One $43 test, one $160 million lab acquisition, and one Danone preferred-provider letter — and the cooperative system 75 years of dairy farmers built has months, not years, to answer for itself.

The next time URUS, ABS Global, Genex/CRI, ST Genetics, or your Select Sires / Semex -affiliated co-op holds a district meeting on your calendar, look at the slide deck the regional manager hands out. Then ask, out loud, in front of your neighbors: “What’s our plan for the GeneSeek close?”

If the room goes quiet, you already have your answer. The publicly announced 2026 dairy genetics stack — Clarifide Plus at $43 a head, the $160 million Zoetis–Neogen lab deal, Danone’s Partner for Growth letter naming Zoetis as preferred testing provider — is reshaping every AI cooperative’s negotiating position through 2030. As of May 1, 2026, none of the major cooperatives most exposed to that shift has published a strategy response.

Your seat at that table. Your kids’ equity in the co-op. The genotyping pipeline three generations of member-owners built. All of it is being decided right now, in rooms where the question hasn’t been asked out loud yet.

This article is built on published program terms, public corporate filings, CDCB evaluation data, NAAB’s 2025 year-end report, USDA NASS Milk Production data, and a peer-reviewed 2025 Journal of Dairy Science study.

What Zoetis Built While the Cooperatives Were Quiet

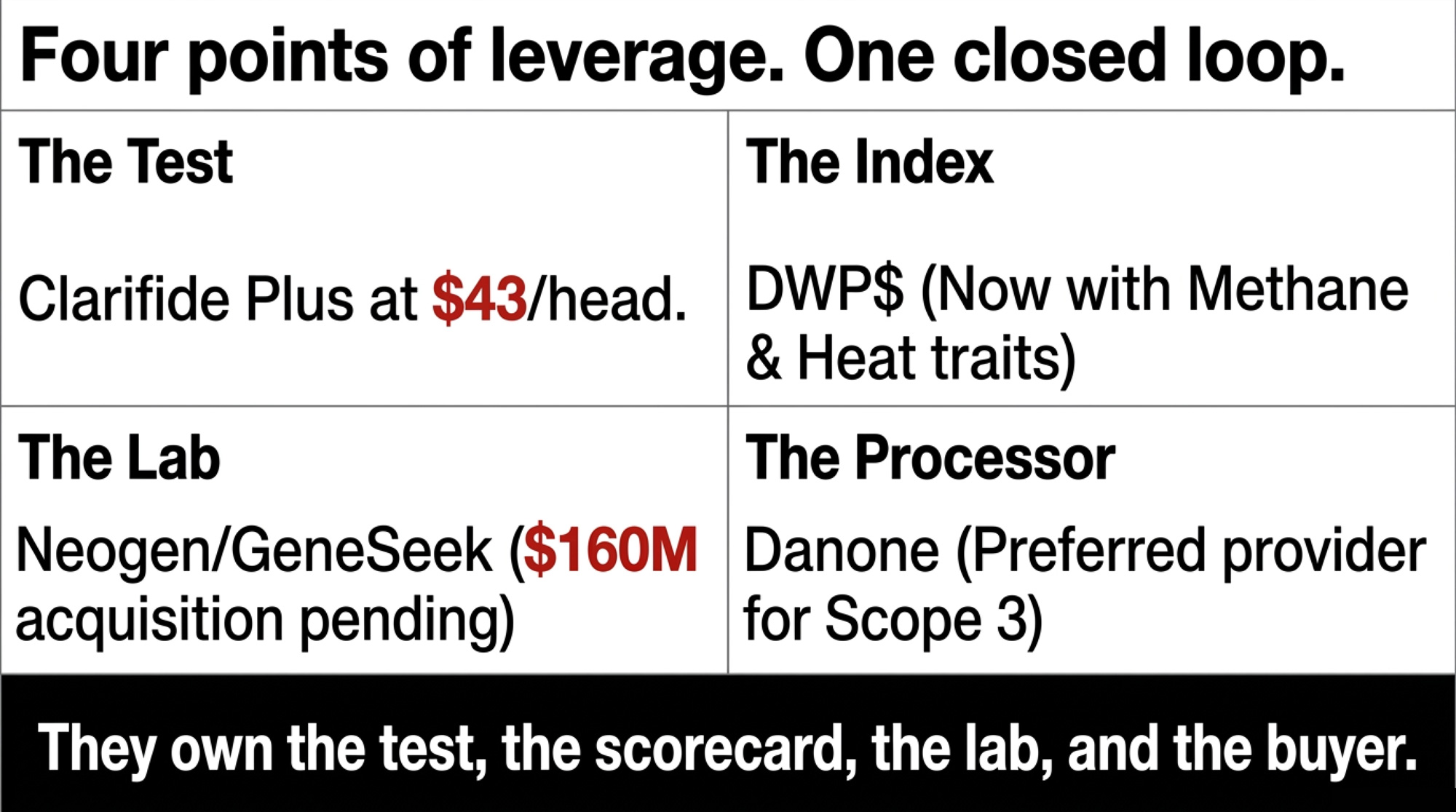

Zoetis doesn’t sell a single straw of semen. But it now sits at four points of leverage in the U.S. dairy genetics chain, and each one was announced publicly, in plain sight.

