A May 2026 federal plan rebranded a pesticide-heavy crop as the “natural choice.” Real milk fits the Make America Healthy Again script better — and the window to say so closes on a competitor’s product decision, not an election.

Executive Summary: Cotton just pulled off the play dairy’s been sitting on: on May 28, USDA’s Rollins and RFK Jr. rebranded a crop tied to roughly 17.5% of world insecticide sales as the MAHA “natural choice,” while real milk — a genuine single-ingredient product — stays silent as plant-based holds about 13% of retail milk dollars. MAHA’s whole frame flipped the question from “how much fat?” to “how processed is this?” and the 2025–2030 Dietary Guidelines now back dairy at every fat level — so your product finally wins on the merits, if anyone says so. The clock isn’t the next election; it’s the morning a major oat brand hits four clean ingredients and claims “minimally processed” first, which they’re already racing toward. This reaches your check whether you ship fluid or cheese: Class I revenue pools across all classes, so a quarter-a-cwt category shift is roughly $5,800 a year on a 250-cow string and about $1,850 on an 80-cow herd. The uncomfortable part — your 15¢/cwt checkoff funds broad “Dairy Does More” advertising, not the raw-milk contrast, partly because co-ops that also process make their margin on value-added lines, not commodity fluid. Read the full piece for the two barn-math scenarios, the ultra-processed trap that snags flavored milk and cheese slices too, and the 30-day question to put to your co-op rep this month.

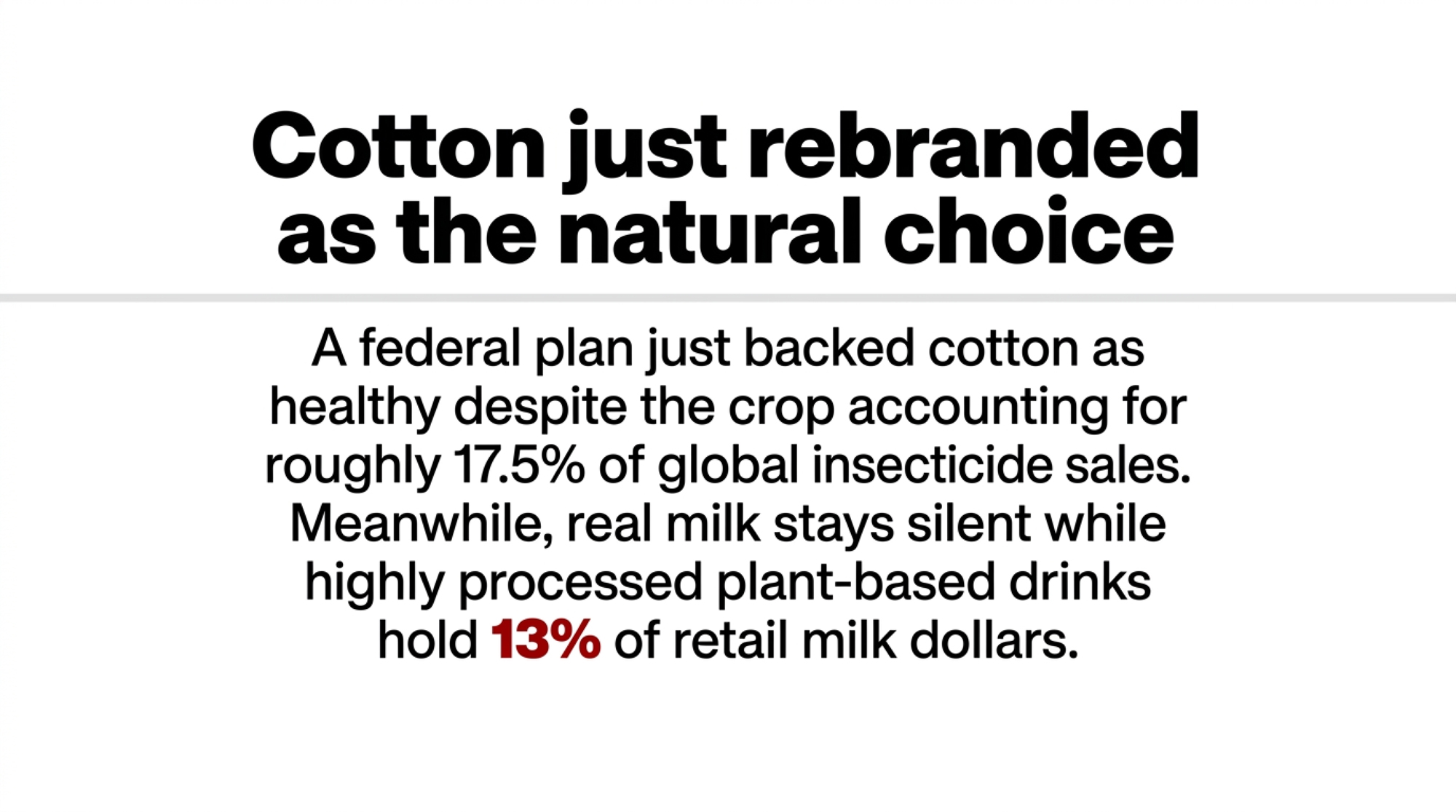

On May 28, 2026, USDA Secretary Brooke Rollins stood at a farm near Marana, Arizona, and launched the Great American Cotton Plan — a federal push to swap synthetic fabrics for American-grown cotton. Within hours, Health Secretary Robert F. Kennedy Jr. backed it under the campaign’s own banner: plant, not plastic. Just like that, a crop that a 2012 international survey tied to roughly 17.5% of global insecticide sales was rebranded as the healthy, natural, American choice within the MAHA movement.

