Mid-size dairies are discovering they have 18 months to pick: premium, scale, or strategic exit

EXECUTIVE SUMMARY: Rabobank’s projection that 7-9% of U.S. dairy operations will disappear annually through 2027 isn’t just another statistic—it represents roughly 2,800 farms making their final milkings each year, with mid-size operations bearing the brunt of this consolidation. What farmers are discovering through hard experience is that traditional 150-400 cow dairies face an impossible equation: spending $35,000-$55,000 annually on calf management labor while those calves generate just $15,000-$30,000 in net returns. Research from Cornell and Wisconsin’s dairy programs confirms that the industry is bifurcating into two distinct models—premium differentiation, which captures 50-75% price premiums for the 20-25% of producers near metropolitan markets, and efficiency-focused operations that achieve costs $3-4 per hundredweight below average through scale and technology. The next 18 months represent a critical decision window, as environmental regulations tighten, the Farm Bill implementation begins, and processor consolidation accelerates the pressure on uncommitted operations. Here’s what’s encouraging: producers who recognize this shift and commit fully to one path—whether premium, efficiency, or strategic transition—are finding renewed profitability and purpose. The conversation isn’t about whether change is coming; it’s about choosing your direction while you still have options to shape your farm’s future on your terms.

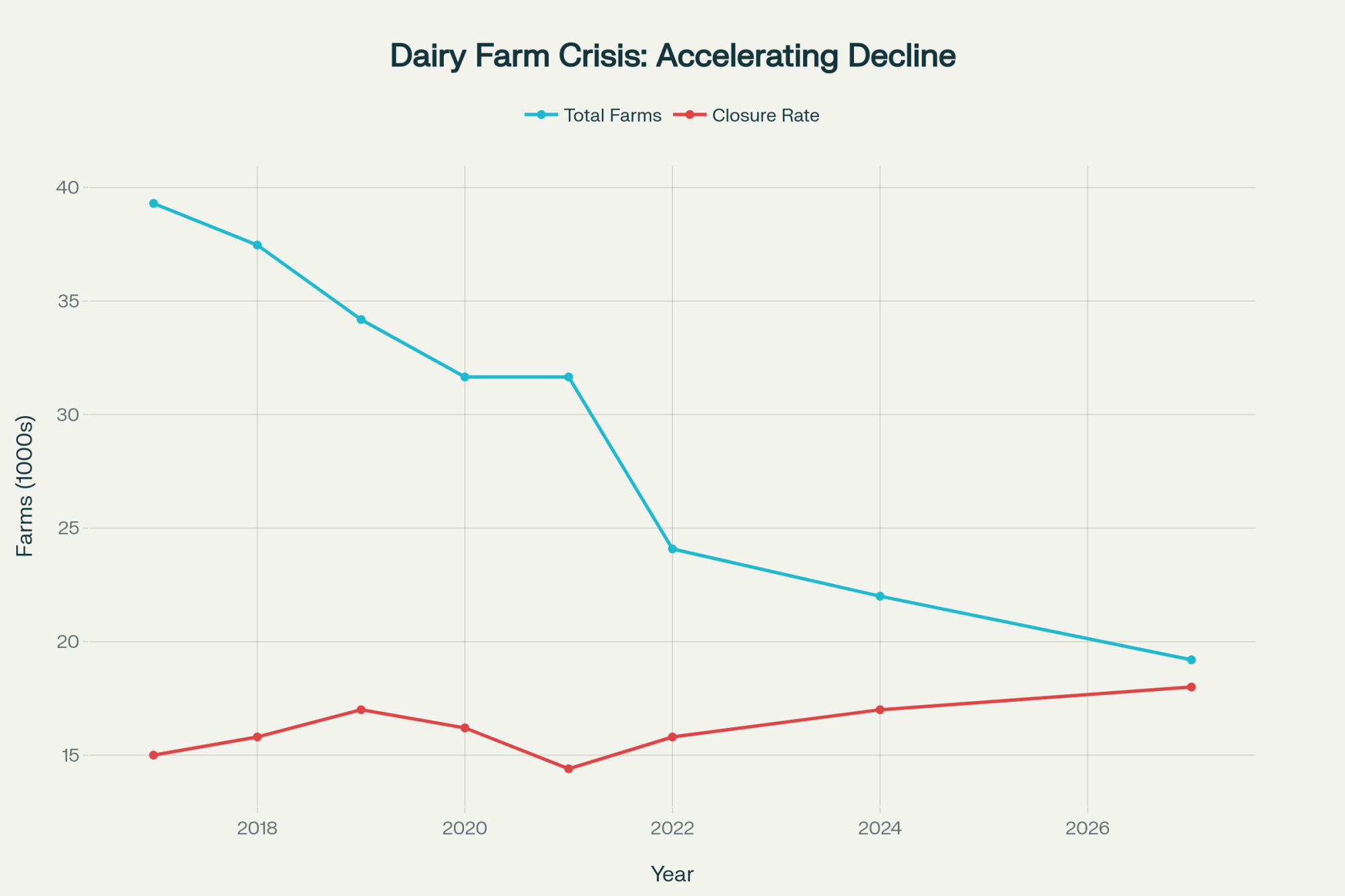

According to Rabobank’s latest North American dairy outlook, we’re losing 7-9% of U.S. dairy operations annually through 2027—that’s potentially 2,800 farms disappearing each year. Walking through a 500-cow operation in County Roscommon last week, where Irish media reports indicate that Department of Agriculture inspections uncovered systematic management failures that had developed over several years, I saw firsthand what happens when mid-sized operations get caught between two increasingly divergent business models.

Here’s why the next 18 months matter: Environmental regulations are expected to tighten in key regions by 2026. The next USDA Farm Bill cycle begins implementation. And consolidation accelerates at a pace that makes waiting increasingly costly. The window for proactive choices is narrowing fast.

Understanding the New Economics of Dairy Farm Profitability

Let me share some numbers that a Wisconsin producer showed me last month, as they reveal the impossible math that breaks traditional dairy models.

Consider a 500-cow operation—substantial by most regional standards, right? With normal breeding patterns, you’re managing approximately 250 bull calves annually. In current markets, based on what I’m seeing in USDA market reports, those dairy bull calves typically bring $50 to $200, depending on breed and season. Even with beef-cross breeding programs—which data from Cornell shows about two-thirds of Northeast dairies have now adopted—prices generally range from $150 to $400 in stronger markets.

