The $3 billion bailout hit producers’ accounts—but the real story is how farmers are turning that relief into resilience and re‑engineering the future of dairy.

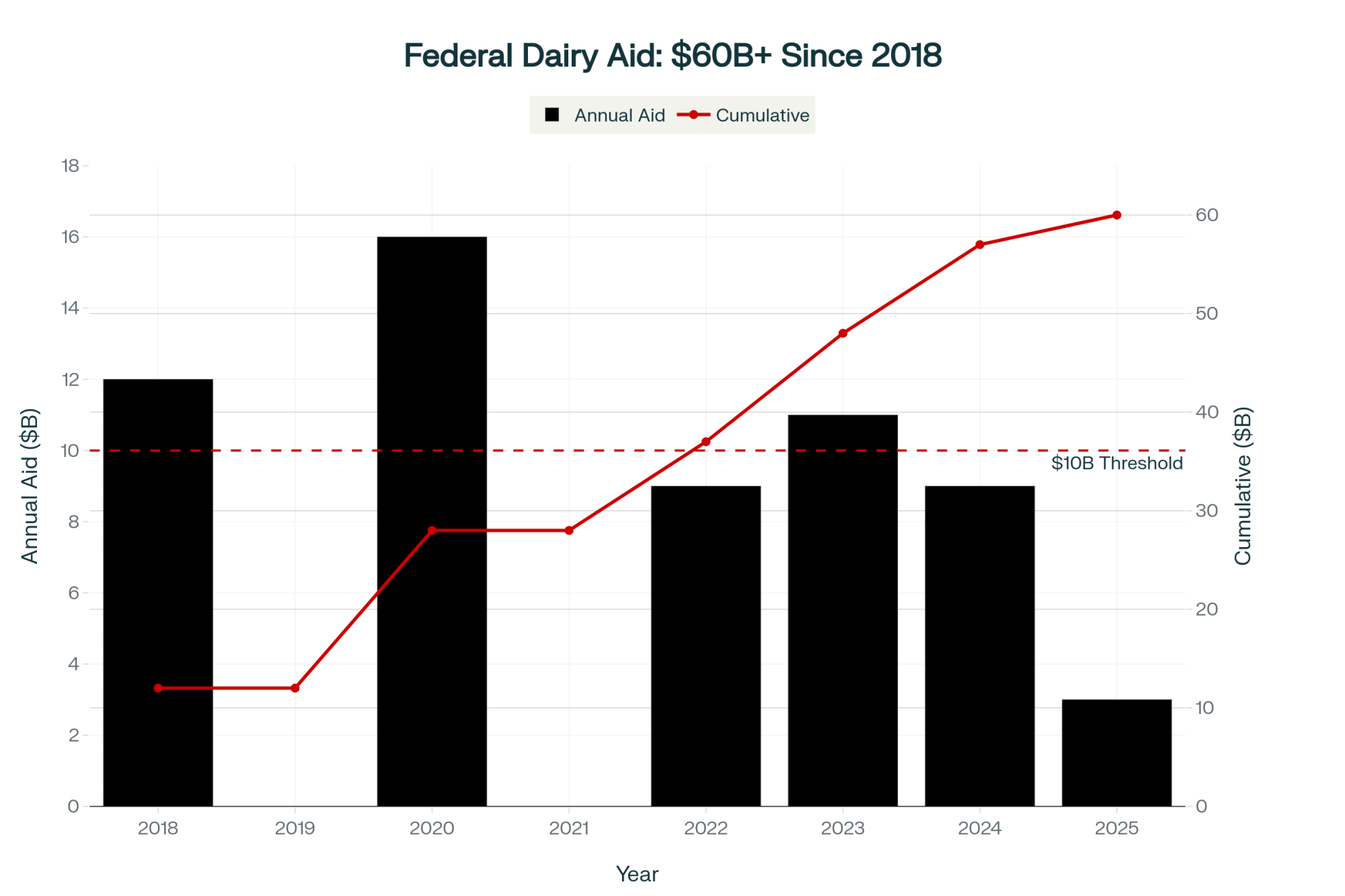

Executive Summary: The USDA’s $3 billion dairy bailout bought farmers time—just not transformation. Since 2018, over $60 billion in federal “emergency” funding has kept America’s milk moving, but it’s also made rescue money feel routine. What’s interesting is how differently producers are responding. In Wisconsin, smaller family herds keep shuttering, while Idaho’s integrated systems keep growing. Yet across regions, many farms are proving that strength now comes from management, not money—from tracking butterfat performance to securing feed partnerships and using Dairy Revenue Protection as standard operating procedure. The article reveals a quiet shift happening in dairy: the producers thriving today aren’t waiting for Washington—they’re building resilience from the inside out.

When the USDA released $3 billion in previously frozen dairy aid earlier this fall, a lot of barns felt the same quiet relief. That check helped cover feed, tide over payroll, or pay for the next load of seed. But here’s what’s interesting—what used to be considered “emergency relief” has quietly become routine.

Since 2018, the government’s Commodity Credit Corporation has distributed over $60 billion in ad‑hoc support to U.S. farmers, according to USDA and Congressional Research Service data. That includes the trade‑war relief payments, COVID‑era CFAP funds, weather‑related disaster programs, and now, this latest round of support. Each program had different names and triggers, yet all share one thing: they’ve made emergency relief feel ordinary.

Looking at this trend, it’s clear that the system doesn’t just respond to volatility—it depends on it.

From Safety Net to Part of the System

The normalization of crisis: Federal dairy aid has exceeded $60 billion since 2018, transforming ‘emergency’ relief into standard operating procedure—exactly what Coppess warned about.

University of Illinois economist Jonathan Coppess put it plainly during a 2025 policy forum: “Every time we call these payments extraordinary, we prove how ordinary they’ve become.”

He’s right. The CCC now spends more than $10 billion each year keeping farm sectors whole when prices collapse. The money buys time—valuable time—for dairy families to stay solvent when margins evaporate. But I’ve noticed something else: those interventions slow the kind of market corrections that might otherwise drive innovation.

In other words, the aid keeps everyone in motion—but it also keeps everyone in the same spot.

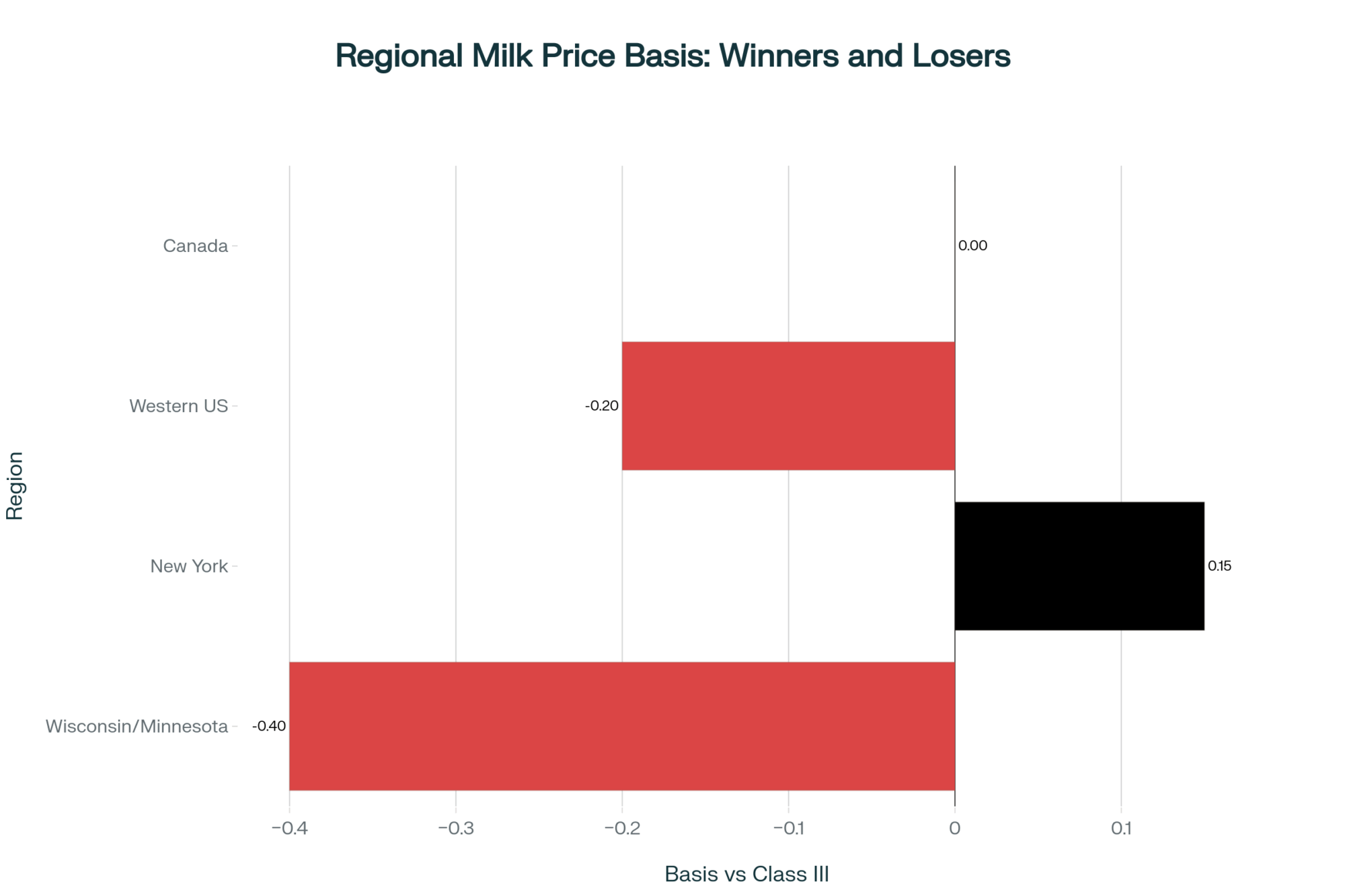

Geography Still Shapes Success

Metric

Wisconsin (Traditional)

Idaho (Integrated)

Impact

Herd Trend 2024

400+ closures

4.2% growth

Consolidation accelerating

Primary Model

Small-mid family farms

Vertically integrated

Structure determines survival

Processor Relationship

Co-op (variable deductions)

Direct long-term contracts

Security vs. volatility

Co-op Deductions

$1-3 per cwt

Minimal/contracted

Margin erosion for traditional

Feed Strategy

Mixed/spot market

Integrated supply chains

Cost predictability advantage

2025 Production Trajectory

Declining

Expanding

Geographic winners emerging

Here’s a sobering contrast.

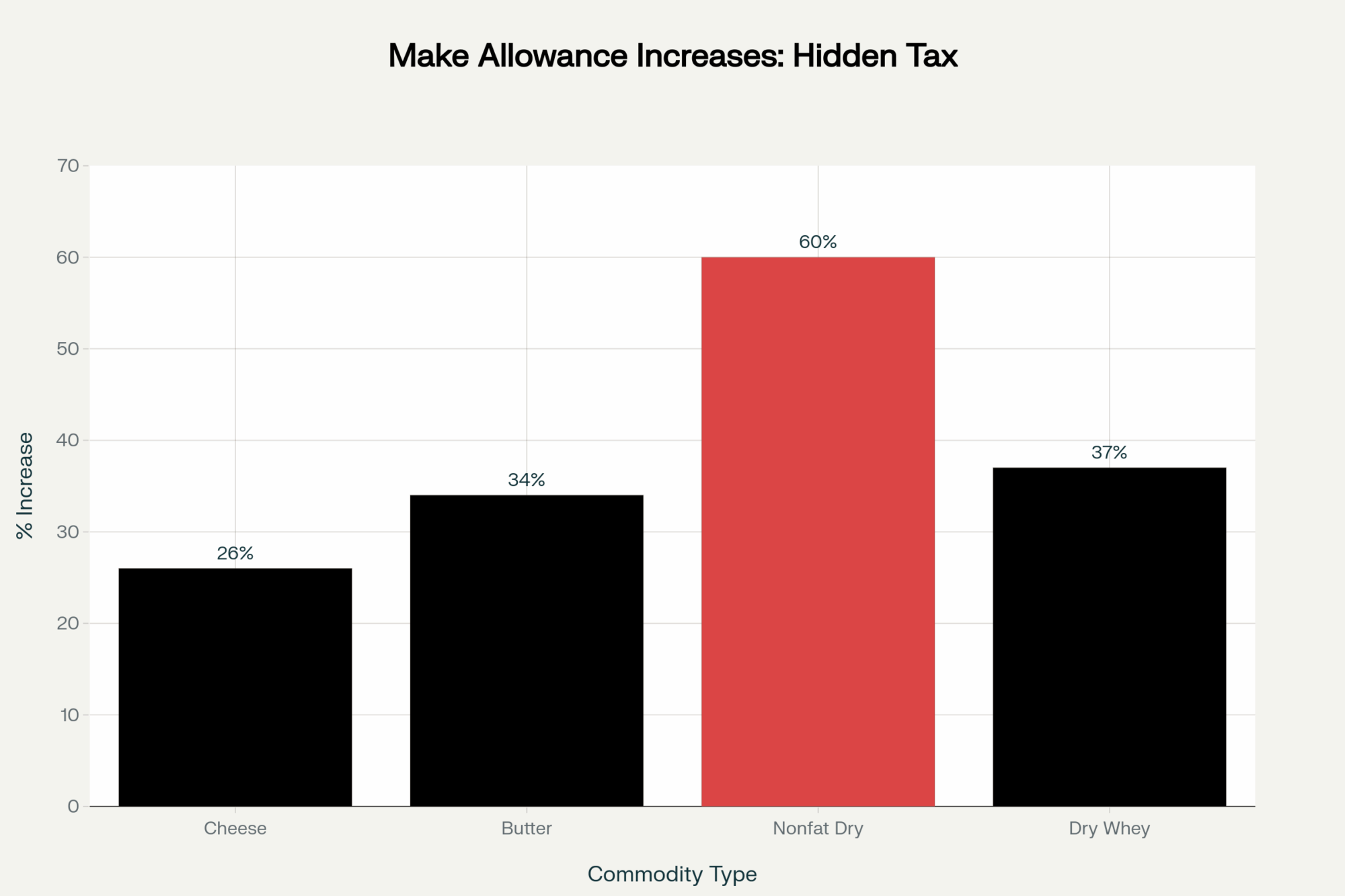

In Wisconsin, USDA NASS reports for 2025 show that over 400 milk license holders closed in 2024, the vast majority small or mid‑sized herds. Co‑op deductions for hauling, marketing, and retained equity often run from $1 to $3 per hundredweight, depending on the service region. Add that to feed pressure, and margins vanish quickly when Class III milk averages around $16 per hundredweight.

