Same nitrogen law, same critical-load maps. Microsoft’s data center got a “tolerance decision” to keep building. The dairy down the road got a buyout letter and an EU-wide ban on ever milking again.

How a court ruling, a vanishing manure exemption, and a cross-border non-compete clause are redrawing dairy country in the Netherlands — and what that pattern looks like, very early, in your region.

Across Dutch dairy country in early 2026, kitchen tables have been carrying the same letter. It isn’t from the bank. It’s from the state, qualifying the operation for “termination with compensation” under the LBV-plus scheme — the Dutch buyout program targeting peak emitters near Natura 2000 reserves. This isn’t a single farmer’s story. It’s the composite scene from the January 2026 Omroep Gelderland / NRC / Follow the Money investigation, walking through how Dutch nitrogen policy actually lands on a fourth-generation dairy.

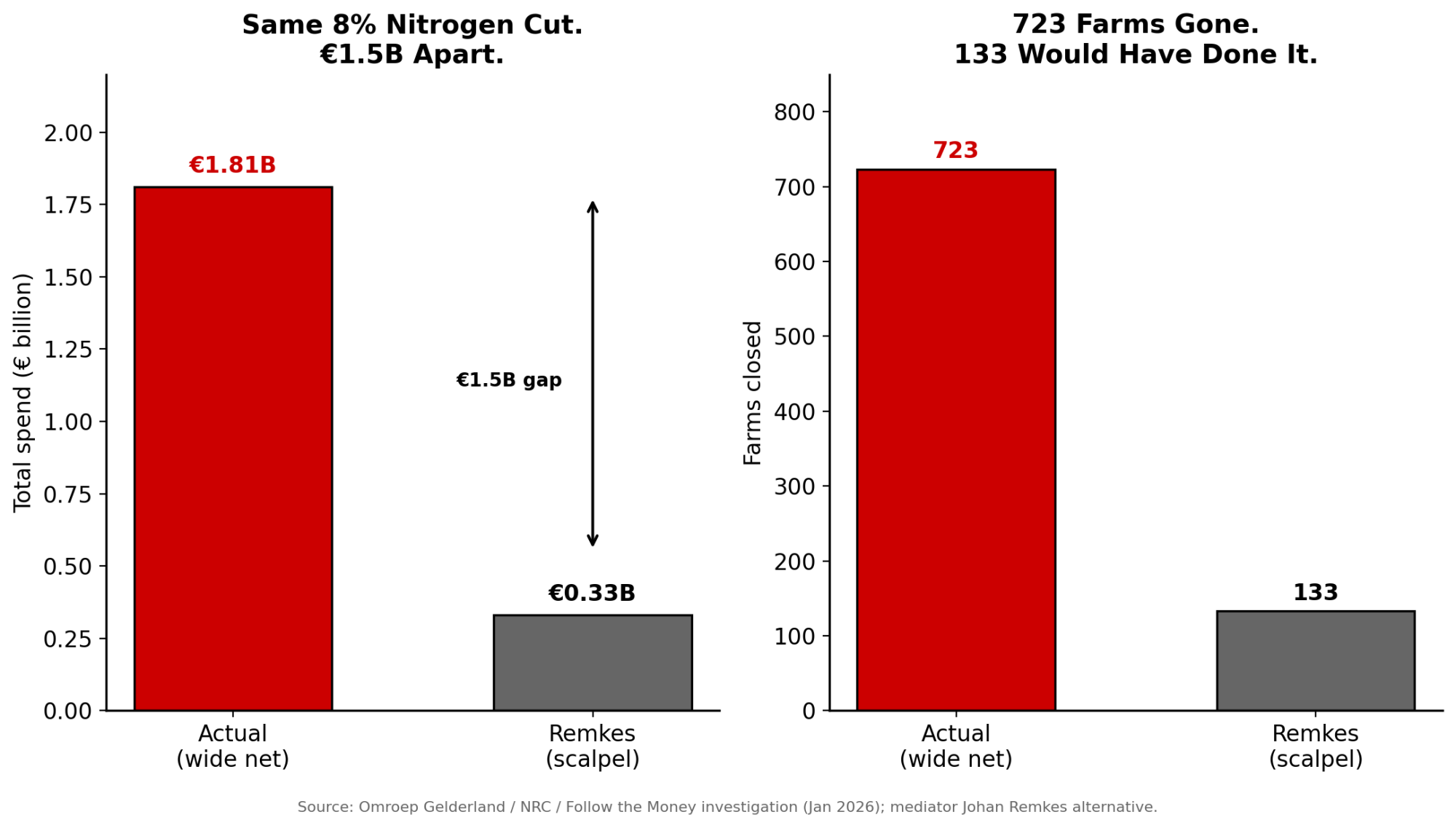

