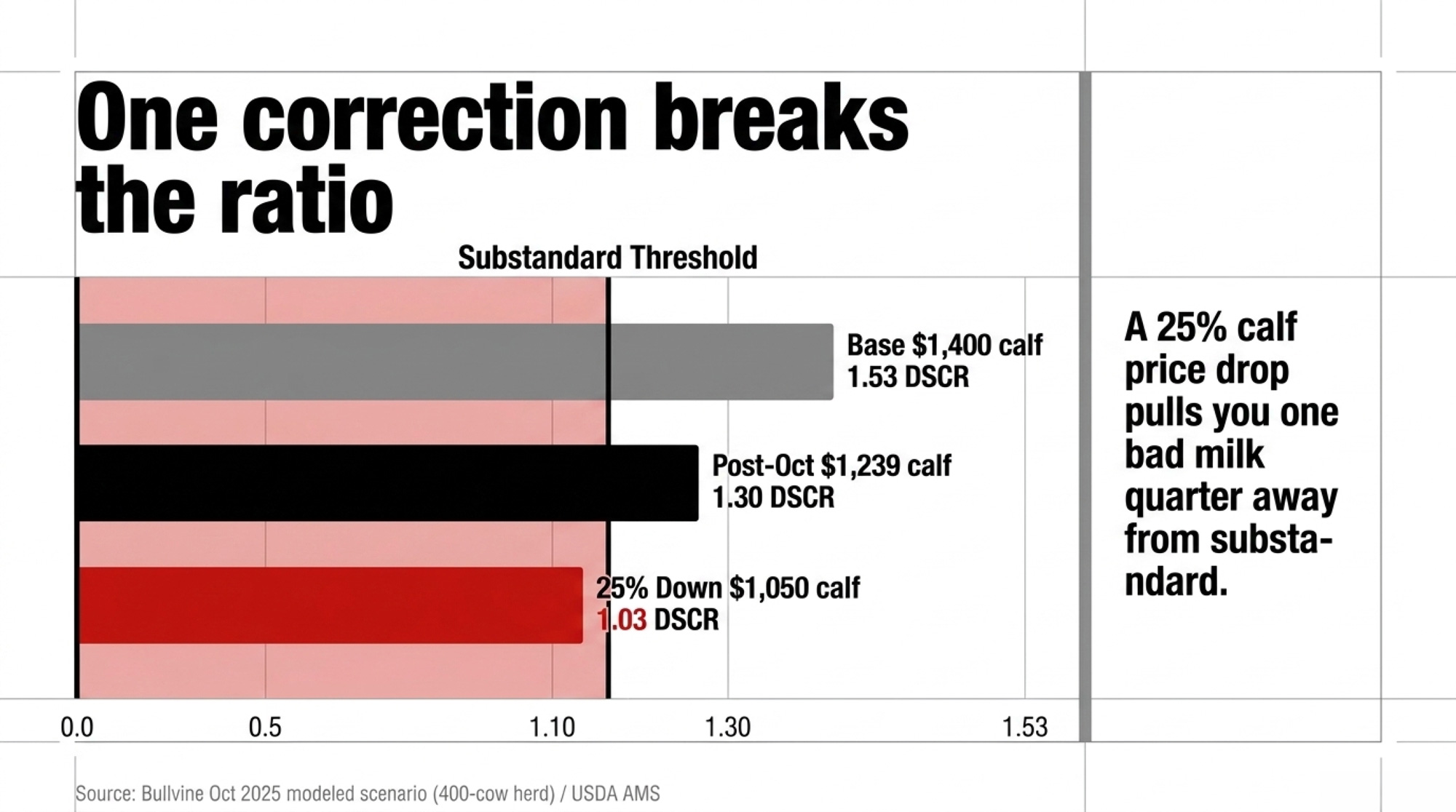

A 12-day October correction knocked $161 off every crossbred calf and pushed a modeled 400-cow DSCR to 1.03. McCarty runs 20,000 cows on a 341-day clock. Your lender already did the math.

