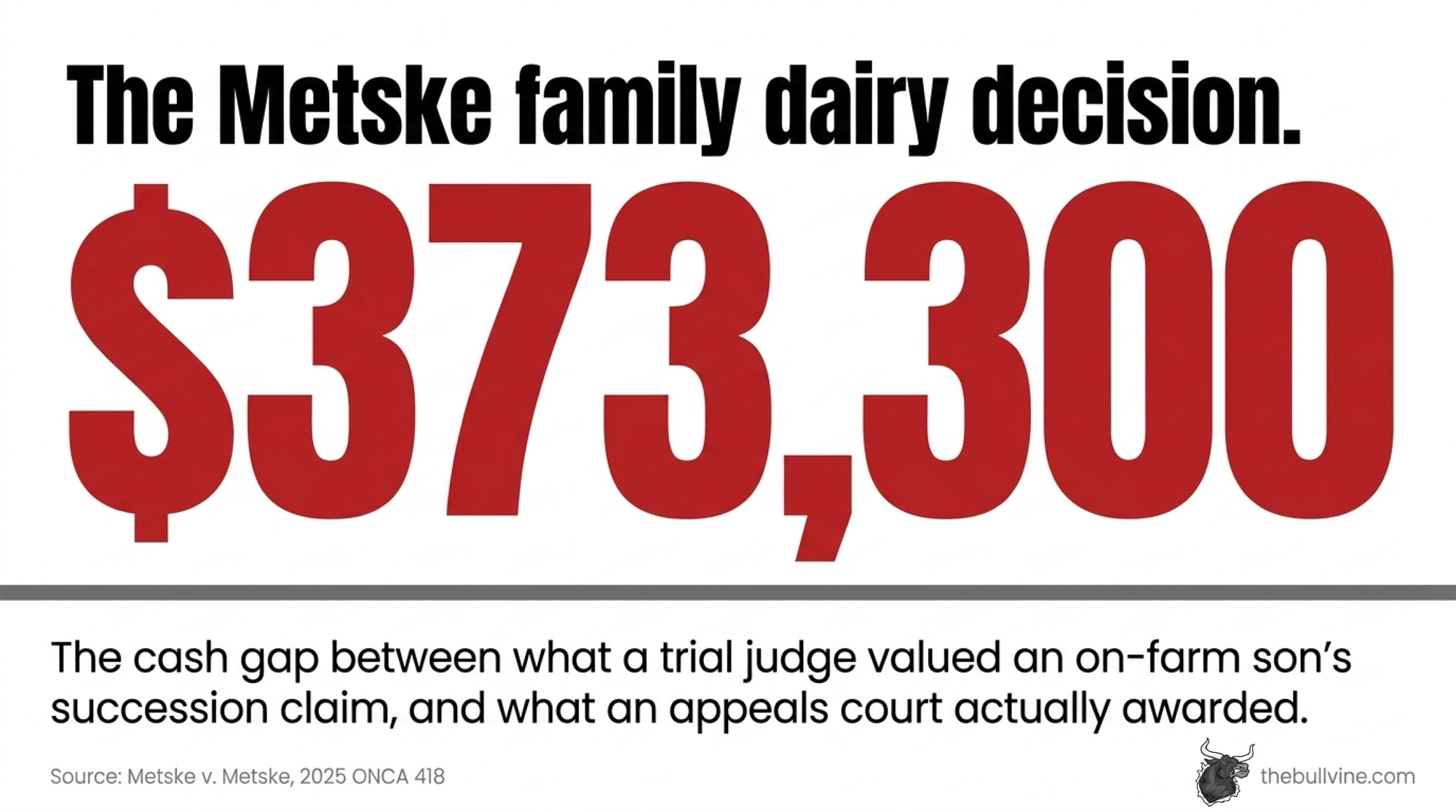

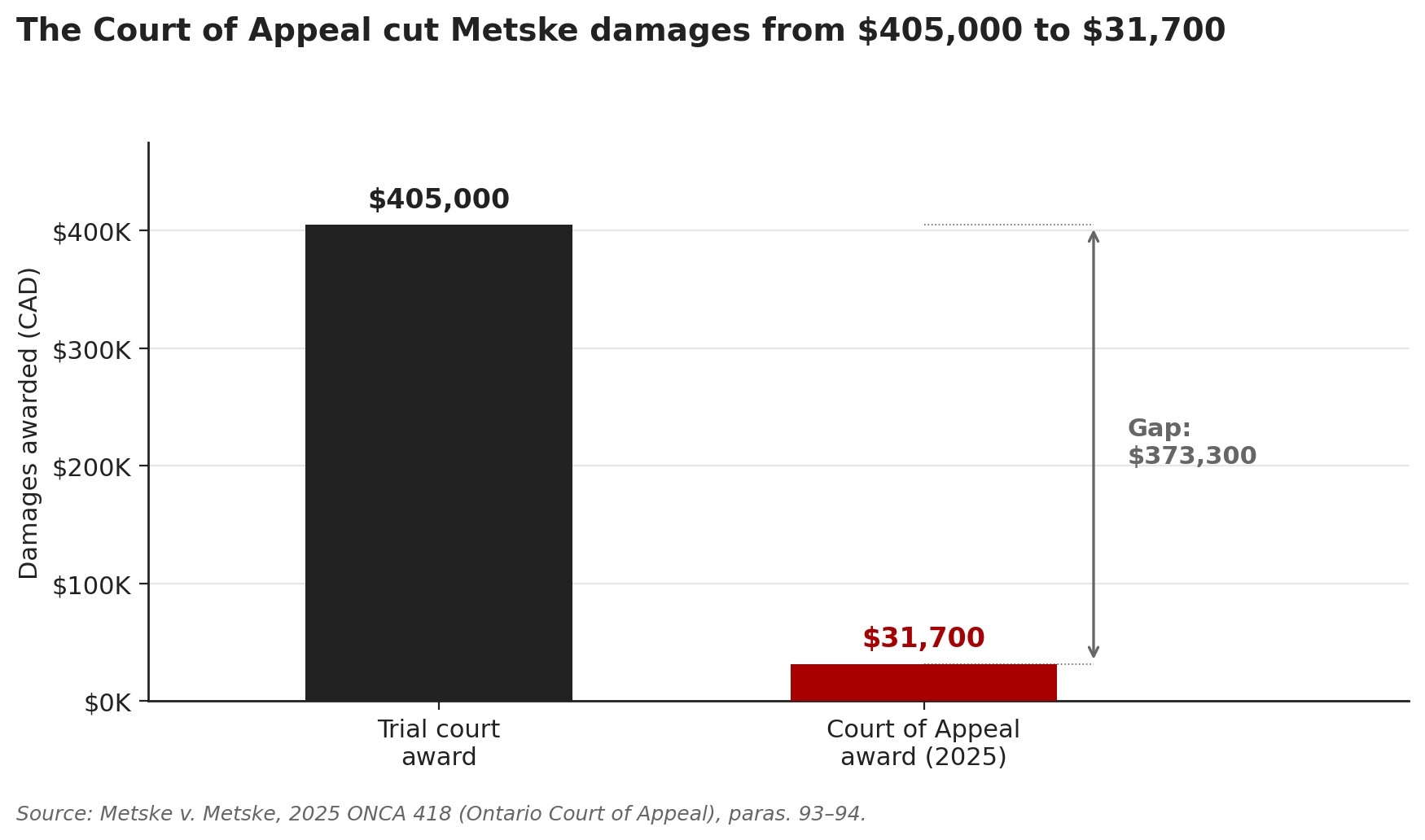

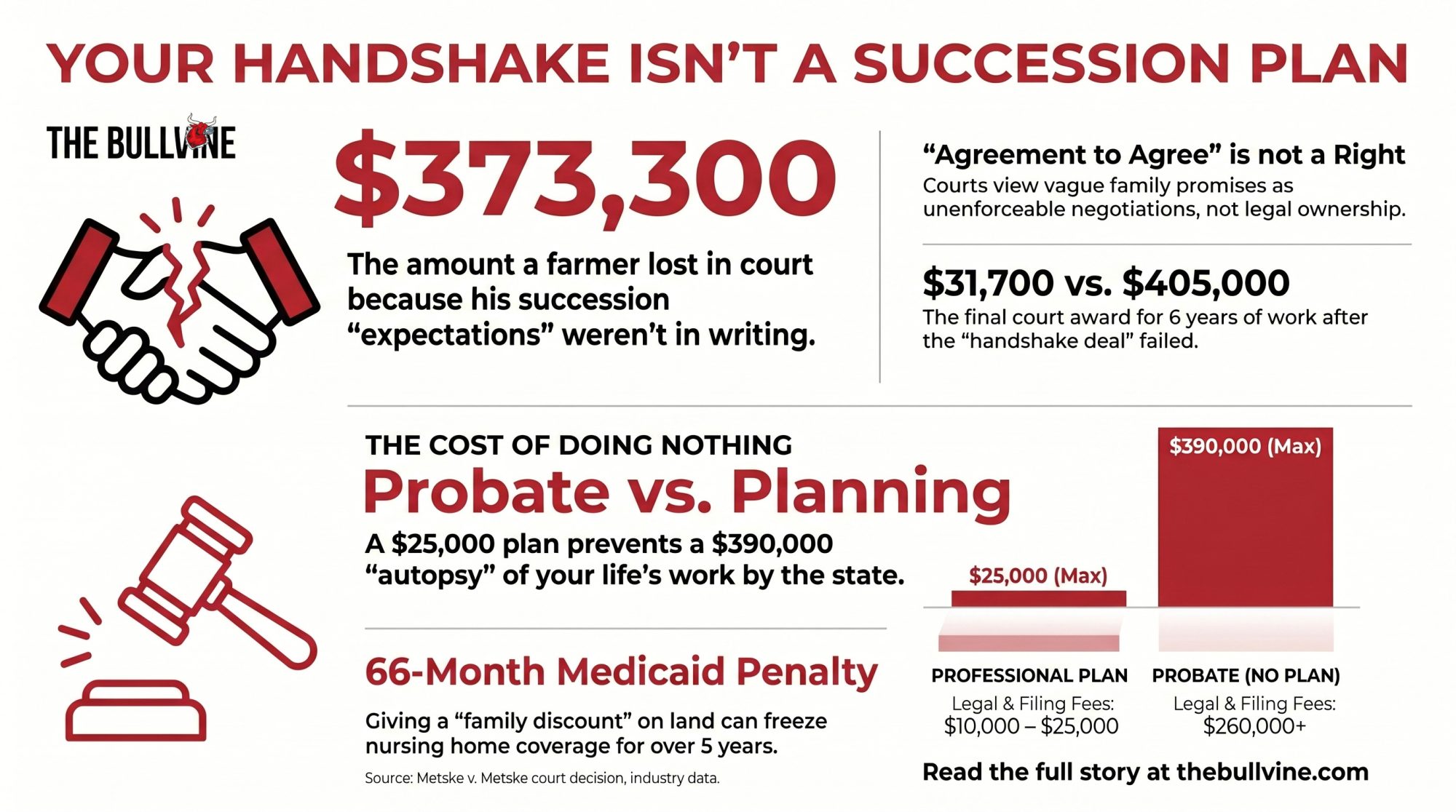

A trial judge valued six years of working the Metske family dairy at $405,000. The Ontario Court of Appeal cut it to $31,700. The $373,300 gap is what a handshake is worth in court.

All facts about the Metske family in this article are drawn from the public Court of Appeal decision Metske v. Metske (2025 ONCA 418) and publicly available legal commentary on that decision from Lerners LLP, Hull & Hull LLP, Weilers LLP, Blaney McMurtry LLP, the Ontario Bar Association, and Law360 Canada. The Bullvine has not contacted the Metske family; the analysis and editorial views are The Bullvine’s alone.

