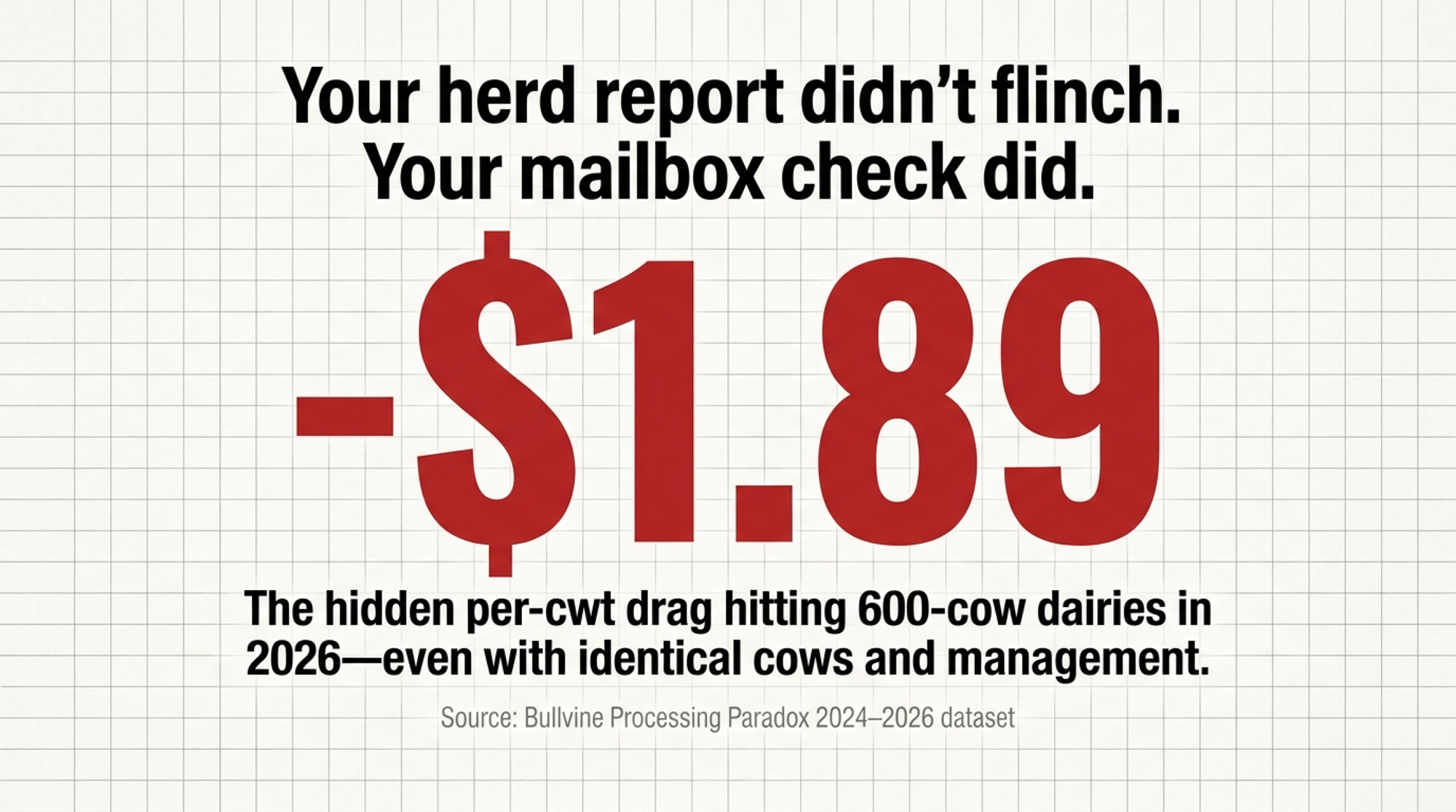

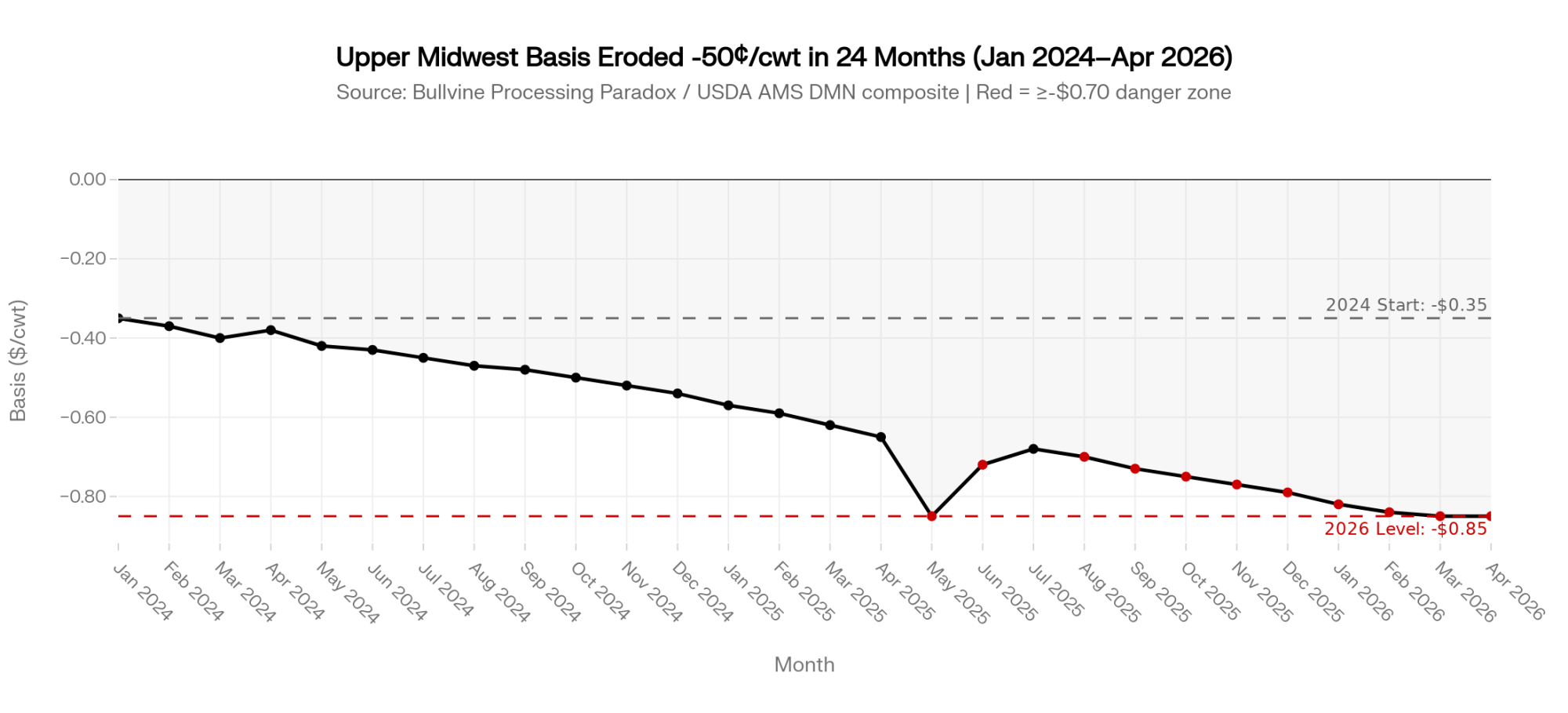

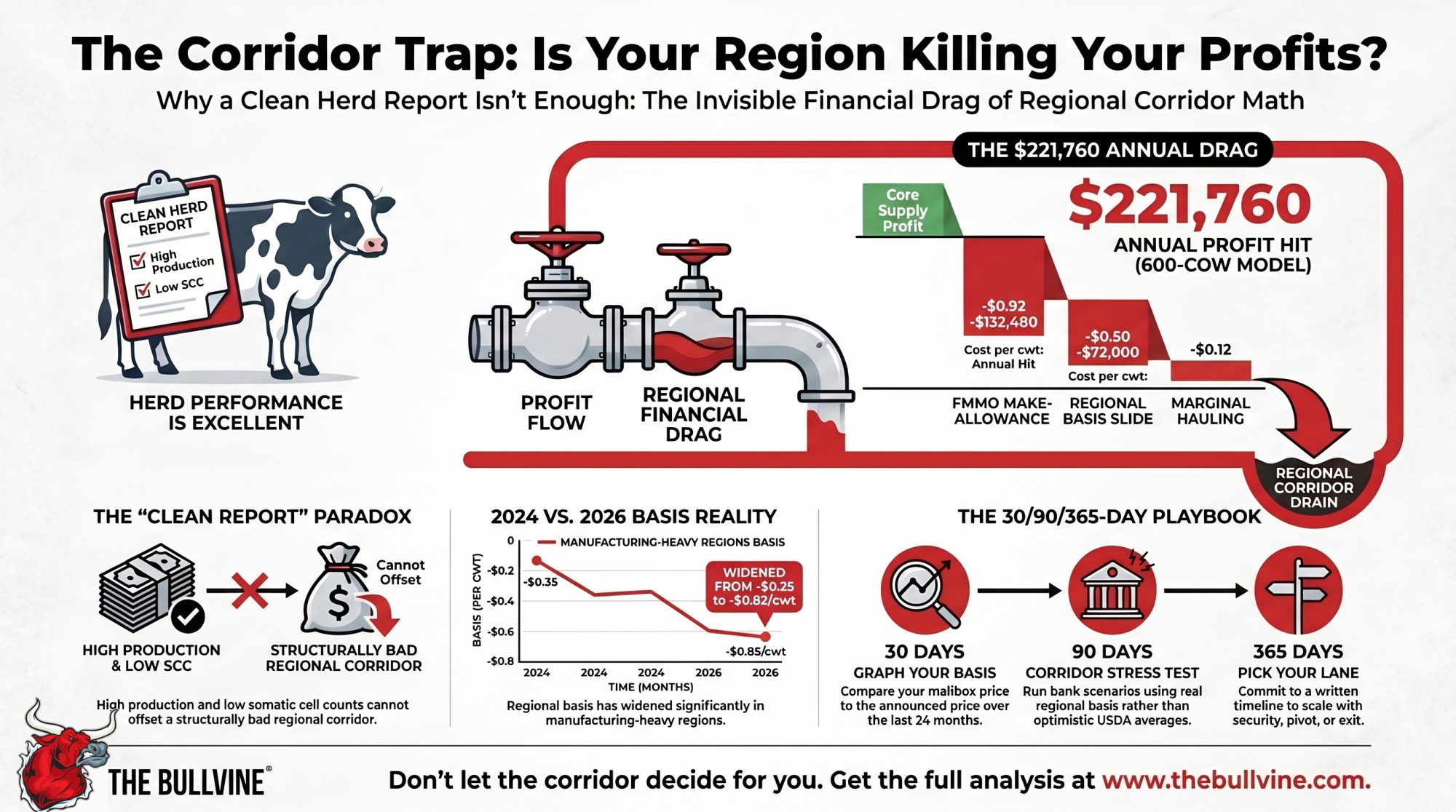

Same cows. Same management. A different corridor — and a $221,760 annual drag. Basis went from ‑$0.35 to ‑$0.85/cwt while the FMMO make‑allowance took another $0.92 off Class III. The herd report still looks clean.

On a 600‑cow Upper Midwest dairy we’ll call Maple Ridge, the all‑in basis on the milk check has moved from roughly ‑$0.35/cwt in 2024 to about ‑$0.85/cwt in early 2026. Same cows. Same management. A different corridor.

USDA ERS’s April 2026 Livestock, Dairy, and Poultry Outlook puts 2026 all‑milk near $20.40–$20.50/cwt, while CME Class III futures for mid‑2026 contracts have traded mostly in the mid‑$16s to upper‑$17s through early Q2 2026 sessions. That $2–$3/cwt gap is the budget anchor argument every dairy lender is now having. Maple Ridge’s gap isn’t on the screen. It’s on the milk check.

Maple Ridge is a composite operation drawn from Bullvine reporting and the Processing Paradox 2024–2026 dataset, used here so we can show real numbers without exposing a real farm’s milk check. The rule‑change inputs are verified against published USDA and Bullvine analysis. The herd‑level inputs are illustrative. Plug in your own.

A 2,000‑cow Western dairy we’ll call Dos Arroyos — also a composite, modeled on the kind of core‑supply contracts Bullvine has documented along the High Plains and I‑29 corridor — is staring at the same kind of basis pressure and adding 400 cows anyway. The processing capacity dairy 2026 question lives right in the gap between those two decisions.

This isn’t a story about milk per cow. It’s about whether your region’s plants want your next pound or not.

