Jarratt logged 69 noncompliance records before the listeria hit. Ten funerals, 7 million pounds pulled, 17 months dark — and the margin damage is already moving upstream to 400-cow herds that never shipped a bad load.

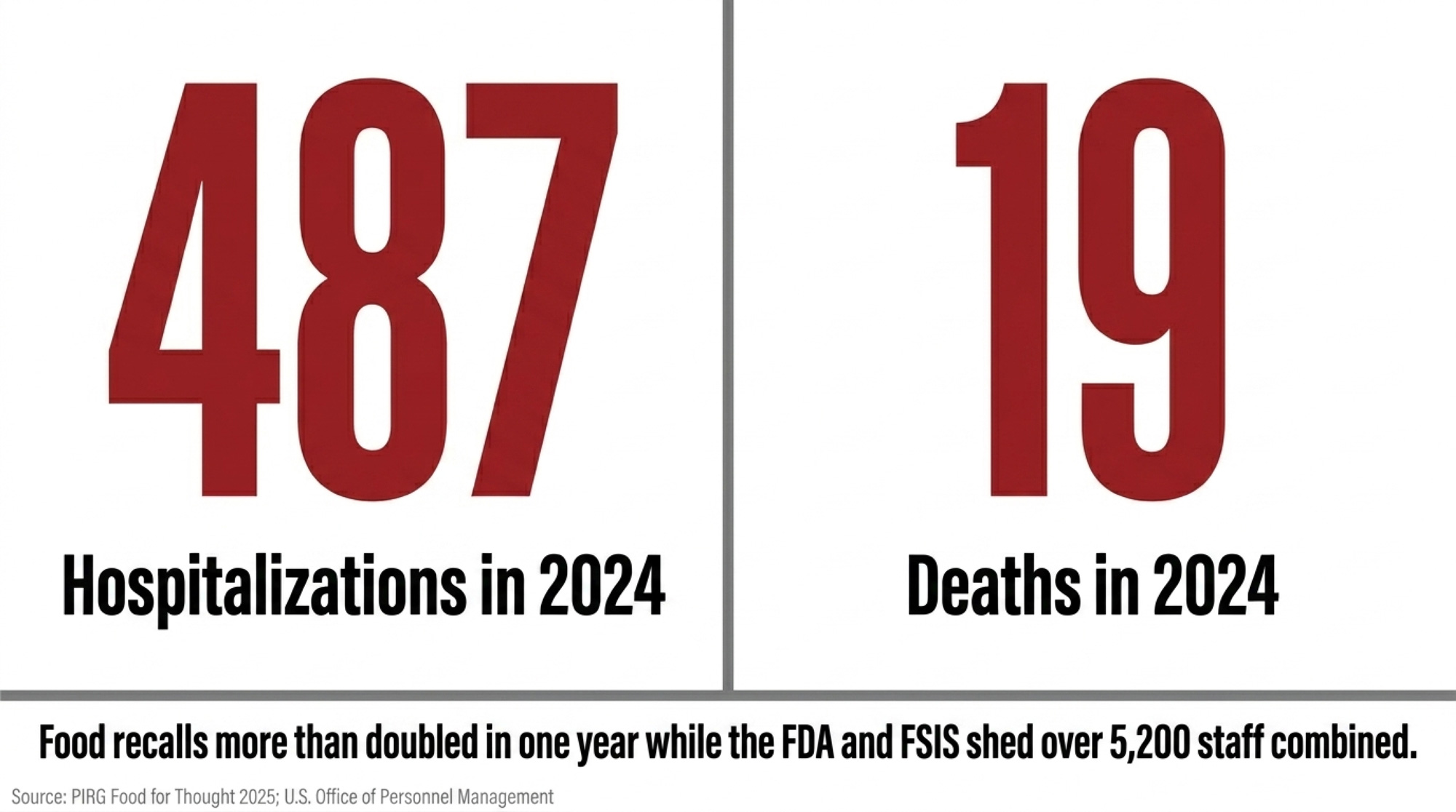

Executive Summary: Boar’s Head’s Jarratt, Virginia plant racked up 69 sanitation noncompliance records before a listeria outbreak killed 10 people, pulled more than 7 million pounds of product, and kept the facility dark for 17 months. That’s one plant in a broader shift: 2024 recall-linked hospitalizations hit 487 and deaths hit 19 — both more than double 2023 — while CDC’s FoodNet quietly de-emphasized listeria as a core target and FDA and FSIS shed over 5,200 staff combined. The dairy side is already in the blast radius — Rizo-López under permanent injunction, Prairie Farms supplemental shakes linked to 14 deaths, and Great Lakes Cheese yanking 1.5 million bags across 31 states on a Class II recall. On a 400-cow herd shipping 300 cwt/day, a 10% downstream intake cut at a $3/cwt discount for 60 days burns about $5,400; a 90-day shutdown scenario runs $16,200 — versus roughly $2,604/year for a basic listeria EMP built on $21.50–$21.86 swabs (Motzer, Trmčić et al., JDS 2025). HACCP self-policing, Talmadge-Aiken enforcement gaps, and co-ops that can’t audit their customers’ drains mean that risk isn’t staying where it was built. If more than 70% of your milk moves through one plant or converter, or your supply contract carries open-ended indemnity and “sole discretion” clauses, you’re carrying downstream plant risk as a fourth pillar next to feed, weather, and price — whether you’ve priced it or not. Read the full piece for the four levers you control, a contract-clause checklist, and the 30-day conversation to have with your co-op before the next recall runs your numbers for you.

In the twelve months before listeria at Boar’s Head’s Jarratt, Virginia plant killed 10 people across nearly 20 states, inspectors walked that facility and wrote up 69 sanitation noncompliance records. Mold on walls. Insects. Condensation over food‑contact surfaces. Meat residue so caked on equipment the inspectors called it “heavy” and “discolored.” Every finding went in the file. The plant kept running.

By the time the recall dust settled, more than 7 million pounds of deli meat were off shelves. Jarratt shut down September 13, 2024. Boar’s Head didn’t resume operations until early February 2026 — about seventeen months later — after what the company called “comprehensive upgrades,” including adoption of USDA’s Alternative 2 Listeriacontrol program and the hiring of its first Chief Food Safety Officer, Natalie Dyenson, in May 2025.

Families who lost loved ones will never see those sanitation records the way you just did. And the dairies feeding milk into the same national retail chains and distribution networks absorbed a financial hit from a failure they didn’t create and never saw coming. This is the dairy recall risk story nobody put on your balance sheet — but it’s already there.

What’s Changing in Food Safety — and Why It Lands on You

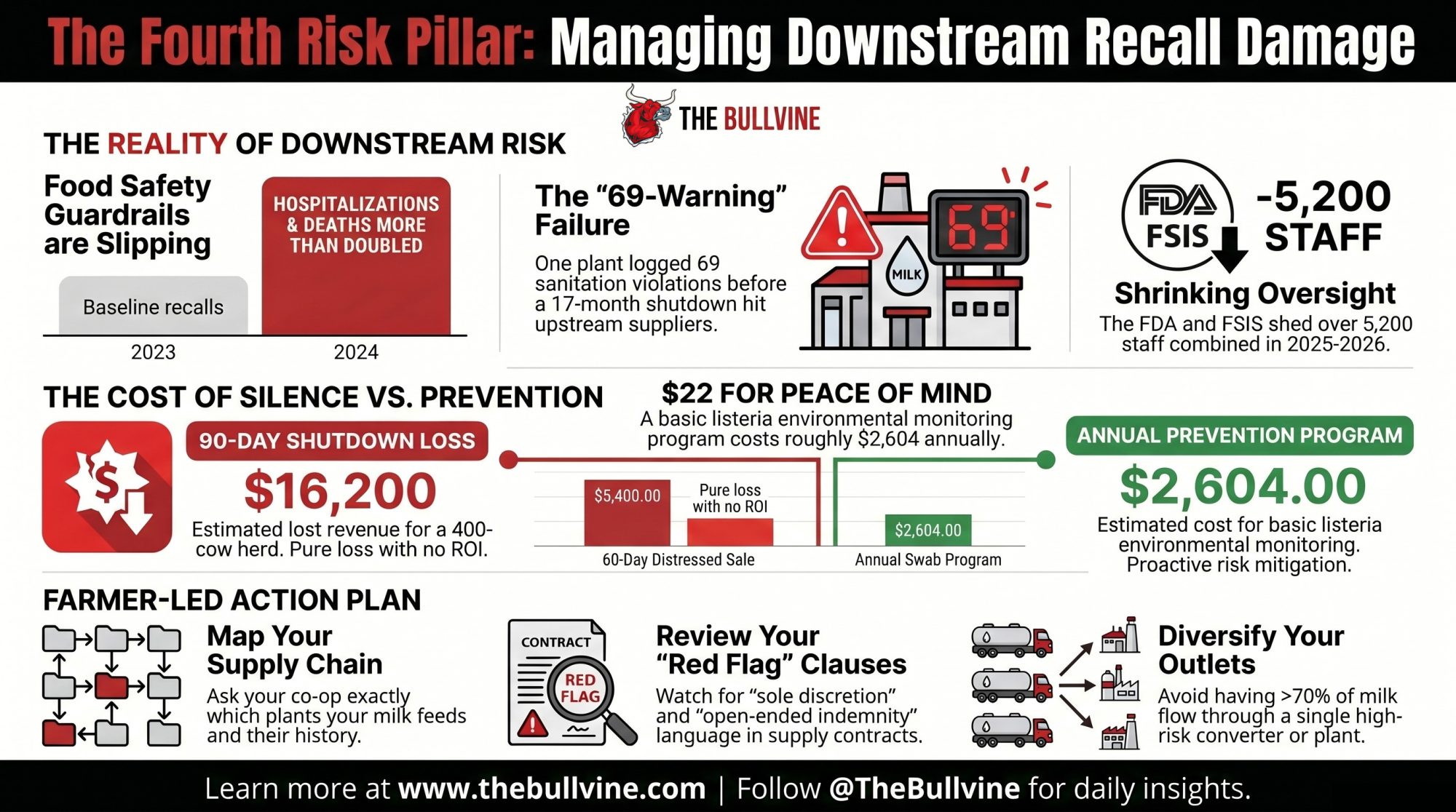

On paper, food safety has never looked more organized: HACCP plans on every wall, third‑party audits, certificates for everything. On the ground, three guardrails are slipping at once.

Recalls are getting more severe, not calmer. In 2024, contaminated food in the U.S. led to 487 hospitalizations and 19 deaths — more than double the 230 hospitalizations and 8 deaths tied to recalls the year before, according to PIRG’s Food for Thought 2025 analysis. Bacteria‑related recalls jumped about 41% year‑over‑year, with Listeria monocytogenes alone driving 65 recalls in 2024, up from 47 in 2023.

