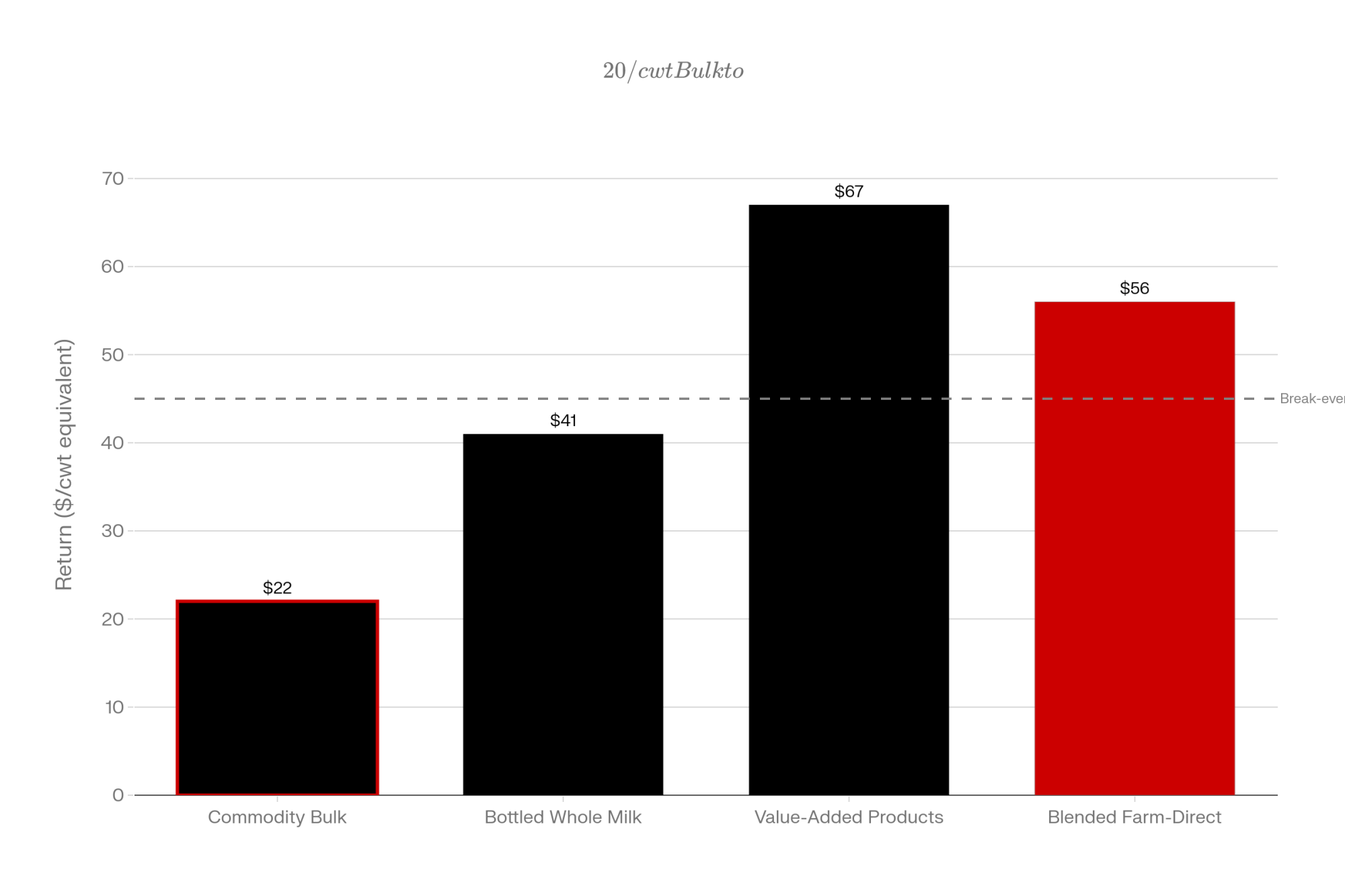

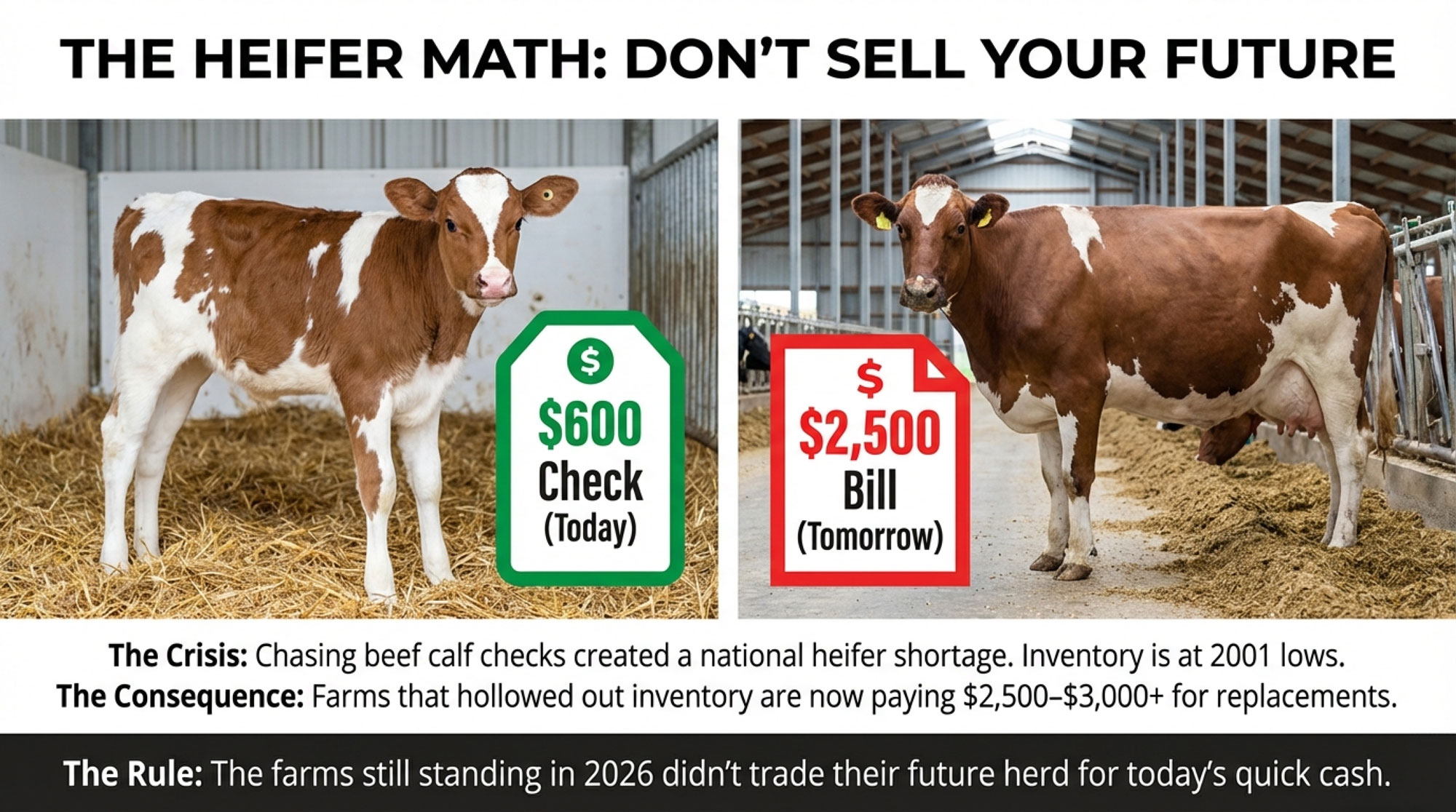

$600 beef calf or $2,500 heifer? The farms still standing in 2026 didn’t trade their future for today’s calf check.

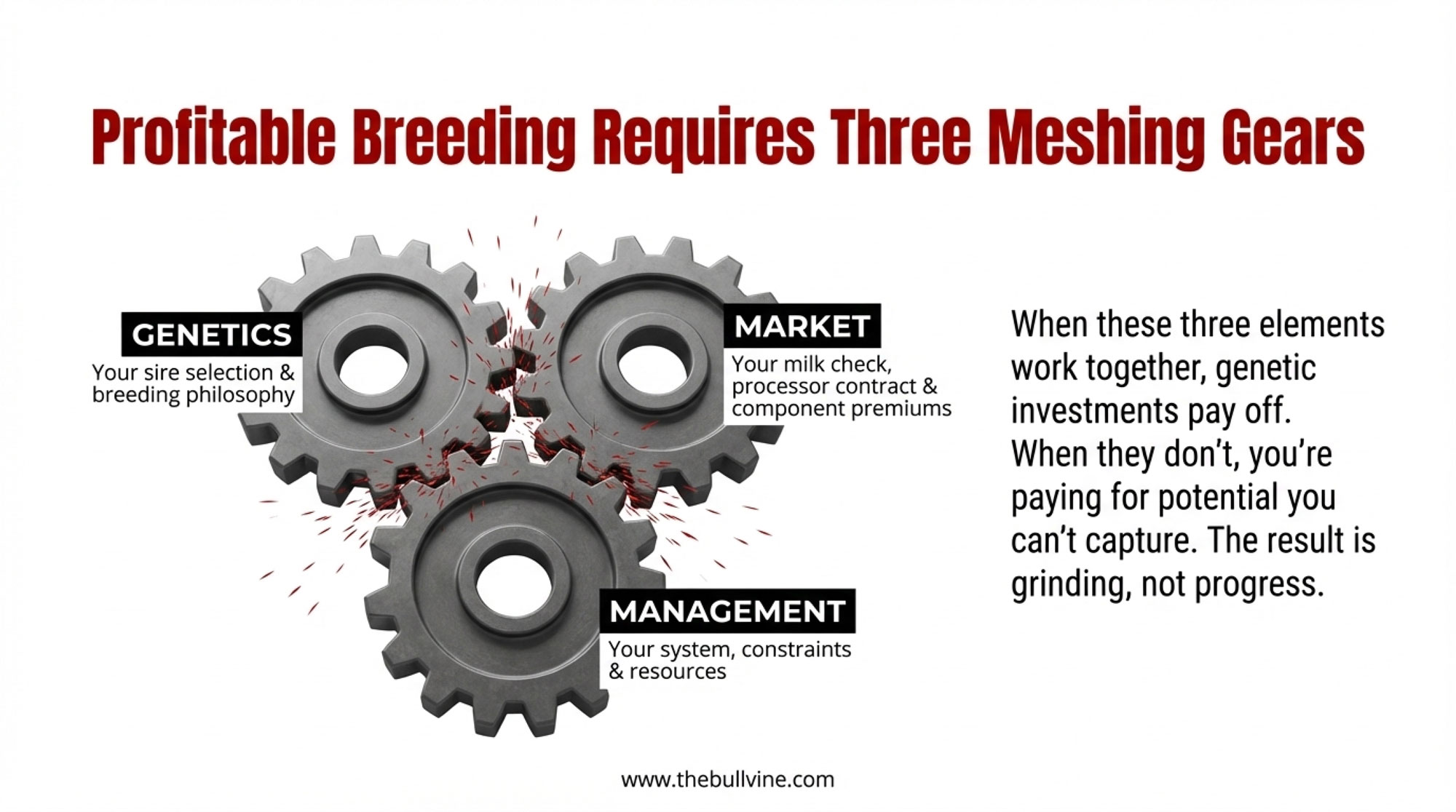

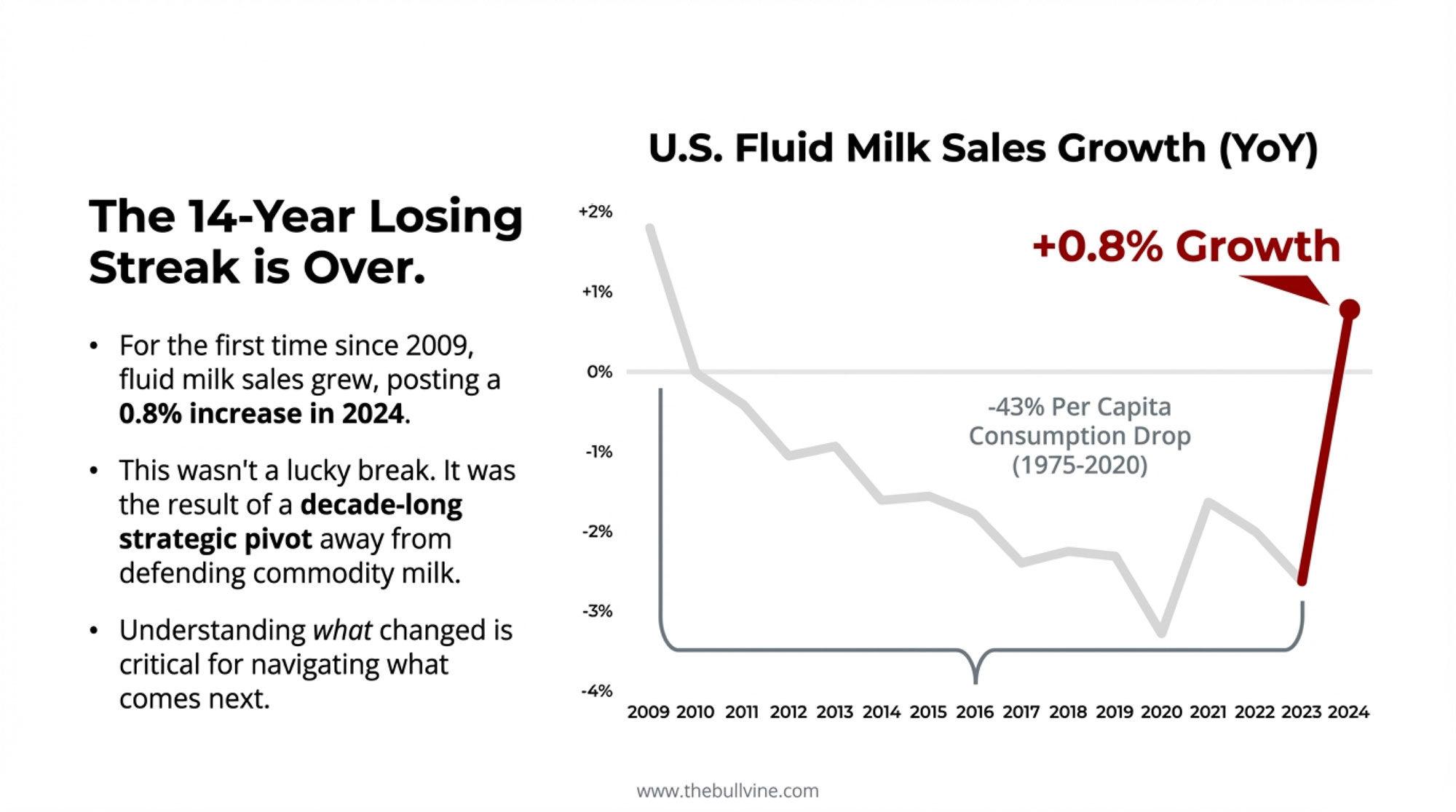

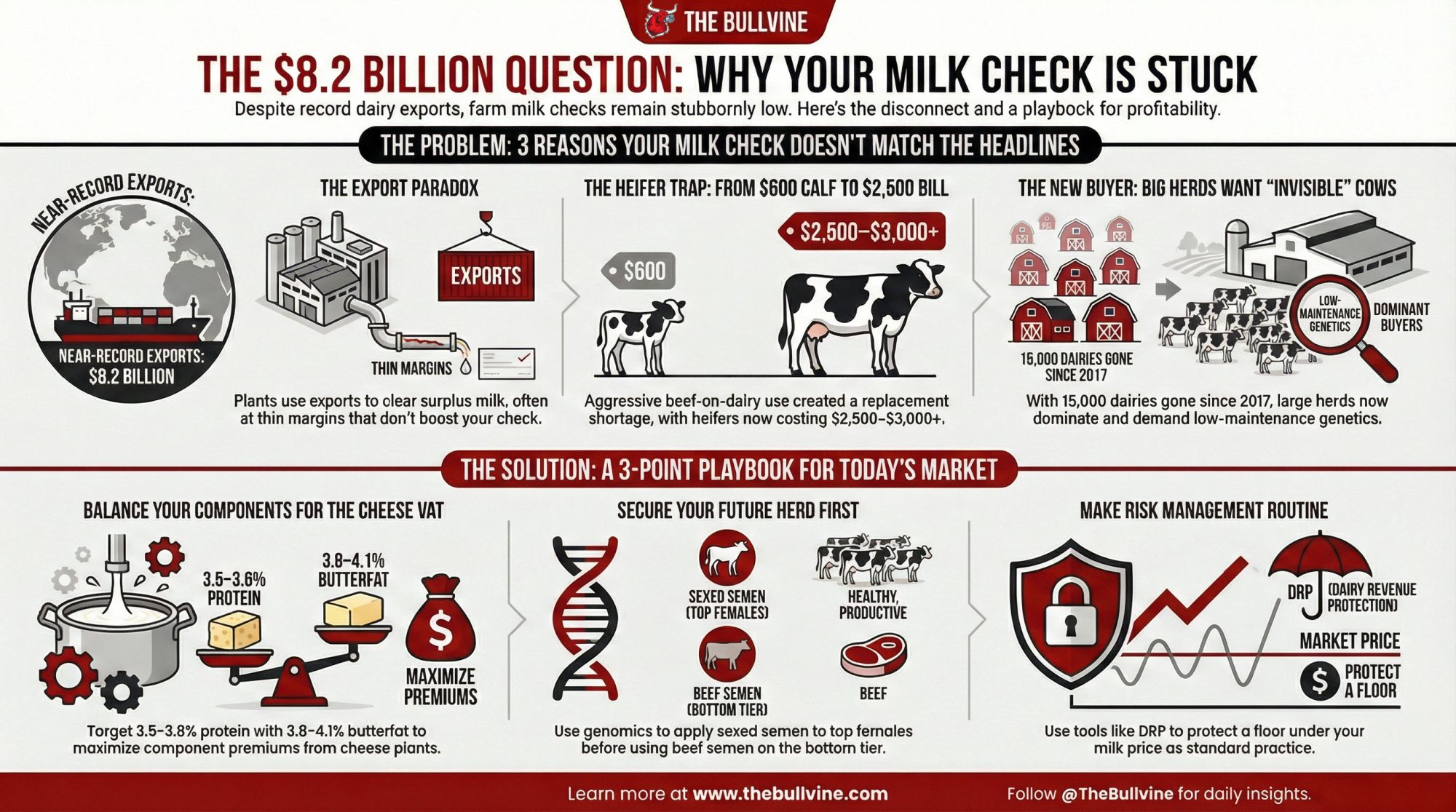

Executive Summary: U.S. dairy exports hit $8.2 billion in 2024, yet milk checks stayed stubbornly flat—and understanding why matters for your next move. The gap comes down to three forces: processing overcapacity that needs export markets to clear marginal pounds, a component shift in which cheese plants now reward protein over extreme butterfat, and a heifer shortage, many herds created by chasing $600 beef calf checks instead of protecting replacements. Today, quality heifers command $2,500–$3,000+, and the math has flipped. Consolidation has reshaped the landscape, too—15,000 dairies exited between 2017 and 2022, with 1,000+ cow herds now producing two-thirds of U.S. milk and demanding “invisible” cows that stay off the treatment list. The operations thriving in this environment share a playbook: components tuned to their plant’s grid, genomics and beef-on-dairy strategies that secure the replacement pipeline, and risk management treated as routine—not a crisis response. The next 12–24 months will separate the farms that planned from the farms that hoped.

You’ve probably lived this. You sit through a winter meeting where someone from the co‑op says, “Exports are strong, global demand looks good, U.S. dairy is well‑positioned.” The slides are full of big numbers. Then you get home, sit down at the kitchen table, open your milk check… and it feels like you’re farming in a different industry than the one they just described.

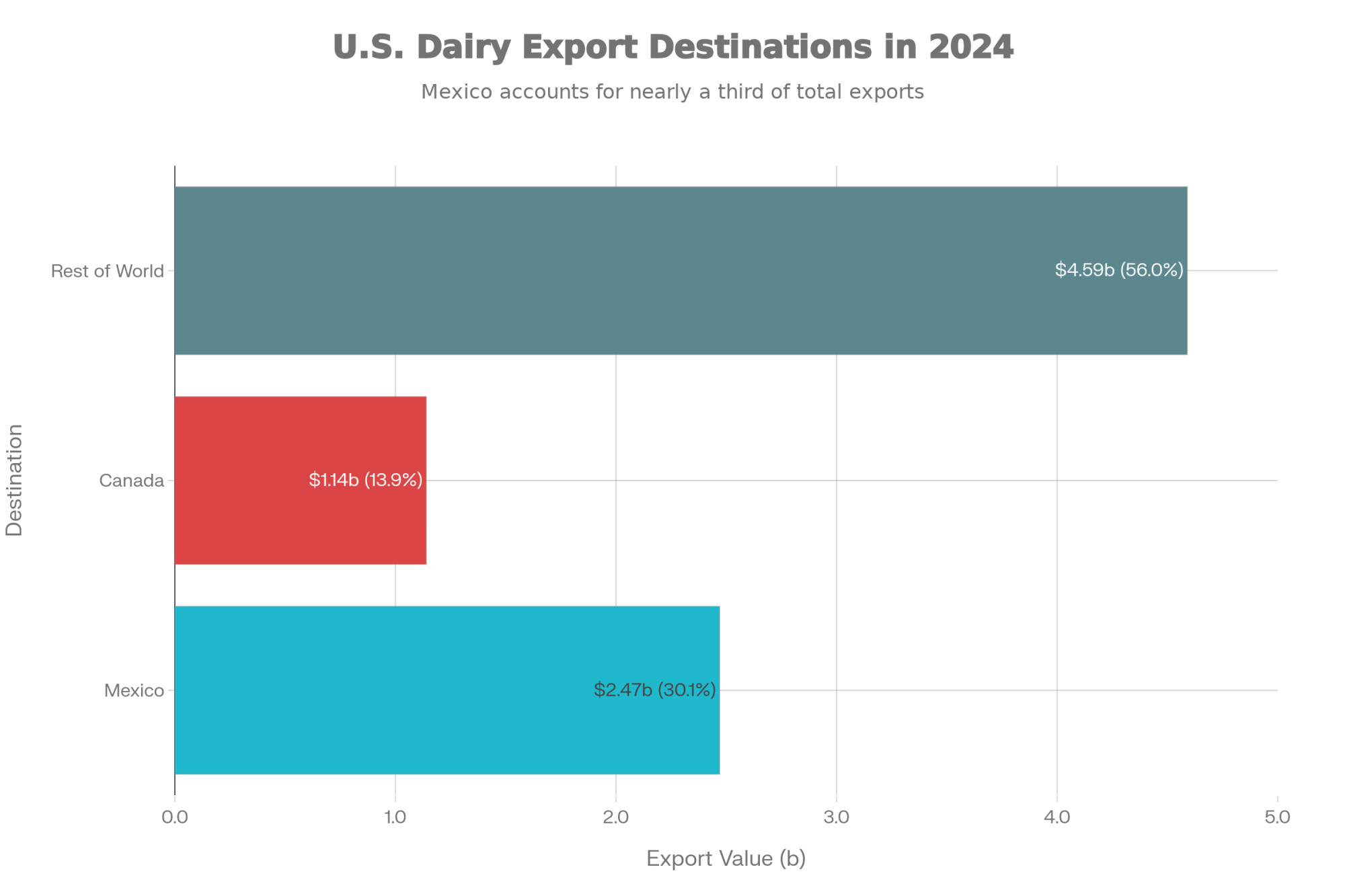

What’s interesting here is that those export numbers really are big. USDA’s Foreign Agricultural Service, in numbers summarized by IDFA, Dairy Processing, Dairy Foods, and Progressive Dairy, put 2024 U.S. dairy exports at about 8.2 billion dollars, the second‑highest export value on record after the 9.5‑billion‑dollar peak in 2022. Mexico took roughly 2.47 billion dollars of that total, and Canada about 1.14 billion, so together those two neighbors account for just over 40 percent of everything the U.S. ships overseas by value. Export coverage from USDEC highlights that Mexico is consistently the top buyer of U.S. cheese and skim milk powder.

Early 2025 commentary from market analysts suggests exports have generally held up reasonably well compared to 2024, with cheese shipments in particular staying firm in several key months. So that “exports are strong” line on the slides isn’t spin.

The question you and a lot of producers are asking is simple: if exports look that good, why doesn’t the milk check feel the same? To get at that, let’s walk through what’s happening at the plant, what’s changed with butterfat performance and protein, why geography still matters, what’s going on in Mexico—and then bring it right back to genetics, beef‑on‑dairy, fresh cow management, and risk decisions on your own farm.

Looking at This Trend from the Plant Side

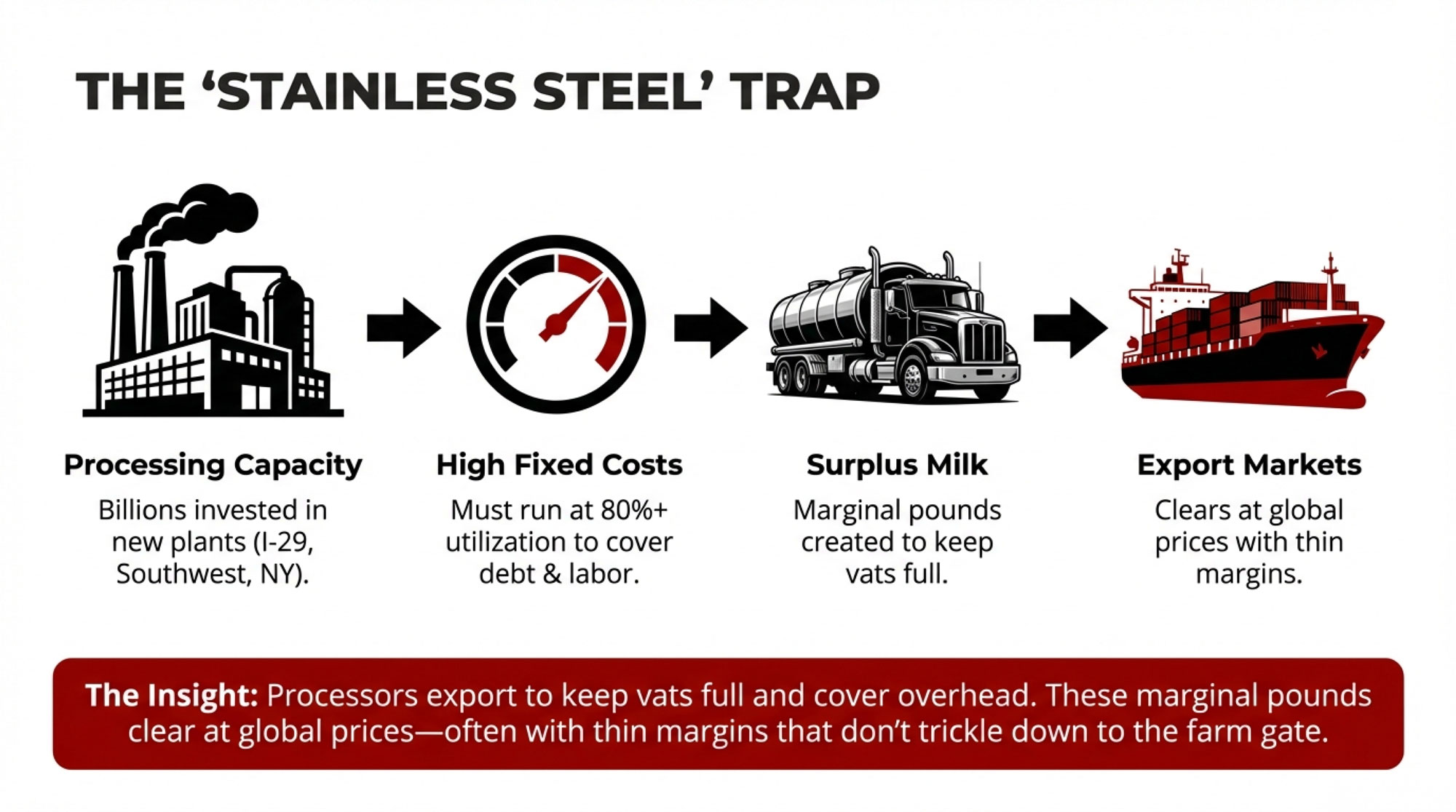

Looking at this trend from the processor’s side is where the fog starts to clear a bit.

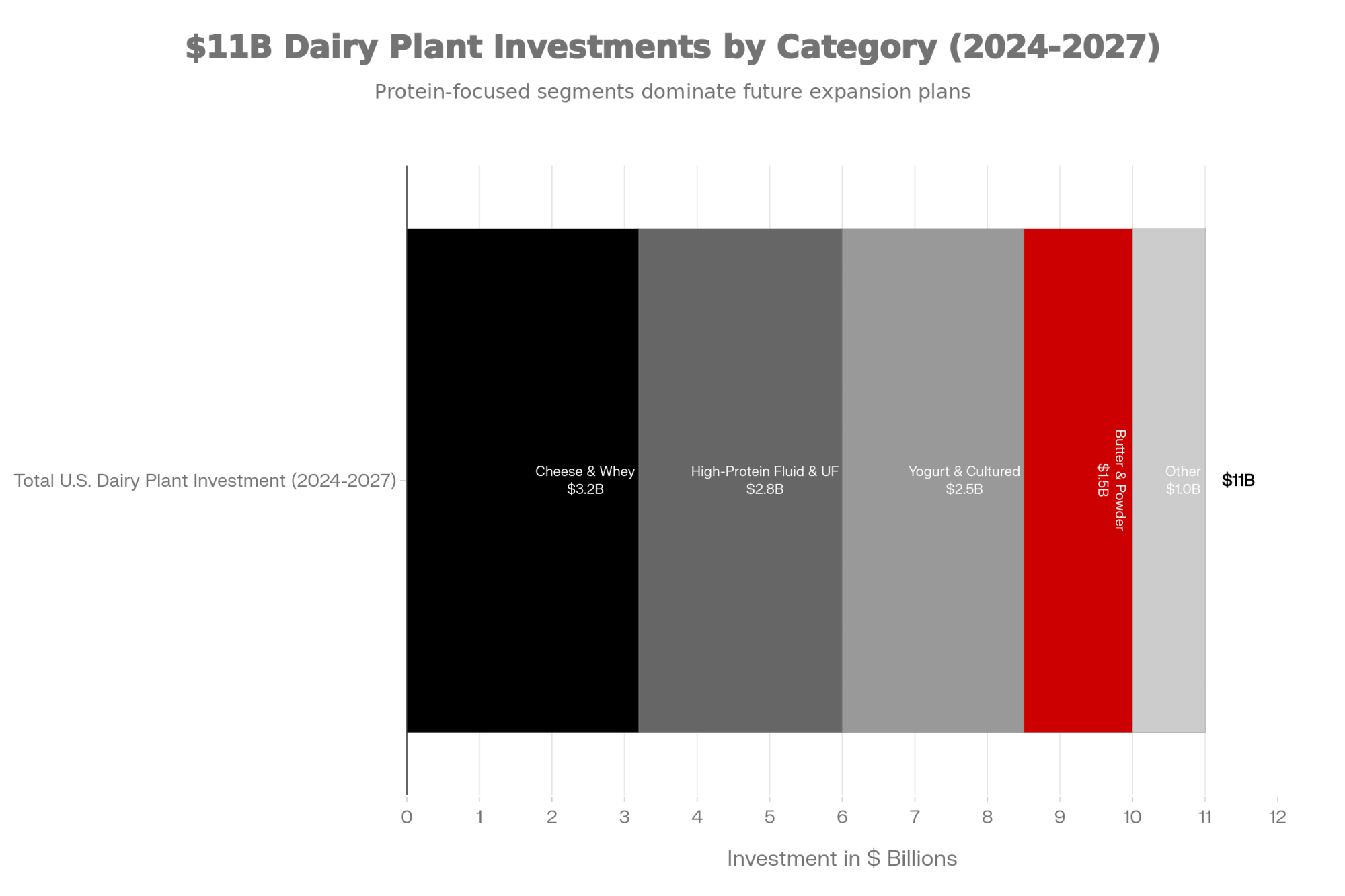

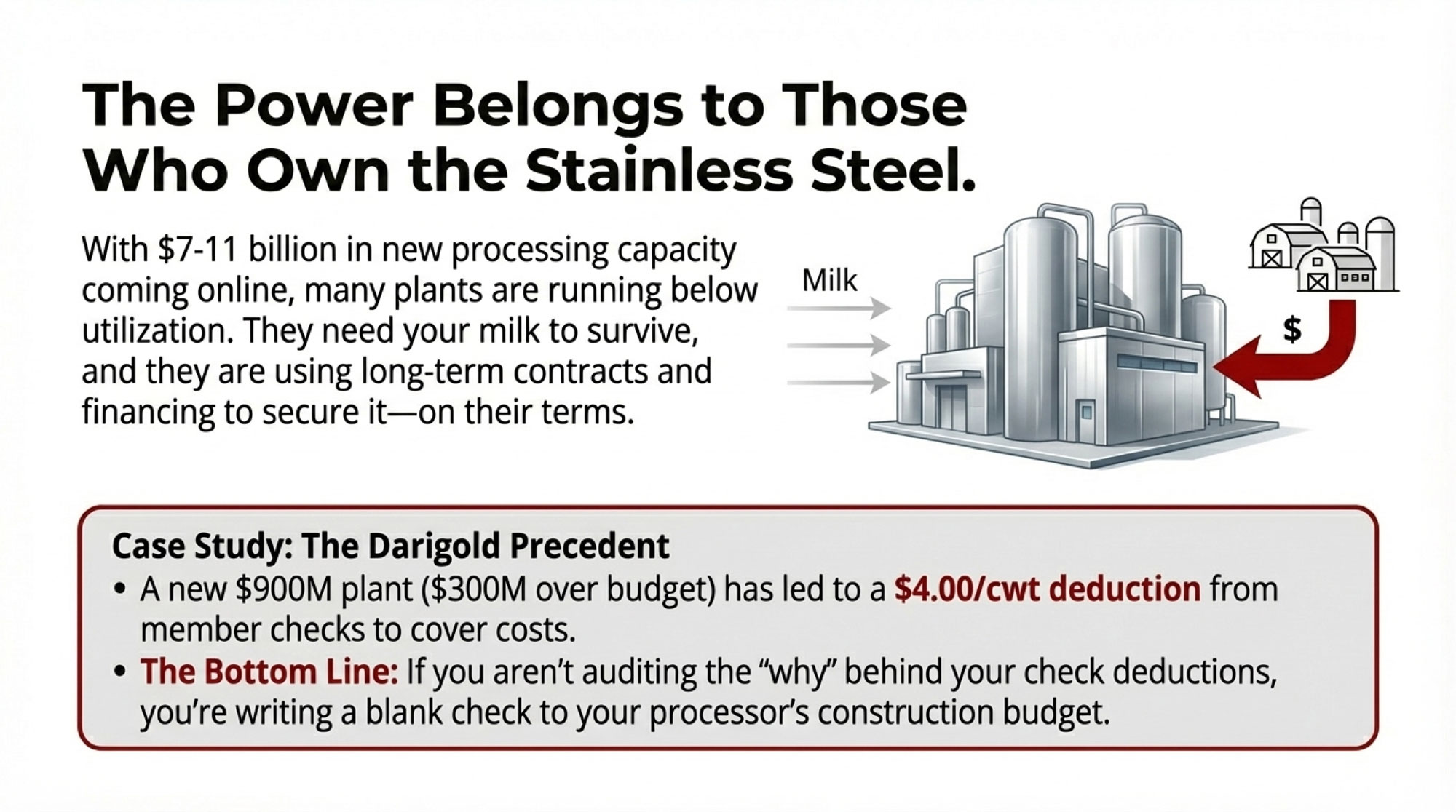

Over the last several years, processors have poured serious money into stainless steel. IDFA and industry analysts have talked about “historic levels” of processing investment, and Hoard’s Dairyman reported that roughly 8 billion dollarsworth of dairy processing projects—new cheese plants, powder facilities, and ingredient expansions—are in the works across the Upper Midwest, Plains, and Southwest. Brownfield Ag News and Dairy Herd have described “widespread growth underway,” citing new or expanded plants in South Dakota, Kansas, Texas, Idaho, and New York.

You see it most clearly along the I‑29 corridor. South Dakota has become one of the fastest‑growing dairy regions in the U.S., as new cheese capacity along I‑29 pulled in cows and capital. Kansas appears in USDA Milk Production reports and Progressive Dairy summaries as another state with steady multi‑year growth, driven by large freestall herds and added processing capacity. In New York, big yogurt and cheese plants—including Chobani’s facility at New Berlin—are regularly flagged in state and federal reports as major buyers anchoring regional milk sheds.

Here’s where the math gets real. Large cheese and powder plants are incredibly capital‑intensive. Dairy economists and plant managers consistently note that these facilities are built to run at high utilization—typically targeting 80 percent or higher—to spread fixed costs over as many cwt as possible. If you build a plant to handle 7 million pounds of milk a day and it only runs at 4 million, your cost per cwt jumps because the debt, labor, utilities, and maintenance don’t shrink just because the milk flow does.

So if the domestic market can only comfortably absorb, say, two‑thirds of what this whole system could produce at profitable prices, the rest has to move somewhere. That “somewhere” is export markets. USDEC summaries show that in 2024, the U.S. shipped record or near‑record volumes of cheese to destinations such as Mexico, South Korea, and Central America, and moved significant quantities of skim milk powder and whey to Asia and Latin America.

From the plant’s point of view, moving that extra product overseas at thin margins is often better than leaving vats idle. From your side of the milk check, those marginal export pounds don’t always create enough added value per cwt—after you factor in global competition, freight, and currency—to show up as a big jump. The plant can spread its fixed costs over a larger volume. You might see a bit better basis at times, but not the windfall “8.2 billion dollars” sounds like on a slide.

That’s the first piece of the export paradox: big export dollars and stubborn milk checks can absolutely coexist.

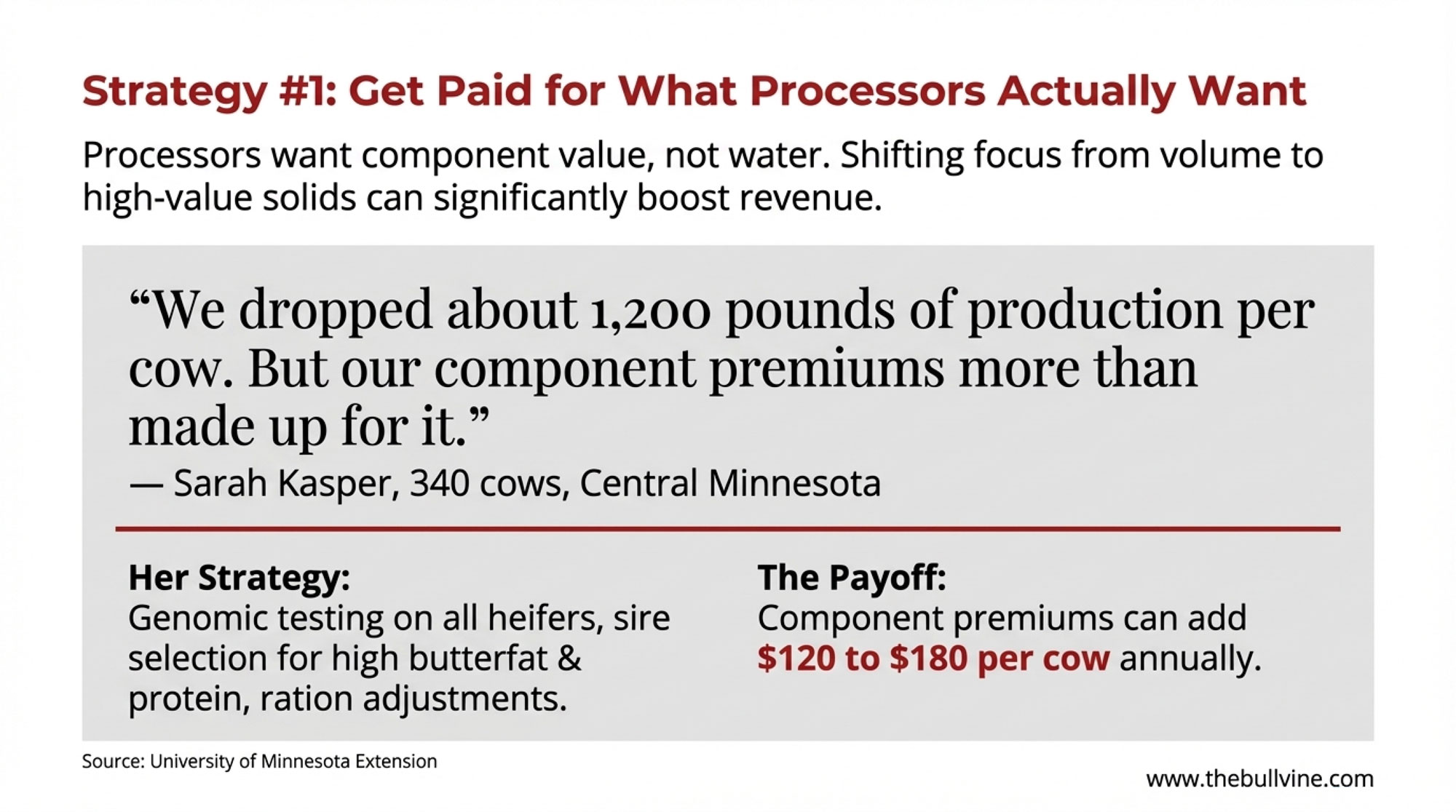

What Farmers Are Finding About Components

Now let’s bring this back into the parlor, because butterfat levels and protein are doing more of the talking on your milk check than many of us expected a few years ago.

