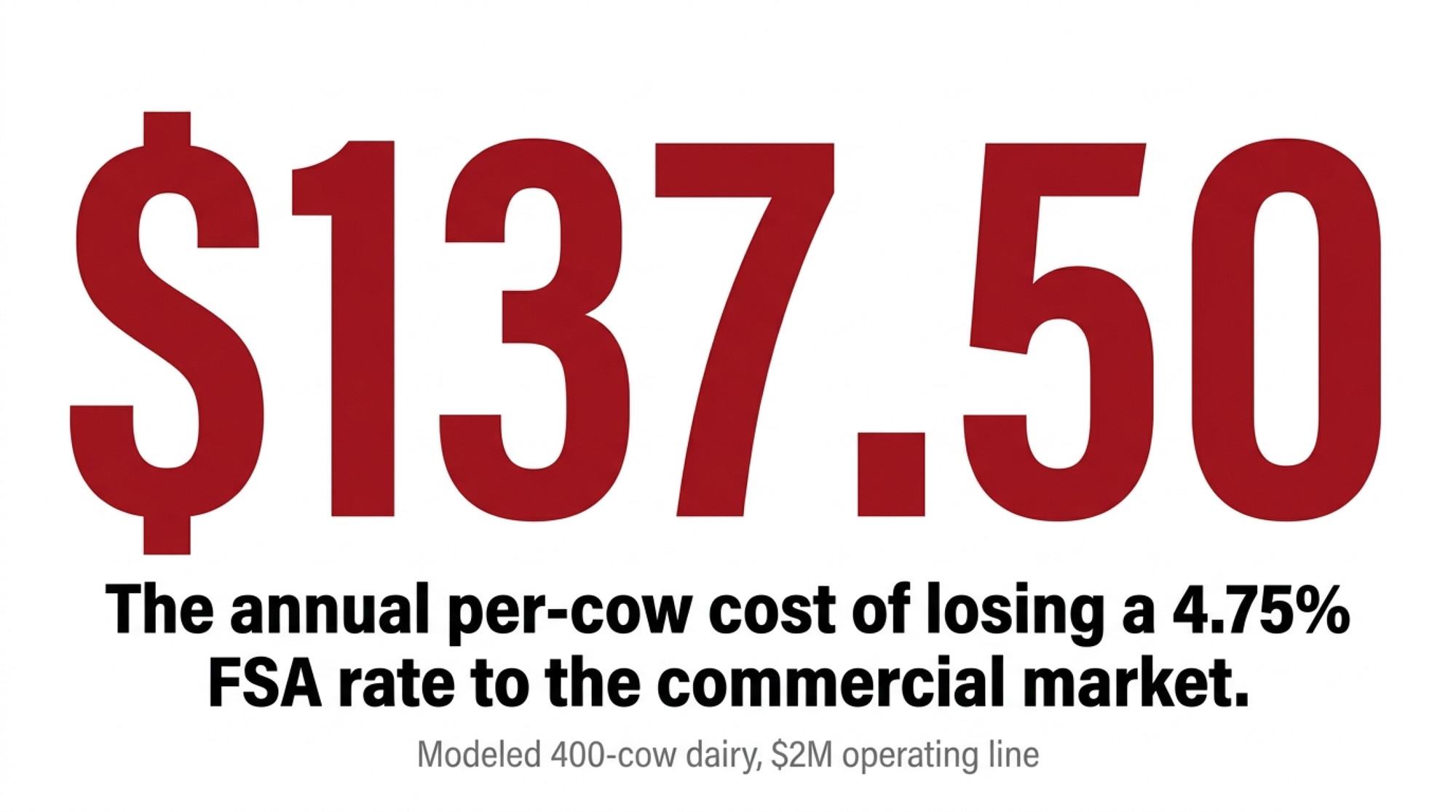

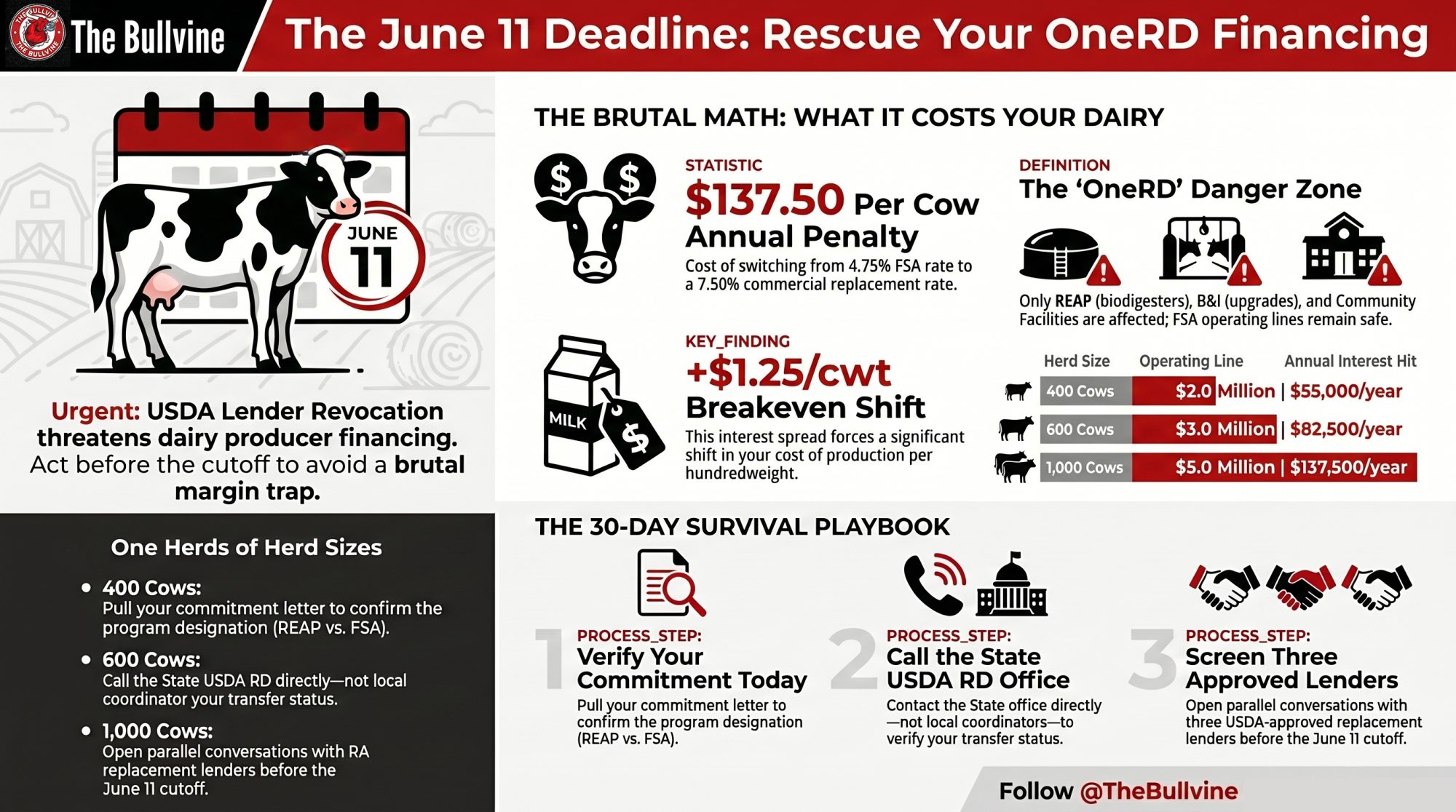

On May 11, your REAP biodigester deal is penciled at 4.75% FSA money. On May 12, your lender lost OneRD approval. That’s $137.50/cow on a 400-cow dairy — and June 11 is the transfer deadline.

Executive Summary: USDA removed 10 lenders from the OneRD-approved list on May 12, and producers with REAP, B&I, or Community Facilities commitments through them have until June 11 to transfer the deal or lose it. The named ten: Bank of Montgomery, Byline Bank, Celtic Bank, Community Bank & Trust – West Georgia, Genisys Credit Union, Greater Nevada Credit Union, North Avenue Capital, Optus Bank, U.S. Eagle Federal Credit Union, and ReadyCap Commercial. One was already in FDIC receivership eleven days before Rollins announced anything. The replacement-rate math is brutal: 4.75% FSA Direct against a 7.50% Q3 2025 Chicago Fed commercial rate runs $55,000/year on a $2M operating line — $137.50/cow on a 400-cow Midwest dairy, a +$1.25/cwt breakeven shift on Cornell DFBS basis. FSA-guaranteed operating lines through these institutions are unaffected; the hit is concentrated on capital projects mid-build. If your DSCR’s been under 1.15x for three months running and your conditional commitment letter is sitting unread, the next 23 days decide whether the project pencils or strands.

Dairy producers working with ten major national and regional lenders have until June 11 to rescue their OneRD infrastructure financing. USDA’s May 12 revocation of OneRD lending privileges for institutions holding roughly $620 million in delinquencies — about 47% of USDA Rural Development’s total delinquent loan portfolio concentrated in just 1% of approved lenders — moved the deadline from theoretical to immediate. Mid-sized operators are facing a brutal reality with REAP biodigesters, B&I-financed processing upgrades, and Community Facilities loans now caught in transfer.

The kind of 400-cow Western Michigan operator running this math today — a modeled scenario based on the named herd-size band and standard REAP guarantee parameters — is staring at a 4.75% FSA Direct Operating rate against a 7.50% commercial replacement rate on a $2 million operating line. That’s $55,000 a year in extra interest, $137.50 per cow. A +$1.25/cwt breakeven shift on the Cornell DFBS basis. The producers feeling that the USDA lender revocation of dairy 2026 will squeeze hardest are the ones whose lenders showed up on the May 12 list — and the State USDA Rural Development office is the contact point the announcement directs them to.

USDA framed the action as accountability. The timeline reads less like enforcement readiness than political cover: the announcement landed eleven days after Community Bank & Trust – West Georgia entered FDIC receivership. For producers mid-application on a REAP biodigester, a B&I-financed processing upgrade, or a Community Facilities loan through any of the ten named institutions, June 11 isn’t an abstraction. It’s the line between a viable capital project and a stranded asset.

What Did USDA Actually Do on May 12 — and What Did They Leave Out?

