A 50,000 MT EU powder quota and a protected cheese-name register say the floor’s gone. The barn math, inside.

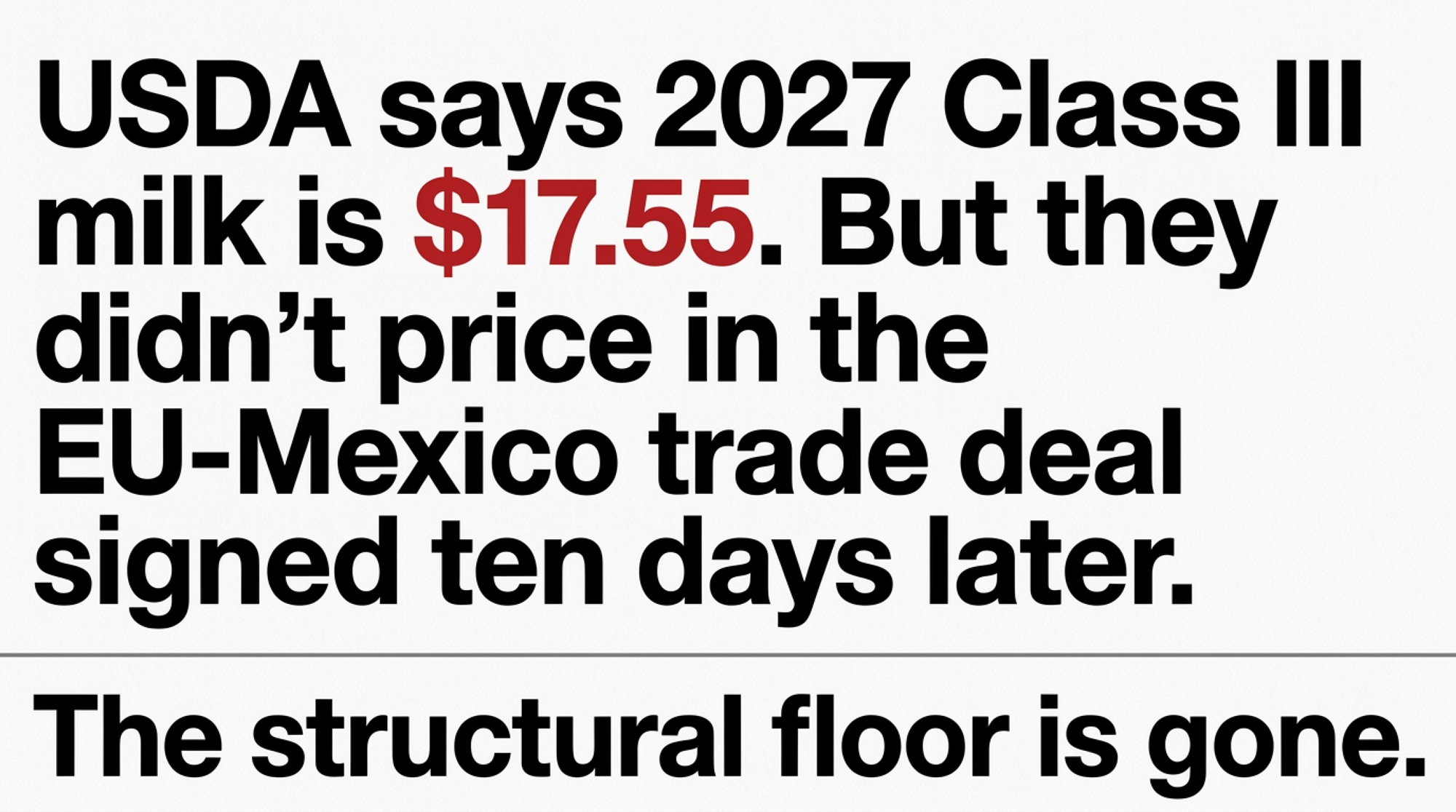

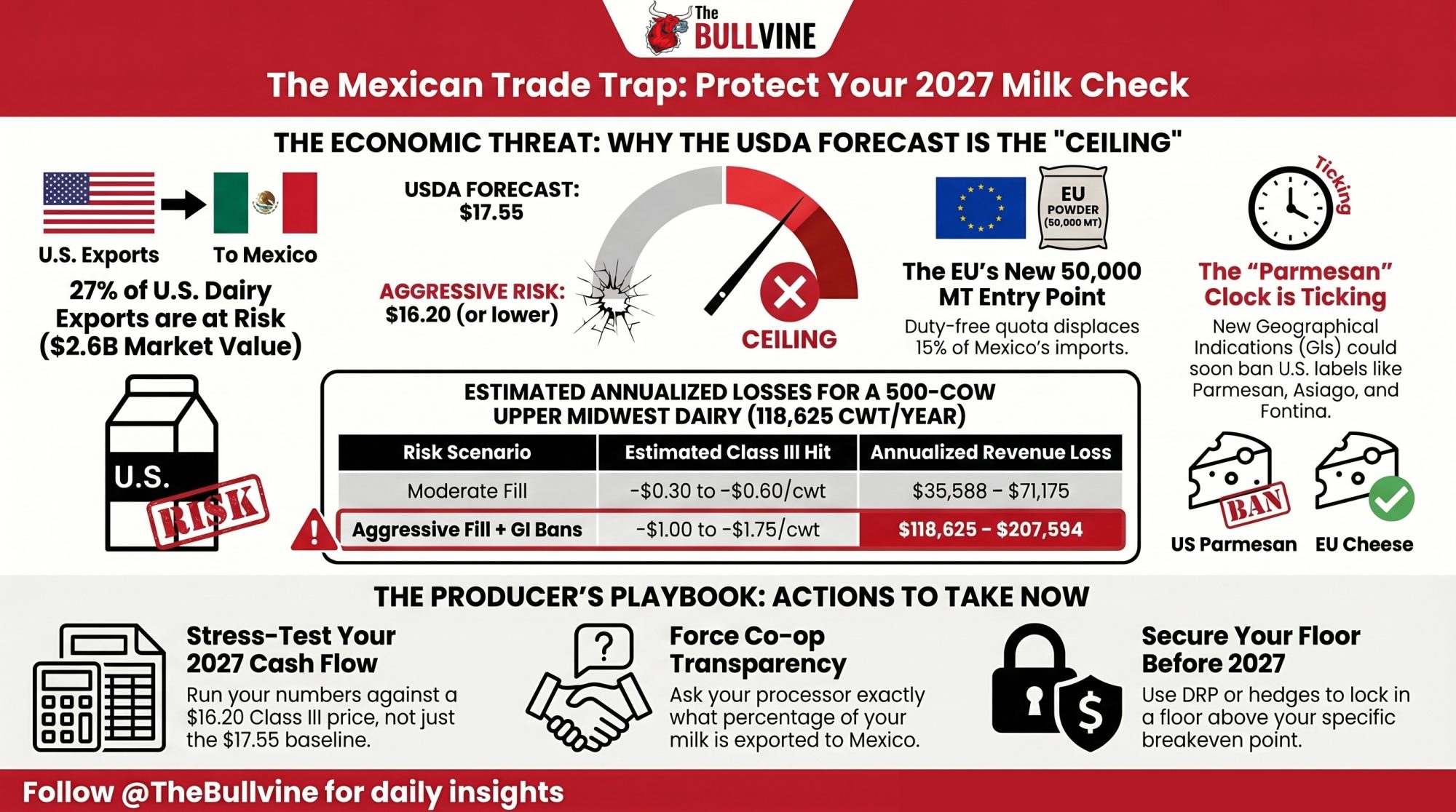

Executive Summary: USDA’s May WASDE put 2027 Class III at $17.55/cwt, all-milk at $20.95, and NDM at $1.575/lb — and that forecast was published ten days before Mexico signed a trade deal with the EU on May 22 that USDA never priced in. The Interim Trade Agreement opens a 50,000 MT duty-free SMP quota (about 15% of Mexico’s 335,000 MT annual import book), 25,000 MT of cheese TRQs, unlimited blue cheese, and — the bigger story — locks in protection for hundreds of EU geographical indications, putting US “Parmesan,” “Asiago,” and “Fontina” labels on the clock with no clear grace period. Mexico is 27% of the US dairy export book by value ($2.6B in 2025, including $1.1B in NFDM/SMP and $965M in cheese), so the displacement risk lands squarely on Upper Midwest Class III milk and Western powder plants. On a 500-cow Upper Midwest dairy shipping ~118,625 cwt/year, the moderate scenario costs $35,588–$71,175; the aggressive GI-enforcement scenario runs $118,625–$207,594. The July 1, 2026, USMCA Article 34.7 review is the last clean leverage point before the iTA likely enters provisional application in late 2026 or early 2027 — same window EU-Mercosur cleared in four months. If your co-op hasn’t stress-tested Mexico exposure or your 2027 hedge book is empty, this piece is the Monday-morning checklist; if you’re already 30–50% covered above breakeven, skim and forward to your lender.

