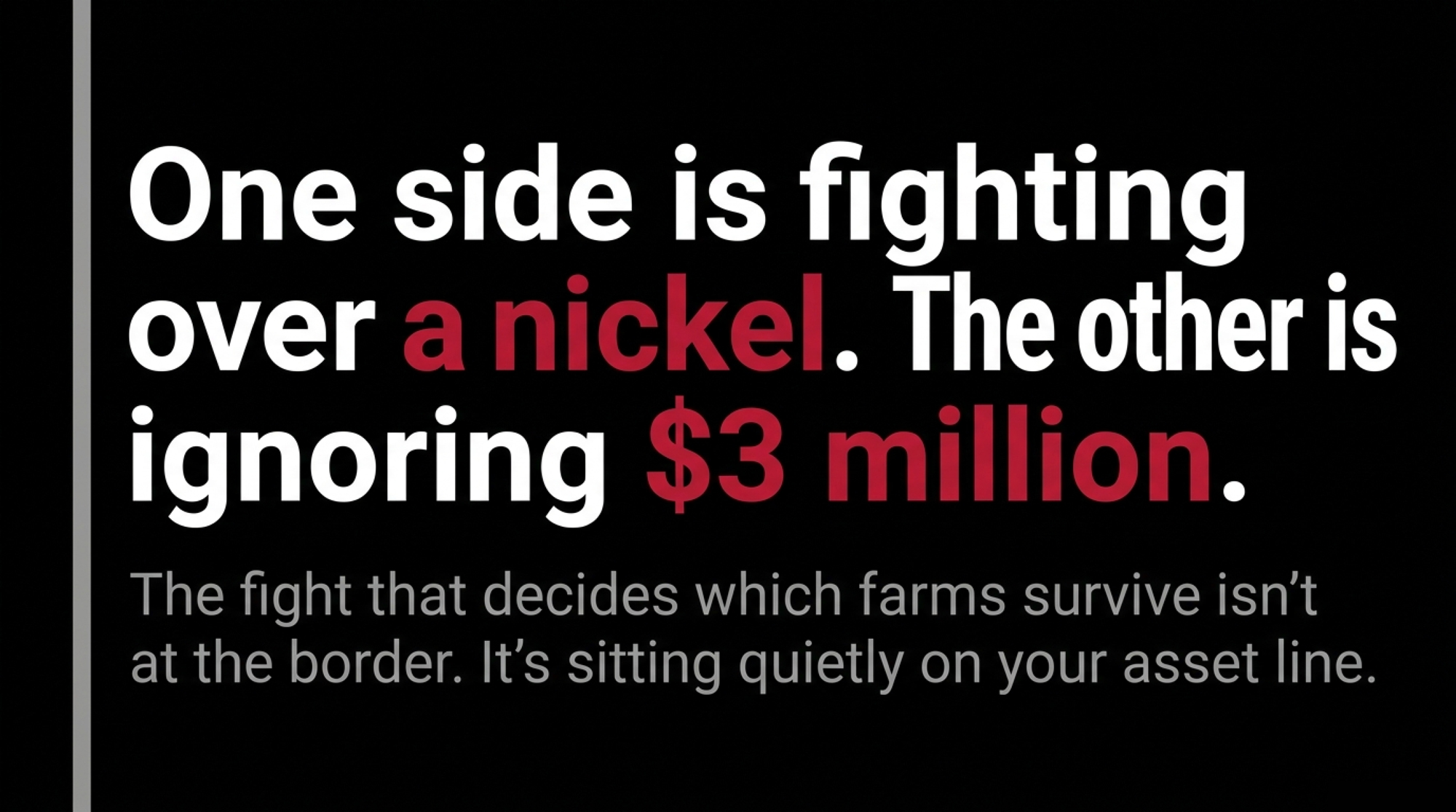

The CUSMA review lit the fuse on July 1, 2026 — but the fight that decides which farms survive isn’t at the border. It’s a nickel per cwt versus a 15% quota drop that quietly turns a bankable 55% balance sheet into 60.4% — and wipes out CA$300K in equity.

Picture two farms — composites, but built from real numbers. A 150-cow operation in Wisconsin, watching Washington rail against Canada “stealing billions” in dairy trade, thinking: finally, somebody’s fighting for us. And a 100-cow farm in Ontario, watching Ottawa hold the line with a brand-new law protecting supply management, thinking: our system won. Both proud. Both patriotic. Both watching the wrong battle while the real risk sits quietly on their own asset line.

Neither farm is a single real operation — they stand in for thousands on each side of the line. But the numbers behind them are real, and they’re the numbers the July 1 CUSMA review dragged into the open. Not a border war over milk. A question about which system leaves its farmers more exposed when the fighting drags on. So let’s put both flags on the table and settle it. Who’s actually winning? And who’s lying to themselves harder?