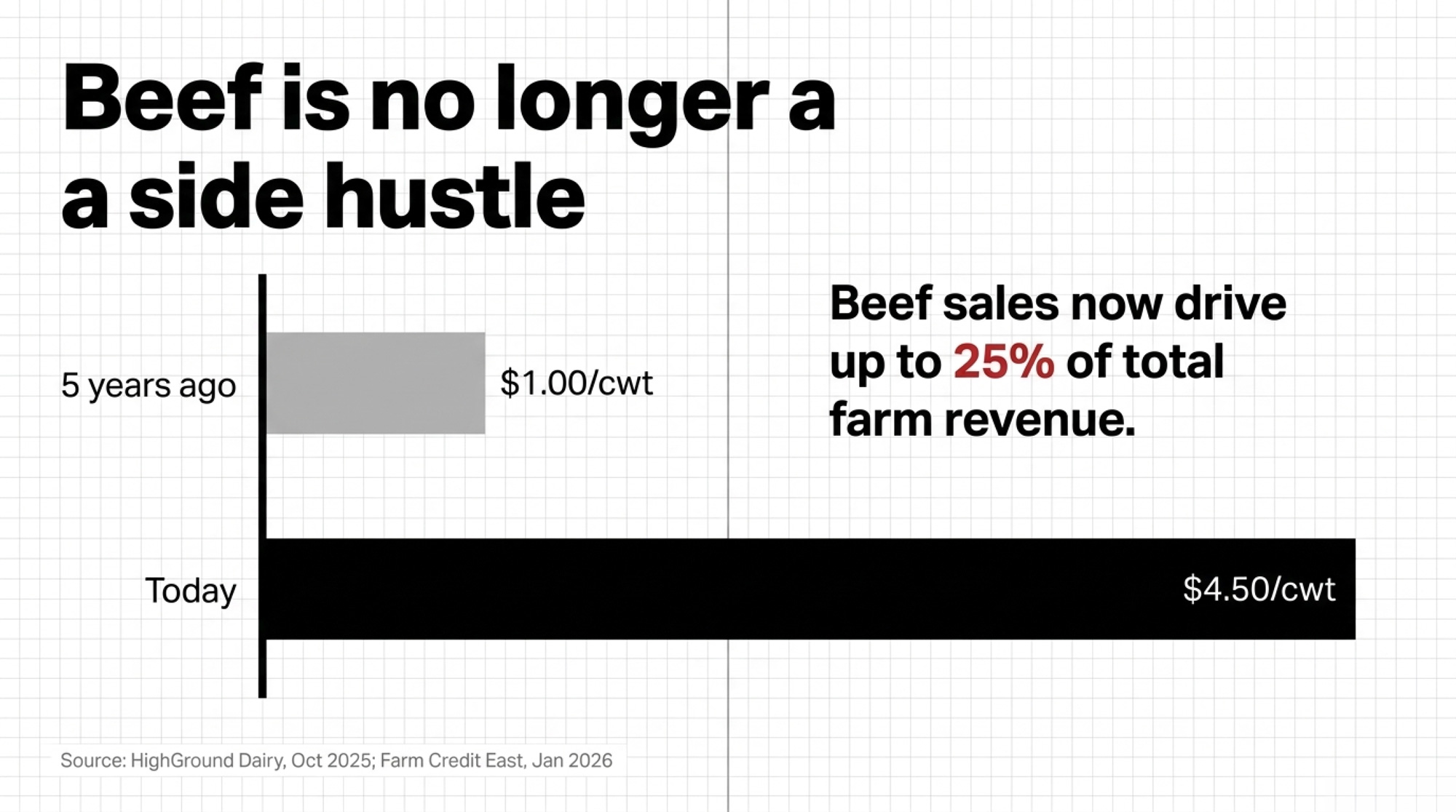

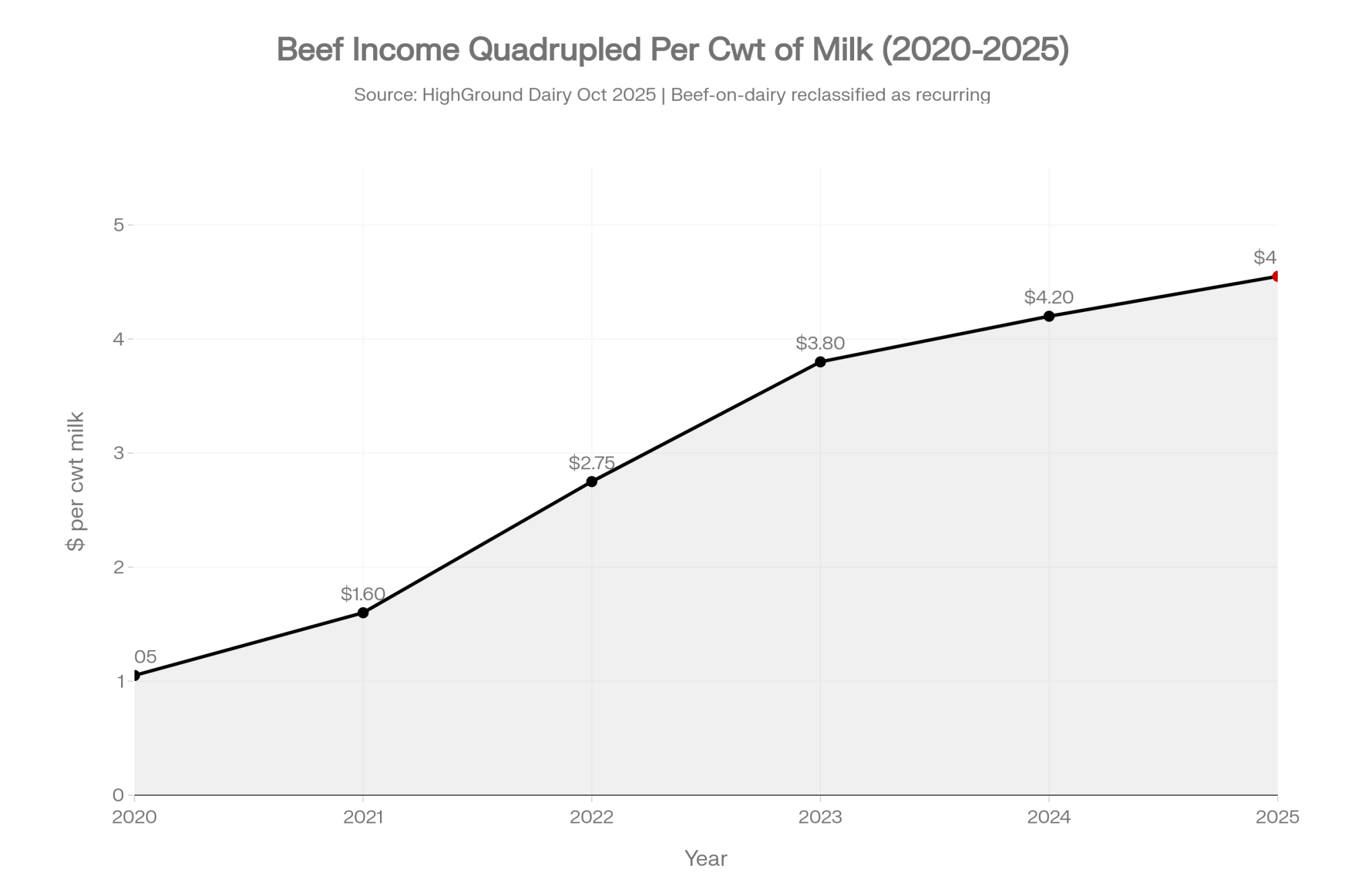

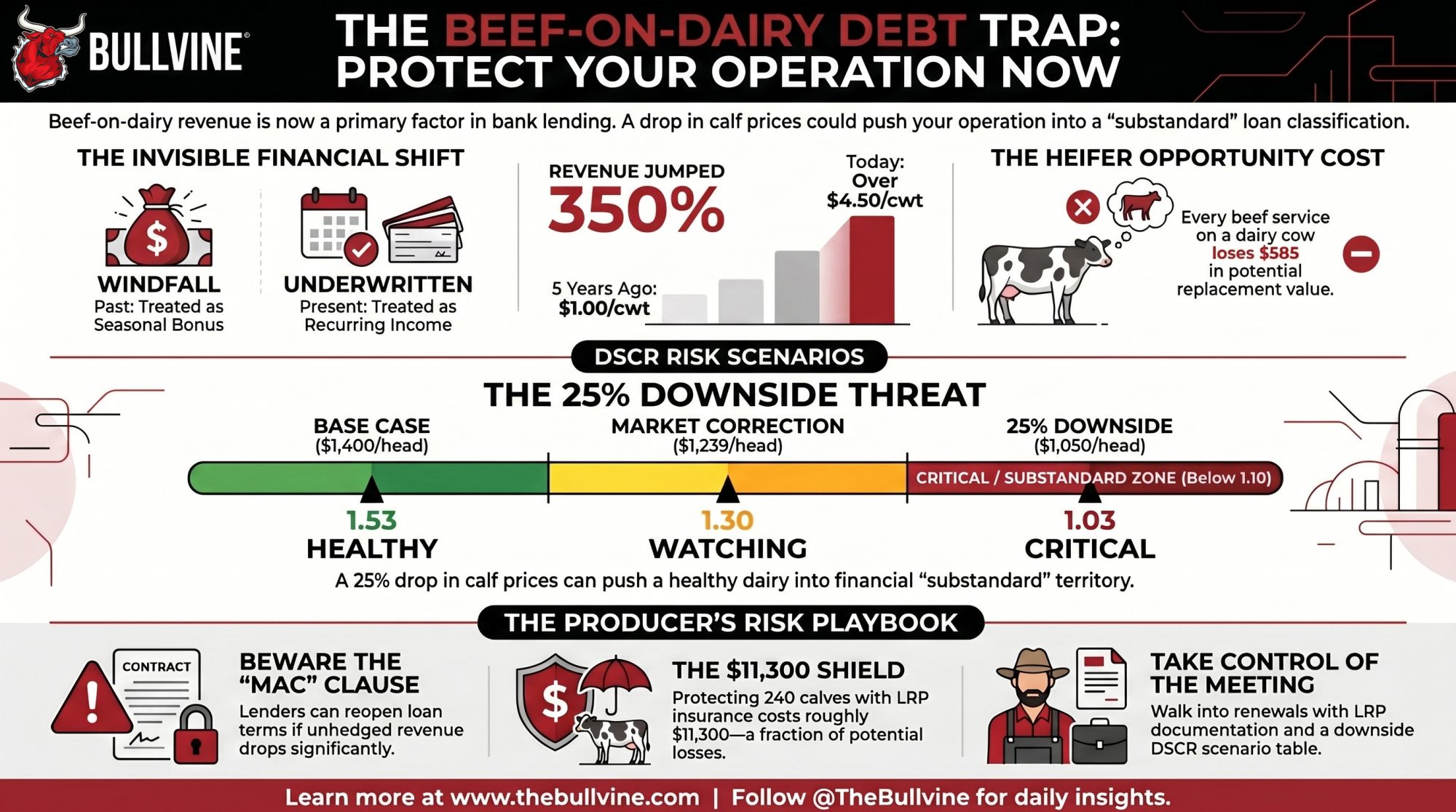

Executive Summary: Beef income now runs above $4.50/cwt for some U.S. dairies — up from just over .00/cwt five years ago, per HighGround Dairy’s October 2025 tracking — and your lender already noticed. Three straight years of six-figure calf receipts moved beef-on-dairy income from the windfall column into the recurring-income column in credit memos across dairy country, so your DSCR and your operating line are now sized around a revenue line you don’t formally hedge.

