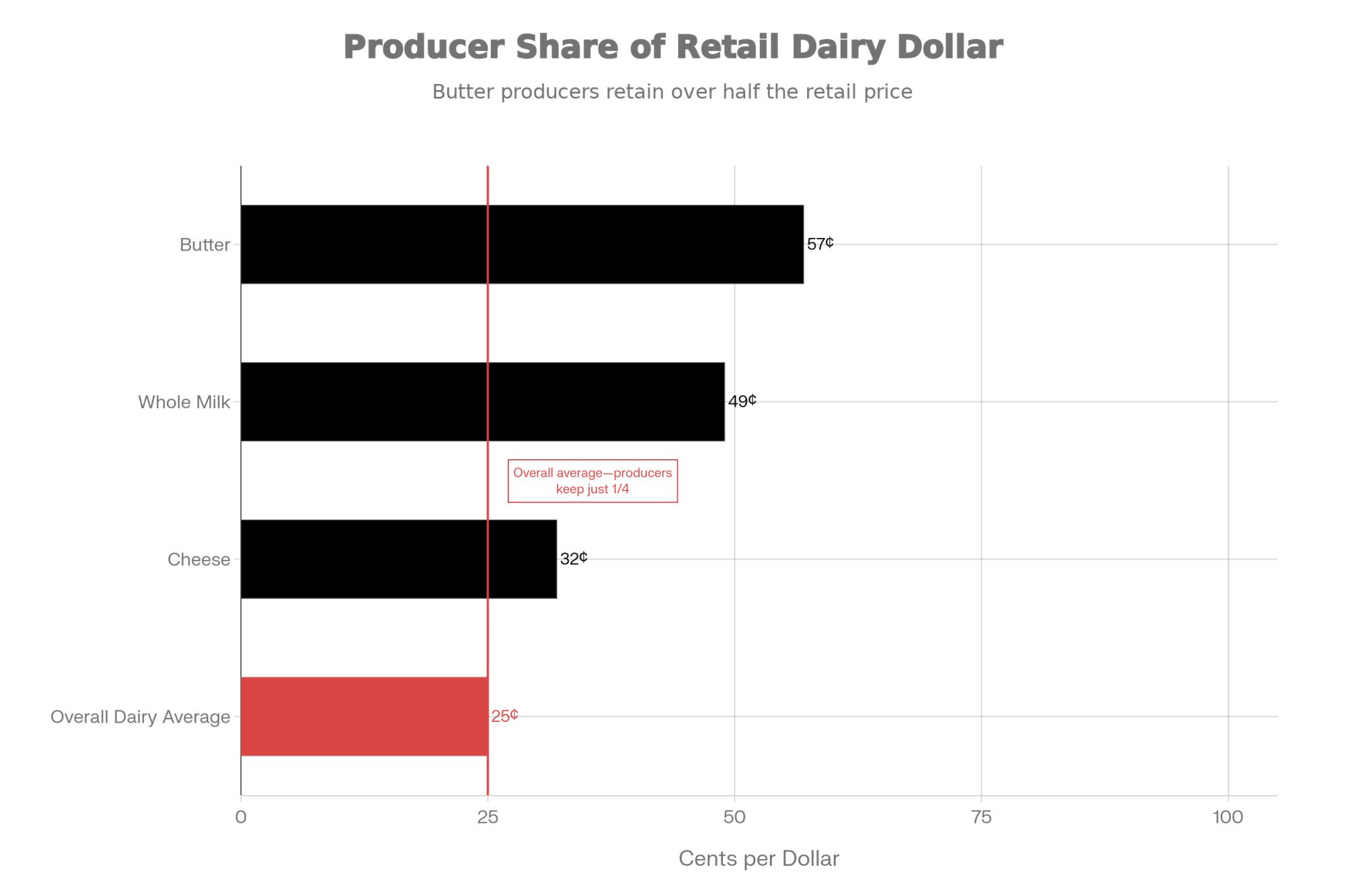

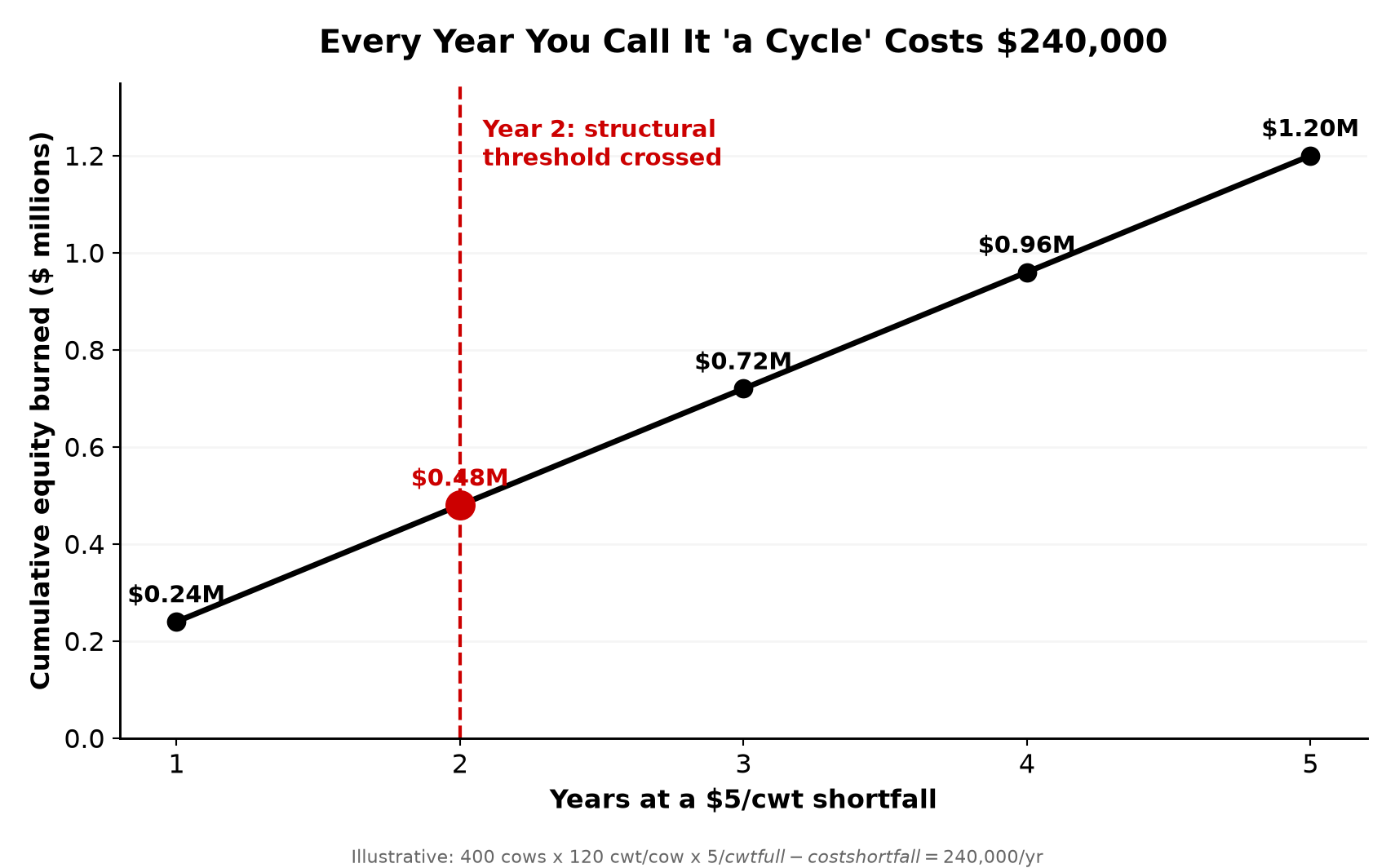

On a 400-cow herd, a $5/cwt shortfall quietly burns about $240,000 a year — and value-added only saves you if the math, the market, and your labor all line up.

On her 25th birthday — April 18, 2026 — Natalie Paino became licensed to make cheese curds from her family’s own milk. Getting there took six years: grant applications, a creamery built inside a shipping container, the full 423-page Pasteurized Milk Ordinance, and two kids born along the way.

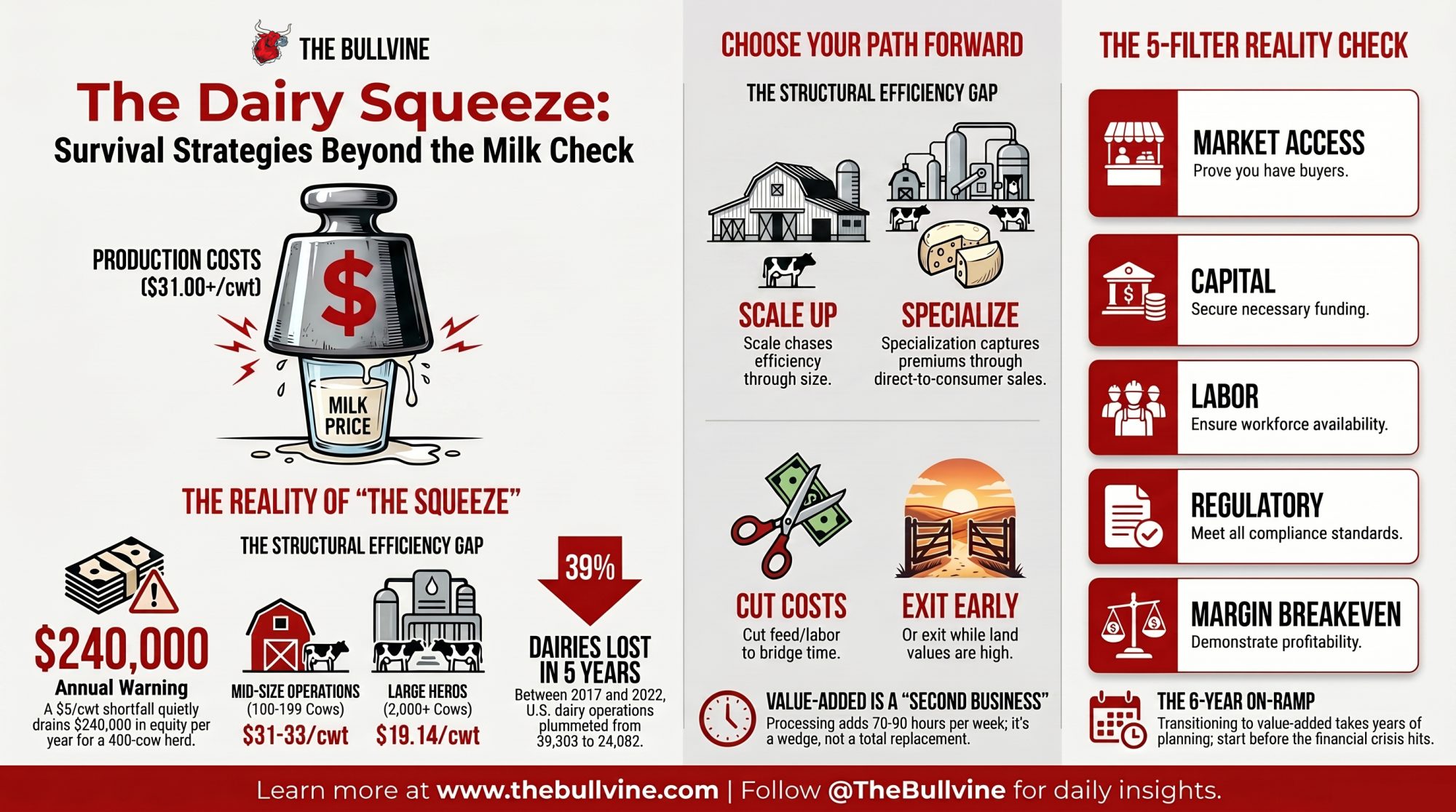

Paino runs Hightail Delivery near Plainfield, Iowa, selling ice cream and fresh cheese curds straight to consumers off the family’s dairy. She didn’t build it because direct sales are trendy. She built it because the commodity milk check stopped making sense — and that’s the same quiet conclusion many mid-size operators are reaching at their own kitchen tables right now. “Milk prices have been pretty poor over the last 40 years,” she told Iowa Food & Family in March 2026. “In fact, they’ve stayed about the same throughout that time, even adjusting for inflation.” That’s not a complaint. It’s a diagnosis — and the numbers back her up.

