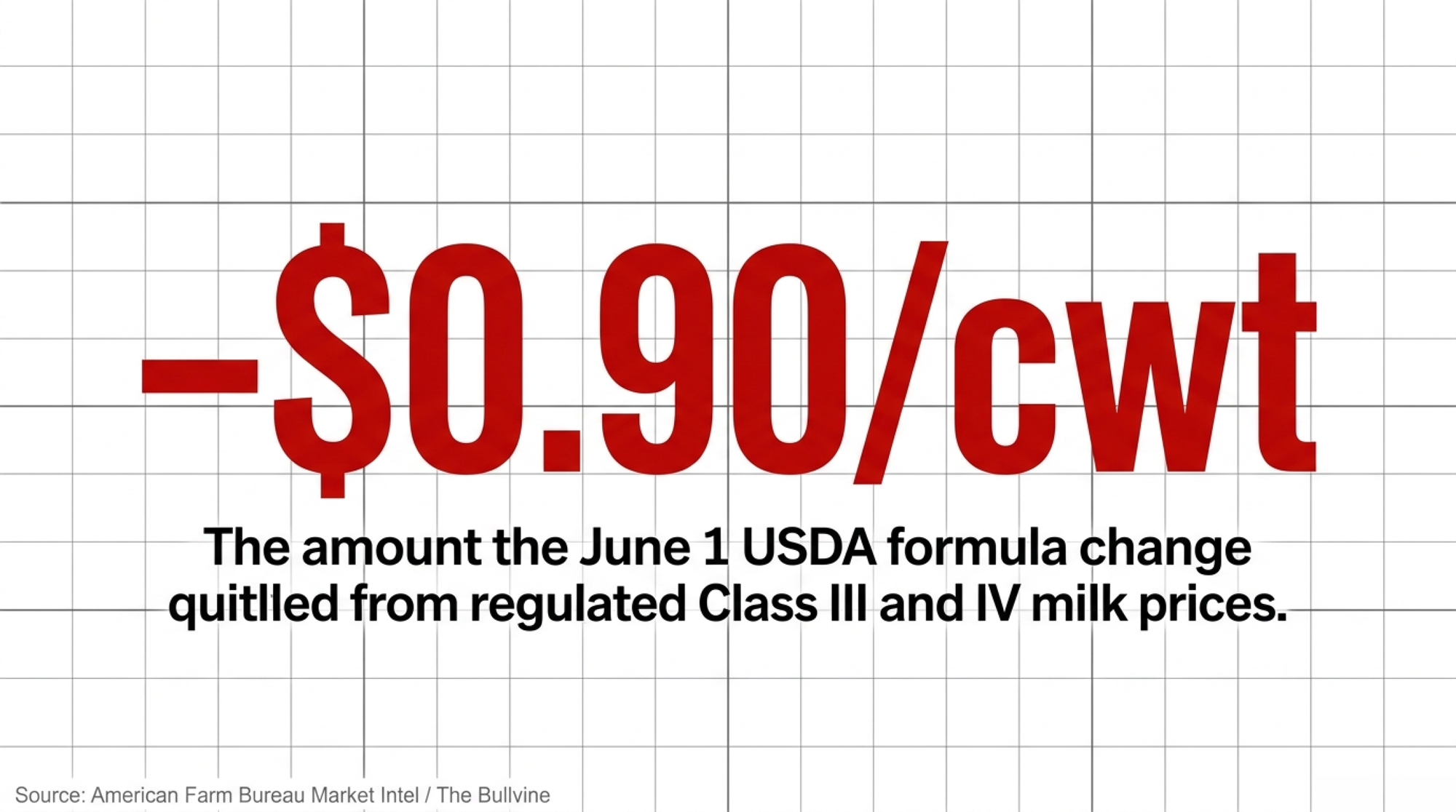

USDA reset make allowances June 1, 2025, and quietly pulled ~90¢/cwt from Class III/IV. On 1,000 cows, that’s about $262,000 a year — and no line on your check says so.

Executive Summary: On June 1, 2025, USDA reset FMMO make allowances for the first time since 2008, and that single formula change pulled roughly 90¢/cwt out of regulated Class III and IV prices — before global oversupply took a nickel. If your milk flows into cheese, butter, or powder across the Upper Midwest, Plains, or West, this hit you hardest, and nothing on your check spells it out. On a 1,000-cow herd shipping 80 lbs/day, that’s about $262,000 a year, gone; run your own pounds times 90¢, and the number scales straight up. AFBF’s Danny Munch clocked Class III down 86¢ and Class IV down 89¢ in the first three months, and here’s the part that stings: it’s structural, not cyclical, so it won’t bounce back when futures rally. Don’t count on shrinking global supply to bail you out either — Rabobank still has 2026 production up about 1%, and USDA has EU deliveries edging up 0.1%, not down. With 2026 all-milk forecast at $20.70, the real question is whether your operation can run 12 months at that number with 90¢ permanently baked into the floor. The move this month: run your DSCR without any DMC or Dairy-RP payments, and if it lands under 1.0x, that’s a lender conversation now — not at renewal.

Picture an Upper Midwest dairy milking 1,000 cows. Same parlor, same cows, same routine that penciled out fine in 2024.

Then the June 2025 milk check came back lighter. And it kept coming back lighter, month after month, with nothing new in the deductions column to point at. Nobody dried off the wrong cows. Nobody blew a ration. The math changed underneath them.

