When the same logo sits on your genomic test, your wellness index, and now the lab behind a big slice of the industry’s DNA cards, the number that matters isn’t just $160 million — it’s the $86,000 you quietly push through that pipeline over five years.

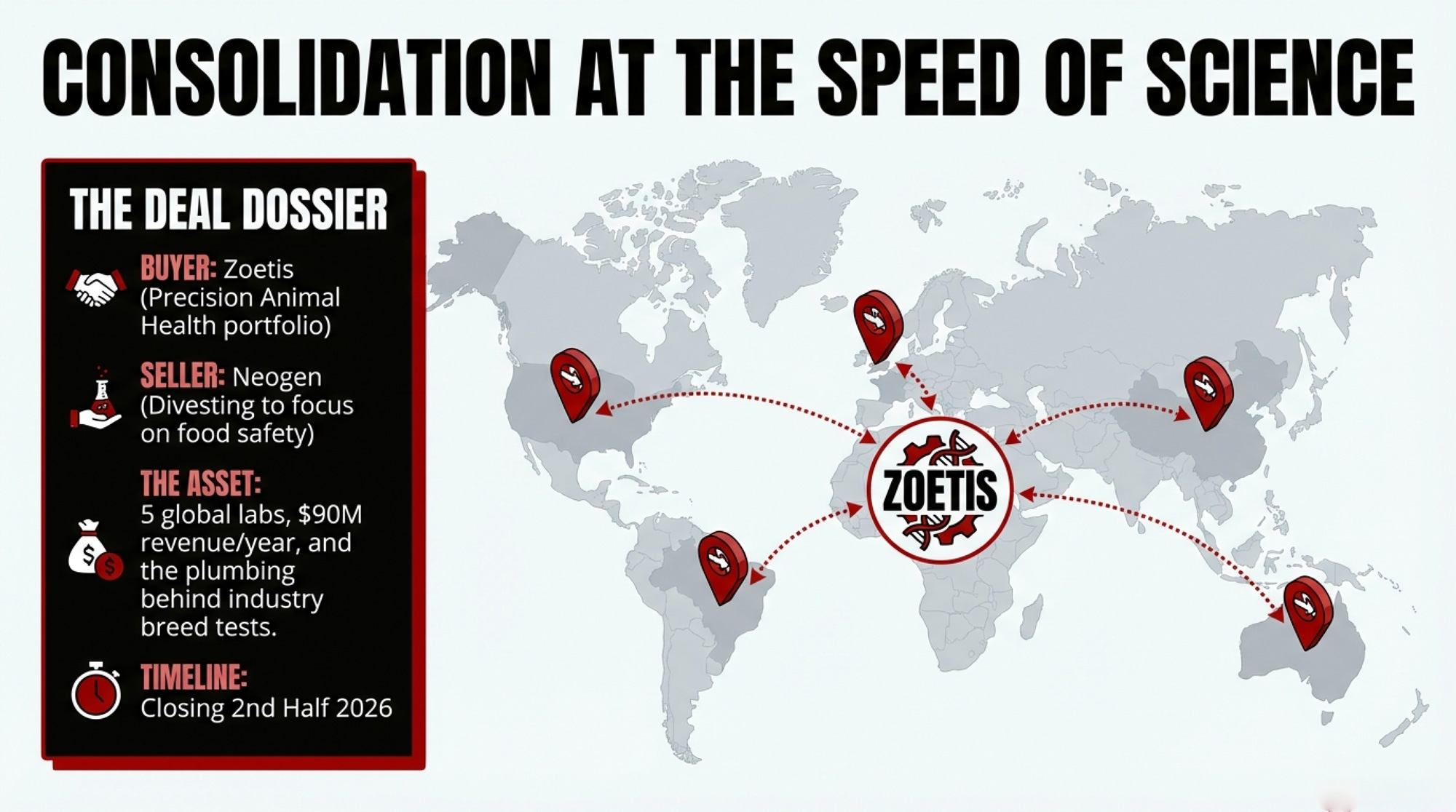

Executive Summary: Zoetis’ just-announced $160 million purchase of Neogen’s animal genomics business is a bet on owning the global DNA pipeline, not just another test brand. Neogen’s unit brings in $90 million in genomics revenue, operates five labs across the U.S., Brazil, Australia, China, and the U.K., and serves customers in 120+ countries, dropping a ready‑made lab network into Zoetis’ Precision Animal Health machine. For a 750‑cow Holstein herd using CLARIFIDE Plus at roughly $43/head, that means around $17,200 a year — about $86,000 over five years — flowing through one company’s genomic loop that now influences breeding, wellness traits, and health protocols. The article shows how that integration can genuinely help (sharper predictions, smoother software, simpler decisions) while also raising switching costs and shifting leverage away from herds, breed associations, and AI programs toward a handful of platforms. It then gives a concrete 30/90/365‑day playbook: audit genomics contracts for data ownership and use, secure export rights, pilot a non‑Zoetis lab as Plan B, and stop letting any single index be the only lens on your genetics and health risk. The core message: you can stay in the Zoetis ecosystem, but before this deal closes in the second half of 2026, you need to decide — and document — who owns your genotypes, how portable they are, and how hard it would really be to change course later.

On March 2, 2026, Zoetis announced it would pay 0 million to acquire Neogen’s animal genomics business, including its GeneSeek laboratories and livestock/companion animal genomics portfolio. Neogen says the net proceeds will primarily go toward debt reduction and a tighter focus on its food safety and animal safety markets, and both companies expect the deal to close in the second half of calendar year 2026, subject to regulatory approvals.

If you’re running 300–1,500 cows or sit on a breed association genetics committee, this isn’t abstract M&A. It means the lab work that used to sit quietly in the background — where your DNA cards went before proofs came back — is on track to sit under the same corporate roof as CLARIFIDE Plus, DWP$, vaccines, mastitis tubes, and digital herd‑software integrations.