At $17.55/cwt — USDA’s May 2026 forecast for 2027 Class III, per the May WASDE — the Upper Midwest dairies that already locked in a 2027 floor are sleeping. The ones whose co-ops haven’t briefed them on the EU-Mexico trade deal are about to learn what 50,000 metric tons of duty-free European powder and a freshly protected EU geographical-indications register do to a Wisconsin milk check. On a 500-cow Class III dairy shipping ~118,625 cwt/year, the moderate displacement scenario takes $35,588 to $71,175 off the top line. That’s the margin over feed dairy 2026 problem nobody on the supply chain side is naming out loud.

Shawna Morris, EVP of trade policy at NMPF, spent the first half of 2026 fighting Canada’s USMCA tariff-rate quota fill rates. The Bullvine’s April 29 analysis took her published USMCA scenarios and modeled a $0.31/cwt twelve-month spread on Class III: +$0.08/cwt upside, -$0.23/cwt downside. Canada-only. Then on May 22, 2026, in Mexico City, Claudia Sheinbaum and Ursula von der Leyen signed the EU-Mexico Modernised Global Agreement (MGA) and the companion Interim Trade Agreement (iTA) — both sides framing it as a counter to Trump tariffs, per Reuters’ coverage from the signing.

The Morris math just got a second pressure point. And it’s bigger than Canada.

Quick Glossary

| Term | Plain English |

| TRQ (Tariff-Rate Quota) | A volume of imports allowed in at a low or zero duty; everything above gets the full tariff. |

| iTA (Interim Trade Agreement) | The fast-track trade-only piece. Needs European Parliament + EU Council. Goes live first. |

| MGA (Modernised Global Agreement) | The full deal — trade plus politics. Needs all 27 EU member states + the Mexican Senate. Years away. |

| GI (Geographical Indication) | A legally protected product name tied to a place (Parmigiano Reggiano, Feta). Blocks competitors from using the name. |

| Basis | The gap between the futures price and what your milk check actually pays. Where co-op exposure shows up. |

