Organic Valley says it’s forced to pay ~$50M a year into a pool for milk it can’t sell. The same June 2025 rule cut your check too. Here’s the pooling math.

Executive Summary

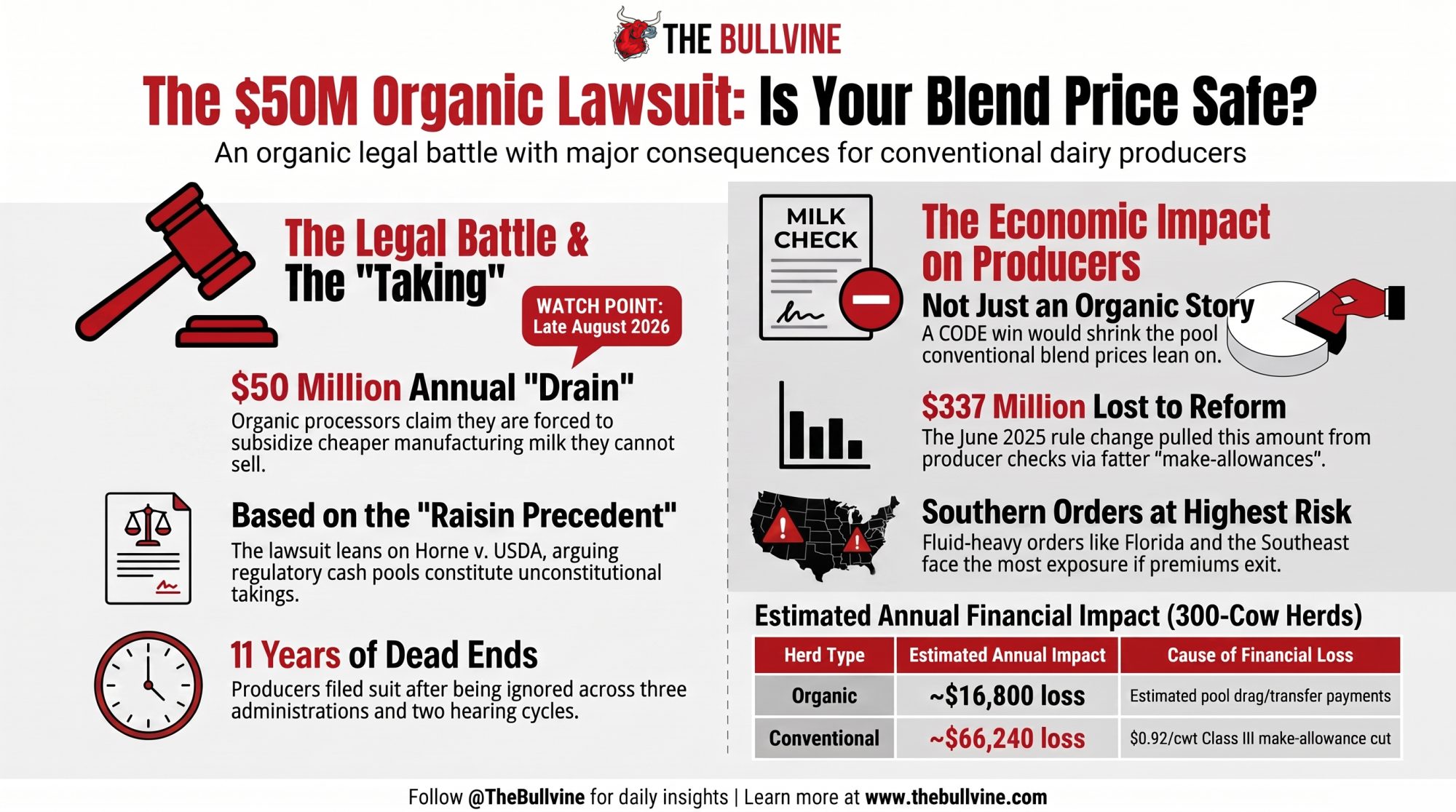

- What happened: On April 28, three of the biggest organic dairies in the country — Organic Valley/CROPP, Aurora, and Horizon — filed four federal lawsuits arguing that Federal Milk Marketing Order pooling is unconstitutional as applied to organic. CROPP alone claims more than $60 million for roughly 1,350 farms and pegs the ongoing drain near $50 million a year.

