$11/lb whey. 69¢ on your milk check. We ran the FMMO barn math on a 300‑cow herd to see where the other $1,500 per cow actually went.

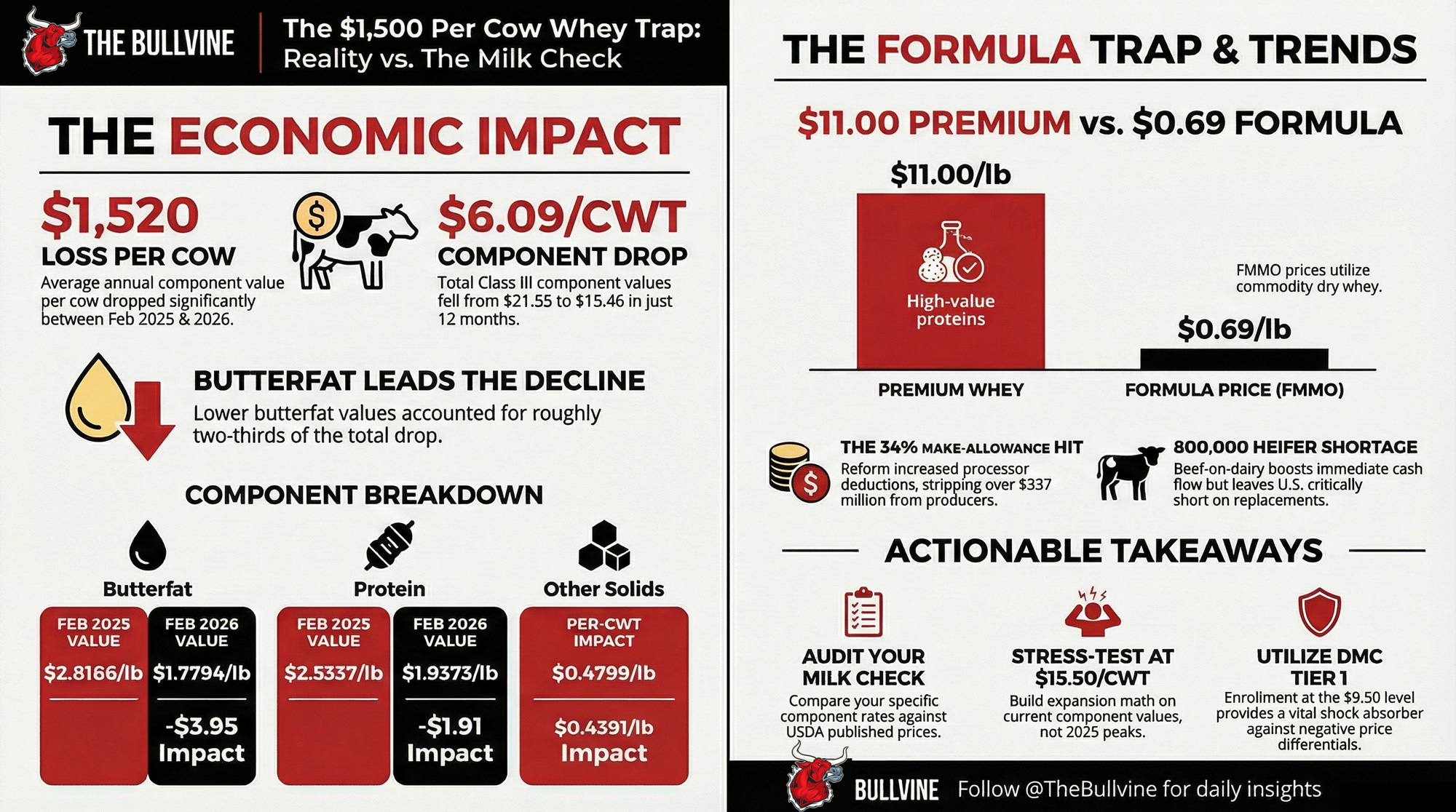

Executive Summary: Your component check dropped about $1,520 per cow from February 2025 to February 2026 while premium whey climbed to $11/lb and plants poured $11 billion into new cheese and whey capacity. FMMO’s new make‑allowance formula now prices other solids off 69‑cent dry whey and higher processor costs, cutting roughly 24¢/cwt from your other‑solids line even as whey markets rally. Butterfat and protein did the rest of the damage, taking total Class III components down about $6.09/cwt — a $450K‑plus swing on a 300‑cow herd. At the same time, beef‑on‑dairy calves are throwing off $500–$800/head, helping cash flow but leaving the U.S. roughly 800,000 heifers short heading into a capacity build‑out. The article walks through barn‑level scenarios if whey and cheese both correct, including how negative PPDs could stack another $1–$2/cwt on top of what you’ve already lost. Then it lays out a 30/90/365‑day playbook: audit your component line against AMS values, stress‑test your DMC and DRP coverage, and rebuild any expansion math around ~$15.50/cwt components instead of 2025 peaks. If you’ve got 200–500 cows on a component order and you’re not sure how much of that $11/lb whey is in your milk check, this is the 10‑minute read to run before your next contract or barn decision.

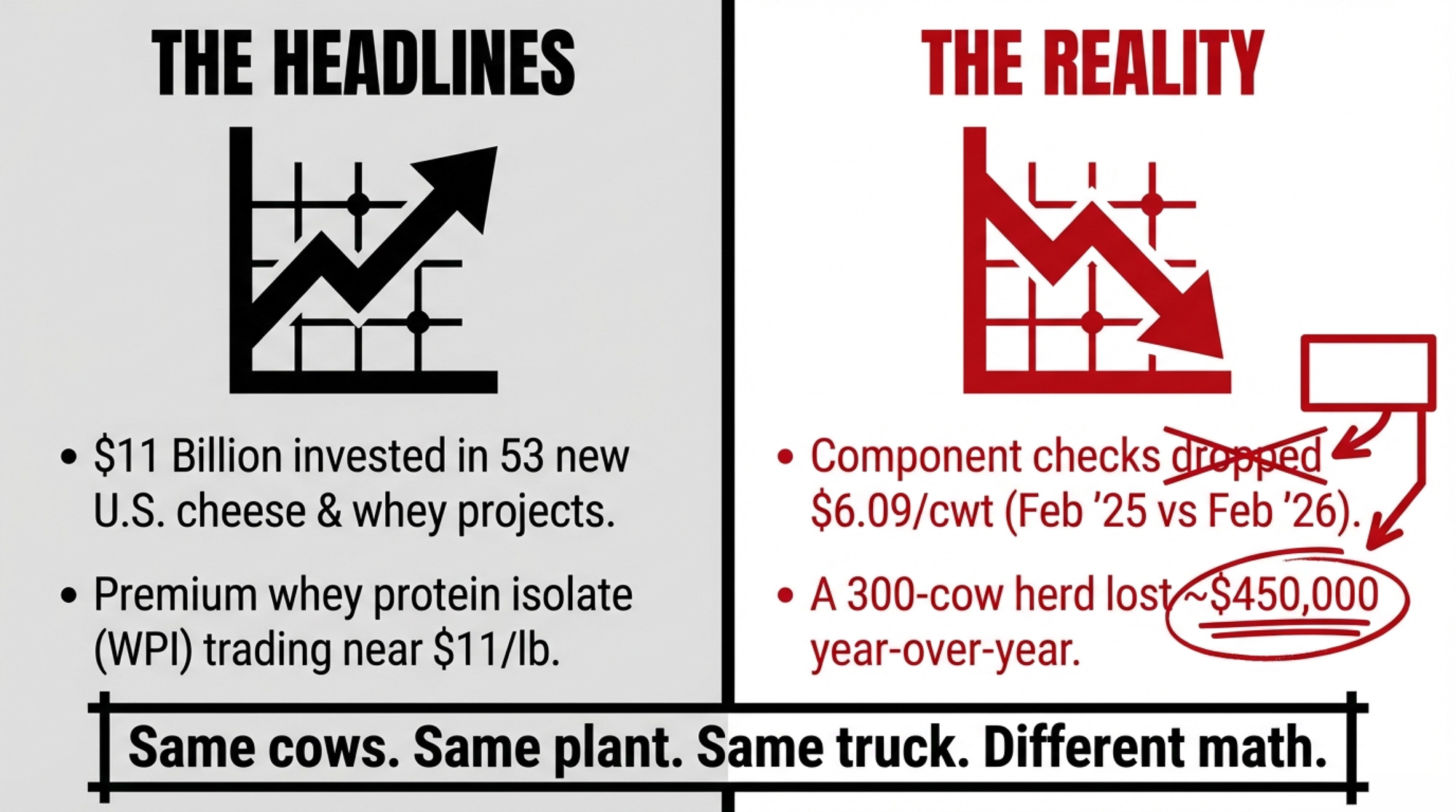

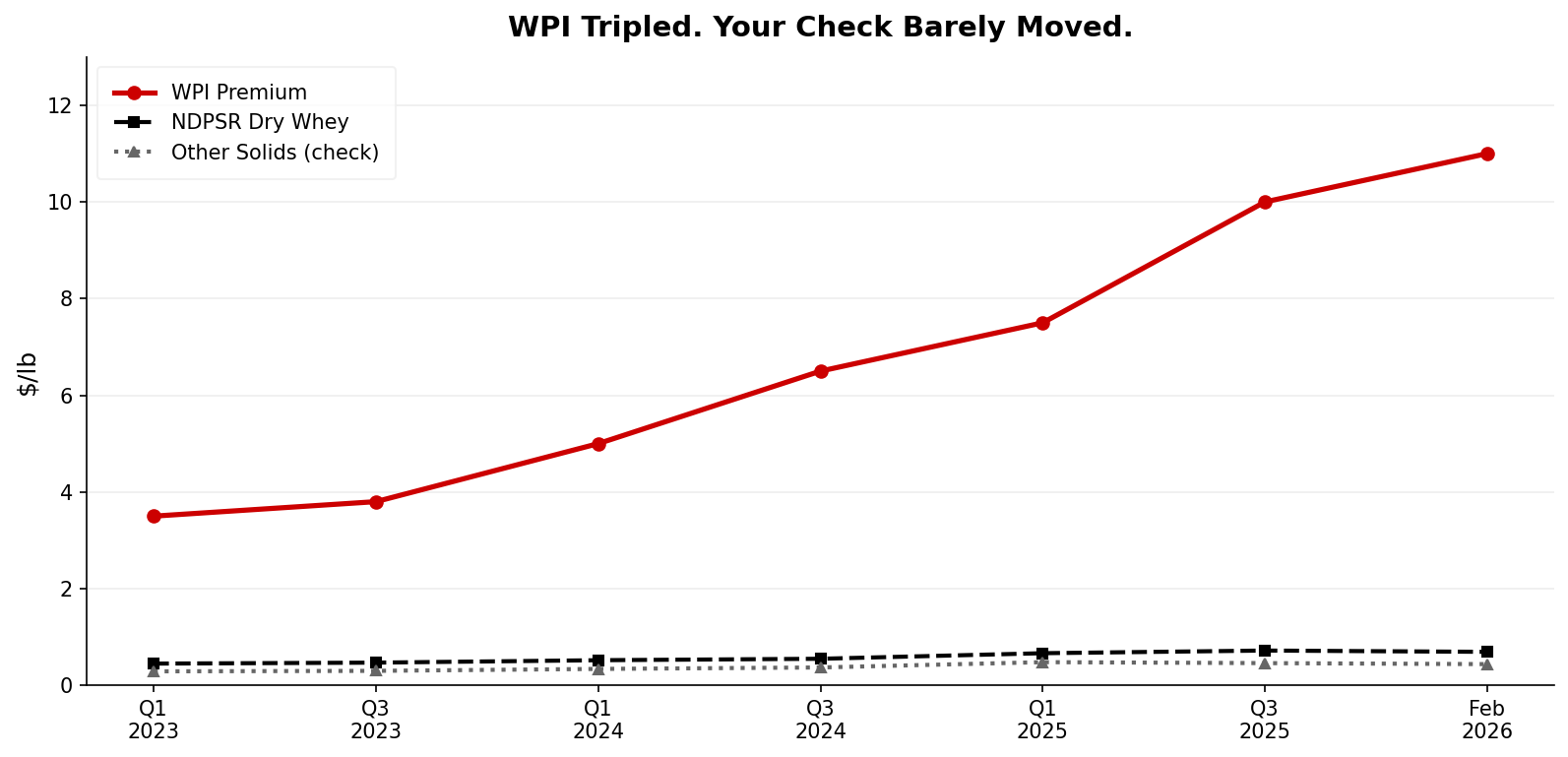

Eleven dollars a pound. That’s where high‑grade whey protein isolate has traded since late 2025, according to Ever.Ag Insight — roughly triple the price three years ago. Cheese plants are sometimes pulling more revenue from the whey stream than the cheese block itself.