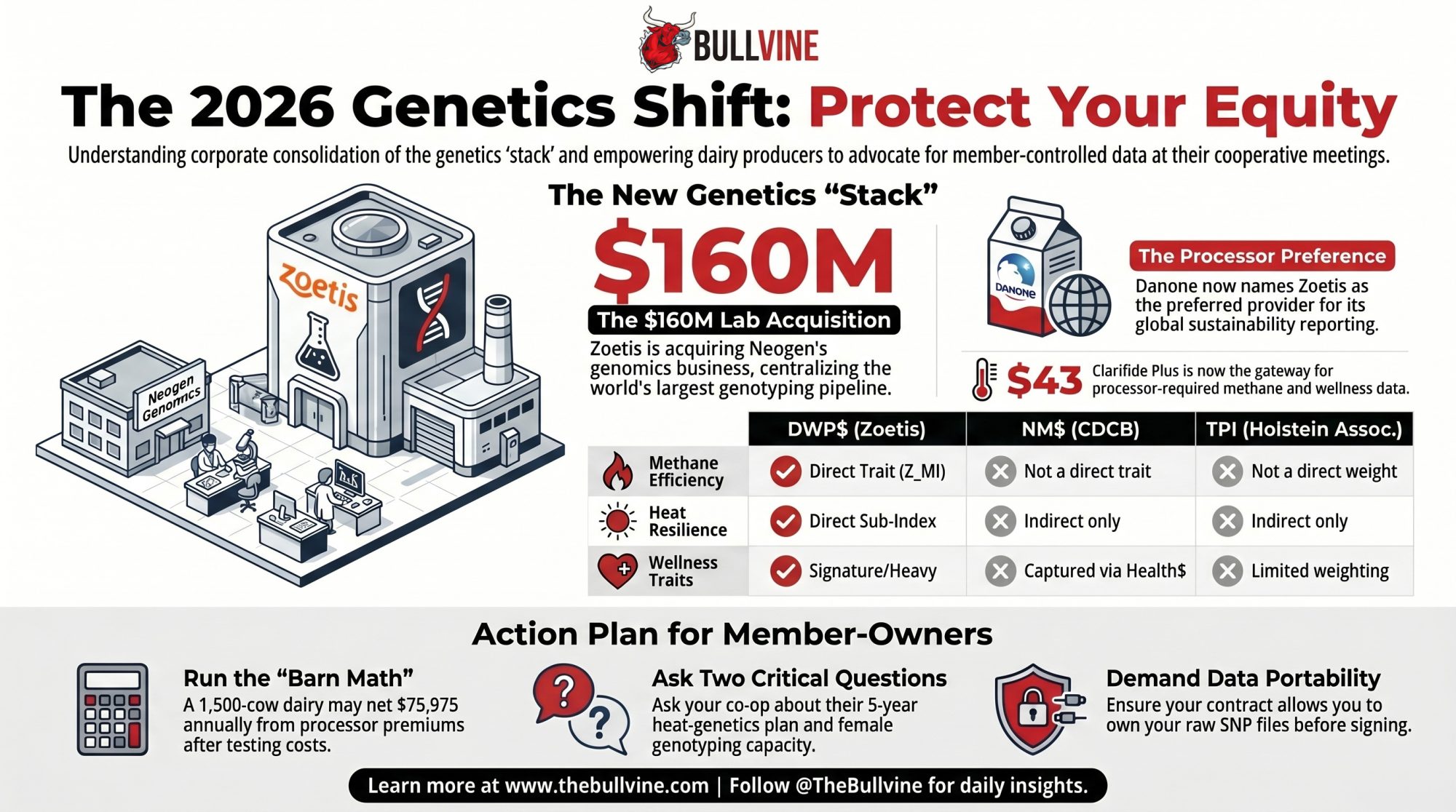

The test. Clarifide Plus runs $43 per Holstein head at Holstein Association USA’s published member rate, accessed May 1, 2026.¹ It’s already among the most widely used genomic tests in U.S. dairy.

The index. Zoetis owns DWP$, the Dairy Wellness Profit index. In April 2026, the company added Milk Methane Intensity (Z_MI) and a new sub-index called DWP$ Heat — built for herds experiencing heat stress 20% or more of the year, roughly 73 days. That’s Florida, Texas, Arizona, the southern San Joaquin, and increasingly the lower Midwest in late summer. For the back-story on how the index was assembled and what’s actually inside it, see our deeper piece on how Zoetis built the DWP$ index.

The lab. In March 2026, Zoetis announced it would acquire Neogen’s animal genomics business — including GeneSeek’s Igenity and GGP portfolios — for $160 million, subject to customary closing adjustments. That business runs roughly $90 million in annual genomics revenue, operates labs across the U.S., Brazil, Australia, China, and the U.K., and serves customers in more than 120 countries. Close is expected in the second half of 2026, pending regulatory approval.

The processor. Zoetis is the preferred genetic testing provider for Danone’s global Partner for Growth program, with DWP$ as the selection index. The two later expanded that partnership to scale testing across Danone’s supplier base for sustainability reporting — methane intensity, nitrogen efficiency, the metrics that feed scope 3 disclosures.

A company with no semen catalog is now the preferred testing provider for one of the world’s largest dairy processors, owns the index that ranks bulls inside that program, and is acquiring the lab that genotypes much of the rest of the industry. That’s the stack. On one page.

| Leverage point | What it is | Key figure | Status / trigger date |

|---|---|---|---|

| The test | Clarifide Plus genomic panel | $43 / Holstein head | Holstein Assn. USA member rate, May 1, 2026 |

| The index | DWP$ (Dairy Wellness Profit$) | Z_MI + DWP$ Heat sub-index added | April 2026 |

| The lab | Neogen animal genomics (GeneSeek, Igenity, GGP) | $160M acquisition, ~$90M annual revenue | Close expected H2 2026, pending regulatory approval |

| The processor | Danone Partner for Growth preferred provider | DWP$ as selection index | Active; expanded for scope 3 reporting |

What 75 Years of Member-Owners Actually Built

Three generations of dairy farmers pooled capital, semen, risk, and bull power so no single member would have to face the genetics market alone. Genex/CRI. Semex. Select Sires-affiliated co-ops — different banners, same logic. Member-owned, member-governed, member-equity. The genotyping pipeline that feeds every NM$ proof you’ve ever read off a sire summary was built on that infrastructure. What’s at stake in the post-GeneSeek environment isn’t whether your cooperative survives. It’s whether the genotyping data, the female reference population your co-op contributes to, and the negotiating leverage your manager carries into a Danone or Saputo or Schreiber meeting — whether all of that stays member-controlled, or gets routed around inside 18 months. That’s not a Zoetis policy question. It’s a member-governance question. And it’s the one your district director almost certainly hasn’t been asked yet.

To be fair to the boards at the major cooperatives, they’re navigating something the cooperative system wasn’t built for. Corporate entities move at the speed of capital. Cooperatives move at the speed of consensus — that’s a feature, not a bug, and it’s the same governance model that built the negotiating leverage worth protecting in the first place. But in 2026, consensus is a luxury members can no longer afford to wait through quietly. The fairness is real. The clock is also real. Both can be true.

Two Questions to Bring to Your Next District Meeting

This is the action that matters most this month. Open the notes app on your phone. Type these two questions out. Read them aloud in front of the room when the floor opens for member questions:

“What’s our plan — capital commitment, timeline, named sourcing partners — for heat-tolerant genetics over the next five years?”

