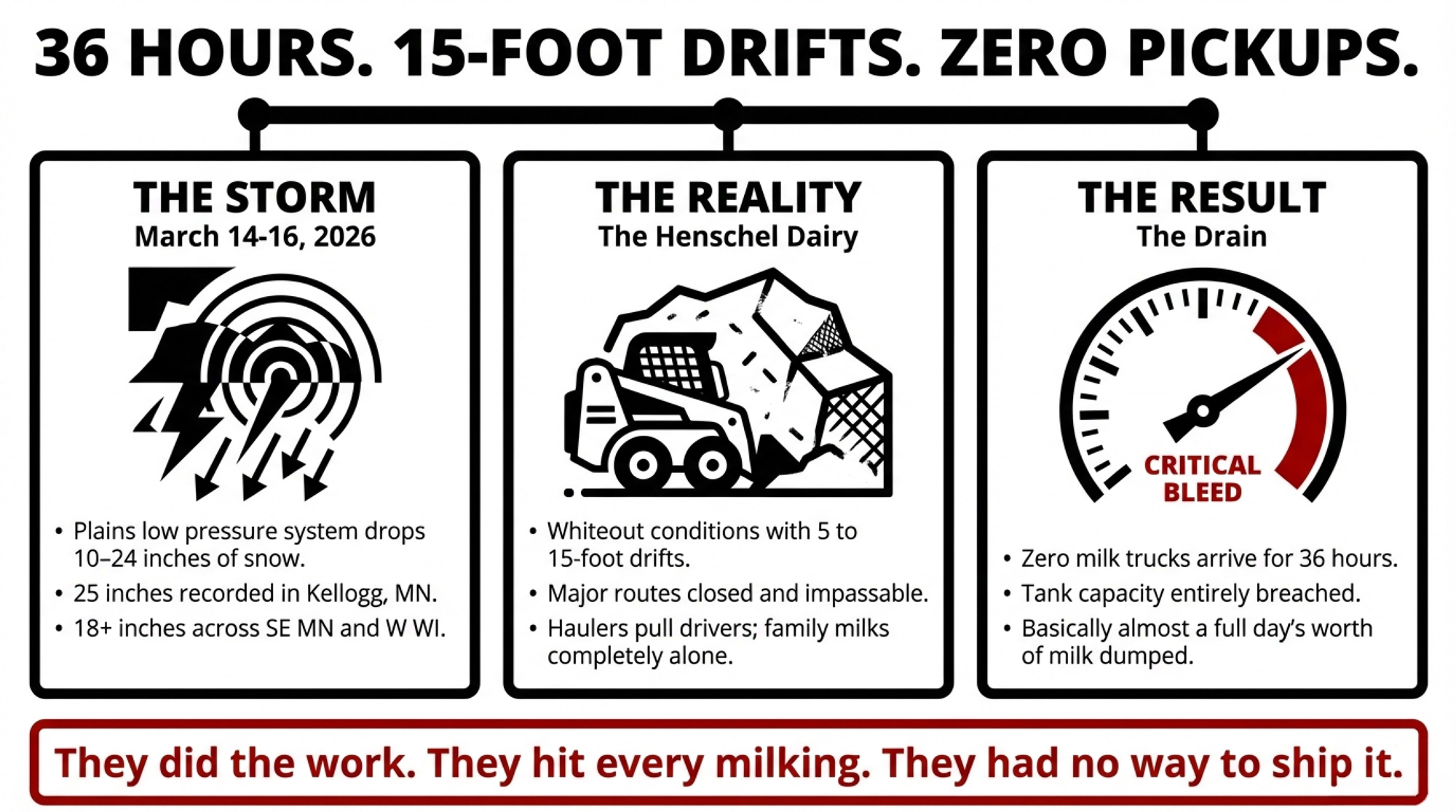

The Henschel family milked through 5‑to‑15‑foot drifts near Manawa — then dumped a full day’s milk because the truck couldn’t come, and no federal program covers the milk you lose.

On the Sunday morning of the March 14–16 blizzard, the Henschel dairy near Manawa, Wisconsin, was buried in snow. Drifts on the lane were higher than the skid steer. The milk truck that usually shows up like clockwork couldn’t reach them. Roads were closed, plows were pulled, and for about 36 hours, they were essentially on their own with cows still milking and a bulk tank running out of room.

Chris Henschel told US Farm Report that they were dealing with “whiteout conditions with snow drifts anywhere from 5 to 15 feet high” around the farm, and that the roads were “impassable for about 36 hours.” Keeping feed in front of cows and milk moving out of the parlor didn’t change one hard fact: the tank only holds so much. In the end, Henschel said they dumped “basically almost a day’s worth of milk because nobody could get to the farm.”

They did the work. They hit every milking. They had no way to ship it. Lay the program rules and the barn math beside that picture, and it’s hard not to see your own risk sitting there too.

When the crew couldn’t reach the barn and the backup was plowing snow, the backup to the backup crew rolled in — the Henschel boys muscling a cart of milk for calves on that blizzard day.

What the March 14–16 Blizzard Really Did to Dairy Roads

This wasn’t a normal March snow that blows through overnight and melts by the weekend. The National Weather Service called it a “historic, record-setting winter storm” — a potent Colorado low that deepened as it tracked from the central Plains toward Chicago and Lake Huron, pulling Gulf moisture into cold air and hammering the Upper Midwest for more than 48 hours.

NWS Green Bay reported a widespread 1 to 2 feet across northeast Wisconsin, with localized amounts exceeding 30 inches from Wausau to Marinette and Door County. Green Bay itself recorded 26.6 inches — its second-largest snowstorm on record. Waupaca County, where the Henschel dairy sits near Manawa, saw 25 to 30.5 inches, with nearby Shawano County reporting up to 33 inches. Snowfall rates hit 4 inches per hour at times, with thundersnow and lightning.

To the west, NWS La Crosse confirmed 25 inches at Kellogg, Minnesota, with similar totals across Trempealeau and Clark Counties in Wisconsin — Independence and Strum both hit 25 inches, Granton 25 inches, and Mondovi 26.6 inches. Peak wind gusts reached 59 mph at Green Bay Airport and 60 mph in De Pere, with 40–55 mph gusts common across the region. NWS La Crosse noted reports of 3‑to‑5‑foot drifts were common; NWS Green Bay documented a 10‑foot drift in Ephraim.

The timing was brutal. Storm onset hit Saturday evening, March 14. Peak winds and whiteouts ran late Saturday into Sunday. Interstates 35, 80, and 94 were all closed for a period on Sunday and Sunday night. NWS Twin Cities confirmed that vehicles became stranded on I‑94 between Eau Claire and Osseo during blizzard conditions, and WisDOT posted “No Travel Advised” across the northern half of the state for an extended period. The worst transport window lasted roughly 24–36 hours, during which rural routes were effectively shut down. If your usual truck hits the yard Saturday night or Sunday morning, a 36‑hour shutdown doesn’t just mean “late pickup.” Depending on your tank size and flow, it can mean “no pickup” before you run out of storage.

US Farm Report and Dairy Herd both described the Henschels’ situation as a “rare milk dump” triggered by this storm, noting that towering drifts blocked every path to the farm. On farms across the region, that translated into township and county plows leaving some dairy roads for last, haulers making the call to stay parked rather than risk drivers in whiteouts, and milk plants adjusting schedules or pausing loads until they knew trucks could actually move.

You can’t change the weather. You can be honest about what it costs — and why all the programs that show up after storms like this barely touch the milk itself.

“Milk Can’t Wait”: The Aid That Showed Up — and What It Missed

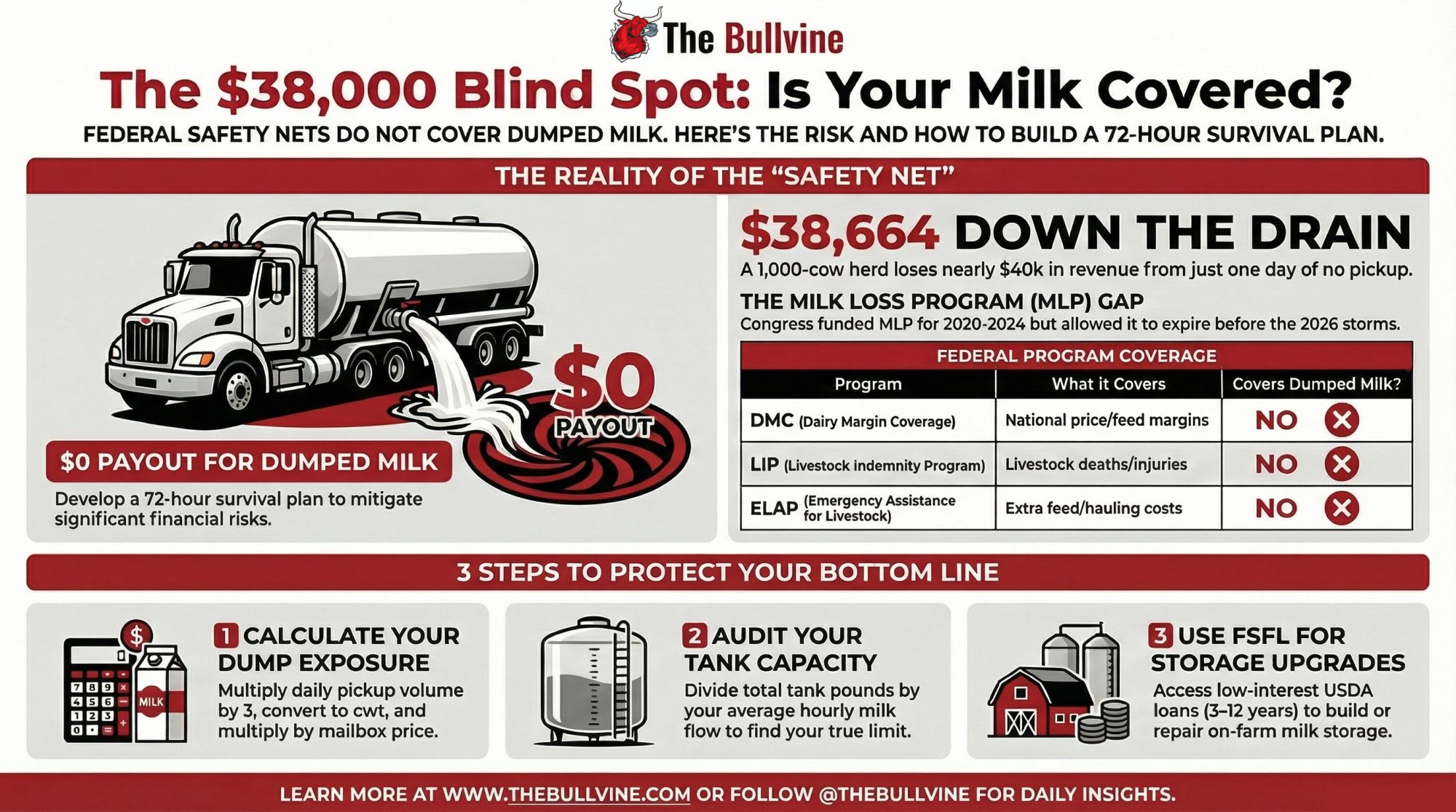

Within days, USDA’s Farm Service Agency in both Wisconsin and Minnesota was pushing reminders about disaster programs. Sandy Chalmers, FSA State Executive Director in Wisconsin, put it bluntly: “Milk can’t wait. When trucks can’t reach farms or processors on time, producers face costly delays and, in some cases, must dispose of milk that can’t be stored.” She urged producers to report “crop, livestock, and infrastructure-related losses” and to contact their county offices.

Here’s what was actually on the table for a storm like this:

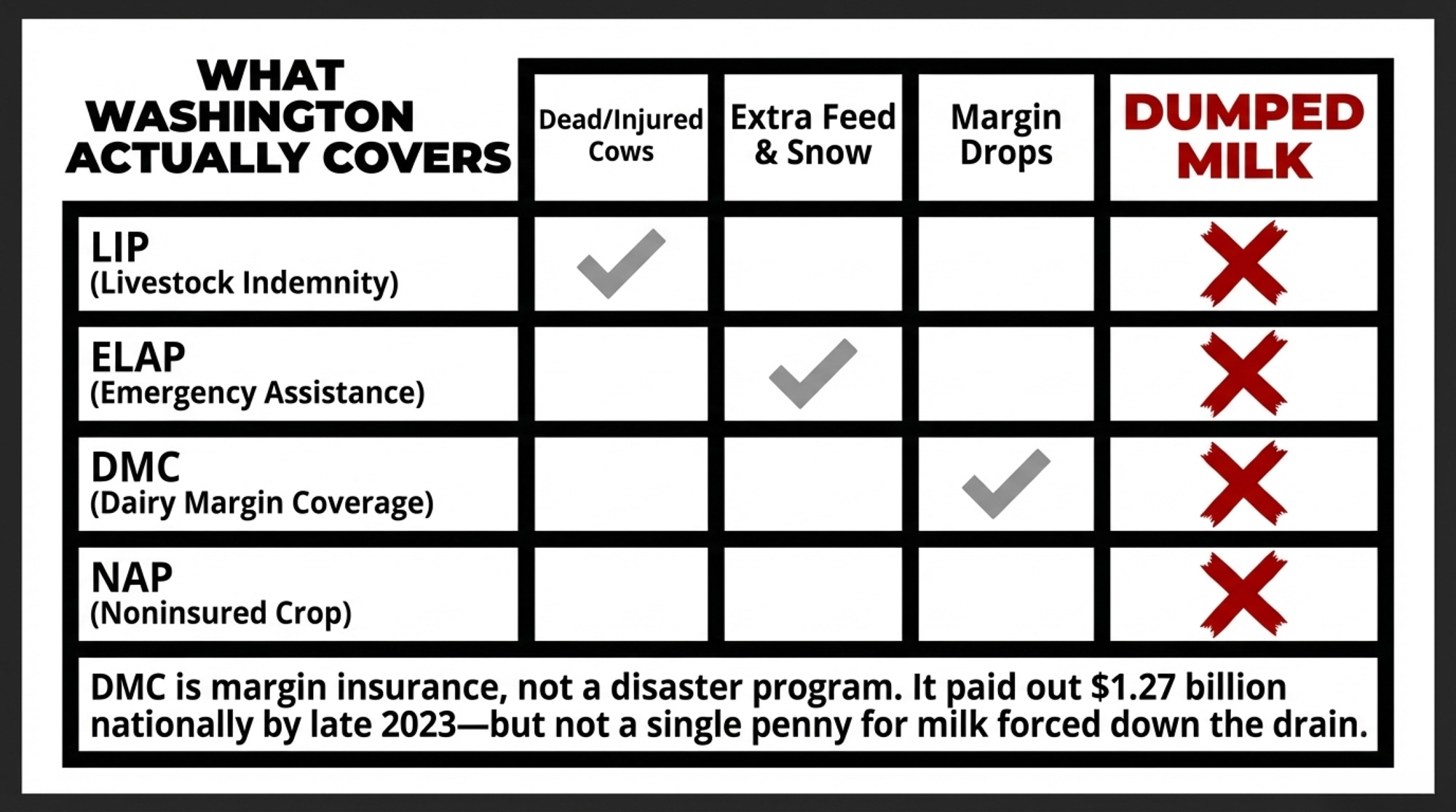

Livestock Indemnity Program (LIP) — Authorized under the 2014 Farm Bill and administered by FSA, LIP pays 75% of the fair market value for livestock deaths above normal mortality due to eligible adverse weather events like blizzards and extreme cold. It can also cover animals sold at a discount after storm-related injuries. Notice of Loss must be filed within 30 calendar days of when the loss becomes apparent.

Emergency Assistance for Livestock, Honeybees, and Farm‑raised Fish (ELAP) — Provides emergency relief for above‑normal feed costs, feed and water hauling, and equipment rental for snow removal when adverse weather makes normal operations impossible. ELAP does not cover milk loss directly, though USDA expanded ELAP in July 2024 to cover milk production losses from H5N1‑infected herds — a different mechanism. Notice of Loss: 30 calendar days from when the loss first became apparent.

Noninsured Crop Disaster Assistance Program (NAP) — Covers non‑insured crops and forage in eligible situations. NAP does not cover milk. A Notice of Loss must be filed within 15 days of the loss becoming apparent — that 15‑day window is shorter than LIP and ELAP, so hay and forage losses from this storm need to be reported fast.

Farm Storage Facility Loan Program (FSFL) — Provides low‑interest financing on 3–12 year terms to build, repair, or upgrade on‑farm storage facilities. USDA’s eligible commodity list explicitly includes milk, and eligible facility types include bulk tanks, so this can apply directly to expanding your on‑farm milk storage capacity. It doesn’t pay for losses, but it can help you build more buffer for the next storm.

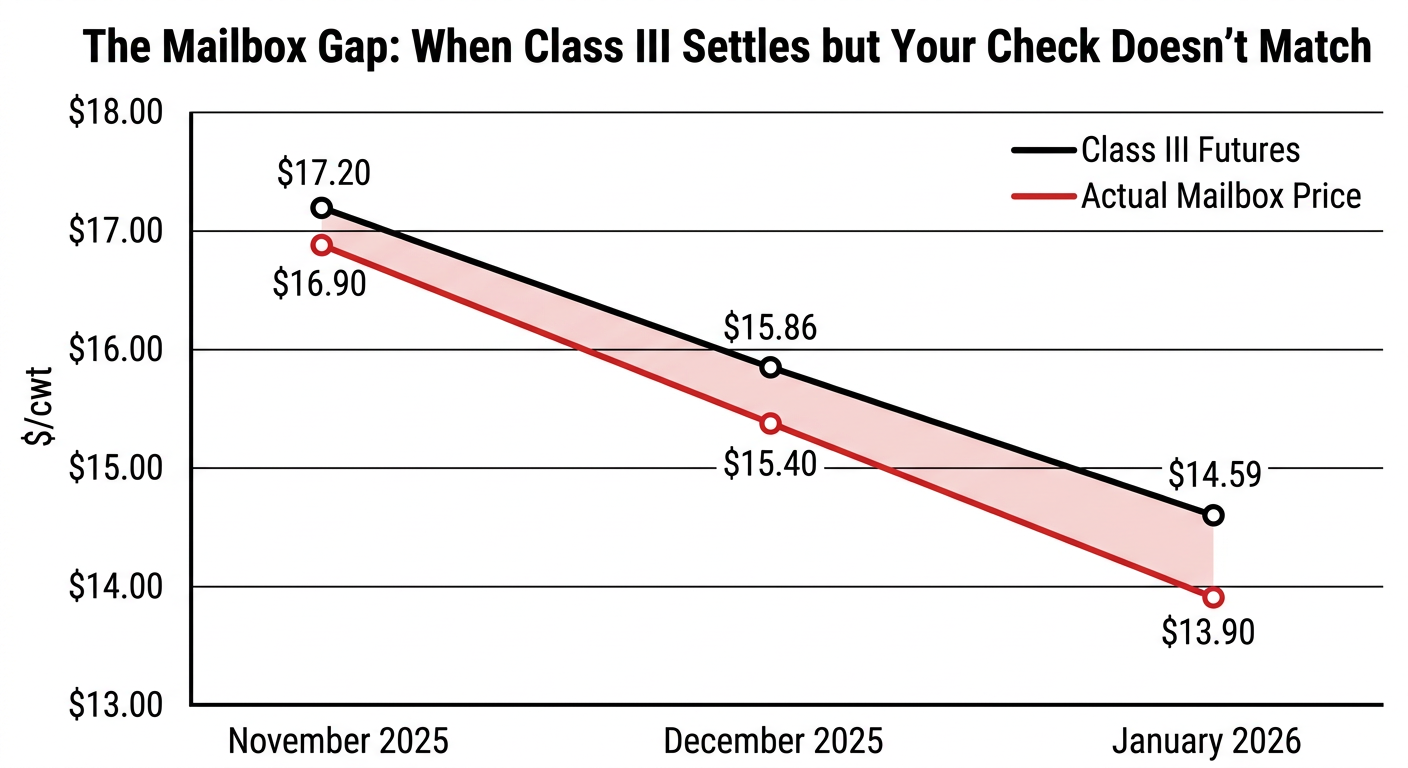

On the margin side, the farm bill politicians in Washington have been celebrating as a “big, beautiful” win for producers, reauthorizing and improving Dairy Margin Coverage (DMC) through 2031. DMC is margin insurance, not a disaster program, but it’s the main federal backstop on dairy revenue. By late 2023, DMC had paid out about $1.27 billion nationally, with Wisconsin topping the list at roughly $272.2 million — around $63,633 per enrolled operation— according to USDA and prior Bullvine analysis.

Bullvine’s DMC work shows margins slipping below $10/cwt by late 2025 and into the mid‑$7s for early 2026, triggering some of the bigger checks in a few years for farms that stayed fully enrolled. Those payouts helped on paper margins. They didn’t do a thing for milk forced down the drain because the road and plant system around you blinked.

On paper, it can look like you’re covered. In the parlor, once you read the fine print, it’s a different story.

Does Any Federal Program Actually Cover Dumped Milk?

Line up USDA’s current tools, and the gap jumps off the page:

Program

What It Covers

Trigger Mechanism

Covers Dumped Milk?

