One month of DMC at $9.50 could pay several years of premiums. The deadline is Wednesday. Have you actually run the math?

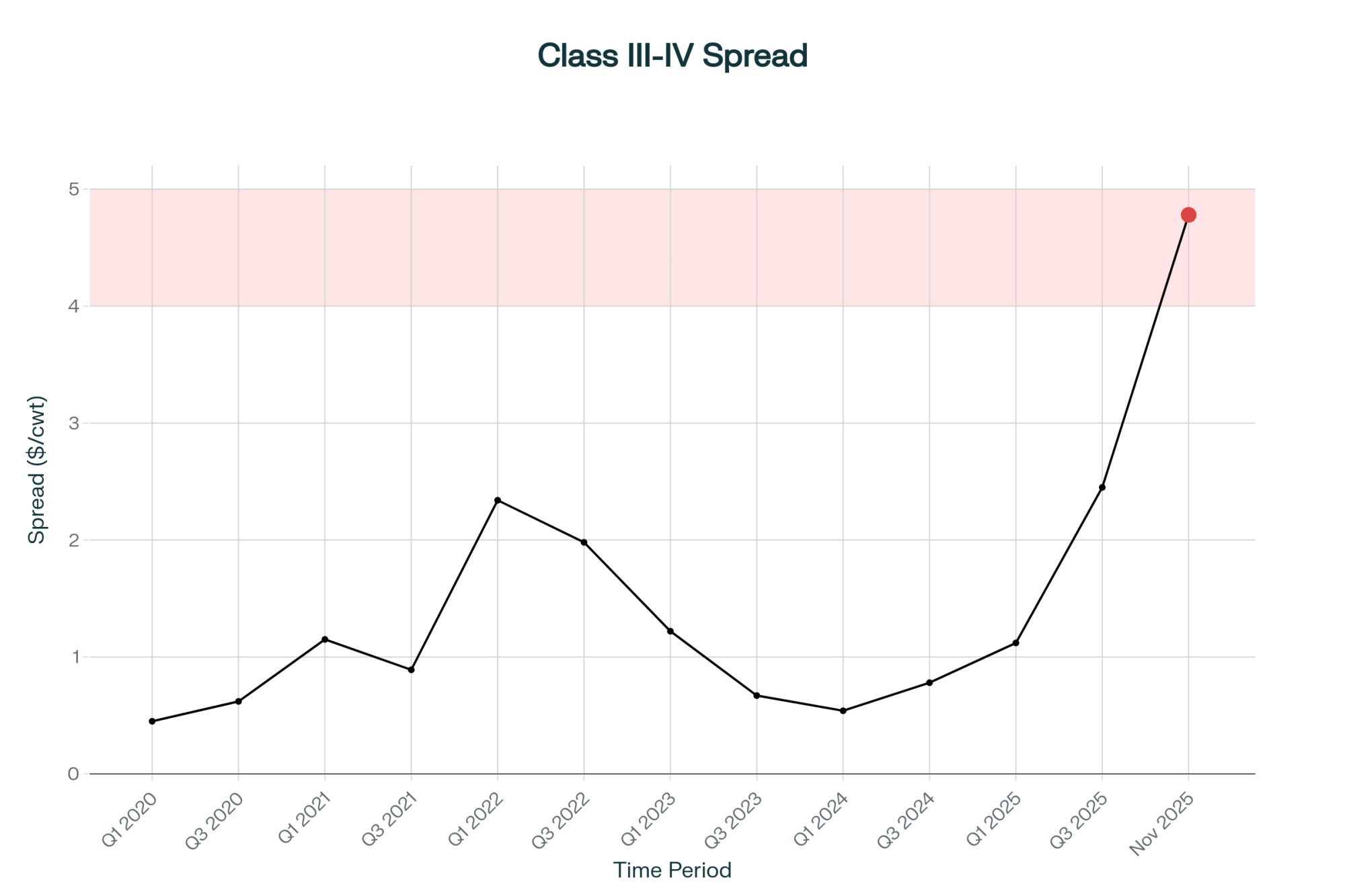

Executive Summary: January’s Class III price fell to $14.59/cwt while March Class IV futures climbed to $19.50, creating a $2.99/cwt spread that works out to about $382,000/year on a 500‑cow herd shipping 70 lbs/cow/day. That gap sits atop June 2025 make‑allowance changes that already skimmed roughly 90¢/cwt from producer checks and is being widened by a global butterfat shortage, a tight U.S. powder market, and a new $75 million USDA butter buy. At the same time, the U.S. dairy herd has grown to 9.58 million cows, the largest in more than 30 years, setting up a spring flush that could pressure prices unless Section 32 purchases and exports keep absorbing product. The one clear positive is Dairy Margin Coverage: with a projected January margin of $7.52/cwt, $9.50 coverage throws off about $1.98/cwt on Tier 1 milk, so a single month’s payment can cover several years of premiums. For a 500‑cow dairy, each combined 0.1% gain in butterfat and protein now adds roughly $46,400/year, making components one of the few levers that improve cash flow without new capital. This article doesn’t just recap those numbers; it walks through barn‑level math and a 30/90/365‑day playbook for lining up DMC enrollment, DRP weighting, component strategy, and Section 179 planning with $16–$17 Class III, not a rosy futures average. It ends with a hard question every producer has to answer: where does your breakeven sit relative to $16.51 Class III, and what are you going to do about it before the DMC window closes?

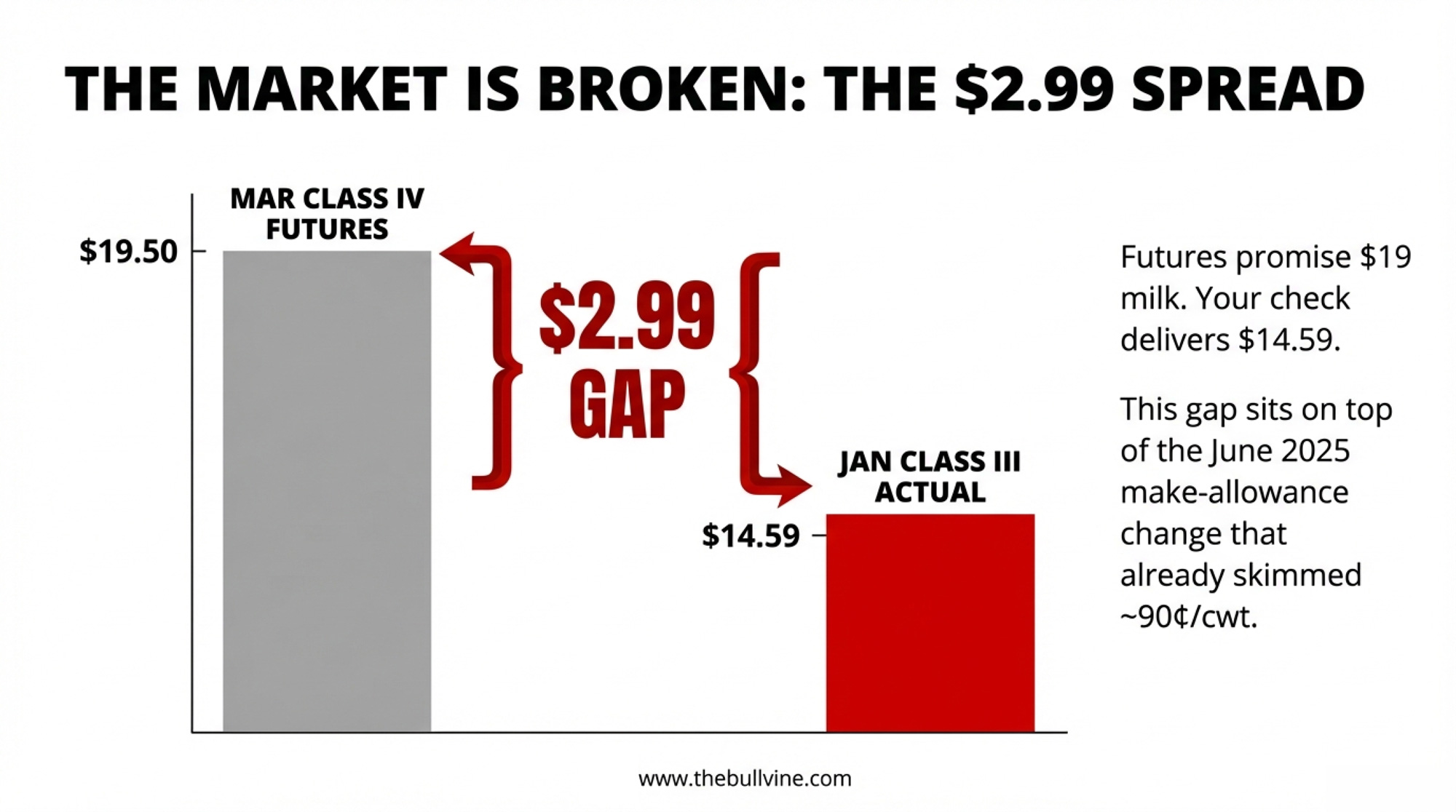

January’s FMMO Class III price landed at $14.59/cwt — down $1.27 from December and the lowest since July 2023’s $13.77. Part of that’s structural: USDA’s June 2025 make-allowance increases shifted roughly 90¢/cwt from producer checks to processor cost recovery. But the bigger story is what happened on the other side of the class divide.

March Class IV futures settled at $19.50/cwt on February 20 — the same day March Class III settled at just $16.51. That’s a $2.99/cwt same-month spread. Nearly three dollars separating what your milk is worth as butter and powder versus cheese, on the same contract month.

That kind of gap doesn’t just show up on a chart. It shows up on your milk check, your DRP election, and your cash-flow projections for the next 90 days.

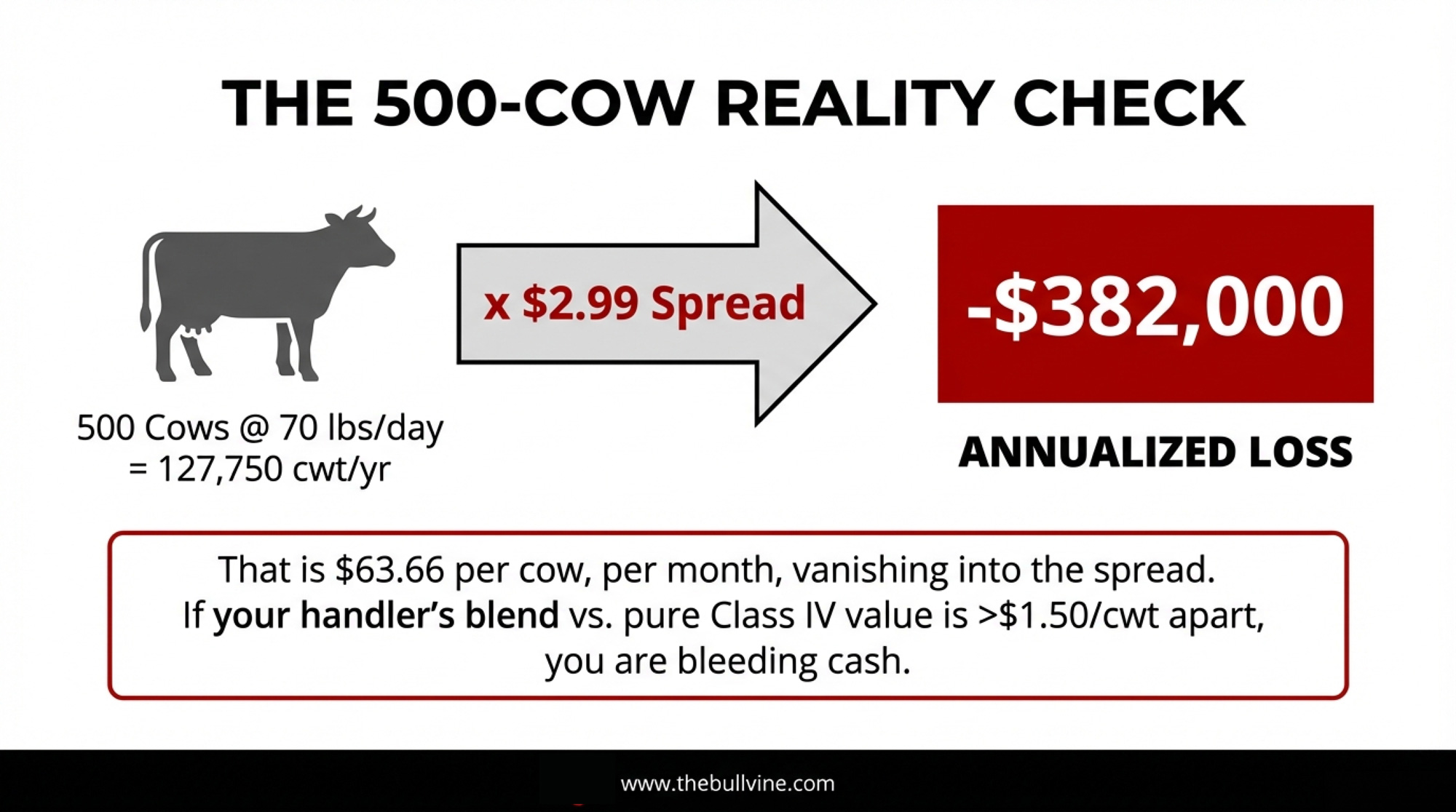

Consider a 500-cow freestall shipping 70 lbs/cow/day — the kind of Upper Midwest operation that entered 2026 staring at roughly $90,000 less operating margin than it had the year before. That was before the Class IV spread blew open. Now the question isn’t just “are margins tight?” It’s “which side of the Class III/IV line is your milk landing on?”

$263 Million in Section 32 Purchases — and the Spread Just Got Wider

For that 500-cow operation already staring at a $2.99 class gap, USDA just added fuel to the fire.

On February 19, Secretary of Agriculture Brooke Rollins announced a $263 million Section 32 purchase of dairy and agricultural products. Of that, $148 million goes to dairy — matching the number NMPF requested in late 2025.

The dairy breakdown:

$75 million in butter — the first major USDA butter purchase in five years

$32.5 million in Cheddar cheese and cheese products

$10 million in Swiss cheese

$20.5 million in fresh fluid milk

$10 million in UHT milk

Traders pushed several CME butter contracts to their daily upper limits on Thursday and Friday. The irony isn’t subtle: a program designed to improve food affordability could temporarily tighten commercial butter supplies and push prices higher. Rush the purchases, and you squeeze an already tight market. Spread them out, and the impact fades. Either way, it lit a fire under Class IV futures that isn’t going out this week.

What Does a $2.99/cwt Class Spread Mean for a 500-Cow Dairy?

The headline number means nothing without per-cow math. So let’s walk it.

A 500-cow herd averaging 70 lbs/cow/day ships roughly 255.5 cwt/cow/year, or about 127,750 cwt annually for the operation.

At March Class IV of $19.50/cwt, that’s approximately $2,491,000 in gross milk revenue annualized at that price. At March Class III of $16.51, it’s roughly $2,109,000.

The same-month gap: $382,000/year. About $31,800/month. $63.66/cow/month.

April’s spread narrows. April Class III settled at $17.30 on February 20, while April Class IV held at $19.50 — a $2.20/cwt spread, or about $281,000 annualized. The futures curve expects some Class III recovery. But March is what’s hitting checks right now.

And no herd receives a pure single-class check. Your milk check is a blend, weighted by your handler’s utilization decisions and the pool. When Class IV runs this far above Class III, depooling accelerates — handlers pull Class IV milk out of the pool because it’s more profitable outside. In Federal Order 30 (Upper Midwest), pooled Class IV producer milk totaled just 1.4 billion pounds in 2025, even as butter and powder production ran strong. Handlers kept that high-value milk outside the pool, and the blend price for everyone who stayed pooled took the hit.

Metric

March Class III ($16.51/cwt)

March Class IV ($19.50/cwt)

Annual Production (500-cow herd, 70 lbs/day)

127,750 cwt

127,750 cwt

Gross Milk Revenue (annualized at this price)

$2,109,000

$2,491,000

Annual Revenue Gap

—

+$382,000 🔴

Monthly Revenue Impact

$175,750

$207,583

Monthly Gap

—

+$31,833 🔴

Per-Cow Monthly Revenue

$292.92

$345.14

Per-Cow Monthly Gap

—

+$52.22 🔴

Run your own numbers. If the gap between your handler’s blend and what you’d get at pure Class IV pricing is more than $1.50/cwt, the rest of this article matters more to your operation than most.

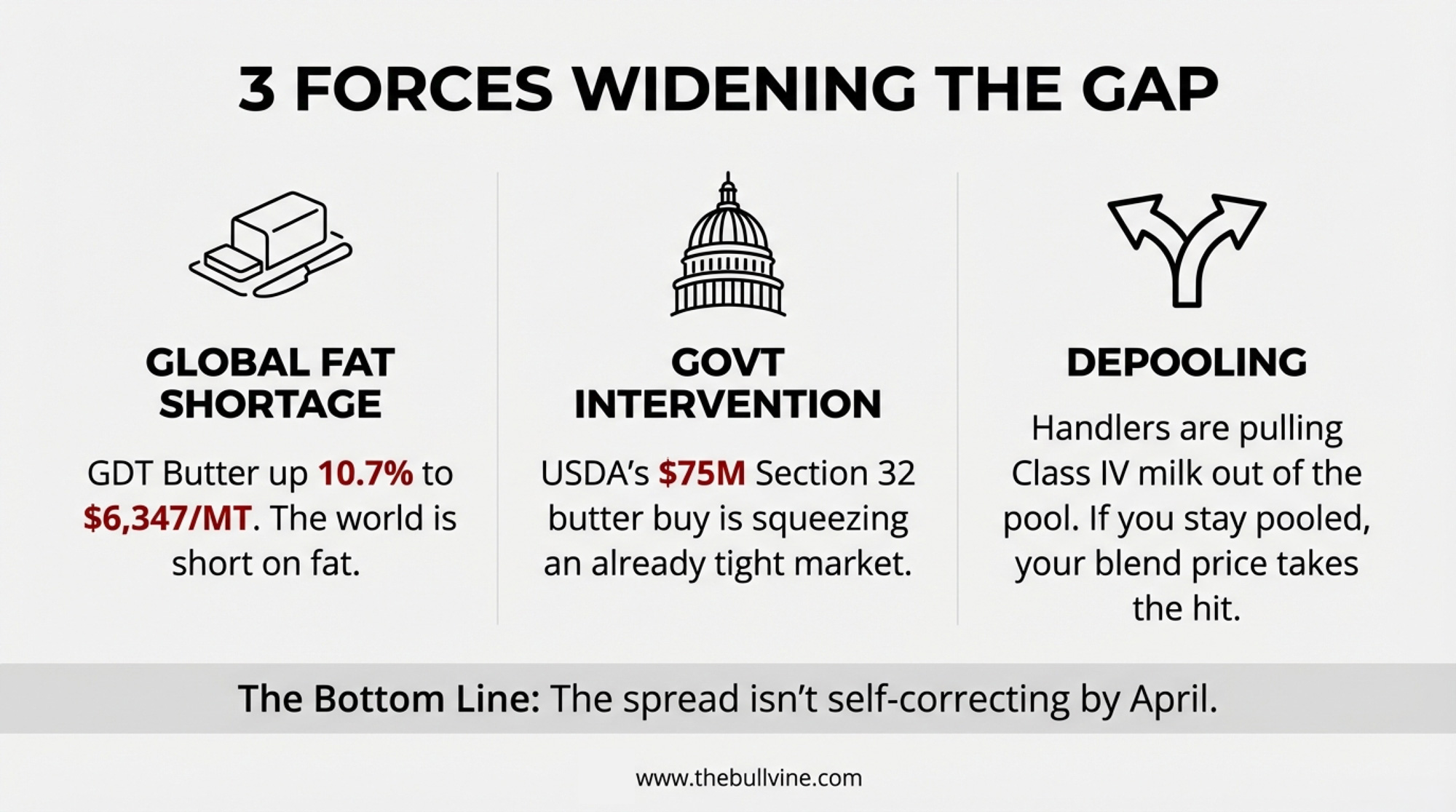

Three Forces That Won’t Let the Spread Self-Correct

For that 500-cow operation watching the spread widen, three structural drivers suggest it isn’t cooling off by April.

Global fat shortage. GDT Event TE398 — the fourth consecutive price increase — saw butter jump 10.7% to $6,347/MT. Anhydrous milk fat climbed 3.8% to $6,751/MT. Butterfat is tight worldwide, not just in the U.S.

U.S. powder premium over world price. CME spot NDM surged to $1.685/lb during the week ending February 20 — the highest since mid-2022. That sits well above the GDT SMP equivalent of roughly $1.44/lb protein-adjusted. The U.S. powder market is especially tight, and it’s dragging Class IV higher.

Government demand is stacked on top. The Section 32 butter buy adds $75 million in new purchasing power to a market already rationed by price. That’s demand creation at the worst possible moment for anyone hoping Class IV cools off.

CME spot butter jumped 16.5¢ to $1.87/lb for the week, a five-month high. Spot cheddar blocks rose 11¢ to $1.4975/lb — competitive, but nowhere near the butterfat rally. Whey fell 4¢ to $0.68/lb, bucking the trend entirely.

The Spring Flush Math Just Got Worse

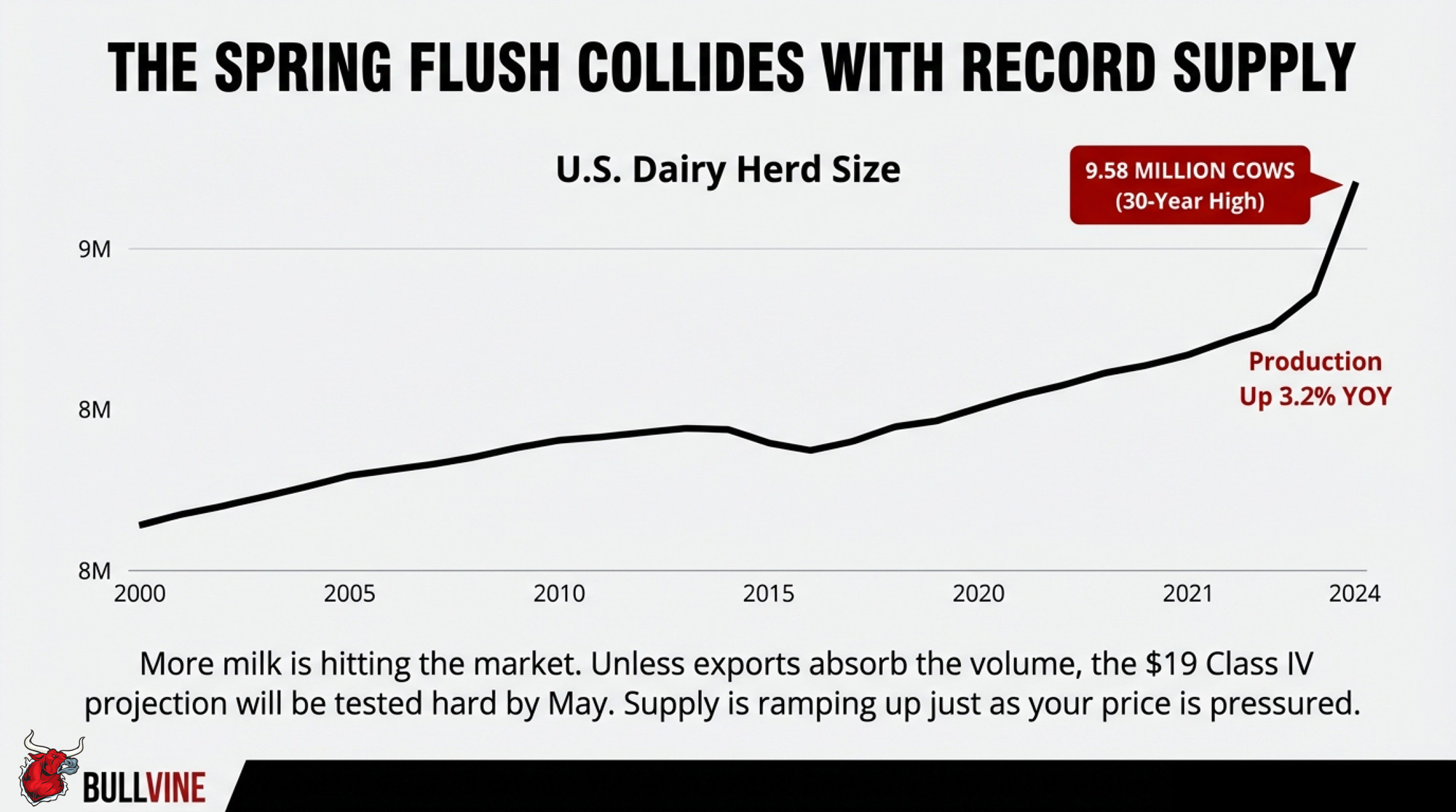

That same 500-cow herd’s spring production ramp is about to collide with the largest national herd in over 30 years.