Tim Metske didn’t lose his family’s 152‑acre Ontario dairy because he misread the milk market. According to the published Court of Appeal decision in Metske v. Metske, 2025 ONCA 418, the key expectations about the barn, the quota, and the land were never reduced to enforceable written terms. The decision records that in spring 2018, after six years of work on his parents’ farm, his mother, Roseanne, notified him and his wife, Amanda, that they had to vacate the property by the end of May.

The court record shows they shipped 96 head through a catalog sale at OLEX — Ontario Livestock Exchange — and moved off‑farm during that transition. A trial judge valued their succession claim at $405,000. The Ontario Court of Appeal reduced that to $31,700 — the net value of $33,700 in concrete and equipment upgrades left behind, minus $2,000 in farmhouse damage. That $373,300 gap is what the court determined informal assurances were worth once enforceable property rights were tested.

If your own dairy farm succession plan mostly lives in people’s heads, the same legal trap sits closer to your parlor than it feels. The core problem: legal structure almost always lags behind the kitchen‑table understanding.

A note on scope: Metske was decided in Ontario, but proprietary estoppel — the legal doctrine at the heart of this case — is a cornerstone of Common Law systems across the U.S., Canada, the U.K., and Australia. The handshake trap doesn’t stop at the border. Probate fees, estate tax thresholds, and Medicaid/long‑term care rules vary by state and province. The probate and Medicaid math below uses Wisconsin as a reference point. Your numbers will differ. The lesson won’t.

Why the Stakes Are Higher in 2025–2026

The legal doctrines behind Metske aren’t new. The economics around them are. USDA NASS 2025 data put Wisconsin farm real estate at about $6,420 per acre and cropland around $7,250 per acre, with most dairy regions across the U.S. and Canada seeing steady or rising land values heading into 2026. A 300‑cow dairy with 400 acres of usable cropland, buildings, equipment, and herd can easily land in the –6 million range on a full balance sheet at those numbers.

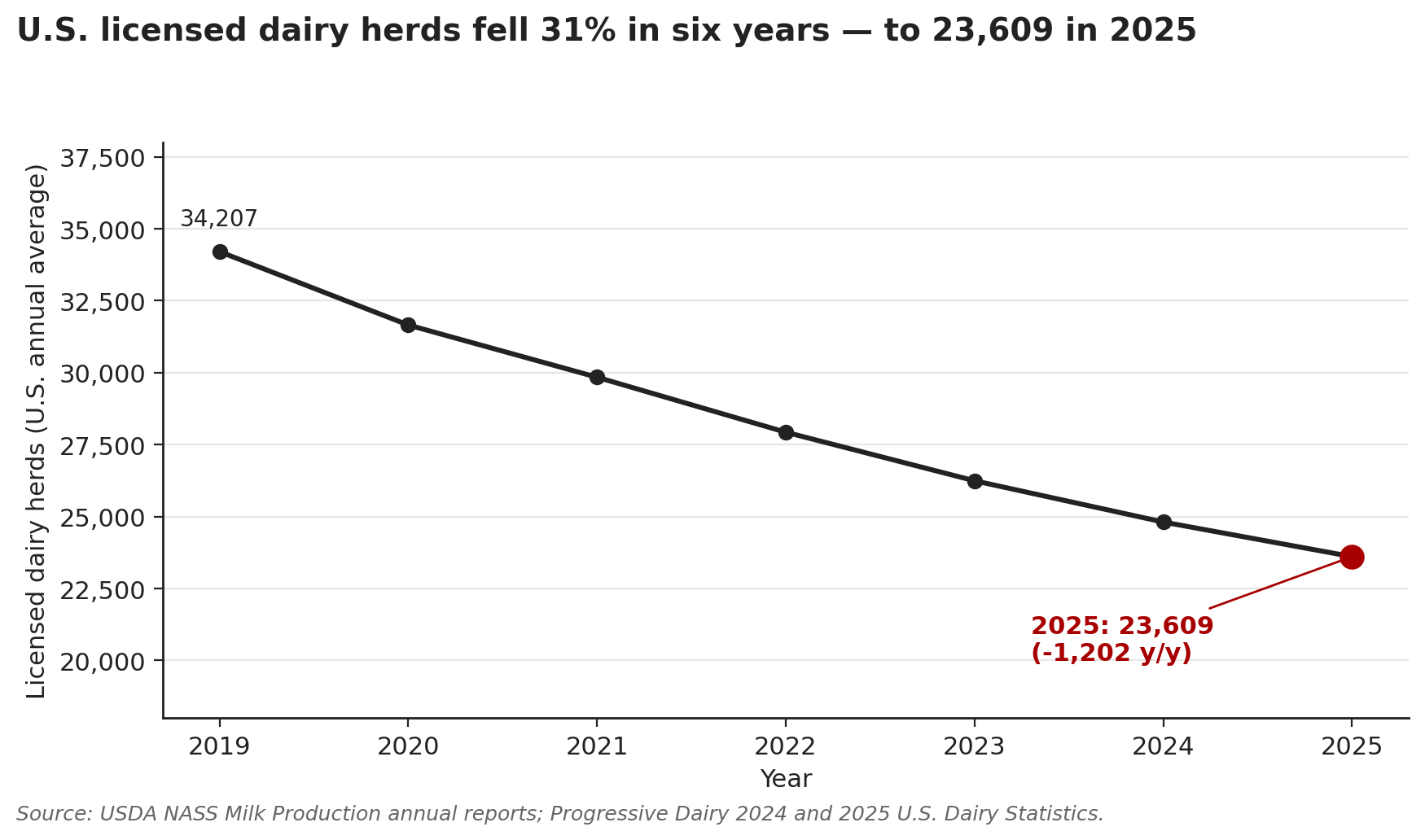

The farm count keeps dropping, too. USDA NASS reported 23,609 licensed U.S. dairies on average in 2025 — a loss of 1,202 operations from 2024, a 4.6% national decline in a single year. Pennsylvania alone accounted for 490 of those exits, an 11.7% single‑year hit (Farmshine, February 2026). Milk price and input costs drive plenty of those exits. But ag lawyers and lenders keep flagging a different pattern: estate disputes, probate delays, and succession breakdowns are turning otherwise viable operations into dispersal catalogs.