The 2027 Trap Hiding Inside USDA’s Own Forecast

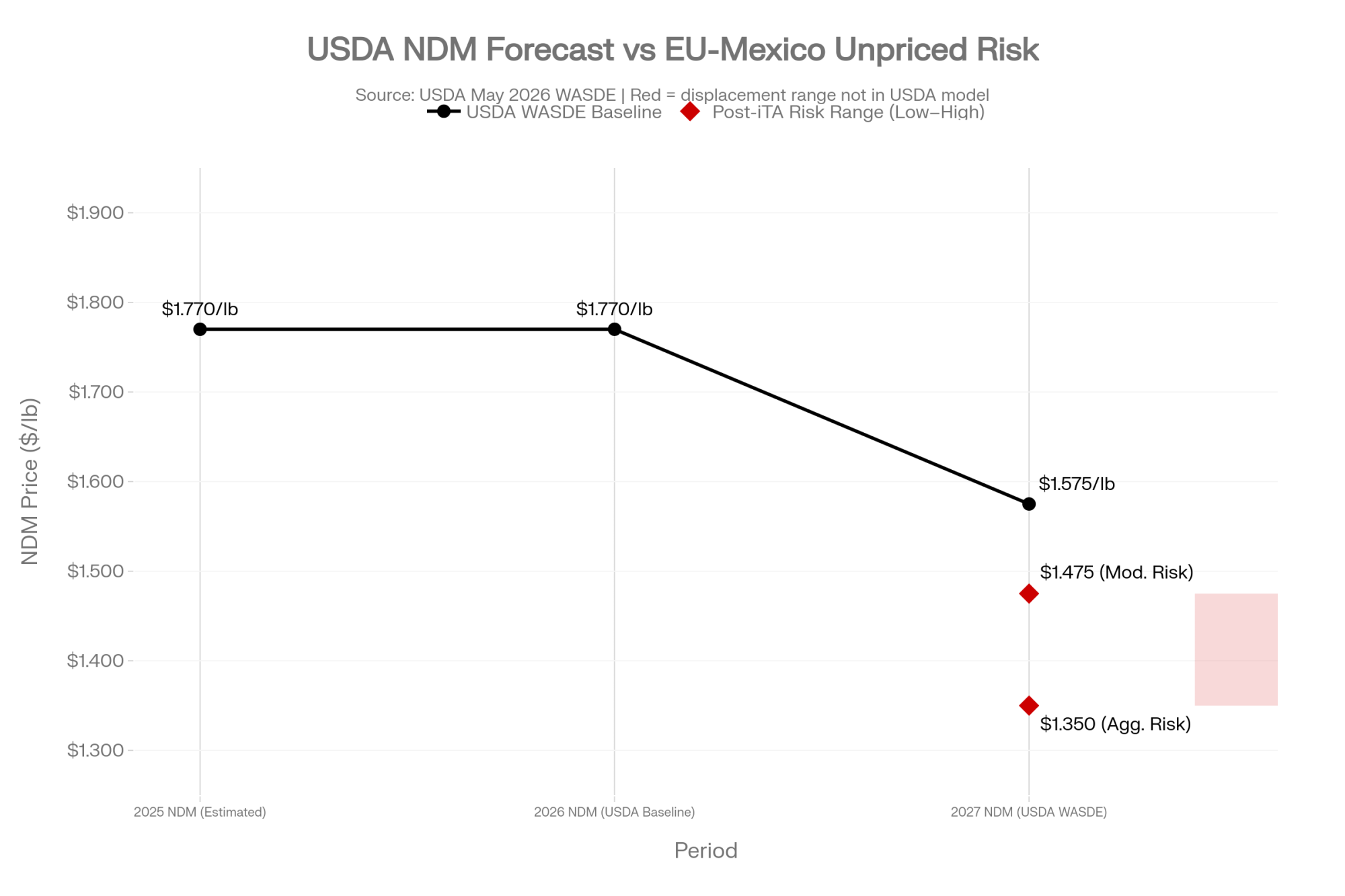

Before Europe ships a kilo, here’s what’s already on paper. USDA’s May 2026 WASDE forecasts 2027 NDM at $1.575/lb, down 19.5 cents from 2026. Whey at $0.640/lb, down 2.5 cents. Class III at $17.55/cwt. All-milk at $20.95/cwt, $0.30 below 2026.

USDA ERS’s May 2026 Livestock, Dairy and Poultry Outlook attributes that 2027 weakness to domestic supply growth and rising per-cow productivity. A supply-side story. Not a trade story.

That distinction matters. WASDE is supply-and-demand accounting, not a trade-shock model. It can’t — and didn’t — incorporate a deal signed days after it published. Mexico displacement risk from the iTA is additive downside USDA hasn’t priced in. The $1.575/lb NDM line is the pre-deal baseline. Not the floor. The starting point.

The deal doesn’t cause 2027 weakness. It removes the structural floor that would normally let prices recover.

What the EU Just Won in Mexico’s Dairy Aisle

The dairy chapter is published and specific. From the European Commission factsheet (qanda_25_249) and Global Dairy Trade’s reading of the agreement text:

| Product | TRQ Volume | Duty at TRQ Rate | Phase-In | US Displacement Risk |

|---|---|---|---|---|

| EU Skim Milk Powder (SMP) | 50,000 MT | 0% | 5-year | High — ~15% of Mexico’s 335k MT annual SMP imports |

| “Other” Cheese | 20,000 MT | 0% within quota | At entry into force | Moderate — direct competition with US “other cheese” |

| Fresh & Processed Cheese | 5,000 MT | 0% within quota | At entry into force | Moderate — quality tier overlap with US product |

| Blue Cheese | Unlimited | 0% (no cap) | Immediate | Low volume, high symbolic precedent |

| EU Geographical Indications | No volume limit | N/A — name ban | At entry into force | 🔴 Critical — bans Parmesan, Asiago, Fontina labels |