The best-case scenario generates approximately $30,000 to $50,000 in gross revenue from the entire calf enterprise. After accounting for transportation, health management, and the typical 8-12% mortality rate that even well-managed operations experience, net returns often fall to $15,000 to $30,000.

Now, here’s where it gets uncomfortable: hiring dedicated calf management costs $35,000 to $55,000 annually, based on current agricultural wage data, excluding benefits and overhead.

You’re spending double on labor what the entire calf enterprise generates.

As one producer in central Wisconsin put it: “That math doesn’t work.” And you know what? It’s not just a Wisconsin problem. Down in the Southeast, where heat stress adds another layer, a Georgia dairyman running 600 cows told me at a recent conference: “Between June and September, my calf mortality jumps to 15%. The cost of climate-controlled housing would bankrupt us, but the losses are killing us slowly anyway.”

What’s happening in Florida is even tougher. A producer near Okeechobee shared that their summer calf mortality can hit 20% without intensive management. “We’re basically choosing between two ways to lose money,” she said.

Learning from Different Models Around the World

What’s particularly revealing is how various countries have addressed these structural challenges. Each approach tells us something about potential pathways forward.

Canada’s Quota System: When Compliance Becomes Valuable

Canadian dairy producers operate within a unique framework. According to recent data from the Canadian Dairy Commission, production quotas in provinces like Ontario currently trade at significant values—tens of thousands of dollars per kilogram of butterfat. A typical 70-cow operation might hold a quota worth well over a million dollars. Their proAction program, mandatory since 2017, ties welfare compliance directly to market access.

“The validation costs us about CAD$400 every two years,” a producer near Guelph told me during a recent Ontario farm tour. “But if we lose compliance, we can’t ship milk. That quota value? Gone. It completely changes how you think about management decisions.”

What I’ve noticed is that Canadian producers rarely discuss cutting corners on animal care. When your compliance is tied to an asset worth more than most people’s retirement funds, you find ways to make it work.

The Netherlands: Environmental Limits as Management Boundaries

The Dutch discovered something fascinating, almost by accident. After EU milk quotas ended in 2015, they implemented phosphate rights to manage environmental concerns. Research from Wageningen shows that this system effectively caps expansion—farmers must either acquire additional phosphate quotas or invest in manure processing, which typically costs between €10 and €25 per ton, sometimes more.