Her work didn’t go unnoticed, either. Iowa State University Extension and Outreach named her a 2025 “Women Impacting Ag” honoree, and in 2026 she took a $10,000 Iowa Farm Bureau “Grow Your Future” award toward the operation. The recognition matters less than what it signals: a 25-year-old built a working dairy business out of a milk check that, by her own account, hasn’t paid in decades.

What’s Changing and Why

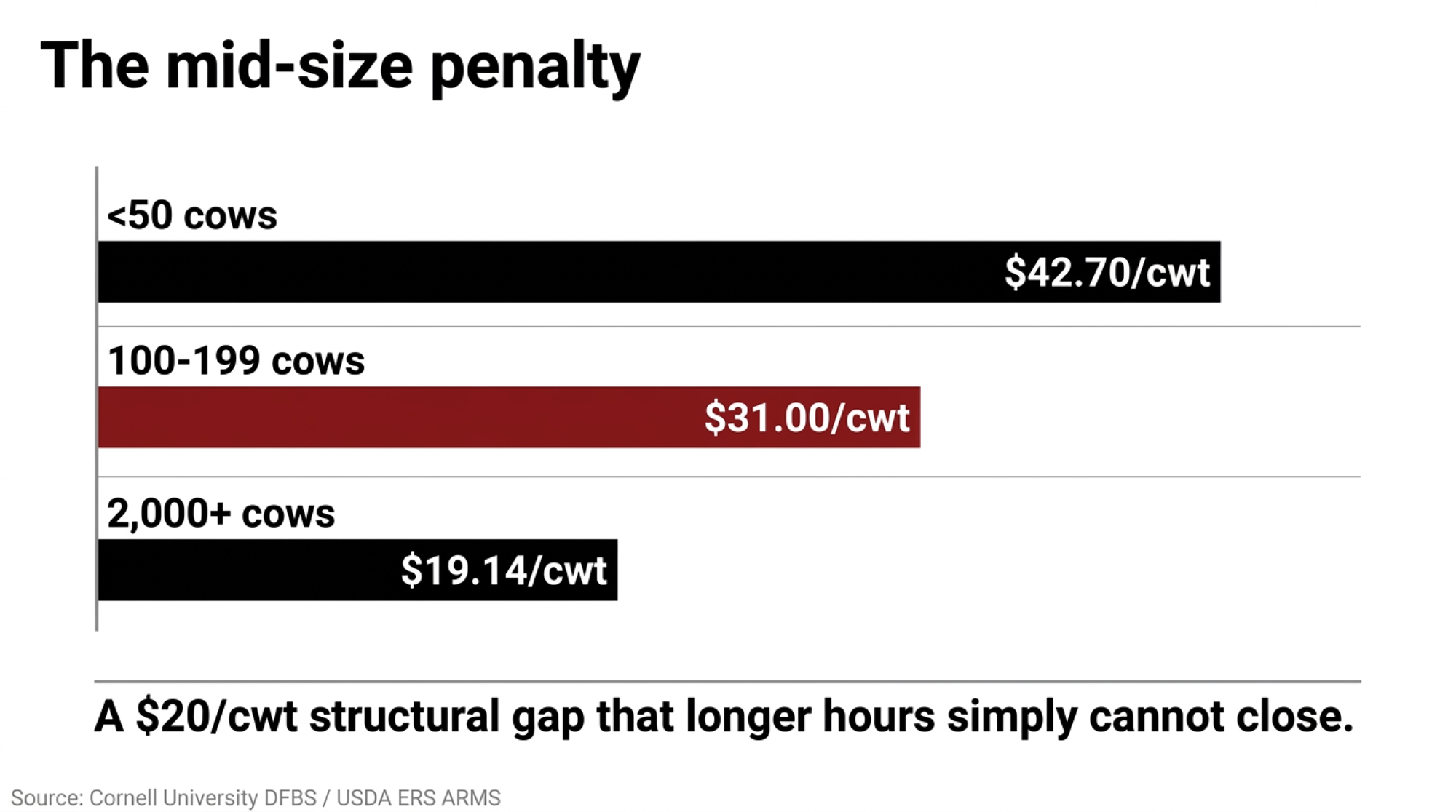

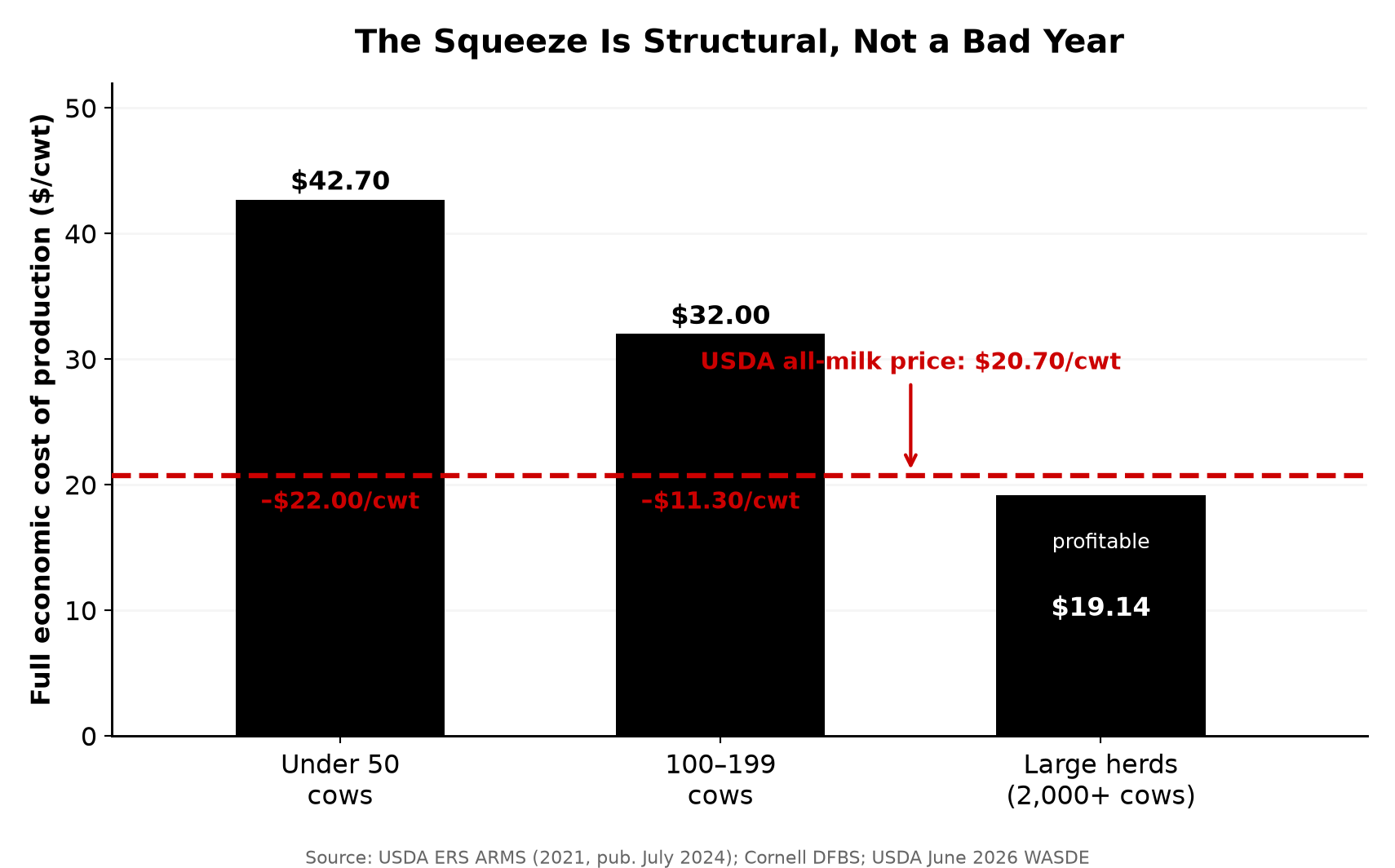

Here’s the gap driving it all. For a 100-199-cow operation, Cornell University’s most recent Dairy Farm Business Summary puts the full cost of production at $31-33/cwt for that size class. USDA’s June 2026 WASDE projects this year’s all-milk price at $20.70/cwt — up from the $18.95 it forecast back in February, but still well short. Even big, efficient herds run $19.14/cwt in full economic cost, per USDA ERS’s 2021 ARMS survey published in July 2024. So the loss shows up before you count a single hour of family labor.

And this isn’t a rough patch you wait out. That same USDA ERS ARMS data shows herds under 50 cows carry full economic costs near $42.70/cwt, while 2,000-plus-cow operations sit at $19.14/cwt — a structural gap of more than $20/cwt that longer hours can’t close. The mid-size disadvantage is baked into purchasing power, labor efficiency, and scale, not effort. A cycle ends. This one hasn’t ended for small- to mid-sized commodity dairy in over a generation.