2026 Status

LIP

Livestock deaths above normal mortality; injured animals sold at discount

National all-milk price minus standardized feed cost (margin)

Monthly margin falls below elected level ($4–$9.50/cwt)

NO

Active — enrolled thru 2031

NAP

Non-insured crops and forage losses

Crop failure / loss event; 15-day NOL requirement

NO

Active — covers crops only

FSFL

Low-interest loans for on-farm storage construction/upgrades

N/A — financing, not indemnity

NO

Active — 3–12 yr terms

MLP

Milk dumped due to qualifying weather — impassable roads, power outages

Physical milk dumped without compensation

YES — BUT 2020–2024 ONLY

EXPIRED — signup closed Jan 23, 2026

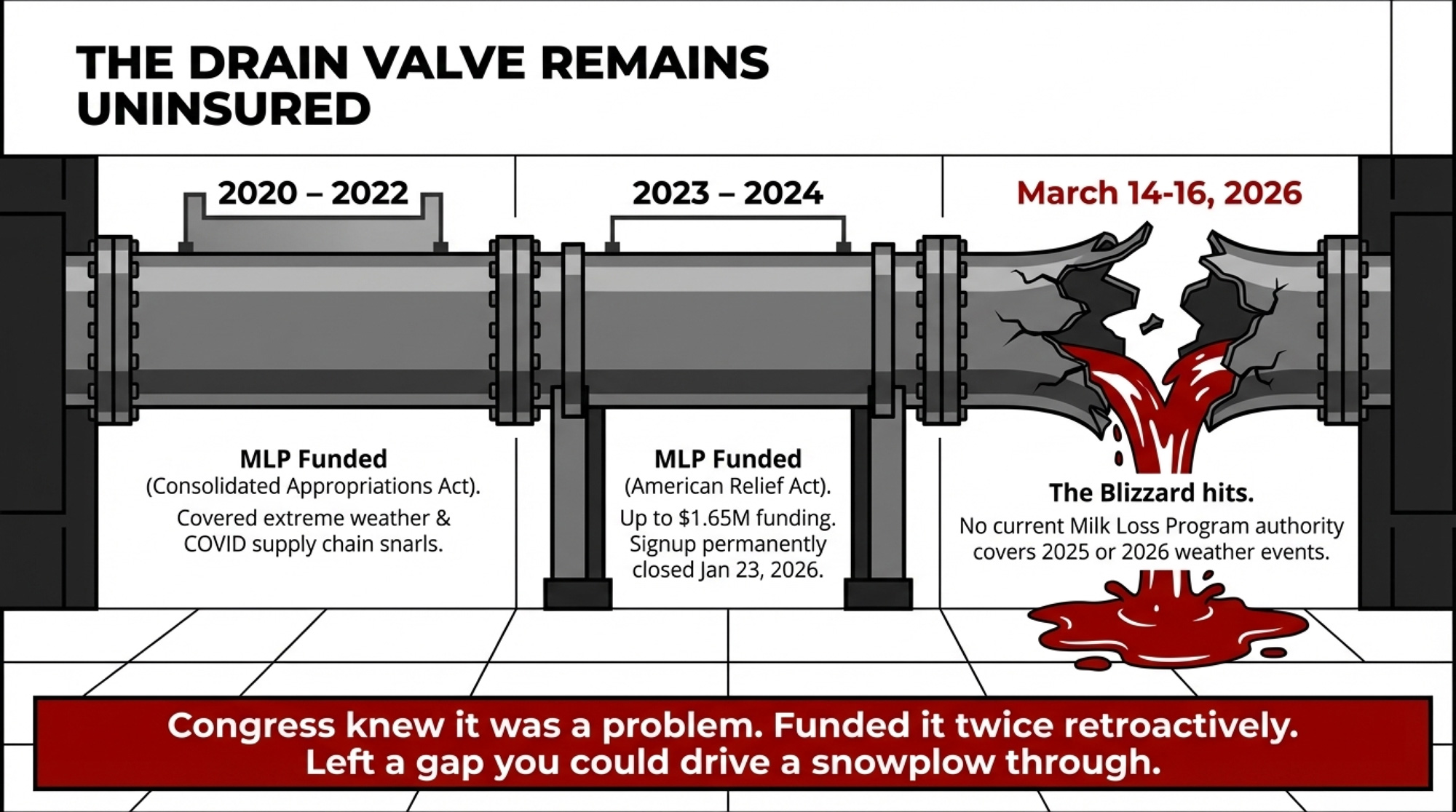

There is one program specifically designed to pay for dumped milk: the Milk Loss Program. Congress has authorized it twice. The first round, under the Consolidated Appropriations Act of 2023, covered eligible losses in 2020, 2021, and 2022 — including extreme weather, supply chain snarls, and COVID‑era processing shutdowns. MLP paid 75% of the milk value for most producers and 90% for underserved producers, including beginning, limited‑resource, and veteran farmers.

The second round, authorized under the American Relief Act of 2025 as part of USDA’s Supplemental Disaster Relief Program, extended MLP to cover qualifying weather events in 2023 and 2024. That signup window opened in late November 2025 and closed in late January 2026 — less than two months before the Henschels’ blizzard.

The March 14–16, 2026, blizzard lands outside both windows. No current MLP authority covers losses for 2025 or 2026. Congress knew about the problem, funded it retroactively twice, and still hasn’t built a permanent program.

So when the Henschels opened that valve, here’s what the safety net really did:

Any calves or cows lost to storm stress or injuries? LIP might cover 75% of their value — but you need to file a Notice of Loss within 30 days, which for this storm means roughly by mid‑April 2026. The application for payment deadline extends to approximately March 1, 2027.

Extra feed, fuel, and snow removal to dig out? ELAP might help — same 30‑day Notice of Loss requirement, with an application deadline of approximately January 30, 2027. fsa. usda

Margins squeezed this winter? DMC sends a check if the national margin falls far enough below your coverage level.

The actual milk they dumped — roughly a full day’s output — sat entirely outside federal coverage in 2026.

That’s not a clerical error. That’s how the net has been structured so far.

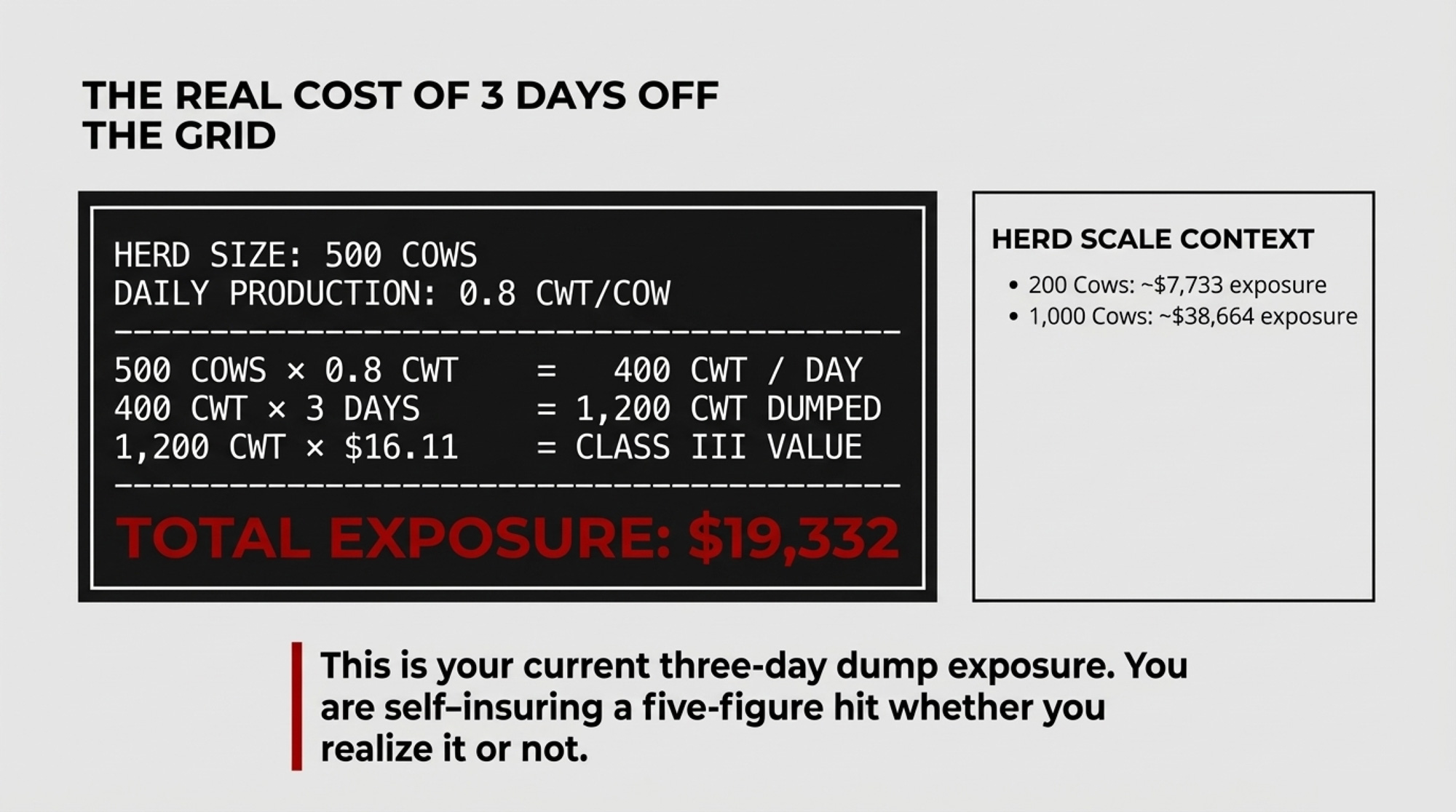

How Much Does 72 Hours Without a Milk Truck Actually Cost Your Operation?

Now put some numbers to what a storm like this means in dollars.

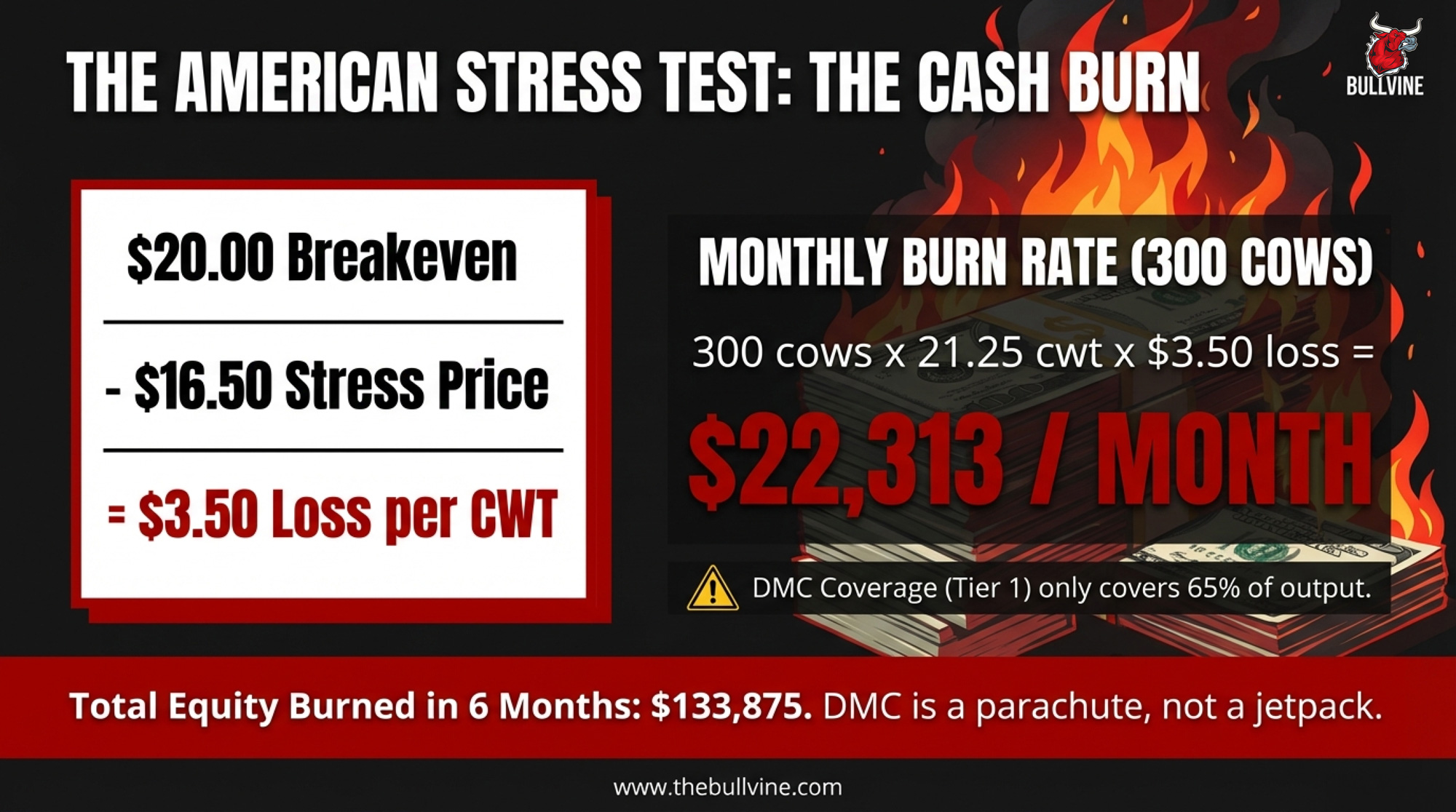

March 2026 Class III futures were trading around $16.11/cwt on the CME. Take a realistic daily production number: 80 pounds of saleable milk per cow per day — 0.8 cwt per cow. Daily revenue per cow at that price: 0.8 cwt × $16.11 = $12.89 per cow per day.

Scale that across a herd and across three days of no pickup:

200 cows: 48,000 lb = 480 cwt. At $16.11 ≈ $7,733 down the drain.

For the Henschels, coverage described them dumping “basically almost a day’s worth of milk” when roads kept trucks out. If you assume a mid‑size herd shipping around 32,000 lb per day — 320 cwt — one dumped day at $16.11/cwt is about $5,155. That’s explicitly example math, not their disclosed volume, but it’s the right scale for a lot of upper‑Midwest family dairies.

Herd Size

Avg Daily Pickup (lbs)

3-Day Pickup (cwt)

At $14.59/cwt (Jan 2026 low)

At $16.11/cwt (March futures)

At $18.00/cwt (strong market)

200 cows

16,000

480

$7,003

$7,733

$8,640

500 cows

40,000

1,200

$17,508

$19,332

$21,600

1,000 cows

80,000

2,400

$35,016

$38,664

$43,200

2,500 cows

200,000

6,000

$87,540

$96,660

$108,000

5,000 cows

400,000

12,000

$175,080

$193,320

$216,000

Here’s the quick version for your own barn:

Grab your last hauler or co‑op statement and find your average daily pickup volume in pounds.

Multiply that number by 3.

Divide by 100 to turn pounds into cwt.

Multiply by today’s Class III or your mailbox price.

That final number is your current three‑day “dump exposure.” Whether you’ve thought about it or not, you’re self‑insuring it.

Does Your Disaster Plan Survive Three Days Without a Pickup?

Most of us say we have a “plan” for storms. What we really have are habits and luck:

The township usually plows us early.

The hauler always finds a way.

The generator has “never let us down.”

Henschel dairy had habits, too. Then they watched the system around them break — drifts higher than the skid steer, I‑94 closed, WisDOT posting “No Travel Advised” across the northern half of the state.

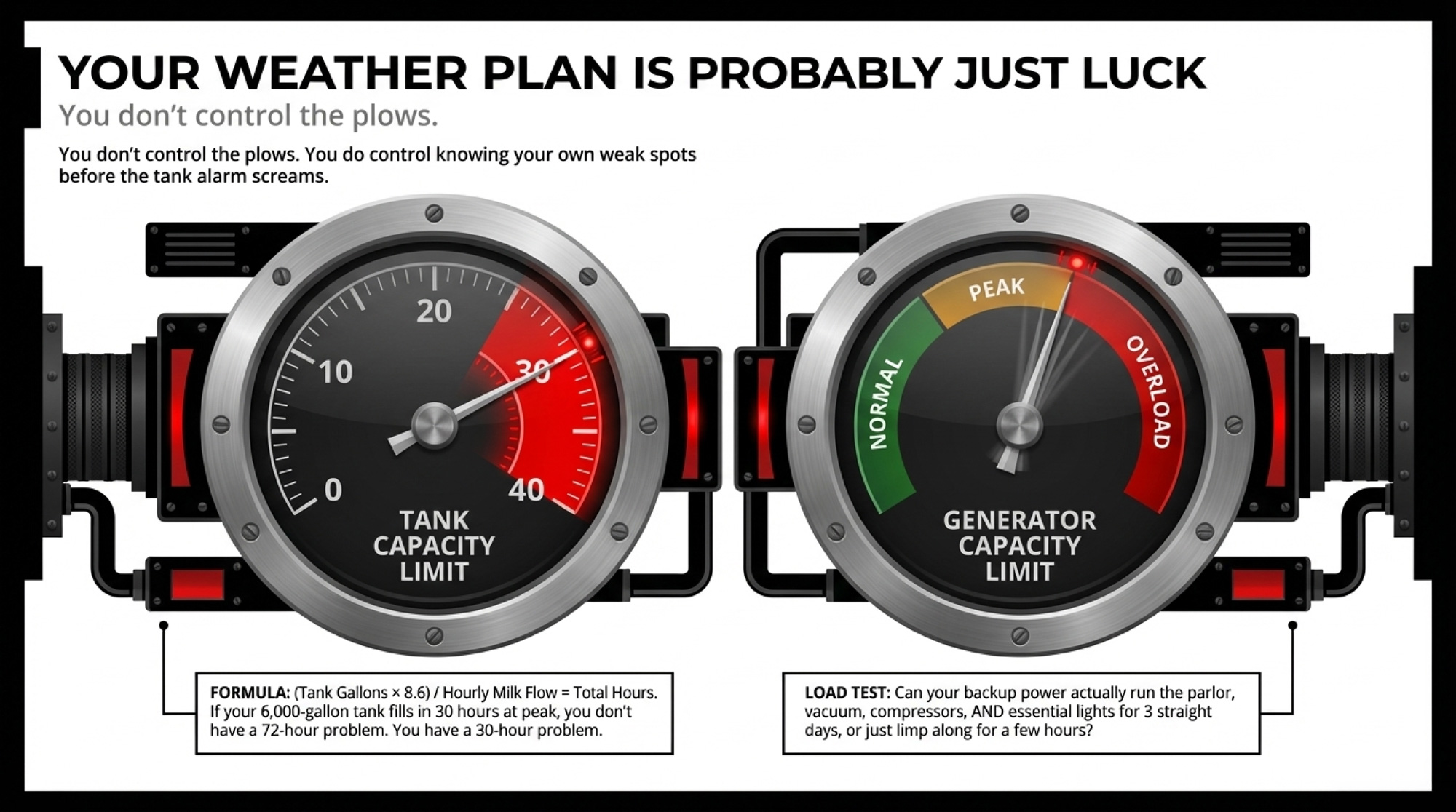

If you want an honest 72‑hour plan, start by knowing your own limits:

How many hours to a full tank? Take your tank size in gallons. Multiply by 8.6 (the weight of a gallon of milk in pounds). Divide by your average hourly milk flow. If your 6,000‑gallon tank fills in 30 hours at peak, you don’t have a 72‑hour problem — you’ve got a 30‑hour one.

What backup storage do you really have? A clean nurse tank you actually trust? Access to a neighbour’s bulk tank under a mutual‑aid agreement? A rented tanker or portable tank you could bring in ahead of a forecast blizzard? USDA’s FSFL program will finance bulk milk storage tanks at low interest rates, so if you’ve been thinking about adding capacity, the loan structure already exists.

What are your hauler’s hard limits? Do they have written rules for when they pull trucks? Will they combine routes, run nights, or send smaller trucks? Who actually decides when routes are suspended, and how do they let you know?

Power and access matter too. If a storm like this takes down the grid, can your generator actually run the parlor, vacuum, compressors, and essential lights for three days, or just enough to limp along for a few hours? If you don’t know the answer, that’s worth a conversation with your electrician before fall.

You don’t control the plows or the wind. You do control whether you know your own numbers and weak spots before the next tank alarm reminds you how tight your margin for error really is.

Options and Trade‑Offs for Farmers

Option

Upfront Cost / Effort

Ongoing Cost

Time to Implement

Covers Which Risk?

Key Limitation

Add on-farm storage (extra tank, nurse tanker)

High — stainless steel, plumbing, wiring; FSFL loans available at low interest

Low — maintenance & cleaning

6–18 months

Buys 12–24 hrs extra buffer

Hauler still won’t come in whiteout; storage has limits

Tighten hauler/processor agreement

Low — phone calls, written plan

None

30 days

Reduces likelihood of no-show

Can’t override DOT road closures; hauler serves many farms

Neighbor/mutual-aid milk pact

Low — a conversation now, co-op paperwork

None

30–60 days

Routes milk to farm with access/storage

Co-op food-safety rules; requires pre-approval before crisis

Push for permanent MLP

Political capital + time

None

1–3 years (Congress)

Creates federal backstop on dumped milk

Program has expired twice; 2026 dumps currently uninsured

You’ve basically got four paths when you think about the “truck can’t come” problem. None are perfect. Each has trade‑offs.

1. Build more on‑farm or shared storage

When it makes sense: you’re milking enough cows that even one dumped day is a five‑figure event, you have physical space, and your lender understands risk management. A 500‑cow herd with 80 lb/cow/day has about $19,332 at risk in a three‑day storm at $16.11/cwt.

What it requires: capital for a larger bulk tank, a second tank, or a nurse tanker. USDA’s Farm Storage Facility Loan Program offers low‑interest financing on 3–12 year terms, and its eligible commodity list specifically includes milk, with bulk tanks listed as eligible facility types.

Risks and limits: you tie up cash in stainless that mostly sits there until the rare bad week. If your hauler and processor can’t or won’t add emergency routes, you may still end up dumping.

2. Tighten hauler and processor agreements

When it makes sense: you’ve got relationship leverage as a long‑term patron with solid quality.

What it requires: honest conversations before the next storm. During this event, WisDOT posted “No Travel Advised” across the entire northern half of Wisconsin – at that point, nobody was running. But for storms short of that, some co‑ops and haulers have emergency pickup or route‑consolidation protocols. If yours doesn’t, that conversation is worth having now.

Your 30‑day move: write a one‑page “storm plan” with hauler and processor contacts, who calls first, and what you’ve agreed to. Tape a copy on the bulk tank, one in the office, and one at home.

3. Build neighbour and community mutual‑aid pacts

When it makes sense: you’ve got another dairy or two within a few miles, and at least one has different exposure — better road, more storage, different hauler.

What it requires: sitting down now and asking, “If your truck can reach you but not us, could you take one load?” Then work with your co‑op on how that milk is ticketed and paid. Some processors are open to cross‑farm loads if quality can be tracked; others need approvals in place.