Here’s the tension. Your lender won’t advance a $500,000 operating line without a signed note. Your processor won’t pick up milk without a contract. And yet the biggest financial transfer your family will ever attempt — moving a multi‑million‑dollar dairy to the next generation — still runs on handshakes and “we all know how this ends” on a lot of farms. Metske shows exactly how little that holds up before a judge.

How the Metske Arrangement Unfolded on Paper

The arrangement described in the court decision follows a pattern common to many family dairy transitions. According to the reasons for judgment, Tim and Amanda bought about 60 cows for roughly $90,000 using a bank loan co‑signed by his father, Martin. They leased the quota, barn, and house from Martin and Roseanne, with the expectation that they would eventually buy 44 kg of quota and, later, the barn and land on terms the trial judge described as “favorable but undefined.”

The business plan filed with the bank assumed fair market value for those purchases. No written discount, no sweat‑equity formula, no fixed price per acre. When Tim sought financing for dairy quota in 2013, the bank required a 10‑year amortization that the projected cash flow couldn’t support. The Court of Appeal found Tim and Amanda’s own bank documents — showing they expected to buy at fair market value — directly contradicted any claim of a guaranteed below‑market transfer.

From 2013 to 2017, the court record shows that Tim and Amanda continued to operate as if a transfer would eventually occur. Martin had twice mentioned a $2 million buyout price in conversation, but nothing was ever written down. They took on barn and building repairs on the understanding that these expenses would fall to the incoming operators. They grew the herd from roughly 60 to 96 head.

In April 2018, Roseanne notified Tim and Amanda that they had to vacate by the end of May. They sent the 96 cows through OLEX and received roughly the same amount for the full herd that they had paid for their original 60 head six years earlier.

From a farm‑family perspective, those years looked like a time of building equity. Legally, the court treated the arrangement as a lease and service relationship — not a transfer of ownership rights.

📌 Go Deeper: We’ve already run the milk cheque math on what delayed succession costs a 400‑cow Wisconsin dairy in “The $2.30/cwt Succession Trap.” That piece covers the per‑cwt bleed. This one covers the legal trap that makes the bleed permanent. Read them together.

Why the Court Said “No Enforceable Promise”

Legally, Tim and Amanda relied on proprietary estoppel — the doctrine that if someone encourages you to believe you’ll get an interest in their land, and you reasonably act on that promise to your detriment, a court can enforce it or compensate you. The core logic is the same whether you’re in Ontario, Wisconsin, or Queensland, even if the labels differ.

The Court of Appeal concluded the test wasn’t met. The judges looked for three things and found gaps in all of them:

- A clear promise or assurance about who would own what, on what terms.

- Reasonable reliance — that it made sense for Tim and Amanda to act as if that promise were real.

- Detriment linked to that promise.

On the promise, the court required a “clear and unambiguous assurance” — not vague encouragement, not general family goodwill, not a willingness to negotiate someday. Twice‑mentioned buyout figures and “favorable but undefined” terms didn’t clear that bar. The Court of Appeal characterized the arrangement as an “agreement to agree,” which Ontario law does not enforce as a property right.

On reliance, the Court of Appeal found that the bank’s cash‑flow concern and the fair‑market‑value assumption in the filed business plan undercut the estoppel argument. The court concluded that continued reliance on a “favourable” transfer — while operating under loan documents that assumed full market value — was not reasonable.

On detriment, the court treated low wages, hard work, and routine herd costs as the ordinary risks of operating a business, rather than losses tied to a broken promise. The only detriment the appeal court quantified was improvements left behind: $33,700 in concrete and equipment upgrades, minus $2,000 for farmhouse damage, leaving $31,700.

Six years. Ninety‑six cows. And, according to the Court of Appeal, the claimed equity resolved to the value of some leftover farm improvements. The decision didn’t turn on character or motive. It turned on a straightforward rule: if you want succession rights, you need a binding agreement, not hope that “we’ll work it out.”

