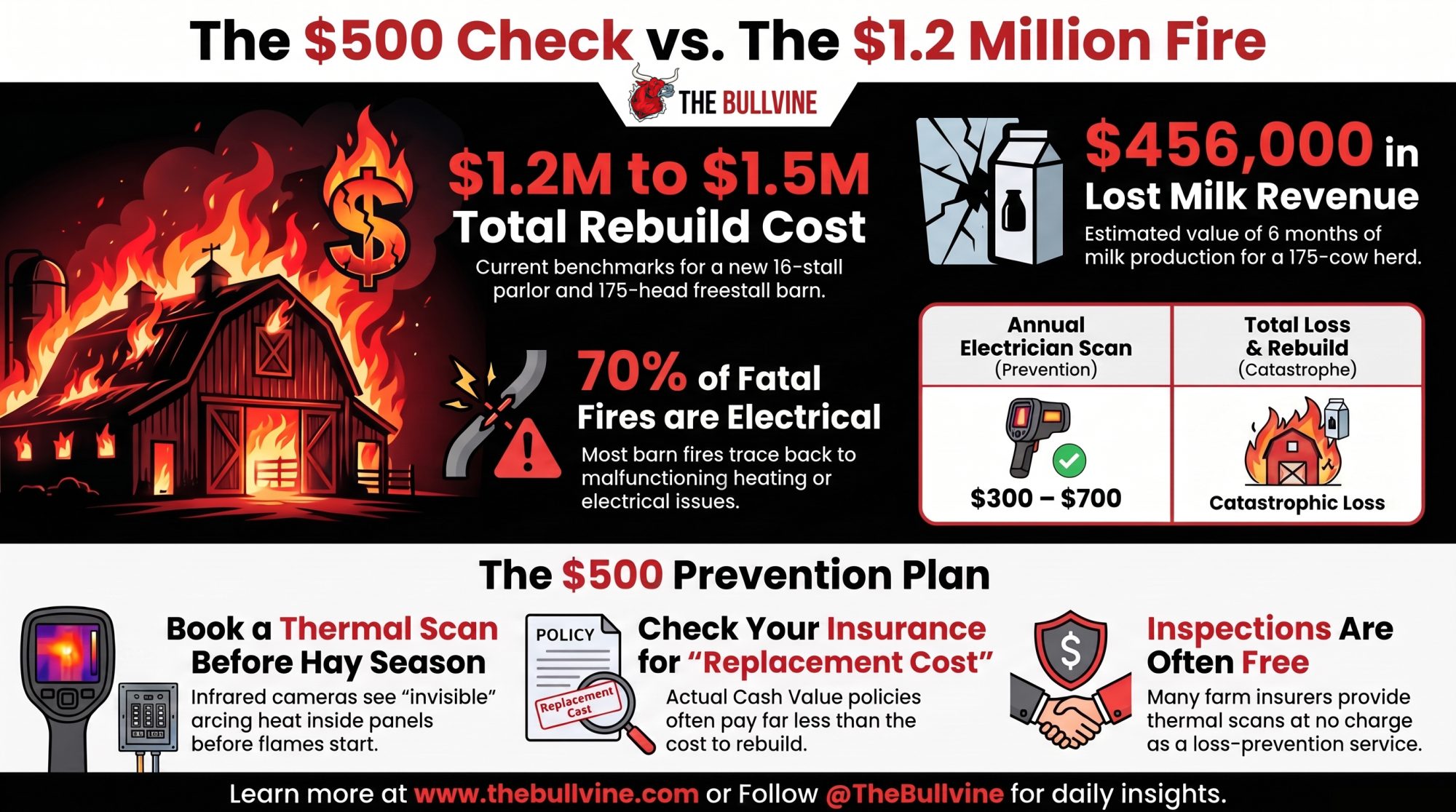

A passerby’s 4:45 a.m. call got all 175 cows out. The barn and parlor? Over $1M, gone. Here’s the ~$500-a-year check that would’ve caught it first.

The short version: Book an electrician’s walkthrough and thermal scan before hay season — $300–$700 a year, often free through your insurer — because the alternative is a $1.2M+ rebuild and roughly $456,000 in lost milk while you figure out where to milk. Guttmann Dairy near West Bend, Wisconsin lived the alternative on June 22. Every cow got out; the barn and parlor didn’t.

At 4:45 on the morning of June 22, somebody who didn’t own a single cow at Guttmann Dairy drove past the farm on Trading Post Trail in the Town of Farmington, Wisconsin, saw flames on the east side of the barn, heard an electrical buzzing sound, and called it in — then alerted the family. That call is why the herd is alive.

The barn and the milking parlor didn’t make it. Total loss. Damage over $1 million. Nobody — no person, no animal, no firefighter — was hurt.

Here’s the part the standard news coverage skipped, and it’s the financial reality that should keep you up at night: the passerby was luck. You can’t schedule luck. But the thing that would’ve caught that buzzing weeks earlier? That you can schedule. It costs about what a routine vet call runs. And almost nobody on a legacy-barn dairy actually does it.

What actually happened at the Guttmann farm

The Fillmore Fire Department got the call and rolled. Crews upgraded it to a box alarm fast, then to a Third Alarm as the structure came up fully engulfed. Before it was over, roughly a dozen departments from three counties worked the scene — most of them volunteer crews who climbed out of their own beds to fight another family’s fire.