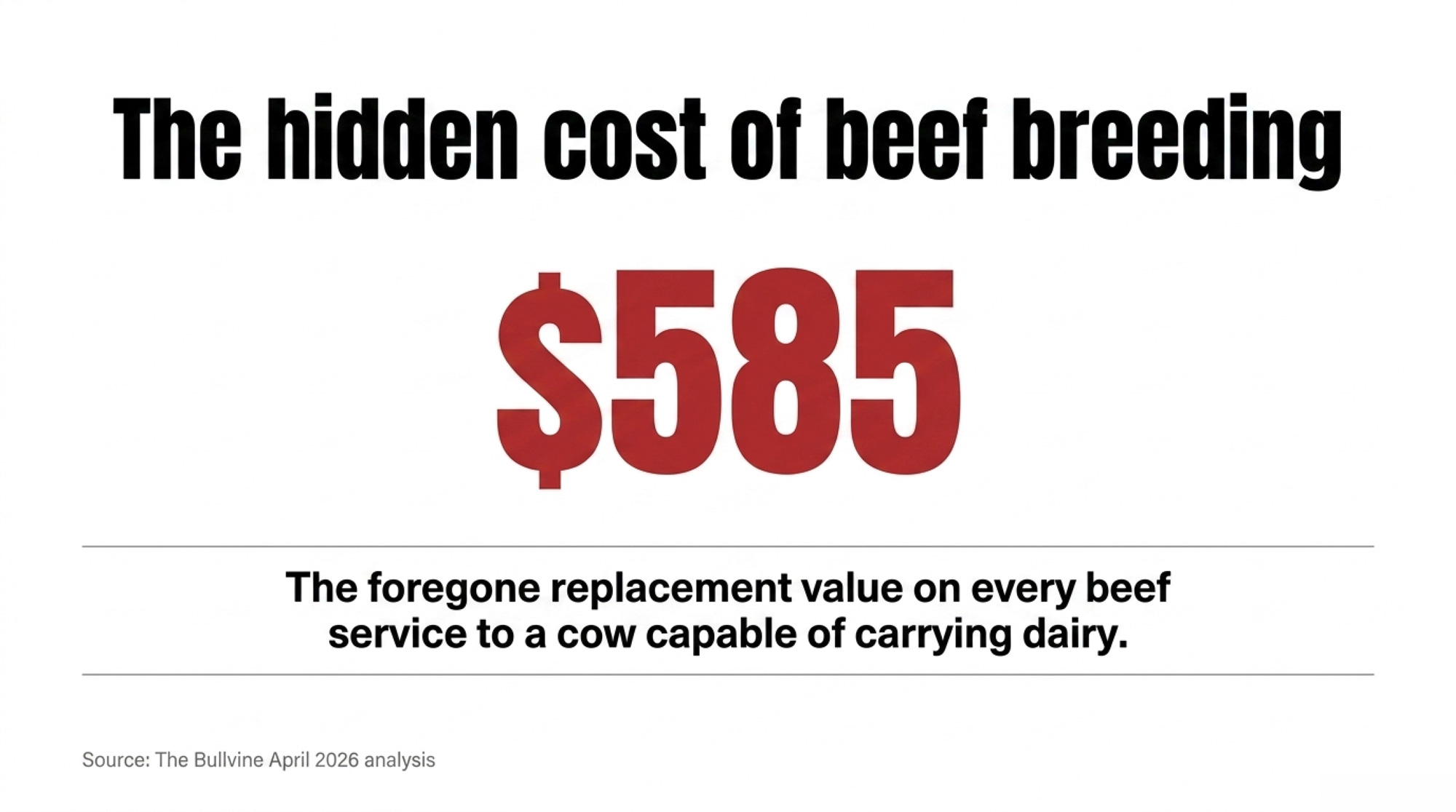

On a 400-cow, 55%-beef-bred operation running 240 crossbred calves per year, a 25% calf-price drop pulls DSCR from 1.53 down to 1.03 — still above water, one bad milk quarter from substandard classification. Add the heifer math — springers at $3,010 national average and $4,100+ top-end in CA/MN, with $585 in foregone replacement value per beef service — and LRP’s ~$11,300/year premium is the small number; the $64,000–$96,000 replacement-purchase bill is the real one.

