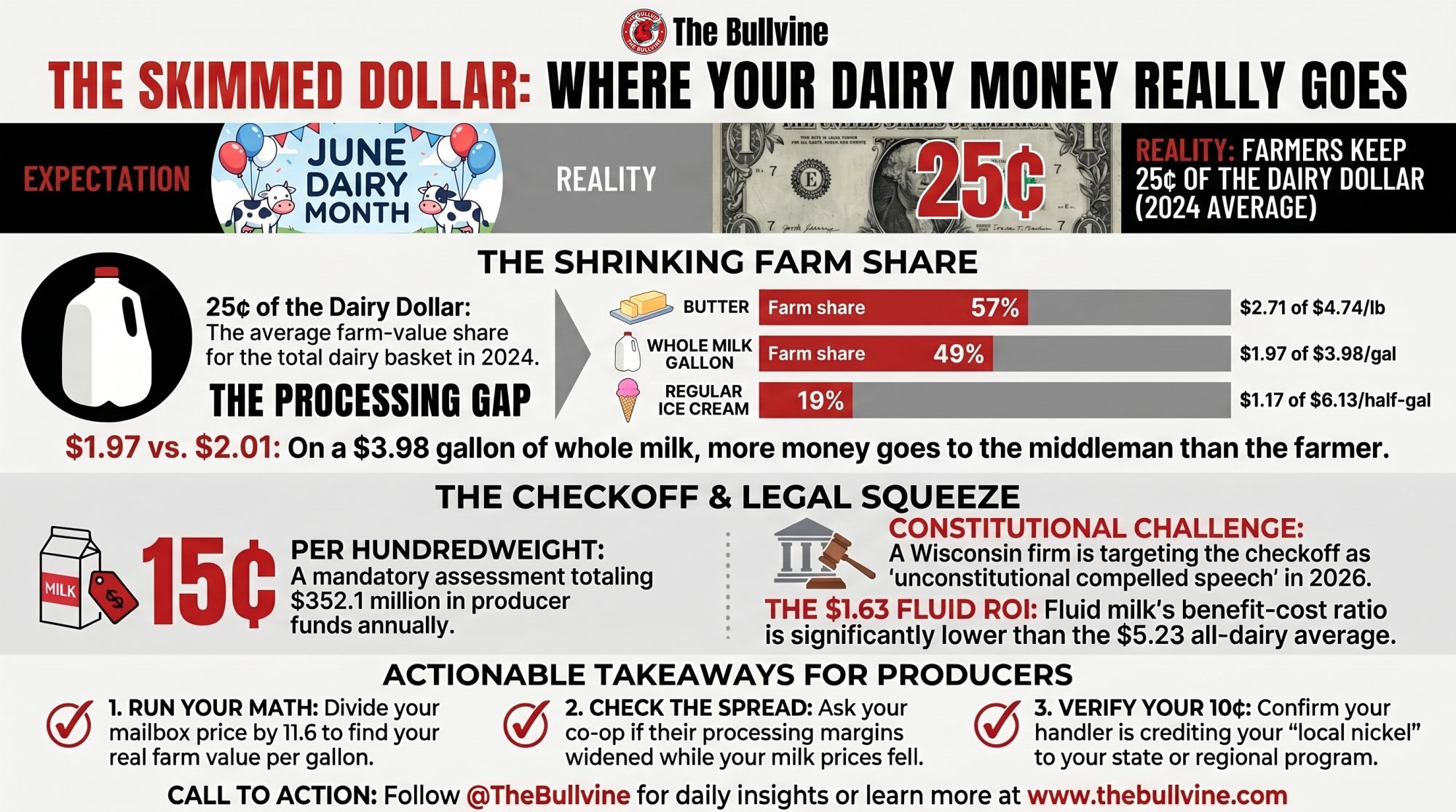

They’ll ask you to pose with a calf this June. Then you go home to the milk check: $1.97 of that $3.98 gallon is yours. The other $2.01 never reaches the tank — and a Wisconsin firm wants a say over your 15¢ next.

Editor’s note: “the Reillys” below is a composite scenario, modeled from public ERS price data and typical Northeast fluid-shipper economics — not a single real farm. Every number attached to them is sourced and real; the operation itself is illustrative, in the same way our $97,000 Breeding Meeting feature was framed.

Picture a 140-cow tie-stall in the St. Lawrence Valley — call them the Reillys, a stand-in for the fluid shippers across the Northeast doing exactly this math. June Dairy Month banners go up at the co-op, the FFA kids hand out string cheese at the county fair, and somebody asks the Reillys to pose with a calf for the local paper. They smile for it. Then they go home and look at the milk check.

Because here’s the question that’s been gnawing at operations like theirs: of the $3.98 a consumer paid for a gallon of whole milk in 2024, how much actually landed in their tank?

About $1.97. The other $2.01 went to everybody between the bulk tank and the dairy case.

