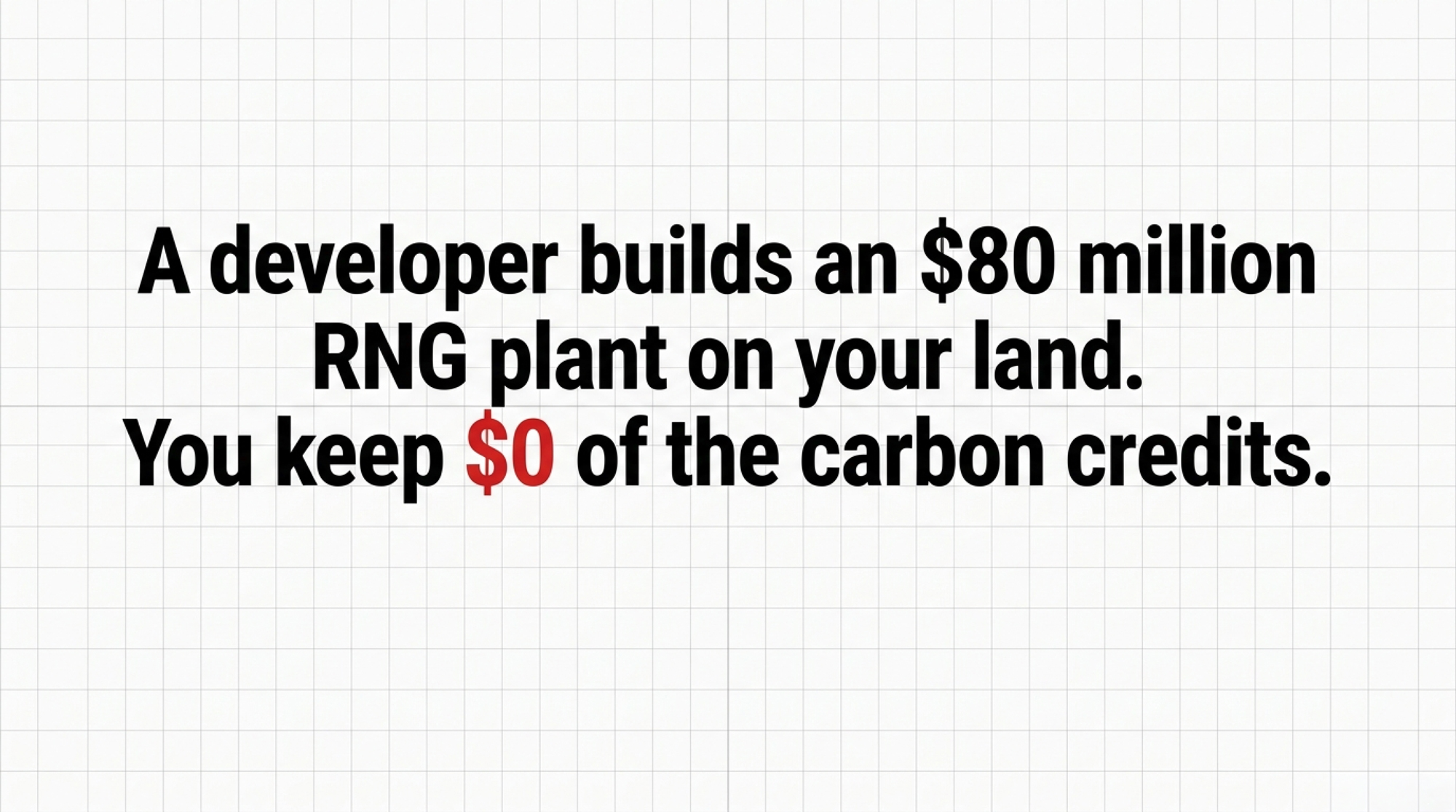

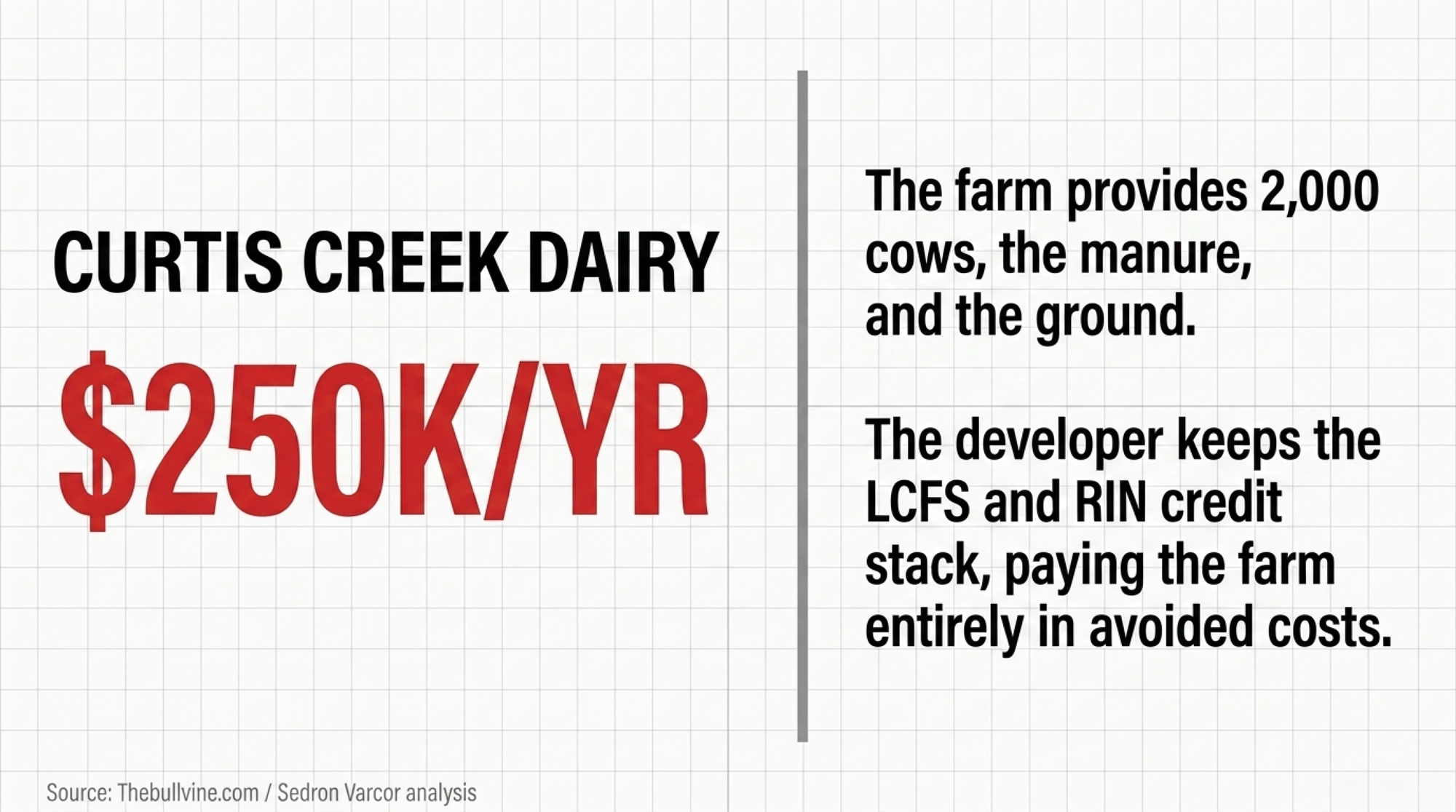

An $80M Sedron Varcor nutrient-recovery plant now sits on Curtis Creek ground, alongside the dairy’s separate anaerobic digester and RNG operation. The farm keeps about $250K/year in avoided costs — and a 20-year manure contract. The credit stack? Not theirs.

| Correction (May 19, 2026): An earlier version of this article incorrectly stated that Sedron operates the anaerobic digesters and produces RNG at Curtis Creek. Sedron’s Varcor system processes digestate into dry fertilizer, liquid ammonium nitrate fertilizer, and clean water; the digester and RNG production are run by a separate party. The article has been updated accordingly. |