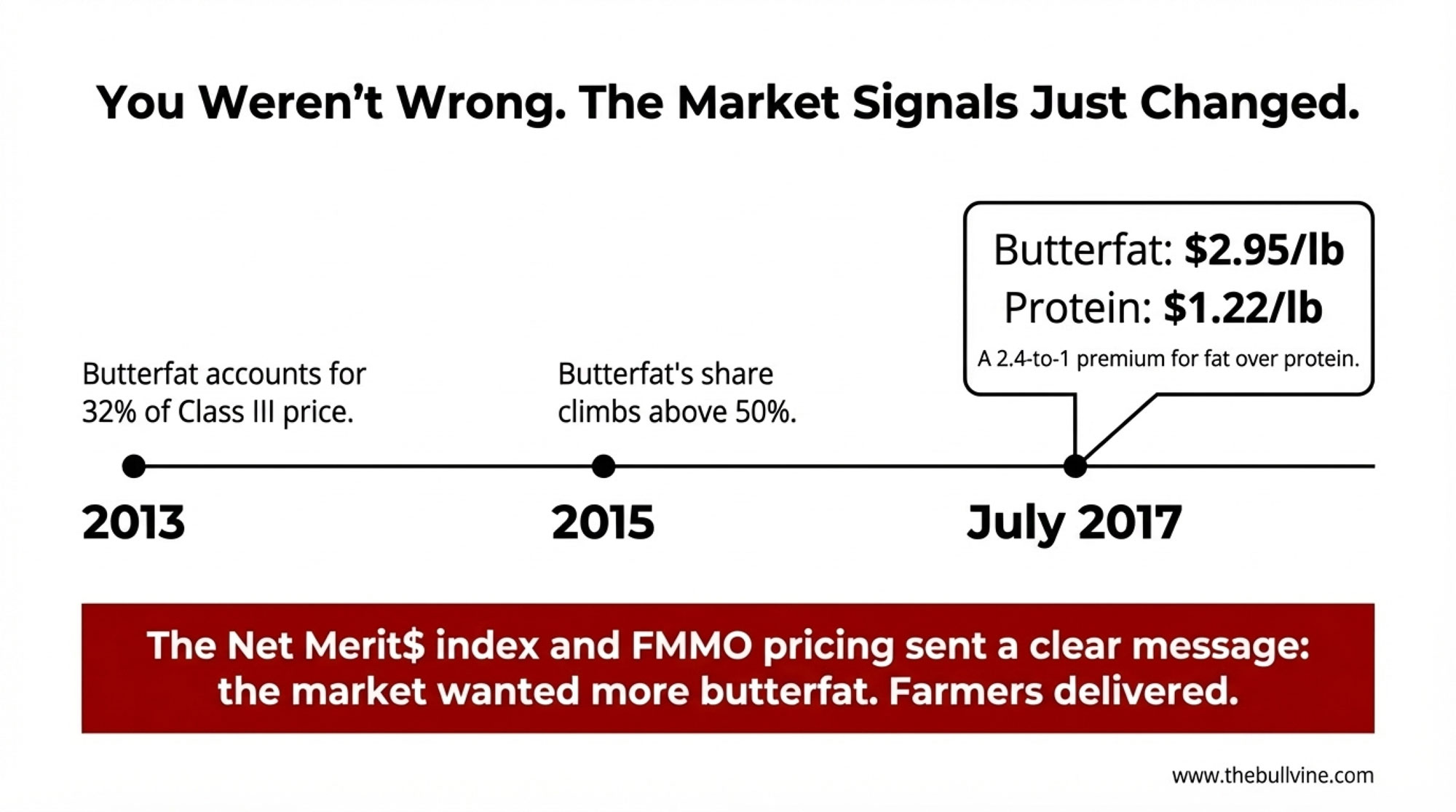

But pull your early‑2026 milk check, and a different number stares back. USDA’s February 2026 Class III component values, at standard test of 3.8% fat, 3.2% protein, and 5.7% other solids, work out to about $15.46/cwt — down from $21.55/cwt in February 2025. That’s a drop of $6.09/cwt, or roughly $1,520 per cow on 25,000 lb shipped.

At the National Farmers Union’s 124th annual convention this March, Wisconsin Farmers Union president Darin Von Ruden dropped a number that landed hard: about $50,000. That’s how much less a 300‑cow dairy operator in southwest Wisconsin received on his January 2026 milk check compared with January 2025. Same cows. Same plant. Same truck. The formulas changed. As Von Ruden told Brownfield Ag News, this wasn’t a model herd or a spreadsheet example — it was a neighbor he’d spoken with the week before.

And the $11 billion pouring into 53 new and expanded U.S. dairy processing projects across at least 19 states, according to IDFA, hasn’t changed that producer’s other‑solids line by a dime.

How Much Whey Value Actually Reaches Your Milk Check?

Almost none. And the formula explains why.

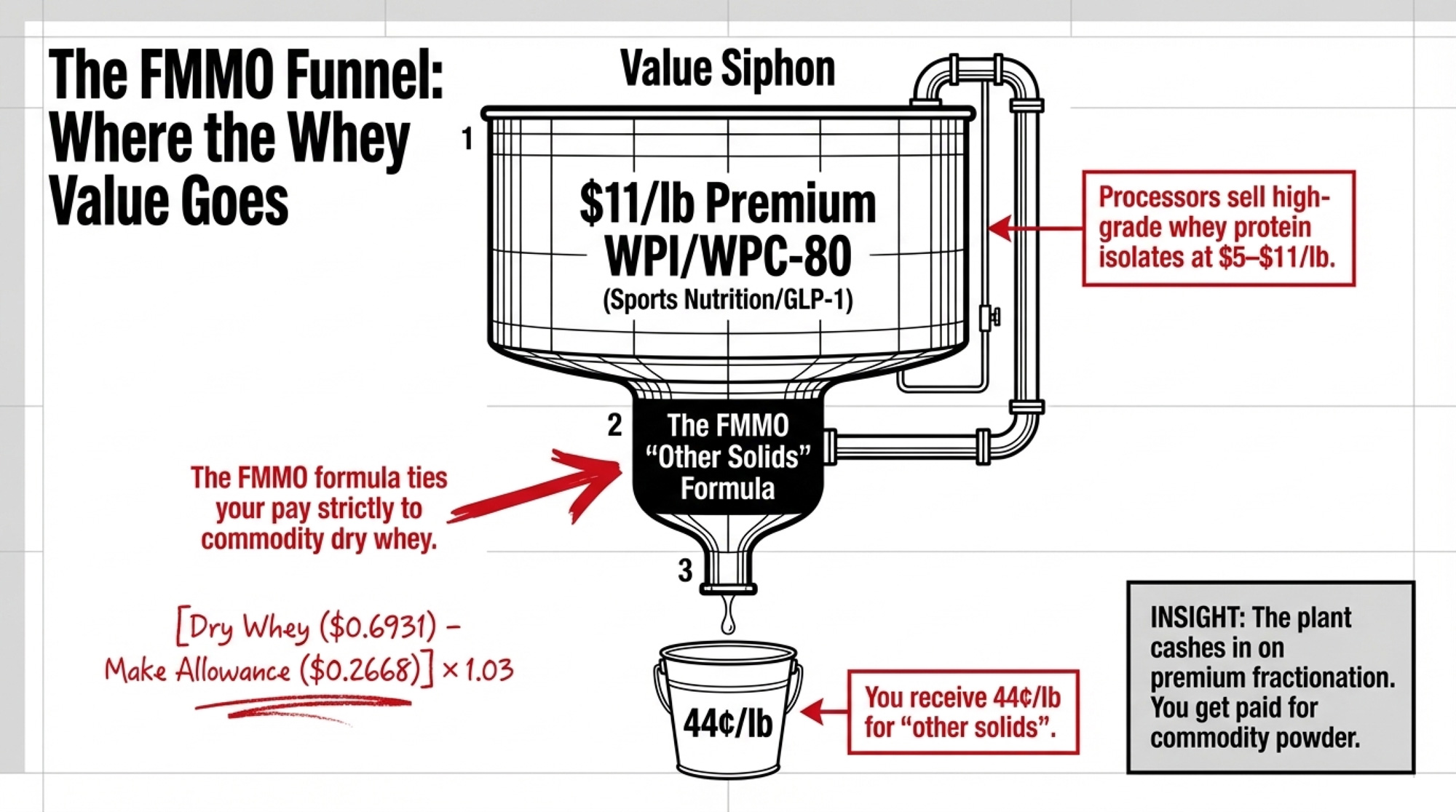

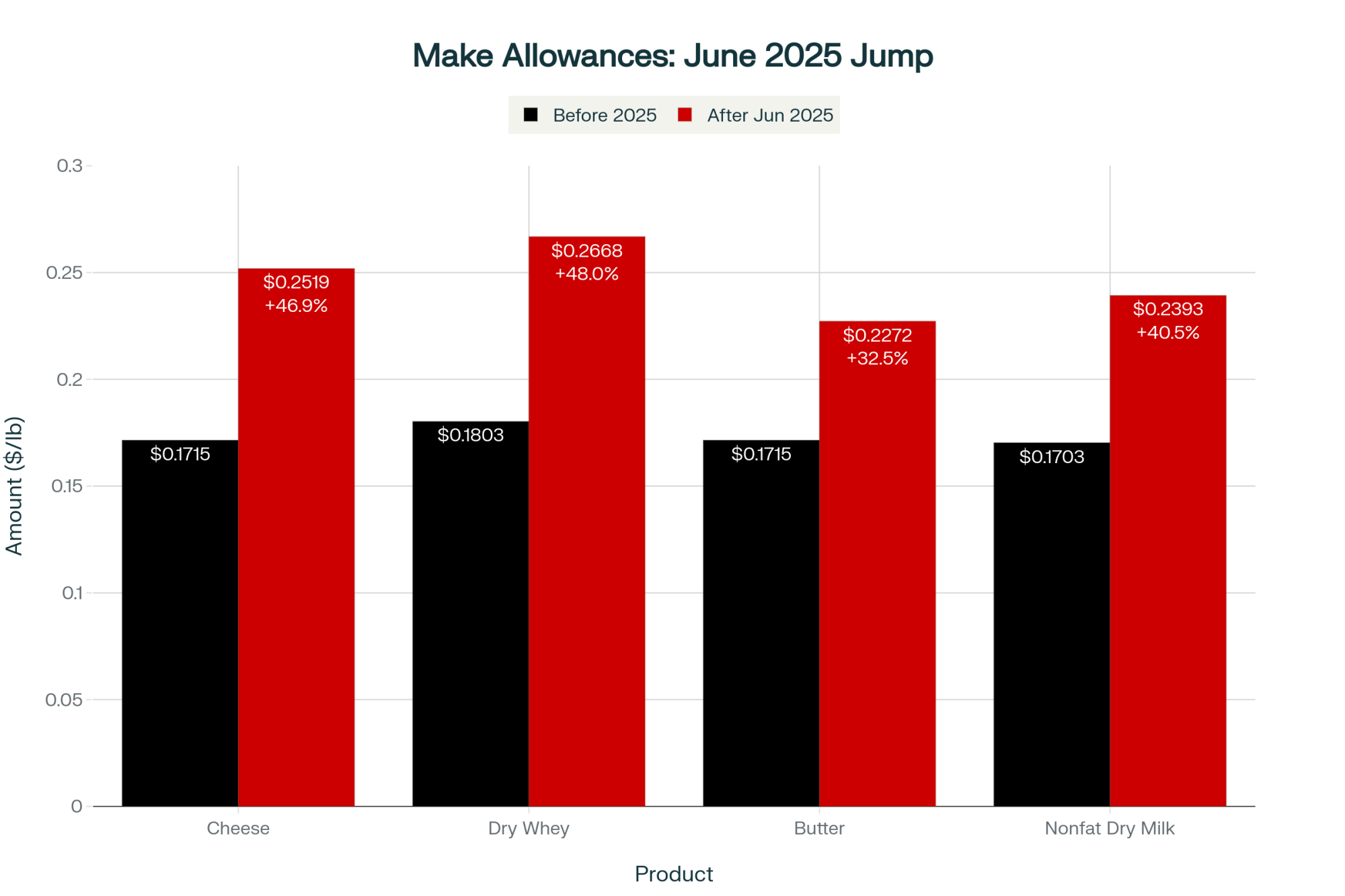

Your “other solids” component — the FMMO line where whey economics should show up — is calculated from commodity dry whey, not the premium WPI or WPC‑80 driving the headlines. Under USDA’s January 2025 Final Rule, effective June 1, 2025:

Other‑solids price = (Dry whey price − $0.2668) × 1.03

USDA’s February 2026 “Announcement of Class and Component Prices” puts NDPSR dry whey at $0.6931/lb. Run the math:

- $0.6931 − $0.2668 = $0.4263

- $0.4263 × 1.03 = $0.4391/lb of other solids.