Meanwhile, Idaho saw 4.2 percent production growth, driven by vertically integrated systems and processor partnerships (Idaho Dairymen’s Association Annual Report 2025). Many herds there ship directly to long‑term contracts with Glanbia Foods or Idaho Milk Products. As CEO , Rick Naerebout says, “Security here comes from being part of someone’s plan.”

That’s becoming the modern split in U.S. dairy. It’s not only about scale—it’s about supply security.

Export Growth Without Equal Payoff

U.S. dairy exports have tripled since 2000, making America the world’s third‑largest dairy exporter, trailing only the EU and New Zealand (USDA Livestock, Dairy and Poultry Outlook, August 2025). It’s an incredible achievement. The challenge is that the extra volume hasn’t meant better milk checks.

The European Commission’s Agri‑Food Trade Report (2025) confirms that EU processors still benefit from export‑enhancing subsidies. And USDA ERS data shows that while New Zealand’s grass‑based systems remain the most cost‑efficient in the world, Americans must rely on grain‑fed cows and higher‑input models.

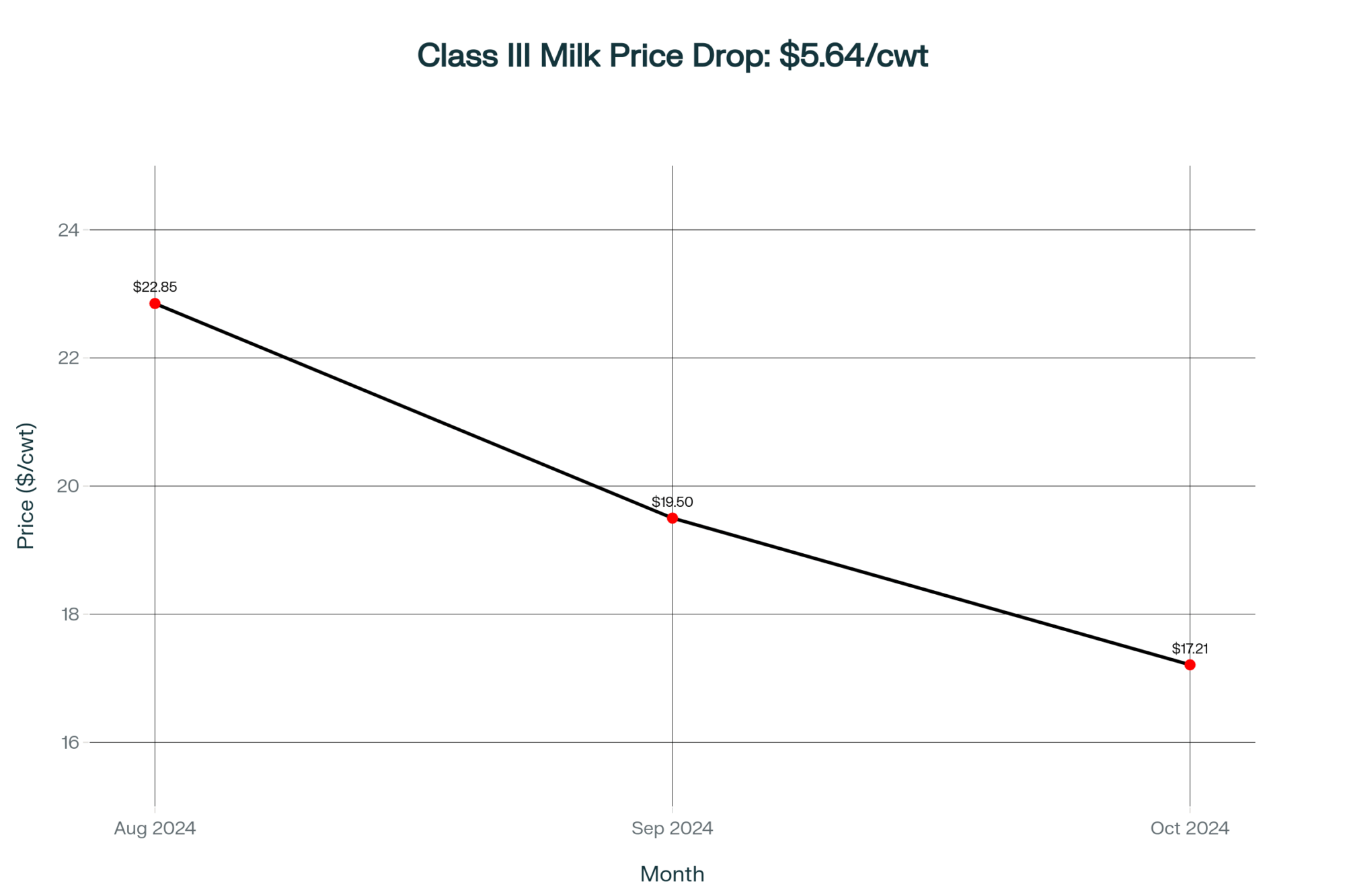

In 2025’s Q3, Class III prices averaged $16.05 /cwt, while breakevens in most regions sat near $18–$20 /cwt(CME Markets and USDA ERS cost‑of‑production reports). Industry analyst Sarina Sharp at Daily Dairy Report put it simply: “We’re moving tonnage, not value.”

Moving tonnage, not value: While U.S. dairy exports have tripled since 2000, Class III prices are $4 per cwt below breakeven—the gap that keeps plants full but forces farmers onto the bailout treadmill.

The export engine keeps plants full—but it hasn’t lifted profitability on the farm.

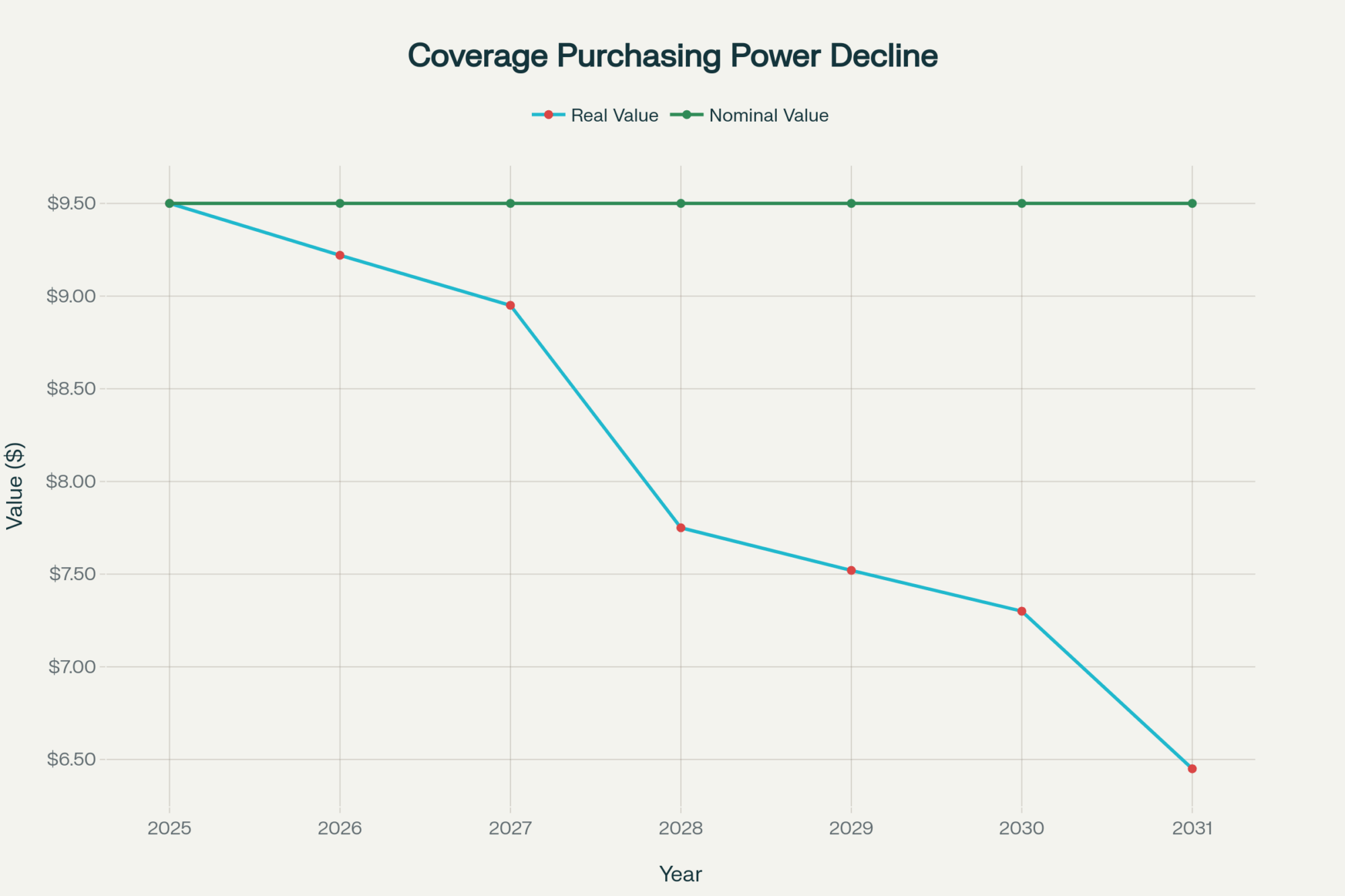

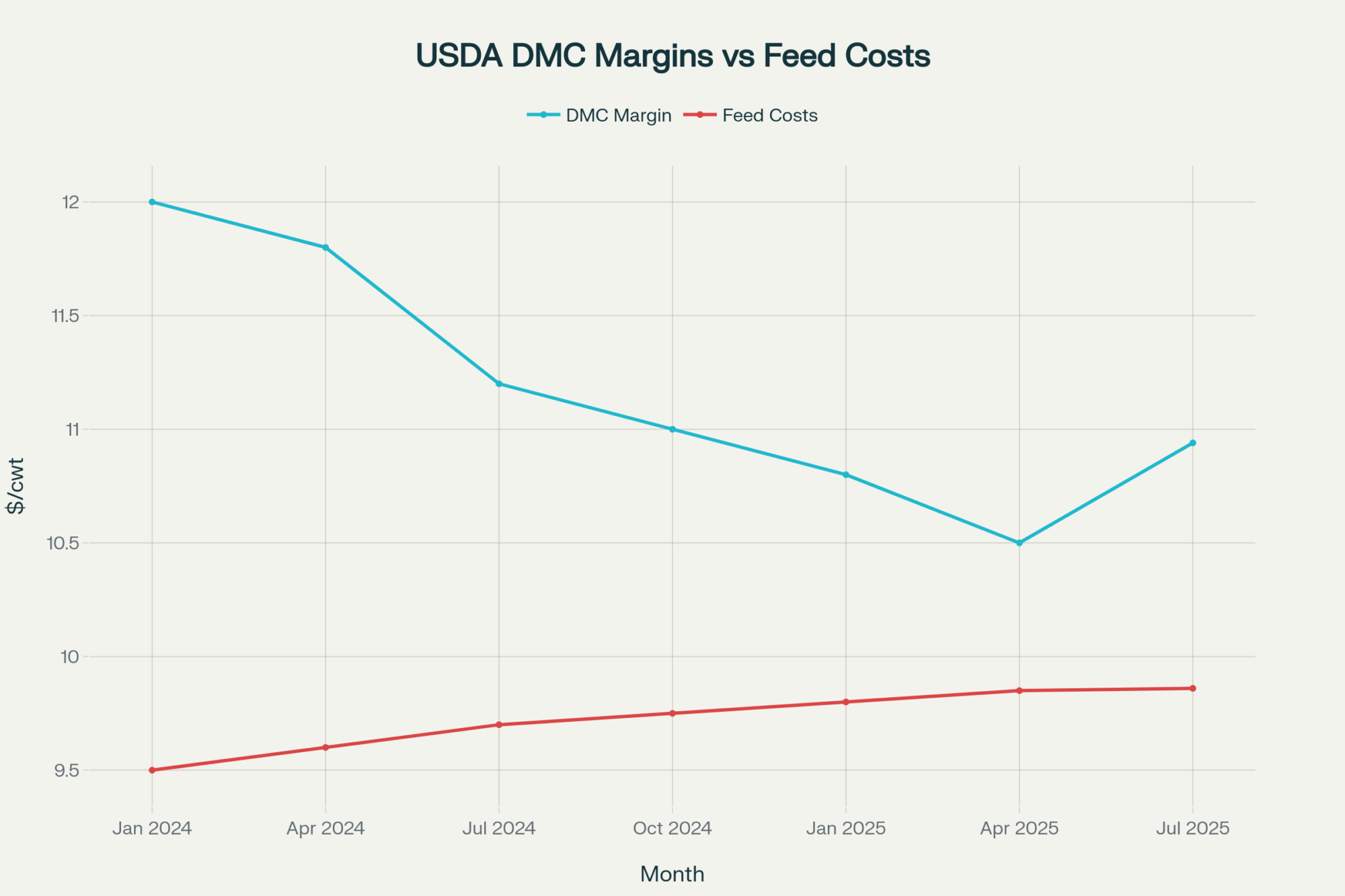

When DMC Numbers Don’t Match Reality

By federal calculations, dairies are doing fine.

