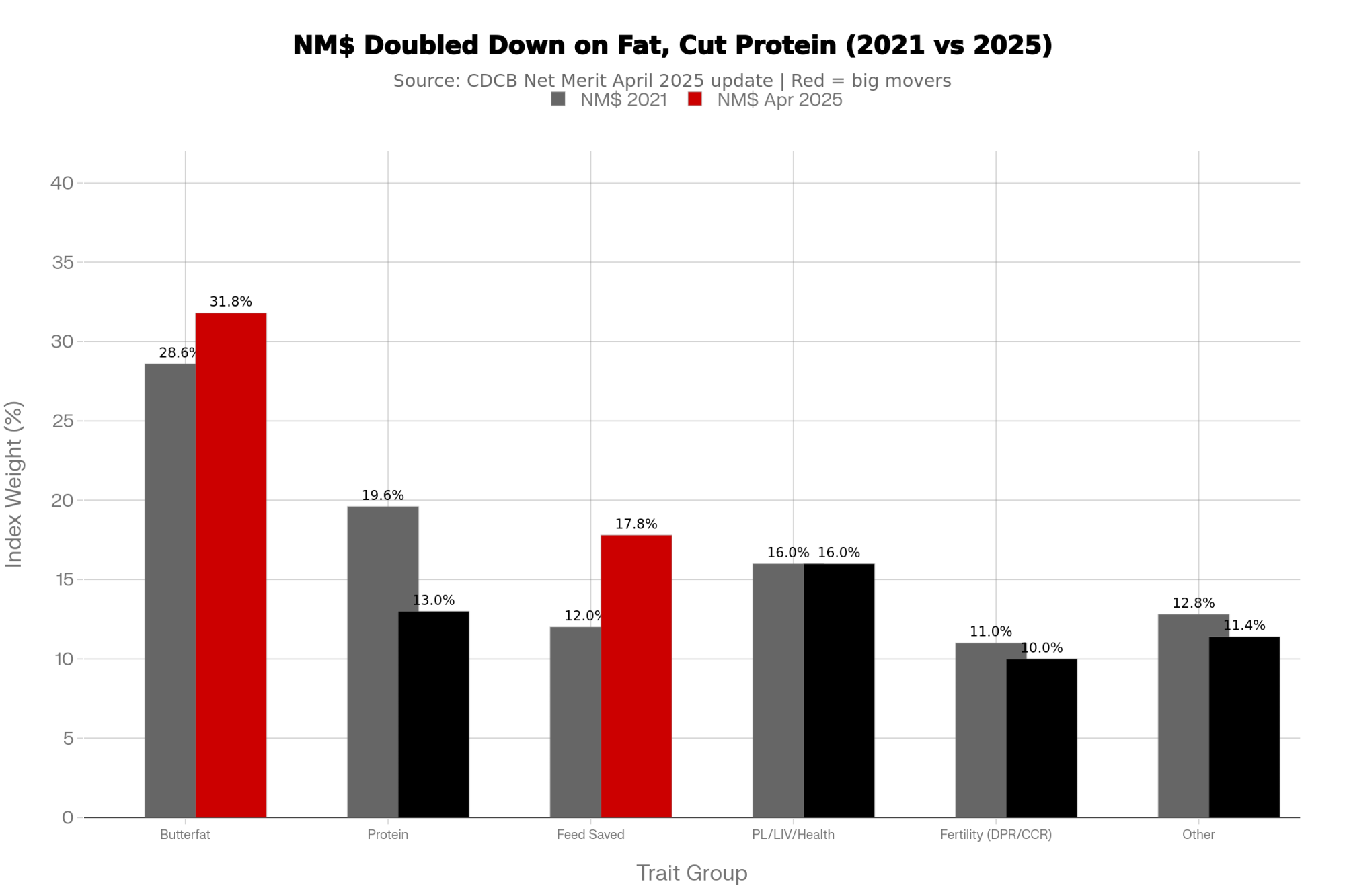

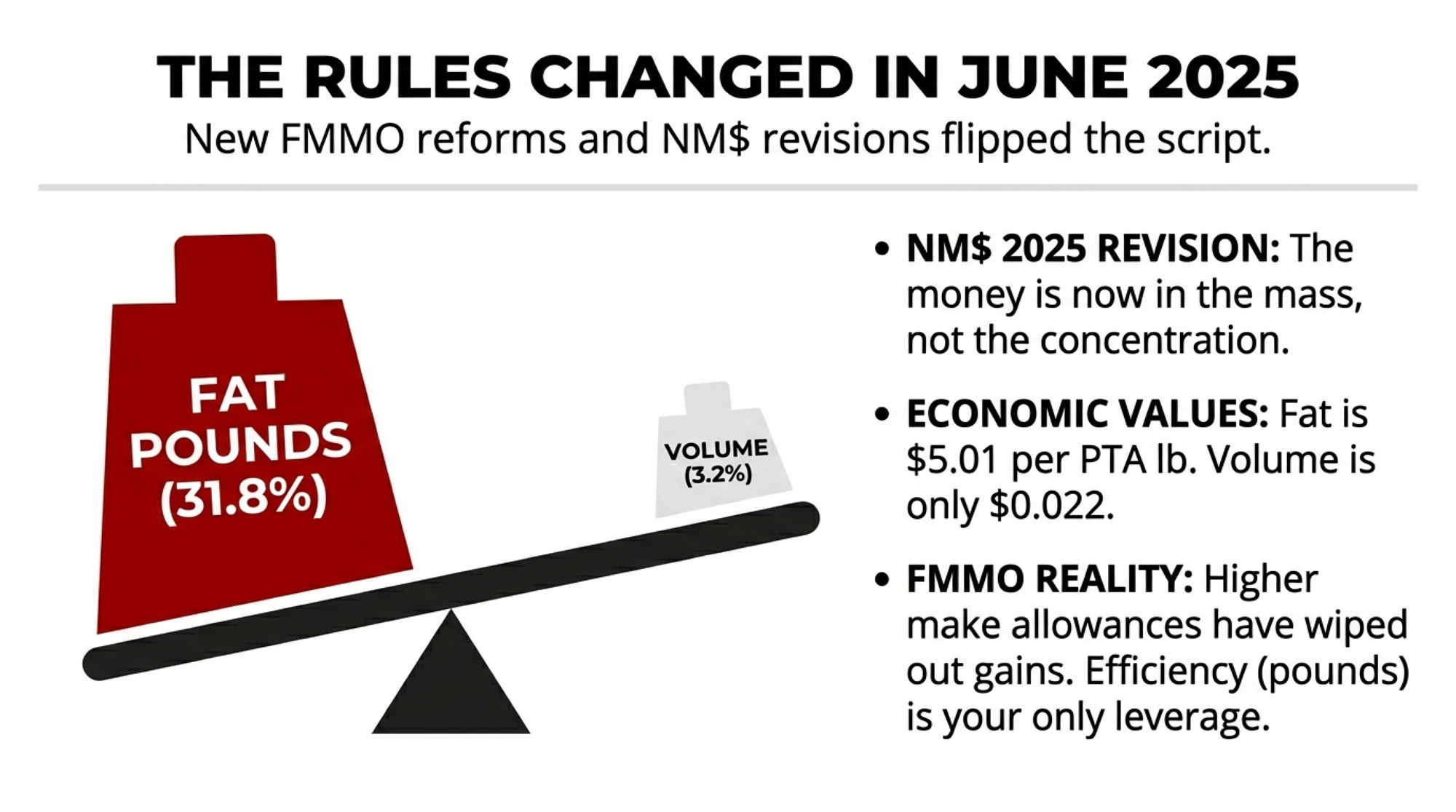

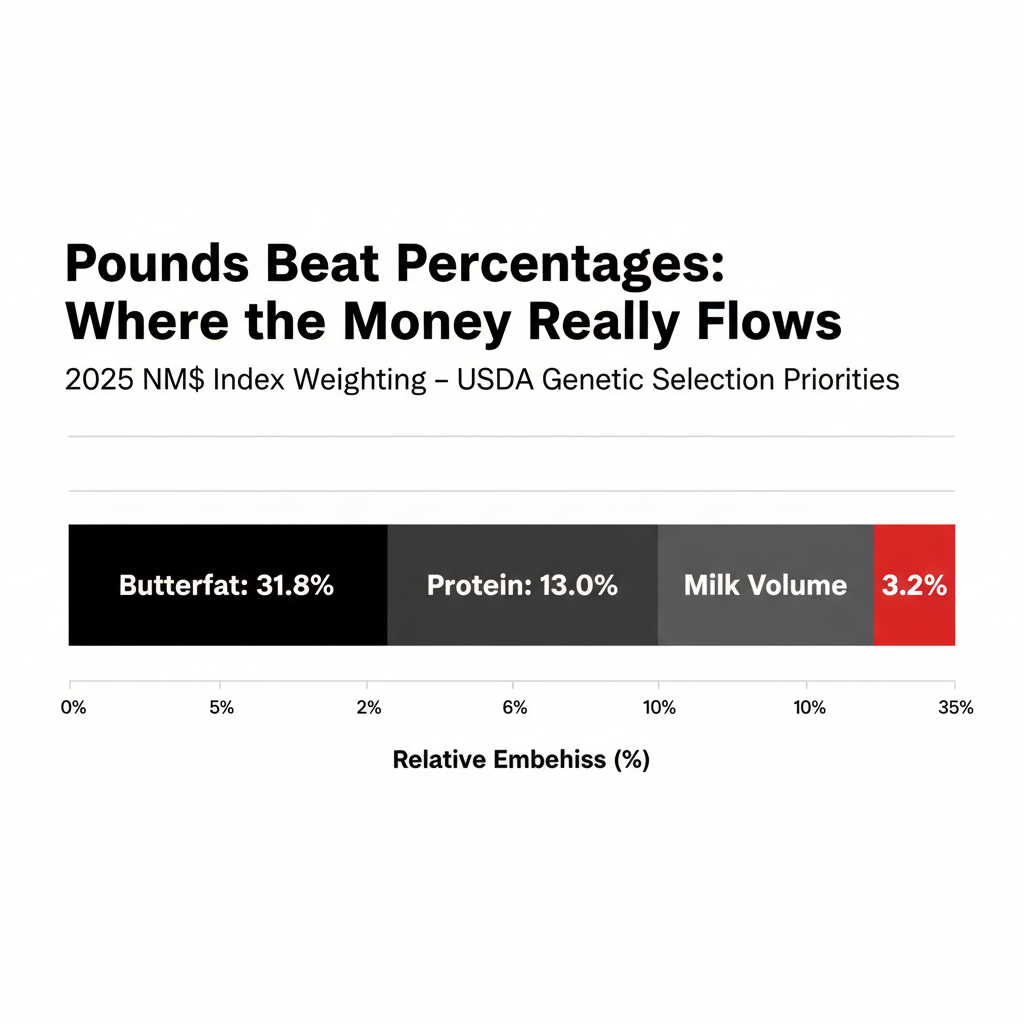

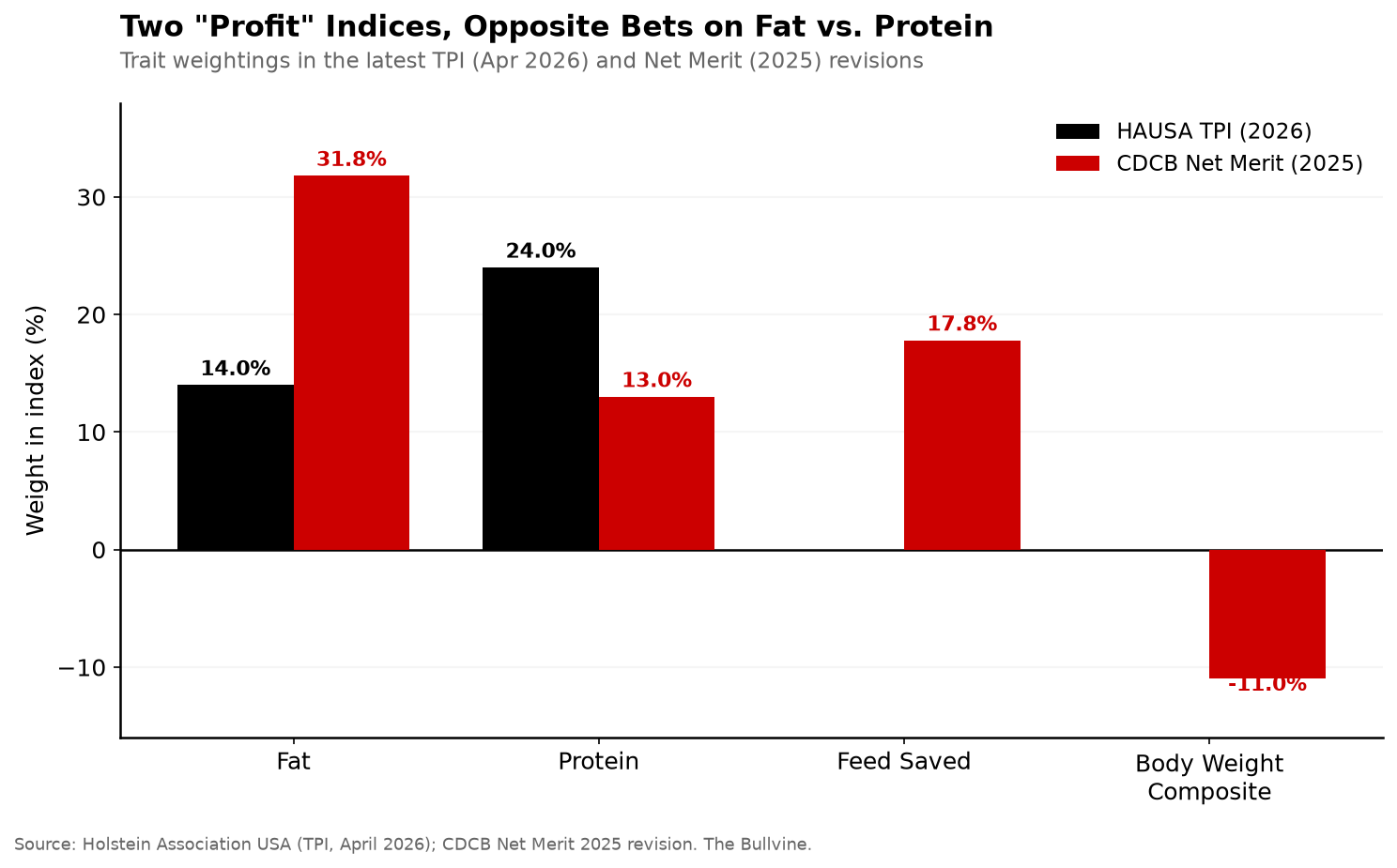

All three are answering different questions, and the numbers now prove it. In April 2026, Holstein Association USA changed its TPI formula to weight protein at 24% and fat at just 14%, up from a 19/19 split. CDCB’s Net Merit 2025 revision went the opposite direction — fat at 31.8%, protein down to 13.0%, with Feed Saved climbing to a combined 17.8% and Body Weight Composite at −11%. Two flagship indices, both claiming to describe a profitable cow, now point in genuinely opposite directions on fat versus protein.

Then there’s the classification change most show barns are still processing. Starting with the May 2026 run, HAUSA set 60 inches as the ideal stature and applied a sliding-scale penalty for cows taller than that — shaving points off the final classification score as height climbs past the limit, so a tall, extreme-framed cow that once scored well can now come in lower on paper for the exact trait that used to help her. The official language is about normalizing size. But underneath it is a harder admission: decades of breeding taller cows collided with feed cost, stall fit, and longevity. The breed association put a measurable penalty on the exact trait the show ring spent a generation chasing.

How This Plays Out on Real Farms

The Lovich story looks like a fairy tale until you read the fine print. They sold both champions. Katrysha went south, and Kandy Cane went to Oakfield Corners Dairy in New York as a four-year-old, well before she walked into Madison as a five-year-old and later reclassified EX-97. For a lot of small tie-stall herds, selling your best cows is how the barn stays viable — the premium on an elite animal funds the operation. And their cows tend to milk well past the age most Holsteins are culled, which flips the whole economics toward longevity rather than peak yield.

The tap that started a dynasty: Lovhill Goldwyn Katrysha is confirmed Grand Champion of the International Holstein Show at World Dairy Expo 2015. Her win put a 72-cow tie-stall herd in Balgonie, Saskatchewan on the map — the first of two World Dairy Expo Grand Champions Michael and Jessica Lovich would breed off cow families and their own eye, not a genomic list, while the rest of the breed narrowed toward it.

