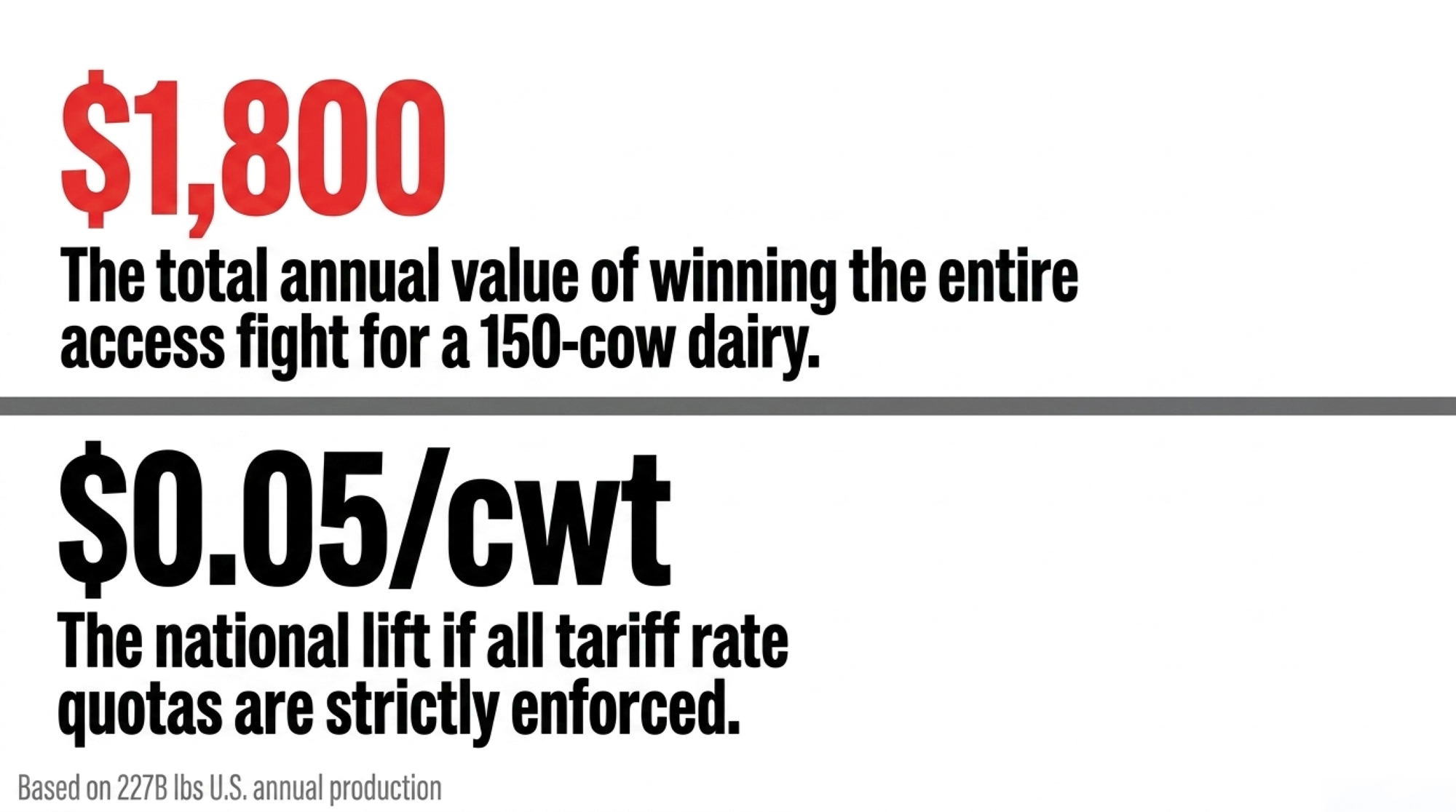

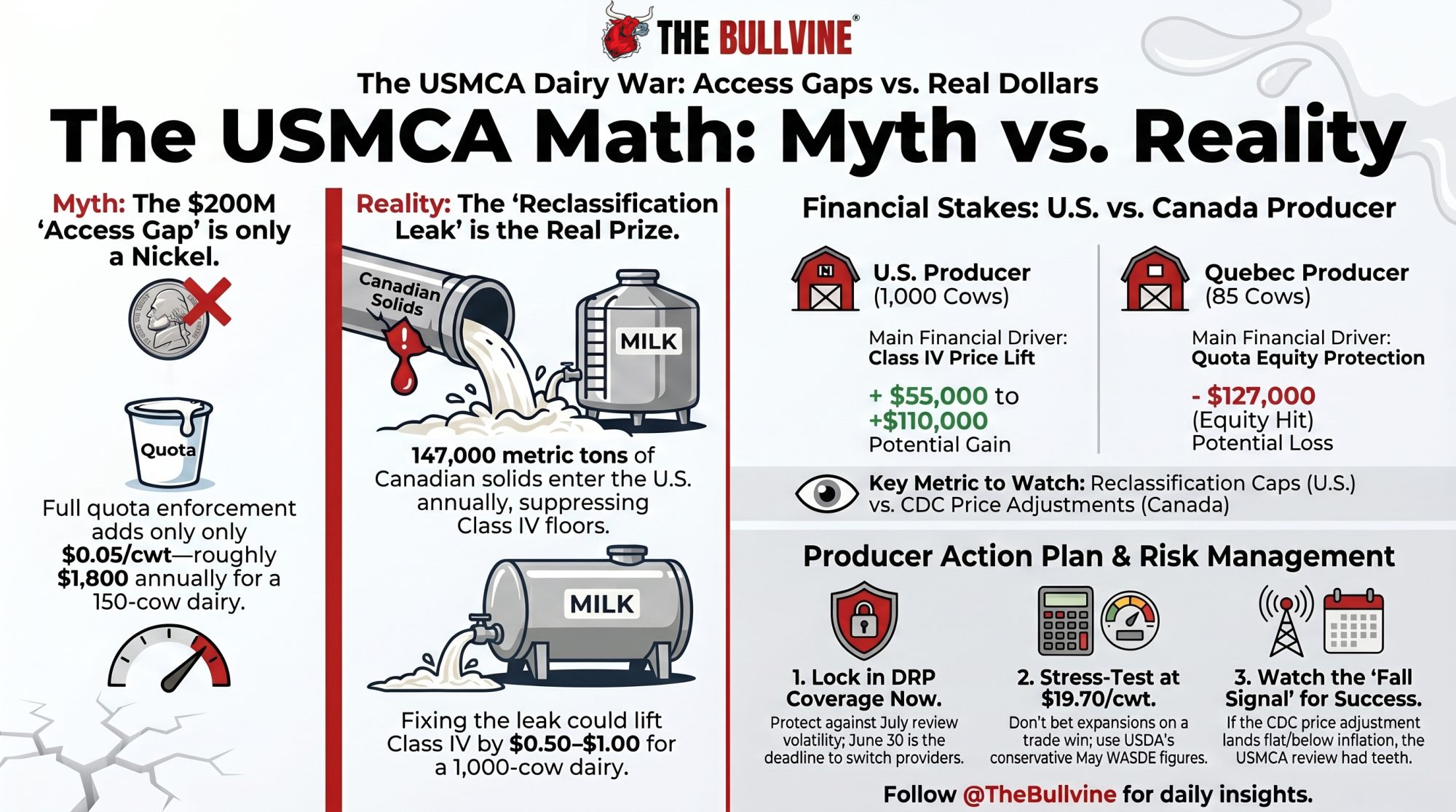

Spread that $200M across 227 billion pounds of U.S. milk and full TRQ enforcement pencils to about a nickel a cwt — $1,800 on a 150-cow dairy. The real Class IV hit is hiding elsewhere.

Executive Summary: When NMPF and USDEC walk into the July 1 USMCA review demanding Canada honor that $200 million in promised dairy access, here’s what they won’t put on the slide: spread across 227 billion pounds of U.S. milk, full TRQ enforcement is worth about a nickel a hundredweight — roughly $1,800 a year on a 150-cow dairy. The money that actually moves your Class IV check is the reclassification leak: 147,000 metric tons of Canadian milk solids landed in the U.S. in 2024 under HTS codes that sit outside USMCA, and the USITC confirmed May 27 they’re priced to suppress your floor. Reverse even half of that and a 1,000-cow Wisconsin dairy picks up $55,000; a full dollar of Class IV lift puts it at $110,000. Flip the border and the same reform threatens C$127,000 in quota equity on an 85-cow Quebec herd — which is why DFC’s Daniel Gobeil is fighting to keep supply management off the table behind Bill C-202. With USDA’s May WASDE pegging 2026 all-milk at $19.70, two moves matter before July: price your DRP coverage now, and stress-test any 2027 expansion below $20 instead of betting it on a Canadian win. Then watch one number — if this fall’s CDC price adjustment lands flat instead of another 2.33% bump, the review had teeth.

When Ted Vander Schaaf testified before the Senate Finance Committee on February 12, 2026, his message was one that most U.S. dairy producers have felt in their milk checks for years: Canada isn’t delivering the dairy market access it agreed to under the USMCA. Vander Schaaf farms in Idaho and owns his share of Northwest Dairy Association, the co-op behind Darigold. He was testifying for the U.S. Dairy Export Council and the National Milk Producers Federation, the two groups leading the charge into the July 1, 2026, USMCA review.