That’s not a grievance — it’s USDA Economic Research Service data, the agency’s own farm-share series, released June 2025. And honestly, for fluid whole milk, 49% isn’t a bad number. It’s the rest of the dairy aisle where the floor fell out. This June, that number collides with a courtroom: a Wisconsin law firm that just settled an 11-month case against USDA says the checkoff every farmer like the Reillys funds is its next target.

The lawyers showed up to the party uninvited

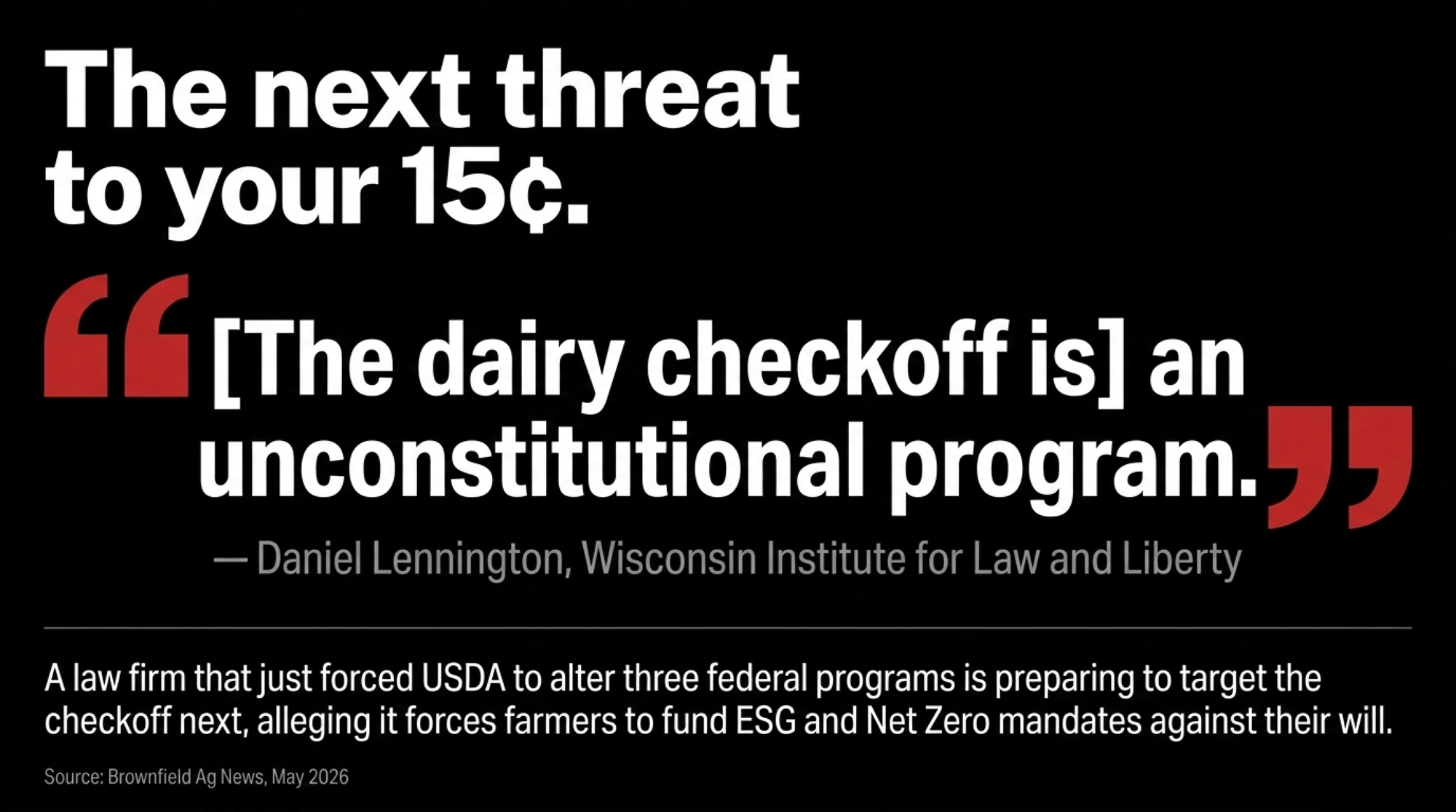

On May 27, 2026, Wisconsin Institute for Law and Liberty deputy counsel Daniel Lennington told Brownfield Ag News the dairy checkoff is “an unconstitutional program.” The timing isn’t subtle. He’s raising the fight during the one month of the year the checkoff is most visible.

Lennington alleges checkoff dollars are flowing into “ESG, environmental social governance programs (including) the Dairy Net Zero program” — work that, in his words, goes “to basically blame dairy farmers and blame cows for global warming,” while requiring “even small farmers to fill out all sorts of disclosures.” The program’s legal mandate, he says, is to promote the purchase of dairy products, “and nothing more.” There’s a factual core under the claim: the Foundation for Food & Agriculture Research announced a $10 million grant supporting dairy’s Net Zero Initiative in 2021, a program co-created with the Innovation Center for U.S. Dairy. The industry casts that work as protecting market access and meeting its 2050 stewardship goals — not as an attack on farmers.