A researcher at Wageningen explained it well during a recent webinar: “We didn’t intend to prevent management overreach. But when expansion requires such significant capital investment, farmers naturally stay within their management capacity.”

Denmark: Market Premiums for Higher Standards

Denmark represents yet another model. Based on industry data from their agricultural council, they’ve implemented enhanced welfare standards beyond EU requirements. More importantly, cooperatives like Arla support these through sustainability incentive programs—real money per kilogram that can add up to thousands of euros annually for an average farm.

Robotic Systems in the Mountain West: A Different Path

What I’ve been watching with interest is how Mountain West producers are approaching this differently. I visited a 240-cow operation near Twin Falls, Idaho, that installed robotic milking units a few years back. “We went from three full-time employees to one,” the owner explained. “The robots cost us several hundred thousand, but we’re saving over $100,000 annually in labor. More importantly, our cows are healthier—somatic cell count dropped significantly.”

That’s not a path for everyone—you need reliable power, technical support within driving distance, and cows that adapt to the system. However, it demonstrates how technology can bridge some gaps for mid-sized operations.

The Emerging Bifurcation: Dairy Consolidation Trends Accelerate

Through conversations with agricultural economists at various land-grant universities, as well as lenders from Farm Credit and other institutions, a clear pattern emerges. As one Cornell economist recently put it: “We’re watching the industry split into two distinct business models, with the traditional middle ground becoming economically unsustainable.”

The Premium Path: Quality and Differentiation

Research from the USDA and analyses from agricultural lenders suggest 20-25% of production is moving toward differentiated markets. These operations capture real premiums—but success requires specific conditions.

Organic Valley’s latest member report shows that their farmers are receiving significantly higher prices—sometimes 50-75% premiums over conventional prices. But achieving this requires patient capital and proximity to premium markets.

A Vermont organic producer who successfully transitioned shared a valuable perspective at a recent conference: “Year one through three, we lost money. Years four through six, we broke even. Since year seven, we’ve been profitable. But that seven-year journey? Not everyone can make it.”

Here’s what consumer research consistently shows: only about a quarter of consumers regularly pay meaningful premiums for differentiated dairy products—and they’re concentrated in metropolitan areas with higher household incomes.

Beyond organic, there’s a young farmer in Texas who’s found success with A2 milk production. “We’re getting a 30% premium selling directly to Houston markets,” she told me. “But it took two years to build the customer base, and we had to change our breeding program completely.”

The Efficiency Model: Scale and Optimization

The majority of production—roughly 75%—continues moving toward efficiency-focused operations. USDA Census data shows the average U.S. dairy herd has grown significantly over recent years, with the largest operations now producing well over a third of the nation’s milk.

Mike, who manages 850 cows near Eau Claire through a combination of owned and leased facilities, shared his approach: “Every decision focuses on efficiency. We utilize precision feeding systems that significantly reduce feed costs. Automated health monitoring catches issues days earlier. Our per-hundredweight production cost runs well below the state average. In volatile markets, that’s survival.”

When milk prices experience significant volatility—as we have seen in recent years—large, efficient operations tend to survive, while smaller farms often struggle to cover their operating costs.

A California producer running 3,000 cows in the Central Valley puts it differently: “We’re not farming anymore, we’re manufacturing. Every process is standardized, measured, and optimized for efficiency. It’s not romantic, but it keeps us in business.”

The Challenge for Mid-Size Operations

Here’s where it gets difficult for operations between 150 and 400 cows—what USDA classifies as mid-size commercial dairies. They’re too small for significant economies of scale but too large for niche marketing approaches.

Research from dairy profitability programs consistently shows farms in this range have the highest per-hundredweight production costs and lowest return on assets. They incur compliance costs similar to those of larger operations but can’t spread them across a sufficient production volume.

A third-generation producer near Viroqua who recently sold his 185-cow operation explained: “We calculated everything honestly. After debt service, family living, and reinvestment needs, we were left with a net annual income of $18,000 for 70-hour weeks. The solar lease on our land now generates $52,000 annually with zero labor.”

This isn’t failure—it’s recognition of changed economics. And you know what? More folks are coming to similar conclusions.