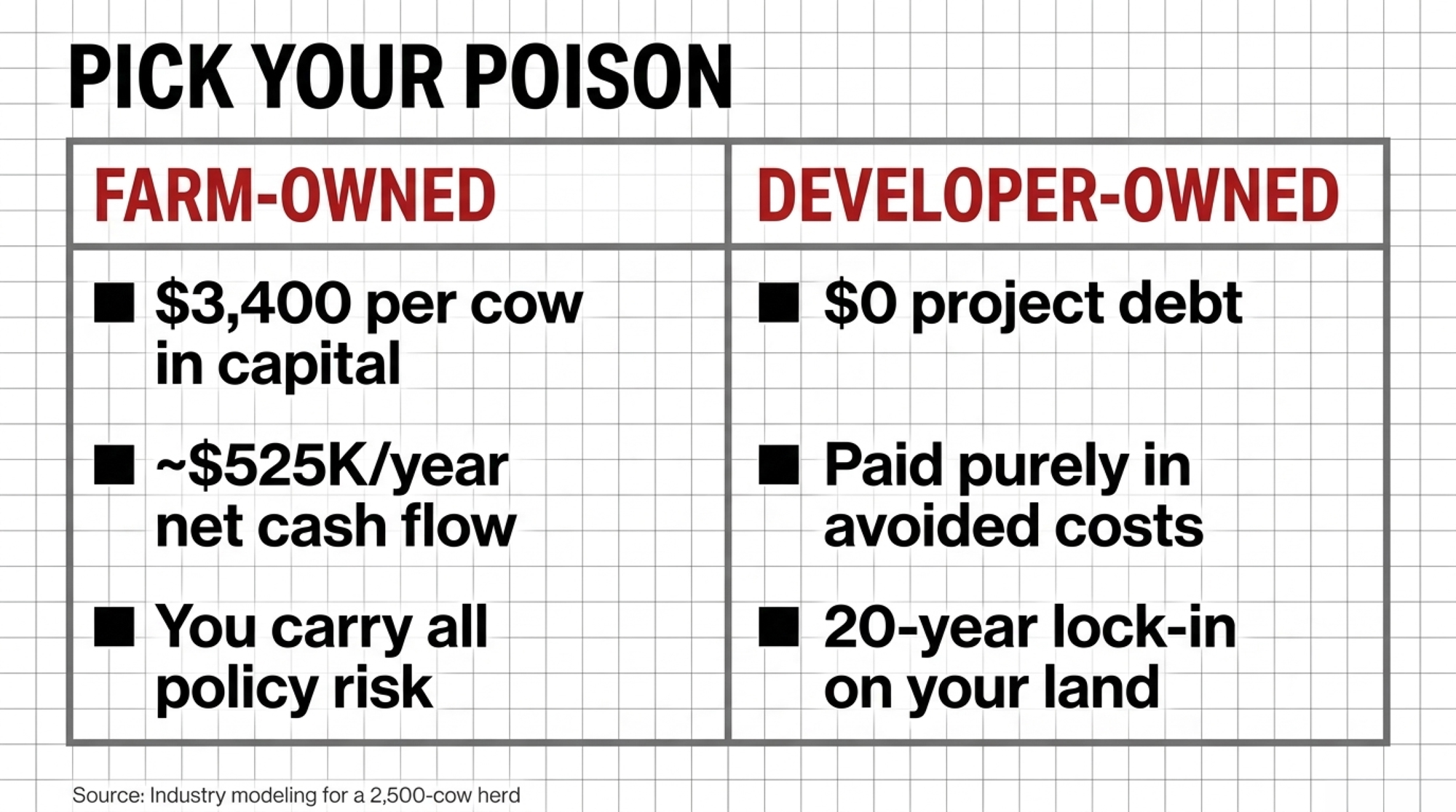

Executive Summary: Curtis Creek Dairy… now hosts an $80M Sedron Varcor nutrient-recovery plant that processes digestate from the dairy’s separate anaerobic digester — and the developer, not the farm, owns the carbon credits. The 2,000‑cow herd (with publicly reported plans toward 3,200) puts up the manure and the land; The RNG developer (not Sedron) owns the LCFS and RIN credit stack tied to gas production. Sedron’s role is downstream nutrient recovery via Varcor. That stack is where the money lives: $3 base gas vs. $60–$90/MMBtu once 2025 LCFS credits ($57.77/ton avg, $40.75–$75.50 range, Stillwater) and D3 RINs (~$2.40 avg, EPA EMTS) are layered in. The farm’s payoff comes in avoided costs — modeled at roughly $250K/year, or about $50–$100/cow on the manure side alone — locked in against a 15–25‑year manure‑supply contract recorded against the property. Compare that to a hypothetical farm‑owned 2,500‑cow build at ~$3,400/cow capital with ~$525K/year net cash flow, and the trade‑off is obvious: stability and zero project debt, or upside and policy risk you carry yourself. With USDA’s REAP grant window paused in early 2026 and similar pitches landing in producer inboxes weekly, the 30‑day move is simple — get any draft term sheet in front of a lender and an attorney who’ve read manure‑to‑energy contracts before they get in front of a pen.

