USDA just rewrote the 2027 livestock insurance rule book. The tools got better. The empty chair on most mid-size dairies didn’t.

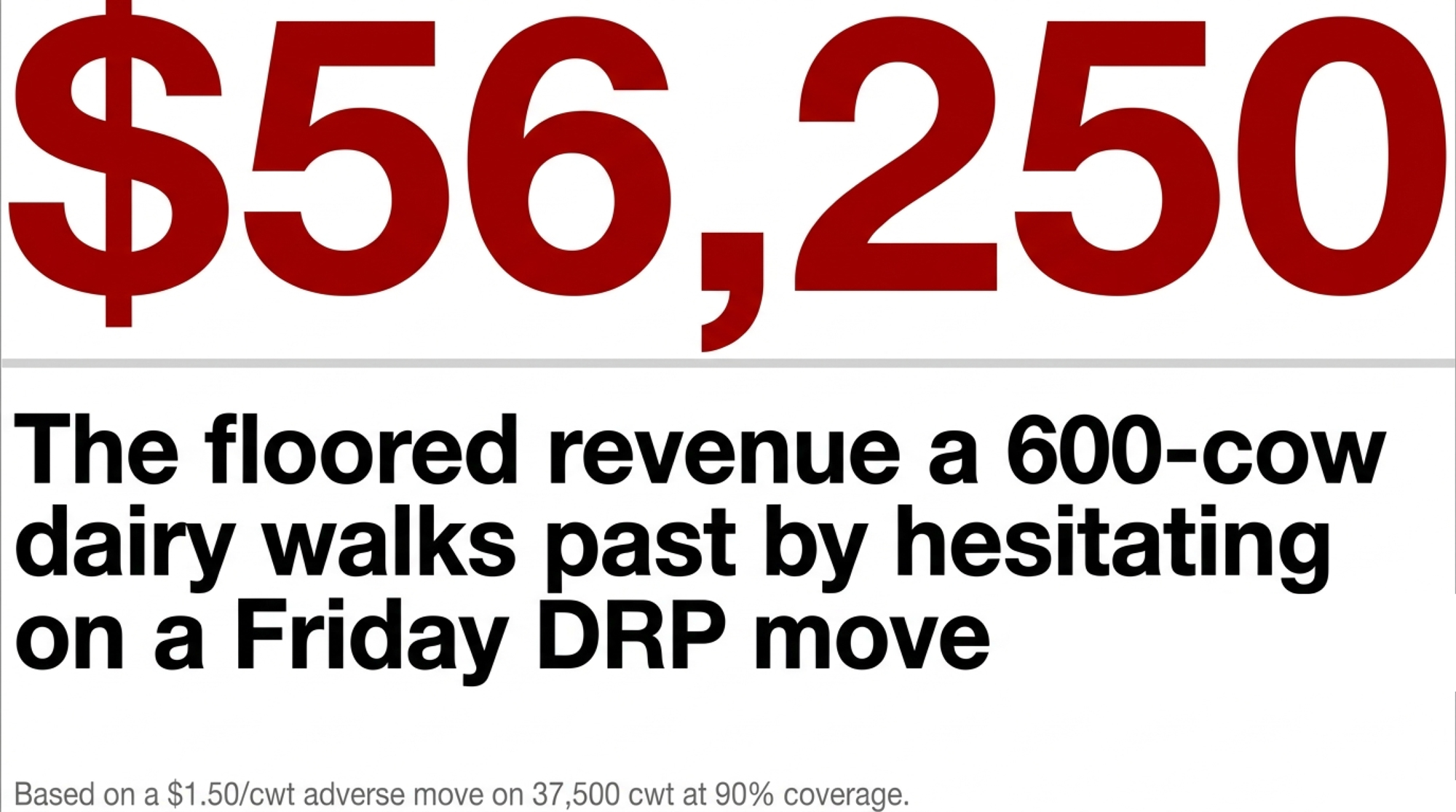

Executive Summary: USDA’s 2027 livestock insurance package — Product Management Bulletin PM-26-024, released May 18, 2026 — extends LRP cull cow coverage to 52 weeks, opens concurrent DRP/LRP/LGM stacking, adds a 6.0–9.0 cwt Unborn Dairy Weight 2 calf category for backgrounded beef-on-dairy, and shifts the DRP sales close to the next calendar day. It also auto-cancels any policy that earns no premium for three consecutive years, which is going to surprise producers who lapsed coverage in 2024–2025. On a 600-cow dairy shipping 37,500 cwt a quarter, hesitating on a $1.50/cwt DRP move at 90% coverage walks past $56,250 in floored revenue — one decision, one quarter. Two hard dates: June 30, 2026 to confirm or transfer your DRP provider, July 1, 2026 to audit which of your existing policies is already ticking toward auto-cancellation. The real question isn’t whether the toolkit got better — it did — but whether anyone on your operation is named, in writing, with authority to lock coverage on a Friday afternoon before Monday’s market move makes the decision for you.

Picture a Friday afternoon in late 2025. RMA had just posted new DRP rates. A 600-cow Upper Midwest dairy got the email from his crop insurance agent late that afternoon: lock about $17.75/cwt on a full quarter of Q4 milk at 90% coverage, and you’ve got a defensible floor going into a soft market.