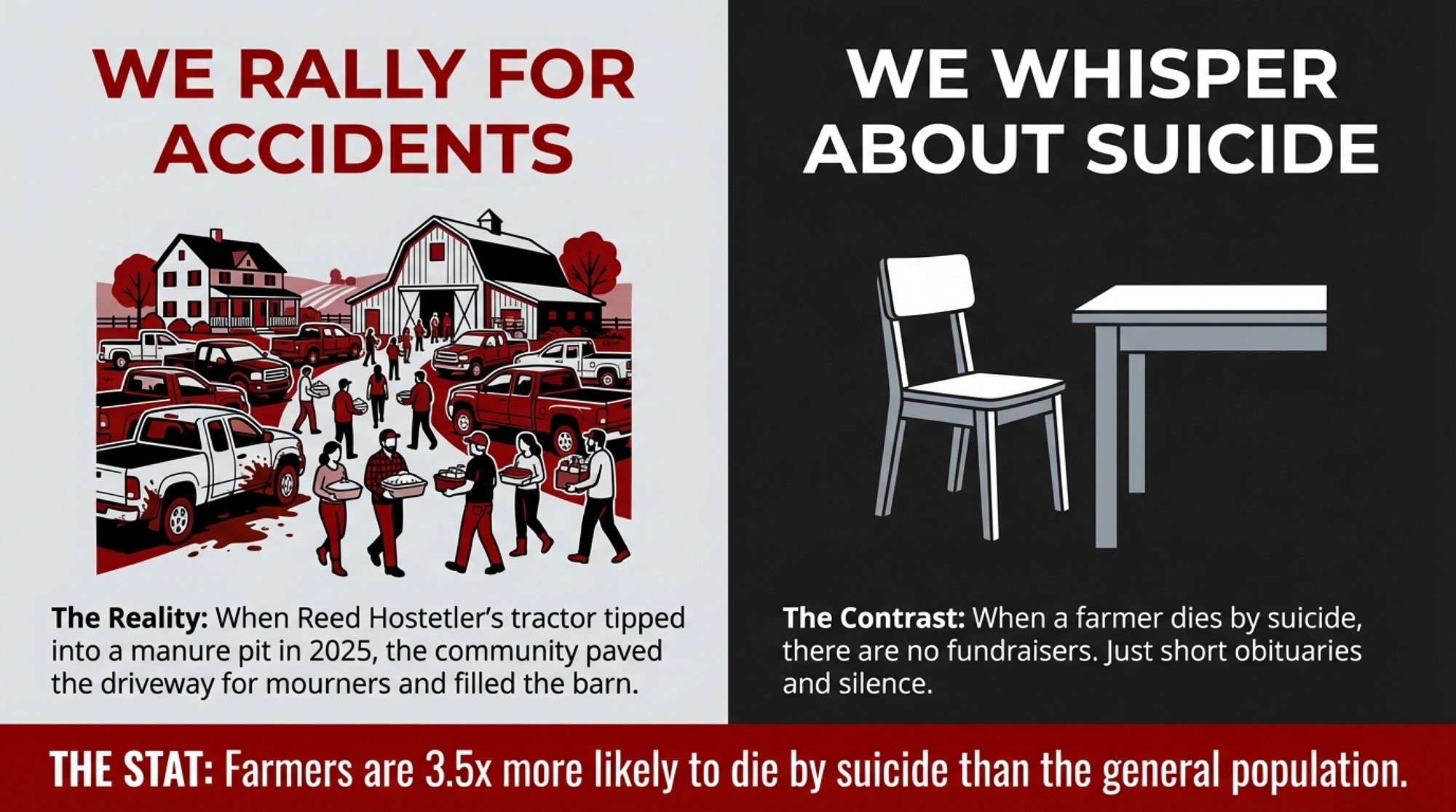

We’ve seen this kind of neighbour network in real crises. When Ohio dairyman Reed Hostetler died in a manure pit accident, neighbours stepped in to run chores, haul feed, and keep the dairy going. That same instinct — organized ahead of time — can keep a blizzard from turning into a five‑figure milk loss.

4. Push for policy change

What it requires: calling your members of Congress and being specific: “Congress funded the Milk Loss Program twice — first for 2020–2022 under the Consolidated Appropriations Act of 2023, then for 2023–2024 under the American Relief Act of 2025. Why does the program keep expiring?”

You can also press your co‑op or processor board. During the 2020 milk‑dump crisis, USDA relief dollars flowed through co‑ops to help cover losses. Ask your buyer, bluntly: “If we’re forced to dump because the road or plant is shut, do you share any of that hit, or are we on our own?”

Bullvine Perspective: The Bill That Brags About DMC and Leaves the Drain Uninsured

The latest farm bill made a big deal out of reauthorizing DMC through 2031 and tweaking margins and coverage levels. They lined up for photo‑ops, telling dairy producers they’d “protected family farms.”

Look at the blizzard math again:

You do the work.

You feed and milk through 5‑ to 15‑foot drifts.

The truck can’t get to you.

You open the valve and dump thousands to tens of thousands of dollars of milk.

DMC pays based on a national margin. It doesn’t care whether your milk is left in a tanker or runs across the floor. LIP and ELAP pay for dead cows, extra feed, and some snow removal. The only program USDA has built to pay for dumped milk — the Milk Loss Program — has been funded twice, retroactively, for events in 2020–2024, and the last signup closed in late January 2026. Less than seven weeks before the Henschels’ tank overflowed.

Congress knew this was a problem. They funded it. Twice. And still left a gap you could drive a snowplow through.

What This Means for Your Operation

If you had any livestock deaths, discounted livestock sales, or major feed disruptions in this storm, your Notice of Loss deadline is roughly 30 days from the event — mid‑April 2026 for March 14–16 losses. Don’t wait. File with your county FSA office now. The application‑for‑payment deadline extends to early 2027, but the Notice of Loss window is the one that catches people off guard.

If your three‑day milk exposure number makes you flinch when you multiply daily pickup × 3 × current Class III, then it’s not a freak event — it’s a business risk you’re actively self‑insuring, and it belongs in the same conversation as debt service and feed contracts.

If you can’t afford more storage, your 30‑day move is to get your paperwork and people in order:document any milk dumps even if they’re not covered yet (you’ll want that record if Congress funds MLP retroactively again), and write down a simple storm plan with hauler and neighbour contacts where everyone can find it.

If you’ve been treating DMC as disaster coverage, remind yourself it’s margin insurance, not milk‑dump insurance. Congress has funded the Milk Loss Program twice for past events and let it expire both times. If you want dumping covered going forward, someone from your area is going to have to say that out loud — using real numbers from storms like this one.

The Bottom Line

Sandy Chalmers was right: milk can’t wait. The Henschels kept cows milking and fed through 5‑ to 15‑foot drifts, and the federal system around them offered help with feed costs and animal losses — but not with the milk they had to dump.

So here’s your kitchen‑table homework: grab your last hauler statement. Multiply your average daily pickup by three days and by today’s price. Are you actually comfortable self‑insuring that number the next time your road disappears under three feet of snow?

If you want the deeper math on how DMC, processor contracts, and USDA dairy disaster assistance actually fit together — and what happens when it’s not the weather but a plant shutdown that stops the truck — keep an eye out for the next “When the Truck Can’t Come” instalments. We’ll be looking at what the AMPI Paynesville strike and shutdown just taught us about stranded milk, and at whether the $17,500 DMC gamble was really the right bet for a storm year like this.

And one more question to chew on while you’re staring at that bulk tank: Do you know where your co‑op actually stands on renewing a permanent Milk Loss Program — and whether they’re truly pushing for it, or just offering sympathy when you’re the one opening the drain valve?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

DMC: The Six-Year Lock-In Gamble or a Big Beautiful Safety Net? – This strategic analysis exposes the hidden costs of the 2026-2031 lock-in, revealing how the “One Big Beautiful Bill Act” actually impacts your long-term liquidity. It provides the high-stakes perspective you need to position your operation against five years of margin volatility.

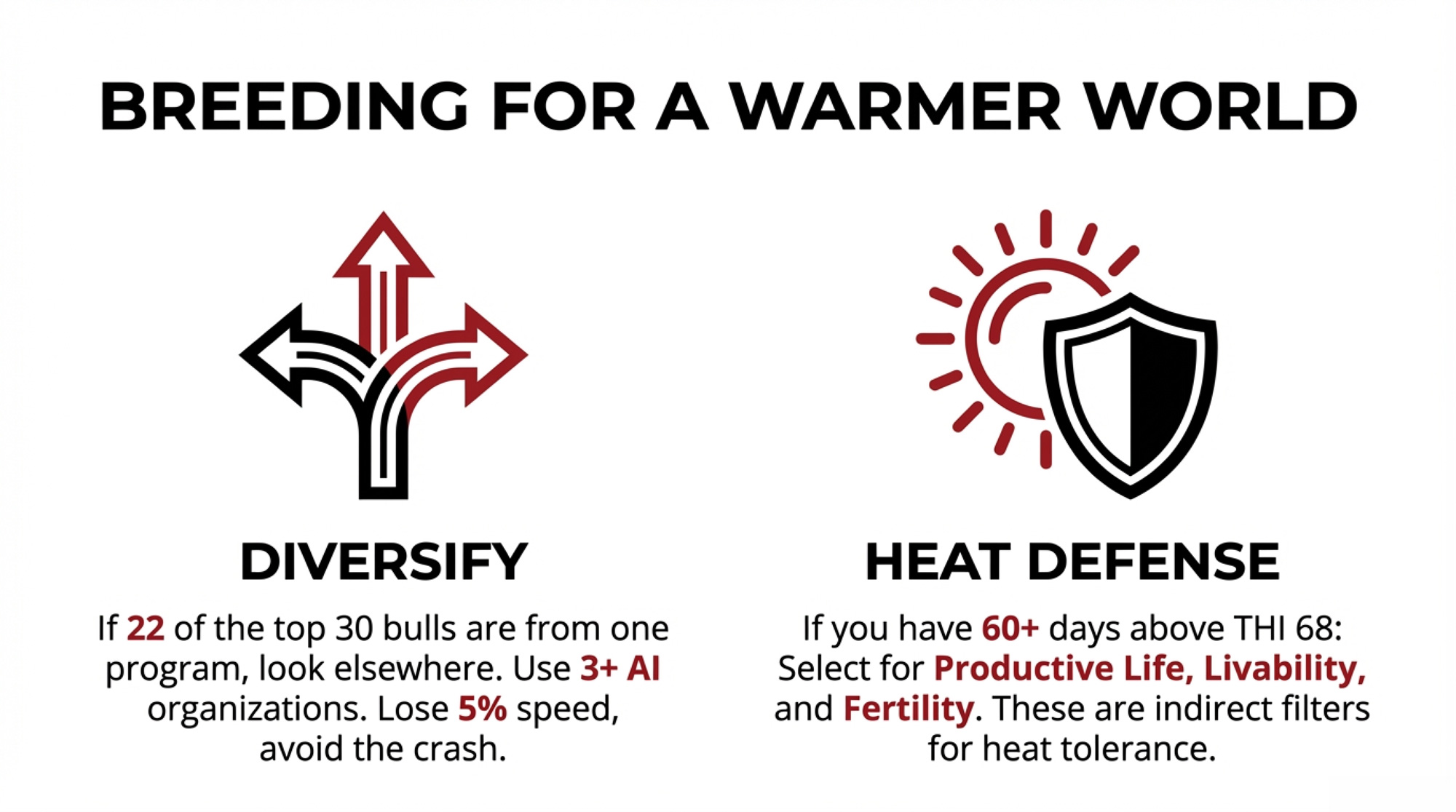

Your Top Heifers All Trace to Three Cow Families. That’s a $93,300-A-Year Trap. – This guide reveals how over-concentrating maternal lines creates a massive capital drain through inbreeding-driven frailty. It delivers a new genetic filter for your genomic sorting, reclaiming diversity and protecting your herd’s physical resilience against the next regional crisis.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

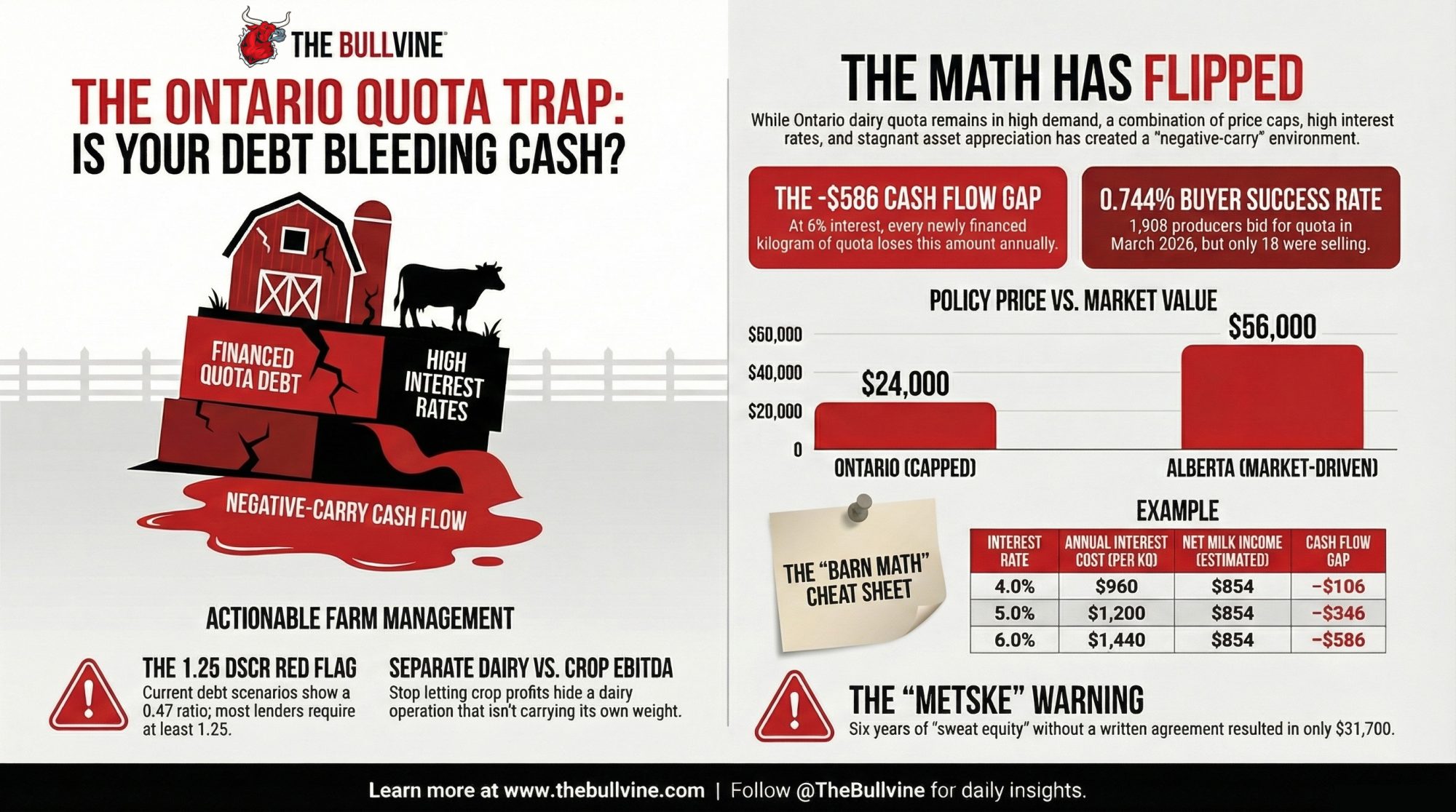

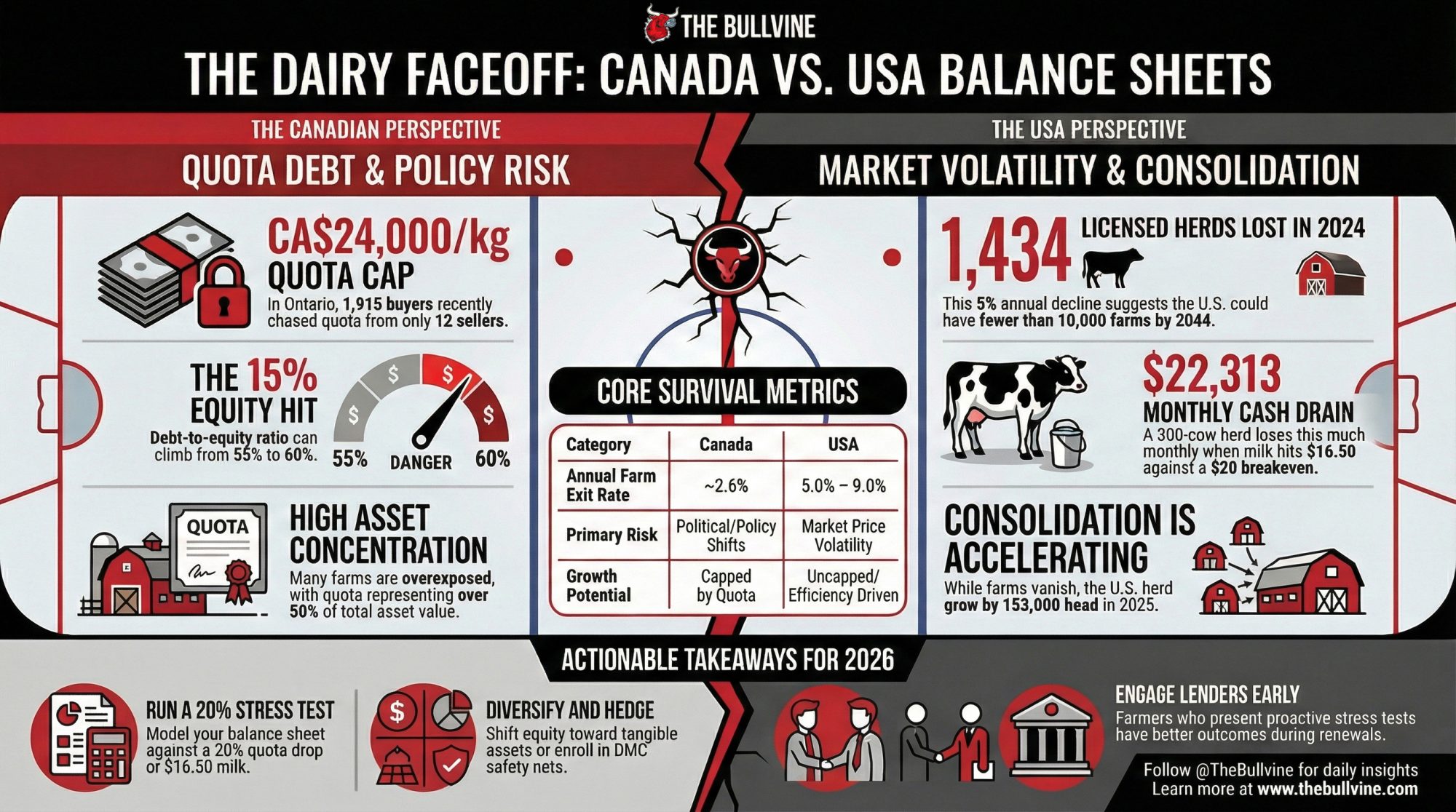

In March, 1,908 Ontario producers bid on quota. Only 190.60 kg traded. Every financed kilogram lost $586 at 6%. The math has flipped — and most farms haven’t noticed yet.

Tim and Amanda Metske ran daily operations on their parents’ 152‑acre Ontario dairy from 2012 to 2018. They invested in quota and cows during those years, working under a family understanding that they’d eventually buy the farm on favourable terms. Martin Metske had discussed a combined price of roughly $2 million — $1 million for the quota, $1 million for the land. But no purchase price, payment terms, or financing structure were ever committed to writing.

When it fell apart, the Ontario Court of Appeal — in Metske v. Metske, 2025 ONCA 418 — awarded $33,700 for tangible improvements, then subtracted a $2,000 counterclaim. Net recovery: $31,700. Six years on a 152‑acre operation carrying millions in Ontario dairy quota, and the court valued the tangible result at less than one kilogram of Alberta quota is worth today.

That number matters well beyond one family. It shows how fast sweat equity evaporates on a farm where the P5 quota cap fixes the single largest asset at $24,000 per kilogram of butterfat per day — a policy number, not a market number. And right now, the math on buying that asset has quietly turned against anyone carrying debt on it.