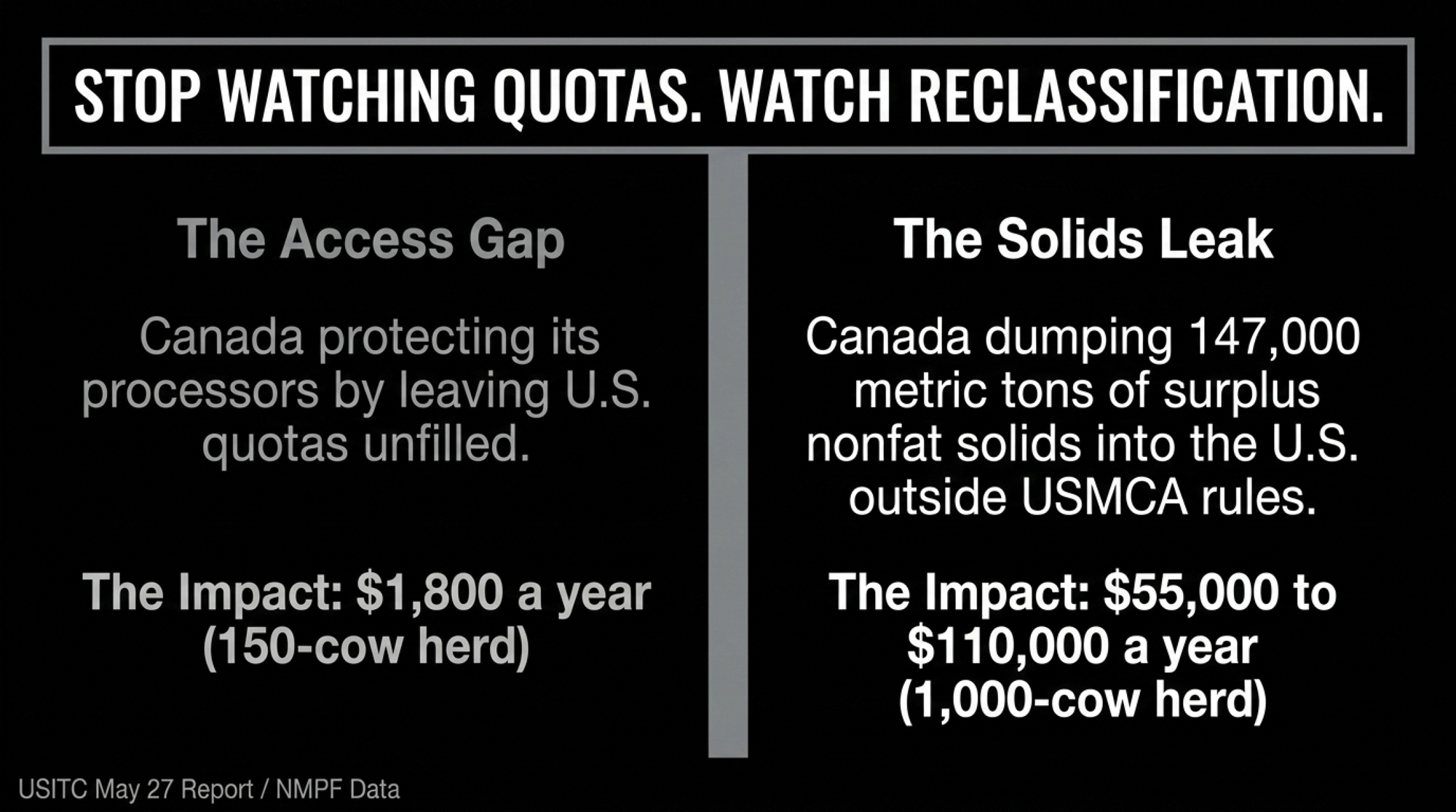

His testimony focused on the access gap — the roughly $200 million a year in Canadian market access that the USMCA promised and that Canada has largely walled off. That’s a real problem. But it’s not the one doing the most damage to your Class IV price. The bigger suppressor has been running quietly since 2020; it doesn’t violate a single quota commitment, and the USITC just put it on the record this week. If you ship Class IV or powder, this is the mechanism worth understanding before July — because the review will either address it or it won’t, and you’ll want to know which one happened.

What’s Actually Changing Heading Into July

USMCA gave U.S. dairy 14 separate tariff rate quota categories into Canada when it took effect in July 2020. Everything within quota enters duty-free. Everything over quota hits a tariff wall — 201% on skim milk powder, 298.5% on butter. Those over-quota rates are prohibitive by design. So the whole game comes down to one question: are the quotas actually getting filled?

Mostly, no. Across the deal’s life to date, the average fill rate across all 14 categories has been around 42%, and 9 of the 14 sit below 50%.

Cheese moves reasonably well at 83% fill. Butter at 81%. But skim milk powder is stuck at 57%, cream at 51%, and yogurt at a dismal 12%.

The quotas exist on paper. Commercial access mostly doesn’t — because Canada hands the bulk of those quotas to its own processors, who have zero reason to import competing U.S. product.

That’s the access fight, and it’s worth having. NMPF and USDEC have pushed it hard, including a formal complaint that led to a 2022 dispute panel decision before Canada rewrote the rules and won the second round in 2023. But here’s the part that hits your milk check more directly than any empty quota: what Canada ships into the U.S. market, not what it refuses to let in.

Don’t Confuse the Access Gap With the Price Hit

Before going further, one honest correction — because the $200 million number gets thrown around in ways that oversell it. Spread that unused access across the roughly 227 billion pounds the U.S. produces a year, and full TRQ enforcement is worth about $0.05/cwt nationally — a back-of-envelope figure, since not every dollar of access converts cleanly to your farm-gate price. Call it a nickel. On a 150-cow Wisconsin dairy producing 24,000 lbs per cow — about 36,000 cwt a year — winning the entire access fight pencils to roughly $1,800 a year. Real money, but not the kind that changes how you run the place.

So if the access gap is a nickel, why does any of this matter to your bottom line? Because the access fight isn’t where the money is. The money is in what Canada ships south, at suppressed prices, under codes nobody’s enforcing. That’s a different mechanism, and it’s bigger.

How This Plays Out on Real Farms

Canada’s supply management system is built around butterfat. Set the price high, control the supply to match what Canadians actually eat in butter and cream. The catch is that every kilogram of butterfat comes bundled with proteins and lactose — the nonfat solids — that the domestic market doesn’t soak up at that managed price. Canada has to move the surplus somewhere.

Before the USMCA, it went through regulated export channels with disciplines attached. After USMCA, a quieter door opened: the surplus moves into tariff codes that sit outside the agreement’s rules. Dairy skim blends and fat-filled milk powder — that’s HTS code 1901.90, for anyone checking — jumped from 77,000 metric tons before USMCA to 166,000 metric tons by 2024. Of that, 147,000 metric tons landed in the United States. A separate protein code went from roughly 76 metric tons a year to 32,000. The product changed classification. The milk solids didn’t.