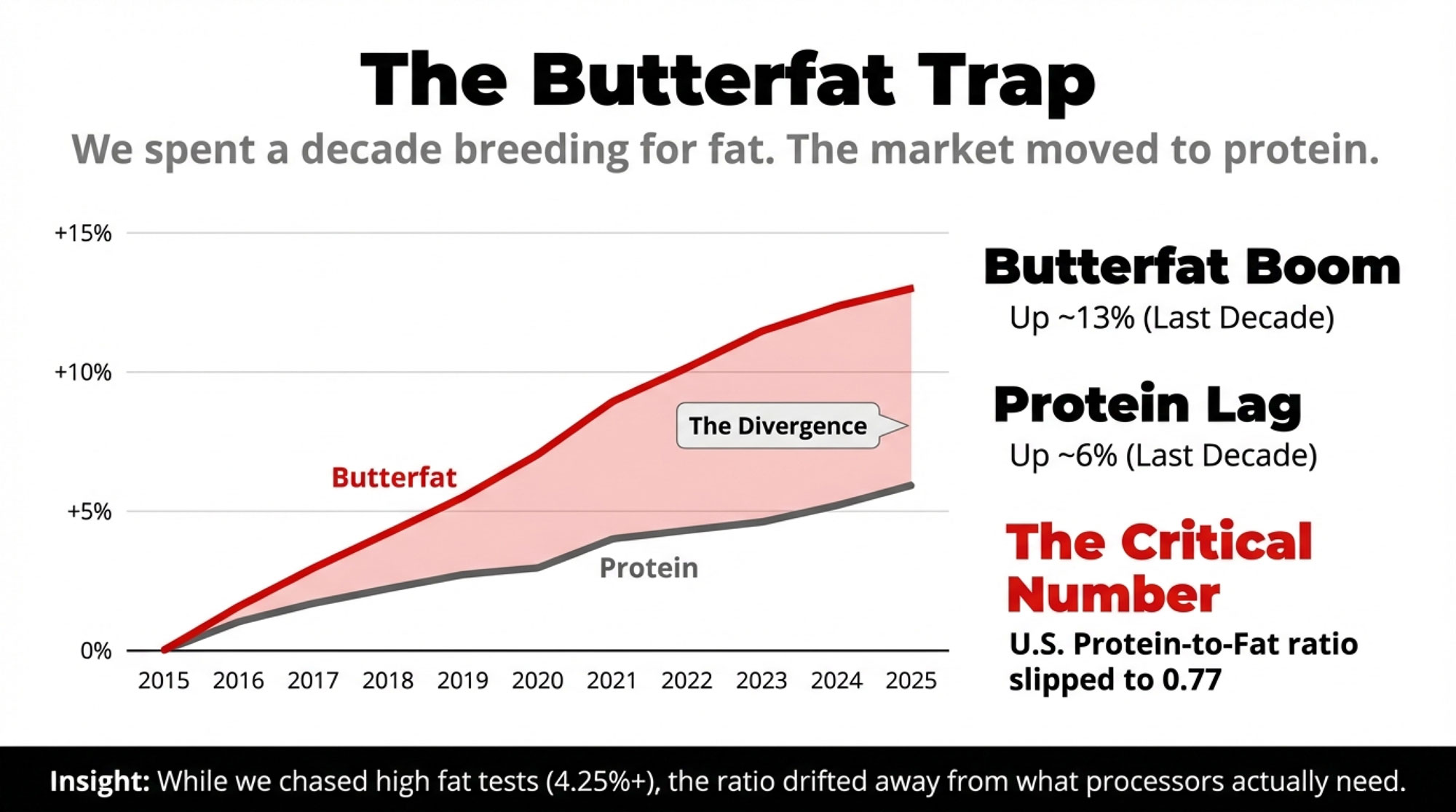

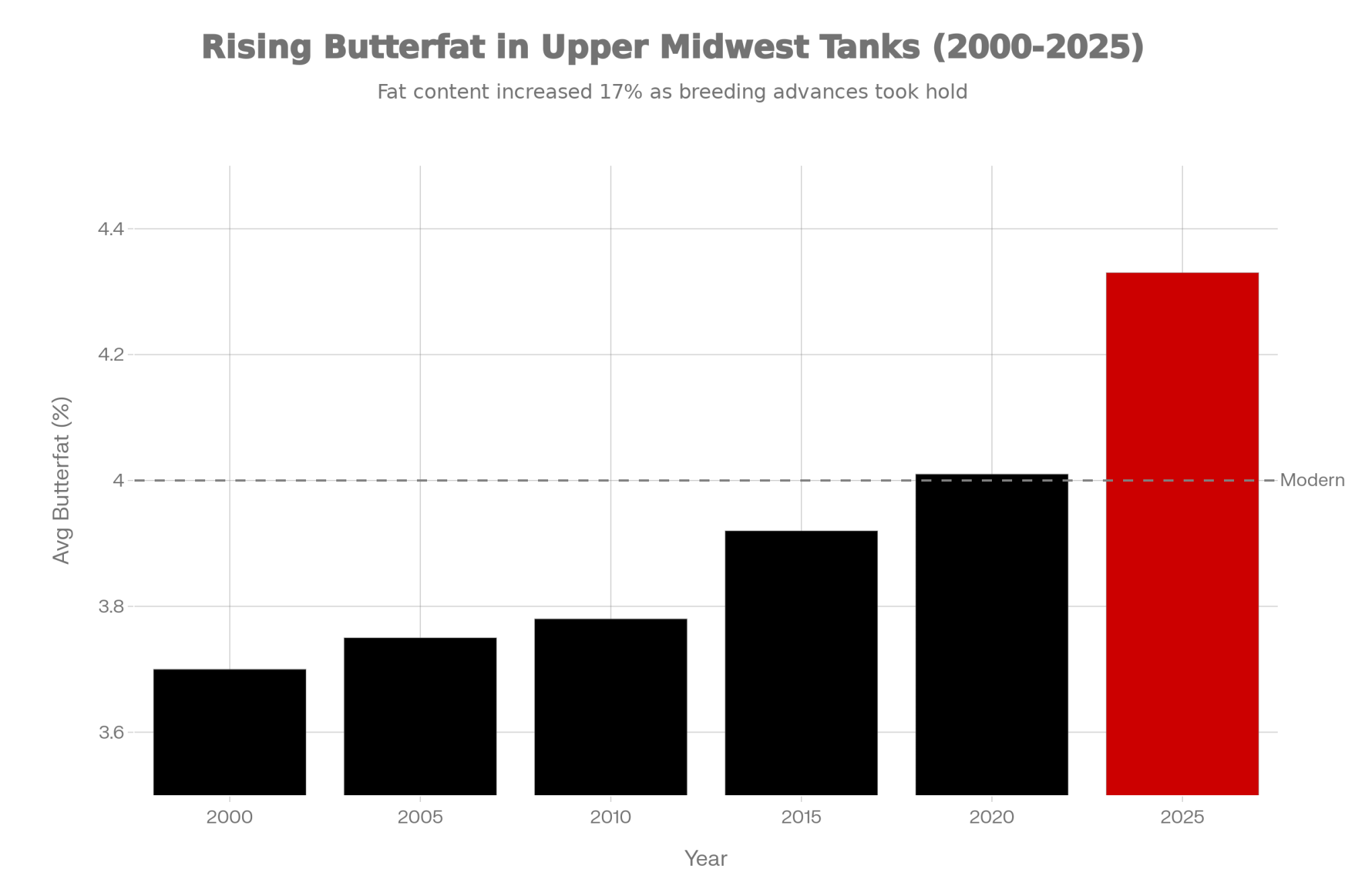

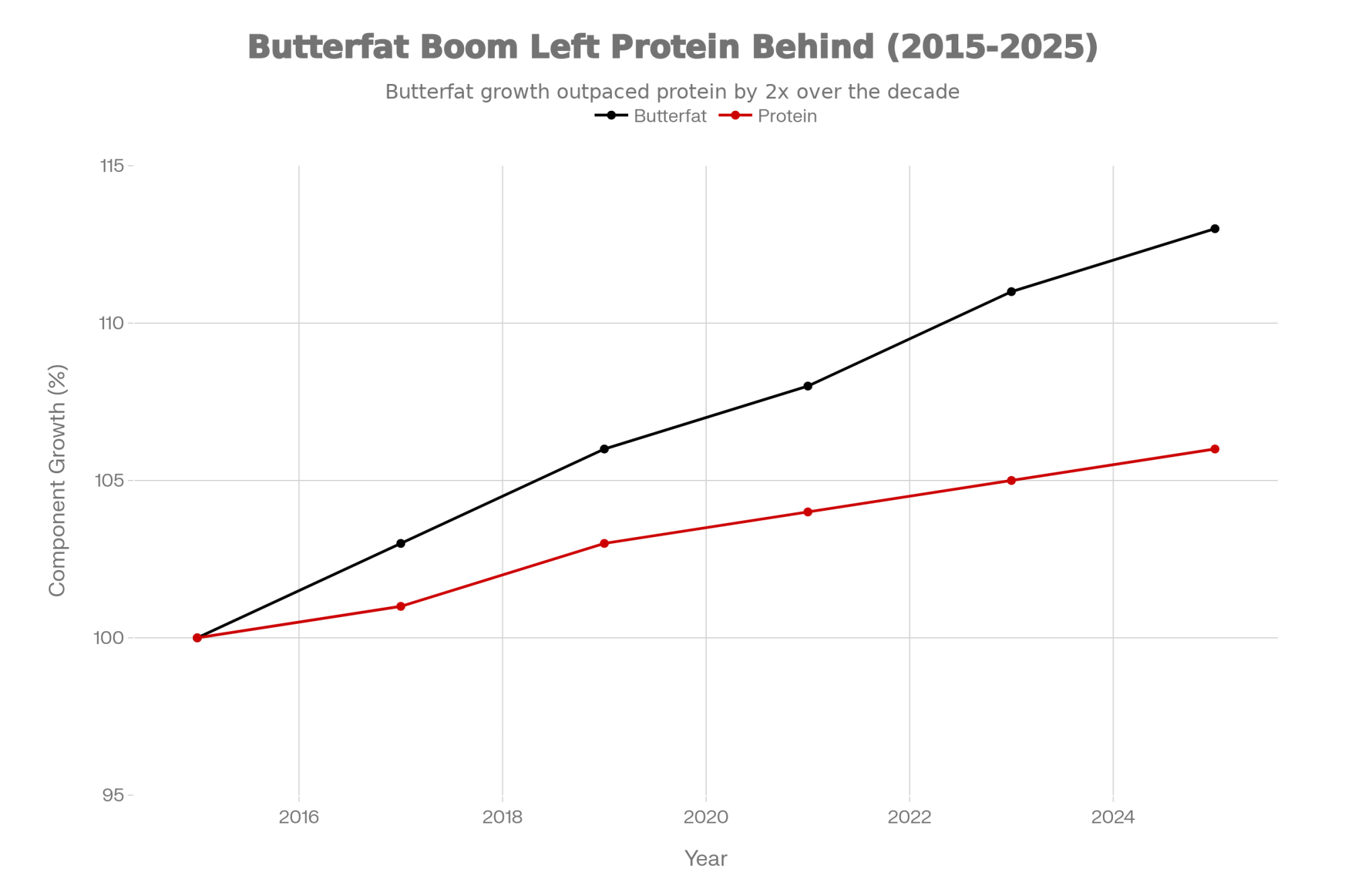

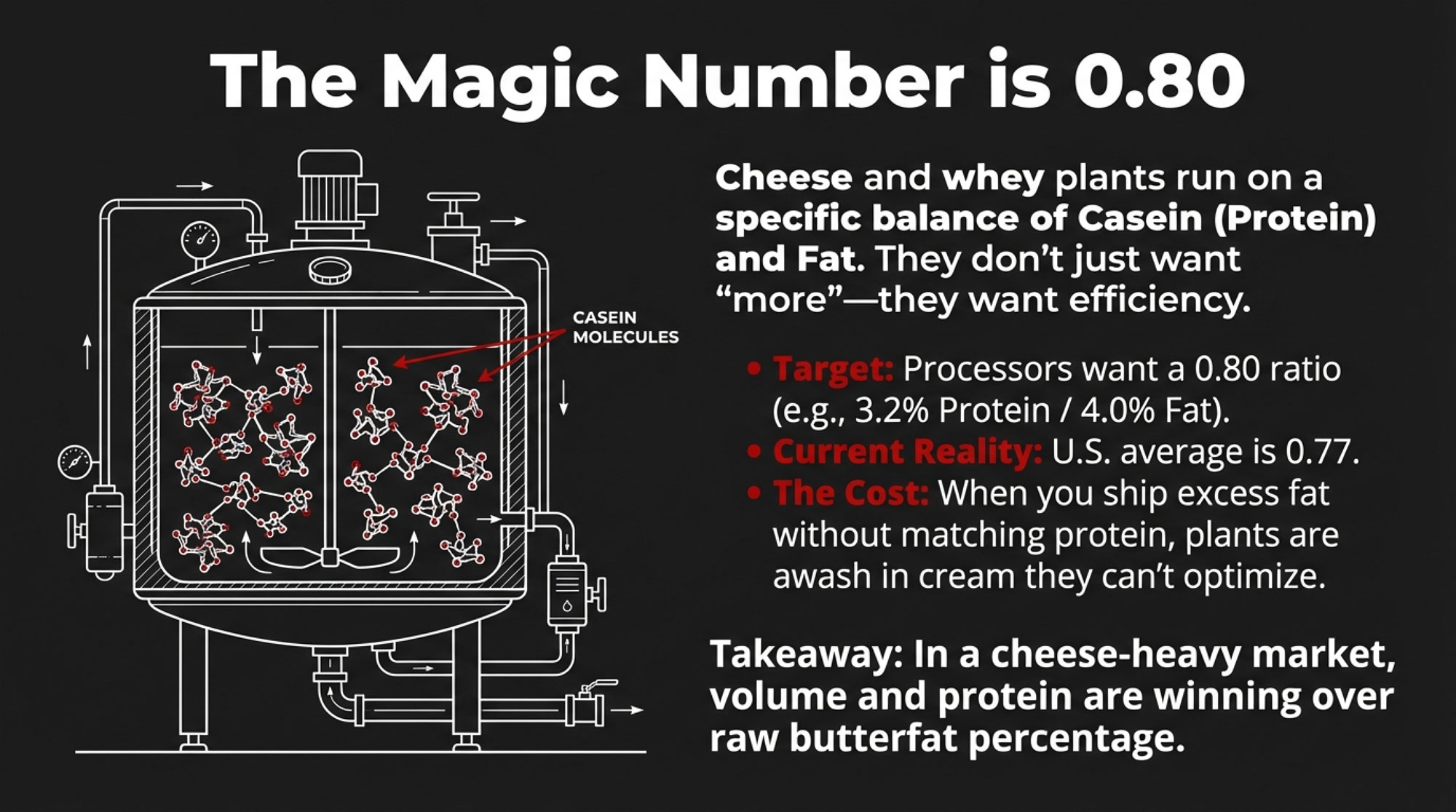

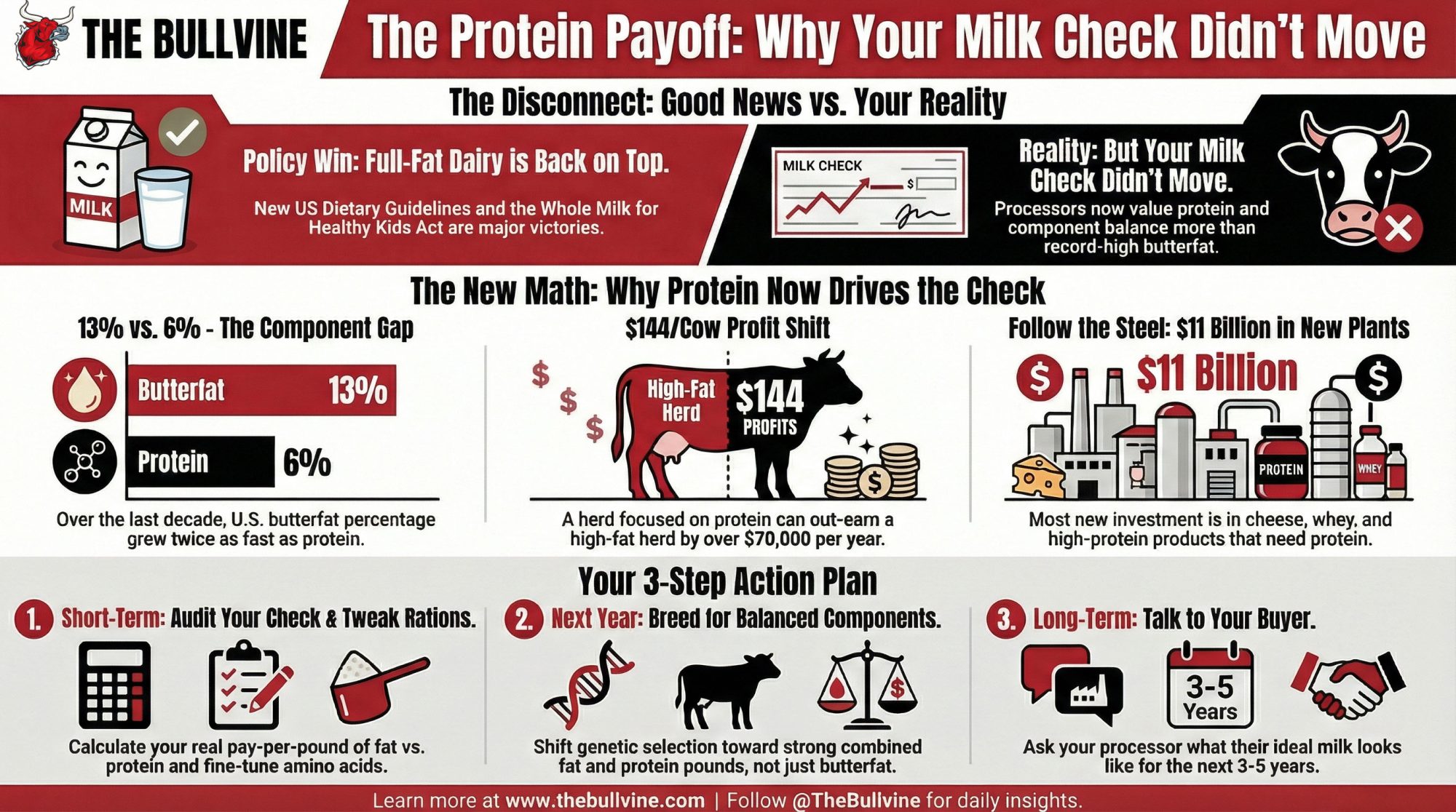

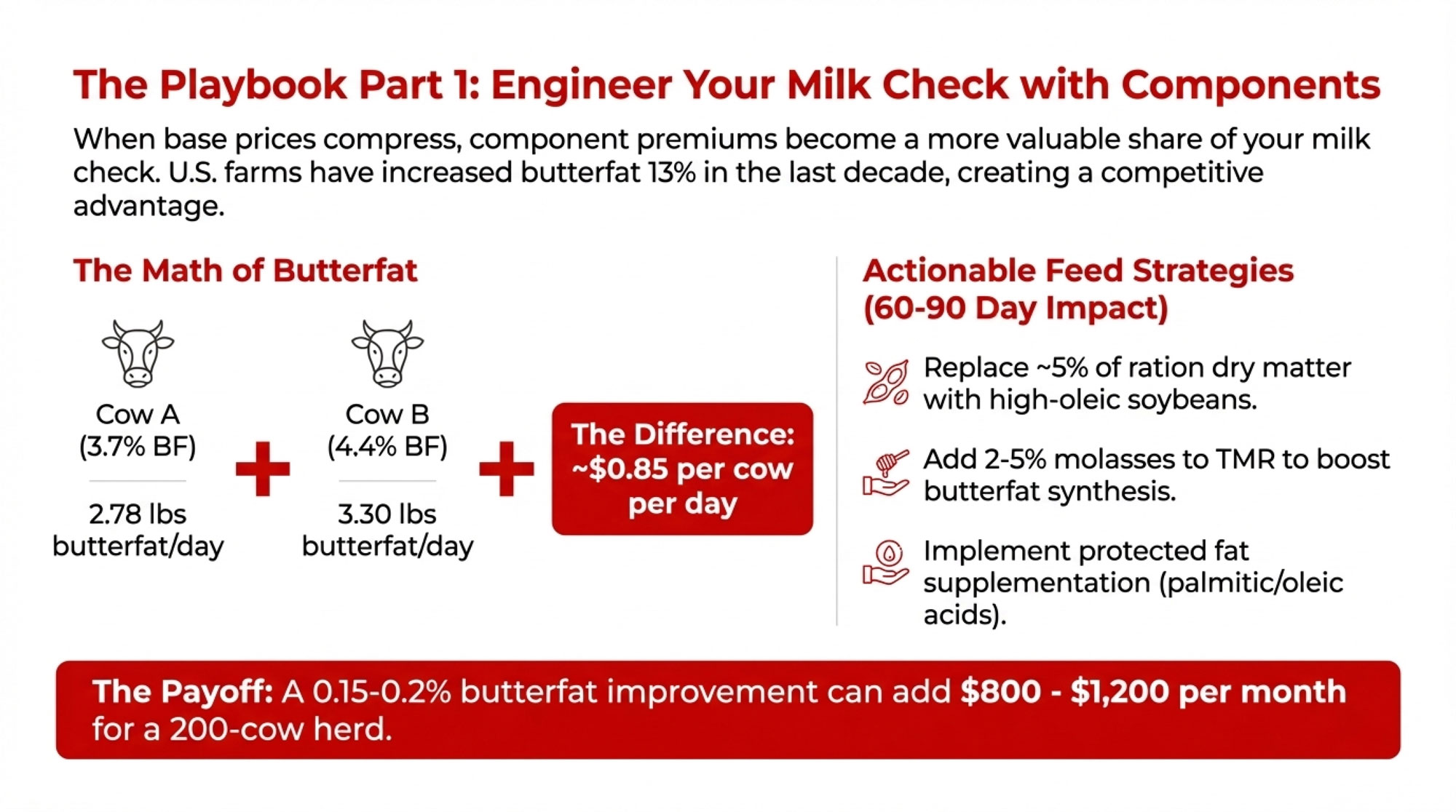

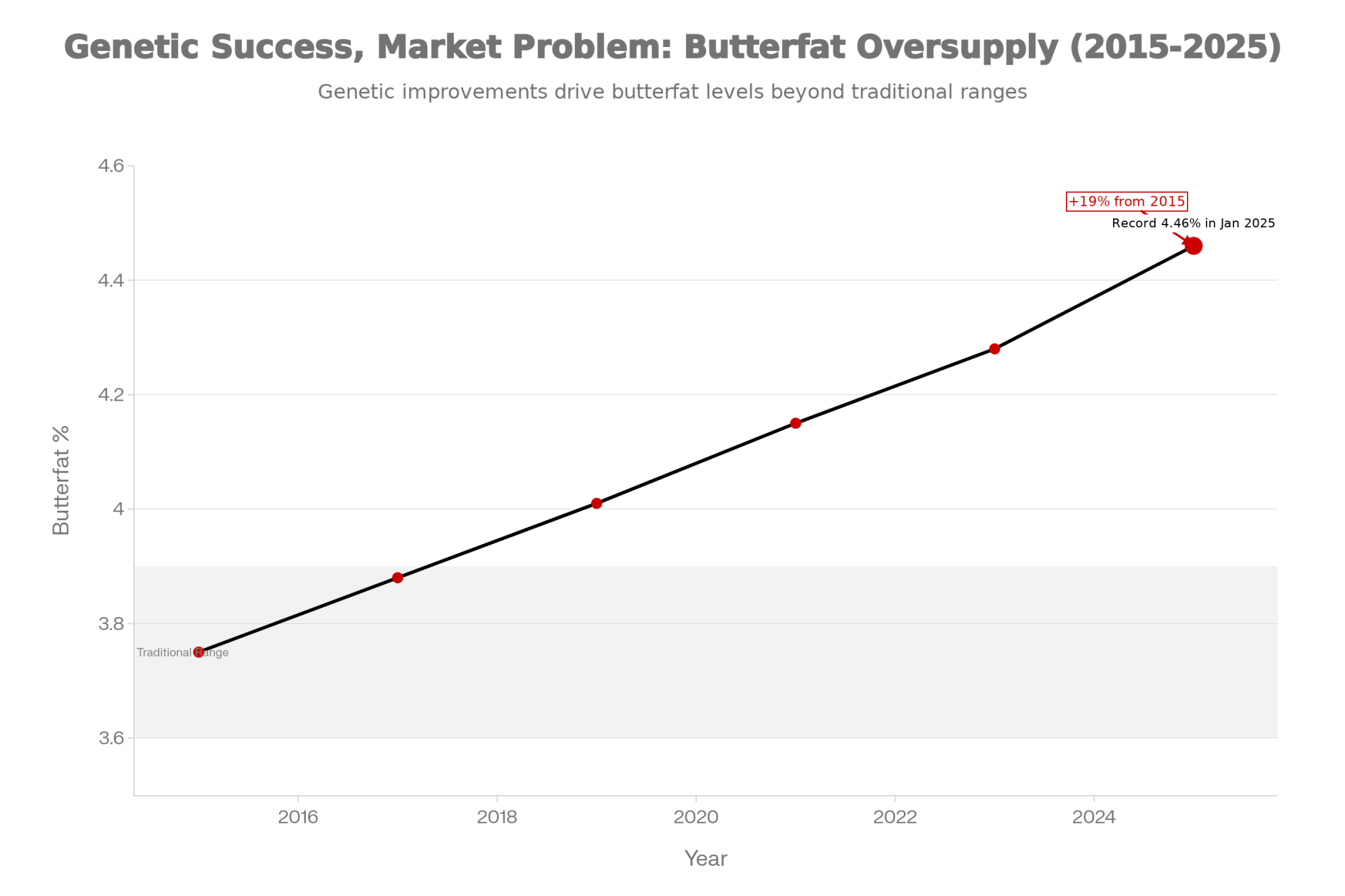

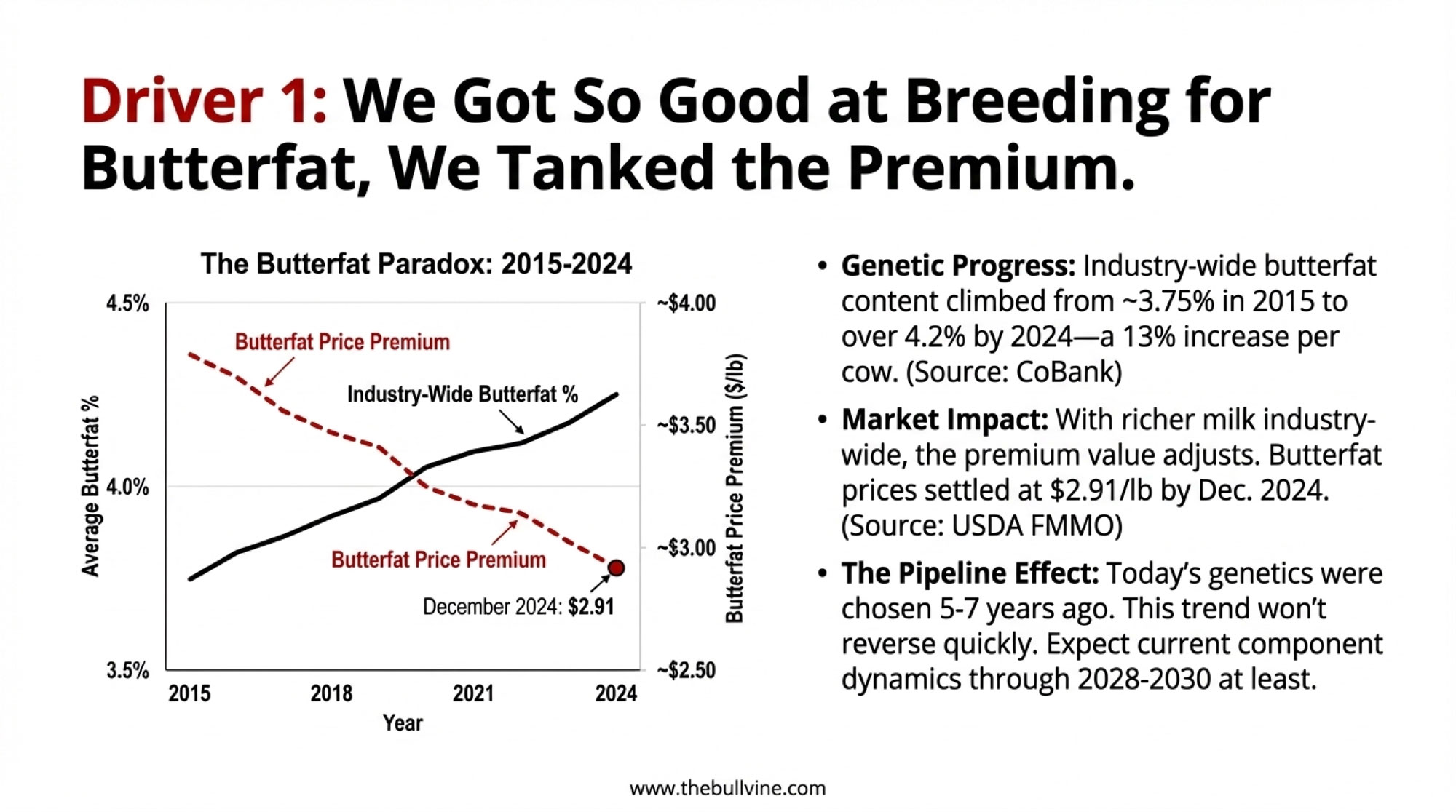

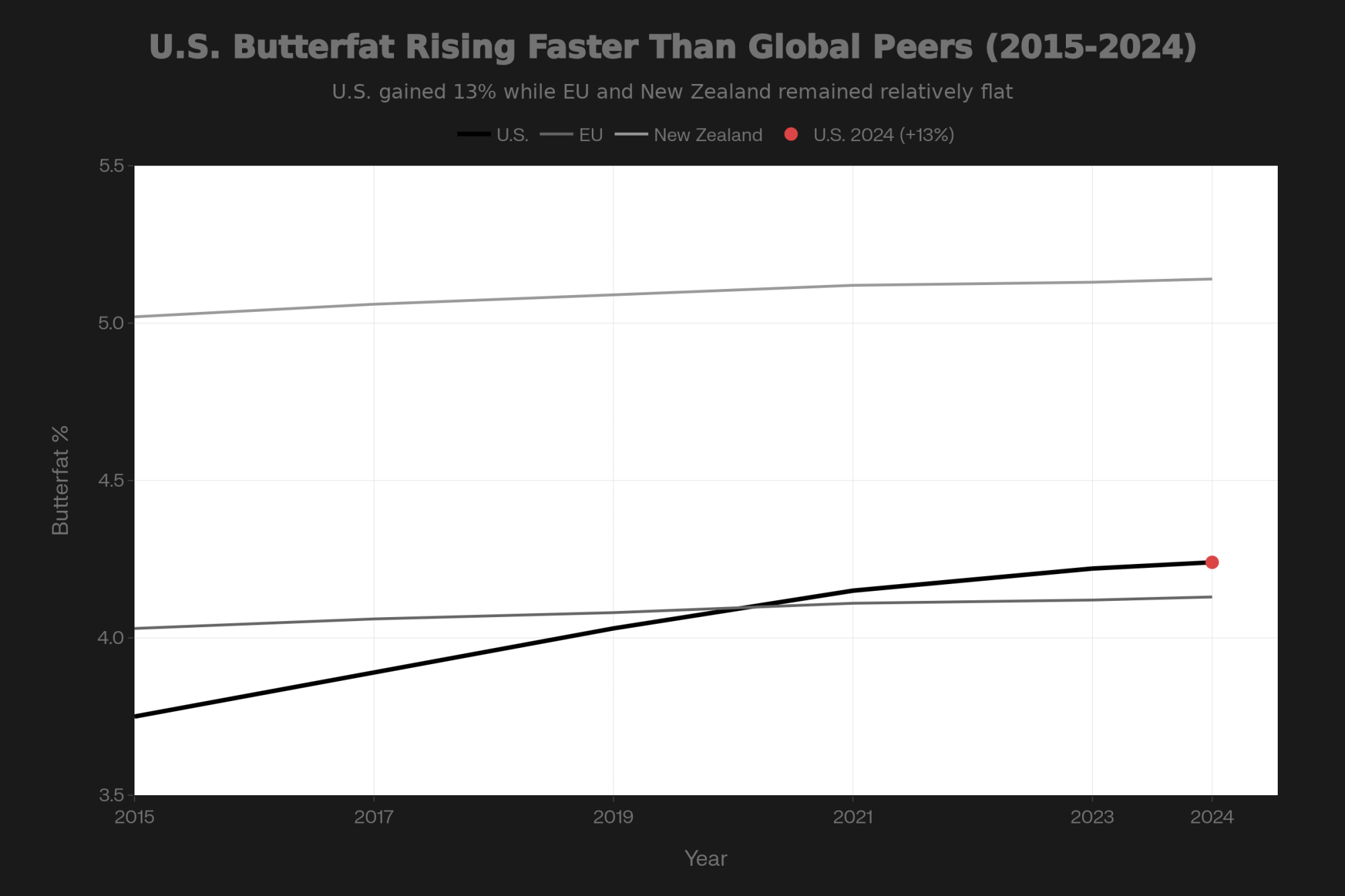

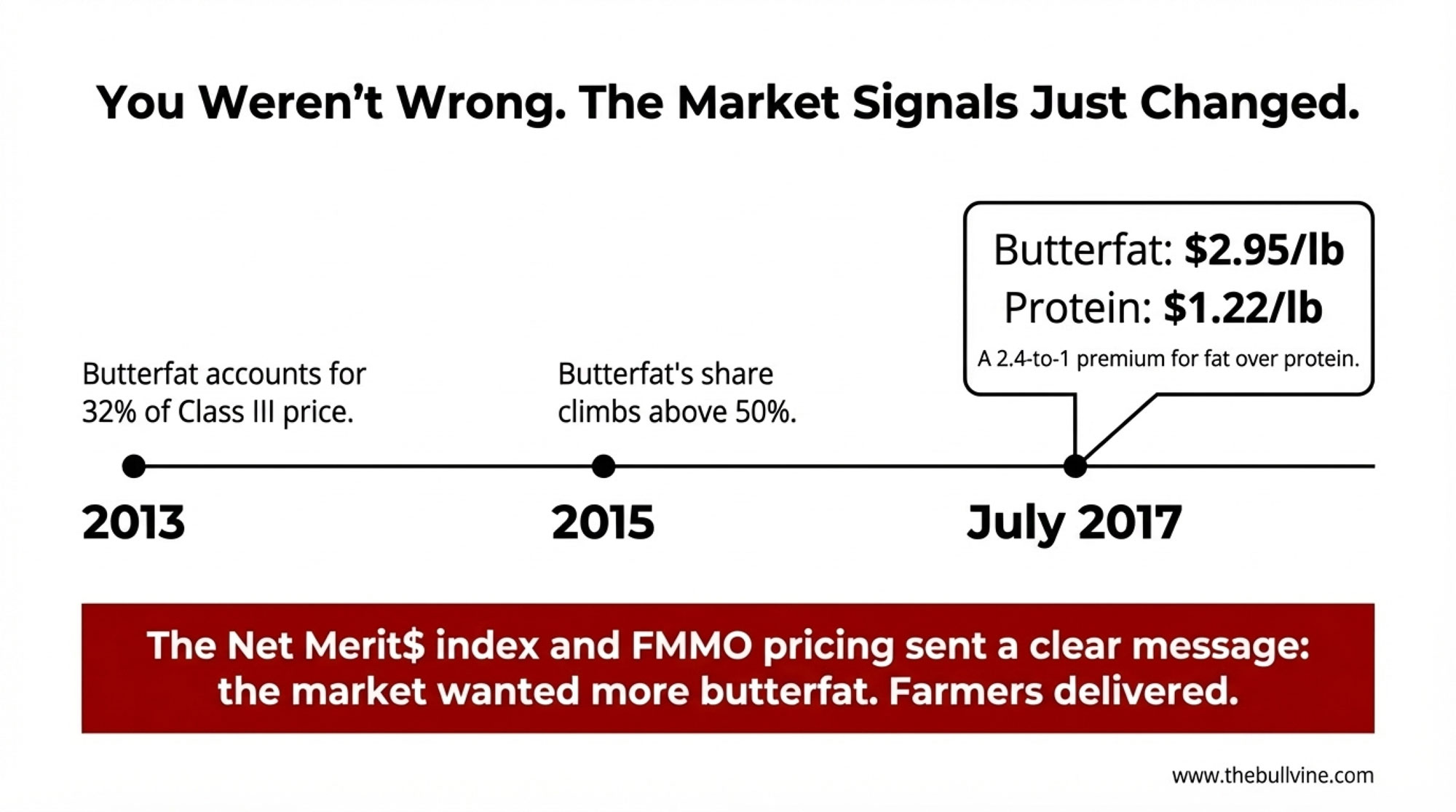

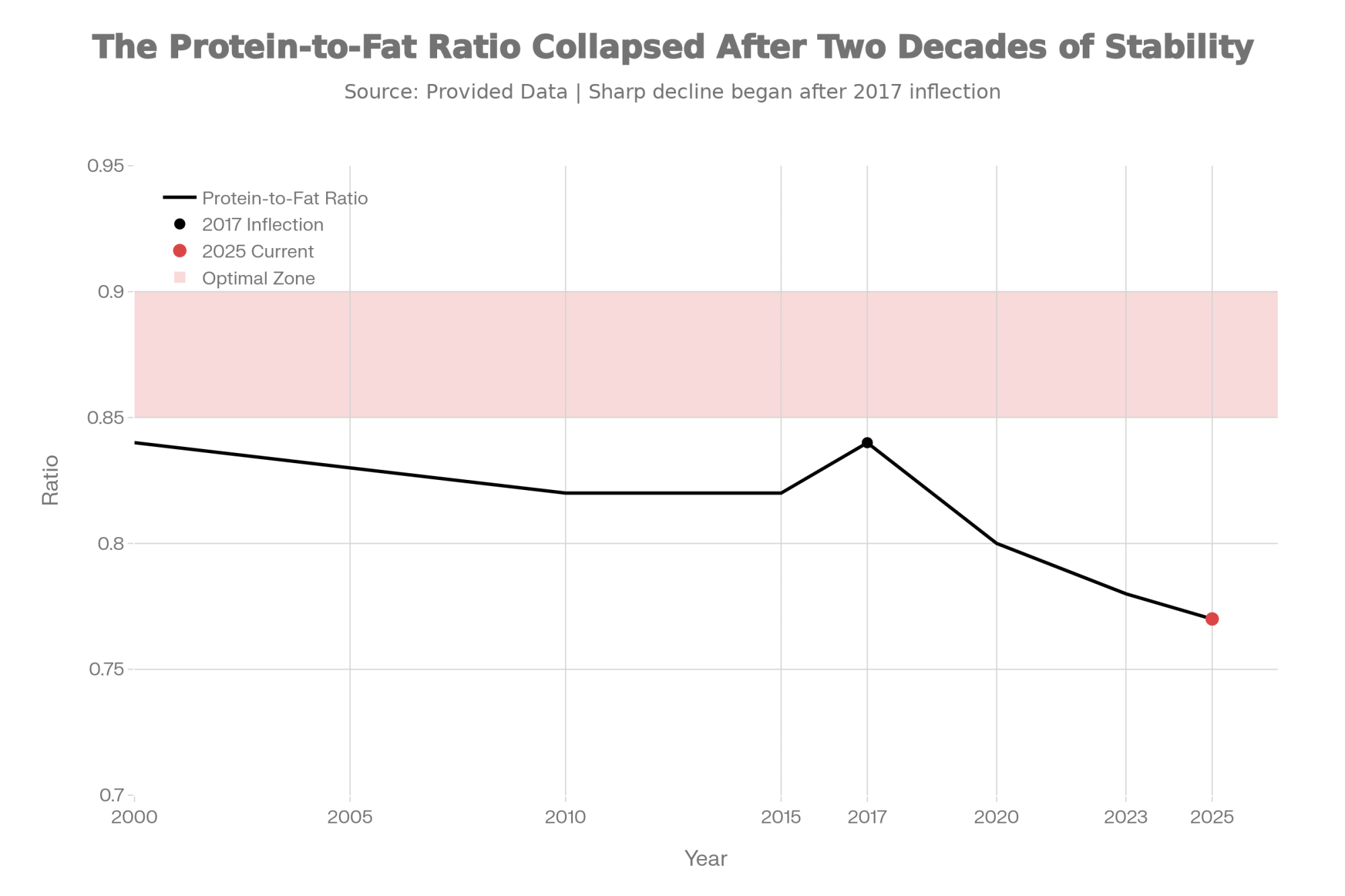

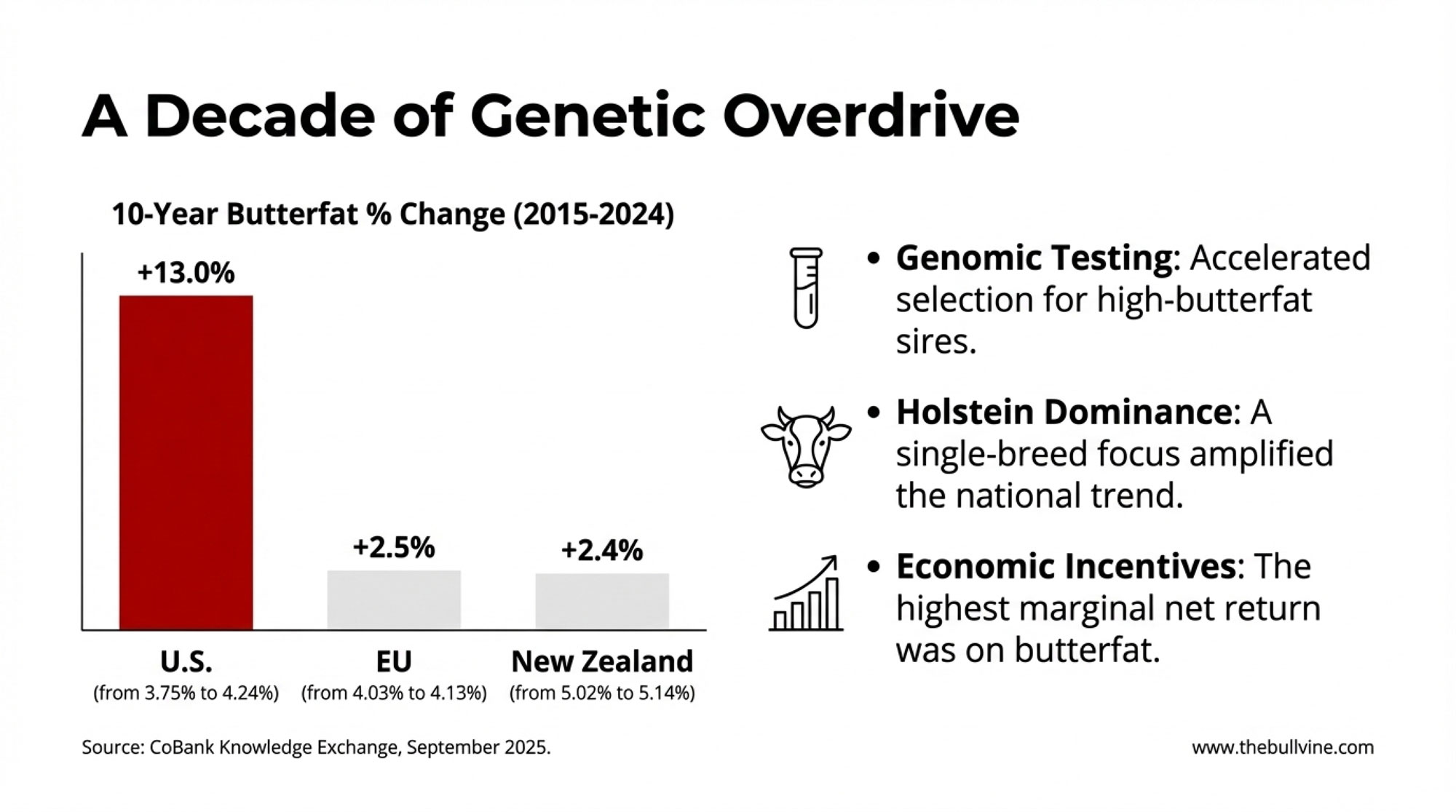

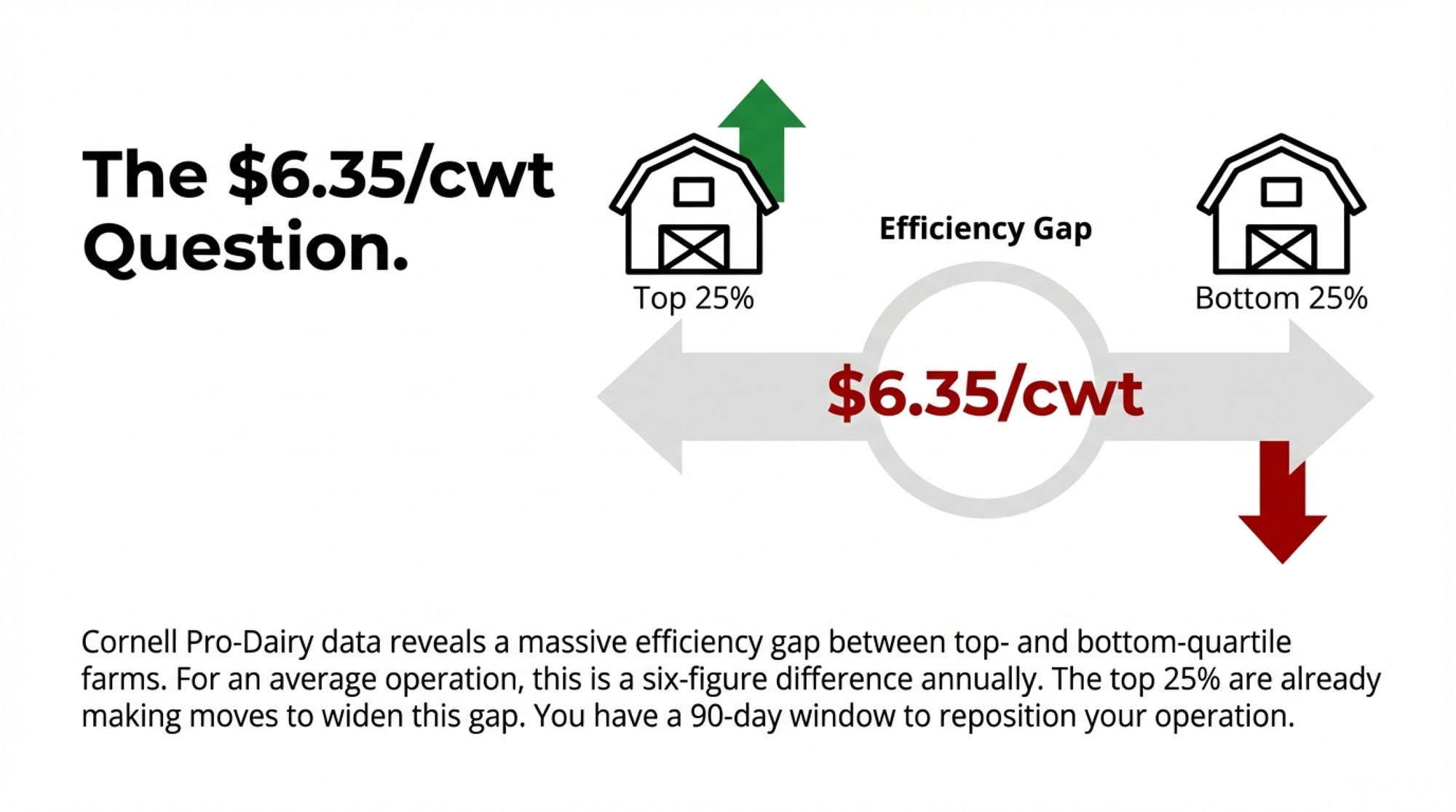

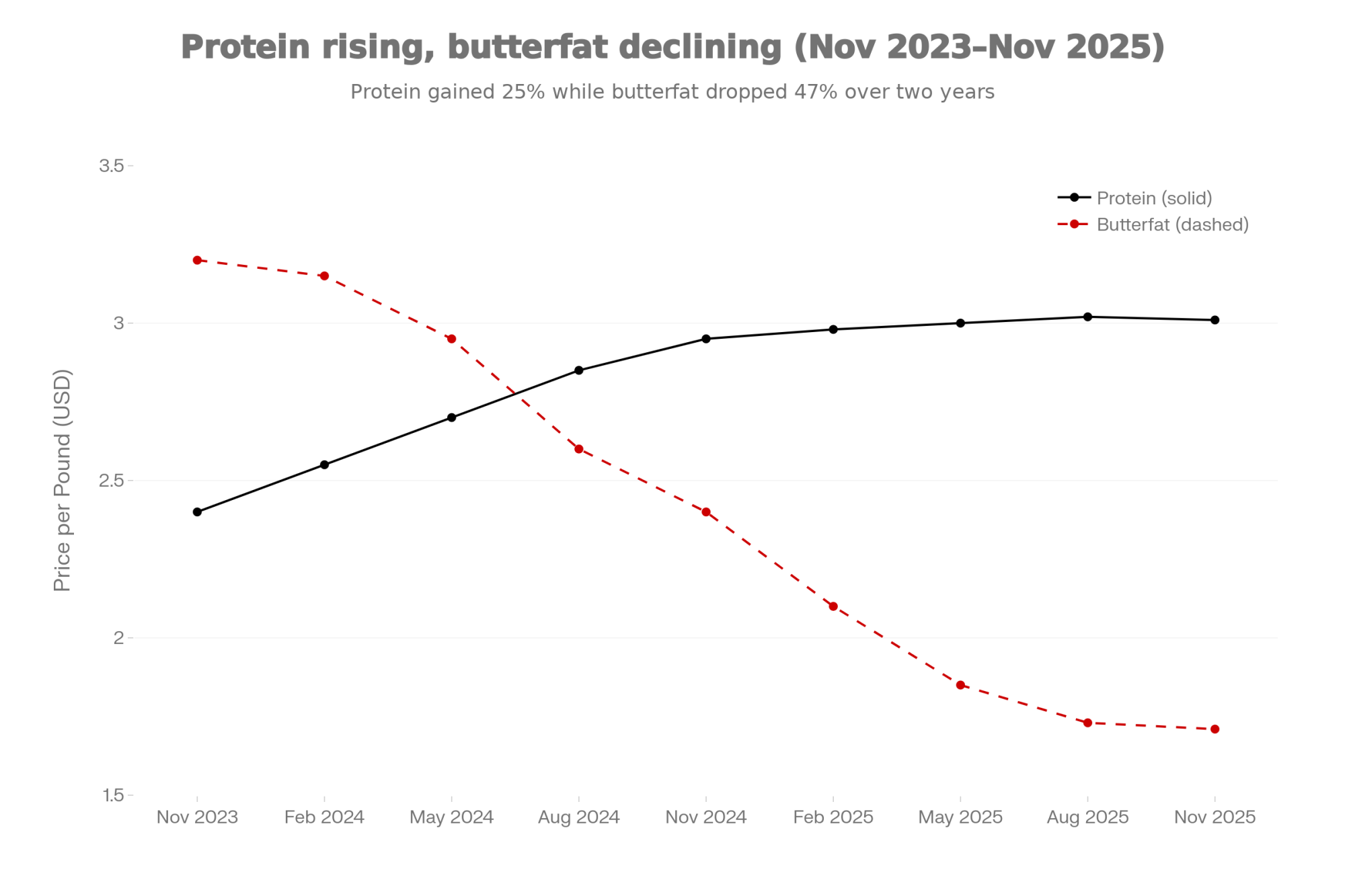

For much of the last decade, butterfat looked like the star. USDA and CME data show U.S. butter prices and per‑capita butter consumption rising, and for many years, Class III and IV values put butterfat at a clear premium over protein on a solids basis. So a lot of us leaned into butterfat—through breeding, rations, and fresh cow management—to capture those butterfat premiums.

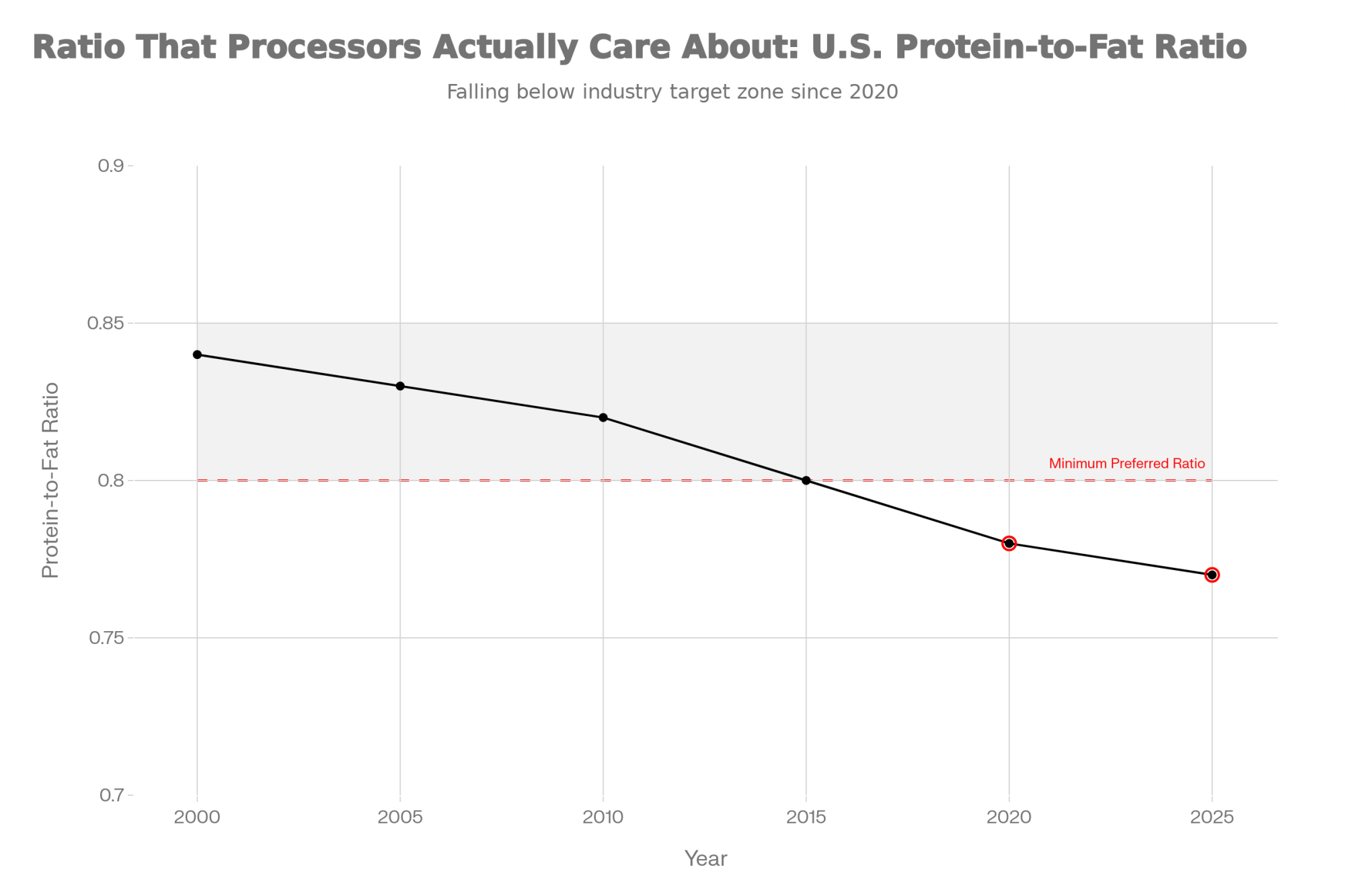

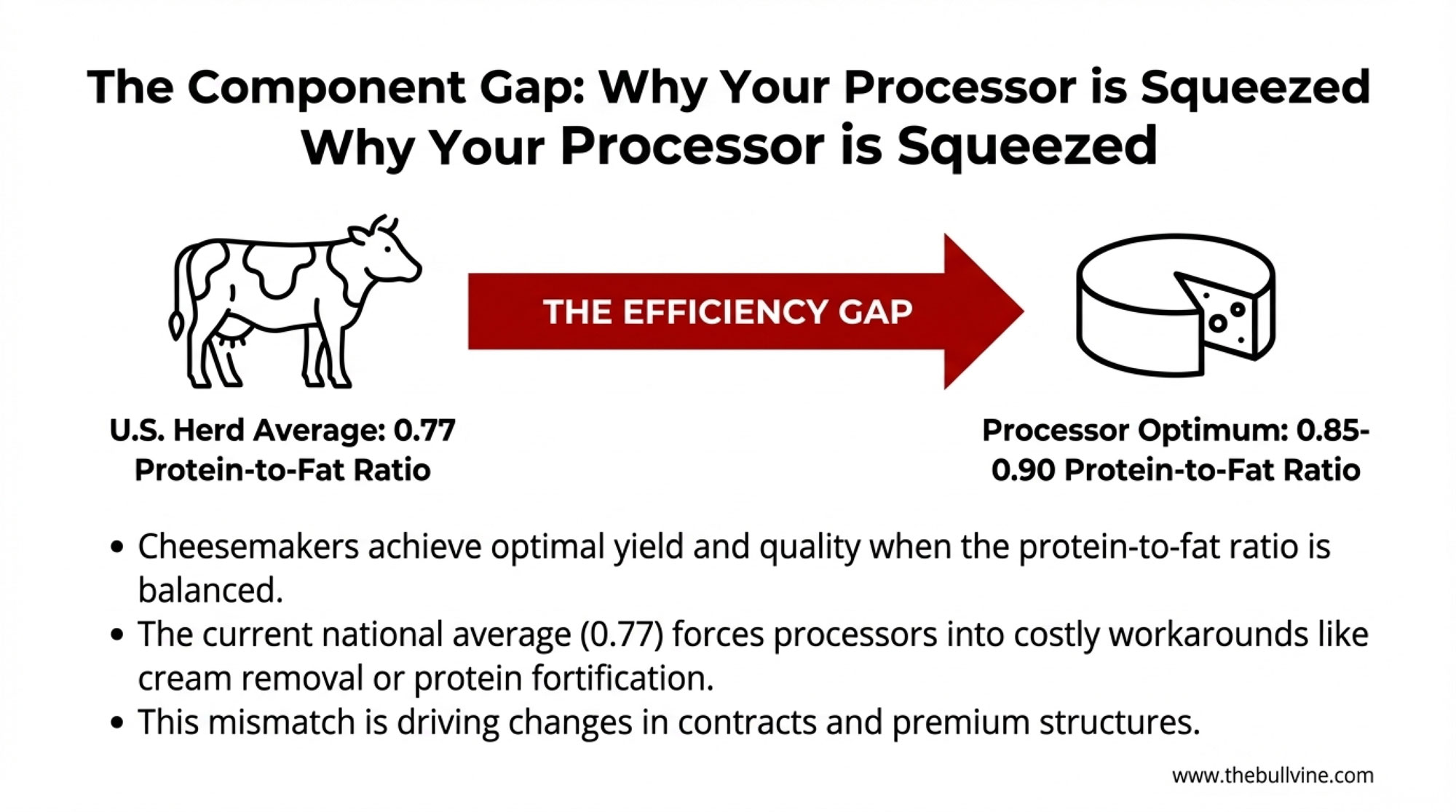

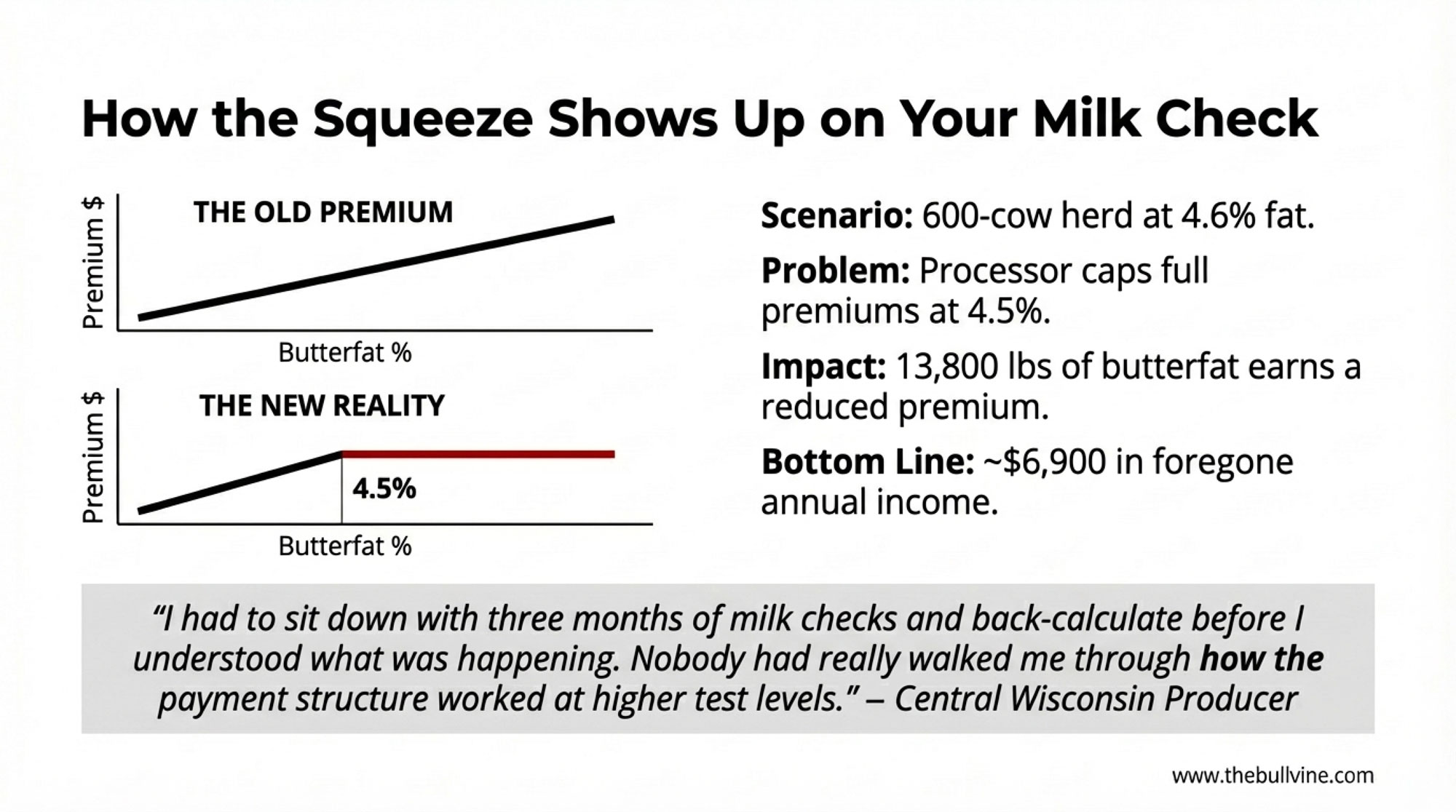

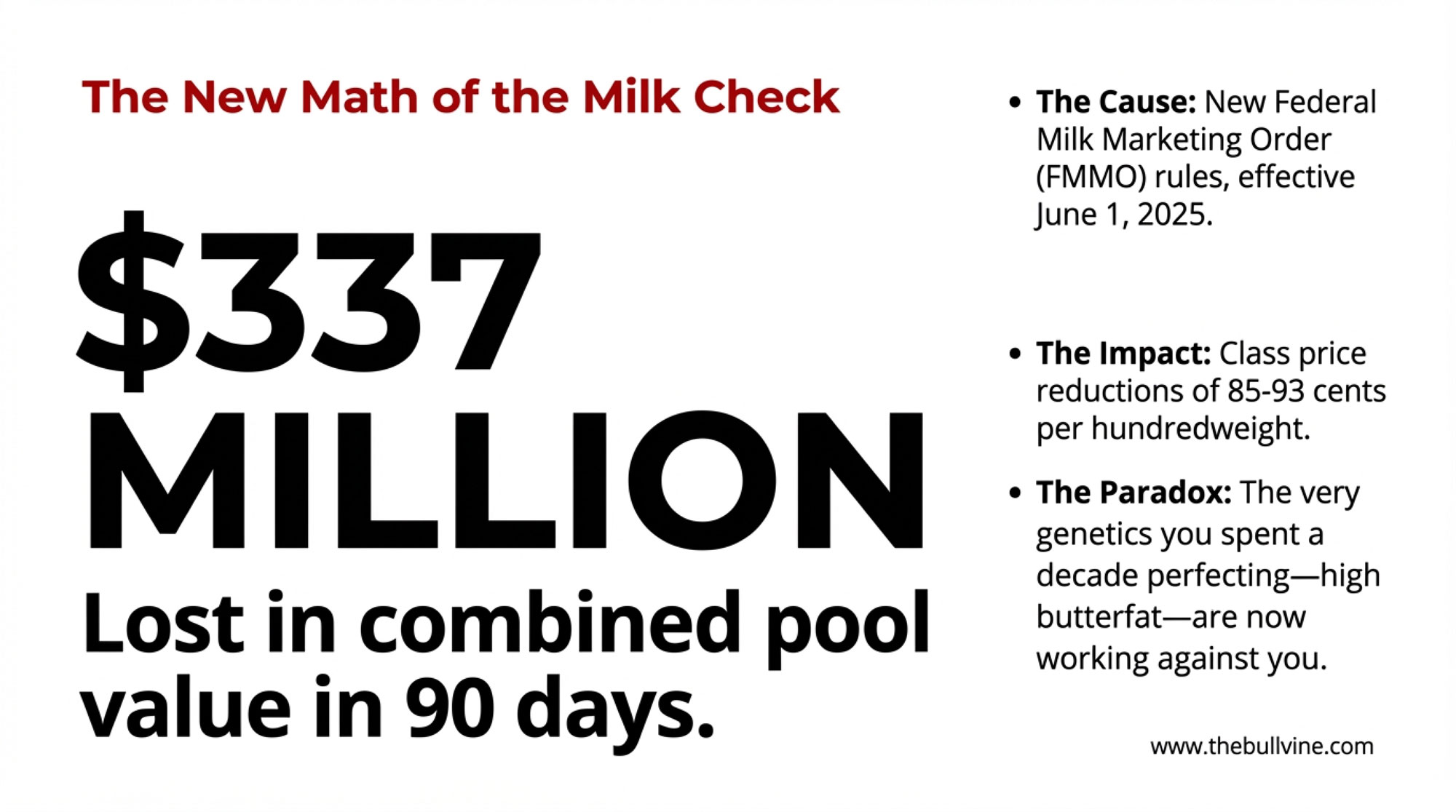

As more milk has flowed into cheese vats, though, the balance has shifted. Cheesemakers live on protein. That’s what builds curd. The Federal Milk Marketing Order Class III formulas use cheese, whey, and butter prices to calculate fat and protein values using specific yield factors. The way those formulas are structured creates a kind of see‑saw: when butterfat prices move sharply higher, the implied value of protein tends to get pulled down, and when butterfat softens, protein can carry more of the pay pool.

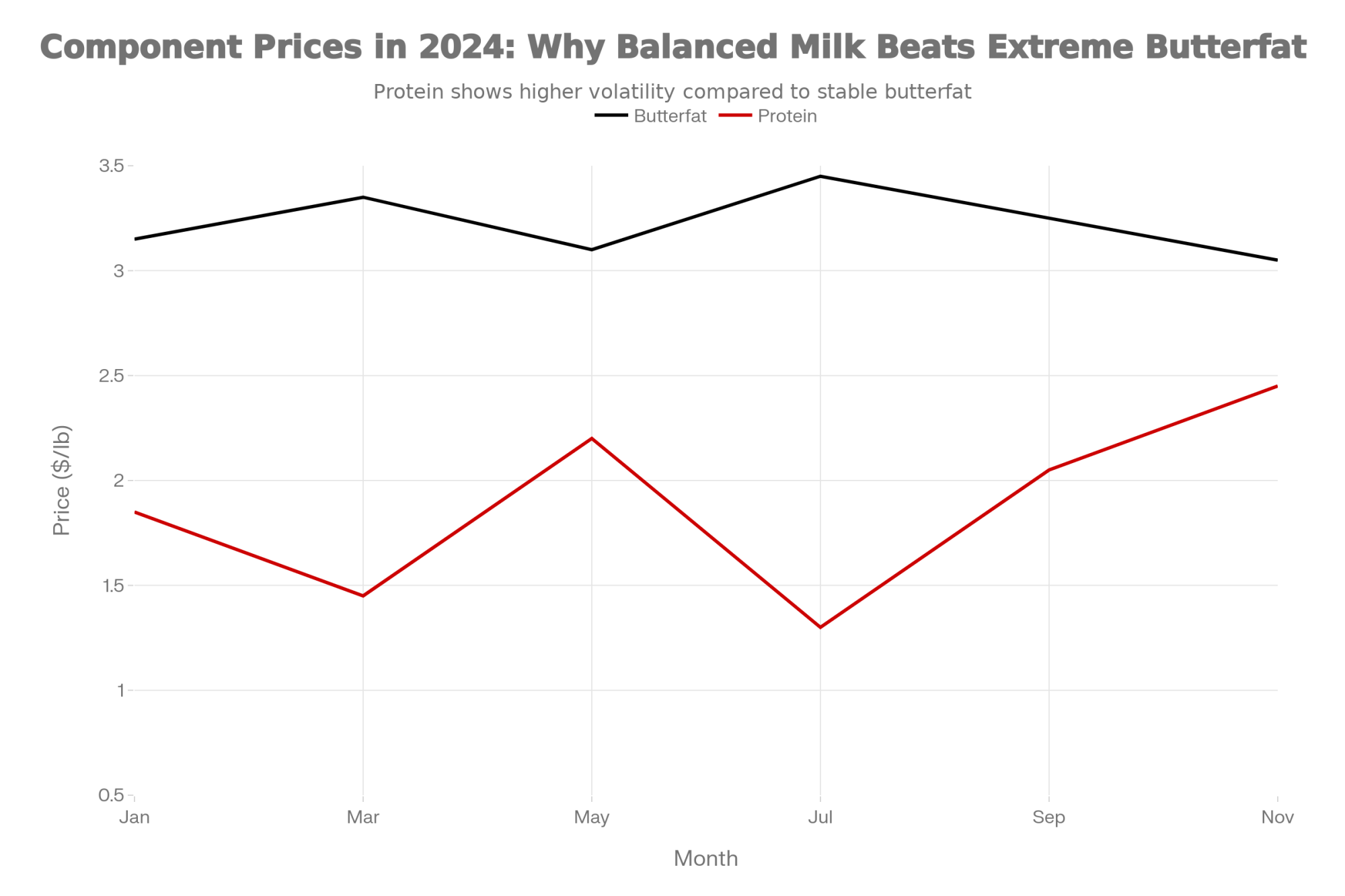

If you look at USDA component price reports across 2024, butterfat values often ran in the 3.00 to 3.50 dollars per pound range, while Class III protein values showed significant volatility—bouncing from around 1.10 to over 2.50 dollars per pound depending on the month. Dairy market updates from MCT Dairies and federal order bulletins highlighted several months where fat was historically strong while protein sagged, reflecting that cheese‑heavy product mix. Analysts like Sarina Sharp with the Daily Dairy Report have talked about co‑ops finding themselves “long on cream” at times, which makes it hard to fully reward sky‑high butterfat tests when protein and cheese demand are really driving the bus.

