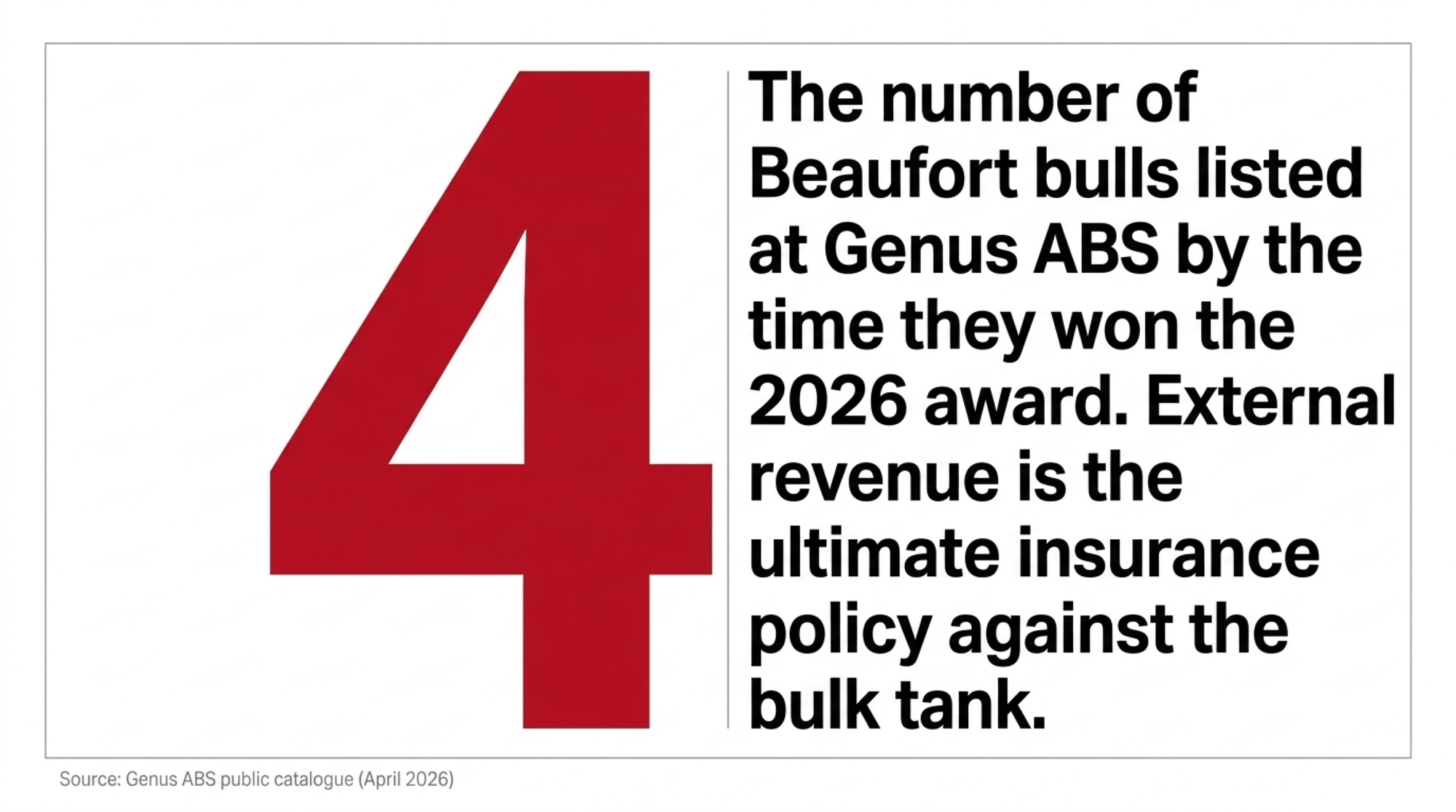

Fifty buyers. £1,409.52 all-in. The Macphersons lost the rented ground, but four Beaufort bulls were already placed at Genus ABS (the UK arm of the US-based bull stud) before the gavel fell. That’s what carried the pedigree to 2026.

On 16 August 2018, the Beaufort British Friesian herd of James and Louise Macpherson was dispersed at Sedgemoor Market, Somerset. Farmers Weekly’s coverage of the sale attributed the dispersal to the loss of rented ground supporting the Macphersons’ Dorset County Council tenancy at Burley Road Farm.

