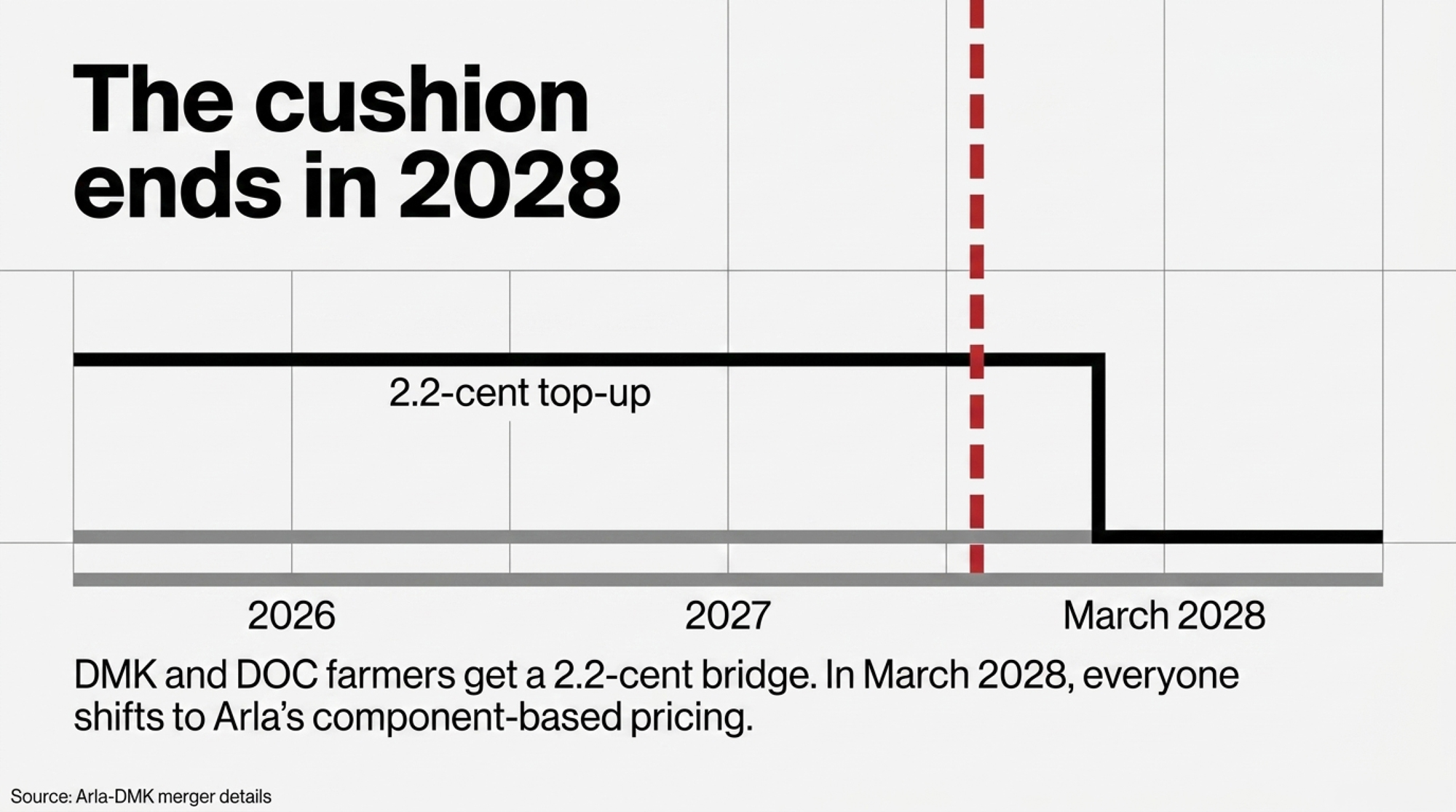

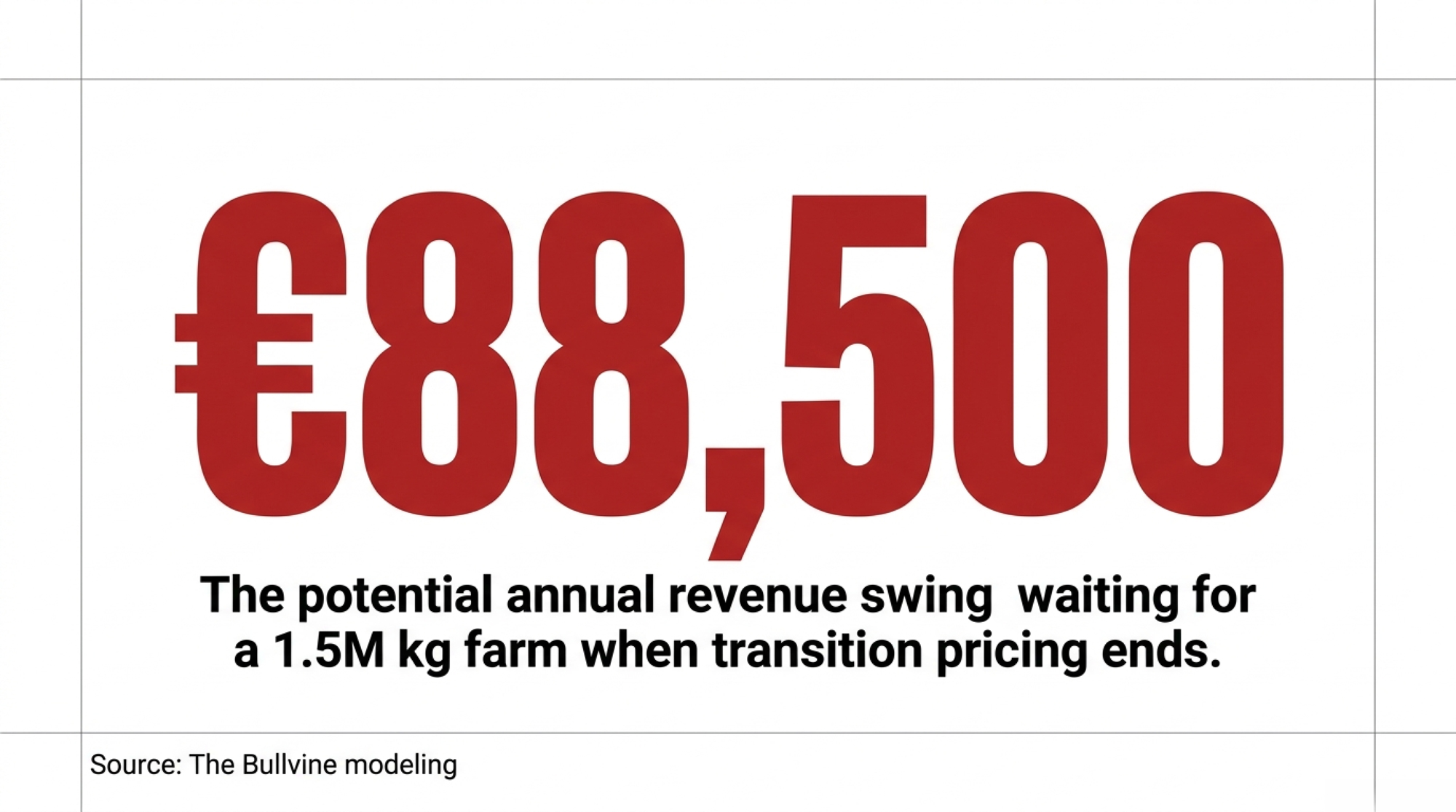

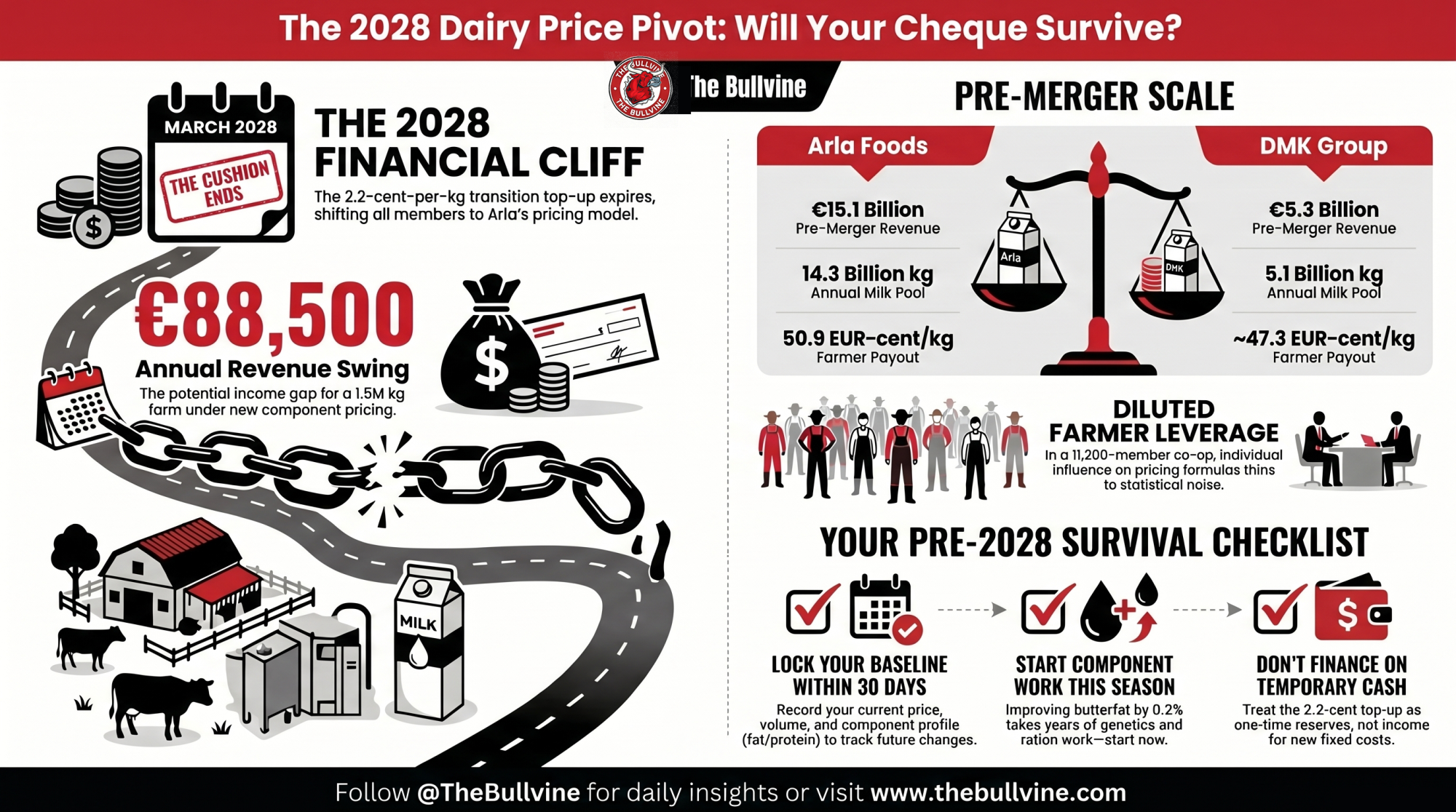

A 2.2-cent top-up cushions DMK and DOC farmers through March 2028. Then component pricing kicks in — and on 1.5M kg, the swing runs to €88,500. Which way does yours break?

