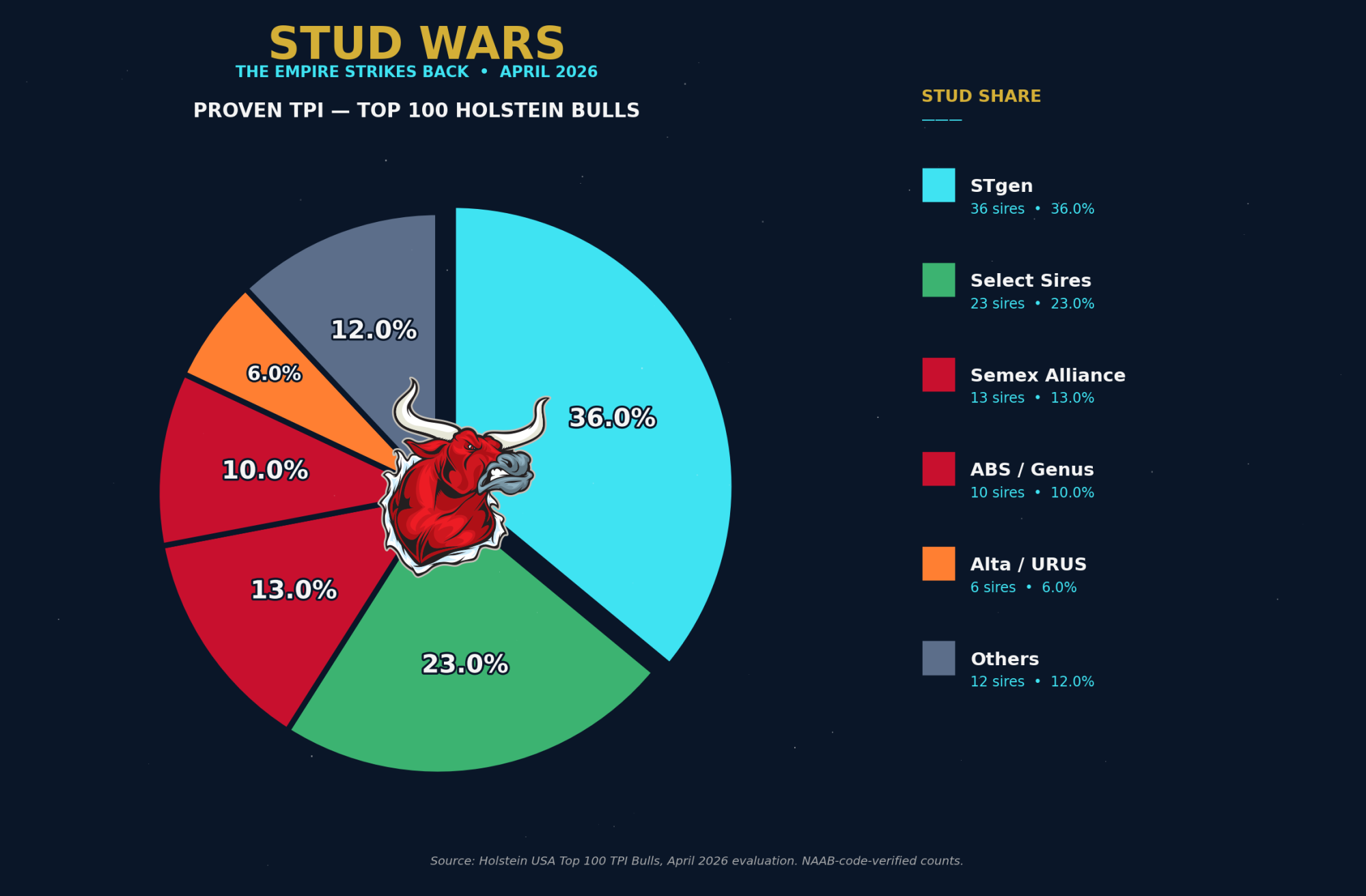

STgen owns 36% of the proven TPI top 100. Select Sires took 29.5% of the genomic top 200. United Sires — an independent breeder co-op founded in 2024 — grabbed 15% of the genomic top 200. And Zoetis just bought the lab pipes everyone else’s DNA flows through.

Three things hit at once on April 7, 2026.

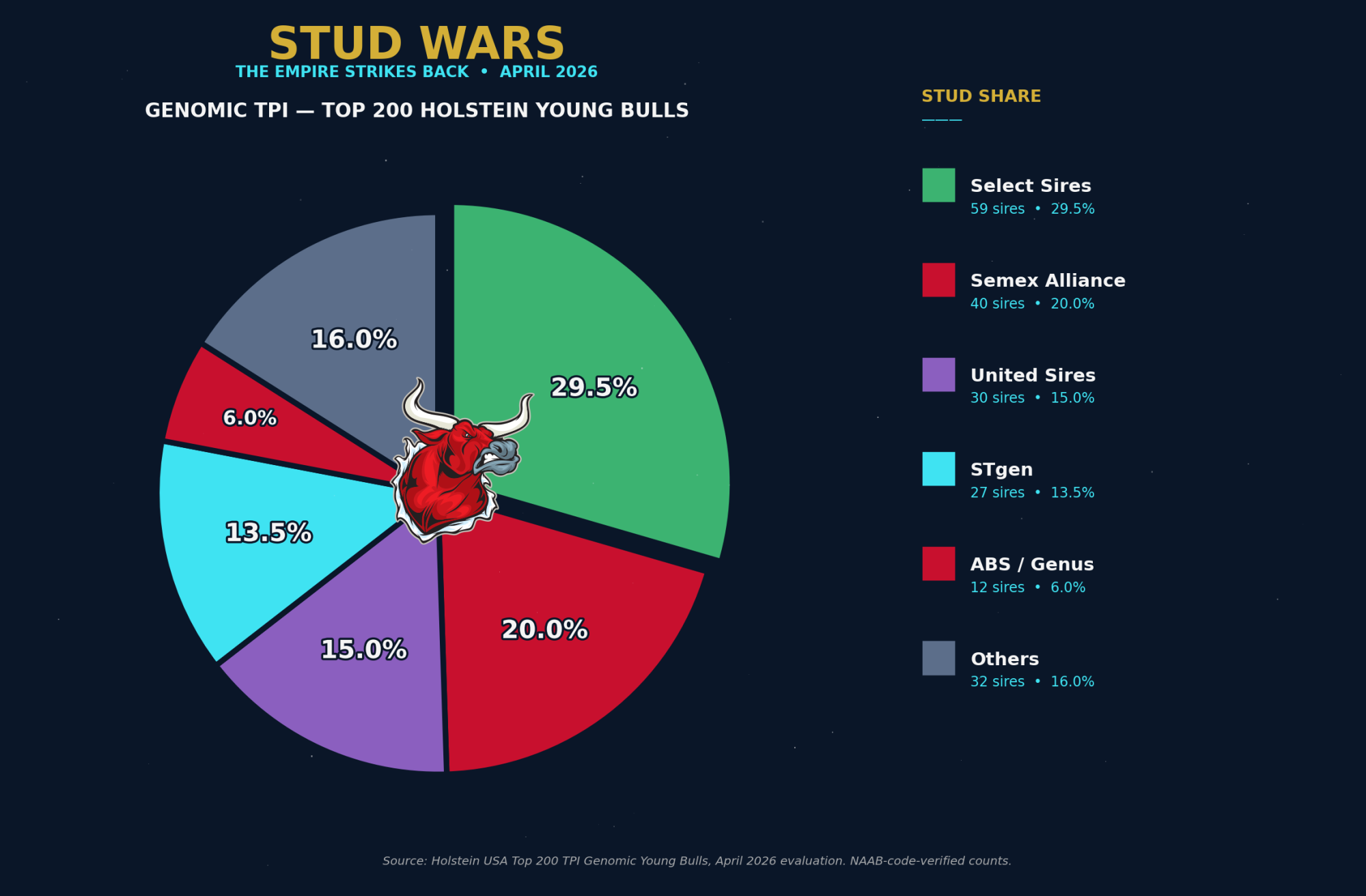

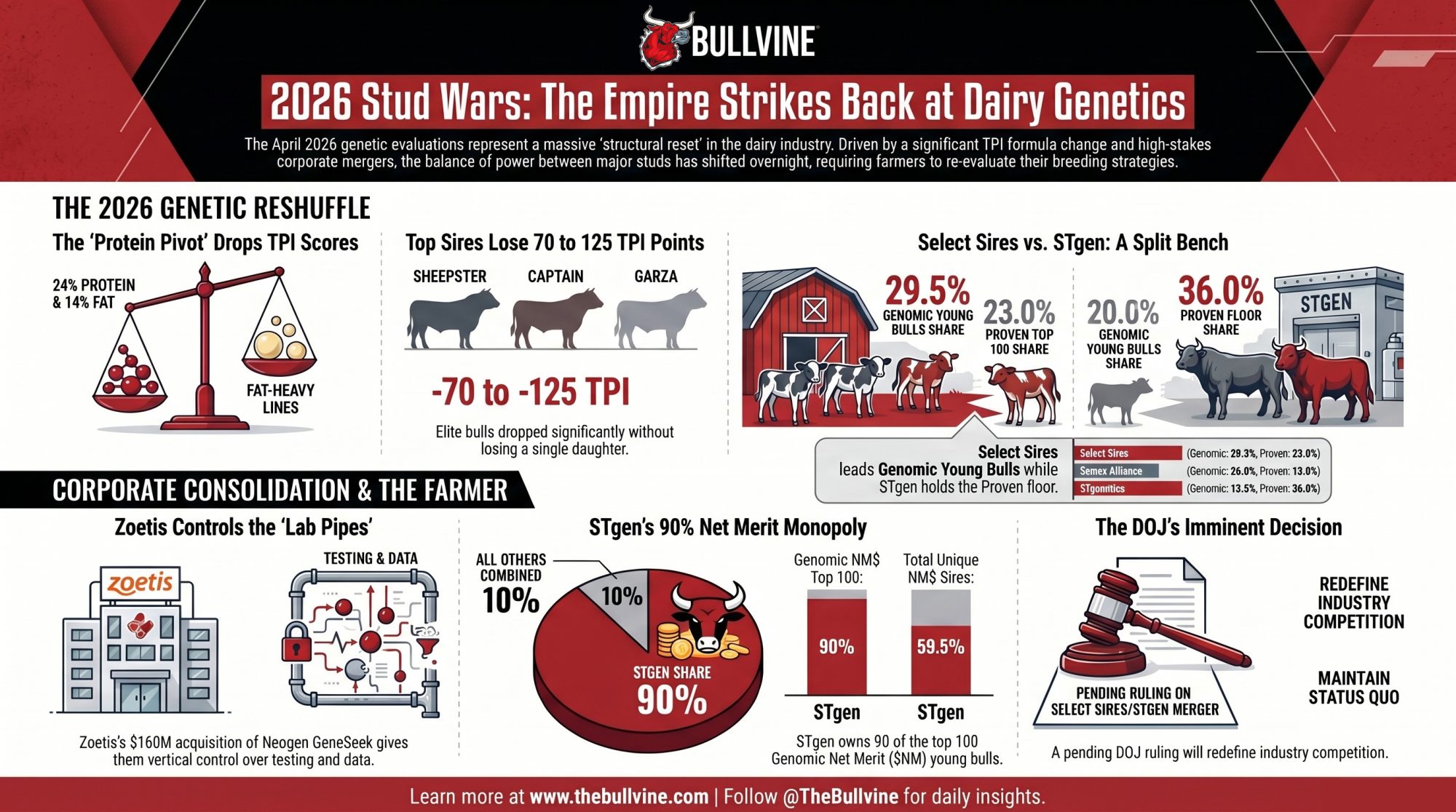

Holstein Association USA detonated a TPI formula change that dropped Garza 125 points, Captain 72, and Sheepster 92 — without a single new daughter. STgen’s elite proven army still owns 36 of the top 100 proven TPI sires even after the formula loss — but the genomic young bull lists tell a different story. Select Sires now owns 59 of the top 200 genomic young bulls (29.5%) — the broadest genomic depth of any single stud. Semex took 40 sires (20%) of the top 200, with 9 of the top 20 spots. United Sires — the breeder-owned independent that launched in 2024 — has grabbed 30 sires (15%) of the top 200 out of nowhere. The genetic galaxy reshuffled overnight.

Meanwhile, the DOJ pulled the Select Sires + STgenetics merger off the shelf and is now “nearing a decision” on whether the largest cooperative distributor in North America gets to merge with the company that owns global sexed-semen patents. And Zoetis — a company that doesn’t sell a single straw of semen — wrote a $160 million check for the lab infrastructure that processes everyone else’s DNA. ABS, meanwhile, completed its full takeover of De Novo Genetics. Three consolidation moves. All upstream of the farmer.

The Bullvine’s position on consolidation hasn’t changed: it’s structural, it’s accelerating, and pretending it isn’t doesn’t help anyone. Whether the DOJ, the FTC, or anyone in Washington is paying attention is another question. The April 2026 sire share analysis isn’t a cleanup of 2025. It’s a structural reset.