Now go look at your bulk tank. Real milk is about as close to a single-ingredient whole food as the dairy case sells. MAHA is openly hunting ultra-processed foods, added sugar, and industrial additives. Cotton had a credibility problem walking in. Dairy doesn’t — and dairy still hasn’t said a word.

That’s the gap worth your attention this month. Not because a slick campaign fixes your milk check overnight, but because someone’s about to decide what “natural” means in the milk aisle, and right now it isn’t you.

What’s Changing and Why

Picture a 250-cow operator in central Wisconsin — the kind of mid-size family dairy that ships to a regional cooperative and watched the whole-milk fight from the cheap seats. (See Editor’s Note: this operator is a disclosed composite, not a single named person.) Why would a farmer like that care about a federal health report? Because the rules of how the government talks about milk decide whether his product sits on the shelf as the healthy default or the old, fatty thing kids aren’t supposed to drink. When MAHA reclassifies what counts as “natural” and “ultra-processed,” it’s not Washington noise — it’s the framing that follows his milk all the way to the carton. That’s the bridge between his barn and the briefing room.

MAHA stopped being a wellness slogan and turned into policy you can point to. The White House published a MAHA assessment report in May 2025 and a strategy report that September, both pinning chronic disease on the “dramatic shift toward ultra-processed foods”. The 2025–2030 Dietary Guidelines followed, and for the first time in decades, federal guidance now backs dairy at every fat level — whole milk, cheese, butter.

That shift is already law in the one place that moves volume on autopilot: the school cafeteria. President Trump signed the Whole Milk for Healthy Kids Act on January 14, 2026, putting whole and 2% milk back on school menus. The bill cleared the Senate in November 2025, passed the House overwhelmingly, and went to the President’s desk as S. 222 — Public Law 119-69.

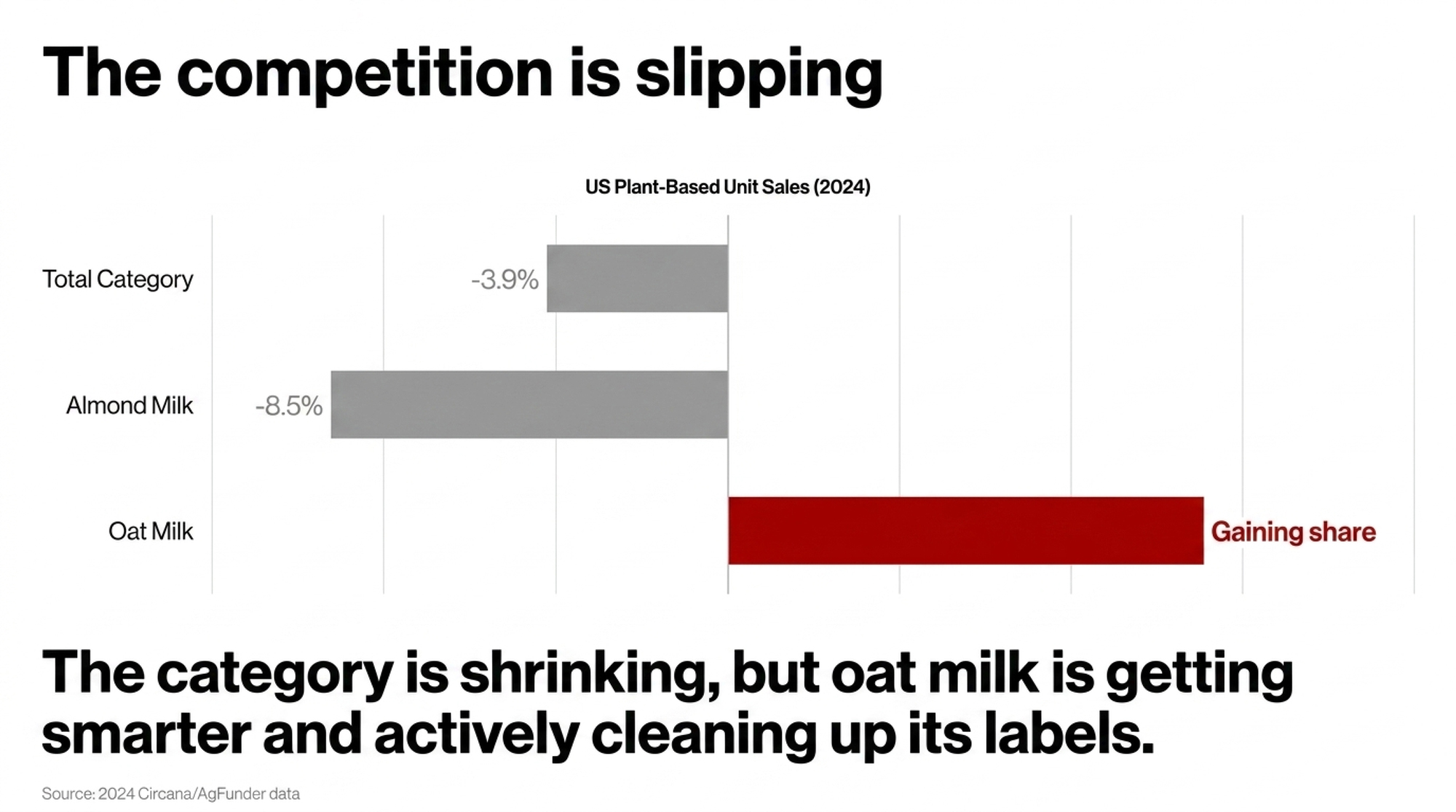

And the competition is slipping. Plant-based dairy lost ground in 2024 — Circana data show US plant-based dollar sales down 2.8% and unit sales down 3.9% that year. SPINS and DairyReporter data point to a chunk of plant-based buyers drifting back to the dairy case. The wind’s at your back, which is exactly what makes the silence so strange.

