Saputo opened 2026–27 at A$8.80/kgMS; farmers wanted A$9.50. On a 400-cow herd that’s roughly A$119,000 a year — and a step-up nobody’s promised won’t cover July.

Executive Summary: The A$119,000 question for southern suppliers this month is whether they can carry Saputo’s A$8.80–8.90/kgMS opening — near the bottom of a board topping out at Bulla’s A$9.95 — when farmers said they needed A$9.50 just to cover surging costs. On a 400-cow Victorian herd shipping around 170,000 kgMS, that A$0.70 gap is roughly A$119,000 a year, and against the top of the board it stretches past A$170,000. ADF president Ben Bennett says processors aren’t gouging — “there’s no fat in the system” with fuel, freight, and exchange rates all biting — but that doesn’t change what an A$8.80 opening does to your July–September cash flow. Producers are betting on a mid-season step-up, except Saputo’s last one was A$0.15/kgMS, came in October, and was tied to exclusive supply — so it never touched the early-season squeeze. With Fonterra exiting its Australian consumer business and Lactalis absorbing Mainland, you’ve also got fewer doors to walk your milk to, which is exactly why a soft opening costs a processor less than it used to. The same lesson travels north: Saputo buys inside Canada’s supply-managed floor but sets its own number in deregulated Australia — so your real protection is the structure under your cheque, not the company on it. Run your own cost of production against the board this month, before July 1, and decide whether you can carry the gap or need to move.

| Cost Driver | Reported Change | Source / Context | Risk Level |

|---|---|---|---|

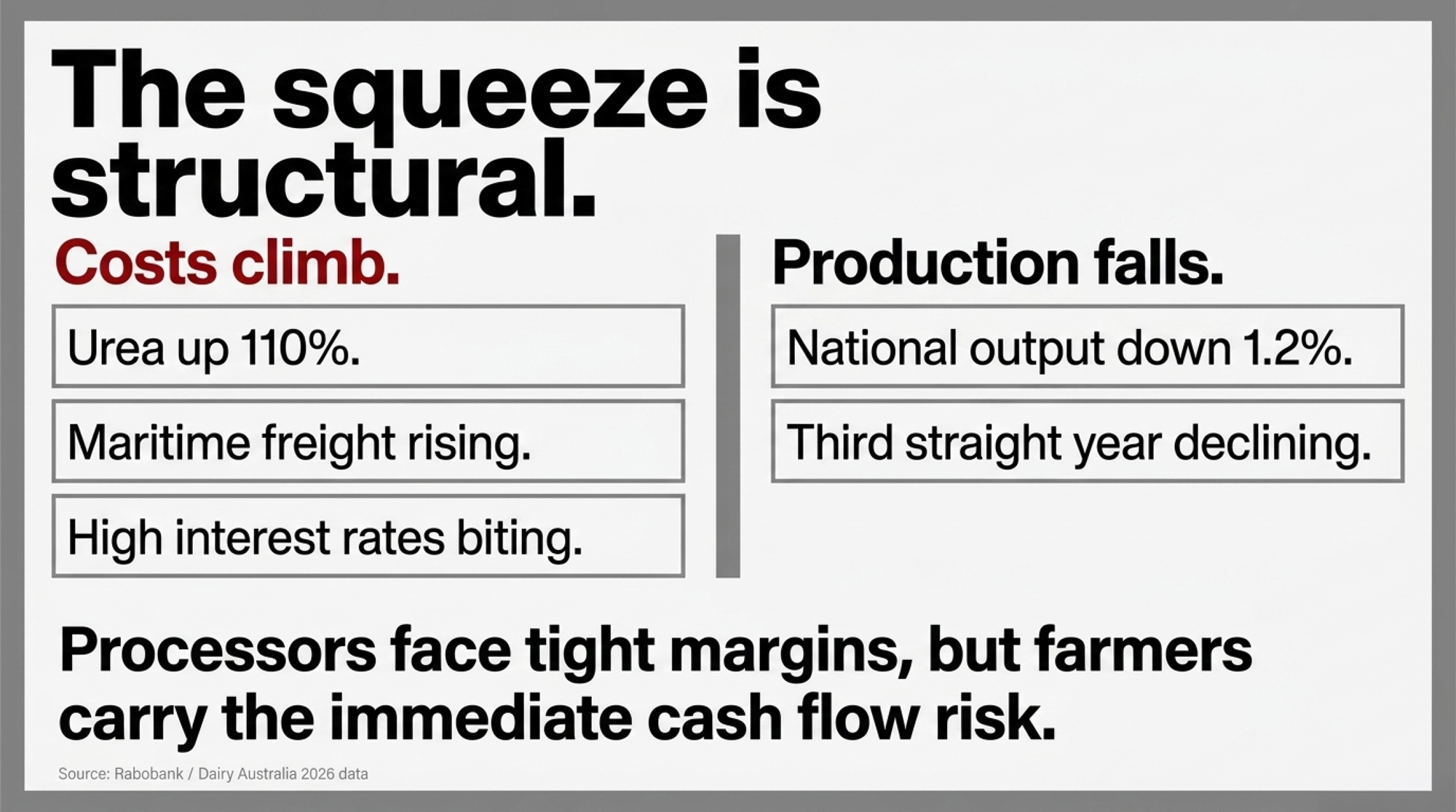

| Urea (nitrogen fertilizer) | ↑ ~110% YoY | Stuart Timms / The Weekly Times | 🔴 Critical |