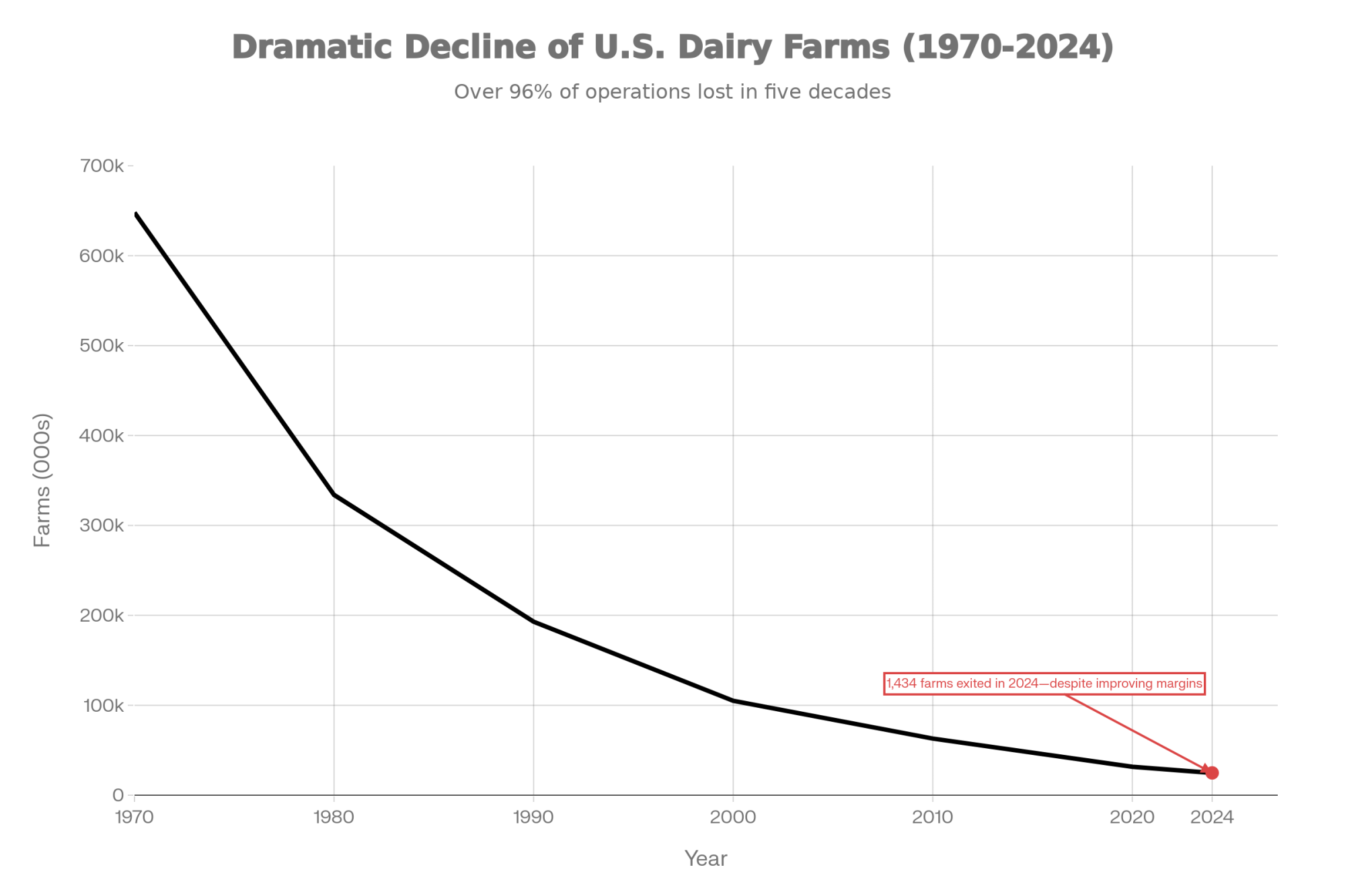

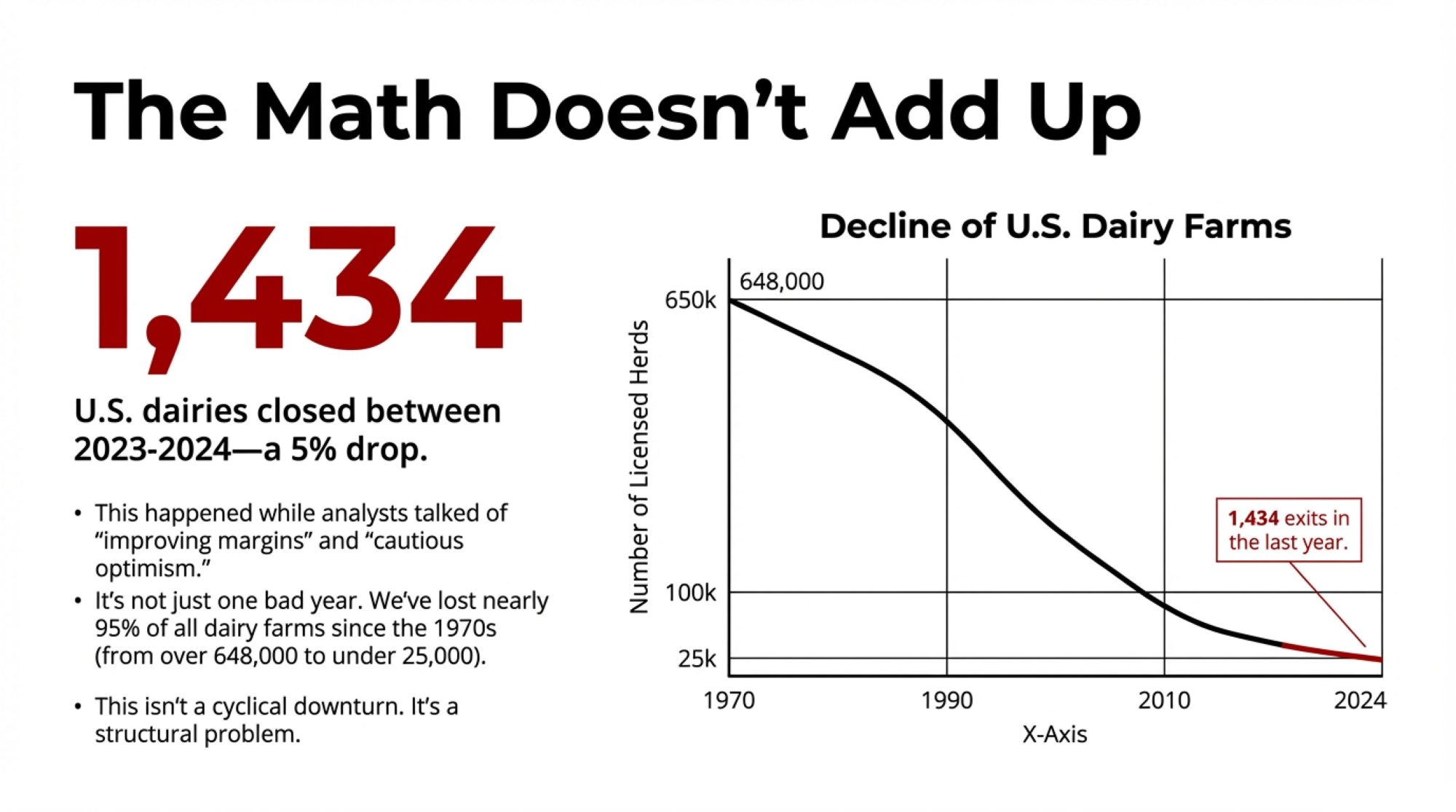

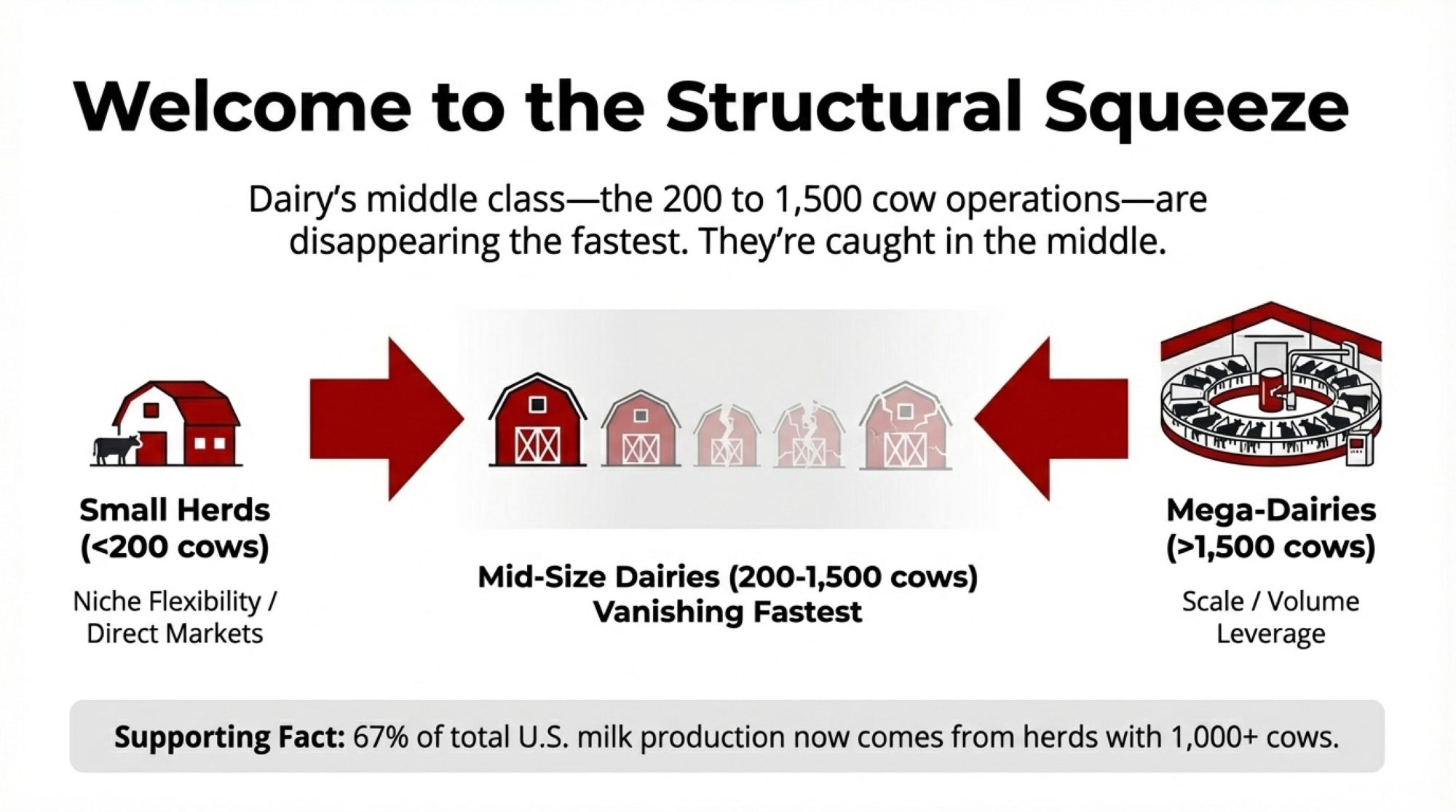

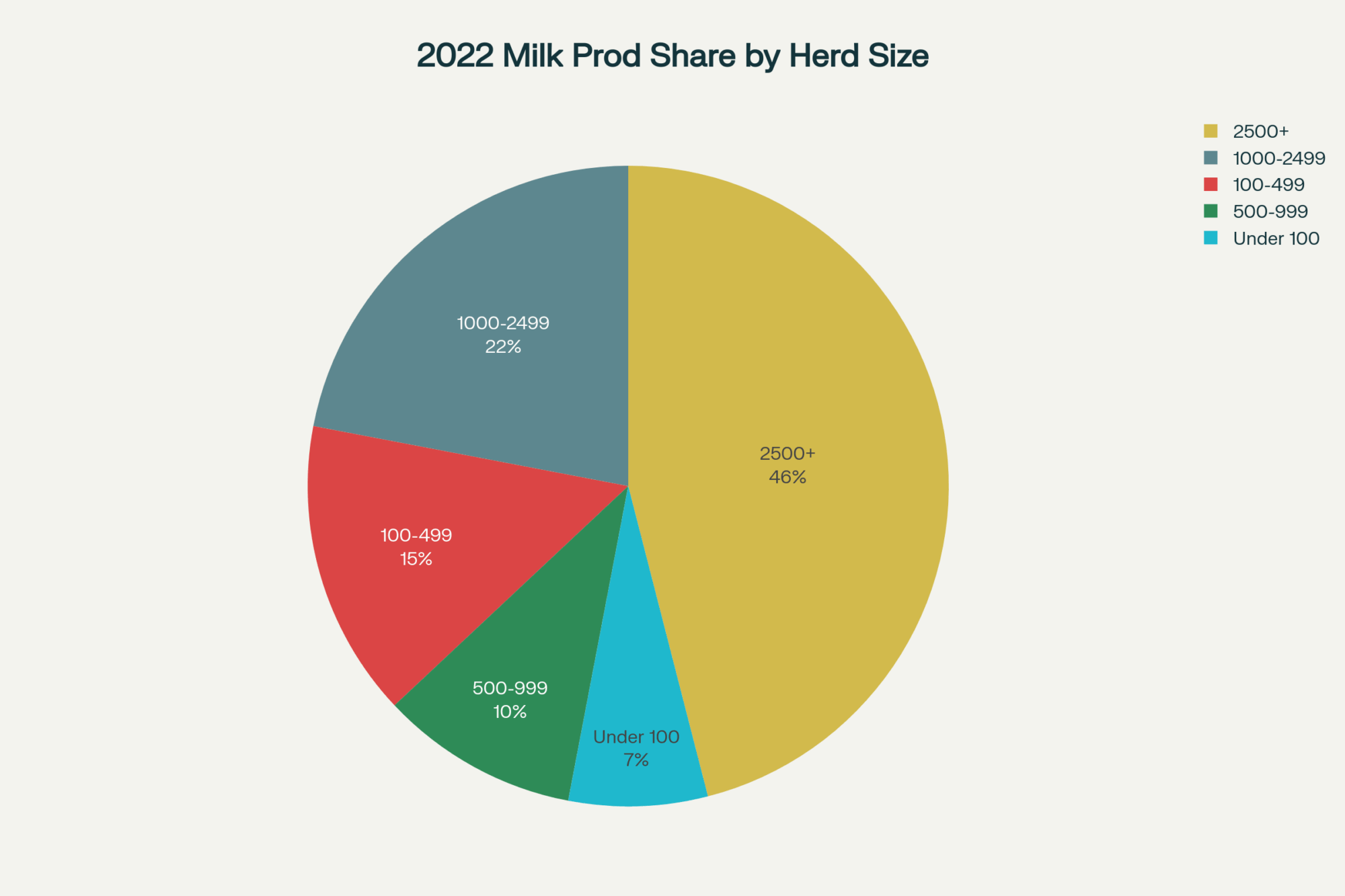

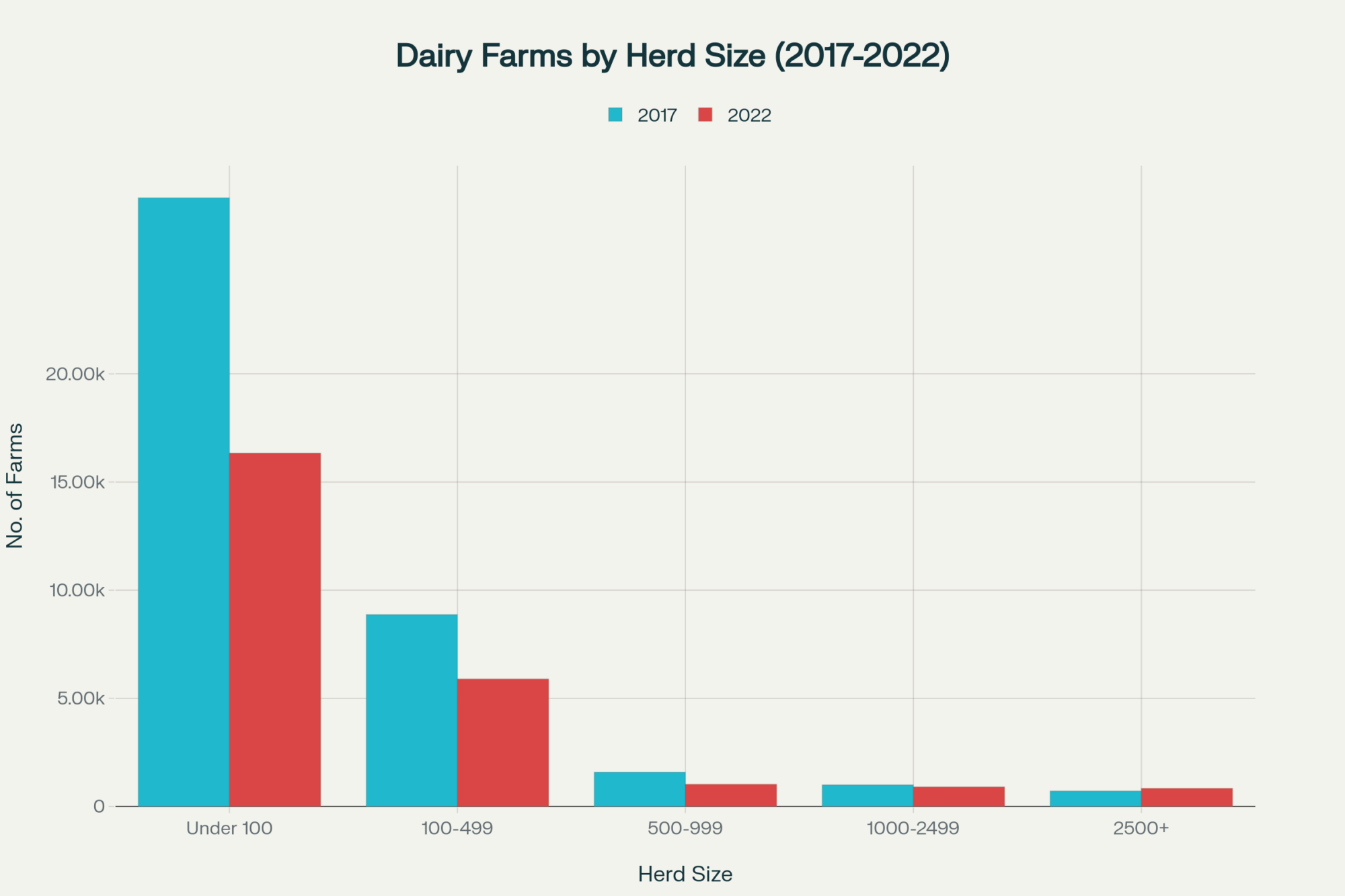

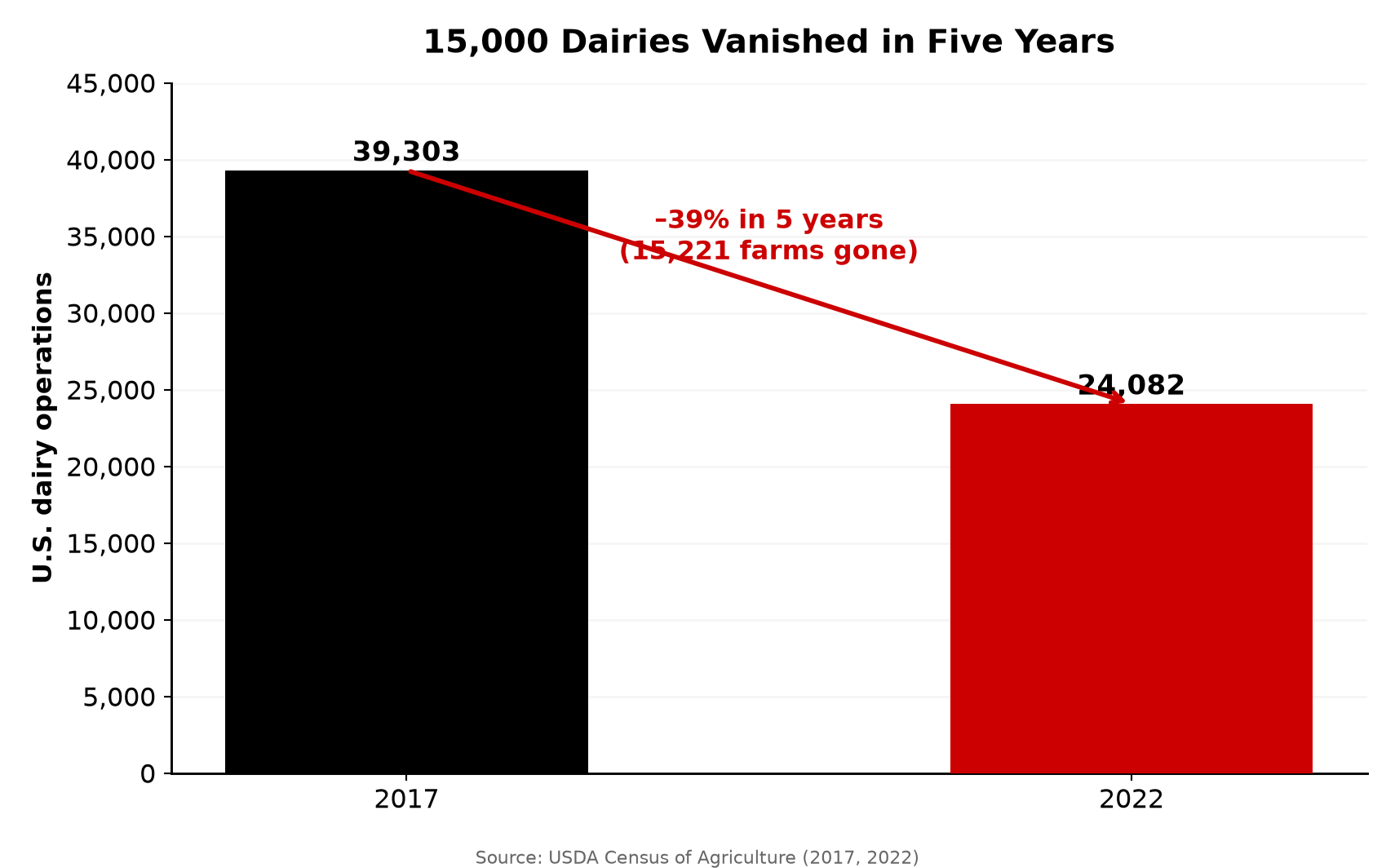

The squeeze lands hardest in the middle. Big enough to be a full-time business, too small to hit the cost efficiencies of a 2,000-cow operation. The 2022 USDA Census of Agriculture counted 24,082 dairy operations, down from 39,303 in 2017 — roughly a 39% drop in five years. The mid-size herd is standing right in its path.

That exit rate isn’t spread evenly. The farms disappearing fastest are the ones too big to run as a hobby and too small to out-buy and out-scale a mega-dairy on feed, labor, and capital. Paino’s own read on the long arc — four decades of flat, inflation-adjusted prices — is exactly the math that’s been quietly thinning that middle for years. Where does your breakeven actually sit? If you haven’t run that number against $20.70 milk lately, that’s the first thing this piece should push you to do.

How This Plays Out on Real Farms

Paino isn’t a one-off. Keegan Donovan was 22 when she and her husband, Brian, launched Millbrook Beef and Dairy in Dutchess County, New York, in 2022 — first-generation farmers who quickly found that the cost of producing their milk outran what they were paid for it. Their answer was to stop shipping commodity milk entirely and sell beef, dairy, pork, and eggs directly off the farm. “You have to be able to bet on yourself,” Keegan told Main Street Magazine in 2024. For two people who started with no land base and no inherited herd, that bet was the whole business plan.

Then there’s Emily Mullen-Niccum, who came back to her family’s Butler County, Ohio, dairy knowing exactly how the commodity story ends there. Her county had gone from 88 dairies in 1970 down to two. She runs about 65 cows through a robotic milker and turns 4,000 pounds of milk a week into 35 product flavors. Her line to DTN/Progressive Farmer in January 2025 lands harder than any margin chart: “Average was over. Nothing bad about Dad or that generation of farmers… However, that generation has forgotten their worth.”

What ties these three together isn’t age or geography. It’s the same calculation, run independently, ending the same way: the milk check alone doesn’t clear the cost of producing the milk, so they each found a buyer who’d pay for something more than a tanker pickup. None of them set out to be a movement. Each one just looked at the same spread between cost and check and decided the tanker wasn’t the only way off the farm.