Last April we called the run The Force Awakens — an emerging order taking shape, polled and gNM$ rebellions challenging the dominant studs. Twelve months later, the Empire is striking back: STgen holding its proven army through a hostile formula change, Select Sires lining up the largest cooperative consolidation in dairy genetics history, and Zoetis executing a vertical lock on the lab pipes that read everyone’s DNA. The rebels who took the genomic top 20 — Semex’s Progenesis line, a brand-new breeder co-op called United Sires — won a battle. The Empire is positioning to win the war.

Methodology: Same Battlefield, New Rules of Engagement

Following the precedent set in our April 2025 analysis, we again use top 200 sires for genomic TPI, top 100 for proven TPI, and the official Holstein Association USA April 2026 evaluation lists drawn from the official CDCB run published April 7, 2026 (Holstein USA; CDCB).

Holstein Association USA implemented the TPI 2026 formula change in this run — production weights shifted from 19% PTA Protein / 19% PTA Fat to 24% PTA Protein / 14% PTA Fat. That’s a 5-point bump for protein and a 5-point cut for fat. Daughter data didn’t change. The math behind the rankings did. This is the largest single TPI formula adjustment in recent memory, and it explains why bulls who were untouchable in December 2025 dropped 70 to 125 TPI points in April without milking a single new daughter (The Bullvine).

Methodology: All April 2026 stud-share figures in this analysis are independent counts of the official Holstein Association USA April 2026 lists, performed using the official NAAB marketing codes as the source of truth for stud assignment. Genomic TPI counts use the Holstein USA Top 200 TPI® Genomic Young Bulls (April 2026, 85% genomic reliability minimum). Proven TPI counts use the Holstein USA Top 100 TPI Bulls (April 2026, ACTIVE or LIMITED semen status, 80% traditional reliability minimum).

Key NAAB code → marketing organization assignments per the official NAAB table: 1 = GENEX Cooperative; 7/9/14/250/507/509 = Select Sires; 11 = Alta Genetics USA; 29/94 = ABS Global; 97 = CRV Holding; 200/777 = Semex Alliance; 288 = ASCOL; 523/551/646 = STgenetics (Inguran); 596/796 = United Sires, LLC (independent breeder co-op founded 2024); 599/799 = Blondin Sires; 719 = RuAnn Genetics. URUS-owned brands (GENEX, Alta, Jetstream, Trans Ova) are reported as separate codes per NAAB and consolidated where editorially useful. April 2025 baselines were independent counts performed at original publication using a different methodology that lumped some breeder codes together; year-over-year comparisons in this article are made cautiously.

For breeders trying to read the new map: the formula change is the single biggest variable in this entire installment. Hold that in your head as you read the tables.

The TPI Saga: A New Hope, Rewritten Mid-Run

Genomic TPI Young Bulls — Top 10 (April 2026)

| Rank | Bull | NAAB | TPI | Stud |

| 1 | Progenesis Timetraveler-ET | 200HO13678 | +3563 | Semex |

| 2 | S-S-I Richard Chichester-ET | 7HO18102 | +3560 | Select Sires |

| 3 | Progenesis Superfreak | 200HO13701 | +3552 | Semex |

| 4 | OCD Whoops Sabotage-ET | 796HO10329 | +3551 | United Sires |

| 5 | S-S-I Stagger Baelum-ET | 14HO18123 | +3547 | Select Sires |

| 6 | Peak AltaGoldenGate-ET | 11HO18042 | +3531 | Alta / URUS |

| 7 | Welcome Gustavsson-ET | 200HO13730 | +3528 | Semex |

| 8 | Beyond Hi-Level-ET | 200HO13044 | +3527 | Semex |

| 9 | Pen-Col AltaGlimpse-ET | 11HO17974 | +3515 | Alta / URUS |

| 10 | Progenesis Tapas-ET | 200HO13681 | +3514 | Semex |

Source: Holstein USA Top 200 TPI® Genomic Young Bulls, April 2026.

Read that table. Five of the top 10 genomic young bulls in the world are 200HO — Semex Alliance. Two are Select Sires (S-S-I lines). Two are Alta/URUS (Peak AltaGoldenGate, Pen-Col AltaGlimpse). One is United Sires (OCD Whoops Sabotage, 796HO). Zero are STgen. The Progenesis line — Timetraveler, Superfreak, Tapas — locked down the top of the list. The 49-point spread between #1 (3563) and #10 (3514) is statistical noise at 65–80% genomic reliability. But the stud ownership pattern? That’s where the story lives.

Genomic TPI Stud Share — Top 200 Holstein Genomic Young Bulls (Verified Counts)

| Stud (NAAB code) | Apr 2026 count | % of top 200 |

| Select Sires (7, 14, 250) | 59 | 29.5% |

| Semex Alliance (200, 777) | 40 | 20.0% |

| United Sires (596, 796) | 30 | 15.0% |

| STgen (523, 551) | 27 | 13.5% |

| ABS / Genus (29, 94) | 12 | 6.0% |

| Alta / URUS (11) | 11 | 5.5% |

| GENEX / URUS (1) | 9 | 4.5% |

| CRV (97) | 8 | 4.0% |

| Independents (El Toro 508/708, A.I. Total 515, Genesis MX 706) | 4 | 2.0% |

Source: Independent count of Holstein USA Top 200 TPI Genomic Young Bulls, April 2026, with NAAB-code-to-stud assignments per the official NAAB marketing codes table.

URUS umbrella — GENEX (1HO) + Alta (11HO) combined = 20 sires (10.0%), the third-largest cooperative group when consolidated.

Two notes on this table.

First, the April 2025 baseline used a different and less rigorous methodology — it lumped “Sexing Tech / Genosource” with breeder-affiliated codes that have since been revealed by official NAAB lookup to be a different organization entirely. With the corrected NAAB-code accounting, the year-over-year comparison should be read as: STgen alone has 13.5% of the genomic top 200 in April 2026 (down from the 39.5% “STgen / Genosource” lumped figure published in 2025). United Sires LLC — a separately-owned independent breeder co-op founded in 2024 with no ownership relationship to STgen — holds a separate 15.0%. The two are independent organizations with independent ownership and independent NAAB codes.

Second, Semex’s 20% matches their own self-reported claim closely. Their Facebook post on April 10 (Semex) reported “45% of the Top 20, 34% of the Top 50, 26% of the Top 100, 20% of the Top 200.” Our verified counts: 45% of top 20, 34% of top 50, 27% of top 100, 20% of top 200. They were on the money.

If you’re keeping score: the 24P/14F formula change penalized bulls heavy on fat — exactly the profile that built Captain, Garza, and Dominance into STgen’s elite proven army. STgen’s deep gNM$ pipeline still benefits from protein-heavy production traits. But on the genomic young bull TPI list — the leading indicator of where the next proven army comes from — Semex’s Progenesis and Beyond pipelines and Select Sires’ S-S-I and Stagger lines, protein-tilted by design, ate the formula change.

This is the imperial-consolidation reversal nobody scripted. STgen didn’t lose because their bulls got worse. They lost because Holstein Association USA changed what “best” means, and Select Sires, Semex, and a brand-new breeder cooperative were already breeding for the new definition.

Proven TPI: STgen’s Empire Holds Despite the Formula

| Apr ’26 Rank | Bull | NAAB | TPI Apr ’26 | TPI Dec ’25 | Δ TPI | Stud (NAAB code) |

| 1 | OCD Trooper Sheepster-ET | 7HO16276 | +3480 | +3572 | −92 | Select Sires (7) |

| 2 | Peak Powerhouse-ET | 1HO16089 | +3448 | +3329 | +119 | GENEX / URUS (1) |

| 3 | SDG-PH Delux Dominance-ET | 551HO04795 | +3437 | +3458 | −21 | STgen (551) |

| 4 | Genosource Captain-ET | 551HO04119 | +3356 | +3428 | −72 | STgen (551) |

| 5 | Terra-Calroy Zuri-ET | 97HO42585 | +3355 | +3375 | −20 | CRV (97) |

| 6 | SDG Cap Garza-ET | 551HO04474 | +3339 | +3464 | −125 | STgen (551) |

| 7 | RMD-Dotterer Bolt Action-ET | 7HO15927 | +3322 | — | new | Select Sires (7) |

| 8 | Cookiecutter Horseshoe-ET | 208HO00356 | +3306 | — | new | Independent (208 primary; 200/777 secondary — Semex distribution) |

| 9 | Peak Powerstar-ET | 200HO12489 | +3299 | — | new | Semex (200) |

| 10 | Peak AltaSamson-ET | 11HO16342 | +3298 | — | new | Alta / URUS (11) |

Source: Holstein USA Top 100 TPI Bulls, April 2026; December 2025 deltas from The Bullvine.

Three things jump off this table.

First, STgen still owns three of the top 8 proven bulls — Dominance, Captain, Garza. Sheepster lost 92 TPI points without losing a daughter. He still sits at rank #1 with 2,359 daughters and 99% reliability. Garza lost 125 points. Captain lost 72. STgen’s elite proven army took the worst formula hit of any stud’s lineup, and they’re still here.

Second, the protein-formula winners are clear. Peak Powerhouse jumped +119 TPI in a single run to become the #2 proven bull in the world (Bullvine). Powerhouse carries the 1HO primary code = GENEX Cooperative (a URUS subsidiary), with secondary URUS codes 511HO and 122HO; the bull is the same Peak-branded URUS production line as the Alta-coded bulls. Peak AltaSamson at #10 carries 11HO = Alta Genetics, also URUS. Combined, URUS owns positions 2 and 10 of the proven top 10. Cookiecutter Horseshoe at #8 is registered under the 208HO Korean code as primary, but the bull is commercially distributed in North America via Semex (secondary codes 200HO and 777HO). Peak Powerstar’s debut at #9 gives Semex a new proven top-10 entry.

Third, the depth still belongs to STgen. 36 of the top 100 proven TPI bulls carry 551HO codes — STgenetics-Inguran, the largest single-stud share in any category we measured.

Proven TPI Stud Share — Top 100 Holstein Bulls (Verified Counts)

| Stud (NAAB code) | Apr 2026 count | % of top 100 |

| STgen (523, 551) | 36 | 36.0% |

| Select Sires (7, 14) | 23 | 23.0% |

| Semex Alliance (200, 777) | 13 | 13.0% |

| ABS / Genus (29, 94) | 10 | 10.0% |

| Alta / URUS (11) | 6 | 6.0% |

| CRV (97) | 5 | 5.0% |

| GENEX / URUS (1) | 4 | 4.0% |

| Independents (RuAnn 719, A.I. Total 515, Korea 208) | 3 | 3.0% |

Source: Independent count of Holstein USA Top 100 TPI Bulls, April 2026, with NAAB-code-to-stud assignments per the official NAAB marketing codes table.

URUS umbrella — Alta (11HO) + GENEX (1HO) combined = 10 sires (10.0%) of the top 100, tied with ABS/Genus.

STgen’s depth on proven TPI is the most surprising finding in this entire run. Despite Garza, Captain, and Dominance each losing ground to the formula change, the broader STgen pipeline behind those flagship names — Brockington, Capn Miguel, Cap Mad Max, Captn Penza, Cap Volos, Cap Rivera, Capn Rodman, Cap Diggory, and dozens more — held position across the top 100. Select Sires gained ground on the genomic side; STgen held depth on the proven side. Both can be true simultaneously.

Running the Numbers: What the 24P/14F Formula Costs (or Saves) Your Mating Program

Take Garza as the worked example. SDG Cap Garza-ET sat at +3464 TPI in December 2025 and dropped to +3339 TPI in April 2026 — a −125 TPI swing with zero new daughter data. His PTA Fat (+140 lbs) and PTA Protein (+50 lbs) didn’t move. The index weighting did.

Practical impact on a 500-cow Holstein herd: if your mating program selects service sires above a +3400 TPI threshold, Garza was in in December and is out in April — same bull, same daughters, same fertility. Multiply that across STgen’s elite proven army (Captain −72, Dominance −21) plus Sheepster (−92) on the Select Sires side, and roughly 30–40% of a typical commercial farm’s previous top-tier proven sire list now sits below older threshold cutoffs.

The fix is mechanical: drop your TPI cutoff by ~75–125 points, or rebuild your selection from PTA Protein and PTA Fat directly instead of relying on the headline index. The math hasn’t changed for milk in the tank. It’s changed for which bulls your computer flags as elite.

Specialty Forces: Type and Red & White

Headline gTPI and proven TPI tables tell you who’s winning the index war. Specialty rankings tell you who’s winning the niches — the breeders who keep buying for udder, feet, and frame; for component-heavy red herds; for a typier cow regardless of what TPI is doing this April. We’ve cross-referenced the EuroGenes April 2026 ranked top-50 lists for Type (PTAT) and Red & White TPI. Both pull from the same Holstein USA April 2026 evaluation as the headline gTPI lists but isolate subsets that don’t surface in the broader rankings.

