Do you think sticking to old breeding strategies will suffice in 2025? Think again.

You know when you’re casually chatting over coffee, and a fellow producer drops that a heifer just fetched $4,200? You choke on your sip, right? That’s how much the dairy breeding scene has flipped today.

The old rules — raise your replacements carefully, cull and churn, milk it out — well, those days are evolving fast.

Here’s the thing.

Across the U.S., replacement dairy inventories are at one of the lowest points seen in decades. We’re talking under 4 million head nationwide, a level not seen since the late 1970s. Prices? Replacement heifers are averaging north of $3,000—with the cream of the crop commanding $4,000 and more at major auctions.

Beef-on-dairy calves aren’t just side hustles anymore—they’re big money.

Premium values for those calves can top $1,000 per head in some regions.

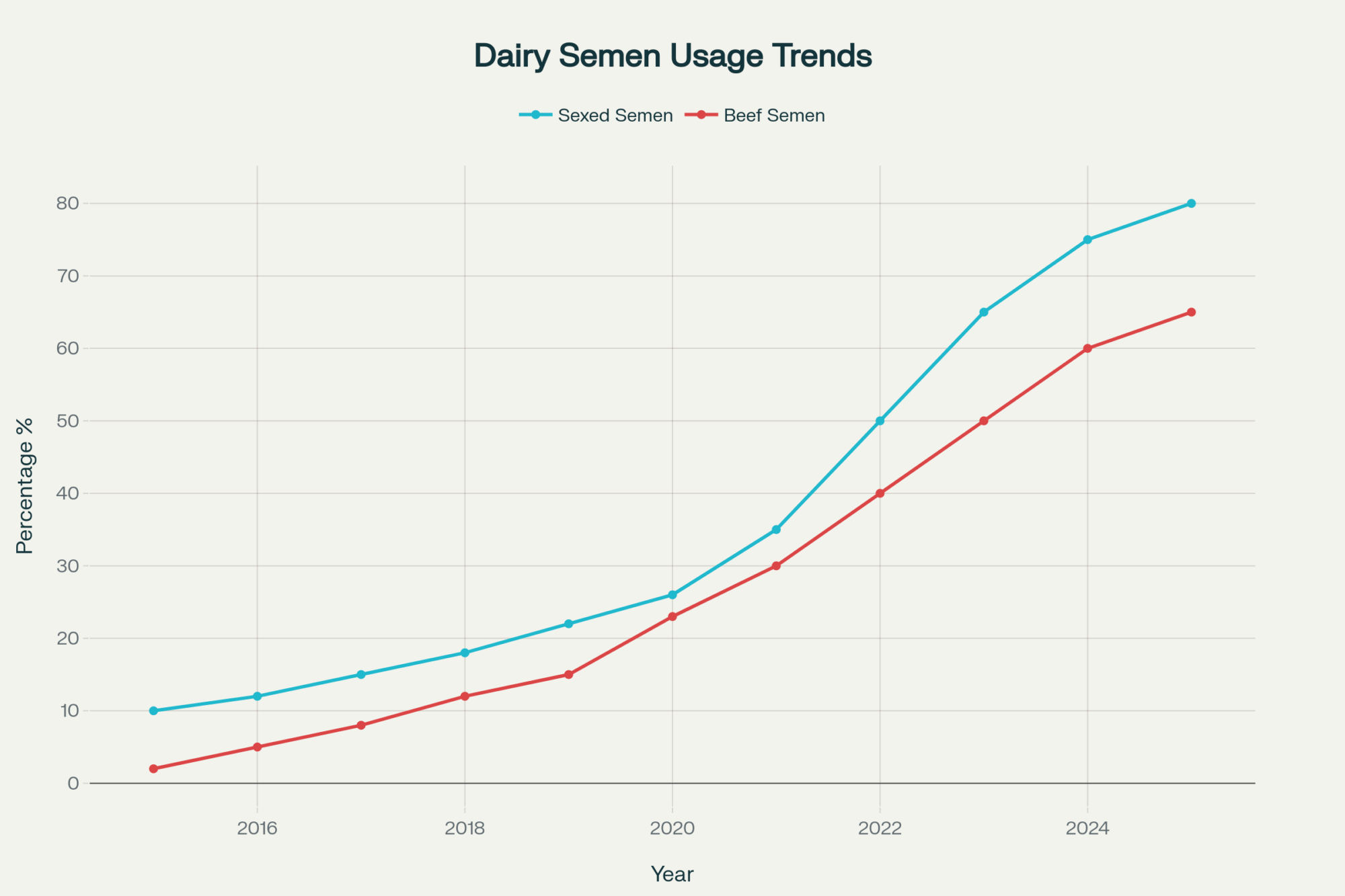

This all stems from a clever yet complex shift: farmers are using sexed semen more than ever to target female replacements among their elite cows, while sending the rest down the profitable beef path.

Sexed semen? It has come a long way, delivering conception rates that reach 80-90% of conventional fertility — typically landing around 45-50% in field conditions. Modern products are achieving gender accuracy rates of 90-97%, significantly higher than the previous standard of 85-90%.

Add in accessible genomic testing that identifies your best cows before breeding, and suddenly you’re precision-targeting your replacement queue while cashing in on beef demand.

But here’s the catch: It’s a balancing act. The more you push into beef, the fewer replacements you create. And when scarcity hits, prices climb.

So, where are folks heading with their breeding strategies?

Plan A: The Rotational Rhythm

Some operators are blocking out breeding cycles — a few months all dairy, then a stint all beef.