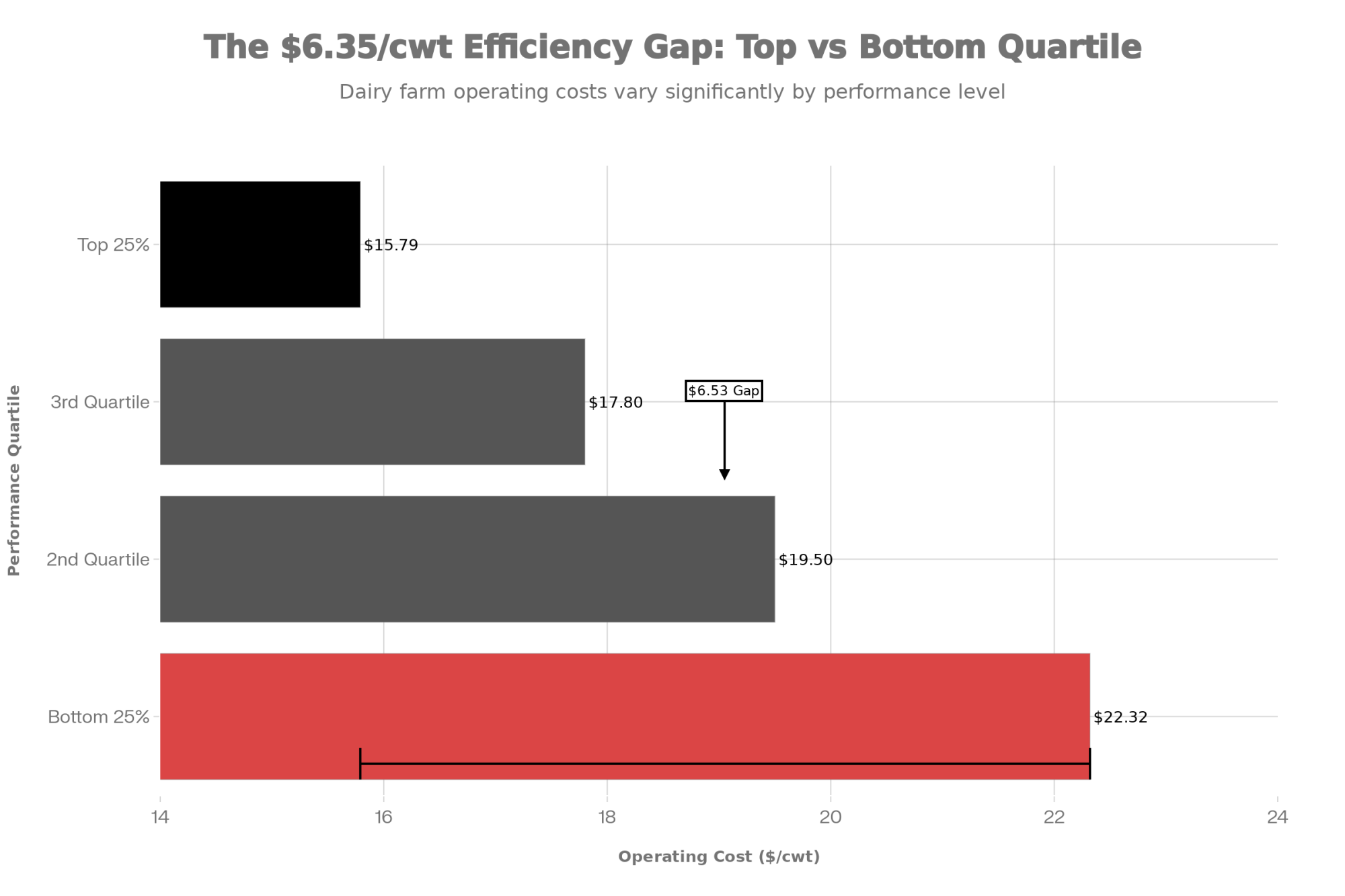

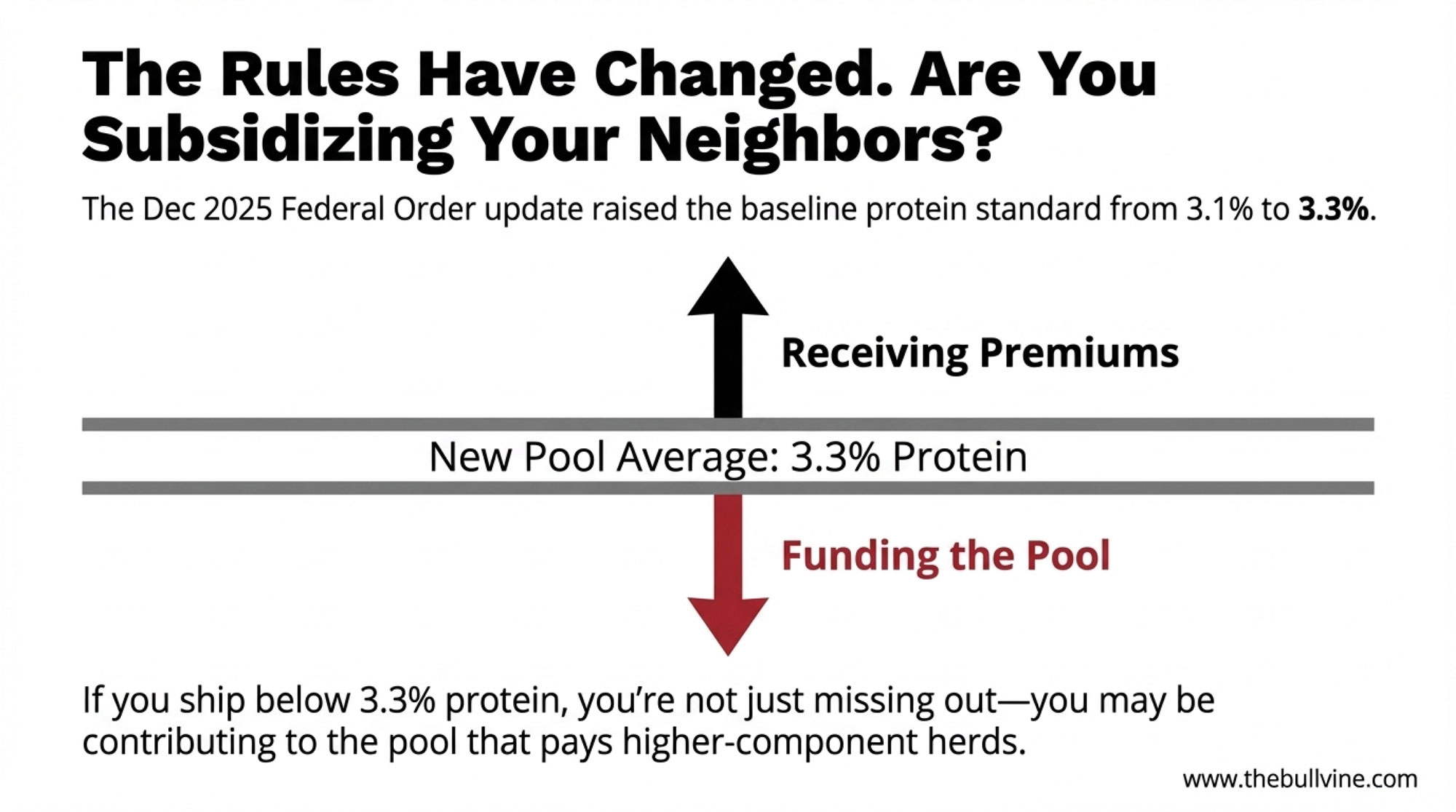

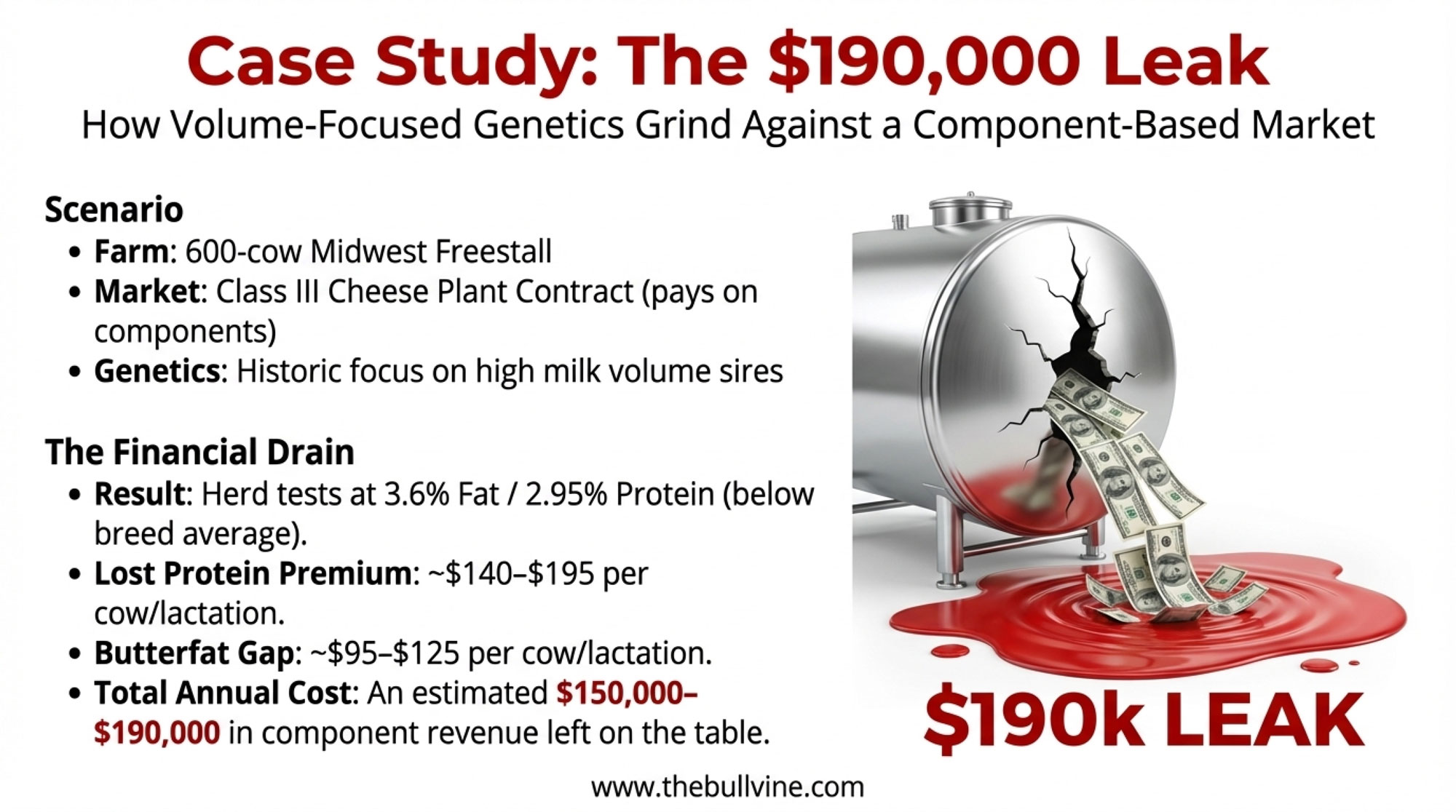

What farmers are finding—and what a lot of field nutritionists and independent advisers will tell you—is that balancedmilk tends to pay better than extreme milk in this environment. Herds averaging around 3.5–3.8 percent protein and 3.8–4.1 percent butterfat, with solid fresh cow management and a smooth transition period, often see more stable component checks than herds that push butterfat into the mid‑4s while letting protein linger around 3.0–3.1 percent. That profile matches what many cheese plants say they want: strong pounds of solids, but in a ratio that actually fits their vats.

| Month | Butterfat ($/lb) | Protein ($/lb) |

|---|---|---|

| Jan | 3.15 | 1.85 |

| Mar | 3.35 | 1.45 |

| May | 3.10 | 2.20 |

| Jul | 3.45 | 1.30 |

| Sep | 3.25 | 2.05 |

| Nov | 3.05 | 2.45 |

If you haven’t done it recently, it’s worth a quick kitchen‑table exercise:

- Take a month’s milk statement and write down the total pounds of fat shipped and total pounds of protein shipped.

- Divide each by the total pounds of milk shipped to confirm your average butterfat and protein tests.

- Then look up that month’s USDA or co‑op Class III/IV component values and see how many dollars per cwt those pounds are really generating.

A recent review on milk quality and economic sustainability points out that herds with better component performance and milk quality tend to show stronger economic sustainability—so long as they aren’t trading away health and fertility to get there. And Mike Hutjens, Professor Emeritus and extension dairy specialist at the University of Illinois, has hammered the same point for years: it’s pounds of fat and protein shipped per cow and per cwt that drive income, not just pretty percentages on the DHI sheet.

This development suggests something important: chasing maximum butterfat at the expense of protein and cow health doesn’t pay the way it once might have. The money today is in a balanced component profile, backed by good transition‑period management and consistent TMRs.

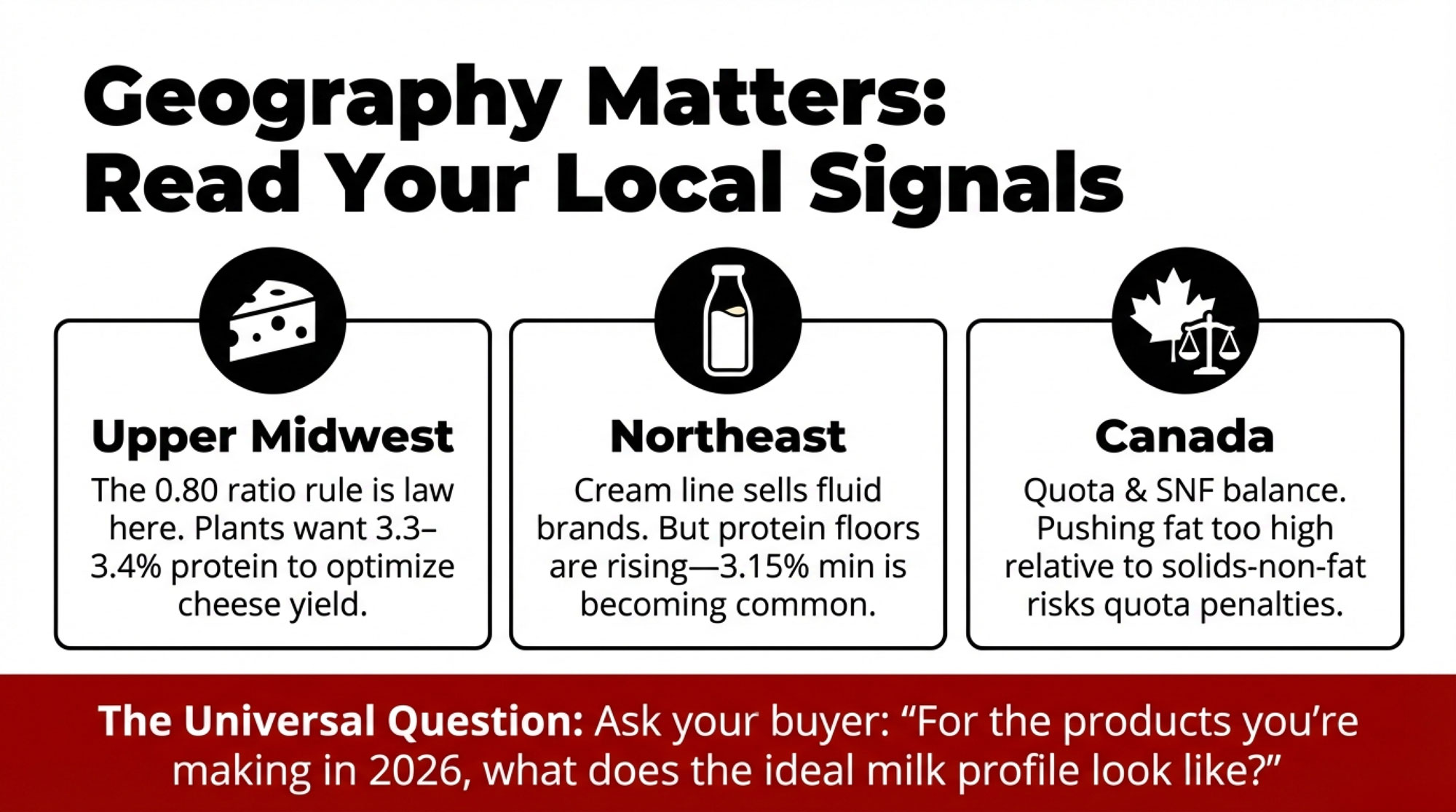

Why Your ZIP Code Still Matters More Than You’d Like

Looking at this trend across regions, it’s hard to ignore how much your postal code still shapes your milk check.

