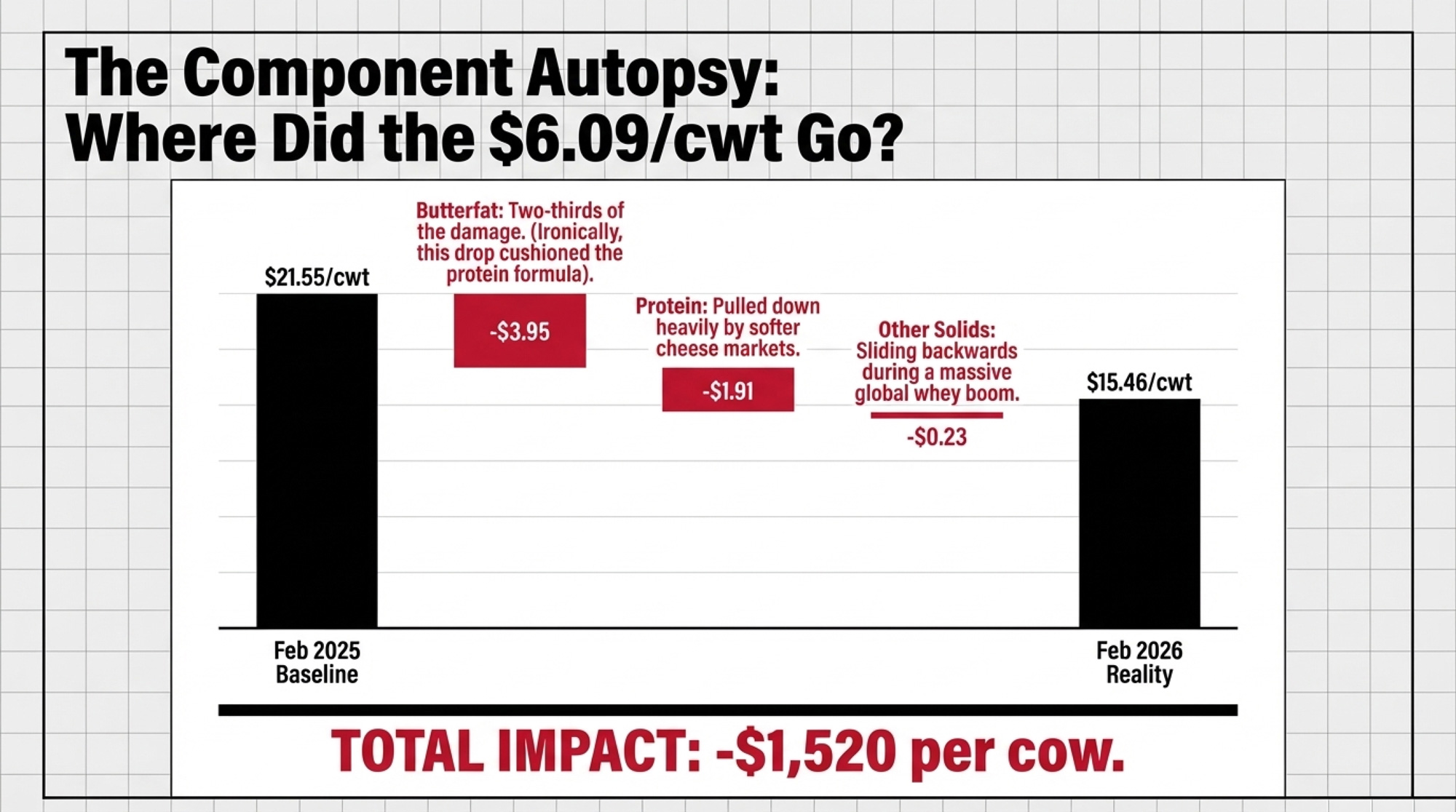

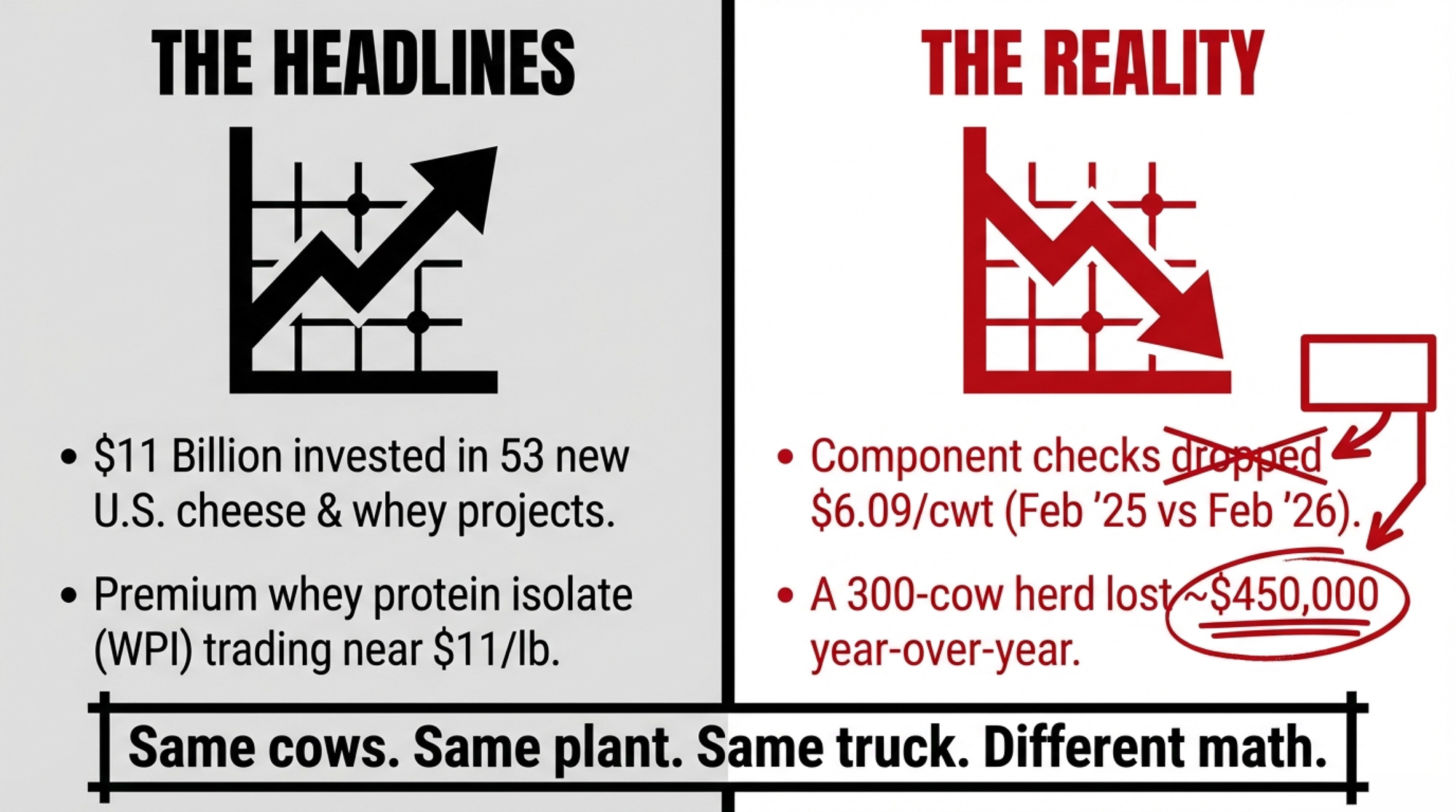

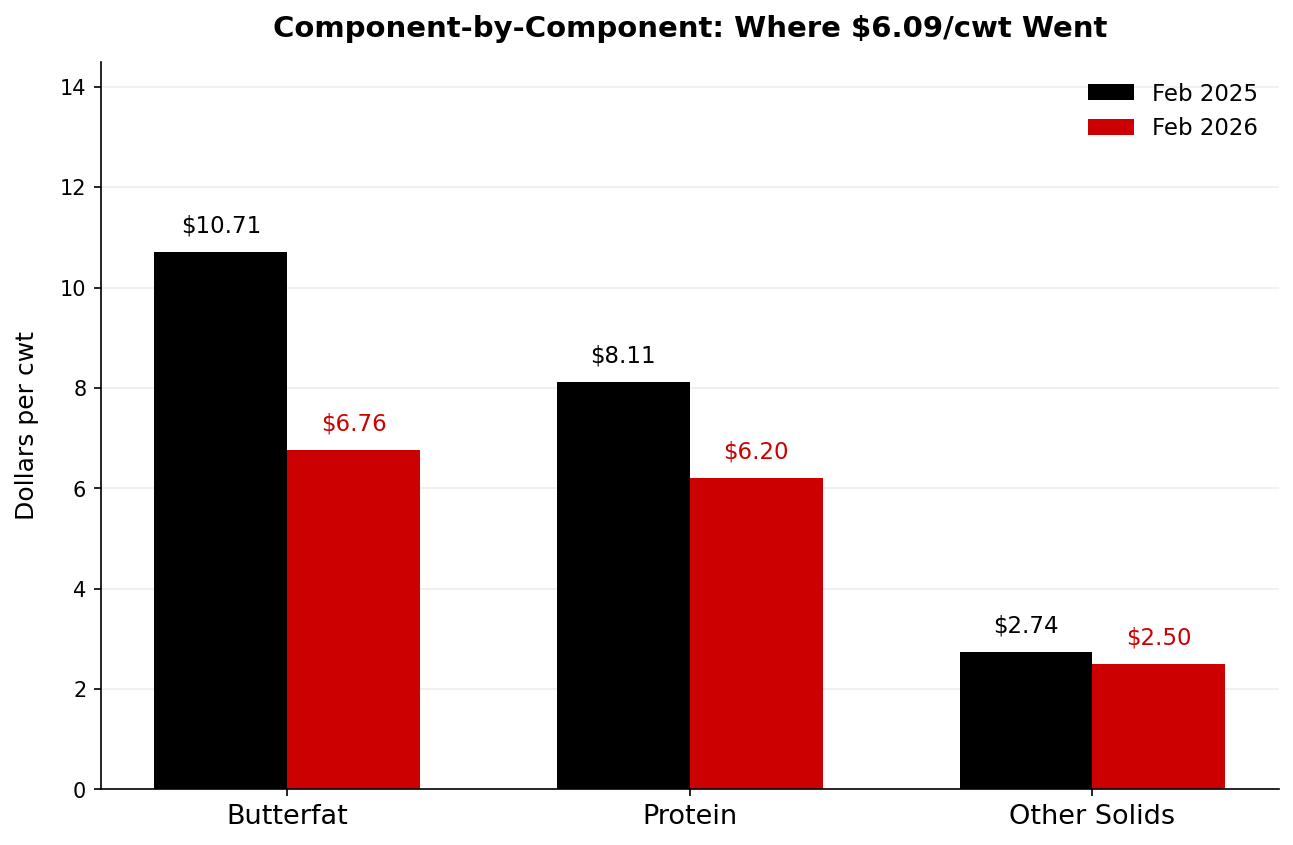

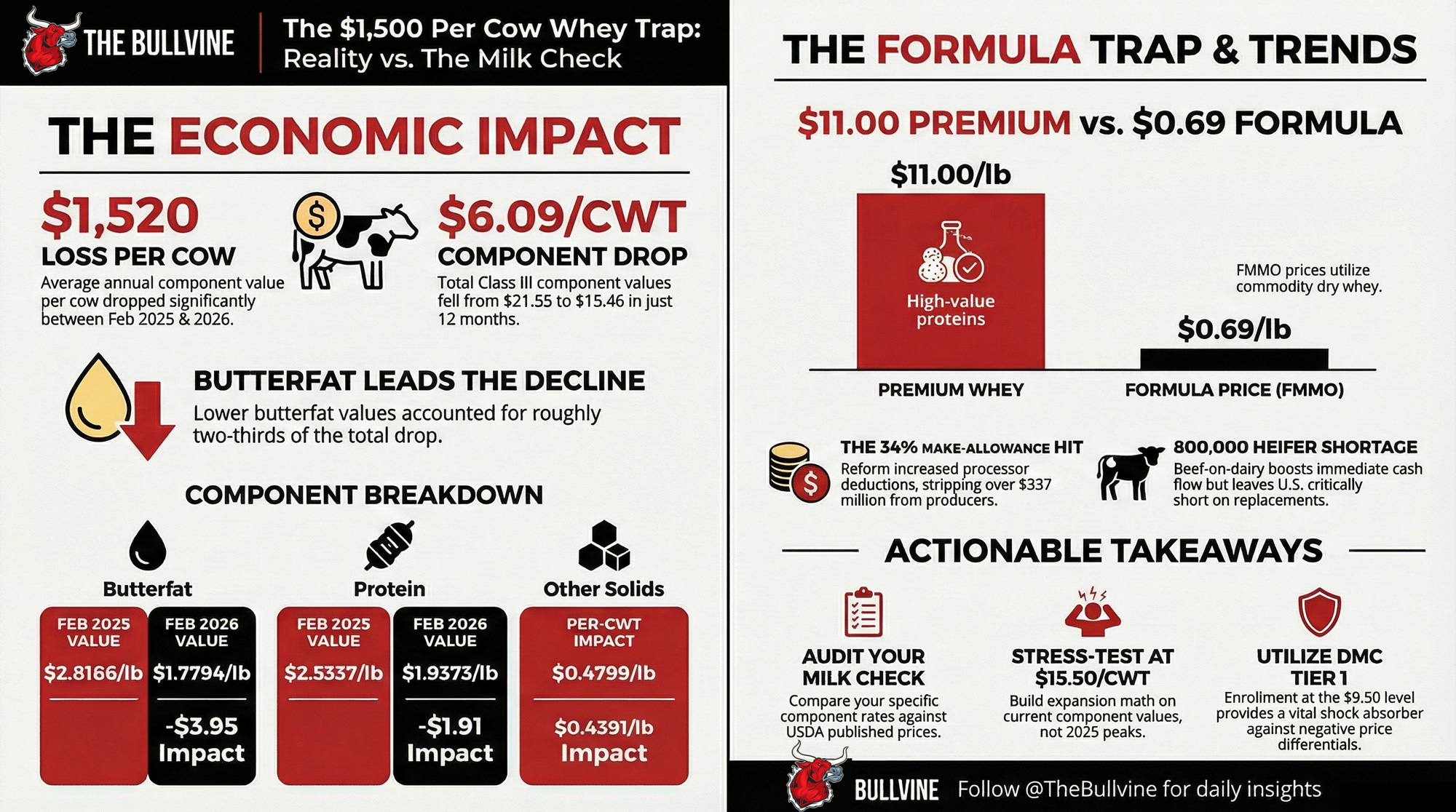

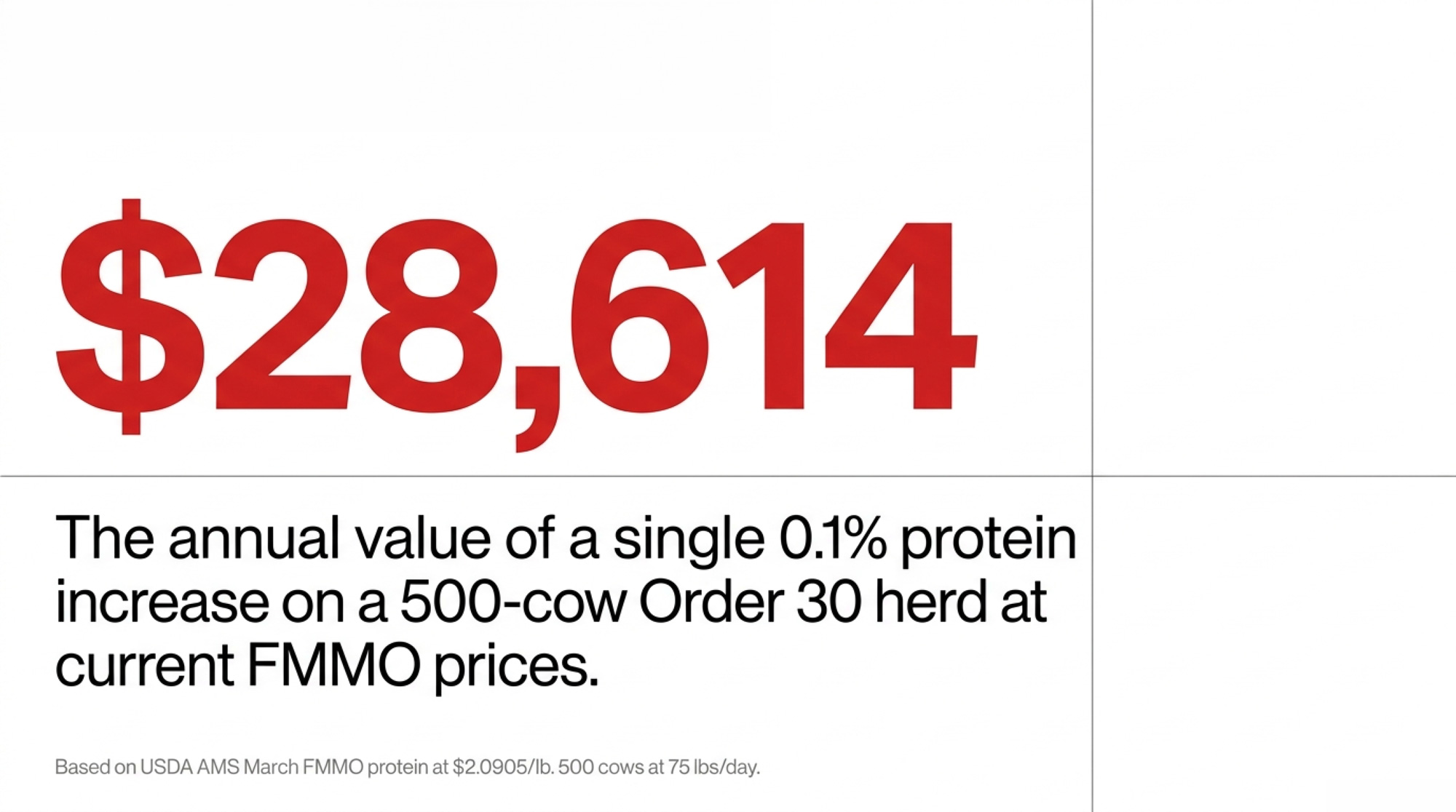

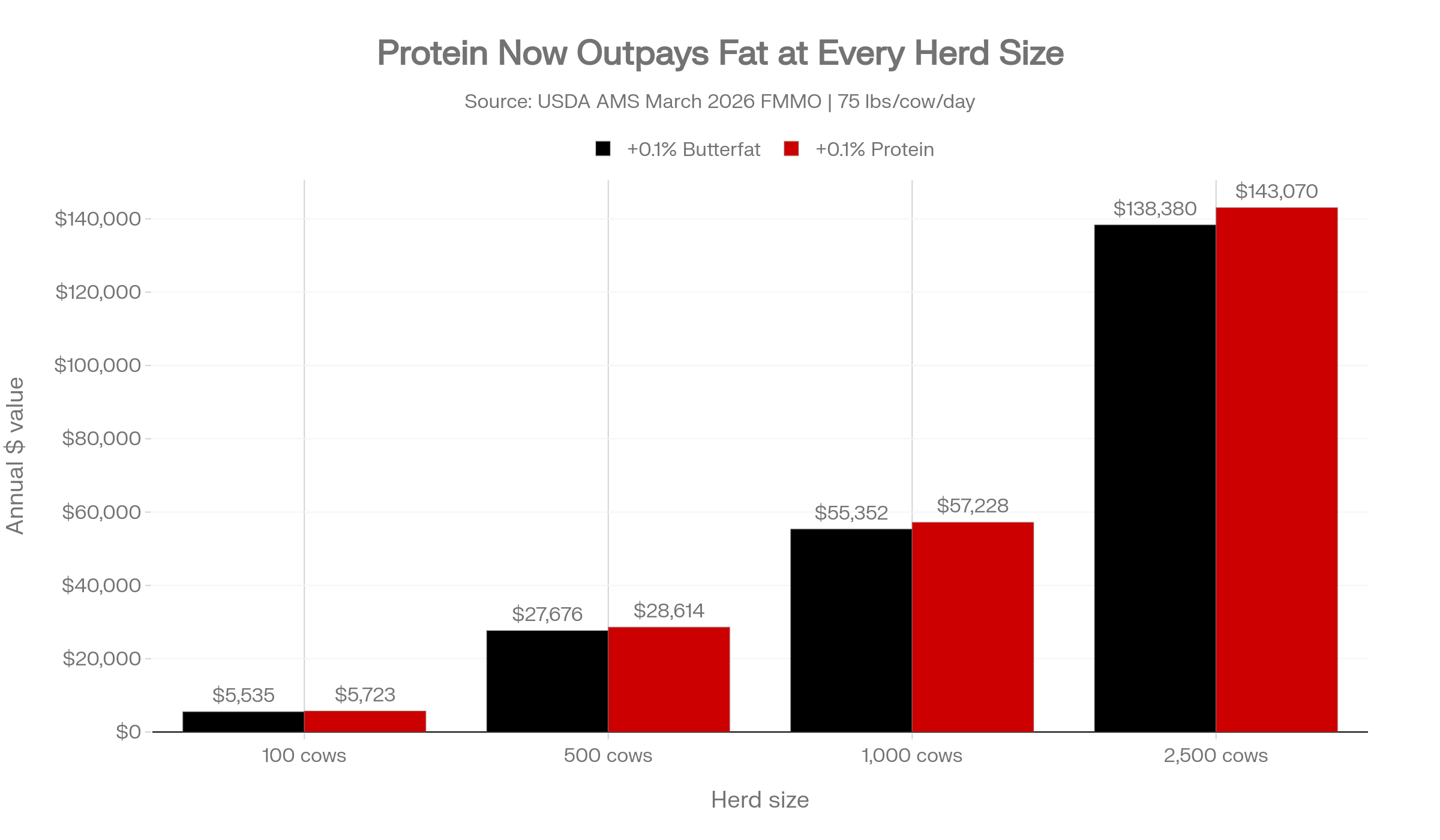

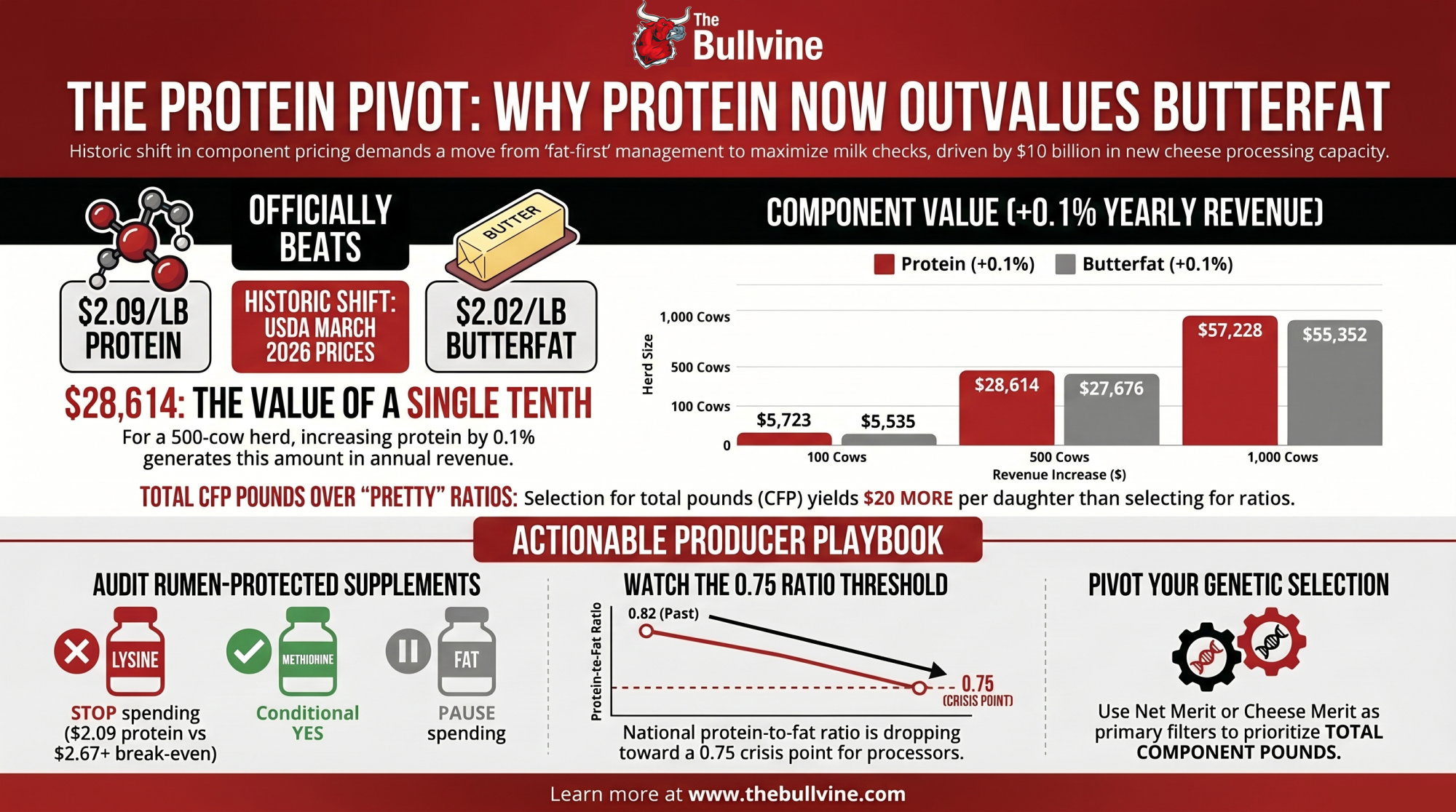

USDA set March protein at $2.0905/lb against butterfat at $2.0220. On a 500-cow Order 30 herd at 75 lbs/day, that tenth is worth $28,614 a year — $938 more than fat. First sustained flip in a decade.

At the March 2026 Federal Milk Marketing Order announcement, USDA AMS set the protein price at $2.0905/lbagainst butterfat at $2.0220/lb — the first sustained stretch in a major cycle where a pound of milk protein outvalues a pound of milk fat. For a 500-cow Wisconsin or Minnesota shipper into Order 30 moving 75 lbs/cow/day, a single tenth-of-a-percent gap in protein now runs $28,614 a year; fat lands close behind at $27,676.

