You think the worst day is when the truck stops. For 15 Harrisburg shippers, the real hit came later — when $985,012 in milk became a risk of a bankruptcy clawback.

Executive Summary: Harrisburg Dairies’ October 2025 shutdown left 15 Pennsylvania farms owed $985,012 for milk that was already sold, with the state’s bond and security fund covering only about 74% of that total. That shortfall exposes the real limits of Pennsylvania’s Milk Producers’ Security Act on a working dairy — it’s built to cover roughly 40 days of milk, not the six to eight weeks of arrears many producers quietly carry. When the company filed Chapter 11 in February 2026, it opened a 90‑day clawback window that could yank money back out of farms’ accounts for checks they’ve already cashed. The article walks through barn‑level math for a 200‑cow herd and a 300‑cow herd so you can plug in your own numbers and see exactly what a 74% recovery means in dollars. It then uses the Dean Foods precedent to explain, in practical terms, how ordinary‑course, subsequent‑new‑value, and contemporaneous‑exchange defenses can cut clawback exposure. The core mindset shift is simple: the Board optimizes for system stability, but you have to optimize for your own balance sheet. The back half is a concrete 30/90/365‑day playbook — from setting a hard limit on unpaid milk, to lining up a backup buyer, to stress‑testing whether your cash flow can survive a three‑month revenue gap if your processor ends up looking like Harrisburg.

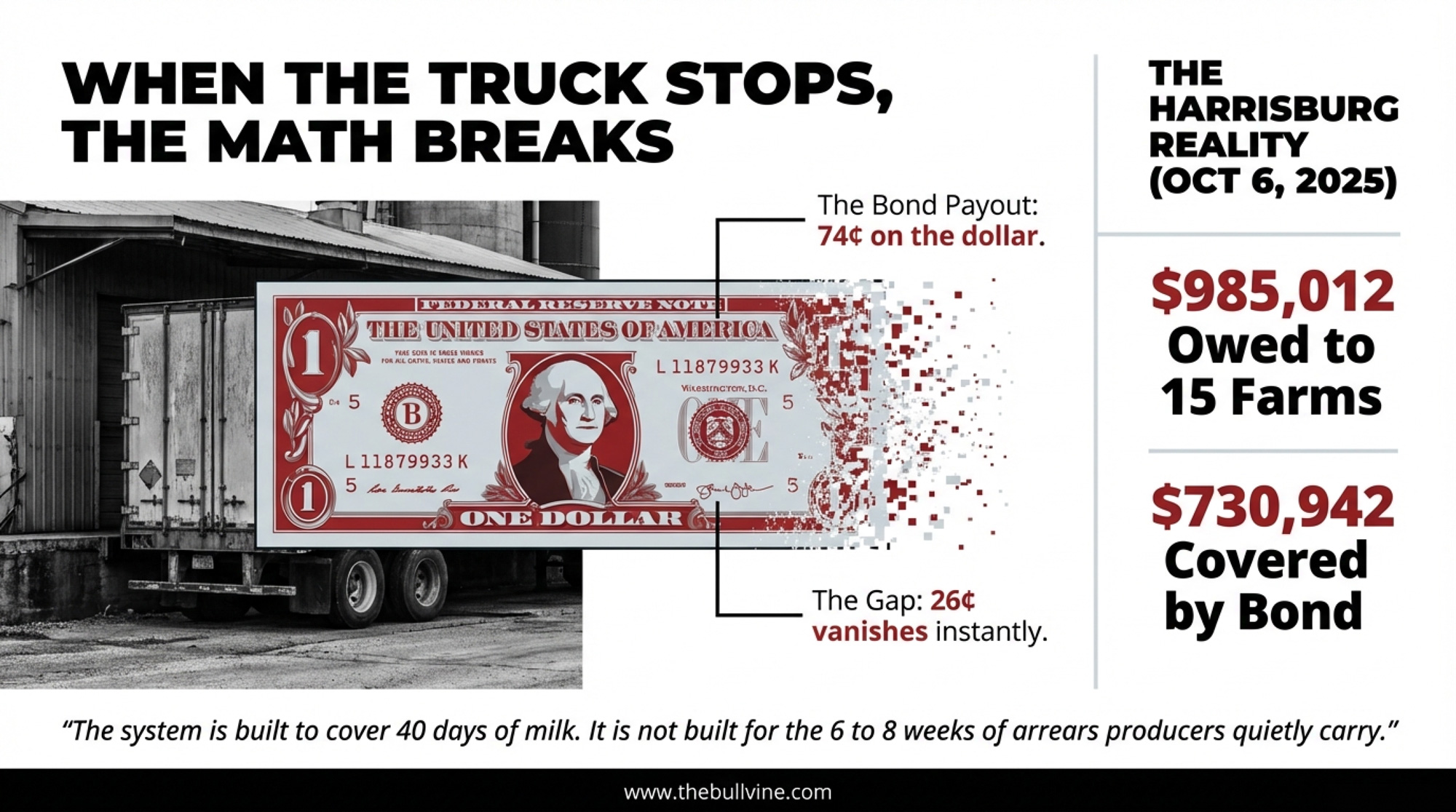

$985,012. That’s the total owed to 15 central Pennsylvania dairy farms when Harrisburg Dairies permanently ceased operations on October 6, 2025, according to Pennsylvania Milk Marketing Board executive secretary Betsy Albright in state milk board records and local coverage from October 2025. The company’s security bond and collateral covered $730,942.29 — roughly 74 cents on every dollar owed. The other 26 cents? That’s the gap the system wasn’t built to close.