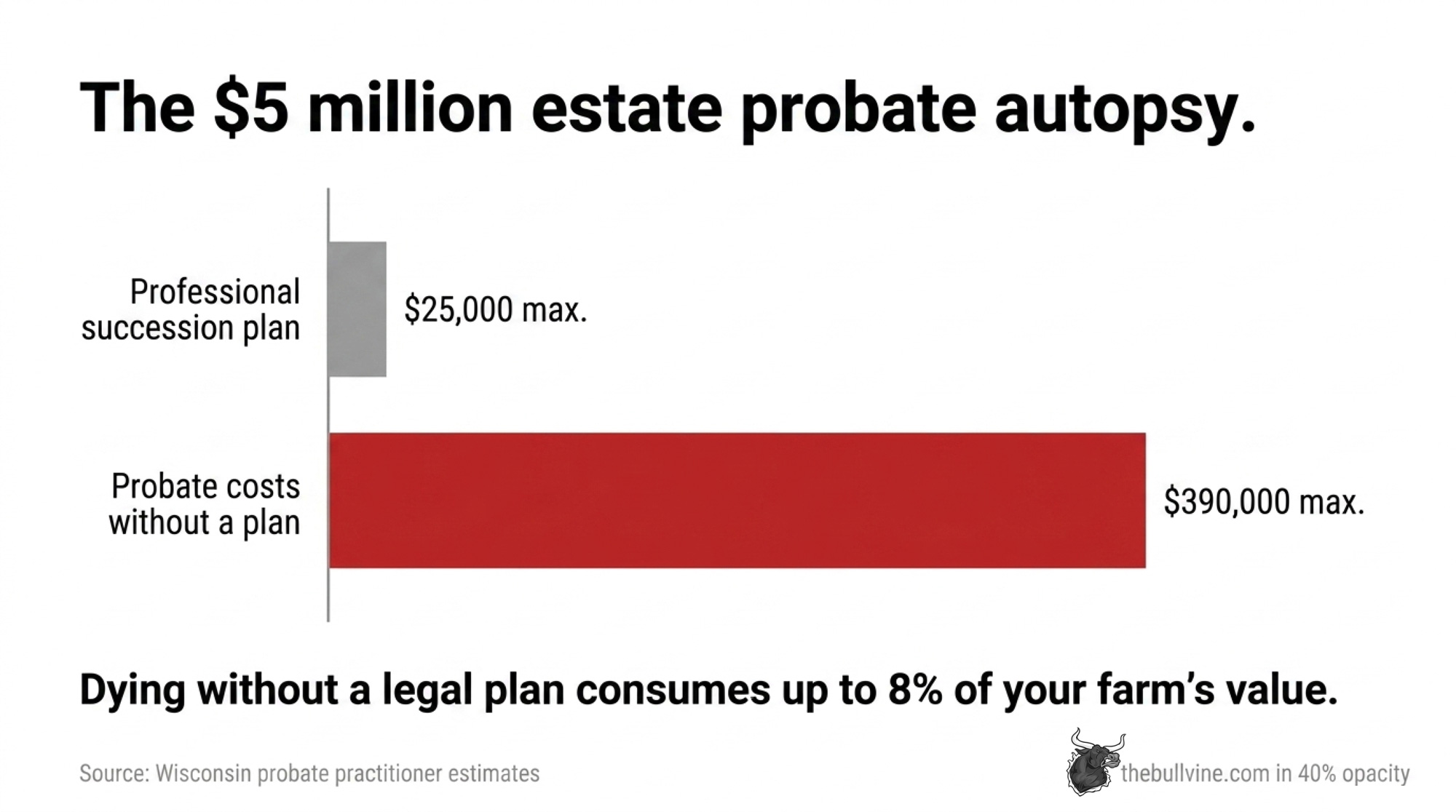

How Much Does Probate Really Eat on a $5 Million Dairy?

That’s the “founder is still alive” side of the trap. The “when Dad dies” side is probate.

If a founder dies with land, buildings, cows, and accounts in their personal name — no trust, no entities — everything falls into the probate estate. For a $5 million operation in Wisconsin, based on published fee ranges from Wisconsin probate practitioners, a realistic probate bill looks more like a feed contract than a rounding error:

| Expense category | Low estimate (USD) | High estimate (USD) |

|---|---|---|

| Court & filing fees (~0.2%) | $10,000 | $10,000 |

| Personal representative fee (~2%) | $100,000 | $100,000 |

| Attorney fees (~3% of estate) | $150,000 | $150,000 |

| Accounting, tax prep & valuations | $35,000 | $100,000 |

| Bond premiums & misc. court costs | $10,000 | $30,000 |

| Total cost of dying without a plan | $305,000 | $390,000 |

| Cost of a professional succession plan | $10,000 | $25,000 |

These figures bracket what Wisconsin probate practitioners typically quote for contested farm estates, though every case varies.

Read those last two rows again. Nobody writes a $20,000 legal cheque cheerfully. It still beats letting the state perform a $390,000 autopsy on your life’s work.

That’s roughly 6–8% of farm value consumed by process over 12–36 months, before anyone touches land transfer tax or income tax. Here’s the barn math you can run right now on your own numbers: take your total estate value, multiply by 0.065 to 0.08, and set it next to a planning fee. If the gap doesn’t make you reach for the phone, read it again.

What Happens to Your Parlor When the Estate Is Frozen?

When an owner dies, the law’s job is to preserve estate value for creditors and heirs — not to keep your parlor on a 10‑minute rotation. Your vet still needs to be paid. Your hauler still backs in before 5 a.m. The probate court doesn’t care.

If Dad dies with everything in his name, here’s what can unfold on a dairy:

- Bank accounts in his sole name may be frozen or restricted until the court appoints a personal representative and issues letters, a process that can take weeks.

- The milk cheque that used to say “John Smith” now belongs to “Estate of John Smith.” The processor might keep paying, but legally, only the court‑appointed rep is supposed to endorse cheques or open new accounts.

- Cows, feed, and equipment in Dad’s name become estate assets. Selling culls, signing feed contracts, or taking on new loans falls to the personal representative — not the widow, not the on‑farm kid — and only after the court signs off.

In real barns, families do whatever it takes to keep cows fed. But if a sibling or creditor later questions those decisions — “Why did you sell those cows?” — the person who stepped up can end up defending every move in front of a judge.

A revocable living trust sidesteps most of that. When the trust owns the land and business interests and names a successor trustee, the hand‑off at death or incapacity occurs under the trust document rather than before a probate judge. Milk cheques keep getting signed. Feed trucks keep backing in. Your parlor doesn’t care who just died.

Only about 12% of family dairy farms make it to the third generation — a number we’ve documented in our coverage of the generational cliff — and how succession choices drive it.

