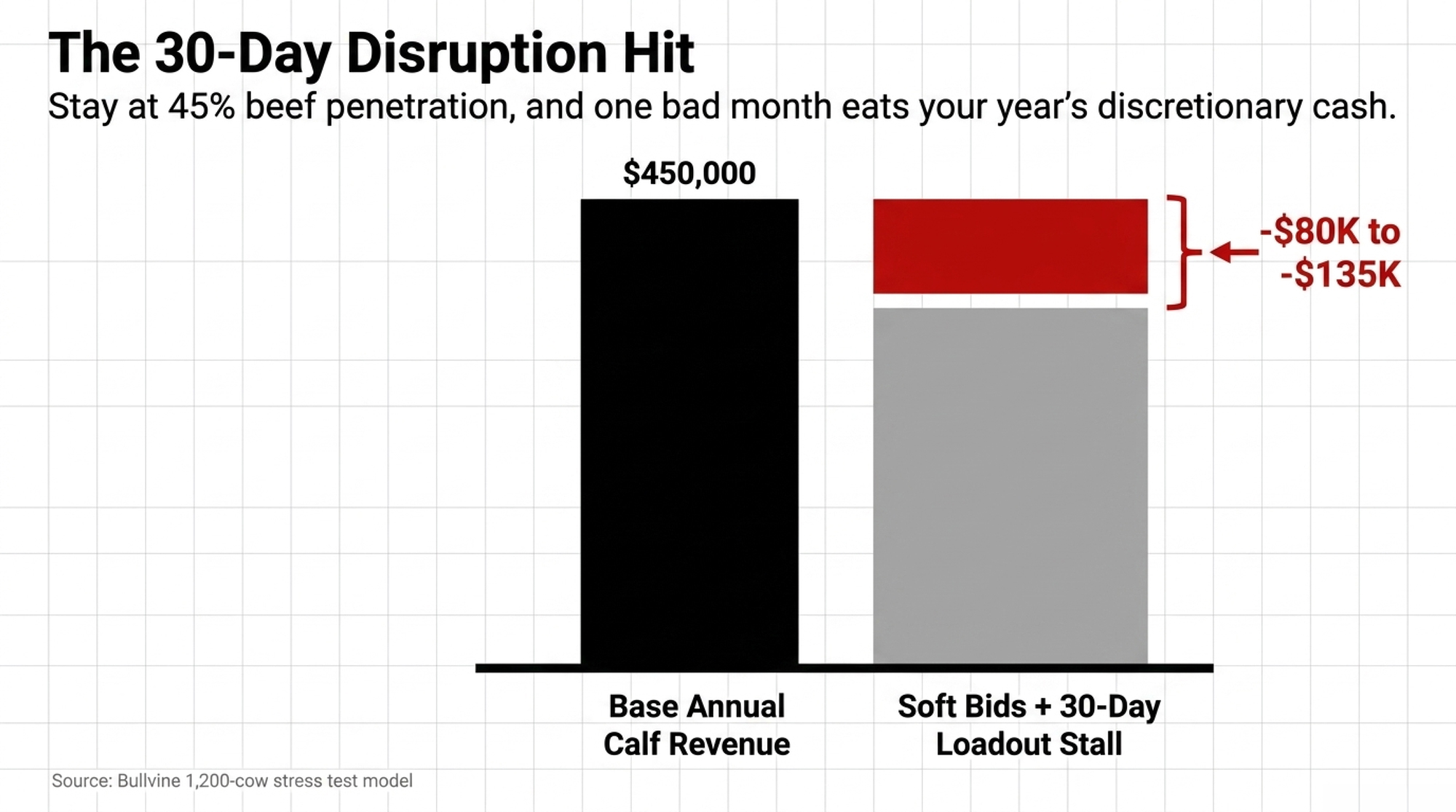

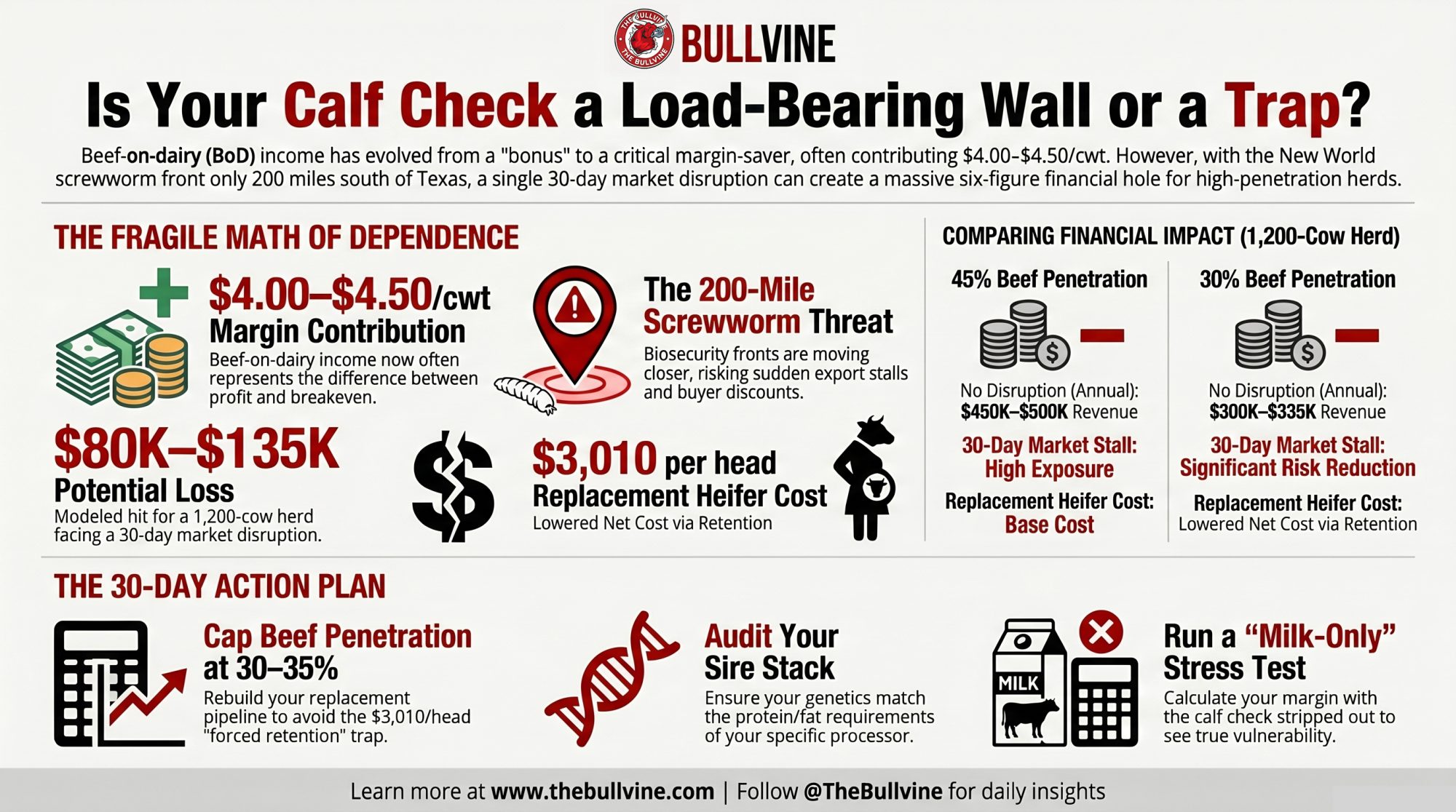

If 45% of your herd is bred to beef and the calf check is worth $4/cwt on margin, a 200-mile screwworm line plus one stalled month of loadouts can stack into an $80K–$135K hole. Run the math now.

Executive Summary: A New World screwworm front sitting 200 miles south of Texas, $11 billion of new export-grade processing stainless going up, and a beef-on-dairy line worth roughly $4.00–$4.50/cwt on the margin-over-feed ledger are now stacked on the same milk check. On a 1,200-cow Panhandle herd running 45% beef, the calf line is pulling $450K–$500K a year — and a partial-year bid discount paired with a single 30-day disruption month models out to an $80K–$135K hit before the extra milk replacer and labor land. Replacement heifers at $3,010/head with an 800,000-head national pipeline shortage mean you can’t just rotate back to dairy semen overnight. The 30-day move is a kitchen-table calculation, not a five-year plan: cap penetration at 30–35%, audit your sire stack against your actual processor’s product mix, and put a basis-and-disruption clause in front of your buyer before the next map dot does it for you.

Picture a 1,200-cow Holstein dairy west of Hereford, Texas. Forty-five percent of the herd is bred to beef. Calves load out at three days old, into a stock trailer headed for a backgrounder up the road. The milk truck rolls the other way — toward Leprino’s new 850,000-square-foot Lubbock cheese plant, designed to process a million pounds of cheese a day off 200 tankers of milk.

That operation is pulling roughly $450,000 to $500,000 a year off beef-cross calves and culls — about $4.00 to $4.50 per cwt on the margin-over-feed ledger, matching the beef-on-dairy economics CoBank and AFBF flagged in their 2026 heifer-pipeline analysis.

Call it feed and labor money. Not bonus money.

Then on May 11, 2025, USDA Secretary Brooke Rollins suspended all live cattle, bison, and horse imports through southern border ports after a New World screwworm detection 700 miles south of Texas. By March 2026, APHIS had the front contained 200 miles south of the Texas line. No worms in your calves. No quarantine on your farm. But that map now sits atop the most concentrated single-line revenue source most Panhandle dairies have built in the last five years.

