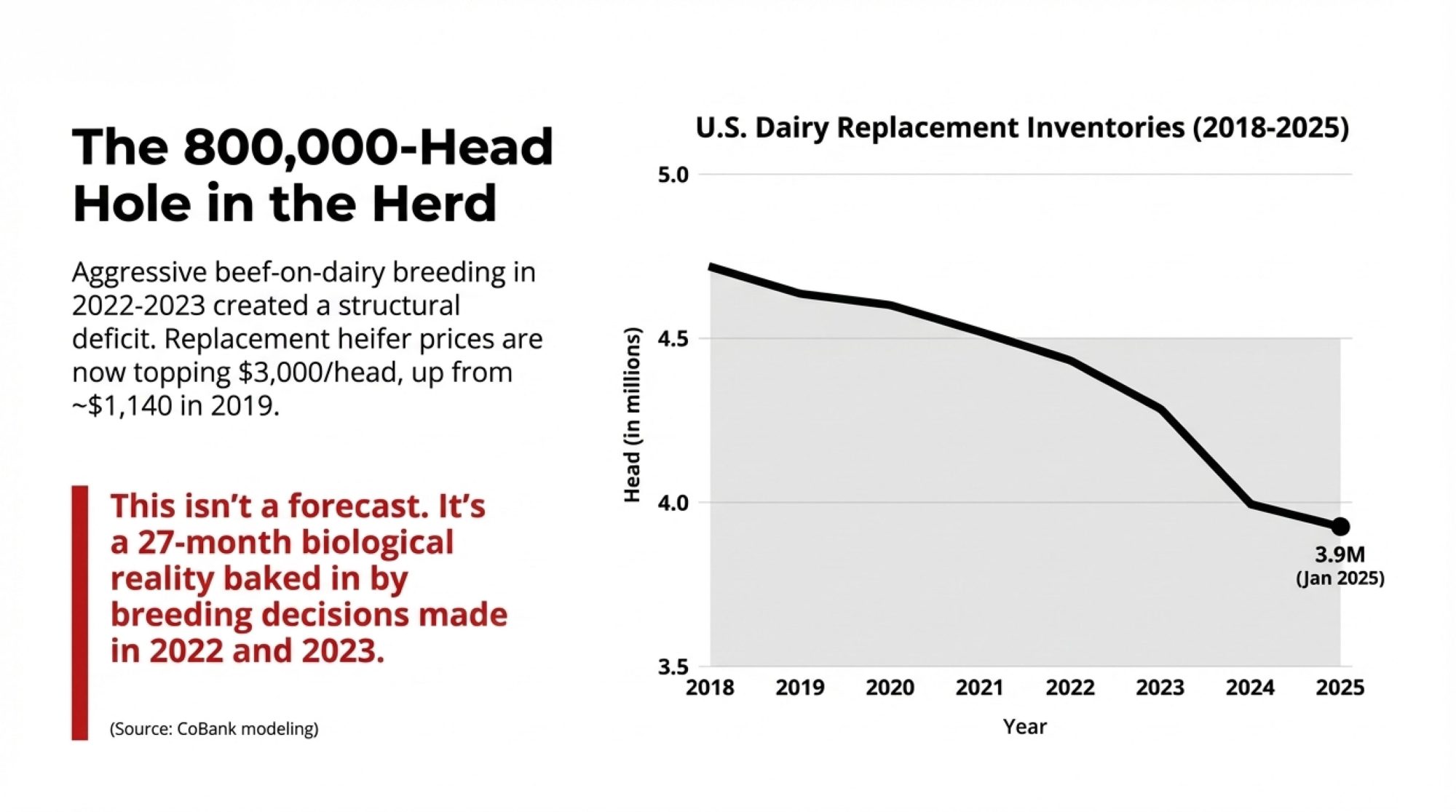

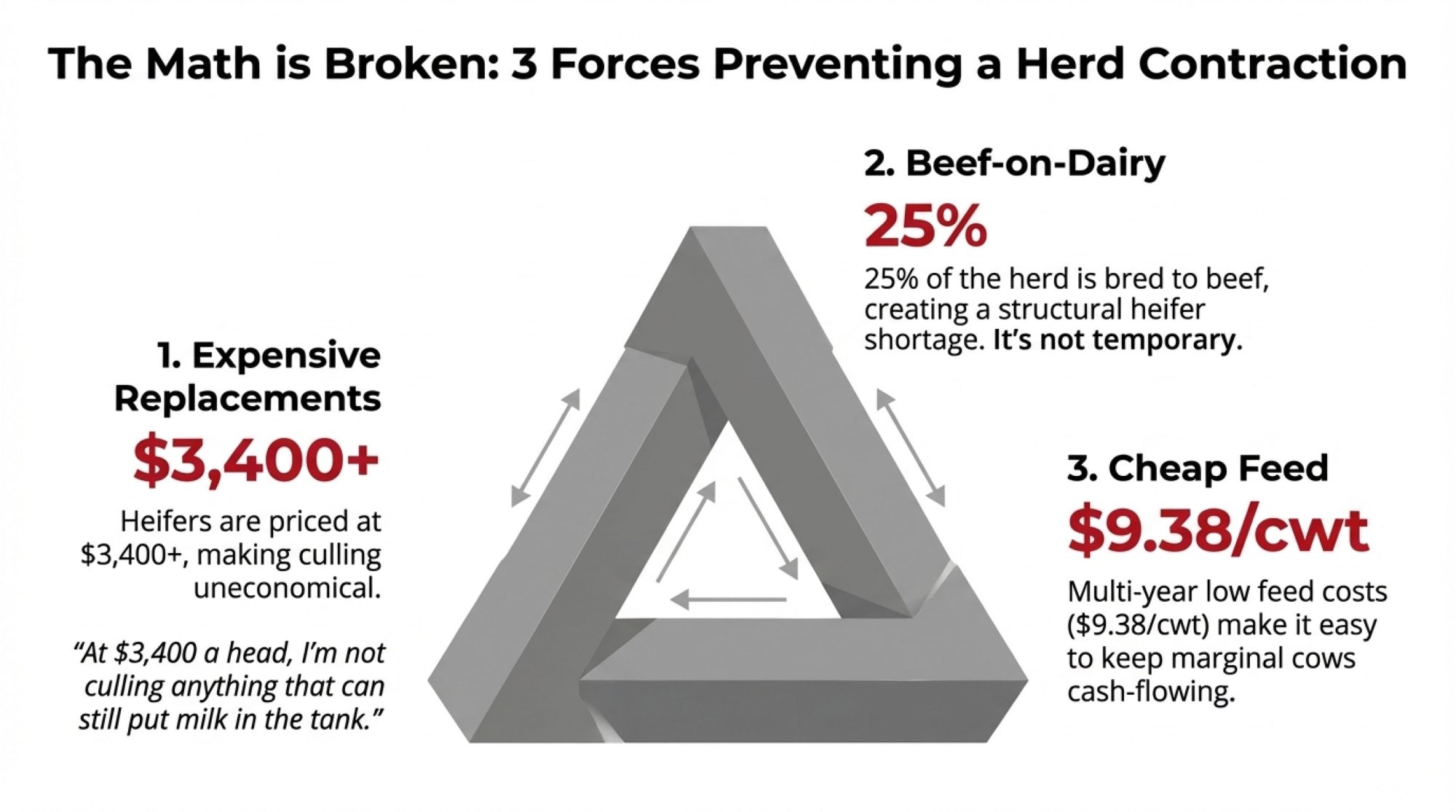

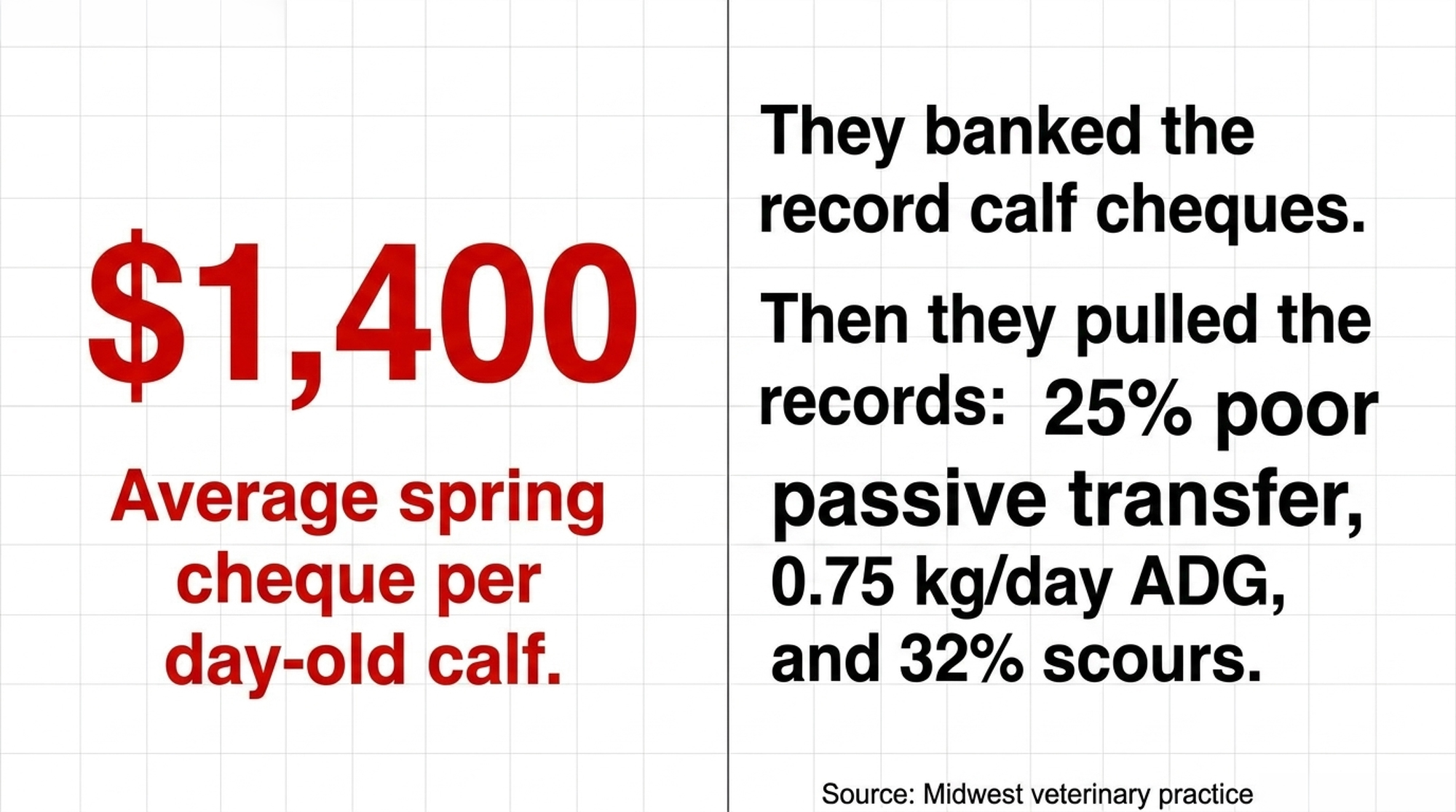

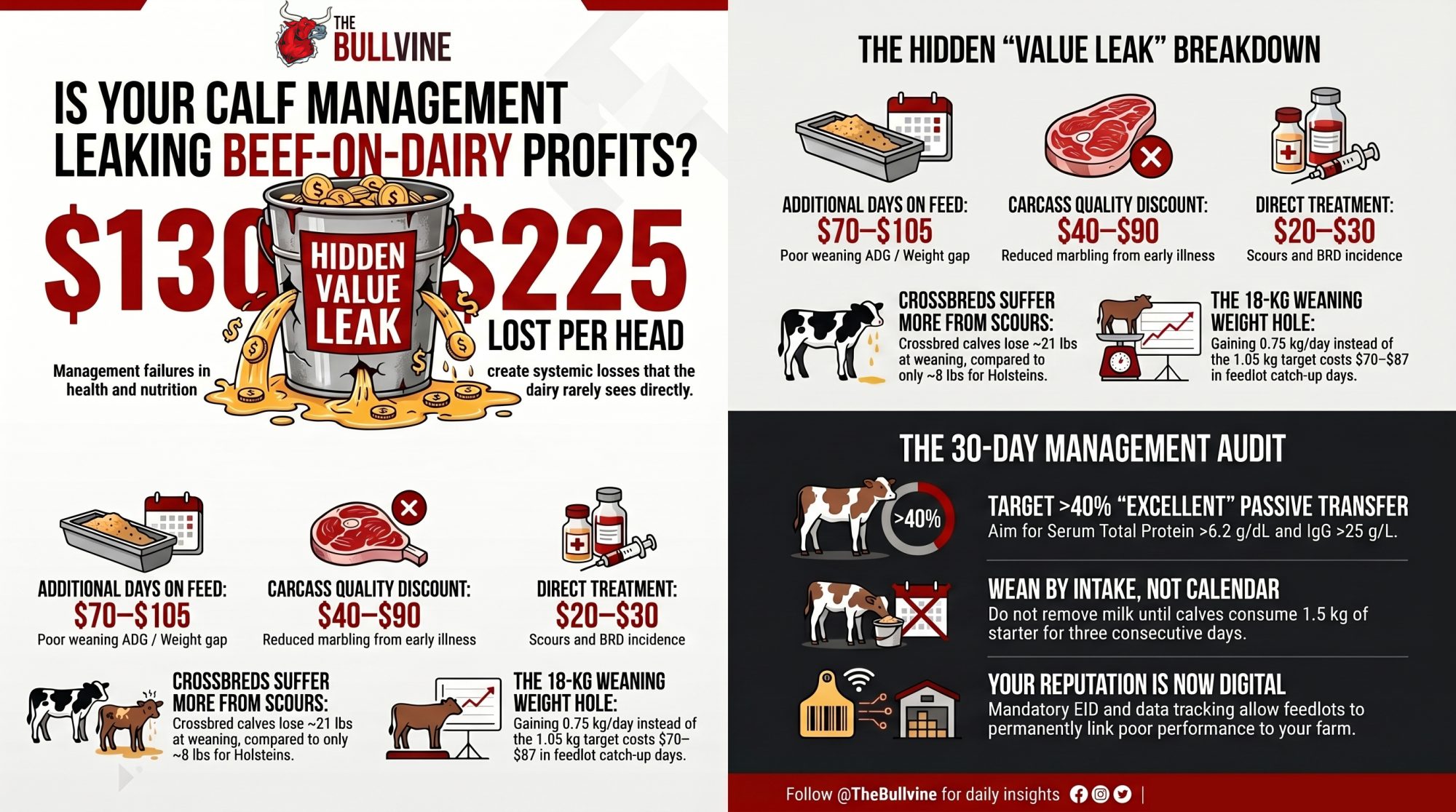

A 1,200-cow Wisconsin dairy banked every $1,400 calf cheque this spring — then pulled six months of records: 25% poor passive transfer, 0.75 kg/day ADG, 32% scours. The feedlot saw it first.

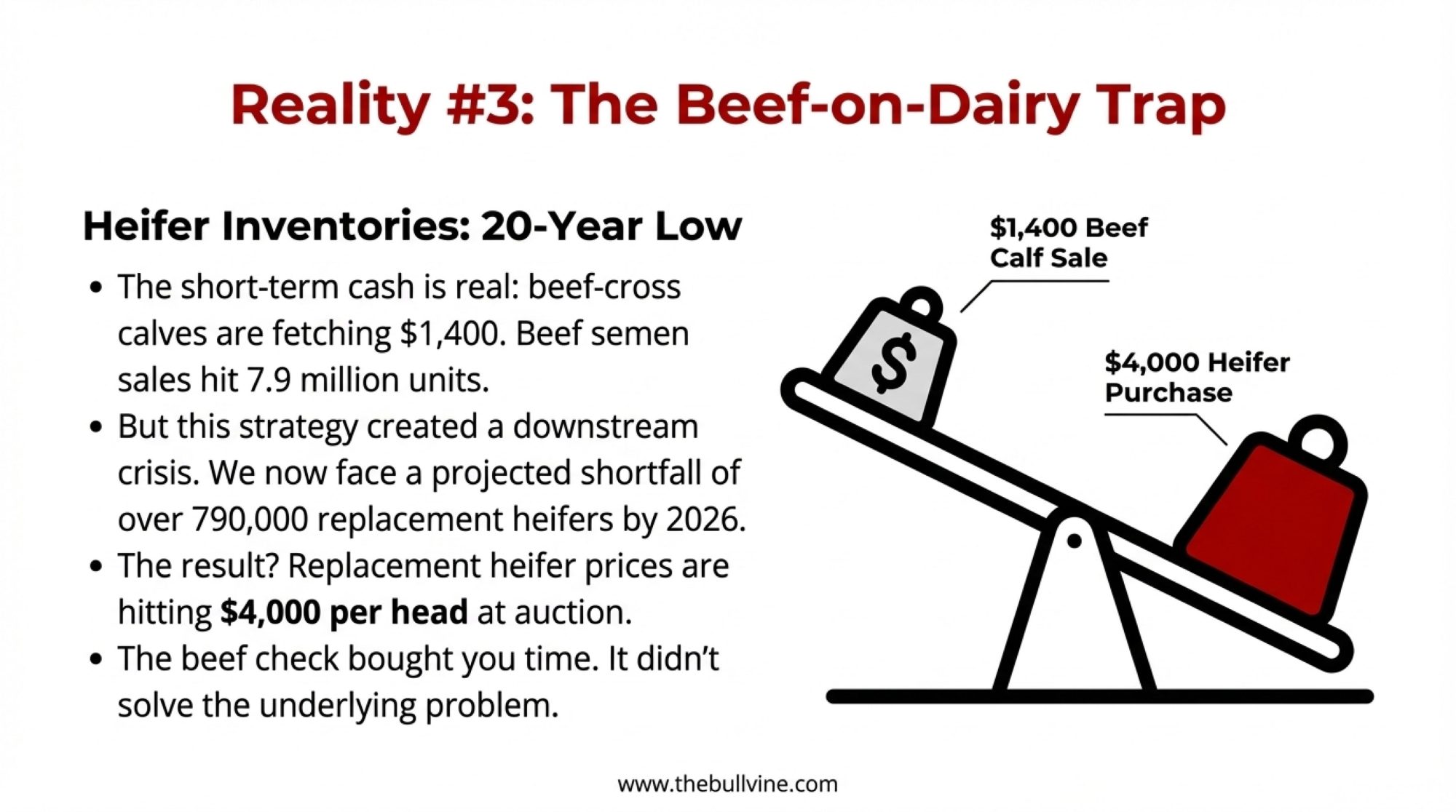

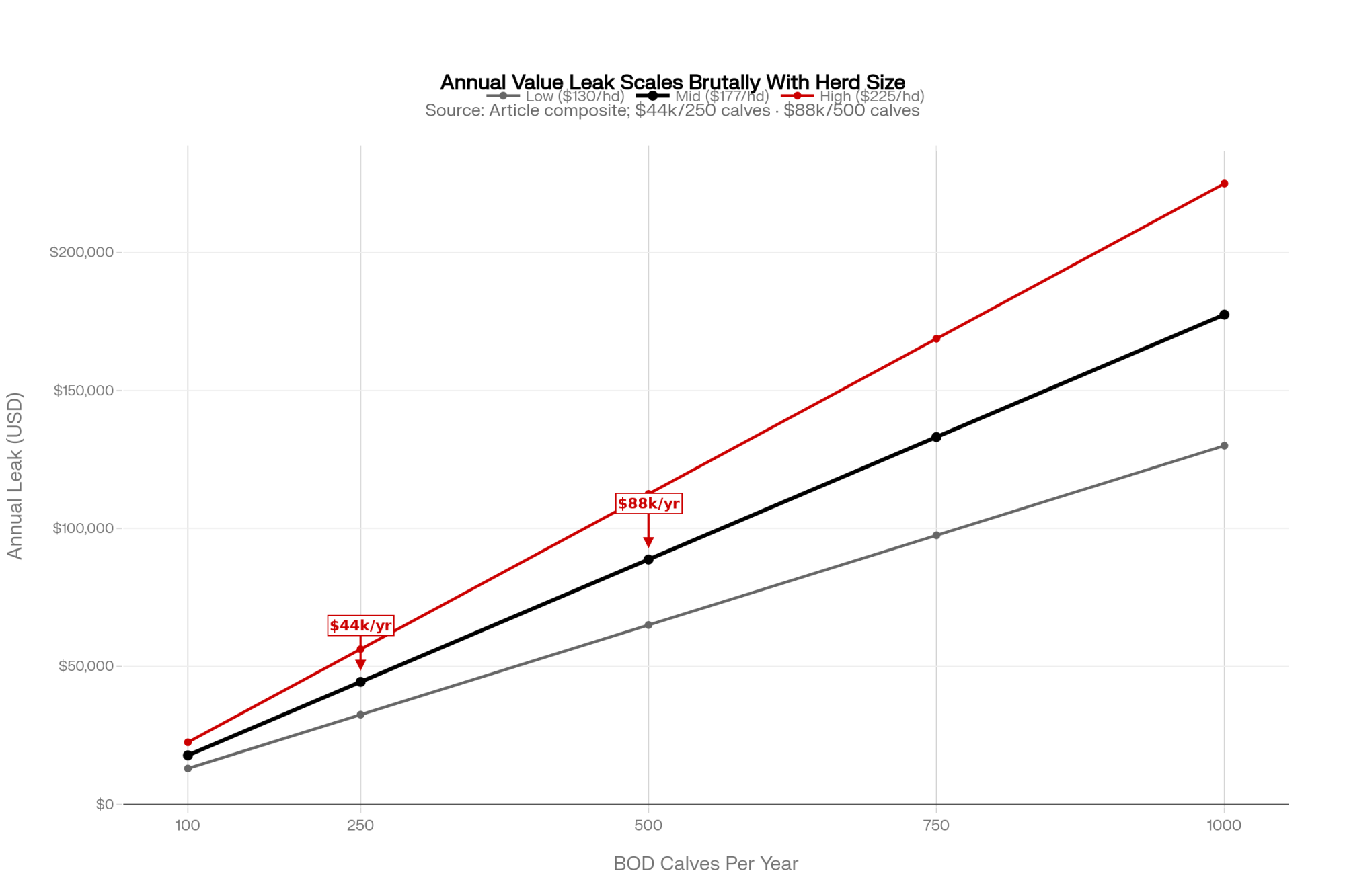

Executive Summary: Day-old beef-on-dairy bull calves are moving off US dairies at $1,350–$1,500 this spring — roughly $400–$600 above straight Holstein bulls per USDA-AMS weekly reporting — and that cheque is propping up margins while the North American heifer hangover drives replacement cost higher. But the same genetics are auditing calf programs in real time: Texas Tech Beef on Dairy Symposium data show crossbreds with scours lose roughly 21 lbs at weaning versus about 8 lbs for Holsteins, and a 0.75 kg/day pre-weaning ADG (vs. a realistic 1.05 kg target) leaves an 18-kg weaning-weight hole that costs the downstream chain $70–$87 per head in catch-up days alone. Stack treatment costs, extra days on feed, and a 10–20-point grid-discount hit on upper Choice and Prime, and the hidden bill runs $130–$225 per head — roughly $44,000 a year on 250 calves, $88,000 on 500. The dairy rarely sees it directly; it shows up as $50–$80 lighter bids the next auction, and USDA’s November 2024 ADT rule plus Source & Age Verification now make that reputation data permanent. Producers with under 40% of calves in “excellent” passive transfer (serum TP >6.2 g/dL, IgG >25 g/L per Lombard et al. 2020) or 60-day scours above 25% are funding elite genetics for someone else. The 30-day move is a serum-TP audit — Brix on every colostrum, blood on two days of calves a week — before the next SimAngus or terminal-sire order. If you can’t pull passive transfer, ADG split, and scours rate in one report by Monday, you don’t have a beef-on-dairy program — you have a hope.

Veterinarians working south-central Wisconsin’s mid-size dairies keep walking into the same story on farm after farm. What follows is a composite of three operations from one Upper Midwest practice — stitched together so no single farm is identifiable, but every number is a real number pulled from real records. On a 1,200-cow dairy in that group, day-old beef-on-dairy bull calves were moving off the property in the ,350–,500 range per head this spring, consistent with USDA-AMS weekly dairy calf and feeder cattle reporting showing beef-on-dairy day-old premiums running roughly 0–0 above straight Holstein bull calves through the first half of 2026. The milk cheque was thin. Beef-on-dairy revenue was doing the heavy lifting. “These crossbreds hardly ever get sick,” the owner told his vet.

Then they pulled six months of records. Passive transfer: 25% of calves in the “poor” category on serum total protein. Pre-weaning average daily gain on the beef-on-dairy calves: 0.75 kg/day — dead-even with his Holsteins. Scours treatments: 32% of calves hit at least once in the first 60 days. Every number he was proud of turned out to be a number he’d never actually pulled. That’s what beef-on-dairy does in 2026. It doesn’t just pay a premium. It audits your calf program whether you want it to or not.

The $1,400 Honeymoon Is Over

Beef semen on dairy cows isn’t a side hustle anymore. It’s a structural piece of the US dairy revenue model. NAAB year-end semen sales reports have tracked beef semen units sold for dairy use in the multi-million-unit range annually since 2021, and USDA reporting from 2022 onward has documented a steady climb in the share of US dairy cows bred to beef sires.