Bullvine Definition — Corridor Math (n.): The calculation of farm profitability based on regional processing capacity, hauling distance to marginal plants, and local basis, rather than national Class III averages. Two farms with identical herd reports can sit on opposite ends of Corridor Math if their plants, hauling lanes, and basis trends diverge.

Quick note for Ontario and Canadian readers: Corridor Math applies under supply management too. The levers change — base allocation, P5 pooling, plant access, CDC pricing signals — but the question is the same: does your buyer’s plant want your next hectolitre, and at what net mailbox price?

How Maple Ridge’s $221,760 Annual Drag Hid Inside a Clean Herd Report

Maple Ridge ships into a cheese‑heavy Upper Midwest milkshed inside Federal Order 30. Components are solid, somatic cell count is low, and debt per cow sits under the $3,500/cow “strong” threshold cited in Cornell PRO‑DAIRY Dairy Farm Business Summary–style benchmarks referenced in the Processing Paradox analysis (Cornell PRO‑DAIRY DFBS, 2024 edition). By the herd report, nothing’s wrong.

The corridor changed around them.

- Bullvine’s Processing Paradox reporting — drawing on USDA AMS Dairy Market News and operator public statements — documented reduced weekend and overtime processing at several Upper Midwest cheese plants through 2024–2025, alongside tighter volume caps and base‑excess plan use. Operators cited labor and energy costs.

- Regional herd consolidation in the same buyer’s draw radius tightened the local milk‑to‑capacity ratio over 2024, consistent with the relocation and consolidation patterns Bullvine has documented along the I‑29 corridor.