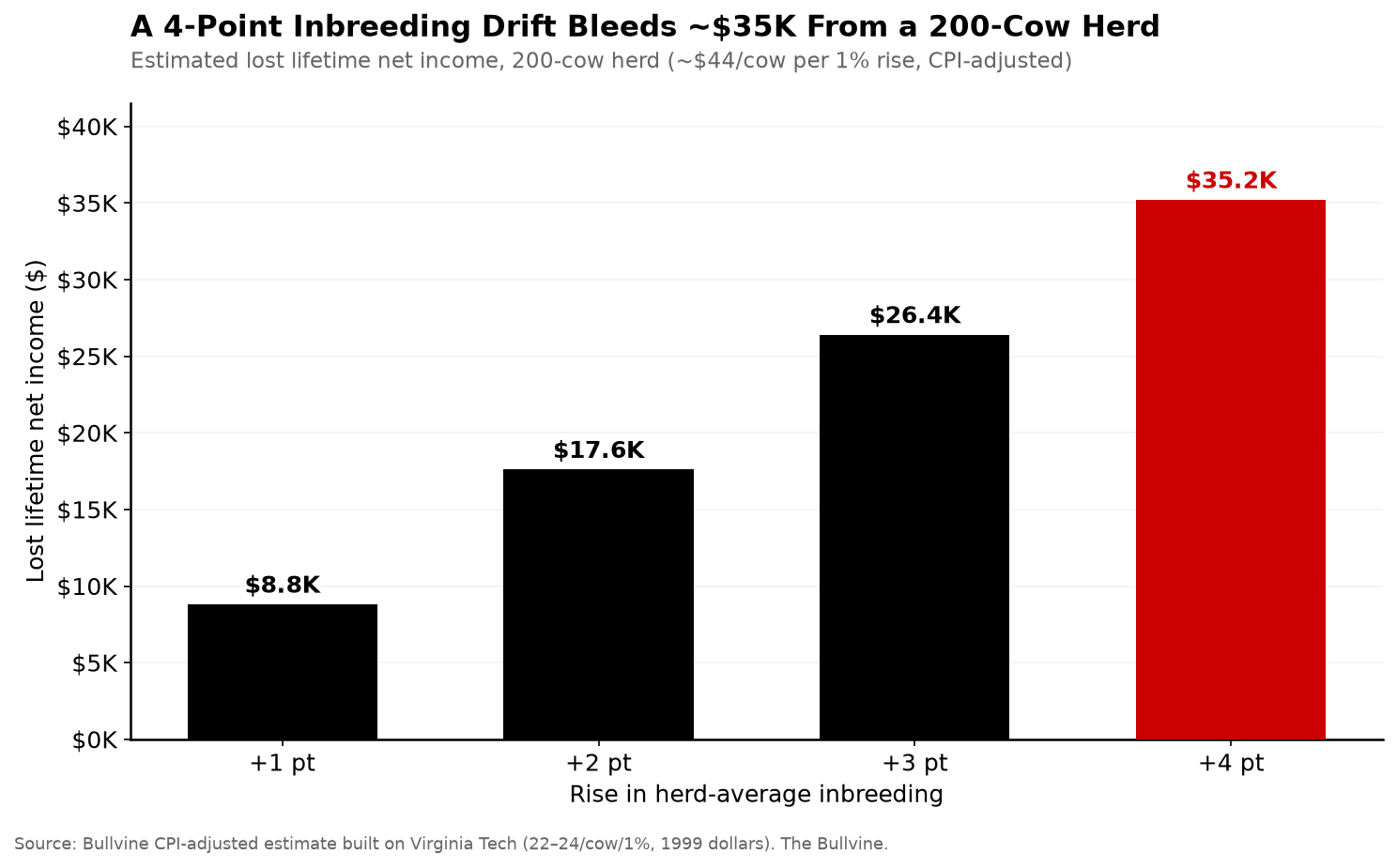

The number that reaches every barn is inbreeding, and it carries a real bill. The Virginia Tech research pegged it at $22 to $24 in lifetime net income per cow for each 1% rise in inbreeding — but that’s in 1999 dollars. Adjust it forward on cumulative inflation alone and the same drag lands near $44 per cow per 1% today (a Bullvine CPI-based estimate — layer in higher modern milk and feed values and the case for the top of that range only gets stronger). Run the math your own way. On a 200-cow herd that lets average inbreeding drift up four points, that’s roughly $35,000 in lost lifetime net income across the herd — not index points on a page, real money bleeding out of the barn. Newer Canadian work backs the mechanism: the Canadian Dairy Network found a cow that’s 10% inbred, versus 5%, loses about 92 kg of milk, 5.3 kg of fat, and 2.6 kg of protein per lactation, adds 1.4 days open, and loses roughly 65 days of productive life. It never shows up on a semen invoice. It hides in open days, mastitis cases, and calves that don’t make it.

Metric (per lactation unless noted)

5% Inbred Cow

10% Inbred Cow

Loss at 10%

Milk yield

Baseline

−92 kg

−92 kg

Fat

Baseline

−5.3 kg

−5.3 kg

Protein

Baseline

−2.6 kg

−2.6 kg

Days open

Baseline

+1.4 days

+1.4 days

Productive life

Baseline

−65 days

−65 days

That’s why this reaches every camp. The show breeder, the Net Merit devotee, and the top-50-list herd are all pulling from an increasingly related bull population, and the compounding cost lands the same way on all of them.

Think of it as three different experiments, not three answers to one question. Show-and-type selection asks whether breeding for conformation and classification produces cows that win and sell. The commercial camp runs a different test entirely: through Net Merit or LPI, does a cow throw the most profit under your actual costs? And the index-first crowd is betting on speed — trust the highest-ranked young bulls, shorten the generation interval, and try to outrun everyone else’s genetic gain.

None of those experiments settles the others, because each measures something different. A judge at World Dairy Expo isn’t scoring feed intake per day or days open. Net Merit ignores ring presence entirely. And the index itself isn’t neutral — it’s an editorial choice about what matters, built on national-average price assumptions that may not match your processor. So when TPI says protein and Net Merit says fat, a breeder who “just uses the index” without checking which one fits their cheque is quietly optimizing for someone else’s barn.

The inbreeding problem sits underneath all three. The top of any genomic list — GTPI or Net Merit — isn’t a random draw. It’s a tight cluster of high-relationship sires that trace back through a handful of grandsires, and the concentration is stark: research finds the vast majority of today’s Holstein AI bulls funnel back to just two ancestral sires, with a single foundation bull, Pawnee Farm Arlinda Chief, still echoing through the population decades later. Ride the list harder, and you stack that relationship faster. CDCB has confirmed its genetic base changes now include Expected Future Inbreeding (EFI) adjustments to account for future inbreeding, not just observed genetic trends — which is why individual PTAs no longer track the base change as cleanly as they once did. When the statisticians pre-discount the future, that tells you something.

How Much Does Sticking With the Wrong Index Actually Cost?

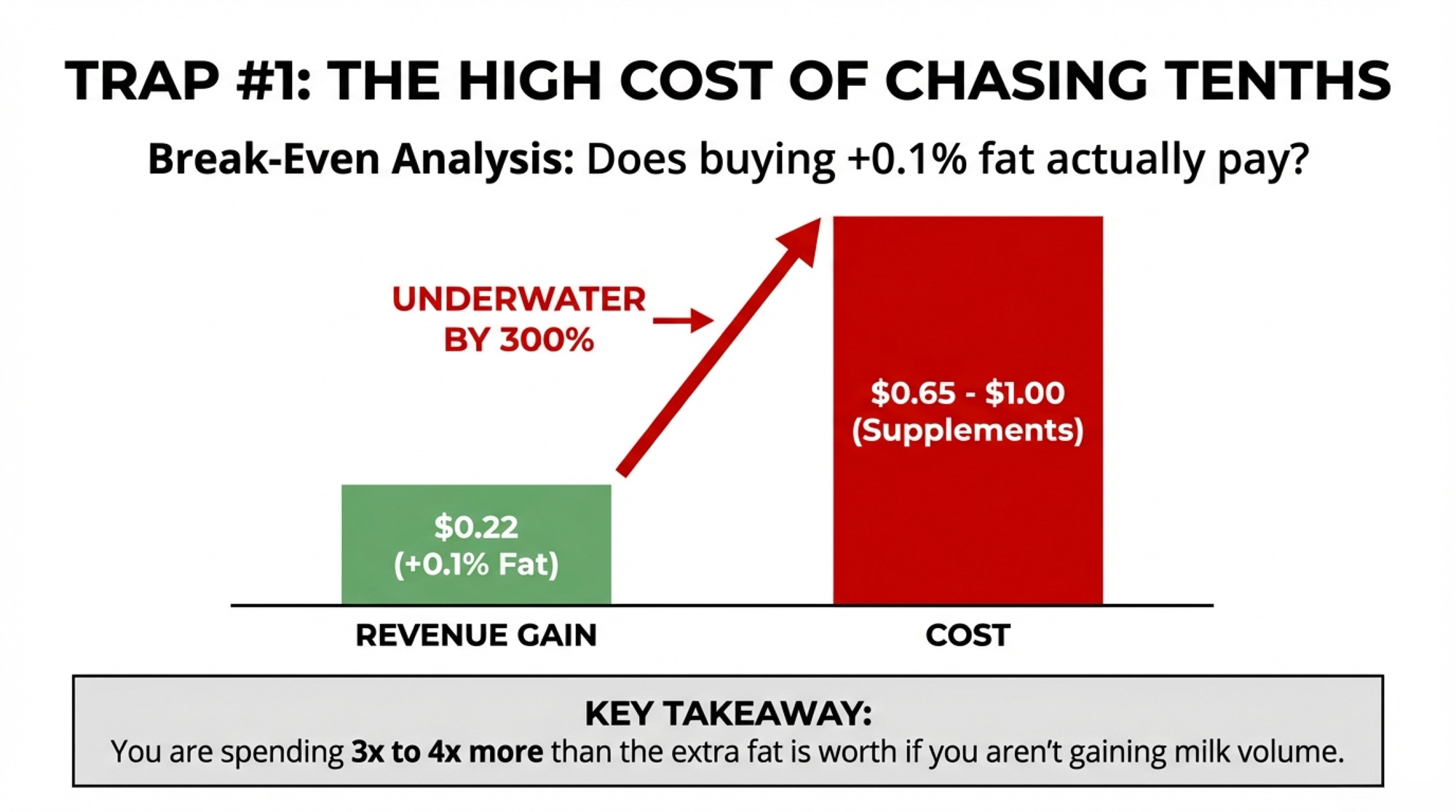

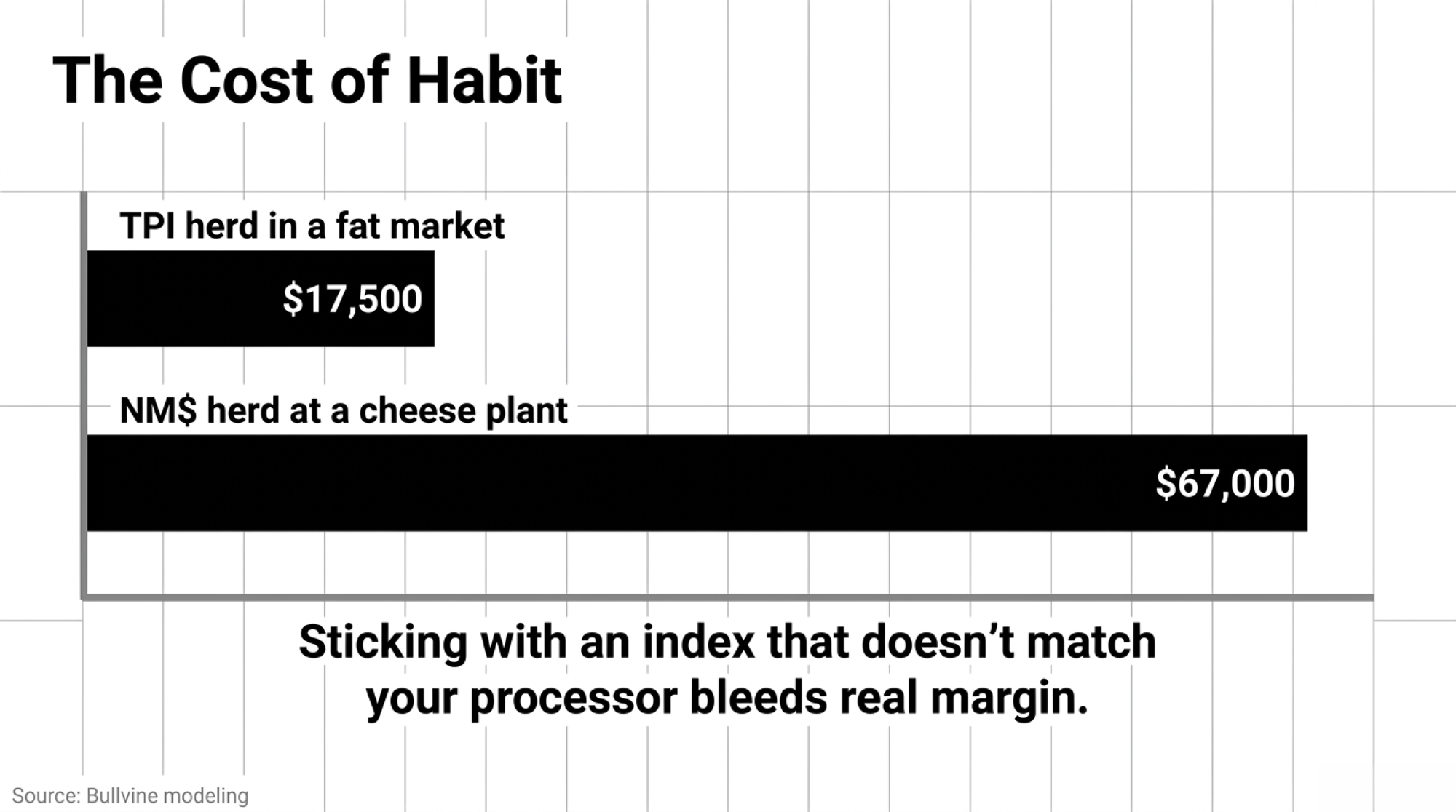

More than most herds realize, and the loss is invisible because it’s “index-approved.” A herd that keeps breeding off TPI out of habit, while getting paid on butterfat, can drift toward higher protein ratios its cheque doesn’t reward at current component prices. Bullvine’s own modeling of the 2026 TPI shift put the exposure as high as $17,500 for a mid-size herd chasing the protein signal in a fat-heavy market — a figure that depends on your herd size and your component spread, so treat it as a scenario, not a guarantee.

The mirror image is just as real. A cheese-plant herd still breeding off Net Merit’s fat signal can leave protein premiums on the table — a gap Bullvine modeled at roughly $134 per cow per lactation, or about $67,000 across 500 cows. Either way, nobody traces it back to the semen order. They blame feed, labor, the processor — everything except the objective function they never chose on purpose.

Barn Situation

Index Being Used

Where It Leaks

Modeled Cost Exposure

Fat-heavy market, chasing protein

HAUSA TPI (2026)

Higher protein ratios the cheque doesn’t reward

~$17,500 (mid-size herd)

Cheese plant, breeding for fat

CDCB Net Merit (2025)

Protein premiums left on the table

~$134/cow/lactation

Same, scaled to the barn

CDCB Net Merit (2025)

Compounded across the herd

~$67,000 (500 cows)

Any herd, wrong index by habit

Either

Blamed on feed, labor, processor — never the semen order

Maybe — and the tie-stall clock makes it more urgent for some. Canada’s updated code of practice requires that continuously tethered cows get untethered freedom of movement, with the key provisions phasing in by 2027.

Connect the dots and the three storylines turn out to be one. HAUSA’s 60-inch stature penalty isn’t an aesthetic call — it’s a structural necessity, because modern Holsteins have been outgrowing the physical dimensions of the tie-stalls and freestalls North American barns were built around. That’s the same logic driving Net Merit’s −11% Body Weight Composite: a bigger cow costs more to feed and fits the barn worse. The logic points one way — a shorter, more genetically diverse cow should fit a retrofitted stall better and carries less of the fertility and health drag that inbreeding stacks on, which is exactly what you want walking into the 2027 deadline. Head in tall and closely related, and you’re solving two problems at once, with only one of them showing up on your classification report.

Options and Trade-Offs for Farmers

Path 1: Pick your index deliberately, then match it to your pay stub. This is the 30-day move. Pull last year’s milk cheques and figure out your actual dollar-per-pound split on fat versus protein. If you’re component-heavy on butterfat, Net Merit’s 31.8% fat weighting likely fits better than TPI’s protein-heavy 2026 formula. It takes an afternoon with your statements and your rep. Skip it, and you leak margin for years while your cows look better on paper.

Path 2: Build an explicit inbreeding ceiling into your mating program. This one’s for any herd riding the top of the GTPI or Net Merit lists year after year. It means telling your mating software — or your rep — a hard limit and holding to it, even when a high-index bull is closely related to your cows. Lactanet notes the average inbreeding level today is roughly 9% and advises aiming matings below that average; its own tools flag %INB so you can screen out mates that push a calf too high. You may give up a few index points per mating. The payoff is not stacking that $22-to-$24-per-cow-per-percent bill — closer to $44 in today’s dollars — that you won’t feel for three years.

Path 3: Borrow across camps instead of picking a tribe. Take the show world’s eye for udders and legs, the commercial index’s discipline on feed efficiency and longevity, and genomic testing’s speed on sorting replacements. Works for most mid-size herds. The trap is doing it by accident — a little TPI, a little Net Merit, a little show type — and ending up with a bull battery optimized for nothing. Lovhill reached the top of the show ring twice by holding one clear standard, not by hedging across three — and that discipline is the part worth copying, whichever camp you land in.

Key Takeaways

If you don’t know your actual dollar-per-pound split on fat versus protein from last year’s cheques, run that number before your next semen order — it decides whether Net Merit or TPI fits your barn.

If your herd’s average inbreeding is at or above the 9% breed average, pull your number from your genetic-management software this month and ask your rep to project it forward before your next mating run.

If your cows skew tall, factor in that the May 2026 stature penalty and Net Merit’s −11% Body Weight Composite now both work against extreme size.

If you show and sell as part of your business model, be honest about whether your plan includes selling your best cows the way the Lovich family did — that’s what made their math work.

If your index “feels safe” because it’s familiar, remember the TPI and Net Merit formulas both changed in the last 18 months — familiarity isn’t the same as fit.

If you’re shipping to a cheese plant with a protein-to-fat ratio below 0.80, run the per-cow math on your own component prices — that’s the danger band where the wrong index quietly costs the most.

Here’s the uncomfortable question worth sitting with. The show breeder confuses a ring result with an economic verdict. The index-first herd confuses trusting the formula with running a strategy. Both outsourced their judgment — one to a judge, one to a formula — and neither stopped to ask whether the thing they trusted still fits the cows they actually need. So which one are you? And when did you last check whether the tool you rely on is optimizing for your barn, or for the average barn someone modeled years ago?

The short version: genetics is an economics question, and the only real mistake is not knowing which experiment you’re running. The longer version — the full cost-per-cow inbreeding math, broken down by herd size and index choice — is where the decisions actually get made. We’re running those numbers in next week’s Bullvine Weekly. If you want to map this to your own operation, that’s where the real math lives.

Hold-to-Proof Cost & Inbreeding Drag Simulator

Map the 2026 TPI/Net Merit formula updates and genetic drag directly to your herd’s bottom line.

200

9.5%

8.0%

Annual Inbreeding Penalty

$0

Annual Index Revenue Leak

$0

Total Invisible Annual Margin Leak

$0

Calculated using updated 2026 genetic values and modern inflationary baselines.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

Dairy Cattle Genetics Explained: TPI, NM$, GTPI and Genomics — Arms you with an immediate operational blueprint to navigate the 2026 formula divergence, showing exactly when to deploy TPI’s high-protein selection versus Net Merit’s aggressive butterfat and feed-efficiency weighting.