Elbe Land and Water brought heavy equipment to pull out a large amount of stored straw so the fire wouldn’t feed on it, and to clear the collapsed structure. Trading Post Trail stayed closed about six hours. Guttmann Dairy milks 175 cows on roughly 600 acres near West Bend, and all of them came through unharmed.

The Fillmore Fire Department said investigators believe an electrical issue caused the fire, and the investigation is ongoing; arson was ruled out. One early report placed the suspected source at an electrical panel just outside the structure. The final fire marshal’s report isn’t out yet, so treat the cause as suspected for now. But “suspected electrical” on an older dairy barn isn’t a whodunit. It’s a pattern with a price tag most operators have never added up.

Why does a buzzing sound mean your barn is at risk?

That noise the passerby heard has a name: an electrical arc. A loose lug, a corroded connection, a wire a mouse chewed over the winter — something’s pushing current across a gap it shouldn’t, throwing heat every second it runs.

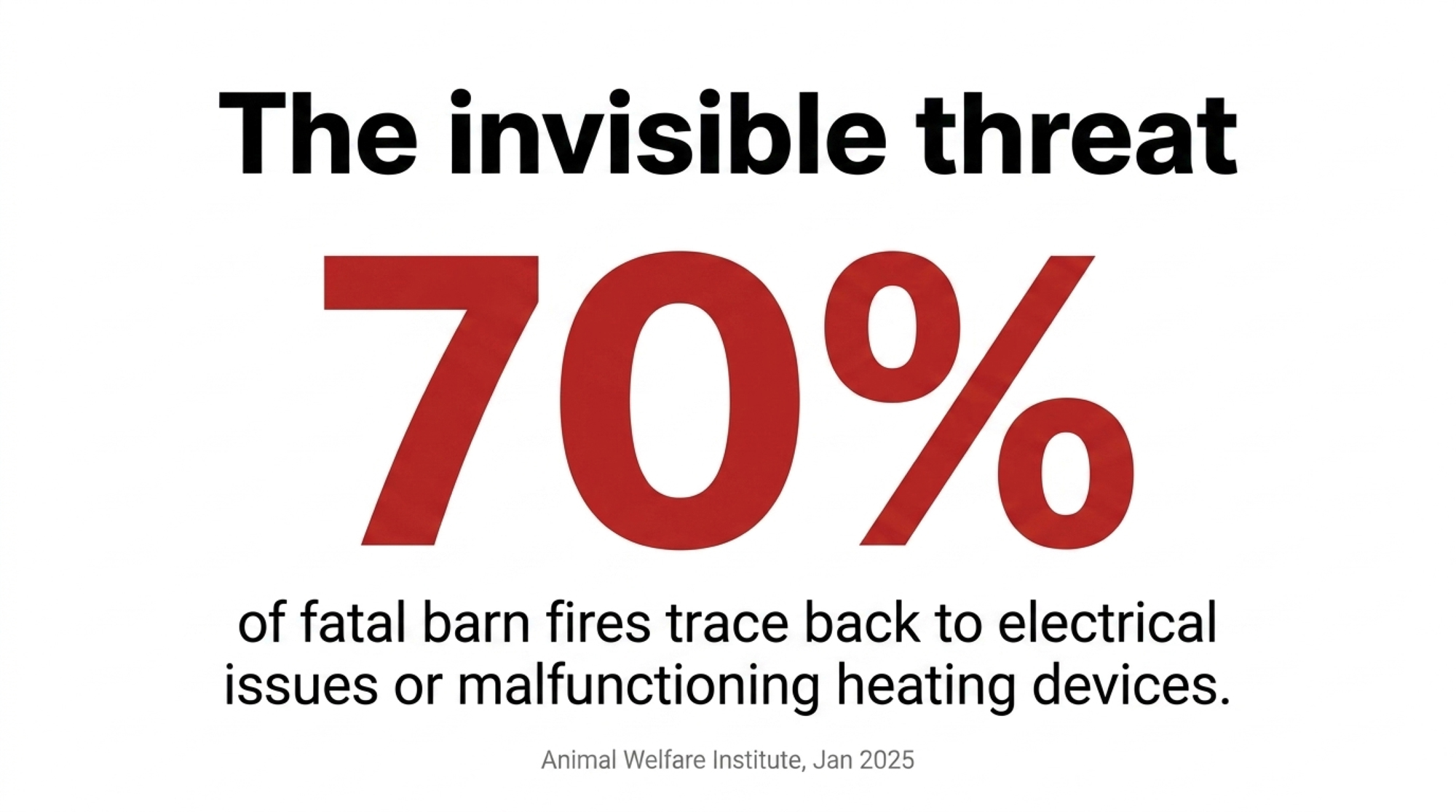

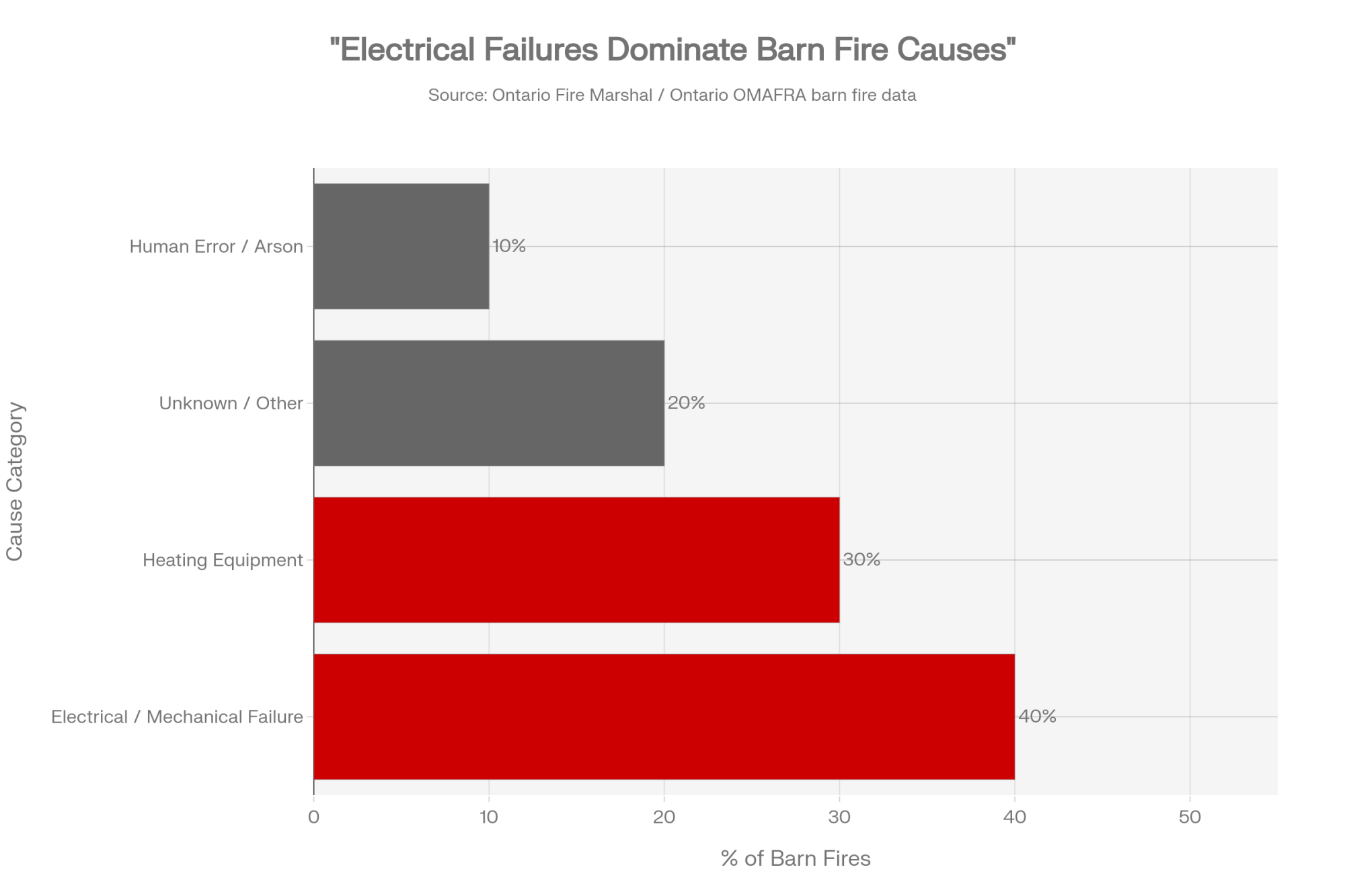

Pull the cause data specifically for barn fires and it gets ugly. In the Animal Welfare Institute’s January 2025 report, of the 111 fatal barn fires where investigators pinned down a cause, about 70% traced back to a malfunctioning heating device or other electrical issue. Canadian numbers tell the same story: the Ontario Ministry of Agriculture puts faulty electrical systems behind roughly 40% of all barn fires, and Ontario’s Fire Marshal logged 113 barn fires in 2023 at an average loss of $808,000 each, with electrical and mechanical failure the leading determined cause. This isn’t abstract — The Bullvine covered the Buckland Holsteins fire near Coaticook, Quebec, in June 2025, where more than 160 head died and the family, too, suspected an electrical cause.