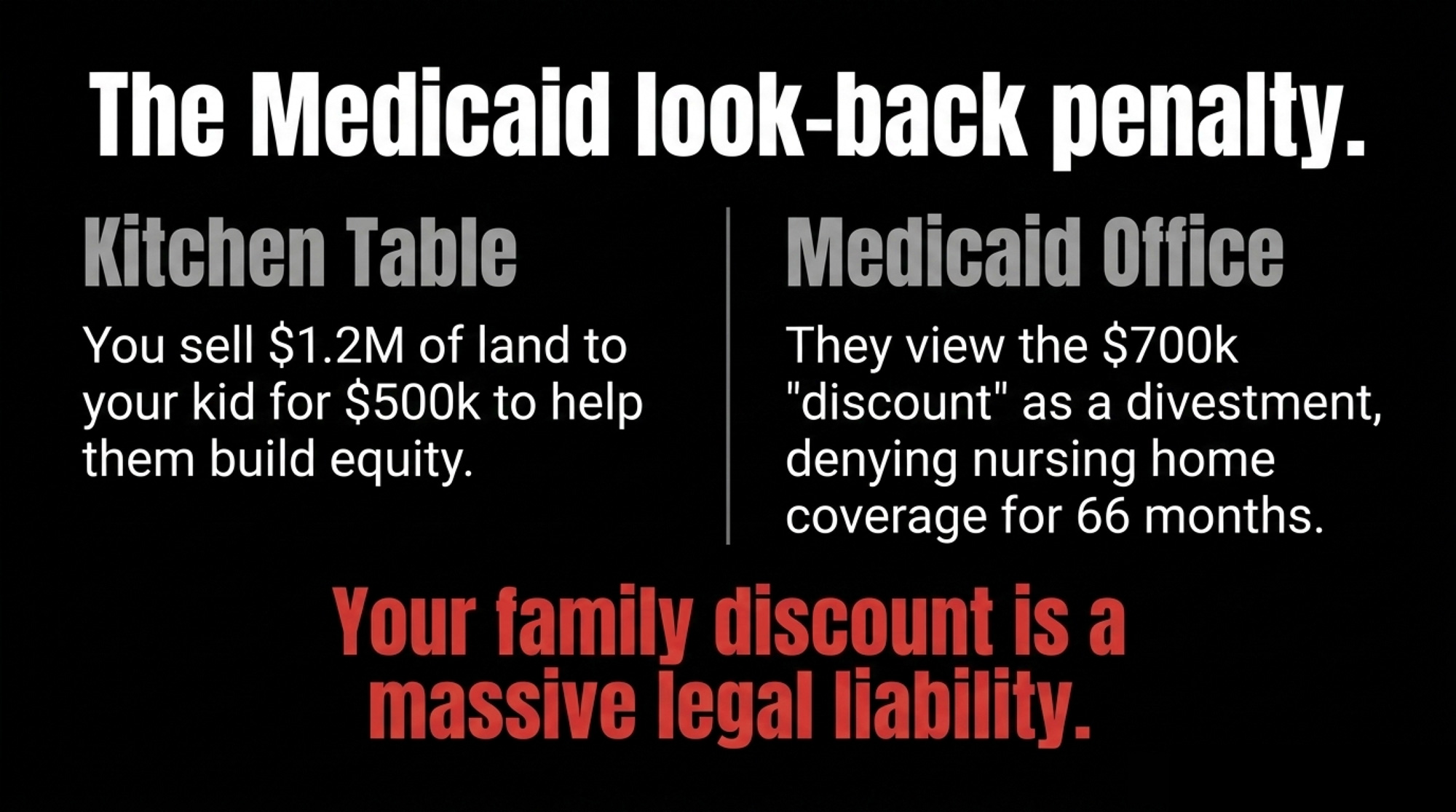

How a 5‑Year Medicaid Look‑Back Turns a “Family Deal” Into a 66‑Month Penalty

Here’s the quiet trap that collides with succession planning as founders age.

Consider an illustrative scenario: a 68‑year‑old owner transfers 150 acres to his son for $500,000 when an appraisal would peg the fair market value at $1.2 million. On paper, it’s a sale. Around the kitchen table, it feels like a family deal. Four years later, he has a stroke and moves into a nursing home. The family applies for Medicaid long-term care.

Medicaid doesn’t just look at what you own the day you apply. It looks back 60 months to find what you gave away or sold below fair market value.

Medicaid sees that land transfer inside the window. It compares $500,000 to the $1.2 million appraised value and treats the $700,000 difference as a divestment — a gift. Wisconsin’s divestment divisor is $352.06 per day, per Wisconsin DHS Operations Memo 25‑20, effective for applications filed on or after January 1, 2026.

The penalty math:

- $700,000 ÷ $352.06 ≈ 1,988 days

- 1,988 days ÷ 30 ≈ 66 months

Medicaid’s answer: “You’re otherwise eligible, but we’re not covering your nursing‑home bill for roughly 66 months.” At Wisconsin’s monthly average private‑pay nursing home rate of $10,708.49 (same memo), the family faces roughly $707,000 out of pocket before coverage kicks in.

The “discount” you thought you were giving the next generation can boomerang as a long‑term care penalty when it falls inside the five‑year window. Mitigation options exist — partial return of assets, narrow hardship waivers — but they’re complicated and fact‑specific. The cleanest path is timing: if you’re going to use irrevocable trusts or deep discounts, do it well outside the look‑back period. This example uses Wisconsin’s 2026 Medicaid rules; specifics vary by state and province.

If any founder in your family is north of 65 and the plan is “we’ll start the transfer after the next project,” you’re not just playing chicken with milk price. You’re playing chicken with that clock.