“What’s our plan to own or control female genotyping capacity so members aren’t dependent on a single outside provider for health and fertility genetic gain after the GeneSeek close?”

Write the answer down. Date it. A serious answer names specific partners — Embrapa, Trans Ova, a domestic IVF lab — with dollar commitments and timelines beating 2028. An answer without partners, dollars, or dates is a signal to keep asking. Re-raise in 90 days. Document each round.

Boards move when members raise issues. The question is whether you’re the member raising this one.

What Data Are Processors Actually Building Their Scope 3 Programs Around?

The farms most exposed are mid-to-large commercial dairies supplying Danone and the processors likely to follow.

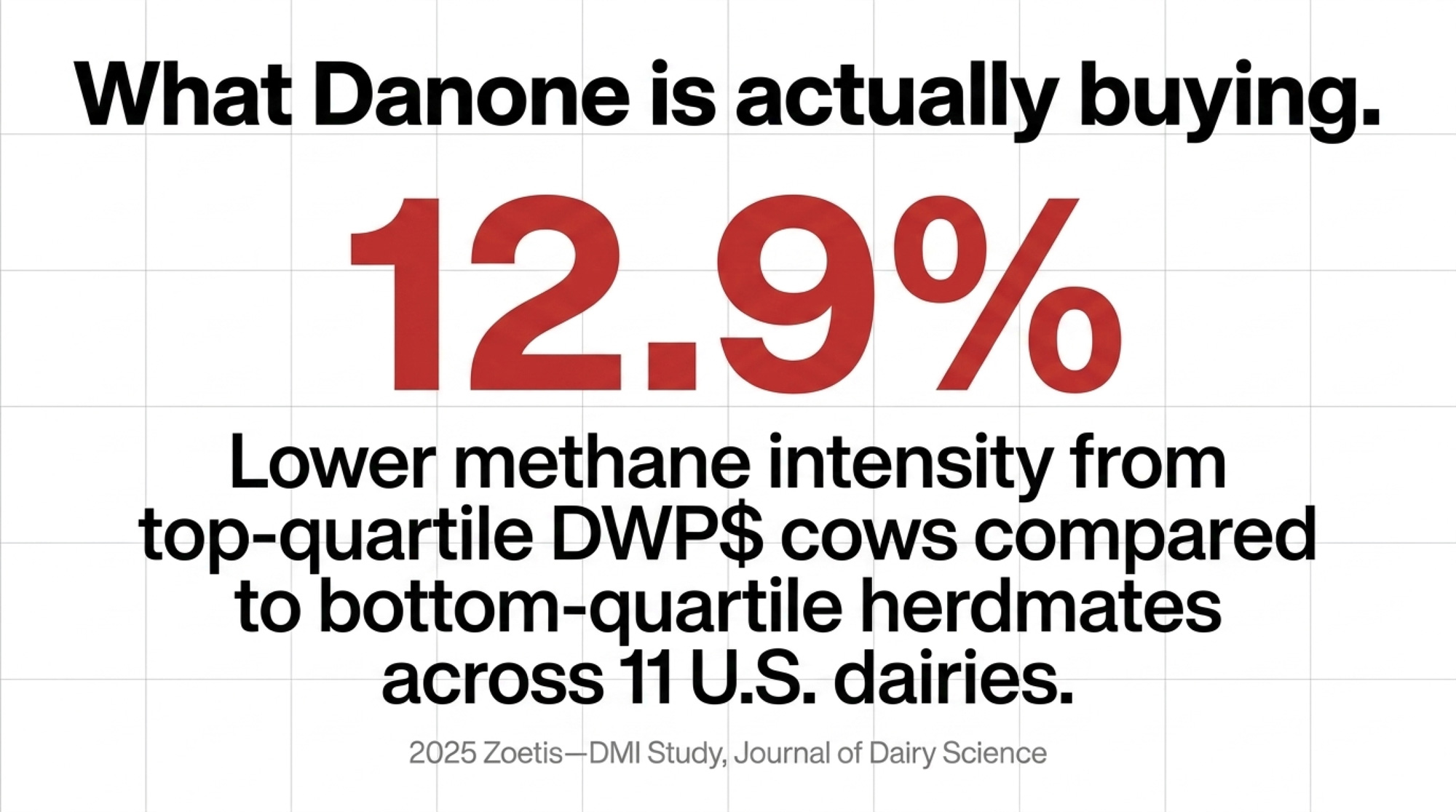

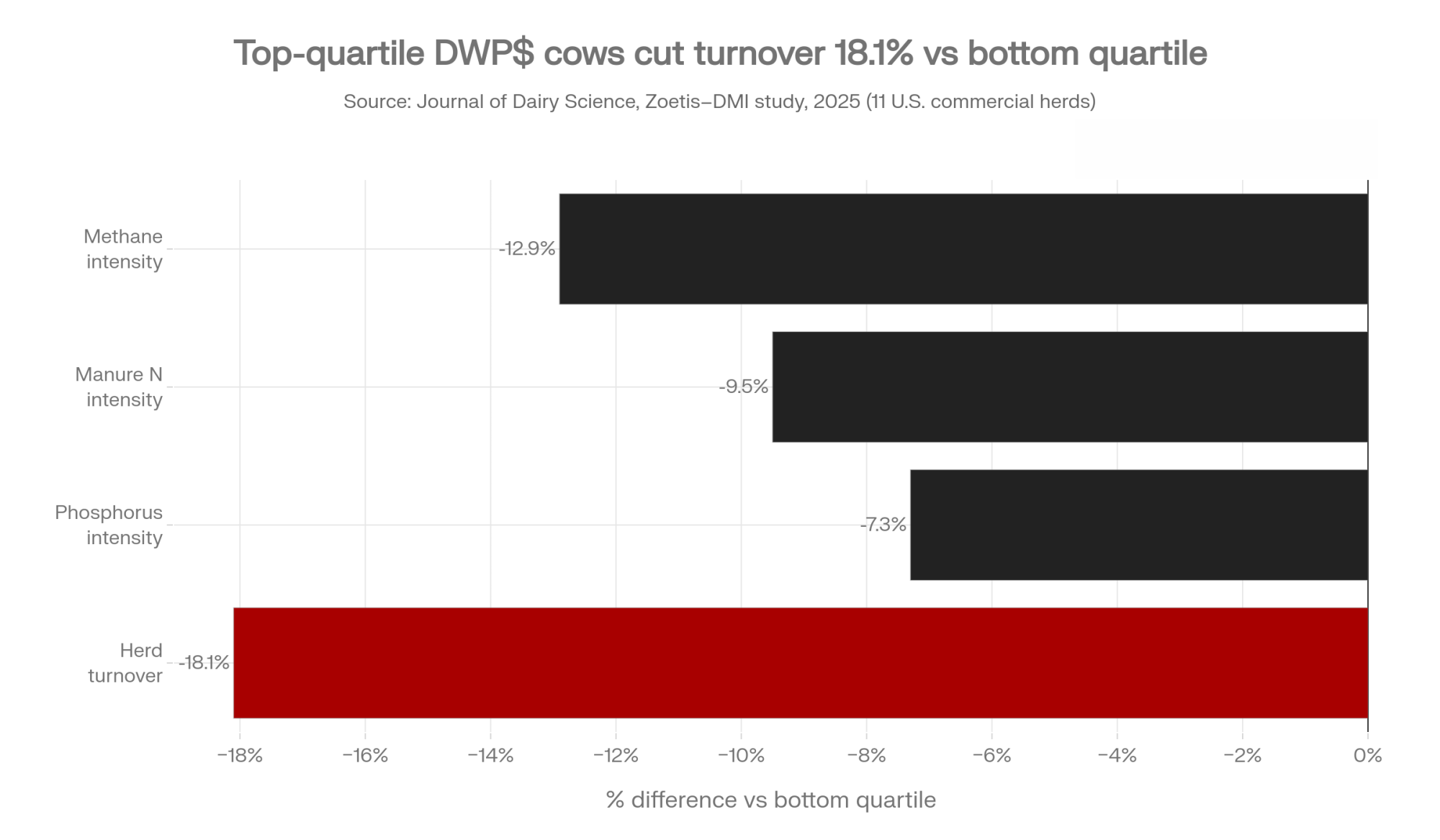

A 2025 Zoetis–Dairy Management Inc. study published in the Journal of Dairy Science — “Reduction of environmental effects through genetic selection” — analyzed cows from the top and bottom DWP$ quartiles across 11 U.S. commercial dairies. Top-quartile cows produced 12.9% lower methane intensity, 9.5% lower manure nitrogen intensity, 7.3% lower phosphorus intensity, and 18.1% lower herd turnover than bottom-quartile herdmates. That’s the dataset processors are now building scope 3 programs around.

Whether your milk check rewards those exact traits is a different question. Whether your cooperative has a counter-proof on the table is a third.

How DWP$, NM$ and TPI Differ on the Traits Processors Now Care About

| Trait category | DWP$ (Zoetis) | NM$ (CDCB) | TPI (Holstein Assn.) |

|---|---|---|---|

| Methane efficiency | Direct trait (Z_MI), added 2026 | Not a direct trait in 2025 NM$ revision | Not a direct trait weight |

| Heat resilience | Direct sub-index (DWP$ Heat), added 2026 | Indirect (fertility, livability) | Indirect (fertility, longevity) |

| Wellness traits | Signature, heavy weighting | Captured via Health$ subindex | Limited direct weighting |

| Components (fat, protein) | Balanced vs wellness/longevity | Substantial weight | Heaviest weight historically |

| Productive Life | Strong weight | Strong weight | Strong weight |

| Type / Conformation | Modest direct weight | Modest direct weight | Heaviest of the three |

Direction, not exact percentages. Each index answers a different question. Your milk check decides which one matters most. Your co-op’s catalog depth decides whether you have alternatives.

How Much Is the Processor Premium Really Worth on Your Operation?

Here’s the barn math. Plug your own herd into one of these and see where the net-out lands.