The “Cliff” That Wasn’t

First, kill the headline that had everyone reaching for the fireworks and the pitchforks. CUSMA didn’t die July 1. The deal runs a 16-year term to July 1, 2036, and July 1, 2026 was a scheduled joint review under Article 34.7 — a checkpoint, not a guillotine. Canada’s chief trade negotiator Janice Charette has framed the review the same way — a checkpoint rather than a cliff. The Bank of Canada’s April 2026 report flagged the review as a significant risk but maintained its base case that the core of the agreement will remain in effect.

But here’s what should worry both camps. If the three countries don’t sign a full extension, CUSMA slips into annual joint reviews — potentially every single year until 2036. Farm Credit Canada’s read: the grievances won’t be settled come July, so tariffs and uncertainty drag on through 2026 and into 2027.

So this isn’t one battle. It’s a ten-year war of attrition. Which makes the only question that matters this: who’s actually exposed when the clock keeps resetting?

Team USA’s Case — And the Gut-Punch Underneath It

Fly the stars and stripes for a minute, because the American producer has a real grievance. USMCA promised US dairy roughly US$200 million a year in new tariff-free access to Canada. Canadian fill rates have run near 42%, meaning more than half of the promised access goes unused — an estimated US$116 million a year left on the table. And in 2024, a CUSMA dispute panel again took up how Canada allocates its dairy import quotas — the core of a years-long fight over whether Ottawa is honoring the deal it signed. That’s not nothing. That’s a deal Canada signed and then, in the US view, quietly boxed shut.

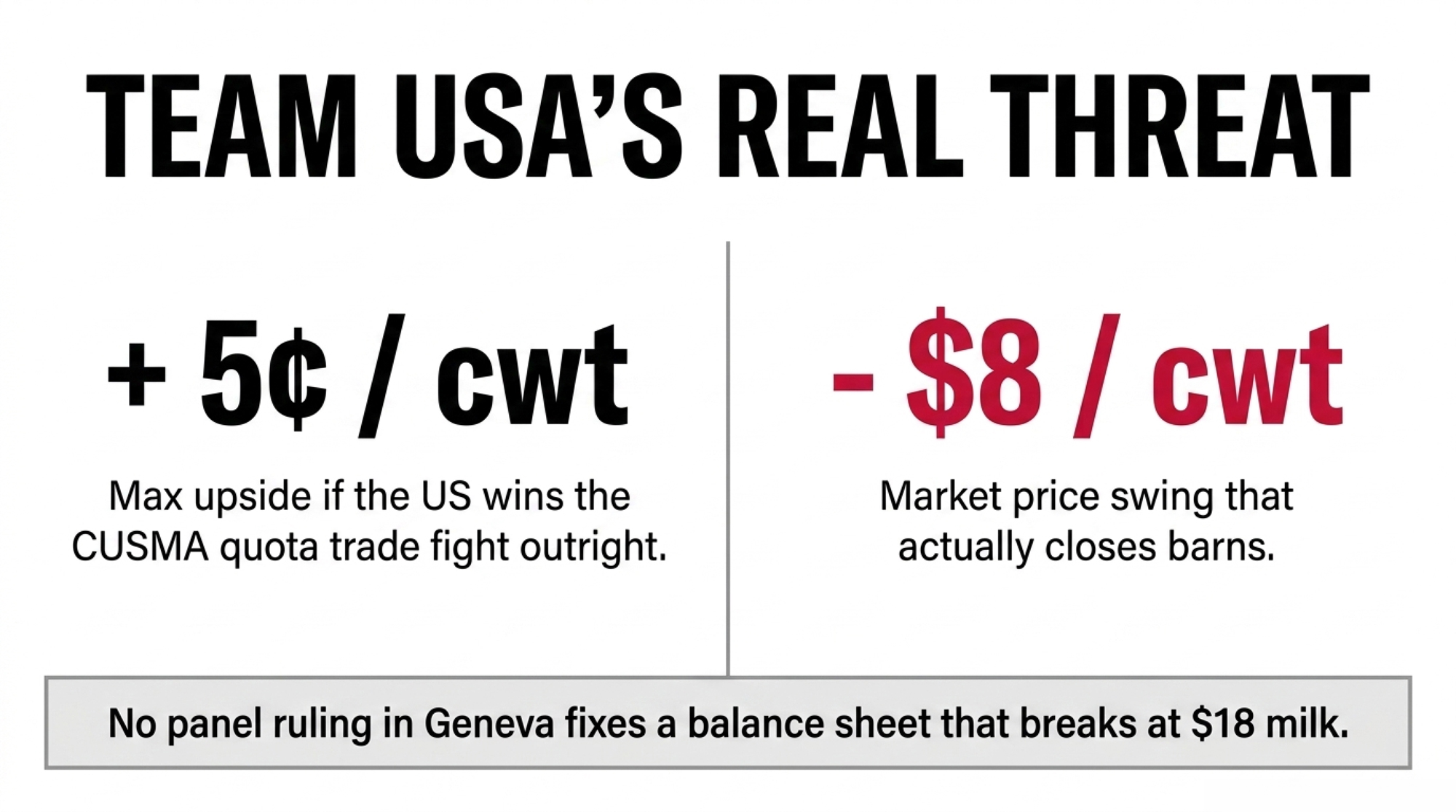

Now the gut-punch. Spread that whole fight across US milk production, and it works out to about five cents per hundredweight. On a 150-cow herd shipping roughly 24,000 lb per cow a year — call it 36,000 cwt — that’s around US$1,800. Real money, sure. Call it a month of feed. But it won’t move the needle on a farm that’s bleeding from somewhere else.