Rob Barley chairs the PMB and co-owns Star Rock Farms, a 1,500-cow Lancaster County operation. When Harrisburg Dairies went dark on Monday, October 6, at least five farms were still actively shipping to the plant — bulk tanks with nowhere to go. “We will do everything possible that the law will allow to help farmers receive the maximum amount of funds available,” Barley told reporters in October 2025. Note the qualifier: what the law allows. All five farms have since been accepted by cooperatives operating in the area, according to Barley. But the milk they’d already shipped and never been paid for — that’s a separate problem.

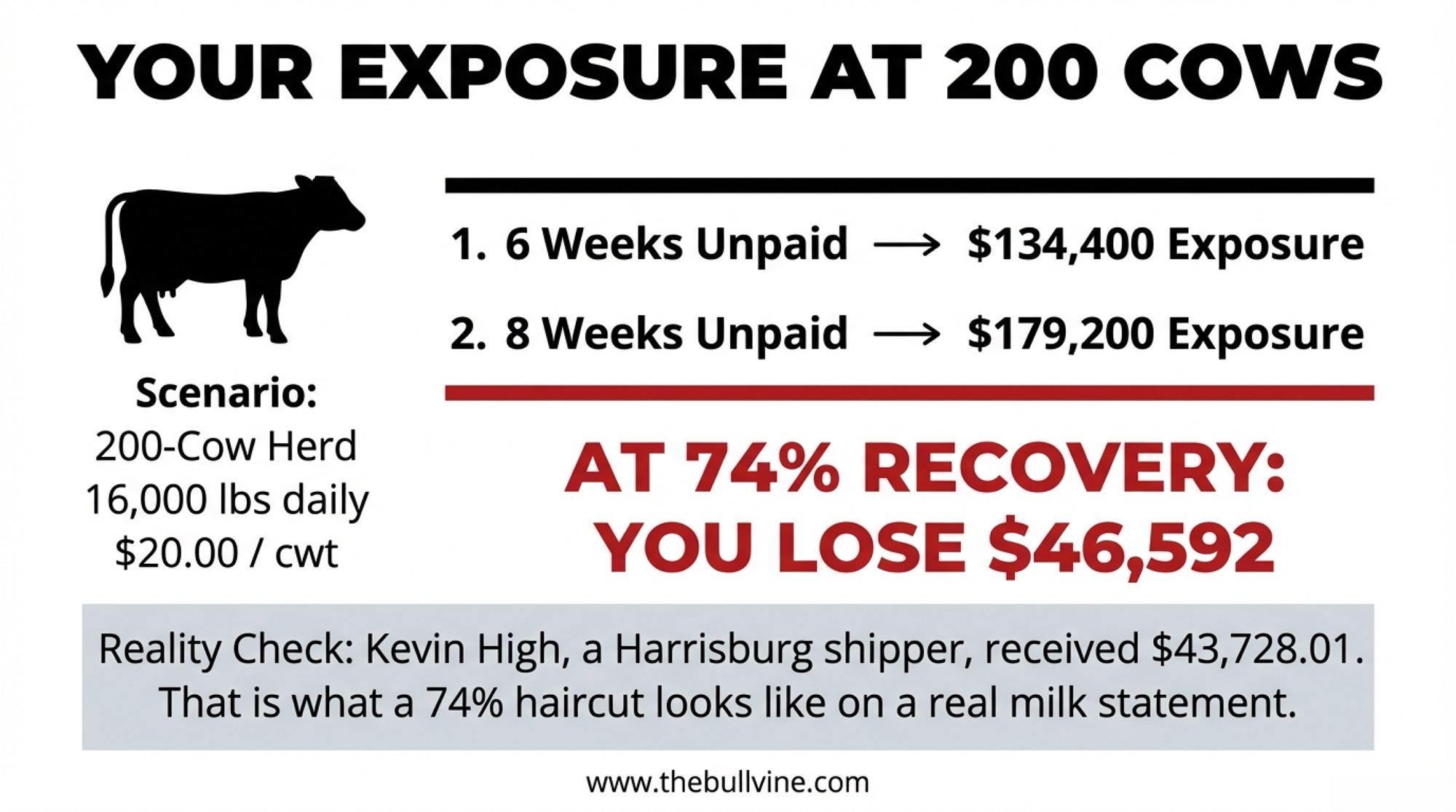

On November 5, 2025, the PMB issued Official General Order A-1021 directing the pro rata distribution of the Harrisburg Dairies security fund and collateral bond proceeds. Kevin High, one of the 15 shippers, was awarded $43,728.01. That’s what 74 cents on the dollar looks like on one farm’s milk statement.