That’s the line you’d cut last in any other year. And it’s the line a single map dot can hit first.

Why the Calf Check Got Load-Bearing

You’ve heard about the stainless for two years. The U.S. processor-investment buildout has cleared $11 billion through 2026, weighted toward cheese, powders, and high-protein ingredients across the Texas Panhandle, Upper Midwest, South Dakota, and Michigan. Texas alone carries Leprino’s Lubbock cheese plant, Hiland’s $100 million Tyler renovation (now over a million gallons a week), and Walmart’s $350 million Robinson fluid plant feeding 650 stores.

Those plants weren’t built for white water. They were built for protein and fat — cheddar, mozzarella, whey protein, milk protein concentrates, butterfat, MPC. Per USDEC’s 2025 calendar-year recap, U.S. dairy exports hit 2.32 million metric tons MSE worth $9.63 billion, with cheese exports up 20% to 613,045 MT and butterfat shipments up 167% to 122,085 MT. Mexico took $2.58 billion of that — the first-ever $2B U.S. dairy market — absorbing 27% of cheese and 43% of NFDM/SMP.

| Export Category | 2025 Volume | YoY Change | Mexico’s Share | Risk Flag |

|---|---|---|---|---|

| Total U.S. Dairy Exports | 2.32M MT MSE / $9.63B | +est. 4–6% value | 27% of total | Medium |

| Cheese | 613,045 MT | +20% | 27% of cheese | HIGH — USMCA review July 2026 |

| Butterfat | 122,085 MT | +167% | ~15% est. | High — single-year surge vulnerable |

| NFDM/SMP | N/A published | Flat–positive | 43% of NFDM/SMP | HIGH — single market dependency |

| Mexico Total Dairy | $2.58B | First ever $2B market | 100% exposure | Tariff/trade risk at USMCA review |

| All Other Markets | ~$7.05B est. | Diversified | <10% each | Low–Medium |

On the producer side, beef-on-dairy quietly became the patch for thin milk-only margins. AFBF and CoBank track replacement heifers past $3,010/head in 2026 — up more than $1,120 in two years — with a national pipeline shortage of roughly 800,000 head. Replacement cost stayed high. Milk-only margins thinned. The calf check covered the gap.