👉 Run those numbers on your own herd — open the Component Value Tracker →

That’s the stake for a mid-size Upper Midwest herd still calibrated to the old fat-premium world. The trap: a decade of fat-first genetics, fat-first rations, and fat-first contracts running headlong into roughly $10 billion in new cheese capacity that needs protein and doesn’t much care about the butter side anymore.

Dairy component economics 2026 isn’t a theme. It’s the math on your next milk check.

This is Issue #1 of The Bullvine Component Value Tracker — a monthly read translating the FMMO announcement into herd-specific dollar decisions, ranking nutrition break-evens against current prices, and scoring where the month’s highest-return component moves actually sit. May 2026 baseline: 58/100 — Maintain and Reposition Toward Protein.

The Signal the Market Already Sent

For eight of the ten years leading into 2025, butterfat paid more per pound than protein. Producers answered the signal. Genetics companies bred for fat. Nutritionists optimized rations for butterfat response. It worked — arguably too well.

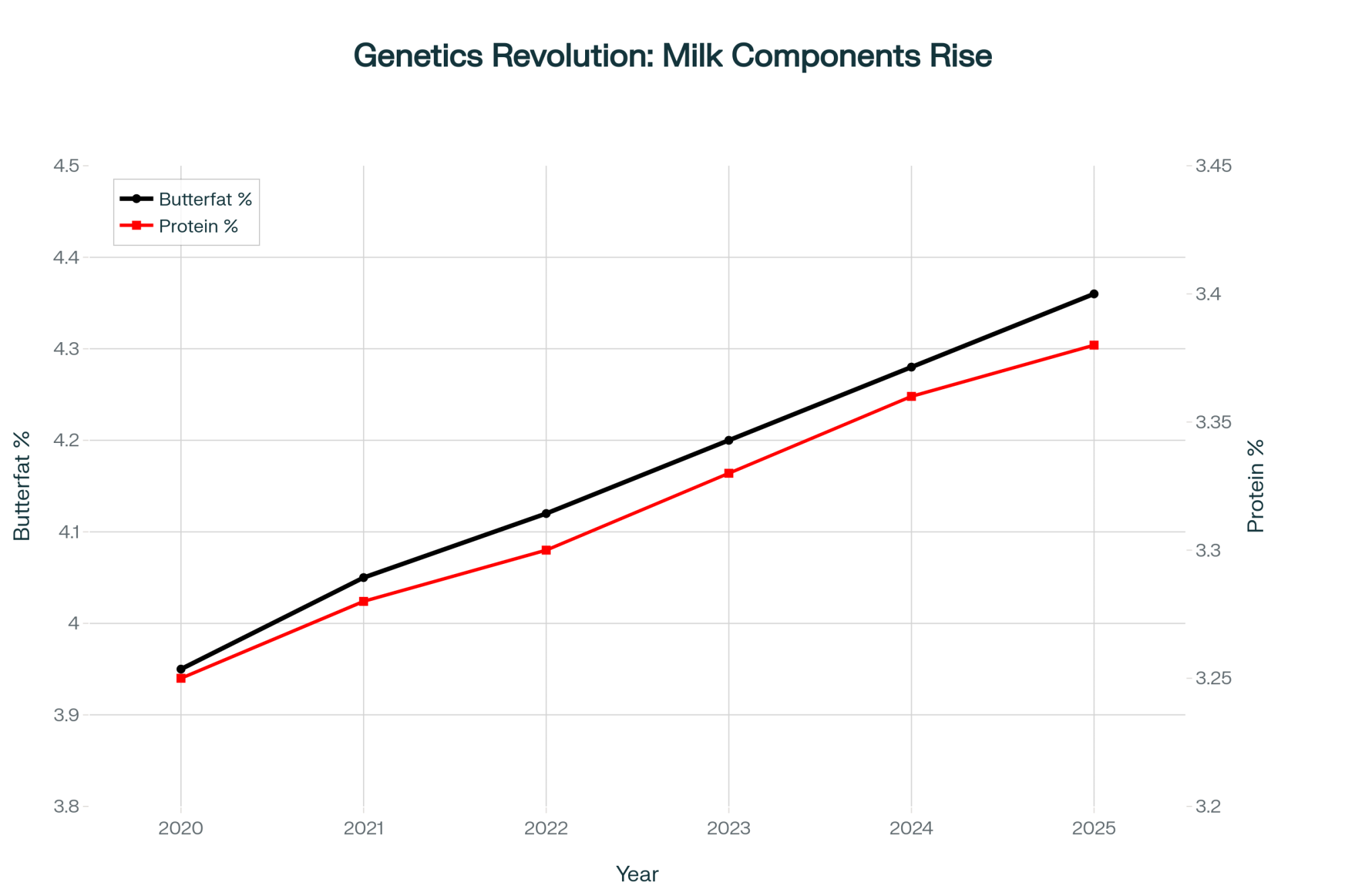

U.S. butterfat climbed 0.58 points between 2015 and 2025, from 3.75% to a record 4.33%, per USDA NASS data compiled by FMMA30 — a 15.5% lift off the 2015 baseline. Over the same window, EU butterfat gained roughly 2.4% and New Zealand roughly 2.5%, per FMMA30’s international comparison. Protein climbed too — 3.11% to 3.29% — but that 5.8% gain only looks healthy until you stack it next to fat running at nearly triple the pace.

