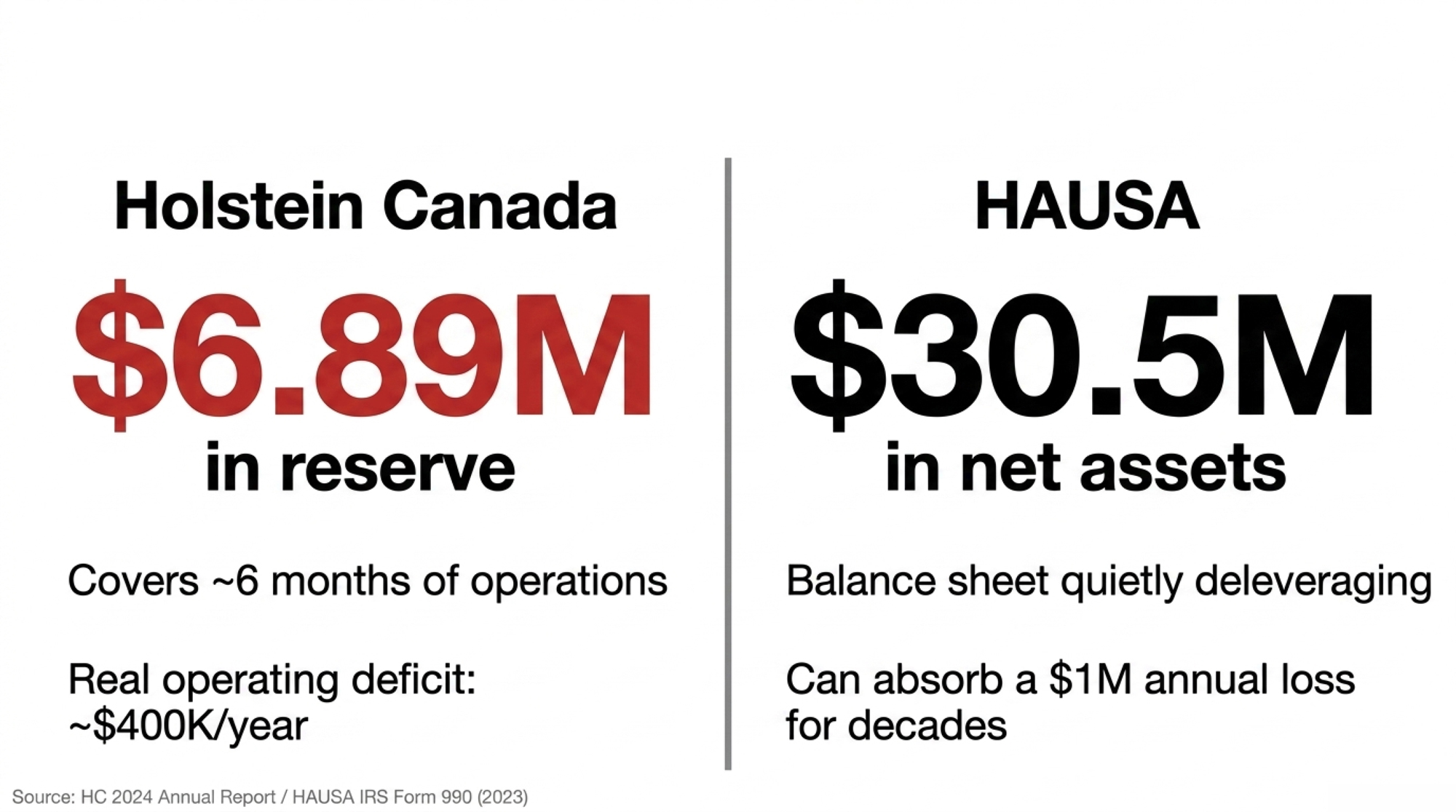

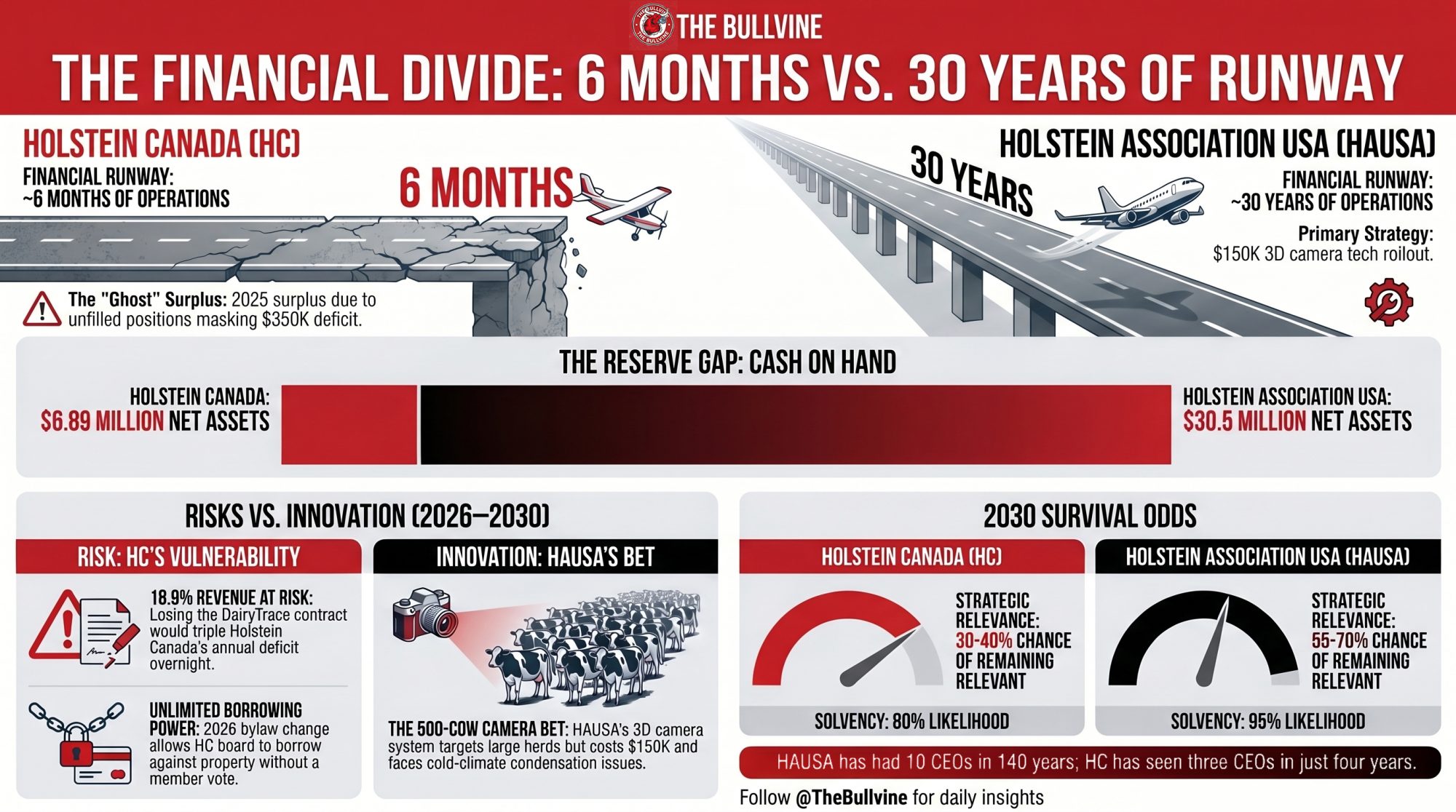

Holstein Canada closed 2025 with $6.89M in reserve. HAUSA sits on $30.5M. One can absorb a DairyTrace contract loss. The other board just quietly took unlimited borrowing power.

Holstein Canada finished 2025 with $6.89 million in reserve against a roughly $16 million annual cost base. Holstein Association USA finished 2023, its most recent IRS Form 990, with $30.5 million in net assets on a revenue base of nearly $17.8 million. That’s the gap. One organization covers its operating losses with investment income and is now betting its 2026 budget on reversing four straight years of classification decline. The other is four years into a 3D camera classification system that could redefine how cows get evaluated, and can afford to be wrong while it figures out whether the technology works.

If you classify with either association, lend to operations that do, or sell genetics into either market, the breed association’s financial outlook for dairy in 2026 matters more than the marketing. Here’s what each path looks like through 2030, the survival odds with reasoning, the realistic solutions on the table, and the questions members need to start asking out loud if either organization’s legacy is going to survive the decade.

Two Numbers and What They Actually Mean