Then May 11, 2025 happened.

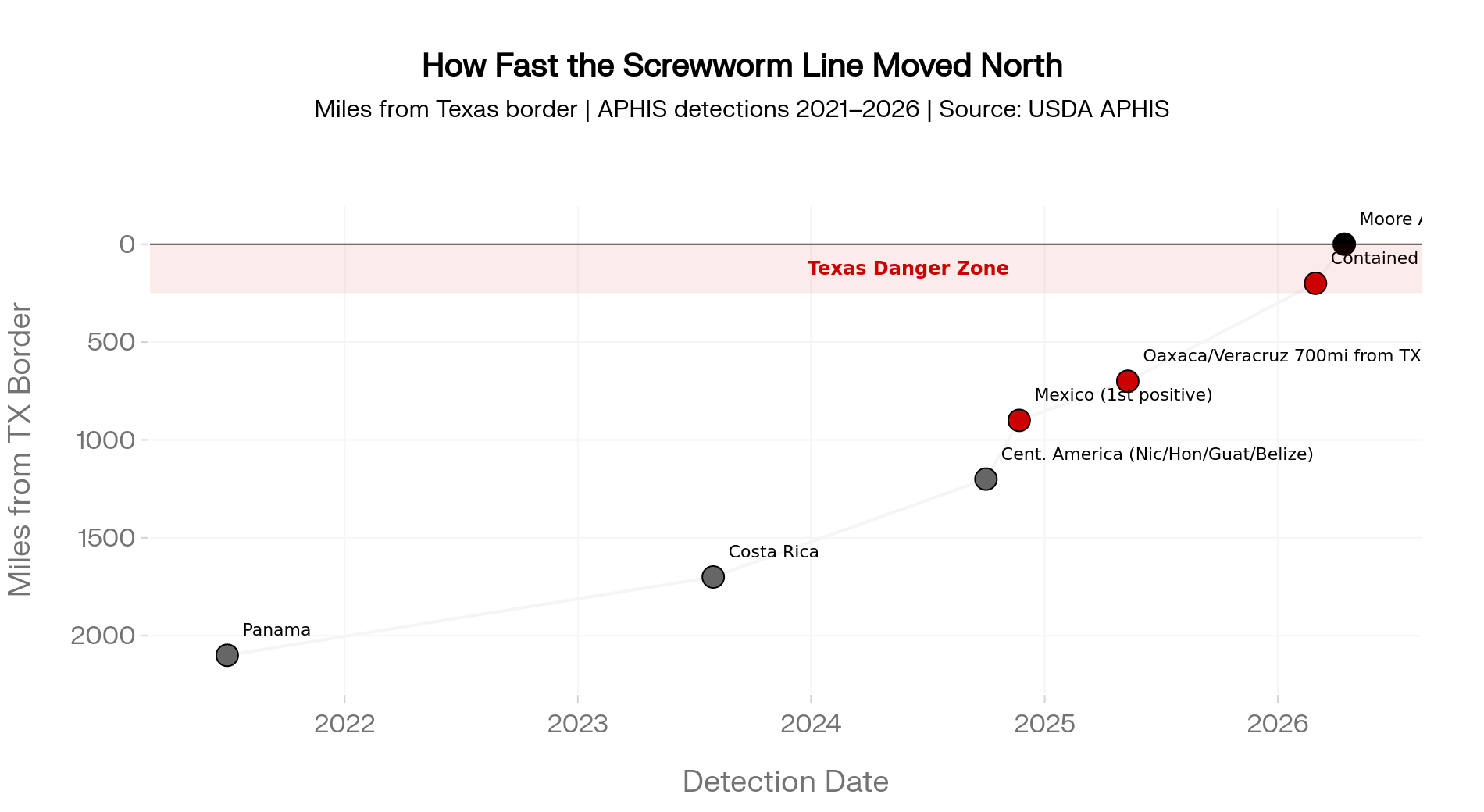

The Path of a Map Dot from Panama to the Texas Line

APHIS data tracks New World screwworm spreading from Panama in July 2021 to Costa Rica in August 2023, then through Nicaragua, Honduras, Guatemala, and Belize by late 2024. Mexico confirmed its first positive on November 22, 2024. By May 11, 2025, detections in Oaxaca and Veracruz — 700 miles south of the U.S. border — triggered Secretary Rollins’s suspension of live cattle, horse, and bison imports through southern border ports.

By March 2026, USDA had the front contained 200 miles south of the Texas border and 800 miles from Arizona. Secretary Rollins announced the agency was evaluating a phased-in, limited reopening starting at the westernmost port — Agua Prieta, Sonora into Douglas, Arizona — because of its distance from active cases.