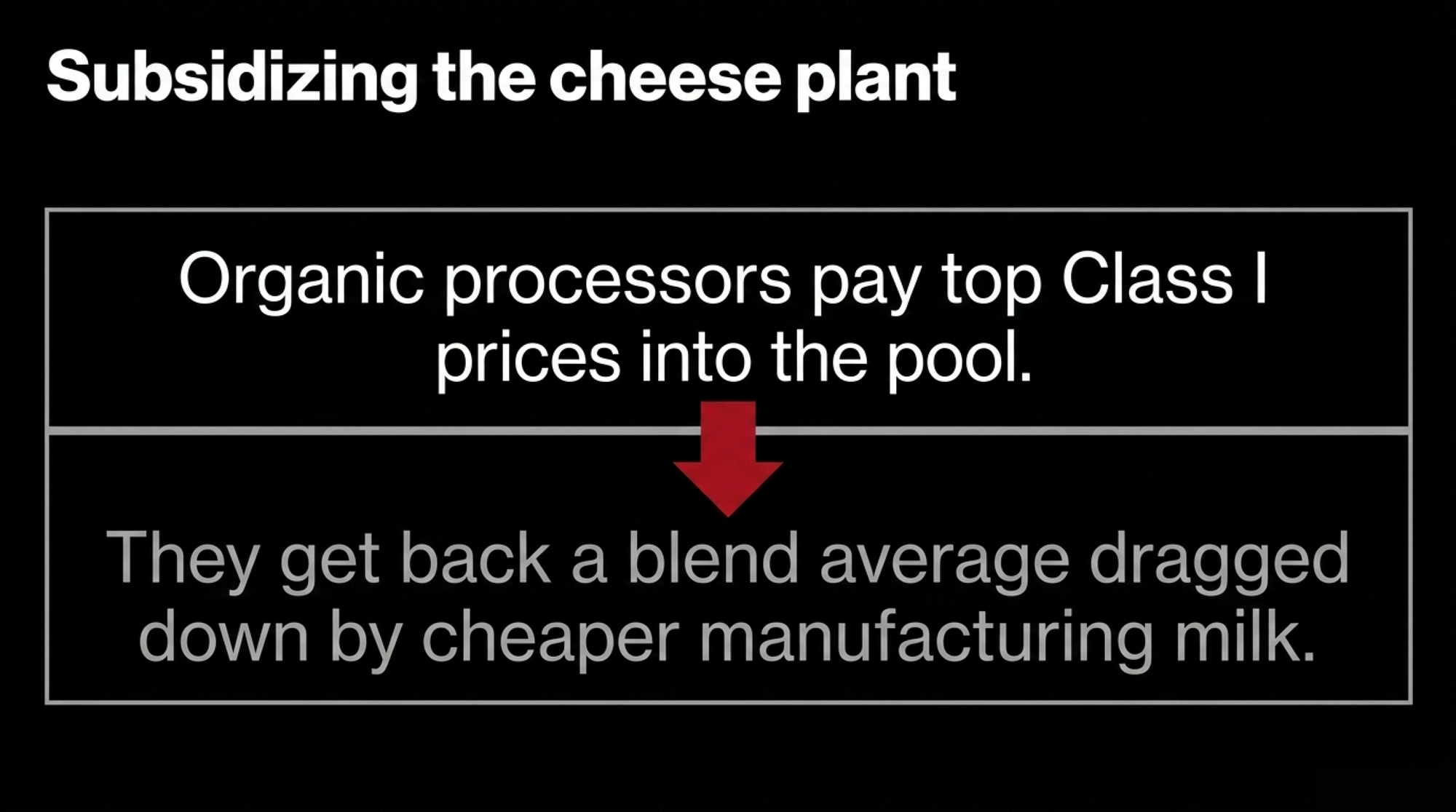

- The mechanism: Organic processors are almost all Class I, so they pay into the pool at the top, then get back a blend average dragged down by cheaper cheese and butter milk — money that lands with the manufacturing handlers.

- The trigger: The same June 2025 AMS rule that cut Class III by about 92¢/cwt and pulled $337 million out of producer checks raised organic’s pool-in payments while shrinking what the pool pays back.

- The legal reality: CODE’s lead claim leans on Horne v. USDA, but Horne involved a physical taking of raisins. Proving a regulatory cash pool is a “taking” is a real legal stretch, and USDA hadn’t responded as of July 9.