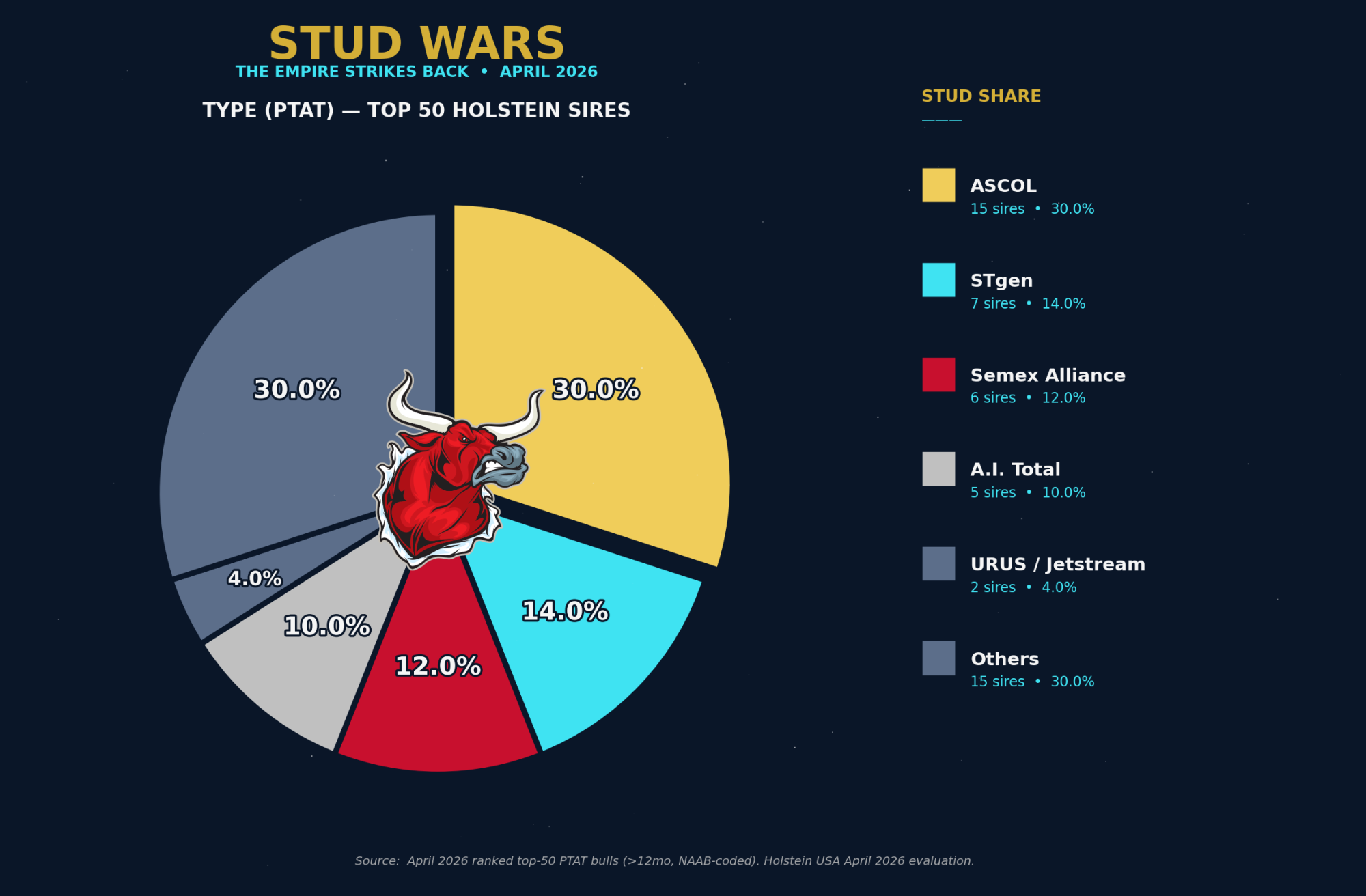

Type (PTAT): The Spanish Empire You Forgot About

| Rank | Bull | NAAB | TPI | PTAT | Stud |

| 1 | Ruann Karat-45955-ET | 719HO45955 | +2647 | +3.92 | RuAnn Genetics |

| 2 | Shg Lego | 515HO00486 | +2307 | +3.84 | A.I. Total (NL) |

| 3 | Redcarpet Story Arc-ET | 730HO00005 | +2215 | +3.78 | Redcarpet Sires |

| 4 | Stone-Front Eyecandy Apollo | 288HO00352 | +2448 | +3.72 | ASCOL (Spain) |

| 5 | Genosource Seenofear-ET | 551HO05904 | +2791 | +3.71 | STgen |

| 6 | Jimtown Nelson-ET | 288HO00321 | +2426 | +3.69 | ASCOL |

| 7 | Curlys Admire | 734HO00157 | +2600 | +3.63 | URUS (Jetstream) |

| 8 | Eclipse Milio-ET | 551HO03708 | +1982 | +3.58 | STgen |

| 9 | Eskdale Hulu Shoutout-ET | 288HO00364 | +2889 | +3.56 | ASCOL |

| 10 | Mr Legacy-Ranch E Atlas-ET | 100HO12395 | +2423 | +3.55 | JLG Custom |

Source: EuroGenes USA Top-Ranking PTAT Bulls, April 2026, drawn from the official Holstein USA April 2026 evaluation.

Type (PTAT) Stud Share — Top 50 Bulls

| Stud (NAAB code) | Apr 2026 count | % of top 50 |

| ASCOL (288) | 15 | 30.0% |

| STgen (523, 551) | 7 | 14.0% |

| Semex Alliance (200, 777) | 6 | 12.0% |

| A.I. Total (515) | 5 | 10.0% |

| Other independents (Showbox 744, Holstein Svc 712, AG3NexGen 733) | 6 | 12.0% |

| Blondin (799) | 2 | 4.0% |

| RuAnn (719) | 2 | 4.0% |

| URUS / Jetstream (734) | 2 | 4.0% |

| Redcarpet (730) | 1 | 2.0% |

| ABS / Genus (94) | 1 | 2.0% |

| Select Sires (250) | 1 | 2.0% |

| Swissgenetics (196) | 1 | 2.0% |

The headline finding is the one nobody outside Europe will see coming: ASCOL — the Spanish breeder cooperative — owns 30% of the top 50 PTAT bulls in the U.S. evaluation, and 3 of the top 10. Stone-Front Eyecandy Apollo, Jimtown Nelson, and Eskdale Hulu Shoutout are all 288HO bulls, all PTAT ≥3.55. STgen has 7 (14%) and a top-10 presence with Genosource Seenofear at #5 and Eclipse Milio at #8. The big U.S. cooperatives — Select Sires (1), ABS (1), GENEX (0) — barely register at the top of the type rankings.

This is not new. PTAT has historically been the most fragmented stud-share category because elite type bulls come from individual breeder programs that license through niche distribution channels rather than the big-five cooperative pipelines. April 2026 just confirms the pattern with verified NAAB-code accounting.

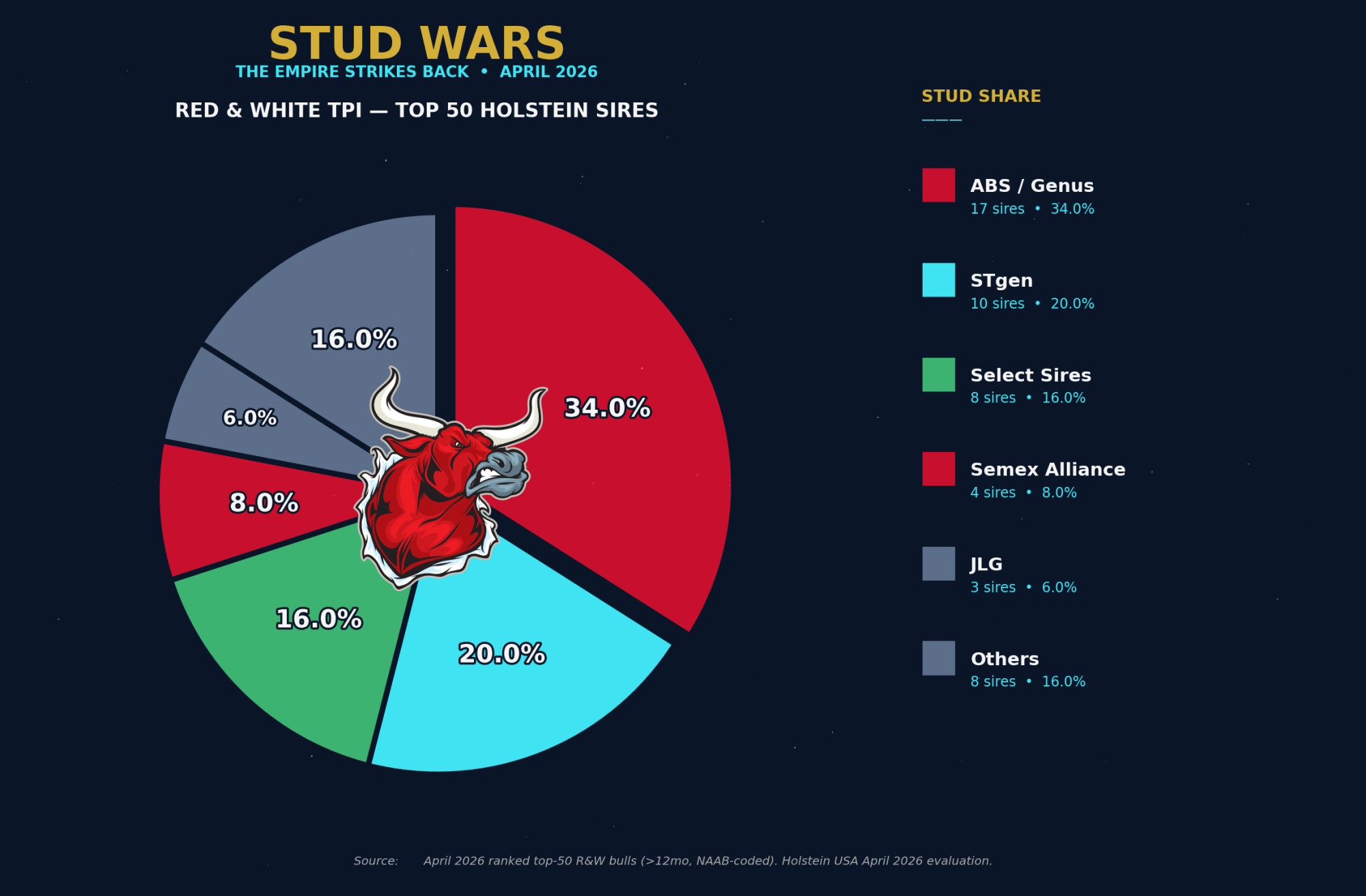

Red & White TPI: ABS’s Quiet Empire

While the gTPI top 200 reshuffled around STgen and Select Sires, the R&W lineup tells a different story — ABS / Genus owns 17 of the top 50 R&W TPI bulls (34%) including 5 of the top 10. The De Novo acquisition is showing up in the rankings.

| Rank | Bull | NAAB | TPI | Stud |

| 1 | Denovo 21873 Okafor-Red-ET | 029HO00951 | +3194 | ABS / Genus |

| 2 | Aprilday Hrok Athens-Red-ET | 250HO18217 | +3180 | Select Sires |

| 3 | Stgen Ocean-Red-ET | 551HO06846 | +3179 | STgen |

| 4 | Ocd Morris Spirit-Red-ET | 551HO06757 | +3177 | STgen |

| 5 | Aprilday Orphs Aesop-Red-ET | 029HO00954 | +3177 | ABS / Genus |

| 6 | Sfh Scudetto Red ET | 029HO22554 | +3177 | ABS / Genus |

| 7 | 3star Patser-Red-ET | 200HO08526 | +3175 | Semex |

| 8 | Siemers Rle Papaya-Red-ET | 007HO17695 | +3174 | Select Sires |

| 9 | Sfh Saviero Red ET | 029HO22562 | +3170 | ABS / Genus |

| 10 | Aprilday Orph Lyon-Red-ET | 029HO00956 | +3168 | ABS / Genus |

Source: EuroGenes USA Top-Ranking Red & White Bulls, April 2026, drawn from the official Holstein USA April 2026 evaluation.

Red & White TPI Stud Share — Top 50 Bulls

| Stud (NAAB code) | Apr 2026 count | % of top 50 |

| ABS / Genus (29, 94) | 17 | 34.0% |

| STgen (523, 551) | 10 | 20.0% |

| Select Sires (7, 14, 250) | 8 | 16.0% |

| Semex Alliance (200, 777) | 4 | 8.0% |

| JLG / Holstein Svc (100, 712) | 3 | 6.0% |

| Alta / URUS (11) | 2 | 4.0% |

| GENEX / URUS (1) | 1 | 2.0% |

| United Sires (796) | 1 | 2.0% |

| Other independents (Cogent 522, Inseme 643, A.I. Total 515, Intermizoo 198) | 4 | 8.0% |

The story in this table is the consolidation of red-and-white genetics under ABS/Genus’s roof. The top R&W bull, Denovo 21873 Okafor-Red-ET (029HO00951) at +3194 TPI, is a De Novo bull — the same De Novo program ABS completed its full takeover of in early 2026. Five of the top ten R&W bulls carry 029HO codes. Of the next 40, ABS owns another 12. Total: 17 of 50 (34%) — the largest single-stud share in any specialty category we counted.