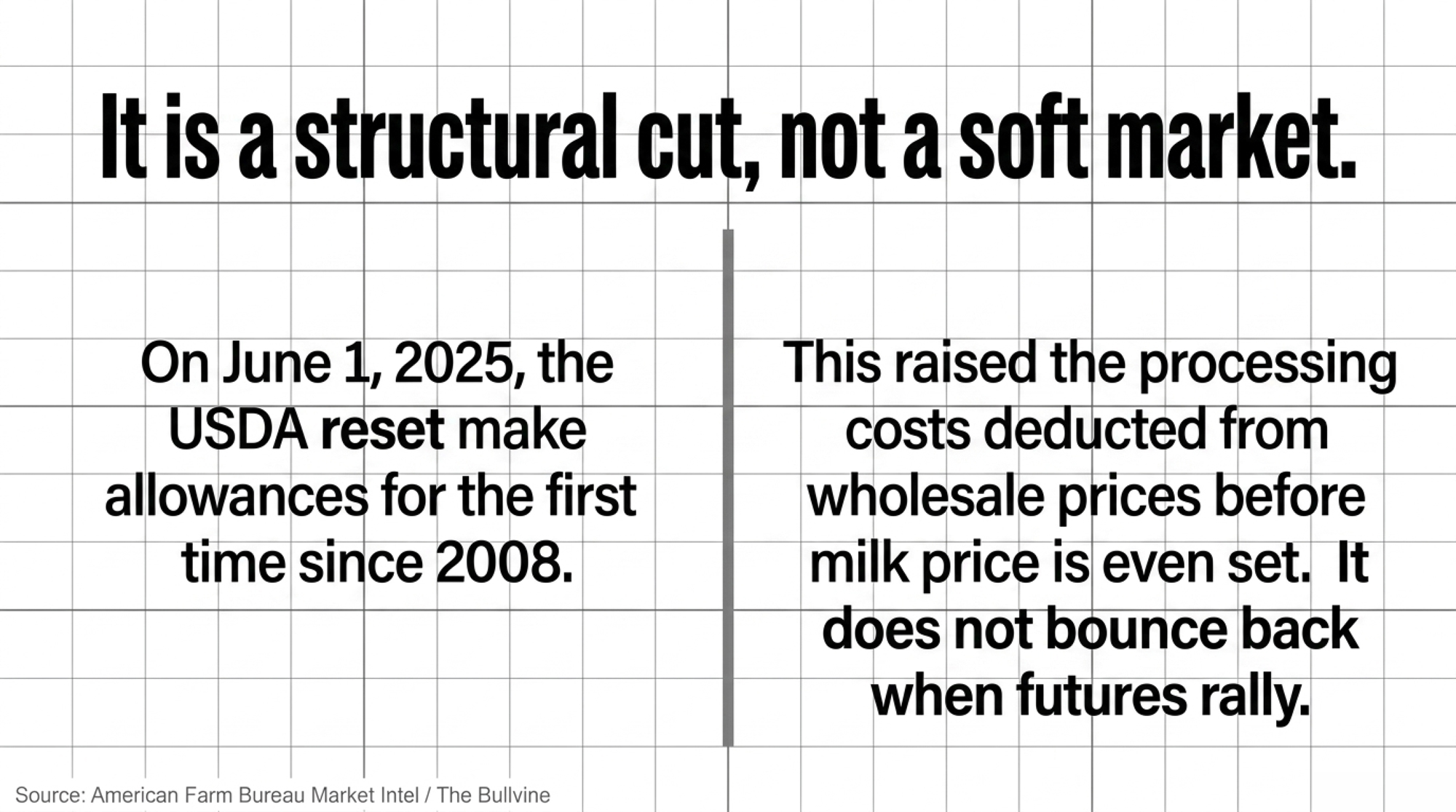

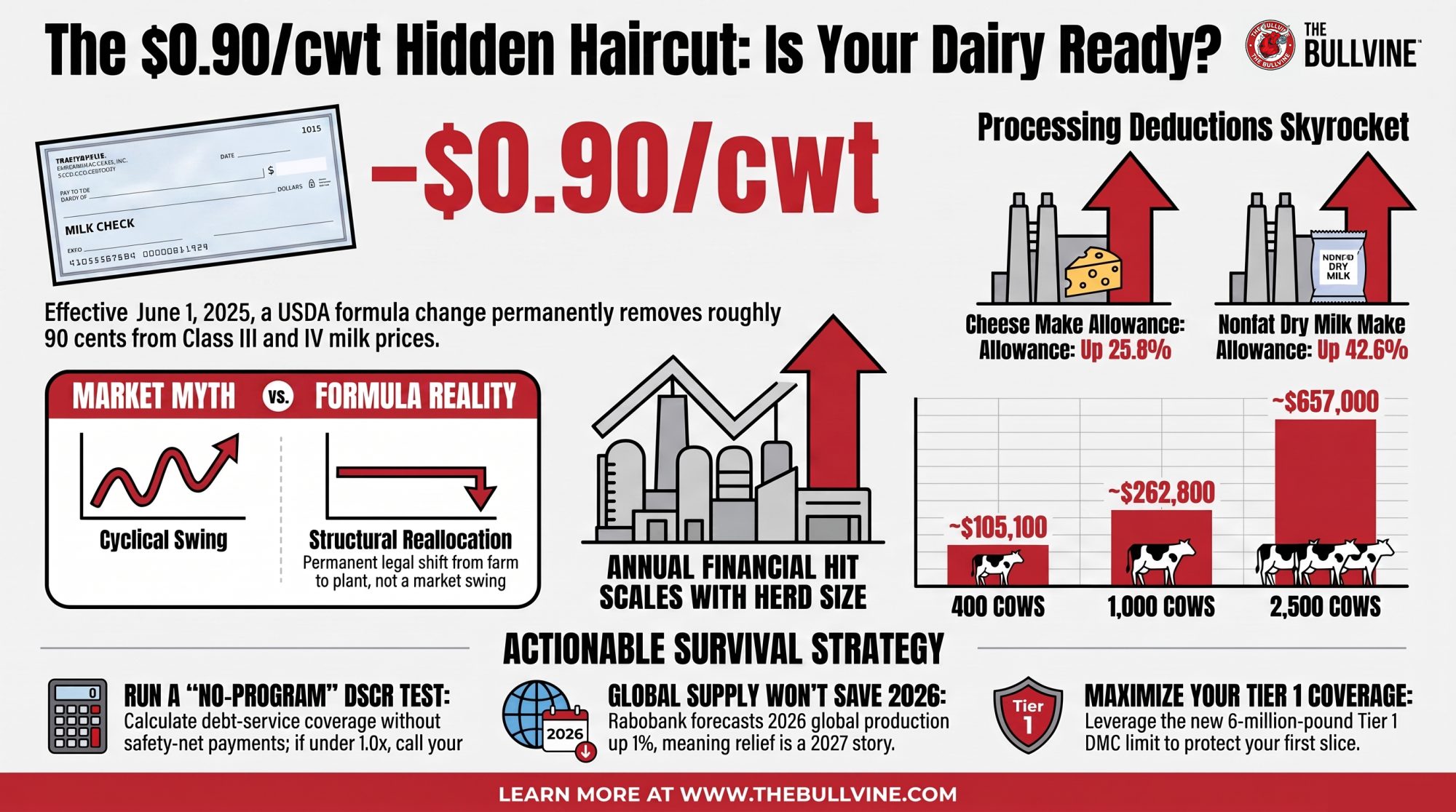

On June 1, 2025, a federal pricing formula quietly shifted. That one change pulled roughly $0.90/cwt out of regulated Class III and IV milk prices — before global supply moved a nickel.

That’s the make-allowance change. And it’s the part of the 2026 squeeze most producers felt in their gut but couldn’t name on paper.

What Actually Changed on June 1, 2025

A make allowance is the processing cost USDA subtracts from surveyed wholesale prices for cheese, butter, nonfat dry milk, and dry whey when it builds your Class III