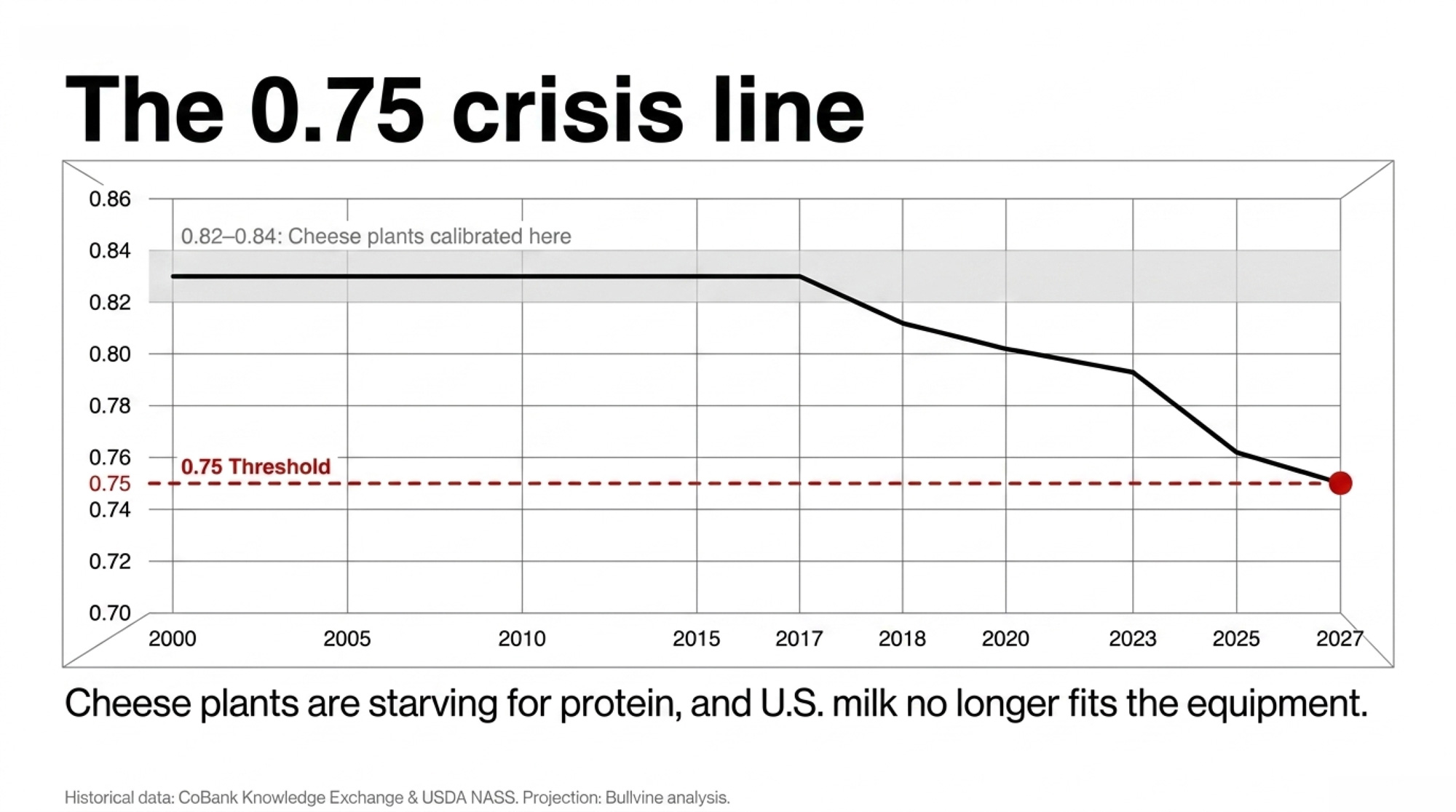

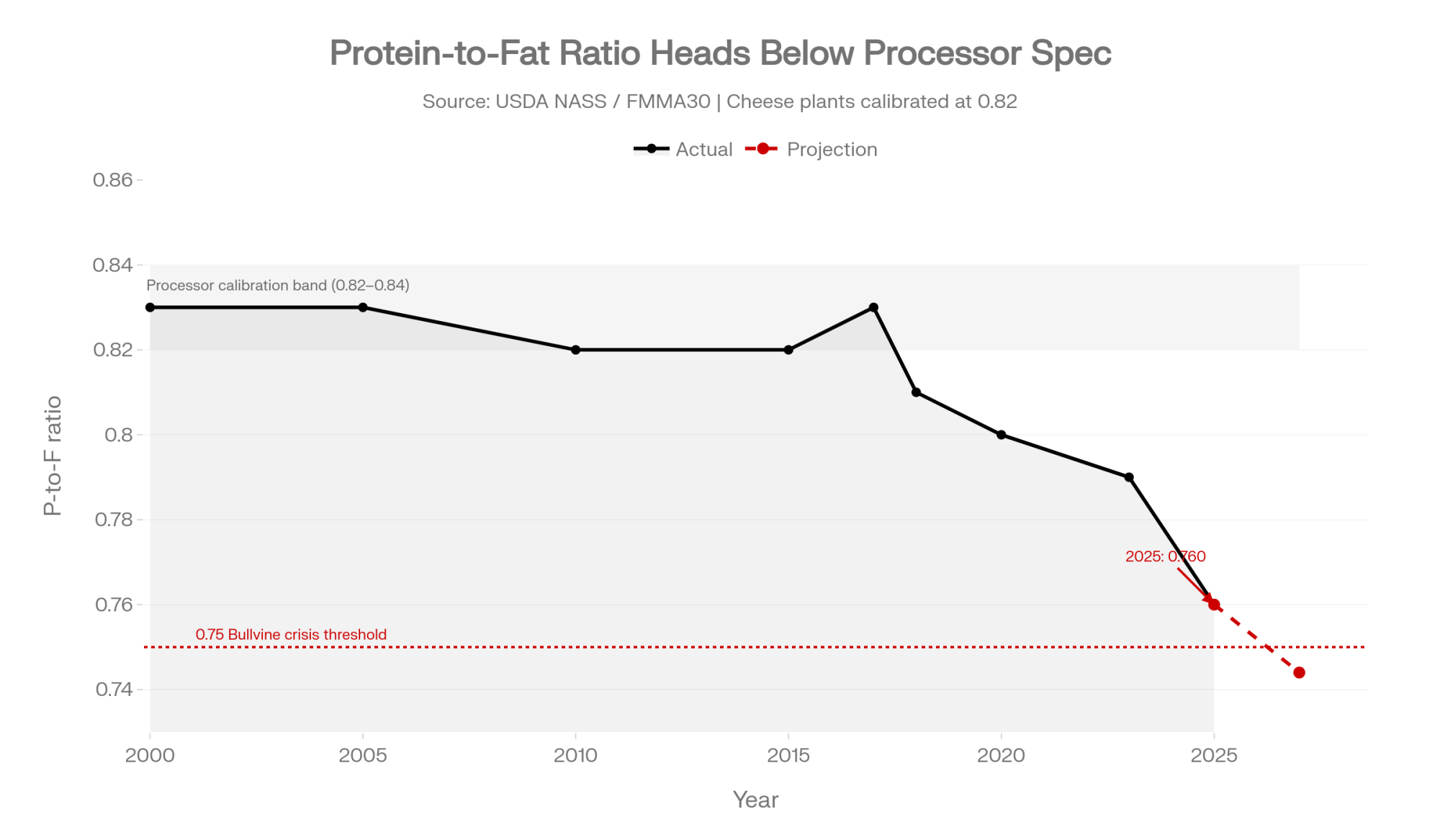

CoBank’s lead dairy economist Corey Geiger flagged the problem in the bank’s September 25, 2025 Knowledge Exchange brief, warning that excessive butterfat can compromise cheese quality and that cheesemakers target a protein-to-fat ratio near 0.80, with ratios significantly below that threshold reducing yield efficiency. At the time, the ratio sat at 0.77. Seven months later, with full-year 2025 butterfat averaging 4.33% against protein stuck at 3.29%, it’s dropped to 0.760 (3.29 ÷ 4.33 = 0.7598).

Over half of U.S. milk now moves into cheese. Those plants were calibrated for 0.82. The milk arriving at the dock doesn’t match the equipment on the other side.

Why Should Upper Midwest Producers Care About the 0.75 Threshold?

From 2000 to 2017, the U.S. protein-to-fat ratio held flat between 0.82 and 0.84, per CoBank’s Knowledge Exchange. That’s the band processors built their plants around. Starting in 2018, the line bent.

| Year | P-to-F Ratio | Context |

| 2000–2017 | 0.82–0.84 | Stable — cheese plants calibrated here |

| 2018 | ~0.81 | Decline begins |

| 2020 | ~0.80 | Geiger’s “near 0.80” cheese-quality target |

| 2023 | ~0.79 | Decline accelerates |

| 2025 full-year | 0.760 | FMMA30 / USDA NASS annual |

| Bullvine crisis threshold | 0.75 | Named in this issue |

| Projected arrival | Late 2027 (~16 months out) | Bullvine projection, ~0.008/year decline |

The Bullvine is putting a stake in the ground: the U.S. protein-to-fat ratio crosses 0.75 within roughly 16 months at current decline rates, and that’s where standardization costs, whey-stream fat losses, and processor basis negotiations visibly reprice Upper Midwest milk checks. If the ratio turns upward before late 2027, the Tracker will say so in writing and retire the call. If it doesn’t, this stops being a chart. It’s the basis for a pricing correction that’s already started.

The structural driver keeping the ratio suppressed is genetics, and the indexes don’t agree on which way out. Holstein USA’s April 2026 TPI revision shifted production weights to 24% protein and 14% fat — a 5-point move in each direction. Top-10% bulls saw an average 34-point TPI decline, with 26.6 of those points attributable to the formula change itself rather than routine evaluation updates. USDA’s Net Merit 2025 moved the opposite direction — 31.8% fat, 13.0% protein. Two major indexes. Two opposite signals. One breeder trying to mate cows this week.

Running the Numbers: What 0.1% Is Worth on a 500-Cow Order 30 Herd

Before you read the rest of this issue, run this math on your own operation.

Scope. 500-cow Wisconsin or Minnesota shipper into FMMO Order 30. 75 lbs/cow/day rolling average. March 2026 FMMO prices.