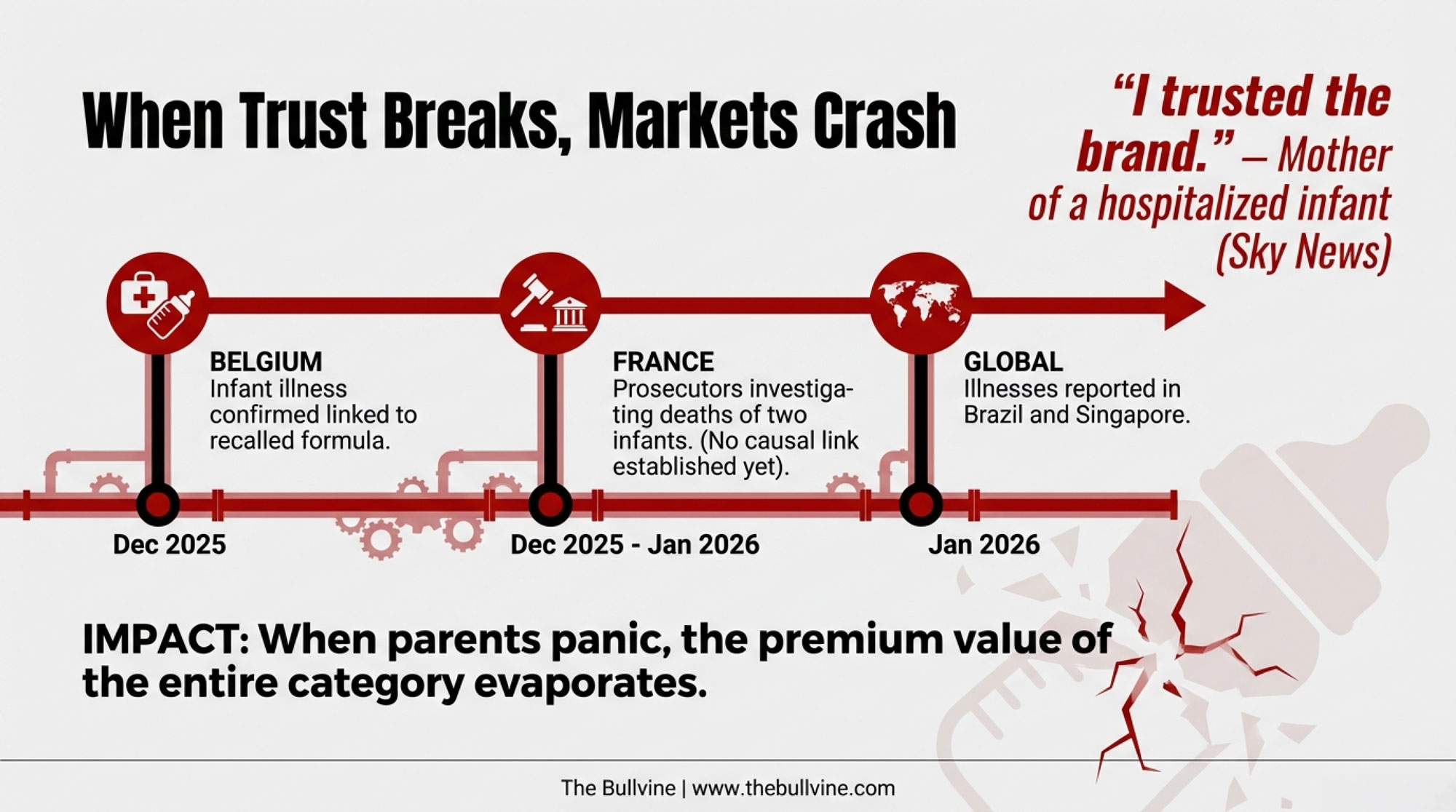

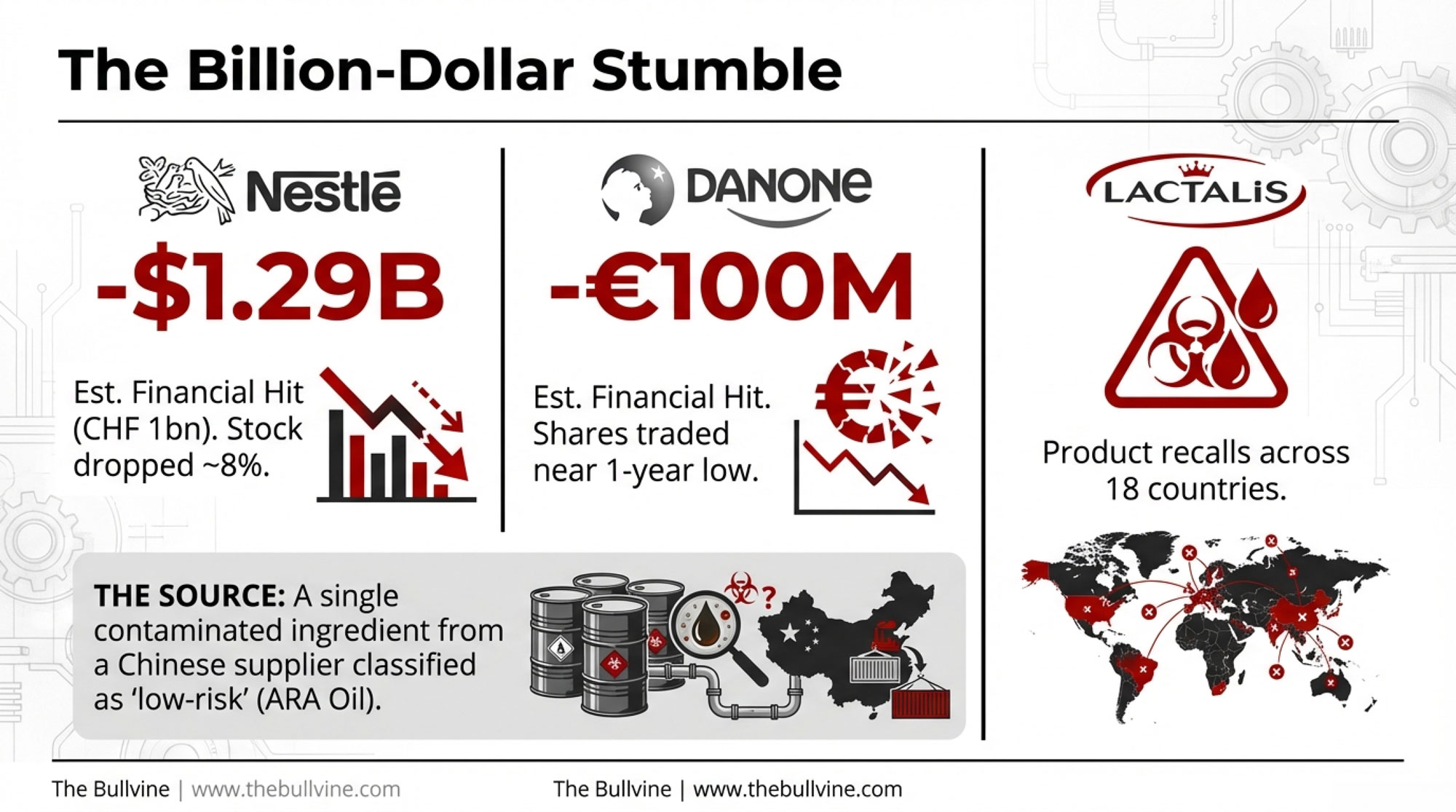

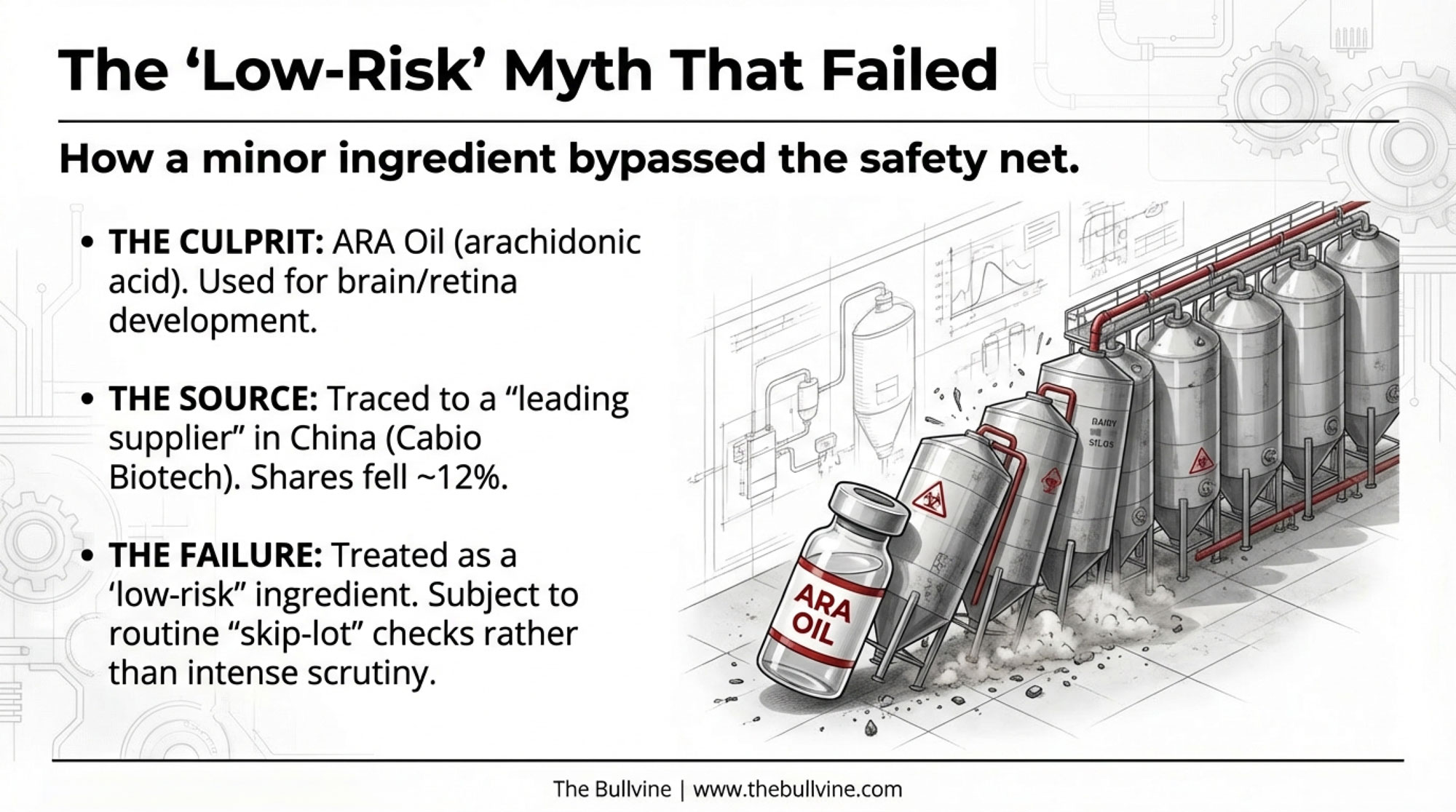

Before you write this off as a deli‑meat story, remember this: Listeria monocytogenes is the great equalizer. It doesn’t care whether the floor drain is in a ham plant in Virginia or a cheese plant in Wisconsin — it thrives in the same damp, cool environments found in deli processing and dairy bottling halls alike. Dairy‑adjacent products were right in the middle of it. Rizo‑López Foods of Modesto, California — a queso fresco and cotija manufacturer — has been linked to 2 deaths and 26 illnesses across multiple states, and now operates under a permanent injunction barring it from manufacturing until it complies with federal regulations.

A separate outbreak tied to frozen supplemental shakes served in medical and long‑term care facilities sickened 42 people across 21 states and killed 14, with illnesses traced back to products manufactured as far back as 2018. Those shakes were made by Prairie Farms Dairy at its Fort Wayne, Indiana facility under Lyons ReadyCare and Sysco Imperial brands. Read that date again. 2018.

The surveillance net that should catch these problems early is fraying. As of mid‑2025, CDC’s FoodNet narrowed its core annual performance targets to Salmonella and Shiga toxin‑producing E. coli, de‑emphasizing the six other pathogens — including Listeria — that used to sit in the same tier. Listeria is still reportable. But it’s no longer a central FoodNet performance benchmark, and the systematic dragnet that used to pull in listeria cases across 10 sites and flag small clusters is now weaker for exactly the bug driving many of the deadliest recalls.

The people doing the watching are stretched thinner. FDA lost 3,859 employees in 2025 and another 473 in early 2026, while FSIS shed 874 employees — roughly 8% of its workforce — in 2025, according to U.S. Office of Personnel Management data summarized by FoodNavigator‑USA. State and local health departments consistently cite limited staff and delayed lab results as major barriers to investigating suspected outbreaks. Fewer people chasing more signals means the subtle ones — low‑level clusters scattered across counties or months — are the first to get missed.

