When Ireland’s grass-fed advantage meets Brussels’ nitrogen limits, everyone’s milk check changes

EXECUTIVE SUMMARY: Ireland’s registration of 54,396 fewer calves this year signals a fundamental shift that’s already reshaping global dairy markets. With the nitrates derogation expiring December 31st, Irish farms face potential nitrogen limits dropping from 250kg to 170kg per hectare — a 32% reduction that could force meaningful herd culls despite EPA data showing river nitrogen at eight-year lows. This matters beyond Europe because Ireland, while producing just 1.5% of global milk, controls approximately €1 billion in annual infant formula exports serving Asia’s booming premium segment, which grew from a 32.8% to a 37% market share this past year. What farmers are discovering through Vermont’s success with GPS-guided manure application — an 18-month payback through reduced fertilizer costs — suggests that technology adoption might be the bridge between environmental compliance and profitable production. December’s Brussels decision will ripple through milk prices globally, but smart producers are already diversifying markets, documenting their environmental performance, and learning from Ireland’s experience that scale doesn’t guarantee survival when regulations shift. The conversation we’re having today about Ireland becomes tomorrow’s reality for dairy regions worldwide, making this the moment to build operational flexibility before regulatory pressure arrives at your farm gate.

I was reviewing the latest ICBF data last week when something really caught my attention. Ireland registered 54,396 fewer calves so far this year — both the Farmers Journal and Agriland confirmed these numbers recently. And you know what? This isn’t your typical seasonal variation. This is something worth understanding.

Here’s what’s interesting: from boardrooms to barn meetings, everyone’s trying to figure out what this means. Industry experts are warning that significant herd reductions could occur in the coming years if the derogation situation doesn’t work out. The scale… well, that’ll depend on what Brussels decides in December. Having watched similar transitions play out in other regions, I think we’re seeing early signs of change that’ll affect all of us, regardless of where we’re milking cows.

Understanding Ireland’s Journey

Let’s discuss how Ireland arrived at this point, as it’s quite a story. When EU milk quotas ended in 2015 — you remember that whole situation — Irish farmers really went for it. The national dairy herd has grown from approximately 950,000 cows to nearly 1.6 million today. Teagasc’s National Farm Survey confirms we’re looking at almost 70% growth in less than a decade.

But it wasn’t just about adding cows. The average herd size increased from around 80 head to 131, based on Teagasc’s People in Dairy Project from May of this year. About 82% of these operations utilize spring-calving systems, which makes perfect sense given Ireland’s grass-growing conditions. It’s a model that works beautifully… if you’ve got their climate.