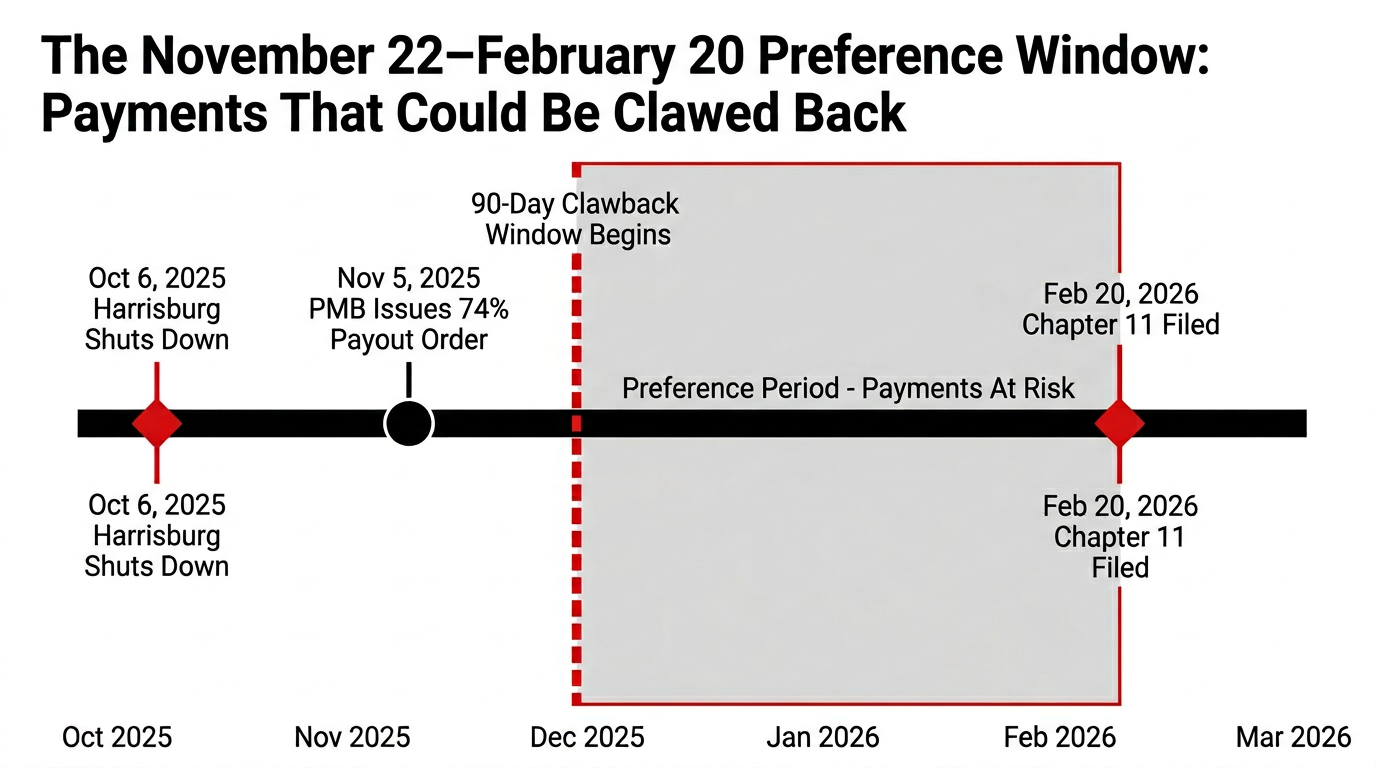

Then, on February 20, 2026, Harrisburg Dairies filed Chapter 11 in Pennsylvania’s Middle District Court (Case No. 1:26-bk-00474, Chief Judge Henry W. Van Eck), represented by Robert E. Chernicoff of Cunningham and Chernicoff PC. Court filings show nearly $4.6 million in assets against roughly $3.6 million in liabilities, primarily loans from Mid Penn Bank, which has filed a Request for Notice. Only about five employees remain, with a pending payroll of $7,624. WGAL reported on February 24 that the company has identified a prospective buyer and is seeking to use cash collateral to reorganize. First Day Motions filed on February 23 included requests for cash collateral use, assurance of utility service, and pre-petition payroll, with an expedited hearing set for February 26 at the Sylvia H. Rambo U.S. Courthouse in Harrisburg.

That filing triggered a second wave of financial exposure — the 90-day preference clawback — that could force farms to return payments they’ve already deposited and spent.

What Actually Breaks When the Truck Doesn’t Show Up

A 200-cow dairy produces roughly 16,000 pounds of milk per day. Without a scheduled pickup, the bulk tank is full in 48 hours. The cows don’t stop. The feed bill doesn’t pause. Every gallon dumped destroys revenue, with the cost already incurred.

But the cascade goes deeper than a full tank. Farmers reported that hauling deductions withheld from their milk checks were not being forwarded to haulers. So the driver who’s supposed to pick up Tuesday’s milk has his own cash-flow crisis — and no obligation to keep showing up for a defunct processor’s route. The weekly payment that was supposed to arrive under the PMB’s special order? It stopped.