- USDA AMS Dairy Market News reported Midwest spot Class III milk trading flat to as much as $7.00 under Class III during the spring 2025 flush cycle, with the deepest discounts in the week ending May 2, 2025 (USDA AMS DMN, April–May 2025 weekly issues).

Stack those forces and a 50¢/cwt basis slide isn’t a mystery. It’s the price tag on a corridor that quietly went long on milk.

The 2025 FMMO modernization sits on top of all this. Bullvine’s April 2026 analysis, The New FMMO Rule Costs a 500‑Cow Dairy $97,750 a Year, pegs the make‑allowance update at roughly $0.85–$0.93/cwt off Class II–IV values once fully phased in, with Class III near $0.92/cwt, based on USDA AMS, Final Rule on Amendments to Federal Milk Marketing Orders (January 2025) and the University of Wisconsin Extension review of the AMS final decision (2025). That’s before a single mile of freight. Before basis. Before a balancing fee.

Deep Dive → The New FMMO Rule Costs a 500‑Cow Dairy $97,750 a Year — Tier 3 pillar, April 2026.

What Does a 50¢/cwt Basis Slide Actually Cost a 600‑Cow Dairy in 2026?

This is where you stop talking corridors and run the numbers like your banker would.

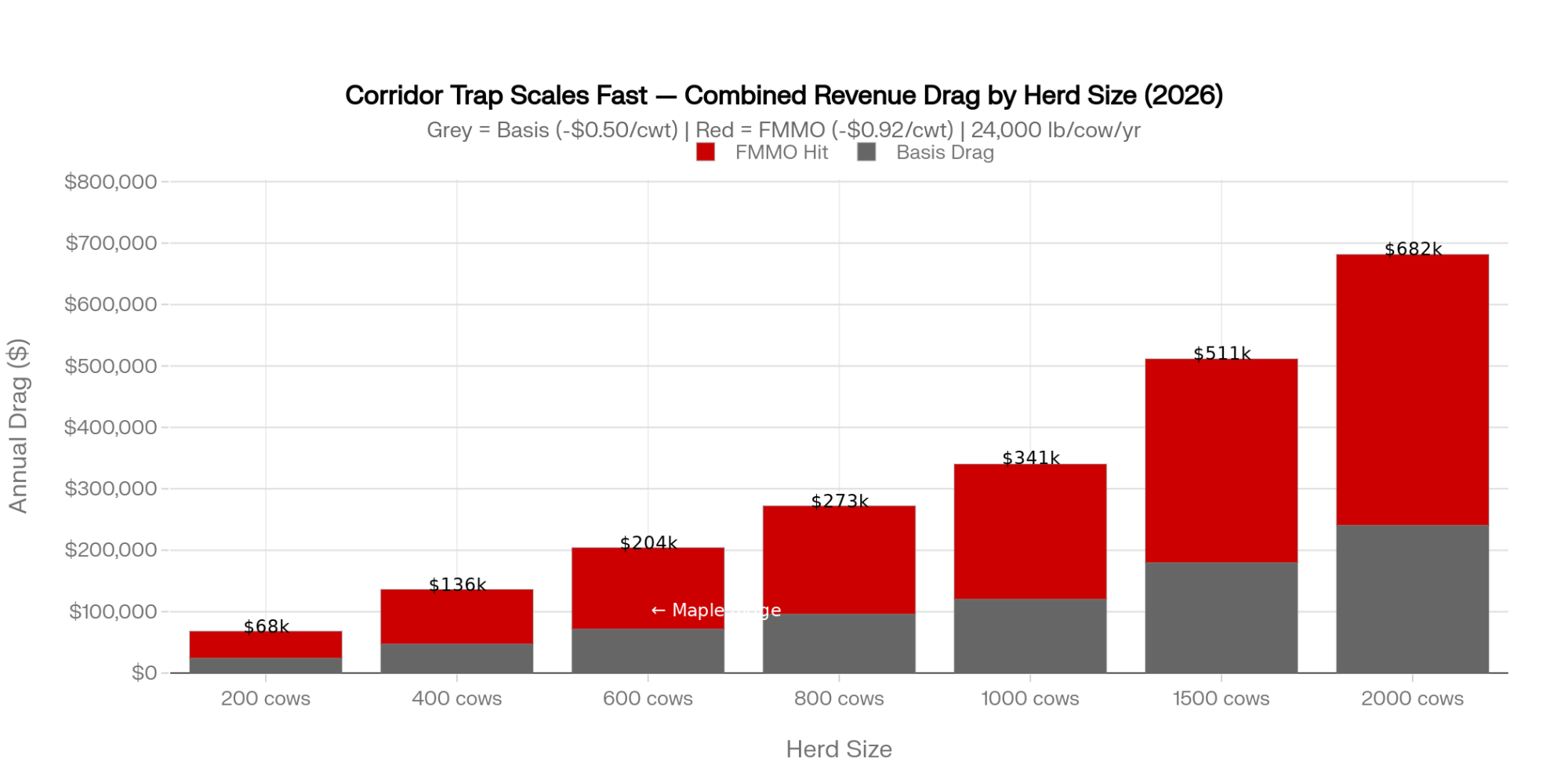

The Maple Ridge 2026 Reality — 600 Cows, Upper Midwest, Illustrative Composite

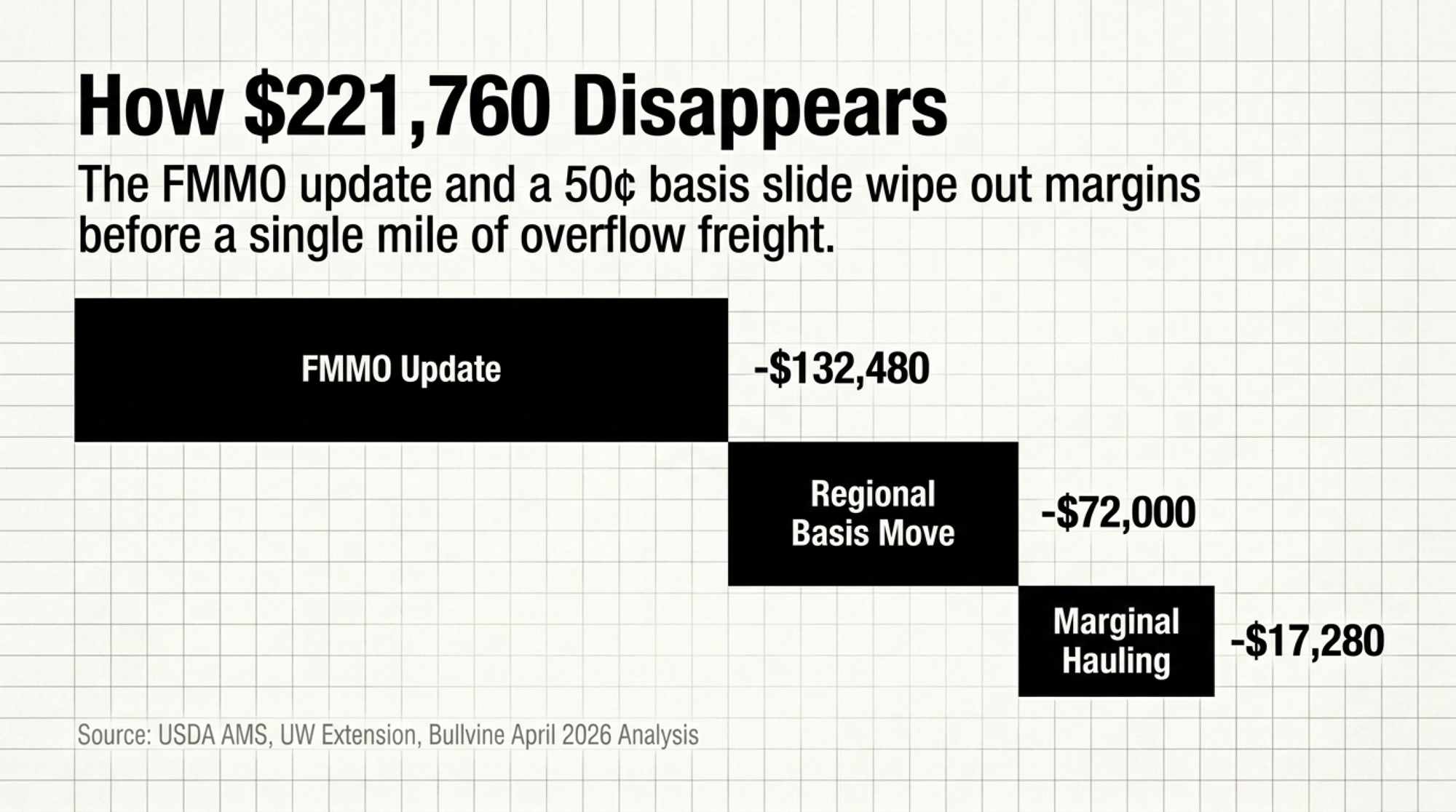

| Factor | 2024 Impact (per cwt) | 2026 Impact (per cwt) | Annual Bottom‑Line Shift vs 2024 |

| FMMO Make‑Allowance | $0.00 | (‑$0.92) | (‑$132,480) |

| Regional Basis | (‑$0.35) | (‑$0.85) | (‑$72,000) on the 50¢/cwt move |