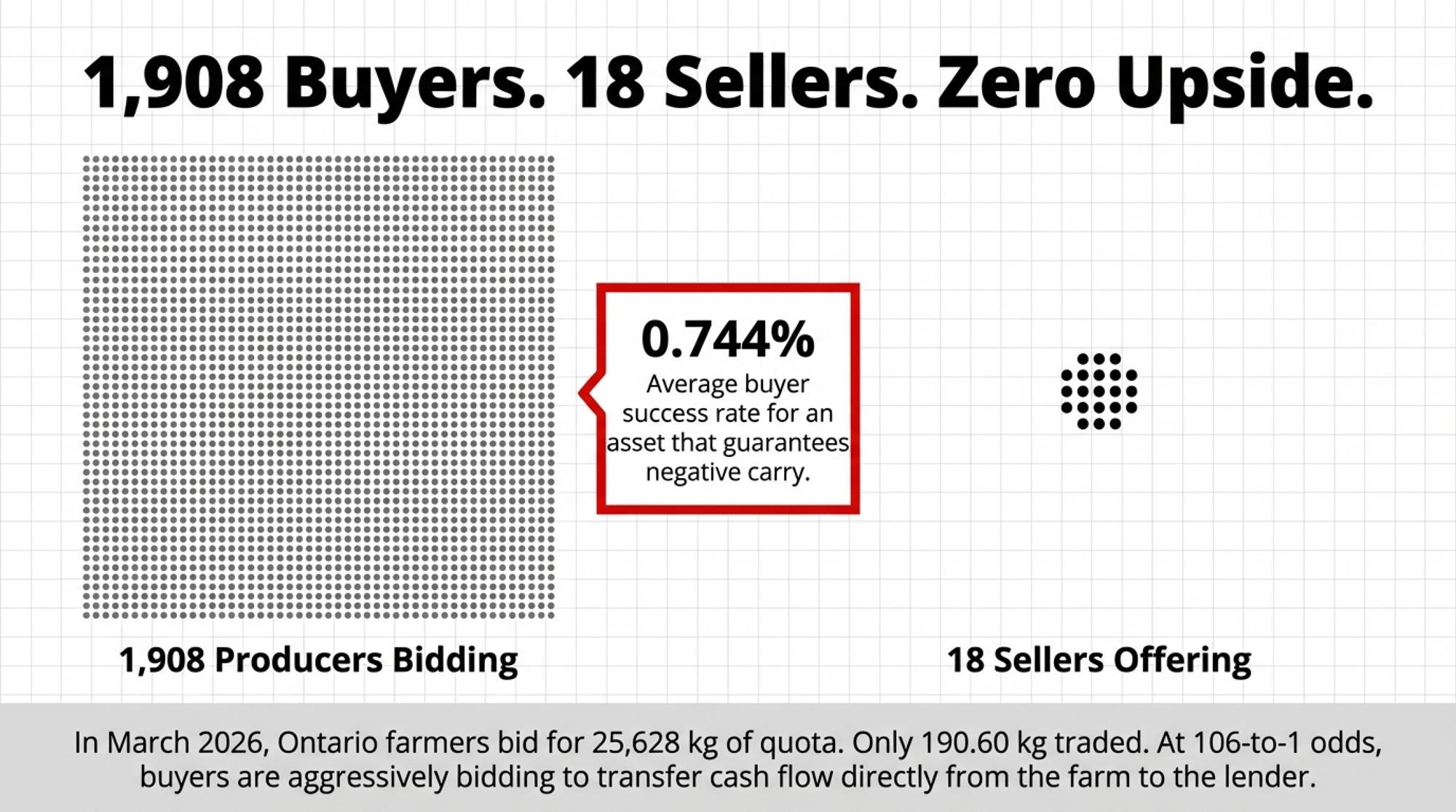

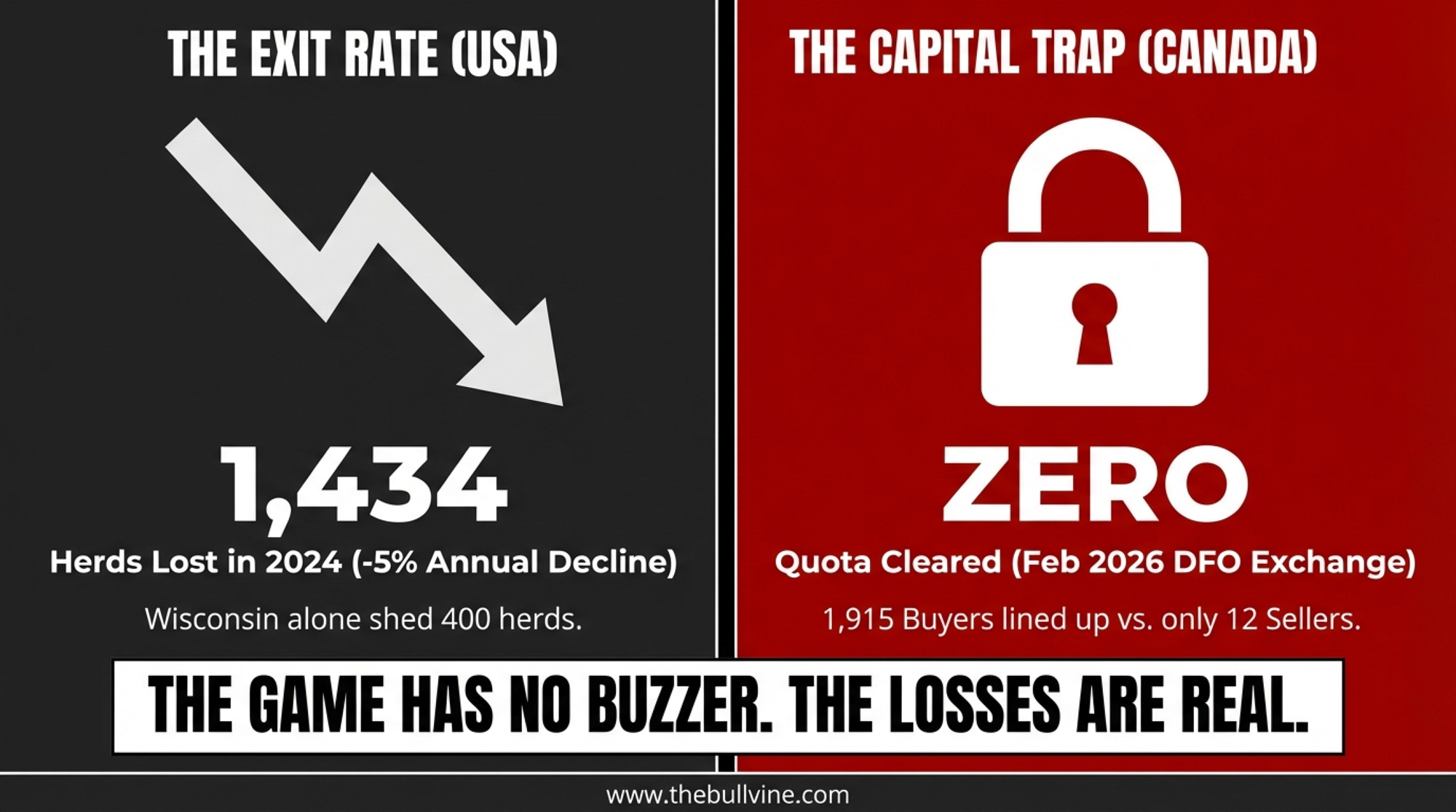

1,908 Buyers. 18 Sellers. Zero Upside.

On March 19, 2026, Dairy Farmers of Ontario released the monthly quota exchange results. The numbers are stark: 1,908 producers placed bids to buy. Just 18 offered quota for sale. All kilograms cleared at the $24,000 cap. Of the 25,628 kg bid by buyers, only 190.60 kg actually traded — what DFO’s own summary calls a “0.744% average buyer success rate.”

A month earlier, it was worse. On the February exchange, 1,915 producers tried to buy. DFO needed 191.40 kg to run even the first allotment round, but only 129.27 kg was offered. The exchange was cancelled outright. Not a single kilogram changed hands.

At roughly 106‑to‑1 by producer count, Ontario farmers are bidding into a market where each newly financed kilogram loses about $586 a year at current rates. That’s not building equity. It’s transferring cash flow from the farm to the lender.

Why Ontario Quota Stopped Growing Your Wealth

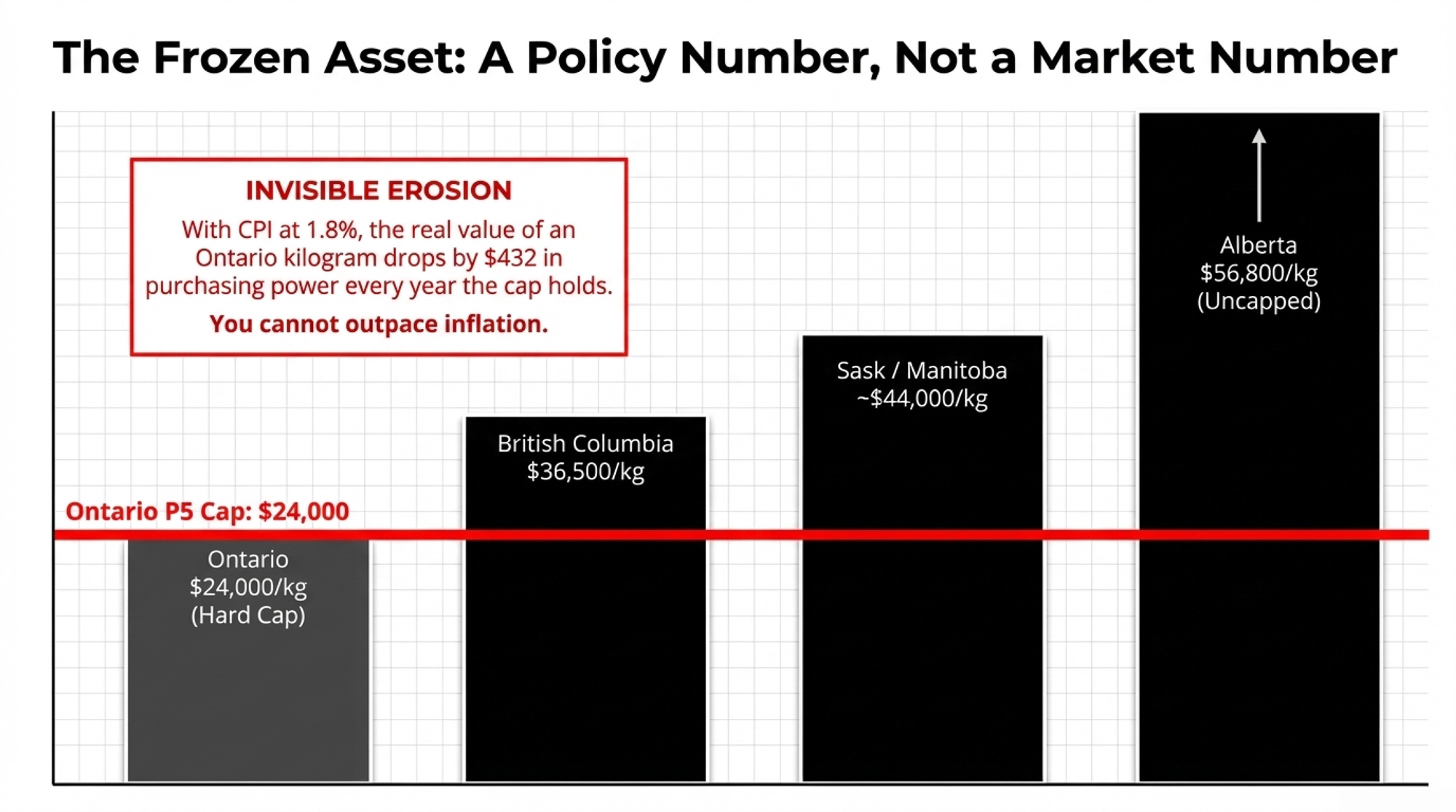

Before the P5 provinces imposed quota price ceilings, values rose steadily. Ontario prices ranged from roughly $17,000 to $22,000/kg around the 1999/2000 dairy year, according to University of Guelph research, and climbed past $40,000/kg in the 2000s before the caps took hold. That capital gain, layered on top of milk income, made quota one of the best‑performing agricultural assets in the country.

The cap shut off that tailwind. At $24,000/kg, Ontario quota is frozen. It doesn’t climb in a good year, track inflation, or compound. With CPI at 1.8% in February 2026, the real value of each kilogram drops by roughly $432 per year in purchasing power — money you won’t recover as long as the cap holds.

Metric

Ontario

Alberta

Current Quota Price (Jan–Feb 2025)

$24,000/kg(policy cap)

$56,648/kg(market price)

Gap vs. Ontario

—

+$32,648/kg

Appreciation Potential

None(hard cap)

Uncapped; market-driven*

Real Value Loss at 1.8% CPI/yr

–$432/kg/yr

Partially offset by price appreciation

Supply Management System

P5 / National

P5 / National

Annual Cash Flow at 6% Financing

–$586/kg

Negative at same rate; higher income potential

Exit Price for Seller Today

$24,000/kg (capped)

~$56,648/kg (market)

Asset Class Behaviour

Fixed liability

Appreciating asset

Look west for proof that $24,000 is a policy number, not a market number. According to AAFC’s monthly quota trade data, Alberta’s exchange averaged $56,495/kg in January 2025 and $56,800/kg in February. British Columbia — which caps at $35,500/kg — traded at that ceiling in January and at $36,500/kg in February. Saskatchewan and Manitoba traded in the $40,000–$44,000/kg range over the same two months. Ontario sits more than $32,000/kg below Alberta. Same supply management system. Same national milk pool. Radically different asset values.

Is Every Financed Kilogram of Ontario Quota Now Underwater?

Here’s the barn math. Stick it on a sticky note beside your desk.

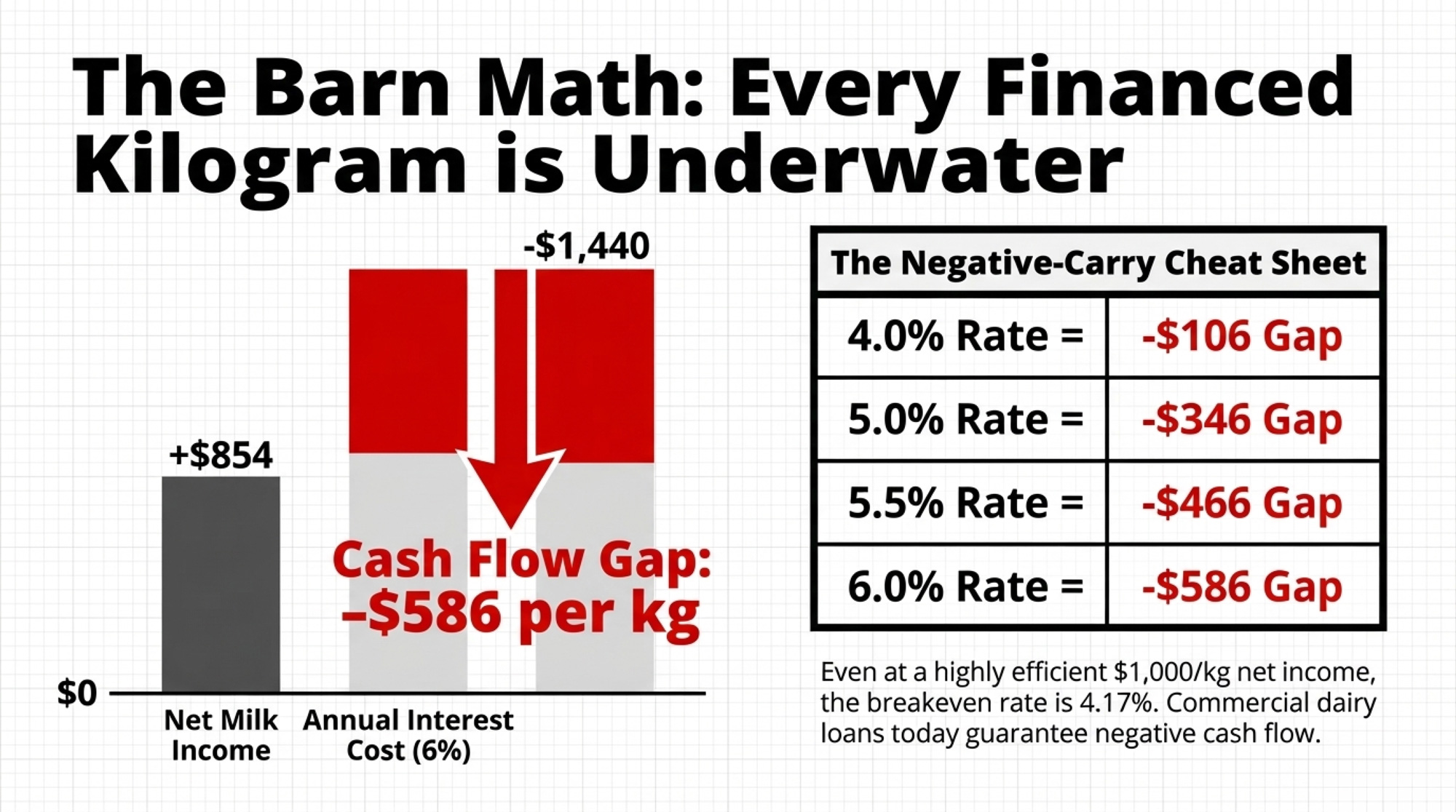

Take one kilogram of Ontario quota at the $24,000 cap. The Canadian Dairy Commission calculated the 2024 cost of production — indexed to the three months ending August 2025 — at $92.82 per standard hectolitre, up 2.72% from $90.36 the previous year. That iCOP result is what feeds the 2.3255% farmgate price increase effective February 1, 2026.

Using current P5 farmgate pricing with that increase baked in, and subtracting cost of production for feed, labour, overhead, and cow depreciation, you land in the ballpark of $854 in net annual milk income per kilogram of quotaon many Ontario herds. That’s The Bullvine’s modeled estimate using current farmgate pricing and recent P5 cost‑of‑production benchmarks — not a DFO or CDC published constant. Your own number will shift with components, feed costs, and overhead. But it’s a defensible mid‑range figure for this math.

The Bank of Canada cut its overnight rate to 2.25% on October 29, 2025, and has held it there through four consecutive decisions — December, January, March — with the next call on April 29. But commercial lenders price quota loans 200–350 basis points above that floor. A rate of 5.5–6% on a quota loan is realistic right now. Nesto’s March 2026 forecast projects no further easing, with bond markets assigning a slight probability of a 0.25% rate hike by October.

Loan Rate

Annual Interest Cost/kg

Est. Net Milk Income/kg

Cash Flow Gap/kg/yr

Rate Needed to Break Even

4.0%

$960

$854

–$106

~3.56%

5.0%

$1,200

$854

–$346

~3.56%

5.5%

$1,320

$854

–$466

~3.56%

6.0%

$1,440

$854

–$586 🔴

~3.56%

If $1,000/kg net

$1,200 (5%)

$1,000

–$200

~4.17%

At $854/kg net income, there isn’t any commercial dairy loan rate on offer today that makes newly financed Ontario quota cash‑flow positive. Even if you’re running tighter than most and clearing $1,000/kg net, your breakeven is only 4.17%. Where’s your rate sitting right now?

Scale it up. Say you’ve picked up 35 kilograms on the exchange in the past few years, all financed at 6%:

35 × $586 = $20,510 of cash leaving your operation every year

That’s interest only. No principal repayment. No new calf barn. Just debt service.

What Did Kyle Horst Find When He Ran His Own Numbers?

Kyle Horst dairy farms with his wife, Jen, and his brother Craig, a school teacher, near Formosa, Ontario. The farm has about 88 kg of butterfat quota, purchased as part of an ongoing operation in 2019.

When Horst enrolled in Chris Church’s Central Dairy Solutions course, he came in carrying the assumption most dairy farmers hold: more milk means more money. Church’s data challenged that head‑on.

“When I started the course, I always thought another litre of milk is obviously more profitable, but he brought that into question with good data,” Horst told Farmtario in August 2025. “I still think high performance through better management is a winner at the end of the day. But simply doing it through added cost is not necessarily financially sustainable.”

Church — DVM, MBA, University of Guelph, and founder of Central Dairy Solutions — spent years as a dairy vet before shifting his focus to farm finance. “I always just figured, as long as we could make more milk, we could make the farm more money,” he told Farmtario. “And that’s about as deep as we’d usually go. And unfortunately, that’s as deep as most of the producers go.” His courses walk Ontario dairies through their quota ranges, from 40 kg to 1,200 kg, using metrics such as operating expense ratio, EBITDA per kilogram of quota, and debt‑service coverage.

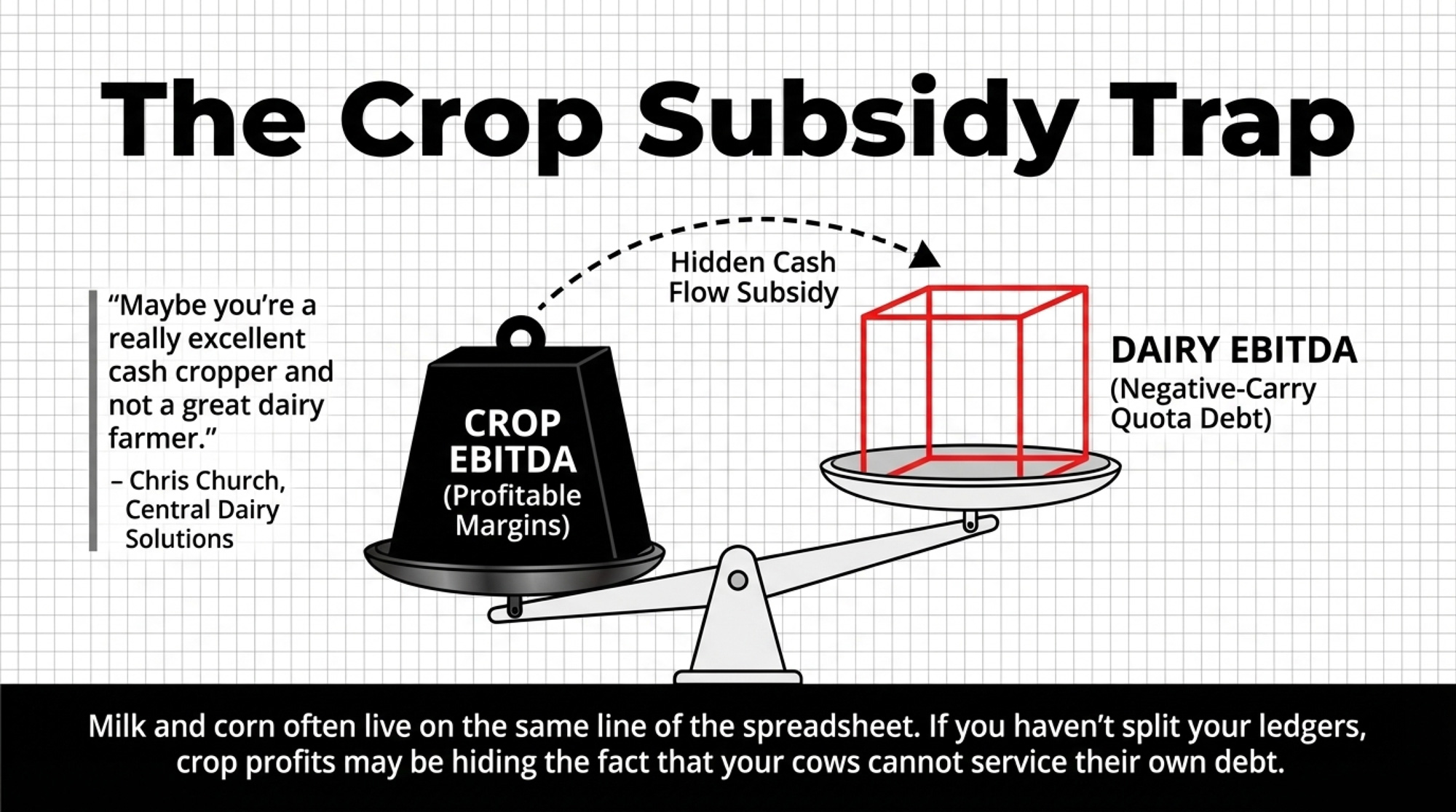

Are You Running a Dairy, a Crop Farm — or Both Without Knowing It?

The Terpstra family milks about 420 cows near Brussels, Ontario. Joe farms with his wife Barb, daughter Emily, and son Cole. Joe and Emily both took Church’s course as part of their succession planning. According to Farmtario, the family has moved to monthly financial reviews, with Emily now managing the books.

It’s exactly the kind of operation where Church’s framework — splitting dairy EBITDA from crop EBITDA — can reveal whether the cows are actually carrying their own weight or riding on crop margins.

“Maybe you’re a really excellent cash cropper and not a great dairy farmer.” — Chris Church, Central Dairy Solutions, Farmtario, August 2025

A lot of farms have never actually separated the financial performance of their dairy from that of their cropping operation. Milk and corn live in the same line on the spreadsheet. As long as the overall farm makes the payment, nobody digs deeper.

But when grain prices drop or weather punches your yields, that cross‑subsidy disappears. The dairy suddenly has to stand on its own. If it can’t, that’s when the bank meeting gets tense. And if your dairy numbers and your crop numbers live in the same line — while you’ve also got leveraged quota in the mix — you might be using crop profits to service a dairy business that, on its own, is financing a negative‑carry asset.