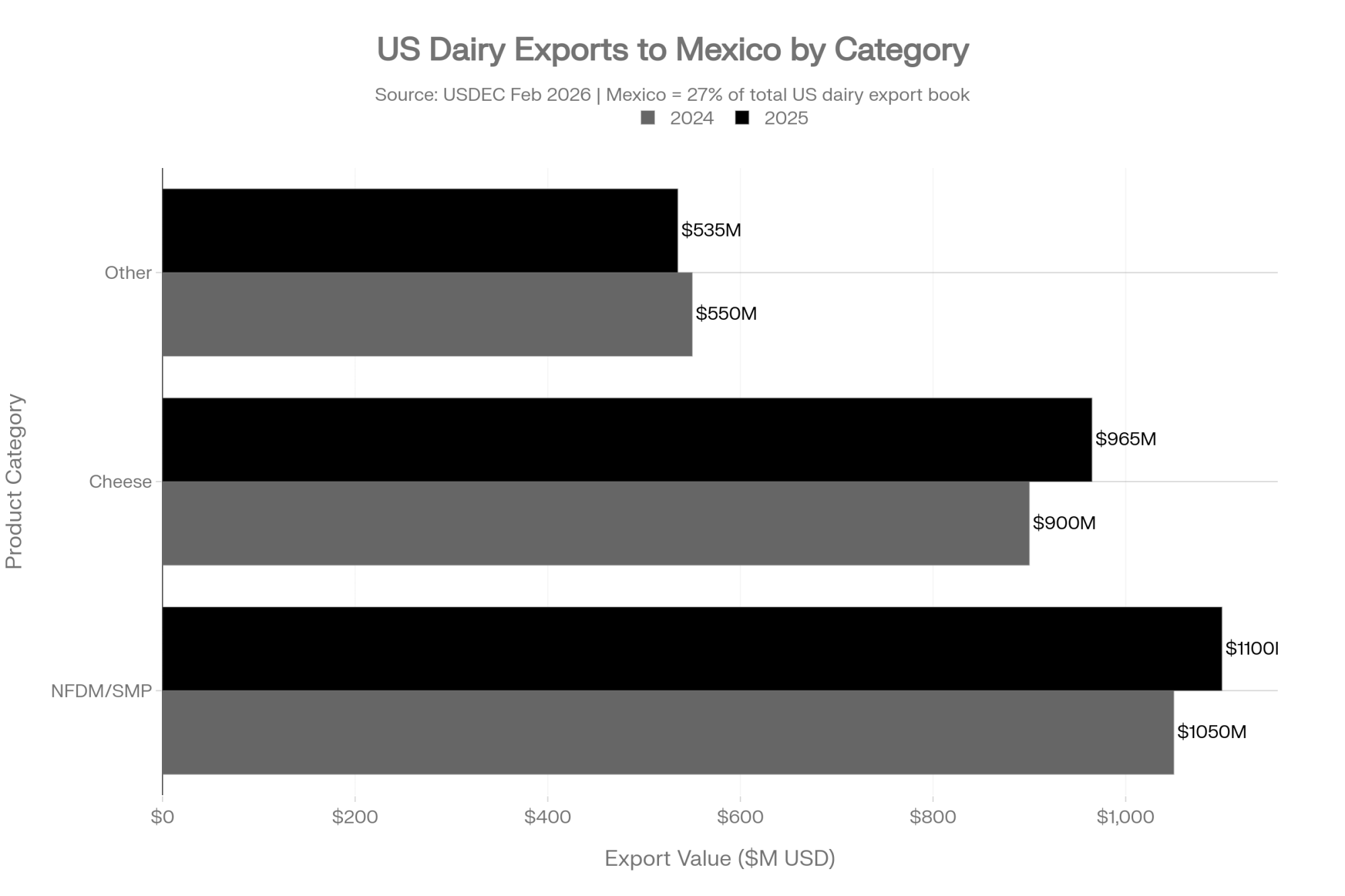

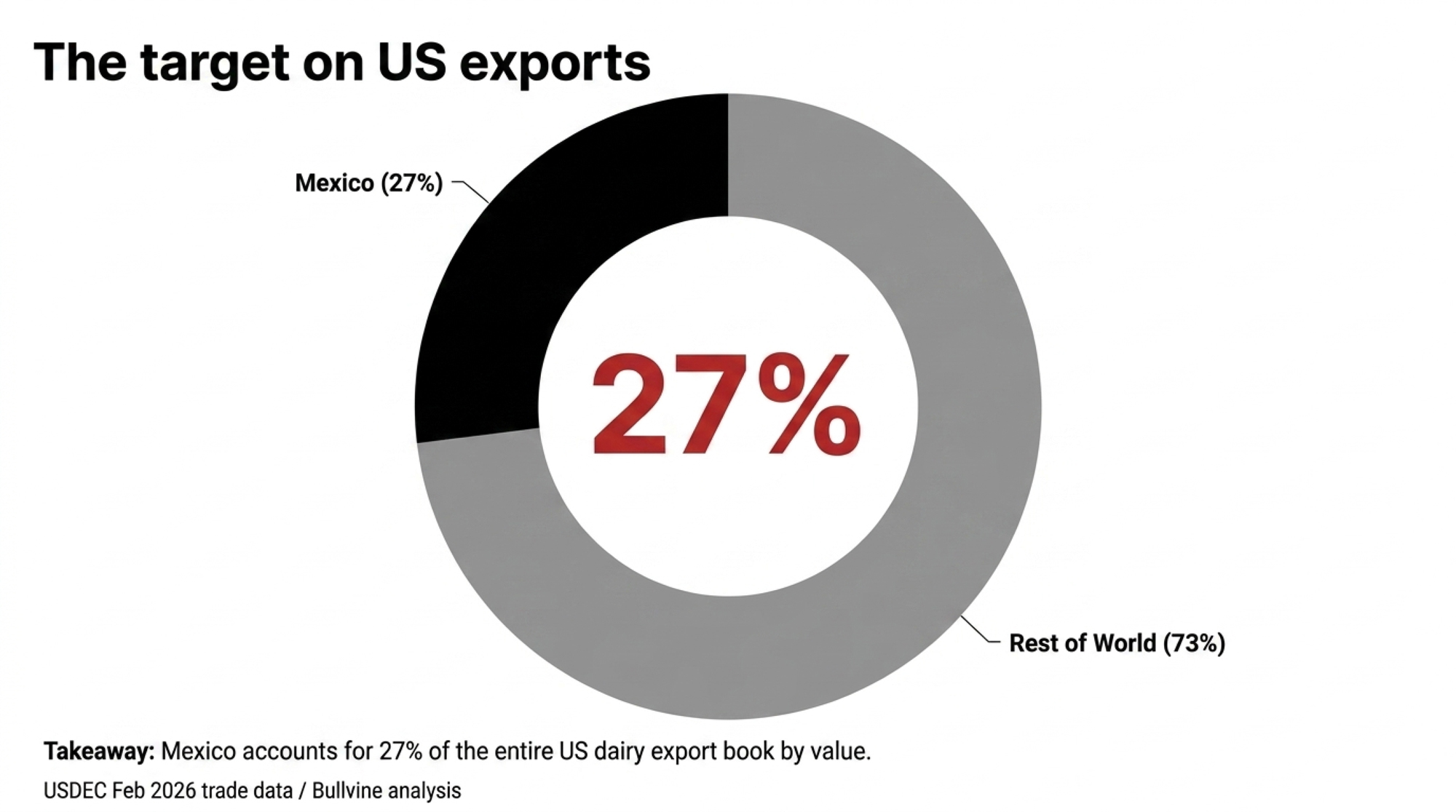

Mexico imports roughly 335,000 MT of SMP annually (2024 baseline, GDT analysis). The 50,000 MT EU TRQ is about 15% of that whole import market. US dairy exports to Mexico hit $2.5 billion in 2024 and $2.6 billion in 2025, with $1.1 billion of that NFDM/SMP and $965 million cheese, per USDEC’s February 2026 trade data release. Mexico is 27% of the entire US dairy export book by value.

“It’s Not in Force Yet” Is Doing a Lot of Work

The deal is signed. It is not yet in force. The iTA needs European Parliament consent plus EU Council adoption — provisional application possible as early as late 2026 or early 2027. The full MGA needs all 27 EU member states plus the Mexican Senate. 2028–2029 minimum.

The closest precedent is EU-Mercosur: signed January 2026, provisional application May 1, 2026, per Dairy Reporter coverage. Roughly four months. If EU-Mexico tracks that pattern, the dairy quotas go live during the 2027 milk year— exactly when USDA already forecasts weaker NDM and whey.

Why Morris’s $0.31/cwt Range Just Became the Light Scenario

The April 29 modeling of Morris’s USMCA scenarios was Canada-only risk. EU-Mexico is additive, not substitutive. Both pressures compound on the same milk check. Five variables make a single-number forecast actively dangerous: TRQ fill rate, implementation timing, the EU-US price spread at activation, GI enforcement pace, and whether USDA updates its baseline mid-year. None of those are knowable today.

Ranges, not point estimates, are the only honest framing. Anchor to a single number and you’ll budget to it. Work in scenarios and you’ve got a hedge plan when one of them prints.