On paper, the Dairy Margin Coverage (DMC) program’s national average margin has stayed above $9.50 for 25 consecutive months (USDA FSA DMC Bulletins, 2025). But back home, budgets tell a different story. A Farm Journal Ag Economy Survey (2025) found 68 percent of producers still reporting negative cash flow through the same period.

The difference is in the math. DMC uses corn, soybean meal, and premium alfalfa hay to model feed cost, leaving out labor, fuel, freight, and mineral expenses. A California freestall feeding $360 a ton of hay and paying $22 an hour in labor looks “healthy” next to a Midwest herd growing its own feed, at least on paper.

As one Wisconsin producer told me, “DMC says I’m comfortable. My milk check says otherwise.”

Where Resilience Is Actually Happening

Management over money: A mere 0.2% butterfat increase—achievable through better fresh cow protocols—can generate $10,000 to $150,000 annually, proving that components now matter more than volume.

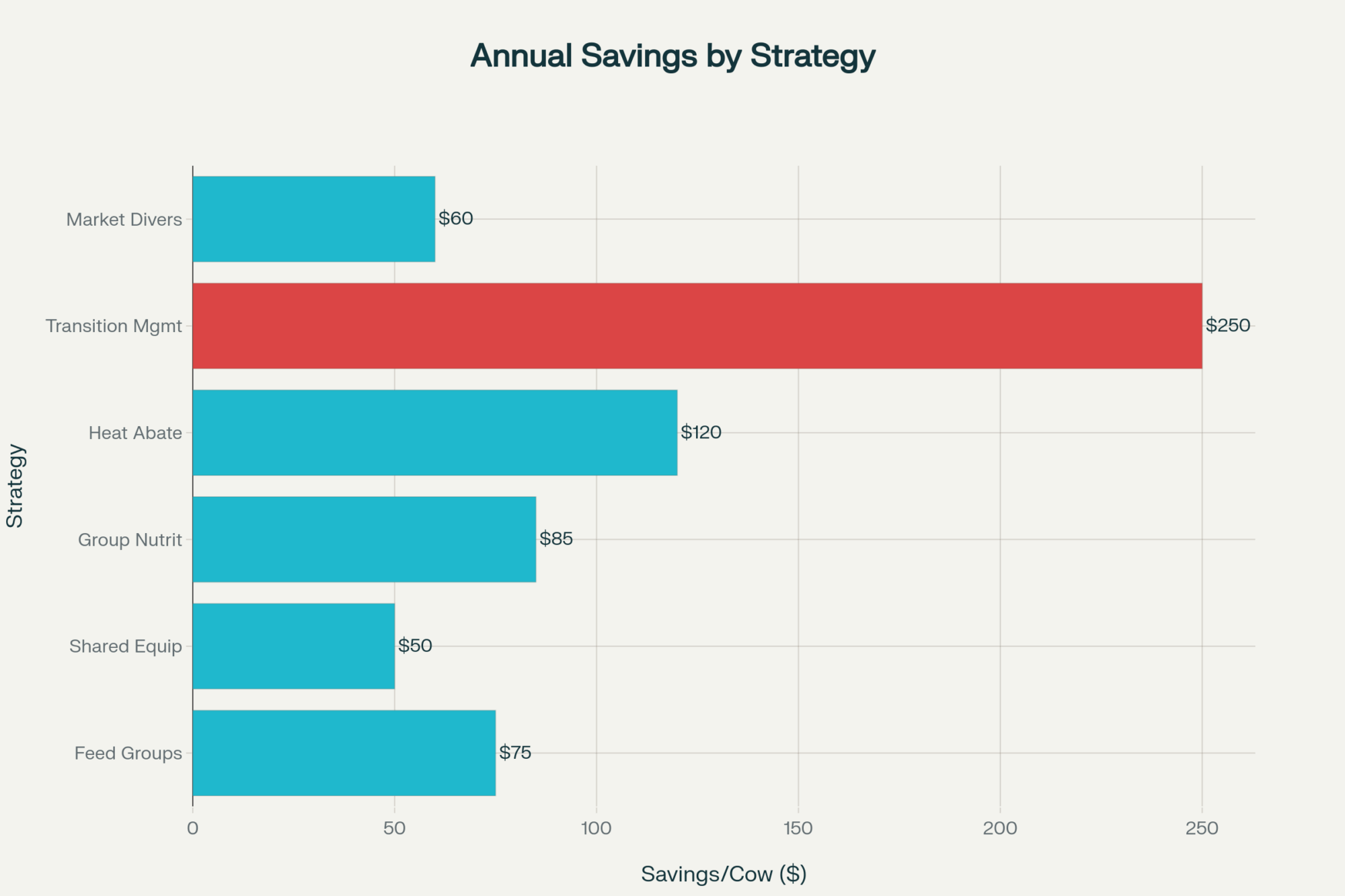

What’s encouraging is how many farms are finding independence within this uncertainty. Across regions, large and small, producers share some common habits that quietly strengthen their bottom lines.

Holding processor relationships close. Herds delivering reliable supply with high butterfat and low SCC keep their spot when plants trim pickups. Consistency is its own insurance policy.

Milking components over volume.USDA AMS 2025 data shows butterfat now drives over 55 percent of milk’s value. Just a 0.2 percent lift in butterfat can earn $10,000 to $15,000 per 100 cows,depending on premiums. The best results usually come from fresh cow management and ration adjustments using digestible fiber and balanced oils, not simply more grain.

Locking in feed and forage partnerships. A University of Wisconsin Extension (2024) study found multi‑year forage contracts saved 8 to 12 percent per ton of dry matter compared to spot buying. Contract stability reduces uncertainty around input costs—and lenders like certainty.

Treating insurance like a feed input. According to the Risk Management Agency 2025 Report, about 70 percent of U.S. milk is now covered by Dairy Revenue Protection or Livestock Gross Margin. Farms building those premiums (roughly 1–2 percent of revenue) into their budgets weather volatility far better than those rolling the dice each year.

Diversifying strategically.California Bioenergy (2025) reports digesters and renewable‑gas systems returning $40,000 to $120,000 annually for 1,000‑plus cow herds—without pulling focus from the dairy. Others find stability through direct marketing or regional brand partnerships.

Measuring profitability monthly.Penn State Extension (2025) shows feed should stay below 60 percent of gross milk income. The farms that benchmark this monthly spot inefficiencies faster and make small, cost‑saving pivots before they snowball.

Planning exits on their own terms. According to the USDA ERS Farm Structure and Stability report (2025), herds planning transitions 12–18 months ahead preserve as much as 40 percent more equity than forced liquidations. Some call that quitting; others call it smart continuity.

Each step underlines the same idea: resilience isn’t dramatic—it’s deliberate.

What the Bailouts Really Buy

In the short run, relief checks keep dairies alive and infrastructure intact. They pay feed bills and save lenders a lot of sleepless nights. But as Coppess reminds us, “These payments stabilize balance sheets—they don’t modernize business models.”

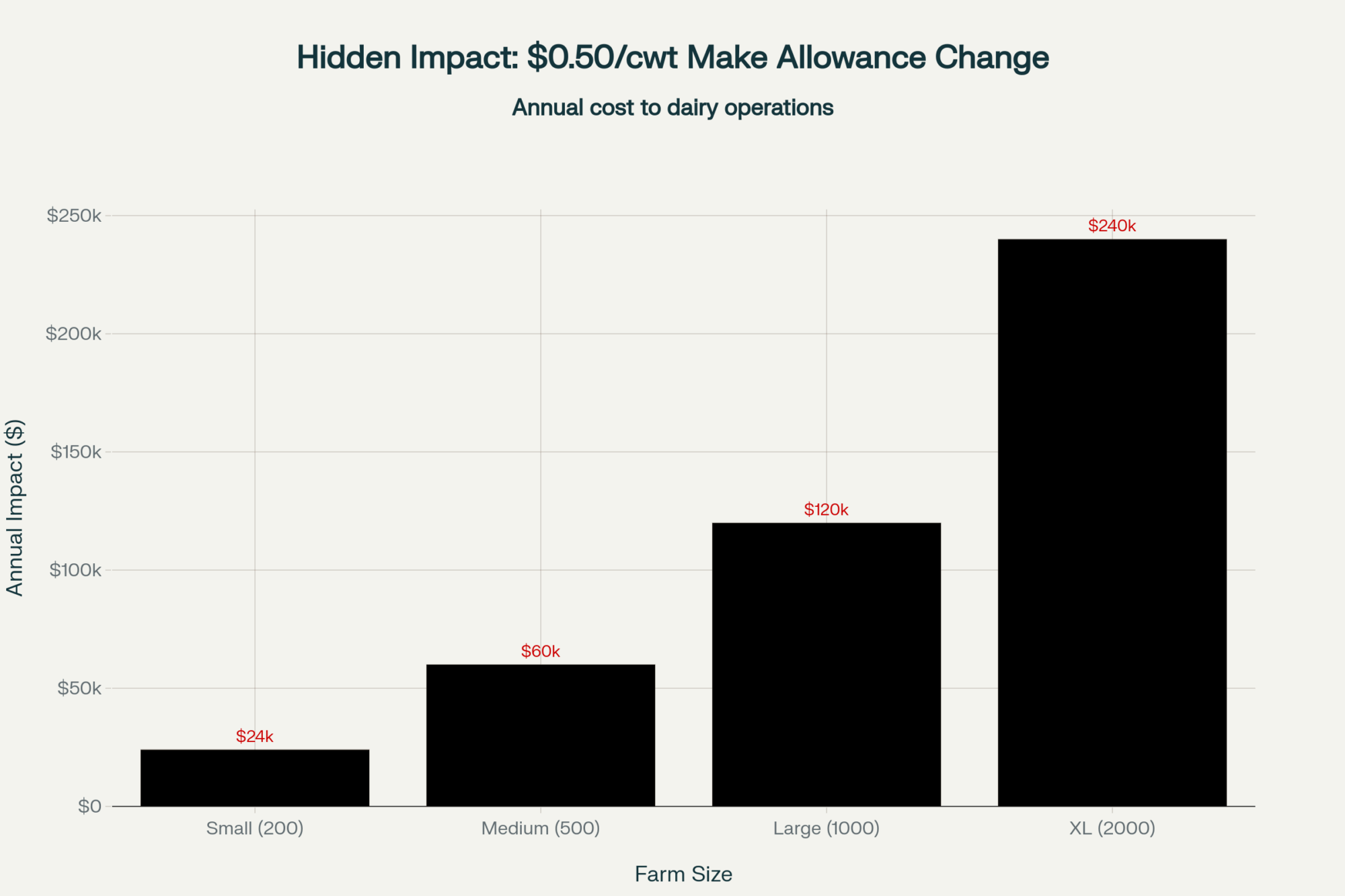

Bailouts treat symptoms, not sources. Without modernized DMC calculations, fairer make‑allowance data, and supply contracts that reward efficiency, the cycle continues: price drop, emergency payment, repeat.

The Bottom Line

Here’s what the 2025 bailout really offers: time.

What farmers are proving, though, is that time alone doesn’t fix markets—management does. Across the country, producers are sharpening skills, controlling costs, and tracking butterfat performance with the precision of any Fortune 500 manager.

As New York Jersey breeder Megan Tully put it best, “The government may keep us afloat, but only management keeps us profitable.”

And there it is. Resilience in dairy right now isn’t a talking point—it’s a mindset. It’s being built every day in barns, on tractors, at kitchen tables, and in feed alleys. One cow, one ration, one decision at a time.

Key Takeaways:

Emergency aid has become standard practice. Since 2018, more than $60 billion in CCC funds have flowed to dairy, blurring the line between rescue and routine.

Farm outcomes now depend on geography and leverage. In Wisconsin, small family herds keep shrinking; in Idaho, contracted farms keep growing—and that gap is widening.

Official margins hide on‑farm reality. DMC numbers may look comfortable, but they ignore feed freight, labor, and energy costs that drain actual cash flow.

Producers are creating their own safety nets. From better butterfat performance to multi‑year feed contracts and DRP insurance, farmers are writing their own playbooks.

Resilience is being rebuilt one decision at a time. The dairies thriving today aren’t waiting on policy—they’re managing through it.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Profit-Driven Persistence: How Dairy Farmers Overcome Challenges to Boost Production – Explores how producers are strategically managing herd growth, breeding, and resource allocation to maintain profitability despite volatility. This article provides actionable tactics for optimizing herd expansion and balancing short-term cash flow with long-term stability.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

The Beef-on-Dairy Paradox: Why Spending More Per Calf Can Earn You More.

You know what’s been keeping me up lately? The price spreads we’re seeing between Holstein bulls and beef-dairy crosses at sale barns across the Midwest. Market reports indicate these spreads have widened considerably, and it’s got everyone talking.