That’s where dairy recall risk management stops being an FDA problem and starts being yours. More recalls, more severe outcomes, less capacity to catch problems before they blow up. Not just a public‑health story. A milk‑cheque story.

How It Shows Up on a 400‑Cow Dairy

If you’re milking 400 cows, shipping clean milk, and passing every antibiotic and PI test, it’s tempting to look at Boar’s Head or Prairie Farms and think, “That’s their mess. We’re fine.”

But money doesn’t move that way.

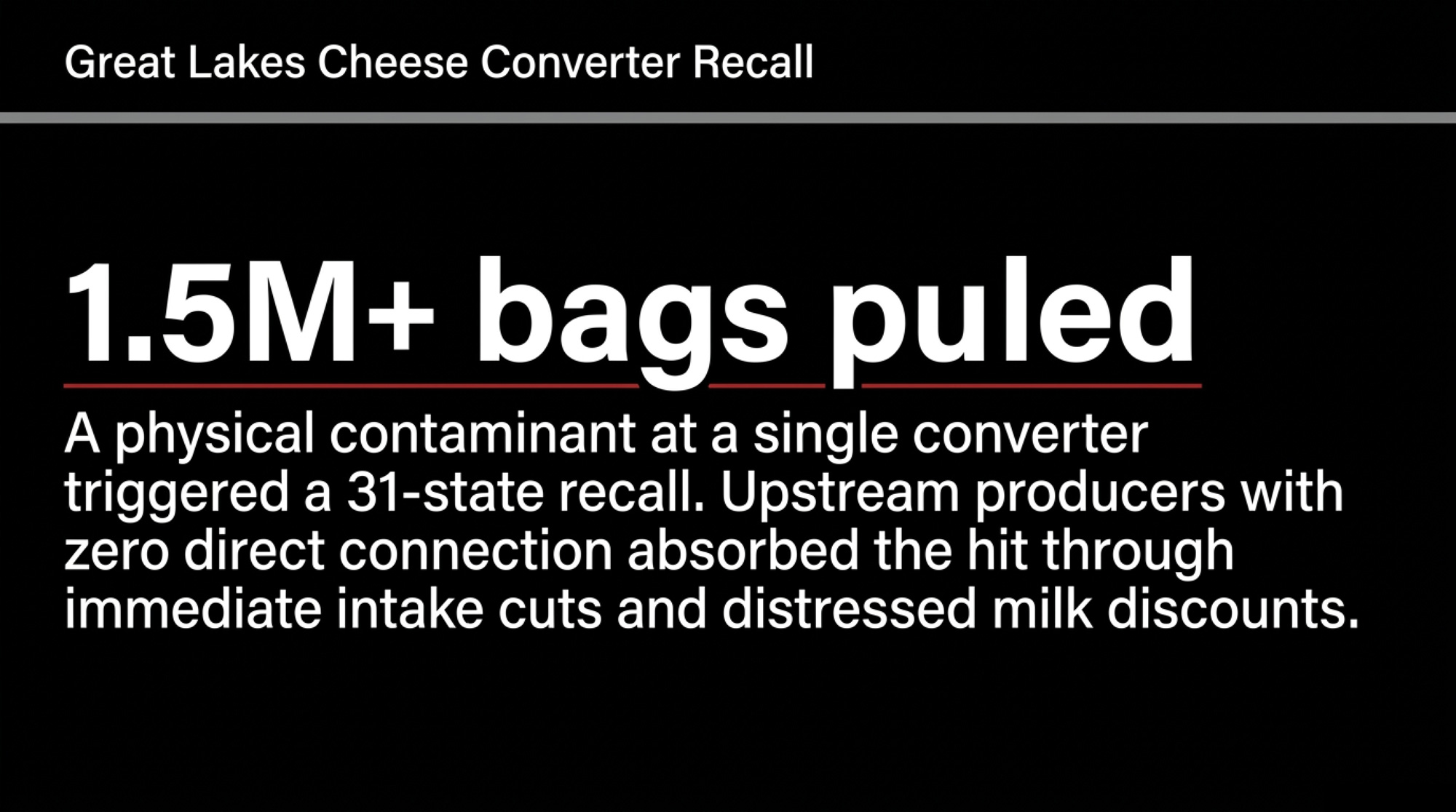

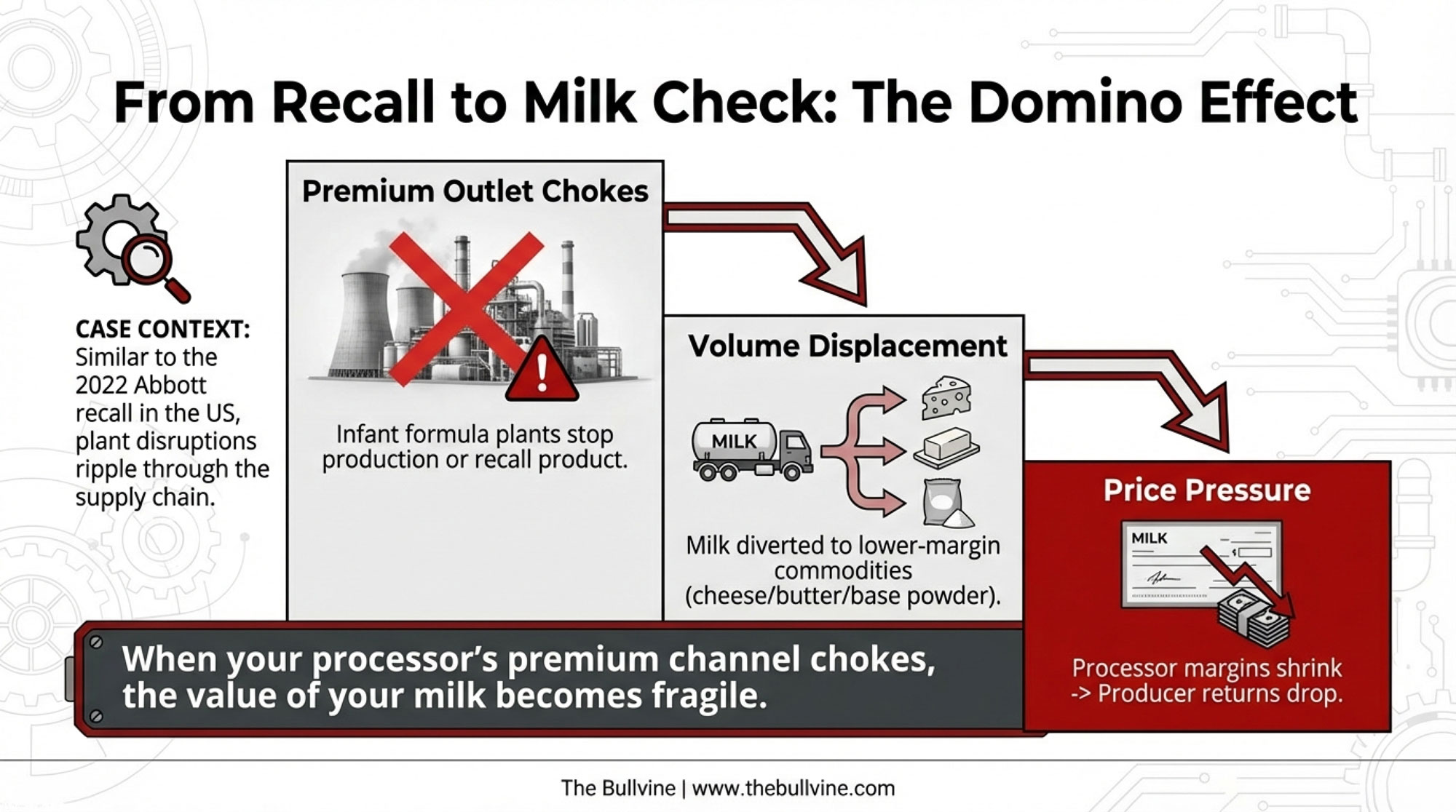

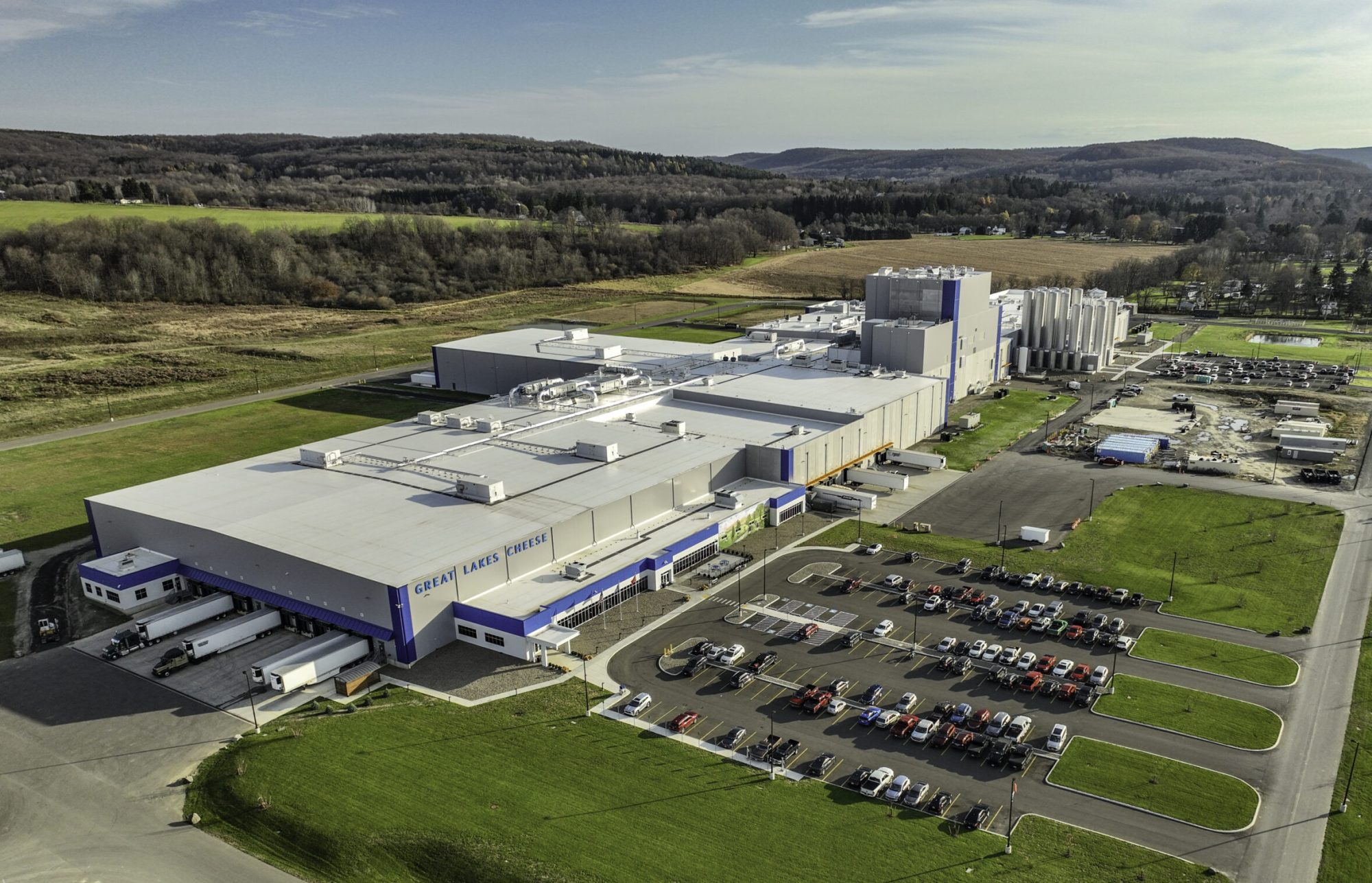

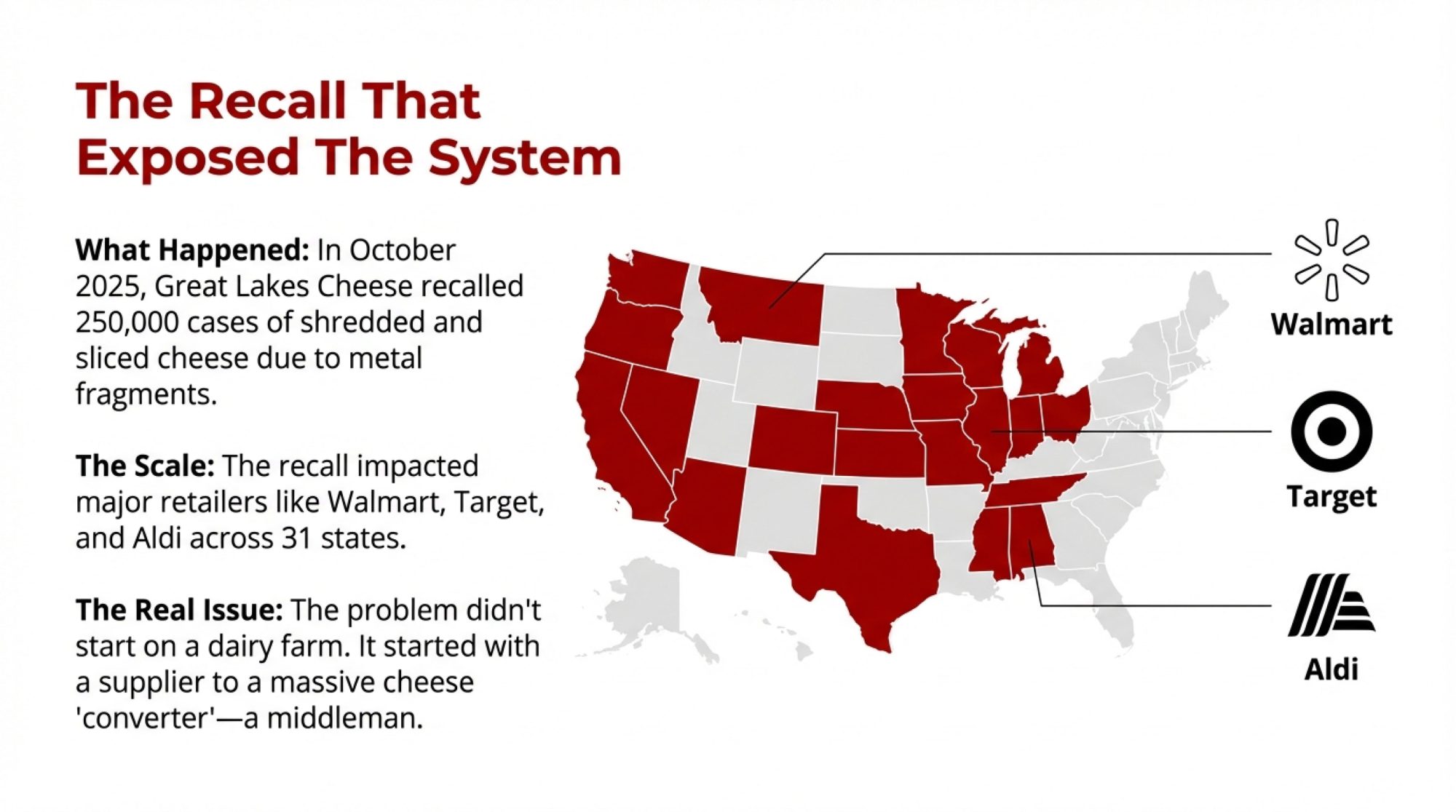

In early October 2025, Great Lakes Cheese initiated a voluntary recall of more than 250,000 cases of shredded and sliced cheese — over 1.5 million bags — sold across 31 states and Puerto Rico under store brands for Walmart, Target, Aldi, Costco, and others after possible metal fragments from a supplier’s raw materials were found in the product. On December 1, 2025, FDA