Formula:

Incremental annual revenue = 0.001 × daily lbs/cow × number of cows × 365 × FMMO component price per lb

Protein at $2.0905/lb:

- 0.001 × 75 = 0.075 extra lbs/cow/day

- 0.075 × 500 = 37.5 lbs/day herd-wide

- 37.5 × 365 = 13,687.5 lbs/year

- 13,687.5 × $2.0905 = $28,614/year

Butterfat at $2.0220/lb:

- 13,687.5 × $2.0220 = $27,676/year

| Herd Size | Daily lbs/cow | +0.1% Butterfat/Year | +0.1% Protein/Year | Combined |

| 100 cows | 75 | $5,535 | $5,723 | $11,258 |

| 500 cows | 75 | $27,676 | $28,614 | $56,290 |

| 1,000 cows | 75 | $55,352 | $57,228 | $112,580 |

| 2,500 cows | 75 | $138,380 | $143,070 | $281,450 |

March 2026 FMMO component prices, USDA AMS. Linear scaling.

Where the $83,000–$140,000 bulk-tank gap comes from. A 500-cow Order 30 shipper at 4.0% fat against a 2025 national average of 4.33% is carrying a 0.33-point fat gap. Three 0.1% increments × $27,676 = roughly $83,000/year in fat alone. Add a 0.2-point protein gap (3.09% vs. 3.29% national), and 2 × $28,614 pulls another ~$57,000/year. The $140,000 upper bound is a composite of two gaps on two components, not one factor. The low end is fat alone.

That’s the money. Not theoretical. Sitting in the bulk tank every month it ships short of county average.

If you’re leveraged. On a 500-cow shop running DSCR closer to 1.1 than 1.3, a captured $56,290 from a combined 0.1%/0.1% component move is the difference between a lender conversation you choose when to have and one your lender chooses for you. Component revenue doesn’t carry the manure tax added volume does — no extra cow, no extra parlor time, no extra lagoon capacity. It’s the highest-leverage margin move currently on the table.

Run the Numbers on Your Herd: The Bullvine Component Value Tracker

Every calculation above is scoped to a 500-cow Wisconsin or Minnesota shipper at 75 lbs/cow/day against March 2026 FMMO prices. Your operation isn’t that one.

The Tracker runs the +0.1% value, the component-gap dollars, and the $17 Class III capital stress-test against your actual numbers — same methodology, your inputs. Plug in your cow count, production level, fat and protein tests, and the dollar numbers move in real time.

Launch the Tracker pre-loaded with this article’s May 2026 baseline — 500 cows, 75 lbs/day, 4.33% fat, 3.29% protein, $2.0220 fat price, $2.0905 protein price, $19.70 USDA all-milk forecast, $16.16 CME Class III futures:

Bookmark the result once you’ve loaded your own cow count, production, and last month’s component tests — that’s your personal Tracker baseline for the Issue #2 refresh against May FMMO prices.

Why Does Chasing a Better Protein-to-Fat Ratio Cost You Money?

Here’s the assumption the “protein market” headlines set up: the right sire in a protein-premium cycle is the one with the best protein-to-fat ratio. Run the dollars at March 2026 prices, and that logic breaks.

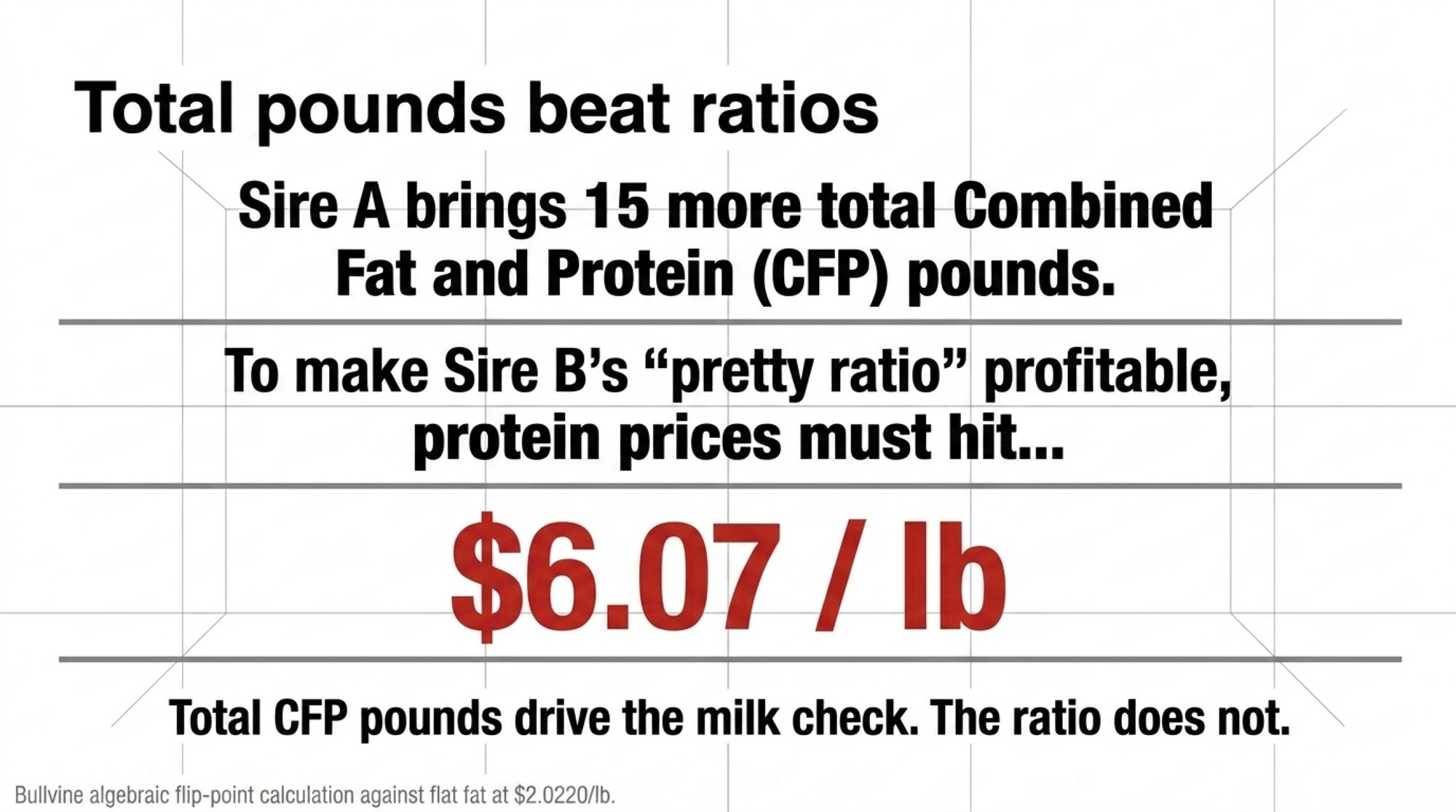

Two sires. Identical on everything else.

| Sire | Fat PTA (lbs) | Protein PTA (lbs) | Fat Value | Protein Value | Total per Daughter/Lactation | Winner |

| Sire A | +45 | +35 | 45 × $2.0220 = $90.99 | 35 × $2.0905 = $73.17 | $164.16 | ✅ +$19.88 |

| Sire B (prettier ratio) | +30 | +40 | 30 × $2.0220 = $60.66 | 40 × $2.0905 = $83.62 | $144.28 | — |

Sire B has the prettier protein-to-fat ratio. Sire A has the heavier check — by $19.88 per daughter per lactation, in a protein-premium market. Total CFP pounds drive the milk check. Ratio doesn’t.

The flip point isn’t where headline logic puts it. Setting Sire A’s value equal to Sire B’s and solving for protein against flat fat at $2.0220/lb:

(45 × $2.0220) + (35 × P) = (30 × $2.0220) + (40 × P) 15 × $2.0220 = 5 × P P = $6.07/lb protein

At flat fat, protein would have to triple from $2.09 to roughly $6/lb before Sire B’s ratio edge overcomes Sire A’s 15-lb CFP advantage. Sire A’s win isn’t marginal. It’s structural — the total-pounds gap is large enough that no realistic protein price flips it.

Picture a Brown County 500-cow operation — a hypothetical herd representative of Order 30 shippers we’ve modeled — that filtered its April sire list on protein-to-fat ratio and surfaced Sire B at the top. Across a typical replacement pipeline of 150 heifers/year and 2.8 lactations per cow in the milking string (Bullvine modeling assumption), that single $19.88/daughter/lactation delta compounds to roughly $8,350/year in steady-state drag once the selection cycles through the lactating herd (150 × 2.8 × $19.88). Filter-the-whole-sire-list style ratio-first selection — not just one sire swap — carries materially more drag; The Bullvine’s April 2026 TPI analysis modeled it at roughly $17,500/year for herds that filtered broadly on ratio across multiple placements.

The ruleset for this mating season:

- Primary filter: Net Merit or Cheese Merit — both balance full economics, not just protein percent

- Sort by: total CFP pounds

- Tie-breaker: protein PTA, when CFP is equivalent

- Don’t: select on protein-to-fat ratio at the expense of total CFP

There’s an interpretive tension inside TPI itself worth flagging — this is Bullvine analysis, not a Holstein USA position. Under the April 2026 formula, one pound of PTA protein carries roughly 1.7× the leverage of one pound of PTA fat in the index. TPI’s own Feed Efficiency formula still values fat at $1.86/lb against protein at $1.75/lb. Same index. Two signals. Trust the price on the milk check, not the coefficient on the ranking sheet.