and IV milk prices. Raise that deduction, and the regulated milk price drops by the same amount — dollar for dollar, per pound of product.

It’s not a market force. It’s a formula input.

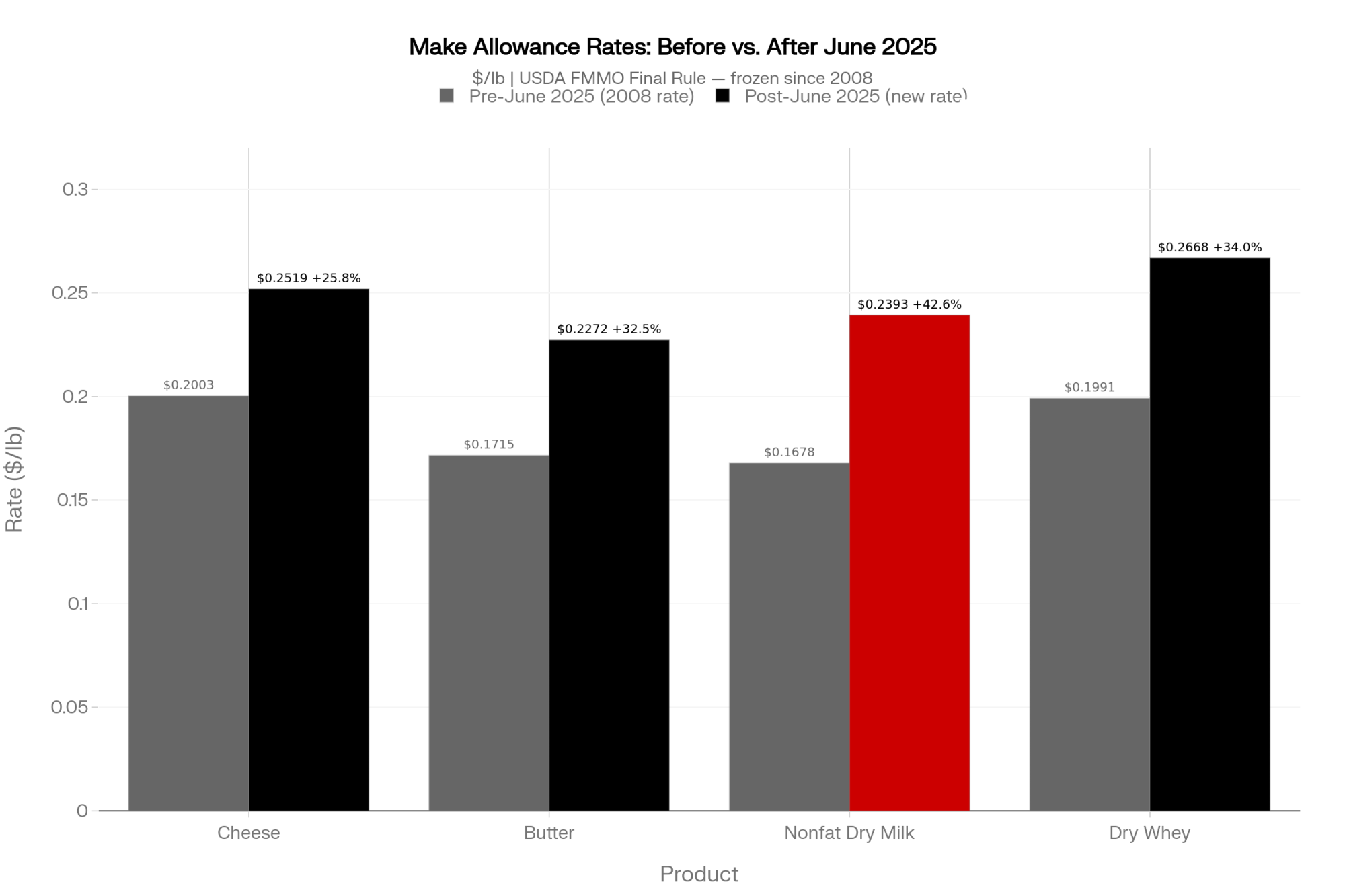

USDA’s final rule reset those allowances effective June 1, 2025: $0.2519/lb for cheese, $0.2272/lb for butter, $0.2393/lb for nonfat dry milk, and $0.2668/lb for dry whey. The old rates — frozen since October 2008 — were $0.2003 for cheese, $0.1715 for butter, $0.1678 for nonfat dry milk, and $0.1991 for dry whey, according to USDA Agricultural Marketing Service rulemaking.