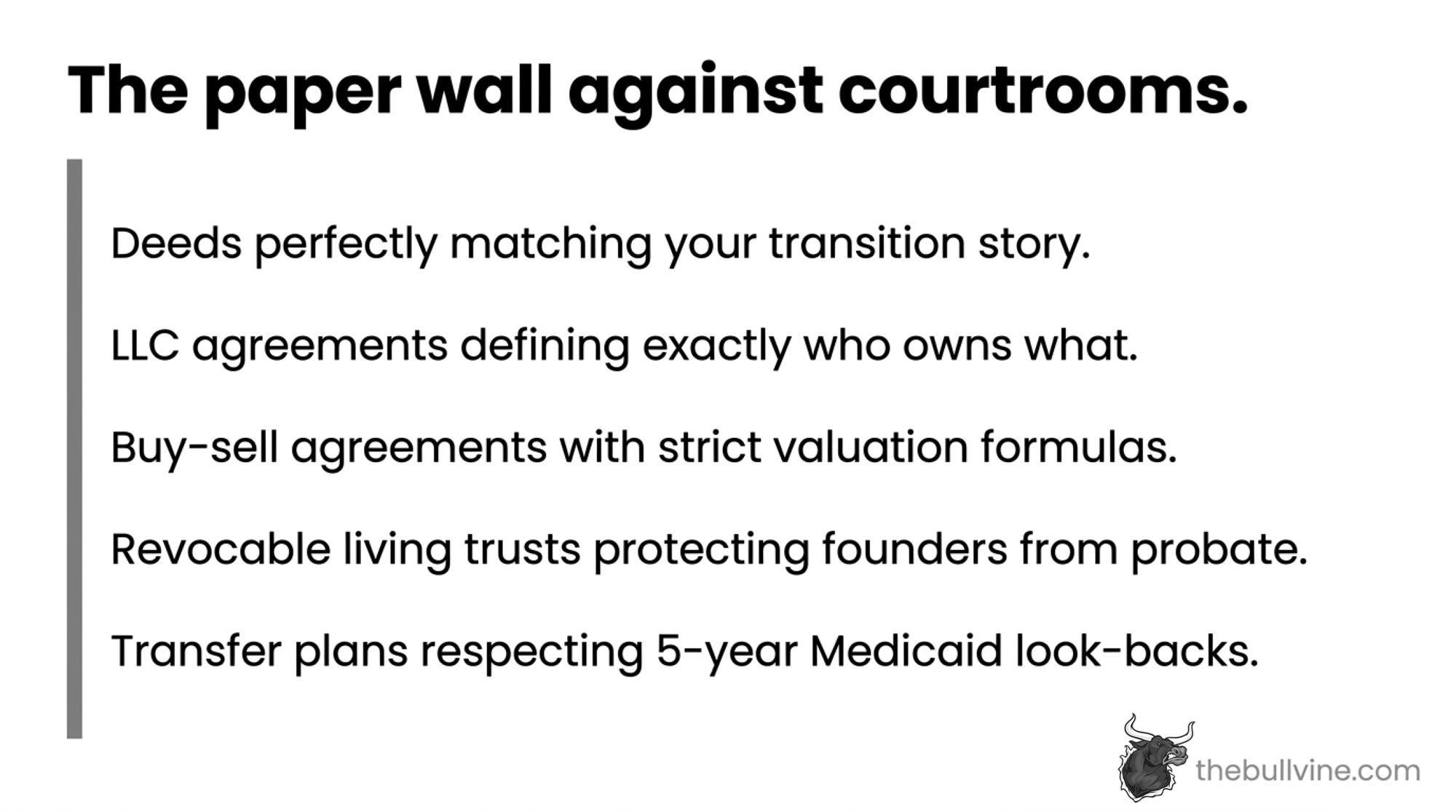

✅ The Seven Legal Pieces That Keep You Out of a Metske‑Style Trap

Save this. Print it. Tape it to the office wall next to the milk cheque.

Lawyers love making this sound like wizardry. It isn’t. The farm plans that actually hold up — in court and on the balance sheet — share the same seven pieces. Miss even one, and there’s a gap a judge or a Medicaid caseworker can drive a truck through.

☐ 1. CLEAN DEEDS THAT MATCH YOUR STORY. Every parcel needs to be titled in the name of the person or entity your plan assumes. If everyone talks like “the LLC owns the land,” but the county recorder still shows Dad on the title, the judge and the bank go with the deed, not the family story. Your 30‑day action: pull every deed from the county recorder’s office and check whose name is actually on it.

☐ 2. AN LLC OR PARTNERSHIP OPERATING AGREEMENT THAT SAYS WHO OWNS WHAT.Percentages, voting rights, profit splits, exit rules — this is where they live. Many dairies now hold land in one entity and cows and equipment in another so that the operating business can transition separately from the dirt. If you don’t have one, you don’t have a business. You have a handshake with a tax ID number.

☐ 3. A BUY–SELL AGREEMENT. The absence of a written buy–sell arrangement is a significant reason the Metskecourt found no enforceable succession rights. A buy–sell spells out who buys if someone dies, divorces, or wants out; how the price is calculated; and how the payments happen. Without one, you’re back to an “agreement to agree,” and Metske shows exactly how courts treat that.

☐ 4. A REVOCABLE LIVING TRUST FOR FOUNDERS. The trust owns the land and entity units. Founders act as trustees while they’re capable. When they die or can’t act, the successor trustee takes over without forcing a full probate on every acre. This is the single document that keeps the probate table above from becoming your family’s reality.

☐ 5. DURABLE FINANCIAL POWER OF ATTORNEY. Gives someone authority to sign cheques, refinance loans, and enter into contracts if the owner is alive but incapacitated. On a dairy, it’s the difference between a stroke triggering an emergency guardianship fight and the on‑farm kid keeping the milk truck rolling.

☐ 6. HEALTHCARE DIRECTIVE AND HEALTHCARE POA. Keeps ugly medical fights from bleeding into succession decisions. When everyone already knows who makes the call on end‑of‑life care, nobody has to use the farm as leverage in those conversations.

☐ 7. A MEDICAID‑SAVVY TRANSFER PLAN FOR ANYONE OVER 65. This is where the five‑year look‑back gets built into the timeline. Maybe it’s an irrevocable trust funded well before any likely nursing‑home stay. It could be a sale at fair market value with installment notes instead of big gifts. The key is that your ag attorney and your elder‑law advisor need to be looking at the same balance sheet.

On a 200–600 cow dairy, getting all seven pieces right typically runs $10,000–$25,000 in professional fees [NEEDS: source — published ag‑law firm fee range or UW Extension farm transfer publication; Menn Law Firm and Ruder Ware LLSC have published fee guidance consistent with this range]. Nobody pretends that’s nothing. Line it up against a $305,000–$390,000 probate bill or a roughly $707,000 Medicaid penalty, and it starts looking like the cheapest insurance policy on the farm.

Are Your “Family Discounts” Worth Anything on Paper?

This is the part nobody wants to talk about at the kitchen table.

Maybe you’ve charged below‑market rent for years because “the kids are taking over anyway.” Maybe you’ve been paying yourself less than a hired manager would cost because you see it as “building equity.” Maybe the on‑farm kid uses equipment at a rate no neighbor could ever negotiate.