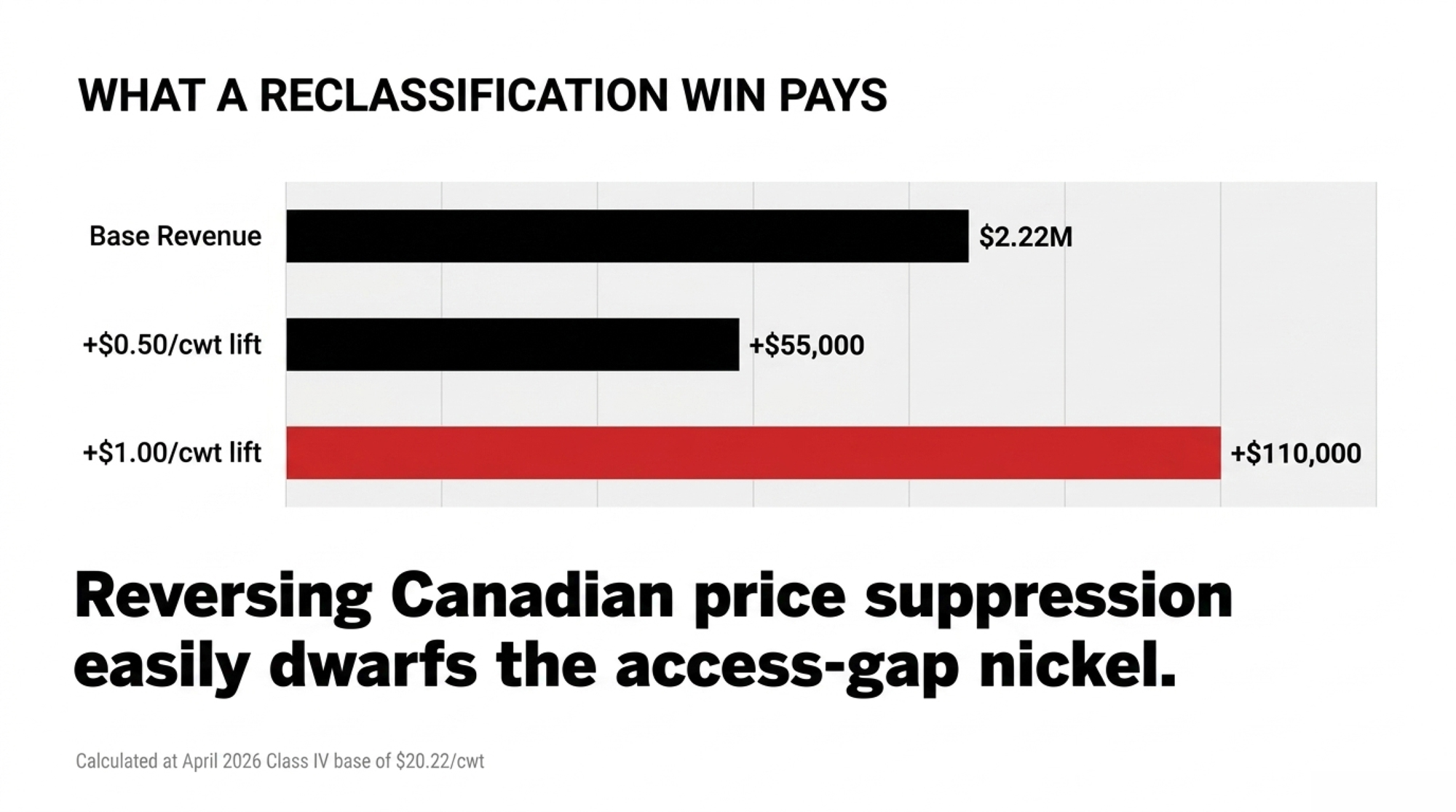

That volume competes head-to-head with U.S.-produced nonfat dry milk and skim powder. It pushes down the clearing price. And that clearing price is what sets your Class IV floor. Run the math on it. Take a 1,000-cow Wisconsin dairy and put a conservative 110 cwt of Class IV-bound milk per cow on the books — not total production, just the share headed to Class IV — that’s about 110,000 cwt a year. At April 2026’s Class IV price of $20.22/cwt, that’s roughly $2.22 million in Class IV revenue. If reversing that suppression lifts Class IV by even $0.50/cwt, you’re looking at $55,000 more on the year. A full dollar puts it at $110,000. That dwarfs the $1,800 access-gap nickel, which is exactly why NMPF’s third ask is the one that matters.

➡️ Go deeper: Why only 42% of U.S. dairy access to Canada gets used — the fill-rate story behind the headline.

What a Wisconsin Cheesemaker Is Actually Watching

This isn’t abstract in Green Bay. BelGioioso Cheese — the Wisconsin specialty maker that ships product both north and south of the border — hosted the Farmers for Free Trade USMCA roundtable on May 7, 2026, putting processors, producers, and Rep. Tony Wied in the same room ahead of the review. BelGioioso President Gaetano Auricchio and VP of Foodservice & Export Frank Alfaro sat on that panel alongside Amber Horn Leiterman, a dairy farmer and Land O’Lakes member-owner of Hornstead Dairy. The panel pointed squarely at Canada’s tariff rate quota system and what they called the offloading of artificially low-priced milk solids as the enforcement gaps the July review has to fix.

Here’s why a cheesemaker cares about a skim-powder problem. Cheese is the one category actually working at 83% fill, so the access side is largely fine for them. But every Wisconsin processor competing for milk is bidding against a Class IV price that imported Canadian solids help hold down — the USITC found the surplus moves at suppressed prices, even if the exact drag in any single month is hard to isolate. Fix the reclassification leak, and the whole nonfat-solids complex firms up. That’s the rising tide a cheese plant feels even when its own TRQ category is full.

The Mechanics Behind the Numbers

Canada’s farmgate price doesn’t float on the market. The Canadian Dairy Commission (CDC) sets it using a formula that’s half cost of production, half consumer price index, adjusted once a year.

