Is your farm positioned to thrive during the longest dairy correction in decades?

EXECUTIVE SUMMARY: The 2025 dairy market correction presents unprecedented challenges, with butter prices plunging 30% since summer and cheddar declining 14% since mid-August, creating margin pressure across all regions. What makes this correction different is its global scope—New Zealand’s milk production surged 14.6% while China’s dairy imports dropped 15%, fundamentally altering traditional market dynamics. Progressive operations are finding stability through anaerobic digesters generating $400-450 per cow annually, though this technology remains accessible primarily to larger farms. Industry projections suggest up to 160,000 dairy operations worldwide may close over the next two years, with asset losses potentially reaching $400 billion globally. However, innovative farmers are adapting through direct-to-consumer marketing, cooperative digester partnerships, and refined transition cow management protocols. The extended 18-to 24-month correction timeline requires strategic thinking rather than simply waiting for recovery. Those who embrace diversification, strengthen local market relationships, and invest in operational efficiency are positioning themselves not just to survive, but to acquire distressed assets and emerge stronger when markets stabilize.

KEY TAKEAWAYS:

- Revenue diversification pays: Anaerobic digesters generate $400-450 per cow annually through carbon credits and renewable energy sales, providing crucial margin protection during price downturns

- Market correction extends longer: Unlike typical 6-9 month cycles, structural factors suggest 18-24 months of pressure, requiring conservative planning and aggressive cost management

- Consolidation accelerates rapidly: Forecasted closure of 160,000+ dairy operations globally creates acquisition opportunities for well-positioned farms while eliminating competitors

- Local markets offer premiums: Direct-to-consumer sales and specialty processing partnerships command 40-60% price premiums over commodity markets during corrections

- Operational excellence becomes critical: Focus on transition cow management, component optimization, and feed efficiency improvements to maintain profitability at lower milk prices

You know, when we sit down with a cup of coffee and talk about markets these days, there’s this feeling that we’re not just going through another typical cycle. This time feels different. Really different.

I’ve been tracking the numbers closely, and what I’m seeing should concern every dairy producer. CME butter prices have dropped about 30% since summer, falling from around $2.62 per pound down to $1.83 by mid-September, according to the latest Dairy Herd Management reports. Cheddar’s been hit too—down roughly 14% since mid-August. But here’s what’s really got my attention: this isn’t just happening here in the States.

Take Wisconsin, where I was talking with producers just last week. They’re telling me the pressure on butterfat performance and milk solids pricing has been relentless. “In past corrections, we’d see some regional breathing room,” one Fond du Lac operator explained. “Maybe when the Midwest got hit, New York or Michigan would hold steady. Not this time.”

The data backs up what farmers are feeling on the ground. We’re seeing volatility that’s literally double the typical market swings, while skim milk powder prices have converged globally. That means those usual price gaps we’ve always counted on for export opportunities? They’re shrinking fast.