A dairy barn is about the worst home you could design for aging wiring. Ammonia eats connections. Washdown moisture finds every gap. Dust and hay chaff settle on the panel face, and mice chew insulation all winter long. The National Electrical Code wrote a whole section — Article 547 — just for farm buildings, because they chew up wiring in ways a house never does. Plenty of 100-to-500-cow family dairies across the Upper Midwest are still running panels put in during the 1970s, ’80s, or early ’90s, long before arc-fault protection was even required. If you’ve spent years chasing unexplained electrical trouble in the barn, you already know how hard these systems are to read.

| Risk Factor | Signs to Look For | Risk Level | Recommended Action | Timeline |

|---|---|---|---|---|

| Panel age >15 years | No arc-fault breakers; old fuse-style boxes | 🔴 HIGH | Thermal scan + electrician evaluation | Within 30 days |

| Ammonia / moisture exposure | Corroded lugs; green-white deposits on terminals | 🔴 HIGH | Clean connections; replace corroded hardware | This month |

| Rodent activity near wiring | Mouse droppings near junction boxes; chewed insulation visible | 🔴 HIGH | Treat as fire countdown; call electrician immediately | This week |

| Pre-hay season dust loading | Visible dust/chaff on panel face; cobwebs on breakers | 🟠 ELEVATED | Blow out panel; schedule scan before first cutting | Before hay season |

| NETA thermal threshold exceeded | >15°C differential between matched components | 🔴 CRITICAL | Per NETA standard: repair immediately | Same day |

| No thermal scan on record | Cannot recall last infrared inspection | 🟠 ELEVATED | Book scan; call insurer first — many cover it free | Within 30 days |

| Aluminum wiring (1965–1973 build) | Silver-colored wire at panel; marked “AL” | 🟠 ELEVATED | Request co-ALR devices or full rewire assessment | This season |

Now put the calendar on top. Summer is peak barn-fire season, and June sits right in the teeth of it. You’re running full ventilation and vacuum load exactly when hay season lays a fresh coat of dust and cobwebs over every panel. Guttmann burned June 22. That timing isn’t a coincidence — that’s the season doing what it does.