Fifty buyers turned up. Bidders came from Cornwall, Carmarthen, Cumbria and across Ireland. A fifth-lactation Rodbrook Milkmaid daughter of Beaufort Milkman sold for 2,600gns (roughly £2,730 at 2018 conversion). The topper hit 3,000gns twice — about £3,150 each — once for the bull Beaufort Kriminal, once for Goonhilly Chad Verity, EX92 in her fourth lactation. All-in average: £1,409.52. Seven years and eight months later, Holstein UK named the rebuilt Beaufort herd the British Friesian Herd of the Year for 2026 — 290 cows near Burton-on-Trent, Staffordshire, four homebred bulls in the Genus ABS catalogue.

The headline reads forced dispersal to national award in seven years. The real story is why the published pedigree survived the trip.

📌 The 50-Cow Test

If you lost your rented ground tomorrow, which 50 cows would rebuild your herd? Not the 50 you like. Not the 50 you’d keep for sentimental reasons. The 50 whose documented maternal families carry enough production, classification, and transmitting ability to rebuild across a 5–7 year window. If you can’t name them in 20 minutes, the breeding plan lives in your head — and the plan evaporates the day the auctioneer shows up.

Forced Dispersals Are the Industry’s Quiet Tail Risk

Forced dispersals are the tail risk the trade press rarely covers — quiet, abrupt, and built into every tenancy agreement, every rented block, and every bTB test. They don’t care how good your cows are. Per FW’s 2018 coverage, the Macphersons lost rented ground that year. Yours might be a landlord selling up, a council estate reviewing its holdings, a bTB breakdown, or a bank conversation you’ve been putting off.

AHDB recorded the GB milking herd at 1.63 million head in October 2025 — the lowest October figure on record, down 0.9% year-on-year — with the total GB dairy herd falling 1.3% to 2.51 million. Producers are leaving, one tenancy and one breakdown at a time.

Breed context sharpens the stakes for British Friesian breeders in particular. AHDB registration figures show British Friesian calf registrations dropped from roughly 100,000 in 2014 — about 7% of GB dairy registrations — to 58,500 in 2023, about 4%. Holstein UK launched the British Friesian Herd of the Year award in 2021 — see how the award has been judged since its 2021 launch — and judges it on classification combined with production.

Inside a shrinking breed, the herds still winning are the ones treating their published pedigree as a capital asset, not a hobby.

What the Beaufort Record Looked Like on Dispersal Day

FW’s 2019 council-farms feature and FarmingUK’s 2026 award coverage report that the Macphersons began in Dorset by buying 55 cows in 2012 — the Rodbrook herd, purchased as a voluntary complete-herd sale from Cheshire breeder Chris Pemberton. A complete-herd acquisition, not a pick-and-choose at auction. You don’t rebuild from documented maternal lines by buying individual animals you like the look of. You rebuild from families.

By the time the sale ring opened in 2018, the young end of the Beaufort herd — 137 cows in their first three lactations — was averaging 8,696kg at 5.03% fat and 3.28% protein on a somatic cell count of 172,000, per FW’s sale report. That’s a working, composition-led British Friesian herd on the numbers, not a show string. The Langley and Goonhilly lines had been added alongside the Rodbrook foundations across six Dorset years, according to FarmingUK’s 2026 award coverage. The EX92 Goonhilly cow that tied for top price is the documented proof the base was deep.

A composition-led herd with VG and EX depth on paper isn’t a trophy cabinet. It’s a portable balance sheet.

Don’t Put All Your Eggs in One Bulk Tank

Here’s what the award coverage didn’t put up front. By the time the sale ring opened in 2018, Beaufort genetics were already moving commercially through Genus ABS — the UK arm of the US-based bull stud. Beaufort Milkman — son of Blackisle Maverick-ET out of Rodbrook Milkmaid 8, whose sire was Rodbrook Barney — was listed Proven in the Genus ABS catalogue. FW’s 2018 dispersal report noted Beaufort Kriminal had “two brothers already at Genus” when he topped the sale at 3,000gns.

Revenue diversification is the insurance policy. If every penny of your cash flow leaves through the bulk tank, one disruption — lost ground, a bTB breakdown, a processor renegotiation — can pull the whole operation down. The public record shows Beaufort spread risk across the milking herd, the AI contract at Genus, and the wider pedigree market for surplus heifers and bulls. By 2026, four Beaufort bulls are listed with Genus ABS across two proof generations.