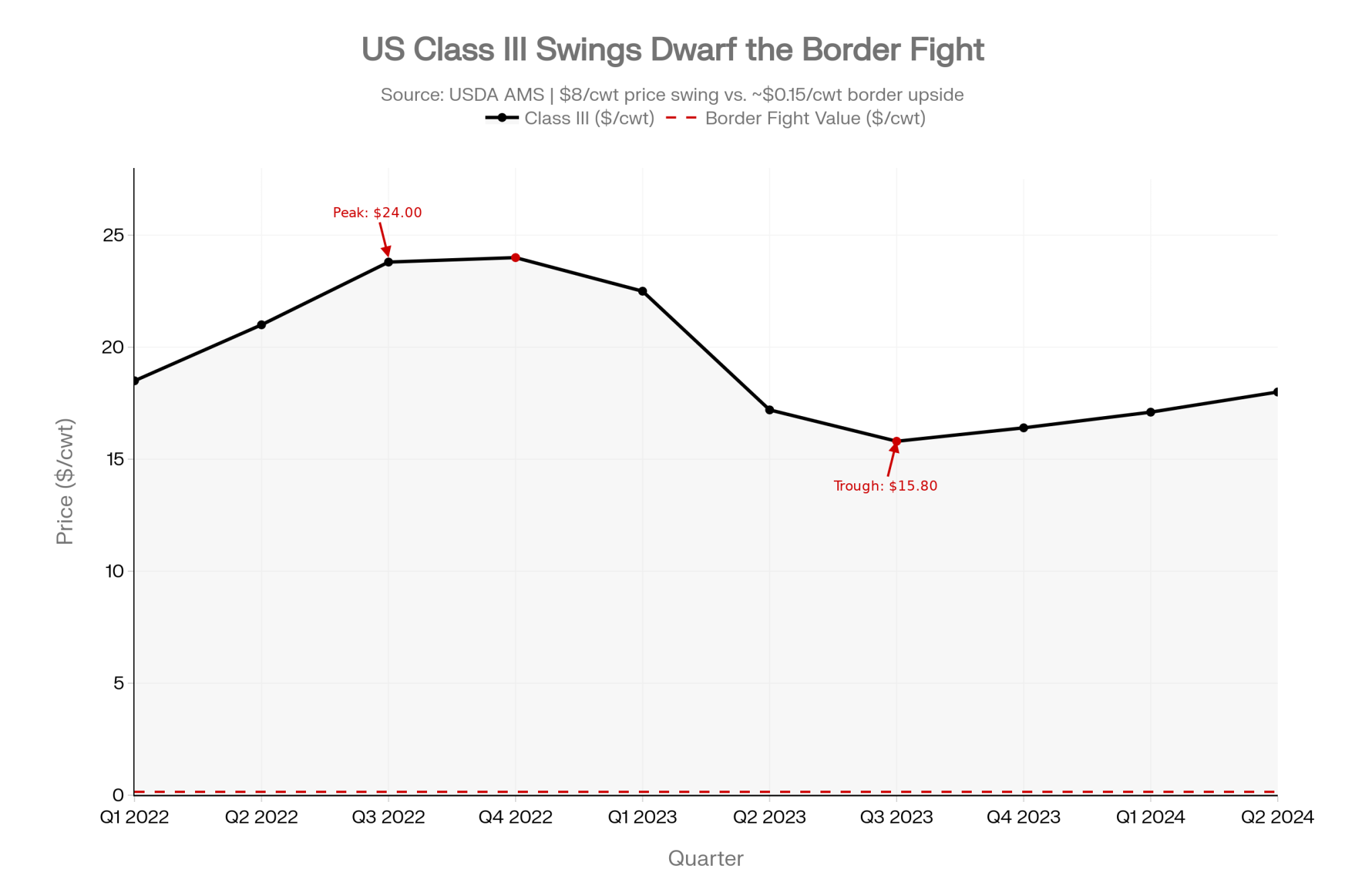

And somewhere else is where American farms actually bleed. US milk prices swing hard — Class III ran near US$24/cwt in mid-2022 and slid to around US$16 by 2023. That’s a US$8 swing per hundredweight, dozens of times larger than the entire border fight — a different order of risk entirely.

