Neil Taylor’s Puddle Hill herd went through the ring after 12 months’ notice. Now up to 100 more UK farms just got the same letter — and your milk contract’s fine print decides whether you lose $260,000 or $78,000.

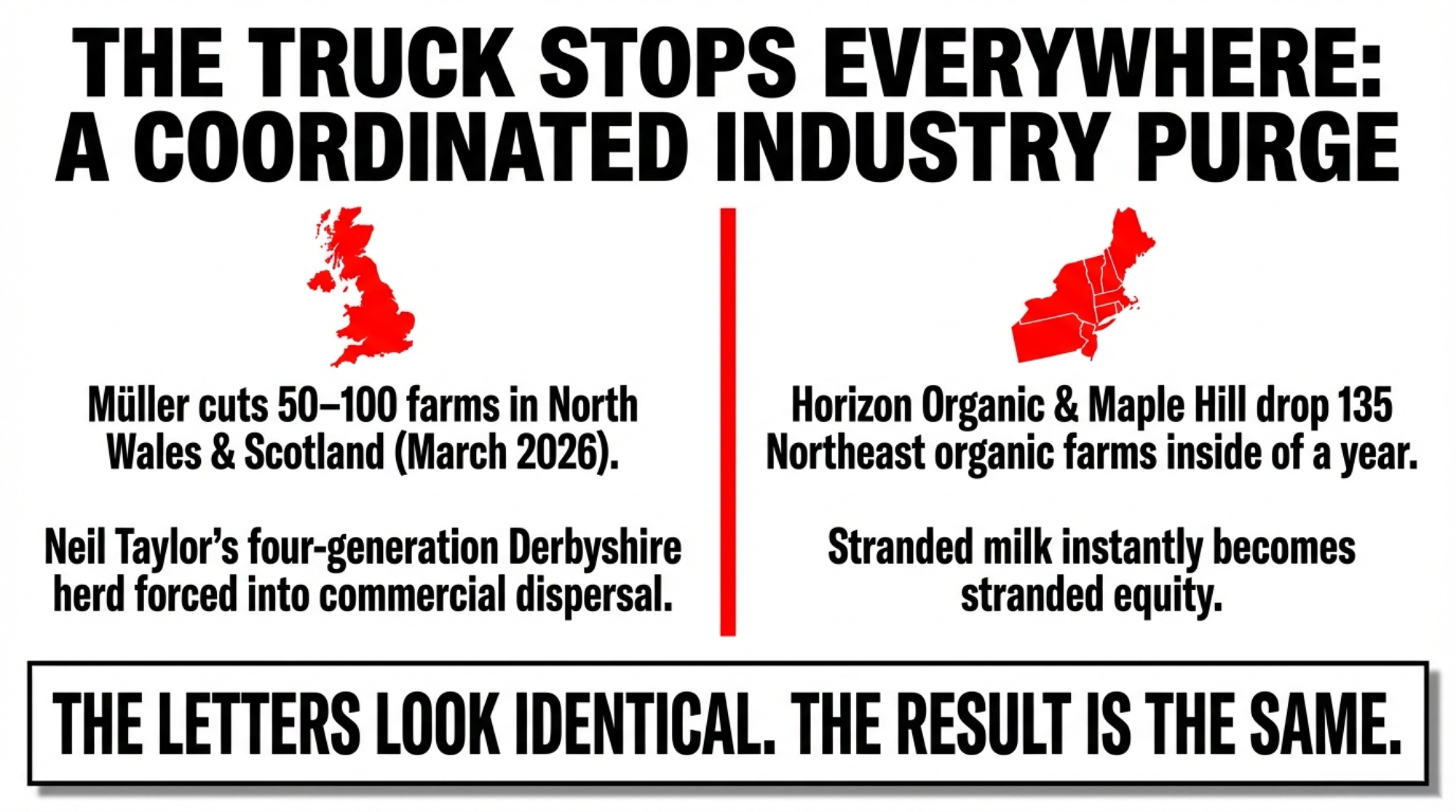

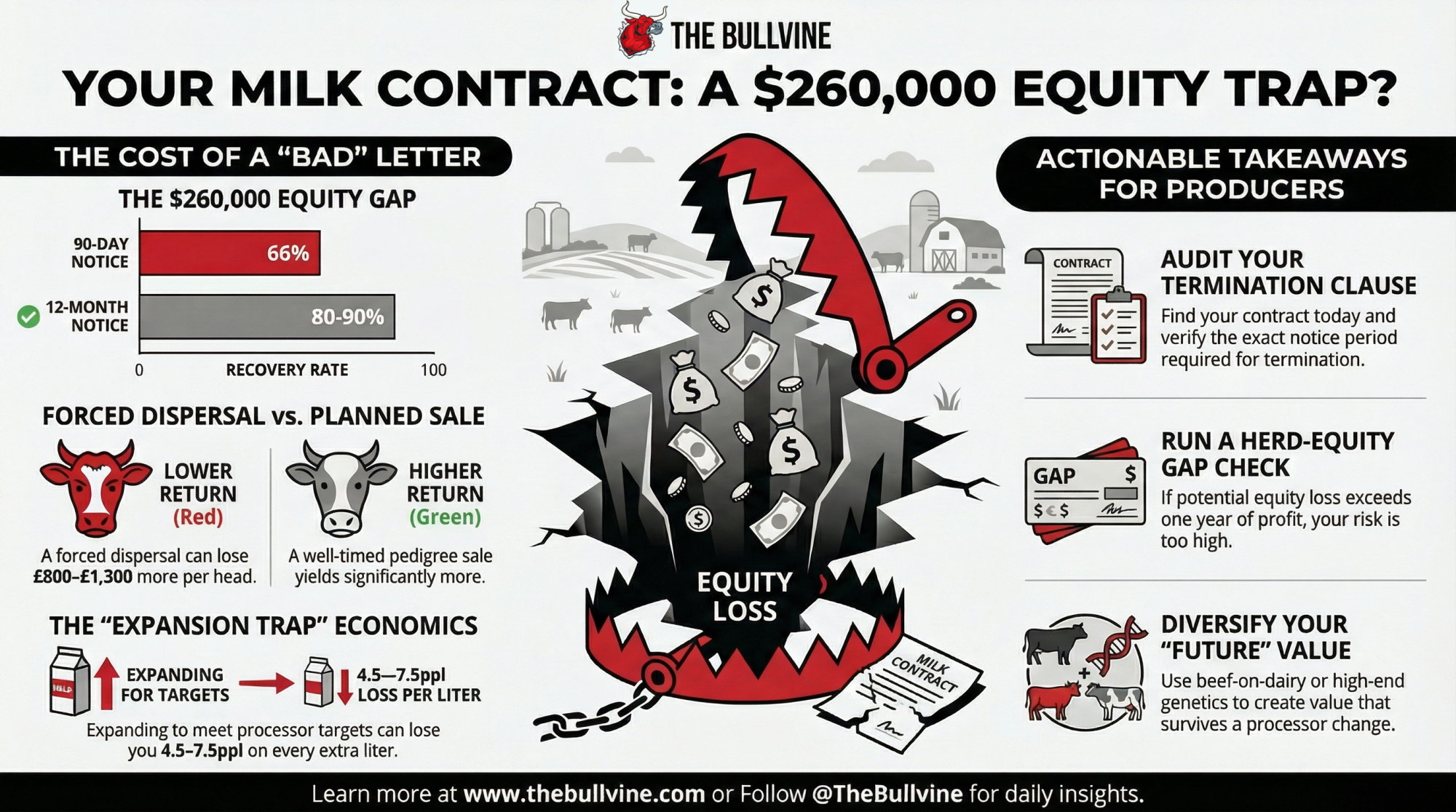

Executive Summary: On a 200-cow herd, the difference between a 12-month and a 90-day termination notice is roughly $260,000 in equity — about 2–3 years of profit gone on timing alone. Müller just proved it again: on March 30, 2026, the processor issued 12-month notices to an estimated 50–100 UK farms in North Wales and Scotland, two years after Neil Taylor’s four-generation Derbyshire herd went through the ring as commercial dispersal cattle under the same kind of letter. This isn’t only a UK pattern — Horizon Organic and Maple Hill dropped 135 Northeast organic farms in 2021–22, and most had even less warning than Taylor got. The expansion trap is equally ugly: at Müller’s current 34.5ppl, adding volume to hit a processor’s target means losing 4.5–7.5ppl on every extra liter before you touch a loan payment. And real auction data shows the gap between a forced dispersal and a well-timed pedigree sale runs £800–£1,300 a head — so how you exit matters almost as much as whether you have to. Pull your contract, run your herd-equity gap against a year of net income, and talk to your lender this month — that checklist applies whether you’re shipping to Müller, a US co-op, or anyone in between.

Neil Taylor is the fourth generation to milk cows at Puddle Hill Farm near Matlock in Derbyshire. He told BBC Farming Today: “I’ve bought them, reared them, I can remember their mums, their grandmas.” Then Müller sent a letter: hit a new production target by the following year, or the contract ends in 12 months. (BBC, July 2024; Farmers Guide, July 2024)

“When I asked how far I’d got to get, they said probably double to what you’re sending now next year,” Taylor told BBC Farming Today. “I couldn’t do it.” Müller has not publicly disclosed the specific volume targets it set for individual farms.

Taylor saw the gap between what Müller was paying and what expansion would actually cost. He sent his cows to market. He and his wife, Bev, have since bought six dairy cows back and plan to raise them for beef. But the dairy herd — the cow families, the genetic equity, four generations of selection — went through the ring as commercial dispersal cattle.

“It’s absolutely devastating,” Taylor told the BBC. “I’ve had 40 years of breeding cows and just to have it taken away from you, it’s a bitter pill to swallow.”

Not Just One Farm: Müller’s Letters Keep Landing

Taylor’s story hit the news in July 2024, but he was just the first to speak up. He told BBC Farming Today he was one of “over a dozen” smaller family farms facing termination. Müller described those affected as “a very small number” of suppliers not meeting its sustainability, welfare, or volume standards, and said all received a full 12-month notice period.