Run the percentages and the jumps are steep: 25.8% on cheese, 32.5% on butter, 42.6% on nonfat dry milk, and 34.0% on dry whey. Those aren’t tweaks. The cheese number alone — a nickel a pound more carved out before the milk price is even set — is what does most of the damage to a III-heavy check, because cheese yield drives the Class III formula harder than anything else. The Bullvine has shown how thin the link already is between what your components are actually worth and what the formula pays you — and this rule widened that gap.

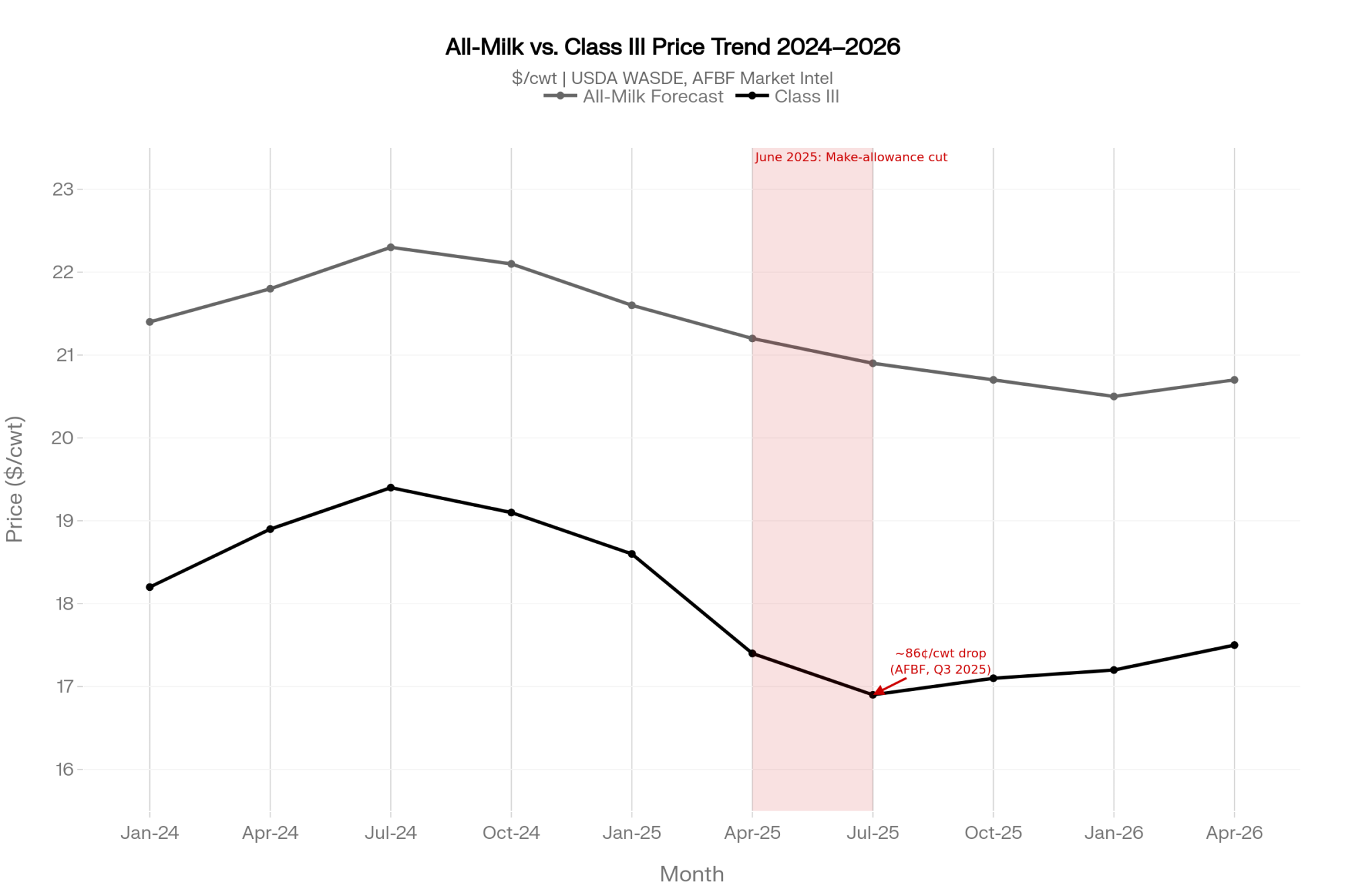

American Farm Bureau economist Danny Munch, tracking the first three months under the new rule, found average Class III prices fell about 86¢/cwt and Class IV about 89¢/cwt, with the make-allowance bump doing most of the damage, per American Farm Bureau Market Intel. The Bullvine’s own breakdown landed close by, at $0.94/cwt on Class III and $0.87 on Class IV.

The spread between those estimates comes down to method and which orders you weight — which is exactly why “roughly 90 cents” is the honest midpoint to plan around.

And who gets hit hardest? If your milk flows into cheese, butter, and powder — the Upper Midwest, the Plains, the West — your mailbox price leans on Class III and IV, so the haircut lands with full force. Fluid-heavy regions feel it less, because more of their value rides on Class I, which the same rule actually nudged higher in spots.

How This Plays Out in the Barn

Here’s what makes it so slippery: nothing on the check screams “USDA just took a dollar.” Class prices simply print lower.

So you blame exports, or China, or “the market” — and the formula change rides along invisible.