Holstein Canada’s $6.89 million reserve covers roughly six months of operations. Per Finance Chair Benoît Turmel at the April 2026 AGM, HC has run operational deficits in five consecutive years averaging $147,000, and the books only stay positive because investment income from the reserve subsidizes the gap. The reserve fund returned 9.28% in 2025, generating roughly $640,000. That’s more than enough to mask a true operating shortfall of about $400,000.

The 2025 reported surplus of $1.01 million was, in CEO Greg Dietrich’s own framing at the AGM, a “ghost.” About $780,000 of it came from staffing matters and staff positions HC didn’t fill. Strip the empty chairs, and the real 2025 operational position was a deficit of nearly $350,000.

Holstein Association USA’s $30.5 million in net assets sits on a balance sheet that’s been quietly deleveraging. Liabilities dropped from $13.3 million in 2020 to $7.6 million in 2023 per IRS Form 990 filings via ProPublica. Even at an aggressive $1 million annual loss, HAUSA has roughly 30 years of runway. HC’s cushion is thinner by a factor of six in absolute dollars.

That asymmetry is the entire story.

Will Holstein Canada Run Out of Money by 2030?

Not under base assumptions. But the trajectory depends on three variables most members don’t track: investment returns, classification volume, and HC’s two DFC-linked service contracts.