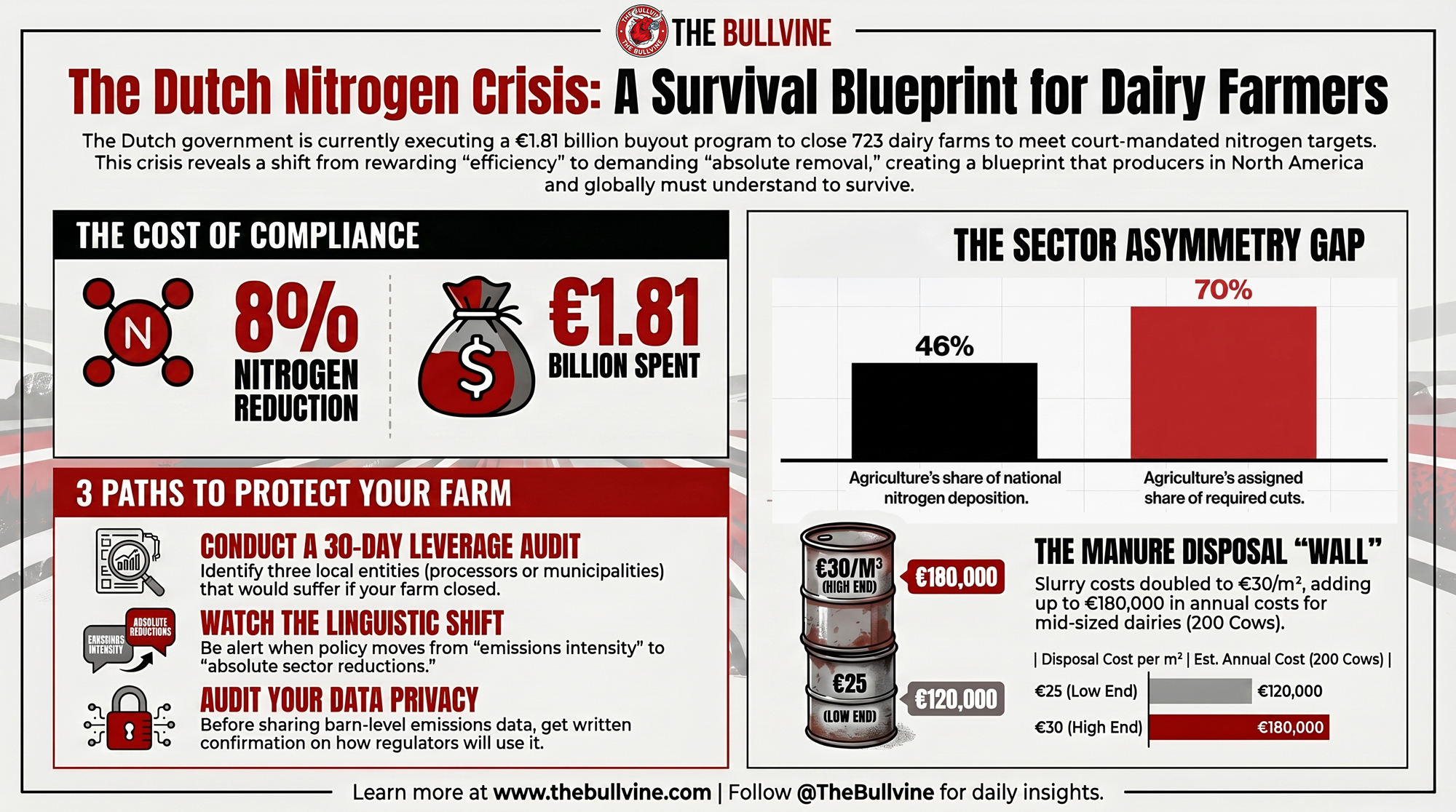

By the time those letters started moving in volume, the cold version of the story looked like this: that same investigation found that the Dutch Ministry of Agriculture had spent €1.81 billion to close 723 farms, resulting in an estimated 8% reduction in the national nitrogen surplus. To understand how a buyout letter ends up on a kitchen table, you have to follow the legal chain backward from 2025.

Why the Dutch Nitrogen Crackdown Started in Court

Dutch nitrogen policy didn’t start as a political program. It started as a permit collapse. In May 2019, the Council of State ruled that the country’s existing framework — the Integrated Approach to Nitrogen, or PAS — violated the EU’s Habitats Directive by issuing permits based on promised future emissions cuts. About 18,000 housing, industrial, and farm projects were paused almost overnight, according to Dutch government estimates, in what locals nicknamed the “nitrogen lockdown.”