Editor’s note: The producer in this opening scene is a composite, drawn from patterns multiple Upper Midwest crop insurance agents describe seeing across their dairy books in 2025. The DRP coverage levels and adverse-move scenario are illustrative. The math reflects real DRP coverage mechanics and reconciles to documented program rules.

He read it between afternoon milking and chores. Told himself he’d think about it over the weekend and call his agent Monday. By Monday afternoon, futures had moved roughly $1.50/cwt. The endorsement at that price was gone. On 37,500 cwt of covered milk for that quarter, the hesitation worked out to about $56,250 in revenue he could’ve floored — and didn’t.

He didn’t lose his farm. He absorbed a quarter’s worth of milk check without protection and went back to work. He’s not unusual. He’s the median dairy operator in America’s current risk landscape — and he’s exactly who USDA’s 2027 livestock insurance updates are aimed at.

The question for every mid-size producer reading this: when the next Friday email lands, who in your operation is actually authorized to say “yes, lock it” before chores?

What’s Changing and Why

USDA’s Risk Management Agency, with FCIC Board approval, dropped a sweeping set of revisions for the 2027 crop year through Product Management Bulletin PM-26-024, released May 18, 2026. The headline changes affect three programs that already touch most serious dairies: Dairy Revenue Protection (DRP), Livestock Risk Protection (LRP), and Livestock Gross Margin (LGM).

The big ones for dairy:

- DRP sales period close moves to the following calendar day — the same window LRP and LGM already use. No more Monday-morning cutoff catching producers who wanted to think over the weekend.

- LRP cull cow coverage extended from 13 weeks to a maximum of 52 weeks under the Fed Cattle Specific Coverage Endorsement.

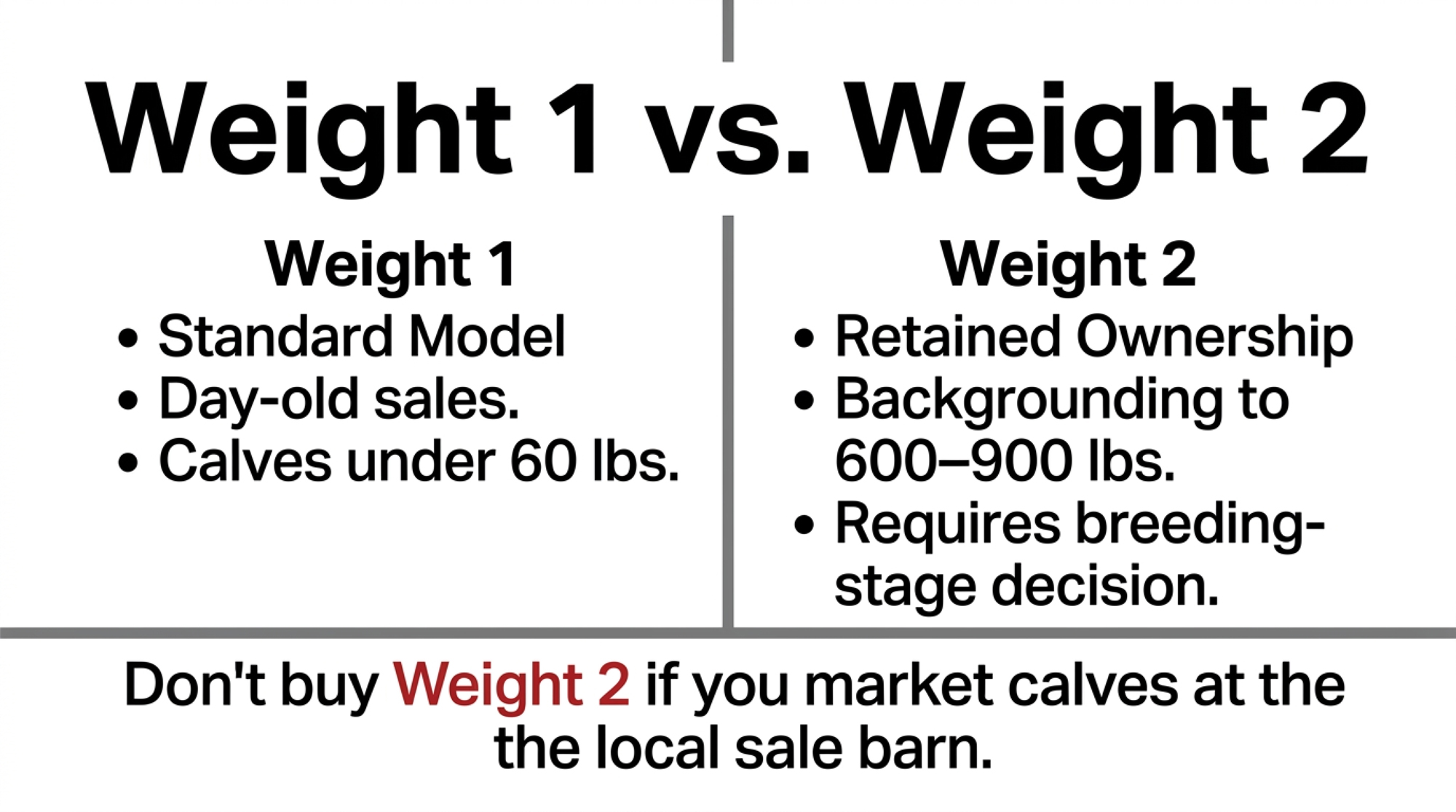

- A new “Unborn Dairy Weight 2” LRP category covers 6.0 to 9.0 cwt target weight calves — built for backgrounded beef-on-dairy crosses, not day-old sales.