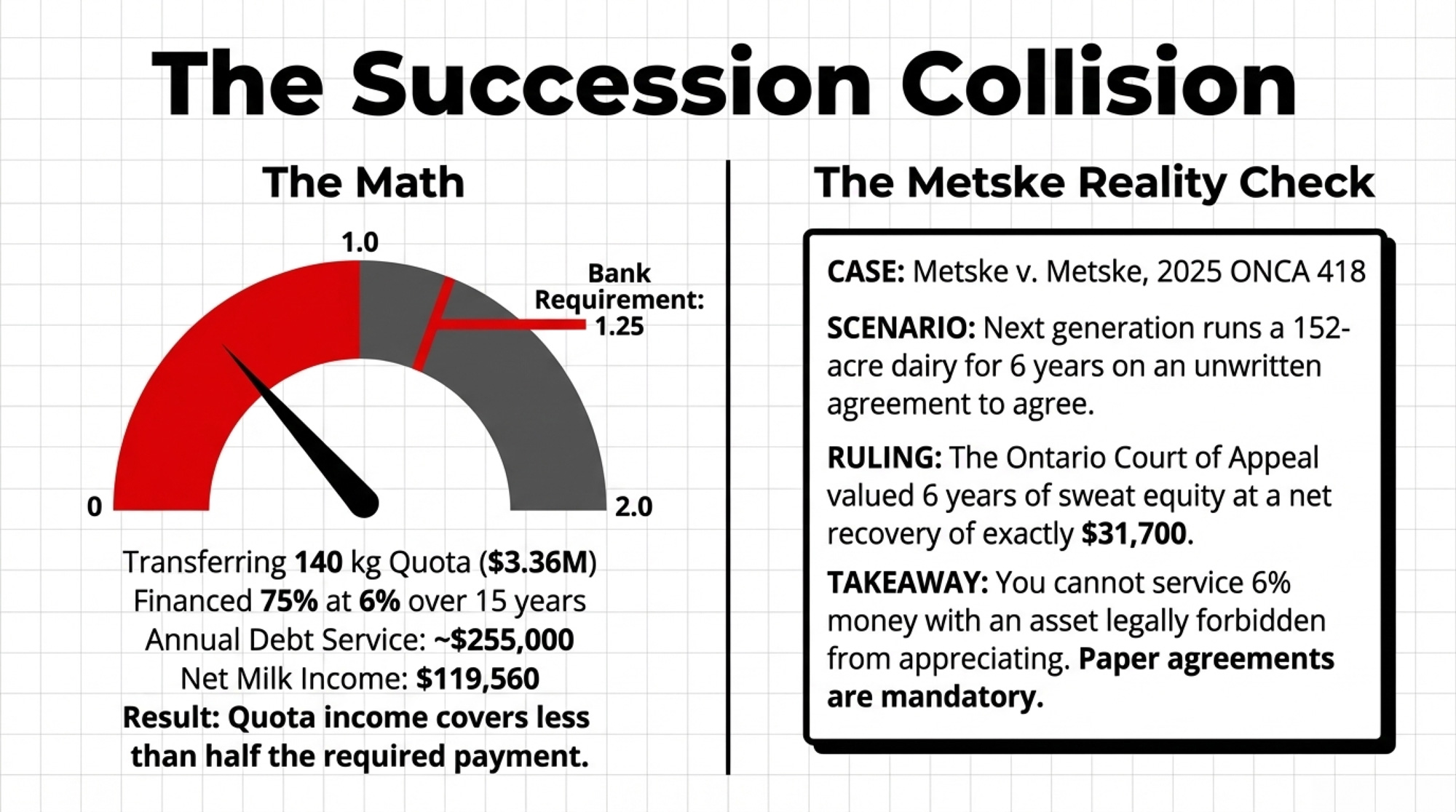

The Succession Collision

This is where the Metske ruling, the quota cap, and the interest rate environment crash into each other.

Most Ontario successions assume the next generation will take over quota — structured as a sale, a gradual buy‑in, or a gift with a vendor take‑back. However you paper it, the incoming operator still has to cash‑flow the debt tied to that quota on their own balance sheet.

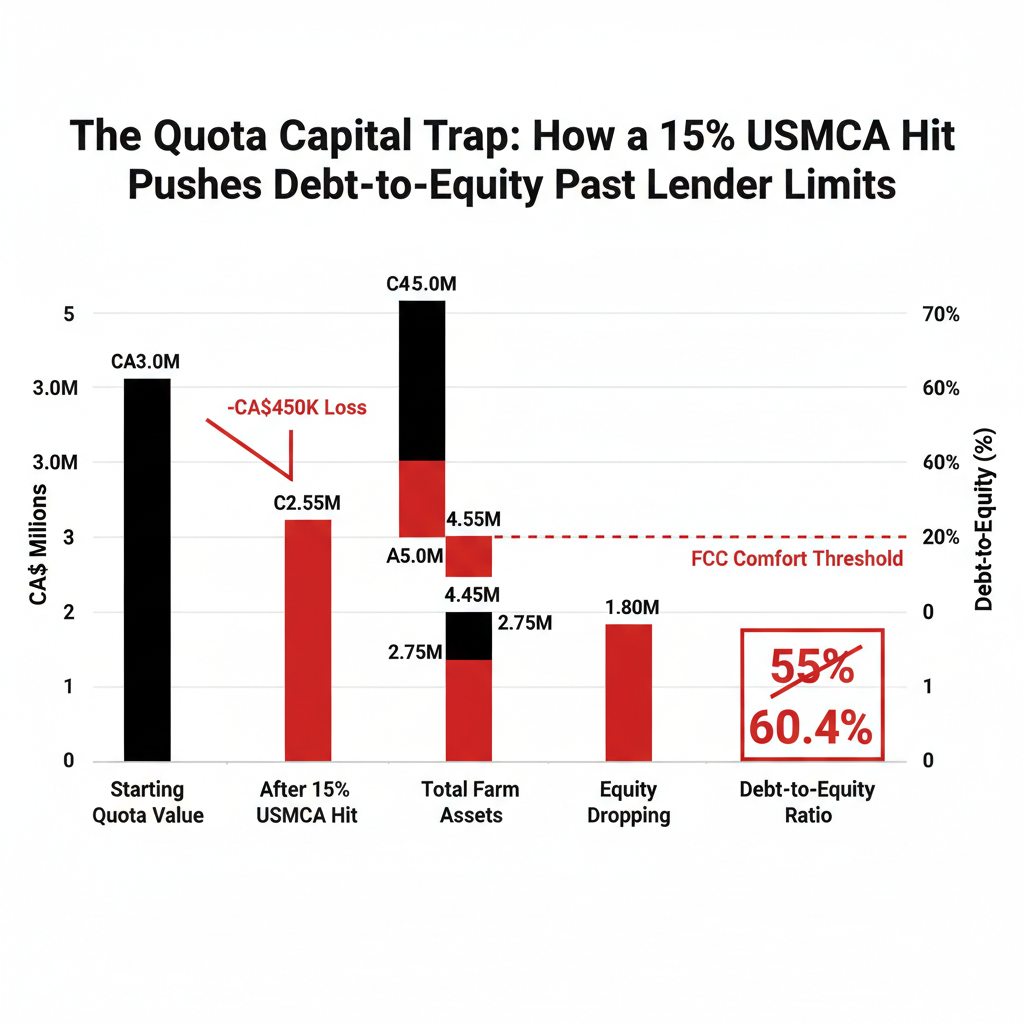

Run a DSCR on a mid‑size scenario:

Quota position: 140 kg of butterfat per day

Quota value at $24,000/kg: $3.36 million

Financing: 75% at 6%, amortized over 15 years

Loan amount: $2.52 million

Annual debt service (P+I): ~$255,000

Net milk income: 140 kg × $854 = $119,560

DSCR: $119,560 ÷ $255,000 = 0.47

Most lenders want at least 1.25. In this scenario, quota income covers less than half the payment. The rest has to come from crops, off‑farm income, parents deferring payments, or more borrowing.

In Metske, the Court of Appeal found the family’s discussions were an “agreement to agree” — too vague to create ownership rights. The parents’ decision to sell their dairy quota separately was held to be a legitimate exercise of autonomy. That’s how six years of contributed labour ended up valued at $31,700.

The P5 boards agreed to increase the saleable quota by 1% as of December 1, 2025, which will slightly dilute your share of the national milk pool. The February 2026 farmgate price bump helps offset that erosion, but doesn’t fix the structural problem: you’re trying to service 5.5–6% money with an asset that isn’t allowed to appreciate.

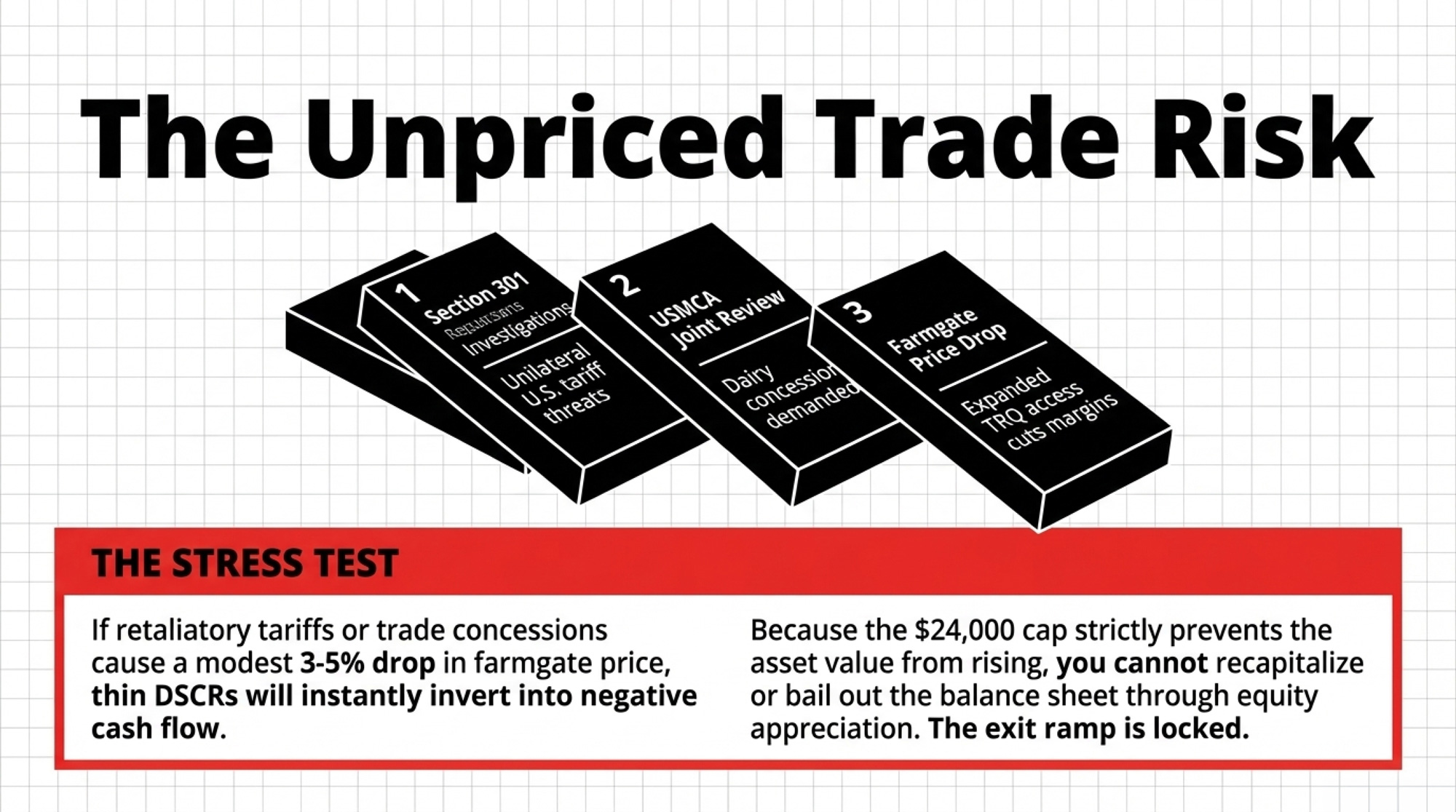

The Trade Risk Nobody’s Priced In

The CUSMA joint review is underway, and it’s not happening in a vacuum. In March 2026, the Trump administration launched Section 301 trade investigations covering Canada and 59 other economies — focused on forced labour and manufacturing overcapacity — after the Supreme Court struck down IEEPA‑based tariffs, according to CBC. USTR fact sheets and the 2026 Trade Policy Agenda make it clear these investigations will feed into the broader USMCA review.

CBC’s coverage notes that U.S. officials have repeatedly flagged Canadian dairy policies as part of a “non‑exhaustive” list of trade irritants. Dairy isn’t the only target, but it’s very much on the table.

Wiens has repeatedly warned that Canada has already conceded roughly 18% of its dairy market access in past trade deals, and that further access would cut directly into domestic production.

Carney has repeatedly said in public that supply management isn’t up for negotiation.

But a Section 301 investigation is different from a negotiation. It’s a unilateral tool the U.S. can use to justify tariffs without Canadian consent. And here’s the link between trade and succession that deserves attention: if a wider TRQ, retaliatory tariffs, or a forced restructuring devalues the exit ramp, the next generation isn’t just fighting to make the numbers work. They’re fighting over a shrinking pie — sale prices might fall at the same time debt loads stay fixed.

Here’s the stress test you can run on your own numbers: assume a modest 3–5% drop in farmgate price if TRQ access expands or tariffs bite. On a farm already running a negative‑carry quota, that price hit drops directly onto your already‑thin DSCR. If a 3–5% decline pushes you below 1.0, you’re into negative cash flow unless something else gives. The quota can’t bail you out by appreciating. The cap keeps that door shut.

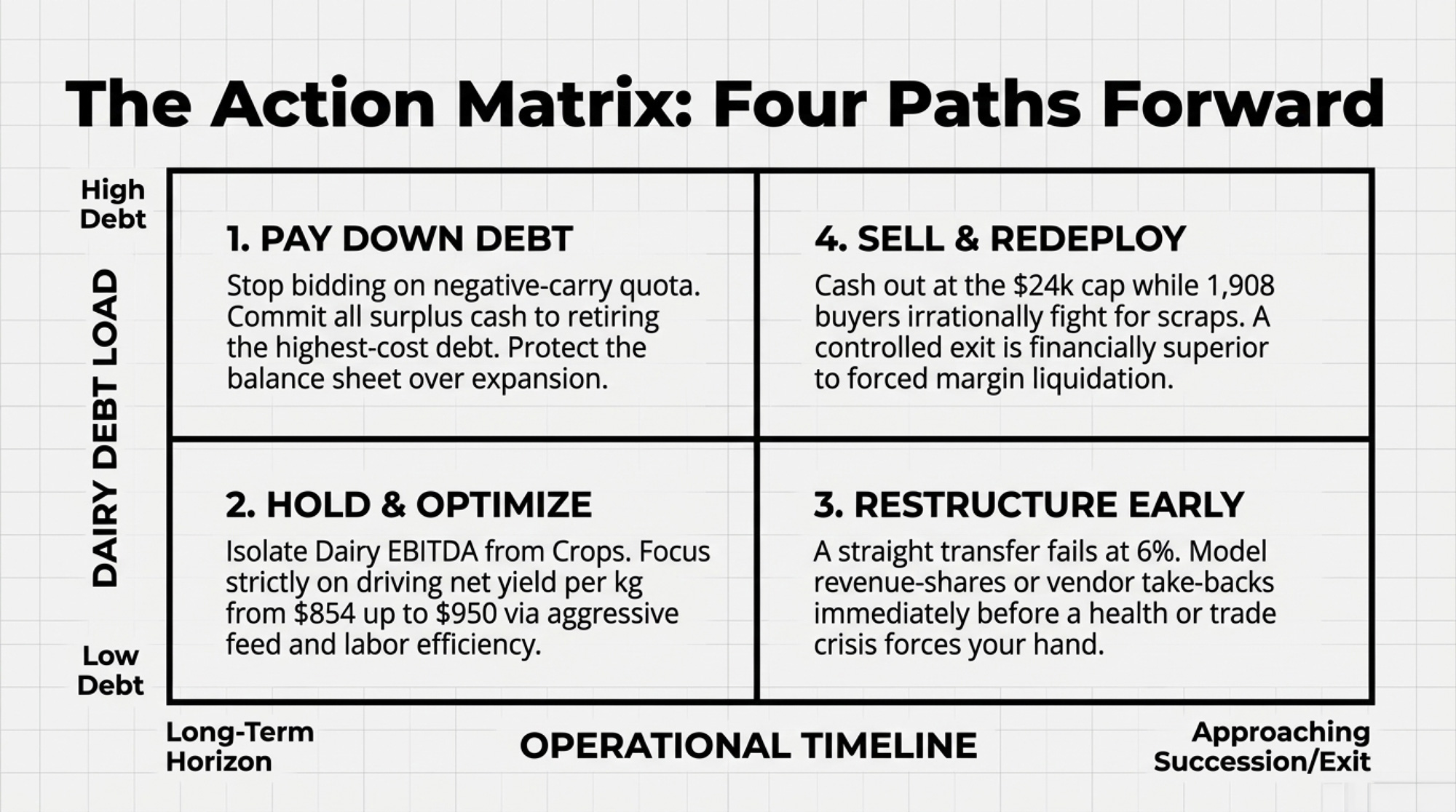

Options and Trade‑Offs for Farmers

Path 1: Pay Down Debt First — Your 30‑Day Action

When it makes sense: You’re carrying quota debt at 5% or higher, and your DSCR is hovering near or below 1.25.

What it requires: One meeting with your lender in the next month. Bring your current loan schedule and ask for a simple ranking: highest to lowest effective interest rate. Then commit your next 12 months of surplus cash to retiring the highest‑cost debt instead of bidding on new quota.

Risk/limits: You won’t grow your quota position while your neighbours might. But right now, negative‑carry quota growth is eating equity. You give up bragging rights to keep your balance sheet intact.

Signals to watch: The BoC has held at 2.25% since October 29. Bond markets currently price a small probability of a rate hike by fall. Even if they cut, commercial quota loan rates would need to drop below roughly 3.6% before newly financed quota stops bleeding cash at $854/kg net income, and below 4.17% even at $1,000/kg. Plug your own numbers into the cheat sheet above.

Path 2: Hold and Optimize What You’ve Got

When it makes sense: Your quota is mostly or entirely paid off, and your net yield per kilogram sits comfortably above your personal opportunity cost.

What it requires: Doing the Church‑style split — separate dairy EBITDA from crop EBITDA and calculate net profit per kilogram of quota. Then tighten the screws on the cost of production: feed efficiency, labour per cow, components, and cull strategy. If you’re earning around $854/kg but could push to $950 through better management, that’s the cheapest “quota purchase” you’ll ever make.

Risk/limits: Inflation quietly erodes your real equity every year the cap holds. At 1.8% CPI, that’s $432/year in real purchasing power per kilogram. You’re not building asset value. You’re milking income from a flat line.

Path 3: Restructure the Succession Before the Bank Does

When it makes sense: You’re within 5–10 years of wanting to step back, and a straight transfer at today’s values and rates produces a DSCR under 1.25 for the next generation.

What it requires: Getting uncomfortable now, not desperate later. Sit down with an ag‑focused accountant and your lender to model alternatives: longer amortizations, revenue‑share structures, vendor take‑backs with interest‑only periods, or partial transfers that let the next generation build equity gradually instead of swallowing a $3‑million loan on day one.

Risk/limits: These structures take time and trust. If you wait until a health scare, a marital split, or a CUSMA/301 shock, you’ll be negotiating with fewer options and less leverage. And here’s the trade risk tied back to your succession: if a 301 finding or wider TRQ devalues quota even 10–15%, the exit ramp the parents are counting on to fund retirement gets shorter — while the next generation faces the same debt load on a less valuable asset.

Path 4: Sell and Redeploy

When it makes sense: Your dairy only cash‑flows when crop income props it up, your debt‑to‑asset ratio keeps climbing, and your kids are lukewarm about taking over.

What it requires: Facing the hardest question in farming: is your equity better deployed in quota, cows, and concrete — or somewhere else? Selling quota into a market where 1,908 buyers are chasing 18 sellers at $24,000/kg turns paper into cash fast. That cash can fund debt elimination, retirement, or a pivot into a different enterprise entirely.

Risk/limits: The risk here is almost entirely emotional. You lose the barn, the routine, the identity. Financially, a controlled exit at the cap is far better than a slow slide into forced liquidation if rates stay stubborn and margins tighten. Right now, 1,900+ buyers are competing for scraps. Last month, the exchange was cancelled because not enough quota even made it to the table. That level of demand won’t last forever.

Key Takeaways

If your blended borrowing rate on quota is above ~3.6%, every new kilogram is cash‑flow negative. At 6%, the gap is –$586/kg/year. Even at a net income of $1,000/kg, breakeven is only 4.17%. Plug your own numbers into the cheat sheet before your next exchange bid.

If the next generation’s DSCR on quota debt alone falls under 1.25, the succession structure needs to change — not your kid’s work ethic. The Metske ruling shows where “we’ll figure it out later” ends: $31,700 for six years of contributed labour.

If you haven’t separated dairy EBITDA from crop EBITDA, you don’t actually know which side of your business is profitable. Church’s Central Dairy Solutions courses are working with Ontario farms from 40 to 1,200 kg — and the answers aren’t always what people expect.

If trade pressure devalues the quota even modestly, the exit and entry ramps both get steeper at the same time. Get the succession on paper now, while the exchange is still massively in the sellers’ favour.

What This Means for Your Farm Right Now

Before the next DFO exchange deadline, ask yourself two questions. When was the last time you ran a real DSCR on your quota loans at today’s rates? And what happens to that ratio if the farmgate price slips 3–5% for a year?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

The Metskes’ $31,700 Wake‑Up Call: What ‘Not Yet’ Costs a $4 Million Dairy – Exposes the brutal financial consequences of delaying your transition plan. It arms you with a 365-day succession playbook to protect millions in equity from the “agreement to agree” legal trap that sank the Metske family.