And here’s the kicker: you can’t see an arcing connection. The hot spot lives inside the box, behind the cover, at a lug that looks fine right up until the morning it doesn’t. A thermal-imaging camera sees it. An electrician’s infrared scan reads the heat coming off every connection and flags the one running hot — weeks or months before it fails. Under the NETA infrared inspection standard, more than a 15°C difference between two components doing the same job is a major discrepancy — repair it immediately. Many farm insurers will run that scan for you at no charge, and most operators have never asked.

What’s cheaper — the inspection or the rebuild?

| Prevention Item | Frequency | Annual Cost | 20-Year Total | Notes |

|---|---|---|---|---|

| Electrician barn walkthrough & panel check | Annual (spring) | $150–$300 | $3,000–$6,000 | Often free via insurer loss-prevention program |

| Thermal imaging scan | Annual (pre-hay season) | $200–$500 | $4,000–$10,000 | Free through many farm insurers — call before booking |

| GFCI outlet protection (wet zones) | One-time retrofit | $15–$30/outlet | $500–$1,500 total | One-time; code-required on new construction since 2002 |

| Arc-fault circuit interrupter upgrade | One-time per panel | $200–$600/panel | $600–$1,800 total | Addresses failure mode, not just symptom |

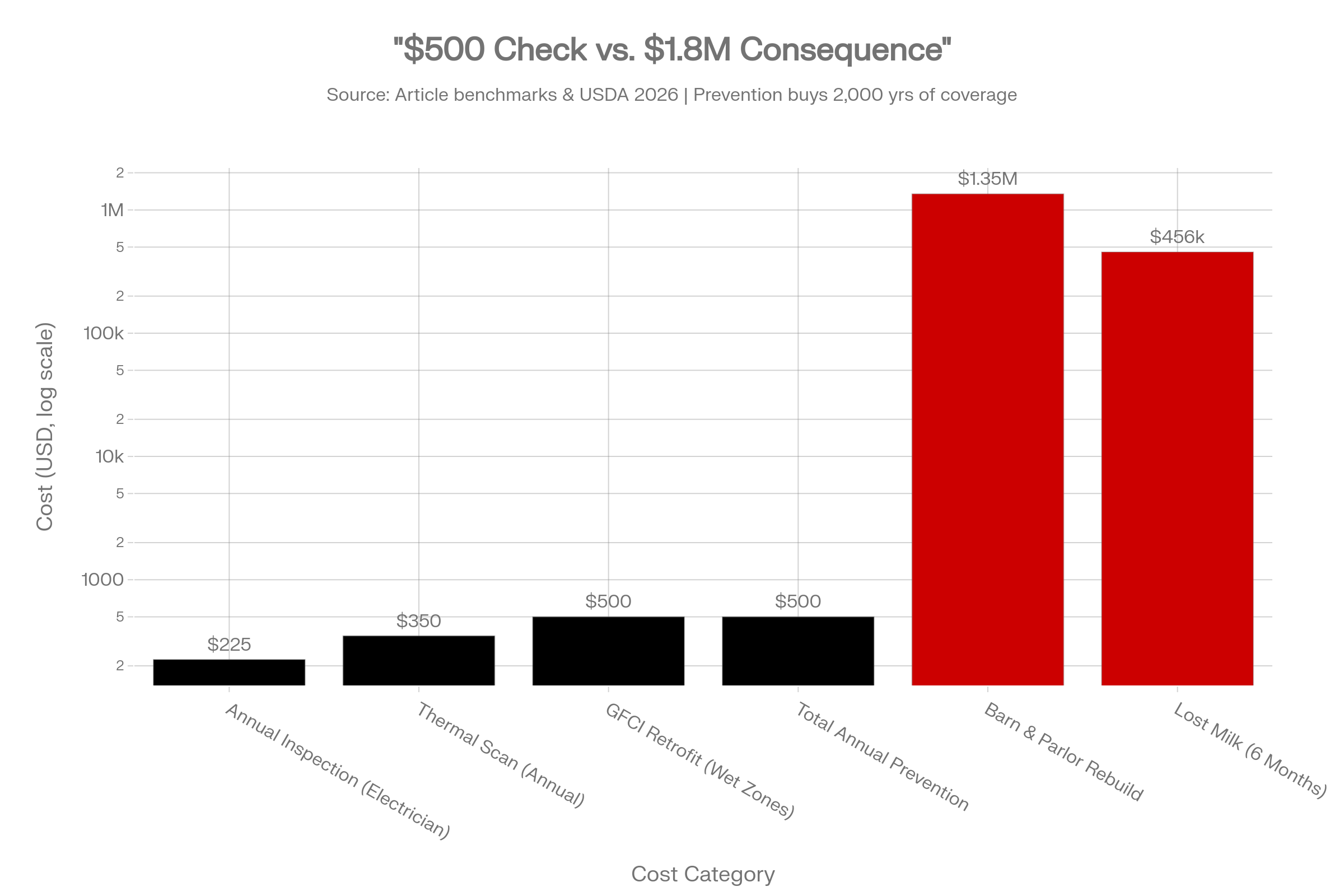

| Total annual maintenance spend | Annual | ~$500/yr | ~$10,000 | Less if insurer covers scan |

| Single total-loss event (rebuild + lost milk) | One event | N/A | $1.8M+ | 🔴 Prevention = $0.04 per $100 of building protected |