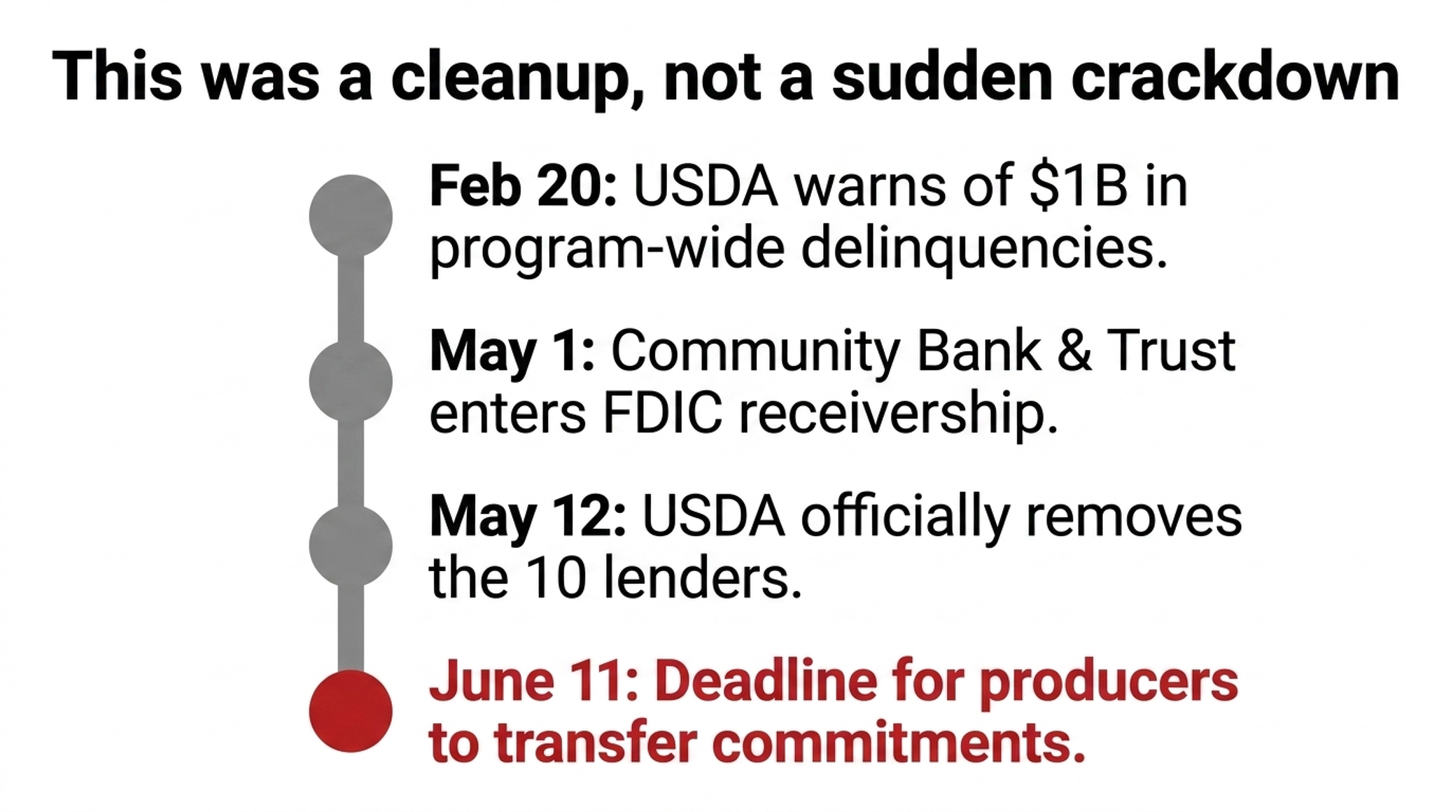

Secretary Brooke Rollins announced the removal of ten lenders from the OneRD Guaranteed Lending Program on May 12. The named ten: Bank of Montgomery, Byline Bank, Celtic Bank, Community Bank & Trust – West Georgia, Genisys Credit Union, Greater Nevada Credit Union, North Avenue Capital, Optus Bank, U.S. Eagle Federal Credit Union, and ReadyCap Commercial.

Here’s what the press release didn’t lead with. Community Bank & Trust – West Georgia was already in FDIC receivership as of May 1, 2026, per the Georgia Department of Banking and Finance. Publicly reported regulatory pressure preceded the May 1 receivership. By the time Rollins stepped to the podium, Georgia state banking authorities had formally seized that institution for eleven days.

Removing a bank already in receivership functions as documentation rather than enforcement. The institution had already been seized.

The timeline gets worse. RBCS Administrator J.R. Claeys sent an open warning letter to 775+ active OneRD lenders on February 20, 2026. That letter disclosed program-wide delinquencies exceeding $1 billion and $300 million in losses realized over the prior 12 months. Eighty-one days passed between Claeys’ letter and the May 12 revocation. Producers who entered conditional commitments through those ten lenders during that window are the ones now racing the clock.

| Lender | State/Region | Primary Sector | Notable Pre-May 12 Status | FDIC/Regulatory Flag |

|---|---|---|---|---|

| Community Bank & Trust – West Georgia | Georgia | Community banking | In FDIC receivership May 1, 2026 — 11 days before removal | ⚠️ Already seized |

| ReadyCap Commercial | National (NJ-based) | SBA/USDA guaranteed lending | High small-business SBA 7(a) delinquency concentration | Elevated |

| North Avenue Capital | National | Commercial RE / hospitality | $168.5M in 90-day delinquencies, CRE/hospitality concentration | ⚠️ High |

| Genisys Credit Union | Michigan (Auburn Hills) | Credit union, 280,000+ members | Active USDA & SBA guaranteed lending; Michigan dairy exposure | Removed |

| Greater Nevada Credit Union | Nevada | Credit union | Rural community lending, OneRD B&I exposure | Removed |

| Byline Bank | Illinois | Commercial banking | Active OneRD originator, FSA guaranteed lines intact | Removed |

| Celtic Bank | Utah | Fintech-adjacent SBA lender | Nationwide USDA program partner | Removed |

| Bank of Montgomery | Alabama | Community banking | Rural community bank | Removed |

| Optus Bank | South Carolina | CDFI-affiliated community bank | Minority depository institution | Removed |

| U.S. Eagle Federal Credit Union | New Mexico | Credit union | Rural Southwest lending | Removed |

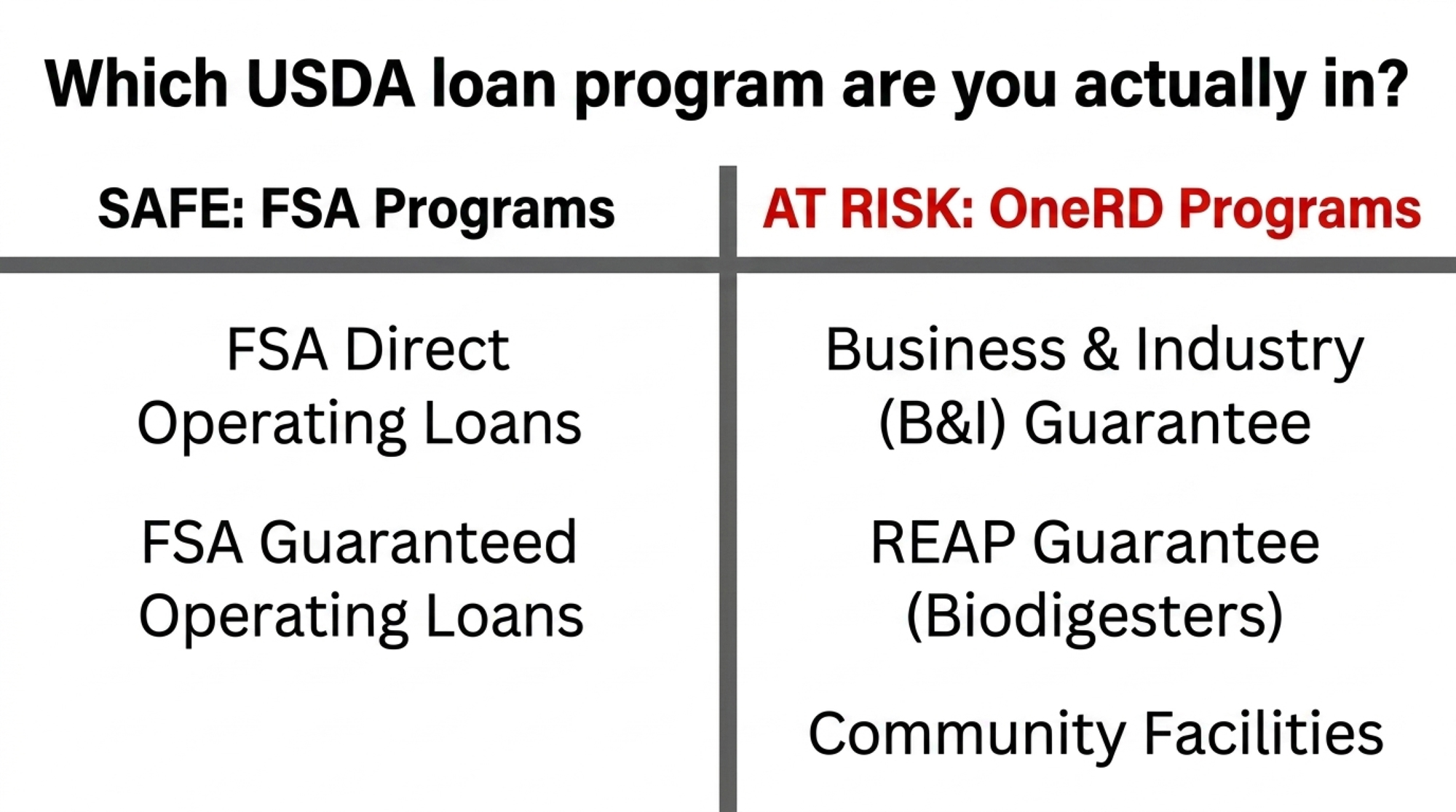

OneRD or FSA: Which USDA Loan Program Are You Actually In?

Before you panic, verify. The OneRD program isn’t a farm operating loan program. It’s a rural business and infrastructure guarantee umbrella covering Business and Industry (B&I), Rural Energy for America Program (REAP), Community Facilities, and Water and Waste Disposal. FSA operating loans run through a completely separate channel — the Farm Service Agency, not Rural Development.

| Loan Type | Administered By | Affected by May 12? | Action Required |

|---|---|---|---|

| FSA Direct Operating Loan | USDA Farm Service Agency | No | No action needed |

| FSA Guaranteed Operating Loan | FSA via commercial lender | No — guarantee survives | Verify with lender in writing |

| OneRD B&I Guarantee | USDA Rural Development | YES | Transfer by June 11 |

| OneRD REAP Guarantee | USDA Rural Development | YES | Transfer by June 11 |

| OneRD Community Facilities | USDA Rural Development | YES | Transfer by June 11 |

| Water & Waste Disposal | USDA Rural Development | YES | Transfer by June 11 |

If your FSA-guaranteed operating line runs through Byline Bank or Genisys Credit Union, your guarantee is intact. The lender can’t originate new OneRD-program loans going forward. If your REAP biodigester, B&I-financed milk processing upgrade, or value-added packaging plant runs through any of the ten — you’re in the window. June 11 applies to existing conditional commitments and new originations through the revoked institutions; closed loans with guarantees already obligated remain in force under standard servicing terms.

How to Check Your Lender’s Status in Three Steps

- Step 1. Go to the USDA Rural Data Gateway at rd.usda.gov/rural-data-gateway and open the Lender Lens portal. Search by lender name. Confirm current OneRD approved status as of the date you’re checking — bookmark the URL with the timestamp.

- Step 2. Cross-reference with your conditional commitment letter. The program designation (B&I, REAP, Community Facilities) and the lender’s tax ID should match. If they don’t, request clarification in writing before calling your State RD office.

- Step 3. Email your loan officer and the lender’s USDA program compliance officer simultaneously. Subject line: “Confirmation of OneRD approved-lender status, file [your loan ID].” Request a written response within five business days.

Why Did USDA Wait 81 Days, and What Did It Cost Producers?

USDA had legal authority under 7 CFR Part 5001 to remove lenders in February. The audit data was sufficient — Claeys’ own letter disclosed it. Bullvine’s read of the timeline: the agency waited for political cover, the kind a visible institutional collapse provides when it frames a broader removal as decisive accountability rather than belated damage control.

Community Bank & Trust – West Georgia’s failure on May 1 provided that frame. Without it, the announcement reads as ten lenders removed for portfolio concentration concerns — a narrative that generates congressional inquiries from delegations representing affected lenders, plus likely litigation. With it, the announcement reads as a cleanup after an already-public failure.

The cost of those 81 days falls on producers who entered binding financing agreements through any of the ten lenders during the window. USDA hasn’t published the commitment-issuance volume by lender for the period. That number is the accountability question that hasn’t been asked on the record.

The 400-Cow Margin Trap at 4.75% Versus 7.50%

The replacement-rate math is where this story stops being an enforcement headline and becomes a barn-level decision. The USDA Farm Service Agency Direct Operating Loan rate sits at 4.750% as of May 1, 2026, per the USDA FSA current rate sheet. The Federal Reserve Bank of Chicago’s Q3 2025 commercial agricultural operating loan rate clocked 7.50%, and the St. Louis District ran 7.78% — the most recent published district surveys, with current commercial quotes likely in a similar range. That’s a 2.75 to 3.00 percentage-point spread between FSA-subsidized capital and the commercial market, displaced borrowers now have to enter.

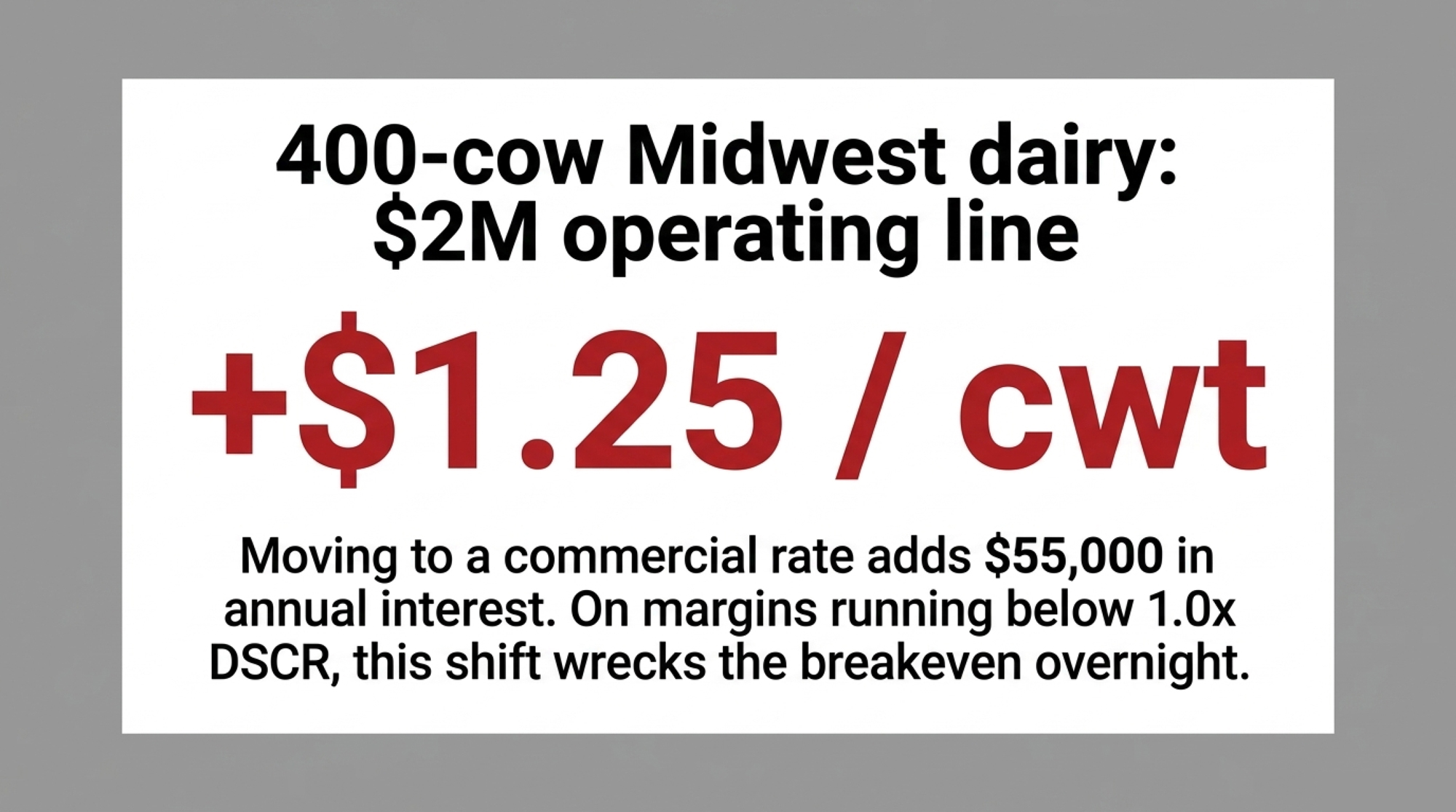

Running the Numbers — 400-Cow Midwest Dairy, $2M Operating Line

Inputs:

- Herd size: 400 cows

- Operating line: $2,000,000 ($5,000 of working capital per cow)

- Annual milk shipped (Cornell DFBS basis, 110 cwt/cow): 44,000 cwt

- FSA Direct Operating rate, May 1, 2026: 4.750% (USDA FSA rate sheet)

- Commercial replacement rate, Q3 2025: 7.50% (Federal Reserve Bank of Chicago / Purdue Center for Commercial Agriculture)

The arithmetic:

- FSA annual interest cost: $2,000,000 × 0.0475 = $95,000/year

- Commercial annual interest cost: $2,000,000 × 0.0750 = $150,000/year

- Annual differential at 2.75 points: $55,000/year

- Per cow per year: $55,000 ÷ 400 = $137.50/cow

- Per cwt shipped (Cornell DFBS basis): $55,000 ÷ 44,000 = +$1.25/cwt breakeven shift

Interest Spread Impact Matrix (Cornell DFBS 110 cwt/cow basis)

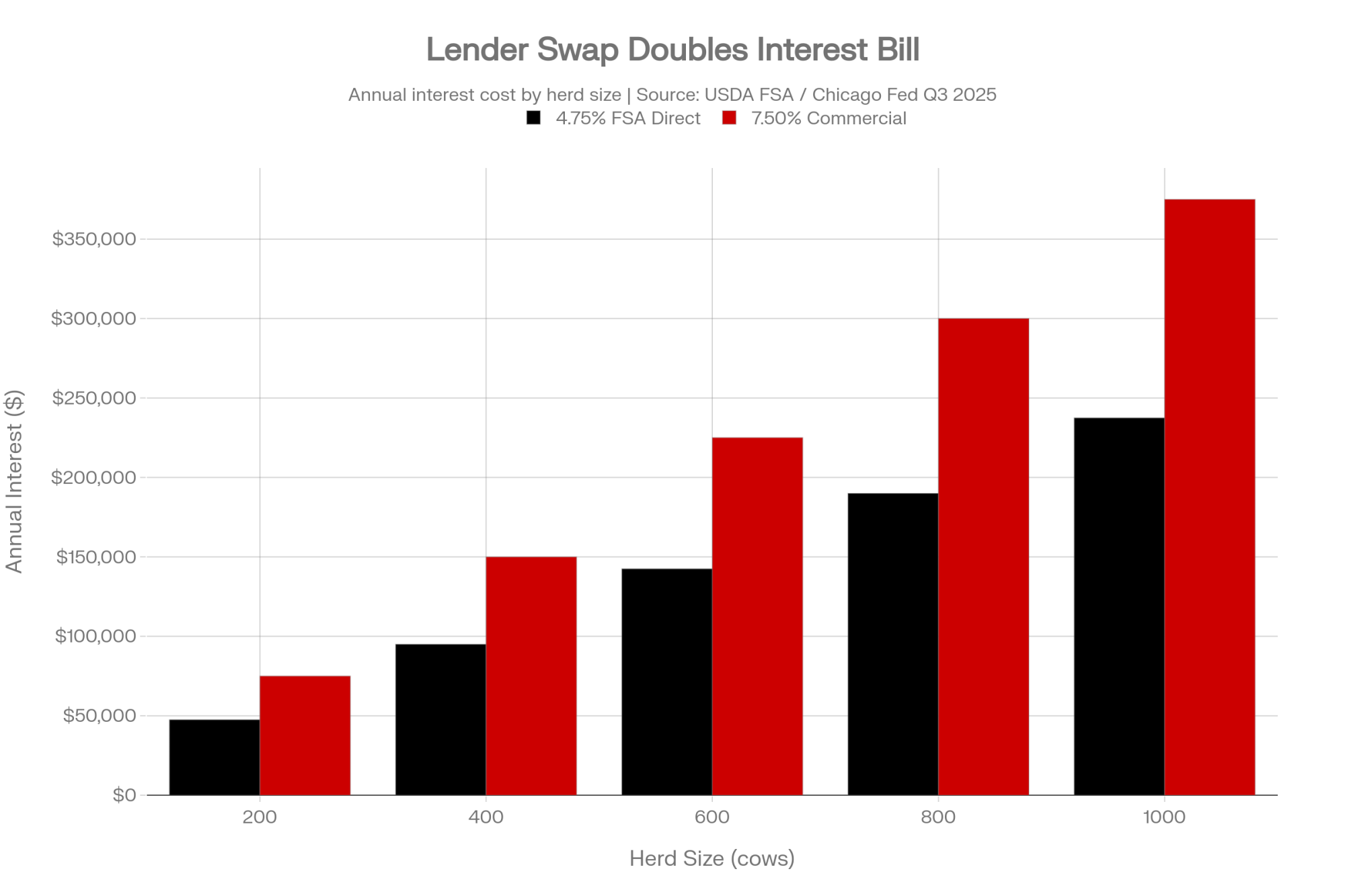

| Herd Size | Operating Line | 1.50% Spread (Guaranteed to Mid-Market) | 2.75% Spread (FSA Direct vs. Commercial) | 3.00% Spread (Severe Commercial Penalty) |

| 400 cows | $2.0M | $30,000/yr (+$0.68/cwt) | $55,000/yr (+$1.25/cwt) | $60,000/yr (+$1.36/cwt) |

| 600 cows | $3.0M | $45,000/yr (+$0.68/cwt) | $82,500/yr (+$1.25/cwt) | $90,000/yr (+$1.36/cwt) |

| 1,000 cows | $5.0M | $75,000/yr (+$0.68/cwt) | $137,500/yr (+$1.25/cwt) | $150,000/yr (+$1.36/cwt) |

Operating-line size assumes $5,000/cow working capital; scale proportionally for differing leverage. The per-cow burden stays constant — $75/cow at 1.5 points, $137.50/cow at 2.75 points, $150/cow at 3.0 points — because the line scales linearly with herd size on that assumption.

Now drop that math into where the dairy economy actually sits in Q2 2026. The USDA ERS all-milk forecast runs $20.40 to $20.50/cwt. Producers in long-milk regions — Idaho, New Mexico, parts of Texas — are realizing $15.00 to $16.97/cwt at the farm gate after basis adjustments, per regional cooperative settlement reporting. Federal Milk Marketing Order formula adjustments implemented earlier in 2026 reduced Class III and Class IV pricing by roughly $0.85 to $0.93/cwt under the current order. Cornell’s 2023 Dairy Farm Business Summary — the most recent published — put bottom-quartile DSCR at 0.36x. Current 2026 conditions remain stressed.

Adding $30,000 to $60,000 in annual interest expense on a 400-cow operation, on top of that structure, compresses margin further on operations already running below 1.0x DSCR.

Why the Old Playbook Doesn’t Work for the Western Michigan Caseload

Take the kind of operator at the top of this article — a modeled scenario, with figures illustrative based on USDA REAP guarantee parameters and the named herd-size band. 400 cows, a $2M operating line through a regional ag bank, and a separate $1.4M REAP conditional commitment through Genisys for an anaerobic digester project that’s 60% complete. The digester financing was the piece that made the project pencil — REAP guarantees compressed lender risk, which compressed the rate, which made the energy savings line up with the debt service. On May 11, the deal was on track. On May 12, the lender lost its OneRD approval. Now everything downstream of that commitment moves to a different institution at a different rate, with a different appraisal, on a 30-day clock.

The Loss of Local Ag Intelligence

Genisys Credit Union, headquartered in Auburn Hills, served 280,000+ members and operated as one of Michigan’s largest credit unions with active USDA and SBA guaranteed lending. Replacing it with a blind entry from a national USDA directory loses two critical assets:

- Local economic nuance. The understanding of unique Lower Peninsula vs. Western Michigan herd dynamics — the difference between a Lower Peninsula 400-cow operation and a 1,200-cow Western Michigan herd — sits inside membership relationships, not lender lists.

- Speed of underwriting. National outfits cannot rebuild a cooperative credit infrastructure on a tight 30-day clock. The institutional knowledge of Michigan dairy operating economics that the credit union represented in its own membership base doesn’t transfer to a directory entry.

Michigan USDA RD invested $889 million across the state in early 2026, with $45 million earmarked for agribusiness and economic development, per the agency’s state announcement. Every project in the OneRD queue at one of the ten removed lenders is either scrambling toward June 11 or already stalled.

The NAC Mirror

North Avenue Capital tells the same story from the other direction. It’s $168.5 million in 90-day delinquencies concentrated in commercial real estate and hospitality categories rather than core agricultural production. The OneRD B&I program’s eligibility-by-geography structure permits any rural business regardless of sector, and NAC’s portfolio reflected that breadth.

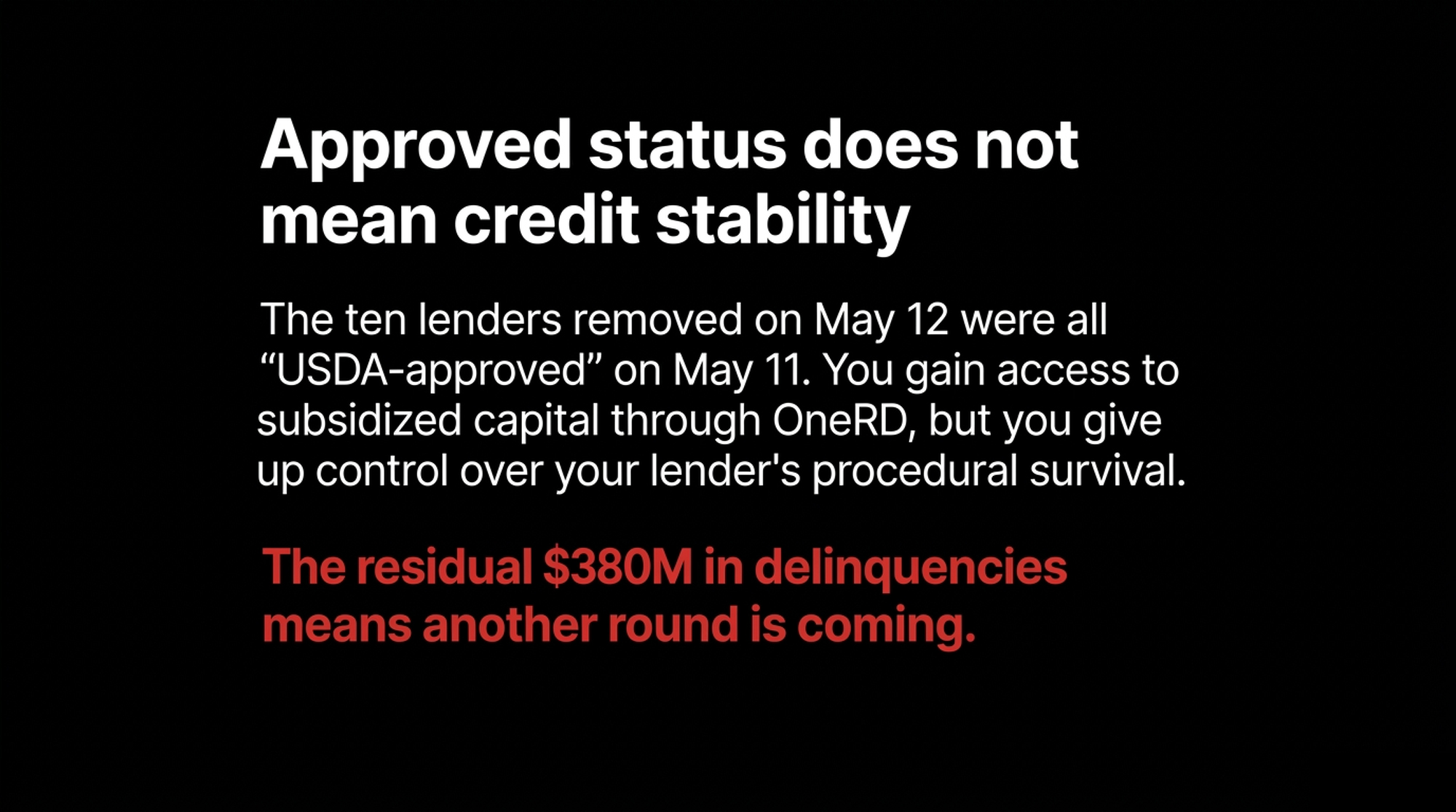

Everyone assumed USDA-approved lender status meant your capital relationship was insulated from federal program risk. The data says it’s a procedural compliance certification, not a credit-quality signal. The ten lenders removed on May 12 were all approved lenders on May 11.

The 30/90/365-Day Playbook for Herds Caught in the June 11 Window

The producers who survive this transition treat the deadline as non-negotiable and work backward from it. The ones waiting for their revoked lender to “figure it out” hit Day 27 with no deal and a contractor sending lien notices.

30-Day Actions — Before June 11

- Pull your conditional commitment letter and your loan note guarantee today. The program designation (B&I, REAP, Community Facilities, FSA Guaranteed Operating) is on the documents themselves. If you can’t find them, request copies from your lender in writing — email both the loan officer and the compliance officer with a timestamped subject line referencing the May 12 revocation.

- Call your State USDA Rural Development office directly, not the local coordinator. Verify current contacts through rd.usda.gov/contact-us/state-offices before the call. Request written confirmation of your conditional commitment status under 7 CFR Part 5001 transfer provisions.

- Open parallel conversations with three approved replacement lenders. Verify approved status through the USDA Lender Lens portal in the Rural Data Gateway before you call. Prioritize Farm Credit (regional association), one regional ag bank with documented dairy expertise, and one second-tier commercial lender with active OneRD volume — not a lender that closes one of these a year.

- Red-flag trigger: If your DSCR has been below 1.15x on lender-method calculations for three consecutive months, this moves to the top of your list today. New-lender independent underwriting will price that exposure aggressively or decline outright. Where this can backfire: walking into a new lender conversation without your own current numbers gives them control of the framing.

90-Day Actions — Through August 2026

- Run your own cash flow stress test before the new lender does. Model $15.00, $18.00, and $20.40/cwt milk against the 7.50% commercial replacement rate. If the project doesn’t pencil at your realistic milk price — not the headline forecast — re-scope before the lender models it for you. What it requires: trailing 12-month financials, a current marketing letter from your buyer, and the original project pro forma showing projected energy savings or processing revenue.

- Negotiate the LTV gap actively. Expect the new lender to compress LTV from 80% on the original guarantee to 60-65% on a partially-completed project — an illustrative range, with actual terms varying by lender and project status. Identify your equity gap source now: subordinated operating advance, equipment lease, contractor financing, or sale-leaseback on paid-off assets. Where this can backfire: closing the gap with unsecured personal debt converts a project problem into a household balance-sheet problem.

- Order your own independent appraisal of any in-progress capital project on Day 11, not Day 18. Half-built REAP infrastructure appraises at salvage value, not completion value. Knowing how low your number is determines your negotiating position.

365-Day Moves — Into 2027

- Diversify your capital sources. USDA-approved lender status is a procedural certification, not a credit-stability guarantee. Build relationships with at least two non-OneRD funding channels — Farm Credit relationship lending, a regional commercial bank with on-balance-sheet ag lending, or a state-level revolving loan fund.

- Coordinate with other producers on capital procurement. Individual mid-sized dairies have limited negotiating leverage. Producer groups aggregating $10-15M in annual capital needs across six to ten operations have real leverage. Wisconsin and Michigan extension offices are the natural coordination point.

- Opportunity signal: If your DSCR holds above 1.25x on trailing 12-month data and your milk basis stays within $1.00 of the regional benchmark, you have negotiating room with new lenders that displaced borrowers under stress don’t. That’s the time to lock terms — not after the next round of revocations forces you into the same scramble.

What the Next Round Looks Like

If ten lenders held 47% of OneRD delinquencies, the residual is roughly $380 million distributed across the 750+ approved institutions Claeys addressed in his February letter. That’s a significant remainder, and it’s not an even spread. Any next-tier institutions would be identifiable from the same loan-level data USDA used to evaluate the ten removed on May 12, though USDA hasn’t made tier-by-tier concentration data public.

The pattern from the May 12 timeline suggests when the next round happens: not when the data crosses a threshold, but when one of them fails publicly and forces USDA’s hand. Producers caught in the next round are likely to be the ones who saw warning signs in regulatory filings — Federal Reserve consent orders, FDIC asset-quality downgrades, trade press reporting on capital adequacy — and assumed USDA would act ahead of the failure. The May 12 sequence suggests otherwise.

What’s the Trade-Off, and What Should You Check?

The ten lenders are the visible cases. The program design — under which USDA backs 80-90% of loss exposure under standard OneRD terms while lenders retain origination revenue and fee income, per USDA Rural Development program documentation — is the structural read of the data. Rollins didn’t change that design on May 12. She removed the most concentrated cases and reset the clock.

You gain access to subsidized capital through OneRD. You give up control over when your lender’s procedural status changes. That’s the trade-off, and it sat invisible until the press release.

Pull your conditional commitment letter this morning. When was the last time your lender provided written confirmation of their current OneRD-approved-lender standing? If the answer is “never,” you’re being treated as a captive borrower — and June 11 is exactly the wrong deadline to learn what that costs.

Key Takeaways

- Ten lenders just lost OneRD approval, and you have until June 11 to transfer any active REAP, B&I, or Community Facilities commitment. FSA-guaranteed operating lines through the same banks are unaffected, so verify which program your file actually sits in before you panic.

- The replacement-rate spread runs $137.50/cow on a 400-cow Midwest dairy at 4.75% FSA versus 7.50% commercial, a +$1.25/cwt breakeven shift on Cornell DFBS basis — small enough to look survivable on paper, large enough to bury a project running below 1.0x DSCR.

- If your DSCR’s been under 1.15x for three consecutive months on lender-method calculations, this moves to the top of your list today; pull your conditional commitment letter, call your State USDA RD office directly, and open parallel conversations with three approved replacement lenders.

- USDA-approved-lender status is a procedural certification, not a credit-stability guarantee — the ten removed on May 12 were all approved on May 11, and the residual $380M in delinquencies across the remaining 750+ institutions suggests another round is a question of timing, not whether.

Run Your Numbers

Snap Check — Pressure-test what a 2.75-point rate jump does to your operation before you walk into a replacement-lender conversation. Snap Check benchmarks your margin exposure quickly so you know where your $/cow and DSCR sit against the 4.75% vs. 7.50% spread driving this story.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The $1.56/cwt Permit Trap Hiding in Your Next Dairy Expansion: Riverview’s 18,855‑Cow Minnesota Fight — Arms you with a concrete formula to calculate time-risk penalties when regulatory delays stall capital execution, exposing how a 7.5% commercial interest rate creates a quiet, devastating cash burn before a single cow enters the parlor.

- Dairy Farm Economics 2026: Milk Pricing, Margins & Risk Playbook — Delivers critical margin forecasts and stress-test scenarios for the current structural squeeze, tracking Class III and IV adjustments alongside robotic return metrics to help you choose whether to aggressively expand, optimize, or exit.

- Key Financial Considerations Before Investing in Dairy Farm Technology — Reveals the vital cost-benefit steps needed to preserve liquidity during volatile credit cycles, forcing producers to calculate real break-even timelines and protect operational cash flow before signing on a high-interest commercial line.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.