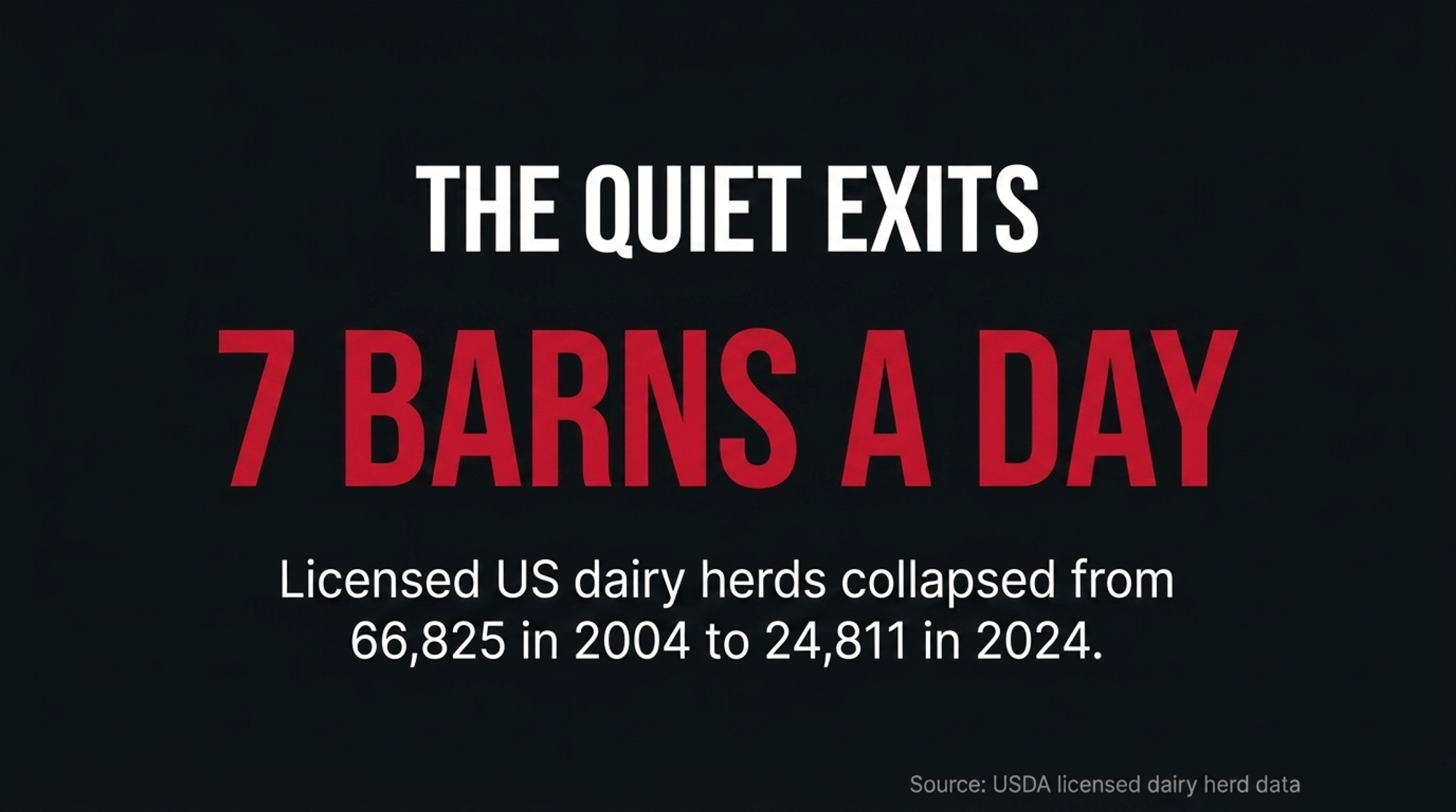

Licensed US dairy herds have collapsed from 66,825 in 2004 to 24,811 in 2024 — roughly 2,500 to 2,800 exits a year lately. About seven barns a day.

The border fight is the loud war. The price cycle is the quiet one that actually closes those barns — and no panel ruling in Geneva fixes a debt-service coverage ratio that breaks at US$18 milk.

What Does the Border Fight Actually Change on a US Milk Cheque?

Not much — and that’s the whole point. Say the US wins the TRQ fight outright and Canada fills every basket tomorrow. The most credible estimates put the upside at five to fifteen cents per hundredweight spread across US production. On that same 150-cow farm — the same 36,000 cwt, just at 15¢ instead of a nickel — the top of the range is roughly US$5,400 a year. A nice cheque. Not a strategy.

Line that up against what the price cycle already does to the same farm. A US$8/cwt swing on that milk is the difference between a comfortable year and a call to the lender. So if you’re American, the honest question isn’t whether Ottawa plays fair. It’s whether your operation clears its debt service when Class III drops back toward US$16 — the number that’s actually been closing seven barns a day. The border is the fight you can watch. Your DSCR is the fight you can win.

Why Aren’t More US Farms Using the Tools Built for Exactly This?