Now the barn math — and watch what it does to the dream version. Take a slightly bigger herd than the one in the headline — 500 cows — and carve off 20% into a direct channel netting an extra $1.50 a gallon. At roughly 70 lbs of milk per cow, that slice is about 800 gallons a day (at 8.6 lbs per gallon), which throws off close to $1,200 a day.Sounds like the problem’s solved. It isn’t. You’re still shipping the other 80% into the same commodity market that’s bleeding money, and that premium only shows up if you actually sell every gallon you process. The direct channel doesn’t replace the milk check. It patches part of the hole the check leaves — and only when the selling works.

The Mechanics Behind the Outcomes

So the first thing to get straight: value-added is a wedge, not a replacement. A 300-cow herd makes around 21,000 lbs of milk a day — far more than a farmstead creamery typically moves. Most operations at this scale process only a fraction of their own volume through premium channels and ship the rest conventionally; UMass Extension warns producers outright that a value-added business may not turn a profit in its first five years. The co-op check doesn’t vanish. It shrinks while a higher-margin slice grows beside it.

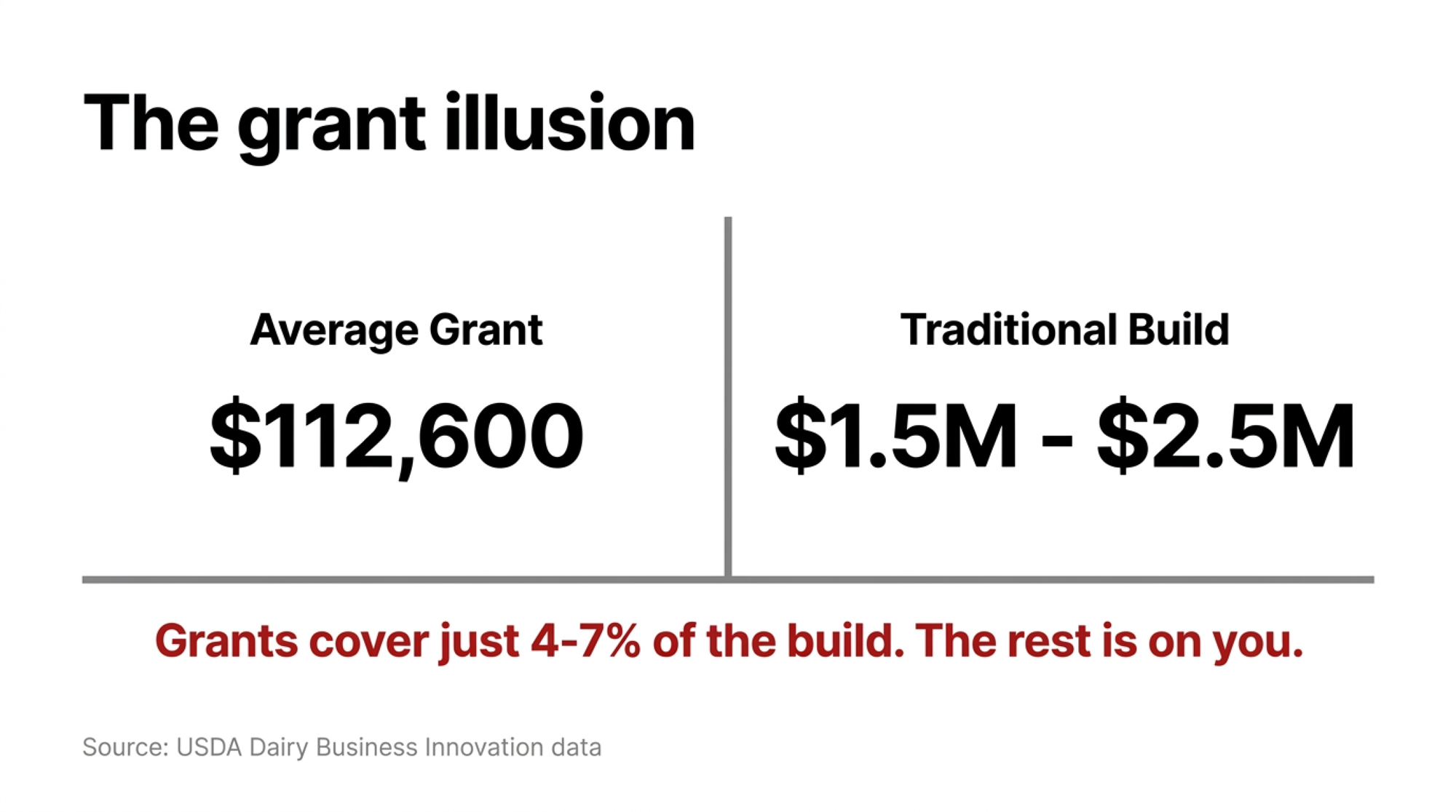

The capital math is humbling, too. A traditional on-farm creamery build runs $1.5-2.5 million, and the average USDA Dairy Business Innovation grant works out to roughly $112,600 per funded entity — about 4-7% of the bill. That’s the number that should stop people cold. Paino dodged it by going small on purpose. “Building a traditional creamery could easily cost millions of dollars,” she said. “So I started researching micro-dairies.” A shipping container isn’t a romantic origin story. It’s how you keep the entry cost from burying you before the first batch sells.

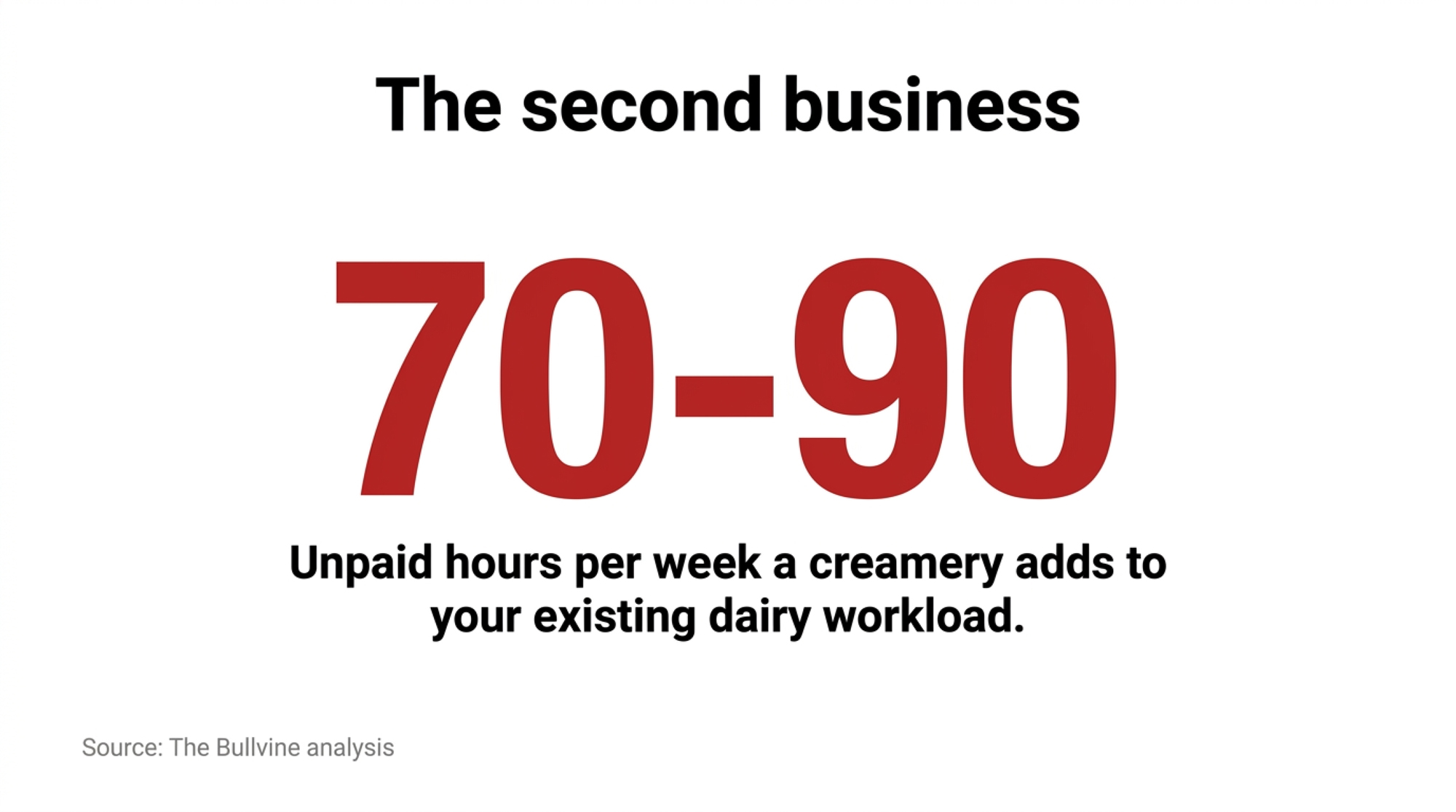

Then there’s the cost nobody pencils in. A Bullvine analysis of a documented creamery operation found that on-farm processing added 70-90 hours per week to a full dairy workload. That’s not a side hustle. That’s a second business stapled to the first one — and somebody in the family has to run it, or you’re hiring it out and watching that $1.50 premium shrink.

Paino’s six-year timeline tells you the rest. The grant applications, the 423-page PMO, the licensing that didn’t clear until her 25th birthday — that’s not slow execution, that’s the actual length of the on-ramp. Anyone who thinks value-added is a quick pivot out of a bad milk year has the timeline backwards. You start building before the crisis, or you’re building during it with no runway left.

What Does This Mean for Your Co-op?