However, what’s interesting—and this is something industry observers are starting to notice—is that not everyone running beef-on-dairy programs is actually making money. Some operations are doing worse than their neighbors who’ve stuck with straight Holsteins. How’s that possible with these market premiums? That’s a question worth exploring.

Different Philosophies, Different Outcomes

The Profit Paradox: Operations investing $150+ per calf in quality nutrition and genetics generate 40-50% higher net returns than cost-cutting approaches

Examining the data that’s emerging, we’re seeing significantly different approaches out there. And honestly, the outcomes are all over the map.

Some folks are understandably focused on keeping costs as low as possible. Makes sense, right? They’re trying to capture beef premiums without spending much extra—using their regular feeding programs, choosing lower-cost genetic options, basically treating beef crosses like slightly different Holstein calves. However, available data indicate that many of these operations capture only a fraction of the available quality premiums. Their net benefit might be positive, but it is often barely so.

It reminds me of that old saying—you can’t starve a profit out of cattle. Yet when feed costs climb, we all feel that temptation, don’t we?

Then you’ve got operations taking more measured steps. They’re investing in better calf nutrition, selecting proven beef genetics, and developing basic tracking systems. Nothing fancy, just steady improvements. Industry patterns suggest that these individuals generally capture most of the available premiums and exhibit reliable positive returns. Good old-fashioned blocking and tackling.

This development suggests something counterintuitive—operations spending the most per calf often generate the highest net returns. Seems backward at first. But when you think about it… they’re the ones with comprehensive data systems, precision feeding, and systematic breeding strategies. All the information we hear about at the winter meetings, but we wonder if it’s really worth it. Turns out, sometimes it really is.

Strategic Implementation Timeline: Building Your Program

Now, I know what you’re thinking—not everyone can transform their operation overnight. Most of us can’t, frankly. So what farmers are finding is a more practical path forward, especially when timing is critical.

Industry patterns suggest successful approaches tend to be gradual. You might start with foundation work—genomic testing on your best cows. Most operations implementing this staged approach report positive cash flow within 18 to 24 months. The $50 per head testing cost typically pays for itself within the first calf crop through better breeding decisions. Select proven beef sires with documented performance records. Nothing experimental, just reliable genetics that work.

The Long Game Wins: Quality-focused beef-on-dairy programs achieve 30% grade improvements by Year 3, while cost-cutting approaches stall at 12%—creating an 18-point performance gap that compounds annually in market premiums.

Industry data shows operations following systematic approaches typically see grade improvements of 20-30% over three-year periods. Start small, keep good records, and adjust as you learn.

And here’s something crucial that dairy nutrition research consistently demonstrates: consistency in calf nutrition matters more than many of us realize. When operations upgrade nutrition for all calves—not just the crosses—it appears to create that stable environment where genetics can really express themselves. The Beef Quality Assurance program, offered through state extension services, provides free resources on this topic. Makes sense when you stop and think about it.

The timing piece is critical here. If you’re considering a more serious commitment to beef and dairy, the biological clock doesn’t wait for our decision-making process, does it? Good breeding decisions made in the coming months should produce calves that hit the market while premiums remain attractive. Every breeding opportunity missed now is one less quality calf when you need it. That’s the unforgiving math of cattle production—nine months of gestation plus feeding time means today’s decisions create opportunities almost two years in the future.

As comfort levels increase, folks scale what’s working. More beef breeding, better feeding systems, stronger market relationships. But it’s gradual. Nobody’s revolutionizing their whole operation in one season.

That three-phase approach typically spans 24-36 months, from the first genomic test to an optimized program: foundation building (6 months), scaling what works (12 months), and then optimization based on actual results (12 months). The timeline matters because breeding decisions made today affect calves that won’t hit the market for nearly two years.

Some opportunities have already passed, honestly. The earliest adoption advantages, those first-mover processor relationships—those ships have sailed. That’s just reality. But industry indicators suggest there’s still a meaningful opportunity here. Regional processors are still developing programs, seeking consistent suppliers who can meet their quality specifications.

The Feed Quality Factor Nobody Talks About

I’ve noticed that when we discuss beef-on-dairy economics, feed quality rarely comes up for discussion. We’re always focused on feed costs, right? But when corn’s relatively affordable, having consistent feed quality might matter even more than the price per ton.

Take molasses, for instance. Most of us never give it a second thought. However, research from university trials on feed quality reveals that the sugar content in generic molasses can vary significantly—documented research shows it ranging from 39.2% to 67.3% in cane molasses samples. That kind of swing can reduce starter intake by up to 18% according to controlled feeding studies. Think about that for a minute… you’re trying to get these valuable crossbred calves off to a strong start, and inconsistent molasses is working against you.

Quality feed companies, such as Kalmbach Feeds, have responded by implementing strict quality standards. Their documentation indicates that they maintain a minimum specification of Total Sugars in their molasses, along with controlled mineral levels and consistent Brix readings. That’s not just marketing talk—it’s measurable consistency that translates to calf performance.

The research backing this is compelling. When molasses quality varies, it affects not only palatability but also other factors as well. It alters rumen fermentation patterns, volatile fatty acid production, and ultimately, how well those expensive beef genetics can be expressed. Recent rumen development research indicates that consistent, quality-controlled molasses can increase butyrate production—and butyrate is crucial for rumen papillae development in young calves.

I understand the appeal of mixing your own rations when ingredients are reasonable. Some operations do it really well. But consider everything involved—mixer maintenance, storage losses, labor time, quality testing, and yeah, that occasional batch that doesn’t turn out quite right. Operations implementing these consistency improvements often report significant performance gains—some seeing a 10-15% improvement in feed efficiency—that more than offset the investment.

Sponsored Post

Regional Differences Matter More Than You’d Think

What farmers are finding is that this beef-on-dairy opportunity plays out really differently depending on where you farm.

In Wisconsin and Minnesota, processor density helps, but those winters… crossbred calves require different management when it’s twenty degrees below zero. Extra bedding, draft protection, maybe some building modifications. Many producers report budgeting extra for winter housing adjustments—it adds up. Consider that heifers may require different housing than steers as well.

Out East—Pennsylvania, New York—it’s a different game. Fewer processors mean every relationship matters more. Programs like National Beef’s AngusLink, Tyson’s Progressive Beef initiatives, or regional programs through American Foods Group offer structured premium opportunities; however, you must consistently meet their specific requirements. The humidity, though… some practitioners report respiratory challenges seem more common with crosses during those muggy summers.

And out West? California and Idaho operations face different challenges altogether. Scale requirements can be daunting—some processors want to see serious volume before they’ll even talk to you. But year-round feeding conditions? That’s a real advantage compared to the Midwest’s weather swings. Additionally, proximity to major feedlots offers various marketing options.

Extension services and breed associations often offer free consultation on genetic selection and program development—resources that many producers don’t realize are available. Some states even offer cost-share programs for genetic improvement. Check with your local extension office about what’s available in your area.

Reading the Market Tea Leaves

Looking at adoption patterns, beef-on-dairy breeding appears to be expanding rapidly across the industry. These premiums we’re seeing will probably hold for a while. But markets being markets, they’ll likely moderate as more producers adopt the practice. Once beef crosses become common enough in the supply chain, that scarcity premium starts to soften—we’ve seen it before with other trends.

The beef cow herd will rebuild eventually—it always does when calf prices stay attractive long enough. There is apparently a new packing capacity in development that should alleviate some current bottlenecks. These things take time, though. Years, not months.

This development suggests that operations building quality-focused programs now might maintain good margins even after scarcity premiums fade. Quality differentiation, operational efficiency, and perhaps some technological advantages—these create value that doesn’t depend entirely on tight supplies.

Let’s Be Honest About Risk

We should discuss potential pitfalls, because things do go wrong in this business.

Crossbred calves may present different management needs. Some practitioners report that they may respond differently to standard protocols, although research in this area is still in its early stages of development. What works for Holsteins doesn’t always translate directly to other breeds. Your vet can provide insights on what they’re seeing locally—it seems to vary quite a bit by region. Labor requirements may also increase, particularly during the critical first 60 days.

Markets shift—we’ve all lived through cycles. If you’re borrowing to expand beef-on-dairy programs, keeping debt conservative makes sense. Financial advisors often recommend maintaining a reasonable debt-to-asset ratio when making long-term commitments.

And processor relationships can change. Plant modifications, ownership transitions, program changes—they happen. Having alternatives, even if they’re not your first choice, provides important flexibility.

Finding Your Own Path

For smaller operations with fewer than 200 cows, success often stems from excellence in basics rather than technology. Good genetics, consistent nutrition, and simple but effective tracking. Consider partnering with service providers for expertise rather than trying to develop everything internally. Operations implementing basic improvements often see meaningful returns when they focus on consistency over complexity.

Mid-sized operations (200-500 cows) often do well with staged approaches. Spreading investments over time, testing at a smaller scale before expanding, leveraging cooperative resources where available. It’s about balancing risk and opportunity, right? These operations typically see the best return on investment when they focus on gradual system improvements rather than dramatic overhauls.

Larger operations face clearer but harder choices. Partial implementation rarely seems to work well at scale. Either build comprehensive systems for long-term positioning or maintain flexibility to adjust as markets evolve.

The Bigger Picture

I’ve noticed that beef-on-dairy reflects broader patterns we’ve seen in agriculture before. When commodity markets experience structural changes, operations that build capabilities and systems often maintain advantages even after initial premiums moderate. We saw it with the adoption of rbST, again with genomic testing, and now with beef-on-dairy.

The operations struggling aren’t necessarily doing anything wrong—they’re optimizing for different constraints. If capital or management bandwidth is limited, focusing on cost control makes perfect sense. But recognizing that this approach may limit access to emerging premiums helps with realistic planning.

Industry consolidation patterns suggest market transitions create both opportunities and challenges. Operations that adapt thoughtfully, building on their strengths while addressing market needs, generally emerge in good shape. Those that either resist change entirely or chase every trend without focus… well, that tends to be harder.

Feed quality consistency—like the molasses example we discussed—genetic selection, and systematic management create value beyond market cycles. Operations investing here position themselves not just for today’s premiums but for whatever comes next.

As we make breeding decisions for calves that won’t reach market for almost two years, thinking about where the industry might be heading matters as much as reacting to today’s prices. The biological lag in cattle production means today’s decisions create tomorrow’s reality—for better or worse.

The beef-on-dairy opportunity seems real, but it’s not uniform or guaranteed. Success likely requires matching strategy to your specific resources, capabilities, and regional context. And, perhaps most importantly, it requires recognizing that in evolving markets, what works today might not work tomorrow.

That’s the challenge—and opportunity—we’re all navigating together. What’s your take on it?

FINAL KEY TAKEAWAYS

The Profit Paradox: The most profitable beef-on-dairy programs often have higher per-calf costs. Their success comes from strategic investment in nutrition and genetics, which generates net returns that significantly outperform low-cost, minimum-effort approaches.

Feed Consistency Trumps Cost: Inconsistent ingredients are a hidden profit killer. Generic molasses, for example, can vary from 39% to 67% sugar, a swing shown to cut calf starter intake by up to 18% and undermine genetic potential. Paying for quality-controlled feed delivers more predictable performance.

Your Strategic Roadmap: Lasting success is built over 24-36 months, not one season. Start with a strong foundation (like genomic testing your best cows), gradually scale what works for your operation, and then optimize using your own carcass data—not industry averages.

Biology Doesn’t Wait: Breeding decisions made today create the calves that will hit the market in late 2027. To build a program that remains profitable even after current premiums soften, the time to invest in quality and consistency is now.

EXECUTIVE SUMMARY

While market premiums for beef-on-dairy calves are strong, profitability varies wildly from farm to farm. The crucial difference isn’t luck; it’s strategy. Industry patterns reveal that producers who strategically invest in superior nutrition, genetics, and management consistently achieve higher net returns than neighbors focused solely on cutting costs. The hidden killer for many programs is feed inconsistency—for instance, when variable sugar content in molasses cuts starter intake by 18%, it sabotages the very genetic potential you’ve invested in. Real success requires a deliberate 24-36 month journey: building a foundation with tools like genomic testing, scaling up proven practices, and optimizing based on your own results. With today’s breeding decisions creating your 2027 market calves, the window is closing to build a quality-driven program that can thrive long-term. In this evolving market, the cost of inaction is proving far greater than the cost of strategic investment.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Maximizing Beef on Dairy Success: Key Strategies for Sire Selection – This guide provides a tactical framework for choosing the right beef genetics. It details how to balance key traits like calving ease, carcass quality, and feed efficiency to drive profitability and avoid common pitfalls in your breeding program.

The Beef on Dairy Revolution: A Deep Dive into the Economics and Market Dynamics – For a strategic perspective, this analysis examines the broader market forces and economic models driving the beef-on-dairy trend. It helps you understand processor demands and long-term supply chain shifts to better position your operation for future profitability.

The Genomic Revolution: How Advanced Genetic Selection is Reshaping the Dairy Industry – This article explores the innovative technology behind the strategies discussed. It reveals how genomic testing provides the precise data needed to make smarter breeding decisions, accelerate genetic progress, and maximize the return on your beef-on-dairy investments.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Cull cows over $2,000 and beef-on-dairy calves near $1,000—why this 90-day window could make or break your 2026 margins

EXECUTIVE SUMMARY: Fall 2025 delivers an uncommon—and urgent—opportunity for U.S. dairy operators. Strong cull and beef-on-dairy calf prices, reported at $2,000+ and near $1,000 respectively, are keeping many herds afloat amid relentlessly flat $17 milk. University and market economists warn these beef premiums look fleeting, with the cattle cycle and supply signals already tightening for 2026. Recent research shows Midwestern breakevens remain high, while only producers invested in butterfat performance and rigorous herd management capture true component bonuses. Meanwhile, export hopes are dimming—contract premiums are now won on genetics, traceability, and relentless cost control. As lenders prepare for summer’s critical cattle inventory and cash flow reviews, operations with intentional plans—whether expanding, pivoting, or winding down—consistently protect more equity. The next three months are a “use it or lose it” window for turning fleeting beef revenue into sustainable resilience. What farmers are discovering is that asking hard questions, running fresh numbers, and pushing for proactivity can make 2026 a year of opportunity—not regret.