The Digester Game-Changer

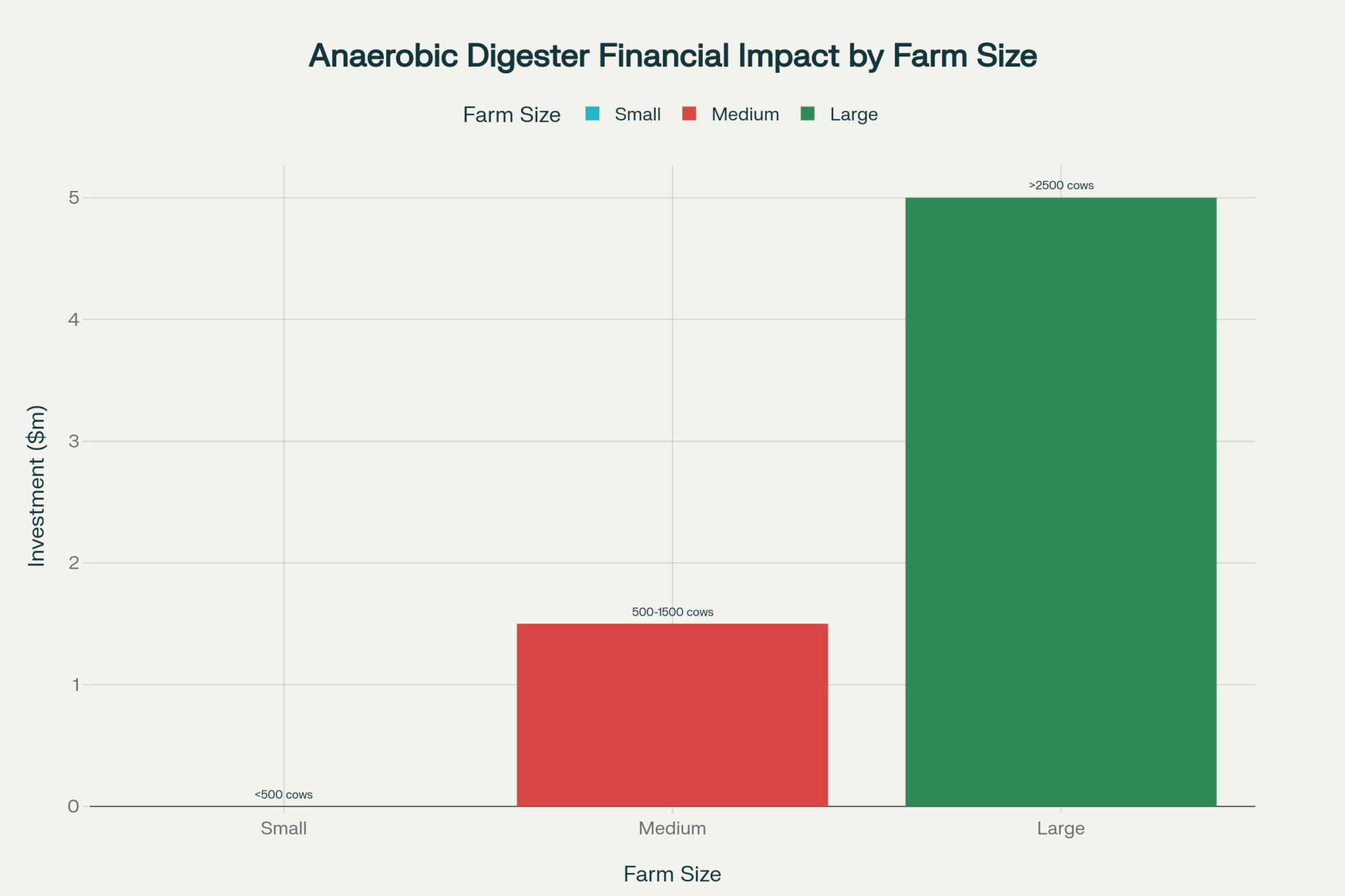

Now here’s where things get interesting—and frankly, a bit concerning if you’re running a traditional operation. Larger farms with anaerobic digesters are playing a completely different game during this downturn.

I recently spoke with a California dairy operator who put it perfectly: “The digester income has really been our saving grace. We’re pulling in about $400 to $450 per cow yearly through energy sales and carbon credits, and it’s smoothing out these wild price swings.” According to EPA AgSTAR program data, these numbers are realistic for operations that can afford the capital investment.

But let’s be honest about the math here. Those digesters typically require multi-million dollar investments and work best for herds of 2,000 cows or more. That puts them out of reach for many family operations.

What’s encouraging, though, is hearing about cooperatives—especially in Quebec and parts of the Midwest—pooling resources to make digester technology more accessible. It’s a promising approach that could level the playing field somewhat.

New Zealand’s Production Paradox

Meanwhile, our friends in New Zealand are dealing with their own interesting situation. Milk production is actually up about 14.6% this season in terms of milk solids, according to their dairy association reports. Farmers there are enjoying some seriously good payouts—around NZ$10.15 per kilogram of milk solids from Fonterra, which represents one of the best rates in recent years.

But here’s the catch that not everyone’s talking about. Fonterra’s balance sheet shows they’ve been dipping into reserves to maintain these high payouts, which obviously can’t continue forever. When the inevitable adjustment comes—probably early next year—it won’t be a sudden cliff but more of a gradual slide over several months.