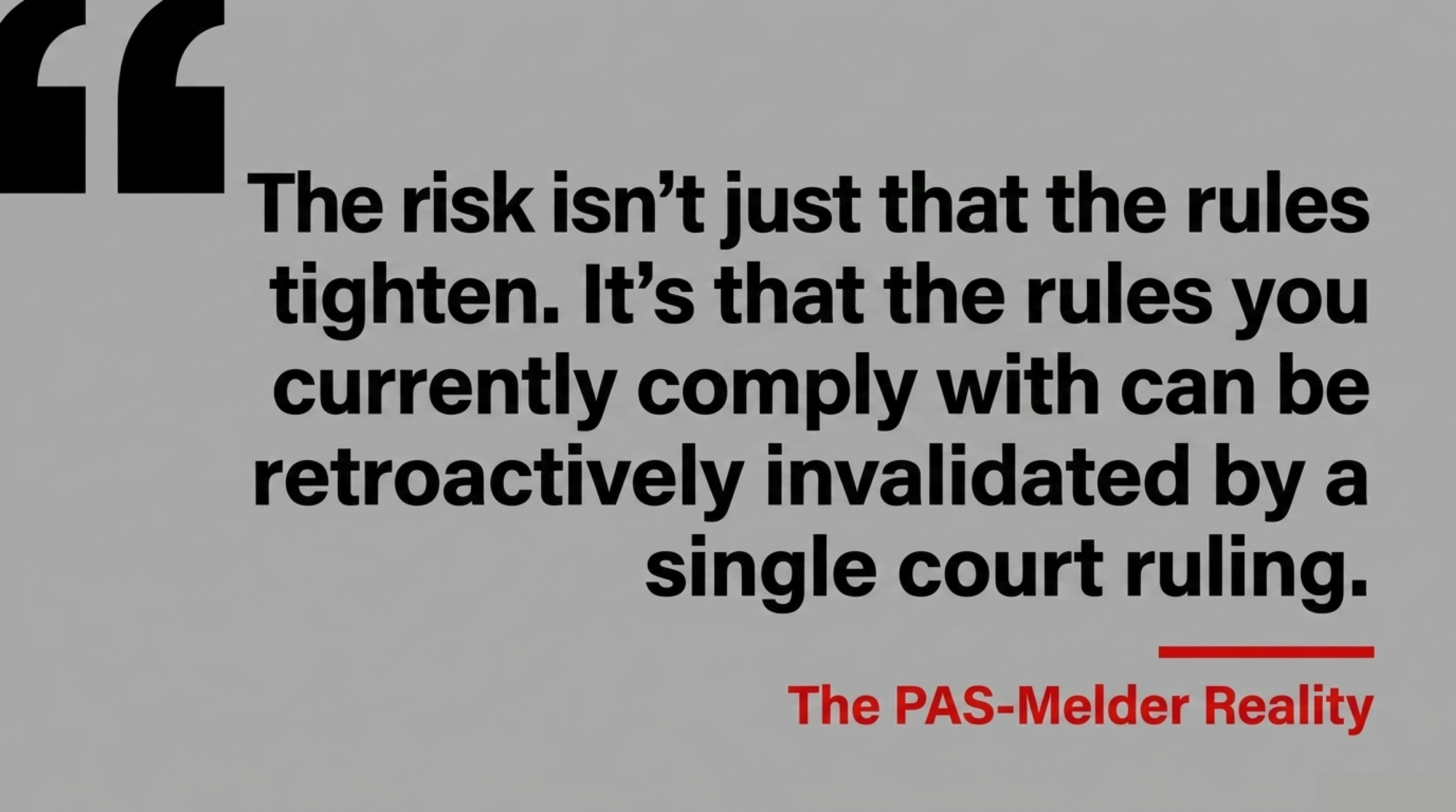

The ruling created a new legal category overnight: the “PAS-melder.” Under the prior Programmatic Approach to Nitrogen, the Dutch government had told thousands of farmers and rural businesses that they could expand or modernize simply by reporting their nitrogen emissions rather than applying for a full environmental permit. After May 2019, those same operations — thousands of them, spanning dairy, pig, poultry, contracting, biomass, and infrastructure — were retroactively found to be without secure permits. Many formally requested legalization. Years on, most still don’t have secure permits. They spent that time in regulatory limbo, having done exactly what the state had asked them to do.

The follow-up came on January 22, 2025, when the District Court of The Hague ruled in favor of Greenpeace and ordered the state to bring at least half of all nitrogen-sensitive nature areas below their critical deposition thresholds by the end of 2030, attached to a €10 million penalty for non-compliance. The court told the government to act with immediate effect, regardless of any pending appeals.

None of this means the underlying ecological pressure isn’t real. Dutch nitrogen deposition has measurable impacts on Natura 2000 ecosystems, and the science behind critical loads isn’t seriously contested. The fight is over which sectors carry the cost of the response — and on what timeline.