This isn’t an idle threat. The same firm just settled the Adam Faust case, in which USDA agreed to strip race- and sex-based “socially disadvantaged” designations from three federal programs — the Dairy Margin Coverage fee, the Loan Guarantee Program, and EQIP — after the U.S. Department of Justice announced on February 9, 2026 that it would abandon its defense of two of them as unconstitutional. They win cases. So when they say the checkoff is next, the Reillys’ co-op delegate is right to pay attention.

To be clear about what this is and isn’t: these are allegations and legal arguments, not court findings. No complaint against the checkoff has been filed yet. And the legal ground is genuinely contested history. A federal appeals court actually struck the dairy checkoff down once — in Cochran v. Veneman (2004), the Third Circuit ruled that compelling Pennsylvania dairy farmers to fund generic milk promotion violated the First Amendment. Then the Supreme Court changed the landscape a year later: its 2005 Johanns v. Livestock Marketing Association decision — a beef checkoff case — held that checkoff promotion is the government’s own speech, and therefore immune from compelled-subsidy challenge. That government-speech doctrine has shielded the dairy program ever since. WILL’s new theory tries to thread that needle: if checkoff dollars fund environmental messaging that falls outside “promotion of the sale and consumption of dairy products,” is it still the government speech Johanns protects? That’s the question no court has been asked in those exact terms.

It’s not the only mandatory dairy program in court this spring, either. In a separate and unrelated case, Organic Valley, Horizon, and Aurora filed constitutional challenges to the Federal Milk Marketing Order system in spring 2026, with a group of Organic Valley farmers adding a Fifth Amendment takings claim. Different program, different argument — but a sign that the legal machinery underneath dairy’s mandatory structures is being tested from several directions at once.

June Dairy Month was always a marketing play — and that’s the point, not the insult

Start with the origin story, because it explains everything that followed. June Dairy Month launched in the late 1930s as “National Milk Month,” a response to a seasonal milk surplus. The goal wasn’t sentiment. It was inventory.

Refrigeration had improved, cows were flush on spring grass, and the market was drowning in milk. The industry needed Americans to drink the surplus before it spoiled. So it built a celebration around the problem.

Nearly nine decades later, the machine is bigger and the surplus never left. USDA’s February 2026 WASDE pegged the 2026 all-milk price at $18.95 per hundredweight, down from a revised $21.17 in 2025. And January 2026’s announced Class III price came in at just $14.59. The cows are still flush. The market’s still long. And June still arrives like clockwork to remind everyone how wholesome it all is.

Here’s the part nobody prints on the banner: the Reillys are paying for the party.

You fund the celebration at 15¢ per hundredweight — and you don’t control most of it

Every hundredweight the Reillys ship carries a 15-cent checkoff assessment, mandated under the federal Dairy Production Stabilization Act of 1983 and the Dairy Promotion and Research Order. Here’s the split most farmers can’t recite from memory: producers can direct up to 10¢ of that 15¢ to a qualified state, regional, or local program — and the other 5¢ goes to the national checkoff, the National Dairy Promotion and Research Board, which funds Dairy Management Inc.

| Checkoff Tier | Amount (¢/cwt) | Who Controls Spending | Benefit-Cost Ratio (fluid milk context) |

|---|---|---|---|

| State/Regional Programs | Up to 10¢ | Farmer-elected boards at state/regional level | Varies by program; farmer has direct delegate influence |

| National (NDPRB → DMI) | 5¢ mandatory | Dairy Management Inc. — not direct farmer vote | $1.63 on fluid milk (1995–2022 eval) ⚠️ |

| Total Producer Assessment | 15¢ | Split as above | $5.23 aggregate all-dairy (most recent Report to Congress) |

| MilkPEP (processors) | Separate: ~2¢/gal equivalent | Processor-governed; funds fluid milk campaigns | Fluid-specific; MilkPEP funds fluid promotion separately |

| 2022 aggregate collected | $352.1M producers + $79.7M MilkPEP | — | $431.8M total checkoff pool |

The dollars are real money in aggregate. In 2022, the most recent audited year in USDA’s September 2024 Report to Congress, the 15¢ producer assessment added up to $352.1 million, plus another $79.7 million from fluid milk processors through MilkPEP. DMI is the entity that turns the national share into demand campaigns — the “undeniably dairy” work, the pizza-chain partnerships, the sports tie-ins.

DMI’s own 2024 audited financials show total revenue of $165.7 million, down from $178.3 million in 2023. Domestic marketing ran $127.1 million; export programs took another $23.7 million. The catch for a fluid shipper: most of where that money lands isn’t something the Reillys vote on.