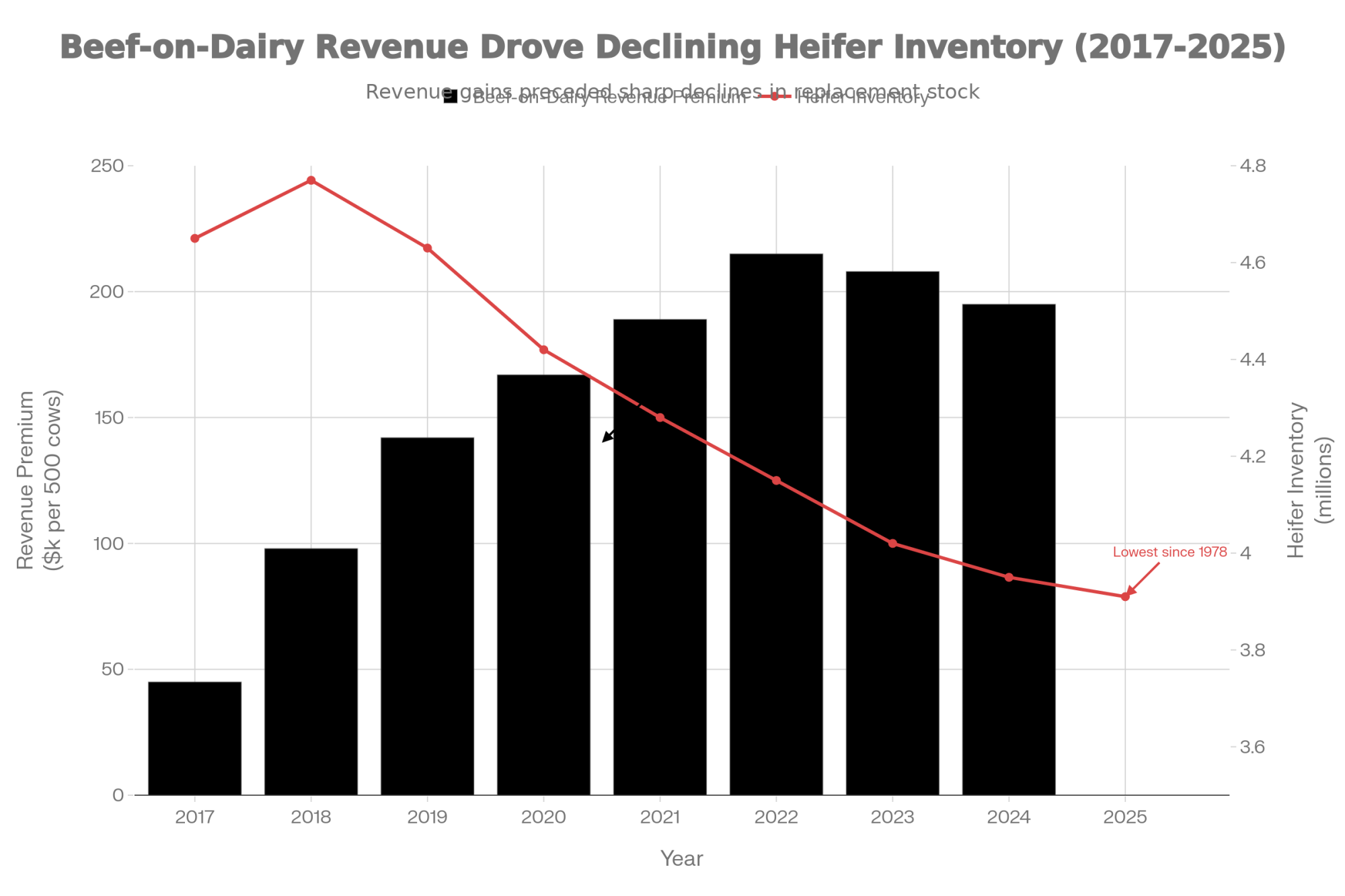

That’s the math that makes a $1,400 calf possible on the front step. And here’s the piece most dairies haven’t processed yet: the beef-on-dairy calf cheque is propping up margins because the North American heifer hangover — documented in USDA NASS January Cattle inventory reports and Rabobank Dairy Quarterly analysis through 2025 — is simultaneously driving replacement costs higher. You are more dependent on that crossbred revenue in 2026 than you were in 2023, not less.

When a Holstein bull calf was worth $200, sloppy colostrum was annoying. When he’s worth $1,400, the same sloppy colostrum is a direct hit to your second-largest revenue line. And the crossbreds themselves are unforgiving in a way Holsteins never were. Research presented through the Texas Tech Beef on Dairy Symposium series has reported that crossbred calves with scours lost roughly 21 lbs of weaning weight versus about 8 lbs for Holsteins hit with the same illness, a finding consistent with the Journal of Dairy Science work of Windeyer et al. (2014) on early-life disease effects on dairy calf weight gain. Higher ceiling. Steeper fall.

The herds most exposed aren’t the ones just starting out. They’re the ones that got comfortable. Mid-size dairies running beef-on-dairy for two or three seasons, still using colostrum and weaning protocols built for Holstein replacements, still weaning on a calendar instead of by starter intake. Those are the farms cashing calf cheques today and losing reputation battles in the feedlot six months from now.

How This Plays Out on Real Farms

On that 1,200-cow operation, the maternity routine hadn’t changed in a decade. Colostrum got fed “when we get to it.” Brix was measured sometimes. Serum total protein — the blood test that tells you whether the antibodies actually made it into the calf — was never pulled, ever. Scours treatments lived in a notebook in the vet’s truck, a pattern Ontario Veterinary College survey work has flagged as widespread: a large share of surveyed herds either don’t record individual calf treatments at all or record them in a format that can’t be analyzed after the fact.

The calf buyer had already noticed, even if the dairy hadn’t. Bids on the last two groups were running $50–$80 a head below what comparable neighbors with tighter calf numbers were getting out of the same auction barns that week. The owner blamed “the market.” The market wasn’t the problem.

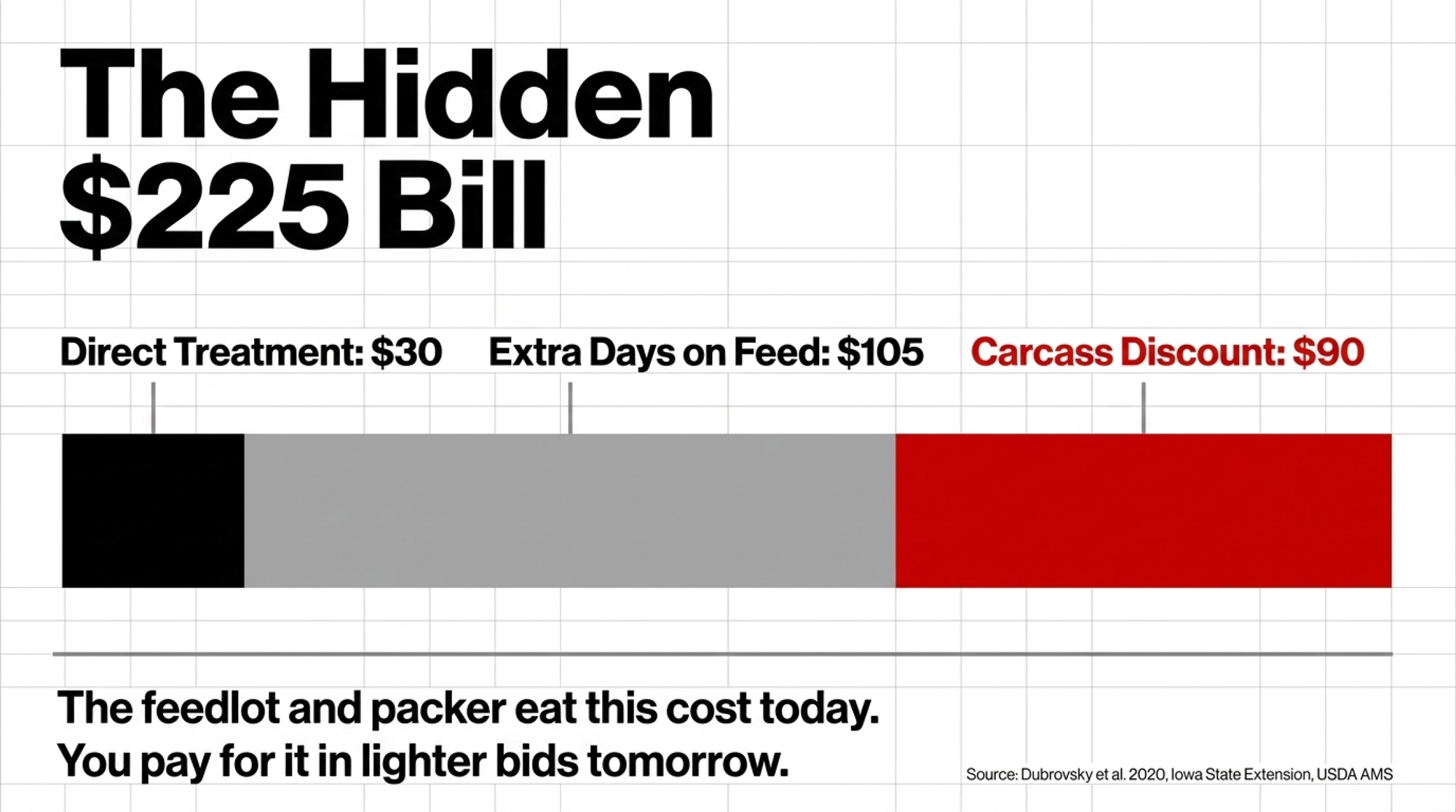

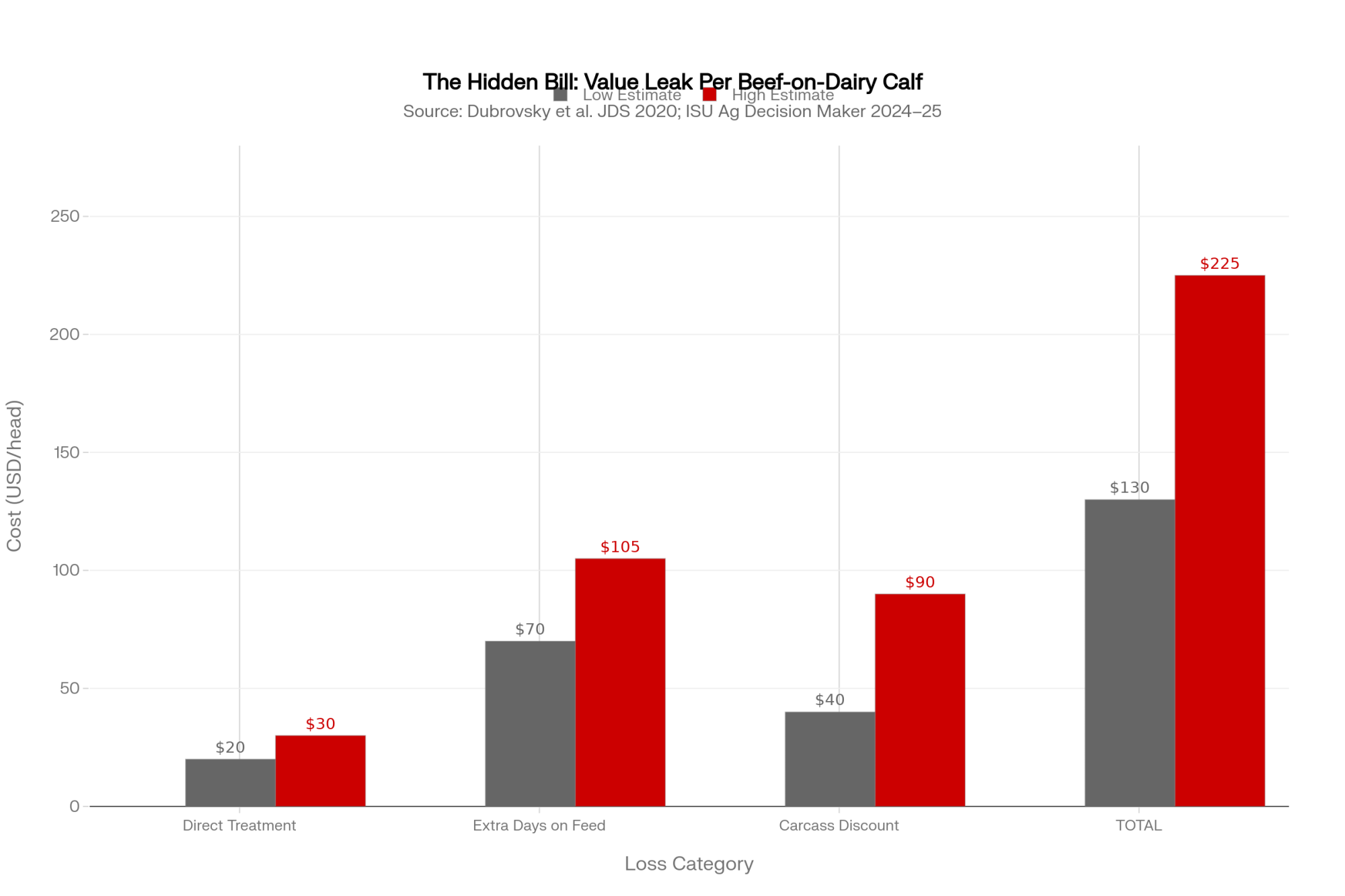

The Hidden Bill, at a Glance

Loss Category

Estimated Cost (per head)

Root Cause

Direct treatment

$20–$30

Scours/BRD incidence

Additional days on feed

$70–$105

Poor weaning ADG / 21-lb weight gap

Carcass quality discount

$40–$90

Reduced marbling from early-life illness

Total value leak

$130–$225

Systemic management failure

Treatment-cost band draws on the Journal of Dairy Science calf-illness economic modeling published by Dubrovsky et al. (2020) and related USDA-ARS work. Days-on-feed costs assume Iowa State Extension’s 2024–2025 Ag Decision Maker custom calf-feeding and yardage surveys, which reported total daily cost of gain in the $3.00–$4.00/day range. The grid-discount band assumes upper Choice and Prime premiums in the $20–$35/cwt range reported through USDA AMS LM_CT155 National Weekly Direct Slaughter Cattle — Premiums and Discounts during 2024–2025.

On a 250-calf operation, the midpoint of that table is roughly $44,000 a year; on 500 beef-on-dairy calves, it’s roughly $88,000. The awkward part? The dairy never sees most of it directly. The feedlot eats the extra days on feed. The packer eats the lighter, lower-grading carcass. You get a $50–$80 lighter bid next round, tell yourself the buyers got cheap, and lose next year’s bid the same way.

Colostrum to Carcass: Where the 0.75 kg/day Gap Actually Costs You

Three things separate herds banking the beef-on-dairy premium from herds quietly leaking it, and none of them live on a genomic test.

Passive transfer is the foundation. USDA NAHMS Dairy 2014 found a substantial share of preweaned heifer calves failed to achieve adequate passive transfer, and Lombard et al. (2020) in the Journal of Dairy Science has since reclassified the targets. Calves with failed passive transfer carry 1.5–2× the risk of diarrhea and pneumonia. Industry guidelines used by Penn State Extension’s CalfCare program, Michigan State Extension, and the Dairy Calf & Heifer Association Gold Standards III now aim for at least 40% of calves in the “excellent” bucket — serum total protein above 6.2 g/dL, IgG above 25 g/L. Plenty of farms running “good Brix” colostrum still have 30–40% of calves sitting in fair or poor when you actually pull blood. Brix tells you about the liquid. Serum TP tells you whether the calf got what you think you gave her.

Passive Transfer Category

Serum TP (g/dL)

IgG (g/L)

Disease Risk vs Excellent

% Farms Hitting 40%+ “Excellent” Target

Excellent

>6.2

>25

Baseline

<50% of US herds

Good

5.8–6.2

18–25

1.2–1.4×

Target threshold

Fair

5.1–5.7

10–17

1.5–1.8×

⚠ Common default

Poor

<5.1

<10

2.0–2.5×

25% of article herd calves

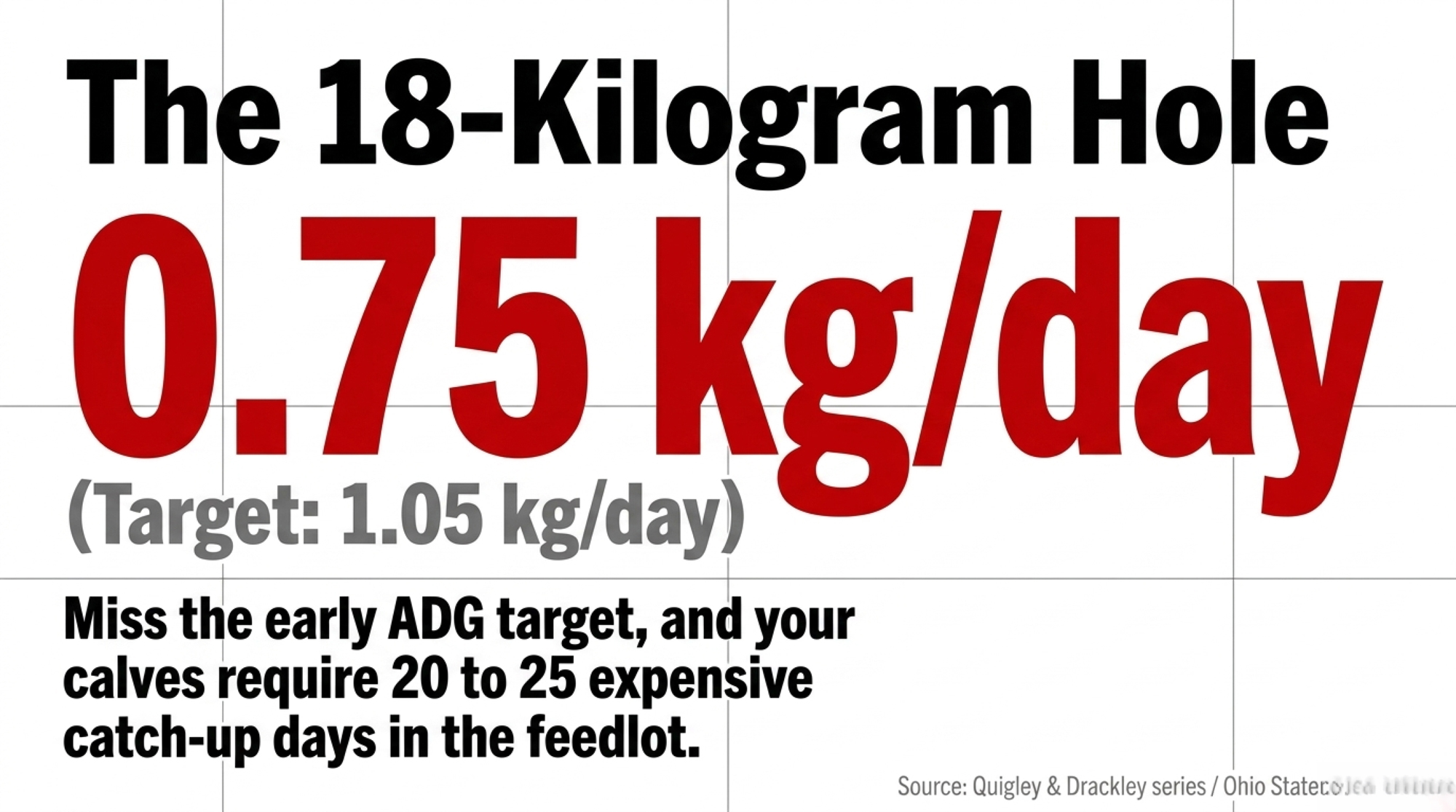

Starter, not milk, drives weaning weight. The Quigley and Drackley line of Journal of Dairy Science research — Drackley (2008) and the Quigley starter-intake series — has shown for two decades that age at first starter intake and starter consumed by 21–28 days are among the strongest predictors of weaning weight. Elite beef-on-dairy programs target 0.9–1.1 kg/day pre-weaning ADG — realistic when calves are eating 0.3–0.5 kg/day of starter by the end of week three and pushing past 1.5 kg/day before the milk comes off.

Here’s what that gap actually costs. If your calves are gaining 0.75 kg/day instead of 1.05 kg/day, the weaning-weight gap over 60 days is (1.05 − 0.75) × 60 = 18 kg. At yardage and feed costs of $3.50/day, that 18-kg deficit takes roughly 20–25 days to close in the feedlot, costing the chain about $70 to $87 in catch-up time alone.

At yardage and feed costs of $3.50/day$3.50/day, that 18 kg deficit takes roughly 20–25 days to close in the feedlot, costing the chain about $70$70 to $87$87 in catch-up time alone. That recovery window assumes typical beef-on-dairy compensatory gain rates reported in Ohio State’s beef × Holstein vs straight Holstein feedlot work (Fluharty et al. and the subsequent OSU beef-on-dairy feedlot study series). The carcass side makes it worse. Ohio State’s growth-performance and carcass-traits data showed measurable advantages for crossbreds on gain, feed efficiency, and carcass value — but those advantages erode when calves arrive with poor early growth or lingering respiratory damage. Penn State extension work on bovine respiratory disease and lung consolidation has linked early BRD to reduced marbling and lower quality-grade outcomes. Lose 10–20 percentage points of calves out of upper Choice and Prime at current grid spreads and the expected-value hit across the lot runs roughly $40–$90 per head. Your day-old cheque looked the same. Your actual value to the chain did not.

The feedback loop is the permanent one. A feedlot typically needs one turn of your calves — 6 to 12 months — to decide whether you’re what your marketing said. They see arrival treatments, gain in the first 60–90 days, then the close-out at harvest. Feeder-cattle research out of Kansas State (Schroeder et al.), UW-Madison, and Superior Livestock tele-auction price analyses has shown consistently that buyers discount negative reputations faster than they reward positive ones — and they rarely tell sellers why.

Why Feedlots Remember — and How EID Makes It Permanent

The reputation problem isn’t anecdotal anymore. It’s digital.

USDA’s Animal Disease Traceability final rule, which made electronic identification mandatory for breeding cattle and bison moving interstate effective November 2024, has accelerated what commercial feedyards were already doing: matching arrival health, gain in the first 60–90 days, and carcass close-out data back to the source dairy through EID tags and lot paperwork. Source and Age Verification programs under USDA Process Verified Programs and equivalent certifications have made those audit trails saleable. A feedlot’s “problem lot” database used to live in a yard manager’s head. It now lives in a database with your farm name next to it.

You don’t get blacklisted with a phone call. You get blacklisted with a quieter bid and a skipped auction. By the time you notice the pattern, the data upstream has already decided for the buyers.

Metric

What the Dairy Thinks

What the Feedlot Records

Data Now Permanent Since

Passive transfer rate

“We feed 4L colostrum”

25% of calves in “poor” category

Nov 2024 (USDA ADT rule)

Pre-wean ADG

“Crossbreds are growing great”

0.75 kg/day — at Holstein floor

Per-lot EID arrival data

60-day scours rate

“We treat when needed”

32% treated ≥ once

Source & Age Verification PVP

Calf health reputation

“Buyers just got cheap”

$50–$80/head bid discount

Lot history, digital & permanent

Carcass outcome

“Not our problem after sale”

10–20pt upper Choice/Prime loss

USDA AMS LM_CT155 grid data

Feedlot feedback

“Nobody tells us anything”

One turn = permanent source score

Kansas State/UW-Madison buyer research

How Much Is a 0.75 kg/day ADG Really Costing You?

Run the numbers on your own herd and the answer isn’t a rounding error. At 0.75 kg/day instead of 0.95–1.1 kg/day, you’re 15–20 kg light at weaning before you factor any post-weaning slump. Against 2026 calf values of $1,350–$1,500, the leak table above puts $130–$225 of value per calf at risk — a meaningful share of the premium the market is currently paying you for crossbred genetics. That math stays ugly whether corn is $4 or $5.

Is Your Calf Program Ready for $1,400 Genetics?

Beef-on-dairy calves were built to outperform. That’s why buyers pay for them. But the outperformance is conditional — on colostrum that actually gets into the calf, on starter that actually gets eaten, on weaning decisions that respect what the rumen is doing rather than what the calendar says.

The honest question isn’t whether your genetics rep sold you the right bull. It’s whether your maternity pen, your colostrum bucket, and your starter pail are holding up their end. A 25% “poor” passive transfer rate on a $200 Holstein bull calf was a rounding error. The same 25% on a $1,400 crossbred is a different conversation, and it’s one the feedlot is already having about you — just not with you.

Options and Trade-Offs for Producers

Path

Core Action

Timeline

Cost

Risk if Ignored

Key Metric

1 — Colostrum Audit

Brix + serum TP protocol

30 days

Low (~$3–8/calf)

Continued value leak

≥40% calves in “Excellent”

2 — Wean by Starter

1.5 kg/day intake threshold

60–90 days

Low (extra MR on slow calves)

18-kg weaning-wt hole

Starter intake Week 3–4

3 — Segment Breeding

30–40% sexed dairy, 50–60% beef

Ongoing

Medium (genomic testing)

⚠ Heifer shortage by 2028

Replacement rate vs cull rate

4 — Feedlot Feedback

Annual data debrief with buyer

Annual

None (relationship cost)

Permanent reputation damage

Arrival health + carcass grades

Path 1 — The “Stop Lying to Yourself” Colostrum Audit (do this within 30 days)

When it fits: any herd that can’t tell you, off the top of its head, the percentage of calves sitting in “excellent” passive transfer.

What it requires: Brix on every first-milking colostrum, a written SOP for volume and timing (4 L within 2 hours of birth, no exceptions), and a rolling serum TP check on a sample of calves at 24–48 hours of age. Pull blood on every calf born across two days a week and run the panel.

Risk and limit: it surfaces problems fast, which means someone has to own the fix. The refractometer is useless if nobody changes what happens between the cow and the calf.

Path 2 — Wean by Starter Intake, Not by Calendar

When it fits: any dairy still pulling milk on a fixed calendar — 42 days, 56 days — regardless of what calves are actually eating.

What it requires: starter in front of calves by day 3–4, buckets dumped and refreshed daily, and a simple rule the barn team can live by: no full milk removal until calves are eating roughly 1.5 kg/day of starter for three consecutive days.

Risk and limit: you’ll extend the milk window on some calves, which costs a few dollars in milk replacer per head in the short run. On $1,400 calves, that’s a bargain.

Path 3 — Segment Your Breeding Instead of Blanket-Beefing It

When it fits: herds using beef semen as a dumping ground for every “low” cow without a genomic plan behind the decision.

What it requires: a genomic framework that puts sexed dairy on roughly the top 30–40% of cows and beef on the bottom 50–60%, with clear calving-ease rules for heifers. Using Angus on first-calf heifers and reserving terminal breeds (Simmental, Charolais, Limousin) for mature cows isn’t a style choice — it’s dystocia management. Watch replacement inventory hard; the heifer hangover reshaping 2026 breeding plans came from over-beefing two and three years ago.

Risk and limit: if your replacement math is off, you’ll fix your calf revenue and break your cow supply at the same time.

Path 4 — Close the Feedlot Feedback Loop

When it fits: any dairy selling more than a truckload of beef-on-dairy calves a year and getting no carcass data back.

What it requires: one structured annual debrief with your primary calf buyer or receiving feedlot — arrival health, gain in the first 60 days, days on feed, carcass weights, grades. EID tagging at birth and BVD-PI ear-notching remove two of the biggest buyer objections at once.

Risk and limit: some buyers won’t share numbers. Sell to the ones who will. The data is worth more than a $20/head bid bump from someone who treats your calves as a black box.

Key Takeaways

If fewer than 40% of your last 30 calves land in “excellent” passive transfer on serum TP, your colostrum program is your first problem — regardless of what Brix says on the bucket.

If your beef-on-dairy pre-weaning ADG isn’t clearly ahead of your Holstein ADG, stop blaming genetics. The crossbreds give you a higher ceiling; management is what’s pinning you to the Holstein floor.