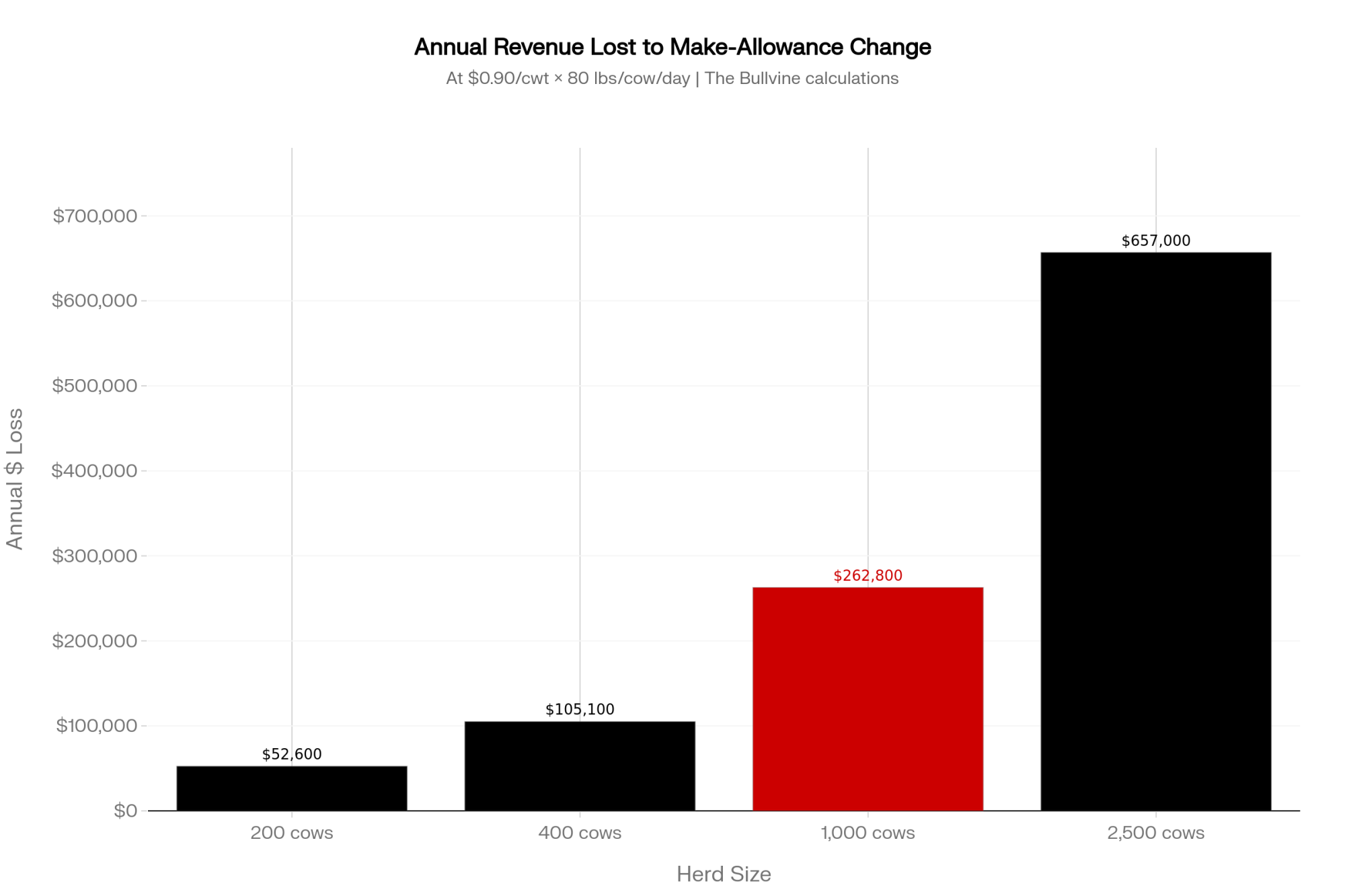

Run the math on that 1,000-cow herd. At about 80 lbs/cow/day — swap in your own average — you’re shipping roughly 292,000 cwt a year. A $0.90/cwt haircut works out to about $262,000 gone — every year — before a single cull cow leaves the yard or a futures contract moves.

The number scales cleanly with herd size, because it’s just pounds times 90 cents. Here’s the same math run across four herd sizes, all at 80 lbs/cow/day:

| Herd size | Approx. annual cwt | Annual hit at $0.90/cwt |

| 200 cows | 58,400 | ~$52,600 |

| 400 cows | 116,800 | ~$105,100 |

| 1,000 cows | 292,000 | ~$262,800 |

| 2,500 cows | 730,000 | ~$657,000 |

The Bullvine ran a version of this on a 400-cow herd and got close to $105,000 a year vanishing into the formula. Plug in your own per-cow production — a 90-lb herd ships more pounds, so the bite is bigger.

And it didn’t land in a vacuum. The rule took effect just as global milk surged through mid-2025, so the cut and the oversupply hit the same checks at the same time — but only the oversupply made headlines. USDA’s June 2026 WASDE lowered the 2026 all-milk forecast by 55¢ to $20.70/cwt — below 2025 and below full economic cost for a lot of mid-size herds.

Stack the structural cut on top of a soft market, and that “$1.25/cwt even when you do everything right” feeling stops being a complaint. It’s arithmetic.

The Mechanics Nobody Walked You Through

Why didn’t this register clearly? Because USDA bundled the bad news with some good.

The same rule package returned Class I to the “higher of” mover and raised Class I differentials in parts of the East — both lift fluid skim values. And there was a genuine offset for high-component herds: updated skim milk composition factors — protein assumptions raised from 3.1% to 3.3%, other solids from 5.9% to 6.0%, nonfat solids from 9.0% to 9.3% — that lift the calculated value of skim milk.

But that piece didn’t take effect until December 1, 2025, a full six months after the make-allowance cut had already been pulling cash out of checks.

| Rule Element | Effective Date | Who It Helps | Who It Hurts | $/cwt Impact |

|---|---|---|---|---|

| Make-allowance rate reset (cheese +25.8%, butter +32.5%, NDM +42.6%, whey +34.0%) | June 1, 2025 | Processors | Class III/IV producers (Upper Midwest, Plains, West) | −$0.86–0.94/cwt |

| Class I “higher of” mover restored | June 1, 2025 | Fluid milk regions (East/Southeast) | No direct impact on Class III/IV | +Variable |

| Class I differentials increased (select Eastern orders) | June 1, 2025 | Eastern fluid producers | — | +Variable |

| Skim milk composition factors updated (protein 3.1%→3.3%; other solids 5.9%→6.0%; nonfat solids 9.0%→9.3%) | December 1, 2025 | High-component herds | Low-component herds | +Partial offset |

| DMC Tier 1 coverage raised to 6M lbs at $9.50 margin | 2026 Farm Bill | Smaller herds (≤6M lbs production) | Large herds shipping 20M+ lbs — Tier 1 covers <25% of volume | Partial floor only |

| Net structural impact on Class III/IV mailbox price | Ongoing | — | All manufacturing-region producers | ~−$0.90/cwt permanent |

That staggered timing is what muddied the water. The big-picture message could stay neutral-to-positive even while the specific message for cheese-and-powder country was brutal: your core class prices just dropped almost a dollar.