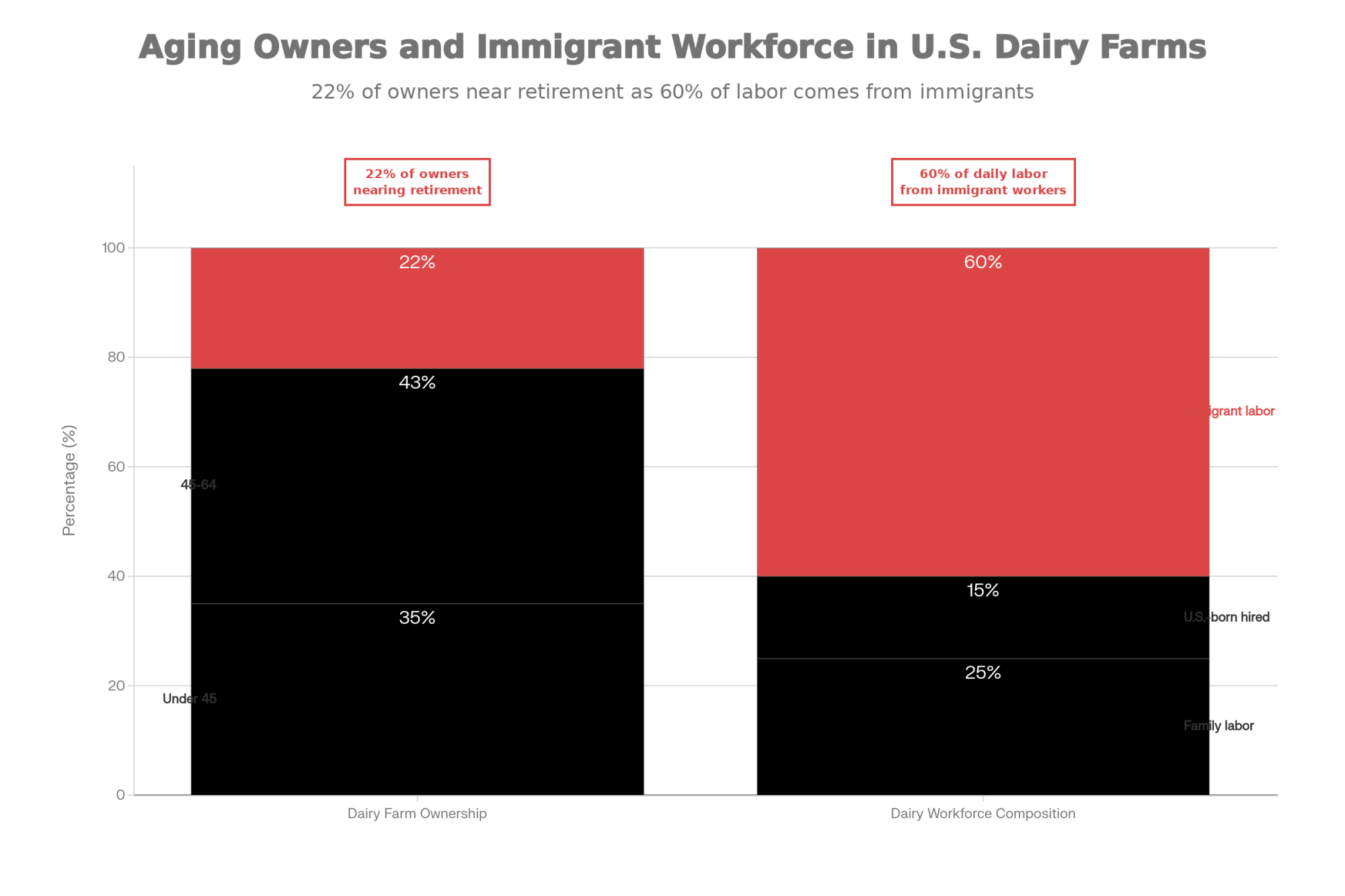

Here’s the angle that doesn’t get talked about enough. Every gallon a young member routes into ice cream or curds is a gallon that doesn’t ride the co-op tanker. And the members most likely to peel off are exactly the ones a co-op needs for the next 30 years — the under-35 crowd, who already make up just 9% of U.S. producers (USDA 2022 Census). When your youngest, most adaptable members start carving off volume, the erosion isn’t just this year’s pounds. It’s the future supply base.

Run the co-op-side math, using that same 500-cow member from above. Shift 20% — roughly 7,000 lbs a day — out of the commodity pool and into their own creamery. Over a year, that’s about 2.5 million pounds of fluid milk leaving the co-op’s book from one farm (7,000 lbs × 365 days; illustrative, built on the herd assumptions above). One farm won’t move a regional co-op. But ten or twenty of them, clustered near the same metro markets where value-added actually works, start to thin the fluid pool on which a balance sheet was built.

The honest read for co-op supply managers: this isn’t a stampede, and there’s no clean public figure yet on how much volume direct channels are pulling out of co-op pools. But the direction is one-way. The members leaving the commodity pool aren’t the ones retiring out — they’re the ones who were supposed to be still shipping in 2050.

Is Value-Added Actually Right for Your Farm?

Before you price a single tank, run the operation through five honest filters. Each one has killed more creamery dreams than bad product ever has. Lay them out as a vertical checklist block — one card per filter, each with the question on top and the hard number underneath — so a reader has to slow down and answer each before scrolling on.

| Filter | The Question | Hard Number | Kill Signal |

| 1 — Market Access | Within reach of a metro market that’ll pay a premium? | Needs a farmers-market track record, not a hunch | No market = no margin |

| 2 — Capital | Can you fund the build without betting the dairy? | Grant covers only 4–7% of a $1.5–2.5M build | Full-scale number sinks most first-timers |

| 3 — Labor | Who runs the second business? | On-farm processing adds 70–90 hrs/week | “We’ll figure it out” = unstaffed second business |

| 4 — Regulatory Load | Ready for the PMO, licensing, inspections? | The PMO runs 423 pages; on-ramp ran 6 years for Paino | Treating compliance as a footnote, not the job |

| 5 — Margin Breakeven | At what volume/price does the premium clear costs? | Budget for no profit in years 1–5 (UMass) | Can’t write the number = a hope, not a plan |

- FILTER 1 — MARKET ACCESS Are you within reach of a metro market with buyers who’ll pay a premium — and can you prove it with a farmers-market track record, not a hunch? UMass Extension’s first question is blunt: are your locations convenient to the consumer? No market, no margin.

- FILTER 2 — CAPITAL Can you fund the build without betting the dairy? The grant covers 4-7%, not half. The rest is on you and your lender — a micro-build like Paino’s container creamery exists precisely because the full-scale number sinks most first-timers.

- FILTER 3 — LABOR Who’s running the second business — the processing, deliveries, licensing paperwork, and marketing? If the answer is “we’ll figure it out,” that’s 70-90 hours a week with no name attached to it.

- FILTER 4 — REGULATORY LOAD Are you ready for the Pasteurized Milk Ordinance, state licensing, and inspection cycles? Paino read all 423 pages of the PMO. That’s the job, not a footnote.

- FILTER 5 — MARGIN BREAKEVEN At what volume and price does the premium actually cover processing, labor, packaging, and spoilage? UMass tells producers straight: budget for no profit in the first five years. If you can’t write that number down, you don’t have a plan — you have a hope.

Clear all five, and value-added is a real wedge against the squeeze. Miss two or more, and you’re building a money pit with a freezer attached.

How Much Does Waiting Actually Cost You?

This is where the clock matters. There’s no tidy figure for how long a struggling dairy drifts before it exits, but the pattern advisors describe is consistent: if off-farm income has bailed out farm operating losses in three or more of the last five years, that’s structural, not a tight stretch. Put real numbers on it. For a 400-cow herd shipping 120 cwt per cow, a $5/cwt full-cost shortfall amounts to about $240,000 a year — straight out of family equity, not the feed mill or the co-op. Every year you call that “a cycle,” that’s the bill.

So the honest question isn’t “will prices come back?” It’s “what is this gray zone costing me every year I keep deciding not to decide?” Bullvine’s modeling puts the critical threshold at two consecutive years of full cost above the all-milk price — past that, you’re funding someone else’s business plan with your own balance sheet. The direction is one-way, and the value-added on-ramp that might offset it runs for years, not months. So the decision and the build can’t be the same conversation.

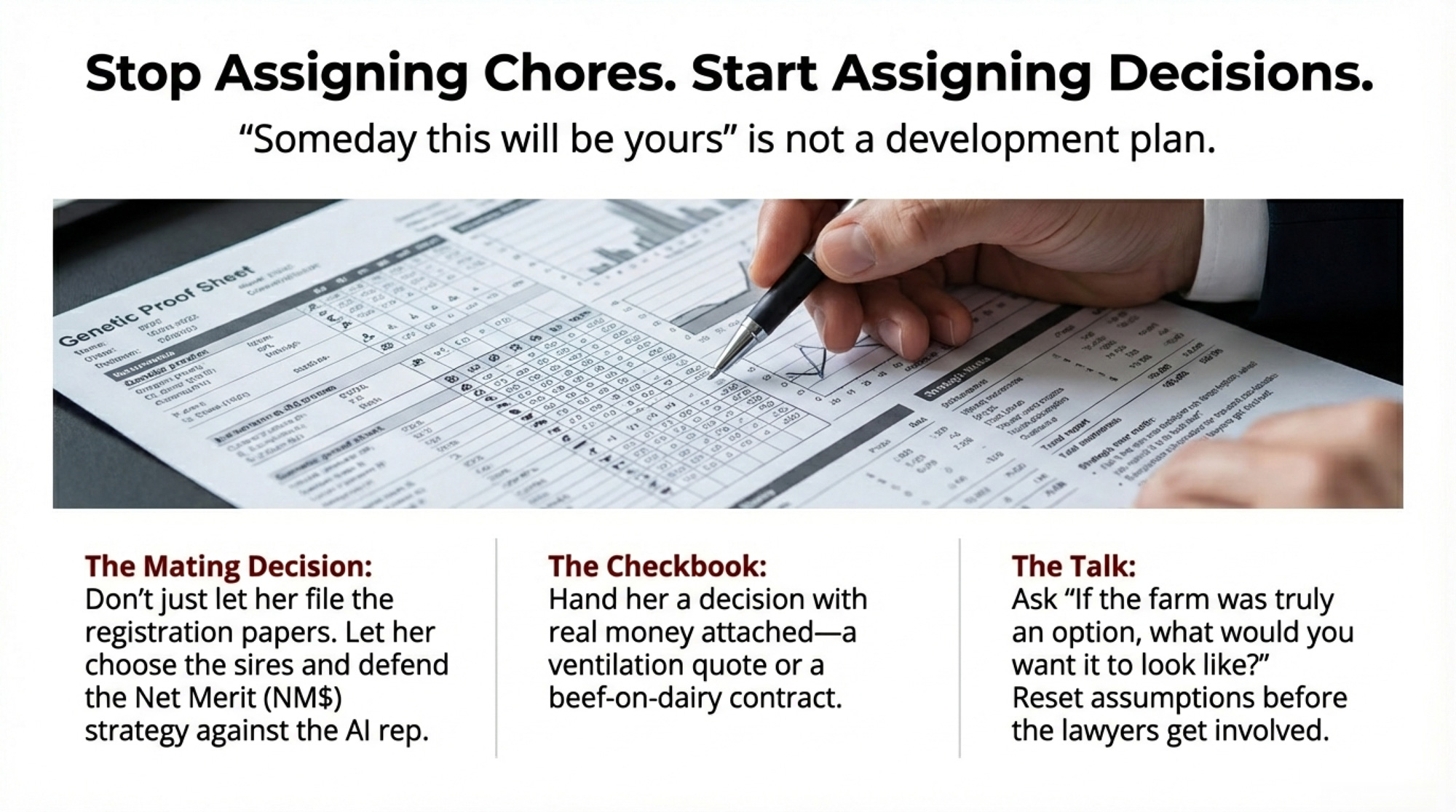

Is Your Inheritance Plan Built on a Real Conversation?