| Maritime freight (Baltic Dry Index) | ↑ Significant YoY | Article (Baltic Dry Index cited) | 🔴 High |

| Fuel & transport costs | ↑ Ongoing | ADF president Ben Bennett statement | 🟠 Elevated |

| Interest rates | ↑ Elevated | Rabobank “limited margin for error” | 🟠 Elevated |

| Labour costs | ↑ Climbing | Rabobank 2026–27 outlook | 🟡 Moderate |

| Exchange rate headwinds | ↑ Unfavorable | Ben Bennett statement | 🟡 Moderate |

| Milk opening price (Saputo) | A$8.80 (–A$0.70 vs benchmark) | Dairy Code disclosure | 🔴 Critical |

Stuart Timms milks 1,000 KiwiCross cows on a pasture-based system at Elingamite North, in western Victoria’s dairy country. His nitrogen fertilizer bill jumped sharply year-on-year, he told The Weekly Times, and he isn’t alone — urea has run up roughly 110%, and maritime freight is up hard on the Baltic Dry Index. The costs climb while the opening price steps down. That’s the squeeze heading into 2026–27, and it’s real cash flow out the door before the season even starts.

And if you ship to a private processor anywhere — Canada or the US included — the mechanics behind it are worth ten minutes. Saputo, one of the dominant buyers in southern Australia, also runs plants across Quebec, Ontario, and Wisconsin.

What’s Changing and Why

The soft opening didn’t land in a vacuum. Western Victorian producers are climbing out of one of the worst dry spells some districts have seen in decades, and a better autumn has finally delivered pasture. A strong March (up 2.8%) wasn’t enough to lift the full 2025–26 season, which still closed down about 0.7%.”

The contraction underneath it is real. Rabobank reports that season-to-date Australian milk production as of January 2026 was down 1.2% year-on-year, and forecasts another 1.2% national decline for 2026–27 — the third straight year of falling output. The bank’s read on the season is blunt: a “limited margin for error,” with fuel, fertilizer, labour, water, and interest costs all climbing. The farms feeling it worst are pasture-based southern manufacturing-pool suppliers in Victoria and Tasmania — operations like Timms’s — who can’t lean on a fresh-milk premium to cushion a flat opening number.

What Did Farmers Actually Ask For?

A$9.50/kgMS. That was the benchmark producers and advocacy groups collectively targeted as the minimum to offset inflation and elevated interest rates. Saputo’s A$8.80 floor sits A$0.70 below that line; even its A$8.90 top end is A$0.60 short.

The processors who released opening prices this week, under the Dairy Code of Conduct’s requirement to publish a month before the financial year, spread across a wide band:

| Processor | 2026–27 opening (A$/kgMS) |

| Bulla | A$9.15–9.95 |

| Dairy Farmers Corporation | A$9.20–9.80 |

| Frestine | A$9.39 |

| Lactalis | A$8.65–9.45 (Mainland) |

| KYValley Dairy | A$8.45–9.29 |

| UDC | A$9.20 |

| Australian Consolidated Milk | A$9.10 |

| Bega | A$9.04 |

| Burra Foods | A$8.90–9.40 |

| Saputo | A$8.80–8.90 |

Note: Opening weighted averages; individual farm-gate prices vary by region, components, and loyalty

That spread is the story: same season, same cost pressures, and Saputo sitting near the bottom of a board that runs all the way up to Bulla’s A$9.95 top end.

A Wound That Goes Back to 2016

To understand why a soft opening stings the way it does, go back to the Murray Goulburn collapse. For decades, Murray Goulburn was the farmer-owned co-op that anchored southern Australian dairy, processing more than a third of the national milk pool. In April 2016, it slashed its farmgate price mid-season, clawing back money farmers had already earned and spent. Suppliers were left carrying debt on milk they’d already shipped.