That matches the published number exactly. Meanwhile, premium WPI trades near $11/lb, and WPC‑80 has approached €20,000/ton in Europe. Those are totally different products from the commodity dry whey that feeds the FMMO formula.

Your other‑solids line is tethered to 69‑cent dry whey and pays 44¢/lb. Your processor’s ingredient desk is selling $5–$11/lb whey proteins into sports nutrition and GLP‑1 diets. That’s the first piece of the disconnect — and it’s the piece Rabobank’s Lucas Fuess has been warning about in interview after interview since late 2025.

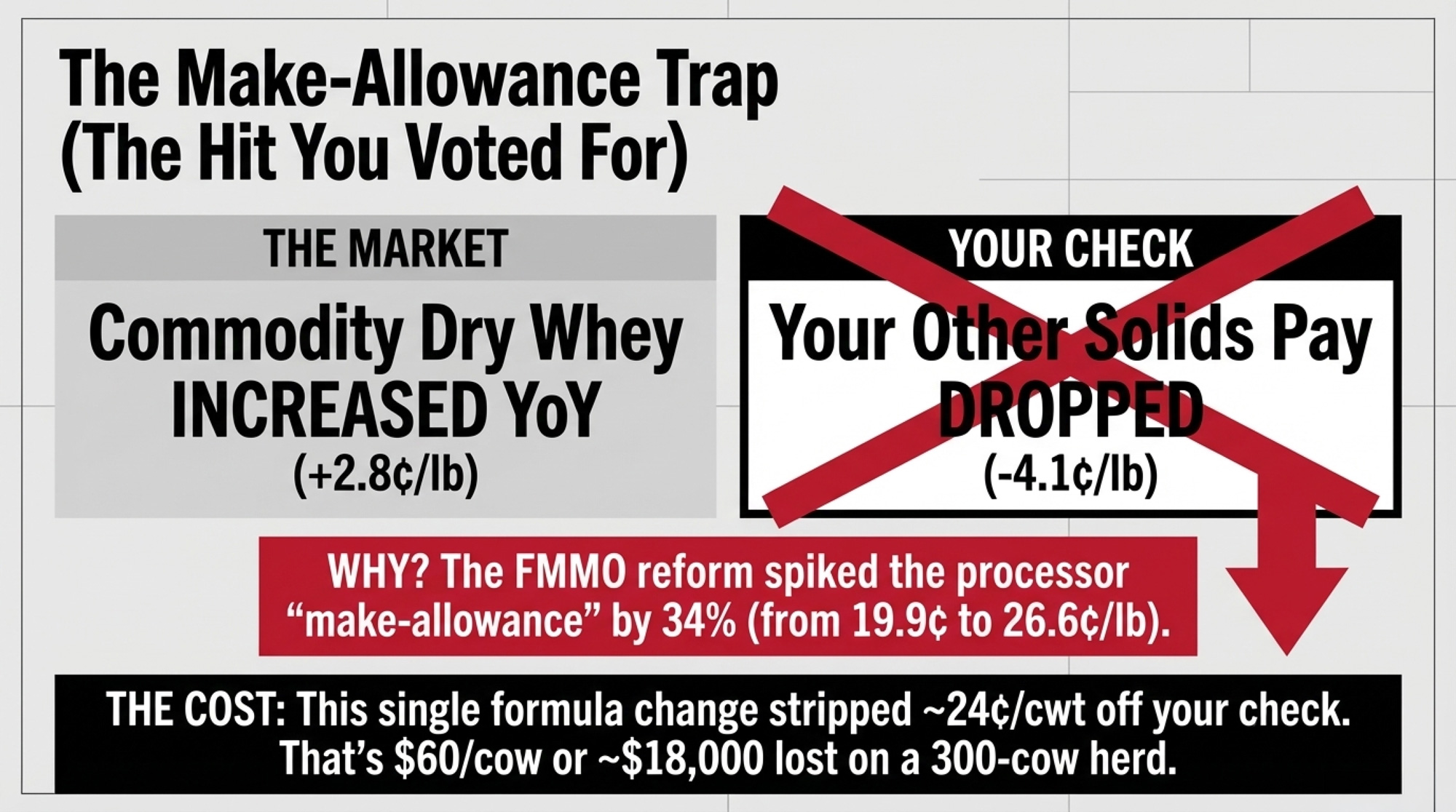

The Make‑Allowance Hit You Voted For

There’s a second piece, and this one was literally on the referendum ballot.

Dry whey did move up year‑over‑year. February 2025’s NDPSR average: $0.6650/lb. February 2026: $0.6931/lb — an increase of 2.8¢/lb. But your other‑solids value didn’t climb. It slid.

- February 2025 other‑solids price: $0.4799/lb (old formula).

- February 2026 other‑solids price: $0.4391/lb (new formula).

Dry whey up 2.8¢. Other solids down 4.1¢/lb.

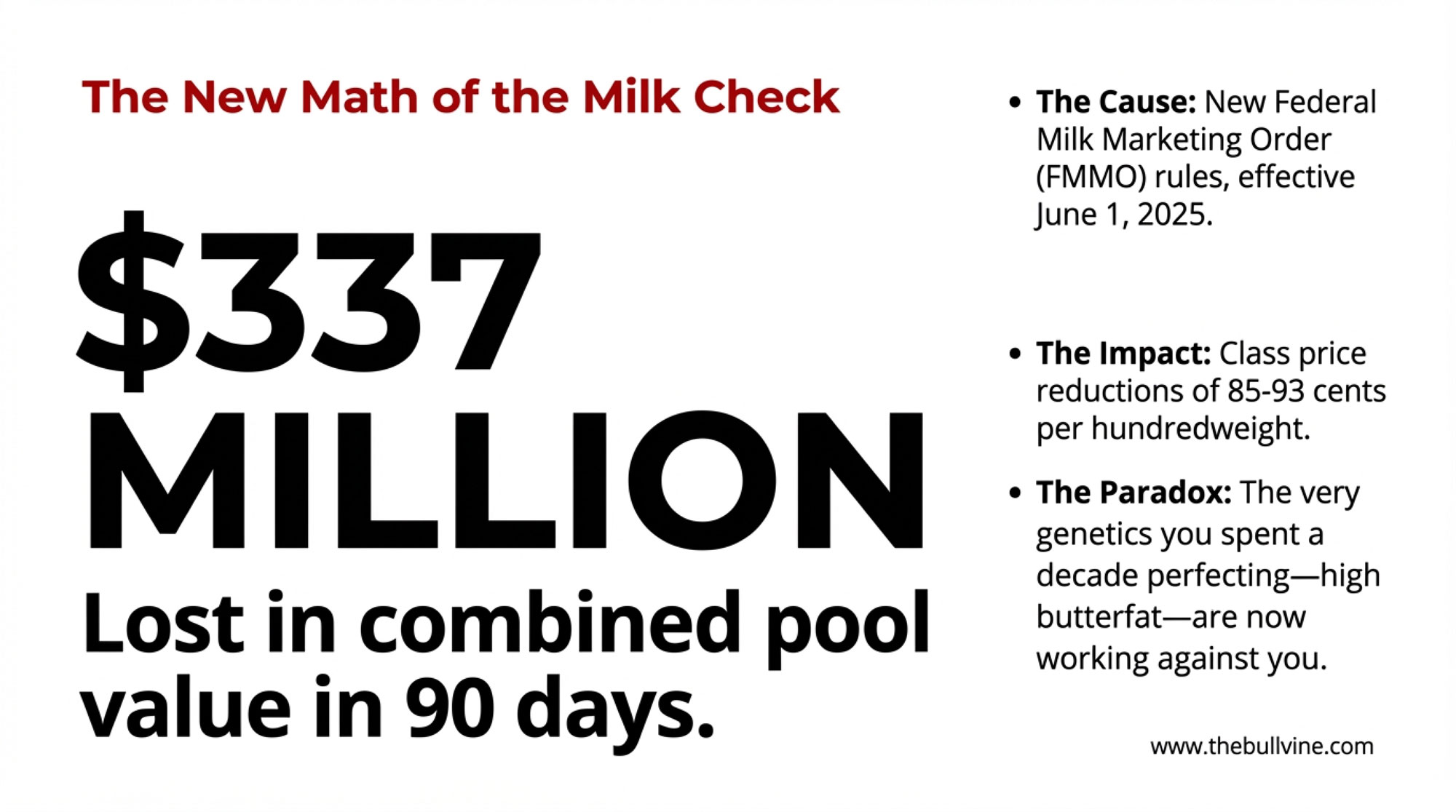

The reason: the FMMO reform raised the dry whey make allowance from $0.1991 to $0.2668/lb — a 34% jump,shifting value from producer to processor. Producers approved it in the December 2024–January 2025 referendum. AFBF economist Danny Munch calculated that in the first three months alone, higher make allowances stripped more than $337 million in combined pool value nationally — class price reductions of 85 to 93 cents per hundredweightdepending on the order (AFBF Market Intel, September 2025). As Munch told Brownfield Ag News, the higher allowances “more than wipe out” the gains from other reforms.

Here’s the barn math at your test level (5.7 lbs OS/cwt):

- 2025 OS component: $0.4799 × 5.7 = $2.74/cwt.

- 2026 OS component: $0.4391 × 5.7 = $2.50/cwt.

That’s 24¢/cwt gone from other solids alone. Over 25,000 lb per cow, roughly $60/cow, and about $18,000 on a 300‑cow herd. Even though dry whey itself went up.