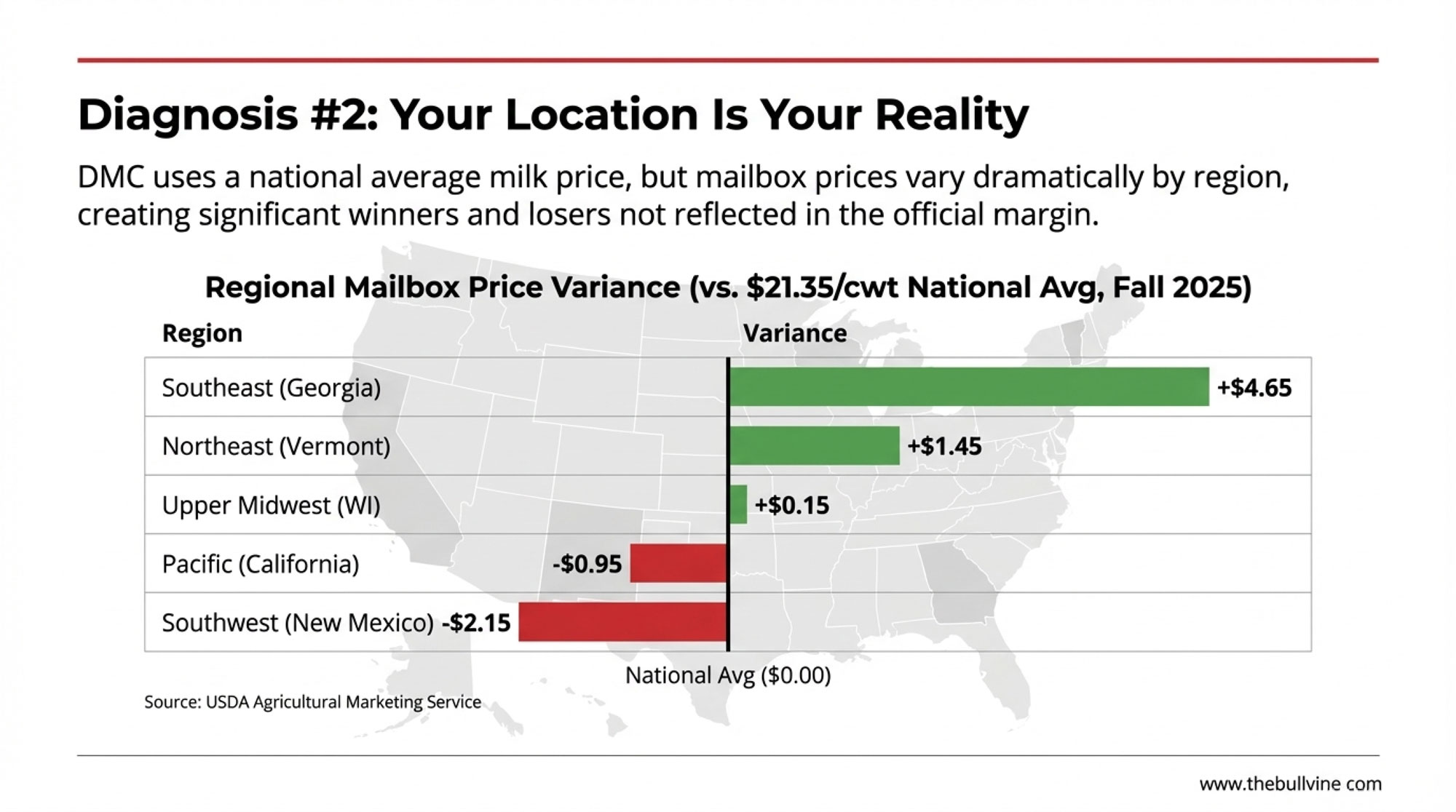

USDA Milk Production reports make it pretty clear that cows and milk have been shifting into certain regions, especially the interior. South Dakota is one of the clearest examples. The state has become a major growth engine as the I‑29 corridor cheese plants and expansions pulled in herds and investment. Kansas appears in USDA and Progressive Dairy statistics as another state with consistent year‑over‑year growth, driven by large freestall operations and added plant capacity. At the same time, USDA/NASS and state reports often rank Michigan near the top for milk per cow, thanks to strong forage programs, cow comfort, and efficient parlors.

What I’ve noticed, looking at those numbers and listening to producers, is that geography flows directly into basis and hauling. A 1,500‑cow freestall in eastern South Dakota, 20 or 30 miles from a modern cheese plant, is playing a different game than a 200‑cow tie‑stall in a New England valley where there’s limited processing and plants are already full. The close‑in herd may save 30–50 cents per cwt on hauling and pick up stronger over‑order premiums and quality incentives because the plant really needs their milk. The more remote herd often pays more just to get milk to town and has fewer realistic buyers if contracts change.

To put some rough numbers on it, imagine a herd shipping 20,000 cwt per month. If better basis and lower hauling together net 0.75 dollars per cwt more than a herd in a less favored location, that’s 15,000 dollars per month, or roughly 180,000 dollars per year. That’s just an example based on USDA and regional data; every farm will have its own version of that spread. But it shows why two herds can read the same export headlines and feel completely different realities when the milk checks arrive.

| Factor | Herd A: Close to Growing Plant (SD, KS, TX) | Herd B: Remote or Declining Region (VT, Upstate NY, Rural West) |

|---|---|---|

| Distance to Plant | 20–30 miles | 80–150+ miles |

| Hauling Cost | $0.25–$0.40/cwt | $0.60–$1.00/cwt |

| Over-Order Premium/Basis | $0.50–$1.25/cwt | $0.00–$0.50/cwt |

| Quality/Volume Incentives | Strong (plant needs milk) | Weak (plant at capacity or shrinking) |

| Monthly Advantage (20,000 cwt) | Baseline | −$15,000 |

| Annual Impact | Baseline | −$180,000 |

It’s not about “good” or “bad” states. It’s about plant geography, infrastructure, and policy. Many producers in the Midwest and Plains will tell you their biggest advantage right now is simply being inside the pull radius of expanding cheese plants. Producers in some Northeast or Mountain West pockets, or even parts of Canada, may have very competitive herds but face higher freight and less processor competition, even while exports are booming.

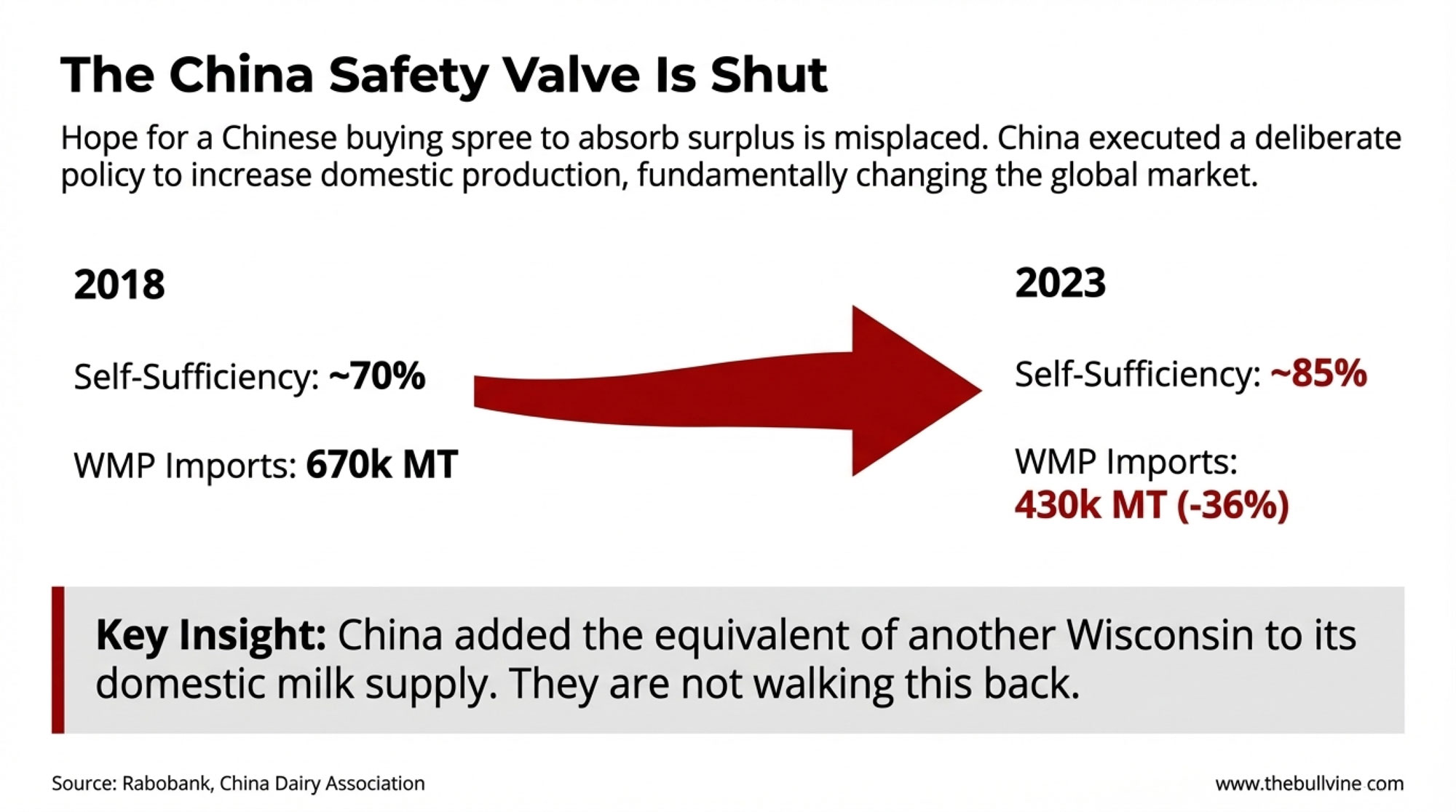

Mexico: Our Best Customer—and a Big Exposure

Now let’s talk about where a lot of those extra cheese and powder pounds actually end up: Mexico.

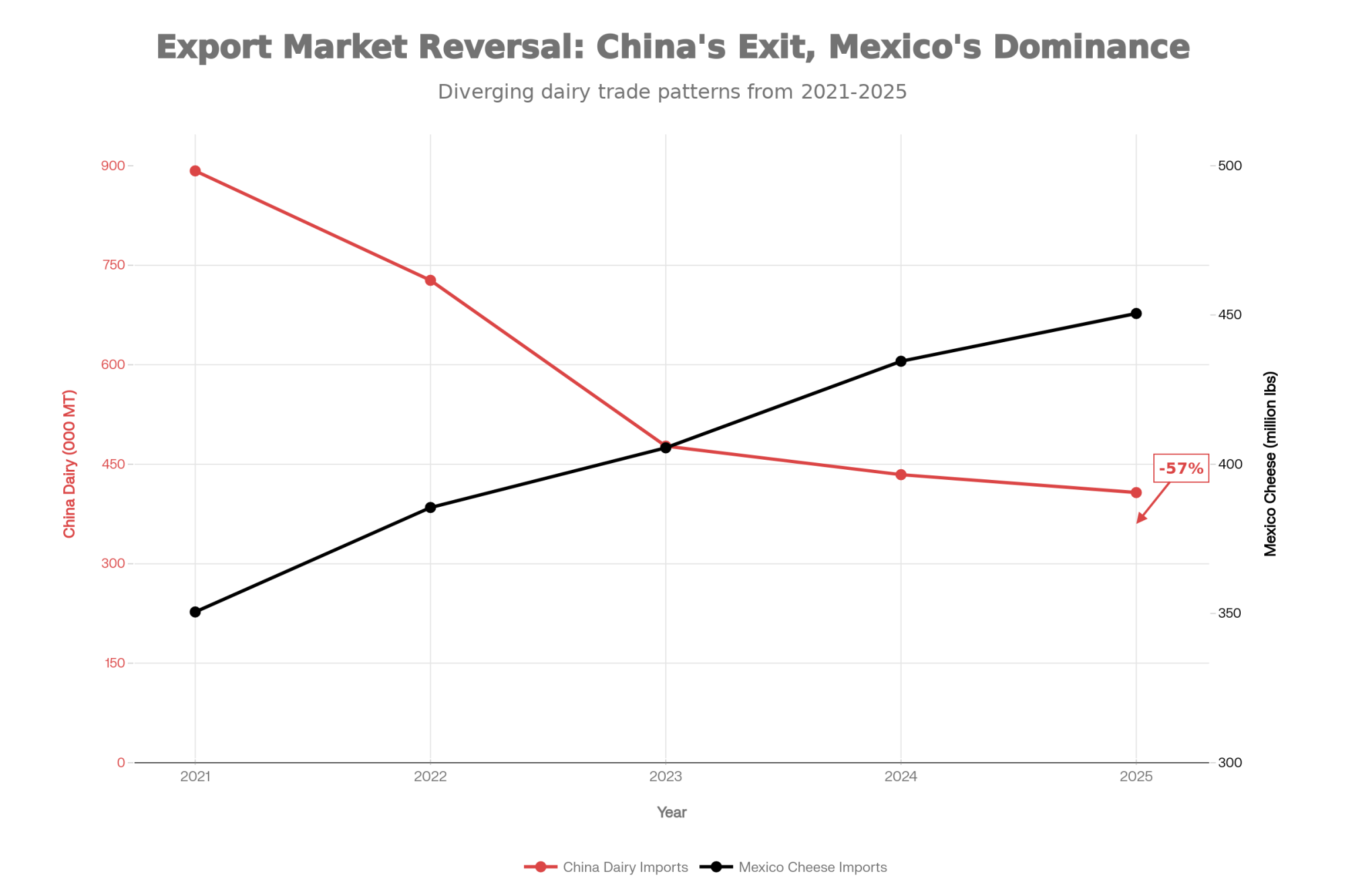

USDA FAS, IDFA, USDEC, and trade outlets like Dairy Processing are all on the same page here: Mexico is the single largest foreign market for U.S. dairy by value. In 2024, the U.S. shipped roughly $2.47 billion in dairy products to Mexico and about $1.14 billion to Canada. Together, Mexico and Canada account for more than 40 percent of U.S. dairy export value, with Mexico consistently the top buyer for U.S. cheese and skim milk powder.

What’s encouraging in the near term is that Mexico is structurally short on milk. CoBank’s export analysis and USDA FAS reports describe a situation where Mexican dairy demand has outpaced domestic production, leaving a persistent gap that imports—mostly from the U.S.—fill. Per‑capita dairy consumption in Mexico is still lower than in the U.S., which gives some headroom for growth as incomes rise. That combination—structural deficit plus room for per‑capita growth—is a big part of why analysts see Mexico as critical to U.S. dairy’s near‑term export outlook.

But there’s another side that matters for your risk. FAS and industry coverage point out that Mexico is investing in its dairy sector, particularly in northern states, where newer farms are increasingly resembling large freestall and dry-lot systems in the U.S. Southwest, with upgraded genetics, improved feed efficiency, and better milk-handling infrastructure. The goal is to trim back some of that import dependence over time.

So what farmers are finding is that Mexico is both a tremendous asset and a concentration point. Over the next one to three years, it’s hard to imagine a strong U.S. export story that doesn’t lean heavily on Mexico. Over a three‑to‑ten‑year window, if Mexico succeeds in significantly boosting its own production, the growth rate of U.S. exports there could slow, or the mix of products could shift—even if the trading relationship remains strong.

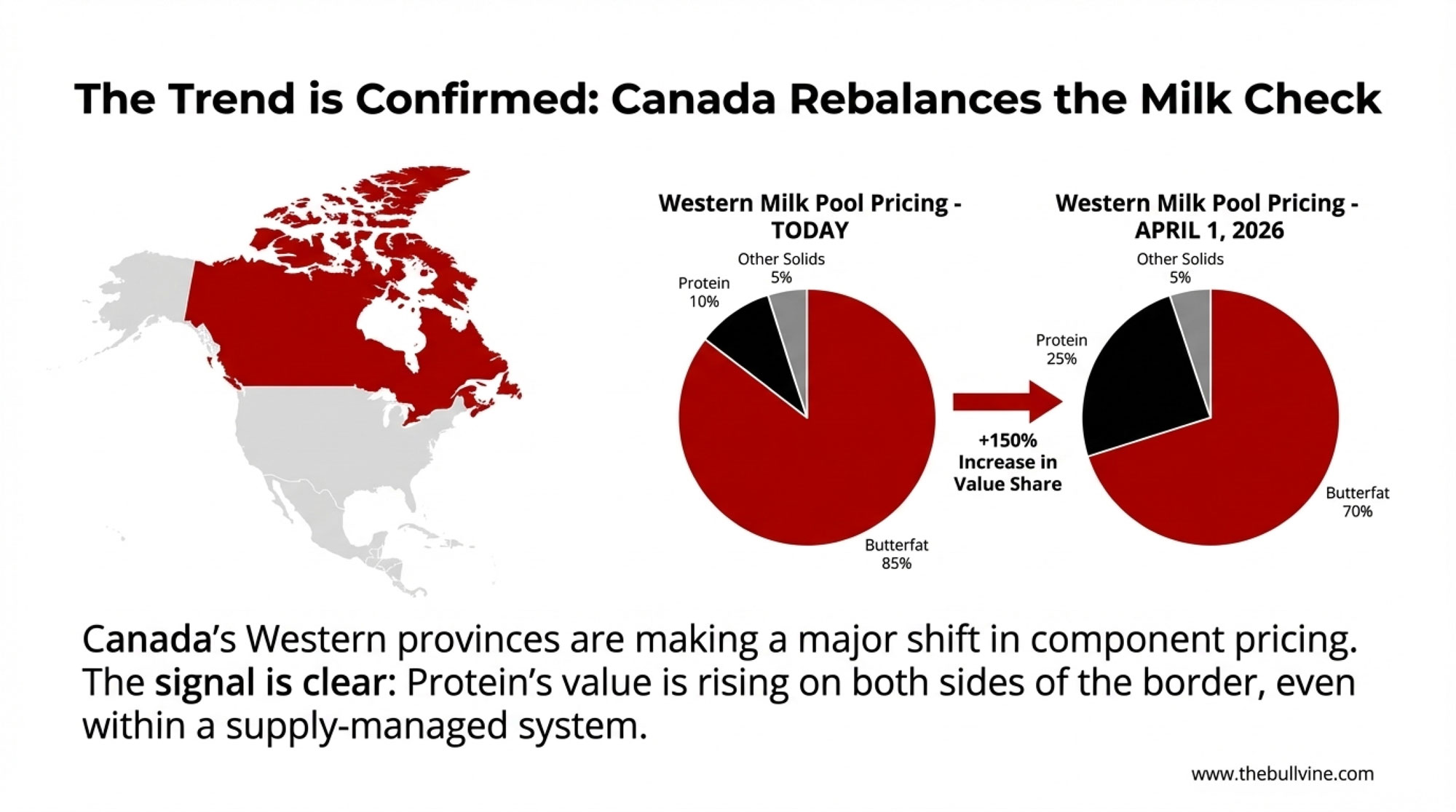

For Canadian readers in Ontario and Quebec, supply management and quota systems buffer your farm‑gate price from a lot of these swings, as multiple analyses of the 2022 Census and Canadian policy have noted. But U.S. export performance and Mexico’s appetite still shape the broader North American environment you’re operating in—especially for processors, trade negotiations, and on‑going USMCA disputes.

One Herd That Fits Today’s Market

Sometimes these big forces are easier to digest when you see how they play out in a real barn.

Top‑Deck Holsteins, a roughly 700‑cow Holstein herd in Iowa, is one of those examples. A recent profile describes Top‑Deck as a freestall operation shipping milk with a rolling herd average around 33,500 pounds per cow per year, built on intentional management and breeding decisions. The exact numbers can move with feed and weather, but the pattern is what matters.

On the cow side, that profile explains that Top‑Deck:

- Pushes forage quality and ration balance hard to drive dry matter intake and feed efficiency.

- Treats cow comfort as a core investment—stall design, bedding, ventilation, and milking routines are all tuned for long lying times and low stress.

- Watches fresh cow management and the transition period closely, with protocols aimed at catching issues early and supporting strong peaks without burning cows out at 30–60 days in milk.

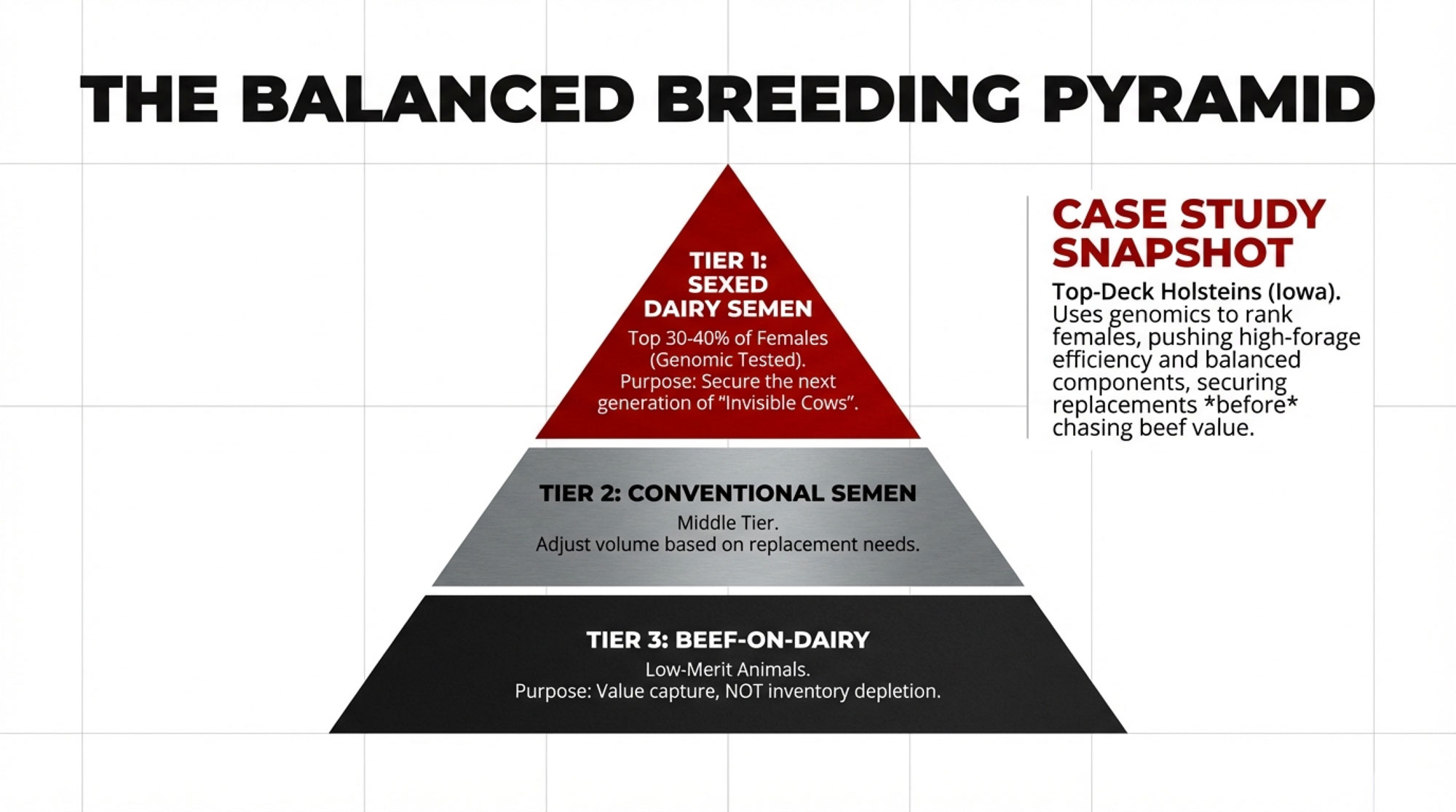

Genetically, Top‑Deck uses genomic testing to rank heifers and cow families, then:

- Uses sexed Holstein semen on top‑merit animals to generate replacements with strong production, components, fertility, and health traits.

- Uses beef semen—often Angus—on lower‑merit animals to produce calves that bring better beef value than traditional Holstein bull calves.

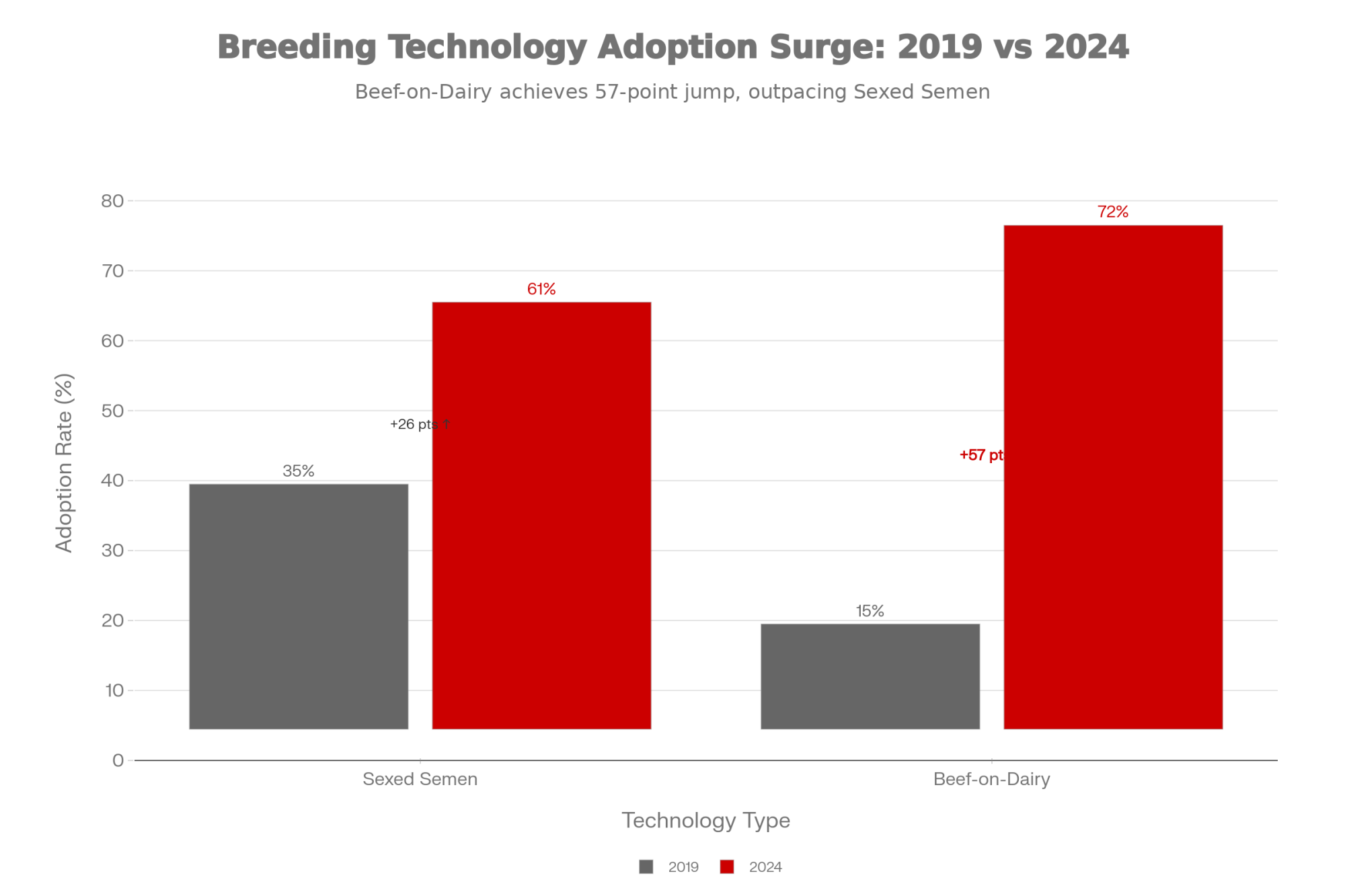

Recent genomic and evaluation‑system reviews in the Journal of Dairy Science and related outlets note that millions of dairy animals worldwide have been genotyped, and that using genomic evaluations with economic indexes has significantly improved progress in production, fertility, and health compared with relying on parent averages. Work from the University of Guelph’s “beef on dairy” research program—funded through the Ontario Agri‑Food Innovation Alliance and national beef research groups—shows that beef‑sired dairy calves, when managed and marketed correctly, can deliver clearly higher prices than straight Holstein bull calves, and that optimizing their early‑life management is key to maximizing value.

What’s interesting here is that Top‑Deck’s approach isn’t about chasing one extreme number. It’s about building cows that quietly ship a lot of pounds of fat and protein, stay healthy and fertile, and leave behind replacements that can do the same—while using beef‑on‑dairy to lift calf revenue. That’s exactly the kind of herd that fits a cheese‑heavy, component‑sensitive, export‑connected world.

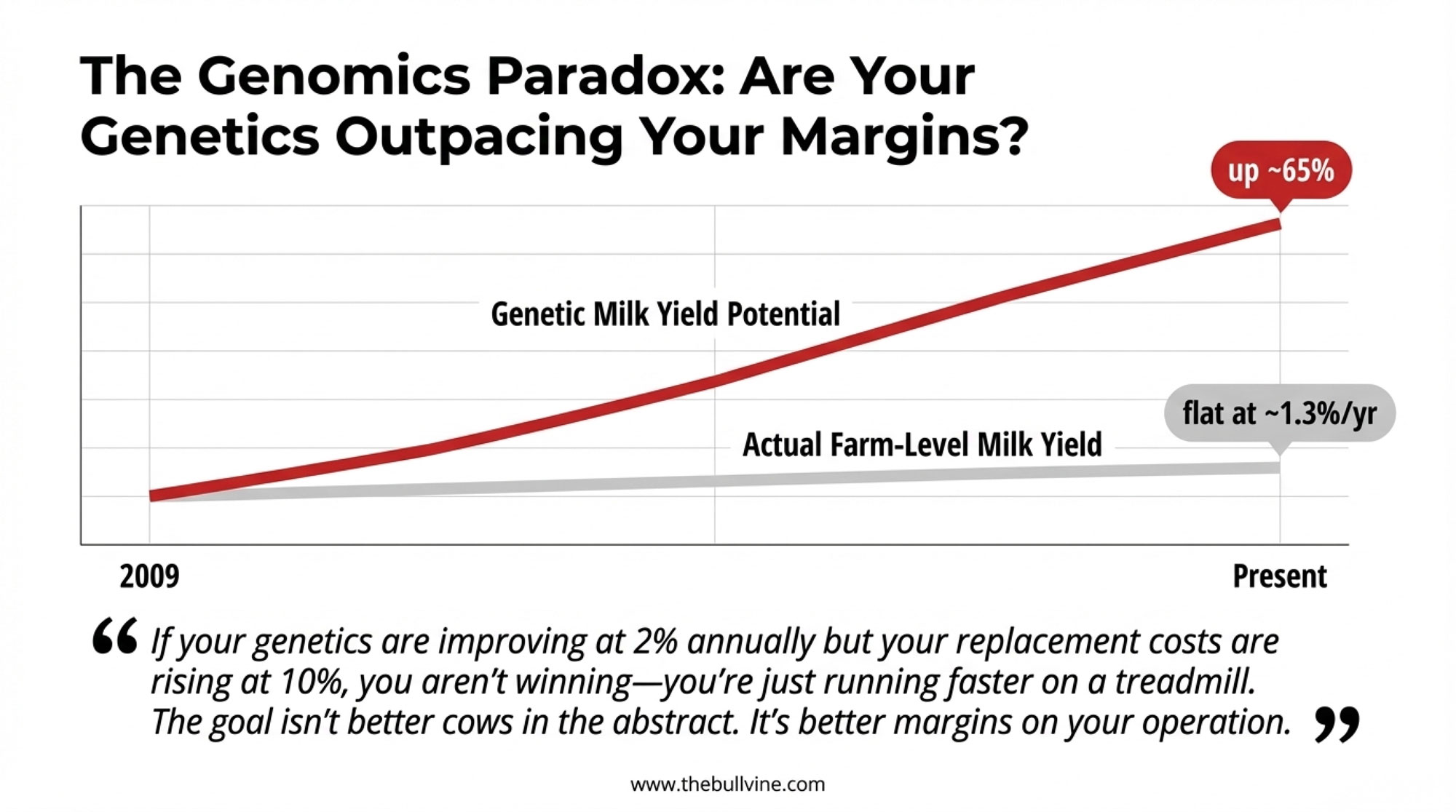

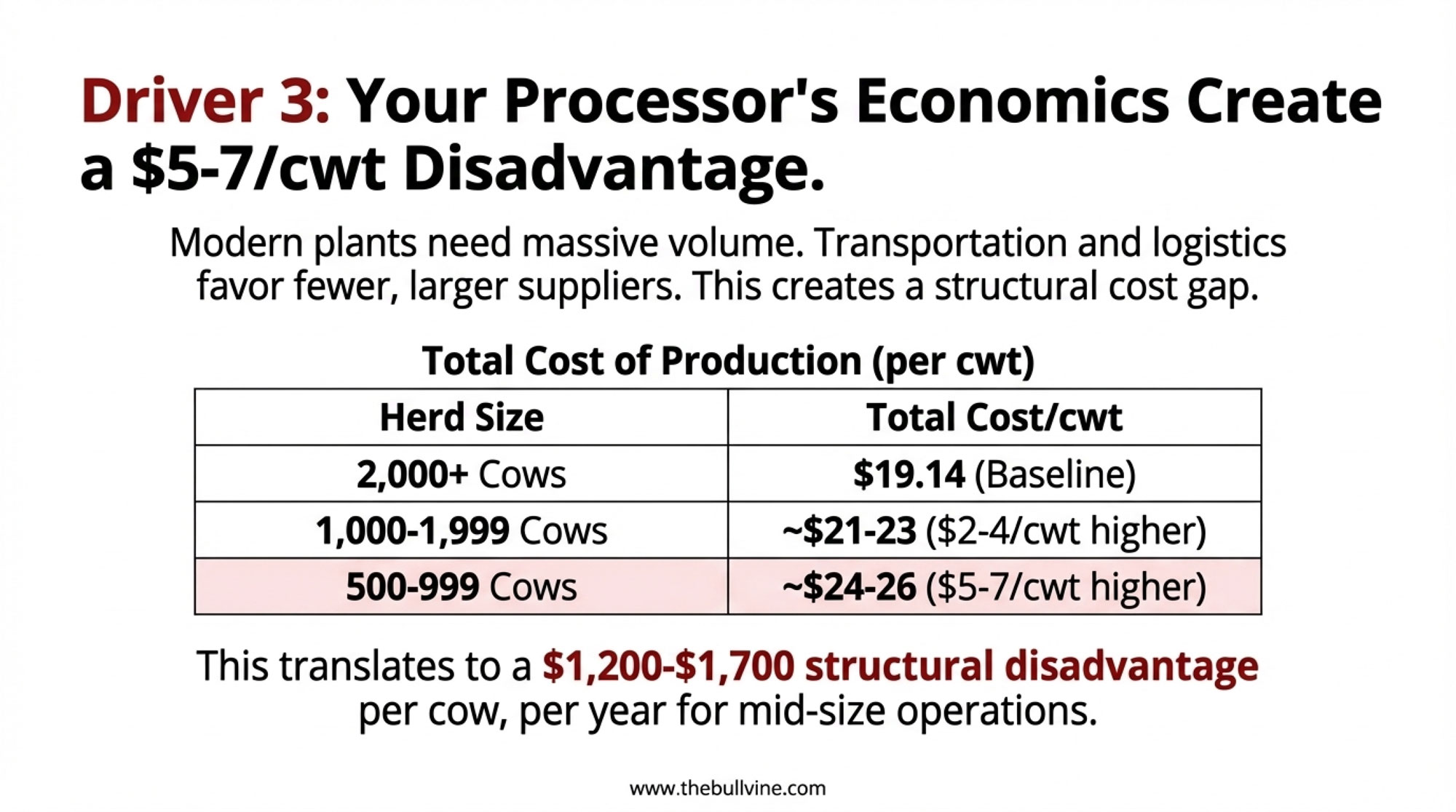

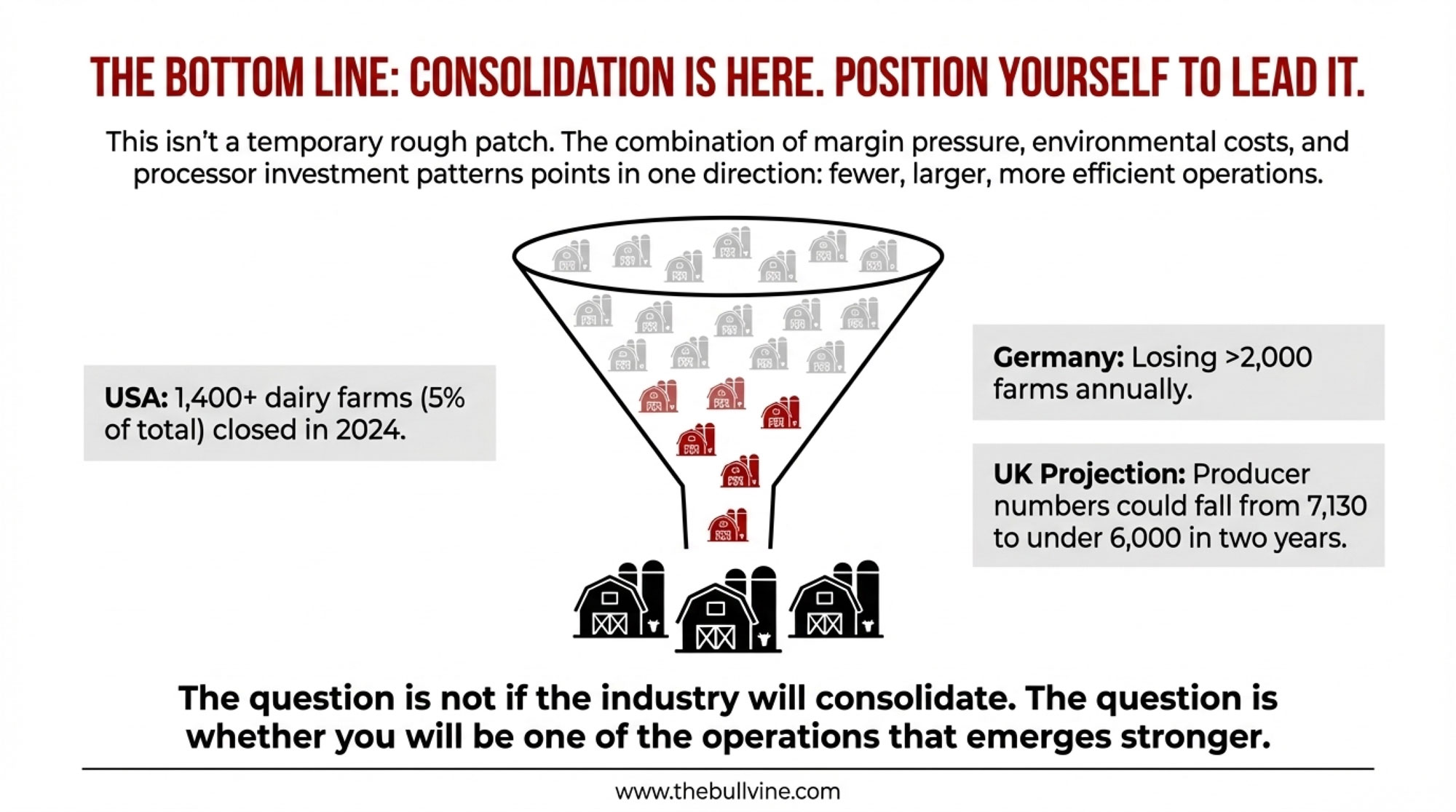

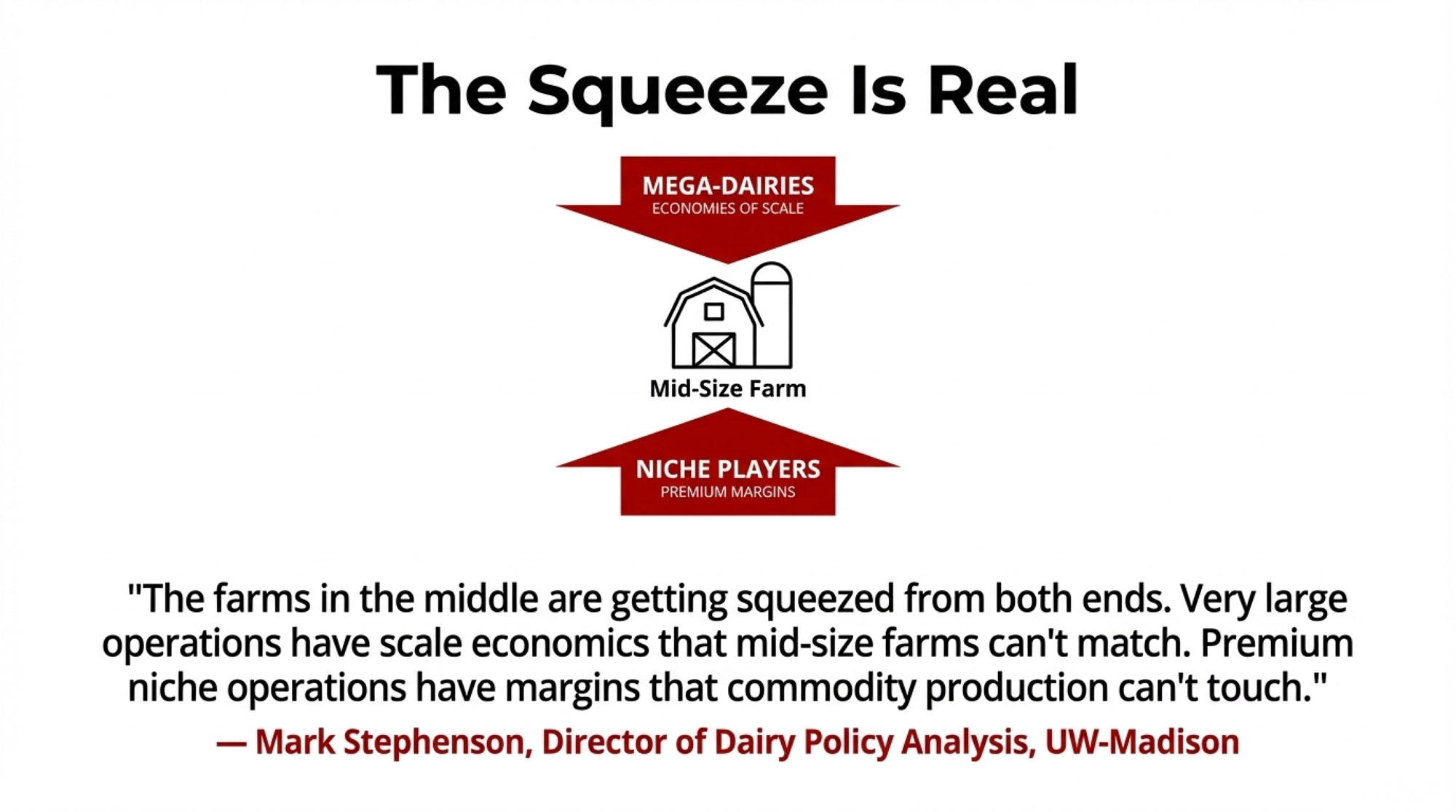

The Consolidation Reality—and What It Means for Genetics

Now let’s punch in the consolidation piece, because this really matters for breeders and for anyone thinking about where their herd fits.