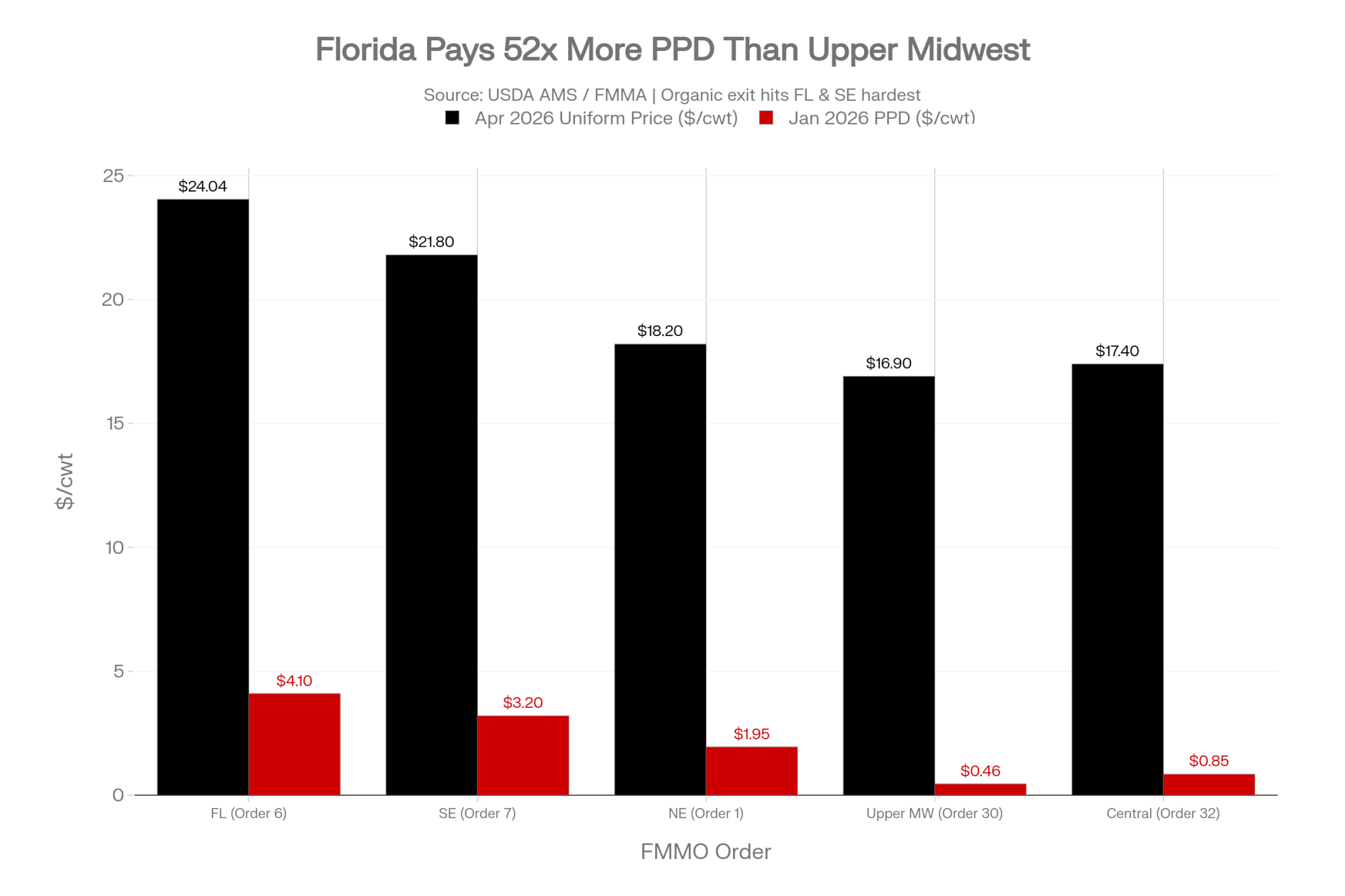

- Why it’s not just an organic story: A win shrinks the pool conventional blend prices lean on, and it bites hardest in fluid-heavy Southern orders like Florida (Order 6, $24.04/cwt in April) and the Southeast — not the Upper Midwest, where January’s PPD was $0.46/cwt.

- The caveat: The dollar figures above $50M are CODE’s own math, not audited findings. Read the arrow, not the number.

- Your move: Before the late-August answer deadline, know which order you’re in and how exposed your blend price is if the biggest premium producers walk out of the pool.

Here’s the number that put USDA in front of three federal judges: about $50 million a year — what the country’s biggest organic dairies say they’re forced to pay into a Federal Milk Marketing Order pool for milk they legally can’t even sell. On the hook are Organic Valley/CROPP, Aurora Organic Dairy, Horizon Organic, and seven named CROPP farmer-members — people like Elvin Ranck in Pennsylvania and Remington Perkins, who, by CODE’s account, runs West Virginia’s first certified organic dairy, filing for roughly 1,350 farms. The trap they’re fighting is the same June 2025 rule change that cut your milk check — and if they win it, the pool your blend price leans on gets smaller.

While framed as an organic dispute, this is an FMMO fight that could fundamentally alter blend prices for conventional fluid milk shippers. The ruling lands on them whether they’ve shipped an organic pound or not.

Who’s Suing, What They Claim, and How Much

On April 28, 2026, three companies filed four separate suits in three federal courts. They call themselves CODE — the Coalition for Organic Dairy Exemption — a descriptive name, not a separately incorporated entity. USDA hadn’t publicly answered any of the four as of July 9, 2026, and docket numbers weren’t confirmable in public PACER records at press time.

| Plaintiff | Court | Core claim | Dollar figure | Source status |

| CROPP/Organic Valley (7 farmer-members) | Court of Federal Claims (D.C.) | Fifth Amendment Takings, class action | >$60M for ~1,350 farms | Filing |

| CROPP/Organic Valley | W.D. Wisconsin | Due process, non-delegation, APA | ~$50M/yr ongoing | Plaintiff estimate |

| Aurora Organic Dairy | D. Colorado | Takings, due process | Part of >$400M since 2006 | Plaintiff estimate |

| Horizon Organic | D. Colorado | Takings, due process | Part of >$400M since 2006 | Plaintiff estimate |

While the headline numbers are massive — reaching up to $400 million since 2006 — it’s critical to note these are the plaintiffs’ internal accounting figures, not audited court findings. Only the $60 million class-action claim traces directly to a filing.

Why Should a Conventional Producer Care About an Organic Lawsuit?

It isn’t an organic lawsuit. Strip the label, and it’s one question: can a pricing law written in 1937 force a legally distinct product to bankroll a pool it can’t draw from — and does that break the Fifth Amendment? The organic-versus-conventional framing is the distraction. The real fight is small-and-differentiated against the industrial pool, argued based on pooling math and constitutional law. (Related: The Bullvine’s July 2, 2026 make-allowance analysis, “$337 Million Disappeared from Milk Checks. Cheese Prices Never Dropped.”)

How the Producer Settlement Fund Actually Moves the Money

Skip the textbook. Every hundredweight in an FMMO gets priced by what it becomes — fluid drinking milk (Class I) pays the most, cheese (Class III) and butter/powder (Class IV) less. The market administrator blends all that value into one uniform price, the minimum every handler pays. Handlers whose milk went to a high-value class pay the difference into the Producer Settlement Fund. Handlers whose milk went cheap draw out of it. The key thing to remember: it’s the handlers who settle with the pool, not the individual farmer.