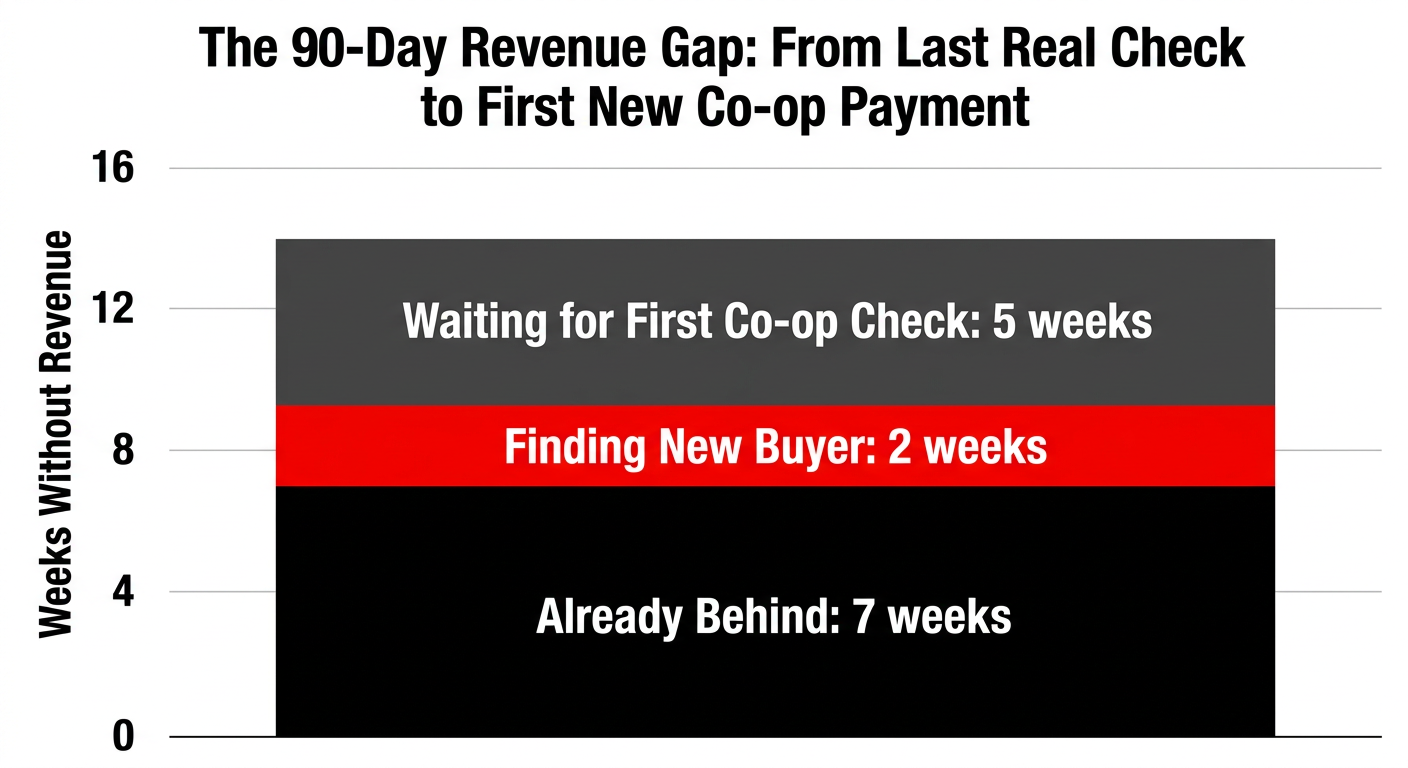

Most of these farms were already six to eight weeks behind on payments when the plant went dark. Finding a new buyer takes weeks, and the first check from a cooperative takes a month or more. The real revenue gap isn’t six to eight weeks. It’s closer to 10 to 12 from the last real payment to the first new check.

One producer told reporters he’d “calculated the risk in staying with Harrisburg Dairies given the prior late payment citations and continued lapses in their required weekly payments.” He stayed anyway. “It’s also a dream, of sorts, to be shipping to a local brand,” another anonymous producer explained. That loyalty — to a 94-year-old local processor — kept them shipping right up until the truck stopped coming. It’s the same generational pull that keeps families tied to the loyalty that keeps a family shipping to the same buyer for generations even when the math says otherwise. And some farms may have stayed simply because route geography, co-op-based programs, or timing barriers left them without a realistic alternative.

How Far Does Pennsylvania’s Milk Security System Actually Go?

Pennsylvania’s Milk Producers’ Security Act requires licensed dealers to file a surety or collateral bond equal to a minimum of 75% of the highest aggregate amount owed to all producers for 40 days during the preceding 12 months. A smaller subset of the roughly 193 dealers licensed by the Board participates in a security fund, posting a minimum 30% bond and making monthly contributions of 2¢ per hundredweight. As of April 2024, the fund held more than $3 million, with more than $100 million in total collateral and surety bonds across all dealers. Pennsylvania is one of only a few states that provide this type of buyer-default protection — worth remembering if you’re shipping to a proprietary plant outside PA.

For Harrisburg, Albright confirmed in news reports that the available security instruments totaled $730,942.29 — against $985,012 owed. The statute is clear: “the moneys available shall be divided pro rata among producers.” No floor. No minimum payout per farm. Kevin High’s $43,728.01 payout shows exactly what that haircut looks like.