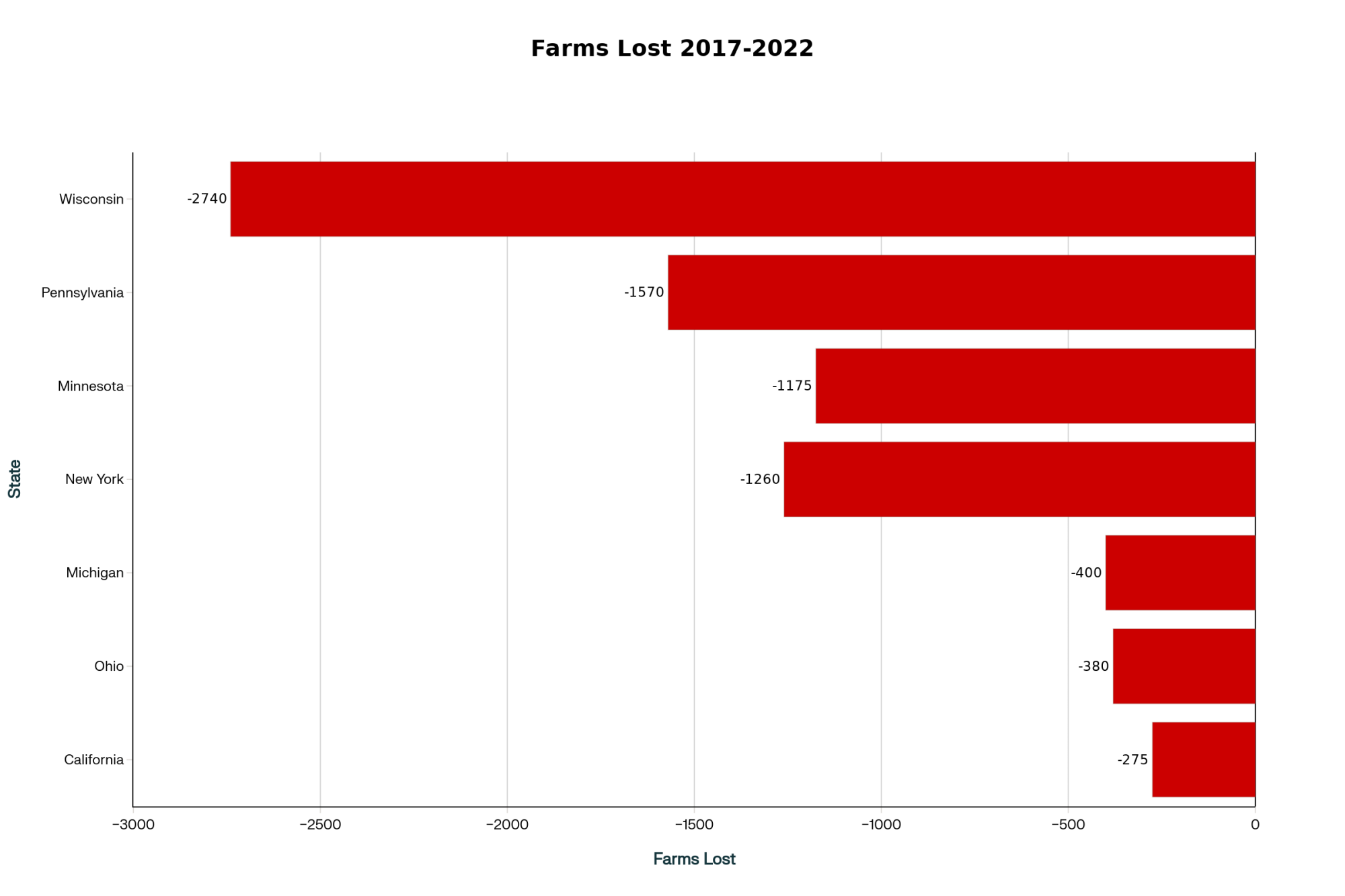

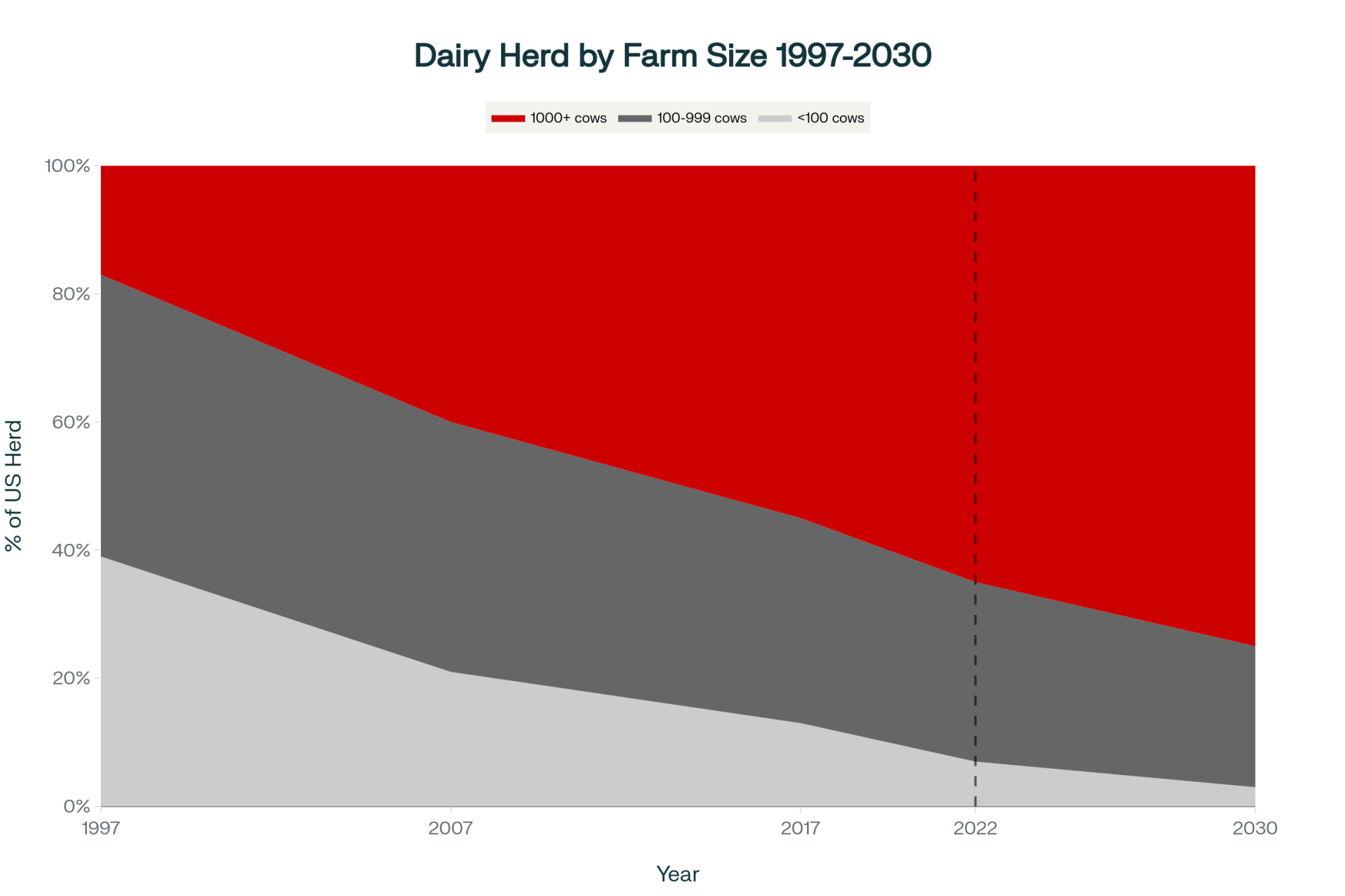

USDA’s January Milk Production report, released February 20, showed total U.S. production at 19.8 billion pounds, up 3.2% year-over-year. The herd itself reached 9.58 million head — up 189,000 cows from January 2025, up 14,000 from December, and the highest total since 1993.

Growth concentrated in the Great Lakes, Texas, and the Northern Plains. Kansas alone added 45,000 cows year-over-year. Wisconsin added 20,000, Idaho 22,000, and Michigan 15,000. On the other side: Washington lost 17,000, Pennsylvania shed 11,000, and New Mexico dropped 8,000. California’s per-cow yields surged 4.6% — from 1,960 to 2,050 lbs/cow in January — with avian influenza fully cleared.

More milk hitting the market should, in theory, ease commodity prices. But the butterfat complex isn’t responding to supply signals the way cheese is. If Section 32 purchases and export demand don’t absorb the extra volume, the futures curve’s $19+ Class IV projection gets tested hard by May, and the spread could narrow from the wrong direction.

But One Thing Already Broke in Their Favor: DMC

Here’s the turn for that 500-cow operation. The safety net they may have treated as an afterthought in 2025 just became the most important enrollment of the decade.

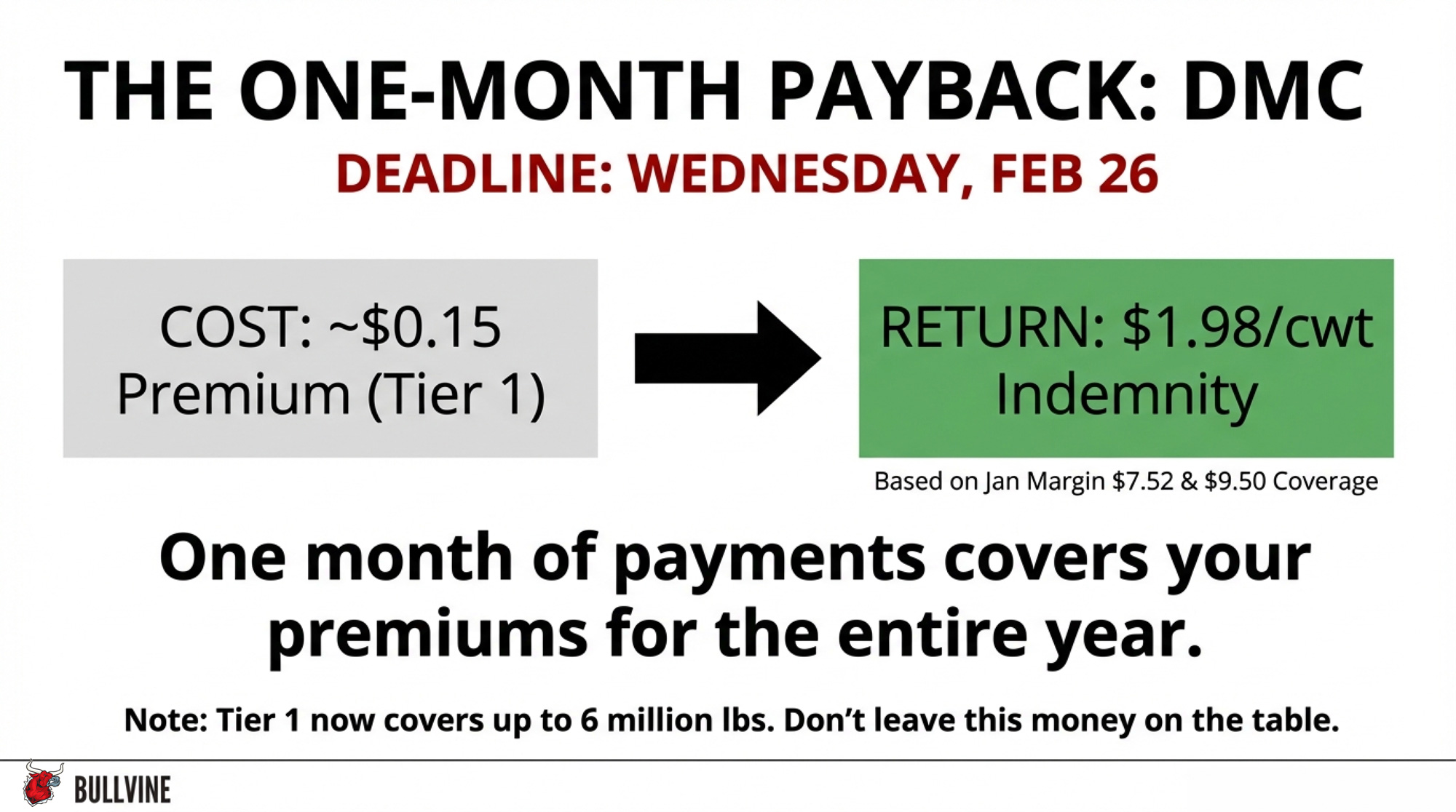

December 2025’s Dairy Margin Coverage margin came in at $9.42/cwt, triggering the first and only payment of 2025 — a thin $0.08/cwt. January doesn’t look thin.

The Center for Dairy Excellence projects the January margin at $7.52/cwt. At $9.50 coverage, that’s a $1.98/cwt indemnity. On 5,000 cwt of monthly Tier 1 production (a 6-million-pound annual allocation), that’s roughly $9,900 in a single month — enough to cover the full year’s premium several times over.

NMPF’s William Loux confirmed the direction: he expects DMC payments through the first quarter and probably through the first half of the year.” USDA projects margins below $9.50/cwt through July.

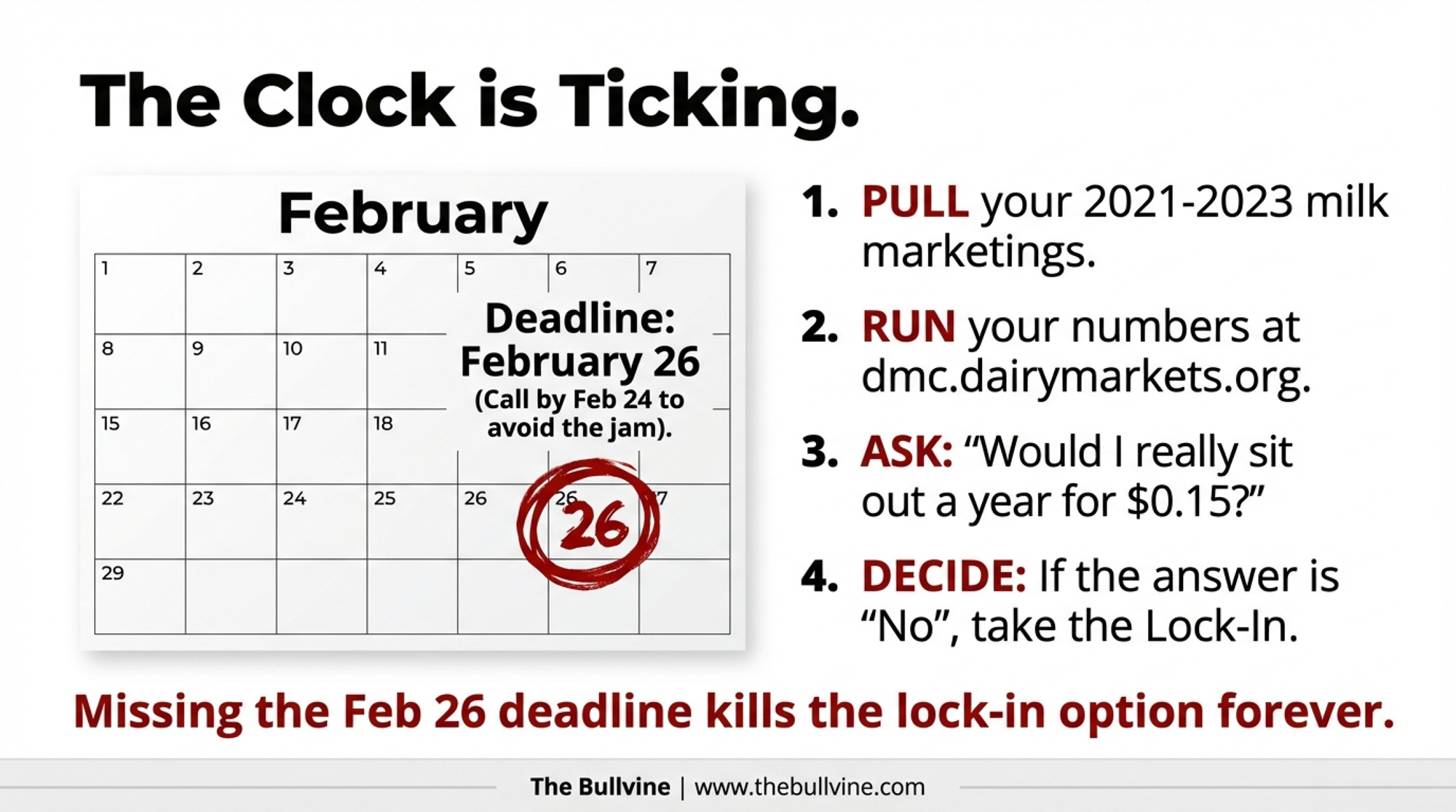

Enrollment closes February 26. Under the One Big Beautiful Bill Act:

Tier 1 expanded from 5 million to 6 million pounds — covering herds up to roughly 250–350 cows at the $0.15/cwt premium for $9.50 coverage.

Highest production year from 2021–2023 becomes your new baseline.

The trade-off is real. You’re committed through 2031 regardless of where margins go. If margins recover to $12+ by 2027, you’re paying premiums on coverage you won’t trigger. But at $7.52 projected margins in January, the payback math is aggressive. If you haven’t enrolled, the decision framework is here.

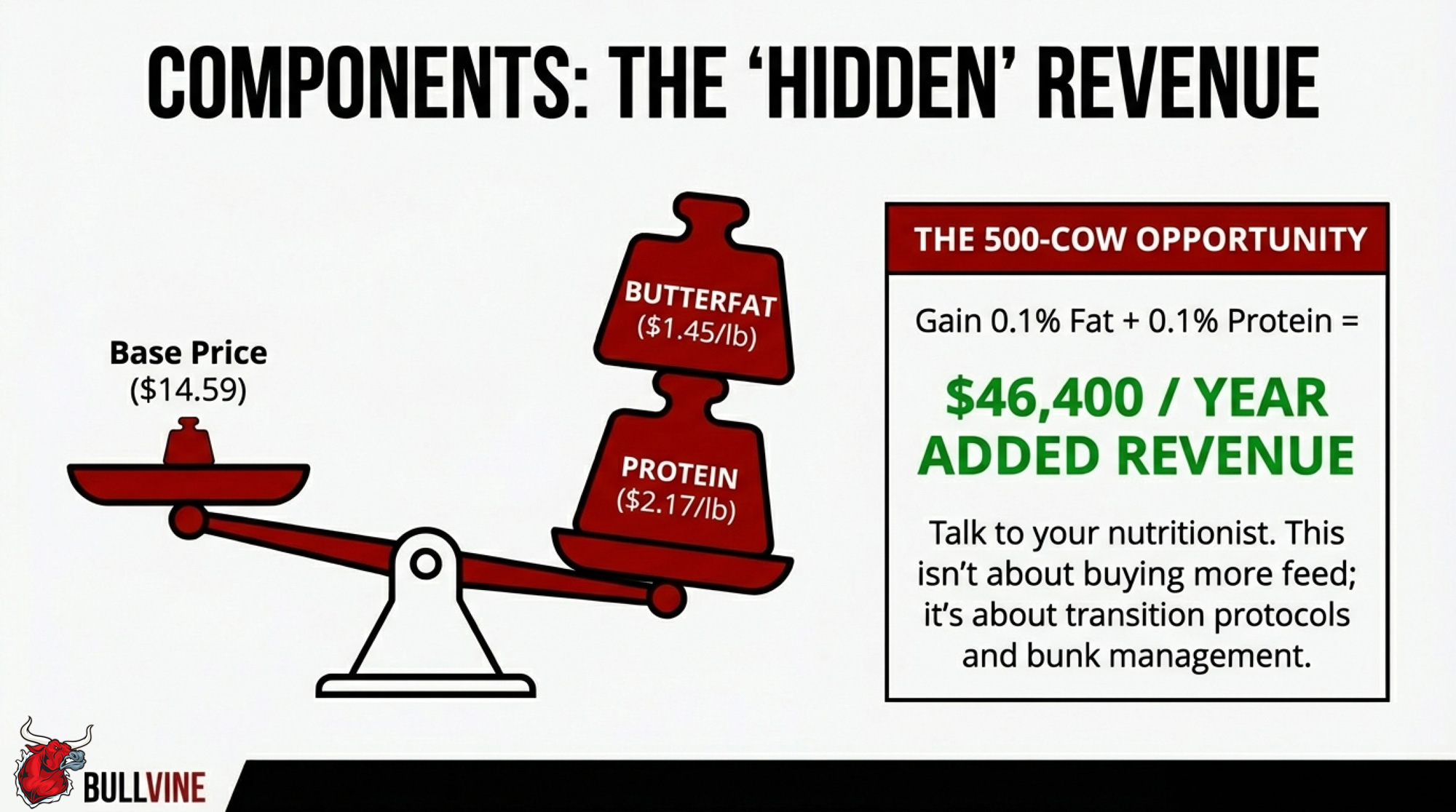

Components: Where the Real Money Hides at $14.59 Milk

January FMMO component prices tell the story: butterfat at $1.4525/lb and protein at $2.1768/lb. In a $14.59 Class III environment — made worse by the June 2025 make-allowance hike that shifted roughly 90¢/cwt to processor cost recovery — components are the difference between breaking even and bleeding cash.

Component Improvement

Additional Production (lbs/year)

FMMO Price ($/lb)

Annual Revenue Gain

0.1% Butterfat

12,775 lbs

$1.4525/lb

+$18,556 🔴

0.1% Protein

12,775 lbs

$2.1768/lb

+$27,809 🔴

Combined 0.1% BF + Protein

25,550 lbs

—

+$46,365 🔴

Per-Cow Monthly Impact (500-cow)

—

—

+$7.73/cow 🔴

Here’s the math on a 500-cow herd shipping 12.775 million lbs/year:

Each 0.1% protein improvement: 12,775 lbs additional protein × $2.1768/lb = $27,809/year

Combined 0.1% gain in both: roughly $46,400/year — or $7.73/cow/month

If you’re below 4.0% fat and 3.1% protein, talk to your nutritionist this week. The herds making component gains aren’t spending more per cow — they’re tightening transition protocols, adjusting TMR formulations, and managing bunk time. Those are $46,000 improvements at the cost of management attention, not capital.

What This Means for Your Operation

This week — before February 26:

DMC enrollment. At the projected January margin of $7.52/cwt, one month’s indemnity at $9.50 coverage equals $1.98/cwt across your Tier 1 production. USDA projects margins below $9.50 through July. The deadline is Wednesday.

DRP weighting review. With a $2.99/cwt same-month Class III–IV spread, your election weighting is the single highest-dollar decision you’ll make this quarter. Call your risk management advisor this week.