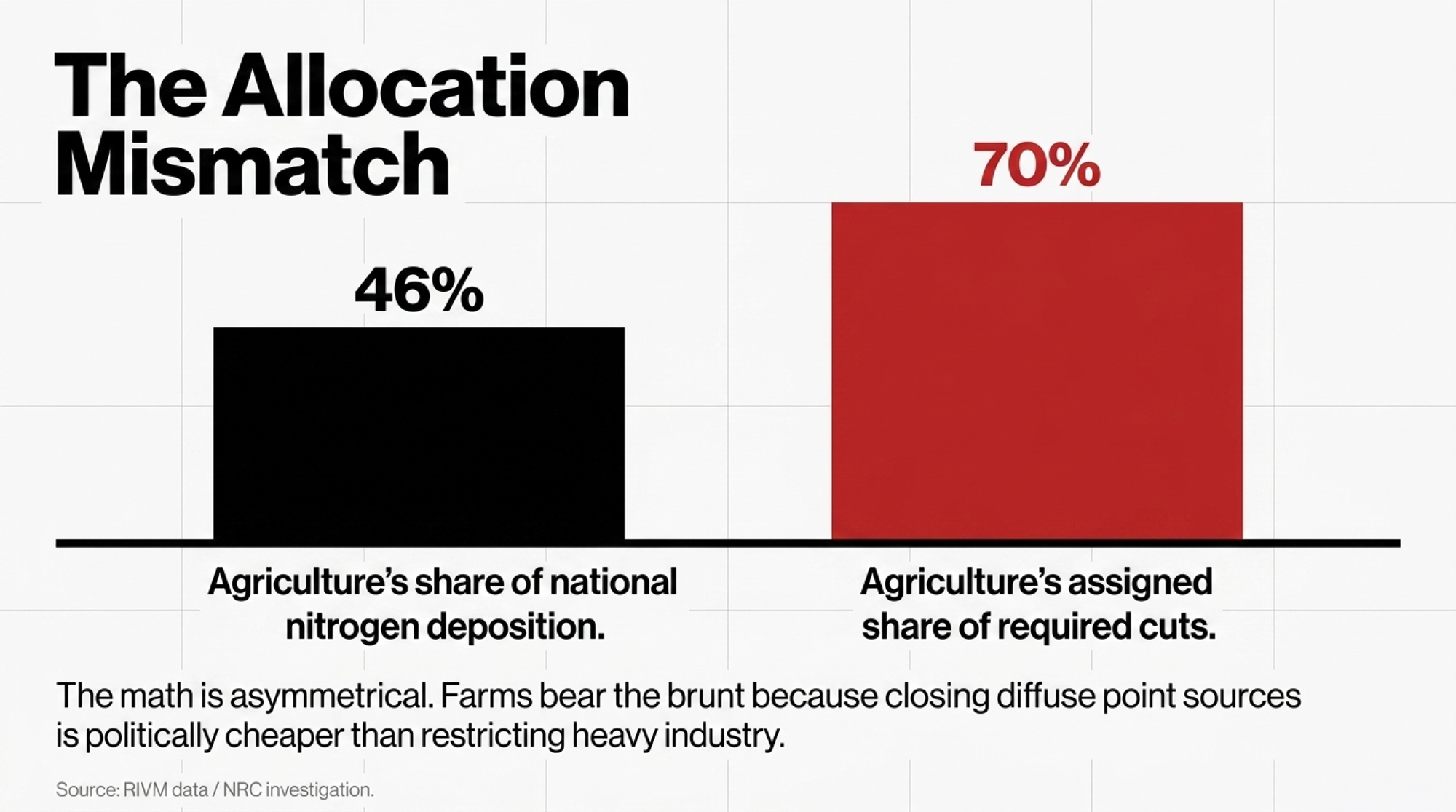

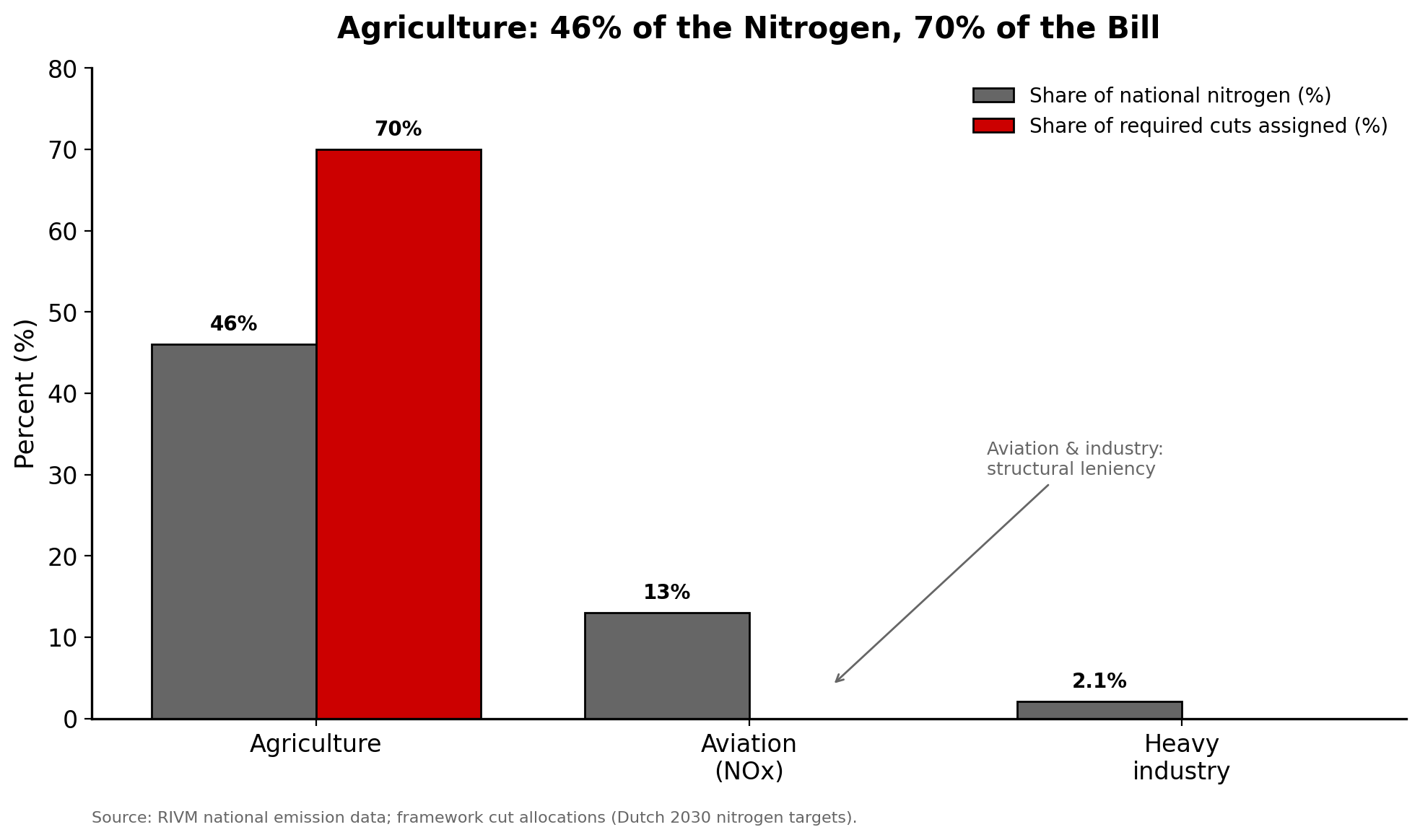

The math is where the asymmetry shows up. Agriculture accounts for roughly 46% of national nitrogen deposition, primarily as ammonia from livestock manure. But under the framework designed to meet those 2030 targets, the sector has been assigned up to 70% of the required cuts. Aviation, with around 13% of nitrogen oxides per RIVM data, has received structural leniency. Heavy industry, at roughly 2.1% per RIVM data, sits inside national economic competitiveness rules that buy it time. That mismatch is the engine driving everything else in this story.

