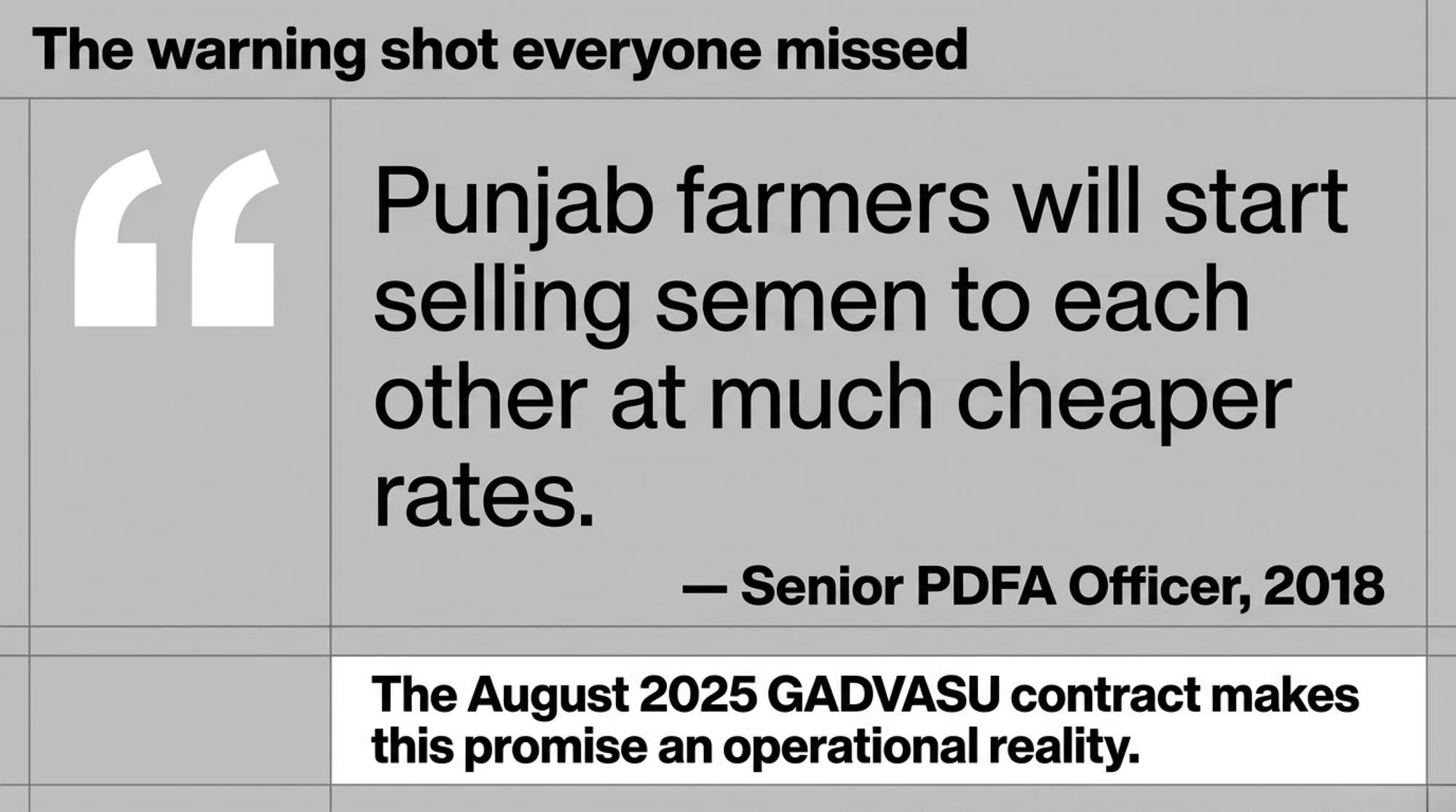

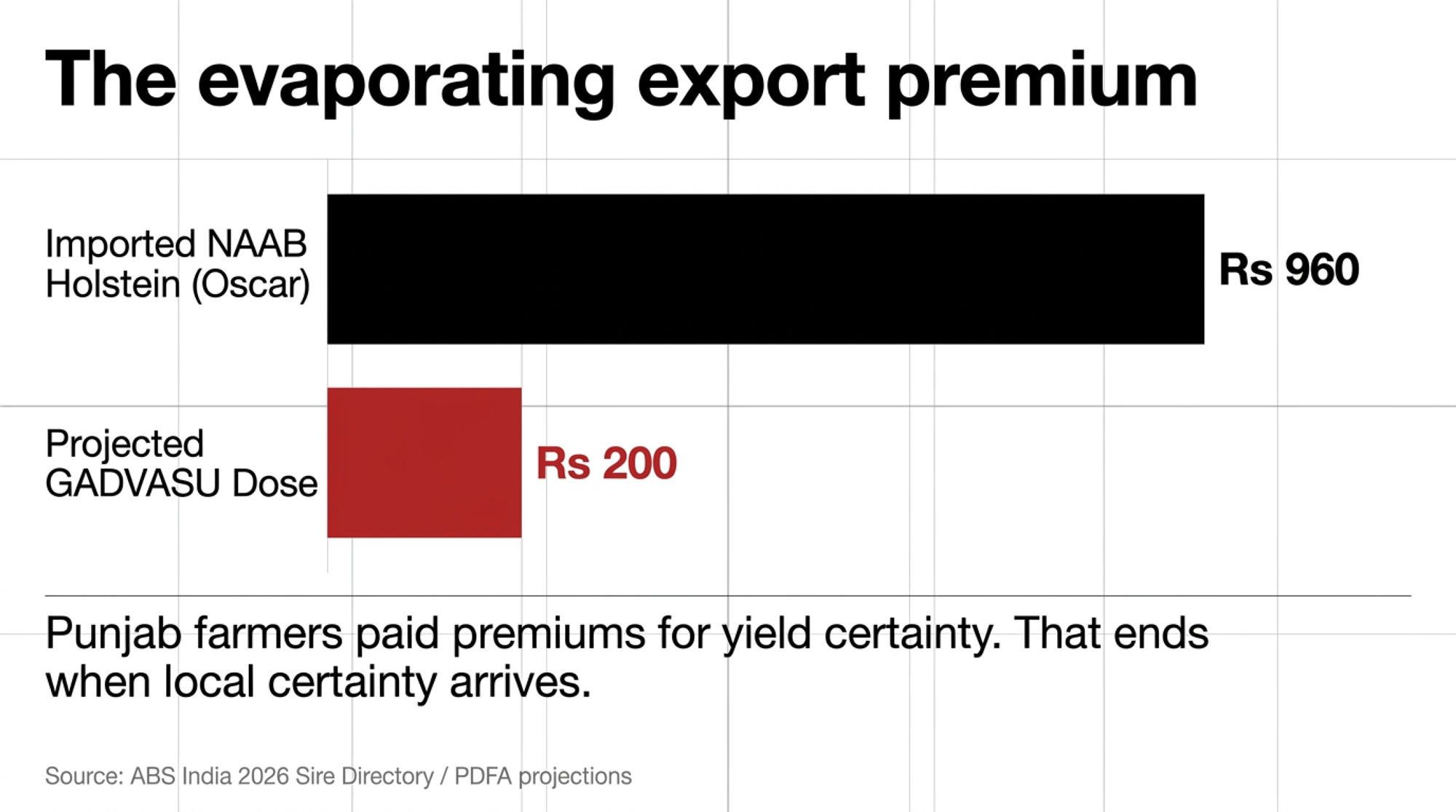

A senior PDFA officer called it in 2018. GADVASU signed the MOU in August 2025. By 2029, Rs 960 imported Holstein straws face Rs 200 locally proven bulls. Who modeled that?

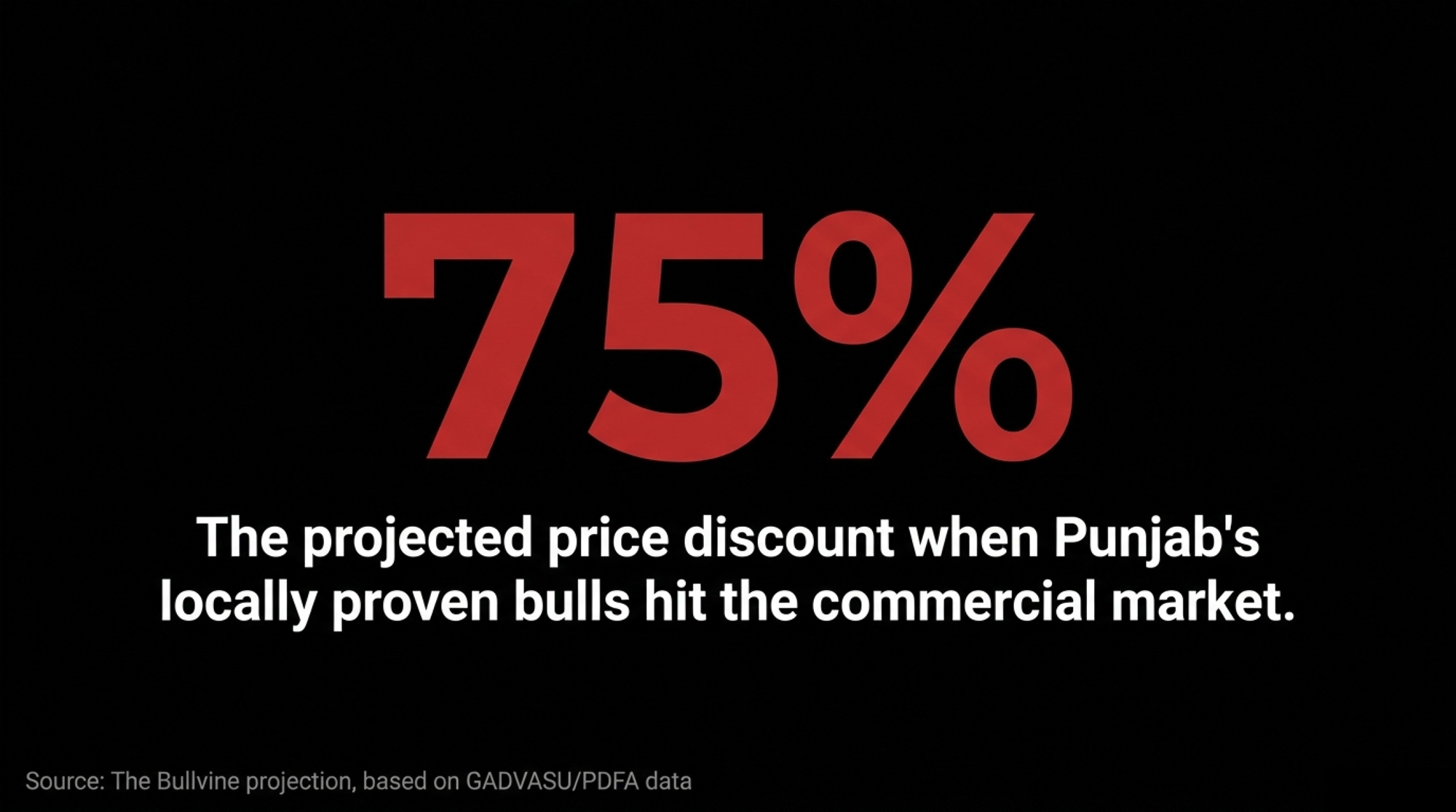

Every North American AI company still counting India as a growth market has a 2029 math problem it hasn’t solved publicly. It’s the moment local reliability meets a roughly 75% price discount. Rs 960 imported conventional semen on one side. A projected Rs 150–250 locally proven GADVASU dose on the other — The Bullvine’s projection, extrapolated from government-subsidized semen pricing and the Progressive Dairy Farmers Association of Punjab’s own 2018 “much cheaper” aspiration. GADVASU hasn’t published commercial pricing. It doesn’t need to yet.