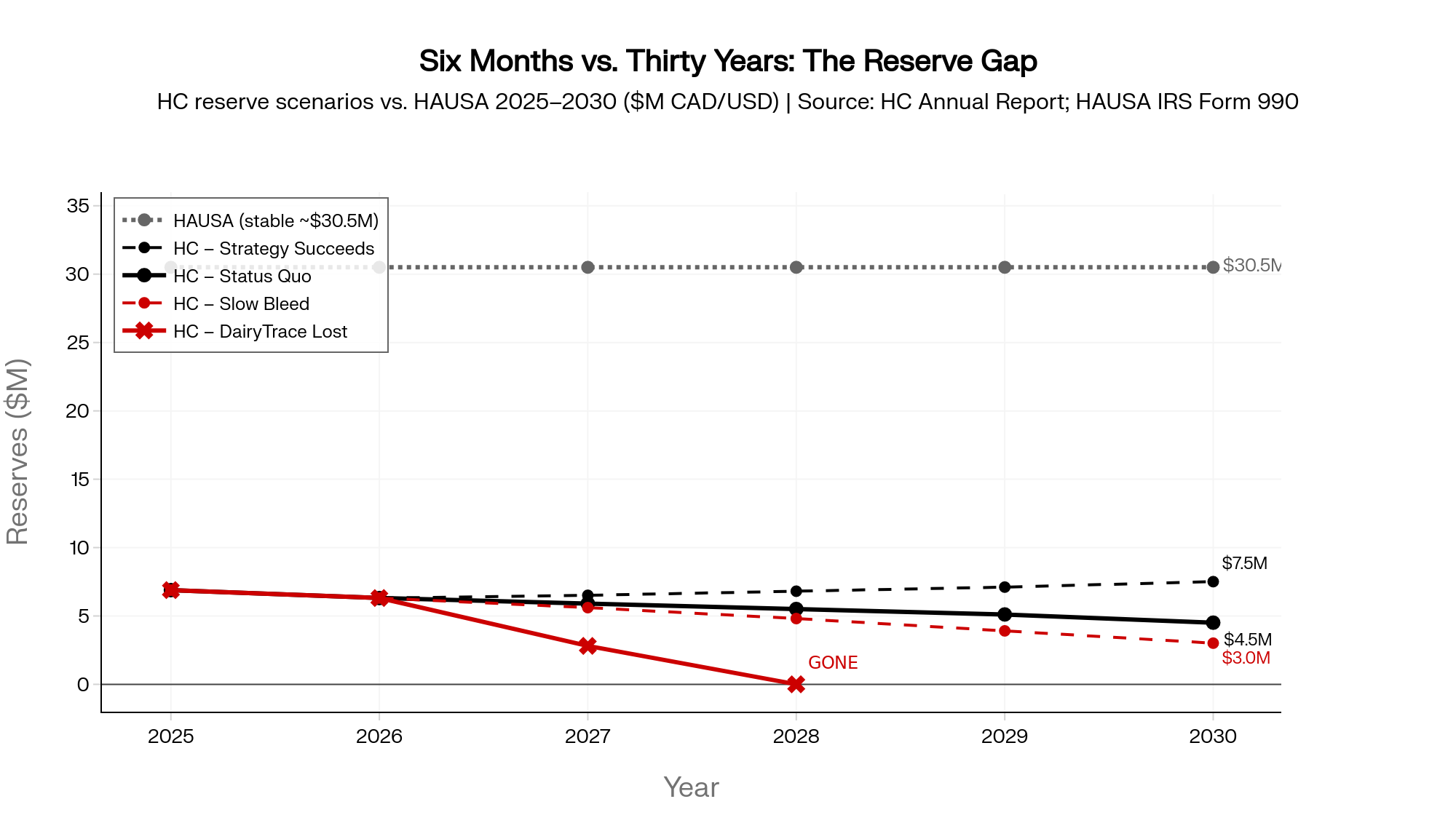

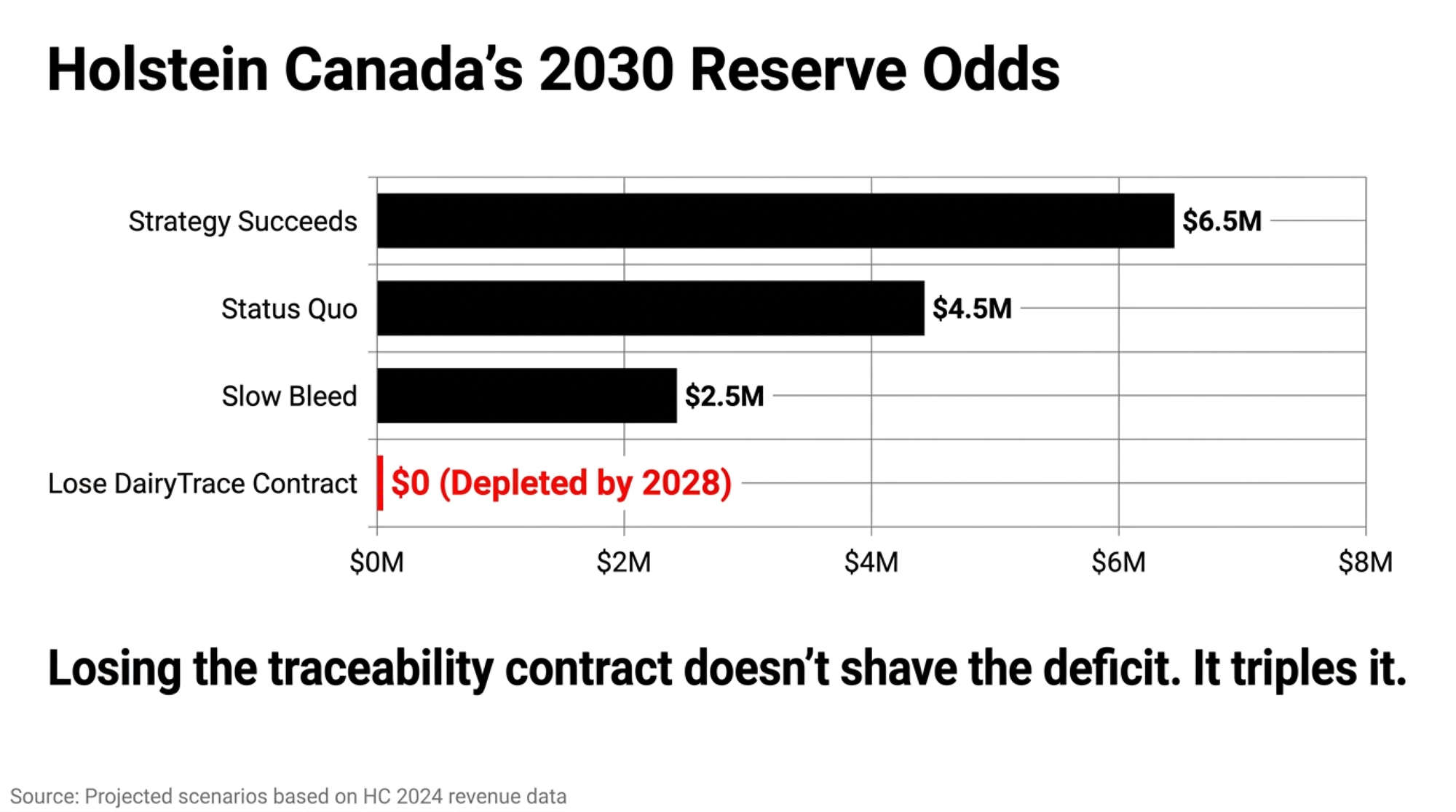

Run the numbers four ways.

| Scenario | 2026 | 2027 | 2028 | 2029 | 2030 | Reserve End-2030 |

| Status quo (9.28% returns hold, deficit ~$400K) | ($584K) | ($400K) | ($400K) | ($400K) | ($400K) | ~$4.5M |

| Strategy succeeds (+20K cows by 2027, both contracts stable) | ($584K) | +$200K | +$300K | +$300K | +$400K | ~$6.5M |

| Slow bleed (returns normalize to 5%, classifications keep falling) | ($584K) | ($700K) | ($800K) | ($900K) | ($900K) | ~$2.5M |

| DairyTrace contract lost ($2.989M revenue gone) | ($584K) | ($3.5M) | ($3.5M) | — | — | Reserve gone by 2028 |