What Counts as “Natural” Just Became a Federal Question

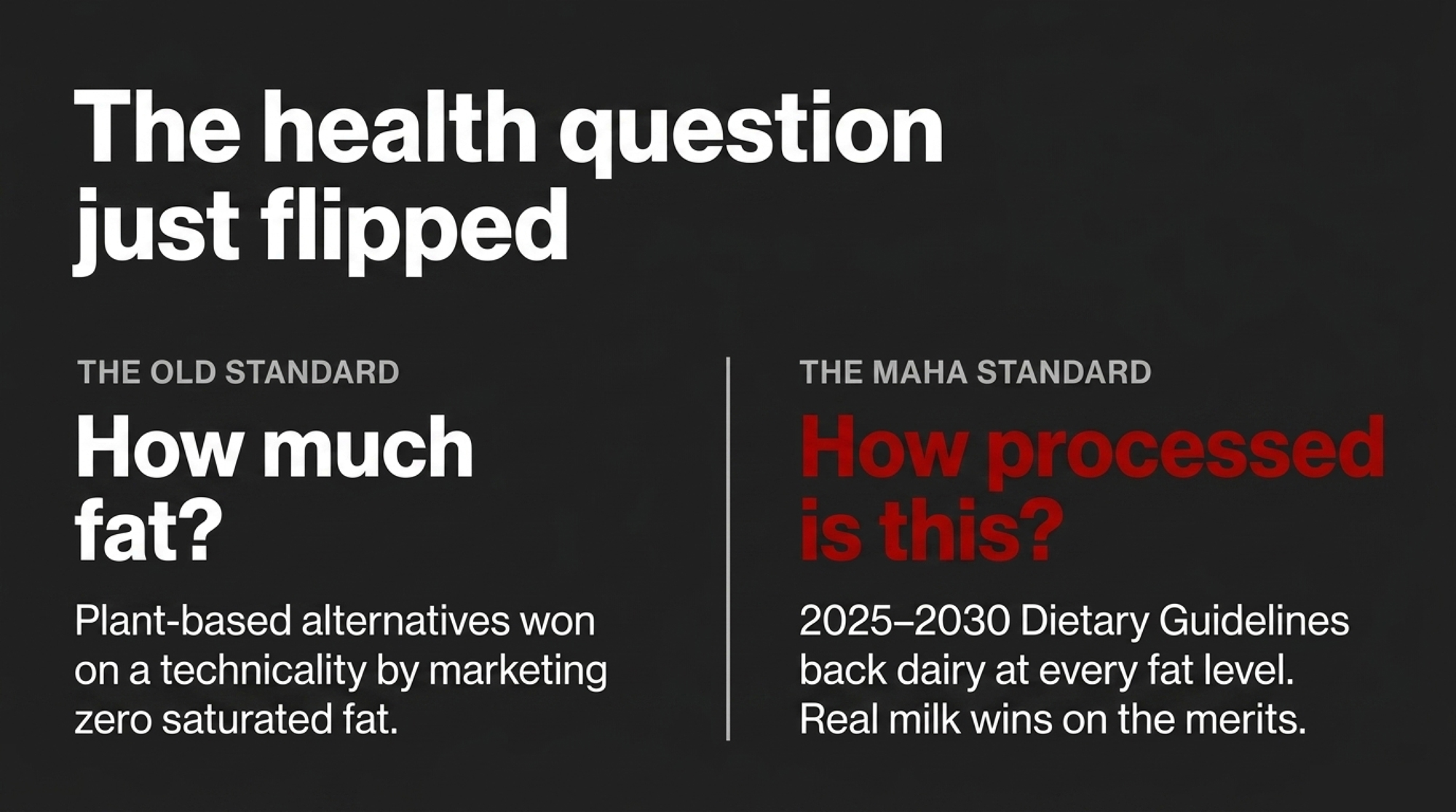

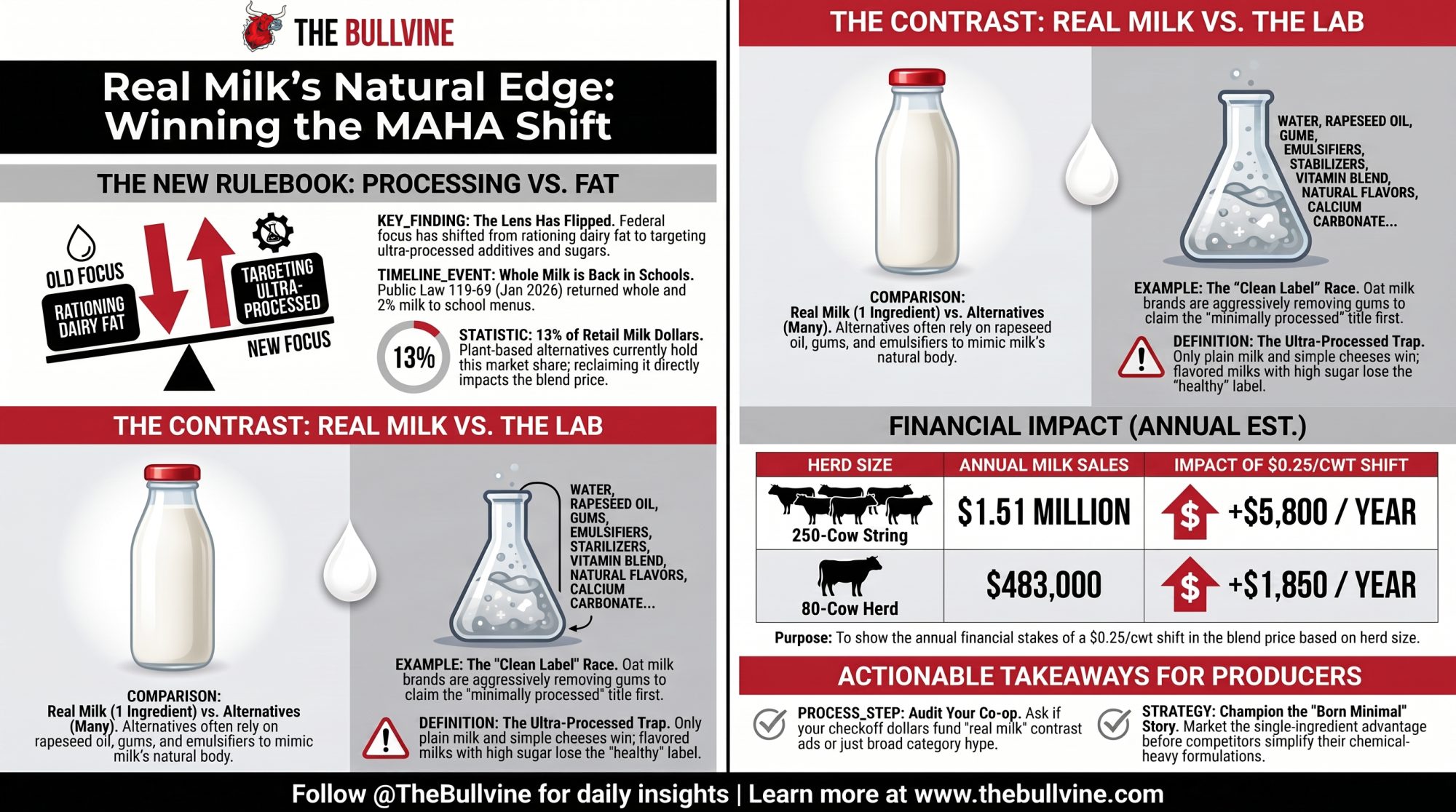

Here’s the shift that matters under your feet. For most of the last fifteen years, federal nutrition policy treated dairy fat as something to ration — low-fat and fat-free only in schools — and saturated fat as the enemy on every guideline chart. That framing built the entire health case for plant-based alternatives, which got to wave a “no saturated fat, no cholesterol” flag at shoppers who’d been told for a decade that’s what mattered.

MAHA flipped the lens. The movement’s whole organizing idea is that the bigger health problem isn’t fat — it’s processing, additives, and added sugar. Once you accept that frame, the scoreboard changes. The 2025–2030 Dietary Guidelines now back dairy at every fat level, including whole milk. So the thing that used to be milk’s liability — fat — stops being the conversation, and the thing that’s always been milk’s quiet strength — a short, recognizable ingredient list — moves to center stage. That’s not a marketing tweak. That’s the federal government changing which question gets asked at the shelf.

When the question is “how much fat?”, plant-based wins on a technicality. When the question is “how processed is this?”, real milk wins on the merits. Dairy didn’t engineer that shift. MAHA handed it over. The only thing left to do is say it out loud — and that’s the part nobody’s doing.

How Cotton Pulled It Off — And Why Dairy Hasn’t

Here’s the part dairy keeps missing: cotton didn’t win on merit. It won on contrast. The crop handed MAHA a villain — plastic microfibers — and a three-word bumper sticker, “Plant Not Plastic”. Nobody made cotton answer for its chemical record, because the White House had already pledged to back off a pesticide crackdown after farm-group pushback and aim its energy at ultra-processed food instead. And the pesticide numbers themselves are contested — that 17.5% figure is cotton’s share of insecticide sales specifically, while the cotton industry’s own fact-checkers argue it’s under 5% of all pesticide sales. Cotton didn’t win that argument. It just changed the subject.