That moment has a source document. In August 2025, PDFA signed a formal MOU with Guru Angad Dev Veterinary and Animal Sciences University — GADVASU, the Ludhiana-based agricultural university that’s been producing HF crossbred semen for years but never at commercial scale. GADVASU Vice-Chancellor JPS Gill described the objective in the language of an import substitution program, noting that high cost and irregular supply of imported semen are hindering genetic improvement at the farm level. The partnership is designed to fix that.

The Warning Shot Everyone Missed in 2018

A senior PDFA officer told ArthaImpact in 2018 exactly what would happen once the pedigree data existed. Punjab farmers, the officer said, would start selling semen to each other at much cheaper rates than the Rs 200–600 they’d been paying for imported straws since the mid-1990s. Almost nobody outside the association heard it properly.

Seven years later, that sentence reads less like an ambition and more like a timeline. The August 2025 MOU is the operational expression of the 2018 promise — elite male calves from PDFA member cows, produced into semen through GADVASU infrastructure, daughter-tested inside the same herds already winning the Jagraon Holstein show. Every structural piece the 1960s-era state programs couldn’t assemble is now in one contract.

The Death of the Export Premium

Punjab isn’t a typical Indian dairy region, and its graduation from genetics buyer to genetics seller isn’t a typical emerging market story. Milk output in the state has grown approximately 172% since 1990. Cattle population over the same period shrank 31%, per eDairy News reporting in August 2025. That arithmetic is the product of 25 years of commercial HF crossbreeding, built on imported North American semen and distributed through a private association infrastructure that operates alongside — but largely independent of — the state government AI system. Bullvine readers tracking India’s 80 million smallholder dairy base will recognize why this commercial elite lane matters so much inside a country still dominated by two-cow households.

PDFA imported its first frozen semen doses from the USA before 2010. World Wide Sires opened direct Punjab operations that year, having already moved 88,000 doses through local distributors, per Business Standard reporting in September 2010. By February 2026, ABS India and Maharashtra’s Chitale Dairy imported live Holstein bulls with TPI values exceeding 3,000 — among the highest-TPI Holstein bulls imported commercially into India on public record. ABS India currently lists bull Oscar (NAAB 29HO22333, TPI 3261, NM$ 844 per the most recent CDCB evaluation published in ABS India’s 2026 Sire Directory**)** at Rs 960 conventional and Rs 2,700 sexed. Those prices sit an order of magnitude or more above what a farmer pays for government-subsidized domestic semen — roughly 48 times for Oscar’s conventional straws and over 130 times for the sexed product versus typical Rs 20 subsidized semen.

Punjab’s commercial dairy farmers have been paying that premium willingly for a generation because the yield math worked. Until now.

How Much Does Imported Holstein Semen Actually Cost a 50-Cow Punjab Dairy?