- LGM cattle weight maximums increased, with target finishing weights bumped accordingly to match current feedyard practice and the LGM dairy margin model.

- Concurrent coverage between similar livestock programs is now explicitly permitted, so a dairy can hold DRP on milk, LRP on cull cows, and LRP on calves at the same time without policy conflicts.

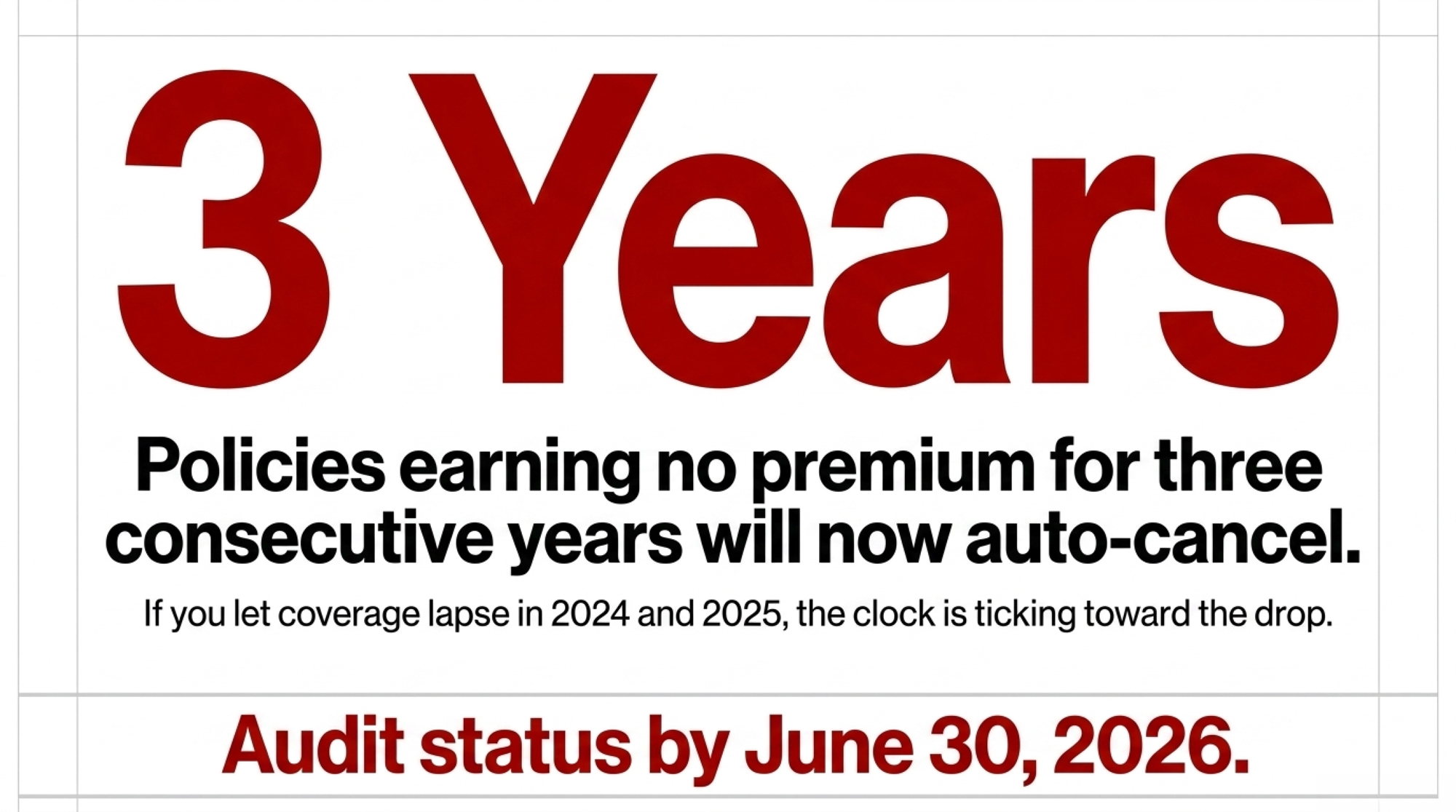

- Policies earning no premium for three consecutive policy years are now subject to automatic cancellation.