Farm groups didn’t speak with one voice, either. Processors had pushed for higher make allowances for years, arguing real costs — energy, labor, packaging — had outrun rates frozen since 2008. That argument isn’t crazy on its face; nobody’s processing milk in 2026 at 2008 cost. But “the rate was stale” and “the producer should eat the entire catch-up in one step” are two very different conclusions, and the rule landed on the second one. Some producer groups swallowed the higher allowances as the price of getting “higher of” back. So the clean “you’re losing 90 cents” line got lost in the trade.

The distinction that matters: this isn’t cyclical. It doesn’t reverse when futures rally. The Bullvine put it bluntly — “that money is now legally reallocated from the farm to the plant.” It’s welded into the floor now.

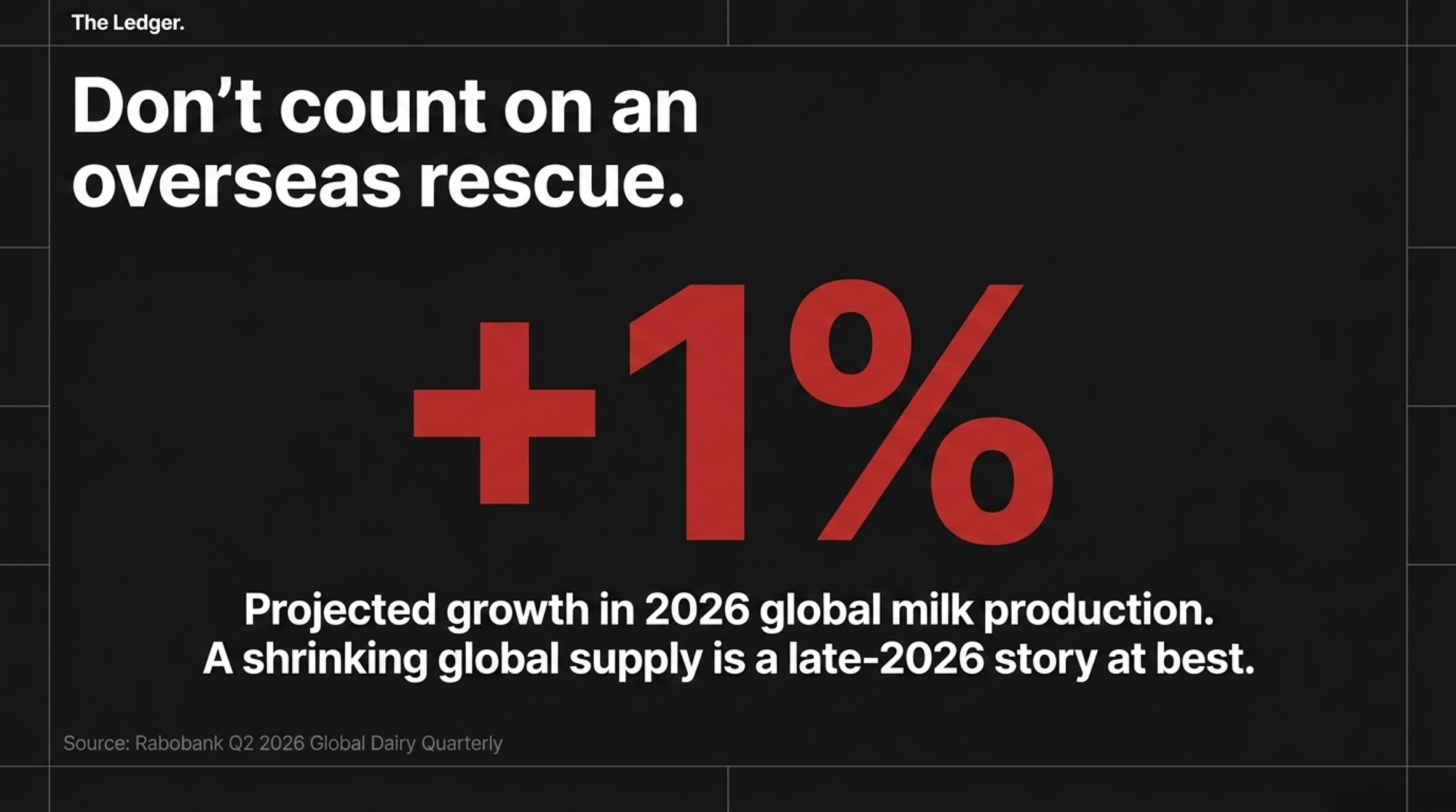

Won’t Slowing Global Milk Bail Out Prices?

Every few weeks a hopeful headline lands: the global wall of milk is finally cresting. And there’s truth to it — Rabobank’s Q2 2026 Global Dairy Quarterly, released in June, has Big-7 output growth peaking and milk supply turning negative by the fourth quarter, down an estimated 1.6% year-on-year.

But here’s the catch most of those headlines skip. Rabobank still pegs full-year 2026 global production up about 1%, following a 3.1% surge in 2025. The slowdown is a Q4 story, not a 2026 story. A herd budgeting on a calendar-year basis won’t feel a fourth-quarter dip until the back end of the year — long after the spring and summer checks are already spent.