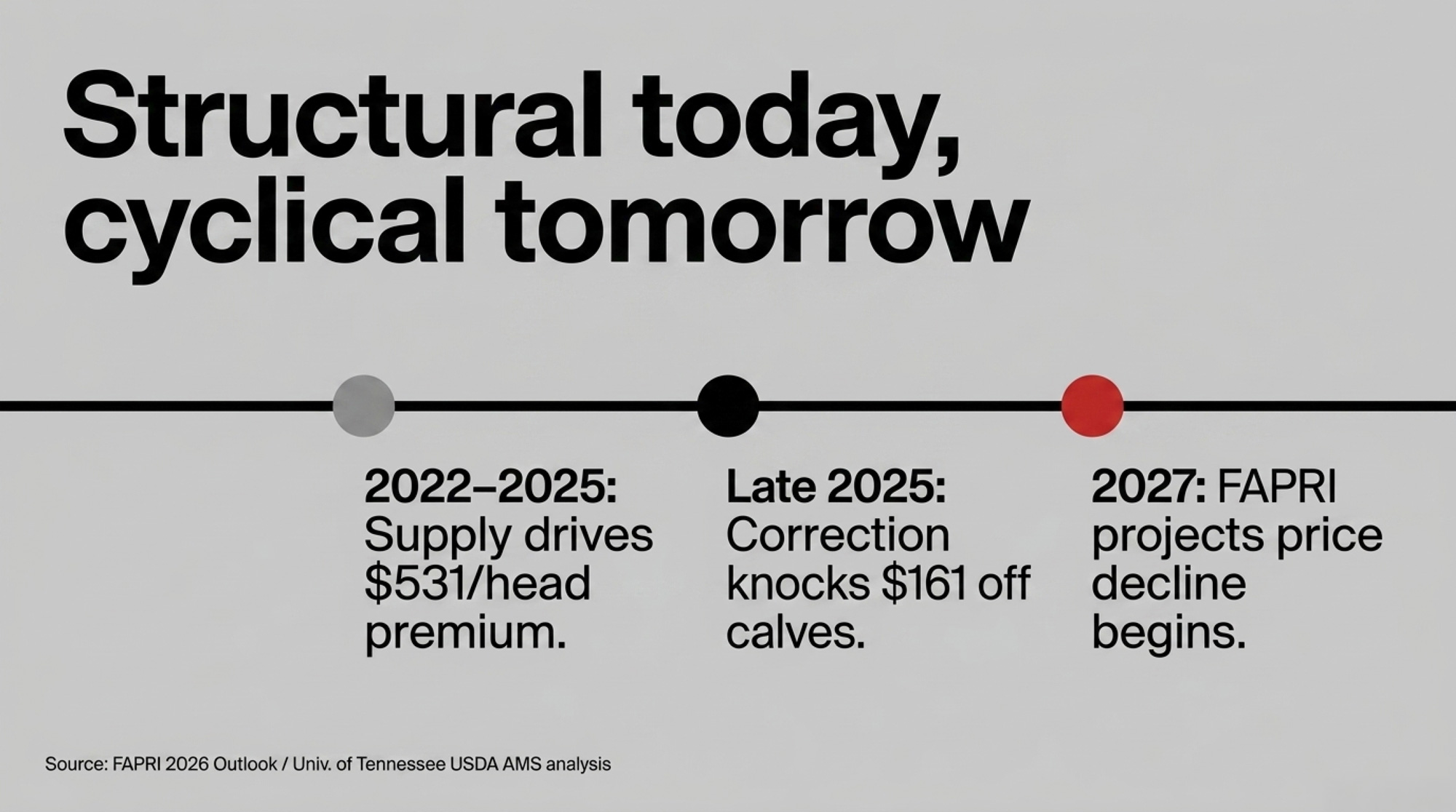

FAPRI projects cattle prices declining from 2027 as the native herd rebuilds, and the $531/head premium crossbreds carry over Holstein calves (University of Tennessee, 2025 USDA AMS data) depends on that tight supply holding. The MAC clause in your operating note lets the lender reopen terms on a material change in risk profile — a six-figure unhedged revenue line correcting 25% qualifies — so the leverage window only opens if you walk in with LRP documentation and a DSCR scenario table before the next credit memo is built.

A 12-day correction in October 2025 knocked $161 off every crossbred calf in the beef-on-dairy pipeline — the difference between $1,400 and $1,239 per head, per USDA AMS feeder data. Class IV milk dropped from $19.16 to $16.17/cwt on CME settlement data in the same window. The Bullvine’s October 2025 modeled scenario put the combined hit on a representative 1,500-cow Midwest dairy at roughly $196,000 in annual revenue. Two unhedged revenue streams. One trade-policy tremor. The beef-on-dairy 2026 barn math most operations hadn’t run finally ran itself.

That wasn’t bad luck. The beef-on-dairy packer risk conversation heading into 2026 isn’t about whether the premium existed. It’s about what the premium quietly became once the lender had watched it land three years in a row.

The Revenue Line Nobody Officially Added

Beef-on-dairy didn’t announce itself as structural change. It crept in as a better calf check. The Holstein bull calf that moved for as little as $50 in some regions in 2019 became a beef-cross worth $1,400 by late 2025.

HighGround Dairy’s October 2025 model tracks the shift. On a per-hundredweight-of-milk basis, beef income — calves plus cull cows — climbed from just over $1.00/cwt five years ago to more than $4.50/cwt today. Farm Credit East’s January 2026 industry outlook found some operations now pulling 20% to 25% of total farm revenue from beef sales, with calf prices running $1,200 to $1,500 per head.

CoBank’s Corey Geiger confirmed in February 2026 commentary that U.S. dairy cow numbers sit at their highest level in 30 years while replacement heifer inventories hit a 20-year low. USDA NASS farm-typology data tracks beef cattle’s share of dairy farm revenue roughly doubling across the 2019–2024 window. Operations running 40–55% beef breeding sit well above that national pattern.

The Kansas Scale Anchor

McCarty Family Dairy is referenced here as an illustrative scale anchor, not as an example of financial distress at that specific operation.

McCarty runs 20,000 cows across its Kansas base, with a scheduled slaughter pipeline of 341 days after birth, per Dairy Herd’s April 2026 reporting from Karen Bohnert. Beef-cross revenue approaches half of the operation’s non-milk income depending on month and market, according to that same reporting. The mechanics a lender applies to a 20,000-cow program are the same mechanics being applied to 400-cow and 1,000-cow operations across the Upper Midwest right now. That’s where the covenant conversation actually lives.

How Your Calf Check Became Underwritten Income

Ag lenders don’t underwrite dairy operations on feel. They underwrite on Debt Service Coverage Ratio — net cash income divided by total debt service. Farm Credit Canada’s October 2025 guidance (the Canadian FCC, not the U.S. Farm Credit System) calls 1.5 healthy and below 1.0 unsustainable. U.S. Farm Credit System associations and regional ag banks apply comparable frameworks with institution-specific thresholds.

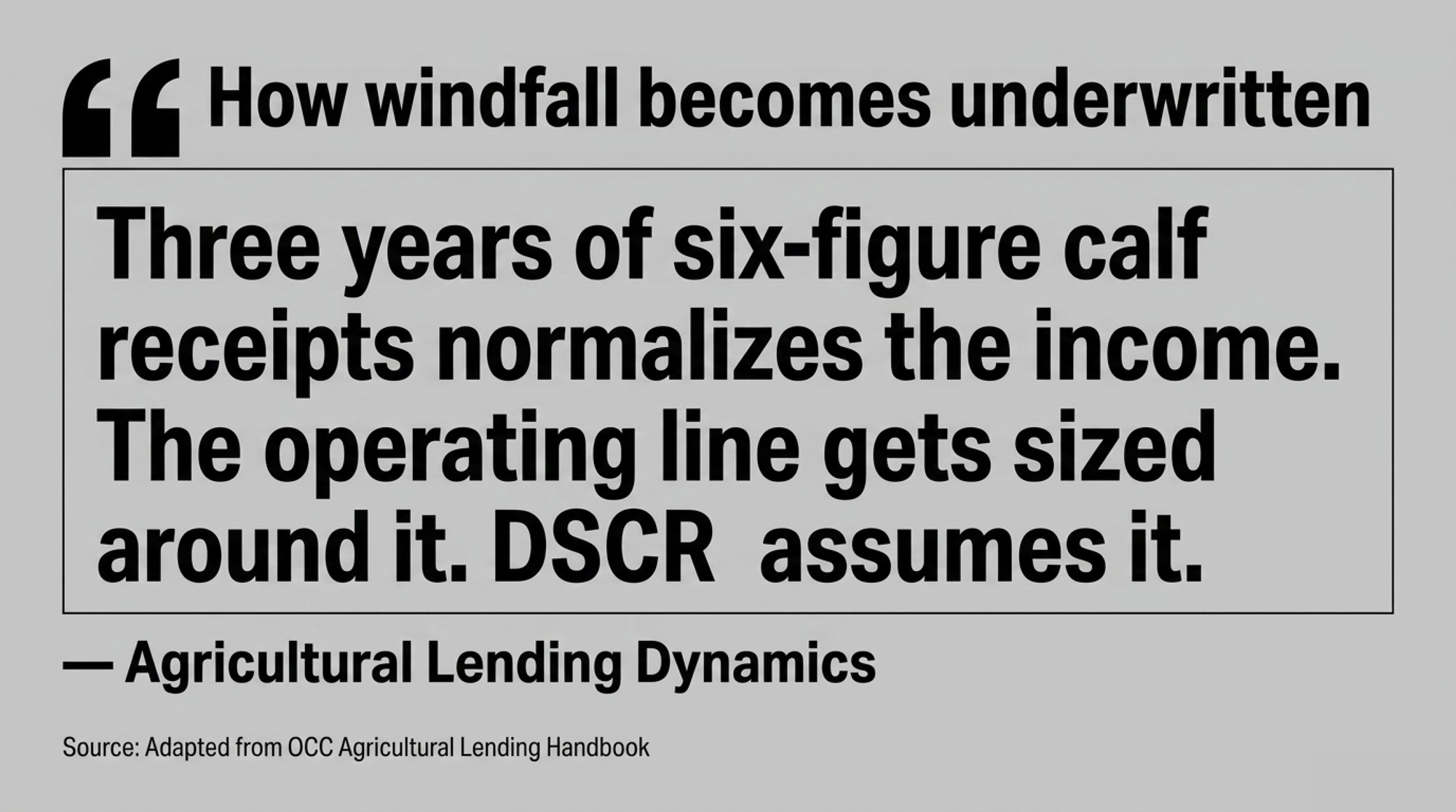

How windfall became underwritten income:

Year 1 — Calf check lands outside DSCR; flagged as windfall income. Year 2 — Lender notes the receipt pattern; income still treated as non-recurring. Year 3 — Three-year consistency rule applies; income normalizes into recurring classification. Year 4 — Operating line sized around it; DSCR now assumes the revenue. October 2025 — Revenue line reprices 11.5% in 12 days; MAC clause activates without further action.

The OCC’s Agricultural Lending Handbook is explicit on the point that matters here. Non-recurring capital gains can’t anchor repayment capacity, but ongoing livestock sales qualify as recurring income when they’re consistent over multiple years. Consistent. That’s the word that moved beef-on-dairy from the windfall column into the baseline column in credit memos across dairy country.

Three years of six-figure calf receipts produces the same classification at McCarty’s scale or at a 500-cow freestall. Income gets normalized. The operating line gets sized around it. DSCR assumes it. Then October 2025 hits, and the line item a producer thought was theirs to manage turns out to be baked into a credit model they never saw.

Running the Numbers: A 400-Cow Dairy Under Three Calf-Price Scenarios

Illustrative model, deliberately scaled down from the 1,500-cow opening scenario to reflect a typical Tier 3 reader operation. Inputs from USDA AMS November 2025 feeder data, HighGround Dairy October 2025, USDA WASDE February 2026, and USDA ERS 2024 Upper Midwest cost-of-production data. Plug in your own numbers.

Inputs

| Input | Value | Source |

| Herd | 400 cows | — |

| Production | 80 lbs/cow/day | — |

| All-milk price | $18.95/cwt | USDA WASDE Feb 2026 |

| Effective crossbred calf yield | ~0.60/cow/year at 55% beef breeding | Industry heuristic |

| Annual calves | ~240 | Derived |

| Base calf price | $1,400/head | Trade data, late 2025 |

| Post-October correction | $1,239/head | USDA AMS Nov 2025 |

| 25%-down scenario | $1,050/head | FAPRI 2026 downside |

| Operating + non-debt fixed costs | ~$2,293,000 (~$5,732/cow) | USDA ERS 2024 Upper Midwest |

| Annual debt service | ~$168,000 | $1.8M @ 7%, 20-yr amortization |

Milk revenue: 400 cows × 80 lbs × 365 days ÷ 100 × $18.95/cwt = $2,213,360

Beef-cross calf revenue by scenario

| Scenario | Calf Price | × 240 Calves |

| Base | $1,400 | $336,000 |

| Post-October correction | $1,239 | $297,360 |

| 25% down | $1,050 | $252,000 |

Cash available for debt service (gross milk + calves − operating − non-debt fixed, divided by $168,000 debt service)

| Scenario | Milk Revenue | Calf Revenue | Costs | Cash Available | DSCR |

| Base | $2,213,360 | $336,000 | ($2,293,000) | $256,360 | 1.53 |

| Post-October correction | $2,213,360 | $297,360 | ($2,293,000) | $217,720 | 1.30 |

| 25% down | $2,213,360 | $252,000 | ($2,293,000) | $172,360 | 1.03 |

[VISUAL OPPORTUNITY: horizontal bar chart of DSCR across the three scenarios with 1.10 watch-list and 1.00 substandard thresholds shaded in red.]

Scale it. A 1,000-cow operation at the same breeding percentage runs roughly 600 calves. A 2,000-cow operation runs roughly 1,200. What triggers lender behavior is the ratio, not the absolute dollar swing.

That 1.03 is the number to stare at. Still above water. Also one bad milk quarter from substandard classification — and the producer won’t know they’re on the watch list until the next renewal conversation.

How Much of Your Revenue Now Depends on the Calf Buyer?

Concentration math is where the industry narrative falls silent. Four firms control roughly 85% of U.S. beef processing capacity per USDA GIPSA/AMS data. Premium packer programs paying top dollar for spec-compliant beef-on-dairy cattle are finite.

Buyer pauses aren’t about conspiracy. They’re logistics. Scheduled packer maintenance shutdowns, cold storage backups when wholesale boxed beef moves slowly, feedyard pen-space constraints, and seasonal labor or transport disruptions all force premium buyers to pause intake or tighten specs on short notice. These are routine events, not edge cases.