The real question for 2026 is blunt: How much control over your genomics and data are you handing to one company — and on what terms — when this closes?

What $160 Million Actually Buys — and What It Doesn’t

Here’s what’s actually changing.

- Buyer: Zoetis Inc. (NYSE: ZTS), “the world’s leading animal health company,” positioning the deal as strengthening its Precision Animal Health portfolio. Jamie Brannan, Zoetis’ Chief Commercial Officer, says the acquisition “brings complementary capabilities that expand predictive insights and individualized care, enabling us to deliver added value to customers.”

- Seller: Neogen Corporation (NASDAQ: NEOG), calling this a “planned divestiture” of its animal genomics business, so it can simplify operations, focus on core food and animal safety markets, and reduce debt. CEO and President Mike Nassif says the sale “allows the company to accelerate de‑leveraging and improve profitability.”

- Asset: Neogen’s animal genomics business, which:

- Generates about $90 million in annual sales as of Neogen’s fiscal 2025.

- Operates five laboratories in the United States, Brazil, Australia, China, and the United Kingdom, plus an office in Canada.

- Serves customers in more than 120 countries, using fixed‑array and sequencing technologies with associated software to support genetic testing.

- Zoetis describes it as a leader in U.S. beef and dairy genomics.

- Price: $160 million, a clean ~1.8× revenue multiple on that $90 million sales base.

- Timeline: Zoetis expects to complete the acquisition in the second half of 2026, and Neogen expects to close by the first half of its 2027 fiscal year, pending regulatory approvals.

That 1.8× revenue multiple tells you how each side sees this. For Neogen, it signals that genomics is a scale‑dependent service line — valuable, but not its primary growth engine, compared with food and animal safety. For Zoetis, rolling a ~$90‑million genomics business into a much larger animal health portfolio is easy to justify if it deepens their Precision Animal Health strategy and tightens the link between genetics, medicines, vaccines, diagnostics, and digital tools.

Zoetis isn’t starting from zero on genomics. They already had:

- CLARIFIDE and CLARIFIDE Plus for dairy, built around genomic predictions and the Dairy Wellness Profit Index (DWP$), with wellness traits aimed at mastitis, metritis, displaced abomasum, ketosis, lameness, twinning, abortion, and more.

- INHERIT Select for beef, positioned as a genomic tool for commercial herds.

- A genetics lab in Kalamazoo, Michigan, is part of their existing Precision Animal Health infrastructure.