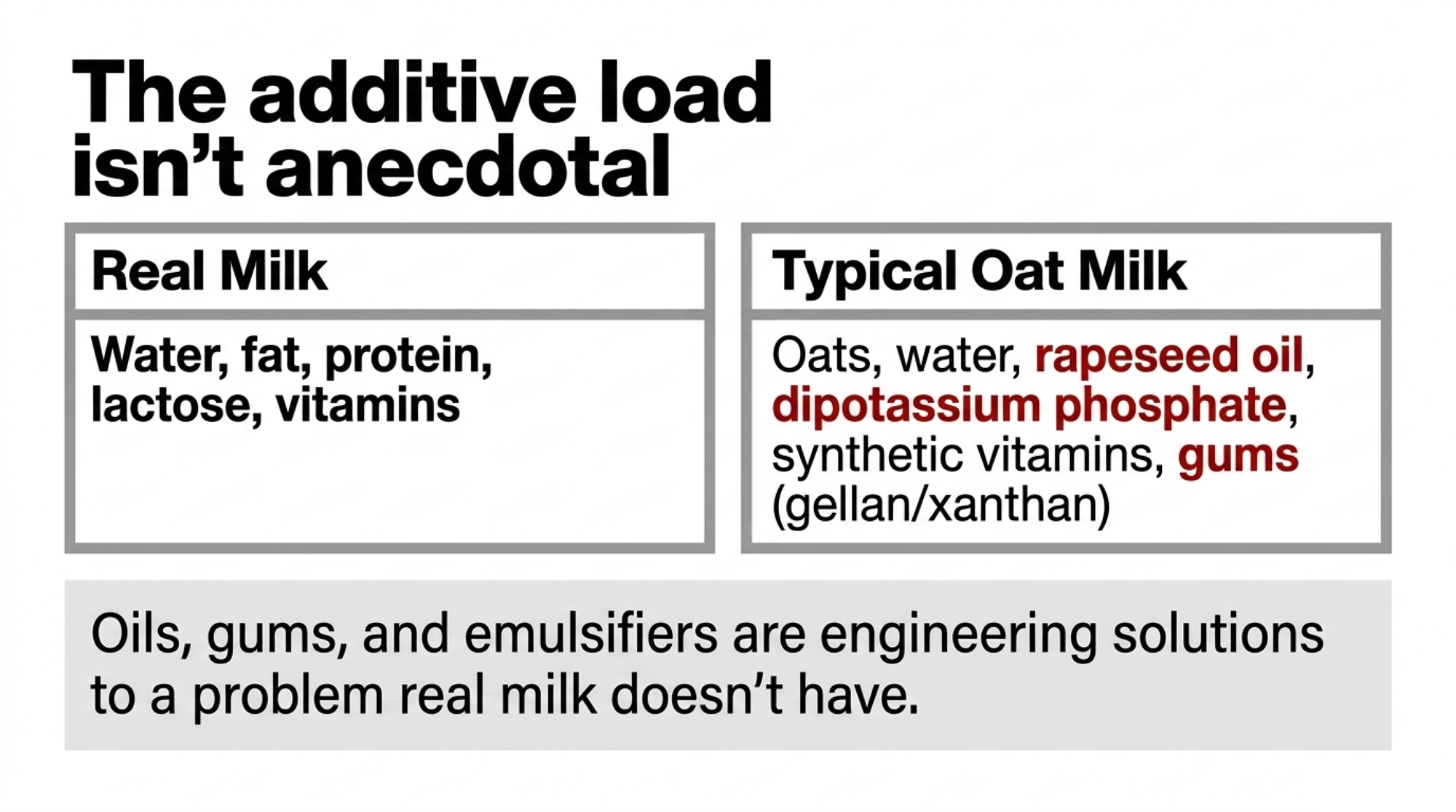

Dairy’s contrast is sitting right there in the carton. Pour a glass of milk: water, fat, protein, lactose, plus the vitamins and minerals that come with it. Pour a typical oat milk and read the back: oats, water, then rapeseed oil, dipotassium phosphate, added calcium, synthetic vitamins, and often a gum like gellan or xanthan to keep it from separating.

