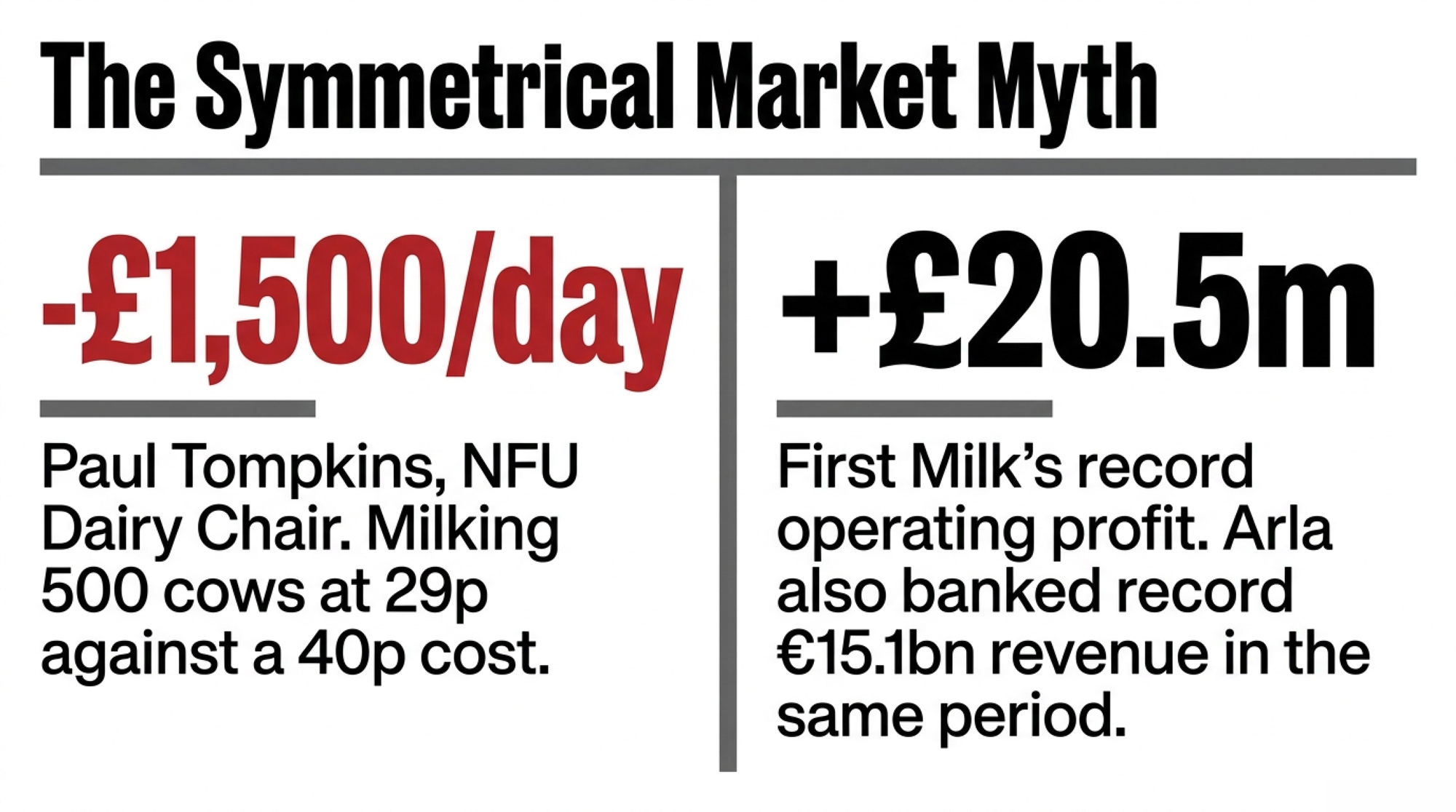

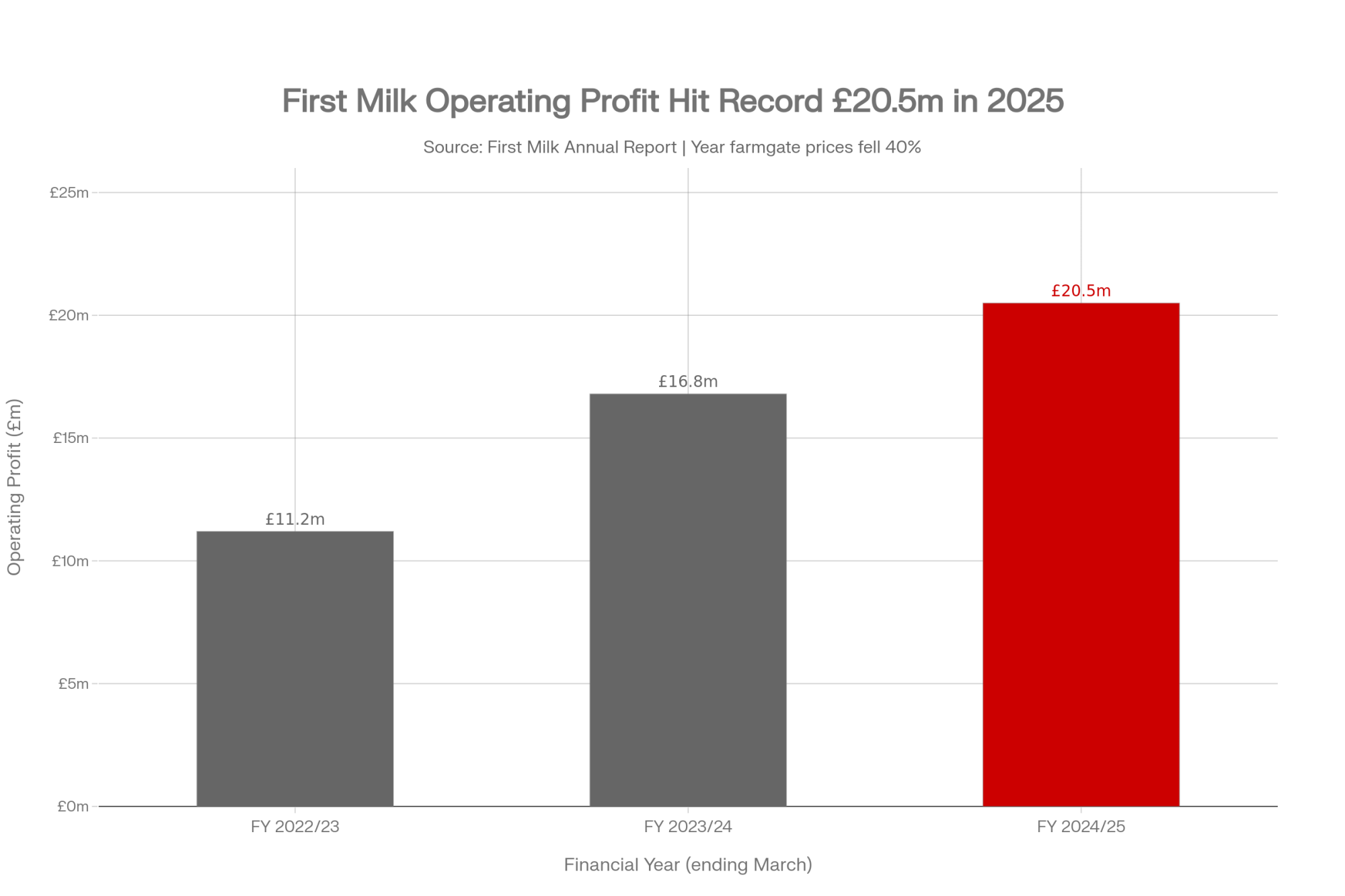

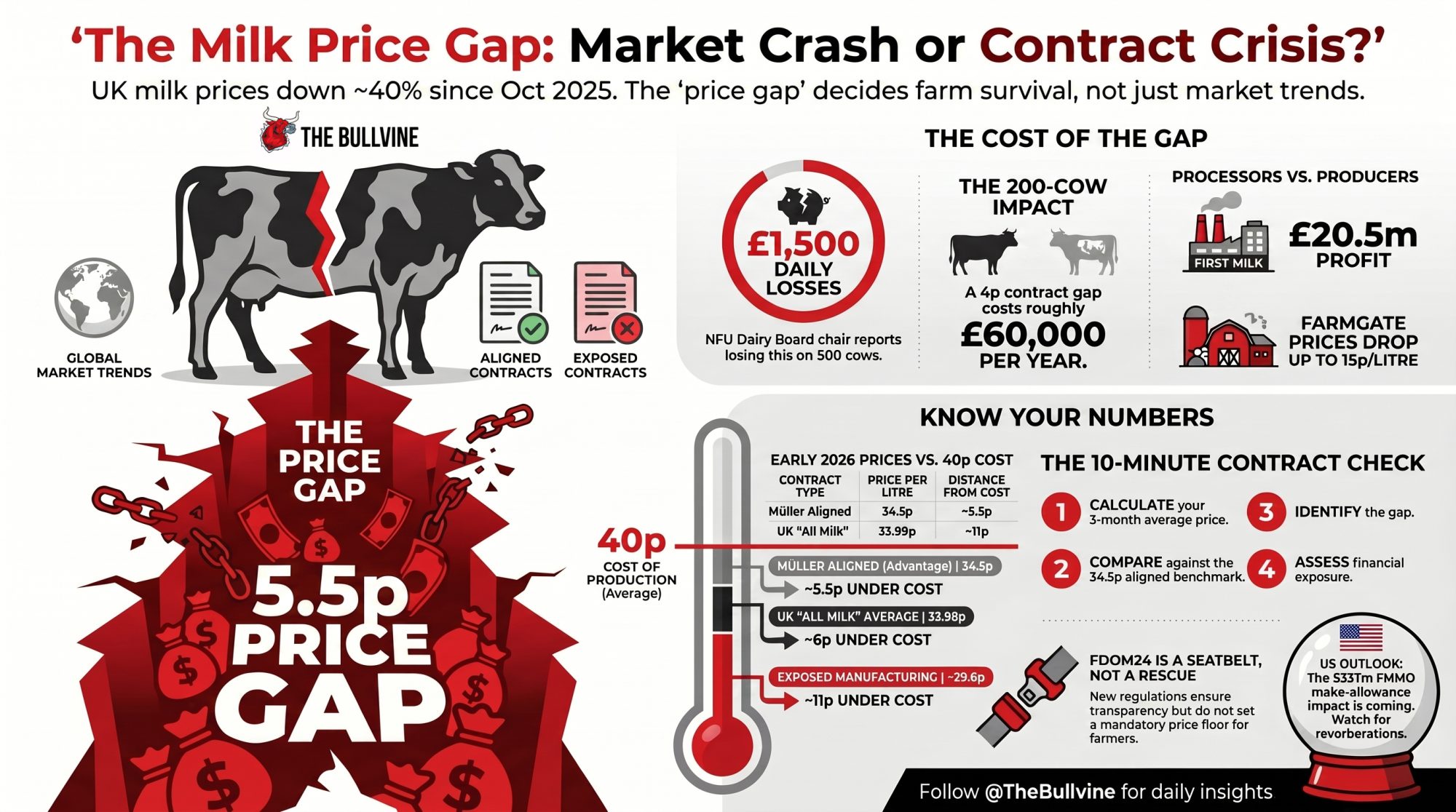

Tompkins chairs the NFU’s Dairy Board and milks 500 cows at 29p against a 40p cost. In its most recent results, First Milk booked a record £20.5m profit. The difference isn’t the market — it’s the contract.