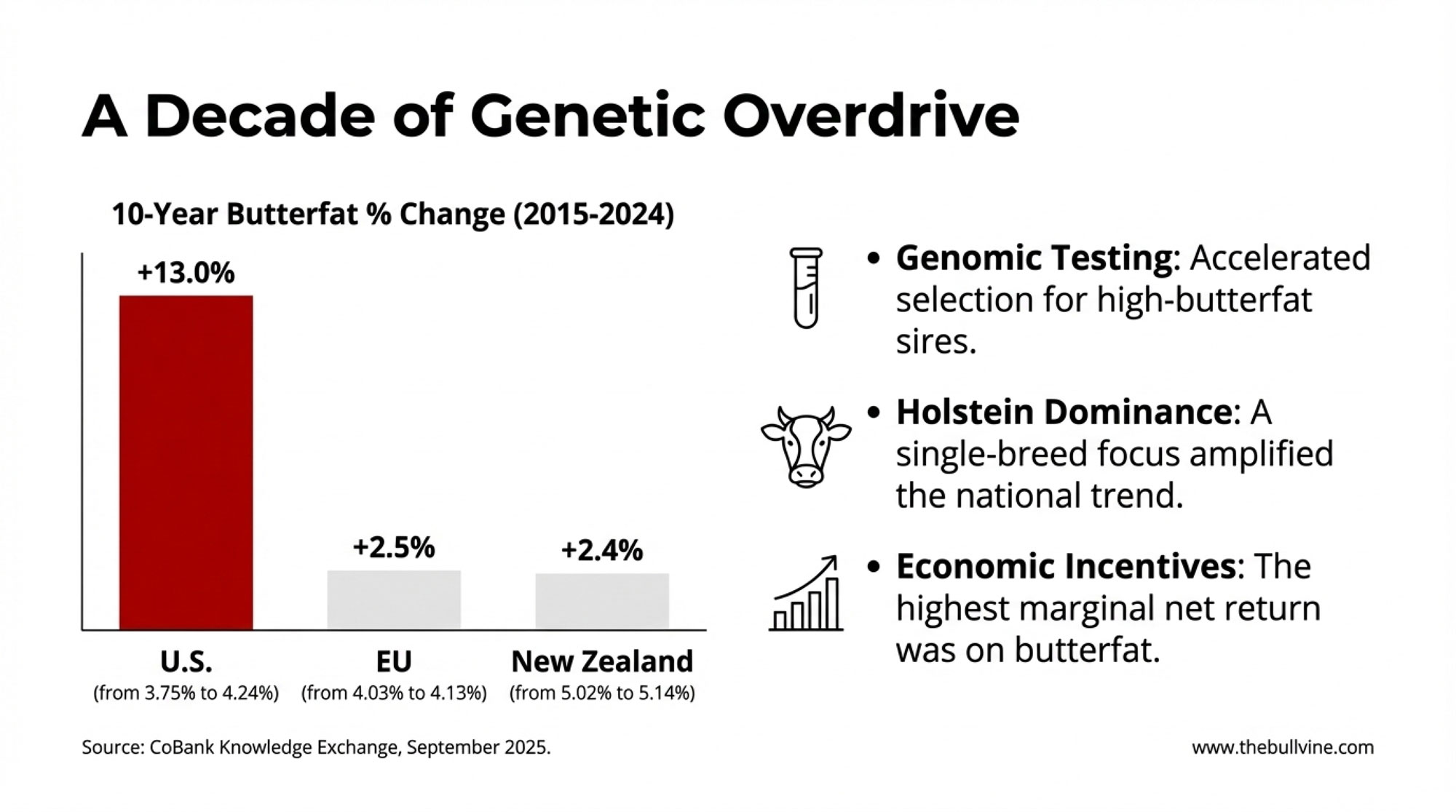

Premium whey triples. Commodity dry whey inches up. The make allowance change eats that small gain and then some. It’s exactly the make‑allowance hit we laid out in the FMMO piece earlier this month.

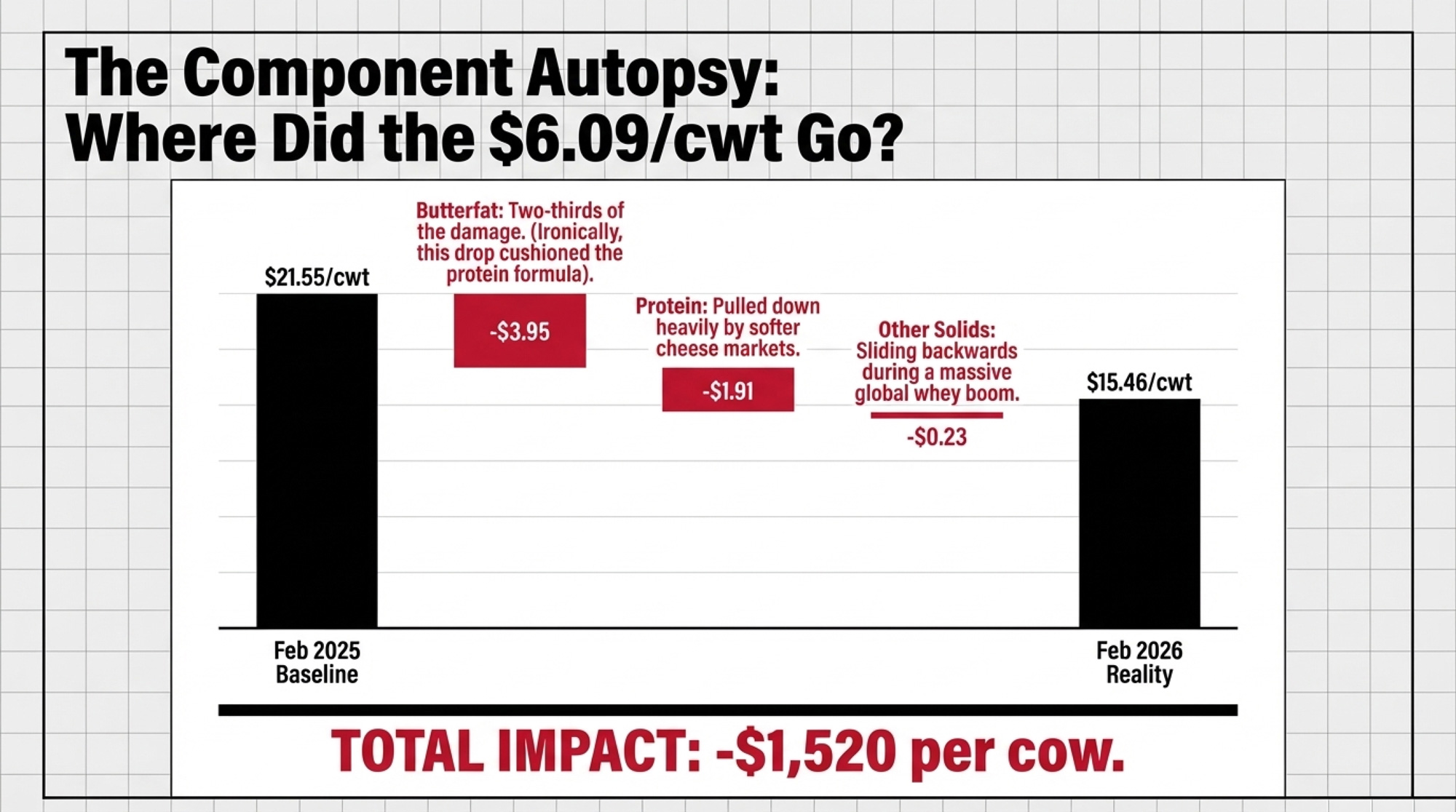

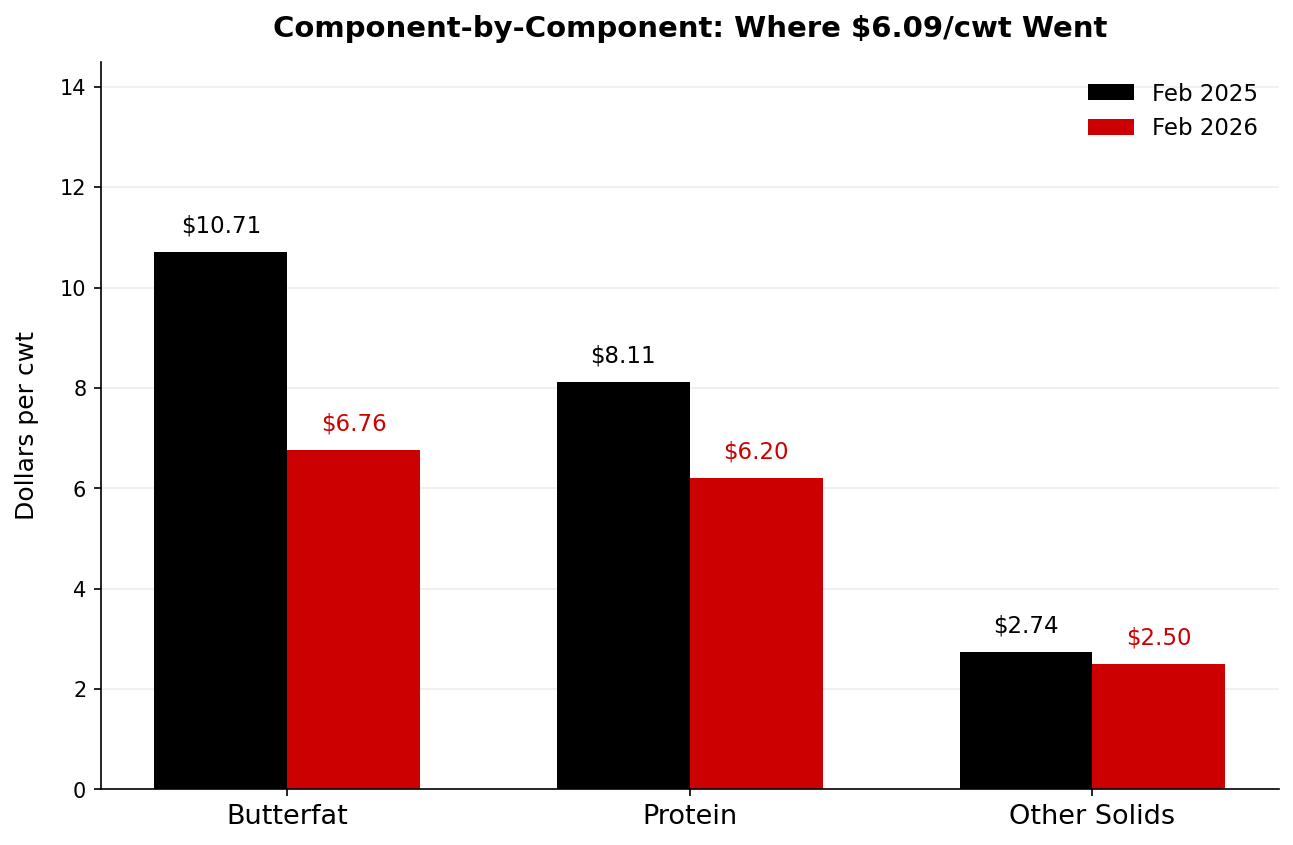

Where Did the ~$6/cwt Actually Go?

The component hit isn’t just whey. It’s the combination of weaker butterfat, softer cheese, and those other solids squeezed all at once.

Using USDA AMS component values for February 2025 vs. February 2026 at standard test:

| Component | Feb 2025 | Feb 2026 | Change/lb | Per‑cwt impact |

| Butterfat (3.8%) | $2.8186/lb | $1.7794/lb | −$1.0392 | −$3.95 |

| Protein (3.2%) | $2.5337/lb | $1.9373/lb | −$0.5964 | −$1.91 |

| Other solids (5.7%) | $0.4799/lb | $0.4391/lb | −$0.0408 | −$0.23 |

| Total | −$6.09/cwt |

Butterfat did about two‑thirds of the damage. Softer cheese pulled protein lower and took another third. Other solids were the smallest slice — but in a whey boom, you’d expect them to be climbing, not sliding.

Per 25,000‑lb cow:

- Feb 2025: $21.55/cwt × 250 cwt = $5,387/cow.

- Feb 2026: $15.46/cwt × 250 cwt = $3,865/cow.

That’s about $1,520/cow gone — roughly $456,000 on Von Ruden’s 300‑cow neighbor. And through all of that, processors with whey-fractionation capacity booked elevated whey-ingredient margins.