If your 60-day scours treatment rate is above 25%, treat it as a five-alarm fire. In the Texas Tech Beef on Dairy Symposium dataset, every case costs roughly triple the weaning-weight penalty a Holstein pays.

If your starter buckets are dusty, caked, or sorted tomorrow morning, your calves aren’t eating enough to hit elite ADG — no matter what the bag label promises.

If you’re still weaning on a calendar, switch to a 1.5 kg/day starter-intake threshold for three consecutive days before full milk removal.

If your primary calf buyer won’t share arrival health, days on feed, or carcass data once a year, assume the worst about how your calves are actually performing — and find a buyer who will.

If you can’t pull passive transfer, pre-weaning ADG split, and scours treatment percentage in the same report by next Monday, you don’t have a beef-on-dairy program. You have a hope.

Your Next Step

Don’t order your next batch of SimAngus or terminal-sire semen until you’ve audited your serum total protein.If you’re under 40% “excellent,” you aren’t ready for elite genetics — you’re funding them for someone else.

This week, put a refractometer, a serum TP kit, and a scale in the calf pens. Pull two days of blood and one week of starter intakes. Then decide whether your calf program deserves your breeding program.

Somewhere downstream, a feedlot is already building a picture of your calves from data you don’t see. The only move that fixes that is deciding to see it first. The week-by-week starter curve and the full colostrum-to-carcass cost model live in Bullvine Weekly and the next Tier 2 playbook — that’s the piece to read before your next sire order.

Run Your Numbers

Calf Feed ROI Tool — Before you pull another $50 off the calf program, run your colostrum, starter, and pre-weaning ADG through the Calf Feed ROI Tool and see whether the cheaper plan is actually funding that $1,400 crossbred — or quietly draining it.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong — Capture your share of the $6,215 monthly performance gap by revealing the reproductive guardrails top earners use. Delivers a blueprint for matching beef semen deployment to specific pregnancy rate tiers and genetic markers.

Boosting Dairy Farm Profits: Using Embryo Transfer and Male-Sexed Beef Semen — Accelerate genetic progress by dismantling the cost barriers of embryo transfer and male-sexed beef semen. Illustrates how leveraging hybrid vigor generates up to 200% higher premiums for your crossbred day-old calves.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

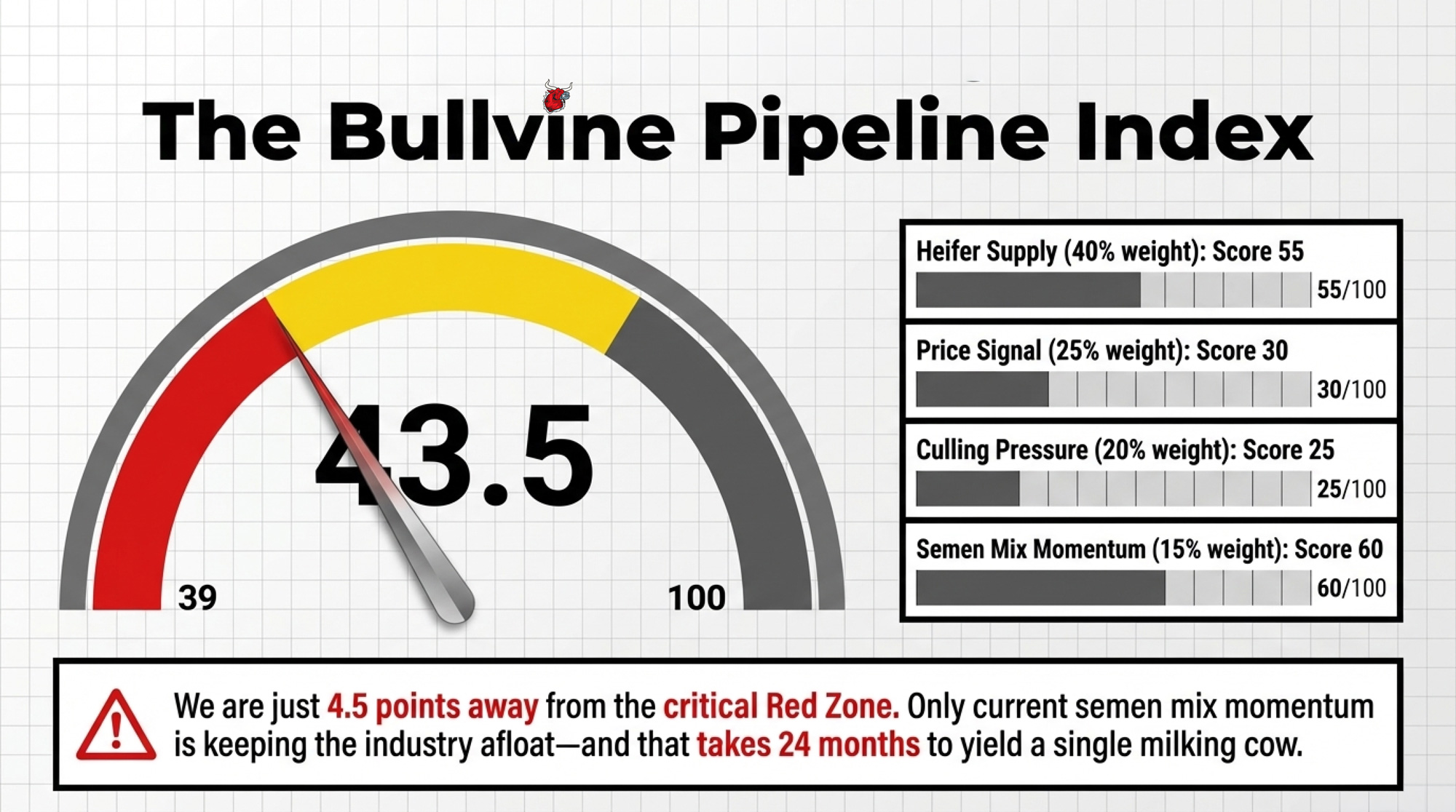

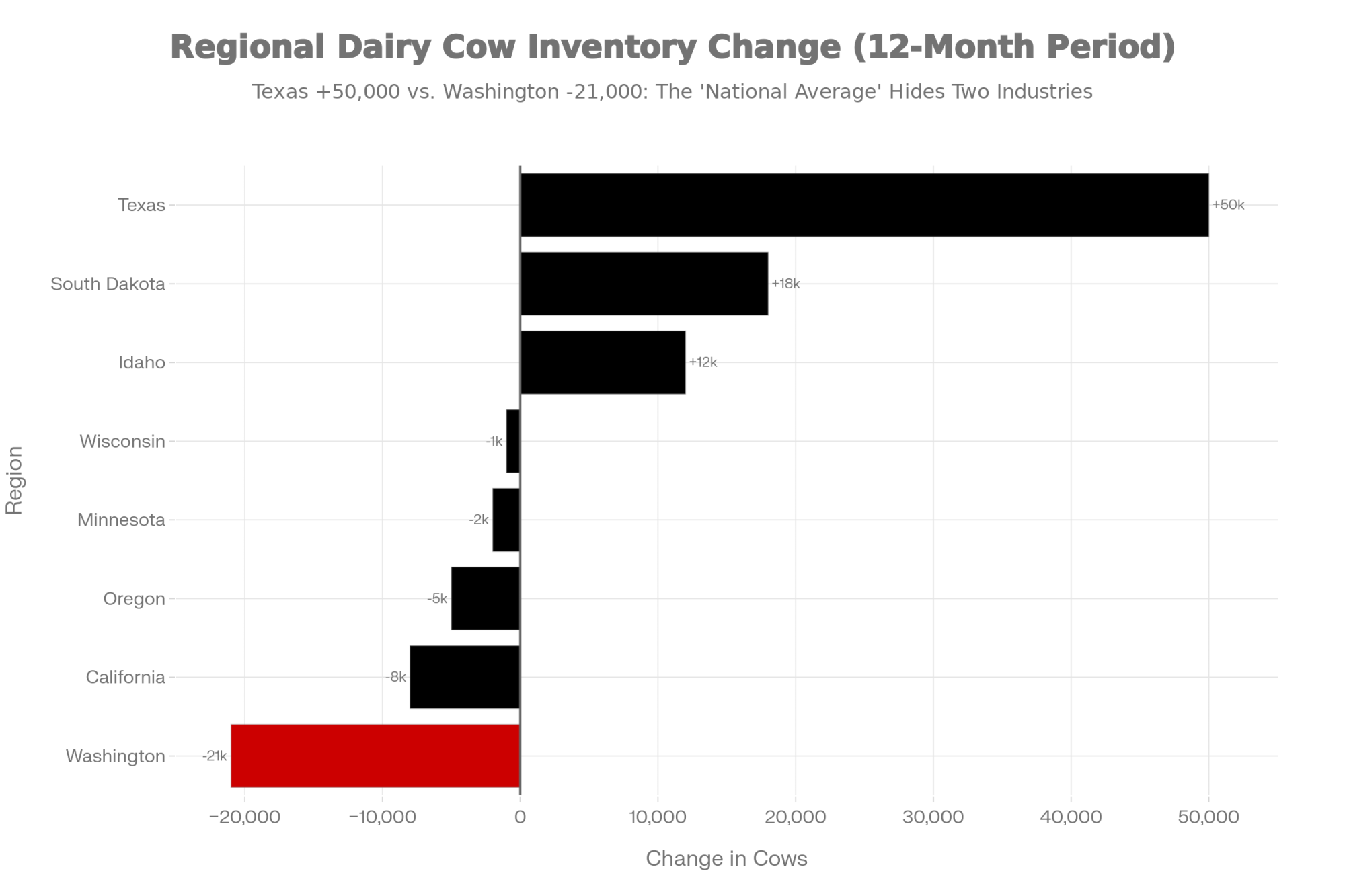

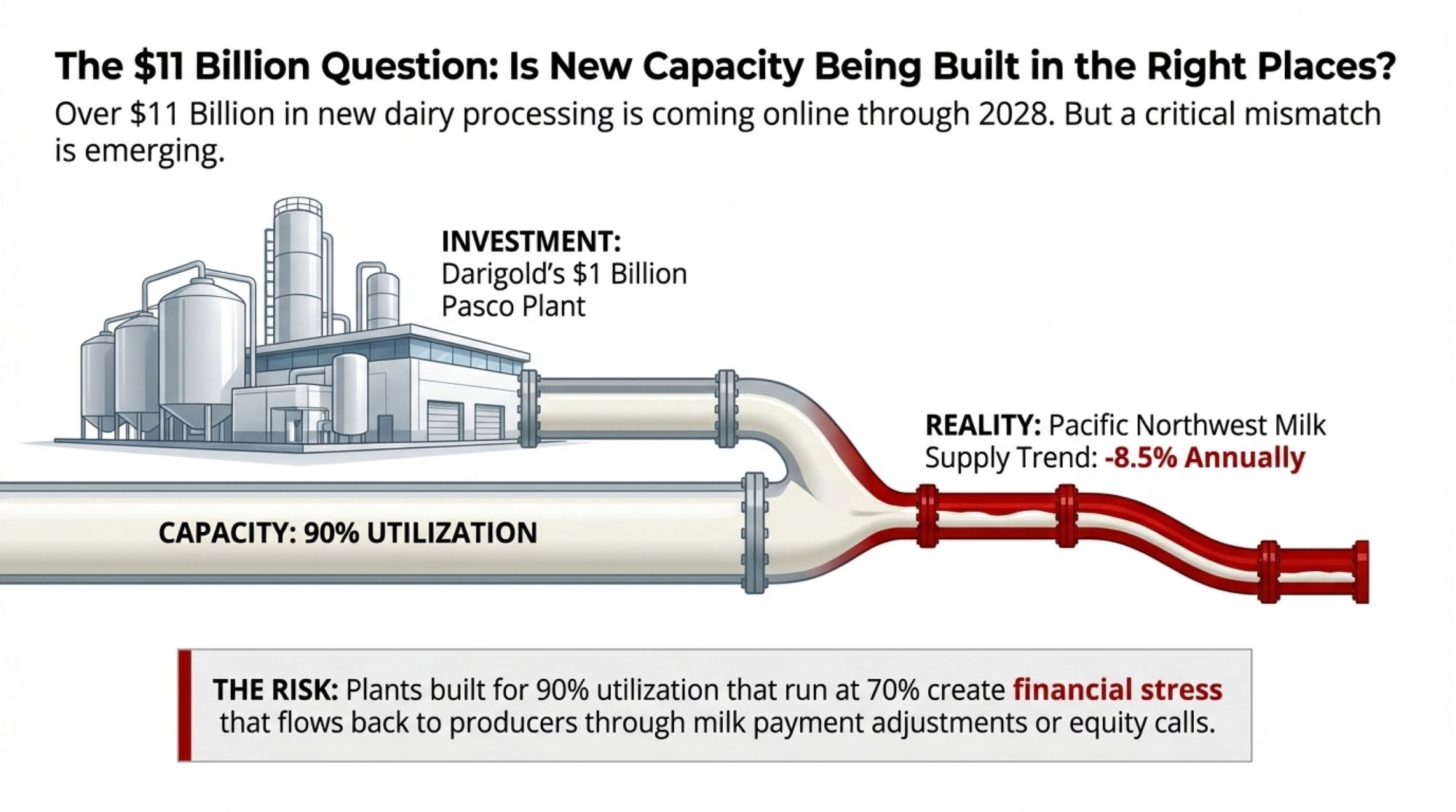

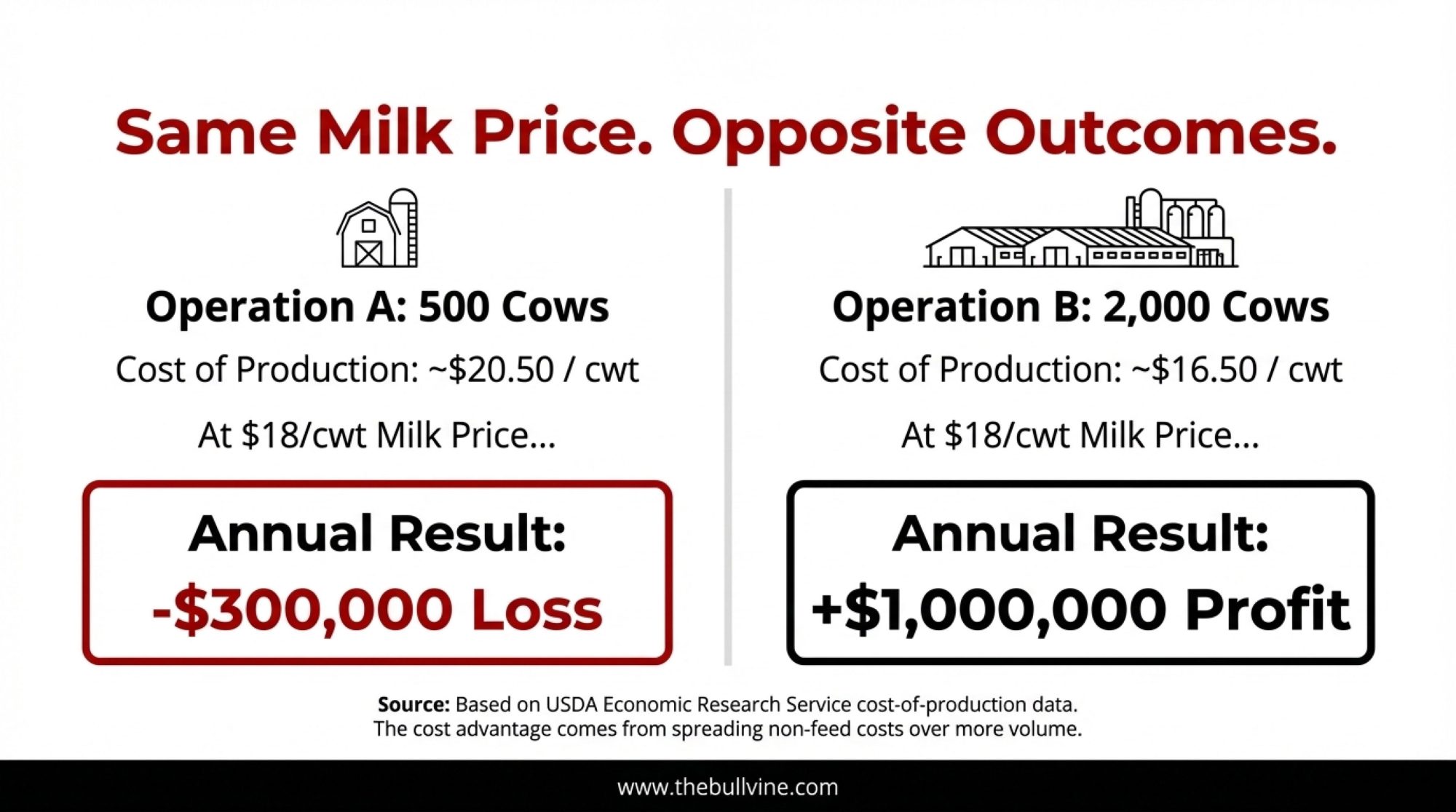

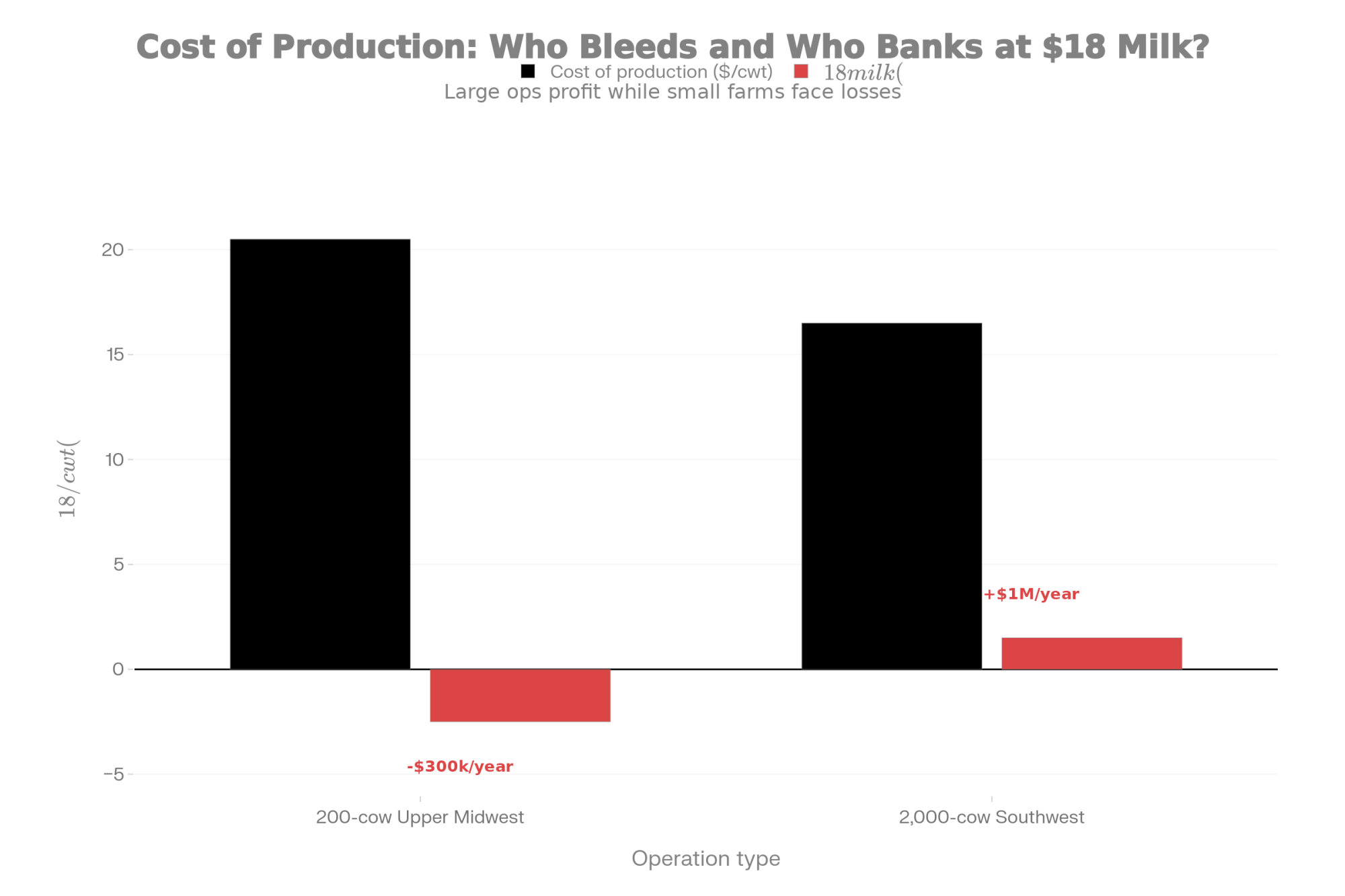

500-cow Panhandle herd, 35% beef through 2023–24. At a $3,010 replacement and a $500 calf, every beef service on a viable dairy dam now costs $583. Pipeline Index: 43.5. Yellow Zone.