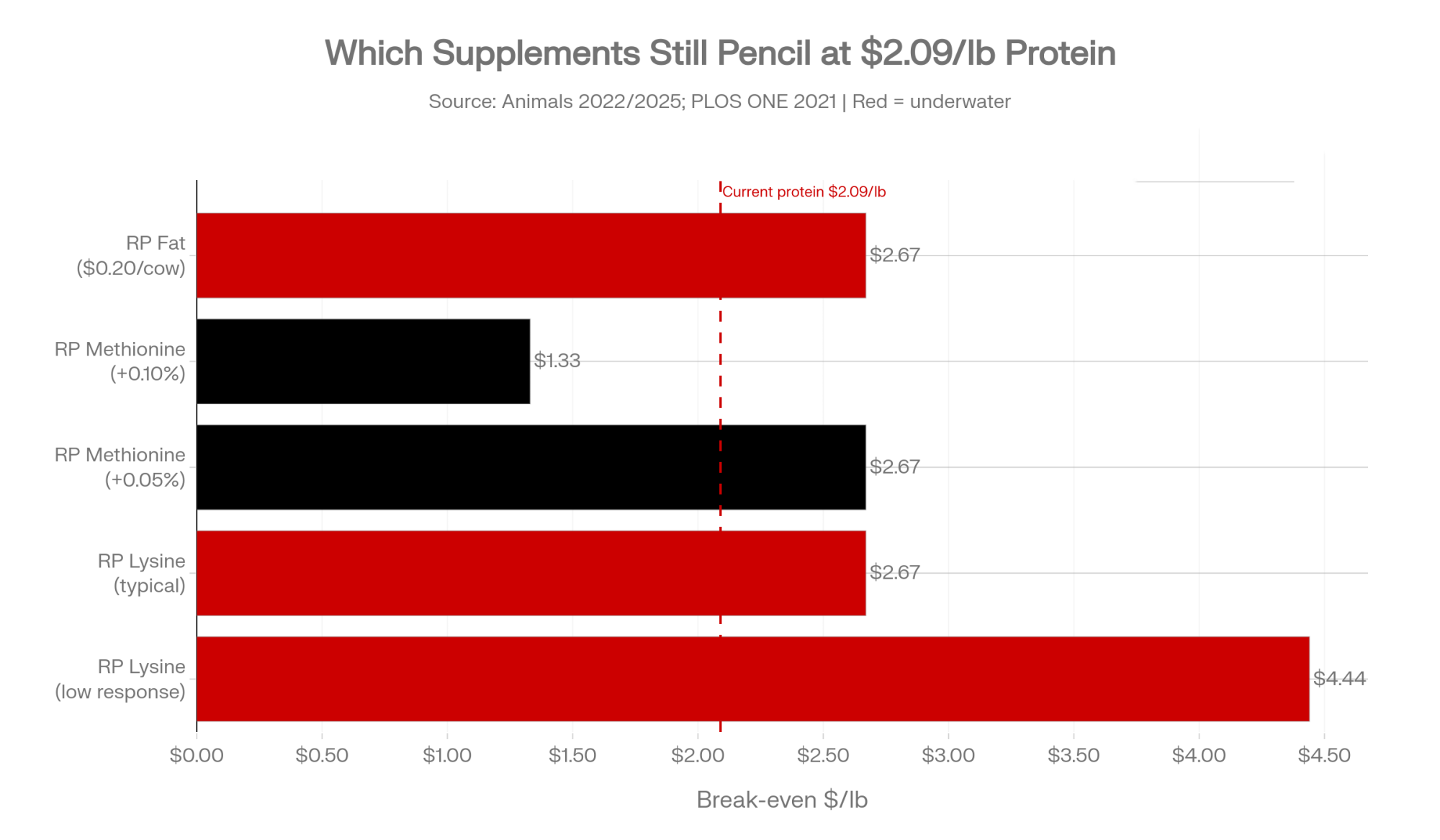

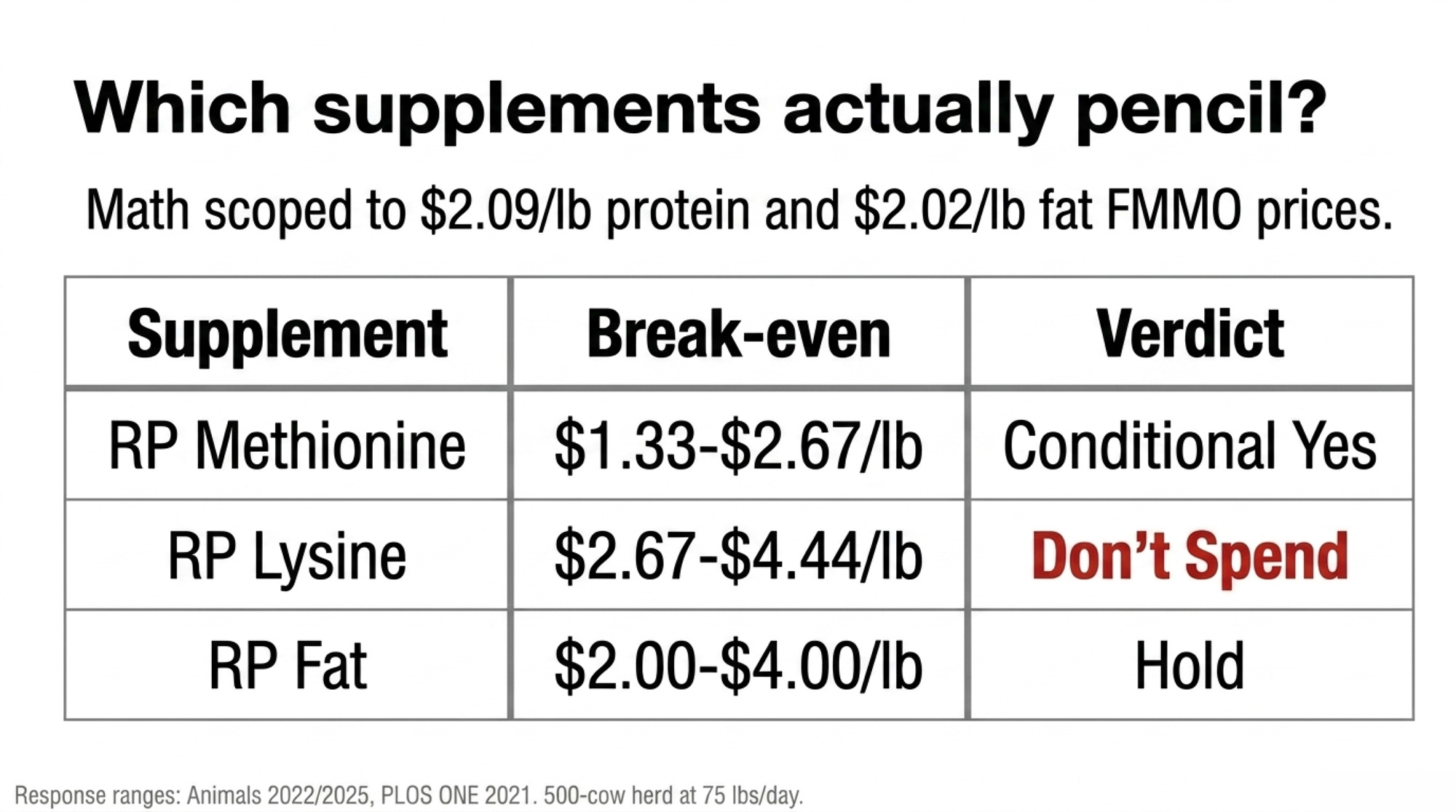

Which Supplements Still Pencil at $2.09/lb Protein?

Component prices shifted. Not every ration has caught up. Break-evens below are scoped to a 500-cow, 75 lbs/cow/day Order 30 operation at March 2026 FMMO prices.

Rumen-Protected Methionine: Conditional Yes

A peer-reviewed meta-analysis in Animals (PMC9219501, 2022) puts RPM’s protein response range at +0.07% to +0.15%, with yield gains of 27–43 g/day. The 2025 combined RPLM paper (Animals, PMC12691028) confirms response is heavily dependent on basal diet and a roughly 3:1 lysine-to-methionine target.

At $0.10/cow/day, +0.05% response:

- Extra protein: 0.0005 × 75 = 0.0375 lbs/cow/day

- Break-even protein price: $0.10 ÷ 0.0375 = $2.67/lb

- Current: $2.09/lb — marginally negative

At $0.10/cow/day, +0.10% response:

- Extra protein: 0.075 lbs/cow/day

- Break-even: $0.10 ÷ 0.075 = $1.33/lb

- Margin vs. current: +$0.76/lb — strongly positive

Methionine pays when the cost is low and the response is real. It doesn’t pay when either assumption slips. That’s a ration-audit conversation, not a standing order.

Rumen-Protected Lysine: Don’t Spend

Commercial RPL response on Holsteins runs +0.03% to +0.08% protein at $0.08–$0.15/cow/day, per trial work summarized in PLOS ONE (pone.0243953, 2021).

- At $0.10/cow/day, +0.05% response: break-even $2.67/lb

- At $0.10/cow/day, +0.03% response: break-even $4.44/lb

Current protein: $2.09/lb. Unless you’ve got 30+ days of bulk-tank data proving outlier response on your herd, lysine’s a ration tax right now. Not a component strategy.

The flip point. Protein above $2.75/lb sustained before lysine pencils at typical commercial response — $0.66/lb of price movement away.

Rumen-Protected Fat: Hold

At March 2026 butterfat of $2.0220/lb, the break-even for RP fat lands at $2.67/lb (at $0.20/cow/day cost and a +0.10% response: $0.20 ÷ 0.075 = $2.667). Current butterfat sits $0.65 below that threshold. The math works only at lower cost or higher verified response — $0.15/cow/day against the same +0.10% response drops break-even to $2.00/lb, right at the current FMMO.

A year ago, with butterfat peaking at $2.95/lb in January 2025 before collapsing 46% to $1.58/lb by December 2025, the math worked early and not at all by year-end. Any response shortfall flips the decision today.

The flip point. Butterfat sustained above $2.67/lb at typical $0.20/cow/day cost, or contract RP fat below $0.15/cow/day with herd-specific +0.10% response confirmed.

| Supplement | Cost/Cow/Day | Response Range | Break-Even (typical) | Current FMMO | Verdict |

| RP Lysine | $0.08–$0.15 | +0.03–0.08% protein | ~$2.67–$4.44/lb | $2.09/lb | Don’t spend |

| RP Methionine | $0.10–$0.14 | +0.07–0.15% protein | $1.33–$2.67/lb (response-dependent) | $2.09/lb | Conditional yes — low cost + verified response only |

| RP Fat | $0.15–$0.30 | +0.10–0.20% butterfat | $2.00–$4.00/lb (cost- and response-dependent) | $2.02/lb | Hold — break-even at or above current FMMO |

Response ranges: Animals 2022 (PMC9219501); Animals 2025 (PMC12691028); PLOS ONE 2021 (pone.0243953). Herd response varies by basal ration, stage of lactation, and product specification.

How Much Does Your FMMO Order Change the Protein Payoff?

Same genetics move. Same ration tweak. Different milk check — because FMMO class utilization dictates how much the market pays for what you improved.

Order 30 (Upper Midwest) routes 83.9% of producer milk to Class III cheese use, per FMMA30 2025 annual data. Wisconsin contributes 69.6% of Order 30 volume; Minnesota adds 21.0%. In a cheese-heavy order, protein dominates.

| FMMO / Region | Class Utilization | P-to-F | Priority |

| Upper Midwest (30) | 83.9% Class III | 0.759 | Protein first at current FMMO prices — highest protein ROI among major orders |

| Southwest (126) / Texas | Expanding cheese | 0.767 | Hilmar + Leprino pulling hard; contract premiums emerging |

| California (51) | Class 4a heavy | 0.763 | Fat premiums compressed; repositioning window |

| Northeast (1) | Balanced I/III | 0.776 | Fluid share moderates protein premium |

FMMA30 Upper Midwest 2025 annual; ratios derived from regional component averages in FMMO reporting.