Net Merit 2025 — Exposes why national genetic indexes lag behind current marketplace realities, tracking the multi-year commodity averages that create a hidden financial mismatch between your tank’s actual value and your long-term breeding goal.

The Proof You Waited Three Years For Averaged a $72 Markdown — Delivers a brutal, data-driven reality check on daughter-proven strategies, demonstrating how holding famous bulls to proof stacks an expensive maintenance bill while sacrificing an entire generation of genetic velocity.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

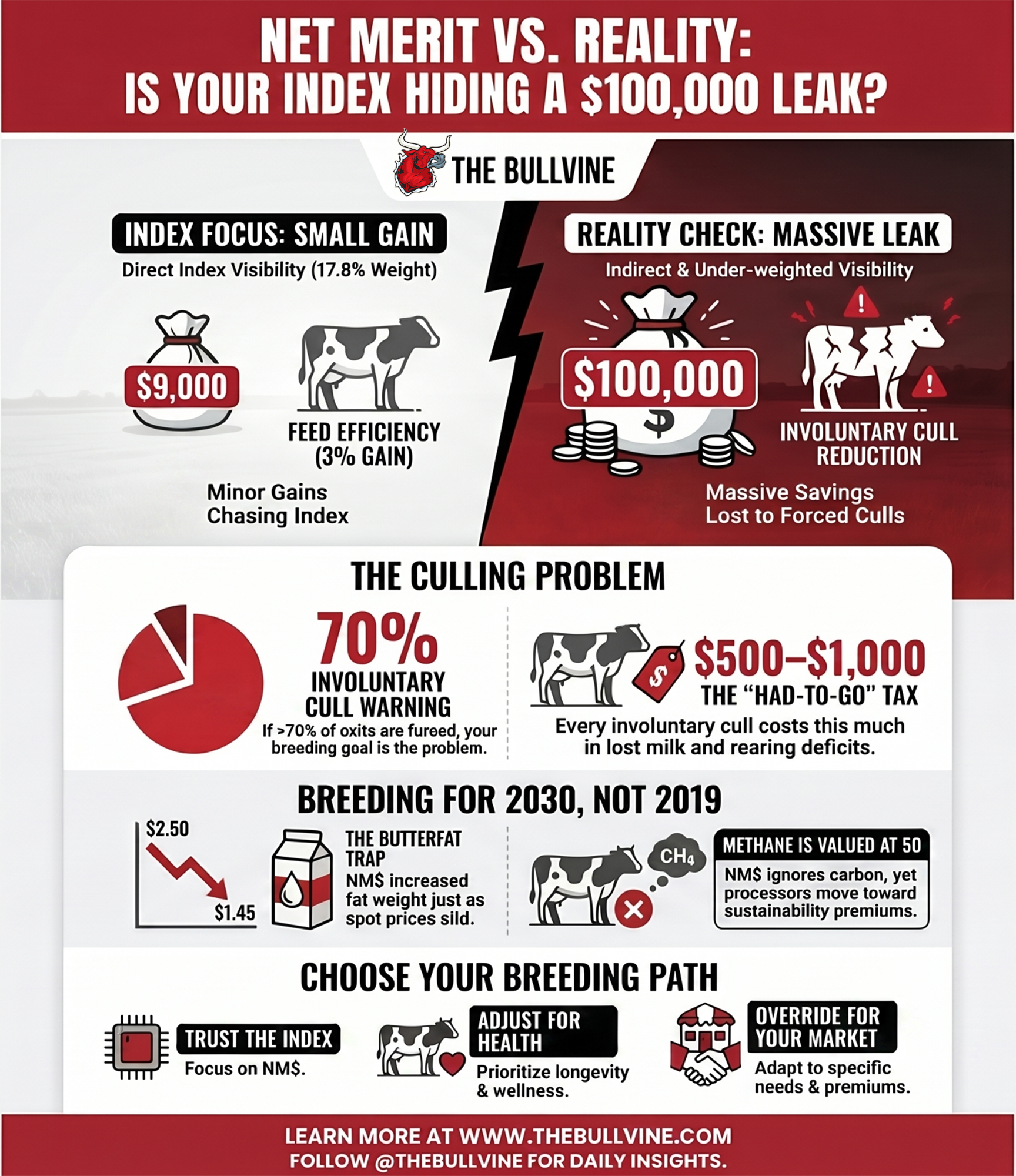

One barn chases $9,000 a year in feed efficiency the index rewards — and loses up to $100,000 out the cull gate it barely scores. Net Merit sees one number. Guess which.

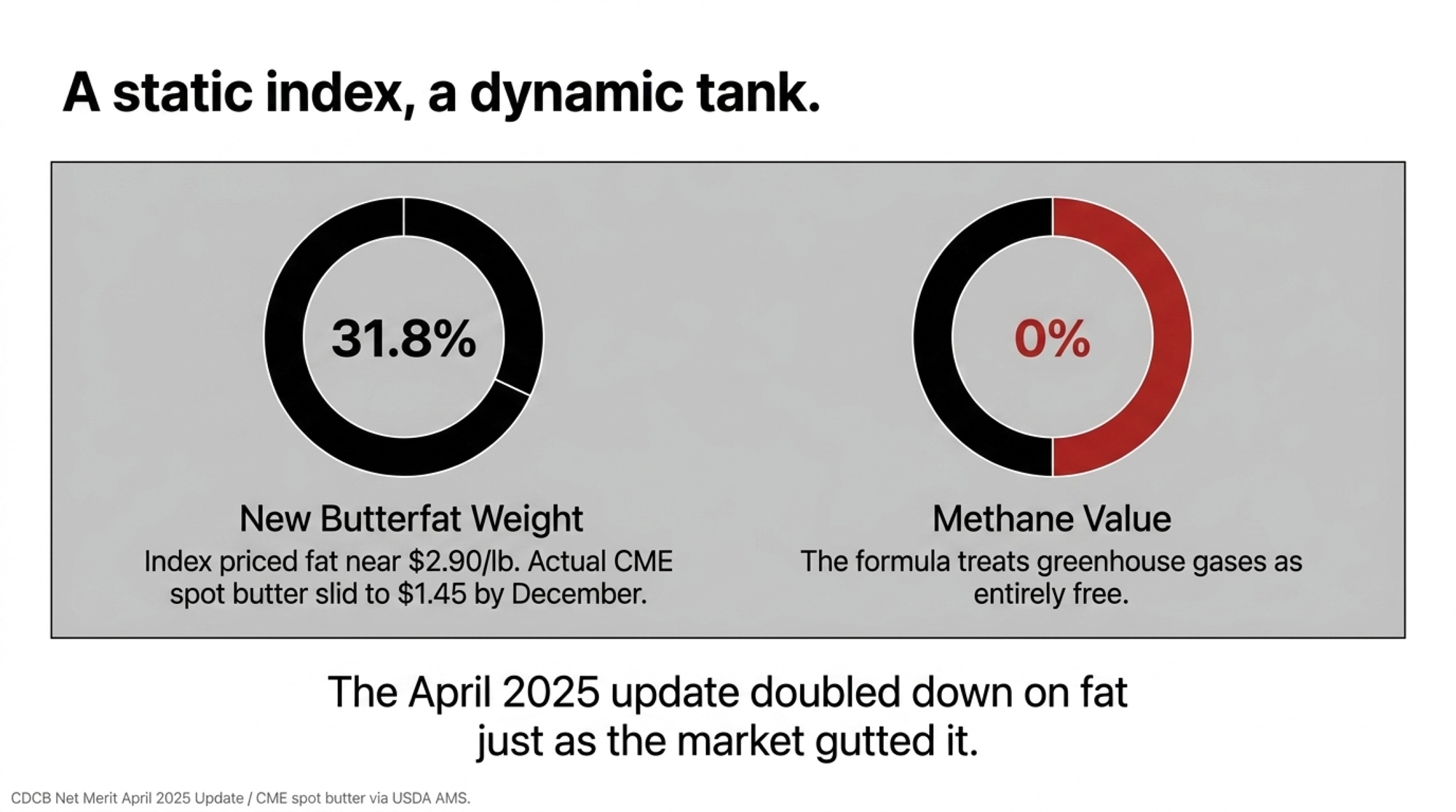

Executive Summary: When CDCB updated Net Merit in April 2025, it effectively priced butterfat near $2.90/lb and methane at $0, pushed the fat weight to 31.8% while cutting protein to 13.0%, and bumped Feed Saved to 17.8% — but the formula re-ranked almost nothing, correlating 0.992 with the old weights for young Holstein bulls. That stability is the trap: it leans on a high-butterfat window that the market already gutted, with CME spot butter sliding from about $2.50/lb in early 2025 to roughly $1.45 by December. For a 1,200-cow, high-output Holstein herd, the bigger blind spot isn’t components — it’s culling. Chasing a genuine 3% feed-efficiency gain is worth maybe $9,000 a year, while 70–100 fewer forced culls is worth $35,000–$100,000 using de Vries-style $500–$1,000/cow modeling, and NM$ only touches that leak indirectly through PL, LIV, DPR, and SCS. Meanwhile, methane sits at $0 even as DFA, Saputo, and FrieslandCampina (already paying €2.63/100kg in sustainability premiums) move toward carbon-graded milk, and the heifers you breed today on a $0 methane value won’t hit the string until 2028–2029. The piece lays out three honest roads — trust the index, adjust it around your own cull and fertility data, or override it with Cheese Merit, EBI, or custom weights — plus a 30-day move: pull your last 12 months of culls, and if more than 70% are involuntary, your breeding goal, not just your transition pen, is the problem.

Editor’s Note: The 1,200-cow western New York Holstein operation in this story is a composite scenario modeled on multiple high-output herds that The Bullvine has reviewed since the April 2025 Net Merit update. The barn math, cull patterns, and adviser conversations are illustrative — drawn from realistic ranges in herd records and published research, not a single farm. All program names, trait weights, researcher names, and economic figures are real and sourced.

Picture the kitchen-table breeding meeting at a 1,200-cow Holstein operation in western New York, late March. Two open laptops. A pot of coffee gone cold an hour ago. A stack of breeding sheets that keeps growing as the herdsman pulls more sire proofs off the printer. This farm is a composite — but the numbers on those sheets are real. For more than a decade, the rule here has been simple: sort by Net Merit, take the top 10 bulls, don’t overthink it.

The vet truck is now a regular fixture at the fresh pen. The hoof trimmer spends most of his day in the high groups. And the cull report shows a rate in the high-30s to low-40s, with most exits starting as a health or fertility problem in the first 60 days.

Sooner or later, somebody at the table asks the question that matters on any operation like this: what is this index actually breeding the herd for in 2030, and does that still match the cows they can keep, and the milk their buyer will want to pay for?

The April 2025 Shift: High-Fat Illusion vs. Genetic Reality

Nobody at this table thinks Net Merit is ‘bad.’ NM$ remains one of the best tools for ranking bulls on expected lifetime profit under typical U.S. conditions. The problem is the gap between the conditions Net Merit assumes and the conditions a herd like this is actually facing now — and will face when today’s calves are in their third lactation.

When the Council on Dairy Cattle Breeding rolled out the updated Net Merit weights in April 2025, the headline changes were clear:

The butterfat weight rose from 28.6% to 31.8%.

The protein weight dropped from 19.6% to 13.0%.

Feed Saved jumped from 12.0% to 17.8%.

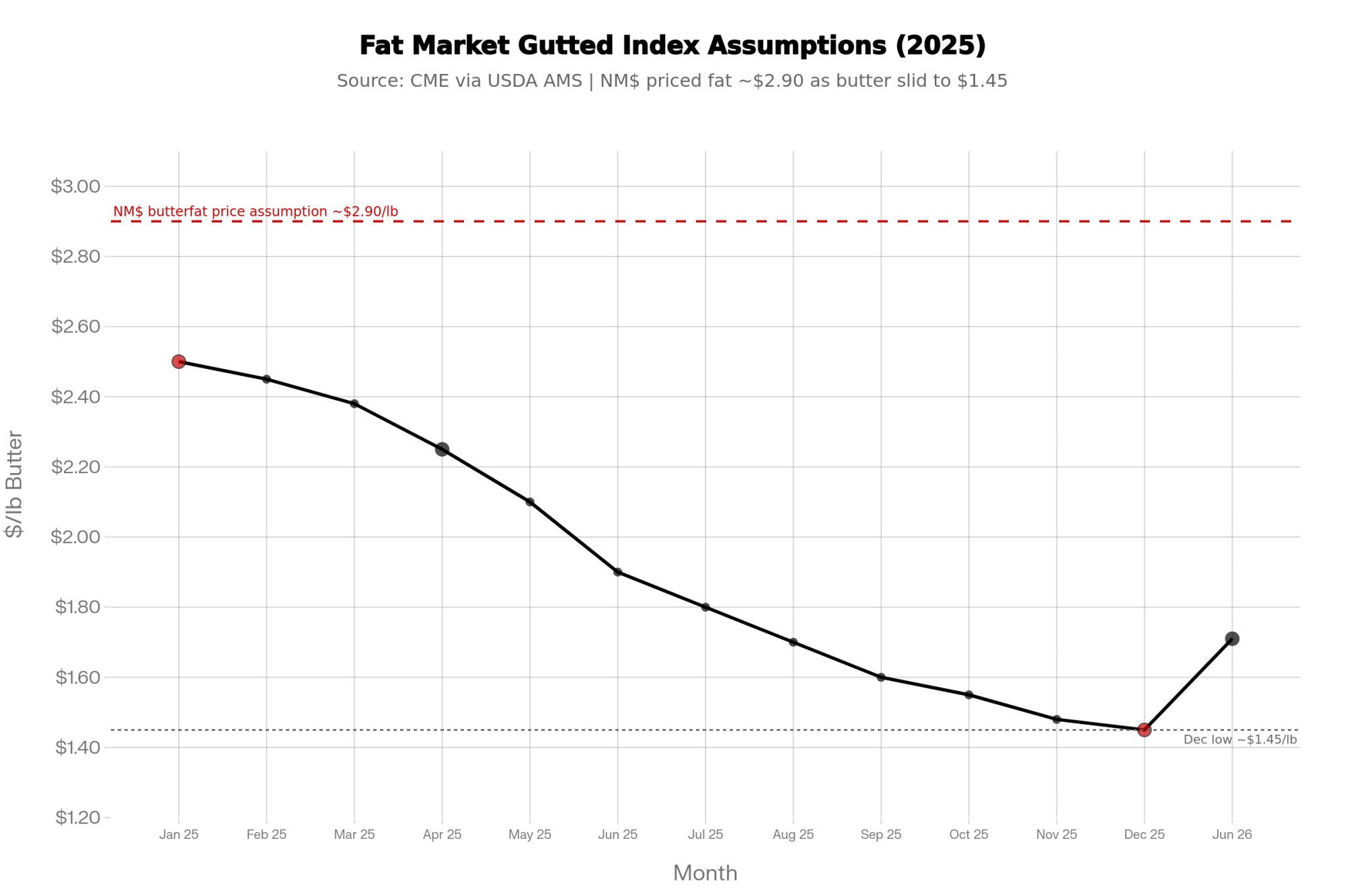

Here’s what that fat-heavy tilt means for your actual milk check. The index is telling your breeding program to chase butterfat hard and ease off protein — but it’s pricing those components off lagging multi-year averages, not what your tank is worth this week. Component values swing, Class prices jump, and a fat-to-protein ratio that looked right when CDCB built the formula can flip before the semen you ordered off it ever produces a milking daughter. A static index will always lag a dynamic tank. So the question isn’t just ‘is butterfat valuable?’ — it’s ‘will it still be priced this way when these matings hit the bulk tank in 2028?’

That’s not a hypothetical. CME spot butter traded near $2.50 per pound at the start of 2025 — right in the window CDCB used to reset those weights — then slid to roughly $1.45 by December and hovered near $1.71 by June 2026 (CME via USDA AMS and trade reporting). The index doubled down on fat just as the market spent a year taking the air out of it. That’s the lag in one commodity within a single year.

Translated into pricing, the update effectively values butterfat at about $2.90 per pound and feed at roughly $0.13 per pound of dry matter, while assigning methane a value of exactly $0 in the index math. CDCB and USDA-ARS used recent rolling averages of milk prices and feed margins — drawn from the years leading into the launch — to reset those economics. Butterfat had been the star during that window, trading near the high-$2-per-pound range in many orders, while protein prices sagged. Feed costs spiked, so Feed Saved was worth more.

Methane, heat tolerance, and welfare penalties weren’t in the equation at all. The official Net Merit documentation is explicit: only traits with a direct, currently measurable impact on farm profit are priced into the index, and greenhouse-gas traits are not yet included. CDCB has stated that traits are added to NM$ only when reliable national evaluations and clear economic values exist, and that greenhouse-gas evaluations are ongoing.

One number from CDCB’s own rollout really lands: the 2021 and April 2025 NM$ indexes correlate at 0.992 for young Holstein bulls and 0.981 for recent progeny-tested bulls. In plain language, almost nothing re-ranked. The same bulls a herd would have picked three years ago still float to the top of the list today — even though the butterfat, protein, and feed markets that drove the new formula look different from when most “top 10 NM$ only” rules began.

A growing number of U.S. processors are publicly discussing scope 3 emissions and sustainability reporting, and several have signaled that future producer payments may be linked to greenhouse gas performance. Nothing on the milk cheque yet. But the direction of travel is obvious.

The Bullvine walked through how the updated formula was built in its coverage ofthe CDCB Net Merit update.

When the Fresh Pen Says “Enough”

The cull report from a herd like this looks a lot like what you see in many high-output Holstein freestall operations. Overall, culling has crept into the high-30s. Sort culls into two piles — voluntary (older, low-producing cows with planned exits) and involuntary (health, fertility, injury, chronic problems) — and most exits are “had to” cows, not “chose to” cows.