| Marginal Hauling (weighted)* | $0.00 | (‑$0.12) | (‑$17,280) |

| Total Drag vs 2024 Baseline | (‑$0.35) | (‑$1.89) | (‑$221,760) |

Weighted across marginal loads, assuming ~30% of volume moves as overflow at an extra $0.40/cwt above the $0.80/cwt core rate documented in the Processing Paradox dataset. At a 15% marginal share, the hauling line is closer to ‑$0.06/cwt, or about ‑$8,640/year.

How to read this table: The Regional Basis line shows the delta vs 2024 — the 50¢/cwt move, not the full 2026 basis cost. The Total Drag row sums the 2026 deltas against that 2024 baseline.

Running the Numbers — Maple Ridge, 600 Cows, Upper Midwest, 2024 vs 2026 (illustrative composite)

Verified inputs: USDA NASS Milk Production 2025 annual production averages; USDA AMS Final Rule on Amendments to FMMOs (January 2025); UW Extension AMS final‑decision review (2025); Bullvine April 2026 New FMMO Rule analysis; Bullvine Processing Paradox 2024–2026 dataset. Illustrative inputs: Maple Ridge’s herd‑level basis trend, marginal‑load share, and hauling differential. Plug in your own numbers and your own statements.

- Herd: 600 milking cows, Upper Midwest, manufacturing‑heavy FMMO.

- Production: ~24,000 lb/cow/year, in line with the 24,390 lb 2025 U.S. average from USDA NASS Milk Production (2025).

- Annual shipped: 600 × 24,000 lb = 14.4 million lb = 144,000 cwt/year.

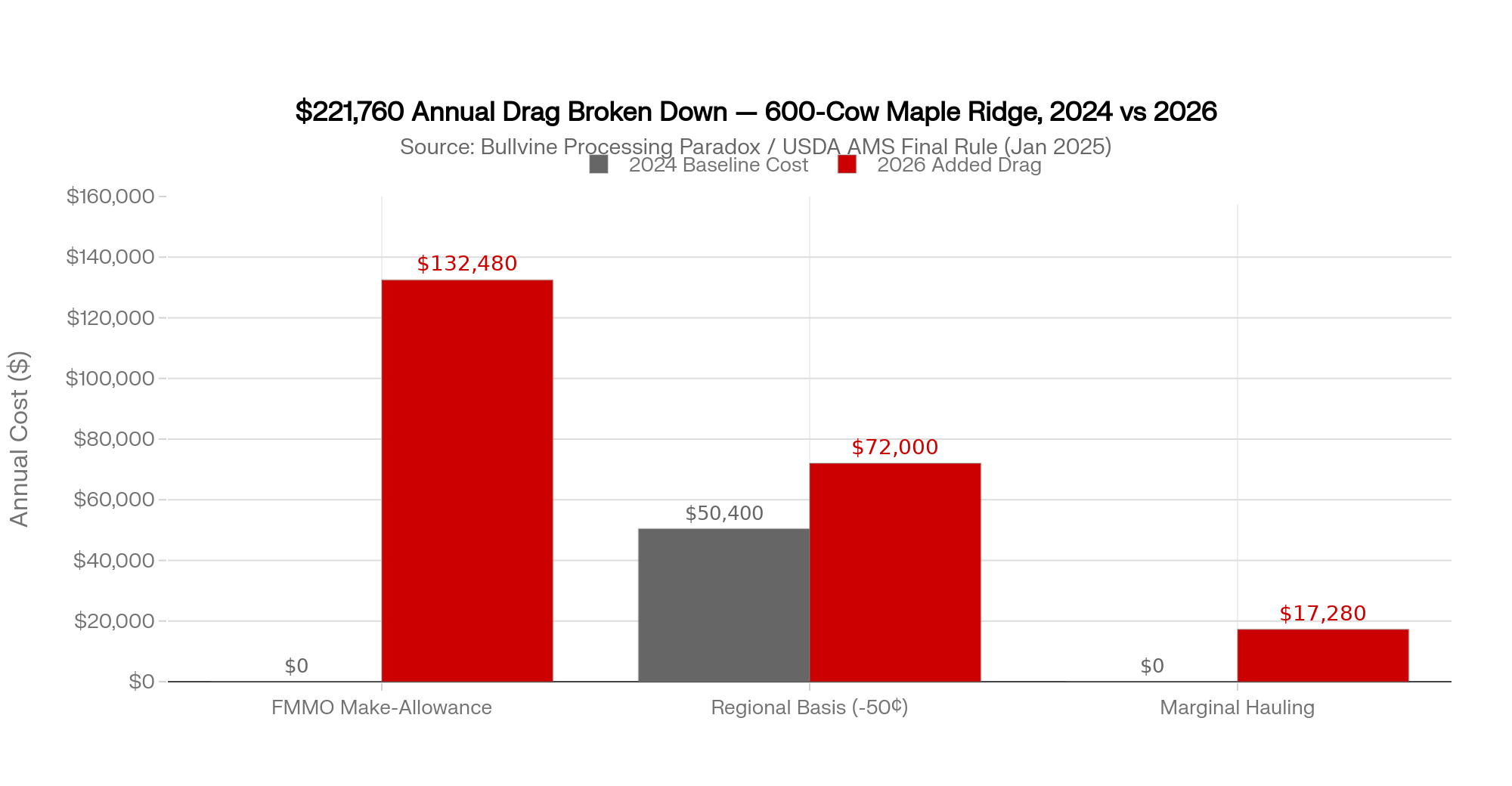

Industry rule‑change impact: 144,000 cwt × $0.92/cwt FMMO Class III hit = ~$132,480/year.