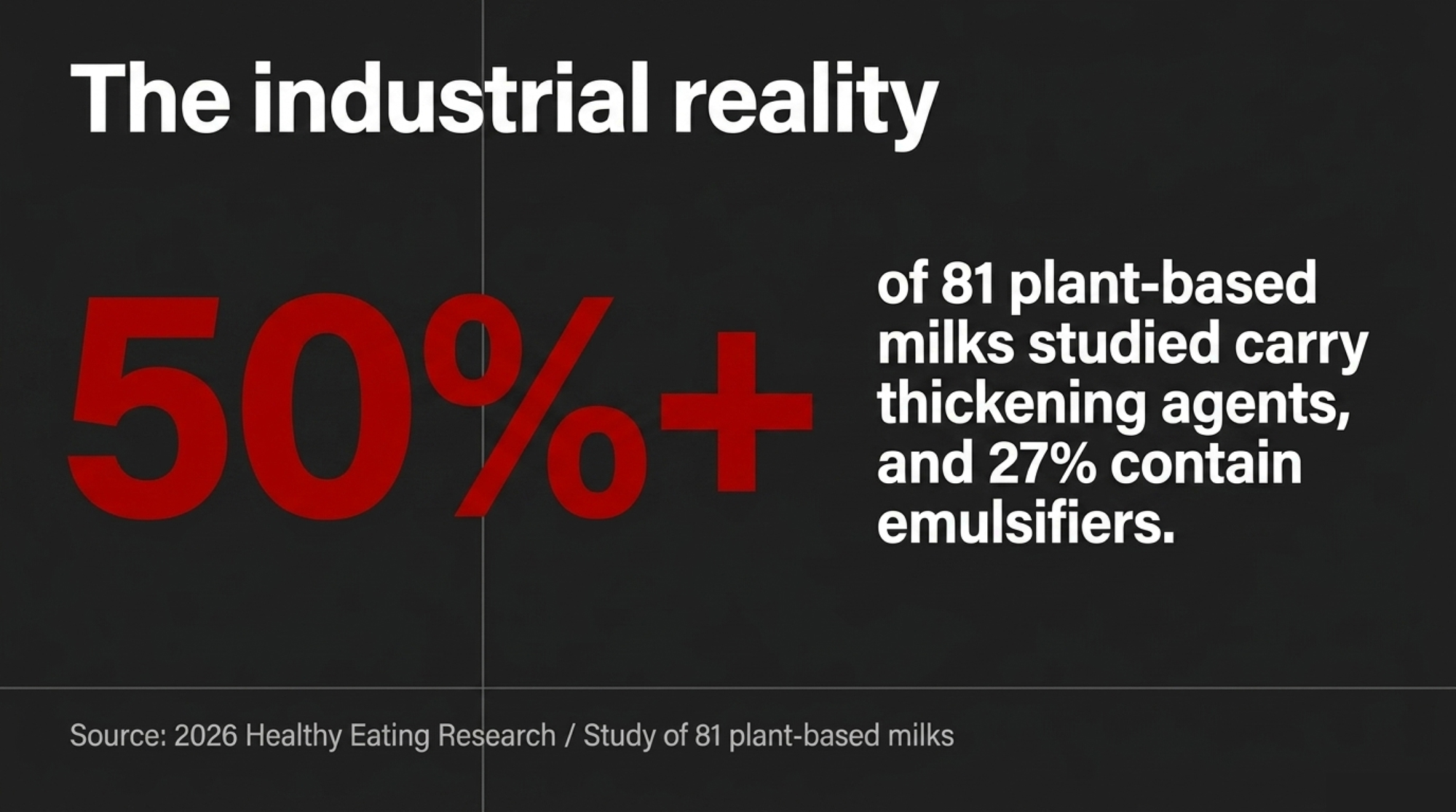

The additive load isn’t anecdotal, either. A study of 81 plant-based milks found more than half carried thickening agents and 27% contained emulsifiers — the exact class of industrial ingredients the MAHA expert panels are flagging. These aren’t there by accident. Oil, gums, and emulsifiers do the work that fat and protein do naturally in real milk: keep the product from separating, give it body in coffee, and stop it from sliding to water at the bottom of the carton. They’re engineering solutions to a problem milk doesn’t have.

The opening isn’t theoretical, either. When Trump signed the whole-milk law in January, AgProud reported it “sparked excitement among many dairy producers and industry leaders,” tying it straight to the broader MAHA push. So the appetite’s there. What’s missing is anyone connecting that win to the bigger contrast cotton just exploited.

How This Plays Out on Real Farms

The economics aren’t abstract. In 2025, plant-based milk held roughly 13% of total retail milk dollars — a multi-billion-dollar slice of the case that used to be yours. That’s not a rounding error. That’s a category someone built while dairy argued about labeling.