Bottom line: The system covers roughly 40 days of exposure. When a dealer falls further behind than that before anyone pulls the trigger, the math breaks.

Running the Numbers: Your Exposure at 200 Cows

Take a 200-cow herd averaging 80 pounds per cow per day at $20/cwt:

- Daily production: 16,000 pounds

- Weekly milk revenue: roughly $22,400

- Six weeks behind: $134,400 in unpaid milk

- Eight weeks behind: $179,200 in unpaid milk

- At 74% recovery, you’re eating $34,944 to $46,592 that no security fund will cover

The 15 Harrisburg farms averaged roughly $65,700 each in total unpaid milk, some substantially more. At a 74% recovery rate, the average unrecovered loss per farm is around $17,000. Plug in your own herd size. At 300 cows, eight weeks at $20/cwt is $268,800. At 74% recovery, you’re absorbing nearly $70,000 in losses.

| Herd Size (cows) | Total Unpaid (8 weeks @ $20/cwt) | 74% Recovery (Security Fund) | Unrecovered Loss |

| 100 | $89,600 | $66,304 | $23,296 |

| 200 | $179,200 | $132,608 | $46,592 |

| 300 | $268,800 | $198,912 | $69,888 |

| 500 | $448,000 | $331,520 | $116,480 |

| 750 | $672,000 | $497,280 | $174,720 |

Could Your Dairy Farm Get a Clawback Letter After Harrisburg Dairies’ Bankruptcy?

The October closure broke daily operations. The February 20 bankruptcy filing broke the legal recovery. Under 11 U.S.C. § 547, payments made during the 90 days before a Chapter 11 filing are considered “preference” payments. The bankruptcy estate can demand repayment of those payments.

Harrisburg’s 90-day window reaches back to approximately November 22, 2025. Any partial payments clearing old balances during that window could be subject to clawback demands — from farms that were already underwater.