STgen’s 20% share comes from a different angle. The 551HO R&W lineup — Ocean, Spirit, Red Lion, Redwood-P, Remington, Sizzler, Genosource Morris, Silver-Elite Ferrari, Silver-Elite Malibu — reflects STgen’s bid to keep R&W relevance through the Genosource production pipeline. Select Sires shows up with 8 bulls (16%), led by Aprilday Hrok Athens-Red at #2.

If you breed red Holsteins commercially, the practical implication is straightforward: the R&W elite is concentrating, not fragmenting. ABS, STgen, and Select Sires together own 70% of the top 50 R&W TPI bulls in April 2026. Independent breeder lines that historically carried R&W (Aprilday, Denovo, Genosource, Stgen) are increasingly inside one of those three corporate umbrellas.

The Economic Theater: NM$ and the Sire-Count Totals

TPI is the breeding-decision proxy. Net Merit (NM$) is the dollars-per-cow-per-lactation proxy — USDA’s lifetime profit estimate for a daughter sired by that bull. If TPI tells you who’s winning the index war, NM$ tells you who’s winning the economics. And nobody who reads sire summaries will be surprised by what the NM$ tables show: STgen owns the NM$ rankings the way Saudi Arabia owns crude oil.

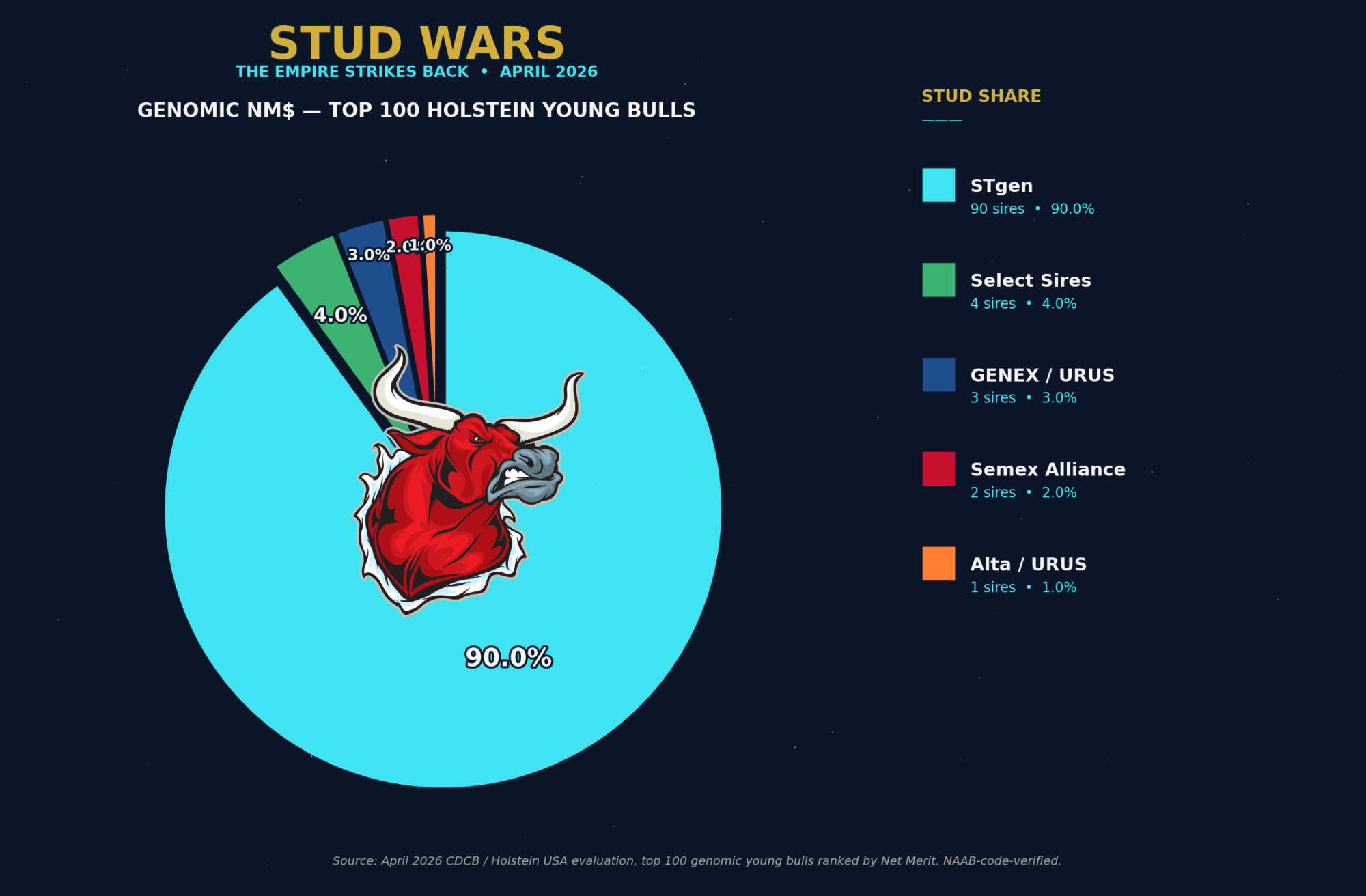

Genomic NM$: STgen’s 90% Empire

| Rank | Bull | NAAB | NM$ | TPI | Stud |

| 1 | Genosource Valkyrie-ET | 551HO07040 | +1308 | +3464 | STgen |

| 2 | Farnear Collateral-ET | 551HO07100 | +1304 | +3410 | STgen |

Source: April 2026 CDCB / Holstein USA evaluation, top 100 genomic young bulls ranked by Net Merit. NAAB-code-verified.

Genomic NM$ Stud Share — Top 100 Bulls

| Stud (NAAB code) | Apr 2026 count | % of top 100 |

| STgen (523, 551, 558) | 90 | 90.0% |

| Select Sires (7, 14, 250) | 4 | 4.0% |

| GENEX / URUS (1) | 3 | 3.0% |

| Semex Alliance (200, 777) | 2 | 2.0% |

| Alta / URUS (11) | 1 | 1.0% |

This is not a typo. 90 of the top 100 genomic NM$ young bulls in the April 2026 evaluation carry STgen NAAB codes (551HO or 558HO). Select Sires has 4. GENEX/URUS has 3. Semex has 2. Alta has 1. Everyone else combined has zero. The Genosource production pipeline — anchored by Captain, Charl, Ripcord, Dominance, and Thorson as foundation sires — is producing genomic young bulls so deep on Net Merit that the rest of the industry barely registers.

This is also the strongest single argument for why the DOJ + Select Sires merger matters. If the deal clears, Select Sires gets distribution rights to 90% of the world’s top genomic NM$ pipeline. If it blocks, every cooperative in North America that wants to sell elite NM$ young bulls has to negotiate with STgen on STgen’s terms.

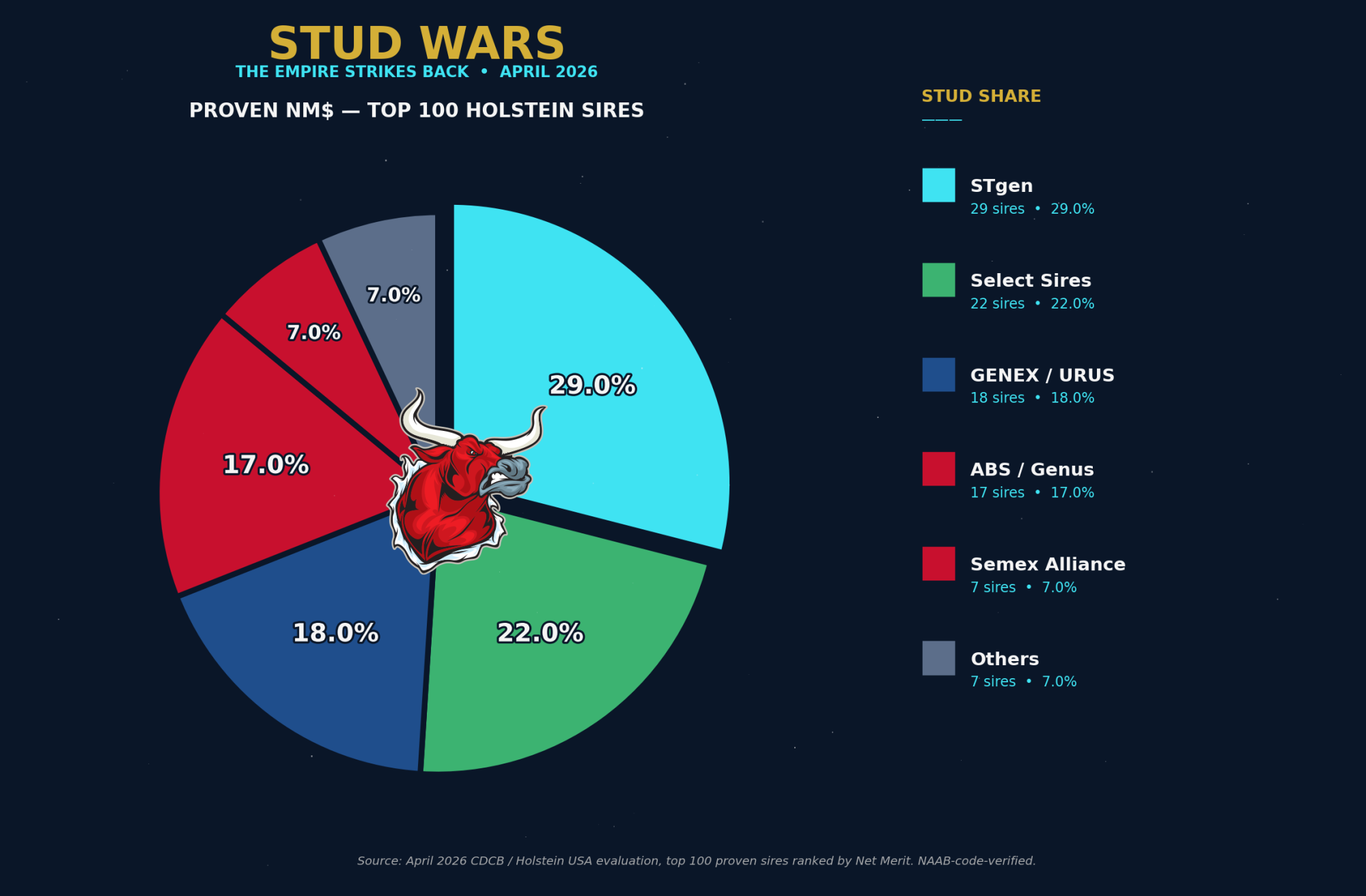

Proven NM$: A Different Five-Way Fight

The proven NM$ list is a different story — wider, more competitive, and shaped by which studs have managed to get high-NM$ Genosource-pipeline bulls daughter-proven before they age out of relevance.

Proven NM$ Stud Share — Top 100 Bulls

| Stud (NAAB code) | Apr 2026 count | % of top 100 |

| STgen (523, 551) | 29 | 29.0% |

| Select Sires (7, 14) | 22 | 22.0% |

| GENEX / URUS (1) | 18 | 18.0% |

| ABS / Genus (29, 94) | 17 | 17.0% |

| Semex Alliance (200, 777) | 7 | 7.0% |

| Alta / URUS (11) | 7 | 7.0% |

Proven NM$ is the most balanced category in the entire April 2026 analysis. Six studs all sit between 7% and 29%. STgen leads at 29% — their proven Genosource pipeline (Dominance #1, Thorson #2, Garza #3, Captain, Jack, John, Vito, Brockington) sweeps the top of the list. But Select Sires (22%), GENEX/URUS via Peak (18%), and ABS/Genus via De Novo (17%) are all within striking distance. The competitive structure here is healthier than anywhere else in the article — four studs have real depth, and any one of them can compete on commercial pricing.