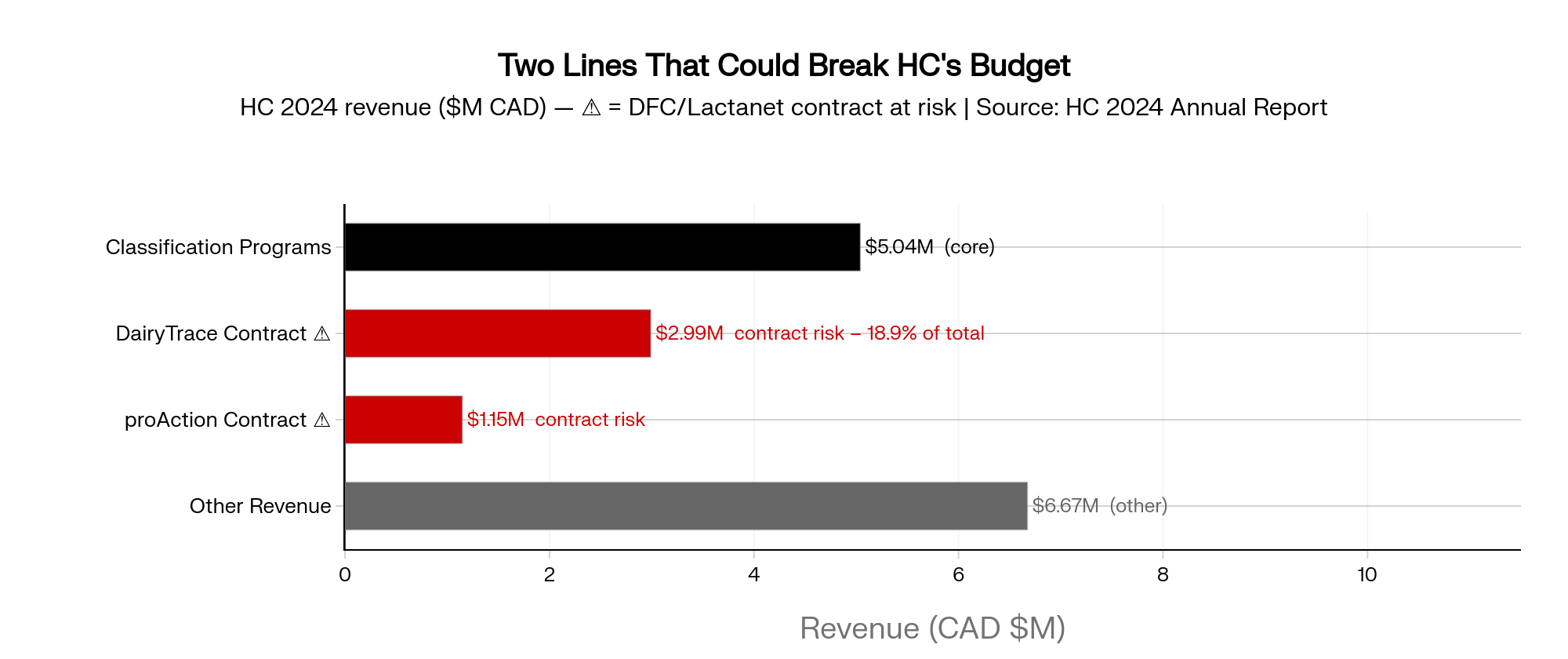

The bottom row is the one to watch. DairyTrace generated $2.989 million in 2024, 18.9% of total revenue per the HC 2024 Annual Report. HC administers DairyTrace customer service outside Quebec under contract with Lactanet, which holds the national DairyTrace program. Quebec is served by Attestra. HC DairyTrace services are the most durable line on HC’s books because they sit inside a single national contract for Canadian dairy cattle traceability, not a registration fee tied to a shrinking heifer pool. They’re also the line that, if lost or repriced at a competitive tender from Lactanet, doesn’t shave the deficit. It triples it.

A note on scope: DairyTrace is a national program, but Quebec’s parallel infrastructure runs through Attestra, so HC’s DairyTrace customer-service footprint runs primarily outside Quebec. That’s the same fault line that shapes how any future HC strategy plays at AGM.

proAction adds a second contract risk on a tighter clock. HC’s 2024 Annual Report notes a renewed two-year DFC contract for proAction Cattle Assessments, booked as “Animal Care Assessments” at $1.147 million in 2024. That’s a smaller line than DairyTrace, but the renewal window is sooner. Lose proAction at tender and the deficit doesn’t triple. It adds roughly $1.15 million to whatever the base case is.

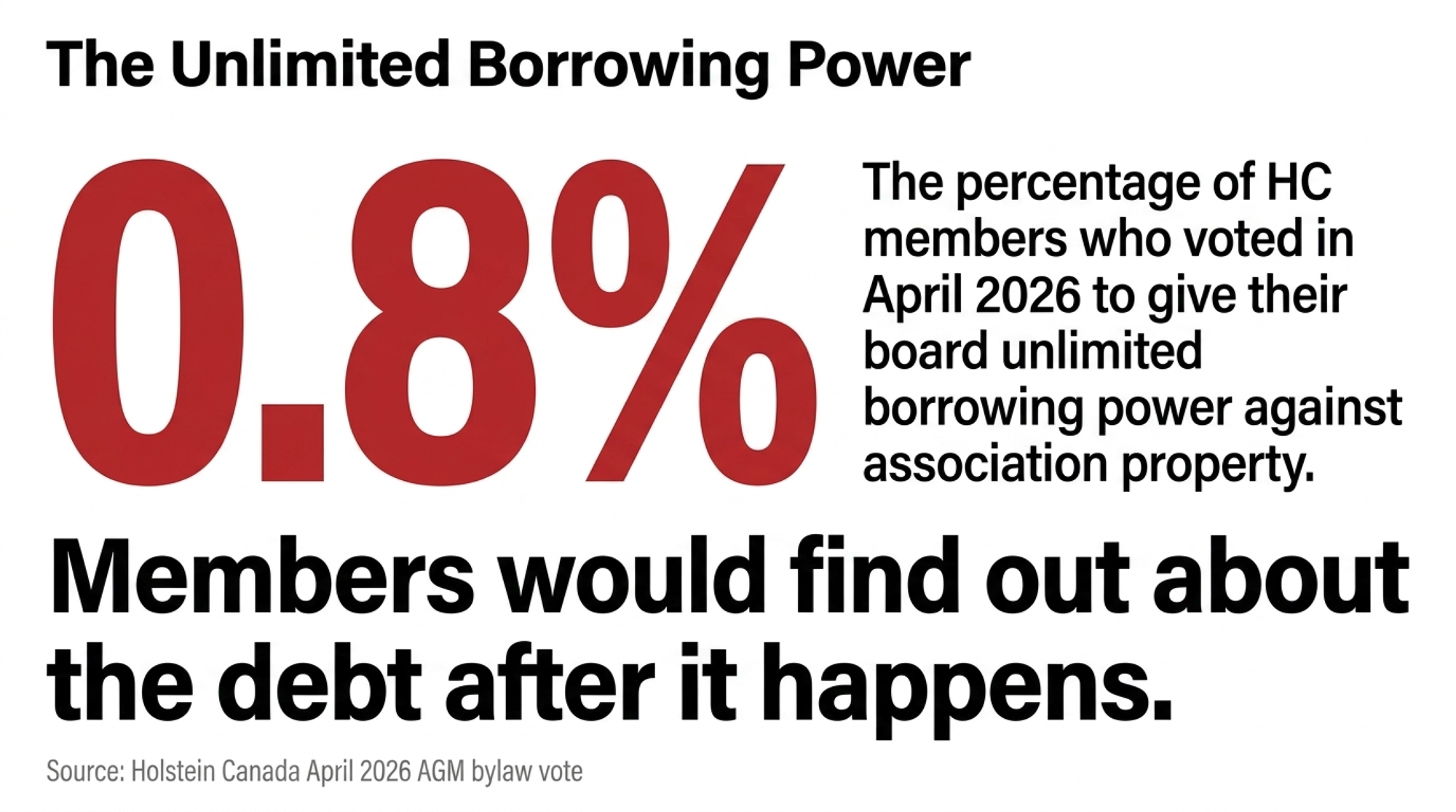

The April 2026 bylaw rewrite passed by 65 of approximately 7,900 members, or 0.8%. It gave the board unlimited borrowing authority against association property without a member vote. That’s not a strategy. That’s the mechanism that gets pulled in a DairyTrace or proAction shock. Members would find out after. (Read more: Holstein Canada’s Governance Rewrite Passed. 0.8% of Members Voted.)