| Date | Event | Impact on Suppliers |

|---|---|---|

| Pre-2016 | Murray Goulburn farmer co-op anchors southern AU dairy | Farmers held ownership stake; co-op structure provided implicit floor |

| April 2016 | MG slashes farmgate price mid-season; claws back earnings | Suppliers left with debt on milk already shipped and spent |

| 2016–17 | MG never recovers; seeks buyer | Structural collapse of farmer-owned processing in southern AU |

| 26 Oct 2017 | Saputo announces MG acquisition | Transition from cooperative model to private multinational |

| 3 April 2018 | ACCC clears acquisition | Regulatory green light; no ownership alternative offered |

| 30 April 2018 | Deal closes at ~A$1.3 billion | Southern suppliers become price-takers from Montreal-HQ processor |

| 2024–25 | Fonterra exits Australian consumer/ingredients business | Fewer independent buyers at the table |

| 2025 | Lactalis absorbs Mainland assets | Further consolidation; supplier switching power weakens |

| June 2026 | Saputo opens 2026–27 at A$8.80 | Lowest major processor on a A$1.50-wide board; no co-op alternative |

The co-op never recovered. Saputo announced the acquisition on October 26, 2017, the ACCC cleared it on April 3, 2018, and the deal closed on April 30, 2018, for roughly A$1.3 billion. Many southern suppliers once owned Murray Goulburn outright; today, they’re price-takers from a Montreal-headquartered processor. That shift in ownership — not any single price — is what shapes how an opening number lands. The vote to sell wasn’t a mistake. It kept plants running when the alternative was collapse. But it was a permanent trade, and ownership doesn’t come back.

The consolidation didn’t stop there. Fonterra is now exiting its Australian consumer and ingredients business — described by Rural News Group as “a major event” for the market — with Lactalis moving on the Mainland assets. Every time a processor changes hands, suppliers wake up with a new owner and a pricing philosophy they didn’t vote for. Fewer buyers at the table means fewer places for your milk to go when an opening price disappoints. That’s the backdrop to this season’s board: a shrinking pool of processors, each one a little less worried about losing you.

How This Plays Out on Real Farms

Run the numbers on a 400-cow Victorian dairy. Assume about 425 kgMS per cow per year — a conservative pasture figure — which lands annual production near 170,000 kgMS. This is a model with stated assumptions, not one farm’s actual books, so treat it as a yardstick you can hold against your own.

| Scenario | Price (A$/kgMS) | Milk income (170,000 kgMS) | Gap vs. Saputo opening |

| Saputo opening | A$8.80 | ~A$1,496,000 | — |

| Lactalis opening | A$9.30 | ~A$1,581,000 | +A$85,000 |

| Farmer benchmark | A$9.50–9.80 | ~A$1,615,000–1,666,000 | +A$119,000–170,000 |

The gap between Saputo’s A$8.80 opening and the A$9.50 benchmark farmers asked for is about A$119,000 a year on this model herd — just 170,000 kgMS times the A$0.70 difference. Move to A$9.80 top end, and the gap stretches past A$170,000. Same cows, same litres. Different number in the tank.

The point isn’t that any single farm sees exactly those figures. But a A$0.60-to-A$1.00/kgMS difference is no rounding error — it’s six figures on a mid-sized herd. A farm of Timms’s size runs more than twice that exposure. Do it for one season, and you tighten the belt and grind through. Do it across three years of falling income, and you start to see why the milk pool keeps draining.

The Mechanics Behind the Outcomes

Here’s what’s easy to miss staring at the opening letter: opening prices are round one, not the final word. Because the national pool has contracted, plants are under pressure to secure raw milk to keep factories full and cover fixed overheads. Producers are hoping that pressure will force competitive step-ups later in the season to stop milk from defecting to rival buyers.

The processors say the soft board reflects a genuinely tight market, not opportunism. Australian Dairy Farmers president Ben Bennett, who farms at Pomborneit near Colac, put it plainly in a statement: “Processors are hurting too. We’re operating in a tight global environment, and everyone in the supply chain needs to get a return. There’s no fat in the system at the moment.” Bennett pointed to exchange-rate movements, Middle East conflict, fuel and freight costs, and a possible strong El Niño as the forces underpinning the conservative numbers. It’s a fair caution — and it doesn’t change what an A$8.80 opening does to a cash-flow plan.

A step-up is discretionary, and history shows the pattern. Saputo’s recent step-up was A$0.15–0.20/kgMS, tied to exclusive supply, and landed mid-season — not in time for the early-season squeeze. Note the timing and the condition: it arrives well into the season, and only for farms on an exclusive agreement. That doesn’t ease the cash squeeze of July through September — for Timms, the same stretch the fertilizer spike hits hardest — and it doesn’t reach farms outside an exclusive agreement. You carry the early-season risk. The processor keeps the choice. And with Fonterra exiting and Lactalis absorbing Mainland, the southern market has fewer independent buyers than a decade ago — so a soft opening costs a processor fewer defections than it once did.

How Much Does Waiting for the Step-Up Actually Cost You?

Do the math on the wait. A step-up of A$0.15/kgMS across a full year on the 400-cow model is worth about A$25,500. But a step-up announced in October only covers part of the season, so the cash that actually lands is less, and none of it touches the July–September stretch when feed bills and a fertilizer spike hit hardest.