Checking in with producers this fall, there’s one urgent takeaway: this is a critical 90-day window to turn temporary beef premiums into lasting resilience for 2026. The evidence is in the numbers—cull cows clearing $2,000 and beef-on-dairy calves pushing $1,000 (USDA National Weekly Direct Cow and Bull Report, October 2025). These premiums are propping up many milk checks stuck at $17. However, as extension economists and market analysts from the University of Wisconsin and Cornell emphasize, these conditions are shifting. We’re staring down the last weeks of this run before cattle cycles and supply buildup set a new tone for the coming year.

What’s interesting here is seeing smart operators use this moment to shore up their businesses—paying down debt, making pro-active facility investments, and building a cash buffer instead of assuming current premiums will last. This development suggests that treating a tailwind as flexibility—not false security—creates real strategic advantage for the next transition period.

The crisis in black and white: milk checks stuck at $17 while breakevens demand $17.50-$18.50, but cull cows and beef calves are throwing off unprecedented cash—turning cattle into the lifeline keeping farms afloat.

The Math of Survival: Breakevens & Components

Revenue Source

2024 Baseline

Fall 2025

Per Cow Impact

100-Cow Herd

Cull Cows (15% rate)

$1,500/head

$2,000+/head

+$75

+$7,500

Beef-Dairy Calves (40% births)

$600/head

$1,000/head

+$160

+$16,000

Component Bonus (3.7%+ protein)

Base milk

+$1.25/cwt

+$31/yr

+$3,100

TOTAL OPPORTUNITY

—

Stack strategies

+$266/cow

+$26,600

🚨 Baseline (No Action)

Wait for recovery

Miss window

-$50 to -$150

-$5K to -$15K

Looking at this trend, most Midwest herds face pre-beef breakevens between $17.50 and $18.50/cwt (UW Center for Dairy Profitability, Fall 2025 Update). Out west, Idaho’s and Texas’s biggest dry lot systems sometimes run at $14–$15/cwt, riding local feed and labor edge. Either way, high butterfat performance is the separating factor. Hitting 3.7% protein or better can mean $1–$1.50/cwt over base—if you’ve invested in genetics, tight fresh cow management, and keep transition periods on track. As many of us have seen, those premiums aren’t accidental; they follow from tough culling decisions and knowing your numbers cold.

That $1-$1.50/cwt component bonus isn’t optional anymore—it’s the difference between red ink and breaking even, between selling out and surviving another season with $17 milk

Export Hopes, Local Contracts

For years, many of us held out hope that another export surge would save the day—especially from China. But this season’s USDA GAIN trade data and Rabobank’s Dairy Quarterly all show it’s growth in cheese and butter, mostly cornered by New Zealand and Europe, that’s outpacing demand for U.S. powder. In the Midwest and Northeast, plants are hungry for consistent, high-component, specialty contracts. Herds that made early investments in A2, organic, or niche certifications find their milk in demand; others should ask whether fluid or low-component contracts will provide enough margin as the cycle shifts.

July Inventory—Lender Stress & Planning Leverage

It’s no surprise to seasoned managers that the USDA July Cattle Inventory Report is more than an annual headcount. When beef prices soften and heifer retention ticks up, lenders across regions—like those briefed by Minnesota Extension and New York FarmNet—run tougher stress tests on farm finances. Farms sitting right at a 1.25x debt service coverage are fine for now, but that can slip fast. Those who restructure or plot a sale while balance sheets are still strong tend to carve out six-figure equity advantages compared to late, forced exits. The lesson, as risk educators preach, is that deliberate action always beats hoping for a bounce.

Three Lanes: Exit, Pivot, or Scale

From kitchen tables in northeast Iowa to group calls with Western Idaho co-ops, three paths are front and center:

Exit with Intention: Producers looking at high debt or retirement are using strong asset values to secure their family legacies, not just chasing another cycle.

Premium Niche Pivot: Some are cutting herd size, chasing premium contracts—A2, grassfed, organic, you name it—with a willingness to meet tough specs on components, health, and traceability. This approach works best when paired with deep processor relationships and quick financial routines.

Expansion: A Tool for the Prepared: Rabobank’s 2025 sector review and extension management profiles agree: disciplined, high-performing herds with fresh cow and labor management dialed in can scale with confidence. For others, fast growth just means fast exposure if things don’t break right.

The north star here? Monthly cost-of-production benchmarking, regular review with lenders, and not waiting to renegotiate contracts until margins are squeezed.

Global Competition & Policy Realities

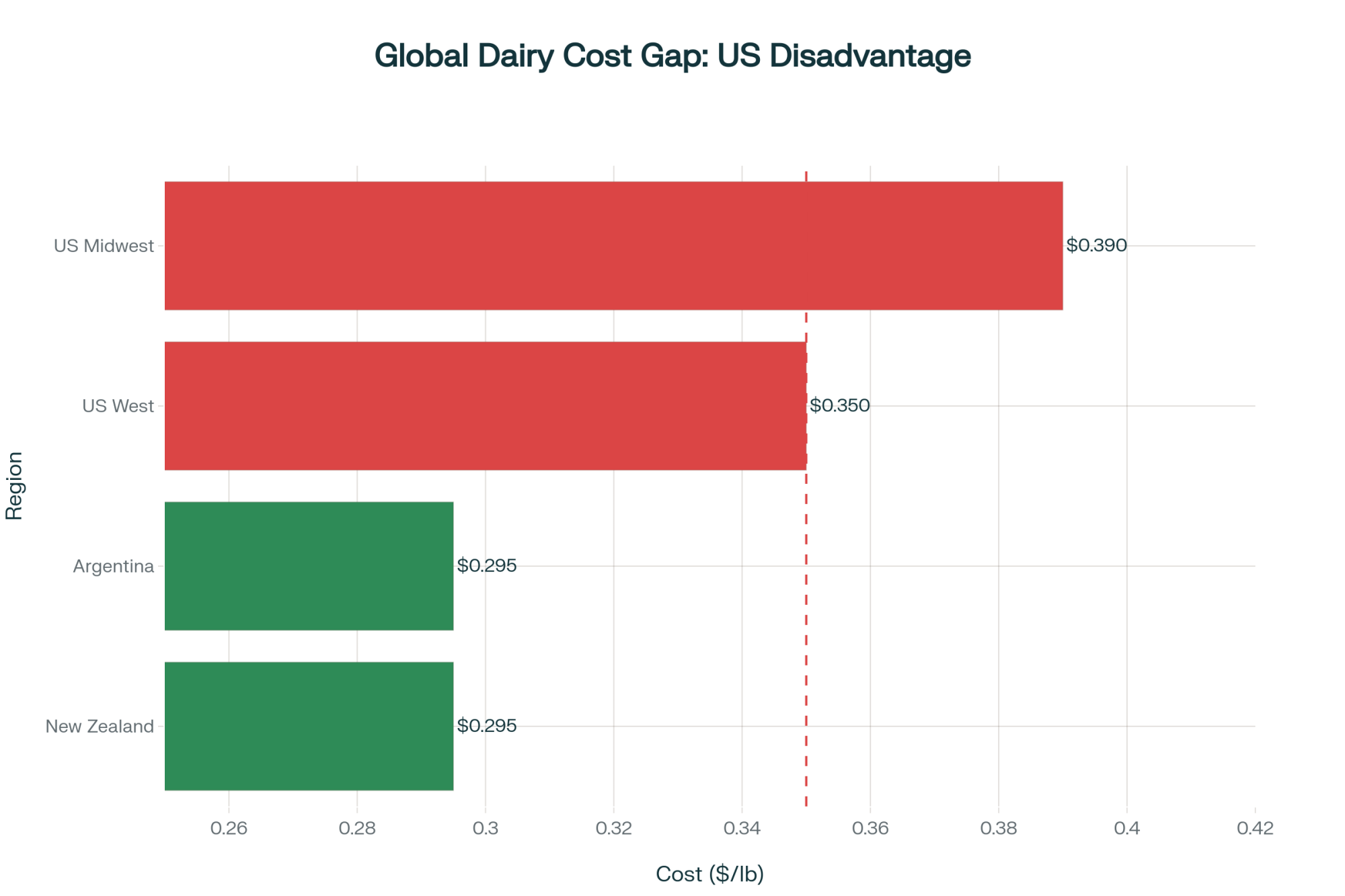

U.S. Midwest producers face a brutal 20-45% cost disadvantage against New Zealand and Argentina—at $0.39/lb versus $0.27-$0.32, every efficiency gain and premium matters when you’re starting in the hole.

It’s worth noting that IFCN’s 2025 benchmarks put leading New Zealand and Argentina herds at $0.27–$0.32/lb. Even top Western U.S. performers run about $0.35, with most Midwest herds closer to $0.39. The gap isn’t destiny: it reflects differences in feed-to-milk efficiency, heifer survival, and transition consistency. Policy backstops like DMC are valuable, and analysis from Cornell and Wisconsin Extension reinforce this: they help good operators stay afloat but aren’t enough to shore up chronic losses over time.

The Myth of the “Deal of the Century”

As expansion talk returns, recent Rabobank analysis and local case studies ring a familiar bell: the “deal of the century” works out for operations already strong on the basics—cost, herd health, labor discipline. Ramped-up purchases without this foundation rarely yield the hoped-for returns and often accelerate operational headaches.

Action Steps: Navigating the 90-Day Window

Here’s the practical bottom line: This window is closing, not expanding. First, benchmark your cost of production with the latest IFCN and extension tools; don’t trust last year’s averages. Next, proactively arrange a review session with your banker—not to plead for relief, but to present your plan for surviving and thriving into next year. Scrutinize your processor or coop contracts and specialty program agreements—will you be the supplier they prioritize in a shrinking market? And take the time this fall to address transition and herd health; waiting until calving issues flare won’t do.

The difference for 2026 will be made by those who act intentionally and aren’t afraid to adjust their course. That’s the mindset that’s kept American dairies resilient through every market twist—and it’s how the smartest operators I know are reading this moment.

KEY TAKEAWAYS

Farms leveraging this fall’s beef premiums could improve net margins by $100 to $200 per cow, while disciplined herd and transition management opens $1–$1.50/cwt in component bonuses (UW Extension, IFCN, Rabobank).

Practical action: Benchmark your cost of production now, meet proactively with lenders to review true breakevens, and secure or re-align premium contracts for 2026 before markets tighten.

Butterfat, protein, and health discipline now outperform volume; herds that master transition periods and component payouts lead in uncertain markets.

The window for turning “luck” into a long-term strategy is closing. Lenders, markets, and export buyers all point to greater volatility ahead for operations not dialed on costs or value.

Across Wisconsin, Idaho, and the Northeast, the most resilient producers are those who build trusted advisor relationships and plan ahead—regardless of herd size or business model.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Navigating Today’s Dairy Margin Squeeze: Insights from the Field – This piece provides tactical field insights for optimizing components and feed strategies. It reveals how targeted nutritional adjustments and culling discipline can directly boost per-cow income, offering an immediate action plan for improving the breakeven numbers discussed in our article.