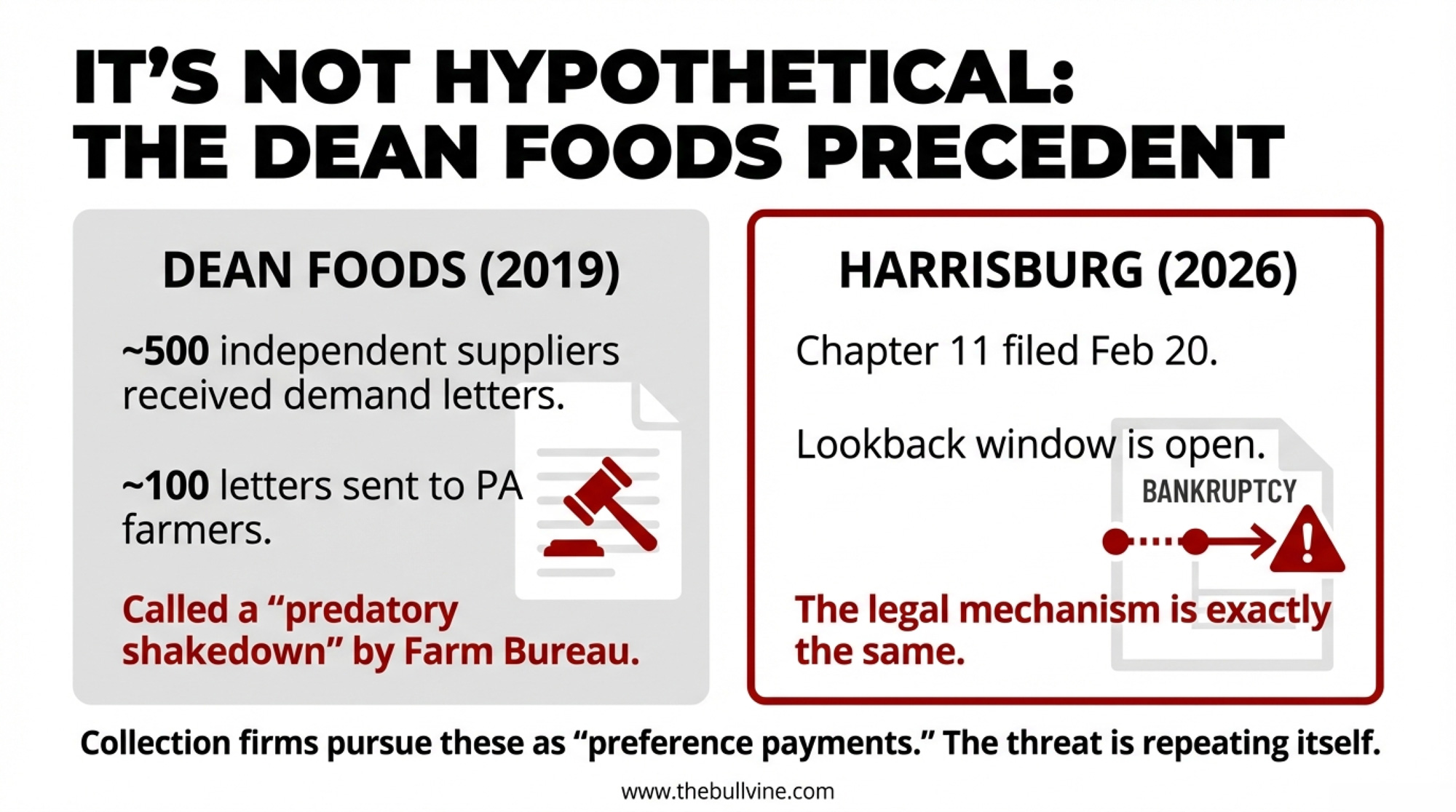

This isn’t hypothetical. When Dean Foods filed Chapter 11 in November 2019 — a collapse The Bullvine covered extensively, from the $850 million DIP financing to how two years of changes led to two major bankruptcies — approximately 500 independent former Dean milk suppliers received demand letters from ASK LLP, a St. Paul, Minnesota firm authorized to pursue preference actions as of September 1, 2020. About 100 of those letters went to Pennsylvania dairy farmers alone. AFBF called the letters “a predatory shakedown,” and General Counsel Ellen Steen demanded ASK withdraw them within 10 business days.

Three defenses cut that exposure — sometimes to zero:

- Ordinary course of business: If that December check looks like how you’d always been paid — same lag, same method — courts often side with you. For milk, where everyone knows standard pay cycles, this defense is strong.

- Subsequent new value: Kept shipping after that payment and never got paid for the later milk? That unpaid “new value” offsets the preference dollar-for-dollar. Got a $28,000 check in December but shipped another $25,000 in unpaid milk afterward? Real exposure drops to $3,000.

- Contemporaneous exchange: If the payment and the milk delivery were roughly simultaneous, there’s no old debt to claw back.

The critical detail from the Dean precedent: the PMMB — working with the Pennsylvania Attorney General’s office and ASK LLP — developed standardized declaration forms that farmers could submit instead of full financial records. ASK agreed to accept the declarations and close files for producers who demonstrated ordinary-course-of-business payments. Board Secretary Carol Hardbarger credited cooperation from the AG’s office, the Center for Dairy Excellence, and the PA Farm Bureau for enabling the quick resolution, a sentiment echoed by Barley.

If Harrisburg Dairies’ estate pursues similar preference actions, that Dean playbook is your template. Don’t pay. Don’t ignore. Get a bankruptcy-savvy ag attorney, pull 12–18 months of invoices and payment dates, and respond with: “We’re evaluating defenses. Extend the deadline.” The broader processor concentration problem driving these collapses — and what your options actually look like — is something we broke down in the consolidation math reshaping who buys your milk.

What Do Dean Foods, Borden, and Harrisburg Dairies Have in Common?