The Beaufort Genetic Engine (public record, as of April 2026)

| Bull | Status | Key Metric | Role in the Rebuild |

| Milkman(BF1088 / 29HO17260) | Proven | Maverick-ET × Rodbrook Milkmaid 8 | Established the Beaufort prefix inside other herds before the dispersal. |

| Karactacus(BF1085 / 29HO17242) | Proven | Born March 2014 | Second Proven Beaufort sire working commercially through Genus. |

| Supersonic(BF1279 / 29HO20412) | Genomic | AHDB April 2025 run: £306 PLI; 3rd in BF PLI rankings; +395kg milk, +29kg combined F+P; Kappa Casein AA | Elite genomic ranking keeping the prefix current post-rebuild. |

| Jackery (BF1285 / 29HO20413) | Genomic | Kappa Casein AB; Red Carrier (*RC); released August 2024 | Niche-market value inside the closed-herd breeding plan. |

The pedigree architecture that carried the herd through the dispersal is the same architecture earning AI income outside the farm. Those aren’t two separate strategies — they’re one. For the long-game logic behind tracking recessives like Red Carrier inside a closed pedigree herd, our Sir Inka May piece covers exactly that kind of decision.

“Our milk buyer is looking for high fat and the Friesians are really good for this — our herd average for 220 cows is 8,400kg at 5.1% fat.” — James Macpherson, quoted in FarmingUK, April 2026

“People said we couldn’t make it work before we started and it’s nice to prove them wrong to a point. It’s an all-consuming life but it’s well worthwhile and I’ve no complaints about it whatsoever.” — James Macpherson, quoted in Farmers Weekly, 2019

Which Cow Families Do You Keep When You Have to Start Over?

The answer visible in the public record is the ones already documented. Rodbrook Milkmaid, the Rodbrook foundation cows, the Langley and Goonhilly lines — all present in FarmingUK’s 2026 award coverage and FW’s 2018 sale report. The specific Beaufort families retained through the move haven’t been publicly itemised, but the Rodbrook Milkmaid, Goonhilly and Langley lines surface in every post-dispersal sale-ring and award reference on the record. A Rodbrook Milkmaid daughter of Beaufort Milkman sold for 2,600gns at Sedgemoor because the rest of the industry could read the same pedigree the Macphersons were reading.

That’s the signal you want your own top families to send — a price outside buyers will pay without needing to see the cow first. For a parallel on how cow-family continuity compounds across generations, our Babe and Britany piece is the cleanest case study on the site.