What the Manure Derogation Collapse Means for Dutch Dairies

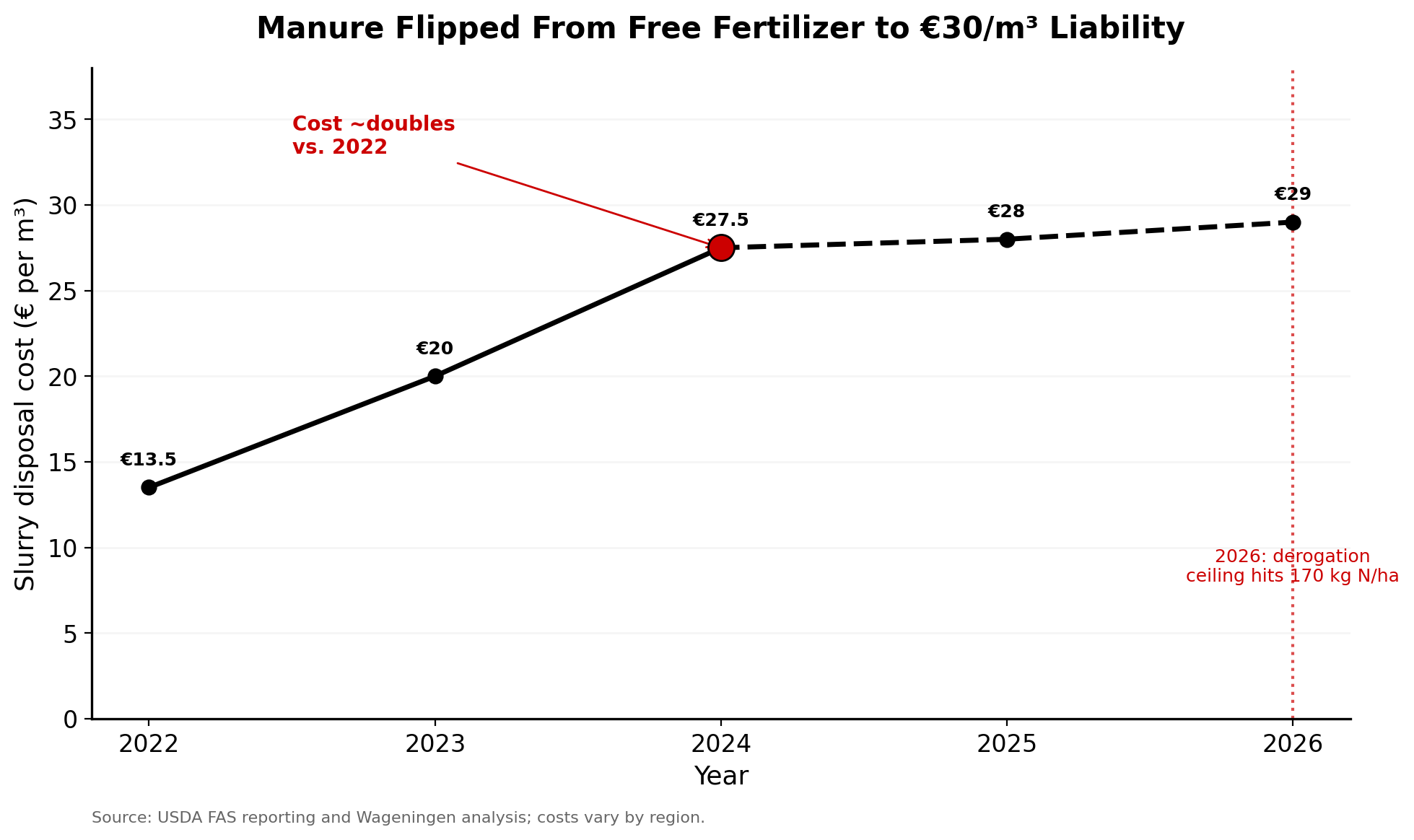

For Dutch dairy producers, the pressure shows up in three reinforcing layers. The first is the manure derogation collapse. Since 2006, Dutch dairies have been legally allowed to apply 230–250 kg of manure nitrogen per hectare on high-yield grass under a special EU exemption. In September 2022, the European Commission set a phase-out: the ceiling drops back to the standard 170 kg N/ha by 2026. By 2024, about 87% of Dutch dairy farms and 94% of pig and poultry operations were producing more manure than they could legally apply on their own land.

The second layer is price. USDA FAS reporting and Wageningen analysis confirm that slurry disposal costs reached €25–30 per cubic meter by 2024, roughly double 2022 levels, with costs varying by region. Try this barn-math moment: a 200-cow Dutch dairy producing slurry at the Wageningen planning norm of 24–30 m³ per cow per year is staring down something on the order of 4,800–6,000 m³ a year. Even partially exporting that volume at €25–30/m³ stacks five- to six-figure annual costs on top of normal operating expenses, before a single new compliance investment.