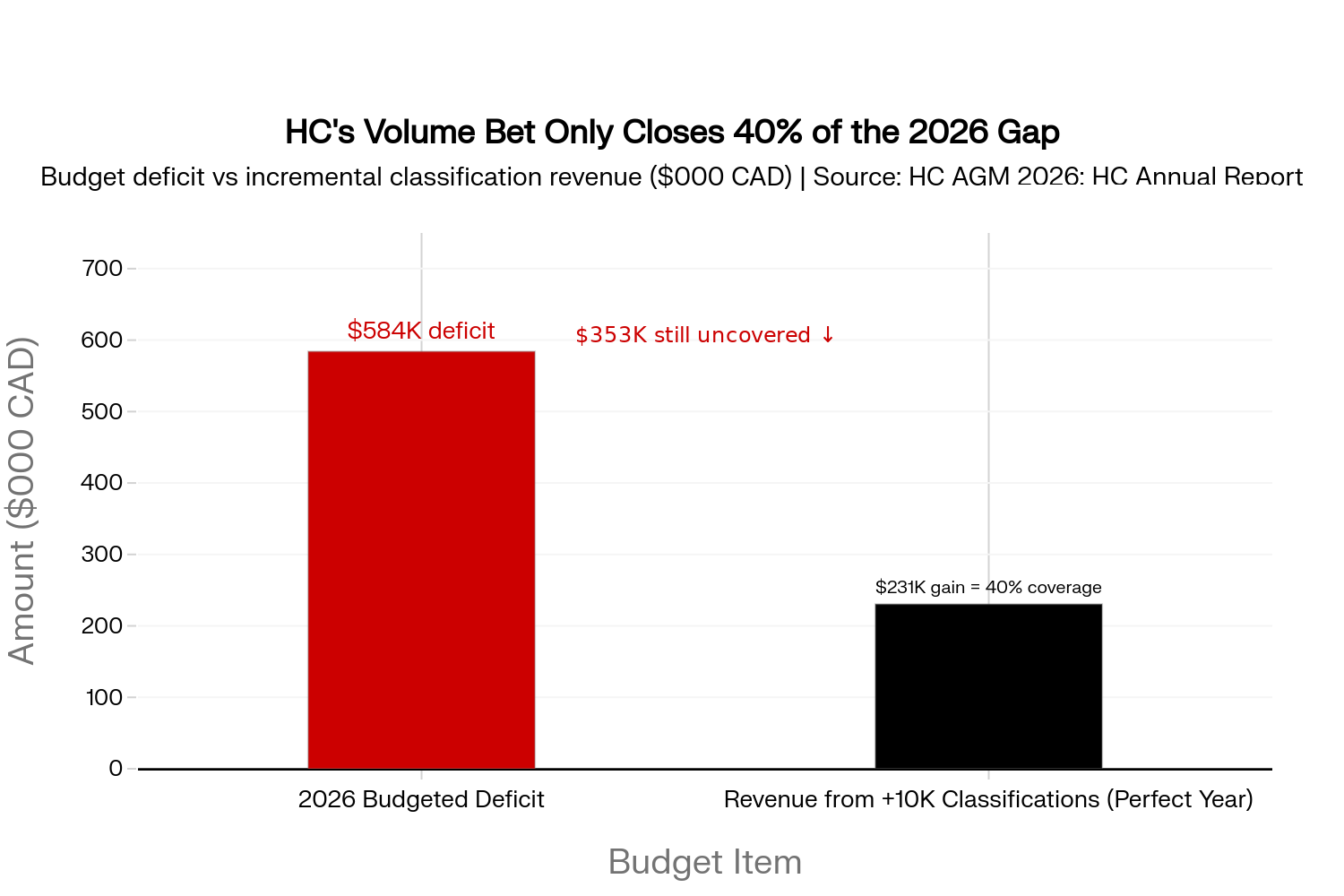

Running the Numbers: HC’s Volume Bet on a 218,000-Cow Base

Per the HC 2024 Annual Report, classification program revenue was $5,039,000 against 218,577 Holstein cows classified. Work it out:

- Revenue per Holstein cow classified: $5,039,000 ÷ 218,577 = $23.06 CAD/cow

- HC’s stated 2026 target: classify 10,000 more cows than 2025

- Incremental revenue at $23.06/cow: 10,000 × $23.06 = ~$230,600 CAD

- 2026 budgeted deficit: $584,000

- Coverage of deficit from perfect execution of classification program: ~40%

Even hitting the volume target closes about 40% of the planned deficit. That’s not a turnaround. That’s a contribution against a hole that’s still getting deeper.

For your operation, the same math runs in reverse. A 200-cow Holstein herd classified annually pays roughly $4,600/year for the service. If HC defends revenue by raising per-cow fees to $30 instead of recovering volume, that’s another $1,400/year coming out of your operating account. HC member Pascal Martin from Quebec asked the right question from the AGM floor: how does the budget assume 10,000 more classifications when you just lost 5,000? The board’s answer was classification visit scheduling tweaks and a new business development hire. No demand evidence was offered.

The structural headwinds aren’t subtle. Per Agriculture Canada and Statistics Canada livestock inventory data, Canadian dairy cow inventory fell from 975,100 in 2018 to 962,400 in 2025. HC-registered calves dropped 17% from 2019 to 2022. Member herds went from 8,621 in 2022 to 8,124 in 2024. Beef-on-dairy keeps reducing the registerable heifer pool.

You can’t manufacture demand that isn’t there. Scheduling efficiency only helps if the cows exist to schedule.