Executive Summary: On June 1, Arla absorbs Germany’s DMK and the Dutch co-op DOC to form Europe’s largest farmer-owned dairy, 11,200 members and €20 billion in revenue trading under one name. DMK and DOC farmers get a 2.2-cent-per-kg transition top-up — but it runs out in March 2028, and that’s the date that matters. After it, everyone shifts to Arla’s component-based pricing, and by The Bullvine’s modeling the annual swing on a 1.5-million-kg operation runs to €88,500 depending on your butterfat, protein, and where butter and powder markets land. The upside is real: the deal scales Arla and DMK’s whey JV right as WPC80 clears €17,000 a tonne in Europe, though that margin reaches you diluted across 11,200 members and split between today’s milk price and tomorrow’s capital projects — not as a cheque marked “your share.” The catch is leverage: at this scale your vote on the pricing formula thins to noise, and even EMB president Kjartan Poulsen, an Arla member himself, says co-ops this big “neither live up to their responsibility nor meet the standards they themselves set out.” Your move before the cushion ends is unglamorous — pull your current price, volume, and components now, and start the butterfat work this season, because it doesn’t move fast. Ask Fonterra’s farmers how long it took to force the brands-versus-milk question; the ones who came out ahead tracked their own numbers early instead of waiting for the reckoning.

Editor’s Note: The two-farmer comparison that opens this piece is a composite scenario, modeled from published DMK, DOC Kaas, and Arla milk-price data — not a single real, named producer. The co-ops have not released farm-level pricing. The figures are sound; the farmers are illustrative.

Picture two dairy farmers, each shipping 1.5 million kg a year. One sells to DMK in Germany at roughly €0.473 per kilogram. The other sells to Arla at about €0.509. Same milk, same workload — and, by The Bullvine’s modeling, a gap of nearly €54,000 a year at that volume. As of June 1, those two farmers are in the same cooperative.

That’s the story sitting under the biggest dairy deal in Europe this year. On May 28, 2026, the European Commission unconditionally approved Arla Foods’ acquisition of Germany’s DMK and the Dutch cooperative DOC. By Arla and DMK’s own announcement, the merger brings together 11,200 dairy farmers across seven countries, 28,800 colleagues, a 19.4 billion kg milk pool, and pro forma revenue above €20 billion — all trading under the Arla name as of June 1. The press releases talk about resilience and food security. But if you’re milking cows in Germany, the question is narrower: will that scale actually show up in your milk cheque? And the honest answer doesn’t land until the transition payments run out in 2028.