categorized it as a Class II recall, meaning the cheese “may lead to temporary or medically reversible adverse health effects” and the probability of serious consequences is remote. No injuries were reported. Still a massive hit: product write‑offs, recall logistics, lost shelf space, and retailer trust on the line.

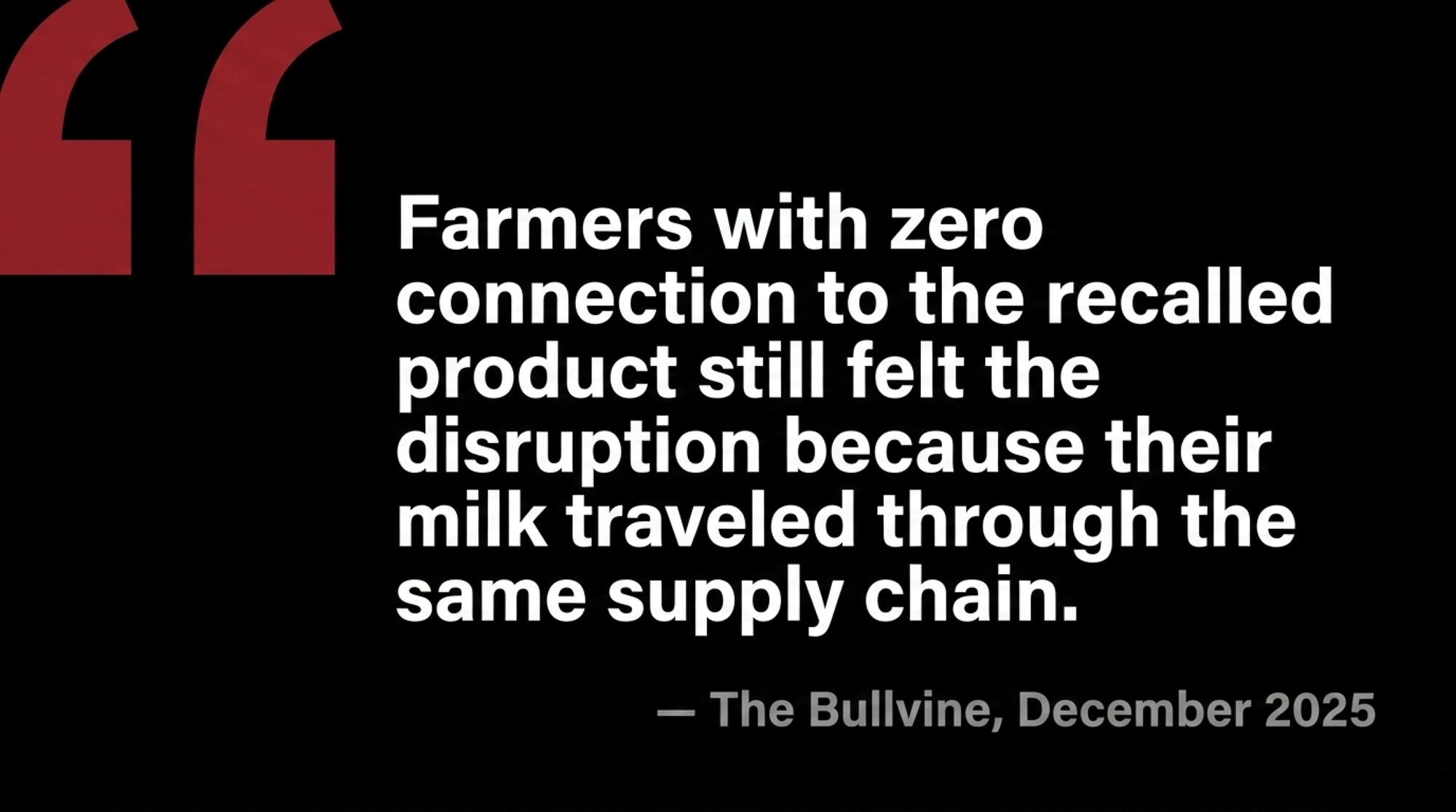

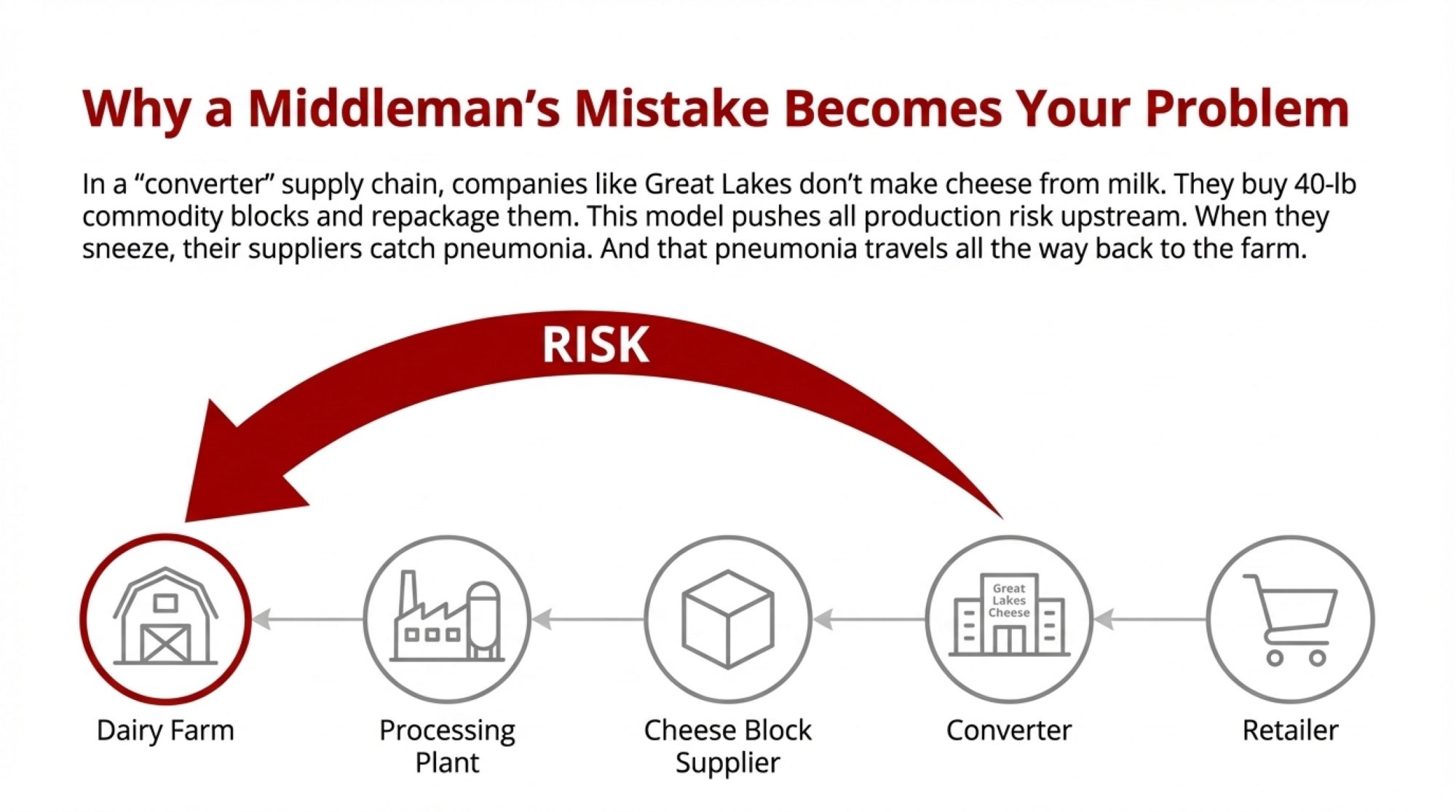

Here’s the part that matters for you. Great Lakes operates primarily as what the industry calls a “converter” — they buy 40‑pound commodity cheese blocks from various suppliers, then shred, slice, and package for retail. When a converter that size pulls back, the ripple moves upstream fast. As The Bullvine reported in December 2025, producers across the Upper Midwest who had no direct relationship with Great Lakes Cheese were already feeling effects — milk intake adjustments, price volatility, and the unsettling realization that something happening several steps down the supply chain was showing up on their bottom line.