Four Years In, HAUSA’s Camera System Still Hasn’t Survived a Winter

Three time-of-flight 3D depth cameras mounted at a milking parlor exit alley. RFID identification. Twenty-six linear traits measured automatically as the cow walks past. Body condition and locomotion indicators on top. Patent pending. Data piped directly to HAUSA for genetic evaluation integration. [INTERNAL LINK: Bullvine October 2025 deep-dive on HAUSA’s Build a Better Cow camera rollout]

The program has been in development for four years under Dr. Jeff Bewley, HAUSA’s Executive Director of Genetic Programs and Innovation. The primary public documentation is Bewley’s 2025 World Dairy Expo presentation and Bullvine’s October 2025 analysis.

What the system doesn’t do, in Bewley’s words at World Dairy Expo: capture final score. “Final score is harder — it’s a 40,000-foot view of the animal that the camera can’t fully capture.” Human classifiers stay in the workflow. The cameras supplement. They don’t replace.

What the system also doesn’t do is pencil out below 500 cows. The estimated installed cost is around $150,000 per farm. The U.S. has roughly 26,290 dairy operations per HAUSA’s Pulse Fall 2024 data. Per USDA NASS structure-of-dairy-farms data, roughly 500 to 800 of them milk above 1,000 cows. That’s the addressable market. Per the same USDA NASS dataset, about 60% of U.S. dairies milk under 100 cows and aren’t part of this conversation at any price.

Cold-climate parlors are also a real problem. Camera condensation in winter milkings shows up in Wisconsin, Vermont, New York, and even most of Canada. Heat shutdowns occur above 105°F and limit Sun Belt deployment. Commercial launch is projected for 2027–2028. The system hasn’t survived a commercial winter yet.

The Governance Tax on Every Other Strategy

Three HC CEOs in four years. Mid-term board president resignation in June 2024. D&O insurance for provincial branches was cancelled in August 2024, with a reinstatement resolution that received no formal progress report a year later. The April 2026 bylaw rewrite, passed by 0.8% of members, referenced regional boundary maps that didn’t exist at time of approval, raised from the floor by Amanda Jeffrey.

Compare that to HAUSA’s transition. John Meyer retired December 31, 2024, after 23 years. Lindsey Worden, an 18-year HAUSA veteran and former COO, took over January 1, 2025. No drama. No revolving door. The 10th CEO in 140 years.

Stability isn’t a strategy. But instability is a tax on every other strategy you try to run.

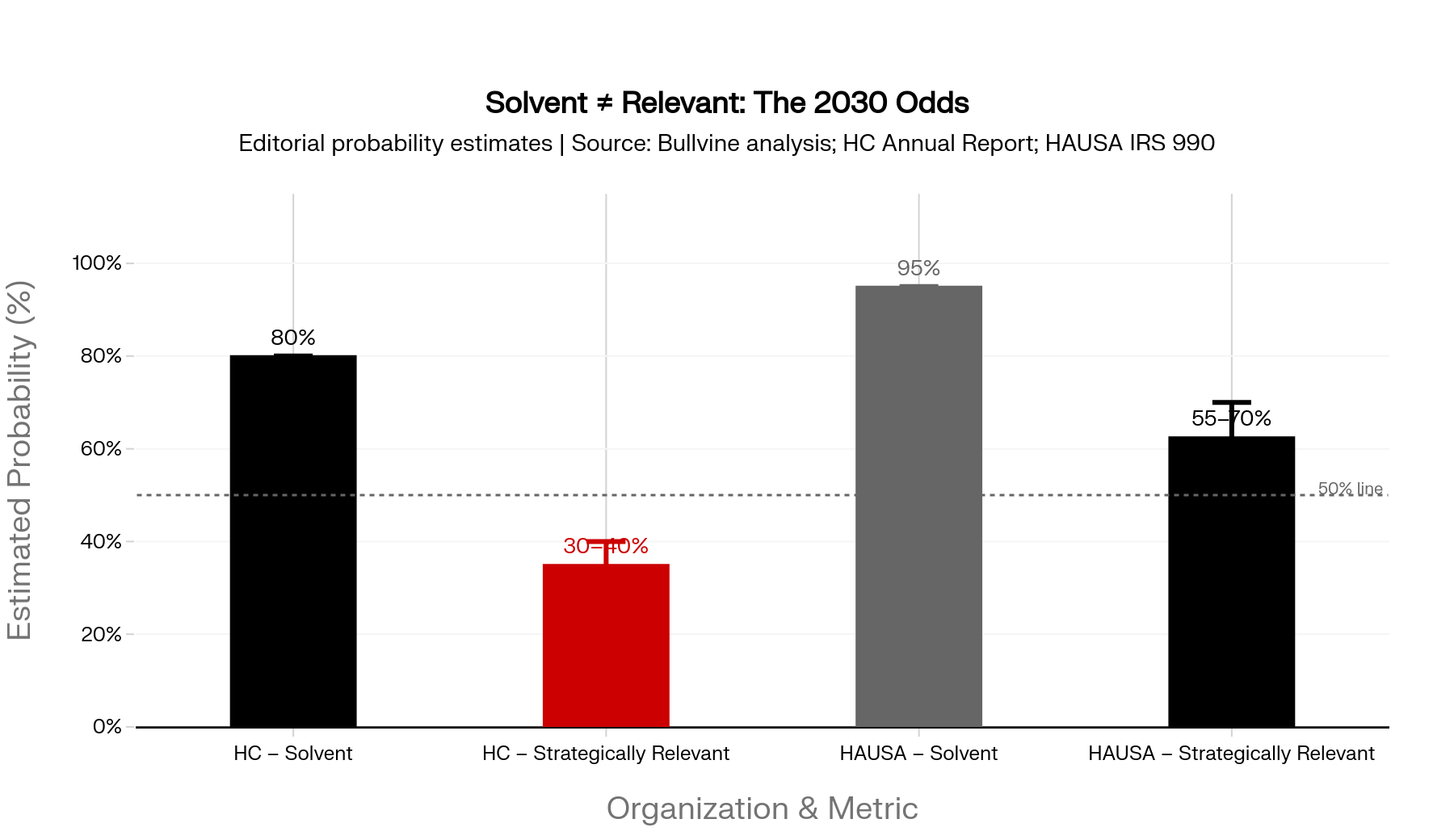

Survival Odds Through 2030

These are informed editorial judgments, not statistical outputs. Reasonable analysts working from the same data could land 10 to 15 points different in either direction.

Holstein Canada, solvent in 2030: ~80%. Reserve at $6.89 million, true deficit closer to $400K net of investment income, status quo lands the reserve around $4.5M by 2030. The realistic threats are a DairyTrace shock or a non-renewed proAction contract, neither of which appears imminent. Solvent, yes.