Then on 30 March 2026, a bigger wave landed. Farmers Weekly reported that Müller issued 12-month termination notices to producers in North Wales and Scotland, with the last milk collections set for 31 March 2027. Industry sources told Farmers Weekly the number is likely between 50 and 100 producers, with more than half offered the option to move to a lower-value ingredients-only contract instead. Grant Hartman, chairman of dairy producer organization MMG Dairy Farmers, confirmed the scope: “There are a number of our members who have unfortunately been served the full 12 months’ notice.” (Farmers Weekly, March 31, 2026)

The NFU confirmed Müller’s cuts affect roughly 1% of its current milk volumes — a small share of the supply base, but a very large share of the affected farms’ futures. (NFU, March 31, 2026)

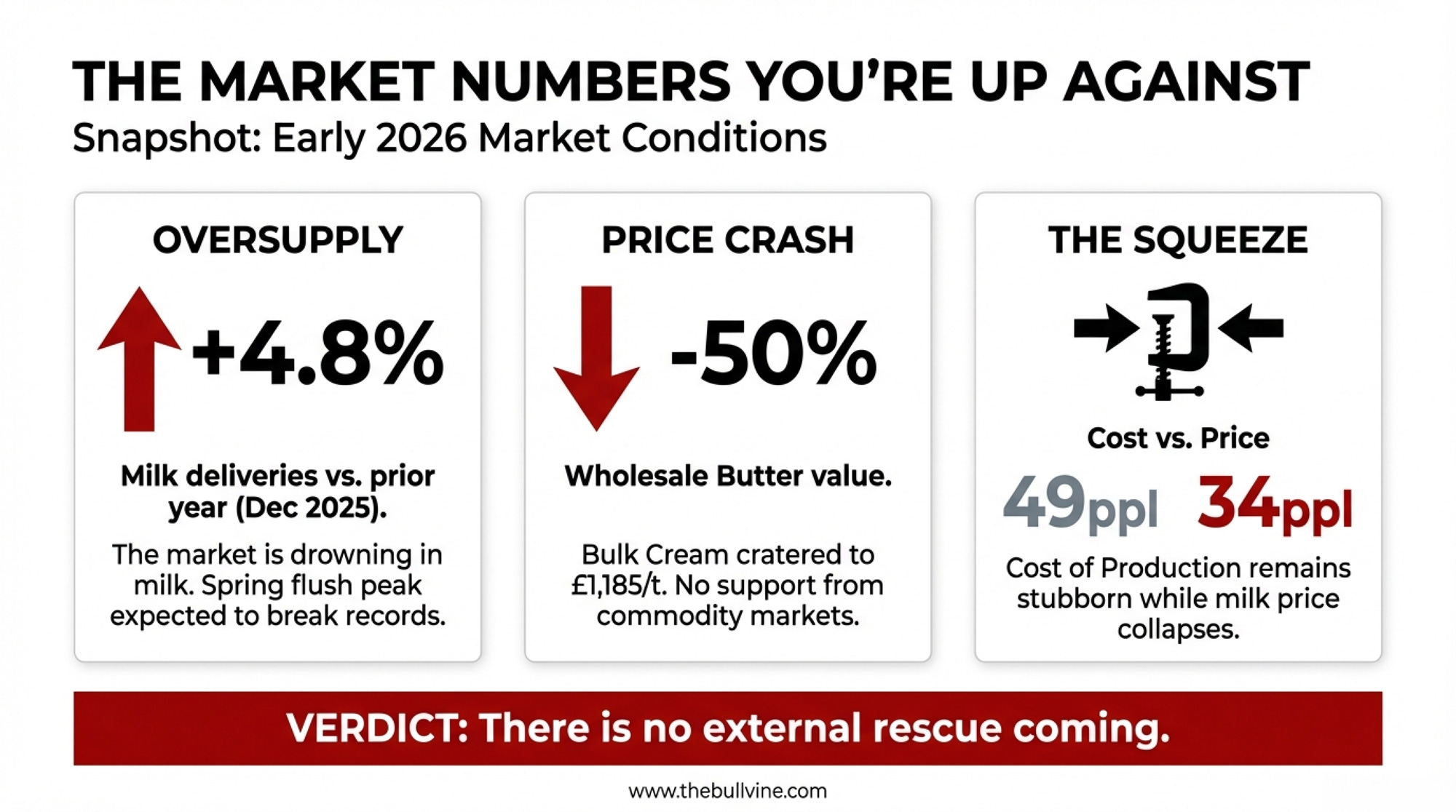

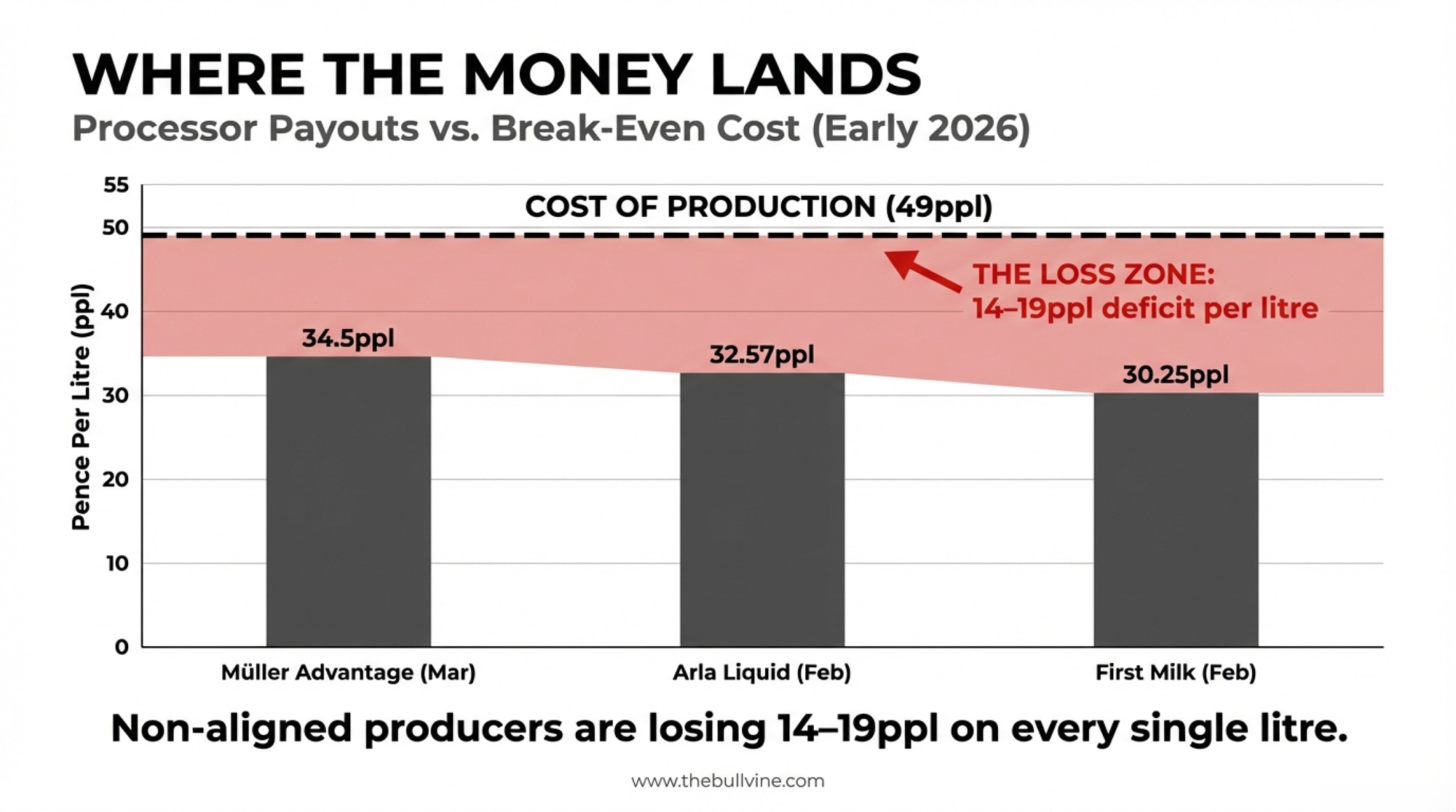

Müller’s agricultural director, Richard Collins, wrote to affected producers: “To ensure we manage our supply of raw milk responsibly and maintain a sustainable balance between milk intake and processing demand, we have no choice but to make adjustments to our supply base.” At the same time, Müller’s Advantage price for March 2026 sits at 34.5ppl— a 1ppl cut from February. For smaller herds already operating on thin margins, those two envelopes arrived in the same period. (IPMS/FarmingUK, January 2026)

When 135 Northeast Dairy Farms Got the Same Kind of Letter

| Factor | Müller (UK, 2024–2026) | Horizon/Maple Hill (US Northeast, 2021–22) |

|---|---|---|

| Farms affected | Est. 50–100 (2026 wave) + prior cases | 135 farms (89 Horizon + 46 Maple Hill) |

| Notice given | 12 months (full legal minimum) | Horizon: ~12 months; Maple Hill: shorter |

| Regulatory backstop | UK Fair Dealing Regs 2024 (new) | None — private contract terms only |

| Processor rationale | “Balance intake and processing demand” | Organic market oversupply |

| Price at termination | 34.5ppl (Müller Advantage, Mar 2026) | Organic premium shrinking vs. conventional |

| Alternative found? | Some offered ingredients-only contract | Organic Valley absorbed ~90 of 135 farms |

| Farms that exited anyway | Neil Taylor + unknown number | Some sold herds, left organic, or quit entirely |

| Farmer quote | “40 years of breeding…a bitter pill” — Taylor | “I could see this coming…not this quick” — Conant |

| Key lesson | Notice ≠ rescue. Time helps, not guarantees. | Alternative buyer ≠ guaranteed. Speed kills equity. |

If you’re reading this from North America and thinking, “That’s a UK problem,” it isn’t.