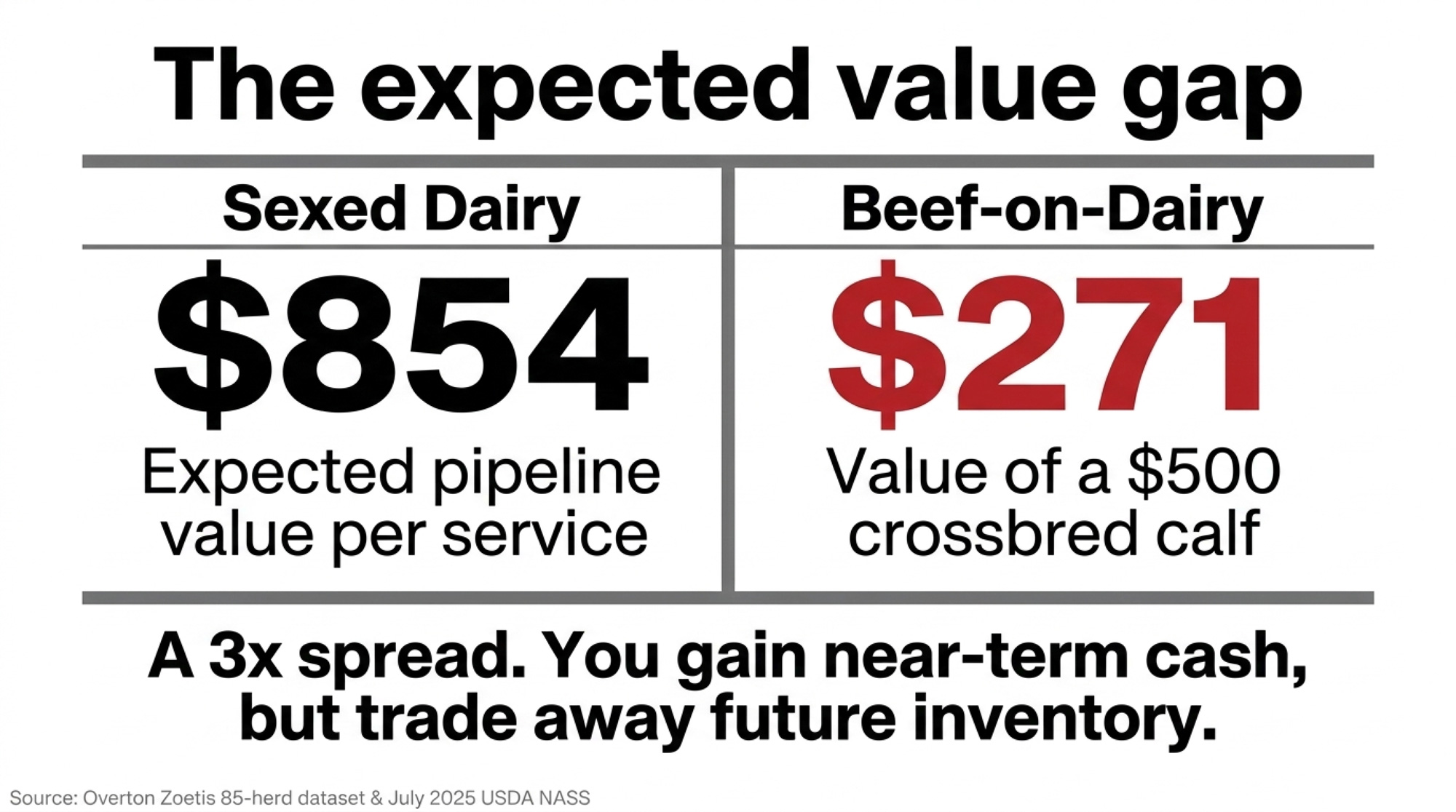

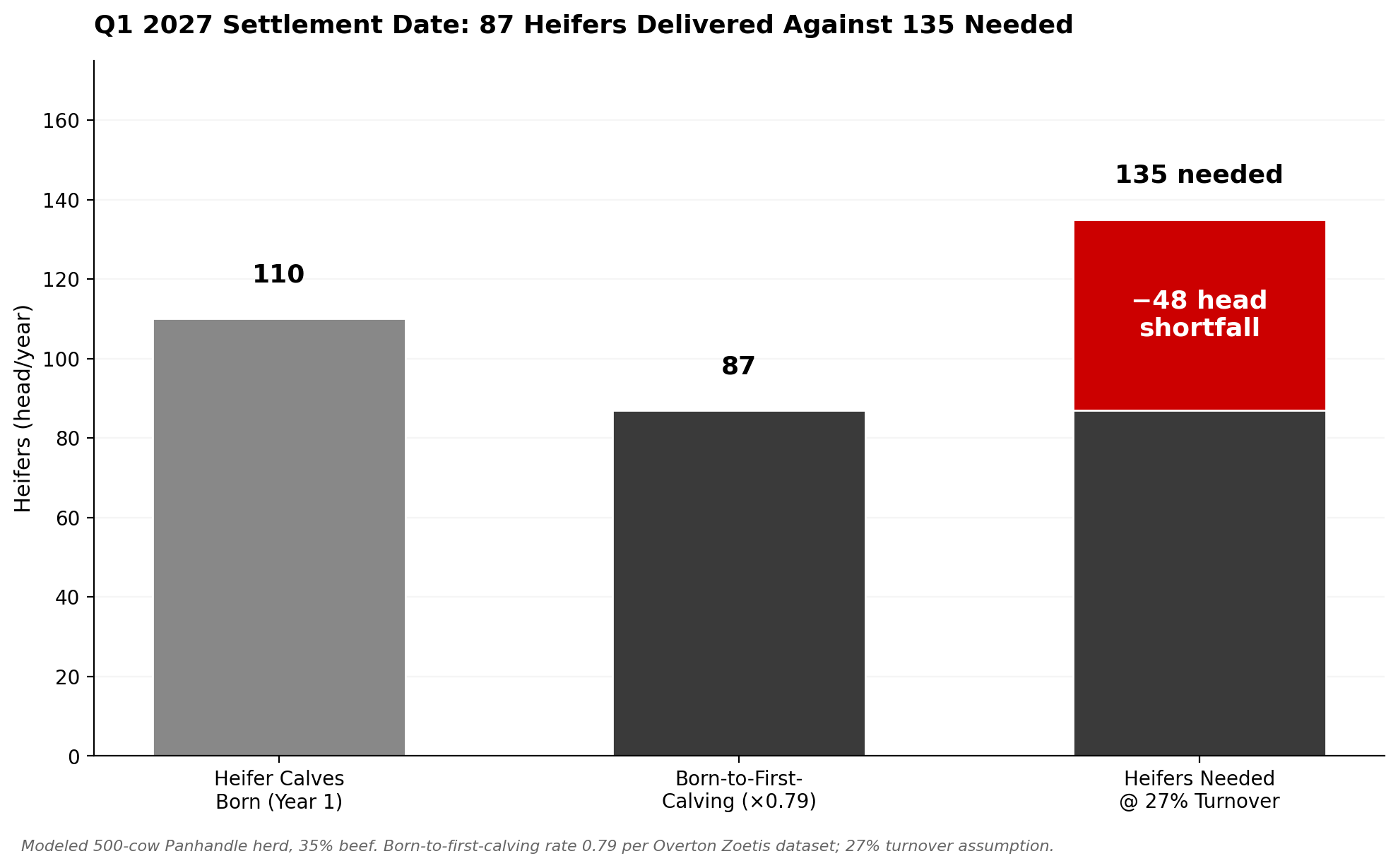

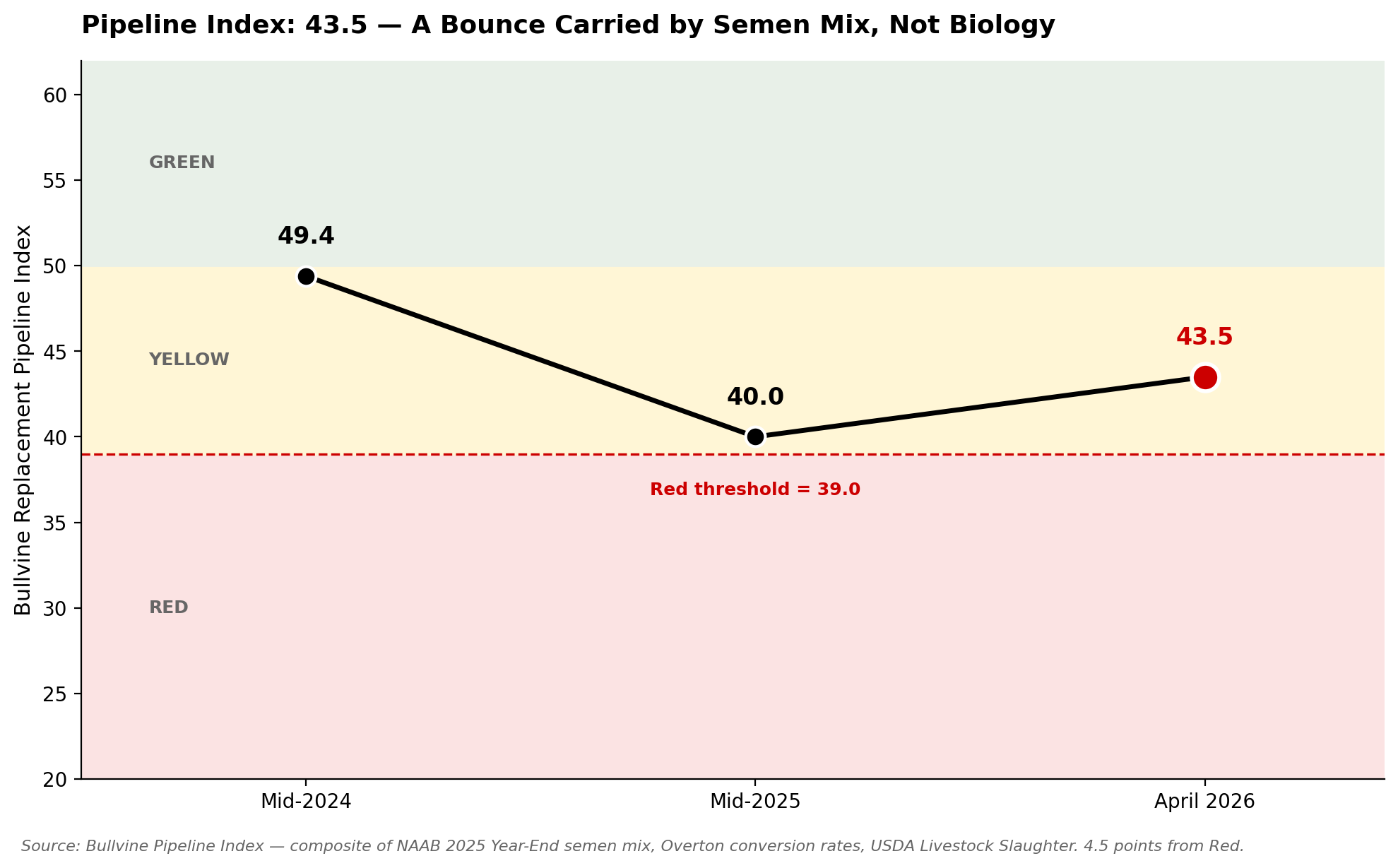

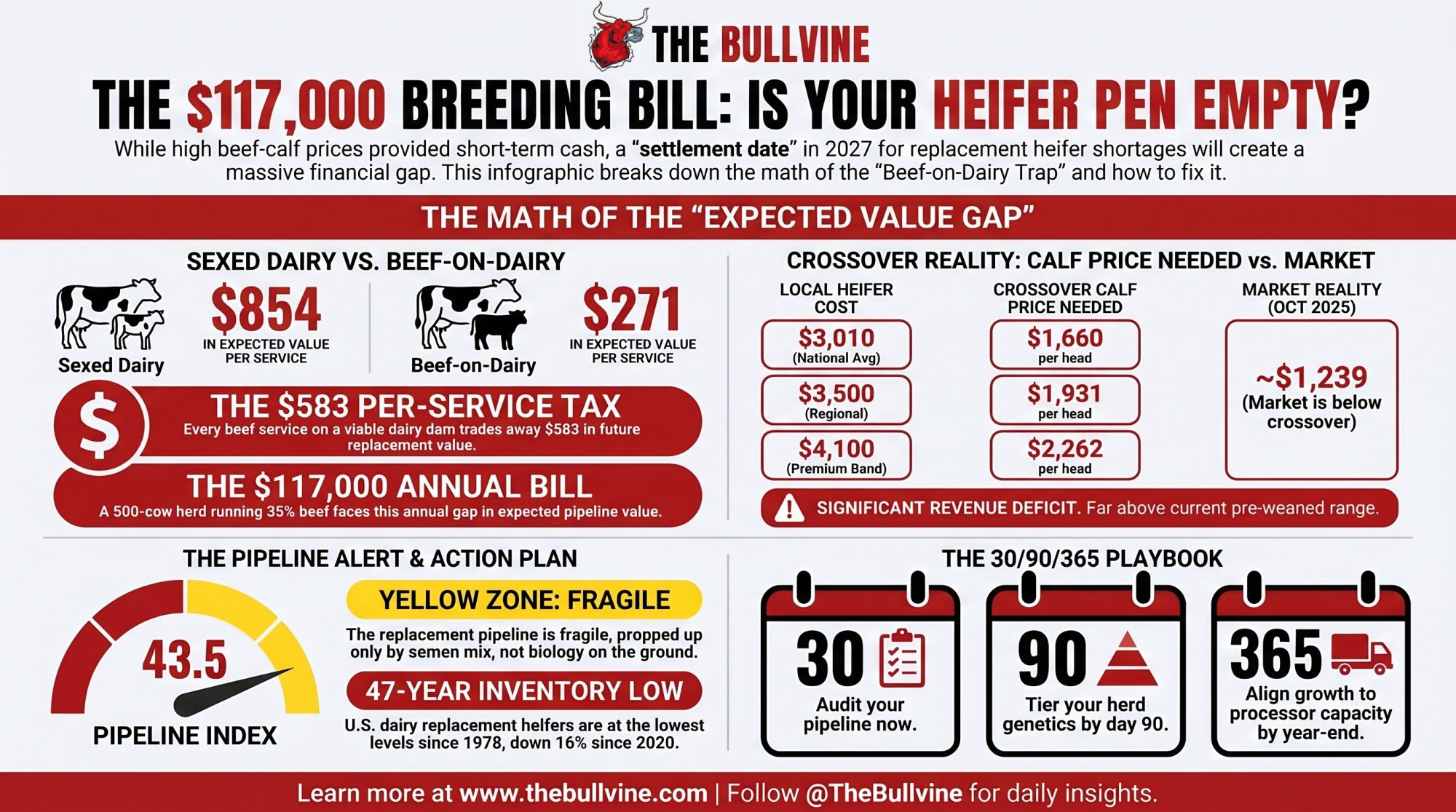

Executive Summary: A 500-cow Panhandle dairy that ran 35% beef-on-dairy through 2023 and 2024 is staring at a $117,000-a-year expected-value gap on its 2026 breeding sheet, with every beef service on a viable dairy dam now costing $583 against a $3,010 national replacement heifer (USDA NASS, July 2025) and a $500 crossbred calf. The Bullvine Replacement Pipeline Index just printed 43.5 — Yellow Zone, 4.5 points from Red — carried almost entirely by semen-mix momentum, not biology on the ground. The math is blunt: sexed dairy delivers $854 per service in expected value, beef-on-dairy delivers $271, and crossbred calves don’t pencil against sexed dairy until they clear $1,660/head at a $3,010 heifer. Settlement date is Q1 2027, when a 27%-turnover herd projects 87 heifers to first calving against 135 needed — 48 head short at spot prices that already ran ,110 in October 2025. The October 2025 correction (/cwt off CME December live cattle in twelve business days, calves from ~,400 to ,239) proved calf revenue and Class III aren’t independent streams — same operation, overlapping signals, correlated downside. Lenders are starting to model this; producer balance sheets generally haven’t caught up. If you ran 30%+ beef the last two cycles, the 30/90/365 playbook inside (plus the LRP Unborn Calves window and the $1,660/$1,931/$2,262 crossover prices) is the math before the heifer pen comes up short.

An archetypal 500-cow Panhandle dairy that ran 35% beef-on-dairy through 2023 and 2024 is looking at a 7,000-a-year expected-value gap on its 2026 beef-on-dairy breeding sheet — math anchored on a late-October 2025 crossbred calf trough near ,239/head reported across regional auction channels and USDA NASS’s July 2025 national replacement milk-cow price of ,010/head. Brad Kooima of KKV Trading has characterized beef-on-dairy, in effect, as a packer’s dream in recent industry commentary: known genetics, predictable gain, a schedulable 341-day pipeline from calf to kill. The Bullvine Replacement Pipeline Index just named the other side of that trade.

43.5 on the Index as of April 2026. Yellow Zone, 4.5 points from Red. Roughly 4.29 million dairy heifers projected by Bullvine’s model to enter the 2027 milking string from 2025 breedings, against a U.S. dairy cow herd near 9.35 millionhead per USDA’s January 1, 2025 Cattle Inventory, and more than billion in new processing steel rising across 19 states per industry build-out tracking.

This is a beef-on-dairy 2026 breeding story. It reads like a credit memo.

Why the Packer’s Dream Is Only Half the Trade

Kooima’s framing points at a real structural gain. Known genetics. Predictable gain. A 341-day pipeline is something native beef never offered the packer-feeder complex at this volume.

CoBank Knowledge Exchange analysis of USDA AMS slaughter-cattle auction data covering March 2024 through February 2025 pegged beef-on-dairy animals at $2,485 at slaughter, native beef at $2,385, and pure dairy at $2,210. Feeder-to-fat value retention ran 81.3% for beef-on-dairy on a $/cwt basis, 72.1% for pure dairy, 69.6% for native beef. Ohio State and Michigan State feedlot trials have documented lower cost of gain on beef-on-dairy steers versus Holsteins, with the spread varying by ration and finishing system.

That efficiency is real. It’s not a packer profit story either. Drovers’ Sterling Marketing Beef Cutout and Packer Margin Tracker has shown deeply negative packer margins through most of 2025 and into spring 2026. Tyson Foods has disclosed materially elevated cattle procurement costs across fiscal 2025 in public filings and announced the closure of its Lexington, Nebraska beef plant.

So where did the supply-chain value come from? NAAB’s 2025 Year-End Report, released March 2026, puts domestic beef-on-dairy semen at 8.1 million units, on top of 10.6 million sexed dairy and 6.0 million conventional. Every beef service on a cow that could carry a viable dairy pregnancy is a dairy heifer that won’t walk into a milking string in 2027.

What Does a $3,010 Replacement Heifer Mean for a 500-Cow Panhandle Herd in 2026?

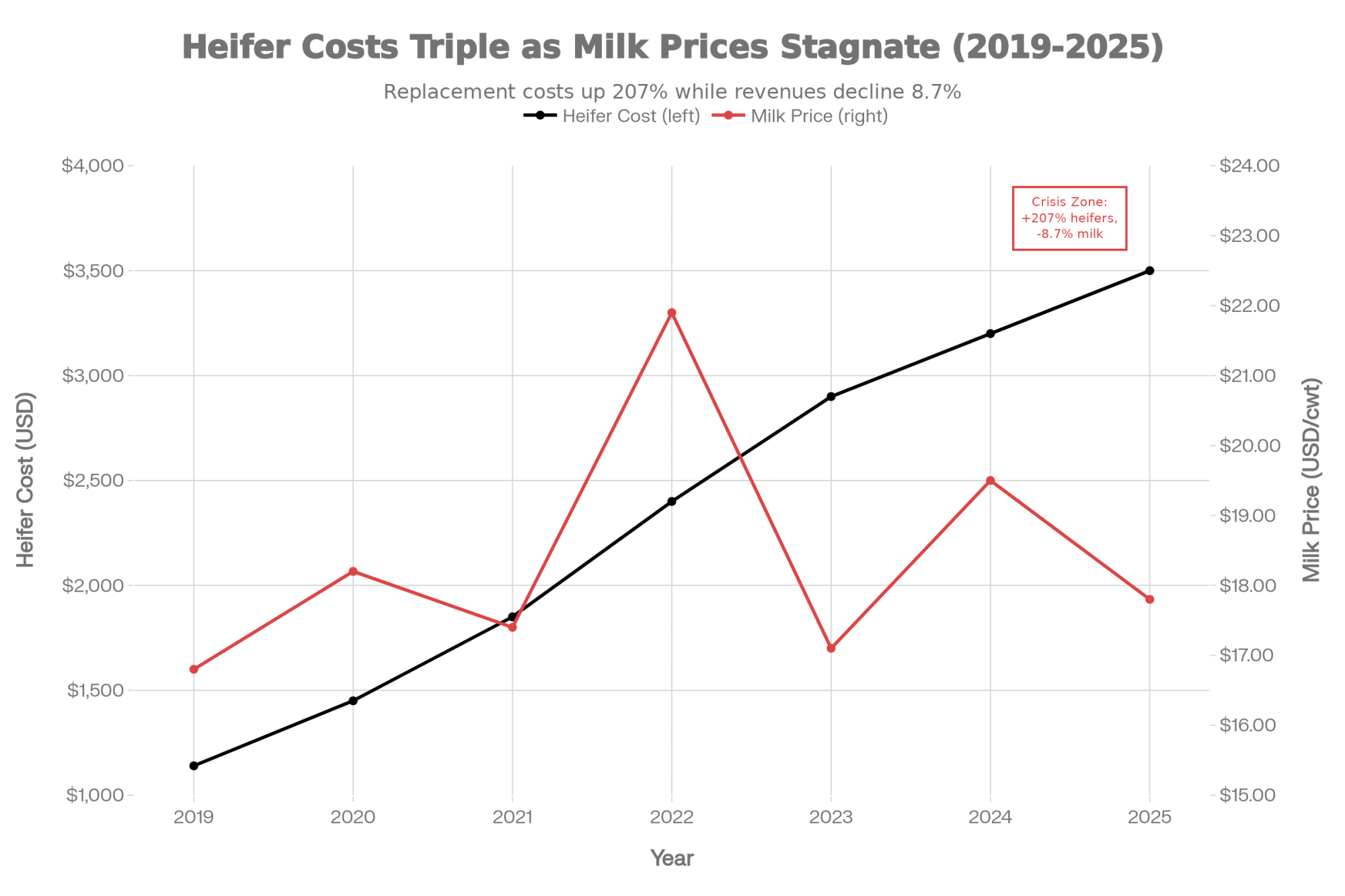

National numbers turn into a breeding sheet fast. An archetypal 500-cow Panhandle dairy shipping to one of the new plants outside Amarillo needs about 135 replacement heifers a year at a 27% turnover rate. At USDA NASS’s July 2025 Agricultural Prices national average of $3,010/head, that’s a $406,350 annual replacement line. In Texas and California premium bands where springers cleared $4,000–$4,500 in late 2025 per regional auction reporting, the number climbs toward $500,000. USDA NASS’s October 2025 reading was already $3,110 — up $100 in three months, up $510 year-over-year.

Run 35% beef on that herd and you’re putting roughly 200 beef services a year on cows that could carry a viable dairy pregnancy. Using Dr. Michael Overton’s Zoetis field dataset from 85 commercial Holstein herds — 42% sexed conception, 57% conventional, 90% and 50% heifer ratios, 95% pregnancy survival, 79% born-to-first-calving — every one of those 200 services trades away roughly $583 in expected replacement value at a $3,010 heifer and a $500 pre-weaned beef calf.

Running the Numbers — The Spread at a Glance

Based on $3,010 national heifer average vs. $500 crossbred calf. Sources: USDA NASS July 2025 Agricultural Prices; Overton Zoetis 85-herd dataset.

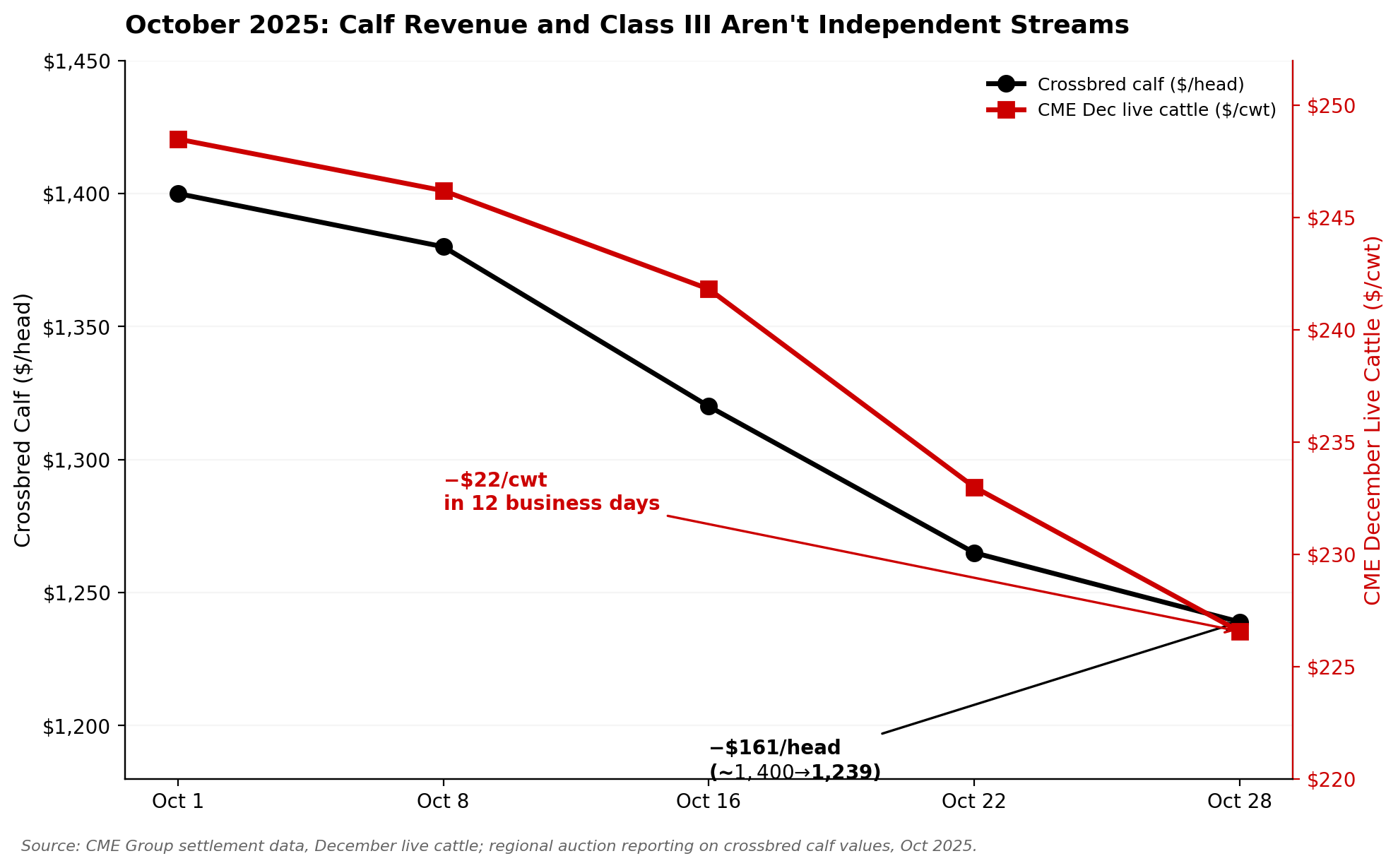

Units note: The October 2025 CME December live cattle move is $/cwt on fat cattle. The ~$1,400 → $1,239 per-head calf move is a different instrument. Both tracked the same signal down.

Heifer-calf baseline: At 35% beef on a 500-cow herd, about 65% of pregnancies are dairy. Against Overton’s conception and heifer-ratio rates, that produces roughly 110 heifer calves/yr. Multiply by 0.79 born-to-first-calving and the herd delivers ~87 heifers to first lactation against 135 needed. That’s the 48-head shortfall the 2027 pipeline has to cover at spot prices.

“$854 per sexed-dairy service. $271 per beef-on-dairy service at today’s $500 calf. The spread is 3x — and the settlement date is 2027.”

What Does the October Correction Actually Say About Calf Price Risk?

Most of the industry filed October 2025 as a blip. It wasn’t.

Per CME Group settlement data, December live cattle futures fell from the mid-$248 range in early October to $241.82on October 16 — a single-session $6.05/cwt drop — and bled to $226.57 by October 28. Roughly $22/cwt in twelve business days. Market analysts linked the move to public presidential commentary that week pressing ranchers on beef prices, and crossbred calf values fell with the futures from roughly $1,400 to near $1,239. Bullvine’s prior modeling on a 1,000-cow / 40%-beef archetype put the annualized revenue impact near $196,000.

The assumption most coverage leaned on: beef-on-dairy is diversification against milk-price weakness. The data says otherwise. USDA AMS Class III printed $14.59/cwt in January 2026 — the lowest since July 2023 — and recovered to $16.16 in March 2026. Thin milk margins, volatile calf revenue, same operation. Both streams moved on overlapping signals, not independent fundamentals.

That’s correlation, not diversification. A different risk structure than the one the 2023 breeding decision was made against.

Red threshold: 39.0 · Distance from Red: 4.5 points

What it is: Bullvine’s proprietary replacement-pipeline health score. It combines NAAB’s domestic semen-sales mix, Overton’s biological conversion rates, and USDA’s weekly Livestock Slaughter data into a single weighted reading (Heifer Supply 40%, Price Signal 25%, Culling Pressure 20%, Semen Mix Momentum 15%). Refreshes quarterly as USDA and NAAB data update.

Read: Fragile recovery. The bounce is carried almost entirely by semen-mix shift, not by biology on the ground. Settlement-date risk for 2027–2028 replacements remains elevated.

The Four Components

Heifer Supply — 55 (weight: 40%). Marginal. Replacement ratio runs near 27 per 100 cows. Why it matters:direct line from current inventory to 2027 milking cows.

Price Signal — 30 (weight: 25%). Red-Zone range, driven by the $3,010 national heifer price. Why it matters:price is the market’s vote on scarcity, and the vote is already in.

Culling Pressure — 25 (weight: 20%). Red-Zone range; retained-cow overhang is keeping today’s milk on. Why it matters: retained cows mask supply tightness now and widen the 2028 gap.

Semen Mix Momentum — 60 (weight: 15%). The one component propping the score up. Sexed dairy climbed to 64% of domestic dairy units used in 2025 per NAAB’s 2025 Year-End Report. Why it matters: the pipeline’s only tailwind — and it won’t produce a milking cow for 24 months.

USDA’s January 2025 Cattle Inventory counted just 3.91 million dairy replacement heifers on U.S. farms — the smallest reading in 47 years, down 16% from 4.61 million on January 1, 2020. Iowa State Extension’s NW Iowa Dairy Outlook (Lee Schulz) has tracked weekly dairy cow slaughter running behind year-earlier across most of the period since September 2023. Bullvine’s modeling pegs cumulative “extra cows kept” at 600,000–611,600 head versus normal culling pace — an extrapolation from the ISU weekly deficit, not a USDA number.

Those retained cows carry milk volume today. They won’t carry a new plant in 2028. The $11 billion in new processing capacity was sized against herd-growth assumptions from 2022–23 that no longer hold.

Why the Operator Who Got the Calf Market Right Got the Settlement Date Wrong

The Panhandle operator who made good money on beef calves through 2023 and 2024 didn’t miscalculate. They executed leg one of a two-leg trade well. What most haven’t done is look up leg two’s price.

That’s not on the operator. It’s on how the trade got sold. One leg at a time. The $900–$1,400 calf checks landed every month through that run. The pipeline cost was deferred, off balance sheet, and only crystallizes when the heifer pen comes up short in Q1 2027.

Some operators ran the full math and took the trade eyes-open. For others, the settlement-date cost didn’t get modeled because the monthly calf check felt like the whole picture. Both positions exist in the data. What’s changed is the spread at the service level: sexed dairy at $854 against beef-on-dairy at $271. More than three times. The crossover doesn’t arrive until beef-cross calves clear $1,660 at a $3,010 heifer. Most markets aren’t in the same zip code.

Will Babler of Atten Babler Risk Management has publicly argued that premium U.S. beef will increasingly be held by dairy producers because of the extra benefits these animals bring to market. He’s right about the premium. The question is whether your animals qualify — traced genetics, breed-society enrollment, direct feedyard relationship — or whether they’re anonymous crossbreds moving through the sale barn at $200–$500 and carrying all the pipeline risk for a fraction of the revenue.