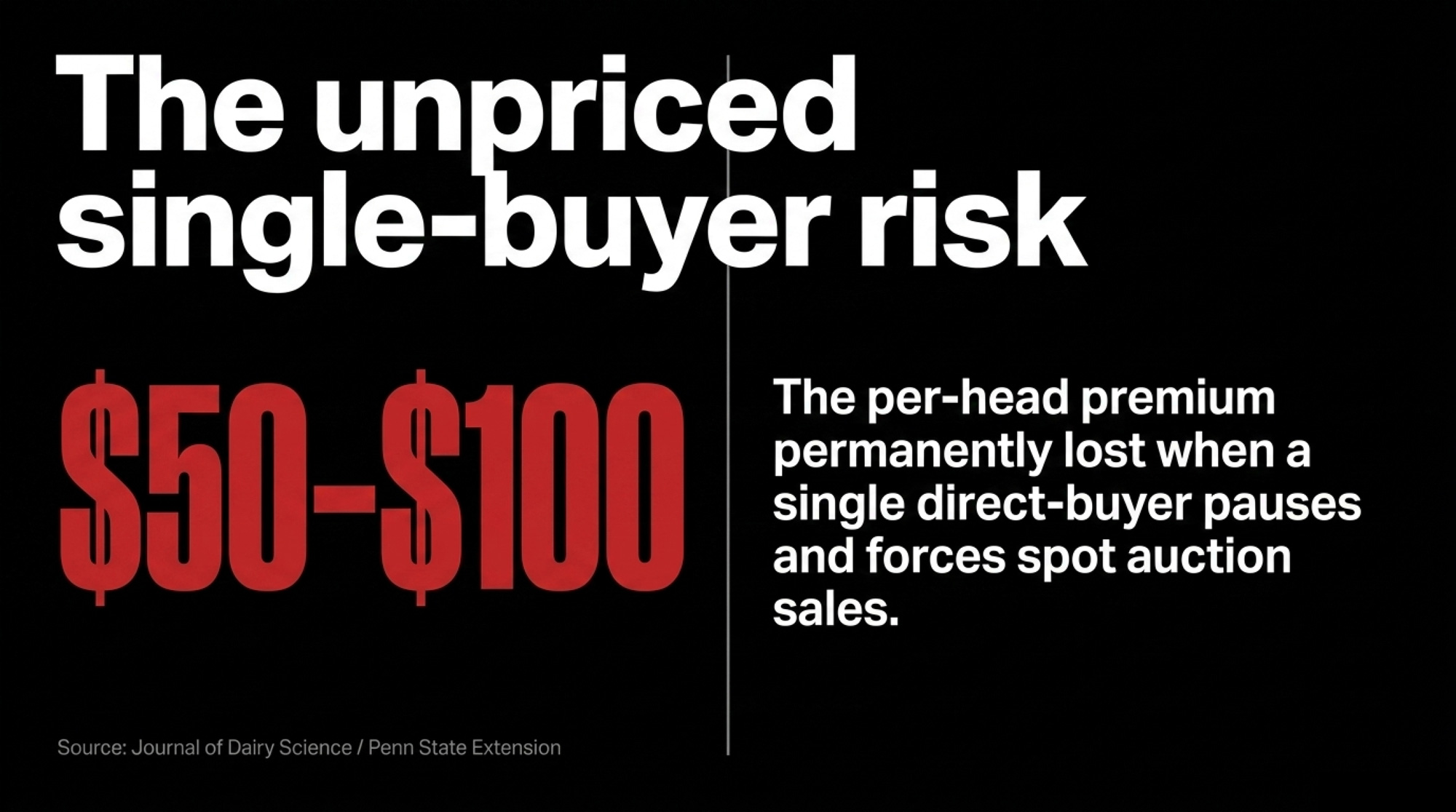

Peer-reviewed dairy-beef channel research in the Journal of Dairy Science and published Penn State Extension work both document that direct-buyer relationships dominate the crossbred calf channel, producing $50–$100/head premiums over auction-based sales. That concentrates risk the way a grain operator’s single-elevator exposure concentrates risk.

Run the numbers on a 400-cow program where 90%+ of 240 calves move through one buyer. The entire $336,000 line reprices the day that buyer adjusts specs. A 60-day pause forces spot sales at auction, typically $50–$100/head below direct-feeder pricing. On 100 head, that’s $5,000–$10,000 in lost premiums per event. Dairy operations haven’t historically run concentration risk for beef revenue because they haven’t historically had meaningful beef revenue. Now they do.

What Happens If Beef-on-Dairy Calf Prices Drop 25%?

This isn’t hypothetical. FAPRI’s 2026 U.S. Agricultural Market Outlook projects cattle prices beginning to decline in 2027 as the native cow herd rebuilds. FCC Agriculture’s December 2025 analysis points the same direction on feeder cattle. Two credible outlooks pointing at the same trajectory on different magnitudes.

| Revenue Share | 400-Cow Operation | Modeled Calf Revenue Drop (25%) | Per-Cow Impact (full herd) | Milk-Equivalent Loss |

| 10% of gross | ~120 calves | ~$37,000 | ~$93 | ~$0.32/cwt |

| 15% of gross | ~192 calves | ~$60,000 | ~$150 | ~$0.51/cwt |

| 20–25% of gross | ~240 calves | ~$84,000 | ~$210 | ~$0.72/cwt |

Modeled impact at sourced inputs. Per-cow column spreads calf-revenue loss across the full 400-cow herd, not per calf. Scale to your own operation.

The Bullvine’s October 2025 analysis pegged the per-cwt hit at $0.54/cwt for a 40%-beef-breeding operation. That maps directly onto this table — enough to flip a marginal year into a restructuring conversation on a revenue stream most producers didn’t formally budget when milk was $22.

The Heifer Bill That Came Due

Beef-on-dairy revenue doesn’t exist in isolation. It compounds with the replacement gap it helped create.

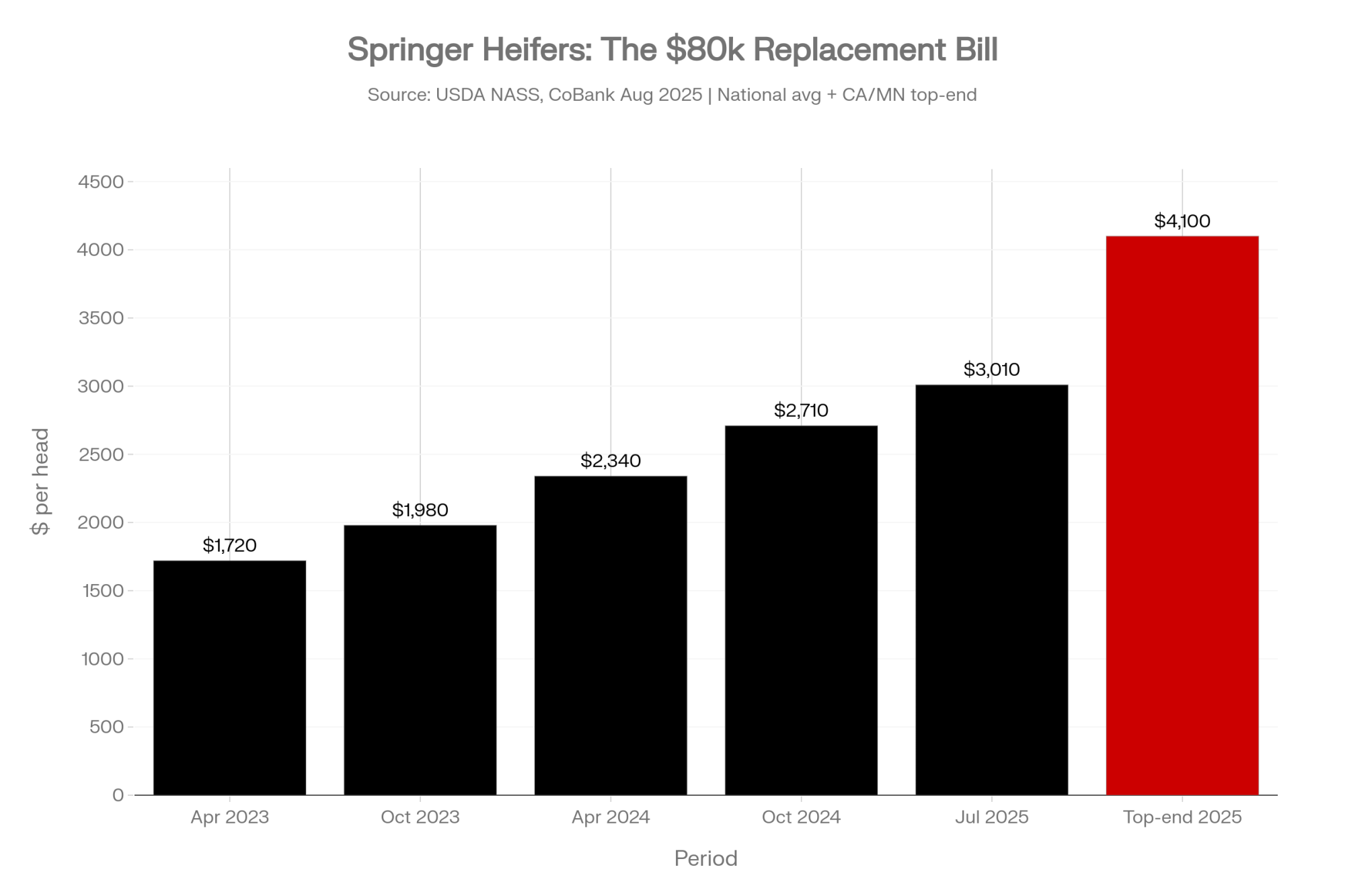

USDA NASS reported dairy replacement inventories at 3,914,300 head in January 2025 — down 18% from 2018. CoBank’s August 2025 Knowledge Exchange analysis projects 438,844 fewer dairy heifers entering 2026 supply versus 2025. Springer heifer prices tracked the squeeze: $1,720/head in April 2023 (national average), $3,010/head by July 2025, with top-end auctions in California and Minnesota clearing above $4,100/head at mid-2025 sales.