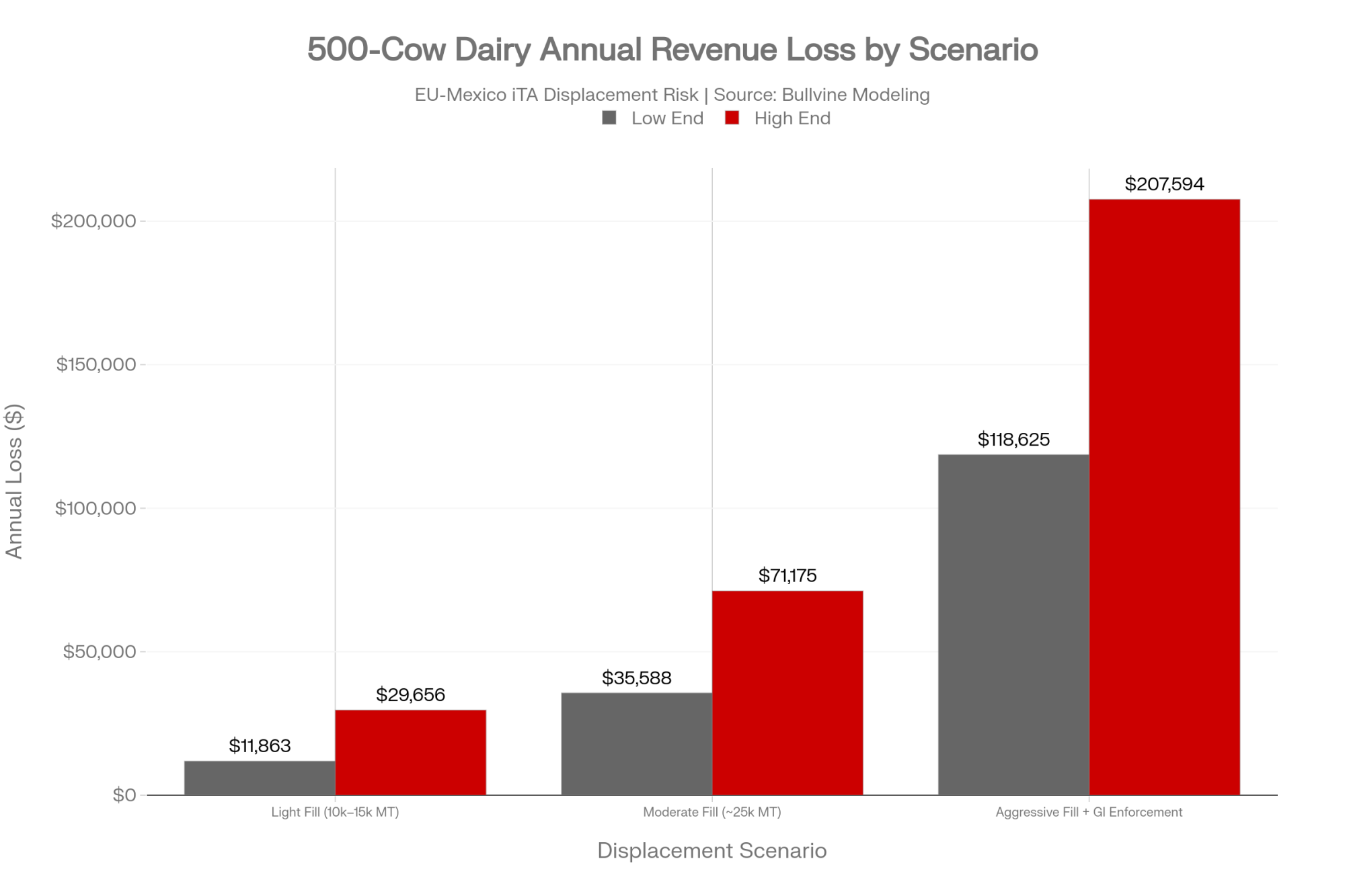

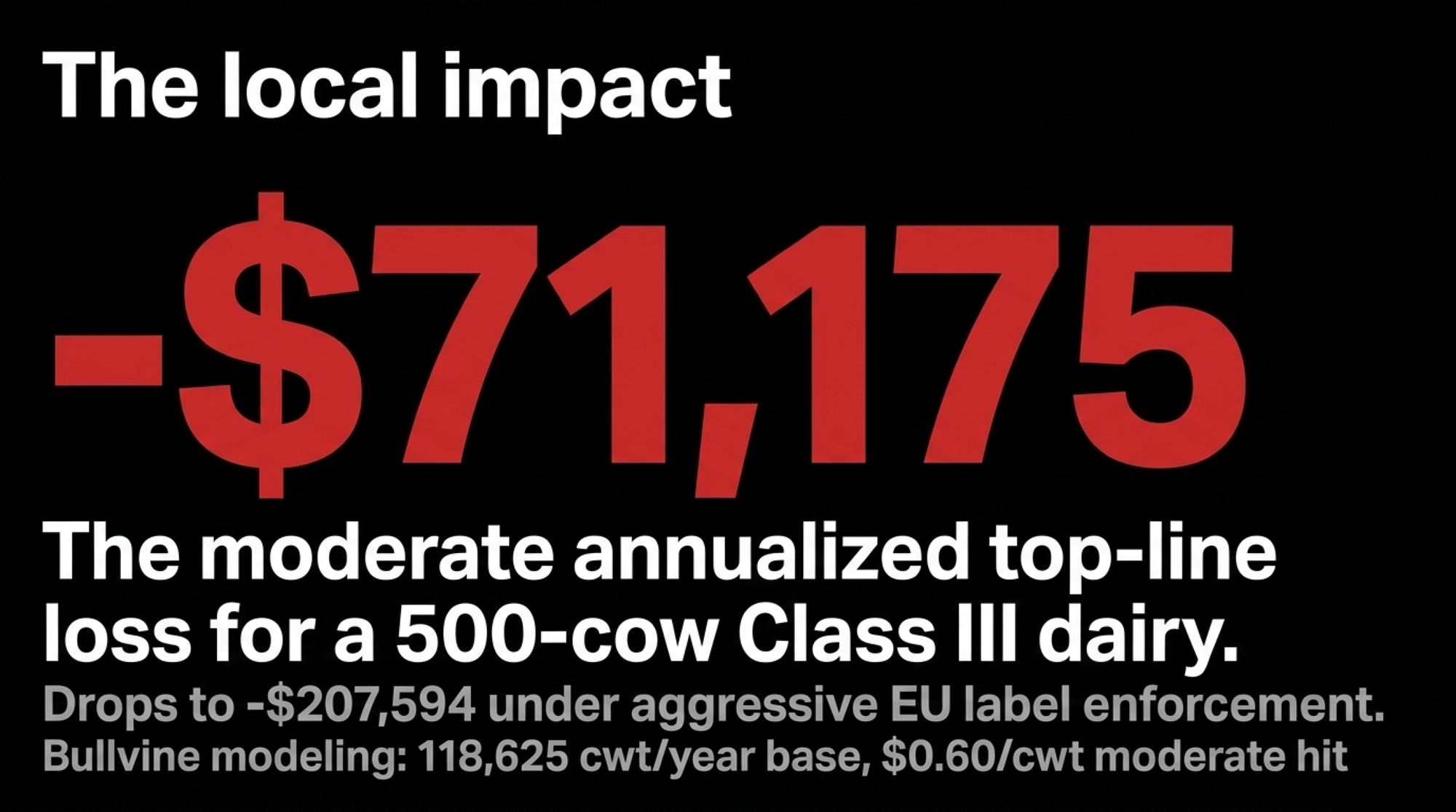

Running the Numbers — 500-Cow Upper Midwest Class III Dairy

Stress-test outputs. Not predictions. Bullvine modeling drawing on USDA and university extension trade-shock literature, extrapolated to the EU-Mexico TRQ structure.