Gregg Doud has framed the reclassification plainly in recent NMPF communications, telling dairy audiences they may be in the beef business more than the dairy business. Lenders have started modeling it that way. Producer balance sheets generally haven’t caught up.

Where Does This Leave Ontario and Supply-Managed Herds?

Different mechanism, same breeding-sheet question. Supply management protects the Canadian milk check in a way the U.S. spot market does not, which blunts the milk-price-weakness argument for riding beef-on-dairy hard. Quota carrying costs and genetic replacement economics still drive the service-by-service EV decision. Beef-cross calves from Ontario herds still move into a North American feedyard market that cleared near $1,239 at the October 2025 trough. The crossover math above holds; the variables that change are your local heifer cost and your calf-sale channel.

The 30/90/365-Day Playbook for Herds That Ran 35%+ Beef in 2023 and 2024

30-Day Actions — Before Your Next Breeding Round

Run your pipeline math. Pull 12 months of heifer-calf births. Multiply by 0.79 for completion to first calving. Compare to herd size × your replacement rate. A 500-cow operation needing 135 heifers/yr but projecting 110 heifer calves × 0.79 ≈ 87 to first calving is roughly 48 head short for 2027–2028. Threshold: any shortfall above 10% of annual demand is a planning problem, not a shopping problem. Where it backfires: if your actual born-to-first-calving rate runs below 79%, the shortfall is bigger than your spreadsheet shows.

Audit beef-on-dairy EV at your own calf price and local heifer cost. EV_beef = your calf price × 0.57 × 0.95. EV_dairy = your heifer cost × 0.42 × 0.95 × 0.90 × 0.79. If the dairy advantage lands near $583/service, decide how many beef services you keep on viable dairy dams. You gain near-term cash. You give up future replacement inventory.

Call your heifer suppliers this week. Ask how far they’re booked and whether they’ll lock numbers 12–18 months forward. If “I’ll just buy later” is the plan, find out whether the supply actually supports that.

💡 Pro Tip — The LRP Window Opens Before the Calf Is Born

Per Farm Credit East’s October 2025 guidance, the USDA RMA’s LRP Unborn Calves program (launched July 1, 2025) lets you floor the price on beef-on-dairy crossbred calves before they hit the ground. Farm Credit East’s worked example shows coverage up to roughly $1,200/head at a post-subsidy premium near $26.20/head, based on a 95-lb target weight and a 395% price adjustment factor. Parameters vary by endorsement length, coverage level, and sale date — confirm current rates with your crop insurance agent.

Most producers miss the window because they don’t realize the coverage is available at breeding-decision time, not at weaning. If you’re making the beef-service call this month, the LRP decision is the same conversation — not a separate one six months later.

Red-flag trigger: If beef revenue runs above 10–12% of gross income (thresholds vary by lender; confirm with yours) and you aren’t carrying LRP on unborn calves, this moves to the top of the 30-day list. LRP is a U.S. RMA program; Canadian producers should consult provincial risk-management options separately. Where it backfires: LRP floors price risk, not local basis risk.

90-Day Actions — Structural Adjustments

Tier your herd and write it into SOPs. Top genetics on sexed dairy. Middle tier mixed. True terminal cows only get beef. Requires: current genomic evaluation, AI technician cooperation, a small conception-rate give-back on sexed services. Where it backfires: aggressive sexed use on a herd running below 20% 21-day preg rate can widen, not close, your pipeline gap.

Forward-book 30–40 springers for Q1 2027 delivery. Heifer developers contacted by Bullvine report contracting 12–18 months forward at typical premiums of $100–$200/head over spot, with 10–20% deposits. Converts a forced peak-market purchase into a known commitment. Where it backfires: if heifer markets soften faster than calf markets, you’re carrying an above-market forward against tighter cash flow.

Cull on profit, not habit. Keep productive older cows if SCC and repro allow. Ship chronic mastitis, repeat breeders, and low-index animals. A retained cow buys you time. She doesn’t buy you margin.

365-Day Moves — Positioning for the Next Cycle

Align your herd plan to your plant. If you’re shipping to new processing steel, decide whether you’re growing, holding, or shrinking. Pipeline, beef percentage, and culling strategy need to match that call — and the processor’s volume expectation. Opportunity signal: if your genetics and repro numbers support program qualification and your local heifer basis is tracking the $3,010 national average rather than the $4,100 peak, 30–40% beef inside a direct-feedyard program can still pencil.

Set hard floors and ceilings. Floor: the minimum beef-calf price where beef services still pencil. Ceiling: the maximum percentage of breedings you’ll put to beef on viable dairy dams. $1,660 at a $3,010 heifer is your north star; $1,931 at $3,500; $2,262 at $4,100.

Recalculate quarterly, not annually. Sexed semen, beef semen, replacement heifers, and calf markets have all moved enough in 24 months that a 2024 analysis won’t hold up in a 2026 credit file. The Pipeline Index refreshes quarterly.

The Trade-Off, Stated Plainly

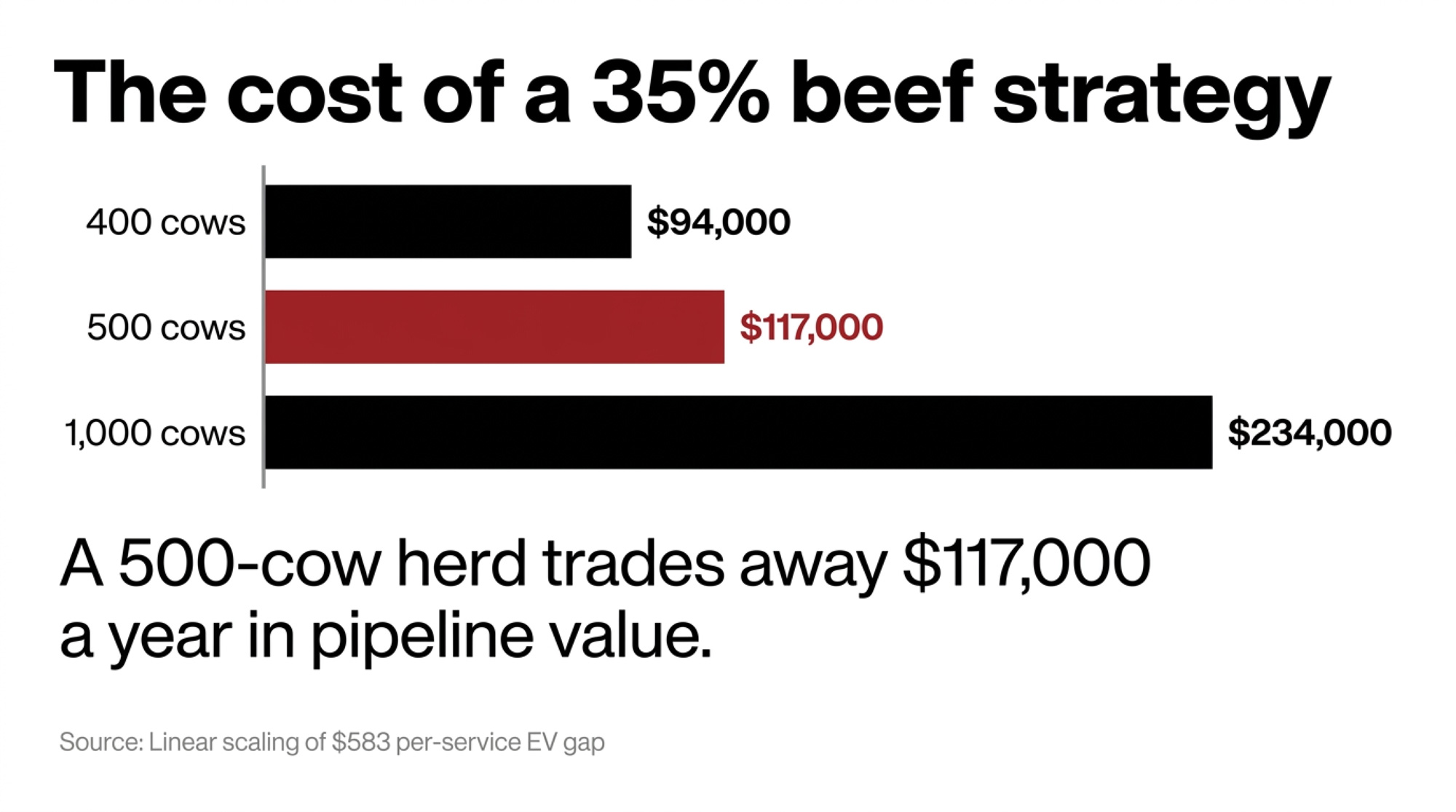

Every beef service on a viable dairy dam is a near-term calf check bought with a 24-month pipeline drawdown. At a $3,010 heifer and a $500 beef calf, that trade costs roughly $583 in expected replacement value per service. At 200 services on a modeled 500-cow Panhandle herd, it’s $117,000 a year. At 4.29 million projected pipeline entries against a 9.35 million U.S. dairy cow herd and billion in new plants, it’s a national structural question. Neither number moves itself. Both settle on a specific date — when the heifer pen is supposed to be full and isn’t.

The crossover prices are the line in the dirt: $1,660 at a $3,010 heifer, $1,931 at $3,500, $2,262 at $4,100. Everything below those prices is a pipeline drawdown with a monthly calf check attached.

The 500-cow Panhandle dairy referenced throughout is an illustrative archetype, not a specific operation. The Bullvine Pipeline Index just put beef calves and replacement heifers on the same invoice — 43.5, Yellow Zone, 4.5 points from Red.

The $117,000 bill is already in the mail. The only question is whether you have the heifers to pay it in 2027, or whether you’ll be writing that check to a neighbor who saw the Yellow Zone coming.

What does your last 12 months of heifer-calf births × 0.79 actually produce — and at what beef-calf price does your own breeding sheet stop building revenue and start building a 2027 liability?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Beef-on-Dairy’s $3,000 Trap: 800,000 Missing Heifers and Who Pays the Bill — Exposes the 800,000-head replacement hole already baked into the 2027 dairy calendar. Mastering this market intelligence allows you to navigate $4,100 price tags and secure elusive processor partnerships before the supply-chain window slams shut.

The Missing Piece in Genomic Selection: Why the Best Herds Still Walk the Pens — Dismantles the “spreadsheet-only” approach to breeding by layering physical structural checks over genomic proofs. Leveraging this hybrid method keeps cows producing into their fourth lactation, effectively slashing your annual heifer replacement draw by 15 percent.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

You’ve run the numbers three times, hoping they’d change. They won’t. For 300-1,000 cow dairies, the math has broken—but your options haven’t. Yet.

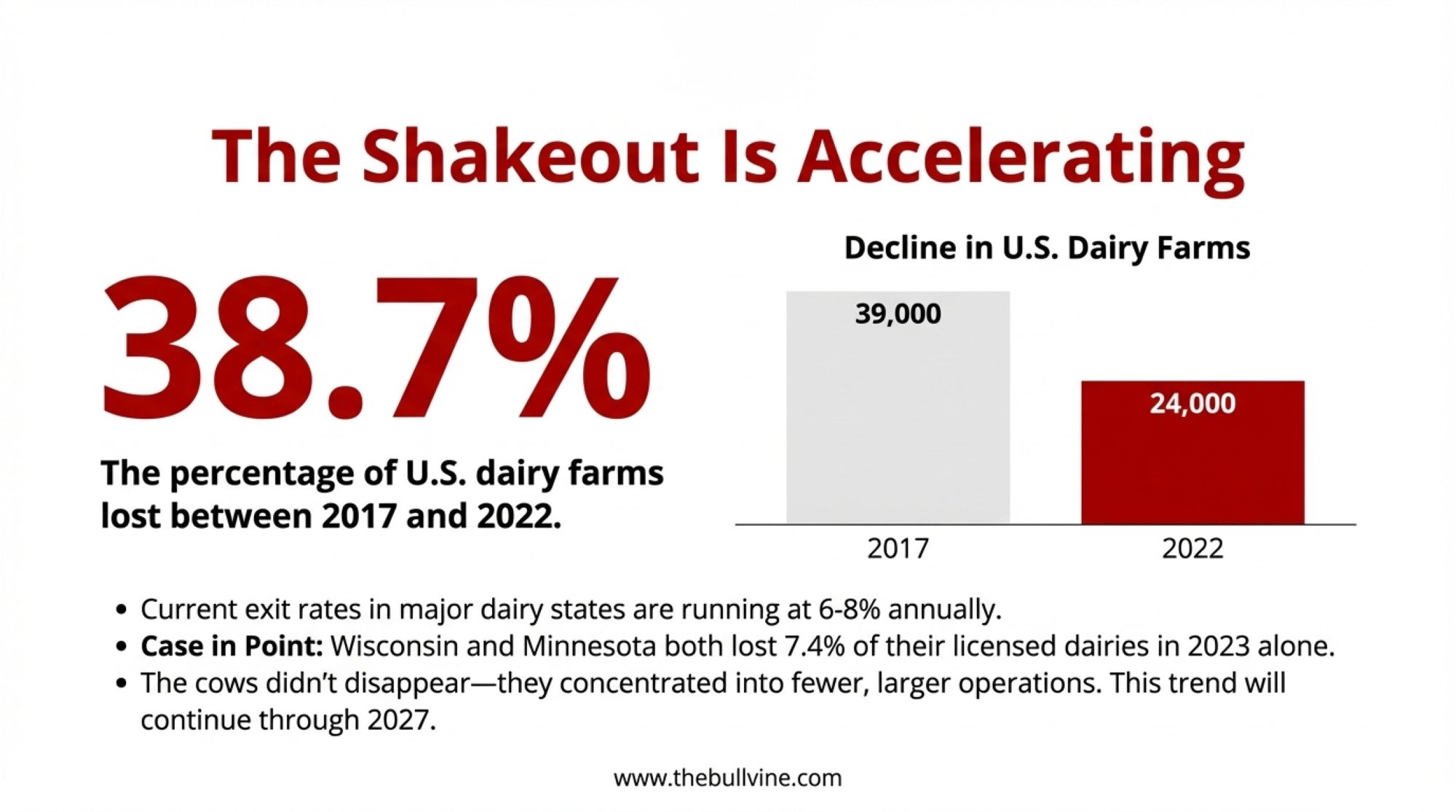

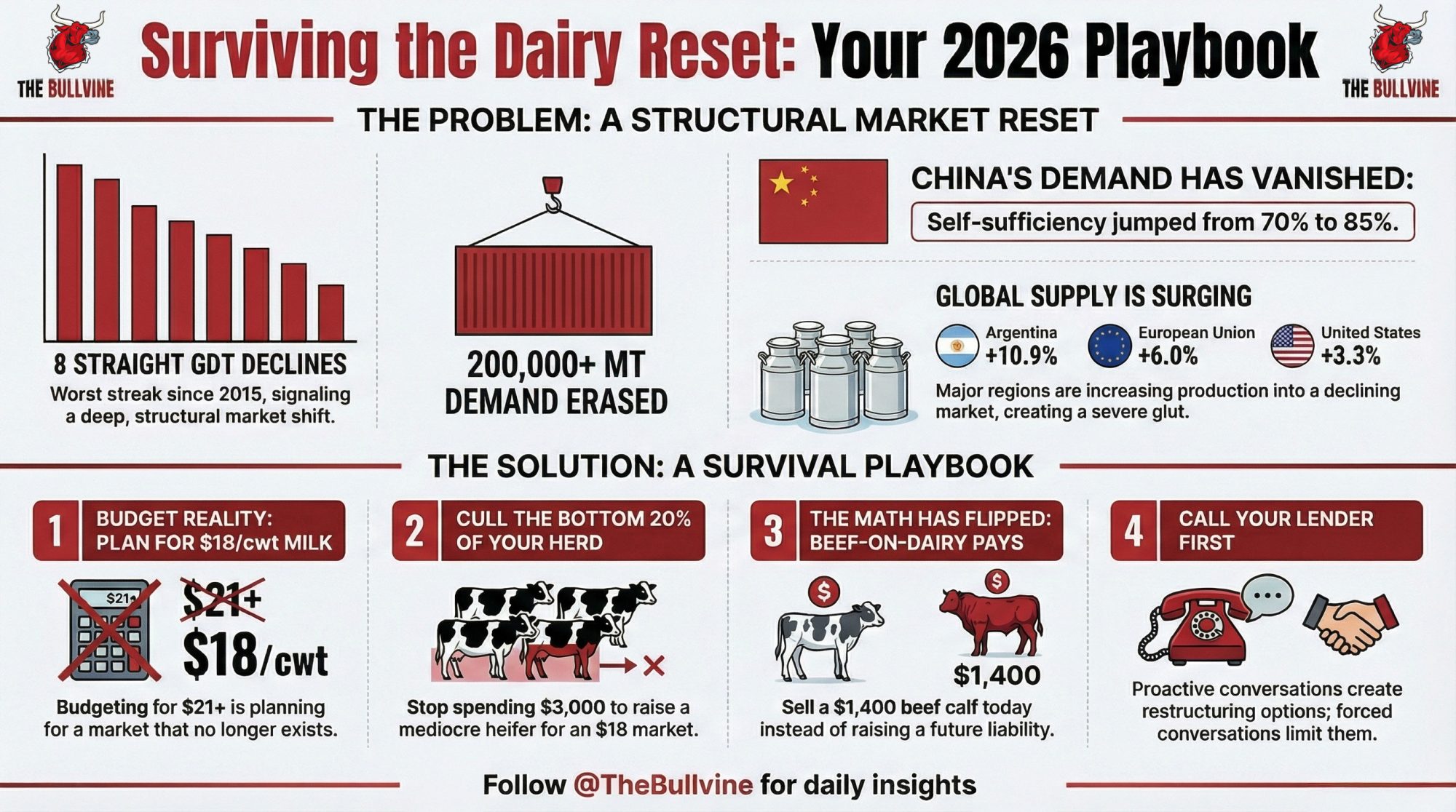

Executive Summary: The economics that sustained mid-size dairy farming are disappearing faster than most producers realize. Heifer prices have tripled since 2019, milk is down $2/cwt from 2024, and component pricing is shifting from butterfat to protein—meaning genetics selected two years ago are now optimized for a vanishing market. For 300-1,000 cow operations, this creates a structural squeeze: too large for specialty positioning, too small for automation to be economically viable. With USDA reporting the lowest heifer inventory since 1978 and Rabobank projecting 2,800 farm closures this year, the pressure is real and accelerating. The paths forward—organic transition, cooperative processing, strategic scaling, or well-timed exit—all require decisions within 12 months. Here’s the verified data, honest analysis, and practical framework you need to choose your path while options remain open.

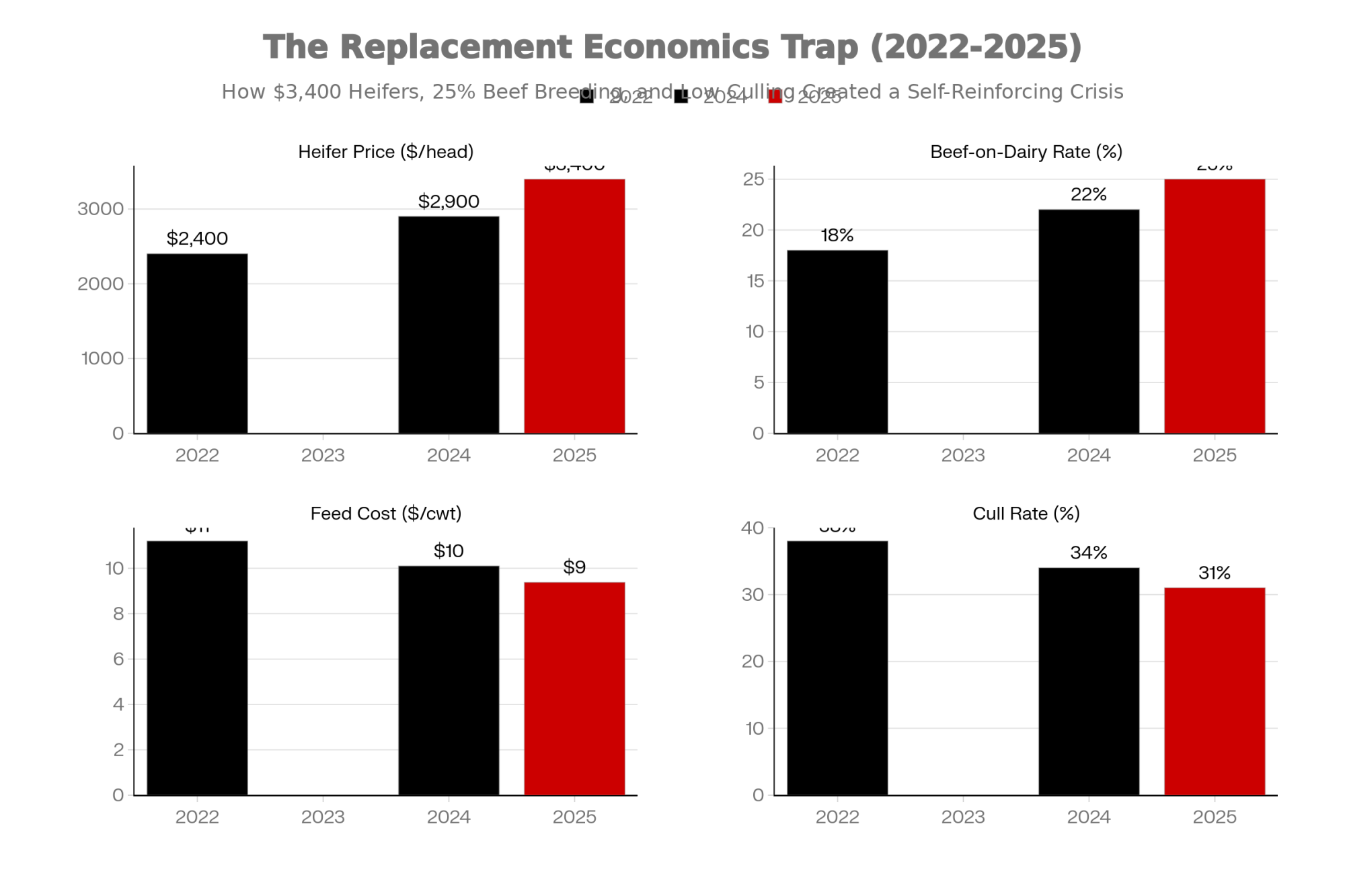

You know that feeling when you run the numbers three times, hoping they’ll come out different? I was sitting with a third-generation Wisconsin dairy farmer last month, and he did exactly that—pulled out his calculator, punched in the same figures again, shook his head.

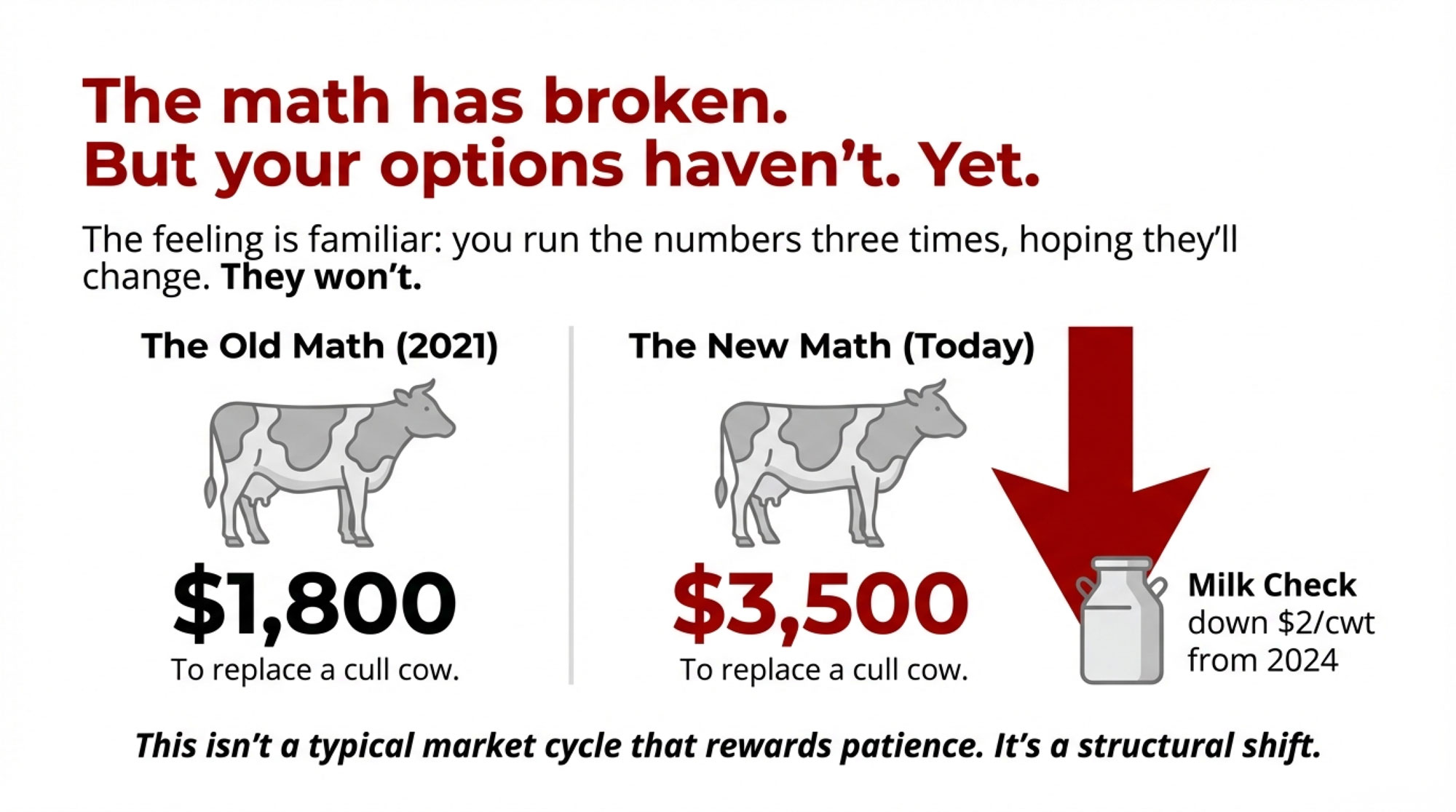

“Three years ago, I could replace a cull cow for eighteen hundred dollars and still make it work,” he told me. “Now I’m looking at thirty-five hundred, and my milk check is down almost two dollars from where it was. Something fundamental has shifted.”

He’s right. And here’s what I’ve been seeing across the industry this year: what’s happening right now isn’t a typical market cycle that rewards patience. Several structural forces are converging at once, creating conditions that favor operations at the extreme ends of the scale spectrum—the very large and the strategically small—while putting real pressure on the traditional middle that’s defined family dairy farming for generations.