What they’re buying now is plumbing and reach: a global lab footprint, thousands of customers who’ve used GeneSeek as their processor, and a large base of Igenity and GGP genotypes feeding evaluations and management tools across species.

| Asset | Zoetis Holdings (Before Deal) | After $160M Neogen Acquisition |

| Genomic Products | CLARIFIDE Plus (dairy), INHERIT Select (beef), DWP$ wellness index | All existing products + Neogen’s Igenity, GGP platforms, sequencing technologies |

| Lab Footprint | 1 genetics lab (Kalamazoo, Michigan) | 6 total labs: U.S., Brazil, Australia, China, U.K., Canada |

| Customer Reach | North America focus via existing distribution | 120+ countries served through acquired lab network |

| Annual Genomics Revenue | Est. $400M+ (within Precision Animal Health segment) | Adds $90M from Neogen genomics business |

| Strategic Control | Owned genomic testing pipeline for proprietary indexes | Also processes DNA for competitors, associations, AI companies |

| Competitive Position | Leading dairy genomics brand | Owns both the test brand AND much of the third-party lab infrastructure |

The 750‑Cow Herd Caught in the New Loop.

Now pull this into a barn you recognize.

Picture a family‑run 750‑cow Holstein herd that’s all‑in on CLARIFIDE Plus:

- Every heifer gets genotyped through CLARIFIDE Plus.

- The breeding program leans heavily on DWP$ and wellness traits that Zoetis positions as predictors of health and profitability.

- The herd‑management software — through Zoetis or partner integrations — pulls genomics directly into the cow card, so DWP$ and wellness scores sit alongside repro, health, and production records.

Meanwhile, another herd in the same region runs Igenity or GGP tests through a breed or AI program that sends DNA cards to Neogen’s GeneSeek labs.

As of March 2, 2026, those routes are set to converge:

- Neogen’s animal genomics business — including its five labs and software — is under a definitive agreement to be sold to Zoetis.

- Zoetis says integrating Neogen’s genomic technologies and data solutions will expand “predictive insights, individualized care, and greater value” across major livestock and companion species.

From the 750‑cow herd’s side of the fence, that means:

- The lab processing a significant share of breed/AI genomics — Neogen’s business — is on track to have the same corporate parent as CLARIFIDE Plus and other Zoetis genomics offerings.

- The company that runs your genomic test, defines your wellness index, integrates with your herd software, and sells you disease‑prevention products will also own a big chunk of the lab capacity behind your neighbors’ tests and some association pipelines you rely on.

That might pencil out just fine. But it’s no longer the same arm’s‑length relationship you started with.