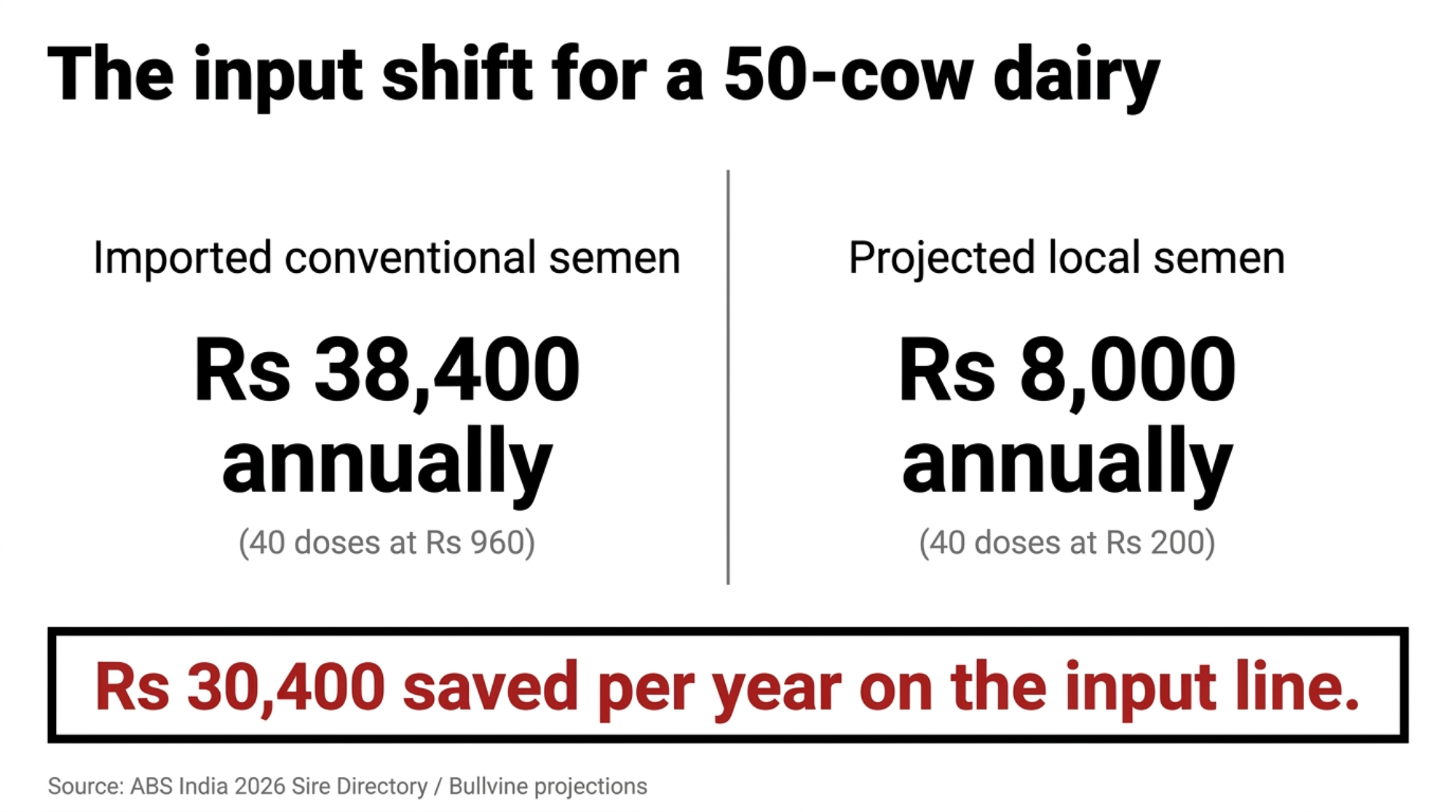

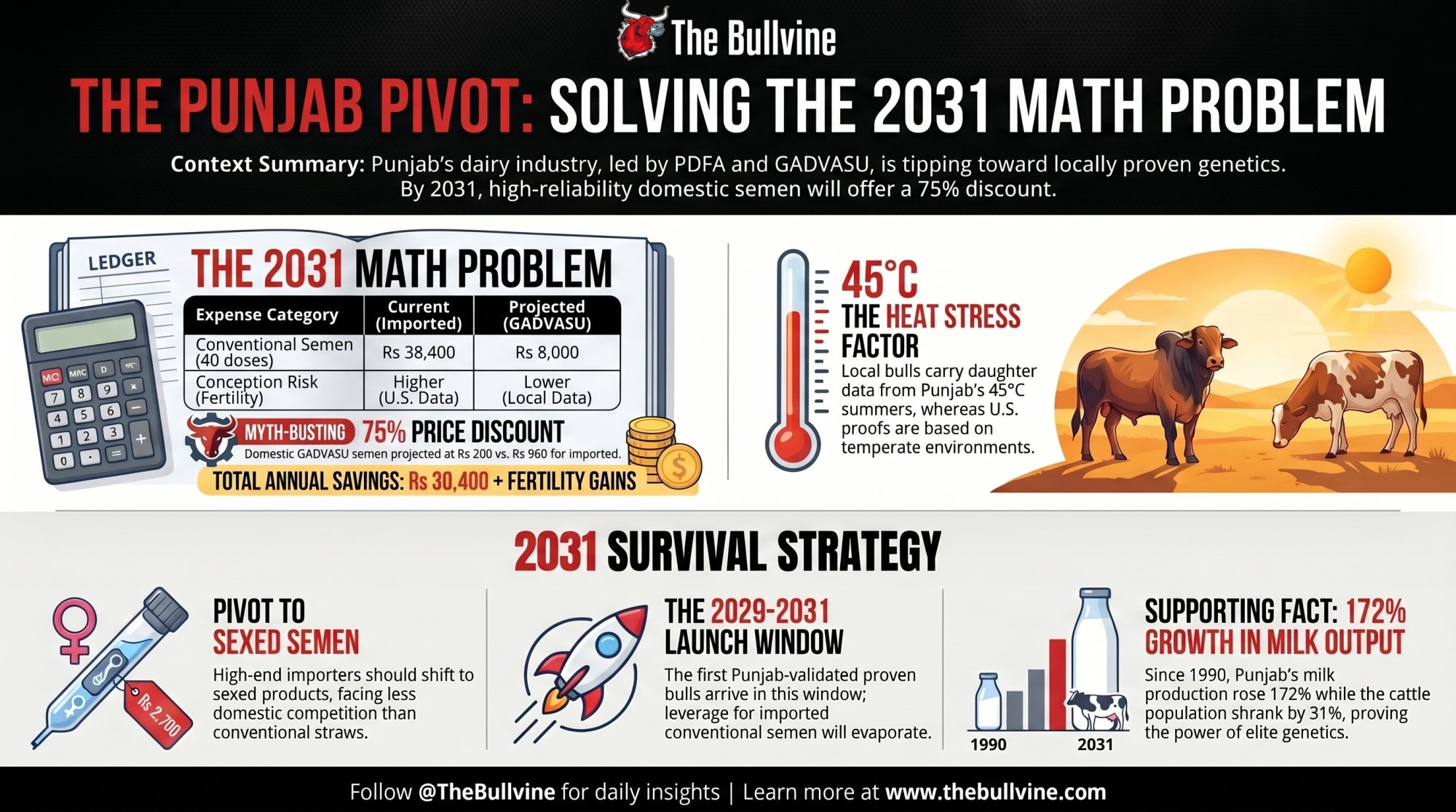

The 2029 Math Problem is straightforward: the moment GADVASU’s first progeny-proven bulls reach commercial distribution, local reliability meets a roughly 75% price discount on conventional semen. A progressive 50-cow operation breeding 40 animals a year absorbs that shift directly on the input line.