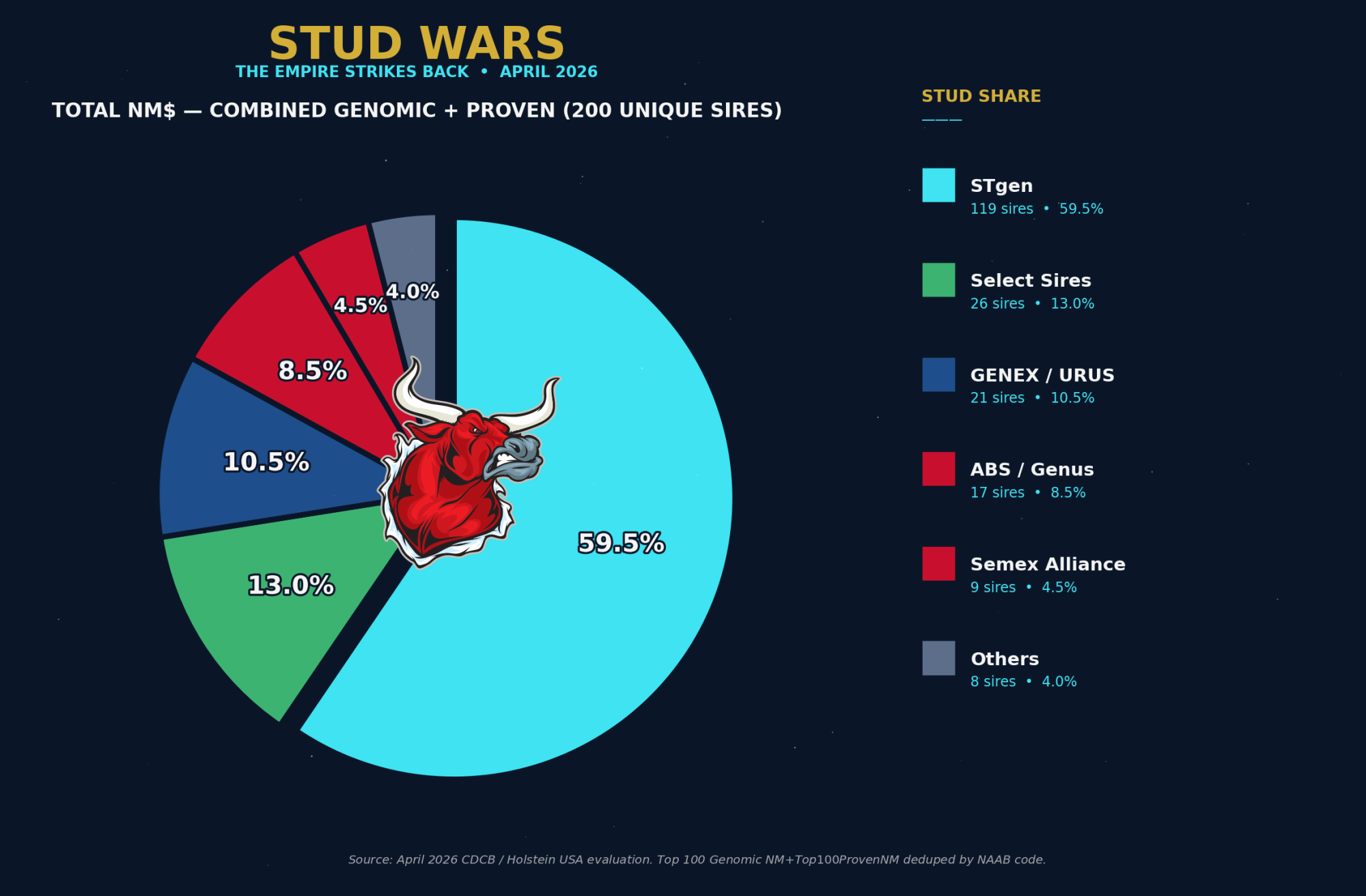

Total NM$: STgen Owns 60% of Both Lists Combined

When you dedupe the Genomic NM$ Top 100 and the Proven NM$ Top 100 by NAAB code, you get 200 unique sires(no bull appears on both lists at the same time). Of those 200, STgen owns 119.

Total NM$ Stud Share — 200 Unique Sires

| Stud | Combined count | % of 200 unique sires |

| STgen | 119 | 59.5% |

| Select Sires | 26 | 13.0% |

| GENEX / URUS | 21 | 10.5% |

| ABS / Genus | 17 | 8.5% |

| Semex Alliance | 9 | 4.5% |

| Alta / URUS | 8 | 4.0% |

[CHART: Total NM$ — Combined Genomic + Proven (200 Unique Sires), April 2026]

STgen owns 59.5% of the combined NM$ map. Select Sires — the largest cooperative distributor in North America — owns 13%. URUS umbrella combined (Alta + GENEX) sits at 14.5%. The DOJ decision is, fundamentally, about who gets to sell the 60% slice that STgen currently produces.

The Combined Sire Count: Who Has the Deepest Bench

The per-category tables tell you who’s winning specific battles. The combined-count tables tell you whose bench is deepest — across every list a commercial breeder might shop from. We’ve deduped each combination by NAAB code so a bull that appears on both the TPI and the NM$ list only counts once.

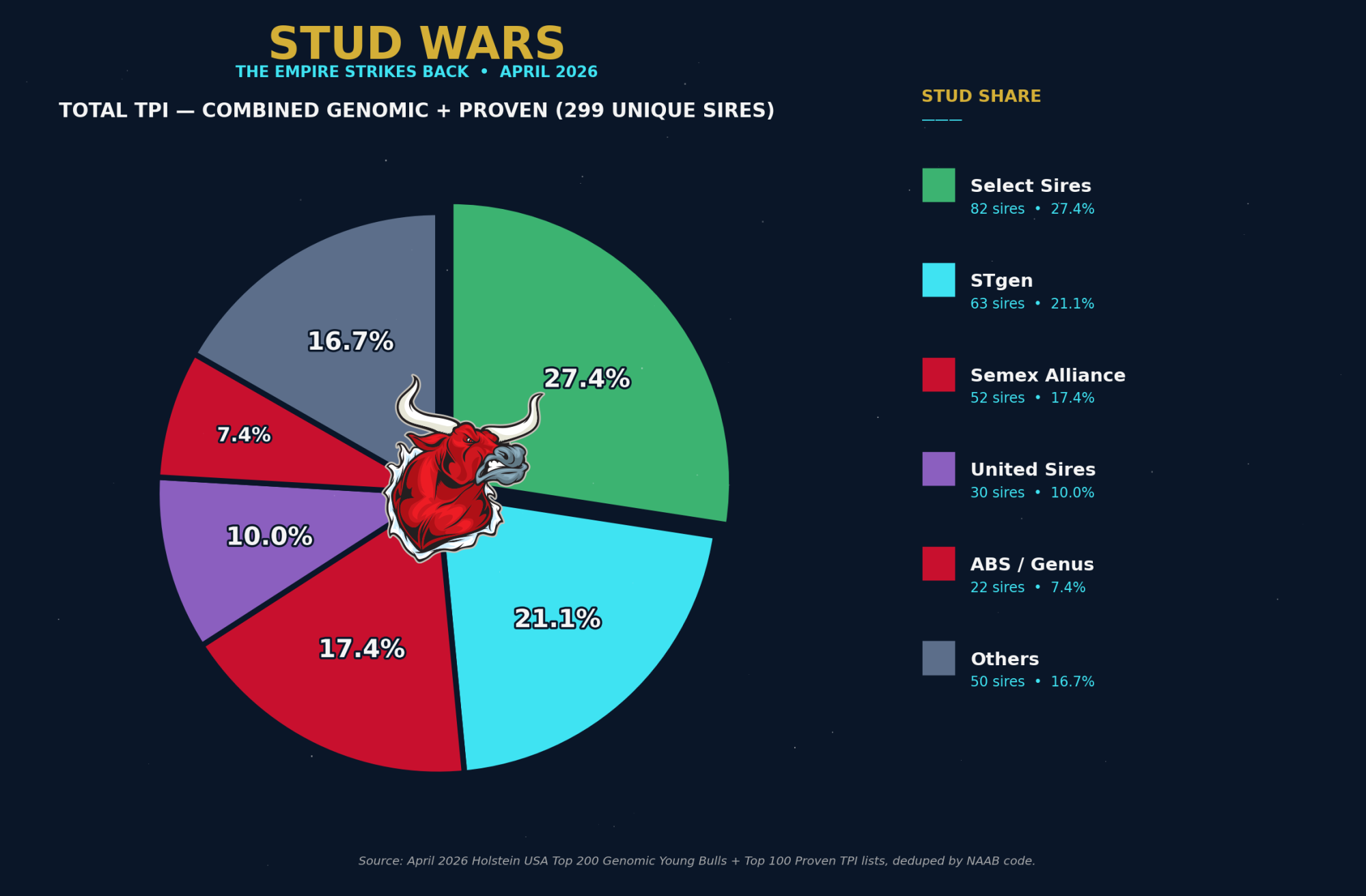

Total TPI — Genomic + Proven Combined (299 Unique Sires)

| Stud | Combined count | % of 299 unique sires |

| Select Sires | 82 | 27.4% |

| STgen | 63 | 21.1% |

| Semex Alliance | 52 | 17.4% |

| United Sires | 30 | 10.0% |

| ABS / Genus | 22 | 7.4% |

| Alta / URUS | 17 | 5.7% |

| GENEX / URUS | 13 | 4.3% |

| CRV | 13 | 4.3% |

| Independents | 7 | 2.4% |

[CHART: Total TPI — Combined Genomic + Proven (299 Unique Sires), April 2026]

Select Sires owns the broadest TPI footprint at 27.4% of all unique TPI-ranked sires (genomic + proven combined). STgen sits at 21.1% — less depth than NM$ but still substantial. Semex’s 17.4% reflects their genomic top-200 strength (40 bulls). United Sires’ 10% from a single year of operation remains the most surprising data point in the entire analysis.

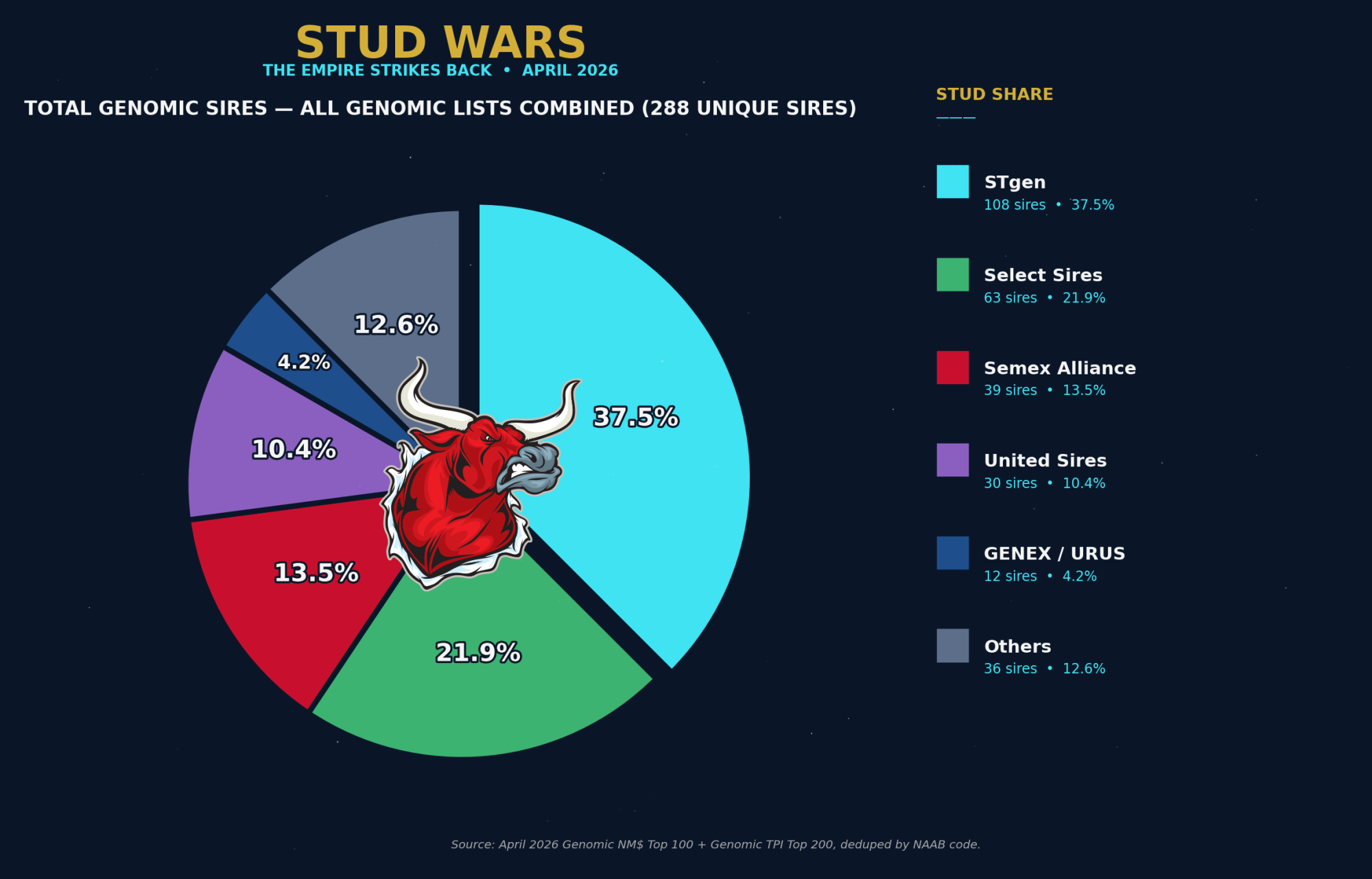

Total Genomic Sires — All Genomic Lists Combined (288 Unique Sires)

| Stud | Combined count | % of 288 unique sires |

| STgen | 108 | 37.5% |

| Select Sires | 63 | 21.9% |

| Semex Alliance | 39 | 13.5% |

| United Sires | 30 | 10.4% |

| GENEX / URUS | 12 | 4.2% |

| Alta / URUS | 12 | 4.2% |

| ABS / Genus | 12 | 4.2% |

| CRV | 8 | 2.8% |

| Independents | 4 | 1.4% |

[CHART: Total Genomic Sires — All Genomic Lists Combined (288 Unique Sires), April 2026]

When you combine the Genomic TPI Top 200 and Genomic NM$ Top 100 — deduped — STgen pulls ahead of Select Sires at 37.5% to 21.9%. The NM$ dominance is what does it: 90 STgen genomic NM$ bulls plus 27 STgen genomic TPI bulls, deduped to 108 unique entries. The genomic future, on these two metrics combined, is overwhelmingly Genosource-pipeline genetics.