I share that not to be pessimistic, but because I think you deserve honest information while meaningful options are still available. And frankly, there are options worth exploring.

What’s Actually Going On

Let me walk through what the data shows, because the way these factors connect matters as much as any single one.

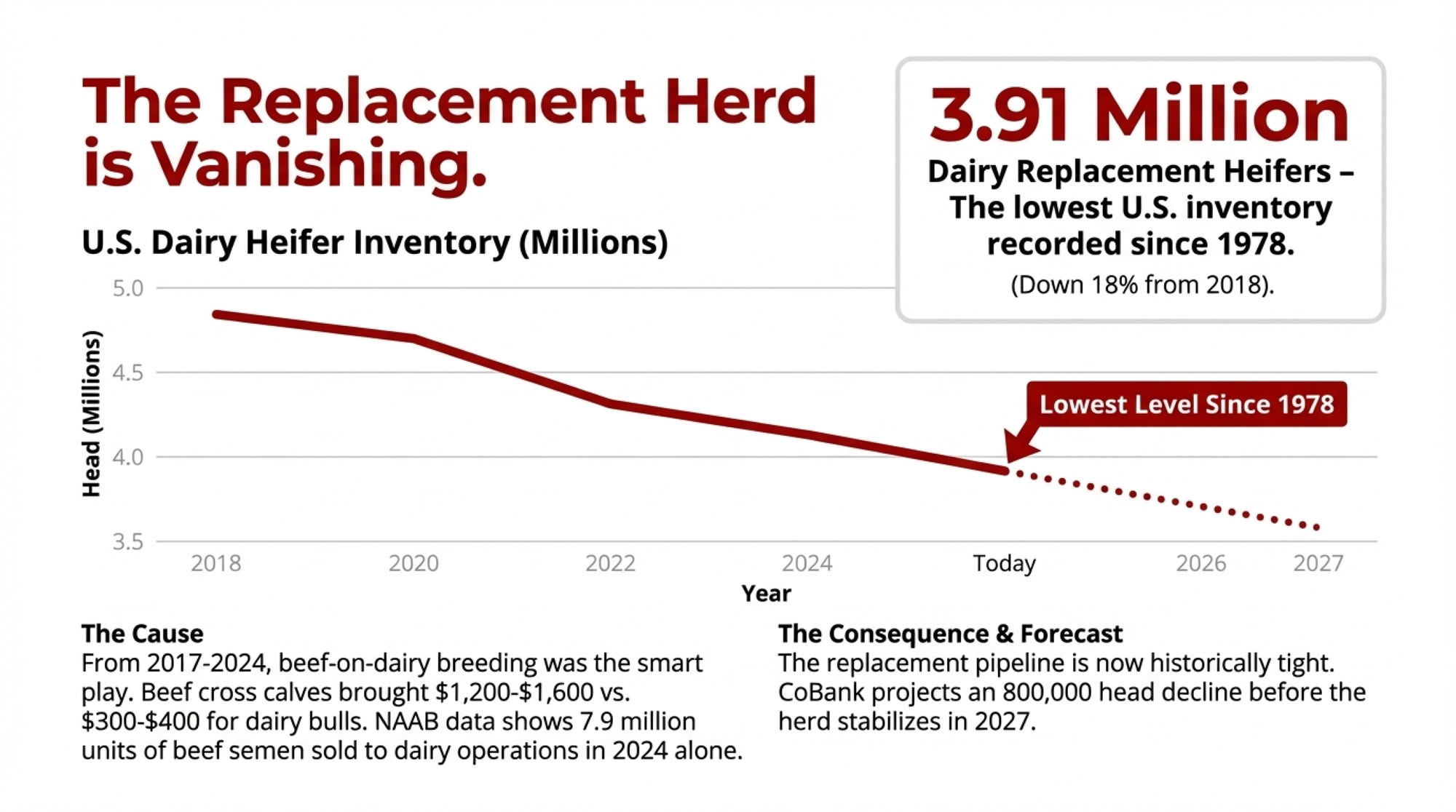

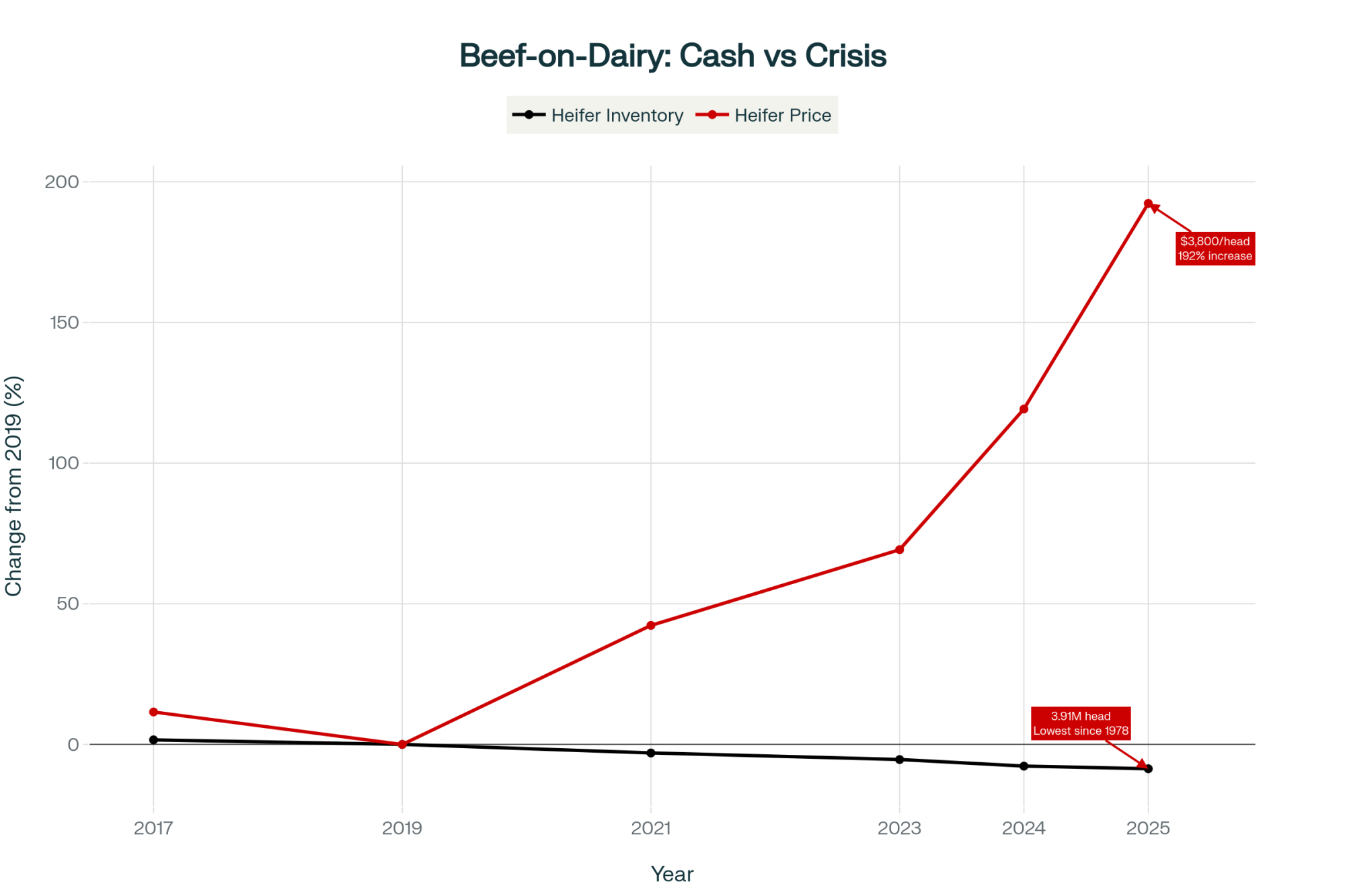

The heifer situation is tighter than most folks realize. USDA’s January 2025 cattle inventory came in at 3.91 million dairy replacement heifers—that’s the lowest level we’ve recorded since 1978. We’re down 18% from 2018 levels. CoBank’s August analysis suggests we’ll see another 800,000 head decline over the next couple of years before things stabilize, probably sometime in 2027.

Now, here’s what’s interesting about how we got here. Between 2017 and 2024, beef-on-dairy breeding took off because the math was genuinely compelling—you probably saw this in your own operation or talked with neighbors who did. Dairy bull calves were bringing $300-$400 at auction, while those beef crossbreds commanded $1,200-$1,600. For a 500-cow operation, that difference meant an extra $200,000 or more in annual calf revenue. Hard to argue with those economics at the time. The National Association of Animal Breeders reported 7.9 million units of beef semen sold to dairy operations in 2024 alone.

The consequence of those decisions—rational as they were—is now arriving. Heifer prices have climbed from roughly $1,140 back in 2019 to $3,000-$4,000 at current auctions. For operations trying to maintain herd size through normal culling cycles, the replacement math looks very different from what it was even two years ago.

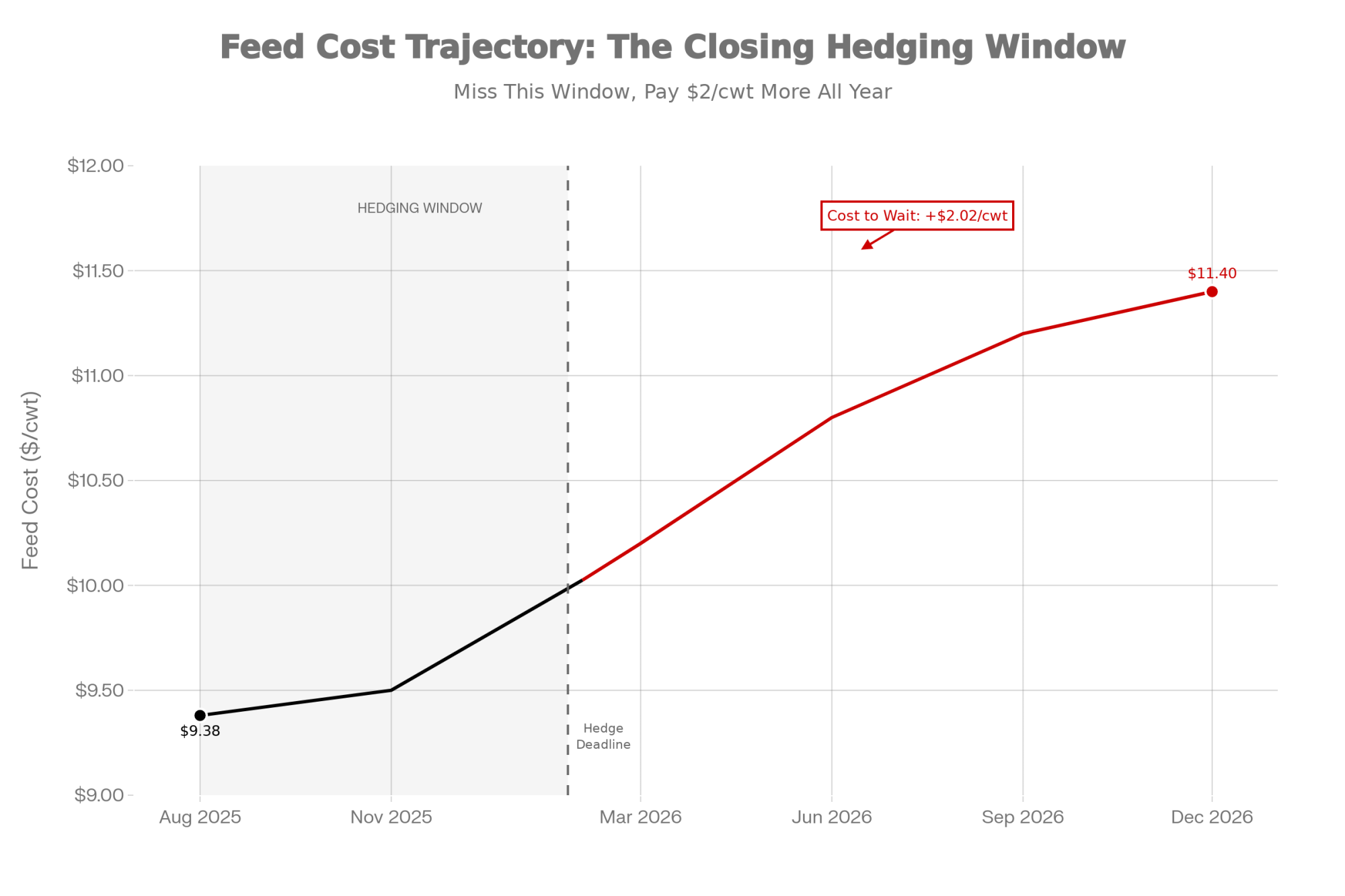

Milk pricing has found a new range. Class III has been trading in that $17-20/cwt corridor through 2025—some months dipping toward the lower end, others pushing higher, but the overall pattern sits $1.50-$2.50 below where we were in 2024. What I find myself thinking about isn’t the decline itself—we’ve all weathered price cycles. It’s the structural factors that suggest this might be more of a new baseline than a temporary dip.

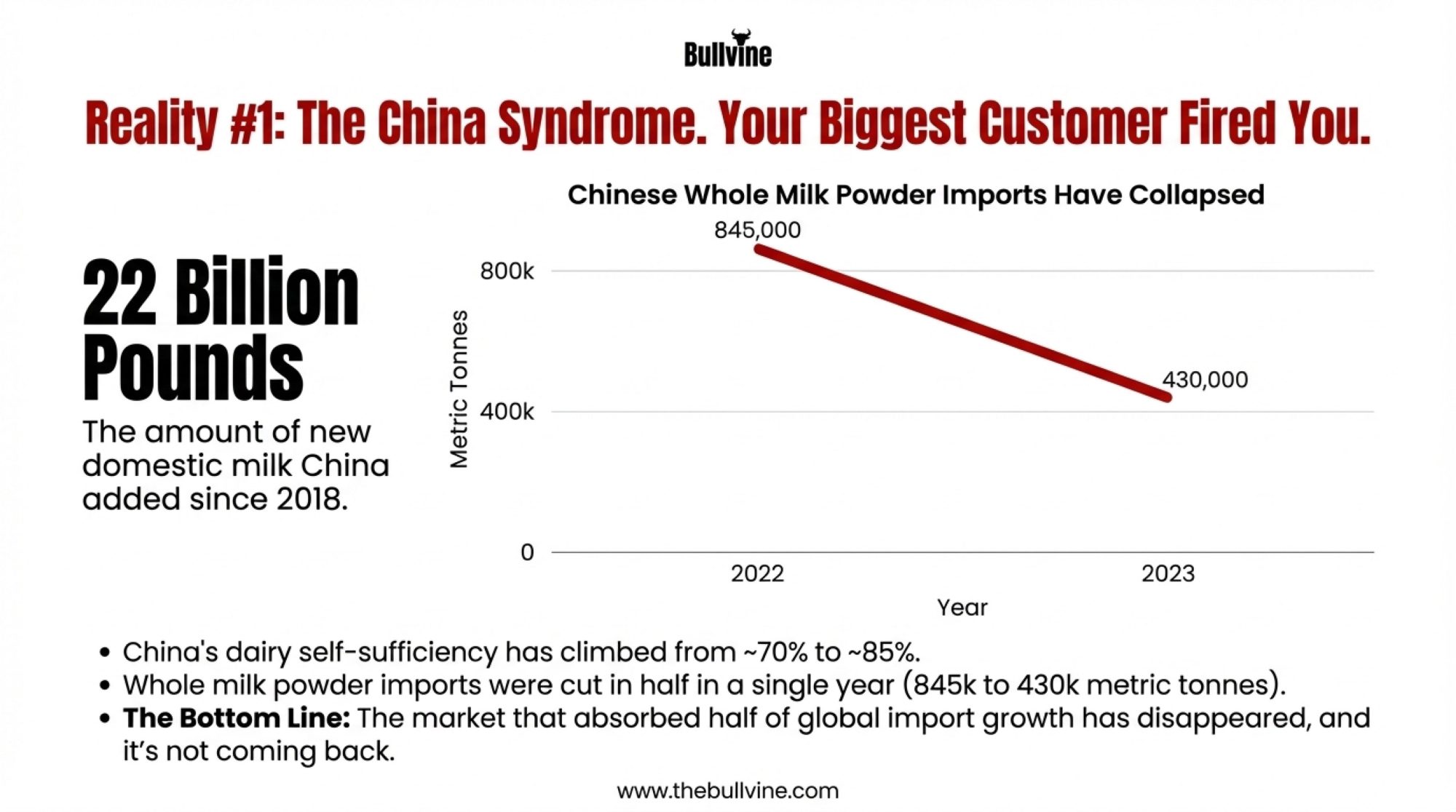

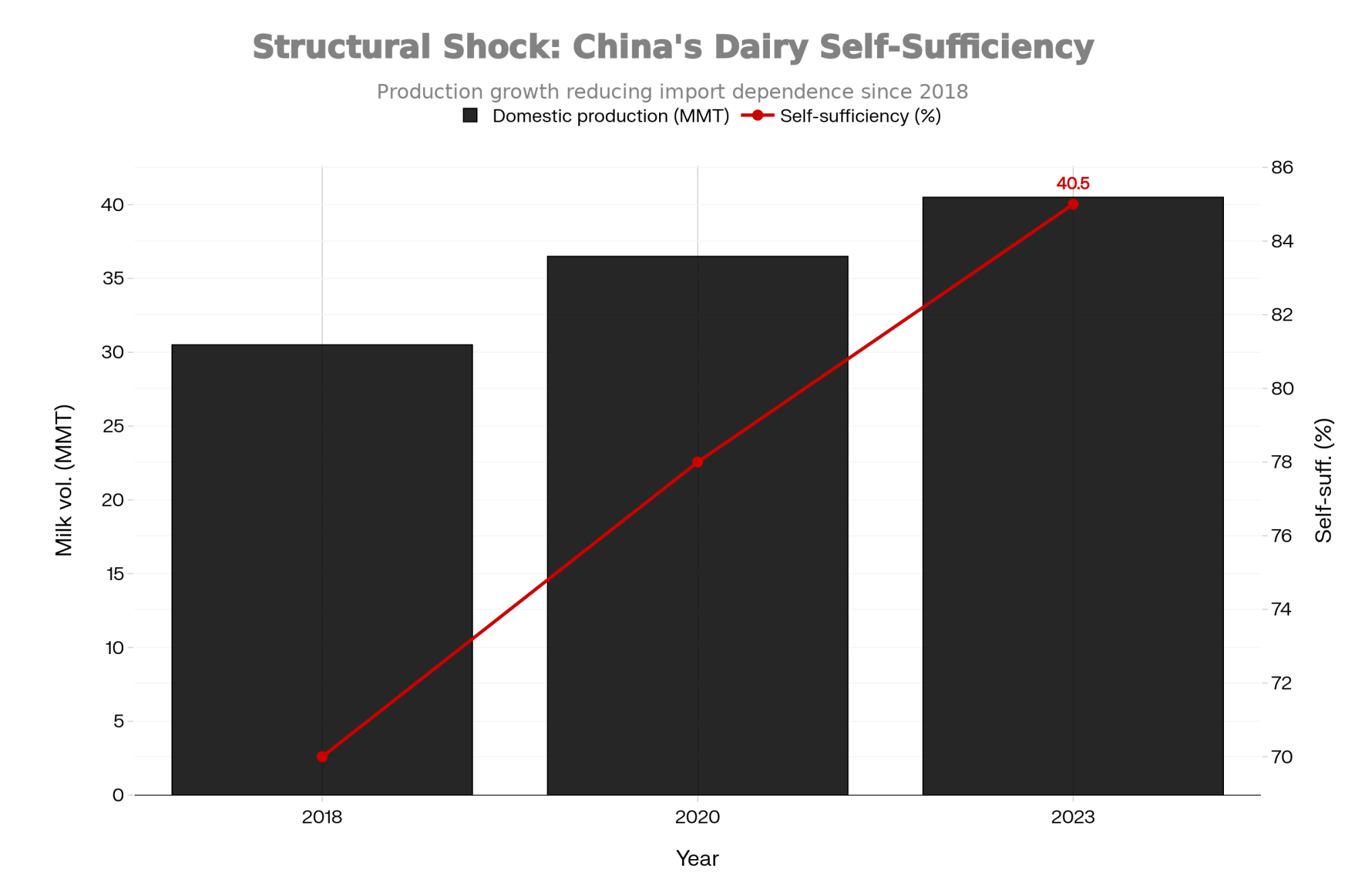

China’s domestic dairy production has expanded significantly, reaching roughly 85% self-sufficiency according to the USDA Foreign Agricultural Service tracking. That compresses what had been a growing export opportunity for U.S. producers. Meanwhile, domestic production continues to expand even as farm numbers decline—larger operations are adding capacity faster than smaller ones are exiting.

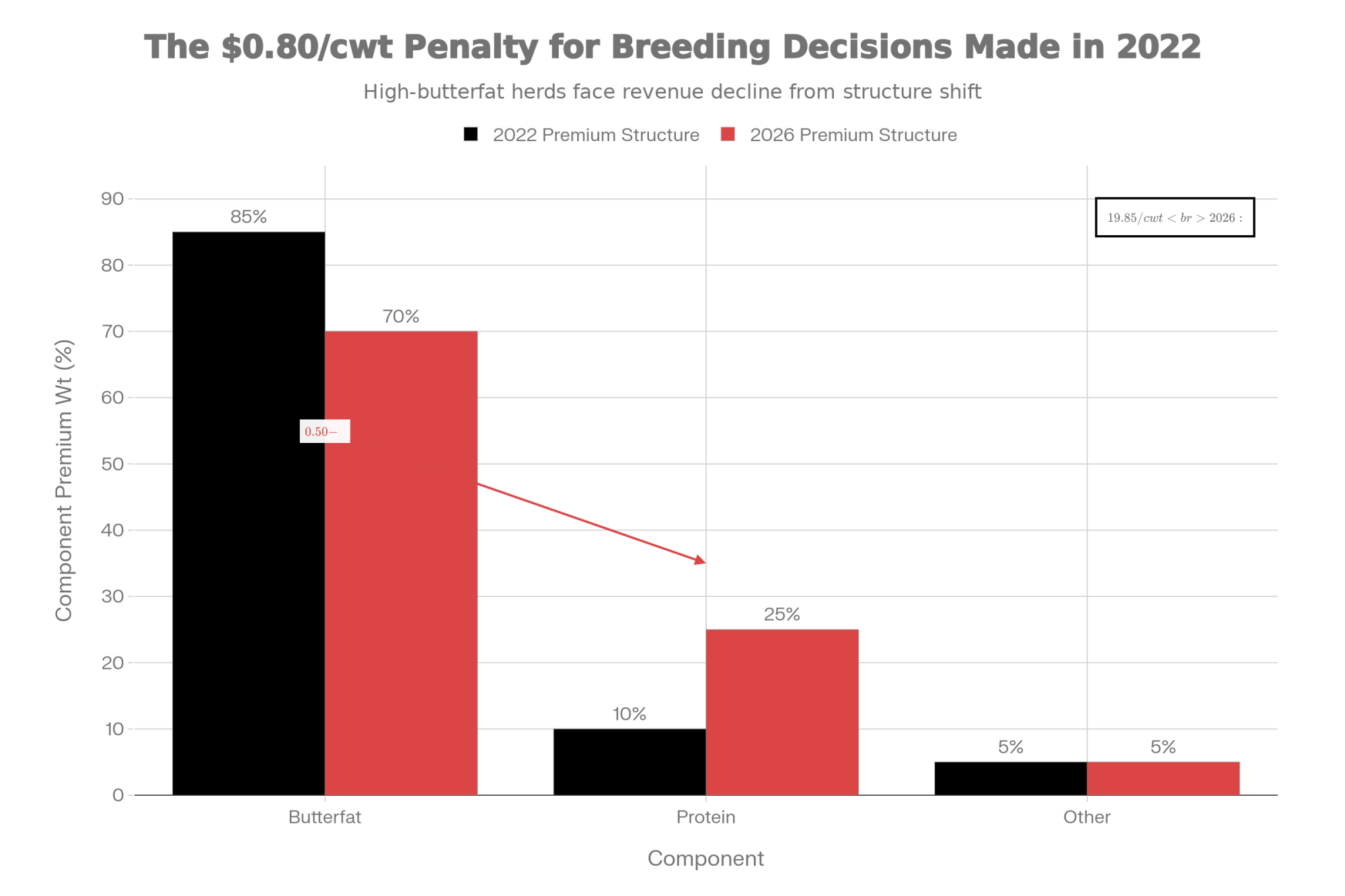

Component economics are shifting in ways that matter. This one’s been on my radar because it affects breeding decisions many of us made years ago. Western Canada’s milk marketing boards announced in October that, effective April 1, 2026, component pricing will move from roughly 85% butterfat emphasis to a 70/25/5 split that weights protein significantly higher than historical norms. You can find the details on the BC Milk Marketing Board’s website.

American processors are beginning to explore similar adjustments. Producers in Wisconsin and Minnesota have mentioned contract offers with $0.30-$0.50/cwt premiums tied to protein content above 3.4%—something that would have seemed unusual three years ago when butterfat commanded all the attention.

Why does this matter right now? Those genetic decisions we made in 2022-2023 are entering the milking herd. They were overwhelmingly butterfat-focused because that’s what the market rewarded at the time. If your tank average is still chasing butterfat because of the bulls you picked in 2022, you’re optimizing for a market that is rapidly evaporating. The premium is moving to protein.

The biological reality of a 24-36 month lag between breeding decisions and production outcomes means some operations may find themselves locked into yesterday’s pricing signals for another full cycle. It’s worth reviewing your current breeding program with this shift in mind—not panic, but awareness and action.

The GLP-1 Factor: A Genuine Shift in Consumer Behavior

Here’s something genuinely interesting from the demand side that I think deserves thoughtful attention.