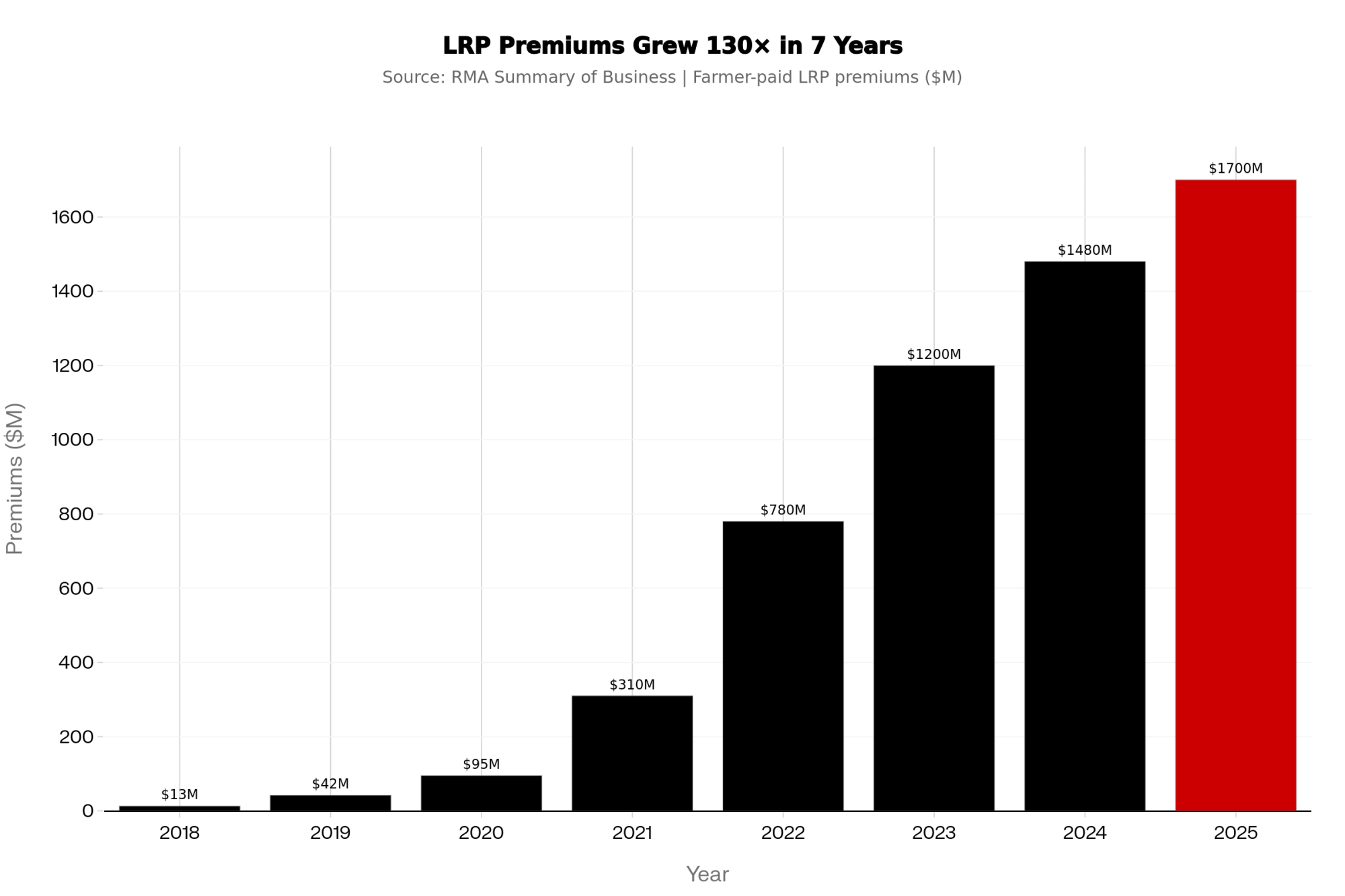

The context matters as much as the changes themselves. Farmer-paid LRP premiums went from about $13 million in 2018 to roughly $1.7 billion in 2025, per RMA Summary of Business data. Insured headcounts climbed from 71,000 in 2017 to about 7.5 million by mid-2025. These programs are no longer a footnote.

In RMA’s May 18, 2026 release, the agency framed the package as expanding coverage options for producers and meeting evolving risk-management needs. Whether the tools actually do that depends on something USDA can’t legislate.

How This Plays Out on Real Farms

The 600-cow scenario in the lede isn’t a one-off. Crop insurance agents working the dairy book describe the same Friday-email-to-Monday-regret pattern across mid-size operations — even as DRP and LRP adoption surges at the larger end of the industry.

Run the cull cow math under the new 52-week rule. Pre-2027, protecting cull revenue meant writing four 13-week endorsements quarterly. Post-2027, a single annual endorsement covers the entire projected cull flow — provided someone actually picks up the phone. The same logic, scaled across herd sizes, produces three very different conversations with a lender.