Texas production ran +10.6% in 2025, Kansas +11.4%, per USDA NASS. Idaho regained the nation’s #3 spot at 18.26 billion lbs of milk, edging Texas’s 18.21 billion by roughly one day’s worth of production. The processing gravity wells driving that growth:

- Hilmar Cheese, Dodge City, KS — $600M, operational since March 2025

- Leprino Foods, Lubbock, TX — approximately $1B complex, ~600 employees, designed for ~1M lbs cheese/day

- Valley Queen, Milbank, SD — expansion completed 2025, anchoring the I-29 corridor

- Leprino, Lemoore East, CA — closing in 2026, driving California capacity losses

Early-2026 trade coverage of High Plains and I-29 corridor contract offers has flagged structural premium tiers rewarding herds that reach roughly 4.2% fat and 3.3% protein. The specific cwt figure varies heavily by plant, co-op, and volume commitment — verify premium language against your own contract before building the number into a budget. What matters here isn’t the exact number at any one plant. It’s that the premium structure exists where the cheese capacity is landing, and it didn’t exist 18 months ago.

California production ran -5.74% in 2025 (USDA NASS), on water scarcity, regulatory pressure, and lost processing capacity. For the dairies that stay, the shift from fat-heavy checks toward protein-relevant ones is a repositioning window. Not a crisis.

Trade-offs to Watch

- Net Merit or Cheese Merit over TPI as your primary screen gives up benchmarking some buyers still reference for genetic marketing. You gain pricing accuracy on the milk check. You give up pedigree shorthand at the auction ring.

- Locking 60–75% of feed at $3.90–$4.10 corn needs equal-weight milk-side coverage. One-sided hedging is worse than no hedge — if corn drops and milk drops with it, you’re paying above-market for feed into a weaker check.

- Genomic-testing 100% of heifers at ~$40/head runs roughly $6,000/year on a 150-heifer pipeline. Payback only lives in the sorting decision. Testing without changing which heifers breed to elite component sires is a $6,000 data subscription.

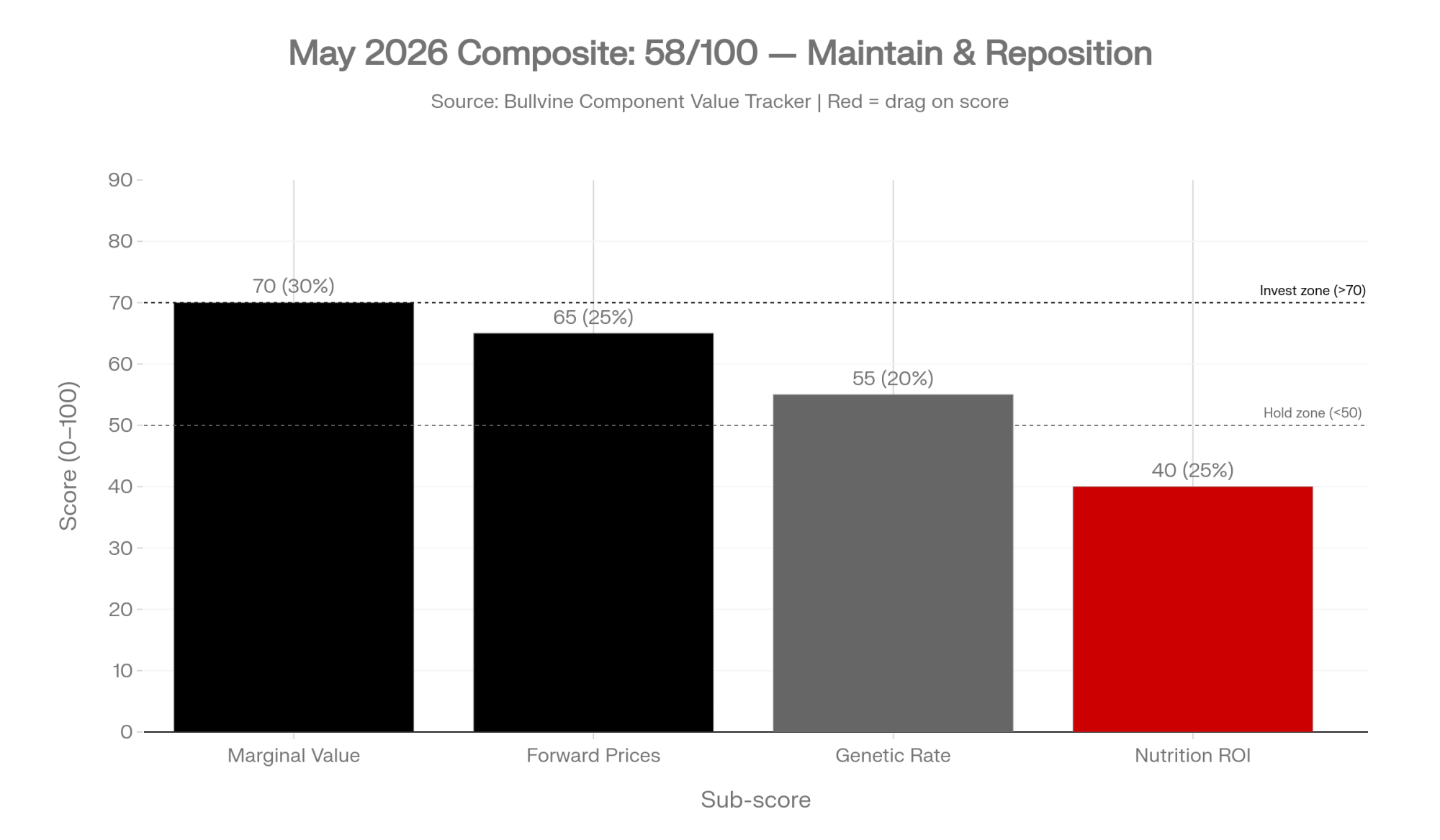

What Does a 58/100 Component Opportunity Score Actually Tell You to Do?

Each Tracker issue compresses four market conditions into one score. May 2026 baseline:

| Sub-Score | Weight | Reading | Score |

| Marginal Value ($/0.1% at current FMMO) | 30% | $27,676 fat + $28,614 protein on 500-cow Order 30 — off 2025 peaks but meaningful | 70 |

| Forward Price Trajectory (CME 6-month) | 25% | Butter and cheese in slight contango from depressed levels — stabilizing, not surging | 65 |

| Genetic Improvement Rate (CDCB trends) | 20% | Fat PTA still outpacing protein PTA; April 2026 TPI starts the correction, pipeline lag is real | 55 |

| Nutrition ROI Opportunity | 25% | Lysine negative; methionine conditional; RP fat break-even at or above current FMMO | 40 |

Composite: (70 × 0.30) + (65 × 0.25) + (55 × 0.20) + (40 × 0.25) = 21.0 + 16.25 + 11.0 + 10.0 = 58.25/100

| Zone | Range | Action |

| Invest Aggressively | >70 | Component premiums justify significant new nutrition + genetics spending |

| Maintain and Reposition | 50–70 | Premiums positive but compressed; genetics and market positioning carry highest forward returns |

| Hold | <50 | Premiums don’t justify added investment |

A 58 doesn’t mean spend everywhere. It means stay in the component game and be ruthless about which marginal dollar goes where. The 40 on nutrition reflects real margin compression — methionine’s the only consistent winner, and only at the low end of cost. The 55 on genetics reflects the lag between what the market wants and what the CDCB pipeline delivers today.

What pushes the score toward 80+: protein sustaining above $2.50/lb as new cheese plants come online; butterfat stabilizing above $2.25/lb; FMMO reform that increases component weight in pricing.

What drops it below 40: both prices falling below $1.75/lb; a feed-cost spike raising all break-evens; component tests plateauing nationally.

The 30/90/365-Day Playbook for a 500-Cow Order 30 Shipper

30-Day Actions

1. Pull last month’s milk check this week and run the 0.1% formula on your own numbers. Compare your protein test to the Order 30 average near 3.29%. The gap has a dollar sign in front of it — and at current prices, that gap’s worth more per pound than it was 18 months ago. Plug actual fat and protein tests into the embedded Tracker at March 2026 FMMO prices.

- Requires: three milk statements, herd size, daily lbs/cow average.

- Red-flag trigger: protein test more than 0.15 points below the Order 30 average = over $40,000/year on the table for a 500-cow herd at current prices. Urgent.

- Watch for: seasonal variation. Compare trailing 12 months, not just last month.

2. Audit every rumen-protected supplement — and stop RP Lysine this month if response isn’t documented. Pull the invoice cost per cow per day. At $2.09/lb protein and typical commercial lysine response rates, the math is underwater by roughly $0.60 to $2.35/lb depending on your inputs. If you can’t show 30 days of bulk-tank data proving outlier response, it’s a ration tax.

- Requires: feed invoices, nutritionist response data, bulk-tank component trend.

- Red-flag trigger: any supplement with implied break-even above $2.09/lb protein or $2.02/lb fat, and no 30-day before-and-after data proving the response — cost to eliminate.

- Watch for: products bundled into larger mixes where per-cow-per-day cost is hard to isolate. Ask for it in writing.

3. Put a methionine kill switch in writing with your nutritionist. +0.05% protein minimum, $0.12/cow/day maximum. Review date on the calendar. No exceptions.

- Requires: nutritionist sign-off, 30-day bulk-tank baseline.

- Red-flag trigger: either threshold violated for 30 consecutive days — pull the product, reset the ration, re-baseline before adding back.

- Watch for: “the response will show up next month.” Put a review date on the calendar and hold it.

4. Before your next breeding decision, ask two questions. “What’s this bull’s total CFP in pounds?” Then: “What’s that worth per lactation at $2.0905 protein and $2.0220 fat?” That conversation surfaces the ratio trap before it ends up in your herd — at current prices, a 15-lb CFP gap between two sires is worth ~$20/daughter/lactation, and no realistic protein price flips that math.

- Requires: current sire-list CFP data, March 2026 FMMO prices in the genetic advisor’s conversation.

- Red-flag trigger: advisor defaults to protein-to-fat ratio or last year’s prices — stop the meeting and reset the reference numbers.

- Watch for: marketing materials built on 2024 component prices. The math has moved.

90-Day Actions

5. Rebuild sire selection criteria around total CFP. Shift from protein-ratio filters to Net Merit or Cheese Merit as the primary screen. Sort by total CFP pounds. Protein PTA as tie-breaker only.

- Requires: a conversation with your genetic advisor using March 2026 FMMO prices, not 2024’s. Bring current herd-average component tests.

- Threshold: if your current bull lineup’s average CFP sits below the breed top 50% on the current CDCB run, you’re leaving component revenue on the table genetics-to-barn is slow to fix.

- Watch for: over-tilting toward protein at the expense of health and fertility. Net Merit and Cheese Merit already hold that balance. Don’t override the index manually for ratio.