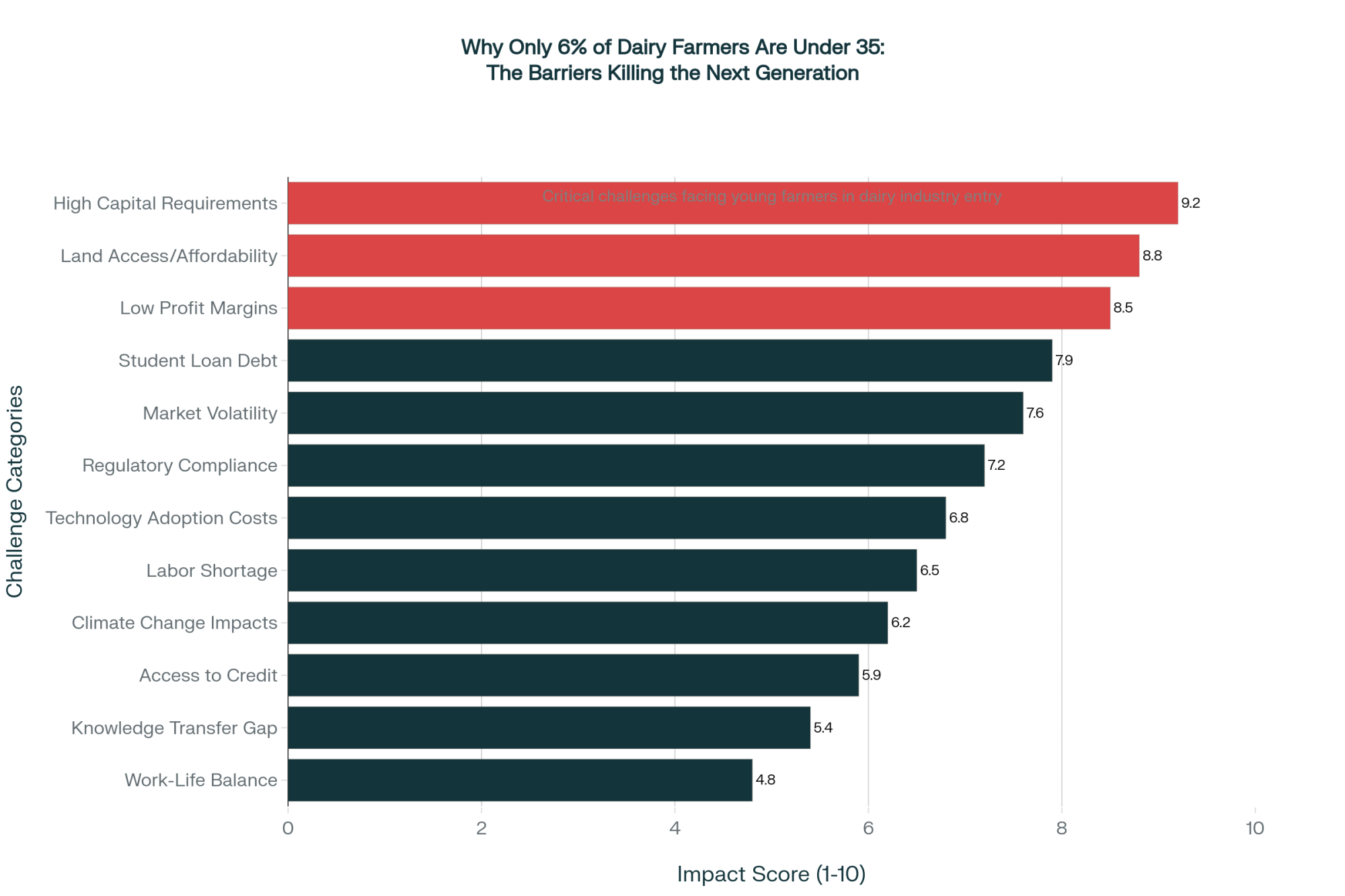

Young Farmers Face Unique Pressures

What worries me most is what I’m hearing from young producers. At a recent young farmer conference in Madison, the mood was notably different than even two years ago.

“My parents want me to take over our 220-cow operation,” a 26-year-old from Minnesota told me. “But the numbers don’t work. I’d need to double the herd size to make it viable, which would mean incurring $2 million in debt. Or transition to organic, which means seven years of uncertainty. Either way, I’m betting my entire future on factors I can’t control.”