The U.S. vs. Canadian Price Disconnect (Spring 2026)

| Metric | U.S. (Wisconsin, 1,000-cow) | Canada (Quebec, 85-cow) |

|---|---|---|

| Farmgate Price | $20.22/cwt (Class IV, Apr 2026) | ~$29/cwt equivalent (C$90.72/hL) |

| Price-Setting Mechanism | Market-determined via USDA class pricing | CDC formula (50% CoP + 50% CPI) |

| Structural Price Gap | — | ~$8–9/cwt structural premium over U.S. |

| Quota Asset Value | None — no quota system | C$2.55M balance sheet (106 kg daily quota × C$24,000/kg) |

| 5% Quota Value Hit | N/A | ~C$127,000 in equity erased |

| Class IV Revenue (est.) | ~$2.22M/yr (110 cwt/cow × 1,000 cows) | N/A — supply-managed pool |

| $1.00/cwt Class IV Lift | +$110,000/yr | Creates pressure on quota confidence |

| Key Risk | Reclassified Canadian solids suppressing Class IV floor | NMPF export cap wobbles C$24,000/kg quota cap |

| July Review Stance | Push for reclassification cap + quota reform | Bill C-202 blocks further supply management concessions |

A hectolitre runs about 2.2 cwt of milk, so the per-cwt conversion bridges the two systems directly.

That gap is the whole point of supply management, and Canada makes no apology for it.

“The U.S. has already secured substantial tariff-free access under the deal.” — David Wiens, President, Dairy Farmers of Canada (March 8, 2025)

The trouble for U.S. producers is that this system inherently generates more nonfat solids than Canada can use at that high price, and the surplus moves south at suppressed values under codes that sit outside USMCA. NMPF pegs the value of Canadian dairy protein exports benefiting from this pricing structure at over $740 million a year.

The USITC report released May 27 added the piece that matters most for July. It confirmed what NMPF and USDEC have long argued: Canada’s milk production quotas, designed to match domestic supply and demand, generate surplus nonfat solids that move into export markets at suppressed prices. U.S. dairy groups have specifically pointed to ventures like the Vitalus Nutrition–Gay Lea Foods partnership in Manitoba, built to process dairy ingredients including milk protein, as the kind of capacity that turns that surplus into export product. USTR Jamieson Greer has the report in hand walking into the review.

What’s at Stake for a Quebec Barn?

Flip the border, and the math runs the other way. Quebec milks roughly 40% of Canada’s cows, and a typical supply-managed dairy there runs around 85 milking cows — well under the 105-cow national average, and a long way from the 1,000-cow Wisconsin operation up top.

That farm’s whole financial model rests on two things:

- A farmgate price near C$90/hectolitre.

- The quota itself — the legal right to ship that milk, which trades at a capped C$24,000 per kilogram of daily butterfat across the P5 pool.

Both are products of the system U.S. negotiators want to crack open. Now run that quota number as an asset.

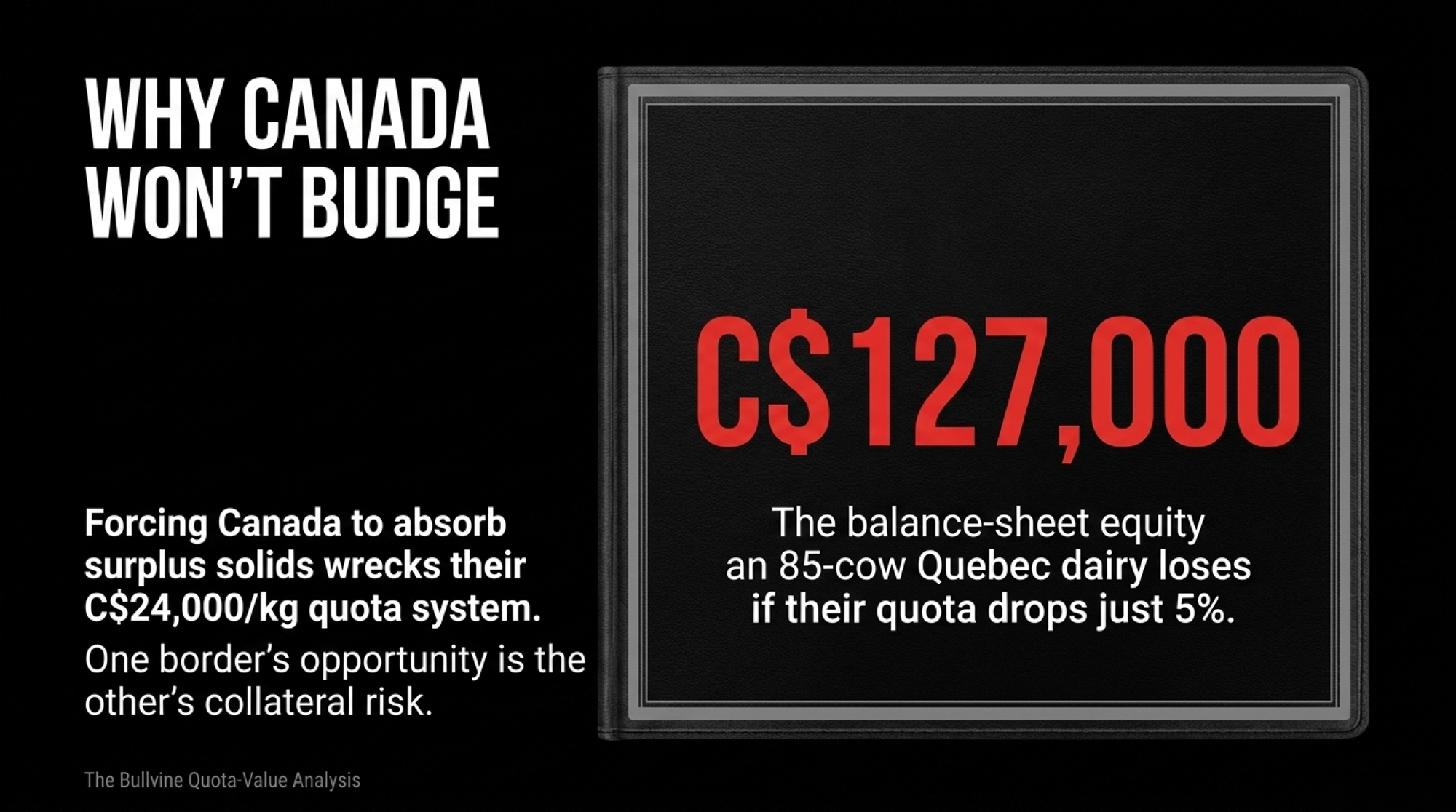

Quebec Quota Value Breakdown (85-Cow Herd Example) 85 cows × 1.25 kg butterfat/day = 106 kg daily quota* 106 kg × C$24,000 cap = C$2.55 million in balance-sheet equity