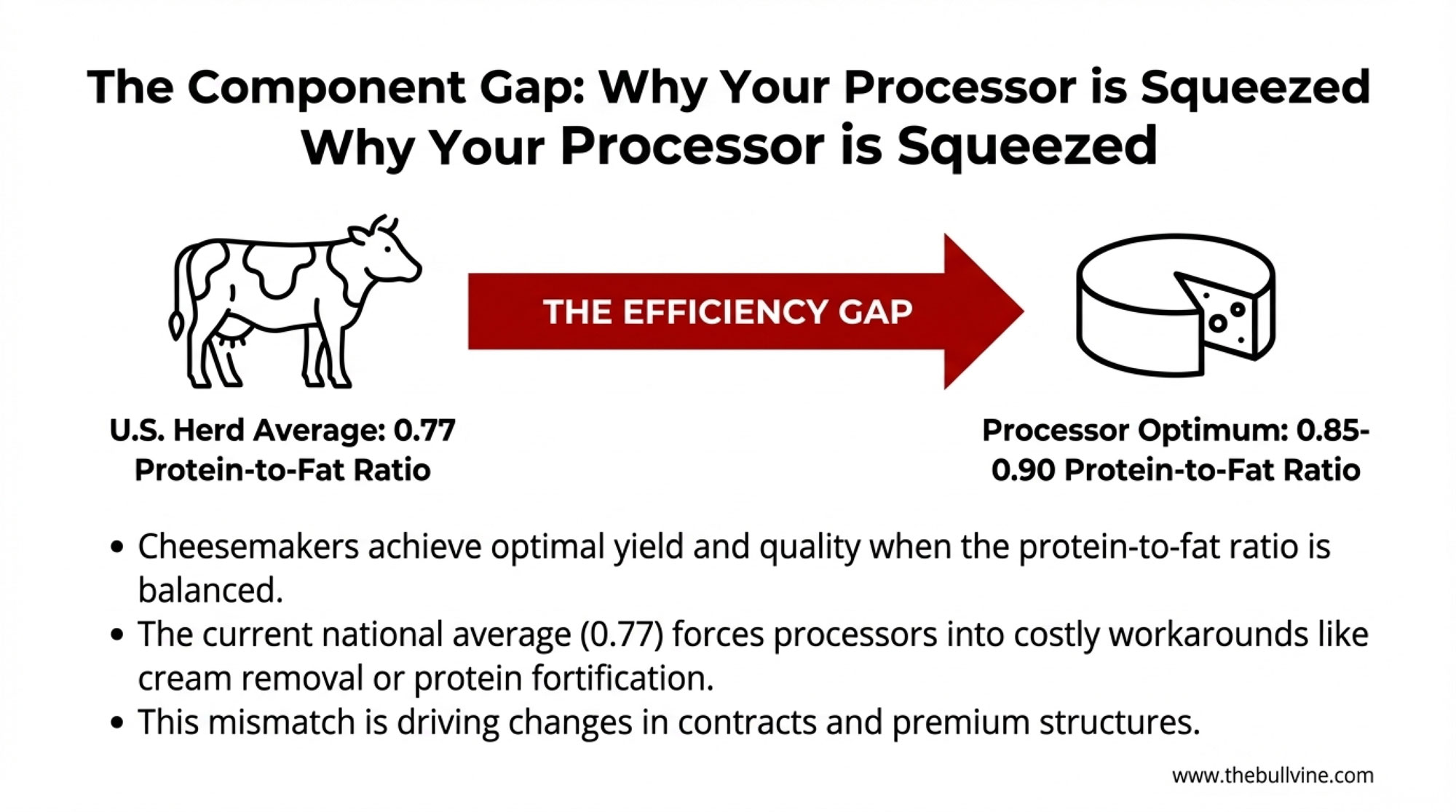

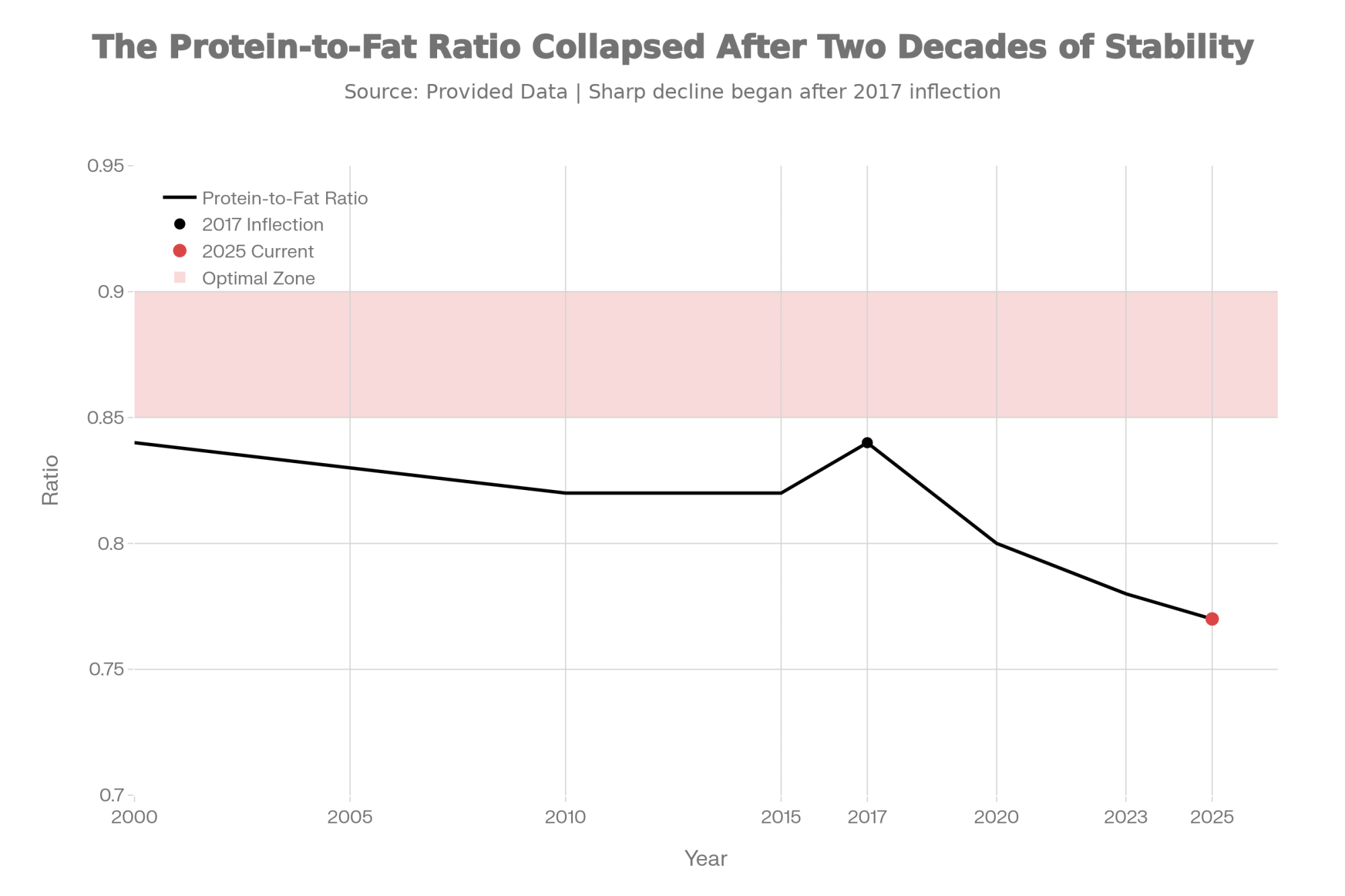

One quirk worth flagging: the FMMO protein formula includes a butterfat deduction. The butterfat drop in early 2026 actually cushioned the protein decline. If butterfat recovers while cheese stays soft, the protein line can fall further, even without another move in cheese.

Who’s Building the Stainless — and Who’s Sharing?

StoneX dairy consultant John Lancaster told DairyReporter that “almost weekly you hear about a small or medium‑sized investment increasing capacity”. Put some names on that $11 billion:

- Glanbia/Southwest Cheese — adding significant WPI capacity in Clovis, New Mexico, through a JV with DFA.

- Idaho Milk Products — investing roughly $200 million in a new protein and powder blending facility.

- Wisconsin Whey Protein — finishing a plant targeting up to 13 million lbs of WPI annually.

- Arla Foods Ingredients contracted with Valley Queen in South Dakota for WPC manufacturing.

- Globally: Fonterra ($50M Studholme expansion, NZ), Tirlán (€126M new facility, Ireland), Amul (doubling a whey plant plus two new builds, India).

Every pound of WPI starts as your cow’s milk going through a cheese vat. The FMMO formula turns that into $0.4391/lb of other solids. The plant’s ingredient desk sells that same stream at several dollars per pound.

| Whey Product | Market Price (Feb 2026) | FMMO Formula Pay | Gap per Pound | Who Captures It |

|---|---|---|---|---|

| Whey Protein Isolate (WPI) | $11.00/lb | $0.4391/lb | $10.56 | Processor ingredient desk |

| WPC-80 | ~$9.00/lb (€20k/t equiv.) | $0.4391/lb | $8.56 | Processor ingredient desk |

| NDPSR Dry Whey | $0.6931/lb | $0.4391/lb | $0.254 | Partially shared via FMMO |

| Commodity Dried Whey Permeate | ~$0.38/lb | Not in formula | N/A | Processor |

Some co‑ops return a slice through patronage dividends or over‑order premiums tied to ingredient economics. In the Upper Midwest, industry sources report some operations have negotiated premiums of $0.20–$0.30/cwt above pool pricing, structured as multi‑year agreements. In a lot of plants, though, any whey value is buried inside the overall component or patronage numbers — not broken out on your statement.

McCully Consulting’s Mike McCully predicts processors will soon be “forced into fights for milk by paying more, meaning some will not get all the milk they need”. That’s your leverage. But only if you know what your milk is worth to the plant buying it — and whether a competing plant within hauling range is offering a clearer premium.

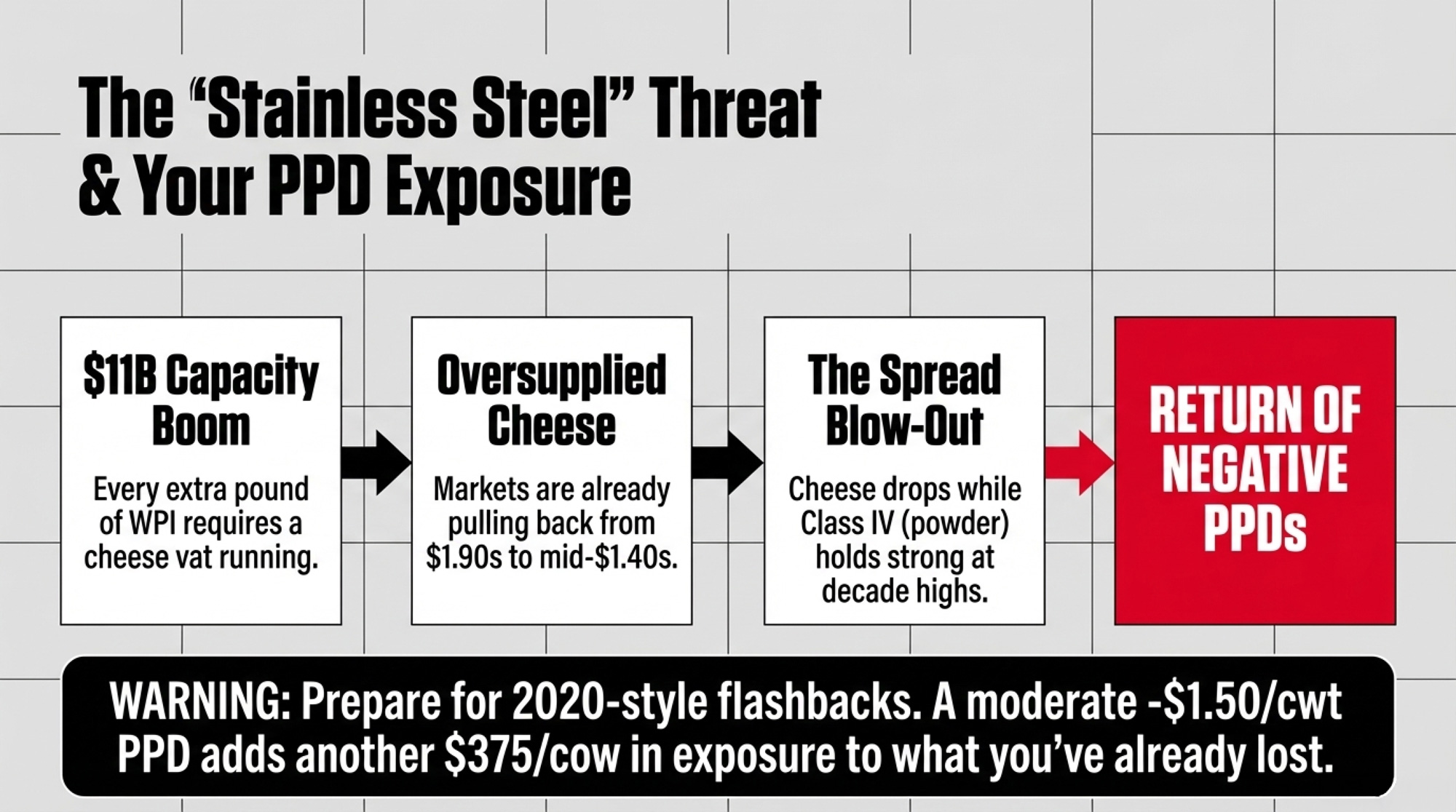

What Happens When $11 Billion in U.S. Dairy Capacity Comes Online?

Every extra pound of premium whey requires another cheese vat running. All that new stainless means more cheese — whether the market is ready or not.