It’s not one monolithic competitor, either — and the breakdown matters for where the contrast bites hardest. Here’s the US retail plant-based milk picture from recent Circana/AgFunder data:

| Segment | Dollar sales trend | Notes |

| Total plant-based milk | −2.8% dollars, −3.9% units (2024) | Category contracting after a decade of growth |

| Almond milk (largest) | −8.5% to ~$1.55B | Biggest segment, falling fastest |

| Oat milk | Gaining share | The one still growing — and the one cleaning up labels first |

That last row is the one to watch. Oat milk is both the rising segment and the one most aggressively simplifying its ingredient list — which means dairy’s cleanest line of attack is aimed at a moving, shrinking-but-smartening target.

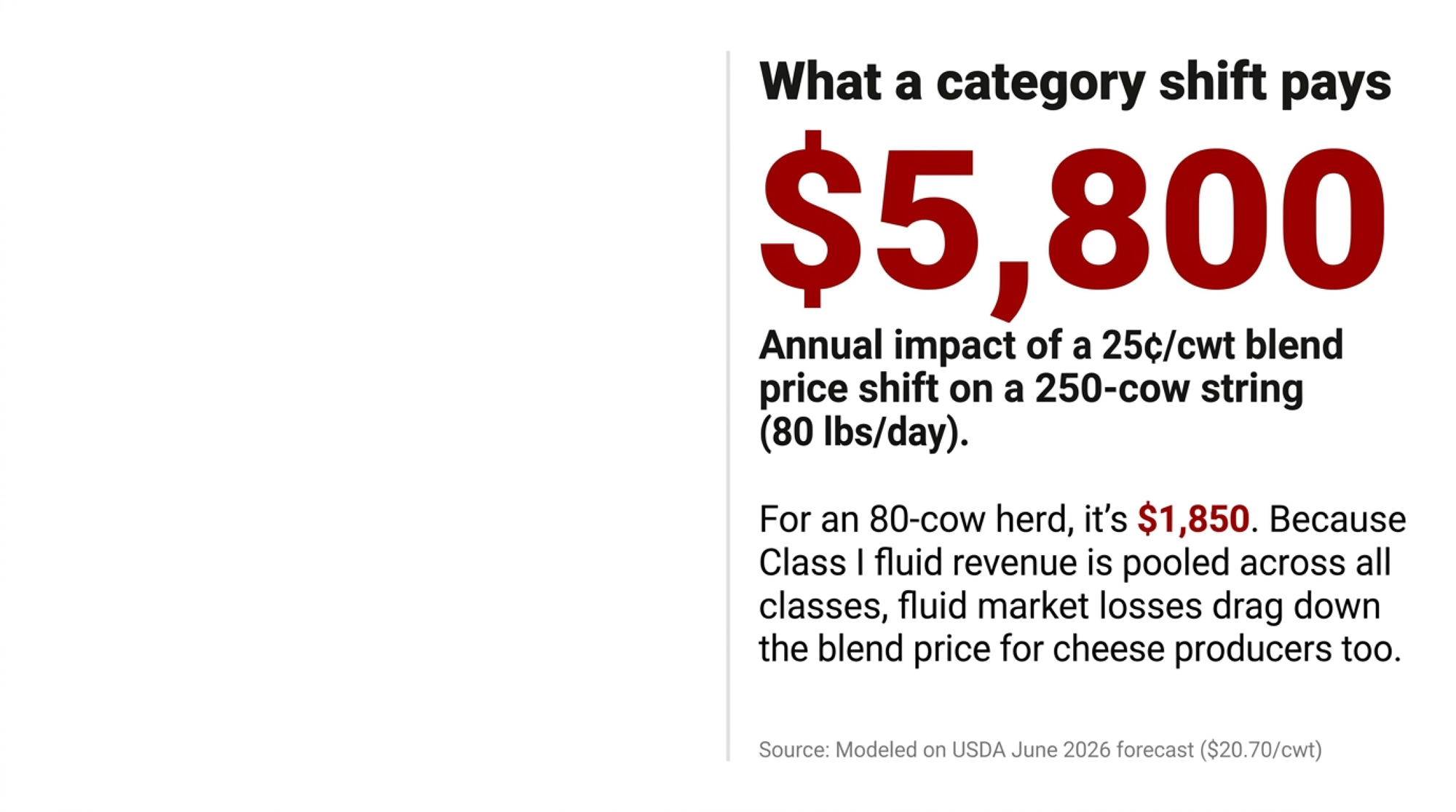

Take that same central-Wisconsin composite operator. Milking 250 cows shipping 80 lbs a day — that’s the milking string, not total head — works out to about 73,000 cwt a year. At USDA’s June 2026 all-milk forecast of $20.70/cwt, that’s roughly $1.51 million in annual milk sales. Demand shifts at the category level land in the blend price every one of those hundredweights gets paid on.