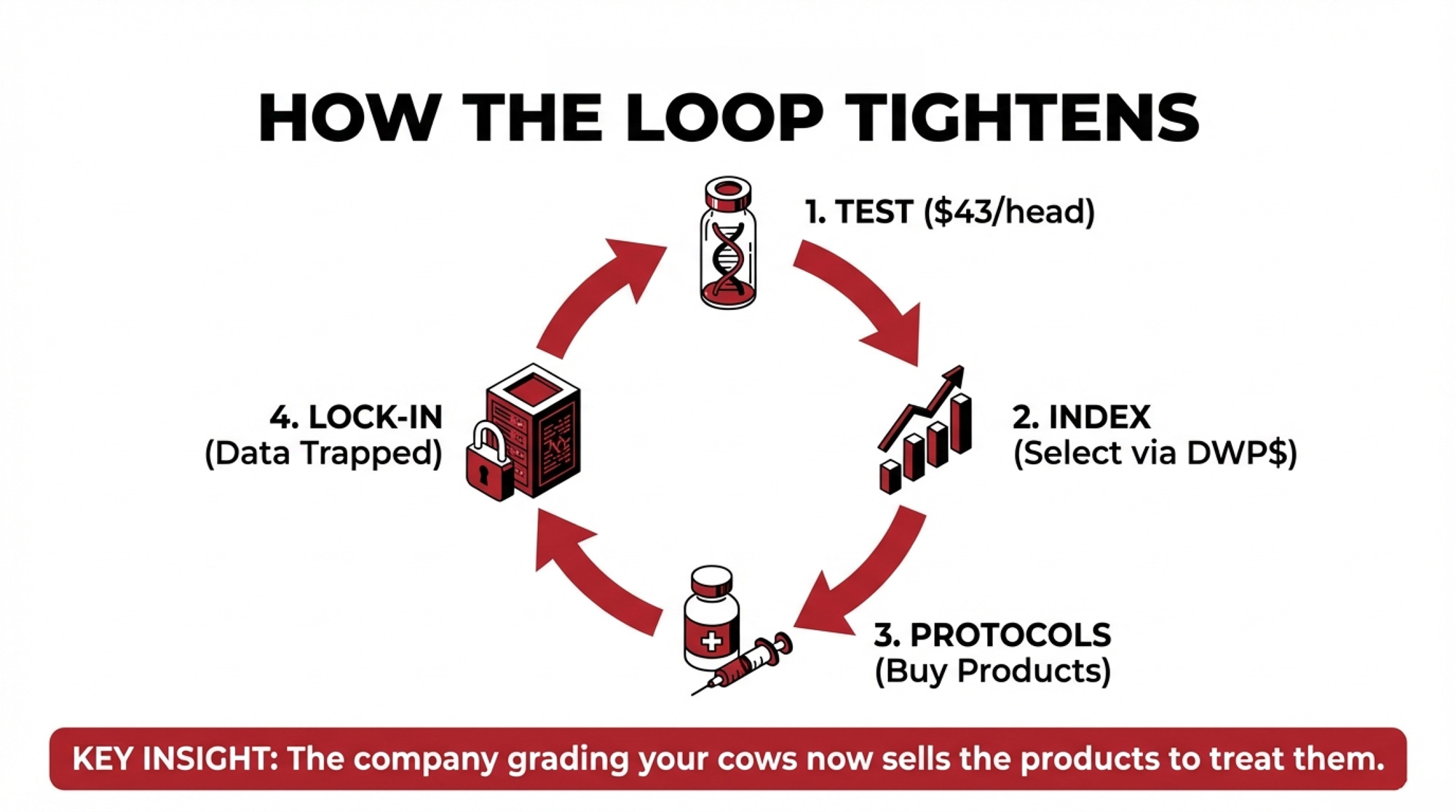

The Genomics Loop: $43 Per Head, 2,000 Animals, One Company

CLARIFIDE Plus isn’t a mystery line item. Holstein Association USA lists CLARIFIDE Plus at around $43 per Holstein animal, with practical costs for many herds in the $40–$50 per head band depending on volume and program.

| Step | Annual Activity | 5-Year Total | Who Benefits |

| Direct Testing | 400 tests × $43 = $17,200/year | $86,000 | Zoetis (lab revenue) |

| Genetic Direction | Selection/culling decisions based on DWP$ index | 2,000 animals shaped by one platform’s trait priorities | Zoetis (proves index “works”) |

| Protocol Adjustments | Est. $10/cow/year targeted health spend (750 cows) | $37,500 | Zoetis (wellness-linked product sales) |

| Switching Friction | Staff retraining, advisor realignment, dual-index period | Opportunity cost: $15,000–$25,000 | Zoetis (customer retention) |

| Total Economic Exposure | $24,700/year | $123,500+ | Platform lock-in achieved |

Now run realistic barn math for that 750‑cow herd:

- You test 400 head per year — heifers plus some key cows.

- You keep that up for 5 years.

- You use one platform’s genomic test and index to steer breeding and culling.

Step 1: Direct testing spend

Using $43 per head as a concrete, sourced test price:

- 400 tests/year × $43 = $17,200 in genomics fees per year.

- 5 years × 400 tests/year = 2,000 animals genotyped.

- 2,000 tests × $43 = $86,000 in direct testing spend over five years.

Your invoices might come in a little lower or higher with discounts and bundling, but you’re still in that neighborhood.

Step 2: Genetic direction

Each year, you and your advisors use those scores to:

- Push sexed semen on the top DWP$ heifers.

- Push beef semen or early culling on low‑index animals.

- Make earlier do‑not‑breed calls when low‑index animals also underperform in the parlor or maternity pen.