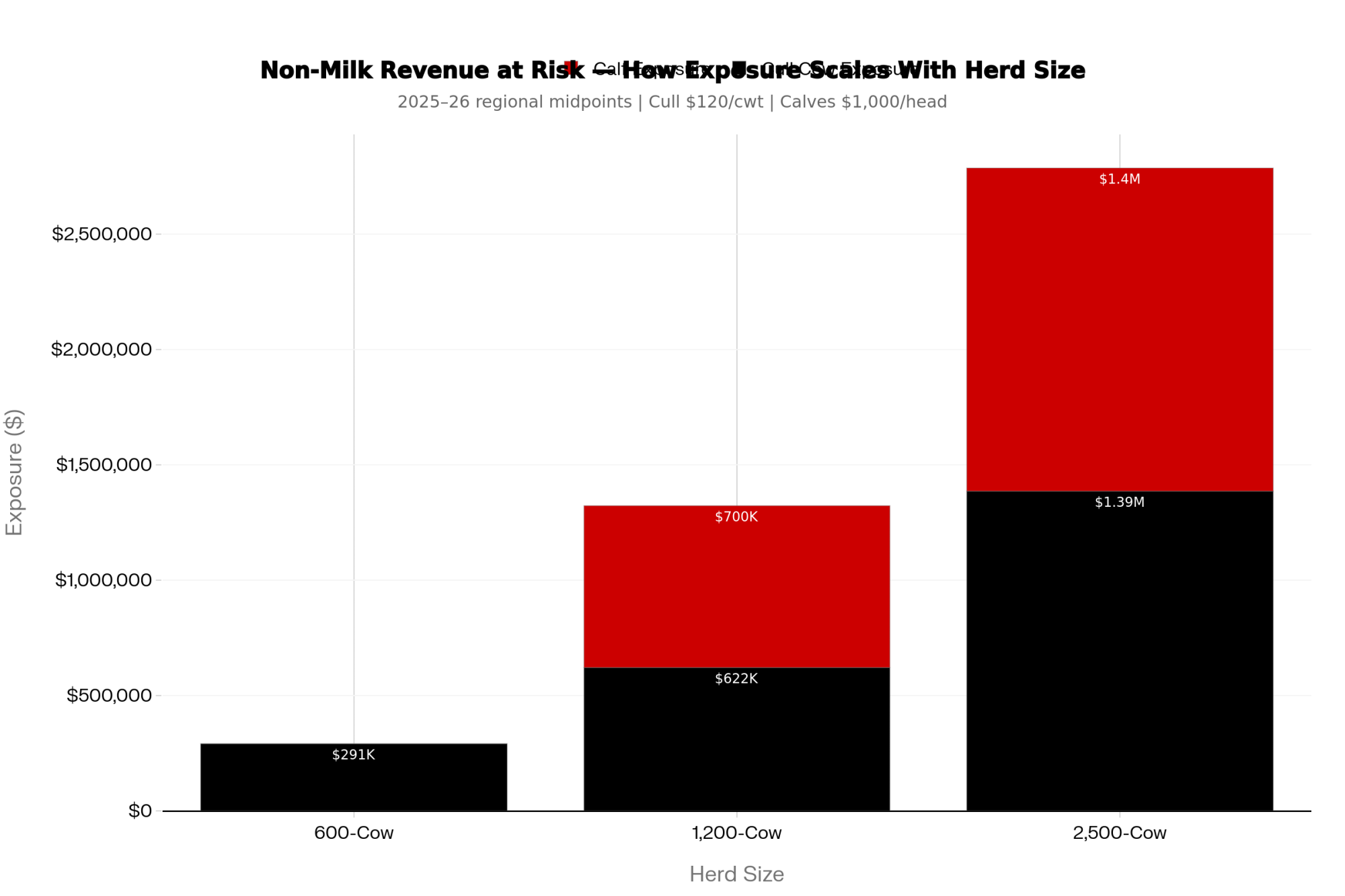

Non-Milk Asset Exposure by Herd Size — A Side-by-Side

The table below uses a $120/cwt midpoint cull price (within the $110–$130 range observed across regional auctions in 2025–2026) and $1,000/head day-old beef-on-dairy calves. Cull weight assumptions reflect typical regional patterns: 1,350 lbs for Upper Midwest Holstein-dominant herds, 1,400 lbs for larger Western and Plains operations carrying heavier-conditioned culls.

Cull and calf prices reflect 2025–2026 regional midpoints. Pull current local auction reports before using these figures for your own planning.