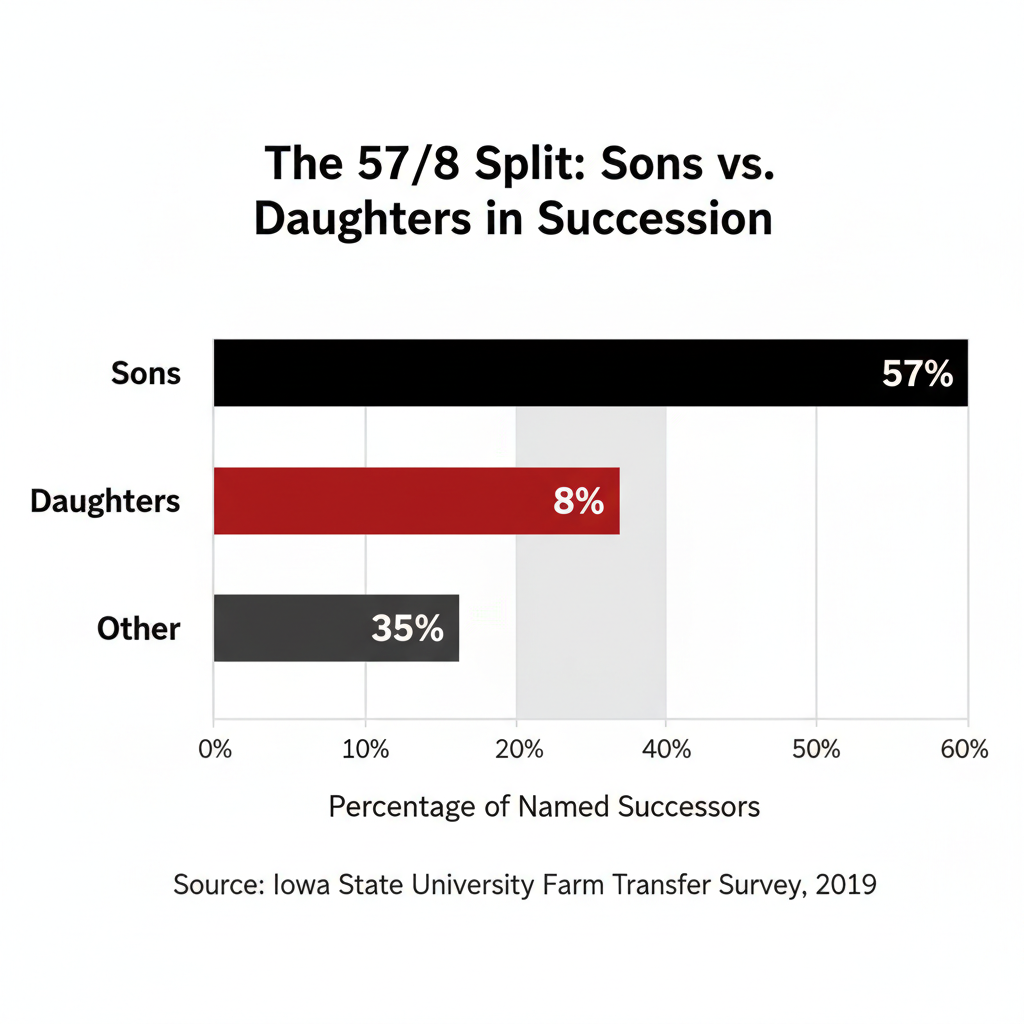

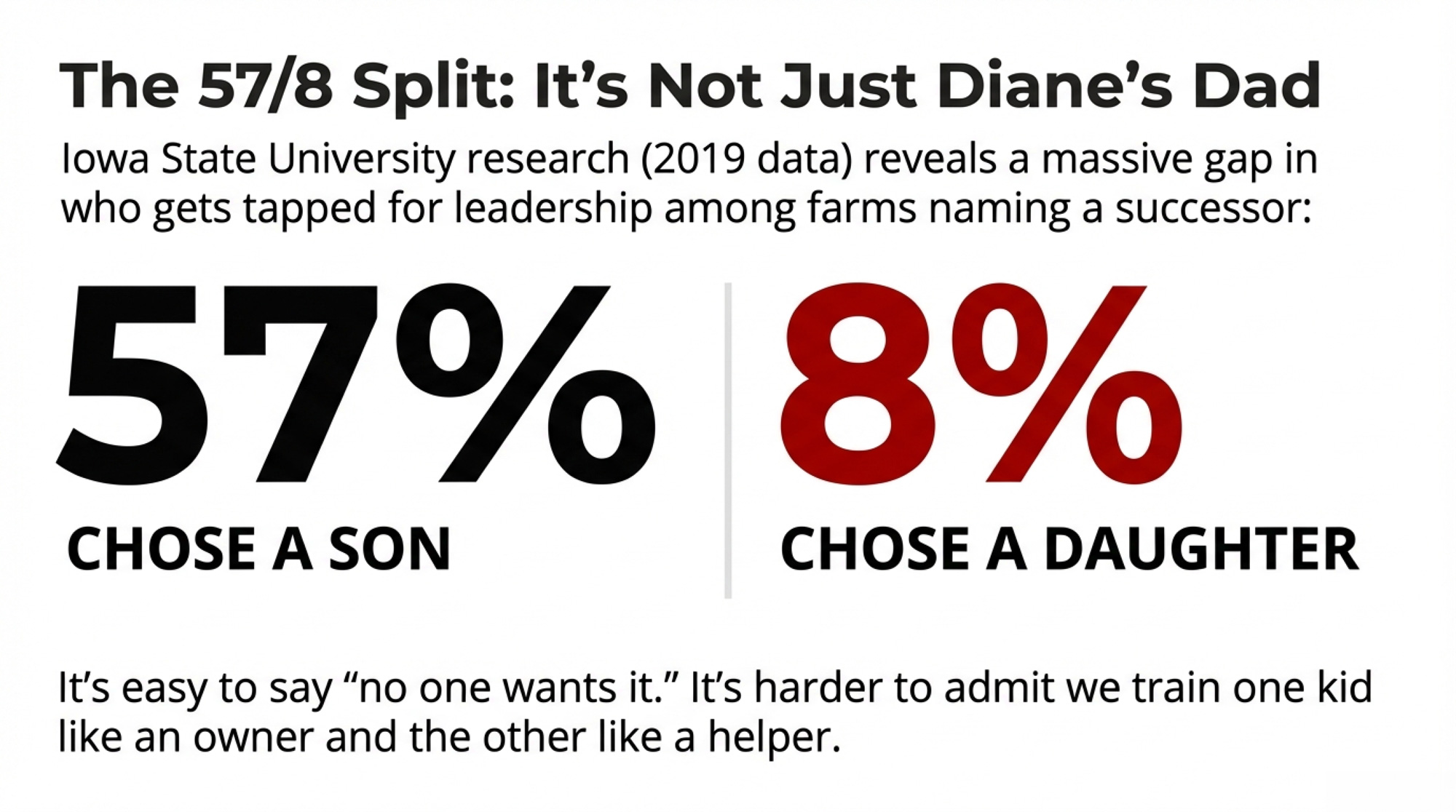

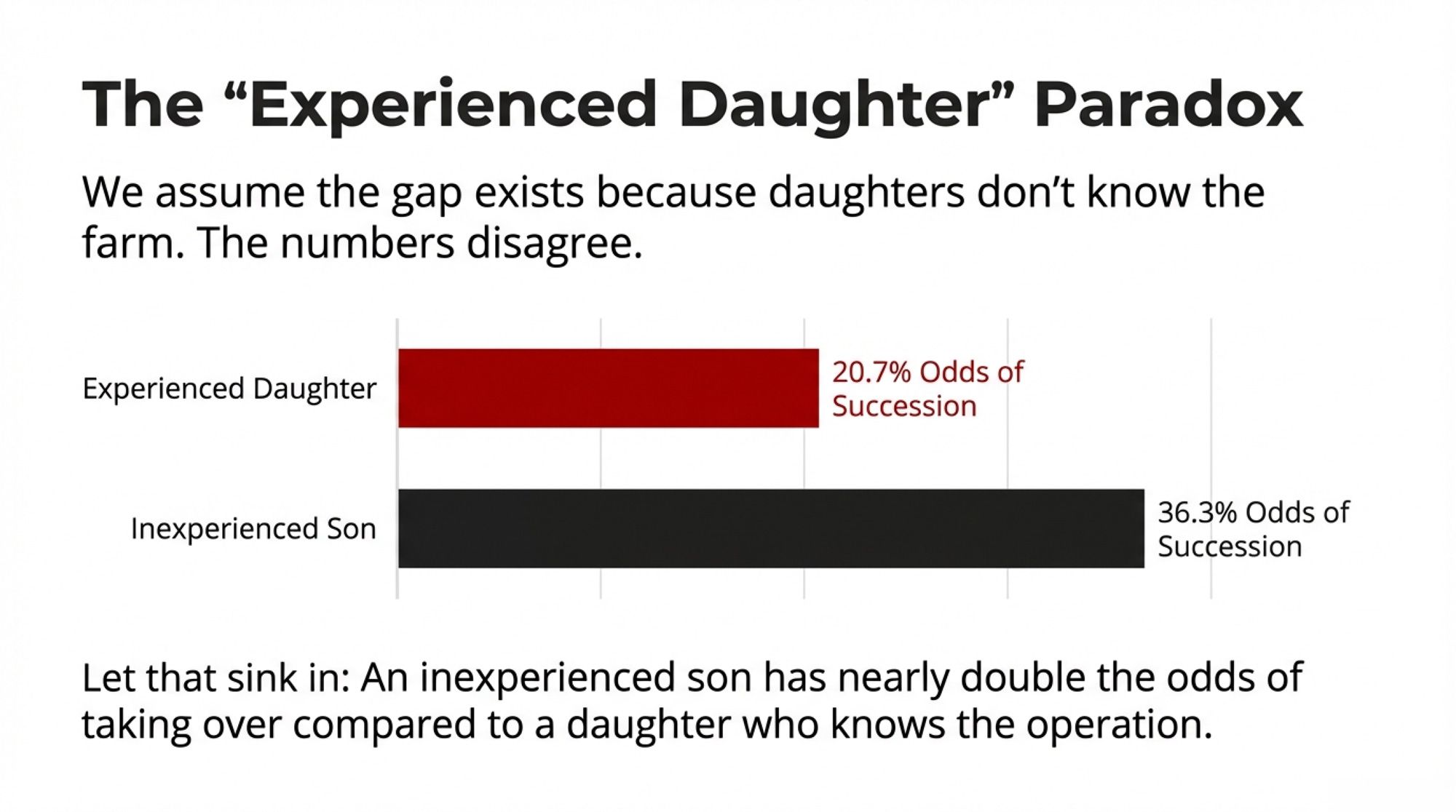

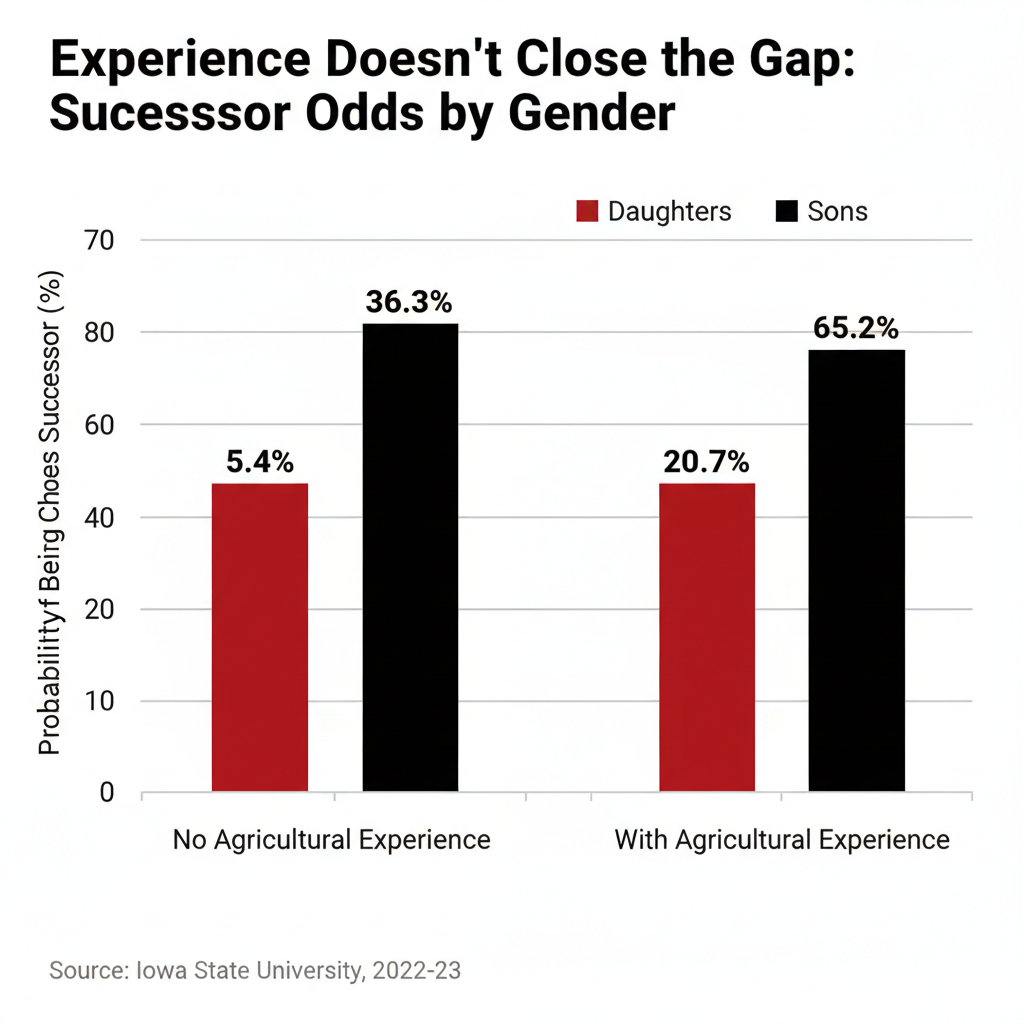

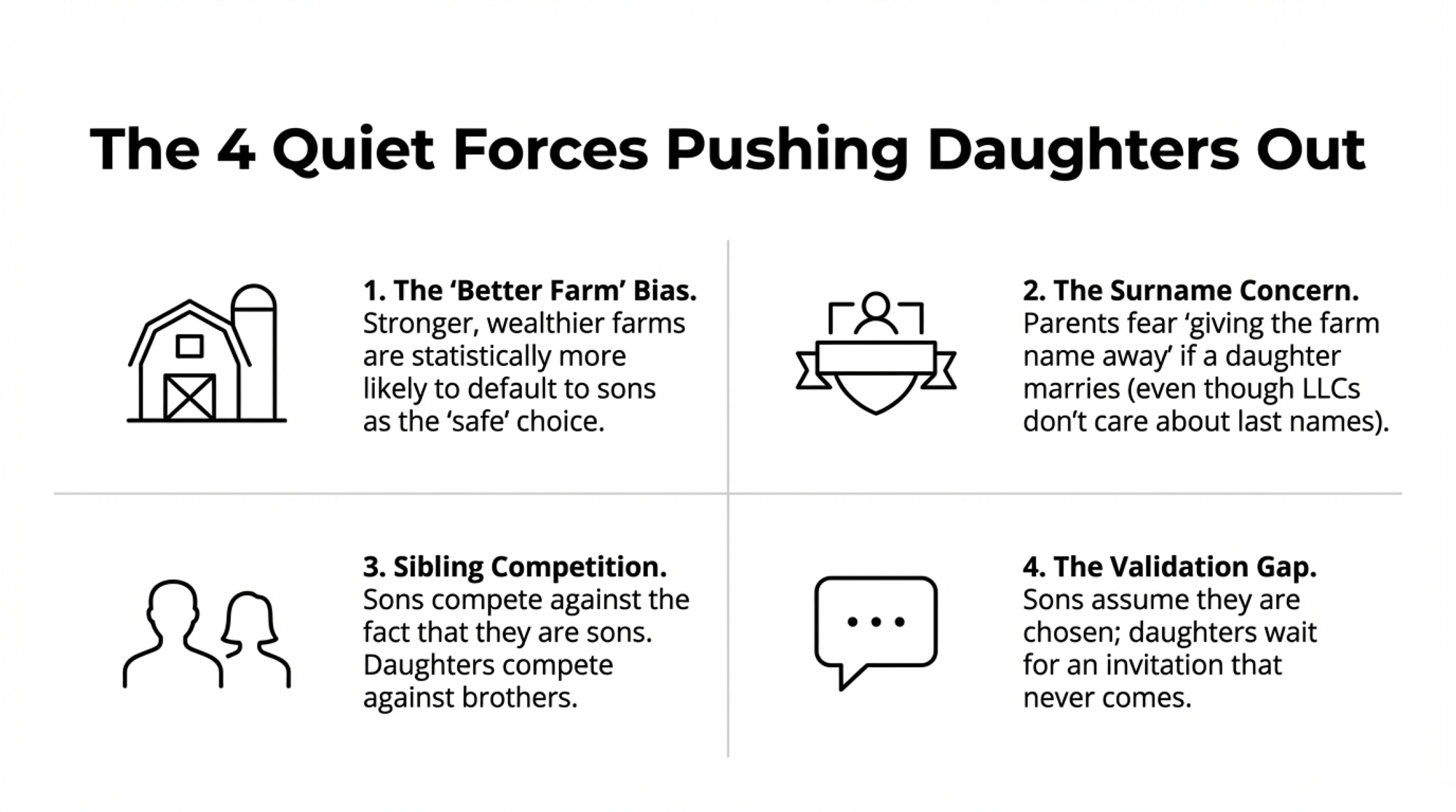

Plenty of operators absorb losses on the quiet assumption that a son or daughter will take over. Be careful with that one. Only 9% of U.S. producers are under 35, and the average age of producers is 58.1 years (USDA 2022 Census). Iowa State research found a daughter’s odds of being the chosen successor climb from about 5.4% to 20.7% when she has real farm experience — though the experience and an explicit plan have to come first, and that figure is Iowa-specific, so treat it as directional rather than national.

Here’s the sharper question underneath it. What are you actually trying to pass on — the land and the history, or this exact commodity business model? They’re not the same thing. Families hand down land and paid-off equipment all the time. Far fewer manage to hand down an unchanged model that’s losing money at today’s prices, and asking a 25-year-old to inherit a margin gap isn’t much of a gift. The young operators in this piece didn’t reject the family farm — they rejected the part of it that didn’t pay, and kept the cows.

Options and Trade-Offs for Farmers

When the commodity math breaks, four structural responses exist. Not all of them are open to every farm. Present these as four side-by-side path cards — each with the move, when it works, and the trap — so a reader can scan straight to the one that fits their balance sheet.

| Path | The Move | Works When | The Trap |

| Scale Up | Chase size efficiency — big herds run $19.14/cwt vs. $42.70 for the smallest | You’ve got equity and lending room | Borrowing toward efficiency you can’t service — millions of capital on an already-underwater sheet |

| Specialize (Value-Added) | Capture the premium — diversified dairies report $25K–$300K/yr in non-commodity income | You’ve cleared all five filters | Build the creamery before proving demand and you’ve bought a pricier way to lose money |

| Cut the Cost Base | Attack feed and labor — the two biggest cost lines | You need a bridge while you decide | Stalls as a standalone — most survivors already trimmed what they can; there’s a floor |

| Exit on Your Terms | Sell while land values hold | No viable successor, no capital for specialization | Waiting until a lender forces the sale instead of choosing the timing |

- PATH 1 — SCALE UP The move: Chase the cost efficiency of size. The biggest herds run at $19.14/cwt full cost while the smallest sit near $42.70, and that gap is widening, not closing. Works when: You’ve got equity and lending room. The trap: Borrowing your way toward an efficiency you can’t service — reaching cost-competitive scale can mean millions in capital on a sheet that’s already underwater.

- PATH 2 — SPECIALIZE (VALUE-ADDED / DIRECT) The move: Capture the premium. Diversified dairies have reported anywhere from $25,000 to $300,000 a year in non-commodity income, depending on scale and channel, while commodity producers fought for pennies at the milk check. The road Paino, the Donovans, and Mullen-Niccum each took. Works when: You’ve cleared all five filters above. The trap: Build the creamery before you’ve proven the demand and you’ve just bought a more expensive way to lose money.

- PATH 3 — CUT THE COST BASE The move: Attack feed and labor — the two biggest lines in cost of production. Works when: You need a bridge while you decide. The trap: As a standalone strategy it stalls — most farms still running have already trimmed what they can, and there’s a floor under how lean you can get.

- PATH 4 — EXIT ON YOUR TERMS The move: Sell while land values hold. Land has held or risen across most regions even as margins fell. Works when: There’s no viable successor and no capital for specialization. The trap: Waiting until a lender forces the sale instead of choosing the timing yourself.