So the real question isn’t “will the price improve?” It’s “can my operation absorb an opening near the bottom of the board for three or four months while I wait on a top-up nobody’s promised — and that’s tied to exclusive supply?” If the answer is no, the step-up isn’t a safety net. It’s a rescue you’re hoping shows up in time.

Why Should a Canadian or US Producer Care About a Victorian Price?

Because the same kind of company operates under very different rules in each market — and those rules, more than the company, determine how much protection is available to the farmer. In Canada, Saputo buys milk within a supply-managed system in which the Canadian Dairy Commission sets the farmgate floor price. In Australia, there’s no administered floor, so the opening number is left to the processor to set, and Saputo’s started at A$8.80. The structure, not the postcode, sets the floor.

None of that is an accusation. Where a system sets a floor, farmers have one; where it doesn’t, the opening number is the processor’s to file. The lesson travels regardless of border: your floor is only as solid as the structure beneath it. If the one thing between your cost of production and your milk cheque is a processor’s discretion, you want to understand that before the next downturn, not during it.

Options and Trade-Offs for Farmers

No single move fixes a soft opening. But suppliers — in Australia and beyond — are working a few real paths.

Pull your supply agreement and read the step-up clause this month

Inside the next 30 days, find the actual language. Saputo’s recent step-up was tied to exclusive supply — is yours? What’s your notice period to switch? This costs you an hour with the contract and a call to your field rep, and the downside is mild: you may learn you’re more locked in than you assumed. Better to know that now than in October.

Benchmark your own cost of production to the cent

The A$9.50 figure was an industry-wide ask, but your real number may sit above or below it. Pull your actual feed, fertilizer, fuel, and labour figures, then run it. There’s no real risk here — and it’s the single most useful number you can carry into any price conversation.

Compare processors on expected season value, not the opening number

This season’s board ran from KYValley’s A$8.45 floor to Bulla’s A$9.95 top — a A$1.50 spread. If you’re free of exclusivity or near a decision, model the likely season-end value, including step-up history, rather than reacting to a single headline. Just remember that with Fonterra exiting and Lactalis consolidating, your switching options are thinner than they were, and switching costs can quietly eat a paper gain.

Watch the supply-contraction signal

A third straight year of national decline eventually changes a processor’s math, because tight supply is the one force that pushes competition onto the opening price. Treat this as the backdrop to every decision above. The catch: “eventually” may move slower than your cash flow can wait.

Key Takeaways

- If you don’t know your exact cost of production in A$/kgMS (or $/cwt), run it this month — you can’t tell whether Saputo’s A$8.80 or anyone’s opening clears your breakeven until you do.

- If your step-up access is tied to an exclusive supply clause, decide before July 1 whether that lock-in is worth the mid-season cents you’re betting on.

- If you’re judging a processor on the opening number alone, stop — this year’s board spanned A$8.45 to A$9.95, so model the likely season-end value before you sign anything.

- If an opening near the bottom of the board would strain your July–September cash flow, treat the step-up as a hope, not a plan, and build your buffer accordingly.

- If consolidation has thinned the buyer base in your region, factor weaker switching power into every contract decision — fewer doors mean less leverage.

- If the only thing under your milk cheque is a processor’s discretion, ask what it would take to put something firmer there — a contract clause, a co-op stake, or a benchmark.

Six months from now, a step-up will probably have landed, and the season-end number will look better than the opening did. The relief will be real. But it’ll be relief you’re renting, not relief you own. So here’s the question worth carrying into the dairy on a cold October morning, after everyone else has moved on: who actually decides where your floor sits — and as the buyers around you keep merging, are you content to leave that decision in someone else’s hands?

Run Your Numbers

Dairy Profit Projector — Saputo’s A$8.80 leaves zero margin on paper, but what does it do to your bottom line? Drop in your herd size, milk price, and ration to see your breakeven milk price, IOFC per cow per day, and whole-herd margin before you sign anything.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Class III Milk Price, DRP, and Your Spring 2026 Risk Plan — Protect your cash flow by sorting risk management into distinct defensive and balanced lanes, arming you with clear market pricing triggers to shield your milk check before margins slide into a danger zone.

- Fonterra’s Bold Gamble: Why The Dairy Giant is Abandoning Consumer Brands — Anticipate structural processing shifts over the next five years as global processors dismantle vertical integration models, exit regional consumer retail spaces, and pivot exclusively toward high-value B2B ingredient manufacturing.

- The Fonterra “Settlement” That Proves Your Co-Op is Playing You for a Fool — Exposes the harsh reality of corporate consolidation by following the money through multi-billion dollar asset sales, proving how processor mergers systematically strip away independent buyer competition and erode farmer bargaining leverage.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.