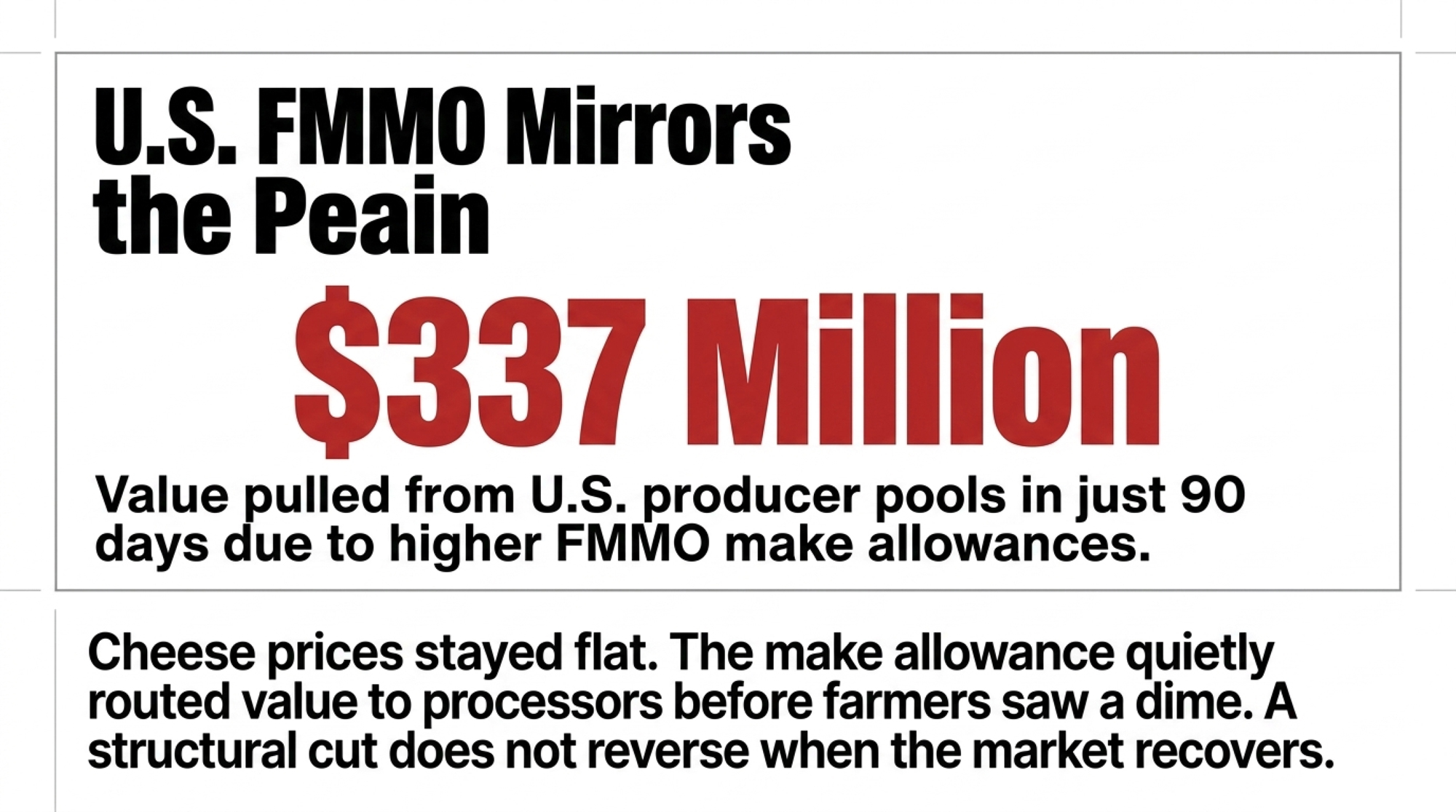

Executive Summary: At 29p a litre against a 40p cost, NFU Dairy Board chair Paul Tompkins was losing more than £1,500 a day in January. Over the same broad period, First Milk posted a record £20.5m operating profit and Arla banked record €15.1bn revenue — so this isn’t symmetric pain, it’s a transfer. UK prices have fallen up to 40% since October 2025, but the number that actually decides your fate is the gap between an aligned contract and an exposed one: Müller’s Advantage holds 34.5p while manufacturing litres sit nearer 29–32p. On a 200-cow herd shipping 1.5m litres, a 4p contract gap is roughly £60,000 a year — and even the aligned farms are now under cost, so the real question is how fast you’re bleeding, not whether. FDOM24 makes your processor show its working, but it sets no price floor, so it’s a seatbelt, not a rescue. Pull your last three milk statements, run your average against the 34.5p aligned benchmark, and if you’re several pence short, the global market isn’t your problem — your contract is. U.S. readers should read it as a mirror: FMMO make allowances pulled $337m out of producer pools in 90 days while cheese prices never dropped.

Paul Tompkins chairs the NFU’s Dairy Board, farms in the Vale of York, and milks a herd of around 500 Holsteins. He told broadcasters in January 2026 that his milk was fetching around 29p a litre against a cost of roughly 40p — leaving him, by his own account, losing more than £1,500 a day.

Sit with that for a second. The man who chairs the national dairy board — who knows milk contracts as well as anyone in the country — can’t price his way out of the hole. That’s not a story about one farmer making bad calls. It’s a story about a milk system where the gap between what you’re paid and what it costs you has become the line between staying in and getting out. And right now, the size of that gap depends largely on which contract you signed.

Why a U.S. reader should care about a UK milk price. This is a British case study, but read it as a crystal ball. The same structure — farmers absorbing the cut while processors hold their margin — is now baked into the 2026 FMMO modernization resets. Higher make allowances that took effect June 1, 2025, cut Class III prices by about 92¢/cwt and, according to AFBF’s modeling, pulled $337 million out of producer pools in 90 days, while cheese and butter prices never dropped. Manufacturing-heavy orders like the Upper Midwest and Central are taking the heaviest pool losses. Different country, different mechanism, identical question: who’s absorbing the loss, and who isn’t?

| Variable | UK Market (2025–26) | US FMMO (2025–26) |

|---|---|---|

| Mechanism of loss | Contract gap: exposed farms paid 29–32p vs 40p cost | Higher make allowances cut Class III by ~92¢/cwt from June 2025 |

| Who absorbs it | Individual farmer on manufacturing/B-litre contract | Producers in manufacturing-heavy orders (Upper Midwest, Central) |

| Processor margin impact | First Milk op. profit up to record £20.5m; Arla €415m net | Processor cost basis reduced; cheese/butter prices unchanged |

| Scale of transfer | UK “all milk” avg down ~22% YoY by April 2026 | $337m pulled from producer pools in 90 days (AFBF modeling) |

| Regulatory buffer | FDOM24: transparency only, no price floor | FMMO: make allowances are built into the formula, not negotiable |

| Farmer leverage | Switch contract if aligned buyer has capacity | Limited — pool participation largely mandatory by order |

| Recovery trigger | Global supply tightening + GDT price bounce | Class III recovery requires cheese/butter to outpace make allowance drag |

| Bottom line | Contract type decides your fate, not the market | Make allowances decide your take, not the commodity price |