*Per-cow daily butterfat and the C$24,000/kg P5 cap drawn from The Bullvine’s quota-value analysis.

That’s not milking equipment or land. That’s the single largest line item, and its value rests entirely on confidence that the managed price holds.

Here’s the squeeze a Quebec producer actually fears: it isn’t the farmgate price drifting down a few percent — it’s what an NMPF-style export cap does to that C$2.55 million quota line. Force Canada to absorb surplus solids domestically rather than export them, and the economics that justify a C$24,000/kg cap start to wobble. Ontario quota already shows the strain: in March 2026, 1,908 producers bid and only 190.6 kg traded, with every financed kilogram at 6% bleeding C$586 a year. Shave even 5% off a C$2.55 million quota base, and that’s roughly C$127,000 in balance-sheet equitygone — dwarfing any single-year farmgate dip. That’s the number Quebec lenders watch. And it explains why DFC Vice-President Daniel Gobeil has fiercely pushed Ottawa to keep supply management off the table — backed by Bill C-202, the law Canada’s Parliament passed barring negotiators from trading away more dairy access. One border’s opportunity is the other’s collateral risk. Same milk molecule, opposite ledgers.

What Does the July Review Actually Decide for You?

The USMCA joint review isn’t a renegotiation by itself. Article 34.7 establishes a structured review in which any of the three countries can put recommendations on the table. NMPF and USDEC filed their asks back in October 2025, and they boil down to three things: open the quota allocation to retailers and food service instead of just Canadian processors, add use-it-or-lose-it penalties for processors who sit on quota, and cap the total nonfat solids Canada can export so the reclassification end-run stops working.

The first two are tune-ups to an existing system. The third is the structural one, and it’s the heavy lift — because Canada argues those reclassified products fall outside USMCA entirely, and it’s leaning on a panel ruling it already won. Canadian trade experts mostly expect the same outcome: more access and tweaked tariff administration, but no dismantling of supply management. Neither side walks in with a clean hand. What you’ll most likely get out of July is a set of commitments whose real value won’t show up until the first full dairy year of implementation, which runs from August 2026 through July 2027. So how do you read whether it actually worked?