Beyond Efficiency: Three Dairy Models Built to Survive $14 Milk in 2026 – Reveals strategic positioning for the next five years by moving past simple volume. It delivers a blueprint for mid-tier stability through enterprise diversification, ensuring your operation remains cash-flow positive even during the harshest market downturns.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

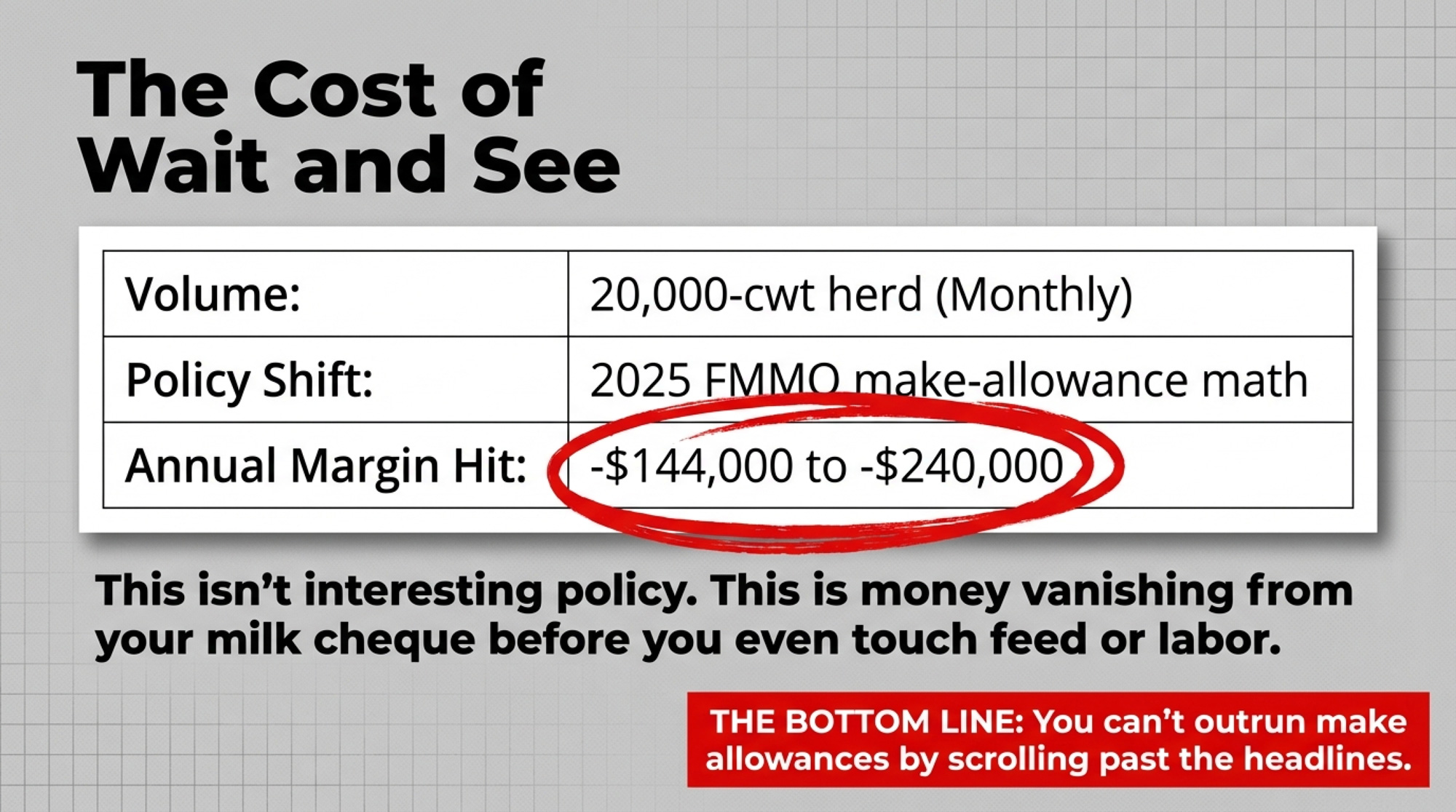

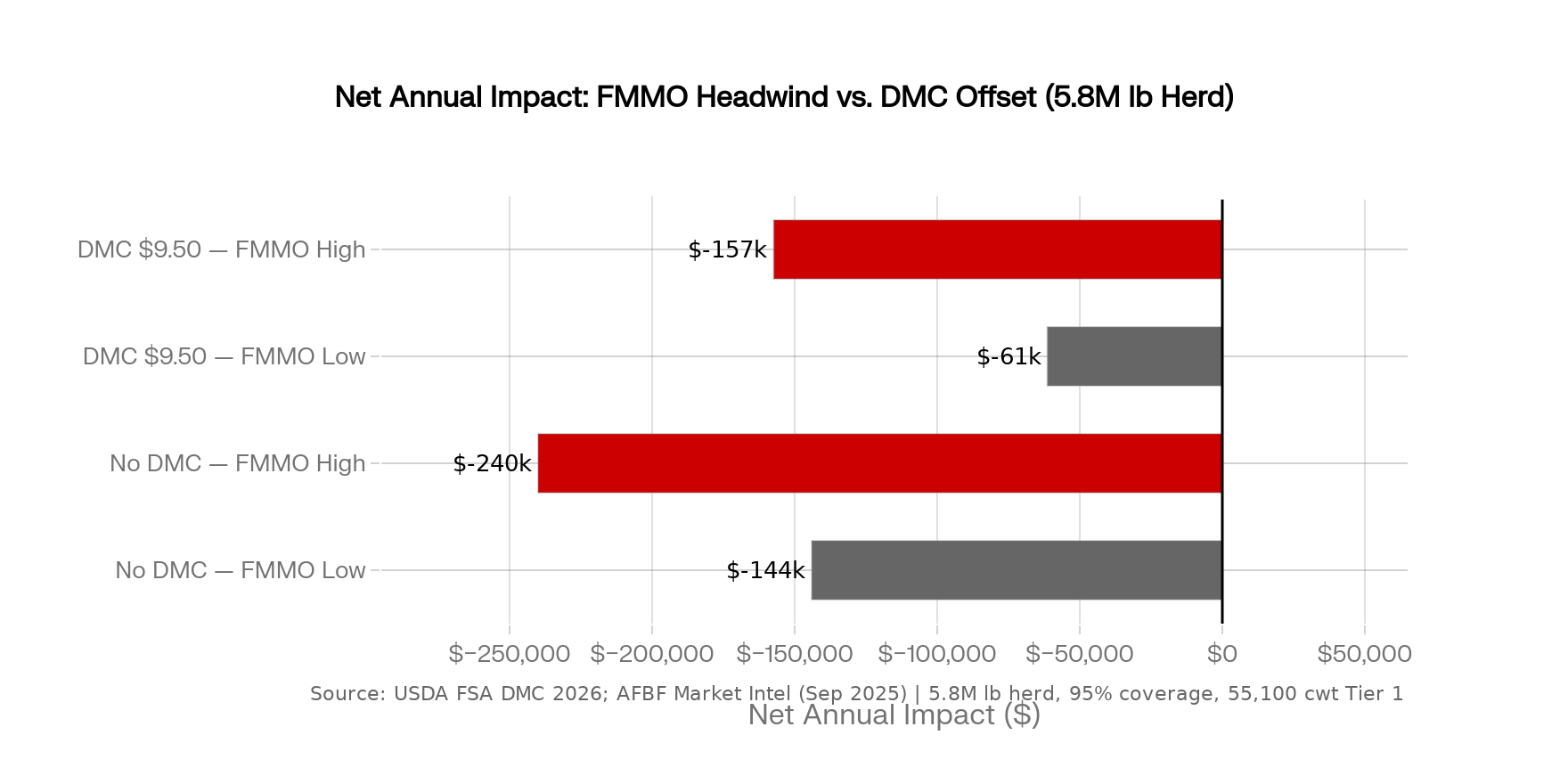

$144,000–$240,000. That’s what a 20,000‑cwt herd can lose in a year from the new FMMO make‑allowance math. Before you shrug, run it through three hard questions.

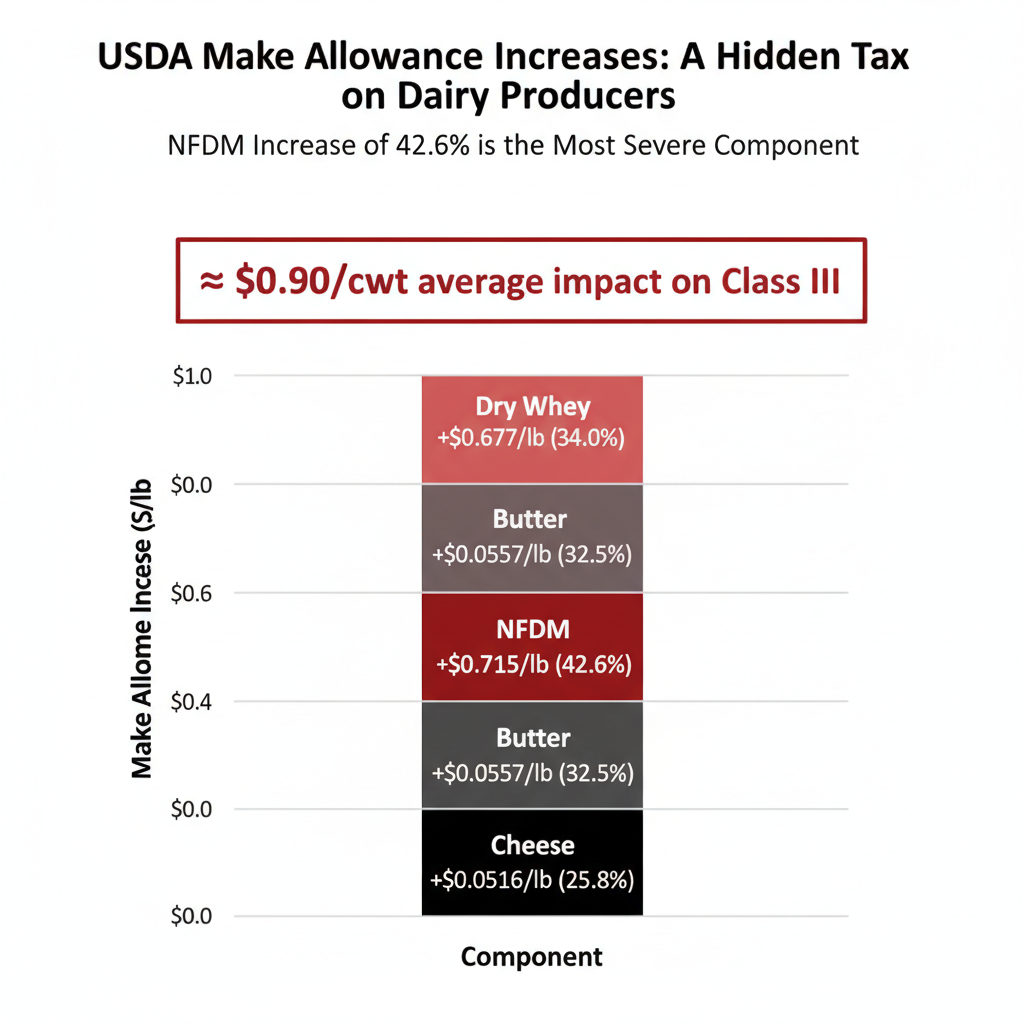

You really see it when you look at how two neighbours handle the same noise. Let’s look at Mark. He’s a composite — built from the kinds of situations central Wisconsin producers are describing this year — but his numbers are real. Mark doesn’t read Federal Register notices. He runs a commercial dairy and measures time in milkings, not hearings. When the new FMMO rules kicked in around June 1, 2025, his co‑op’s economist didn’t send him a white paper. She sent him a number: AFBF economist Daniel Munch’s September 2025 Market Intel showed roughly 85–93¢/cwt in class‑price reductions from higher make allowances — and more than $337 million pulled from producer pool value in the first three months alone.

For his order and plant mix, she translated that into a working range: expect somewhere around $0.60–$1.00/cwt less on each cheque over the next year. Mark ships about 20,000 cwt a month. At the low end, that’s $12,000 gone every month — roughly $144,000 over 12 months. At the high end, closer to $240,000. That’s not “interesting policy.” That’s whether you keep the loan officer relaxed and the feed mill paid on time.

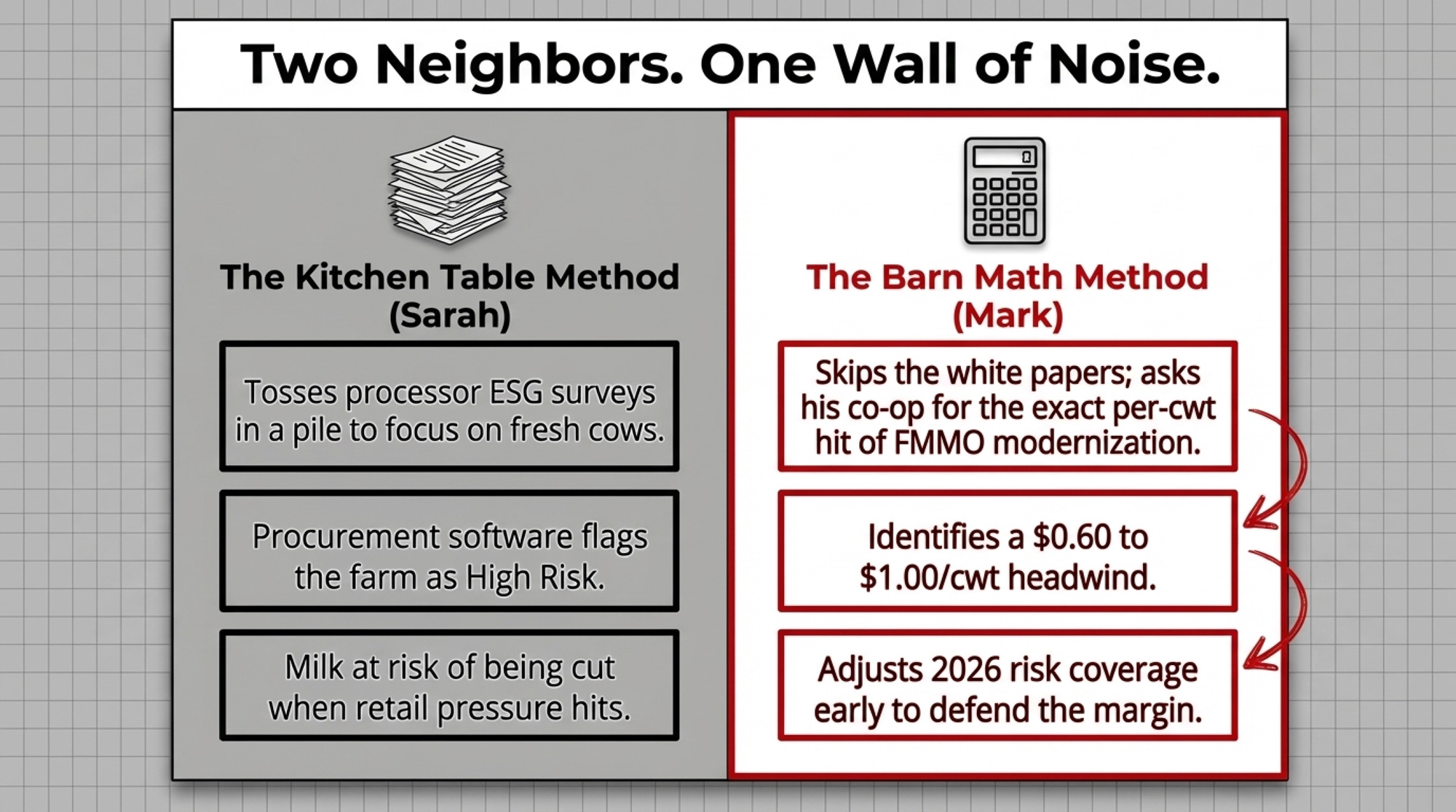

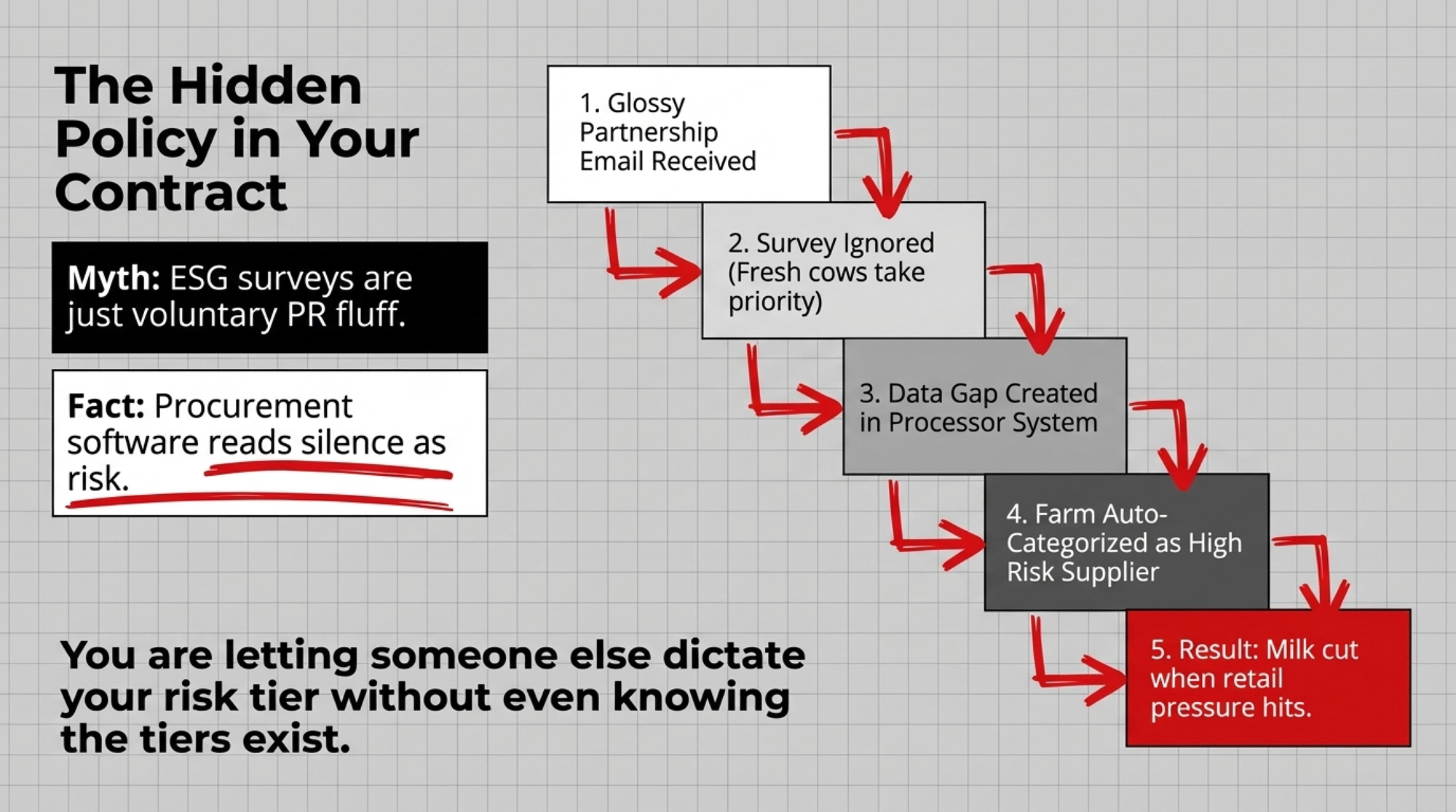

Now picture the producer down the road — call her Sarah. She’s a composite, too, built from the ESG experiences multiple farms have described to us. Sarah tossed a new “Supplier Code of Conduct” email from her processor into the pile on the kitchen table. It linked to a glossy brochure about sustainability, asked her to complete an online questionnaire about manure, energy, and welfare, and used words like “partnership” and “journey.” Fresh cows in the pen and a scraper that wouldn’t start. The survey could wait.

A year later, the tone from procurement on these programs was different at some plants. Supplier codes and ESG surveys were feeding internal risk‑sorting tools that grouped farms by perceived risk level, tied to “time‑bound corrective action” language and, on paper, potential termination if issues weren’t addressed. ESG and procurement teams were using that data to show management which suppliers looked lower‑ or higher‑risk.

Mark and Sarah faced the same wall of noise: FMMO modernization, Dairy Margin Coverage 2026 changes, USMCA review chatter, ESG pressure from retailers and banks. The difference wasn’t that Mark cared more about policy. He just ran every headline through three questions before he gave it his time. Sarah didn’t have a filter at all.

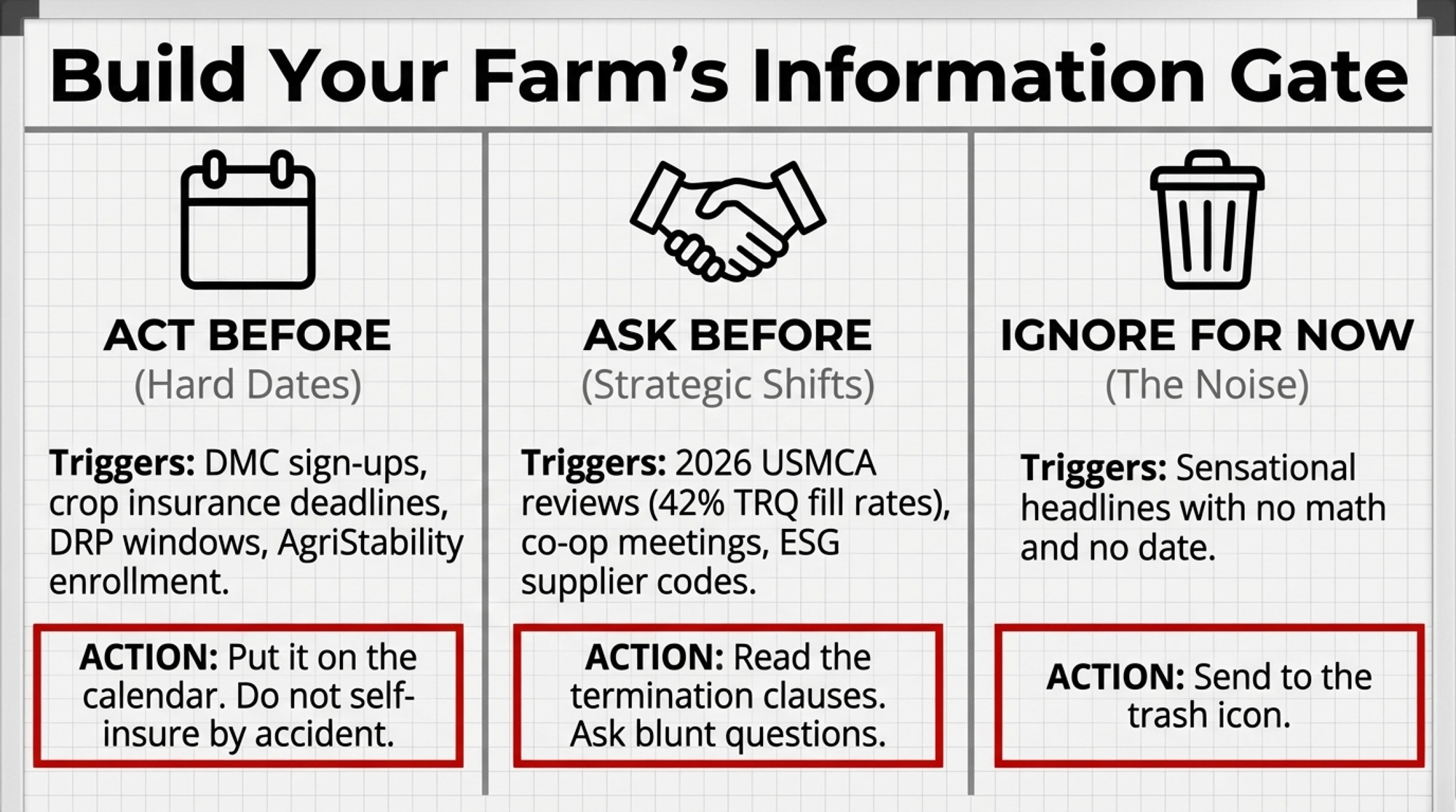

Here’s how you steal those three questions for your own operation — and stop letting policy eat hours of your week without giving anything back to your margin.