There’s no single “official” cost of an involuntary cull, but economic modeling summarized by Albert de Vries and others puts the loss in the $500–$1,000 per cow range when you fold in lost future milk, replacement rearing cost, and health costs. And here’s why the timing hurts so much. Lose a second-lactation cow at 45 days in milk, and you’re not losing an average cow — you’re losing her at the exact moment she’s climbing toward peak yield, the most productive stretch of her life. She never gets the chance to milk back the rearing deficit she ran up as a heifer. You ate two years of feed, labor, and opportunity cost raising her; she’s three weeks from paying it back, and she leaves on the cull trailer instead. Do that 70 to 100 times a year, and the leak isn’t a rounding error — it’s much of the problem.

Cull Pattern

Involuntary Share

Estimated Annual Leak

Likely Genetic Signal

Recommended Action

Mostly older, low-producing cows

<30% involuntary

Minimal ($5k–$15k)

Program working; monitor components trend

Stay Path 1; re-check butterfat vs. protein pricing quarterly

Mix of health + low production

40–60% involuntary

Moderate ($20k–$45k)

Fertility and health traits under-weighted

Move to Path 2; add DPR/CCR and SCS floors

Dominated by fresh-cow disease, lameness, infertility

>70% involuntary

High ($50k–$100k+)

Breeding goal misaligned with system pressure

Path 2 or 3 immediately; audit sire stack for PL, LIV, hoof health

High culls concentrated in first 60 DIM

>65% involuntary

High + rearing cost unrecovered

Transition risk baked in genetically

Full genetic audit; consider Nordic/EBI sires for robustness

For 1,200 cows with a cull rate near 40%, even modest improvements in involuntary culling add up fast — and they add up to a number that dwarfs anything achievable by chasing feed efficiency alone.

A genuine 3% improvement in feed use (genetics + management together) on 30,000 cwt shipped, at a Northeast purchased-feed cost around ~$10/cwt, consistent with recent Cornell PRO-DAIRY / Northeast Dairy Farm Summary benchmarks

Per-unit economics

$500–$1,000 per involuntary cull saved (de Vries-style modeling)

3% of ~$300,000 annual feed cost

Annual impact

$35,000–$100,000/yr

~$9,000/yr (more if your landed feed cost runs higher)

Source of the gain

Cows staying in the herd long enough to pay off rearing cost

Smaller cow size + intake efficiency in the Feed Saved PTA

Visible in the index?

Indirectly via PL, LIV, DPR, SCS — all under-weighted relative to this leak

Directly via Feed Saved (17.8% weight)

🔴 The P&L Blind Spot

High-output herds are chasing roughly $9,000 a year in marginal feed-efficiency gains the index explicitly rewards — while quietly leaking up to $100,000 a year through transition wrecks and forced culls the index barely sees. One number sits on the spreadsheet your breeding program optimizes for. The other walks out on the cull trailer.

So why is a breeding goal still leaning as hard on production and Feed Saved as the national average?

“We Bred Exactly What We Asked For”

A decade of sire choices on a farm like this tells an ordinary story. The team chased high NM$ and TPI, especially big milk and components. Less weight on body condition and “middle,” more on tall and angular. They eventually bolted on Productive Life and SCS filters once the cost of mastitis and early exits became impossible to ignore.

The cows walking the freestall alleys in 2025 are the predictable result. Powerful milkers, especially in first and second lactation. But many fresh cows dive into a deep negative energy balance — the window Cornell and PRO-DAIRY transition research has long flagged as the highest-risk stretch for high-output Holsteins — that drops them right on the edge between “profitable” and “problem.”

In our reporting on transition cow disease across high-output Holstein herds, one pattern keeps surfacing: genetics now produce cows that can out-milk the ability of an operation to keep them healthy through the first 60 days. Good transition management still helps. But genetics quietly loads the dice against you before the calf is even born.

Cornell’s NYSCHAP transition-cow benchmarks draw the alarm lines in hard numbers: displaced abomasum at or above 6% (target under 3%), milk fever at or above 5% (target under 2%), retained placenta at or above 10% (target under 8%). Herds that have selected hard on production for years tend to flirt with those lines unless genetics and transition management are pulling in the same direction.

Lay health and culling patterns next to a genetic trend, and what shows up isn’t a “transition program” problem. It’s a breeding-goal problem that’s been compounding across multiple sire generations.

If you want the mechanics, The Bullvine breaks down how feed efficiency is actually measured in its primer onresidual feed intake.

Net Merit: Where It Still Helps and Where It’s Blind

This isn’t “abandon NM$.” It’s knowing what Net Merit is genuinely good at for a herd like this — and where it’s blind.

Where NM$ still shines:

Ranks bulls for lifetime profit under average U.S. confinement herd economics, assuming FMMO-style component pricing and no carbon price.

Keeps obviously risky sires — very poor somatic cell, extremely low fertility, weak livability — out of the tank.

Provides a consistent national yardstick to compare bulls, cow families, and herds.

Where NM$ goes blind for this kind of herd:

Feed efficiency. The Feed Saved trait combines actual feed intake data, where available, with the body weight composite. A big slice of that PTA still comes from smaller cows, not necessarily cows that convert feed more efficiently at the same size. For a herd already pushing milk per stall hard, smaller isn’t automatically better if it means less “middle” to handle higher output.

Environment. Methane and other environmental externalities are valued at $0 in the NM$ formula. Any future carbon premium or deduction from a processor is invisible to the index, which leaves any herd thinking about methane efficiency or low-carbon dairy genetics working off-index.

How it plays in robots. Udder and teat composites that work fine in a parlor can be a headache in AMS barns. Robot herds have learned the hard way that rear teats too close together are one of the quickest ways to make a robot hate your cow. National udder composites weren’t originally built around AMS needs.

Responsiveness. The April 2025 update didn’t add any new traits and barely moved bull rankings overall, despite real changes in butterfat prices and feed costs. That’s a deliberate trade-off CDCB makes to keep the national index stable: changes that re-rank too many bulls or invalidate years of breeding decisions are, by design, hard to push through quickly.

For a herd with a full fresh pen, a high share of involuntary culls, and a processor warming up for sustainability scoring, NM$ is still useful — but more as a minimum standard than the steering wheel.

Trust the Index, Adjust It, or Override It?

Here’s where the kitchen-table conversation gets honest. Three roads forward. And which one you take isn’t a personality test — it’s dictated by how far your herd has drifted from the “average U.S. parlor herd” the index assumes.

Start at Path 1. The further your reality sits from that national average, the further down the line you move. Cull report still looks normal, and your processor’s quiet on carbon? Trust works. Watching involuntary culls climb, and fresh-pen disease creep toward those NYSCHAP alarm lines? You’re already past Path 1, whether you’ve admitted it or not. Running robots, grazing, or staring down a processor sustainability contract? You’re at Path 3. Find the road that matches what you’re actually living — then decide whether it still fits the next decade.

Selection Path

Primary Sort Tool

Key Assumption

What You Give Up

Red Flag Trigger

Path 1 — Trust NM$

NM$ top 10–20 bulls

Avg U.S. confinement economics, FMMO pricing, no carbon price

Direct control over methane, AMS udder fit, index lag

Involuntary culls >70%; fresh-pen disease at NYSCHAP alarm lines

Path 2 — Adjust Around Your Data

NM$ as gatekeeper + custom minimums

Your DPR, CCR, mastitis, and hoof floors override top-end ranking

Some NM$ points at top of list

High forced-cull rate + processor starting carbon conversation

Path 3 — Override the Index

Cheese Merit / EBI / NTM / custom weights

Your system (robots, grazing, OAD) differs materially from national average

Single national ranking; smaller reference populations

You are here if: Your primary sire-selection rule is “sort by NM$, take the top 10–20 bulls, move on.”

What it assumes: Average U.S. confinement herd economics, FMMO-style component pricing, no carbon price, and a herd structure close to the national mean.

What you give up: Direct emphasis on the traits NM$ doesn’t price — methane, heat tolerance, AMS-specific udder design — plus any responsiveness to the gap between your milk cheque and the index’s pricing assumptions.

Honest tell: If your involuntary cull share is climbing and your fresh-pen disease rates are flirting with NYSCHAP alarm levels, “trust” is quietly costing you the leakage in the table above.

Path 2 — Adjust Around Your Own Data

You are here if: You use NM$ as a gatekeeper but layer your own minimums on top.

What it looks like in practice: A hard floor on Daughter Pregnancy Rate and Cow Conception Rate. More weight on mastitis resistance and hoof health, where credible proofs exist. A preference for bulls with real feed-intake data behind their Feed Saved PTAs, not just a smaller body weight composite. Acceptance that you’ll give up some top-end NM$ points to get cows that stay in the herd longer.

What you give up: Some short-term genetic merit on the top-line index number.

Honest tell: If your composite herd looks like the New York one in this story — full fresh pen, high involuntary culls, processor talking carbon — this is usually the right starting road.

Path 3 — Override the Index

You are here if your future system looks materially different from the “average U.S. parlor herd.”

What it looks like in practice: Cheese Merit or Grazing Merit as your primary sort instead of NM$. Irish or Nordic sires were brought in because EBI and NTM placed greater weight on fertility, pasture performance, and emissions. Or rough custom economic weights built off your own numbers — your feed costs, your culling pattern, your labor situation, and the language in your processor’s contract.

What you give up: The simplicity of a single national ranking, and reference populations that may be smaller for some traits.

Honest tell: Robots, grazing, OAD, processor sustainability scoring, or a strong components-only payment structure are all signs the override path is worth a serious look.

A composite herd like this New York operation usually lands between Path 2 and Path 3. Keep an NM$ threshold but stop insisting on only top-10 bulls. Weight health, fertility, livability, and moderate stature harder when picking sires. Hunt for bulls with credible feed-efficiency stories. And look at EBI-bred and Nordic sires with curiosity instead of writing them off as “pasture bulls from somewhere else.”

The agreement that emerges around the table is usually the same: cows that stay in the herd and pay off their rearing cost deserve more weight in the breeding goal than cows that leave after one or two rocky lactations.

What Does a Case of Ketosis Really Mean for Your Genetics?

Most of us talk about genetics and picture proofs before pens. The health patterns in your fresh pen are exactly where your index choices show up.

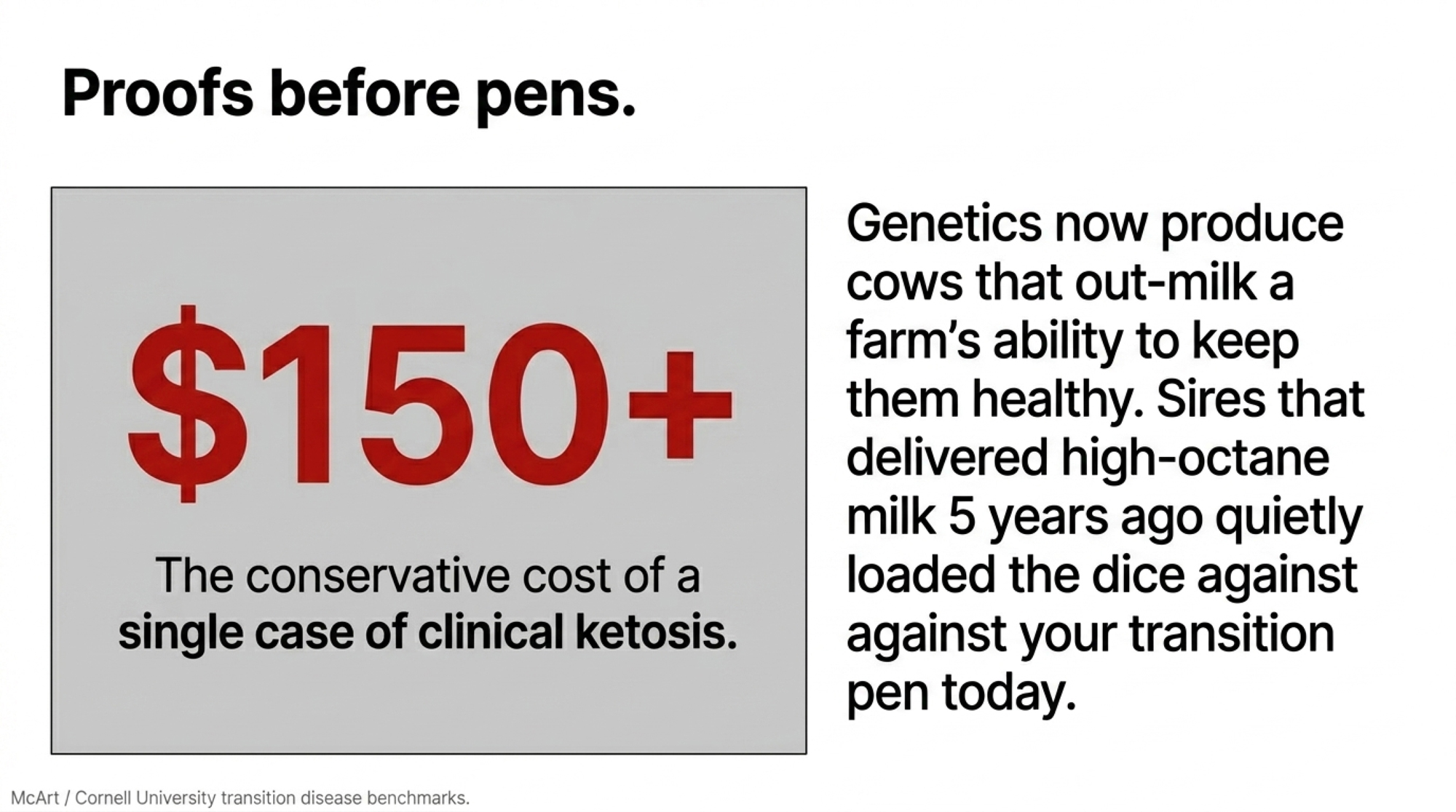

Take ketosis. Cornell research led by Jessica McArt and recent extension summaries put a single case of clinical ketosis in the low hundreds of dollars per cow — published estimates range from roughly $117 to over $230 per case once treatment, lost milk, reproduction delays, and added culling risk are factored in. The exact number depends on the system and prices, but it’s not trivial.

Run the example off this herd’s scale:

1,200 cows, with 10% hitting some form of ketosis in early lactation. That’s 120 cases.

If better genetics and management together trimmed that by 20%, that’s 24 fewer cases.

Use a conservative blended estimate of around $150 per case to stay on the low end of published ranges, and you’re looking at about $3,600 a year back in your pocket.

You’re not retiring on that number. But stack it with fewer DAs, fewer down cows, better fertility, and a few more cows making it into third and fourth lactation, and now you’re talking real money.

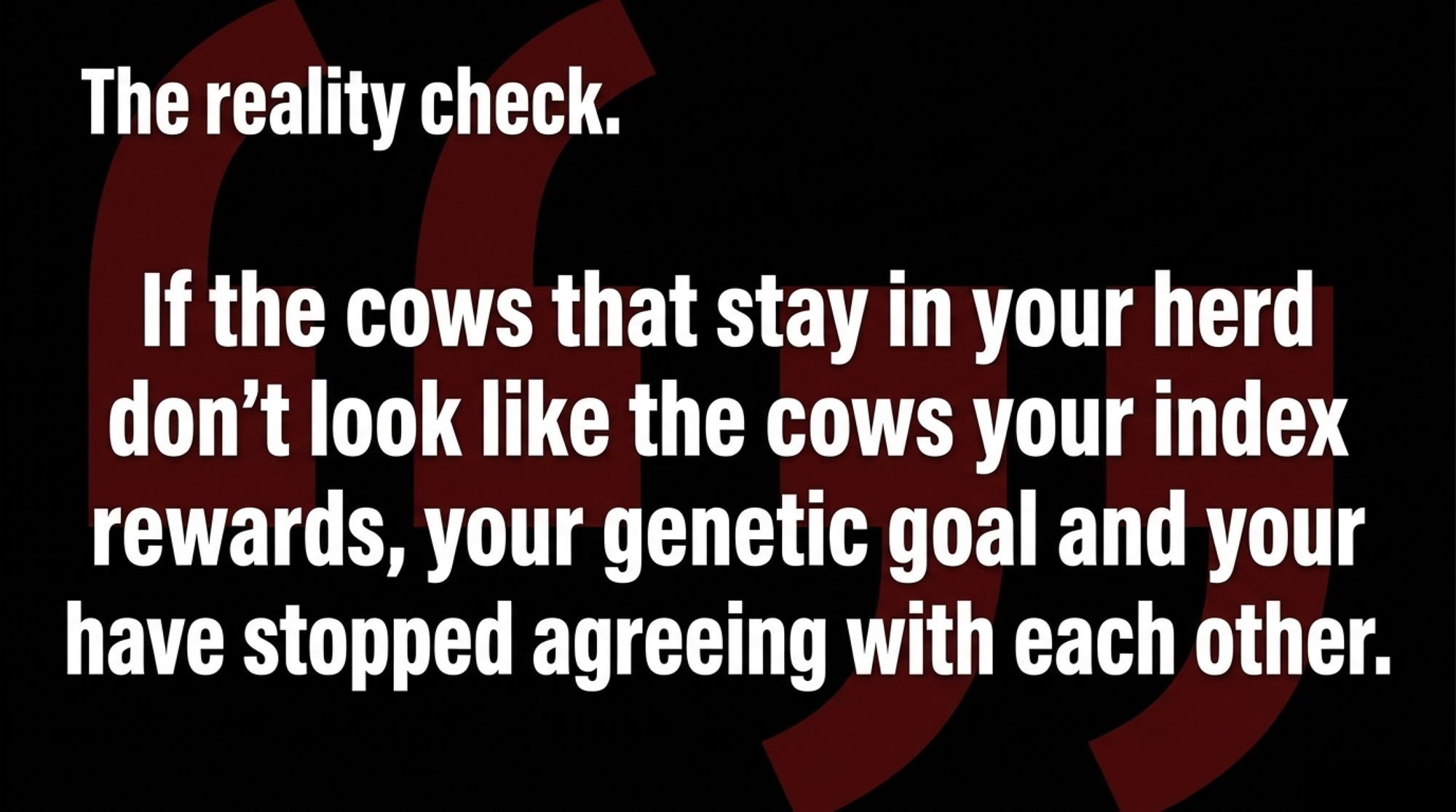

Changing trait weights doesn’t magically fix everything. But the cows getting sick now are partly the product of mating decisions made 5–10 years ago. The same proofs that gave you high-octane milk can quietly raise the odds that cows tip over in a high-pressure transition program. And if the cows that stay in your herd don’t look like the cows your index rewards, your genetic goal and your business have stopped agreeing with each other.