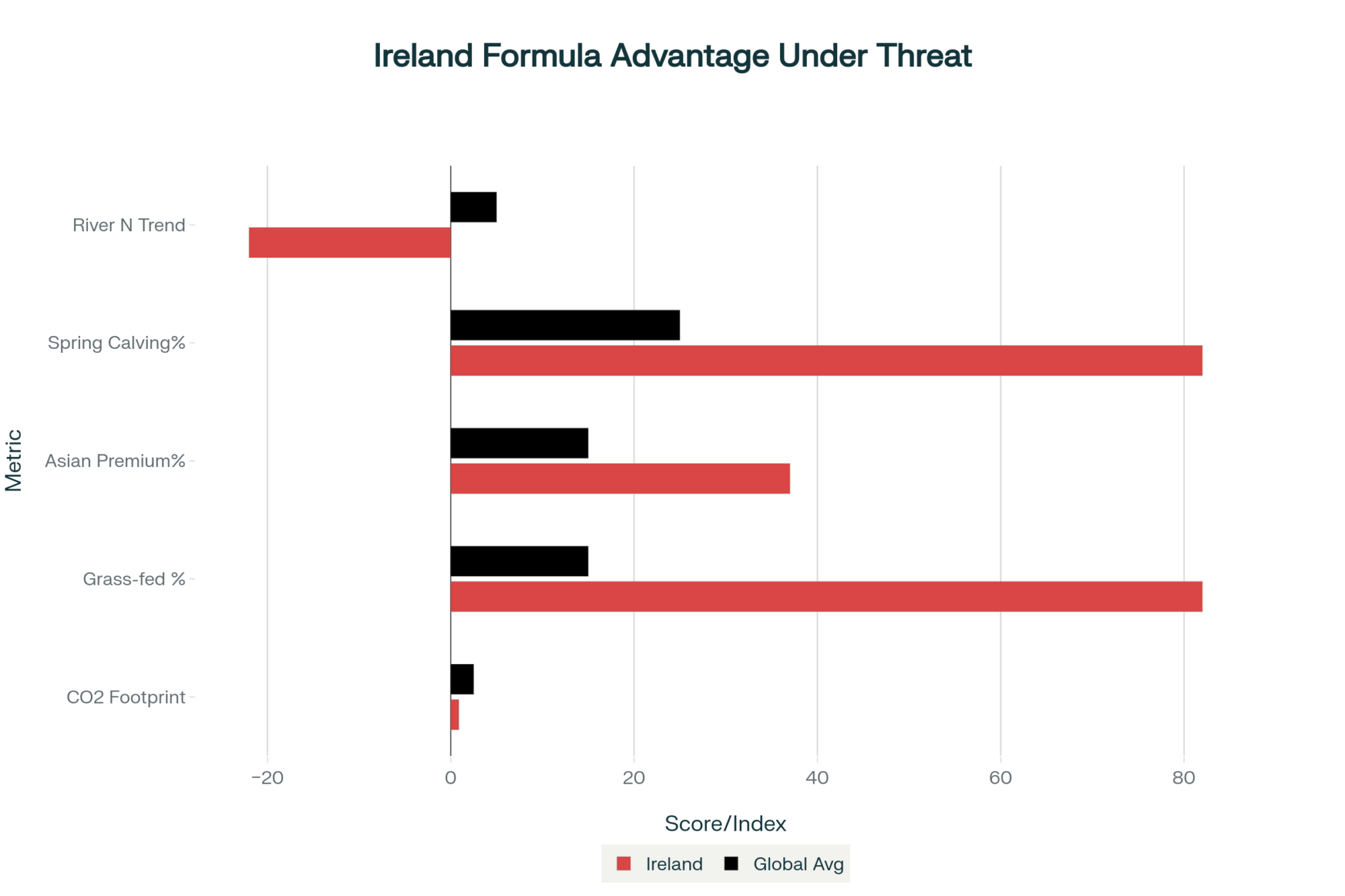

What’s particularly noteworthy is the efficiency they maintained during this expansion. Frank O’Mara’s research team at Teagasc has documented a carbon footprint of just 0.88 kg CO2e per kilogram of fat- and protein-corrected milk. The global average? That’s running around 2.5 kg. So you can see why people pay attention to what happens over there.

The investment required was substantial. The Irish Farmers Association documented about €2.2 billion in farmer investment during the post-quota expansion period, with processors adding another €1.3 billion in capacity. That’s real money, borrowed against real assets.

December’s Decision Point

Now here’s where things get really interesting. December 31st is when Ireland’s nitrates derogation expires. For those unfamiliar with European regulations, the derogation permits qualifying farms to apply up to 250kg of nitrogen per hectare annually — significantly exceeding the standard 170kg limit. Most Irish farms have already reduced their stocking rates to 220kg as of January 2024, and maintaining that level is uncertain.

What I find encouraging is that the Netherlands submitted their derogation extension request back in July, according to Agriland’s reporting. So Ireland won’t be negotiating alone, which might influence how things play out in Brussels.

I’ve been talking with several Irish producers about this, and their frustration is understandable. The EPA monitoring shows nitrogen in Irish rivers hit an eight-year low in 2024 — that’s real environmental progress, which RTÉ covered back in March. Yet Brussels added these new requirements under the Habitats Directive, demanding individual assessments for 46 different catchments. I mean, can you imagine managing that paperwork while you’re trying to keep fresh cows healthy during transition?

“Good data is becoming as important as good genetics” — Wisconsin dairy producer on technology adoption

Denis Drennan from ICMSA has been pretty clear that milk prices need to stay strong in 2025 just to cover the increasing regulatory burden. And with co-ops reporting notable year-over-year reductions in deliveries during parts of this year — the magnitude varies by region and month — those newly expanded processing plants are facing some real challenges.