Corridor basis impact: $0.50/cwt move × 144,000 cwt = ~$72,000/year.

Marginal hauling drift (illustrative scenarios):

- Scenario A — 15% marginal: 144,000 × 0.15 × $0.40 = ~$8,640/year.

- Scenario B — 30% marginal: 144,000 × 0.30 × $0.40 = ~$17,280/year.

Combined drag range: ~$213,000–$222,000/year, against an operation that hasn’t changed cows, ration, or management since 2023.

Scale the basis‑only piece to your herd:

- 400 cows shipping ~96,000 cwt: 50¢/cwt basis move = ~$48,000/year.

- 1,000 cows shipping ~240,000 cwt: same move = ~$120,000/year.

The herd report didn’t flinch. The mailbox check did. That’s the gap most barn KPIs aren’t built to catch.

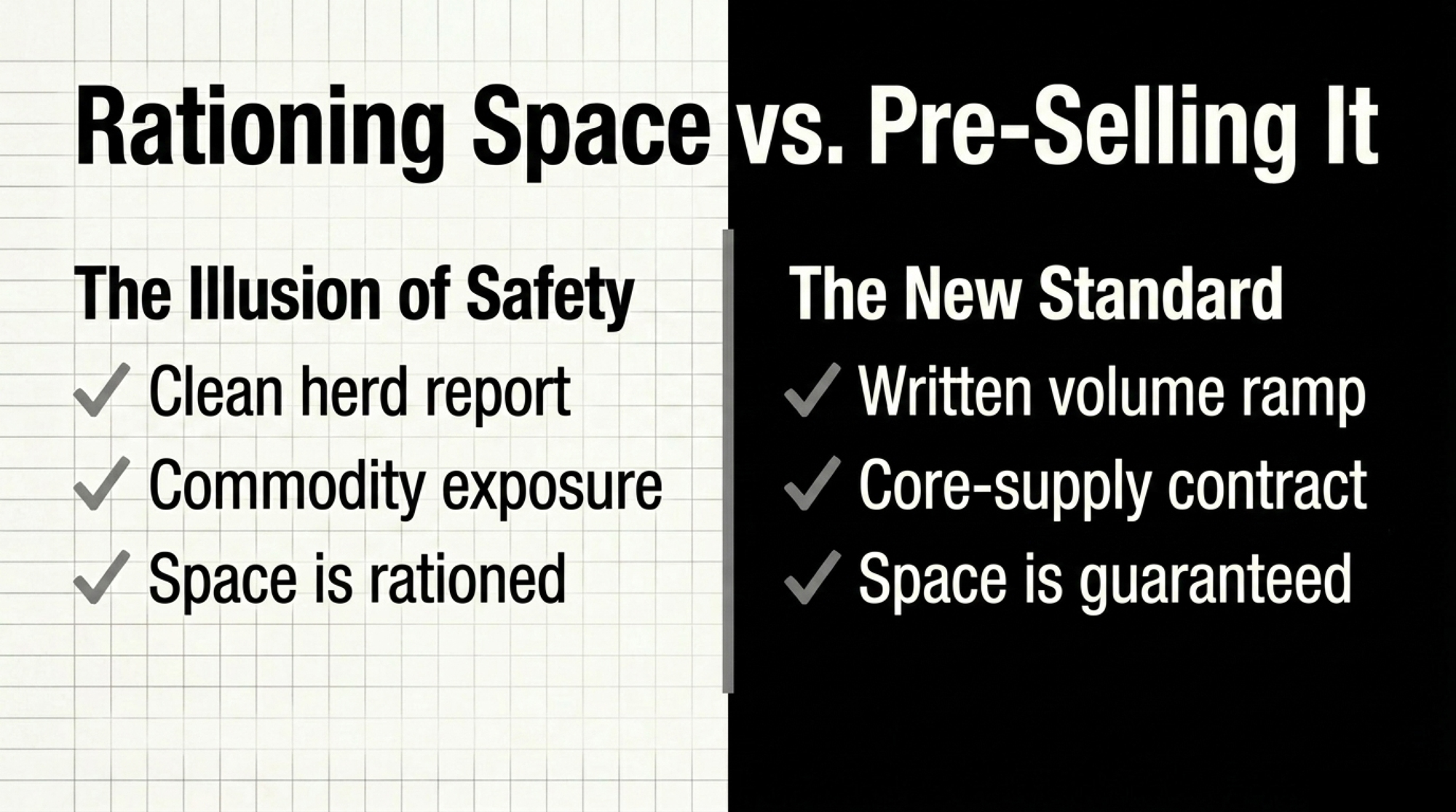

The Continental Divide: Rationing Space vs Pre‑Selling It

While the Upper Midwest is rationing space, the High Plains is pre‑selling it. The difference isn’t the cows. It’s the contract.

| Factor | Maple Ridge (Upper Midwest) | Dos Arroyos (High Plains/I-29) |

|---|---|---|

| Herd size | 600 cows | 2,000 cows (+ 400 planned) |

| Federal Order | FO-30 (cheese-heavy) | High Plains / non-pooled |

| 2026 All-in Basis | -$0.85/cwt | ~-$0.35/cwt (core supply) |

| FMMO Class III impact | -$0.92/cwt (2025 rule) | -$0.92/cwt (same rule) |

| Marginal hauling (overflow) | $1.10–$1.20/cwt | <$0.80/cwt within 60 mi |

| Plant capacity status | Rationing / base-excess | Pre-sold / volume ramp |

| Core supply status | Swing/dispensable | Written core-supply contract |

| Total 2026 annual drag vs 2024 | -$221,760 | Largely offset by contract premiums |

| Robot/capex DSCR (corridor case) | 1.05–1.10× (yellow light) | >1.25× (green) |

| Strategic path | Pivot, exit, or reposition | Scale with concrete |

| Regional farm count trend | -630 farms, 2022–2025 | Expansion corridor |

Most producers can name the bull behind their best heifer. Few can name the closest plant project in their draw radius. Dos Arroyos can.

Their state, by the headline numbers in Processing Paradox 2024–2026 (USDA NASS state‑level Milk Production, 2014 vs 2024), looks bad. New Mexico shed roughly 2.2 billion pounds of annual milk and about 83,000 cows over that decade. California gave back more than 2.0 billion pounds and around 72,000 cows. The Ogallala Aquifer projection — up to 70% of the aquifer’s saturated thickness potentially unusable in the Texas Panhandle expansion zone within 20 years, per the Texas Tech and USGS‑linked aquifer research cited in Processing Paradox — isn’t a footnote.