Now run it smaller, because most of the country isn’t milking 250. An 80-cow herd shipping the same 80 lbs a day moves about 23,360 cwt a year — call it $483,000 in milk sales at that same $20.70. The percentages don’t care about your herd size. A category shift that nudges the blend price a quarter a hundredweight is roughly $5,800 a year on the 250-cow string and about $1,850 on the 80-cow herd. Small money? Run it across five years and a barn full of decisions you’re already making, and it stops feeling small.

Why Should the Cheese Guy Care About Fluid Milk?

Here’s the part that catches people who figure they’re insulated because their milk goes to cheese, not the jug. Under federal milk marketing orders, Class I fluid revenue gets pooled and shared across all classes through the blend price. So when fluid premiums get drawn down, the money that flows back into the pool shrinks — and that haircut reaches the cheese and butter guys too, not just the bottlers.

A weaker fluid category doesn’t stay in the fluid lane. It pulls down the blend everyone draws from. You can be shipping every pound to a cheese plant and still feel a fluid-milk fight you thought wasn’t yours. That’s the quiet mechanics of pooling, and it’s exactly why “let the fluid guys worry about it” is the wrong read on this one.

The Ultra-Processed Trap: Not every gallon wins this fight. Flavored school milk, processed cheese slices, and dessert-style yogurts trip the ultra-processed wire just as fast as oat milk does. The strategy only works if the industry champions its raw heroes and reformulates the rest.

| Product | Ingredient Count | Added Sugar | Industrial Additives | MAHA Pass/Fail |

|---|---|---|---|---|

| Whole milk (plain) | 1 | None | None | ✅ Passes |

| 2% milk (plain) | 1 | None | None | ✅ Passes |

| Natural cheese (aged cheddar) | 4 | None | None | ✅ Passes |

| Plain Greek yogurt | 2–3 | None/trace | None | ✅ Passes |

| Flavored school milk (chocolate) | 8–10 | ~20g/serving | Carrageenan, gums | 🟥 Fails |

| Processed cheese slices | 10–14 | Low | Emulsifiers, phosphates | 🟥 Fails |

| Flavored protein dairy drink | 12–18 | 10–20g | Stabilizers, artificial flavor | 🟥 Fails |

| Sweetened fruit yogurt | 8–12 | 15–25g/serving | Pectin, colorings | 🟥 Fails |

The Mechanics Behind the Outcomes

The engine here is MAHA’s definition of “ultra-processed.” A 2026 Healthy Eating Research expert panel recommends flagging foods that carry at least one industrial ingredient you’d never keep in your own kitchen — emulsifiers, flavorings, colorings — paired with high added sugar, sodium, or saturated fat. Under that lens, plain milk and simple cheese land on the clean side of the line. Most plant-based milks don’t.

But that same lens cuts both ways, and pretending otherwise is how dairy loses credibility. DairyReporter, summarizing the Lancet’s ultra-processed series, said it plainly: the evidence on whether ultra-processed dairy like cheese slices and flavored yogurt actually harms health “remains limited” and mixed. Overclaim, and the first reporter who reads an ingredient panel hangs you with it.

Cotton left its awkward bits in the footnotes and led with the contrast. Dairy can do the same — champion the heroes, quietly reformulate the rest — but only if it stops treating every SKU in the case as equally worth defending. The FDA’s dye ban and GRAS overhaul are already forcing that reformulation conversation on processors, so the raw-versus-processed split isn’t hypothetical — it’s the full risk-and-reward picture of MAHA for dairy already playing out.

How Much Does Waiting Actually Cost You?

The real deadline isn’t a vote. It’s a product decision sitting on a competitor’s whiteboard. Plant-based brands are already cleaning up their labels — Circana flagged “more simple ingredients, specifically no gums or oils” as a leading 2025 innovation theme in the category. MALK rolled out a shelf-stable almond milk in July 2025 with four ingredients and no gums or fillers. FoodNavigator called the ultra-processed backlash a “watershed moment,” pushing the whole category toward “fewer, more recognizable ingredients”.

So picture the morning a major oat or almond brand hits three or four ingredients and plants its flag in the “minimally processed” space first. Your cleanest advantage blurs overnight. The fight stops being real milk versus an industrial drink and becomes animal protein versus plant protein under the same health halo — same shelf, same claim, much harder sell. And the category isn’t going away: global plant-based milk forecasts run from about $21 billion in 2026 to $46 billion by 2035. It’s not dying. It’s reformulating.

Is Your Checkoff Actually Fighting This Fight?