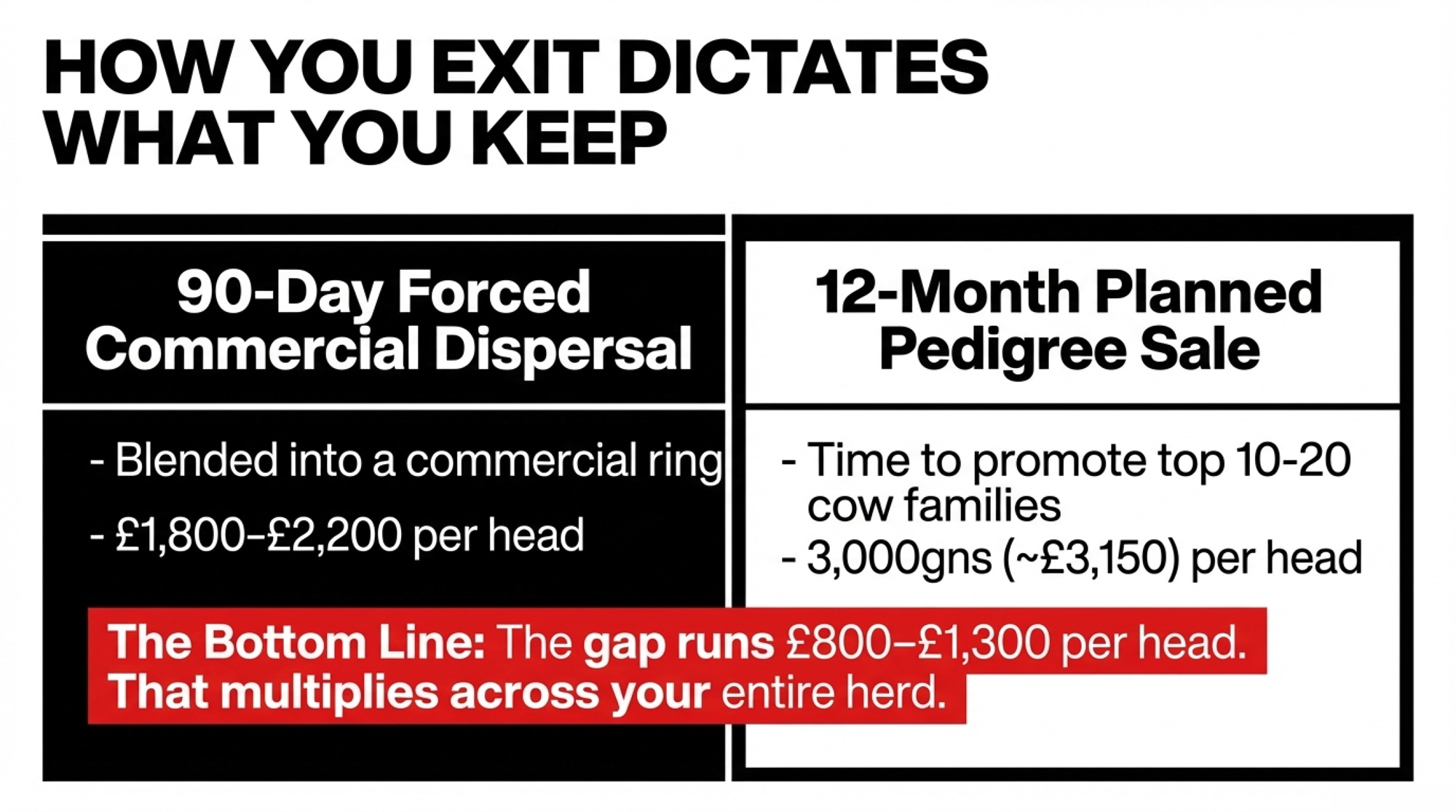

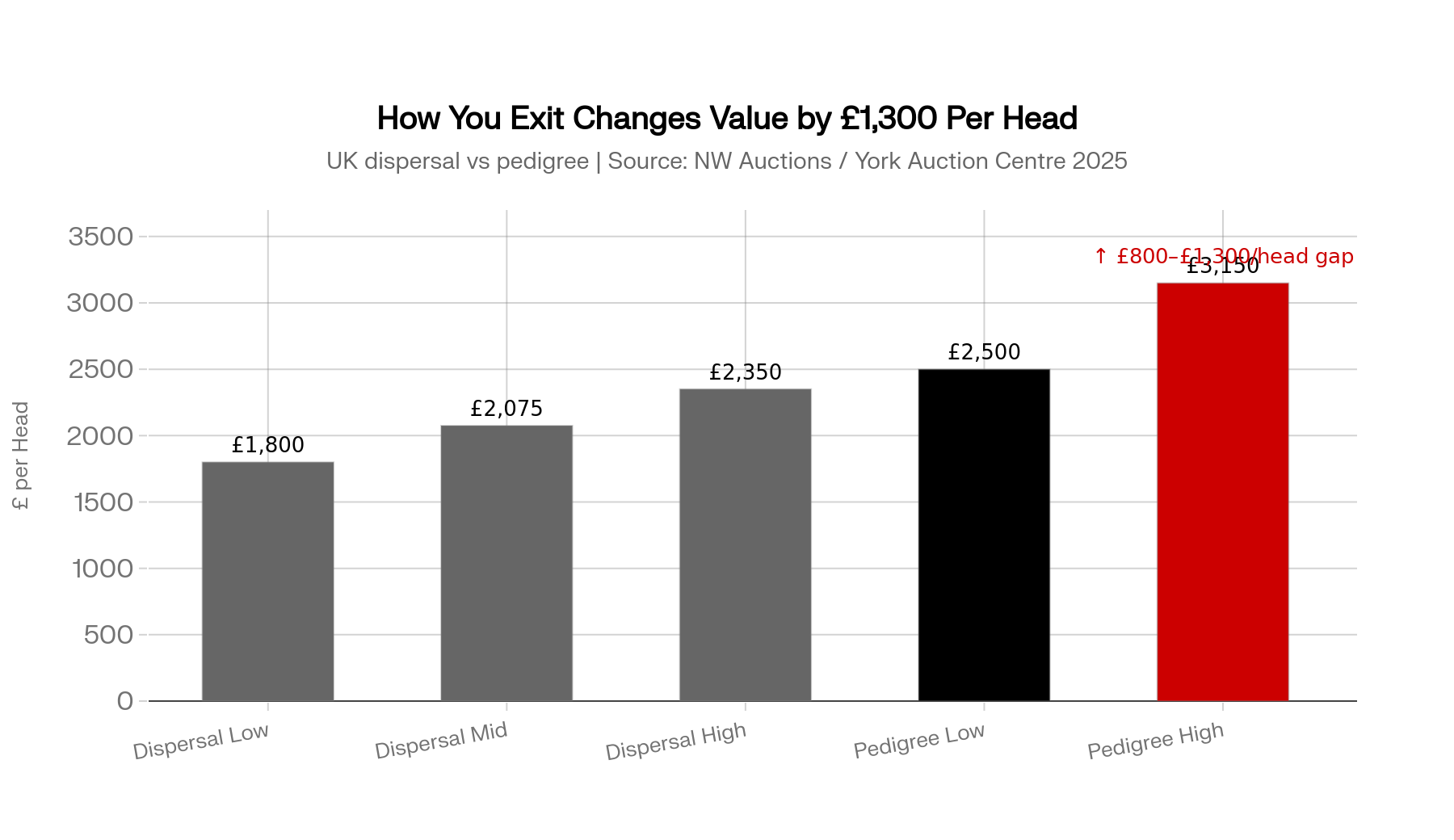

The £700,000 Ghost: What Does a 290-Cow Rebuild Actually Cost?

The income gap is the figure that stops most breeders cold. Based on 2019 UK pricing, a 290-cow herd losing a full year of production is staring at a hole in the balance sheet north of £700,000. A dispersal cheque is a band-aid; the published pedigree and the outside AI revenue are a far bigger part of the cure.

Exact Beaufort rebuild figures aren’t public and won’t be invented here. Orders of magnitude are still useful if you’re running anything bigger than a hobby herd. The table below stacks the 2018 Sedgemoor cheque against the scale of a single-year income hole at 2019 milk prices and a 2018 infrastructure comparator.

Dispersal Cheque vs. Rebuild Hole

| Line | Figure | Source / Formula |

| 2018 Sedgemoor gross (all published lots) | ~£306,000 | 217 lots at £1,409.52 all-in average, FW 17 Aug 2018 |

| 2018 UK greenfield new-build (structures + silage only) | £1.1m+ | FW 2018 build feature |

| 2019 UK farmgate milk price band | 28.80–29.35 ppl | Defra monthly releases via AHDB |