What’s Actually Changing

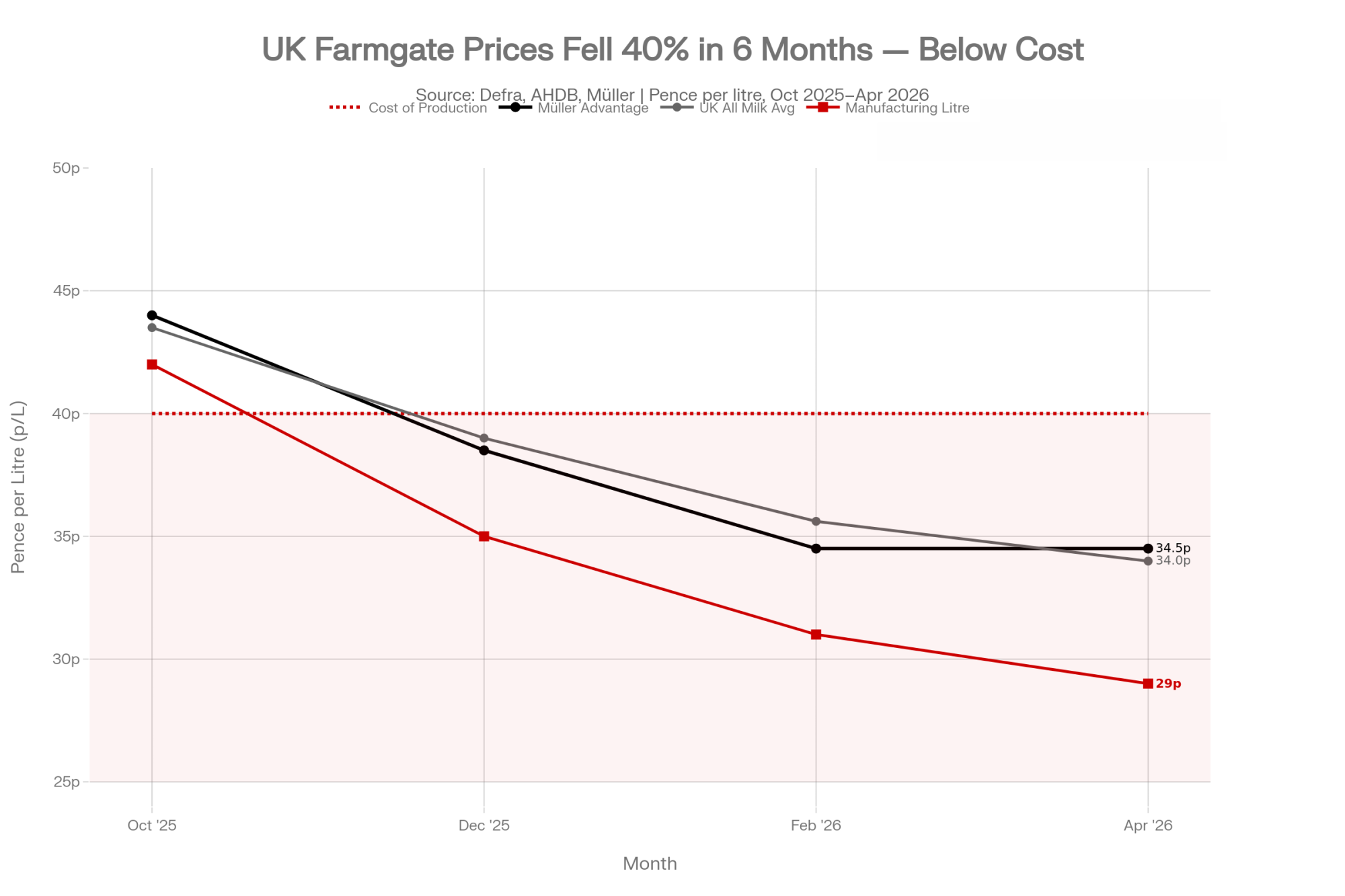

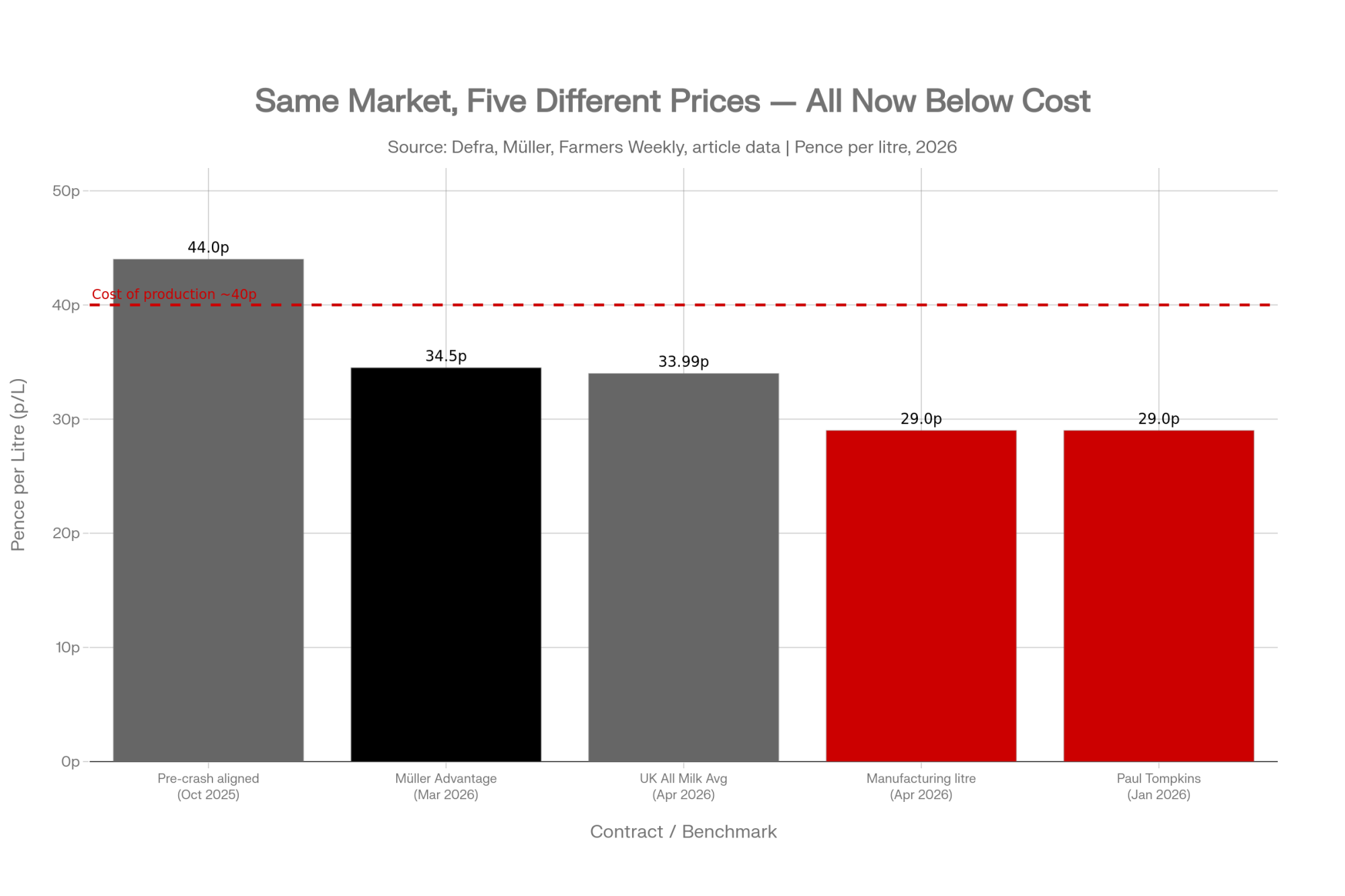

UK milk prices have fallen fast and hard. Processor payments to many farmers have dropped by up to 15p a litre — around 40% — since October 2025, according to Reuters, as a wave of global production has swamped the market. Some contracts that were paying 48p have fallen to 32p.

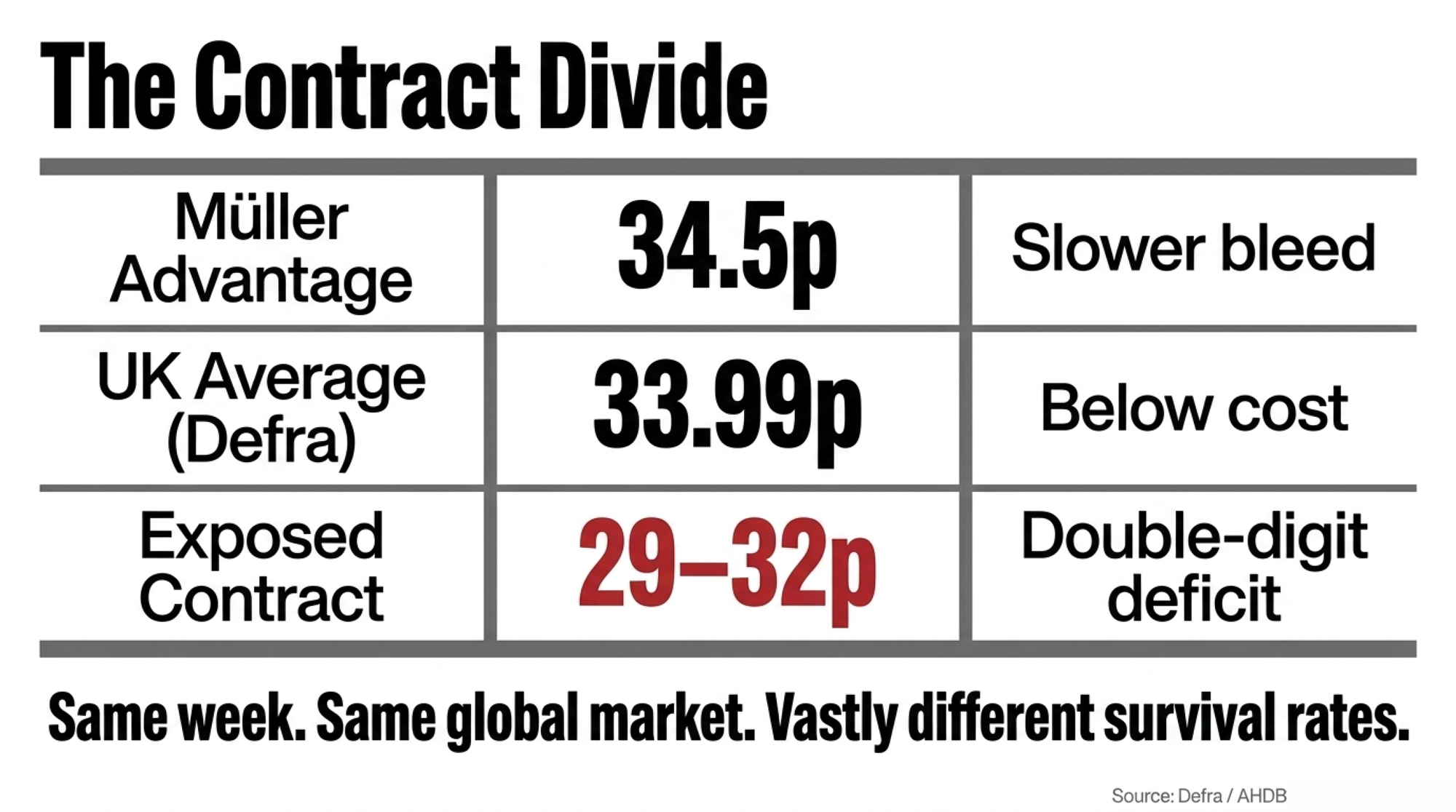

But the headline number hides the real story. Two farmers in the same county, milking similar cows, shipping similar volumes, can be living in completely different realities this spring. Arla cut its conventional price by 3.5p in December to 39.21p, and has since trimmed it further into the mid-30s by early 2026. Müller cut its aligned Advantage price to 34.5p from 1 March 2026. Manufacturing and B-litre contracts fell further and faster.

That divide is the whole game now. The spread between a held aligned price and an exposed manufacturing litre can run into double digits per litre — in the same week, in the same market. One farmer’s contract is cushioning the crash. The other is passing the whole thing straight through to the bank account.

Read more: The Contract Clause Deciding Which UK Dairies Survive 2026

How This Plays Out on Real Farms

Put the gap in barn terms, because that’s where it stops being abstract.