Now watch where organic gets stuck. Organic processors are almost all Class I. They pay in at the top, then get back the blend average, dragged down by all that cheaper cheese and butter milk. The gap doesn’t evaporate — it lands with the handlers who ran the cheap manufacturing milk.

Pay in at the top. Get back the average. Subsidize the cheese plant. Every month.

Adam Warthesen, Organic Valley’s VP of Government and Industry Affairs, pegs the transfer at more than $400 million out of organic since 2006 — about $50 million a year now. Both figures are CODE’s own math. No neutral party — not USDA, not a land-grant economist, not Farm Bureau — has independently run them in any source found for this piece. Believe the arrow. Don’t yet bank the number.

The June 2025 Rule Change That Lit the Fuse

You felt this one. The USDA AMS final rule, published January 17, 2025 and effective June 1, did five things.

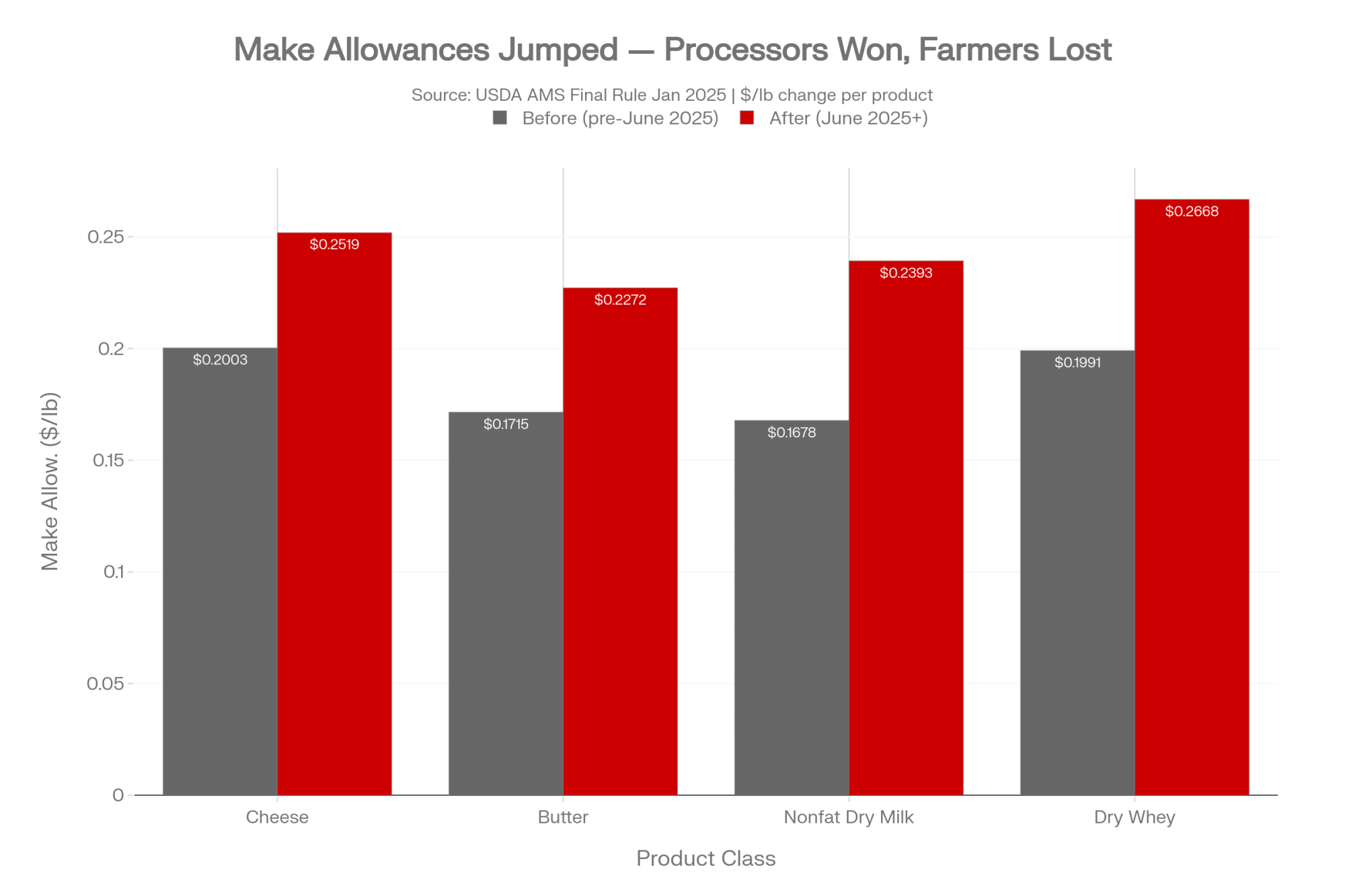

- Raised make allowances — the processing-cost credits in Class III/IV. Cheese went from $0.2003 to $0.2519/lb; butter, from $0.1715 to $0.2272/lb; nonfat dry milk, from $0.1678 to $0.2393/lb; dry whey, from $0.1991 to $0.2668/lb.

- Restored the “higher-of” Class I mover, scrapping the 2019 average-of-plus-74-cents formula.

- Raised Class I location differentials.

- Dropped the 500-lb barrel cheddar from the Class III formula.

- Updated skim composition factors, effective December 1, 2025.

That make-allowance change cut roughly 92¢/cwt from the Class III price and pulled about $337 million from producer milk checks — money that now stays with processors, even though cheese prices never dropped to match. Across all classes, the reform netted a $231.9 million decline in pool revenue in its first three months.