But there are success stories too. I met a 28-year-old in Pennsylvania who took over her family’s 180-cow operation and immediately began bottling milk on the farm. “We’re capturing $4 more per gallon than commodity pricing,” she said. “It was scary taking on the debt for processing equipment, but we’re actually profitable now.”

Data from beginning farmer programs shows dairy has the lowest rate of young farmer entry among agricultural sectors—just 6% of dairy farmers are under 35, compared to 8% across all agriculture. That should concern all of us.

Technology’s Role and Limitations

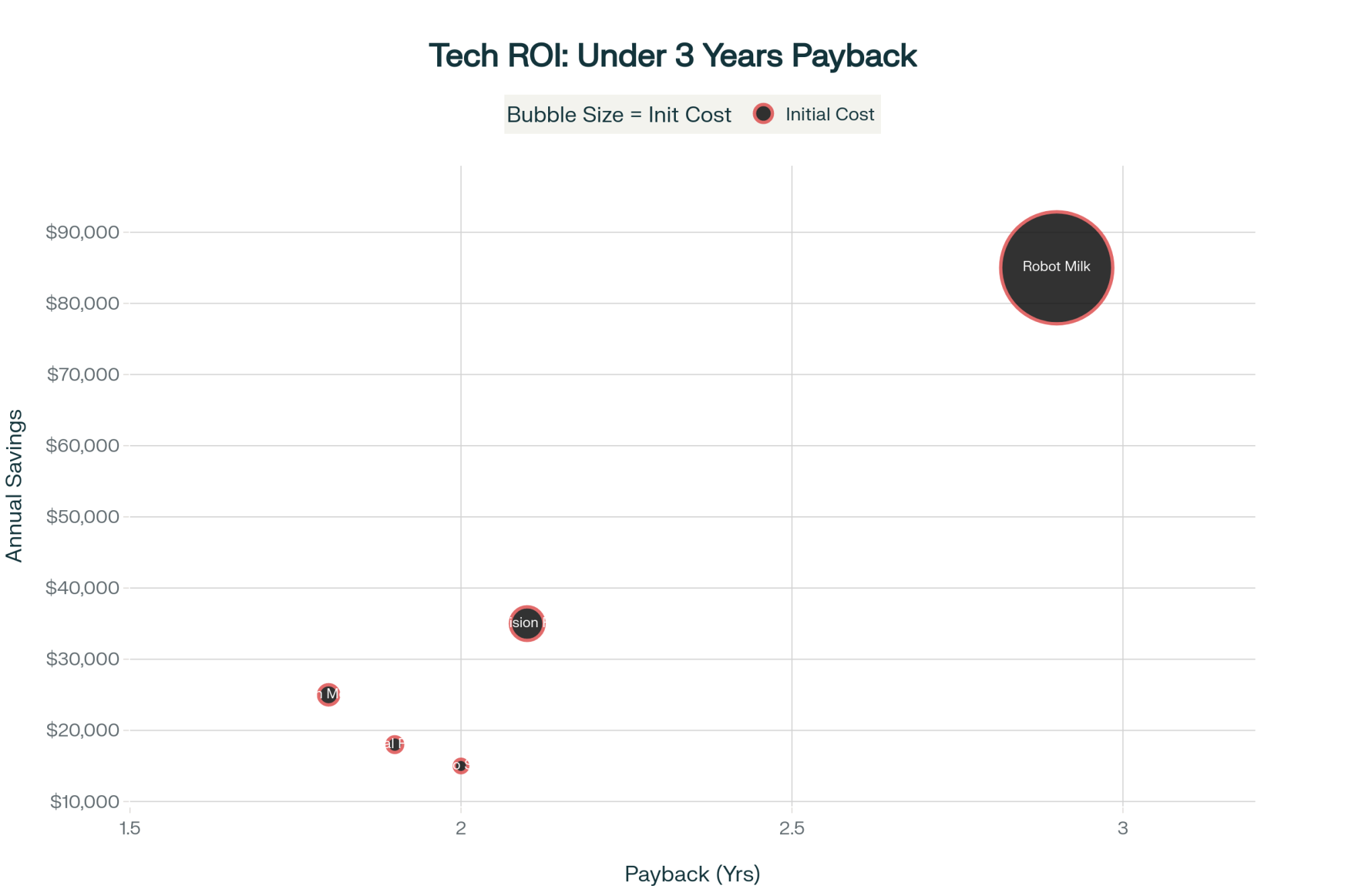

Examining precision dairy technologies reveals genuine benefits. Recent research in dairy science journals indicates that automated health monitoring can significantly reduce treatment costs and improve conception rates. Several Wisconsin producers report real improvements from adoption.