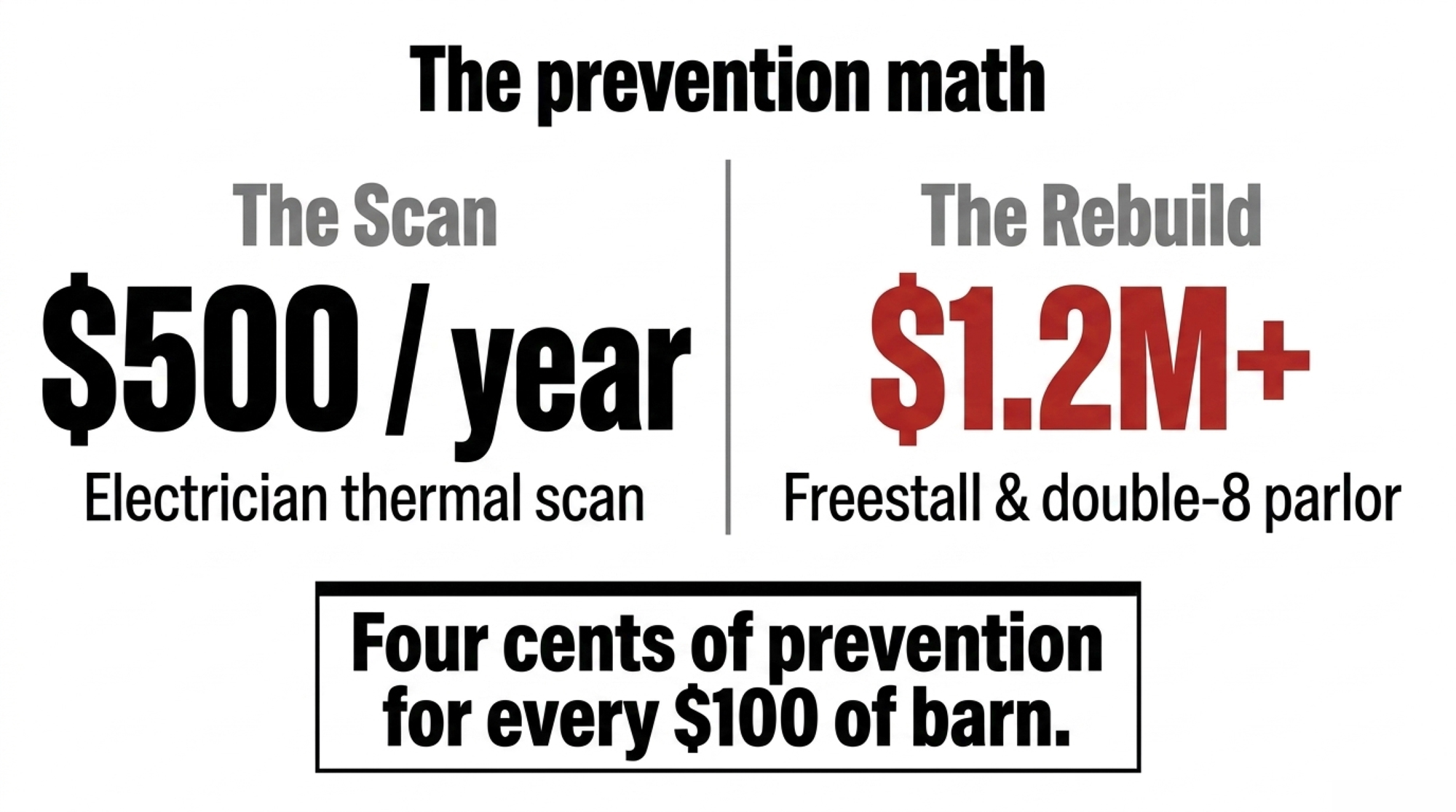

This is where the Guttmann story stops being sad and starts being useful. Put the two numbers side by side and let the arithmetic pick the winner.

Start with prevention. A licensed electrician’s barn walkthrough and panel check runs somewhere around $150 to $300, depending on your barn’s size and how many panels you’ve got. Add a thermal scan at $200 to $500 — or free, if your insurer offers it as a loss-prevention service. GFCI protection for your wet zones runs $15 to $30 per outlet installed. Call it a working budget of $300 to $700 a year, and less if the insurer covers the scan. Costs are directional and vary by region and barn size.