What’s Changing and Why

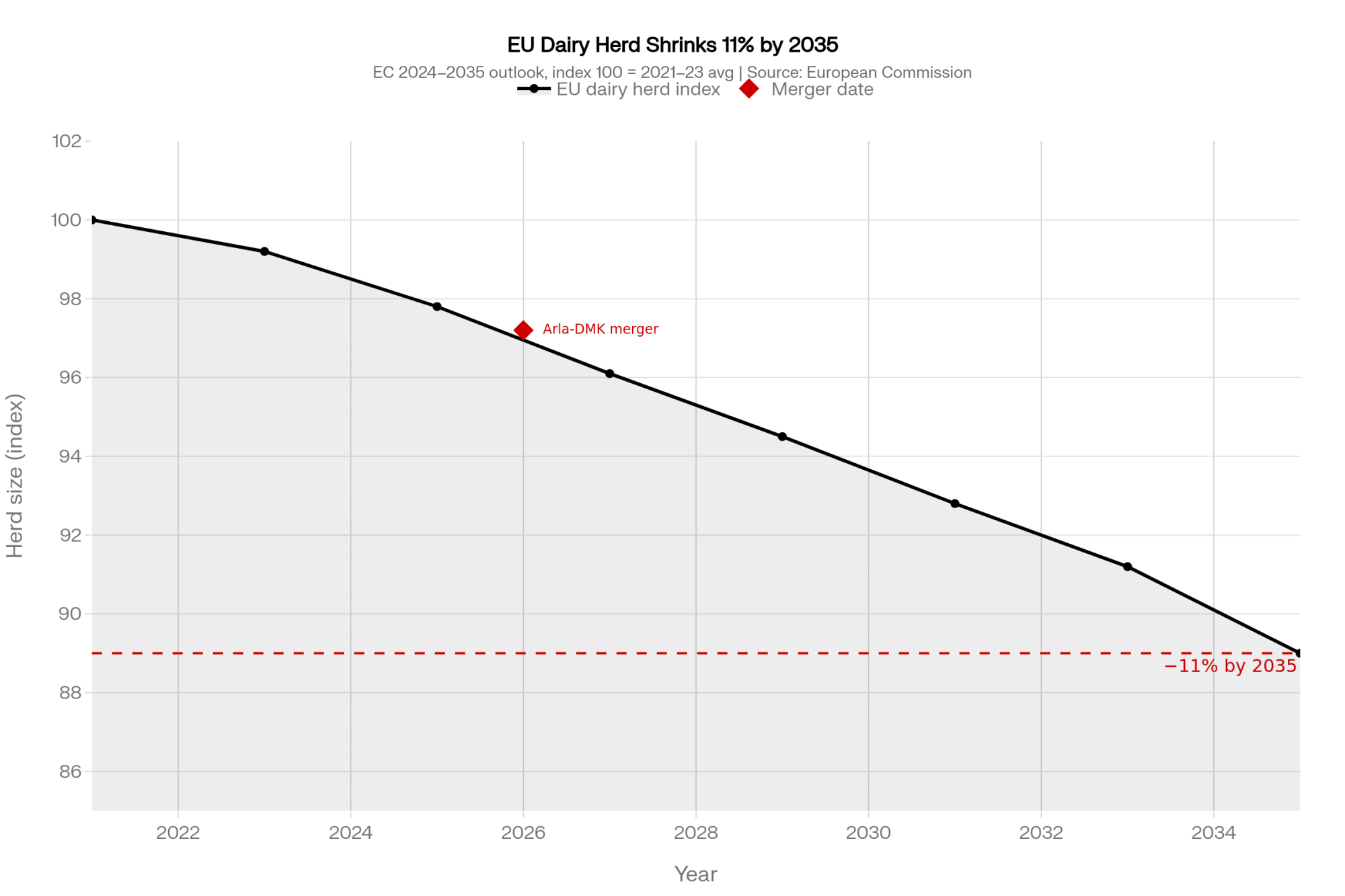

European milk production is shrinking, and that’s the engine behind all of this. The European Commission’s 2023–2035 outlook projected the EU dairy herd would contract by 13% by 2035 relative to the 2021–2023 average; its newer 2024–2035 edition softened that to an 11% decline, but the direction is the same either way. Stack on input-cost pressure, tightening environmental rules, and a handful of grocery chains setting the terms, and cooperatives face a blunt choice. Get bigger, or get squeezed between the global processors above them and the retailers below.

| Dimension | DMK/DOC Farmers — Now | Arla-DMK Farmers — Post-March 2028 |

|---|---|---|

| Milk pricing model | Flat regional rate (~€0.473/kg) | Component-based: butterfat, protein, quality |

| Transition support | +€0.022/kg top-up, paid quarterly | Top-up expires; no published replacement floor |

| Annual revenue swing (1.5M kg) | Stable, predictable | ±€88,500 depending on components & markets |

| Commodity risk | Absorbed by co-op balance sheet | Transferred to individual farm P&L |

| Governance weight | Regional co-op structure | 1 farm voice across 11,200 members, 7 countries |

| Whey/ingredients upside | Limited direct access | Scaled JV — but diluted into performance price |

| Butterfat premium signal | Minimal pricing incentive | Direct revenue impact per 0.1% BF shift |

| Walk-away leverage | Moderate — regional alternatives exist | Shrinking — fewer large buyers as herd contracts |

| Producer org rights (EU law) | Standard cooperative rules apply | Same — lighter transparency obligations than arms-length processors |

| Key action deadline | Baseline audit before June 1, 2026 | Component/nutrition work before March 2028 |

That’s why consolidation is sweeping the continent. FrieslandCampina merged with Milcobel — a deal that took effect January 1, 2026 — to form a cooperative worth roughly €14 billion, and now Arla-DMK clears €20 billion. The two partners aren’t strangers, either — they’ve jointly run a whey-processing venture for over a decade, so this is a deepening of an existing relationship rather than a leap into the dark.