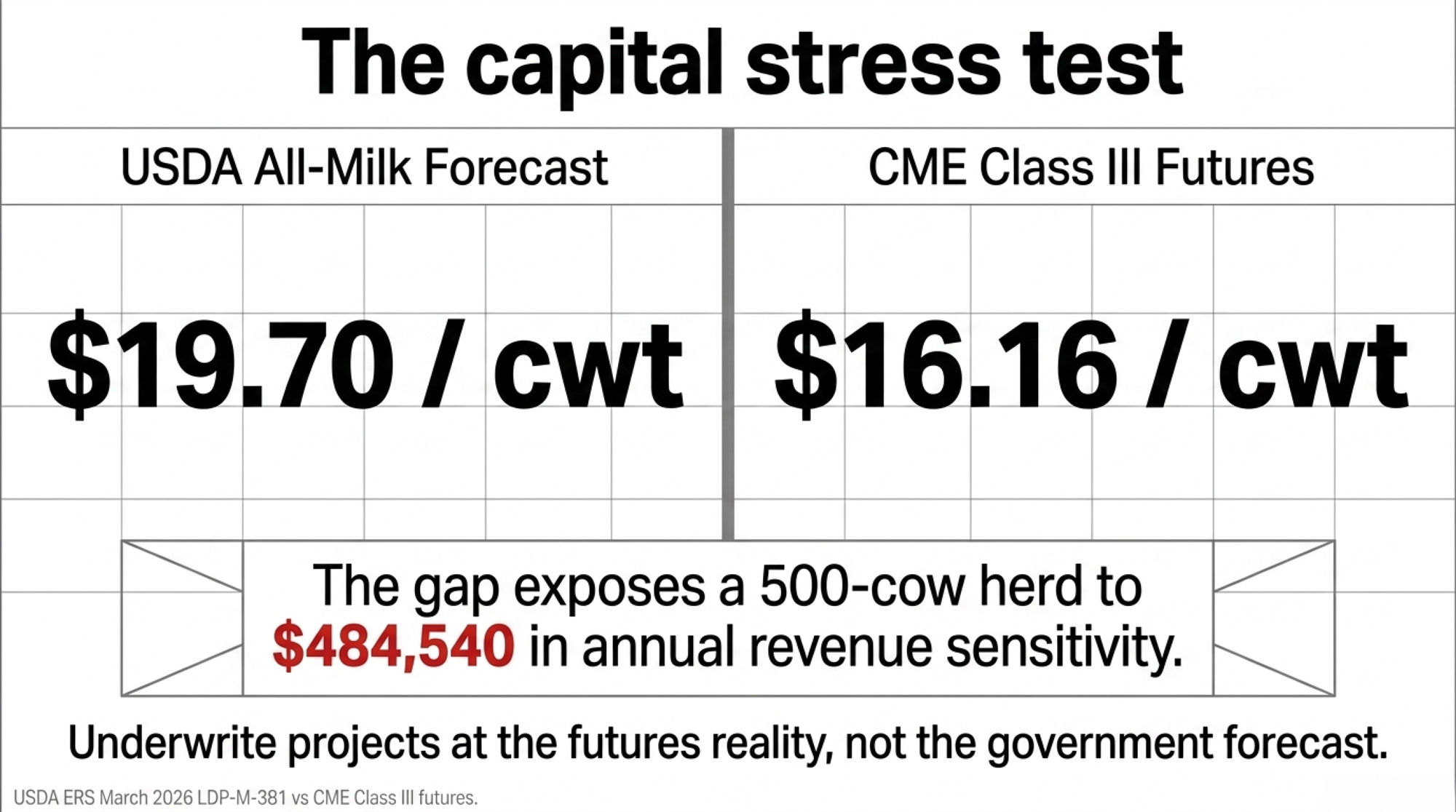

6. Stress-test every capital project at $17 Class III, not $19.70 all-milk. USDA’s March 2026 LDP-M-381 outlook projects 2026 all-milk at $19.70/cwt; CME Class III futures at the same moment traded closer to $16.16/cwt. A $3.54/cwt gap between the government forecast and the market’s own price signal is real-money exposure on any capital underwriting. On a 500-cow herd shipping roughly 136,875 cwt/year (500 × 75 × 365 ÷ 100), that’s approximately $484,540/year of revenue sensitivity between the two benchmarks — enough to break a project that only pencils at the USDA forecast. The gap between the government forecast and the futures board is the gap between a project that survives and one that breaks the operation.

- Requires: your CPA or lender running sensitivity on barn, robot, and equipment purchases at $17 Class III.

- Threshold: if a project’s DSCR drops below 1.2 at $17 milk for three consecutive months, treat as a luxury, not a necessity.

- Watch for: contractors and equipment sellers pitching against the USDA forecast. The futures market is the one you hedge.

7. Lock in 60–75% of feed needs when corn projects at $3.90–$4.10/bu. Per the source economic analysis cited in this issue’s methodology, corn in that band yields roughly $11.56/cwt feed cost — manageable against current Class III.

- Requires: cash flow for the hedging strategy, or a relationship with your co-op’s risk management service.

- Threshold: corn in-band → lock. Corn above $4.25/bu with basis strengthening → wait for pullback or shorten coverage horizon.

- Watch for: locking feed without also locking enough milk. You want both sides covered, not just the cost side.

365-Day Moves

8. Map your FMMO basis against the processing gravity wells. If you sit within draw radius of Lubbock, Dodge City, or an I-29 corridor plant, you have pricing leverage producers 200 miles farther out don’t. Structural demand from ~$10B in new cheese processing supports protein prices for the next two to three years. Renegotiate before capacity is fully committed.

- Requires: 12 months of basis data against your plant vs. Order 30 statistical uniform price.

- Opportunity signal: basis tightened to within $0.30/cwt of the Statistical Uniform Price while your component tests exceed county average — room to ask for contract improvements.

- Watch for: short-term premiums written with pull-back triggers tied to volume. Read the basis-when-volumes-fall clause specifically. It’s the clause nobody reads until it triggers.

9. Track the 0.75 milestone quarterly. If the national ratio hits 0.75 on the late-2027 projected timeline, processor standardization costs accelerate and basis pressure increases on fat-heavy, protein-light herds. Herds repositioned 12–18 months ahead feel it least.

- Requires: Tracker updates plus your own herd’s component trend line.

- Opportunity signal: national ratio stabilizing above 0.76 for three consecutive months = evidence the market is self-correcting. Different strategy.

- Watch for: short-term seasonal swings masking a trend reversal. Quarterly, not monthly.

10. Genomic-test for component direction, not just rank. At $30–$40/head, genomic testing identifies the top 20–30% of heifers worth breeding back to elite component sires. Bottom tier goes beef-on-dairy to capture beef-cross value while the pipeline tightens on components.

- Requires: ~$40 × testing population + time to integrate results into breeding decisions.

- Threshold: if your current replacement pipeline runs less than 25% genomic-tested heifers and you milk 500+, the sorting decision pays back within the replacement cycle at current component prices.

- Watch for: testing without changing what you do with the data. ROI lives in the sorting decision, not the test itself.

The market already repriced. Your milk check is catching up. Every month the operation stays calibrated to the old fat-premium world is a month of compounding gap against herds that already moved. You gain cushion on components here. You give up flexibility on ration-by-habit there.

Two questions to take to your next milk meeting. What does your processor contract actually say about basis when Order 30 cheese utilization exceeds 85%? And what’s your real margin over feed per cwt this month versus 90 days ago — at $2.0905 protein, not last year’s number?

Key Takeaways

- March 2026 FMMO flipped the component stack: protein at $2.0905/lb now beats butterfat at $2.0220, and on a 500-cow Order 30 herd at 75 lbs/day, every tenth of protein is worth $28,614 a year.

- The national protein-to-fat ratio hit 0.760 in 2025 against cheese plants calibrated for 0.82; if you ship into Order 30, you’ve got roughly 16 months before the 0.75 line starts showing up in basis conversations.

- At current prices, total CFP pounds drive the milk check — not protein-to-fat ratio. If your sire list is sorted on ratio, you’re leaving roughly $20 per daughter per lactation on the table and you won’t outrun that math until protein triples.

- Stress-test every 2026 capital project at $16.16 CME Class III, not USDA’s $19.70 all-milk forecast. The $3.54/cwt gap is about $484,540/year of revenue sensitivity on a 500-cow herd — the difference between a project that survives and one that doesn’t.

Methodology and Sources

Scope. All barn math uses March 2026 USDA AMS FMMO component prices (protein .0905/lb, butterfat .0220/lb) on a 500-cow Wisconsin/Minnesota operation shipping into FMMO Order 30 at 75 lbs/cow/day, unless stated otherwise. Prices refresh with each month’s FMMO announcement. The interactive Component Value Tracker at thebullvine.com/tools lets readers substitute their own herd parameters against the same formulas and price inputs.

Bullvine projections, labeled as such. The 0.75 crisis threshold, the ~16-month timeline, the Component Opportunity Score methodology, the ~$8,350 Brown County single-sire-swap scenario, the $17,500 broad-filter ratio-trap estimate, and the 150-heifer/2.8-lactation replacement-pipeline assumptions are proprietary Bullvine modeling — published here for the first time.

External sources. USDA AMS FMMO March 2026 component prices; FMMA30 Upper Midwest 2025 annual class utilization and international component comparison; USDA NASS Milk Production Reports, February and March 2026; USDA ERS Livestock, Dairy, and Poultry Outlook, March 2026 (LDP-M-381); CoBank Knowledge Exchange, “While U.S. Leads Milk Component Growth, Butterfat May Be Growing Too Fast,” September 25, 2025; Holstein Association USA Geneticist Insights, April 2026; Select Sires / CDCB April 2025 Base Change documentation; Animals meta-analysis of rumen-protected methionine (PMC9219501, 2022); Animals combined RPLM supplementation study (PMC12691028, 2025); PLOS ONE rumen-protected methionine trial (pone.0243953, 2021).

Learn More

- USDA Recommended Decision on Federal Milk Marketing Order (FMMO) Modernization: What Producers Need to Know — Exposes the structural shifts in FMMO pricing that favor higher protein and solids yield. Gains clarity on federal formula changes that dictate your check’s floor, ensuring you position the herd for the next decade of regulation.

- Boosting Bulk Tank Components: Feeding Strategies to Increase Fat and Protein — Delivers a tactical roadmap for troubleshooting bulk tank slumps and identifies the specific nutrition levers that move fat and protein tests. Arms you with the math to determine which ration adjustments pay for themselves.

- The Changing Face of Selection – TPI® and Jersey Genetic Indices to be Updated April 2024 — Dismantles outdated breeding goals by explaining the genetic formula updates that prioritize component volume over fluid production. Shows why selecting for higher PTA fat and protein is the only way to insulate your future pipeline.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.