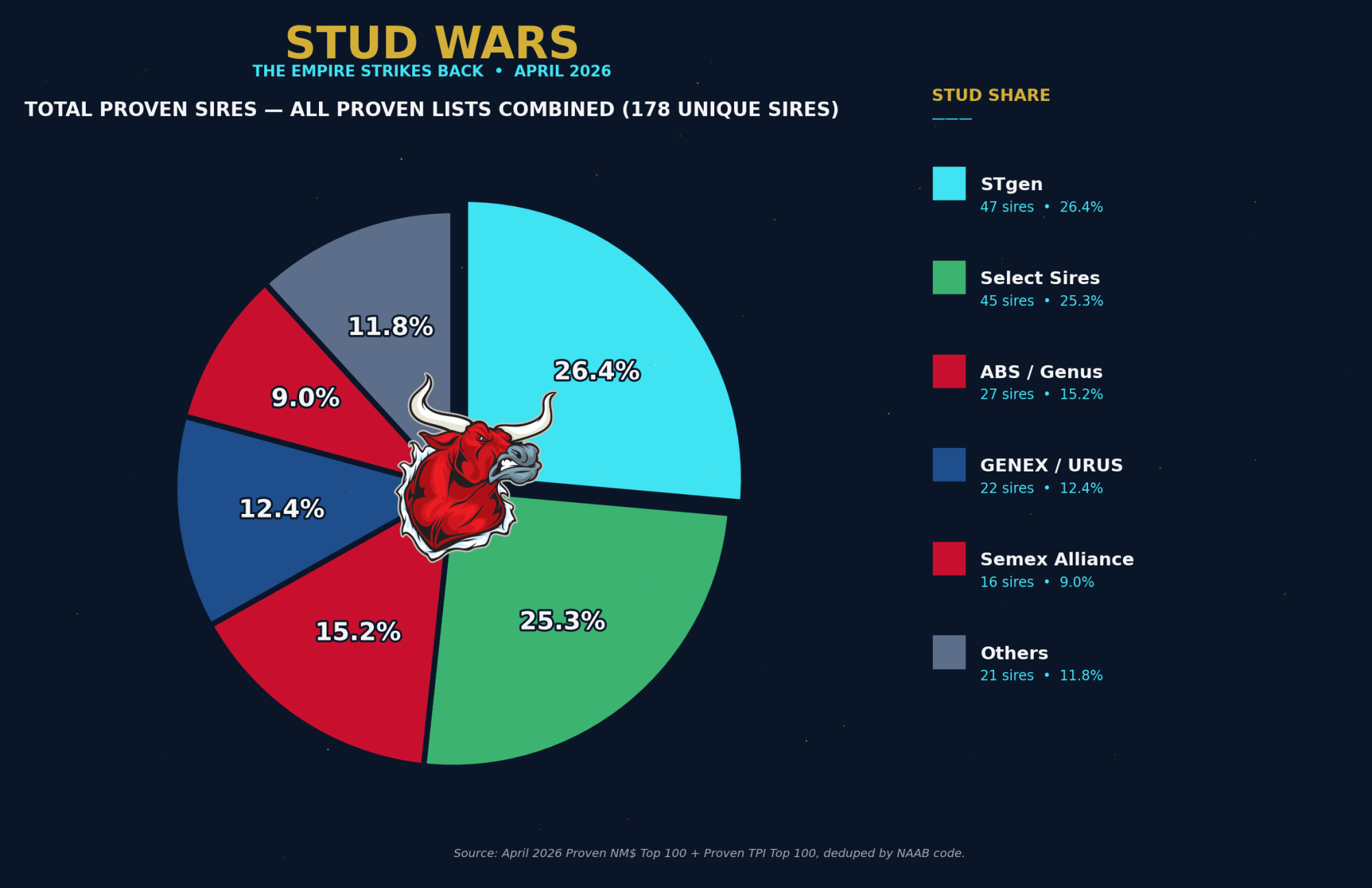

Total Proven Sires — All Proven Lists Combined (178 Unique Sires)

| Stud | Combined count | % of 178 unique sires |

| STgen | 47 | 26.4% |

| Select Sires | 45 | 25.3% |

| ABS / Genus | 27 | 15.2% |

| GENEX / URUS | 22 | 12.4% |

| Semex Alliance | 16 | 9.0% |

| Alta / URUS | 13 | 7.3% |

| CRV | 5 | 2.8% |

| Independents | 3 | 1.7% |

[CHART: Total Proven Sires — All Proven Lists Combined (178 Unique Sires), April 2026]

Proven sire counts — across both TPI and NM$ — are the most balanced in the entire article. STgen and Select Sires are within one bull of each other (47 vs 45). ABS, GENEX, and Semex all have meaningful proven depth. This is the category most resistant to consolidation pressure: proven sires take 5-7 years to develop, the pipeline can’t be acquired overnight, and four to five studs all have genuine elite proven inventory.

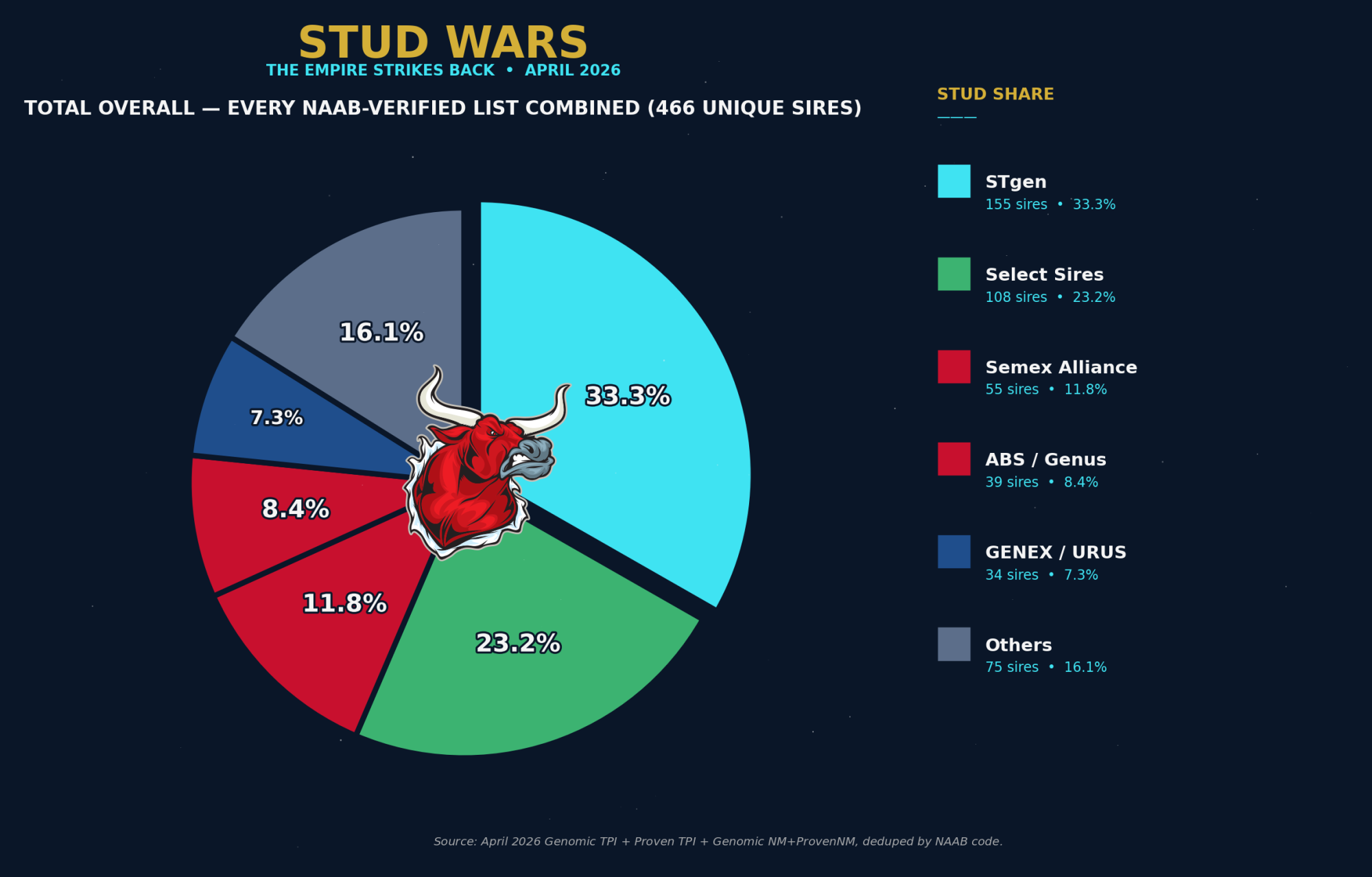

Total Overall — Every NAAB-Verified List Combined (466 Unique Sires)

| Stud | Combined count | % of 466 unique sires |

| STgen | 155 | 33.3% |

| Select Sires | 108 | 23.2% |

| Semex Alliance | 55 | 11.8% |

| ABS / Genus | 39 | 8.4% |

| GENEX / URUS | 34 | 7.3% |

| United Sires | 30 | 6.4% |

| Alta / URUS | 25 | 5.4% |

| CRV | 13 | 2.8% |

| Independents | 7 | 1.5% |

This is the master scoreboard. Combine the Genomic TPI Top 200, Proven TPI Top 100, Genomic NM$ Top 100, and Proven NM$ Top 100 — dedupe everything by NAAB code — and you get 466 unique elite sires in the April 2026 evaluation. Of those, STgen owns 155 (one in three). Select Sires owns 108 (just under one in four). Together those two studs control 56.5% of the entire elite sire universe.

If the DOJ approves the merger, a single combined entity controls 56.5% of the elite Holstein sire population in North America — by deduplicated NAAB count, across every metric Holstein USA and CDCB rank. Every conversation about whether the merger is pro-competitive or anti-competitive starts with that number — but it’s not the whole story.

What the Rankings Don’t Tell You

We owe readers the second half of this conversation, because the rankings analysis above tells one true thing and is silent on a second, equally true one.

What the rankings tell you: who supplies the bulls that clear the elite-tier reliability and ranking thresholds Holstein USA and CDCB use to publish official lists. That’s a useful filter. If you’re looking for the deepest bench of high-NM$ genomic young bulls, the data says you go to STgen. If you’re looking for the broadest spread of TPI-ranked sires across both genomic and proven categories, you go to Select Sires.

What the rankings do not tell you: how many straws of semen each stud actually sells. And the gap between those two numbers is wider than most articles in our category admit.

The honest read — the one most stud-share articles avoid because it complicates the headline numbers — is that today’s farmers don’t buy semen on an index. They buy on minimum thresholds across multiple traits, then on price, then on relationships, then on what the rep happens to be selling that month. Index rank is a filter on the upstream side; it’s a smaller input to the downstream purchase decision than ranking articles like this one tend to suggest. Senior executives at every major U.S. stud will say that privately. Some will say it on the record. The structural argument is sound, and it’s been sound for at least a decade.

The 4,000-Bull Universe

NAAB’s 2025 year-end report — the official trade-association volume data — puts U.S. bovine semen production at just under 66 million units across all categories (NAAB 2025 Year-End Report, March 11, 2026). Holstein dairy semen alone accounts for roughly 13.8 million units, or 83.5% of total dairy units sold (dairynews.today summary of NAAB 2025).

At an industry-average of roughly 15,000 straws sold per active bull per year, doing the math says the U.S. Holstein semen market requires roughly 4,000 actively-selling bulls to produce that 60-million-unit volume. The Holstein USA Top 200 Genomic + Top 100 Proven combined represents 300 bulls. The combined NM$ Top 200 represents another 200 (with significant overlap to TPI). The full “NAAB-verified elite universe” we counted in the prior section — 466 unique sires — represents roughly 12% of the bulls that actually move semen in the U.S. market.

The other 88% — roughly 3,500 bulls — don’t appear in any of the rankings this article counts. They sell straws anyway, often in significant volume, into market segments the rankings don’t capture.

Twenty Sub-Markets, Not One

The U.S. dairy genetics market isn’t one market. It’s at least 20 sub-markets with overlapping combinations. Every farmer who has shopped a sire catalog already knows this. The rankings industry tends to flatten it:

- Component-driven herds buying for fat and protein percentage

- Type-focused herds buying for udders, feet, and frame regardless of TPI

- Polled-only buyers paying premiums for heterozygous P/PP genetics

- Sexed-conventional split decisions varying by parity and reproduction protocol

- Beef-on-dairy programs filtering on terminal-cross profitability, not Net Merit

- A2A2 buyers; organic operations; robot-fit conformation; high-component breed preferences

- Geographic preferences — a Wisconsin component buyer and a California production buyer don’t shop the same sires

Each of those segments has its own minimum thresholds across multiple traits, its own price ceilings, and its own bull preferences. A bull ranked #50 on the genomic TPI list may be the wrong choice for 18 of those 20 sub-markets and the right choice for two. The rankings are a starting filter, not a buying decision.