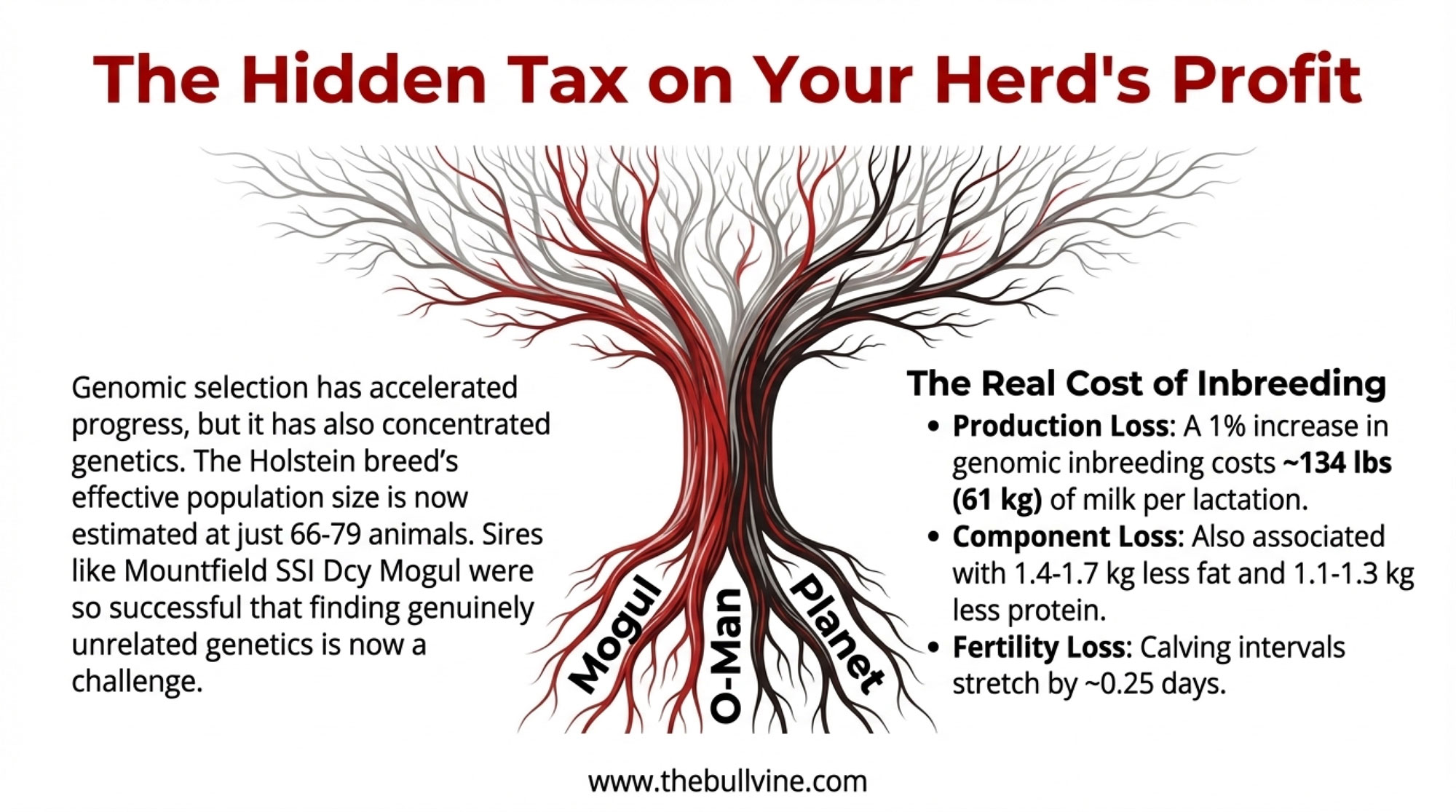

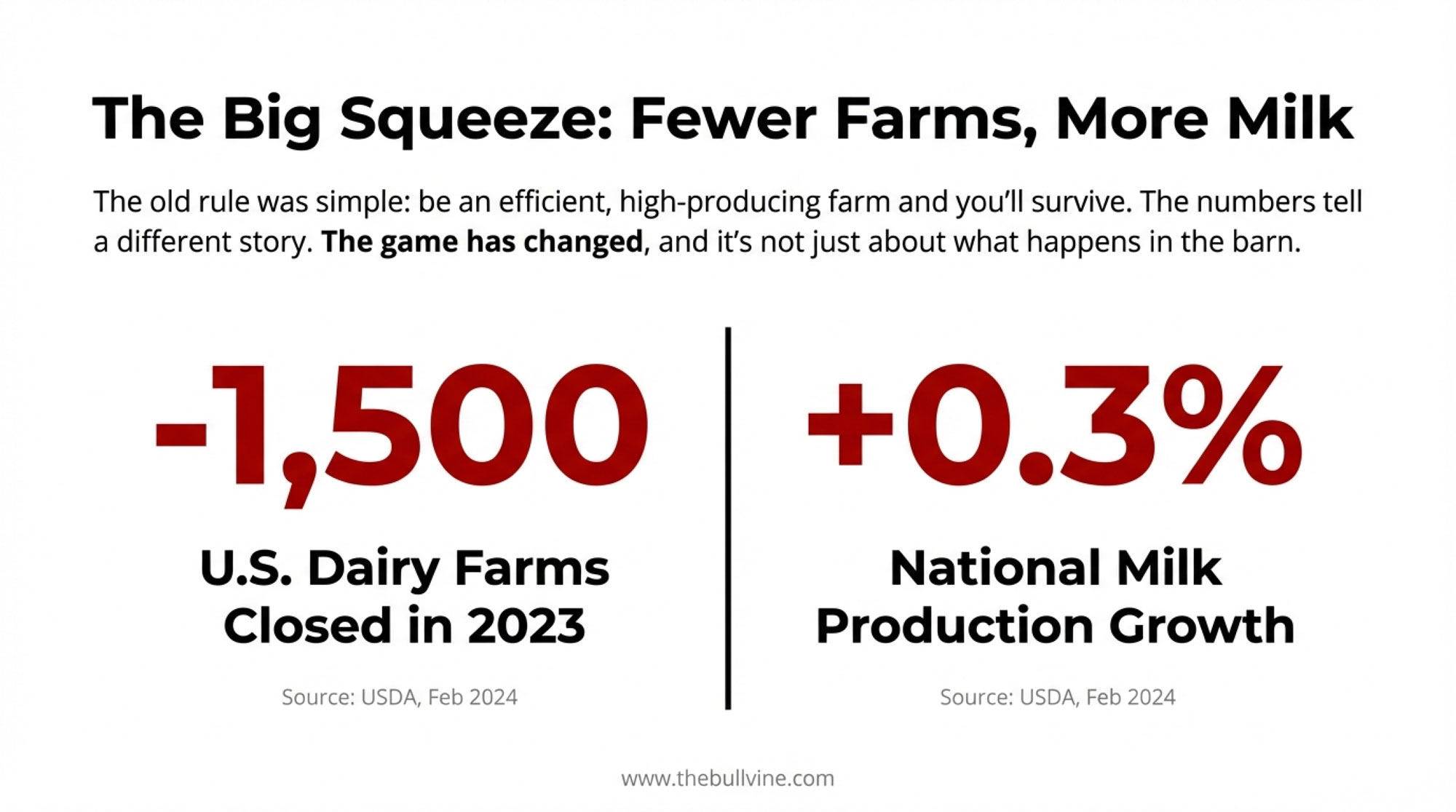

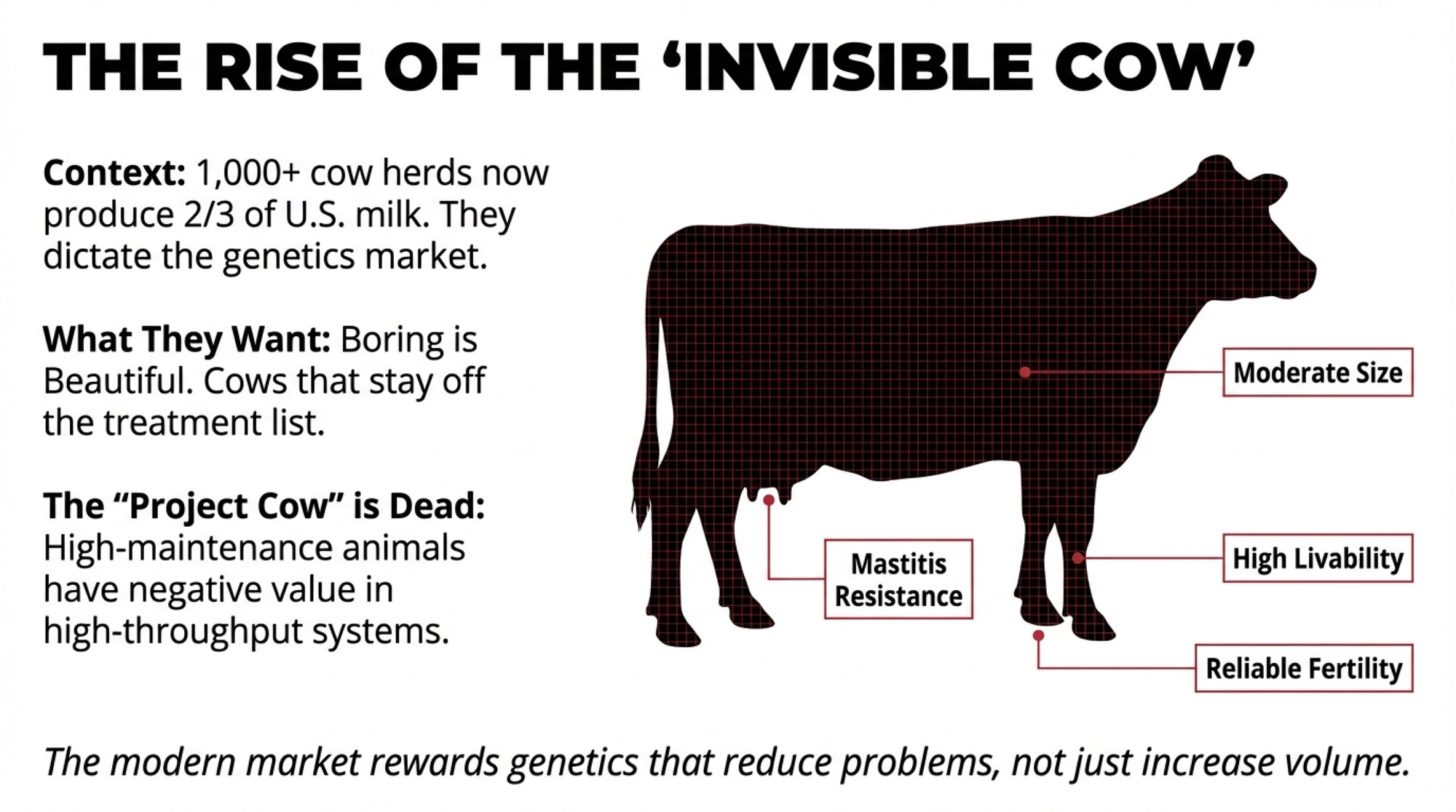

The 2022 Census of Agriculture shows U.S. dairy farm numbers dropping from 39,303 in 2017 to 24,082 in 2022. That’s roughly a 39 percent decline—about 15,000 dairies gone in five years—even as total U.S. milk production climbed roughly 5 percent, on about 9.4 million milk cows. Rabobank analysis cited in those same reports estimates that herds with more than 1,000 cows now produce around two‑thirds of U.S. milk by value, up from around 60 percent in 2017.

On top of elemental market forces, environmental and labor policies are nudging in the same direction. California, Washington, and other states have tightened manure, water, and methane rules, pushing dairies toward digesters, lagoon covers, and more sophisticated nutrient management systems—investments that are easier to justify on a 2,000‑cow dairy than on an 80‑cow tie‑stall. Labor and immigration constraints also tend to hit smaller farms harder, while larger operations often have more tools to recruit, pay, and house workers.

So the center of gravity has shifted. The buyers of genetics and semen are increasingly large freestall and dry-lot herds milking 1,000, 3,000, or 10,000 cows, not just smaller family herds picking bulls at a local sale. And those large herds are demanding a specific type of cow.

European and Scandinavian research has started using the phrase “invisible cows” to describe the ideal animal in large, modern dairy systems: basically trouble‑free, almost boring cows that don’t show up on the treatment list, have few metabolic or hoof problems, calve easily, breed back reliably, and quietly ship components that fit the plant’s grid. U.S. management and genetics advisers are framing similar ideas—focusing on cows that minimize disruptions in high‑throughput, labor‑tight environments.

What I’ve noticed, talking with large‑herd managers and AI folks, is that this is changing the genetic marketplace. Big herds don’t want “project cows” that constantly need special attention. They want cows that are almost invisible day‑to‑day:

- Strong on productive life and livability.

- Good mastitis resistance and udder health.

- Sound feet and legs that keep them moving to the bunk and parlor.

- Fertility and calving traits that keep fresh cow problems to a minimum.

- Moderate size with solid feed efficiency.

| Trait Category | Old Priority (Show Ring / Single Trait) | 2025 Large-Herd Priority (“Invisible Cow”) |

|---|---|---|

| Production | Max milk volume or max butterfat % | Balanced pounds of fat + protein shipped per cow/year |

| Health | Treat problems as they come | Mastitis resistance, low SCC, minimal treatments |

| Fertility | Secondary concern | Strong heat detection, conception rate, calving interval |

| Calving | Some assistance acceptable | Calving ease (sire & maternal), low stillbirths |

| Longevity | Cull and replace as needed | Productive life, low cull rate, multiple lactations |

| Structure | Extreme dairy form, show-ring style | Sound feet/legs, good locomotion, moderate frame |

| Temperament | Not formally selected | Calm, easy to handle in high-throughput parlors |

| Feed Efficiency | Rarely considered | Moderate intake, strong component output per lb DMI |

For breeders, that has two big implications. First, there’s an opportunity for those who can breed and market families that consistently deliver these trouble‑free, “invisible” cows and back it up with real herd performance. Second, there’s risk if a herd or breeding program stays focused only on show‑ring traits or single‑trait extremes without a clear economic story tied to big‑herd, high‑throughput systems.

As herds get larger, the market is slowly but surely rewarding genetics that reduce problems rather than create them.

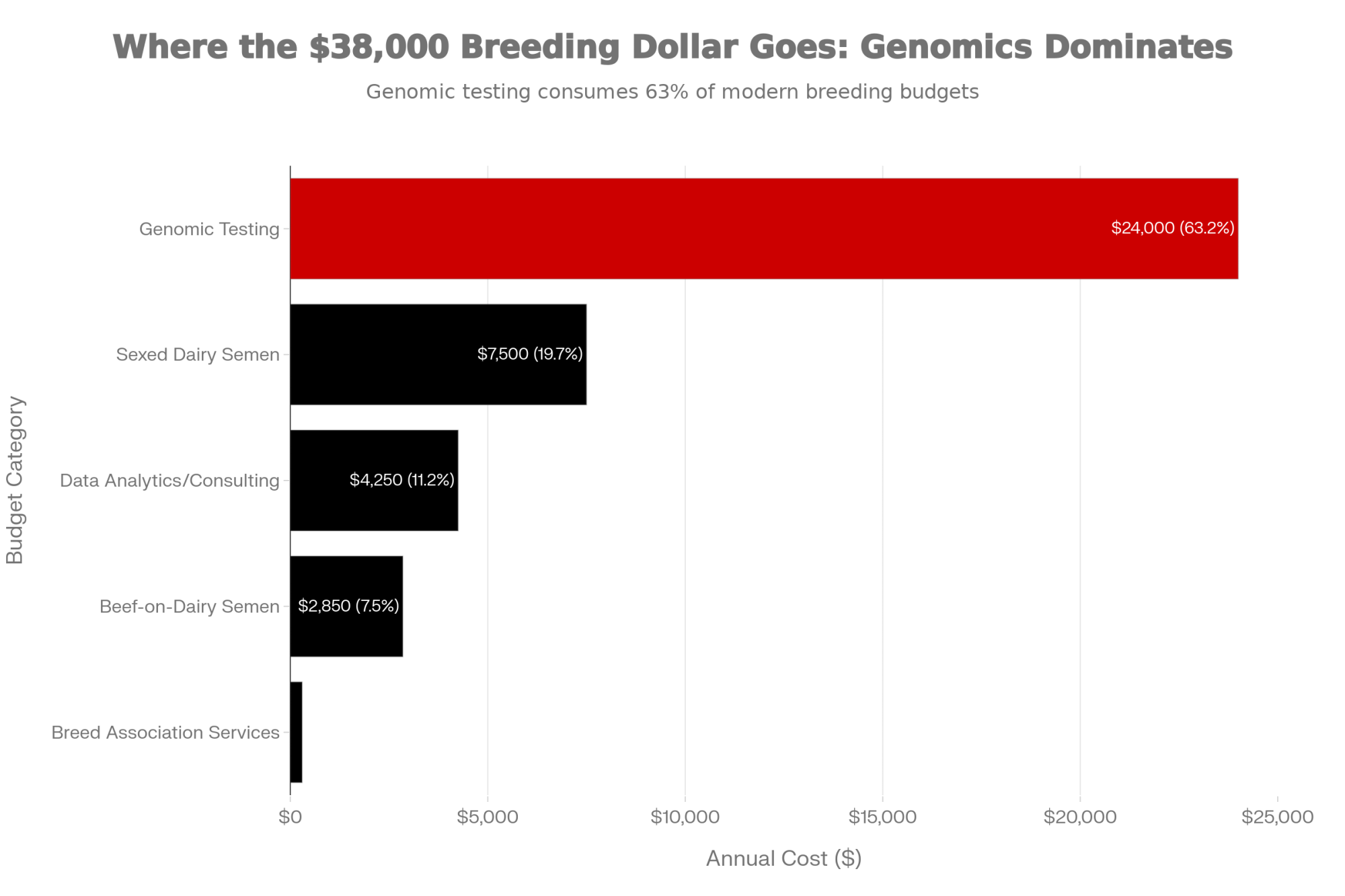

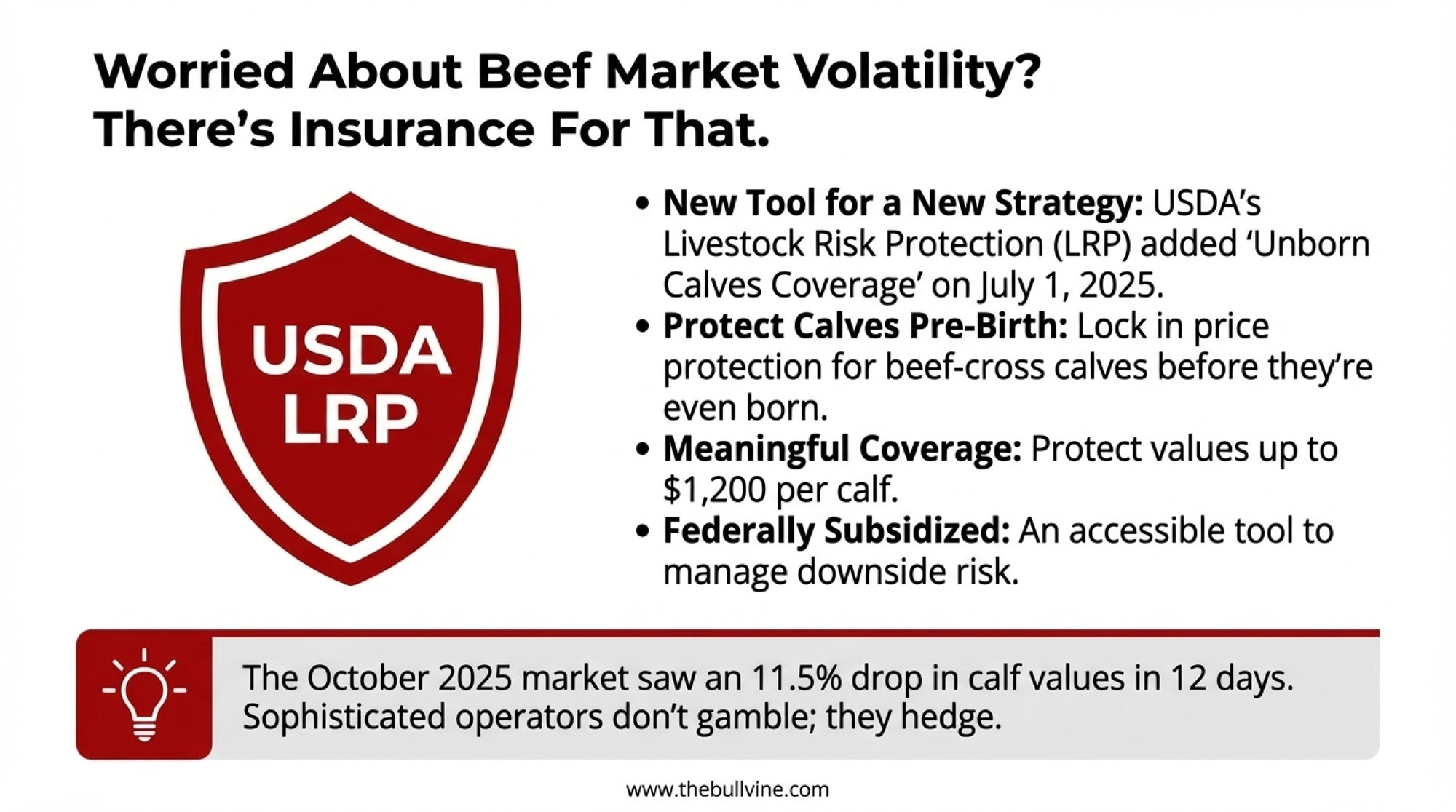

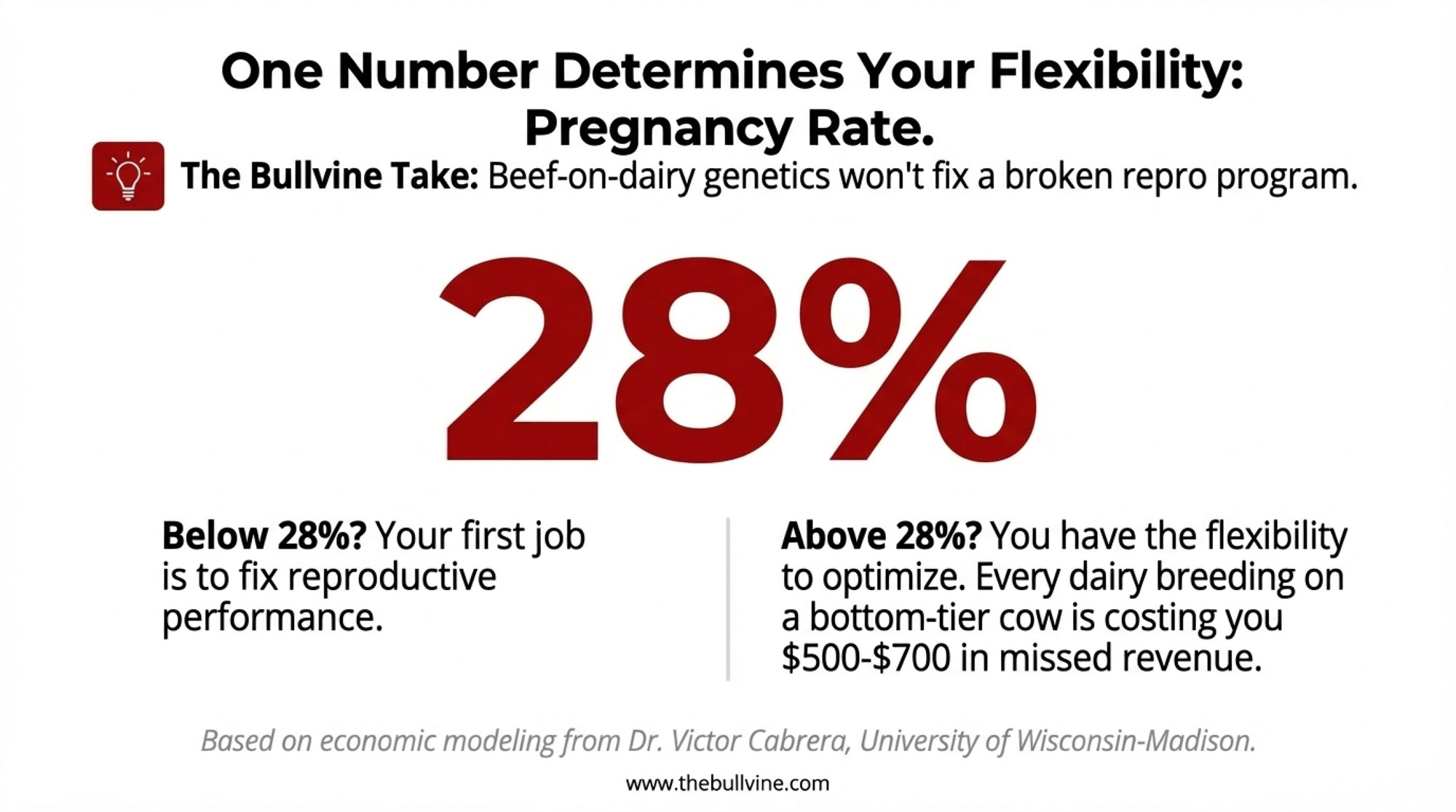

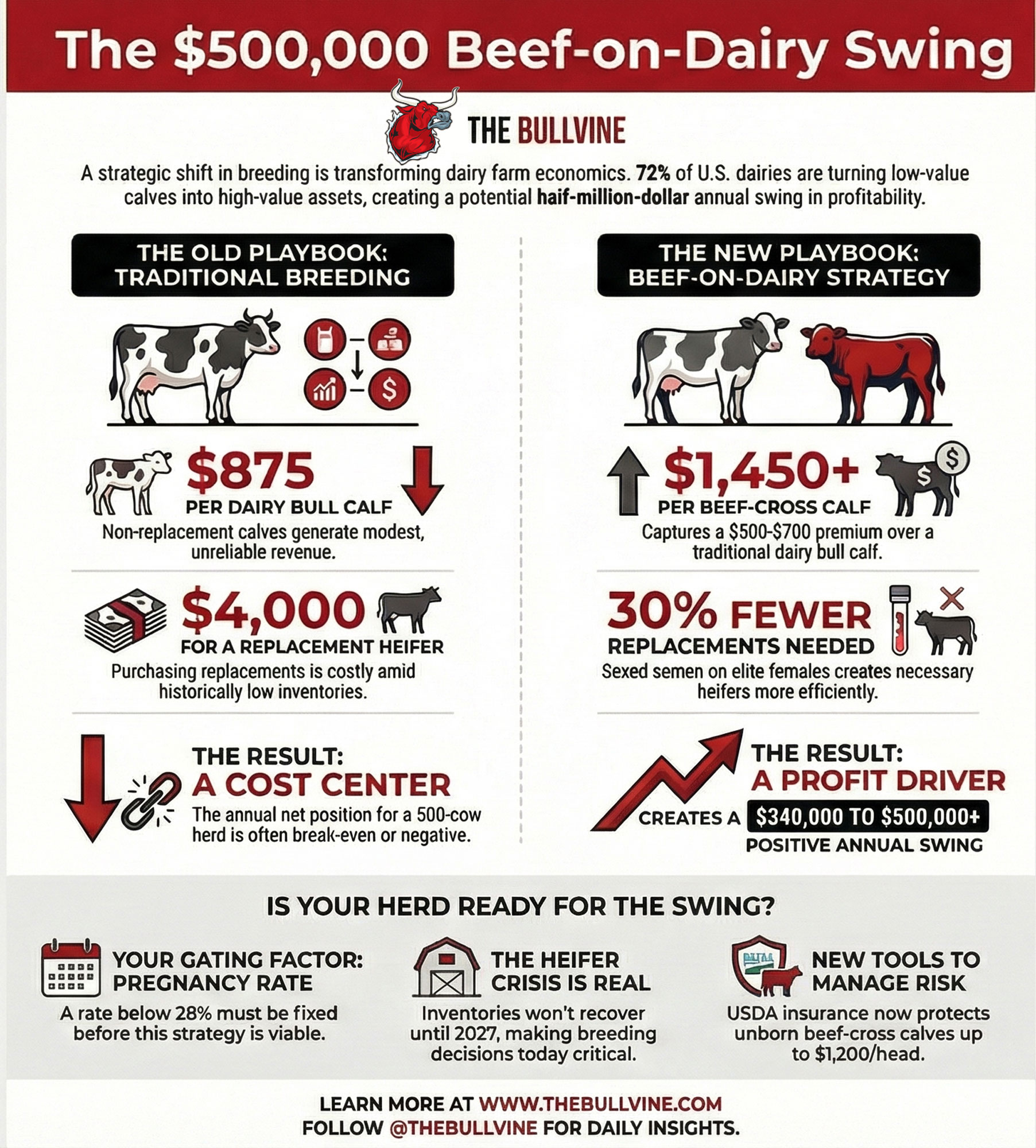

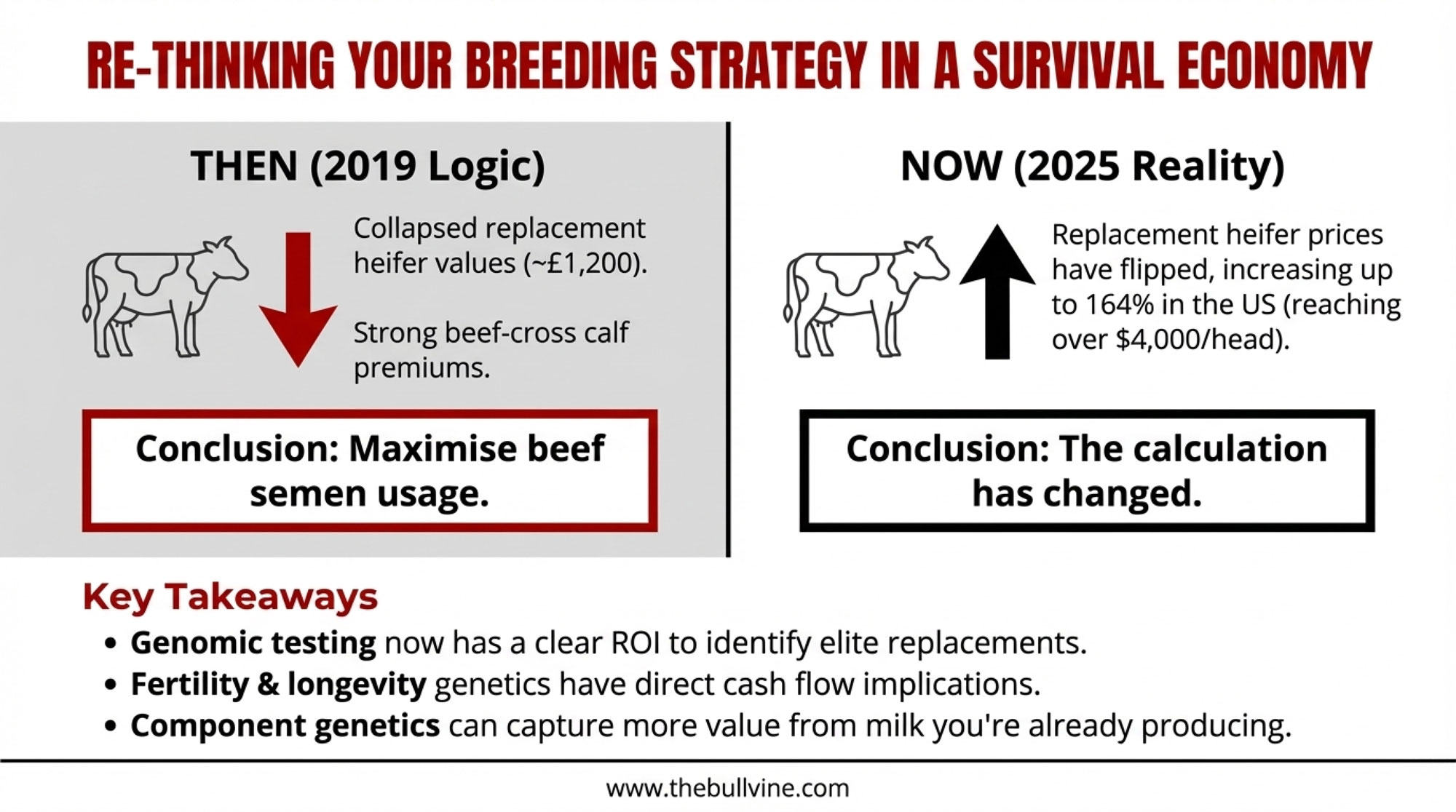

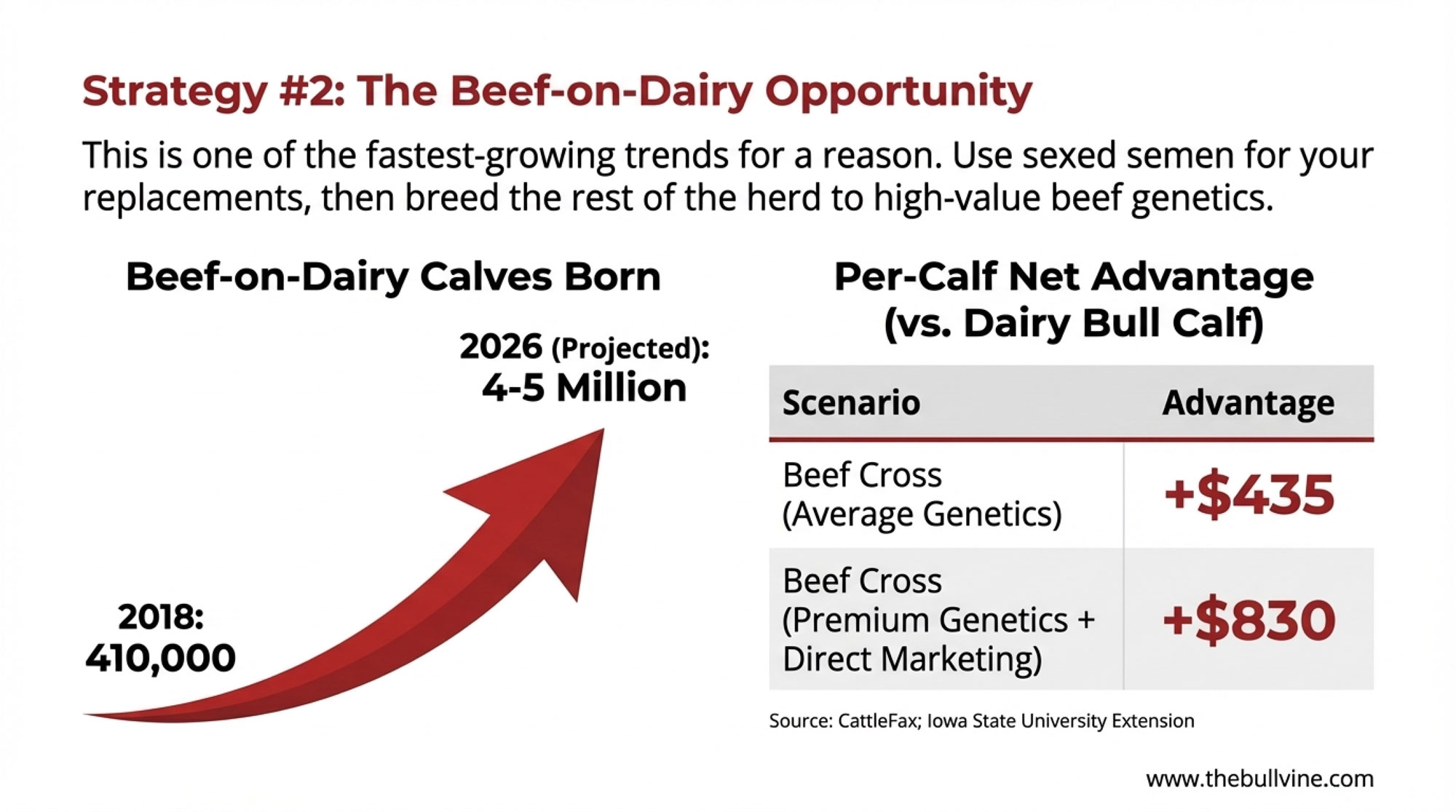

Beef‑on‑Dairy: Cash Cow or Heifer Trap?

Now let’s lean into beef‑on‑dairy and replacements, because this is where a lot of operations are feeling both opportunity and pain.