This isn’t a “transition program” problem that showed up in 2025. It’s a long-running genetic strategy that never got updated as the economics and farm realities shifted around it.

Is Your Index Already Behind Your Processor?

The other source of tension at the table isn’t the vet bill. It’s the milk buyer.

Several large U.S. processors — Dairy Farmers of America among them, with its publicly committed net-zero greenhouse-gas goal by 2050 and ongoing scope-3 reporting, and Saputo with its publicly stated commitment to reduce absolute scope 1 and 2 emissions and to engage suppliers on scope-3 emissions by 2030 — have lined up sustainability targets that put farm-level emissions on the table. Nobody knows exactly what the premium and deduction structure will eventually look like. But at some point, a kilogram of milk from a low-footprint herd won’t be treated the same as a kilogram from a higher-footprint one.

International examples are the warning shot. In November 2022, Ireland’s Economic Breeding Index added a dedicated carbon sub-index, which ICBF and Teagasc set at a 10% weighting of the total EBI — putting a monetary value on emissions at €80 per tonne of carbon dioxide. Teagasc and ICBF data show cows bred under EBI have become measurably more carbon-efficient per kilogram of milk solids, mostly through higher fertility, better solids, and tighter calving patterns, diluting emissions per unit of output.

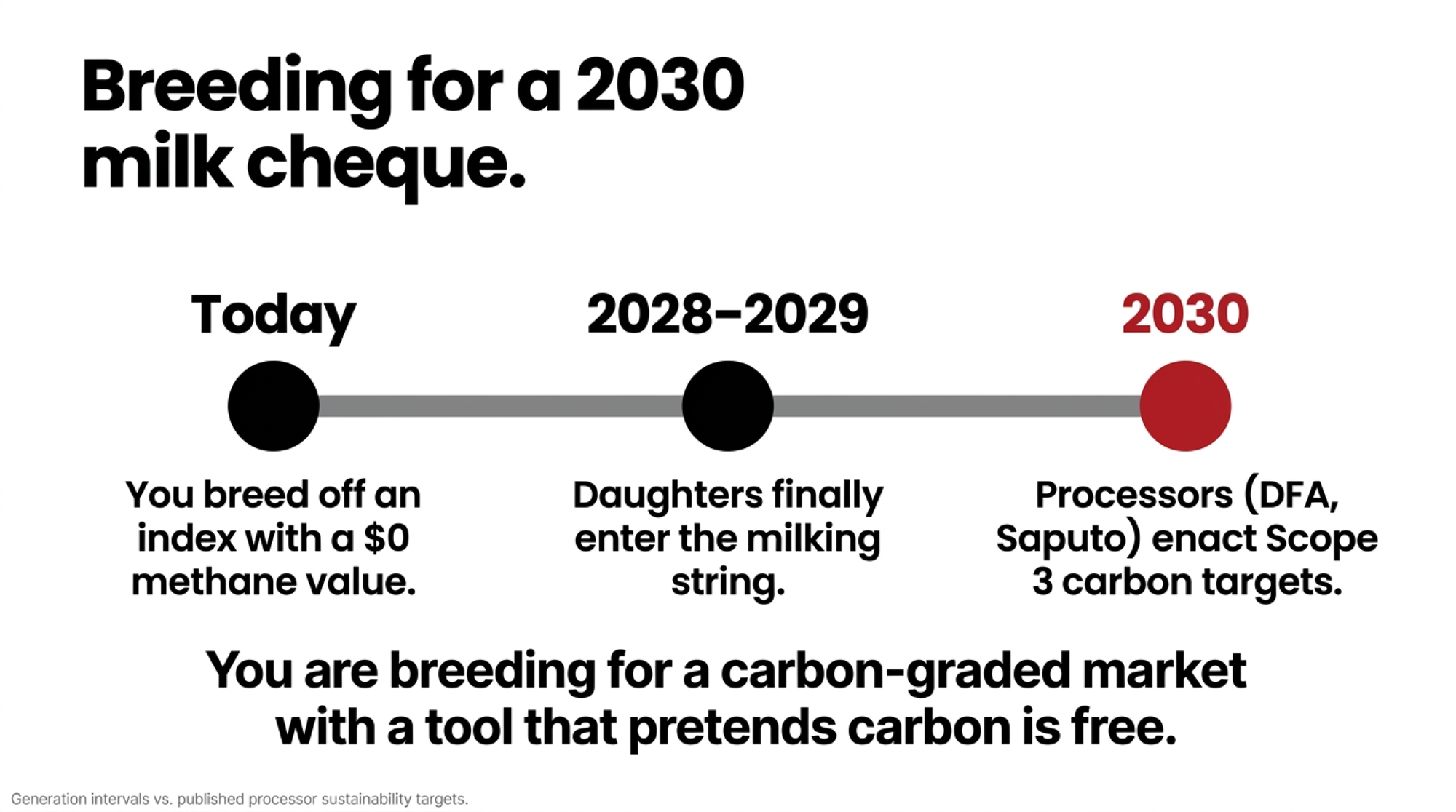

Now factor in the clock that makes this urgent: a dairy animal’s generation interval runs roughly 3 to 4 years. Breed off a “$0 methane value” index today, and the heifers you’re creating won’t even enter the milking string until 2028 or 2029 — and they’ll be in your herd for years after that. So if a U.S. processor lands a carbon premium or deduction by the turn of the decade, the cows facing that penalty are being conceived right now, off an index that prices their emissions at nothing. You’re not breeding for today’s milk cheque. You’re breeding for a milk cheque you can’t see yet, with a tool that pretends carbon is free.

Dutch dairy co-op FrieslandCampina already runs the real-world version of this on the milk cheque. The co-op paid out more than €245 million in sustainability premiums to member farms for 2023 — averaging €2.63 per 100 kg of farm milk — with about €190 million of that flowing through the Foqus planet sustainable-development incentive system, and the remaining €55 million-plus tied to special milk flows such as organic and PlanetProof. The exact split shifts year to year, but the principle is fixed: greenhouse-gas and sustainability performance is already cash on a Dutch milk cheque.

Net Merit still values methane at $0, even after the April 2025 update. For a herd that sells embryos or bulls, or supplies a processor already thinking in carbon accounting, that mismatch matters. If your index assumes greenhouse gases cost nothing and your buyer’s long-term plan treats them as a real liability, you’re breeding into a gap that shows up somewhere — on your milk cheque, in your access to certain programs, or in how marketable your genetics are to buyers further down the sustainability path.

For a herd like this, that’s the final nudge. Nobody wants to discover in 2030 that their genetics were perfect for a 2023 milk cheque and badly misaligned with a carbon-graded market.

Pull your last 12 months of cull records and sort them into “voluntary” and “involuntary.” If more than 70% of your culls are involuntary, and infertility, lameness, mastitis, and transition disease top the list, that’s a strong sign you need more genetic emphasis on health, fertility, and robustness — not just better management.

Ask your genetics adviser one specific question about Feed Saved. For the bulls you’re using, how much of their Feed Saved PTA is attributable to true feed intake data versus just smaller body size? If the answer leans heavily on body weight composite, you’re mainly selecting for smaller cows, not necessarily cows that convert feed better at the same size.

Compare your milk cheque to the index’s pricing assumptions. Net Merit’s updated weights lean toward butterfat and protein values that reflect recent U.S. component prices, with a heavier emphasis on fat than on protein. If your market pays more aggressively for protein, or your fat price has already slid from those highs — and it slid hard through 2025 — give Cheese Merit or a custom trait profile more weight alongside NM$.

Look at your 5-year system plan, not just this proof run. Are robots, grazing, or alternative housing in the pipeline? Start filtering now for the traits that matter in those systems — teat placement and udder depth for robots, fertility and feet for grazing — instead of assuming the national composite will automatically produce the right cows.

Do one “override the index” exercise in the next 30 days. For your next semen order, deliberately pick two or three bulls that aren’t in your usual top-10 NM$ list but rank strongly for the traits your own numbers say matter most. Track their daughters separately. See whether they match the kind of herd you actually want to milk.

Use your own numbers to set genetic red lines. If your records show that DAs, metritis, or down cows at certain levels destroy your margin, work with your adviser to set minimum thresholds for relevant traits — not just maximum NM$ points — and stick to them.

Key Takeaways

If your cull report is dominated by cows you “had to” ship, that’s not just a transition management story — it’s feedback on your breeding goal. Genetics and management pull on the same rope. Adjust only one end, and the herd won’t move very far.

Net Merit’s updated weights make it a solid national index, but it’s built on 2021–2024 economics with zero value on methane and limited direct emphasis on the traits that keep cows in a high-pressure system. Use it as a baseline, not a blind autopilot.

Your own data is the best starting point for adjusting or overriding the index. The three biggest leaks in your P&L — usually involuntary culls, fresh-cow disease, and labor around “problem cows” — should drive more of your trait emphasis than they probably do today.

If your processor, lender, or genetics customers are already talking about sustainability and 2030 targets, your breeding program is in the sustainability business whether you like it or not. The genetics you choose now will decide whether your herd fits those programs or constantly fights them.

A herd like this, the New York composite, still looks at NM$ every proof run. The difference, once the conversation goes honestly, is that it becomes one lens, not the whole picture. The sire list bends toward cows you can keep, and toward a milk cheque your buyer is likely to be writing in 2030, not 2019.

If you laid your last ten years of sire choices next to your last 12 months of cull reasons and vet bills, would those two stories look like they came from the same farm — or is it time to redraw your genetic target?

Run Your Numbers

Herd Health ROI Calculator — This article puts the cull-gate leak at up to $100,000 a year. Plug in your own culling rate, replacement heifer cost, and mastitis incidence to see what slowing those forced exits is actually worth on your herd — before you blame the breeding goal or the transition pen.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

If your inbreeding is over 9.99% and FSAV isn’t on your proof sheet, Net Merit 2025 is using you — not the other way around.

Executive Summary: Net Merit 2025 added a $57‑per‑point “weight tax” on big Holsteins by cutting Body Weight Composite to ‑11% and lifting Feed Saved to 17.8% of NM$, pushing the breed toward smaller, feed‑efficient cows. Fat now carries 31.8% of the index, protein just 13%, and cow/heifer Livability has more pull, so the model rewards components and survival over sheer size. New calf‑health evaluations — CDCB’s DIAR/RESP and Lactanet’s Calf Health RBVs — reveal that daughters of top 5% sires stay healthy 15–18 percentage points more often than daughters of the worst bulls, and a single respiratory event costs about 121 kg in first‑lactation milk. Meanwhile, average inbreeding for Canadian Holstein heifers hit 9.99% in 2024, and JDS work shows recent inbreeding hurts longevity more than older, diluted inbreeding, raising real questions about how we’re using genomics. Rosy Lane Holsteins leans hard into NM$, FSAV, and calf‑wellness indexes, but still filters out extreme‑stature bulls and ignores classification that doesn’t help profit, showing how to use the system without letting it run the herd. The practical playbook: pair NM$ with reliability, make FSAV and calf health non‑negotiable filters, keep your top three bulls below ~40% of expected future inbreeding, and, in the next 30 days, sit down with your proofs to see if Net Merit’s priorities actually match how your farm makes money.

While you’re scraping stalls or checking heaters, three people you’ve never met just changed the value of every cow in your barn. In a quiet Maryland office park, the USDA recalculated the “ideal” Holstein — and if your cows are “too big” on Body Weight Composite, they just picked up a $57‑per‑point penalty for lifetime Net Merit.

The math lives in Beltsville. The consequences land in your parlour. The April 2025 Net Merit revision didn’t just shuffle a few bulls; it hard‑wired a new answer to a simple question: what kind of Holstein is worth breeding in 2026?

This is the story of the scientists who set that answer — and Rosy Lane Holsteins in Wisconsin, where Lloyd Holterman refuses to let those formulas be the whole story.

Quick Facts: What Changed in Net Merit 2025

Body Weight Composite (BWC): -11% emphasis in NM$.

Fat vs Protein: Fat 31.8%, Protein 13% of NM$ emphasis.

Feed costs in the model:58% of milk income (39% marginal, 19% maintenance).

“Weight tax”: +1.0 BWC = -$57 lifetime NM$ per daughter.

Genetic gain: Genomics roughly doubled NM$ gain per bull from $40 → $85/year.

Those aren’t trivia numbers. They’re the new rules your proof sheet is playing by.

From Coin, Iowa, to Every Proof Sheet in North America

The modern proof system didn’t start with DNA chips. It started with a kid from Page County, Iowa, who didn’t begin his animal breeding career until he was nearly 40.

Charles Roy Henderson grew up on a general livestock farm, served as an Army Nutrition Research Officer during World War II, and earned his PhD in genetics and animal breeding from Iowa State in 1948 at age 37. At Cornell, he developed best linear unbiased prediction — BLUP — the math that finally separated herd effect from genetic effect. It let evaluators ask: Is this cow actually superior, or just in a better barn?

USDA adopted Henderson’s herdmate comparison method in 1962, replacing the old daughter–dam comparisons. By 1989, BLUP‑based Animal Model evaluations were running in the U.S., with other countries following through the 1990s.

There was still a massive bottleneck. A young bull went into AI around two, his daughters calved, finished a lactation, and the proof didn’t publish until the bull was seven or eight. Only about 1 in 8–10 bulls “graduated” from progeny testing, and each active bull represented a $350,000–$400,000 investment in semen collection, daughter sampling, and promotion.

Genomics blew that up. Illumina’s 50K SNP BeadChip hit the market in 2007, the bovine reference sequence landed in Science in April 2009, and USDA’s Animal Genomics and Improvement Laboratory launched official genomic evaluations for Holsteins and Jerseys in January 2009. Generation interval collapsed — suddenly, you could get a genomic PTA on a bull before he was old enough to breed.

Paul VanRaden joined the USDA’s Animal Improvement Programs Laboratory after his Iowa State PhD in 1986. His name is on a long list of methods you see every time you open a proof sheet — but Net Merit is the one that hits your pocketbook most directly.

Henderson’s BLUP told you which cow was genetically better. VanRaden’s Net Merit dollar index (NM$) tells you which cow should make you more money over her lifetime. It rolls multiple production, fertility, health, and conformation traits into a single lifetime profit estimate — and every revision is another set of judgment calls about what matters, and how much.

Where the 2025 Change Hits Your Herd

The April 2025 NM$ revision increased the emphasis on butterfat and reduced the emphasis on protein, reflecting actual component price trends in recent years. It also shifted weight from Productive Life toward cow and heifer Livability, based on stronger cull cow and heifer calf markets.

The bigger jolt is in body weight and feed efficiency. New feed‑intake data from more than 8,500 Holstein and Jersey lactations showed that maintenance feed costs were higher than previous models assumed. In plain language: big cows cost more to keep milking than the old Net Merit math gave them “credit” for.

So BWC now sits at ‑11% emphasis in NM$. For every extra point of BWC, the model knocks about $57 off that cow’s lifetime Net Merit — mostly for maintenance feed, but also for housing and replacements.

Big cows = big feed bills the model sees no profit

Here’s the barn‑math version:

Your bull team averages +1.0 BWC over breed average.

NM$ says that’s about ‑$57 lifetime NM$ per daughter.

Across 100 daughters, that’s roughly $5,700 in lifetime NM$ drag for that sire choice compared to a BWC‑neutral bull.

You can argue with the model. But you can’t pretend it’s not there.

Why Did Fat Leapfrog Protein?

VanRaden’s team also re‑estimated the true genetic cost of components. Genomic and sire regressions suggested that, genetically, fat takes as much or more feed to produce than protein. That’s the opposite of what older phenotypic regressions implied when they just watched cows and feed trucks.

The feed‑side math behind this revision assumes feed costs equal 58% of milk income — 39% for marginal production and 19% for maintenance. Combine that with the new Feed Saved trait (FSAV), and you see where the wind is blowing:

FSAV is 17.8% of NM$ when you add its BWC and Residual Feed Intake components together.

If you’re not looking at FSAV on your proofs, you’re ignoring almost a fifth of the index you think you’re using.

The subtext is pretty clear: do more milk from less feed, land, and carbon, or get left behind.

Wiggans: The Infrastructure Nobody Sees

If VanRaden designed the engine, George Wiggans made sure it was street‑legal and still running when you opened your proofs this morning.

Theory doesn’t help anybody if it can’t be computed, delivered, and trusted. Wiggans spent his career sorting out genotype management, data quality control, and the nuts and bolts of turning millions of milk, type, and health records into evaluations that AI organizations can actually ship. He was central to the push that got Canadian AI studs to contribute DNA to a shared U.S.–Canada reference population before genomic proofs went live, which still underpins most North American Holstein genomic evaluations.

Every chip you send in has to survive that QC pipeline. The genotype is checked against reported parents, then against the entire database to catch swapped samples or mis‑ID’d animals. If it doesn’t add up, it doesn’t make it into the evaluations.

In a 2022 Frontiers in Genetics paper, Wiggans and Carrillo showed that the U.S. genomic‑selection era roughly doubled the rate of NM$ gain: from about $40 per bull per year (2005–2009) to roughly $85 per bull per year from 2010 onward. The genetic trend lines are real. Whether those gains match your own herd’s priorities is a different question.

What Kills Your Calves Before They Ever Milk?

John Cole is part of the generation pushing genomic evaluations into the ugly stuff that never makes it to the parlor: dead or wrecked calves.

Across multiple datasets, about 75% of preweaned calf mortality comes from just two buckets: diarrhea and respiratory disease. To put numbers on the genetics behind that, CDCB and partners pulled together 207,602 diarrhea records and 681,741 respiratory disease records from calves born between 2013 and 2024. Those data streams feed the new U.S. genomic evaluations for calf diarrhea (DIAR) and respiratory disease (RESP), officially launched in April 2026. Lactanet rolled out its own Calf Health RBVs for Holsteins in August 2025.

The heritability looks low at first glance: about 0.026 for diarrhea resistance and 0.022 for respiratory resistance. Translate that: only 2–3% of the variation in those health outcomes is explained by genetics in the current models. Zoetis’s earlier proprietary Calf Wellness index (CW$) reported slightly higher figures due to differences in traits, models, and data sources.