After five years, a large share of your milking herd has been shaped by one company’s definition of “profitable genetics” — the way DWP$ weights milk, fat, protein, fertility, and wellness traits.

That’s powerful if DWP$ lines up with your economics. It’s limiting if you ever decide you want different trade‑offs.

Step 3: Downstream product spend

Those wellness traits don’t just sit in a report. They steer protocols.

Zoetis describes its Precision Animal Health vision as predicting, preventing, detecting, and treating disease using integrated tools across medicines, vaccines, diagnostics, and digital solutions. On a CLARIFIDE Plus herd, that often turns into:

- High mastitis‑risk genetics? More aggressive mastitis prevention and treatment programs.

- High lameness risk? Tighter hoof‑health schedules, trims, and monitoring.

- Transition disease risk? Higher‑touch dry‑cow and fresh‑cow protocols backed by specific products.

Nobody’s forcing these choices, but when the same company provides the risk scores and sells the tools, it’s easy for more of your per‑cow health spend to gravitate there over time.

Even modest shifts add up. If wellness‑driven protocols increase targeted health spend by:

- $10 per cow per year across 750 cows, that’s $7,500/year.

- Over 5 years, it’s $37,500 in additional health spending guided by the same platform.

You may get every dollar of that back in avoided disease. The point is that your genomics, protocols, and product choices are now tightly coupled to one ecosystem.

Step 4: Switching cost

Fast‑forward to 2031.

You decide you’d like to:

- Move some or all genotyping to a non‑Zoetis, CDCB‑approved service lab, or

- Shift your primary emphasis from DWP$ to a national index like NM$, TPI, or PRO$, alongside your own KPIs.

You’re not just changing who prints your reports.

You’re:

- Re‑training staff who’ve lived in DWP$ bands and wellness trait lists.

- Re‑aligning conversations with genetics advisors, vets, and lenders.

- Managing a period where different indexes don’t always agree on which cows are “top” and which are “bottom.”

Each turn of the loop made the system easier. It also raised the friction if you ever want to step partly outside it.

What Does This Deal Change for a 750‑Cow Herd?

| Step | What You Do/Spend | What Zoetis Gains |

| 1. Testing | 400 tests/year → $17,200/year → $86,000over 5 years | Lab revenue and a larger genomic dataset |

| 2. Selection | Herd bred and culled to a single platform index | Evidence their index “works” + genetic direction aligned to their trait priorities |

| 3. Protocols | Wellness traits steer more targeted health programs | Product sales linked to genomic risk and integrated Precision Animal Health offerings |

| 4. Switching | Higher friction if you try to move labs or indexes after 5+ years | Stickier customers and more leverage in commercial negotiations |

That’s the decision pipeline Zoetis is paying $160 million to tighten.

Why Many Producers Will Choose the Loop Anyway

There are plenty of good reasons herds will lean into this ecosystem on purpose.

Zoetis and Neogen both emphasize that combining their genomics businesses will expand “predictive insights,” “individualized care,” and “highly accurate, scalable genetic testing,” giving customers deeper views on animal health, productivity, and sustainability across species.

For a 700‑cow operation juggling labor, data overload, and disease pressure, that upside looks like:

- Sharper predictions. A larger combined genomics business — more samples, traits, and species — can support more robust trait predictions, especially for wellness and health.

- Less friction. Results that feed directly into herd software and decision tools cut the time you spend moving files and reconciling systems.

- Cleaner conversations. When your genomics, wellness traits, and protocols use the same language, it’s easier for your team to pull in the same direction.

So it’s perfectly rational for a herd to say: “We’ll accept more dependence if the tools keep improving and the economics hold up.”

The risk isn’t using the loop. It’s using the loop without knowing how to exit it or what happens to your data if you ever need to.

When “Neutral” Labs Aren’t Neutral Anymore

For breed associations, AI companies, and public genomics projects, the immediate tension isn’t about convenience. It’s about governance.

From Zoetis and Neogen’s own descriptions, Neogen’s genomics business has been:

- Serving customers in more than 120 countries,

- Operating five laboratories in the U.S., Brazil, Australia, China, and the U.K., plus an office in Canada, and

- Acting as a leader in U.S. beef and dairy genomics.