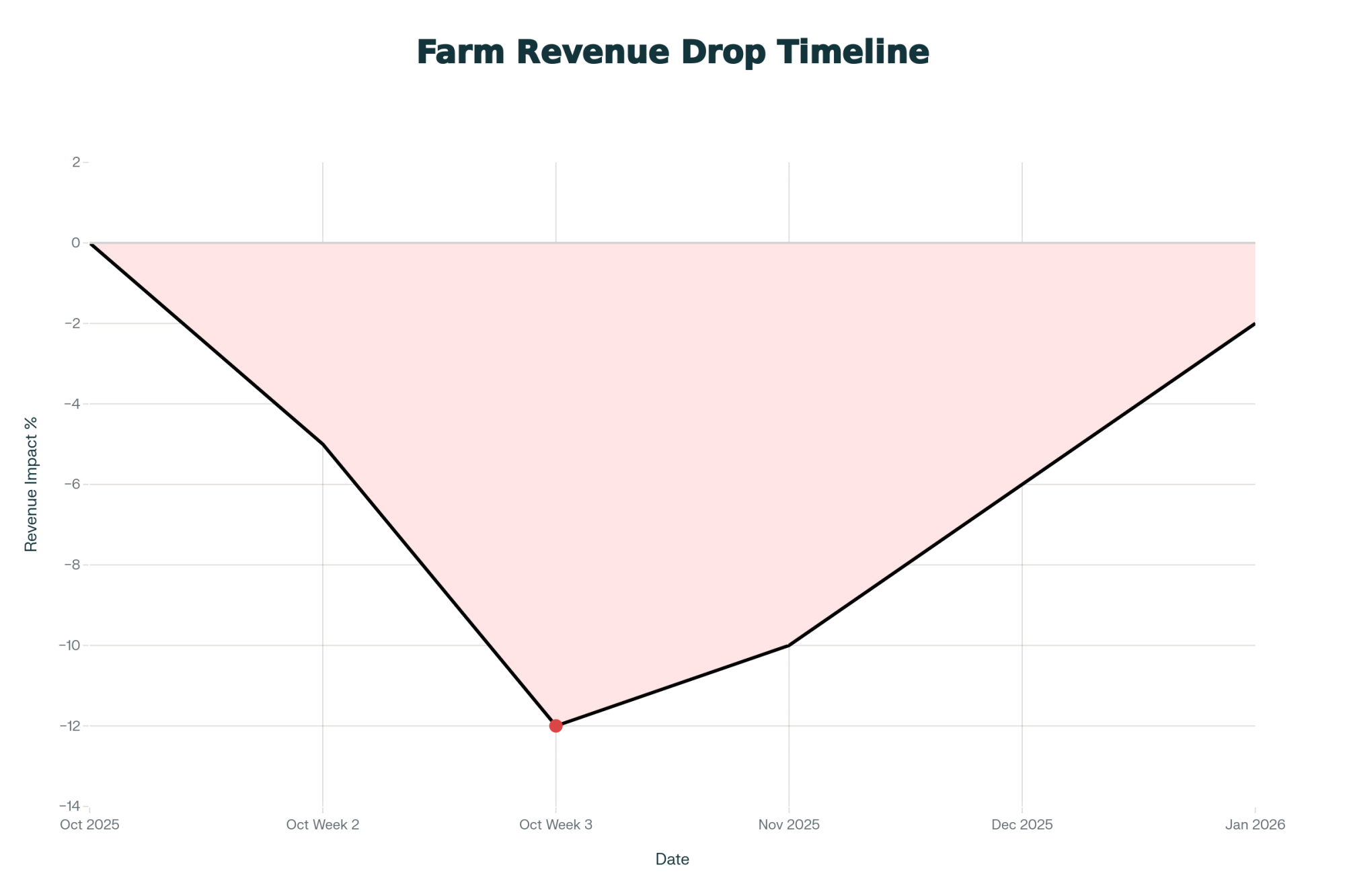

Here’s what that looks like on paper. On a 400‑cow herd averaging 75 lb/day, you’re shipping roughly 300 cwt/day. That 75 lb/day figure is a planning midpoint — adjust up or down for your own rolling herd average. If a downstream recall forces your co‑op to dial you back 10% for 60 days and that 30 cwt/day has to clear into a distressed market at a $3/cwt discount, you’ve just eaten around $5,400 in lost revenue over two months. Nothing to do with your ration, your SCC, or your parlor routine. Something changed in someone else’s plant — the pain still moved upstream.

The Cost of Prevention vs. the Cost of a Recall

| Metric | The “Distressed” Reality (60 Days) | The Prevention Strategy (Annual) |

| Activity | 10% intake cut / distressed sale on a 400‑cow herd | 120 environmental swabs + targeted repairs |

| Daily / Unit Cost | $90.00 / day | $21.70 / swab |

| Total Financial Hit | $5,400.00 | $2,604.00 |

| Business Impact | Pure loss (no ROI) | Risk mitigation / insurance |

Illustrative planning numbers — substitute your own cwt/day and discount.

That’s the mild version — a physical contaminant that didn’t kill anyone. When listeria gets into the mix, like at Jarratt or in those supplemental shakes, the recalls are larger, the shutdowns measured in months instead of weeks, and the retailer reaction harsher. The bigger the shock, the more aggressively cost and risk get pushed back through processors, co‑ops, and finally onto you.

Why the System Fails Upstream Producers

So why does someone else’s listeria problem keep showing up in your pay statement instead of staying where it started? A lot of it comes down to how the rules are written — and what they actually reward.

HACCP is built to reward paperwork first, pathogen control second. Processors write their own hazard analyses and critical control points. Inspectors mostly verify those plans exist and the records are filled out. At Jarratt, USDA’s post‑outbreak review found thermometer calibration records in the plant’s HACCP files didn’t match what devices were actually reading on the floor. On paper, the system looked fine. In the coolers, listeria was quietly doing its job.

Many listeria controls live in sanitation SOPs and environmental monitoring programs rather than as “stop‑the‑line” CCPs that automatically shut down production when a threshold is crossed. If a plant treats listeria as a cleaning nuisance instead of a production‑stop issue, management can understaff cleaning, rush changeovers, and still pass audits because the documentation looks tidy. Jarratt’s reopening under the more stringent USDA Alternative 2 Listeriacontrol program — which adds post‑lethality treatments or increased testing — is itself an admission the plant’s earlier controls weren’t enough.

Talmadge‑Aiken agreements can document problems without forcing plants to stop. Jarratt wasn’t inspected by federal FSIS staff day‑to‑day. It fell under a Talmadge‑Aiken agreement where Virginia state inspectors operated under federal authority.

Layman’s definition: Under Talmadge‑Aiken agreements, state inspectors do the footwork, but they’re technically enforcing federal (USDA) standards. It’s a “partnership” that, as Jarratt proved, can sometimes leave accountability gaps — plenty of paperwork generated, not enough production‑stopping force.

Those inspectors wrote up 69 sanitation noncompliance records between August 2023 and August 2024. Each generated a corrective‑action entry. None triggered the kind of sustained production halt and teardown that might have cleared a persistent listeria problem before those deaths and hospitalizations. Only after the outbreak did USDA promise clearer expectations for oversight, tougher enforcement of federal food‑safety laws, and comprehensive federal training for Talmadge‑Aiken inspectors at that plant — exactly the things most producers assumed were already in place.

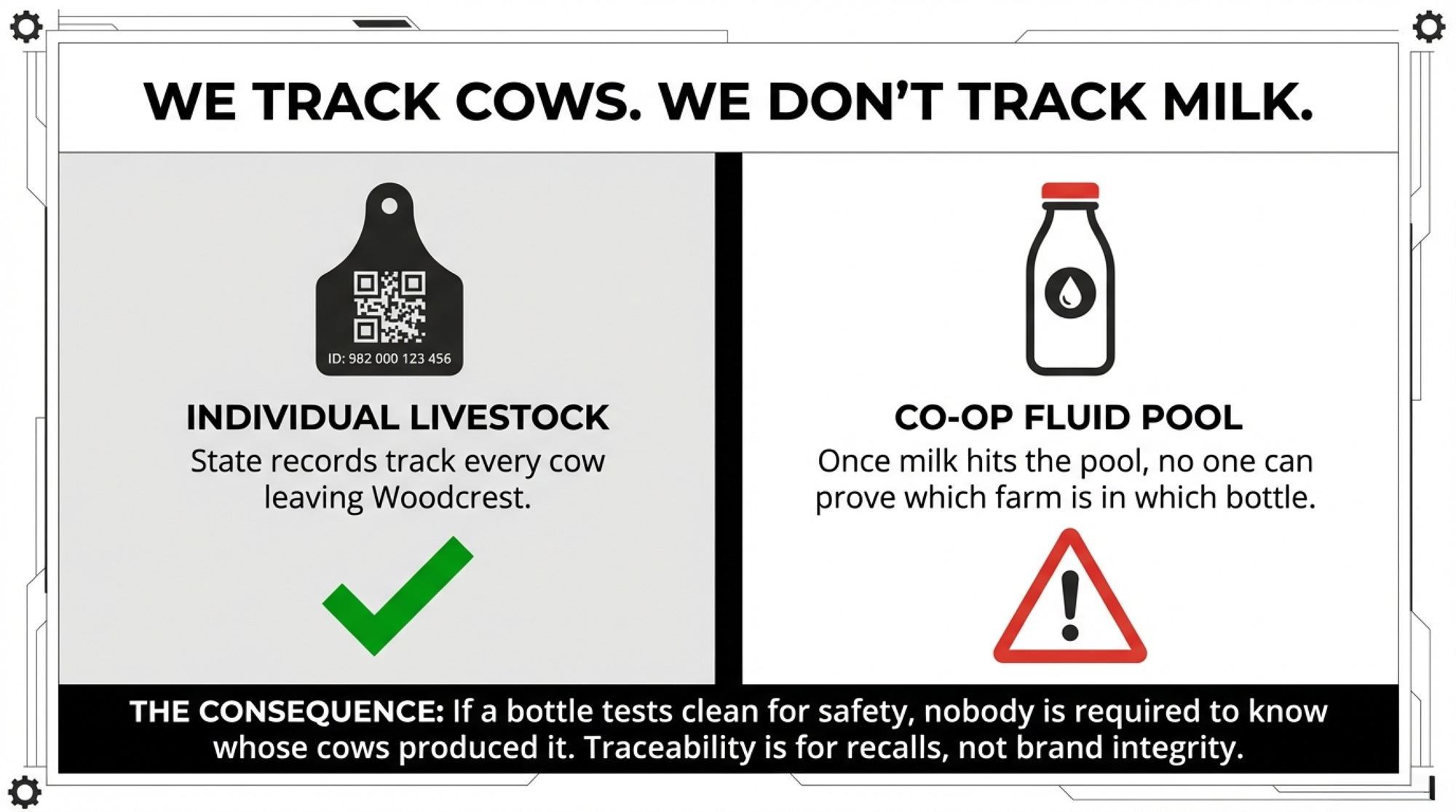

Your co‑op’s job is to move milk and chase price, not audit every converter’s drains. Most co‑ops don’t own the shredders, blenders, and co‑packers where a lot of recall risk actually sits. Their main levers when a customer has a problem are to redirect loads, renegotiate terms, or adjust member intake. They can’t walk into a customer’s plant, rewrite their HACCP plan, or force them to start paying for a real environmental monitoring program. The Great Lakes situation made that dynamic plain: farmers with zero connection to the recalled product still felt the disruption because their milk traveled through the same supply chain.