Production baseline: 500 cows × 65 lbs/cow/day × 365 days ÷ 100 = 118,625 cwt/year (65 lbs/day held conservative against USDA NASS Milk Production data for early 2026.)

Class III hit × annual cwt = annualized milk-check exposure.

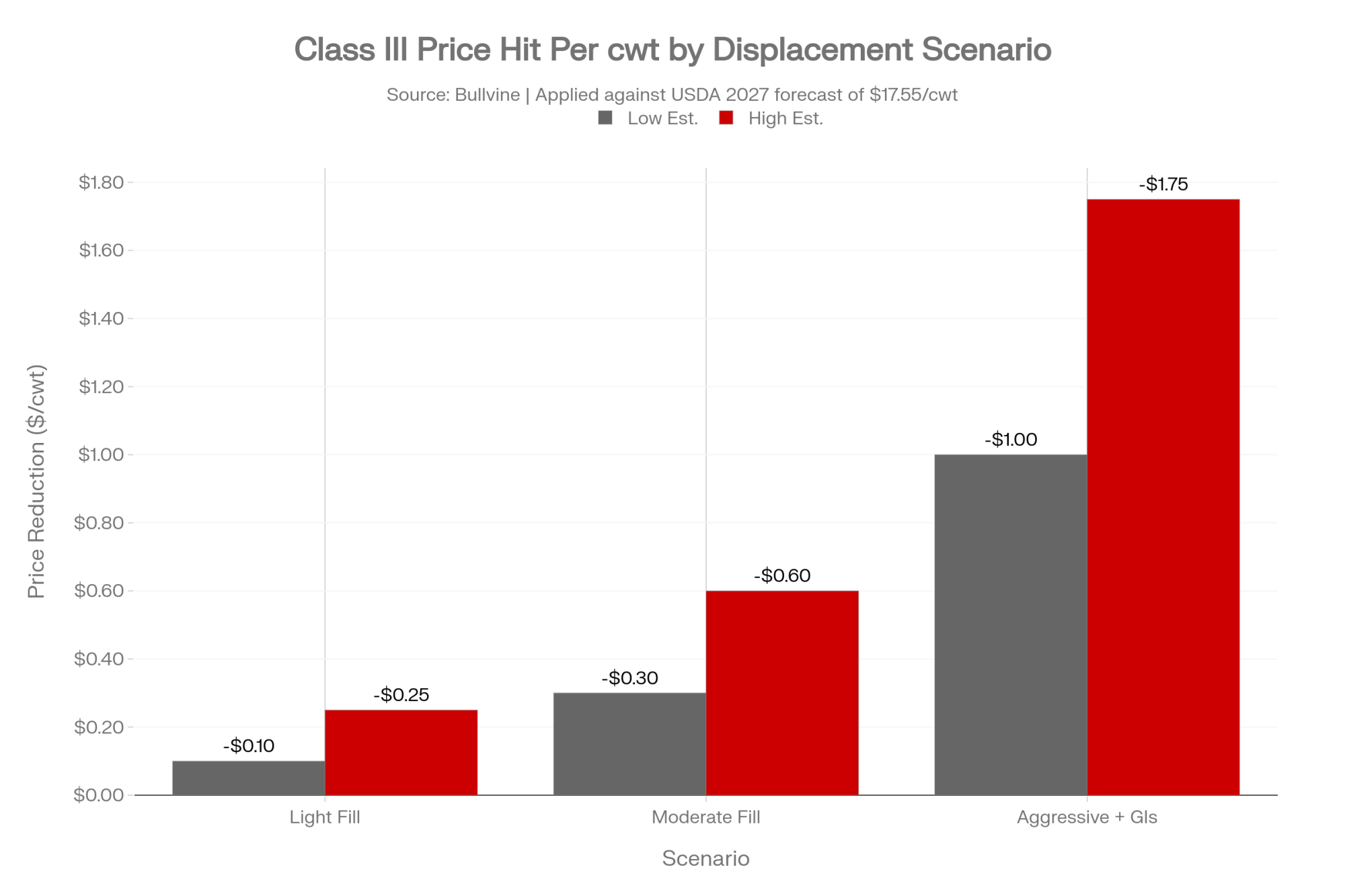

| Scenario | Market Penetration / GI Action | Estimated Class III Hit | Annualized Loss (500-Cow Dairy) |

| Light Fill | EU SMP fills 10k–15k MT (~3–4% of Mexico’s annual SMP imports). | -$0.10 to -$0.25/cwt | -$11,863 to -$29,656 |

| Moderate Fill | EU SMP fills ~25k MT (7–8% share) + 5% EU cheese capture (~9,600 MT against US cheese-to-Mexico volume of ~192,778 MT in 2024, per USDEC). | -$0.30 to -$0.60/cwt | -$35,588 to -$71,175 |

| Aggressive Fill + GIs | Full TRQ utilization + active GI enforcement banning US “Parmesan” and “Feta” labels. | -$1.00 to -$1.75/cwt | -$118,625 to -$207,594 |

Plug your own cwt and your own breakeven into the same arithmetic. Same shape, different dollars.

Run Your Numbers

Dairy Profit Projector — Stress-test your 2027 milk check against the moderate ($0.30–$0.60/cwt) and aggressive ($1.00–$1.75/cwt) EU-Mexico displacement scenarios in this article. Plug in your herd size, ration, and current futures, and see exactly where breakeven, IOFC, and margin per cwt break before the iTA goes provisional.

Why Are EU Geographical Indications a Bigger Threat Than the Tariff Quota?

Here’s the part producers aren’t hearing from their co-ops: the GI provisions matter more than the volume quotas.

A TRQ is a volume valve. EU exporters can ship up to 50,000 MT of SMP into Mexico at 0% duty. Whether they fill it depends on the EU-US price spread, which Dairy Reporter pegged in Q4 2025 with EU prices running roughly 40% above US prices. The quota wouldn’t fill aggressively on day one. Capacity for displacement, not immediate displacement.