Here’s the piece aimed at organic. Under the restored higher-of, the base Class I skim price each month equals the higher of the advanced Class III and Class IV skims. For July 2026, USDA’s advanced price sheet put the base Class I price at $21.33/cwt, down $0.85 from June. Organic processors are Class I handlers. Higher Class I means a bigger check into the pool, and fatter make allowances shrank what the pool hands back in the blend. Organic pays more in, pulls less out — both levers yanked the same way on June 1, 2025.

Running the Numbers: What the Pool Costs, Organic vs. Conventional

The 300-Cow Organic Herd

Organic cows milk well below conventional — regional organic data runs roughly 10,000 to 19,000 lb/cow/year depending on grain and pasture rules, so call it 16,000 lb/cow (160 cwt) as a working middle. For a 300-cow herd, that’s about 48,000 cwt a year.

Now the drag per cwt, and here’s where you have to be careful, because CODE’s own numbers point two directions. Spread the $50 million-a-year claim across the roughly 1,350 farms and their volume, and the annual burden lands near $0.35/cwt. Take instead the $60 million class-action claim — a cumulative compensation ask, not an annual flow — and the implied per-cwt figure runs higher. They aren’t the same measurement, and stacking one on the other double-counts. Use the annual figure for a yearly comparison.

- Pool drag (CODE-implied annual): roughly $0.35/cwt.

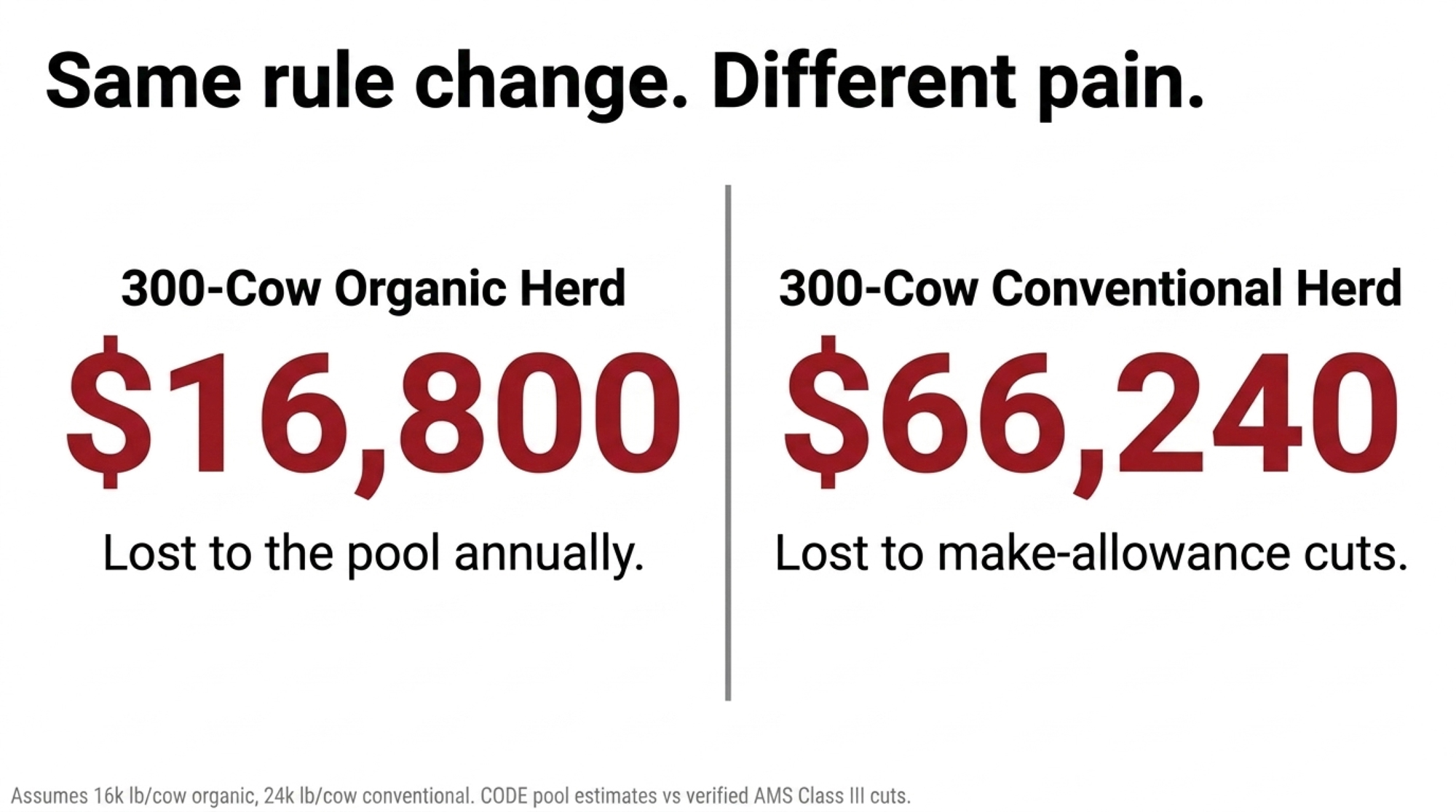

- Annual PSF transfer for a 300-cow organic herd: 48,000 cwt × $0.35 = about $16,800 per year, leaving that herd’s pool position for the conventional system.