What’s particularly problematic is how farmers typically respond to declining payouts. They tend to push production even higher, trying to make up for lower per-unit revenue with increased volume. Makes perfect sense from their perspective, but it keeps the global market flooded with supply exactly when we need less.

China’s Changing Role

And then there’s China—the market that used to be our safety valve. Their dairy imports have dropped about 15% recently, according to USDA Foreign Agricultural Service data and Rabobank research. They’re pushing hard toward domestic milk production despite higher feed costs, and you can see this shift reflected in how they’re using dairy ingredients—moving from imported powders to locally produced products.

This represents a fundamental change in global dairy trade patterns. Where China used to come in with big buying sprees whenever prices softened, we can’t count on that anymore.

What the Timeline Really Looks Like

Piecing all this together, the data suggest we’re probably looking at a market correction that stretches 18 to 24 months before things truly stabilize. That’s significantly longer than the typical 6-9 month cycles we’re used to.

The consolidation numbers are sobering. Industry analysis based on USDA census data and current trends suggests as many as 160,000 dairy operations worldwide could close during this period, with asset losses potentially reaching $400 billion globally as farms get liquidated at distressed prices.

But it’s not all doom and gloom. I’ve seen some remarkable adaptation happening.

Real-World Success Stories

There’s a producer near Fond du Lac who started layering direct-to-consumer sales alongside regular contracts—it’s helped cushion the financial blow considerably. Around the Northeast, smaller farms are crafting local brands that command genuine premiums from consumers who value the farm story.

In California’s Central Valley, some larger operations are weathering this storm because they tightened their efficiency measures back when times were good. They’re now positioned to acquire distressed assets at significant discounts, potentially.

What This Means for Your Operation

If you’re running an operation under 1,200 cows, this is the time to investigate partnerships for renewable energy projects seriously. Look hard at your transition cow management—those improvements in fresh cow protocols can make a real difference during tight periods. And explore local market niches where your farm’s story might command premium pricing.

For those managing larger herds, prioritizing investments in alternative revenue streams isn’t optional anymore—it’s essential. Consider moving aggressively on digester projects, carefully scouting acquisition opportunities, and tightening cost controls across the board.

Don’t think of this as a sprint to the finish line. The road ahead is long, with challenges and opportunities wrapped together.

Learning from History

Remember, we’ve navigated major industry transformations before. The shift to artificial insemination. The evolution from tie-stall barns to parlor systems. The adoption of computerized feeding. Each transition seemed overwhelming at the time, but the industry emerged stronger and more productive.

Those who embraced change didn’t just survive—they thrived in the new environment.

The Path Forward

What’s your next move going to be? Are you positioning for adaptation or just hoping to ride this out?

Let’s keep the conversation going and share what’s working. The best lessons often come from our collective experience, especially during challenging times like these.

Market Snapshot:

- CME butter: down ~30% since summer 2025

- Cheddar prices: off ~14% since mid-August

- New Zealand milk solids: up 14.6% this season

- Fonterra payout: NZ$10.15 per kg milk solids

- Digester revenue: $400-450 per cow annually

- China imports: down ~15% in 2024-25

- Projected closures: 160,000+ operations globally

- Asset impact: ~$400 billion potential losses

It’s a challenging landscape, but together we can navigate it by sharing knowledge, strategies, and keeping our focus on adaptation rather than just survival.

Thanks for thinking this through with me—here’s to keeping the coffee warm and the conversations productive.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- 11 Proven Strategies to Lower Feed Costs and Boost Efficiency on Your Dairy – This article provides tactical, actionable steps for reducing feed costs and improving operational efficiency, essential for maintaining profitability during market downturns. It complements the main article’s focus on cost management with specific, practical strategies.

- Global Dairy Market Dynamics: Navigating Volatility and Strategic Opportunities in 2025 – This piece offers a detailed, strategic look at the global economic forces reshaping the dairy market, including new regulations and shifting trade patterns. It provides a macro-level understanding of the trends discussed in the main article.

- The Carbon Credit Goldmine: How Forward-Thinking Dairy Producers Are Turning Methane Reduction into Cash Flow – While the main article mentions anaerobic digesters, this piece goes deeper into the technology and economic models. It reveals how producers can generate significant revenue from carbon credits, a key diversification strategy for the future.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.