In August 2021, Danone’s Horizon Organic sent termination letters to 89 organic dairy farms across the Northeast — including 28 in Vermont, 14 in Maine, 17 in Washington County, New York, and the balance in New Hampshire and other New York counties — with contracts ending August 31, 2022. Vermont Agriculture Secretary Anson Tebbetts told VTDigger the terminations were “a significant problem because these farmers have few choices on where to sell their milk.” Dean Conant, who’d been selling milk to Horizon for 14 years from his farm in Randolph, Vermont, began reaching out to other buyers when he received the letter. Nobody had room. (VTDigger, August 2021)

“I could see this coming,” Conant told VTDigger. “I didn’t think it was gonna be this quick.”

Then Maple Hill terminated contracts with an additional 46 organic farmers in eastern New York. That’s 135 farm families in one region, inside of a year, told their buyer was done with them. Organic Valley eventually offered to pick up as many as 90 of those farms — but by the time the offer came, some had already sold herds, exited organic, or quit entirely. (VTDigger, March 2022)

Abbie Corse, an organic dairy farmer on the board of the Northeast Organic Farming Association of Vermont, put it plainly: “These aren’t just jobs. These aren’t just pieces of the economy. These are entire lives that are tied up in a farm.” If you want a closer look at what happens when the truck stops showing up with zero warning, AMPI’s Paynesville plant shutdown is a case study in how fast stranded milk turns into stranded equity.

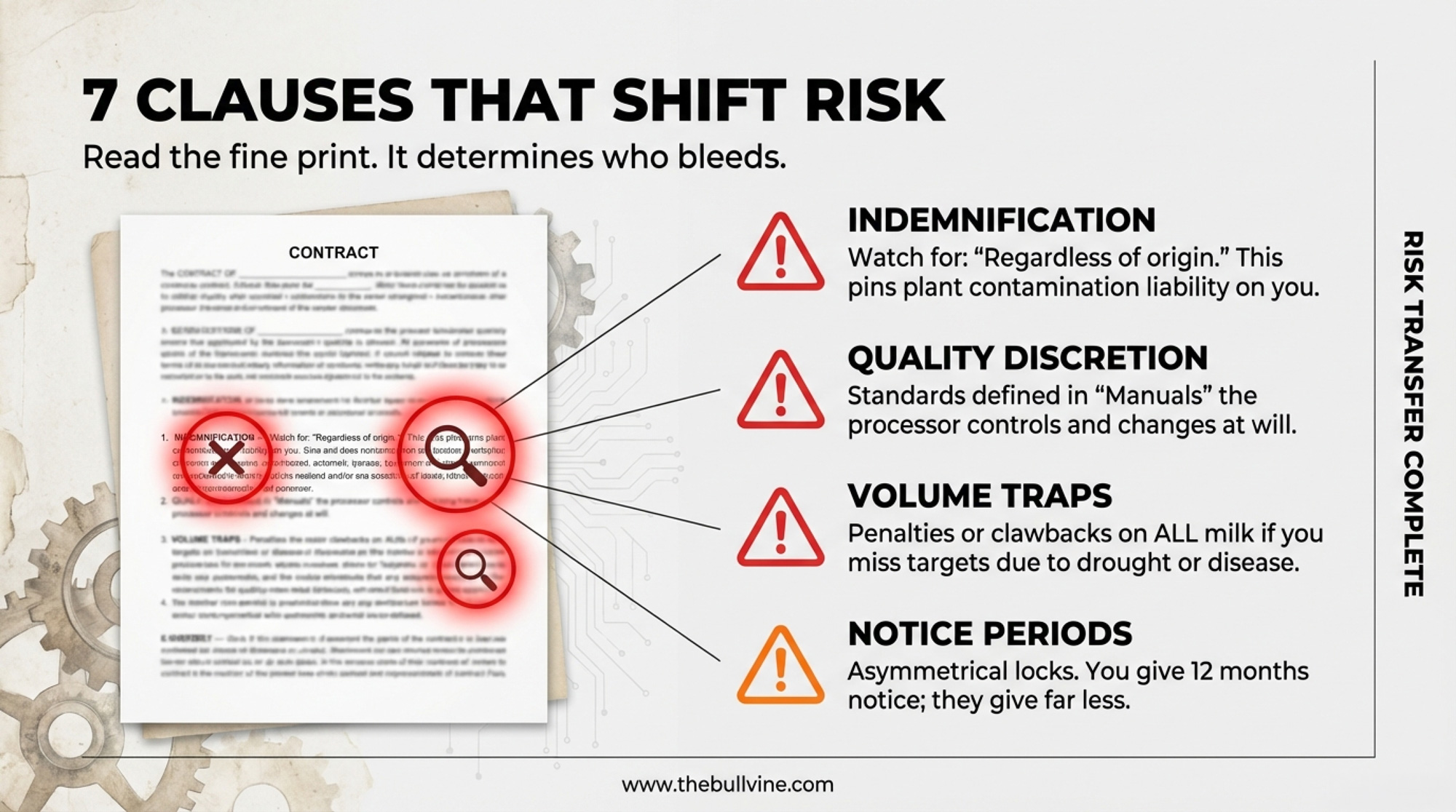

The Rulebook Helped on Paper — Not in the Parlor

Part of the backdrop here is the UK’s new Fair Dealing Obligations (Milk) Regulations 2024. Those rules require processors to give at least 12 months’ notice to terminate a milk-supply contract, offer farmers at least 21 days to consider new contracts, and spell out transparent pricing mechanisms instead of one-sided “take it or leave it” terms.

On those measures, Müller complied. Taylor and the 2026 wave of affected farms all received the full year’s notice. The NFU confirmed this: “Where producers receive no less than 12 months’ notice of any no-fault termination, milk buyers are likely to be complying with that aspect of the regulations.” But the NFU also urged affected producers to seek independent legal advice and contact the Supply Chain Adjudicator if anything seemed off.

| Notice Period | Jurisdiction Example | Herd Recovery Rate | Equity Lost (200-cow/$780k) | Risk Level |

|---|---|---|---|---|

| 30 days | US — some private contracts | ~60–65% | $273,000–$312,000 | 🔴 CRITICAL |

| 60 days | US — some state minimums | ~65–68% | $250,000–$273,000 | 🔴 HIGH |

| 90 days | Pennsylvania (state rule) | ~68–72% | $218,000–$250,000 | 🔴 HIGH |

| 6 months | Some UK pre-2024 contracts | ~75–80% | $156,000–$195,000 | 🟡 ELEVATED |

| 12 months | UK Fair Dealing Regs 2024 | ~82–88% | $94,000–$140,000 | 🟡 MANAGEABLE |

| 18+ months | Best-practice co-op bylaws | ~90–95% | $39,000–$78,000 | 🟢 LOW |

The trouble is, the regulations protect the process of being dropped more than the equity you’ve built. They can’t turn an uneconomic expansion into a good bet. And they don’t guarantee you’ll have the time or market conditions to sell decades of breeding as anything more than commercial dairy cows.

On this side of the Atlantic, even that level of protection often doesn’t exist. Federal Milk Marketing Orders deal with minimum price formulas, not private contract terms or notice periods. In Pennsylvania, the state Milk Marketing Board pushed a change from the old 28-day minimum to a 90-day notice for contracts covered by state rules, after some farmers received short-notice terminations and struggled to find new buyers. In many other regions, your “notice period” is whatever your co-op bylaws or individual milk contract says — and for some, that’s still 30 or 60 days, or nothing in writing at all.