University of Wisconsin Extension trials documented impressive wins in calf health with this approach—’all-in, all-out’ nursery management slashed respiratory disease cases by 35%.

But it’s a rollercoaster on cash flow — you get big spikes and dry spells.

It’s tailor-made for places like Wisconsin and Minnesota, where seasonal labor patterns and feed costs make it a viable option. Down south? Trickier. University of Georgia research indicates that dairy cows face heat stress indexes exceeding 72 for extended summer periods, prompting operators to shift breeding windows to cooler months and invest heavily in cooling systems.

Plan B: Go Big with the Heifers

These operators put all their eggs in the surplus replacement basket. It’s potentially lucrative — think serious revenue streams — but the ride’s bumpy.

Industry observers report mixed results: profits soared during the hot streak, but operators felt the pinch when prices cooled off.

CoBank analysts warn this boom could bust—replacement inventories may bounce back by 2027 as more producers adjust breeding strategies.

The challenge? You’re betting big on market timing, and the University of Missouri Extension estimates that raising costs will be $2,640 per heifer from birth to freshening.

Plan C: The Genetic Leapfrog

Some farms are hitting pause on raising their own replacements, flooding calf sales with beef calves, all to buy in elite genetics.

It’s high-stakes — skipping years of gradual genetic gain in one purchase.

The risks? Disease introduction (the highest-risk activity for transmission) and today’s sky-high prices for elite animals often exceed the combined savings from beef calf sales and avoided raising costs.

The Quiet Game-Changer: Male-Sorted Semen

Here’s something most producers aren’t considering yet: male-sorted semen for precision market targeting.

University of Idaho research found all-steer loads earned $5,180-6,746 more per truckload than mixed-sex groups—serious money if you’ve got the right marketing channels.