The conventional-to-conventional savings isn’t transformational on its own. The real shift is somewhere else.

| Expense Category | Current (Imported) | Projected (GADVASU) | Savings / Impact per 50-Cow Herd |

| Conventional Semen | Rs 38,400 (@ Rs 960) | Rs 8,000 (@ Rs 200) | Rs 30,400/year |

| Sexed Semen | Rs 108,000 (@ Rs 2,700) | Import-only through 2033 | Minimal near-term shift |

| Conception Risk | Higher (U.S. proofs vs 45°C) | Lower (Local daughter data) | 1–2 repeat services avoided |

| Reliability Moat | U.S. CDCB infrastructure | Local PDFA member herds | Loss of import data monopoly |

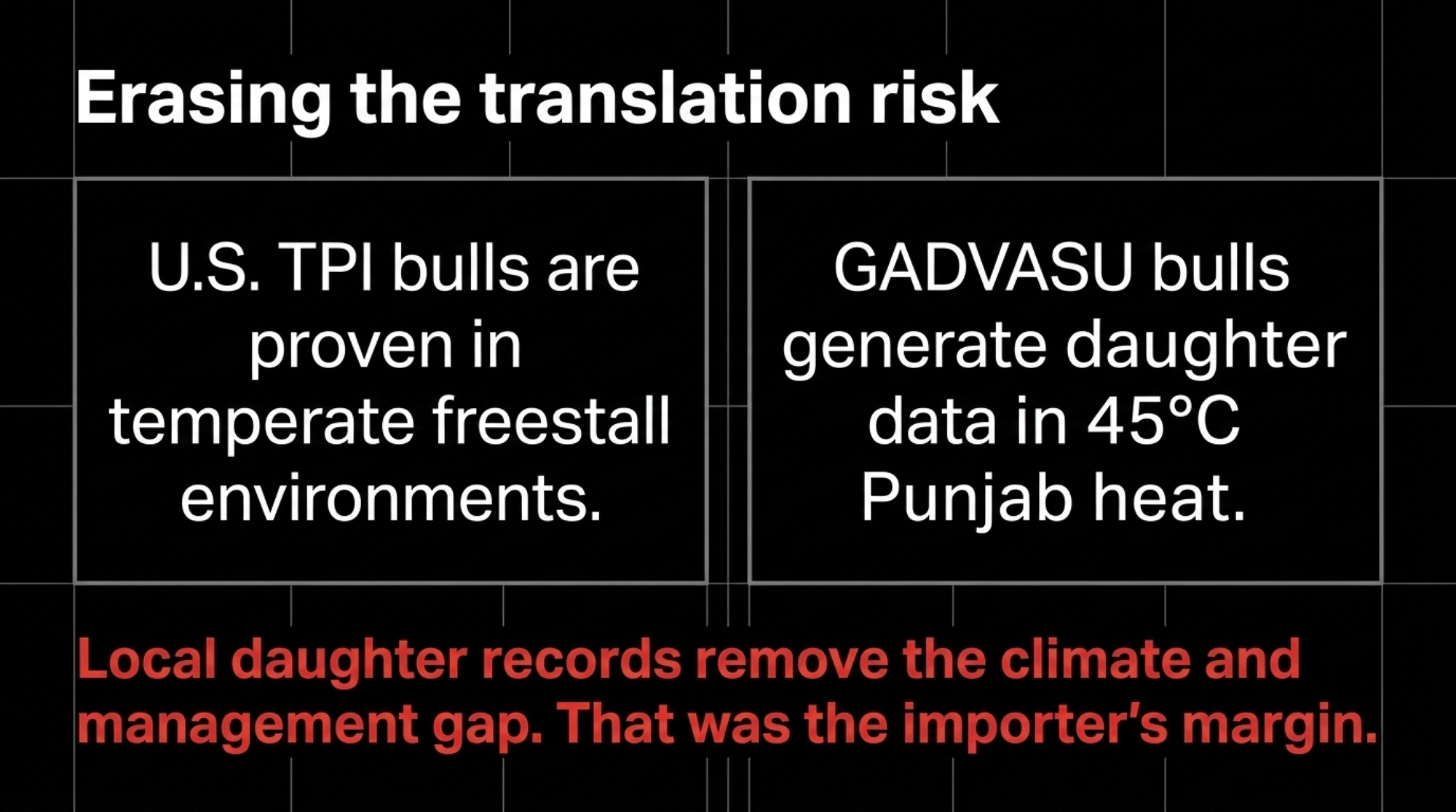

A TPI 3261 North American bull is evaluated for fertility on daughter records collected across U.S. commercial herds — temperate freestall environments, not 45°C Punjab heat. A GADVASU bull with daughter data generated inside PDFA member herds — same TMR formulations, same parlor routines, same ambient conditions — removes that translation risk. That’s margin that was accruing to North American genetics suppliers to begin with, and in the post-graduation market, it disappears from the value chain.