That’s not lost revenue — these farms still clear $35–$45/cwt in organic pay. It’s the cash walking out the pool door. Warthesen claims that June 2025 lifted organic’s pool burden by about 60%; the direction holds, but the exact percentage is CODE’s estimate and varies with the order, volume, and butter-cheese spread each month.

The Conventional Herd, Same Rule Change

Conventional cows milk far harder — figure roughly 24,000 lb/cow (240 cwt), so a 300-cow herd runs near 72,000 cwt. That’s why the cwt totals differ between these two boxes even at the same cow count. Apply the verified 92¢/cwt Class III make-allowance cut:

- 300 cows (~72,000 cwt): 72,000 × $0.92 = about $66,240 a year, gone.

- 500 cows (~120,000 cwt): 120,000 × $0.92 = about $110,400 a year.

Same rule change. Two producers. The conventional herd’s dollar hit is bigger — it’s a measured make-allowance loss straight off USDA’s own class-price math, not a contested pool estimate — and yet it’s the organic side that went to court. Plug in your own herd’s rolling average and the arithmetic doesn’t change.

| Metric | 300-Cow Organic | 300-Cow Conventional | 500-Cow Conventional |

|---|---|---|---|

| Est. milk yield/cow | 16,000 lb (160 cwt) | 24,000 lb (240 cwt) | 24,000 lb (240 cwt) |

| Annual herd volume | ~48,000 cwt | ~72,000 cwt | ~120,000 cwt |

| Per-cwt impact | ~$0.35/cwt pool drag | $0.92/cwt make-allow. cut | $0.92/cwt make-allow. cut |

| Annual dollar hit | ~$16,800 | ~$66,240 | ~$110,400 |

| Organic pay base | $35–$45/cwt | ~$18–22/cwt blend | ~$18–22/cwt blend |

| Source quality | CODE estimate — unaudited | USDA-verified class price math | USDA-verified class price math |

The 11-Year Paper Trail Before Anyone Filed

CODE didn’t skip the line. In 2015, the Organic Trade Association asked USDA to exempt organic fluid handlers from PSF payments above a threshold. NMPF, DFA, Agri-Mark, Land O’Lakes, and ten co-ops lined up against it; OTA withdrew by January 2017 with no hearing held. The 2023–24 national FMMO hearing in Carmel, Indiana, ran 49 days and accepted 21 proposals — organic’s weren’t among them. USDA’s Final Decision landed November 2024 with organic’s submissions unaddressed. CODE filed formal Section 15A petitions in May 2025; they’re still pending. Then, on April 28, four lawsuits were filed.

Eleven years. Two hearing cycles. Three administrations. Same answer every time.

What’s the Constitutional Argument — and Is It Real?

CODE makes four claims. Every one is a plaintiff allegation; none adjudicated; USDA hasn’t answered.

| Legal Claim | What CODE Argues | Key Precedent | USDA’s Likely Counter | Relative Strength |

|---|---|---|---|---|

| Fifth Amendment Takings | Mandatory PSF payments = taking of private property without just compensation | Horne v. USDA(2015) — raisin physical taking | Regulatory cash pool ≠ physical seizure; courts give regulators more latitude over money than goods | Medium — Horne is real but the fit is a stretch |

| Due Process | Organic gets no usable benefit from a pool it can’t draw commodity supply from | General 14th/5th Amendment doctrine | Organic processors voluntarily entered a regulated market knowing pooling was mandatory | Weak-to-medium — voluntary entry undermines this |

| Non-Delegation | Private industry groups (NMPF, DFA) effectively blocked organic’s proposals from reaching a hearing | APA structural limits on delegation | Hearing process followed statutory AMAA procedures; all proposals subject to the same rules | Weak — hardest to win at district level |

| APA (Arbitrary & Capricious) | USDA ignored organic’s FMMO reform submissions in its 2024 Final Decision | Motor Vehicle Mfrs. v. State Farm(1983) | USDA considered and implicitly rejected organic’s submissions through the public record | Medium — strongest if organic can document procedural gaps |

The Fifth Amendment Takings claim is the heavyweight: mandatory PSF payments take private property without just compensation. The precedent is Horne v. USDA (2015), in which the Supreme Court ruled 8-1 that a marketing order requiring raisin growers to physically surrender part of their crop to a government reserve was a per se taking.

Here’s the catch, and it’s a real one. In Horne, the government physically took raisins — tangible property it hauled off. In CODE’s case, USDA isn’t seizing milk; it’s telling a handler what to do with their money through a regulatory pool. CODE’s hurdle is proving that a regulatory cash-balancing mechanism constitutes a physical or categorical “taking” of private property, not just an economic regulation that handlers dislike. Courts have long given regulators more room on money than on physical goods. That gap is exactly where USDA will push back.

The other three claims round it out: due process (organic gets no benefit from a pool it can’t draw supply from), non-delegation (CODE alleges private industry groups effectively pick which proposals reach a hearing and blocked organic’s), and an APA claim (ignoring organic’s submissions was arbitrary and capricious). Horne is real and decided. Whether a cash cross-subsidy fits inside it is the live question — and it’s not frivolous.

The Case for the Other Side — Without the Hedging

USDA hasn’t filed its answer. The conventional defense is real, so put it on the table straight.

The strongest card isn’t legal; it’s arithmetic. Organic lost a vote it was always going to lose, then went to court. The 2025 changes were approved by a two-thirds supermajority of pooled producers in separate referenda under the Agricultural Marketing Agreement Act of 1937. Organic accounts for about 3% of the pool volume. The system is built to let 97% outvote 3% — that’s the design, and it’s held up for 90 years.