Why This Matters Globally

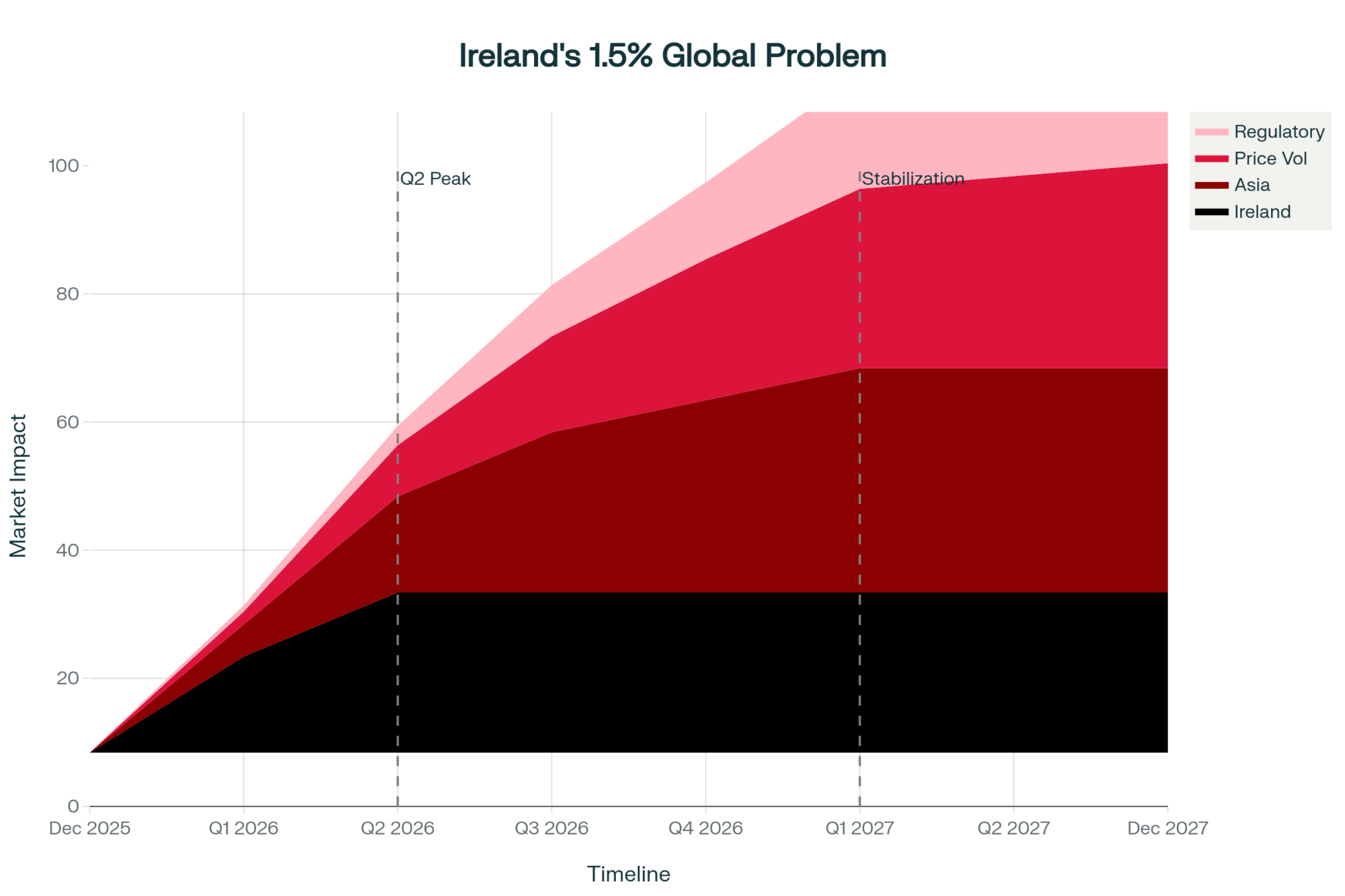

This is where Ireland’s situation becomes everyone’s business. Despite producing only about 1.5% of global milk, Teagasc research from June indicates that Ireland generates approximately €1 billion in annual infant formula exports, with six major manufacturers operating there. That concentration of expertise… it’s not something you can quickly replicate elsewhere.

The Asian market dynamics are particularly relevant here. Analysis from July shows China’s premium infant formula segment grew from about 32.8% to 37% market share over the past year. These consumers specifically want products with verified grass-fed credentials—and they’re willing to pay for them.

You know, the nutritional advantages from grass-based systems — higher CLA levels, better omega-3 profiles — that’s not just marketing. Those are measurable differences that processors can document. However, here’s the thing: these advantages stem from specific climate conditions, decades of infrastructure development, and genetics selected for grass-based production… you can’t just flip a switch and replicate that.

Similar challenges are playing out in California, where water restrictions shape production decisions, or in the Northeast, where land costs drive different operational choices. Each region has its unique pressures. In Canada, supply management adds another layer of complexity, while Australian producers navigate drought cycles that make Ireland’s consistent rainfall look like a paradise.