Rabobank’s Fuess warned in March 2026 that these expansions “could temporarily lead to an oversupplied market and reduce cheese prices in the near term as the market works to absorb the additional output”. Cheese has already pulled back from around $1.90/lb a year ago to the mid‑$1.40s in early 2026.

Exports are doing their best to bail the boat. USDEC data show U.S. dairy exports started 2026 with 12% year‑over‑year volume growth in January — the biggest January on record — with cheese up 11%, butter up 187%, and NFDM/SMP up 19%.

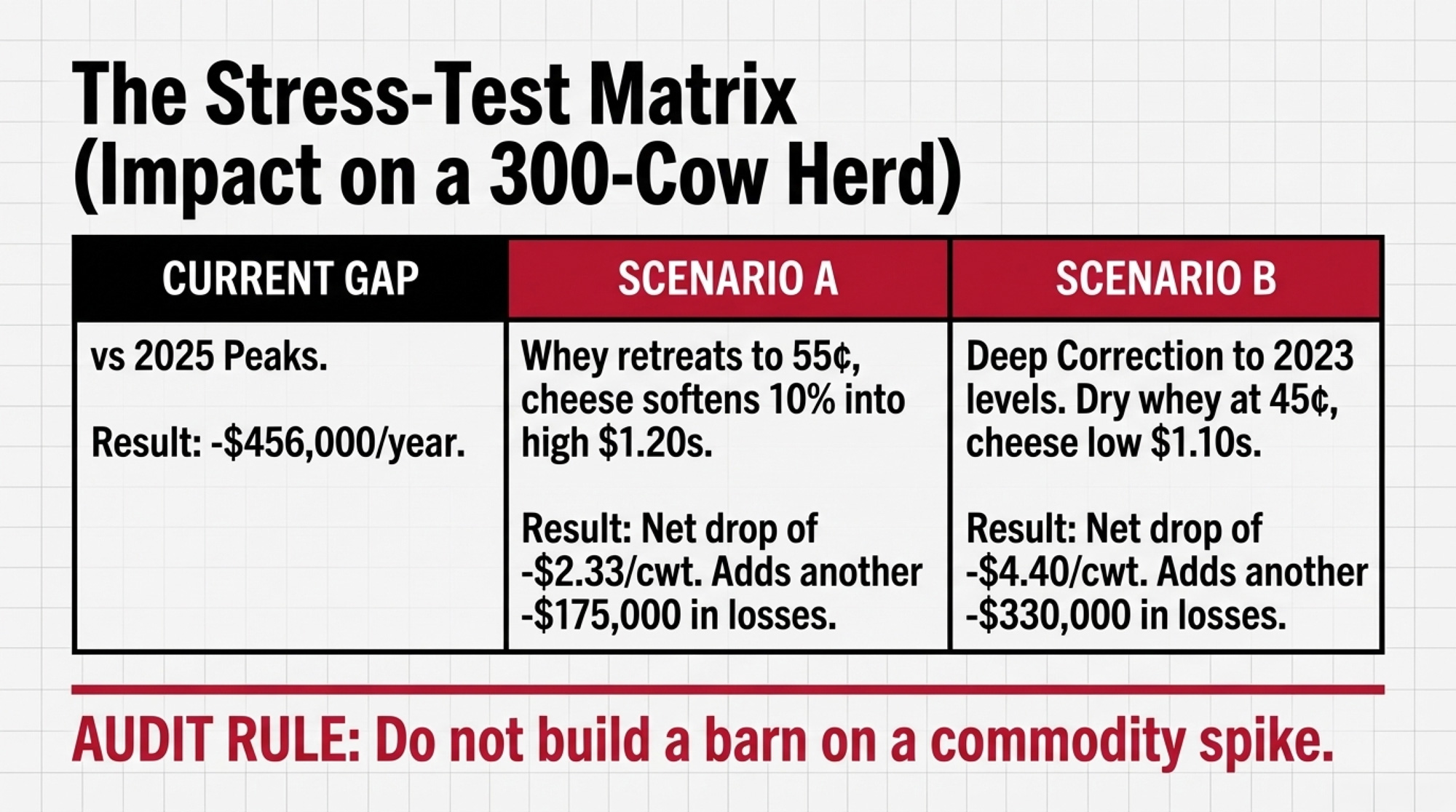

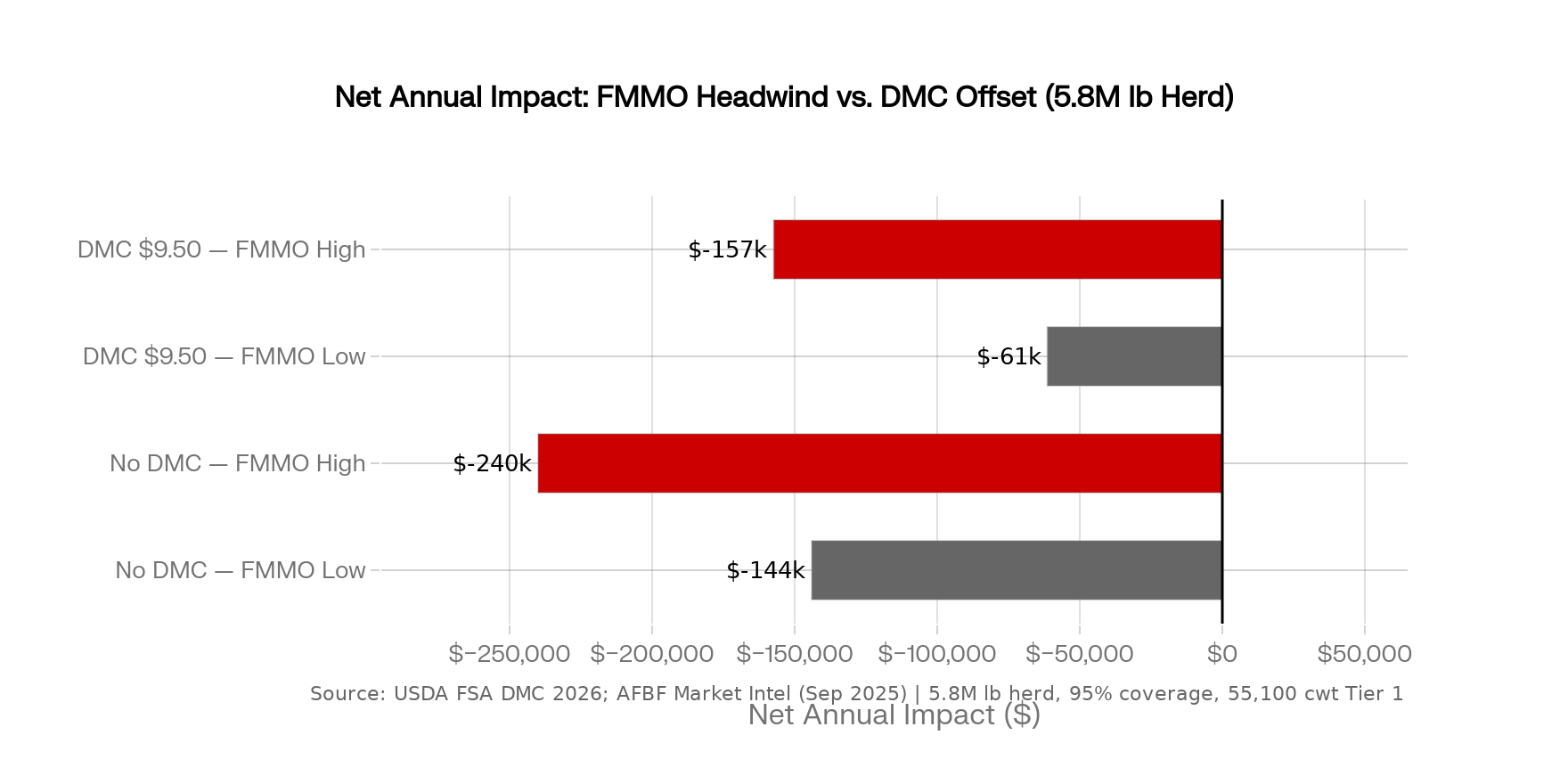

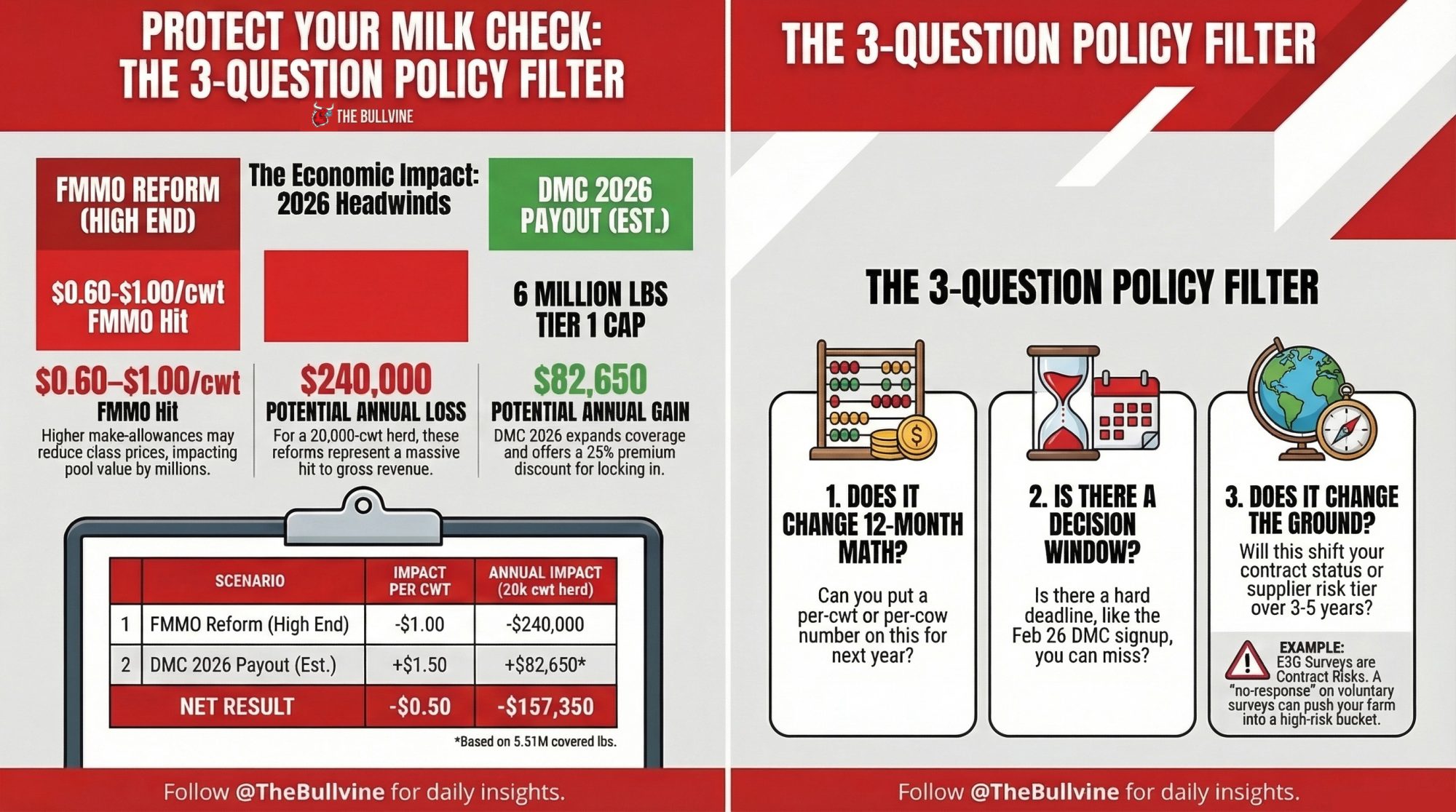

But here’s the stress test. Using the USDA’s component formulas and historical price ranges, two downside scenarios:

Scenario A — Whey retreats, cheese softens:

- Dry whey slides to $0.55/lb (mid‑2025 levels). Cheese eases ~10% into the high‑$1.20s.

- Other solids drop to roughly $0.29/lb. Protein falls to mid‑$1.40s/lb.

- Net: about −$2.33/cwt from February 2026 levels → −$582/cow → −$175,000/year on 300 cows.