Their corridor still tells a different story.

Dos Arroyos isn’t ahead because they’re better farmers. They’re ahead because they bought Processing Security in writing before they bought concrete. The era of producing milk and hoping for a check is over inside their basin.

The corridor’s public cheese build‑out — Hilmar (Lubbock, TX project announced 2021), Leprino (Lubbock, TX complex announced 2022), and Valley Queen (Milbank, SD expansion announced 2022) — sets the public context, per each operator’s project announcements and Processing Paradox.

The contract terms described below are a Bullvine composite of corridor practice, drawn from Processing Paradox. They are not attributable to Hilmar, Leprino, Valley Queen, or any other named processor.

- Dos Arroyos’s milk feeds into the $1.6 billion High Plains and I‑29 cheese build‑out underway since 2020.

- Their 2025 supply agreement, as composited from Processing Paradox, carries defined base‑excess terms, component premiums tied to plant product mix, and a written volume ramp.

- That ramp is what makes the 400‑cow expansion pencil. In the composite, throughput is committed in writing before concrete is poured. The base‑excess clause prices growth pounds inside core‑supply terms for the duration of the ramp, not at swing‑load discounts.

- Their marginal load travels under 60 miles to a plant still bidding for volume, not rationing it.

The assumption that “Western dairy is doomed” doesn’t survive a corridor‑level read. The assumption that Upper Midwest dairy is structurally safe because it’s always been there doesn’t either. The Upper Midwest lost roughly 630 farms between 2022 and 2025 while regional milk climbed to 43.2 billion pounds (Bullvine Processing Paradox, drawing on USDA NASS, 2024–2026). The volume stayed. The mid‑size families didn’t.

Must‑Read → The $11 Billion Dairy Rush: Growth Corridor or Dead Zone? — Tier 3 hidden gem.