Next 90 days — through the spring flush:

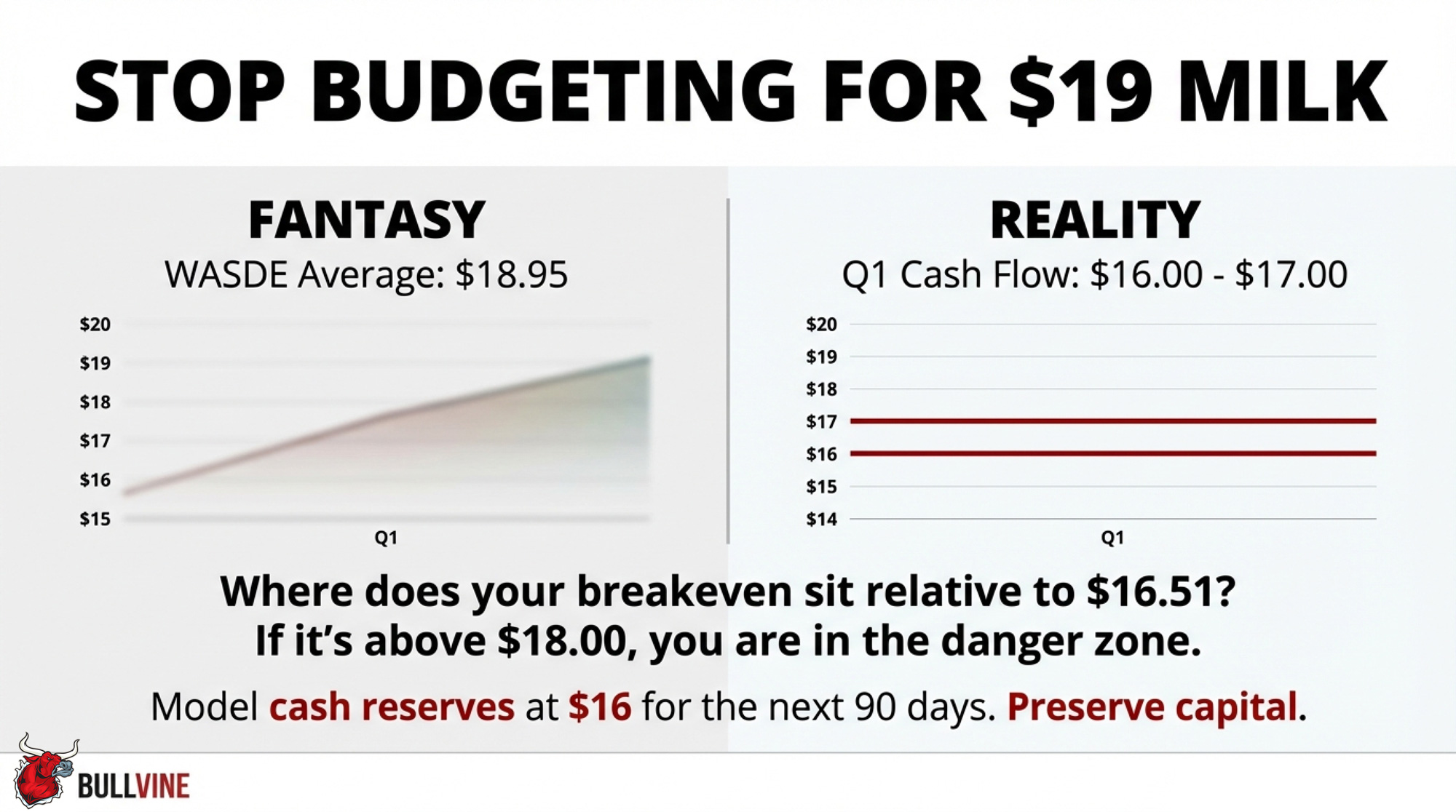

Model cash flow at $16–$17 Class III, not the $18.95 annual WASDE average. Your March and April checks reflect January and February commodity prices, which were ugly. If your all-in cost of production sits above $18/cwt, model your cash reserve at $16 Class III for Q1 and count the months of runway.

Pull your handler’s utilization report. In Federal Order 30, Class IV depooling thinned the pool all through 2025. If you don’t know where your milk is classified, you can’t evaluate whether this spread is working for or against you.

Push components hard. At January’s $1.4525/lb butterfat and $2.1768/lb protein, each tenth of a percent in BF and protein combined is worth $46,400/year on a 500-cow herd. Talk to your nutritionist about transition cow protocols and bunk management — that’s where the cheapest gains live.

By year-end:

Section 179 planning. The OBBBA raised Section 179 expensing to $2.5 million with 100% bonus depreciation through 2030. But borrowing to buy equipment to save on taxes only works if you can service the debt at $16 milk. Run those numbers with your accountant before your lender does.

Watch the July USMCA review. The mandatory six-year joint review hits July 1, 2026. Canada and Mexico bought $3.6 billion in U.S. dairy in 2024 — roughly 44% of the $8.2 billion total export value that year. In 2025, U.S. dairy exports surged to a confirmed $9.51 billion, nearly matching the $9.54 billion record set in 2022. But Canada’s TRQ fill rates still average just 42%. NMPF’s Shawna Morris argues that Canada remains “technically compliant with USMCA’s text, commercially limiting in practice.” If you’re in a co-op with significant North American export exposure, the July outcome shapes your 2027 milk price more than anything on the CME right now.

Key Takeaways

If your handler’s blend is more than $1.50/cwt below a pure Class IV value, this spread is actively costing your herd real money.

At $7.52/cwt projected January margin, one DMC indemnity month at $9.50 can pay several years of premiums on your Tier 1 volume — but only if you’re enrolled before February 26.

Each combined 0.1% gain in butterfat and protein is worth about $46,400/year on a 500-cow herd at today’s component prices.

The Bottom Line

The futures curve says relief is coming. Your January check says it hasn’t arrived yet. That 600-cow Wisconsin freestall operation profiled in The Bullvine’s January analysis — the one facing a $250,000 margin gap between full cost of production and what 2026 futures actually deliver? They stress-tested at $16 milk, trimmed 50–75¢/cwt from their breakeven through tighter heifer programs and lease renegotiations, and showed their lender a plan built off conservative numbers. The lender, seeing they were budgeting off realistic prices and actively adjusting, worked with them on amortization flexibility.

The producers who come out of this spring in good shape won’t be the ones who waited for $19. They’ll be the ones who ran their numbers at $16 and made decisions accordingly.

Where does your breakeven sit relative to $16.51 Class III? That’s the only number that matters this week.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Dairy Tech ROI: The Questions That Separate $50K Wins from $200K Mistakes – Cut through the trade-show hype and discover which innovations actually move the needle. This guide exposes the $200,000 mistakes in automation, arming you with the scale-specific ROI benchmarks that separate profitable disruptors from the struggling.

The Sunday Read Dairy Professionals Don’t Skip.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

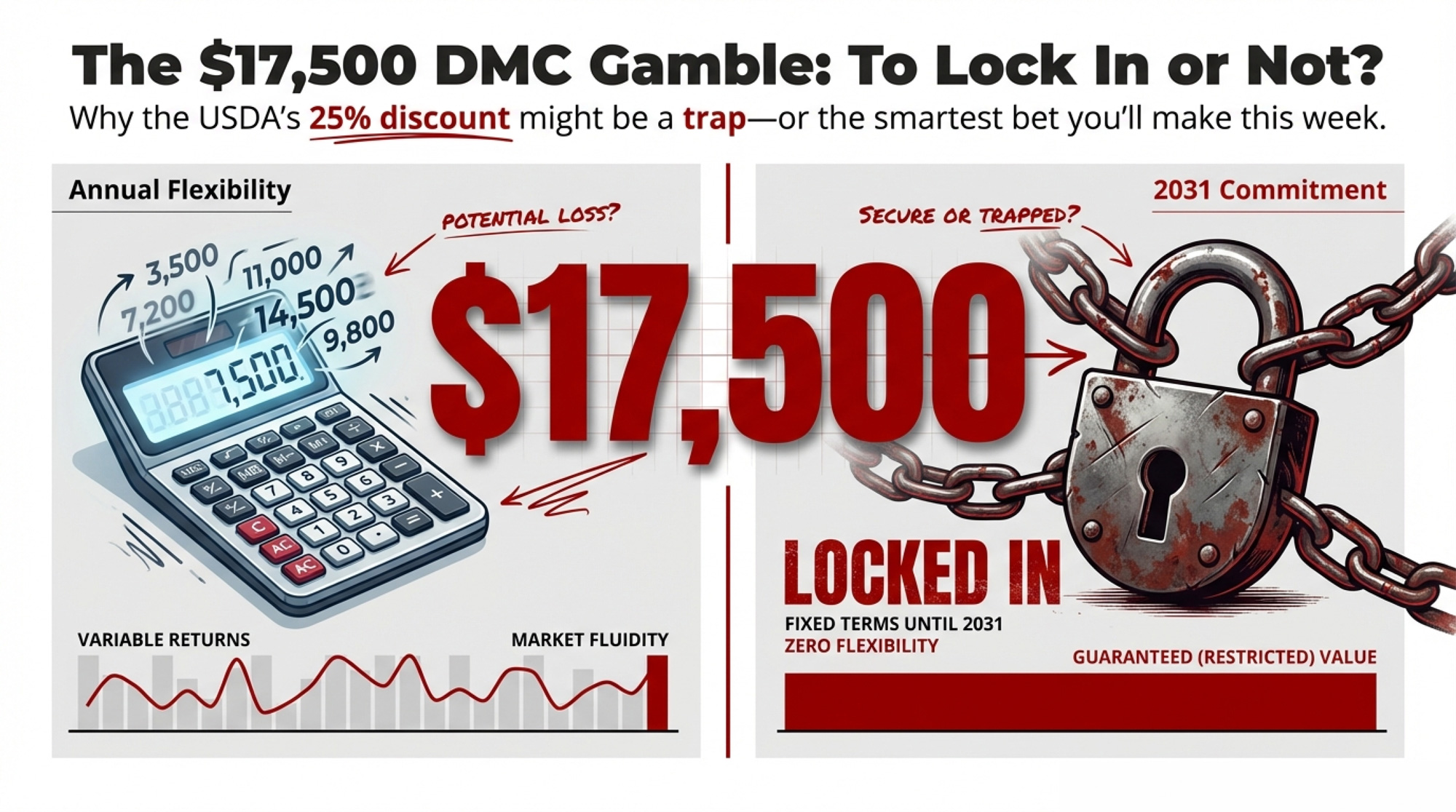

USDA’s 25% premium discount only pays off if margins stay compressed five of the next six years. That’s never happened.

Executive Summary: Wisconsin dairies are a week from the 2026 Dairy Margin Coverage deadline, and 68% still aren’t enrolled even though January’s projected DMC margin of $7.52/cwt would generate about $1,564 per million pounds — enough to cover a full year of Tier 1 premiums at $9.50. The article breaks down how the new 6‑year lock‑in, with its 25% premium discount, only comes out ahead if you’d enroll in at least five of the next six years, and how locking in anyway can turn into a $17,500 premium drag for a 200‑cow herd when margins stay strong in four of those years. ⚡ But that analysis comes with an important caveat: at $0.15/cwt, the enrollment hurdle is low enough that a rational producer looking at futures would likely have enrolled in most years — which makes the lock‑in more defensible than it first appears. The article walks through full barn math for 200‑ and 500‑cow operations, shows how the 6‑million‑pound Tier 1 cap leaves half the milk on a 500‑cow herd uncovered, and puts 2023’s record $1.27 billion in DMC payouts — $63,633 per enrolled Wisconsin dairy — in context as the benchmark for what this program delivers when margins compress. Instead of generic advice, you get four specific paths — annual DMC, 6‑year lock‑in, lower‑tier coverage, or skipping DMC and leaning on DRP/LGM for the rest of your milk — with clear trade‑offs spelled out for each. The playbook is simple: pull your 2021–2023 milk marketings, run the USDA DMC calculator with your actual cwt, and call FSA by February 24, so you know exactly what you’re betting before you sign a contract that runs through 2031.

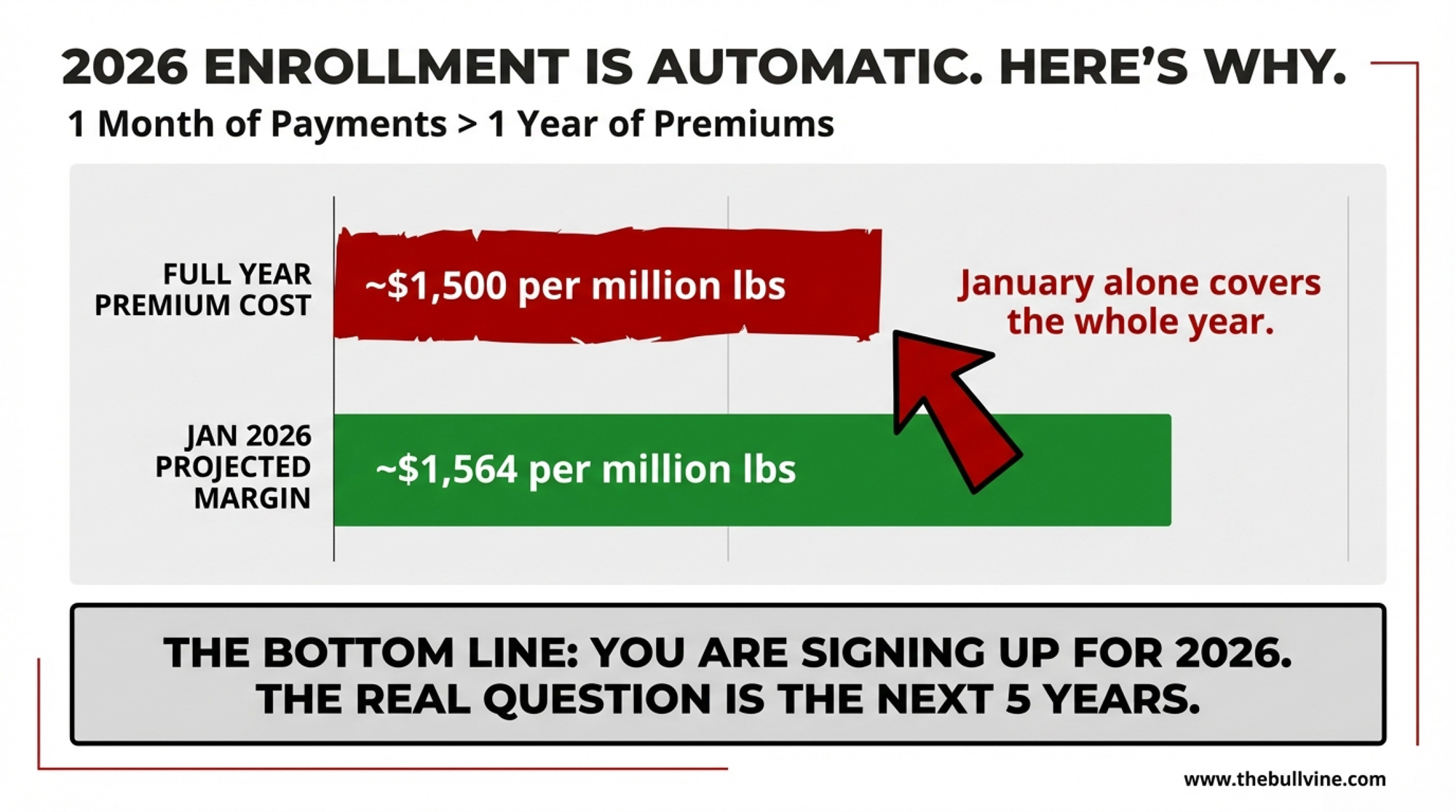

January 2026 Class III settled at $14.59/cwt — the weakest month since early 2024. And as of February 17, roughly 3,500 Wisconsin dairy operations still hadn’t enrolled in Dairy Margin Coverage for 2026. Katie Detra at Wisconsin’s Farm Service Agency shared that just 1,616 producers had completed DMC signup — only 31.5% of the state’s 5,116 licensed dairy farms. The deadline is February 26.

DMC doesn’t use Class III directly. The program’s margin formula takes the national All-Milk price and subtracts a standardized feed cost. But the pressure is running in the same direction. As of February 2, the Center for Dairy Excellence projected the January 2026 DMC margin at $7.52/cwt. At $9.50 coverage, that’s a $1.98/cwt indemnity — and CDE noted that January alone would produce “about $1,564 on a million pounds of production covered under Tier 1, which would cover premium costs” for the entire year.

One month’s payment covers your annual premium. For 2026, the enrollment decision is close to automatic. The six-year lock-in checkbox sitting next to it on the form? That’s a different conversation entirely—and nobody’s walking producers through the math.

From 80% to 31% — What Happened in Wisconsin?

Here’s the part that doesn’t add up. As of early 2024, 80 percent of Wisconsin dairy farmers were enrolled in DMC — the highest participation rate in the country, per Wisconsin Farm Bureau Federation. WFBF President Brad Olson called it “a critical farm safety net program during tough times.”

Fair warning on the comparison: that 80% figure was a final-year enrollment count. The current 31.5% is a mid-signup snapshot with six days left. Deadline rushes always close the gap. But even so, the pace is way off.

Some of the lag is structural. Wisconsin lost 545 dairy operations between January 2024 and today — down from 5,661 to 5,116. Some of those lost farms were DMC enrollees. Others are mid-transition, selling cows or passing the herd to the next generation, and a six-year commitment is the last thing they want. Still others have built hedging programs around Dairy Revenue Protection and see DMC as redundant on their first 6 million pounds.

But the margin picture has shifted underneath all of them. December 2025’s DMC margin came in at $9.42/cwt — just barely triggering the year’s first and only payment, a thin $0.08/cwt. That was the warm-up act. CDE’s January 14 outlook projects the full-year 2026 average margin at $8.51/cwt, starting at $7.37 in January and not climbing above $9.50 until November. If that forecast holds, ten months trigger payments — a total net indemnity of $8,300 per million pounds of Tier 1 covered production, after premiums but before sequestration.

Katie Burgess, director of risk management at Ever.Ag, projected “payouts of more than $1 per hundredweight for January through April, and then some smaller payments for May through July as well.” Mike North, also at Ever.Ag, as been blunt with producers: just “get it.”

They’re right about 2026. The harder question is whether you should lock your elections through 2031.

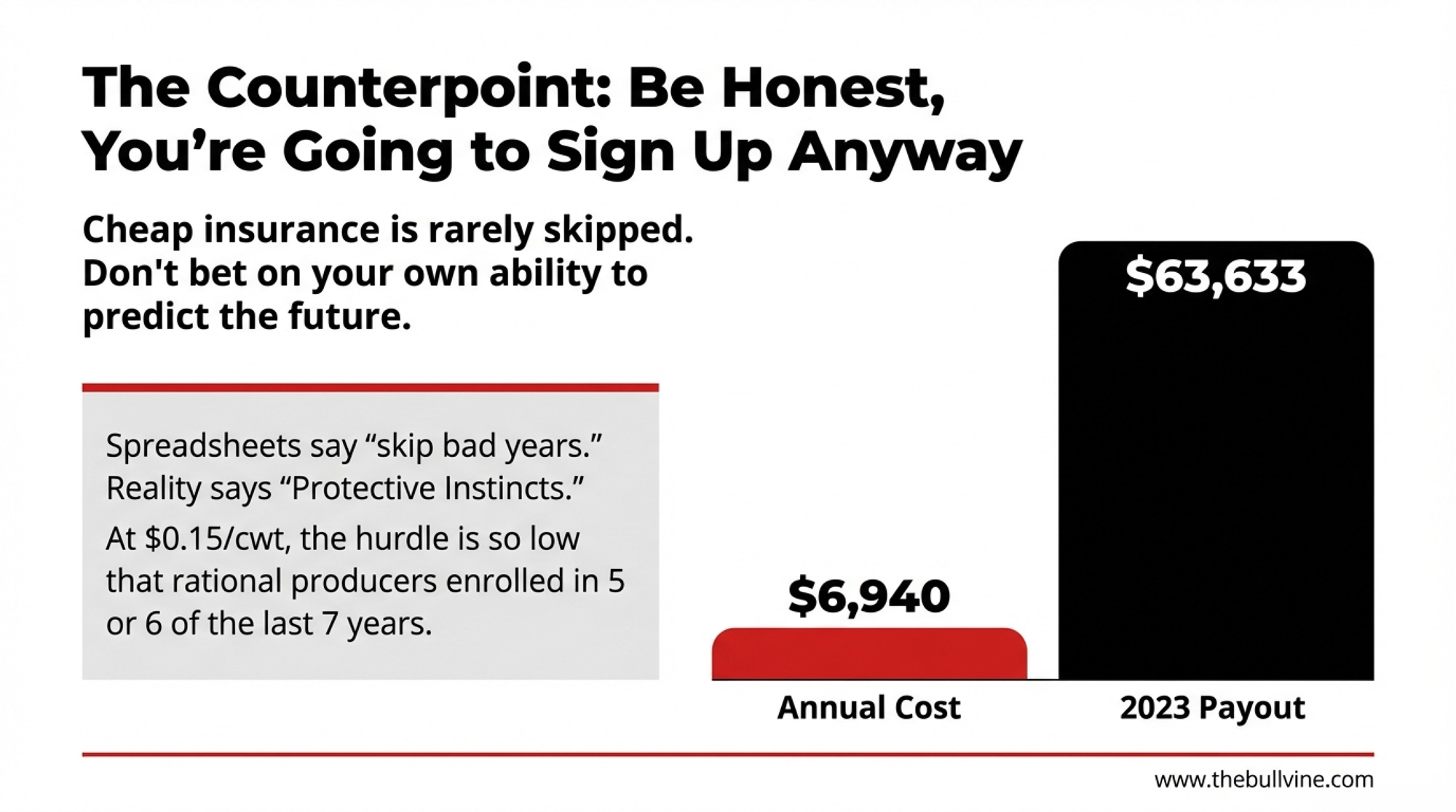

What 2023 Should Remind Every Producer About DMC

Before digging into the lock-in math, it’s worth anchoring on what DMC actually delivers when margins compress hard — because the numbers aren’t theoretical.

In 2023, DMC triggered payments in 11 of 12 months at $9.The 50 coverage. At the level of average enrolled dairy, received indemnity payments of $2.80/cwt per month. Through the first nine months alone, total program payouts reached $1.27 billion — surpassing the previous annual record of $1.187 billion set in 2021. Wisconsin led all states at $272.2 million, averaging $63,633 per enrolled operation.

July 2023 hit the floor: a $3.52/cwt margin, the lowest in DMC history. At $9.50 coverage, that was a $5.98/cwt indemnity in a single month.

Put that in barn math for a 200-cow herd at 95% Tier 1: one month at $5.98/cwt on 3,800 covered cwt = roughly $22,724 from one month of milk. The annual premium was about $6,840. One July check covered three years of premiums.

Here’s the full payout history at $9.50 Tier 1 coverage:

Year

Months Triggered

Total Payouts

Avg Per Enrolled Dairy

2019

7 of 12

$451.6M

$19,306

2020

5 of 12

$234.0M

$17,324

2021

11 of 12

$1.187B

$62,214

2022

2 of 12

$83.7M

$4,656

2023

11 of 12

$1.27B+

$74,553

2024

~5 of 12

$36.9M est.

$2,356 est.

2025

1 of 12

Minimal

~$0.08/cwt (Dec only)

Two things jump out. First, the big-payment years are massive — 2021 and 2023 alone combined for roughly $2.46 billion in indemnities. A single year of compression can dwarf a decade of premiums. Second, the non-payment years (2022, 2024, 2025) are real. At $0.15/cwt, you’re not losing much in those years — but you are paying premiums for coverage that didn’t trigger.

That second point matters for the lock-in question. More on that below.

What Changed Under the New Law

The One Big Beautiful Bill Act, signed July 4, 2025, reauthorized DMC through 2031 with three changes that shift the math.