How Processors Are Adapting

The processing sector they’re really scrambling right now. Companies like Danone, Glanbia, and Kerry Group invested hundreds of millions based on growth projections that seemed reasonable at the time. Now they’re looking at potential supply drops while those fixed costs aren’t going anywhere.

What I’m hearing is that processors are stress-testing all kinds of options. Some are exploring powder reconstitution for specific applications, others are recalibrating their product mix, and many are focusing on supply diversification. But when your competitive advantage is rapid conversion from farm to finished product — that speed-to-value that’s so critical in infant nutrition — workarounds have limitations.

According to industry contacts, processors aren’t waiting for December. They’re actively reviewing supply chain contingencies, adjusting portfolios, and working through various scenarios. Many are now seeking long-term supply diversification contracts in other low-cost regions. It’s pragmatic planning in uncertain times.

Technology’s Growing Role

| Technology Type | Investment Cost | Payback Period | Annual Savings | Regional Example |

| GPS-guided manure application | $45,000 | 18 months | $30,000 | Vermont (fertilizer reduction) |

| Robotic milking systems | $175,000 | 48 months | $43,000 | Wisconsin (labor + efficiency) |

| Precision feed management | $25,000 | 24 months | $15,000 | Ireland (compliance ready) |

| Heat detection collars | $15,000 | 12 months | $16,000 | Netherlands (conception rates) |

| Environmental monitoring | $8,000 | 15 months | $6,500 | California (water compliance) |

Something that really caught my attention was ICBF’s September update to their Economic Breeding Index. The Farmers Journal reported that average EBI values dropped about €83 per animal — not because genetics suddenly went bad, but because they shifted the base cow from 2005-born to 2015-born animals. That’s the industry recalibrating for new realities.

The technology adoption gap is becoming really apparent. Farms with advanced parlor management systems, comprehensive data collection… they’re navigating these challenges differently. When you have automated heat detection improving conception rates, robotics helping with consistency — and we’re talking $150,000 to $200,000 for quality robotic systems — these are no longer luxuries. They’re becoming necessities.

A producer I know in Wisconsin put it well: “The difference between operations that invested in precision technology five years ago and those that didn’t is becoming a chasm. This includes everything from advanced feed efficiency sensors and GPS-enabled manure application systems that maximize nutrient use, to automated health monitoring collars. Good data is becoming as important as good genetics.”

And here’s the ROI that’s catching attention: one operation in Vermont saw their investment in GPS-guided manure application pay back in 18 months through reduced fertilizer purchases and improved compliance documentation. That’s the kind of return that makes technology adoption a no-brainer, especially when regulatory pressure continues to build.

Regional Variations Matter

Not every part of Ireland faces the same challenges, which is worth thinking about. The southeast, with its free-draining soils and longer growing seasons, operates under different conditions than those in the northwest, which deal with heavier ground. Spring-calving herds — that’s about 82% of Irish operations, according to Teagasc — they’ve got all their nutrient management concentrated into tight windows.

These variations… they really make you wonder about one-size-fits-all regulations. You’ve got farms achieving excellent bulk tank counts, managing transition periods effectively, keeping their herd health metrics strong — but they’re facing challenges based on nitrogen calculations that might not fully account for grass-based efficiency.

Looking at Three Possible Scenarios

| Scenario | Timeline | Key Outcomes |

| Managed Adjustment | Q1-Q2 2026 | Derogation renewed with tighter restrictions. Modest production adjustments, premium markets tighten, and some global price movement. Processors adapt toward higher-value products. |

| Political Compromise | Q2 2026 | Farmer advocacy leads to compromise. Technology investments enable progress in maintaining production. Politicians declare victory, farming continues. |

| Sharp Contraction | Mid-2026 onwards | Minimal derogation renewal. Significant production drops within 18 months. Premium market disruption, price volatility, supply gaps. |

What This Means for Your Operation

So what should we take away from all this?

First, regulatory dynamics are accelerating everywhere. What starts in Brussels has a way of showing up in other jurisdictions. Environmental regulations are increasingly shaping how we farm, whether we’re in California dealing with methane rules, Wisconsin managing nutrient plans, or anywhere else.

Second, if you have genuine production advantages — whether that’s organic certification, grass-fed systems, local market access, or any other unique aspect of your operation — now’s the time to document and protect those advantages. Ireland’s grass-fed position took generations to build. Once it’s gone, it’s gone.

Third, market relationships need diversification. When supply gets tight, operations with multiple outlets generally fare better. That’s not pessimism — it’s risk management. And beyond just infant formula, Irish dairy also supplies significant volumes to specialty cheese makers and premium butter operations across Europe. Those alternative channels become crucial when primary markets shift.