For years, much of that work sat under Neogen as a third‑party service:

- Associations sent member DNA for genotyping under genomic‑enhanced evaluations.

- AI companies used Neogen’s platforms (Igenity, GGP) to genotype bulls and commercial heifers.

- Government and research projects used its lab network for large‑scale testing.

Neogen’s incentive was straightforward: provide accurate, timely testing and invest in genomics technology as a service line.

Once those labs move under Zoetis’ roof, the questions change:

- What do the firewalls really look like? Zoetis says it’ll integrate Neogen’s genomic technologies and data solutions into its Precision Animal Health offering while “supporting continuity for colleagues and customers” and building on Neogen’s genomics legacy. Partners will want clarity on how individual customer data is segregated and protected.

- What visibility does a lab owner get, even without individual IDs? Aggregate volume, array choice, and project timing can reveal a lot about what breeds, studs, and associations are doing.

- Who benefits most from data aggregation? Associations may own members’ genotypes, but Zoetis’ ownership of the lab business gives it more visibility into patterns than a standalone, service‑only lab would.

Zoetis is open about using this acquisition to “advance animal health through innovation, data, and technology,” and to empower customers with tools for healthier animals and sustainable production. That’s legitimate. The flip side is that it also concentrates influence — as both lab vendor and product competitor — in fewer hands.

If Consolidation Keeps Rolling, Where Does It End?

The Zoetis–Neogen deal fits a familiar pattern from seeds, crop protection, and precision ag:

- Products evolve into platforms.

- Platforms build data moats.

- Data moats raise switching costs — and leverage shifts toward the platform owners.

In animal genetics, current signals already point to:

- A global market where animal genetics and genomics continue to grow as producers chase productivity, health, and sustainability gains.

- A small top tier of players — Zoetis, major genetics companies, and large animal health providers — controlling most of the genomics and evaluation stack.

If current consolidation trends continue, it’s easy to picture a world where:

- Four to six dominant platforms effectively steer most genetics and health decisions on commercial herds.

- Genomics becomes a feature inside integrated solutions (software + products + advisory) rather than a standalone service you can easily shop for.

- Independent labs focus on niche work or act as backup routes for organizations that deliberately keep a second lane open.

For mid‑size dairies, the risk creeps in quietly:

- Platform indexes and wellness scores become the default language for your team and advisors.

- The easiest tools — usually the ones tied to your main platform — get used by default.

- By the time you question the relationship, your replacement strategy, cull logic, and protocols may all be tuned to a single system.

The myth is: “If this stops working, we’ll just switch.”

The reality, if you don’t plan, is: “We’d like to switch, but the friction is too high, and the whole farm thinks in one platform’s numbers.”

The Turn: It’s Not “Stay or Go” — It’s “On What Terms?”

You’re not going to stop Zoetis and Neogen from closing this deal. Regulatory reviews may tweak conditions, but the labs will likely sit under Zoetis by late 2026.

What you do control is how boxed in you are when that happens.

The real decision over the next 12–18 months is:

- Do you keep using Zoetis‑linked genomics on default terms, or

- Do you keep using them while locking in better data and exit terms to maintain leverage?

Most producers and associations will stay in the ecosystem because:

- The tools are strong and already integrated.

- The workflows are familiar.

- Evaluating alternatives takes time and focus.

That’s fine — as long as you treat lab and data contracts like infrastructure decisions, closer to choosing a milk buyer or lender than picking a glove supplier.

That means pushing for:

- Clear language that your farm or organization owns your raw genotypes.

- Guaranteed data portability — the right to export complete genotype files with IDs in standard formats if you move some or all volumes.

- Tight data‑use provisions — especially around using your genotypes, even de‑identified, to train proprietary tools.

- A transition clause that obligates cooperation if you shift business elsewhere.

You don’t have to leave. You don’t want to discover your options are gone the day you actually need them.

The Playbook Before This Deal Closes

Here’s a practical, time‑bound framework.

In the Next 30 Days: Read the Fine Print Like It’s a Milk Contract

Before the announcement fades:

- Pull your genomics agreement or program terms.