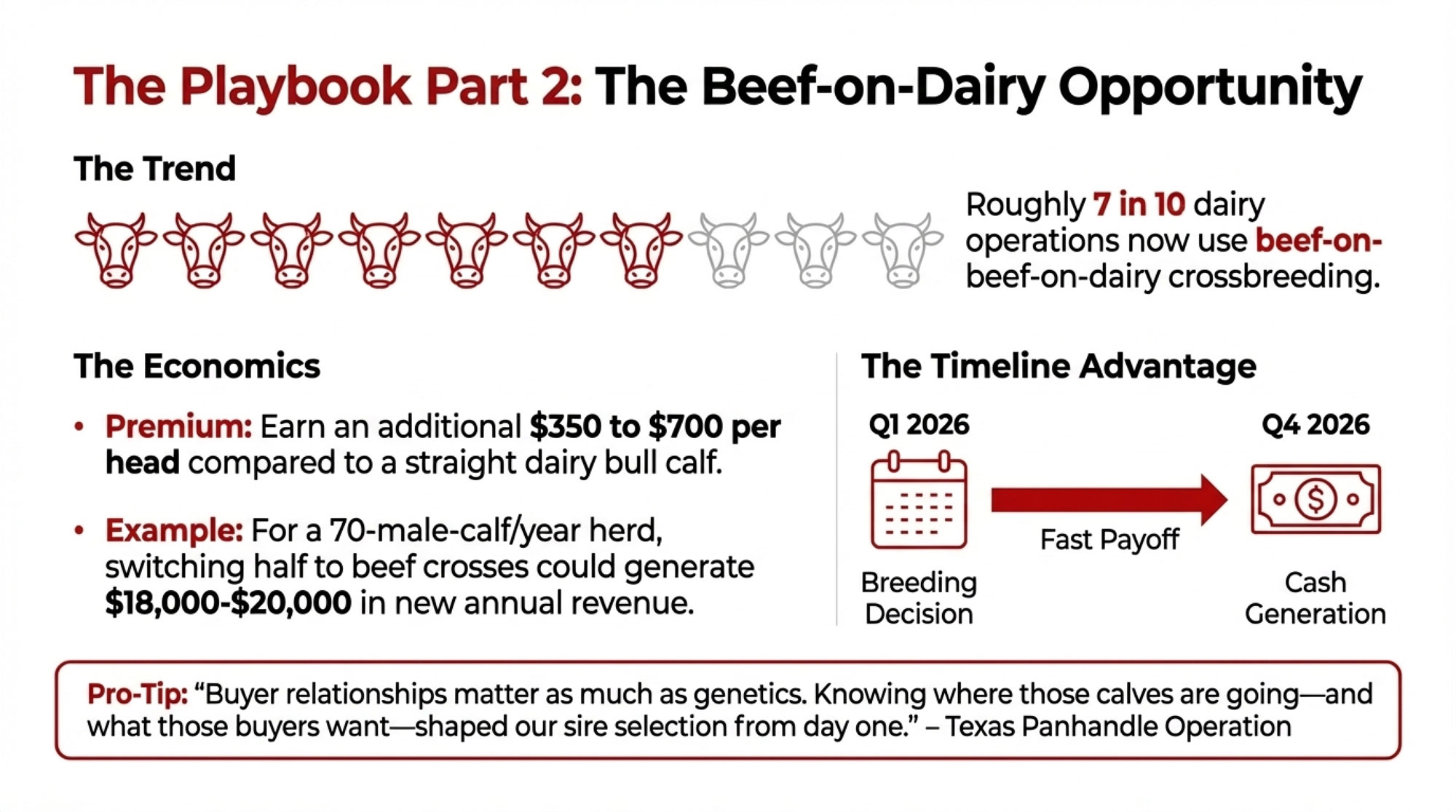

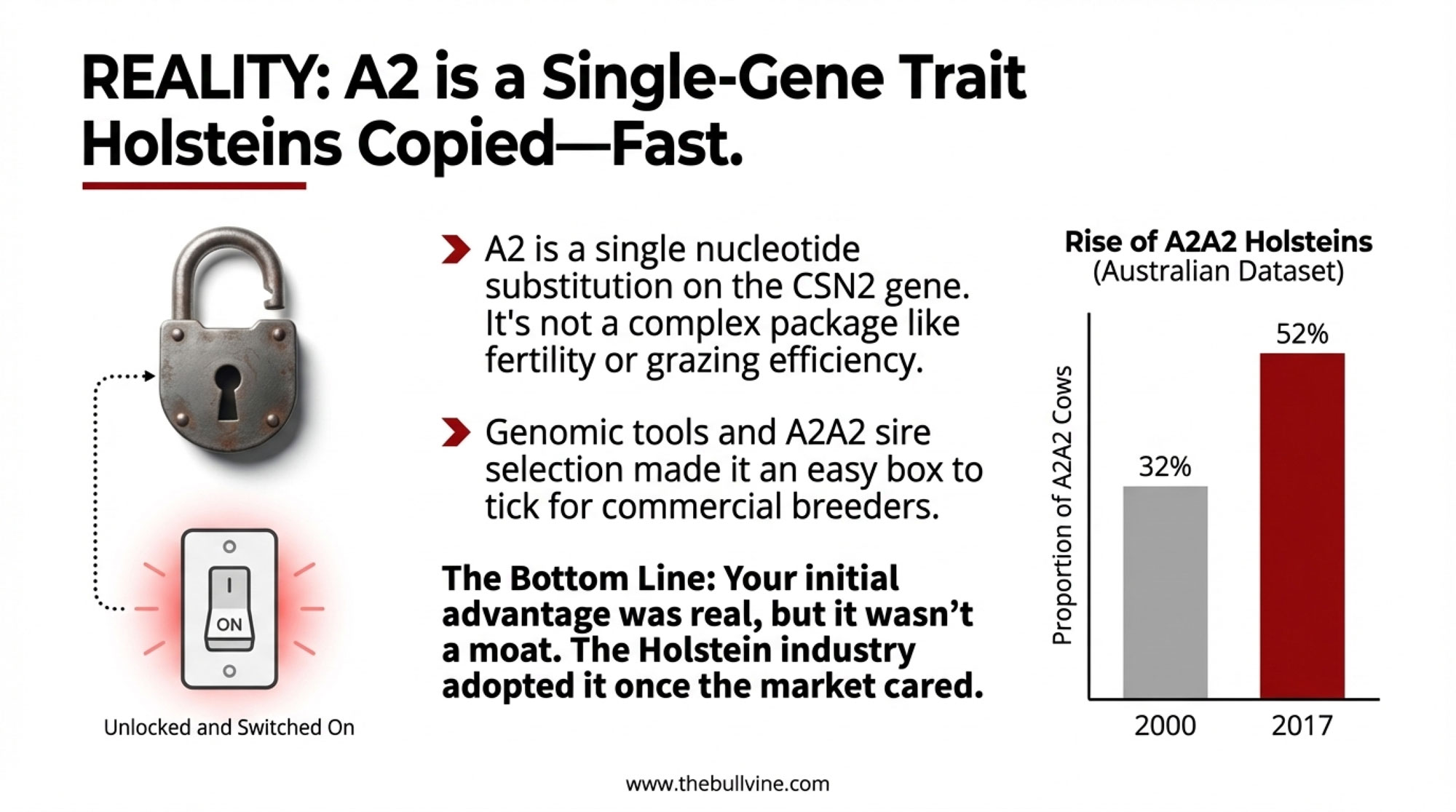

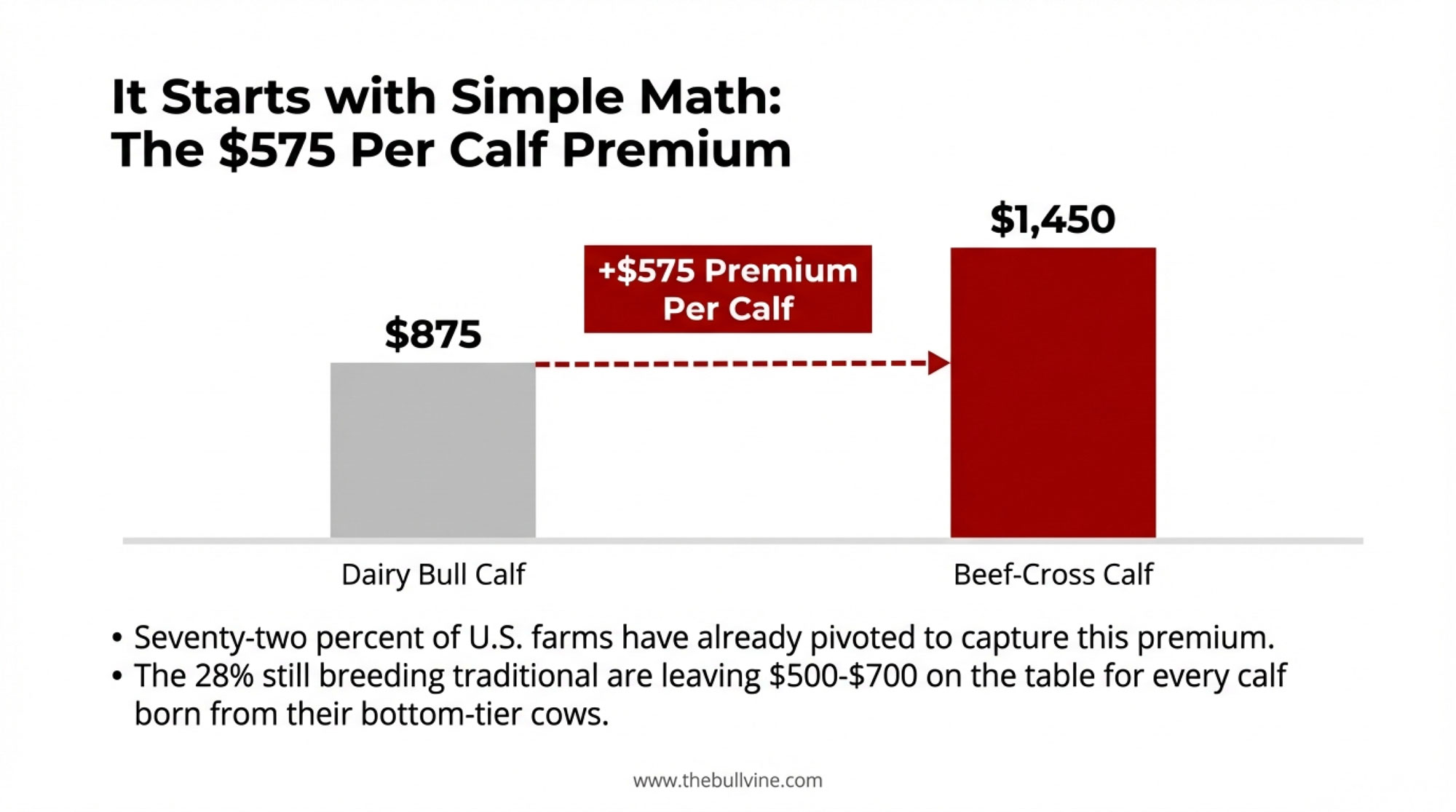

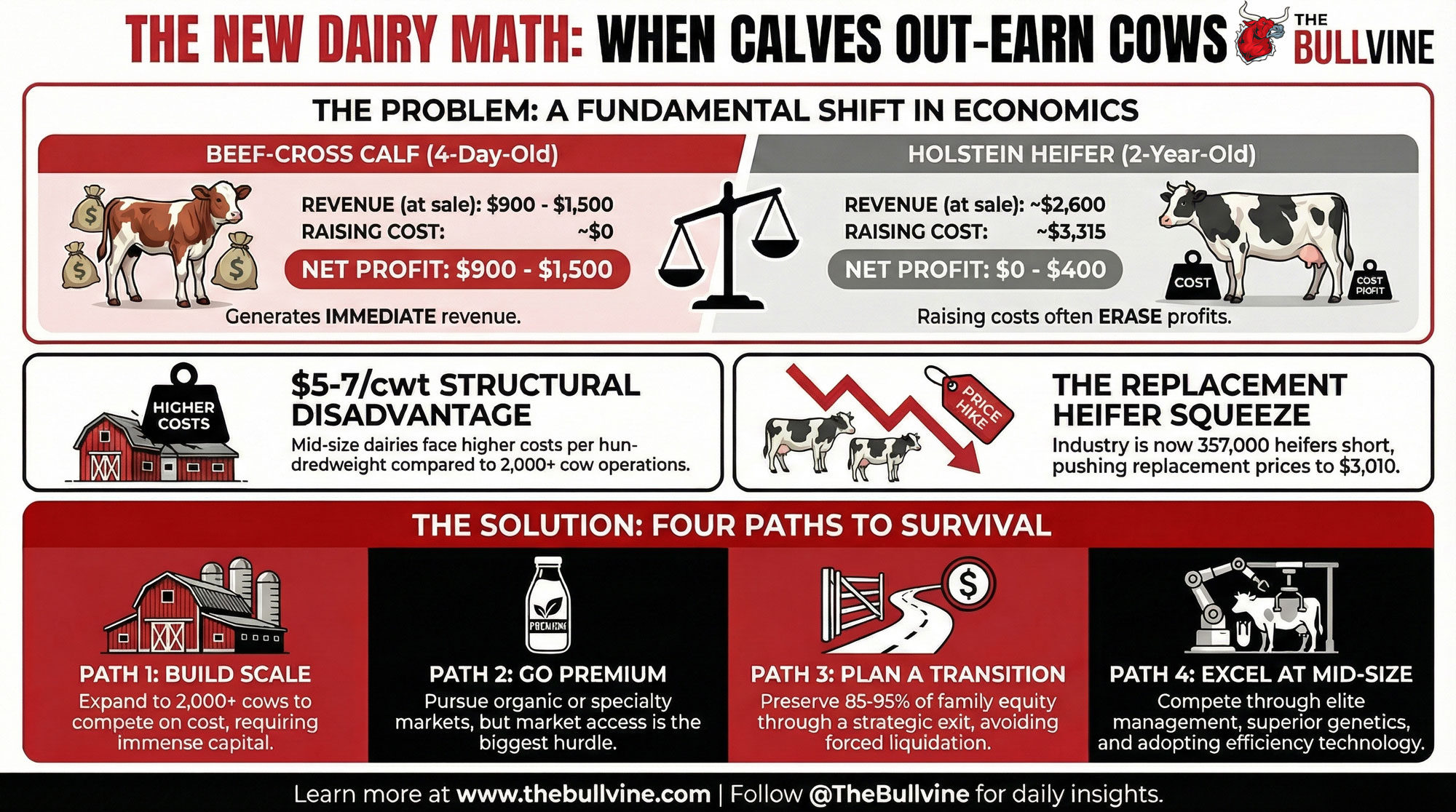

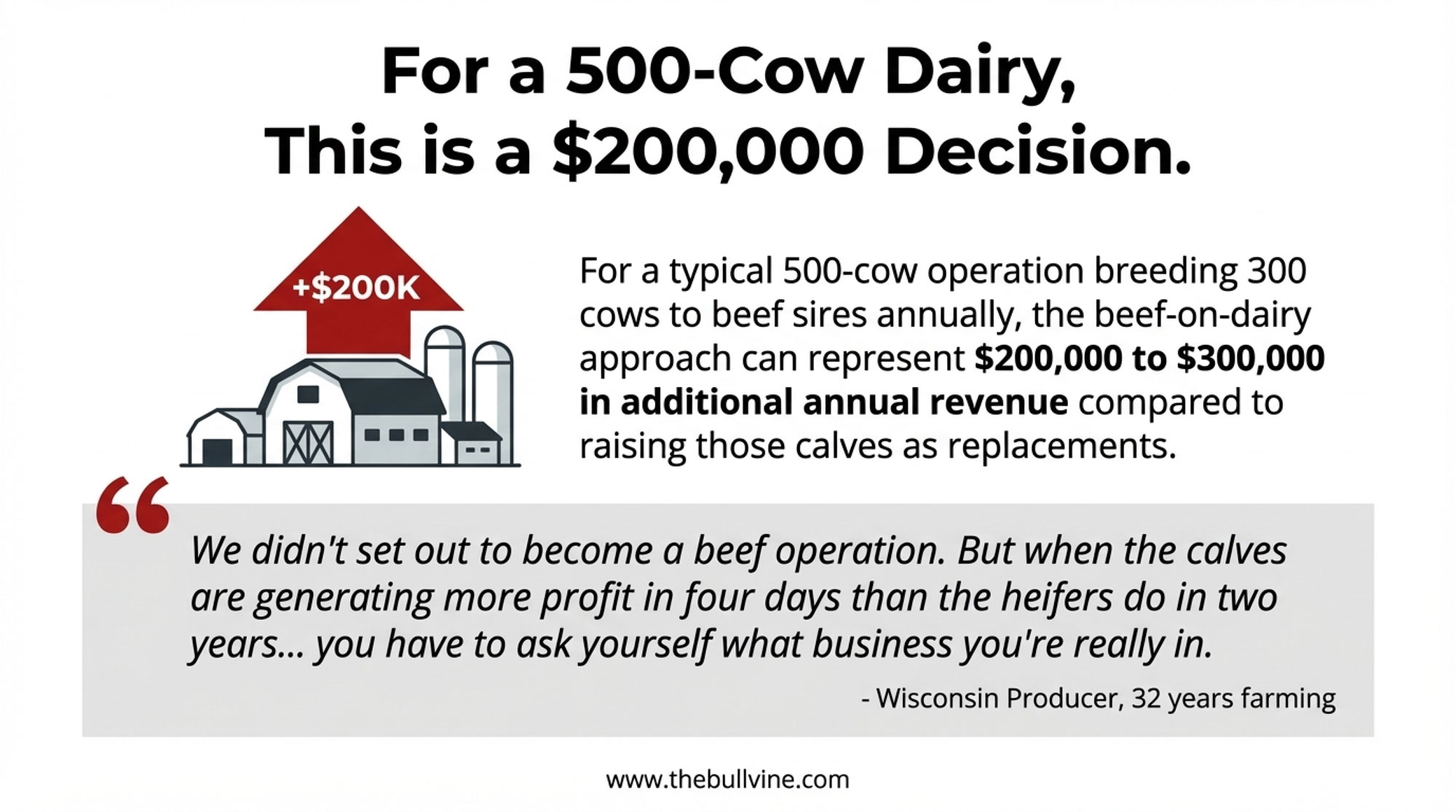

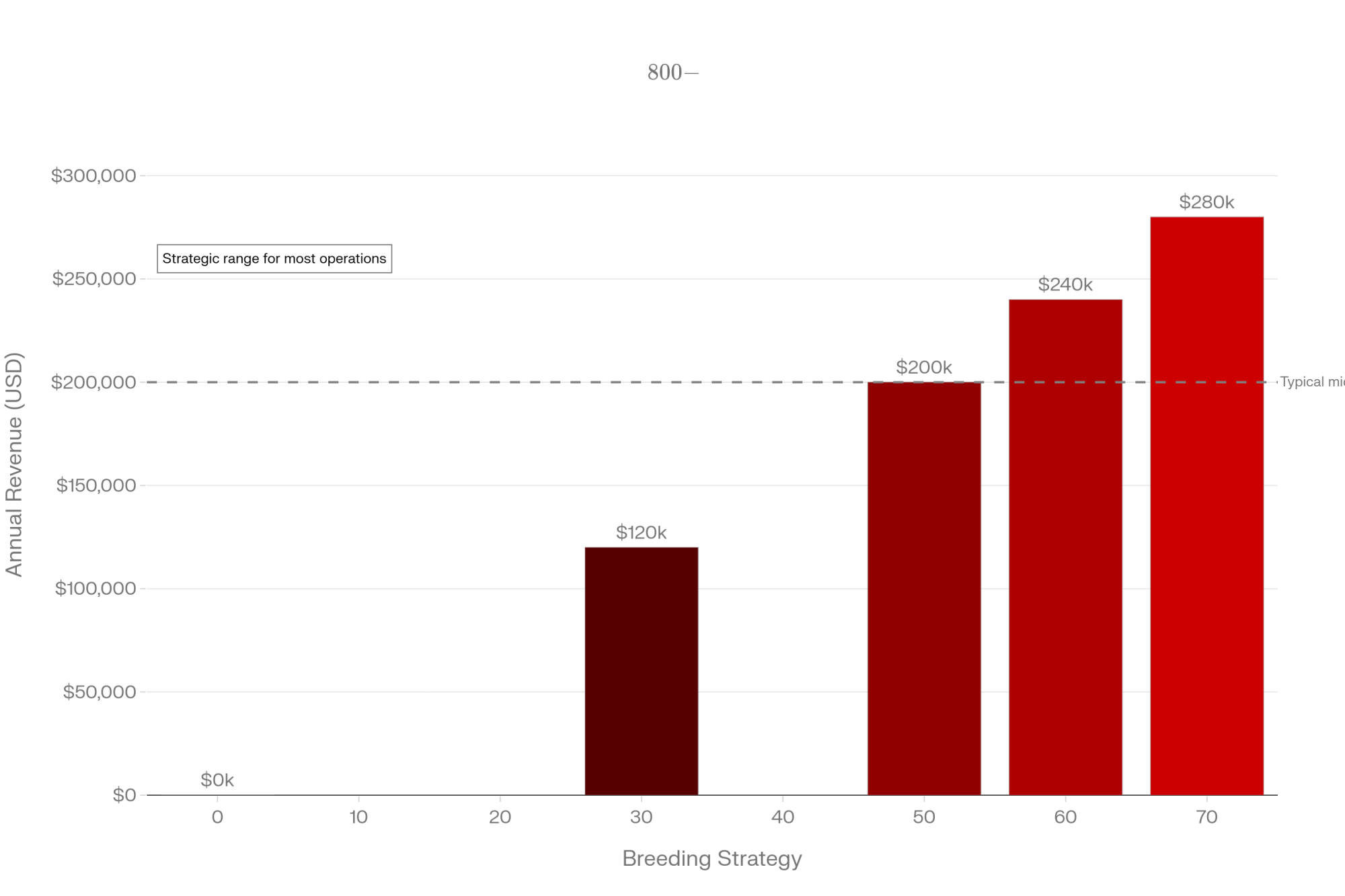

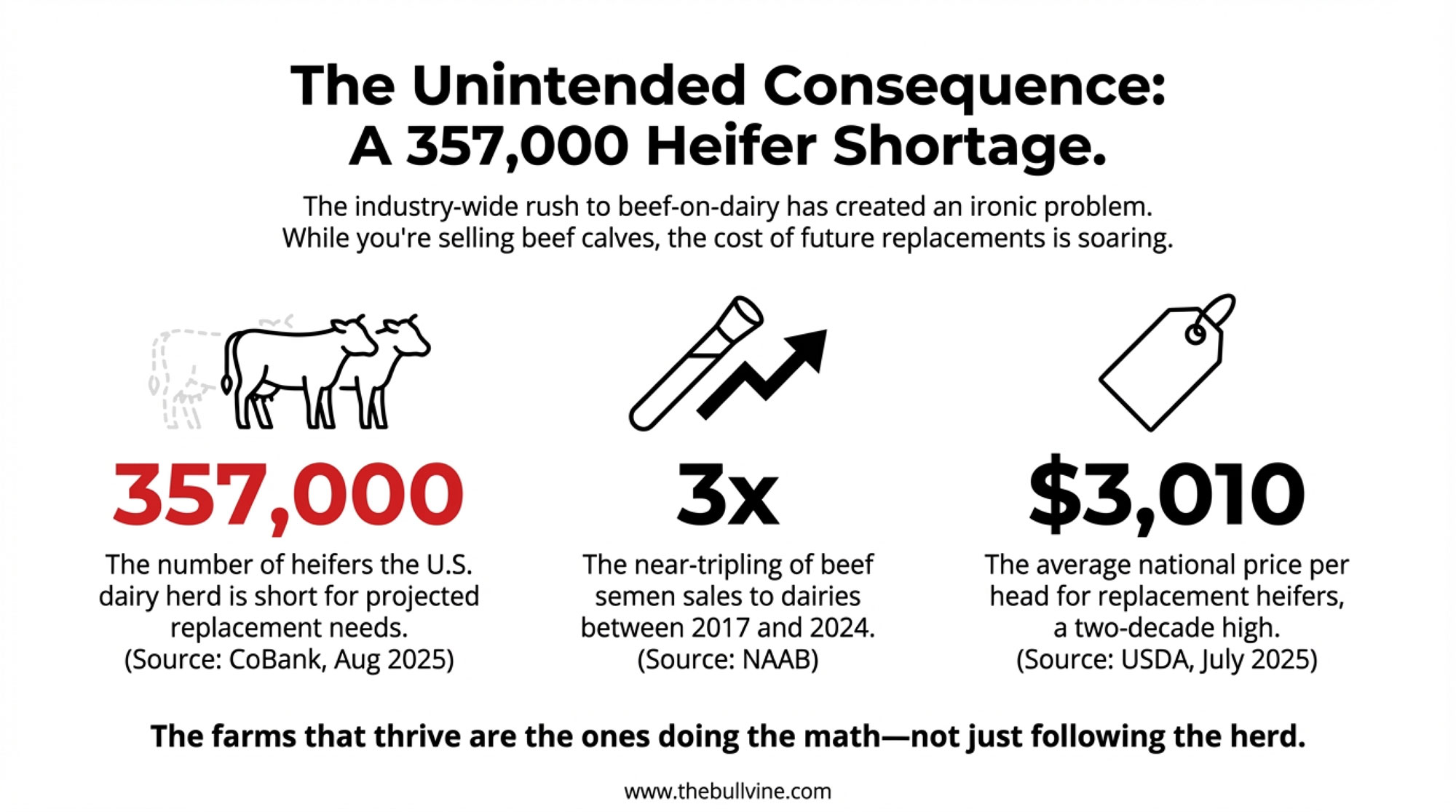

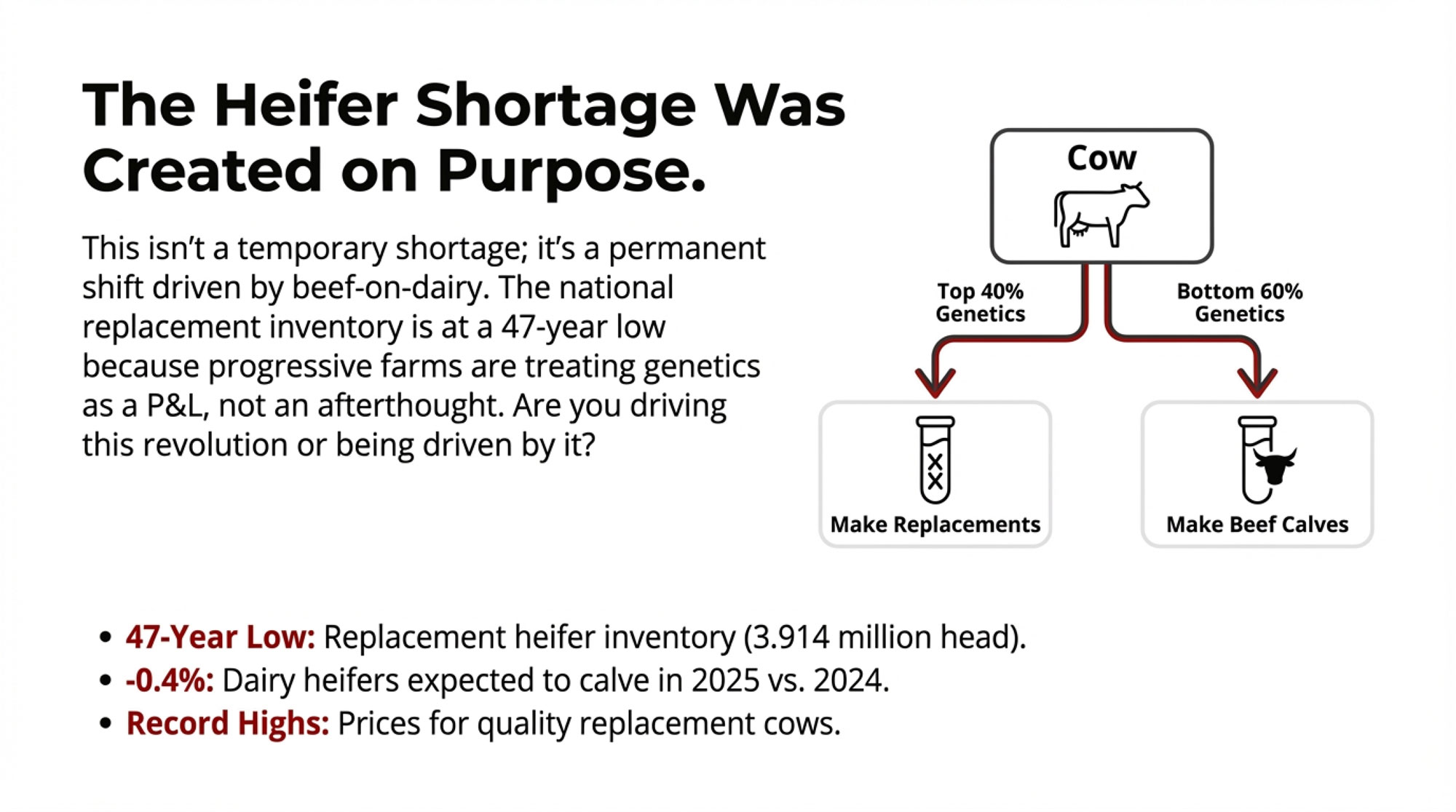

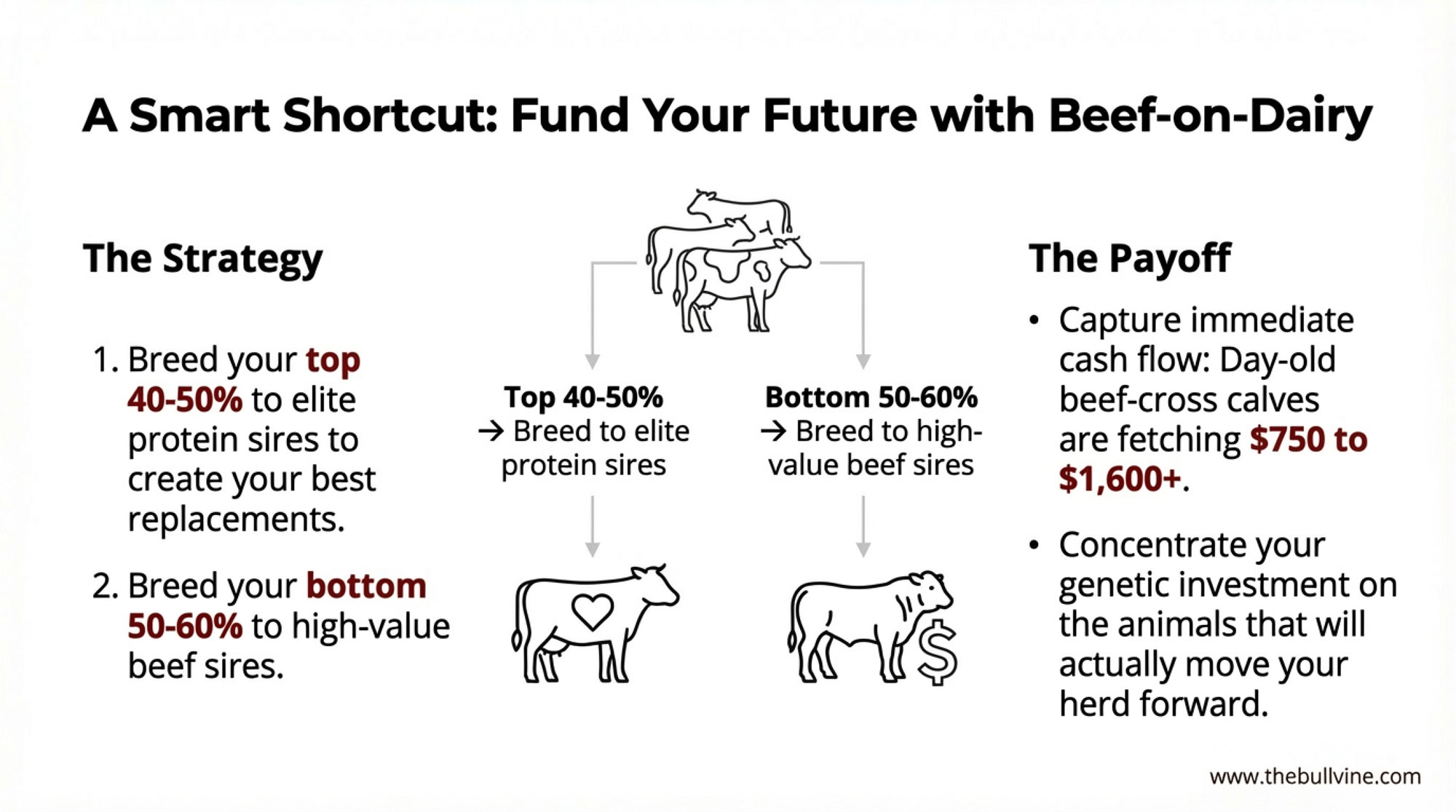

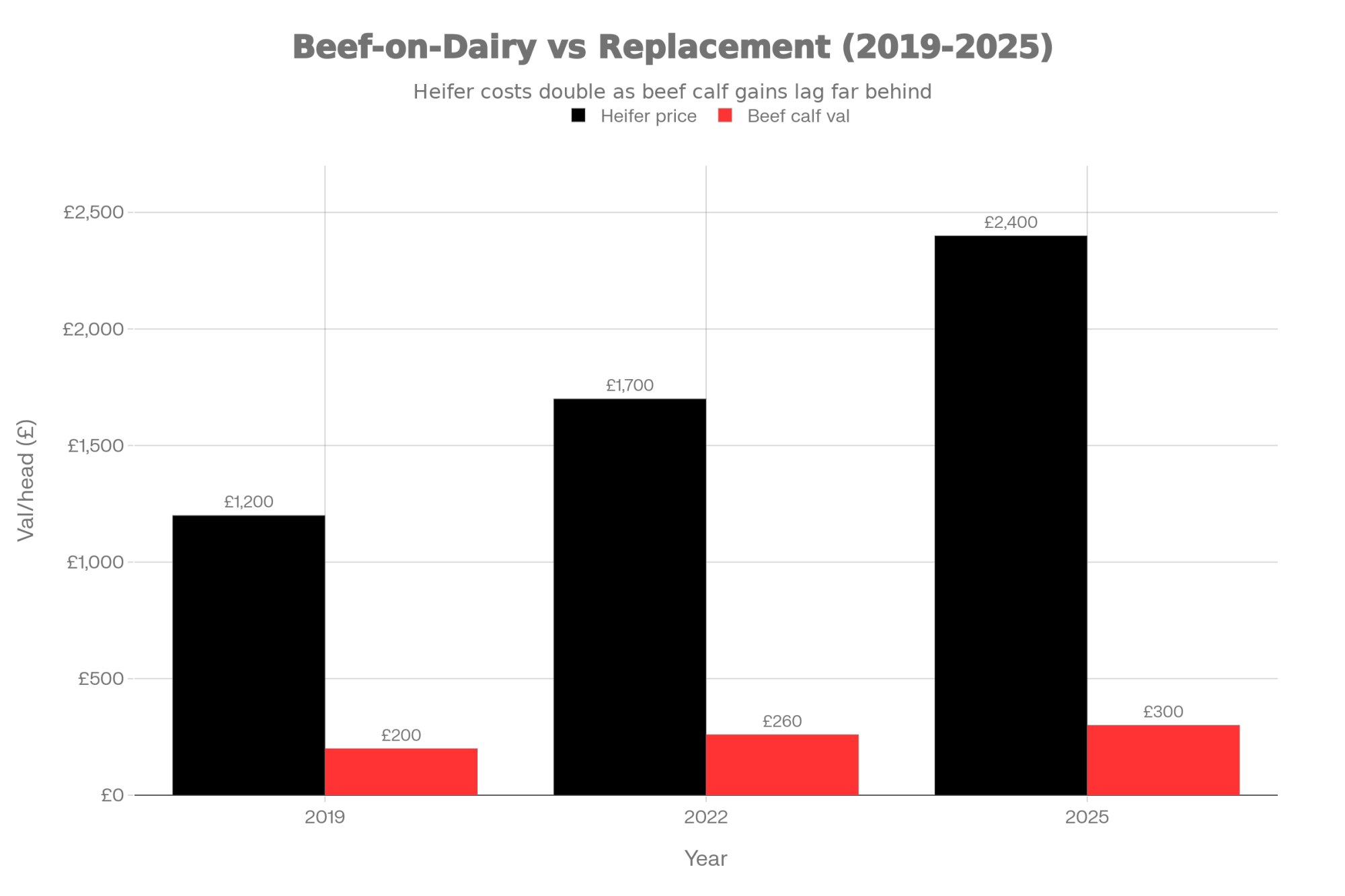

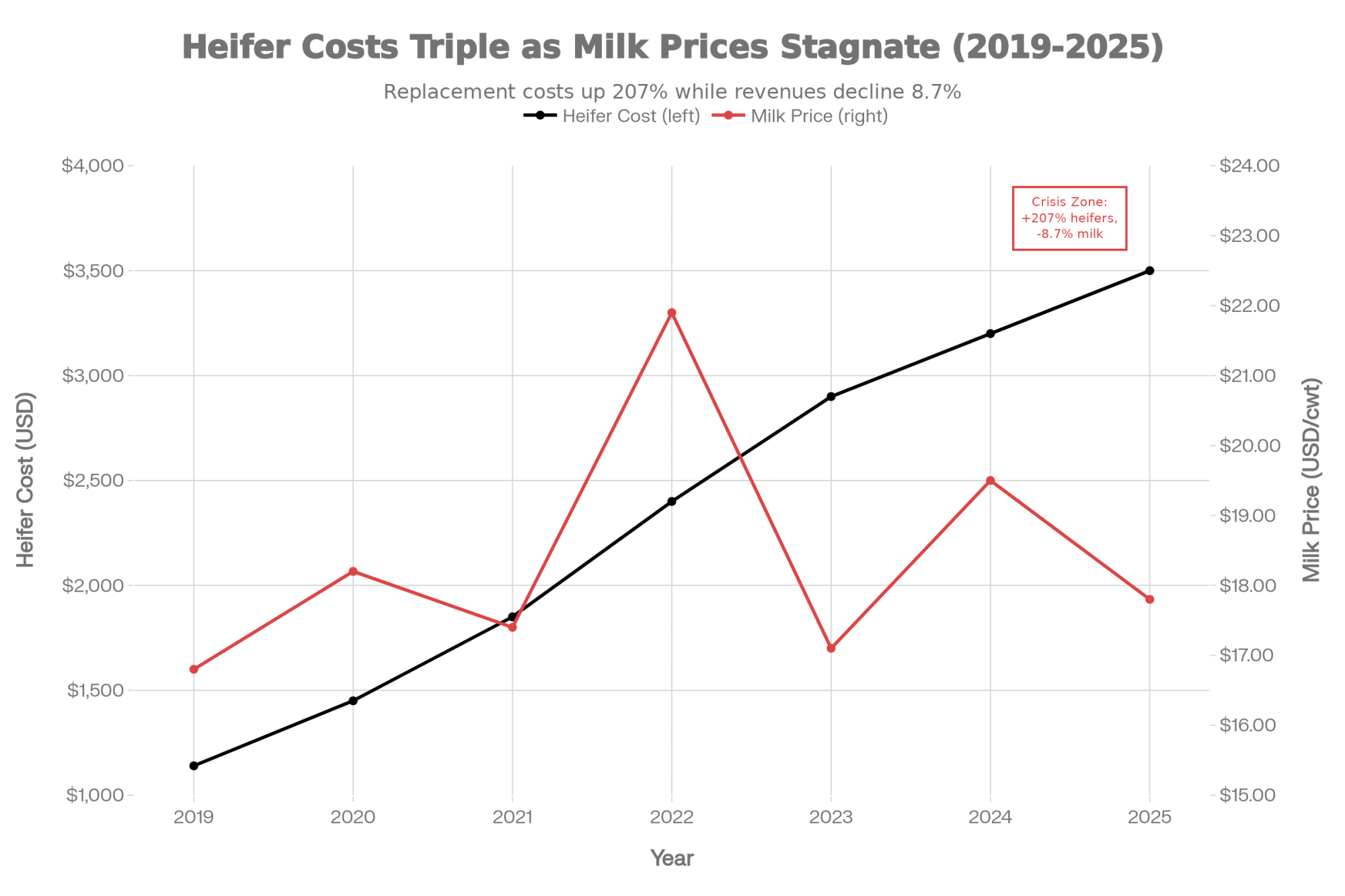

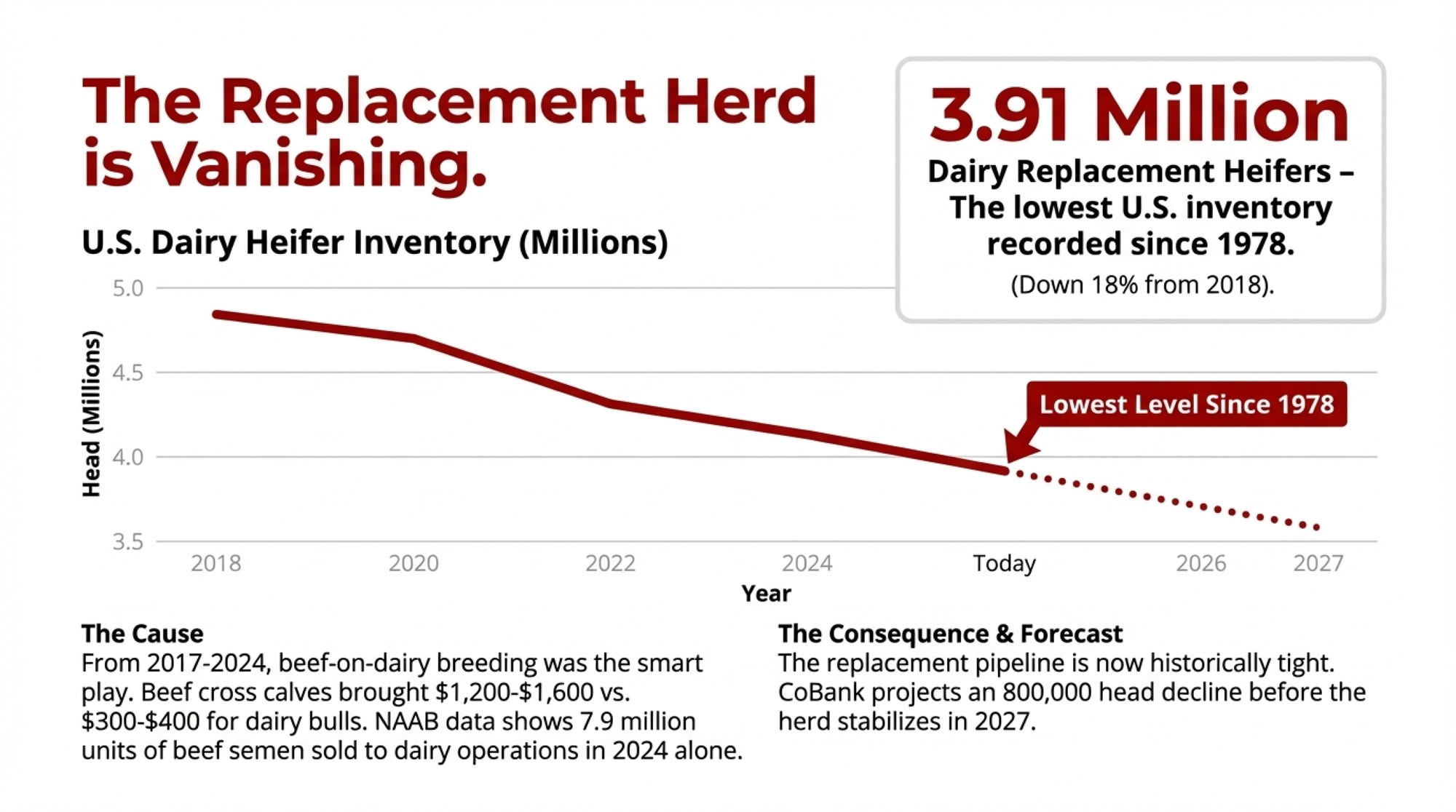

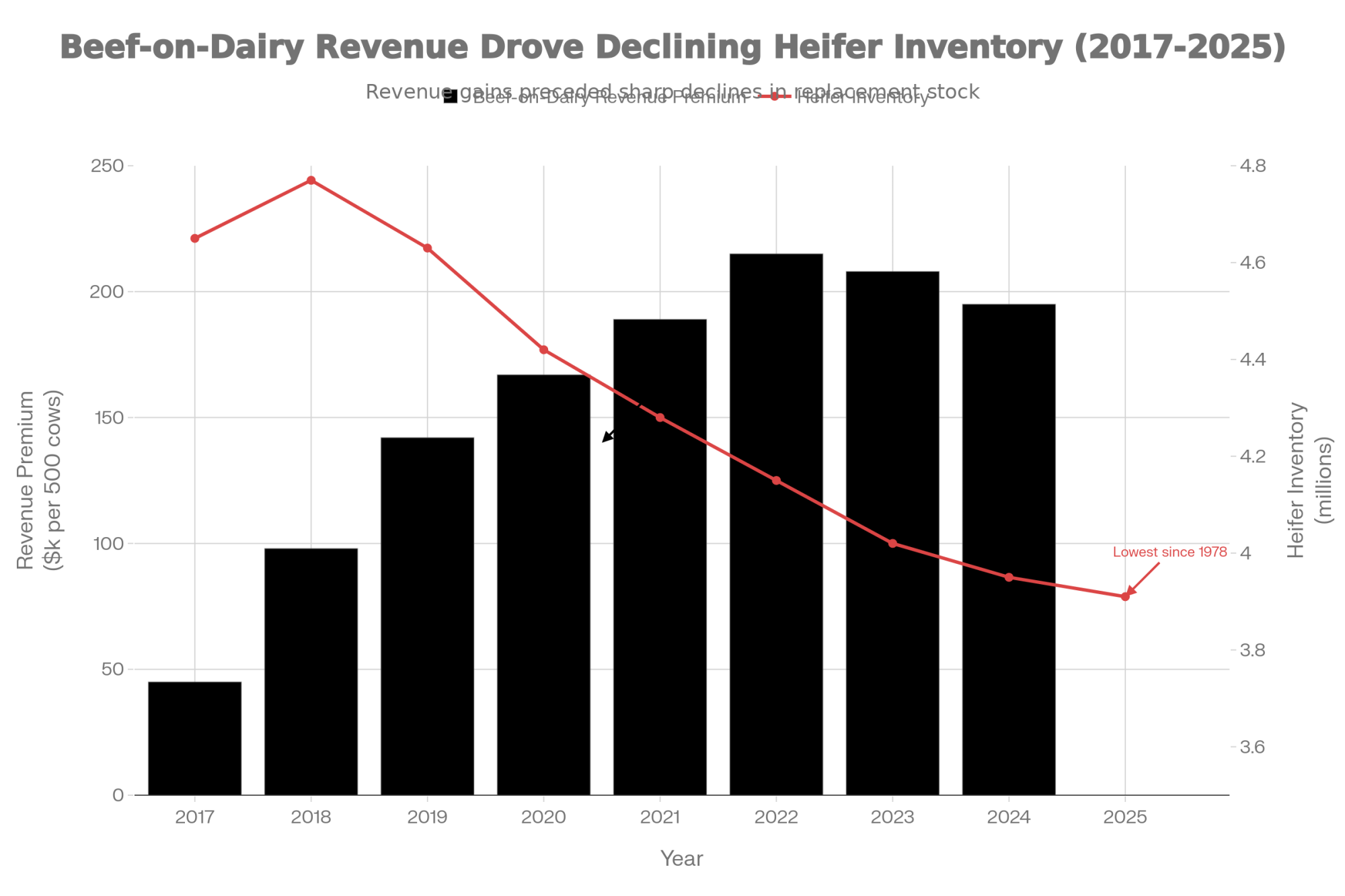

Over the last several years, beef semen sales into dairy herds have surged. CoBank analysts and semen company data indicate that beef semen units going into dairy cows have roughly tripled compared to the late 2010s, with estimates that 7–8 million beef units were sold into U.S. dairies in 2024 alone. The attraction is obvious: in many markets, newborn beef‑on‑dairy calves can bring 600 to 900 dollars per head in the first week, while Holstein bull calves often lag well behind that.