Run it the other way, and the pinch gets sharper. At the low end — 4,800 m³ at €25 per m³ — that’s €120,000 per year. At the high end — 6,000 m³ at €30 — it’s €180,000. Even if the farm only has to export a third of its slurry because it can still spread the rest on its own ground, you’re looking at €40,000 to €60,000 in additional annual costs for a 200-cow operation. That’s not a line item. That’s the difference between a profitable year and a loss for many family-scale dairies, and it shows up before anyone even factors in the buyout conversation.

| Scenario (200-cow dairy) | Volume (m³/yr) | Rate (€/m³) | Annual disposal cost |

| Low end, full export | 4,800 | €25 | €120,000 |

| High end, full export | 6,000 | €30 | €180,000 |

| Export ⅓ only, low rate | 1,600 | €25 | €40,000 |

| Export ⅓ only, high rate | 2,000 | €30 | €60,000 |

| Per-cow planning norm | 24–30 m³/cow | — | Profit-vs-loss swing for family-scale |

Here’s the part that should land hardest for a North American reader. The same cost mechanism is embedded in California’s spread limits, Ontario’s nutrient management plans, and Ireland’s own derogation fight — Ireland’s exemption was cut to 220 kg N/ha in its most recent European Commission review, and Dutch producers are watching it because they’ve already lived through the next chapter. When application ceilings tighten, manure flips from a free fertilizer asset to a metered disposal liability almost overnight. The Dutch just hit the wall first.

The third layer is the buyout itself. The EU-approved LBV (€500 million) and LBV-plus (€975 million) schemes target livestock sites near vulnerable Natura 2000 areas. LBV pays up to 100% of “losses incurred” on closure; LBV-plus pays up to 120% for peak emitters, plus demolition costs. The catch is in the covenant. Signing means permanent closure of that production capacity and a legal ban on restarting the same livestock activity anywhere in the Netherlands or the wider EU. The state buys the business, not the land — leaving the underlying parcel free to be rezoned for housing, industry, or data infrastructure.

Why the Same Nitrogen Law Treats Two Emitters Very Differently

Why does this travel? Three structural reasons.

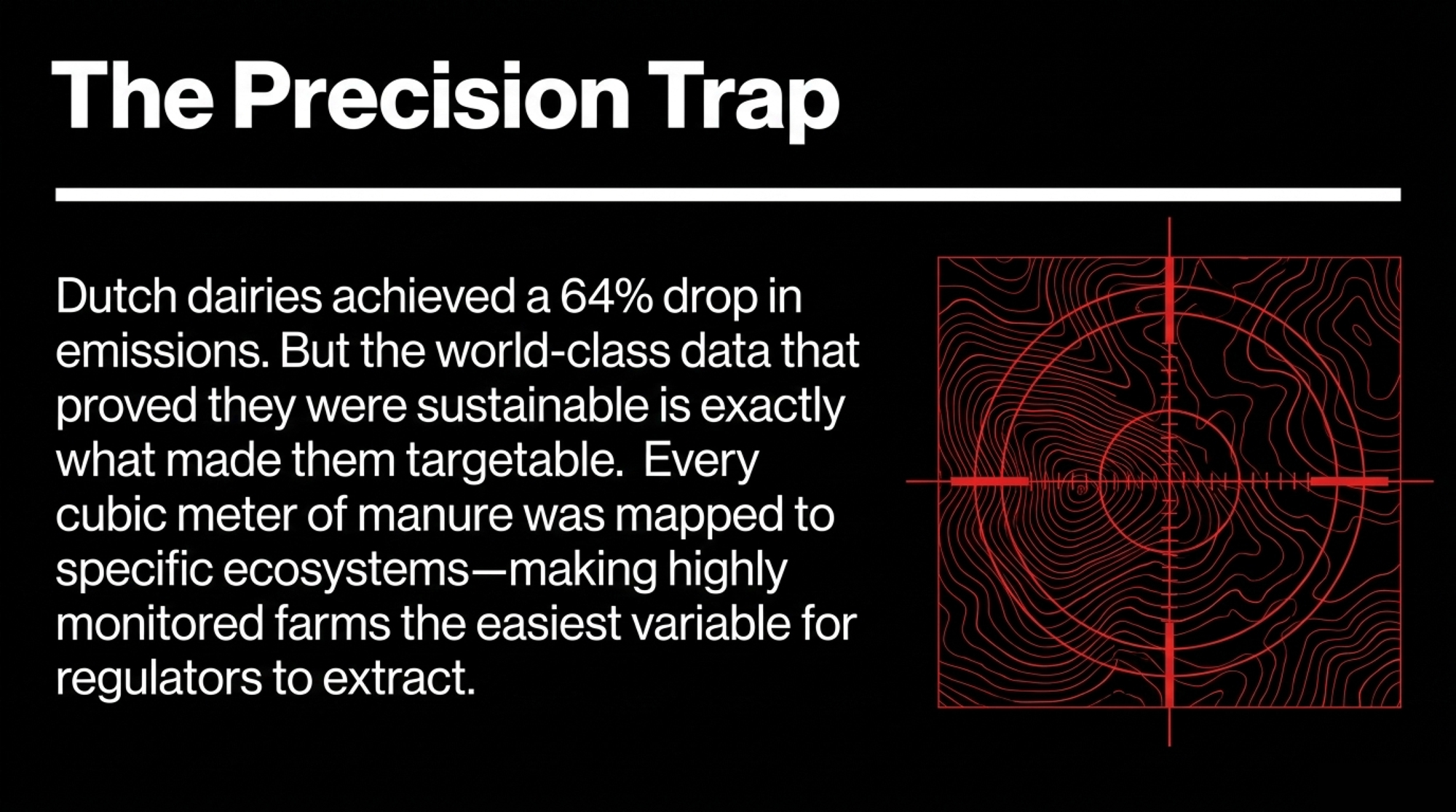

Once a court locks in a hard cap on local nitrogen deposition, somebody has to allocate scarce “nitrogen space” between sectors. Agriculture turns out to be the cheapest, fastest place to extract reductions. It’s spatially diffuse — tens of thousands of small point sources you can shut one at a time without triggering a single big political fight. And it’s politically fragmented — dairy, pig, and poultry producers don’t show up as one unified corporate lobby; they show up as individual permit holders. It’s also already heavily monitored — every animal is registered, every cubic meter of manure is tracked, and the RIVM’s National Emission Model for Agriculture (NEMA) links farm-level inputs to specific Natura 2000 polygons.