| 2019 Beaufort NMR Gold Cup qualifying-year average | 8,629kg across 218 lactations | NMR Gold Cup release |

| 290-cow zero-milk-cheque year (Defra 2019 ppl band) | ~£703,000–£712,000 | 290 × 8,629kg × 0.97 L/kg × 28.80–29.35 ppl |

| 150-cow zero-milk-cheque year (illustrative at 8,000kg / 29 ppl) | ~£340,000 | 150 × 8,000kg × 0.97 L/kg × 29 ppl — illustrative comparator; not sourced to a specific 150-cow herd |

Litre-per-kilogram conversion of 0.97 applied throughout, consistent with roughly 4% fat / 3.3% protein British Friesian composition.

Plug your own yield and current milk price into the same formula to see what a zero-milk-cheque year costs on your farm. A sale cheque of that scale doesn’t close a hole that size on its own. Operations that rebuild after a forced dispersal typically combine retained-heifer value, pre-placed AI revenue, and land capital committed ahead of the sale. FW’s 2019 council-farms coverage notes the Macphersons had bought their Staffordshire land before the Sedgemoor sale.

For the full cost-per-cow economics across herd sizes, we’re building that Tier 3 model as a dedicated Bullvine Weekly feature — see our earlier UK farmgate milk price coverage for the input side of the same equation.