GI enforcement is an architecture story. It permanently tilts which products are legally allowed on Mexican shelves under US-familiar names.

Mexico moves fast when it decides to. NOM-051 front-of-pack labeling, effective October 2020, ended exemptions overnight, per USDEC member alerts from that period. SAT (Mexican customs) became the enforcement authority at port of entry. US dairy shipments without compliant Spanish labels were detained until relabeled. USDEC negotiated a 60-day non-enforcement grace period because non-compliant product was technically subject to sanction on day one.

Replace “missing sugar icon” with “the word ‘Parmesan’ on a US cheese label,” and you have the GI enforcement playbook. Mexican regulators have shown they can flip the switch.

The 8-year transition period that’s getting all the attention applies only to Feta, and only for prior users who relabel with prominent origin statements, per USDA FAS Mexico’s February 2026 GAIN report. Names like Parmesan, Asiago, Gorgonzola, and Fontina don’t appear with explicit grace periods in the public summaries. NMPF’s December 2025 USMCA brief said it directly: Mexico still hasn’t codified its USMCA common cheese name commitments into domestic regulation, and the EU GI package now creates an explicit conflict with those USMCA obligations.

What Happens at the July 1, 2026 USMCA Review?

USMCA Article 34.7 requires a joint review on July 1, 2026 — the structural decision on whether to extend the agreement another 16 years or enter a six-year wind-down. USTR Jamieson Greer told the House Ways and Means Committee in May 2026 that the dairy dispute would either be resolved soon through USMCA negotiations or settled through an enforcement action.

NMPF and USDEC have filed coordinated priorities, including pushing Mexico to codify USMCA common cheese name protections into domestic law. Mexico just signed a deal in May 2026 committing it to protect the EU GI package — a list that, in the read of trade observers, conflicts with the USMCA cheese-name protections US negotiators thought they’d locked in.

When that contradiction lands on the desk of IMPI (Mexico’s industrial property institute), the Secretaría de Economía, and COFEPRIS, the structural incentives appear to pull toward Brussels. The EU GI list is numerically defined and clean to administer. USMCA’s common name protections are open-textured and procedural.

July 1 is the last obvious leverage point before the EU GI clock starts running.

| USMCA Review Outcome | Cheese-Side Implication |

| Best case | Greer extracts binding Mexican commitments to treat Parmesan, Feta, etc. as customary terms protected under USMCA. |

| Worst case | Review consumes its energy on Canada’s TRQ fill rates; Mexico’s common-name obligations get punted to a side letter. |

What If You Ship to a Canadian Processor?

Canadian supply management is buffered from direct EU-Mexico exposure on the production side. The bigger Ontario and Quebec read is structural: if US Class III softens on Mexico displacement, global benchmarks that influence quota valuations and processor negotiations face downward pressure on review years.

Bill C-202 protects supply management from USMCA concessions. It doesn’t insulate Canadian milk against global price transmission. EU-Mercosur landing provisional in May 2026 plus EU-Mexico signed in May 2026 is the EU actively building a dairy trade network that routes around the North American architecture. That’s the slower-moving story Canadian producers should be tracking through the back half of 2026.

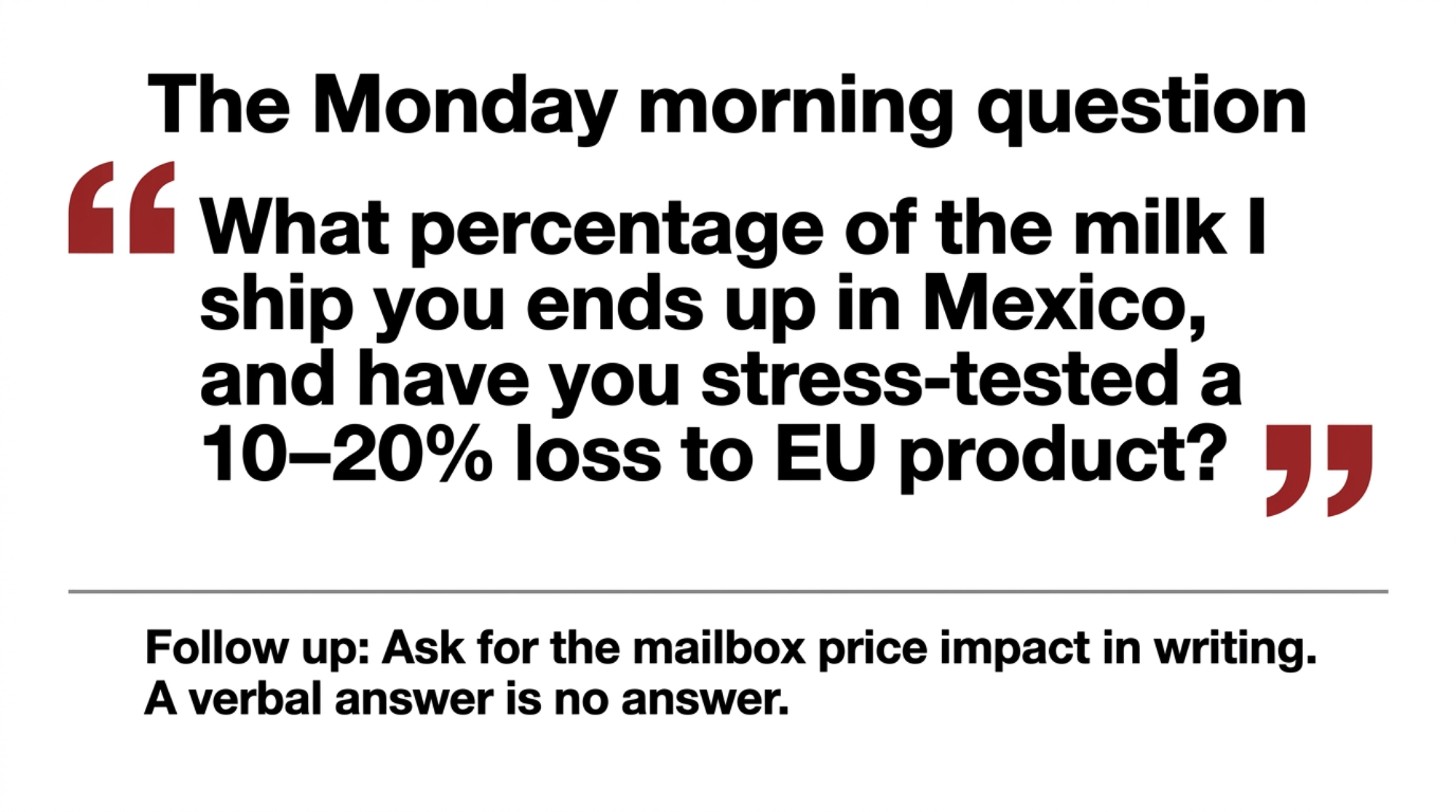

What Question Should You Be Asking Your Co-op on Monday Morning?