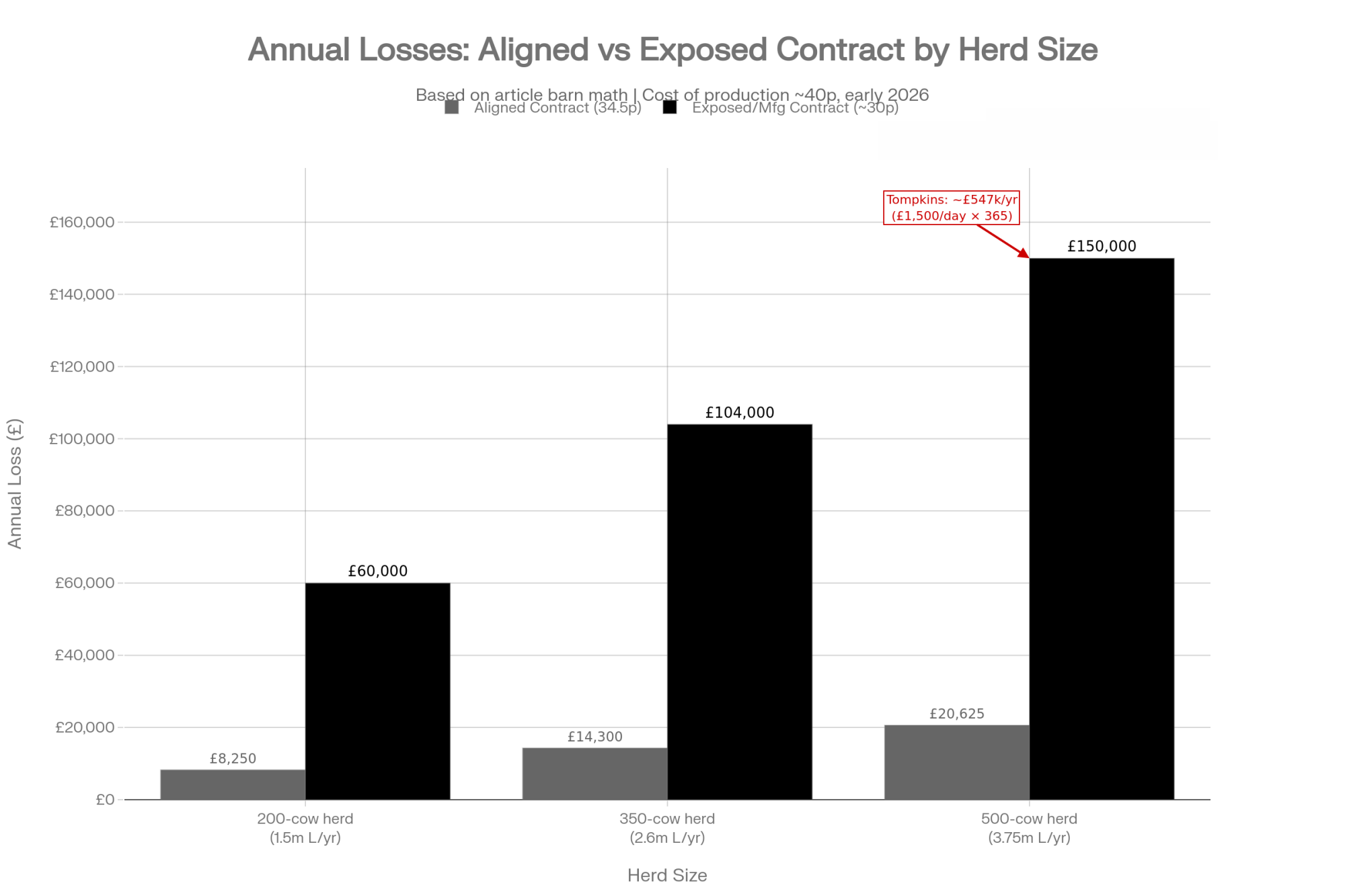

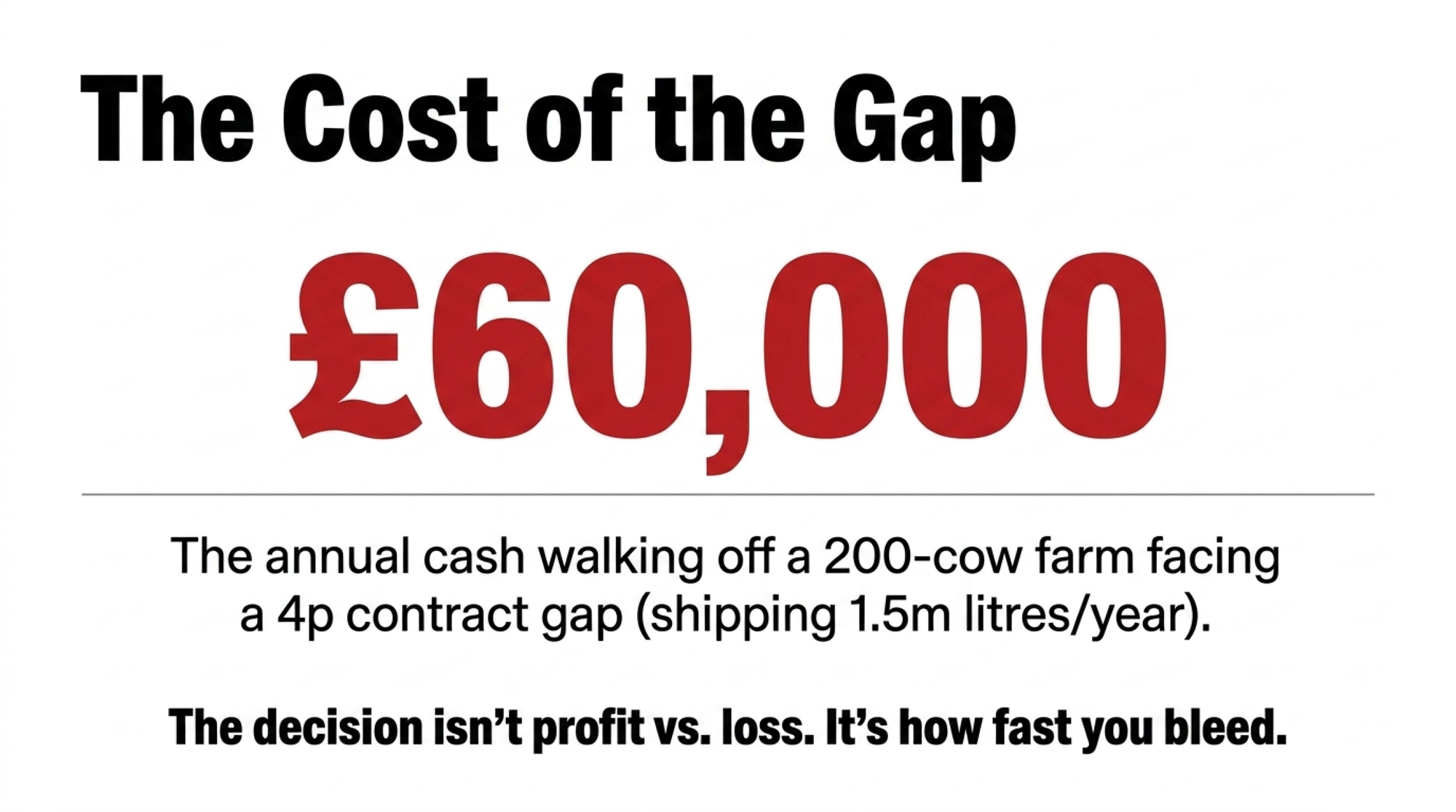

Tompkins reckons he’s losing more than £1,500 a day on around 500 cows. He’s not alone at that scale — Farmers Weekly reported some larger farms losing more than £1,000 a day as the collapse bit. Now scale it down to a 200-cow herd. Say you’re shipping around 1.5 million litres a year and your contract leaves you 10p short of cost. That’s £150,000 walking off the farm over twelve months — before a single other cost line moves.

And here’s why you can’t just turn the tap down to stop it. You can’t turn a dairy herd on a sixpence. Cut feed, and you risk yield, fertility, and next season’s performance. Sell cows, and you lose the genetics you spent years building — and you still owe on the buildings. The cost side is stubborn. When the milk price drops like a stone, nothing else politely shrinks to match.

The exits, when they come, come quietly — one family at a time. That’s the part that doesn’t show up in a market report until it’s already happened.

The Mechanics: Why the Same Market Pays Two Prices

Here’s the part that’s hard to swallow if you’re on the wrong side of it. The crash looks like a pure market event from the outside, and a lot of it is. The main driver is global oversupply — 2025 was a strong year for grass and for cows, and the extra milk had to go somewhere. GB production for the 2025/26 season hit a record, with December deliveries running several percent above the prior year, per AHDB.

The same stretch that squeezed farmgate prices saw processors post strong results. First Milk, a farmer-owned co-op, reported its best year ever for the year to March 2025 — turnover up 20% to £570 million and operating profit climbing to £20.5 million, from £16.8 million. Arla reported record revenue of €15.1 billion for 2025 with net profit of €415 million. Both have publicly tied those results to factors such as strong ingredient and protein demand rather than to liquid-milk margins. As a co-op, First Milk’s profits also flow back to its farmer members.

So why do two farms in the same market end up so far apart? Strip it back, and the reason is structural, not a stitch-up. On an exposed contract, the farmgate price is contractually the most movable number in the chain, so it tends to adjust first when the market falls. A processor can lean on its ingredients arm or efficiency programs to protect its own margin; the individual farmer on a manufacturing litre doesn’t have those levers. If that mechanism sounds familiar to a U.S. reader, it should — it’s the same logic by which higher FMMO make allowances quietly route value to the processing side before the farmer sees a dime.

The price picture, in one place

Here’s the same crisis laid out as a handful of numbers on one page. This is the gap, in pence per litre, against a cost of production sitting near 40–49p depending on the system:

| What you’re shipping on | Price per litre (early 2026) | Position vs. cost of production |

| Müller aligned Advantage | 34.5p (from 1 March 2026) | Several pence under cost |

| Arla conventional | Mid-30s (after Dec + further cuts) | Several pence under cost |