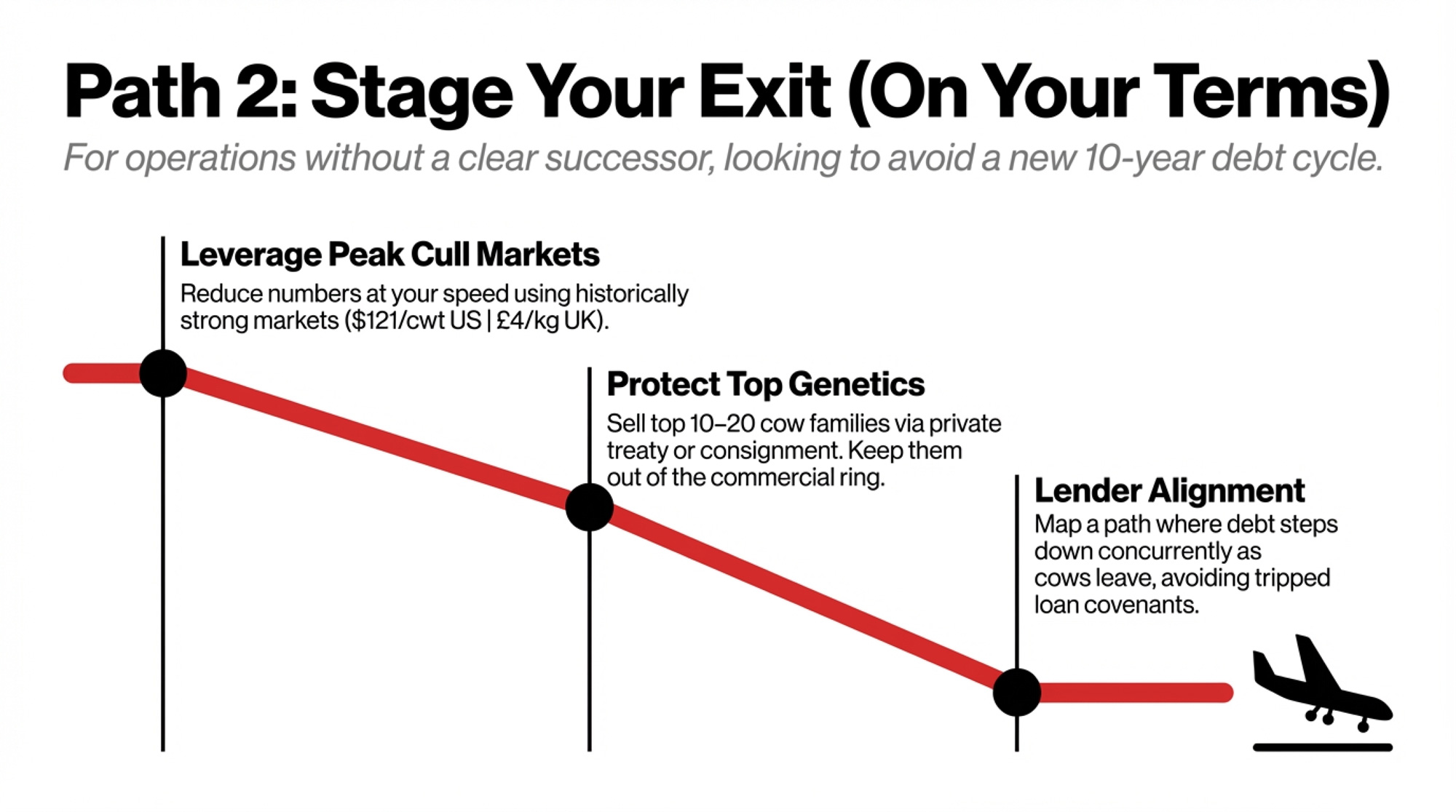

Options and Trade-Offs for Pedigree Breeders

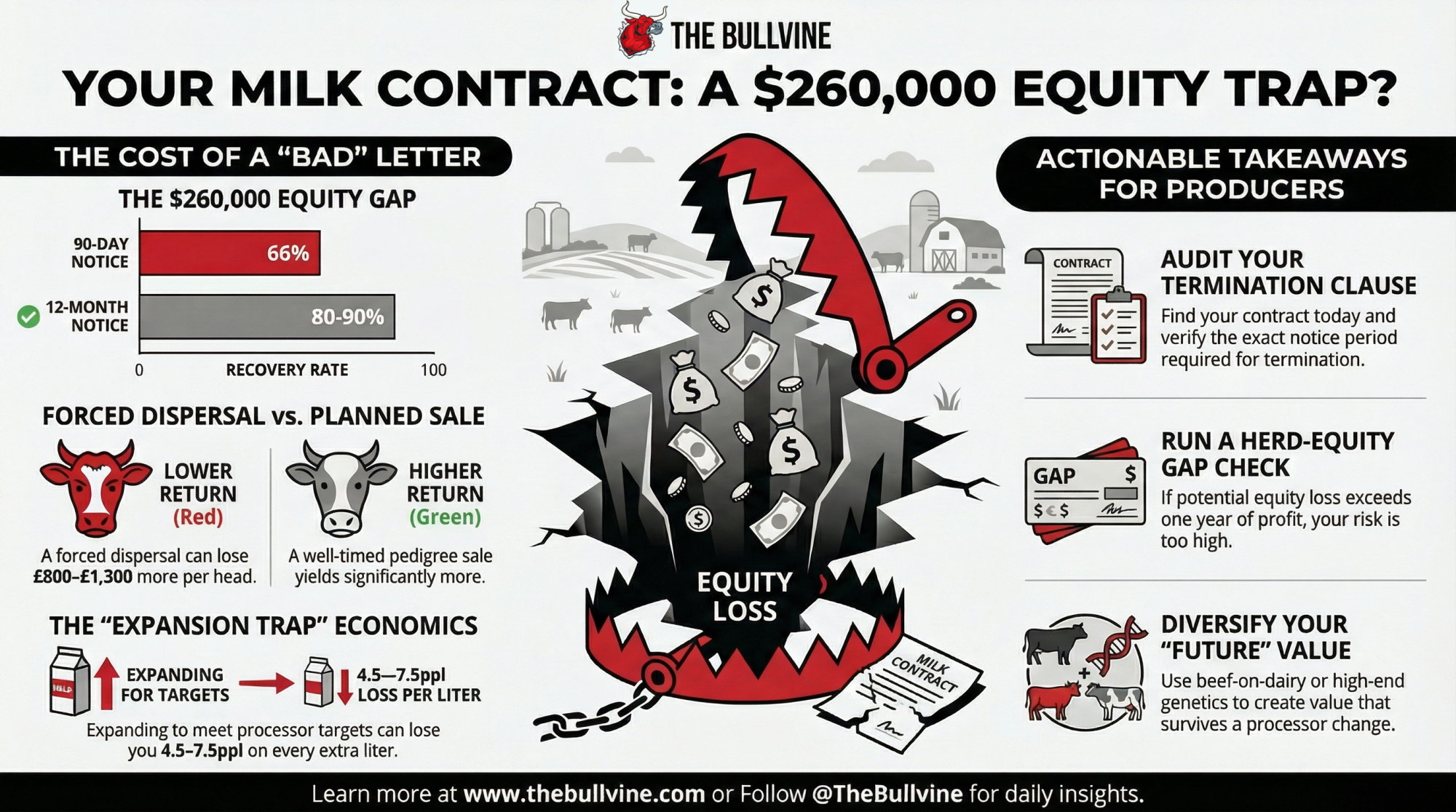

Most pedigree breeders will never run a dispersal. The mechanics visible in the Beaufort public record still apply if you’re facing a tenancy renewal, a bTB test, a succession event, or a landlord conversation you’ve been putting off.

1. Document your top cow families — and rank them by production depth, not individual EX score. (30-day move.) Pull two generations of NMR records this month. Rank your maternal lines by average combined fat-and-protein yield across the family. Write down the top three. As a rule of thumb — not a breed-society standard — any family that hasn’t produced a VG87+ daughter in two consecutive lactations isn’t a top family; it’s a decent family. There’s a difference, and a dispersal exposes it. Risk: you may find you have one deep family and a lot of average cows. That’s useful information. Act on it now, not after.

2. Build external revenue from your best genetics — before the farm needs the money. Per FW’s 2018 reportingand the Genus ABS public catalogue, Beaufort Milkman was listed Proven at Genus before Sedgemoor, and Kriminal had two brothers already placed. If getting a homebred bull into a national stud feels out of reach, the small version of the test still works: have you ever sold semen, embryos, or pedigree heifers off your top family at a premium to the commercial market? If the answer is no, your genetics haven’t been priced by anyone outside your fence. For the same arc told through an AI stud’s lens, our “65 Cows to 10,000” feature is worth the detour. Risk: takes years to build and requires genetics that are genuinely competitive, not just registered.

3. Bank stored semen from your best homebred bulls out of your deepest families. Not every homebred bull justifies it. Pick the ones out of your deepest families. As a rule of thumb — not a breed-society standard — a reasonable floor is 20 doses minimum from any bull out of a VG88+ dam with three generations of confirmed production depth. For context on what genetic influence looks like when it’s fully separated from the home farm, our Walkway Chief Mark piece is the benchmark. Risk: storage and collection cost is real money, and the insurance doesn’t pay out unless something goes wrong.