USDA’s 5-Prong Eradication Strategy is doing the heavy lifting. A $21 million renovation of the sterile-fly facility in Metapa, Mexico is producing 60–100 million flies per week on top of Panama’s 100 million. Moore Air Base in South Texas, completed in 2025, began dispersing sterile flies in northern Mexico in mid-April 2026, ramping toward 500 million flies per week.

That’s the backdrop for any Panhandle or Southwest herd shipping to the new plants, running 40–45% beef, and counting on calf cheques to balance the books. The hero map graphic above traces APHIS detections from Panama in 2021 through the March 2026 200-mile containment line, with the Lubbock, Tyler, and Robinson plants layered on top. Trace the dots north and the geographic overlap is the whole story.

Running the Numbers on a 1,200-Cow Stress Test

Here’s the math the way a Panhandle producer would run it on a yellow pad.

Base revenue — the calf line

- 1,200 cows × 45% beef-on-dairy = 540 beef matings/year

- Net of typical 10–15% dairy-program losses (conception failure, abortion, stillbirth, early neonatal): ~460–490 weaned beef-cross calves

- Net per beef-cross calf, Panhandle/High Plains range, day-old to short-weaned: $900–$1,200, working from regional sale-barn and direct-to-backgrounder bids tracked through Q1 2026

- Annual beef-cross calf revenue, before culls: $432,000–$576,000

Base revenue — total margin contribution

- Modeled milk volume: 1,200 cows × 80 lb/cow/day × 365 ÷ 100 = 350,400 cwt/year (adjust to your own bulk-tank average)

- At $4.00/cwt beef-and-cull contribution: ~$1.40 million/year

- At $2.00/cwt beef-and-cull contribution: ~$700,000/year

Disruption Scenario 1 — a year of soft bids

In comparable past USDA biosecurity events, calf buyers in border-proximate corridors have responded with bid discounts and tighter loading rules. This analysis models a 10–15% discount band as a working assumption — pressure-test it with your own buyer.

- 10% × $432K = –$43,200

- 15% × $576K = –$86,400

- Working envelope: –$43,000 to –$86,000 over the year

Disruption Scenario 2 — a 35% disruption month

Calves delayed, bids soft, movement slowed for 30 days during peak-sales window. Peak calf-sales months commonly carry 2–4× a flat 1/12 share, so the in-window concentration runs hotter than it would on a smooth annual line.

- 35% × $450K–$500K total beef line = –$157,500 to –$175,000 over the year

- Compressed into a single 30-day peak window: –$30,000 to –$60,000 during that month

Combined mid-stress hit

A partial-year discount stacked with a single 30-day disruption month — the realistic case for a containment scare or a stalled phased reopening — lands the modeled hit at roughly $80,000 to $135,000 before the extra milk replacer, bedding, and labor on calves the buyer wants older. A full-year 35% disruption pushes that toward $175,000.

Now plug your own herd in. A 400-cow operation runs 116,800 cwt/year. At $2.00/cwt in beef-and-cull income, that’s $233,600 a year — a parlor overhaul, a year of principal, or the cushion between cutting feed and not.

| Herd Size | Annual cwt (80 lb avg) | Beef-Cull Income @ $4.00/cwt | 25% Bid Haircut | 35% Disruption Month | Combined Mid-Stress Hit |