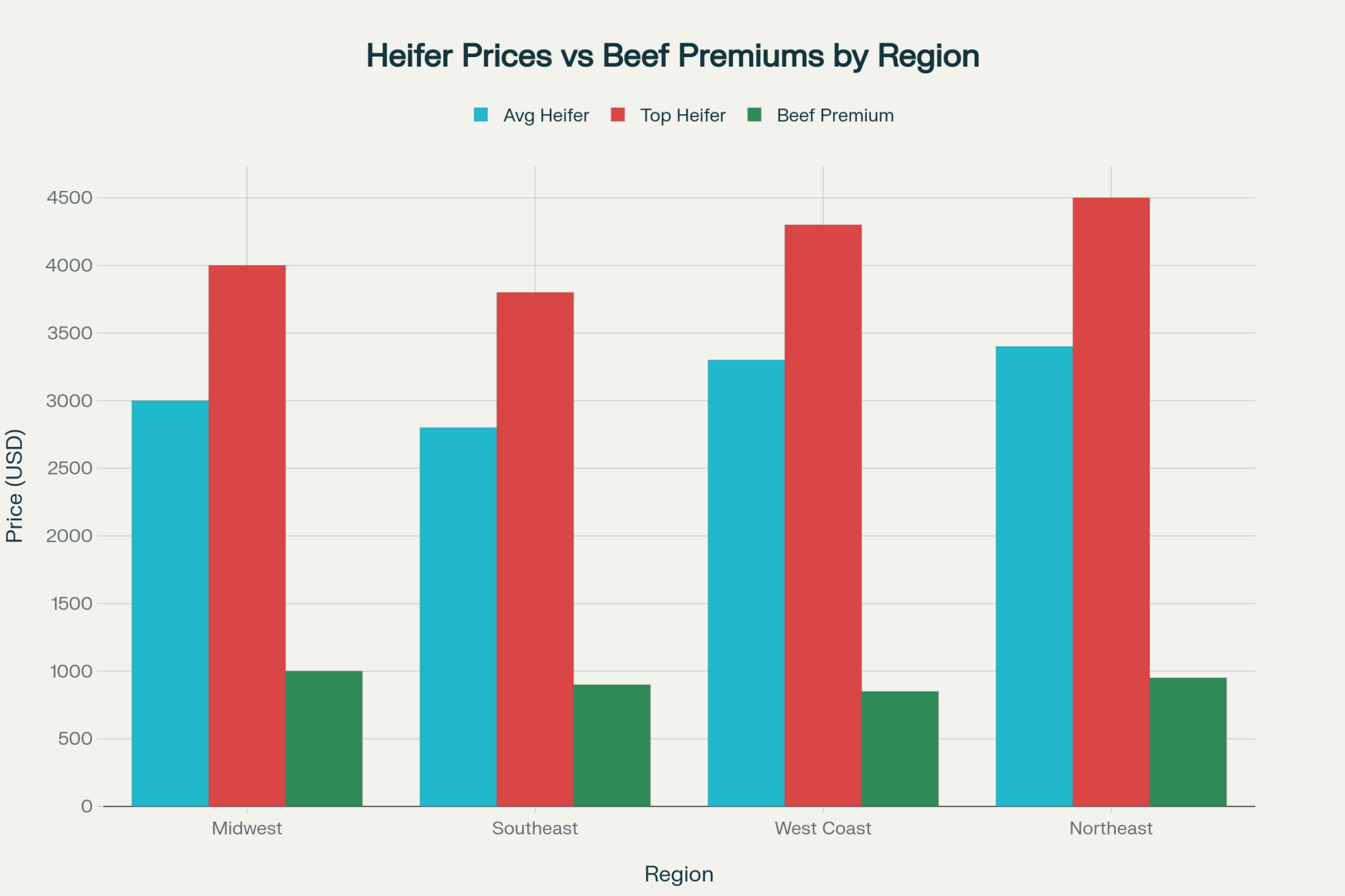

The Map Matters

Success depends heavily on location:

Upper Midwest: Feed costs run 8-12% below the national average, and seasonal labor patterns fit rotational breeding naturally. Perfect territory for batch approaches.

Southeast: Heat stress management becomes critical. Operations are installing high-volume fans, adding shade structures, and shifting feed timing to cooler hours.

West Coast: California wages average $20.48/hour, compared to $19.11 nationally. High labor costs push toward automation, but proximity to premium markets creates opportunities.