Here’s the frustrating part. The federal programs designed to blunt that US$8 swing already exist — and plenty of farms leave them on the shelf. Dairy Margin Coverage pays out when the national milk-feed margin falls below the coverage level you buy, and Dairy Revenue Protection lets you lock a floor under your quarterly milk revenue. Neither is a handout, and neither is complicated once you’ve run it once.

The catch producers cite is cost and paperwork — premiums due when margins look fine, forms that feel like busywork in a good year. That’s exactly the wrong time to judge them. And the program’s most affordable coverage tier is built for the family-scale operation — it applies to a base slice of your production history, which, for a herd the size of that 150-cow Wisconsin farm, covers all of its milk at essentially the cheapest rate. If that’s your farm and you’re not enrolled, you’re leaving your best-fit risk tool on the shelf while arguing about a nickel at the border.

Team Canada’s Case — And Its Own Gut-Punch

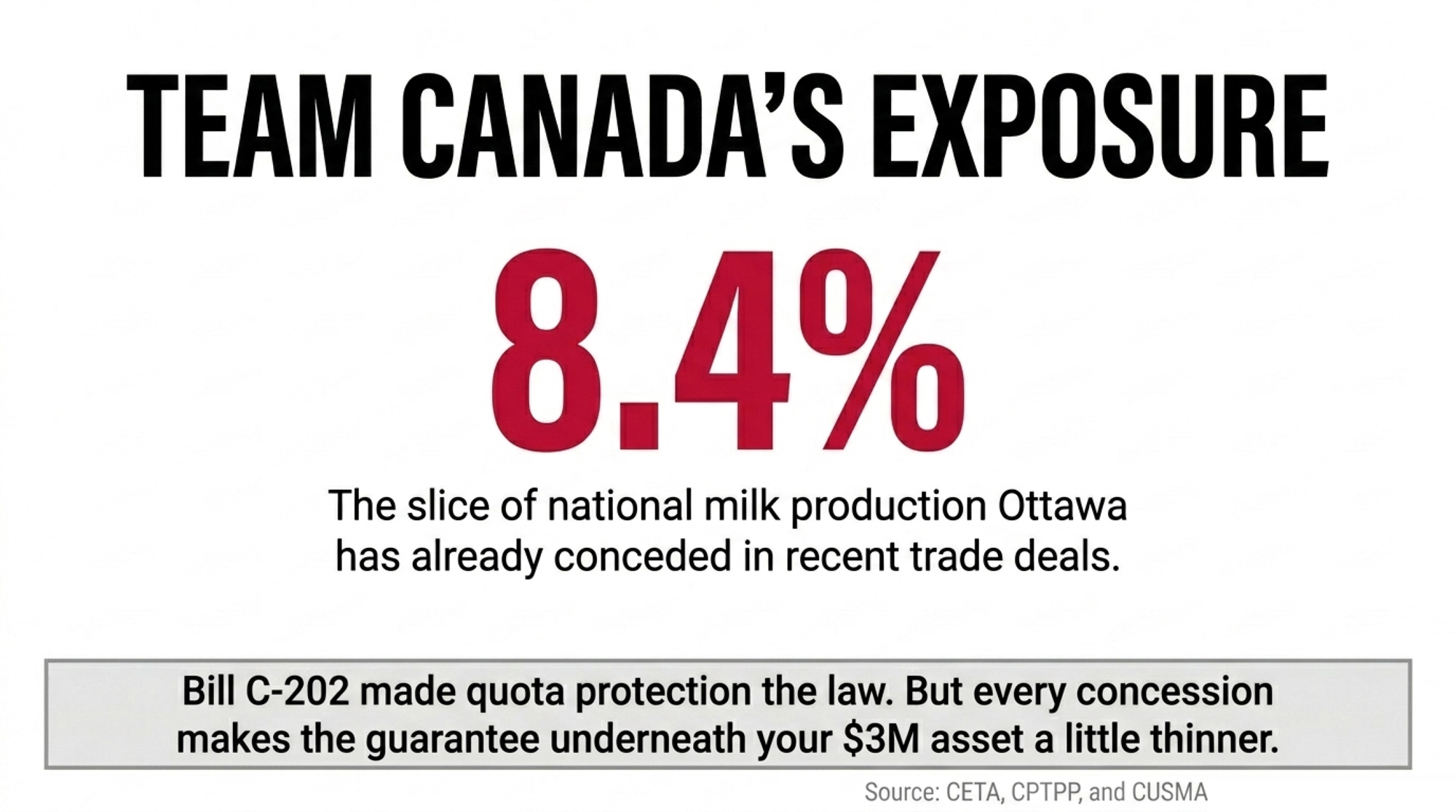

Now raise the Maple Leaf. The Canadian producer’s pitch is stability, and the numbers back it. Supply management delivers a steadier milk cheque, and Ottawa just made it law that nobody can trade it away. Bill C-202 received Royal Assent on June 26, 2025, replacing an earlier version that died when Parliament was prorogued. The trade minister now legally can’t raise import quotas or cut over-quota tariffs on dairy, poultry, or eggs. That’s settled law now, not a proposal — which is what makes the “off the table” framing real. Fortress sealed. Flag planted.