Why This Isn’t Another Government Semen Program That Won’t Scale

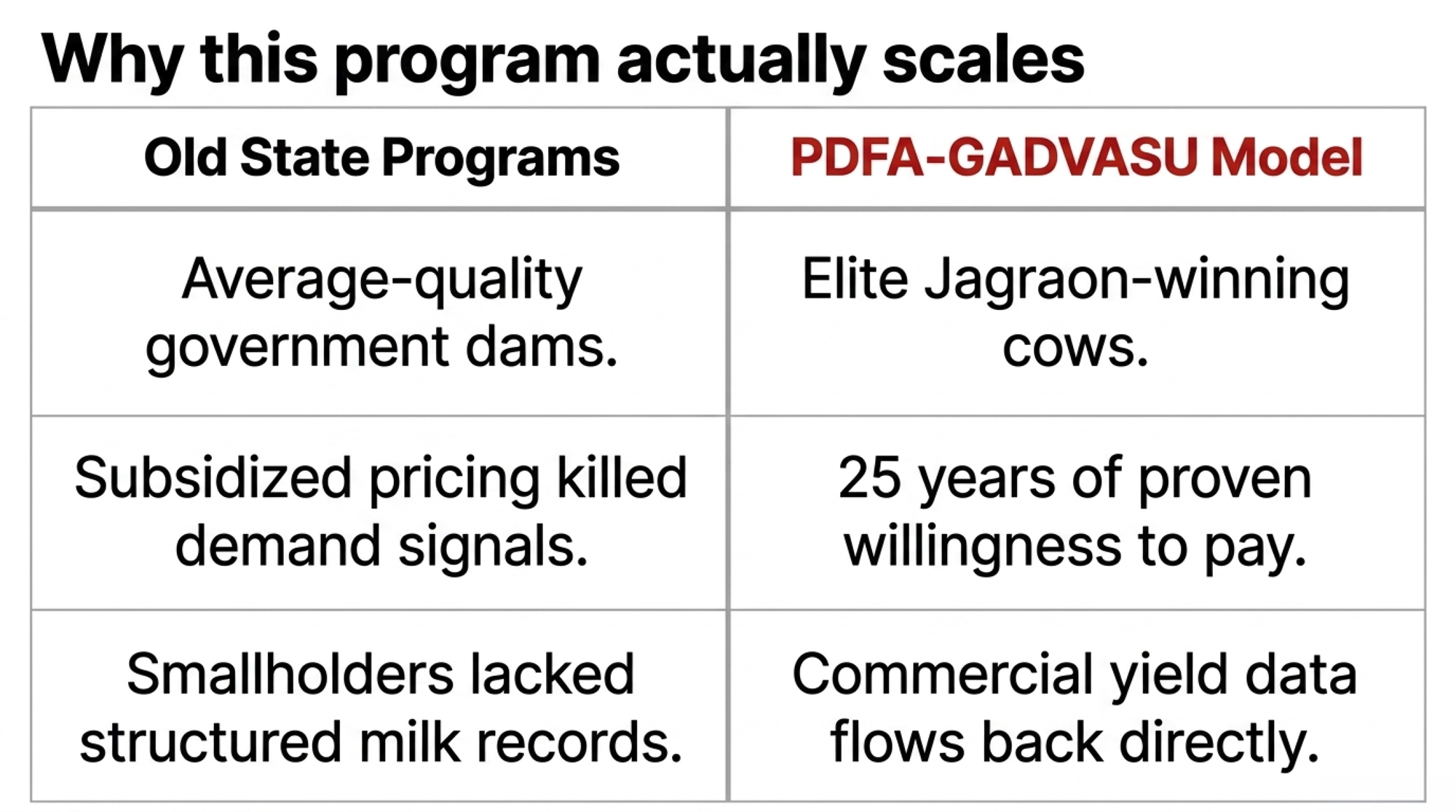

India has been running progeny testing programs since the 1960s. None cracked the premium commercial market, for structural reasons that have nothing to do with capability.

Government programs tested bulls from government herds, which meant the genetic ceiling was set by average-quality dams. They distributed semen through government AI networks at subsidized prices, which killed the price signal that would tell the program which bulls the market actually valued. And they struggled to generate rigorous daughter data because smallholder farmers don’t maintain structured milk recording.

The PDFA-GADVASU arrangement flips every one of those failure modes. Elite male calves will be selected from PDFA member cows — the same animals that win the Jagraon Holstein show, the ones already averaging 5,000+ litres per lactation per 2018 ArthaImpact reporting on the original PDFA pedigree plan. The PDFA has 25 years of documented farmer willingness to pay Rs 200–600 for imported premium semen, which is the demand signal telling the program what traits matter. And PDFA member farms already track yield data to justify their purchasing decisions, so the daughter records flow back into the evaluation system through commercial channels that already exist.

What remains is execution risk, not structural risk. The one worth watching: Indian progeny testing protocols require daughter records from several hundred animals per bull, distributed across multiple herds and agro-climatic zones. If PDFA’s participating farms cluster too tightly geographically, the resulting proofs could be challenged as region-specific rather than broadly applicable. That’s a known stumble point in previous Indian programs, and a real thing to monitor over the next three years.

How Fast Does Punjab’s Semen Advantage Actually Arrive?