Now the rebuild. Here’s what it costs to put a barn and parlor back up at current benchmarks:

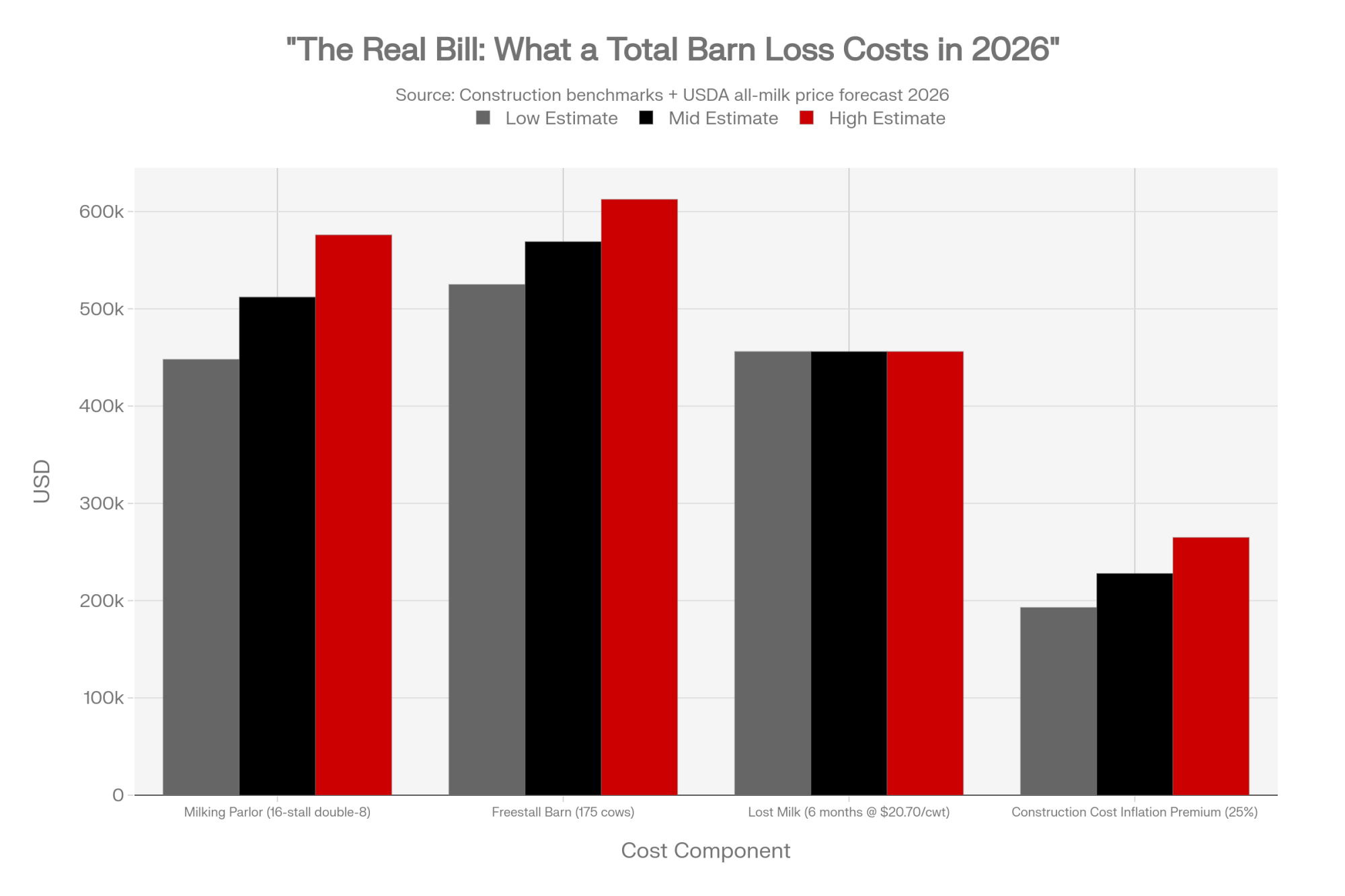

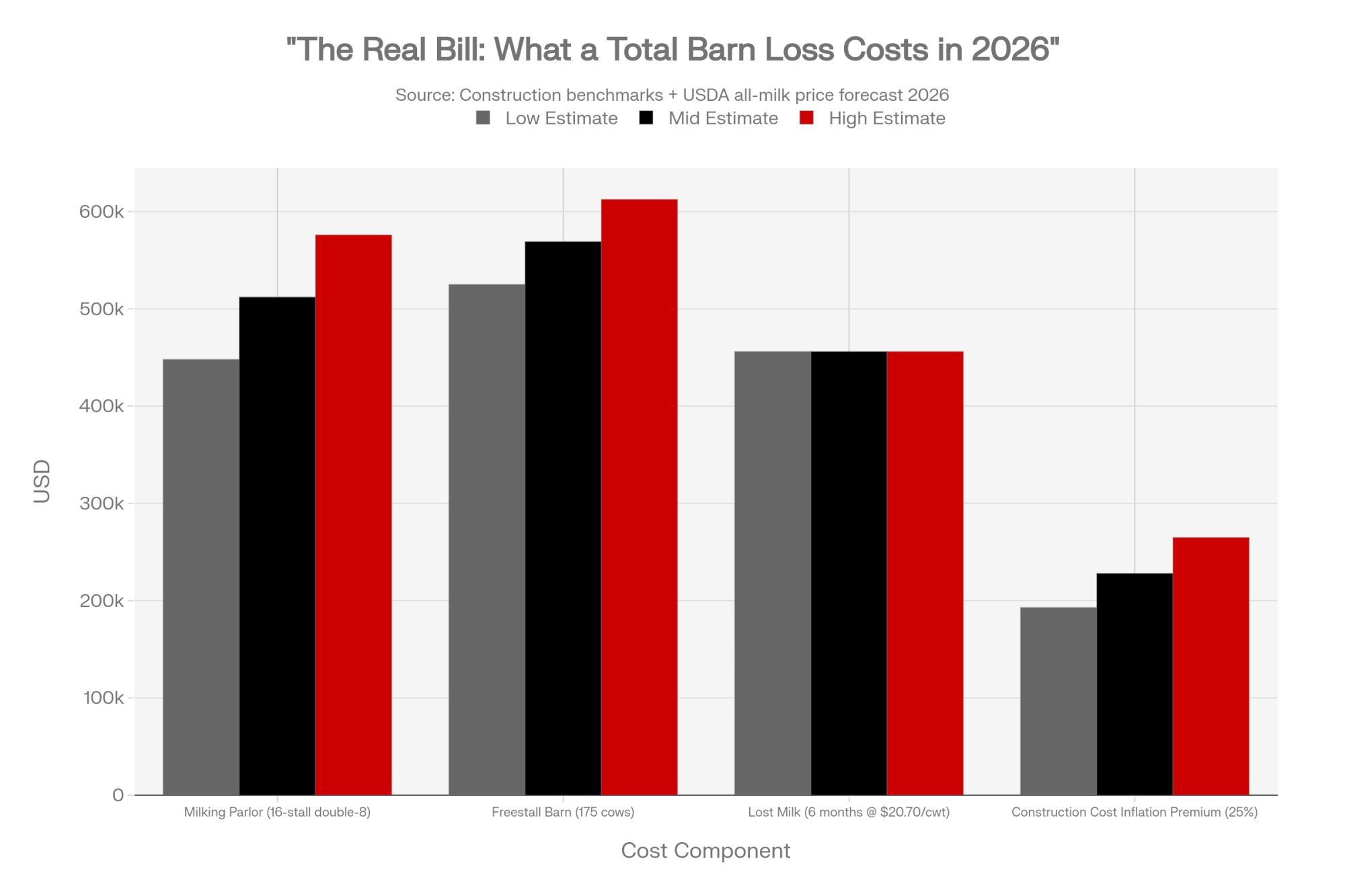

The Rebuild Reality (current benchmarks)

- New parlor with structure: $28,000 to $36,000 per milking stall

- Double-8 parlor (16 stalls): $448,000 to $576,000 — about $512,000 at the midpoint

- Freestall barn: $3,000 to $3,500 per cow — roughly $525,000 to $613,000 for a 175-head herd

- Total estimated cost: $1.2 to $1.5 million, once you fold in the 15–35% construction-cost inflation since those 2022 benchmarks were set

That squares with the “over $1 million” Washington County put on the Guttmann loss.

Here’s the barn-math moment worth mapping to your own place. Say you spend $500 a year on an inspection and a scan. Over 20 years, that’s $10,000 — real money, no argument. Against it sits a rebuild north of $1.2 million. Run the ratio: you’d have to inspect that barn every year for more than 2,000 years before the prevention spend added up to a single total loss. Put it the other way — the annual check costs roughly four cents for every $100 of building you’re protecting. Name another decision on your operation that pays like that.

Where do you milk tomorrow morning?

The rebuild isn’t the whole bill. There’s a second number nobody budgets for, and it starts running while the concrete’s still curing.

The Guttmanns had an answer to this one. Within a day, the milking herd was moved to local farms and was already being milked the next morning — the machinery of a dairy community doing what it does when a neighbor goes down. That’s not luck. That’s a network of nearby operations with parlors and the room to absorb someone else’s cows on a moment’s notice.

Run the number that arrangement is quietly covering. Wisconsin cows averaged 25,599 pounds each in 2025 — about 70 pounds a day — so a 175-cow herd puts up roughly 12,250 pounds of milk every single day that has to go somewhere. Six months of that milk at USDA’s $20.70/cwt 2026 all-milk forecast is around $456,000 in milk value alone, before you count hauling, temporary housing, or the labor of milking at somebody else’s place twice a day. That’s the question the wire story never asked. If your parlor burned tonight, where do your cows get milked at 5 a.m. tomorrow — and if you can’t name the farm, that’s your homework from this whole story.