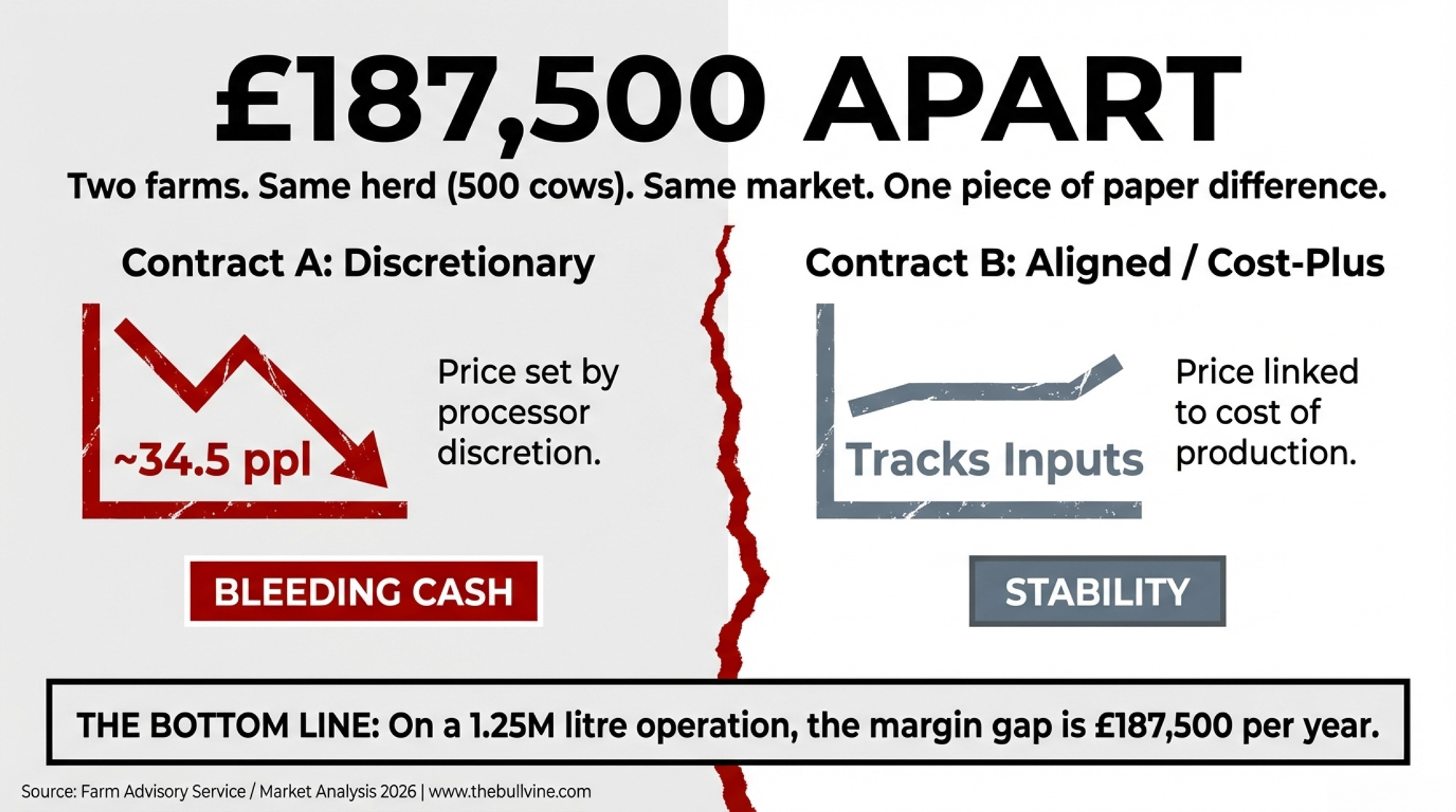

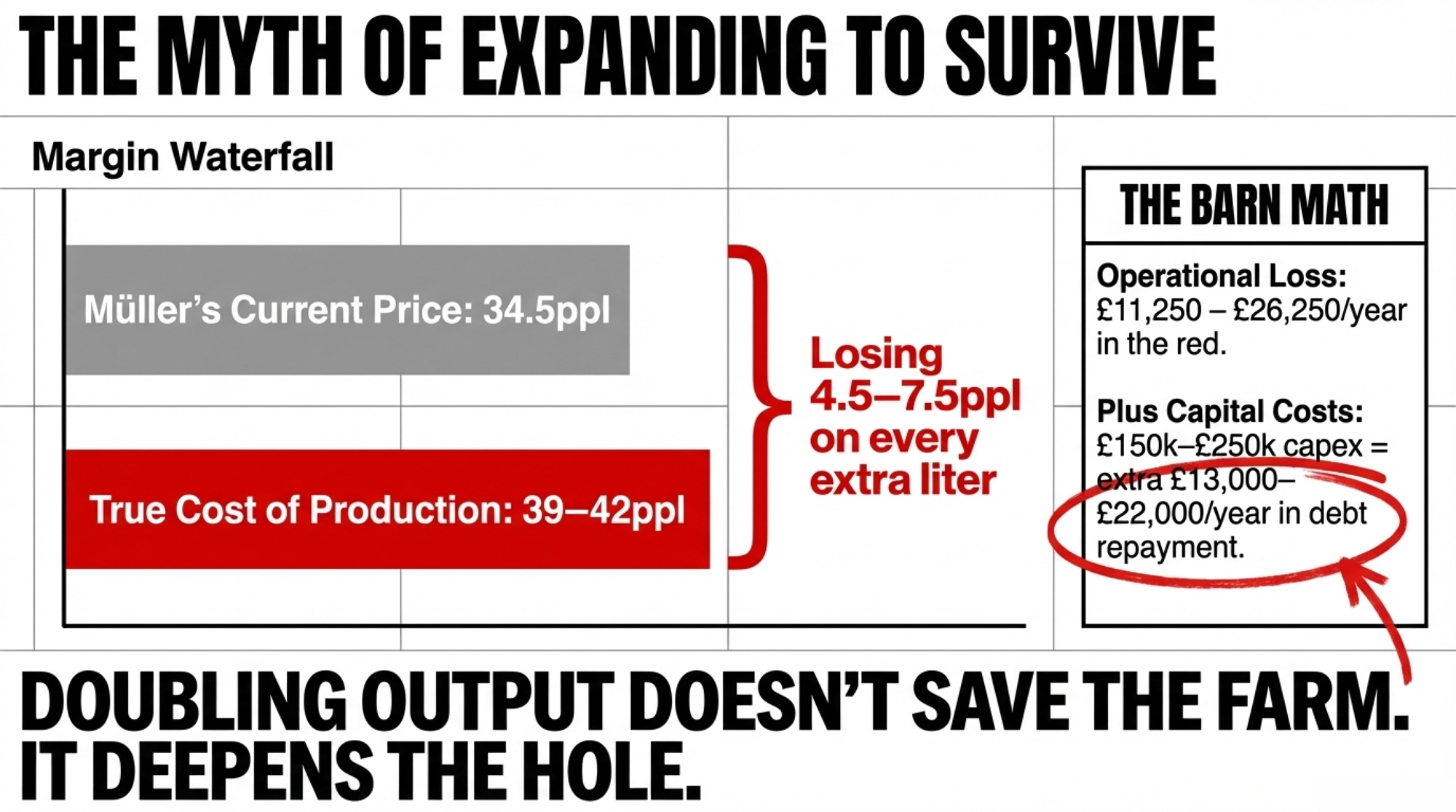

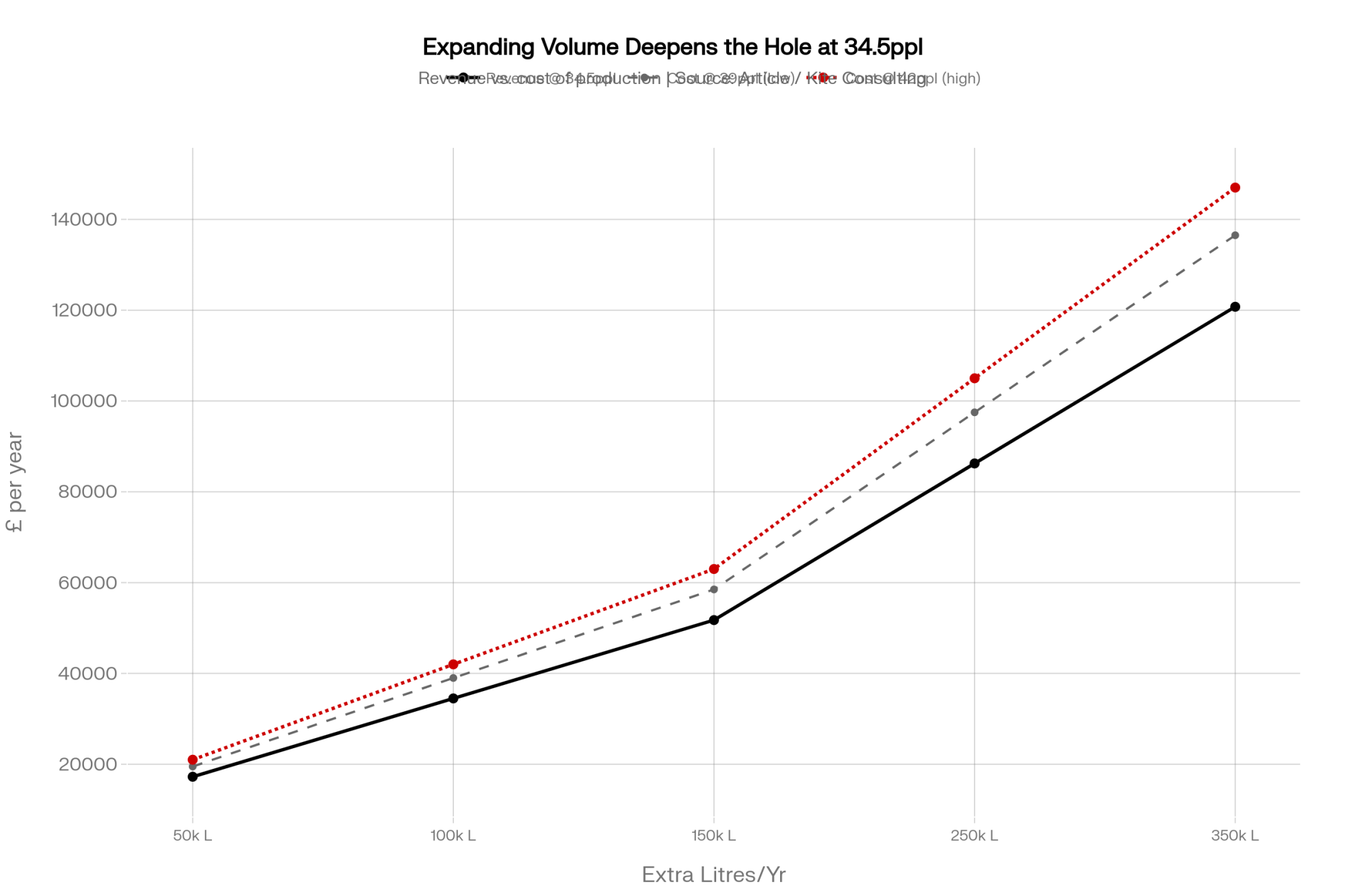

How Does Expansion at 34.5ppl Actually Pencil?

Taylor’s supposed option was simple on paper: expand enough to meet Müller’s volume expectations, and the truck keeps coming. But the economics behind that “option” aren’t theoretical.

Cost-of-production estimates vary widely by farm, region, and method. Albert Goodman’s 2025 farming profitability review noted that the AHDB average farmgate price topped 46.56ppl in October 2025 and that “many dairy farms making healthy profits well over £1,000 per cow” — but also warned that with global oversupply pushing prices down, “there is already talk of it going below 30 pence per litre, which is below current breakeven price for many dairy farmers.” Kite Consulting’s climate-resilience work, based on data from over 850 UK dairies, adds another 2.4ppl over ten years for the average farm to cover slurry storage, silage capacity, and land improvements — roughly £472,539 per farm over that period, based on an average herd of 236 cows. (Albert Goodman, February 2026)

Run a quick barn-math check on the kind of expansion someone in Taylor’s position would face. Say you add 250,000–350,000 liters a year to hit a new target. At 34.5ppl, that extra milk brings in about £86,250–£120,750. If your true cost of production — even at the lower end of current estimates, say around 39–42ppl once you include resilience investments — those same liters cost somewhere in the range of £97,500–£147,000 to produce. You’re losing roughly 4.5–7.5ppl on every extra liter. That’s somewhere between £11,250 and £26,250 a year in the red — before you make a single loan payment on the new capacity.