Policy Headline

Changes 12-Mo Math?

Decision Deadline

3–5 Year Ground Shift

Bucket

FMMO make-allowance changes (Jun 2025)

YES — $0.60–$1.00/cwt

Already in effect

Class I formula, pool dilution

🔴 Act Now

DMC 2026 Tier 1 expansion to 6M lbs

YES — up to $0.15/cwt savings

Feb 26, 2026

6-year lock-in at 25% discount

🔴 Act Now

USMCA 2026 joint review

Indirect — TRQ fill rates avg 42%

2026 review milestones

Market access, import competition

🟡 Watch

ESG supplier survey (processor)

Not directly — risk tier risk

Varies by contract

Audit/termination clause risk

🟡 Watch

Canada NPF 2028 consultations

No — 2028+

Jan 2026 input window

Safety net depth (AgriStability)

⚫ Ignore for Now

Carbon tax adjustments

Marginal — varies by province/state

Ongoing

Input cost creep

⚫ Ignore for Now

What’s Actually Changed — FMMO Reform 2026 and the Rest of the Noise

On the U.S. side, USDA’s final FMMO decision raised make allowances, butter, nonfat dry milk, and whey, updated product composition factors, adjusted some Class I differentials, and returned the Class I mover to the higher of Class III or IV starting June 1, 2025. In that first look‑back, Munch’s AFBF Market Intel analysis calculated that higher make allowances alone trimmed 85–93¢/cwt off class prices and removed more than $337 million from combined producer pool value in the first three months. Composition factor updates add back around $110 million over the first half‑year — real money, but it doesn’t erase the hit.

Dairy Margin Coverage shifted under your feet, too. For 2026, USDA’s Farm Service Agency reset each farm’s production history to the highest annual marketings from 2021, 2022, or 2023 and expanded Tier 1 coverage from 5 million to 6 million pounds. The 2026 sign‑up window is also your one shot to lock in a coverage level and percentage for 2026–2031 in exchange for a 25% discount on Tier 1 premiums. Enrollment opened mid‑January and closes February 26, 2026, according to FSA national and state office reminders. Miss that, and you’re self‑insuring Tier 1 for the year.

Zoom out further, and trade is humming in the background. The 2026 joint review of the USMCA will reopen questions about dairy access among the U.S., Canada, and Mexico. USMCA promised U.S. dairy roughly $200 million in new annual access to the Canadian market — about 3.6% of Canada’s dairy consumption — but tariff‑rate quota data show average fill rates of only about 42%, with 9 of 14 quotas below 50% in 2022/23. That under‑use has already fuelled formal USMCA disputes and plenty of frustration among U.S. dairy groups and negotiators.

Then there’s “policy by contract.” Supplier codes from global processors say it plainly: they only partner with suppliers who comply with environmental, welfare, and labour requirements, they reserve audit rights, and they can terminate relationships if high‑risk issues aren’t corrected. ESG supply‑chain planning guidance tells those processors to score suppliers on risk, audit the flagged ones, and prioritise low‑risk milk when retailers and banks squeeze.

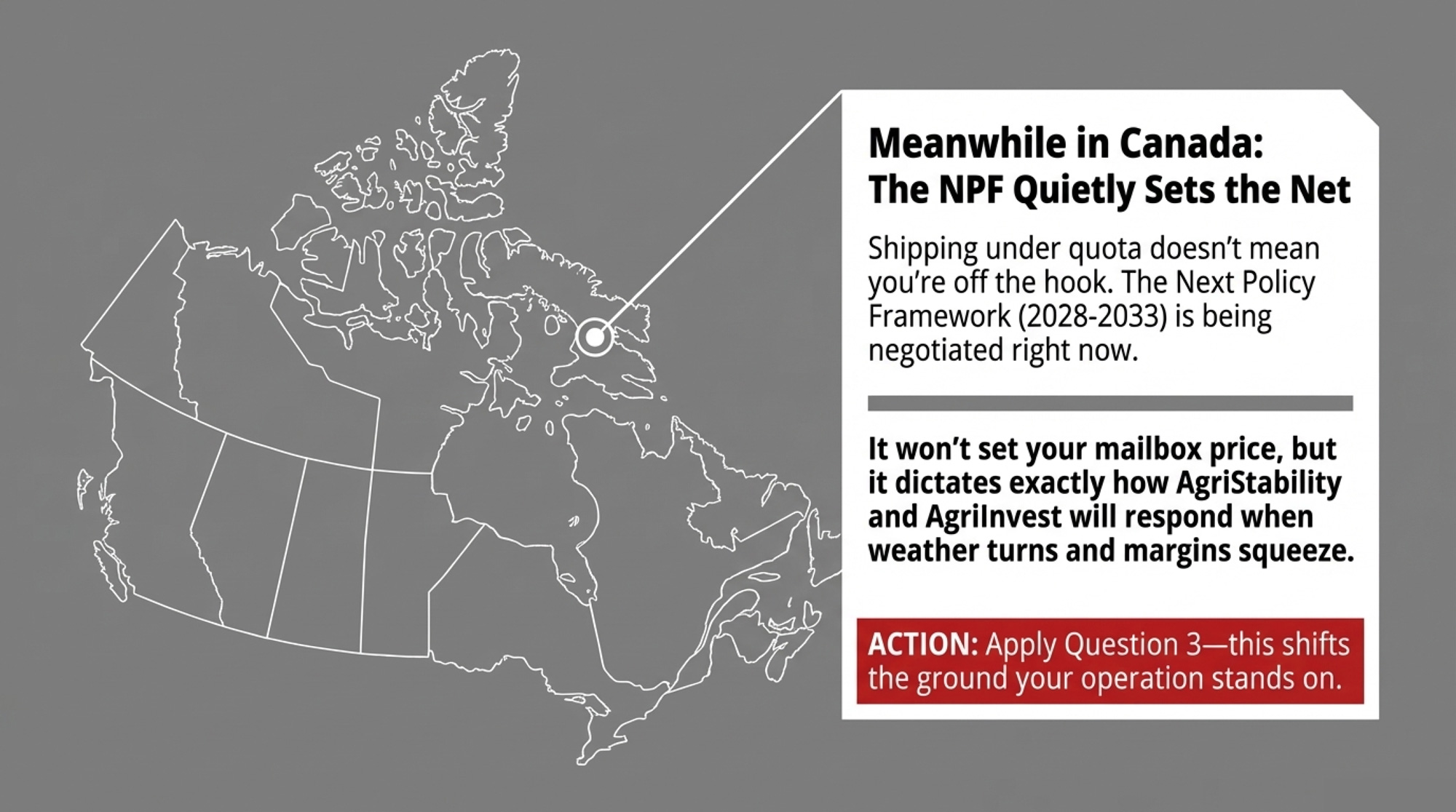

Meanwhile, North of the Border

If you’re shipping under quota, your stress looks different — but you’re not off the hook.

In Canada, the Sustainable Canadian Agricultural Partnership (Sustainable CAP) runs from 2023 through March 31, 2028, as the main framework behind AgriStability, AgriInvest, AgriInsurance, AgriRecovery, and cost‑shared sustainability and innovation programs. Ottawa launched consultations in January 2026 on the Next Policy Framework (NPF) that will replace it for 2028–2033. Federal and provincial governments are now gathering input on priorities like competitiveness, climate resilience, and risk management as they shape the next five‑year agreement.

For Canadian producers, that framework plays a role similar to that of DMC and other federal tools in the U.S. It doesn’t set your mailbox price, but it shapes how AgriStability, AgriInvest, and other supports respond when margins squeeze. You may not see “NPF 2028” printed on your milk cheque — but it quietly decides how deep the safety net is when weather and markets turn.

Every one of those pieces lands in your feed as “news.” The reality: only a few change your numbers, your deadlines, or your ground in a way that deserves more than a skim.

The Barn Math — DMC 2026 Lock‑In Versus the FMMO Headwind

Back to Mark and that FMMO reality check.

Using that 85–93¢/cwt class‑price impact range and a realistic view of his order’s utilization and plant mix, his co‑op’s economist told him to plan for something in the neighbourhood of $0.60–$1.00/cwt less on his cheque over the next year. Not a perfect model. A band you can work with.

Instead of burying that in prose, here’s how it looks on paper — with a DMC year that lines up with what you’ve already seen when margins got ugly.

Scenario

Impact per cwt

Monthly (20,000 cwt)

Annual Impact

FMMO (Low End)

−$0.60

−$12,000

−$144,000

FMMO (High End)

−$1.00

−$20,000

−$240,000

DMC 2026 Payout*

+$1.50

+$30,000

≈+$82,650 (5.51M lbs covered)

*Example uses a 5.8M‑lb production history at 95% coverage (55,100 cwt) and a hypothetical $1.50/cwt average annual DMC payment — similar to some of the worst 2019–2020 margin months when modelled over a full year; used here as a stress‑test scenario, not a forecast.

For that 5.8M‑pound herd:

Covered pounds = 5.8M × 0.95 = 5.51M lbs.

Covered cwt = 5.51M ÷ 100 = 55,100 cwt.

Tier 1 premium at $0.15/cwt for $9.50 coverage — the 2026 Tier 1 rate listed by Penn State Extension with the 25% lock‑in discount baked in — comes to 55,100 × 0.15 ≈ = $8,265.

Margin history from 2019–2025 includes several years where DMC payments at higher coverage levels more than covered annual premiums for many herds. It doesn’t take many bad months with average payments around $1.50/cwt to repay an $8,265 premium on that volume.

The ESG Side of the Cheque

Now look again at Sarah’s composite.

Her processor’s supplier code spelled out that they partner only with suppliers who comply with environmental, labour, and animal‑welfare requirements — and that they can audit farms, request documentation on emissions, energy, manure, and welfare, and require action plans if they find problems or data gaps. High‑risk suppliers get corrective action plans with deadlines. Failure to address issues can end the relationship.

That first survey email sounded optional. But in 2026, a no‑response on an ESG survey usually isn’t neutral — in many supplier‑risk systems, it’s treated as a data gap that pushes your farm toward the “higher‑risk” bucket, right alongside weak paperwork or unresolved issues. ESG and procurement teams are already using that data to rank suppliers for audits and, when things get tight, decide whose milk is simplest to keep.

ESG Response Status

How Processor Software Reads You

Typical Consequence

Timeline Risk

Survey completed, no flags

Low-risk supplier

Priority in milk volume allocation

Stable

Survey completed, gaps noted

Medium-risk

Corrective action plan requested

30–90 day window

Survey ignored / no response

High-risk (data gap = red flag)

Audit triggered; at bottom of volume-cut list

Immediate

Repeated non-response

Unacceptable supplier risk

Potential relationship termination

Contract cycle

Survey completed + audit passed

Verified low-risk

Retailer/bank ESG credit for processor

Positive long-term

Good or bad, that’s how their software reads you.

You can’t outrun make allowances by scrolling your phone. The lesson is simpler: you need a fast way to decide whether a headline belongs in your barn math, your calendar, or your trash folder.

The Three‑Question Filter That Keeps Policy in Its Place

You don’t need to enjoy politics to protect your milk cheque. You need three questions you can ask about any policy headline, email, or rumour in under two minutes.

“Does this change my math within 12 months?”

“Does this create a decision window I can actually miss?”

“If this keeps marching for 3–5 years, does it change the ground my operation stands on?”

Here’s what each one is really asking.

How Much Does This Change Your 12‑Month Math?

This is your first cut. Any change that touches your milk price formula (FMMO changes, premiums, hauling adjustments), your safety‑net math (DMC rules, AgriStability margins), or known costs (carbon taxes, labour rules, feed subsidies) deserves a quick “can I put a believable per‑cwt or per‑cow number on this for the next year?”

For FMMO, you’ve already got a starting point: AFBF’s 85–93¢/cwt class‑price hit from higher make allowances. Once you run that through your order’s utilization and your plant’s product mix, it becomes a $0.60–$1.00/cwt working range for your cheque. For DMC, FSA and Extension have already laid out how the new 6M Tier 1 cap and production‑history reset change which part of your volume gets covered cheaply.

If you can’t get to a range for your own operation with help from one or two trusted sources, you either need better sources — or that headline probably doesn’t belong in your “urgent” pile.

How Much Does Waiting 30 Days on FMMO or Dairy Margin Coverage 2026 Actually Cost?

“Wait and see” feels reasonable when you’re tired, and the numbers are fuzzy. Sometimes it is. The trick is stopping it from becoming your default answer to everything that makes your head hurt.

Take that 5.8M‑pound DMC farm. If you shrug and let February 26 slide, you’ve decided to self‑insure Tier 1 for the year — even though margin history from 2019–2025 shows several years where DMC payments at high coverage more than covered premiums for many herds. That decision might be fine if your cost of production is low and you’re comfortable riding the margin. It’s not fine if you just never sat down with a pencil because somebody forwarded a scary link about something else that failed all three questions.

FMMO is the same story. If AFBF’s analysis and your plant’s product mix suggest a realistic $0.60–$1.00/cwt headwind on average mailbox prices once everything bakes in, “wait 30 days” doesn’t improve the forecast. It just pushes back when you revisit risk coverage, tighten cost targets, or re‑evaluate expansion projects that only work at pre‑reform prices.

The real question isn’t “Could this analysis be off?” It’s this: if that range is right and you do nothing, can your operation carry it for a year at current feed, interest, and labour? If your gut says no, waiting isn’t neutral anymore.

Is Your Contract Language Already Writing Policy for You?

On the operational side, a lot of the policy that will matter most to your farm over the next five years isn’t hiding in Parliament or Congress. It’s in contracts.

Supplier codes from global dairy companies are clear on three points. They expect compliance with specific environmental, animal‑welfare, and labour standards — often referencing local law and sometimes going beyond it. They reserve the right to audit your operation, request documentation, and require action plans if they identify problems or data gaps. And they give themselves the option to end relationships with suppliers who don’t correct high‑risk issues within set timelines.

ESG planning guidance tells these companies to categorise suppliers as low, medium, or high risk, then prioritise lower‑risk suppliers when squeezed by retailers, banks, or emission‑reduction commitments. Data you send — or don’t send — in that first “voluntary” survey directly feeds those scores.

If you haven’t read the ESG, audit, and termination sections of your own supplier code or milk contract in the last year, you’re letting someone else decide what risk tier your farm occupies without even knowing the tiers exist. You might be perfectly comfortable where you are. Or you might find out you’re at the bottom of the list only when volume cuts land on your desk.

Options and Trade‑Offs for Farmers

You can’t turn the policy tap off. You can decide how much gets past your gate. Here’s how producers are using the three‑question filter — and what each path demands.

Barn Math First, Politics Later

When it makes sense: You’re already using at least one risk tool (DMC, DRP, crop insurance) and you’re comfortable with a pencil and a calculator.

What it requires: Any time a big headline shows up — FMMO tweaks, DMC changes, USMCA review drama, ESG survey — ask yourself: “Can I get a credible per‑cwt range for this on my farm in the next 12 months?” If yes, what does that look like on your monthly cwt? Lean on one or two trusted sources for the heavy lifting — your co‑op economist, Extension, or a piece that translates policy into cheque math.

Risks/limits: If you don’t have those sources, you risk either underplaying real hits (like making allowances) or overreacting to noise. And barn math is only as honest as your breakeven — if the base numbers are fiction, the filter won’t save you.

The Calendar and Contract Gate

When it makes sense: You’re not spending evenings reading market intel, but you’ll respect hard dates and signatures.

What it requires: Put a single sheet or whiteboard in the office with three columns: “Act Before,” “Ask Before,” and “Ignore For Now.” “Act Before” gets DMC sign‑ups, crop insurance deadlines, DRP windows, and any AgriStability/AgriInvest enrollment dates on your side of the border. “Ask Before” applies to the USMCA 2026 review, co‑op meetings, and any session where your buyer explains their plan. “Ignore For Now” gets headlines that don’t pass any question and carry no date.

Risks/limits: If nobody owns updating that sheet weekly, it becomes wallpaper. Someone — you, a partner, the family member who actually reads this stuff — has to be the designated filter and move items between columns as things develop.

Treat ESG as Contract Risk, Not PR

When it makes sense: Your milk goes to a processor selling into big retail or export markets, and their website is full of “net‑zero,” “scope‑3,” and “responsible sourcing” language.

What it requires: Read every supplier code, sustainability annex, and contract update your buyer sends. Highlight anything about ESG data, audits, “continuous improvement,” or termination. Ask blunt questions: “If I don’t fill out this survey, what happens to my status?” and “Are you scoring suppliers? If so, how?” You don’t have to like the answers. But you’re making decisions with eyes open instead of assuming good farming speaks for itself.

Risks/limits: This won’t stop ESG from coming. It keeps you from being blindsided when procurement starts treating ESG like quality or SCC. If you strongly disagree with the direction, the bigger decision is whether to stay in that buyer’s system at all.

Install a Designated Filter in 30 Days

When it makes sense: You’re running 200–500 cows, you don’t have a “policy person,” and every week someone different is forwarding “urgent” links into the family group chat.

What it requires (within 30 days): Choose one person — the owner, a partner, or a family member who actually reads — and make it their explicit job to filter the policy. Give them 20–30 minutes once a week to run every headline, email, or rumour through the three questions and sort them: “Act Now,” “Watch,” or “Noise.” Only “Act Now” items go on the weekly meeting agenda. “Watch” items get a look at the end of the month. “Noise” dies on their notepad.

Risks/limits: Only works if everyone agrees to respect the filter. If you still treat every Facebook thread like an emergency, you’re back to chaos. But if you back the filter, you trade random panic for a predictable, small time cost that protects a very large cheque.

Key Takeaways

If you can’t get to a realistic 12‑month per‑cwt impact for your own volume, a policy headline doesn’t outrank chores. Ask your co‑op, Extension, or a trusted source to turn it into barn math first.

If there’s a date on it — DMC signup, a USMCA review milestone, a supplier‑code acknowledgment, a contract auto‑renewal — treat it as a decision window, not background noise. Saying nothing before the deadline is still a decision; it might not be the one you’d pick on purpose.

If your main buyer talks about ESG, net‑zero, or “responsible sourcing,” treat supplier codes and sustainability surveys like policy notices, not marketing fluff. Read the audit, data, and termination clauses and decide whether you’re willing to live in the tier they assign you.

If your production history sits between 5 and 6 million pounds, the 2026 DMC upgrade to a 6M Tier 1 cap and six‑year lock‑in changed your numbers enough that “same as last year” isn’t a safe default. Run the new math or call your FSA office now.

If your order’s best estimates point to a $0.60–$1.00/cwt headwind from FMMO changes once make allowances and utilization settle, ignoring it isn’t neutral. Either your balance sheet carries that for a year, or you adjust risk coverage, costs, or capital plans now.

The Bottom Line

The three questions didn’t make the noise go away for producers like Mark. They made it obvious which pieces belonged in barn math, which belonged on a calendar, and which belonged in the trash icon. Farms like Sarah’s didn’t have that filter. By the time they realised their “voluntary” ESG survey had been feeding into a risk-tiering system, their buyer already had a list of farms flagged as harder to keep when things got tight.

So, does your operation look more like Mark’s — pencil to cheque, questions before panic — or more like Sarah’s, finding out about the tiers a year late?

The question isn’t whether policy is getting louder. It’s whether, if FMMO tweaks, a missed DMC cycle, or an ESG‑driven contract change knocks $0.75/cwt off your cheque next year, you’d catch it early enough to move — or hear about it from a neighbour in the parlour after the fact.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The Hidden Contract Clause That Could Cost Your Dairy $55,000 in 2026 – This report uncovers high-stakes liability shifts in 2026 milk contracts that could erase 44% of your net profit. It delivers an immediate 30-day survival checklist to dodge these disruptive costs and protect your family equity.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

They started with grade cows and manure on their trousers. They built every genomic proof you chase today.

The year was somewhere in the mid‑2000s, and if you were lucky enough to lean on the rail at World Dairy Expo with a coffee in your hand, you felt it. The big banners and spotlights still belonged to the cow show—the Goldwyns, the Durhams, the glossy strings from famous prefixes—but when the sire lists went up on the bulletin boards outside the Coliseum, a different set of names rose to the top in black and white: Durham. Goldwyn. O‑Man. Rudolph. Shottle. Marshall. Mountain.

Now, the thing about that era is this: if you judged the future by those glossy ads and center‑spread photos, you’d have sworn the next great sires would all come out of investor barns with brass nameplates and full‑time fitters. But what a lot of people didn’t realize was that the real engine of change was turning miles away—in grade‑started herds where the breeder’s trousers were more likely streaked with manure than show sheen, and where the biggest “promotion” was a good proof and a paid‑off feed bill. Between roughly 1991 and 2010, a handful of farmer‑bred bulls, show‑ring architects, and fitness warriors quietly built the cow population that genomics would later “discover.”

Most of those bulls and cows are long gone now, except in the pedigrees. This is the story of how they earned their place there.

Act I – Hillsides, Sale Rings, and the Bulls Nobody Expected

If you want to understand how this Golden Age began, you don’t start in Madison or Toronto. You start on a Vermont hillside in 1946.

Everett’s Hills and the Mathematics of Manure

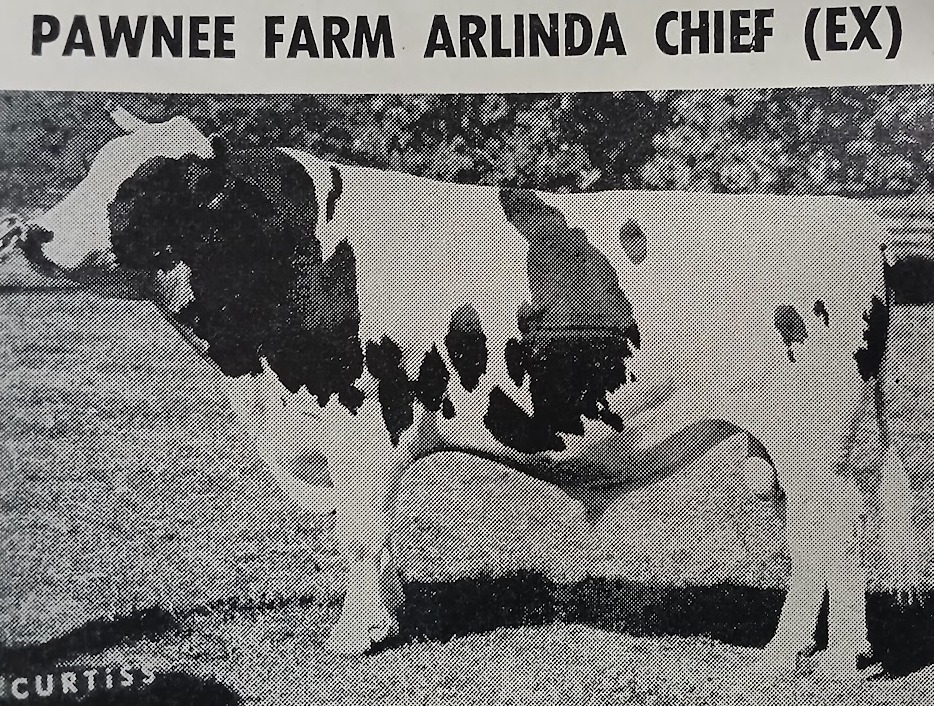

Bis‑May Farm sat in the rolling hills around Moretown, Vermont, about 17 miles west of Montpelier. It wasn’t a show palace. Everett and his father, Ralph, started with a grade herd; a few cows had papers, but most just had to earn their keep in a tie‑stall barn where every empty stanchion hurt. In 1950, they bought Kearsarge Governor Jean from C. Leland Slayton in New Hampshire, and a few years later, Everett’s fascination with the old Mount Victoria Rag Apple cattle pushed him to buy nine Canadian cows rich in Rag Apple blood, including Marie Pabst Lochinvar.