The Bullvine’s April 2026 analysis put a number on the breeding decision itself — every beef service on a cow capable of carrying a viable dairy pregnancy represents 5 in foregone replacement value at current heifer prices.

The Replacement Gap Math (400-cow herd, 55% beef breeding)

- LRP premium on 240 calves at 90–95% coverage: ~$11,300/year after RMA subsidy

- Replacement shortfall: 4–6 percentage points = 16–24 heifers short annually

- Heifer replacement cost at $4,000/head: $64,000–$96,000

- Per beef service on a cow capable of carrying dairy: $585 foregone replacement value

LRP is the $11,300 problem. Replacements are the $80,000 midpoint problem.

Producers pulling back beef breeding percentages are responding to the second number, not the first. The LRP obligation just made the total cost legible.

The Turn: Why Some Producers Got This Right Before October

They weren’t smarter about beef. They were smarter about cattle cycles.

| Decision Lever | Cycle-Aware Operator | $1,400-Calf Believer | 2026 Consequence |

| Beef breeding % of herd | 35–40% (capped) | 50–60% | Replacement gap 4–6 pts |

| Replacement pipeline | Intact, internal | Purchase-dependent | $64k–$96k annual bill |

| LRP coverage on calves | 90–95%, pre-enrolled | Reactive / none | ~$11,300 premium vs. unhedged loss |

| Buyer concentration | 2–3 documented buyers | 1 buyer, >60% volume | $5k–$10k per 60-day pause |

| Calf income treated as | Windfall / hedged | Baseline / underwritten | MAC clause exposure on correction |

| DSCR stress-test run | $1,050 / $125 / $18.00 | None formally | Watch list without warning |

Operators who lived through 2015–2016 — when feeder cattle fell roughly 40% in 18 months as the U.S. herd rebuilt after the 2012 drought liquidation — didn’t read the 2022–2024 calf premium as permanent. They harvested it. They hedged it. They capped beef breeding at 35–40%. They kept the replacement pipeline intact. They treated the calf check as windfall, not baseline.

Producers who built their 2026 structure around $1,400 calves made a forecasting error that was understandable given the information available in 2023 — two years of exceptional premiums, a compelling packer narrative, and every trade publication calling it a structural transformation. The incentive to believe it was permanent was enormous, and that’s the miscalculation. A familiar error in commodity agriculture — confusing a favorable cycle for a new normal, and sizing a permanent cost structure around a temporary price. McCarty’s 341-day pipeline isn’t the risk. Building a 400-cow version of it around $1,400 calves is.

What Does Your Operating Note Actually Say?

Most dairy operating notes don’t contain explicit “maintain LRP coverage” language. What they do contain is material adverse change language — MAC clauses — giving the lender the right to reopen terms if a borrower’s risk profile shifts materially.

Letting a documented hedge lapse can qualify. So can a six-figure revenue line correcting 25% in a single cycle. The lender doesn’t need a specific insurance covenant to act. They have the MAC clause.

Pinion Global’s April 2026 lender guidance is published on this point: 2026 credit reviews are rewarding producers who walk in with documented risk management strategies, not just trailing actuals. Farm Credit East’s February 2026 dairy outlook pointed in a similar direction, suggesting LRP-covered beef income should be treated more like DRP-protected milk — hedged variable income rather than unmanaged baseline.

Three practitioner-cited thresholds drive the cascade:

- DSCR below 1.10 — the informal watch list. Consistent with OCC “special mention” risk-grading guidance. Your credit grade shifts internally, the loan officer moves from annual to quarterly monitoring, and nothing happens visibly.

- DSCR below 1.00 — substandard territory. OCC handbook guidance requires formal classification. Capital reserving requirements change on the lender’s side, and a workout plan is required within a defined timeframe.

- High debt-to-asset plus persistently weak DSCR — the liquidation analysis line. The loan moves into liquidation analysis rather than workout. At that point, the options a lender is legally permitted to offer are different from the options a producer needs.

| DSCR Band | Lender Classification | What Changes Internally | What Producer Sees |

| ≥ 1.50 | Healthy / Pass | Annual review cadence | Normal renewal |

| 1.10 – 1.49 | Acceptable | Loan officer flags trend | Nothing visible |

| 1.00 – 1.09 | Special Mention (Watch List) | Quarterly monitoring, credit grade shifts | Unchanged rate; extra info requests |

| Below 1.00 | Substandard | Capital reserving up, workout plan required | Covenant letter, restructure talks |

| Below 1.00 + high D/A | Doubtful / Liquidation | Moves off workout track | Options narrow to asset sale |