Now layer on the capital. For a smaller operation looking at a more modest step — buying 30–50 cows at £1,800–£2,500 a head plus the housing, slurry, and parlor upgrades those extra cows need — you’re easily into a £150,000–£250,000 capital project. Farm borrowing costs have risen significantly from the ultra-low levels of recent years, and HCR Law noted in February 2026 that “the longer-term ‘floor’ for rates appears higher than before.” At current farm lending rates, that kind of project adds roughly £13,000–£22,000 a year in repayments. (HCR Law, February 2026)

Taylor told the BBC he “couldn’t do it.” Under those prices and costs, doubling output doesn’t save the farm. It deepens the hole. Grant Hartman’s advice to the 2026 cohort echoes that: don’t make “knee-jerk reactions,” but “take stock, assess the position.”

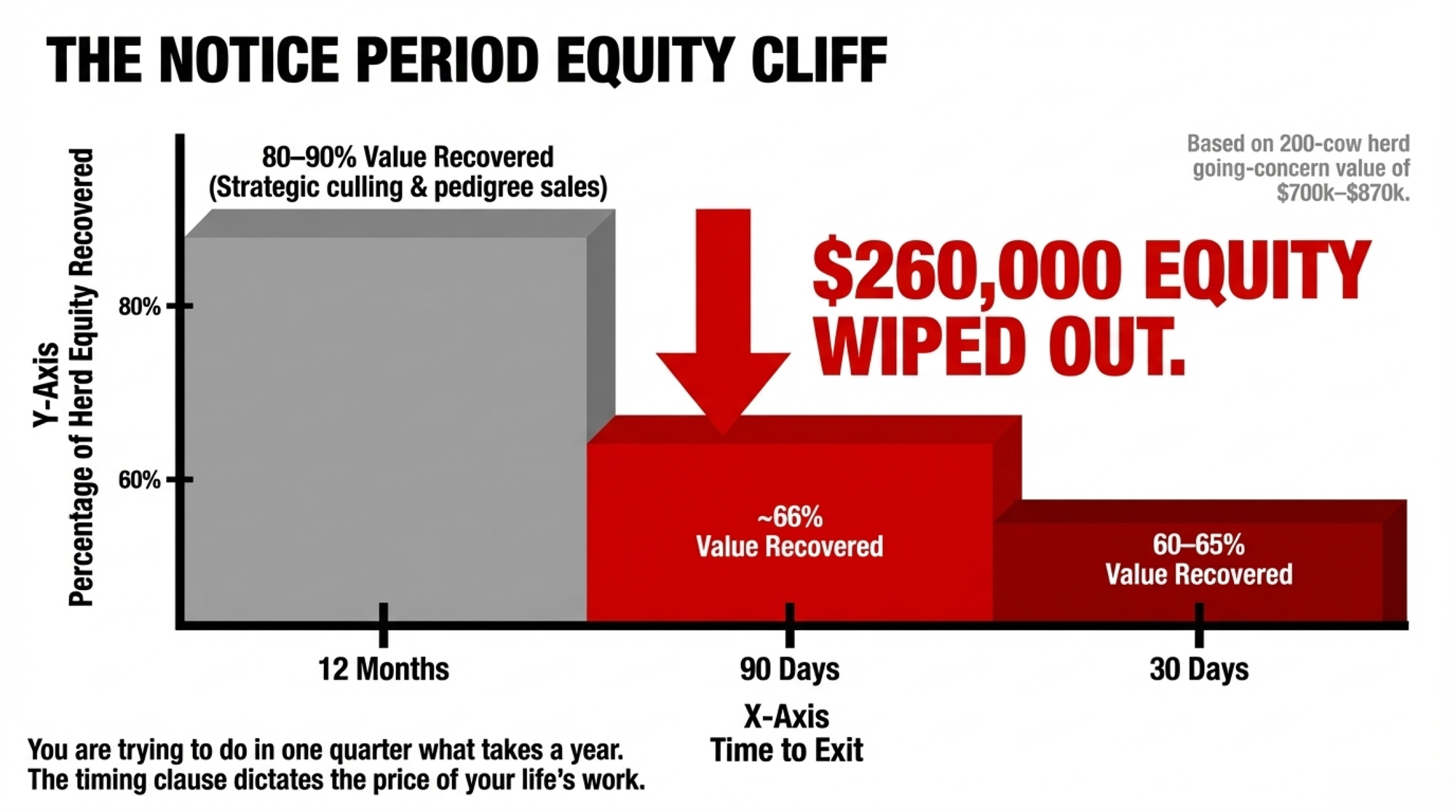

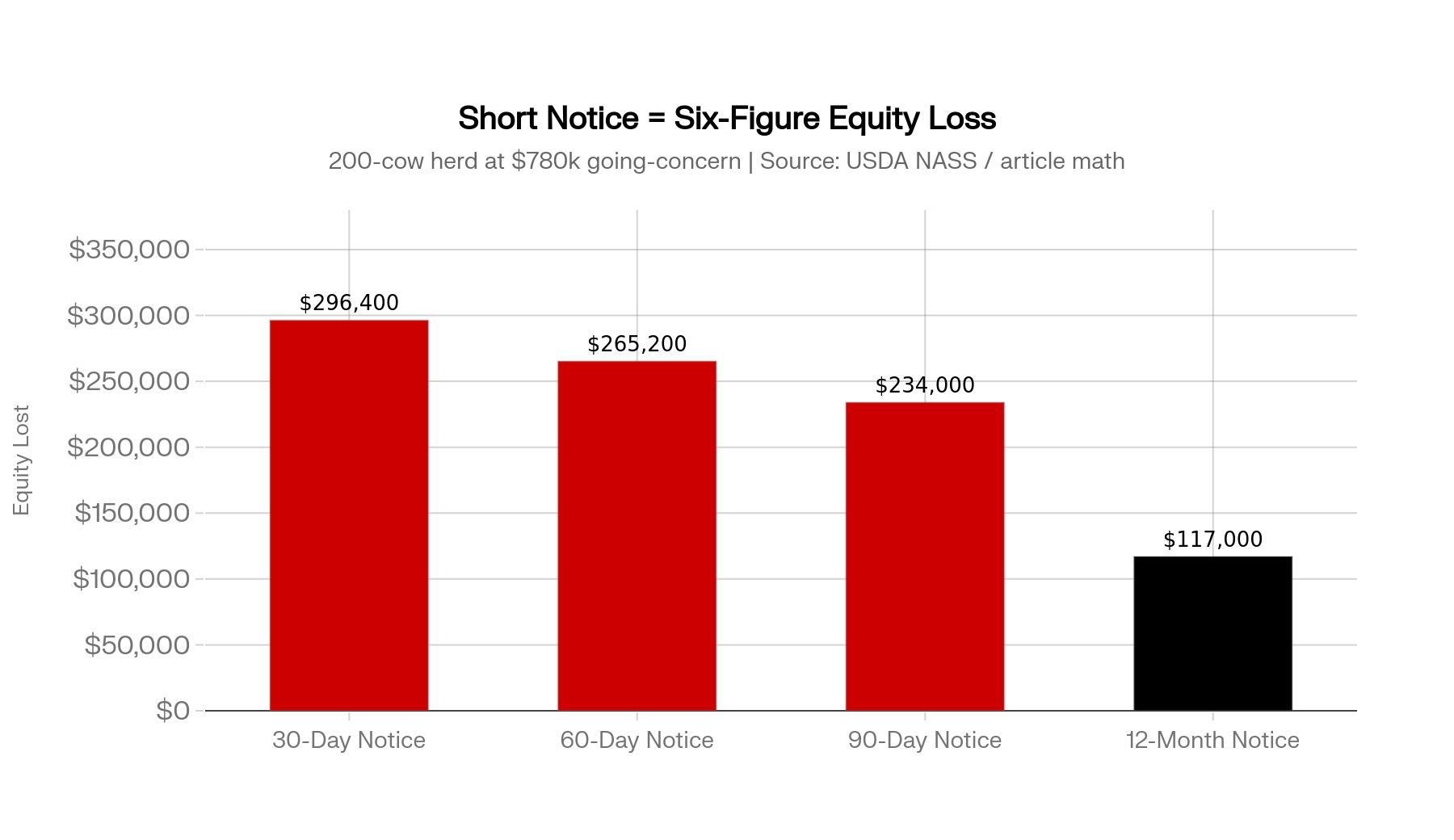

How Much Does Losing 60 Days of Notice Actually Cost Per Cow?