That’s how 69 ignored warnings at someone else’s plant, or a multi‑year listeria problem in someone else’s product line, quietly turns into intake cuts, lost premiums, and more volatile contracts for you.

What This Rising Dairy Recall Risk Really Means for Your Operation

In practical terms, the biggest food‑safety risk to your business might not be in your bulk tank or your milking routine. It might be the plant your milk flows into, the converter they sell to, and the brand that ends up on the package.

You already manage the risk inside your fence: mastitis, repro, feed costs, weather. You probably use DMC, DRP, or forward contracts to keep milk price swings from wrecking your cash flow. This is a fourth risk pillar sitting alongside those three: downstream plant and contract risk.

It’s uncomfortable because it lives outside your control. But that doesn’t mean you’re powerless. It means you can’t treat “regulation” as a safety net and assume if something were really dangerous, someone would shut it down. Jarratt ran for a year under 69 documented violations. Rizo‑López stayed in business until a permanent injunction followed multiple illnesses and deaths. The Prairie Farms supplemental shake outbreak ran from 2018 case onsets until the FDA closed its investigation in May 2025 with 42 illnesses and 14 deaths on the books.

The system will sometimes leave bad plants running much longer than you’d expect. So you start with the question most of us avoid: how exposed are you if your main plant goes dark?

How Much Could a 90‑Day Plant Shutdown Really Cost You?

Forget Boar’s Head for a second. Picture your own milk truck.

If your primary processor shut down for 90 days — listeria, metal fragments, equipment failure, enforcement action, whatever — what actually happens to your milk? Do you know which plants are your first and second outlets? Could your co‑op redirect your volume within a week? Would you be on full quota, reduced, or dumping? Have you asked?

Take that same 400‑cow herd shipping about 300 cwt/day. If 20% of your volume — 60 cwt/day — suddenly has to move into lower‑value channels at a $3/cwt discount for three months, the math looks like this:

- 60 cwt/day × $3/cwt = $180/day

- $180/day × 90 days = $16,200

Plug your own cwt/day and discount to see where you land. You can argue about whether $3/cwt is the right number for your market. You might think your co‑op could shift you into something better. That’s exactly the point. For a lot of farms, those are guesses — not numbers.

As The Bullvine reported in December 2025, the herds that rode the Great Lakes disruption best weren’t necessarily the biggest or fanciest. They were the ones who’d already mapped their supply chain. They already knew:

- Where their milk actually goes

- What backup outlet exists if a plant shuts

- How long they can ride a disruption before it forces ugly decisions

Everyone else found out mid‑crisis.

Is a $22 Swab Test Really Worth More Than Your Premium Channel?

If you do any on‑farm processing — fresh cheese, bottled milk, ice cream, even a modest cream line — the math on basic listeria environmental monitoring isn’t that scary.

A 2025 Journal of Dairy Science study by Motzer, Trmčić, and colleagues looked at nine small‑ and medium‑sized dairy processors and found total annual environmental monitoring program (EMP) costs ranged from $1,187 to $55,531per plant, depending on size and intensity. The sponge swab and lab fee together ran about $21.50–$21.86 per sample.

Take 10 targeted swabs a month — drains, floor‑wall junctions, under equipment where it’s always damp — and that’s 120 swabs a year. At roughly $21.70 each, you’re in the ballpark of $2,604 a year. That’s not nothing. But stack it against the $5,400 intake‑cut hit from the earlier two‑month example, and the EMP starts looking less like a line item and more like the cheapest insurance policy you’ll buy all year.

Even if you’re only shipping raw milk, the environmental hygiene logic still applies. Listeria monocytogenes loves cold, wet, nutrient‑rich environments. It forms biofilms on stainless steel and in drains that survive standard sanitizers. Research has shown 10‑day‑old listeria biofilms on stainless steel can resist both quaternary ammonium and chlorine — the same products most parlors and plants rely on every day.

You probably don’t need a full lab in your milk house. But you can:

- Fix cracked concrete and low spots where water pools.

- Get rid of dead‑leg piping and places where milk or wash water sits.

- Keep drains in bulk tank rooms and load‑out areas surgically clean.

- Run a few indicator swabs a year through your vet or local lab as a sanity check that your own environment isn’t part of the problem.

Options and Trade‑Offs for Farmers

You don’t get to rewrite HACCP rules or hire back CDC epidemiologists. You do get to decide how much of this downstream risk you carry blind.

Here are four levers you control.

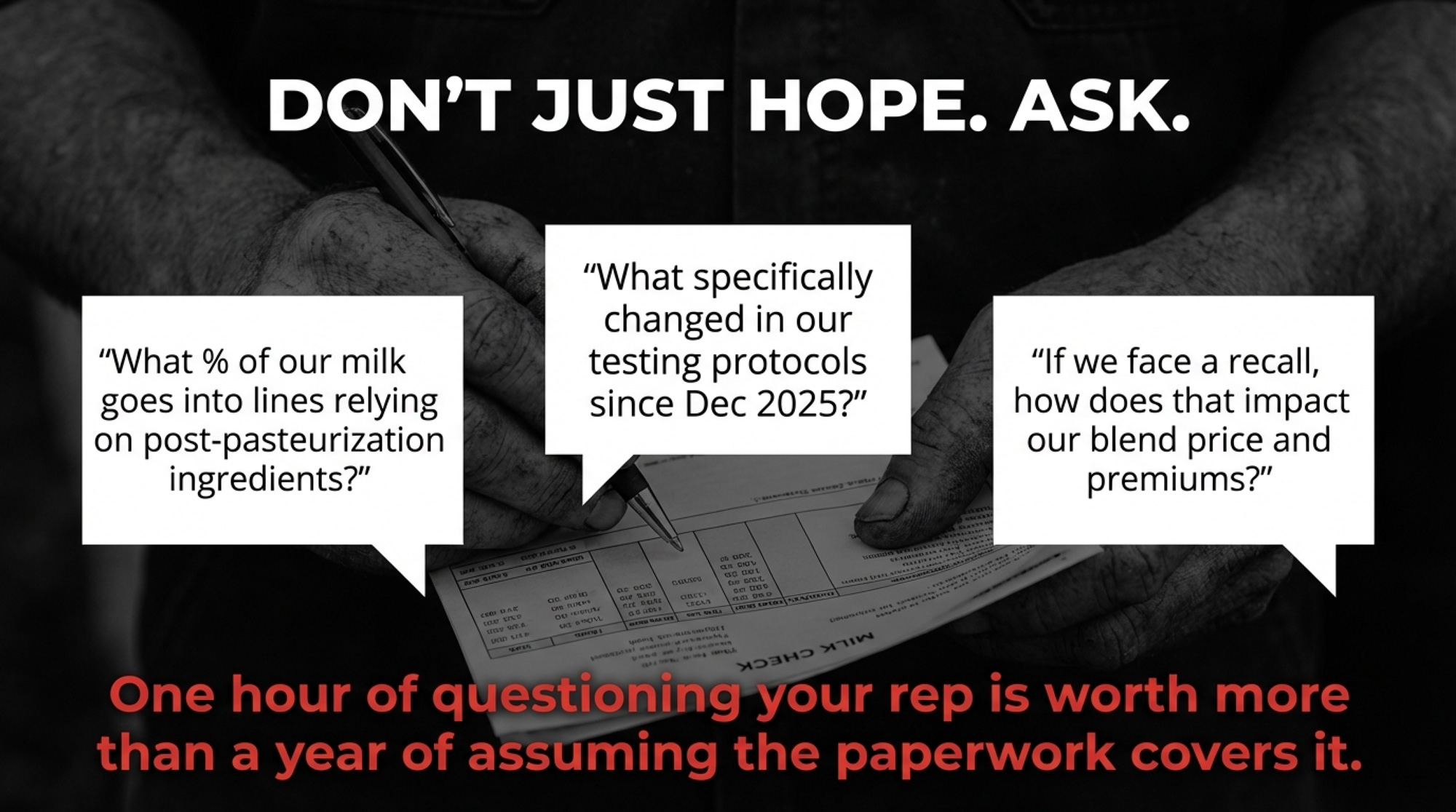

1. Ask where your milk really goes — and do it in the next 30 days.

Within the next month, sit down with your co‑op or buyer and ask three blunt questions:

- Which specific plants does my milk typically go to?

- What products do those plants make — fluid, commodity powder, shredded cheese, RTE meals, infant formula?

- Have those plants or their major customers been involved in recalls or enforcement actions in the last five years?

If the answers are detailed and transparent, that tells you something. If they’re vague or “we don’t really track that,” that tells you something else. As The Bullvine reported in December 2025, the Upper Midwest producers who’d already mapped their supply chain had more room to react than those caught off guard by the Great Lakes ripple.

- When it makes sense: Always — this is the lowest‑cost move you can make.

- What it requires: A phone call and a willingness to listen.

- Risks/limits: You might learn you’re more concentrated than you thought. That’s uncomfortable, but ignorance doesn’t make the risk go away.

2. Don’t put all your volume into one high‑blast‑radius channel.

If 80–100% of your milk is tied to one plant — or flows through a single converter like Great Lakes that feeds dozens of retail brands across 31 states — you’re more exposed than a neighbour whose milk is split across fluid, cheese, and powder.

You might still choose the higher‑risk, higher‑premium outlet. Just treat it like you treat forward contracting: consciously, with eyes open.

- When it makes sense: When you have any say in program enrolment or buyer mix.

- What it requires: Understanding where your milk ends up and being willing to say “no” to all‑in deals that pay a bit more but concentrate your risk.

- Risks/limits: Diversifying outlets can mean giving up some premium today for more resilience tomorrow. Only your balance sheet can answer if that trade works.

3. Read your contracts like they were written for the day after a recall.

If you’re in any kind of direct‑supply or specialty program, pull out your milk supply agreement and look for three phrases:

- “Indemnify and hold harmless” — especially if it covers “any contamination‑related loss,” not just issues you directly control.

- “Sole discretion to adjust volume or price” — particularly for vague triggers like “market disruption” or “customer quality concerns.”

- Fuzzy definitions of “non‑compliance” that could include someone else’s ingredient failure or a downstream recall.

Those phrases don’t automatically make a contract bad. But they do shift more risk onto you when something goes wrong down the line.

- When it makes sense: Any time a contract is renewed or a new premium program is pitched.

- What it requires: A careful read, maybe a conversation with your lender, accountant, or a lawyer who’s seen these clauses before.

- Risks/limits: Pushing back may cost you a premium or a buyer. Accepting them without understanding may cost you much more later.