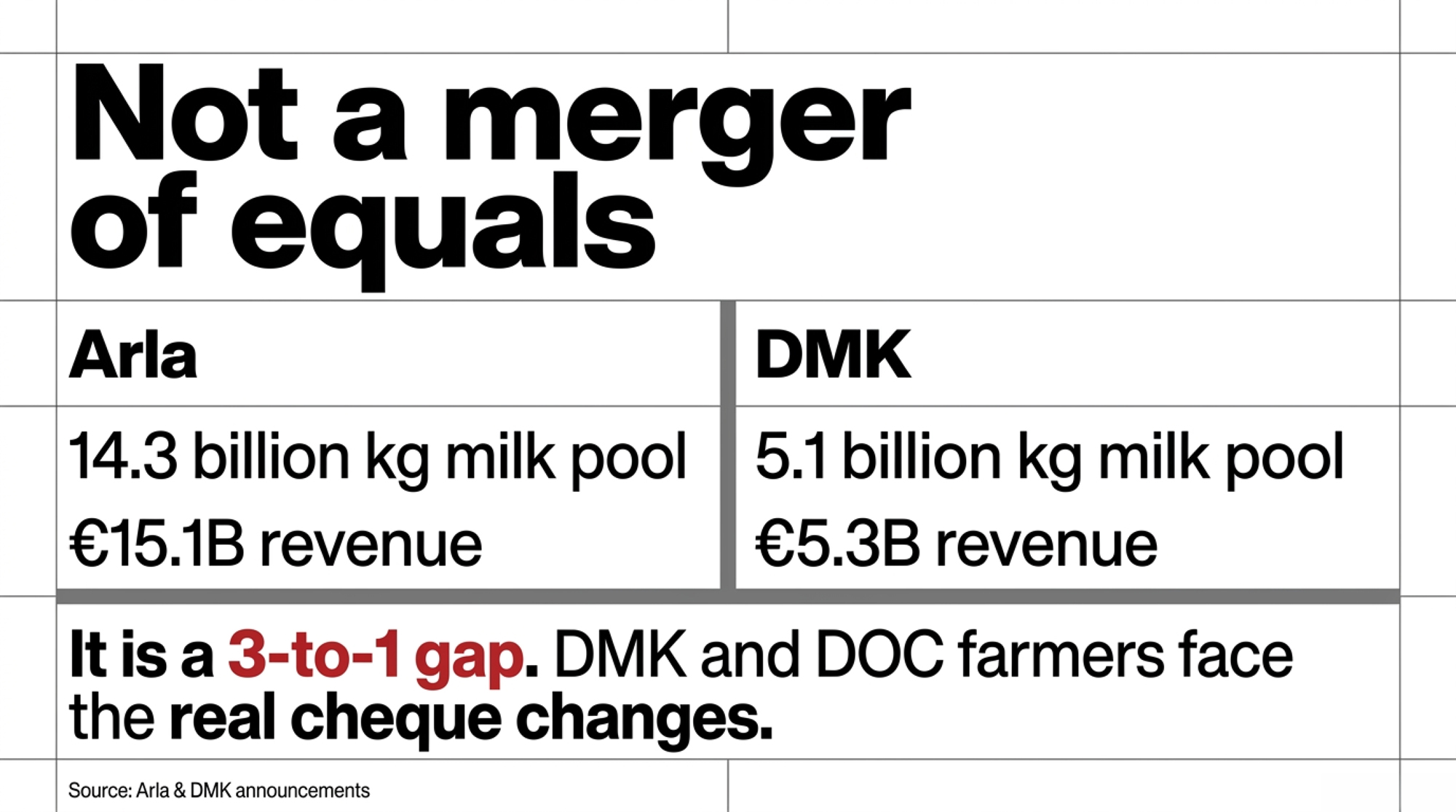

Who feels it most? German and Dutch producers — and the reason sits in the raw scale gap between the two sides.

| What each side brings | Arla | DMK |

| Revenue into the deal | €15.1 billion | €5.3 billion |

| Milk pool | 14.3 billion kg | 5.1 billion kg |

| Recent farmer payout | 50.9 EUR-cent/kg performance price — its second-highest ever | Revenue down 6.7%, partly as producers walked after the deal was announced |

That’s not a merger of equals — it’s nearly a 3-to-1 gap on both revenue and milk. Arla members already sit toward the top of the pricing scale. DMK and DOC farmers are the ones whose cheques face the real change, and some voted with their feet before the ink was dry.

Don’t Forget the Dutch Side

DMK gets most of the attention because it’s the bigger of the two acquired co-ops, but DOC Kaas is the third party in this deal, and its farmers face the same pricing question on the same timeline. DOC is the Dutch cooperative folded in alongside DMK, and its members receive the same 2.2-euro-cent transition top-up through March 2028. Same bridge, same cliff at the end of it.

The Dutch piece matters for a reason beyond size. Producers in the Netherlands are already squeezed by some of the tightest environmental and nitrogen rules in Europe, so a DOC farmer weighing the post-2028 pricing switch is doing so on top of herd-size and land-use pressures that a German or Danish member may not feel as acutely. The merger doesn’t change those rules. It just changes who buys the milk and how the cheque gets calculated. So if you’re a DOC member, the transition-year math in this piece is yours too — and the regulatory backdrop only sharpens the case for knowing your numbers cold before the cushion ends.

How This Plays Out on Real Farms

The merger softens the immediate blow with a bridge payment. From 2026 through 2028, DMK and DOC Kaas farmers receive an extra 2.2 euro cents per kilogram, paid quarterly and drawn from the merged entity’s common equity — not by cutting anyone’s current price. The schedule runs in installments through to a final payment in March 2028. Genuine money in the near term. But a bridge, not a raise.

Here’s where it gets real for herds at your scale. When the top-up ends in 2028, every member shifts onto Arla’s component-based pricing — milk value set by butterfat, protein, and quality rather than a flat regional rate, as laid out in DMK’s milk-price model summary. According to The Bullvine’s modeling, that can swing annual revenue for a 1.5 million kg operation by as much as €88,500, depending on your components and where commodity markets land — the full scenario assumptions are in our component-pricing breakdown. That’s a modeled range, not a published Arla figure; the co-op hasn’t released a farm-level formula.

Think about what an €88,500 swing covers. A year and a half of tractor payments. A full parlour renovation. The farms that come out ahead are the ones with strong butterfat and protein levels and enough cash reserves to ride out volatility. The marginal producers are the ones who tend to exit in the years after, and in a shrinking market, that attrition tightens the milk pool on its own, with no formal decision required and no one announcing a cut. That’s how pay-for-quality systems work everywhere, not a quirk of this deal.

The Mechanics Behind the Outcomes

Component pricing isn’t a trick. It’s standard across much of the dairy world, and it genuinely rewards quality milk. But it also hands you commodity risk the cooperative’s balance sheet used to absorb. Your cheque now rides global butter and powder markets you don’t control.

The deeper tension sits one level up. The same cooperative that’s supposed to fight for high milk prices for its members is also the buyer trying to source raw milk as cheaply as it can. Arla and DMK both frame “the highest possible milk price” as the core purpose of the merged co-op. But at 11,200 members across seven countries and several languages, your individual influence shrinks toward statistical noise.

Picture how a decision actually gets made in a co-op this size. You don’t vote on the milk-price formula at your kitchen table. You elect a district representative, who sits on a regional council that sends delegates to a board of representatives, which hires the management team that runs the pricing model day-to-day. By the time a pricing decision reaches you, it’s passed through three or four layers — and at each one, your single farm’s weight gets diluted against thousands of others. That’s not corruption. It’s arithmetic. Kjartan Poulsen — an Arla member himself, and president of the European Milk Board — argues cooperatives at this scale “neither live up to their responsibility nor meet the standards they themselves set out.”

There’s a regulatory wrinkle most farmers never hear about, too. As Poulsen and the European Milk Board frame it, this is a structural feature of EU cooperative law, not of any one co-op: because members own the business, the contract-transparency rules that bind arms-length processors often don’t apply, and members generally can’t form independent producer organizations to negotiate price. So a large cooperative can operate under lighter pricing-transparency obligations than a standard processor contract, while the farmers inside it have fewer outside tools to push back. You gain scale. You give up leverage.

The Whey Upside: Does the Margin Come Back to You?

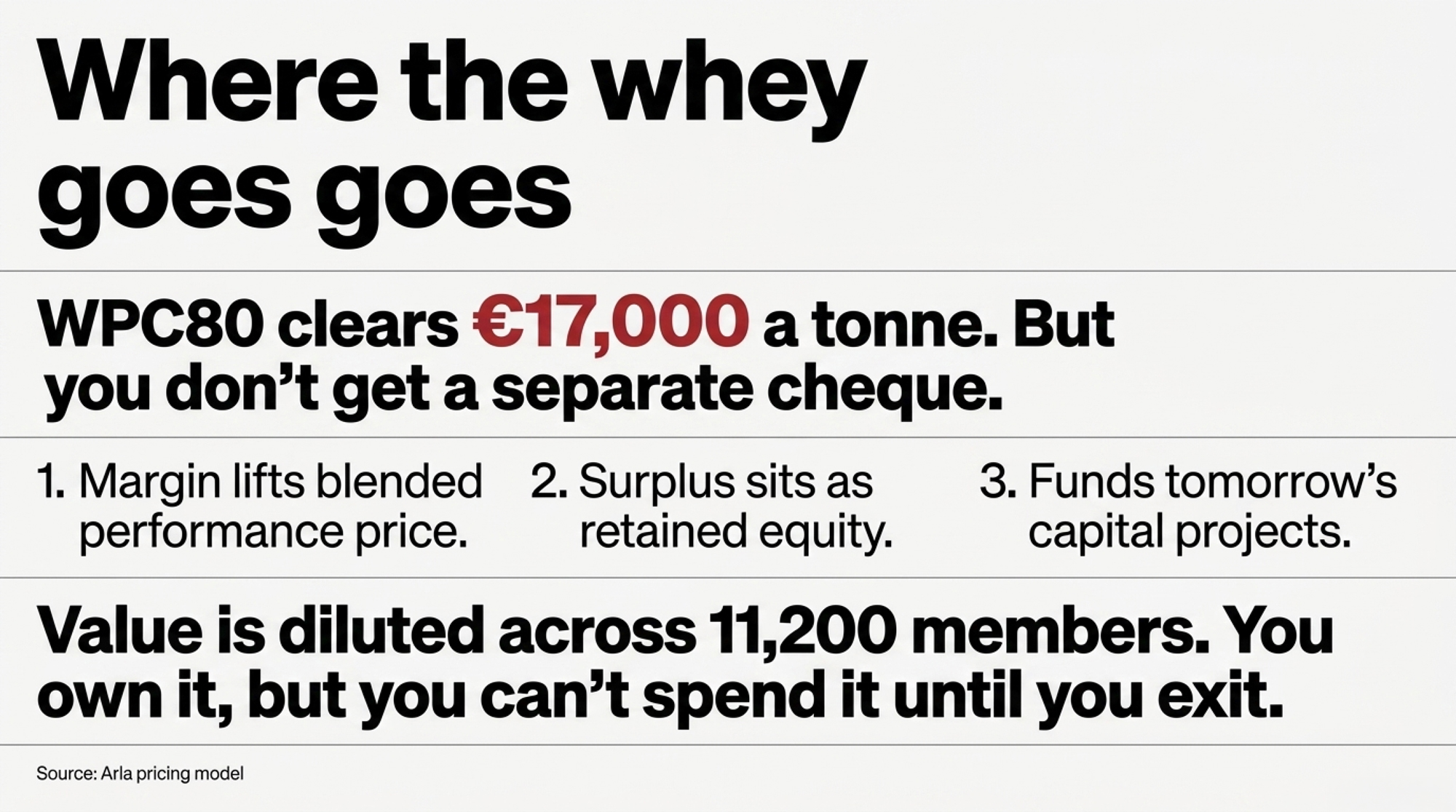

Now, the genuinely promising part of this deal. The whey protein and ingredients business is Arla-DMK’s strongest card. WPC80 — whey protein concentrate, the high-value stuff bound for sports nutrition, infant formula, and clinical nutrition — hit nearly €17,000 per tonne in Europe and over €18,000 in the US in spring 2026, driven by structural supply bottlenecks and surging protein demand. The existing whey joint venture already turns DMK’s cheese-stream byproduct into that product, and the merger scales it hard.

Follow the milk to see why that matters. Cheesemaking turns only about a tenth of your milk into cheese — the rest, the bulk of it, leaves the vat as whey. For decades, that stream was a disposal cost; now it’s the highest-margin product in the building. A merged co-op with a bigger cheese footprint generates more whey, and more whey at €17,000 a tonne is real money. The question is whose money.

In Arla’s model, the answer runs like this. Arla pays members a single performance price — a blended per-kilo figure that already accounts for whatever it earns downstream, including ingredients — and what isn’t paid out is retained as member equity on the cooperative’s balance sheet. So whey margin doesn’t arrive as a separate cheque marked “your share of WPC80.” It either lifts the performance price for everyone, or it sits as retained equity funding the next dryer or acquisition — value you technically own but can’t spend until you exit the co-op. That’s the real mechanism behind the tease. Ingredient profit reaches you diluted across 11,200 members and split between today’s milk price and tomorrow’s capital projects, and you don’t get a vote on that split line by line. DMK’s materials promise that the merger will “further grow the value of our milk,” but there’s no published formula that ties whey EBITDA to your individual price. Until there is, “grows the value of our milk” and “raises my cheque this year” are not the same sentence — and that’s the question worth raising out loud at your regional meeting.

Options and Trade-Offs: Your Pre-2028 Sequence

No single path fits every operation, but the order matters. These four moves run from “this week” to “before the cushion ends” — work them in sequence, because each one sets up the next.

Step 1 — Within 30 days: lock down your baseline. Pull your milk statements and write down three numbers: your exact current price, your trailing 12-month volume, and your component profile (butterfat %, protein %, somatic cell average). It takes an afternoon, it carries zero risk, and it’s the only way you’ll know — once component pricing fully takes over in 2028 — whether the new math is rewarding your milk or quietly clipping it. Skip this, and you’re flying blind into the switch.

Step 2 — This quarter: decide what the 2.2-cent top-up is for. Treat it as one-time income, not a raise — push it into working-capital reserves or component-improving nutrition, not new fixed costs. That works if your operation is stable, but it takes discipline while the cash flow feels good. And don’t finance a tractor on money that disappears in 2028.

Step 3 — This season: start the component work, because it’s slow. Lifting butterfat 0.2–0.3% takes ration work, genetics decisions, and forage quality — none of it moves fast. Begin before the March 2028 cutoff, not after, especially with European processors already signalling they want less butterfat than farmers have been breeding for. Start now, or you’ll be adjusting after the window closes.

Step 4 — Before the cushion ends: know your walk-away number. UK cost analysis puts structural unprofitability for many farms at around €0.38–0.43/kg, depending on cost structure and debt — a German or Dutch figure may look different. Run a 12-month cash flow at three milk prices: current, 10% down, and 15% down. If the 15%-down case sinks you, build the contingency plan now, while the transition cushion still exists.

Run alongside all four — the governance play: work your regional council, not just the central board. Arla runs through regional farmer structures, and the merged co-op pledges “representation and decision making among all members.” Show up in 2026–2027, while the cooperative still needs farmers’ goodwill to ensure smooth integration. One farm won’t reshape a €20 billion pricing model — but a documented record of asking the hard question is leverage you’ll want later.

How Much Does Waiting Until 2028 Actually Cost You?

The honest answer: nobody can hand you a hard post-2028 figure yet, because the long-run pricing formula hasn’t been published in farm-level detail. And that’s exactly the problem. The leverage you hold today comes from the cooperative needing your cooperation to integrate smoothly. Once the bridge payments stop in March 2028 and the new model locks in, that leverage shifts toward management.

Look at Fonterra for the cautionary version. New Zealand’s farmer-owners spent years debating how far their cooperative should chase consumer brands versus focus on the milk pool. In October 2025, they settled it — voting to sell the entire Consumer and associated businesses (Mainland Group) to Lactalis for NZ$4.22 billion, with 88.47% of votes cast in favour. A decisive verdict that the cooperative’s best returns came from milk, not brands. The lesson for Arla-DMK members isn’t the outcome — it’s the years it took farmers to force the question. The ones who fared best didn’t wait for the collective reckoning. They tracked their own numbers early.

Is Your Herd’s Component Profile Ready for the Switch?