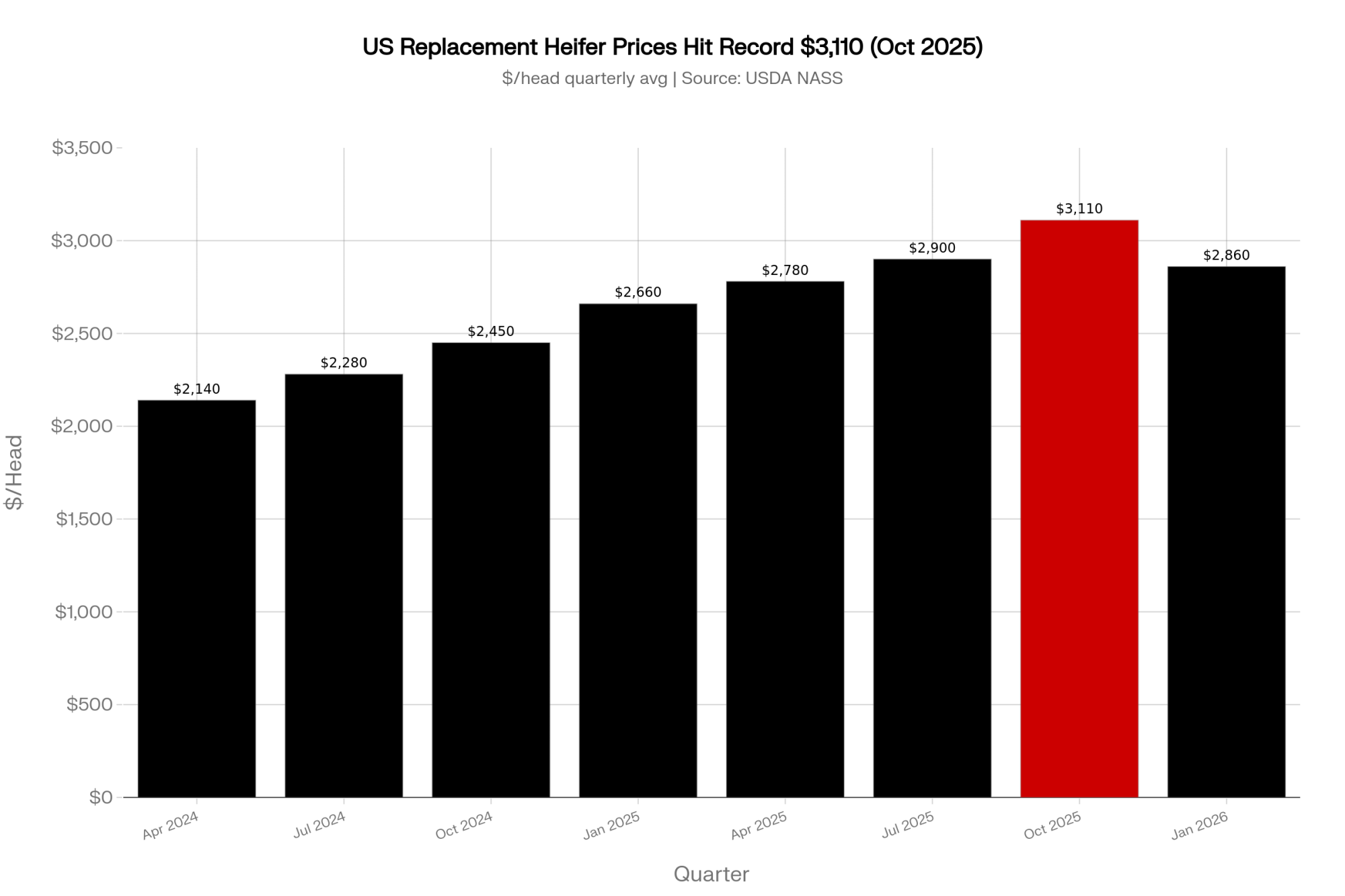

Notice periods look like lawyer talk until you hang them on a real herd. Take a 200-cow US dairy with about 80 replacements and peg the going-concern value off USDA-tracked replacement prices. Those have climbed steeply — from about $2,140 per head in April 2024 to $2,660 in January 2025 and a record $3,110 in October 2025, according to USDA NASS quarterly estimates. By January 2026, the average eased back to $2,860 per head. For a deeper look at what those per-head numbers mean for your culling and replacement decisions, the $3,110 heifer trap is worth your time.

Using recent prices, a reasonable working herd value for 200 cows plus 80 replacements sits in the neighborhood of $700,000–$870,000.

With a genuine 12-month notice period and a plan, you can often recover something like 80–90% of going-concern value. That means time to market cows privately, structure a going-concern sale, and time to cull and heifer sales into stronger points in the price cycle.

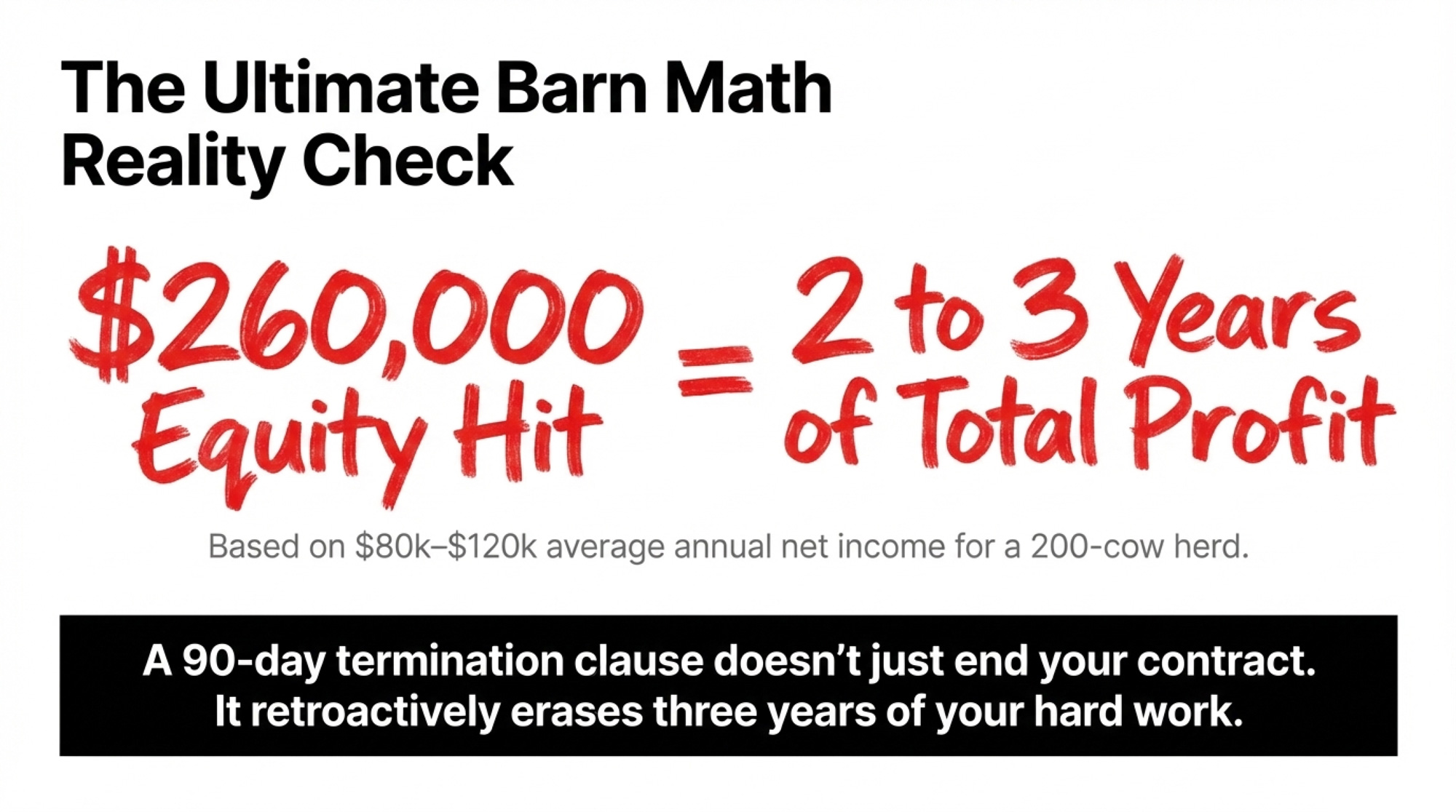

On a 90-day clock, it changes fast. You’re trying to do in one quarter what usually takes a year or more. In many dispersal situations, recovery drops toward two-thirds of the going-concern value. On a herd valued at roughly $780,000 (midpoint of our range), that gap works out to around $260,000 in equity wiped out — compared to maybe $78,000–$156,000 left on the table with a full year’s notice. Tighten that to 30 days, the kind of window some producers saw in past contract terminations, and you may only see 60–65% of going-concern value.

Here’s the barn math in plain language. If that 200-cow herd generates somewhere in the range of $80,000–$120,000 a year in net income — a figure that swings enormously by region, debt load, and management — a $260,000 equity hit from a 90-day forced dispersal represents roughly 2–3 years of profit gone because of how much time your notice clause gave you. The UK’s 12-month rule didn’t save Taylor’s herd. But it gave him time to organize the dispersal and protect more value than many North American producers could on 60 or 90 days’ notice.

Options and Trade-Offs for Farmers

Stack those numbers up — Taylor’s four-generation herd, 50–100 more UK farms on the clock, 135 Northeast organics dropped in a single year — and the pattern is obvious. Processors will continue reshaping their supply bases. You can’t control that. You can control how exposed your equity is when they do.