|---|---|---|---|---|---|

| 400 cows | 116,800 cwt | $467,200 | -$26,600 | -$35,100 | -$28K–$44K |

| 800 cows | 233,600 cwt | $934,400 | -$53,200 | -$70,200 | -$57K–$88K |

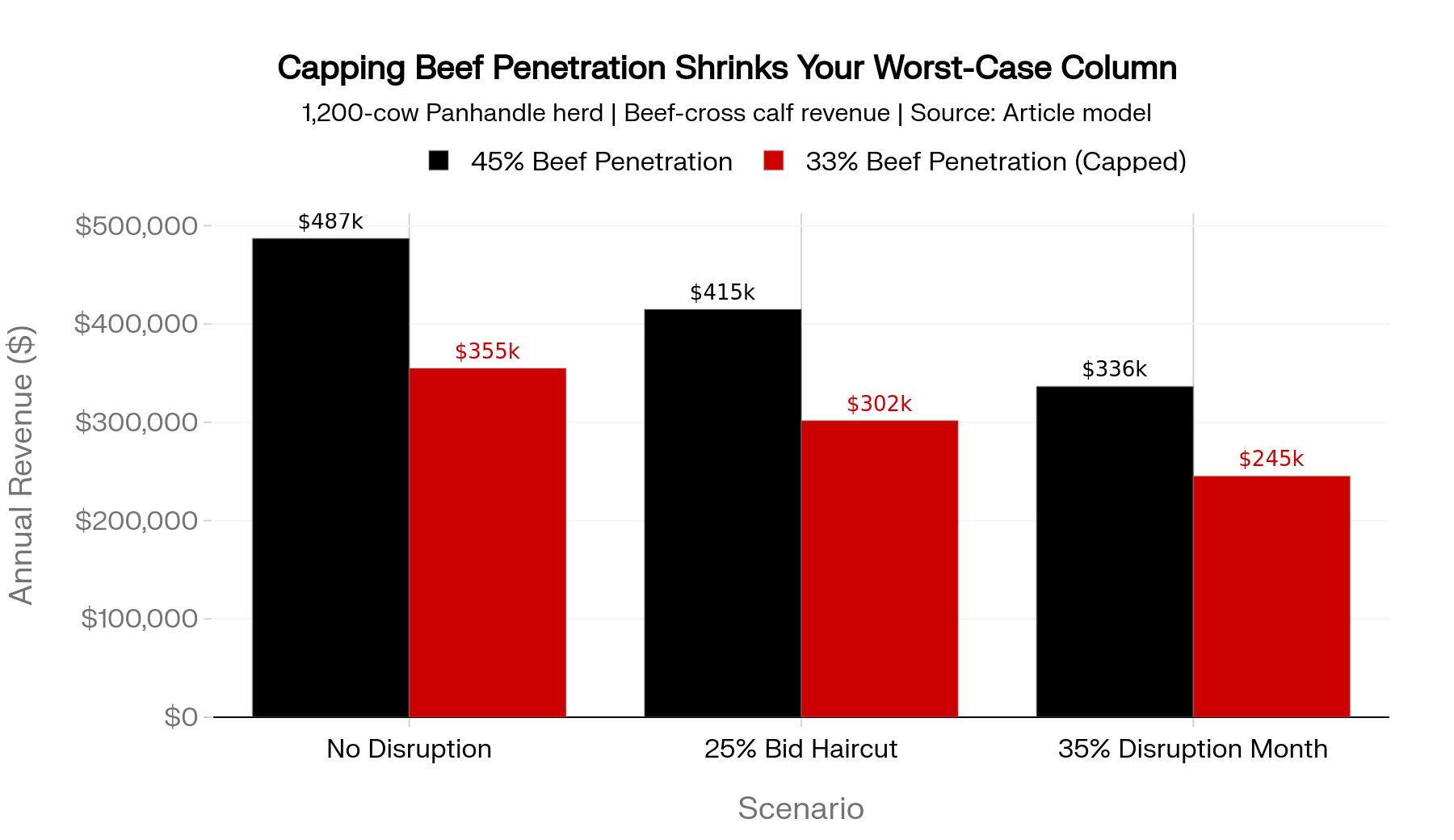

| 1,200 cows | 350,400 cwt | $1,401,600 | -$80,000 | -$105,300 | -$80K–$135K |

| 2,000 cows | 584,000 cwt | $2,336,000 | -$133,400 | -$175,200 | -$133K–$224K |

| 3,500 cows | 1,022,000 cwt | $4,088,000 | -$233,500 | -$306,600 | -$233K–$392K |

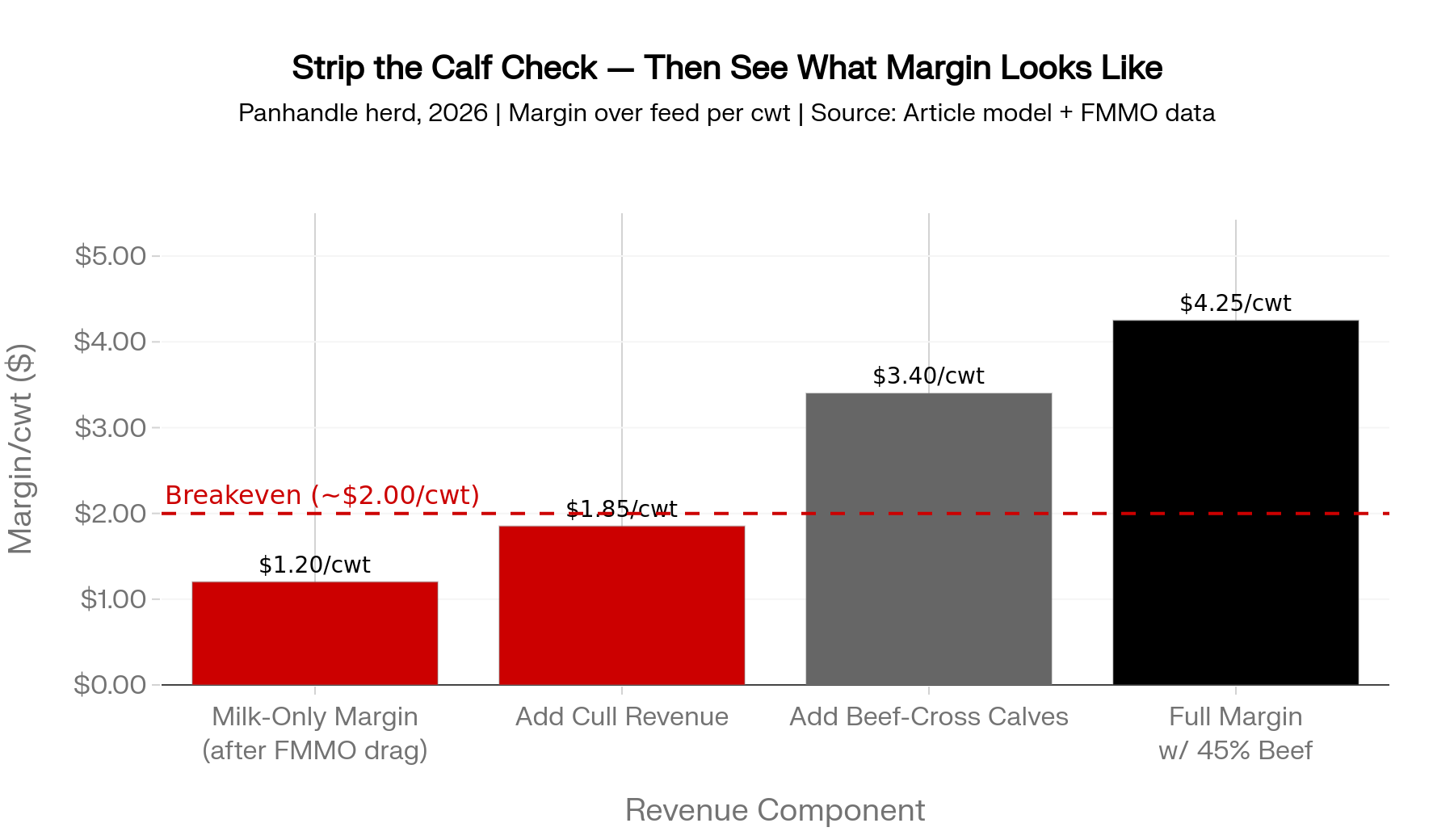

What’s Your Milk-Only Margin Without the Calf Check?