Carl Ramsey doesn’t really manage a manure lagoon anymore. He carries the title Manager of Digester Operations at Curtis Creek Dairy in Newton County, Indiana — a role that started as Farm Manager back in 1999 and has since grown into oversight of a 7.5‑million‑gallon DVO plug‑flow digester and a 50,000-square-foot Sedron Varcor facility that processes digestate from the dairy’s digester into dry fertilizer, liquid ammonium nitrate fertilizer, and clean water. Curtis Creek is milking about 2,000 cows today, with publicly reported plans to grow toward 3,200, but the real story sits on the other side of the flush barn — an $80 million Sedron Varcor plant that recovers nutrients and water from digestate. The pipeline gas and California carbon credits come from the dairy’s separate digester/RNG project. “Their facility is going to use the manure from our cows for the basis of their feedstock,” Ramsey told Brownfield Ag News in May.

If you’re being courted for a digester or RNG project, this is the kind of deal that’s likely headed your way.

What’s Actually Changing Around the Manure Pit

For most of dairy’s history, manure has been a cost and a compliance headache. You scraped it, stored it, hauled it, and hoped the inspector didn’t show up the week after a big rain. Early digesters didn’t change that much. They knocked down odor and spun a generator, but the economics were usually thin — low power buy‑back rates, high maintenance, and more than a few farms quietly shutting them off after a rough run.