Here’s the gut-punch for Team Canada. That protected system runs on quota — and quota is where the real exposure hides. Farm Credit Canada’s 2026 report pegs mid-size quota holdings near CA$2.5 million, at CA$24,000 to CA$27,000 per kilogram of butterfat. Our 100-cow Ontario example runs a bit higher — about CA$3 million in quota — which is where the barn math below starts. Either way, it’s the biggest asset on the balance sheet. And it’s not a commodity price you can hedge — it’s a value that exists only because the political system says it does.

That system’s already been chipped away three times.

CETA, CPTPP, and CUSMA combined opened access equal to about 8.4% of national milk production. Ottawa’s answer each time: up to CA$4.8 billion in compensation to producers, plus CA$497.5 million to processors.

Concede a slice, pay the compensation, declare the fortress intact. The new law even hints at the fear underneath it. If quota value were truly bulletproof, you wouldn’t need a statute swearing you’ll never trade it away.

Could Quota Values Actually Re-Rate — Or Is That Fear Talking?

Fair question. Nobody’s predicting a crash, and no lender or ag-economics body has published a model calling for one. But you don’t need a crash to feel it — you need a slow squeeze, and the pieces for one are already on the board. Three trade deals have opened access equal to about 8.4% of production, and C-202 has removed dairy as a bargaining chip for the next round. Each concession moves more foreign product inside the fence; the guarantee behind your quota gets a little thinner each time.

Here’s why that matters for the price of a kilogram of butterfat. Quota holds its CA$24,000-to-CA$27,000/kg value because the system guarantees you a buyer at a set return. Weaken that guarantee — more import share, a thinner effective utilization rate — and the asset starts to look less bulletproof to the next buyer, and to your lender. Provincial boards cap how fast quota prices can move, which slows any re-rate but doesn’t put a floor under the underlying value. And with Ottawa’s only remaining tool being the compensation cheque, the political durability of quota value sits dead center of the next decade. The data on exactly how past concessions moved quota values is thin — but the direction of the pressure isn’t in dispute.

How Much Would a 15% Quota Drop Actually Cost Your Equity?