Cole’s message in presentations and industry pieces has been consistent: don’t let the low heritability numbers fool you. Once you’re doing the basics right on colostrum, hygiene, and housing, adding genetic resistance can still move many calves out of the treatment pen and into the parlor.

The Genetic Spread, in Real Daughters

Lactanet clearly summarized the genetic spread in an August 2025 calf health article and a companion presentation. Among officially proven Holstein sires:

For respiratory disease, daughters of the top 5% sires by calf health RBV stayed healthy (no recorded RESP case) about 71% of the time; daughters of the bottom 5% sires were healthy only about 54% of the time.

For diarrhea, daughters in the top 5% were healthy about 69% of the time, compared with roughly 53% for those in the bottom 5%.

That’s not “nice‑to‑have.” That’s a lot of treatments, mortalities, and delayed heifers tied directly to the bulls you pick.

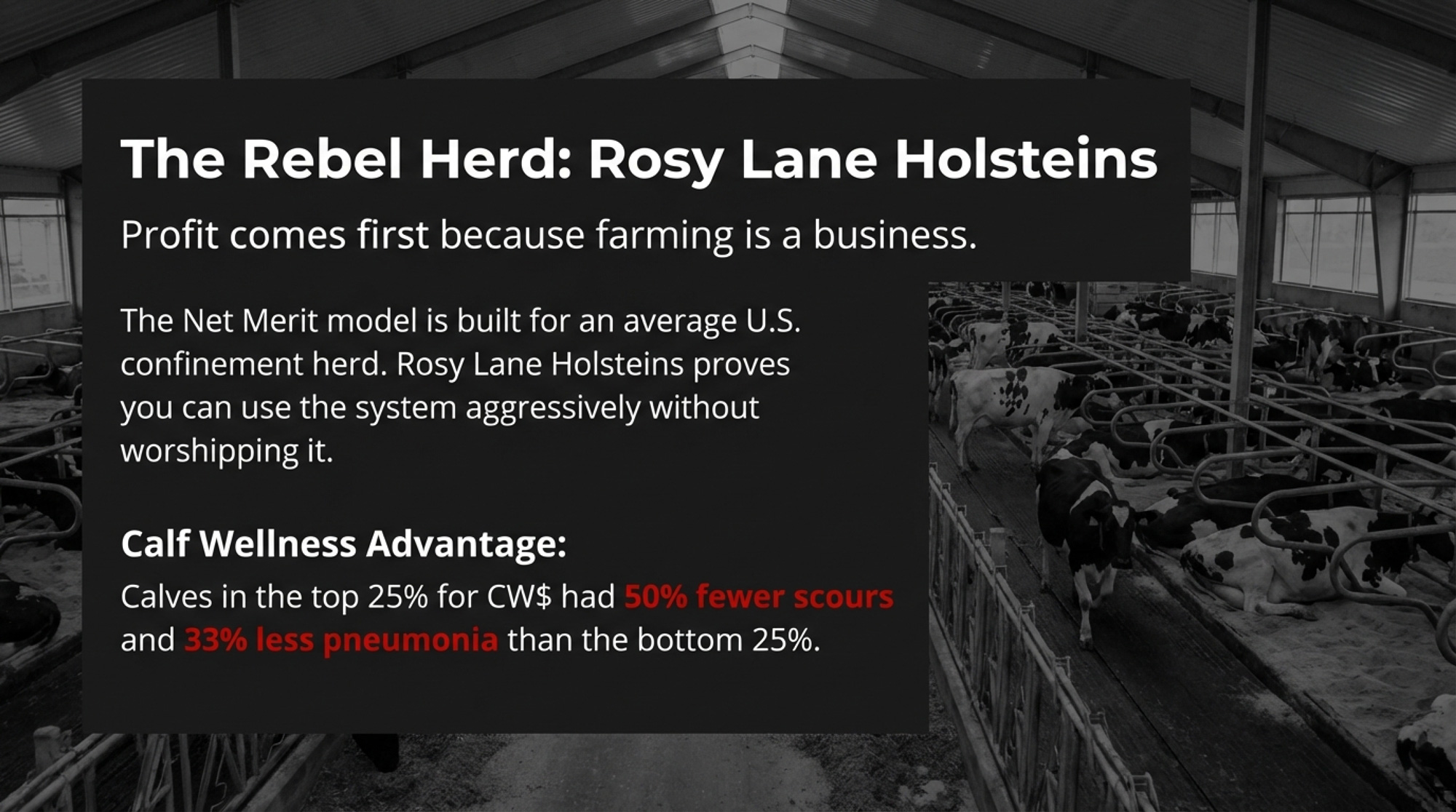

Rosy Lane Holsteins saw similar real‑world spreads years earlier when it leaned heavily into Zoetis’s Calf Wellness index. A WW Sires case study reported that calves in the top 25% for CW$ at Rosy Lane logged about 50% fewer scours cases and roughly 32% fewer pneumonia cases than calves in the bottom 25% over a 12‑month window — tracked with ultrasound to catch subclinical pneumonia that never showed as a full‑blown “trainwreck.”

An often‑cited study summarized in Farmtario’s 2025 calf‑health coverage showed that heifers with a recorded respiratory disease event produced 121 kg less milk in first lactation. Stack that across a whole age group, and you feel it in the tank.

Genetics won’t fix sloppy colostrum or filthy hutches. But if you’re already holding preweaned mortality in the 3–4% range, calf health genetics is one of the few levers left to push toward that 1–2% elite zone.

What Data Actually Feeds Your Genomic Proof?

Data Source

What It Captures

Who Provides It

Key Blind Spot

DHI/DHIA test

Monthly production, components, SCC

Techs or automated meters

Only ~40% of U.S. herds on some form of official test

Classification

Linear type traits and composites

Breed‑association classifiers

In Canada, only first‑lactation scores feed official type proofs

Genomic labs

SNP genotypes (e.g., 50K → ~54,001 usable markers)

DNA from hair, blood, ear notch

Minor breeds have thin reference populations

Producer health records

Mastitis, metabolic disease, calf health events

Producers via herd software

Only a minority of farms consistently log calf health events

Those gaps matter. The DIAR and RESP national datasets are over 97% Holstein and Jersey — roughly 80% Holstein, 17% Jersey — which makes the models strong for those breeds and less robust for everyone else. If you’re milking registered Holsteins on test and logging health, the system sees you. If you’re off test, crossbred, or light on health records, you’re asking the index to guess.

Does the System See Your Herd — or Just the Average?

Genomic selection was intended to mitigate inbreeding. The sales pitch: if you can see exactly which genes each calf got, you can manage inbreeding smarter. In reality, progress has been messier.

Lozada‑Soto and co‑authors (2024, Journal of Dairy Science) showed that in Nordic Holstein and Jersey populations, yearly inbreeding rates increased after genomic selection took off, and the effective population size for Nordic Holsteins dropped from 54.3 to 42.8. Doekes et al. (2019, Journal of Dairy Science) found that recent inbreeding — long runs of homozygosity in the genome — hurts longevity more than older, “diluted” inbreeding.

You see that on‑farm, as good‑looking heifers that fall apart too soon for reasons you can’t fully blame on your nutritionist or hoof trimmer.

So you’re stuck with a double‑edged sword:

Genomics doubles genetic gain in traits the index rewards.

Key traits like heat tolerance, methane emissions, and temperament still don’t have official U.S. evaluations. The index can’t weigh what it doesn’t measure. If those matter on your farm, you’re into custom selection, not blind NM$ chasing.

On the Canadian side, Lactanet’s August 2025 inbreeding update pegged average inbreeding for Holstein heifers born in 2024 at 9.99% — a full percentage point higher than 2014. That’s your benchmark when you run your own mating reports.

Rosy Lane Holsteins: Using the System, Not Worshipping It

The Net Merit model is built for an “average” U.S. confinement herd. Rosy Lane Holsteins, just outside Watertown, Wisconsin, is one of the operations proving you can use that system aggressively without letting it run the show.

Lloyd Holterman and the Rosy Lane team have been clear for years: profit comes first because farming is a business.In a 2014 Bullvine profile and later Zoetis/WW Sires features, Holterman laid out a strategy that still makes some breeders twitch:

Sort bulls by NM$ first, not TPI or show‑ring appeal.

Avoid bulls that crank up Stature; favor moderate‑sized, wide, durable cows.

Stop classifying if the scores aren’t helping profit decisions.

When Rosy Lane compared its cows, Holterman told The Bullvine they found that shorter, wider, better‑conditioned cows “far outlived their higher‑scoring herd‑mates while having fewer foot problems and better fertility.” We later quoted his joking shorthand for what can happen when people chase pure type without thinking about fertility: cows that are “tall, pretty and infertile.” (Read more: ROSY-LANE HOLSTEINS – “Don’t Follow the Herd!”)

That line isn’t a scientific verdict on TPI. It’s one breeder’s sharp reminder that an index built for show cows and an index built for profit aren’t the same tool.

Rosy Lane also leaned early into Calf Wellness genetics. The Zoetis/WW Sires case study from their herd showed calves in the top quartile for CW$ had around half the scours and one third fewer pneumonia cases than bottom‑quartile calves — not because management changed, but because the sire list did. That’s exactly the kind of “make the data pay” story the Beltsville team hopes other herds can copy.

Holterman’s bottom line hasn’t changed: use the tools, but never forget your own milk cheque.

The Bullvine Verdict: Who Gets to Decide What a “Good” Holstein Looks Like?

Here’s the uncomfortable truth: if you don’t know how NM$, FSAV, and calf health evaluations work, someone else is making your breeding strategy — even if you’re the one signing the semen bill.

Beltsville’s job is to define an average profitable Holstein in 2025: moderate size, high components, better feed efficiency, fewer dead calves, and fewer young cows leaving early. That’s not a bad target.

But your farm isn’t average. Your milk contract might reward protein harder than fat. Your freestalls and robot boxes might punish tall, wide cows. Your land base might mean feed is your bottleneck, not cow numbers. Or you might be okay trading some NM$ for show‑ring presence or niche milk premiums.

Net Merit is a strong starting point. It’s just blunt. Rosy Lane is a live example of how a herd can lean hard into Net Merit, calf wellness, and FSAV — and still make their own calls about size, type, and classification.

The real question isn’t “Is Net Merit right?” It’s “Does Net Merit, as currently weighted, line up with the way money actually moves through your operation?”

What This Means for Your Operation

Always read NM$ with reliability beside it. An NM$ +1,000 bull at 75% reliability is a strong estimate; at 95% reliability, it’s a proven moneymaker relative to the base. They’re not interchangeable, and low‑reliability bulls can move 150+ NM$ in a run.

Match your index to your contract. If your cheque pays on components, CM$ or Pro$ might match better than NM$ if you’re fluid and volume-heavy. NM$ is still the best fit. The index choice isn’t a religion — it’s a business decision that should be revisited at least annually as prices shift.

Find FSAV on your sire summary — or ask why it’s missing. With 17.8% combined weight in NM$, FSAV is now a core trait, not a side note. A bull that looks good on milk and components but is weak on FSAV may not pencil once you factor in feed and maintenance.

Use genomics to diversify, not concentrate. Spreading risk across at least 5 genomic sires is cheap insurance. One young bull can re‑rank hard; a group of five rarely does. If your top 3 sires account for more than ~40% of your herd’s expected future inbreeding, that’s a practical red flag to add diversity.

Treat Net Merit as your first filter, not your only one. Rosy Lane uses NM$ as the gate, then rejects bulls that push Stature too high. You might do the same for calving ease, A2A2, polled, robot suitability, or grazing traits, depending on your system.

Put calf health on the table if you’re already nailing management. Once your basic colostrum, housing, and hygiene are solid, DIAR/RESP and tools like CW$ can start doing noticeable work in the background.

Key Takeaways

If your expected inbreeding is higher than 9.99%, it’s time to adjust your mating plan. That 9.99% is Lactanet’s average for Canadian Holstein heifers born in 2024. Run your own mating reports. If your next calf crop is well above that, add two or three outcross or lower‑inbreeding bulls before the next breeding cycle.

If a bull drops more than ~150 NM$ between proof runs, he should lose some tank share. That kind of swing is normal for low‑reliability genomic sires, but it’s your cue to slow his usage and bring in a replacement rather than riding him for another year, hoping he comes back.

If your top 3 bulls contribute more than ~40% of your herd’s expected future inbreeding, you’ve got a concentration problem. That number isn’t a magic line — it’s a simple threshold that tells you when you’ve leaned too hard on a couple of “hot” sires.

If FSAV isn’t in your sire selection process yet, you’re ignoring 17.8% of the index you think you’re using.That’s a lot of money and feed to leave on the table when you’re already fighting ration costs.

The Bottom Line

In the next month, carve out half an hour with your genetic advisor or semen rep. Pull up your proofs, look at BWC, FSAV, reliability, and expected inbreeding side by side — and ask one question: “Does the way I’m using these tools actually match how my farm makes money?”

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

The $212,000 Bulk Tank Lie Hitting Upper Midwest Dairies – Exposes the high-test trap that’s quietly draining your bank account. You’ll gain a concrete 4-point playbook to stop chasing percentages and start shipping the component pounds that actually drive your 2026 milk check.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Every time you pull up a sire list, there’s one question you almost never ask: what am I not measuring that’s already costing me money?

February 2003. Snow coming down sideways in a drafty barn at the Wisconsin Holstein Convention Sweetheart Sale. Experienced breeders — guys who’d driven hours through a Wisconsin winter to be there — were heading for the exits. The auctioneer’s voice was getting that tired, frustrated edge as bidding stalled out on a five-year-old Holstein whose rump “wasn’t entirely balanced.”

Matt Steiner called in from Pine-Tree Dairy in Ohio. He’d never laid eyes on the cow in person. Her second lactation ran 31,880 pounds at 4.1% fat and 3.2% protein — respectable, not revolutionary. He bid $8,100 for what everybody else in the room saw as just another decent cow past her prime.

Wesswood-HC Rudy Missy-ET EX-92 — the “unbalanced” Wisconsin sale cow whose $8,100 phone bid quietly rewrote Holstein genetics for the next 20 years.

But here’s the part of that story nobody tells. The same breeding system that produced Missy — the same genomic toolkit that doubled annual genetic gain to 109 kg/year for milk in registered Holsteins (García-Ruiz et al., 2016, PNAS) — was simultaneously dragging 198 fertility genes and 67 immunity genes in the wrong direction. For 20 years. And the industry didn’t catch it.

The question that should bother you: what’s getting dragged sideways in your herd right now?

How Fast the Engine Actually Runs

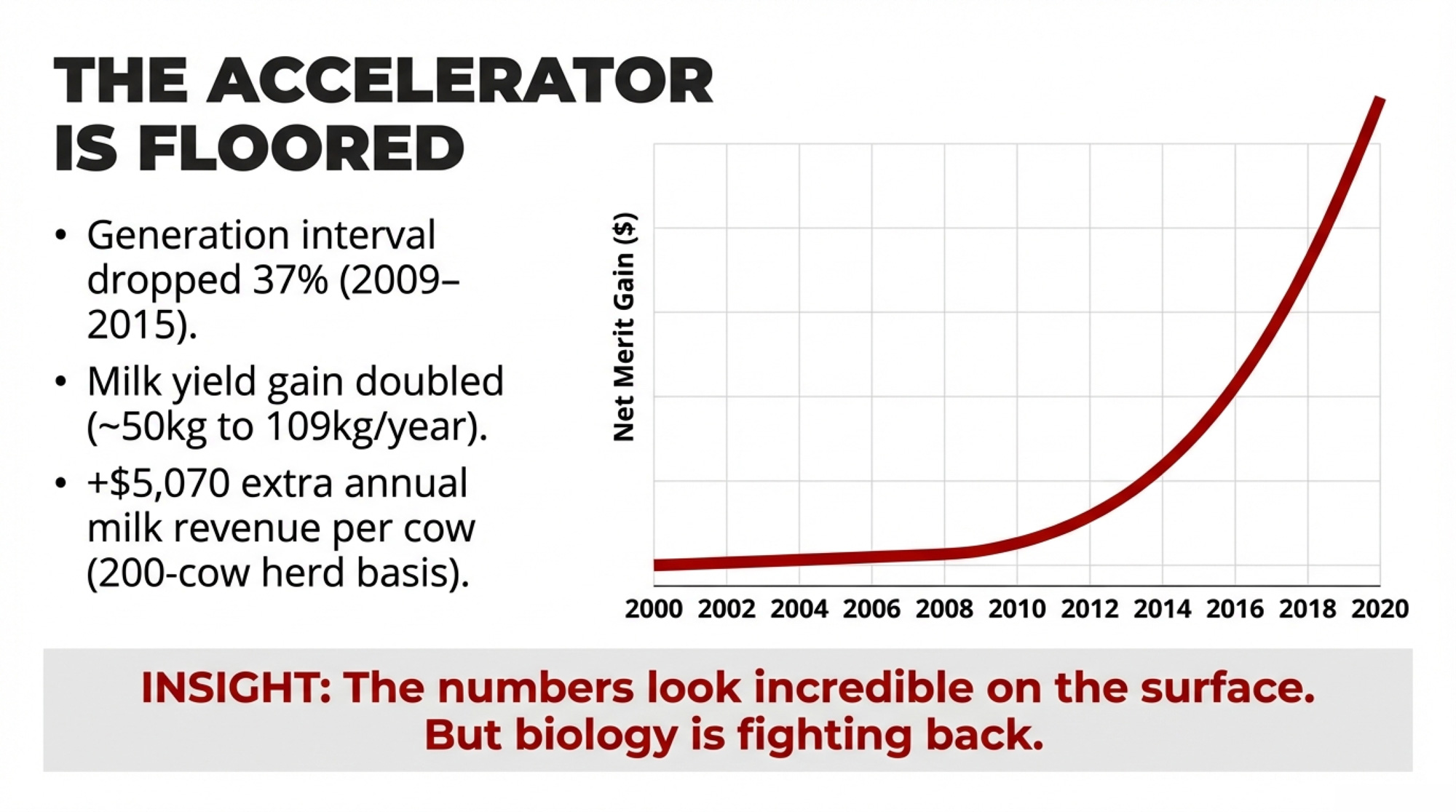

Before 2009, you waited five to seven years for a bull’s daughters to start milking before you knew if he was any good. Genomic selection rewired that math completely. Paul VanRaden and colleagues at USDA helped architect a system that estimates merit at birth, and the speed gain was dramatic. Across all four selection pathways that drive Holstein genetics (sire-of-bulls, sire-of-cows, dam-of-bulls, dam-of-cows), the combined generation interval dropped from 21.4 years in 2009 to 13.5 years by 2015 — a 37% reduction in just six years (García-Ruiz et al., 2016, PNAS). The sire-of-bulls pathway collapsed the fastest, from about 7 years to under 2.5.