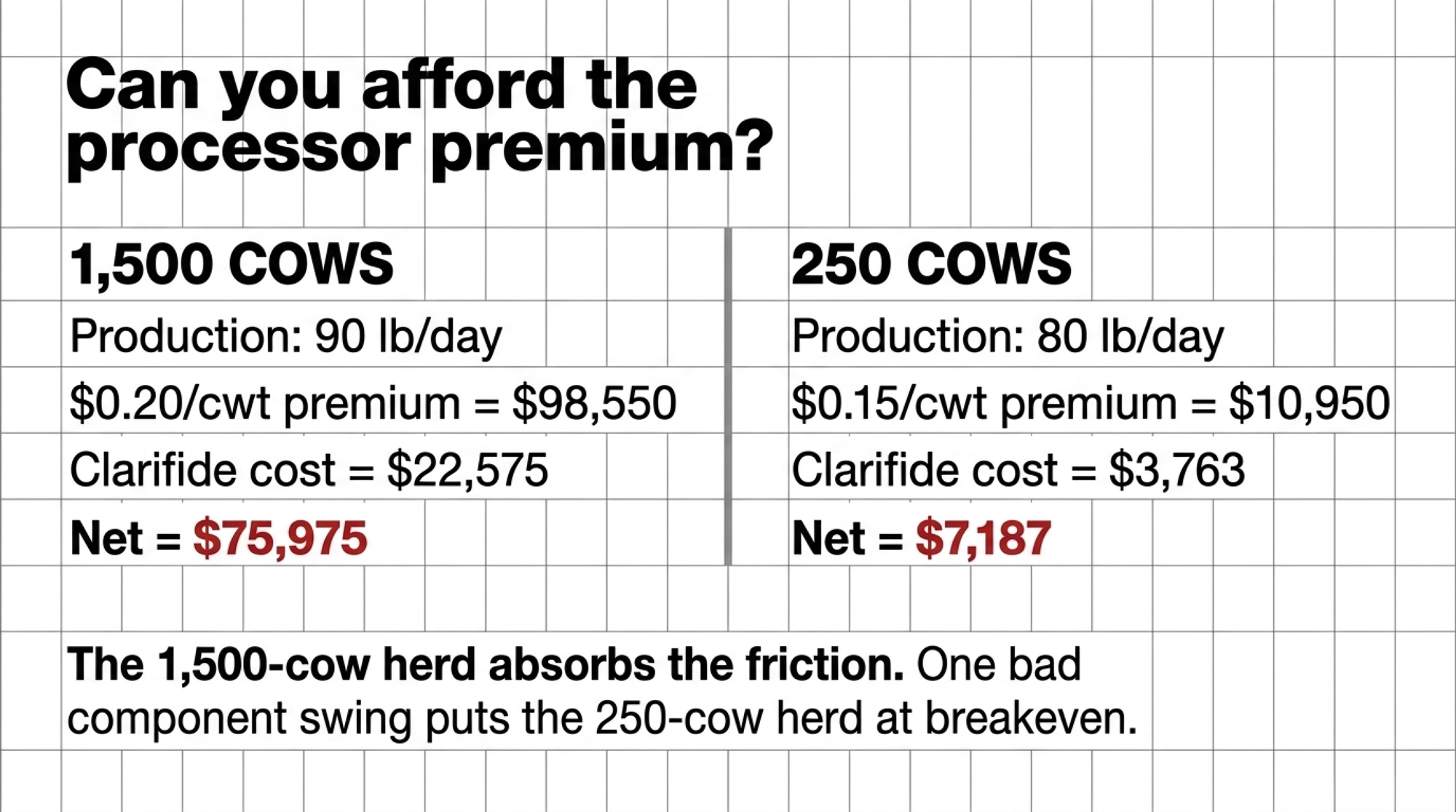

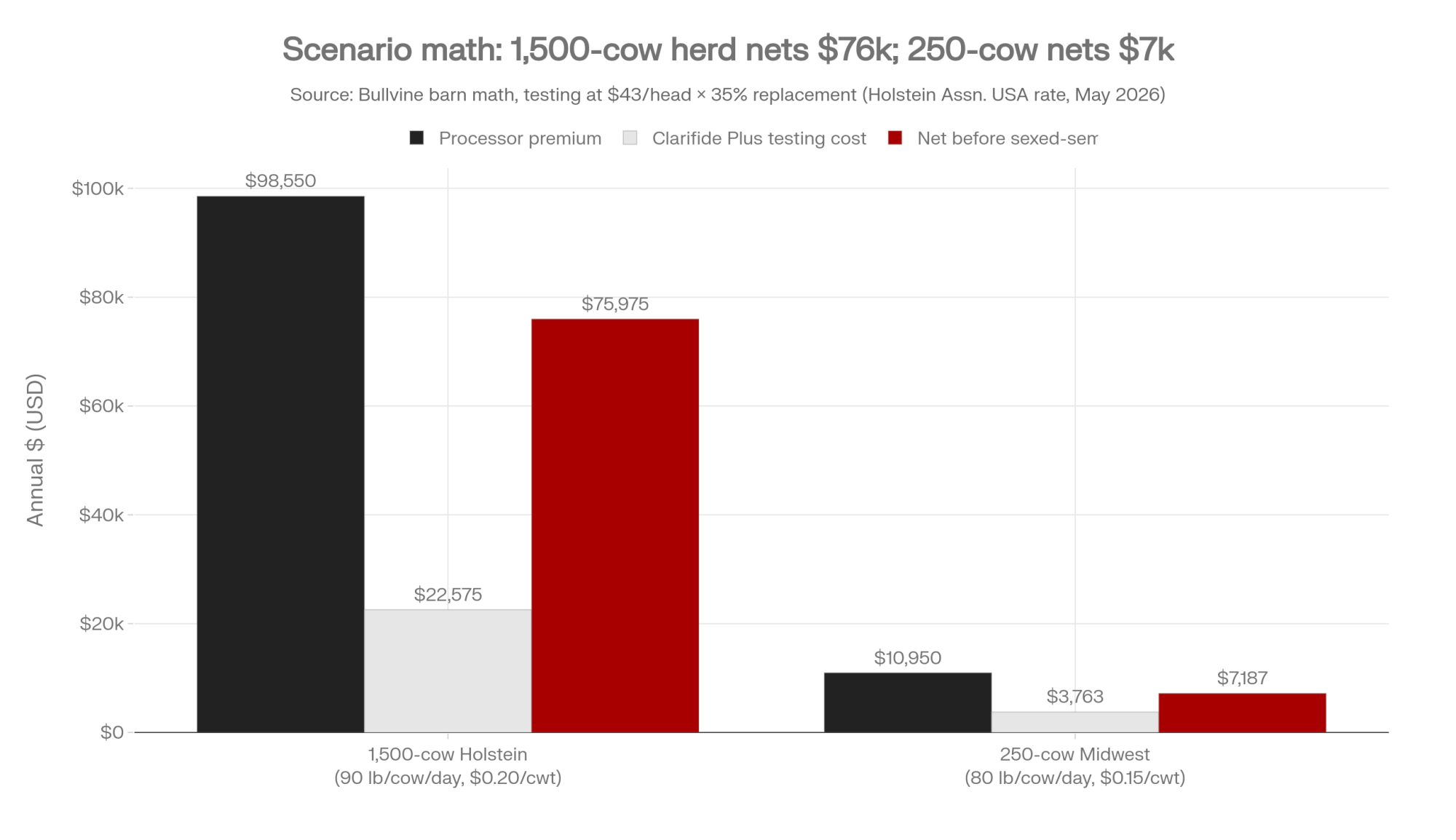

Scenario A — 1,500-cow Holstein operation, 90 lb/cow/day

| Input | Value |

| Cows in milk | 1,500 |

| Daily production per cow | 90 lb (above the U.S. herd average of ~66–67 lb/day implied by USDA NASS Milk Production, late 2025)² |

| Total annual production | 49,275,000 lb = 492,750 cwt |

| Premium at $0.20/cwt | $98,550 |

| Annual Clarifide Plus testing (1,500 × 35% × $43)³ | ~$22,575 |

| Net at $0.20/cwt before sexed-semen differential | ~$75,975 |

Scenario B — 250-cow Midwest herd, 80 lb/cow/day

| Input | Value |

| Cows in milk | 250 |

| Daily production per cow | 80 lb |

| Total annual production | 7,300,000 lb = 73,000 cwt |

| Premium at $0.15/cwt | $10,950 |

| Annual Clarifide Plus testing (250 × 35% × $43)³ | ~$3,763 |

| Net at $0.15/cwt before sexed-semen differential | ~$7,187 |

These are gross figures. Before the sexed-semen price differential. Before any component-yield drift if your contract pays butterfat and protein harder than DWP$ weights them. Before any year-one Danone signing subsidy.