Holstein Canada, strategically relevant in 2030: ~30–40%. Classification volume has fallen for four straight years. Member herds are contracting from 8,621 in 2022 to 8,124 in 2024. With Lactanet already holding the national DairyTrace program above HC, and without a credible shared-services arrangement or a defensible expansion of HC’s contract footprint, the trajectory is toward an organization that exists but doesn’t matter much.

HAUSA, solvent in 2030: ~95%. No realistic five-year scenario runs HAUSA out of money. The 5% accounts for catastrophic events not visible in current data.

HAUSA, strategically relevant in 2030: ~55–70%. The high end assumes cameras deploy by 2028, 200–500 large herds adopt, and continuous conformation data becomes what AI companies and dairy farms pay for. The low end is cold-weather problems plus large-herd drift to genomic-only evaluation via Zoetis CLARIFIDE and other DNA testing organizations. Solvent in either case. The gap between 55% and 70% is whether the camera bet works.

What Could Save Holstein Canada and HAUSA by 2030?

Neither board can fix everything. But there are specific paths that could change the trajectory, sorted by how plausible they actually are.

1. Sustainability data services layered on the DairyTrace customer-service role. Probability: ~35%. Upside if it works: $1–3M CAD/year in new revenue. HC sits on the customer-service interface for the only national Canadian dairy cattle traceability dataset, even though Lactanet holds the program. Processors and federal programs need carbon intensity, antibiotic use, and longevity metrics for ESG (environmental, social, governance) reporting, supply contracts, retailer audits, and federal climate programs. The raw material exists. What’s missing is a productization strategy negotiated with Lactanet and a data licensing framework HC has never built. This is the single highest-leverage move on the board, and it requires a partner conversation HC can’t dodge.

2. HC–Lactanet shared services arrangement. Probability: ~50%. Upside: $500K–$2M CAD/year in HC cost reduction, plus extended relevance. A formal split where HC handles classification field work plus DairyTrace customer service and Lactanet handles data infrastructure and genetic evaluation. Not a merger. Quebec representation at 43% of HC membership and Lactanet’s DFC mandate make full consolidation politically unworkable, especially since Quebec runs its own parallel traceability through Attestra. But Dietrich spent ten years on Lactanet’s Genetic Evaluation Board. The relationships are deep enough to negotiate this. The risk: branch politics treats it as the first step toward HC dissolution, and Quebec resolutions block it at AGM.

3. HAUSA cameras commercialize on schedule. Probability: ~55%. Upside: $250K–$1M USD/year in incremental data subscription revenue, plus relevance retention with the 500–800 large U.S. herds that drive genetic progress. The science is published. The patent is filed. The cold-climate condensation problem is engineering, not physics. HAUSA has four years of R&D and the balance sheet to absorb a delayed launch. The risk is adoption stalling at 50–100 farms because the $150K capital outlay doesn’t pencil for operators who already get most of what they need from Zoetis CLARIFIDE or other genomic testers.

4. Phenotypic data licensing to genomics companies. Probability: ~25% near-term, higher long-term. Upside: $500K–$3M/year for either organization if pursued aggressively. Both associations sit on decades of individual animal conformation scores correlated with production and health records. Zoetis, Semex, and ABS have built machine learning models that need exactly this kind of data. HAUSA is structurally better positioned because of AgriTech Analytics in Visalia and Bewley’s analytics mandate. HC has higher-quality national data but no disclosed commercialization infrastructure. Neither has made it a public priority. That’s the missed opportunity, not the impossible one.

5. Premium tiering: charging serious genetics customers high prices. Probability: ~40% at HAUSA, ~15% at HC.HAUSA already has Holstein COMPLETE, Classic, and Standard tiers. The cameras are inherently a premium product for large operations. Repositioning is structurally feasible. HC has a much harder version of this problem because its DairyTrace customer-service role and national herdbook role require it to serve all members, not just elite breeders. Two-tier service models within a national registry are politically expensive to execute and tend to fracture branch and provincial relationships.

6. Cross-border merger of HC and HAUSA. Probability: under 5%. Upside: theoretically substantial. Practically: not happening. Discussed informally for 20+ years. The cultural gap between the Canadian bilingual branch structure and the U.S. state federation, plus regulatory differences and currency complexity, makes it implausible. Given HC’s current governance turmoil, HAUSA would be absorbing a liability rather than gaining a partner. Useful to mention so it can be set aside.

| Solution | HC Probability | HC Upside (CAD) | HAUSA Probability | HAUSA Upside (USD) | Verdict |

|---|---|---|---|---|---|

| Sustainability data services on DairyTrace | ~35% | $1–3M/yr new revenue | N/A | N/A | HC’s highest-leverage move — requires Lactanet deal |

| HC–Lactanet shared services | ~50% | $500K–$2M/yr cost cut | N/A | N/A | Politically viable; Quebec branch is the obstacle |

| Camera system commercializes on schedule | N/A | N/A | ~55% | $250K–$1M/yr subscriptions | Science is solid; cold-climate engineering is not |

| Phenotypic data licensing to genomics cos | ~25% near-term | $500K–$3M/yr | ~25% near-term | $500K–$3M/yr | Missed opportunity for both — neither has built the infrastructure |

| Premium tiering (elite vs standard service) | ~15% | Modest | ~40% | Moderate | HAUSA feasible; HC can’t tier a national registry |

| Cross-border HC–HAUSA merger | < 5% | Theoretically large | < 5% | Theoretically large | Not happening — set it aside |

The high-probability moves aren’t transformational. The transformational move, sustainability and adjacent data-service expansion negotiated through Lactanet, is low-to-medium probability and entirely dependent on whether HC’s leadership has the political capital and credibility to execute it.

What Members Need to Ask, Out Loud, On the Record

Boards respond to the questions members put in writing. Both organizations were built by breeders who showed up. The next decade depends on whether enough members still do.

Five questions HC members should be putting to the board in writing:

- What is the DairyTrace contract renewal date with Lactanet, and what’s the plan if HC’s customer-service delivery role goes to competitive tender?

- HC’s 2024 Animal Care Assessment revenue from the proAction Cattle Assessments contract was $1.147 million. What’s the renewal date on the current two-year DFC agreement, and what’s the plan if the contract isn’t renewed or goes to tender?

- Under what circumstances would the board exercise the unlimited borrowing authority granted in the April 2026 bylaw rewrite, and what disclosure will members receive before debt is taken on?