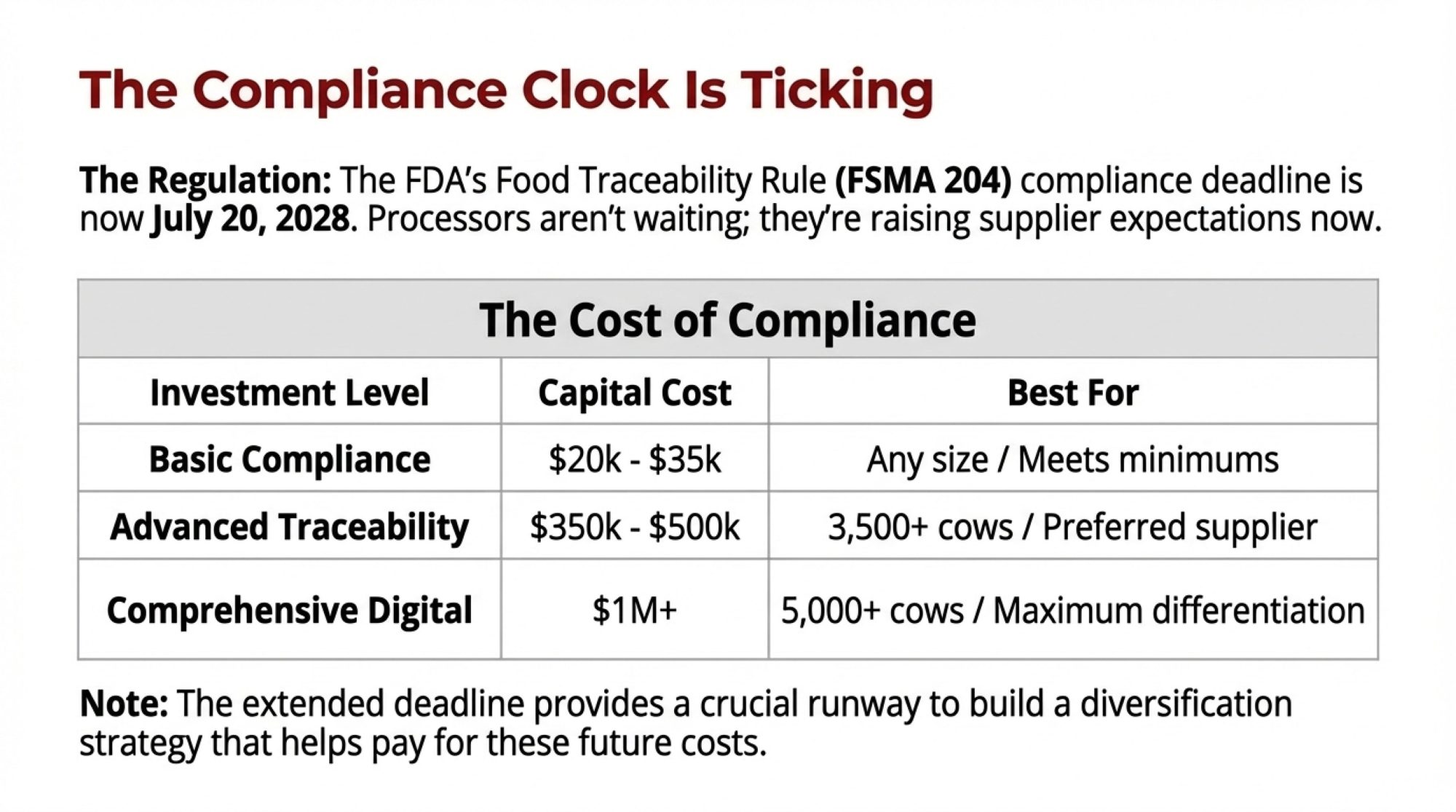

4. Match your own risk controls to your exposure over the next year.

If you run a farmstead creamery or sell direct, a basic listeria EMP — 5–10 swabs a month in the highest‑risk spots — is reasonable at about $2,604 a year. If you only ship raw milk, focus on environmental fixes: eliminate standing water, repair broken surfaces, and make sure the path from bulk tank to tanker is as close to biofilm‑free as you can make it.

Think of this as sliding a dial. The more your milk ends up in high‑risk, high‑value products, the more it makes sense to spend a little to make sure your own environment isn’t the weak link. Boar’s Head just spent seventeen months and serious capital retrofitting Jarratt with the kind of environmental monitoring they should have had all along. A basic version of that same principle costs you $2,604.

- When it makes sense: Over the next 12 months, especially if you’re adding processing or targeting premium RTE channels.

- What it requires: Some cash, time, and honesty about “gross spots” you’ve been ignoring.

- Risks/limits: You might find something you have to fix. That’s the whole point.

Key Takeaways

- If more than about 70% of your milk flows through a single plant or converter, treat that as a red‑line concentration level and run the 90‑day shutdown math on your own numbers before the next recall runs it for you.

- If your co‑op or buyer can’t clearly tell you which plants your milk feeds and what their recall history looks like, assume nobody is actively managing that risk on your behalf — and start asking tougher questions this month.

- If your supply contract includes open‑ended indemnity language and “sole discretion” volume or price cuts after “market disruptions,” flag it for review before you count on that premium holding.

- If a 10–20% intake cut at a $3/cwt discount for 60–90 days would put you in a cash‑flow bind, compare that number to a $2,604 EMP or some concrete and drain repairs — and decide which one is really “too expensive.”

- If your milk ends up in RTE products, fresh cheeses, or supplemental shakes, treat environmental testing around the bulk tank room as part of the cost of being in that market, not an optional extra.

The uncomfortable truth is this: you can run a tight herd, ship clean milk every day, and still get sideswiped because a plant you’ve never walked through treated listeria like a paperwork problem instead of a reason to stop the line.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- Heat Kills Bird Flu: Are You Doing Enough to Protect Your Dairy Operation? — Adopt specific heat treatment parameters and biosecurity protocols revealed by Cornell research to neutralize H5N1 risks. Arms your operation with precise temperature/time targets that protect workers, calves, and bulk tank integrity during active outbreaks.

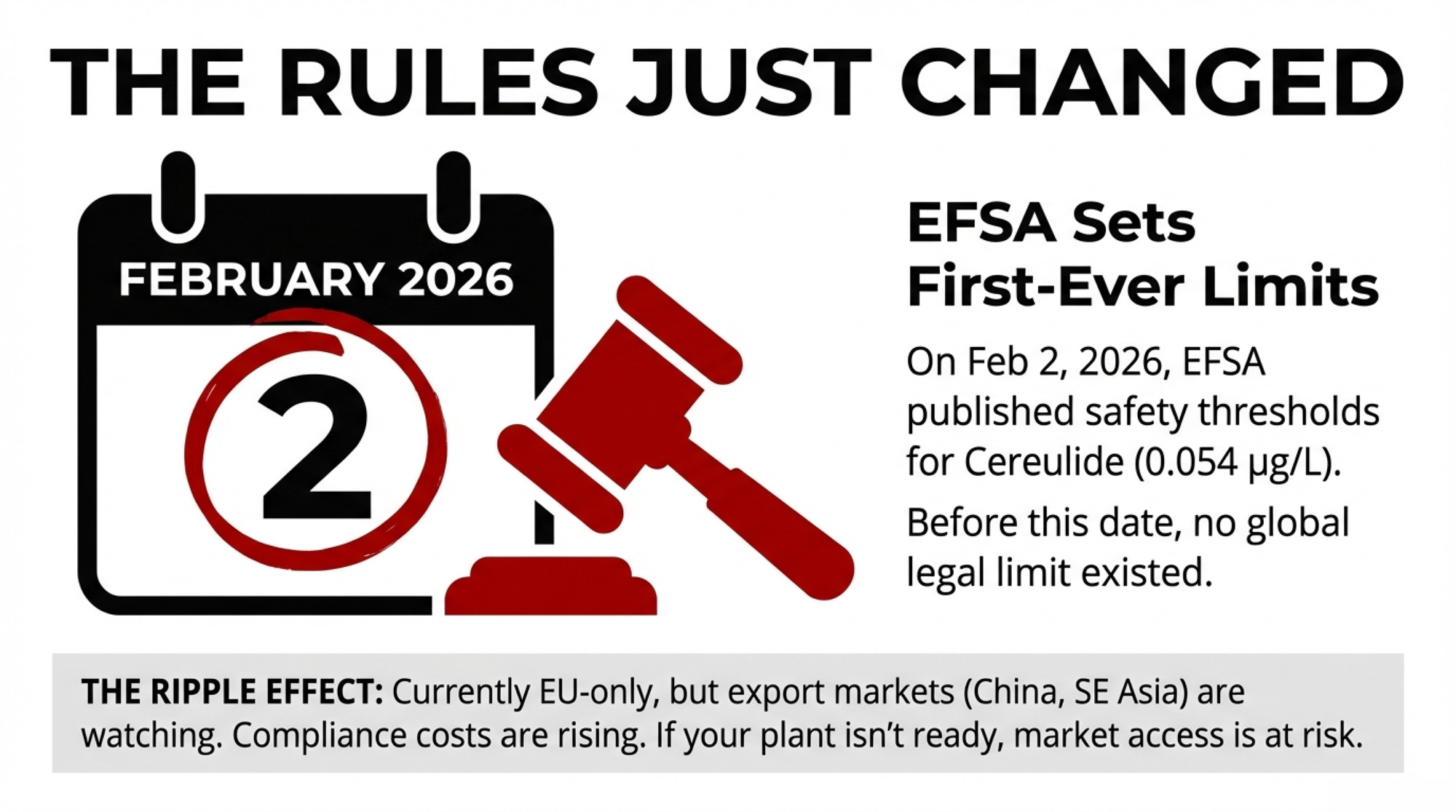

- The $125‑Million Recall Precedent: How the 2025 Formula Crisis Exposes Dairy’s Contract and Milk Cheque Risk — Reevaluate your milk marketing agreements as global buyers shift risk classification for post-pasteurization ingredients. Exposes the $125-million financial ripple effect of ingredient failures and why your current contracts may leave your margin unprotected.

- The Digital Dairy Revolution: How IoT and Analytics Are Transforming Farms in 2025 — Secure your bulk tank integrity using in-line sensors that detect quality shifts before they impact your cheque. Demonstrates how new sensor platforms turn passive monitoring into proactive mitigation, shielding your eligibility for high-value premium markets.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

![Generate SEO elements for this The Bullvine article targeting dairy industry professionals:

ANALYSIS REQUIREMENTS:

Identify the article's primary topic and target audience (dairy farmers, industry professionals, agricultural specialists)

Focus on practical, implementation-oriented keywords that dairy professionals would search for

Consider both technical dairy terminology and business/profitability terms

DELIVERABLES:

1. SEO Keywords (5 keywords):

Create a comma-separated list of relevant keywords mixing:

Primary dairy industry terms (dairy farming, milk production, herd management, etc.)

Technology/innovation terms if applicable (precision agriculture, automated milking, genomic testing, etc.)

Business/economic terms (dairy profitability, farm efficiency, ROI, cost reduction, etc.)

Geographic terms if relevant (dairy industry trends, global dairy, etc.)

2. Focus Keyphrase:

Develop a 2-4 word primary keyphrase that captures the article's core topic and would be commonly searched by dairy professionals seeking this information.

3. Meta Description (under 160 characters):

Write a compelling meta description that:

Summarizes the article's main value proposition

Naturally incorporates the focus keyphrase and 1-2 keywords

Appeals to dairy industry professionals

Includes a benefit or outcome (cost savings, efficiency gains, profit increases, etc.)

Uses action-oriented language that encourages clicks

4. Category Recommendation:

Suggest the most fitting category from The Bullvine website (e.g., Dairy Industry, Genetics, Management, Technology, A.I. Industry, Dairy Markets, Nutrition, Robotic Milking, etc.) where this article should be published for maximum relevance and engagement.

FORMAT REQUIREMENTS: Present results in this exact format:

SEO Keywords: [keyword1, keyword2, keyword3, keyword4, keyword5]

Focus Keyphrase: [primary keyphrase]

Meta Description: [compelling description under 160 characters with natural keyword integration]

Category Recommendation: [Best-fit category from The Bullvine’s options]

DAIRY INDUSTRY CONTEXT: Ensure all elements appeal to dairy farmers, agricultural specialists, and industry professionals seeking practical, profitable solutions for their operations.](https://www.thebullvine.com/wp-content/uploads/2025/09/Google_AI_Studio_2025-09-08T17_37_41.620Z.png)

USDA Proposes Return to ‘Higher-Of’ Method for Fluid Milk Pricing: What It Means for Dairy Farmers

Learn how USDA’s plan to bring back the ‘higher-of’ method for milk pricing might affect farmers. Will this change help dairy producers? Find out more.