Does it work? Depends what you’re measuring. USDA’s congressionally mandated evaluation, authored by Texas A&M economist Oral Capps Jr., pegs the aggregate all-dairy benefit-cost ratio at $5.23 per dollar spent for the 1995–2022 period — meaning the model estimates $5.23 in economic value for every checkoff dollar. That’s a government-published number, and it’s the strongest case for the program.

But read the category breakdown in the same report, because not all dairy dollars perform alike. Butter returned $17.73 per dollar invested. Cheese returned $3.87. Exports, $8.63. And fluid milk — the product the Reillys anchor to — came in dead last at $2.68, the lowest-returning category of everything the checkoff promotes. Cheese, butter, and exports carry the program; the jug barely keeps pace. We laid that gap out in our recent breakdown of where the checkoff money actually goes. So when the checkoff celebrates June, the dollars are largely working for cheese and exports. The Reillys’ fluid-milk dollar is along for the ride.

Why do you keep half a fluid gallon but only a quarter of the basket?

Now the line that matters most. And it needs a careful read, because two different USDA numbers get mashed together constantly.

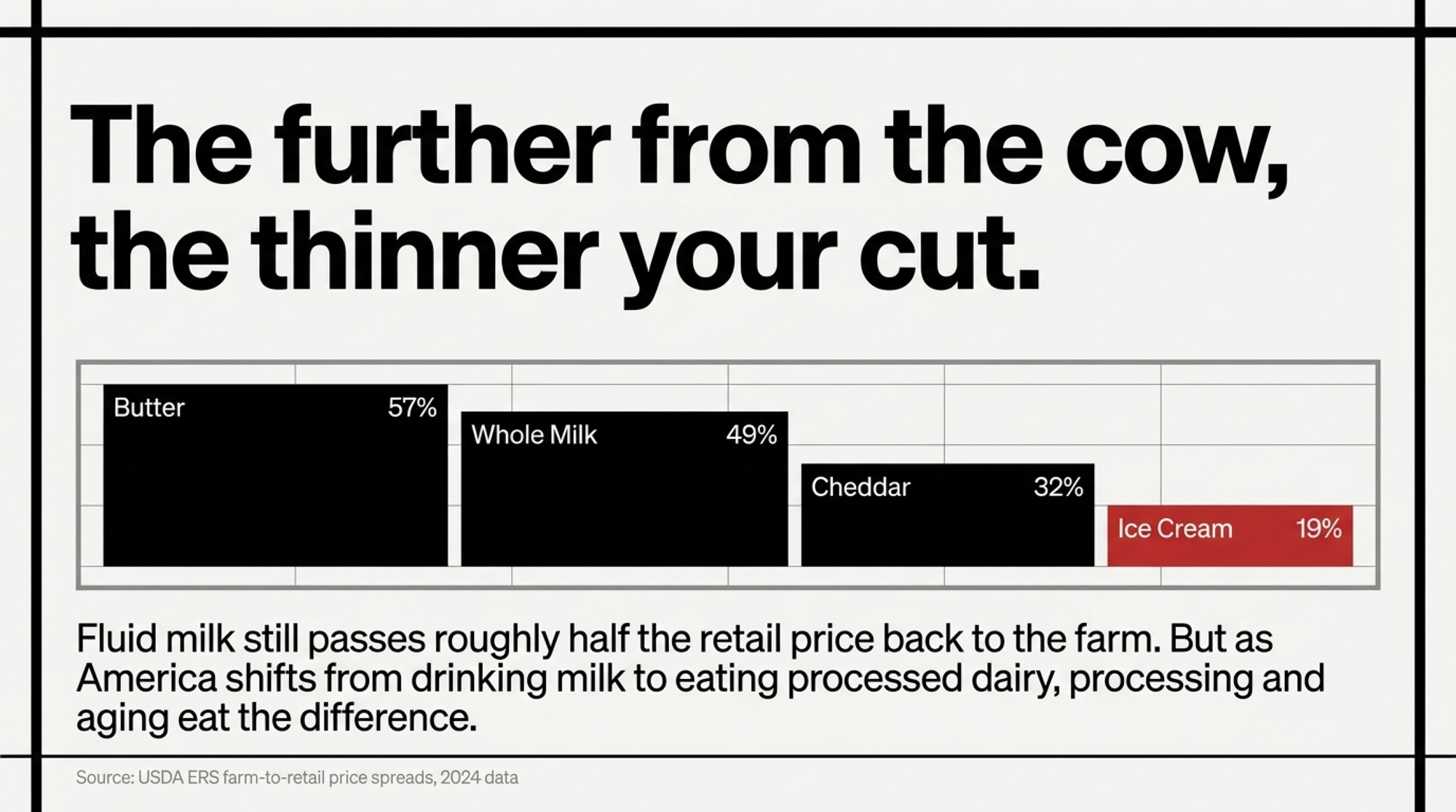

For a gallon of fluid whole milk, the farm share was 49% in 2024 — $1.97 of a $3.98 retail gallon, up from 47% the year before. The point figures move year to year, so treat any single year as a snapshot, not a trend line. Fluid milk still passes roughly half the retail price back to the farm.

For the total dairy basket — milk, cheese, butter, yogurt, ice cream, all of it — the farm-value share sat at 25% in 2024, up from 23% in 2023 but down from 28% in 2022. Here’s the contrast that should ruin the Reillys’ appetite:

| What’s being measured | Farm share, 2024 | What it tells you |

| Butter | 57% ($2.71 of $4.74) | Less processing, bigger farm slice |

| Whole milk gallon | 49% ($1.97 of $3.98) | Half the retail price still gets back to you |

| Cheddar cheese | 32% ($1.80 of $5.66) | Processing and aging eat the difference |

| Total dairy basket | 25% | Processed product keeps three-quarters downstream |

| Regular ice cream | 19% ($1.17 of $6.13) | The further from raw milk, the thinner your cut |

Source: USDA Economic Research Service, farm-to-retail price spreads, released June 2025. Butter and ice cream prices are per pound and per half-gallon, respectively.

Why the gap between 49% and 25%? Because America stopped drinking milk and started eating processed dairy. Cheese, ice cream, and value-added products carry far more processing and marketing value downstream — and almost none of it flows back to the farm gate. The more the dairy case tilts toward processed product, the smaller the Reillys’ slice of the total basket, even when their fluid share holds steady. We traced that erosion in our piece on how the milk dollar collapsed to 25¢. It’s the part of the story the June Dairy Month banner has never centered on.