Scenario B — Deeper correction:

- Dry whey returns to $0.45/lb (closer to 2023 levels). Cheese drops ~20% into the low‑$1.10s.

- Other solids fall to roughly $0.19/lb. Protein slides toward $1.00/lb.

- Net: about −$4.40/cwt → −$1,100/cow → −$330,000/year on 300 cows.

Scenario A isn’t far‑fetched. NDPSR dry whey sat in the 50–60¢ band for stretches of 2024 and 2025.

Now add the hidden multiplier: PPDs. If cheese drops while Class IV holds firm — CME nonfat dry milk has been trading at some of its strongest levels in more than a decade, near $1.94/lb in March 2026 — the spread blows out, and negative Producer Price Differentials come back. In 2020, some orders saw PPDs past −$4 to −$8/cwt. Even a moderate −$1.50/cwt PPD adds another ~$375/cow in exposure.

If you lived through 2020–2021 negative PPDs, you know this isn’t theoretical. And it’s exactly the kind of peak‑price trap that backfired for Kiwi producers when Fonterra built budgets around NZ$9.70 milk.

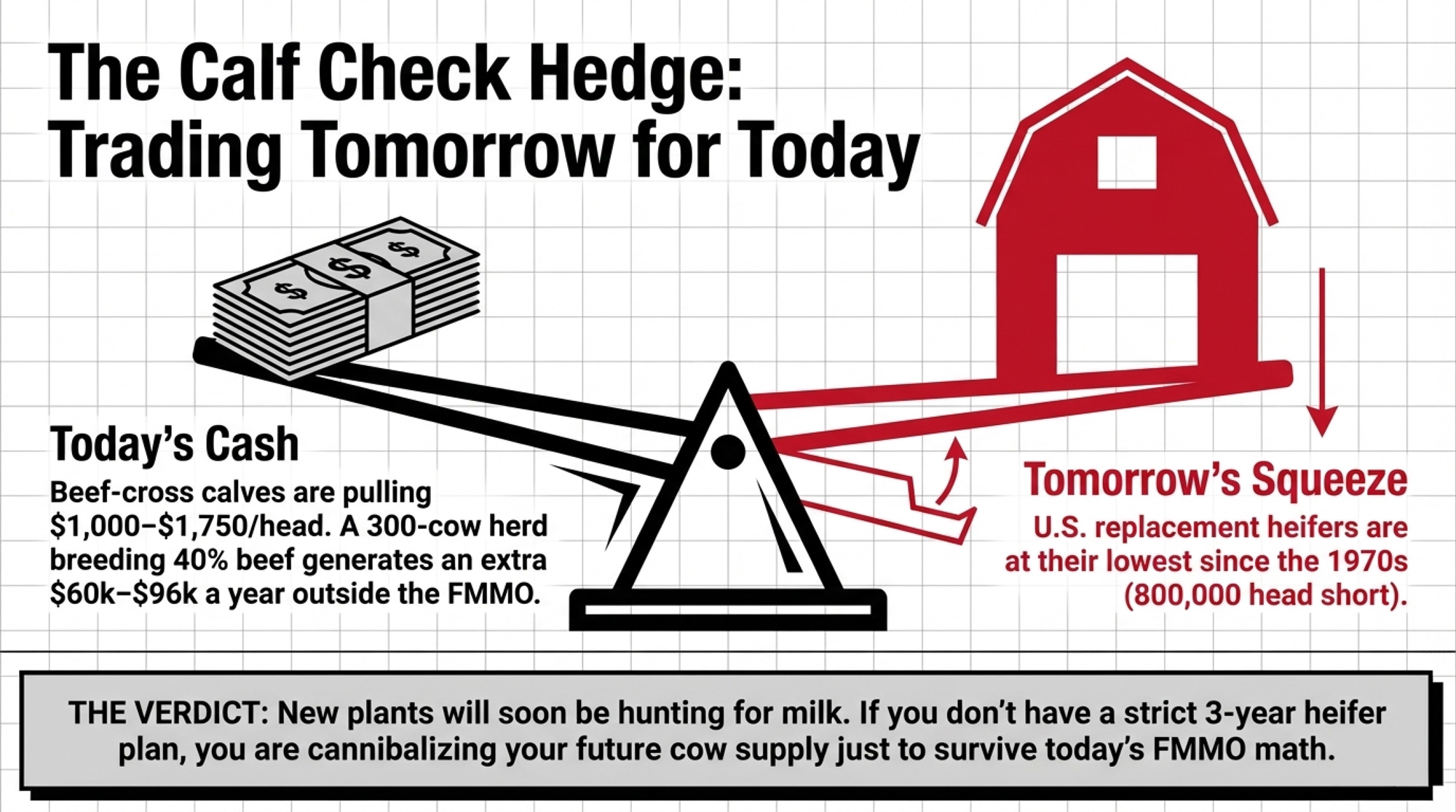

The Calf Check: One of the Few Hedges Hitting Cash Today

While the FMMO formula fails to capture the $11/lb whey premium, beef‑on‑dairy is one place producers are actually winning back margin in cash.

In strong Wisconsin markets, beef‑cross calves have brought up to $1,750 a head, with Premier’s January 2026 report listing beef‑dairy crosses at $1,000–$1,750. Holstein bull calves, by comparison, sit in the $700–$1,150 range.

That extra $500–$800 per calf functions as a de facto hedge. On 300 cows breeding 40% to beef semen, that’s 120 calves generating roughly $60,000–$96,000/year that never touches a federal order.

The trade‑off is real, though. USDA’s January 1, 2026, cattle report puts U.S. dairy replacement heifers at 3.905 million head — the lowest since the late 1970s and about 16% below January 2020. CoBank dairy economist Corey Geigerprojects the gap at roughly 800,000 fewer replacements across 2025–2026 before inventories begin to rebound sometime in 2027. As Geiger put it: “We don’t see a rebound until 2027, and that will be up 285 thousand, but you’ve got to remember, that’s going to be after 800 thousand fewer heifers”.

Fewer replacements mean fewer cows when all that new stainless steel starts hunting for milk. That takes you straight back to McCully’s question: “Who won’t get the milk?”

Beef‑on‑dairy props up your cash and tightens the supply that new capacity needs. But it comes with a shelf life — and if more than half your AI program is going to beef without a three‑year heifer plan, you’re trading tomorrow’s cow supply for today’s calf check. We walked through exactly how that math can break on a 400‑cow herd last week.

What This Means for Your Operation

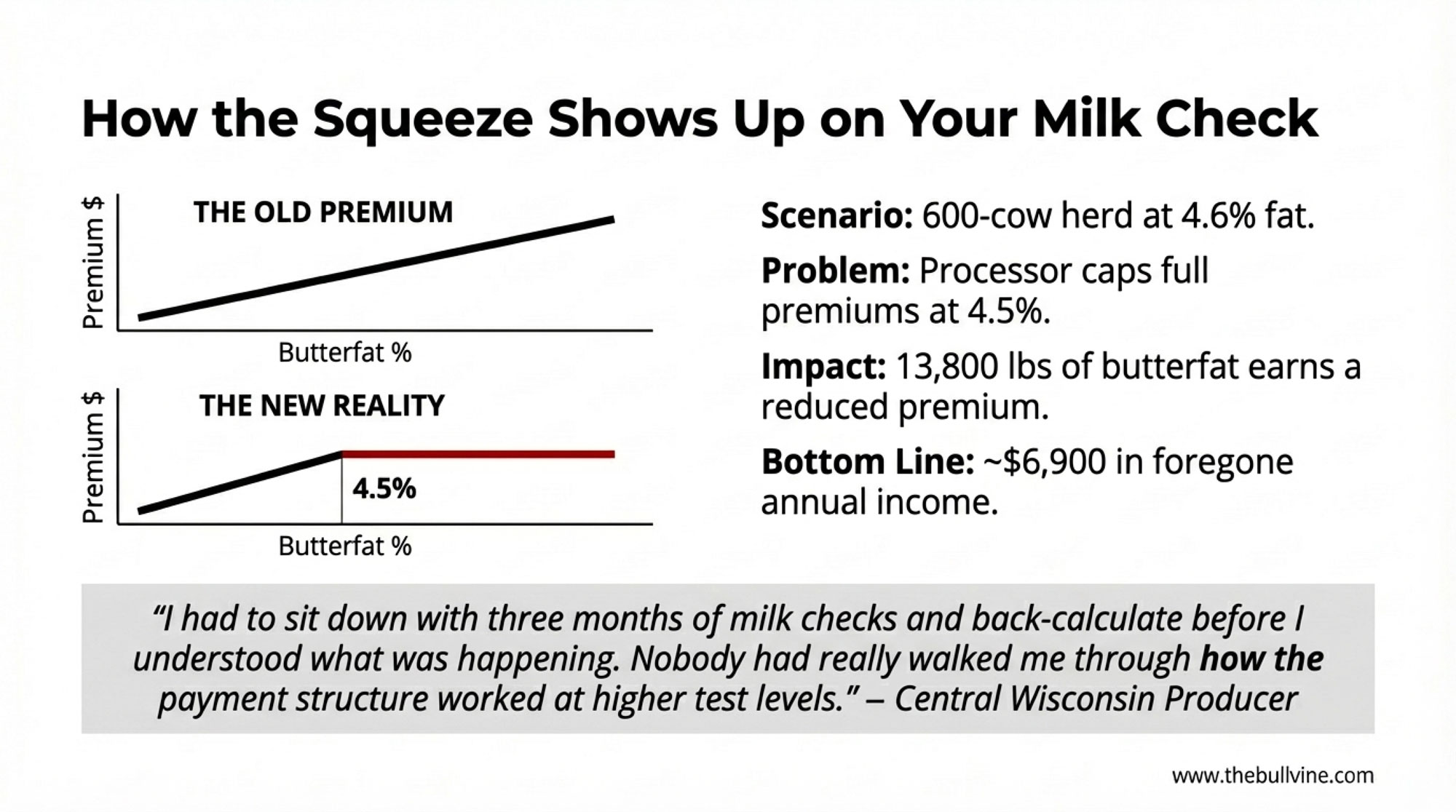

- Your component check has already absorbed roughly $1,520/cow from February 2025 to February 2026 — about $456,000 on 300 cows. If your expansion budget or debt‑service math is built on early‑2025 component values, you’re building on a number that isn’t there anymore.

- The FMMO reform alone shaved about $60/cow off your other‑solids line via the higher make allowance — roughly $18,000/year on 300 cows — even as processors booked stronger whey ingredient margins.

- You need to know what your plant does with whey and how they share it. If your co‑op’s annual report shows whey ingredient revenue growing faster than patronage per cwt, that gap is worth understanding — and worth raising at your next member meeting.

- Beef‑on‑dairy calves at $1,400–$1,750 are real margin, but they’re also tightening heifer supply in ways that make the coming milk bidding wars more brutal. Your beef‑to‑dairy AI ratio needs to line up with your three‑year heifer plan, not just this month’s calf check.

- Negative PPDs are the hidden multiplier. With Class IV buoyed by strong powder and cheese under pressure, the setup looks uncomfortably similar to 2020 and late 2024. Model another $1–$2/cwt of exposure.

- Don’t build a barn on a commodity spike. Stress‑test every expansion pro forma at about $15.50/cwt component value, not $21. If it doesn’t cash‑flow there, you’re not investing — you’re betting.

- Price the haul to a competing plant. If whey capacity is being added within hauling range, ask directly what the over‑order premium is and how ingredient economics show up in their payment structure. McCully’s “who won’t get the milk?” question is where your leverage comes from.