4. Close the herd now — while the decision is still voluntary. Closed-herd discipline forces better selection because you can’t buy your way out of a weakness. FarmingUK’s 2026 coverage notes the Beaufort rebuild ran with Collycroft and Catlane lines introduced in measured steps alongside the Rodbrook, Langley and Goonhilly foundations. Trade-off to name honestly: closed-herd discipline buys you genetic continuity; open-herd flexibility buys you speed of correction. You can fix a known weakness faster with the right imported semen than by breeding it out over four generations. Risk: closed herds with shallow family depth compound weakness fast. This only works if the documentation from move #1 is real.

What This Means for Your Operation

An 80-cow pedigree herd doesn’t rebuild from the same playbook as a 400-cow one, but the audit questions are identical. On a smaller herd, your top three families probably represent most of your milking string — documentation matters more, not less, because you have no redundancy. On a 200-cow herd, the risk isn’t depth; it’s that average cows from average families are eating feed that should be going to your foundation animals. On a 400-cow herd, the risk is that nobody on the farm can name the top families off the top of their head, because day-to-day management has moved past individual cow recognition.

Run the same audit at any scale. If a forced decision took you to 50 cows next month, which 50 would you keep — and are they on paper?

Key Takeaways

- If you can’t name your top three cow families from memory by production-and-classification depth, your breeding plan isn’t documented. Spend an afternoon on it this month.

- If your farm closed tomorrow and none of your genetics would still be working in somebody else’s barn, that’s your gap. Start building external revenue now, not after a disruption forces the question.

- If you’re running a closed pedigree herd without banked semen from your best homebred bulls out of your top families, you’re carrying physical risk you don’t need to carry. Rule-of-thumb floor: 20 doses per bull, VG88+ dam families, three generations of production depth.

- If you haven’t mapped your rented-ground exposure as a percentage of your total feed base, you don’t know what your dispersal trigger looks like. Do that this quarter, not after the landlord letter arrives.

- If your breed’s classification and production thresholds have moved in the last three years and you haven’t updated your selection criteria, you’re breeding against yesterday’s standard. Check the current Holstein UK British Friesian Herd of the Year criteria and use it as a benchmark, not just an award target.

- If your 30-day, 90-day, and 365-day breeding plan all live only in your head, that’s the single biggest fragility in your operation. A rebuild starts with what’s documented, not what’s remembered.

The Real Question

The Beaufort herd won Herd of the Year because what got sold at Sedgemoor wasn’t the whole of what mattered. What mattered was already documented in the Genus ABS catalogue, in NMR’s qualifying record, and in the Rodbrook, Langley and Goonhilly lines FarmingUK’s coverage traces back to 2012. Awards come and go. The documentation either exists or it doesn’t — and you find out which one on the day somebody else decides how fast you have to move.

When was the last time you actually audited your maternal lines on paper rather than in memory? And if a buyer called tomorrow about your best homebred bull, what would the documentation you send them actually say?

Sources: publicly reported coverage in Farmers Weekly (2018), Farmers Weekly (2019), FarmingUK (April 2026), the Holstein UK 2026 award release, the Genus ABS public catalogue, and public records from AHDB, NMR and Defra. James and Louise Macpherson were not interviewed for this piece.

Learn More

- Why the Smartest Dairy Operators Are Unlocking Over $150,000 in Potential Returns While Others Get Blindsided by Market Chaos — Arms you with a specific ROI breakdown for labor automation and feed efficiency. It bridges the Beaufort income-gap strategy with actionable technology shifts that stabilize margins when market volatility strikes your balance sheet.

- From $1.5 Million to $150000: The Dairy Genetics Shakeout and Your Next Move — Exposes how corporate consolidation is hollowing out independent seedstock revenue. It challenges the Beaufort model of genetic ownership, providing a 12-month survival map for breeders who want to capture value before their windows close.

- Washington Just Handed Dairy Farmers a $68 Billion Gift, But Here’s Why Most Won’t Unwrap It Properly — Dismantles the volume-over-value myth by leveraging the latest component-focused risk management shifts. It delivers an aggressive edge on capitalizing on the 2026 policy overhaul while competitors remain bogged down by traditional production biases.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.

The Sunday Read Dairy Professionals Don’t Skip.Every week, thousands of producers, breeders, and industry insiders open Bullvine Weekly for genetics insights, market shifts, and profit strategies they won’t find anywhere else. One email. Five minutes. Smarter decisions all week.