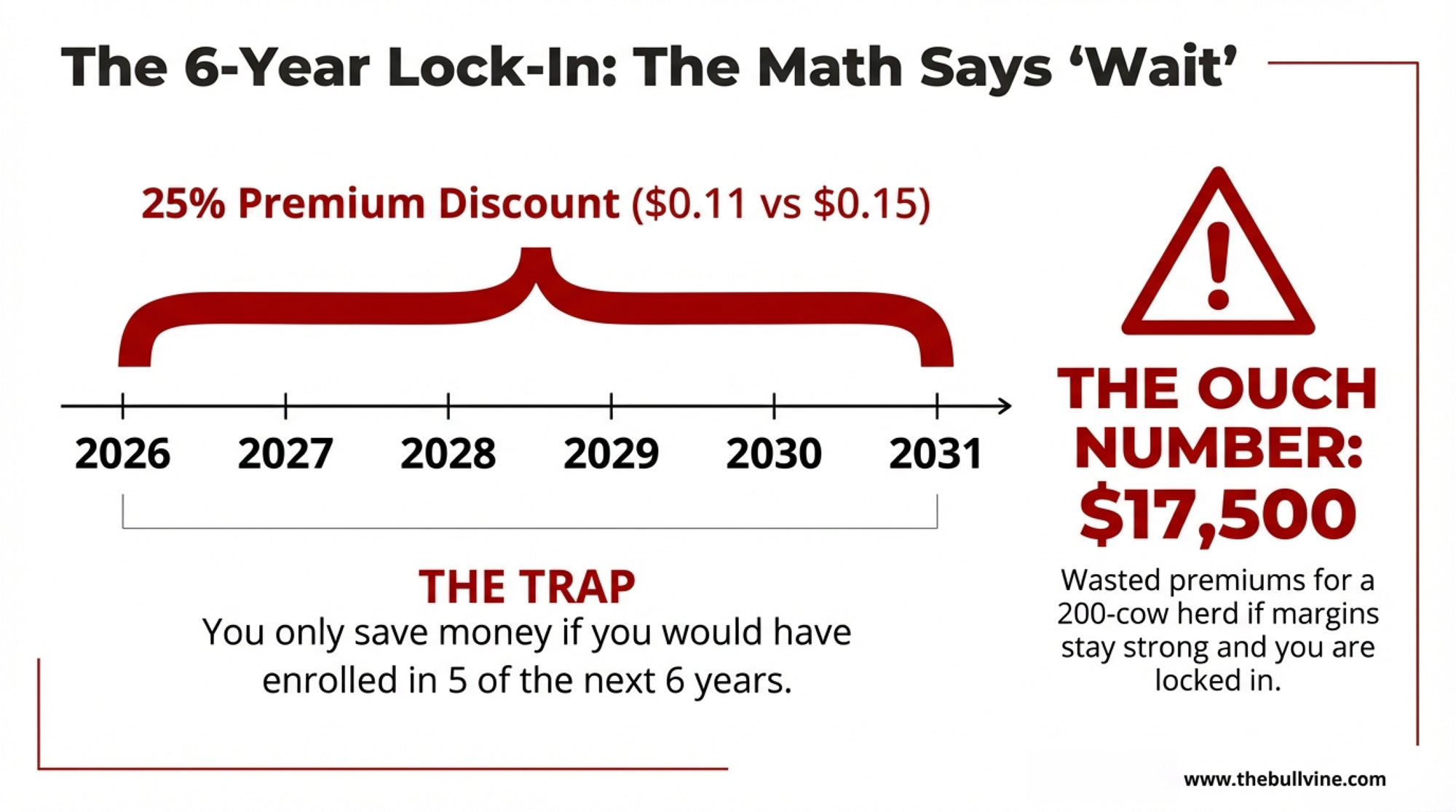

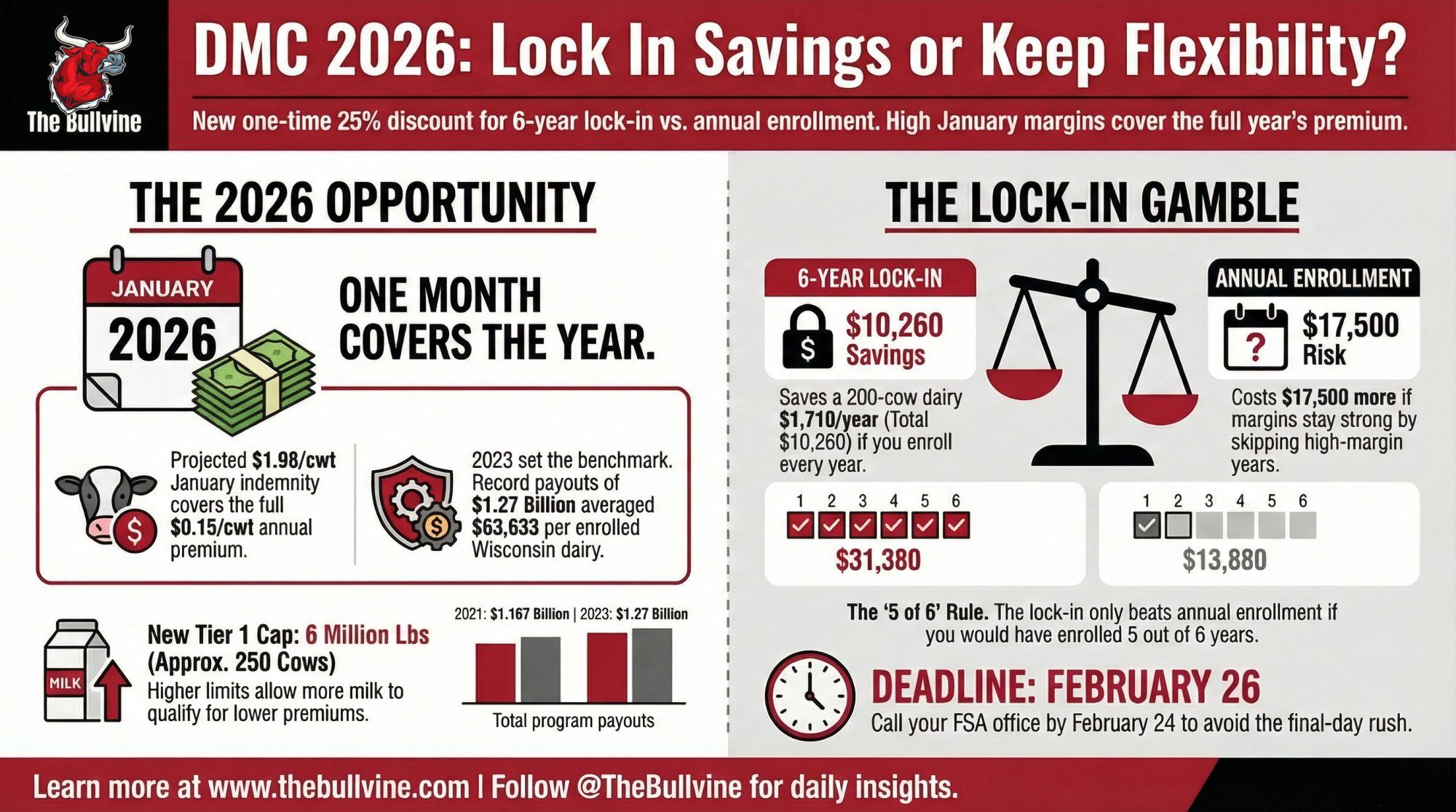

Tier 1 coverage went from 5 million to 6 million pounds. A 250-cow herd shipping 24,000 lbs/cow now fits entirely inside Tier 1. Every operation gets a fresh production history based on the highest annual marketings from 2021, 2022, or 2023. And the new wrinkle: lock your elections for all six years and get a 25% premium discount.

FSA program manager Doug Kilgore confirmed this lock-in is a one-time election — available only during 2026 enrollment. Skip it now, and it’s gone for the life of the program.

Sandy Chalmers, Wisconsin’s FSA State Executive Director, outlined the base case on February 17: “At $0.15 per hundredweight for $9.50 coverage, risk protection through Dairy Margin Coverage is a cost-effective tool to manage risk and provide added financial security for your operations.”

At fifteen cents a hundredweight, she’s right. That’s the easy part.

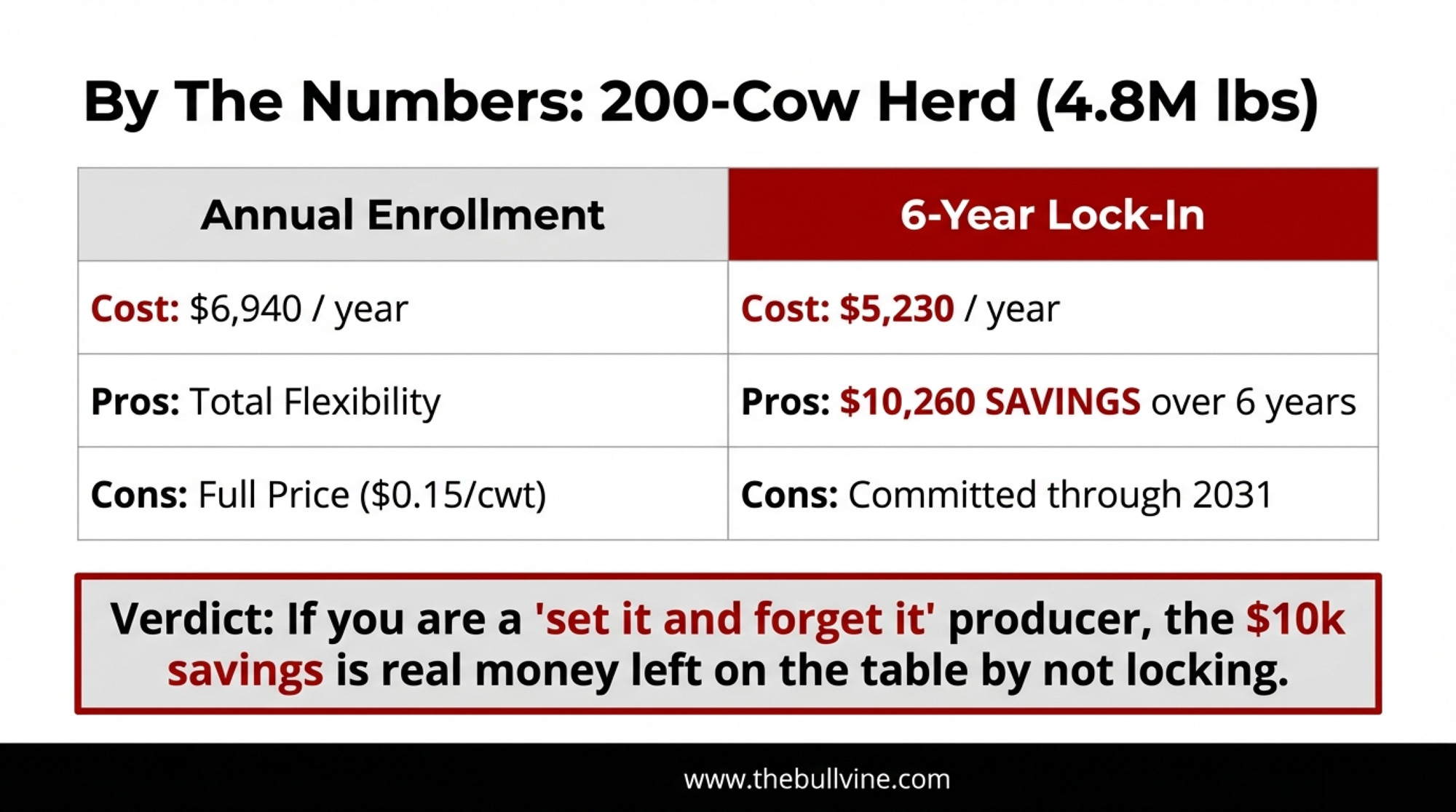

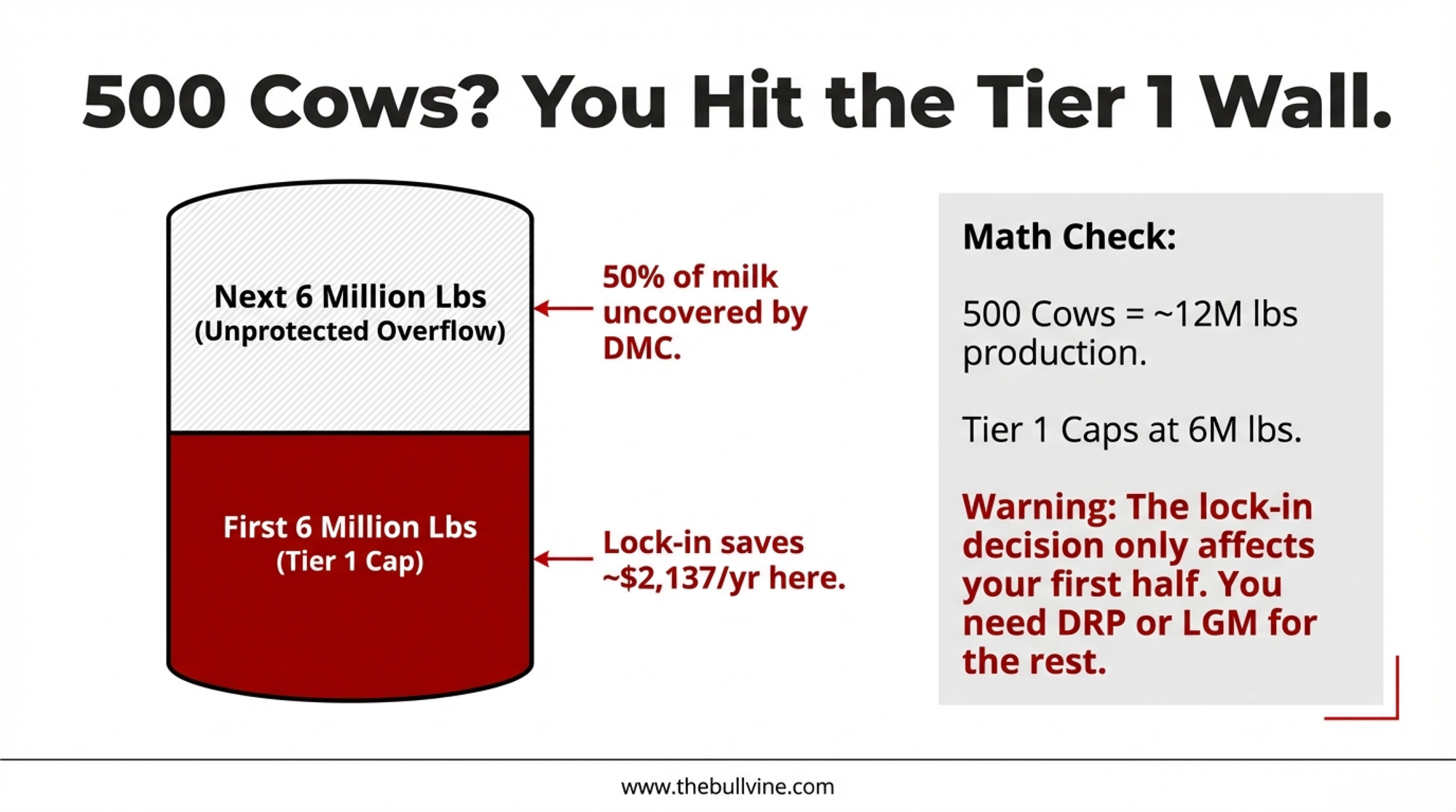

How Much Does DMC Actually Pay a 200‑Cow Dairy?

A 200-cow operation averaging 24,000 lbs/cow ships 4.8 million pounds — comfortably inside the 6-million-pound Tier 1 cap. At $9.50 coverage and 95% enrollment, the premium is $0.15/cwt.

Annual savings from the lock-in: $1,710/year, or $10,260 over six years.

Now look at January alone. CDE’s $1.98/cwt projected indemnity on that 200-cow herd: 3,800 cwt of monthly covered production × $1.98 = roughly $7,524 on one month’s milk. That single payment exceeds the entire annual premium.

If margins track CDE’s January 14 forecast for the full year, total net indemnity on 4.56 million covered pounds would land around $37,800 for 2026. That’s a projection, not a guarantee — forecasts shift month to month. But it shows the scale of what’s sitting on the table.

And on a 500‑Cow Operation?

Scale up, but know where the wall is. A 500-cow dairy at 24,000 lbs/cow produces 12 million pounds. Tier 1 caps at 6 million. Half of your milk is unprotected.

January’s projected indemnity: 4,750 monthly cwt × $1.98 = $9,405. One month covers the premium. Scale CDE’s full-year projection the same way — $8,300 per million covered pounds × 5.7 million — and you’re looking at roughly$47,310 in net indemnity for 2026 on the Tier 1 portion alone.

But the other 6 million pounds? Nothing. Tier 2 premiums jump to a maximum of $8.00 coverage with rates running dramatically higher — that’s why most advisors treat DMC as a Tier 1 play and layer DRP on top for the rest.

William Loux, senior vice president of global economic affairs at the National Milk Producers Federation, put it this way: “The uncertainty in dairy markets is not going away anytime soon. So DMC, DRP — these are great programs to utilize.”

Should You Lock In DMC for 6 Years?

This is where the 25% discount starts to get complicated. Leonard Polzin, dairy markets and policy specialist at UW–Madison Extension, ran the margin history, and his numbers frame the decision.

The lock-in only beats annual enrollment if you’d sign up in at least 5 of the 6 years. Here’s what that looks like for a 200-cow dairy:

Scenario

Lock-In Cost (6 yrs)

Annual Cost

Differencefor

Enroll all 6 years

$31,380

$41,640

Lock-in saves $10,260

Enroll 5 of 6

$31,380

$34,700

Lock-in saves $3,320

Enroll 3 of 6

$31,380

$20,820

Annual savings are $10,560

Enroll 2 of 6

$31,380

$13,880

Annual saves $17,500

That bottom row. You’ve paid $17,500 in premiums for coverage that barely triggered.

So how often do margins actually compress for five or six straight years? Polzin checked. From 2019 through 2025, 39 of 84 months fell below $9.50. Payment runs averaged 4.88 months. Non-payment runs averaged 4.33 months. As his analysis notes, “margins tend to move in episodes rather than in isolated one-month shocks” — and “the relevant risk is frequently the duration of tight margins and the associated working-capital strain, not only whether a single-month payment occurs.”

The margin oscillates. It doesn’t stack up in neat multi-year compression streaks.

But Here’s the Honest Counterpoint: What Did Futures Show at Decision Time?

The table above assumes you’d skip enrollment in years when margins ended up running above $9.50. That’s hindsight. You don’t have hindsight at enrollment time — you have futures.

And here’s what producers actually knew at each deadline:

Enrollment Year

Deadline Window

Market Signal at Signup

Would a Rational Producer Enroll?

Actual Result

2019

Early 2019

Tight margins expected

Yes

7 months triggered; $19,306/op

2020

Late 2019

Uncertain; premium cheap

Probably

5 months; $17,324/op

2021

Early 2021

Feed costs rising

Yes

11 months; $62,214/op

2022

Late 2021

Milk recovering, feed high

Uncertain — but $0.15/cwt is cheap insurance

2 months; $4,656/op

2023

Extended to January 31, 2023

FSA Administrator: “early projections indicate payments are likely for the first eight months”

Absolutely

11 months; $74,553/op

2024

February 28 – April 29, 2024

Jan margin hit $8.48, first payment triggered before enrollment opened

Probably

~5 months; $2,356/op

2025

January 29 – March 31, 2025

Futures projected ~$12.50/cwt average margins

Maybe skip — but premium is just $0.15/cwt

1 month; ~$0.08/cwt

At $0.15/cwt, the enrollment hurdle is remarkably low. A 200-cow herd pays $6,940 for a full year of $9.50 coverage. In 2023, that $6,940 returned roughly $63,000. Even in the weakest year on record — 2022 — the premium amounted to about $1.44/cow/year. Most producers would enroll on cheap-insurance logic alone in all but the most obviously strong-margin years.

Look at that column honestly: a rational producer reviewing futures at each enrollment deadline would likely have enrolled in five or six of the last seven years. Only 2025 gave a clear “skip” signal — and even then, some producers enrolled because the premium was effectively a rounding error against downside protection.

That changes the lock-in math. If you’re the kind of operator who enrolls most years anyway — and the historical enrollment rate of 73–80% of eligible dairies suggests most producers are — the lock-in’s $10,260 in savings over six years is real money you’d leave on the table by staying annual.

The lock-in loses when you’re disciplined enough actually to skip enrollment in good-margin years. Polzin’s data shows that the years 2022, 2024, and 2025 all had weak or zero payouts. But the question isn’t whether good-margin years exist. It’s whether you’d actually sit out when the premium is $0.15/cwt and the downside is missing a 2023-style year.

Loux captured the tension: “It’s good that DMC is paying out, but it’s almost always better for prices, and better for dairy farmers, if they don’t.”

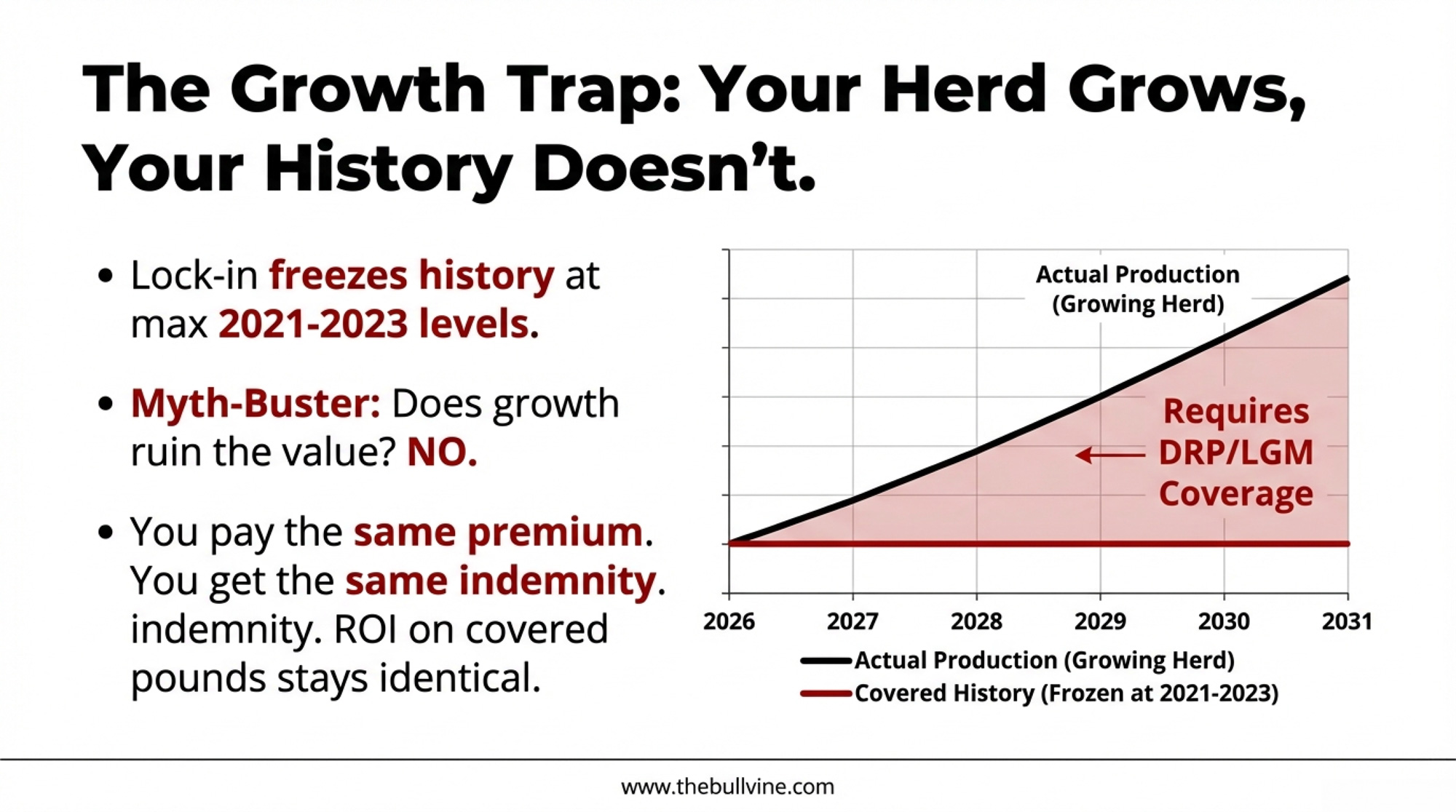

What Happens When Your Herd Outgrows Your History?

Lock in for six years, and your production history freezes at your best year between 2021 and 2023. Your herd doesn’t.

Say your best history year was 170 cows. You’re milking 200 now. That history — 4,080,000 lbs at 95% enrollment — gives you 3,876,000 covered pounds. Here’s the part that trips people up: the dollars don’t change as you grow. The premium stays the same. The indemnity payment stays the same. You’re buying coverage on a fixed number of pounds — same check out, same check in, regardless of what’s happening with your actual herd size.

What does change is the share of your total production that has margin protection underneath it:

Year

Actual Production

Covered Lbs

% Covered

Annual Premium

Indemnity per $1/cwt Trigger

2026

4,800,000 (200 cows)

3,876,000

80.8%

$5,914

$38,760

2028

5,198,000 (217 cows)

3,876,000

74.6%

$5,914

$38,760

2031

5,845,000 (244 cows)

3,876,000

66.3%

$5,914

$38,760

Notice the last two columns — they’re identical every row. The DMC math on your covered pounds doesn’t erode. You pay the same premium. You get the same indemnity. The ROI on the covered portion is unchanged whether you’re milking 200 cows or 244.

The real issue is what’s growing outside that coverage. By 2031, a third of your actual production has zero margin protection. That milk generates revenue in good months and unprotected losses in bad ones. It’s not that DMC got worse — it’s that your unprotected exposure got bigger, and you need to manage it separately.

For a 500-cow herd, this gap exists from day one. You’re producing 12 million pounds and covering 6 million — half your milk is already outside DMC, regardless of herd growth.