Strip out beef-on-dairy and cull income. What’s left?

That’s the question to put to your CPA and your lender this month. On a herd carrying $4.00–$4.50/cwt of beef-and-cull contribution, the answer often lands at or just below breakeven on milk alone — especially with the 2025–2026 FMMO make-allowance updates dragging another $0.85–$0.93/cwt off Class II, III, and IV values. That isn’t diversification. That’s dependence.

Then the second question, the one that decides your breeding plan: if you couldn’t ship a single beef-on-dairy calf for 30 days, what percentage of your herd could you afford to have bred to beef and still pay your bills and keep enough replacements?

At 45% penetration, a 30-day disruption pushes most operations into cutting exactly the things that wreck herd performance 6–12 months out. Repro herd checks stretch from every two weeks to “when we can.” Cows tagged for culling stay another lactation because the math on $3,010 replacements doesn’t pencil. Pregnancy rate slips. Days open creep. The calf cheques that saved this year quietly lock you into needing them even more next year.

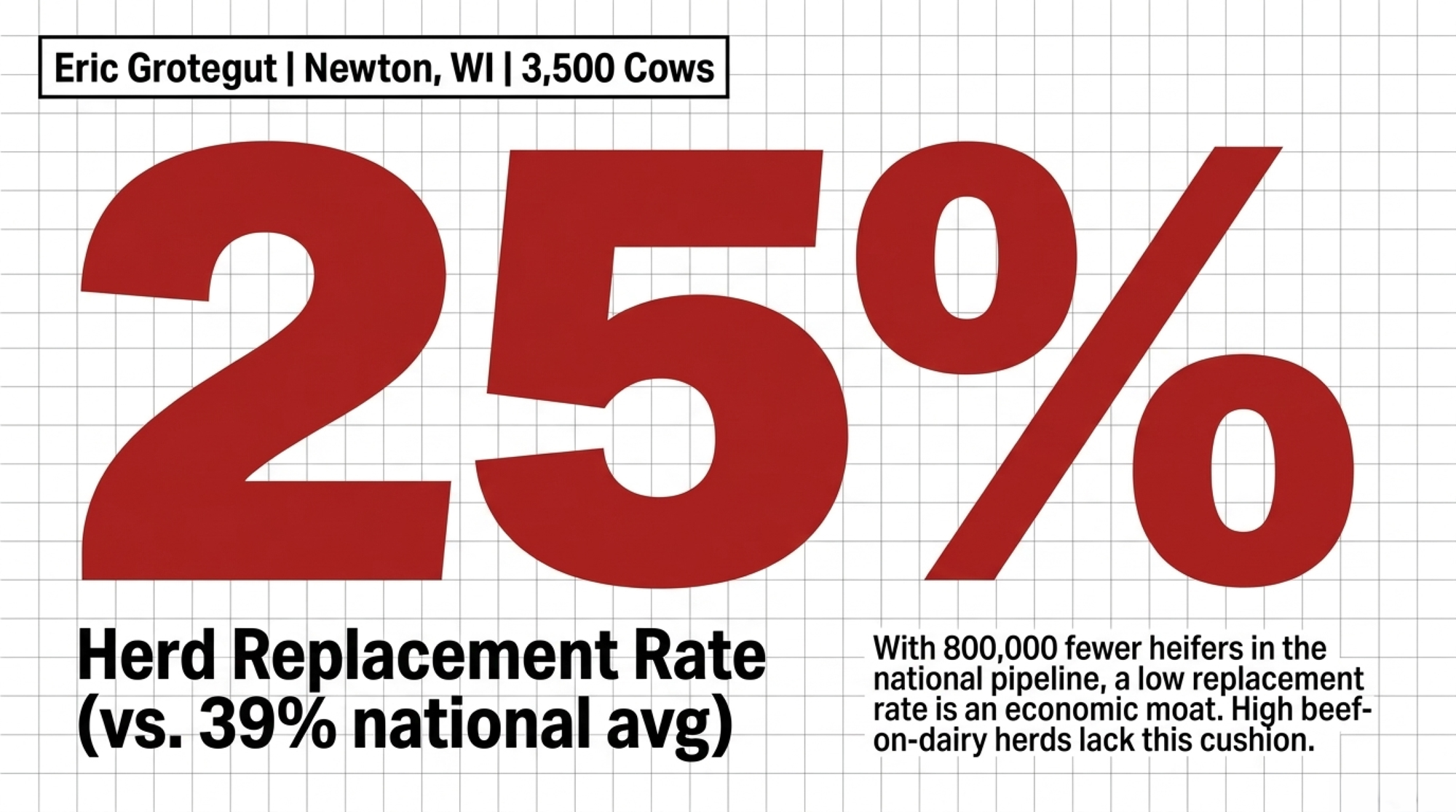

Eric Grotegut’s 3,500-cow operation in Newton, Wisconsin runs a 25% replacement rate against a 39% national average. That gap is now an economic moat, not a curiosity — and it’s exactly the cushion a 45%-beef Panhandle herd doesn’t have when the trailer can’t load.