Metske illustrates a hard legal reality: unless those breaks live in formal documents — a buy–sell formula, a unit‑ownership schedule, a written discount on an appraised price — a court may not treat them as the next generation’s equity.

The Court of Appeal recognized only $31,700 of net improvements as Tim and Amanda’s recoverable interest. Six years of reduced wages, reinvested labor, and herd‑building didn’t translate into equity because the court found no clear and unambiguous assurance the farm would transfer on favorable terms — and the bank documents pointing to fair market value undercut any claim it would.

Same principle in non‑quota systems. If your on‑farm heir rents 400 acres well under market rate, that discount is real money. But unless it’s baked into an ownership formula or a buy–sell agreement, it won’t automatically convert to equity before a judge. It’s worth understanding how marriage, divorce, and ownership structure can quietly shift who actually owns your dairy — because those dynamics compound the same risk.

Options and Trade‑Offs for Farmers

You don’t have to turn your family into a boardroom. But you do have to choose a path on purpose.

Path 1: Treat the farm plan like a bank loan. When it makes sense: clear on‑farm successor, serious land value, at least one off‑farm heir. What it requires: over the next 90 days, sit everyone down and answer three questions — who gets the operating business, who gets the land, and what “fair” looks like for non‑farm heirs. Take those answers to an ag‑savvy attorney and build or update the LLC agreement, buy–sell, trust, and POAs. Risks: you’ll surface hard feelings now instead of letting them detonate at the funeral. Someone may hear “no” for the first time. That conversation is hard. Probate is harder.

Path 2: Use insurance to level the table — and keep it fresh. When it makes sense: the farm can’t cash‑flow a full‑value buyout of off‑farm heirs, but you can afford premiums. What it requires: a realistic valuation of land, cows, and buildings every 5–10 years, with life insurance sized to roughly cover what off‑farm heirs won’t get in dirt or cows. Risks: policies that made sense when the farm was $1.5M can be wildly undersized at $5M. Skip the updates, and you’re handing your off‑farm kids a lawyer’s phone number instead of a cheque.

Path 3: Admit it’s a business sale, not a gift. When it makes sense: the next generation can’t stroke a cheque for fair market value today but can run a profitable operation over time. What it requires: a clear valuation formula — appraisal with a defined sweat‑equity discount — long‑term amortization, and often a “farm pension” where founders live off land rent or entity distributions. Risks: successors have to run lean enough to service the buyout. Founders may need to accept that the final transfer step happens at death to get the tax result everyone wants. If any founder is nearing long‑term care, this path has to be coordinated with elder‑law counsel to stay outside the 60‑month window.

Path 4 — Your 30‑Day Move: Stop pretending the handshake is a plan. When it makes sense: if you’ve read this far, it’s you. What to do this month:

- Pull every deed, will, LLC/partnership document, and life insurance policy tied to the farm.

- Make two lists: who thinks they’re getting the farm, and whose names are actually on those documents.

- If those lists don’t match, book an agricultural attorney within 60 days. Bring both lists and your latest balance sheet.

Risks: You may discover the story you’ve been telling around the kitchen table never had a legal backbone. That’s a lousy Monday morning. But it beats finding out at the funeral — or in a courtroom, as the published Metske decision makes painfully clear.

Key Takeaways

- If your succession plan only exists in conversations, assume a court could treat your on‑farm heir as a tenant, not a future owner. Don’t shake hands on another season — book an attorney meeting before your next herd check.

- If any founder in your family is over 65 and you’re planning a deep “family discount” on land or quota, assume Medicaid will count the gap as a divestment if nursing‑home care arrives within five years. Build the transfer outside the 60‑month window or reframe it as a documented sale at fair market value.

- If your total asset value exceeds your state’s small‑estate threshold (for example, $50,000 in Wisconsin under Wis. Stat. §867.03), treat a revocable living trust as mandatory — not optional. The probate math on a $5M dairy puts the break‑even against planning fees inside the first death in the family.

- If the names on the deed, the LLC units, the life insurance beneficiary form, and the will don’t all point to the same successor, fix the mismatch this quarter. That gap is exactly what fuels the next Metske‑style dispute.

- If you’re counting on sweat equity or a family discount to reduce your buyout price, require it in writing before you invest another year of labor. Courts won’t back‑fill a formula just because “everyone knew what we meant.”

You don’t have to draft contracts at the kitchen table. But you do have to accept that courts, banks, Medicaid offices, and title companies all speak one language — and it isn’t “you know what we mean.”

Ask yourself this week: if a judge looked only at your paperwork tomorrow — no stories, no memories, no handshake promises — who would they say owns your dairy? How much would they say it’s worth? And who would they say has the right to run it? If that answer doesn’t match what you thought, now’s the time to fix it. For the deeper milk‑cheque math on how delayed succession quietly bleeds dollars per cwt off your operation, we unpacked that in “The $2.30/cwt Succession Trap.” That’s where the spreadsheets live. This piece is your nudge to pick up the phone before your own handshake becomes Exhibit A.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Who Really Owns Your Dairy? Three Ways to Stop Divorce and Succession Turning Unpaid Spousal Work into a Land Sale — Arms you with a winter playbook to document “invisible” labor and map legal ownership before family shifts trigger a liquidation. This operational guide prevents unpaid work from becoming a high-stakes liability during succession.

- The $586‑Per‑Kilo Dairy Quota Trap: Why New Ontario Quota at 6% Bleeds Cash Every Year — Breaks down the negative-carry math that turns debt-fueled growth into an equity-shredding machine. Gain the strategic foresight to prioritize debt retirement over expansion when current interest rates collide with flat-line asset caps.

- Only 12% of Dairy Farms Reach Generation Three – A 2025 Court Ruling Exposes Why Succession Fails and How to Fix It — Dismantles the “equal inheritance” myth and delivers a 90-day triage plan for equitable transfers. Follow the money through separate entities for land and cows to ensure the next generation survives a 4.6% industry contraction.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.