The practical question isn’t “is my DMC eroding?” — it’s “what am I doing about the growing share of milk that DMC was never designed to cover?” That’s where DRP, LGM, or self-insurance need to enter the conversation. Kilgore confirmed: locked-in operations must pay premiums annually and certify they’re commercially marketing milk every year. There’s no pause button and no off-ramp — but the coverage you’re paying for delivers the same dollar protection it always did.

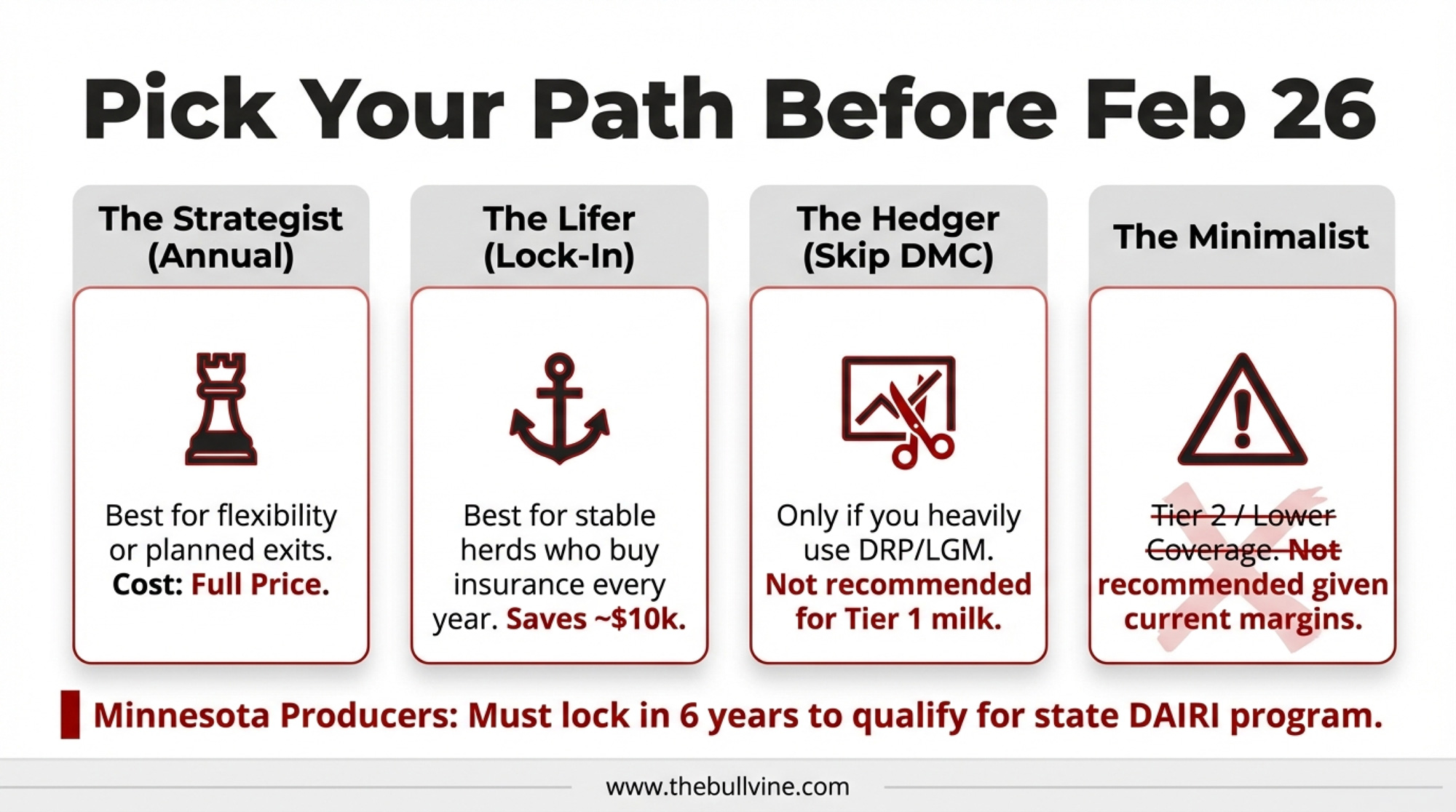

Four Paths Before February 26

Path 1: Annual enrollment at $9.50, Tier 1. No lock-in. Best for growing herds, operations expecting margin recovery within 2–3 years, or anyone facing a major change before 2031. Cost: $6,940/year (200-cow) or $8,650/year (500-cow), paid only in the years you choose. You sacrifice $1,710–$2,137/year in premium savings. You keep full flexibility.

Path 2: The stable-herd lock-in. Fits operations that closely match their 2021–2023 history, plan to milk through 2031, and would realistically enroll most years anyway, which the enrollment history suggests is most producers. Savings: $10,260–$12,825 total. But it can’t be reversed. Premiums are due by September each year, regardless of conditions. If 2028 turns out to be a $12 margin year, you’re still writing that check. ⚡

Think you’ll weigh the lock-in decision next year? You won’t have the option. This election is only available during the 2026 enrollment. Miss it, and it’s gone permanently.

Path 3: Enroll at a lower coverage tier. Dropping from $9.50 to $8.00 cuts your Tier 1 premium and reduces your exposure if margins recover faster than expected. But it also slashes your indemnity in the months that matter most. Run both scenarios at dmc.dairymarkets.org with your actual production numbers before deciding.

Path 4: Skip DMC entirely. Only makes sense if you’re running active DRP or LGM hedging and are comfortable walking away from the cheapest margin protection available on your first 6 million pounds. Note: operations with unpaid 2025 premiums can’t get a 2026 contract until the balance clears.

Minnesota producers — one more variable. Your state’s DAIRI program requires a 6-year DMC commitment to qualify for state-level dairy assistance. That alone could tip the math.

What This Means for Your Operation

Pull your 2021–2023 milk marketings now. Your production history is the highest of those three years. If it sits well below current output, know that your DMC coverage on those pounds still delivers the same dollar protection — but you’ll need DRP or LGM for the uncovered portion. ⚡

Be honest about your enrollment behavior. How many of the last seven years would you have enrolled? Not in hindsight — looking at what futures showed at each enrollment deadline. At $0.15/cwt, most producers enrolled in five or six of seven. If that’s you, the lock-in’s $10,260 in savings is real. If you’re disciplined enough to skip when futures signal strong margins, annual gives you that optionality.

Remember what 2023 delivered. Wisconsin dairies enrolled in the program averaged $63,633 in indemnity payments. Those that weren’t? Zero. At $0.15/cwt, the annual cost of not being covered in a compression year dwarfs a decade of premiums.

Call your local FSA office by February 24—not the 26th. Phone lines jam on deadline day. Paperwork takes longer than you expect. Find your office at farmers.gov/service-locator.

DMC payments are taxable income and are subject to a 5.7% sequestration, per OMB’s FY2026 report. On a $1.98/cwt January indemnity, that shaves roughly $0.11/cwt before the check hits your account. Plan with your accountant.

Within 3–5 years of a transition? A six-year commitment may outlast your timeline. Annual enrollment preserves every option.

Key Takeaways

If you’d realistically enroll most years anyway — and at $0.15/cwt, the enrollment history suggests most producers would — the lock-in saves $10,260 on a 200-cow herd. The 25% discount represents genuine savings if your enrollment behavior aligns with historical norms.

If you’re disciplined enough to skip enrollment when futures signal strong margins, annual enrollment preserves that optionality. Polzin’s data shows margins ran above $9.50 for all or most of 2022, 2024, and 2025 — skipping those years saves more than the lock-in discount.

Growing herds don’t lose DMC value on covered pounds — same premium, same indemnity, same ROI. But the uncovered share of your total production continues to grow each year. If current production exceeds your 2021–2023 high by more than 15%, layer DRP or LGM on the exposed portion now.

If your debt-service coverage ratio sits below 1.3, the lock-in’s predictable cost may matter more to your lender than flexibility. Have that conversation before the 26th.

The six-year election disappears after 2026 enrollment. Annual is the default. After February 26, the option is permanently gone.

The Bottom Line

Pull your milk statements. Plug your numbers into the USDA calculator — yours, not the ones in this article. And before you check that lock-in box, answer one question honestly: in the last seven years, how many times would you have sat out enrollment at $0.15/cwt?

If the answer is one or two, the lock-in probably makes sense. If you’d have skipped three or more annual wins.

Make the call before February 24. When January’s official DMC margin drops, you’ll know exactly what your decision was worth.

We’ll have that scorecard next month.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

The 90-Day Reckoning: What Your Milk Check Is Really Saying About 2026 – Delivers a strategic playbook for the upcoming consolidation period by revealing structural shifts in 2026 budgets. It helps you calculate your true “red line” to keep you solvent and liquid while peers face the exit.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

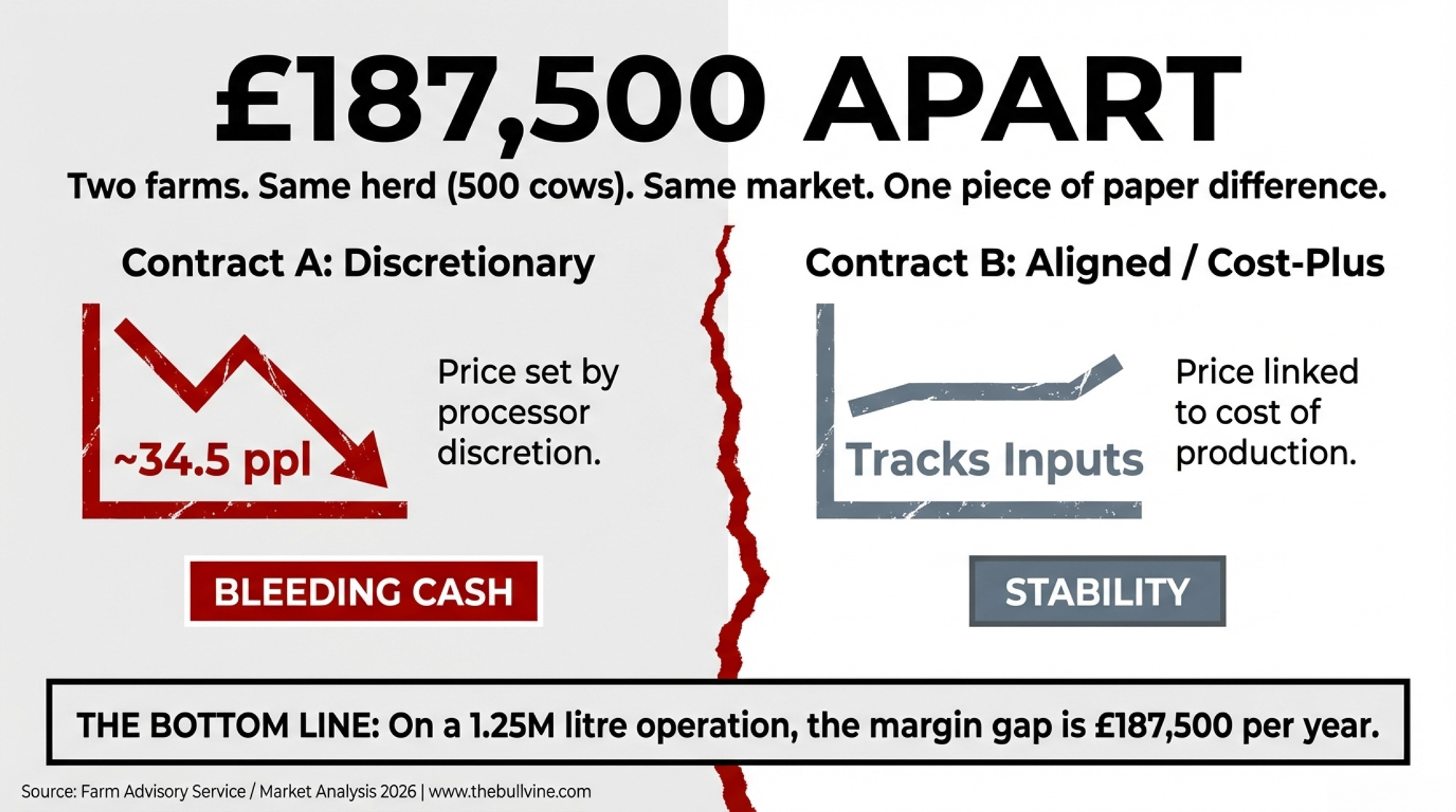

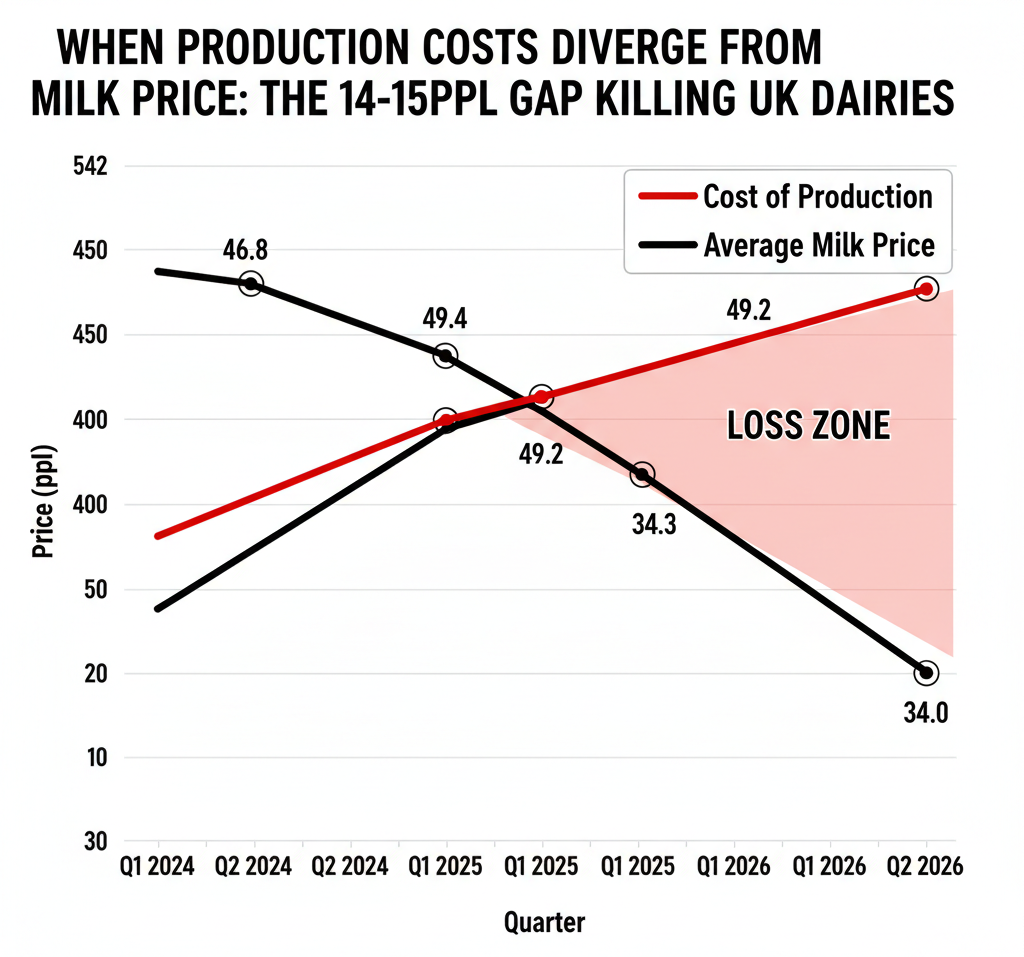

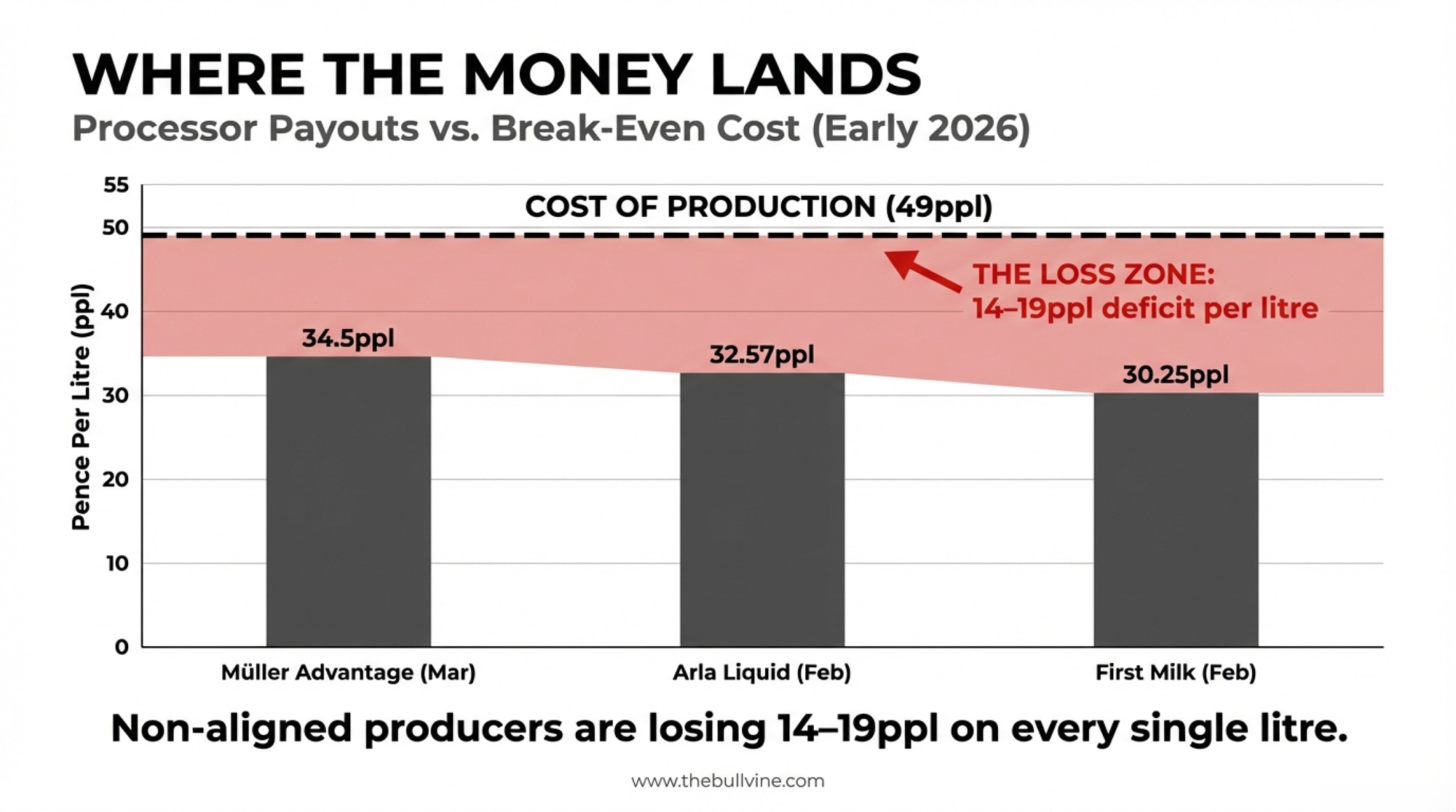

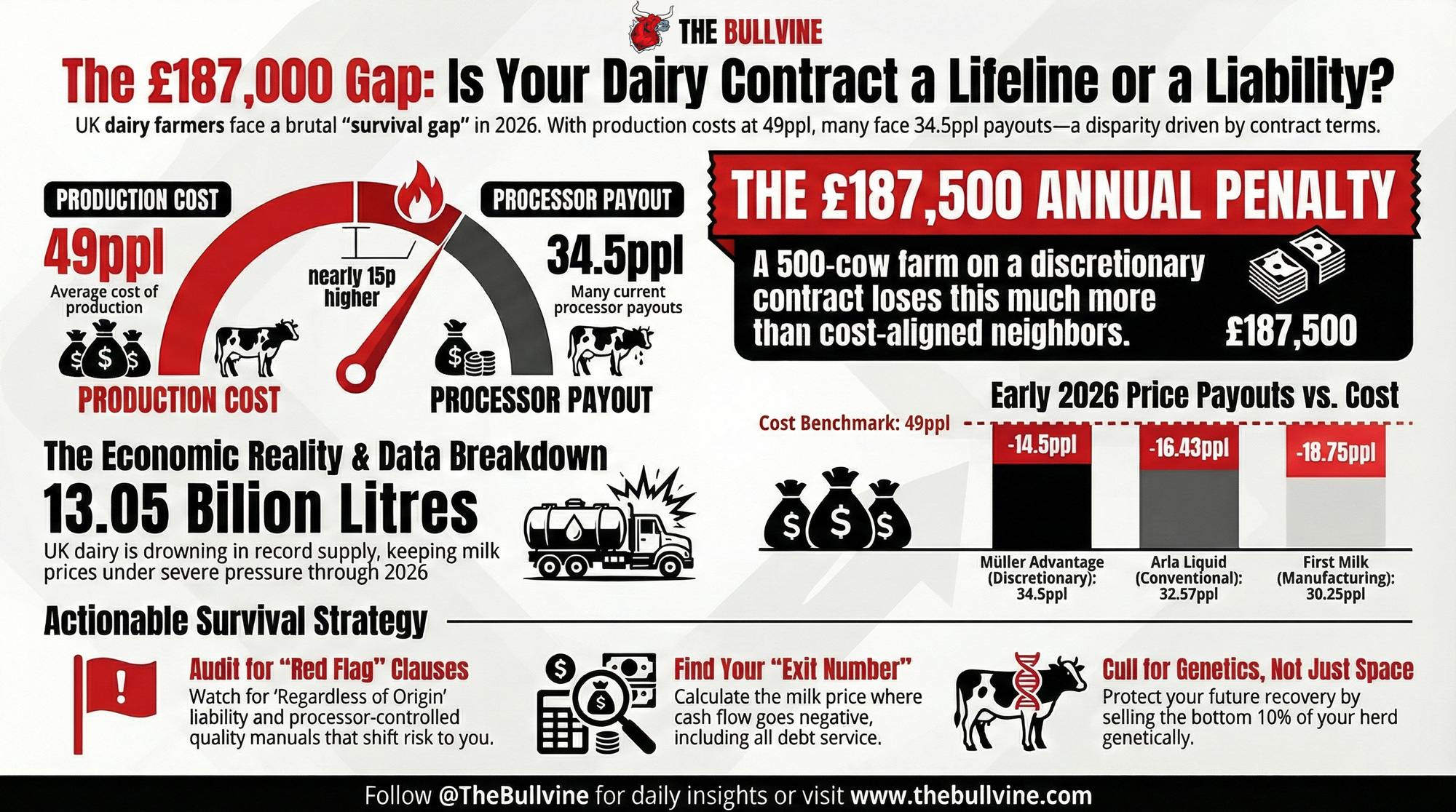

When milk is worth 34.5ppl, and it costs close to 49ppl to produce, your contract decides whether you survive this squeeze or bleed cash until the bank decides for you.