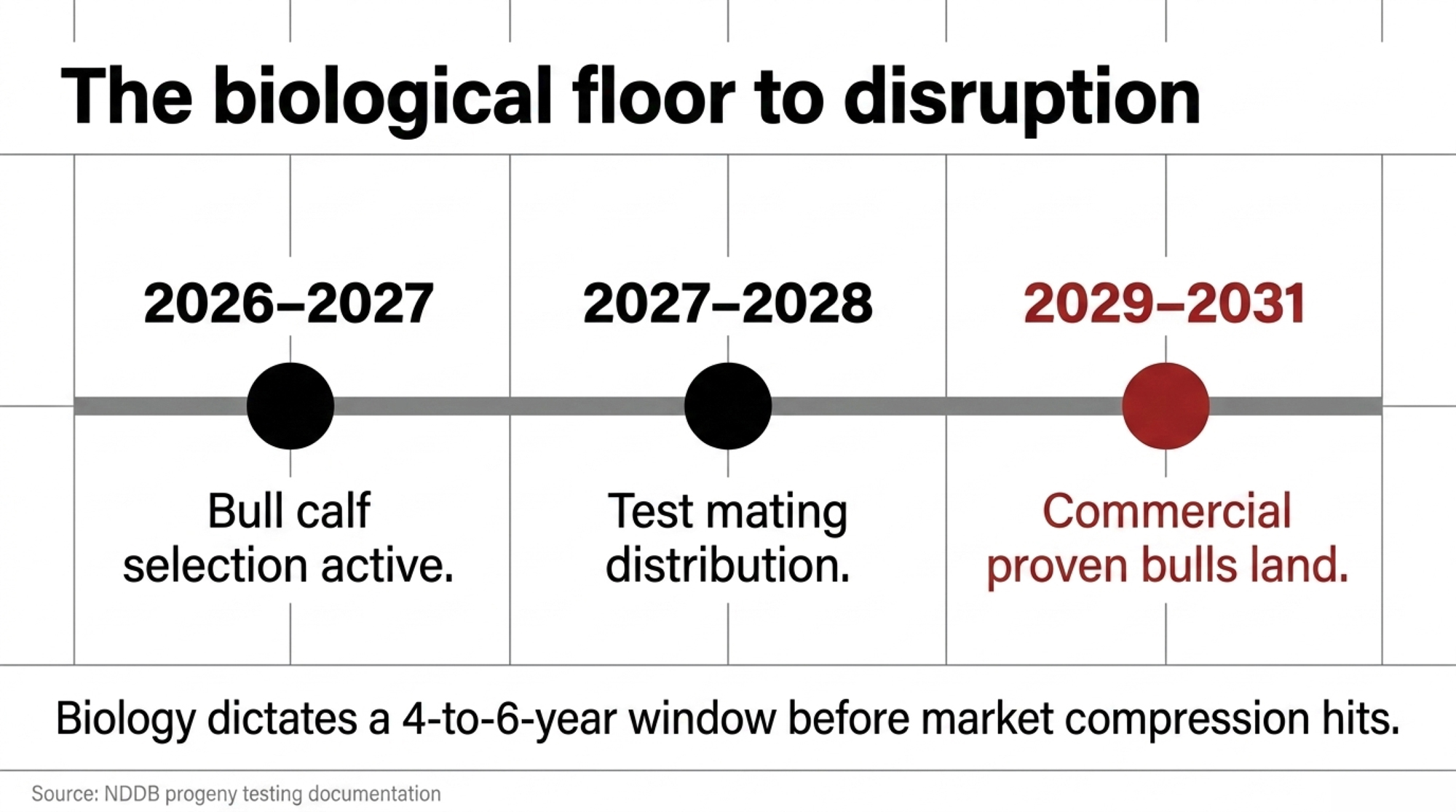

Cattle have a roughly 9-month gestation, and a heifer reaches first calving around 24 months of age. First lactation records require another 305 days. Add the daughter-record threshold and multi-zone distribution requirement, and that sets the biological floor on how fast a proven bull can reach market. NDDB documentation describes conventional progeny testing as under a five-year cycle from calf selection to proven bull status.

Which puts the GADVASU timeline in approximate terms. Bull calf selection active now through 2026–2027. Test mating distribution 2027–2028. First daughter data and commercial proven bulls landing 2029–2031 at the earliest. Full progeny-tested domestic lineup with genomic layer operational 2032–2035.

The market compression doesn’t hit when GADVASU launches. It hits when the first Punjab-validated proven bulls arrive at roughly a fifth of imported pricing, carrying conception rate data from PDFA herds. That’s a four-to-six-year window. Whether it gets used to build the next business or to extract the last revenue from the current one depends on ownership structure — cooperatives like CRV and Semex are structured to tolerate that investment horizon, as NAAB’s record $327.6 million export year coverage makes clear about the cooperative-vs-corporate revenue divide. For publicly-traded genetics businesses answerable to quarterly reporting, in our view the organizational case is harder to build.

What Changed Between 2015 and 2025

In 2015, the Punjab government briefly proposed restricting imported semen, in a move USDA FAS reporting from August of that year framed as protecting the state AI delivery system that competed with private distributors. Ten years later, the same state government publicly backed the GADVASU genomics infrastructure underpinning the PDFA partnership.

The political economy flipped for four reasons worth studying if you’re a progressive breeder in a state that hasn’t made this transition.

Punjab’s per-cow yield gap became a government accountability problem rather than a technical observation. The national policy frame shifted toward genomics through the Rashtriya Gokul Mission, making state genetics investment a path to central matching funds rather than a standalone expense. The smallholder constituency that state semen stations were designed to serve eroded as Punjab’s dairy sector consolidated into commercial operations. And the PDFA, with a large and well-attended annual Jagraon expo and documented yield improvements across member farms, became a constituency the state government could no longer afford to work around.

That’s the playbook other Indian states will need to execute. Build the commercial network first, accumulate demonstrated results, organize the political constituency, then approach the state government for infrastructure backing. PDFA took years of steady network-building to complete that sequence. No MOU shortcuts it. Gujarat, with Amul’s cooperative scale and existing milk recording density, is the obvious candidate state to watch for the next credible replication attempt — but Amul’s smallholder orientation may cut against the elite-dam selection that makes the Punjab model work.

The Data Monopoly Is the Only Moat Left

Here’s the part most trade coverage misses. North American genetics companies aren’t just selling straws into India. They’re selling certainty — the TPI number, the NM$ number, the reliability percentage, the whole decades-long apparatus of CDCB evaluation infrastructure that makes Oscar’s TPI 3261 a credible purchase decision for a farmer 12,000 kilometres away. It’s the same data moat that underpins the broader battle for Holstein’s genetic direction in every major dairy market.

That certainty is the moat. Price was never the moat. Indian farmers have always had cheaper options; they paid Rs 960 because the data was real and the domestic equivalents weren’t.

The moment GADVASU starts generating its own certainty — Punjab-validated daughter data from PDFA herds, under local heat stress and local management — the moat evaporates. What’s left is a straw-for-straw price comparison that North American suppliers cannot win.

Which puts a question on the table that’s uncomfortable enough nobody in the industry wants to ask it out loud: are the big AI houses ready to compete on price, or are they going to keep selling U.S. daughter-proof certainty to farmers in a 45°C Punjab summer? Because those are the two options. There isn’t a third.

The 2031 Survival Checklist: Strategic Directives

Strategic Directive 1 — Commercial HF operator in Haryana, Maharashtra, or Karnataka: The replication window is approximately now through 2028. State programs launched before GADVASU’s proven bulls establish interstate market share will have a defensible position. Programs launched after 2030 will be competing against a validated Punjab reference population they can’t match on reliability. What it demands: a private farmer association with procurement scale, a university research partner willing to produce commercial semen, and elite commercial dam density sufficient for rigorous progeny testing. Chitale Dairy has the institutional capacity to anchor a Maharashtra version. Where it backfires: if your state’s smallholder-focused cooperative sector blocks the commercial elite program politically, or if your farmer base lacks the recording discipline that makes daughter data usable.