That last point is the quiet kicker. The same precision data that earned Dutch farmers their reputation as world-leading sustainable producers — a 64% drop in NOx and ammonia emissions between 1990 and 2018, and a 57% drop in nitrogen surplus by 2023 — also pinpointed them as the most cleanly quantifiable units to remove. The system rewarded them with maps that made them targetable.

Large industrial projects have faced very different rules on the same legal turf. Microsoft’s Hollands Kroon hyperscale data center, built on agricultural land roughly 50 kilometers outside Amsterdam, was granted a “tolerance decision” by the local environment authority — the regulator’s own term — that permitted construction to continue while its nitrogen footprint was still being assessed. In Amsterdam, the FTM/NRC investigation reported that a three-tower Microsoft project was approved as three separate smaller permits during the same period the 2022 national hyperscale moratorium was in effect. In Zeewolde, a Meta campus equal to 310 American football fields was planned on reclaimed agricultural polder land before being canceled in 2022 amid political pushback.

Look at what the construction phase alone demands. A hyperscale data center build runs diesel generators, hundreds of truck movements, and heavy machinery for months — all nitrogen-emitting, all on the same critical-load maps that flag a dairy barn. The difference isn’t the chemistry. It’s that a data center arrives as one large applicant a government wants to keep, with lawyers and a permitting strategy, while a dairy arrives as one of tens of thousands of individually liable permit holders. Same nitrogen law. Two enforcement cultures. Neither Microsoft nor Meta responded to questions about those decisions in time for publication.

| Factor | Dairy operation | Hyperscale data center |

| Regulatory treatment | Retroactively unpermitted; buyout letter | “Tolerance decision” — build continues during assessment |

| Status under the law | One of tens of thousands of liable permit holders | Single large applicant the government wants to keep |

| Permitting strategy | Individual; limited national appeal | Lawyers; 3-tower project split into 3 smaller permits |

| Nitrogen-emitting construction phase | Standing barn on critical-load map | Diesel generators, hundreds of truck trips — same maps |

| Land outcome | Closed, rezonable for housing/industry/data | Built on former agricultural land |

How Much Does the Math Actually Punish the Middle?

The number that should land hardest is buried in the per-farm math. Dividing the €1.81 billion across the 723 closed farms works out to roughly €2.5 million per operation, based on a blended average that includes scheme spending, administration, and demolition support, as reported in the Omroep Gelderland / NRC / FTM investigation. On paper, that sounds generous. The covenant is what reframes it. Read against the covenant terms, the payment functions as compensation for exit, not transition — it ends the business, locks the land out of livestock use, and bars the family from restarting the same activity anywhere in the EU.

The same investigation flagged a sharper alternative. Mediator Johan Remkes argued that targeting only the largest peak emitters near Natura 2000 borders could have delivered the same 8% nitrogen reduction by closing roughly 133 farms for €330 million. That’s a €1.5 billion gap between two policy choices — wide net versus precise scalpel — and it isn’t an environmental cost. It’s a political one. For producers in North America, this is the math worth memorizing: when a regime decides to cast a wide net rather than a precise one, mid-sized family operations are exactly the size that gets caught first — and as the PAS-melder cohort learned, the risk isn’t only that the rules tighten. It’s that the rules you currently comply with can be retroactively invalidated by a single ruling on the framework itself.

Is Your Operation in the “Easy to Remove” Band?

Dutch farmers ran the wrong diagnostic five years too late. The one worth running today comes down to three structural features that made certain farms the first targets:

- Highly invested mid-to-large family farms with recent CAPEX in low-emission housing, robots, and nutrient tech, making them visible in every dataset.

- Locations near sensitive ecosystems, water sources, or other regulated zones where future buffer requirements could compress operations regardless of compliance history.

- Reliance on regulatory exemptions — like the manure derogation — whose removal could be triggered by a single EU- or court-level decision, with limited national appeal.

If two or three of those describe your operation, you’re in the same structural band that took the heaviest hit in the Netherlands. That doesn’t mean exit. It means being deliberate, now, about leverage and visibility before the lines on a map are drawn.

| Structural feature | Lower exposure | Higher exposure (Dutch-pattern) |

| Capital profile | Older facilities, low recent CAPEX | Recent low-emission housing, robots, nutrient tech — visible in every dataset |

| Location | Distant from sensitive zones | Near Natura-style reserve, water source, or buffer zone |

| Regulatory footing | Owns full permit, no exemption reliance | Depends on a derogation removable by one court/EU ruling |

| Herd size band | <80 or >800 cows | 80–800 mid-family band — big enough to track, small to lobby |

| Verdict | Watch and document | Prioritize legal/policy engagement now |

Options and Trade-Offs for Farmers

The Dutch story doesn’t predict what happens in Wisconsin, Ontario, Cork, or California. But the early signals are visible enough to act on. California’s SB 1383 mandates a 40% cut in dairy and livestock methane from 2013 levels by 2030. Canadian federal climate policy commits to a 30% reduction in methane emissions from 2020 levels by 2030 under the Global Methane Pledge, with longer-horizon discussions tied to the 2050 net-zero target. Ontario continues to review and tighten its nutrient management framework under the existing Nutrient Management Act. Four paths are emerging.