Through his college years, Everett had pored over Holstein‑Friesian World, thumbing through pictures of Montvic Rag Apple Gladiator and the rest of Thomas Macaulay’s great cattle. The Mount Victoria dispersal had already happened in 1942. The sale was over. But in his mind, those cows still had something to say.

Here’s the thing—Everett believed the math. There are thousands of farmer‑breeder herds. There are only a handful of Pabsts, Skokies, and Carnations. If great sires come from good cows, and there are vastly more good cows in ordinary barns than in famous ones, where do you think most of the real genetic power is hiding?

When he became chairman of the little Central Vermont Breeding Association, whose entire A.I. battery was Jersey bulls, he pushed the group to buy a Holstein: Walker Homestead Dawn, proven at Howacres in Vermont for high butterfat test and “exceptionally good type.” They did. Everett used him so heavily that when Dawn died, he bought 100 extra doses and kept right on breeding Dawn daughters.

Out of that web of grade cows, Rag Apple immigrants, and Dawn blood came three bulls no one would have picked out of a show catalog: Bis‑May Astro Jupiter, Bis‑May Tradition Cleitus, and Bis‑May S‑E‑L Mountain.

Mathematical probability, with manure on its boots.

Jupiter: Astronaut’s “Second Son” and the Brood Cow Maker

In the Paclamar Astronaut era, the headlines went to Bridon Astro Jet, and rightly so. But at Eastern A.I. in Ithaca, New York, there was another Astronaut son quietly doing the heavy lifting: Bis‑May Astro Jupiter, born in 1972. He was out of Bis‑May P Admiral Jana VG‑88‑GMD, a high‑lifetime Irvington Pride Admiral daughter backed by Bis‑May Homestead June, one of Everett’s precious Walker Homestead Dawn cows.

Jupiter’s daughters had that farmer’s wish‑list look—usually only medium for stature, but wide in the muzzle and chest, deep in the rib, and carrying big, capacious rear udders that could hold up to full meters of milk. The New York cow Welcome Jupiter Gala VG‑GMD‑DOM put up 31,360 pounds of milk at 4.1 fat as a 2‑11 365‑day record—a state record when she made it. When you asked her breeder, Bill Peck of Welcome Stock Farm, what kind of cow he wanted to breed, he’d tell you: “wide in the muzzle, wide in the chest, and wide in the udder.” When you asked which family did that best, he pointed straight at the Jupiter Galas.

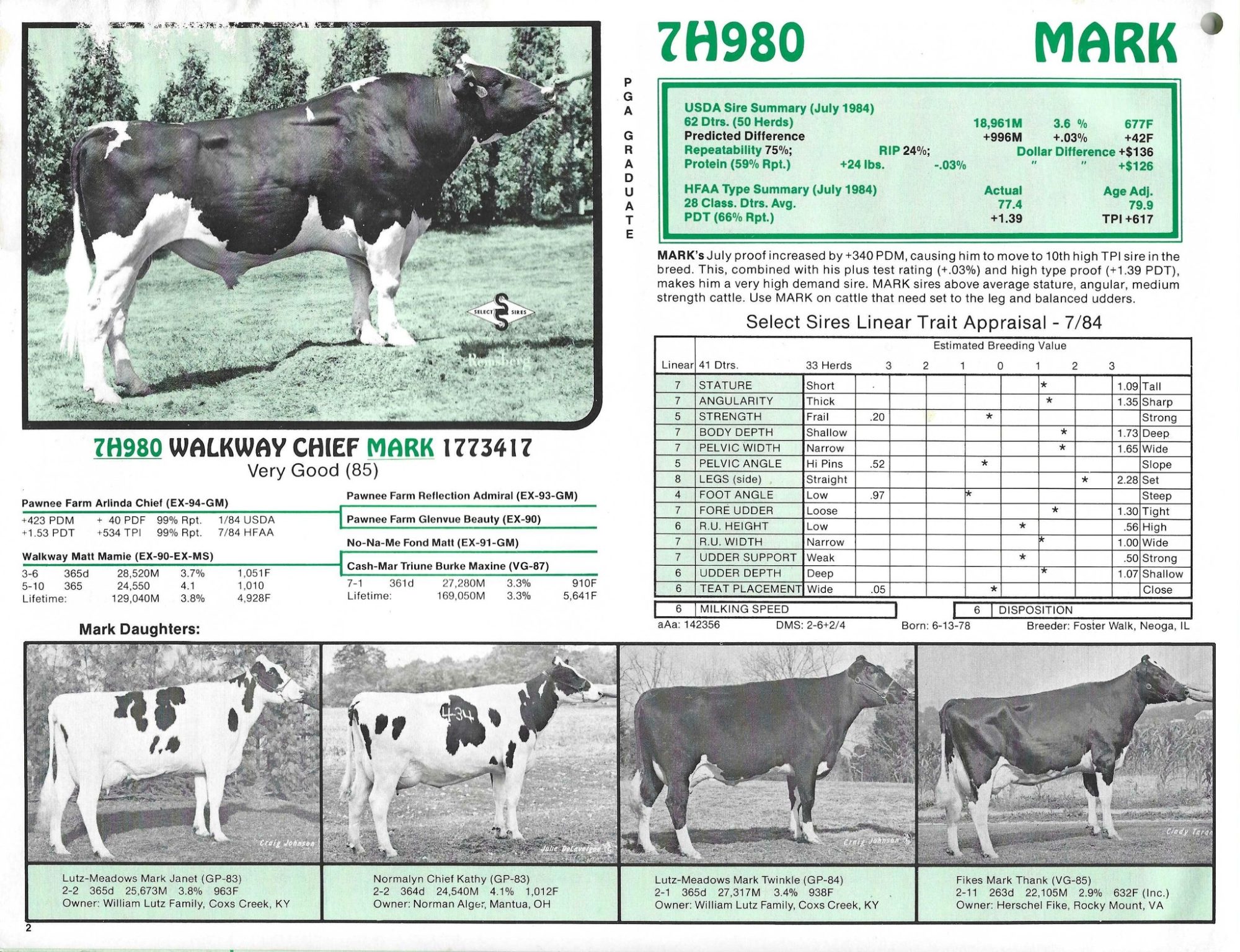

Gala’s daughter, Welcome Valiant Gingersnap VG‑GMD‑DOM, produced Mark CJ Gilbrook Grand VG‑GM by Walkway Chief Mark, and Grand, in turn, became the double grandsire in the pedigree of Braedale Goldwyn—siring both Shoremar James (Goldwyn’s sire) and Braedale Gypsy Grand (Goldwyn’s maternal granddam).

So every time you see a Goldwyn daughter step into the ring at Madison, there’s a little strand of Bis‑May Astro Jupiter and Walker Homestead Dawn hiding in the fine print of that pedigree.

On the home farm, another Jupiter daughter, Bis‑May Jupiter Mabel VG, made a top record of 31,159 milk, 3.6 fat, and 3.3 protein—but she only classified Good Plus for udder. Her dam line, back through Zion‑View Amys Prince and U.N.H. Burke Ideal Graduate, was all about body capacity and power. The Maynards bred Mabel to the udder specialist Cal‑Clark Board Chairman, and the resulting daughter, Bis‑May Chairman Merri VG‑87‑DOM, made two heifer records, both over 28,600 pounds, with 3.3 protein.

Midway through Merri’s second lactation, they flushed her to Lekker Valiant Royalty. When they consigned Merri and her five Royalty pregnancies to the North‑East Kingdom Sale, Steve Smith and Chet Crosby of Shade‑E‑Lane bought the package for $14,500. One of those Royalty calves would make the whole thing look cheap.

Mountain: The “Poor‑50” Bull Whose Daughters Didn’t Read His Proof

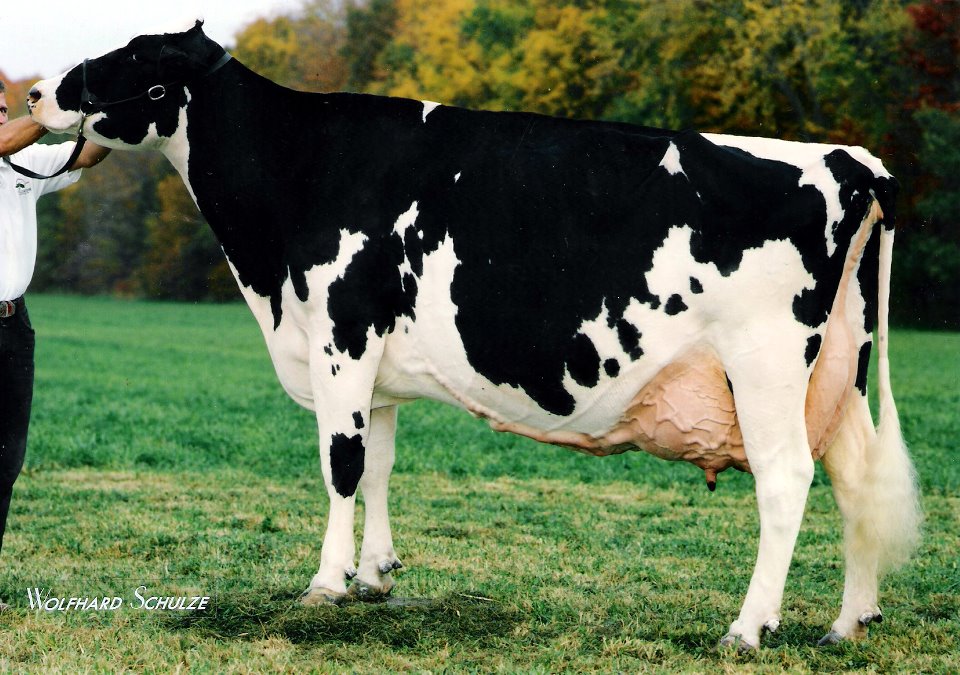

To‑Mar Mountain Helen VG — a stylish Bis‑May S‑E‑L Mountain daughter whose frame, udder, and balance give breeders a rare visual glimpse of what the famous 50‑point “homely anti‑hero” was actually capable of siring.

Under the Shade‑E‑Lane roof, one of those Royalty calves grew into Bis‑May S‑E‑L Mountain. He was proven at Sire Power in Pennsylvania. He had two flush brothers. When Sire Power analyst Steve Neeley had to choose between them, he did what sire analysts do: he looked at type, frame, legs, and testicles—because bigger testicles meant earlier and heavier semen production. Mountain got the nod.

Then the classifier came.

The classification report on Mountain is one of those documents you’d frame if you like irony: “Poor. Fifty points. Straight legs and almost no middle.” That’s almost comical in an era when Good still meant something—back when a 50‑point score really meant “don’t bother taking his picture.” For a moment, you can imagine folks at the stud wondering if they’d backed the wrong brother.

But the classification sheet didn’t tell the whole story. As Mountain daughters freshened, their proofs started rolling in, and they were “pumping out the protein like nobody’s business,” as one contemporary account put it. They weren’t all pretty, but they were resilient producers with better‑than‑average type and solid milk.

When A.I. centers started using Mountain sons because of those daughters, the people rose in protest. Holstein‑Friesian World and the Holstein Association were flooded with cranky letters about a 50‑point bull being used as a sire of sons. The cows didn’t care. They just milked.

From that “homely anti‑hero” came an elite trio of 100% U.S. blood bulls scattered around the globe: Jesther CV in France, Etazon Addison in the Netherlands, and Elite Mountain Donor in Australia. Another daughter, Emerald‑Acr‑SA Tannice VG, produced Emerald‑Acr‑SA Dawson, a popular protein sire in the early 2000s.

Think about that for a second. In a time when breeders still slapped bull pictures on the fridge, one of the defining protein sires of his era was a 50‑point bull whose best “photo” might have been his proof sheet.

Cleitus: The Milk Bull That Slipped in the Side Door

If Mountain taught the industry not to judge a bull by his picture, his herdmate Bis‑May Tradition Cleitus EX‑GM taught it not to judge a bull by his dam’s index.

When Bis‑May Conductor Coral VG‑88‑GMD‑DOM, a tall, deep‑bodied Wapa Arlinda Conductor daughter out of Bis‑May Bold C Coconut VG‑87 (by Nicolk Sunshine Bold Chief), dropped an early Sweet‑Haven Tradition son in 1987, his numbers were low enough that the first A.I. stud the Maynards approached turned him down. Tradition semen was hard to get, and Coral’s index didn’t look like bull‑mother material on paper.

Eastern A.I. remembered what Jupiter had done for them and decided to roll the dice. The young bull they took was named Bis‑May Tradition Cleitus.

Cleitus grew into one of the key production sires of his time and one of the best Elevation grandsons in the books. His best son, Norrielake Cleitus Luke EX‑GM, stood at Alta Genetics in Alberta and sired Dixie‑Lee Aaron EX‑GM and Lexvold Luke Hershel GM, both out of Mascot daughters. Aaron daughters clicked beautifully with O‑Bee Manfred Justice to produce bulls like Long‑Langs Oman Oman VG‑GM, while Hershel’s sons included Sandy‑Valley Bolton EX‑GM, a big milk and protein bull that earned a reputation as a serious freestall sire.

Norrielake Cleitus Luke EX‑GM — the powerful Alta Cleitus son whose Aaron and Hershel lines carried Bis‑May blood straight into Oman Oman, Bolton, Snowman, and the protein‑driven pedigrees of the genomic age.

Another Cleitus son, Paradise‑R Cleitus Mathie EX‑GM, was selected by Charlie Will for Select Sires and sold upwards of two million doses, making him the highest semen seller in Holstein history at the time.

By the late 1990s and early 2000s, you could hardly scan a top TPI or Net Merit list without bumping into Cleitus, Luke, Aaron, or Hershel in the pedigree. Everett’s Hill Farm in Vermont had done exactly what his probability instincts predicted: stock the A.I. shelves from farmer‑bred cows.

Act II – Madison Architects and Fitness Warriors

All that milk, type, and protein needed a frame to live on—and a body that would last long enough to pay for itself. That’s where the second act of this Golden Age really takes hold.

Dellia, Durham, and Five Years at the Top of Madison

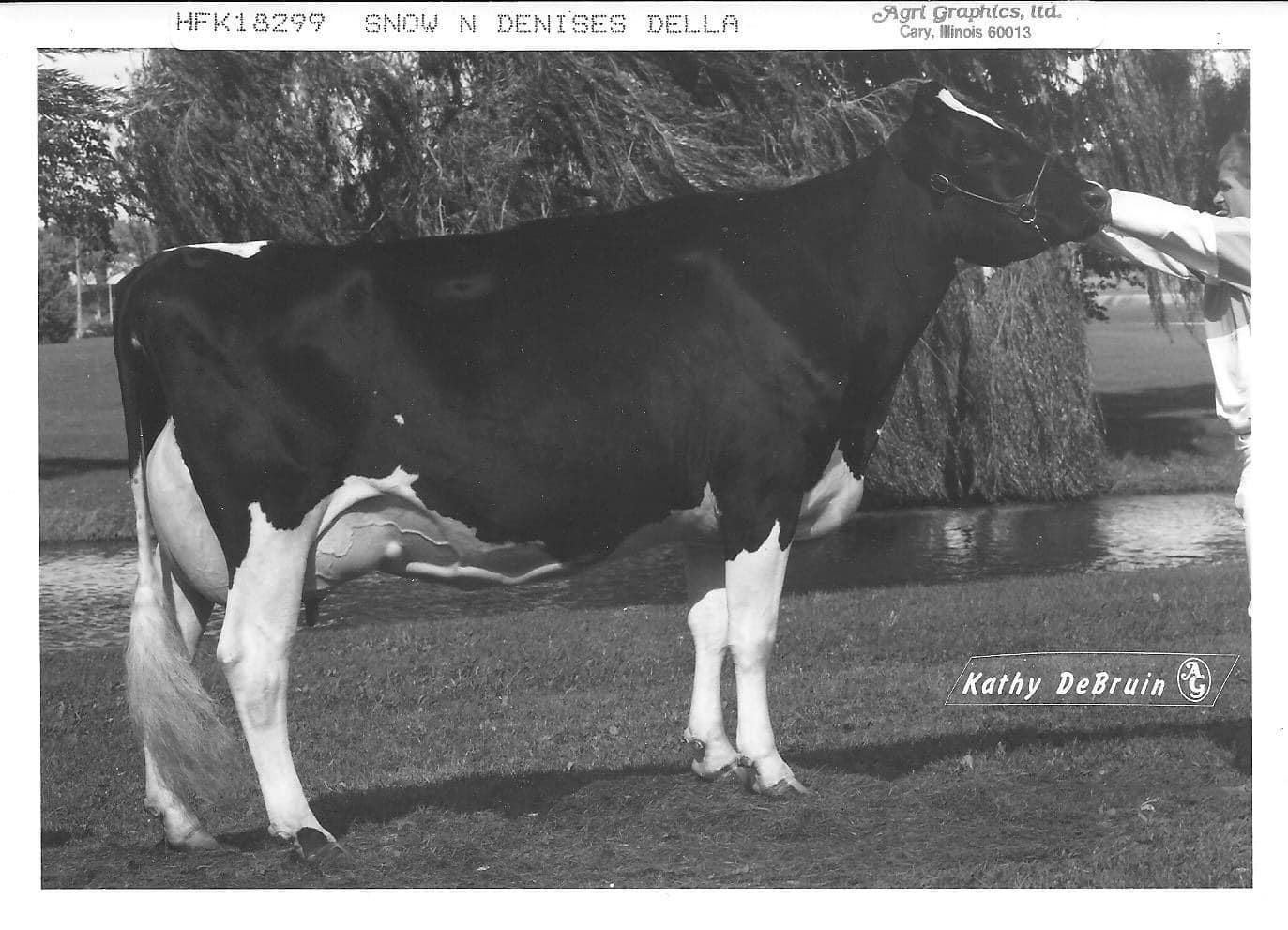

Snow‑N Denises Dellia EX‑95‑2E‑GMD‑DOM wasn’t bred as a glamour cow. She was a Bell x Mark granddaughter developed by Bob Snow and young herdsman John Steinhoff out of a hard‑doing family that had to travel down a pasture, cross a creek, and walk back up to the barn every day. By all accounts, there were nights when she walked into the parlor carrying three gallons of sand in her udder.

Frank Regan saw Dellia and couldn’t shake her from his mind. He came back. Looked again. Eventually, he bought her, on the condition that she show one more time at the Wisconsin Spring Show in 1991 before heading to Regancrest in Iowa.

The night before the show, Dellia looked a little drawn. So the crew did what cow people do: they fed her four bales of hay, warmed up her beet pulp—Dellia liked it that way—and let her settle down. The next day, judge Niles Wendorf walked her out first in the four‑year‑old class, gave her the best udder, and slapped her grand champion of the show. That creek‑bottom cow had just crossed a completely different kind of river.

Back at Regancrest, Frank called Select Sires’ Charlie Will. “What should I use on her?” he asked. The answer came back: Emprise Bell Elton, a Bell son whose daughters were building a reputation for udders, feet, and legs, and longevity. The Dellia x Elton flush produced four sons. First choice went to Japanese buyers for $20,000. The second choice went to Alta Genetics for similar money. Select Sires took the third bull, Regancrest Elton Durham. The Regans used the fourth.

Nobody in that semen office knew they’d just picked up the bull who’d become Premier Sire at World Dairy Expo five years in a row, 2003 through 2007—a run that, as the Durham profile notes, may stand for a very long time.

Sheeknoll Durham Arrow EX — a signature Regancrest Elton Durham daughter, captured in her World Dairy Expo moment, showing exactly the kind of balanced frame and welded‑on udder that kept her sire on the Premier Sire podium for five straight years.

The thing about Durham daughters is that you could pick them out from the stands: long bodies, flat and wide rumps, and udders that looked like they’d been hung with a level—high rear udders, smooth fore udders, clean teat placement. More than one dairyman has said his Durhams weren’t always the highest milk cows on the test sheet—but they were some of the most trouble‑free cows he ever milked. They bred back, they walked well, and they often looked their best at four and five—exactly when the milk check really starts to count.

Durham sons—Mr. Sam, Duplex, Damion, Modest, Drake, D‑Fortune, Primetime—filled type lists from Canada to Europe. His daughters—Kamps‑Hollow Altitude, Lylehaven Lila Z, MD‑Delight Durham Atlee, Regancrest‑PR Barbie, Scientific Debutante Rae—founded families that still show up behind modern genomic stars.

Looking back, the signs were there: Durham gave the breed a blueprint for “classic” dairy cow architecture exactly when the industry was learning to care about cell counts, fertility, and productive life as much as it cared about banners.

If Durham was the architect of style, Braedale Goldwyn GP‑Extra was the finisher who wouldn’t leave a seam out of place.

Goldwyn was born January 3, 2000, a Semex young sire out of Braedale Baler Twine VG‑86, the Maughlin Storm daughter of Braedale Gypsy Grand VG‑88, both cows deeply rooted in Sunnylodge breeding. His sire was Shoremar James GP‑Extra, a Mark CJ Gilbrook grandson out of an Aerostar daughter.

His pedigree is a masterclass in line breeding. Goldwyn carries three close crosses to Madawaska Aerostar (through James, Storm, and Moonriver), and three to Walkway Chief Mark (through James, Gypsy Grand, and Sunnylodge Chief Vick). There’s also a tight knot in the ninth, tenth, and eleventh dams involving Hays Inspiration and Ajax Sovereign B, both tied to Montvic Rag Apple Sovereign and the anchor Dutch cow Vrouka 9198 H.H.B.—the same foundation that produced Osborndale Ivanhoe.