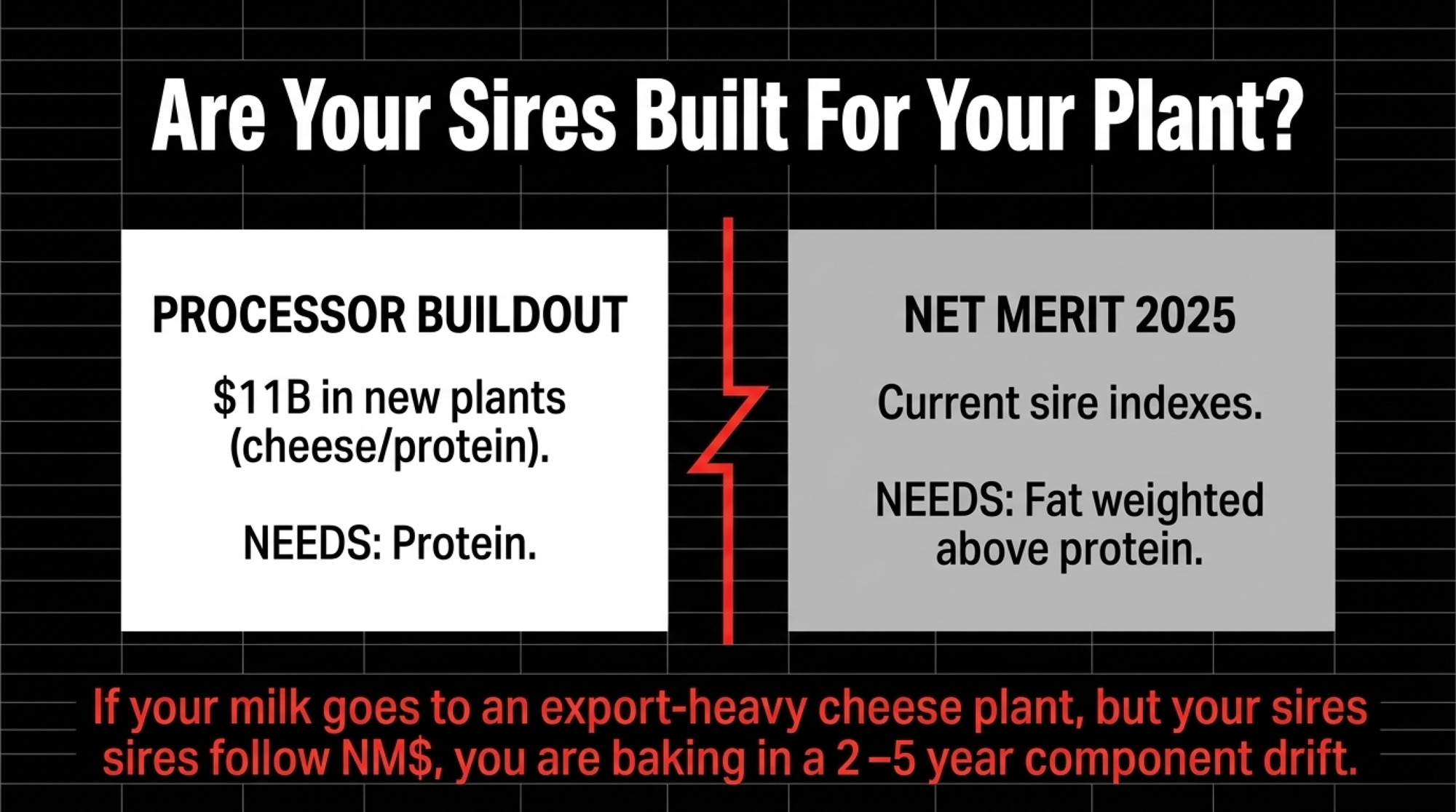

Are Your Sires Built for the Plant That’s Buying Your Milk?

Processors don’t see your bank statements. They see loads, lab sheets, and contracts.

Leprino’s Lubbock plant runs on a million pounds of cheese a day. Hiland’s Tyler expansion quadrupled output to over a million gallons a week. Walmart’s Robinson plant pulls fluid milk for 650 stores. Those capital budgets assumed steady milk flow and a steady component profile — and your selection index has a vote in whether they get it.

The current CDCB and breed-association indexes are not pointing the same direction. Net Merit 2025 weights fat above protein on the production side. The Holstein Association’s TPI revisions over the last several years have raised protein weighting to recognize cheese and whey demand. Lactanet’s LPI, in its current published formula, runs roughly a 60% protein / 40% fat split on the production component for Canadian Holsteins.

If your milk’s going to an export-oriented cheese or protein plant but your sires are locked onto an index that rewards a different solids mix, there’s a gap. Component progress takes 2–5 years to show in the bulk tank. Catching the mismatch this year is cheaper than catching it in 2028.