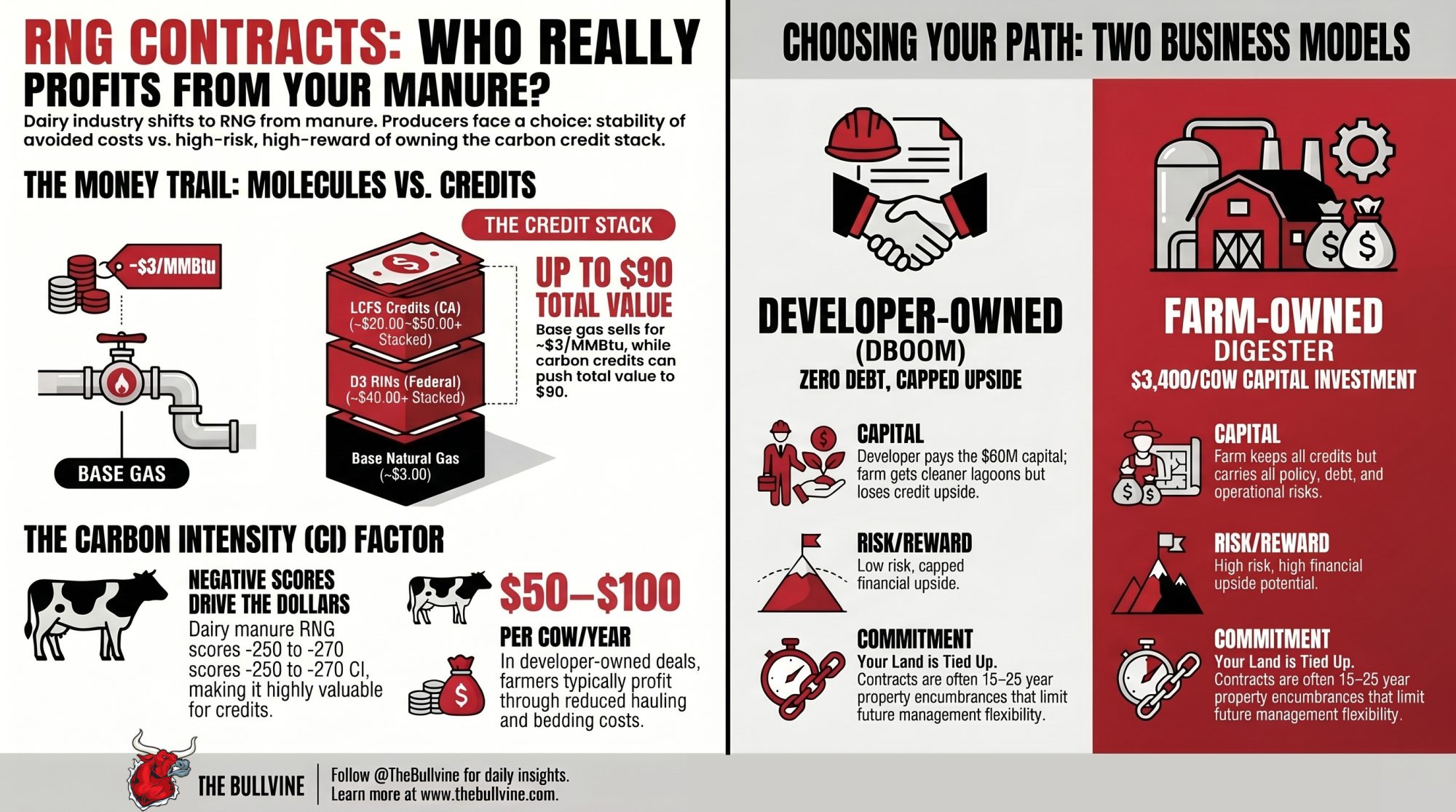

Curtis Creek represents a different era. Here, manure flows first to the dairy’s anaerobic digester, which produces RNG. The leftover digestate is then piped to Sedron’s Varcor plant for nutrient and water recovery, which is backed by private‑equity firm Ara Partners. Your cows and land become the steady input for a facility whose real profit centre is not the gas molecule itself, but the environmental “attributes” attached to it.

That’s where the money gets interesting. A million BTUs of methane might sell for roughly $3 at the city gate, but the credit stack on dairy RNG is where the real dollars sit. In 2025, D3 cellulosic RINs — the federal credits tied to dairy RNG — averaged about $2.40 per RIN, based on EPA EMTS data and trade press averages. California’s LCFS credit price averaged $57.77 per metric ton CO₂e that same year, with trades ranging from $40.75 to $75.50 and a credit‑clearance market price ceiling indexed up toward $275.39 per ton in 2026 (CARB and Stillwater Associates, 2025–26). When your project scores a deeply negative carbon intensity (often ‑250 to ‑270 g CO₂e/MJ for dairy manure RNG), those numbers stack fast.

Translation: this isn’t a milk‑cheque play. It’s a credit‑market play, and the policy math decides who eats.

Quick glossary for your boardroom brain

- MMBtu: million British thermal units — the unit gas is sold in.

- RIN (D3): Renewable Identification Number under the Renewable Fuel Standard, cellulosic biofuel category.

- LCFS: California’s Low Carbon Fuel Standard credit; pays for displacing fossil fuel based on carbon intensity.

- CI score: carbon intensity, in grams CO₂‑equivalent per megajoule. Dairy manure RNG often scores deeply negative.

- DBOOM: Design‑Build‑Own‑Operate‑Maintain. The developer owns and runs the plant; you provide manure and site access.

How This Plays Out on a Real Farm

At Curtis Creek, manure handling is no longer just a herd‑side job — Ramsey’s title, Manager of Digester Operations, captures the shift. According to Sedron’s public materials, the site processes 200 million gallons of digestate a year, which means feedstock consistency, throughput, and biology are now operational priorities alongside the scraper schedule. The farm provides the cows, the manure, and the ground. Sedron provides the $80 million Varcor facility, the plant staff (about four full‑time employees on their payroll), and the contracts with the pipeline and credit markets.

That’s a real change in scope for a role that started as Farm Manager in 1999. The cows still come first, but on this site, the lagoon now functions as the feedstock source for an industrial process feeding the pipeline.

Sedron’s own materials describe Curtis Creek as a 200‑million‑gallon‑per‑year processing site and their flagship agricultural project. The Varcor system takes digestate and separates it into three product streams: clean, nearly pathogen‑free water; roughly 37,000 tons a year of dry organic fertilizer; and a liquid ammonium nitrate fertilizer, per Sedron’s Varcor product spec. The digester/Varcor complex sits alongside a 1.7 MW solar array that helps power the site and farm, supported by a 0,000 USDA REAP grant documented in USDA Rural Development’s 2024 Indiana Earth Day release. For a glimpse of where lower‑tech nutrient recovery is heading, it’s worth comparing this with the lower‑tech nutrient recovery bet one farm is making with worms instead of distillation.

In the forensic modeling for a Curtis Creek–scale setup, the avoided‑cost value comes in around $250,000 per year, conservatively — that’s lagoon dredging avoided, bedding replaced with dry solids (worth $20,000–$50,000 annually), water reuse, and solar‑offset energy. In other words, the dairy sees its manure problem shrink and some line items drop.

Now stack that against a farm‑owned version, using industry‑typical barn math instead of Curtis Creek’s internal books. A hypothetical 2,500‑cow digester, built and owned by the farm, takes on about $8.5 million in capital cost. Under conservative assumptions:

- Gross revenue (gas plus credits): about $2.83 million/year

- Operating cost: about $1.1 million/year

- Debt service (7%, 10‑year term): about $1.21 million/year

You’re left with roughly $525,000 a year in net cash flow. That’s the upside. The downside: every swing in RIN and LCFS prices hits you directly.

At 45,000 MMBtu/year of gas output, a stacked value of per MMBtu means about .7 million in credit‑driven revenue before operating costs. That credit‑driven upside is a big part of why private capital is so interested in these projects. The real question is how much of that flow will ever reach your farm account.

How Much Money Actually Flows Back to Your Farm?

Short answer: in a typical developer‑owned deal, your gain shows up more in avoided costs than in a direct share of credit revenue.

In most DBOOM‑style deals, the developer’s profits come primarily from the credit stack, not the base gas price. On the farm side, the payoff usually shows up as avoided cost rather than a cheque tied to every RIN or LCFS credit. That’s still real money. But unless the contract ties your compensation to RIN or LCFS prices, your avoided‑cost benefit stays flat even if credit prices climb. We’ve dug into how carbon contracts are reshaping farm balance sheets if you want to see how this plays out beyond manure.

What kind of avoided cost are we talking about?

- $50–$100 per cow per year in reduced lagoon dredging and handling.

- Bedding savings using dry separated solids, modeled at $20,000–$50,000 a year on a Curtis Creek–size herd.

- Distilled water reused for cows and irrigation instead of pumping new water.

- Solar and digester heat offsetting roughly $139,850/year in farm electricity.

| Benefit Category | Low Estimate | High Estimate | Per-Cow Range (2,000 cows) | Notes |

|---|---|---|---|---|

| Lagoon dredging avoided | $50K/yr | $100K/yr | $25–$50/cow | Depends on lagoon size and frequency |

| Dry solids bedding replacement | $20K/yr | $50K/yr | $10–$25/cow | Replaces purchased sand/straw |

| Water reuse (irrigation/cows) | $10K/yr | $30K/yr | $5–$15/cow | Site-specific; distilled effluent quality |

| Solar & digester heat offset | ~$140K/yr | ~$140K/yr | ~$70/cow | Based on $139,850/yr REAP-supported array |

| Total avoided cost | ~$220K/yr | ~$320K/yr | ~$110–$160/cow | Article models ~$250K/yr mid-point |

On a 2,000‑cow herd, that $50–$100/cow range is $100,000–$200,000 a year, before bedding and power savings. That’s meaningful — especially if your lagoon headaches are getting worse — but it’s also a capped upside. Your side doesn’t automatically rise with higher LCFS or RIN prices unless the contract says so.

And those credits move. In 2025, LCFS credits traded between about $40.75 and $75.50 per ton, with an average around $57.77 (Stillwater Associates LCFS data, 2025). That’s after sliding from earlier levels that pushed up close to the program’s price ceiling. Meanwhile, D3 RINs sat around $2.40 on average in 2025, with futures already pricing in some policy uncertainty. Terrain’s 2025 “Economic Sustainability of Dairy Digesters” report, prepared for the Farm Credit System, was blunt: the feasibility of dairy digesters producing RNG “hinges on the value of LCFS, RIN credits and tax incentives,” not just base gas value.

From a lender’s point of view, that means an RNG project is only as strong as the policy stack it sits on. Layer a 15–25‑year manure‑supply contract on top of that, recorded against your land, and they have to think hard about what happens to your debt‑service coverage and collateral if credit prices dip mid‑contract.

Is Your Land’s Future Tied Up for 25 Years?

For a lot of projects, it can be.

A typical RNG contract runs 15 to 25 years and is often recorded as an encumbrance against the property, which means it shows up in a title search. If you ever want to sell the farm, bring in a partner, or carve out land for development, a recorded manure‑supply obligation and a large industrial plant on site can narrow the pool of potential buyers and influence how they look at price.

The contract is usually built around a feedstock guarantee. You’re committing to:

- A minimum volume of manure.

- A certain solids content and methane potential.

- Operating practices that won’t dilute or disrupt the feedstock.

That’s where flexibility can disappear. If the document says a change in bedding or ration that lowers gas yield brings “lost gas” penalties, you’re effectively treating your manure as a tightly specified feedstock. You need to decide whether living inside those limits for 20 years fits how you want to run the herd. Before you sign anything that touches feed, it’s also worth running through what a methane‑reducing additive actually costs per cow on your operation.

Force‑majeure language matters too. If H5N1 or another disease forces a depopulation, you want the supply guarantee clearly paused without penalties, not a lawyer arguing that “disease risk was foreseeable.” Those are the lines you want to see in black and white, not just implied in a brochure.

| Contract Clause | 🔴 Red Flag Language | 🟢 Green Light Language |

|---|---|---|

| Credit ownership | “All attributes, RINs, LCFS, and low-carbon premiums assigned to Developer” | Farm retains or receives revenue share on RINs/LCFS above a price floor |

| Feedstock specification | Penalty triggered by bedding or ration changes that affect gas yield | Reasonable tolerance range (+/–15%) with no penalty |

| Contract term | 20–25 years with no exit clause | 15-year base with mutual renewal options or buyout provisions |

| Title encumbrance | Agreement recorded against fee title with no subordination clause | Subordinated to farm’s primary lender; carve-out for sale |

| Force majeure | Disease risk listed as “foreseeable” or not listed | Explicit coverage: disease depopulation, regulatory shutdown, Act of God |

| Decommissioning | Silent on removal responsibility | Developer solely responsible for removal and site restoration |

| Expansion rights | Developer has right of first refusal on herd expansion manure | Farm retains full rights over additional cows and future infrastructure |

Options and Trade‑Offs for Farmers

Three main models are on the table for most dairies. Each trades a different mix of capital, control, and upside.

Farm‑owned digester

- When it makes sense: Big herds with capital room, strong tax appetite, and the desire to own the upside.

- What it requires: Comfort with policy risk, a solid O&M plan, real offtake agreements, and a lender fluent in RNG.

- Risks/limits: Long payback if credits soften; potential to strain your balance sheet; a new operational discipline on top of your cows.

You put up the capital — roughly $3,400 per cow for a plug‑flow system without distillation, plus about $440/cow/yearin operating cost. You own the digesters, the gas upgrading, and usually the interconnect. You also own the credits, the downtime, and the policy risk.

30‑day action: if a developer sends you a proposal, ask them for a build‑cost estimate for a farm‑owned system and ask your lender for a term sheet. You don’t have to build it. You just need real numbers to compare. Then run that same capital against your next‑best options — pellet‑free robotics, spray drones, cow‑comfort work — using your own numbers and Bullvine’s ROI pieces as benchmarks. If $3,400/cow in digester capital can’t beat the return on a robotics or cow‑comfort upgrade on your farm, that’s a loud signal. The $36,740‑per‑200‑cows robotics math is a good starting comparison.

Developer‑owned (DBOOM)

- When it makes sense: You want manure headaches reduced and you’re okay trading upside for stability.

- What it requires: Comfort with a long‑term manure contract, clarity on title encumbrance, and trust in the developer’s staying power.

- Risks/limits: Limited share in credit booms; dependence on a third party’s solvency; less flexibility in future herd or management changes.

Curtis Creek is the textbook example. Sedron designs, builds, owns, operates, and maintains the Varcor nutrient-recovery plant. The anaerobic digester and RNG facility are owned and operated separately by the developer under their own DBOOM-style arrangement. You put up no project capital, take on no project debt, and get paid in avoided costs and, sometimes, a modest lease or royalty.

The big trade‑off is control. A DBOOM contract will spell out how much manure you must supply, what you can and can’t do that might affect gas yield, and for how long. As of early 2026, USDA has halted new REAP grantapplications while it rewrites program rules and rescinds earlier funding notices, even as the guaranteed loan side of REAP remains open (USDA Rural Development; Brownfield Ag News; DTN, 2026). That means the grant layer that helped sharpen Curtis Creek’s solar economics may not be available in the same way for the next wave of projects.

Community hub

- When it makes sense: Mid‑size farms in a cluster, or regions where a hub exists or is planned.

- What it requires: Haulage or piping to the hub, coordination with neighbouring farms, and a clear tipping‑fee and revenue‑share formula.

- Risks/limits: You’re one step removed from the credits; your economics depend on decisions made at the hub and policy levels you don’t control.

Think Fair Oaks: several dairies in a region truck or pipe manure to a central digester and RNG upgrading plant. You might pay a small hookup or haul fee and get a tipping fee or revenue share back. The key is the tipping‑fee math. What does it cost you per cow to get manure to the hub, and what do you get back per MMBtu or per ton? Put those numbers next to your lagoon, hauling, and nutrient‑plan costs, not just on a “feel” basis. If you’re weighing capital between manure and other operations, the 980‑acre breakeven on owned spray drones is another useful side‑by‑side.

| Metric | Farm-Owned Digester | DBOOM (Curtis Creek model) | Community Hub |

|---|---|---|---|

| Capital cost (per cow) | ~$3,400/cow | $0 | Low (haulage/hookup only) |

| Annual net cash flow | ~$525K/yr | ~$250K avoided cost | Varies (tipping fee + revenue share) |

| Owns RINs & LCFS credits | Yes | No — developer keeps all | Partial (hub-level split) |

| Contract length | Negotiable | 15–25 years | 10–20 years typical |

| Title encumbrance risk | Low | High — recorded on property | Moderate |

| Policy price exposure | Full (you carry all downside) | Shielded | Partial |

| O&M responsibility | Full | O&M responsibility (Varcor): Sedron, 4 FTEs on Sedron payroll. O&M responsibility (digester/RNG): separate developer. | Hub operator |

| Best fit | Large herds, capital + tax appetite | Farmers prioritizing stability | Mid-size farms in a cluster |

30‑day action: if an RNG pitch has landed in your inbox, get the draft term sheet — even a non‑binding one — into the hands of (1) an attorney who’s read manure‑to‑energy contracts before, and (2) your primary lender. Ask both of them one simple question: “What’s the worst‑case scenario for our farm in this deal?”

Key Takeaways

- If your avoided‑cost benefit in a DBOOM offer comes out under about $80/cow/year on your numbers, you’re likely giving away too much of the manure value for too little return.

- If the contract hands all “attributes” — RINs, LCFS credits, and any low‑carbon‑milk premiums — to the developer, assume you’ve sold your future green‑milk story along with your gas.

- If a routine ration or bedding change would trigger “lost gas” penalties, you’re effectively signing up for a tightly specified feedstock supply role — decide if you can live with that for 20 years.

- If decommissioning responsibilities aren’t clearly spelled out, assume that taking the plant off your land could become your problem down the road.

- If $3,400/cow in digester capital can’t beat the ROI on robotics, drones, or cow‑comfort investments on your own farm, don’t let a “free money” pitch rush your decision.

- If you’re a mid‑size herd, don’t write off digesters until you’ve checked whether a community hub option exists within hauling distance.

- If your lender and lawyer haven’t seen an RNG agreement before, make sure they do — in full — before anyone at your farm touches a pen.

You don’t have to become an energy trader to milk cows in 2026. But if your manure is about to feed a multimillion‑dollar industrial plant, you do need to know whether you’re trading that manure for durable value or just getting cleaner lagoons while someone else rides the credit stack.

So, if a Sedron‑style pitch showed up on your phone tomorrow, which version of the deal would actually fit your balance sheet and your family’s plans — farm‑owned, developer‑owned, or a community hub? And just as important, what happens to that deal if the credits that make it all pencil don’t hold?

Run Your Numbers

Farm Benchmark Snap Check — Before you sign a 20‑year manure‑supply contract, pressure‑test the offer against your own herd. Plug in your cow numbers and avoided‑cost line items to see whether a DBOOM deal clears the $80/cow threshold — or quietly trades your manure value away.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The Carbon Credit Conversation: What’s Really Happening on Dairy Farms Today — Secure your share of the upcoming $130-per-acre 45Z tax credit using proven farm-level methods. Real-world cash flow data from Midwest operations demonstrates exactly how targeted solar installations and feed additives rapidly defend operational margins.

- The State of the Dairy Industry 2026: Policy, Markets & Change — Mandatory climate laws and Scope 3 reporting are transforming abstract environmental metrics into concrete business risks. Following the money on processor-level carbon insetting ensures your dairy remains competitive ahead of tightening milk supply contracts.

- The $73-a-Cow Gap Hiding in Your 2027 Bovaer Contract — Breaks down the hidden math behind Bovaer feed additives to expose a $73-per-cow revenue shortfall. You can close this dangerous margin gap without adding another budget line item by deploying overlooked genomic selection tools instead.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.