| UK “all milk” average (Defra) | 35.61p early 2026, 33.99p by April, down ~22% YoY | Below cost |

| Exposed manufacturing / standard litre | ~32p, some toward 29p | Double-digits under cost |

Read that table against your own milk statement, and one thing jumps out. The top of the column and the bottom are separated by several pence a litre, and on a million-plus-litre operation, every penny is real money. The lower row isn’t a different market. It’s the same market, paid through a different contract. That’s the lever most of this debate ignores.

What Are the Aligned Farms Actually Getting?

This is where the “it’s just the market” story falls apart. Müller’s aligned Advantage farmers are sitting on 34.5p. A producer shipping on a manufacturing litre is looking at something nearer 29–32p. Same week, same wall of milk, same global oversupply — and a gap that can run 3–5p, sometimes more.

Now run that gap as barn math.

The contract gap, in money you’d recognize A 200-cow herd (~1.5m litres/year) with a 4p contract gap loses ~£60,000 a year. A 500-cow herd at Tompkins’ scale, on the same 4p gap, loses ~£150,000 a year. None of that turns on how well you milk cows. It’s the contract line on your statement.

Here’s the uncomfortable part: even the aligned farms are now at a loss. With production costs at 40p and beyond, a 34.5p Advantage price still loses money — it just bleeds more slowly. So the contract decision isn’t “profit versus loss” right now. It’s “how fast am I bleeding, and how long can I last at that rate?” For many farms, that’s the only question that matters this spring.

Read more: 28p vs. £300 Million: The 2025 Milk Price Gap Nobody’s Explaining

Does FDOM24 Actually Protect You?

The government’s answer was the Fair Dealing Obligations (Milk) Regulations 2024 — FDOM24 — with contracts required to comply by 9 July 2025. It forces processors to be transparent about how they set price changes and gives you clearer terms and notice. Genuine progress, and the NFU fought for it for more than a decade.

But it’s a seatbelt, not a rescue helicopter. FDOM24 makes a processor explain how it sets the number. It doesn’t set a floor under it. You’ll get a clearer paper trail showing exactly how your price was cut — which is useful at renewal, and cold comfort at the bank. Read the small print on notice periods and exclusivity before you assume the regulation has your back.

| FDOM24 Provision | What It Delivers | What It Doesn’t Deliver | Risk Level |

|---|---|---|---|

| Price change transparency | Processor must explain how price is changed | No floor under the price itself | 🔴 HIGH |

| Notice periods | Clearer advance warning of cuts | Doesn’t prevent a cut from happening | 🔴 HIGH |

| Contract term clarity | Legible terms at renewal | Doesn’t stop exclusivity or volume lock-in | 🟡 MEDIUM |

| Dispute resolution pathway | Formal route to challenge a change | Slow; cold comfort mid-crisis | 🟡 MEDIUM |

| Aligned benchmark reference | Sets a comparator for negotiation | Not a contractual guarantee | 🟡 MEDIUM |

| Price floor mechanism | — | Not included | 🔴 HIGH |

| Emergency minimum price | — | Not included | 🔴 HIGH |

How Do You Tell If It’s the Market or Your Contract?