- Path 1 — Read the policy language, not just the rules. Watch for the shift from “emissions intensity per kg of milk” to “absolute sector reductions by year X.” Intensity targets reward efficiency. Absolute targets reward removal. The Dutch experience shows how fast that quiet linguistic shift translates into farm closures. Risk: this means real time spent reading consultation drafts and provincial or state climate plans, not just farm media summaries.

- Path 2 — Build leverage you don’t currently have. (30-day action.) Dutch farms were structurally exposed because they were spatially diffuse and politically fragmented. Mid-band family operations sit in the same vulnerable middle — big enough to show up in every dataset, small enough to lack corporate-scale lobbying clout. Within 30 days, take a hard look at where your operation has irreplaceable value: an anchor supplier to a regional plant, a watershed steward, an employer in a rural municipality, a source of distinct genetics. Document it. If you can’t name three institutional parties — processor, municipality, watershed group — who would experience real loss if you closed, you have a leverage gap to fix this month. Trade-off: this strengthens your political position, but it also reveals your dependency map to potential acquirers.

- Path 3 — Don’t volunteer your data without understanding the long arc. ESG dashboards, sustainability premiums, and methane-reduction cost-shares all require detailed barn- and field-level reporting. Today, that data flows into corporate sustainability reports. The Dutch case is a warning that the same datasets will serve as the basis for future regulatory targeting. Trade-off: you may need that data to access premiums or grants, but it’s worth asking — in writing — exactly how regulators will and won’t use it downstream.

- Path 4 — Engage upstream, not downstream. Dutch farmers lost the legal architecture fight before they realized it was happening. The Greenpeace ruling, the Habitats Directive interpretation, and the LBV covenant design were all settled in courtrooms and ministries — not in barns. When it makes sense: now, while methane and nutrient frameworks in your region are still in pilot or consultation phase. What it requires: working with your dairy organizations on the legal and judicial side, not just the agronomic one. Central trade-off: every hour spent on policy is an hour not spent on barn-level efficiency, but the Dutch case shows efficiency alone doesn’t buy you a future when the legal architecture has already been written. The PAS-melders are the proof: thousands of farms that followed the law to the letter were left in legal limbo not because they did anything wrong, but because the framework they relied on was struck down above their heads.

Key Takeaways

- If your regional climate or nutrient policy is shifting from “intensity per unit” to “absolute sector reductions by date,” treat that as a Dutch-pattern signal worth tracking month by month.

- If your jurisdiction tightened application or storage rules, run the manure cost math at current rates and project it forward for 24 months before signing your next CAPEX commitment.

- If you can’t name three institutional parties — processor, municipality, watershed group — who’d experience real loss if your farm closed, you have a leverage gap to fix in the next 30 days.

- Before signing up for any sustainability program that requires barn- or field-level emissions data, ask in writing how regulators may use that data over the next 5–10 years.

- If your operation falls in the 80–800-cow mid-family band and has recent environmental CAPEX near a sensitive area, prioritize legal and policy engagement through your dairy organization over the next 90 days.

- Map your 2030 compliance scenario against two cases: a 30% absolute reduction target and a hard local deposition cap. If neither fits your balance sheet, you have a strategy gap, not a compliance gap.

- If your dairy organization isn’t currently tracking the legal framework itself — not just the emissions rules but the court rulings and consultation drafts that shape them — that’s the PAS-melder gap. Close it before the next ruling, not after.

A Question Worth Asking Before the Letter Arrives

The Dutch story isn’t really about the Netherlands anymore. It’s about which parts of that pattern arrive in your region, in what order, and how much warning you get.

So here’s the question worth carrying back to your kitchen table this week: what would it take for your farm to be structurally un-replaceable in your region — not just efficient, not just compliant, but so woven into the local food system, land base, and community that you’re the last operation a planning office could justify pushing out?

Run Your Numbers

Consolidation Clock — 5-Question Decision Engine — Five questions, sixty seconds. It turns herd size, cost position, succession, and capital access into one signal: expand, hold, pivot, transition, or exit. Find out which structural band you’re in before a planning office decides for you.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Dutch Dairy Farmers Face 30-40% Income Loss Due to Manure Crisis: Report by Wageningen Economic Research — Exposes the immediate financial damage of the derogation collapse, detailing how stricter nitrate limits and surging disposal fees slash operating income by up to €40,000 annually for intensive family operations.

- Ireland’s 54000 Missing Calves Signal the Regulatory Storm Heading Your Way — Explores how European environmental mandates force massive pre-emptive herd culls across Ireland, arming global producers with a clear timeline of how regional processing sectors contract when nitrogen limits drop from 250kg to 170kg.

- The Carbon Credit Goldmine: How Forward-Thinking Dairy Producers Are Turning Methane Reduction into Cash Flow — Delivers a contrarian blueprint for monetizing absolute emission mandates, showing how high-performing dairies can weaponize barn data to build new revenue streams via credit programs before regulations turn manure into a strict liability.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.