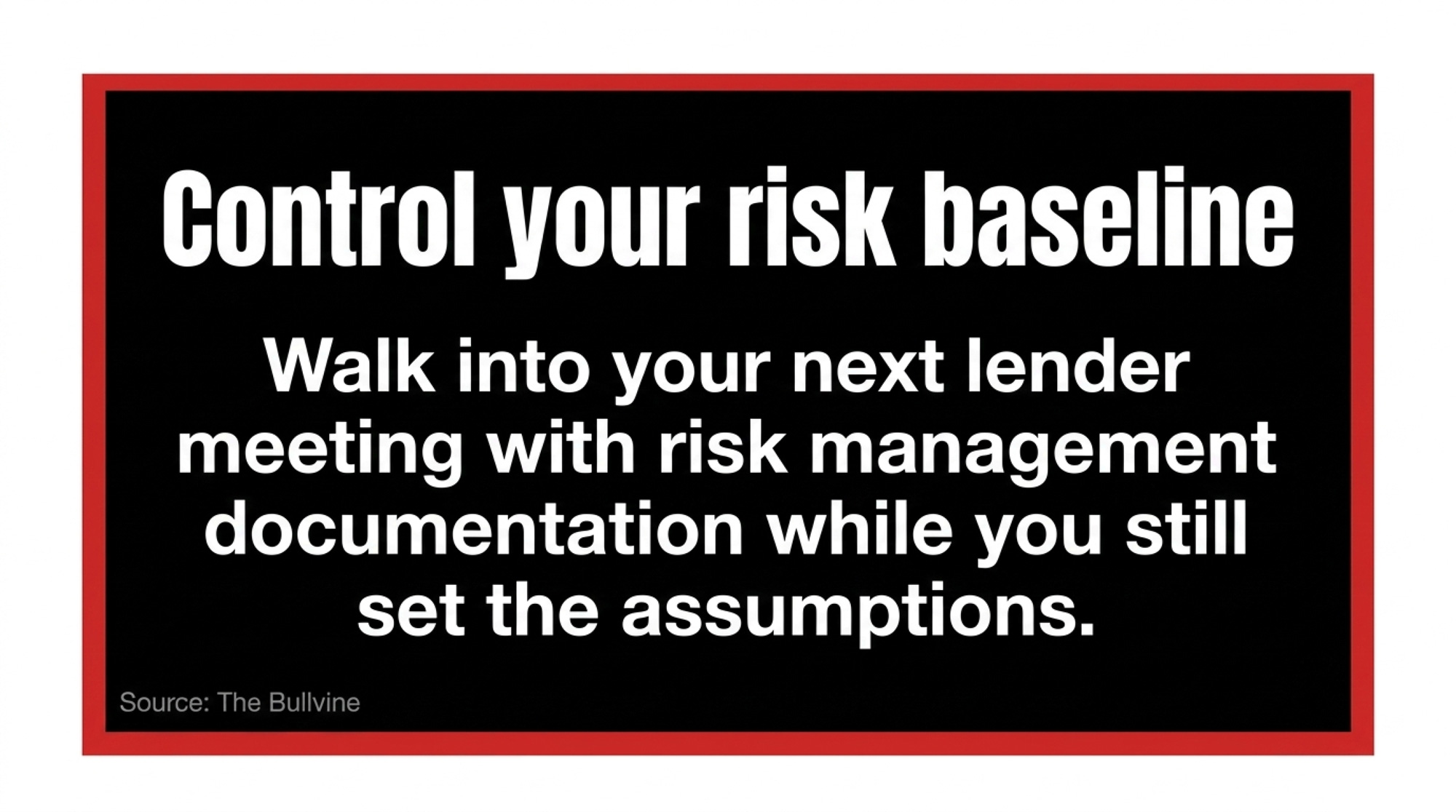

That leverage window only opens if a producer walks in before the lender builds the next credit memo around unhedged assumptions.

The 30/90/365-Day Playbook for Herds Like McCarty’s

30-Day Actions — Urgent Checks

1. Audit calf-sale buyer concentration. Pull your last 12 months of calf sales by buyer and spec. If one buyer received more than 60% of volume, you have single-buyer concentration risk. Price your calves at your regional auction spot to establish the discount baseline if that buyer changes terms.

- Requires: your own sales records plus one USDA AMS auction report

- Red-flag trigger: DSCR below 1.20 for two consecutive review periods on your lender’s calculation method — treat as urgent, not strategic

- Where it backfires: shopping buyers too aggressively without documentation can cost you your current buyer’s priority list

2. Enroll LRP on the current and next calf crop at 90–95% coverage. Net premium after RMA subsidy on a 240-calf program runs roughly $11,300 per year at current schedules.

- Requires: a crop insurance agent call and 5–7 business days

- Where it backfires: buying LRP reactively after a correction gives you protection without leverage — enroll before the next renewal, not after the next crisis

3. Calculate your beef revenue share of gross. Above 10–12%, your lender is probably already treating it as recurring income whether you are or not.

90-Day Actions — Structural Adjustments

1. Model a formal downside scenario. $1,050 calves, $125/cwt cull cows, milk at $18.00/cwt simultaneously. Does the operation survive 12 months at those levels without restructuring?

- Requires: 2–3 hours with your books and your CPA or farm financial advisor

- Threshold: if that scenario puts your DSCR below 1.10, you’re on a watch list the lender hasn’t told you about yet

2. Contact at least two alternative calf buyers. Feedyards, backgrounders, direct-to-packer programs — document their current specs and pricing. You don’t need to change buyers. You need to know your options.

3. Bring risk-management documentation to your lender as a mid-year update. Your LRP endorsement, a one-page DSCR scenario table, and a written breeding plan — framed as risk management, not remediation.

- What it does: changes which number the lender stress-tests at renewal

- Where it backfires: walking in without documentation lets the lender set assumptions you didn’t help shape

365-Day Moves — Strategic Positioning

1. Set a formal revenue concentration cap. Bullvine’s October 2025 analysis and Farm Credit East guidance both point toward 10% of gross as the threshold where beef revenue should carry the same formal risk management infrastructure as milk.

2. Align your genetics program with your replacement math. If your herd needs 22% replacement annually and you’re breeding 55% to beef, you need 98%+ conception and zero heifer death loss to break even on inventory — math that rarely works at scale. Genomic-tiered breeding typically yields 35–40% effective beef breeding on screened animals without starving your replacement pool.

3. Negotiate written buyer agreements. Documented premium specifications, price-determination methods, and advance-notice terms for spec changes. Most buyers will provide this. Most producers haven’t asked.

- Opportunity signal: if your beef basis has narrowed and your milk margin over feed has held through Q3 2026, you have room to negotiate firmer terms before the next buyer renewal

What This Means for Your Operation

Three specifics, tied to numbers you can check this week:

- If beef revenue exceeds 10–12% of gross, it’s already in your lender’s recurring-income model. Act on that assumption or let someone else set it.

- If you’re above 55% beef breeding with replacement purchases at current heifer prices, you’re arbitraging two cyclical markets against each other — and both cycles project correction into 2027.

- If your operating note contains standard MAC language and you’re carrying unhedged beef revenue, a single-cycle correction can trigger covenant review without any action on your part.

The Trade-Off at the Heart of It

Beef-on-dairy isn’t the problem. Running it like a side hustle when it’s become a business line — that’s the problem.

Operations that scaled beef breeding to 50–60% built revenue streams worth hundreds of thousands of dollars annually at 2025 prices, per Bullvine modeling across representative herd sizes. That revenue was transformative when milk margins compressed. None of that is in dispute.

What’s also real: FAPRI projects cattle prices declining from 2027 as feeder supply rebuilds with cow-calf profitability driving retention. The $531/head premium a beef-cross commands over a Holstein calf — per the University of Tennessee’s 2025 analysis of USDA AMS data — depends on tight native supply. A structural advantage today that turns cyclical from 2027 forward.

Producers who weather the transition will already know three things about their own operation: how much of the gross comes from beef, how many buyers that revenue depends on, and what the operation looks like at 25% lower calf prices. Most can answer the first. Fewer can answer the second. Almost none have formally answered the third.

Which of those three numbers could you pull up before dinner tonight — and what does your operating note actually say about material changes to your risk profile?

Key Takeaways

- If beef revenue is already north of 10–12% of your gross, your lender is treating it as recurring income whether you classified it that way or not — and the MAC clause in your operating note doesn’t need your permission to reopen terms.

- Run the 25%-down scenario on your own numbers before your next renewal: $1,050 calves, $125/cwt culls, $18.00/cwt milk. If that combination drops your DSCR below 1.10, you’re on a watch list nobody’s told you about yet.

- LRP at roughly $11,300/year on a 240-calf crop is the small hedge. The $64,000–$96,000 replacement-heifer bill behind 55% beef breeding is the one that actually moves the balance sheet — and $585 in foregone replacement value rides on every beef service to a cow that could’ve carried dairy.

- FAPRI has cattle prices turning down from 2027 as the native herd rebuilds, so the $531/head crossbred premium is structural today and cyclical tomorrow. Walk into your lender with LRP documentation and a DSCR scenario table while you still set the assumptions.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- $3,010 Per Heifer. 800,000 Short. Your Beef-on-Dairy Bill Is Due. — Arms you with the math to survive the 800,000-heifer shortage by exposing the $144,000 capital gap hidden in beef-on-dairy premiums. Verifies the 18% pregnancy rate threshold required to avoid a permanent replacement inventory collapse.

- The $16600 DMC Farm Bill “Win” vs a 0.9x DSCR: The 2026 Decision for 400‑Cow Herds — Delivers a brutal test for business-model viability by stripping away subsidy illusions to reveal your ‘no-program’ DSCR. Forces the decision between disciplined cost-culling and a controlled exit before lender intervention mandates the outcome.

- $1 Labor or $200,000 Debt? The Robotic Milking Bet That Could Make or Break Your Dairy — Protects your capital by exposing the robotic milking trap where $200,000 in annual payments creates a captive-buyer relationship. Dismantles the labor-savings myth to reveal the 7-year red-ink runway required before automation generates a true upside.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.