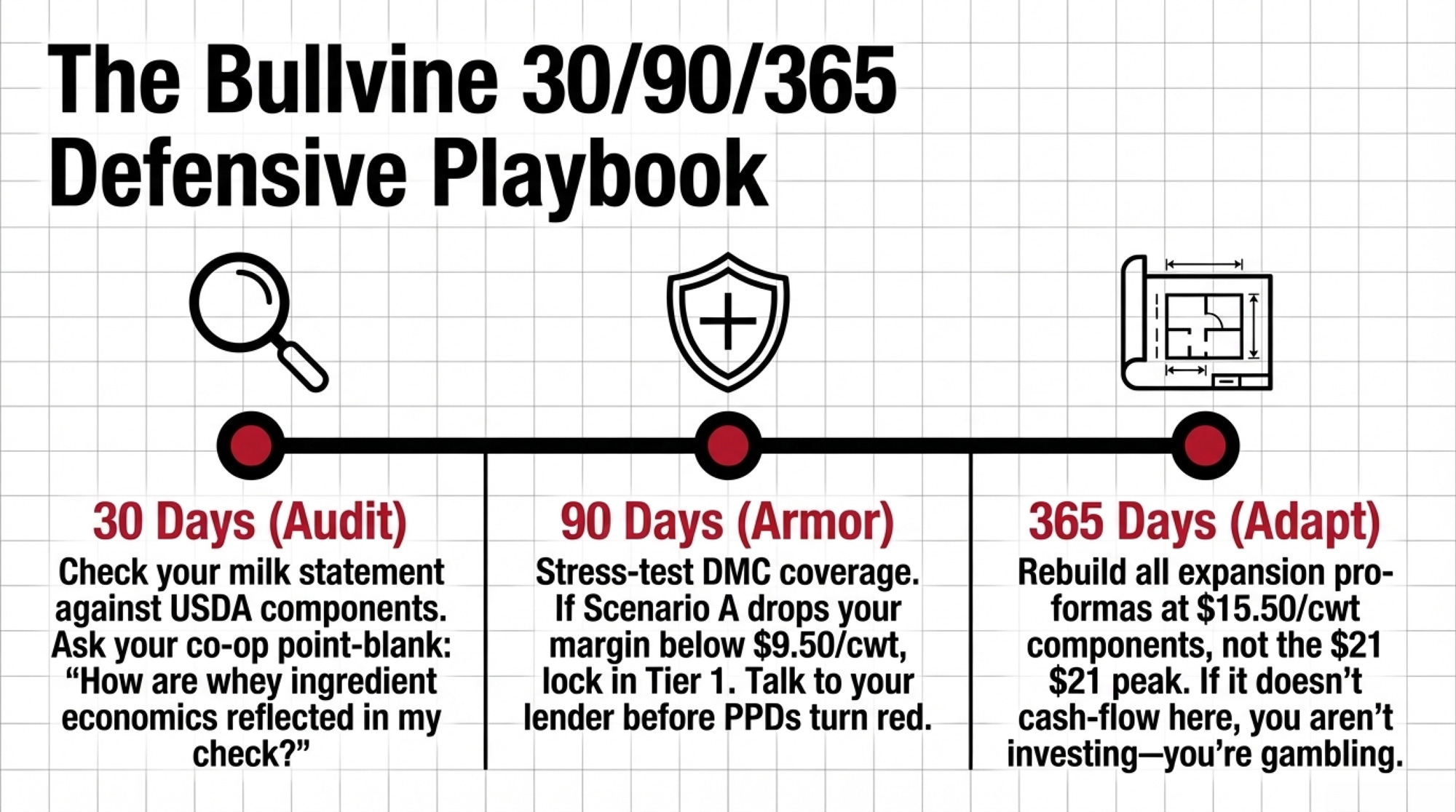

Your 30/90/365‑Day Playbook

| Timeframe | Key Action | Target Benchmark | Red Flag Threshold | Tool / Source |

|---|---|---|---|---|

| 30 Days | Audit milk check vs. USDA values | Protein: $1.9373/lb; OS: $0.4391/lb; Fat: $1.7794/lb | >$0.15/cwt below FMMO after hauling | USDA AMS February 2026 component prices |

| 30 Days | Request co-op whey breakdown | Patronage per cwt growing with ingredient revenue | Whey revenue growing faster than patronage | Co-op annual report / equity statement |

| 90 Days | Stress-test DMC coverage | Tier 1 at $9.50 (up to 6M lb) | Margin drops below $9.50 in Scenario A | USDA DMC / Center for Dairy Excellence |

| 90 Days | Model PPD exposure | $0/cwt PPD | PPD turns -$1.50/cwt or worse | Class III vs. Class IV spread monitor |

| 12 Months | Re-run expansion pro forma | Base case: $15.50/cwt components | Only pencils out above $20/cwt | Internal proforma, lender review |

| 12 Months | Price hauling alternatives | Confirm over-order premium structure | Plant within haul range offers no premium | McCully/StoneX consultant framework |

Within 30 days: Audit your check against USDA component values.

Pull your last three milk statements. Compare your protein, other solids, and butterfat rates to USDA’s February 2026 published component prices: protein at $1.9373/lb, other solids at $0.4391/lb, butterfat at $1.7794/lb.

If your combined protein‑plus‑other‑solids payment runs more than $0.15/cwt below the FMMO values after hauling and marketing deductions, call your co‑op and ask one direct question: “How are whey ingredient economics reflected in my component check?”

If you get a non‑answer, request the co‑op’s annual financial report and equity statement. Compare ingredient revenue to patronage distributions. That gap — if it’s growing — is the conversation to bring to the next member meeting. It’s the kind of thing that costs real money when you put off the hard financial questions.

Within 90 days: Stress‑test your DMC coverage and talk to your lender.

USDA’s January 2026 DMC margin landed at $7.81/cwt, triggering a $1.69/cwt indemnity for herds enrolled at the $9.50 Tier 1 level. February’s margin was projected to be around $8.07/cwt by the Center for Dairy Excellence.

Walk your own numbers through Scenario A:

- Knock $2.33/cwt off your current component value.

- Layer in a −$1.50/cwt PPD if you’re in an order that’s likely to go negative.

- See where your income‑over‑feed margin lands relative to $9.50/cwt.

If the margin drops below $9.50 in that scenario, the expanded Tier 1 coverage — now up to 6 million pounds under the One Big Beautiful Bill Act — is likely your cheapest shock absorber.

Then bring both scenarios to your lender. Ask specifically: what debt‑service coverage ratio would they need to see — 1.2×? 1.3×? — to stay comfortable if those margins showed up for 12 months. Better to push that conversation now than have your banker push it when the PPD turns red.

Within 12 months: Rebuild your expansion math around post‑reform prices.

Run every major capital decision at three component levels:

- $15.50/cwt — roughly where early‑2026 Class III components sit.

- $19.20/cwt — a 2025‑style “good year” average.

- Scenario A with a −$1.50 PPD — your personal worst‑case stress.

You don’t control whether WPI stays at $11 or glides down to $6. You do control whether your business can survive both.

Key Takeaways

- If your expansion or refinance pencils out only at a $20+ component value, you’re exposed. Re‑run at $15.50/cwt and see if it still holds water.

- If you can’t see whey in your milk check, assume it’s not there. Plan your cash flow on FMMO components alone until your statement or co‑op report shows a clear whey‑linked premium.

- If more than half your AI is going to beef without a three‑year heifer plan, you’re trading future cow supply for today’s calf check. Make sure that’s intentional.

- If you’re not enrolled at $9.50 DMC Tier 1 and you’re running 200–500 cows, you’re choosing to self‑insure against a whey/cheese/PPD shock. Do the math with your lender, not in your head.

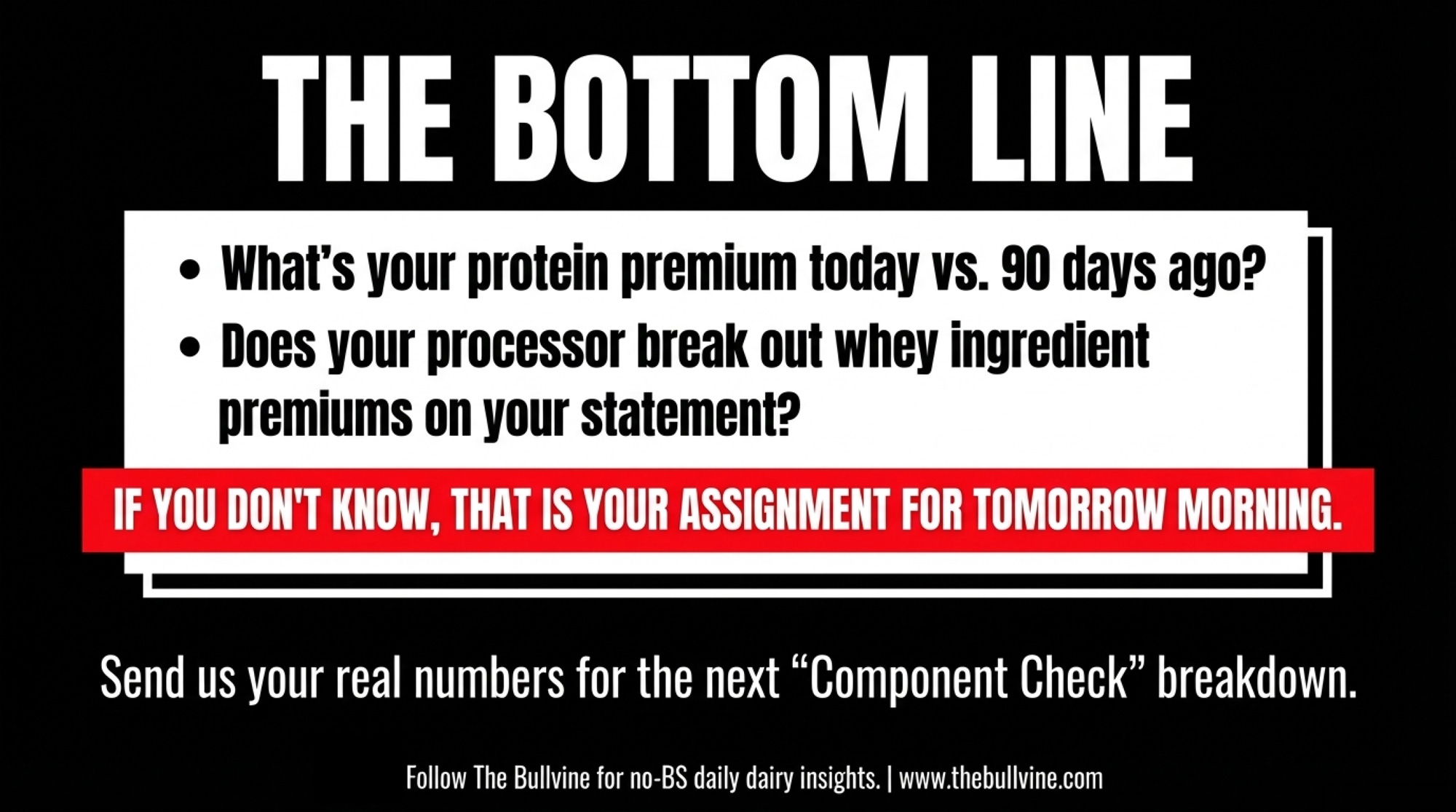

The Bottom Line

What’s your protein premium per cwt this month versus 90 days ago? Does your processor break out whey solids or ingredient premiums anywhere on your statement? And if you’re in a co‑op, how did last year’s patronage per cwt move compared to the co‑op’s reported whey ingredient revenue?

If you don’t know any of those answers, that’s your 30‑day assignment.

Next in “Component Check”: we run the math on how the April DMC margin and the whey premium interact on a 500‑cow milk check. If you want us to use your real numbers, send them.

This analysis uses publicly available USDA data, published analyst commentary, and FMMO pricing formulas. It’s intended as economic education and decision support for dairy producers, not as investment advice or a recommendation regarding any specific co‑op, processor, or financial product.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- 76% of Your Dairy Checkoff Funds Cheese and Exports. How Much ROI Hits Your Fluid Milk Check? – Reveals how to execute a 30-day “Accountability Dashboard” audit. This guide arms you with the specific formulas to calculate your individual checkoff ROI and identifies whether your processor’s product mix is quietly devaluing your daily shipments.

- USDA Says $18, Futures Say $16: The $150K Gap That’s Rewriting 2026 Dairy Budgets – Exposes the dangerous disconnect between government forecasts and real-world futures markets. This strategic analysis delivers the $17/cwt “capital test” you must run to ensure your long-term expansion plans don’t collide with the $11 billion processing capacity surge.

- Beef-on-Dairy’s $3,000 Trap: 800,000 Missing Heifers and Who Pays the Bill – Breaks down the disruptive math of the national replacement shortage. This report delivers the “guard rails” for reproduction and genetic planning, ensuring you capture immediate beef-cross premiums without accidentally triggering a $60,000-a-year heifer bill by 2027.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

Join the Revolution!

Join the Revolution!