Options and Trade-Offs for Your Operation

| Strategy Path | Best For | What It Requires | Annual Cost/Upside | Where It Fails |

|---|---|---|---|---|

| Cap BOD at 30–35% | Herds >40% BOD in border corridors | Genomics file, sire audit, sexed dairy semen | Reduces worst-case hit by ~$45K–$90K | Replacement pipeline at $3,010/hd balloons cost before milk benefits show |

| Stay at 40%+ BOD, hedge it | Solid milk-only margin; deep buyer relationships | DRP coverage + forward calf contracts + written biosecurity SOP | $450K–$500K/yr maintained — if bids hold | No fully approved NWS treatment outside emergency use; vet confirmation required |

| Realign sire stack to your plant | Signed/pending contracts at cheese or whey plants | Plant product-mix confirmation + sire portfolio audit | Component drift correction saves 2–5 yrs of mismatch cost | Index mismatch means 2 yrs selecting for traits your plant doesn’t pay for |

| Renegotiate contract now | Basis within benchmark; component margin above breakeven | Contract, willingness to walk, specific asks on basis & disruption clauses | Locks in protection before July 2026 USMCA review | Wait until after a disruption and the plant writes its own terms |

Path 1 — Cap beef penetration at 30–35%, starting this month

When it makes sense: any herd above 40% beef in a border-proximate or export-heavy corridor. Re-mate the bottom 25–30% of cows on genomics and production. Shift sexed dairy semen onto the top 35% to rebuild replacement flow over two years.

What it requires: a current genomics file, a sire portfolio audit, a semen rep, and a written breeding-plan reset.

Where it fails: with replacement heifers at $3,010/head and a national pipeline shortage near 800,000 head, over-rotating to dairy semen balloons replacement cost before the milk-cheque benefits show up. The forced-retention trap — keeping low-producing cows because replacements are unaffordable — costs an estimated $500–$600 per cow in lost daily yield.

Forward signal: if APHIS holds the 200-mile containment line and the Agua Prieta–Douglas phased reopening proceeds without setbacks, the discount risk on day-old calves compresses and you can scale beef back up.

Path 2 — Stay at 40%+ beef but treat it like the high-leverage bet it is

When it makes sense: your milk-only margin is genuinely solid without the calf check, and your buyer relationships are deep enough to ride out a 30-day soft patch.

What it requires: actual hedging — DRP and forward calf contracts where available — plus a written biosecurity SOP for navel and wound management on every calf, aligned with APHIS’s farm-level surveillance guidance.

Where it fails: the U.S. has no fully approved NWS treatment regime for cattle outside emergency-use channels. Confirm current FDA CVM and APHIS status with your vet before any treatment decision.

Path 3 — Realign your sire stack to your actual processor

When it makes sense: you’ve signed or are about to sign a contract with one of the new cheese or whey plants — Leprino Lubbock, Agropur Lake Norden’s whey-protein expansion, fairlife’s $650 million Coopersville buildout — and your current sire portfolio was picked for a different pay pattern.

What it requires: written product-mix confirmation from your plant or co-op, a sire portfolio audit with your genetics rep, and patience. CDCB benchmarks plus genomic sorting now make this a measurable shift, not a guess.

Where the wheels come off: misalign the index and you spend two years selecting for traits the plant doesn’t pay for.

Path 4 — Renegotiate the contract before the next disruption does it for you

When it makes sense: your basis has narrowed to within a typical regional benchmark while your component-adjusted margin over feed stays above breakeven. That’s leverage.

What it requires: the contract on the table, willingness to walk if the answer is “we’ll let you know,” and a clear ask on component premiums, basis on volume disruptions, and how the plant treats your loads if exports stall 30–60 days. Mexico is 27% of U.S. cheese exports and the July 2026 USMCA Joint Review under USTR Jamieson Greer is the next hard deadline. Your contract should anticipate it.

Where it backfires: wait until after a disruption and the plant writes its own basis terms.

Key Takeaways — Decisions, Not Restatements

- If your milk-only margin sits at or below breakeven once you strip the calf check and apply the $0.85–$0.93/cwt FMMO make-allowance drag, the calf check is no longer diversification. It’s load-bearing — and it should be hedged or capped.

- If a 30-day, 35% disruption forces you to cut repro, hoof care, or replacement flow, your current beef penetration isn’t defensible. Recalibrate the cap before the next map dot, not after.

- If your co-op can’t tell you the export-exposure percentage of your pooled milk — and what its plan looks like if Mexico’s $2.58 billion of U.S. dairy demand stalls 30–60 days — that’s a board-level conversation. Not a maybe-next-quarter conversation.

- If your sire stack is selecting on a different solids mix than your plant pays for, you have 2–5 years of component drift baked in already. Audit it this quarter.

- 30-day action: pull last year’s beef-on-dairy income line by line, pull your last three milk checks, and calculate milk-only margin over feed per cwt with beef and cull income stripped out and the FMMO drag applied. 90 minutes at the kitchen table. Run it monthly, not annually.

So pull the contract. Pull the milk checks. Run the numbers with the calf cheque stripped out. What does your processor agreement actually say about basis when volumes fall? And how does your real margin over feed per cwt this month compare to 90 days ago, with the calf check pulled out of the equation?

Then pull last month’s beef-on-dairy line and ask three operators on your bulk-tank route what theirs looks like. The number that surprises you is the one to act on.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $3,000 Heifer Hangover: How Beef‑on‑Dairy Emptied Your Pipeline and Left the U.S. 800,000 Head Short — Breaks down the severe financial toll of buying replacement heifers during an 800,000-head pipeline deficit, mapping out a 30-day strategy to protect your margin-over-feed ledger from skyrocketing youngstock replacement costs.

- Protein Will Drive Your 2026 Milk Check: Are Your Components Still Built for the Butterfat Era?— Exposes why cheese plants are pushing back on fat-heavy milk, delivering the precise dietary adjustments and regional component targets required to align your bulk tank with export-driven processing demands.

- TPI 2026 Part 2: The $300/Cow Pounds‑vs‑Percent Trap Plants Actually Care About — Dismantles the structural flaws of selection indexes that reward pure milk volume over true casein density, arming component-heavy herds with the exact genomic benchmarks needed to maximize cheese-grid milk checks.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.