| Metric | 600-Cow Dairy | 1,200-Cow Dairy | 2,500-Cow Dairy |

|---|---|---|---|

| Annual cull rate | 30% | 32% | 33% |

| Annual cull cows (head) | 180 | 384 | 825 |

| Avg cull weight | 1,350 lbs | 1,350 lbs | 1,400 lbs |

| Cull cow revenue exposure | ~$291K | ~$622K | ~$1.39M |

| Day-old beef-on-dairy calves/yr | Variable | ~700 | ~1,400 |

| Calf value exposure (@$1,000/hd) | Variable | ~$700K | ~$1.4M |

| Combined non-milk exposure | ~$291K | ~$1.3M | ~$2.7M |

| Annual milk volume (25K lbs/cow) | 150,000 cwt | 300,000 cwt | 625,000 cwt |

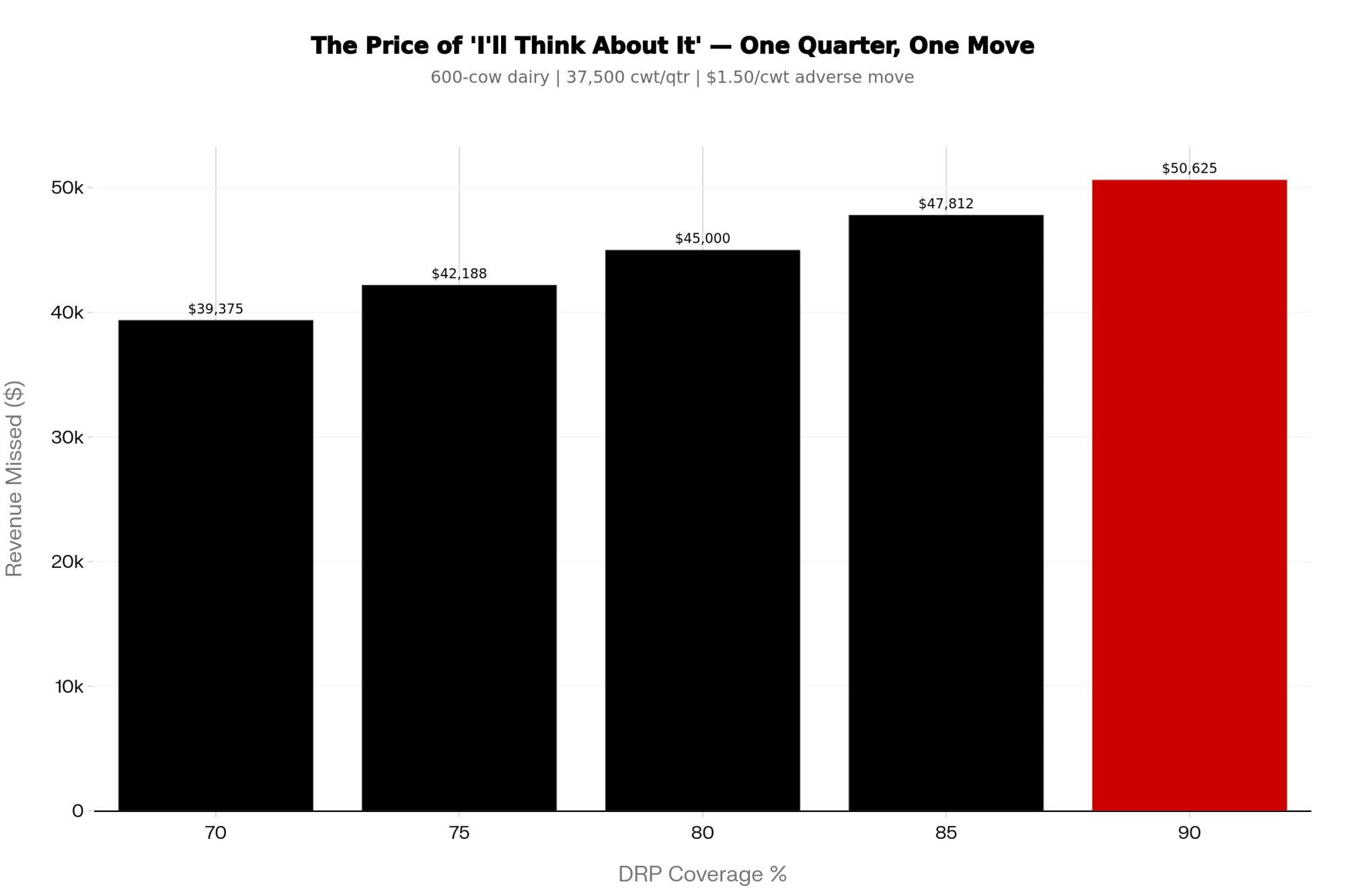

| Missed floor @ $1.50/cwt adverse, 90% coverage/quarter | $50,625 | $101,250 | $210,938 |

| Named risk decision-maker present? | 🔴 Rare | 🟡 Sometimes | 🟡 Inconsistent |

| Written authority playbook? | 🔴 Rare | 🟡 Sometimes | 🟡 Inconsistent |

| Typical risk role | Missing | Controller or adviser | Controller or CFO |

Calf counts at the 1,200-cow and 2,500-cow lines assume roughly 55–60% of the herd is bred to beef. Adjust to your own breeding share before concluding.

Read across any row, and the governance question changes character. At 600 cows, the dairy is making decisions about a quarter-million-dollar cull stream with no one formally watching the windows. At 2,500 cows, the dairy is running roughly $2.7 million in non-milk exposure through a finance function that may have the right title but not the written authority to execute on a Friday afternoon.

The dairies running layered portfolios well almost always have a named risk person — a family member, a controller, or a contracted adviser through outfits like Crop Growers, AgCountry, or GreenStone — whose job description includes “watch the windows.” The dairies sitting at 600 cows with no defined risk role tend to use one program reactively, lapse on it for two years, and then scramble back to the agent during a downturn. The new three-year cancellation rule will surprise some of those operators.

The Mechanics Behind the Outcomes

The 2027 changes reduce mechanical friction. They don’t reduce decision complexity. If anything, they raise it.

| 2027 Change | What It Fixes | What It Doesn’t Fix | Who It Helps |

|---|---|---|---|

| DRP closes next calendar day | No more Sunday-night panic; weekend rates are actionable | Producers with no pre-agreed trigger rule still won’t act | Active DRP users with a named decision-maker |

| LRP cull cow coverage extended to 52 weeks | Eliminates quarterly re-writing; one annual endorsement | Doesn’t protect dairy-cull basis vs. beef-breed index spread | Dairies with predictable, planned culling cycles |

| New LRP Unborn Dairy Weight 2 (6–9 cwt) | Opens federal floor for backgrounded beef-on-dairy | Decision must precede breeding — sale-barn timing is too late | Retained-ownership operations only |

| Concurrent DRP + LRP + LGM stacking | Complete multi-stream risk architecture now federally possible | Requires half-day/quarter of recordkeeping + engaged adviser | Operations ≥750 cows with dedicated risk bandwidth |

| 3-year no-premium auto-cancellation | Cleans up lapsed, inactive policies automatically | Will silently cancel policies operators think are still active | Nobody — this is a trap for lapsed users |

| LGM cattle weight maximums increased | Better alignment with actual feedyard finishing weights | Still settles on futures index, not local basis | Beef-on-dairy operators in retained-ownership models |

DRP timing is genuinely easier now. The next-calendar-day window means a Friday rate posting can be acted on through the weekend without the old Sunday-night panic. That fixes a real friction point for active users. It doesn’t help producers who never had a rule for when to lock coverage in the first place.