What does your insurance actually cover — and what won’t it?

Say the worst happens anyway. Now it’s not whether you’re insured — it’s how. And most operators don’t find out until an adjuster is standing in the ashes.

Two gaps eat dairy families alive after a parlor fire. The first is cash value versus replacement cost. If your 30-year-old parlor is written on an actual-cash-value policy, the check reflects what a depreciated old parlor is “worth” — not what it costs to rebuild new. A published farm-insurance explainer lays the trap out plainly: whatever an older parlor is insured for on a cash-value policy is roughly what you’ll get, often far below the cost to rebuild. The second gap is co-insurance. Most farm policies carry an 80% to 90% co-insurance clause, and if your barn’s insured below that share of true replacement value, you eat a penalty on every claim.

| Coverage Question | What Most Operators Assume | What Many Policies Actually Pay | Risk Flag |

|---|---|---|---|

| Barn/Parlor Valuation Basis | Full replacement cost to rebuild new | Actual cash value — depreciated 30-yr-old structure | 🔴 Often 40–60% less than rebuild cost |

| Co-Insurance Clause | Not aware it exists | 80–90% of insured value required; penalty if under-insured | 🔴 Penalty applied to everyclaim if barn is undervalued |

| Business Interruption Trigger | Pays when parlor burns down | Requires “necessary suspension of operations” — milking off-farm may not qualify | 🔴 Operator keeps milking, insurer may deny BI claim |

| Extra Expense Coverage | Assumed included | Often excluded or capped — trucking, rental facilities, custom milking fees | 🔴 $50K–$100K in emergency logistics may be out-of-pocket |

| Electrical Panel Endorsement | Standard policy covers all fire causes | Some policies exclude “gradual deterioration” of aging infrastructure | ⚠️ Depends on policy language — verify in writing |

Business interruption is the sneaky one — coverage that doesn’t always cover the interruption. It usually requires a “necessary suspension of operations.” But a dairy scrambles. You find a neighbor’s parlor, you hire a custom milker, you keep the milk moving. Does the policy still pay when you’re milking off-farm — or only if you stop cold? And the extra costs — the hauling, the rental, and the custom-milking contract — covered, or on you?