Yet technology alone won’t resolve structural challenges. Studies consistently find that most commercially available precision dairy systems haven’t been independently validated for all their claims.

As one precision dairy specialist noted at World Dairy Expo: “Technology amplifies good management. It doesn’t replace it or change basic economic realities.”

Carbon Credits and Environmental Opportunities

One emerging opportunity that’s still developing: carbon markets. California’s Air Resources Board offset program now includes dairy digesters, paying substantial amounts per metric ton of CO2 equivalent reduced. A large operation with a digester can generate $150,000 to $200,000 annually in carbon credits.

But here’s the catch—digester installation costs run into the millions, and you need consistent manure management to make it work. Plus, these programs favor larger operations that can afford consultants to navigate the complexity.

“It’s another way the big get bigger,” a medium-sized producer in California told me, shaking his head. “We looked at it, but the upfront costs and ongoing management requirements put it out of reach.”

What The Next 18 Months Will Bring

Based on regulatory filings, market projections, and discussions with industry analysts, several trends are accelerating toward critical decision points:

Environmental Regulations (By June 2026):

- California’s methane reduction requirements are getting real teeth

- The Netherlands is continuing with a significant reduction in dairy cow numbers through buyout programs

- Wisconsin is implementing new phosphorus limits affecting hundreds of farms in sensitive watersheds

Market Consolidation (Accelerating Now):

- That 7-9% annual reduction in farm numbers continues through 2027

- Processor consolidation is creating fewer, larger milk buyers with stricter requirements

- Premium market growth is slowing from the previous rapid expansion

Economic Pressures (Building Through 2026):

- Federal Reserve keeping interest rates elevated through at least mid-2026

- Input costs are stabilizing but remaining well above pre-2020 levels

- Labor availability is declining, with visa costs increasing significantly

What farmers are finding is that these pressures compound each other. It’s not just one challenge—it’s all of them hitting simultaneously.

Making Strategic Decisions: Your Three Paths Forward

After analyzing hundreds of operations across different models, three viable strategies emerge. And honestly? There’s honor in all three choices.

Path 1: Commit to Premium Differentiation

Requirements:

- Location within a reasonable distance of metropolitan markets with substantial populations

- Capital for a multi-year transition period (typically several hundred thousand for a 200-cow operation)

- Willingness to develop direct marketing relationships or join an established cooperative

First Three Steps:

- Contact established premium cooperatives for transition planning—they offer mentorship programs

- Engage the USDA Natural Resources Conservation Service for transition funding opportunities

- Develop realistic cash flow projections with significant revenue discounts during transition

Success Example: A Vermont farm transitioned its 220-cow herd to organic production over a six-year period. They’re now grossing significantly more per hundredweight than regional conventional averages. “The transition nearly broke us,” the owner admits, “but we’re now set for the next generation.”

Path 2: Scale for Efficiency

Requirements:

- Access to capital for expansion (typically thousands per cow for facilities and equipment)

- Management systems for larger operations

- Ability to weather significant price volatility

First Three Steps:

- Develop an expansion feasibility study with an agricultural lender—many offer specialized dairy expansion analysis

- Investigate management partnerships or qualified labor sources

- Implement precision management technologies, starting with feed management, for the fastest return

Success Example: Three neighbors in Idaho formed an LLC, consolidating their operations into a single, larger facility. Shared labor, bulk purchasing, and professional management significantly reduce costs. “Individually, we were struggling. Together we’re competitive.”

Path 3: Strategic Transition

Requirements:

- Honest assessment of long-term viability

- Understanding of asset values and alternative uses

- Willingness to preserve equity while options exist

First Three Steps:

- Obtain a professional business valuation, including all assets

- Investigate alternative land uses (solar leases can generate substantial annual income in suitable locations)

- Consult a tax advisor regarding timing and structure

Success Example: A family converted their dairy to custom heifer raising and leased cropland, maintaining expertise while eliminating unprofitable segments. “We kept what we’re good at, eliminated what wasn’t working, and actually improved our quality of life.”