Strategic Directive 2 — Progressive breeder in UP, Rajasthan, or MP: You’ll be a buyer of Punjab genetics, not a competitor. Start positioning now to access PDFA-network semen when it reaches interstate distribution. The generational commercial HF adoption lag in these states isn’t closable on a useful timeline. This month, pull your last two lactation records and benchmark your top 10% cows against published GADVASU or NDRI crossbred HF performance data. If your best cows sit where Punjab’s middle tier sat five years ago, you’re buying Punjab genetics in 2030, not building your own.

Strategic Directive 3 — Importer of premium North American semen today: Conventional imported semen at Rs 960 is the product category most exposed to domestic substitution once GADVASU’s proven bulls reach market. Sexed semen at Rs 2,700 holds longer because the flow cytometry technology doesn’t get domestically replicated on the same timeline. Shift your import mix toward sexed product and genomic-tested young bulls with defensible Indian-condition fertility data. The elite operation running 200+ cows will always have a reason to access the top 1% of global genetics. On the pricing and quality trajectory this article describes, the case for bulk-purchasing commodity conventional imports starts to erode around 2031.

Strategic Directive 4 — ABS, CRV, Semex, ST Genetics strategist: Each of these companies operates comparable international genomic evaluation, embryo, and sexed semen programs globally. The India-specific question is how quickly the local entity activates those capabilities for Punjab-network farms. If you don’t have a local progeny or genomic partner anchored inside India by 2027, the 2029–2031 compression window will arrive with your leverage already gone. At that point, the options narrow to pricing the conventional product at domestic parity, retreating to sexed and embryo specialty, or shifting the growth narrative to the next emerging market.

A realistic caveat before you plan around this timeline. The scenario above assumes GADVASU executes on the MOU at the pace PDFA needs. Previous Indian progeny testing programs have stumbled on exactly this point. If execution slips three years, the compression window moves with it — but it doesn’t close.

What This Means for Your Operation

- Are your replacement heifers being bred to genetics that will still command a premium in 2031, or are you paying import prices for a product category about to see domestic substitution pressure?

- If your state has elite commercial HF herds but no PDFA equivalent, who in your region is positioned to organize one — and what’s your role in that conversation?

- Does your current farm recording system generate data rigorous enough to contribute to a regional genomic reference population if one gets built?

- For breeders outside Punjab: have you mapped which imported bulls are producing the best daughters under your specific management conditions, or are you buying on catalog TPI alone?

- Is your sexed semen penetration where it should be given the shifting economics of conventional product?

- The genetic distance between your top-tier cows and your commercial middle — wider or narrower than five years ago? That ratio determines your exposure to market-leveling genetics arriving at low prices.

- If you’re an AI distributor or dealer in India, what does your 2031 revenue model actually look like, and have you pressure-tested it against a scenario where Punjab-proven semen is commercially available at Rs 200 per dose?

Key Takeaways

- If you’re commercially breeding HF crossbreds outside Punjab and your state has no PDFA equivalent in motion by 2028, you’re positioned as a genetics customer — not a producer — through at least 2040. Plan your sourcing relationships accordingly.

- If your operation currently pays Rs 900+ per conventional imported straw, assume that product category will face meaningful domestic substitution pressure by 2031. Migrate your premium spend toward sexed semen and genomic-tested young sires in the next 24 months.

- If you’re a genetics company with India exposure, the 2026–2028 window is the one where pricing leverage and data-relationship leverage are still on your side. After GADVASU’s first proven bulls land, both compress in the same direction.

- If you’re evaluating a state-level genetics program in Haryana, Maharashtra, or Karnataka, the non-negotiable variables are elite commercial dam density, a university production partner, and structured daughter-recording discipline. Missing any one and the program produces interesting research, not commercial competition.

The Question Sitting in Your Parlor

The comfortable read on Punjab’s story is that it’s an outlier — specific conditions, specific institutional history, not replicable in your state or your operation. That read is half-true and half-excuse. The generational lag in HF commercial crossbreeding is real biology. The PDFA network’s years of social infrastructure aren’t instantiated by decree. Those barriers are genuine.

But the policy lever that could compress the replication timeline from fifteen years to seven exists, and it’s not expensive. A national HF crossbred genomic reference population — tens of thousands of genotyped daughters across multiple states, linked to NDDB’s existing milk recording infrastructure — would make genomic pre-selection viable everywhere commercial dairy farms exist. The cost is a rounding error in the current national genetics budget. The decision to build it hasn’t been made because the political constituency organized around it hasn’t been assembled.

So the question for readers outside Punjab isn’t whether the graduation is coming. It’s whether your state’s commercial dairy sector — and your own barn within it — will be a supplier or a customer when it arrives.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Stud Wars April 2026 — The Empire Strikes Back — Follows the money on the latest CDCB evaluation reshuffle, revealing how single studs capture 36% of top-100 lists. Arms you with hard market-share data to negotiate next year’s contracts before global price compression hits.

- Kooima Called Beef-on-Dairy a Packer’s Dream. Your 2027 Heifer Pen Just Sent the $117,000 Bill. — Protect your replacement pipeline from the beef-on-dairy trap. Dismantles the diversification myth with a $583-per-service breakdown, showing why chasing quick calf checks leaves 500-cow herds brutally short on $3,010 heifers just as scarcity hits.

- The $45 Holstein Genomic Test: Three Blind Spots CDCB’s April Reset Missed — Hidden premiums exist outside the commercial index. Exposes the structural flaws in standard $45 SNP chips that completely ignore maternal DNA, showing why legacy breeders flushing proven cow families hold a pricing edge technology cannot replicate.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.