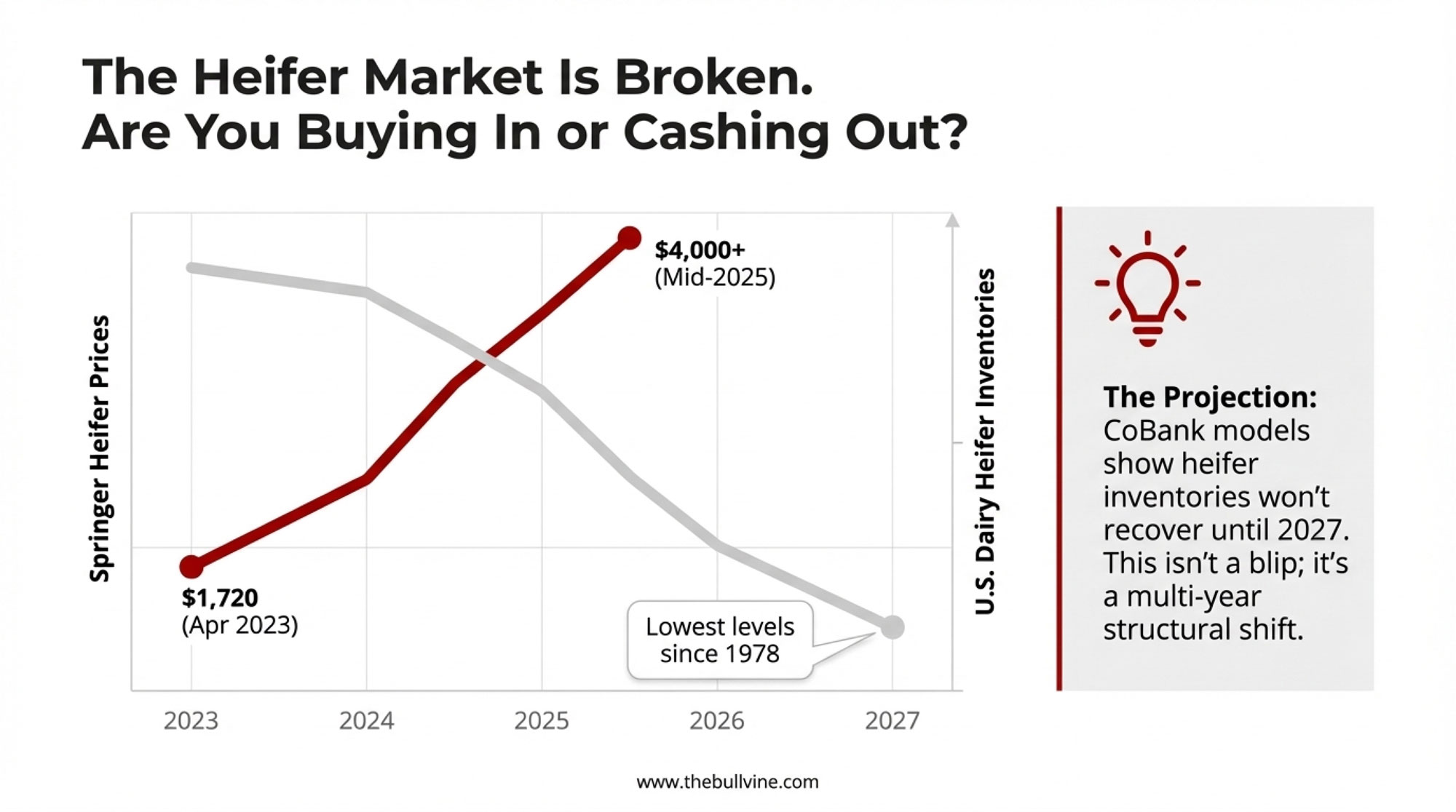

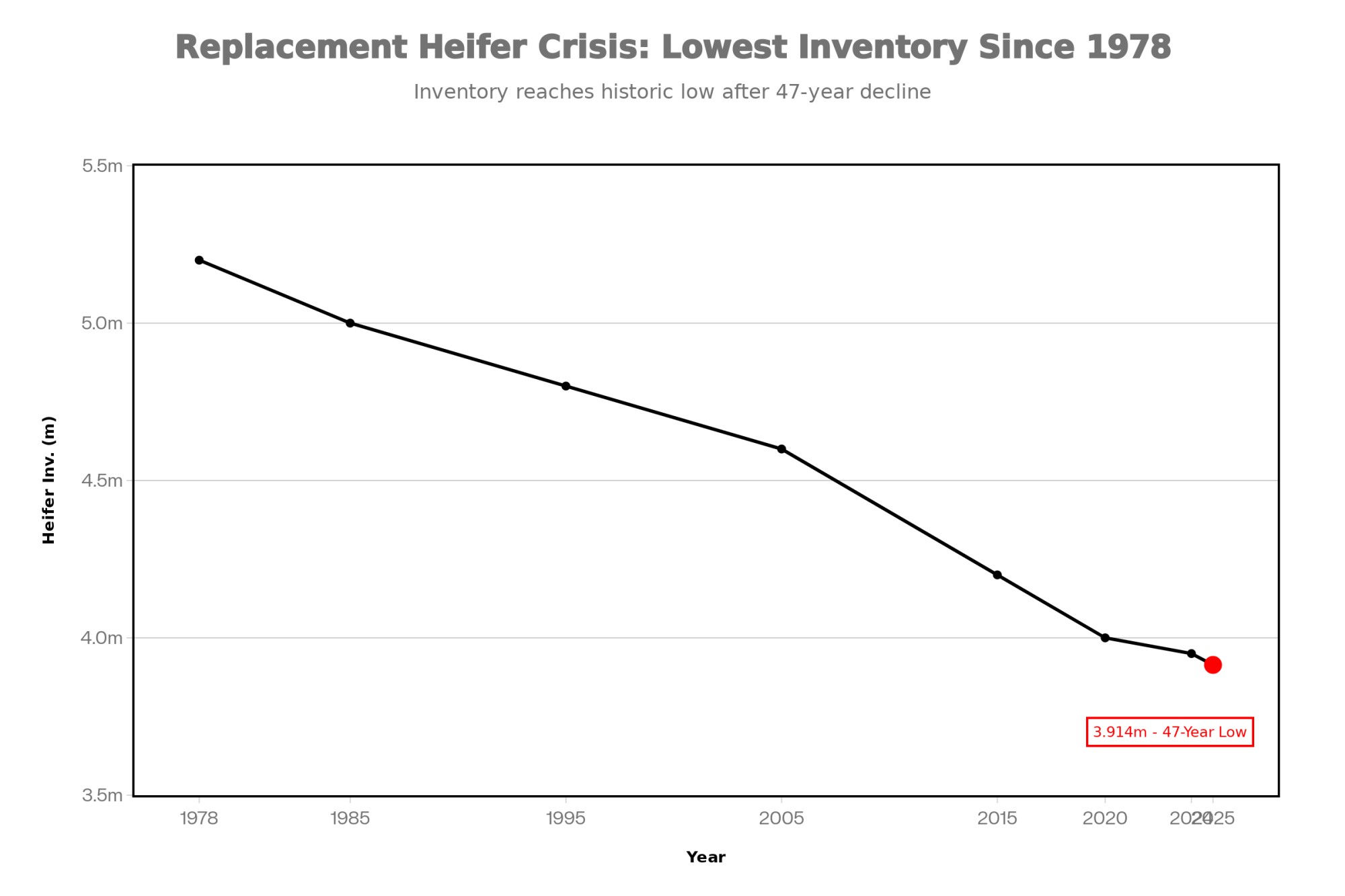

At the same time, USDA’s annual Cattle reports and independent analyses have been ringing the bell on dairy replacement inventories. A 2024 Farmdoc Daily review noted that just 2.59 million dairy heifers were expected to calve and enter the herd that year—the lowest since USDA began tracking that series in 2001. More recent updates and CoBank commentary suggest replacement inventories have been revised downward multiple times and remain historically tight.

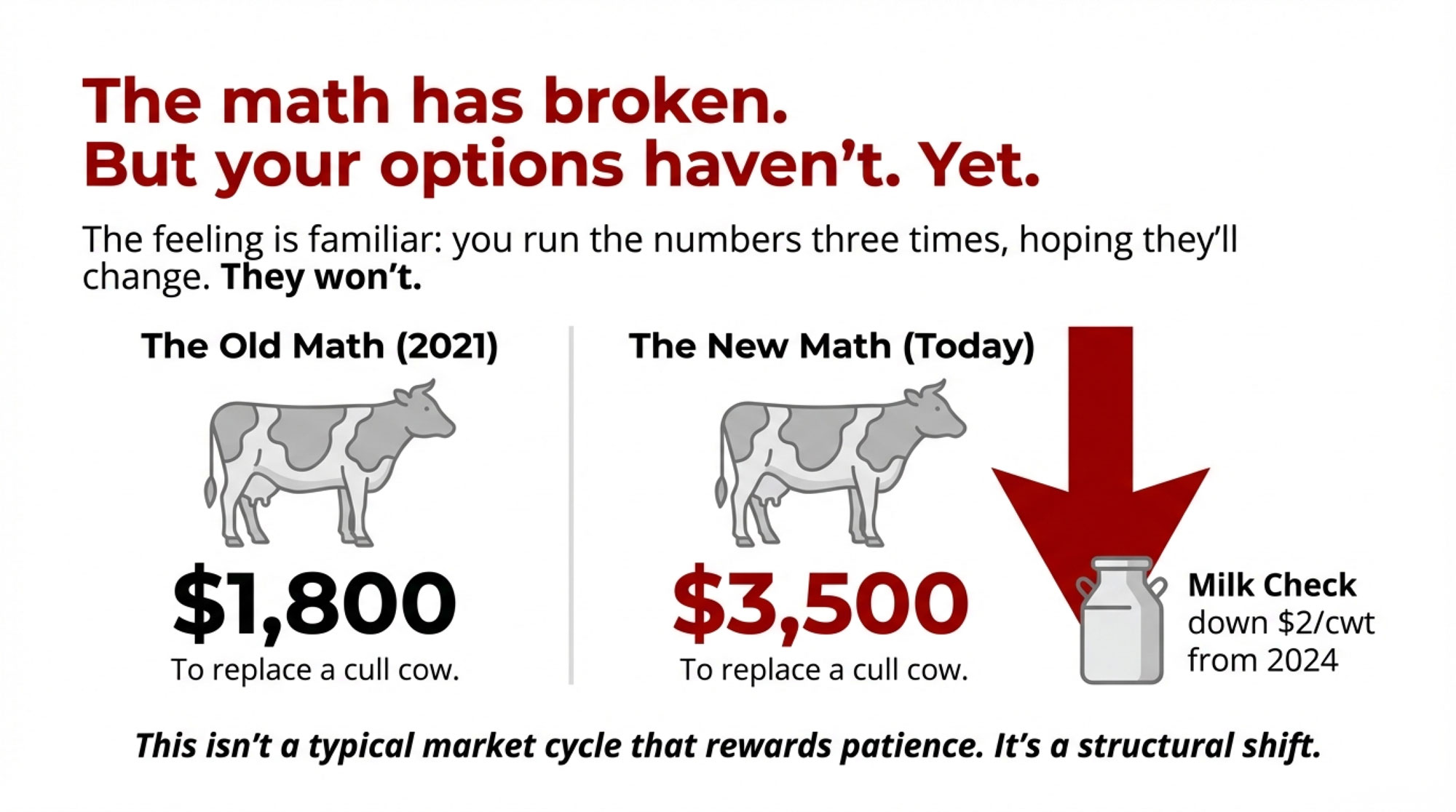

On the price side, USDA’s Agricultural Prices reports show average dairy replacement heifer values moving into the 2,200 to 2,700 dollar range in many regions over 2023–2024, with springing heifers at auctions commonly bringing 2,500 to 3,000 dollars, and top lots in some Midwest and Western states touching 3,600 to 4,000 dollars. Several economic studies and extension bulletins peg the cost of raising a replacement heifer from birth to calving around 1,700 to 2,400 dollars, depending on the system—confinement, dry lot, or pasture.

So here’s the hard truth many of us are dealing with: a lot of farms leaned into beef‑on‑dairy so aggressively—because that 600–900 dollar beef calf check looked awfully good—that they’re now staring at 2,500‑plus replacement heifer prices when they want to expand or even just maintain herd size. Analysts in Dairy Herd have gone so far as to say that America’s heifer shortage is actively limiting expansion and that the “big money in beef‑on‑dairy” is one of the key drivers.

For a Bullvine reader, the warning needs to be crystal clear:

Don’t sell your future for a 300‑dollar calf check today.

| Decision Point | Today’s Cash | Cost to Raise | Market Price | Real Economics |

|---|---|---|---|---|

| Beef-on-Dairy Calf | $600–$900 | $0 (buyer’s problem) | N/A | Immediate income, no future cow |

| Holstein Bull Calf | $150–$250 | $0 (buyer’s problem) | N/A | Minimal income, no future cow |

| Keep & Raise Heifer | $0 today | $1,700–$2,400 | $2,500–$3,600 | 24-month investment, future production |

| Annual Impact (100 beef calves) | +$60,000–$90,000 | Clear | −$250,000–$360,000 in replacement costs | Net position depends on replacement needs |

In some markets, the calf check is 600 or 800 dollars, not 300, but the principle is the same. Beef‑on‑dairy is a powerful tool when it’s aimed at the bottom of the herd with a clear replacement plan. Used without a plan, it can hollow out your future cow herd and leave you paying top-of-the-market prices to fill stalls.

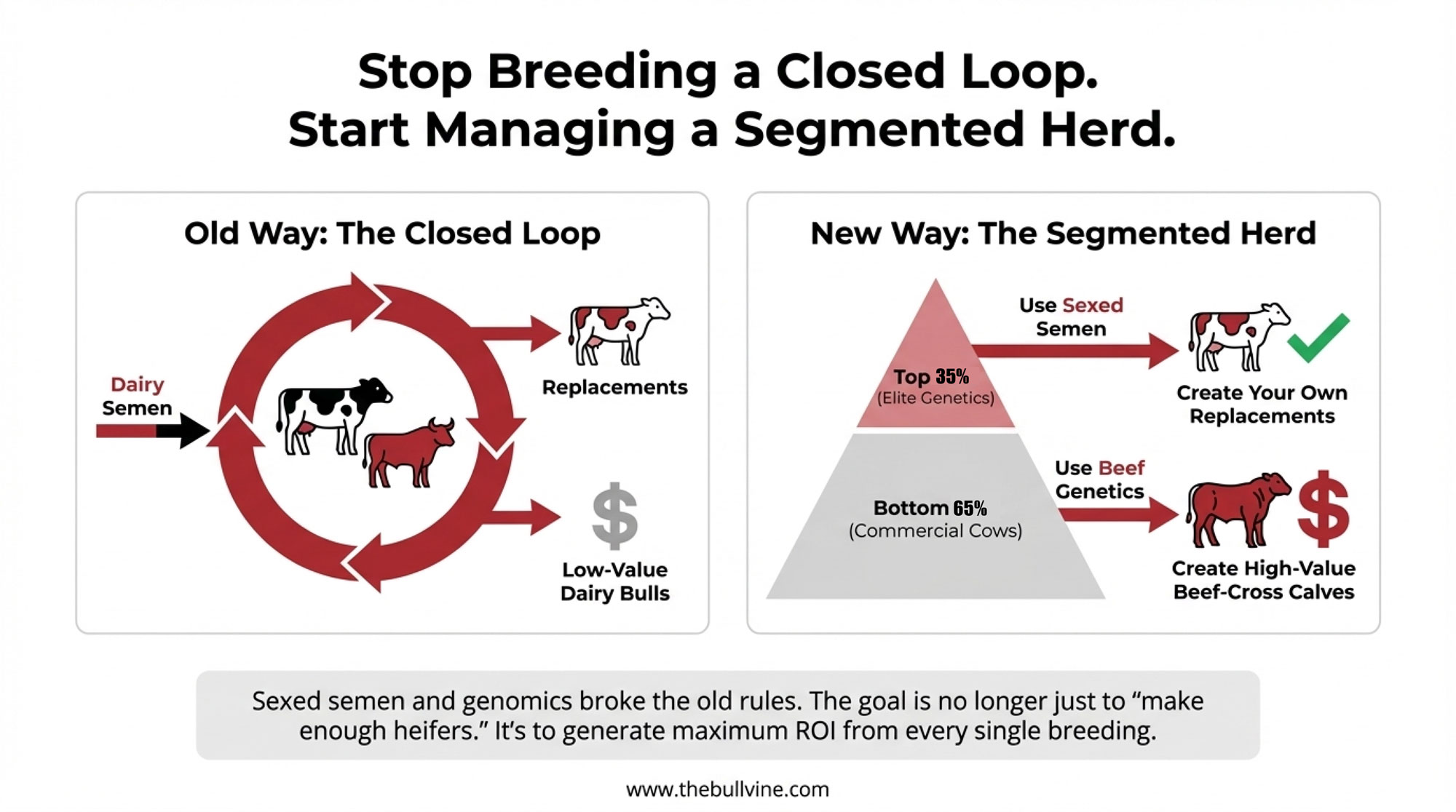

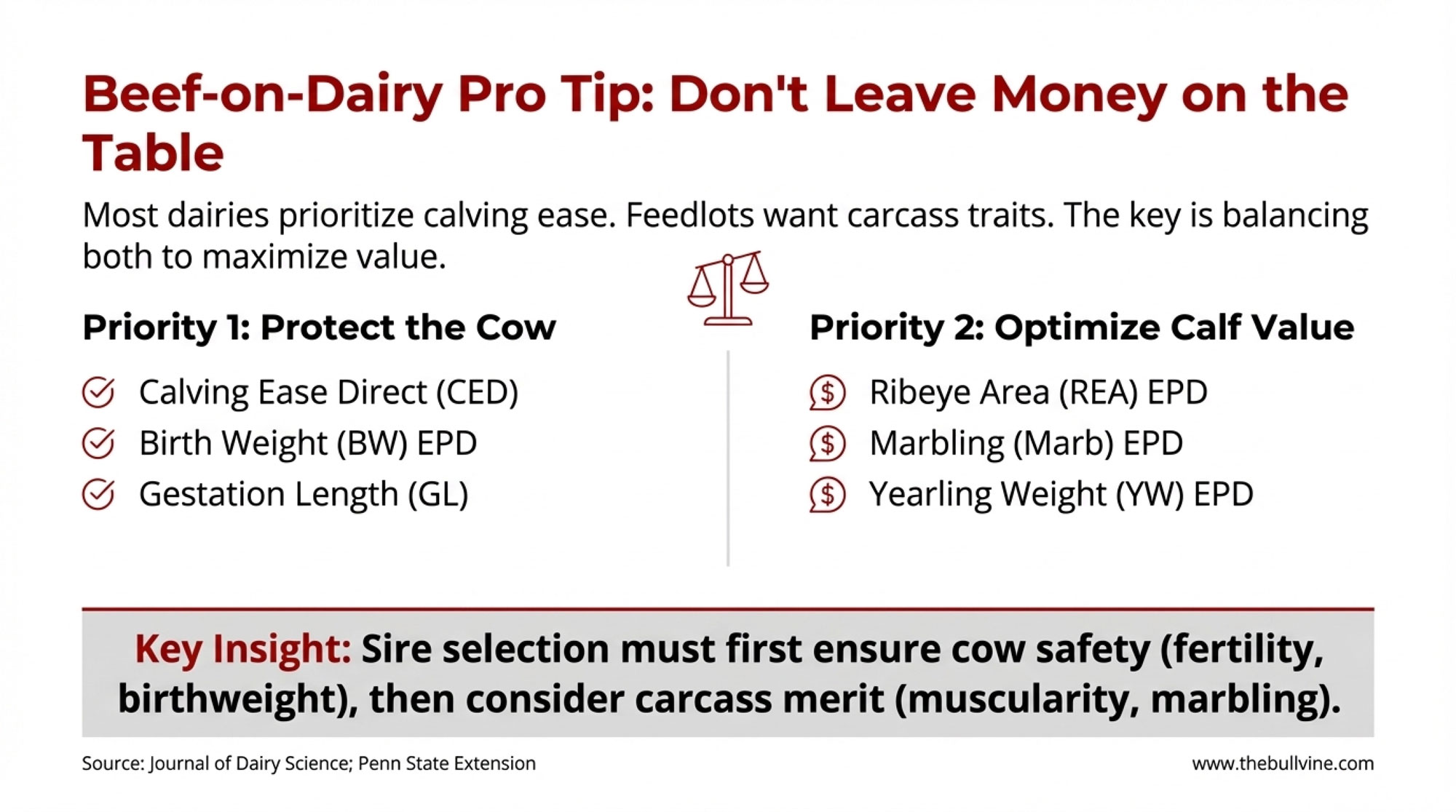

The sweet spot, based on both research and what well‑run farms are doing, looks something like this:

- Top 30–40 percent of females: Genomic‑tested and top‑merit cows and heifers get sexed dairy semen to generate replacements.

- Middle group: Conventional dairy semen, adjusted up or down depending on your replacement needs.

- Bottom end: Clearly identified low‑merit cows and heifers get beef‑on‑dairy semen to turn them into higher‑value calves.

And that plan isn’t static. It gets revisited each year as calf, beef, and replacement markets change. But the order of operations doesn’t change: protect your future herd first; chase beef calf checks second.

What Farmers Are Finding Works Right Now

Talking with producers from Wisconsin to South Dakota, from Idaho to Ontario, three themes keep showing up on farms that seem to be navigating all this better than most.

Breeding for Profit and “Invisible” Cows

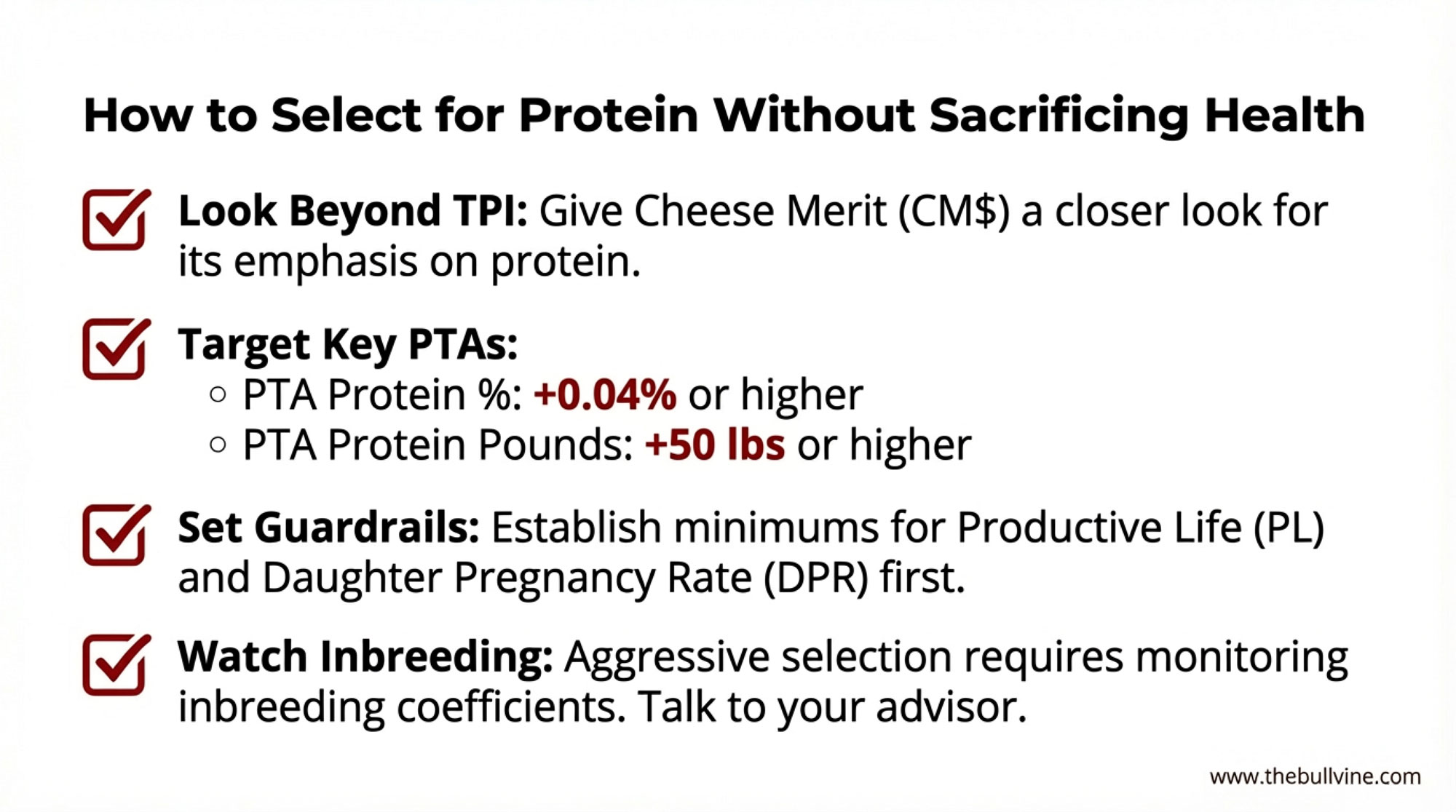

Looking at this trend in breeding decisions, the herds that look most resilient aren’t chasing a single extreme trait. They’re using tools like genomic selection, economic indexes, and on‑farm records to build cows that are profitable and low‑drama.

Peer‑reviewed work on dairy genetics and national evaluation systems, summarized by the Council on Dairy Cattle Breeding and others, shows that genomic selection combined with economic indexes like Net Merit (U.S.) and Pro$ or LPI (Canada) can significantly improve progress in production, fertility, and health traits compared to traditional selection. That’s the backbone of how most major AI studs and progressive herds are making mating decisions today.

On the farms I’ve seen, a practical genetics plan often looks like this:

- Use a profit index (Net Merit, Pro$, LPI) as the main filter rather than picking bulls off a single trait like butterfat or total milk.

- Inside that pool, favor bulls that nudge both fat and protein percentages modestly upward while maintaining or improving fertility, udder health, and productive life.

- Put real weight on traits that keep cows in the herd: mastitis resistance, hoof health and locomotion, calving ease, and overall robustness.

In that context, many commodity‑oriented herds are targeting cows with butterfat around 3.8–4.0 percent, protein in the mid‑3s, and reproduction performance that aligns with their culling and replacement plans. That doesn’t win you banners at a show, but it tends to win you more predictable component checks, fewer headaches, and a cow that’s “invisible” in the best way—just quietly doing her job.

Turning Genomics and Beef‑on‑Dairy into Everyday Tools

Genomics and beef‑on‑dairy aren’t fringe ideas anymore—they’re everyday tools for a growing number of herds.

Recent genomic reviews indicate that genomic evaluations can roughly double the accuracy of selecting young animals compared to using parent averages alone, especially for complex traits such as fertility and health. Breeding programs that use sexed semen on the top tier of females and beef semen on the bottom tier to accelerate dairy genetic gain while also lifting calf value.

On many commercial farms, that has turned into a straightforward three‑tier system like the one above. The key shift on farms that are doing it well is that they’ve stopped guessing:

- They genomic‑test at least a subset of heifers to identify which families deserve replacements.

- They run replacement‑need projections based on real cull rates, expansion plans, and age at first calving.

- They adjust the proportion of sexed, conventional, and beef semen to hit those replacement targets rather than just chasing what the calf market looks like this month.

University of Guelph research and beef‑on‑dairy extension materials emphasize that dairy‑beef cross calves can command solid premiums over straight Holstein bull calves when marketed correctly, but they also warn that early‑life management and health are critical to capturing that value. The farms that treat beef‑on‑dairy as a strategic tool—not just a quick cash grab—are the ones turning it into a durable advantage.

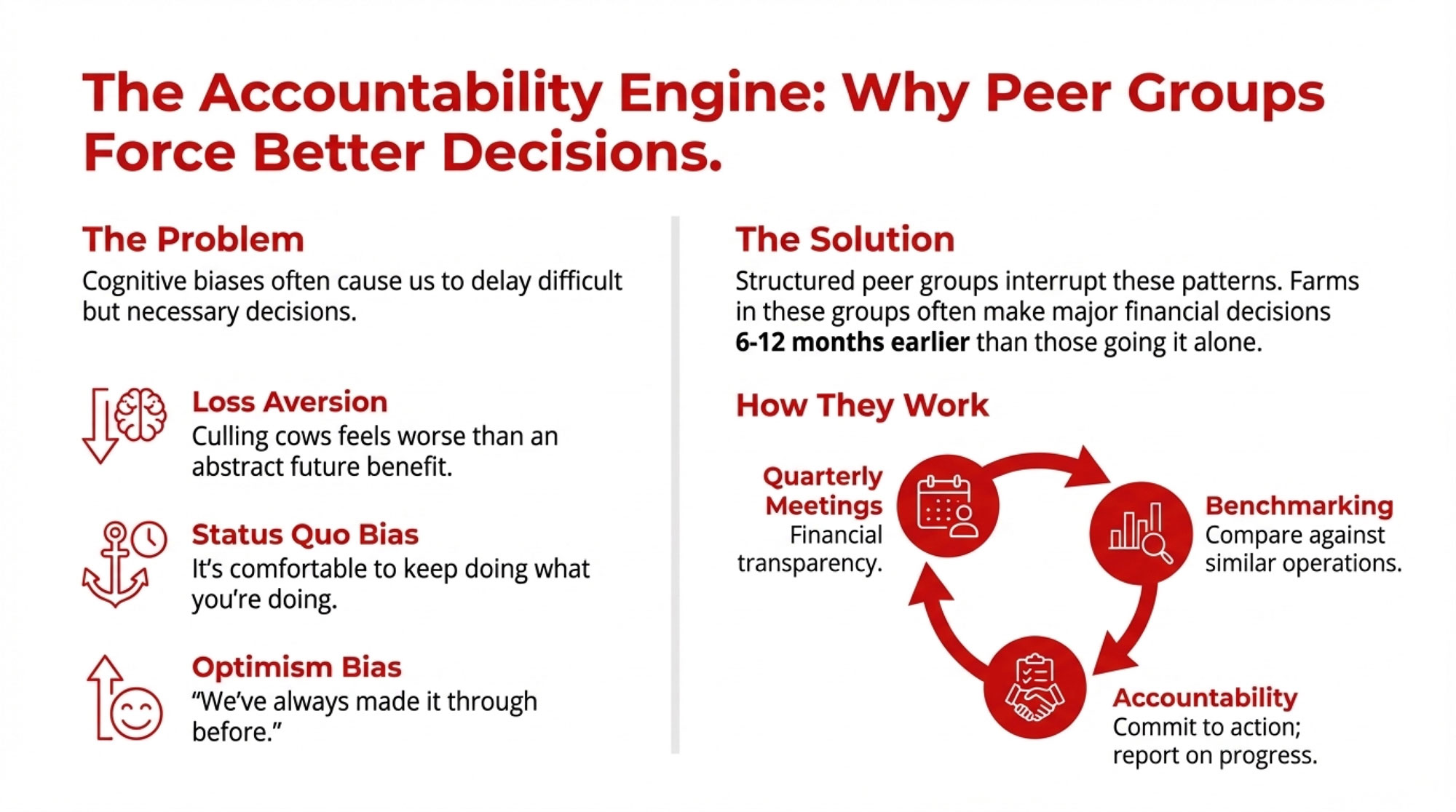

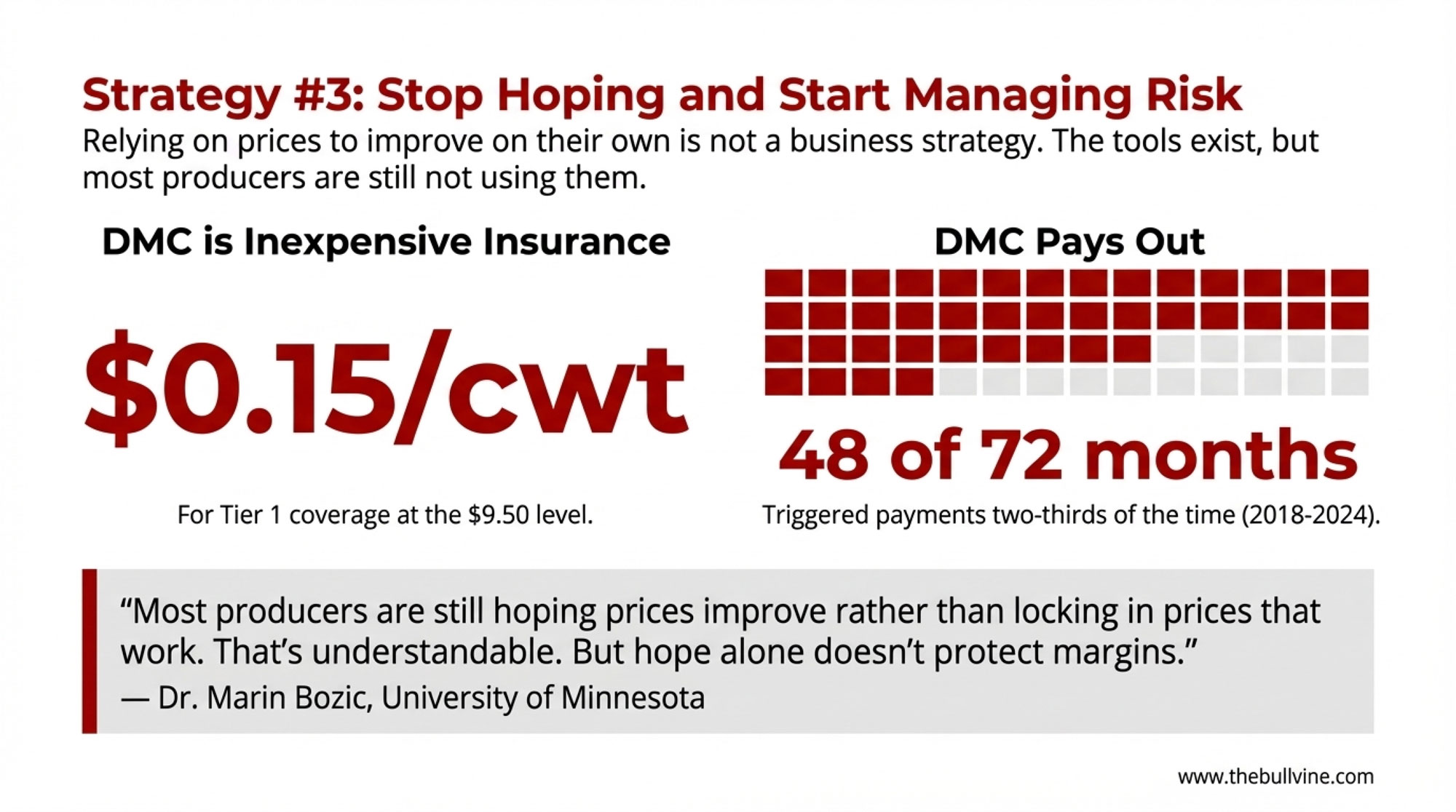

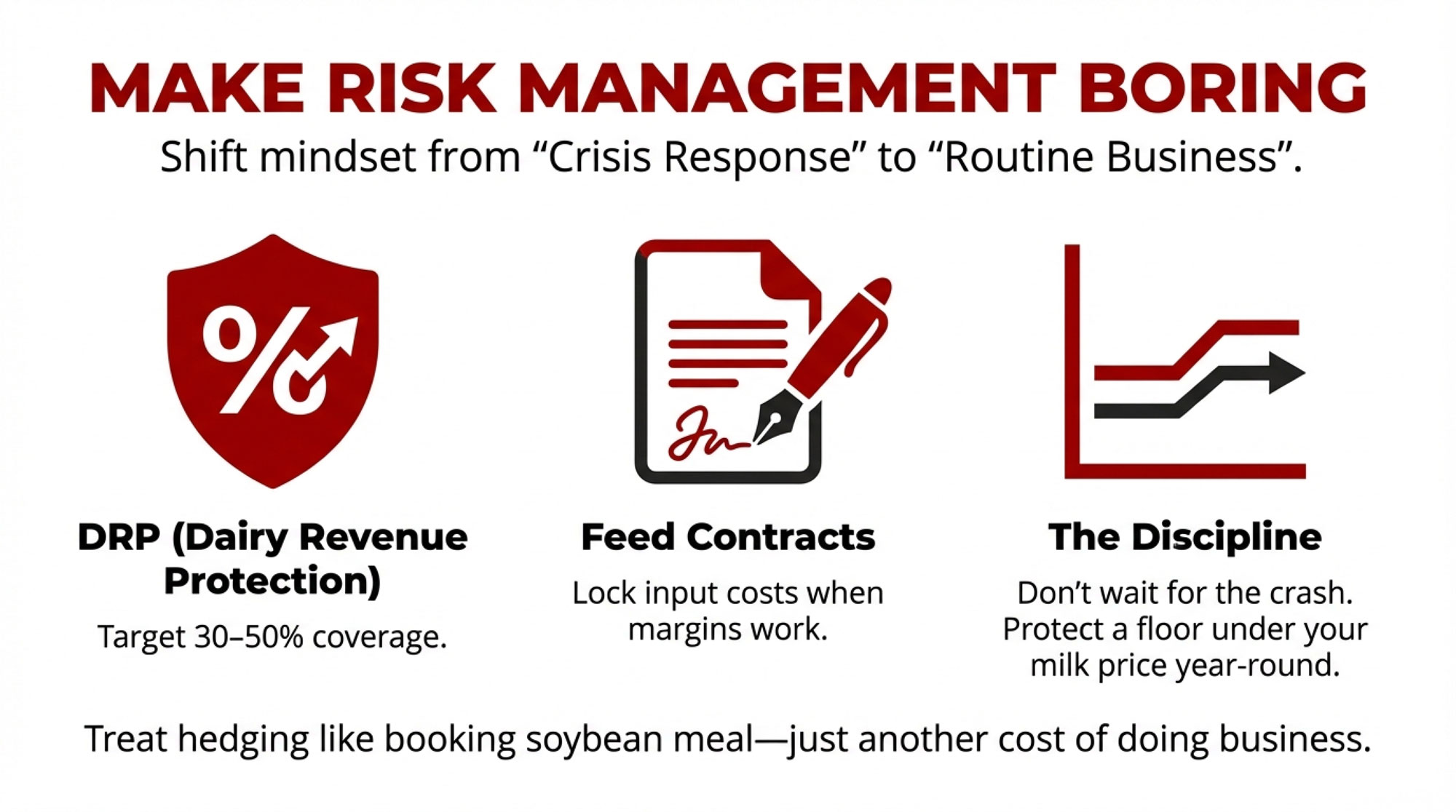

Making Risk Management Routine Instead of a Panic Button

The third big shift isn’t genetic or nutritional—it’s in how farms treat price risk.

Extension economists and dairy market advisers have been pushing for years now that tools like Dairy Margin Coverage and Dairy Revenue Protection should be part of a routine risk plan, not just something you sign up for when prices crash. Herds that quietly use DRP or basic options strategies year after year to put a floor under part of their milk price while leaving some upside open.

What many advisers suggest, as a starting point, is that producers consider protecting something like 30–50 percent of their expected milk production with DRP, options, or fixed‑price contracts when forward prices cover their cost of production and debt needs. It’s not a rule; it’s a range that seems to work for a lot of operations. Some herds are comfortable covering more, while others are less comfortable, depending on their balance sheets and risk tolerance.

A simple example might look like this:

- A 900‑cow herd in Wisconsin, selling mainly into Class III, uses DRP to set a revenue floor under part of its projected spring and summer milk based on its typical butterfat and protein tests and the markets it ships into.

- At the same time, the herd forward‑contracts a portion of its corn and soybean meal when futures plus local basis give them a feed cost that supports a margin they can live with.

The rest of the milk and feed stays unhedged, leaving room to benefit if markets move higher. The point isn’t that 900 cows in Wisconsin need this exact plan. The point is that treating risk tools as normal business practice—as much a part of the job as booking soybean meal—can turn wild swings into manageable bumps.

From conversations with producers who’ve made that shift, the hardest step usually wasn’t understanding the math. It was deciding to stop waiting for the next crisis to start learning.