The 52-week cull cow extension only pays off if your culling pattern is predictable enough to write a single annual endorsement against. For dairies pulling cows reactively as they fail rather than on a planned cycle, shorter-window endorsements may still fit better. The decision work just shifted from your agent’s calendar to yours.

Concurrent coverage is the structural change with the biggest implications. Three programs covering three revenue streams — milk, calves, culls — give you a more complete risk architecture than dairy has ever had access to under federal subsidies. But the same head still can’t be insured under multiple policies simultaneously, which means head-level recordkeeping (breeding logs, pregnancy checks, birth records, marketing receipts within strict calendar windows) becomes part of the compliance work. That’s manageable with the right adviser. It’s a paperwork trap without one.

The bigger surprise sits in the Unborn Dairy Weight 2 category. Most beef-on-dairy dairies still sell calves under 60 lbs within two weeks of birth — a pattern consistent with industry surveys and how DFA’s beef-on-dairy programs are structured. That’s Weight 1 territory, and those operators have already had unborn calf coverage available since July 2025. Weight 2 is built for a different model: dairies retaining calves through backgrounding to 600–900 lbs, often as part of profit-sharing arrangements with feedyards. The same pattern points to a directional shift over the last several years, visible in beef-on-dairy semen sales and retained-ownership pilots.

If you’re not in that game today, Weight 2 isn’t your tool. If you’re considering moving toward retained ownership, the floor is what makes the math work.

How Much Does Hesitation Actually Cost on a Mid-Size Dairy?

Here’s the math behind the lede, plain and simple. A 600-cow herd at 25,000 lbs/cow annual production ships 150,000 cwt a year. Divide by four quarters, and you get roughly 37,500 cwt of milk per quarter. At 90% coverage with a $1.50/cwt adverse move, that’s 37,500 × $1.50 = $56,250 in floor revenue you walked past.

That’s one decision, one quarter, one program. Repeat the pattern across cull cow timing, calf coverage windows, and DRP layering across four quarters, and the cumulative cost of “I’ll think about it” easily reaches into six figures over a couple of years.

The compounding effect is what most producers underestimate. A dairy that misses one DRP window per year, lets cull cow coverage lapse during calm markets, and never engages with calf LRP isn’t catastrophically wrong any single year. They’re structurally exposed across cycles. When a real downturn lands, peers with consistent — even modest — coverage typically absorb less of the hit, though specific outcomes vary by program use, timing, and local basis. Risk advisers writing publicly about DRP timing describe the same pattern: producers wait for prices that feel “good enough,” and the window closes.

Who in Your Operation Owns the Friday Decision?

This is the question every mid-size dairy needs to answer before July 1, 2026. On most 600-cow operations, the role is simply missing. The crop insurance agent emails when they remember. The lender raises it once a year at the annual review. The producer is between parlor and TMR mixer when the email lands, and “let’s see what Monday looks like” feels safer than committing on a Friday afternoon.

The dairies that use DRP and LRP well share one structural feature. Someone is named, in writing, with explicit authority to execute coverage decisions according to a pre-agreed playbook. That person can be a family member, a controller, or a contracted adviser through AgCountry, GreenStone, or a similar lender-aligned risk desk. What matters is that ownership has explicitly said that if they follow the rules everyone agreed on, no one gets to second-guess after the fact. That permission structure is what keeps the role from defaulting to whoever happens to read the email first.

Options and Trade-Offs for Farmers

Four practical paths most mid-size dairies should be evaluating right now. One is a 30-day move; the others stretch into the 2027 crop year.

Path 1: Audit your existing policy status before July 1, 2026 — this is your 30-day action.

The new three-year no-premium cancellation rule is quiet and easy to miss. If you’ve held a DRP or LRP policy that hasn’t earned a premium since 2024, it’s at risk. Call your agent this week and confirm policy status. The June 30, 2026 DRP provider transfer deadline also closes the window to switch agents before the 2027 crop year begins. This is the lowest-effort, highest-payoff move on the list — and the one most likely to be skipped.

Path 2: Use the 52-week cull cow LRP if your culling is predictable — but understand what the index actually protects.

A 600-cow herd with a stable culling rhythm can write one endorsement covering the year’s projected cull flow, lock a price floor against the CME Feeder Cattle or Fed Cattle Index, and stop scrambling quarterly. Here’s the trade-off an experienced peer would push you on. LRP settles against the CME Feeder Cattle Index or Fed Cattle Index, both of which are structurally built around beef-breed cattle. A Holstein cull already carries a structural quality and yield discount at slaughter relative to beef-breed counterparts. A Jersey cull carries an even larger one. The LRP coverage you write protects against a drop in the broader cattle market — directional declines in the index. It does not protect against a blowout in the dairy-beef basis differential. If beef cull prices hold steady but dairy-cull discounts widen because of a quality or yield spread shift, your endorsement won’t pay even though your local cull check did. That’s the gap to size before you sign.

Path 3: Layer concurrent coverage if you’re above 750–1,000 cows.