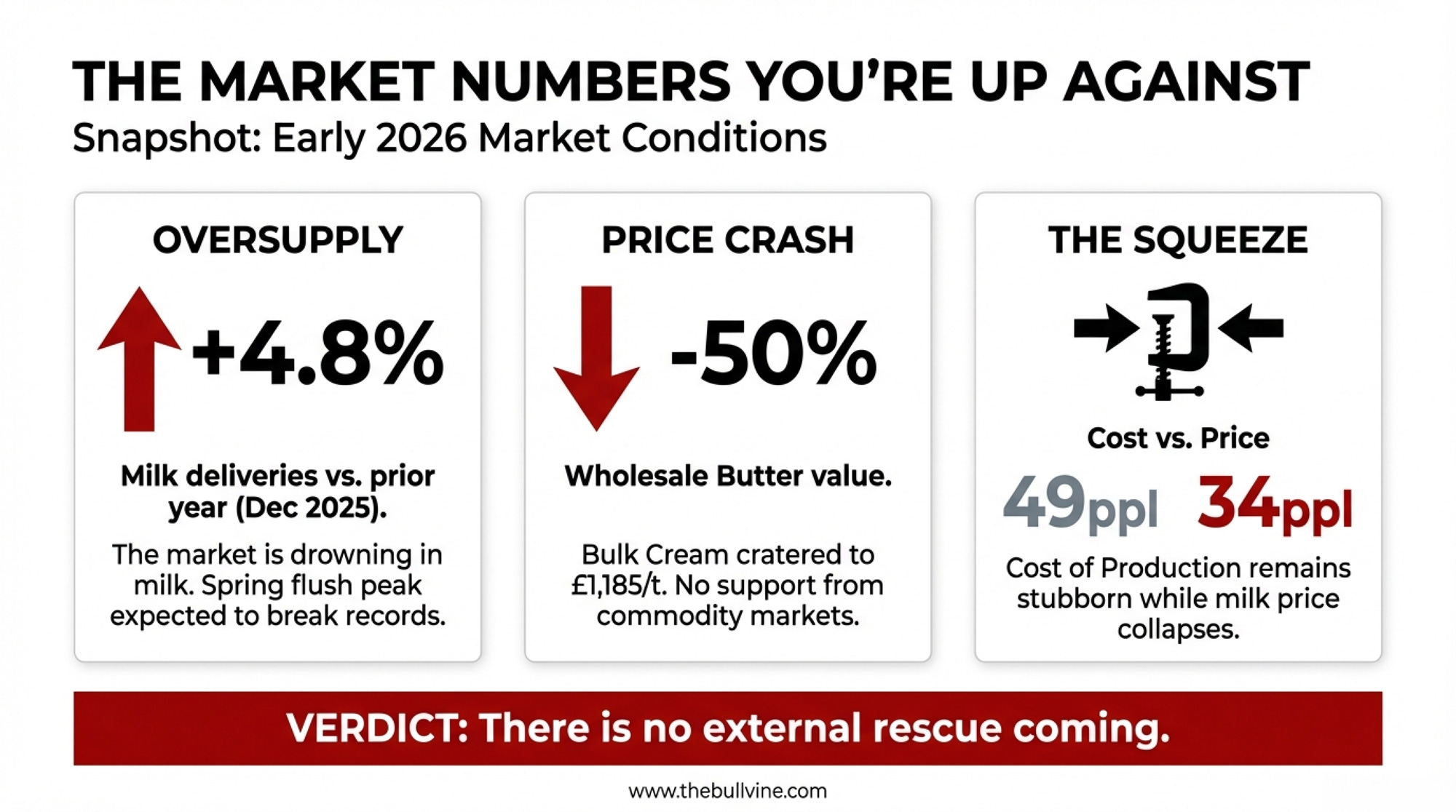

EXECUTIVE SUMMARY: Two farms. Same county. Same herd size. One loses £187,500 more this year—the only difference is the contract. UK milk sits at 34.5ppl while production costs hit 49ppl (FAS Scotland, January 2026), leaving farmers on processor-discretionary deals 14-15ppl underwater on every litre. AHDB forecasts no relief until H2 2026 at the earliest. Seven contract clauses are doing the damage—from indemnification language that pins processor-facility contamination on you, to volume traps that trigger clawbacks when drought cuts your output. The UK’s Fair Dealing regulations gave farmers a complaints process, but in ASCA’s first twelve months, not one producer filed formally; nine called in confidence, then went silent. For non-aligned operations with less than six months of cash, the decision window isn’t approaching—it’s here.

Two farms. Same county. Same herd size. Same brutal market.

One loses close to £190,000 more this year than the other.

The difference isn’t just Müller’s March 2026 price cut to 34.5ppl. It’s not only the record milk glut or the butter crash. It’s what’s written in the contract—specifically, which operation bears the downside when processors slash farmgate prices, and which has terms that track costs and provide a floor.

Aligned retail contracts held steady in January 2026. Processor-discretionary deals dropped 1-4ppl. Meanwhile, The Dairy Group—reporting through Scotland’s Farm Advisory Service in January 2026—put the average cost of production at 48.5ppl for 2024/25, with a forecast of 49.2ppl for 2025/26. That means many non-aligned farms are now producing milk for roughly 14–15ppl more than they’re being paid.

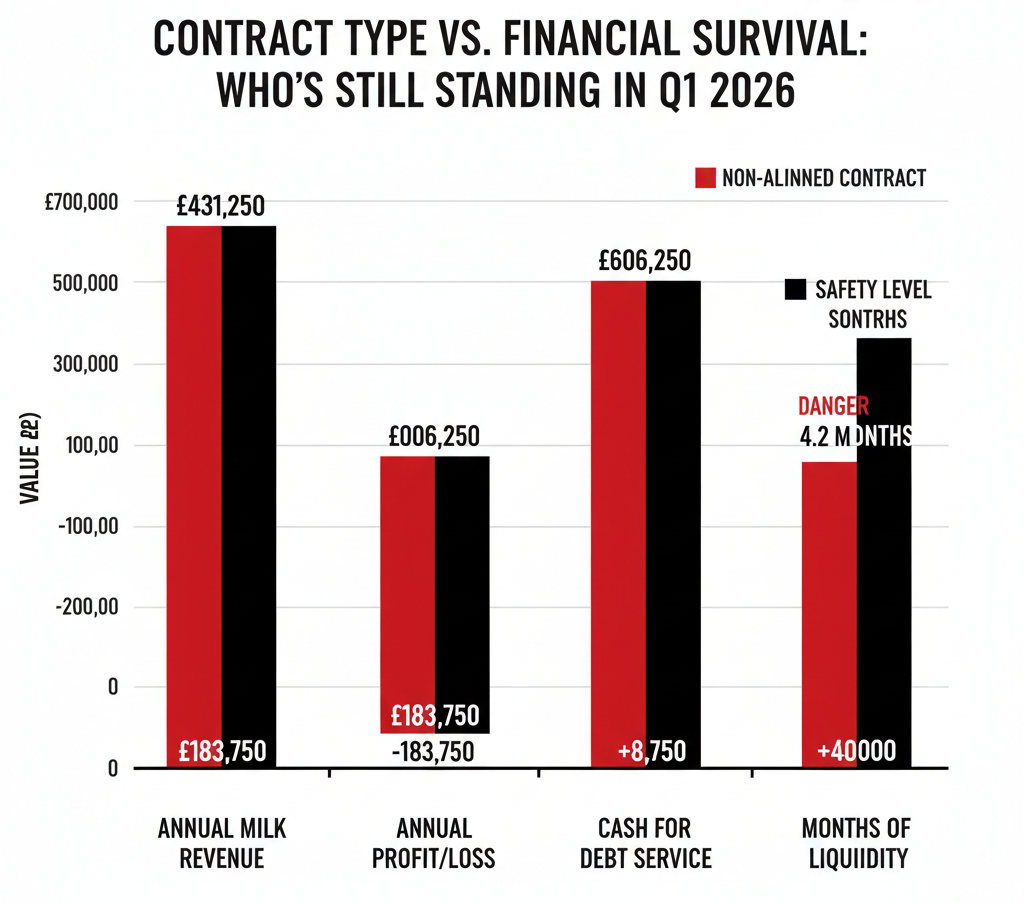

On a 500-cow operation producing 1.25 million litres annually, that 14–15ppl gap represents roughly £175,000–£187,500 per year in lost margin compared with a neighbour on a cost-of-production-linked contract facing the same market.

Farm Parameter

Farm A (Non-Aligned)

Farm B (Aligned Retail)

Difference

Herd Size

500 cows

500 cows

—

Annual Production

1.25M litres

1.25M litres

—

Milk Price (Early 2026)

34.5 ppl

48.5 ppl

+14.0 ppl

Cost of Production

49.2 ppl

49.2 ppl

—

Margin per Litre

-14.7 ppl

-0.7 ppl

+14.0 ppl

Annual Loss/Profit

-£183,750

-£8,750

£175,000

“Prices are falling fast while costs remain high,” said Bruce Mackie, chair of NFU Scotland’s Milk Committee, in December 2025. “Processors must communicate clearly and fairly with suppliers.”

The UK now has regulatory teeth—the Fair Dealing Obligations (Milk) Regulations 2024 and the Agricultural Supply Chain Adjudicator to enforce them. But in ASCA’s first 12 months, not a single formal complaint landed across the entire industry. Nine farmers rang up in confidence. None followed through.

Is the regulation toothless, or are farmers too terrified of their milk buyer to bite back?

The Market Numbers You’re Up Against

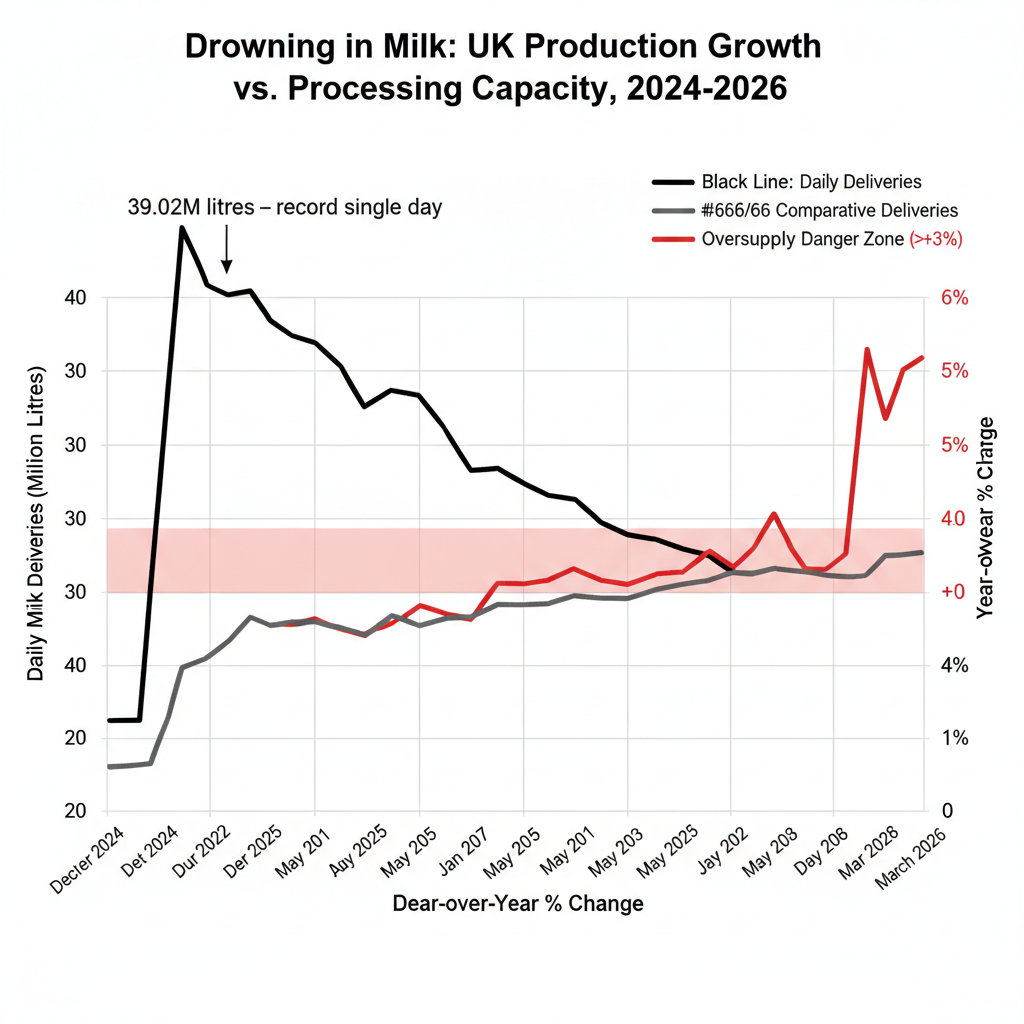

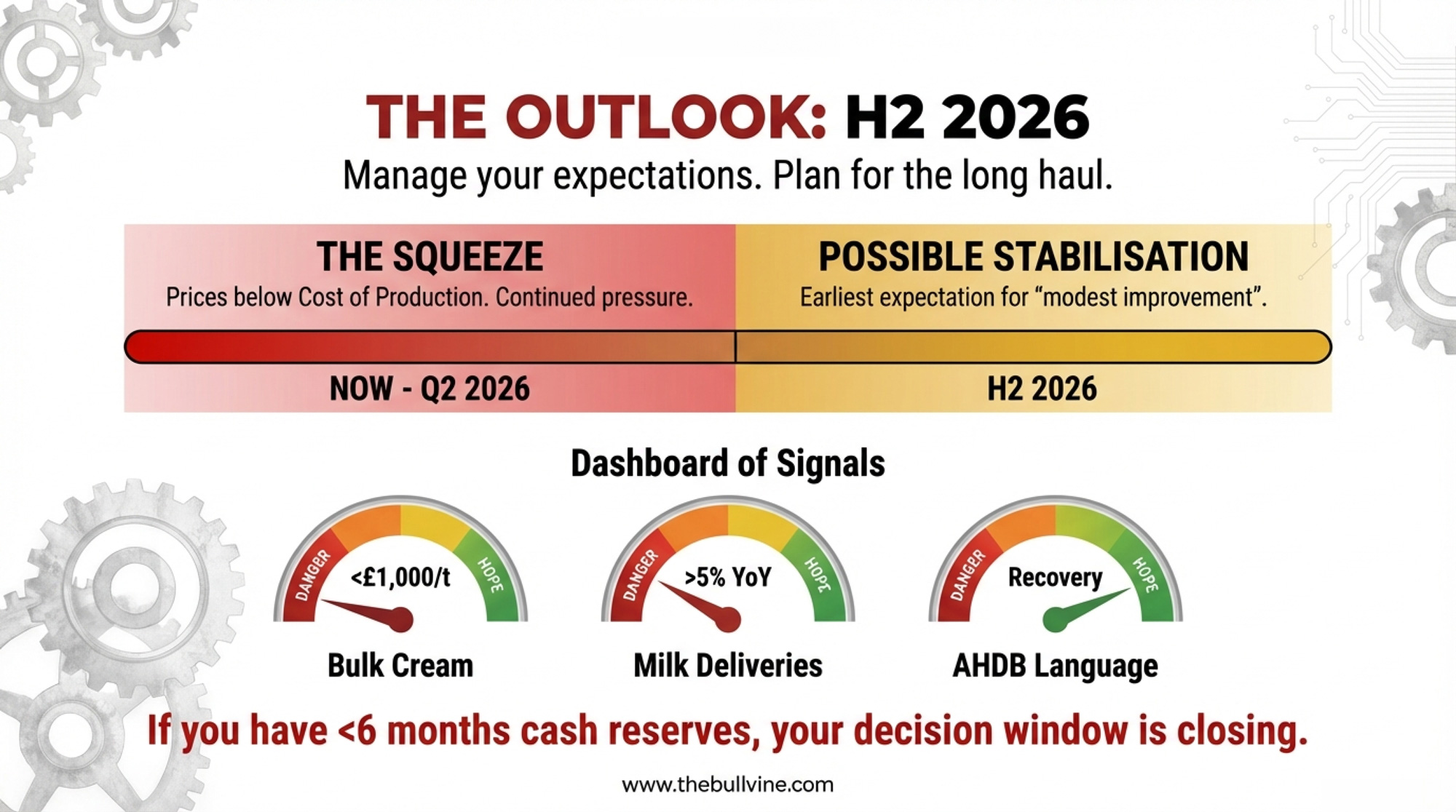

UK dairy entered 2026 drowning in milk. December 2025 deliveries averaged around 35.6 million litres daily—4.8% above the prior year, according to AHDB. Total GB production for 2025/26 is forecast at a record 13.05 billion litres. Spring flush 2025 peaked at 39.02 million litres on May 4—the highest single-day volume ever recorded.

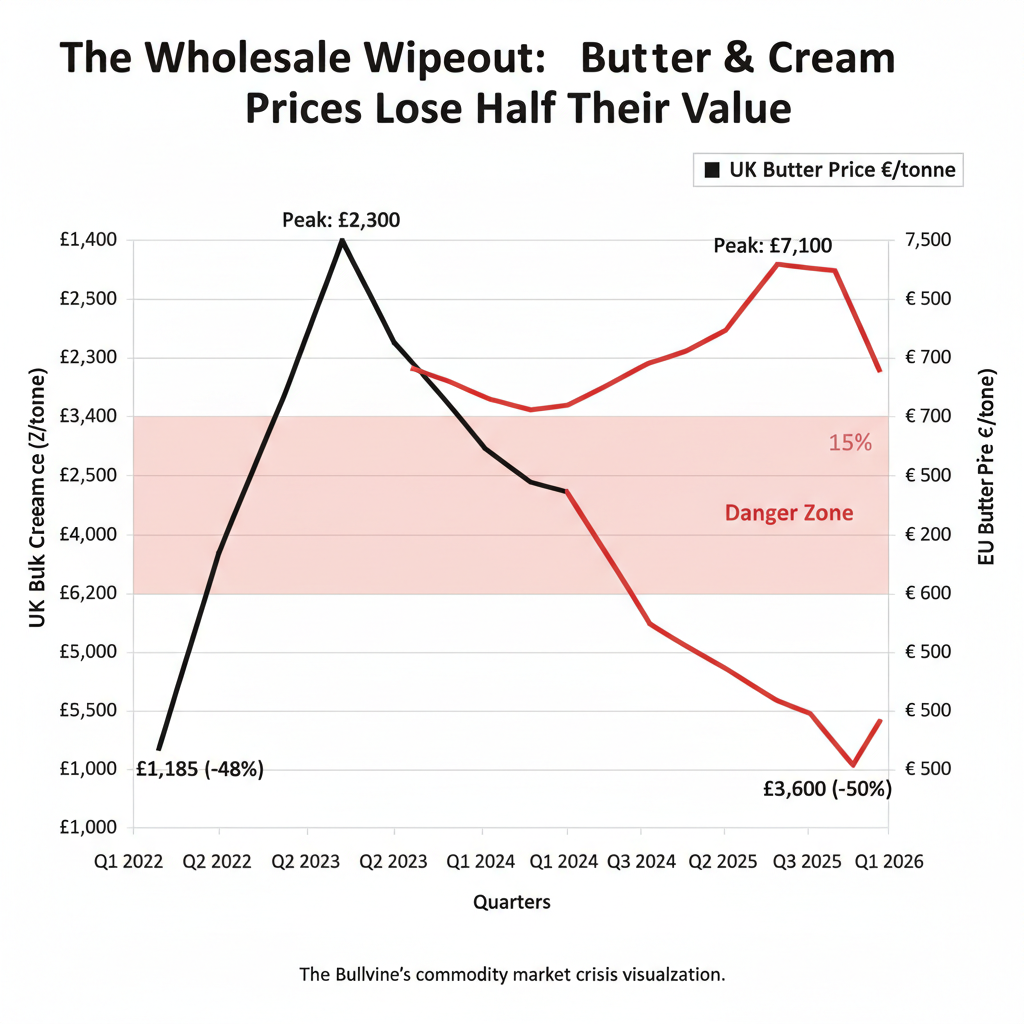

Wholesale markets buckled. Bulk cream cratered to £1,185 per tonne in January 2026, down 10% from December, per AHDB. UK wholesale butter averaged £3,600 per tonne for the month—AHDB notes it “has now lost over half of its value since the peak.” European butter slid below €4,000 per tonne in late January, down from over €7,000 at the 2022 high.

AHDB’s January 2026 outlook didn’t mince words: milk prices are “set to stay under pressure through the first half of 2026” with only “modest improvement” expected later. Rabobank’s Q4 2025 update pegs global supply growth at just 0.12% for 2026, with actual decline not expected until the first half of 2027.

FAS Scotland confirms it plainly: milk price was below the cost of production for most of 2025 and remains so heading into spring.

If your contract amplifies downturns, you’re staring down at least six more months of pain with no structural relief on the horizon.

A Global Problem, Not Just a UK One

While this analysis focuses on UK contracts and FDOM regulations, producers across the globe are fighting the same battle between discretionary and formula-based pricing.

In the US, the gap between Federal Milk Marketing Order Class III prices and actual processor pay has sparked renewed debate about order reform—with some co-ops offering cost-plus contracts while others stick to commodity-based formulas. EU producers face similar tensions as intervention prices sit well below production costs in many member states. The contract structures differ, but the fundamental question is identical: who absorbs the pain when markets turn?

UK farmers have FDOM. American producers have FMMO reform debates. EU farmers have CAP negotiations. None of these frameworks have yet solved the core imbalance: processors can pass risk down; farmers can only absorb it or exit.

Where the Money Actually Lands

The split between contract types has become stark.

Sainsbury’s Sustainable Dairy Development Group suppliers operate under cost-of-production models that flex with input costs. When feed and energy prices spike, the farmgate price rises. When wholesale markets collapse, the formula cushions the fall. These suppliers saw modest price bumps in early 2026.

Farmers locked into processor-discretionary deals—where pricing follows wholesale swings or processor margin targets—caught the full blow:

Processor

Contract Type

Early 2026 Price

Müller Advantage

Manufacturing (March)

34.5ppl

First Milk

Manufacturing (February)

30.25ppl

Arla

Liquid (February, GB conventional)

32.57ppl

Set those against a cost of production near 49ppl, and many non-aligned producers are losing 14–19ppl on every litre.

Metric

Non-Aligned (Red)

Aligned Retail (Black)

Annual Milk Revenue

£431,250

£606,250

Annual Profit/Loss

-£183,750

-£8,750

Cash Available for Debt Service

-£50,000

+£40,000

Months of Liquidity Remaining

4.2 months

18+ months

On 1.25 million litres, a farm stuck at 34.5ppl instead of cost-linked pricing is effectively giving up £175,000–£187,500per year compared with a neighbour whose contract moves with costs. At 1.5 million litres and a 14ppl loss, you’re looking at roughly £210,000 in negative margin before you pay a penny on capital or debt.

Switching sounds nice. But with synchronized cuts across processors, alternatives aren’t materially better for most farms right now. And FDOM’s 12-month notice requirement means any move you make today won’t take effect until 2027.

Producers from Southwest England to Yorkshire are living the same reality: identical market conditions, wildly different cheques depending on what they signed 12–24 months ago.

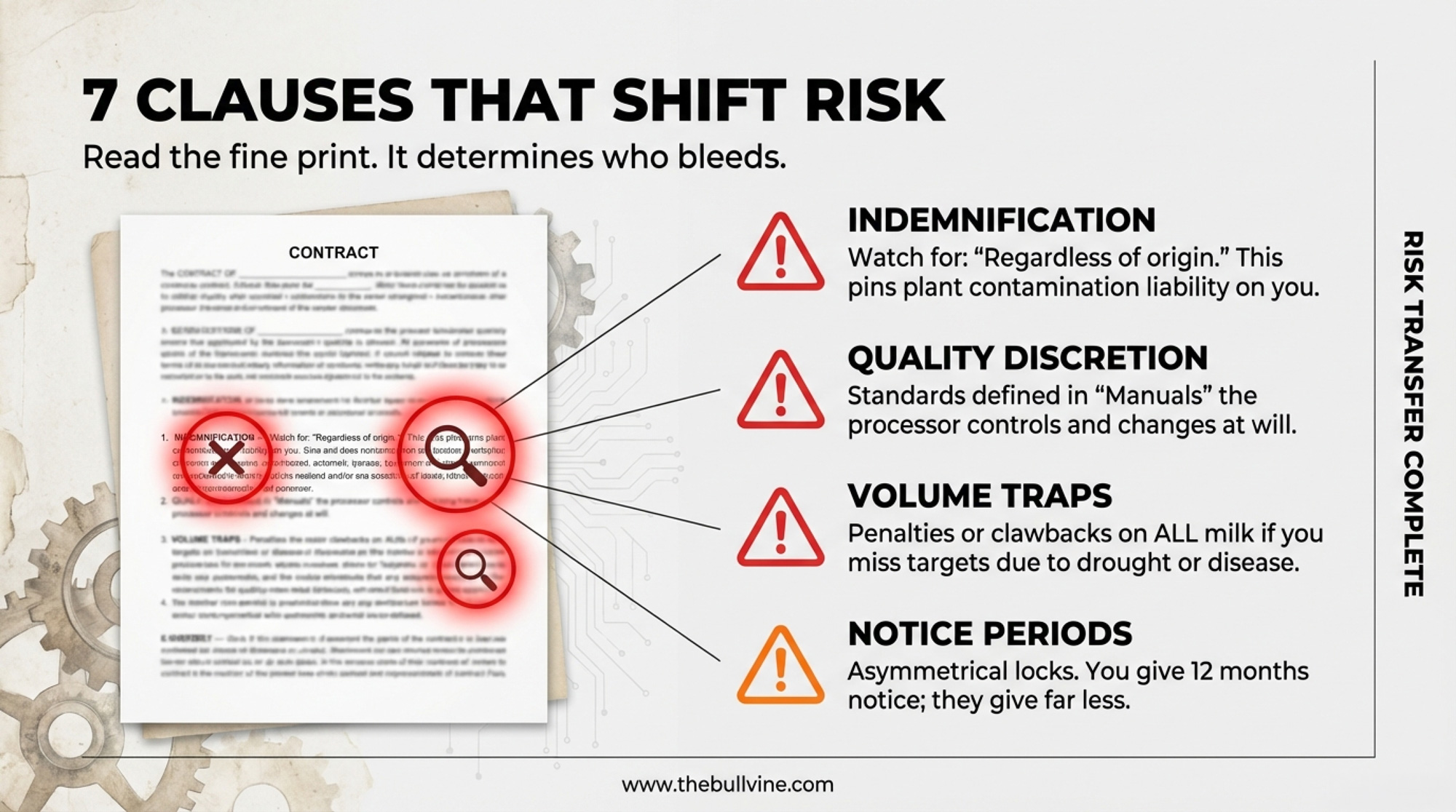

Seven Clauses That Shift Risk Onto Your Back

What separates a protective contract from a loaded gun isn’t the headline price. It’s the fine print.