So why doesn’t your check recover? Because the milk’s still coming. The U.S. is forecast to keep growing for the full year, and even Europe isn’t pulling back the way the “shrinking EU herd” story suggests — USDA’s Foreign Agricultural Service, in its June 2026 update, actually has EU cows’ milk deliveries edging up 0.1% in 2026 to about 148.6 million metric tons. That’s not a contraction. That’s flat-to-higher from the one region everyone keeps expecting to ride to the rescue.

The wall doesn’t come down until production actually contracts and stays there — and Rabobank doesn’t see that holding until late 2026 into 2027.

The Bullvine has laid out who actually blinks first in the global milk picture — worth a read if you’re tempted to bank on an overseas rescue.

How Much Does Doing Nothing Actually Cost You?

This is the question worth sitting with at the kitchen table. On a 1,000-cow herd shipping about 24,000–25,000 cwt a month, a $1.00/cwt shortfall against what you budgeted is roughly $25,000 a month — just under $300,000 a year.

The Bullvine’s risk math frames the smaller version cleanly: on 9,000 cwt, every $1.00/cwt gap is $9,000 a month.

Dairy Margin Coverage helps — but know exactly where it stops. Tier 1 coverage rose from 5 to 6 million lbs for 2026, with subsidized protection up to a $9.50 margin. That’s a genuine lifeline on your first 6 million pounds.

But a 1,000-cow herd ships around 29 million pounds, which leaves roughly 23 million pounds with no Tier 1 net under it. DMC puts a floor under part of your milk. It doesn’t fix a model that’s underwater before debt service.

If you want the coverage tables and lane-by-lane strategy, the full 2026 risk playbook breaks it down.

What This Means for Your Operation

Strip away the policy talk and it comes down to three things you can do something about. First, the make-allowance cut is now part of your structural cost of doing business, the same way a higher haul rate or a tighter component schedule would be — so it belongs in your budget as a permanent line, not a bad-luck footnote you expect to bounce back.

Second, the size of the hit scales directly with how many pounds you ship, which means your highest-production strings are also where the formula takes the most. That’s not a reason to pull production. It is a reason to make sure every one of those pounds is either hedged, contracted, or priced into a margin you can actually live with.

Third, the relief everyone’s waiting on — shrinking global supply — is a late-2026-into-2027 event at best, and Europe isn’t even cooperating with the story yet. Budget for the world you’re milking in now, not the one the optimistic headlines keep promising. If your 2026 cash-flow plan assumes a second-half price rally, stress-test it against milk staying near $20.70 and see whether the year still closes in the black.

Is Your Breakeven Number Written Down — or Just a Feeling?

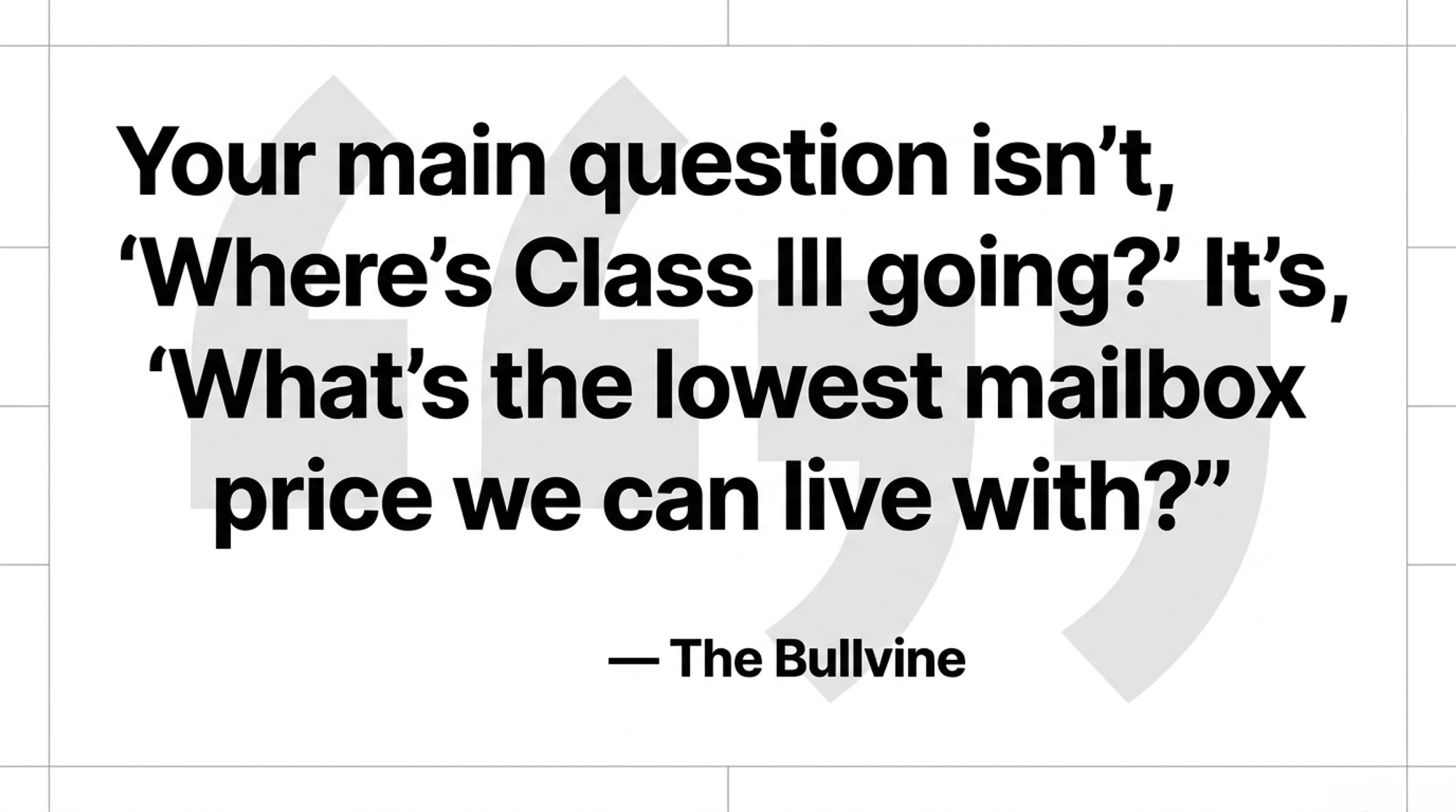

Here’s the one risk-management question most operators aren’t asking out loud: What’s the lowest mailbox price and margin over full cost you can ride for 12 straight months before you’re forced to cut cows, change the model, or get out — and what protection actually kicks in at that line?