- What is the formal status of HC’s working relationship with Lactanet, and is a shared-services arrangement under discussion?

- What does the 2030 strategic plan look like under three scenarios: both contracts stable, DairyTrace lost to a Lactanet tender, and proAction not renewed?

For HAUSA members, the three open questions that matter most are the realistic commercial launch date for the Build a Better Cow camera system against the original four-year timeline, how the cold-climate condensation problem gets solved before deployment in Wisconsin, the Northeast, and the Upper Midwest, and what HAUSA’s data licensing strategy with AI companies actually looks like, including how member-generated phenotypic data gets valued and protected. The 12% nominal decline in program services revenue over the last 11 years sets the clock on all three.

For both HC and HAUSA members, there are two questions every member should answer for themselves before the next AGM or convention. What does your last classification or registration invoice actually buy you in dollar terms, marketing premium, export eligibility, show eligibility, breeding value, and if that line item disappeared tomorrow, what changes in your P&L and what doesn’t? And: is your breed association still your partner, or has it become your competitor for the same data, the same dollars, and the same producer attention?

These aren’t gotcha questions. They’re the questions any breeder with three generations in a herdbook should be able to ask without apology. The April 2026 HC bylaw rewrite passed because 99.2% of members didn’t vote. That’s the math. Boards govern as much as members let them.

Boards of directors also have an obligation to direct management to communicate the association’s vision for 2030 and beyond, including the concrete plan to deliver value for breed membership and breed services.

Neither association is in great shape. One of them can afford to be wrong while it figures out the next moves. The other can’t.

If your most recent classification invoice is up materially from 2023, where did the increase come from, and does the value you get back justify the trend?

How We Know What We Know

Sources used in this analysis:

- Holstein Canada 2024 Annual Report (revenue lines, classification volumes, DairyTrace customer-service revenue of $2.989M / 18.9% of total revenue, Animal Care Assessment revenue of $1.147M from the renewed two-year DFC proAction Cattle Assessments contract, member-herd counts)

- Holstein Canada April 2026 AGM — public remarks by Finance Chair Benoît Turmel and CEO Greg Dietrich; floor questions from Pascal Martin and Amanda Jeffrey; bylaw vote results

- Lactanet as the national DairyTrace program holder; HC delivers customer service outside Quebec under contract with Lactanet

- Attestra as the Quebec traceability service provider running parallel to DairyTrace

- Holstein Association USA IRS Form 990 filings (2020, 2023) via ProPublica Nonprofit Explorer (net assets, liabilities, program services revenue). HAUSA’s 2024 and 2025 Form 990s were not yet posted on ProPublica at the time of analysis.

- HAUSA Pulse Fall 2024 (U.S. dairy operation count of ~26,290)

- USDA NASS structure-of-dairy-farms data (herd-size distribution: ~60% of U.S. dairies under 100 cows; ~500–800 operations above 1,000 cows)

- Dr. Jeff Bewley, World Dairy Expo 2025 presentation (Build a Better Cow camera system specifications, “final score” quote, and timeline)

- Bullvine October 2025 analysis (camera system reporting and large-herd adoption assumptions) Read more: Holstein’s Automated Classification Cameras: Why They’ll Work for 500-Cow Dairies but Maybe Not Yoursv

- Statistics Canada and Agriculture Canada livestock inventory data (Canadian dairy cow inventory 2018–2025)

Derived figures shown in the article: revenue per Holstein cow classified ($5,039,000 ÷ 218,577 = $23.06 CAD/cow); incremental revenue at HC’s 2026 volume target (10,000 × $23.06 = ~$230,600); deficit coverage ($230,600 ÷ $584,000 = ~40%); 200-cow operator annual classification spend (200 × $23.06 = ~$4,600); proAction-loss impact (~$1.147M added to base-case deficit).

Survival probabilities (HC ~80% solvent / ~30–40% strategically relevant; HAUSA ~95% solvent / ~55–70% strategically relevant) and the six-solution probability/upside ranges are informed editorial judgments based on the sources above. They are not statistical outputs. Reasonable analysts working from the same data could land 10–15 points different in either direction.

Limitations: Holstein Canada does not publish full line-item financials at the granularity this analysis would prefer. The DairyTrace customer-service contract sits under Lactanet’s national program, and the proAction Cattle Assessments contract sits directly with DFC on a two-year cycle, so the two contract risks operate on different counterparties and different timelines. HAUSA’s IRS Form 990 reports program services revenue in aggregate and does not split out registration, classification, and AgriTech Analytics revenue at the line-item level.

Key Takeaways

- Holstein Canada’s $6.89M reserve covers about six months of operations, and the real operating deficit is closer to $400K once you strip out investment income and unfilled staff positions. HAUSA’s $30.5M gives it roughly 30 years of runway to absorb mistakes Holstein Canada can’t afford.

- HC carries two DFC-linked contract risks, not one. DairyTrace customer service ($2.989M in 2024) sits under a Lactanet contract and turns a $584K deficit into a $3.5M one if lost at tender. proAction Cattle Assessments ($1.147M in 2024) sits under a renewed two-year DFC contract on a tighter renewal clock and adds roughly $1.15M to whatever the base case is if not renewed. The April 2026 bylaw rewrite already handed the board unlimited borrowing power to plug either gap without member approval.

- HAUSA’s camera bet only pencils above 500 cows at roughly $150K installed, and it hasn’t survived a commercial winter yet. Solvency isn’t the question for HAUSA. Relevance with the 500–800 large U.S. herds that drive genetic progress is.

- Members need to decide whether their breed association is still a partner or has become a competitor for the same data, the same dollars, and the same producer attention, and whether the board they vote for is the one making that call.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Holstein’s Automated Classification Cameras: Why They’ll Work for 500-Cow Dairies but Maybe Not Yours — Arms you with a sharp capital expenditure reality check by calculating the 3–5 year payback timeline required for 500-cow herds against the prohibitive 11-year barrier facing smaller operations eyeing automated evaluation technology.

- Did Genomics Really Deliver What We Think It Did? $238,000 Says Yes – If You Steer It Right — Exposes the structural market shift driving the contraction of traditional breed registry programs by tracking how slashed sire generation intervals accelerated lifetime profit benchmarks by $221 annually.

- The $7,200 Lameness Fix That Beats $45,000 Technology (40-50% Reduction Proven) — Dismantles the tech-first industry narrative with raw financial data proving that low-cost, disciplined herd-management protocols deliver a rapid 4–6 month payback while outperforming six-figure data platforms on commercial operations.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.