This is the uncomfortable part, and it’s worth asking out loud. You pay 15¢/cwt into the national checkoff, and a DMI-commissioned analysis, backed by USDA research at Texas A&M, estimates that this adds roughly $1/cwt to the all-milk price. The 2026 “Dairy Does More” campaign is built to broaden how people think about dairy across milk, cheese, yogurt, and kefir — the whole portfolio, not the one-ingredient hero.

| Checkoff Activity | 2026 Campaign Focus | Who Benefits Most | MAHA-Aligned? |

|---|---|---|---|

| “Dairy Does More” broad campaign | Portfolio awareness: milk, cheese, yogurt, kefir | Processed dairy brands, co-op value-added lines | 🟡 Partial |

| School nutrition programming | Whole milk law implementation (S. 222) | Fluid milk producers | ✅ Yes |

| Export/trade promotion (cheese & butter) | 76% of cumulative checkoff value | Commodity cheese shippers | 🟡 Indirect |

| “Real milk vs. ultra-processed” contrast | Not funded in 2026 (per article) | Fluid milk farmers | 🟥 Absent |

| GLP-1 / high-protein dairy messaging | Emerging — yogurt, kefir focus | Cultured/protein dairy | 🟡 Partial |

| Reformulation support (reduce additives) | Not a stated checkoff priority | Processed dairy processors | 🟥 Absent |

There’s a structural reason for that. The big farmer-owned cooperatives don’t just market your milk; they own processing plants and sell finished product, and the margin logic there matters. A gallon of plain fluid milk is a low-margin commodity, while value-added processed lines — cheese, cultured products, branded items — capture more of the retail dollar at the plant level. In our view, that’s the built-in tension of the dual role: an organization that both buys members’ milk and sells processed products has more incentive to grow the high-margin processed business than to sharpen a “real milk is the clean choice” message that mostly lifts low-margin fluid sales. The co-ops, for their part, describe themselves as farmer-owned and focused on returning value to members. Either way, when your checkoff gets graded on broad reputation numbers, the safe play is to defend the whole portfolio. That institutional inertia leaves an open contrast on the table untouched — a familiar symptom of what happens when your co-op becomes your competitor.

Options and Trade-Offs for You

A lot of this gets decided above your milkhouse — at the co-op, the checkoff, the trade group. But the strategy shapes your check, so know the paths and where each one breaks.

Strategy 1: Weaponize the “Born Minimal” Contrast. Drive the message of one-ingredient milk versus industrial plant-based formulations before the alternatives clean up their labels — and they’re already moving, with “no gums or oils” a leading 2025 innovation theme. Works while plant-based is still mostly multi-ingredient and additive-heavy. Needs checkoff and trade groups to anchor on the contrast. Breaks if the industry won’t admit flavored and heavily processed dairy sit on the wrong side of the line.

Strategy 2: Cash in the School-Milk Win. Capitalize on the new law and USDA’s school-meal standards — this one’s mostly free, since the law’s already signed. The catch: flavored school milk is capped at no more than 10 grams of added sugar per 8 fluid ounces under the USDA’s final rule, so your SKUs have to stay strictly under that limit for the clean story to hold.

Strategy 3: Ride the GLP-1 High-Protein Wave. GLP-1 households eat yogurt at nearly three times the average rate, per Mintel, and that demand favors high-protein, nutrient-dense formats. The risk: a lot of high-protein dairy drinks are themselves ultra-processed, so you can’t lead the “clean” argument with them.

Your 30-Day Move: Before you close this tab — call your co-op or state checkoff rep this month and ask one direct question: is any 2026 promotion money funding a MAHA-aligned “real milk” message, or is it all broad category advertising? You’re entitled to know where your 15¢ goes, and the answer tells you whether anyone above your milkhouse is actually running this play.

Key Takeaways

- If your co-op or checkoff can’t name a single MAHA-specific “real milk” campaign for 2026, treat that as a flag worth raising at your next district meeting — the policy window is open now, not next year.

- If any dairy product made with your milk relies on added sugar or emulsifiers, assume it falls on the ultra-processed side under emerging federal definitions — and build your messaging around the products that don’t.

- When a national plant-based brand hits four clean ingredients, your “minimally processed” edge starts shrinking — watch new launches as your real clock, not the election calendar.

- If you ship to school channels, confirm your flavored-milk SKUs sit under the 10g added-sugar cap before you lean on the “healthy choice” line.

- If your co-op also processes, ask how its promotion priorities line up with low-margin fluid demand versus the higher-margin value-added products it sells.

What Happens If Dairy Lets This One Pass?

So here’s the question to chew on before your next co-op meeting: if a plant-based brand gets to a four-ingredient carton and looks MAHA in the eye first, what’s left of dairy’s “natural” advantage — and is your operation built for a world where “milk” is just a protein preference, not the default healthy choice on the shelf?

We’re breaking down the full checkoff math by herd size, too — where your 15¢/cwt actually goes and what it returns at your scale, given that 76% of the cumulative value is tied to cheese and exports. That’s the piece to read if you want the real numbers behind this one, not just the argument.

EDITOR’S NOTE: The 250-cow and 80-cow central-Wisconsin operators referenced in this article are disclosed composite scenarios modeled from typical mid-size and small Upper Midwest family dairies, not single named individuals. All figures attached to them — herd size, daily shipment, cwt, and milk-sales math — are illustrative and built only from the sourced USDA price and standard production assumptions cited in the piece.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Same Milk, Different Payday: How Your Processor’s Product Mix Shapes Your Future — Arms you with six critical questions to negotiate the best price by auditing your plant’s utilization matrix. Connects to a steady $1/cwt premium spread that directly protects long-term farm equity.

- You Won the Whole Milk Fight. Here’s Why Your Milk Check Didn’t Move. — Exposes why political policy victories in the cafeteria do not automatically lift your blend price unless your herd’s protein-to-fat ratios match the component values that modern processors actually pay for.

- Dairy checkoff lawsuit: Faust sues over your 15¢/cwt — Dismantles the regulatory plumbing of your mandatory checkoff assessments by tracking the legal challenge against spending on corporate ESG initiatives. Delivers a financial stress test detailing your multi-year cash exposure during the litigation window.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.