Most producers won’t ask this. The ones who do will get a real answer or learn how prepared their co-op is.

The question, word for word:

“What percentage of the milk I ship you ends up in products exported to Mexico, and have you run a Class III and cheese price stress test assuming we lose 10–20% of that Mexico volume to EU product under the new EU-Mexico trade deal?”

Follow it immediately with:

“Show me, in writing, the price range you used in that stress test and how it changes our mailbox price if Class III trades $0.50–$1.50/cwt under USDA’s current 2027 forecast.”

If they can’t answer cleanly, you’ve learned something about the analysis behind your milk check. That’s information you can act on.

The 30/90/365-Day Playbook for Herds Like Morris’s Constituents

The action isn’t “monitor the situation.” It’s repositioning your floor before the iTA enters provisional application.

30-Day Actions

| Action | What It Requires | Trigger / Threshold | Where It Backfires |

| Pull your last three milk checks. Calculate margin over feed per cwt using actual feed bills, not modeled ration costs. | Milk check stubs, feed invoices, an hour at the kitchen table. | Establish your real breakeven, written down. | Modeled ration costs understate your real exposure. |

| Call your DRP agent. Ask: “If 2027 Class III trades $16.50 or lower because Mexico takes less of our powder and cheese, what coverage keeps my floor above breakeven?” | DRP-licensed advisor. | Forces a calculation, not an opinion. | Vague answers signal the wrong advisor. |

| Locate your existing 2027 coverage position. | 5 minutes with your hedge file. | Red flag: DSCR under 1.2 for three straight months under your lender’s method + zero 2027 coverage = top of the list. | Treating zero coverage as a default rather than a decision. |

90-Day Actions

| Action | What It Requires | Trigger / Threshold | Where It Backfires |

| Move from 0% to 30–50% covered against the moderate displacement scenario. Use DRP endorsements that floor at or above breakeven if Class III settles in the $16–$17 band. Larger operations: structured puts or option collars. | Current breakeven, premium budget, advisor with DRP authority. | Hedge to your breakeven, not to your hopes. | Over-hedging at a temporarily soft price locks in pain that may not arrive. |

| Get explicit with your processor or co-op about Mexico exposure in your milk’s product mix. Push for basis transparency and ask about export-exposed risk-sharing pools. | Contract document, willingness to push, possibly a board-level conversation if member-governed. | Written answer required. | A verbal answer is no answer. |

| Re-run 2027 cash flow against three Class III scenarios — $17.55 (USDA baseline), $17.00 (moderate), $16.20 (aggressive). | Updated cost-of-production model. | Find where debt service coverage breaks. That’s the number you protect. | Stress-testing only the optimistic scenario. |

365-Day Moves

| Action | What It Requires | Trigger / Threshold | Where It Backfires |

| Watch two implementation triggers: European Parliament vote on the iTA (likely late 2026) and Mexican COFEPRIS labeling guidance updates referencing GI terms. | News-feed discipline. | Either signals provisional application is imminent. | Treating “signed” and “in force” as the same thing. |

| If July 1 produces binding Mexican commitments on common cheese names, reduce hedge ratios or extend out the curve. | Coverage flexibility. | Opportunity signal: Class III futures rally above $18.00 on a clean USMCA outcome + margin over feed holds positive = layer in 2028 coverage at better strikes. | Reducing coverage before the ink is dry. |

| If the review stalls or punts the common-names issue, treat 2027–2028 as a structurally weaker price environment. Adjust herd size, heifer inventory, and capex accordingly. | Lender alignment, board buy-in. | Sustained Class III below $17.00 with no near-term policy catalyst. | Cutting heifer inventory during a weather-driven price spike that masks the underlying displacement. Read the basis, not the headlines. |

What Your Contract Actually Says

A year from now, in June 2027, some producer is going to call his marketer with Class III at $16.20 on the screen and ask why the EU-Mexico deal didn’t show up in any conversation he had this spring. The conversation that follows is brutal: triage the cash flow, hedge what’s left of 2027 and 2028, cut heifers that aren’t earning their keep, and walk into the lender’s office with updated numbers before the lender walks into yours.

The question that prevents that call is the one your contract probably doesn’t answer in plain language. What does your processor actually do with your milk, and who pays the price when one of their export markets sees a 50,000 MT European TRQ open up overnight?

Hedging now buys margin certainty. The cost is upside if the deal stalls or the EU never fills its quota. Real trade. Named numbers on both sides.

Pull your contract today. Find the basis clause, the export risk language, and the volume penalty terms. If you can’t find them or don’t understand them, your contract is an answer to a question that’s already changed.

What does your current processor contract say about basis when 27% of the US dairy export book by value gets a new competitor — and where does your real margin over feed per cwt sit this month versus 90 days ago?

Key Takeaways

- The May 22 EU-Mexico trade agreement introduces unpriced, additive downside risk that transforms USDA’s 2027 Class III forecast of $17.55 from a conservative baseline into a hard price ceiling.

- Strict enforcement of 336 European geographical indications poses a swift structural threat that could abruptly block US cheese labels like Parmesan and Feta from Mexican retail shelves.

- Producers must establish a true, kitchen-table breakeven margin over feed now and move toward a 30% to 50% covered position before provisional application shifts global trade architecture.

- Demanding immediate basis transparency and running multi-scenario cash flow stress tests with your co-op determines whether your processor contract can handle a more competitive export landscape.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Class III Milk Price, DRP, and Your Spring 2026 Risk Plan — Arms you with execution strategies for defensive, balanced, and aggressive risk management lanes. It details five critical herd numbers needed on paper to establish a floor that protects thin operating cash cushions against unexpected market swings.

- The 400-Cow Margin Trap: When $14.59 Milk Bleeds $425K in 2026 — Exposes the hidden economic cost of multi-year equity erosion driven by four-figure replacement heifers. This analysis delivers a structural blueprint to stress-test your three-year cash flow against softening WASDE price projections and tight lender thresholds.

- DAIRY TRADE DECEPTION: How the US-Canada USMCA Deal Failed American Farmers — Dismantles the political rhetoric surrounding North American market access by revealing dismal 42% tariff-rate quota fill rates. It highlights how domestic regulatory maneuvers and structural trade barriers continue to insulate processors, routing global price shocks directly to US checkbooks.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.