Second card: voluntary entry. Organic processors entered a regulated market knowing that participation was mandatory. Courts don’t love a plaintiff who signs up for the game, then calls the rulebook unconstitutional when the score turns.

Third, NMPF’s genuine point is that the pool isn’t pure extraction. It sets a floor nobody can lowball under and keeps marketing orderly — the whole Depression-era reason it exists. The counter is just as sharp. None of that answers Horne. “You benefit from stability” didn’t save the raisin reserve, and “you knew the rules” gets weaker when the rules changed under organic in 2025 by a vote it couldn’t win. Two real arguments. That’s why this won’t settle on a napkin.

Does a CODE Win Actually Shrink Your Pool?

Yes — but smaller and more targeted than the headline suggests, and not where most people assume.

Everyone pictures the Northeast as fluid country. It isn’t anymore. Order 1’s Class I utilization has run in the high-20s to low-30s percent in recent months, and sat near 20% in 2024. The truly Class I-heavy orders are the Southeast (Order 7) and Florida (Order 6), which run on skim-fat pricing and post the highest uniform blend prices in the country — Florida’s statistical uniform price hit $24.04/cwt this past April against far lower manufacturing-order prices. That’s where an organic exit from the pool actually bites a conventional blend price. In Upper Midwest cheese-and-butter country, a multiple-component-pricing order where January 2026’s PPD was just $0.46/cwt, you’d barely feel it.

Organic accounts for about 3% of total U.S. milk and a larger share of Class I fluid. Pull it out, and the net payers shrink; the Class III and IV plants that currently receive PSF money get a little less. Spread CODE’s ~$50M/year across the affected orders and the per-cwt hit is real but small.

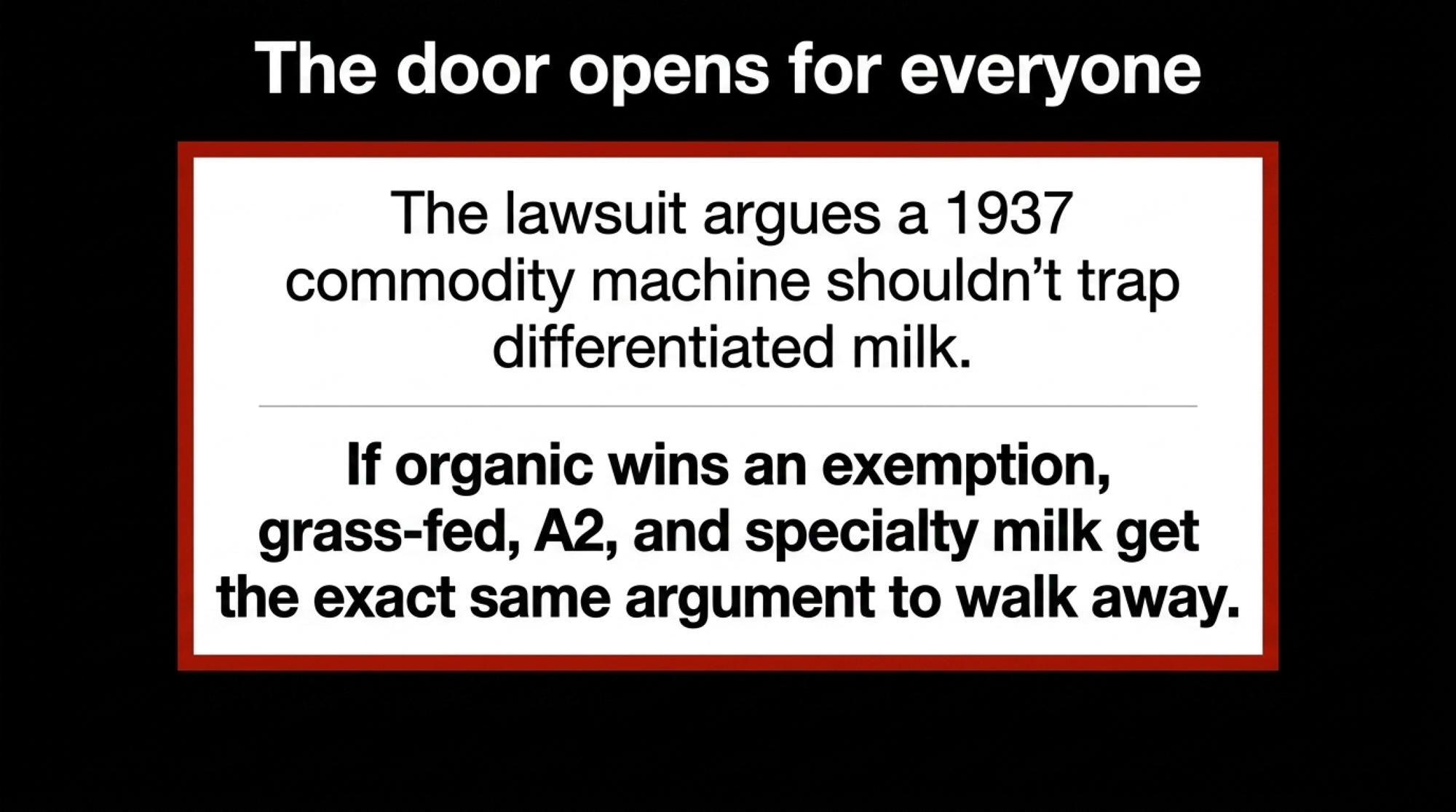

Here’s the bigger question, the one that should keep co-op boards up at night. CODE isn’t only asking for an organic carve-out. They’re arguing the FMMO was never built for a differentiated market — that a 1937 commodity machine structurally punishes any product that’s legally distinct, sells at a premium, and can’t swap commodity milk into its supply chain. Win on that, and grass-fed, A2, and high-protein specialty milk all get the same argument, ready-made. That’s not a certainty. It’s a door — and CODE just showed everybody where it is. (See also The Bullvine’s coverage of building-component premiums and differentiated-milk market position.)