“But milk’s a bargain” — true, and that’s exactly the trap

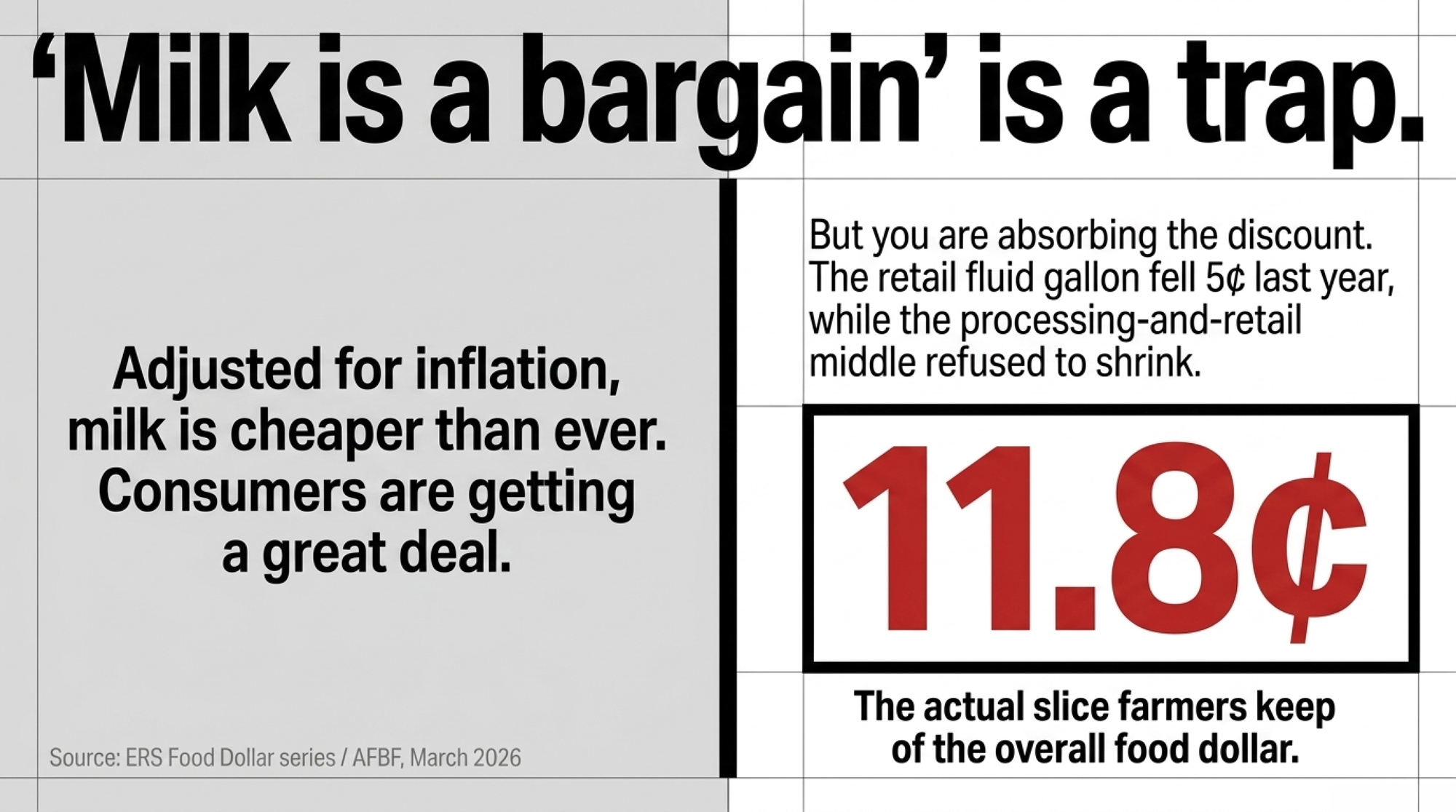

Here’s the defense you’ll hear, and it isn’t wrong. Adjusted for inflation, milk is cheaper than it was when the Reillys poured their last freestall. Consumers are getting a deal.

The problem is who’s absorbing the discount. The 2024 ERS data shows the moving parts: the retail whole-milk gallon actually fell five cents year over year, while the farm value rose nine cents — so that year, fluid milk’s farm share ticked up. But zoom out to all food and farmers kept just 11.8¢ of every dollar in 2024, down from 12.1¢ the year before, according to ERS’s Food Dollar series as summarized by the American Farm Bureau Federation in March 2026. After expenses, the same AFBF analysis puts farmers’ and ranchers’ combined net at 5.8¢ of the food dollar. The processing-and-retail middle is where the money sits, and it isn’t shrinking.

So “milk is a bargain” is true. The Reillys are just not the ones setting the price of the bargain.

How do you run the math on your own gallon — before the cake gets cut?