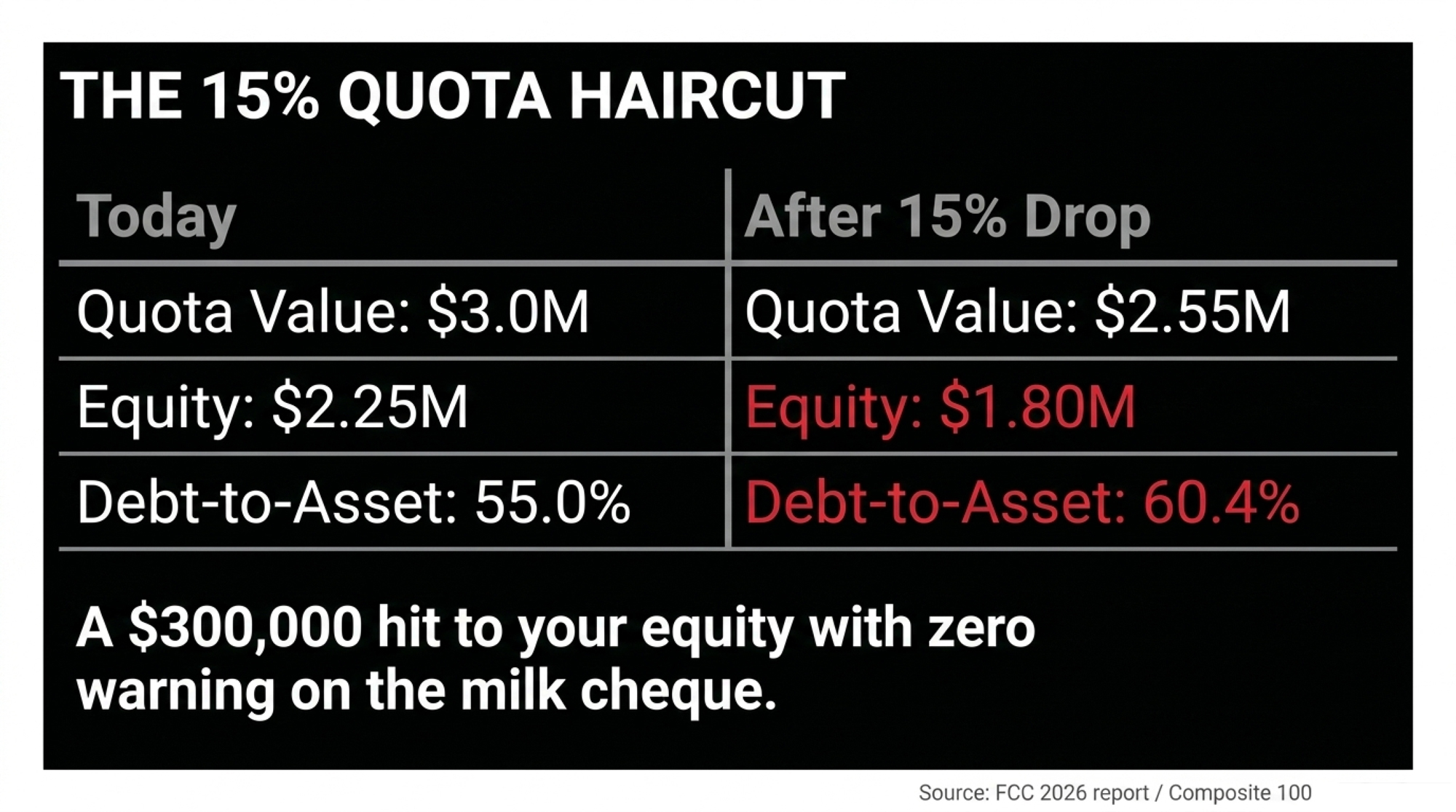

Here’s the barn math that should make a Canadian producer put down the flag and pick up a calculator. Take that 100-cow Ontario farm: CA$5.0 million in assets, CA$3 million of it quota, CA$2.75 million in debt, CA$2.25 million in equity. Debt sits at about 55% of assets — comfortable, bankable, nothing a lender blinks at.

Now knock 15% off the quota. CA$3.0 million becomes CA$2.55 million. Same cows. Same milk. Same components. But equity drops to CA$1.80 million, and debt climbs to roughly 60.4% of assets — the kind of shift that moves a farm from a routine renewal to a sit-down with the bank. A 10-to-20% haircut on that CA$3 million is a CA$300,000 to CA$600,000 hit to your equity, with zero warning on the milk cheque.

And here’s the part that makes it personal: that same cut lands differently depending on where your leverage sits. A farm that paid its quota down over the years absorbs the hit and stays comfortably bankable. A farm that expanded recently at peak quota prices — far more debt against the same asset — can get pushed from a routine renewal into a hard conversation with the lender. Same milk cheque. Same haircut. Wildly different phone call. The question isn’t whether quota drops. It’s where your leverage sits when it does — which is exactly what the 30-day stress-test below is built to tell you.

So Who’s Actually Winning the Border War?

Depends on which risk scares you more. Here’s the honest scoreboard, side by side.

| Risk Dimension | 🇺🇸 Team USA (150-cow Wisconsin) | 🇨🇦 Team Canada (100-cow Ontario) |

|---|---|---|

| Milk Price Stability | Volatile — US$8/cwt swings in a single year | Regulated, formula-based — predictable |

| The Trade Fight’s Real Value | ~5–15¢/cwt upside if US wins outright | 8.4% of production already conceded |

| Annual Impact on 150/100-cow Farm | ~US$1,800–$5,400/year max gain | Quota re-rate risk: CA$300K–$600K equity |

| Debt-to-Asset at Risk | Dependent on milk price / DSCR | 55% → 60.4% on a 15% quota drop |

| Biggest Structural Threat | Price cycle + ~2,500–2,800 farm exits/yr | Quota value linked to political system |

| Freedom to Grow / Export | High — open market, export upside | Capped — C-202 seals dairy as non-tradeable |

| Government Risk Backstop | DMC, DRP — voluntary, no price floor | CA$4.8B in compensation paid to date |

| What Producers Are Watching | Ottawa’s TRQ fill rates | Washington’s tariff threats |

| What They Should Be Watching | Their DSCR at US$18 milk | Their D/A ratio after a quota haircut |

Read it straight, and nobody sweeps. On price stability, Canada wins — no argument. On scale, export upside, and freedom to grow, the US wins. But on the risk each side refuses to look at? It’s a tie in the worst way. The American’s chasing a rounding error at the border while the price cycle eats his neighbors. The Canadian’s sleeping on a six-figure asset he’s never once stress-tested. Both flags flying. Both fighting the wrong battle.

Is Your Farm Watching the Wrong Border?

The instinct on both sides is to watch the other country. Americans watch Ottawa’s “unfair” quota walls. Canadians watch Washington’s “400% tariff” soundbites and Trump’s threats. But for the US producer, the milk cheque barely moves either way — the real war is a debt-service coverage ratio nobody’s tested against the next price dip. And for the Canadian producer, Washington’s mood is a sideshow. The variable that could reset your net worth is whether quota values hold through ten years of annual reviews. Everyone’s watching the border. The risk is in the barn.

Options and Trade-Offs: Your Move by Border

Panic isn’t the point. Nobody can put a probability on a quota re-rate, and no lender or ag-economics body has published a formal model predicting one. Most farms on both sides have rehearsed the wrong risk. Here’s the playlist — Canadian balance-sheet homework first, then the American risk-management moves.