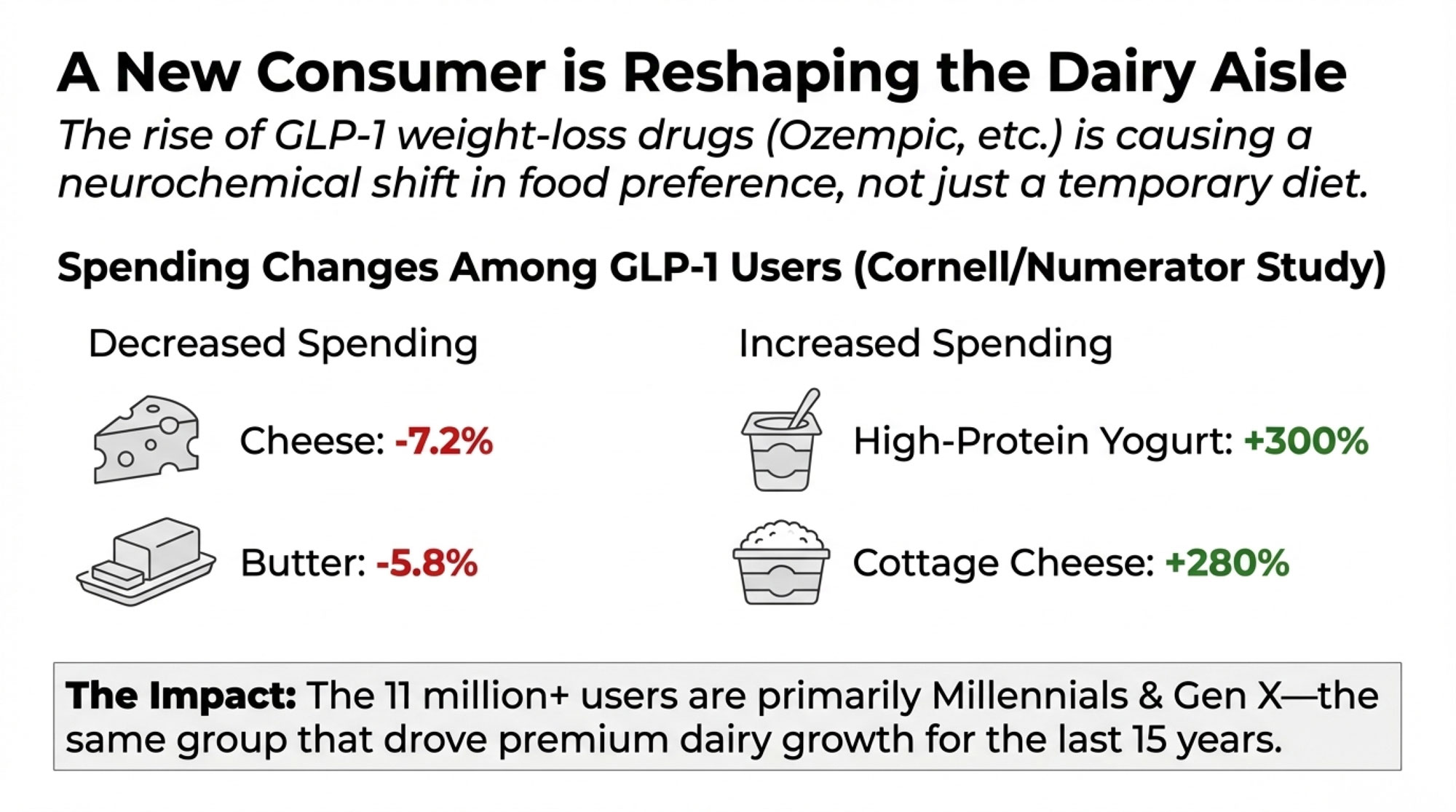

A collaborative research effort between Cornell University and Numerator, which tracks household purchasing data across more than 100,000 households, published findings analyzing how consumers using GLP-1 weight-loss medications are changing their eating habits. The patterns were notable:

Cheese spending down 7.2%

Butter down 5.8%

Ice cream down 5.5%

High-protein yogurt up nearly triple

Cottage cheese purchases up 280%

As of mid-2025, IQVIA data shows approximately 11 million Americans are actively using GLP-1 medications, with that number steadily increasing. Now, there’s been confusion about Medicare coverage—let me clarify what actually happened. The Trump administration declined to extend Medicare coverage for weight-loss-only indications back in April 2025. But commercial coverage continues expanding, costs are moderating, and most healthcare analysts expect the user base to keep growing through 2026.

What makes this different from typical diet trends is the underlying mechanism. These medications don’t just suppress appetite temporarily—they appear to shift food preferences by affecting dopamine pathways.

“Users report that high-fat foods simply become less appealing. That’s a different kind of demand pattern.”

We’re not talking about willpower or temporary restriction. We’re talking about neurochemical changes that persist as long as patients remain on medication—and many of these drugs are prescribed long-term.

The demographic profile matters too. According to the Numerator data, 71% of GLP-1 users taking these drugs for weight loss are Millennials or Gen X—the same consumer groups that drove premium dairy category growth over the past fifteen years.

What’s encouraging is the flip side of this data: protein-focused dairy is growing dramatically. Operations positioned to serve that demand—high-protein yogurt, cottage cheese, protein-enhanced products—are seeing real opportunity. The question becomes whether your operation can participate in that shift.

Labor Economics: A Threshold Worth Understanding

Farms have always dealt with labor challenges—that’s nothing new. But the current cost structure warrants careful examination.

The H-2A program restructuring established tiered wage requirements. In Michigan—a reasonable proxy for Midwest dairy regions—the Adverse Effect Wage Rate for experienced agricultural workers is $18.15/hour, according to Department of Labor data. But that base wage significantly understates actual costs.

Once you factor in employer-provided housing (required under H-2A), transportation, insurance, payroll taxes, and turnover replacement costs… many operations I’ve talked with are seeing all-in costs of $19-$21/hour. A 600-cow dairy requiring 2.5 full-time-equivalent milking positions now faces annual labor costs exceeding $140,000 just for parlor staffing.

What’s interesting is how this interacts with scale. Larger operations spread specialized positions across more cows, reducing per-unit labor cost. They can also more readily justify automation investments—which brings me to a topic that deserves nuanced discussion.

The Automation Question at Different Scales

The numbers here tell a more complicated story than equipment marketing materials often suggest.

For a 100-130 cow operation, a two-robot system (Lely, DeLaval, or comparable) plus barn modifications, feed integration, and installation runs somewhere in the $430,000-$740,000 range based on late 2025 dealer quotes. That’s getting fully operational with adequate support infrastructure.

For a 600-cow dairy, you’re looking at 8-10 robots minimum—now we’re talking $1.5-$2.5 million in total investment. The per-cow economics shift dramatically depending on how that fixed cost gets distributed.

Industry research and extension analyses suggest payback periods vary significantly with herd size. Smaller operations often face 15-20+ year payback at current financing rates, while larger operations with 2,000+ cows may achieve returns in under 10 years. These aren’t hard rules—individual circumstances matter enormously—but the pattern is worth understanding.

And there’s the financing dimension. A dairy lender I spoke with (he asked to remain anonymous, given client relationships) put it directly: “We’re looking at debt service coverage ratios very carefully. A producer comes in wanting financing for robotics, but their margins have compressed significantly over the past two years. That’s a challenging loan to structure, even when the long-term investment thesis makes sense.”

This isn’t to say automation is wrong for mid-size operations—some are making it work beautifully. But the economics require an honest assessment of your specific situation.

What Processors Are Building Toward

The processing side of this equation often gets discussed abstractly. Let me make it more concrete.

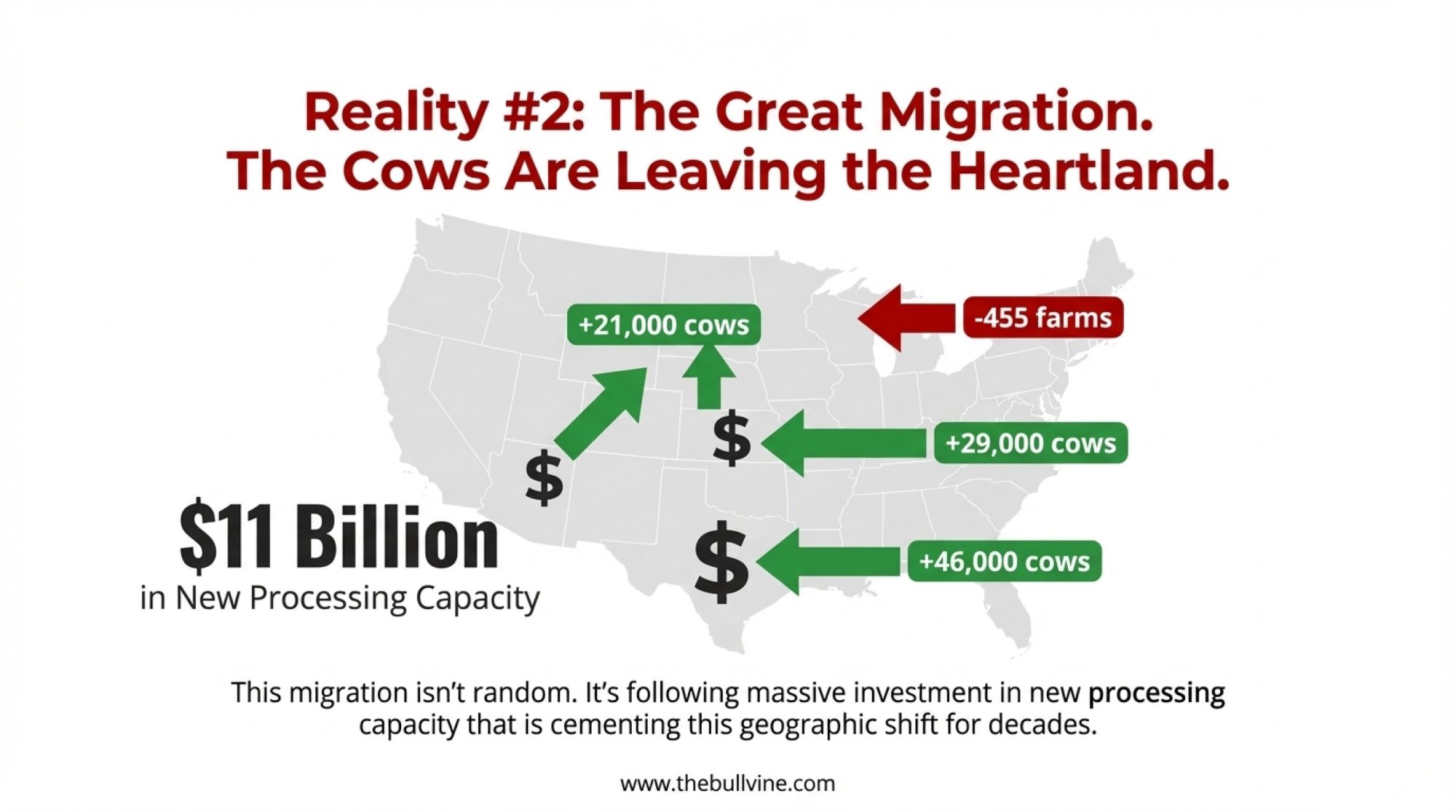

The International Dairy Foods Association released October data showing that between 2024 and 2027, U.S. dairy processing capacity expansion totals more than $11 billion in announced investments across 19 states. New cheese plants, expanded fluid milk processing, protein isolation facilities—substantial infrastructure.

What’s particularly noteworthy isn’t the investment volume alone. It’s the supply relationship structure underlying it. Major facility expansions—Hilmar in Kansas, Valley Queen in South Dakota, Glanbia and Leprino projects—are largely being built around long-term supply agreements with operations milking 2,000 cows or more.

A dairy cooperative field representative in the Upper Midwest explained the underlying economics: “A 600-cow operation represents maybe 60,000 pounds of milk daily. For a plant processing 8 million pounds, that’s less than 1% of the supply. The transaction costs of managing that relationship—quality monitoring, logistics, payment processing—are roughly the same whether it’s 60,000 pounds or 600,000 pounds.”

He was careful to add that cooperatives remain committed to their member base. “But producers need to understand the economics their buyers are navigating. The pressure toward consolidation has structural roots.”

So What Does “Viable” Actually Mean Right Now?

This is where I want to be careful to distinguish between what the data clearly show and what represents my analytical interpretation.

Operation Size

Per-Cow Labor Cost

Automation ROI Payback

Processor Leverage

Premium Access

2025 Viability Status

<100 cows

$520/cow/year

20+ years (not viable)

Minimal

Direct-to-consumer, organic

Viable if specialty

100-300 cows

$465/cow/year

15-20 years

Low

Organic, grassfed possible

Transition required

300-600 cows

$410/cow/year

12-18 years

Moderate

Limited at current scale

⚠️ High pressure zone

600-1,000 cows

$385/cow/year

10-15 years

Moderate

Scale too large for specialty

⚠️ Severe structural squeeze

1,000-2,500 cows

$315/cow/year

8-12 years

Strong

Component optimization focus

Structurally advantaged

2,500+ cows

$245/cow/year

6-10 years

Preferred supplier

Contract leverage

Dominant position

The data shows that operations above 1,000 cows have structural advantages in the current environment—lower per-unit fixed costs, automation ROI that pencils out more readily, processor leverage, and stronger capital access. The data also shows that specialty operations under 300 cows can achieve premium pricing that fundamentally changes the economics—several dollars per hundredweight above conventional for organic, significantly more for direct-to-consumer channels.

What I can’t tell you with precision is exactly how many operations will exit or consolidate, or over what timeline. When I suggest that traditional 400-1,000 cow conventional commodity operations face structural rather than cyclical challenges, that’s my analytical conclusion from watching these forces converge—not an official forecast from USDA or university research.

The trajectory raises legitimate questions. Rabobank’s analysis projects that approximately 2,800 dairy operations will close in 2025. If structural factors continue operating as they have—and I don’t see any obvious near-term reversal mechanisms—exit rates could remain elevated.

Dairy Category

GLP-1 User Consumption Change

Current U.S. GLP-1 Users

Projected Annual Market Impact

Strategic Implication

Cheese

-7.2% ⚠️

11 million

-$840M category pressure

Declining demand for commodity cheese milk

Butter

-5.8% ⚠️

11 million

-$320M category pressure

Butterfat premium erosion accelerating

Ice Cream

-5.5% ⚠️

11 million

-$675M category pressure

High-fat dessert categories vulnerable

Fluid Milk (whole)

-3.1% ⚠️

11 million

-$180M category pressure

Commodity fluid milk continues secular decline

Greek Yogurt

+185% ✓

11 million

+$920M category opportunity

Protein-focused growth accelerating

Cottage Cheese

+280% ✓

11 million

+$450M category opportunity

Dramatic protein-demand spike

High-Protein Beverages

+195% ✓

11 million

+$615M category opportunity

Emerging premium protein channel

Skyr / Icelandic Yogurt

+220% ✓

11 million

+$285M category opportunity

Ultra-high protein positioning working

The dynamics play out somewhat differently across regions. California operations face additional water cost and regulatory pressures that compound the structural challenges we’ve discussed. Idaho’s rapid consolidation has created different competitive patterns, with fewer mid-size operations surviving the squeeze. Texas and New Mexico dairies navigate the economic impacts of heat stress, which affect both production and labor. But the underlying forces—hierarchal costs, component shifts, processor consolidation, labor thresholds—are similar across geographies.

Here’s what’s equally important to acknowledge: different producers in different circumstances will navigate this very differently. I’ve talked with 800-cow conventional operations in Wisconsin, genuinely optimistic about their positioning—strong processor relationships, manageable debt, recent automation investment. I’ve talked with 500-cow operations in the same region that see no viable path forward without fundamental restructuring. Context matters enormously.

Paths That Are Working

Let me share what I’m observing in operations as they find viable paths forward, because genuine success stories exist alongside the challenges.

The organic transition continues to offer meaningful premium for operations willing to commit to production system changes. Operating margins for organic dairy typically exceed conventional operations substantially—though specific returns vary considerably by region, market relationships, and transition management. Several producers who converted from larger conventional operations emphasized that they had to reduce herd size significantly to make organic economics work long-term.

One Vermont organic producer—she runs about 200 cows and has been active in regional organic dairy advocacy—described her experience: “We ran 450 conventional cows for fifteen years. When we converted in 2019, we dropped to 200 and actually increased net income. The gross revenue decline was scary initially, but the margin improvement proved real.”

The transition period requires careful planning and an adequate financial runway. It’s not a quick fix, but it’s working for operations that approach it strategically.

Cooperative processing models are emerging in several regions and merit attention. The concept: multiple mid-size operations collectively invest in processing capacity—typically Greek yogurt, high-protein products, or specialty cheese—to capture value-added margins on a portion of their milk.

One Minnesota cooperative involving four farms with a combined 1,800 cows reports routing 25% of collective production through a small processing facility they financed together. That portion generates roughly twice the commodity price. The remaining 75% continues through traditional channels.

“We didn’t have the scale individually to make processing investment work,” one participating farmer explained. “Together we did.”

This model won’t fit every situation, but it represents creative thinking worth exploring.

Strategic positioning toward protein-focused products is another path to gaining traction. Some operations are pivoting toward products that align with GLP-1-influenced consumption patterns—high-protein yogurt, cottage cheese, protein-enhanced beverages. Rather than resisting the demand shift, they’re moving with it.

→ Confidential consultation with ag financial advisor and equipment appraiser

A Necessary Conversation About Timing

I want to address something directly that industry coverage sometimes avoids.

For some operations facing the structural challenges discussed here—compressed margins, elevated replacement costs, processor relationship pressure, automation economics that don’t pencil out, no clear specialty pivot—strategic exit while asset values remain elevated may represent the soundest financial decision available.

Choosing to exit under these circumstances isn’t failure. It’s asset management.

It’s recognition that structural economics have shifted in ways that particular operational configurations can’t accommodate. The industry changing isn’t any individual producer’s fault.

Current asset values remain relatively favorable. USDA market data shows slaughter cattle prices elevated, with bred dairy heifers commanding $2,800-$3,200 at many auctions. Used equipment markets haven’t yet flooded with liquidation inventory. Agricultural real estate values in productive regions remain firm.

These conditions won’t persist indefinitely if exit rates accelerate as structural pressures suggest they might.

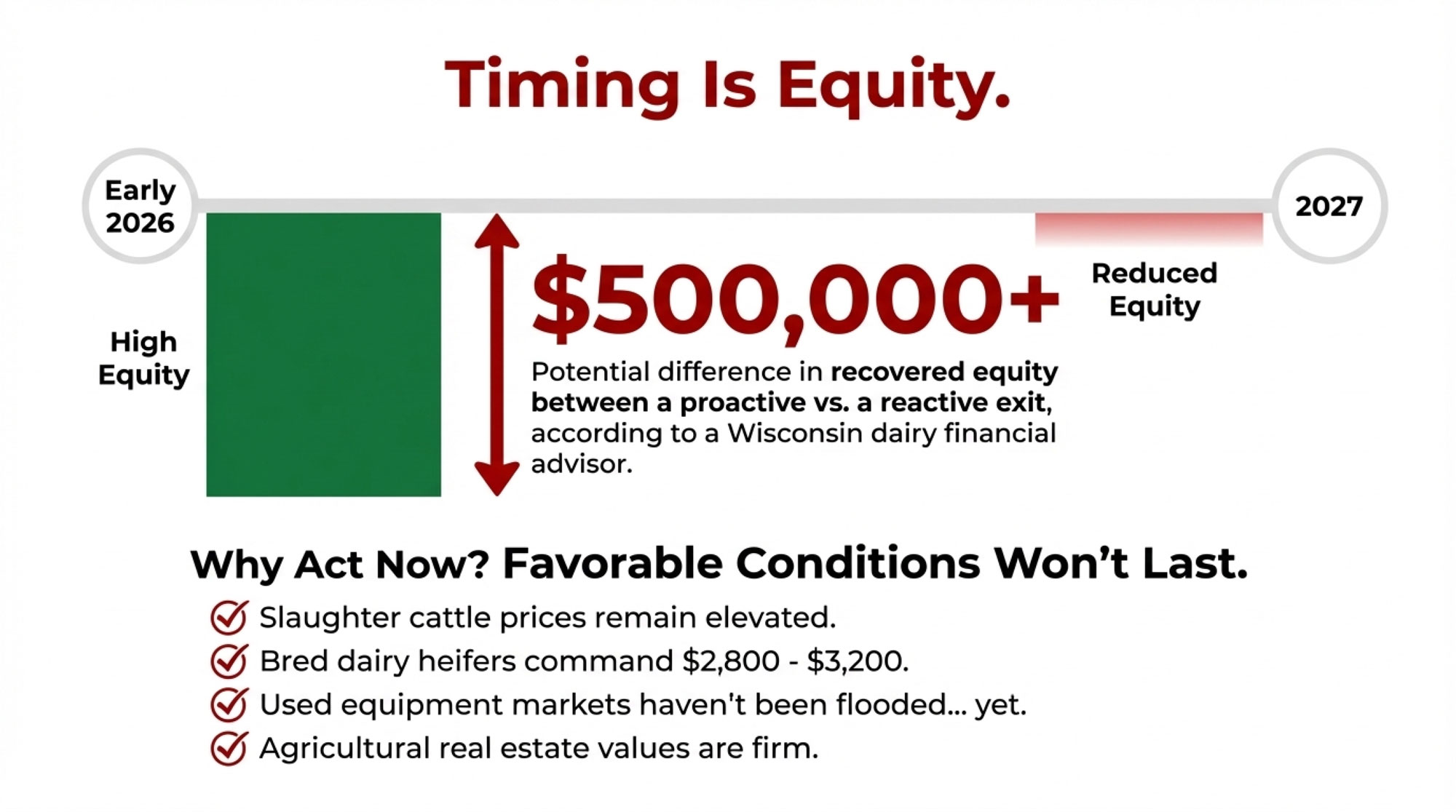

A financial advisor working exclusively with Wisconsin dairy operations framed it this way: “The difference between a proactive exit in early 2026 and a reactive exit in 2027 can exceed half a million dollars in recovered equity for a mid-size operation. That’s not about farming ability—it’s about timing.”

What I’d Tell Someone Navigating This

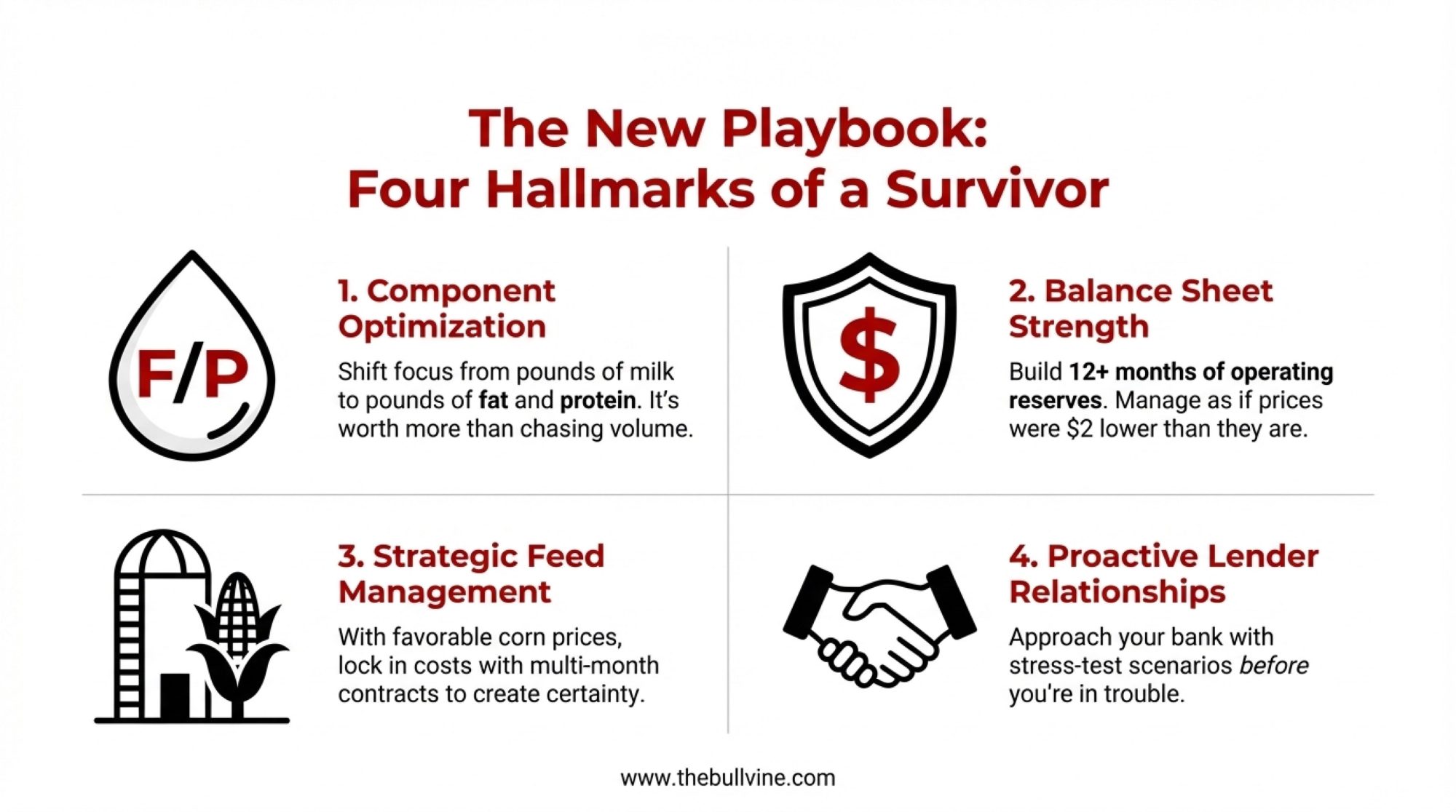

If I were sitting across from you working through these realities—and I’ve had many such conversations this year—here’s what I’d want you to understand:

The structural forces are real, but they’re not uniform. Your specific circumstances—debt levels, processor relationships, facility condition, labor situation, geographic positioning, family involvement, personal goals—matter enormously. There’s no single right answer that applies universally.

The timeline for proactive decision-making appears compressed. Whether you’re considering specialty transition, cooperative participation, strategic investment, or planned exit, the window for making deliberate choices rather than reacting to crisis seems to be the next six to twelve months. Asset values, credit access, and market options tend to deteriorate once financial stress becomes externally visible.

Professional guidance matters more than usual. This isn’t a moment for figuring everything out alone. State agricultural extension services offer transition planning resources—Wisconsin’s Center for Dairy Profitability and Cornell’s PRO-DAIRY program have developed tools specifically for this environment. The Farm Financial Standards Council maintains directories of qualified agricultural financial consultants. USDA’s Farm Service Agency administers loan programs supporting organic transition or operational restructuring.

Consider what you actually want. Beyond financial analysis lies a personal question: What do you want your life to look like in three years? Five years? Sometimes the right answer is to continue farming dairy under restructured circumstances. Sometimes it means preserving the equity you’ve built and redirecting it elsewhere. Both can represent good decisions depending on your situation and values.

A producer working through organic transition planning after thirty years in conventional dairy offered a perspective that’s stayed with me: “The industry I came up in doesn’t exist anymore. That’s not my fault—that’s just what happened. What I do about it is my choice.”