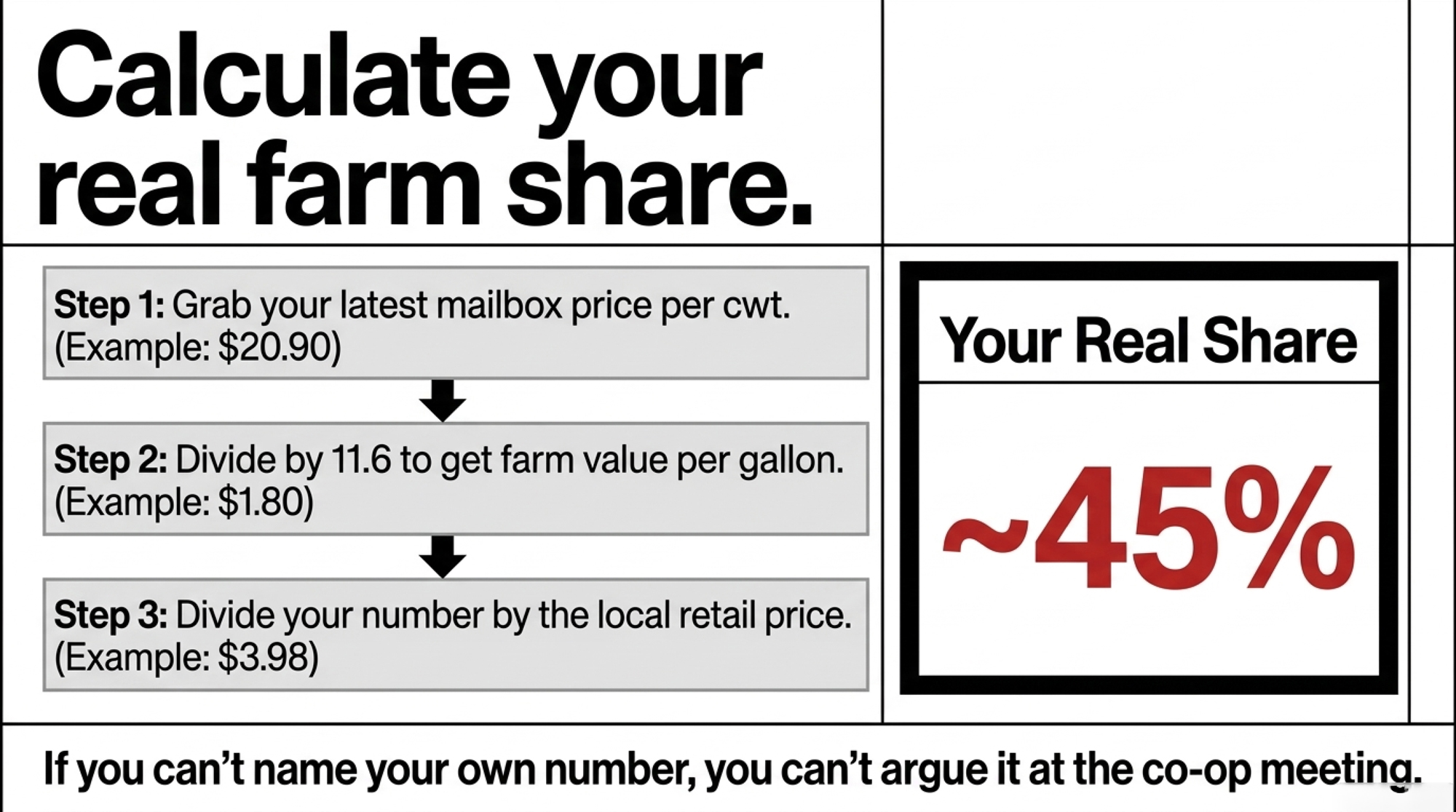

You don’t need a spreadsheet for this. Five minutes at the kitchen table turns a vague grievance into a number you can take to a lender or a co-op meeting. Here’s the four-step version the Reillys ran:

Step 1. Grab your latest mailbox price per hundredweight.

Step 2. Divide it by 11.6. (A gallon is about 8.6 lbs of milk, so a hundredweight covers roughly 11.6 gallons.) That’s your farm value per gallon.

Step 3. Stack it against the $3.98 retail gallon.

Step 4. Divide your number by $3.98. That’s your real farm share.

Run it at two prices and watch how exposed a fluid shipper is:

| Milk price | Farm value per gallon | Share of the $3.98 gallon |

| $20.90 mailbox | ~$1.80 | ~45% |

| $14.59 Class III (Jan 2026) | ~$1.26 | ~32% |

That bottom row uses a raw Class III base, not a mailbox price — so it’s a floor, not what actually hits a check after premiums and producer price differential. Either way, the point holds: you keep somewhere between a third and a half of a fluid gallon, and a lot less once the milk turns into cheese or ice cream.

Now the checkoff side. Shipping roughly 38,000 hundredweight a year (see the methodology note for the assumption behind that), the Reillys’ 15¢/cwt assessment comes to about $5,700 leaving the tank annually — and up to 10¢ of it can be directed to a qualified state program, with the national nickel funding DMI regardless. A 200-cow herd at the same per-cow output crosses $8,000; a 500-cow dairy clears $20,000. Small money per cow. Real money in aggregate — and most of it spent without a direct vote.

What does your processor’s product mix do to your check?

Here’s the operational piece the farm-share average hides. Two farms can ship identical milk and bring home different money, depending on what their buyer makes with it. A co-op spinning your milk into private-label fluid and commodity cheddar passes back a thinner slice than one selling branded specialty product, because every processing step downstream eats into the share that can flow back to raw milk.

That’s why the Reillys’ real exposure isn’t the national 25% — it’s their own buyer’s spread. If their co-op’s processing margin widened last year while the farmgate price fell, the squeeze this article describes is happening inside their own supply chain, not just in an ERS chart.

Options and trade-offs for your operation

This isn’t a problem you fix with a better breeding decision or a tighter ration. It’s structural. But three moves sit inside the Reillys’ control — and yours.

Pull your co-op’s annual report and check the spread — within 30 days. Find the processing margin alongside the farmgate price they announced. Then ask one question: did that spread widen when milk prices fell last year? You’re a member-owner. You’re allowed to ask. Costs nothing but an afternoon. The catch: a co-op that won’t break out processing margins has told you something too.

Confirm where your 10¢ is going, and weigh the checkoff against your product mix. You can’t opt out — it’s mandatory, and that’s exactly the fight WILL is picking. But up to 10¢ of your 15¢ can be credited to a qualified state or regional program where farmer-elected boards direct the spending. Pull a milk settlement statement, find the checkoff line, and confirm with your handler. And if you ship into a fluid market like the Reillys, fluid’s $2.68 benefit-cost ratio — the lowest of any category the checkoff funds — says the national promotion is doing the least for you. A reason to lean on your delegates, loudly.

Watch the WILL case as a real variable, not background noise. If a constitutional challenge is filed and advances, the assessment and how it’s spent could come under pressure within a couple of years. That’s not a reason to build your budget around it. It is a reason to know where your producer organizations stand before the question reaches you. The risk: these cases move slowly, and nothing may change for a long time.

Key takeaways

- If you ship into a fluid market, the checkoff has returned $2.68 per dollar on your product — the lowest of any category it funds, versus $17.73 for butter — so push your co-op delegates on spending priorities rather than assuming the promotion works for you.

- If you can’t name your own farm-share number, you can’t argue it. Run the four-step gallon math before your next lender or co-op meeting.

- If your 10¢ isn’t credited to a qualified state program, you’re losing local governance, not money — confirm with your handler this week.

- If your co-op won’t show you its processing margin next to the farmgate price, treat that opacity as data — and ask louder.

- If the WILL challenge is filed and advances, expect the checkoff’s structure and spending to come under pressure; know your producer org’s position now.

So what’s your real number?