AI and Precision Tech: What’s Actually Changing the Game for Dairy Farms in 2025? – Explore the innovation and technology driving modern profitability. This article breaks down the real-world ROI for precision tools like AI-driven feeding and automated health monitoring, showing how strategic tech investments can slash input costs and enhance herd efficiency.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

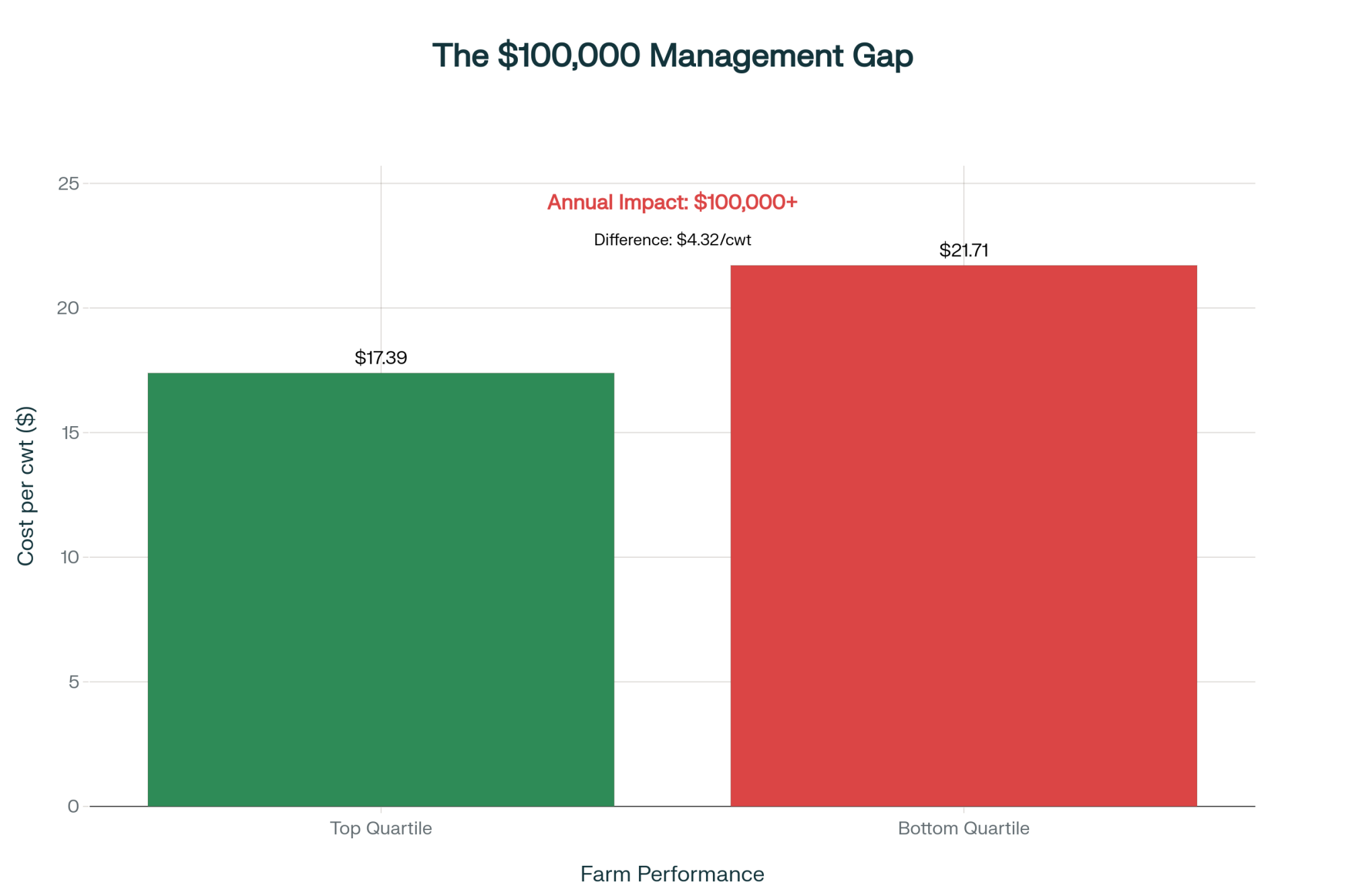

Cornell study shows 150-cow dairies outearning 500-cow operations by $100K. The secret? It’s not what you think.

Cornell data reveals a $100,000 performance gap that has nothing to do with size. Here’s the 3-phase plan to capture it.

You know that feeling when you’re driving past one of those massive new dairy facilities? All that shiny equipment, those huge freestall barns stretching as far as you can see… makes you wonder sometimes about where smaller operations fit in all this, doesn’t it?

But here’s what’s really fascinating—and Cornell’s 2023 Dairy Farm Business Summary has been documenting this for years now—the profit differences between well-run and poorly-run farms of the same size are actually bigger than the differences between small and large operations.

“The profit differences between well-run and poorly-run farms of the same size are actually bigger than the differences between small and large operations.”

Think about that for a minute. We spend so much time worrying about scale, but what Cornell’s latest benchmarking data shows is that a really well-managed 150-cow dairy in the top quartile can generate significantly better returns per cow than a 500-cow operation that’s struggling with management. Same milk prices, same basic input costs, completely different bottom lines.

The numbers really spell it out. Top performers were hitting around $17.39 per hundredweight in operating costs. Bottom performers? They were running $21.71. On a 150-cow herd producing 24,000 pounds per cow annually… well, you can do the math. That’s over $100,000 difference we’re talking about. And that has nothing to do with how many cows you’re milking.

The $100,000 Management Gap: Top-performing 150-cow dairies achieve operating costs of $17.39/cwt versus $21.71/cwt for bottom performers—proving management beats scale every time. Same herd size. Same milk prices. Completely different bottom lines.

Critical Success Factor: Never skip phases. Foundation must be solid before pursuing transformation.

Small Dairy Farm Management: The Real Story Behind Consolidation

Dairy farm consolidation from 2017-2024 shows 15,221 operations closing—but with 40-45% of farmers lacking successors and average age at 58, this reflects retirement demographics, not management failure

But when you actually dig into who’s leaving—and the 2022 Census of Agriculture really shows this clearly—the average dairy farmer is now 58 years old. Somewhere between 40 and 45% don’t have anybody lined up to take over.

“That’s not business failure, is it? That’s retirement.”

I was talking to a producer near me last week who’s selling out next spring. He’s 64, his back’s giving him trouble, and his kids have established careers elsewhere. He actually had a pretty good year financially. But when you can barely get out of bed some mornings and your daughter’s doing well as a nurse practitioner with actual weekends off… the decision kind of makes itself.

There’s also the land value situation to consider. Out in California’s Central Valley, I heard about a 300-cow operation sitting on 40 acres near Modesto. With water costs skyrocketing and developers offering several million for the land… can you really blame them for taking it? Same thing’s happening in Pennsylvania, upstate New York, anywhere near growing communities.

What’s encouraging for those planning to stay is seeing how different successful models are emerging. Vermont’s Agency of Agriculture organic sector data show that smaller organic operations, typically 100 to 200 cows, are achieving solid profitability. Meanwhile, USDA Economic Research Service research indicates conventional operations generally need much larger scale—often over 2,000 cows—to hit similar per-cow returns.

So it’s not that small, can’t work. It’s so that small has to work differently.

The $100,000 Management Difference: Where Excellence Shows Up

That $4-5 difference per hundredweight—on a 150-cow operation, we’re talking serious money that has nothing to do with scale.

Labor Efficiency Makes or Breaks You

The Hidden $75,000: Labor efficiency creates a massive competitive advantage—top-performing dairies achieve 50+ cows per worker versus 35-40 for struggling operations. The gap compounds through better parlor workflows, reduced wage costs, and operational flexibility. No capital investment required.

The benchmarking programs consistently show top operations getting 50-plus cows per full-time worker. Struggling farms? They’re down around 35-40.

I know a farm in Pennsylvania—150 cows, really efficient setup, running with 2.5 people total. Another operation nearby, same size, needs 4.5 people. At today’s wage rates… finding good help isn’t getting cheaper, as we all know… that difference alone can save or cost you $75,000 annually.

“We restructured our workflows last year,” one producer told me recently. “Went from 4.5 people down to 3 just by fixing bottlenecks in our parlor routine. Saved us $75,000 annually.”

Feed Efficiency: Not What You’d Expect

Here’s what’s interesting about feed costs. Looking at various state data, top farms aren’t necessarily spending less on feed per hundredweight. Often it’s about the same—around $9.60. But their income over feed cost? Way higher.

They’re not feeding cheaper. They’re feeding smarter. Better forage quality from optimal harvest timing. More precise ration formulation based on actual testing instead of guesswork. Walking those bunks twice daily, making adjustments based on what you see. Keeping waters clean, stalls comfortable, catching that fresh cow that’s a little off before she crashes.

It’s consistency. Every single day. Even when you’re tired.

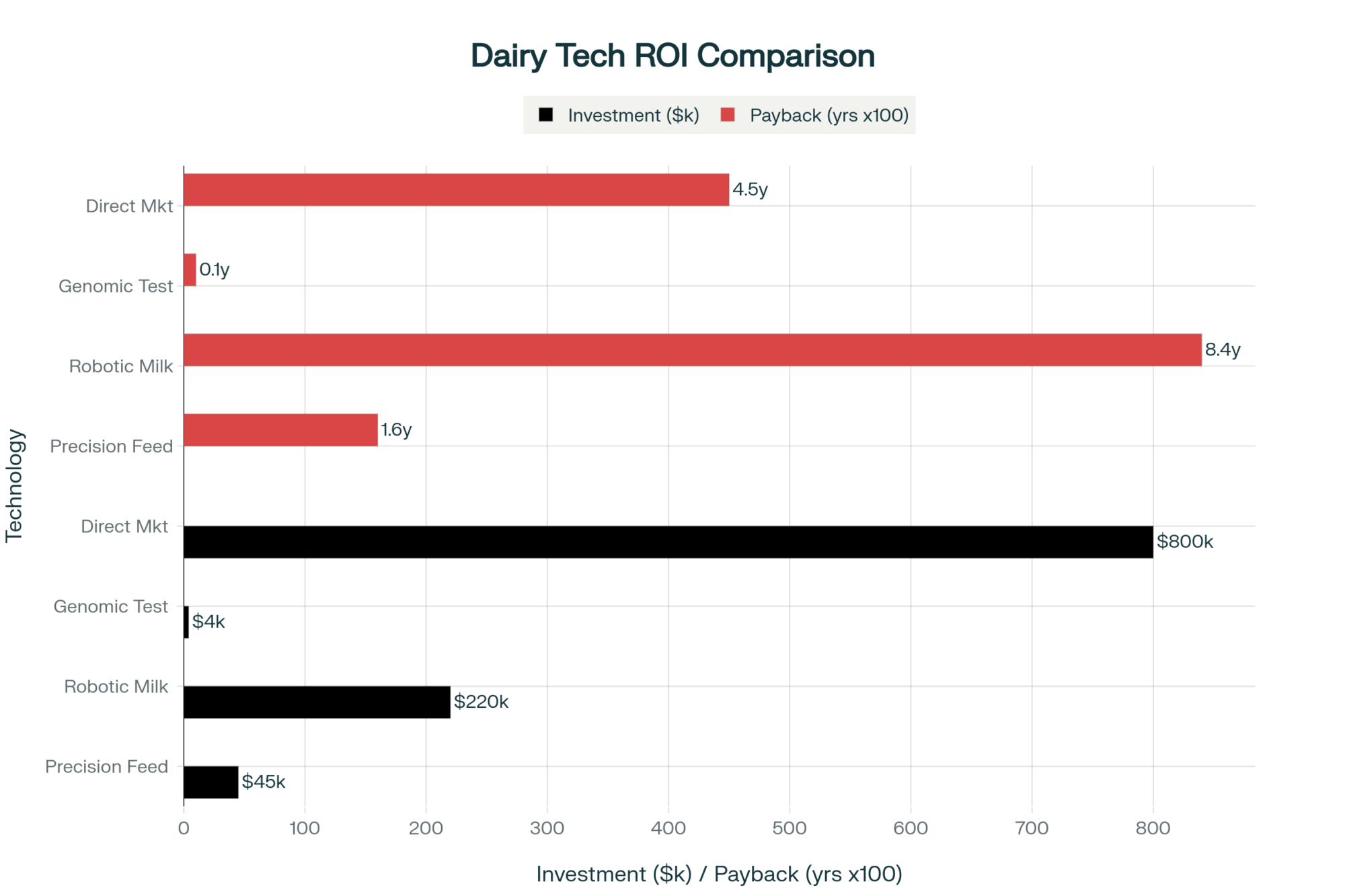

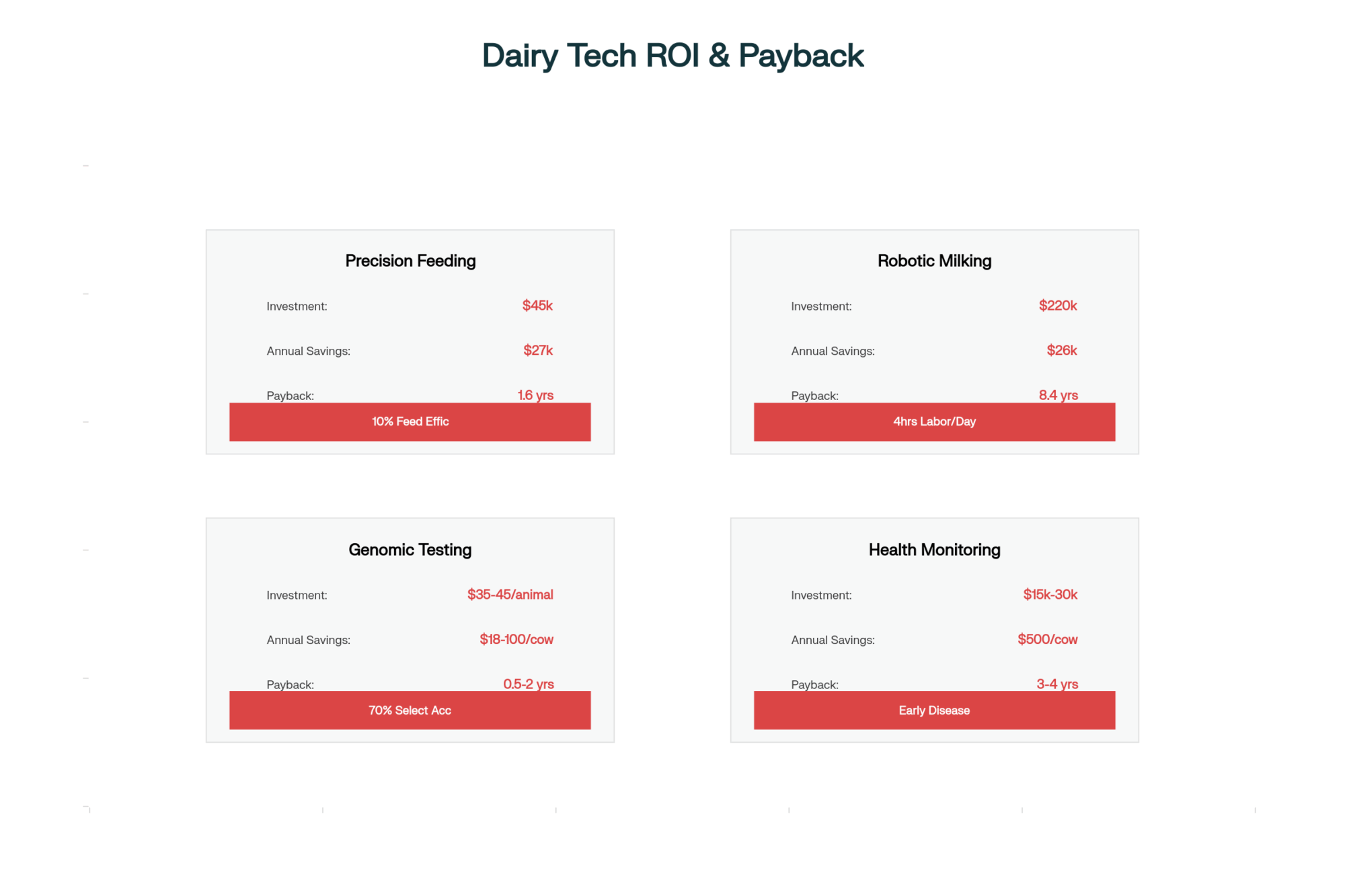

Robotic Milking Economics: The Truth Nobody Wants to Hear

Let’s have an honest conversation about robots. Everyone’s got an opinion—they’re either the future or a complete waste. Truth is somewhere in the middle.