This is the question worth answering before your next milk cheque lands. You can do it tonight — three statements and a calculator, ten minutes at the kitchen table.

The 10-minute contract check. Step 1 — Pull your last three milk statements and work out your average received price per litre across them. One number. Step 2 — Find the published UK average: Defra put the UK “all milk” figure at 35.61p in early 2026, falling to 33.99p by April, down 22.3% year-on-year, and AHDB updates processor price changes regularly. Step 3 — Compare against an aligned benchmark: Müller’s Advantage sits at 34.5p today, roughly what a held contract is paying. Step 4 — Read the gap: if your number is several pence under that aligned benchmark, the global market isn’t your main problem. Your contract is.

One of those problems corrects when supply tightens. The other only corrects when you take action. (U.S. readers: the same test works on a milk check — print January 2025 and January 2026 statements, strip out the Class III, IV, and butter moves, and whatever gap is left is structural, not a bad month.)

What Does Doing Nothing Actually Cost?

There’s a perfectly rational way to ride this out — if your contract genuinely covers your costs and your relationship with your processor is solid, waiting for the cycle to turn is a real strategy. It has turned before. AHDB even noted firmer tones at the January Global Dairy Trade event, with most products ticking up a percent or two.

But “wait for recovery” is only a plan if your balance sheet survives the wait. AHDB cautioned the bounce could be a dead-cat blip, with record volumes flowing into the spring flush keeping prices under pressure. And the official average kept falling — Defra had the UK at 33.99p by April 2026. Run it against Tompkins’ own numbers: at more than £1,500 a day, even a few months’ wait is six figures gone. On a 200-cow herd losing 10p a litre, six more months is roughly £75,000. The question isn’t whether you believe in the cycle. It’s whether your overdraft does.

Options and Trade-Offs

Contract type isn’t carved in stone. But the better roads need you moving before the window shuts, not after.

Get onto a retail-aligned contract — start asking this month. Aligned pools held better than exposed contracts because they price off cost trackers rather than the spot market — Müller’s Advantage at 34.5p still beats a 29–32p manufacturing litre. Your 30-day move is finding out which aligned buyers are taking on supply, what they require, and where your farm fits. Works when: you’re a liquid milk producer with steady volume and quality. Risk: seats come with strings — volume commitments, exclusivity, specification, sometimes investment. You trade flexibility for a steadier price.

Look hard at direct vending — if you’ve got the footfall. On-farm vending is returning £1.20–£1.60 per litre against wholesale near 33p, with around 400 machines now operating nationally; a unit costs roughly £15,000–£30,000. Works when: you’re near consumer traffic or already run a farm shop. Risk: demand is local and finite — it’s a margin play on a slice of your milk, not a replacement for the underlying wholesale contract.

Run the organic numbers — but respect the lead time. Organic has held a wide premium over conventional — Arla’s organic price sat near 56p against conventional’s mid-30s in early 2026. Works when: you’ve got a financial runway and a buyer lined up. Risk: transition runs two to three years, with upfront costs, and the premium market has a ceiling — a wave of conversions could thin it out.

Key Takeaways

- If your received price is more than 3–4p under what comparable aligned farms are getting today — Müller Advantage is at 34.5p — you’re not just riding the market. Your contract is the problem. That’s a call to your advisor this week, not next quarter.

- On a 200-cow herd, a 4p contract gap is roughly £60,000 a year; a 10p shortfall to cost is about £150,000. If you’re on an exposed deal, find out which aligned buyers are taking supply inside 30 days.

- FDOM24 upgraded your contract’s terms, not your price. Before you renew, know exactly what it does and doesn’t protect. It’s a seatbelt, not a rescue.

- Even aligned farms are under cost right now. The question isn’t profit versus loss — it’s how fast you’re bleeding and how long you can last at that rate.

- If you’re farming under a U.S. FMMO, run the same logic on your make-allowance drag: a ~92¢/cwt structural cut doesn’t reverse when the cheese price recovers.

- “Wait for the cycle” is only a plan backed by a balance sheet. If the January GDT bounce proves to be a blip, can your overdraft carry you through to the real recovery?

The cycle will turn. It always does. The real question is whether your specific contract, your overdraft, and the recovery timeline are pointing the same way — or whether you’re carrying a structural gap that a market rebound won’t close on its own.

So pull the statements. Run your number against what your neighbor on an aligned contract is getting. Then decide whether you’re fighting the market or fighting your contract, because those are two different fights with two different exits. If you want the full breakdown — the contract-by-contract barn math by herd size, what the aligned-buyer applications actually demand, and where the real numbers sit — that’s what we’re laying out in this week’s Bullvine Weekly.

⚠️ Before you carry this one alone. If the numbers on your own statements are keeping you up at night, you don’t have to sit with it by yourself. This kind of pressure is heavy, and reaching out is the strong move, not the weak one.

UK — RABI: free, confidential, 24/7 — 0800 188 4444.

UK — Farming Community Network: 03000 111 999, answered in person 7am–11pm, every day of the year.

US — 988 Suicide & Crisis Lifeline: call or text 988, 24/7.

US — Farm Aid Farmer Hotline: 1-800-FARM-AID (1-800-327-6243), Mon–Fri 9am–9pm ET (Spanish line available).

Canada — National Farmer Crisis Line: 1-866-FARMS01 (1-866-327-6701), 24/7, English and French.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Coles and Brownes Just Exposed The $386000 Hole In Your Milk Contract — Arms you with a 90-day cash exposure protocol to stress-test your operation against hidden processor volume caps. Details the exact formula to calculate unpriced counterparty liability on automated milking infrastructure before your bank forces a debt covenant workout.

- The $20 Milk Paradox: Solving 2026 Dairy Basis Risk — Delivers the strategic blueprint to navigate the widening gap between headline USDA price predictions and real-world regional clearing basis. Follows the money on the permanent class-price cuts triggered by recent federal order make-allowance amendments.

- The $11 Billion Reality Check: Why Dairy Processors Are Banking on Fewer, Bigger Farms — Exposes the structural processing shift that has quietly pre-secured supply through mega-dairy exclusive agreements. Explains why a permanent cost-of-production variance forces rapid tier consolidation, rendering conventional commodity price cycles obsolete for independent operators.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.