Rank Doesn’t Equal Price (or Volume)

The price-list reality every commercial breeder has noticed but the rankings industry rarely addresses: the difference in semen price between a bull ranked #50 and a bull ranked #500 is, on most published stud price lists, pennies. Once a bull clears a buyer’s minimum thresholds — NM$ above some floor, PTA Protein above some floor, fertility and calving ease acceptable — price is determined more by the buyer’s price ceiling than by the bull’s rank. Studs know this. Buyers know this. The rankings industry rarely admits it.

The practical implication: a stud with 90% of the genomic NM$ top 100 does not have 90% of U.S. dairy semen market share. Not 80%. Not 70%. Not even 30%. STgen’s actual share of U.S. domestic dairy semen volume sits in the single digits by NAAB volume data, well below their 33.3% share of the deduplicated elite-rankings universe and dramatically below their 90% genomic NM$ concentration.

ABS Global is the cleanest counter-example. ABS holds roughly 6% of NAAB-verified elite genomic + proven counts (12 genomic top 200 bulls, 10 proven top 100 bulls) but commands a much larger share of actual U.S. straws sold than that ranking presence would suggest — driven by R&W depth (34% of the R&W TPI top 50), polled depth, beef-on-dairy programs, and decades of cooperative-distribution relationships with commercial herds. The rankings undercount ABS’s commercial footprint by a substantial multiple.

The Bigger Consolidation Story Sits at the Lab Level

The rankings analysis above counts bulls. The bull-distribution mergers in the next section reshuffle which studs sell which bulls. But the most consolidated structural shift in U.S. dairy genetics in 2025–26 is happening at a layer most articles in this category don’t even count: the genomic-test labs.

The Zoetis + Neogen GeneSeek merger consolidates the genomic-test infrastructure layer, not the bull-distribution layer. Neogen describes itself in its own filings as a “leader in U.S. beef and dairy genomics,” operating five labs serving 120+ countries with $90 million in annual genomics revenue (Zoetis-Neogen $160M deal coverage, March 2, 2026). Zoetis already operates the Kalamazoo, Michigan, genetics lab that processes a substantial share of CDCB-approved CLARIFIDE Plus tests.

CDCB does not publish lab-by-lab volume breakdowns publicly, so the post-merger Zoetis + Neogen share of CDCB-approved genomic-test volume isn’t independently auditable from open sources. Multiple senior industry executives we’ve talked to put the post-close concentration above 75% of U.S. CDCB-approved genomic test volume. We’re reporting that estimate as the directional industry view, not as a CDCB-published statistic. The directional case is supported by Zoetis’s stated Precision Animal Health strategy, Neogen’s self-description as the dominant U.S. genomics service provider, and the absence of any third CDCB-approved lab operating at comparable scale.

If the post-close concentration is even directionally in that range, the lab-pipe consolidation is a more concentrated structural shift than any of the bull-distribution mergers in this article. Every breeding decision driven by genomic data — whether the test is branded CLARIFIDE Plus, Igenity, GGP, or a breed association card — increasingly flows through one corporate parent’s lab infrastructure. The DOJ + Select Sires + STgenetics decision shapes who sells your bulls. The Zoetis + Neogen close in H2 2026 shapes who reads your DNA. The second is harder to escape than the first.

What This Means for How You Read This Article

Everything in the rankings tables above is verified, NAAB-coded, and accurately describes who supplies bulls that clear Holstein USA’s and CDCB’s elite-tier thresholds in April 2026. None of it tells you what straws are selling, where, at what price, to whom. The rankings are inputs to a small fraction of the buying decision. The actual U.S. dairy semen market is structured by component preferences, R&W demand, polled preference, beef-on-dairy economics, sub-regional buyer relationships, and price ceilings — and most of those signals don’t appear in any ranked list.

The studs who run the largest sire-summary marketing campaigns know this. The breed associations who publish the rankings know this. Now you know it too. Use the rankings as one filter among many, not as a proxy for who controls the market.

The Corporate Battlefield: Three Wars, One Year

Here’s where the April 2026 installment diverges hardest from any prior Stud Wars piece. The sire-share tables tell you who’s winning the bull selection war. The corporate tables tell you who controls the rules.

Battle 1: The DOJ Decision That Reshapes Everything

In August 2023, Select Sires (Plain City, OH) and Inguran LLC — better known as STgenetics — signed a letter of intent to combine production and R&D functions (Select Sires/STgen press release). The deal would marry STgen’s roughly 60 global sexed-semen sorting facilities and the patent-backed SexedULTRA 4M technology with Select Sires’ cooperative distribution to about 30,000 farmer-owners across 27 U.S. states.

The Biden DOJ shelved it. Antitrust concern: combining the dominant sexed-semen technology platform with the dominant cooperative farm-level distribution channel creates dual gatekeeping at both critical bottlenecks.

Then in July 2025, Select Sires’ annual report stated the organization was again pursuing the combination — “hoping for better chances with the second Trump administration” (Farm Progress, April 20, 2026; Beef Magazine, April 24, 2026).

As of April 2026, the DOJ is “nearing a decision.”

If the merger clears: the combined entity pairs the largest U.S. cooperative distribution network with the sexed-semen sorting technology behind roughly 30% of sex-selected semen sold globally. ABS keeps building IntelliGen, CRV keeps running its own sorting facility, and every other stud has to either license the combined entity’s sorting technology or develop independent sorting from scratch. Smaller cooperatives without access to either technology face a hard squeeze.

If the merger blocks again: STgen and Select Sires reach a strategic dead end. STgen has built sorting capacity ahead of demand it expected the merger to channel. Select Sires has been unable to acquire significant intellectual property of its own. Both organizations would need to find new strategic paths in a market where the cost-of-entry for sorting tech is climbing.

This isn’t an academic concern. The DOJ decision changes who can sell what to whom, at what cost, on what timeline, for the next decade. It’s the most consequential pending transaction in North American dairy genetics. And the call is coming.

Battle 2: Zoetis Buys the Pipes

On March 2, 2026, Zoetis Inc. announced a definitive agreement to acquire Neogen Corporation’s animal genomics business for $160 million (Neogen Investor Relations; The Bullvine).

That price — about 1.8× the unit’s annual revenue of roughly $90M — almost undersells what Zoetis is actually buying.

Neogen GeneSeek operates 5 genomic labs (U.S., Brazil, Australia, China, UK), serves customers in 120+ countries, and includes the Igenity and GGP platforms. These labs process DNA tests for AI companies, breed associations, public genetic evaluation systems, and farmers running parentage and genomic predictions. Many of those customers compete directly with Zoetis’s own CLARIFIDE Plus genomic test.

Post-close — expected second half of 2026, pending regulatory clearance — Zoetis owns:

- The branded test product (CLARIFIDE Plus, DWP$)

- The wellness index used to rank bulls (DWP$ — recently updated to add residual feed intake, methane, and heat resilience traits)

- The processor-mandated supply chain (Danone CLARIFIDE Plus partnership announced 2024)

- The lab infrastructure that processes competitor DNA

If you’re a breed association routing samples through GeneSeek labs, those labs are now owned by the company whose proprietary index (DWP$) competes with your association’s official rankings. If you’re a non-Zoetis AI company, the lab handling your young-bull screening and parentage tests just changed parents. If you’re a farmer on a Danone supply contract, the company that mandated your CLARIFIDE Plus testing also owns the lab pipeline behind it — same vendor, both ends.

This is the kind of structural move that doesn’t show up in NAAB volume tables but reshapes who has leverage at every contract negotiation for the next decade. No DOJ challenge has been announced. The deal is on track to close on Zoetis’s timeline.

Battle 3: The Gene-Editing Door Opens

On April 30, 2025, the U.S. FDA granted approval to Genus PIC’s PRRS-resistant pig (PIC press release; National Hog Farmer). On January 23, 2026, Health Canada and CFIA followed (PIC).

That’s the first FDA approval for a gene-edited food animal — period. Bigger context: Genus PLC went on to form an accelerated joint venture with Beijing Capital Agribusiness for PIC China (51% BCA / 49% Genus, formed January 31, 2026), receiving $160M in gross cash on the deal (Genus plc preliminary results; Vox Markets).

For dairy cattle genetics, the implications are direct:

- The regulatory pathway works. The FDA “low-risk determination” framework is no longer theoretical. It’s been used.

- The constraint on commercial gene-edited cattle is no longer FDA approval — it’s processor and retailer acceptance.

- The Genus China JV structure is a working template for getting gene-edited livestock genetics into restricted markets.

Acceligen’s PRLR-SLICK heat-tolerant cattle got their FDA low-risk determination back in 2022 (FDA risk assessment). Brazil’s CTNBio approved gene-edited Holsteins in 2023, and commercial herds are in production. The UK Precision Breeding Act took full effect on November 13, 2025, covering livestock. The EU reached provisional agreement on its New Genomic Techniques regulation on December 4, 2025 — focused initially on plants, with livestock to follow.

For Stud Wars purposes: gene editing isn’t the stud-versus-stud fight yet. It’s the regulatory ceiling everyone’s waiting on. April 2025 to April 2026 is the year that ceiling started moving up.

The IVF Sub-War: URUS vs. Semex

While the headlines went to mergers and gene editing, Trans Ova Genetics (URUS subsidiary) and Boviteq (Semex subsidiary) executed parallel franchise-style IVF expansion campaigns through 2025 and into 2026. The independent IVF market is being divided between URUS and Semex on a country-by-country basis.

| Operator | 2025–2026 Moves |

| Trans Ova (URUS) | Acquired ReproLogix (Sept 2025); Quebec IVF lab with Evolygen (Sept 2025); Saskatchewan lab with Bovigen (Mar 2026); Ireland Extension Site with Target Genetics (Mar 2026); small-ruminant expansion with RSG (Mar 2026) |

| Boviteq (Semex) | Nosawa as Japan licensee (Jan 2025); Boviteq Arizona OPU/IVF lab at Arizona Dairy Co. (May 2025); Diamond Genetics as Netherlands partner (Feb 2026) |

Sources: Trans Ova press releases, Semex press releases.

Vytelle, the largest non-aligned IVF player, hasn’t announced new funding in our research window but stayed active at CattleCon and rolled out its Vytelle.io data platform and ASSURE recipient screening tool (Vytelle). The independent IVF lane is narrowing.

On December 19, 2025, Semex purchased Semex Holland from Bles Dairies, effective December 31, 2025, adding direct distribution in the Netherlands, Denmark, and Belgium (Semex) — 2.6 million cows of new direct-distribution territory.

CRV (Dutch co-op) announced a 150-FTE restructuring on November 12, 2024, in response to projected decline in Dutch and Belgian dairy/beef cattle numbers (CRV). FY2024–25 results showed €3.8 million operating profit, recovering from a €4.2 million loss the prior year (CRV January 2026 update). On the bull side, CRV’s Terra-Calroy Zuri-ET sits at #5 in the Holstein USA proven top 100 — the only CRV bull in the global proven top 10.

VikingGenetics quietly executed two structural moves that won’t show up in NAAB stats for years: a direct U.S. subsidiary operationalized in 2025, and a first internal IVF lab at the Assentoft bull station in Denmark (VikingGenetics 2024 Annual Report). Total revenue €35.1 million; small absolute numbers, but structurally Viking is positioning for a direct-to-American-farmer model that bypasses traditional U.S. distribution. That’s not an Empire move. That’s a flanking maneuver.

The Volume Game: NAAB 2025 Numbers

Stud market share doesn’t pay anyone’s bills. Semen sales do. The NAAB 2025 year-end report (published March 11, 2026) shows the headline numbers North American studs are working with:

| Metric | 2025 | YoY |

| Total U.S. bovine semen units | ~66M | −4% |

| Total domestic dairy units | 16.5M | +2% |

| Gender-selected dairy | 10.6M | +6% |

| Gender-selected as % U.S. dairy AI | 64% | +3 pts |

| Conventional dairy domestic | 6.0M | −5% |

| Beef-on-dairy domestic | 8.1M | 0% |

| Heterospermic beef (pooled) | ~2M | −28% |

| Total dairy exported | 28.3M | −8% |

| Beef semen exported | 5.5M | +13% |

| Total export value (record) | $327.6M | +0.6% |

The story in those numbers: gender-selected dairy semen is now 64% of all U.S. dairy AI — up another 3 points in a single year and well past 60% as a permanent baseline. Beef-on-dairy looks saturated at 8.1M units, flat for two consecutive years, capped by farms unable to afford losing more replacement heifers. Heterospermic beef (pooled multi-sire) crashed 28% off its 2024 peak — the trial bubble has burst, and traditional sire-identified beef-on-dairy is reasserting.

Crucially, in February 2025, China effectively closed to U.S. semen exports through retaliatory tariffs (NAAB analysis cited in industry coverage). China was the #1 export market four years running. Total dairy exports fell 2.5 million units. Other markets and beef-semen growth absorbed the dollar value, keeping the export total at a record $327.6 million — but the volume hit landed on every major U.S. stud’s books.

For Stud Wars positioning, the volume story rewards three things in 2026: dominant sexed-semen production capacity, beef-on-dairy lineup depth, and meaningful non-China export reach. STgen has #1. Select Sires has #2. URUS and ABS are in #3 contention with growing IVF and beef-cross programs.