If you farm in Canada:

| Farm Size | Quota Value (Baseline) | Equity (Baseline) | D/A (Baseline) | –10% Quota Drop | –15% Quota Drop | –20% Quota Drop |

|---|---|---|---|---|---|---|

| 60-cow (Starter) | CA$1.8M | CA$1.0M | ~55% | –CA$180K → 58.9% | –CA$270K → 61.3% | –CA$360K → 63.8% |

| 100-cow (Mid-size) | CA$3.0M | CA$2.25M | ~55% | –CA$300K → 58.2% | –CA$450K → 60.4% | –CA$600K → 62.5% |

| 200-cow (Large) | CA$6.0M | CA$4.5M | ~55% | –CA$600K → 57.8% | –CA$900K → 59.7% | –CA$1.2M → 61.6% |

- Run the haircut stress-test yourself — within 30 days. Take your current quota value, cut it 10%, 15%, and 20%, and recalculate your debt-to-asset ratio and loan-to-value.

- When it makes sense: any farm carrying quota as major collateral.

- What it takes: an afternoon and your last balance sheet.

- The risk of skipping it: you learn where your covenants sit from your lender, not from yourself.

- Ask your lender their own haircut assumptions. Your bank or FCC may already discount the quota internally when sizing up your position.

- When it makes sense: before your next operating-line renewal.

- What it takes: one direct conversation.

- The payoff: you find out if the bank already values your equity lower than you do.

If you farm in the US:

- Treat the TRQ fight as gravy, not a plan. Even a fully “fixed” quota system moves you five to fifteen cents per cwt.

- The real levers: your DSCR, and whether you’re actually enrolled in DMC and DRP.

- The limit: no ruling in Geneva saves a balance sheet that breaks at US$18 milk.

- Check your risk-management coverage before the next sign-up window. DMC and DRP are built to blunt exactly the price swings that close barns, and the most affordable coverage favors family-scale herds.

- When it makes sense: any herd exposed to margin collapse — which is all of them.

- What it takes: a sign-up window and premiums paid even when margins look fine.

- The trade-off: small guaranteed cost now versus an uncovered margin collapse later.

For both sides:

- Grow margin before volume. For Canadians, C-202 walls off big export-driven growth, so the edge is cost per litre and better components. For Americans, chasing volume into a price trough is how good herds go under.

- The Canadian catch: financed quota at around 6% interest already bleeds cash on a negative carry, so buying more into a possible re-rate stacks the risk.

Key Takeaways

- If quota is your largest asset and a 15% cut pushes your debt-to-asset ratio past your lender’s comfort zone, you’ve found your real exposure — not the one on the news.

- If you bought quota recently at peak values with high leverage, you’ve got the thinnest equity cushion to absorb a re-rate. Model it before your next renewal.

- If you’re American and your DSCR can’t survive a US$18 milk year, fix that before you spend one more minute on a TRQ fight worth about 5¢/cwt.

- If you’re not enrolled in DMC or DRP, you’re leaving the tools built for exactly these price swings unused — check your coverage before the next sign-up window.

- If you see dairy compensation getting reframed as “temporary” or “transitional” in Canada, or risk-tool cuts moving through a US Farm Bill, that’s your signal the ground is shifting under your system.

The border war makes for great fireworks on both sides. But the fight that decides whether your farm will still be standing in ten years isn’t happening in Washington or Ottawa. It’s happening on your own balance sheet — and most operations on both sides of the line have never run the numbers.

So pick your battle, but pick the right one. If you’re American, would your farm survive the next price crash without a single Canadian container crossing the border? And if you’re Canadian, if your quota value dropped 15% tomorrow, would your lender notice before you did? We’re breaking down the full head-to-head — the quota-haircut model by herd size beside the US risk-tool playbook — in an upcoming Bullvine deep-dive. That’s where the real numbers live, for both flags.

The Bullvine Balance Sheet Stress-Tester

Stop watching the news. Run your actual numbers below.

Learn More

- The $586‑Per‑Kilo Dairy Quota Trap: Why New Ontario Quota at 6% Bleeds Cash Every Year — Arms you with the cash-flow math behind capped Canadian quota financing at 6% interest. You learn why buying new quota at negative carry bleeds $586 per kilogram annually and how to reallocate capital to optimize debt instead.

- USMCA 2026: The $200M Question – Why Only 42% of U.S. Dairy Access to Canada Gets Used — Exposes the hidden regulatory loopholes keeping over half of the promised $200 million trade access out of reach. It delivers the precise timeline and market-positioning rules needed to coordinate long-term pricing adjustments directly with your milk processor.

- What Lactalis’s 270-Farm Cut Really Means for Every Producer — Dismantles the belief that hard work beats scale by breaking down the structural shift forcing mid-size operations to adapt. You gain specific strategies to pivot toward premium divisions boasting high 15% to 20% operating margins.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.