Holding DRP on milk, plus LRP on culls and calves, gives lenders a complete, protected revenue picture. The combined documentation supports DSCR covenants and borrowing base calculations. The trade-off: this requires either dedicated risk management bandwidth or a highly engaged agent. Plan on roughly a half-day a quarter of bookkeeping, plus a standing 30-minute call with your agent the week each program’s window opens — minimum. Below 750 cows, the administrative cost likely outpaces the marginal protection benefit unless you’ve already built the governance to run it.

Path 4: Consider Weight 2 only if you’re moving toward retained ownership.

Day-old calf sellers stay in Weight 1. The Weight 2 category opens real options for dairies backgrounding their own beef-on-dairy crosses at 700–900 lbs, with endorsement windows that run through the months leading up to marketing. The trade-off: the decision has to precede breeding, not weaning. Operators thinking about calf coverage at the sale barn have already missed the window.

For each path, the honest filter is the same. Do you have someone in the operation whose job is to watch the trigger and execute? If not, fixing that comes first.

Is Your Operation Already Behind on the Risk-Governance Curve?

Lenders are moving — quietly, in advisory blogs and credit committee conversations — from “DRP is encouraged” toward DRP/LRP governance as the new baseline for serious dairies. Farm Credit advisory content across 2026 increasingly treats LRP as standard equipment rather than exotic — an assumption embedded in stability-planning guidance from multiple Farm Credit associations. The shift from Phase 1 to Phase 2 is happening in the language before it shows up in the term sheets.

If your last conversation with your lender included the phrase “let’s talk about your risk plan” — and you didn’t have a one-page answer ready — you’re already in the Phase 2 conversation. You just may not have noticed.

Key Takeaways

- If you’ve held a DRP or LRP policy that earned no premium in 2024 or 2025, call your agent before June 30, 2026 to confirm status. The new three-year cancellation rule may already be ticking on your policy.

- If your culling is predictable enough to forecast a year out, run the 52-week LRP cull cow numbers — but pull your local dairy-cull basis against the CME Feeder Cattle and Fed Cattle indices before assuming the endorsement is full protection.

- If you’re still selling beef-on-dairy calves under 60 lbs, Weight 1 is your category. Weight 2 is for retained-ownership operations and demands a breeding-stage decision, not a sale-barn one.

- If your herd is above 750 cows and your lender is asking about layered coverage, treat concurrent DRP + LRP + LRP as a borrowing base conversation, not a checkbox.

- If you’re at 2,500 cows with a controller but no written risk playbook, the gap between “we have someone who could do this” and “someone is authorized to do this” is what will cost you in 2027.

- If nobody in your operation can answer “who locks coverage when the trigger hits?” — fix that before you fix anything else. Name the person, write the playbook, give them authority.

- If your last conversation with your lender got vague when risk management came up, your next one likely won’t.

Grade Your Own Farm’s 2027 Risk Readiness — Before You Close This Tab

Print this. Screenshot it. Tape it to the office door. Answer yes or no, today.

- ☐ I can name, in 10 seconds, the person on my farm authorized to lock DRP or LRP coverage on a Friday afternoon without calling me first.

- ☐ That authority is written down somewhere — even one paragraph — and the lender, the agent, and ownership have all seen it.

- ☐ I know whether each of my active DRP and LRP policies earned premium in 2024 and 2025, and I’ve confirmed status before the new three-year cancellation rule applies.

- ☐ I’ve made a deliberate decision before June 30, 2026 about whether to keep or transfer my DRP provider for the 2027 crop year.

- ☐ I’ve sized my annual cull cow exposure against the 52-week LRP option and pulled my local dairy-cull basis against the CME Feeder Cattle and Fed Cattle indices, not assuming the index protects my actual check.

- ☐ If I run beef-on-dairy, I know which weight category (1 or 2) matches how I actually market calves — and I haven’t bought the wrong one.

- ☐ If my herd is above 750 cows, I’ve modeled what concurrent DRP + LRP + LRP would do to my DSCR and borrowing base, and I’ve shared that with my lender before they ask.

- ☐ The last time my lender said “let’s talk about your risk plan,” I had a one-page answer ready.

Six or fewer checks means you’re in the Phase 1 group lenders are quietly moving past. Seven or eight means you’re already running the playbook the 2027 toolkit was built for.

Run Your Numbers

Farm Benchmark Snap Check — Pressure-test where your operation sits before the next DRP window opens. The tool flags margin exposure, non-milk asset risk, and the governance gaps that turn a $1.50/cwt market move into a $56,250 hole on your milk check.

Closing

So the question isn’t whether USDA built better tools for 2027. They did. The question is whether your operation has someone whose job description includes acting on them before Friday afternoon turns into Monday regret.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Class III Milk Price, DRP, and Your Spring 2026 Risk Plan — Arms you with a defensive, balanced, or aggressive playbook to sort five core operational metrics—including production, components, and basis—into real-time DRP pricing triggers before calling your crop insurance agent.

- The 400-Cow Margin Trap: When $14.59 Milk Bleeds $425K in 2026 — Exposes the catastrophic gap between cash and economic breakevens, walking strategic planners through forward debt-service coverage ratio stress tests to protect equity from high replacement liabilities and repriced term debt.

- Beef-on-Dairy at 45%? A Screwworm 200 Miles South Just Rewrote Your Calf Math — Dismantles the standard herd-diversification narrative by demonstrating how a single biosecurity disruption or regional bid haircut triggers a six-figure blow to non-milk margins when beef penetration scales too high.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.