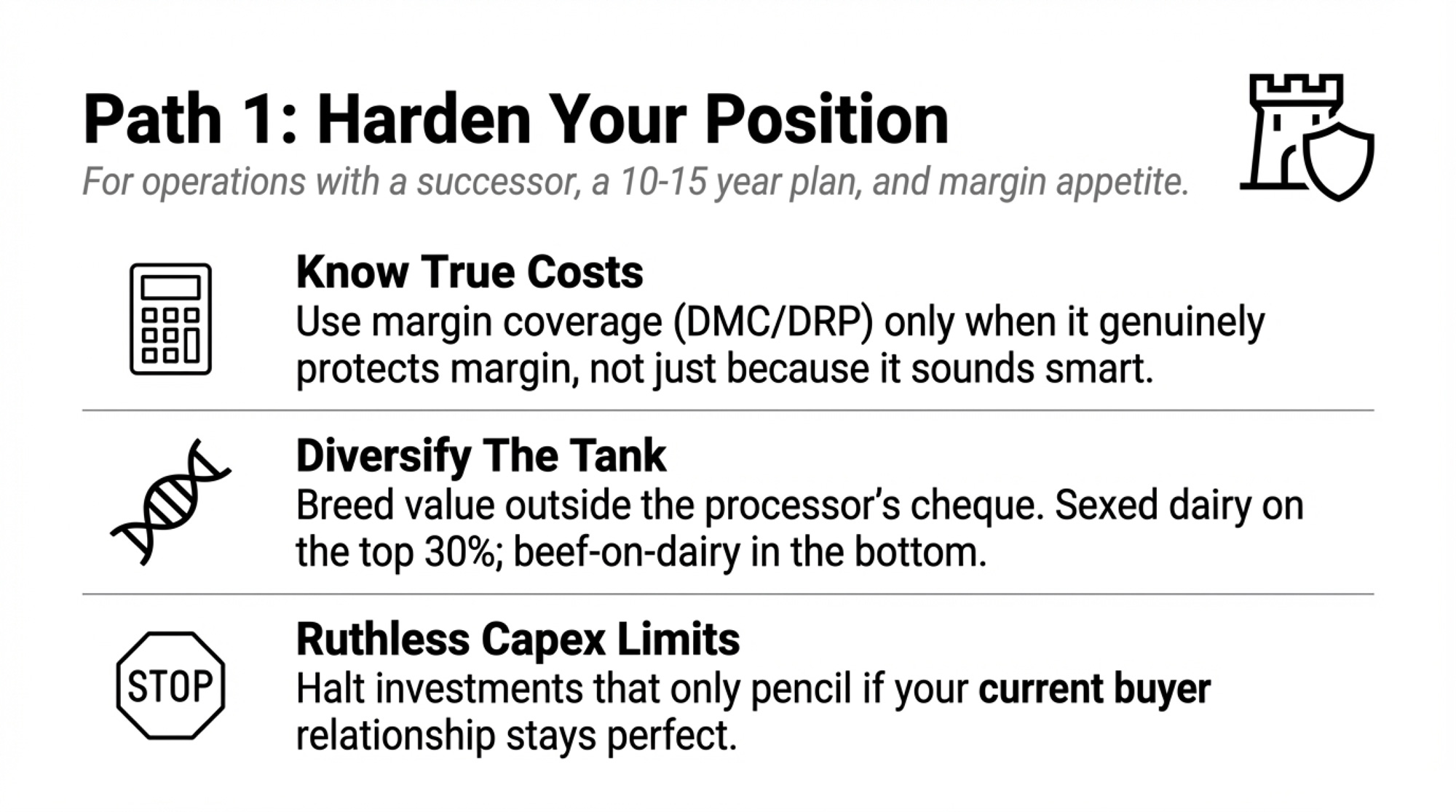

Path 1: Harden to stay with your current buyer

When it makes sense: You’ve got a successor, a clear 10- to 15-year plan, and enough appetite to reinvest if the margin is there. You want to be one of the suppliers they fight to keep.

What it requires:

- Knowing your true cost of production — and using tools like Dairy Margin Coverage or DRP only when they actually protect margin at your volumes, not because they sound smart. If you’ve never looked at who really controls the cheque in consolidated markets, that context matters here.

- Breeding so little of your future lives only in the bulk tank: more sexed dairy on the top 30–40% of the herd, more beef-on-dairy in the bottom end, and at least a pocket of genetics that holds value outside your processor’s cheque.

- Being ruthless on capex that only makes sense if this exact relationship stays perfect — those extra stalls, parlor extensions, or robots that don’t improve your flexibility or exit options.

- Quietly building secondary outlets. A standing conversation with another plant in your hauling radius. A limited on-farm product line. Even just being a known quantity to another co-op, so you’re not a total stranger if you ever need to call.

Risks and limits: You may give up expansion speed. You might watch a neighbor add 150 cows while you spend money on slurry storage and debt structure. But if the truck stops coming, you’re the one with a safer notice clause, a clear equity number, and a lender who already knows you’ve thought about this.

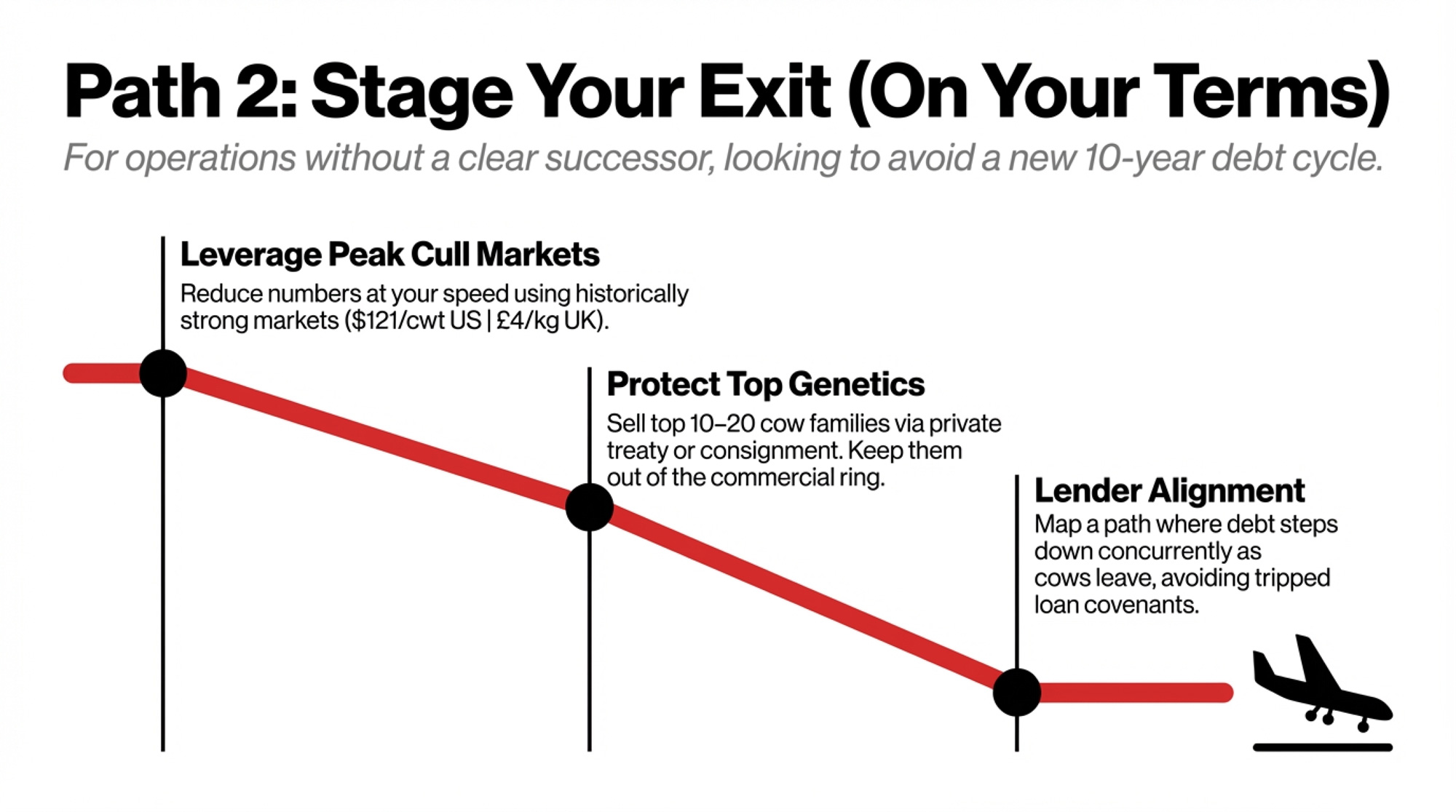

Path 2: Stage an exit on your terms, not in 90 days

When it makes sense: You don’t see a clear successor. You’re not keen to start another long debt cycle in your 50s or 60s. When you look at the barn math on a forced sale, the equity you stand to lose is more than a year or two of net profit.

What it requires:

- Using today’s strong cull and beef markets to reduce numbers at your speed, not under a deadline. The USDA reported 2024 annual average cull cow prices at $127/cwt — the highest on record —, and while December 2024 eased to $121/cwt, the market remains historically strong. Albert Goodman’s UK review noted beef prices “continued to increase” with liveweight cattle around £4/kg and supply down 1% year-over-year. Conditions like these won’t last forever.