That might be with Zoetis directly, a stud, a breed association, or a vet/genetics service that bundles testing. - Circle language on:

- Data ownership

- Data use (especially “de‑identified,” “aggregated,” “research,” “product development”)

- Term, automatic renewal, and termination

- Ask your contact three blunt questions:

- Who legally owns my raw genotype files — me, the association, the vendor, or some combination?

- Can I get a full export, with animal IDs, in a standard format if I move labs?

- Will my herd’s genotypes be used to train proprietary tools without a separate, explicit data‑sharing agreement?

If the answers are fuzzy and the contract doesn’t match them, that’s not a problem for tomorrow. That’s a now problem.

In the Next 90 Days: Build a Real Plan B Lab

You may never use it. You’ll still sleep better knowing it exists.

- Identify at least one non‑Zoetis, cattle‑focused genotyping lab that’s compatible with CDCB or your national evaluation system. holsteinusa Get specifics: pricing, turnaround time, data formats, and how they deliver results back to you or your association.

- Run a pilot batch.

- Choose a defined group (e.g., a heifer cohort).

- Send samples through both your current program and the alternative lab.

- Confirm that:

- Results from the alternative lab plug into your existing evaluation system.

- Service and communication are solid.

- You can easily map data back into your farm or association records.

Spending roughly the cost of 50 tests to learn how hard it is to move volume is cheap insurance compared to discovering you’re stuck mid‑dispute.

In the Next 365 Days: Rebalance Who Really Steers Your Decisions

As the Zoetis–Neogen integration moves from press release to day‑to‑day reality:

For 300–1,500‑cow herds:

- Split your steering wheel.

- Keep using CLARIFIDE Plus, DWP$, and wellness traits if they’re working; Zoetis and its partners built those tools for a reason.

- But cross‑check big moves with at least one independent lens:

- National indexes (NM$, TPI, LPI, PRO$, etc.).

- Your own data on culls, mastitis, lameness, stillbirths, and reproduction.

- Get your advisory team aligned.

Sit down with your genetics advisor, vet, nutritionist, and lender and ask:- “Whose index are we effectively breeding to?”

- “How much of our herd strategy assumes this one platform’s view of genetic value and health risk is the truth?”

For breed associations and genetics committees:

- Write a lab and data policy on purpose, not by default.

- Define expectations: independence, firewall standards, audit rights.

- Decide how often you’ll review lab partnerships and under what conditions you’ll diversify volume.

- Keep a non‑Zoetis lane open.

- Even if most samples continue flowing through Zoetis‑owned labs for cost and performance reasons, maintain a meaningful stream through at least one other approved lab.

- That stream is your insurance policy; you don’t want to build it from scratch under pressure.

What This Means for Your Operation

Turn this from news into checks you actually run.

- In the next 30 days, read your genomics contract line by line.

If it doesn’t clearly say who owns your genotypes and how you can export them, that’s your first negotiation target. - Ask for written data‑use boundaries.

Push for language that says your genotypes won’t be used to train proprietary tools without a separate, explicit agreement you sign. - Know at least one backup lab by name and price.

Make a call, get a quote, and ask exactly what it would take to send 50 heifers through their system. - Test the switching friction with a small pilot.

Don’t wait until you’re unhappy with pricing or terms to find out your data is badly stuck in one ecosystem. - Stop letting any single index be the only truth.

On your next breeding or cull list, compare your platform index with at least one national index and your own health and cull data before you finalize. - If you’re on a genetics committee, get this on the agenda.

Ask staff to map where member DNA goes, who has access, and what it would take to move 10–20% of volume elsewhere over the next 1–3 years. - Treat genomics and lab choice like a processor or lender decision, not a glove order.

The wrong glove order is annoying. The wrong lab contract can shape your herd’s genetics and negotiating power for a decade.

Key Takeaways

- Zoetis isn’t just buying five labs and $90 million in sales. It’s buying a global genomics business that plugs into its Precision Animal Health strategy and tightens the loop between your DNA, your herd software, and its products.

- At roughly 1.8× revenue, Neogen is signaling genomics is a scale‑driven service line for them, not their main growth engine. For Zoetis, that same business is another gear in a much larger machine for animal health and diagnostics.