Send your agent these three questions this week — in writing, and get the answers in writing. Screenshot them, or paste them straight into an email:

1. Today’s replacement vs. depreciated cash value: Is my barn and parlor insured at today’s full, inflation-adjusted replacement cost, or a depreciated actual cash value?

2. Off-farm business interruption: If my parlor is a total loss, does my business-interruption coverage pay out if I temporarily milk my herd at a neighbor’s farm, or only if I shut down operations entirely?

3. Extra-expense coverage: Does my policy cover the emergency logistical costs — temporary facilities, emergency trucking, and custom-milking fees — while I rebuild?

A verbal “yeah, you’re covered” is worth nothing at 4:45 a.m. Paper only.

Options and trade-offs: where to put your first $500

Book the electrician’s walkthrough and thermal scan — this month. This one’s for every operator running a panel older than 15 years, which is most legacy barns in the region. It takes a phone call and a few hundred dollars, and your insurer may cover the scan outright. The limit: a scan is a snapshot, not a monitor. It catches what’s hot the day it runs, so make it a spring ritual, not a one-and-done — before hay season, while the dust load is still light. That’s the 30-day move.

Retrofit GFCI and arc-fault protection on the wet-zone and parlor circuits. Bigger spend, deeper fix — it goes after the failure mode instead of the symptom. It earns its keep when the walkthrough turns up aluminum wiring, corroded connections, or a panel that predates modern protection standards. The trade-off is real dollars up front and a licensed electrician’s time. But it’s the difference between finding tomorrow’s hot spot and never letting it happen.

Build the continuity plan before you need it. The Guttmanns had neighbors ready to take their cows within a day. Do you? Line up which operation could physically absorb your string, learn your co-op’s emergency protocol, and keep your hauler’s number where you can grab it half-asleep. And watch this signal: as herds in your area consolidate and parlors get bigger, the number of neighbors who could absorb 175 extra cows twice a day keeps shrinking. The backup that existed five years ago may not exist next spring. Confirm it now, not in the smoke.

Key Takeaways

- If your panel is older than 15 years and hasn’t been thermally scanned, book the scan within 30 days — call your insurer first, because many run it free.

- If you can’t name the operation where your cows would milk tomorrow morning, you’ve got a hope, not a plan — fix it with two phone calls this week.

- If your parlor sits on cash-value coverage, assume the check won’t rebuild it, and get the replacement-cost answer in writing before you need it.

- If you spot mouse droppings near a junction box, treat it as a fire countdown, not a pest problem — rodent-chewed insulation is a documented ignition source.

The Guttmanns got every cow out because a stranger heard a noise and made two phone calls before dawn. As one neighbor put it after the smoke cleared: this family will rebuild, no one was hurt, and no cows were lost — which is what matters most. But luck doesn’t run on a schedule. The inspection does — about $500, before hay season, before 5 a.m.

So carry one honest question back out to your own barn this morning: when’s the last time anyone looked inside your panel? If the answer is “I can’t remember,” you already know your next move. To help you take it, we’ve put a downloadable insurance-gap worksheet and the full per-stall prevention model inside this week’s Bullvine Weekly — the deeper barn math the daily coverage skips.

The Barn-Math Exposure Calculator

Plug in your farm’s metrics to calculate your true capital risk, daily interruption losses, and custom prevention payback ratio.

Your panel age or lack of thermal scanning flags your operation as a high hazard. Book an inspection immediately.

You would need to inspect this barn every year for 3,080 years before the $500 annual check spend matches a single total loss event.

Reporting note: Incident details are drawn from the Washington County Sheriff’s Office (Case #2026-22892) and Wisconsin news coverage (TMJ4, WHBL, Fox6, WISN, Wisconsin State Farmer) and Dairy Star’s July 11 report on the farm. The fire’s cause remains under investigation and is reported here as suspected electrical; investigators have ruled out arson. Rebuild and lost-revenue figures are estimates built on published construction benchmarks and USDA production and price data, with stated assumptions — they are not based on the Guttmann family’s actual policy or losses.

Learn More

- $1000 in Diesel or $10000 Down the Drain: The Storm Math Every Dairy Needs Before the Next Big Blow — Arms you with critical generator load calculations and fuel reserves to prevent a $10,000 power-outage loss, showing how preparation beats scrambled crisis-management when your mechanical infrastructure fails.

- Vagts, Normans, Haldersons: $18 Million in Stray Voltage Verdicts. And a $3000 Test No One Told Them Existed. — Exposes the insurance loopholes and utility testing blind spots that cost dairy families hundreds of thousands in unrecoverable milk losses, detailing how a slow-motion electrical issue can bypass standard property policies.

- Is Stray Voltage Stealing 20 Pounds Per Cow from Your Dairy? — Delivers the technical facts on how resistance differences alter the electrical currents cows actually feel, helping you identify low-voltage ground leaks that quietly drag down production and claw back daily margins.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.