Financially, the results are hard to argue with. Annual Net Merit gains climbed from $13 during 2000–2004 to more than $85 after 2010 (nominal dollars). Fat yield accelerated 173%. Protein yield, 156%. And the daughter pregnancy rate — which had been flat or declining for decades — finally reversed direction, rising to +0.26% per year.

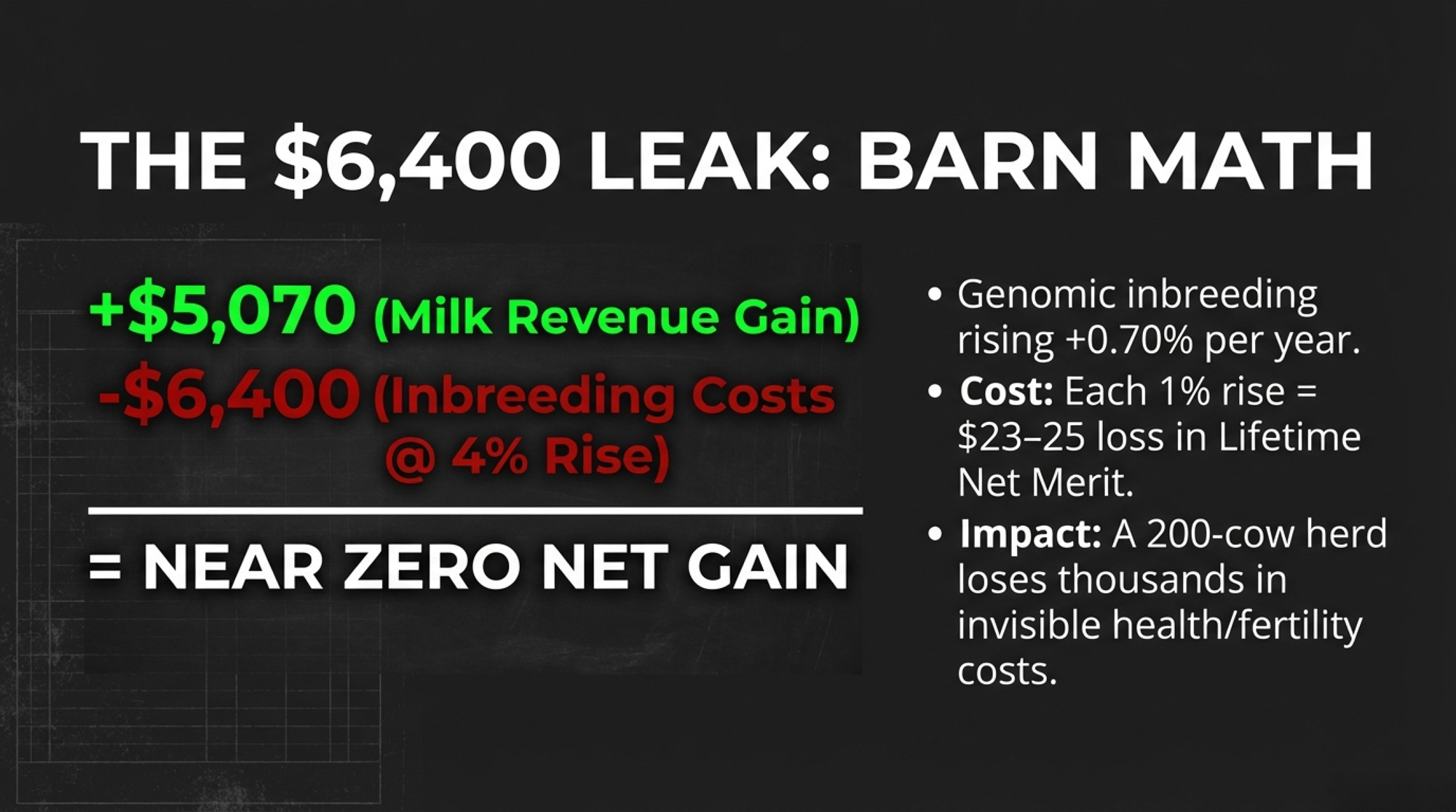

Here’s a way to feel that in your bulk tank. On a 200-cow herd averaging 85 lbs/day, the post-genomic milk yield acceleration alone (from ~50 kg/year to 109 kg/year for registered Holsteins) translates to roughly an extra 130 lbs of milk per cow per year in genetic potential over what the old system would have delivered. At a $19.50/cwt mailbox price, that’s about $5,070 in additional gross milk revenue across your herd annually — and it compounds every generation. Adjust that number for your regional mailbox price, but the scale holds. The record-breaking component shifts reshaping dairy’s economics are a direct product of this acceleration.

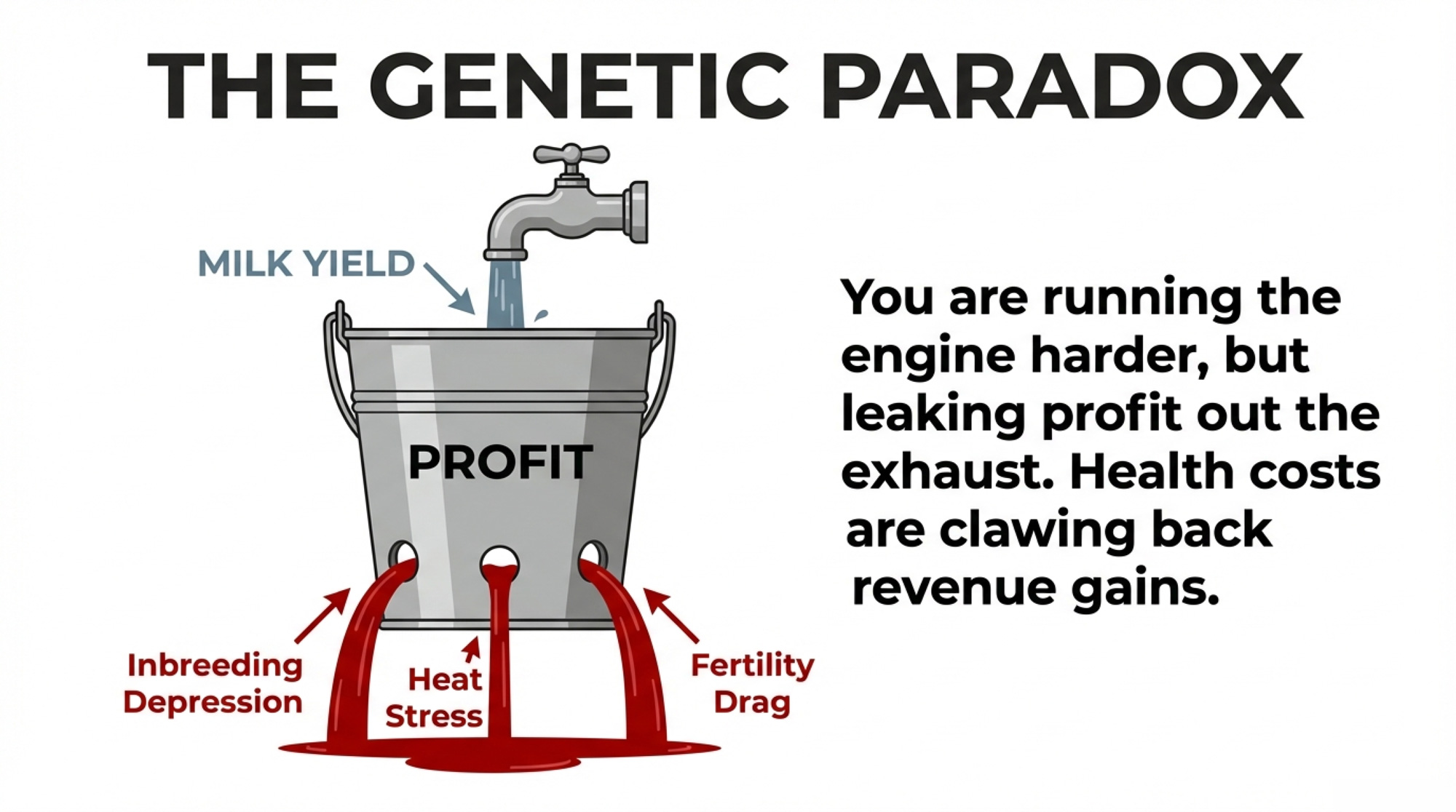

But the engine has a blind spot. And it’s biological, not mathematical.

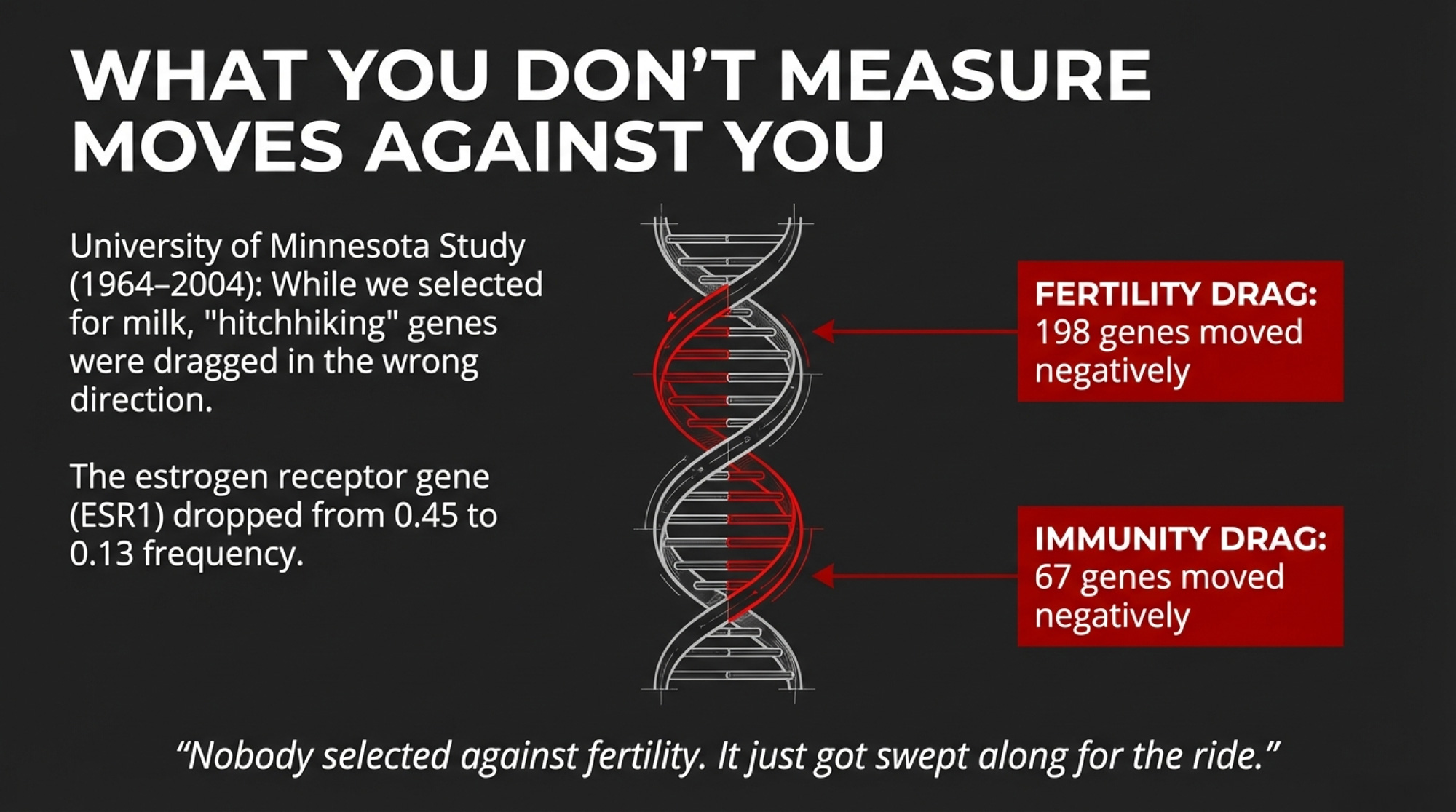

What Happened When Nobody Was Measuring Fertility

The University of Minnesota’s research herd at the Southern Research and Outreach Center in Waseca did something nobody else bothered to do: they maintained an unselected Holstein control line alongside the commercially selected national population from 1964 onward. Same management. Same feed. Different genetics.

By 2004, the selected population had increased milk yield by 79%, from 6,309 kg to 11,324 kg. It had also lost roughly 30 additional days for successful conception compared to the control cows living right next door (Ma, Cole, Da & VanRaden, 2019, BMC Genomics 20:128).

That fertility decline wasn’t nutrition. Wasn’t repro protocols. Purely genetic. A breeding consequence nobody planned for.

The genome-level analysis revealed the mechanism. Within 234 chromosome regions shaped by four decades of milk selection, researchers found 198 genes involved in reproduction and 67 genes involved in immune function whose allele frequencies had shifted as collateral damage. The estrogen receptor gene ESR1 decreased from 0.45 to 0.13. The MHC region on chromosome 23 — the heart of immune diversity — showed significantly decreased heterozygosity.

Category

Count

Fertility genes negatively affected

198

Immunity genes negatively affected

67

Total chromosome regions under selection

234

Nobody selected against fertility or immunity. Those genes just happened to sit near milk-boosting alleles on the same chromosomes, and they got swept along for the ride. Geneticists call it hitchhiking. Producers who lived through the collapse in conception rates in the 1990s just called it expensive.

(This hitchhiking analysis comes from a single study using the unique Minnesota control line — the only unselected comparison herd of its kind. The broader fertility decline is independently confirmed across both the U.S. and Israeli dairy populations.)

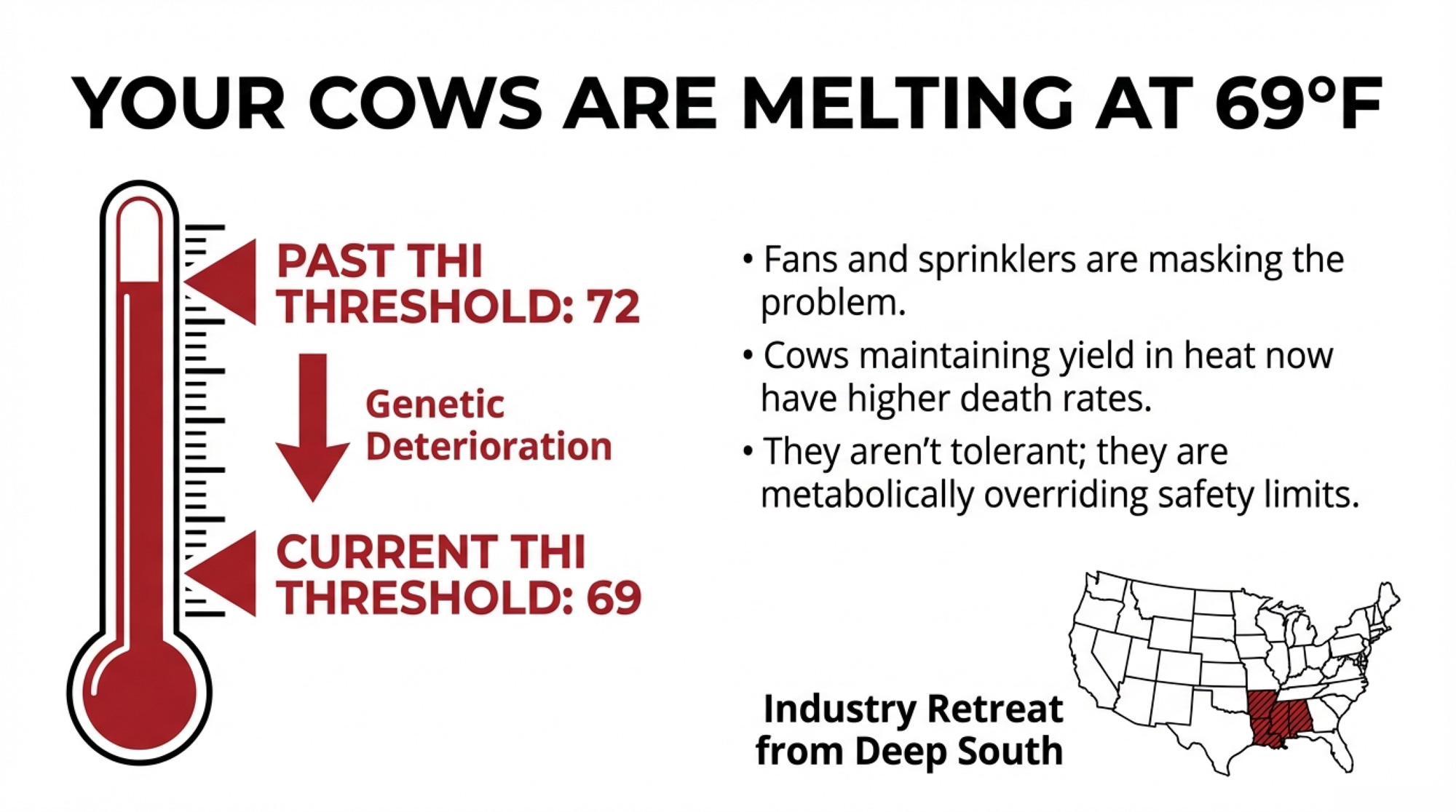

Is the Same Thing Happening to Heat Tolerance Right Now?

The fertility crash is old news — the industry course-corrected, and genomic selection actually reversed the decline. The real question: where is the same pattern building today?

Heat tolerance is eroding, and almost nobody is selecting against it. Research led by Ignacy Misztal at the University of Georgia and Luiz Brito at Purdue found that the temperature-humidity index (THI) threshold where Holsteins start losing production has dropped from 72 to 69 over the past two decades (Misztal, Brito & Lourenco, 2024, JDS Communications 6(3):464–468). Your cows start suffering heat stress at lower temperatures than cows bred a generation ago.

And the grim part: cows that maintain production during heat stress peaks show an increased likelihood of death. They’re not tolerating the heat. They’re metabolically overriding their body’s protective shutdown. The authors note that better fans, sprinklers, and tunnel ventilation may actually be masking an even larger genetic deterioration underneath.

With the exception of Australia, dairy cows are not directly selected for improved heat tolerance anywhere in the world. In Alabama, Mississippi, and Louisiana, dairy has already become economically unviable — these states don’t even appear in the 24 major dairy states NASS tracks monthly (Misztal et al., 2024). A quiet testament to how completely the industry has retreated from the Deep South.

If your herd faces more than 60 days per year above THI 68, this isn’t an abstract research finding. It’s your next fertility crash in slow motion.

The Inbreeding Bill Coming Due

Genetic diversity is narrowing faster under genomics, not slower. A study of 74,485 Italian Holstein cows found the annual inbreeding rate based on runs of homozygosity (ROH) was +0.32% per year before genomic selection. After genomic selection took hold, it jumped to +0.70% per year (Ablondi et al., 2022, Frontiers in Veterinary Science8:773985). That’s above the 1% per generation threshold FAO considers critical for long-term sustainability.

Category

Value

Pre-Genomic Annual Rate (Italy)

0.32%

Post-Genomic Annual Rate (Italy)

0.70%

U.S. Cumulative Increase 2010–2020

168%

It isn’t just an Italian problem. U.S. Holstein inbreeding climbed from about 5.7% in 2010 to 15.2% by 2020 — a 168% jump — with CDCB analysis putting the cumulative cost to the national herd at an estimated $6.7 billion (The Bullvine, 2025 year-end review).

Metric

Annual Impact (200-cow herd)

What’s Driving It

Extra Milk Revenue (Genomic Gain)

+$5,070

109 kg/year genetic gain vs. 50 kg/year pre-genomic (registered Holsteins, $19.50/cwt)

Inbreeding Drag (4% increase)

−$4,800 to −$6,400

$23–25/cow lifetime NM$ loss per 1% inbreeding, annualized over 3–4 year turnover

Net Realized Gain (Conservative)

+$270 to +$1,070

On fast-turnover herds, inbreeding wipes out nearly all the genomic advantage

Net on Fast-Turnover Herds

−$1,330 (loss)

Herds replacing >35% annually can lose more than they gain

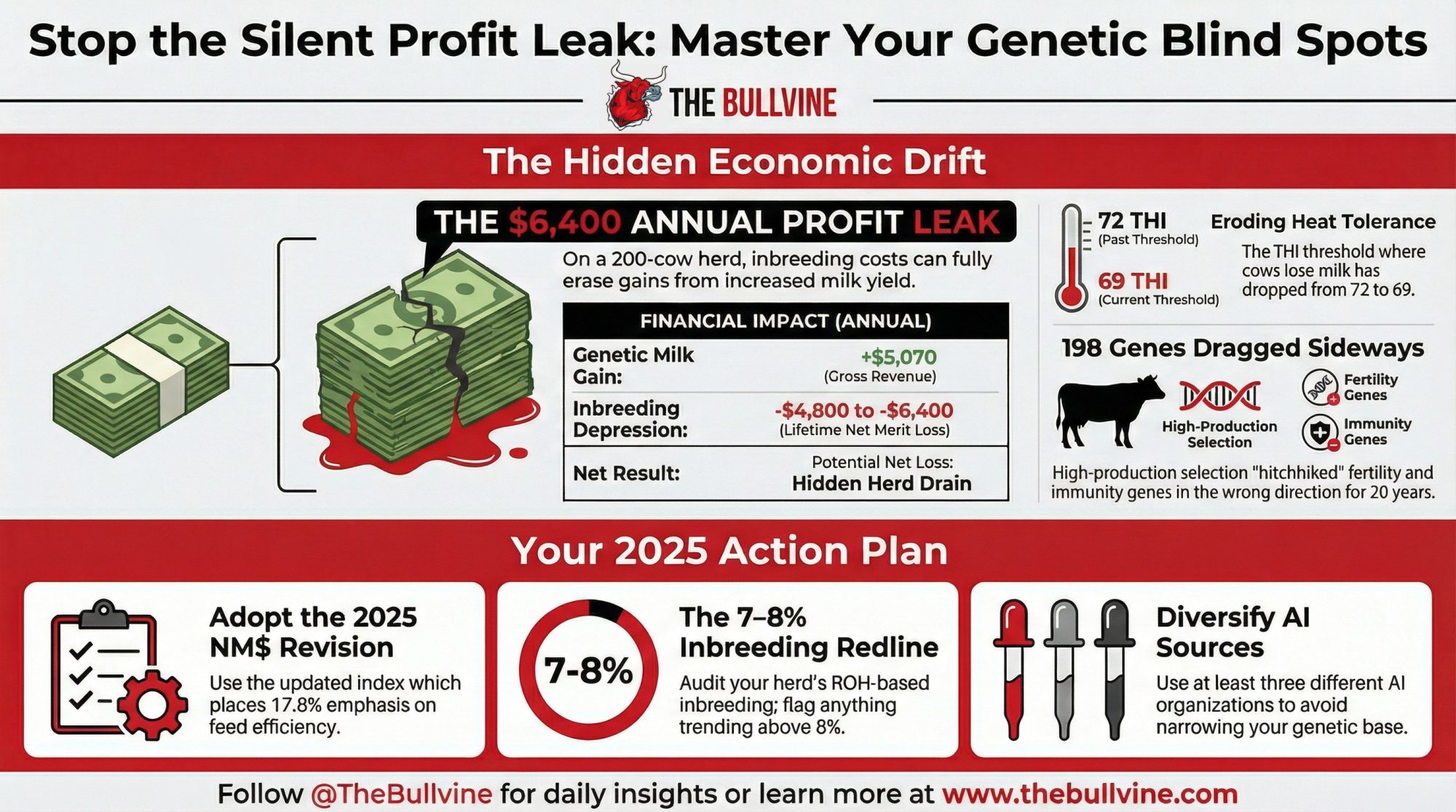

Here’s where the barn math gets uncomfortable. Each 1% increase in inbreeding costs roughly $23–25 off a cow’s lifetime Net Merit (USDA-ARS, 2025 NM$ revision). Go back to that 200-cow herd. If your average genomic inbreeding crept up 4 percentage points over the past decade — and given that the national average jumped 9.5 points in ten years, 4% is conservative — that’s about $96 per cow in lifetime profit quietly erased. Spread across a herd that turns over every three to four years, you’re looking at roughly $4,800 to $6,400 per year leaking out through health costs, fertility failures, and shortened productive life, depending on your actual turnover rate. Remember that $5,070 in extra annual milk revenue from faster genetic gain? At most turnover rates, inbreeding depression is clawing back nearly all of it — and on herds that turn over faster, the loss actually exceeds the gain. You’re running the genetic engine harder, and a big chunk of what it produces is leaking out the other side.

(Note: the $5,070 figure is gross milk revenue at $19.50/cwt; the $4,800–$6,400 range is annualized lifetime Net Merit loss, which captures health, fertility, and longevity effects beyond milk alone. They’re not identical units, but the scale of the offset is real — and the barn-math range depends on how quickly your herd turns over.)

Options and Trade-Offs for Your Next Breeding Decisions

The fertility crash lasted 20-plus years because nobody measured the trait being eroded. Heat tolerance, inbreeding, and resilience are in a similar position today. Here’s what you can actually do about it — with the honest trade-offs attached.

Action

When to Act

What You’re Hedging Against

Trade-Off

ROH Inbreeding Audit

If genomic inbreeding >7–8%

$23–25 lifetime NM$ loss per 1% increase; $4,800–$6,400/year drag on 200-cow herd

Restricting matings may slow genetic progress 5–15%

Weight Productive Life + Livability

If you face 60+ days above THI 68

Heat tolerance declining; THI threshold dropped from 72 to 69 over 20 years

May sacrifice 3–5% genetic gain on other traits

Diversify Across 3+ AI Programs

If top 5 bulls all trace to one program

Genomic inbreeding rising 0.7%/year; 22 of top 30 NM$ bulls from one program (Dec 2025)

Aggressively avoiding related matings costs ~5–15% progress

Contribute AMS/Activity Monitor Data

If you’re running precision dairy tech

Next hitchhiking problem: feeding the reference population so crashes get caught in 5 years, not 20

Consistent data entry discipline required

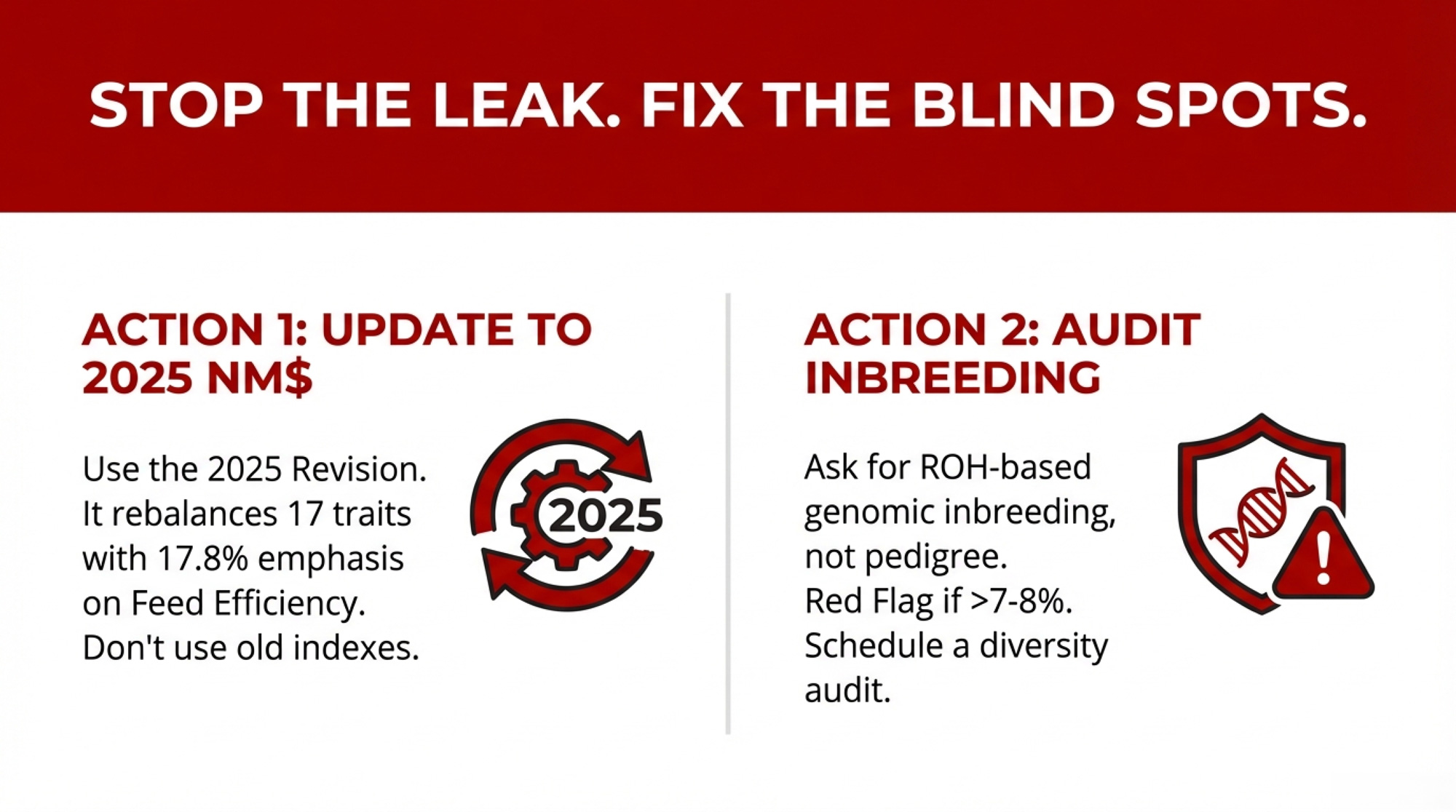

Confirm you’re using CDCB’s 2025 NM$ revision — and don’t override it. The updated index rolled out alongside the April 2025 base change. It now balances 17 traits for lifetime profitability, with feed efficiency (FSAV) carrying 17.8% of total emphasis — a substantial shift from prior weightings. If your genetics provider hasn’t updated to the 2025 revision, it’s worth a quick conversation; the trait emphasis shifted enough that older weightings are optimizing for a different market than the one you’re selling into. But even the right index can’t save you from yourself: if your top five bulls all rank in the top 20 for a single component while sitting below breed average for productive life, you’re running a single-trait program no matter what the index says. David Dyment at AG3 has built his program on exactly this principle — “consistency over unpredictability,” as he puts it — betting that balanced functional genetics outlast flavor-of-the-month rankings. The trade-off: you’ll pass on some high-component bulls that look great on paper. The fertility crash is what happened when the industry overrode balanced selection often enough.

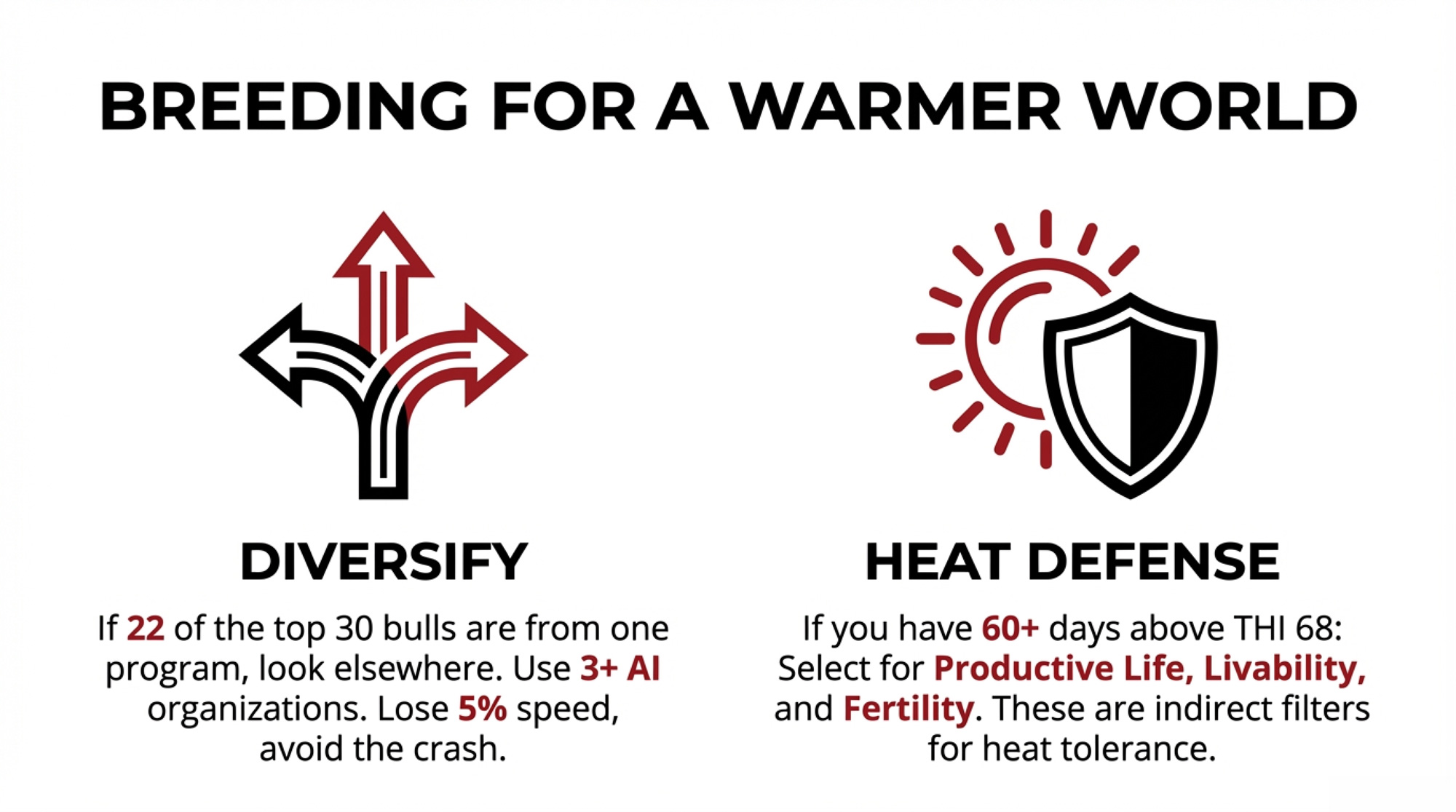

Ask your genetics advisor for your herd’s ROH-based genomic inbreeding — this month. Pedigree coefficients underestimate actual homozygosity. In Italian Holsteins, pedigree inbreeding averaged 0.07 while genomic inbreeding was more than double at 0.17 (Ablondi et al., 2022). As a general rule of thumb, many geneticists start flagging concern when genomic inbreeding crosses 7–8% for Holsteins — there’s no official industry threshold, but herds above 9% should seriously consider a diversity audit. CDCB provides genomic inbreeding estimates — if your genetics provider isn’t using ROH-based calculations in mating plans, you’re flying partly blind. Diversify your sire lineup across at least three AI organizations. The trade-off: aggressively avoiding related matings can slow genetic progress — estimates vary, but the general range is somewhere around 5–15% depending on how restrictive you get. That’s a real cost. But inbreeding depression quietly eating your gains from the inside is worse — and that $4,800-to-$6,400-a-year leak on a 200-cow herd is real money.

If you’re in a heat-stress region, start weighting for it now. Increasing emphasis on productive life, livability, and fertility provides indirect selection pressure for thermotolerance — these traits correlate positively (Misztal et al., 2024). The trade-off: you may sacrifice 3–5% of genetic gain on other traits. In a warming climate, that’s a hedge worth paying for. If you’re south of the Mason-Dixon or running herds in the Central Valley, this isn’t optional — it’s self-defense.