- A typical 750‑cow herd testing 400 head a year at around $43/head is putting roughly $17,200/year — about $86,000 over five years — through one genomic loop. That loop shapes genetics, protocols, and, eventually, your flexibility.

- Mid‑size dairies (roughly 300–1,500 cows) are often the most exposed to platform lock‑in. You’re big enough that the loop meaningfully affects your economics, but not always big enough to dictate terms.

- There are real upsides — sharper predictions and cleaner workflows — that many herds will choose on purpose. The smart play is to enjoy those benefits while making sure your data ownership, portability, and Plan B lab are nailed down in writing before the labs change hands.

The Bottom Line

When you sit down at the desk tonight, don’t just skim the $160 million headline.

Pull your latest genotyping invoice, find the program terms it points to, and circle every line that spells out who owns your data, who can use it, and what it takes to walk away.

Then ask yourself, honestly: Is that language strong enough for the $17,200 a year you’re putting through this pipeline?

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- McCarty’s $40 Genomic Test Exposed a 28% Error – and a $104,750 Leak on a 500-Cow Dairy – This field-tested breakdown reveals how a simple genomic panel exposed a six-figure profit leak for one 500-cow herd. It arms you with concrete sorting tactics to stop wasting rearing capital and immediately fix your bottom-line execution.

- 2025 Dairy Year in Review: Ten Forces That Redefined Who’s Positioned to Thrive Through 2028 – This strategic analysis exposes the structural shifts—from the 800,000-head heifer deficit to shifting culling math—reshaping the next three years. It delivers the foresight needed to navigate milk price volatility while securing your operation’s long-term market access.

- The Hidden Cost of Lameness: Is AI Exposing Dairy’s Biggest Profit Thief? – This feature reveals how AI-driven camera monitoring is becoming the new frontier for slashing $337-per-case lameness losses. It delivers a high-tech roadmap for early detection and precision breeding that provides an immediate, massive early-adopter advantage.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.

![Generate SEO elements for this The Bullvine article targeting dairy industry professionals:

ANALYSIS REQUIREMENTS:

Identify the article's primary topic and target audience (dairy farmers, industry professionals, agricultural specialists)

Focus on practical, implementation-oriented keywords that dairy professionals would search for

Consider both technical dairy terminology and business/profitability terms

DELIVERABLES:

1. SEO Keywords (5 keywords):

Create a comma-separated list of relevant keywords mixing:

Primary dairy industry terms (dairy farming, milk production, herd management, etc.)

Technology/innovation terms if applicable (precision agriculture, automated milking, genomic testing, etc.)

Business/economic terms (dairy profitability, farm efficiency, ROI, cost reduction, etc.)

Geographic terms if relevant (dairy industry trends, global dairy, etc.)

2. Focus Keyphrase:

Develop a 2-4 word primary keyphrase that captures the article's core topic and would be commonly searched by dairy professionals seeking this information.

3. Meta Description (under 160 characters):

Write a compelling meta description that:

Summarizes the article's main value proposition

Naturally incorporates the focus keyphrase and 1-2 keywords

Appeals to dairy industry professionals

Includes a benefit or outcome (cost savings, efficiency gains, profit increases, etc.)

Uses action-oriented language that encourages clicks

4. Category Recommendation:

Suggest the most fitting category from The Bullvine website (e.g., Dairy Industry, Genetics, Management, Technology, A.I. Industry, Dairy Markets, Nutrition, Robotic Milking, etc.) where this article should be published for maximum relevance and engagement.

FORMAT REQUIREMENTS: Present results in this exact format:

SEO Keywords: [keyword1, keyword2, keyword3, keyword4, keyword5]

Focus Keyphrase: [primary keyphrase]

Meta Description: [compelling description under 160 characters with natural keyword integration]

Category Recommendation: [Best-fit category from The Bullvine’s options]

DAIRY INDUSTRY CONTEXT: Ensure all elements appeal to dairy farmers, agricultural specialists, and industry professionals seeking practical, profitable solutions for their operations.](https://www.thebullvine.com/wp-content/uploads/2025/09/Google_AI_Studio_2025-09-08T17_37_41.620Z.png)