The 1,500-cow operation has the volume to absorb the friction. The 250-cow operation is one bad component-pay swing from breakeven. If you’re a Wisconsin cheese-milk herd paid hard on components, or a Southern operation whose biggest profit leak is summer fertility — exactly the herds Zoetis is targeting with DWP$ Heat — DWP$ alignment may or may not match how your milk check actually gets built. Run your own math against your own contract before you renew.

Where Will Catalog Pressure Show Up First in Your AI Rep’s Order Sheet?

Indexes improve by consuming data. The one with preferred-provider testing across thousands of farms refines itself faster than one relying on voluntary contributions. Over five to seven years, in our analysis, DWP$ is on track to lead among major U.S. indexes on the traits processors care about — methane, feed efficiency, wellness — because of Zoetis’s vertically integrated testing-plus-index position. The 2025 JDS study is the first peer-reviewed proof point for that thesis.

The compounding runs downstream fast. More processors layer in Clarifide. Studs feel pressure to shift young-sire sampling toward DWP$-ranking bulls. Sampling slots are finite. A slot that doesn’t fit processor demand is a slot unlikely to recover cost.

That’s not Zoetis policy in any direct sense. It’s market dynamics responding to a structural shift. By April 2026, in our analysis of the public NAAB genomic young-sire list, the top tier of genomic Net Merit young bulls in the U.S. showed sharp concentration in a single stud’s NAAB code (methodology available on request). That’s the precedent for what catalog compression looks like when it works through to a published bull list.

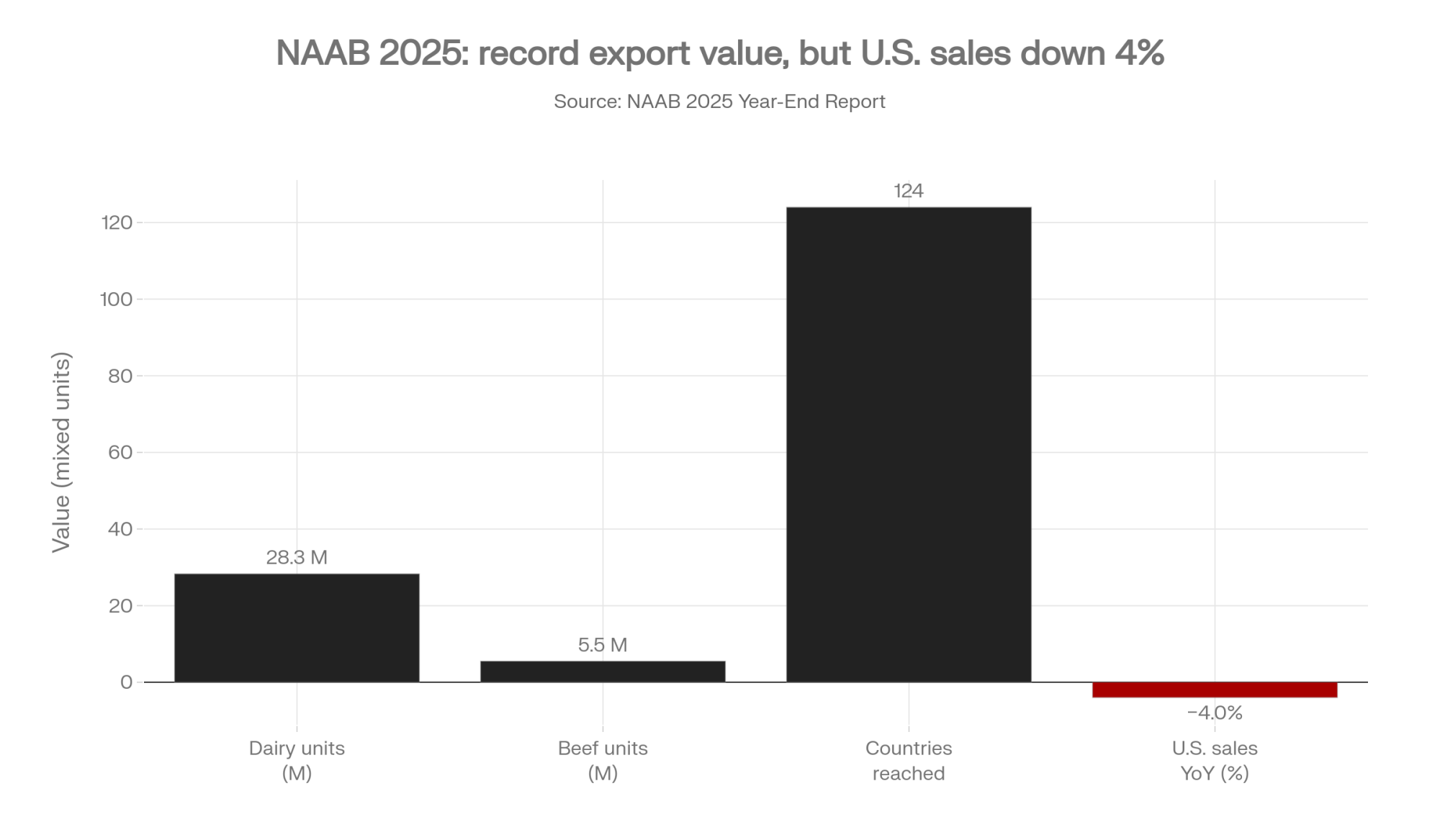

NAAB’s 2025 year-end report shows U.S. bovine semen sales down roughly 4% year-over-year. Export value reached a record $327.6 million even as total export units fell. China exited the U.S. market in early 2025. Dairy units exported settled at 28.3 million; beef exports rose to 5.5 million. U.S. genetics now reach 124 countries, up from 108 the prior year — and a clear majority of all dairy semen produced by NAAB members in 2025 left the country.

The structural pressure to watch is catalog compression outside the flagship top tier. The bulls most exposed in your cooperative’s next two catalogs are the slot 40–80 specialists: outcross health-trait sires, daughter-pregnancy-rate-leading bulls without methane-efficiency rank, show-type longevity sires whose proofs were built around classification rather than wellness data, A2A2-plus-component specialty sires for cheese-milk niches DWP$ doesn’t reward. That’s our read, not NAAB-confirmed sampling-mix data. Your cooperative’s next two catalogs will tell you if it’s right.