At-a-Glance: Where Each Stud Stands After April 2026

| Stud (NAAB codes) | Genomic top 200 | Proven top 100 | Specialty position | Biggest 2025–26 catalyst |

| Select Sires (7, 14, 250) | 29.5%(59/200) | 23.0% (23/100) | Federation distribution; balanced TPI depth | DOJ decision on STgen merger |

| Semex Alliance(200, 777) | 20.0%(40/200) | 13.0% (13/100) | Progenesis/Beyond pipelines; 12% of Type top 50 | Holland acquisition; Boviteq IVF expansion |

| United Sires(596, 796) | 15.0%(30/200) | 0.0% (0/100) | Independent breeder co-op founded 2024; Whoops/Howland-P pipeline | Emergence as 4th-largest genomic player in 18 months |

| STgen (523, 551) | 13.5% (27/200) | 36.0%(36/100) | Proven depth; gNM$ leadership | Pending DOJ + Select Sires merger; formula loss on TPI |

| ABS / Genus (29, 94) | 6.0% (12/200) | 10.0% (10/100) | R&W TPI 34% (17/50); 5 of top 10; De Novo pipeline | Genus FY25 +53% AOP; De Novo full takeover |

| Alta / URUS (11) | 5.5% (11/200) | 6.0% (6/100) | URUS Peak production line via Alta | Powerhouse +119 (carried by GENEX code) |

| GENEX / URUS(1) | 4.5% (9/200) | 4.0% (4/100) | URUS Peak production line via GENEX | Powerhouse #2 proven |

| URUS umbrella combined (Alta + GENEX) | 10.0% (20/200) | 10.0% (10/100) | Trans Ova IVF franchise; Genetics Australia JV | Powerhouse +119; Australia JV |

| CRV (97) | 4.0% (8/200) | 5.0% (5/100) | Terra-Calroy Zuri (#5 proven); data platform pivot | Restructuring; €3.8M profit recovery |

| ASCOL (288) | n/a (gTPI) | n/a (proven) | Type 30% (15/50); 3 of top 10 PTAT | Spanish breeder co-op dominates U.S. PTAT rankings |

| Independents | 2.0% (4/200) | 3.0% (3/100) | Niche specialty (proven: RuAnn 719, A.I. Total 515, Korea 208; genomic: El Toro 508/708, A.I. Total 515, Genesis MX 706) | RuAnn Karat #1 PTAT (+3.92); Cookiecutter Horseshoe at #8 proven |

| Zoetis (non-stud) | n/a | n/a | DNA lab + DWP$ + Danone | $160M Neogen GeneSeek deal |

| Acceligen / LIC / gene-edit | n/a | n/a | Regulatory watchers | Genus PRP FDA + Canada approvals |

The Bullvine Bottom Line

This is the most structurally consequential Stud Wars installment we’ve published since the series started in 2013.

The TPI 24P/14F formula change cost STgen significant headline TPI position on the genomic young bull list and rewarded protein-tilted Select Sires, Semex, and URUS-affiliated lineups (Peak via both GENEX 1HO and Alta 11HO codes). But STgen’s proven army held — 36 of the top 100 proven TPI bulls still wear 551HO (STgenetics-Inguran). The Empire didn’t fall on the proven list. They got reshuffled on the genomic young bulls.

The DOJ decision on the Select Sires + STgen merger is the next domino. It will reshape U.S. sexed-semen access, cooperative leverage, and the cost-of-entry for every smaller stud and every farmer-owned organization for the next decade. Either outcome — clearance or block — locks the industry into a path with no easy reversal.

The Zoetis + Neogen GeneSeek transaction is the deal nobody outside genomics testing fully understood at the time. Owning the test, the index, the processor mandate, and the lab infrastructure simultaneously is a vertical lock. Neither the DOJ nor the FTC has signaled concern. That alone should worry breed associations, AI cooperatives, and farmers who care about who reads their genomic data.

The PIC PRRS-resistant pig FDA approval and Canadian clearance unlock a gene-editing pathway that cattle programs have been waiting on. Acceligen, LIC, ABS, and CRV all have programs in motion. Three to five years out, the bull catalog conversation could include polled, heat-tolerant, and disease-resistant edits — and the studs who positioned early will lead.

NAAB’s 2025 numbers tell the underlying market story. Sexed semen is 64% of U.S. dairy AI. Beef-on-dairy hit a saturation ceiling at 8 million units. China’s tariff closure took a 2.5 million unit chunk out of dairy exports. Total volume down 4%, total export dollars at record. Less semen, sold at higher prices, into more diverse markets.

The April 2026 run is the moment the genomic balance of power shifted. Semex took the genomic top 20 — 9 of the top 20 genomic young bulls in the world are 200HO. Select Sires owns the broadest genomic depth at 29.5% of the top 200. STgen still owns proven depth (36%) and gNM$ economics. United Sires — a brand-new breeder co-op — captured 15% of the genomic top 200 in 18 months from a standing start. The IVF map is being redrawn weekly. And the corporate rules of the game are about to be rewritten by the DOJ and Zoetis, not by anyone breeding bulls.

Last April’s run was a New Hope. This April’s is the Empire striking back — not at any single bull or breeder, but at the genomic insurgency itself, through formula changes, mergers, and a vertical lock on the lab pipes. STgen’s army held the proven floor. The corporate empire is positioning to define every contract negotiation, every lab routing decision, and every cooperative’s leverage for the next decade.

And the rankings that everyone in this article has been counting? They’re a useful filter for who supplies elite-tier bulls. They’re not a measure of who sells the straws. STgen owns 90% of the genomic NM$ top 100 and a single-digit share of U.S. domestic dairy semen volume. ABS has a 6% ranking presence and a much larger commercial footprint than that suggests. The 4,000-bull selling universe is shaped by 20-some sub-markets, minimum-threshold buying, and price ceilings the rankings don’t capture. The studs know it. Now readers know it too.

In the immortal words of Yoda: “Always in motion, the future is.” Especially when Holstein USA changes the formula, the DOJ wakes up, and Zoetis writes a $160 million check.

May the Force — and a sharp eye on stud share — be with you.

What This Means for Your Operation

- Re-rank your active sire list against the 24P/14F formula. Bulls you trusted on TPI in December 2025 may be 50–125 points lower in April 2026 with no daughter data shift. If your mating program drives selection from a TPI cutoff, reset the threshold or risk over-narrowing or over-widening your bull list.

- Audit your single-source dependencies before the corporate rules change. Whether the Select Sires + STgen merger clears or blocks, the industry’s structure in 2027 will be meaningfully different. If you’re locked into single-source semen supply or single-source genomic testing, build optionality now.

- Watch the Zoetis–Neogen close in H2 2026. If you’re on CLARIFIDE Plus, a Danone supply contract, or any breed-association DNA test routed through GeneSeek labs, your genomic data is moving to a single corporate owner. Know who reads your DNA.

Key Takeaways

- 24P/14F formula reshuffled the entire genomic deck: Garza −125 TPI, Sheepster −92, Captain −72, all without daughter changes. Powerhouse +119 became the run’s signature winner.

- Genomic top 200 verified counts (NAAB-code accurate): Select Sires 59 (29.5%), Semex 40 (20.0%), United Sires 30 (15.0%), STgen 27 (13.5%), ABS/Genus 12 (6.0%), Alta/URUS 11 (5.5%), GENEX/URUS 9 (4.5%), CRV 8 (4.0%).

- Proven top 100 verified counts: STgen 36 (36.0%), Select Sires 23 (23.0%), Semex 13 (13.0%), ABS/Genus 10 (10.0%), Alta/URUS 6 (6.0%), CRV 5 (5.0%), GENEX/URUS 4 (4.0%).

- Type (PTAT) top 50 verified counts: ASCOL 15 (30.0%), STgen 7 (14.0%), Semex 6 (12.0%), A.I. Total 5 (10.0%). RuAnn Karat-45955-ET is the #1 PTAT bull at +3.92.

- Red & White TPI top 50 verified counts: ABS/Genus 17 (34.0%), STgen 10 (20.0%), Select Sires 8 (16.0%), Semex 4 (8.0%). Denovo 21873 Okafor-Red-ET tops R&W at +3194 TPI — a De Novo (ABS) bull.

- Genomic NM$ top 100 — STgen owns 90 of 100 sires (90.0%): Select Sires 4, GENEX/URUS 3, Semex 2, Alta/URUS 1. The single most concentrated category in the entire analysis.

- Proven NM$ top 100: STgen 29 (29.0%), Select Sires 22 (22.0%), GENEX/URUS 18 (18.0%), ABS/Genus 17 (17.0%), Semex 7 (7.0%), Alta/URUS 7 (7.0%) — the most balanced category.

- Total NM$ (200 unique sires — deduped): STgen 119 (59.5%), Select Sires 26 (13.0%), GENEX/URUS 21 (10.5%), ABS/Genus 17 (8.5%), Semex 9 (4.5%), Alta/URUS 8 (4.0%).

- Total Overall (466 unique elite sires across all 4 NAAB-verified lists): STgen 155 (33.3%), Select Sires 108 (23.2%), Semex 55 (11.8%), ABS/Genus 39 (8.4%), GENEX/URUS 34 (7.3%), United Sires 30 (6.4%), Alta/URUS 25 (5.4%). Combined STgen + Select Sires = 56.5% of the entire elite sire universe.

- United Sires LLC — a breeder-owned independent co-op founded in 2024 (596/796 NAAB codes) — captured 15% of the genomic top 200 from a standing start. Largest emergent player of the year.

- STgen still owns the proven floor: 36 of the top 100 proven TPI bulls. Even with Garza, Captain, Dominance taking formula hits, the depth held.

- Cookiecutter Horseshoe at #8 proven is registered under the 208HO Korean code as primary, but commercially distributed in North America via Semex (200HO/777HO secondary codes).

- DOJ decision on Select Sires + STgenetics merger is imminent and will define 2027–2030 industry structure.

- Zoetis paid $160M for Neogen GeneSeek — controlling test, index, processor mandate, and lab pipes simultaneously. Closes H2 2026.

- NAAB 2025: sexed dairy at 64% of all dairy AI; beef-on-dairy flat at 8.1M units; China tariff closure cost ~2.5M dairy units of exports.

Methodology Note

All April 2026 stud-share figures are independent counts of official Holstein Association USA April 2026 evaluation lists, drawn from the official CDCB run published April 7, 2026 (CDCB). NAAB-code-to-stud assignments follow the official NAAB marketing codes table as the source of truth.

Genomic counts use the Holstein USA Top 200 TPI® Genomic Young Bulls, April 2026, which requires 85% genomic reliability for production and type. Proven counts use the Holstein USA Top 100 TPI Bulls, April 2026, which requires ACTIVE or LIMITED semen status and 80% traditional reliability minimum.

Specialty Type (PTAT) and Red & White TPI counts are independent NAAB-code counts of the EuroGenes April 2026 ranked top-50 PTAT and R&W bull lists, which are curated from the same Holstein USA April 2026 evaluation as the headline gTPI/proven lists but isolate the type and R&W subsets.

Genomic NM$ Top 100 and Proven NM$ Top 100 counts are independent NAAB-code counts of the official CDCB April 2026 high-ranking bull lists sorted by Net Merit. Combined-category totals (Total NM$, Total TPI, Total Genomic Sires, Total Proven Sires, Total Overall) are produced by deduplicating across each component list by NAAB code so a sire that appears on multiple lists is counted exactly once.

Polled gTPI, polled NM$, and Jersey JPI ranked lists weren’t available in the same downloadable format this run; standalone polled and Jersey stud-share tables are held until bull-by-bull verification is possible rather than relying on stud self-reports.

Key NAAB code → stud assignments used in this analysis: 1 = GENEX Cooperative; 7/9/14/250 = Select Sires; 11 = Alta Genetics USA; 29/94 = ABS Global; 97 = CRV Holding; 200/777 = Semex Alliance; 288 = ASCOL; 523/551/558/646 = STgenetics-Inguran (Sexing Technologies / Genosource collapse to a single STgen entry); 596/796 = United Sires LLC (independent breeder co-op founded 2024, no STgen relationship); 599/799 = Blondin Sires; 719 = RuAnn Genetics. Where bulls have multiple secondary codes (e.g., Cookiecutter Horseshoe primary 208 with secondary 200/777), the primary code is used for stud assignment.

The URUS umbrella encompasses Alta Genetics (11HO), GENEX Cooperative (1HO), Jetstream Genetics (534/634/664/734), Trans Ova Genetics (264), and VAS data services. We report Alta and GENEX separately at the official NAAB level and consolidate as “URUS umbrella” where editorially useful.

April 2025 baselines as published in the original Stud Wars: April 2025 used a less-rigorous methodology that lumped breeder-affiliated codes together. Year-over-year comparisons in this article have been made cautiously and are noted where the methodology has tightened.

National averages may not reflect your region or operation. Have data we got wrong? Email editor@thebullvine.com

Read Next

- TPI 2026’s $17,500 Protein Trap: Breeding Holsteins for a Protein Market That Doesn’t Exist

- Powerhouse Up 119, Rozline Down 626: The April 2026 Holstein Proof Reset

- Zoetis + Neogen’s $160M Genomics Deal: The Hidden Cost of Letting One Company Own Your Pipeline

- Stud Wars April 2025: The Genetic Force Awakens (the prior installment)

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.