The Fourth Option: Cooperative Formation

What’s interesting is there’s potentially a fourth path emerging—small groups of producers forming new cooperatives. I’m watching a group of five 200-cow operations in Ohio that are exploring joint processing and marketing. “Individually we’re too small for premium markets, too big for farmers markets,” one explained. “Together we might have something.”

| Factor | Premium Path | Efficiency Path | Strategic Exit |

| Initial Investment | High ($500K) | Very High ($2M+) | Minimal |

| Time to Profitability | 5-7 years | 3-5 years | Immediate |

| Market Access | Limited/Regional | Global/Commodity | N/A |

| Labor Requirements | High Skilled | Automated/Tech | N/A |

| Regulatory Compliance | Complex | Standard | Minimal |

| Milk Price Premium | 50-75% | 0% | 0% |

| Risk Level | Medium | High | Low |

| Success Rate (%) | 25 | 60 | 90 |

Looking Ahead: The Industry We’re Building

The dairy industry continues evolving toward this bifurcated structure. This isn’t a temporary disruption—it’s structural realignment driven by global economic forces.

What encourages me is seeing producers who’ve found their path and committed fully. Whether it’s the organic producer in Vermont finally turning profits, the Wisconsin operation that merged with neighbors to achieve scale, or the family that transitioned to custom heifer raising—success comes from clear decisions and full commitment.

The industry needs both models. Premium producers cater to consumers who are willing to pay for specific attributes. Efficient operations meet global demand for affordable nutrition. What it can’t sustain is the uncertain middle ground where costs exceed commodity returns but premiums remain out of reach.

For those committed to the future of dairy, multiple viable paths exist. The key is choosing one that aligns with your resources—financial, geographic, and personal—and executing fully. Half-measures don’t work in this environment. They never really have, but now it’s obvious.

As spring flush approaches in a few months, Holstein operations may have different considerations than Jersey farms when it comes to component pricing and efficiency models. But regardless of breed, the fundamental choice remains the same.

The conversation we need isn’t about whether this transformation is happening—it’s about how individual producers will navigate it successfully. That decision window remains open, but based on every indicator I’m tracking, it won’t stay open past 2026.

Choose your path. Commit fully. Execute well. The future belongs to those who do.

KEY TAKEAWAYS

- The calf enterprise math reveals the deeper crisis: Mid-size dairies are spending $35,000-$55,000 on labor to manage calves worth $15,000-$30,000 net—and that’s just one symptom of why farms with 150-400 cows show the highest production costs and lowest returns according to Wisconsin’s Center for Dairy Profitability

- Three proven paths forward, each with specific requirements: Premium differentiation needs proximity to metro markets and 5-7 year transition capital; efficiency scaling requires $8,000-$12,000 per cow expansion investment; strategic transition preserves equity through alternatives like solar leases generating $800-$1,200 per acre annually

- Regional solutions vary, but the timeline doesn’t: Whether you’re dealing with Southeast heat stress pushing calf mortality to 20%, California’s methane regulations, or Wisconsin’s phosphorus limits affecting 580 farms—the 18-month window before 2026 regulatory changes remains constant

- Technology amplifies but doesn’t replace fundamentals: Automated health monitoring reduces treatment costs by 18% and robotic systems save $100,000+ annually in labor, but as precision dairy specialists confirm, these tools work only within economically viable business models

- Young farmers face unique pressures requiring creative solutions: With only 6% of dairy farmers under 35 (versus 8% across agriculture), successful transitions involve innovations like on-farm bottling, capturing $4 more per gallon, or forming new cooperatives where five 200-cow operations achieve together what they couldn’t alone

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Generate $15,000+ Annual Carbon Revenue: The Dairy Producer’s Guide to Getting Paid for Going Green – This guide reveals strategic methods for turning methane reduction into a profit center, using feed additives and Section 45Z to generate $15,000+ annual revenue. Learn how to utilize government cost-share programs to finance your environmental transition.

- Why This Dairy Market Correction Feels Different – and What It Means for Our Farms – Dive deeper into the 18- to 24-month market correction driven by global forces like China’s import drop and New Zealand’s production surge. This analysis reveals why aggressive cost management and diversification are critical to surviving and acquiring assets.

- Robotic Milking Revolution: Why Modern Dairy Farms Are Choosing Automation in 2025 – This case study-rich piece debunks the myth that robots are only for massive dairies, proving that mid-sized farms (200-500 cows) see the best ROI and labor savings. Discover how automated precision data improves health and production.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.