Most producers can rattle off their rolling herd average from memory but can’t name that floor. The Bullvine said it plainly: “Your main question isn’t, ‘Where’s Class III going?’ It’s, ‘What’s the lowest mailbox price we can live with and still pay the bills and keep the lender comfortable?'”

Write the number down. Then tie specific hedges, DMC coverage, and cull triggers to it.

If you can’t name it, you’re not managing risk — you’re hoping the wall of milk spares your yard.

Options and Trade-Offs

Producers are handling this squeeze a few different ways. None is a silver bullet, and each one costs you something. Here’s how they stack up — scan the bold, then dig into the one that fits your operation:

- Layer DMC and Dairy-RP together: This remains a no-brainer for 2026, especially with the 6-million-pound Tier 1 bump. Just remember: DMC only protects your first slice; Dairy-RP has to handle the rest without capping your upside too heavily if the market rallies.

| Protection Tool | Coverage Trigger | Max Covered Volume | Approx. Annual Premium | Addresses Structural Cut? | Lender Comfort? |

|---|---|---|---|---|---|

| DMC Tier 1 (2026) | Margin < $9.50/cwt | 6M lbs (~75 cows) | ~$800–$1,200 subsidized | No — formula loss not a DMC trigger | Partial — floor on first slice only |

| DMC Tier 2 | Margin < $9.50/cwt | Unlimited (unsubsidized) | Rises steeply above 6M lbs | No | Partial |

| Dairy-RP (Class III/IV floor) | Declared price < insured level | Up to ~100% of production | $0.05–$0.15/cwt depending on coverage % | Yes — if floor set below current prices | Yes — quantifiable hedge |

| DMC + Dairy-RP layered | Combined triggers | Full production volume | $0.08–$0.20/cwt combined | Best available | Strongest lender case |

| No program | — | — | $0 | No | DSCR risk: <1.0x on many 1,000-cow herds |

| Futures hedge only | CBOT Class III | Variable | Basis risk + margin calls | Partial — doesn’t recover formula loss | Depends on structure |

- Run a “No-Program” DSCR Test within 30 days: Calculate your debt-service coverage ratio without any safety-net payments. If your herd sits below the 1.15x–1.25x benchmark your bank demands — The Bullvine’s 400-cow analysis found one at just 0.9x even after a $16,600 DMC “win” — you need a proactive conversation with your lender today, not at loan renewal.

- Audit your basis and your buyer: This matters most in manufacturing regions, where plant closures or consolidation can widen basis $2–3/cwt. The risk you can’t hedge is the one to name out loud: a buyer that simply stops taking your extra milk.

- Tighten breeding and replacement decisions before the cushions thin: Beef-on-dairy premiums and strong cull prices have been quietly masking the milk-margin problem — and both could face pressure by late 2026. The trade-off is real: more dairy replacements means giving up some beef-cross cash flow today.

Key Takeaways

- If you ship to a Class III/IV-heavy order, treat roughly $0.90/cwt of your 2025–26 price drop as structural, not market — and build your cash flow as if it’s permanent.

- Multiply your annual cwt by $0.90. If that number rattles you (a 1,000-cow herd: about $262,000; a 2,500-cow herd: north of $650,000), it belongs in your 2026 budget, not your blind spot.

- Run your DSCR without program payments this month. If it’s under 1.0x, that’s a lender conversation now — not at renewal.

- Don’t budget around a global supply rescue. Rabobank still has 2026 production up about 1%, and even the EU is edging up, not down — so the relief is a late-2026-into-2027 story at best.

- Watch your cushions. If beef-on-dairy premiums or cull prices soften while milk stays flat, the margin you thought you had disappears fast.

- Write down your 12-month floor — the lowest mailbox price you can survive — and attach a specific action to it before futures test that line.

So — Where Does Your Floor Actually Sit?

If milk holds near $20.70 and that make-allowance cut stays baked in, can your operation run 12 months at that number without leaning on the cushions? It’s not rhetorical. It’s the question your lender will ask at renewal, and the one your milk buyer is already modeling.

Pull last June’s milk check and this one, lay them side by side, and see how much of the gap you can actually explain. The part you can’t? Some of that is the formula.

Calculate Your Structural Make-Allowance Hit

Enter your herd size or annual milk volume to see the real impact of the USDA formula shift on your operation.

*Based on a baseline structural loss midpoint of $0.90/cwt across Class III and Class IV pricing formulas following the June 1, 2025 FMMO modifications.

Editor’s Note: The 1,000-cow operation described below is a composite scenario, modeled from typical Upper Midwest herds shipping to Class III and IV markets. It does not represent any single real farm. The dollar figures are drawn from USDA, the American Farm Bureau, and published Bullvine calculations, as cited throughout.

Learn More

- $50K Gone: Von Ruden Reveals FMMO Make Allowance’s 300-Cow Dairy Gut Punch — Exposes the exact math behind the 90-cent regulatory deduction and equips you with a 30-day milk statement verification checklist to separate structural formula hair-cuts from normal commodity price drops.

- Class III Milk Price, DRP, and Your Spring 2026 Risk Plan – The Bullvine — Arms you with a concrete risk-management playbook that outlines defensive, balanced, and aggressive positioning strategies to shield uncovered milk volume from devastating multi-thousand-dollar monthly margin swings.

- Squeezed Out? A 12-Month Decision Guide for 300-1,000 Cow Dairies — Dismantles outdated breeding priorities by mapping out the fundamental structural pivot from butterfat to protein, proving how genetics selected two years ago are running directly into a vanishing market.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.