Practical Considerations by Operation Size

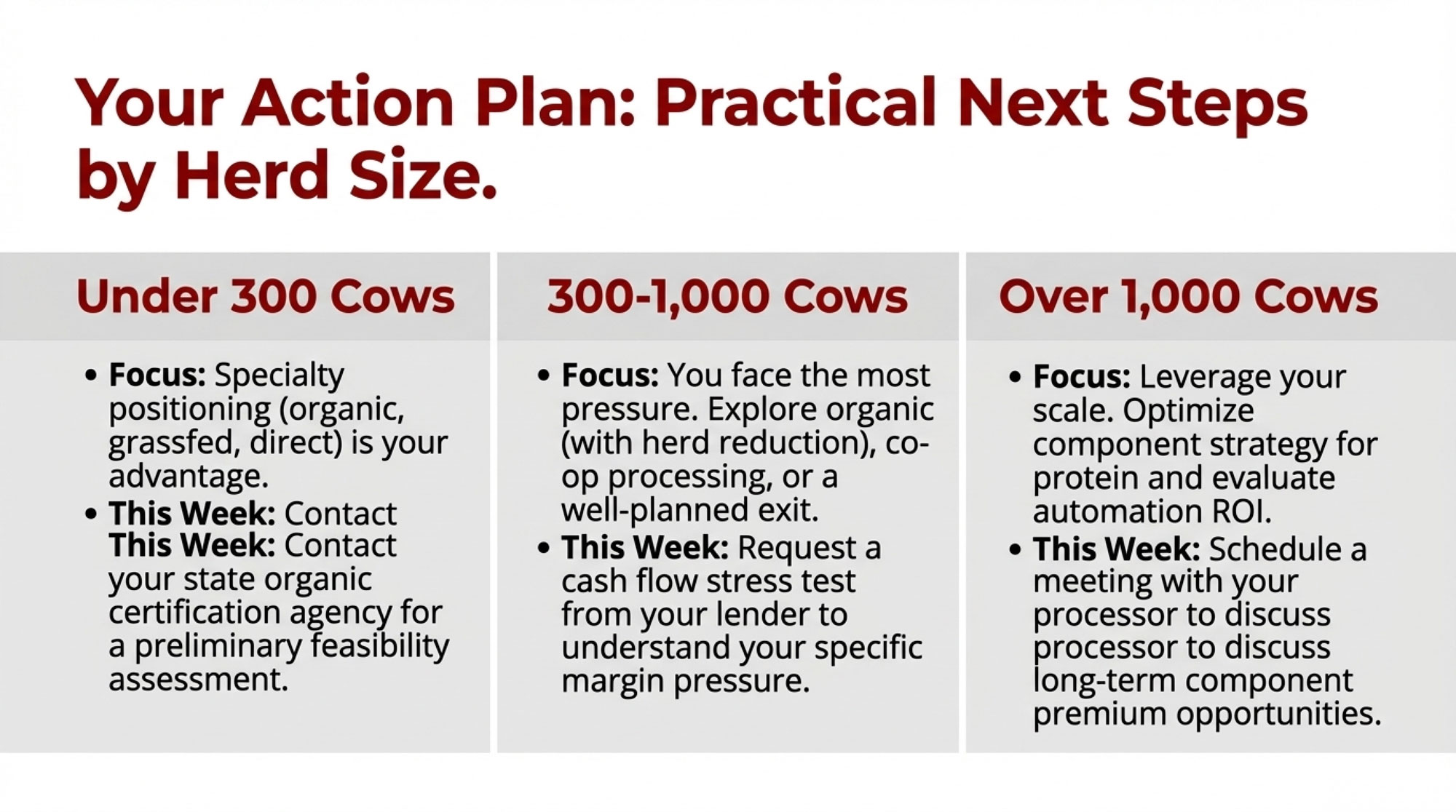

For operations under 300 cows:

Specialty positioning—organic, grassfed, direct-to-consumer—offers economics that commodity production increasingly struggles to match

Your scale disadvantage in commodity markets can become an advantage where authenticity and direct relationships matter

Organic certification typically requires 18-24 months of transition planning; raw milk licensing varies significantly by state

State organic certification agencies and NODPA offer valuable transition guidance

This week: Contact your state organic certification agency to request a preliminary feasibility assessment for your operation

For operations of 300-1,000 cows:

This scale faces the most significant structural pressure—large enough that specialty positioning at current capacity is difficult, but not large enough for automation economics to work straightforwardly

Viable paths worth exploring: organic conversion with strategic herd reduction, cooperative processing partnerships, or well-planned exit

Timeline for decision-making matters; consultation with dairy financial specialists before mid-2026 seems prudent

Conversations with neighboring operations about cooperative arrangements may reveal unexpected opportunities

This week: Request a cash flow stress test from your lender or farm financial consultant to understand your specific margin pressure under various price scenarios

For operations above 1,000 cows:

Automation ROI becomes more favorable at this scale; systematic robotics evaluation is appropriate if not already undertaken

Processor relationships and component optimization—particularly protein—represent strategic priorities worth attention

Structural advantages in labor efficiency, purchasing leverage, and capital access provide meaningful flexibility

Expansion through the acquisition of exiting operations may warrant consideration depending on circumstances

This week: Schedule a meeting with your processor contact to discuss long-term supply relationship options and component premium opportunities

For all operations regardless of size:

Breeding program review with attention to emerging component economics favoring protein

Recognition that GLP-1 demand impacts appear structural rather than cyclical

Early lender conversations if refinancing or restructuring might become necessary

The dairy industry has weathered profound changes before and will continue producing the milk, cheese, and products consumers depend on. What’s shifting is who produces them and at what scale—and that transition is happening faster than many anticipated.

For individual producers, the essential insight is this: the forces reshaping dairy economics appear structural rather than cyclical. Making strategic decisions—whether restructuring toward specialty production, joining cooperative arrangements, investing in scale and automation, or executing an orderly exit—tends to preserve options and equity that waiting erodes.

The producers who navigate this most effectively share a common characteristic: they make deliberate choices based on a realistic assessment of their specific circumstances rather than hoping that general conditions will improve on their own.

The choice belongs to each of you. The information needed to make it wisely is increasingly available.

Key Takeaways:

Heifer economics have flipped: Prices tripled ($1,140 → $3,500+), and inventory is at its lowest since 1978. Every replacement costs $2,000+ more than it did three years ago.

Protein is overtaking butterfat: Component premiums are shifting. Review your breeding program now—genetics from 2022 may be optimized for a vanishing market.

The middle is disappearing: 300-1,000 cow operations face a structural squeeze—too large for specialty pivots, too small for automation ROI to work.

Four paths, one timeline: Organic transition, cooperative processing, strategic scaling, or planned exit. All require action before mid-2026.

Timing is equity: Asset values favor decisions made now. The difference between proactive and reactive exit can exceed $500,000 in recovered value.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong – Reveals how to balance calf revenue with replacement needs using a specific tiered breeding framework to maximize profitability without creating a terminal “financial time bomb” for your herd’s future.

Robot Revolution: Why Smart Dairy Farmers Are Winning with Automated Milking – Demonstrates how to effectively transition to robotic systems, providing specific benchmarks for labor savings, production increases, and the 2025 ROI math required to justify high-capital automation investments in a tight-margin environment.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Everyone’s celebrating 2025’s wins. Almost nobody’s asking how heifer shortage, processor overcapacity, and component changes interact—and what to do about it. The complete 2025 strategic analysis.

Walk into any dairy industry gathering in late 2025, and you’ll hear the same narrative: FMMO passed, DMC extended, $11 billion in new plants. What you won’t hear is how the heifer shortage just made half of those “wins” irrelevant for the next 30 months.

Industry associations called it progress. Most coverage treated these as separate wins.

Here’s what that narrative misses. These ten developments aren’t independent stories—they’re interconnected forces that fundamentally reshaped who’s positioned to thrive and who’s scrambling for the next five years. Some created real strategic advantages, others masked structural problems that are surfacing now, and a few are going to prove costly for producers who waited too long to respond.

What follows is what actually happened in 2025, beyond the headlines.

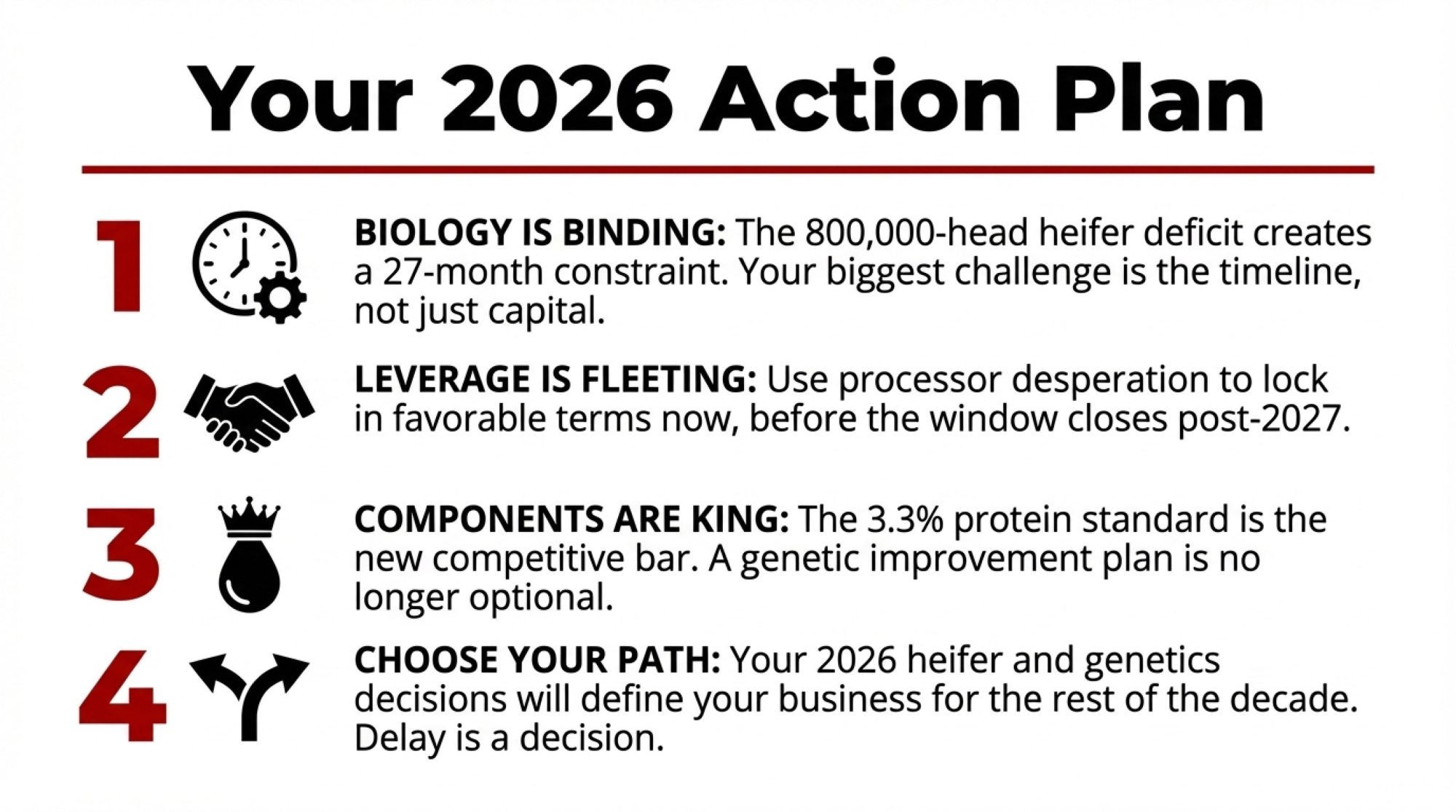

The Heifer Shortage: How Beef-on-Dairy Breeding Created a 27-Month Supply Constraint

Visit any Upper Midwest or California auction barn in mid-2025, and you saw the same scene playing out: replacement heifers averaging above $3,000 per head—up from around $1,140 back in April 2019, according to CoBank’s August report. Premium animals with strong genetics were commanding significantly higher prices.

And here’s the thing. This isn’t a pricing problem you hedge or a policy issue you lobby. It’s a biological constraint that binds for 24 to 30 months, and there’s no shortcut around the gestation and growth timeline.

Dairy replacement inventories dropped to 3,914,300 head in January 2025, down 18% from 2018 levels, according to the USDA’s Cattle Inventory report. CoBank’s modeling shows heifer inventories will shrink by an estimated 800,000 head over the next two years before beginning to rebound in 2027. That 800,000-head deficit isn’t a projection—it’s already baked into the system based on breeding decisions made in 2022 and 2023.

The cause is straightforward, you know. Producers spent 2022-2023 breeding 60-70% of their herds to beef semen because beef-on-dairy calves brought $1,200-$1,800 while dairy bull calves fetched $50—numbers documented throughout that period in Progressive Dairy and Hoard’s Dairyman market reports. The short-term cash flow looked smart. The long-term math created a structural deficit we’re living through now.

How the Math Actually Works

Several Wisconsin producers have described similar experiences in industry discussions, with operations reporting they thought 65% beef breeding in 2022 was conservative. Looking back now, they realize those decisions created their own shortage problem.

Here’s how it plays out. An 800-cow herd with a 35% replacement rate and 85% completion needs roughly 330 heifer calves annually. Heavy beef breeding during 2022-2023 dropped that to 65-70 calves per year, creating a 260-heifer annual shortfall. Scale that behavior across the country and you get the 800,000-head hole CoBank documented in their August sector analysis.

The Timeline Won’t Speed Up

From the moment you switch back to sexed dairy semen, you’re staring at 27 months to first calving: nine months gestation plus 18-24 months to freshening. Even with perfect execution, it won’t be until mid-to-late 2028 before replacement inventories feel healthy again.

What keeps coming up in conversations—and I’ve heard this from producers across three regions now—is how quickly this creates a cascade of impacts we’re already seeing:

Culling math flips entirely. That marginal cow you would have shipped for chronic lameness or weak production now represents a different equation. Culling brings in $2,200-$2,400 at current cull cow prices, but forces a $3,000+ replacement purchase. You’re suddenly in the hole rather than keeping a marginal producer for one more lactation.

This is clearly evident in USDA livestock slaughter data. Dairy cow slaughter trailed year-ago levels for 94-98 of the past 100+ weeks through November 2025, with cumulative declines exceeding 550,000 head. Producers are keeping cows they would have shipped two years ago, which suppresses turnover and drags on herd-average production efficiency.

Expansion plans die or get completely redesigned. A planned 250-cow expansion at previous heifer pricing would cost nearly twice as much at current rates. That kind of capital increase pushes projected returns well below most lender thresholds for dairy expansion projects.

Producers who are still expanding have pivoted strategies entirely—chasing 24,000-26,000 pounds per cow through better genetics and management, buying fresh cows instead of heifers, or locking in long-term heifer contracts at fixed prices with neighboring operations or heifer growers. Each approach has tradeoffs, but they’re all designed to work around the heifer constraint rather than pretend it doesn’t exist.

Every breeding decision becomes capital allocation. You can’t afford to waste pregnancies on beef calves, but you also can’t dump expensive sexed semen on low-merit cows that deliver weak daughters. The new logic emerging across progressive herds: sexed dairy on the top 40% for genomic multipliers, conventional dairy on the middle 40% for higher conception rates, and that 50/50 gender split, limited beef on the bottom 20% to purge genetics you don’t want to propagate.

“The ones who treated it like a temporary price spike are learning that biology doesn’t negotiate.”

The operators who recognized this constraint early in 2025 rewired breeding protocols, slowed or reshaped expansion plans, and leaned into their newfound leverage with processors hunting for milk.

$11 Billion in New Stainless: When Processing Capacity Outran Milk Supply

By mid-2025, new and expanded dairy processing projects added capacity to process nearly 20 million pounds of milk per day, according to industry announcements compiled by Dairy Foods magazine.

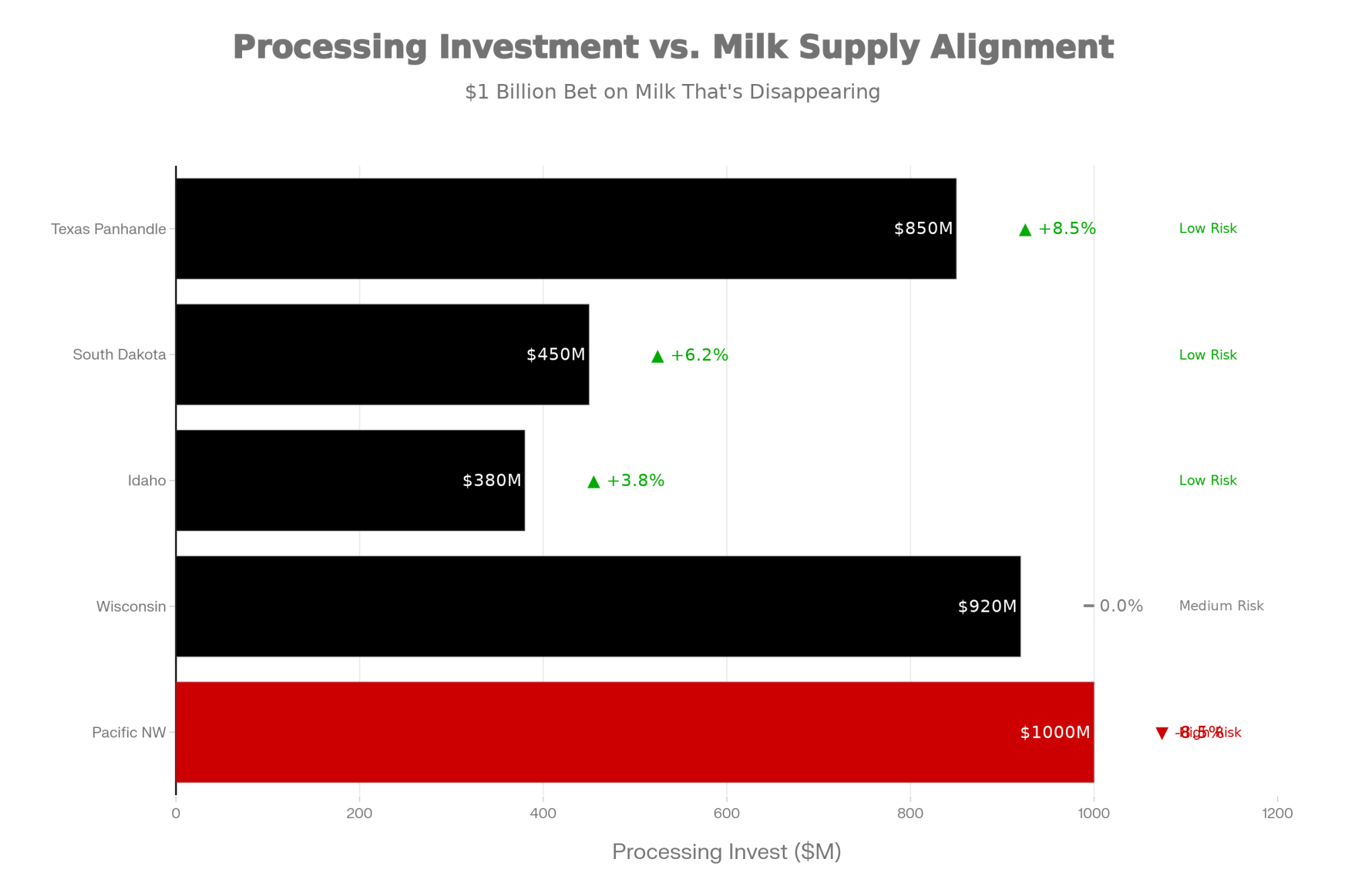

Chobani announced a $500 million expansion in Twin Falls, Idaho, and broke ground on a $1.2 billion plant in Rome, New York, designed to process 12 million pounds of milk daily. Once at full capacity, Chobani will purchase an estimated 6 billion pounds per year. Darigold opened a $1 billion facility in Pasco, Washington, processing up to 8 million pounds daily. Hilmar Cheese launched a cutting-edge facility in Dodge City, Kansas. California Dairies and several other processors added significant capacity throughout the year.

Now, historical U.S. milk production growth has run about 1.5-2% annually, according to USDA data. Food processing facilities typically need to operate at 80-85% utilization to meet their return targets and justify capital deployment.

Biology just vetoed those growth assumptions.

Replacement heifer inventories fell to 20-year lows, with the pipeline expected to shrink further before rebounding after 2027, as CoBank’s dairy economists documented. Producers kept marginal cows longer, and national cow slaughter stayed unusually light, but per-cow efficiency gains produced a one-time volume bump rather than sustainable long-term growth.

The tension is explicit in industry commentary. “Farmers are shipping more milk components, which is most important as 80% of U.S. milk flows into manufactured dairy products,” said Corey Geiger, CoBank lead dairy economist, in their August report. “With the amount of new processing capacity coming online across the country, the ability for milk production to keep up with the demand is worth noting. Given the historically high prices for dairy replacements to enter the milking string, dairy farmers are planning two to three years out for expansions.”

In other words, these plants were built on growth assumptions just as biology capped supply, which shifts negotiating leverage toward producers who can reliably deliver milk.

What Processor Desperation Actually Looks Like

Processors don’t publicly admit supply desperation. They telegraph it through behavior patterns we’ve been tracking throughout 2025.

If a plant historically pulled milk from a 100-150 mile radius and starts recruiting 300-500 miles out, that signals supply desperation. If you’re 50 miles from that plant while they’re wooing farms 400 miles away, you’re their lowest-cost, lowest-risk volume source. That’s leverage worth understanding.

Volume bonuses, consistency premiums, multi-year price floors, richer component incentives, and co-funded capital projects signal that standard pool pricing isn’t securing enough milk. Industry sources report that some operations have negotiated arrangements, including premiums of $0.20-$0.30 per hundredweight above pool pricing, structured as multi-year agreements with processor co-financing for replacement heifers at favorable interest rates. Essentially, processors are using their cheaper cost of capital to lock in a reliable milk supply.

Plants sold as 24/7 engines running three shifts can’t hide if they’re stuck at two shifts, hiring below announced job numbers, or taking frequent maintenance downtime. If they built for 80-85% utilization and are running in the low-60s, every extra million pounds you can commit moves their return needle meaningfully.

The window for producer leverage is real but temporary. Once replacement inventories rebuild after 2027-2028 and milk supply catches up to the $11 billion of new capacity, processors drift back toward classic commodity behavior: more milk than needed, less desperation, harder-edged pricing.

Between now and then, producers who understand the supply-demand mismatch have a once-in-a-cycle opportunity to lock in better premiums, real partnership terms, and multi-year structures that still look attractive when the leverage pendulum swings back. These opportunities typically don’t announce themselves with flashing lights—they show up as unusual persistence from field reps or surprising openness to negotiation on terms that were non-starters six months ago.

FMMO Component Factor Changes: The Permanent Repricing of Standard Milk

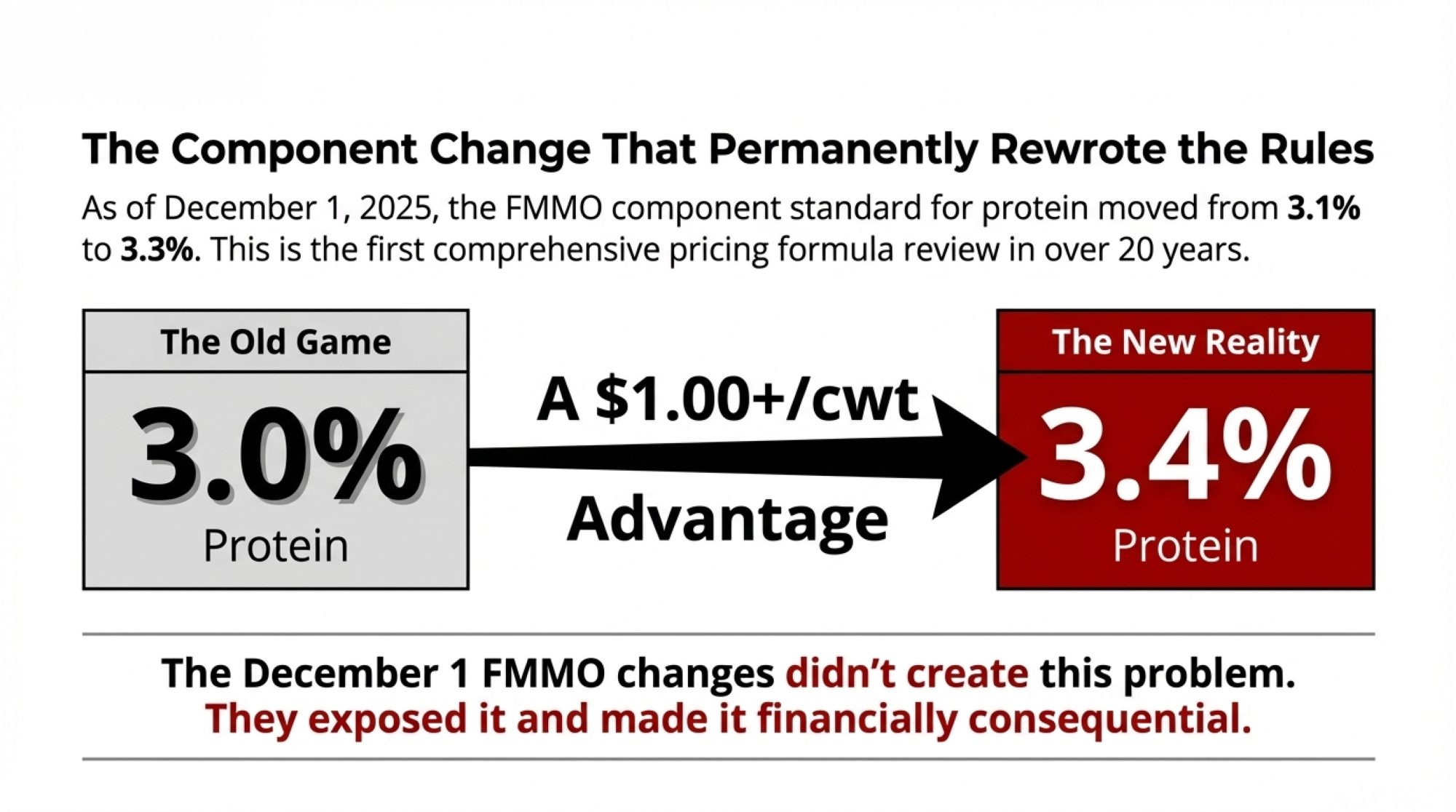

December 1, 2025, marked a fundamental shift in how milk gets valued. The component standard updates moved to 3.3% protein, 6.0% other solids, and 9.3% nonfat solids, according to the USDA’s Agricultural Marketing Service final rule published in October.

These aren’t technical adjustments—they’re a permanent repricing of what counts as standard milk.