Why Maple Ridge’s Owner Stopped Trusting the Old Lender Spreadsheet

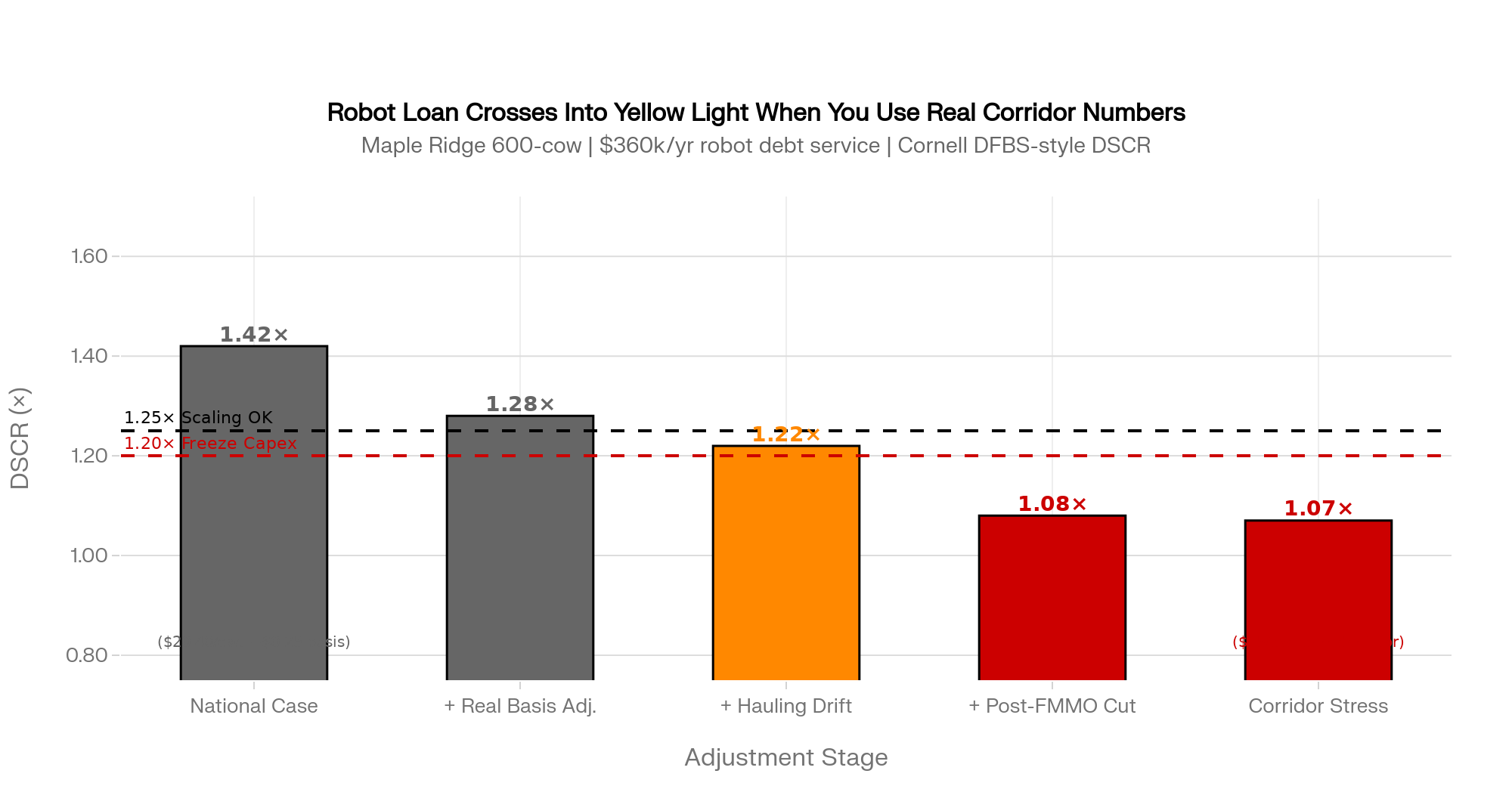

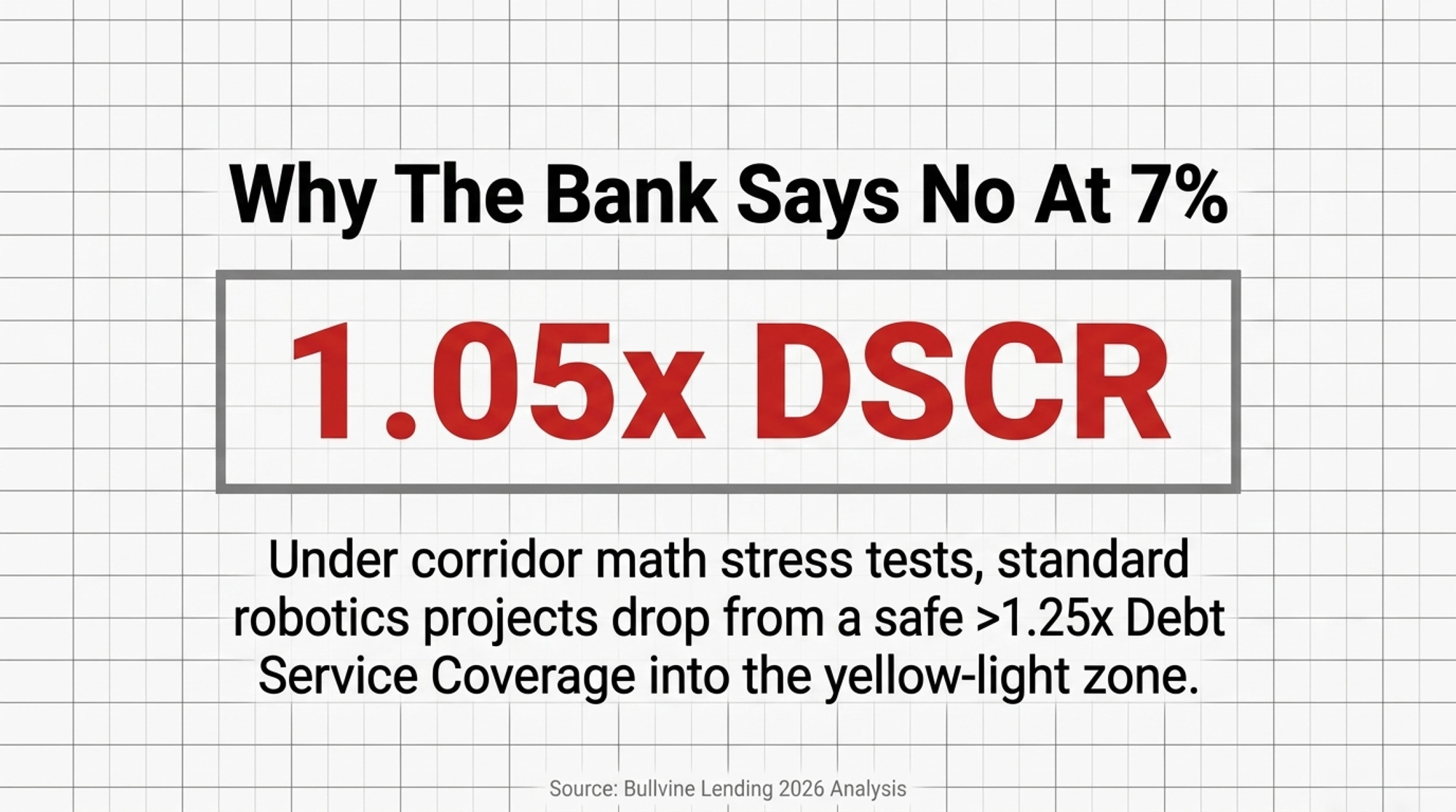

The turn for Maple Ridge came in early 2026, in a robotic milking conversation with a regional ag lender.

The opening was familiar. Rolling 12‑month averages. A USDA‑style price near $20.40/cwt for 2026, pulled from ERS and WASDE ranges. A generic stress test at $15/cwt with a flat ‑$0.25/cwt basis. Ag operating loans in the mid‑7% range, consistent with the lender environment Federal Reserve district and Purdue Center for Commercial Agriculture outlooks have tracked through late 2025 and into early 2026.

On those numbers, robots penciled.

Maple Ridge’s owner put three different numbers on the table.

- A real trailing 24‑month all‑in basis: ‑$0.85/cwt, not ‑$0.25/cwt.

- Marginal hauling reality from this composite operator’s dispatch profile: about $1.10–$1.20/cwt on overflow loads, versus the $0.80/cwt core rate documented across Processing Paradox herds.

- Post‑FMMO Class III math reflecting the ~$0.92/cwt make‑allowance hit per the UW Extension review and the Bullvine April 2026 analysis, instead of pre‑2025 class values.

Bullvine’s 2025–2026 lender reporting describes the same pattern in plainer terms. The binding constraint isn’t a lower headline price. It’s a lower effective floor once basis, hauling, and post‑FMMO Class values are layered in.

A robotic milking project at this herd profile typically carries roughly $360,000/year in annual debt service on the parlor and related infrastructure portion of the loan, drawn from Bullvine’s prior reporting on robotic ROI in the 300–600 cow range and standard amortization on 7%‑range term money. Re‑run with the corridor inputs above against that debt service, the project moved from comfortably above 1.25× DSCR into the 1.05–1.10× range under a $15/cwt corridor stress case — the “yellow light” zone Cornell DFBS‑style benchmarks (referenced in Processing Paradox) flag for tighter scrutiny.

The DSCR shift is illustrative. The inputs that drove it are real: the basis trend, the marginal hauling, the post‑FMMO Class values, and the debt service.

The robots didn’t become impossible. They became a different decision.

The question is no longer “how do we squeeze more milk out of this barn.” It’s “do we want to leverage 7%‑range money against a corridor that’s losing capacity, or use that equity to reposition?”

Deep Dive → Dairy Lending 2026: Why Your Banker Says No at 7% Money — prior Tier 3 economics analysis.

What Maple Ridge’s 24‑Month Basis Trend Means For Your Operation

Maple Ridge’s herd report stayed clean while its corridor quietly repriced every cwt. That’s the lesson worth carrying off this page: cost per cwt and milk per cow defend the milk check only as far as your buyer’s plant has room for your next pound. Corridor structure decides how much of any cost or component advantage you actually keep.

There are three honest paths from here, and you don’t get to skip the diagnosis to pick one.

- Scale with a processor. Real only if your buyer puts core‑supply status, base terms, and component premiums in writing, and your corridor‑aware DSCR holds.

- Pivot to a premium or niche channel. Smaller volume, higher complexity, slower onboarding, but partial escape from commodity basis.

- Plan an orderly exit or relocation. Preserves equity in a structurally bad basin; forecloses generational continuity in the existing barn.

The trade‑off underneath all three: speed of decision versus depth of corridor diagnosis. Move too fast and you lock in the wrong path. Stall and the basis keeps deciding for you.

The 30/90/365‑Day Playbook for Herds Like Maple Ridge’s

Adapt the thresholds to your own statements and your own basin. Don’t copy them.

30‑Day Actions — urgent checks

- Pull 24 months of milk checks and graph all‑in basis: mailbox − announced price, including hauling and any “marketing” or “balancing” adjustments.

- Requires: bookkeeping time, statements, a spreadsheet.

- Red‑flag trigger: basis widened by more than 25¢/cwt over 18 months without a corresponding national price move.

- Backfire risk: averaging across very different months hides flush‑season pain. Look at flush separately.

- Separate loads into core versus marginal. Calculate actual hauling cost per cwt on overflow loads.

- Requires: dispatch tickets, co‑op statements, an hour of cross‑checking.

- Red‑flag trigger: marginal‑load hauling 50% or more above your core rate.

- Watch for: milk‑check formats that combine freight with basis or place it under “other,” making marginal hauling hard to isolate.

- Confront your field rep with three direct questions, on the record. Are we core, swing, or dispensable supply over the next 5–10 years? Where do our marginal loads physically go, and at what discount, when milk is long? What plant additions or closures are in your 3–5‑year network plan?

- Requires: one meeting, no spin in your own answers.

- Red‑flag trigger: vague answers or “we’ll get back to you” on all three.