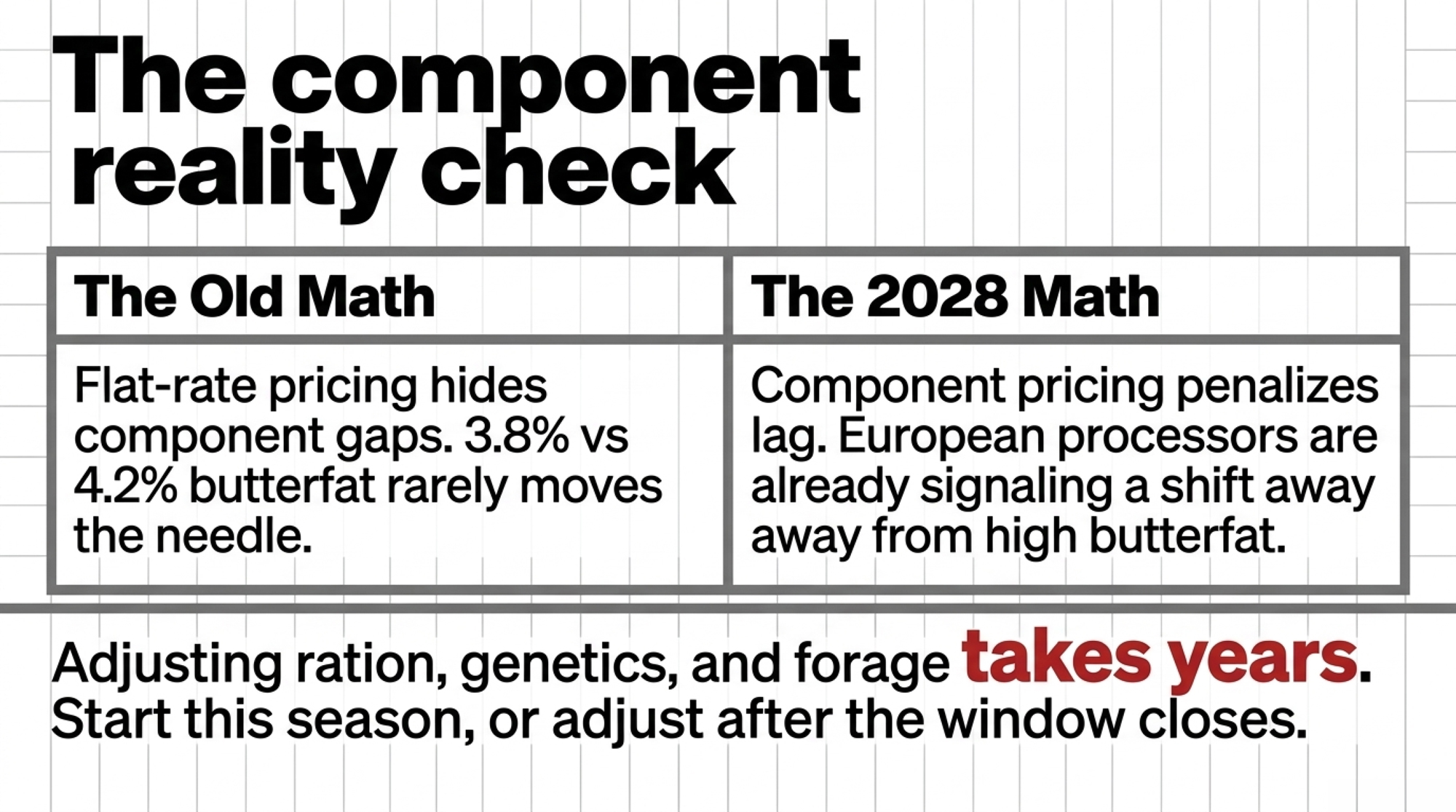

Under a flat-rate structure, the gap between a herd at 4.2% butterfat and one at 3.8% might not move your cheque much. Under component pricing, that same gap can meaningfully change annual revenue on a 1.5 million kg farm — and it’s a live issue right now, with European processors already signalling they want less butterfat than farmers have been breeding for. That’s not a rounding error. That’s whether your kid can take over the operation.

The window to adjust components is now, during the transition years — not once the new math is fully live in 2028. Nutrition tweaks, genetics decisions, and forage quality all move the needle, but slowly. If your butterfat and protein are out of step with where your processor’s premiums are headed, that’s the number to start working this season. Where does yours sit right now?

Your Decision Triggers

If you only act on one thing this year, make it the first row. Each trigger below maps a situation to a move and a deadline — pull the dates onto your own calendar.

| If this is you | Do this | By when |

| You ship to DMK or DOC | Write down your exact current price, 12-month volume, and component profile so you have a baseline | Before June 1, 2026 |

| You’re getting the 2.2-cent top-up | Bank it or spend it on components — run the post-2028 cashflow before committing it to anything fixed | This quarter |

| Your butterfat/protein is out of step with your processor’s premium signals | Start ration and genetics work — component shifts take years | This season |

| A 15%-below-current milk price would break you | Run a three-scenario cashflow and build the contingency plan while the cushion exists | Before March 2028 |

| You want a say in the post-2028 formula | Get to your regional council meetings and ask for the pricing math in writing | 2026–2027 |

| You don’t know your walk-away price | Calculate the per-kg point where you burn equity every month | Before the cushion ends |

What’s Your Number?

The merger will almost certainly succeed as a business. The open question is whether “Europe’s largest farmer-owned cooperative” still behaves like a cooperative at 11,200 members across seven countries — or whether scale quietly turns member-owners into shareholders in a €20 billion food company. We won’t know until the cheques arrive after 2028. And management, fair to say, knows a great deal more about that answer right now than you do.

So before the transition years lull anyone to sleep, two questions are worth sitting with. Where does your breakeven actually sit? And could your operation absorb an €88,500 revenue swing if components and commodity markets turn against you simultaneously? You now own a piece of the biggest dairy cooperative on the continent. The only thing that determines whether that’s an asset or a slow squeeze is whether you’re watching your own numbers as closely as their management watches theirs.

Key Takeaways

- The 2.2-cent top-up runs out in March 2028. Treat it as one-time money, not a raise — bank it or put it toward components, and don’t finance anything fixed on it.

- Once component pricing takes over, the swing on a 1.5-million-kg farm runs to €88,500 depending on your butterfat, protein, and where butter and powder land. Pull your current price, volume, and components now so you’ve got a baseline.

- Lifting butterfat 0.2–0.3% takes ration, genetics, and forage work that doesn’t move fast. Start this season, not after the cutoff.

- At 11,200 members your vote on the pricing formula thins out, so work your regional council in 2026–2027 while the co-op still needs farmer goodwill to integrate.

Run Your Numbers

Component Value Tracker — Before 2028 turns butterfat and protein into your milk-check math, run the Component Value Tracker to see what 0.1 point of fat or protein is actually worth in your herd — and pressure-test whether your components leave you on the winning or losing side of that €88,500 swing.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $28614 Tenth: Why Upper Midwest Protein Is Now Worth More Than Fat — Delivers the exact financial formula to reprice your component strategy under shifting processor premiums, proving why a single tenth of a point of protein now outvalues butterfat and shifting your immediate nutritional ROI.

- The $19 Milk Trap: How 2026 Prices Quietly Drain a 400‑Cow Dairy’s Equity — Exposes the deep structural tension between a mega-cooperative’s processing margins and your farm-gate price, arming producers with a 30-day playbook to stress-test equity before single-buyer leverage locks out your mid-sized operation.

- Why 88% of Fonterra Farmers Just Voted to Sell Their Brands for 12 Cents on the Dollar — Breaks down the mathematical destiny behind multi-billion-dollar asset liquidations, revealing how production-weighted voting and mounting debt pressure force family operations to trade long-term corporate brand equity for immediate cash survival.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.