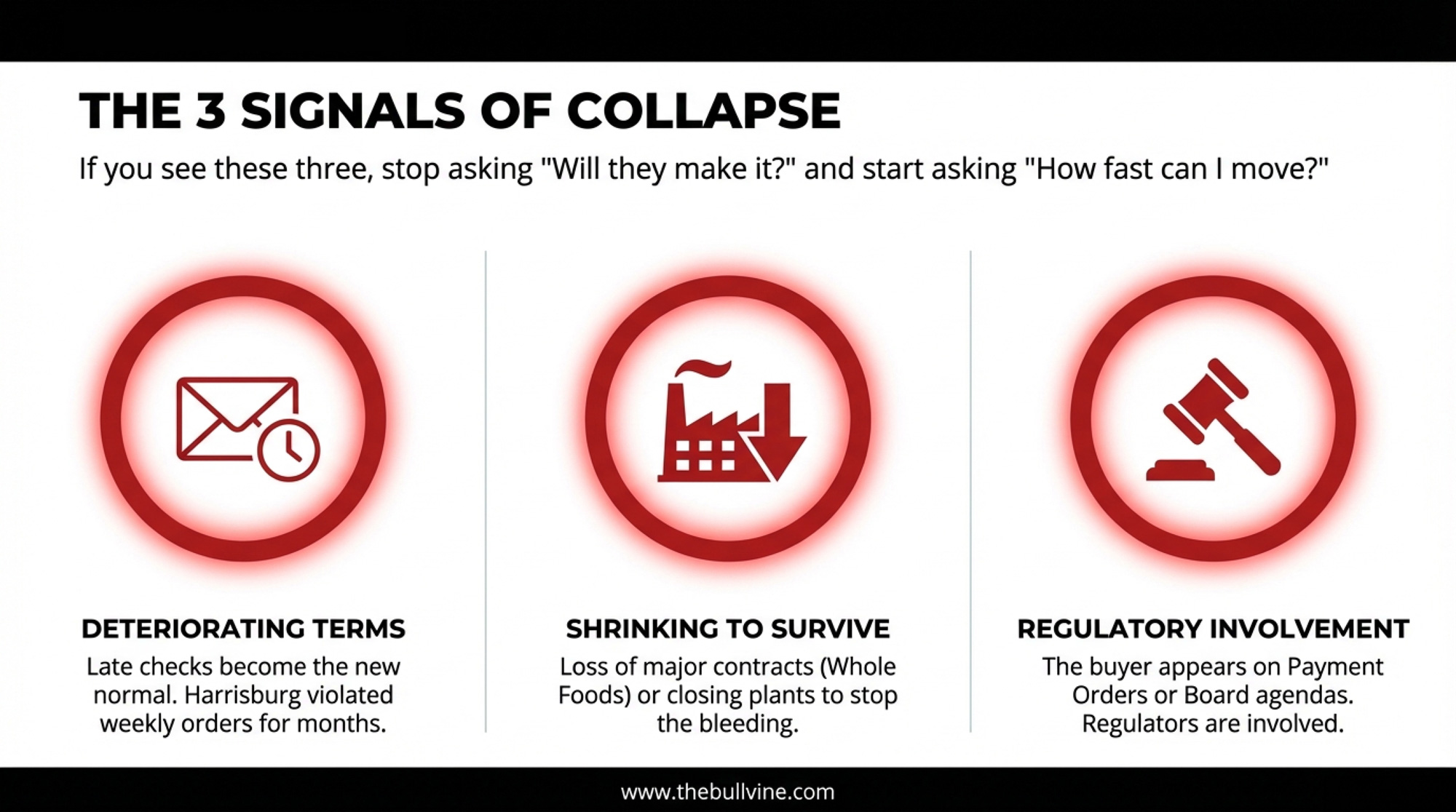

Here’s the uncomfortable pattern: in each of these cases, regulators had documented evidence of deterioration months before the collapse — and chose to keep the processor operating.

Harrisburg Dairies was under a weekly payment order since September 2023. By May 2025, the PMB had evidence of violations dating back to at least December 2024 and found grounds to revoke the dealer’s license. They chose not to. “Doing so would not serve the best interests of the Pennsylvania dairy industry,” the Board ruled on May 7, 2025, according to PMMB Sunshine Meeting minutes from May 7, 2025 and local coverage summarizing the Board’s decision. The Board’s decision reflected a structural tension built into the Act itself: revoking a license protects producers from future losses but can strand current shippers with no buyer at all.

Instead: stricter conditions, a higher bond, and weekly payments at 110% of the previous month’s lowest class price. “They lost a big customer. There wasn’t much we could do but give them the 28 days. We also made sure someone could take the milk from those farms,” Barley told news reports in July 2025. Pennsylvania has limited processing capacity, and the alternative to an imperfect processor is sometimes no processor at all. Doug Eberly, PMB chief counsel, confirmed the termination approval was narrow: “This is not a blanket approval — it applies only to this particular volume loss.”

Two consequences followed. Arrears stretched from two to three weeks behind in mid-July to six to eight weeks by early October. And milk volume continued to flow through a processor whose bond covered only 74% of producer exposure.

The common assumption: “If it gets really bad, the Board will shut them down before I get too exposed.”

| Collapse Indicator | Dean Foods (2019) | Borden (2020) | Harrisburg (2025) |

| 1. Payment Terms Deteriorate | Failed Oct 2019 Class I obligations before Nov 12 filing | Needed court permission to pay Dec 2019 milk bills | Weekly payment order since Sept 2023, violated for months |

| 2. Company Shrinks to Survive | Closed 6+ facilities, carried >$1B net debt | Filed Ch 11 in Jan 2020 citing debt load | Lost Whole Foods (229K lbs/wk), terminated 7 farms July 2025 |

| 3. Regulatory Involvement Escalates | Active FMMO issues, public scrutiny | Court oversight of payments | PMB payment order, license revocation debate |

The data says otherwise. The Board optimizes for system stability — keeping enough processing capacity alive so farms have somewhere to send milk tomorrow. You need to optimize for your own balance sheet.

Three signals showed up 6–12 months before each of these collapses:

- Payment terms deteriorate and never recover. Not one late check — a new, worse normal. Dean failed to make October 2019 Class I obligations to most regional FMMOs in the month before its November 12 filing, according to The Milkweed. Harrisburg’s weekly order was violated for months before closure.

- The company shrinks to survive. Harrisburg lost its Whole Foods Market contract — 229,116 pounds per week — then terminated seven Lebanon County farms in July 2025 to match the volume loss. Dean closed at least a half-dozen facilities and carried more than $1 billion in net debt as of its November 2019 filing. The Walmart second-plant story tells that same tale from the other side — 18 months after Walmart’s first plant opened, Dean filed.

- Regulators become characters in the story. Payment orders, missed pool payments, PMB hearings, and special oversight. Borden needed court permission to pay the December 2019 milk bills. When your buyer’s name starts appearing regularly on regulatory hearing agendas, treat it as a serious risk signal — not a guarantee of failure, but a pattern that preceded every processor collapse examined here.

The moment you see all three on the same timeline, stop asking “Will they make it?” Start asking “How fast can I move my milk?”

Your Buyer Just Got a Payment Order. Now What?

If your processor is on a payment order right now, you’re in the window where Harrisburg’s farms found themselves in mid-2025. Here’s the playbook they wish they’d had.