The 30/90/365-Day Playbook for Herds Like Ranck’s

In the next 30 days — run the urgent checks.

- Know your order and how it prices. If you ship into Florida (Order 6) or the Southeast (Order 7), you’re in a skim-fat order that pays a single uniform blend price directly — that blend value is your exposure, and it’s among the highest in the country. If you’re in a component-pricing order like the Upper Midwest, your check reflects fat, protein, and other solids plus a PPD, and your exposure to an organic exit is far smaller.

- Map your blend-price exposure, not a “pool draw.” Individual farmers don’t settle with the Producer Settlement Fund — handlers do. What matters for you is how much of your order’s blend value rides on Class I utilization that a premium-milk exit could thin out.

In the next 90 days — make the structural moves.

- Calendar USDA’s answer deadline and read what USDA files. Under Federal Rule of Civil Procedure 12(a)(2), the government gets 60 days from service, putting the window into roughly late August 2026 depending on the actual service date. A motion to dismiss on standing means USDA is dodging the merits; a head-on Horneargument means a durable fight.

- If you sit on a co-op board in a high-Class-I order, ask your GM one question: if organic exits the pool, what happens to our blend price — and who’s next in line behind them? Just don’t overreact to a lawsuit that’s 12–24 months from any ruling.

Over the next 365 days — position for the outcome.

- Model your blend price under a scenario where premium milk leaves the pool. If you’re manufacturing-heavy and your handlers draw from the PSF, a shrinking pool of net-payer handlers is a slow structural risk worth pricing into your next contract cycle.

- Track the parallel fight — USDA still hasn’t ruled on CODE’s Section 15A petitions, filed back in May 2025. Sitting on them can itself become an APA issue and reshape the timeline.

Realistic ruling horizon: 12–24 months minimum. Don’t expect a district decision before late 2027. But August tells you which movie you’re watching. (Background: The Bullvine’s ongoing coverage of the Class III/IV price squeeze on family-scale operations.)

What This Means for Your Operation

The FMMO was built in 1937 for a market where milk was milk. The market it’s policing in 2026 has organic, grass-fed, A2, and specialty premiums the law never imagined and can’t substitute. CODE isn’t trying to burn the pool down — they’re asking three federal courts one question: can a Depression-era commodity system force a legally distinct product to pay for a pool it doesn’t use?

Lose, and nothing changes. Win small, and a couple of fluid-heavy Southern orders lose a little blend value. Win big — on the theory, not just the exemption — and the wall around your pool has a door in it. You gain nothing by waiting until the ruling to run your own numbers.

So here’s the contract check that matters more than the headline: know your order, know how it prices, and know how much of your blend value rides on Class I milk staying in the pool. What does your check look like if the biggest premium producers in the country win the right to walk out?

Key Takeaways

- This isn’t an organic fight — a CODE win shrinks the pool your blend price leans on, and it bites hardest in fluid-heavy Southern orders like Florida (Order 6) and the Southeast, not the Upper Midwest.

- The $50M/year, $60M class, and $400M-since-2006 figures are CODE’s own math, not audited findings. Read the arrow, not the number, until USDA answers.

- The lawsuit leans on Horne v. USDA, but Horne was a physical taking of raisins. Proving a regulatory cash pool is a “taking” is a real stretch, so don’t assume this wins.

- Before the late-August answer deadline, know your order and how it prices — Florida and the Southeast pay a uniform blend directly, so your whole blend value is what’s exposed.

Legal claims attributed to CODE and its members throughout; USDA had not publicly responded as of July 9, 2026. Docket numbers for the April 28 filings couldn’t be found in public PACER records at press time. The $50M/year, $60M class, $400M since 2006, and ~60% pool-burden-increase figures originate with CODE/Organic Valley and have not been independently verified. FMMO class prices, make allowances, uniform prices, and PPDs are sourced from USDA AMS and Federal Order market administrator sources. The ~$0.35/cwt annual organic pool-drag figure and the 16,000 lb/cow organic and 24,000 lb/cow conventional yields are labeled estimates. The Bullvine editorial team will source party and expert commentary separately.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The USDA Formula Change No Milk Check Explains — Arms your spreadsheet with the exact math behind the June 2025 make-allowance hikes that quietly stripped 90¢/cwt from your milk check long before market oversupply moved a single nickel.

- 25 extra miles is where your milk check starts bleeding — Delivers a blueprint to calculate your localized exposure to long-haul routing changes, proving why an extra 25 miles of transit instantly transforms hauling from standard background noise into a major margin drain.

- You Only Get 15.9¢ of the Food Dollar: A Dairy Farmer’s Playbook for Hauling, Co‑ops, and Premium Milk — Explores the necessary financial boundaries for specialty shipments, establishing a non-negotiable 15% to 20% net premium hurdle rate you must clear before shifting volume into niche A2, organic, or lactose-free contracts.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.