Different Starting Points, Different Options

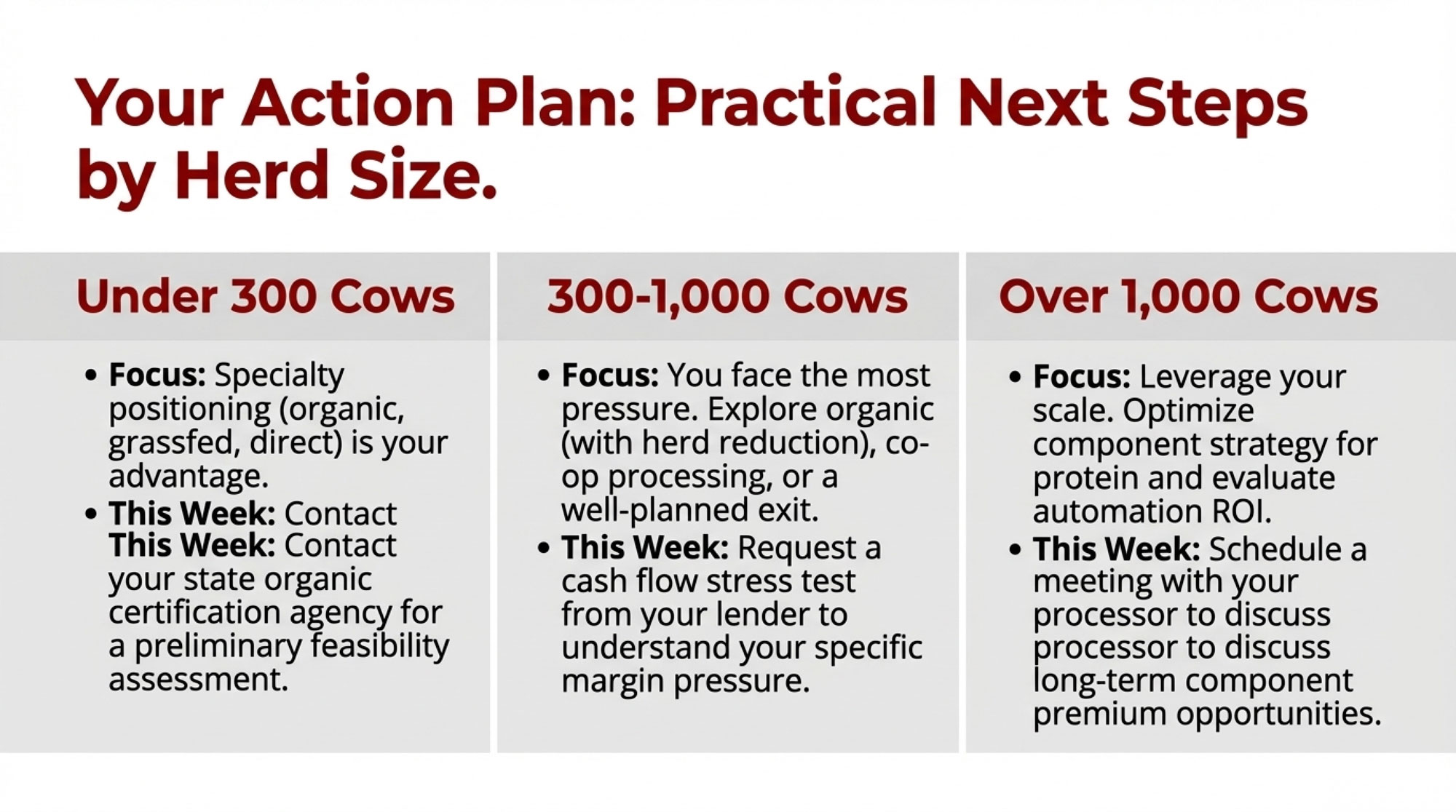

Given all this, the logical question is: “So what does this mean for my farm?” The honest answer depends on your size, your location, and your timeline. But some patterns show up pretty consistently.

Larger Herds Close to Growing Plants

If you’re milking 800–3,000 cows in eastern South Dakota, western Kansas, the Texas Panhandle, southern Idaho, or near growing plants in Wisconsin or New York, you’re in a spot where processors need your milk. That doesn’t solve everything, but it’s a real advantage.

On farms like yours that seem to be in decent shape, you usually see:

- Sharp focus on components and cow flow. Butterfat and protein targets are tuned to what nearby cheese and ingredient plants actually pay for, and fresh cow management during the transition period is geared to support strong peaks without wrecking cows.

- Structured breeding and replacement plans. Genomics and sexed semen build replacements from the top of the herd; beef‑on‑dairy is used thoughtfully on the bottom end to boost calf revenue without starving replacements.

- Habitual risk management. DRP, DMC, options, and feed contracts are used when the math works, not just when the market is already in free fall.

- Cautious growth decisions. Expansion plans are stress‑tested against lower milk prices and higher costs, often with lender and adviser input, not just modeled on today’s strong basis.

Mid‑Size Herds in Stable Regions

If you’re running 400–800 cows in places like Wisconsin, Michigan, Pennsylvania, Vermont, or Southern Ontario, you’re big enough to feel serious capital pressure but not always big enough to be your plant’s top priority.

Mid‑size herds that look resilient tend to:

- Drive the cost of production hard. They lean into cow comfort, parlor throughput, and ration consistency to get into the top third of their region’s cost curve, using benchmarks from lenders, extension, and trade media.

- Make themselves “must‑keep” suppliers. Plants know they can count on them for consistent volume, strong quality, and components that fit the product mix.

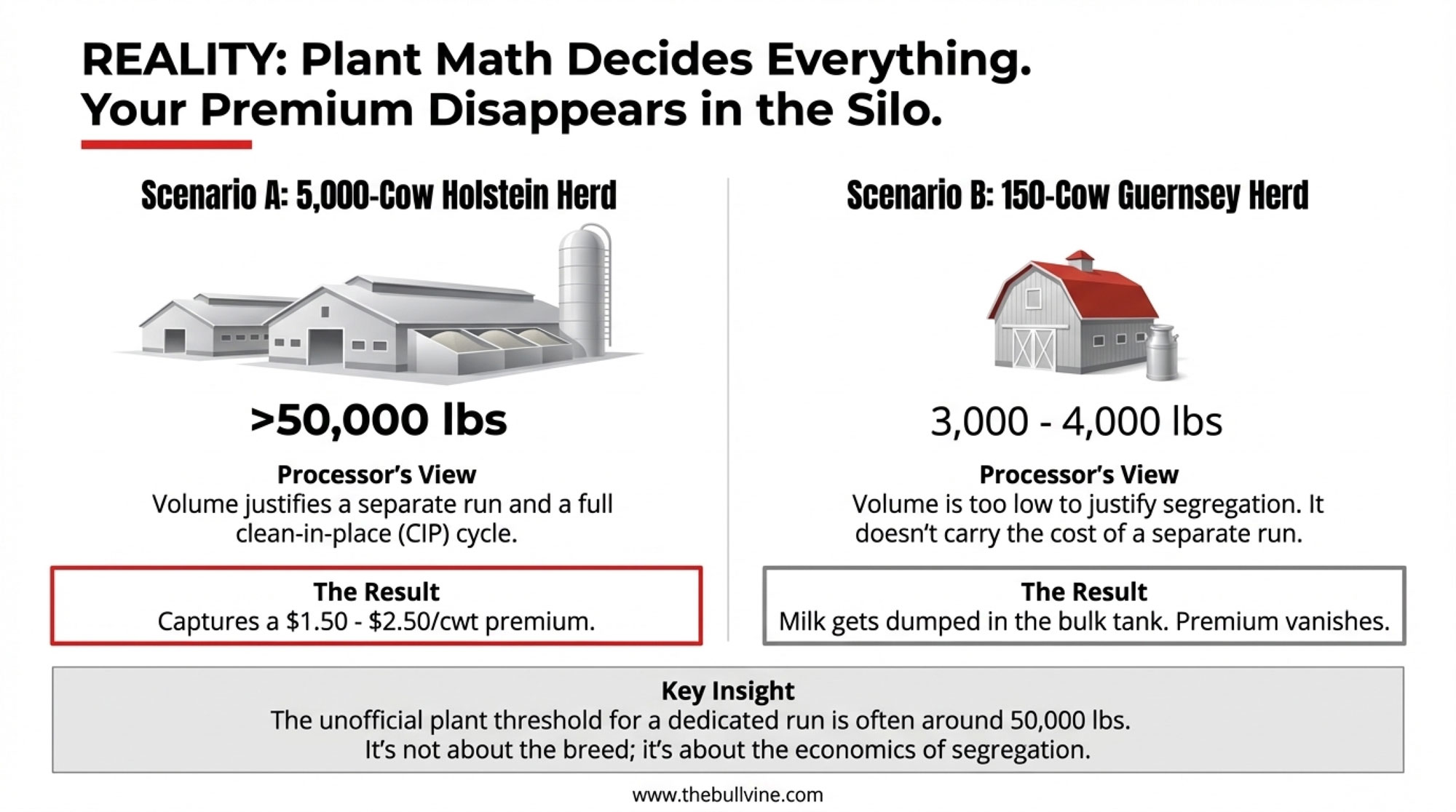

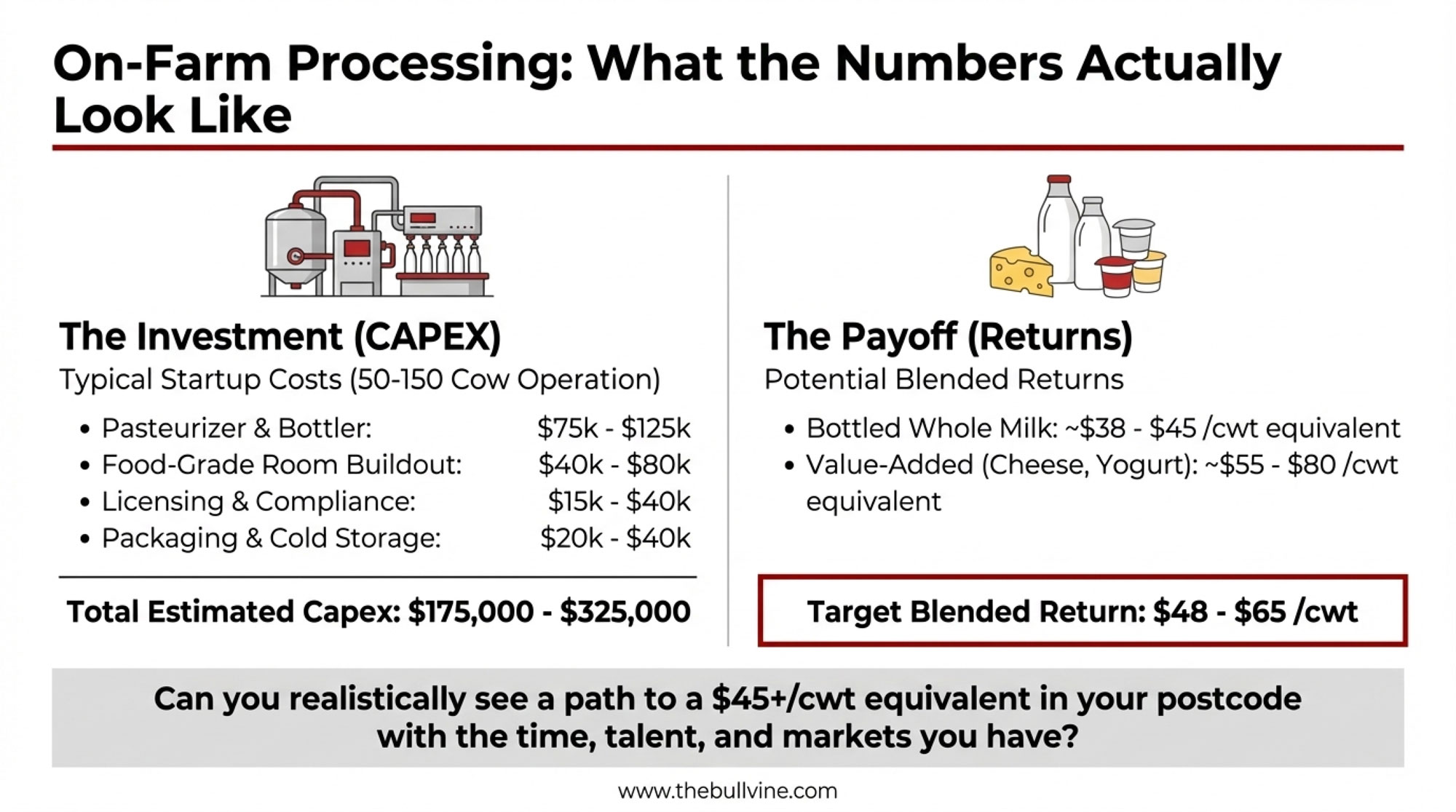

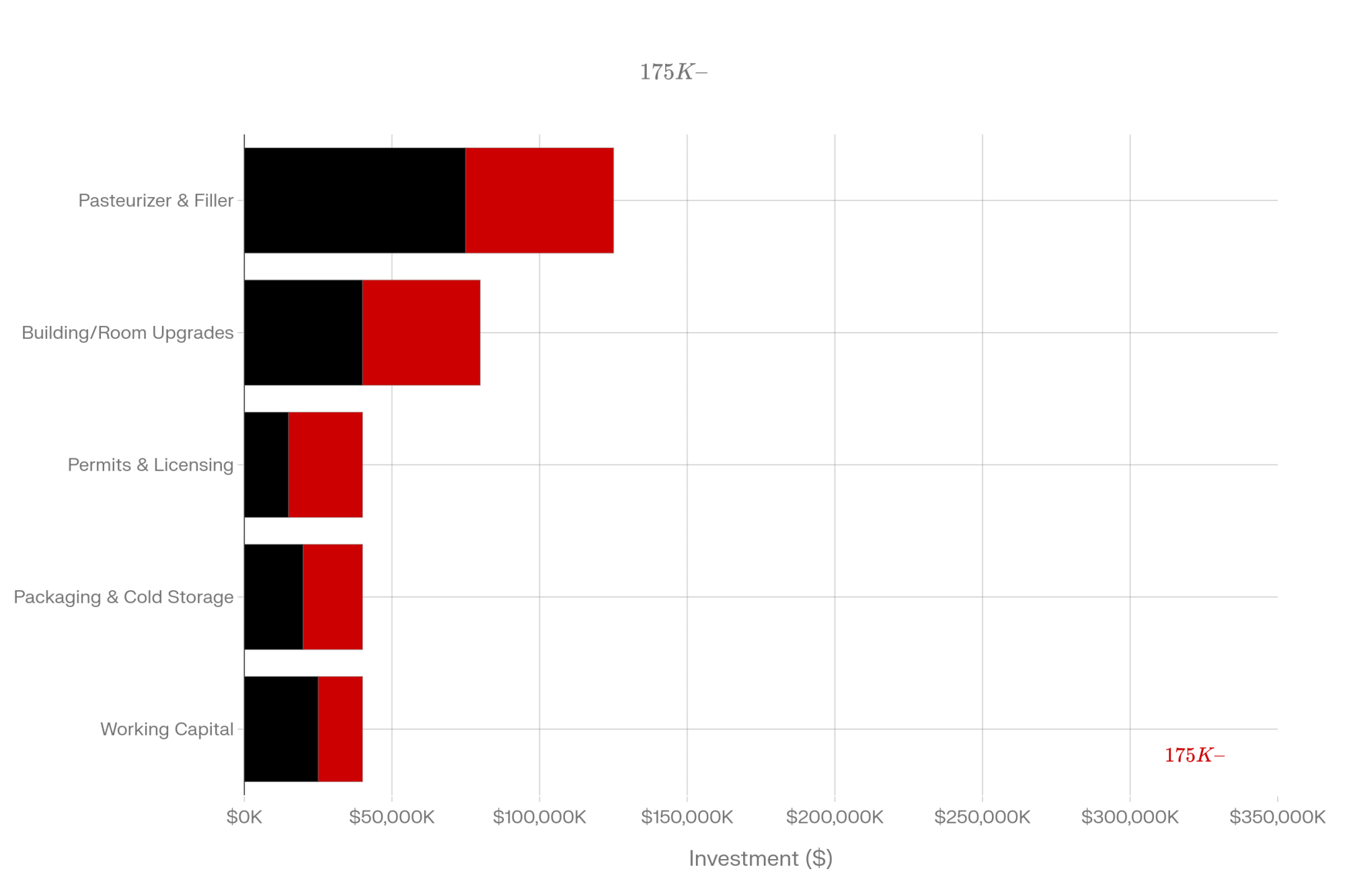

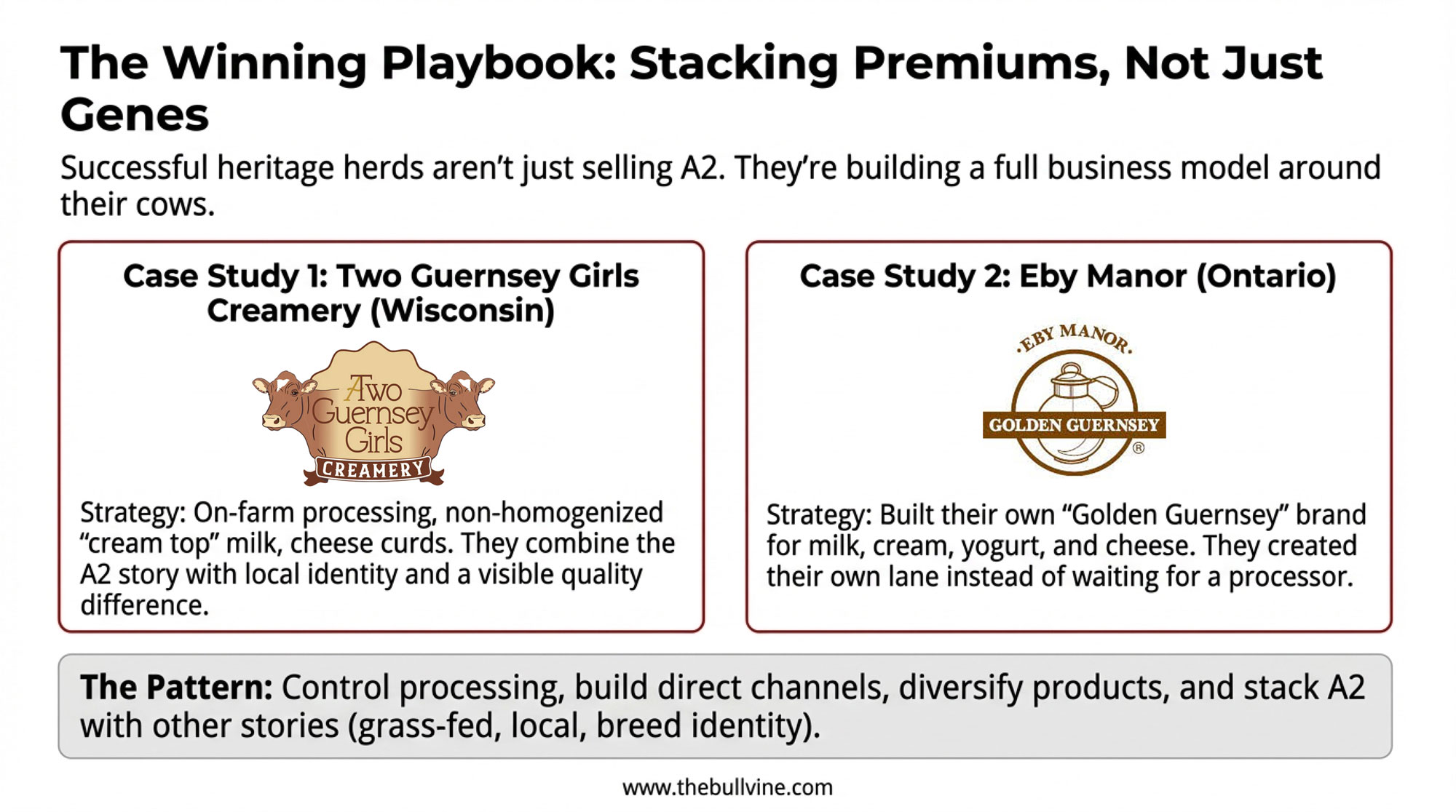

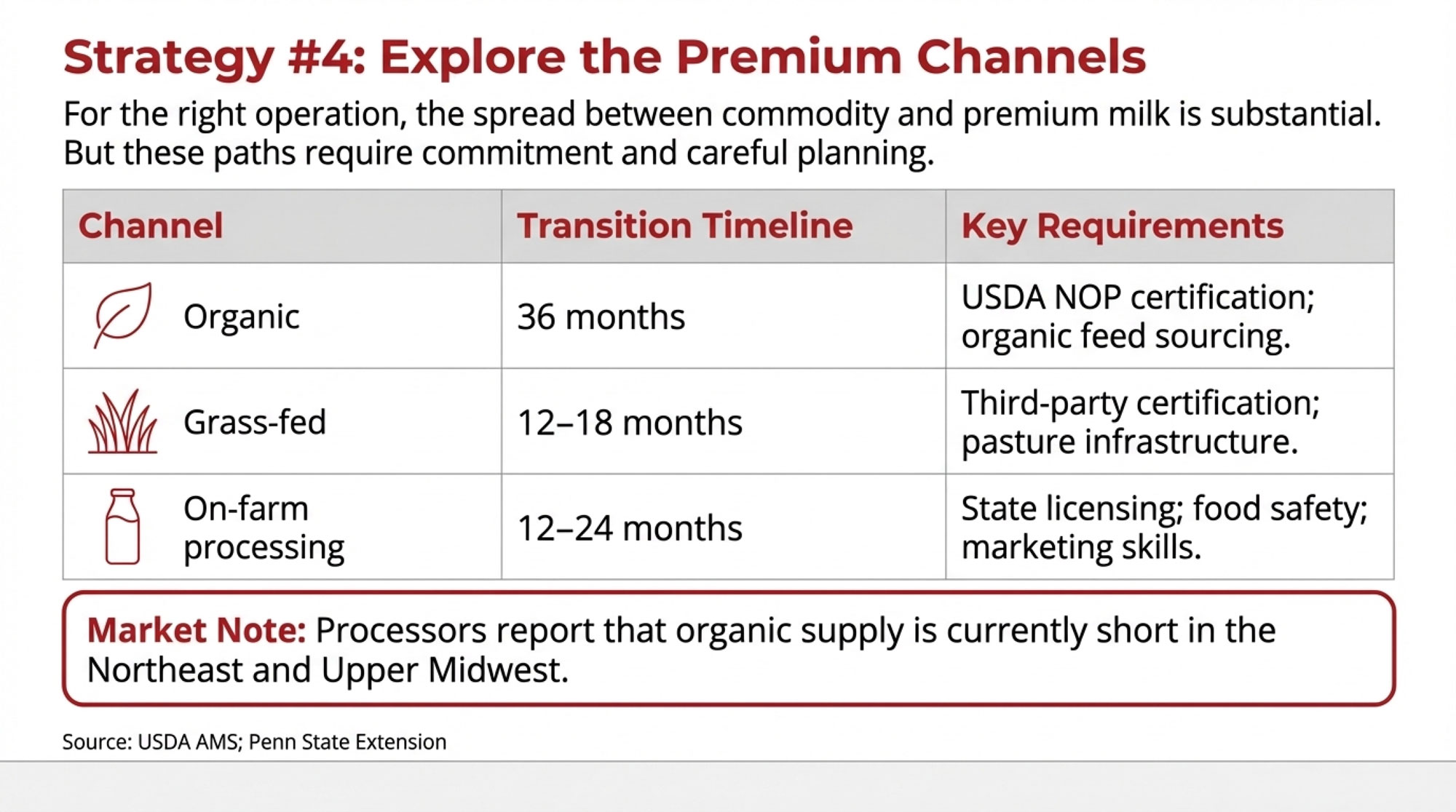

- Explore niches where they truly fit. Some find success with organic, grass‑fed, A2A2, on‑farm processing, or regional branding—especially in the Northeast and Upper Midwest—but only when local demand and the family’s temperament for marketing line up.

- Treat succession and timing as strategic variables. Major upgrades or expansions are tied to clear family plans for who wants to be there in 5–10 years, not just to what the bank will finance.

Smaller or More Isolated Herds

If you’re milking 50–200 cows in a rural pocket far from growing plants, or in a region losing processing, the export‑driven, capacity‑heavy system frankly isn’t built with you in mind.

Smaller herds in that position that manage to stay in the driver’s seat often:

- Get brutally honest about cost and equity trends. They know, in numbers, whether they’re gaining ground, treading water, or slowly slipping.

- Decide what role the dairy plays. For some, the dairy is still the primary economic engine. For others, it’s part of a mix with off‑farm jobs, cash crops, custom work, or direct‑marketing businesses. That choice shapes everything else.

- Explore niches carefully, not desperately. On‑farm processing, direct‑to‑consumer sales, or agritourism can work—especially near population centers—but only when location, market, and family skills align. They’re not automatic lifelines.

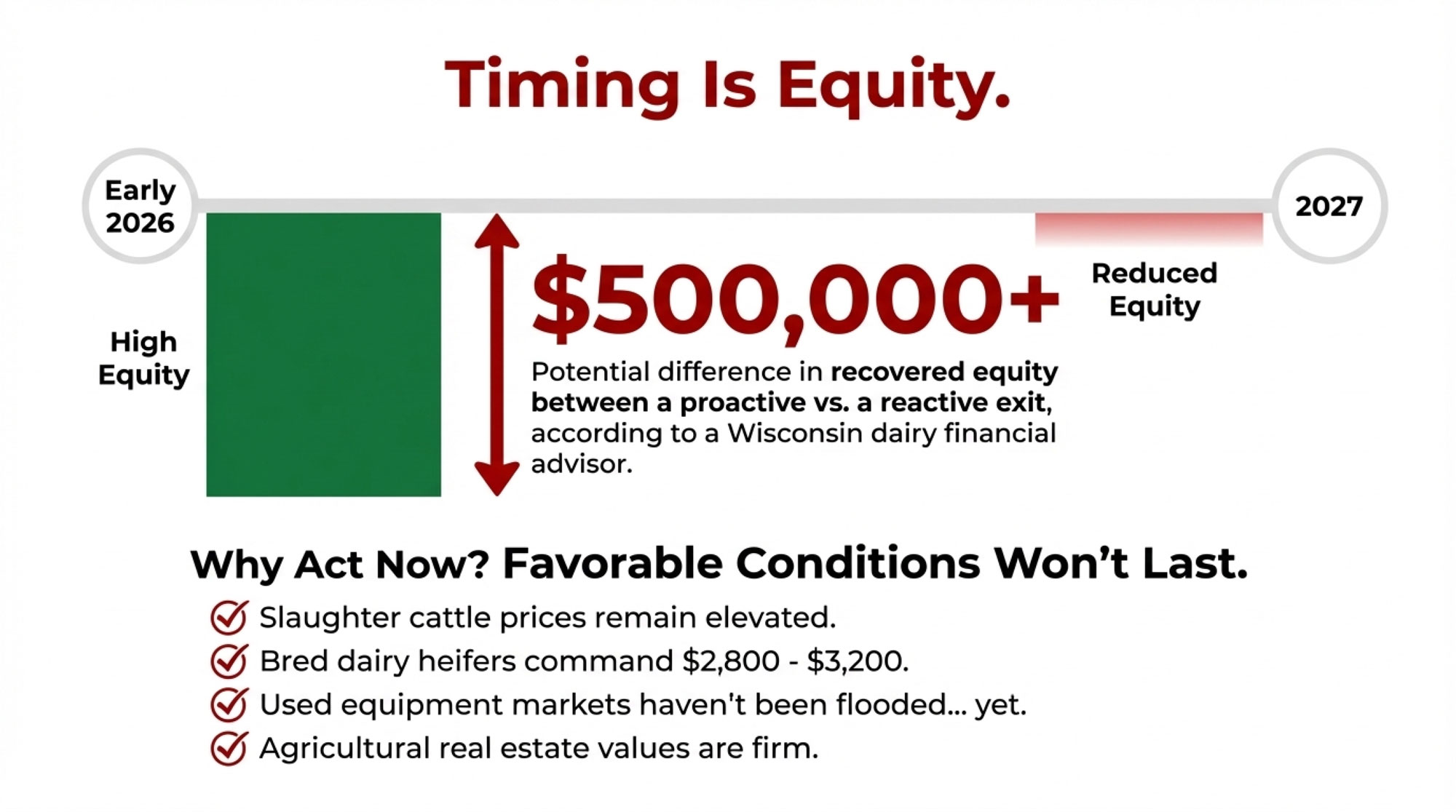

- Plan early for transitions. The most successful exits or step‑downs start with early, candid conversations with family, lenders, and advisers—before external forces make the decision for them.

A Few Practical First Steps

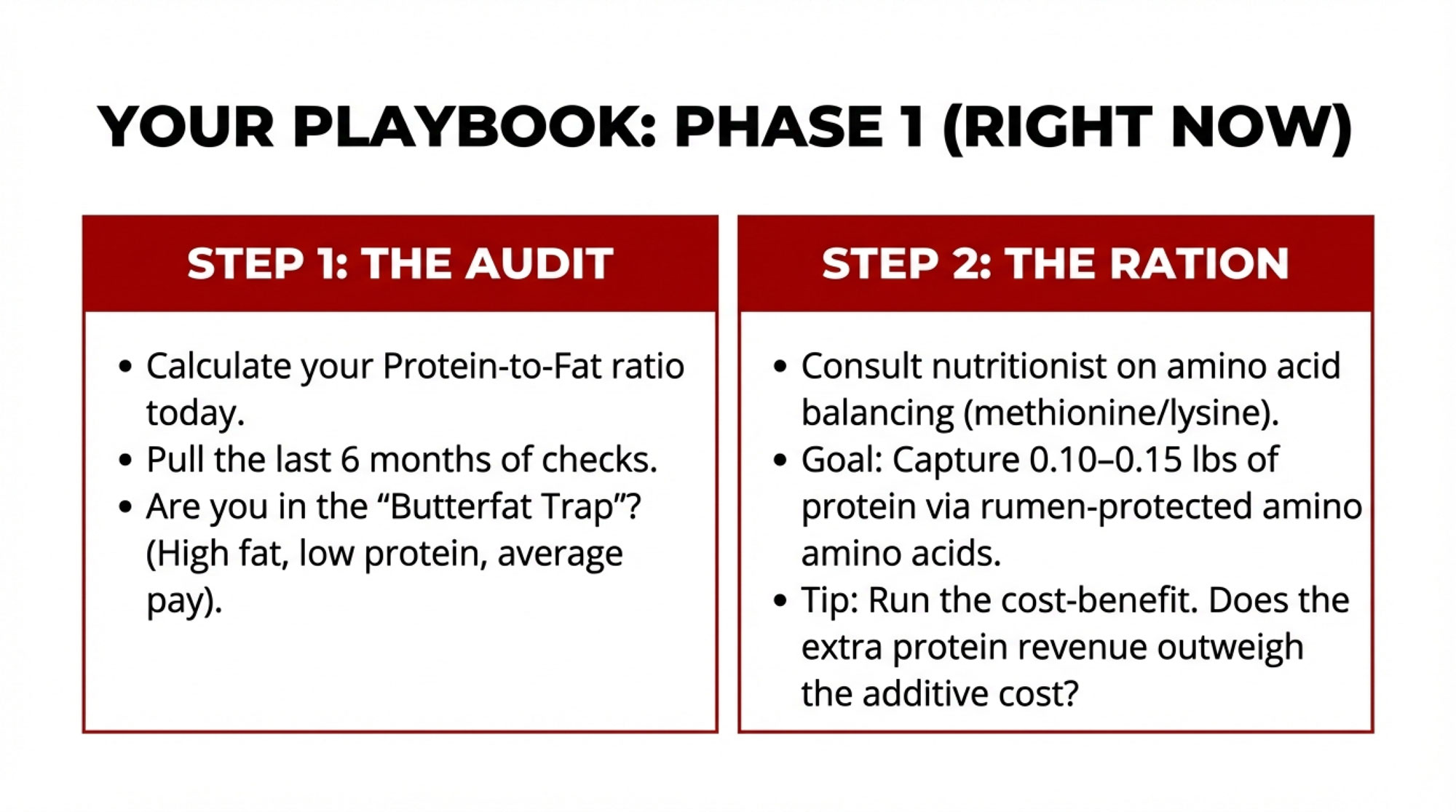

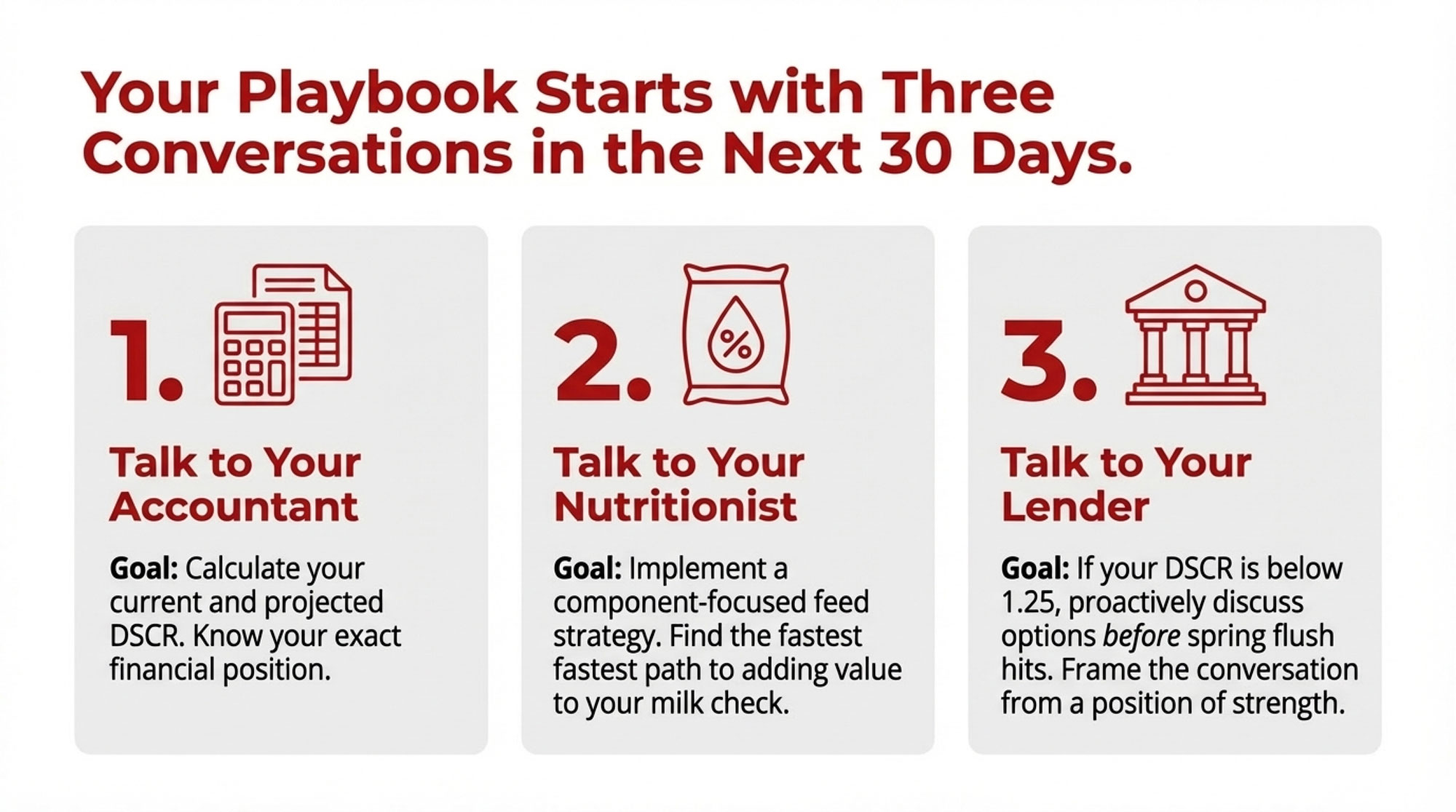

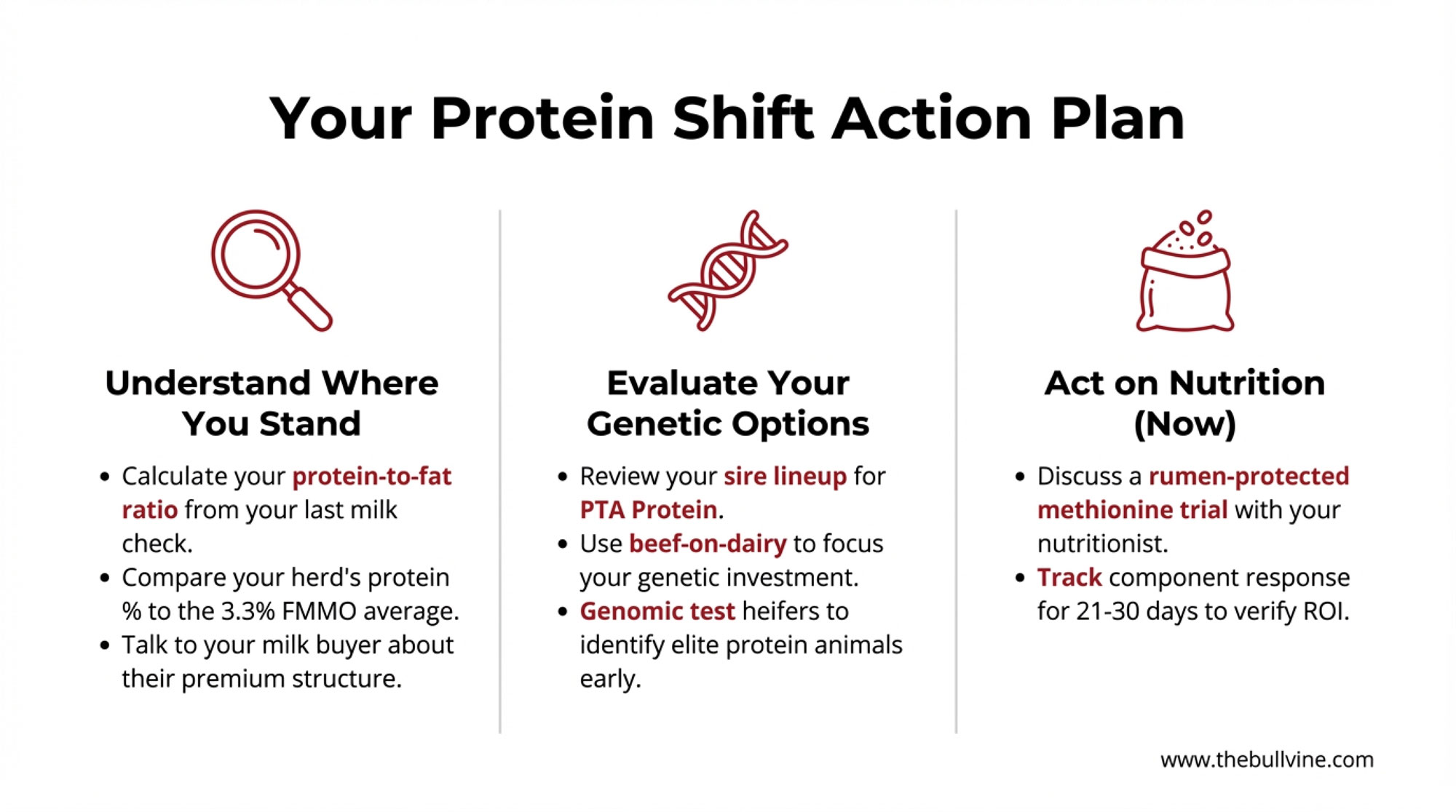

If you’re looking at your own numbers and wondering where to start, here are a few simple, concrete steps that many producers have found useful:

- Pull a year’s worth of milk checks and component reports.

Work out your true average butterfat and protein tests, and—more importantly—your pounds of fat and protein shipped per cow and per cwt. Then talk with your field rep or plant contact about how that profile lines up with what your leading buyer wants and pays best for. - Map your replacement needs before you map beef‑on‑dairy.

Sit down with your records and figure out your real replacement rate and any expansion plans. Estimate how many quality dairy heifers you’ll need calving in over the next two to three years. Use that number to double-check how much beef‑on‑dairy your breeding program can truly support without putting you in the heifer penalty box. - Pilot genomic testing on a subset of heifers.

Work with your AI rep or herd vet to test a group, rank them, and use that ranking to decide who gets sexed dairy semen and who gets beef. Treat this as a learning process, not a one‑off experiment. - Schedule an hour with a risk adviser.

Sit down with someone from your co‑op, a dairy‑focused broker, or an extension economist and ask them to walk you through what it would look like to protect roughly 30–50 percent of your expected milk and some of your feed at prices that cover your costs and debt needs. Then adjust that percentage based on your own risk tolerance and lender expectations. - Run a stress‑test budget.

Put together a simple cash‑flow scenario at a lower milk price—say 13–14 dollars Class III—and slightly higher feed costs. See where the pinch points are. Use that information to decide whether your next move should be to tighten costs, adjust debt, lock in some margins, pursue measured growth, or plan a gradual pivot.

Three Questions Worth Asking Yourself

As you work through all that, three blunt questions keep coming up in good kitchen‑table conversations:

- Do my components actually fit my buyer’s product mix and pricing grid—or am I leaving money on the table chasing the wrong butterfat/protein profile?

- Am I using genomic tools and beef‑on‑dairy with a clear replacement strategy—or am I selling my future herd for today’s calf checks?

- Do I have even a basic risk plan for the next 12–24 months, or am I still gambling that spot markets will treat me kindly?

The Bottom Line

At the end of the day, the export headlines and your milk check are telling different parts of the same story. The export dollars keep plants running and markets open. The milk check reflects how that big system—stainless steel, global competition, butterfat and protein pricing, consolidation, geography, heifer supply, and policy—lines up with your cows, your barn, and your ZIP code.

What I’ve noticed, sitting at a lot of kitchen tables and in a lot of barn offices, is that once you really understand those connections, the whole situation feels a little less random. You won’t control the world price of cheese. But you can control how your herd is bred, how your fresh cows come through the transition period, what your cost of production looks like, and whether you use the genetics, beef‑on‑dairy, and risk tools that are already on the table.

There isn’t one right answer. For some operations, the smart play will be to lean in and grow with the local plant. For others, it’ll be carving out a well‑defined niche that truly fits their region and family. And for some, the bravest and best decision will be planning a thoughtful transition that protects family, equity, and sanity. The key is making that call with clear eyes, honest numbers, and a solid grasp of the forces that are shaping all of us—whether we like them or not.

Key Takeaways

- $8.2B exports, stubborn checks: Record dairy shipments didn’t lift every milk check because expanded plant capacity needs export markets to clear marginal pounds—at margins that rarely flow back to producers.

- Protein now drives the pay grid: Cheese plants reward curd yield, not extreme butterfat. Herds balancing 3.5–3.8% protein with 3.8–4.1% fat are capturing more consistent component premiums than single-trait chasers.

- Beef-on-dairy created a heifer crisis: Replacement inventories fell to their lowest since 2001. Farms that grabbed $600 beef calf checks now face $2,500–$3,000+ heifer bills—proof that short-term cash can cost long-term cows.

- Big herds are buying “invisible” cows: 15,000 dairies exited in five years; 1,000+ cow operations now ship two-thirds of U.S. milk. They’re paying for genetics that deliver fertility, health, and components—not project cows that hit the treatment list.

- Three moves that separate planners from hopers: Tune your component profile to your plant’s grid, use genomics and beef-on-dairy with a locked-in replacement plan, and treat DRP and feed hedges as standard practice—not emergency measures.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $4,000 Heifer: Seven Strategies to Navigate the New Dairy Economy – Reclaim your margin with a tactical breakdown of the “Raise vs. Buy” math. This guide arms you with the leverage needed to negotiate with lenders while surviving $3,000 replacements in a historically tight-supply market.

- 2025’s Dairy Dilemma: Record Exports, Falling Checks, and What Every Producer Must Decide Next – Exposes the “Volume over Value” trap where being the world’s cheapest cheese supplier bleeds your bottom line. Gain the strategic foresight to outmaneuver the coming Mexican production pivot and Southeast Asia’s critical processing shift.

- The December Genetic Reckoning: Former Champions Fall, New Kings Rise, and Your 2026 Strategy Just Changed – Reveals the “Invisible Cow” dominance reshaping global Holstein rankings. Learn to manage genomic volatility and leverage concentrated bloodlines to build the low-drama, high-component herd that modern processors and large-scale managers demand.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.