- Escalate if your DSCR has been under 1.20× for three straight months on your lender’s or CPA’s standard method. This list moves to the top of the next 30 days.

90‑Day Actions — structural adjustments

| Input | Standard Lender Model | Corridor-Aware Model | Difference |

|---|---|---|---|

| All-milk price used | $20.40–$20.50/cwt (USDA ERS 2026) | $15.00/cwt (corridor floor) | -$5.40–$5.50/cwt |

| Basis assumption | -$0.25/cwt (generic flat) | -$0.85/cwt (trailing 24-month actual) | -$0.60/cwt |

| FMMO Class III values | Pre-2025 class values | Post-rule: -$0.92/cwt make-allowance | -$0.92/cwt |

| Marginal hauling % | 0% (core rate only) | 15–30% of volume at overflow rate | +$0.06–$0.12/cwt |

| Effective floor (combined) | ~$20.15/cwt | ~$13.71/cwt | -$6.44/cwt |

| Robot project DSCR result | >1.25× ✓ (pencils) | 1.05–1.10× ✗ (yellow light) | Crosses freeze threshold |

| Capex decision | Proceed | Freeze or resize | Material divergence |

| Risk to lender if national model used | Low (on paper) | High (basis keeps widening) | Model blind spot |

- Force a corridor‑aware stress test at your bank. Two scenarios, side by side.

- National case: USDA‑style all‑milk price, flat basis, generic hauling.

- Corridor case: post‑FMMO Class values reflecting the 2025 make‑allowance changes (per the UW Extension review and Bullvine’s April 2026 analysis), your trailing 12–24‑month basis minus another 25–50¢/cwt, and marginal‑load hauling on at least 15–30% of volume.

- Requires: milk check history, dispatch records, current contract, lender model.

- Threshold: corridor‑case DSCR below 1.20× should freeze any non‑essential capital project.

- Backfire risk: if a lender won’t run the corridor case alongside the national case, factor that into your read of how flexible the relationship is likely to be when margins tighten.

- Pressure‑test a “minus 10–15% intake” scenario. If your primary buyer cut your base by 10–15% tomorrow, where does that milk go, and at what discount?

- Requires: honest conversations with two or three alternative buyers.

- Threshold: if you can’t name a plant and a realistic price within two to three weeks, your marketing risk is bigger than your production risk.

- Watch for: verbal interest that disappears when you ask for a number.

- Revisit any contracted or planned capital project — robots, freestall expansion, parlor upgrade — against the corridor case, not the national case.

- Requires: vendor flexibility, willingness to walk back announced plans.

- Threshold: re‑size, re‑time, or shelve if the corridor case pushes DSCR below 1.20×.

- Backfire risk: sunk‑cost thinking on deposits and engineering work.

Deep Dive → Robotic Milking ROI Under 500 Cows — Tier 2 management pillar.

365‑Day Moves — strategic positioning

- Pick your lane on a written timeline: scale, pivot, or exit. Bullvine’s December 2025 piece, Squeezed Out? A 12‑Month Decision Guide for 300–1,000 Cow Dairies, lays out the logic.

- Requires: a family or partnership meeting that ends with a decision, not another meeting.

- Opportunity signal: if a buyer puts core‑supply status, base terms, and component premiums in writing, and your corridor‑aware DSCR stays above 1.25×, scaling is defensible.

- Backfire risk: leveraging into hope without both a written commitment and a corridor‑aware model.

- Condition any expansion on a written processor commitment. No contract, no concrete.

- Requires: legal review of base‑excess and force‑majeure clauses.

- Threshold: walk away if base‑excess deductions are deeper or longer than the plant’s own escape clauses.

- Evaluate relocation or premium transition before equity erosion makes the call, if you sit in a legacy region with no new steel within reasonable hauling distance. Processing Paradox closure analysis documents a $15,000–$45,000/quarter equity erosion range across negative margin cycles (Bullvine, 2024–2026).

- Requires: appraisals, tax planning, succession conversations 12–24 months before any move.

- Opportunity signal: if a growth‑corridor buyer expresses written interest in backing a relocated supply, that timing window is real but short.

- Watch for: emotional attachment overriding the math. This is where families lose the most.

Must‑Read → Squeezed Out? A 12‑Month Decision Guide for 300–1,000 Cow Dairies — Tier 3 pillar, December 2025.

From the human side → More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run — what the corridor squeeze looks like at the kitchen‑table level.

What This Means On Your Next Statement

Maple Ridge’s 50¢/cwt basis slide didn’t show up in herd software, ration sheets, or somatic cell graphs. It showed up in 24 months of milk checks — and it turned a robot decision into a corridor decision. Dos Arroyos sees the same pressure on the horizon and is leaning into it because its composite contract and its plants give it room.

Your next pound of milk is worth what your corridor is willing to pay for it, less what hauling and base‑excess take on the way there.

Pull your current milk supply agreement and your last three milk checks tonight. Find the language that governs base‑excess, hauling, and any “marketing” or “balancing” adjustments. Match that language against the basis trend you’ve actually lived since 2024.

What does your current processor contract say about basis and base‑excess when your region’s milk goes long — and does that language describe the corridor you’re still in, or the one you used to be in?

Key Takeaways

- A clean herd report won’t save you from a bad corridor. Maple Ridge’s 50¢/cwt basis slide plus the post‑2025 FMMO Class III hit stacks to ~$1.89/cwt — about $221,760/year on 600 cows shipping ~144,000 cwt.

- Stress‑test on your real basis, not the USDA all‑milk price. If your lender won’t run a corridor case with trailing 24‑month basis and 15–30% marginal hauling, the spreadsheet that says robots pencil isn’t the one you should bet on.

- The capex question changed shape. Below 1.20× DSCR on the corridor case, freeze any non‑essential project. Below 1.25× even with national‑case math, scaling isn’t defensible without a written core‑supply commitment.

- Pick your lane on a written timeline — scale, pivot, or exit — inside 12 months. Stall, and the basis keeps deciding for you while $15K–$45K/quarter of equity quietly walks off the farm.

This analysis uses composite operator profiles (Maple Ridge, Dos Arroyos) drawn from Bullvine’s Processing Paradox dataset. Contract structures described are illustrative composites and do not describe the actual contracts of any named processor.

Learn More

- The New FMMO Rule Costs a 500-Cow Dairy $97,750 a Year – Before a Mile of Freight — Arms you with the specific math to navigate the 2025-2026 make-allowance phase-in. It reveals how an 85–93¢/cwt hit on Class III and IV milk prices can trigger structural losses of nearly $100,000 annually for 500-cow herds.

- Squeezed Out? A 12-Month Decision Guide for 300-1,000 Cow Dairies — Delivers a tactical 12-month survival framework to protect family equity as mid-size dairies face a $5-7/cwt cost disadvantage. This guide helps you identify your strategic path—scale, specialty, or exit—before market forces choose for you.

- Dairy Lending 2026: Why Your Banker Says No at 7% Money — Exposes the cold math inside your banker’s underwriting model as 7% interest rates add $1.07/cwt to debt service. This briefing reveals the stress-test thresholds needed to secure capital while protecting your 1.0× debt-service coverage ratio.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.