The cows don’t know it’s June. They’ll eat the same ration, fill the same tank, and somebody in a boardroom will still build a campaign around it. The party’s real. So is the 25¢. The Reillys will pose with the calf again next year, because that’s who they are — but they’ll do it knowing exactly what their gallon is worth and exactly what their 15¢ is buying.

Methodology note. Farm-share and price figures are from USDA Economic Research Service farm-to-retail price-spread data, released June 2025 (2024 reference year): whole milk farm share 49% ($1.97 farm value / $3.98 retail gallon, up from 47% in 2023); butter 57% ($2.71 / $4.74 per lb); cheddar 32% ($1.80 / $5.66 per lb); regular ice cream 19% ($1.17 / $6.13 per half-gallon); total dairy basket 25% (23% in 2023, 28% in 2022). The 11.8¢ all-food farm share and 5.8¢ net figure are from ERS’s Food Dollar series, 2024 reference year, as summarized by the American Farm Bureau Federation, March 2026. Checkoff structure: 15¢/cwt assessment under the Dairy Production Stabilization Act of 1983 and Dairy Promotion and Research Order; producers may direct up to 10¢ to qualified state/regional programs, with 5¢ going national to the National Dairy Promotion and Research Board, which funds Dairy Management Inc. (per USDA AMS). The 2022 assessment totals ($352.1M producer; $79.7M MilkPEP processor) and all benefit-cost ratios are from USDA’s 2022 Dairy Report to Congress (published September 2024; covering 1995–2022; quantitative evaluation by Texas A&M economist Oral Capps Jr.): aggregate all-dairy BCR 5.23; fluid milk 2.68; cheese 3.87; butter 17.73; export 8.63; DMI-specific spending 6.51. (The fluid-milk BCR had fallen across prior evaluations — 3.26, then 1.91, then 1.63 — before rising to 2.68 in the current report.) DMI revenue figures ($165.7M in 2024; $178.3M in 2023; $127.1M domestic marketing; $23.7M export) are from DMI’s 2024 audited financial statements. Milk prices are from USDA WASDE/ERS (February 2026 WASDE: 2026 all-milk $18.95/cwt; 2025 revised $21.17/cwt; January 2026 announced Class III $14.59/cwt). Legal matters: the checkoff challenge is attributed to Daniel Lennington of the Wisconsin Institute for Law and Liberty as reported by Brownfield Ag News (May 27–28, 2026); the Adam Faust settlement details are from WILL’s May 2026 release and reflect the DOJ’s February 9, 2026 announcement; the $10M FFAR grant to dairy’s Net Zero Initiative was announced in 2021. Cochran v. Veneman (3rd Cir. 2004) struck the dairy checkoff down on First Amendment compelled-speech grounds; Johanns v. Livestock Marketing Association (U.S. 2005), a beef-checkoff case, established the “government speech” doctrine that has shielded checkoff programs since. The Federal Milk Marketing Order challenges by Organic Valley, Horizon, and Aurora are separate from the checkoff and were filed in spring 2026. Barn math: the ~$5,700 figure assumes a 140-cow herd at approximately 75 lbs/cow/day over 365 days (~38,300 cwt) × $0.15/cwt; per-herd figures scale at the same per-cow output. Gallon conversion uses 1 gallon ≈ 8.6 lbs of milk. All figures are USD.

Limitations. National averages may not reflect your region, herd size, product mix, or operation. Single-year farm-share figures are snapshots, not trends. Benefit-cost ratios are model estimates from a single congressional evaluation, not farm-level guarantees.

Conflict of interest. The Bullvine has no business relationship with Dairy Management Inc., the Wisconsin Institute for Law and Liberty, the Foundation for Food & Agriculture Research, or any party named in this article.

Corrections. Spot an error? Tell us. We correct publicly, at the top of the article, dated.

This article is based on reporting and public records available as of June 1, 2026. The legal claims described are allegations, not court findings. “The Reillys” is a disclosed composite scenario, not a single real farm; all attached figures are sourced.

Learn More

- 18.95 Milk, 19.14 Costs: USDA’s 2026 Milk Price Upgrade Still Leaves Your Dairy in the Red — Breaks down the widening gap between the federal all-milk price baseline and actual operational costs, arming you with the precise margin numbers needed for short-term feed and cash-flow budgeting.

- From 52¢ to 25¢: Where Your Milk Dollar Goes Now and 3 Ways to Reclaim Your Share — Exposes the long-term structural erosion of the farmer’s slice of the consumer dairy basket over the last four decades, mapping out multi-year strategic positioning moves to combat downstream retail capture.

- The $3 Milk Trap: How 2026’s Class III/IV Spread Becomes a $382,000 Hit on a 500-Cow Milk Check — Dismantles standard pricing assumptions by calculating how regional processing bottlenecks and component pricing imbalances penalize specific component pools, delivering an aggressive financial warning for risk-management plans.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.