The move that fits any of these — and you can start it this month: pull your last 12 months of milk checks, feed bills, debt service, and labor, and calculate your real cost per hundredweight, your own and your spouse’s labor included at $18-22/hour. Most operators in trouble are flying on feel instead of a current number. You can’t pick a path until you know which side of breakeven you’re actually standing on.

Run Your Own Number First

Dairy Profit Projector — This whole piece comes down to one question: would your farm make money at $20.70 milk? Run your herd through the Projector to pressure-test breakeven milk price, IOFC, and your next 12 months of margin before you pick a path — or decide value-added is worth the six-year build.

Key Takeaways

- If you haven’t calculated full cost per cwt — family labor included at $18-22/hour — in the last 12 months, do it before month’s end. Every other decision waits on that number.

- If your full cost of production stays above the $20.70 all-milk projection for two consecutive years, the gap is coming out of family equity — treat that as the line, not a rough patch.

- If government payments (nearly 29% of net farm income nationally in 2026) are covering operating losses rather than topping up profit, read that as a signal, not a cushion.

- If you’re eyeing value-added, model it on a slice of your volume — not all of it — clear all five filters, and budget for no profit in years one through five.

- If a grant is what makes your creamery plan pencil, the plan doesn’t pencil. The average DBI grant covers about 4-7% of the build.

- If you’re starting a value-added build to escape a bad year, you’re already too late for that year — Paino’s on-ramp ran six years. Start before you need it.

- If you’re a co-op supply manager and your under-35 members are floating direct-channel ideas, treat retention of that group as a volume-planning issue now, not a problem for later.

- If you’ve got no named, willing successor who’s actually seen the numbers, stop absorbing losses “for the next generation” until you’ve had that talk.

What’s Your Number?

So here’s what’s worth sitting with tonight. Strip out the off-farm paycheck and the government check — would this farm still make money at $20.70 milk? And if not, which of the four paths actually fits your balance sheet and your zip code? Most operators already know the answer in their gut. The numbers just make it sayable — and they tell you which door to walk through while you still get to choose. Natalie Paino ran her version of that math at 18 and spent six years acting on it. The question isn’t whether she’s unusual. It’s whether the math that pushed her is sitting on your kitchen table too.

If you want the deeper math — the full cost-per-cwt model broken out by herd size, plus the real capital and labor behind a value-added build before you sign anything — that’s where the next pieces pick up. Start with our breakdown of why the milk-check math stopped working, run the numbers in our honest creamery ROI piece, and if you’re a co-op member or manager, the milk-price coverage is where the supply-side story keeps developing.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Dairy Tech ROI: The Questions That Separate $50K Wins from $200K Mistakes — Arms you with the exact formulas to evaluate automation, showing why unglamorous tech like activity monitors beats robots with a fast 7-to-14-month payback while highlighting how infrastructure failures wipe out potential margins.

- The Great Dairy Migration: How Regional Economics Are Reshaping America’s Milk Map — Exposes the brutal geographical realities forcing dairies to relocate, breaking down how regional labor spikes and a $23.56 per cwt scale gap dictate which zip codes survive the decade.

- Bred for Success, Priced for Failure: Your 4-Path Survival Guide to Dairy’s Genetic Revolution — Delivers a stark blueprint to escape the commodity treadmill by detailing the genetic-economic paradox, showing how breeding for elite efficiency only pays when matched with $42-to-$48 per cwt niche markets.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.