Pull slots 40–80 in the next catalog. Count what’s missing.

Options and Trade-Offs

Pick the path that fits how your milk check is built and how much room you’ve still got.

Path 1 — Participate with a parallel scorecard. Stay in Clarifide/DWP$ for processor compliance. Run your own mating logic underneath it, weighted to what your milk check actually pays for. Works when the processor premium is meaningful and your contract pays traits DWP$ underweights. Requires a breeding consultant or software workflow that shows DWP$ and NM$ rankings side by side. The risk: your AI rep’s default view is DWP$-framed. You have to actively ask for the second view every time.

Path 2 — Diversify your testing providers now, while you still can. Before you renew any testing contract, negotiate data-portability terms or split testing between Clarifide and an alternative — Neogen-GeneSeek pre-close, CDCB-based panels, a cooperative-run program. The H2 2026 close narrows the window on pre-close options. The risk: your nutrition software, vet platform, and mating program increasingly default to one data feed. Break one integration and three break with it.

The Switching-Cost Trap — read this before you sign anything.

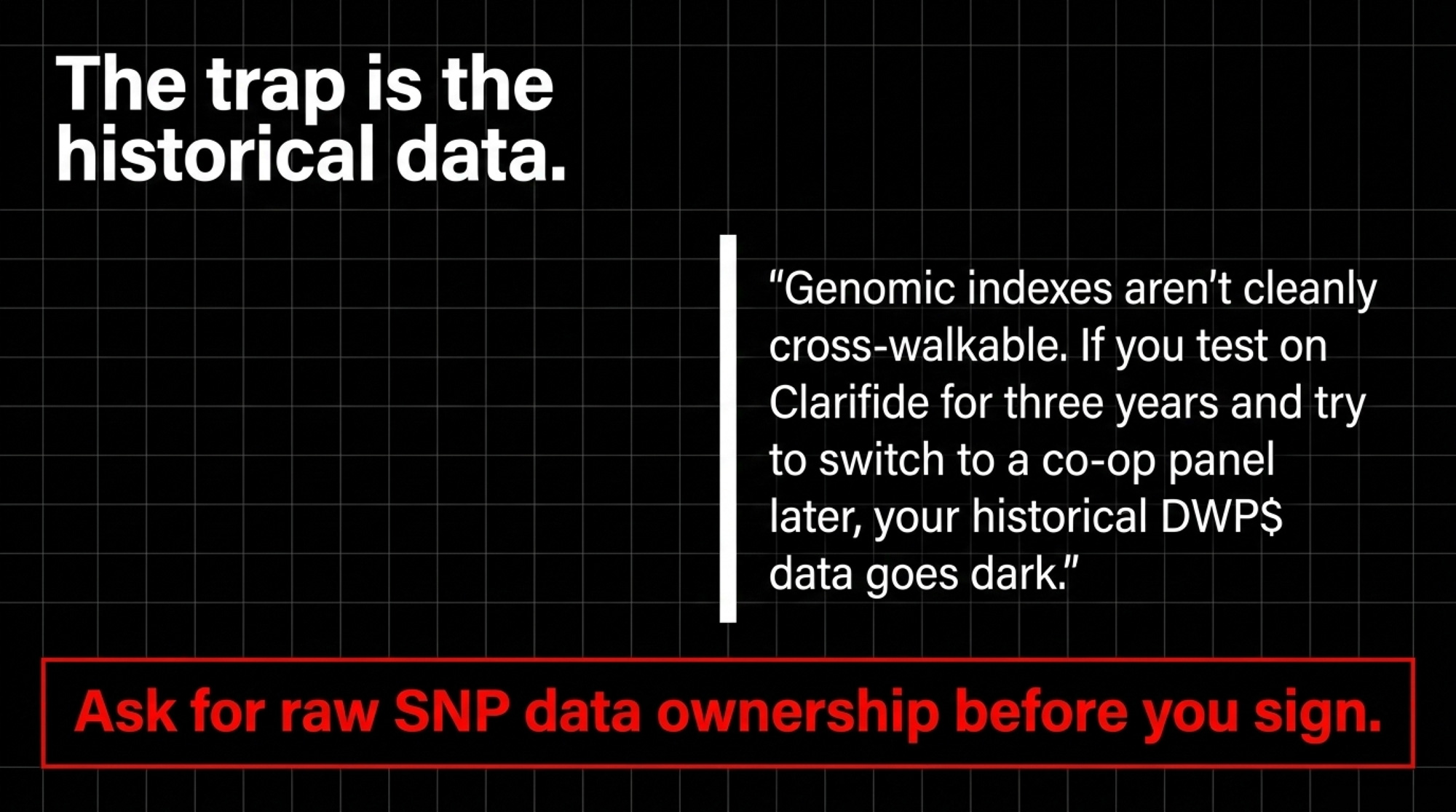

The harder cost in Path 2 isn’t the per-head test fee. It’s what happens to three years of historical rankings if you switch later.

Genomic indexes don’t translate cleanly across providers. The underlying SNP genotype usually does — once a genotype is on file with CDCB, it gets imputed to the same 80K-marker reference base regardless of which chip generated it. What doesn’t translate is the index ranking. DWP$ is Zoetis. NM$ is CDCB. TPI is Holstein Association. Each one weights traits differently, and a cow’s rank on one is not her rank on another.

So if you stay on Clarifide for three breeding crops and then want to move to a CDCB-based panel or a co-op program, the question isn’t whether to re-test the cattle. It’s whether your testing contract gives you export rights to the raw SNP file — and whether your genotypes were deposited with CDCB at the time of original testing. With those two boxes checked, a parallel evaluation costs a fraction of a re-test. Without them, you’re stuck either re-pulling samples or accepting that your historical DWP$ rankings and your forward-going scorecard live on different rulers.

Before you sign any testing contract this year, ask three questions in writing: Who owns the genotype file? Can you receive the raw SNP data, not just the index output? And can you re-run that data through a competing index without paying for a second test? Get the answers in the contract, not over the phone.