Clause

The “Red Flag”

Risk Level

Indemnification

“Regardless of origin.”

High

Quality Discretion

Processor-controlled manuals

High

Volume Traps

Clawbacks on total delivery

High

Delayed Payments

Loyalty bonuses forfeited on exit

Medium

Confidentiality

No carve-outs for advisors

Medium

Notice Period

12-month asymmetrical locks

Medium

Dispute Resolution

Multiple steps before external review

Medium

Indemnification scope is where real damage hides. Standard language covers losses from your breach or negligence—fair enough. Expanded versions using “regardless of origin” or “arising from or related to the milk supplied” can pin liability for contamination at processor facilities squarely on your operation.

Agricultural attorney Ross Janzen, dissecting US contracts for Progressive Dairy in 2018, flagged this pattern: direct-buy contracts may hold producers “directly liable, not only for their own milk, but milk from other producers or the entire plant.” The mechanics apply similarly to UK contracts.

Quality standard discretion creates similar exposure. If your contract defines requirements by referencing a “Quality Manual,” the processor can rewrite whenever they like, and your pricing can shift mid-term without triggering any formal amendment clause.

Volume commitment traps bite hardest during downturns. What happens when you fall short? Some contracts treat under-delivery—even from drought or disease—as a material breach, triggering price clawbacks on all milk delivered.

Contract Clause

The “Red Flag” Language

Risk Level

What It Means When Prices Fall

Indemnification Scope

“Regardless of origin” or “arising from or related to”

HIGH

You’re liable for contamination at processor facilities—not just your milk, potentially entire plant batches. Legal exposure can exceed annual revenue.

Quality Discretion

“As defined in Quality Manual” (processor-controlled)

HIGH

Processor can rewrite quality standards mid-contract, triggering price penalties or rejection without contract amendment. Zero farmer input.

Volume Traps

Clawbacks or penalties on “total delivery” if minimums missed

HIGH

Miss volume targets (drought, disease, market exit)? Processor claws back pricing on all milk delivered, not just shortfall.

Delayed Payments

Loyalty bonuses or “end-of-year” payments tied to contract completion

MEDIUM

Walk away mid-contract? You forfeit 6–12 months of accrued payments—effectively a financial hostage clause.

Confidentiality

No carve-outs for “advisors,” “legal counsel,” or “lenders”

MEDIUM

Can’t share terms with solicitor, accountant, or bank without breach. Makes informed decision-making nearly impossible.

Notice Period Asymmetry

12-month producer notice, 30–90 day processor notice

MEDIUM

You’re locked in for a year; they can exit or cut pricing in 90 days. Risk runs one direction.

Dispute Resolution Barriers

“Escalation process” requiring processor internal review first

MEDIUM

Multiple hoops before external adjudication. Designed to exhaust you before you reach ASCA or legal remedy.

Your Contract Audit Checklist

Before your next contract conversation, nail down these eight items:

[ ] Indemnification scope: Does the clause include “regardless of origin” or similarly broad language?

[ ] Quality standards: Defined in the contract, or in external manuals, that the processor controls?

[ ] Volume commitment remedies: What happens if you miss minimums due to factors outside your control?

[ ] Payment timing: What chunk of your stated price depends on future behaviour?

[ ] Notice period symmetry: How much warning do you owe versus what they owe you?

[ ] Title transfer point: When does ownership move, and who carries risk during haulage?

[ ] Confidentiality carve-outs: Can you share terms with your solicitor, accountant, and lender?

[ ] Dispute resolution path: How many hoops between “I have a problem” and external review?

Four Realistic Paths Forward

You’re not going to strong-arm better terms out of your processor. Academic research on dairy supply chains shows that farmers’ bargaining power is well below that of processors. A 500-cow unit doesn’t rewrite standard contract language.

So what can you actually do?

Path 1: Audit for Intelligence

Contract auditing isn’t about renegotiating—it’s about knowing your exposure before the next price cut lands. Map how clauses interact. What happens if you trip the quality threshold while also missing the volume threshold?

Best for: Anyone who hasn’t done this in the last 12–18 months. Requires: 2–3 hours with your contract and a calculator. Downside: None—this is baseline due diligence

Path 2: Find Your Exit Number

Your exit price isn’t simply the cost of production. Cornell economists have shown the rational exit threshold often sits below variable cost because of “option value”—the potential gain from hanging on and catching a recovery. But debt changes that math fast.

The number that matters: At what milk price does cash flow go negative, including debt service? That’s your hard line.

Best for: Non-aligned contract holders carrying significant debt. Requires: Honest cash flow work with your accountant. Downside: Waiting for “confirmation” while cash drains out

Path 3: Position Without Committing

There’s groundwork you can lay before triggering any notice clock:

Talk to other processors. Exploring alternatives doesn’t breach exclusivity—shipping milk elsewhere does. Options are thin in early 2026. But knowing that is intelligence.

Run lender scenarios. “What happens if prices stay here through Q3?” Their answer tells you how much runway you actually have.

Compress costs strategically. NFU Scotland, in a November 2025 advisory, encouraged farmers to “reduce output slightly—selling poorer performing cows while cull prices remain high” to ease cost pressure. But don’t just sell cows—sell your bottom 10% genetically to protect future recovery. When margins turn negative, the embryo budget and top-tier semen are often the first casualties. Make culling decisions that preserve your genetic trajectory, not just your tank space.

Best for: Producers with 6–12 months of cash left. Requires: Uncomfortable conversations with lenders. Downside:Cut too deep, and you hobble your recovery capacity

Path 4: Build a Paper Trail

If pricing looks opaque or inconsistent, document everything. Under FDOM, processors must respond to pricing queries within 7 working days. If they don’t, that’s something concrete for ASCA.

Best for: Anyone who suspects their contract breaches FDOM rules. Requires: Systematic logging of every price notification and query. Downside: The confidential route may produce no visible outcome; the formal route puts you on their radar

Signals to Watch Through Q3 2026

Bulk cream leads the farmgate by 2–3 months. January’s £1,185/tonne—down 10% month-on-month—signals near-term pressure continues. AHDB sees “positive movements” starting but warns fats remain under “severe pressure.”

SMP and cheddar show early stabilisation. AHDB reports SMP up £80 (5%) to £1,810/tonne in January; cheddar recovered £30 to hit £2,860/tonne. But AHDB cautions that “stabilisation should not be mistaken for recovery.”

Milk deliveries versus year-ago gauge supply-side pressure. With volumes running nearly 5% above the prior year heading into spring flush, processing capacity stays strained through May.

ASCA activity tells you whether the regulator has any bite. If formal complaints stay in single digits through April while prices sit below the cost of production, the framework isn’t working as Parliament intended.

Why Nobody’s Talking

Here’s the part that doesn’t show up in market reports: why you’re not hearing individual farmers’ stories.

The producers getting hit hardest—the ones sliding toward exit—are the least likely to speak publicly. In farming culture, financial distress still feels like personal failure. Going on record about contract pressure invites lender scrutiny, community judgement, and processor retaliation.

As NFU Scotland’s Bruce Mackie put it in December 2025: “The dairy supply chain depends on farmers being able to plan and invest with confidence. Sudden, unjustified price drops damage that confidence and threaten not just individual businesses but the resilience of Scotland’s rural economy and food security.”

ASCA built confidential channels precisely because farmers fear reprisals. That’s the right protection—but it also keeps the pain invisible. Processors see aggregate data across their supplier network. Individual farmers see only their own situation and wonder if they’re alone.

You’re not. The aggregate numbers—nearly 5% oversupply, butter down more than half, costs near 49ppl against prices in the low-to-mid 30s—represent thousands of operations running the same brutal calculations.

What This Means for Your Operation

If you’re on an aligned retail contract: Your immediate exposure is limited. Don’t waste the breathing room. Build cash reserves and pay down debt—the cushion you create now determines your options when conditions shift.

If you’re not aligned with 6+ months of cash, you’ve got time to watch. Track these triggers:

Bulk cream dropping toward £1,000/tonne signals more farmgate pressure

UK deliveries staying 5%+ above year-ago into spring signals capacity strain

AHDB language shifting from “pressure” to “recovery” signals inflection

Book your lender scenario conversation before April 1.

If you’re non-aligned and have less than 6 months of cash on hand, the math is unforgiving. Run your exit threshold calculation this week. Have the lender conversation now. If two warning signs fire together—cash flow negative, cream still sliding, deliveries elevated—your decision window is closing fast.

Key Takeaways

At current price and cost levels, the gap between aligned and non-aligned contracts can reach 14–15ppl—roughly £175,000–£187,500 a year for a 500-cow, 1.25M-litre operation.

Contract auditing is intelligence, not leverage. You may not change the terms, but you can understand where the landmines are.

Risk is shifted onto your books across seven areas: indemnification, quality discretion, volume penalties, delayed payments, confidentiality, notice asymmetry, and dispute barriers.

Exit decisions come with a 12-month lag under FDOM notice rules. Staging preparation preserves options without starting the clock.

Every credible forecast points to H2 2026 at the earliest for meaningful recovery. AHDB: stabilisation “should not be mistaken for recovery.”

When culling to compress costs, cull genetically—not just economically. Protect your herd’s trajectory for the recovery.

Cash runway is the bottom line. Under six months at current prices means fundamentally different choices.

Your contract didn’t create this oversupply. It didn’t crash butter prices. But it decides which side of that £175,000–£187,500 divide you’re standing on while you wait for conditions to turn.

Pull out your contract this week. Work through the checklist.

Which side of the gap are you on?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

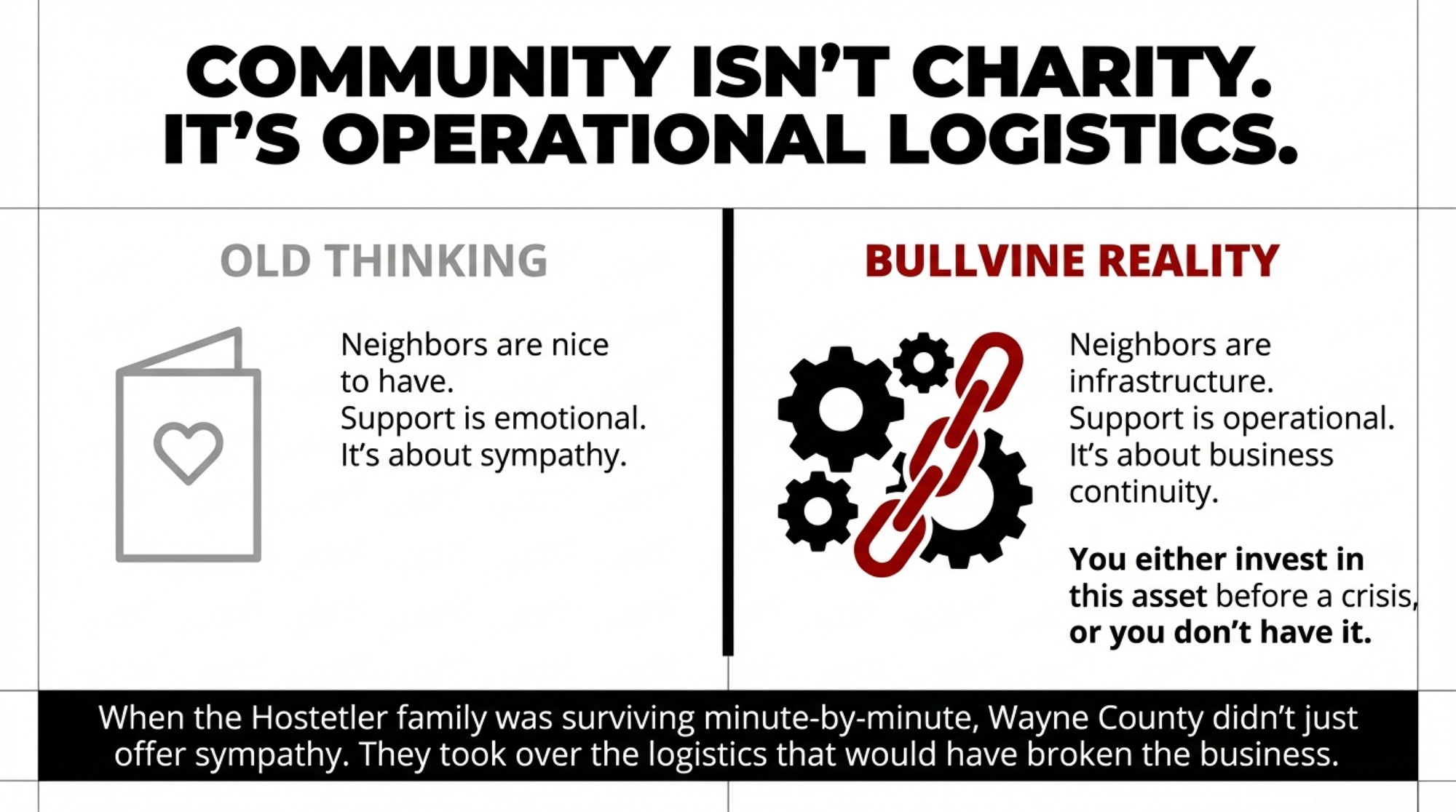

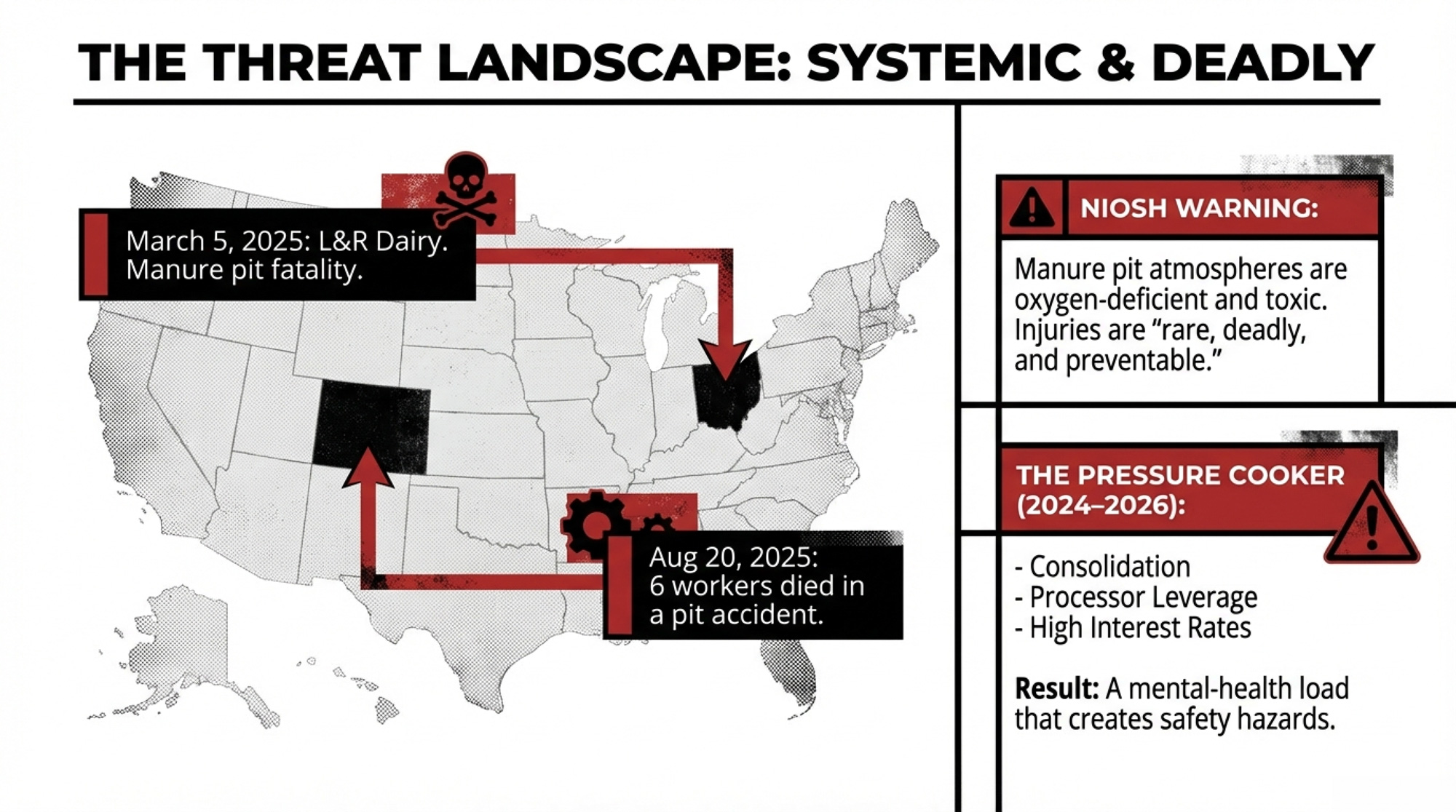

One year after Reed Hostetler’s death at L&R Dairy in Ohio, his community is still proving what farm safety and resilience look like when farmers refuse to let one of their own stand alone.

Executive Summary: Reed Hostetler was 31, co-owner of L&R Dairy in Ohio, and father of three when his tractor tipped into the manure pit on March 5, 2025. He didn’t survive. What his community built in the year since—a barn transformed into a funeral venue, tractors lined up in tribute, months of meals, chores, and quiet financial support that never stopped—is a blueprint every dairy should steal. This article connects Reed’s death to the systemic pit risks that killed six at a Colorado dairy five months later, and to the margin and mental-health pressures squeezing farm families through 2024–2026. It delivers a concrete playbook: phone trees, neighbor check-ins, youth crisis roles, safety protocols that don’t vanish when one person does. The core argument is blunt—community is infrastructure, and the operations that have it recover faster when everything falls apart. Nearly one year later, the only question is whether your road is ready.

The faces behind the “Lead Like Reed” legacy: For the Hostetler family, community isn’t just a sentiment—it is the vital human infrastructure that ensures no dairy operation has to face its darkest day alone.

On March 5, 2025, a 31-year-old dairy farmer drowned after his tractor tipped into the manure pit at L&R Dairy in Marshallville, Ohio. Reed Hostetler was a husband, a father of three young kids, and co-owner of the family operation. He was also, by every account, the kind of guy who showed up when his neighbors needed help.

Almost a year later, his community is still showing up for his family. And that’s the part of this story you can actually copy.

You’re not getting a safety manual here. You’re getting something harder to build and more important to have: a real-world playbook for community resilience and dairy farm safety, forged in the worst possible way.

From Barn Wedding to Barn Funeral

Years before the accident, Reed and Abby Hostetler were married in the main barn at L&R Dairy. Same beams. Same alley. Same cows shuffling in the background.

In March 2025, that same barn became the gathering place for family and friends to say goodbye.

Hosting a large crowd in a working dairy barn isn’t just sweeping the alley and stacking a few straw bales. It’s parking logistics, liability questions, shuttle coordination, sound systems, seating, and making sure the space looks like a celebration of a life, not a Tuesday afternoon herd check.

The Hostetlers didn’t have to figure any of that out on their own.

Neighbors and friends showed up days ahead to pressure-wash walls, scrape alleys, and transform the barn into a place where a casket and grieving family could stand with some dignity. Local companies and neighbors brought gravel and equipment to shore up the lane before vehicles started rolling in. Shuttle buses ran from Marshallville Park, so the yard and road didn’t lock up.

While the family was just trying to survive minute by minute, the community quietly handled the logistics that would have broken them.

Reed and Abby’s three kids—Baer (4), Claire (2), and Axe (1) at the time—were too young to remember most of it. But they’ll hear it for the rest of their lives: the barn was full. People came. We weren’t alone.

That’s not sentimental. That’s an asset. You either have it before a crisis—or you don’t.

The Tractor Line That Said What Words Couldn’t

A mourner puts their hand on a forage harvester parked outside Reed Hostetler’s funeral service, which was held at his family dairy farm March 12. Reed died March 5 after an accident at the farm (Jane Schmucker photo).

There’s a sound you don’t forget: a line of tractors and semis idling in low gear outside a church or a farm. Not parade noise. Heavier. Slower. You feel it in your chest.

At Grace Church in Wooster, where the reception was held, tractors, semis, trucks, and implements lined the parking lot and road as a silent, steel-and-diesel guard of honor.

Local equipment dealers, co-ops, and farmers coordinated the lineup. Once the first few units were committed, the rest followed. Some of the tractors were polished. Others still carried field mud and manure dust. That mix mattered. It wasn’t a show. It was the working dairy community saying, “He was one of ours.”

As one neighbor put it, it was the hardest funeral they’d ever been to—not just because of who they lost, but because of what they watched happen around the family.

Among friends and neighbors, a simple phrase started making the rounds:

“Lead like Reed.” If something needed doing—hay to chop, kids to watch, cows to milk—people asked, “What would Reed do?” and then they just did it. No committee. No sign-up sheet. Just action.

You don’t get that kind of reputation overnight. You build it one favor, one late-night call, one “yeah, I’ll be there” at a time.

When Our Community Needs Help, Help Comes

Most tragedies follow a pattern: three days of intensity, three weeks of fading attention, and then a long, quiet stretch where the family is expected to “get back to normal” while everything inside them is still upside down.

That’s not how this played out.

Weeks and months after the funeral, people kept showing up: groceries, diapers, dinners; neighbors stepping in for chores unannounced; friends checking in not once but over and over.

Abby has said that seeing people show up changed how she thinks about community—and how she plans to show up the next time someone else needs help. That shift, from “How will we survive this?” to “How do we pay this forward?” is the proof that community isn’t just nice. It’s infrastructure.

The support didn’t stop at the farm gate.

Green Elementary’s PTO organized a “Dine to Donate” night at a local Applebee’s, using a “student day off” incentive to bring in more families and raise money for the family. The dollars helped. The message mattered more: “Your school sees what your family is going through. You’re not invisible.”

A crowdfunding campaign drew donations from people who knew the Hostetlers well and from others who only knew them as “the young dairy family in Ohio.” It turned years of quiet relational equity into real, practical support when the family needed it most.

Someone told Abby that because of the way Reed lived, he’s still taking care of his kids even after his death. In strictly financial terms, that’s true. But the bigger truth is this: he’d invested in people, and when it all went sideways, those people cashed that investment in for his family.

Who Reed Was—and Why It Matters Now

Reed wasn’t just “helping out” on the home farm. He was co-owner of L&R Dairy, part of the next generation taking over and pushing the operation forward.

He’d hiked the entire Appalachian Trail. He’d ridden bulls. He’d done mission work in Thailand. Back home, he was the guy who could fix nearly any piece of machinery on the place and still make time to talk with a neighbor in the yard. Neighbors remember him as the kind of person you’d see under a mixer wagon at 11 p.m. and then at someone else’s place the next morning, making sure their chopper started.

Like most dairy producers, Reed knew manure pits are dangerous spaces. He wasn’t inexperienced or careless around equipment. But as this tragedy shows, sometimes the margin between “busy day” and “life-changing day” is just physics and bad timing.

At home, Reed and Abby were in the same season a lot of you are in right now: three little kids, a 24/7 operation, and a calendar that only worked because somebody gave up sleep. Abby picked up nursing shifts at the hospital and was learning more of the farm side to help cover when family needs shifted.

They were raising calves, raising kids, and—often without noticing—raising the bar on what it means to be part of a community.

The wave of support after the accident didn’t appear out of nowhere. It came from years of small decisions: taking a call instead of letting it go to voicemail, showing up with a skid steer when a neighbor’s barn burned, buying a few extra tickets for a school fundraiser, saying yes when something needed doing.