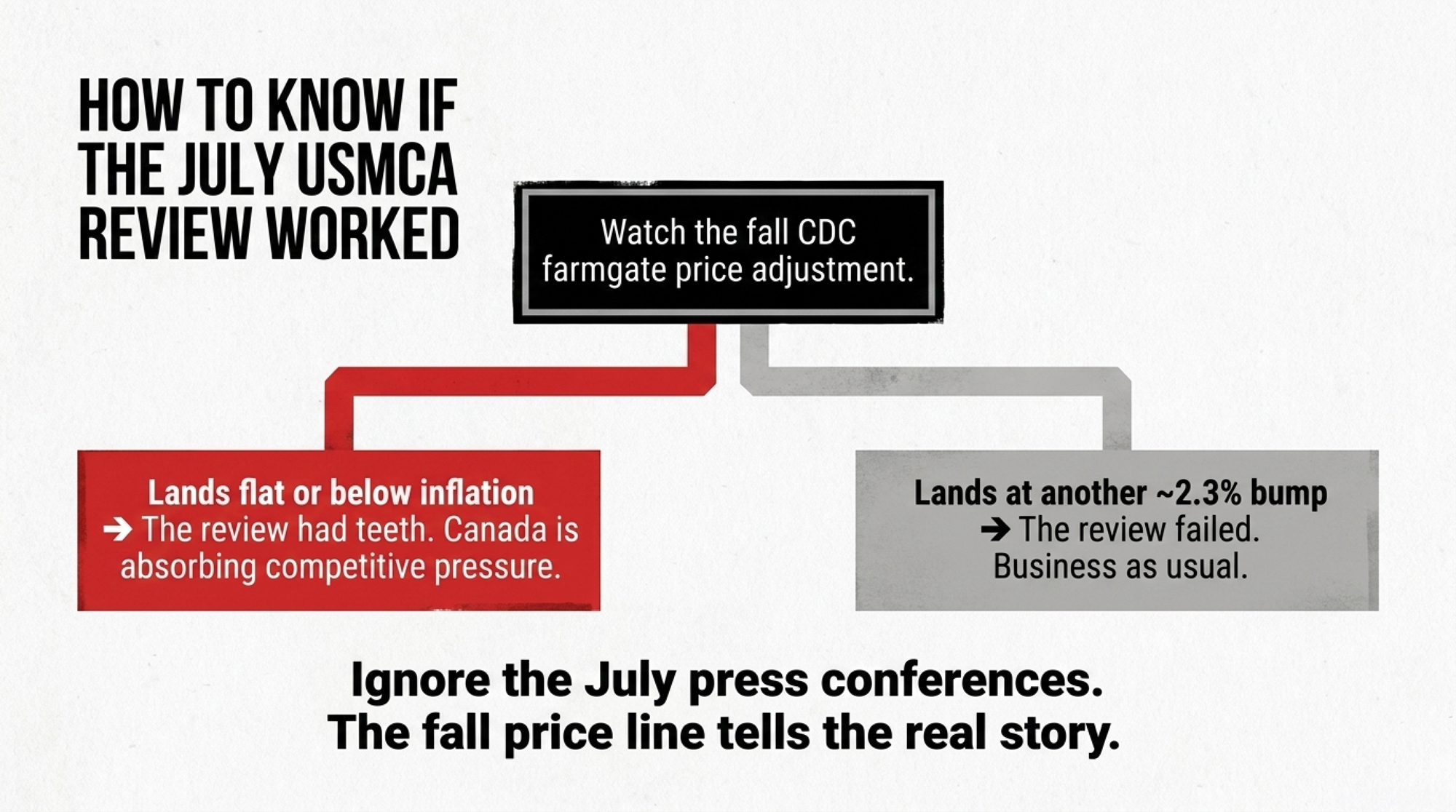

How Do You Know If July Delivered Anything Real?

Watch one number, not the whole circus. The Canadian Dairy Commission announces its annual farmgate price adjustment each fall — and the last one, effective February 1, 2026, was a 2.33% increase. For years, it’s tracked inflation, a steady climb. If this fall’s announcement lands flat or below inflation, it means Canada’s pricing system is starting to absorb real competitive pressure. That’s your first hard evidence the review had teeth.

If the CDC posts another comfortable inflation-linked bump, you’ve got your answer too: the fight produced process language and a working group, not market access. The press conferences in July will tell you almost nothing. The fall price line will tell you most of what you need to know.

| Signal | What It Means If True | Farm Action |

|---|---|---|

| CDC Fall Price Announcement: Flat or below inflation | ✅ Review had real teeth — Canada’s pricing system absorbing competitive pressure | Monitor Class IV — structural improvement may follow; revisit 2027 expansion math upward |

| CDC Fall Price: Another ~2.33% CPI-linked bump | ❌ Process language only — no market access change | Keep DRP coverage in place; stress-test 2027 plans at $19.70/cwt; don’t build on a Canadian win |

| First 2026–27 TRQ fill data (Aug–Oct 2026): Fill rates rise meaningfully | ✅ Quota reform commitments have teeth | Expect modest uplift in skim powder and yogurt categories; revisit co-op mix exposure |

| TRQ fills stay near 42% average | ❌ Structural quota allocation unchanged | Access fight gains are cosmetic; reclassification cap is only reform that matters for Class IV |

| Reclassification cap announced with enforcement mechanism | ✅ The big one — Class IV suppression mechanism addressed | Price upside of $0.50–$1.00/cwt potentially real; revisit DRP coverage level upward |

| No reclassification language in outcome statement | ❌ USMCA 2.0 on dairy = USMCA 1.0 | Hold existing coverage; assume $20/cwt baseline through 2027 |

Options and Trade-Offs for Producers

Lock in DRP coverage before July — this is your near-term move. Dairy Revenue Protection exists for exactly this kind of known-event risk, and coverage is available daily for quarters running out through the first quarter of 2027. July 1 is a fixed date with an uncertain outcome; Greer has openly said exit, revision, and renegotiation are all live options. You can’t control the outcome, but you can put a floor under your Class IV exposure at today’s futures before the announcement moves anything. One scheduling note worth knowing: if you’re thinking about switching DRP providers, that’s a once-a-year move with a June 30, 2026, deadline. The trade-off on coverage itself: premium cost against a price that may not move much either way.

Ask your co-op what share of its volume moves through under-filled TRQ categories. A co-op heavy in cheese is sitting in the one category that’s actually working at 83% fill. One leaning on skim powder or yogurt is exposed to the categories where reform matters most. This costs you nothing but a phone call, and the answer tells you how much your milk check is actually riding on the July outcome. If they can’t answer it, that’s worth knowing too.

Don’t build your 2027 expansion on a Canadian win. A $0.50-to-$1.00/cwt Class IV lift is plausible if July produces commercial-grade language — but it’s been “almost there” before, and the 2023 panel went Canada’s way. Stress-test any expansion at $19.70/cwt, the figure USDA’s May WASDE landed on after a 75-cent upward revision off February’s $18.95 — still down from the revised 2025 average of $21.17. If the numbers don’t hold there, have the lender conversation before July, not after a disappointment. The trade-off is real: wait too long for clarity, and you miss a window to act; move on a hoped-for recovery, and you’ve bet the operation on a negotiation.

Key Takeaways

- When someone sells you the $200 million access gap as a milk-check game-changer, run the nickel. Full TRQ enforcement is about $0.05/cwt nationally — roughly $1,800 on a 150-cow dairy. The reclassification fight is where the real Class IV money sits.

- Class IV feeling structurally low, even when butter and powder demand look fine? It might be. Roughly 147,000 metric tons of reclassified Canadian protein hit the U.S. market in 2024, and the USITC says that surplus moves at suppressed prices.

- Not covered on Class IV through Q3 2026? Price the DRP decision now — coverage is available daily, and a provider switch carries a June 30 deadline.

- Got a co-op leaning on skim powder or yogurt? Your milk check has more riding on July than a cheese plant’s does. Call them and ask.

- A 2027 plan that only pencils above $21/cwt is a plan on thin ice. Run it again at $19.70 — USDA’s May WASDE 2026 all-milk figure — and decide before July whether the math survives without a USMCA bump.

- Farming under quota in Quebec or Ontario? The line to watch isn’t the farmgate price — it’s whether an export cap shakes confidence in the value of the quota. On an 85-cow herd, a 5% hit to a C$2.55 million quota base is roughly C$127,000 in equity.