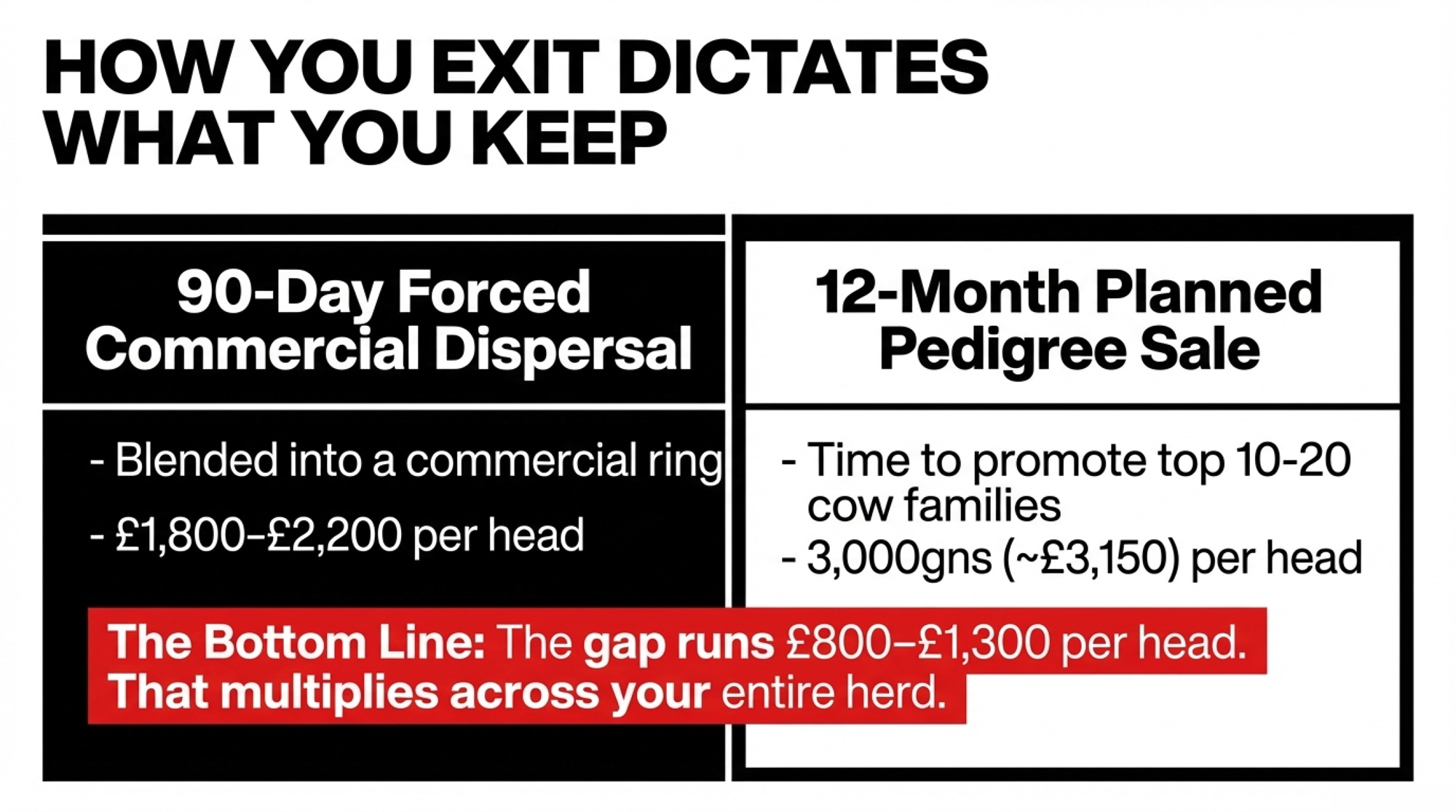

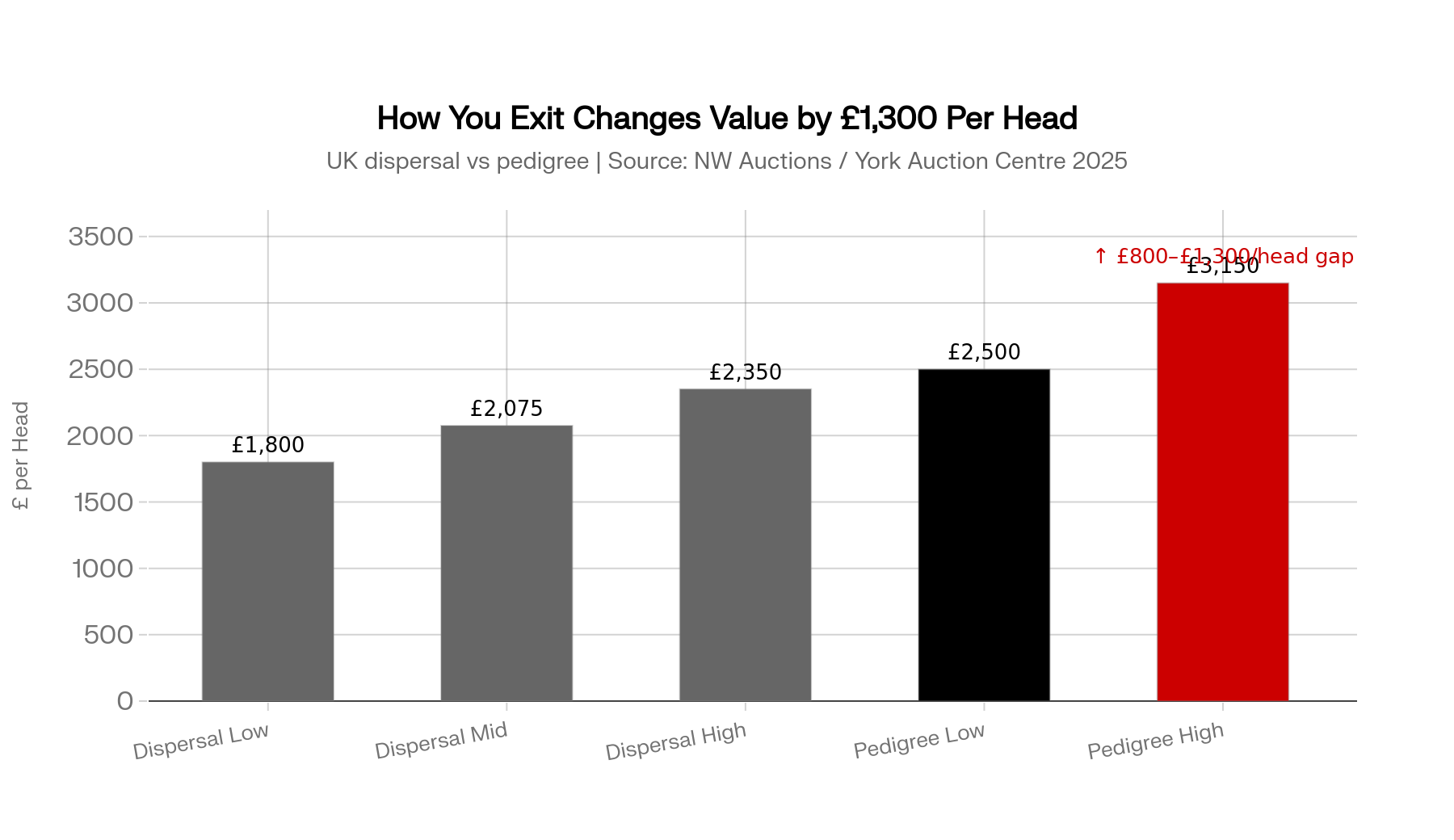

- Identifying your top 10–20 cow families and selling them differently — private treaty or consignment sales with time to promote, rather than letting them blend into a commercial ring. Taylor’s herd went through dispersal as commercial cattle. To see what that gap looks like in practice: at the July 2025 WB Winder & Co dispersal at Crooklands (J36), Holstein Friesians topped at £2,350 for a second-calver, with most of the herd selling £1,800–£2,200. Compare that to pedigree dairy cattle at York Auction Centre the same period clearing 3,000gns (roughly £3,150) for a fresh-calved cow. The gap between a dispersal and a well-marketed pedigree sale can run £800–£1,300 a head — and it multiplies across an entire herd. (North West Auctions, July 2025; York Auction Centre, October 2025)

- Sitting down with your lender to map a “glide path” where debt comes down as cows leave, so one bad letter doesn’t trip loan covenants or force a land sale.

Risks and limits: Emotionally, this is the hardest path. Shrinking or planning to wind down can feel like failure. The reality is the opposite: it’s protecting what decades of work have built, rather than gambling it on someone else’s procurement strategy.

Forward-looking signal for both paths: If you see your buyer trimming price while issuing termination notices to “non-aligned” suppliers — as Müller has done in both 2024 and 2026 — move this from “someday” to “now.” If organic plants or speciality processors in your region are consolidating, as Horizon and Maple Hill did across the Northeast, don’t assume your contract is immune. Those are your early-warning lights.

Path 3 (30-Day Action): Know your clause and your gap

Even if you’re not sure which camp you’re in, there’s one path that fits almost every operation — and you can do it within the next 30 days.

- Pull your processor or co-op contract — or call and get a copy — and mark the termination and notice sections. If you’ve never actually read the termination clause in your milk contract, this is the week to find it. The NFU’s advice to UK farmers applies everywhere: seek independent legal advice if anything about the notice terms is unclear.

- Run a simple herd-equity gap: use a realistic replacement value per head in your region (USDA’s latest quarterly estimates have ranged from $2,860–$3,110 over the past two quarters), subtract a realistic cull value ($121/cwt was the US average in December 2024 per USDA), multiply by your total cows and heifers, and compare that number to your average annual net profit. If the gap is bigger than a year of profit, you’re carrying serious processor risk. For a deeper look at how that replacement-vs-cull math works at the cow level, the $3,000 Heifer Hangover breaks it down.

- Book a short meeting with your lender and lead with, “We’re not in trouble, but we want to understand how exposed our herd equity is if our buyer changes terms or drops us.” That one conversation often decides whether you have options if something shifts — or whether you feel boxed in.

Key Takeaways

- If the herd equity you’d lose in a forced exit is bigger than a year of net profit, you’re not fine — you’re exposed. That’s your threshold to either harden your position or start staging an exit instead of hoping your contract always renews.

- If your contract gives you less than 90 days’ notice, time is your most valuable asset. You might not fix the clause tomorrow, but you can make sure you have a cull plan, a lender plan, and at least one potential alternative outlet lined up before you ever need them.

- If most of your future is priced as anonymous bulk milk, shift some of it into value that survives a processor change. Beef-on-dairy calves, a pocket of genetics that sell on their own merit, a modest direct-sale channel — none of these replace the milk cheque, but they give you more landing spots when buyers move.

- If your next big capex project only pencils with this buyer and this route, hit pause and rerun the numbers with your equity gap on the table. Grant Hartman’s advice to the latest wave of Müller farmers — don’t make “knee-jerk reactions,” but “take stock” — applies to expansion decisions too.

The Bottom Line

Asked whether he’ll ever retire, Taylor told BBC Farming Today he hopes to be fit enough to keep farming for “another 20 odd years.” He isn’t leaving farming. He’s leaving a contract that didn’t pencil — and starting over with six cows and a beef plan.

The question for you isn’t whether Müller treated him fairly under the law. It’s whether you’re running your numbers as if your processor could give you 90 days — or as if they’ll always need your milk the way they do today. If you want the deeper math on how to calculate your own processor-dependency ratio and which contract clauses move the needle most, keep an eye on the Bullvine newsletter and the upcoming playbook on processor risk. And if you want a gut-check on how fast milk can become unmarketable when trucks or buyers disappear, the Henschels’ story is the case study you don’t forget.

Complete references and supporting documentation are available upon request by contacting the editorial team at editor@thebullvine.com.

Learn More

- $60 Million in Unpaid Milk, 150 Families Wrecked: The 4-Question Processor Risk Audit Every Dairy Needs – Arms you with a 4-question risk audit to stress-test your cash runway before payments slow. This protocol exposes hidden exposure and delivers a 72-hour emergency plan, ensuring you’re the one holding the cards if your buyer falters.

- The Great American Dairy Heist – Who Really Owns Your Milk Check in 2025? – Exposes the hierarchy of power behind the $11 billion processing boom and reveals why 834 mega-dairies now dictate your future. Gain the strategic leverage needed to navigate massive industry consolidation and secure your market access through 2028.

- 211,000 More Dairy Cows. Bleeding Margins. The 2026 Math That Won’t Wait. – Breaks down the structural reset where beef-on-dairy premiums have broken the traditional culling cycle. You’ll master the new math of protein-focused genetics and replacement-pipeline scarcity to maintain high-margin performance while your neighbors chase empty volume.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.