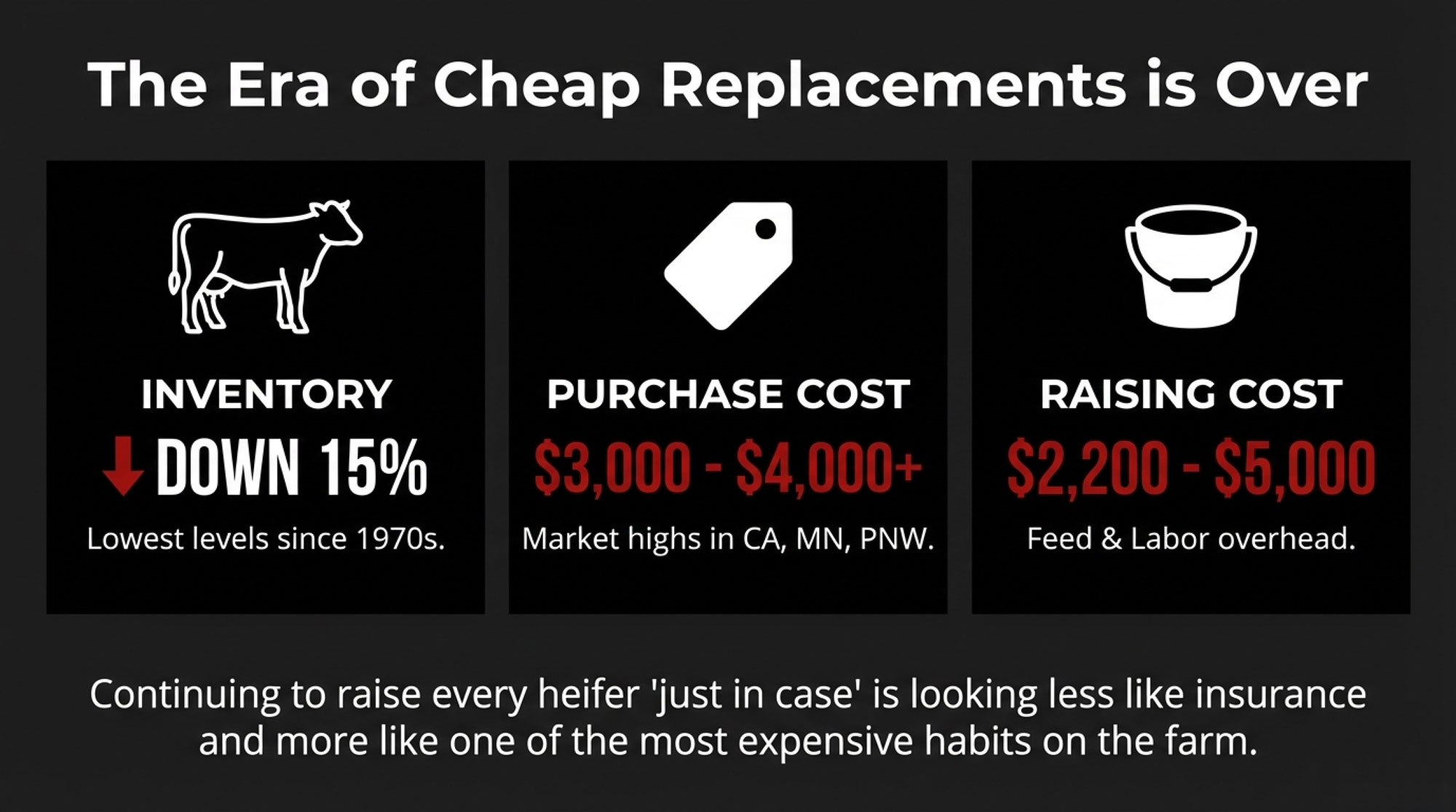

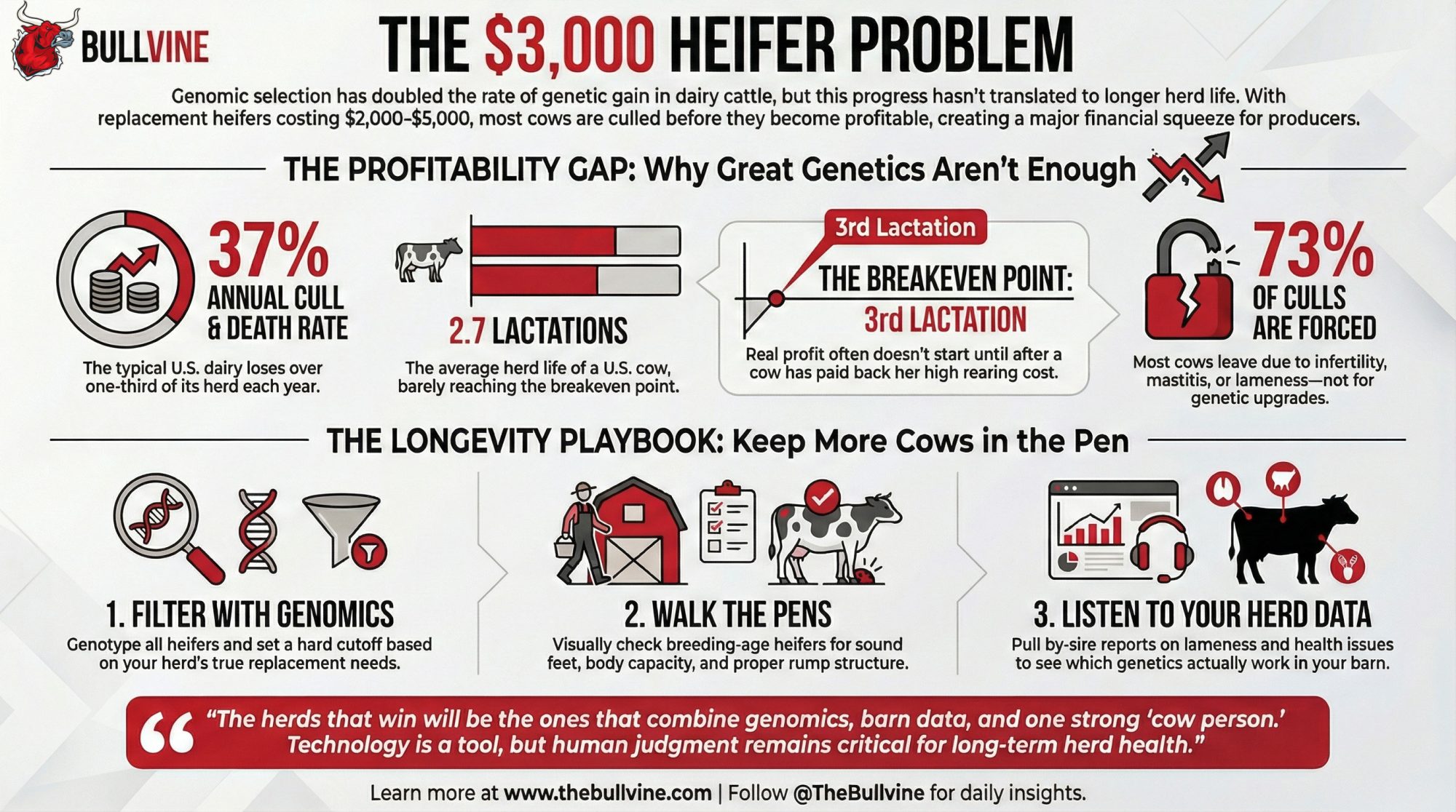

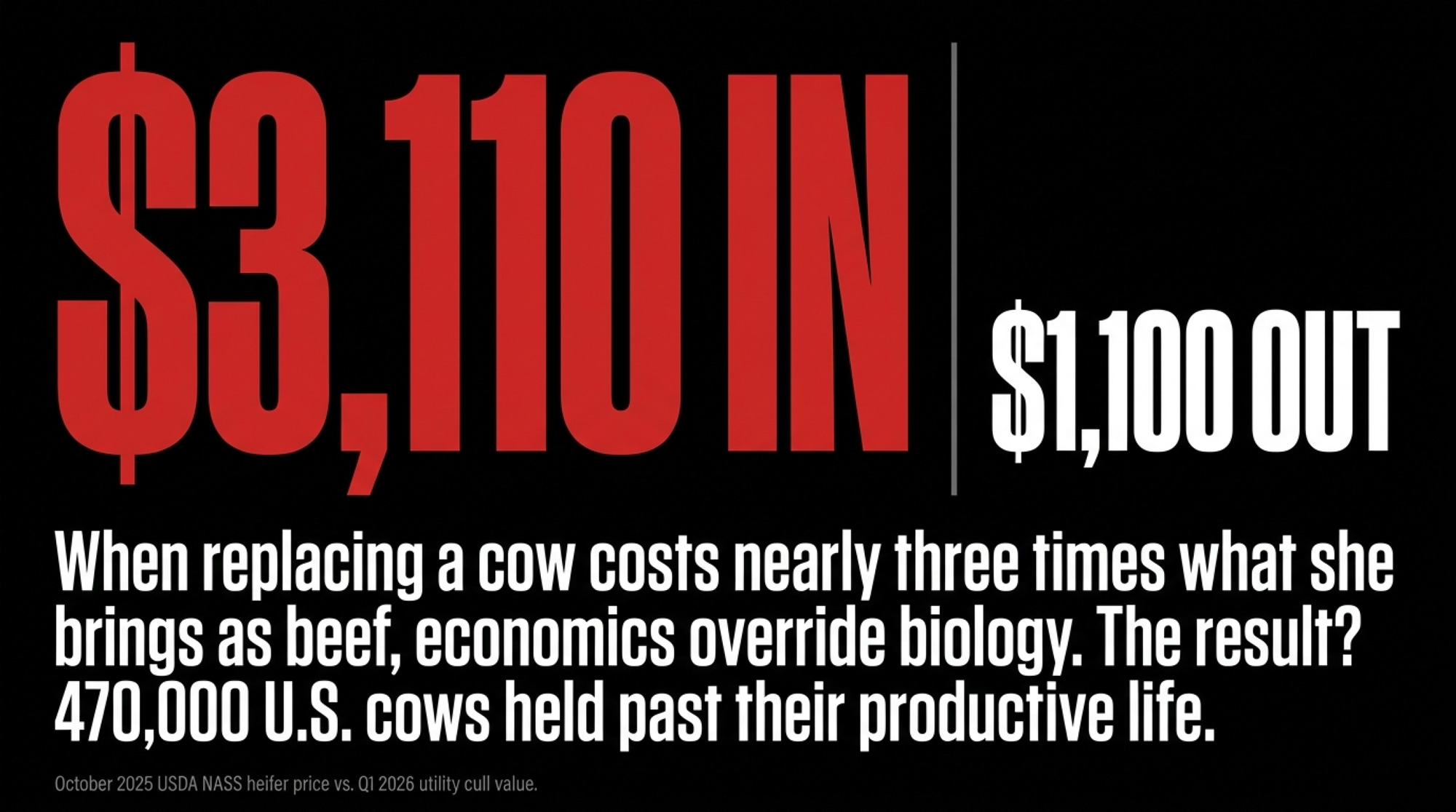

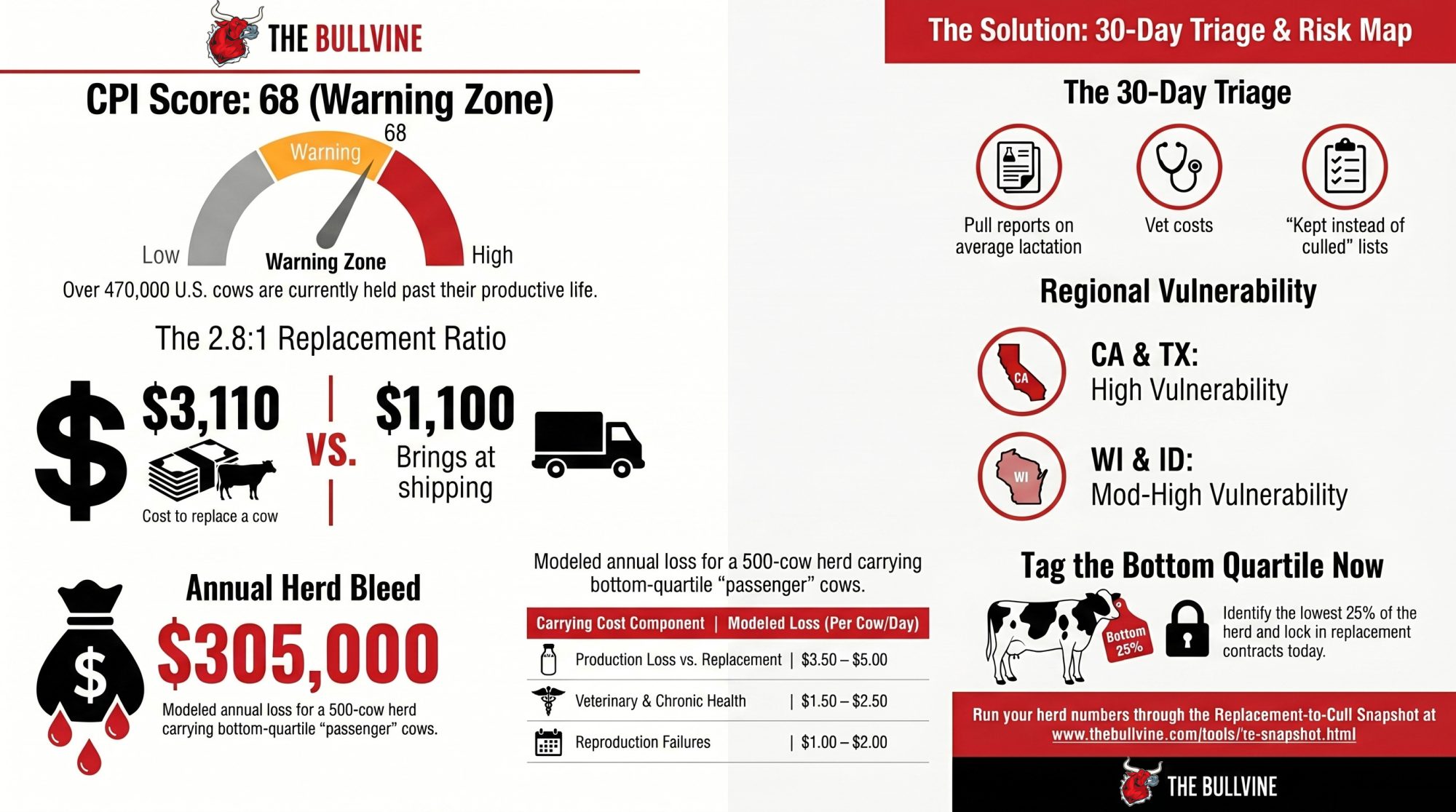

$3,110 to replace her. $1,100 to ship her. That ratio is why ~470,000 U.S. cows are still in stalls they’d have left in 2019 — and why The Bullvine’s CPI just flipped to 68. Warning Zone.

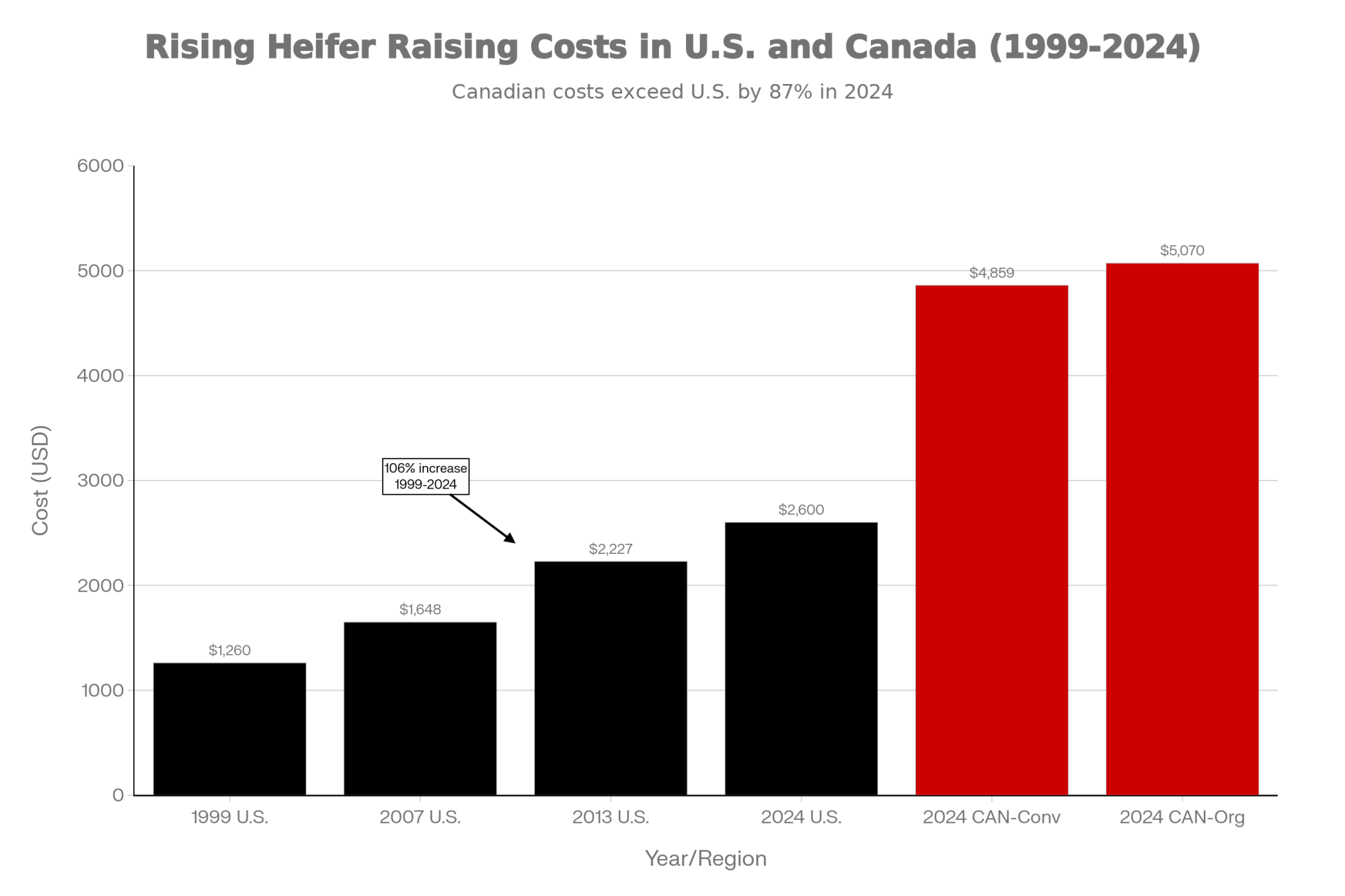

Picture a 500‑cow Wisconsin‑style herd sitting across from its lender this spring. Margin over feed dairy 2026 math says $255,000–$305,000 a year is walking out of that barn in the Bullvine model — a $205,500 milk‑over‑cost gap plus $50,000–$100,000 in bottom‑quartile carrying cost. Every culling decision runs into the same wall: the October 2025 USDA NASS Agricultural Prices release (the most recent heifer series) recorded replacement dairy heifers at a record $3,110/head.

The scene above is a composite drawn from Bullvine modeling on a representative Wisconsin 200–700 cow family operation. Milk price and cost‑of‑production inputs are national ranges applied to a Federal Order 30 (Upper Midwest) representative herd; your Order and cost structure will shift the output. Numbers throughout this piece are USDA and industry sourced; the operator is illustrative.

The cull check on the other side? Roughly $1,100/head for dairy utility cows, with better cuts clearing $1,400–$1,600in hot beef markets (USDA AMS National Weekly Cull Cow & Bull Summary, Q1 2026 range — see methodology appendix for the specific weekly reports used). That puts the replacement‑to‑cull ratio between 1.9:1 and 2.83:1.

| Market Case | Cow/Heifer Value | Replacement-to-Cull Ratio | Editorial Read |

| Dairy utility cull | $1,100/head | 2.83:1 | Maximum pressure to defer culling |

| Strong beef-market cull | $1,400/head | 2.22:1 | Still expensive to replace |

| Hot beef-market cull | $1,600/head | 1.94:1 | Better exit value, but not enough relief |

| Replacement dairy heifer | $3,110/head | Baseline | The price wall driving the trap |

When replacing a cow costs nearly three times what she brings as beef, the economics override the biology. That’s how you get to The Bullvine’s modeled estimate of roughly 470,000 U.S. cows held past their productive life — the first piece of the trap.

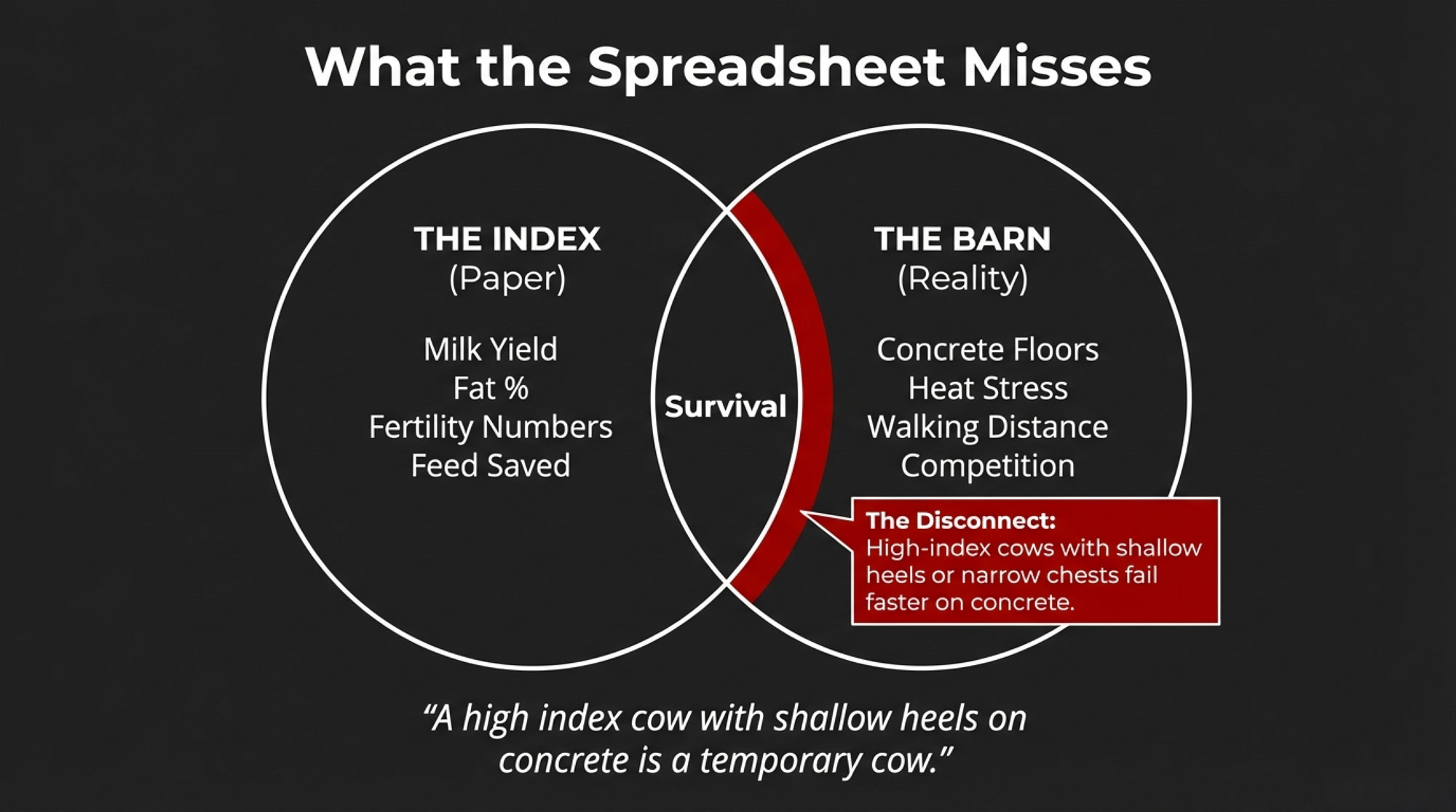

“The most expensive cow in your barn isn’t the high‑index yearling you just bought. It’s the lame third‑lactation cow you can’t afford to cull.”

The Most Expensive Cow In Your Barn Isn’t The Heifer

The most expensive cow in your barn isn’t the high‑index yearling you just bought.

It’s the lame third‑lactation cow you can’t afford to cull.

She’s giving somewhere around 60 lb/day. Vet bills stack. Repro has stalled. Every instinct says ship her — until you look at the heifer market and flinch.

That flinch, repeated across the country for 18 months, is the structural story of 2026 U.S. dairy.

The Retention Trap Your P&L Won’t Show You

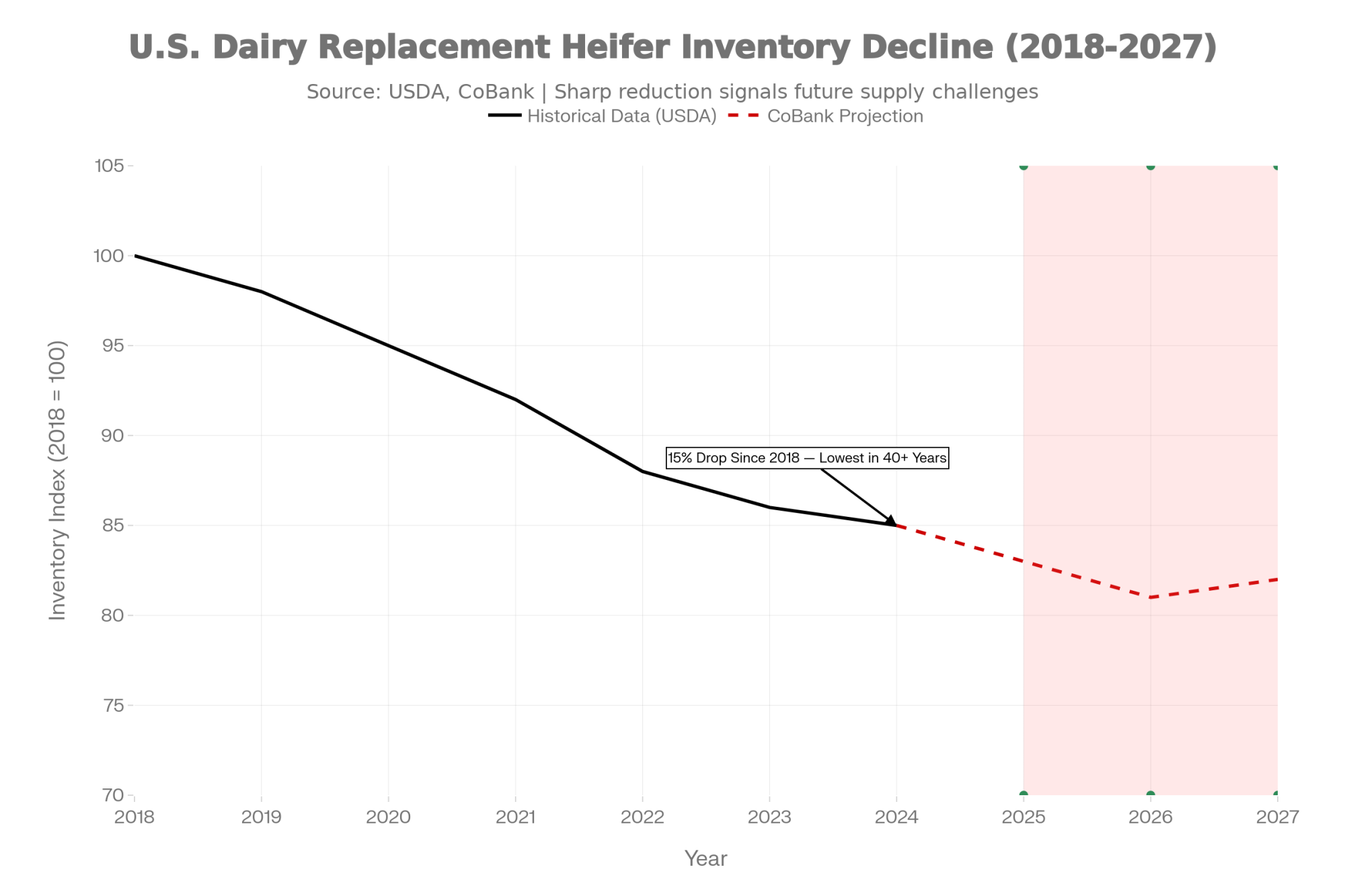

On paper, the U.S. herd looks strong. USDA NASS reports February 2026 milk cow inventory at 9.62 million head, up 211,000 year‑over‑year — the largest U.S. monthly inventory since 1994 per the NASS historical milk cow series (specific comparison month cited in methodology appendix). Total 2025 milk output ran roughly 232 billion lb, up about 2.6% over 2024.

Everyone assumed that meant expansion. It doesn’t. It’s hoarding — and the slaughter data says so in plain English.

Since September 2023, U.S. producers have culled an estimated 611,600 fewer dairy cows than the five‑year rolling pace, per USDA AMS weekly Federally Inspected slaughter data (Sept 2018–Aug 2023 baseline, roughly 3.0M head/yr; full baseline table in the methodology appendix). 2025 dairy cow FI slaughter totaled around 2.53 million head — the lowest U.S. annual FI total since 2011 based on AMS federally inspected series.

Co‑op briefings track the heifer shortage daily. Almost nobody is tracking what’s piled up on the other side of the barn.

The Shadow Loss Your P&L Won’t Flag

Your P&L is lying by omission. It tracks what you spent on feed, but it ignores the 10 lbs of milk you didn’t ship because a lame cow is occupying a prime stall. That’s the Shadow Loss — and it’s the most dangerous number in your barn.

The Bullvine‑modeled $50,000–$100,000/year bottom‑quartile drag on a 500‑cow herd isn’t a P&L line. It’s a shadow loss. Modeled range; actual values vary by herd, region, and breeding program. The underlying carrying‑cost methodology draws on USDA price data, typical herd records, and extension‑style budgets, triangulated against the Cornell Dairy Profit Monitor framework, Miner Institute reproductive economics, and Penn State Extension dairy decision tools.

Want your own number fast? The Bullvine Replacement‑to‑Cull Snapshot at thebullvine.com/tools/rc-snapshot.html takes your herd size, current heifer price, local cull value, and deferred‑cow count and spits out a herd‑specific pressure read with a prioritized bottom‑quartile action list. Same math as the published CPI. Your inputs.

How Deferred Culling Bleeds A 500‑Cow Wisconsin Herd

The Bullvine CPI workup models the bottom 20–25% of a typical herd carrying roughly – per cow per day in drag once production loss, vet cost, reproduction failures, and stall opportunity cost are stacked. These are Bullvine‑modeled ranges built on extension‑style budgets, not cited external point values; the full derivation sits in the carrying‑cost worksheet.

| Carrying‑Cost Component (Bottom Quartile) | Modeled $/Cow/Day | Why It Matters |

| Production loss vs a younger replacement | .50–.00 | Aging cows commonly trail herd average at –/cwt milk, per CDCB lactation‑curve data and extension references cited in the worksheet. |

| Veterinary costs (lameness, mastitis, metabolic) | .50–.50 | Chronic issues compound with lactation number. |

| Reproduction failures (extra days open, repeats) | .00–.00 | Each extra open day past mid‑lactation costs real margin. |

| Stall opportunity cost | .00–.50 | Every bottom‑quartile cow blocks a springing heifer. |

| Total modeled carrying cost | .00–.00 | The barn math on the “cheap” cow you kept. |

Running the Numbers: 500‑Cow Wisconsin‑Style Herd

Inputs: 500 cows | 75 lb/cow/day | –/cwt milk (national range) | –/cwt all‑in cost of production (national range) | Federal Order 30 representative; your Order and cost structure will shift the output | Modeling base: Bullvine CPI using USDA ERS Cost of Milk Production framing.

Step 1 — Daily and annual production 500 × 75 = 37,500 lb/day = 375 cwt/day 375 × 365 ≈ 136,875 cwt/year

Step 2 — Margin gap (if COP runs ~$1.50/cwt above milk price)

Note: this margin gap partially overlaps with the component‑premium gap discussed in “The $11 Billion Sorting Machine” below. Don’t stack them.

136,875 × $1.50 ≈ $205,500/year negative margin

Step 3 — Bottom‑quartile drag 100 cows × $8–$12/day × 365 ≈ $292,000–$438,000 gross

Net of replacement‑cost offset: the “drag” is the incremental loss from keeping the old cow versus a replacement in the same stall — it nets out the replacement cow’s own production contribution, her own vet/feed load, and ordinary depreciation. The Bullvine model assumes ~75% of the gross carrying cost offsets against that counterfactual, leaving ≈$50,000–$100,000/year net drag. Full derivation in the carrying‑cost worksheet.

Step 4 — Total modeled bleed

| Loss Layer | Low Case | High Case | What It Means |

| Annual production | 136,875 cwt | 136,875 cwt | 500 cows × 75 lb/day |

| Milk-over-cost gap | $205,500/year | $205,500/year | Negative margin at $1.50/cwt gap |

| Net bottom-quartile drag | $50,000/year | $100,000/year | Deferred cows occupying better stalls |

| Total modeled bleed | $255,500/year | $305,500/year | The lender-facing number |

| Per cow equivalent | $511/cow/year | $611/cow/year | Pain spread across the whole herd |

Modeled for an illustrative 500‑cow Wisconsin operation on national milk and COP ranges. Your number will differ. Plug your own cow count, pounds, COP, and bottom‑bucket count into the Replacement‑to‑Cull Snapshot at thebullvine.com/tools/rc-snapshot.html for a herd‑specific output.

That’s the formula your lender is already running. Write it on your own whiteboard.

More from The Bullvine — Tier 3 economics: Why Your 2026 Budget Is Lying to You: USDA $18.95 Milk vs. $19.14 Costs.

Why Did The Bullvine Build A New Index For This?

The CPI exists because no one else was tracking the inverse of the heifer shortage. Every co‑op briefing reports how few heifers are coming. None publish how many cows are still in the barn that should have already left.

To The Bullvine’s knowledge, the CPI is the first published composite index scoring deferred culling and the replacement shortage together as a single trackable number. USDA doesn’t publish it. Land‑grant extensions don’t. The gap was real. The math could be done. Here’s how.

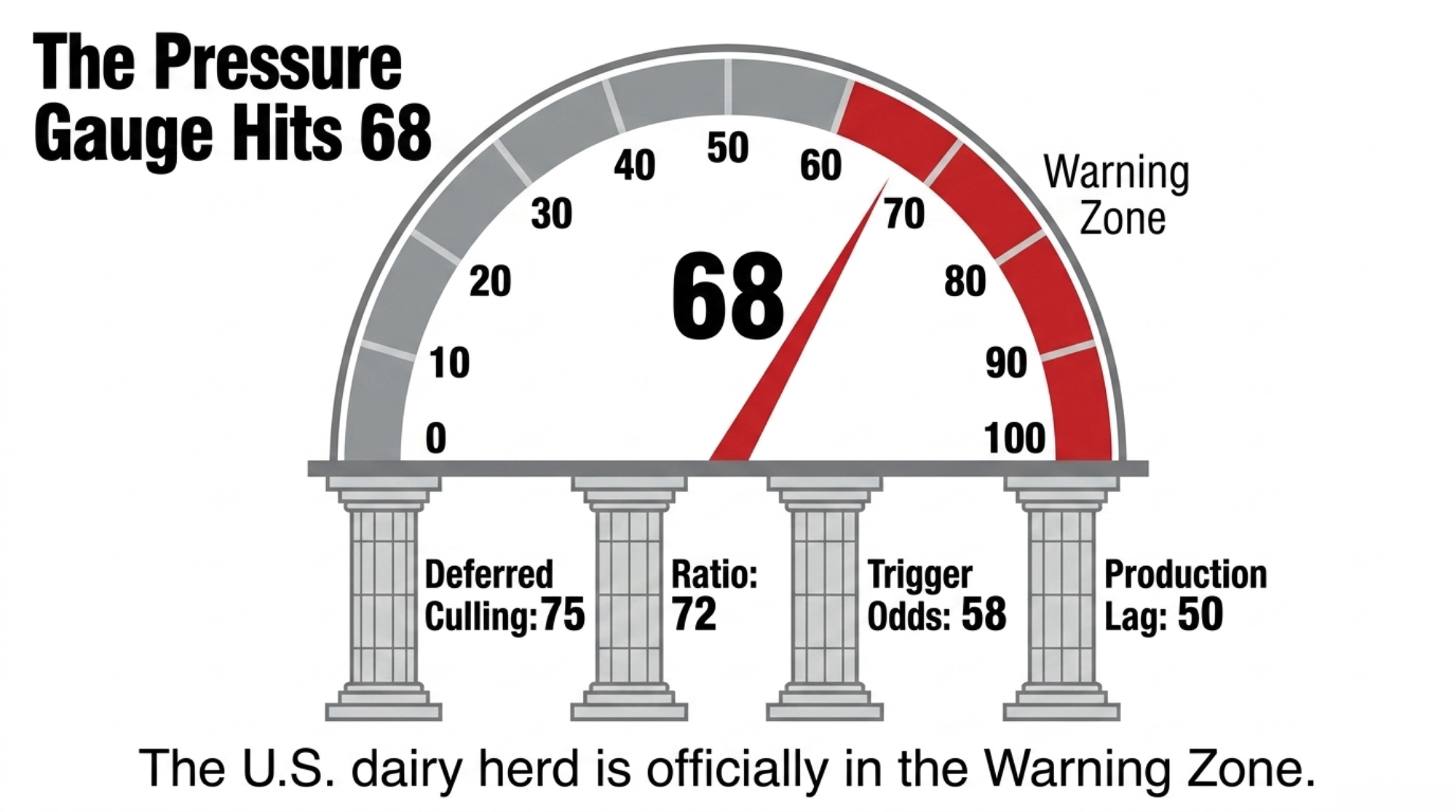

How The CPI Reads The Herd

Four components composite into a 0–100 score, updated monthly. Inputs and weights are public.

| Component | What It Measures | Current Value | Sub‑Score | Weight |

| Deferred Culling | Cows retained past productive life | ~470,000 head | 75 | 30% |

| Replacement‑to‑Cull Ratio | Economic incentive to defer | 2.83:1 | 72 | 25% |

| Production Lag | Genetic potential vs actual yield | ~144 lb implied vs 200–220 lb trend | 50 | 20% |

| Trigger Odds | Probability of a correction catalyst | Borderline high | 58 | 25% |

| Composite CPI | April 2026 | — | 68 | — |

The Volatility Premium: Why The Reading Is 68, Not 65

The straight weighted composite lands at 65.0 (75×0.30 + 72×0.25 + 50×0.20 + 58×0.25 = 22.5 + 18 + 10 + 14.5). The published reading of 68 carries a three‑point Volatility Premium on top of the raw math.

Here’s why. The four sub‑scores weight correction risks as if they add linearly. They don’t. HPAI exposure doesn’t just stack on top of deferred culling — it multiplies the weight of it, because the same aging cows are the animals most likely to drop hard in a disease event. Class III sub‑$16 for multiple prints doesn’t just add pressure — it compounds against a heifer market above $3,000, because producers facing both can’t cull or replace their way out.

The Volatility Premium quantifies that convergence risk in a single digit. Future monthly releases publish both the raw weighted composite and the premium‑adjusted reading side by side, so you can see when trigger‑convergence is doing the work and when it isn’t.

Deferred Culling — 30% weight

USDA AMS weekly FI slaughter since September 2023 runs ~611,600 head below the five‑year rolling baseline (Sept 2018–Aug 2023, roughly 3.0M head/yr; baseline table in the methodology appendix). Net of eventual exits and natural attrition, The Bullvine’s central estimate is ~470,000 head retained past productive life — plausible range 350,000–550,000 depending on assumed mortality and voluntary exit rates.

Even at 350,000, this component still scores in the 70+ band. The Warning Zone read doesn’t depend on the headline number being exact.

Replacement‑to‑Cull Ratio — 25% weight

$3,110 October 2025 USDA heifers against a $1,100 dairy utility cull gives a headline 2.83:1. On a stronger cull (~$1,600 in hot beef markets), the ratio drops toward 1.9:1. Either read, the economics tell producers to wait.

Production Per Cow — 20% weight

USDA NASS puts 2025 per‑cow production at 24,390 lb, up 218 lb over 2024 — essentially on pace with the 200–220 lb/yr genetic trend implied by CDCB data. February 2026 per‑cow production came in at 1,899 lb, just 12 lb above February 2025. If that February pace held for all 12 months, the implied annual gain would run near 144 lb — short of genetic potential.

That’s a conditional read, not a measured 12‑month result. But it’s where the Warning Zone signal lives.

Trigger Probability — 25% weight

- Class III: $14.59 Jan 2026, $14.94 Feb 2026, $16.16 Mar 2026 (USDA AMS class prices).

- April 2026 WASDE projects 2026 average Class III at $16.90/cwt.

- Corn ending stocks ~2.127B bu, 14.6% stocks‑to‑use, season‑average $4.15/bu (April 2026 WASDE‑670).

- IDFA capacity tracker tallies $11B+ in new or expanded U.S. dairy processing capacity through 2028, across 50+ projects in 19 states (October 2025 release).

One more sub‑$16 Class III print and this leg alone pushes CPI deeper into Warning — before the Volatility Premium even recalculates.

What The CPI Doesn’t Tell You

The CPI is a national composite. It reads industry‑wide pressure — not your barn.

- Regional variance. California and New York face different correction probabilities at the same national score.

- Herd‑size variance. Large‑herd financial dynamics differ from family operations.

- Genetic merit. Strong and weak breeding programs feel the same national CPI differently.

- Beef‑on‑dairy mix. Herds heavy on beef‑cross calf revenue face different replacement math.

- Trade shock. Export collapse shows up only through sustained Class III pressure inside Component 4.

Regional and herd‑size CPIs are in development as Phase 2. For a herd‑specific read today, run your numbers through the Replacement‑to‑Cull Snapshot at thebullvine.com/tools/rc-snapshot.html.

What Does CPI 68 + $3,000 Heifers Mean For Your Herd?

The Bullvine built this Decision Matrix so this doesn’t stay theoretical.

| CPI Score | Heifers >$3,000 | Heifers $2,000–$3,000 | Heifers <$2,000 |

| 30–50 (Stable–Building) | Normal cull pace; map 2027 replacement pipeline. | Normal cull pace; opportunistic purchases. | Cull freely; replace aggressively. |

| 50–70 (Building–Warning) | Identify lowest‑quartile cows; lock replacement contracts. | Accelerate culling of obvious passengers. | Cull hard and refresh herd age. |

| 70–80 (High Warning) | Cull lowest quartile only as fast as replacements allow. | Cull aggressively; secure replacements now. | Maximize herd turnover. |

| 80+ (Correction Imminent) | Cull aggressively only if replacements secured. | Cull now; expect heifer prices to react. | Full herd refresh, if balance sheet allows. |

At CPI 68 with >$3,000 heifers, the U.S. sits in the 50–70 × >$3,000 cell. Translation: tag your bottom quartile and pre‑position replacement access now — not after the correction starts.

Companion analysis — Tier 3 economics: The $3,000 Heifer Hangover: How Beef‑on‑Dairy Emptied Your Pipeline.

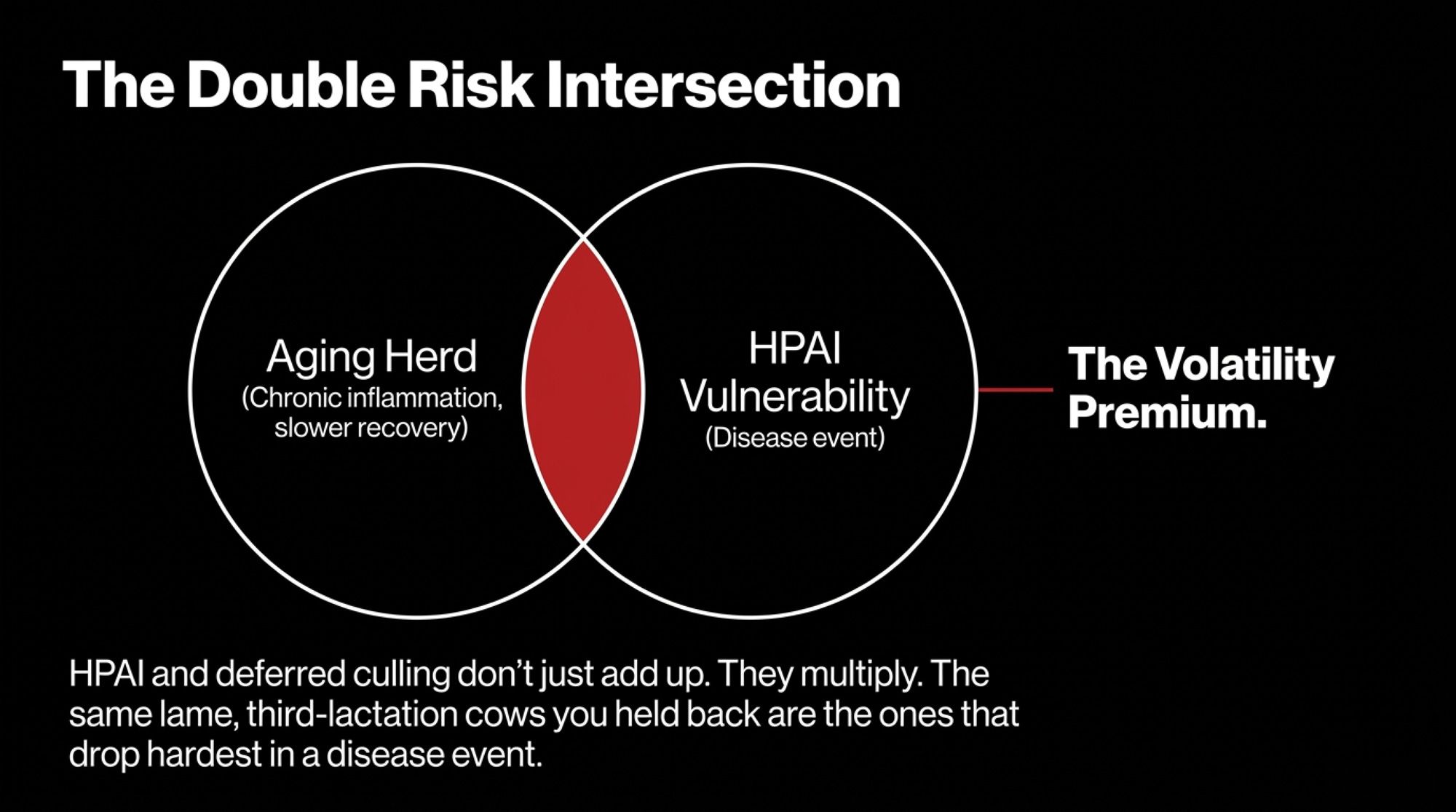

Why HPAI Makes Deferred Cows A Double Risk

Older, deferred cows aren’t only an economic problem. They’re also the animals most at risk in a disease event.

Immune function declines with age. Third‑, fourth‑, and fifth‑lactation cows carry more cumulative stress, more chronic inflammation, and slower recovery than first‑ and second‑lactation cows. They’re more likely to carry subclinical mastitis, lameness, or metabolic issues that blunt immune response — a pattern consistent with published veterinary literature on age‑linked immune competence in lactating cattle in the Journal of Dairy Science and Veterinary Clinics of North America: Food Animal Practice.

In an HPAI event, those are the cows that drop hard in milk, recover slowly, and are most likely to be culled post‑outbreak. A herd that has been deferring culls for 18 months is, by definition, stacked with those animals. CPI 68 plus an HPAI event isn’t risk on top of risk. It’s the same risk hitting the same cows twice. That’s what the Volatility Premium is pricing.

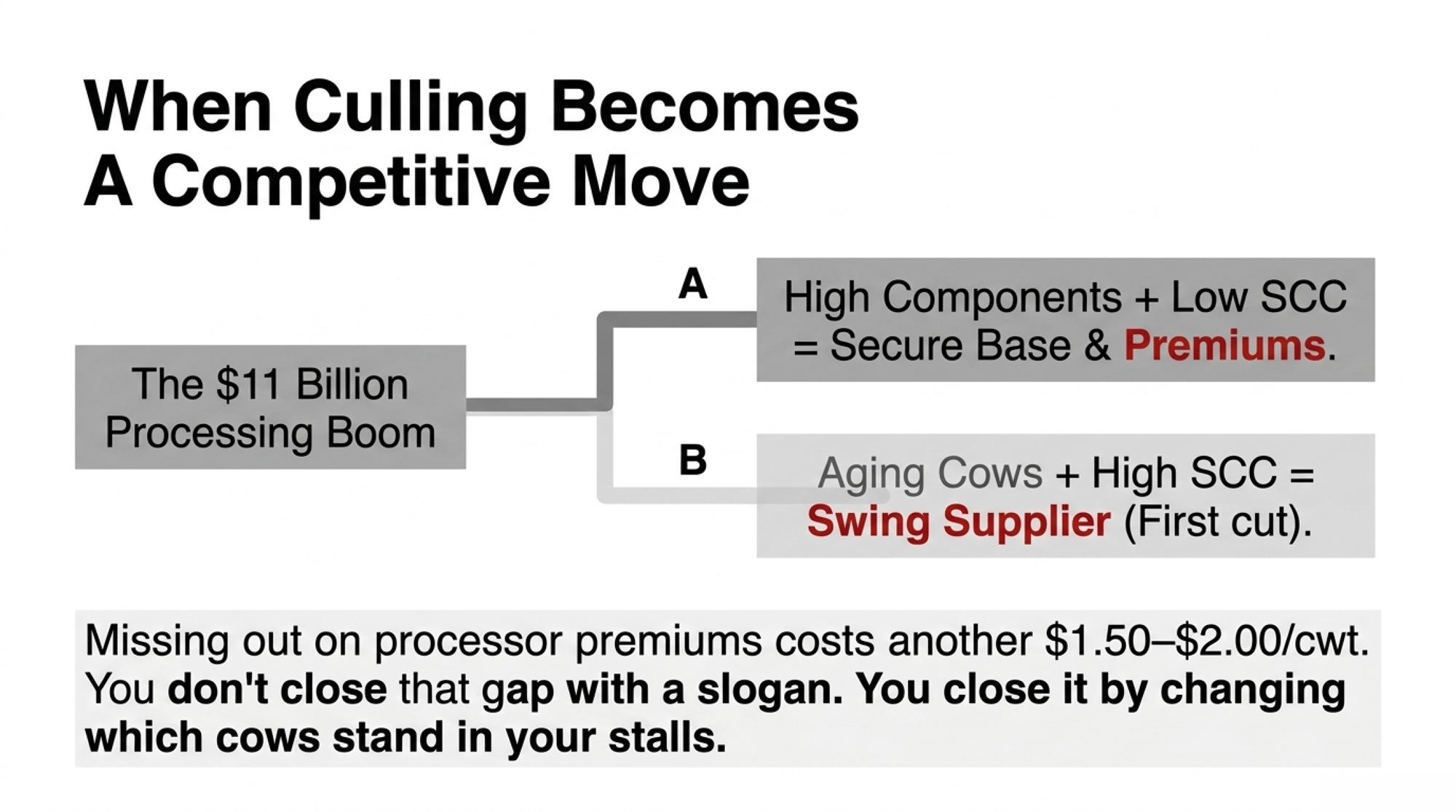

The $11 Billion Sorting Machine

Processors are pouring concrete for plants the deferred herd can’t fully service. IDFA tracks $11B+ in new and expanded U.S. dairy processing capacity through 2028 — 50+ projects in 19 states, heavy on cheese, whey, and high‑protein ingredients. Those plants are built for high‑component, low‑SCC milk running 12 months a year.

What does $11 billion in new concrete actually need? Components. SCC that doesn’t kill shelf life. Supply they can count on.

Two farm‑level outcomes:

- High‑component, low‑SCC herds get base volume and more secure deals.

- Average‑component, higher‑SCC herds drift into “swing supplier” territory — first cut when plants are long, last in line for premiums.

This component/quality gap partially overlaps with Step 2 in the barn‑math box above. Don’t stack them.

Missing $1.50–$2.00/cwt in component and quality premiums on 136,875 cwt is $205,000–$274,000/year in Bullvine modeling. Same order of magnitude as the deferred‑culling bleed. You don’t close that gap with a slogan. You close it by changing which cows stand in your stalls.

Continue the series — Tier 3 analysis: The $11 Billion Dairy Rush: Your 18‑Month Window to Lock in Processor Premiums.

The 438,844 Missing Heifers

The culling mess exists because of the heifer mess.

CoBank’s Dairy Heifer Inventories to Shrink Further Before Rebounding in 2027 (August 2025), read alongside USDA Cattle inventory data, implies approximately 355,000 fewer dairy replacements in 2025 than 2024, and another ~440,000 fewer in 2026 than 2025 (specific CoBank table referenced in the methodology appendix). Dairy heifers over 500 lb now sit just under 4 million head, a 20‑year low per USDA Cattle Jan 2026.

The deficit traces to the 2023–24 beef‑on‑dairy wave — sexed semen on the top, beef semen on the rest, beef‑cross calves clearing $400–$800/head above Holstein bull calves per Livestock Marketing Information Center weekly summaries and trade‑press auction reporting across 2023–24. Calf checks cashed. Replacement gap now.

CoBank’s outlook is blunt: inventories shrink through 2026 and only start rebounding in 2027. Until then, a structural heifer deficit runs underneath everything. That’s why The Bullvine runs the CPI and the Pipeline Tracker™ as a pair — one asks how many cows should have already left, the other asks how many heifers are actually coming 24 months out.

When 470,000 Cows Finally Move

Deferred culling doesn’t unwind politely. When some producers ship, more follow. The Bullvine’s scenario modeling, anchored to USDA slaughter and production data, sketches four plausible paths.

| Scenario | Trigger | Cows Exiting | Timeline | Milk Impact | Modeled Class III Effect |

| Slow Release | No major trigger | ~150,000 | ~12 months | ~ –1–2% | +$0.50–$1.00/cwt |

| Moderate | Class III <$16 for 3+ months | ~300,000 | 6–9 months | ~ –3% | +$1.50–$2.50/cwt |

| Full Correction | Multiple financial triggers converge | ~470,000 | ~90 days | ~ –5% | +$2.00–$3.00/cwt |

| Extreme (tail risk) | Financial triggers + disease event | ≥600,000 | <3 months | ~ –6% or more | +$3.00–$5.00/cwt |

These are modeled illustrative scenarios, not forecasts. The Extreme row is tail risk — a correction lining up with an HPAI event — and it’s the shape lender stress tests commonly include.

Drop Full Correction onto a 1,000‑cow, 75 lb/cow/day herd: 1,000 × 75 ÷ 100 × 365 = 273,750 cwt/year × $2.50/cwt = $684,375/year extra gross milk revenue if the rally lands in your tank.

Whether you keep that –/cwt depends on whether your cow mix and components qualify for the premium tier when the move hits. That’s the barn math on the upside.

Where Does The Pain Hit First?

Not evenly. Vulnerability scoring below reflects structural variables — herd size, replacement sourcing, cost structure — and is not an assessment of any individual operation or lender book.

| State | Feb 2026 Herd (000 head) | YoY Change | Vulnerability | Key Risk |

| California | 1,712 | +3 | HIGH | Largest herd; high costs; culled hard and early in the 2018–19 exit wave. |

| Texas | 718 | +34 | HIGH | Expansion built on purchased replacements. |

| Wisconsin | 1,290 | +25 | MODERATE–HIGH | 200–700 cow backbone squeezed on costs. |

| Idaho | 724 | +24 | MODERATE–HIGH | Growth state; replacement‑dependent. |

| New York | 653 | +21 | MODERATE | Aging infrastructure; cash‑flow‑driven deferral. |

Data source: USDA NASS Milk Production, February 2026.

California carries 1.712M cows and added just 3,000 head YoY. High replacement costs, water, and regulation load every culling decision. When margins compressed in 2018–19, California culled hard and early — a likely early indicator pattern worth watching in the national herd this cycle.

Texas grew by 34,000 cows to 718,000 — the biggest state gain, leaning most heavily on purchased replacements. A correction mid‑ramp means depreciating cows paid for at the top.

Wisconsin added 25,000 cows to 1.29M, but the backbone is still 200–700 cow herds. Those operators don’t carry the contract leverage of mega‑herds and are most likely holding marginal cows because no replacement path pencils without torching cash flow.

Idaho grew by 24,000 cows to 724,000 — replacement‑intensive throughput. Correction mid‑expansion is a double squeeze.

New York added 21,000 cows to 653,000, behind a cluster of announced regional processing projects tracked by The Bullvine against IDFA and New York State Ag & Markets filings. Specific project‑dollar totals are posted on the CPI methodology subpage. Deferred culling there is often cash‑flow‑driven.

Lender screening rule: fastest growth + highest reliance on purchased replacements = most exposed when the CPI climbs.

Breeding Your Way Out Of The Next Trap

If CPI 68 says clear your bottom 25%, the next question is who stands in those stalls next.

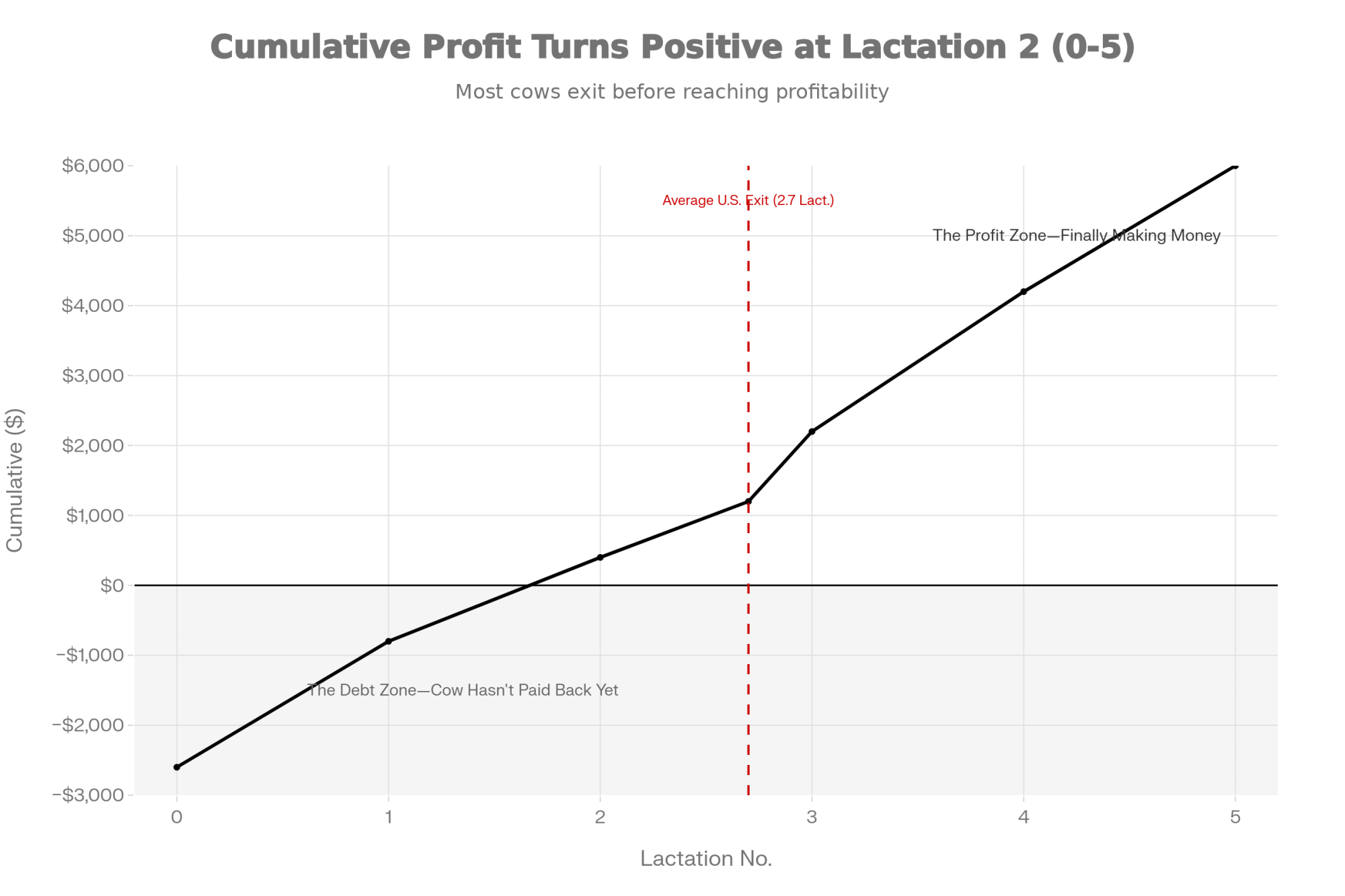

Paying $3,110 for a replacement only pencils if she stays out of the bottom quartile long enough to earn back. Extension cost work implies roughly a three‑lactation payback window at today’s heifer prices and milk values, while average U.S. productive life continues to run well short of that window in CDCB genetic trend reporting.

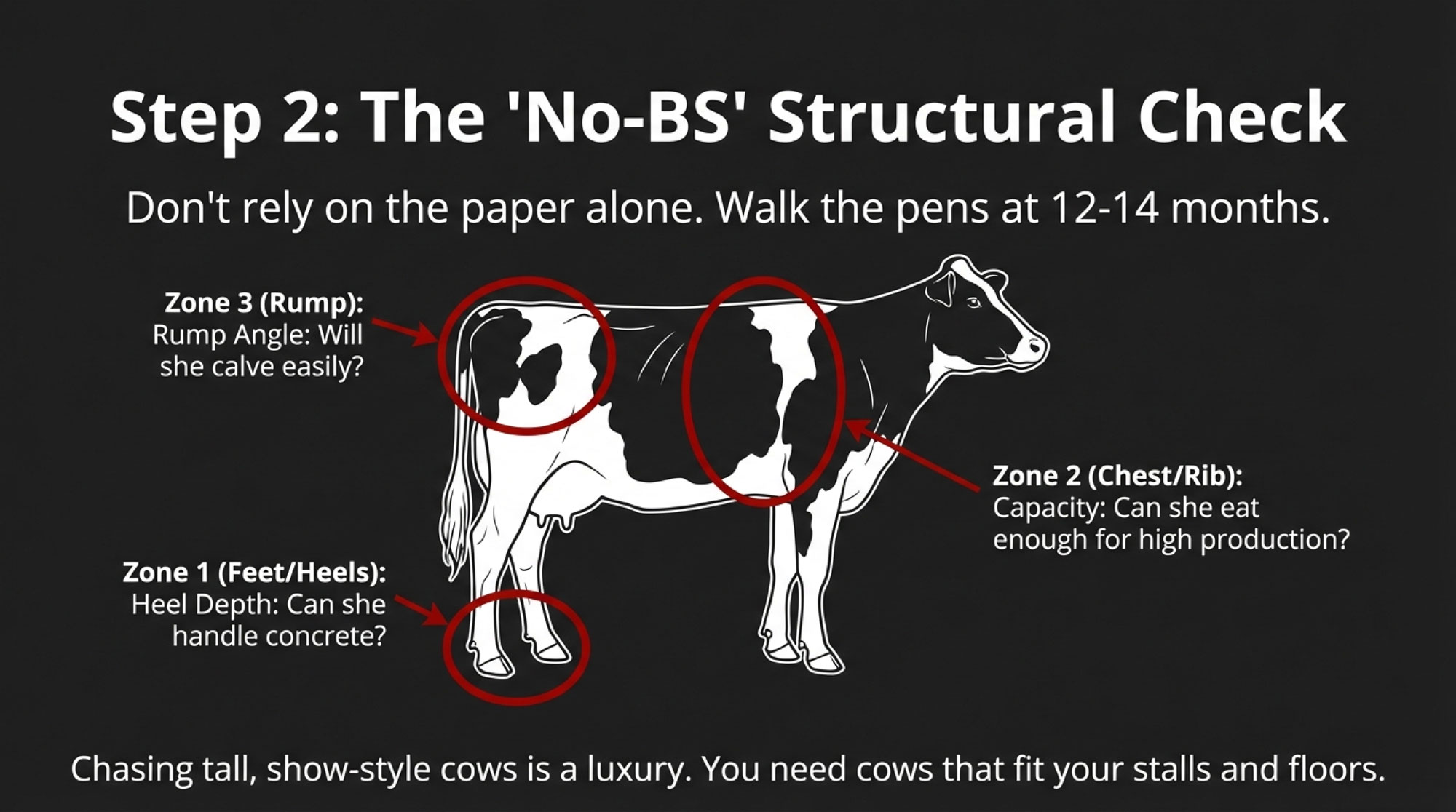

More herds are quietly shifting sire lists away from one more notch of yield and toward Productive Life, Daughter Pregnancy Rate, and health traits. In a $3,000‑heifer world, you’re better off with cows you still like in third lactation than cows you’re debating at second.

Companion genetics read — Tier 2: Sire Selection for Longevity in a High‑Heifer‑Cost Cycle.

The 30‑Day “pull three reports” step below pairs with this hidden‑gem analytics piece: Reading Your DHIA Report Like a Lender.

The 30/90/365‑Day Playbook for 200–700 Cow Deferred Herds

30‑Day Actions: Triage

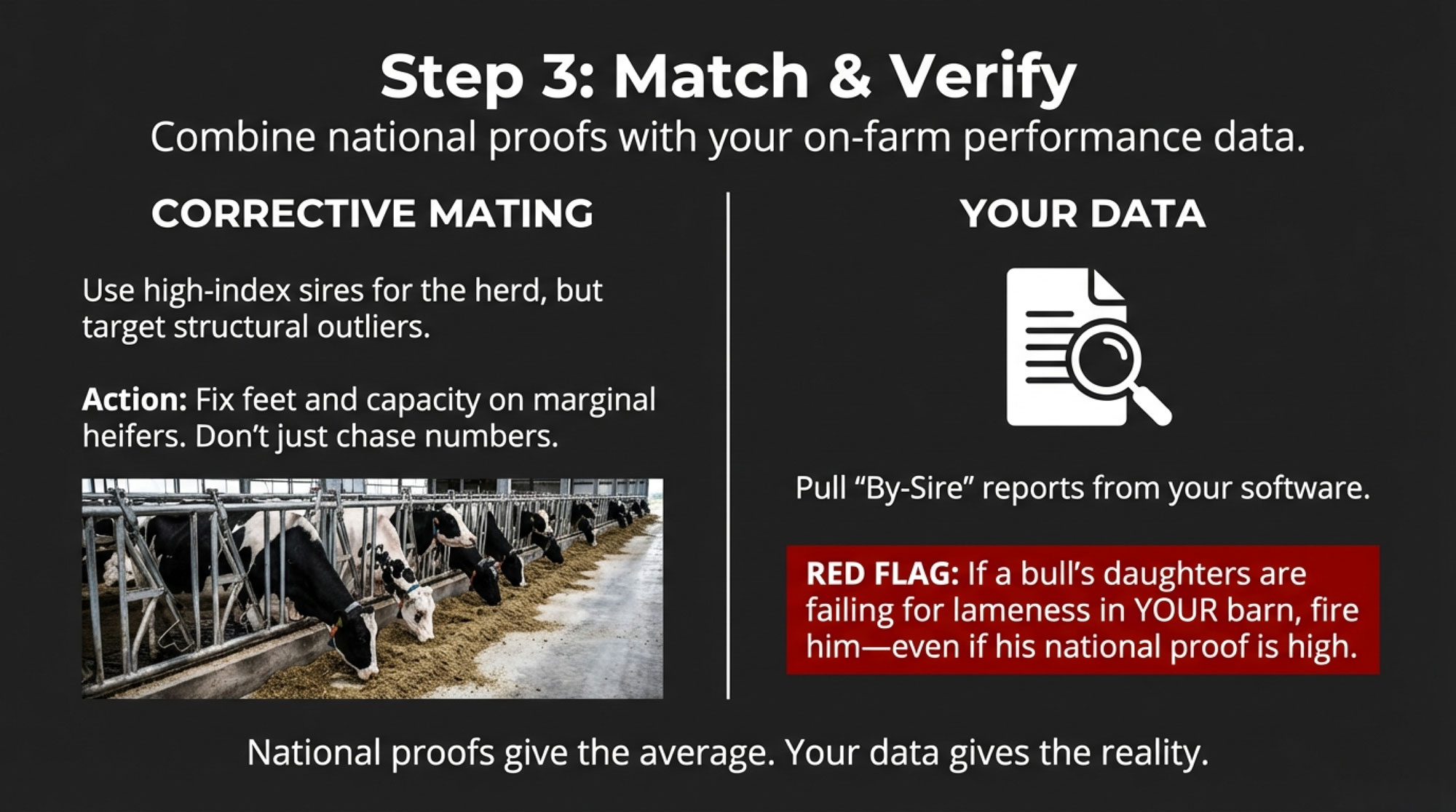

Pull three reports from your herd software. Average lactation, vet cost per cow YoY, and a “kept instead of culled” list (cows you held in 2024–25 that would have shipped in 2019–20). Feed those numbers into the Replacement‑to‑Cull Snapshot the same afternoon. Requires: DHI and repro records, 20 minutes. Trigger: Average lactation >2.8 and vet cost/cow up YoY = you’re in the deferred cohort. Backfires when: You cull off software rank alone without checking repro status; some bottom‑rank cows are fresh and will climb.

Build your bottom‑quartile list. Rank by production, SCC, lameness, and days open. Tag each cow “ship within 6 months” or “re‑test at 6 months.” Requires: DHIA records and DC305/PCDart. Trigger: If your DSCR has been under 1.2 for three consecutive months on your lender’s reporting standard, treat the top third as urgent. DSCR covenant language varies — confirm with your loan officer. Backfires when: You empty stalls you can’t refill. Pair with the 90‑day replacement step below.

90‑Day Actions: Structural

Ship 25–35 cows from the bottom‑quartile list (8–12/month). Start with obvious passengers. Recheck vet cost/cow, bulk tank SCC, and daily shipped milk at Month 3. Requires: Replacement access or accepted lower cow count; freight and packer capacity. Trigger: If none of those three indicators improve, the hole is deeper than culling alone can fix. Backfires when: You ship without securing replacements and permanently shrink your base — fine if that’s the plan, a problem if it isn’t.

Lock replacement access. Heifer‑raising contracts, forward purchase agreements, or more sexed semen on your top 35–40%. Requires: 6–9 months for sexed semen to move through the pipeline; legal review on any forward contract. Trigger: Heifer prices break above $3,200 nationally, or your local replacement market tightens — pull this forward. Backfires when: Forward contracts signed at the top lock in peak prices. Build optionality where you can.

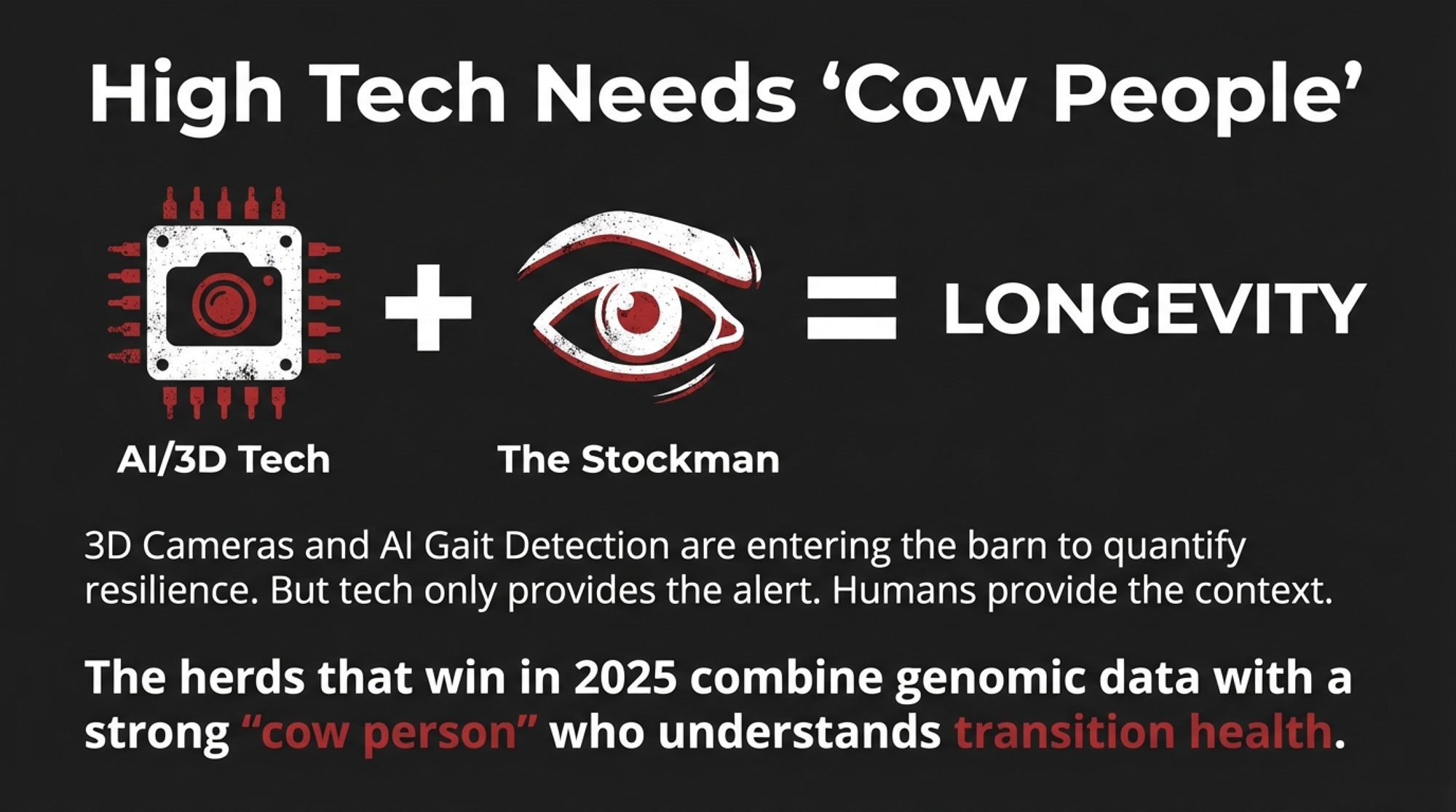

Tighten sire criteria on PL, DPR, and health. Requires: Genomic testing infrastructure and a breeding advisor aligned on PL/DPR weighting. Trigger: Average lactation trending up while production lags genetic trend = aging structurally, not just cyclically.

365‑Day Moves: Strategic

Clear 80–100 of the original bottom‑quartile cows; re‑run the diagnostic. Requires: Committed 12‑month cull and replacement schedule; lender in the loop. Trigger: Modeled annualized losses narrow by $50,000+ and cash‑flow draw slows — keep restructuring. Opportunity signal: If your components and SCC move you up a processor premium tier while Class III rallies into the Moderate or Full Correction band, you capture margin expansion your aging‑cow peers won’t. Backfires when: You keep a cow just to “earn back” the $1,000 you already spent on her vet bills. That vet check is gone. The only question left is what she produces tomorrow forward versus what a replacement produces in the same stall. Sunk cost is not a strategy.

Decide honestly at Month 12. Narrow the losses and rebuild, or plan a managed exit while cattle and heifer values still give you an equity‑preserving off‑ramp. Requires: Real data, not optimism. Accountant and lender at the table. Trigger:Equity ratio drifting below your lender’s covenant floor + two consecutive years of sub‑1.2 DSCR = managed‑exit conversation, not “one more year.” Backfires when: You wait for “one more good year” while deferred peers finally ship. That’s when heifer prices correct against you and cull prices soften.

Lender/advisor move: map CPI against your regional herd mix. Fastest‑growth, purchased‑replacement states (TX, ID) sit in a different risk band than flat regions. Portfolio exposure isn’t uniform.

The Turn: When Culling Becomes A Competitive Move

Run that same 500‑cow Wisconsin‑style herd forward 12 months in the model.

Average lactation is down. Vet cost per cow is flattening. Components trend toward the processor’s premium tier. The $205,500 margin gap hasn’t disappeared — but the $50,000–$100,000 bottom‑quartile drag has mostly retired.

A deferred‑herd peer down the road is still waiting. When the correction hits, everyone ships the same month. That’s when the lender’s “Can we afford to cull?” question flips to the only one that matters: Can we afford not to?

The CPI is a pressure gauge, not a guilt trip. Some cows are worth holding — young age structure, flat vet cost, production matching genetic expectations. If those conditions don’t describe your barn, the math isn’t ambiguous. Just uncomfortable.

What This Means For Your Operation

- Pull those three reports in the next 30 days and set them beside your last three milk checks. If you won’t, you’re not managing this risk — you’re hoping it doesn’t land on you.

- Run your numbers through the Replacement‑to‑Cull Snapshot today. Three minutes of inputs, a herd‑specific pressure score, a prioritized bottom‑quartile list, and a 30/90/365 plan calibrated to your barn.

- Three or more “yes” answers on the CPI diagnostic puts your behavior inside the 470,000‑cow deferred bucket. Fix it with a 12‑month plan, not one cull load.

- Watch Class III and your local heifer market together. Three straight sub‑$16 prints + heifer softening = shift from “prepare” to “act.”

- Plan culls, replacements, and sire selection on one whiteboard. A CPI‑driven cull plan that isn’t tied to replacement access and sire strategy just sets up the next deferred trap.

- Lenders and co‑ops: TX and ID expansion herds sit in a different risk tier than flat Northeast regions. Map your portfolio accordingly.

I grew up on a dairy farm where we knew every cow by name. We also knew when it was time to let one go.

That instinct hasn’t changed. But at $3,110 a replacement, the economics have overridden the instinct for hundreds of thousands of U.S. producers. The CPI is how we get the instinct back into the data.

— Andrew Hunt, Founder, The Bullvine

Run Your Herd Through The Replacement‑to‑Cull Snapshot

The Bullvine Replacement‑to‑Cull Snapshot

Your herd. Your numbers. Your pressure score.

Enter your cow count, current heifer price, local cull value, average lactation, vet cost per cow, and deferred cull count in the form below. The tool returns:

- A herd‑specific pressure score with sub‑component breakdown.

- A prioritized bottom‑quartile action list.

- A 30/90/365 plan calibrated to your inputs.

- A shareable PDF output you can bring to your lender or co‑op advisor.

Tool is editorial. Inputs are anonymized unless you opt in to a consulting follow‑up. The pressure score uses the same component math and weights as the published CPI and is not influenced by consulting engagements — see methodology below.

Methodology Note: How The Culling Pressure Index™ Is Built

The Culling Pressure Index™ is a monthly composite that quantifies deferred culling pressure in the U.S. dairy herd and estimates correction probability.

Update cadence. Published monthly, on the second Tuesday after the USDA NASS Milk Production release. Next update: Tuesday, May 12, 2026.

Version. CPI v1.0, April 2026.

Data inputs by component.

- Component 1 — Deferred Culling (30%). USDA AMS weekly FI Dairy Cow Slaughter vs a five‑year rolling baseline (Sept 2018–Aug 2023, ~3.0M head/yr). Full baseline table in appendix.

- Component 2 — Replacement‑to‑Cull Ratio (25%). USDA NASS Agricultural Prices for replacement heifers; USDA AMS National Weekly Cull Cow & Bull Summary for cull values (specific weekly reports cited in appendix).

- Component 3 — Production Lag (20%). USDA NASS Milk Production monthly data vs CDCB published genetic trends.

- Component 4 — Trigger Probability (25%). CME Class III futures, USDA Agricultural Prices, USDA WASDE corn stocks‑to‑use, IDFA processing capacity announcements.

Weighting rationale. 30% deferred culling (lagging indicator of accumulated risk); 25% ratio (economic driver of deferral); 20% production lag (herd‑quality drag); 25% trigger probability (correction timing).

Composite reading. The straight weighted composite for April 2026 is 65.0. The published reading of 68 includes a three‑point Volatility Premium for trigger‑convergence signals (HPAI × deferred culling, sustained sub‑$16 Class III × $3,000+ heifers). Future releases publish the raw and premium‑adjusted readings side by side.

Governance. The CPI score is editorial and is not influenced by Bullvine consulting engagements. Methodology changes are disclosed in monthly updates and historical scores are restated side‑by‑side. The embedded Replacement‑to‑Cull Snapshot at thebullvine.com/tools/rc-snapshot.html uses the same component math and weights as the published CPI.

Known limitations. State‑level data lags national data by 30–60 days. CDCB genetic trend data is smoothed annually. The natural‑attrition assumption behind the 470,000 retained‑cow estimate carries a sensitivity range of 350,000–550,000 head.

Versioning. v1.0 → v1.1 → v2.0. Material methodology changes will be flagged in monthly updates. Historical scores will be restated and presented as “as‑published” and “restated” series.

FAQ

What is the CPI? A monthly composite index, published by The Bullvine, scoring deferred culling pressure in the U.S. dairy herd and estimating correction probability.

Where does the data come from? USDA AMS FI slaughter, USDA NASS Milk Production and Agricultural Prices, CDCB genetic trends, CME dairy futures, USDA WASDE corn stocks‑to‑use. All inputs public.

What is the Volatility Premium? A qualitative adjustment on top of the raw weighted composite that prices trigger‑convergence risk — specifically HPAI exposure multiplying (not just adding to) deferred‑culling risk, and sustained sub‑$16 Class III compounding against $3,000+ heifer prices.

How is the Replacement‑to‑Cull Snapshot different from the published CPI? The published CPI scores the national herd monthly. The Snapshot at thebullvine.com/tools/rc-snapshot.html applies the same component math to your herd’s inputs and returns a herd‑specific score and action list. Both use the same methodology.

How is CPI different from the Pipeline Tracker™? Pipeline Tracker projects replacement heifer supply 24 months out. CPI measures retained‑cow pressure today. Together they form the most complete U.S. dairy supply read published.

Can I cite it? Yes. Recommended format: “The Bullvine Culling Pressure Index™, [Month Year]”

Does The Bullvine sell anything based on it? Yes — disclosed plainly. The Bullvine offers herd‑specific consulting engagements applying the CPI framework. The published CPI score and the Snapshot tool output are editorial; neither is influenced by consulting engagements.

Challenge The Model

Substantive challenges to the methodology are welcome. Write to cpi-feedback@thebullvine.com. Every substantive critique gets reviewed. Material responses are published in monthly updates.

Learn More

- From “Worst Dairy” to Zero Lame Cows: How CDCB’s New h² = 0.27 Trait Could Rewrite Lameness Genetics | The Bullvine — Saves you $337 per clinical case by leveraging mobility PTAs with triple the heritability of traditional scores. This field report delivers a 30/90/365-day playbook to slash lameness using CattleEye cameras and strategic sire filtering.

- The $3,000 Heifer Hangover: How Beef‑on‑Dairy Emptied Your Pipeline and Left the U.S. 800,000 Head Short | The Bullvine — Exposes the structural 800,000-heifer gap currently hollowing out barn capacity and processor security through 2027. This analysis follows the money on how beef-on-dairy profits cashed today jeopardize your operation’s long-term expansion and equity.

- The $3,500 Calf Question: What Dairy Farmers Need to Know About April 2026’s New CDCB Calf Health Evaluations | The Bullvine — Arms you with a tactical roadmap for April 2026’s new CDCB calf health evaluations to reduce mortality by 38%. It dismantles traditional rearing logic to deliver a 50% reduction in scours cases using data-driven genetic selection.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.