- Want one signal instead of fifty headlines? Watch this fall’s CDC price announcement. Flat or below inflation means the review bit. Another raise on the order of the 2.33% bump in February 2026 means it didn’t.

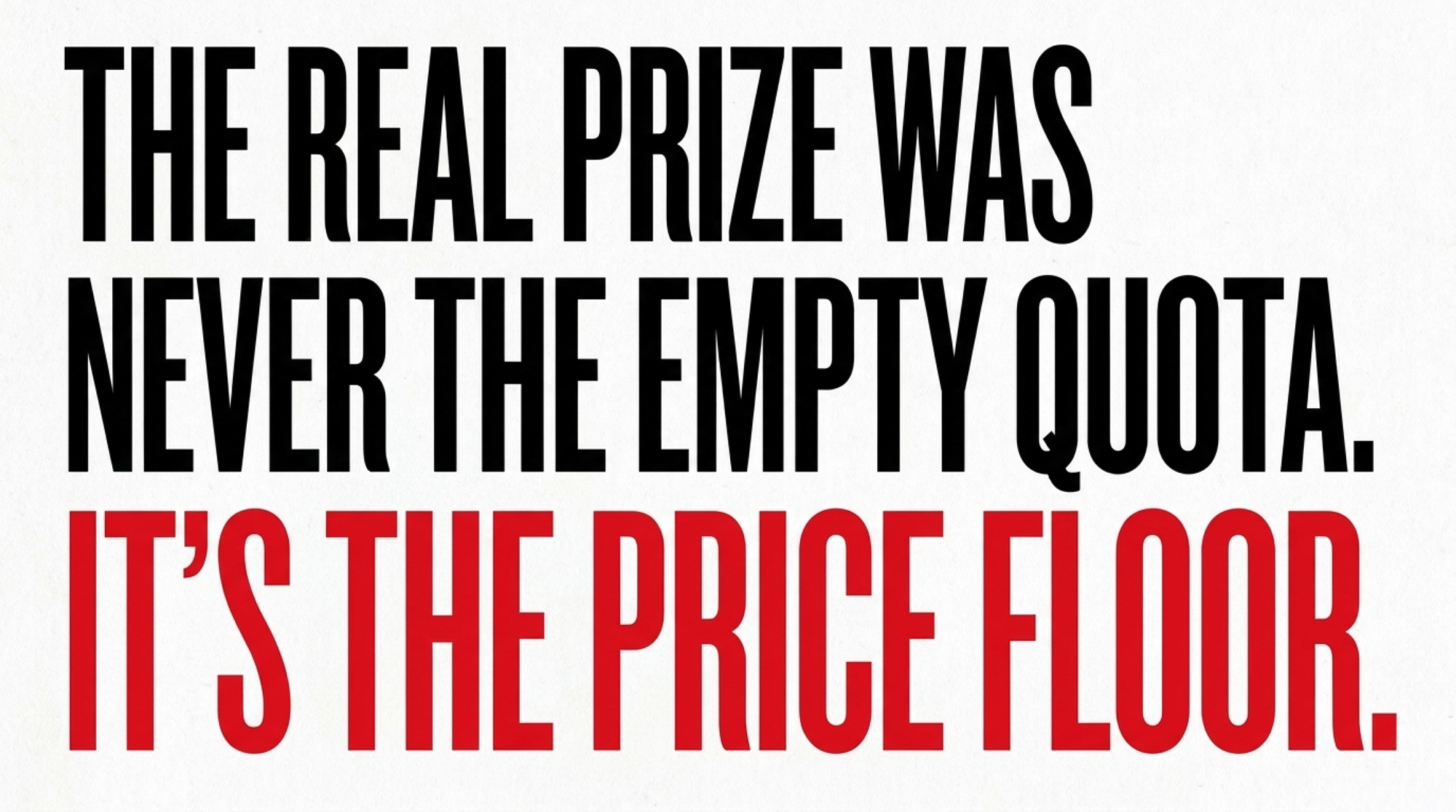

Vander Schaaf went to Washington to make the case that Canada owes U.S. dairy more than it’s delivering. He’s right that the access is short, but the nickel-per-hundredweight access math tells you the real prize was never the empty quota. It’s the price floor. And Gobeil, a province away, is just as right that the same reform that firms up your Class IV price puts real equity at risk on a Quebec balance sheet. The producer reading this before morning milking doesn’t get to vote on the July outcome. You only get to decide how exposed your operation is when it lands. So where does your breakeven actually sit right now, and how much of your 2027 milk check are you quietly counting on a trade win to deliver?

Run Your Numbers

Dairy Profit Projector — Before you bank on a USMCA bump, drop in your herd size and milk price to see where your breakeven and margin per cwt actually land. Stress-test 2027 at $19.70 instead of $21, and find out if your plan survives without a Canadian win.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The DRP Window Sitting Open on Most Mid-Size Dairies — Arms you with immediate risk-management tactics before the USMCA review, exposing how newly modified, weekend-friendly DRP rules allow mid-size herds to efficiently lock in revenue floors and protect multi-quarter milk-check exposure.

- The $900/Cow Hit You Can’t Outbreed by April: Western Canada’s 70/25/5 Reckoning — Delivers the critical operational strategy needed to survive the cross-border protein shift, breaking down exactly how a new payment ratio penalizes high-fat, lower-protein herds by up to $100,000 annually.

- The $586‑Per‑Kilo Dairy Quota Trap: Why New Ontario Quota at 6% Bleeds Cash Every Year — Exposes the brutal balance-sheet reality facing supply-managed producers, dismantling the illusion of quota security by proving how current financing rates and hard caps drain thousands in cash flow from expanding operations.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.