Wisconsin Extension and Minnesota Extension have done thorough economic analyses. For a 200-cow operation, you’re looking at close to a million dollars all in. The robots themselves run $250,000 to $300,000 each; you need about three for 200 cows, plus barn modifications, software, training… it adds up fast.

Annual operating costs? Figure $40,000 to $60,000 between maintenance contracts, parts, and electricity. When you run realistic payback calculations—not the dealer’s sunny projections—you’re often looking at 20-plus years. Sometimes 25 or 30.

Yet farms keep installing them. And many swear by them.

Here’s why: it’s not about immediate payback. Statistics Canada’s latest agricultural census data and university research consistently show farms with automated milking are significantly more likely to have younger family members interested in taking over.

“The financial payback is marginal at best. But my 24-year-old son, who was planning to leave farming? He’s now fully engaged. My daughter, studying ag business, sees a future here. What’s that worth?”

For older farmers—and let’s be honest, we’re not getting any younger—reduced physical demands can mean farming another decade versus selling. One Wisconsin producer was ready to quit at 55 because his knees were shot. Installed robots, now he’s 62 and planning to continue until 70.

Premium Market Access for Small Dairies: Reality Check

Strategy

Investment

Time to ROI

Annual Return

Risk Level

Accessibility

Component Premiums

Minimal

Immediate

$20K-$30K

Low

High

Organic Certification

$150K-$300K

3+ years

$165K-$470K

High

Limited

Direct Sales

$150K-$300K

3-5 years

Variable

Med-High

Medium

Everyone talks about capturing premiums like it’s simple. Go organic! Sell direct! Problem solved!

Extension studies from Penn State and Cornell suggest you need $150,000 to $300,000 in extra working capital to survive the transition. Even after certification? Organic Valley and Horizon maintain regional quotas. NODPA producer surveys show many new organic farms only receive premium prices on partial production initially.

“It’s a marathon where you’re not sure the finish line exists until you cross it,” as one Vermont producer who completed the transition described it.

Direct Sales Infrastructure: Major Investment Required

Direct sales can work—retail prices obviously exceed farm gate values. But infrastructure costs are substantial.

Meeting health department requirements, installing pasteurization equipment, bottling lines, developing HACCP plans… Penn State Extension and Cornell Small Farms Program estimate $150,000 to $300,000 minimum for compliant facilities.

Building a customer base takes time, too. Most operations report 3-5 years to achieve meaningful volume. “Year one, we sold 50 gallons weekly and questioned our sanity,” a New York producer now moving 30% of production direct told me. “Year five, we’re at 500 gallons and hiring staff.”

Component Premiums: The Accessible Opportunity

Here’s what’s realistic for most operations—component premiums. Major processors are paying real money for high-protein, high-butterfat milk.

Current typical Northeast processor premiums (October 2025):

Chobani (Rome, NY): $0.75-$1.25/cwt for 3.3%+ protein

DFA: $0.50-$1.00/cwt for consistent 3.25%+ protein

Upstate Niagara: $0.40-$0.80/cwt for SCC under 100,000

Various cooperatives: $0.30-$1.50/cwt for butterfat over 3.8%

Getting from 3.0% to 3.3% protein through genetics and nutrition management generates $20,000-30,000 annually for a 150-cow herd. That’s achievable for pretty much any operation willing to focus on it.

Why Community Connections Generate Real Returns

I know sponsoring the 4-H livestock auction feels like charity. But the USDA Economic Research Service and Colorado State research documents that local food spending generates 1.8-2.6 times its value in local economic activity.

More directly, those connections pay off unexpectedly. When you need harvest help, and neighbors show up. When you’re expanding and the town supports your zoning request. When you need workers and people recommend their kids.

“Half our township board had either bought beef from us or had kids in 4-H projects we supported,” a Midwest producer told me about his manure storage permit. “That permit sailed through.”

Farms with strong community ties consistently report better employee retention, stronger bank relationships, and higher grant success rates. When regulations change, connected farms get flexibility. Isolated operations get compliance notices.

Your Strategic Path Forward

Looking at successful operations that have really turned things around, there’s a clear pattern.

First, they fix fundamentals. Labor efficiency, operating costs, and working capital. This alone can improve cash flow by tens of thousands annually.

Then they capture accessible wins. Component bonuses, quality premiums, maybe beef-on-dairy genetics. Things requiring minimal capital but adding meaningful revenue.

Only after achieving operational excellence and financial stability do they tackle major transformations—organic transition, direct sales, robotics. By then, they have management skills and a financial cushion to handle it.

The farms that fail? They jump straight to transformation, thinking it’ll save them without fixing underlying problems. Doesn’t work that way.

Making the Tough Exit Decision

Not everyone can make this work long-term. That’s okay.

If you’re consistently unable to cover costs. If you’re approaching retirement without succession. If health is failing and stress is overwhelming…

I’ve seen too many burn through equity trying to save something unsaveable. There’s no shame in selling with equity intact. That’s smart business, not failure.

“At first it felt like giving up,” a respected producer who sold at 62 told me. “Now, doing some consulting, enjoying grandkids—I realize it was my smartest business decision.”

The Bottom Line for Small Dairy Success

The industry is consolidating—24,082 farms now versus 39,303 in 2017. Those numbers are real.

But consolidation doesn’t mean small farms are doomed. What’s happening is sorting. Farms with strategies matching their capabilities thrive. Those competing on the wrong metrics struggle.

Your 150-cow dairy trying to beat a 5,000-cow operation on commodity cost per hundredweight? That’s like your local hardware store trying to beat Home Depot on lumber prices. Won’t work.

But competing on quality, flexibility, specialized products, customer relationships, and community connection? Different game entirely. Winnable game. Cornell’s data proves it. Wisconsin’s successful small farms demonstrate it. Vermont’s thriving organic dairies live it daily.

The question isn’t whether small dairies can survive. Plenty are doing better than surviving. The question is whether you’ll play the game that fits your size and situation.

“Good management at any size beats poor management at every size.”

Because ultimately—and this is what all the research confirms—management quality and strategic fit matter far more than scale.

That’s something we can all work on, regardless of herd size.

Key Takeaways:

THE PROFIT TRUTH: Management quality drives a $100,000+ annual profit gap between same-sized dairies—Cornell data proves top 150-cow operations consistently outearn bottom-performing 500-cow dairies

THE EFFICIENCY EDGE: Before buying robots, hit these benchmarks: 50+ cows/worker (saves $75K), operating costs under $18/cwt, and 40% working capital reserves—most farms can achieve this without major investment

THE SMART MONEY PATH: Follow this exact sequence or fail: Fix fundamentals first (Year 0-2), capture component premiums second ($20-30K/year), only then pursue transformation (organic/robots/direct sales)

THE PREMIUM REALITY: Component premiums pay faster than going organic: Getting to 3.3% protein adds $20-30K annually with minimal investment vs. a 3-year organic transition requiring $150-300K working capital

THE COMMUNITY ROI: Your 4-H sponsorship isn’t charity—it’s strategy: Farms with strong community connections report 3.8-year employee retention (vs. 11-month average) and 23% lower borrowing costs

Executive Summary:

Cornell’s 2023 data definitively proves what progressive dairy farmers have long suspected: management excellence beats scale every time, with well-run 150-cow operations outearning poorly-managed 500-cow dairies by over $100,000 annually. The critical difference lies not in technology or size but in achieving operational benchmarks—top performers hit $17.39/cwt operating costs and 50+ cows per worker, while bottom quartile farms struggle at $21.71/cwt and 35-40 cows per worker. This comprehensive analysis reveals a proven three-phase strategy where successful small dairies first fix fundamentals (saving $50-100K), then capture accessible premiums like component bonuses ($20-30K), before attempting any transformation, such as organic transition or robotics. While the industry has consolidated from 39,303 to 24,082 farms since 2017, this largely reflects the reality that 40-45% of aging farmers lack successors, not the failure of small-scale dairy economics. The path forward is clear: compete on management quality, specialized products, and community relationships—not commodity volume. For the 150-cow dairy willing to execute this strategy, the opportunity hasn’t just survived consolidation; it’s actually grown stronger.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

The 10 Commandments of Dairy Farming: Expert Tips for Sustainable Success – This guide provides a tactical framework for mastering the fundamentals discussed in Phase 1. It details actionable best practices in animal welfare and nutrition that directly translate to lower operating costs and higher efficiency, forming the bedrock of profitability.

The Robot Revolution: Transforming Organic Dairy Farms with Smart Tech in 2025 – Exploring a Phase 3 transformation, this article offers a focused case study on technology adoption within the high-value organic sector. It demonstrates how to weigh the true ROI of automation, balancing innovation with the core values of a specialized market.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

From Indiana barns to show rings around the world…

Once in a generation, someone comes along who changes how we see the Jersey cow—and how we see each other. That was Ronnie Lee Mosser, 77, whose deep cow sense was matched only by his profound kindness.

The Quiet Strength Behind a Confident Smile

You could spot Ronnie in any show ring. Hat tipped just enough to catch his eyes, clipboard in one hand, and that steady grin that spoke louder than any call on the mic. He didn’t just judge Jerseys—he read them. Every set of legs, every udder, every walk through the ring was, to him, a story: a testament to the breeder’s patience, the family behind the barn, and the promise that the Jersey breed still carries bright into the future.

Beginning January 7, 2002, Ronnie joined the American Jersey Cattle Association (AJCA) as a Type Traits Appraiser, eventually earning promotion to Senior Appraiser in August 2008. Over two decades, he logged thousands of miles appraising more than 158,700 Jersey cows across the country before transitioning to part-time in March 2022. His steady work ethic and deep cow sense made him a cornerstone of the AJCA classification program—setting a standard not just for how to evaluate cattle, but for how to live with purpose.

More Than a Job—A Calling

Ronnie’s passion carried him far beyond Indiana, where he served as field representative for both Indiana and Kentucky Jersey breeders. He judged shows at every level—across the U.S. and internationally in Canada, Brazil, Colombia, Ecuador, Guatemala, and Argentina—and stood in center ring at events like the National Jersey Jug Futurity and the Premier National Junior Jersey Show. He taught AJCA classification methods to appraisal teams around the world, spreading the gospel of good type and honest evaluation.

Yet, even on the biggest stage, he never lost sight of the cows—or the kids—who made it all matter. As a regular ringman for All American Jersey events and national sales, Ronnie brought energy and expertise that elevated every event he touched.

Lessons from Pleasant Ridge

At his home farm in Geneva, Pleasant Ridge Jerseys became more than a breeding operation—it was a testament to family values and Jersey excellence. The farm regularly sponsored All-American classes, supporting youth and the broader Jersey community. Their cattle earned consistent recognition, including Pleasant Ridge Kid Rock Ella, who claimed Junior Champion and first fall yearling at the 2024 All-Americans.

Behind every ribbon was a simple truth Ronnie repeated often: “Good cows come from good people.” He believed that sound breeding decisions and sound character always walked hand in hand.

And he lived that wisdom daily—through early mornings, late nights, and countless conversations in barn alleys, show pens, and sale rings. Summers found him on the fair circuit with his grandchildren, passing on not just show techniques but life lessons. If you stayed long enough, Ronnie would leave you with more than advice. He’d leave you believing in yourself.

He is survived by his wife and children, who continue the tradition at Pleasant Ridge, carrying forward his love of the breed and the values he instilled.

Voices from the Jersey Family

In the days following his passing, hundreds from around the world shared memories that painted the same picture: a man who made everyone feel valued, welcomed, and inspired.

“Ronnie had a way of making you feel like you mattered. Every time I talked to him, I walked away smiling.”

“He was more than a judge—he was family to anyone who loved a Jersey cow.”

“I first met Ronnie at the All American in Louisville in 1978. I thought he was a rockstar, but he quickly became a friend I could call my own.”

“What he loved more than the little brown cow was his family.”

Across continents, from 4-H barns to show arenas, people remember his laughter, his fairness, and the way he brightened every barn alley he entered. As one friend said simply, “Another great one is gone—but what a gift it was to know him.”

The Man Who Made You Feel Seen

Ask anyone who crossed paths with Ronnie, and you’ll hear it: he had a way of making you feel seen. Whether you were a first-year showman or a seasoned breeder, he met you with respect and patience. He could give correction without sting and encouragement without fanfare. His honesty was as solid as his handshake—and just as memorable.