Northeast: Smaller herds require flexibility, but proximity to high-value markets is beneficial. High-quality animals fetch $ 4,500 or more at regional sales.

Counting the Real Costs

Let’s talk dollars, because that’s where strategy meets reality.

Most operators know growing an animal from calf to first-calf heifer soaks up around $2,500—and that’s with tight management on feed, housing, and health.

Your financial picture for a 100-cow operation looks roughly like this:

- A rotational approach requires approximately $ 100,000 or more upfront to grow heifer batches while pursuing beef payouts.

- A surplus heifer strategy involves investing substantial capital in raising additional animals, relying on market timing to maximize returns.

- Genetic leapfrog concentrates cash on buying elite quality but risks price volatility.

One market swing and your calculations change completely.

Note: These figures represent direct costs related to calf and replacement management—separate from milk revenue and other farm expenses.

What This Really Means

Look, it’s no longer simple.

The smart operator balances short-term cash from beef, long-term genetic progress, and risk tolerance — then adjusts based on what actually works in their situation.

Because the days of just milking cows and raising calves are long gone.

The producers who master this complexity? They’re positioning for years of competitive advantage.

We’re witnessing a fundamental shift from commodity milk production to strategic genetic and market portfolio management.

So what’s your play? Testing rotational breeding? Banking on the heifer market? Or planning a genetic upgrade?

Drop your thoughts below — let’s turn coffee-shop talk into real-world strategies.

KEY TAKEAWAYS

- Leverage sexed semen with nearly 90% reliability to craft premium heifers and capitalize on beef-on-dairy premiums up to $1,000 per calf – start genomic testing your herd this month to identify breeding targets.

- Adopt rotational breeding for disease control, reducing respiratory illnesses by 35% while managing cash flow fluctuations. Perfect for Midwest operations with seasonal labor patterns.

- Explore the strategic purchase of elite heifers with an eye on the 2025 market’s high prices and risks – it’s a significant upfront cost, but can potentially leapfrog genetics by 5-10 years in one purchase.

- Don’t underestimate genomic testing – knowing your cows’ genetics sharpens breeding decisions and improves herd profitability. With replacement costs exceeding $ 2,500 per heifer, precision pays.

- Tailor your strategy by region: Northern states are well-suited for batch breeding approaches, while southern dairies require heat mitigation and adapted scheduling to avoid summer calving disasters.

EXECUTIVE SUMMARY

This isn’t your grandpa’s dairy breeding anymore. Dairy replacement inventory in the U.S. hit a 40-year low, and with fewer heifer calves born, prices soared past $3,000 – topping $4,000 in hotspots. Meanwhile, beef-on-dairy calves pull premiums up to $1,000 each, turning genetics and breeding choices into your new profit center. Tech like sexed semen now reliably produces female replacements, while beef semen turns the rest into gold. And with genomic testing, you can zero in on your best cows. This trend shakes up your bottom line and offers clever producers a new road to boost profitability – now’s the time to explore and adapt.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More:

- Beef on Dairy in 2025: Turning Calf Premiums into Real Profit Without Blowing Up Your Herd – This article moves from “why” to “how,” offering practical strategies for selecting the right beef sires and managing crossbred calves to maximize premiums. It reveals methods for turning a market trend into a consistent, high-value revenue stream on your operation.

- Boost Your Dairy Farm’s Health: Vital Ratios for Financial Fitness and Growth – Before changing your breeding strategy, you need to know your numbers. This piece reveals the key financial ratios you must track to manage the significant cash flow shifts and investment risks discussed in the main article, ensuring profitability through the market cycle.

- The Genomic Revolution: How Next-Gen Breeding is Creating Super Cows – Go deeper than just “breed the best.” This piece explores how to leverage genomic data to accelerate genetic gain and create more profitable, efficient cows. It reveals advanced methods for using technology to build a herd that thrives in the modern economy.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.