Path 3 — Source heat-tolerant genetics directly. If you’re in the South, parts of the West, or the lower Midwest, build a relationship with a Brazilian genetics supplier or a domestic IVF program working with Gyr-Holstein or SLICK-edited genetics. Trigger: summer THI in the upper-70s-to-low-80s range across an extended window — roughly where Zoetis itself recommends DWP$ Heat — and conception rates dropping by more than 5 percentage points across three consecutive summers. The risk: your traditional cooperative supplier probably can’t serve this need, creating a sourcing split you’ll need to manage.

Worth saying plainly as we head into the May–September heat window: DWP$ Heat is a software answer to a hardware problem. Genomic selection inside an existing Holstein population can shift what your daughters inherit at the margin. It cannot change what a Holstein is — a black-and-white animal selected over 75 years for cool-climate fluid-milk production, with body mass and coat type that limit how she dissipates heat at peak summer THI. Gyr-Holstein crosses and SLICK-edited cattle are a different physical platform: shorter coats, smaller body mass, sweat-gland density bred for the tropics. The honest question isn’t “is my DWP$ Heat score high enough?” It’s “do I need a different cow?” For most herds the answer is no — Holsteins still pay best where heat stress is occasional. For Florida, South Texas, Arizona, and the southern San Joaquin, where the answer is increasingly maybe, the Path 3 conversation isn’t optional anymore.

Path 4 — Stay loud at the cooperative. This is the 30-day action. The two questions earlier in this article aren’t a one-time ask. Walk them into the next district meeting on your calendar. Bring them on your phone. Read them aloud. Write the answer down, date it. Talk to two neighbors before the meeting and ask them to do the same. Re-raise in 90 days. Boards respond to repeated, specific, member-coordinated pressure. They do not respond to a single member raising an issue once. The cost is your time and a little social friction. The alternative is having the answer handed to you in 2028 by someone who wasn’t elected by your district.

The 30/90/365 Horizon

| Horizon | Action | Trigger |

|---|---|---|

| 30 days | Read data-ownership clauses (raw SNP file, portability, re-run rights); bring district-meeting questions; talk to two neighbors | Renewal letter on file or expected within 12 months |

| 90 days | Negotiate portability terms; open tropical-genetics conversation; re-raise at next district meeting | THI / fertility decline ORrenewal date inside H2 2026 |

| 365 days | Track slots 40–80; commit to scorecard or diversification path; document board responses | Next two catalog cycles published |

Key Takeaways

- If your processor has mentioned Clarifide, sustainability testing, or scope 3 reporting in any conversation this year, assume a similar letter could land within 6 to 18 months. Negotiate data-portability terms — including raw SNP file access — before you sign, not after.

- If DWP$ rankings on your last 30 sire selections diverge from your NM$ or TPI rankings by more than your milk-check structure can absorb, you’re breeding against a scorecard that doesn’t match how you get paid.

- If your summer conception rate has dropped more than 5 points across three consecutive summers, the question isn’t whether to chase a higher DWP$ Heat score. It’s whether the Holstein is the right physical platform for your zip code at all. Put tropical, SLICK-edited, or DWP$ Heat-aligned genetics on your supplier conversations this quarter.

- If your cooperative can’t name partners, dollar commitments, and timelines when asked the Path 4 questions, treat that as an unanswered question. Re-raise in 90 days. Keep asking.

- If thinning shows up at slots 40–80 in your cooperative’s next two catalogs, that’s the leading indicator of R&D compression — visible 18 to 24 months before it shows up in flagship marketing.

What Kind of Cooperative Do You Want to Belong to in 2030?

Three generations of dairy farmers decided no member should face the genetics market alone. That decision built shared genotyping pipelines, member-owned data, and the negotiating leverage that has kept U.S. genetics competitive in 124 export markets and in your own barn. None of that is guaranteed to survive a structural shift it doesn’t see coming.

The cow-level economics — full DWP$-versus-NM$ math broken down by contract type and herd size — live in next week’s Bullvine Weekly. That’s where the spreadsheet sits: plug in your own components, your own premium, your own replacement rate, and see where the net-out lands.

But the question that actually matters this month isn’t the spreadsheet. It’s the one you bring to your next district meeting, in front of the neighbors whose kids might still be milking cows in 2050. What kind of cooperative do you want them to belong to?

Editorial note: This article reflects publicly available information as of May 1, 2026. Updates and any post-publication responses will be reflected in subsequent coverage.

¹ Holstein Association USA, Genomic Testing Services price schedule, accessed May 1, 2026: Clarifide Plus Medium-Density SNP Test + Dairy Wellness Traits & Polled at $43 per Holstein animal (member rate). Industry-wide practical costs typically run $40–$50 per head depending on volume and program tier.

² USDA NASS Milk Production monthly report, late-2025 release: U.S. average production per cow for the most recent reported month was 1,963 lb, putting annualized U.S. herd-average in the 24,000–24,400 lb/cow/year band, equivalent to roughly 66–67 lb/day on a steady-state basis.

³ 35% reflects a typical Holstein heifer-replacement rate; operations generally run 30–40% depending on cull rate. Figures rounded to the nearest dollar; testing-cost rows reflect 35% of milking herd as a straight multiplier. Adjust to your own heifer inventory before applying.

Disclaimer: The Zoetis–Neogen $160 million transaction is structural in scope, but individual outcomes vary by state, processor contract, regional milk pricing, herd size, and cooperative affiliation. The barn-math figures above are illustrative benchmarks, not universal forecasts. Run your own numbers against your own contract before any breeding, testing, or supplier decision.

Learn More

- Beyond the Milk Check: How Dairy Operations Are Building $300,000 in New Revenue Today — Arms you with the math to capture hidden premiums beyond basic component pricing. Breaks down how successful herds stack beef-on-dairy and efficiency gains to build a $300,000 buffer against the very margin compression Zoetis-type contracts often create.

- The Dairy Mirage: How the Industry’s ‘Fixes’ Are Finishing Off the Farmer — Dismantles the illusion that industry ‘solutions’—from co-ops to proprietary indices—are designed for your benefit. Exposes the extraction system that profits from farm losses, urging a pivot toward scale or specialization before the system cashes you out.

- When 110 Brazilian Gyr Cows Changed Everything: The Dairy Shift Tropical Producers Can’t Ignore — Reveals the physical limits of the Holstein platform in a warming climate. Delivers a blueprint for using heat-adapted Gyr genetics to stabilize summer production, offering a ‘hardware’ alternative to the genomic ‘software’ fixes promised by newer indices.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.