Carrying His Legacy Forward

Ronnie’s passing leaves a silence in the Jersey community, but his lessons continue to speak. They echo in the rhythm of the milking parlor, in the steady hand of young appraisers he trained, and in every show ring where the next generation steps forward to do things the right way.

He taught us that excellence isn’t about chasing banners—it’s about grace, grit, and gratitude.

Ronnie Mosser lived those values to the last mile. And though the clipboard is laid down, his voice still travels with us all—steady, fair, and kind.

Lessons from Ronnie’s Life

Respect Before Recognition: He valued people more than positions, and cows more than competition.

Integrity in Every Call: Whether scoring one of his 158,700 cows or guiding a youth, his fairness defined him.

Legacy in Mentorship: He measured success not by ribbons earned, but by confidence built in others.

Service Information: The Mosser family will receive friends on Friday, October 24, 2025, from 12:00 PM to 8:00 PM at Downing & Glancy Funeral Home, 100 N. Washington St., Geneva, IN. Additional service details will be announced. In lieu of flowers, the family suggests memorial contributions to the American Jersey Cattle Association Youth Programs or a charity of your choice.

The Bullvine joins the Mosser family, the AJCA, and breeders everywhere in celebrating a man whose work made cows better—and people stronger.

Why sell brands posting 103% profit growth? 10,700 farmers decide Oct 30 if $320k now beats legacy forever.

EXECUTIVE SUMMARY: Fonterra’s proposed $3.8 billion sale of its consumer brands to Lactalis presents 10,700 farmer shareholders with one of the cooperative dairy’s most consequential decisions—vote by October 30 on whether to cash out brands that have shown a remarkable turnaround. The consumer division’s operating profit surged from NZ$146 million to NZ$319 million year-over-year (103% growth), driven by expanding sales of South Asian packaged milk powders and the UHT market in Greater China, according to Fonterra’s Q3 financials. This valuation—between 10 to 15 times earnings with a 15-25% premium over typical dairy transactions—suggests that Lactalis sees long-term value in New Zealand’s grass-fed reputation, which took generations to build. With Fonterra carrying NZ$5.45 billion in debt at 39.4% gearing, the board views this sale as a means to balance sheet strengthening, although farmers must weigh the immediate capital needs against surrendering their connection to consumer markets. What farmers are discovering through discussions from Taranaki to Canterbury is that this vote transcends individual operations—it could reshape global cooperative strategies, as the boards of DFA, Arla, and FrieslandCampina watch closely. The decision ultimately asks whether farmer cooperatives can compete in consumer markets or should retreat to ingredients and processing. Each shareholder must evaluate their operation’s specific needs, succession plans, and vision for dairy’s future before casting a vote that, once done, can’t be undone.

You know that feeling when you’re doing evening chores and something on the news makes you stop and really think? That’s been happening a lot lately with this Fonterra situation. Back in August, they announced they’re selling their consumer brands to Lactalis—the French dairy giant—for NZ$3.845 billion, according to their official announcements. Could increase to $4.22 billion, including the Australian licenses.

And here’s what has got me, and many other farmers, talking… With 10,700 farmer shareholders voting on October 30, we’re looking at something that could change how we all think about cooperative dairy.

The Numbers We’re All Trying to Figure Out

So here’s what’s interesting about the financial performance, and I’ve been digging through Fonterra’s Q3 reports to get this straight. The consumer division—encompassing Mainland cheese, Anchor butter, and Kapiti specialty products—saw its operating profit increase from NZ$248 million to NZ$319 million in Q3, representing approximately a 29% rise, according to their FY25 financial presentations.

Now, where that 103% figure comes from gets a bit specific—it’s actually the quarter-on-quarter comparison. When comparing Q3 this year to Q3 last year, the consumer division’s operating profit surged 103%, increasing from approximately NZ$146 million to NZ$319 million. That’s impressive growth, anyway you slice it, driven largely by higher sales volumes of packaged milk powders in South Asia and UHT milk in Greater China, according to their quarterly updates.

I’m not sure about you, but that timing leaves me scratching my head a bit. After years—and I mean years—of hearing “just wait, the turnaround is coming,” it finally arrives. And now we’re selling?

What I’ve found interesting in the latest annual reports is the valuation itself. When you adjust for standalone costs, Lactalis is paying somewhere between 10 and 15 times earnings, with a premium of about 15 to 25 percent over what these deals typically cost. That’s… substantial. They’re clearly seeing something valuable here. And it makes you wonder—could this affect Fonterra’s position as one of the world’s largest dairy exporters? That’s something worth thinking about.

Key Facts at a Glance:

Sale price: NZ$3.845 billion (potentially $4.22 billion)

Voting date: October 30, 2025

Farmer shareholders: 10,700

Consumer operating profit: NZ$319 million in Q3 FY25 (up from NZ$248 million)

Quarter-on-quarter growth: 103% (Q3 FY25 vs Q3 FY24)

Current debt: NZ$5.45 billion

Gearing ratio: 39.4%

Different Farms, Different Calculations

Here’s the thing about this vote—and this is what makes it so complicated—it means something different for every operation and every region.

Take farmers supplying milk to Te Rapa, one of Fonterra’s largest manufacturing sites, down in Waikato. The plant produces over 300,000 tonnes of milk powder and cream products annually, according to Fonterra’s operational data. If you’re one of those suppliers, you’re probably thinking more about the ingredients side of the business since that’s where your milk’s likely going anyway.

However, if you’re in a region that supplies plants producing consumer products—such as some of the operations near cheese plants or butter facilities—this sale hits differently. You’ve been directly involved in building those brands.

If you’re running a smaller herd, maybe 400 to 600 cows, like a lot of farms in Taranaki or up in Northland, that potential payout could be a game-changer. We’re talking real money that could help with debt from that new rotary you put in, or finally let you upgrade that aging effluent system. With feed costs where they are and milk prices doing their usual dance, breathing room matters. Though it’s worth noting—depending on how the payout’s structured, there might be tax implications to consider. That’s something to discuss with your accountant before counting chickens.

But then… and this is where I keep getting stuck… these brands weren’t built overnight. Your milk, your parents’ milk, probably your grandparents’ milk, went into building that New Zealand dairy reputation. What’s that worth over the next 20 years? Hard to put a number on it, really.

Now, if you’re running 2,000-plus cows—like some of those bigger operations down in Canterbury or Southland—you might be looking at this differently. Many of those farms are already pretty commodity-focused anyway. For them, maybe the immediate capital for expansion or debt reduction makes more sense than holding onto consumer brands they feel disconnected from.

And then there’s everyone in between. I was speaking with a farmer near Rotorua last week who runs approximately 850 cows. She’s torn. “The money would help,” she said, “but I keep thinking about what we’re giving up. My daughter’s interested in taking over someday—what kind of industry am I leaving her?”

Farmers in regions more dependent on the consumer business—those near plants that have historically focused on value-added products—may feel this more acutely than those in regions with heavy milk powder production. It’s not just about the money; it’s about what part of the value chain your community has been connected to.

Consider the rural communities as well. When farm families have more capital, it flows through the local economy—equipment dealers, feed suppliers, the café in town. But long-term? If we lose that connection to consumer markets, what happens to the value of what we produce? And what about future cooperative dividends, considering that those higher-margin consumer products will not contribute to them?

Why Lactalis Wants In

The French aren’t throwing this kind of money around without good reason, that’s for sure. According to industry analysis, several factors are converging simultaneously.

First, there’s the Asian market access. But honestly, I think it’s more than that. It’s that grass-fed story we’ve built over decades—you know what I mean? That image of cows on green pastures, the clean environment, the careful breeding programs we’ve all invested in. Lactalis knows they can’t just create that from scratch.

And think about it—how many years of getting up at 4 AM, dealing with wet springs and dry summers, constantly working on pasture management and milk quality… all of that goes into that premium reputation. You can’t just buy that off the shelf.

What’s also interesting is how this compares to what’s happening in other markets. In the States, cooperatives like DFA have been under similar pressure. Europe’s seeing the same thing with Arla and FrieslandCampina facing questions about their consumer strategies. Down in Australia, Murray Goulburn farmers went through a similar experience with Saputo a few years ago; it might be worth asking them how that worked out.

I haven’t heard any major farming organizations take official positions on this yet, but you can bet they’re watching closely. The implications go beyond just Fonterra.

The Financial Reality Check

Now, we can’t pretend Fonterra hasn’t had some rough patches. Is that a Beingmate investment in China? Lost NZ$439 million according to their financial reports from a few years back. Other ventures also didn’t pan out.

According to their latest interim reports, they’re carrying NZ$5.45 billion in net debt, with a gearing ratio of 39.4%. That’s… well, that’s a fair bit of debt. So you can understand why the board might see this sale as a way to clean things up.

But here’s my question—and maybe you’re thinking the same thing—are we selling the profitable parts to fix past mistakes? Because that’s kind of what it feels like.

There’s also the environmental regulation side of things to consider. With nutrient management rules becoming increasingly stringent every year, some farmers are wondering if having more capital now might help them meet these requirements. It’s another factor in an already complicated decision.

And let’s not forget about currency. The NZ dollar’s been all over the place lately. Receiving a lump sum payment now versus relying on favorable exchange rates for future dividends… that’s something else to consider.

What This Means Beyond the Farm Gate

Here’s something to chew on—what happens in New Zealand doesn’t stay in New Zealand anymore. Not in today’s global dairy market.

I was speaking with a fellow who ships to a cooperative in Wisconsin last month, and he mentioned that their board is already receiving questions about their consumer brands. “If Fonterra’s doing it, why aren’t we?” That kind of thing. And you know how these conversations go—once one big cooperative makes a move, others start wondering if they should follow.

We’ve all seen what happens when cooperatives become just milk suppliers to companies that own the brands. The whole bargaining dynamic changes. Ask any of those farmers who used to supply Dean Foods in the States how that worked out. Once you’re just a supplier, not a brand owner… well, it’s a different game entirely.

There’s also something to be said about cooperative governance here. This entire situation may serve as a wake-up call about who we elect to boards and what questions we ask them. Perhaps we should be more involved in these strategic decisions before they reach the voting stage.

Questions That Keep Coming Up

Winston Peters made some good points in Parliament about this whole thing—and regardless of what you think of politicians, the questions were valid. What exactly are the terms of these supply agreements with Lactalis? I mean, if New Zealand milk becomes relatively expensive compared to, say, European or South American sources, what happens then?

These aren’t just theoretical worries. They’re the kind of practical concerns that could affect milk checks for years to come. And honestly? Farmers deserve clear answers before voting on something this big.

If you want to dig deeper into the details, Fonterra’s shareholder portal has the full transaction documents. Your local discussion group is likely covering this topic as well—it might be worth attending the next meeting to hear what your neighbors are thinking. And for those wondering about the voting process itself, it can be conducted in person at designated locations, by proxy if you are unable to attend, or through postal voting—details should be included in your shareholder materials that were distributed last month.

Regarding the timeline, if farmers vote ‘yes’ on October 30, the deal is likely to close in early 2026, pending receipt of regulatory approvals. That’s when you’d see the money, but also when the brands would officially change hands.

Thinking It Through

So, where’s all this leave us with October 30 coming up? Well, like most things in farming, it depends on your situation.

If your operation needs capital right now—and I know many that do, given current margins—this payout could be exactly what keeps you going. There’s absolutely no shame in prioritizing your farm’s survival. We all do what we need to do.

However, if you’re thinking longer term, especially if you have kids showing interest in taking over someday, you have to wonder what you’re giving up. These brands represent decades of dedication and hard work by New Zealand farmers. All those early mornings, all that attention to quality… once those brands are gone, they’re gone.

Two Different Roads

If this sale goes through, Fonterra will essentially become an ingredients and processing company. That’s a pretty fundamental shift from what the cooperative has been. We’d be supplying milk primarily for ingredients markets, with Lactalis controlling the consumer-facing side of things.

If farmers vote no? Well, that’s a statement too, isn’t it? We still believe that farmer cooperatives can compete in consumer markets. This might even encourage other cooperatives around the world to continue building their brands rather than selling them off.

The Bottom Line

You know what really strikes me about all this? Sure, the money’s important—nobody’s saying it isn’t. However, it’s really about what we think dairy farming should be in the future.

Those brands—Mainland, Anchor, Kapiti—they mean something. They’re the result of generations of farmers getting up before dawn, dealing with whatever the weather throws at us, and constantly working to improve. That connection to consumers, that ability to capture value beyond the farm gate… once you hand that over, you don’t get it back.

The vote’s coming whether we’re ready or not. Whatever you decide, make sure it’s something you can live with—not just when that check clears, but years down the road when you’re looking at what the industry’s become.

Because here’s the truth: once this is done, there’s no undoing it. Dairy farmers everywhere will be watching closely to see what New Zealand decides. And whatever way it goes, it will influence how cooperatives think about their future for years to come.

Take your time with this one. Discuss it with your family, and chat with your neighbors at the next discussion group meeting. Get all the information you can from Fonterra’s shareholder resources and those quarterly reports they’ve been putting out. Consider discussing the tax implications with your accountant as well. This is one of those decisions that really does shape the industry for the next generation.

Make it count.

KEY TAKEAWAYS:

Immediate financial impact varies by operation size: Smaller 400-600 cow farms could see debt relief equivalent to 18 months operating costs, while 2,000+ cow operations might fund expansion—but all sacrifice future dividend streams from consumer products showing 103% profit growth.

Regional implications differ based on plant specialization: Farmers supplying Te Rapa’s 300,000 tonnes of milk powder production think differently than those near cheese and butter facilities who’ve directly built these consumer brands over generations.