The USDA plans to bring back the ‘higher-of’ pricing method for fluid milk, a move intended to modernize federal dairy policy based on a comprehensive 49-day hearing that evaluated numerous industry proposals. This method picks the higher price between Class III (cheese) and Class IV (butter and powder) milk, which could signify a notable shift for the dairy industry. Previously, the 2018 Farm Bill had replaced the ‘higher-of’ system with an ‘average-of’ pricing formula, averaging Class III and IV prices with an additional 74 cents. While switching back might benefit farmers, it also introduces risks like negative producer price differentials in 2020 and 2021. The USDA’s proposal seeks to mitigate these challenges and provide farmers financial gains amidst modern dairy economics’ complexities.

Understanding the Federal Milk Marketing Order (FMMO) System

The Federal Milk Marketing Order (FMMO) system, established in 1937, plays a crucial role in ensuring fair and competitive dairy pricing. It mandates minimum milk prices based on end use, providing price stability for dairy farmers and processors across the U.S. Each FMMO represents a distinct marketing area, coordinating pricing and sales practices.

The ‘higher-of’ pricing method for Class I (fluid) milk has long been integral to this system. It sets the Class I price using the higher Class III (cheese) or Class IV (butter and powder) price, offering a financial safeguard against market volatility. This method ensures dairy producers receive a fair price despite market fluctuations.

However, the 2018 Farm Bill introduced an ‘average-of’ formula, using the average of Class III and IV prices plus 74 cents. While aimed at modernizing milk pricing, this change exposed farmers to greater risk and reduced earnings in volatile periods like 2020 and 2021.

A Marathon Analysis: Unraveling Modern Dairy Policy over 49 Days in Indiana

The marathon hearing in Indiana highlighted the complexities of modern dairy policy. Spanning 49 days, from Aug. 23, 2023, to Jan. 30, it reviewed nearly two dozen industry proposals. This intensive process reflected the sophisticated and multifaceted Federal Milk Marketing Order system as stakeholders debated diverse views and intricate data to influence future milk pricing.

Decoding Dairy Dilemmas: The “Higher-Of” vs. “Average-Of” Pricing Methods

The “higher-of” and “average-of” pricing methods are central to understanding their impact on farmers’ incomes. The “higher-of” process, which uses the greater of the Class III (cheese) price or Class IV (butter and powder) price, has historically provided a safety net against dairy market fluctuations. This method ensured farmers got a better price, potentially safeguarding their income during volatile times. Yet, it increased the risk of negative producer price differentials, which reduced earnings in 2020 and 2021.

On the other hand, the “average-of” method, introduced by the 2018 Farm Bill, calculates the price as the average of Class III and IV prices plus 74 cents. While this seems balanced and predictable, it often fails to deliver the highest financial return when either Class III or IV prices exceed expectations. Farmers have noted that this method might not reflect their costs and economic challenges in volatile markets.

The “higher-of” method often offers better financial outcomes during favorable market conditions but brings increased uncertainty during unstable periods. Conversely, the “average-of” method offers stability but may miss optimal pricing opportunities. This debate within the dairy industry over the best formula to support farmers’ livelihoods continues. Thus, the USDA’s proposal to revert to the “higher-of” method invites mixed feelings among farmers, whose earnings and economic stability are closely tied to these pricing mechanisms.

Examining the Potential Implications of the USDA’s Return to the ‘Higher-Of’ Pricing Method

The USDA’s return to the ‘higher-of’ pricing method, while potentially beneficial, also presents some challenges that the industry needs to be aware of. This approach, favoring the higher Class III (cheese) or Class IV (butter and powder) prices, seems more beneficial than the ‘average-of’ formula. However, deeper insights indicate potential challenges that need to be carefully considered.

The ‘higher-of’ method usually leads to higher fluid milk prices but poses the risk of negative producer price differentials (PPDs). When the Class I price far exceeds the average of the underlying class prices, PPDs can become negative, as seen during the harsh economic times of 2020 and 2021, exacerbated by the COVID-19 pandemic.

Negative PPDs can hit farmers’ financial stability, making it harder to predict income and manage cash flows. This reflects the delicate balance between gaining higher milk prices now and ensuring long-term financial reliability.

The 24-month rolling adjuster for extended-shelf-life milk introduces further uncertainty. Its effect on milk pricing needs to be clarified, potentially causing fluctuating incomes for farmers in this segment.

In conclusion, while the ‘higher-of’ pricing method may offer immediate benefits, risks like negative PPDs and uncertain impacts on extended-shelf-life milk pricing demand careful consideration. Farmers must balance these factors with their financial strategies and long-term sustainability plans.

New Horizons for ESL Milk: Navigating the 24-Month Rolling Adjuster Amidst Market Uncertainties

Under the USDA’s new proposal, regular fluid milk will revert to the ‘higher-of’ pricing. In contrast, extended-shelf-life (ESL) milk will follow a different path. The plan introduces a 24-month rolling adjuster for ESL milk to stabilize prices for these longer-lasting products.

Yet, this change brings uncertainties. Laurie Fischer, CEO of the American Dairy Coalition, questions the impact on farmers. The 24-month adjuster is untested, making it difficult to foresee its effects amid fluctuating market conditions. ESL milk’s unique production and logistics further complicate predictions.

Critics warn that the lack of historical data makes it hard to judge whether this method will help or hurt farmers. There’s concern that it could create more price disparity between regular and ESL milk, potentially straining producers reliant on ESL products. While USDA aims to tailor pricing better, its success will hinge on adapting to real-world market dynamics.

Make Allowance Controversy: Balancing Processor Profitability and Farmer Finances

The USDA also plans to increase the make allowance, a credit to dairy processors to cover rising manufacturing costs. This adjustment aims to ensure processors are adequately compensated to sustain profitability and operational efficiency, which is expected to benefit the entire dairy supply chain.

However, this proposal has drawn substantial criticism. Laurie Fischer, CEO of the American Dairy Coalition, argues that the increased make allowance effectively reduces farmers’ milk checks, disadvantaging them financially.

Pivotal Adjustments and Economic Realignment in Dairy Pricing Formulas

The USDA’s proposal adjusts pricing formulas to match advancements in milk component production since 2000. This update ensures that farmers receive fair compensation for their contributions.

The proposal also revises Class I differential values for all counties to reflect current economic realities. This is essential for maintaining fair compensation for the higher costs of serving the fluid milk market. By reevaluating these differentials, the USDA aims to align the Federal Milk Marketing Order system with today’s economic landscape.

Recalibrating Cheese Pricing: Transition to 40-pound Cheddar Blocks Only

Another critical change in USDA’s proposal is the shift in the cheese pricing system. Monthly average cheese prices will now be based solely on 40-pound cheddar blocks instead of including 500-pound cheddar barrels. This aims to streamline the process and more accurately reflect market values, impacting various stakeholders in the dairy industry.

Initial Reactions from Industry Leaders: Balancing Optimism with Key Concerns

Initial reactions from crucial industry organizations reveal a mix of cautious optimism and significant concerns. The National Milk Producers Federation (NMPF) showed preliminary approval, noting that USDA’s proposal incorporates many of their requested changes. On the other hand, Laurie Fischer, CEO of the American Dairy Coalition, raised concerns about the make allowance updates and the impact of extended-shelf-life milk pricing, fearing it might hurt farmers’ earnings.

Structured Engagement: Navigating the 60-Day Comment Period and Ensuing Voting Procedure

To advance its proposal, USDA will open a 60-day public comment period, allowing stakeholders and the public to share insights, concerns, and support. This process ensures that diverse voices within the dairy industry are heard and considered. Once the comment period ends, USDA will review the feedback to gain a comprehensive understanding of industry perspectives, informing the finalization of the proposal.

Afterward, the USDA will decide based on the collected data and input. However, the process continues with a voting procedure where farmers pooled under each Federal Milk Marketing Order (FMMO) cast votes to approve or reject the proposed amendments. Each Federal Order, representing different regions, will vote individually.

This voting process is crucial, as it directly determines the outcome of the proposed changes. For adoption, a two-thirds majority approval within each Federal Order is required. Suppose a Federal Order fails to meet this threshold. In that case, USDA may terminate the order, leading to significant changes in how milk pricing is managed in that region. This democratic approach ensures that the final policies reflect majority support within the dairy farming community, aiming for fair and sustainable outcomes.

Regional Impacts: Navigating the Complex Landscape of FMMO System Changes

The proposed changes to the Federal Milk Marketing Order (FMMO) system are bound to impact various regions differently, given each Federal Order’s unique economic landscape. Federal Order 1, covering most New England, eastern New York, New Jersey, Delaware, southeastern Pennsylvania, and most of Maryland, may benefit from more favorable fluid milk pricing due to the higher-of method. With significant urban markets, this region could see advantages from updated Class I differential values addressing the increased costs of serving these areas.

On the other hand, Federal Order 33—encompassing western Pennsylvania, Ohio, Michigan, and Indiana—might witness mixed outcomes. This area has substantial dairy manufacturing, especially in cheese and butter production, which could gain from the new cheese pricing method focusing on 40-pound cheddar blocks. However, the higher make allowance might stir controversy, potentially cutting farmers’ earnings despite adjustments for rising manufacturing costs.

The future remains uncertain for western New York and most of Pennsylvania’s mountain counties, which any Federal Order does not cover. These areas could feel indirect effects from the new proposals, particularly the revised pricing formulas and allowances, which could impact local milk processing and producer price differentials.

While the higher-of-pricing method may benefit farmers by securing better fluid milk prices, the regional impacts will hinge on each Federal Order’s specific economic activities and market structures. Stakeholders must examine the proposed changes closely to gauge their potential benefits and drawbacks.

The Bottom Line

The USDA’s push to reinstate the ‘higher-of’ pricing method for fluid milk marks a decisive moment for the dairy industry. The 49-day hearing in Indiana underscored the complexity of the Federal Milk Marketing Order (FMMO) System. Key aspects include reverting to the ‘higher-of’ pricing from the 2018 ‘average-of’ formula, new pricing for extended-shelf-life milk, and the debate over increased make allowances. Significant updates to pricing formulas and cheese pricing methodologies were also discussed.

The forthcoming vote on these changes is critical. With the power to reshape financial outcomes for dairy farmers and processors, each Federal Order needs two-thirds approval to implement these changes. Balancing modern dairy policy advancements with fair profits for all stakeholders is at the heart of this discourse.

Ultimately, these decisions will affect dairy practices’ economic landscape and sustainability nationwide. This vote is a pivotal moment in the evolution of the American dairy industry, demanding informed participation from all involved.

Key Takeaways:

Summary:

The USDA plans to reintroduce the ‘higher-of’ pricing method for fluid milk, a move aimed at modernizing federal dairy policy. This method, which selects the higher price between Class III and Class IV milk, could be a significant shift for the dairy industry. The 2018 Farm Bill replaced the ‘higher-of’ system with an ‘average-of’ formula, averaging Class III and IV prices plus an additional 74 cents. This change could benefit farmers but also introduce risks like negative producer price differentials (PPDs). The Federal Milk Marketing Order (FMMO) system ensures fair and competitive dairy pricing, and the ‘higher-of’ method usually leads to higher fluid milk prices but also poses the risk of negative producer price differentials (PPDs). Negative PPDs can impact farmers’ financial stability, making it harder to predict income and manage cash flows. The 24-month rolling adjuster for extended-shelf-life milk introduces further uncertainty, potentially causing fluctuating incomes for farmers. The USDA’s proposal to increase the make allowance, a credit to dairy processors, has been met with criticism from industry leaders. The USDA will open a 60-day public comment period to advance its proposal. The proposed changes to the FMMO system will impact various regions differently due to each Federal Order’s unique economic landscape.

Learn more: