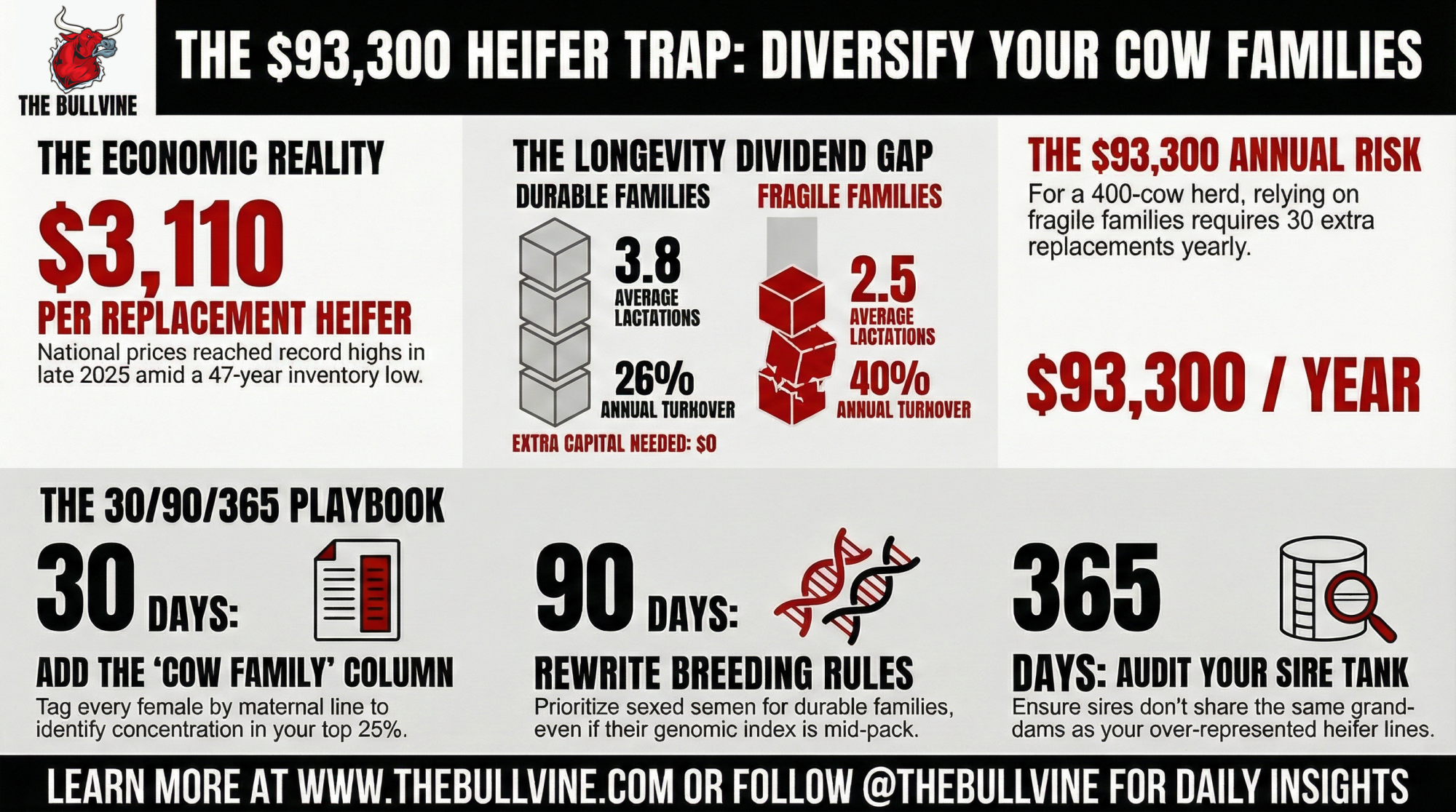

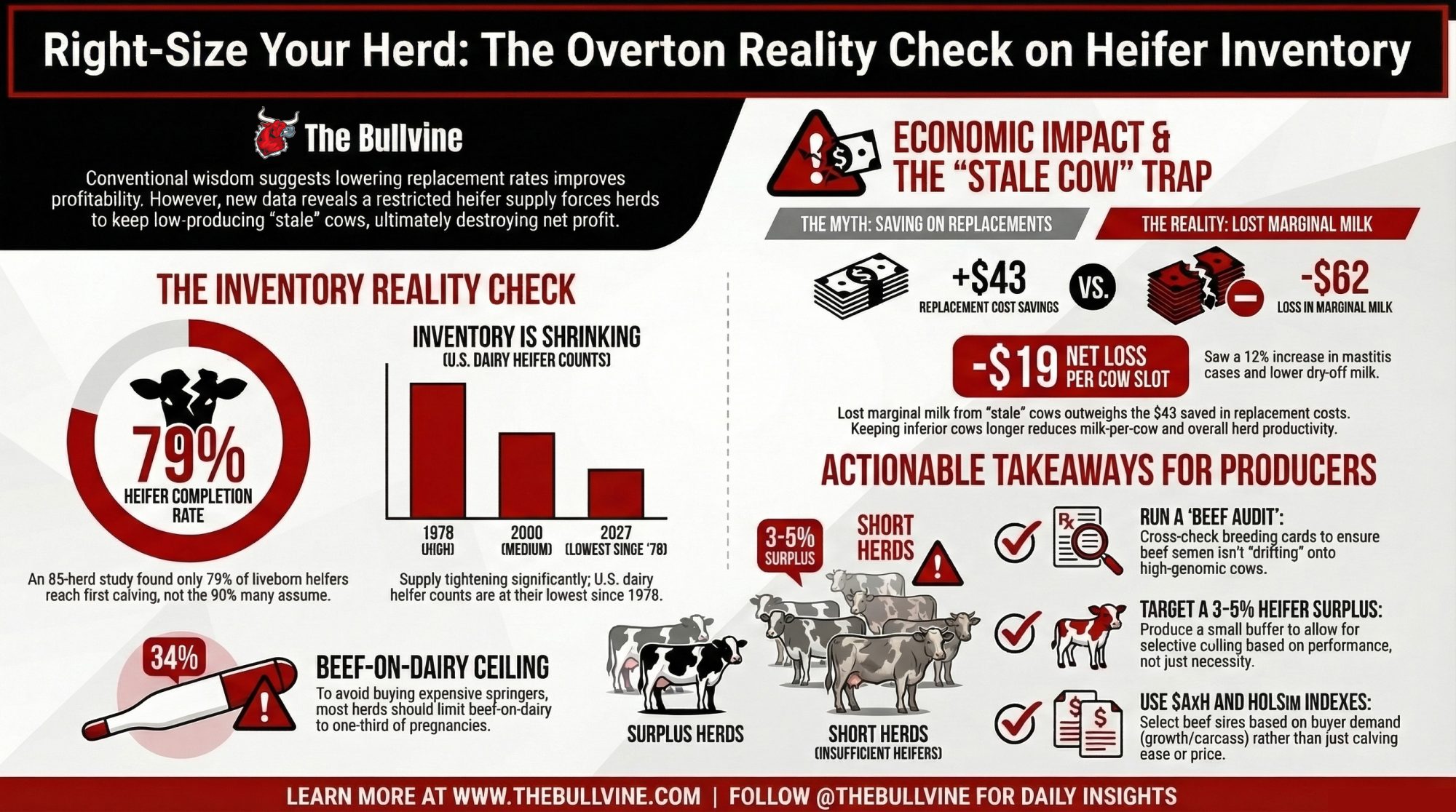

Overton’s 85-herd study found a 79% heifer completion rate. That math says most herds can only afford about one-third of pregnancies as beef-on-dairy.

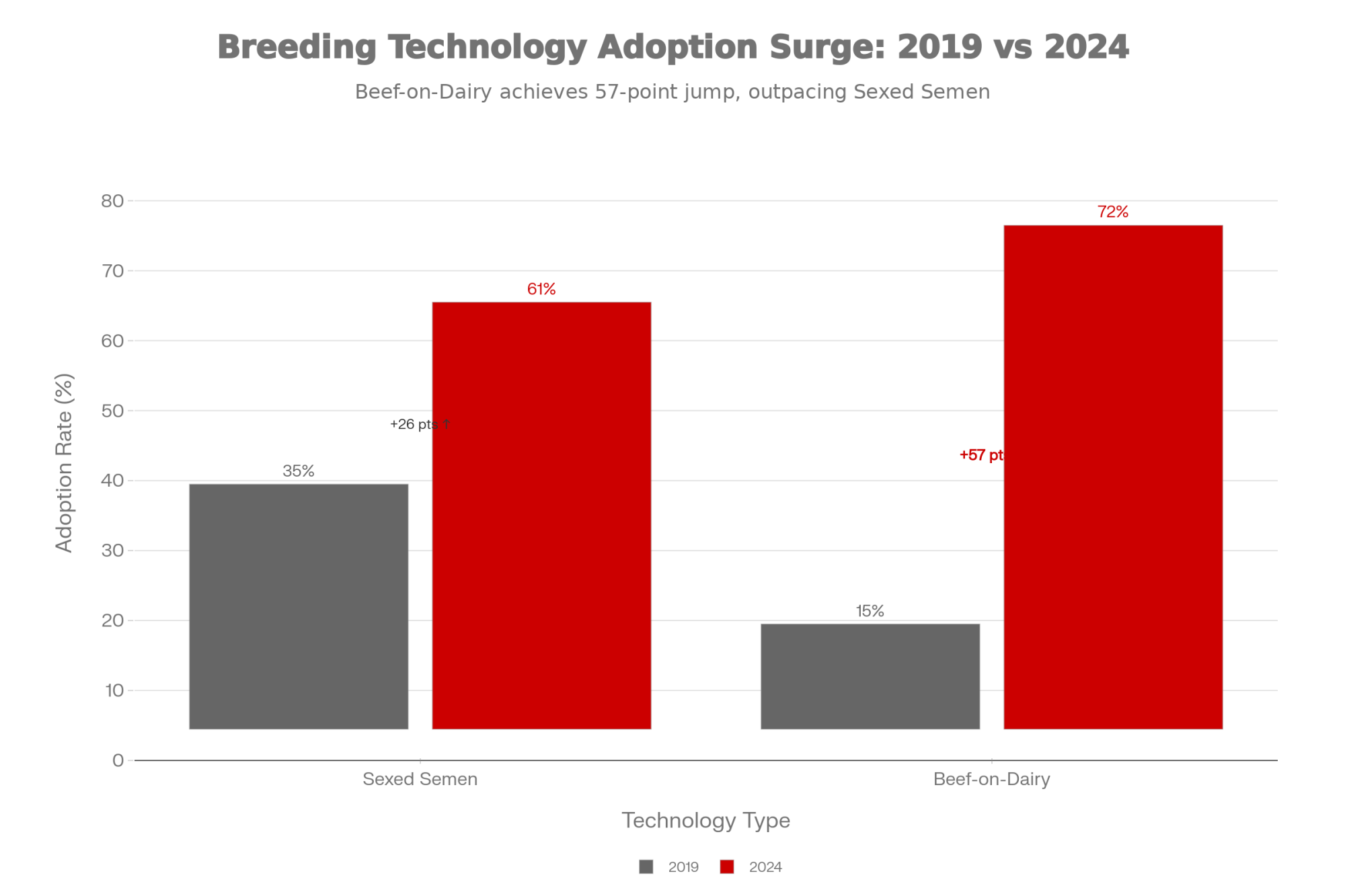

Executive Summary: Beef-on-dairy has been a bright spot on many milk cheques, but new numbers show plenty of herds are quietly overbreeding to beef and starving their future heifer supply. In an 85-herd dataset presented at the 2026 High Plains Dairy Conference, Mike Overton found an average 79% heifer completion rate from liveborn heifer calf to first calving, not the 90% many breeding plans assume. Layer that on top of CoBank’s forecast that U.S. dairy heifer inventories will shrink by roughly 800,000 head before rebounding in 2027, and the room for error on replacement planning almost disappears. For a typical 500-cow herd using sexed and conventional semen, realistic math often limits beef-on-dairy to about one-third of pregnancies if the goal is to avoid buying springers back at record prices instead of producing them at home. This article walks you through that “Overton reality check” step by step, then shows how to audit breeding cards for parlor drift, tighten tier-based breeding rules, and reverse-engineer your beef sire lineup from your buyer’s cheque using tools like $AxH and HOLSim. It finishes with a 30-day beef-audit checklist and annual replacement-pipeline review so you can keep beef-on-dairy as a profit center without blowing a hole in your 2028 milking string.

The breeding cards were supposed to confirm the plan.

A herd manager spread a week’s worth of cards across the office table, grabbed a red marker, and circled every beef mating. It didn’t take long before everyone in the room could see it: beef semen on cows that weren’t truly bottom‑third genetics, chronic mastitis cows bred again instead of marked DNB, and a lot more red circles than the “about 25% beef” the farm thought it was running.

That gap between the breeding plan in your head and the breeding cards in your hand is exactly where this story sits. In 2025–26, with heifer numbers tight and beef‑on‑dairy still hot, getting that gap wrong isn’t a rounding error — it’s a replacement pipeline problem waiting to surface right when you least want to be buying springers.

The 21% Leak: Why Your Heifer Pipeline Is Thirstier Than You Think

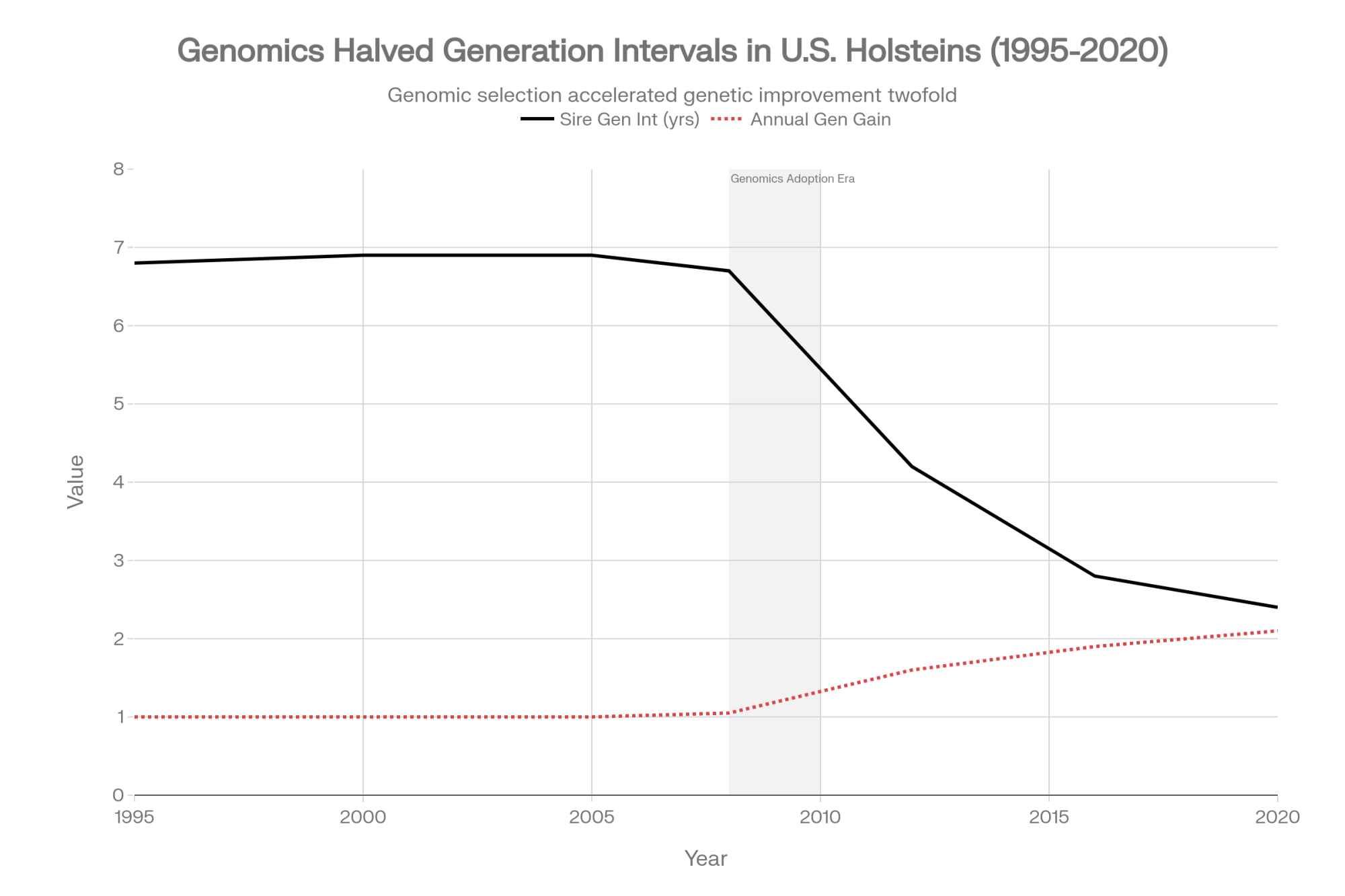

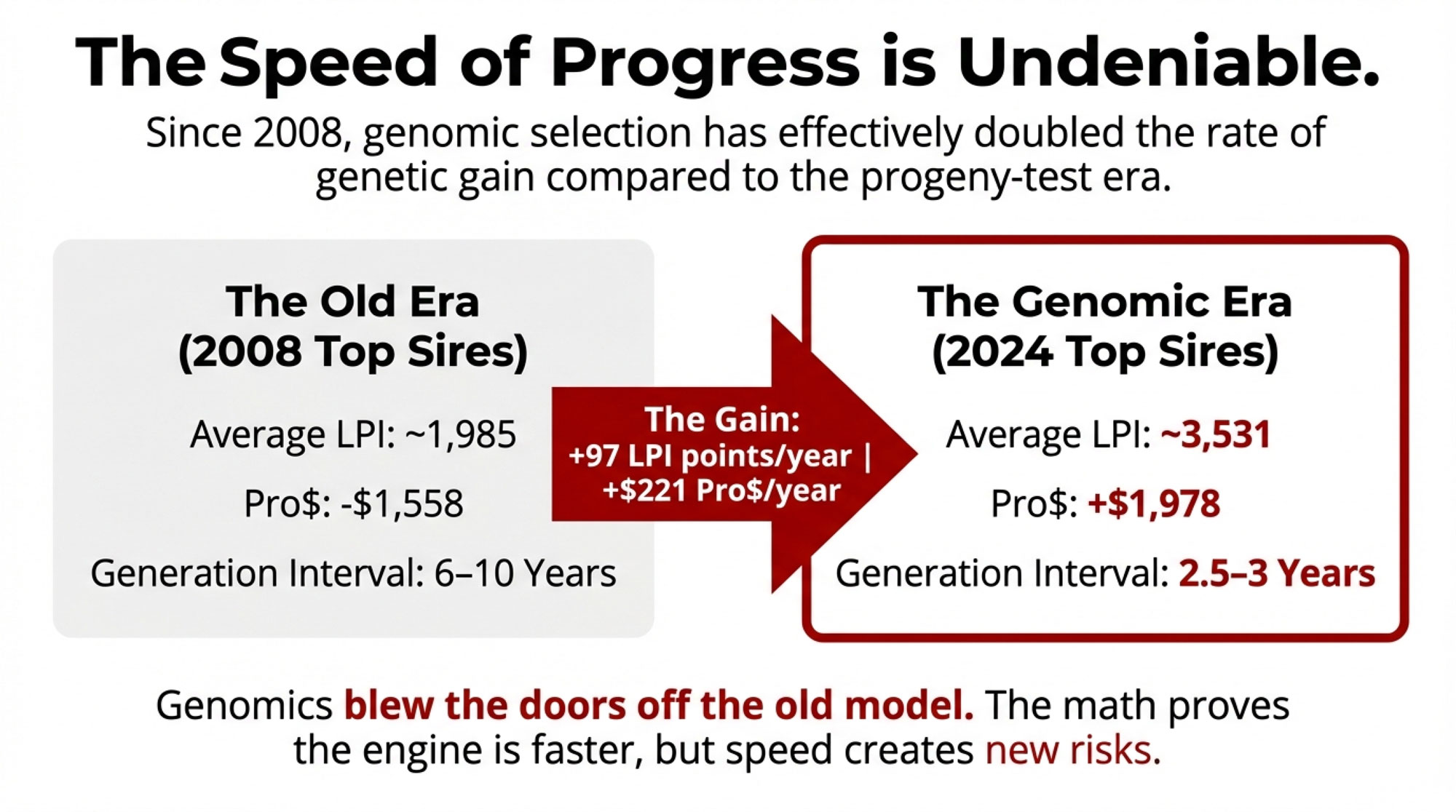

Veterinarian and dairy economist Mike Overton went looking for hard numbers on replacement risk when he analyzed data from 85 commercial U.S. herds and presented it at the High Plains Dairy Conference in Amarillo, Texas, on March 3–4, 2026.

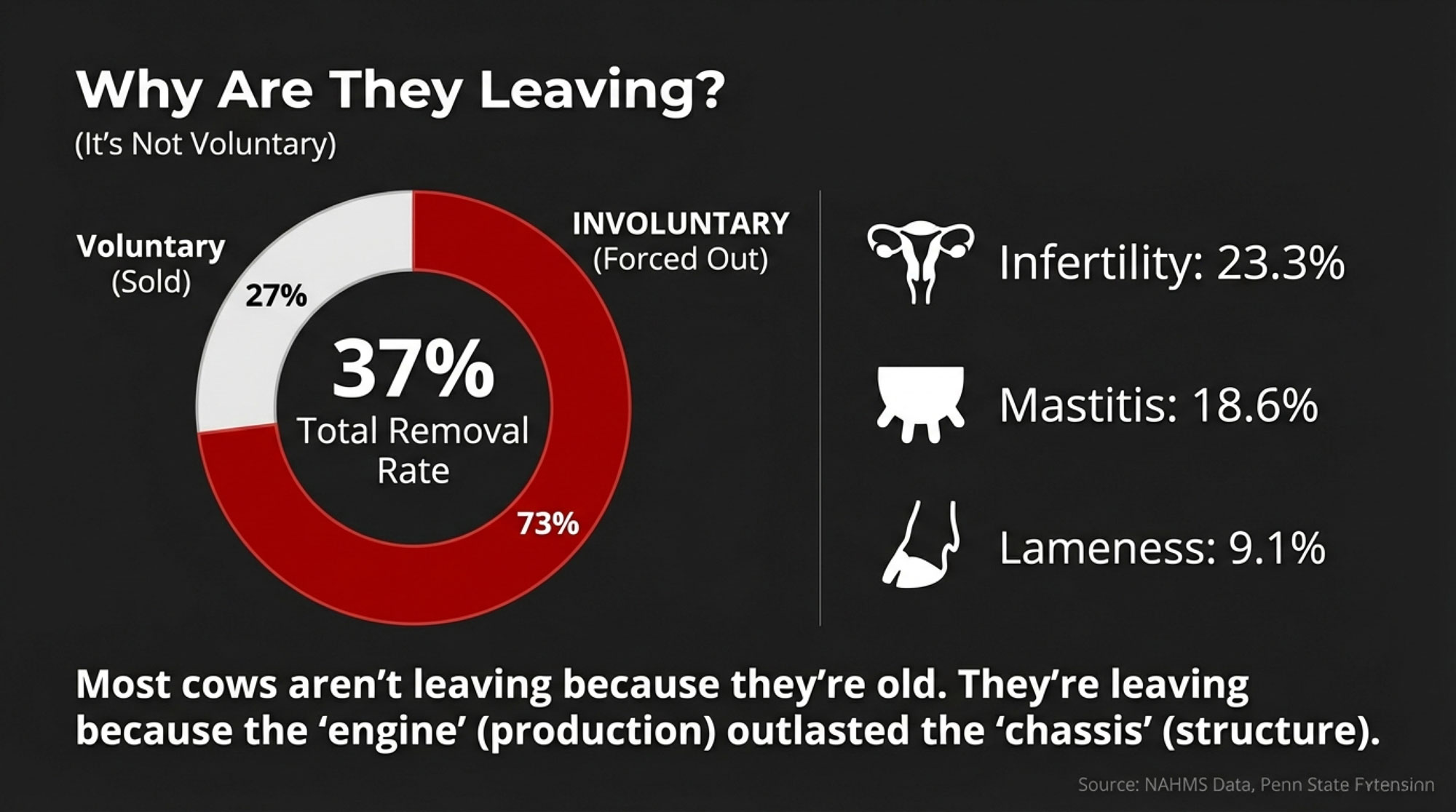

Across those herds, the average heifer completion rate from liveborn heifer calf to first calving was about 79%, with most herds landing between 74 and 84%. Just over one in five heifer calves never make it into the milking string. Some are lost at, or shortly after birth, some in the calf and grow‑out phases, some to disease or injury, and some are culled before they ever freshen.

Overton’s point to the HPDC crowd was blunt: a lot of operations are still planning their replacement needs as if nearly every heifer calf eventually freshens. His datasets say those assumptions are quietly loading risk into every decision about sexed semen usage, beef‑on‑dairy percentage, and whether a herd will be forced to compete in a record‑high springer market a couple of years down the road.

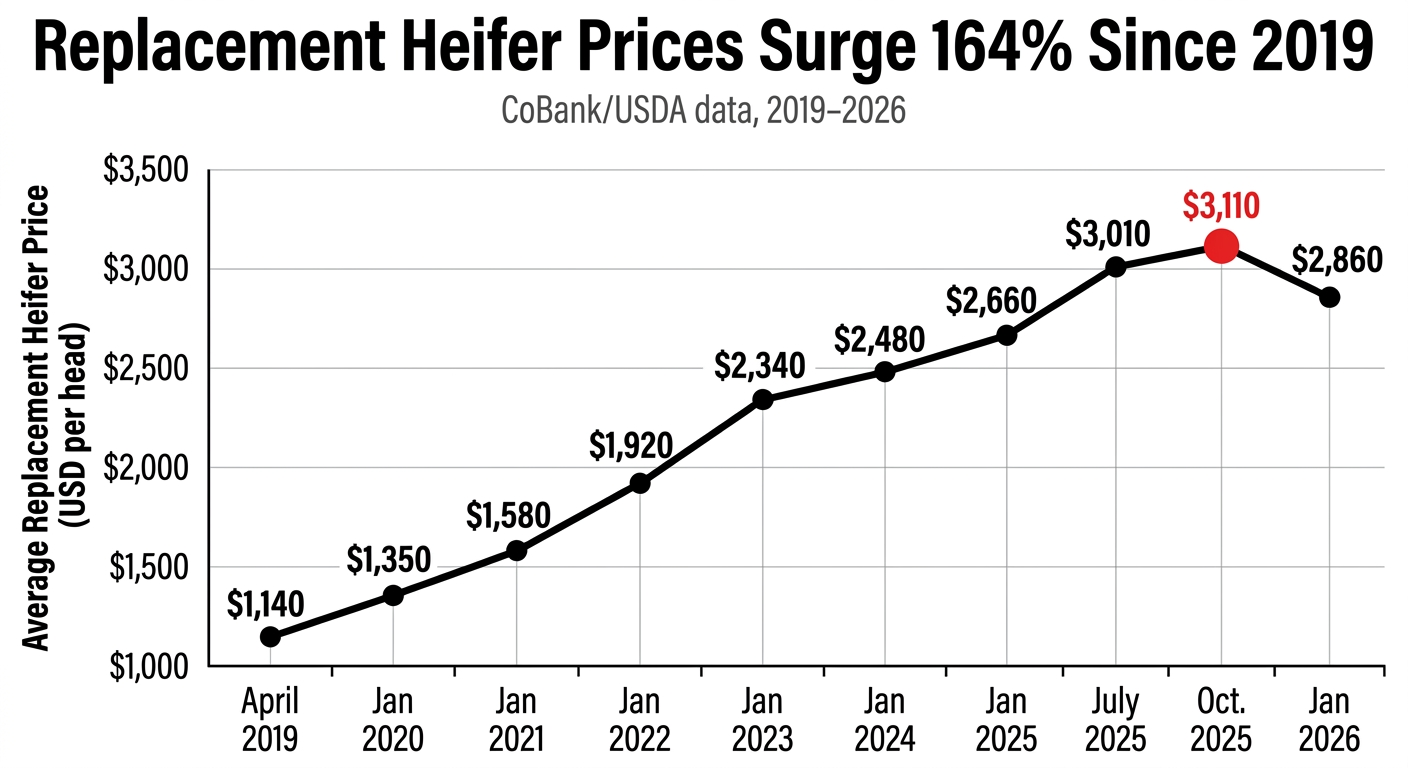

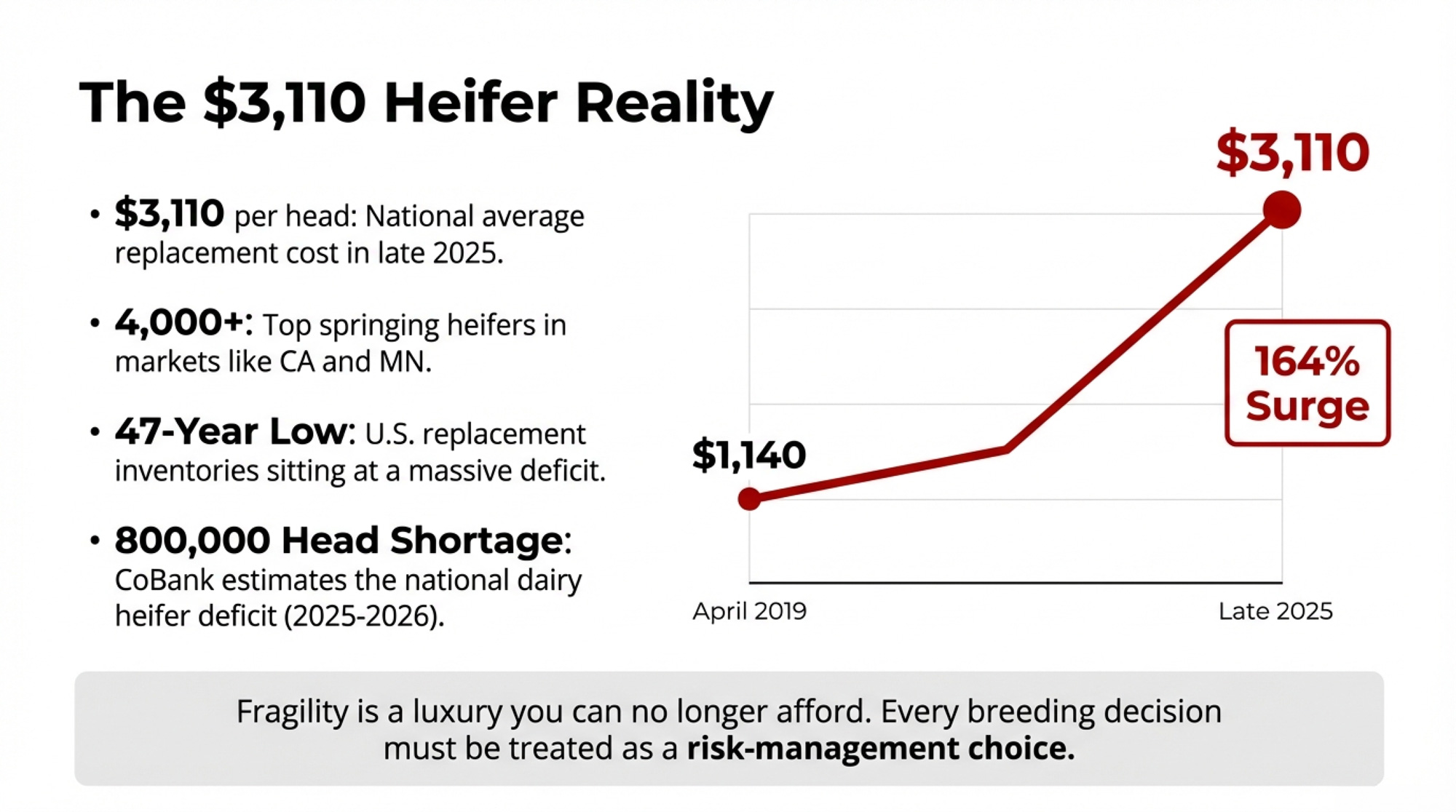

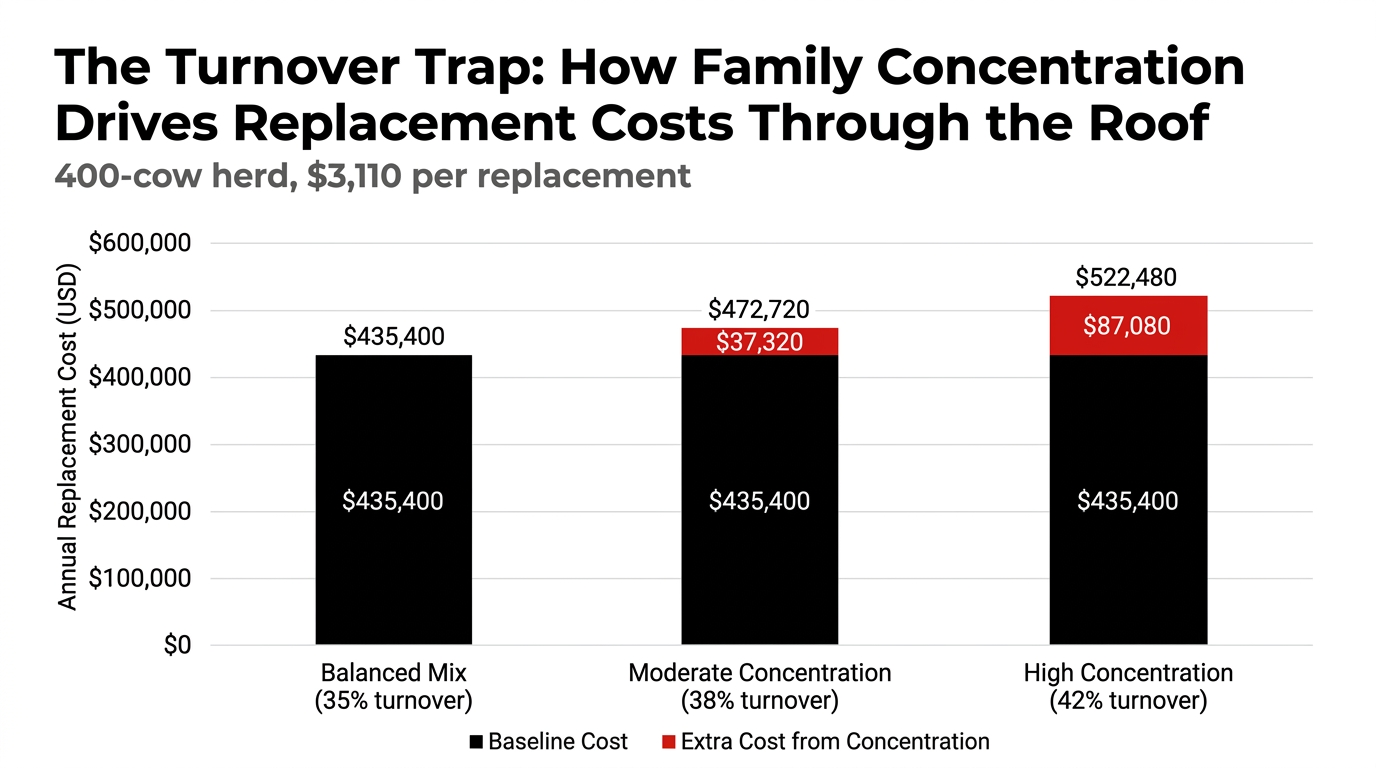

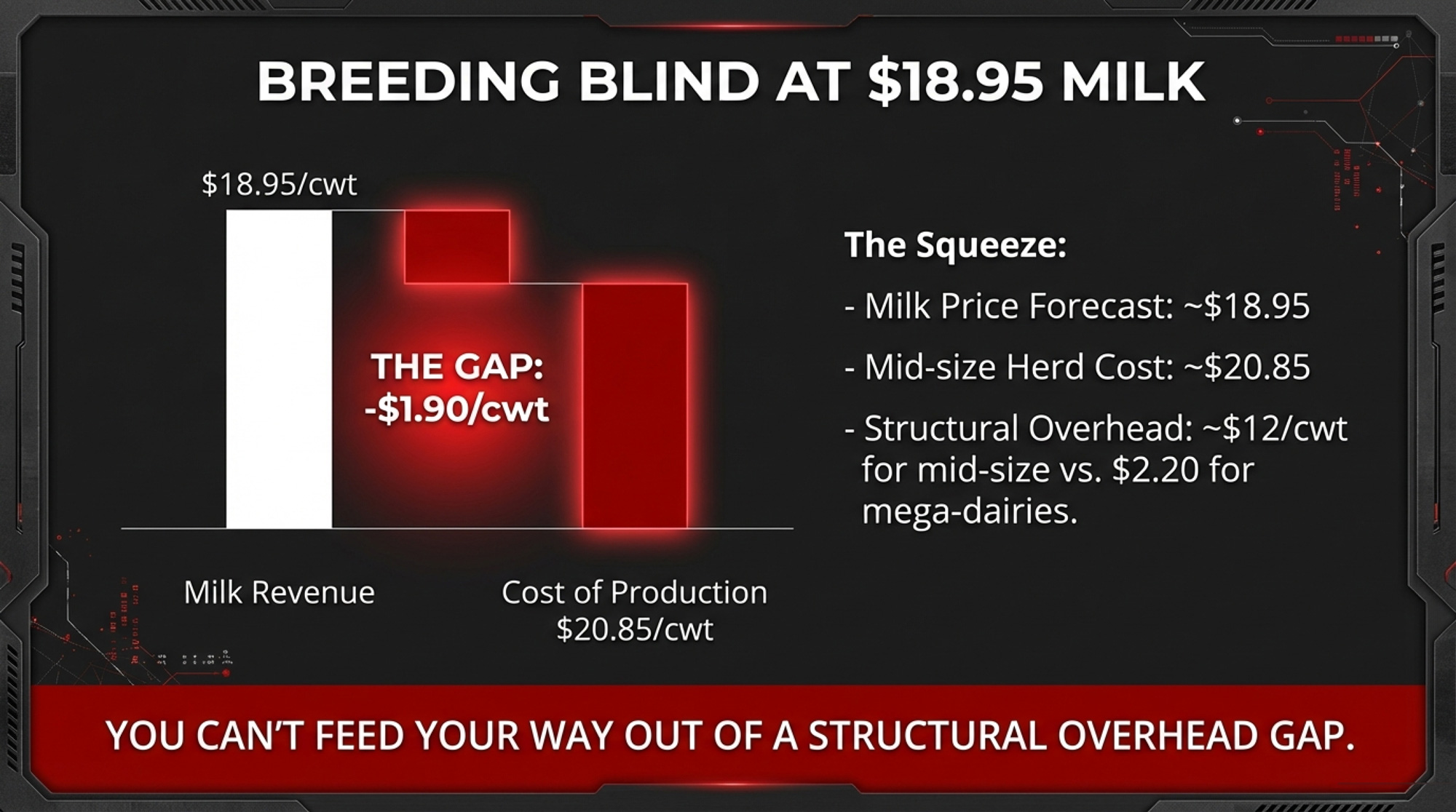

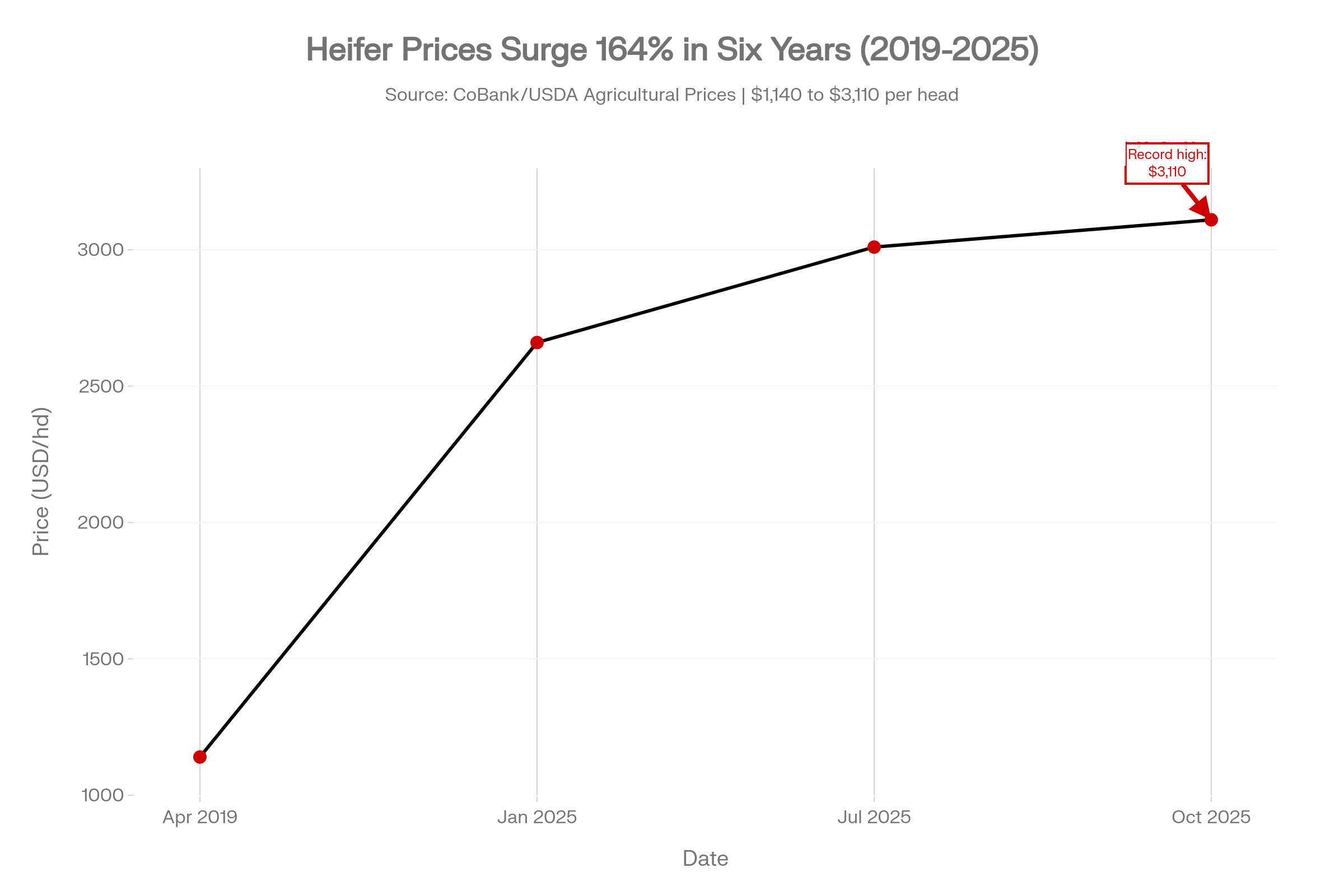

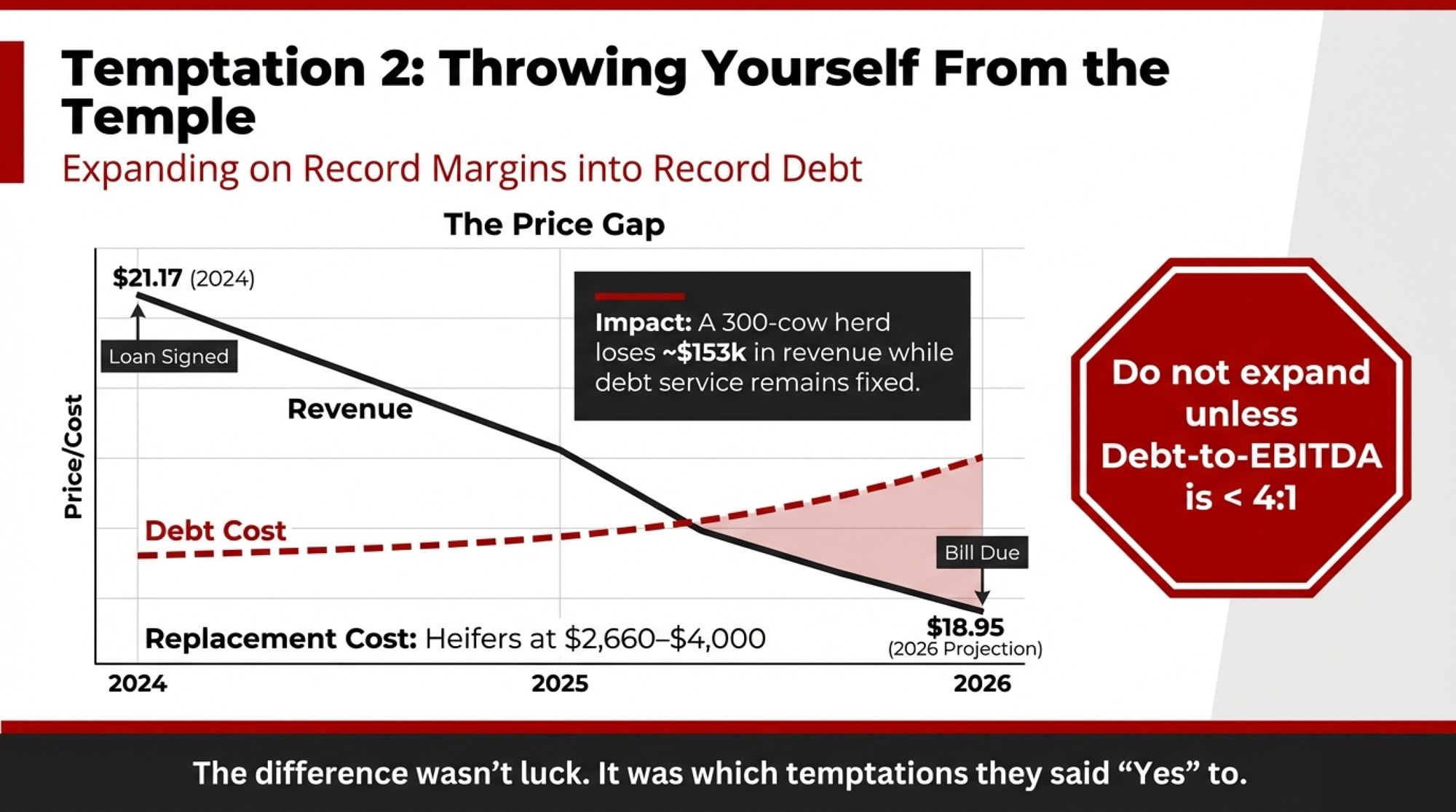

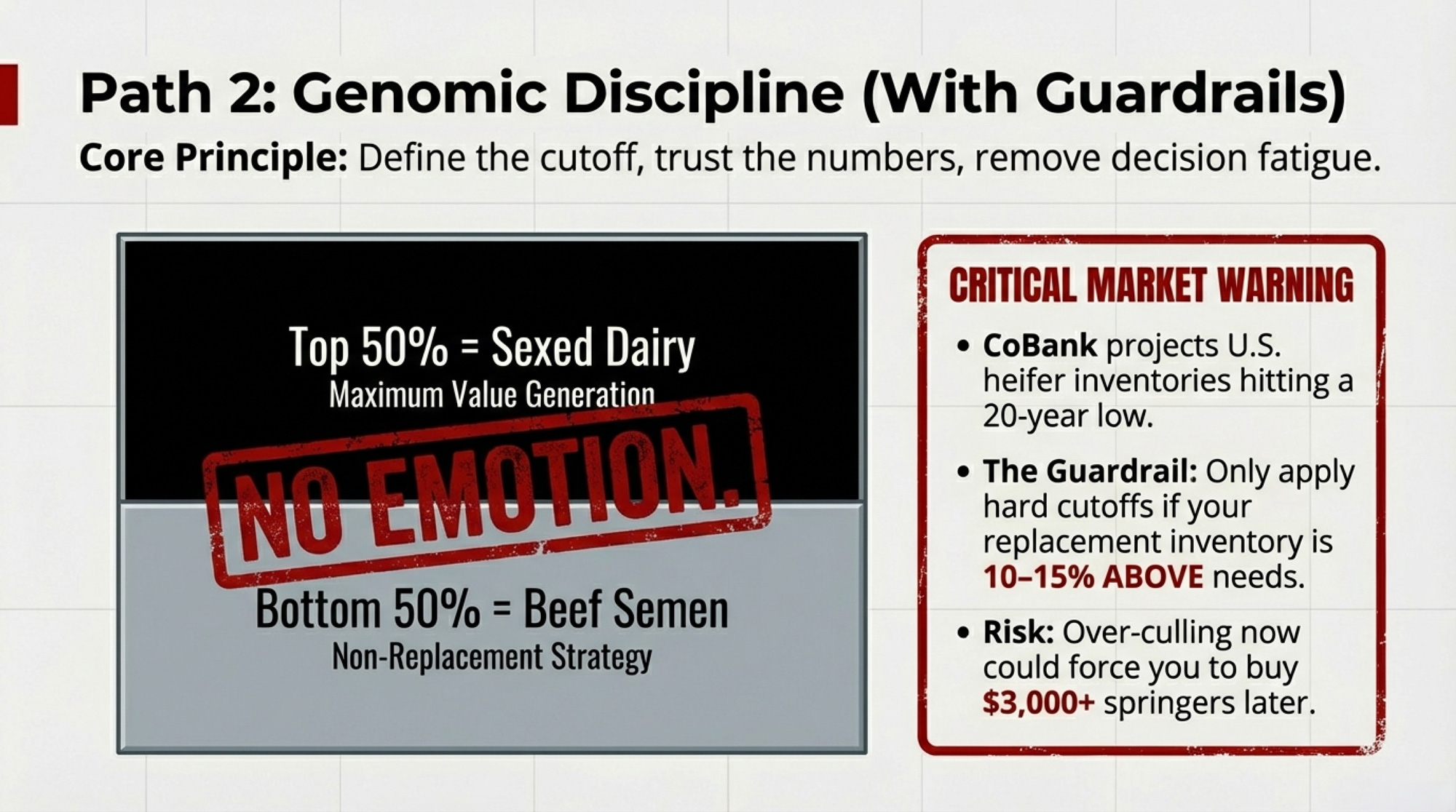

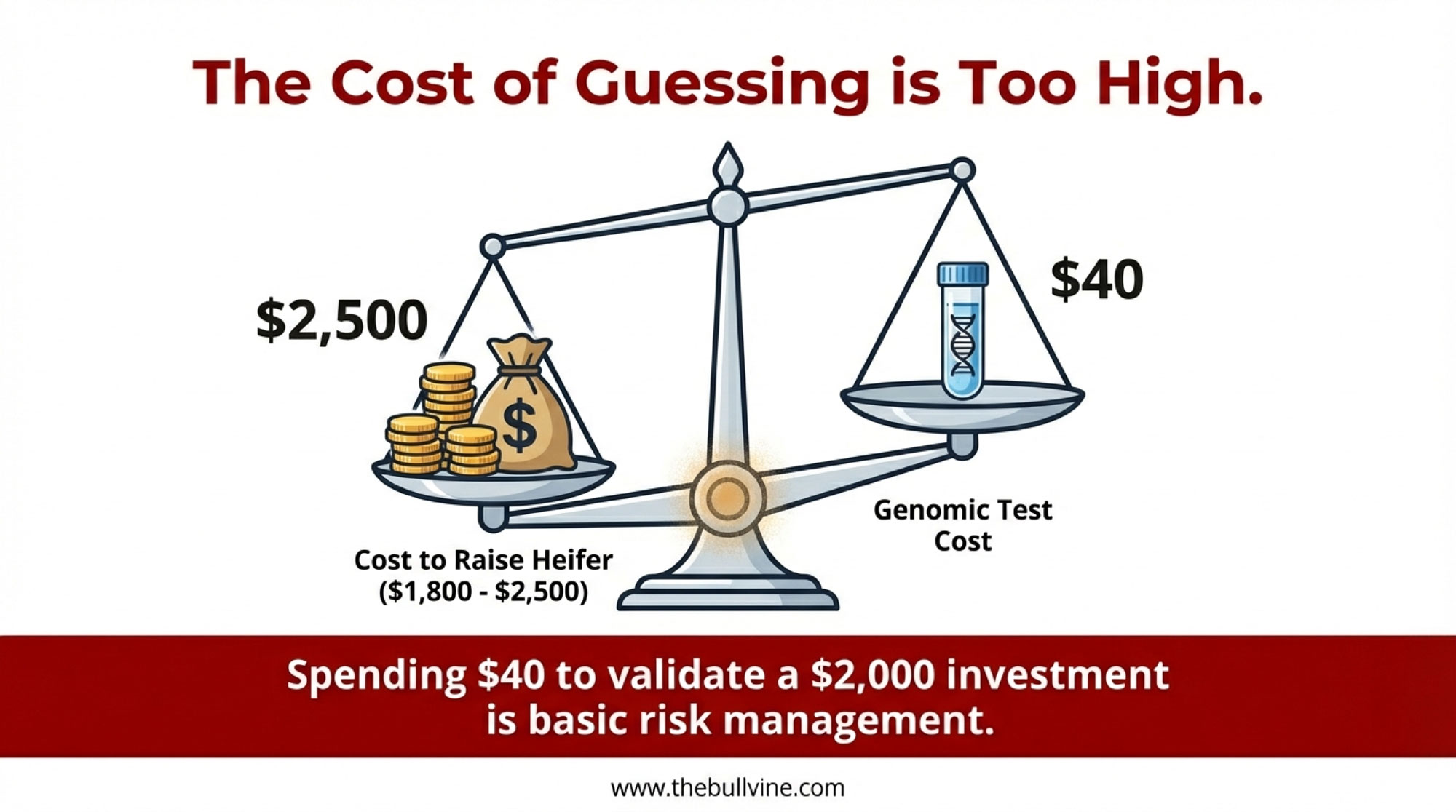

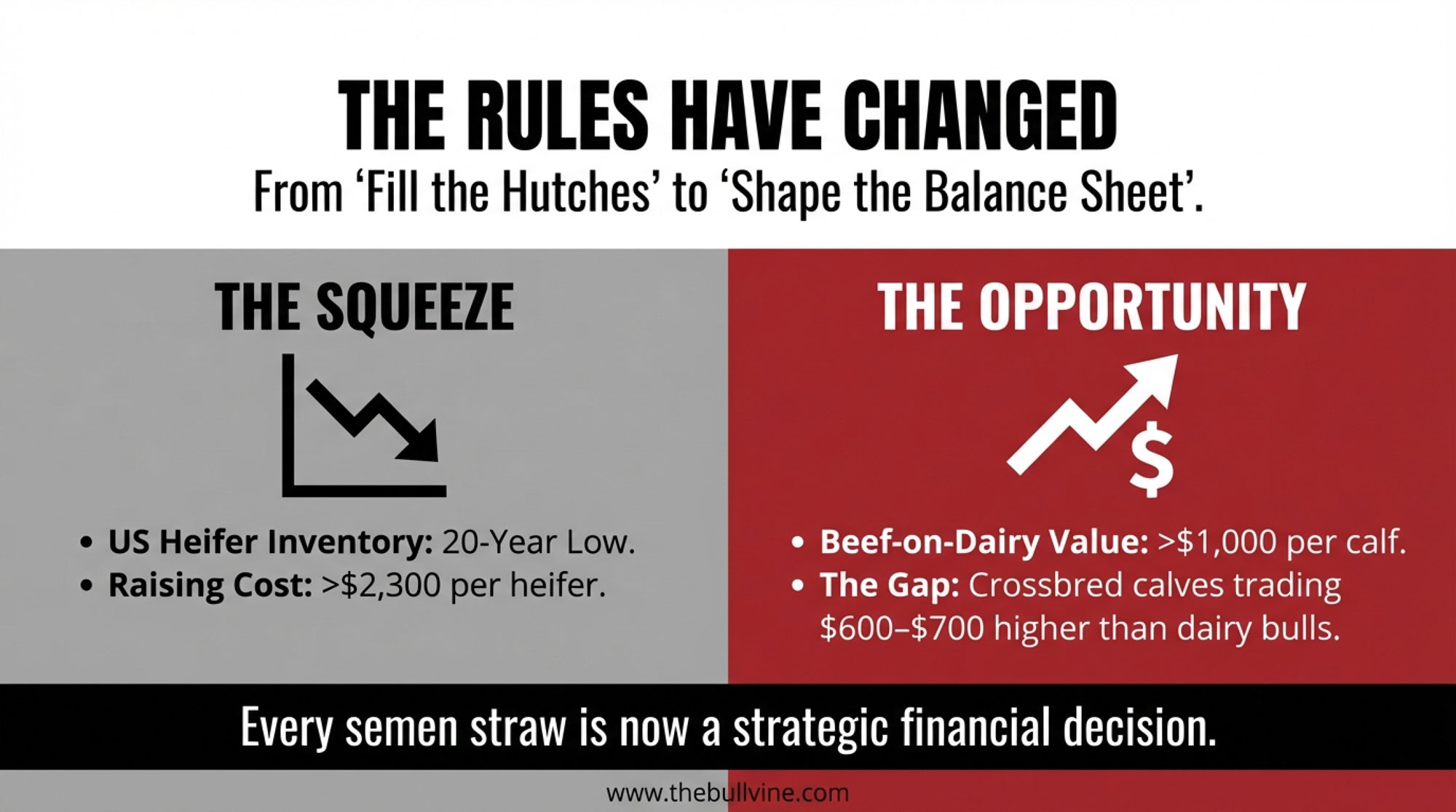

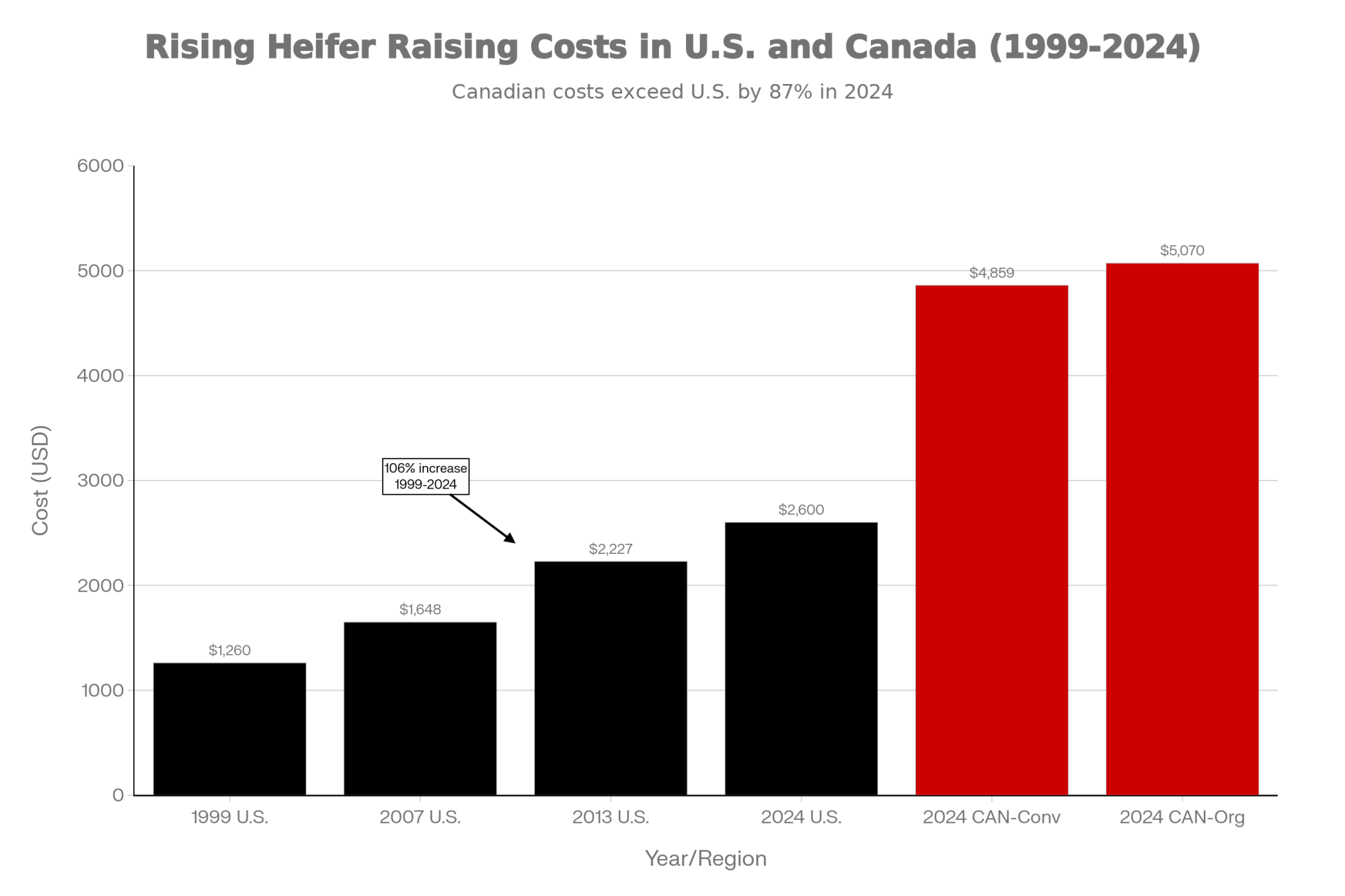

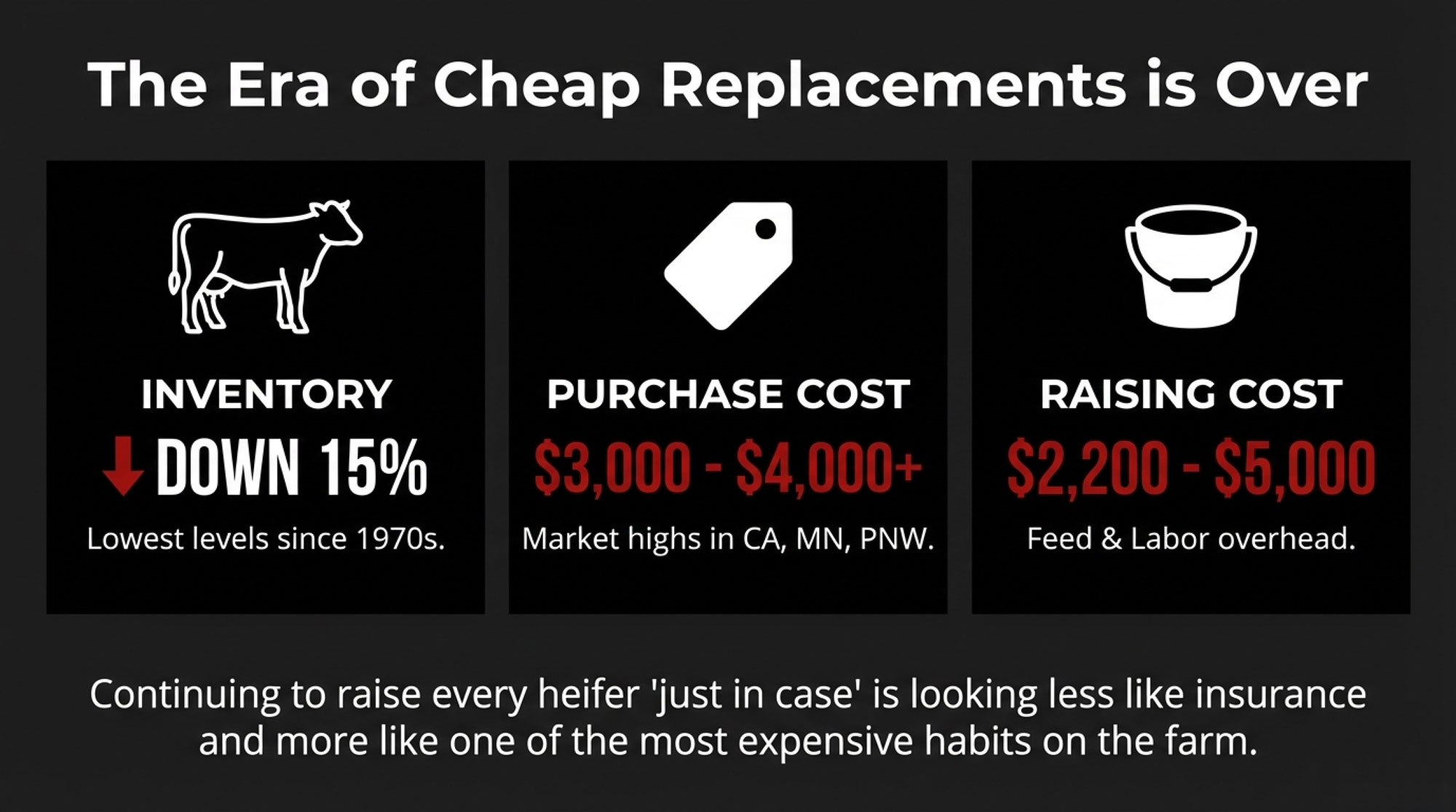

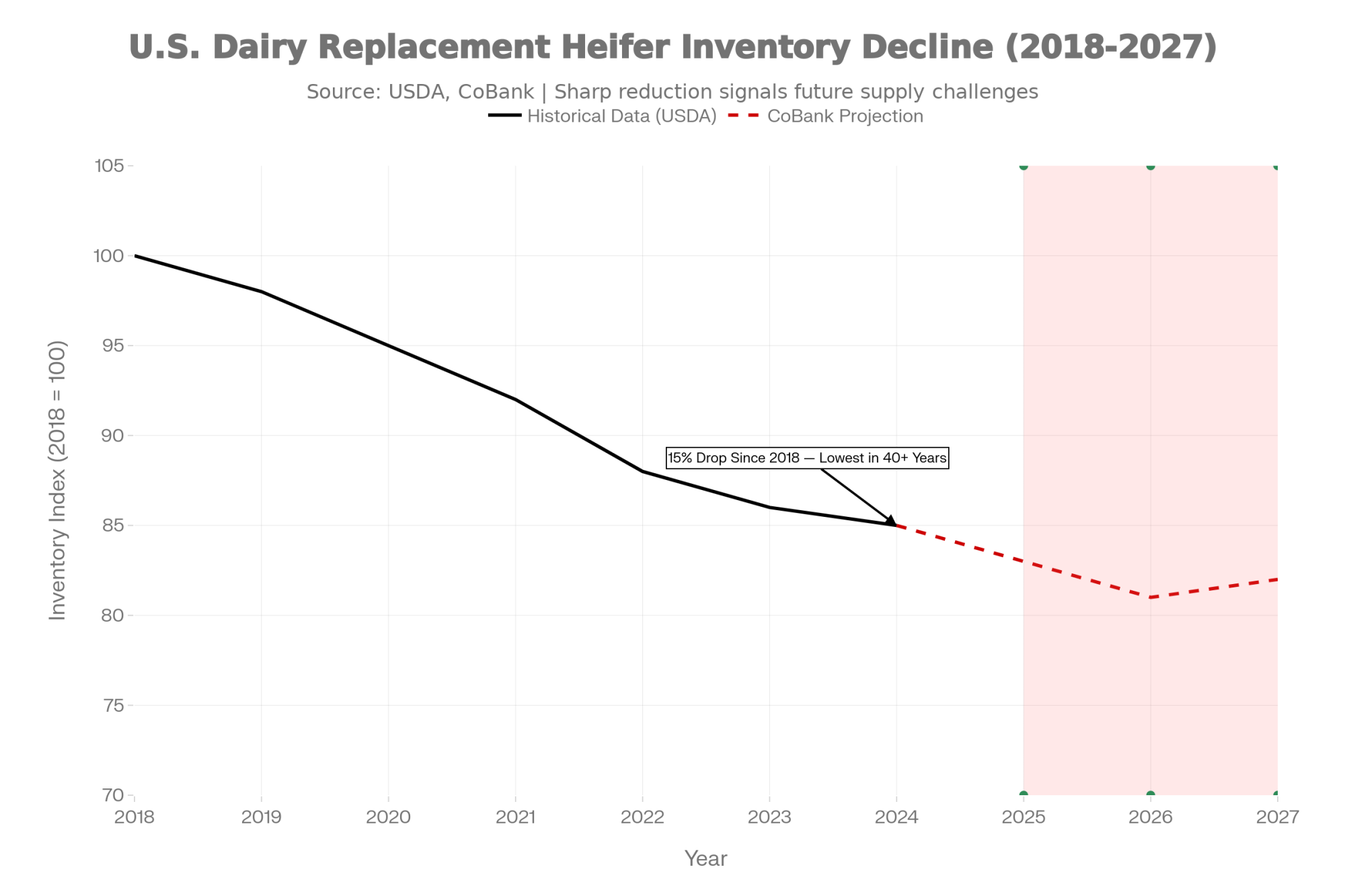

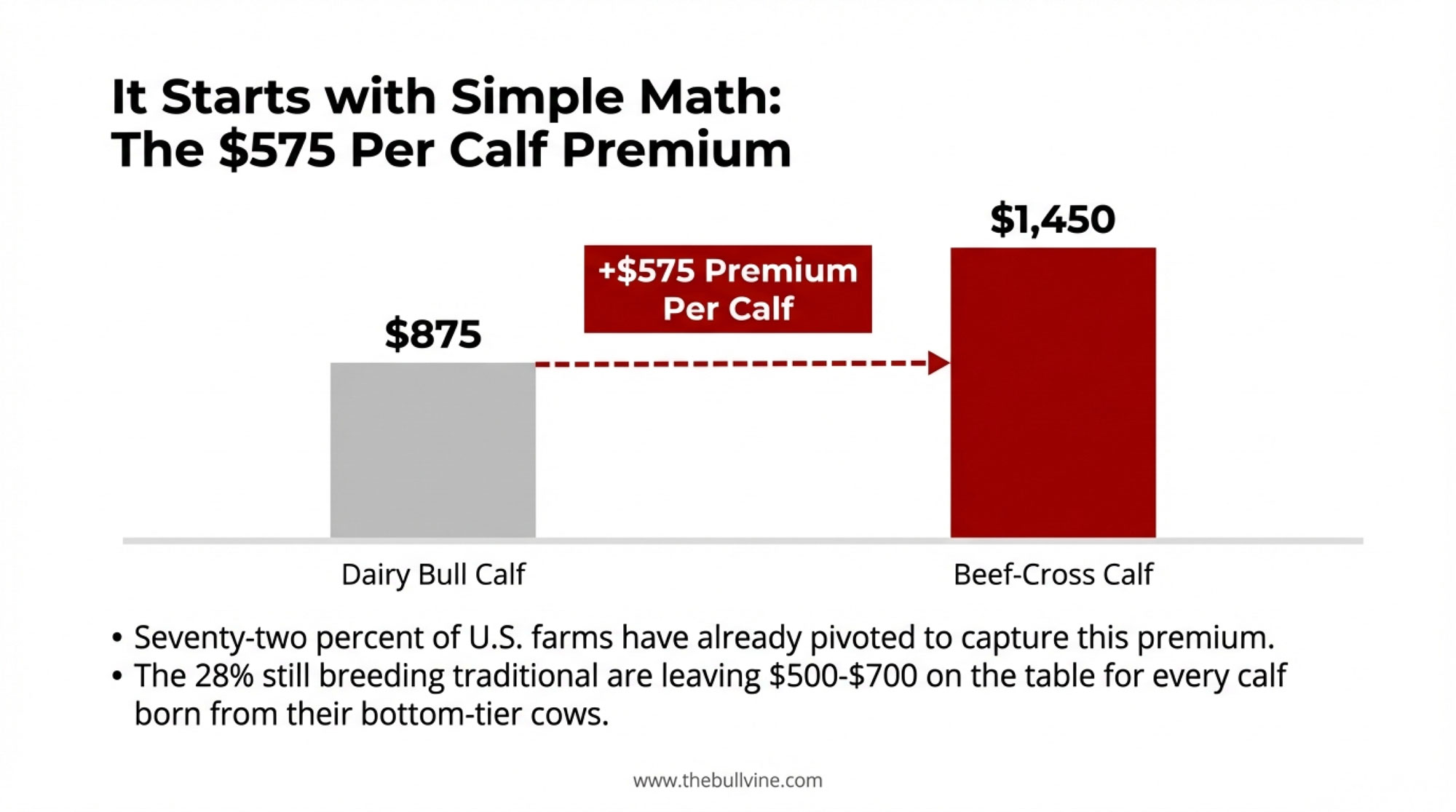

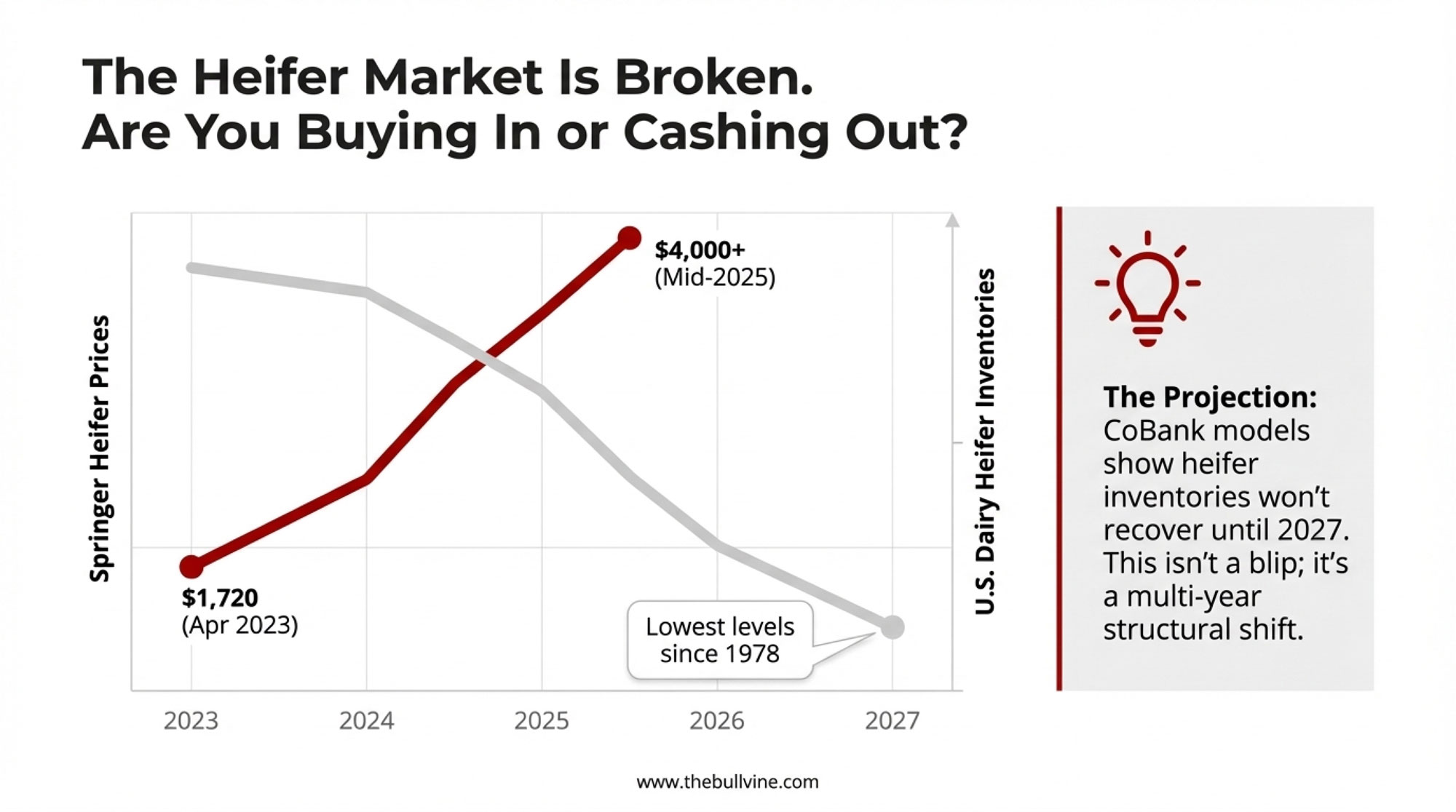

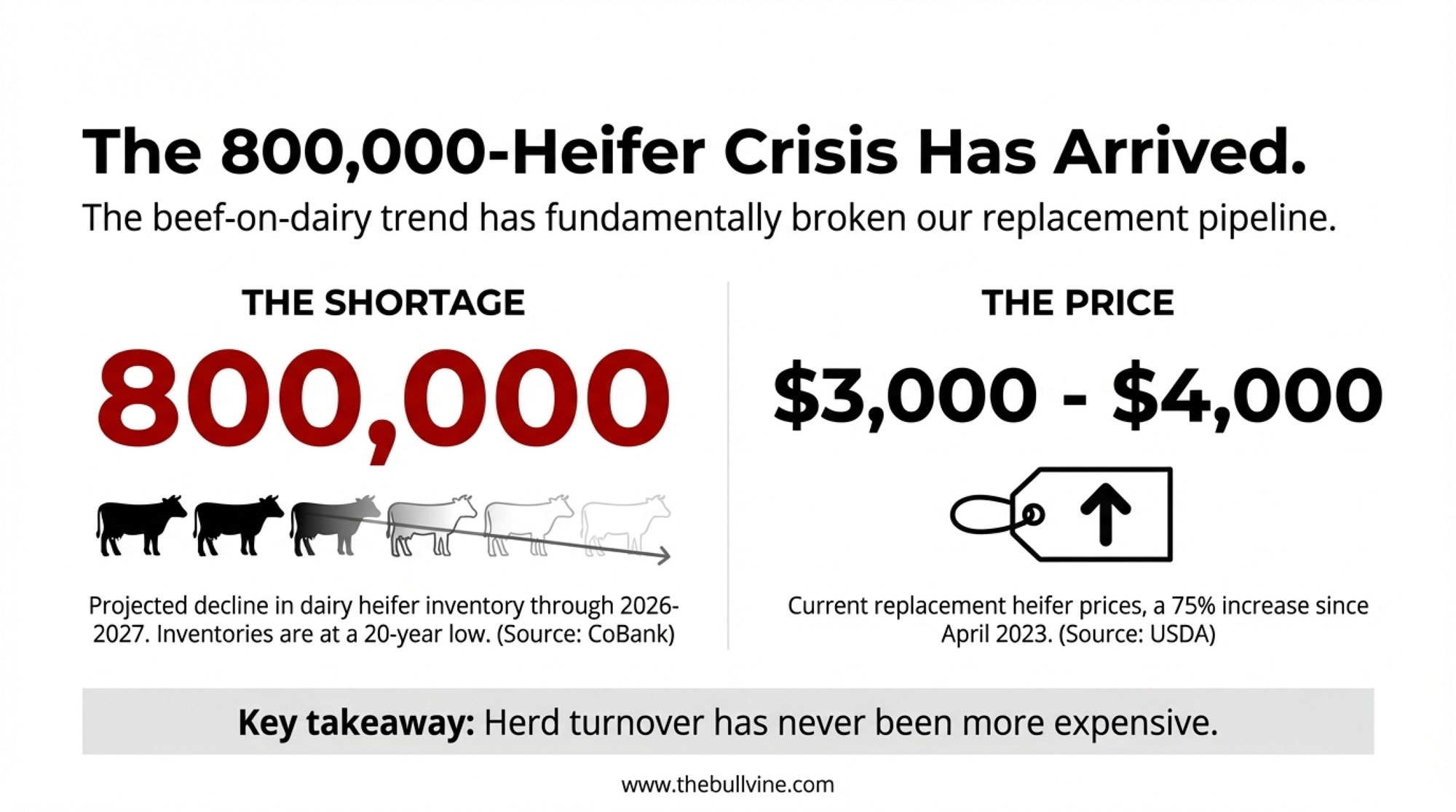

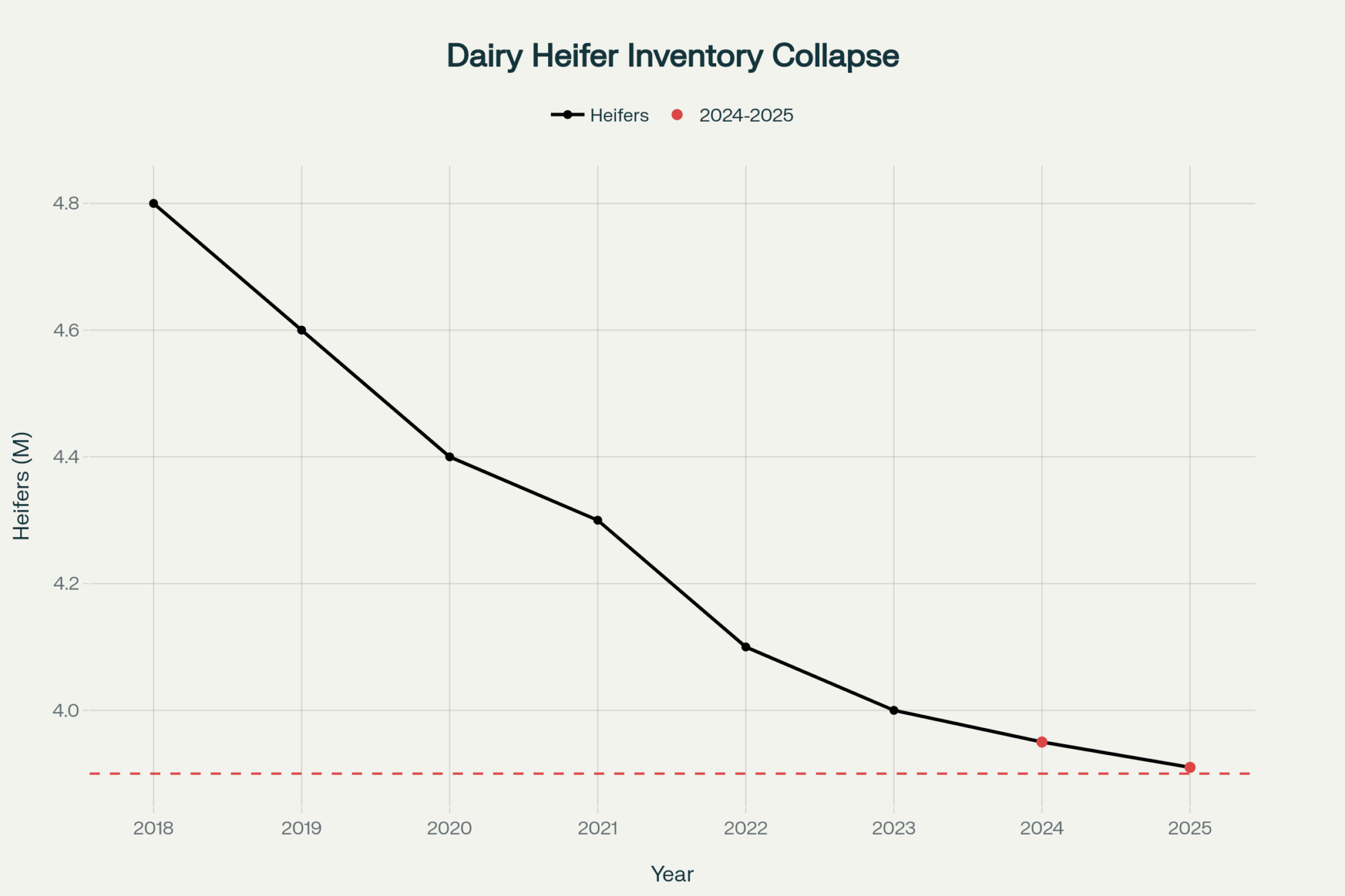

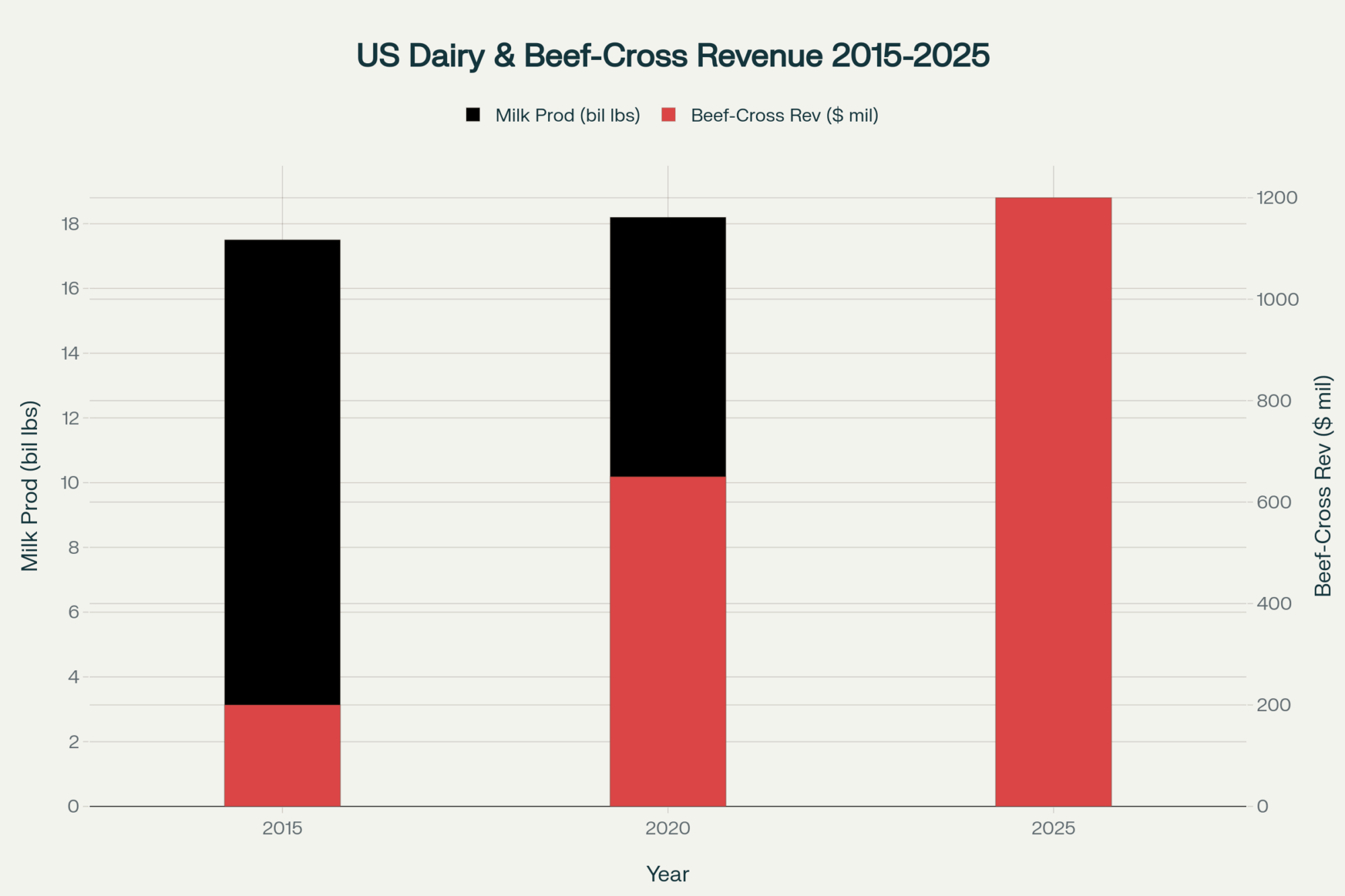

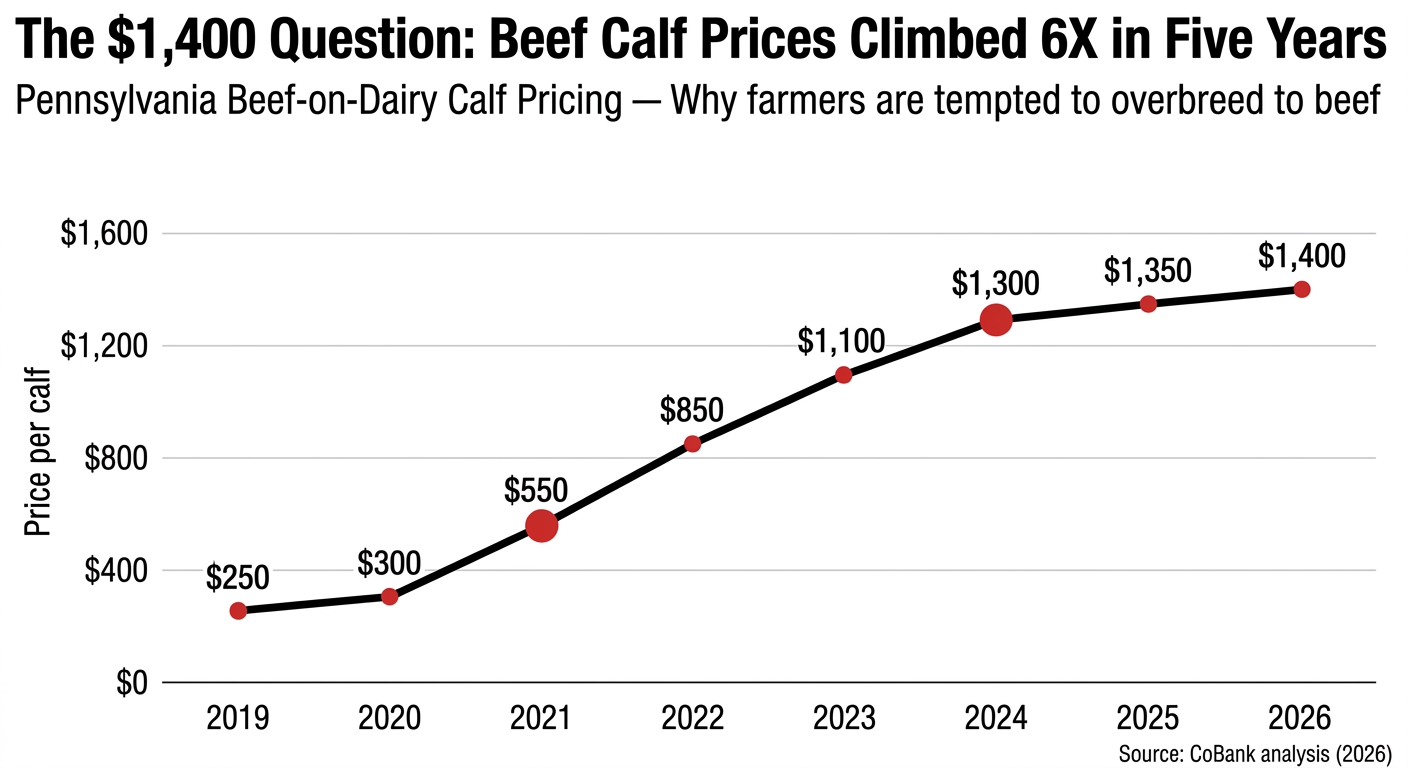

The national backdrop doesn’t leave much margin for error. USDA’s January 1, 2025, cattle estimates put dairy heifers 500 pounds and over at 3.914 million head, the lowest count in that category since 1978. CoBank’s August 2025 Knowledge Exchange report projected dairy heifer inventories would shrink by roughly 800,000 head over the following two years before beginning to rebound in 2027, with heifer prices already at record highs and potentially moving well beyond $3,000 per head in some markets as supply tightens. When $3,000‑plus springers are the new normal, pretending your herd runs at 90% heifer completion when the real number is closer to 79% is an expensive fantasy.

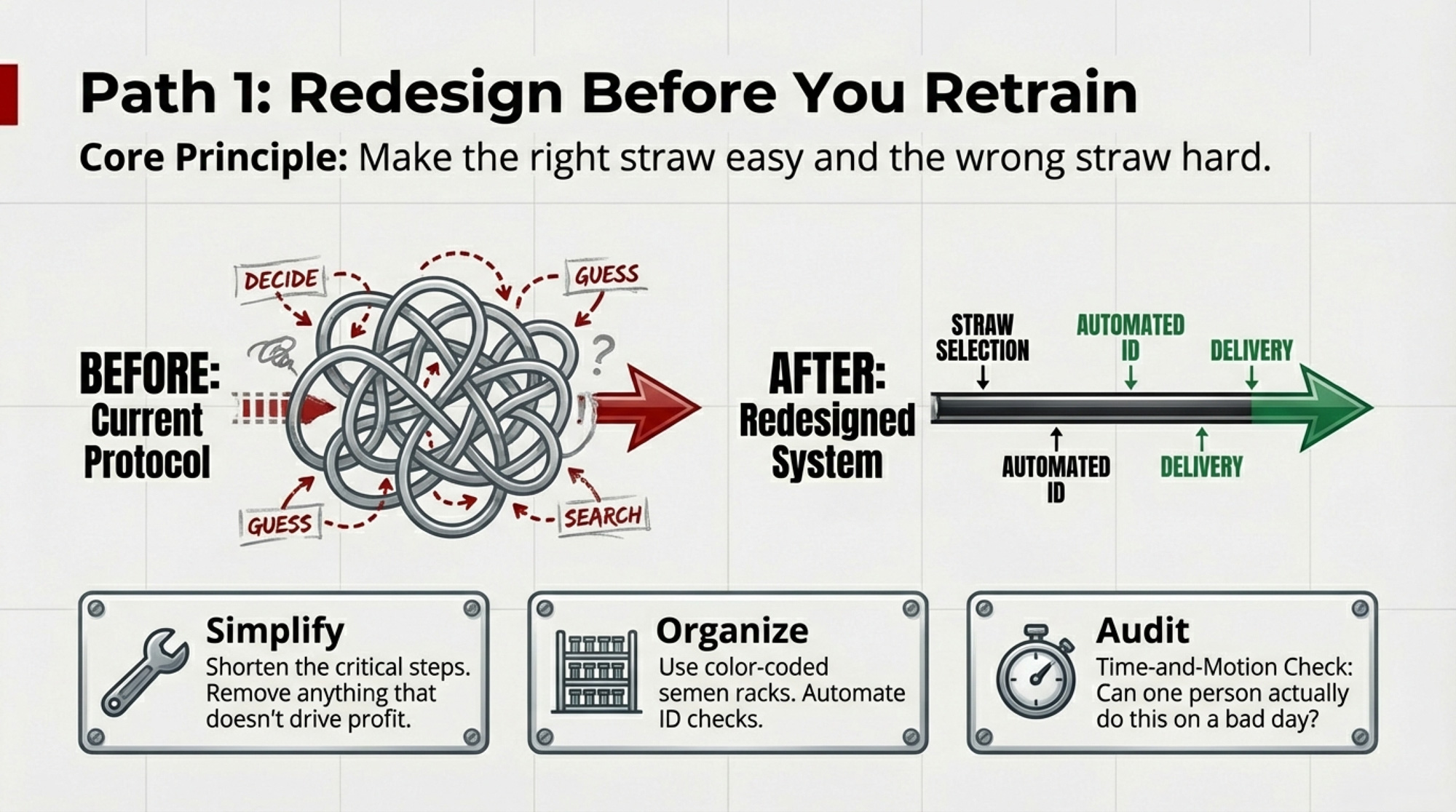

Parlor Drift: Is Your 4:00 a.m. Tech Killing Your Genetic Progress?

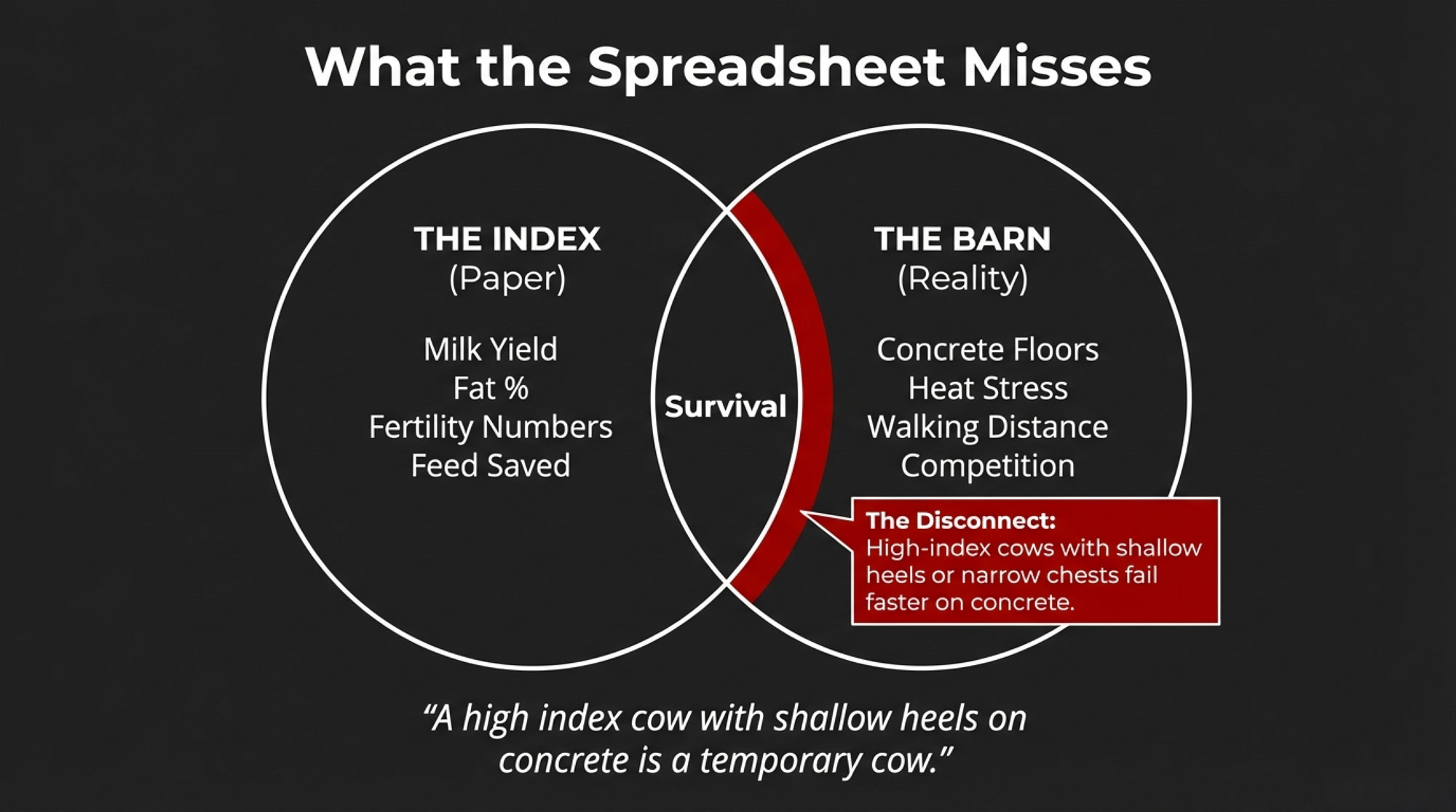

On paper, the breeding strategy in a lot of progressive herds already sounds sharp.

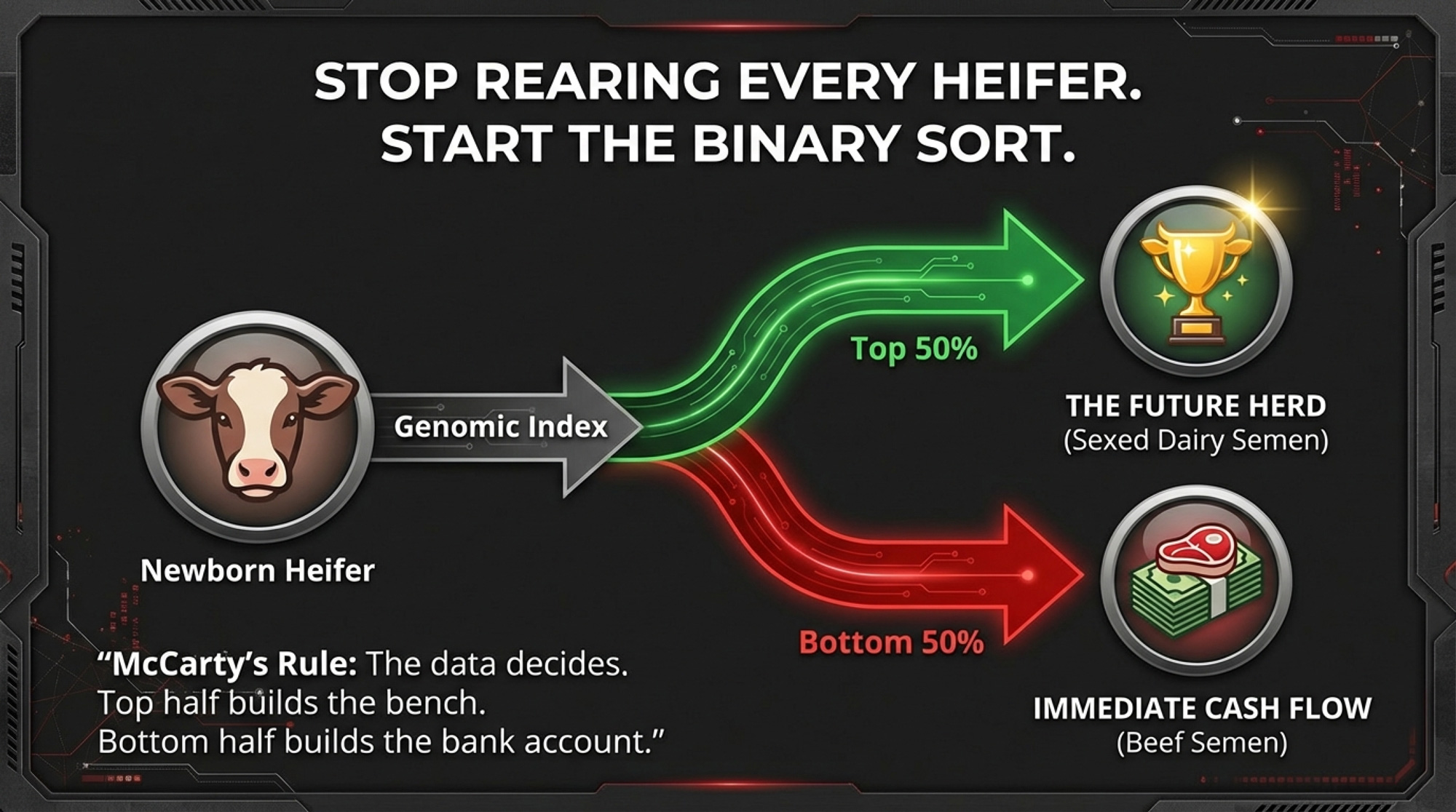

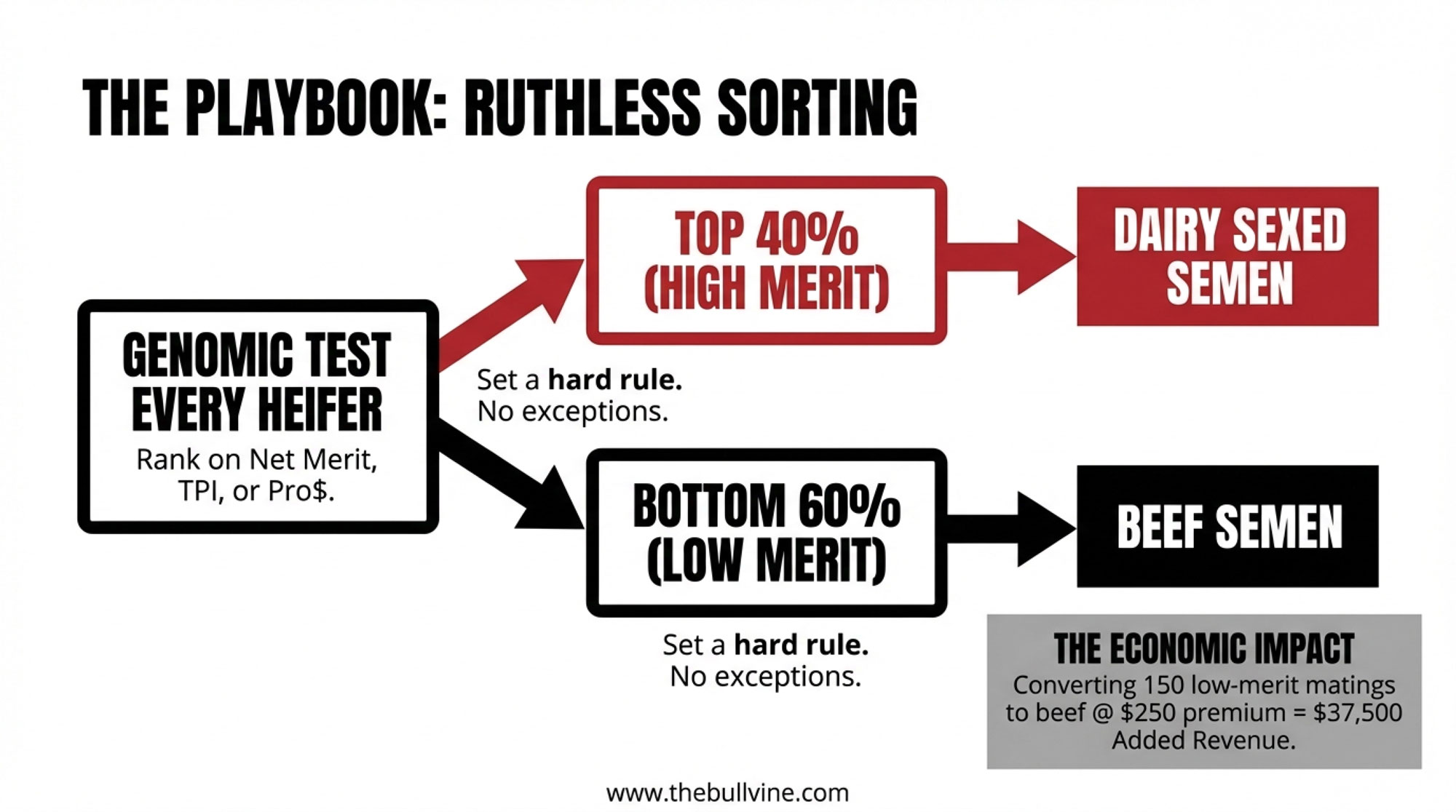

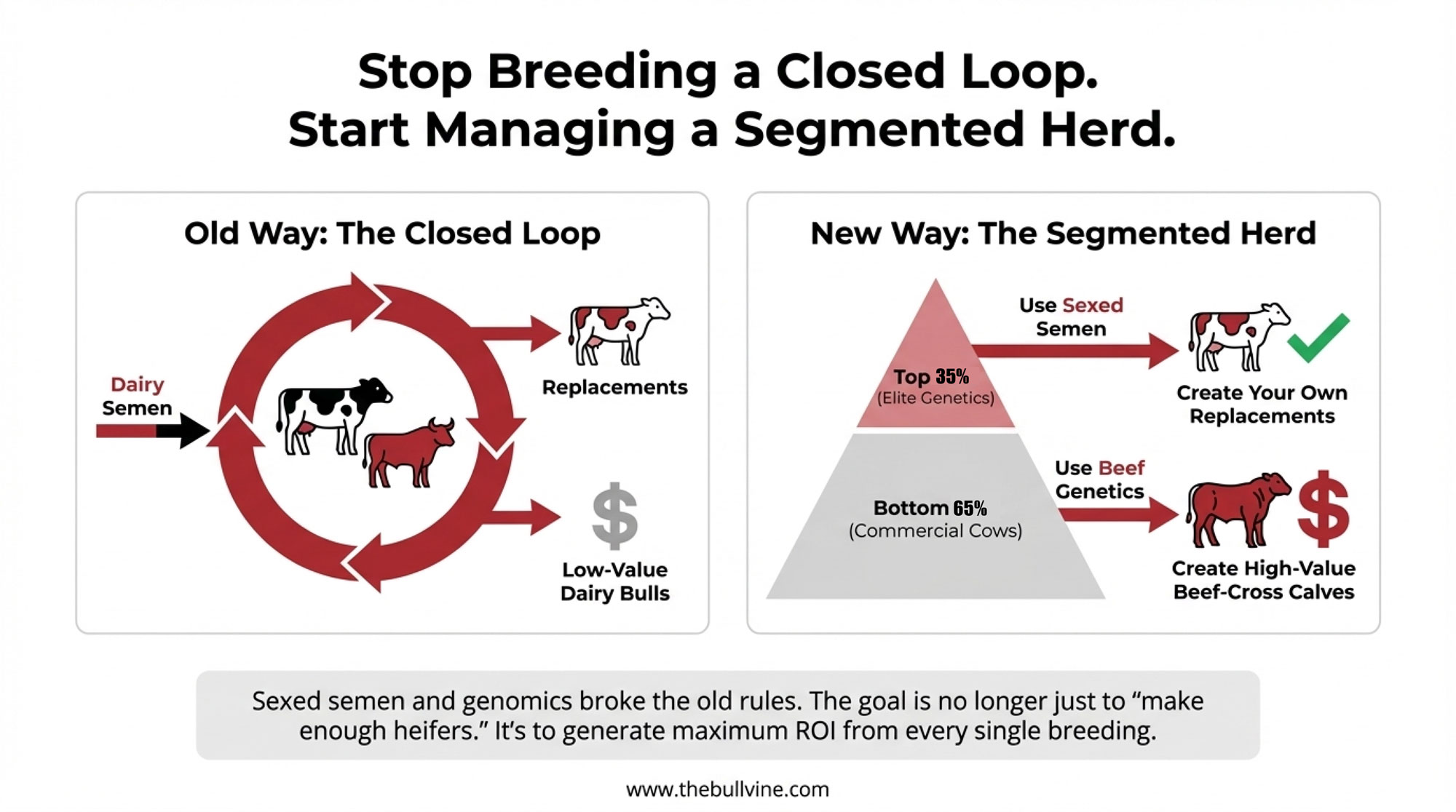

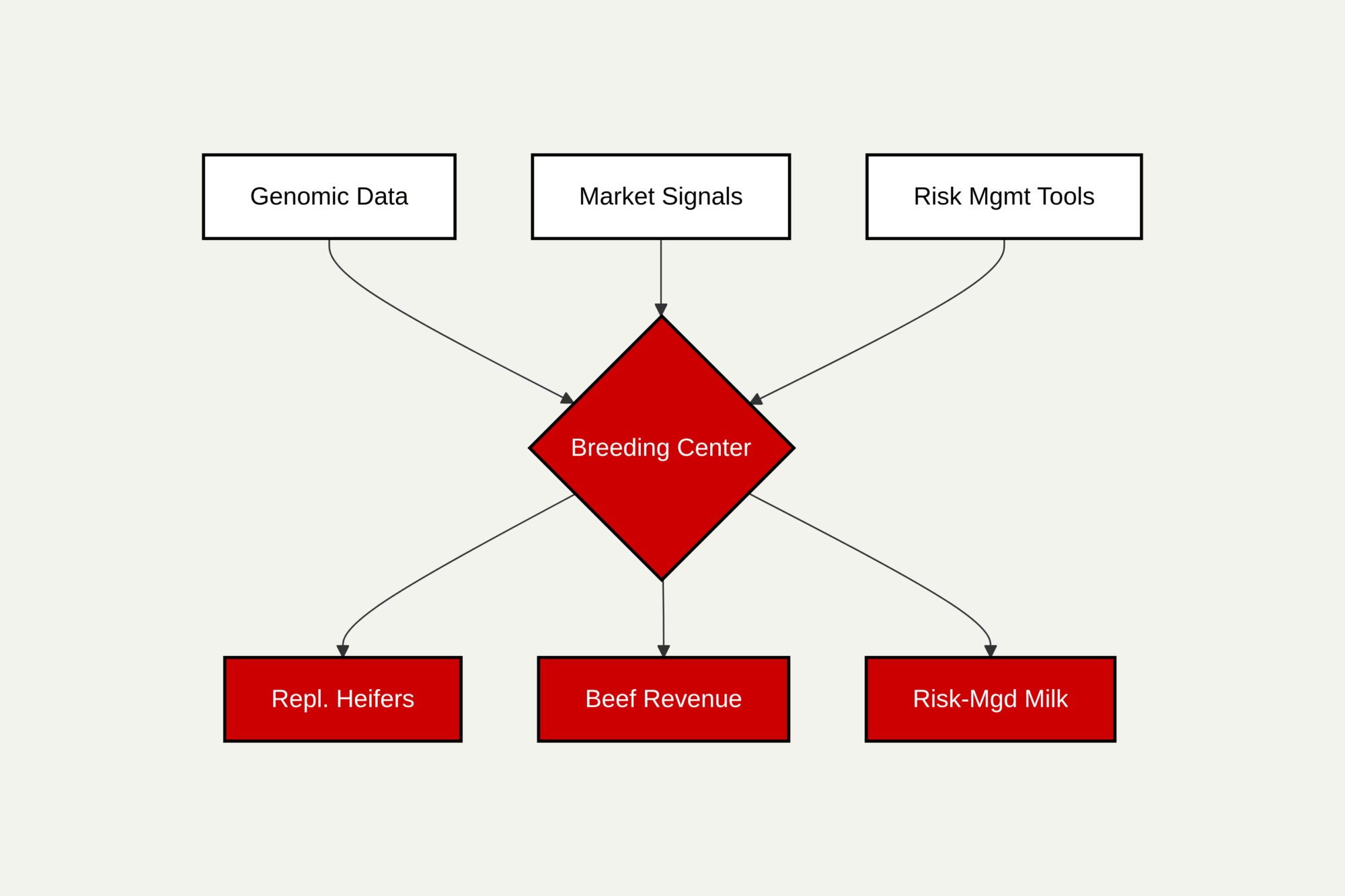

The binder in the office usually says something like: the top genomic tier and key cow families get sexed dairy semen; the middle third get conventional dairy; the true bottom third get beef from carefully chosen Angus or SimAngus sires; and obvious problem cows are DNB. That’s the clean terminal‑program diagram you walk through with your vet, nutritionist, and semen rep.

The decision about which straw goes in which cow doesn’t happen on that whiteboard, though. It happens at 4 a.m. in the parlor.

If today’s list says “breed these 14 cows” without telling the tech who gets sexed, who gets conventional, who gets beef, and who shouldn’t be bred at all, the plan starts to leak:

- A high‑genomic heifer that missed first service on sexed gets conventional “just this once” so she’s not open again.

- A third‑lactation cow, the crew is sick of treating, gets beef because she was open again, not because she’s truly bottom‑tier genetically.

- A lame, stale cow that should be hard DNB gets a straw anyway because she’s already in the headlocks and the tank is right there.

- A cow flagged for beef on the list gets conventional dairy because the tech grabbed the wrong tank canister, and nobody caught it until reconciliation — if reconciliation happens at all.

None of those calls look crazy in isolation. Stack them up over 52 weeks, and it’s easy for a beef target in the mid‑20s to creep into the low‑ or mid‑30s without anyone ever sitting down and saying, “Let’s change the plan.” Until someone reconciles pregnancies by semen type against the replacement math, that drift stays invisible.

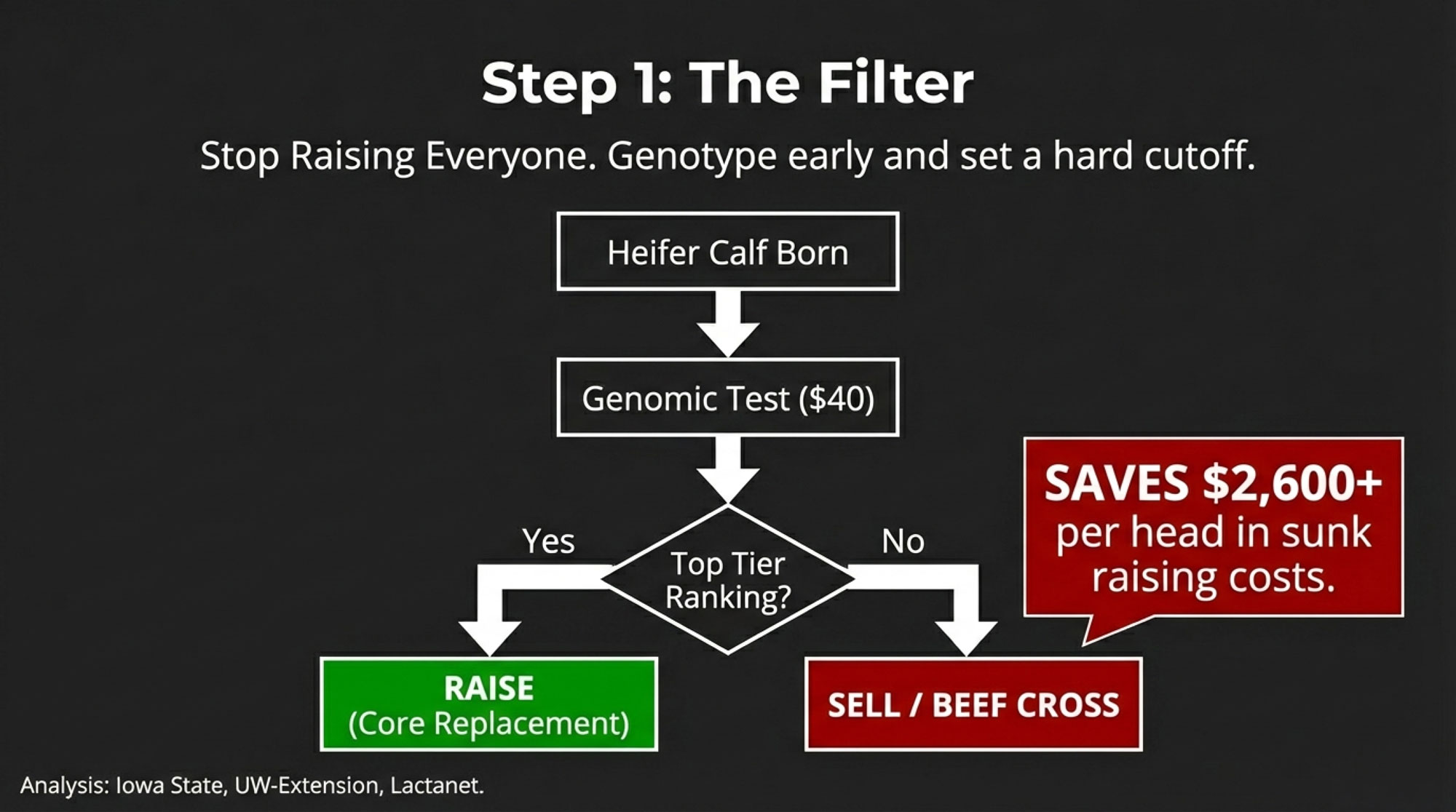

If you haven’t done it recently, a simple 20‑minute “beef audit” on your breeding cards is eye‑opening. Grab a recent week, highlight every beef mating, and cross‑check those cows against your genomic or index‑based tier list and DNB list. When more than a handful of beef straws are landing on cows that aren’t truly bottom‑tier, the day‑to‑day realities in the parlor are quietly pulling the program off the plan.

The 500-Cow “Overton Reality Check.”

Overton’s 79% completion figure isn’t just an interesting stat to quote at meetings. It’s the anchor for a simple backward pipeline calculation you can run on your own herd to find your real beef‑on‑dairy ceiling.

Here’s how a hypothetical 500‑cow herd looks when you put the math side by side with typical planning assumptions:

| Metric | Your Value (Est.) | The “Overton” Reality Check |

| Herd Size | 500 | 500 |

| Replacement Rate | 35% (what you’d like) | 37% (what many herds actually run) |

| Heifers Needed | 175 | 185 (+15 buffer = 200) |

| Completion Rate | 90% (goal in your head) | 79% (85‑herd actual) |

| Heifer Calves Needed | 194 | 253 |

| Beef Ceiling | ~50% of pregnancies (on paper) | ~34% of pregnancies (with sexed + conventional mix) |

Walking through the right‑hand column in barn‑math terms:

- At a 37% annual cull/turnover rate, you need 185 replacements to stand still (0.37 × 500 = 185).

- Add a modest 3% buffer for flexibility — about 15 extra heifers — and you’re targeting 200 heifers calving in per year.

- At a 79% heifer completion rate, those 200 heifers require roughly 253 heifer calves born alive (200 ÷ 0.79 ≈ 253).

- If 60% of your dairy pregnancies use sexed semen (≈90% heifers) and 40% use conventional (≈50% heifers), the weighted average female fraction per dairy pregnancy is about 0.74.

- To get 253 heifer calves at 0.74 heifers per pregnancy, you need about 342 dairy‑sired pregnancies per year(253 ÷ 0.74 ≈ 342).

Total pregnancies per year in a 500‑cow herd vary with the reproduction program, but for illustration, say you generate around 520 pregnancies annually. In that scenario:

- 520 total pregnancies − 342 dairy‑sired pregnancies needed = 178 pregnancies available for beef.

- 178 ÷ 520 ≈ 34% of pregnancies.

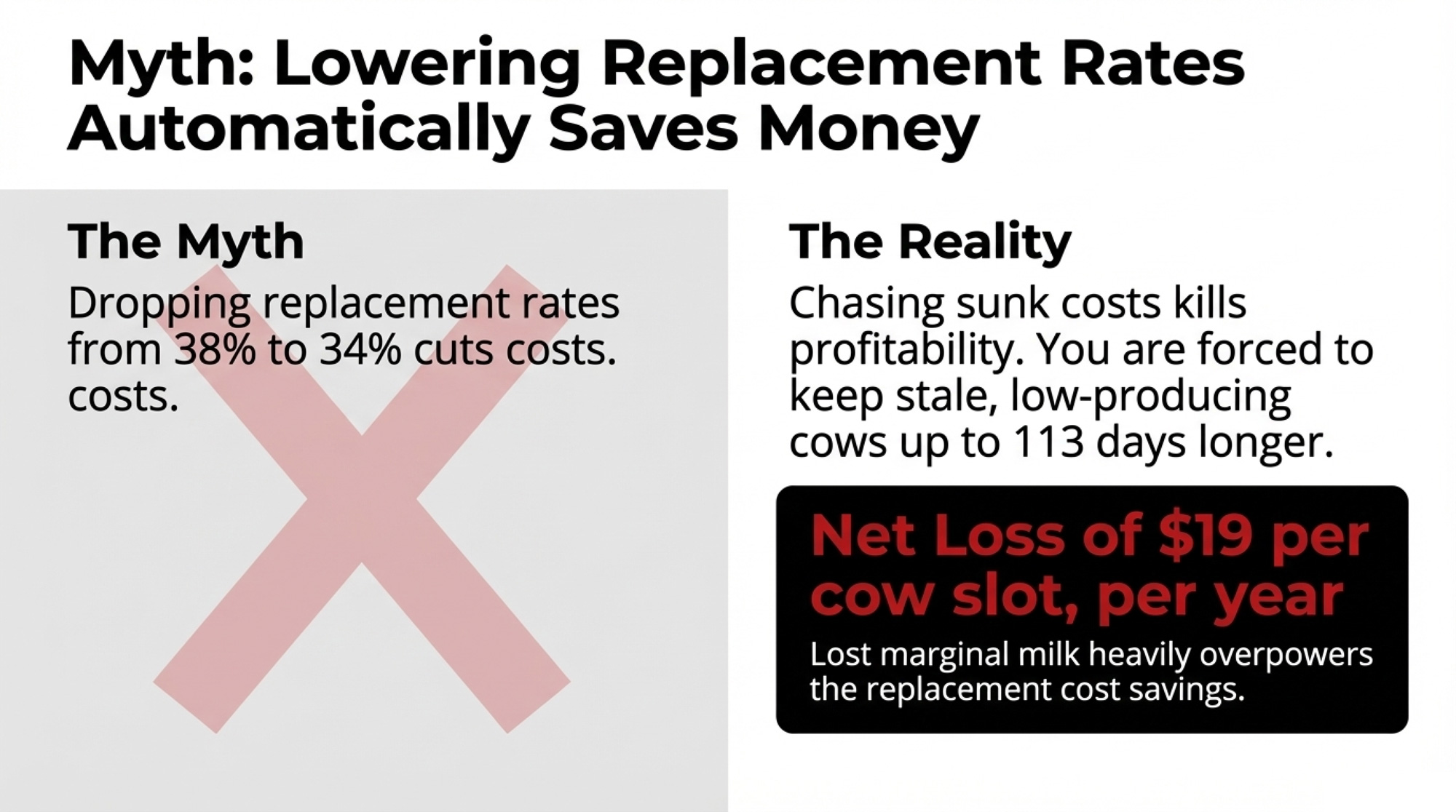

That 34% isn’t a magic industry standard. It’s the ceiling in this particular example with these assumptions. If your actual completion rate is lower than 79%, your safe beef ceiling drops. Dial back sexed semen usage — or see weaker conception on sexed — and it drops again. Want more than a 3% heifer surplus to sell into a strong replacement market? It drops further still.

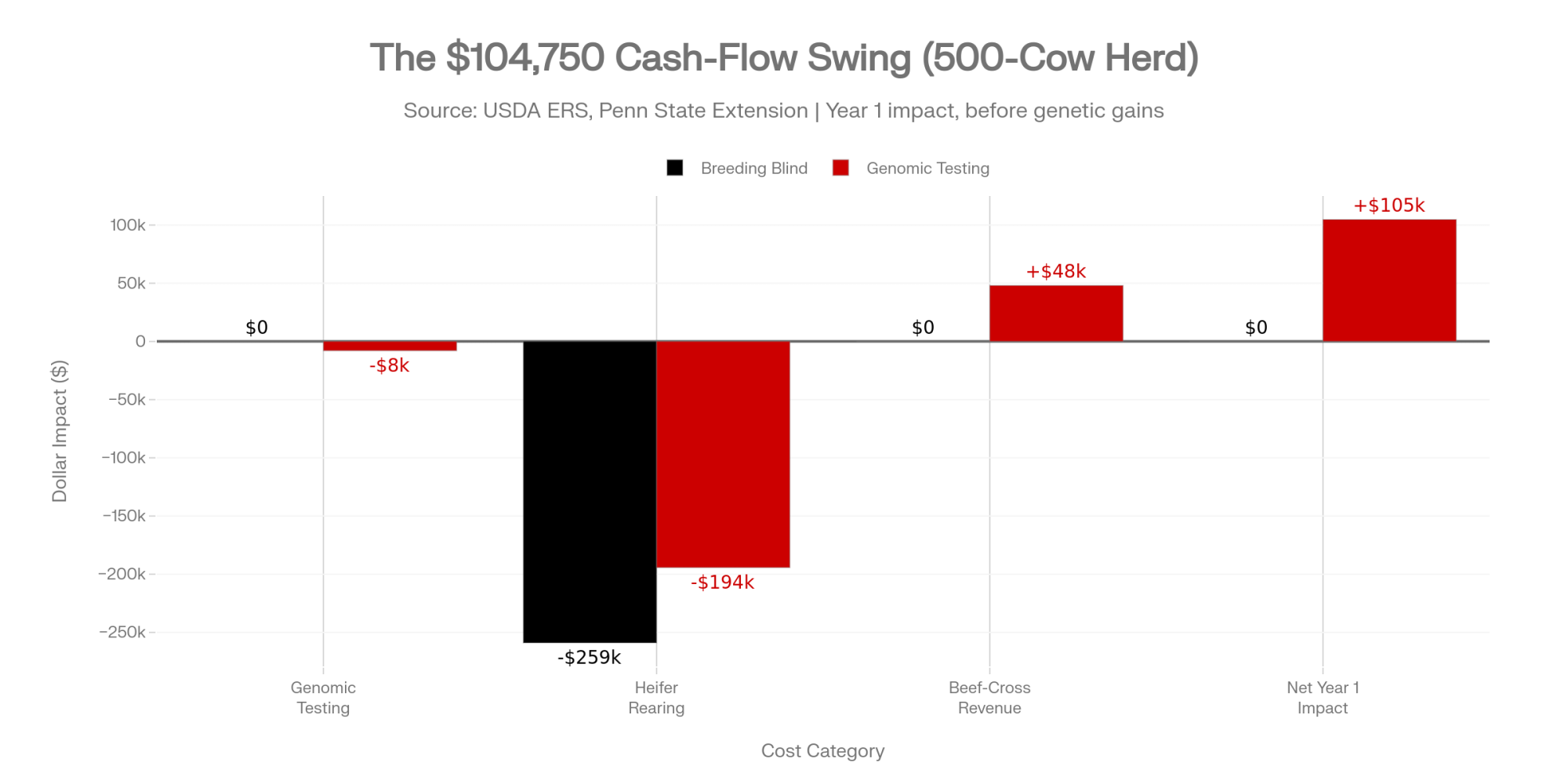

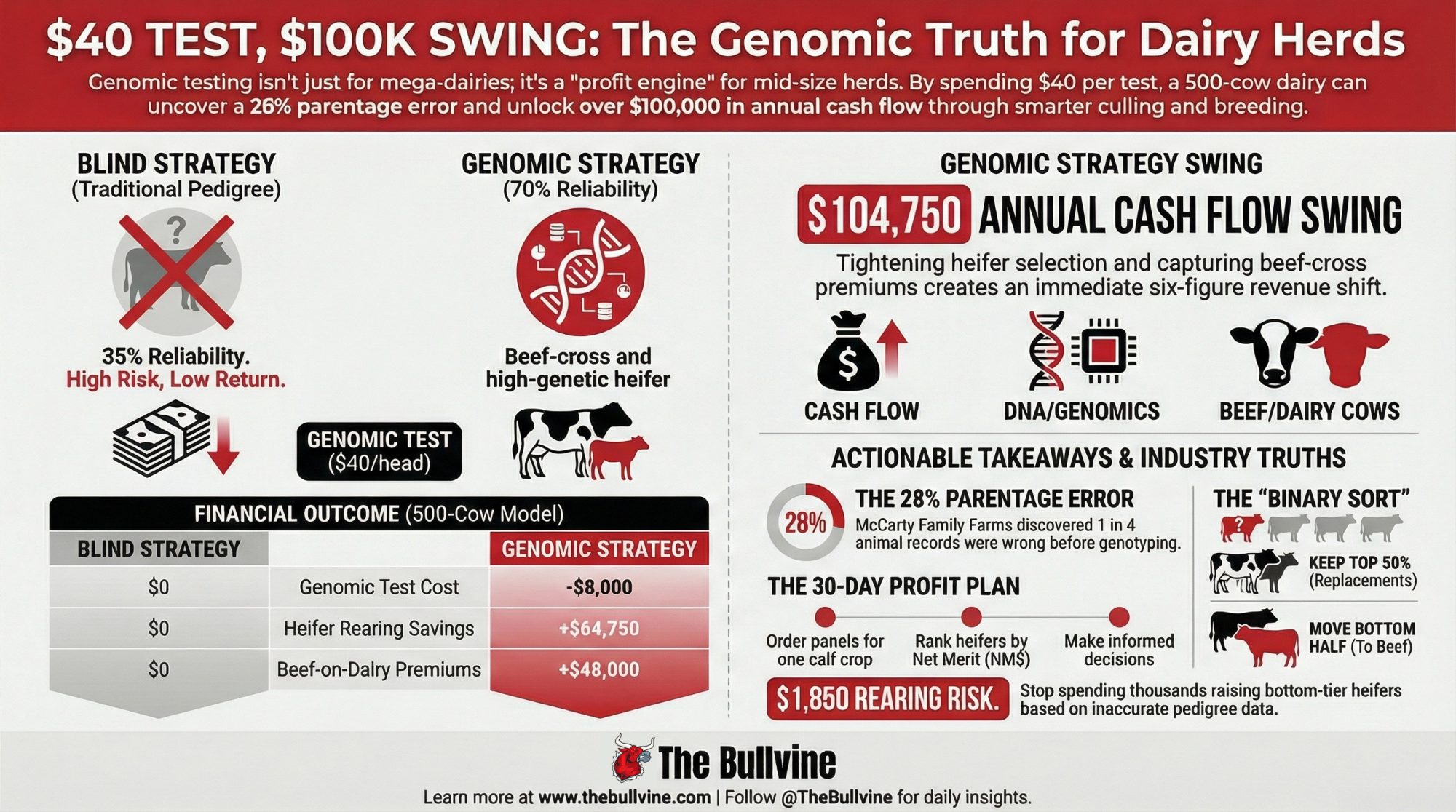

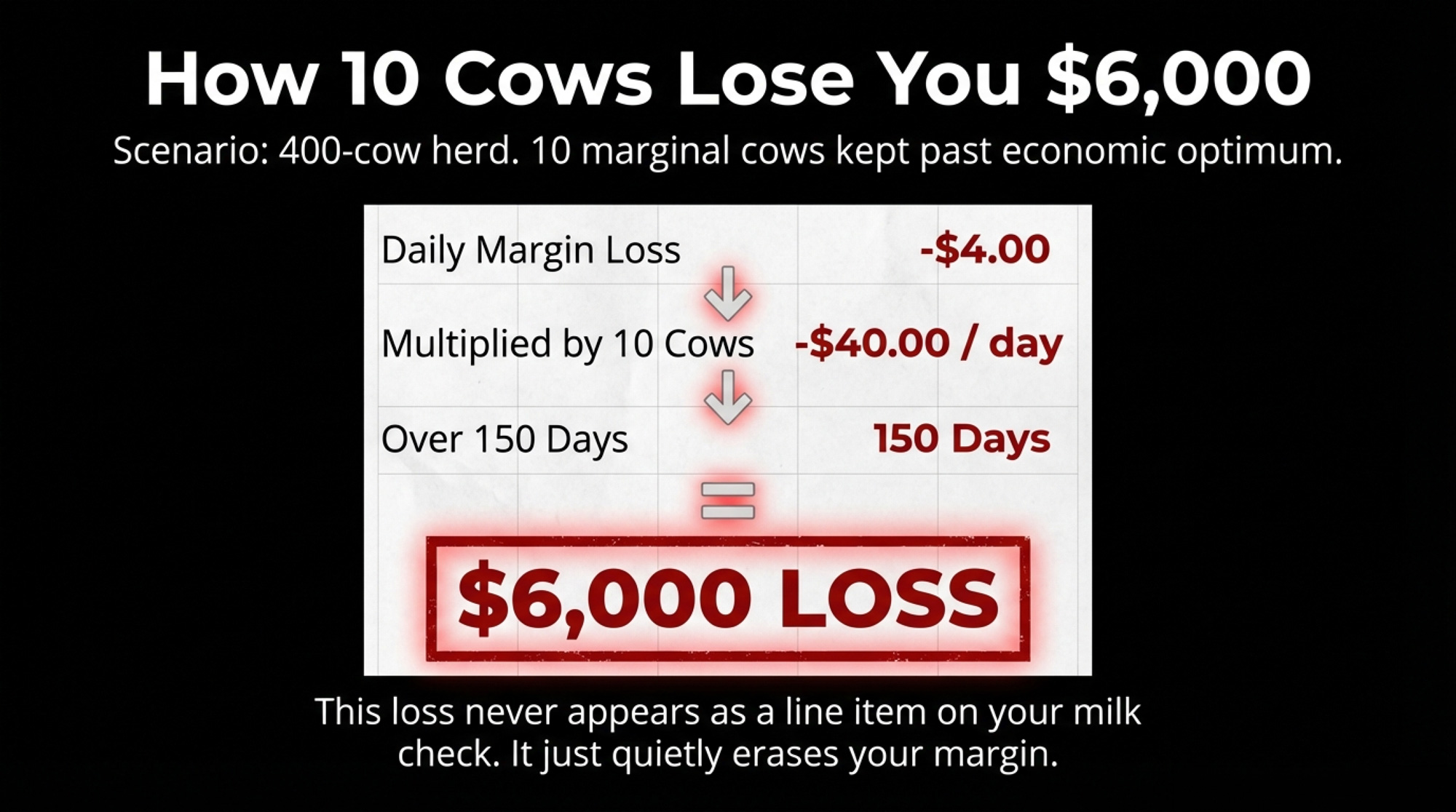

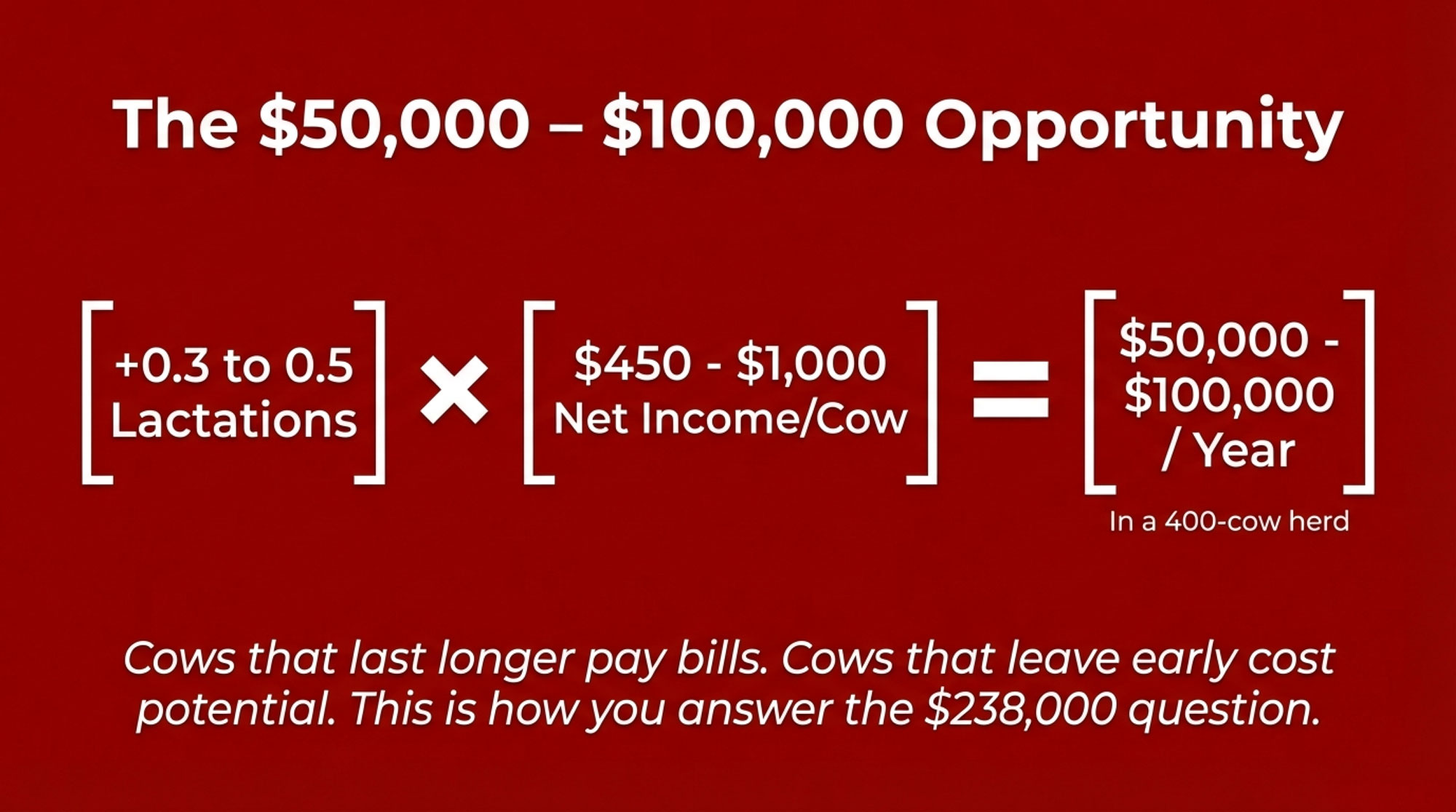

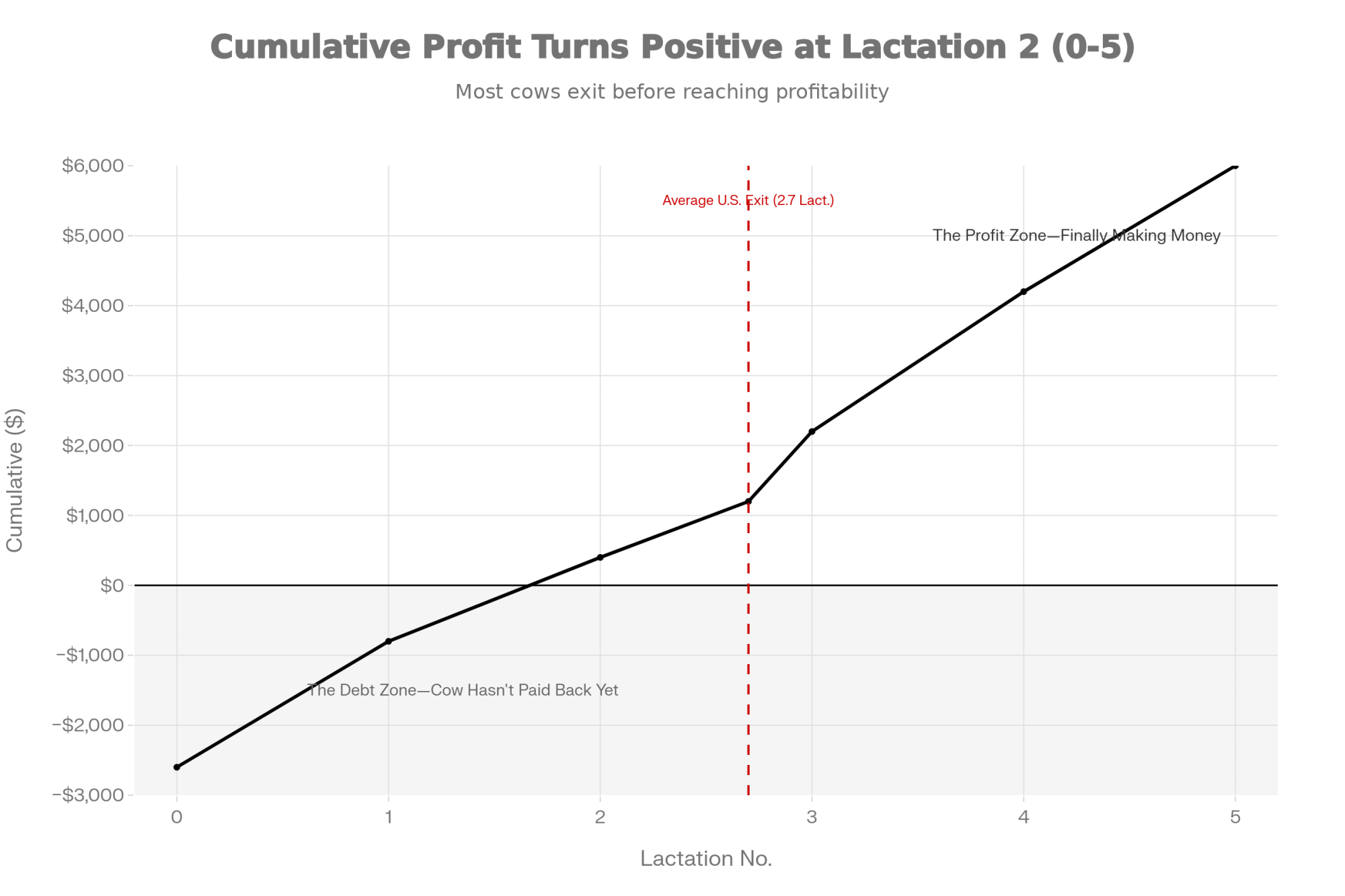

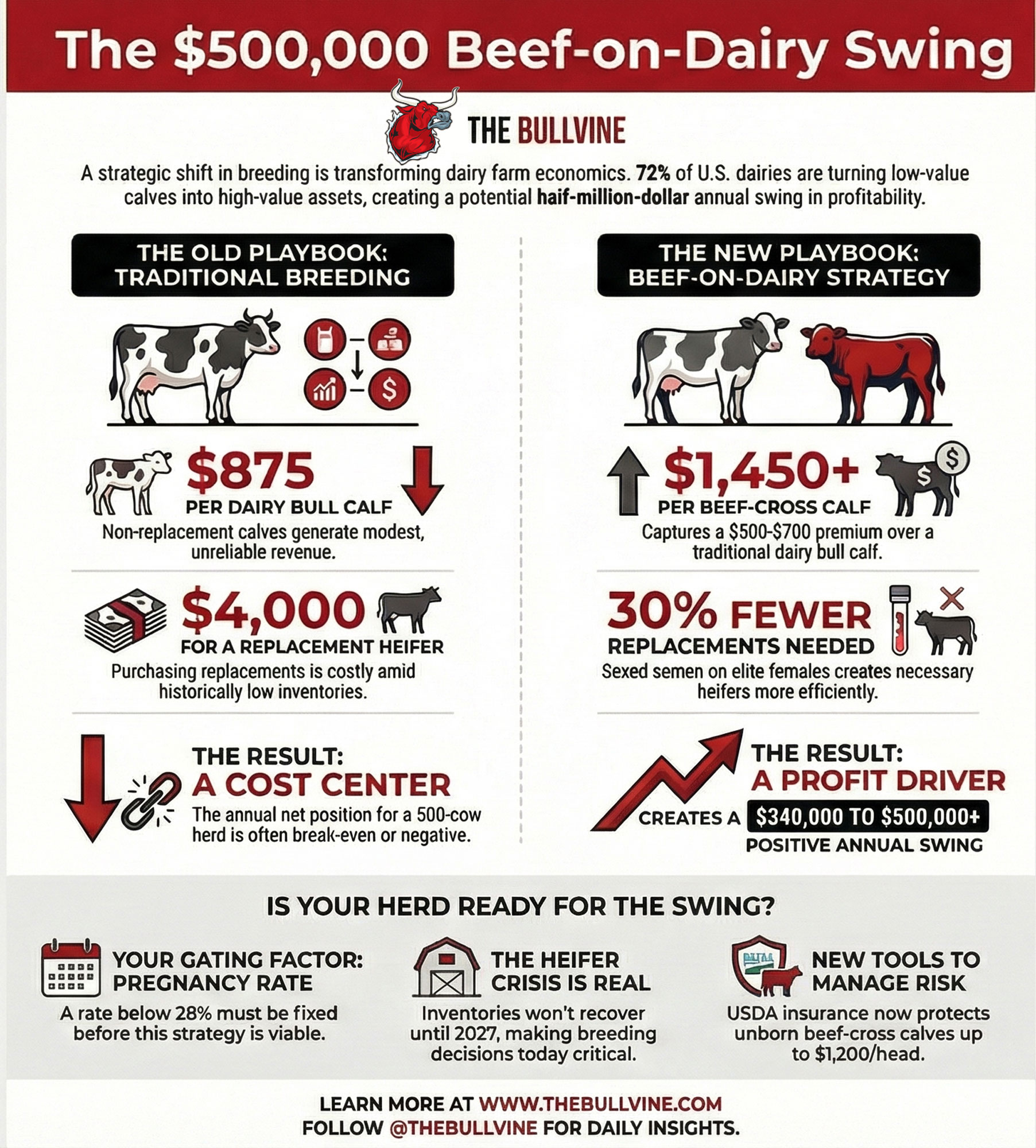

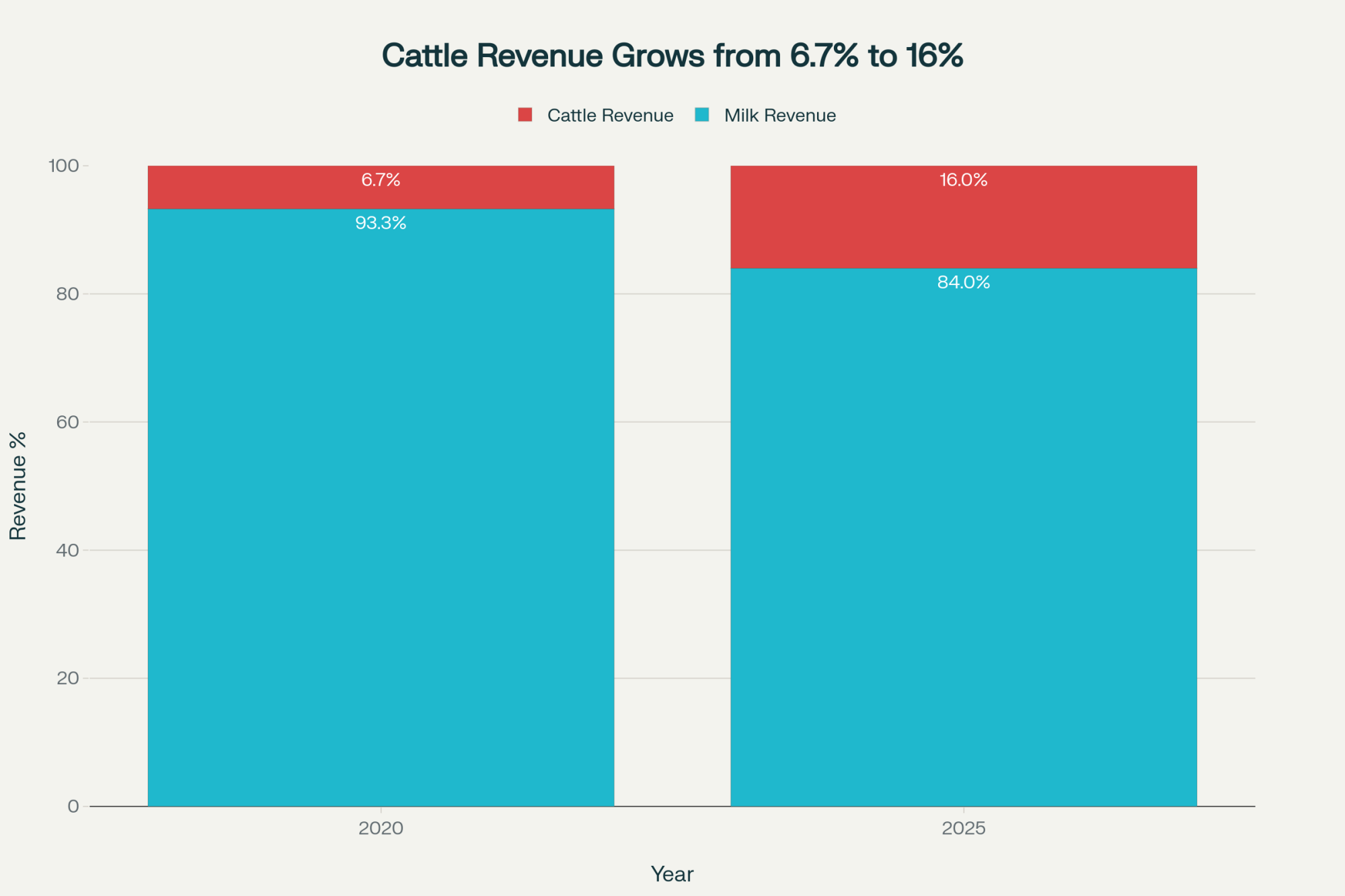

Overton showed how the math scales on a larger herd in that same HPDC talk. In one 2,500‑cow scenario from his presentation, he modeled using sexed dairy semen versus beef semen on the final 100 pregnancies. Once he included three‑year replacement costs, his model showed the sexed semen strategy generating about $216,000 more net value than the beef‑semen strategy on those same 100 pregnancies. Most of that difference came from not having to buy high‑priced springers into a market where $3,000‑plus per head isn’t rare.

The calf cheque from beef is visible right away. The springer cheque is delayed and much less fun to write. The arithmetic doesn’t care which one feels better.

| Decision | Beef-on-Dairy Pregnancy | Sexed Dairy Pregnancy | Difference |

|---|---|---|---|

| Immediate Calf Value | +$1,200 (beef calf) | +$750 (dairy heifer calf) | +$450 to beef |

| Heifer Raised | 0 | 1 @ $1,700 raising cost | -$1,700 to beef |

| Springer Purchased Later | -$3,200 | $0 | -$3,200 to beef |

| Net Present Value | -$2,000 | +$850 | -$2,850 net loss for beef |

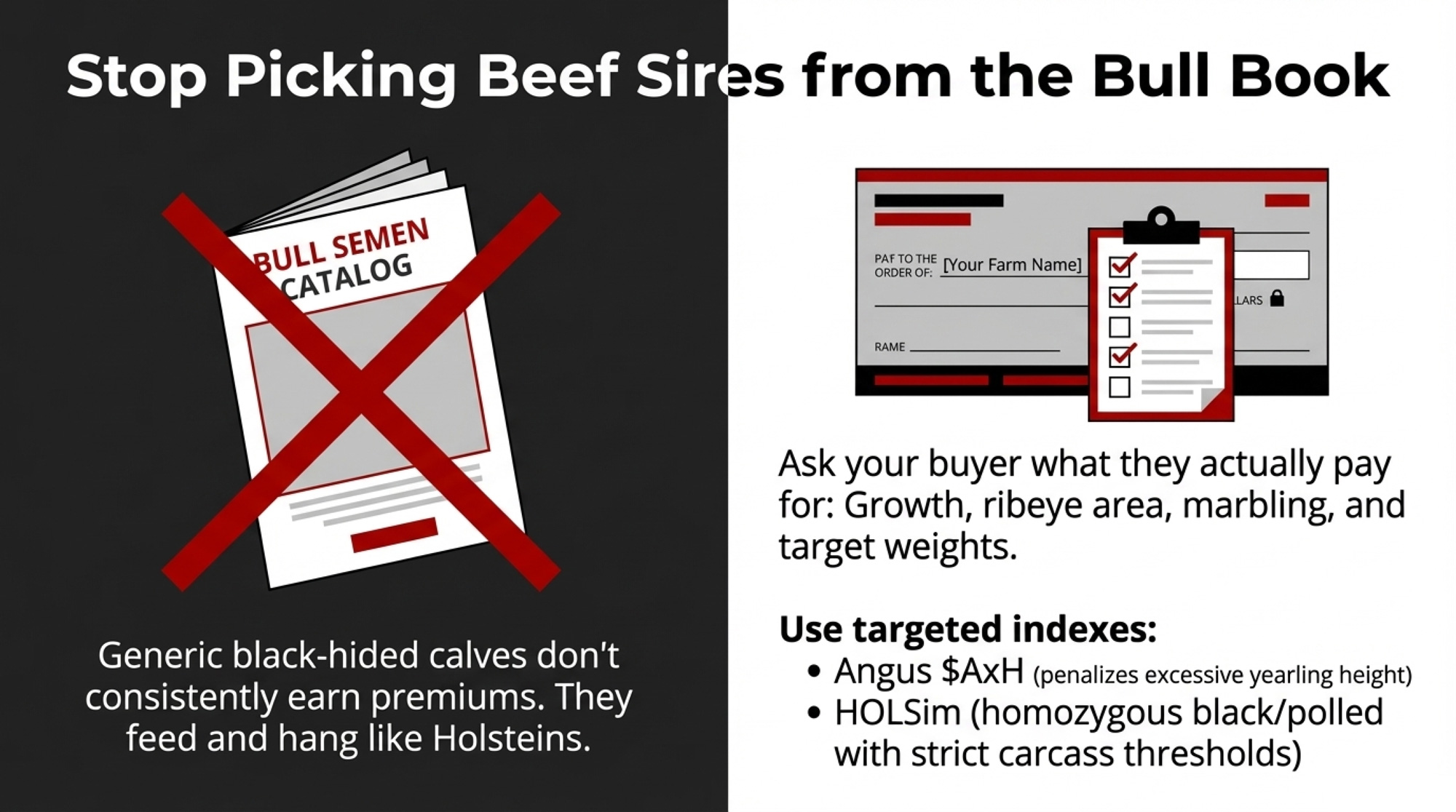

Are You Breeding for the Bull Book or the Buyer’s Cheque?

Once you’ve got a handle on how many pregnancies you can safely point at beef‑on‑dairy, the next question is uncomfortable and simple: are you picking beef bulls for your buyer, or for your semen catalog?

Plenty of herds still select beef semen on a mostly dairy‑centric checklist — calving ease, conception rate, semen price, and maybe coat color — instead of starting with the traits their calf buyer actually pays for. Meanwhile, calf buyers and feedlots are looking at a different checklist: calves that grow, hang a decent carcass, and are consistent enough they don’t need a spreadsheet to figure out what they’re feeding.

Extension and university work — including Kansas State’s analysis of Holstein and beef‑dairy cross calves in video auctions — shows that well‑bred beef‑on‑dairy calves often sell above straight Holstein steers on a per‑hundredweight basis, narrowing the gap to native‑beef calves in many sales. Generic black‑hided calves that still feed and hang like Holsteins don’t earn those premiums consistently.

Instead of guessing, start that conversation at the other end of the chain. Ask your buyer:

- What breed or breed type do you actually want on these calves — straight Angus, or are SimAngus/HOLSim crosses on the table if they’re black and muscled?

- Do you need predominantly black‑hided calves for your program?

- Are you insisting on polled calves?

- At what weight do you buy — day‑old, 250 pounds, 500 pounds, or heavier?

- Are you paying primarily on live weight, or is there carcass/grid feedback that matters?

Those answers translate directly into trait priorities on the sire side: growth and feed efficiency to hit target weights, muscling and ribeye area to avoid “dairy‑type” carcasses, marbling to hit Choice or better, moderate frame consistently, and the calving ease you need on Holstein or Jersey dams. Color and horn status become hard filters, not catalog fluff.

On the genetics side, two indexes do a lot of heavy lifting:

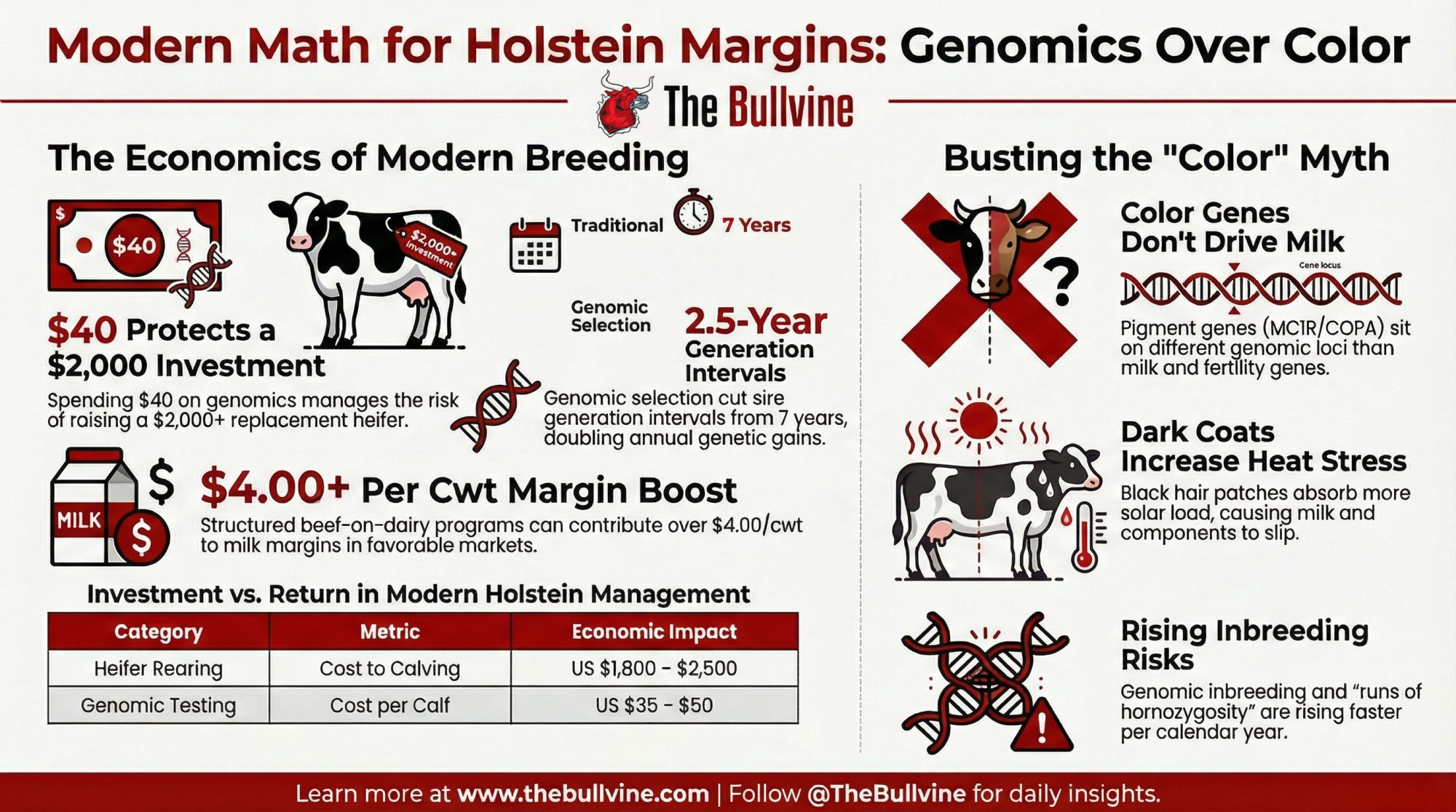

- The Angus $AxH index was developed specifically for Angus sires used on Holstein dams. It blends calving ease, growth, muscling, and marbling while penalizing excessive yearling height — directly addressing the carcass‑length and cut‑size issues common in straight Holstein steers. In one Angus Genetics Inc. summary from 2022, just 15 of 9,690 sires ranked over 150 on $AxH, which tells you how small the truly elite slice was at that point.

- The HOLSim program, a joint effort between Holstein Association USA and the American Simmental Association, launched in 2019 and designates SimAngus bulls that are homozygous black and homozygous polled and exceed a Holstein‑specific terminal index threshold, balancing calving ease and carcass traits. Eligible bulls must be SimAngus with a breed composition of 3/8 to 3/4 Simmental, with the balance Angus.

Beef semen used in dairy herds has often been cheaper on average than top‑end terminal options, as Dairy Herd and Progressive Dairy have both noted. The real question isn’t whether you can save a few dollars per straw. It’s whether the sires you’re using actually work for the person writing the cheque.

For many 200‑ to 1,000‑cow herds, the practical move isn’t a 20‑bull lineup. It’s a small, consistent group — often three to five sires — that rank well on $AxH or HOLSim and match your buyer’s spec sheet. And then the discipline to stick with them. No off‑list bulls go in the tank “just this once.” No “cleaning out the tank” by throwing calves into the pipeline, your buyer didn’t ask for.

- Don’t just take the cheque; demand the data. Ask for carcass or grid information back from your buyer, where possible. If your high‑index beef‑crosses aren’t consistently grading Choice or Prime, you’re giving away leverage on next year’s price discussion — and you won’t know it until you ask.

📖 Recommended Reading:

Overton’s heifer inventory deep‑dive — “A new perspective on right-sizing your heifer inventory.”

Can You Get the Beef-on-Dairy Benefit Without Fancy Tech?

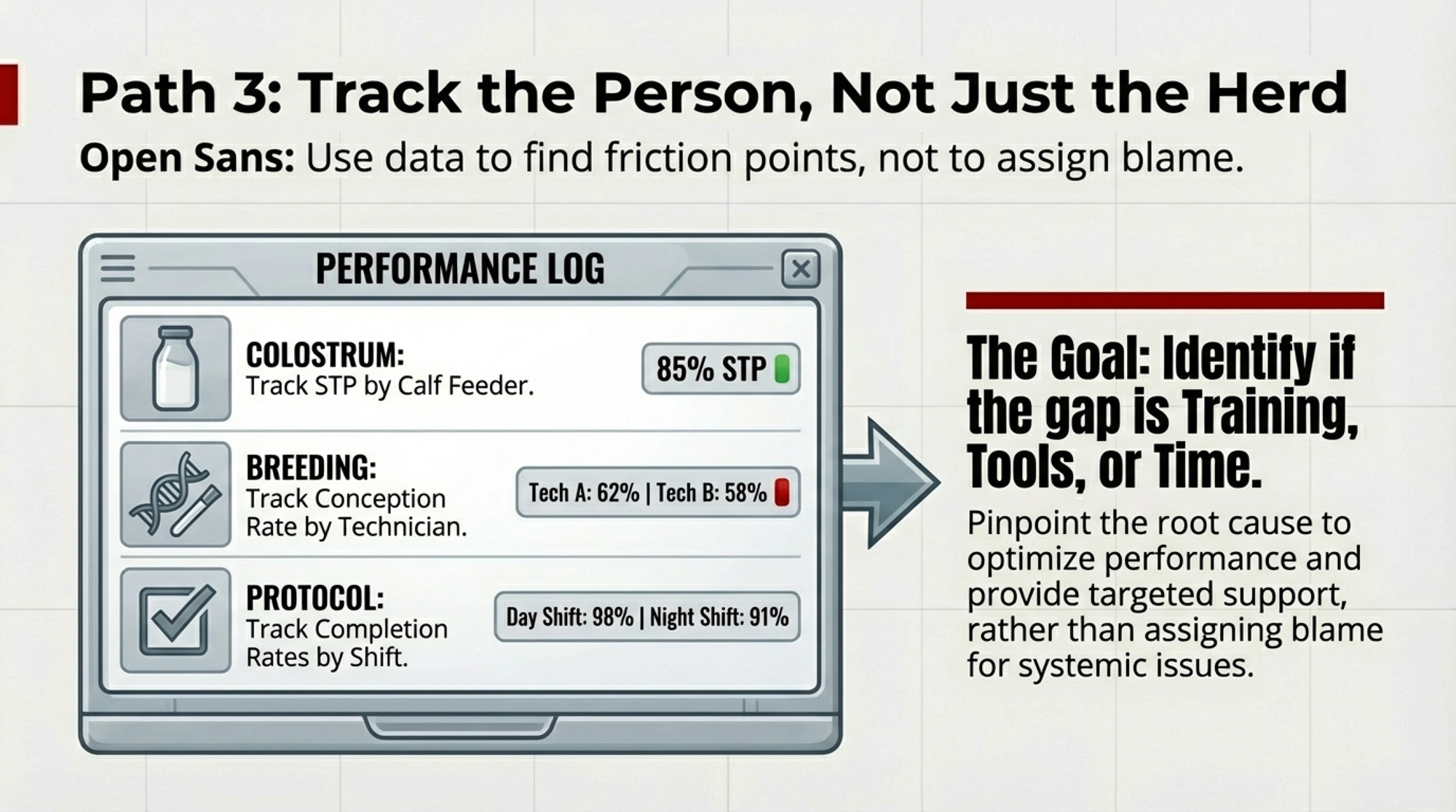

A lot of the breeding‑strategy case studies making the rounds right now feature fully integrated setups: automated sort gates, activity monitors feeding into DairyComp or BoviSync, cow‑level breeding reports, semen assignment protocols. If you’re there already, great.

Plenty of 200‑ to 800‑cow herds aren’t there yet. And they’re not going to install a six‑figure tech stack to straighten out beef usage.

You don’t need another app to remove most of the slop from your program. You do need a clear, written plan, a slightly smarter breeding sheet, and a ruthless 20 minutes once a week.

The minimum viable system looks something like this:

- Write a one‑page breeding policy and hang it where cows actually get bred. Define top, middle, and bottom tiers using your genomic or index ranking. In one line per tier, spell out which semen types are allowed on which services. Then list your DNB criteria in plain language — chronic mastitis, chronic lameness, multiple failed services, stale lactation, whatever fits your herd.

- Print a color‑coded cow list out of your genomic file or herd software. Sort by your chosen index (NM

, or a custom ranking), then tag green for top, yellow for middle, red for bottom. Put a dot or symbol next to the cows you already know should be DNB. Keep that list beside the breeding cards, not in the office drawer.

- Add one column to your breeding card or work list: “Tier + Allowed Semen.” When the tech goes to breed cow 4123, they don’t just see an ID. They see “green — sexed only” or “red — beef only.” If “Angus” gets written next to a green cow, that mismatch is easy to spot on Friday.

- Block 20 minutes once a week for a three‑count audit:

- Count how many beef straws went to green or yellow cows instead of red.

- Count how many services were sexed, conventional, and beef — and compare that mix to the replacement plan you just ran with your own numbers.

- Count how many cows marked as DNB on your list still got bred.

You won’t get a slick dashboard out of this. You will get a clear yes‑or‑no answer to a hard question: is your beef‑on‑dairy program being driven by your genetic and replacement plan, or by whoever happened to be standing in the parlor with an AI gun at 4 a.m.?

What This Means for Your Operation

Think of this as a set of reality checks, not a recap:

- Within 30 days, run the breeding‑card beef audit. Pick a recent week, highlight every beef mating, and cross‑check each cow against your genomic tier list and DNB list. If more than a third of your beef straws are landing on cows that aren’t truly bottom‑tier, it’s a sign the day‑to‑day realities in the parlor are quietly pulling the program off the plan.

- Calculate your own heifer completion rate instead of guessing. Take a recent calf crop, divide the number of heifers that actually calved in by the number of live heifer calves born in that group. If you’re near Overton’s ~79% average — or below — your safe beef‑on‑dairy percentage is tighter than it looks in your winter planning meeting.

- Run the backward pipeline math once a year. Start with herd size and actual replacement rate, add a small buffer, then work back through your real completion rate and sexed/conventional mix to find how many dairy pregnancies you need. Whatever’s left is your genuine beef ceiling. If your current beef percentage is higher than that, you’re pre‑loading a replacement deficit.

- Sit down with your calf buyer or integrator before your next semen order and get their specs in writing: breed, color, horn status, target weight, and how they pay. Build your beef sire list backward from that conversation using $AxH or HOLSim bulls that fit, instead of forward from whichever bull picture looks best in the catalog.

- Make the breeding sheet match your plan. If you’re asking staff to remember which cows get what semen type in their heads, you’re almost guaranteeing drift. The moment you write “green — sexed only” and “red — beef only” on the card, you’ve given people a fair chance to hit the target.

- Watch the opportunity cost, not just the calf cheque. In a market where replacement heifers can sell well above $3,000 per head, that extra $150–$200 on a beef‑cross calf can disappear fast if you later have to buy a heifer to replace the one you didn’t create. The gap is on the order of a couple of thousand dollars, not a rounding error.

Key Takeaways

- If you don’t know your own heifer completion rate, you’re guessing about how much beef‑on‑dairy your herd can afford — and Overton’s 85‑herd dataset suggests those guesses are often 10 points too optimistic.

- If your breeding cards and your genomic tier list don’t line up on where beef semen is actually going, you’ve got more of a beef‑on‑dairy storyline than a fully enforced strategy.

- If your beef sire lineup came from the bull book forward instead of from the buyer’s cheque backward, you’re likely leaving premiums on the table — especially if you aren’t tracking whether those calves are actually grading Choice or Prime once they reach the packer.

- If you can’t explain — in one hallway conversation — how many dairy pregnancies you need each year to protect your replacement pipeline, it’s a sign you don’t yet have full control over how beef‑on‑dairy fits into your herd.

The Bottom Line

The heifer shortage isn’t going to disappear this year or next. Beef‑on‑dairy isn’t going away either. On Monday morning, before you do anything else with the next semen delivery, grab last week’s breeding cards, a highlighter, and your genomic list — and find out whether your beef‑on‑dairy program is protecting your 2028 milking string or just making it more expensive to buy back later.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Beef-on-Dairy’s $6,215 Secret: Why 72% of Herds Are Playing It Wrong – Gain total control over your monthly margins with specific reproductive “guard rails” that separate top-tier earners from the rest. It delivers a clear Monday-morning blueprint for maximizing revenue by matching semen types to your pregnancy rate.

- 9.57 Million Cows, 3.9 Million Replacements: Genetics Built This Dairy Herd Paradox – and 2027 Ends It – Protect your 2028 milking string by exposing the structural reset of the heifer market and the price cliff ahead. It reveals how to position your operation now, recalculating culling math to avoid the $4,000 replacement trap.

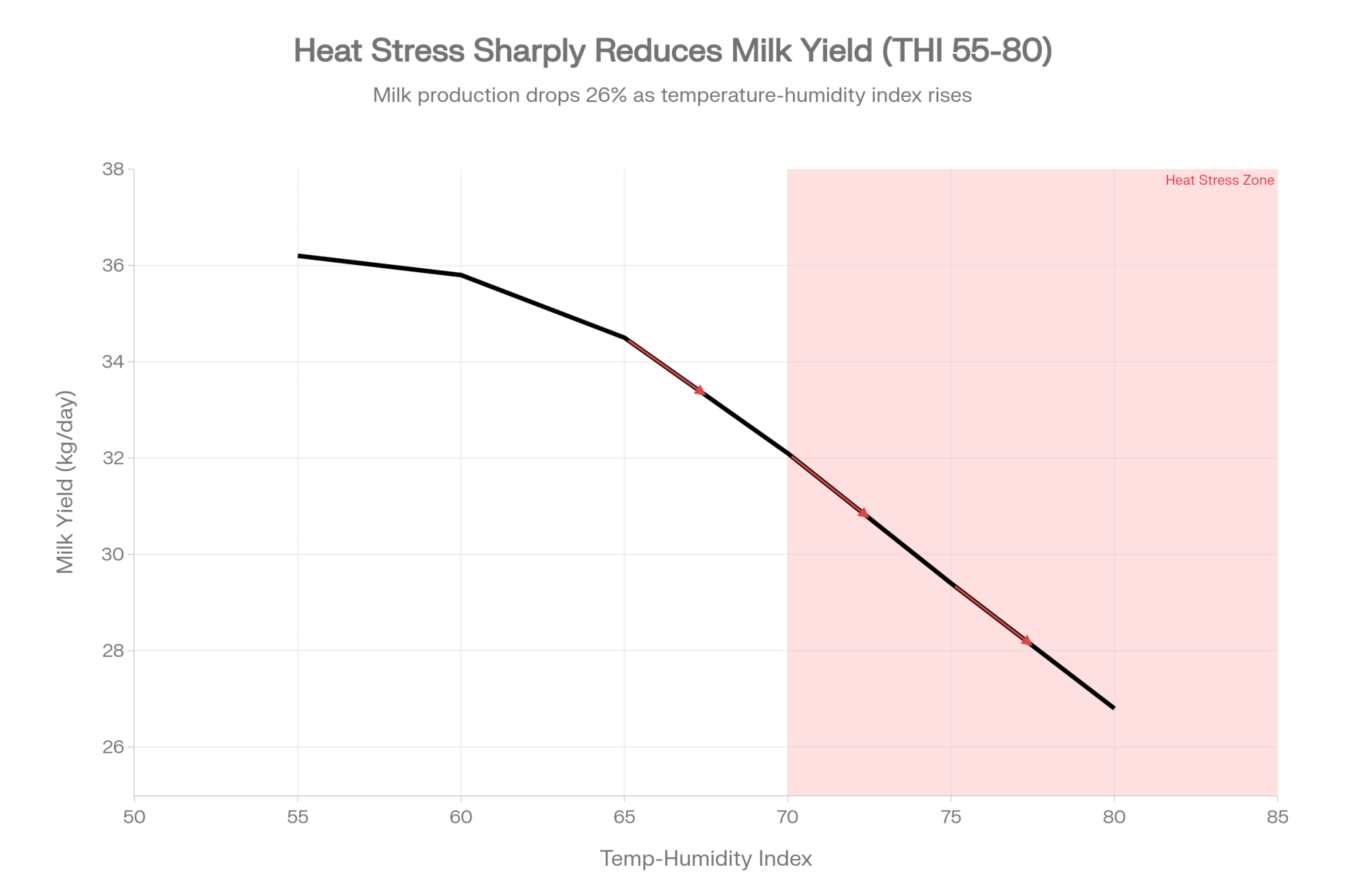

- Stop Breeding by Color: Genomics, Heat Stress and Beef-on-Dairy Math That Can Add Over $4/cwt to Holstein Margins – Capture an extra $4/cwt by replacing visual “eye” selection with hard genomic data. It breaks down the hidden connection between heat stress and coat color that current breeding strategies ignore, handing you a massive efficiency edge.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.