This week (30-day actions):

- Document everything. Pull 12–18 months of milk statements, deposit dates, component data, and payment timelines. This is your evidence for ordinary-course and new-value defenses if clawback letters arrive.

- Know your number. Calculate your unpaid balance in dollars and days. Set a hard threshold: “We will not carry more than 30 days of unpaid milk with this buyer.” For a 200-cow herd at $20/cwt, that’s roughly $96,000. If that figure makes your stomach turn, you have your answer.

- Make two phone calls. Contact at least two alternative buyers — co-ops or other plants in your draw. Ask bluntly: “If my current buyer fails, how fast could you start picking up?” The farms that moved before October had already started those conversations. The ones still there on October 6 were caught without a backup.

Next 90 days:

- Call your lender before they call you. Your operating lender is watching the same PMB orders you are, updating your risk profile without telling you. Say this: “Here’s our exposure, here’s our Plan B, here’s the working capital we’ll need for a 60-day cash gap. Are you in or out?”

- Stress-test for a three-month revenue gap. Harrisburg’s farms were 6–8 weeks behind at closure, then waited another month-plus for first checks from new buyers. That’s roughly 90 days of revenue disruption. If your operation can’t survive that without the banker making survival decisions for you, your financial structure needs work, regardless of processor risk. We’ve written extensively about the liquidity buffer that separates farms that survive a revenue gap from those that don’t.

This year (365-day actions):

- Track your buyer’s regulatory record. PMB sunshine meeting minutes and docket entries are public. Harrisburg’s problems were documented for over two years before closure. Treat those filings like forward-price signals.

- Stay transition-ready. Keep SCC strong, records current, and relationships warm with at least one alternative buyer. Our deep dive on keeping your components and SCC where a co-op field rep says yes, lays out the protocol.

Red flag: Your buyer is on a payment order AND has lost a major customer or closed a facility in the past 12 months. That’s two of three collapse indicators active.

Opportunity: Your co-op field rep confirms route capacity and 30-day pickup timeline. That’s your exit ramp — keep it open. But understand what the equity retained on your co-op milk check actually costs you before you sign.

Key Takeaways

- If your buyer is more than 21 days behind on payment, your exposure already exceeds the PA Milk Security Act’s 40-day bond coverage window — and the gap widens every week you keep shipping. Run the math from the 200-cow example above with your own herd size.

- If you received any payment from a distressed processor within the 90 days before their bankruptcy filing, pull your records now. Your ordinary-course-of-business defense depends on documentation you can produce — not on what you remember.

- If your processor has been on a payment order for more than six months, you’re past the warning-signal stage. Two of Harrisburg’s three pre-collapse indicators (deteriorating terms + regulatory involvement) are already active. The only question is whether the third (shrinking to survive) has started.

The Number That Decides Who Survives the Transition

Consider two operations on the same route in Harrisburg. Same buyer, same October 6 closure. The one with modest debt and three months of breathing room rides it out — switches to a cooperative, absorbs the equity retained on the new milk check, moves on. The one with maxed-out operating credit and razor-thin liquidity hits a 60-day payment gap, and suddenly the banker — not the co-op — is making the survival call.

Processor risk and leverage risk are the same animal when the plant goes dark.

That anonymous Harrisburg producer who told news reports he’d “calculated the risk in staying” — he did the math and stayed. The bond covered 74 cents. Kevin High’s $43,728.01 check from the PMB tells you what the 74 cents actually buys. The other 26 cents is a hard lesson in the distance between what the system promises and what it delivers.

Pull your last three milk statements. How many days behind is your buyer right now? Multiply your daily production by that number, then by your pay price. That’s your current uninsured exposure — and the only forecast that matters before Tuesday’s truck doesn’t show up.

| Days Behind | 100 Cows | 200 Cows | 300 Cows | 500 Cows | 750 Cows |

| 15 days | $12,000 | $24,000 | $36,000 | $60,000 | $90,000 |

| 21 days | $16,800 | $33,600 | $50,400 | $84,000 | $126,000 |

| 30 days | $24,000 | $48,000 | $72,000 | $120,000 | $180,000 |

| 45 days | $36,000 | $72,000 | $108,000 | $180,000 | $270,000 |

| 60 days | $48,000 | $96,000 | $144,000 | $240,000 | $360,000 |

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- The 18-Month Window: Why Your Lender Knows Your Dairy’s in Trouble Before You Do – Reveals the specific financial benchmarks your banker uses to flag insolvency months before you do. This guide arms you with the exact healthy, warning, and high-risk ranges for debt-to-equity and margin-over-feed costs to protect your credit.

- More Milk, Fewer Farms, $250K at Risk: The 2026 Numbers Every Dairy Needs to Run – Breaks down the brutal math of the $250,000 margin gap facing 500-cow dairies in 2026. This analysis delivers a concrete playbook for closing that gap through targeted heifer program cuts and smarter supply network positioning.

- Revolutionizing Dairy Farming: How AI, Robotics, and Blockchain Are Shaping the Future of Agriculture in 2025 – Exposes how AI-milking robots and blockchain tracking are weaponizing consumer trust to secure 15% price premiums. This article reveals the ROI-driven technologies that turn your herd into a high-margin profit engine while your competition stalls.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.