Fourth, technology adoption is shifting from optional to essential. Being able to document your environmental performance, optimize inputs, and adapt quickly —that’s increasingly what separates operations that thrive from those that just survive.

And here’s something interesting — scale no longer guarantees success. Some of Ireland’s most efficient large operations face real challenges because they’re over nitrogen thresholds, while smaller operations with direct market access and flexibility sometimes prove more adaptable.

The Human Side

Behind every statistic are real families making tough decisions. UCD’s School of Psychology published research in August showing nearly all Irish farm families report work-family conflict, with younger, debt-leveraged farms particularly affected.

These aren’t abstract business decisions. When families have mortgaged generational land to build facilities, they might not be able to fully use… that pressure extends way beyond finances. I’ve witnessed similar situations unfold in various dairy regions, and the stress on rural communities is indeed a real concern.

For those needing support, organizations such as Farm Aid in the US (1-800-FARM-AID), the Farm Community Network in the UK, and the Irish Farmers Association’s member support services offer resources for farmers facing transition pressures. There’s also the International Association of Agricultural Producers, which offers global support networks. Please don’t hesitate to reach out if you need assistance.

Where We Go from Here

What’s happening in Ireland represents more than just regional adjustment. We’re watching environmental objectives, food security needs, and agricultural economics intersect in real time. This dynamic between production efficiency and regulatory requirements… it’s not unique to Ireland. It’s emerging globally.

Those 54,396 fewer calves aren’t just numbers. They’re the leading edge of changes that’ll influence global dairy markets over the next several years. How this affects your operation depends largely on the decisions you’re making right now.

December’s derogation decision will have far-reaching consequences that extend well beyond Ireland. Smart producers are already considering various scenarios and building operational flexibility to adapt to changing market conditions. Most importantly, they’re learning from Ireland’s experience to prepare for similar challenges that might emerge closer to home.

Because if there’s one thing that’s becoming clear, it’s this: success in modern dairying requires understanding both market fundamentals and regulatory dynamics. Political and policy factors are increasingly influencing decisions that were once purely economic in nature. Recognizing and adapting to this reality may well determine which operations thrive in tomorrow’s dairy industry.

The conversation continues, and we’re all part of it. How we respond collectively to these challenges will shape dairy farming for the next generation. What strategies are you implementing to prepare for these changes? Share your thoughts and experiences — because learning from each other is how we’ll navigate this transition successfully.

KEY TAKEAWAYS

- Technology ROI beats regulatory burden: Vermont operations seeing 18-month payback on $150,000-200,000 precision systems through 20-30% fertilizer savings and streamlined compliance documentation — making tech adoption essential, not optional

- Market diversification matters more than size: Irish farms over nitrogen thresholds face elimination despite peak efficiency, while smaller operations with direct sales to specialty cheese and premium butter markets show better resilience — suggesting 3-5 market outlets minimum for risk management

- Environmental progress isn’t protecting producers: Ireland achieved EPA-verified eight-year low nitrogen levels while maintaining 0.88 kg CO2e per kg milk (vs. 2.5 kg global average), yet still faces production cuts — document your sustainability metrics now before regulators set the narrative

- Premium markets concentrate risk: China’s grass-fed infant formula segment commands 50% price premiums, but Ireland’s potential 15-25% production drop threatens €1 billion in exports — operations dependent on single premium channels need contingency plans by Q1 2026

- Regional advantages require active protection: Ireland’s grass-fed position took generations to build through climate, genetics, and infrastructure, but December’s decision could eliminate it overnight — whether you’re organic, pasture-based, or locally focused, start building your verification systems today

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Feed Smart: Cutting Costs Without Compromising Cows in 2025 – This tactical roadmap for 2025 reveals how to save up to $470/cow/year by focusing on strategic feed procurement and NDF digestibility targets. Learn essential cost-saving methods to protect your margins from rising regulatory pressures.

- Why the Global Dairy Market is Making Waves in 2025 (and What That Means for You) – Discover how market shifts, including 14% Southeast Asian cheese premiums, require urgent risk diversification and hedging strategies. This article provides the strategic context needed to build operational resilience against policy-driven price volatility.

- Robotic Milking Revolution: Why Modern Dairy Farms Are Choosing Automation in 2025 – Get the hard numbers justifying technology investment by reviewing the 4-7 year robotic payback period. Learn how automation delivers 60% labor reduction, improves component quality consistency, and provides the data necessary for proactive health and compliance management.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.