None of those actions looked like “strategy” at the time. Together, they’re the reason people felt personally responsible for being in that barn and that driveway when everything fell apart.

You can’t fake that after the fact. You either build it before you need it, or you don’t have it.

Why One Ohio Manure-Pit Accident Should Change How Your County Shows Up

It’s tempting to file this under “heartbreaking story from another state” and move on. That’d be a mistake.

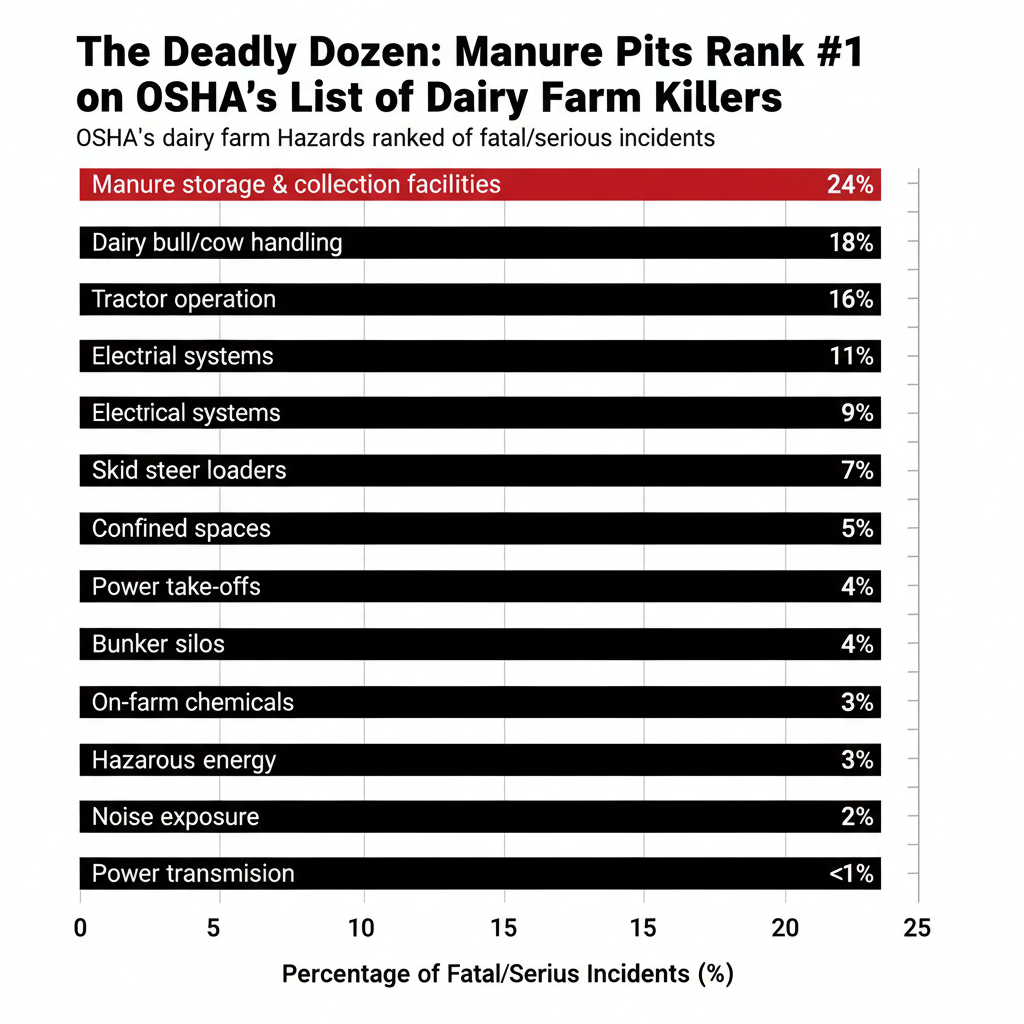

Manure pits have been recognized as a deadly hazard for decades. In a 1993 bulletin titled “Manure Pits Continue to Claim Lives,” NIOSH warned that the oxygen-deficient, toxic atmosphere in manure pits has “claimed many lives” and that hydrogen sulfide, methane, and other gases can overcome workers within seconds when conditions line up the wrong way. A 2012 clinical review published in the Journal of Agromedicine described manure-pit injuries as “rare, deadly, and preventable,” noting that while these incidents don’t happen often compared to other farm injuries, the fatality rate is extremely high once something goes wrong.

And it’s not just Ohio.

On August 20, 2025, six workers—including a 17-year-old—died in a manure-pit accident at Prospect Valley Dairy in Keenesburg, Colorado. Investigators and local reports indicate that a contractor doing routine work likely triggered a hydrogen sulfide release and was overcome almost immediately. Five other workers went in after him in attempts to rescue him. None of them came back out.

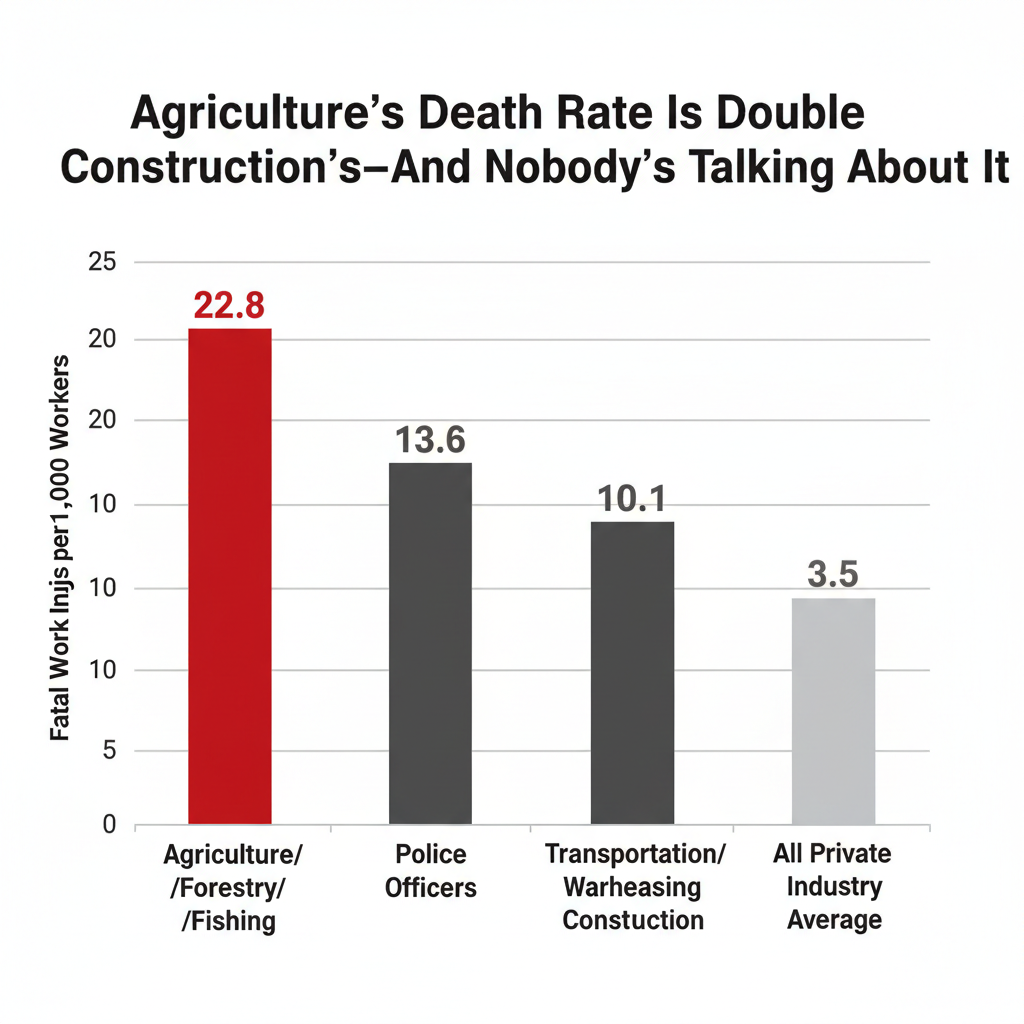

When The Bullvine looked back at 2025’s defining dairy stories, Reed’s death in Ohio and the Colorado tragedy both made the list for the same reason: they exposed how thin the margin really is between an ordinary workday and a permanent hole in a family, a workforce, and a local dairy economy. These aren’t freak one-offs. This is systemic risk we’ve tolerated for too long.

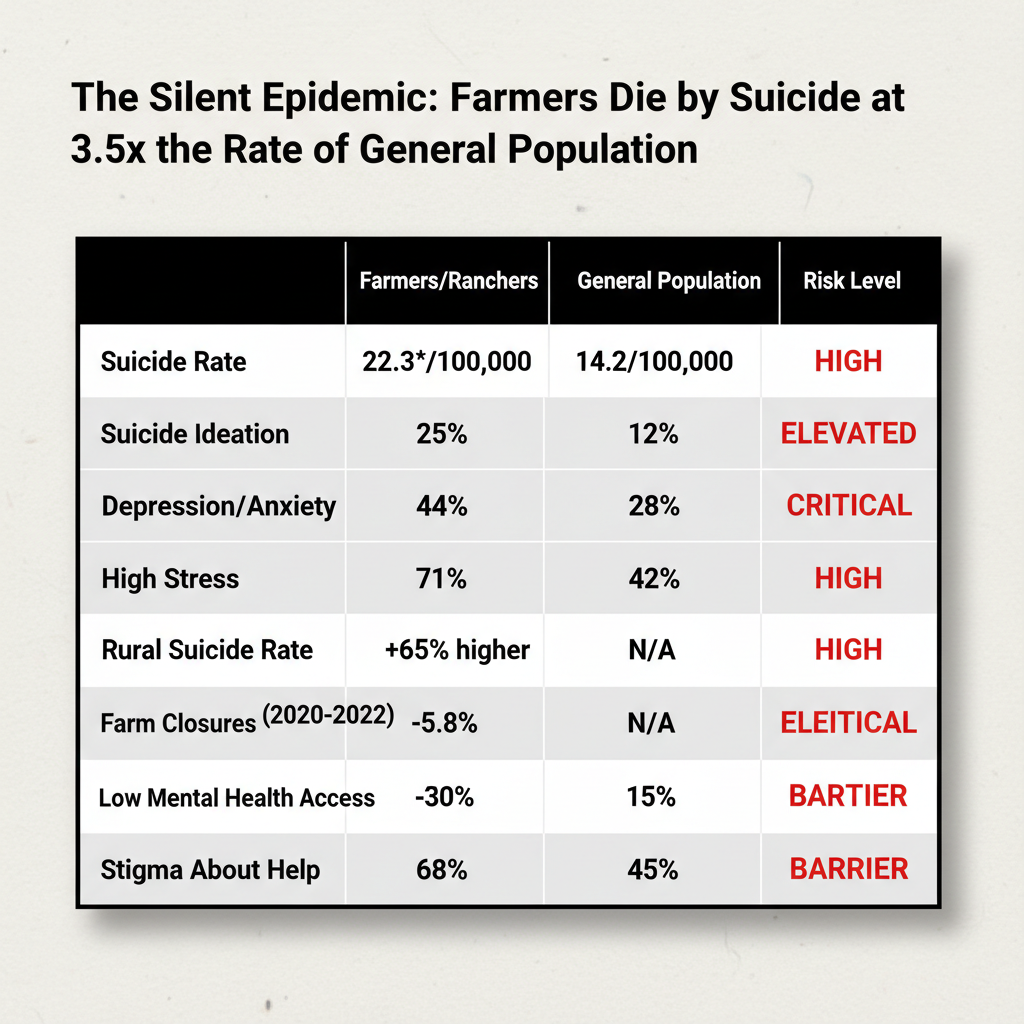

Now layer that on top of 2024–2026 realities—consolidation, processor leverage, stubborn input costs, labor shortages, and interest rates that haven’t dropped the way anyone hoped. You’ve got a mental-health load that doesn’t show up on your milk check but absolutely shows up in your barn and your house.

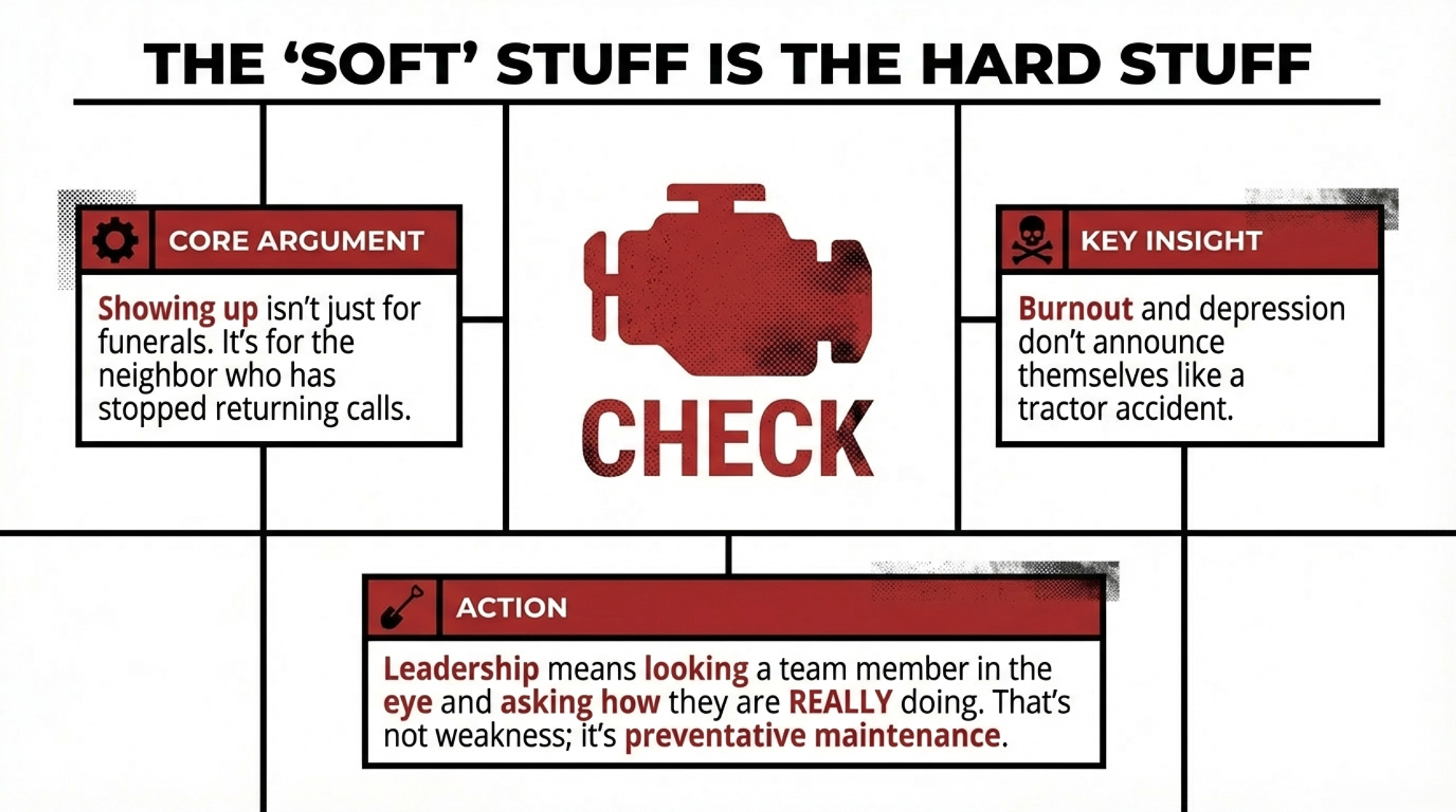

You know people in this business who are running close to the edge—physically, mentally, and financially. “Showing up” can’t just mean after a visible accident. It has to include watching for the quieter stuff: the guy who stops returning calls, the coworker making more mistakes than usual, the family where one bad month of prices seems to hit harder than it should.

Mini-Moments That Show What “Showing Up” Actually Looks Like

Big headlines are built from small, unglamorous decisions. A few details from Wayne County are worth stealing outright.

The food. Abby jokes that Wayne County people sure know how to cook. For weeks, the kitchen counters stayed full: hot casseroles, snack trays, grab-and-go items for the kids. The food itself wasn’t the point. The point was the message: “You don’t have to think about supper tonight. We’ve got that piece.”

The quiet chores. One neighbor made a habit of showing up early, doing a full round of chores, and leaving before anyone could say thank you. Calves fed, pens cleaned, gates latched. No Facebook post, no photo, no public pat on the back. Just work done when the farm needed fewer decisions, not more.

The school connection. Green Elementary’s PTO could’ve checked the “we sent a sympathy card” box and moved on. Instead, they organized the restaurant fundraiser and used a “student day off” incentive to bring in more families. They told the kids, in actions: “Your school sees what your family is going through. You’re not invisible.”

The tractors. Those machines parked outside the church didn’t fix anything on paper. What they did was silently tell Reed’s kids: “Your dad mattered to a lot of people.” Ten years from now, those kids will remember that wall of iron as clearly as any words they heard.

None of these actions use the word “community.” They don’t have to. They define it.

What This Means for Your Operation

If you strip away the emotions, what Wayne County proved is simple: community is infrastructure. You either invest in it before you need it, or you find out what it costs not to have it when everything goes wrong.

Farm families that aren’t alone recover faster—financially and operationally—because chores, crops, and kid logistics don’t collapse alongside grief. That’s not soft thinking. That’s business continuity.

Here are the hard questions worth asking this month:

If a tractor rolled or a fire started on your place tomorrow, who are the first three people who would be in your yard without being asked?

If it happened to a neighbor instead, would anyone automatically assume you were one of those three?

If you had to line up 20 tractors and trucks as a sign of respect, who would answer that call—and who wouldn’t notice?

Who on your team or in your circle has been quieter, shorter-tempered, or more withdrawn than usual lately—and when was the last time you looked them in the eye and asked how they’re really doing?

If you can’t rattle off names without thinking too hard, you don’t have a phone tree. You have a hope and a prayer.

And if you sign the checks or make the schedule, you’re the one who can change that.

What You Can Actually Do This Month

If you’re wondering where to start, here’s the short list.

Build a simple phone tree now. Don’t overcomplicate it. Aim for at least 8–10 key people on your road, in your church, and in your school community. Decide who calls whom in the first 15 minutes if there’s an accident, sudden death, major health crisis, or barn fire. Write it down where people can actually see it—in the milk house, office, or group chat.

Pick three farms to check on. Not with a text. With a quick call or visit. Ask, “How are you doing—really?” and be ready for the answer to take longer than you planned.

Involve your youth on purpose. 4-H and FFA clubs can own “comfort” jobs in a crisis: cards, posters, freezer meals, calf chores. Give them clear roles so they grow up knowing how to show up instead of watching from the sidelines.

Talk about mental health out loud. Put it on the agenda at your discussion group, local dairy association meeting, or men’s breakfast. Share one real story, even if it’s uncomfortable, and be the one who goes first. Make it normal to say, “I’m not okay right now,” before someone breaks. That’s not weakness; it’s maintenance. If you or someone on your team feels overwhelmed, talk to your doctor, a trusted advisor, or a local mental-health provider.

Practice before the crisis. Help each other with harvest, planting, big herd moves, or barn clean-outs, so you already know how to work together. You’ll spend a few hours now—or you’ll scramble from zero on your worst day.

Tie safety and support together. As you review protocols around pits, lagoons, and confined spaces—gas monitors, ventilation, entry rules—ask yourself: “Who else knows this? Who would enforce it if I’m not here?” If there’s any task on your farm that only one person can do safely, that’s a red flag. Train at least one backup and write down the protocol. Safety that only lives in your head isn’t safety.

None of this replaces hard safety work around manure pits, lagoons, and confined spaces. You still need lock-out/tag-out, proper equipment, training, and clear protocols.

But when safety systems fail, insurance is slow, milk prices are tight, and official help ends—this is what catches people.

Key Takeaways

Community doesn’t appear out of thin air in a crisis. It’s built on years of small, quiet favors when nothing is on fire.

Kids are watching. Who shows up, who kneels down to their level, who keeps coming back after the casseroles are gone—that’s what they’ll remember long after the details fade.

Leadership on a dairy isn’t just about numbers and banners. It’s about who you are when someone down the road is in trouble.

“Showing up” includes the quiet stuff. Burnout, withdrawal, depression—these don’t announce themselves the way a tractor accident does. Check on your people before they break.

Safety that lives only in your head is a liability. If nobody else on your operation knows your protocols or would enforce them without you, that’s a gap you can fix this week.

Lead Like Reed

Underneath all the grief, this is a story about assets—just not the kind your accountant can depreciate.

On the hard-numbers side, you chase efficiency, butterfat, component premiums, and labor stability because the economics of 2024–2026 don’t leave much slack. If you’re not on top of genetics, feed, and contracts, you get run over. We all know that.

On the human side, there’s another question that matters just as much to long-term survival: when—not if—something goes very wrong, is your farm part of a community that knows how to respond?

That’s not a feel-good side issue. It’s about whether your family, your workforce, and your local dairy ecosystem can take a hit without collapsing.

So here’s the challenge, almost a year after Reed’s accident:

Look at your own road. Who would need you if something happened tomorrow?

Look at your own barn. Who would you call first if it was your tractor in the pit, your fire, your heart attack in the parlor, or your brain finally saying “enough” after too many bad months in a row?

Look at your own kids and grandkids. What stories do you want them telling 10 years from now about how your community handled hard things?

Reed didn’t get a vote on what happened on March 5, 2025. His brothers did everything they could in a window that physics, machinery, and toxic gas had already stacked against them. His wife, kids, and parents didn’t choose any of it.

What they did get—and what they’re still getting a year later—is a community that decided they weren’t going to carry it alone. A community that turned a barn into both a wedding hall and a sanctuary of grief. A community that lined up tractors, cooked meals, ran fundraisers, and kept showing up long after the news cycle moved on.

Support Type Wayne County Response Typical Farm Crisis Response Immediate Response (0-3 days) 20+ neighbors in yard day 1, full chore coverage Family handles alone, maybe 1-2 calls Funeral/Memorial Logistics Barn transformation, shuttle buses, tractor line, parking coordination Funeral home handles, family figures out details Food/Meals Weeks of daily hot meals, grab-and-go for kids, coordinated delivery 3 days of casseroles, then silence Financial Support Crowdfunding, school fundraiser ($5,000+), sustained donations Maybe a GoFundMe, no follow-up Chore/Labor Coverage Daily unannounced chore coverage for weeks, crop/haying help 1 week if lucky, then “back to normal” School/Kids Support PTO-organized fundraiser, student engagement, visible recognition Sympathy card, kids expected to cope alone Long-Term (3+ months) Ongoing check-ins, continued meals, relationship maintenance “How are you holding up?” texts, no action Phone Tree/Coordination Pre-existing relationships, clear roles, no central organizer needed Confusion, duplicate efforts, gaps in coverage Mental Health Follow-Up Community members trained to recognize signs, ongoing support “Let us know if you need anything” (passive) Business Continuity Farm operations maintained, no production loss, equity preserved Operations suffer, milk quality drops, financial losses compound

You can’t control every accident or every market swing. You can control whether anybody in your circle ever has to face one alone.

So the next time you hear about a farm accident, a diagnosis, or a sudden death—whether it’s in your county or three states away—don’t just shake your head and scroll on.

Ask yourself, honestly: “What would ‘lead like Reed’ look like where I live?”

Then do one concrete thing this month to make sure no farmer on your road has to stand alone when their barn—or their mind—goes dark.

Week

Action Item

Output/Deliverable

Time Required

✓

Week 1

Build your phone tree

List of 8-10 names: neighbors, church, school contacts who would respond in first 15 minutes if something went wrong

2 hours

☐

Week 2

Make 3 farm check-ins

Call or visit 3 farms in your area—ask “How are you doing, really?” and be ready for the answer to take longer than you planned

3 hours

☐

Week 3

Assign youth crisis roles

Meet with local 4-H/FFA club—define specific “comfort jobs” (cards, posters, freezer meals, calf chores) youth can own during next community crisis

1.5 hours

☐

Week 4

Put mental health on agenda

Add mental health discussion to your next dairy association meeting, men’s breakfast, or discussion group—share one real story and go first

1 hour

☐

BONUS: Practice Before Crisis

Help a neighbor with harvest, planting, big herd move, or barn cleanout so you already know how to work together when everything falls apart

Completed joint work project with neighboring farm

4-6 hours

☐

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.